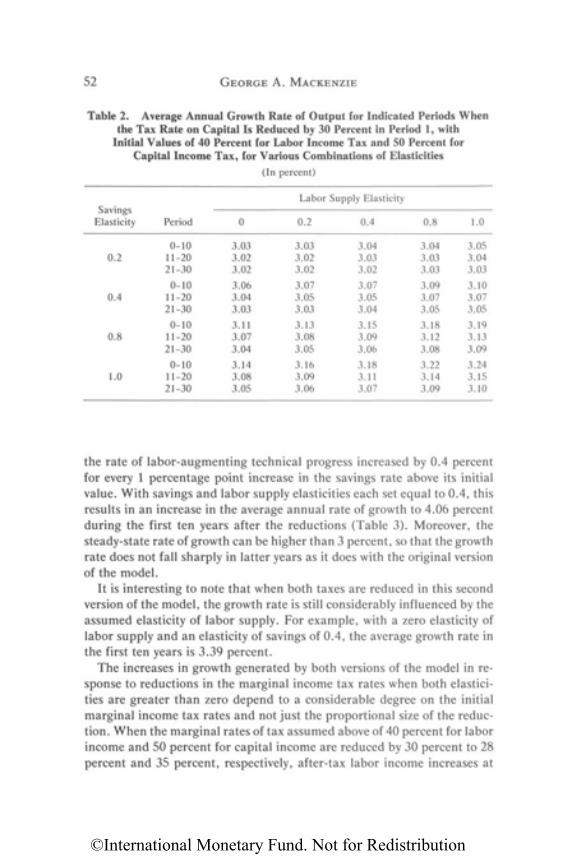

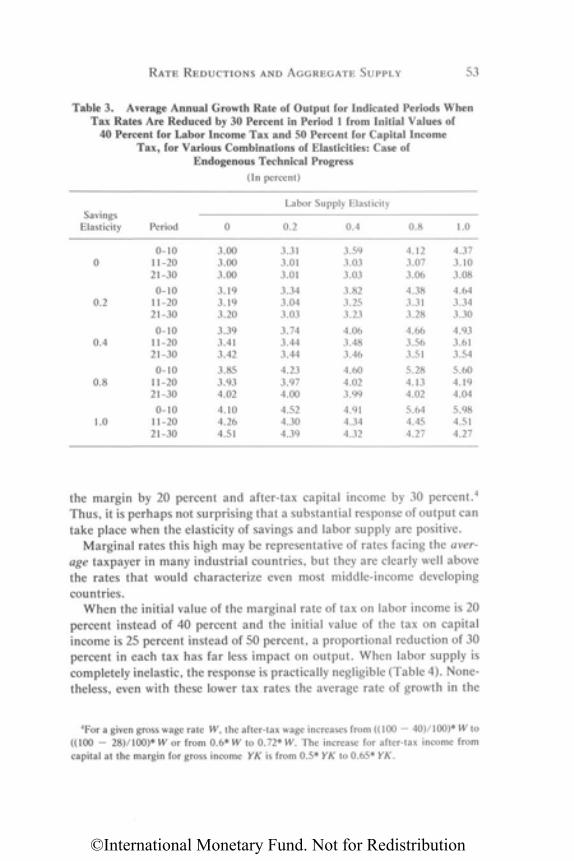

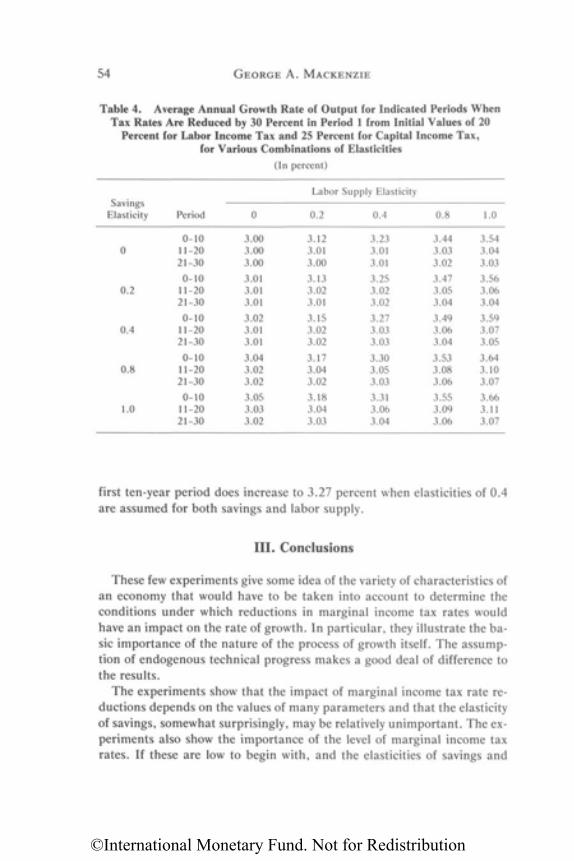

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Ved P. Gandhi

Liam P. EbrillGeorge A. MackenzieLuis A. Manas-Anton

Jitendra R. ModiSomchai Richupan

Fernando Sanchez-UgarteParthasarathi Shome

International Monetary FundWashington, D.C. • 1987

SUPPLY-SIDETAX POLICY

Its Relevance toDeveloping Countries

©International Monetary Fund. Not for Redistribution

© 1987 International Monetary FundReprinted March 1995

Cover design by the IMF Graphics Section

Library of Congress Cataloging-in-Publication Data

Supply-side tax policy.

Bibliography: p.1. Taxation-Developing countries. 2. Supply-side

economics-Developing countries. I. Gandhi, Ved P.(Ved Parkash)HJ2351.7.S86 1987 336.2'009172'4. 87-29890ISBN 0-939934-91-4

Price: $20.00

©International Monetary Fund. Not for Redistribution

Contents

Foreword vii

Preface ix

Part I. Overview and Summary

Chapter 1. Relevance of Supply-Side Tax Policy toDeveloping Countries: A Summary Ved P. Gandhi 3

Scope of Supply-Side Economics 4The Scope of the Studies and Overall Conclusions 11Validity and Relevance of Popular Supply-Side Tax Policy 16Tax Policy for Efficiency and Growth 28Supply-Side Tax Reforms for Developing Countries 33

Part II. Income Taxes and Growth: Evidence onPopular Supply-Side Tax Policy

Chapter 2. A Simple Model of the Effects of Income TaxRate Reductions on Economic Growth andAggregate Supply George A. Mackenzie 45

Incorporating Marginal Income Tax Rates in theOne-Sector Neoclassical Model 47

Assumed Elasticities and Simulation Results 49Conclusions 54

Chapter 3. Are Labor Supply, Savings, and InvestmentPrice-Sensitive in Developing Countries? A Survey of theEmpirical Literature Liam P. Ebrill 60

Labor Supply 62Savings Behavior 69Investment Behavior 75Conclusions 82

i i i

©International Monetary Fund. Not for Redistribution

iv CONTENTS

Chapter 4. Optimal Taxation of Financial Savings inDeveloping Countries: Relevance ofSupply-Side Tax Policies Liam P. Ebrill 91

Institutional Background 92Evaluation of Reform Proposals 95Conclusions 109

Chapter 5. Income Taxes and Investment:Some Empirical Relationships forDeveloping Countries Liam P. Ebrill 115

The Theoretical Framework 116Empirical Results 123Conclusions 133

Chapter 6. Determinants of Income Tax Evasion:Role of Tax Rates, Shape of Tax Schedules, andOther Factors Somchai Richupan 140

Standard Models of Tax Evasion 141Theoretical Studies on Factors Affecting Tax Evasion 147Empirical Studies on Factors Affecting Tax Evasion 755Limitations of the Literature 158The Role of Tax Factors 161The Role of Nontax Factors in Developing Countries 166Conclusions 172

Chapter 7. Evidence on the Laffer Curve:The Cases of Jamaica and India Liam P. Ebrill 175

The Supply-Side Approach 176Supply-Side Effects and the Personal Income Tax 180Overview and Conclusions 192

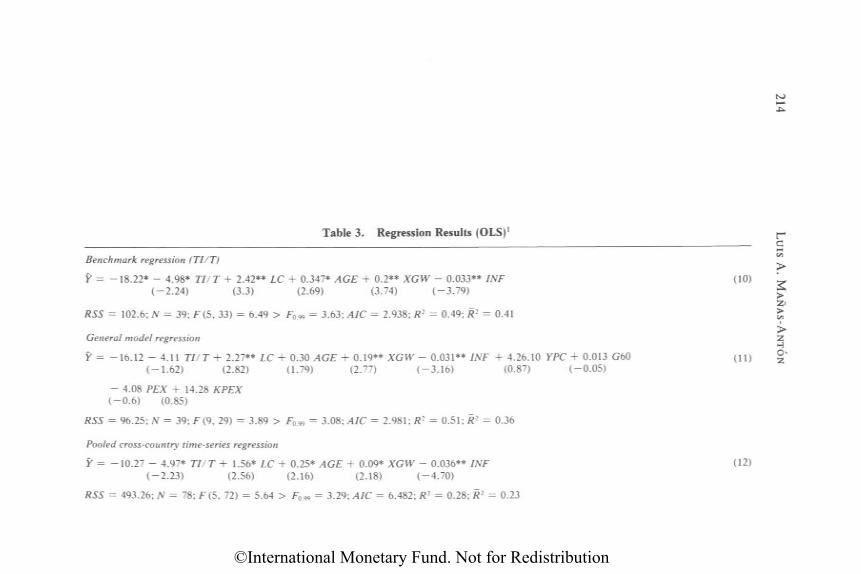

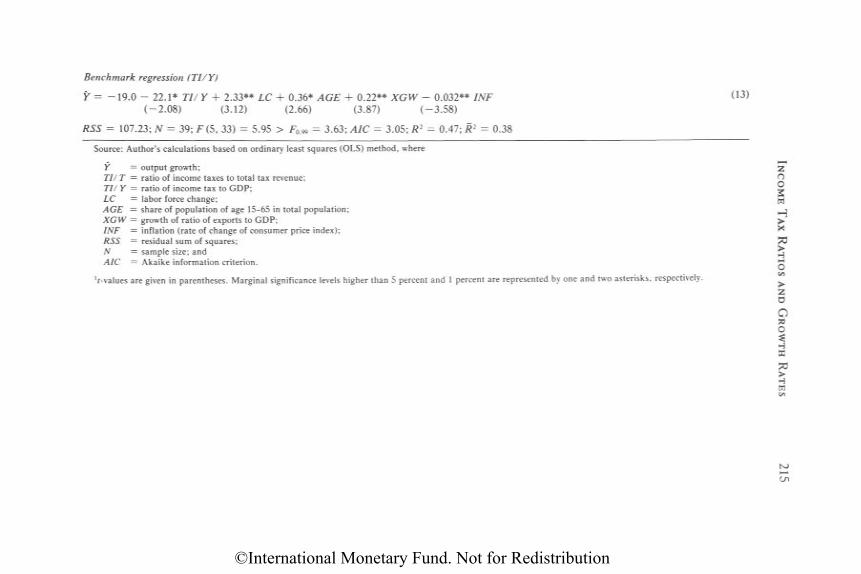

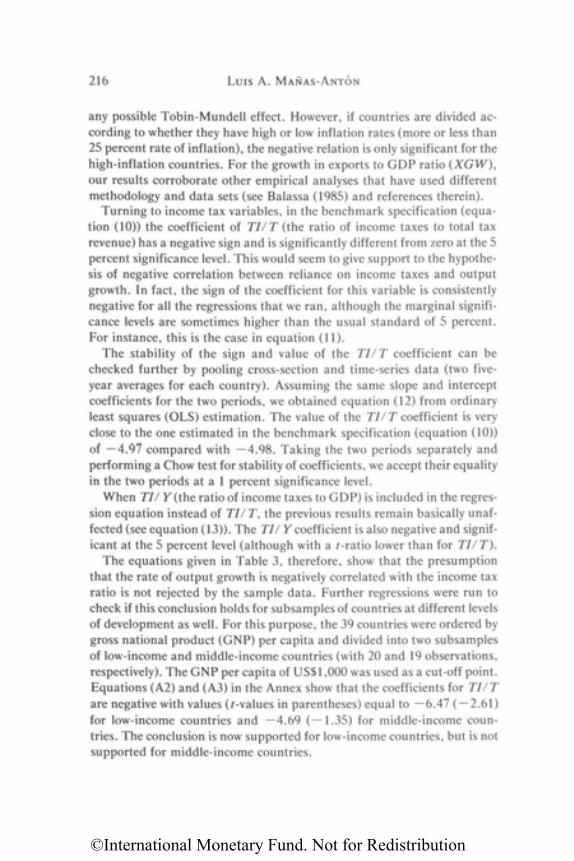

Chapter 8. Relationship Between Income Tax Ratios andGrowth Rates in Developing Countries:A Cross-Country Analysis Luis A. Mañas-Anton 198

Strategy of the Empirical Analysis 200Empirical Analysis 207Concluding Remarks 217

©International Monetary Fund. Not for Redistribution

CONTENTS V

Part III. Tax Policy for Efficiency and Growth:Aspects of Basic Supply-Side Tax Policy

Chapter 9. Tax Structure for Efficiency and Supply-SideEconomics in Developing Countries Ved P. Gandhi 225

Supply-Side Objectives of the Tax System—in Theory 226Tax Bases for Supply-Side Economics or Efficient

Tax Bases 232Rate Design for Supply-Side Economics or Optimal

Tax Rates 236A Popular Supply-Side Economist Versus an

Optimal Tax Economist 239A Tax System Dictated by Popular Supply-Side Economics:

Some Implications 241

Chapter 10. Rationality of Income TaxIncentives in Developing Countries:A Supply-Side Look Fernando Sanchez-Ugarte 250

The Economic Rationality for Tax Incentives 252General Considerations in the Design of Tax Incentives 258The Efficiency of Specific Tax Incentives 262The Effectiveness of Tax Incentives 269Concluding Remarks 273

