1 THE POTENTIAL OF DISTRIBUTED SOLAR IN GHANA A RESEARCH BRIEF JANUARY 2017

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

THE POTENTIAL OF DISTRIBUTED SOLAR IN GHANA

A RESEARCH BRIEF

JANUARY 2017

2

ForwardA transformation of the electric power sector is emerging across the developed countries of the world. This is an industry that has remained

largely unchanged since it’s inception, with technology disrupting established business models and enabling a more sustainable way to generate

and deliver electricity to customers. In this context, emerging markets across the world are well positioned to leap frog developed economies in

the way that they plan their energy future. An opportunity to build a more distributed, clean, and equitable electric grid is here today for countries

across Africa and Southeast Asia.

Unreliable electric power is a stifling impediment to growth in developing nations. As mobile phones have transformed the business landscape of

Africa, the distributed energy industry holds vast potential in granting or improving energy access to a large segment of the population. There is

opportunity to expedite service to off-grid communities while enhancing reliability in urban areas that commonly experience interruptions.

It takes long periods to build large central generating facilities, particularly in markets like Africa with financing challenges and risk profiles that

often stifle the flow of foreign investment. Therefore, it is an absolute necessity to evaluate both grid-connected and off-grid renewable energy

systems to deliver power to a growing population across the continent. A diverse ecosystem of entrepreneurs, multi-national corporations,

financial investors, and policy makers have embraced the opportunity that solar energy offers for both economic development and social good.

There is no “one-size-fits-all” solution that can be instituted across the continent, countries, or regions. This series of research is aimed that

supporting these initiatives through identification of the key challenges and opportunities across developing markets and the stakeholders that

are driving to address them.

3

AcknowledgementsThis study has been made possible by our sponsor and a diverse group of stakeholders contributing their insights. We thank all that have taken the time to provide input into this research brief.

Project Sponsor:

Contributing Stakeholders:

Gertrude N. Koomson, Volta River Authority (VRA)Dr. Kwame Ampofo, Ghana Energy Commission (GEC)Frederick Kenneth Appiah, Ghana Energy Commission (GEC) Lambert Faabeluon, Ghana Energy Protection Agency (EPA)Jabesh K. Ammissah-Arthur, Arthur Energy AdvisorsNick Ayitey-Wallace, Siginik EnergyDr. Daniel Davies, SolarCenturyAnthony Carvalho, Nexant

Project Author:Alexander Pischalnikov, Energy Industry Advisor

LEGAL DISCLAIMER: The analysis and presentation of this study does not constitute investment advice. The views and data presented are that of the author, and are not indicative of or associated with any other company or affiliate.

4

IntroductionThis study is performed as an independent research project to assess the barriers and opportunities of the distributed solar energy market in

Ghana. As one of the most developed countries in West Africa, Ghana enjoys a rather high rate of electrification (above 75%). However, this is

not fully indicative of the access to power that Ghanaian have across the country. The rural electrification rate hovers close to 50%. In addition to

this, Ghana’s average electricity tariff is very high, relative to both West Africa and the rest of the world.

The reliability of Ghana’s electric supply is notoriously bad, which has profound effects on the economy and standard of living. Dumsor, as it is

referred to by the locals, is a term used to describe the “persistent, irregular, and unpredictable electric power outages” that plague the country.

According to a report by the Institute of Statistical Social and Economic Research (ISSER), a Ghanaian based think-tank, since 2010 the

economy has lost over $24 billion dollars due to the energy crisis.

This confluence of factors makes Ghana one of the most attractive African markets for investing in both Residential and Commercial/Industrial

solar development – whether they be off-grid or grid connected. However, significant challenges remain in spurring this development. As the

power sector in Ghana goes through a significant transformation, distributed and off-grid solar can be a momentous contributor to achieving

energy policy objectives and securing a reliability of electric power supply.

