Swedbank June 2013

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Swedbank

June 2013

2

Table of contents

1. Financial performance 3

2. Liquidity and funding 15

3. Cover pool data 27

4. Swedish economy 33

5. Swedish housing and mortgage market 39

6. Appendix 47

1. Financial performance

3

• Stable NII

– Repricing

– Funding costs

– Lower deposit margins

• Net gains and losses

one-off gain in Q4 12

• Lower costs

• Continued good asset quality

• Ukraine and Russia discontinued

operations

Robust earnings

4

Financial performance - Group results

SEKm Q1 12 Q4 12 Q1 13 ▲Q/Q ▲Y/Y

Net interest income 4 895 5 346 5 353 7 458

Net commission income 2 398 2 502 2 388 -114 -10

Net gains and losses 979 830 557 -273 -422

Total income 9 072 9 437 9 082 -355 10

Total expenses 4 327 4 142 4 043 -99 -284

Profit before impairments 4 745 5 295 5 039 -256 294

Impairment of tangible assets 40 141 85 -56 45

Credit impairments -96 -76 60 136 -156

Tax 1 108 786 976 190 -132

Profit from continued ops. 3 693 4 427 3 918 -509 225

Profit from discontinued ops. -279 -174 -390 -216 -111

Profit for the period 3 410 4 252 3 525 -727 115

Return on equity, % 14.1 16.9 13.8

ROE continuing operations, % 15.3 17.5 15.3

Cost/income ratio 0.48 0.44 0.45

Source: Swedbank Mar 31, 2013

Stable results

• Stable NII

• Solid asset quality

• New organisation

5

Financial performance - Retail

SEKm Q1 12 Q4 12 Q1 13 ▲ Q/Q ▲ Y/Y

Net interest income 3 371 3 353 3 332 -21 -39

Net commissions 1 538 1 554 1 589 35 51

Total income 5 346 5 255 5 377 122 31

Total expenses 2 429 2 474 2 406 -68 -23

Profit before

impairments 2 917 2 781 2 971 190 54

Credit impairments 21 91 55 -36 34

ROE, % 28.4 28.0 27.9

C/I ratio 0.45 0.47 0.45

Source: Swedbank Mar 31, 2013

Good return

• Stable NII

• Low activity in Corporate Finance

• Structural challenges in Equities

• Solid credit quality

6

Financial performance - Large Corporates & Institutions

SEKm Q1 12 Q4 12 Q1 13 ▲ Q/Q ▲ Y/Y

Net interest income 728 795 783 -12 55

Net commissions 485 536 419 -117 -66

Total income 2 071 1 857 1 814 -43 -257

Expenses excl variable

staff costs 661 668 646 -22 -15

Variable staff costs 105 75 88 13 -17

Profit before

impairments 1 305 1 114 1 080 -34 -225

Credit impairments 17 162 74 -88 57

ROE, % 18.9 18.3 16.7

C/I ratio 0.37 0.40 0.40

Source: Swedbank Mar 31, 2013

Focus on costs

• Stable NII in local currency

• Increased customer activity

• Recoveries

• Increased efficiency in focus

7

Financial performance - Baltic Banking

SEKm Q1 12 Q4 12 Q1 13 ▲ Q/Q ▲ Y/Y

Net interest income 910 760 742 -18 -168

Net commissions 386 366 388 22 2

Total income 1 468 1 289 1 281 -8 -187

Total expenses 629 633 586 -47 -43

Profit before

impairments 839 656 695 39 -144

Credit impairments -134 -329 -70 -259 -64

ROE, % 14.6 13.3 12.6

C/I ratio 0.43 0.49 0.46

Source: Swedbank Mar 31, 2013

Income distribution Q1 2013

8

Financial performance – Income

Source: Swedbank Mar 31, 2013

Lending and deposits

64%

Treasury, Trading and

Capital Markets

6%

Asset Management

11%Payment,

Cards8%

Insurance3%

Share of P&L of associates

2%

Other6%

Sweden 79%

Estonia 5%

Latvia 4%

Lithuania 4%

Other 8%

Continued strengthening capital position

• 13-15% CET1

• CRD/CRR IV – less impact

• IRB Advanced

• Waiting for regulatory clarity

9

Financial performance - Capital situation

* As of 2012 incl. IAS 19

16.7 17.3

15.416.4

2007 2008 2009 2010 2011 2012 Q1 13

Common Tier 1 capital ratio

Basel 2* Basel 3

15.45%0.14% 0.14%

0.24%

0.55%

-0.13

16.38%

Q4 2012 Profit Q1 IAS 19 RWA change Q1

SME & CVA

(Basel 3)

Other Basel 3

changes

Q1 2013

Changes in B3 CET1 ratio Q4-Q1

Increase Decrease

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

Proposed 2013 Proposed 2015

Supplemental capital (Equity, AT1 and/or T2), 1.5% + 2.0%

Countercyclical buf fer (Equity), 0-2.5%

Capital conservation buf fer (Equity can be used in stressed scenario), 2.5%

Swedish SiFi buf fer (Equity), 3% (2013), 5% (2015)

Min. requirement (Equity), 4.5%

Swedish capital requirement proposal • Delayed, earliest implementation end of 2013

10

Source: The Ministry of Finance, the Riksbank and the Swedish FSA

13.5-16%

12%

10%

15.5-18%

Proposal 2013 Proposal 2015

Financial performance - Capital situation

Risk weights – do they matter?

• Transparency

• Regulatory requirement

• Tool for ranking risk

• No steering tool – emphasis on stress tests instead

─ Internal capital allocation process

11

0,00%

0,05%

0,10%

0,15%

0,20%

0,25%

2009 2010 2011 2012

Loan loss ratio corporate portfolio

Swedbank, Sweden Handelsbanken

0%

10%

20%

30%

40%

50%

60%

70%

80%

Swedbank Sweden total IRB

Handelsbanken total IRB

Swedbank Sweden corporate IRB

Handelsbanken corporate IRB

Average risk weight corporate exposure class

2009 2010 2011 2012 ,Sweden

s

Financial performance - Capital situation

Strong credit quality

• Continued high credit quality in Sweden

• Slower net recoveries in

Baltic Banking

• Exiting Russia and Ukraine

12

Financial performance – Asset quality

Credit impairments, SEKm Q1 12 Q4 12 Q1 13

Retail 21 91 55

Large Corporates & Institutions 17 162 74

Baltic Banking -134 -329 -70

Estonia -78 -242 -54

Latvia -21 86 4

Lithuania -35 -173 -20

Swedbank Group -96 -76 60

31.7

10.3

0

5

10

15

20

25

30

35

Q1 11 Q2 11 Q3 11 Q4 11 Q1 12 Q2 12 Q3 12 Q4 12 Q1 13*

SEKbn Impaired loans

* Russia and Ukraine reported as discontinued operations.

