Sustainable Homeownership Donna Greene- Regional Diverse Segments Manager Delaware Governor Housing Conference October 7, 2014

Sustainable Homeownership Donna Greene- Regional Diverse Segments Manager Delaware Governor Housing Conference October 7, 2014.

Dec 14, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Sustainable Homeownership

Donna Greene- Regional Diverse Segments Manager

Delaware Governor Housing Conference

October 7, 2014

Agenda

Discussion topics: Current market conditions The first-time homebuyer segment First-time homebuyer characteristics Products and programs to help first-time homebuyers

purchase a home Wells Fargo’s commitment to first-time homebuyers Tools and resources to help first-time homebuyers Financial Reform

– Qualified Mortgage/Non-qualified Mortgage

– Ability to Repay

Questions

2

3

First-time homebuyersUnderstanding the segment and their financing needs

Current market condition

Customer characteristics and market conditions may impact first-time homebuyers: Low inventory Competing with cash buyers/investors Credit readiness Understanding the homebuying process Product options and cost Savings for a down payment Preparation for sustainable homeownership

4

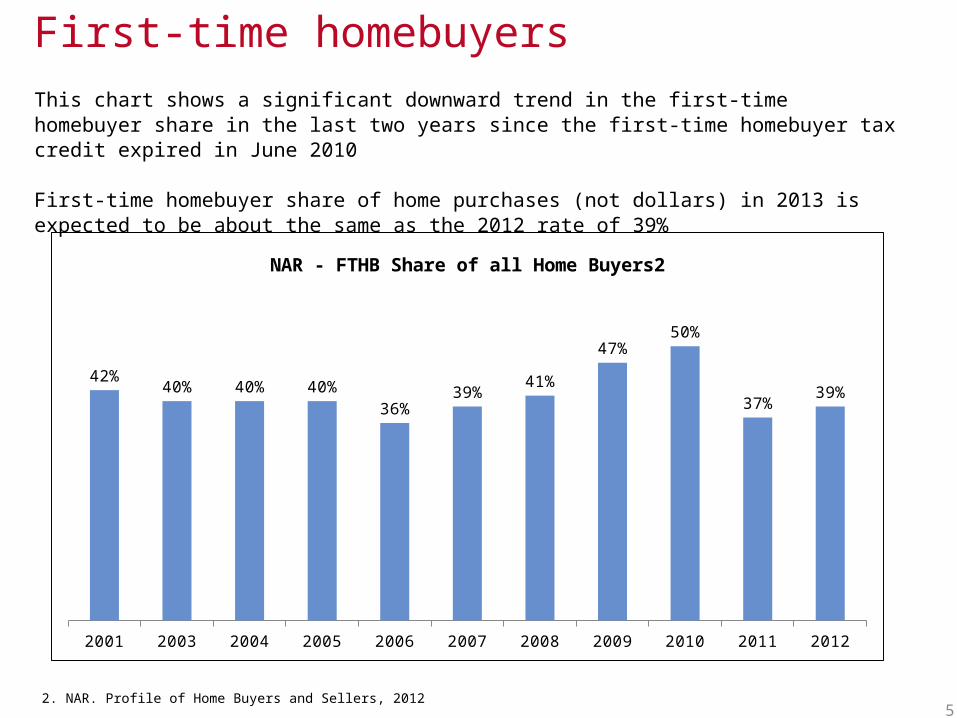

This chart shows a significant downward trend in the first-time homebuyer share in the last two years since the first-time homebuyer tax credit expired in June 2010

First-time homebuyer share of home purchases (not dollars) in 2013 is expected to be about the same as the 2012 rate of 39%