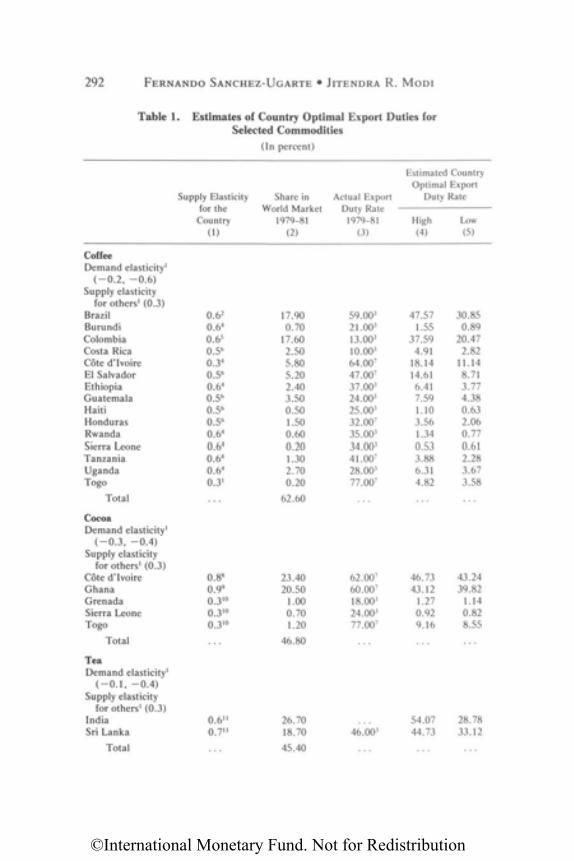

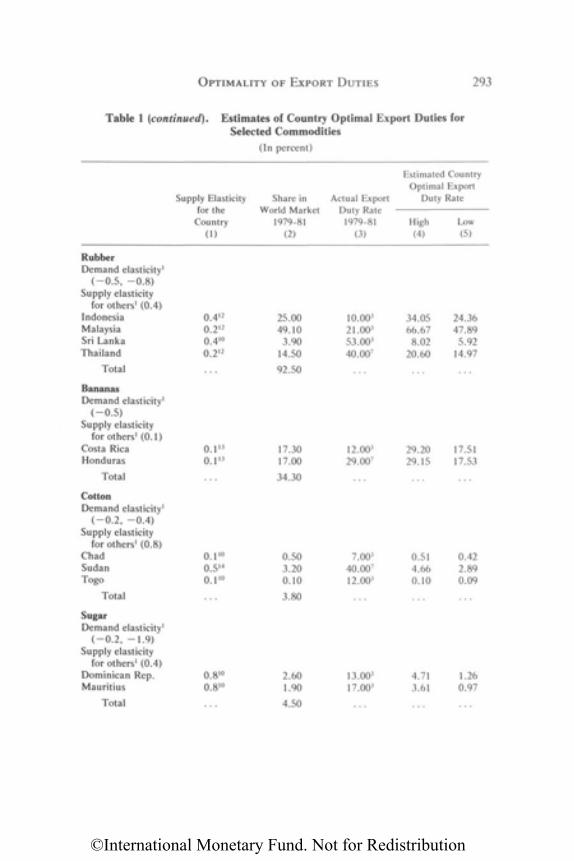

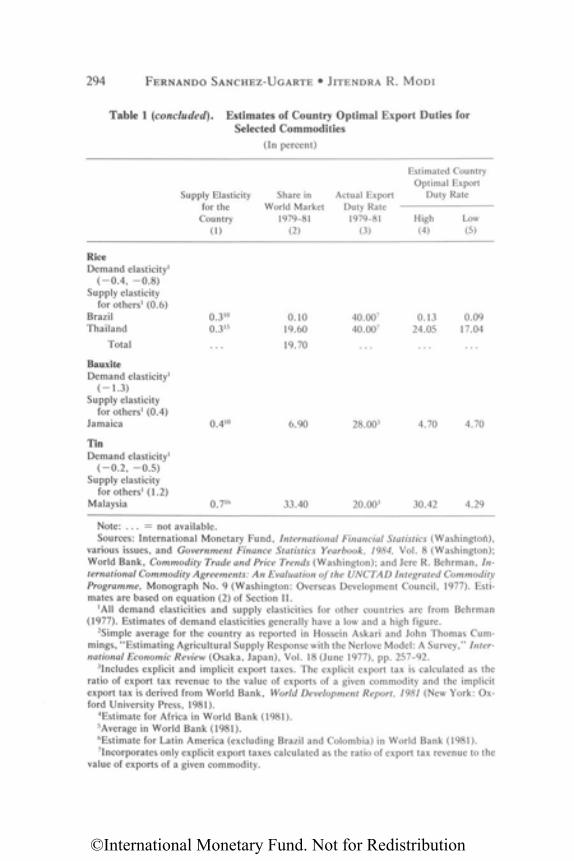

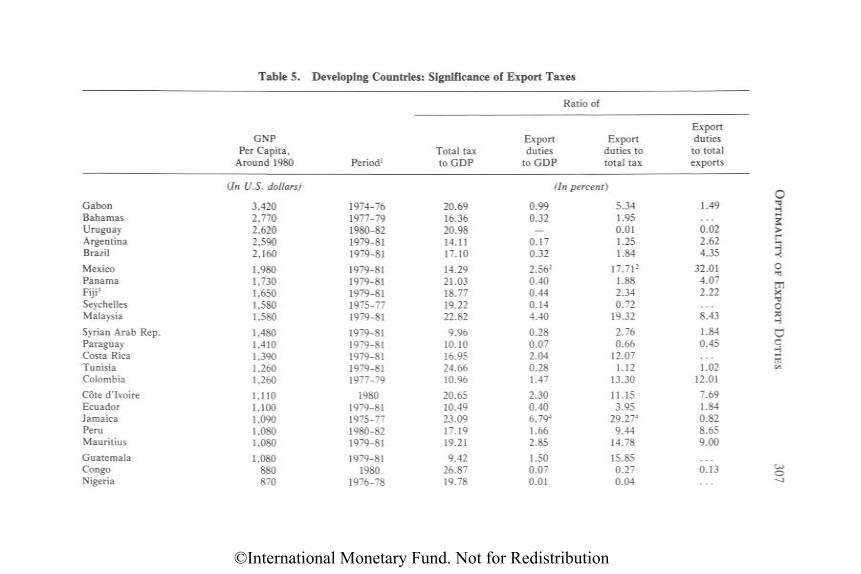

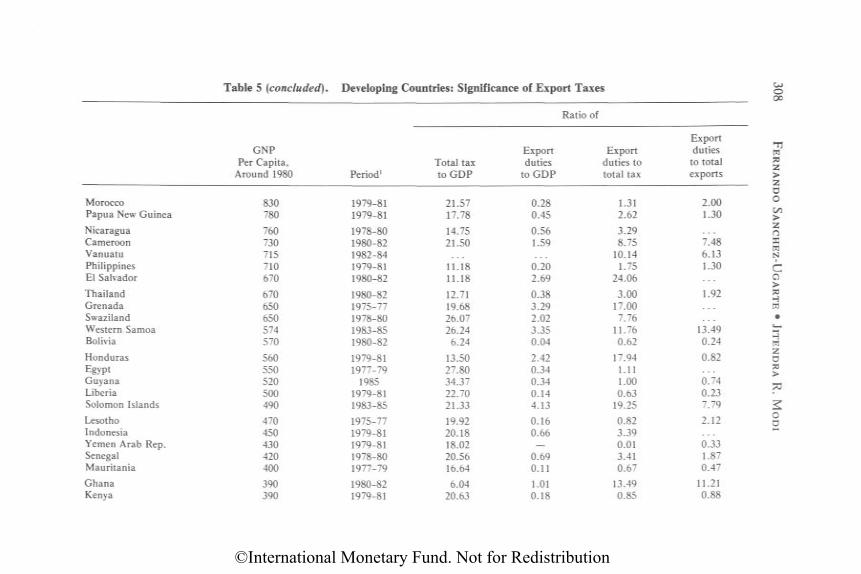

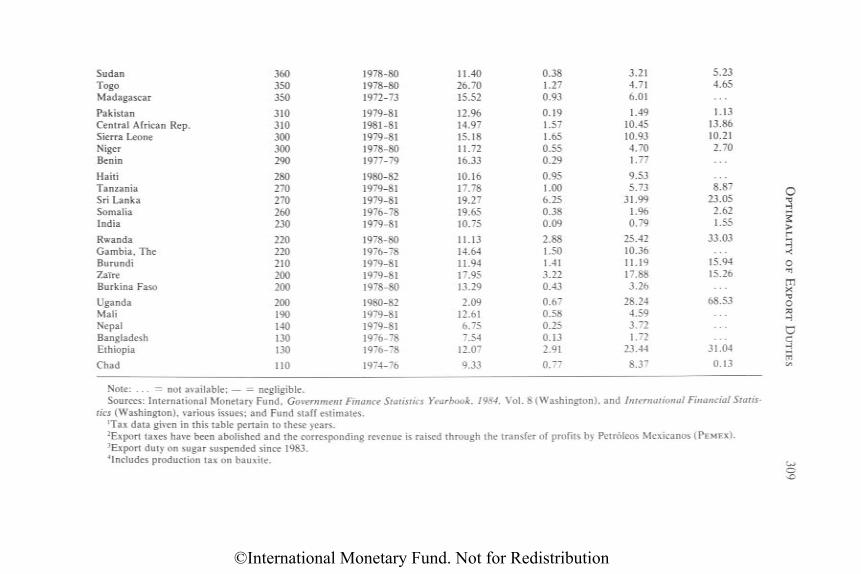

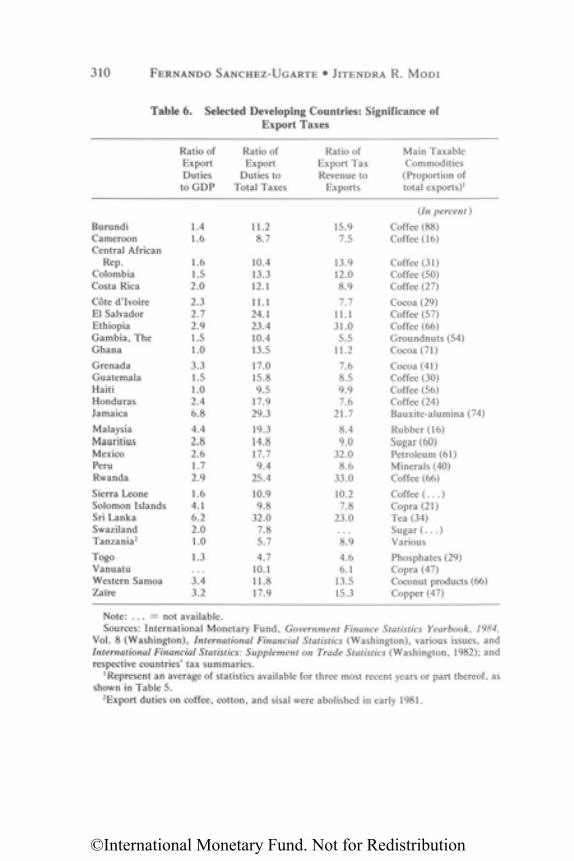

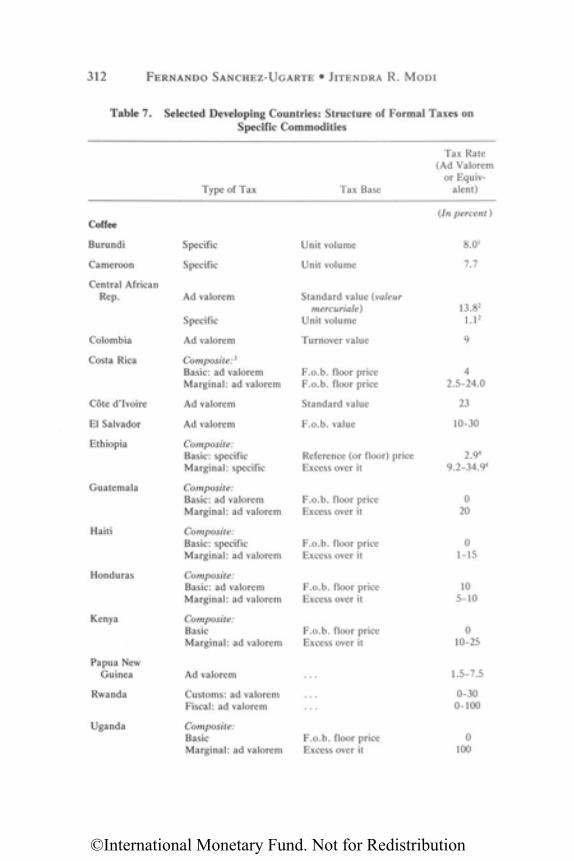

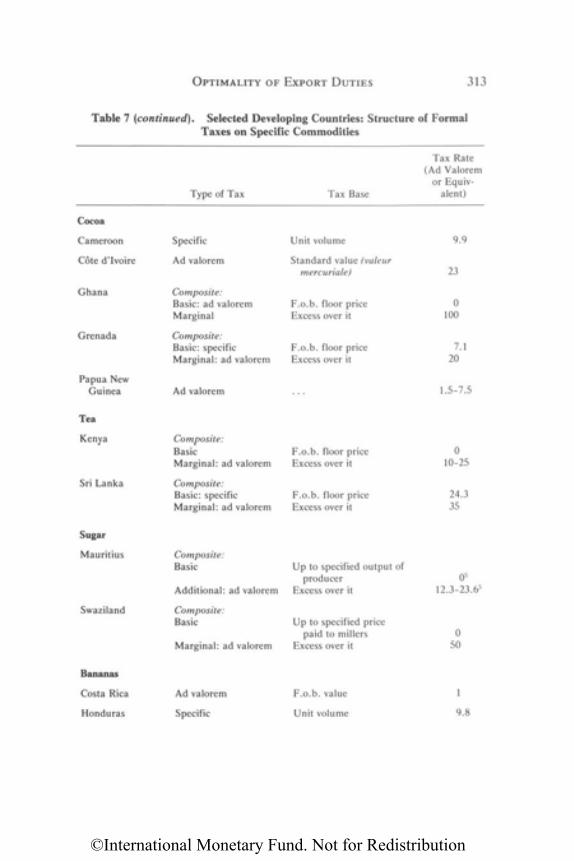

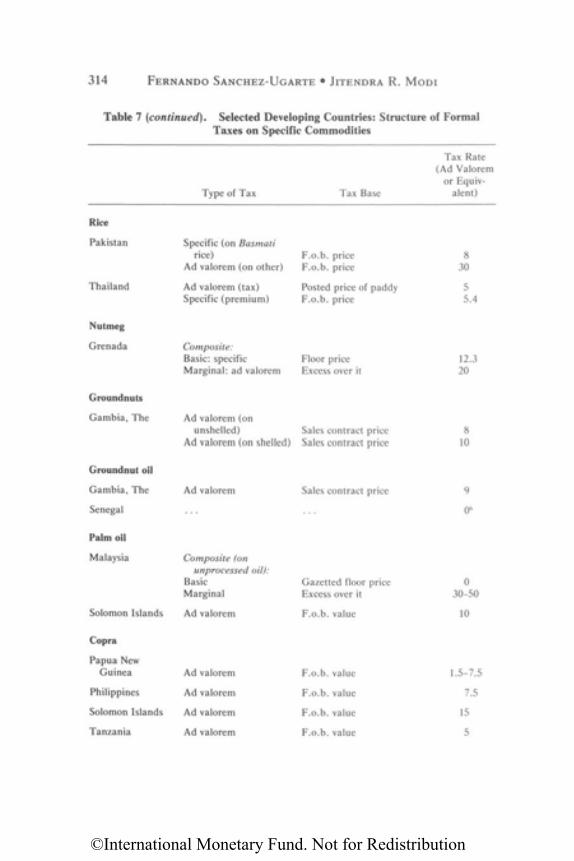

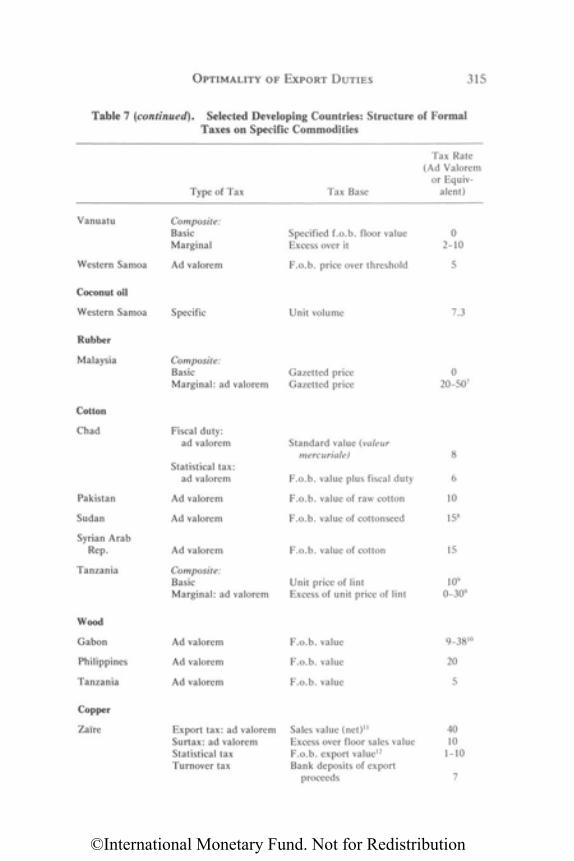

Chapter 11. Are Export Duties Optimal inDeveloping Countries? Some Supply-Side ConsiderationsFernando Sanchez-Ugarte and Jitendra R. Modi 279

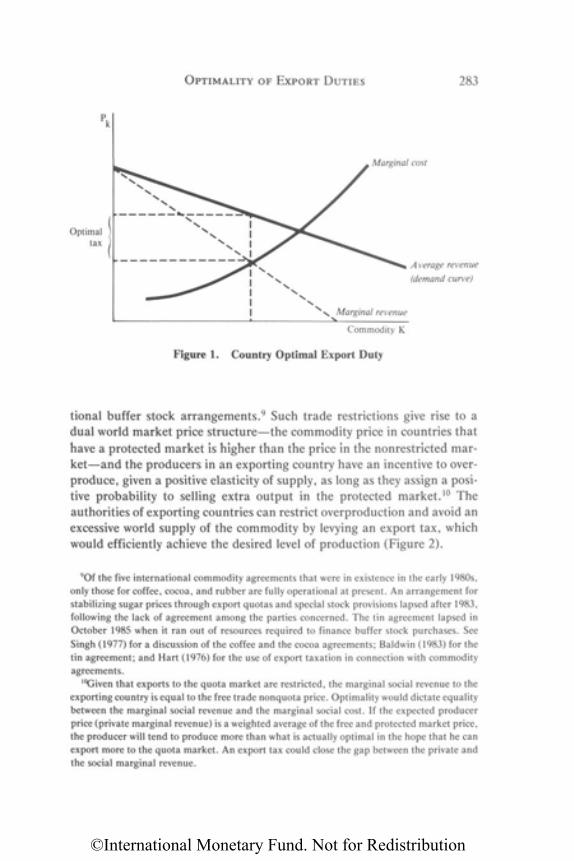

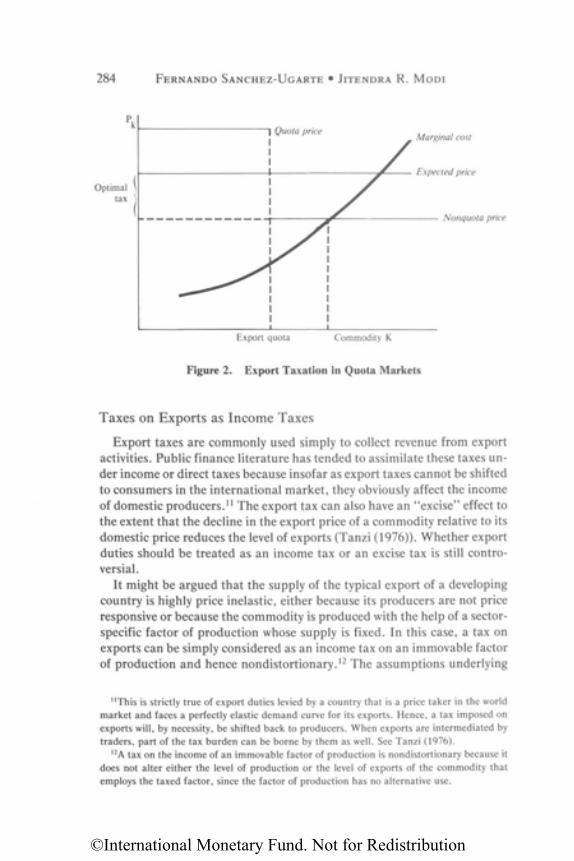

The Rationale for Export Taxes 281Methodology for Estimating Country Optimal Export