Swedish household loans(90% mortgages)

Shipping and offshore, Transportation

Manufacturing

Other corporate lending

Latvian lending

Other property management

Residential properties

Agriculture and forestry

Hotels and restaurants, Retail

64%

12%

4%

3%

8%

Lithuanian lending

2%

6%

Estonian

Asset portfolios – low risk

13

Source: Swedbank, Mar 31 2013

Financial performance – Asset quality

Tenant owner associations

Rating strategy – same level as the best rated Nordic banks

14

Source: Swedbank Mar 31, 2013

Short Long Short Long BFSR* Short Long

Swedbank A-1 A+ P-1 A2 C- F1 A+

Swedbank Mortgage A-1 A+ P-1 A2

Covered bonds AAA Aaa

* Bank Financial Strength Rating

S&P FitchMoody's

Financial performance – Credit ratings

2. Liquidity and funding

15

0

200

400

600

800

1 000

1 200

1 400

Q1 20130

200

400

600

800

1 000

1 200

1 400

Q1 2013

Core balance sheet* structure

16

Liquidity and funding

CEE lending

Estonia

Other corporate

lending, Sweden &

other Nordic countries

Other private, Sweden

Swedish

mortgage loans

Senior

Covered

bonds

Deposits

CET1

Suppl. cap

Government guaranteed debt

Source: Swedbank, Mar 31, 2013

Assets Liabilities SEKbn SEKbn

* Simplified balance sheet

Wholesale funding strategy

• Main internal liquidity measure is survival horizon (accumulated cash-flows)

• Covered bonds less volatile than senior unsecured debt

• Secure presence in senior unsecured debt markets

– OC level

– Liquidity reserve

– Structural subordination

17

Liquidity and funding

Source: Swedbank, Dec 31, 2012

0

1 000

2 000

3 000

4 000

5 000

6 000

7 000

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1980 1990 2000 2005 2010 2012

Deposits and retail bonds (LHS) Equities (LHS)

Pension savings and mutual funds (LHS) Other f inancial assets (LHS)

Total f inancial assets (RHS)

18

Covered bond strategy

Swedish households’ financial assets

Source: Statistics Sweden “Hushållens ställning“, Mar 2013

Liquidity and funding

Maturity, years

EUR/USD

SEK 150-200bn

Other*

SEK 50-85bn

Sweden

SEK 300-375bn

<5Y 3-7Y >7Y

SEKbn

-20%

-10%

0%

10%

20%

30%

40%

0% -5% -10% -15% -20% -25% -30% -35% -40% -45% -50%

OC, Q113

0

20

40

60

2013 2014 2015 2016 2017 2018 2019-

Senior unsecured debt

Senior unsecured debt strategy

19

Source: Swedbank, Mar 31, 2013, nominal amounts

• Limited need given Swedbank’s balance sheet structure

• Secure OC

• Fund liquidity reserves

Senior unsecured debt maturity profile

SEKbn

Over-

colla

tera

lisation

House price drop

House price sensitivity of the cover pool

Liquidity and funding

0

20

40

60

80

100

120

Covered bonds Senior unsecured

Lower funding needs

• LCR 139% (Swedish FSA definition FFFS 2012:6)

• NSFR 93%

• SEK 120bn in funding plan 2013 to meet total maturing debt FY 2013 of SEK 86bn of

which SEK 46bn for the remainder of 2013

20

Liquidity and funding

Term funding issuance – completed and planned

SEKbn

Source: Swedbank, Mar 31, 2013, nominal amounts

0

10 000

20 000

30 000

40 000

50 000

60 000

Domestic CP ECP/CD USCP Yankee CD French CD

Q4 12

Q1 13

0

10 000

20 000

30 000

40 000

50 000

60 000

70 000

Domestic CB

Euro CB USD CB (144A)

Other CB Senior unsecured

FY 2012

Q1 13

Conservative funding plan

21

Long-term debt issued

• Issued SEK 40bn of term-funding in Q1

• Term funding plan in 2013 of SEK 120bn, full-year maturities of SEK 86bn

Liquidity and funding

Outstanding short-term debt SEKm SEKm

Source: Swedbank, Mar 31, 2013, nominal amounts

Liquidity reserve

22

1 95% of the securities in the liquidity reserve per Q3 2013 are rated AAA

According to the template defined by the Swedish Bankers' Association

2 84% of the additional liquid assets fulfill the Liquidity Reserve definition by the Swedish Bankers’ Association except

from that they are held outside the Treasury department. 3 82% of the additional assets are rated AAA

Liquidity and funding

Source: Swedbank Fact book, Mar 31, 2013

Additional liquid assets, Group2, 3

56 472

SEKm

Cash and holdings in central banks 210 251

Deposits in other banks available overnight 1 290

Securities issued or guaranteed by sovereigns, central banks or multilateral development banks 27 751

Securities issued or guaranteed by municipalities or public sector entities 378

Covered bonds 58 284

- Issued by other institutions 58 284

- Own issued

Securities issued by non-financial corporates

Securities issued by financial corporates (excl. covered bonds) 2 532

Other

Total1

300 486

SEKbn

Days forw ard

0

50

100

150

200

250

300

0 20 40 60 80 100 120 140 160 180 200 220 240 260 280 300 320 340 360365

Prolonged survival horizon

23

Liquidity and funding

SEKbn

Source: Swedbank Mar 31, 2013

Days forward

0

50

100

150

200

250

300

350

400

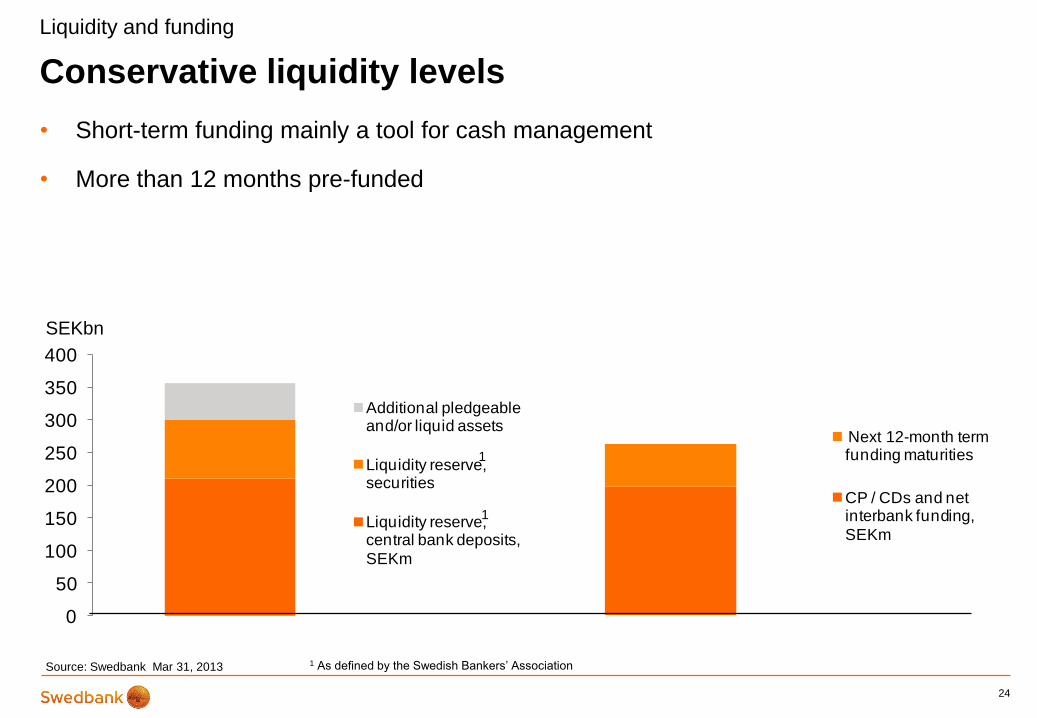

Next 12-month term funding maturities

CP / CDs and net interbank funding,

SEKm

0

50

100

150

200

250

300

350

400

Additional pledgeable and/or liquid assets

Liquidity reserve, securities

Liquidity reserve, central bank deposits,

SEKm

Conservative liquidity levels

• Short-term funding mainly a tool for cash management

• More than 12 months pre-funded

24

SEKbn

Source: Swedbank Mar 31, 2013

Liquidity and funding

1 As defined by the Swedish Bankers’ Association

1

1

Asset encumbrance

25

Liquidity and funding

Source: Swedbank Facts Q1 2013

1) Repoed securities on balance sheet.

2) Collateral posted under CSA agreements, gross (3-year, SEKm,

High: 21 572, Low : 10 945, Average: 13 975).