52. NAR. Profile of Home Buyers and Sellers, 2012

First-time homebuyers

2001 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

42%40% 40% 40%

36%39%

41%

47%50%

37%39%

NAR - FTHB Share of all Home Buyers2

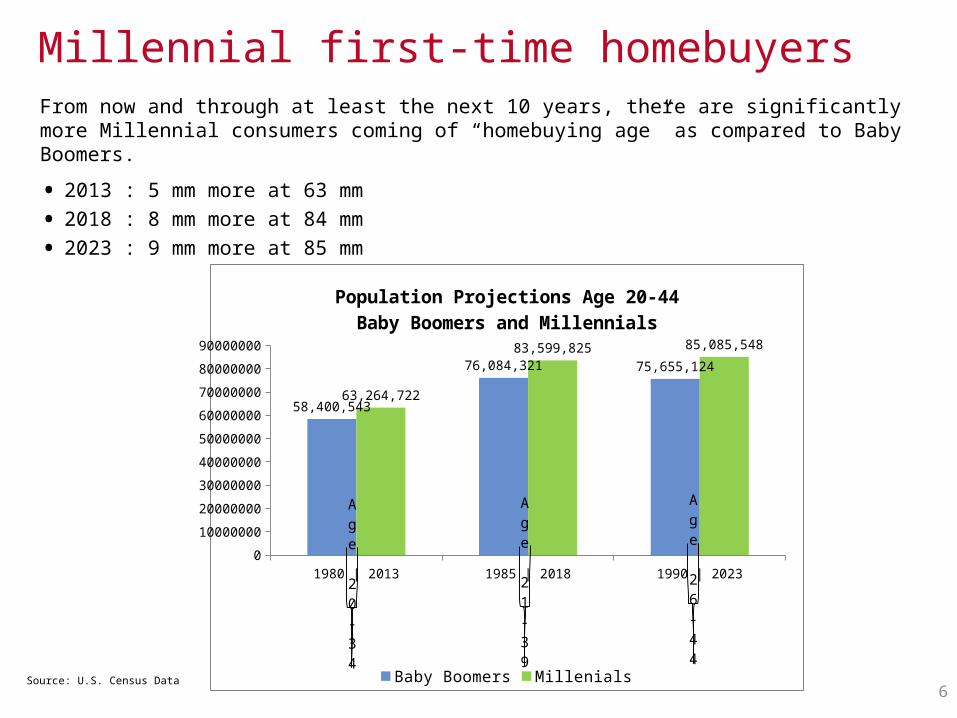

Millennial first-time homebuyersFrom now and through at least the next 10 years, there are significantly more Millennial consumers coming of “homebuying age” as compared to Baby Boomers.

• 2013 : 5 mm more at 63 mm

• 2018 : 8 mm more at 84 mm

• 2023 : 9 mm more at 85 mm

6

1980 | 2013 1985 | 2018 1990 | 20230

10000000

20000000

30000000

40000000

50000000

60000000

70000000

80000000

90000000

58,400,543

76,084,321 75,655,124

63,264,722

83,599,825 85,085,548

Population Projections Age 20-44Baby Boomers and Millennials

Baby Boomers Millenials

Age 21-39

Age 26-44

Age 20-34

Source: U.S. Census Data

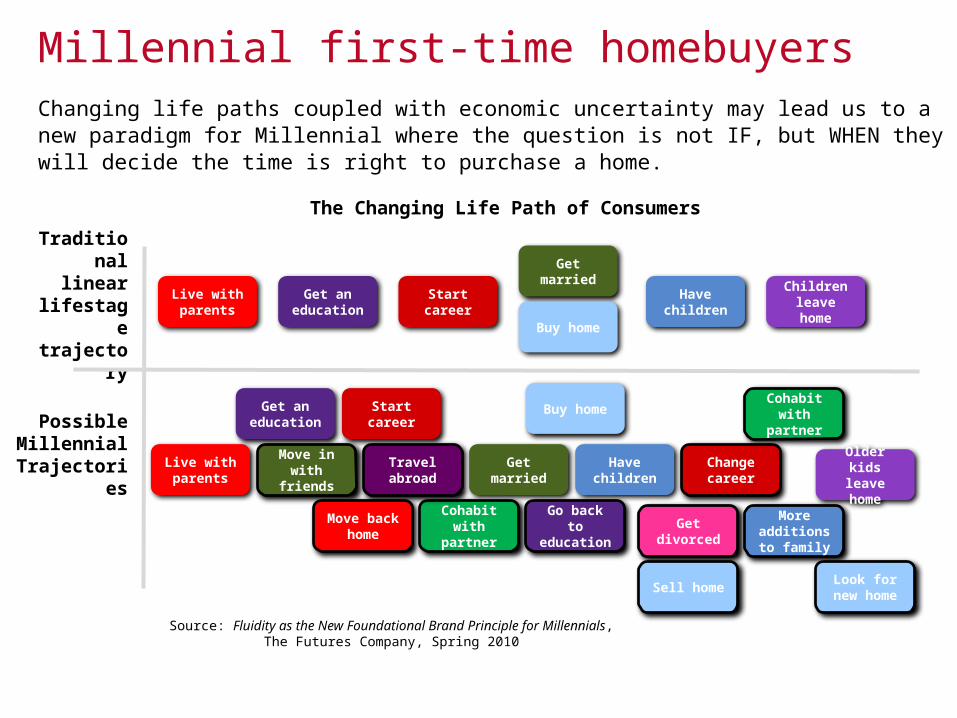

Changing life paths coupled with economic uncertainty may lead us to a new paradigm for Millennial where the question is not IF, but WHEN they will decide the time is right to purchase a home.