Duties and Their Effects 287Appraisal of the Impact of Existing Export Taxes 291Conclusions 305

Chapter 12. Limitations of the Role of Tax Policy inEconomic Development Parthasarathi Shome 321

The Determinants of Development 322Tax Policy and the Determinants of Development 327Concluding Remarks 330

©International Monetary Fund. Not for Redistribution

vi CONTENTS

Appendices

Appendix I. Statistical TablesJitendra R. Modi, Somchai Richupan, and Chris Wu 337

Appendix II. Selected Bibliography 386

©International Monetary Fund. Not for Redistribution

ForewordThe decade of the 1980s is likely to be remembered as the time when tax

reform became fashionable around the world. Not only many industrialcountries but also many developing and centrally planned countries havefelt the need to reform, sometimes drastically, their tax systems. While inearlier periods reforms often had the objective of raising revenue and ofmaking the tax system more progressive, during the 1980s most tax re-forms have been revenue neutral in intention, if not always in actualresults, in spite of the large fiscal deficits that have characterized many ofthese countries. The main objective of the recent reforms has been the re-moval of obstacles to growth. In the industrial countries, the concernabout the relationship between the tax system and the rate of economicgrowth has been heightened by the high and increasing unemploymentrates that have accompanied the slowdown of their rate of economicgrowth in recent years. In the developing countries, there has been the re-alization that heavy debt burdens could only be reduced by acceleratingthe rate of growth of these economies. Furthermore, in view of the lowlevels of income in these countries, growth had always been a major objec-tive for their policymakers.

In this period, both economists and policymakers have rediscovered theimportance of supply-side aspects of economic policy. While up to recentlyeconomic policy had been driven by the Keynesian assumption that regu-lating aggregate demand would go a long way toward achieving whatevereconomic objectives the policymakers wanted to achieve, during the 1980sthe focus of policymakers' attention shifted from the demand to the supplyside of the economy. They came to believe that it would be possible tosqueeze a larger growth rate out of the existing resources if certain changeswere made in economic policies. For the tax system, these changes wereoften thought to require reductions in tax rates accompanied by broaden-ing of bases. They also required reductions in the differential treatments ofeconomic sectors and economic activities.

In spite of the fact that many observers think of the Fund as an institu-tion concerned mainly with stabilization, it has, in fact, always paid atten-tion to the objective of economic development. As a consequence, it wasnatural that it would be influenced, like everybody else, by the currentthinking about the role of incentives in general and tax incentives in partic-ular. The Fund has paid increasing attention to the structural components

vii

©International Monetary Fund. Not for Redistribution

viii FOREWORD

of adjustment policies. It has accepted the conclusion that without majorstructural adjustments developing countries might achieve stability, butonly at the cost of a slower rate of growth. Stability with growth requiresthat many changes in the structure of their economies must take place inthese countries. There must be changes in the external sector through theliberalization of imports and the removal of impediments to exports, inaddition to the more traditional adjustments in the exchange rate. Theremust be changes in the financial markets, through the removal of obstaclesto the flow of financial resources within the economy, through the raisingof real interest rates to realistic levels, and through the reduction of theproportion of total credit that is administratively allocated. There must berealignments in relative prices in order to eliminate disincentives to pro-ducers, when the prices that they receive are too low to keep them produc-ing the cash crops for which the countries have comparative advantages.There must also be changes in the relative prices of consumer goods toreduce the consumption of products that must be imported or that couldbe exported in larger quantities.

The restructuring of economies will inevitably involve also the reform ofthe tax system. This is the aspect addressed in this book. Under the direc-tion of Ved Gandhi, Chief of the Tax Policy Division, the Fiscal AffairsDepartment has made a systematic attempt at surveying what is knownabout the disincentive effects of taxes. This research has relied on hardevidence in order not to be swayed by claims that may be fashionable butthat are often not fully substantiated. This reliance on hard evidence hasobvious scientific merits, but it has also some shortcomings. The merits arethat the conclusions reached are based on firm evidence. The shortcom-ings are that those conclusions are based on work which has already beendone; that work may itself have been biased by earlier preconceptionsabout the effect of taxes. In any case, I hope that enough interesting con-clusions are provided by this book to make it a valuable addition to theliterature on taxation in developing countries. I also hope that policymak-ers will find some of its conclusions useful for the conduct of their eco-nomic policy. I should perhaps conclude by adding that the views pre-sented reflect the thinking of the authors and do not necessarily reflectofficial Fund positions.

VITO TANZI

DirectorFiscal Affairs Department

©International Monetary Fund. Not for Redistribution

Preface

A striking feature of the 1980s has been the sharp decline in the rates ofgrowth witnessed by countries in the developing world. According to theWorld Bank's World Development Report, 1986, the average annual rateof growth of these countries declined from 6.6 percent during 1965-73 and5.4 percent in 1973-80 to 2 percent in 1982 and 1983 (Statistical AppendixTable A.3, page 115). Countries all over Africa as well as Latin Americaand the Caribbean have experienced a significant erosion of the standardof living of their populations in recent years, as their economic growthrates have fallen far short of their population growth rates, and there islittle hope for early reversal of these trends. Given the uncertain prospectsfor growth, many economists have expressed the belief that exclusive reli-ance on traditional demand management policies, which can certainlyachieve successful stabilization around a trend growth path, may not beenough to improve economic welfare and that these policies may have to becombined with policies aimed at raising the trend growth path itself. Thisbelief has renewed the interest of economists and policymakers alike in thedeterminants of growth and supply-side economics with its fundamentalclaim to enhancing the country's potential for growth.

Although supply-side economics addresses all aspects of aggregate sup-ply, it focuses particularly on the appropriate role of government in en-couraging growth through its expenditure and taxation policies. This bookexamines the relevance to developing countries of the tax policy recom-mendations of supply-side economists and attempts to delineate policyguidelines to ensure that fiscal management enhances rather than inhibitsgrowth and efficiency in the wider economy.

The book is the product of a research project initiated in 1984 in theFiscal Affairs Department of the International Monetary Fund to assessthe relevance to the special circumstances of developing countries of taxpolicy aspects of the popular supply-side revolution in the United States.The main emphasis of the popular version of this revolution has been tostress the negative effects of high income tax rates on incentives to pro-duce, save, and invest and, through these, on the growth of the economy.

Assessing the relevance of supply-side tax policy for developing coun-tries is no easy task. First, there are many forms of taxes and the effects ofeach tax on incentives have many aspects. Effects of tax rates, the primary

ix

©International Monetary Fund. Not for Redistribution

x PREFACE

focus of the popular supply-siders, on the behavior of the economic agentsare interwoven with the type and scope of the tax base, tax reliefs, and taxincentives, and many other special provisions of the tax system. Second,tax policy frequently interacts with other economic policies of the govern-ment in very many complicated ways so that the economic effects of a taxcut become a function of the institutional and economic policy environ-ment within which it operates. Furthermore, statistical and other informa-tion relevant to estimating the disincentive effects of various tax policies orthe incentive effects of the reform of such policies are not readily available.

The book does not purport to be comprehensive; it covers only selectedaspects of supply-side tax policy. In particular, it attempts to deal with thefollowing eleven questions:

• What are the most important price elasticities that determine the ef-fects of income tax reductions on aggregate supply?

• How price-sensitive are labor supply, savings, and investment in de-veloping countries?

• To what extent do income tax policies, given certain other economicpolicies, reduce financial savings in developing countries?

• To what extent do income and corpopate tax policies, given generoustax incentives and other tax provisions, reduce corporate investmentin developing countries?

• Do high and progressive income tax rates significantly increase in-come tax evasion in developing countries?

• Are there certain examples from the developing world where a reduc-tion of top marginal income tax rates has increased government reve-nue significantly in the short run as predicted by the "Laffer curve?"

• What is the econometric evidence on the negative relationship be-tween reliance of developing countries on income taxes and theirgrowth rates?

• What will the tax systems of developing countries look like in theory ifincentives and efficient allocation of resources were the major concernof policymakers?

• How efficient are the generous tax incentives that are frequently givento investors in developing countries in order to induce economicgrowth?

• Under what circumstances are export duties justified on grounds ofefficiency and growth?

• What is the precise role of tax policy in removing the various struc-tural bottlenecks to economic development and helping the growth ofdeveloping countries?

©International Monetary Fund. Not for Redistribution

PREFACE xi

Chapters 2 through 12 deal with each of these questions, while Chapter 1brings together the findings and conclusions of the analyses and suggestsideas for supply-side tax reform relevant for developing countries.

The research project was carried out by a staff team headed by Ved P.Gandhi of the Tax Policy Division of the Fiscal Affairs Department. Inaddition, the team consisted of Liam P. Ebrill, Jitendra R. Modi, SomchaiRichupan, Fernando Sanchez-Ugarte, and Parthasarathi Shome. The pa-pers included in this book were prepared by the staff members as and whenthey found time in the course of their regular operational work for theFund. The papers by George A. Mackenzie and Luis A. Mañas-Antonwere not prepared as a part of the project; the former was completed be-fore the research project was initiated, while the latter was prepared whenthe author served as a summer intern in the Tax Policy Division.

The research project was a cooperative effort, and the author of eachpaper has benefited from the comments of the other members of the staffteam. In addition, many friends and colleagues in the Fiscal Affairs De-partment, as well as in other departments of the Fund, took pains to readthe draft papers and provide guidance, and their advice is gratefully ac-knowledged. The team is particularly indebted to Vito Tanzi, Director ofthe Fiscal Affairs Department, who took interest in the research projectfrom its inception, provided an exciting environment, and guided the workof the team; the book owes a great deal to him. The team also wishes tothank Alan Tait, Leif Muten, Robert Schneider, Richard Hemming,Sheetal Chand, David Nellor, and Charles Sisson, who gave constructivecriticisms on one or more draft papers. Extensive comments on the entiremanuscript and valuable suggestions were received from Professor RoyBahl of Syracuse University and Professor Charles McLure, Jr., of Stan-ford University and the authors wish to express their gratitude to them.However, none of the foregoing can be held responsible for any errors oromissions that may remain. The authors also wish to express appreciationfor the painstaking and skillful editing of the manuscript by Esha Ray.Finally, thanks are due to Lyndsey Livingstone and Ahwerah Vichailak fortheir patience and superb job of typing and retyping successive drafts ofeach paper until the final manuscript stage.

VED P. GANDHI

©International Monetary Fund. Not for Redistribution

This page intentionally left blank

©International Monetary Fund. Not for Redistribution

PART I

Overview and Summary

©International Monetary Fund. Not for Redistribution

This page intentionally left blank

©International Monetary Fund. Not for Redistribution

1Relevance of Supply-Side Tax Policy to

Developing Countries

A Summary

Ved P. Gandhi

Within the short span of a few years, "supply-side economics" has cometo be considered in some quarters to be the "new" economics that is mostrelevant to policymaking for solving the economic problems of the 1980s.However, the basic propositions of supply-side economics, including thebelief that taxes affect economic behavior and the substitution effects oftaxes are important for the efficient allocation of resources, are as old asneoclassical economics itself. What is new is the conviction of some supply-side economists that a substantial reduction of tax burdens, in general,and the rates of income tax, in particular, will have significant effects onthe level of output and growth rates. In 1984, the Fiscal Affairs Depart-ment of the International Monetary Fund undertook a research project toanalyze the relevance to developing countries of the tax policy recommen-dations of supply-side economics made in the context of developed coun-tries. This volume contains the studies that were prepared as part of thisresearch project.

As explained in greater detail in Section I of this chapter, there are atleast two interpretations of supply-side economics, and, consequently, ofsupply-side tax policy—the traditional or the "basic" view and the new orthe "popular" view. Most of the studies included in this book assess thevalidity of the arguments of popular supply-side economics, while othersdeal with the validity of selected propositions of basic supply-side eco-nomics.

The volume is in three parts. Part I provides an overview and summaryof findings and conclusions. Part II presents seven papers reviewing theevidence on the validity of popular supply-side tax policy. Part III contains