3) Of w hich accrued interest of assets in the cover pool, SEK 2 389m

as of Q1 2013

4) Collateral pledged in securities lending activities and w ith

exchanges

5) Reversed repos are included.

6) All type of securities, including securities non pledgeable at central

banks, of w hich 80% are rated AAA, 2% are rated below A-

and 8% are not rated.

7) Of w hich accrued interest of assets in the cover pool

overcollateralisation, SEK 831m as of Q1 2013

8) Type of loans; Residential 84.3%, Forestry & Agriculture 15.4%,

Commercial 0.3%.

Encumbered assets - distribution by type of liability (row) and asset (column)

SEKm

Government

debt

instruments

Central banks

and

supranational

debt

instruments

Covered

bonds

Debt

instruments

issued by

credit

institutions

Securities

issued by

corporate and

other issuers ABS

Mortgage

loans Cash Total

Central bank funding 0

Intraday settlement 1 028 10 772 11 800

Repurchase agreements 1) 18 448 12 765 31 213

Derivatives 2) 74 1 949 13 125 15 148

Covered bonds 3) 514 795 514 795

Other 4) 0 736 284 1 020

Total 19 550 0 25 486 736 0 0 514 795 13 409 573 976

Financial assets pledged for insurance policy holders 109 813

Unencumbered assets - additional assets available for secured funding

SEKm

Government

debt

instruments

Central banks

and

supranational

debt

instruments

Covered

bonds

Debt

instruments

issued by

credit

institutions

Securities

issued by

corporate and

other issuers ABS

Mortgage

loans Cash Total

Securities 5, 6) 30 948 11 213 73 812 12 671 8 238 984 137 866

Cover pool over-

collateralisation 7) 192 782 192 782

Cover pool eligible assets 8) 12 031 12 031

Total 30 948 11 213 73 812 12 671 8 238 984 204 813 0 342 679

Total assets 1 917 227

26

3. Cover pool data

27

28

Rating, S&P / Moody’s AAA / Aaa

Total pool size SEK 704.3bn

Geographic distribution Sweden 100%

Current OC-level 37.0%

Weighted average seasoning 2 63 months

Average LTV 3, 4

– WA LTV on property level (Max LTV) 58%

Non-performing loans 5 None

Fixed /Floating interest loans 6

– Fixed 44%

– Floating 56%

Repayment structure 7

– Amortising 44%

– Interest only 56%

Average loan size SEK 447 280

Number of loans outstanding 1 574 581

Number of borrowers 1 132 671

Number of properties 745 558

Dynamic pool Yes

1 As per Mar 31, 2013

2 Public sector loans not included

3 Index valuation as per Mar 31, 2013 4 Maximum LTV: Residential 75%, Commercial 60%, Forest and Agriculture 70% 5 Past due loans > 60 days are not eligible for the cover pool 6 Floating interest loans < 365 days 7 Property level of cover pool

Cover pool data1

Source: Swedbank Fact book, Mar 31, 2013

Swedbank’s cover pool

Swedbank is a labeled issuer of

the ECBC Covered Bond Label

Foundation

(www.coveredbondlabel.com )

Cover pool data

29

Swedbank’s cover pool

Source: Swedbank, Facts, Mar 31, 2013

Geographical distribution - Sweden 100% Q1

% 2013

North 6.7

Norrbotten county (BD) 1.5

Västerbotten county (AC) 2.4

Västernorrland county (Y) 1.6

Jämtland county (Z) 1.3

Middle (including Stockholm) 43.9

Dalarna county (W) 2.3

Gävleborg county (X) 2.2

Värmland county (S) 2.2

Örebro county (T) 2.6

Västmanland county (U) 2.7

Uppsala county ( C) 4.0

Södermanland county (D) 2.7

Stockholm county (including Stockholm) (AB) 25.2

South (including Göteborg and Malmö) 49.4

Västra götaland county (Including Göteborg) (O) 17.4

Östergötland county (E) 4.1

Jönköping county (F) 3.7

Halland county (N) 3.7

Kronoberg county (G) 2.3

Kalmar county (H) 3.4

Skåne county (including Malmö) (M) 12.5

Blekinge county (K) 1.8

Gotland county (I) 0.6

100.0

Type of loans

%

Residentials 91.0

of w hich Single-family housing 60.6

of w hich Tenant ow ner rights 16.2

of w hich Tenant ow ner association 9.8

of w hich Multi-family housing 4.5

Public 1.4

Commercial 0.3

Forest & Agricultural 7.3

100.0

0%

5%

10%

15%

20%

25%

30%

35%

40%

00-10 10-20 20-30 30-40 40-50 50-60 60-70 70-75

0%

5%

10%

15%

20%

25%

00-10 10-20 20-30 30-40 40-50 50-60 60-70 70-75

Cover pool loan-to-value distribution

30

Swedbank’s cover pool

Source: Swedbank, Mar 31, 2013

• Weighted average LTV 58%

LTV distribution per property1 LTV distribution by volume1, 2

1 Public loans of 1.4% of the cover pool are excluded as they are either guaranteed by a Swedish municipality or the

government and have therefore no LTV assigned to them. 2 LTV distribution as defined by the Association of Swedish

Covered Bond Issuers (www.ascb.se)

-0.10%

0.00%

0.10%

0.20%

0.30%

0.40%

0.50%

Residential Forest & Agriculture

31

Source: Swedbank Mar 31 2013

• Total accumulated Swedish mortgage loan losses since 1982 of SEK 7.4bn (size of

total loan book SEK 746bn)

– Main part incurred during the years of 1992 and 1993

– Around 20% in the private segment

Insignificant credit loan losses in Swedbank Mortgage

Financial performance – asset quality

Credit impairments, Swedbank Mortgage

%

32

4. Swedish economy

33

A balance sheet in favourable condition

• Sweden’s financial assets continue to exceed its liabilities

34

Swedish economy

Source: OECD Economic outlook 92 (table 33), Dec 18, 2012

-40

-20

0

20

40

60

80

100

120

2011 2012F 2013F

General government net financial liabilities % of nominal GDP

35

A budget in balance

Swedish economy

Source: OECD Economic outlook 92 table 27, Dec 18, 2012

Budget balance as a percentage of GDP

• Budget framework since early 1990’s – to stabilize and achieve long-term sustainability

in the public finances

– Mandatory public sector excess savings target of 1% of GDP on average over a business cycle

– Mandatory ceiling for the state and pension system expenses (3 years ahead)

