Running head: Quantitative Analysis: Comcast and Time Warner Cable Merger 1 Quantitative Analysis: Comcast and Time Warner Cable Merger Samuel Sutanto MBA 531 February 16, 2014 Ryan Gunhold

Sutanto_QuantitativeAnalysis_APA

Aug 08, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Running head: Quantitative Analysis: Comcast and Time Warner Cable Merger 1

Quantitative Analysis: Comcast and Time Warner Cable Merger

Samuel Sutanto

MBA 531

February 16, 2014

Ryan Gunhold

Quantitative Analysis: Comcast and Time Warner Cable Merger 2

Quantitative Analysis: Comcast and Time Warner Cable Merger

Introduction

Comcast announced on February 13, 2014 an agreement to acquire 100 percent of Time

Warner Cable’s 284.9 million shares outstanding for more than $45 billion in equity value. The

transaction will generate $1.5 billion in operating efficiencies; increased Internet speed for Time

Warner Cable customers, more high-definition offerings, and cheaper future service deployment.

This means the deal would merge the biggest and the second-biggest cable television

operators in the U.S. The merger will combine their customers, reaching 30% of all American

subscribers in 19 out of 20 U.S largest metropolitan regions and provides them with immense

power against content providers. The deal could face an uphill battle against the antitrust law,

which some has called on federal regulators to reject the merger. Comcast and Time Warner

Cable need to gain approval from Federal Communications Commission (FCC) and either

Department of Justice or Federal Trade Commission.

Comcast and Time Warner Cable are the largest providers to offer the “Triple Play”, a

service that combines TV, Internet and phone services. Both companies do not compete with

each other because none of their customer markets overlap; instead they mainly compete with

DirecTV and Dish Network which partner with local telephone companies to offer DSL

connections.

Comcast Company Overview

Comcast Corporation is a Philadelphia-based media, entertainment, and communications

company, mainly involved in the cable system operation through Comcast Cable, and production

Quantitative Analysis: Comcast and Time Warner Cable Merger 3

and distribution of media content through NBC Universal. Apart from a broadband

infrastructure, Comcast is an expertise in Video on Demand (VoD) services, digital telephone

and high speed Internet. Since acquiring NBC Universal in 2011, Comcast is the world’s largest

media corporation, owning 26 TV Stations, 20 Cable Channels, and several production facilities.

At the end of FY2012, Comcast’s cable systems served 22 million video customers, 19.4

million high-speed Internet customers and 10 million VoIP customers in 53.2 million homes and

businesses in 39 states. This makes Comcast the largest cable company in the US without any

close competitors to its scale and reach.

Time Warner Cable Company Overview

Time Warner Cable is a provider of video, high-speed data and voice services to

residential and business customers, over its broadband cable systems. Based in New York, the

company’s business services include networking and transport services, managed and outsourced

information technology (IT) solutions, and cloud services. Increasing adoption to cloud

technology placed Time Warner Cable (through its subsidiary NaviSite) to offer enterprise-class,

cloud-enable hosting, managed applications and services.

Time Warner Cable is the second largest cable company, serving 12.2 million video

subscribers; 12.3 million high-speed data subscribers; and 5.2 million voice subscribers across

29 states.

Quantitative Analysis: Comcast and Time Warner Cable Merger 4

Antitrust Law Issue

The two cable giants merger will likely face scrutiny from antitrust enforcers because of

the deal’s potential to reshape pay TV and broadband markets in the United States.

Even though the merger between Comcast and Time Warner Cable will create a

behemoth, it would not reduce competition in any relevant market. Comcast owns cable systems

in Chicago, San Francisco, and Seattle among many other cities, while Time Warner Cable owns

cable systems in key areas, including New York City, Southern California, and Texas. Out of the

top 50 market areas in the country, Time Warner Cable and Comcast only overlap in 3 cities:

New York City, Kansas City and Louisville, but operates in different zip codes.