Source: Fluidity as the New Foundational Brand Principle for Millennials, The Futures Company, Spring 2010

Traditional linear

lifestagetrajectory

Possible Millennial

Trajectories

Live with parents

Cohabit with

partner

Get divorced

Move in with friends

Get an education

Start career

Get married

Have children

Travel abroad

Children leave home

Live with parents

Get an education

Start career

Have children

Go back to education

Get married

Move back home

Change career

Cohabit with

partner

More additions to family

Older kids leave home

Buy home

Buy home

Sell homeLook for

new home

The Changing Life Path of Consumers

Millennial first-time homebuyers

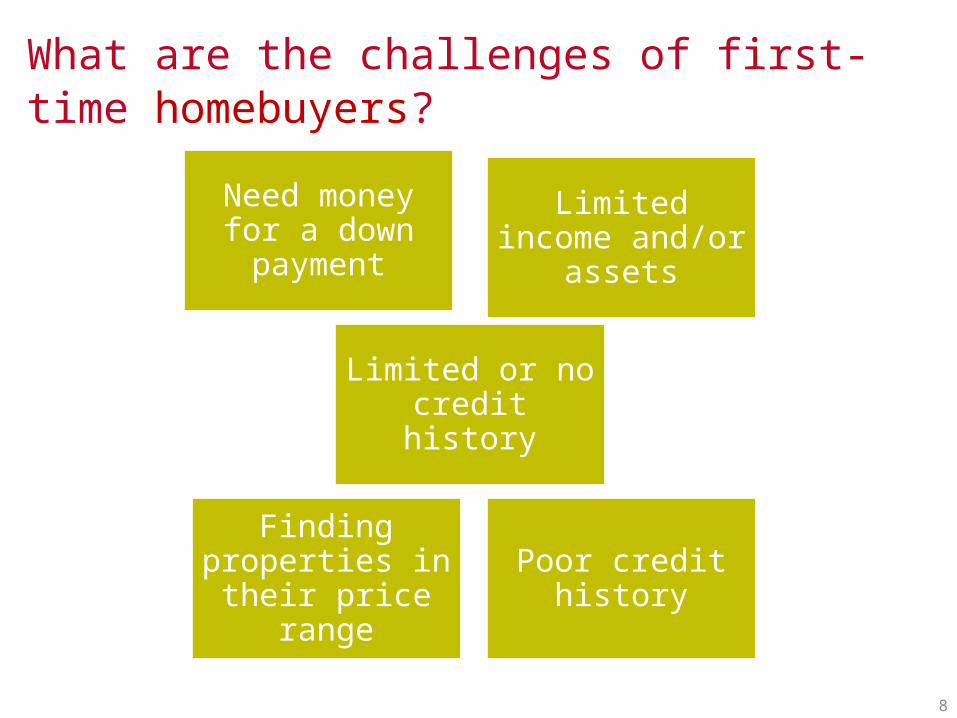

What are the challenges of first-time homebuyers?