Swedish historic budget balance as a percentage

of GDP

-12

-10

-8

-6

-4

-2

0

2

2010

2011

2012F

2013F

-8

-6

-4

-2

0

2

4

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012F

2013F

2014F

36

Savings

Swedish economy

Source: OECD Economic Outlook 92, table 23, Dec 18 2012

Household saving rates % of disposable income

-10

-5

0

5

10

15 1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012F

2013F

Sweden

Germany

Norway

US

Finland

Denmark

0

200

400

600

800

1 000

1 200

1 400

1 600

1 800

2005 2006 2007 2008 2009 2010 2011 2012 Q1 130

20

40

60

80

100

1999 2001 2003 2005 2007 2009 2011 2013F

Euro area

France

United Kingdom

Germany

Denmark

Sweden

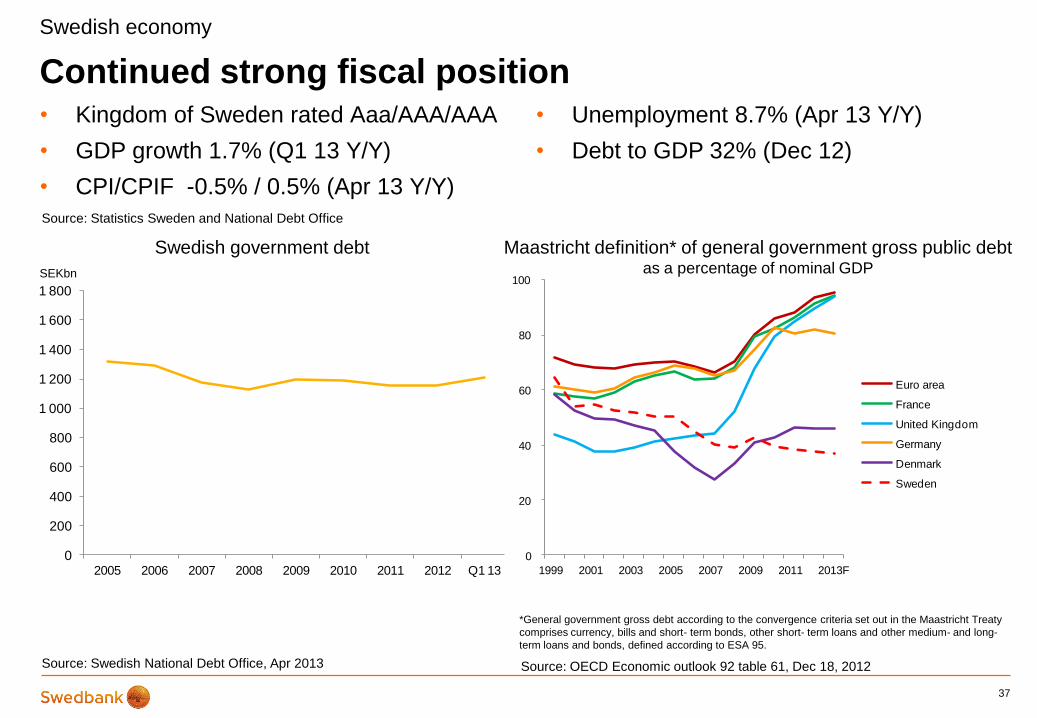

• Kingdom of Sweden rated Aaa/AAA/AAA

• GDP growth 1.7% (Q1 13 Y/Y)

• CPI/CPIF -0.5% / 0.5% (Apr 13 Y/Y)

37

Continued strong fiscal position

Source: OECD Economic outlook 92 table 61, Dec 18, 2012

Swedish government debt

Swedish economy

SEKbn

Maastricht definition* of general government gross public debt as a percentage of nominal GDP

Source: Statistics Sweden and National Debt Office

Source: Swedish National Debt Office, Apr 2013

*General government gross debt according to the convergence criteria set out in the Maastricht Treaty

comprises currency, bills and short- term bonds, other short- term loans and other medium- and long-

term loans and bonds, defined according to ESA 95.

• Unemployment 8.7% (Apr 13 Y/Y)

• Debt to GDP 32% (Dec 12)

0

20 000

40 000

60 000

80 000

100 000

120 000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Import Export

Exports – key factor for growth

38

Swedish economy

Source: Statistics Sweden, Mar, 2013

Top 10 export countries, Feb 2013, %

Exports and imports trend per month, SEKm Current prices

Data up to and including Feb 2013

Current account balance as % of GDP

Source: OECD – Economic outlook 92, table 51, Dec 18, 2012

-6

-4

-2

0

2

4

6

8

10

12

2007 2008 2009 2010 2011 2012F 2013F

Sweden

Germany

Denmark

Italy

Finland

France

United States

United Kingdom

Canada

0

2

4

6

8

10

12

5. Swedish housing and mortgage market

39

Swedish mortgage market

• No securitisation (on balance sheet), no sub-prime market, no 3rd party origination, restricted buy-

to-let market

• 70% home ownership1

• Rental market is regulated

• Transparent credit information (credit information agency, www.uc.se)

– Publicly available information regarding income, debt, payment track record etc

• Consumer credit legislation requires affordability calculations including stress test of higher interest

rate

• Very limited debt forgiveness possibilities (full recourse)

• Strong social security and generous unemployment benefit system

40

Swedish housing and mortgage market

1 Source: Boverket, 2011

0

2

4

6

8

10

12

14

03 04 05 06 07 08 09 10 11 12 13

Annual percentage change

Pace of household borrowing declines

• House prices stabilize

• Credit growth abates

• LTV development impacted by changed origination standards

41

House-price development (2007=100) Household borrowing growth

0

20

40

60

80

100

120

140

2007 2008 2009 2010 2011 2012 2013

HOXSWE HOXFLATSWE HOXHOUSESWE

Source: Swedbank, Statistics Sweden and Valueguard (HOXSWE= Total, HOXFLATSWE= Tenant owner rights, HOUXHOUSESWE= Single family houses)

%

Swedish housing and mortgage market

Real estate prices – Sweden 12 months development

42

Swedish housing and mortgage market

Single-family homes1 Tenant-owner rights2 Combined3

12M Δ

12M Δ

12M Δ

Apr/12 -2% 2% -1%

May/12 -2% 3% -1%

Jun/12 -1% 4% 0%

Jul/12 0% 4% 1%

Aug/12 2% 4% 3%

Sep/12 2% 5% 3%

Oct/12 1% 6% 3%

Nov/12 3% 7% 4%

Dec/12 4% 7% 6%

Jan/13 3% 7% 5%

Feb/13 4% 7% 5%

Mar/13 3% 7% 5%

Source: Valuegard www.valuegard.se (Based on data from Mäklarstatistik), 1 HOXHOUSESWE, 2 HOXFLATSWE, 3 HOXSWE

Debt servicing ability of the households will remain good

43

Swedish housing and mortgage market

Swedish household financial assets and liabilities to disposable income

Source: Riksbanks’ financial stability report 12:2. Nov 2012, chart 3:10.

%

0

100

200

300

400

500

600

700

71 74 77 90 83 86 89 92 95 98 01 04 07 10

Total wealth Real wealth Liquid wealth Debts

Note. Liquid wealth refers mainly to cash, bank deposits, bonds and shares. Own financial saving is total saving excluding collective and real saving.

0

10 000

20 000

30 000

40 000

50 000

60 000

70 000

80 000

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Apartment buildings Single-family dwellings

44

Housing investments at a conservative level

Housing completions, apartments in Multi-family dwellings

and Single-family houses in Sweden Housing investments as a percentage of GDP (4Q moving average)

Swedish housing and mortgage market

Number of apartments

Source: Statistics Sweden, Mar 2013 (data as per FY 2012) Source: Reuters Ecowin, Oct 20, 2012 (data as per Q2 2012)

0

2

4

6

8

10

12

14

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

Spain

Eurozone

Denmark

UK

USA

Sweden

As per 31 Dec 2012, 24,524 apartments were completed during 2012

0

200 000

400 000

600 000

800 000

1 000 000

1 200 000

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Acc increase in population

Acc increase in housing starts

Population growth far exceeds housing unit growth

45

Source: Statistics Sweden, Mar 2012, 1 Boverket

Population- and housing growth

Number of homes / persons

Swedish housing and mortgage market

• 60%1 of the Swedish population live in Municipalities with housing shortage

Population growth far exceeds housing unit growth

46

• Trend more pronounced in the three largest cities, (index 1990=100)