If the merger is approved, Comcast will acquire Time Warner Cable’s customers in New

Jersey and Connecticut and add major markets such as Los Angeles and Dallas. In return,

Quantitative Analysis: Comcast and Time Warner Cable Merger 5

Comcast will extend open Internet access rules to Time Warner Cable customers and offer

affordable broadband access to low-income families, schools, and communities.

Satellite TV companies such as Dish, DirecTV, Verizon’s FiOS and AT&T’s U-verse

will still compete with one company in many of the regions.

The merger won’t affect the customers much, however Comcast plan to divest 3 million

subscribers in exchange for regulatory approval so their combined customer base of 30 million

would represent just under 30% of the U.S pay television video market.

The most significant impact will affect media providers. Being the dominant national

company gives them the advantage to negotiate with cable networks and content providers. The

bigger the company gets the more leverage it will be to exert on the networks that depend on it

for distribution. On an extreme case the company has the power to stop airing certain stations,

like what happened to CBS in August 2013 when Time Warner Cable pulled CBS stations off

the air in several cities for a month due to their disagreement over transmission fees.

Herfindahl-Hirschman Index (HHI) on Pay-TV

Herfindahl-Hirschman Index is a commonly accepted method to measure market

concentration. The index counts the market share of not just the top four or eight firms, but all

firms. The more unequal the market share, the greater is the index. The more numerous the

firms, the lower is in the index. Because of these properties, HHI is used as one factor in the

Department’s of Justice Merger Guidelines.

HHI are ranked on a scale of 0 to 10,000 with 0 representing Perfect Competition, and

10,000 representing Monopoly. If an industry scores above 2,500, it’s considered “highly

concentrated”. If it scores between 1,500 and 2,500, it’s considered “moderately concentrated.”

Quantitative Analysis: Comcast and Time Warner Cable Merger 6

Any merger that increases an industry’s HHI by more than 200 points in a highly concentrated

market, or more than 100 points in a moderately concentrated market, will alert the Department

of Justice.

HHI = s12 + s2

2 + s32 + … + sn

2

Monopoly HHI: 1002 = 10,000,

Duopoly with 50/50 market share HHI: 502 + 502 = 5,000,

Triopolies with same market share HHI: 33.332 + 33.332 + 33.332 = 3,332.67, and so on.

Port-Merger HHI Industry Concentration

Change between Pre-merger HHI and Post-merger

HHI

Antitrust Action

Less than 1,500 Not concentrated Any amount No ActionBetween 1,500 and

2,500Moderately concentrated

100 or more Possible Antitrust Challenge

Greater than 2,500 Highly concentrated 200 or more Antitrust Challenge virtually certain

Roughly there are about 100 million U.S. homes with some form of paid TV service.

Comcast and TWC have about 22 million and 11 million subscribers. Using Multimedia

Research Group, Inc. (MRG)’s recent statistic about the top eight pay-TV providers, rough pre-

merger estimate of the industry’s HHI is 1,815, which means the industry is moderately

concentrated.

Quantitative Analysis: Comcast and Time Warner Cable Merger 7

Top 8 U.S. Pay-TV Operators’ Subscribers, 4Q12

Service Provider Total Subscribers (4Q/2012)

% of Total Subscribers (Sn)

Sn2

Comcast 21,995,000 26.01% 676.52DirecTV 20,080,000 23.75% 564.06DISH Network 14,056,000 16.62% 276.22Time Warner Cable 12,030,000 14.23% 202.49Verizon 4,700,000 5.56% 30.91AT&T 4,500,000 5.32% 28.30Charter 3,989,000 4.72% 22.18Cablevision 3,197,000 3.78% 14.29Others 21,995,000 26.02%Total 84,547,000 100% 1814.99

Source: Company financials, compiled by MRG

But if we merge Comcast and Time Warner Cable total subscribers and divest 3 million

(as planned by Comcast) and transfer them to other service providers, the pay-TV industry’s

nationwide HHI become 2,383, an increase of 568 points.