Need money for a down payment

Limited or no credit history

Limited income and/or assets

Finding properties in their price

range

Poor credit history

8

9

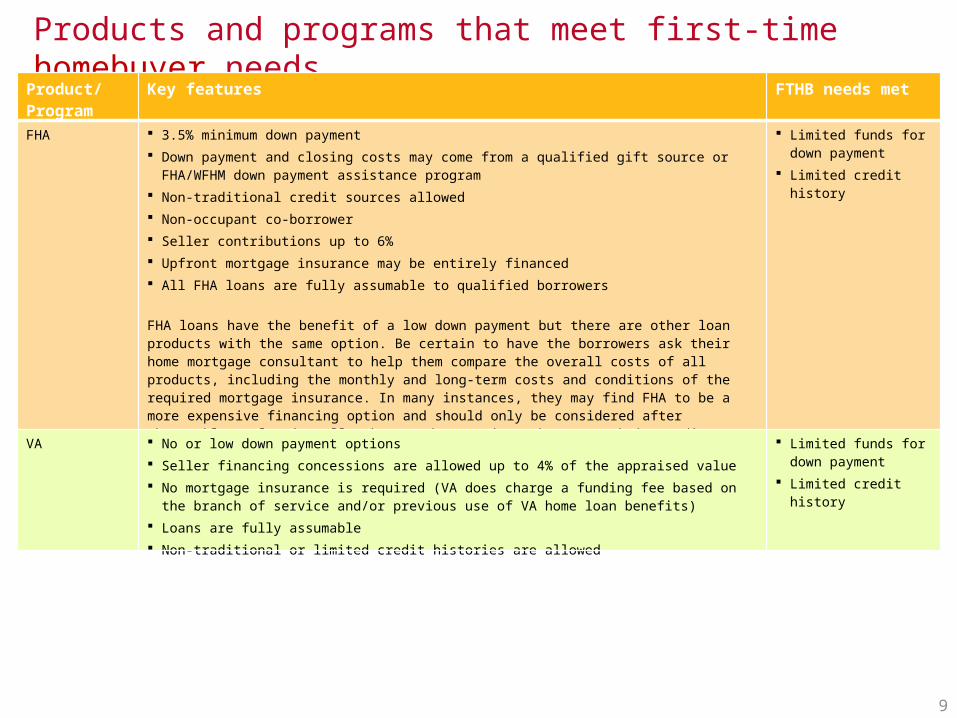

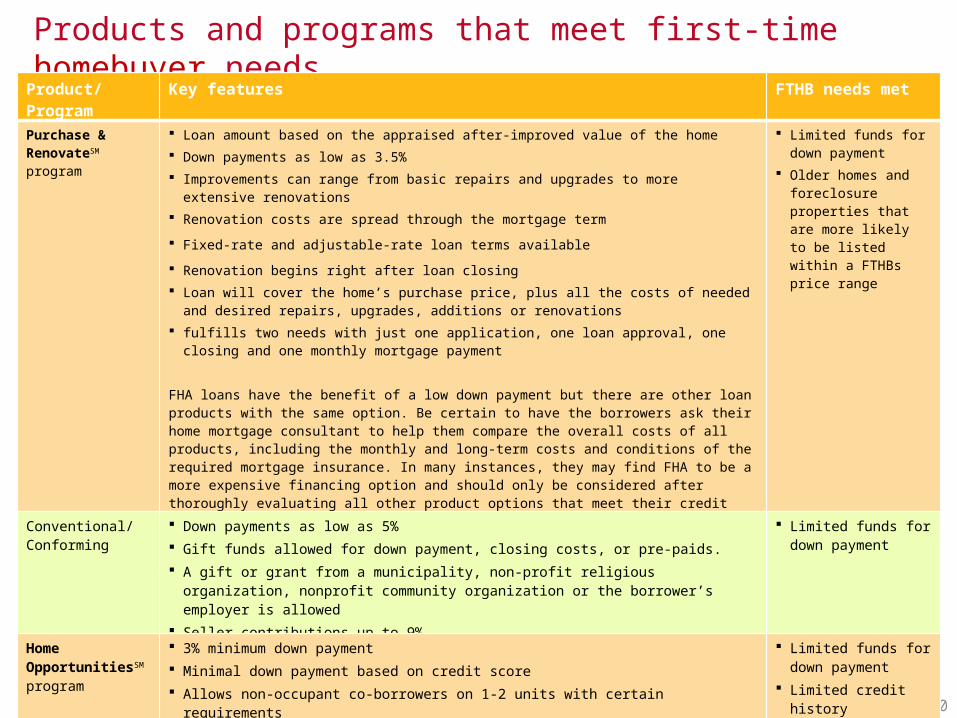

Products and programs that meet first-time homebuyer needs

Product/ Program

Key features FTHB needs met

FHA 3.5% minimum down payment Down payment and closing costs may come from a qualified gift source or FHA/WFHM

down payment assistance program Non-traditional credit sources allowed Non-occupant co-borrower Seller contributions up to 6% Upfront mortgage insurance may be entirely financed All FHA loans are fully assumable to qualified borrowers

FHA loans have the benefit of a low down payment but there are other loan products with the same option. Be certain to have the borrowers ask their home mortgage consultant to help them compare the overall costs of all products, including the monthly and long-term costs and conditions of the required mortgage insurance. In many instances, they may find FHA to be a more expensive financing option and should only be considered after thoroughly evaluating all other product options that meet their credit qualifying and financial needs.

Limited funds for down payment

Limited credit history

VA No or low down payment options Seller financing concessions are allowed up to 4% of the appraised value No mortgage insurance is required (VA does charge a funding fee based on the branch of

service and/or previous use of VA home loan benefits) Loans are fully assumable Non-traditional or limited credit histories are allowed

Limited funds for down payment

Limited credit history

10

Products and programs that meet first-time homebuyer needs

Product/ Program

Key features FTHB needs met

Purchase & RenovateSM

program

Loan amount based on the appraised after-improved value of the home Down payments as low as 3.5% Improvements can range from basic repairs and upgrades to more extensive

renovations Renovation costs are spread through the mortgage term

Fixed-rate and adjustable-rate loan terms available

Renovation begins right after loan closing Loan will cover the home’s purchase price, plus all the costs of needed and desired

repairs, upgrades, additions or renovations fulfills two needs with just one application, one loan approval, one closing and one

monthly mortgage payment

FHA loans have the benefit of a low down payment but there are other loan products with the same option. Be certain to have the borrowers ask their home mortgage consultant to help them compare the overall costs of all products, including the monthly and long-term costs and conditions of the required mortgage insurance. In many instances, they may find FHA to be a more expensive financing option and should only be considered after thoroughly evaluating all other product options that meet their credit qualifying and financial needs.