01

5

0 1 0 3

0 30 2

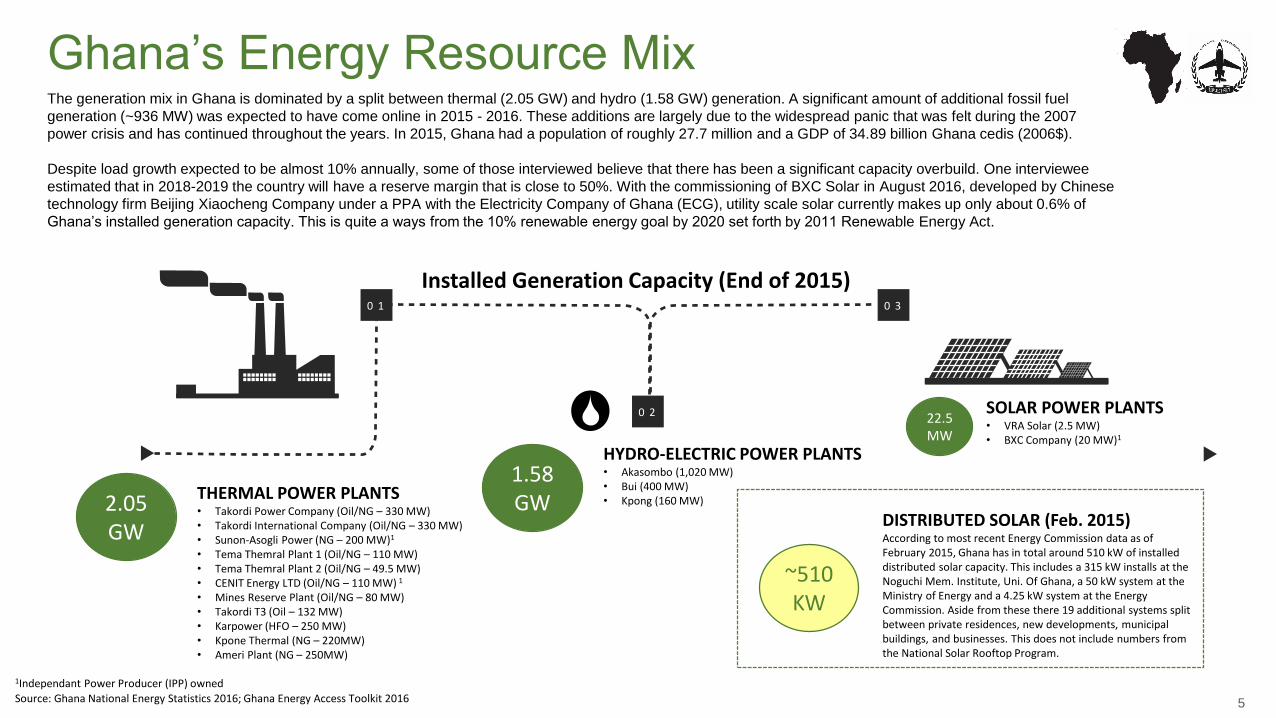

Ghana’s Energy Resource MixThe generation mix in Ghana is dominated by a split between thermal (2.05 GW) and hydro (1.58 GW) generation. A significant amount of additional fossil fuel

generation (~936 MW) was expected to have come online in 2015 - 2016. These additions are largely due to the widespread panic that was felt during the 2007

power crisis and has continued throughout the years. In 2015, Ghana had a population of roughly 27.7 million and a GDP of 34.89 billion Ghana cedis (2006$).

Despite load growth expected to be almost 10% annually, some of those interviewed believe that there has been a significant capacity overbuild. One interviewee

estimated that in 2018-2019 the country will have a reserve margin that is close to 50%. With the commissioning of BXC Solar in August 2016, developed by Chinese

technology firm Beijing Xiaocheng Company under a PPA with the Electricity Company of Ghana (ECG), utility scale solar currently makes up only about 0.6% of

Ghana’s installed generation capacity. This is quite a ways from the 10% renewable energy goal by 2020 set forth by 2011 Renewable Energy Act.

2.05GW

THERMAL POWER PLANTS• Takordi Power Company (Oil/NG – 330 MW)• Takordi International Company (Oil/NG – 330 MW)• Sunon-Asogli Power (NG – 200 MW)1

• Tema Themral Plant 1 (Oil/NG – 110 MW)• Tema Themral Plant 2 (Oil/NG – 49.5 MW)• CENIT Energy LTD (Oil/NG – 110 MW) 1

• Mines Reserve Plant (Oil/NG – 80 MW)• Takordi T3 (Oil – 132 MW)• Karpower (HFO – 250 MW)• Kpone Thermal (NG – 220MW)• Ameri Plant (NG – 250MW)

1.58 GW

HYDRO-ELECTRIC POWER PLANTS• Akasombo (1,020 MW)• Bui (400 MW)• Kpong (160 MW)

22.5MW

SOLAR POWER PLANTS• VRA Solar (2.5 MW)• BXC Company (20 MW)1

Source: Ghana National Energy Statistics 2016; Ghana Energy Access Toolkit 2016

~510 KW

DISTRIBUTED SOLAR (Feb. 2015)According to most recent Energy Commission data as of February 2015, Ghana has in total around 510 kW of installed distributed solar capacity. This includes a 315 kW installs at the Noguchi Mem. Institute, Uni. Of Ghana, a 50 kW system at the Ministry of Energy and a 4.25 kW system at the Energy Commission. Aside from these there 19 additional systems split between private residences, new developments, municipal buildings, and businesses. This does not include numbers from the National Solar Rooftop Program.