Top 8 U.S. Pay-TV Operators’ Subscribers, Post Comcast & TWC Merger

Service Provider Total Subscribers (4Q/2012)

% of Total Subscribers (Sn)

Sn2

Comcast + Time Warner Cable

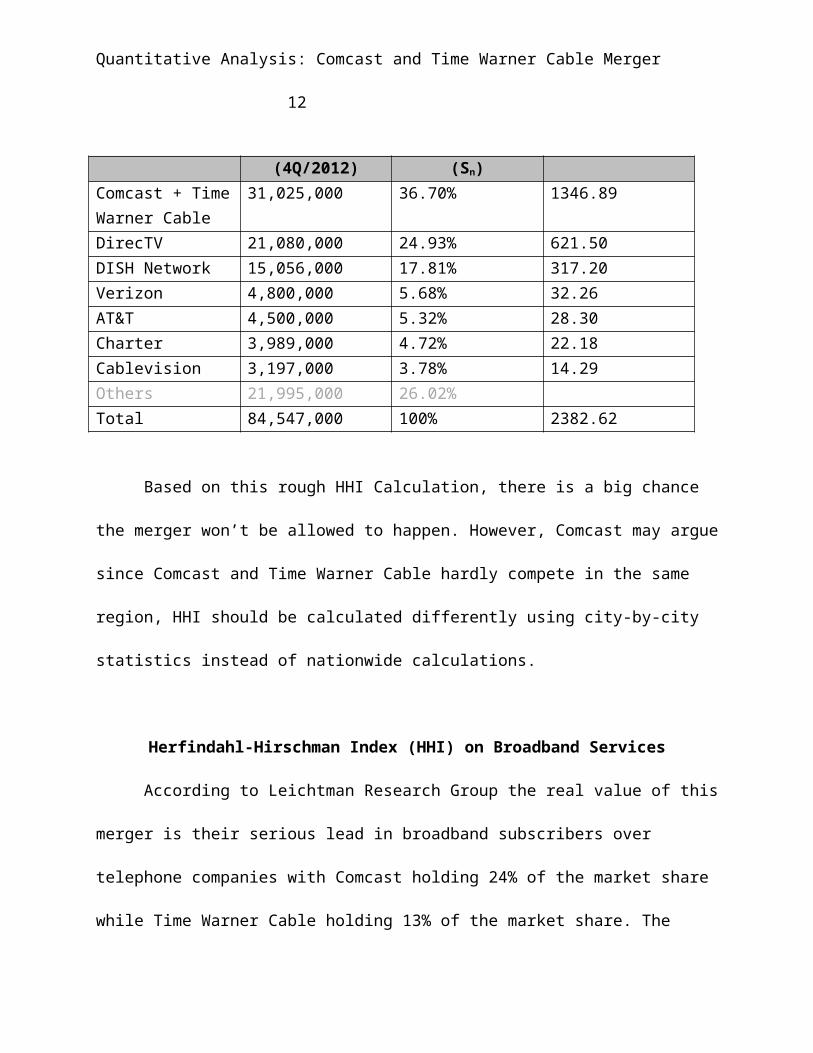

31,025,000 36.70% 1346.89

DirecTV 21,080,000 24.93% 621.50DISH Network 15,056,000 17.81% 317.20Verizon 4,800,000 5.68% 32.26AT&T 4,500,000 5.32% 28.30Charter 3,989,000 4.72% 22.18Cablevision 3,197,000 3.78% 14.29Others 21,995,000 26.02%Total 84,547,000 100% 2382.62

Quantitative Analysis: Comcast and Time Warner Cable Merger 8

Based on this rough HHI Calculation, there is a big chance the merger won’t be allowed

to happen. However, Comcast may argue since Comcast and Time Warner Cable hardly compete

in the same region, HHI should be calculated differently using city-by-city statistics instead of

nationwide calculations.