3

©International Monetary Fund. Not for Redistribution

4 VED P. GANDHI

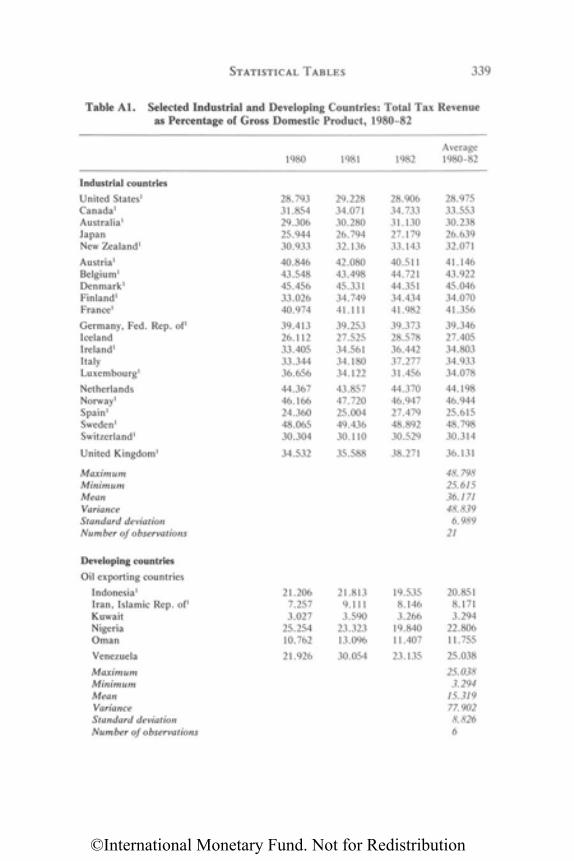

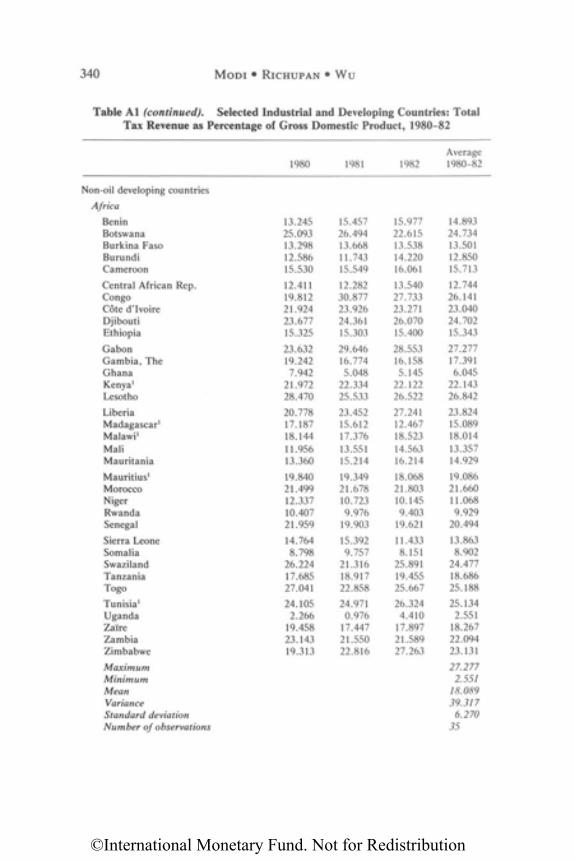

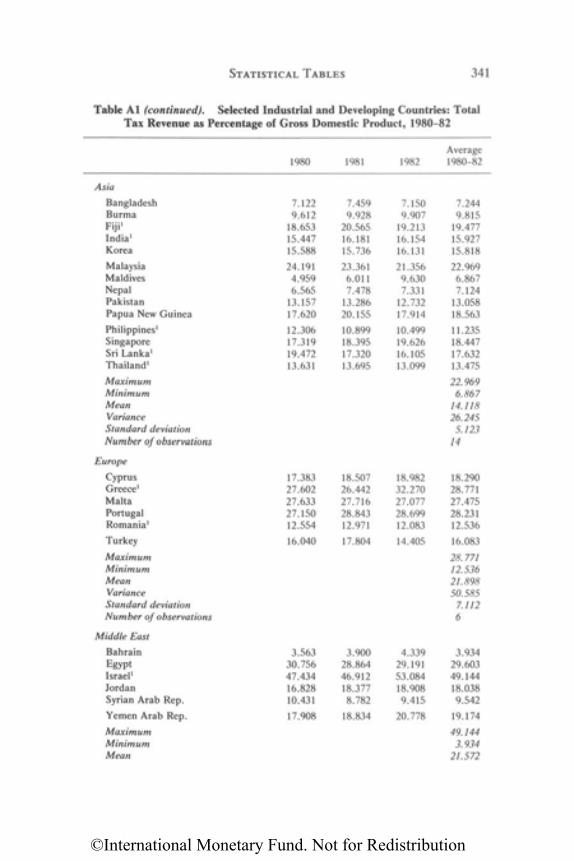

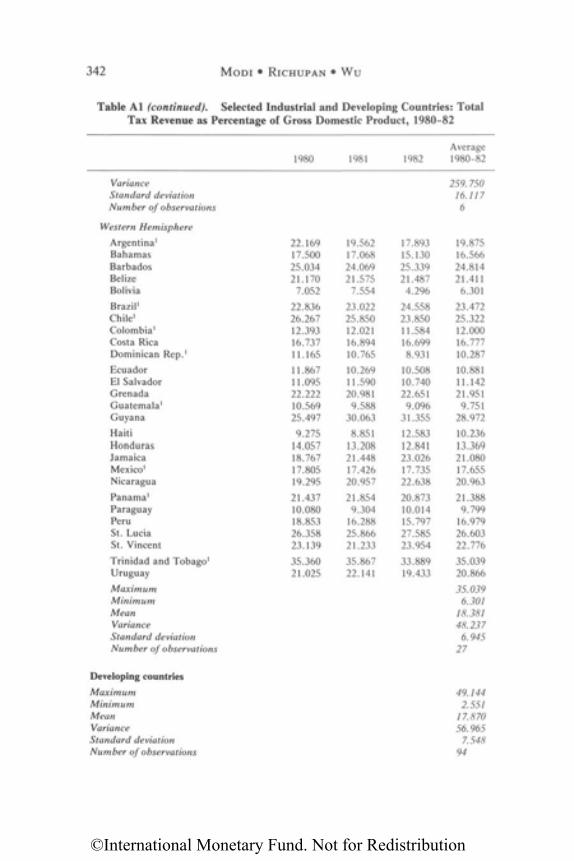

four papers dealing with selected aspects of basic supply-side tax policy ortax policy for efficiency and growth. The book also has two appendices.Appendix I contains statistical information that is readily available on therevenue structures of developing and developed countries relevant to thevarious studies. Appendix II presents a selected bibliography of publica-tions on popular supply-side economics of interest to the general reader.

The term supply-side economics originated in the United States in themid-1970s primarily as a reaction to government economic policies basedon Keynesian macroeconomic theory and represents a new way of lookingat government economic policies.1 The term, however, has evolved overtime and has come to mean different things to different people. It is, there-fore, important at the outset to clarify in broad terms what supply-sideeconomics stands for and then to define with greater precision those as-pects of supply-side tax policy that have received the most attention in theUnited States and whose relevance is analyzed in the context of developingcountries in the papers included in this volume.

These concepts are explained in Section I of this chapter. Section II de-scribes the scope of the project and the broad conclusions reached under it.Sections III and IV contain the main findings and conclusions of individ-ual papers on the validity and relevance of popular supply-side tax policyand tax policy for efficiency and growth. Finally, Section V summarizesseveral supply-side-oriented proposals for tax reform that have emergedfrom the various studies.

I. Scope of Supply-Side Economics

Supply-side writers have founded their work on the strong convictionthat free markets, with few exceptions, allocate resources most efficiently.2

This belief drives both their economic tenets and the way they view politicsand the social order.

On the political side, supply-side economists see governments, which areusually monopolists and not subject to the requirement of profit maximi-zation, as inherently inefficient because of their lack of market disciplineand as subject to a tendency to grow without bound. Because the agents ofgovernment have personal objectives which, by definition, differ from the

1Bartlett (1985, p. 18) points out that the term was coined by Professor Herbert Stein of theUniversity of Virginia in April 1976, as described in Stein (1984, p. 241).

2Supply-siders accept that the existence of pure public goods, such as defense and internalsecurity, and some merit goods, such as protecting the welfare of the extremely needy, pro-vides a rationale for social action. However, they believe that policymakers would not neces-sarily provide even these goods in the optimum quantity or at the lowest possible cost.

©International Monetary Fund. Not for Redistribution

SUPPLY-SIDE TAX POLICY: A SUMMARY 5

goals of the society at large, neither politicians nor bureaucrats in policy-making positions can be trusted to act effectively in the social interest.3

On the economic side, the belief that any policy that distorts free-market-determined relative prices distorts resource allocation has led sup-ply-siders to espouse at least three important propositions that have majorconsequences for government policy. (1) Most government regulationsaimed at protecting consumers and workers are generally costly and inde-fensible in terms of their cost-benefit ratios; eliminating them would,therefore, improve resource allocation in the economy; (2) most welfareand entitlement programs discourage work effort (including retraining);limiting access to such programs to the really needy would, therefore, re-store work incentives; and (3) personal income tax is inherently biasedagainst work effort (on the ground that work is taxed but leisure is not), aswell as against savings (since income saved is taxed twice, while incomeconsumed is taxed only once) and investment (since productive investmentis taxed but unproductive investment is not) and that high marginal in-come tax rates exacerbate these biases significantly; reducing marginalincome tax rates would, therefore, increase labor supply, savings, and in-vestment. As will be shown below, many of the propositions of supply-sideeconomists are implicit in the behavioral and market structure assump-tions made by most neoclassical economists.

In general, thus, supply-side economists emphasize minimizing the dis-tortions in market-determined relative prices that result from regulations,subsidies, and high income taxes and believe that the reduction of suchdistortions would encourage savings and production by allowing the eco-nomic incentives of a free market to work. They also believe that the pri-vate sector is generally capable of bringing about sustained economicgrowth, so that there is no need to tolerate the inefficiencies of large gov-ernment in the economy. At least two interpretations of supply-side eco-nomics, and, consequently, of supply-side tax policy have evolved withinthis general framework over time. These interpretations have been referredto in this volume as basic supply-side economics and popular supply-sideeconomics.

Basic Supply-Side Economics: Return to Classical andNeoclassical Economics

The first interpretation, basic supply-side economics, is simply an appli-cation of classical and neoclassical economic theory to government policy-

3The political philosophy underlying supply-side economics derives from the writings ofDowns (1957), Buchanan and Tullock (1969), Niskanen (1971), and Breton (1974).

©International Monetary Fund. Not for Redistribution

6 VED P. GANDHI

making. According to this view of supply-side economics, government eco-nomic policies should focus on aggregate supply rather than on aggregatedemand. As aggregate supply is the result of the economic behavior of pro-ducers, they, rather than consumers, should be considered the drivingforce in the economy and their economic behavior should be considered themost important determinant of real and nominal economic activity. Asgovernment economic policies can, and frequently do, have significantnegative substitution effects (drive economic agents away from rational—welfare maximizing—economic decisions), they should be structured insuch a way so as to minimize the substitution effect.

If one follows this interpretation, supply-side economics is essentially nodifferent from mainstream classical and neoclassical economics. It empha-sizes the objective of efficient allocation of resources more than any otherobjective of economic policy and recognizes the importance of negativesubstitution effects of government economic policies and, particularly, oftax policies. These beliefs were also held by Smith, Say, Mill, Marshall,Pigou, and Ramsey and others who obviously were supply-siders long be-fore the term was coined.

A basic supply-side economist believes that government tax policy can,and does, create a "wedge" between pretax and posttax producer prices aswell as rates of return to factors of production and, given the negative sub-stitution effect, is likely to distort the economic behavior of producers aswell as the suppliers of factor inputs. Given the importance of efficientresource allocation to aggregate output, a basic supply-side economistseeks to reduce distortions in resource allocation that individual taxes andtax structures can cause. Distortions can arise because of a number of fac-tors such as (1) the economic aggregate or the base on which taxes arelevied; (2) tax rules and provisions that affect the taxable base for individ-ual producers and factor suppliers; (3) the height of nominal tax rates andthe degree of progression in the tax rate schedule; and (4) the interactionbetween inflation, the taxable base, and tax liabilities. A basic supply-sideeconomist is one who seeks to reform all of these aspects of a tax structure.

The recommendation that tax policy be reformed along these lines isalso not new; it is well known in public finance literature. Most books ontraditional public finance, for example, contain detailed analyses of theeffects of various forms of taxation on the efficiency of resource allocation.4

The relative merits of income and consumption as alternative tax bases

4Recent literature on "optimal taxation" also deals extensively with this subject. The opti-mal taxation literature takes this objective and the neoclassical framework as starting pointsbut reaches very different conclusions on tax reform. For a discussion of the difference be-tween a supply-side tax economist and an optimal tax economist, see Gandhi (Chapter 9).

©International Monetary Fund. Not for Redistribution

and their possible effects on savings are frequently discussed at length.Similarly, the effects of alternative tax rules and provisions—relating todepreciation allowances and inventory valuation, loss-offset and carry-forward privileges, debt versus equity, etc.—on capital formation, risk-taking, and financial policies are discussed in considerable detail in theliterature. The argument that the "excess burden" of a tax depends on thenominal rate of the tax is also well known to students of public finance.5

The resource allocation costs of the lack of inflation-adjustment of the in-come tax system, which have been dealt with extensively as the rates ofinflation have accelerated in the 1970s, are also well known.

Thus, basic supply-side tax policy would seem to be no different fromthe views of fiscal economists who, on efficiency grounds, recommend thereform of (1) the economic base on which taxes are levied; (2) various taxbreaks and loopholes that signify distortionary economic signals; (3) thelevels and progressivity of nominal tax rates; and (4) tax rules and provi-sions that raise the effective tax rates in inflationary times. If these are theaims of supply-side tax policy, then fiscal economists such as Pigou,Simon, Haig, Kaldor, Harberger, Feldstein, Boskin, and McLure obvi-ously were supply-siders long before the term "supply-side tax policy" wasconceived.6

In a sense, supply-side economics is as old as economics itself, if all thatit stands for is that efficiency of resource allocation is an important objec-tive of economic policy and that market-determined resource allocation isbasically optimal. Most economists would find it hard to disagree with itscontents in theory and under normal circumstances. As a clone of classicaland neoclassical economics, basic supply-side economics contains policyprescriptions based on the latter's specific assumptions relating to, first,what the proper role of the government should be and, second, how devel-oped the commodity and factor markets are or how well they function. But

5The argument that "excess burden" rises monotonically with the nominal tax rate belongsto the partial equilibrium tax theory. According to this argument, an income tax by its verynature causes an excess burden vis-a-vis a lump sum tax (i.e., it causes a reduction of utility inexcess of that which would have occurred had the tax been collected as a lump sum) and thatpartial equilibrium analysis suggests that, in an economy completely free of distortions, in-cluding distortions caused by other taxes, the higher the rate of tax, the higher the excessburden. In fact, under highly simplified assumptions regarding the shapes of demand andsupply curves, the excess burden of a tax (which is not lump sum) is given by the square of therate of the tax. Theoretically, thus, the rate of the tax does have a very significant effect on theeconomic behavior of the taxpayers. See Rosen (1985, Chapter 12).

6Ture (1982b), Hall and Rabushka (1983), and the authors of the report by the U.S. Trea-sury Department (1984) also belong to the basic supply-side school since they seek tax reformin a wider sense, as described above.

SUPPLY-SIDE TAX POLICY: A SUMMARY 7

©International Monetary Fund. Not for Redistribution

8 VED P. GANDHI

one can still question whether both of these assumptions are strictly validin the special circumstances of developing countries. To what extent, forexample, should one whole-heartedly accept the "appropriate" role of thegovernment implicit in supply-side economics (as well as in classical andneoclassical economics) which states that the main aim of the governmentshould be ensure an efficient allocation of the economy's resources throughprivate initiative and enterprise and that all other roles of state, such as itsrole as an active agent of income redistribution or of economic stabilizationor of the growth of the economy, whenever in conflict with the former,should receive lesser priority? Similarly, to what extent should one acceptthe fundamental faith of supply-side economists (as well as of classical andneoclassical economists) that private markets are capable of delivering"appropriate" levels of goods and services and that, in the interest ofachieving maximum welfare of the society, governments should ensure asmooth working of free markets and provide few goods and services otherthan essential public goods, such as defense and internal security?

Popular Supply-Side Economics: Elasticity Optimism

It is not the views of the basic supply-siders, however, that have caughtthe public attention since the mid-1970s. Rather, it is the views of what canbe called popular supply-side economics and the extravagant claims madeby its proponents for efficiency-enhancing government economic policies,in general, and income tax policies, in particular, that have become thesubject of major debate in the United States and other developed coun-tries.7 The major proponents of popular supply-side economics have writ-ten a number of articles and books during the last few years.8

Of the many policy recommendations of popular supply-side economics,the lowering of marginal income tax rates is the most important and alsothe best known. As one leading popular supply-side economist has stated,"The term supply-side economics has in recent years become closely asso-ciated with . . . a set of policy prescriptions, the most prominent of whichhas been a recommendation that tax rates be lowered both in the UnitedStates and in many other countries."9

Never before have economists given so much importance to the marginal

7Cf., Feldstein (1986).8For the views of popular supply-siders, see Laffer and Seymour (1979); Meyer (1981); U.S.

Congress (1981); Bartlett (1982); Fink (1982); Raboy (1982); Hailstones (1982a, 1982b); Ro-berts (1982, 1984); Gilder (1981); and Canto, Joines, and Laffer (1983). Also see Appendix IIfor additional references.

9Canto, Joines, and Laffer (1983, p. ix).

©International Monetary Fund. Not for Redistribution

SUPPLY-SIDE TAX POLICY: A SUMMARY 9

rates of income taxation, and particularly to the top marginal income taxrates, and made reduction of the progressivity of income taxation the cen-terpiece of reform of government economic policies. This elevation by pop-ular supply-siders of nominal marginal income tax rates to such a height isa reaction to two major trends of recent years.

First, it is a reaction to the perceived overwhelming equity bias of tradi-tional literature on taxation. With its preoccupation with the ability-to-paybasis of taxation and the principles of sacrifice, traditional literature gen-erally justifies the progressivity of nominal rates of income taxation.

Second, it is a reaction to the progressive income tax systems found in allcountries. The progressivity has been accentuated in recent years becauseof the interaction between rates of inflation and tax brackets based onnominal incomes, as a result of which taxpayers have been constantlypushed into higher income brackets during inflationary times and havebeen subjected to even higher tax rates under unindexed income tax sys-tems.10 Such steep progressivity, in the opinion of popular supply-siders,intensifies the relative price effects and biases of taxation and creates"crushing" effects on all incentives to produce.11

Therefore, the first characteristic of popular supply-siders that setsthem apart from basic supply-side economists is their preoccupation withtax policy and, within tax policy, a focus on the nominal progressivity ofincome taxation and the top marginal income tax rates rather than on thereform of the tax system in all its aspects.

Another characteristic that distinguishes the popular supply-siders fromthe basic supply-siders is the extravagance of their claims with regard tothe effects of a reduction of marginal income tax rates on the economy. It istheir conviction that because the negative substitution effects of incometaxes are extremely high, reductions in marginal income tax rates willresult in "rapid growth, dramatic increases in tax revenue, a sharp rise insaving, and a relatively painless reduction in inflation."12 The popularsupply-siders believe that a reduction in marginal income tax rates, espe-cially the top rates, would increase the supply of labor significantly by in-ducing marked shifts from leisure to work and from nonmarket to marketactivity as after-tax wages increase, thereby raising marketed output andslowing down the rate of inflation. It would also increase the supply ofsavings and capital significantly by encouraging large shifts from con-

10"Under current law, everyone will face the top rate sooner or later," Kemp (1981, p. 94).11Wanniski(1981, p. 38).l2This is how Feldstein (1986, p. 27) has summed up the position of popular supply-siders;

he, however, does not believe in it.