Limited funds for down payment

Older homes and foreclosure properties that are more likely to be listed within a FTHBs price range

Conventional/ Conforming

Down payments as low as 5% Gift funds allowed for down payment, closing costs, or pre-paids. A gift or grant from a municipality, non-profit religious organization, nonprofit

community organization or the borrower’s employer is allowed Seller contributions up to 9%

Limited funds for down payment

Home OpportunitiesSM program

3% minimum down payment Minimal down payment based on credit score Allows non-occupant co-borrowers on 1-2 units with certain requirements Reduced mortgage insurance coverage Down payment Assistance Programs (DAPs) allowed

Limited funds for down payment

Limited credit history

11

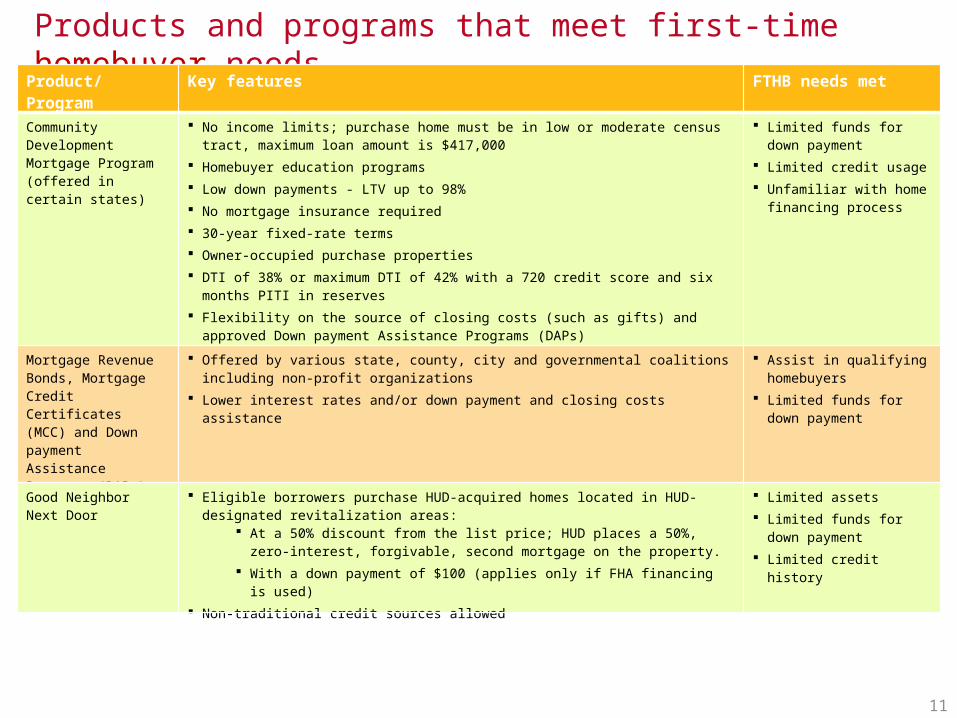

Products and programs that meet first-time homebuyer needs

Product/ Program

Key features FTHB needs met

Community Development Mortgage Program(offered in certain states)

No income limits; purchase home must be in low or moderate census tract, maximum loan amount is $417,000

Homebuyer education programs Low down payments - LTV up to 98% No mortgage insurance required 30-year fixed-rate terms Owner-occupied purchase properties DTI of 38% or maximum DTI of 42% with a 720 credit score and six months PITI

in reserves Flexibility on the source of closing costs (such as gifts) and approved Down

payment Assistance Programs (DAPs) No cash reserve requirements for Standard CDMP

Limited funds for down payment

Limited credit usage Unfamiliar with home

financing process

Mortgage Revenue Bonds, Mortgage Credit Certificates (MCC) and Down payment Assistance Programs (DAPs)

Offered by various state, county, city and governmental coalitions including non-profit organizations

Lower interest rates and/or down payment and closing costs assistance

Assist in qualifying homebuyers

Limited funds for down payment

Good Neighbor Next Door

Eligible borrowers purchase HUD-acquired homes located in HUD-designated revitalization areas:

At a 50% discount from the list price; HUD places a 50%, zero-interest, forgivable, second mortgage on the property.

With a down payment of $100 (applies only if FHA financing is used) Non-traditional credit sources allowed

Limited assets Limited funds for down

payment Limited credit history

Wells Fargo is committed to responsible lending and advancing sustainable homeownership. We want to see all consumers achieve their homeownership goals and stay comfortably in their homes for years to come. And that begins with helping people understand all the aspects and obligations of purchasing a home, so they can realistically assess their own readiness and be better able to make informed decisions.

Resources that may help your homebuyers prepare for successful homeownership: My FirstHomeSM – Online education program The Wells Fargo Home Lending Learning and Planning Center –

online resources center My Home Roadmap – aids borrower in becoming mortgage ready