Source: Statistics Sweden

Swedish housing and mortgage market

128

115

60

70

80

90

100

110

120

130

140

Stockholm Population

Stockholm Housing stock

120

114

60

70

80

90

100

110

120

130

140

Gothenburg Population

Gothenburg Housing Stock

129

113

60

70

80

90

100

110

120

130

140

Malmoe Population

Malmoe Housing Stock

126

114

60

70

80

90

100

110

120

130

140

Top three cities population

Top three cities housing stock

Appendix

47

This is Swedbank

48

The Bank for the many people, households and businesses

49

Latvia

Population 2.0m

Private customers 0.9m

Corporate customers 84 000

Branches 54

ATMs 417

Cards 1.0m

Employees 1 738

Lithuania

Population 3.0m

Private customers 2.0m

Corporate customers 87 000

Branches 81

ATMs 503

Cards 1.9m

Employees 1 948

Estonia

Population 1.3m

Private customers 1.0m

Corporate customers 118 000

Branches 57

ATMs 496

Cards 1.1m

Employees 2 408

Sweden

Population 9.5m

Private customers 4.0m

Corporate customers 263 000

Organisations 67 000

Branches 308

ATMs 444

Cards 3.8m

Employees 7 920

This is Swedbank

Source: Swedbank Fact book Q1, 2013

0

10

20

30

40

50

60

Sweden Estonia Latvia Lithuania

Mortgage lending

Corporate lending

0

10

20

30

40

50

60

Sweden Estonia Latvia Lithuania

Deposits Private

Deposits Corporate

Market leading retail franchise in all home markets

50

% %

Source: Source Sweden: Statistics Sweden (SCB)

Source Estonia: Estonian Central Bank

Sources Latvia: Association of Commercial Banks of Latvia (ACBL) & The Financial and Capital Market Commission (FCMC)

Source Lithuania: Association of Lithuanian Banks (LBA)

This is Swedbank

Market shares, Deposits February 2013

• Largest retail bank and fund manager in Sweden

Market shares, Lending February 2013

0 200 400 600 800 1000 1200

Other* 3.3%

Lithuania 2.9%

Latvia 2.4%

Estonia 4.3%

Sweden 87.1%

Swedish Mortgage loans (private+corp)

Other corporate (incl. LC&I, Sweden)

Other

Sweden – the dominating home market

• Total lending to the public amounts to SEK 1,183bn (as per Q1 2013), out of which

around 87% is originated in Sweden

• Estonia makes up 45% of total lending in the Baltics

51

Source: Swedbank Fact book Q1 2013, page 37

This is Swedbank

* Russia & Ukraine, Denmark, Norway, Finland and NY Branch

Lending distributed by countries (Q1 2013)

SEK 1 030bn

Baltic market fundamentals

• Legal and institutional framework

• Fiscal position

• Market concentration

• Absence of “irrational” players

• Sophisticated product penetration

• Swedbank retail and deposit incumbent

• GDP / capita less than half of Sweden’s

• Risk mitigators

– Loan-to-deposit restriction

– Group governance model

52

Estonia

Latvia

Lithuania

This is Swedbank – Baltic banking

Source: Swedbank

Customer requirements drive new ways of banking

• Focus on functionality and ease of use

53

This is Swedbank - Retail banking

0

5

10

15

20

25

30

Jan 2010 Jan 2011 Jan 2012 Jan 2013

millionMonthly logins Swedbank and Savings Banks

Mobile bank Internet bank

Source: Swedbank Mar 31, 2013

Fast increase of digital usage

• Internet Bank, private and corporate (since March 1997)

– Number of users: >3.5 million

• Mobile Bank, private (since Dec 2009)

– Number of users: >1.3 million

• Mobile Bank Youth (since March 2013)

– Number of users: 6 700

• Mobile Bank Corporate (since March 2013)

– Number of users: >8 000

• Ipad (since Oct 2012)

– Number of users: >200 000

• Swish (since Dec 2012)

– Number of users: ~100 000

54

This is Swedbank - Swedbank and Savings Banks

Source: Swedbank Mar 31, 2013

Financial performance

55

Peer comparison – Swedbank top 1 or 2 in all key metrics

56

Business position

• Peer group definition - jurisdiction matters

Reported YE 2012 figures Swedbank SHB SEB Nordea Danske DnB

Rating, long-term (S&P/Moody's/Fitch) A+/A2/A+ AA-/Aa3/AA- A+/A1/A+ AA-/Aa3/AA- A-/Baa1/A A+/A1/A+

Rating, short-term (S&P/Moody's/Fitch) A-1/P-1/F1 A-1+/P-1/F1+ A-1/P-1/F1 A-1+/P-1/F1+ A-2/P-2/F1 A1/P-1/F1

RoE, %* 14.1 14.4 10.8 11.5 3.6 10.9

RoCET1, % 19.2 17.6 13.6 15.2 4.4 11.5

Pre-provision RoCET1, % 26.2 22.8 17.8 24.6 19.6 18.0

CET1 Basel 2, % 17.4 18.4 16.4 13.1 14.5 12.1

CET1 Basel 3, % 16.1 16.5 14.3 11.8 12.5 12.1

CET1 IAS 19, % 15.4 16.4 13.1 11.6 12.5 12.1

C/I ratio, % 46.3 46.3 60.5 50.7 55.8 50.2

Credit impairment ratio, % 0.06 0.08 0.08 0.27 0.74 0.25

Impairment (gross) as % of total gross loans 1.11 0.45 1.07 1.94 6.54 2.05

LCR, % 130 136 113 127 121 n/d

NSFR, % 91 n/d n/d n/d n/d n/d

*ROE calculated as average of equity for Q1 and Q4 for comparable reasons (otherwise communicated 14.4% calculated as an average for all quarters 2012)

n/d = not disclosed

Strategic focus areas

• ROE target of 15%

– Efficiency

– Repricing

– Increase share of wallet

– Capital efficiency

• Lowest risk – lowest funding costs

– Buffers

• Customer offering

– Internet banking own profit center – further investments

– Improved advisory capability – further investments

• Continue de-centralisation

57

Financial performance - business position

Asset quality

58

Provisions – well provided for

59

Asset quality

Provision ratios, % Q1 13

Retail 70

LC&I 76

Baltic Banking 52

Group 57

* Russia and Ukraine reported as discontinued operations.

11 91510 951

9 934

7 077

4 429

2 4782 040

1 774

1 545

1 420

65.0% 63.7% 65.2%61.9%

57.0%

0

5 000

10 000

15 000

20 000

25 000

Q1 12 Q2 12 Q3 12 Q4 12 Q1 13*

SEKm

Individual provisions Portfolio provisions Provision ratio

Source: Swedbank Mar 31, 2013

Corporate portfolio drives capital efficiency

60

Asset quality - Retail

94

24

104

Total portfolio SEK 222bn

Swedbank Mortgage AB

Swedbank Finans AB

Other

Segments excl. Swedbank

Mortgage and Swedbank Finance

Volume

(SEKbn)

Secured

(%)

Agriculture 5.9 81

Manufacturing 9.7 74

Public sector and utilities 5.1 92

Construction 4.7 82

Retail 9.0 88

Transportation 1.9 85

Shipping 0.1 95

Hotels and restaurants 3.1 91

Information & communication 0.9 46

Finance and insurance 2.0 66

Property management 49.4 97

Professional service 6.7 65

Other 6.0 72

Total 104.4 87

Source: Swedbank Mar 31, 2013

15

5

4

24 26 25

24 23

0

10

20

30

Q1-12 Q2-12 Q3-12 Q4-12 Q1-13

SEKbn

Shipping and Offshore

Offshore Tanker Other

61

• Exposure to Shipping & Offshore sector

was SEK 23.5bn plus unutilised

commitments of SEK 7.7bn

– Portfolio duration 4-5y

– Average fleet age 7y

– Strong employment profiles

Asset quality – Large Corporates & Institutions

0 5 10 15 20

SEK

EUR

USD

NOK

JPY

Shipping and Offshore portfolio by currency

Q1-13

Q4-12

0,5

6,8

1,6

3,5

1,2

1,9

0,2

2,3

0,7

1,4

0,7

0,9

1,6

0 2 4 6 8

Cruise

Drilling & exploration

Oil service

Supply

Accommodation

Floating production

Chemical

Product

Crude oil

Gas (LNG/LPG)