Installed Generation Capacity (End of 2015)

1Independant Power Producer (IPP) owned

6

The Changing Structure of Ghana’s Power Sector

Ghana’s power sector is in a state of significant flux and transformation. Changes

are either currently underway or proposed across the value chain – from

generation, transmission, to distribution. Although this creates uncertainty as to

what the end state might look like, and subsequently adds risk for investors. It is

yet to be seen how and if the restructuring will create a more stable and

economically viable power sector.

- De Regulation of the Wholesale Power Market: The Transmission business

was formerly controlled by the VRA, whereas now GridCo has the

responsibility of operating the bulk transmission system. The vision set forth

by the Ministry of Power and the Energy Commission is to establish a fully de-

regulated wholesale power market, which would promote competition and in

turn lower electricity prices.

- Volta River Authority (VRA) Selling Off Non-Core Business Units: The

VRA owns and operates the vast majority of the generation in Ghana. It was

announced in November 2016 that in order to focus on it’s core generation

business, the VRA would be selling off it’s interests in businesses related to

real estate, hospitals, agriculture, and schools.

- Electric Company of Ghana (ECG) Privatization: Ghana’s largest

distribution utility is a state owned entity that has experienced considerable

financial strain in recent years. As part of a condition to access a $500 million

Millennium Challenge Compact grant from the US Government, the company

must be privatized. Consider controversy has surrounded this issue.

It is important to notice and commend the duties of policy makers and regulators

in Ghana’s energy sector. The Ministry of Power, Ghana Energy

Commission, and Public Utilities Regulatory Commission play vital roles in

charting the country’s energy future and have introduced progressive reforms in

moving towards a more sustainable electric industry.

Ghana Grid Company (GridCo) – 50Hz @ 16kV, 225 kV and 330kV

Volta River Authority (VRA) BUI HydroSunanAsogli

CENIT Thermal

Power Exchange

(Cote d’Ivore)

Electricity Company of Ghana (ECG)(~1500 MW)

NEDCO(~160 MW)

Mines(~225 MW)

VALCO(~70 MW)

Bulk Trans Customers

(~160 MW)

Export(~139 MW)