©International Monetary Fund. Not for Redistribution

10 VED P. GANDHI

sumption to savings, thereby lowering interest rates. Finally, it would redi-rect resources from unproductive investment and nonmarket activity tomore productive uses of capital and market activity, thereby lowering unitcosts, raising productivity, and removing supply bottlenecks. In short, areduction of marginal rates of income taxes will significantly change theeconomic behavior of households and businesses in favor of work, savings,and productive investments and against leisure, consumption, and unpro-ductive investments. Lower top marginal income tax rates and less pro-gressive income taxation would also greatly discourage tax avoidance andreduce tax evasion. In a word, the popular supply-siders believe that theshort-run price elasticity in the behavior of various economic agents is ex-tremely large. Feldstein, therefore, rightly points out, "what distinguishedthe new [popular] supply siders from the traditional [basic] supplysider . . . was not the policies they advocated, but the claims that theymade for those policies."13

It is this elasticity optimism that also underlies the "Laffer curve," sup-ported by all popular supply-siders. According to its author, ArthurLaffer, government revenues first rise with tax rates (as long as tax ratesare in the "normal range"), reaching a peak (the "Laffer hill"), and thenfalling (as tax rates rise to a "prohibitive range").14 A reduction of incometax rates from the prohibitive range is believed by Laffer and all leadingpopular supply-siders to result in a very large expansion of economic activ-ity and tax compliance, and hence income tax revenues.15

Thus, the popular supply-side economist aims to reduce the "excise-ness" (relative price effects) of income tax rates.16 As high marginal in-come tax rates have large negative substitution effects, the popular supply-siders would like particularly to see the marginal rates of personal incometax reduced and expect significant increases in output and real incomes

13Feldstein (1986, p. 27).14For an elaboration of the Laffer curve, see Canto, Joines, and Laffer (1983, pp. 2-24) and

Wanniski (1983, pp. 97-115). The Laffer curve is not essential to the basic premise of supply-side economics that leaner governments are better.

15Comments on the Laffer curve can be found in Hemming and Kay (1980), Blinder (1981),Moszer (1982), Henderson (1982), Buchanan and Lee (1982), Fullerton (1982), Mirowski(1982), and Malcolmson (1986). For a test of the validity of the Laffer curve in one developedcountry and two developing countries, see Feige and McGee (1983) and Ebrill (Chapter 7),respectively. Also see Wanniski (1983, Chapter 11).

16See Kemp (1981, p. 68). Comments on supply-side economics can be found in Tobin(1982).

©International Monetary Fund. Not for Redistribution

SUPPLY-SIDE TAX POLICY: A SUMMARY 11

even in the short run.17 They believe that an income tax cut would actuallyincrease tax revenue (by moving the economy back from the "prohibitiverange" of the Laffer curve) rather than raise the budget deficit, because itwould unleash an enormously depressed supply of labor and work effortand reduce tax evasion. And even if a tax cut did lead to an increasedbudget deficit, that would not "crowd out" resources available for privateinvestment and capital formation, because a tax cut would significantlyraise the private savings rate by increasing the after-tax rewards to savers.Nor would the increased budget deficit result in inflation, because in-creased nominal demand resulting from a budget deficit would bematched by an increased supply of goods and services, resulting from in-creased incentive to work and save, due to the tax cut.18

To conclude Section I, the tax systems as well as economic and otherconditions of developing countries are quite different from those of devel-oped countries. Therefore, the views of popular supply-side economists ontax policy, espoused primarily in the context of developed countries, aswell as the validity of market and other assumptions made by basic supply-side economists, need to be scrutinized closely before appropriate conclu-sions can be drawn regarding the nature of tax reforms that would be ofrelevance to developing countries.

II. The Scope of the Studies and Overall Conclusions

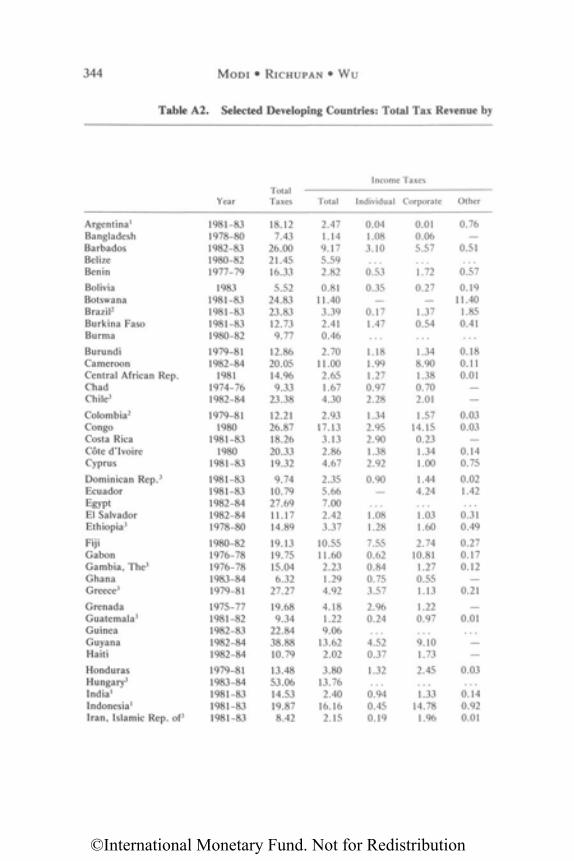

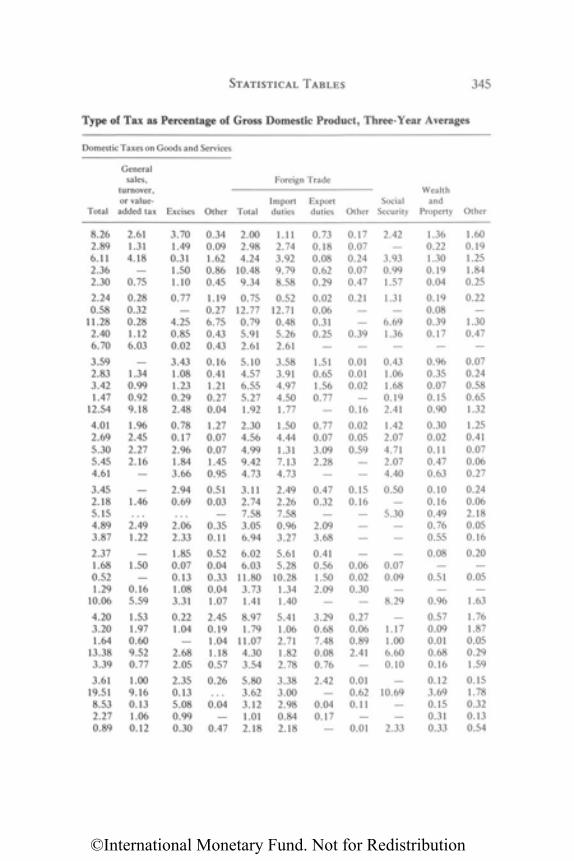

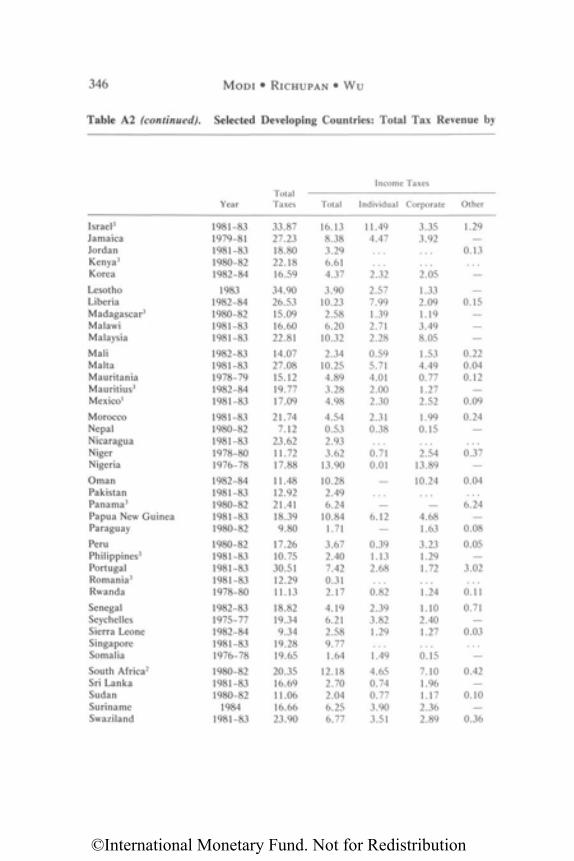

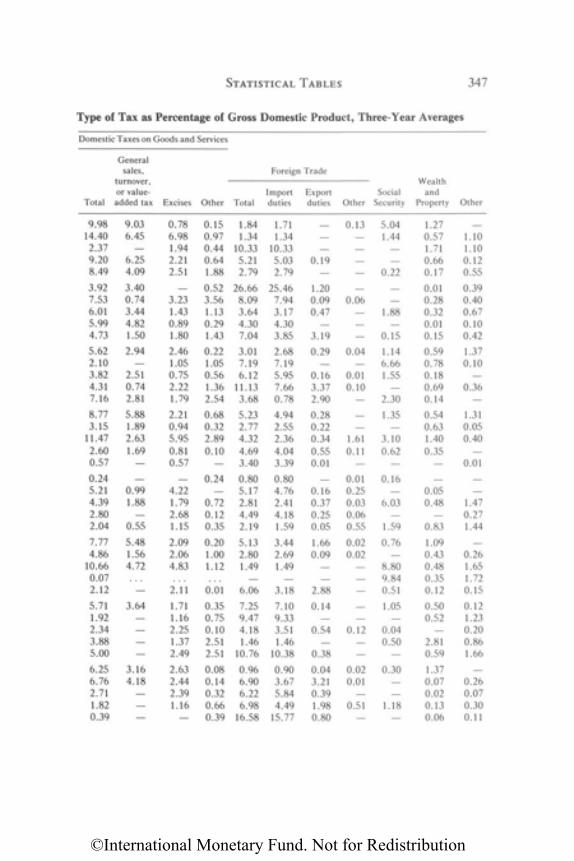

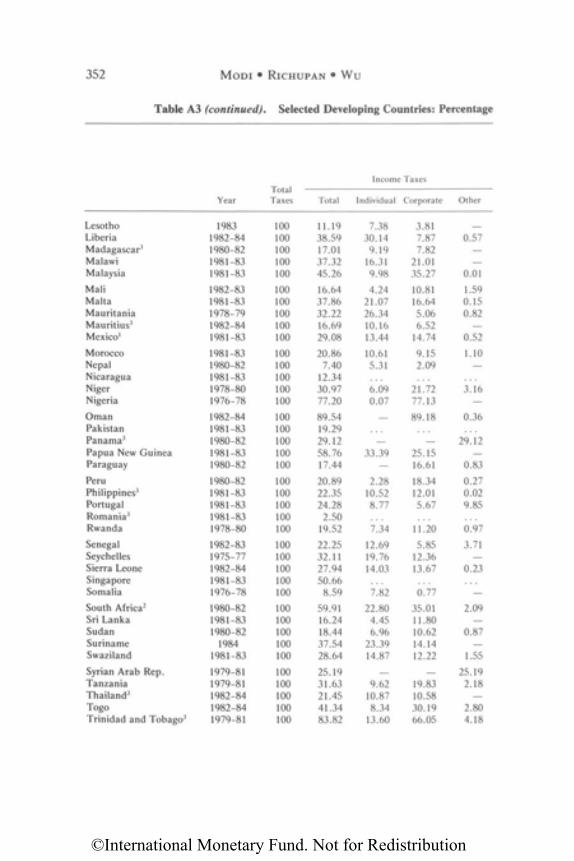

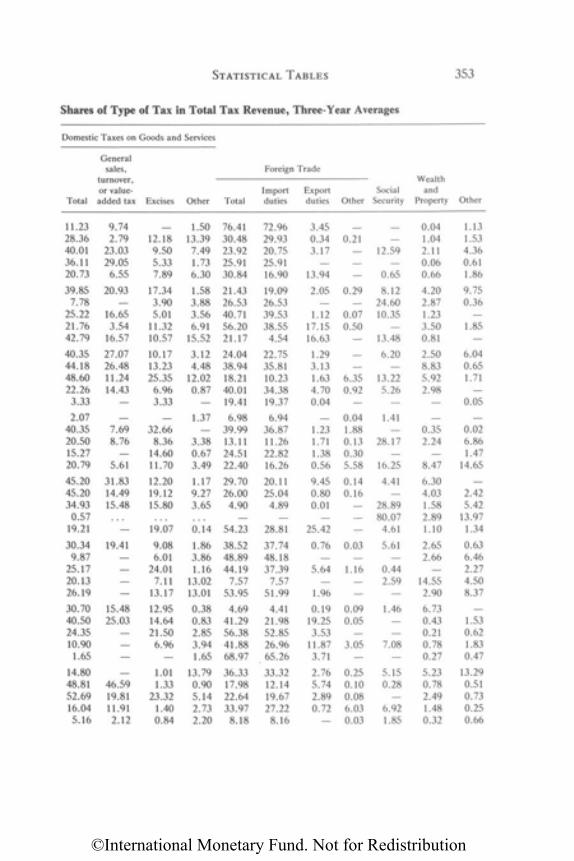

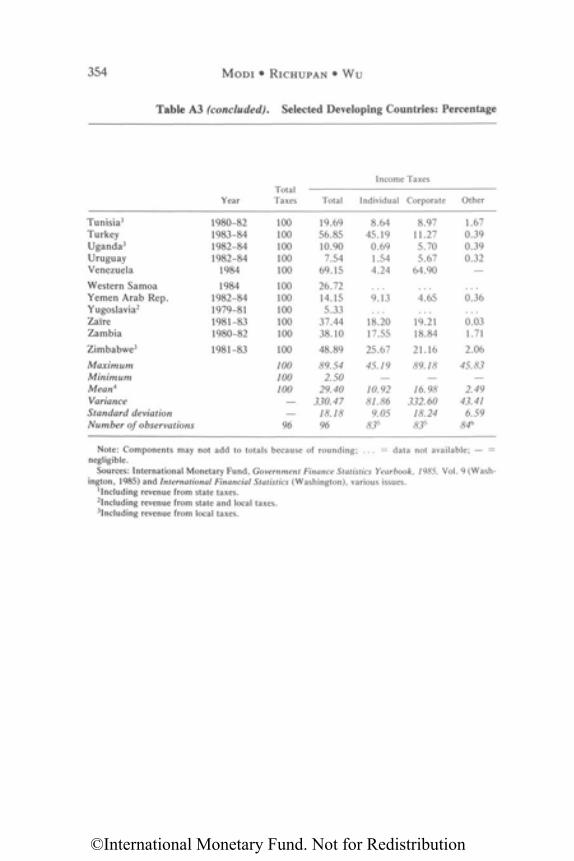

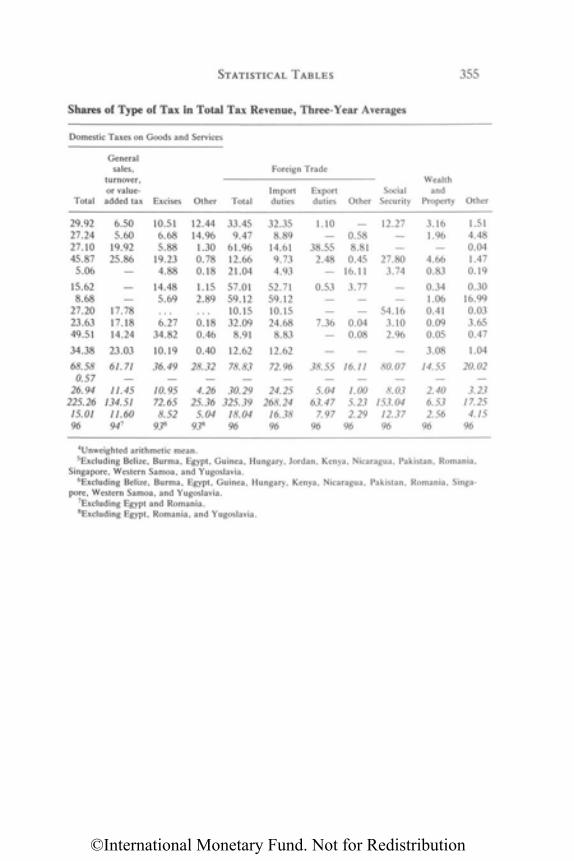

Sections II and III highlight the findings and conclusions of individualstudies included in this book. However, it is important to define the scopeof the studies as well as clarify what the studies do and do not cover. Mostdeveloping countries depend on import duties and domestic commodity

17Wanniski (1981, p. 43) and Ture (1982a, p. 26). The nominal marginal tax rates areimportant for incentives, while the average effective tax rates are important for their implica-tions about the size of government and income distribution. Both Wanniski and Kemp wouldlike to see the marginal income tax rates ultimately range between 5 percent and 35 percent.See Wanniski (1981, pp. 45-46 and p. 49) and Kemp (1981, p. 52). Both of them favor thetop rate of 35 percent, which is merely expression of an opinion and is not derived from anytheoretical or economic arguments. The popular supply-siders do not want, as one mightthink, to do away with progressivity in the marginal rates of income taxation in the short run,although they would probably prefer a flat but low rate income tax in the long run. In theiropinion, excessive progressivity of tax rates is often evaded and avoided, and never achievesthe intended reduction in income inequalities.

