Supplementary Analysis: Republic of Paraguay Primary Credit Analyst: Delfina Cavanagh, Buenos Aires (54) 114-891-2153; [email protected] Secondary Contacts: Dominica Zavala, Sao Paulo 55 11 3039 7719; [email protected] Sebastian Briozzo, Mexico City (52) 55-5081-4524; [email protected] Table Of Contents Rationale Outlook Summary Statistics: Institutional And Governance Effectiveness: Advancement Of The Structural Reform Agenda Faces Some Resistance In Congress Economic Analysis: Increasing Resilience To Negative Economic Trends In The Region External Analysis: Strong External Position Will Moderately Weaken In The Coming Years Fiscal Analysis: Rising Political Tensions And Increasing Expenses In Public Works Will Test The Limits Established By The Fiscal Responsibility Law Monetary Policy Analysis: The Inflation-Targeting Regime Has Become More Effective, Yet Dollarization Remains High Local Currency Rating, T&C Assessment WWW.STANDARDANDPOORS.COM/RATINGSDIRECT JUNE 25, 2015 1 1409081 | 302092998

Supplementary Analysis: Republic of Paraguay · Dominica Zavala, Sao Paulo 55 11 3039 7719; [email protected] Sebastian Briozzo, Mexico City ... Supplementary Analysis:

Aug 26, 2018

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Supplementary Analysis:

Republic of Paraguay

Primary Credit Analyst:

Delfina Cavanagh, Buenos Aires (54) 114-891-2153; [email protected]

Secondary Contacts:

Dominica Zavala, Sao Paulo 55 11 3039 7719; [email protected]

Sebastian Briozzo, Mexico City (52) 55-5081-4524; [email protected]

Table Of Contents

Rationale

Outlook

Summary Statistics:

Institutional And Governance Effectiveness: Advancement Of The

Structural Reform Agenda Faces Some Resistance In Congress

Economic Analysis: Increasing Resilience To Negative Economic Trends In

The Region

External Analysis: Strong External Position Will Moderately Weaken In The

Coming Years

Fiscal Analysis: Rising Political Tensions And Increasing Expenses In Public

Works Will Test The Limits Established By The Fiscal Responsibility Law

Monetary Policy Analysis: The Inflation-Targeting Regime Has Become

More Effective, Yet Dollarization Remains High

Local Currency Rating, T&C Assessment

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT JUNE 25, 2015 1

1409081 | 302092998

Table Of Contents (cont.)

Related Criteria And Research

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT JUNE 25, 2015 2

1409081 | 302092998

Supplementary Analysis:

Republic of Paraguay

This report supplements our research update "Paraguay Outlook Revised To Positive On Greater Resilience To Weak

Regional Economies; 'BB/B' Ratings Affirmed," published on June 16, 2015. To provide the most current information,

we may cite more recent data than that stated in the previous publication. These differences have been determined not

to be sufficiently significant to affect the rating and our main conclusions.

Rationale

The ratings on the Republic of Paraguay reflect its sound economic

performance, anchored by prudent macroeconomic policy and strengthening

economic institutions, as well as the steps it is taking to boost infrastructure.

Sovereign Credit Rating

BB/Positive/B

These factors are balanced by Paraguay's still developing political institutions that will continue to challenge the

government's ability to implement its agenda.

Standard & Poor's Ratings Services projects GDP to grow 4%-4.5% in the next three years. Although the process of

diversifying the economy is advancing, Paraguay's economic performance is still relatively vulnerable to

weather-related risks and commodity price shocks. Paraguay's strong external position is likely to moderately weaken

in the next three years as a result of the current account deficits, after several years of surpluses. External deficits will

be mainly a result of lower agricultural commodity prices and the government's investment strategy, which will result

in greater industrial-related imports. However, we expect the country's external position to remain relatively robust

thanks to low external debt and solid external assets supported by gradual economic diversification. Paraguay's still

developing political institutions will likely hold back the full implementation of key reforms. President Horacio Cartes'

Administration will continue facing resistance from within its own political party and in Congress as it advances its

reform plans, as well as challenges related to the weak implementation capacity of key public-sector institutions.

Paraguay's economy grew 4.4% in 2014 despite the weakness of its trading partners and low soya prices, reflecting less

volatility and dependence on the agricultural commodity price cycle. Despite a weather-related drop in electricity

production, which represents more than 10% of GDP, resilient economic growth was a result of a boost in private

investment from the construction, livestock, service, and industrial sectors. Rising manufacturing investments, mainly

from the fast-growing "maquila" (or manufacturing) industry--although from a low base--along with the industrialization

of the agricultural production chain, will help to gradually reduce the economy's still heavy reliance on agriculture.

Economic weakness in Brazil and Argentina will constrain Paraguay's re-exports to those countries. Despite noticeable

advances in economic resilience over the past year, Paraguay has yet to fully demonstrate a longer track record in

withstanding shocks from external events, in particular those related to its main trading partners, such as Brazil and

Argentina. Also, because dollarization remains fairly high (almost 50% of total credits are denominated in dollars), a

significant depreciation in the guarani coupled with inadequate policy response could raise risks of deposit outflows

and external volatility.

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT JUNE 25, 2015 3

1409081 | 302092998

We expect real growth of 4.3% in 2015 and 4.5% over the next two years, although greater infrastructure investment

and advances in structural reforms could provide a material upside to this forecast. Still, Paraguay remains a

low-middle-income country, with per capita GDP estimated at $4,461 for 2015. We expect 3% per capita GDP growth

over the next two years.

Paraguay has solid external indicators, which gives the country flexibility to withstand unexpected external shocks.

International reserves have risen steadily over the past five years, reaching $7.1 billion at the end of May 2015 from

$6.3 billion in May 2014. Narrow net external debt to current account receipts has consistently decreased over the past

decade, to -17.2% in 2014 (from 98% in 2002). We expect Paraguay's narrow net external debt to reach -18.5% of

current account receipts, and gross external financing requirements to reach 14.7% of usable foreign exchange

reserves plus current account receipts in 2015. We expect external indicators to remain solid over the next three years.

Despite government efforts to attract investments from outside, foreign direct investment (FDI) has been modest at

about $283 million in 2014 (less than 1% of GDP).

We project that net general government debt will reach 10.8% of GDP in 2015 and will be 12%-14% of GDP in the next

three years, on average. Interest payments are likely to consume 2.2% of government revenues in 2015 and 2.3% on

average in the next three years. In 2013, the government issued its first bond in the international capital markets--a

$500 million 10-year bond (with a reopening of the original issue in 2015 for an additional $280 million) and another

30-year bond in 2014 for US$1 billion, totaling $1.780 billion of sovereign bond debt. It has no external issuances

planned until 2016.

We believe that it may be difficult for the government to comply with Paraguay's Fiscal Responsibility Law's target, as

Congress passed a 2015 budget with spending and deficit numbers that exceed the law's limits. We also believe that

the public-private partnership (PPP) law might make it more difficult to adhere to the fiscal deficit of 1.5% of GDP in

2015 and beyond. To achieve the target in 2015, the government will have to rein in expenses, especially given the

surge in expenses in late 2014, and contain the political pressures for more spending in 2016. We expect moderate

progress in increasing the tax collection and improving compliance. However, even if fully reaching the Fiscal

Responsibility Law (FRL) target remains challenging, we believe that the law continues to provide an important anchor

for fiscal prudence over the medium term.