Dry bulk

Container

RORO

Shipping and Offshore Portfolio by subsegment

Q1-13

Q4-12

Shipping and Offshore

SEKbn

bn

Source: Swedbank Mar 31, 2013

Agriculture

• Segmentation definitions – Corporate Agriculture: Businesses

that derive their main income from

agricultural activities

– Private Investments: Private individuals who

own agricultural properties for residential or

investment purposes

• Lending to the agricultural sector SEK

63.3bn – Corporate Agriculture: (58%)

• Agriculture 45%

• Forestry 13%

– Private Investments (42%)

• Residential: 20%

• Forestry: 22%

62

Asset quality

Agriculture 45%

Forestry 13%

Private: Forestry

22%

Private: Residential

20%

Liquidity and funding

63

Structure of the Swedish domestic covered bond market

• Benchmark system established in early 1990s

• Tap issuance enhances liquidity and reduces execution risk

– Continuous daily issuance

– Buy-backs against issuance of longer tenors

– Total issue size often peak at SEK 40-60bn

• Market making at pre-set bid/offer spreads

64

Source: Swedbank

Liquidity and funding

0

200

400

600

800

1 000

1 200

1 400

1 600

2007 2008 2009 2010 2011 2012 Q1 13

SE

Kb

n

Swedbank Mortgage Total excl. Swedbank Mortgage

1 0621 149 1 113 1 075 1 128 1 134 1 103

1 015883

0

5

10

15

20

25

30

35

40

0

200

400

600

800

1 000

1 200

1 400

1 600

2008 2009 2010 2011 2012F 2013F 2014F 2015F 2016F

Government debt % of GDP

The Swedish covered bond market

65

Swedish Domestic Covered Bonds, in SEKbn Public debt projections 2012-2016

Source: Actual and forecast from government budget statement, Sep 20, 2012

• Domestic covered bonds represent approximately 1/3 of GDP and 1/2 of the total

Swedish bond market

Source: www.ascb.se , Mar 31, 2013

Liquidity and funding

% SEKbn

0

10

20

30

40

50

60

70

80

Jun 13 May 14 Mar 15 Sep 15 Jun 16 Mar 17 Dec 17 May 20

SPI 177 SPI 166 SPI 182 SPI 183 SPI 184 SPI 185 SPI 186 SPI 180

2009-12-31 2010-12-31 2011-12-31 2012-03-31

2012-06-30 2012-09-30 2012-12-31 2013-03-31

Swedbank’s domestic covered bonds

66

Source: Swedbank, Mar 31, 2013

Liquidity and funding

SEKbn

29%

18%

35%

10%

34%

66%

2% 6%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2007 Q1 2013

5 years +

1-5 years

3-12 months

0-3 months

0

5

10

15

20

25

30

35

40

45

50

Q3 09

Q4 09

Q1 10

Q2 10

Q3 10

Q4 10

Q1 11

Q2 11

Q3 11

Q4 11

Q1 12

Q2 12

Q3 12

Q4 12

Q1 13

Total capital market funding Covered bond funding

Fundamental change of maturity profile

67

Average maturity profile of outstanding market

funding

Source: Swedbank, Mar 31, 2013

Months

SEK

673bn

SEK

767bn

• 2007 – 64% of wholesale funding < 12 months, SEK 13bn in central bank deposits

• Q1 2013 – 28% of wholesale funding < 12 months, SEK 210bn in central bank deposits

Liquidity and funding

0

50

100

150

200

2013 2014 2015 2016 2017 2018 2019-

Government guaranteed debt

Senior unsecured debt

Covered bonds

68

Long-term funding maturity profile

• FY 2013 maturities amount to nominal SEK 86bn, of which SEK 46bn remains

68

Long-term funding maturity profile

Source: Swedbank Mar 31, 2013

Liquidity and funding

SEKbn

0

50

100

150

200

250

300

Assets Liabilities

Assets held for sale

Interest-bearing securities

Lending to the public

Loans to credit institutions

Cash and balances with central banks

Deposits and borrowings from the public

Amounts owed to credit institutions

Debt securities in issue

Limited need for USD-funding

69

SEKbn

• USD-funding need covered for more than 12 months

• Issued USD 1bn of covered bonds (144a) and USD 1bn of senior (144a) YTD 2013

Source: Swedbank Fact book, Mar 31, 2013

Liquidity and funding

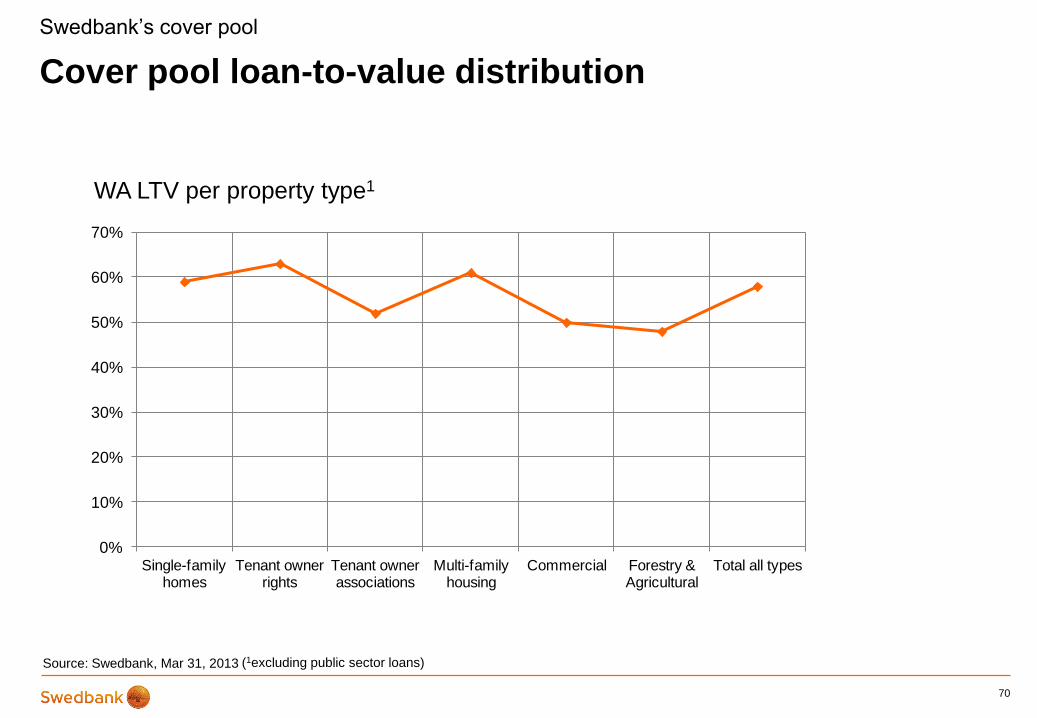

Cover pool loan-to-value distribution

70

Swedbank’s cover pool

Source: Swedbank, Mar 31, 2013 (1excluding public sector loans)

WA LTV per property type1

1 0%

10%

20%

30%

40%

50%

60%

70%

Single-family homes

Tenant owner rights

Tenant owner associations

Multi-family housing

Commercial Forestry & Agricultural

Total all types

The Covered Bond Act entered into force on July 1, 2004 and is over-sighted by the Swedish FSA. Its main characteristics are:

Dual recourse to the issuer and cover pool

Dynamic, regulated pool of assets, frequently monitored by the Swedish FSA via appointment of an

independent inspector

Regulated valuation of cover pool assets which remain on the balance sheet

The cover pool may consist of certain mortgage credits, public credits and supplemental assets. There is no requirement to segregate mortgage and public credits.