12

Wells Fargo Home Mortgage’s commitment to first-time homebuyers

13

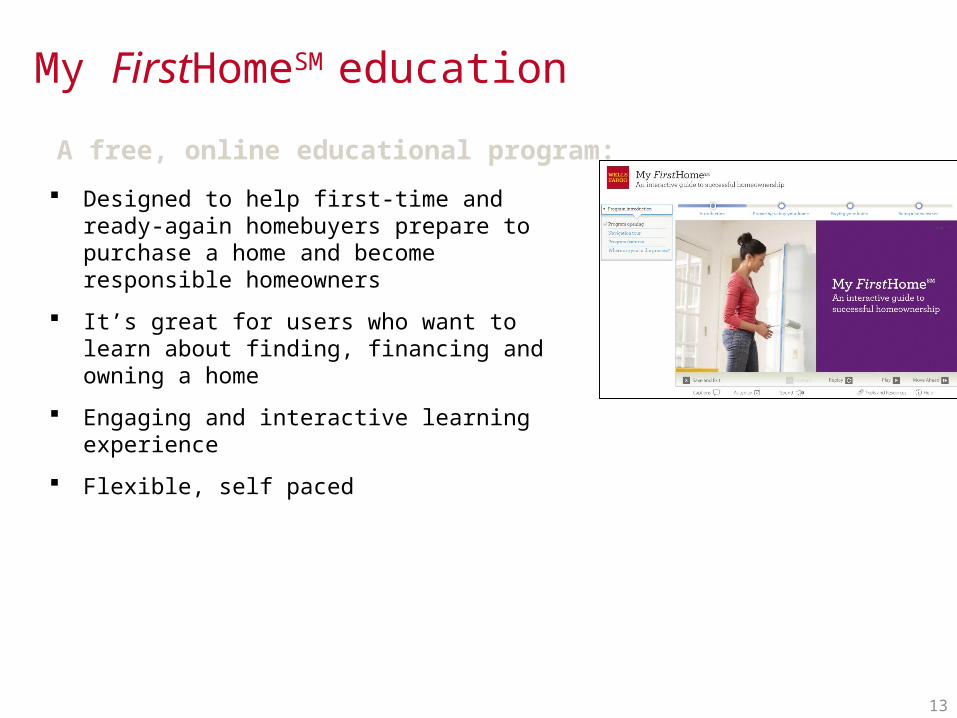

Designed to help first-time and ready-again homebuyers prepare to purchase a home and become responsible homeowners

It’s great for users who want to learn about finding, financing and owning a home

Engaging and interactive learning experience

Flexible, self paced

A free, online educational program:

My FirstHomeSM education

14

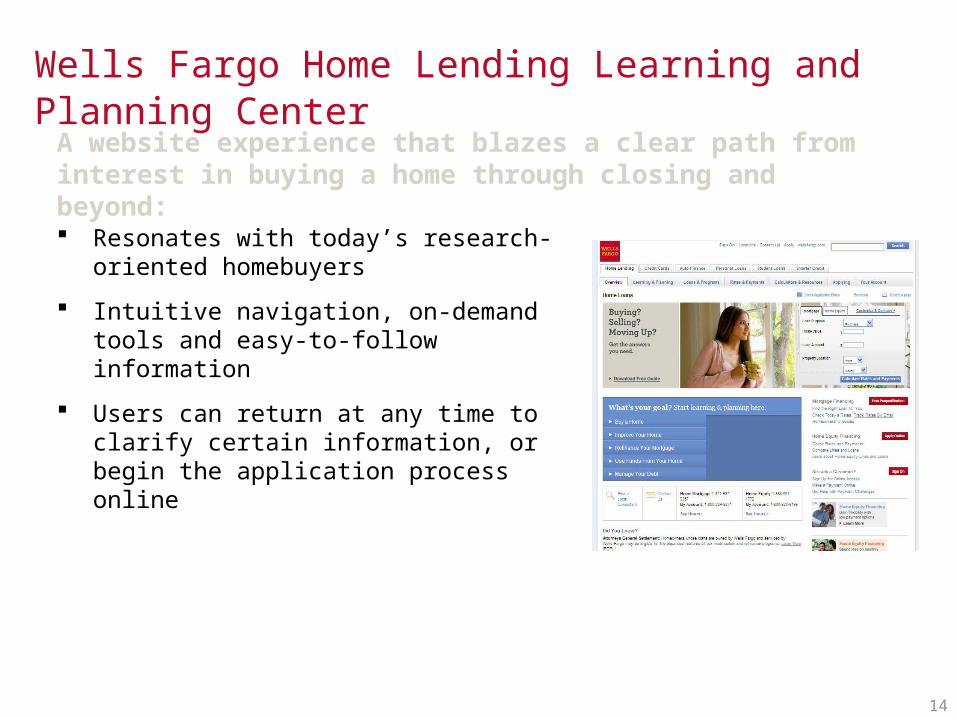

Wells Fargo Home Lending Learning and Planning Center

Resonates with today’s research-oriented homebuyers

Intuitive navigation, on-demand tools and easy-to-follow information

Users can return at any time to clarify certain information, or begin the application process online

A website experience that blazes a clear path frominterest in buying a home through closing and beyond:

We have many additional tools and resources to support first-time homebuyers in their journey to buy their first home:

Mortgage Product Guide First-time Homebuyers Guide Home Financing Process Checklist First-time Homebuyer Workshops Product Options Tool Mortgage Calculators Homebuying Checklists

15

Tools and resources to help first-time homebuyers

16

Key terms: QM/Non-QM and Ability to Repay (ATR)

Financial Reform

17

What is the Financial Reform Act?