Paraguay has made progress toward adopting an inflation-targeting monetary policy. The central bank cut its policy

rate by 25 basis points (bps) in its latest meeting (in March), to 6.25%. We expect that inflation will continue to decline

and will reach the target of 4.5% for 2015. We believe core inflation will remain at 4%. Nevertheless, high dollarization

in the Paraguayan economy still limits monetary policy flexibility. Domestic credit in dollars remains high at about

49%, and about 43% of deposits are in dollars, as of March 30, 2015. However, an elevated level of international

reserves sustains confidence in the stability of Paraguay's currency.

Outlook

The positive outlook reflects a one-in-three chance that we could raise the ratings in the next one to two years. For

this, gaining a track record in economic resilience and further institutionalizing fiscal policy will be important. Likewise,

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT JUNE 25, 2015 4

1409081 | 302092998

Supplementary Analysis: Republic of Paraguay

reinforcing the country's regulatory and institutional framework to reduce uncertainties while also strengthening the

implementation capacity of key government agencies to boost public investment projects could enhance Paraguay's

economic prospects over the next two years. Continued economic growth and resilience, as well as better fiscal policy

with a proven track record, could result in an upgrade.

Conversely, we would consider revising our rating outlook to stable if we perceive a weakening commitment to

policies that sustain macroeconomic stability, or an inadequate response to adverse external developments. Also,

further political polarization that could block or reverse the government's structural reform agenda and disrupt

economic policy implementation could result in an outlook revision to stable. The resulting decline in investor

sentiment and economic growth could weaken Paraguay's credit profile, leading to a downgrade.

Summary Statistics:

Table 1

Paraguay--Summary Statistics

2008 2009 2010 2011 2012 2013 2014 2015f 2016f 2017f 2018f

Nominal GDP (bil. US$) 18.50 15.93 20.05 25.10 24.60 28.90 30.98 31.26 32.55 34.38 36.64

GDP per capita (US$) 2,967.2 2,510.3 3,103.5 3,818.5 3,677.9 4,248.1 4,487.7 4,460.8 4,575.7 4,762.3 5,000.1

Real GDP growth (%) 6.4 (4.0) 13.1 4.3 (1.2) 14.2 4.4 4.3 4.5 4.5 4.5

Real GDP per capita growth

(%)

4.5 (5.7) 11.1 2.5 (2.9) 12.3 2.8 2.8 3.0 3.0 3.0

Change in general

government debt/GDP (%)

3.6 (2.2) (1.5) (1.2) (0.8) 2.8 4.1 2.7 2.4 2.1 2.0

General government

balance/GDP (%)

2.2 0.0 1.2 0.7 (1.8) (1.9) (1.6) (2.0) (1.9) (1.8) (1.8)

General government

debt/GDP (%)

25.2 23.5 18.1 15.1 13.8 14.9 17.5 19.0 20.0 20.5 20.9

Net general government

debt/GDP (%)

17.9 14.2 8.0 4.8 4.2 5.2 6.2 10.8 12.4 13.6 14.5

General government interest

expenditure/revenues (%)

6.5 4.2 3.6 1.7 1.6 2.0 2.3 2.4 2.5 2.6 2.6

Other dc claims on resident

nongovernment sector/GDP

(%)

24.8 30.2 34.5 38.9 42.9 46.1 49.9 51.4 53.5 55.2 55.9

CPI growth (%) 10.2 2.6 4.7 8.3 3.7 2.7 5.0 3.0 4.0 4.0 4.0

Gross external financing

needs/CARs plus usable

reserves (%)

84.3 78.4 84.0 85.8 86.4 82.1 82.0 81.3 81.2 81.7 81.2

Current account

balance/GDP (%)

1.0 3.0 (0.3) 0.4 (2.0) 1.7 (0.3) (1.2) (1.6) (2.0) (2.0)

Current account

balance/CARs (%)

1.7 5.4 (0.5) 0.8 (3.8) 3.2 (0.7) (2.6) (3.3) (4.1) (4.2)

Narrow net external

debt/CARs (%)

4.7 (5.2) (4.3) (8.5) (13.2) (13.9) (17.2) (18.5) (18.4) (18.6) (18.7)

Net external liabilities/CARs

(%)

127.5 128.4 93.0 77.3 80.7 64.1 69.6 67.9 62.8 58.4 54.2

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT JUNE 25, 2015 5

1409081 | 302092998

Supplementary Analysis: Republic of Paraguay

Table 1

Paraguay--Summary Statistics (cont.)

Note: Savings is defined as investment plus the current account surplus (deficit). Investment is defined as expenditure on capital goods,

including plant, equipment, and housing, plus the change in inventories. Other depository corporations (dc) are financial corporations (other

than the central bank) whose liabilities are included in the national definition of broad money. Gross external financing needs are defined as

current account payments plus short-term external debt at the end of the prior year plus nonresident deposits at the end of the prior year plus

long-term external debt maturing within the year. Narrow net external debt is defined as the stock of foreign and local currency public- and

private-sector borrowings from nonresidents minus official reserves minus public-sector liquid assets held by nonresidents minus

financial-sector loans to, deposits with, or investments in nonresident entities. A negative number indicates net external lending. The data and

ratios above result from Standard & Poor's own calculations, drawing on national as well as international sources, reflecting Standard & Poor's

independent view on the timeliness, coverage, accuracy, credibility, and usability of available information. CARs--Current account receipts.

f--Forecast.

Institutional And Governance Effectiveness: Advancement Of The StructuralReform Agenda Faces Some Resistance In Congress

• President Cartes from the ruling Partido Colorado (PC) secured key policy victories during his first year in office,

including the FRL and a strategy for increasing infrastructure investment, yet his Administration is now facing a

more challenging political environment in the implementation stage.

• Amid municipal, Colorado Party primary elections and 2015 budget negotiations, legislative obstruction is

becoming a bigger issue as the government faces resistance to some of its plans, which highlights Paraguay's still

evolving political institutions.

• Even though continuity in prudent macroeconomic policy and strengthening economic institutions reflect

Paraguay's sound economic policymaking, government institutions still have weak implementation capacity, which

is currently subjected to polarization from the political cycle.

Paraguay's weak political environment continues to constrain full implementation of key reforms. Limited institutional

capacity remains a key constraint to Paraguay's economic development. President Cartes managed to launch a set of

key structural reforms at the beginning of his term, including a landmark tax reform in the dominant agricultural sector,

which would boost fiscal revenues; a strategy for furthering infrastructure development based on the PPP Law; a

Freedom of Information Law to increase transparency in public institutions (Paraguay ranks 150 out of 175 countries

in Transparency International's 2014 Corruption Index); and the FRL limiting political interference in fiscal policy.

Nonetheless, the Cartes Administration is facing some resistance from within his political party and in Congress as he

struggles to advance his reform plans.

Strong forces within the Colorado Party remain polarized and fragmented. As the Colorado Party's primaries and

municipal elections are looming, President Cartes is increasingly facing political resistance to his market-oriented

agenda and plans to create a more investor-friendly and inclusive economy. This includes reforming the country's

notably inefficient public sector, opening up some state-owned enterprises of private participation, and making

advancements in critical infrastructure development and human capital. Yet risks have increased during this year's

political cycle as the government's strategy to improve the country's precarious infrastructure still runs some risks.

Congress is currently debating the possibility of modifying some key articles from the PPP Law, or even repealing it.

