Not for distribution SUSTAINABLE FORESTRY INVESTMENT Cary Wingfield Raditz, CFA

SUSTAINABLE FORESTRY INVESTMENT

Jan 11, 2016

SUSTAINABLE FORESTRY INVESTMENT. Cary Wingfield Raditz, CFA. Total Global Forestry Investment. Total investable and leasable global forestlands estimated > 870 million ha Value > US$480 billion Forestry investment growing 20% p.a. for 20 years US$35 billion invested mainly in US - PowerPoint PPT Presentation

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Not for distribution

SUSTAINABLE FORESTRY

INVESTMENTCary Wingfield Raditz, CFA

Not for distribution

07-Jun-07 Cary Wingfield Raditz, CFA p2

Total Global Forestry Investment

Total investable and leasable global forestlands estimated > 870 million ha

Value > US$480 billion Forestry investment growing 20%

p.a. for 20 years US$35 billion invested mainly in US US$20 billion held by institutional

investors

Not for distribution

07-Jun-07 Cary Wingfield Raditz, CFA p3

Timber: the Investment Class

Predictable biological growth Asset growth= forest growth Inventory=stored on the stump Strong historical returns Moderate risk High returns on risk* Portfolio diversification

characteristics * Sharpe ratio

Not for distribution

07-Jun-07 Cary Wingfield Raditz, CFA p4

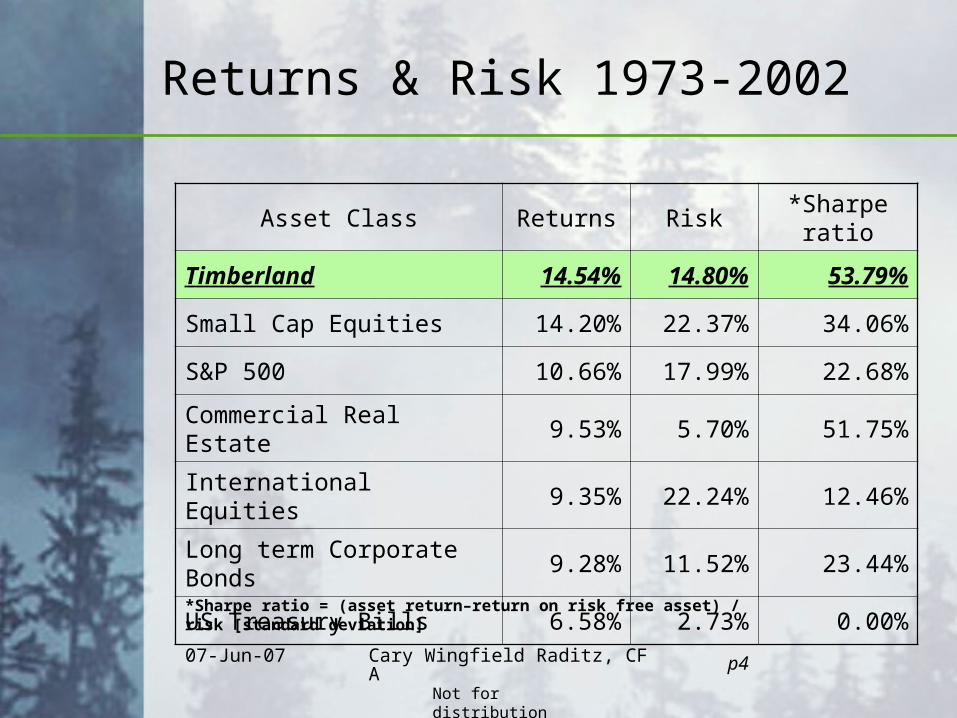

Returns & Risk 1973-2002

Asset Class Returns Risk*Sharpe

ratio

Timberland 14.54% 14.80% 53.79%

Small Cap Equities 14.20% 22.37% 34.06%

S&P 500 10.66% 17.99% 22.68%

Commercial Real Estate 9.53% 5.70% 51.75%

International Equities 9.35% 22.24% 12.46%

Long term Corporate Bonds

9.28% 11.52% 23.44%

US Treasury Bills 6.58% 2.73% 0.00%

*Sharpe ratio = (asset return–return on risk free asset) / risk [standard deviation]

Not for distribution

07-Jun-07 Cary Wingfield Raditz, CFA p5

Attributes of Return

Biological tree growth Timber price changes Changes in the value of the

underlying land asset Non-timber forest products and

services—ancillary cash flows

Not for distribution

07-Jun-07 Cary Wingfield Raditz, CFA p6

Timber Reduces Portfolio Risk

Not for distribution

07-Jun-07 Cary Wingfield Raditz, CFA p7

Investment Suitability of Timber

> 10 years = illiquid Long-term institutional portfolios Endowments, foundations, pension

funds, insurance companies, high-net worth

Matches maturity of longterm assets to maturity of longterm liabilities

Low correlation to equities and fixed income provides diversification

Certified forestland suitable for socially responsible investors

Not for distribution

07-Jun-07 Cary Wingfield Raditz, CFA p8

Investment Vehicles

Purchase forestland—manage timber assets

Forestry product equities Forestry product bonds REITS—real estate investment trusts TIMOS—Timber Investment