The Financial Reform Act was passed in July 2010 to establish new requirements to govern banks, insurance companies and hedge funds, as well as other publicly- and privately-held companies in the financial services industry. The act also impacts mortgage brokers, correspondent lenders, originators and servicers.

In January 2013, the Consumer Financial Protection Bureau (CFPB) issued seven rules implementing many elements of the Dodd-Frank Wall Street Reform and Consumer Protection Act, the official name of the Financial Reform Act. These rules impact a broad range of mortgage banking activities, from origination to servicing to the secondary market.

18

Wells Fargo Home Mortgage is currently adhering to these new regulations

Financial Reform includes new laws and regulations impacting

all mortgage lenders and changing the way Wells Fargo – and

the entire financial industry – will do business in the future. The

new regulations intend to protect consumers and prevent

abusive underwriting practices that contributed to the mortgage

crisis.

19

What are the seven Financial Reform rules that were issued January 2013?

1. Ability to Repay/Qualified Mortgage

2. High-Cost Mortgage and Homeownership Counseling

3. Appraisal Delivery Requirement

4. Appraisal Standards for Higher-Priced Mortgage Loans

5. CFPB Servicing Standards

6. Loan Origination Compensation

7. Escrow Requirements (took effect June 1, 2013)

20

Ability to RepayLargest impact to your buyers

For customers, the Financial Reform change that will have the most impact is the Ability-to-Repay (ATR) rule. This rule will require customers to provide additional documentation to support their ability to repay their mortgage.

It requires lenders to obtain and verify information showing that customers have the capability to pay their mortgage debt or home equity loan obligation. Generally, Wells Fargo already meets the rule’s standards with our current underwriting policies and processes.

This regulation creates minimum underwriting standards lenders must use in confirming a customer’s ability to repay their loan according to the loan terms.

21

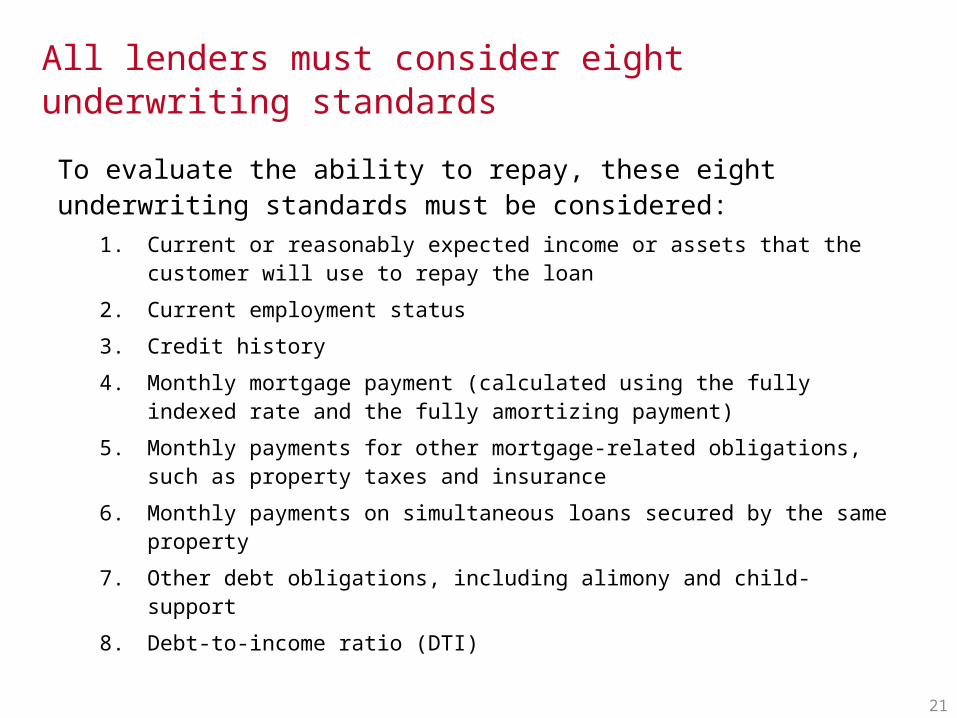

All lenders must consider eight underwriting standards

To evaluate the ability to repay, these eight underwriting standards must be considered:

1. Current or reasonably expected income or assets that the customer will use to repay the loan

2. Current employment status

3. Credit history

4. Monthly mortgage payment (calculated using the fully indexed rate and the fully amortizing payment)

5. Monthly payments for other mortgage-related obligations, such as property taxes and insurance

6. Monthly payments on simultaneous loans secured by the same property

7. Other debt obligations, including alimony and child-support

8. Debt-to-income ratio (DTI)

22

All lenders will be held to the same standardsDepending on when a consumer last experienced the mortgage origination process, they may have to provide more information to lenders when applying for a mortgage. It’s important to be proactive in informing your clients on what to expect as a result of Financial Reform. For example, they should know that all lenders are required to:

Make a reasonable and good faith determination that the consumer has the ability to repay the loan according to its terms.