Likewise, Congress and members of Mr. Cartes' own party voted last year to raise the proposed budget deficit from the

limit of 1.5% of GDP to 3.4% of GDP. This would be in direct violation of the FRL. As budget negotiations begin this

year, the risks of this happening again persist, especially taking into account the local government elections. From a

rating perspective, establishing the FRL as a reliable fiscal anchor is elemental, and adhering to the legislation and

strengthening its track record of implementation is essential.

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT JUNE 25, 2015 6

1409081 | 302092998

Supplementary Analysis: Republic of Paraguay

Anti-Cartes factions have emerged within the president's own party lines in Congress, reflecting, in part, his position as

an outsider from the traditional leadership. As President Cartes pushes forward his modernizing agenda, he will have

to deal with the political system, which in essence is based on old-fashioned political patronage. Also, as municipal

elections approach this year, the Colorado Party and its leadership are increasingly fragmented. In this manner,

compromising within traditional factions of the Colorado Party is most likely.

The government has begun tackling long-standing structural weaknesses, which should aid Paraguay's developing

institutions. Paraguay's political institutions remain influenced by vested interest groups and vulnerable to red tape and

corruption despite a process of greater economic institutionalization. Commendable efforts have been made to

maintain Paraguay's relatively stable macroeconomic framework. We believe there will be continuity in economic

policy and a gradual strengthening of macro policymaking. A higher level of institutionalization will allow the

government to develop the country's infrastructure. One of the keys to this will be the Administration committing to

improve technical expertise, particularly in areas such as customs, which remain dominated by vested interests.

Nonetheless, the current government has achieved improvements in tax collection, which has created more space for

public investment.

Likewise, the Cartes Administration has made important strides to increase government transparency with the recently

adopted Freedom of Information Law, which requires disclosure of public-sector employees' remuneration. This is a

step forward in improving Paraguay's weak institutional quality and rule of law. Ameliorating these institutional

elements is critical to improving the country's business conditions to attract investment and strengthen productivity.

Protection of property rights remains feeble, and acquiring title documents for lands can take more than two years.

The judicial system remains inefficient and vulnerable to vested interests, and advancing the judicial reform is vital to

strengthening institutions. This would build on the efforts the government has taken to protect private and foreign

investment.

Even though President Cartes has committed to poverty reduction, social divisions and rural security pressures have

heightened. Combating extreme poverty and income inequality via conditional cash transfer programs has continued

with this Administration, and President Cartes has introduced his own plan to combat extreme poverty (Sembrando

Oportunidades). However, social unrest has increased, stemming from the damage caused by the floods in 2014, which

highlighted the chronic deficiencies in urban infrastructure that ail mainly poor families. Land reform remains largely

unaddressed, and periodic invasions by peasants and by a small guerrilla group named Paraguayan People's Army,

whose attacks are isolated to certain rural areas, are likely to continue. This group has become more active over the

years, even as President Cartes has taken a stronger stance against them by giving the military a leading role to

combat them.

Economic Analysis: Increasing Resilience To Negative Economic Trends In TheRegion

• Paraguay's economy grew 4.4% in 2014 despite the weakness of its trading partners and low soya prices, reflecting

less volatility and dependency on the agricultural commodity price cycle.

• Increasing new manufacturing investments, mainly from the fast-growing maquila industry, along with the

industrialization of the agricultural production chain, will help, over time, to limit the economy's overreliance on

primary agricultural activities.

• We expect real growth of 4.3% in 2015 and 4.5% over the next two years, although greater infrastructure investment

and advances in structural reforms could provide a material upside to this forecast.

• Paraguay remains a low-middle-income country, with per capita GDP estimated at $4,461 for 2015. We expect 3%

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT JUNE 25, 2015 7

1409081 | 302092998

Supplementary Analysis: Republic of Paraguay

GDP per capita growth over the next three years.

Economic growth slowed to 4.4% in 2014 from record growth of 14.2% in 2013, but it remains buoyant. Paraguay's

economy rebounded in 2013 from a drought the year before. In 2014, the healthy economic expansion benefited from

private investment and agro-industrial activity. Even though the country's main trading partners weakened and soya

prices fell, we expect 4.3% real growth this year as investment projects and lower oil prices sustain economic

expansion. Growth last year resulted mainly from the construction, livestock, and industrial sectors. The most dynamic

sector by far was construction, leading the way with 14.9% year-over-year growth, mainly because of private-sector

projects. Livestock picked up, with 10.5% growth, boosted by the reopening of international markets to meat products.

Manufacturing (led by the fast-growing maquila industry) and mining grew a solid 8.3%, and the service sector by

6.4%. Paraguay has been capitalizing on low growth and unfavorable economic conditions in Brazil and Argentina.

This has provided Paraguay with an opportunity to gradually emerge as an alternative for different investments (such

as auto parts, basic chemical industries, and food processing), making use of its relative advantages, such as cheaper

labor, low tax burden, and cheap and abundant energy.

On the other hand, a weather-related drop in electricity production was the main drag on growth. As a main

component in Paraguayan GDP, the production of the two largest hydroelectric dams, one operated with Brazil (Itaipu)

and the other with Argentina, accounts for about 10% of Paraguay's total GDP, 12% of fiscal revenue, and 17% of

exports. The electricity sector posted a 6.4% contraction, hurt by the reduction in water volumes resulting from the

drought. Lastly, agriculture, which generally plays a leading role in the Paraguayan economy, grew a weak 1.5%. So

far, according to preliminary data from the IMAEP (monthly economic activity indicator), the index rose to 4.6% by

March 2015 and 8.5% on a yearly basis, led mainly by the construction industry and livestock and service sectors.

We project growth of 4.5% in 2015-2018--close to the economy's trend growth. However, this may be subject to some

volatility from the agricultural sector, in particular the primary sector because Paraguay is still vulnerable to

weather-related risks and commodity price shocks. We expect infrastructure development to complement sources of

growth over the next three to four years. Growth should be boosted by infrastructure investment and projects

developed through the public and private partnership program, low oil prices, and a rebound in electric energy

generation.

Four key PPP projects could have positive productivity effects in the country. These investments are two major roads

(about US$400 million and currently the most advanced project); the modernization of Asuncion's airport (US$250

million); the dredging and maintenance of hydro-way Paraguay-Parana ($105 million); and the rehabilitation,

improvement, and expansion of the routes connecting the two most populated cities, Ciudad del Este and Encarnacion

($685 million). However, the weakness of Paraguay's trading partners as well as the low prices of soya could limit

growth to some extent in 2015. Paraguay's economy is fairly open, among the highest in the region, with total

registered exports and imports at 80% of GDP according to Interational Monetary Fund (IMF) figures. This means

commodity prices could have a big impact on Paraguay's economy, and a continued decline in soya prices will not

only reduce profits rather than production, but could also hurt business confidence and withhold investment and

output.

Advances in investments have been slow despite initial plans. Paraguay has important bottlenecks that are

bureaucratic, as well as political, with attempts to revise the PPP law to give Congress more decision-making power in

choosing the companies involved in the investments. Likewise, important government agencies still lack the

experienced human capital and abilities to execute not only these types of investments, but also to sustain the desired

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT JUNE 25, 2015 8

1409081 | 302092998

Supplementary Analysis: Republic of Paraguay

level of public works. Attempting to address these bottlenecks, government authorities are outsourcing the project

management of a variety of public investments to specialized international consulting firms. In 2015, we expect

investment to GDP to be 17.3% and remain at about 18% from 2016-2018.