18Keynes also believed in tax cuts, but only if they were not accompanied by expenditurecuts, so as to make fiscal deficits stimulative during recessions. Popular supply-siders, on theother hand, do not consider the size of the budget deficit to be of any macroeconomic rele-vance. See also Bechter (1982).

©International Monetary Fund. Not for Redistribution

12 VED P. GANDHI

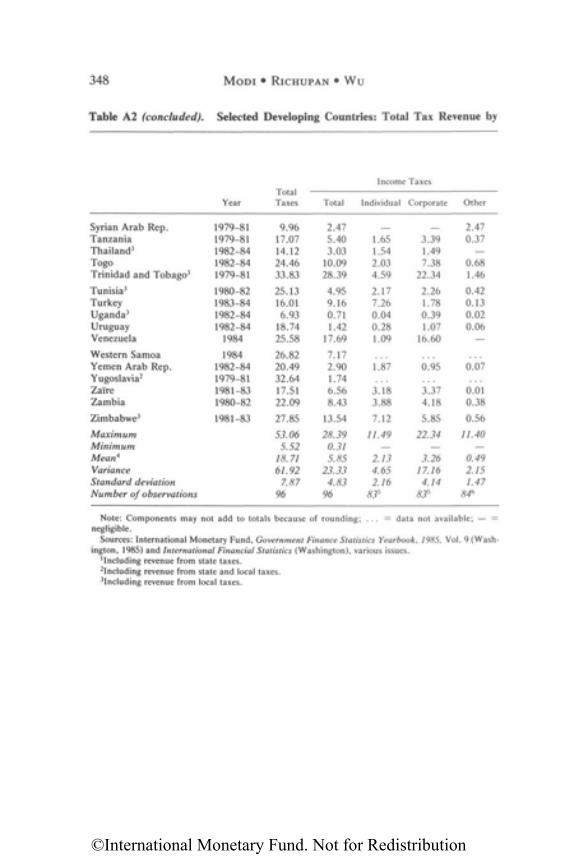

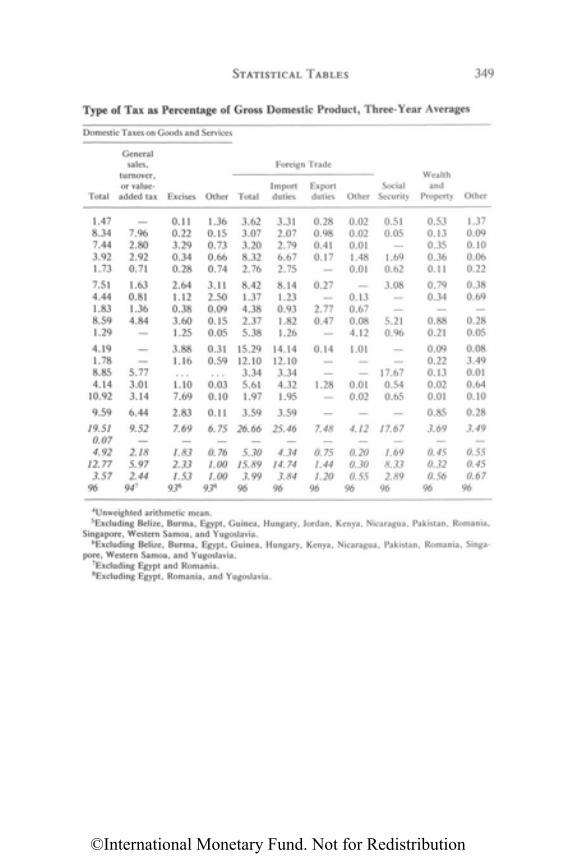

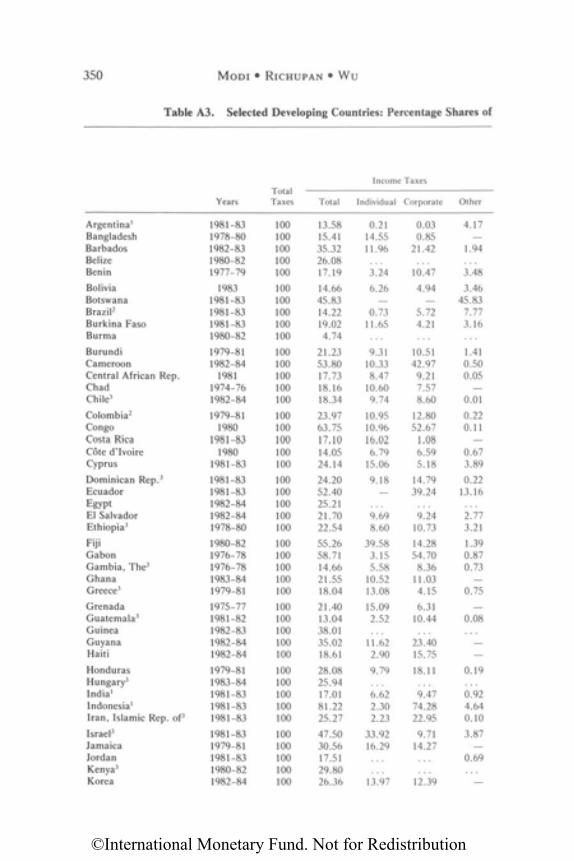

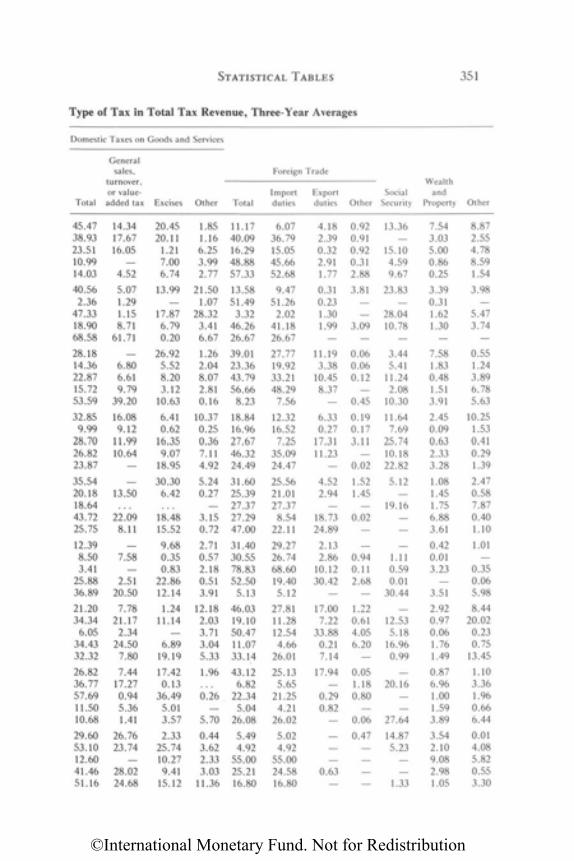

taxes to a significant extent (see Tables A2 and A3 in the Statistical Ap-pendix) and some countries depend heavily on mineral taxation. Thesetaxes have not been analyzed from a supply-side perspective in this book inview of existing research on the subject.19 The supply-side effects of exces-sive effective protection, implicit in the high and complicated structures ofimport duties prevalent in most developing countries, are well known inthe literature on international trade and development economics. Also wellknown are their negative effects on the efficiency of resource allocation,export prospects, and growth rates, especially when they are combinedwith quotas and other trade restrictions, as is also usually the case in devel-oping countries.20 Various studies carried out by the World Bank and theFund have also convincingly alluded to the distortionary effects and anti-export biases of high import duties. Papers produced in the Fund's FiscalAffairs Department have reviewed natural resource taxation and excisetaxation in developing countries, respectively, from the viewpoint of effi-ciency.21 The studies prepared under this research project, therefore, con-centrated primarily on the economic effects of direct taxes, viz., incometax, corporation tax, and export duties, and attempted to review their opti-mality in the real (second-best) world prevalent in developing countries.22

19Nontax revenue policies of the government, including prices charged for various govern-ment services as well as outputs of autonomous public enterprises, can also have taxes orsubsidies implicit in them. The supply-side effects of such implicit taxes, if any, were notanalyzed under the research project either.

20For a theoretical exposition of and empirical evidence on this see Corden (1974, 1975).Empirical work on the effect of foreign trade regimes on the economic development of tendeveloping countries has been carried out under the auspices of the National Bureau ofEconomic Research. The results of this work are summarized in Bhagwati (1978) andKrueger (1978). See also Balassa (1971).

21See Palmer (1980), Nellor (1984), and Ferron (1986).22Given the importance of foreign investment to the growth of most developing countries,

the effects of tax policies on foreign investment should have been covered. However, this wasomitted because experience shows that foreign investment decisions are usually affected by anumber of economic (e.g., market size, availability of raw materials and skilled manpower),financial (e.g., development of capital market, registration and financial disclosure require-ments for mobilizing domestic equity), institutional (e.g., entry and ownership regulations),and political factors, and tax policy is frequently of lesser importance in these decisions. Tothe extent tax policy is important, however, it seems from the survey of the literature that eachdeveloping country's tax policy will have to be tailor-made to suit its special circumstances. Inthis process, all tax rules and tax incentives (not tax rates alone) affecting the net return onretentions in, and remittances from, the "host" developing country will have to be reformed.The tax policies of neighboring countries and of countries in similar situations will have to betaken into account. Full account will also have to be taken of the tax systems of the "home"country of potential investors, including the availability of tax deferral, tax sparing, and for-eign tax credit provisions. The scope of the double taxation treaty agreements between the

©International Monetary Fund. Not for Redistribution

SUPPLY-SIDE TAX POLICY: A SUMMARY 13

Although the research project focused primarily on the tax policy recom-mendations of the popular supply-side economists and their relevance todeveloping countries, some comments on the objective of efficient resourceallocation emphasized by all supply-side economists seem necessary. De-veloping countries have some very special circumstances which make theneoclassical model (achievement of efficient allocation of resourcesthrough primary reliance on private initiative and enterprise) underlyingsupply-side economics less than fully valid. Many of these countries, espe-cially the low-income ones, suffer from a number of disadvantages, such as(1) highly skewed income distribution; (2) "population trap," that is, largeand rapidly growing population with high levels of absolute poverty; (3)large structural unemployment, both rural and urban, with little hope of asolution for want of appropriate labor-intensive technology; (4) dominanceof agriculture, particularly less-productive peasant agriculture, sometimesresulting from existing land tenure systems; (5) unstable prices of exportcommodities; and (6) lack of adequate economic infrastructure, educa-tion, and human resources.23 Thus, to the extent that the governments ofsuch countries have to concern themselves with objectives other than theefficient allocation of given resources, for example, income redistribu-tion,24 economic stabilization,25 or the creation of social and economic in-frastructure for economic growth,26 the supply-side approach generally hastended to be seen as being of limited relevance to these countries. Simi-larly, to the extent that most factor, product, and financial markets areinadequately developed in these countries, their development by the gov-ernment has been considered an important objective in itself. As a result,the role of the state has been seen as far larger than that "implicit" in thesupply-side approach.27 Finally, as Shome (Chapter 12) stresses, savings

"host" country and the "home" country will also need to be considered. Finally, the nature offoreign investment (whether it is "footloose" or "country-specific") and its volatility as well asthe existence of tax havens will also be relevant. For the importance of some of these factorssee International Monetary Fund (1985b). Also see Ebrill (Chapter 3).

23Cf., Todaro (1985, especially Part II).24There is ample evidence that the distribution of income is far more skewed in developing

countries than in developed countries. See Lecaillon and others (1984, especially Table 9and p. 41).

25See Killick and others (1984, especially Part I).26Cf., World Bank (1980, especially pp. 36-39 and Chapters 5 and 6).27As Todaro (1985) has pointed out, "whether one likes it or not, Third World governments

must inevitably assume a more active responsibility for the future well-being of their countriesthan the governments of the more developed nations. . . . Central to this new role will beinstitutional and structural reform in the fields of land tenure, taxation [to mobilize resourcesfor investment, lacking private financial markets], asset ownership and distribution, educa-

©International Monetary Fund. Not for Redistribution

14 VED P. GANDHI

alone are not enough for growth, they require "complementary factors" ifthey are to become investment in reality, especially the removal of externalconstraints (such as foreign exchange availability) and domestic con-straints (such as expanding the size of the market, facilitating the transferof technology, and establishing adequate financial intermediary institu-tions).28 Also, growth by itself would not mean development unless it isaccompanied by certain institutional reforms involving human capital for-mation and the creation of essential social and economic structure, agri-cultural reforms, population control, etc. Growth and development of de-veloping countries are, thus, objectives that are much more complex thanensuring the efficient allocation of given resources only, and they call for amuch bigger role of the state than supply-side economists are perhaps will-ing to concede.

The broad conclusion of the research project is that the supply-side taxpolicy which focuses on marginal income tax rates alone (the popular ver-sion) is too narrow and is of limited relevance to many developing coun-tries, especially the low-income countries. The view of supply-side tax pol-icy which stresses broadening the tax base and rationalizing the rates ofnot only income tax but also of other taxes so as to remove all tax-relateddistortions (the basic version) is of greater relevance to such countries.29 Inaddition, the research project has established that the impact of the taxsystem of a developing country on the potential for its development de-pends on a variety of factors such as (1) the reliance of the tax system onincome-related taxes; (2) the interaction between tax rates, the tax base,specific tax incentives for savings and capital formation, and the tax ad-ministrative capacity, as they each affect savers and income earners; (3)the rate of inflation and the degree of inflation-indexation of depreciationand other provisions of the tax system, which determine the effective taxburdens of producers and income earners and their after-tax rewards; (4)the interaction between tax policy and other macroeconomic policies of thegovernment, which affects the prices of foreign exchange, capital, and la-bor; and (5) the degree of imperfection in or the level of development of thelabor market, the capital market, the foreign exchange market, financial

tional and health delivery systems, credit rationing, labor market relations, pricing policies,the organization and orientation of technological research and experimentation . . . and thevery machinery of government and planning itself" (pp. 526-27).

28Cf., Streeten (1979, pp. 21-52).29Recent income tax reform efforts in Indonesia, India, the Philippines, and Jamaica and a

few other developing countries reflect this strategy. See Gillis (1985), India, Ministry of Fi-nance (1985), Yoingco (1986), and Bahl and others (1987) for descriptions of these efforts.

©International Monetary Fund. Not for Redistribution

SUPPLY-SIDE TAX POLICY: A SUMMARY 15

institutions, credit markets, etc. As is shown by the papers that follow,these factors are of fundamental importance and developing countrieshave some very special circumstances with respect to all of these, so thatthe advice of lowering the marginal income tax rates must be examined inthis wider context. Once this approach is taken, the high degree of elastic-ity and growth optimism, which the popular supply-siders frequently takefor granted subsequent to a reduction of high marginal income tax rates,must be moderated in the special circumstances of the developingcountries.

More specifically, the research project has established that while thepopular view of supply-side tax policy (that the height of nominal tax ratesmatters for incentives) has to be valid for developing countries, other taxand nontax factors are equally important, if not more important forgrowth and development. While tax policy undeniably affects the behaviorof taxpayers, factors such as inflation and rigid nontax policies of develop-ing countries are frequently more severe disincentives to economic agents.Similarly, though labor supply, financial savings, and investment in devel-oping countries do respond to economic incentives and tax policy, they arefrequently affected by market imperfections and institutional factors aswell and their price elasticities tend to be low in the short run. In relation toincome taxation in particular, the finding is that the overall reliance ofdeveloping countries, particularly the low-income ones, on this tax is ex-tremely low. Hence, any policy reform in the area of income taxation can,at best, be expected to have a limited impact on the growth of the economy.Furthermore, while the present nominal levels of personal income taxationare high in many developing countries, their negative economic effects oncapital incomes are frequently neutralized, partially if not fully, by the verygenerous tax incentives granted to savers and investors. Indeed, loweringmarginal personal income tax rates, while at the same time broadening thetax base and removing the liberal tax incentives in order to contain theshort-run revenue loss, in the context of many developing countries couldwell lead to an increase in the tax burden on savings and investments.There is also some evidence that in developing countries, given their infla-tionary situations, the disincentive effects of high rates of taxes other thanindividual income tax, such as of export duties, and certain provisions ofcorporation tax, such as historic cost depreciation, first-in-first-out basisof inventory valuation, and other provisions, are far greater than those ofhigh marginal income tax rates on individuals. In light of all this, severalefficiency and growth-oriented tax reform ideas have emerged from theresearch project, which are consistent with the views of basic supply-sidetax policy. These are highlighted in Section V, below.