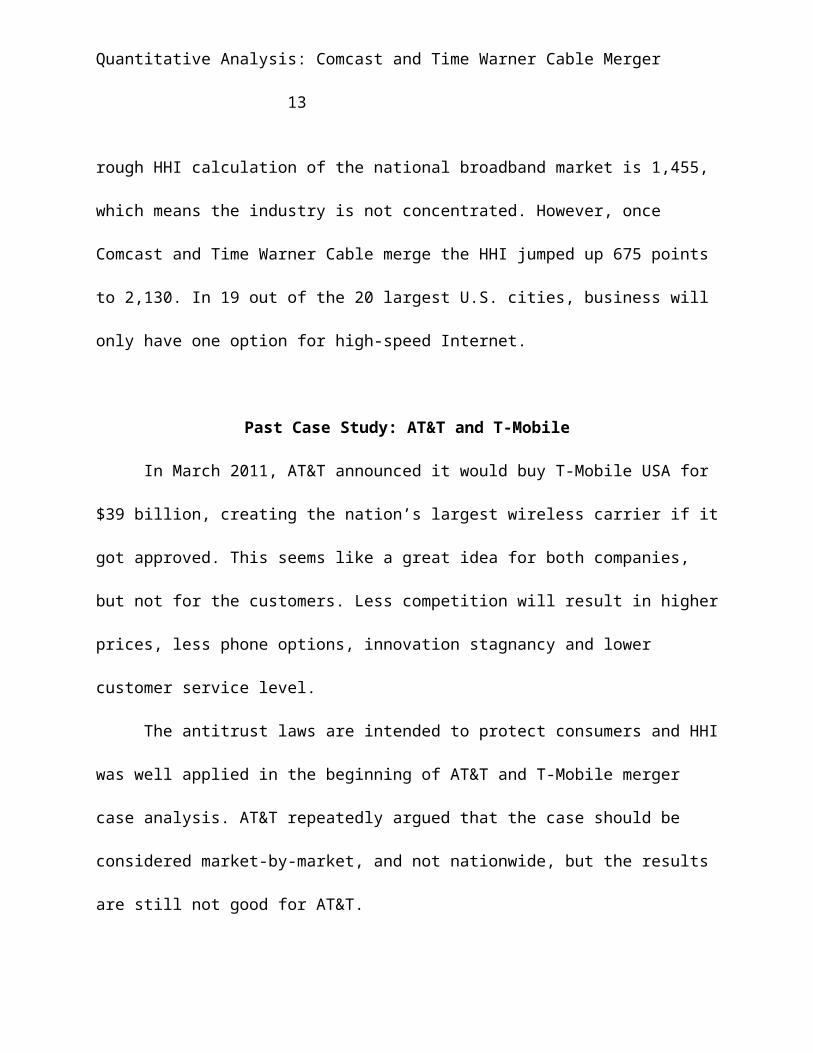

Herfindahl-Hirschman Index (HHI) on Broadband Services

According to Leichtman Research Group the real value of this merger is their serious

lead in broadband subscribers over telephone companies with Comcast holding 24% of the

market share while Time Warner Cable holding 13% of the market share. The rough HHI

calculation of the national broadband market is 1,455, which means the industry is not

concentrated. However, once Comcast and Time Warner Cable merge the HHI jumped up 675

points to 2,130. In 19 out of the 20 largest U.S. cities, business will only have one option for

high-speed Internet.

Past Case Study: AT&T and T-Mobile

In March 2011, AT&T announced it would buy T-Mobile USA for $39 billion, creating

the nation’s largest wireless carrier if it got approved. This seems like a great idea for both

companies, but not for the customers. Less competition will result in higher prices, less phone

options, innovation stagnancy and lower customer service level.

The antitrust laws are intended to protect consumers and HHI was well applied in the

beginning of AT&T and T-Mobile merger case analysis. AT&T repeatedly argued that the case

should be considered market-by-market, and not nationwide, but the results are still not good for

AT&T.