Continued efforts to improve business conditions will be critical to keep attracting investments. According to the World

Bank's 2015 Doing Business Survey rankings--which measure countries according to the ease of doing

business--Paraguay's ranking has improved to 92 from 124 in 2010 (with 1 being the best country, and 189 being the

worst). Improving the effectiveness of the judicial system, strengthening property rights, and streamlining bankruptcy

procedures would improve the business climate and help attract new investment.

External Analysis: Strong External Position Will Moderately Weaken In TheComing Years

• International reserves have risen steadily over the past five years, reaching $7.077 billion at the end of May 2015

from $6.332 billion in May 2014.

• We estimate that, for 2015, gross external financing requirements will represent about 14.7% of current account

receipts. We expect this trend to continue over the next three years.

• We expect Paraguay's narrow net external debt to reach -18.5% of current account receipts, and gross external

financing requirements will likely reach 81.3% of usable reserves plus current account receipts in 2015.

• FDI has been modest at about $283 million in 2014; attracting it remains a critical objective for the government.

Paraguay posted a small current account deficit of about 0.34% of GDP in 2014 and is likely to run a small deficit of

1.2% of GDP in 2015 onward, based on lower world market prices for agricultural products. The Paraguayan economy

has continuously benefited from the technological changes and innovation currently going on in soya production. A

boom in export volumes, despite declining prices, has led to current account surpluses. Even though lower world

market prices for agricultural products will affect earnings from exports over the coming years, this could be partly

offset by volume growth from technological efficiency gains in production, as well as advances in the industrialization

of agricultural exports alongside favorable livestock prices (meat), a key export. Lower oil prices and, therefore, fuel

prices could also help contain a weakened trade balance as imports for industrial inputs rise in a context of increasing

public and private investment. We estimate a small current account deficit in 2015 of about 1.2% of GDP, and we

project minor deficits of less than 2% of GDP for 2016-2018. Apart from the changes in terms of trade, we expect that

the main driver of the current account deficit will be inputs related to investment in infrastructure, which would draw

in decreased imported inputs (mainly capital goods and services from investment-related activities). As a result of

rising international reserves and the growth in goods exports, Paraguay's external liquidity remains relatively strong.

Consequently, we expect gross external financing needs to represent 81% of current account receipts and usable

reserves on average over the next three years.

Several Brazilian and Asian companies are setting up assembly plans in Paraguay as well as increasing the number of

companies under the maquila regime, which could propel FDI growth. Export concentration, however, is still high,

with roughly two-thirds of exports coming from three agricultural sectors: soya, beef, and vegetable oils and

derivatives.

Public-sector external debt has generally decreased over the years, though it rose in the past two years after successful

international bond issuances. We project public-sector external debt will reach 26.8% of current account receipts in

2015 and remain around 26% over the next two years. In 2014, it reached 24.7% of current account receipts, down

from almost 100% in 2002. In 2013, the government issued its first bond in international capital markets--a $500

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT JUNE 25, 2015 9

1409081 | 302092998

Supplementary Analysis: Republic of Paraguay

million 10-year bond (with a reopening of the original issue in 2015 for an additional $280 million) and another 30-year

bond in 2014 for US$1 billion, totaling $1.780 billion of sovereign bond debt. Over the past five years, the government

has made net repayments to official creditors. Most private-sector external debt is trade related to the agri-business

sector--the income of which is also in foreign currency.

Paraguayan authorities have recently revised the country's international investment position to include the external

liabilities of the two large binational hydroelectric dams (Itaípu and Yacyretá). This moved Paraguay into a sizable net

external liability position and made the stocks more consistent with the balance of payment flows, as well as brought

data reporting standards in line with IMF standards. The creditors are the same government owners (50% of

ownership corresponds to Paraguay), and the debt is payable with the export of the energy produced in the dams. We

believe that the reclassification of binational dams as residents does not present an ultimate risk. Overall, this revision

doesn't alter our analysis because debt amortization and interest payments previously expressed through trade and

services account flows are now shown in the income account and capital and financial account. Thus, we have decided

to treat the binational dams' debt as more analogous to FDI-related debt.

Fiscal Analysis: Rising Political Tensions And Increasing Expenses In PublicWorks Will Test The Limits Established By The Fiscal Responsibility Law

• Complying with the FRL is essential to anchor solid public finances, especially after Congress passed the 2015

budget with higher spending and deficit numbers.

• Prospects of fiscal consolidation have weakened as public works expenditure accelerated. In order to achieve the

target in 2015, the government would have to rein in expenses, especially given the surge in expenses in late 2014,

as well as contain the political pressures for the 2016 budget negotiations.

• We estimate net general government debt to GDP of 10.6% in 2015 and 12%-14% for fiscal 2016-2018. If the

anchors the FRL imposes remain in place, this would remain low.

By approving the FRL, the government committed to comply with a fiscal ceiling, though it might end up having to be

more flexible. After running fiscal surpluses every year since 2004, Paraguay reported moderate fiscal deficits since

2012, mainly after large public-sector wage increases. The government started to run deficits in 2012, and debt began

to increase in terms of GDP, although from very low levels. We expect gross general government debt to reach a low

18.8% of GDP by year-end 2015 and remain at similar levels over the next three years.

Continuing with the fiscal reform agenda and strengthening the fiscal framework will remain critical to limiting political

interference in fiscal policy. The FRL establishes a deficit ceiling to the central government of 1.5% of GDP, restricts

the yearly growth in current primary expenditure to 4% plus inflation, and links salary increases in the public sector to

the minimum wage. The FRL aims to avoid the recent experience of steep public-sector salary increases during

election years, which led to deteriorating fiscal dynamics. The law adds limits on expenditure growth during an

election year. Nonetheless, the 2015 budget Congress approved increased spending 36% from 2014, resulting in a

3.4% of GDP deficit. The budget law also created a legal exception whereby capital spending financed by sovereign

bond issuances would be excluded for the deficit calculation. Even though Congress decided to ignore the FRL in late

2014, we expect the executive to resist congressional pressure to increase spending.

Fiscal policy tightening will be challenging as a large part of the fiscal stimulus done during 2012-2013 was focused on

current expenditure--particularly wage increases--which will be difficult to rein in. Still, institutional locks, which

prevent new borrowings from being used to finance operating expenditure, continue to work (based on the Financial

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT JUNE 25, 2015 10

1409081 | 302092998

Supplementary Analysis: Republic of Paraguay

Administrative Law passed 10 years ago and later reinforced by the State Financial Administration Modernization

Law). Besides, poorly managed state-owned enterprises and the public pension system coupled with the participation

of the private sector in infrastructure projects could pose some fiscal risks. The possibility of allowing private operators

to participate in improving the operation of state-owned enterprises has diminished with the current political climate.

As for infrastructure projects, it will be important for the government to remain cautious and prudent when assessing

contingent risk in each contract and project. All in all, securing the institutional capacity to manage PPP projects will

be essential in order for the country to reap its benefits.

Improvements in tax collection efforts remain a priority and crucial given the country's high level of informality and tax

evasion. Revenue increases in the past two years reflect the government's efforts to improve taxpayer compliance.

Paraguay's underlying weakness when it comes to public finances remains high given the level of labor informality,

which will keep tax revenue as a percentage of GDP low. This will prove even harder to tackle despite recent reforms

that introduced the personal income tax and the new agricultural tax. Likewise, weak institutions further complicate

expenditure oversight and limit the quality for the government's spending. Moreover, Paraguay's tax ratio, at 13.6% of

GDP, is low and depends largely on indirect taxation. Tax measures that Congress approved in recent years focused

more on raising formality in the economy, thereby making the success of tax administration dependent on the ability

of the tax agency to enforce the changes--rather than on increasing tax rates. Over the past two years, Congress

increased some tax rates and created some new taxes.