©International Monetary Fund. Not for Redistribution

16 VED P. GANDHI

III. Validity and Relevance of PopularSupply-Side Tax Policy

This section summarizes the findings and conclusions of the papers con-tained in Part II of the book which assess the validity and relevance of thepolicy prescriptions of popular supply-side economics in the context of thespecial circumstances of developing countries.

Validity of Popular Supply-Side Tax Policy

The validity of the popular supply-side tax policy prescription for devel-oping countries requires positive answers to the following five questions.

• Are labor supply, savings, and investment highly price-sensitive?• Do income tax policies (tax rates combined with liberal tax incentives

for savings) significantly reduce savings, especially the availability offinancial savings?

• Do income tax policies (tax rates combined with generous tax incen-tives and other tax provisions affecting investors) significantly reduceinvestment?

• Do high and progressive income tax rates significantly increase in-come tax evasion?

• Have government revenues increased significantly in the short run, inline with the Laffer curve, when top marginal income tax rates havebeen reduced?

A positive answer to all these questions in the institutional and economiccircumstances of the developing world would imply that the tax policy pre-scriptions of the popular supply-side school are valid and require carefulconsideration by the policymakers of developing countries. Six papers in-cluded in Part II of this book attempt to answer the above-mentioned fivequestions, while the seventh paper reviews some econometric evidence onthe interrelationship between reliance of developing countries on incometaxes and their growth rates.

Price Responsiveness of Labor Supply, Savings,and Investment

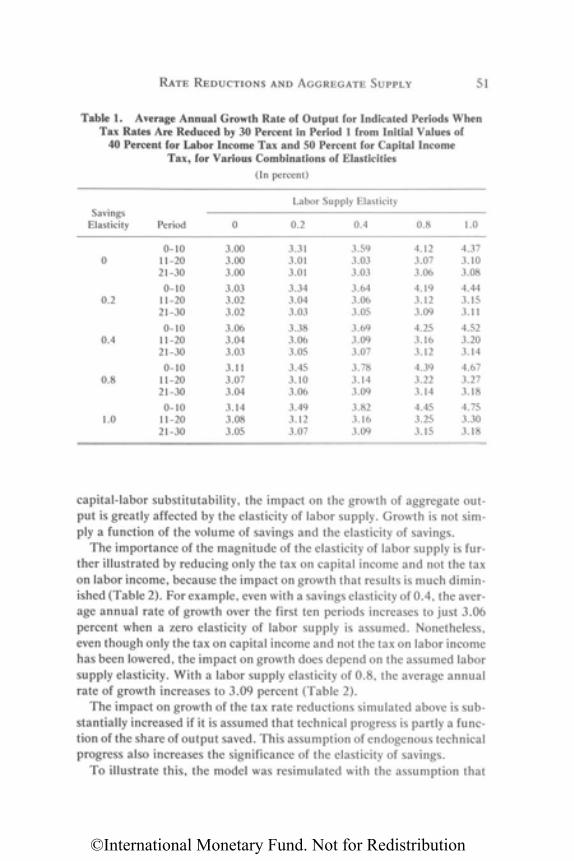

Using some simple macroeconomic models, Mackenzie (Chapter 2) es-tablishes that, theoretically, a reduction of income tax rates can have ag-gregate supply effects as well as effects on aggregate demand and liquidity.However, he also shows that the supply effects are far less significant thanthe demand and liquidity effects unless the income tax reductions are dras-tic and the price elasticities of labor supply and savings are very high. Toillustrate his point, he takes the readily available empirical estimates of

©International Monetary Fund. Not for Redistribution

SUPPLY-SIDE TAX POLICY: A SUMMARY 17

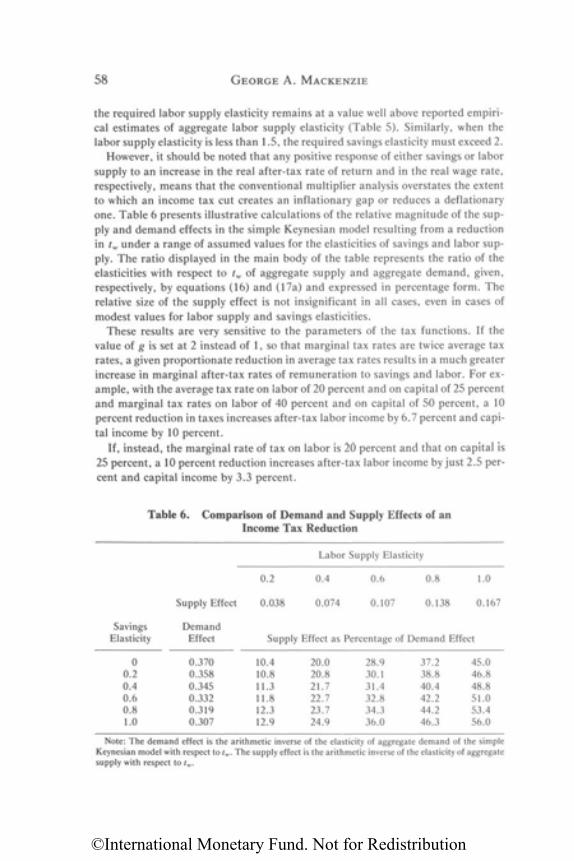

elasticities for a well-integrated and well-functioning competitive marketeconomy as that of the United States. (Economies of some middle-incomedeveloping countries may well have similar features.) Even for such aneconomy, he establishes that for the income tax cut to be self-financing,labor supply elasticity will have to be 15, when savings elasticity is assumedto be within the limits of reported empirical research. He shows that if thelabor supply and savings elasticities are low (as they, in fact, are for theUnited States where savings elasticity has been estimated by some studiesto be between 0.2 and 0.4 and labor supply elasticity has been estimatedto be around 0.2), the increases in the rate of growth of real output wouldnot be particularly great in the first ten years following a significant reduc-tion of income tax rates. He estimates that a 20 percent across-the-boardreduction of income tax rates for both capital and labor, given a savingselasticity of 0.4 and a labor supply elasticity of 0.2, and other economicparameters similar to those of the U.S. economy, will raise the averageannual growth rate of 3 percent over a ten-year period to at most 3.14 per-cent. In the extreme case, when both elasticities equal 1.0 and the tax rateon labor incomes is reduced by 20 percent and that on capital incomes by50 percent, the average annual growth rate of 3 percent over a ten-yearperiod increases to 3.77 percent. Mackenzie, thus, concludes from his the-oretical analysis that some positive supply-side effects are certain from anacross-the-board reduction of income tax rates but how large the effect willbe will depend upon the price elasticities of labor supply, savings, and in-vestment. The size of these elasticities is an empirical question and mustdepend on the structural features of the economy or economies in question.However, on balance, the potential impact of sweeping income tax ratecuts on the growth rates of a representative economy of the type some mid-dle-income developing countries may have does not seem to be very high.

Ebrill (Chapter 3) surveys the empirical evidence on the price respon-siveness of labor supply, savings, and investment in developing countries.He finds a dearth of solid empirical work and the direct evidence on priceresponsiveness to be rather limited. He, therefore, looks for indirectevidence.

On labor supply, he reviews studies on subjects such as rural-urban mi-gration, the effects of minimum wage laws, and the determinants of earn-ing functions and concludes that "some indirect support" does exist for theproposition "that supply-side considerations have a role in the determina-tion of the equilibrium wage" (p. 67). He also concludes that "althoughthe empirical work supports the existence of a well-defined aggregate laborsupply function, it appears not to be very elastic" (p. 67). In rural areas, inparticular, the evidence is that labor supply decisions are determined by avariety of factors other than the wage rate (labor markets are frequently

©International Monetary Fund. Not for Redistribution

18 VED P. GANDHI

interlocked with other factor markets and widespread land-lease contractsand sharecropping arrangements make for imperfect labor markets). As aresult, the labor supply function is price inelastic.

On savings, he finds that savings data in developing countries are veryinadequate and that the development economics literature has dealt littlewith the question of interest elasticity of savings. Ebrill, therefore, seeksout indirect evidence again. Most available estimates of consumption func-tions in developing countries, for example, reveal that aggregate savingsare affected more by income as well as by noneconomic factors, such asdemographic factors, income distribution, life span, occupational pat-terns, and urban-rural distinction, than by interest rates. However, theempirical literature evaluating the effects of financial repression (artifi-cially low interest rate ceilings) widely prevalent in developing countriesdemonstrates that financial savings may be sensitive to changes in interestrates. He, therefore, concludes that "even though aggregate savings maynot be very interest-sensitive, the allocation of that aggregate between con-ventional financial assets and alternatives such as curb market funds andworks of art is indeed responsive to economic incentives" (p. 74). Ofcourse, changes in income tax rates may be powerless in influencing eventhe allocation of aggregate savings if financial policy is "wrong."

On investment, Ebrill finds much of the empirical evidence from devel-oping countries to be against the neoclassical framework which explainsinvestment simply in terms of the cost of capital. Foreign investment is saidto be influenced by factors such as the presence of natural resources,proven record of economic performance of a country, threat of expropria-tion, degree of urbanization, and the availability of advanced infrastruc-ture rather than by the availability of fiscal incentives. Domestic invest-ment, on the other hand, is shown to be influenced by factors such as theavailability of domestic savings, retained earnings of businesses, public in-vestment outlays in support of private productive activity, trade policy,and the degree of protection, and, in the specific case of agricultural in-vestment, by distortions associated with price support systems and market-ing boards. Ebrill, therefore, concludes that while investors do react toeconomic incentives, "investment [in developing countries] is influencedby a number of factors" (p. 81).

Ebrill sums up his findings on the subject of price responsiveness in de-veloping countries as follows: "Although the empirical literature examin-ing the impact of tax policy on labor supply, savings, and investment leavesmuch to be desired, it nonetheless appears that changes in tax policy willhave some effects. The behavior of these aggregates appears, however, tobe determined as much by other elements. . . . Given the existence ofwidespread market failure in many developing countries, the impact of

©International Monetary Fund. Not for Redistribution

SUPPLY-SIDE TAX POLICY: A SUMMARY 19

changes in tax policies may be quite difficult to predict. . . [and] it may bethe case that a more promising supply-side approach might be one thatalso aims at alleviating the most obvious sources of market failure" (p. 82).

Tax Policies and Financial Savings

What is the optimal tax policy toward financial savings in developingcountries and is the sharp reduction of marginal income tax rates its mostimportant element? In Chapter 4, Ebrill reviews the existing literature insearch of a theoretical answer to these questions and finds that the litera-ture is inconclusive; in addition, the literature does not adequately accom-modate the special circumstances of developing countries. He identifies atleast four characteristics of developing country situations (they exist in alldeveloping countries although their magnitudes may vary): (1) artificiallylow interest rate ceilings which, given the rates of inflation, frequentlyresult in financial repression; (2) relatively underdeveloped financial insti-tutions and capital markets; (3) the existence of unorganized capital mar-kets; and (4) the use of compulsory savings schemes by the governments.

Ebrill then develops a modified illustrative optimal tax framework totake into account some of the characteristics of the financial structures ofdeveloping countries, in particular the existence of financial repressionand curb markets. To start with, his model shows that, under normal cir-cumstances, the optimal tax on financial savings depends on its own-priceelasticity. While the evidence indicates that financial savings are interest-elastic to some degree, he admits that no useful point estimates can bemade of the relevant price elasticity and, therefore, of the optimal taxrates. Once, however, the special circumstances of developing countriesare taken into account, the model suggests that the optimal taxation offinancial savings changes. If the degree of financial repression in a devel-oping country is large, and if for some reason this distortion cannot beremoved, his modified optimal tax framework indicates that "a subsidyrather than a tax is appropriate" (p. 106). In turn, if the use of subsidies isprecluded for fiscal or other reasons, then "consumption . . . is more ap-propriate than income as a tax base" (p. 106).

Ebrill argues that the optimal tax treatment of financial savings dependscritically on the degree of financial repression, which varies widely bothacross countries and over time. "Accordingly, there is no single recom-mended policy such as reducing marginal tax rates. Each country has to beconsidered individually" (p. 108). Depending on the particular countrythat is under consideration, "the optimal tax treatment of financial sav-ings runs the gamut from subsidies to substantial taxation" (p. 92).

©International Monetary Fund. Not for Redistribution

20 VED P. GANDHI

Tax Policies and Investment

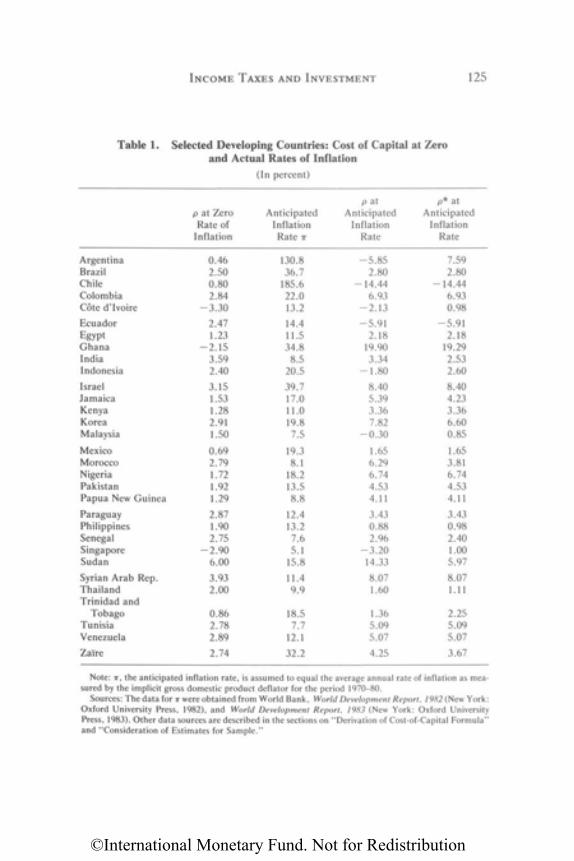

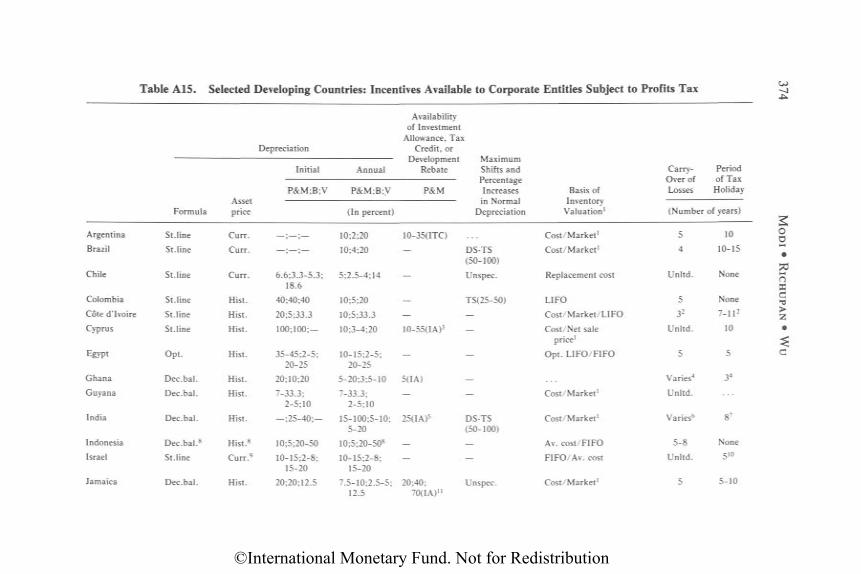

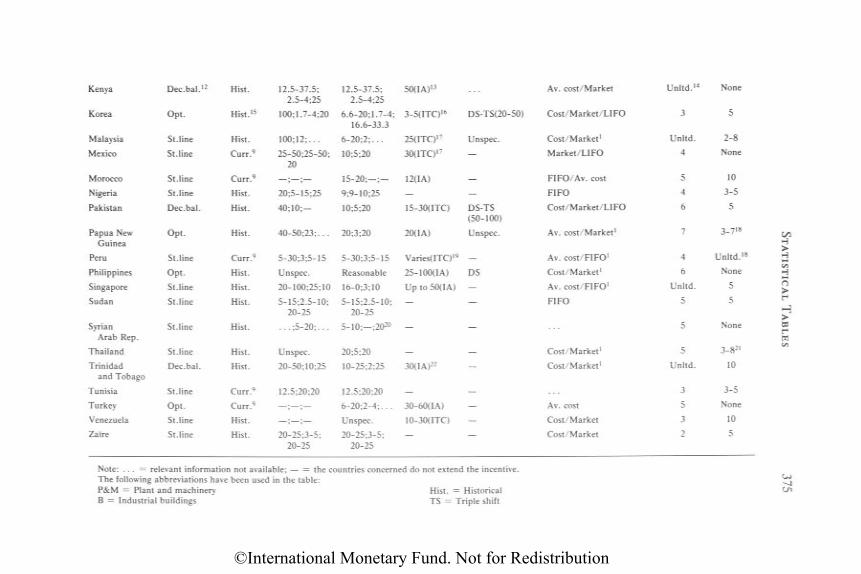

The rate of tax affects the cost of capital and, therefore, affects the levelof investment—this much is built into the neoclassical framework of in-vestment behavior. In many developing countries, the nominal rate of cor-poration income tax is high but, as Table A15 in the Statistical Appendixshows, tax incentives and deductions for investment are relatively liberaland it is the combination of both of these, along with the rate of inflation asit interacts with capital allowances, capital gains, and interest deductibil-ity provisions, that determines the cost of capital. In Chapter 5 Ebrill re-views the income and corporate tax structures of 31 developing countriesand makes cost-of-capital estimates. His results show that "Indeed . . .the tax system in many countries subsidizes the cost of investment at lowinflation rates." At high rates of inflation, on the other hand, their tax sys-tems (especially those featuring depreciation allowances and inventory val-uations based on historic costs) are such as to be a "source of investmentdisincentives." For several countries with very high inflation rates, he findsthe disincentive effects to be pronounced (p. 126).