Quantitative Analysis: Comcast and Time Warner Cable Merger 9

In New York, the combination of AT&T and T-Mobile would acquire 43.7 percent of the

market, resulting in an HHI of 3,335, an increase of 951; In Chicago, it would acquire 48.1

percent of the market and an HHI of 3,189, an increase of 1,114; and in Seattle, it will acquire

53.2 percent of the market with an HHI of 4,044, an increase of 1,366. These numbers are way

above the 200 HHI increase limit.

In 96 of the top 100 markets, the HHI is over 2,500, which means the industry is highly

concentrated. In all of the 40 markets, the increase exceeds the guideline limit of 200. If

nationwide is calculated as a whole, the HHI is 3,100 and the increase would be just under 700.

Quantitative Analysis: Comcast and Time Warner Cable Merger 10

The next step analysis was to explore on barriers of entry, T-Mobile’s replacement,

higher efficiencies and lower prices in high concentration industry. The Justice department

concluded each case with a resounding “no” and further analysis showed that the merger was

AT&T’s way to eliminate “maverick competitor” and solidify AT&T’s leading market position

in major areas.

If this merger was not stopped, there is a possibility that Verizon will merge with Sprint,

creating a national duopoly, resulting in negative impacts on competitions and less choice for

consumers.

Comcast and Time Warner Cable Merger Possible Results

Comcast and Time Warner Cable emphasized that their networks do not overlap, which

means the deal is not a simple horizontal merger. Horizontal merger such as AT&T and T-

Mobile were more vulnerable to being blocked by antitrust officials. Telecoms and satellite

rivals would still face the same number of competitors in each market.

Their subscribers have consistently ranked the companies with the lowest customer

satisfaction in both pay-TV industry and Internet service providers industry. According to

Harvard Law Professor, Susan Crawford, the merger will probably will cause the price to

increase without any corresponding improvement in service.

Sarah Morris, Senior Policy Counsel for the Open Technology Institute at New America

Foundation mentioned that cable companies serve as gatekeepers for a number of

communications services. This merger represents unprecedented move to consolidate market

even further. There will be fewer competitive incentives to invest in network infrastructure, and

will likely lead to higher prices and less innovation.

Quantitative Analysis: Comcast and Time Warner Cable Merger 11

The increased size and market power Comcast will get from the merger is one of the

regulators’ concerns. Industry battles with content providers in the past 2 years resulted in

multiple outages of popular programming due to clash over rising content costs.

However, the biggest concern is the combined company’s control over broadband access

to more than one-third of consumers in the country. Content providers, broadcast networks, and

other competitors that rely on the broadband services to reach viewers, such as Netflix and

Amazon, are worried about the merger.

According to HHI calculations the merger is unlikely to be approved, but Comcast has

received regulatory approval every single time. They have researched, lobbied from the early

stage, and laid the groundwork for counter arguments against regulators. There is sizable chance

for this merger to be approved.

Quantitative Analysis: Comcast and Time Warner Cable Merger 12

References

Alvear, J. (March, 2013). Cable vs. Satellite vs. IPTV Subscribers in the US. MRG Executive

Brief. Retrieved

from http://www.mrgco.com/wp-content/uploads/2013/03/PTV101013_Cable-Satellite-

and-IPTV-Brief-2013.pdf

Baker, L. B. (February 13, 2014). Comcast takeover of Time Warner Cable to reshape U.S. pay

TV. Reuters. Retrieved from http://www.reuters.com/article/2014/02/13/us-comcast-

timewarnercable-idUSBREA1C05A20140213

Bishop, B. (February 13, 2014). Why you should be scared of Comcast and Time Warner Cable

merging. The Verge. Retrieved from

http://www.theverge.com/2014/2/13/5407932/comcast-and-time-warner-a-very-dark-

cloud-with-a-tiny-silver-lining

Chon, G., Steel, E. (February 13, 2014). TWC battle will test Comcast’s regulatory skills.