Maximum LTVs: Residential 75%, Agricultural 70%, Commercial 60%

Maximum 10% commercial loans and 20% supplemental assets in cover pool

Regular monitoring of the property values, revaluation of property prices in case of significant drop (generally interpreted as 15% drop)

No mandatory over-collateralisation (OC)

Regional constraint on collateral assets (Mortgage - EEA, Public - OECD)

The cover pool value shall always exceed the aggregate value of claims (including derivatives)

A sound balance in terms of FX, interest rates and maturities must be achieved. It is deemed to exist when the present value of the cover pool at all times exceed the present value of liabilities (including derivatives), even on a stressed basis. Present value cover must hold even after 1% upward and downward shift in the yield curve and a 10% change in the currency

Non-performing assets in the cover pool which are more than 60 days overdue must be disregarded for the purposes of the matching tests

Holders of covered bonds and relevant derivative counterparties benefit from a priority claim over the cover pool should the institution be declared bankrupt and rank pari passu ahead of unsecured creditors and all other creditors of the institution in respect of assets in the cover pool

The registered assets in the cover pool, the covered bonds and any relevant derivative contracts are required to be maintained as a unit and kept segregated from other assets and liabilities of the bankruptcy estate of the institution. The administrators-in-bankruptcy are then required to procure the continued timely service of payments due under the covered bonds and any relevant derivative contracts

Overview of the Swedish covered bond legislation

71

Swedish covered bond legislation

Loan-to-value ratios and other limitations

Matching requirements

Benefit of a priority right over the cover pool

Administration in event of bankruptcy

The Covered Bond Act

Source: www.ascb.se

Funding sources

72

Swedbank AB Swedbank Mortgage AB*

* 100% guaranteed by parent company

- Irrevocable

- Unconditional

- Timely

** Limited by cover pool size

100% owned

Liquidity and funding

Source: Swedbank, Mar 31, 2013

Program Limit

Long Term

Global MTN USD 40bn

Domestic MTN SEK 60bn

USD Senior (144a / Reg.S) USD 15bn

NSV (stand alone doc.)

Short Term

Domestic CP SEK 80bn

European CP/CD EUR 6bn

US CP USD 15bn

Yankee CD USD 10bn

French CD EUR 4bn

Finnish CD EUR 4bn

Program Limit

Long Term

Domestic Benchmark CB Unlimited**

EMTN CB EUR 25bn

USD Covered bonds (144a / Reg.S) USD 15bn

Domestic MTN CB SEK 150bn

Norwegian Benchmark CB Unlimited**

Registered CB (stand alone doc.)

Short Term

Domestic CP SEK 50bn

Swedish economy

73

74

Swedish economy

• Real economic growth declined to 1.2% in 2012 from 3.7% the

year before. Despite the slowdown, economic activity held up

surprisingly well in the last two quarters of the year, and labour

market developments were supported by a stronger-than-

expected employment growth

• We expect GDP growth to remain weak in the first half of 2013

before picking up steam. Overall, for 2013 and 2014, we

forecast real growth at 1.6% and 2.7%, respectively. In

particular, household consumption will drive growth, and

economic policy will remain expansionary.

• In 2012, economic growth decelerated to 3.2%, primarily due

to weakened foreign demand and the contraction of export-

oriented manufacturing. Growth was primarily driven by public

investments in buildings and infrastructure, financed by EU

transfers and CO2 quota sales.

• Boosted mainly by domestic demand, GDP growth is expected

to reach 3.3% in 2013 and accelerate to 4.2% next year, with

additional support from exports. Investment growth will

decelerate as government investments will decrease. Private

consumption will contribute the most to economic growth.

• The economy expanded by 5.6% in 2012, driven by exports

and stronger domestic demand. Inflation has slowed sharply

as domestic price pressures are weak and global price

dynamics benign. Latvia has applied for euro area

membership and is expected to join it on January 1, 2014

• The GDP growth forecast for 2013 is raised to 4.3% (4.1%

before) as lower inflation will support private spending.

Inflation is revised down to 1.1% this year but will pick up to

3.5% in 2014. GDP growth will speed up to 5% in 2014, as the

global outlook improves and the personal income tax rate is

cut.

• Growth remained strong at the end of last year, mainly due to

booming exports. Companies postponed some of their

investments and slashed inventories, but we do not expect

this trend to continue. Last year, for the first time, foreign trade

was in surplus.

• We keep our GDP growth forecast at 4.0% for both 2013 and

2014. Real net wages are expected to grow faster this year

and the next, due to lower inflation and likely lower labour tax

rates. We have cut the inflation forecast for 2013 to 2.5%, but

euro accession is far from certain.

Sweden

Estonia

Latvia

Lithuania

Source: Swedbank Economic outlook, Apr 10, 2013

Government debt

• Around 15% in foreign currencies

Swedish economy

SEKbn 2011 2012F 2013F

Government debt in the beginning of the year 1188 1158 1167

Primary financing need excluding sell-off's -79 6 -4

Sale of government assets -23 0 0

Interest cost on government debt 34 26 19

Net financing need -68 32 15

Corrections of debt 22 -6 4

Money-market assets (annual change) 16 -17 0

Government debt change -30 10 19

Government debt at year end 1158 1167 1186

0

10

20

30

40

50

60

70

80

90

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012F

2013F

Debt to GDP ratio, % – historic distribution Government net financing need

Source: Swedish National Debt Office, Jul 2012

-8

-6

-4

-2

0

2

4

6

8

10

1995 1998 2001 2004 2007 2010

0

1 000 000

2 000 000

3 000 000

4 000 000

5 000 000

6 000 000

Resources Expenditures

Import

GDP

Gross investments

Public consumption

Privat consumption

Export

Swedish GDP breakdown

76

Swedish economy

Source: Statistics Sweden, Mar, 2013

GDP growth From corresponding quarter previous year , %, fixed prices

Data up to and including Q4 2012

0% 2% 4% 6% 8% 10% 12% 14%

Subsidies on products

Agriculture,forestry, f ishing

Education, health and social work

Electricity, gas, steam and air …

One and two family houses, secondary …

Financial services and insurance activities

Transport and storage

Management of real estate

Information and communication

Construction

Real estate activities

Scientif ic, technical and admin. Act

Wholesale and retail trade

Other value added

Taxes on products

Manufacturing industry

GDP production approach at market price

The output of the Swedish economy SEKm

Housing and mortgage market

77

Mortgage loans – risk-adjusted returns before volume

• Risk reduction – a long-term necessity

─ Price

─ Loan-to-value

─ Amortization

• Market shares

─ Risk-adjusted returns before volume

─ Defend business position

78

Swedish housing and mortgage market

Mortgage margins

0

10

20

30

40

Dec-0

5

Jun-0

6

Dec-0

6

Jun-0

7

Dec-0

7

Jun-0

8

Dec-0

8

Jun-0

9

Dec-0

9

Jun-1

0

Dec-1

0

Jun-1

1

Dec-1

1

Jun-1

2

Dec-1

2

Swedbank's share of monthly

growth

Share of housing lending

balance (Sweden statistics) 0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

1.2%

Jan-0

8

Mar-

08

May-0

8

Jul-08

Sep

-08

No

v-0

8

Jan-0

9

Mar-

09

May-0

9

Jul-09

Sep

-09

No

v-0

9

Jan-1

0

Mar-

10

May-1

0

Jul-10

Sep

-10

No

v-1

0

Jan-1

1

Mar-

11

May-1

1

Jul-11

Sep

-11

No

v-1

1

Jan-1

2

Mar-

12

May-1

2

Jul-12

Sep

-12

No

v-1

2

Jan-1

3

Private, back-book of which f loating of which f ixed

Private net mortgage lending market share

Jan 2008 – Dec 2012, %

Source: Swedbank, Mar 31, 2013

Price development

79

Swedish housing and mortgage market

Source: SCB and Swedbank

Real estate price to disposable income, index 1993= 100

0

50

100

150

200

250

Structural interest rate decline key to affordability

80

Household indebtedness and interest expenditures after tax as

percentage of disposable income

Source: Riksbanken, Financial Stability Report 2012:2, Nov, 2012, chart 3.5

Swedish housing and mortgage market

% %

0

2

4

6

8

10

12

14

16

18

20

22

0

20

40

60

80

100

120

140

160

180

200

220

93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

Debt ratio (left scale) Interest ratio (right scale)