Verify and document, through independent third-party records, the information they used to make that credit determination.

With the new rules, all lenders will be held to the same, specific standard to help advance sustainable homeownership.

23

Documentation customers must provideLenders must look at a customer’s financial records and verify the information with reliable third-party records such as:

1. A copy of a tax return filed with the IRS or state taxing

authority

2. A record the lender maintains for an account of the customer

held by the lender

3. Documents or other records prepared or reviewed by an

appropriate person other than the customer, the lender, or the

mortgage broker, or an agent of the lender or mortgage broker

Qualified Mortgage vs non-Qualified MortgageLenders are allowed to originate non-QM loans but they still must meet the ATR requirements.

A new classification – Qualified Mortgage (QM) – refers to a specific set of loan parameters, that when met, ensure the borrower has met all the ATR requirements. Such loan parameters include: specific product, documentation, points/fees and debt-to-income requirements (not to exceed 43%).

24

All lenders can originate both QM and non-QM mortgages. Lenders will have the ability to determine their own approach to originating non-QM loans. Wells Fargo is committed to providing credit to credit-worthy borrowers that may not fit QM standards but do meet the Ability-to-Repay requirements and Wells Fargo’s credit policies.

Examples of Non-Qualified Mortgages (non-QM) include loans with:

Terms longer than 30 years

Interest-only payment feature

Balloon payment Negative amortization Debt-to-income (DTI)

ratio higher than 43%

25

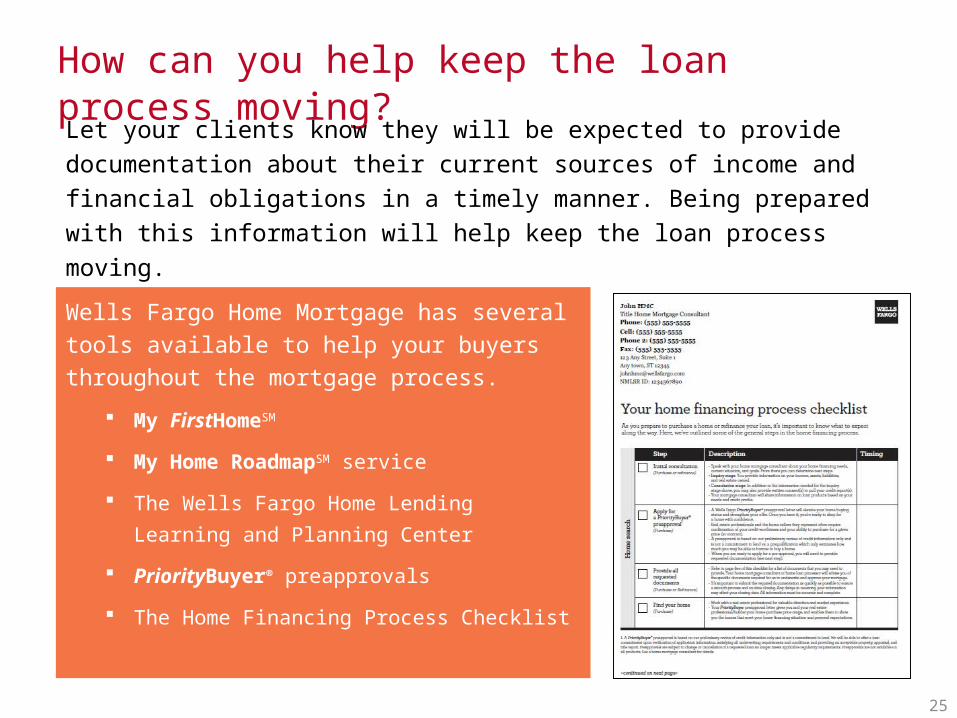

How can you help keep the loan process moving?

Wells Fargo Home Mortgage has several tools available to help your buyers throughout the mortgage process.

My FirstHomeSM

My Home RoadmapSM service

The Wells Fargo Home Lending Learning

and Planning Center

PriorityBuyer® preapprovals

The Home Financing Process Checklist

Let your clients know they will be expected to provide documentation about their current sources of income and financial obligations in a timely manner. Being prepared with this information will help keep the loan process moving.

26

Wells Fargo remains focused on helping all of our

customers succeed financially while complying with

the changes that affect the home lending business.

This information is for real estate, builder, legal and financial planning professionals only and is not intended for distribution to consumers or other third parties. Information is accurate as of date of printing and is subject to change without notice. Wells Fargo Home Mortgage is a division of Wells Fargo Bank, N.A. © 2013 Wells Fargo Bank, N.A. All rights reserved. NMLSR ID 399801. 107189 12/13

Related Documents