Strengthening budget practices and maintaining favorable debt dynamics is vital. Finding sources to finance the deficit

will be manageable via domestic and foreign creditors. With Paraguay's public debt coming from moderate levels, a

potential deficit above the 1.5% target would not pose an immediate risk for fiscal sustainability precisely. Still, we

believe meeting the FRL requirements while also strengthening the budget processes will provide the government with

more solid fiscal performance and discipline. Going forward, we will look for a growing track record of compliance

with the new restrictions to determine whether they have become real anchors of fiscal sustainability. As in other Latin

American countries, the emergence of legislation like the FRL or PPP in Paraguay may not constitute significant

structural fiscal improvements.

Debt burden

Paraguay's general government debt has remained stable at low levels. We expect gross general government debt to

reach 18.8% of GDP by year-end 2015. Paraguay issued its first bond in the international capital markets in early 2013,

raising $500 million, with a reopening of the same issuance in 2015 for an additional $280 million (whose funds were

used mainly to rollover debt). The government successfully launched a second round of sovereign bond issuance for

$1 billion due in 2044, aimed mainly at boosting investment projects as well as assisting other sectors of the economy.

Out of the total $1.780 billion issued, over $1 billion has been transferred to fund key investment projects, with

priorities in public works, electricity, and social housing.

Past low fiscal deficits or small surpluses led to a low net general government debt to GDP equivalent of 6.19% at

year-end 2014. We estimate it will be 10.6% in 2015 and 12%-14% for fiscal 2016-2018. If the anchors the FRL

imposes remain in place, this would remain low.

Most of the Paraguayan government's debt is external (68% of total debt stock) and distributed evenly across

multilateral agencies (33.1%), domestic (16.1%) and international bonds (30.2%), the $890 million perpetual bond

(15.3%) issued by the government in December 2012 to capitalize the central bank, and--to a lesser extent--bilateral

lenders (5.3%). Paraguay's main multilateral creditors are the Inter-American Development Bank (20.9%), World Bank

(7.3%), Japan Bank for International Cooperation (3.8%), and Corporacion Andina de Fomento (2.9%) at concessional

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT JUNE 25, 2015 11

1409081 | 302092998

Supplementary Analysis: Republic of Paraguay

terms. Paraguay's debt structure has changed after the international issuances, given that before public debt was

concentrated mainly with multilaterals. Even though improvements have been made in terms of information quality

produced by the debt management office, we believe additional strengthening will be necessary for the government to

issue debt more frequently in the global markets despite its low debt levels. Currently, the government issues about

$280 million per year of debt denominated in local currency.

The government faces limited contingent liabilities based on our Banking Industry Country Risk Assessment (which

reflects economic and industry risks) and Paraguay's ratio of gross assets of other DC to GDP of 65%.Paraguay's

public-sector enterprises are nine entities performing a wide variety of activities, such as public utilities, transport

infrastructure (airport, ports, and railroad), and commercial activities, including fuel import and distribution,

telecommunications, and the production of alcoholic beverages and cement. The largest public-sector enterprises are

mainly the Administración Nacional de Electricidad (ANDE), Administración Nacional de Navegación y Puertos

(ANNP), Direccion Nacional de Aeronáutica Civil (DINAC), Industria Nacional del Cemento (INC), and Petróleos

Paraguayos (PETROPAR). Some proceeds from both sovereign bond issuances went into financing investments in the

main public-sector enterprises such as ANDE (US$87.6 billion) and INC (US $24 billion. Although Paraguay's

state-owned enterprises generate a small operating surplus, they generally are unable to cover the investment needs

from their own revenues. As most tariffs are regulated below costs and investment capacity is very weak, most public

companies have low efficiency levels and face challenges in their limited operational performance.

Monetary Policy Analysis: The Inflation-Targeting Regime Has Become MoreEffective, Yet Dollarization Remains High

• The central bank cut its policy rate by 25 bps last meeting to 6.25%, reflecting the central bank's expectation that

inflation will continue to decline toward the new target of 4.5% for 2015.

• We expect domestic credit to grow about 12% annually, down from 20% in 2014, which is good news.

• The amount of domestic credit and deposits in dollars remains high at about 49% and 43%, respectively, as of

March 30, 2015.

Monetary policy credibility has progressed with improvements in the effectiveness of Paraguay's inflation-targeting

regime. Inflation came down to the lower end of the targeted range in mid-2014 and remains on target, suggesting a

credible policy commitment. Even though consumer prices increased at the beginning of the year, inflation is still low

and core inflation, which excludes regulated services and fuels, remained below target. A drop in commodity prices

helped contain inflationary pressures, though we expect inflation will remain at 4% during the year, consistent with the

depreciation of the guarani. For 2016, we expect inflation to be at the center of the central bank's target range

(4%-4.5%), given our expectations that monetary policy will remain focused on keeping inflation close to the target.

Paraguay could benefit from stronger financial intermediation and lower dollarization, which remains fairly high.

Domestic capital markets are still in an early stage of development, with very little secondary market trading of

government securities, which limits the ability to conduct monetary policy through repurchases and reverse

repurchases. Furthermore, the economy is highly dollarized. Foreign currency credit to the private sector as a share of

total credit rose to about 49% as of March 30, 2015, from about 45.7% as of May 2014 and remains slightly higher than

the 2005 levels (about 47%). It will be important for the central bank to work toward policies that facilitate a gradual

reduction in dollarization because bank deposits and loans in foreign currency account for nearly half of the total,

reflecting mainly the high agricultural export earnings over the past years. These have outpaced domestic currency

loans and deposits. However, a high level of international reserves gives investors greater confidence in the stability of

Paraguay's currency.

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT JUNE 25, 2015 12

1409081 | 302092998

Supplementary Analysis: Republic of Paraguay

The government initiated the recapitalization process of the central bank to prevent any perceptions that the

inflation-targeting regime could be compromised given its financial position. According to the IMF, the central bank

has an annual loss of about 0.5% of GDP, reflecting the costly sterilization of its foreign exchange reserves. Since it was

crucial to recapitalize the central bank, the central government issued a perpetual bond to the monetary agency in

local currency for $886.34 million in 2012. The government is also changing course by making non-renumerated

interest payments on the central government's large deposits held at the central bank.

Strong credit growth, particularly in foreign currency, could increase risks to Paraguay's financial system.Domestic

credit has grown rapidly; total credit rose 29.3% from April 2015 to April 2014. This involved a 19.3% rise in credits in

local currency and a strong 41.1% increase in credits in foreign currency. At the same time, nonperforming loans in the

banking system remain low at 2.06% of total loans as of Dec. 31, 2014, similar to levels a year earlier.

New banking and central bank laws will help prudential oversight. In our view, the Paraguayan government's legal

and regulatory framework for banking supervision, especially for cooperatives, continues to evolve. Cooperatives now

account for roughly one-fifth of total financial system assets and attend to many small savers. Cooperative sector

nonperforming loans are high, at 7.9% among the largest institutions as of September 2014. Its regulator, Instituto

Nacional de Cooperativismo (INCOOP), which is under the Ministry of Agriculture, is working toward creating a

greater financial safety net as current regulatory and supervisory powers are relatively weak. The government

supervises these assets less rigorously, and they have weaker provisioning requirements than banks. However the new

law submitted to Congress in 2015 should help update the central bank's outdated regulatory powers. The new law

aims to extend the powers of the regulator authority and enable more transparent and efficient (risk-based) oversight

via the bank superintendent.