Financial Times Media. Retrieved from http://www.ft.com/intl/cms/s/0/78f84a72-94d0-

11e3-af71-00144feab7de.html?siteedition=uk#axzz2tTgUxjjO

Comcast Corporation SWOT Analysis. (2013). Comcast Corporation SWOT Analysis, 1-13.

Comcast. (February 13, 2014). Time Warner Cable To Merge With Comcast Corporation To

Create A World-Class Technology And Media Company. Comcast. Retrieved from

http://corporate.comcast.com/news-information/news-feed/time-warner-cable-to-merge-

with-comcast-corporation

Faber, D., Belvedere, M. J. (February 12, 2014). Comcast CEO: Time Warner Cable deal 'pro-

competitive'. CNBC. Retrieved from http://www.cnbc.com/id/101413235

Quantitative Analysis: Comcast and Time Warner Cable Merger 13

Fernholz, T. (February 13, 2014). Why the Time Warner-Comcast merger isn’t going to happen

—at least the way it looks today. Quartz. Retrieved from

http://qz.com/177162/why-the-time-warner-comcast-merger-isnt-going-to-happen-at-

least-the-way-it-looks-today/

Gelles, D. (February 12, 2014). Comcast Deal Seeks to Unite 2 Cable Giants. New York Times

Deal Book. Retrieved from http://dealbook.nytimes.com/2014/02/12/comcast-set-to-

acquire-time-warner-cable/

Goldman, D. (February 13, 2014). Comcast deal to face antitrust hurdles. CNN Money.

Retrieved from http://money.cnn.com/2014/02/13/technology/comcast-time-warner-

antitrust/

Gustin, S. (February 14, 2014). Massive Cable Deal Means Your Bill May Jump. Time Business

& Money. Retrieved from http://business.time.com/2014/02/14/comcast-deal-consumers/

Ingram, D. (February 14, 2014). Comcast turns to Davis Polk for Time Warner Cable merger.

Reuters. Retrieved from http://www.reuters.com/article/2014/02/14/us-usa-antitrust-

comcast-idUSBREA1D17I20140214

Investopedia. (February 13, 2014). Herfindahl-Hirschman Index - HHI. Investopedia. Retrieved

from http://www.investopedia.com/terms/h/hhi.asp

Lauria, P. (February 13, 2014). Why The Comcast-Time Warner Cable Merger You Hate Will

Be Approved Anyway. Buzzfeed Business. Retrieved from

http://www.buzzfeed.com/peterlauria/why-the-comcast-time-warner-cable-merger-you-

hate-will-be-ap

Quantitative Analysis: Comcast and Time Warner Cable Merger 14

Manne, G. (December, 2011). FCC Report On AT&T's T-Mobile Merger Is Just Appalling.

Forbes. Retrieved from http://www.forbes.com/sites/beltway/2011/12/02/the-fcc-report-

on-atts-t-mobile-merger-is-just-appalling/2/

Media Data Base (2013). Comcast/NBC Universal, LLC. Retrieved from

http://www.mediadb.eu/en/data-base/international-media-corporations/

comcastnbcuniversal-llc.html

Multimedia Research Group, Inc. (2013). Cable vs. Satellite vs. IPTV Subscribers in the US.

Multimedia Research Group. Retrieved from http://www.mrgco.com/blog/cable-vs-

satellite-vs-iptv-subscribers-in-the-us/

NCTA. (2012). Top 25 Multichannel Video Service Customers (2012). Retrieved from

https://www.ncta.com/industry-data/item/217

O’Toole, J. (August 6, 2013). Time Warner Cable blacks out CBS stations for millions as fee

spat continues. CNN Money. Retrieved from

http://money.cnn.com/2013/08/02/news/companies/cbs-time-warner-blackout/

index.html?iid=EL

Pasick, A. (February 13, 2014). A Comcast-Time Warner Cable deal would combine two of