Management Organizations Private equity partnerships

Not for distribution

07-Jun-07 Cary Wingfield Raditz, CFA p9

Environmental Issues

Climate change Soil and freshwater

conservation Loss of biodiversity Forest systems play a critical

role in managing environmental problems

Not for distribution

07-Jun-07 Cary Wingfield Raditz, CFA p10

Forestland Management Methods

Clear cutting (controversial) Pure conservation—tax deductible

gifts of forestland Sustainable forestry management

—”pure play” Forestry operations includes

processing Certified forests (FSC)—biodiversity Non-timber forest products (NTFPs) Capturing PES cash flows--e.g., CERs Structured methods—e.g. easements

Not for distribution

07-Jun-07 Cary Wingfield Raditz, CFA p11

Tropical Forestry Investments

Fast growing in tropics (short rotation) High discount for Emerging Markets risk Controversial (Equator Principles) Lessons learned: Mitigate country risk

(management, rigorous internal controls, portfolio diversification)

:Factor costs of poor infrastructural :Neutralize corruption risk :Coop local community participation in forest

management :Certify forests :Manage non-timber forest products :Monitize tradable carbon emissions rights

(CERs)

Not for distribution

07-Jun-07 Cary Wingfield Raditz, CFA p12

Payments for Eco-services

Carbon sequestration--CERs Water use rights—local (New York

City) Biodiversity—FSC certified (Precious

Woods) Eco-tourism (Texas Inland—hunting

rights) Conservation easements (USA e.g.,

Forest Legacy Trust) Tradable development rights (USA

locally regulated)

Not for distribution

07-Jun-07 Cary Wingfield Raditz, CFA p13

Implications for Investment Valuation

Value = Σ of discounted future cashflows

NTFPs and PES are real options When exercised: PES provide

ancillary cash flows “Value enhancements” Reduce illiquidity in afforestation PES converge private good and

public good agenda

Not for distribution

07-Jun-07 Cary Wingfield Raditz, CFA p14

Timber Conservation Strategies

1. Pure Conservation

2. Sustainable Harvesting

3. Creative Structured Solutions

4. Example: Selling Easements

Not for distribution

07-Jun-07 Cary Wingfield Raditz, CFA p15

1. Pure Conservation

No return of principal or income Forestland gift is tax deductible Appropriate for land having

special value or unsuitable for logging

Example: green belts near urban centers, old-growth riparian forests

Not for distribution

07-Jun-07 Cary Wingfield Raditz, CFA p16

2. Sustainable Harvesting

Land harvested sustainably (< 6% of board ft/year)

Sub-optimal timber returns, but is still solid investment

Short-term positive impact on environment

Either requires very long investment horizon or sale of most of land to capture principal and return on capital

Not for distribution

07-Jun-07 Cary Wingfield Raditz, CFA p17

3. Structured Solutions

Incorporate PES Tax sensitive strategies--

Easements Partner with non-profit govt and

NGOs (Sierra Club) Structure for socially

responsible investment market

Not for distribution

07-Jun-07 Cary Wingfield Raditz, CFA p18

Selling Easements

Conservation easements Development easements Optimal or near optimal

investment returns Fair short term/Good long term environmental

impact Requires foundation and non-

profit funds

Not for distribution

07-Jun-07 Cary Wingfield Raditz, CFA p19

Easement Return and Impact Benefits: Conserve wildlife habitat, clean

watersheds, prevent urban sprawl, preserve valuable forestland

Purchase land with merchantable timber Agree to environmental easement on the

property at beginning Satisfy the environmental guideline test Provide investors tax-deductible

contributions Through careful replanting, return the

ecosystem to its natural pre-logging state At end of term, put the land into permanent

conservation through a land trust

Not for distribution

07-Jun-07 Cary Wingfield Raditz, CFA p20

Is it Time to Invest?

Opportunities for creative, sustainable solutions

New SRI listings in capital markets Select opportunities in emerging

markets Environment awareness will increase

value of certified wood New international protocols will

increase demand and price of carbon and other PES

Not for distribution

07-Jun-07 Cary Wingfield Raditz, CFA p21

Sources of Information

www.forest-trends.org Private placement

memorandum Initial public offering prospectus Hancock Timber Resource

Group www.hnrg.com Rights and Resources

www.rightsandresources.org

Related Documents