Relating the share of gross domestic investment in gross domestic prod-uct (GDP) to his cost-of-capital estimates for 31 developing countries,Ebrill shows that while after-tax cost of capital has a significant impact oninvestment levels, other variables, especially the rate of inflation and thegrowth of exports, are equally important which, at least, "raises the ques-tion of which is the most promising path for policy to take" (p. 132).

He concludes, therefore, that strong policy recommendations concern-ing the effectiveness of income and corporate tax rate reductions alone forencouraging investment in developing countries should be resisted and at-tention should be paid to controlling inflation and alleviating distortions toexports. All this suggests "that supply-side based tax reform proposals[advocated by popular supply-siders] are only of limited use" (pp. 133-34)and additional tax reforms, such as indexation of depreciation allowancesor taxing corporations on a cash flow basis (i.e., full expensing of all in-vestment and disallowing the deductibility of interest payments on debt),are equally important.

Progressivity and Income Tax Evasion

The effect of high and progressive taxation on income tax evasion iscommonly taken for granted and with ample justification. Richupan(Chapter 6) surveys the theoretical and empirical literature on income taxevasion to locate the basis of this perceived relationship. He concludes that"the theoretical literature does not support the claim that an increase inthe tax rate will lead to an increase in tax evasion" (p. 148) or "that a

©International Monetary Fund. Not for Redistribution

SUPPLY-SIDE TAX POLICY: A SUMMARY 21

progressive tax rate schedule stimulates tax evasion" (p. 151). The empiri-cal studies on the subject are, however, sketchy and indirect and do notyield a definitive conclusion on the subject.

Richupan, however, finds that the theoretical literature containsstronger conclusions regarding the role of other tax and nontax factors inencouraging income tax evasion. In particular, high penalty rates and highprobability of detection are shown to have a negative effect on tax evasion.Income tax evasion is also shown to be strongly influenced by nontax fac-tors such as the type of income and perception of fiscal equity. In the spe-cial circumstances of developing countries, nontax factors such as pricecontrols, government regulations, and civil service salaries, are all shownto contribute positively to income tax evasion.

Thus, Richupan ends up doubting the effect that a reduction of incometax rates alone or even income tax reforms generally will have on the degreeof income tax evasion which is far higher in developing countries than indeveloped countries.

Evidence on the Laffer Curve

One important assumption of popular supply-side economics is that iftax rates are sufficiently high (the "prohibitive range") then a reduction intax rates would lead to an increase in tax revenues. The implicit assump-tion in this relationship is that the substitution effect of a tax cut is positiveand the factor elasticities are very large.

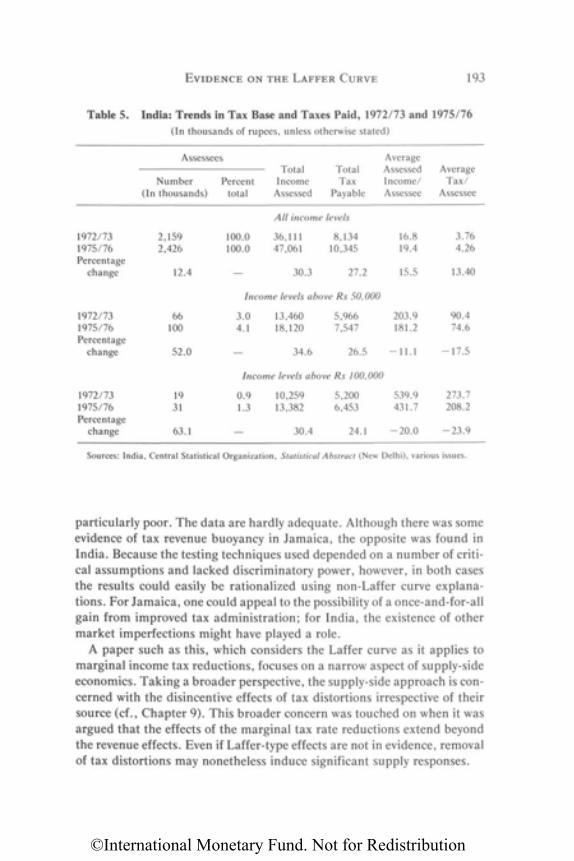

Ebrill (Chapter 7) tests the validity of this assumption and the Laffercurve with data from Jamaica and India, two developing countries that hadvery high marginal income tax rates and where in the 1970s the top mar-ginal income tax rates were significantly reduced. He points out that anideal test of the Laffer curve would involve relating income tax yield amongthe highest income groups with proxies for tax rate reductions and otherexplanatory variables. Using the data for PAYE taxpayers in Jamaica be-tween 1979 and 1981 only, and adjusting it for changes in income distribu-tion, real growth rates, and inflation over time, Ebrill concludes that "dataare consistent with the existence of a Laffer curve in Jamaica" (p. 188);however, he mentions many reservations about this conclusion. Data avail-ability is better for India and Ebrill's analysis of the effects of a marginalincome tax reduction introduced in that country in 1975 leads him to con-clude that "the data on India, at least for the years selected . . . do notsupport the Laffer curve hypothesis" (p. 192).

Ebrill recognizes the limitations of his methodology, which had to betailored to use the available (rather poor quality and inadequate) data, andadmits that existence of market imperfections, improvements in income

©International Monetary Fund. Not for Redistribution

22 VED P. GANDHI

tax administration, and other variables may account for his results. Never-theless, he concludes that "assertions to the effect that developing coun-tries are operating in regions of the Laffer curve, where tax rate reductionswould lead to revenue increases, should be treated with caution" (p. 175)and that "the results [obtained for Jamaica and India] could easily be ra-tionalized using non-Laffer curve explanations" (p. 193). He, therefore,cautions that none of his results can be seen as a complete endorsement ofthe narrow (popular) supply-side approach (marginal income tax rate re-ductions) and that the broader (basic) supply-side approach (removal oftax distortions irrespective of the source) may still induce significant sup-ply-side response.

The answers to the five questions set out at the beginning of this subsec-tion can be summed up as follows. Although there is some indirect evi-dence that the assumptions underlying the popular supply-side tax policymay be valid for developing countries, the research has highlighted manyother factors, special to the circumstances of developing countries, whichmay be of equal or greater importance to the expansion of labor supply,savings, and investment as well as the reduction of income tax evasion,considered desirable by supply-side economists. In particular, the researchshows that developing countries need to pay attention to the developmentof labor and capital markets and to removing other economic policy distor-tions such as high minimum wages, overvalued exchange rates, interestrate ceilings, and inflationary financing of the budget. Even in the area ofincome tax policy, the alternatives of inflation-adjustment of depreciationallowances and inventory valuations, conversion of income tax to someform of consumption tax (i.e., the exemption of savings or, at least, a mod-eration of the tax burden on capital incomes), and the replacement of acorporation tax based on profits by a tax based on cash flow may affectsavings and investment more significantly than a simple reduction of mar-ginal income tax rates. Similarly, raising income tax penalties and increas-ing the probability of detection of income tax evaders, through legislativeand administrative improvements, may also be more effective in reducingincome tax evasion in developing countries than just lowering marginal taxrates and reducing the progressivity of income taxation.

Thus, the conclusion of the research is that it is not that the popularsupply-side tax policy prescription of reducing the excessively high mar-ginal income tax rates, in the interest of improving growth prospects, isinvalid but that there are other important tax and nontax determinants ofthe behavior of economic agents and economic growth in developing coun-tries. The fact that developing countries are quite heterogeneous and thattheir governments must, at this stage of development, pursue a variety ofobjectives (including redistribution, economic stabilization, and mobiliz-

©International Monetary Fund. Not for Redistribution

SUPPLY-SIDE TAX POLICY: A SUMMARY 23

ing revenue for providing essential social and economic infrastructure andits maintenance) further complicates the task of arriving at a unique con-clusion about the levels and structure of taxation that will be valid for alldeveloping countries. Advice on tax policies must, therefore, struggle withthis multiplicity of objectives; in doing so it must also take into account theuses to which government revenues are put and assess their economic andsocial necessity.30

Relevance of Popular Supply-Side Tax Policy

In assessing the relevance to developing countries of the popular view ofsupply-side tax policy, one needs to assess the reliance of developing coun-tries on income taxes, in particular (1) the relative importance of incometax revenues in such countries; (2) the height of their income tax rates; and(3) the scope and generosity of various tax reliefs to savings and invest-ments and the impact of these on the effective tax rates on capital incomes.These topics are treated below. Furthermore, one also needs to considerthe empirical evidence on the growth rates of the developing countries thatrely heavily on income taxes, which is explored by Mañas-Anton in Chap-ter 8.

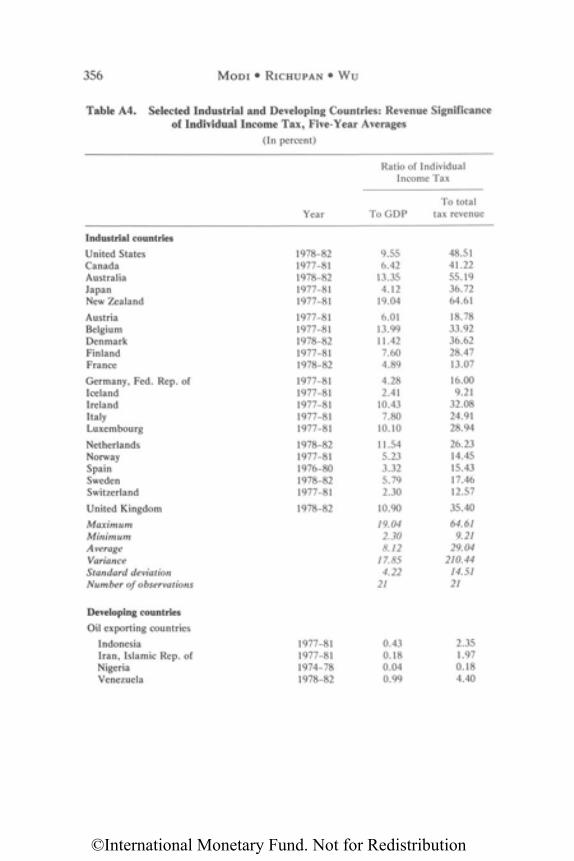

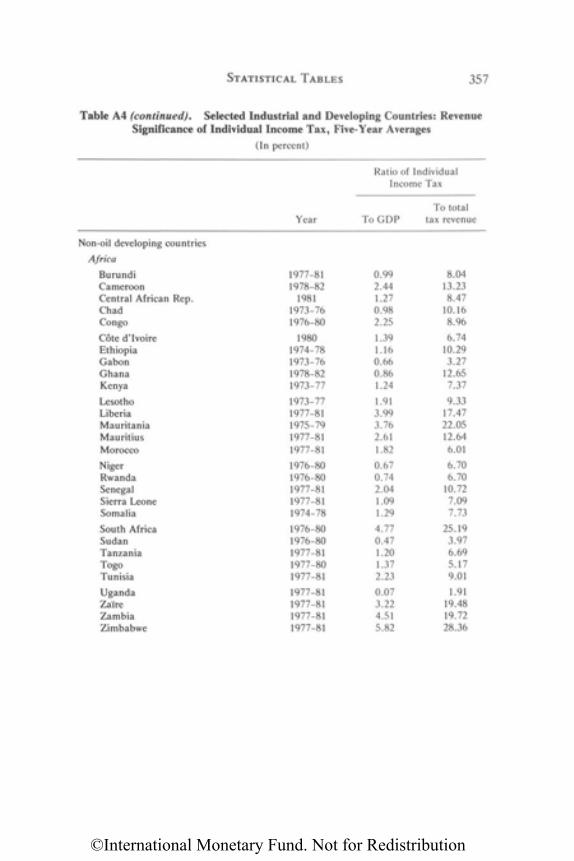

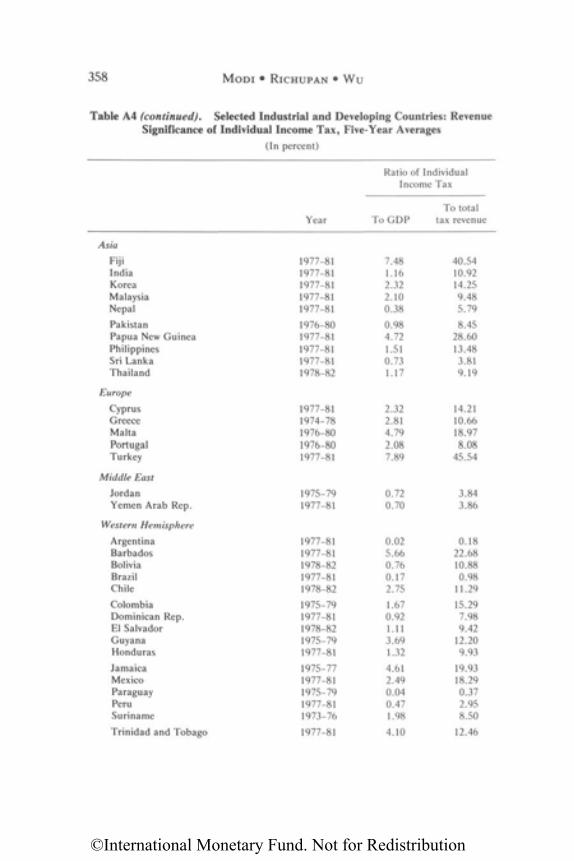

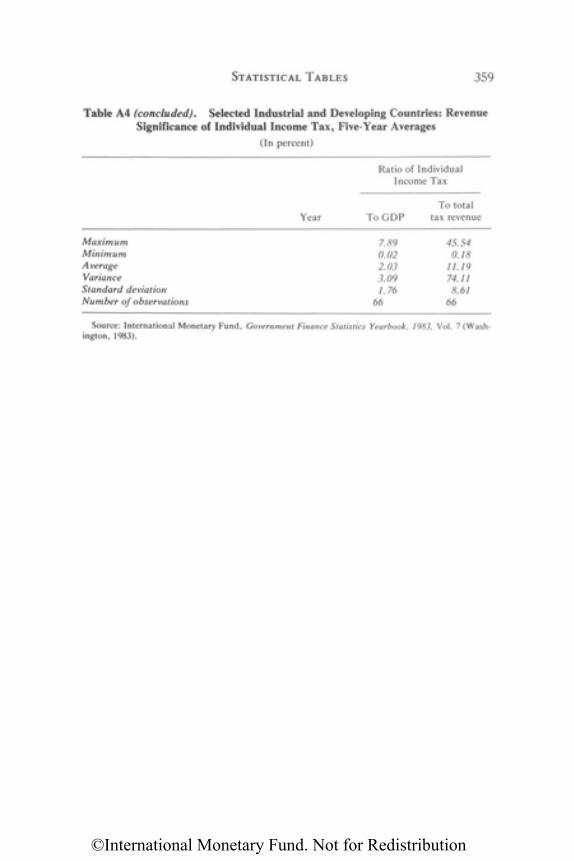

Relative Insignificance of Individual Income Taxation

The data given in Tables A2-A4 in the Statistical Appendix confirm thatthe individual income tax is a relatively unimportant source of revenue inmany developing countries, particularly in those that do not have large andsignificant mining sectors. While there are important differences amongcountries of the developing world, on average, the individual income taxaccounts for only 2 percent of GDP and 11 percent of all tax revenue, com-pared with 8 percent and 29 percent, respectively, in developed countries.From a limited number of developing countries for which it has been possi-ble to collect information (see Tables A5 and A6 in the Statistical Appen-