America’s most-reviled companies. Quartz. Retrieved from

http://qz.com/176883/a-comcast-time-warner-cable-deal-would-combine-two-of-

americas-most-reviled-companies/

Pepitone, J. (October 31, 2013). Time Warner Cable lost 300,000 subscribers amid CBS

blackout. CNN Money. Retrieved from

http://money.cnn.com/2013/10/31/technology/time-warner-cable-cbs/

Quantitative Analysis: Comcast and Time Warner Cable Merger 15

Roose, K. (February 13, 2014). This Math Formula Shows Why the Comcast—Time Warner

Cable Deal Should Be Blocked. New York Magazine News & Politics. Retrieved from

http://nymag.com/daily/intelligencer/2014/02/why-comcasttime-warner-cable-should-be-

blocked.html

Samuelson, W. F., Marks, S. G. (2012). Managerial Economics. Danvers, MA: John Wiley &

Sons, Inc.

Santoli, M. (February 13, 2014). Comcast and Time Warner Cable merger: What it means for

consumers. Yahoo! Finance The Daily Ticker. Retrieved from

http://finance.yahoo.com/blogs/daily-ticker/comcast-to-acquire-time-warner-cable-

143000745.html

Schoenberg, T. (February 13, 2014). T-Mobile Antitrust Challenge Leaves AT&T With Little

Recourse on Takeover. Bloomberg Technology. Retrieved from

http://www.bloomberg.com/news/2011-08-31/u-s-files-antitrust-complaint-to-block-

proposed-at-t-t-mobile-merger.html

Segan, S. (March 20, 2011). AT&T Buys T-Mobile: Great For Them, Bad For You. PC

Magazine. Retrieved from http://www.pcmag.com/article2/0,2817,2382267,00.asp

Sherman, E. (February 13, 2014). Comcast and Time Warner merger could be bad for

customers. CBS Money Watch. Retrieved from http://www.cbsnews.com/news/comcast-

and-time-warner-merger-could-be-bad-for-customers/

Stewart, J. B. (September 9, 2011). Antitrust Suit Is Simple Calculus. The New York Times

Business Day. Retrieved from http://www.nytimes.com/2011/09/10/business/att-and-t-

mobile-merger-is-a-textbook-case.html?pagewanted=all&_r=0

Quantitative Analysis: Comcast and Time Warner Cable Merger 16

Szalai, G. (February 13, 2014). Time Warner Cable Stock Hits High on Comcast Deal, Charter

Drops. The Hollywood Reporter. Retrieved from

http://www.hollywoodreporter.com/news/time-warner-cable-stock-hits-680026

Time Warner Cable Inc. SWOT Analysis. (2013). Time Warner Cable Inc. SWOT Analysis, 1-

8.

Topper, J. (February 12, 2014). Free Press: Comcast-Time Warner Cable Merger Would Be a

Disaster for Consumers. Freepress. Retrieved from http://www.freepress.net/press-

release/105771/free-press-comcast-time-warner-cable-merger-would-be-disaster-

consumers

Tsukayama, H. (February 13, 2014). Comcast, Time Warner Cable could merge: What would

happen to my service? The Washington Post. Retrieved from

http://www.washingtonpost.com/business/technology/comcast-time-warner-to-merge-

what-happens-to-my-service/2014/02/13/b285f81e-94b4-11e3-83b9-

1f024193bb84_story.html

U.S Department of Justice and the Federal Trade Commission. (August 19, 2010). Horizontal

Merger Guideline. U.S Department of Justice and the Federal Trade Commission.

Retrieved from http://www.justice.gov/atr/public/guidelines/hmg-2010.html#4b

Wang, G. (August, 2011). AT&T/T-Mobile Merger: More Market Concentration, Less Choice,

Higher Prices. Yankee Group Focus Report. Retrieved from

http://web.yankeegroup.com/rs/yankeegroup/images/2011AT%26T-T-Mobile-Merger-

Report.pdf

Quantitative Analysis: Comcast and Time Warner Cable Merger 17