Local Currency Rating, T&C Assessment

The local currency rating on Paraguay is 'BB', the same as the foreign currency rating because Paraguay has a

still-developing domestic capital market, which limits the sovereign's ability to conduct monetary policy through active

secondary market trading.

The 'BB+' transfer and convertibility assessment is one notch higher than our 'BB' long-term foreign currency

sovereign credit rating. It reflects Standard & Poor's opinion that the likelihood of the sovereign restricting access to

foreign exchange that Paraguay-based nonsovereign issuers need for debt service is lower than the likelihood of the

sovereign defaulting on its foreign currency obligations. Paraguay's relatively open foreign exchange regime and

outward-oriented economic policies suggest that the likelihood of resorting to such restrictions in a downside scenario

is lower than in more interventionist sovereigns.

Table 2

Paraguay--Selected Indicators

2008 2009 2010 2011 2012 2013 2014 2015f 2016f 2017f 2018f

Economic indicators

Nominal GDP (bil.

LC)

80,734.8 79,117.2 94,934.3 105,203.2 108,832.3 124,853.1 138,259.9 148,352.9 160,962.8 174,644.7 189,489.5

Nominal GDP (bil.

US$)

18.5 15.9 20.0 25.1 24.6 28.9 31.0 31.3 32.5 34.4 36.6

GDP per capita (US$) 2,967 2,510 3,103 3,819 3,678 4,248 4,488 4,461 4,576 4,762 5,000

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT JUNE 25, 2015 13

1409081 | 302092998

Supplementary Analysis: Republic of Paraguay

Table 2

Paraguay--Selected Indicators (cont.)

Real GDP growth (%) 6.4 (4.0) 13.1 4.3 (1.2) 14.2 4.4 4.3 4.5 4.5 4.5

Real GDP per capita

growth (%)

4.5 (5.7) 11.1 2.5 (2.9) 12.3 2.8 2.8 3.0 3.0 3.0

Real investment

growth (%)

32.1 (12.5) 22.7 10.8 (13.5) 20.2 10.6 7.0 7.0 7.0 7.0

Gross domestic

investment/GDP (%)

16.4 13.8 16.2 17.1 15.1 15.4 16.4 16.8 17.2 17.5 18.0

Gross domestic

savings/GDP (%)

17.4 16.8 15.9 17.5 13.0 17.1 16.0 15.5 15.6 15.6 16.0

Real exports growth

(%)

0.9 (8.2) 19.9 6.2 (6.7) 18.4 0.9 7.0 5.0 5.0 5.0

Unemployment rate

(average %)

5.7 6.4 5.7 5.6 4.9 5.0 5.5 5.5 5.5 5.5 5.5

External indicators

Narrow net external

debt/CARs (%)

4.7 (5.2) (4.3) (8.5) (13.2) (13.9) (17.2) (18.5) (18.4) (18.6) (18.7)

Gross external

financing

needs/CARs plus

usable reserves (%)

84.3 78.4 84.0 85.8 86.4 82.1 82.0 81.3 81.2 81.7 81.2

Net external

liabilities/CARs (%)

127.5 128.4 93.0 77.3 80.7 64.1 69.6 67.9 62.8 58.4 54.2

Current account

balance/GDP (%)

1.0 3.0 (0.3) 0.4 (2.0) 1.7 (0.3) (1.2) (1.6) (2.0) (2.0)

Current account

balance/CARs (%)

1.7 5.4 (0.5) 0.8 (3.8) 3.2 (0.7) (2.6) (3.3) (4.1) (4.2)

Trade balance/GDP

(%)

5.7 7.1 4.4 3.4 2.3 5.8 3.3 1.6 1.0 0.4 0.2

Net FDI/GDP (%) 1.1 0.6 1.1 2.2 3.0 0.2 0.8 1.1 1.4 1.4 1.3

Net portfolio equity

inflow/GDP (%)

0.0 0.0 0.0 0.4 2.0 1.7 4.2 1.0 0.9 0.9 0.8

Short-term external

debt by remaining

maturity/CARs (%)

3.8 7.2 7.7 8.5 9.6 8.1 9.8 12.1 11.4 10.8 10.3

Reserves/CAPs

(months)

2.6 3.8 3.4 3.1 3.6 3.4 4.1 4.8 4.8 4.7 4.7

Fiscal indicators

Change in general

government

debt/GDP (%)

3.6 (2.2) (1.5) (1.2) (0.8) 2.8 4.1 2.7 2.4 2.1 2.0

General government

balance/GDP (%)

2.2 0.0 1.2 0.7 (1.8) (1.9) (1.6) (2.0) (1.9) (1.8) (1.8)

General government

primary balance/GDP

(%)

3.3 0.8 1.8 1.0 (1.5) (1.6) (1.2) (1.5) (1.5) (1.3) (1.3)

General government

revenue/GDP (%)

15.8 17.5 17.1 18.0 19.0 17.2 17.9 18.3 18.5 18.7 19.0

General government

expenditures/GDP

(%)

13.6 17.5 15.9 17.3 20.8 19.1 19.4 20.2 20.5 20.5 20.7

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT JUNE 25, 2015 14

1409081 | 302092998

Supplementary Analysis: Republic of Paraguay

Table 2

Paraguay--Selected Indicators (cont.)

General government

interest

expenditure/revenues

(%)

6.5 4.2 3.6 1.7 1.6 2.0 2.3 2.4 2.5 2.6 2.6

General government

debt/GDP (%)

25.2 23.5 18.1 15.1 13.8 14.9 17.5 19.0 20.0 20.5 20.9

Net general

government

debt/GDP (%)

17.9 14.2 8.0 4.8 4.2 5.2 6.2 10.8 12.4 13.6 14.5

General government

liquid assets/GDP (%)

7.3 9.4 10.0 10.3 9.6 9.7 11.4 8.2 7.6 7.0 6.4

Monetary indicators

CPI growth (%) 10.2 2.6 4.7 8.3 3.7 2.7 5.0 3.0 4.0 4.0 4.0

GDP deflator growth

(%)

9.3 2.0 6.1 6.2 4.7 0.4 6.1 2.9 3.8 3.8 3.8

Other dc claims on

resident

nongovernment

sector growth (%)

63.5 19.4 37.0 25.1 14.0 23.2 19.8 10.7 13.0 11.9 9.9

Other dc claims on

resident

nongovernment

sector/GDP (%)

24.8 30.2 34.5 38.9 42.9 46.1 49.9 51.4 53.5 55.2 55.9

Note: Savings is defined as investment plus the current account surplus (deficit). Investment is defined as expenditure on capital goods, including

plant, equipment, and housing, plus the change in inventories. Other depository corporations (dc) are financial corporations (other than the central

bank) whose liabilities are included in the national definition of broad money. Gross external financing needs are defined as current account

payments plus short-term external debt at the end of the prior year plus nonresident deposits at the end of the prior year plus long-term external

debt maturing within the year. Narrow net external debt is defined as the stock of foreign and local currency public- and private-sector borrowings

from nonresidents minus official reserves minus public-sector liquid assets held by nonresidents minus financial-sector loans to, deposits with, or

investments in nonresident entities. A negative number indicates net external lending. The data and ratios above result from Standard & Poor's own

calculations, drawing on national as well as international sources, reflecting Standard & Poor's independent view on the timeliness, coverage,

accuracy, credibility, and usability of available information. CARs--Current account receipts. CAPs--Current account payments. FI--Financial

institutions. f--Forecast.