0

200

400

600

800

1 000

1 200

1 400

1 600

1 800

Jan

-05

Jul-

05

Jan

-06

Jul-

06

Jan

-07

Jul-

07

Jan

-08

Jul-

08

Jan

-09

Jul-

09

Jan

-10

Jul-

10

Jan

-11

Jul-

11

Jan

-12

Jul-

12

Jan

-13

Vilnius

Nr.of deals EUR/m2

0

200

400

600

800

1 000

1 200

1 400

1 600

1 800

Jan

-05

Jul-

05

Jan

-06

Jul-

06

Jan

-07

Jul-

07

Jan

-08

Jul-

08

Jan

-09

Jul-

09

Jan

-10

Jul-

10

Jan

-11

Jul-

11

Jan

-12

Jul-

12

Jan

-13

Riga

Nr.of deals EUR/m2

Baltic countries

81

Real estate prices

Source: Land book database

0

200

400

600

800

1000

1200

1400

1600

1800

Jan

-05

Jul-

05

Jan

-06

Jul-

06

Jan

-07

Jul-

07

Jan

-08

Jul-

08

Jan

-09

Jul-

09

Jan

-10

Jul-

10

Jan

-11

Jul-

11

Jan

-12

Jul-

12

Jan

-13

Tallinn

Nr.of deals EUR/m2

Source: Swedbank, Estonian Land Board

Source: Swedbank, State Enterprise Centre of Registers

LTV-distribution, %

Q1 2013 Q4 2011 Q4 2010

Estonia 67 75 86

Latvia 133 149 161

Lithuania 91 96 97

Swedish Riksbank’s Financial Stability Report

82

Transparency index for liquidity reporting, European banks

83

Swedish Riksbank’s financial stability report

0 20 40 60 80 100

Handelsbanken

Nordea

SEB

Swedbank

Note. The transparency index specifies the quality and scope of the banks' public reporting of liquidity risks. The higher the higher the level, the higher the quality and scope. The grey bars

represent global banks. The chart shows the Swedish banks and a sample of European banks (grey bars).

Source: The Riksbank’s Financial Stability Report 2013:1, chart 1:4

Report NSFR

at least once

a quarter

Handelsbanken Nordea SEB Swedbank

Financial

Stability

Report

2013:1

Minimum level observed

Partly observed

Not observed

Table 1:3 Public reporting of NSFR

Core Tier 1 capital ratio according to Basel II

84

Swedish Riksbank’s financial stability report

0 5 10 15 20

Crédit Agricole

RBS

Banco Santander

Raif feisen

Société Générale

Barclays

BBVA

UniCredit

Intesa Sanpaolo

DNB

Deutsche Bank

BNP Paribas

Lloyds

Commerzbank

HSBC

Nordea

Danske Bank

SEB

Credit Suisse

Swedbank

Handelsbanken

UBS

Source: The Riksbank’s Financial Stability Report 2013:1, chart 1:6

Equity in relation to total assets

85

Swedish Riksbank’s financial stability report

0 2 4 6 8 10 12

Handelsbanken

SEB

Nordea

Swedbank

%

Source: The Riksbank’s Financial Stability Report 2013:1, chart 1:7

Note. The measure specifies the capital of the Swedish banks and of a sample of European banks (grey bars) in relation to their total assets, with reductions for reverse repos, derivatives and

insurance assets. The measure should not be confused with the Basel Committee's leverage ratio.

CET1 ratios according to Basel III

86

Swedish Riksbank’s financial stability report

Note. The CET 1 ratios are stated according to the Riksbank's own calculations in accordance with the Basel III Accord. On 1 January 2013, the revised accounting standard IAS 19 "Compensation

to employees" were implemented. The revision primarily refers to defined pension plans and entails the reporting of accumulated actuarial gains and losses directly against equity, which may have

effects on reported CET 1 ratios.

Source: The Riksbank’s Financial Stability Report 2013:1, chart 1:12

%

0

2

4

6

8

10

12

14

16

18

20

Handels-banken

Nordea SEB Swedbank

March 2012

June 2012

September 2012

December 2012

March 2013

The major Swedish banks’ liquidity coverage ratio (LCR)

87

Swedish Riksbank’s financial stability report

0

20

40

60

80

100

120

140

160

Handels-banken

Nordea SEB Swedbank

%

Source: The Riksbank’s Financial Stability Report 2013:1, chart 4:16

Note. LCR according to the Swedish FSA:s regulations FFFS 2012:6. Does not correspond to the Basel Committee's revised LCR from 2013.

The Riksbank’s structural liquidity measure

88

Swedish Riksbank’s financial stability report

0

20

40

60

80

100

120

Handels-banken

Nordea SEB Swedbank

December 2010

December 2011

December 2012

%

Source: The Riksbank’s Financial Stability Report 2013:1, chart 4:17

Note. For a detailed description of the Riksbank’s structural liquidity measure, see Method for stress tests of the banks liquidity risks. Article in Financial Stability Report 2010:2. Sveriges

Riksbank.

0

20

40

60

80

100

120

140

160

180

70 80 90 100 110 120 130 140

The Riksbank’s short-term and structural liquidity measures

89

Swedish Riksbank’s financial stability report

Swedbank

Handelsbanken

Nordea

SEB

Source: The Riksbank’s Financial Stability Report 2013:1, chart 4.19

Short-term liquidity measure (days)

Str

uctu

ral liq

uid

ity m

easure

(per

cent)

Note. The dashed lines show the mean value, the grey dots illustrate a group of European banks.

0

2

4

6

8

10

12

14

16

18

20

Q1 13

13 14 15 Q1 13

13 14 15 Q1 13

13 14 15 Q1 13

13 14 15

Handelsbanken Nordea SEB Swedbank

CET1 ratios according to Basel III, initially and in the stress test

90

Swedish Riksbank’s financial stability report

Source: The Riksbank’s Financial Stability Report 2013:1, Table A:5 and chart A.3

%

2013 2014 2015 2013 2014 2015 2013 2014 2015 2013 2014 2015

Profit before impairments 14.6 14.6 14.6 34.3 34.3 34.3 12.2 12.2 12.2 16.0 16.0 16.0

Impairments -17.3 -18.3 -17.9 -39.2 -41.0 -39.1 -16.0 -17.1 -16.2 -13.2 -14.1 -13.5

Operating profit -2.7 -3.7 -3.3 -4.9 -6.7 -4.8 -3.8 -4.9 -4.0 2.8 1.9 2.5

CT1 capital, end of year (Basel II) 84 80 76 181 174 169 85 80 75 81 82 83

RWA end of year (Basel II) 502 501 503 1 488 1 495 1 519 616 619 627 482 484 490

CT1 capital ratio, Basel II 16.6% 15.9% 15.1% 12.1% 11.6% 11.1% 13.8% 12.9% 12.0% 16.8% 16.9% 16.9%

CT1 capital ratio, Basel III 16.1% 15.4% 14.6% 11.0% 10.5% 10.0% 12.1% 11.2% 10.3% 15.9% 16.0% 16.0%

SHB Nordea SEB SwedbankStress test

2015 regulatory cap

2013 regulatory cap

Related Documents