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT JUNE 25, 2015 15

1409081 | 302092998

Supplementary Analysis: Republic of Paraguay

Chart 1

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT JUNE 25, 2015 16

1409081 | 302092998

Supplementary Analysis: Republic of Paraguay

Chart 2

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT JUNE 25, 2015 17

1409081 | 302092998

Supplementary Analysis: Republic of Paraguay

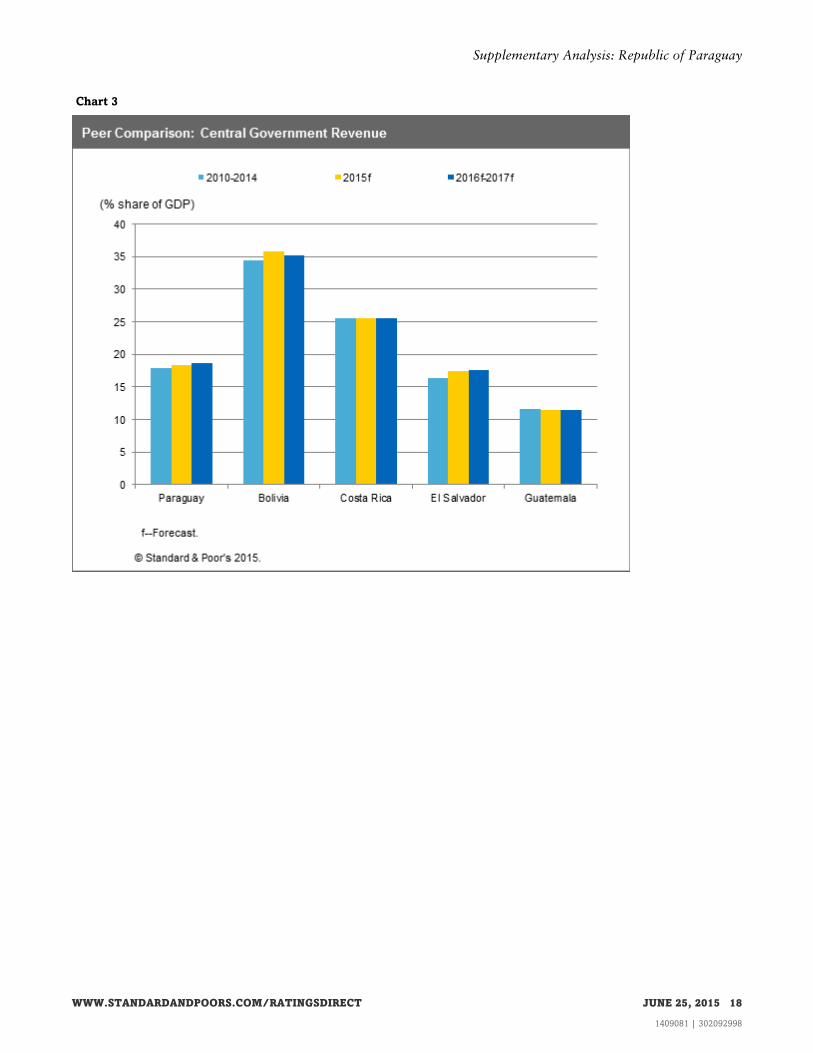

Chart 3

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT JUNE 25, 2015 18

1409081 | 302092998

Supplementary Analysis: Republic of Paraguay

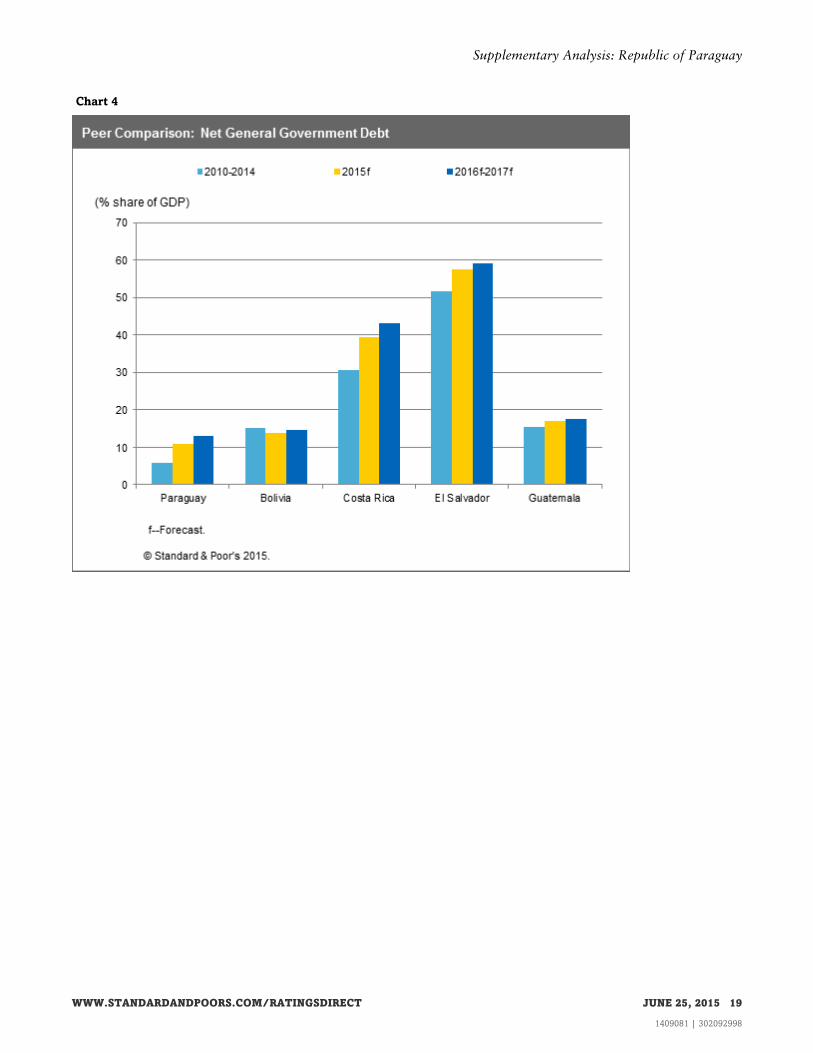

Chart 4

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT JUNE 25, 2015 19

1409081 | 302092998

Supplementary Analysis: Republic of Paraguay

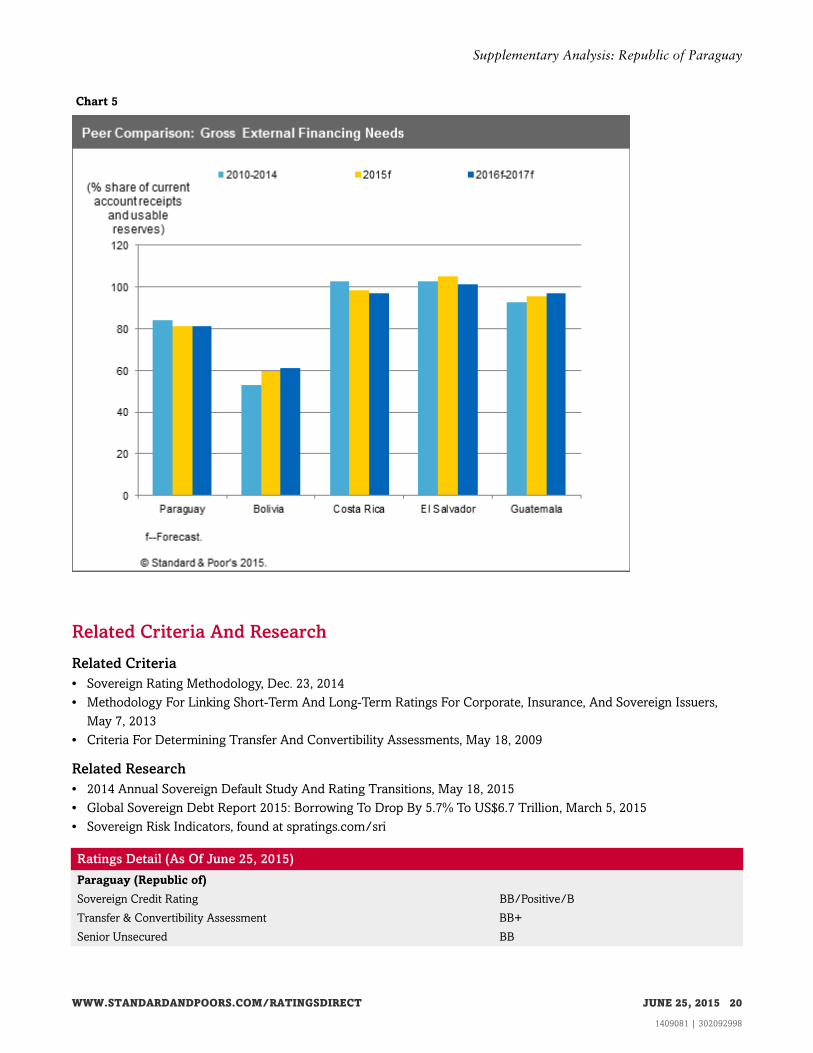

Chart 5

Related Criteria And Research

Related Criteria

• Sovereign Rating Methodology, Dec. 23, 2014

• Methodology For Linking Short-Term And Long-Term Ratings For Corporate, Insurance, And Sovereign Issuers,

May 7, 2013

• Criteria For Determining Transfer And Convertibility Assessments, May 18, 2009

Related Research

• 2014 Annual Sovereign Default Study And Rating Transitions, May 18, 2015

• Global Sovereign Debt Report 2015: Borrowing To Drop By 5.7% To US$6.7 Trillion, March 5, 2015

• Sovereign Risk Indicators, found at spratings.com/sri

Ratings Detail (As Of June 25, 2015)

Paraguay (Republic of)

Sovereign Credit Rating BB/Positive/B

Transfer & Convertibility Assessment BB+

Senior Unsecured BB

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT JUNE 25, 2015 20

1409081 | 302092998

Supplementary Analysis: Republic of Paraguay

Ratings Detail (As Of June 25, 2015) (cont.)

Sovereign Credit Ratings History

16-Jun-2015 BB/Positive/B

11-Jun-2014 BB/Stable/B

29-Aug-2012 BB-/Stable/B

25-Jun-2012 BB-/Watch Neg/B

30-Aug-2011 BB-/Stable/B

23-Aug-2010 B+/Positive/B

*Unless otherwise noted, all ratings in this report are global scale ratings. Standard & Poor's credit ratings on the global scale are comparable

across countries. Standard & Poor's credit ratings on a national scale are relative to obligors or obligations within that specific country. Issue and

debt ratings could include debt guaranteed by another entity, and rated debt that an entity guarantees.

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT JUNE 25, 2015 21

1409081 | 302092998

Supplementary Analysis: Republic of Paraguay

S&P may receive compensation for its ratings and certain analyses, normally from issuers or underwriters of securities or from obligors. S&P

reserves the right to disseminate its opinions and analyses. S&P's public ratings and analyses are made available on its Web sites,

www.standardandpoors.com (free of charge), and www.ratingsdirect.com and www.globalcreditportal.com (subscription) and www.spcapitaliq.com

(subscription) and may be distributed through other means, including via S&P publications and third-party redistributors. Additional information

about our ratings fees is available at www.standardandpoors.com/usratingsfees.

S&P keeps certain activities of its business units separate from each other in order to preserve the independence and objectivity of their respective

activities. As a result, certain business units of S&P may have information that is not available to other S&P business units. S&P has established

policies and procedures to maintain the confidentiality of certain nonpublic information received in connection with each analytical process.

To the extent that regulatory authorities allow a rating agency to acknowledge in one jurisdiction a rating issued in another jurisdiction for certain

regulatory purposes, S&P reserves the right to assign, withdraw, or suspend such acknowledgement at any time and in its sole discretion. S&P

Parties disclaim any duty whatsoever arising out of the assignment, withdrawal, or suspension of an acknowledgment as well as any liability for any

damage alleged to have been suffered on account thereof.

Credit-related and other analyses, including ratings, and statements in the Content are statements of opinion as of the date they are expressed and

not statements of fact. S&P's opinions, analyses, and rating acknowledgment decisions (described below) are not recommendations to purchase,

hold, or sell any securities or to make any investment decisions, and do not address the suitability of any security. S&P assumes no obligation to

update the Content following publication in any form or format. The Content should not be relied on and is not a substitute for the skill, judgment

and experience of the user, its management, employees, advisors and/or clients when making investment and other business decisions. S&P does

not act as a fiduciary or an investment advisor except where registered as such. While S&P has obtained information from sources it believes to be

reliable, S&P does not perform an audit and undertakes no duty of due diligence or independent verification of any information it receives.

No content (including ratings, credit-related analyses and data, valuations, model, software or other application or output therefrom) or any part

thereof (Content) may be modified, reverse engineered, reproduced or distributed in any form by any means, or stored in a database or retrieval

system, without the prior written permission of Standard & Poor's Financial Services LLC or its affiliates (collectively, S&P). The Content shall not be

used for any unlawful or unauthorized purposes. S&P and any third-party providers, as well as their directors, officers, shareholders, employees or

agents (collectively S&P Parties) do not guarantee the accuracy, completeness, timeliness or availability of the Content. S&P Parties are not

responsible for any errors or omissions (negligent or otherwise), regardless of the cause, for the results obtained from the use of the Content, or for

the security or maintenance of any data input by the user. The Content is provided on an "as is" basis. S&P PARTIES DISCLAIM ANY AND ALL

EXPRESS OR IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF MERCHANTABILITY OR FITNESS FOR

A PARTICULAR PURPOSE OR USE, FREEDOM FROM BUGS, SOFTWARE ERRORS OR DEFECTS, THAT THE CONTENT'S FUNCTIONING

WILL BE UNINTERRUPTED, OR THAT THE CONTENT WILL OPERATE WITH ANY SOFTWARE OR HARDWARE CONFIGURATION. In no

event shall S&P Parties be liable to any party for any direct, indirect, incidental, exemplary, compensatory, punitive, special or consequential

damages, costs, expenses, legal fees, or losses (including, without limitation, lost income or lost profits and opportunity costs or losses caused by

negligence) in connection with any use of the Content even if advised of the possibility of such damages.

Copyright © 2015 Standard & Poor's Financial Services LLC, a part of McGraw Hill Financial. All rights reserved.

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT JUNE 25, 2015 22

1409081 | 302092998

Related Documents