Source: Ghana Energy Access Toolkit 2016

IPPs

7

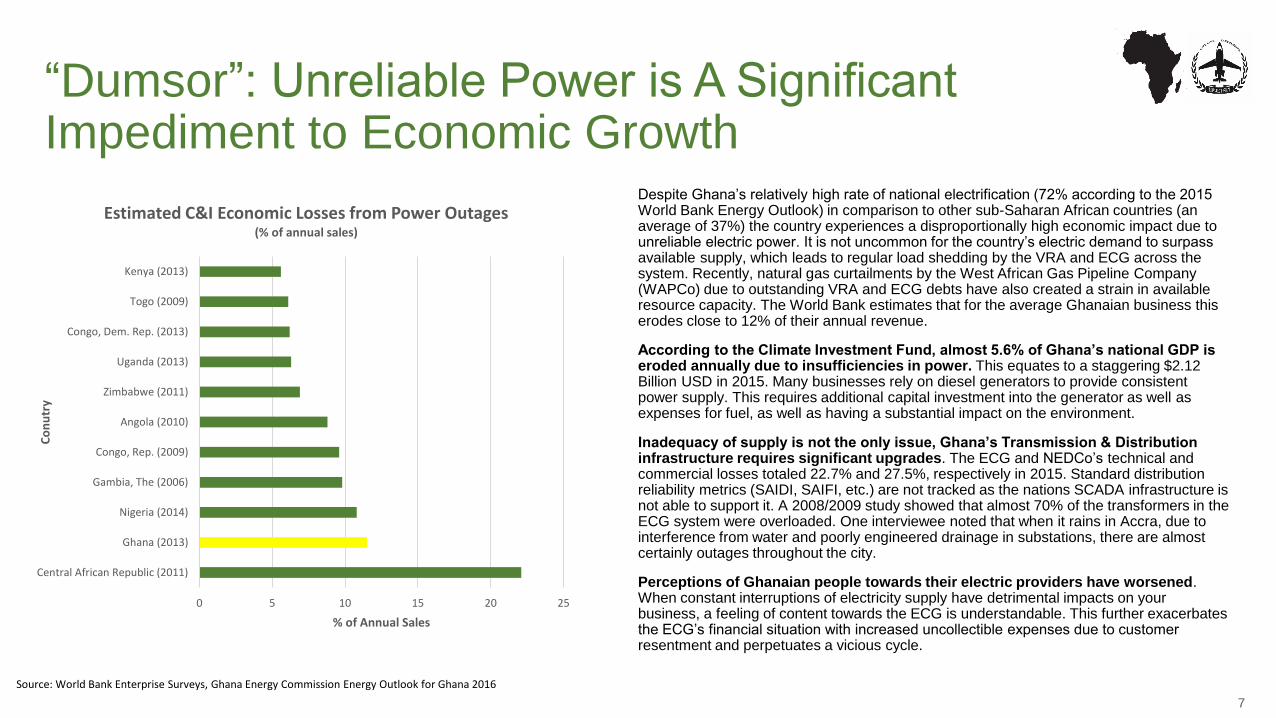

“Dumsor”: Unreliable Power is A Significant Impediment to Economic Growth

Despite Ghana’s relatively high rate of national electrification (72% according to the 2015 World Bank Energy Outlook) in comparison to other sub-Saharan African countries (an average of 37%) the country experiences a disproportionally high economic impact due to unreliable electric power. It is not uncommon for the country’s electric demand to surpass available supply, which leads to regular load shedding by the VRA and ECG across the system. Recently, natural gas curtailments by the West African Gas Pipeline Company (WAPCo) due to outstanding VRA and ECG debts have also created a strain in available resource capacity. The World Bank estimates that for the average Ghanaian business this erodes close to 12% of their annual revenue.

According to the Climate Investment Fund, almost 5.6% of Ghana’s national GDP is eroded annually due to insufficiencies in power. This equates to a staggering $2.12 Billion USD in 2015. Many businesses rely on diesel generators to provide consistent power supply. This requires additional capital investment into the generator as well as expenses for fuel, as well as having a substantial impact on the environment.

Inadequacy of supply is not the only issue, Ghana’s Transmission & Distribution infrastructure requires significant upgrades. The ECG and NEDCo’s technical and commercial losses totaled 22.7% and 27.5%, respectively in 2015. Standard distribution reliability metrics (SAIDI, SAIFI, etc.) are not tracked as the nations SCADA infrastructure is not able to support it. A 2008/2009 study showed that almost 70% of the transformers in the ECG system were overloaded. One interviewee noted that when it rains in Accra, due to interference from water and poorly engineered drainage in substations, there are almost certainly outages throughout the city.

Perceptions of Ghanaian people towards their electric providers have worsened. When constant interruptions of electricity supply have detrimental impacts on your business, a feeling of content towards the ECG is understandable. This further exacerbates the ECG’s financial situation with increased uncollectible expenses due to customer resentment and perpetuates a vicious cycle.

0 5 10 15 20 25

Central African Republic (2011)

Ghana (2013)

Nigeria (2014)

Gambia, The (2006)

Congo, Rep. (2009)

Angola (2010)

Zimbabwe (2011)

Uganda (2013)

Congo, Dem. Rep. (2013)

Togo (2009)

Kenya (2013)

% of Annual Sales

Co

nu

try

Estimated C&I Economic Losses from Power Outages(% of annual sales)

Source: World Bank Enterprise Surveys, Ghana Energy Commission Energy Outlook for Ghana 2016

8

Industry Trends & Regulatory PolicyGhana enjoys one of the highest rates of electrification throughout West Africa. However, this is not indicative of how reliable the country’s electric supply is. Due to a confluence of factors – including deficiencies in capacity and deterioration of the distribution infrastructure – the reliability of electricity is very low. It is very difficult to quantify the actual magnitude of this problem, as there is a lack of standardized reporting for reliability performance, particularly at the distribution level. Generally, these two issues are “lumped together” when referring to the consistency of electric supply.

In addition to this, the cost of electricity is Ghana is substantially higher than it’s peers across Africa. This leads to challenges across the energy value chain – from being unable to economically export surplus energy to other West African countries to a large amount of theft and uncollectible debt from the nation’s largest distribution utility, the Electric Company of Ghana.

Despite these challenges, recently instituted and proposed energy policies show that there is initiative being taken in promoting installation of more solar resources. The Ghana Ministry of Power and Energy Commission have developed plans to increase both utility scale and distributed solar generation throughout the country through the National Rooftop Solar Program and the Feed-In-Tariff.

02

9

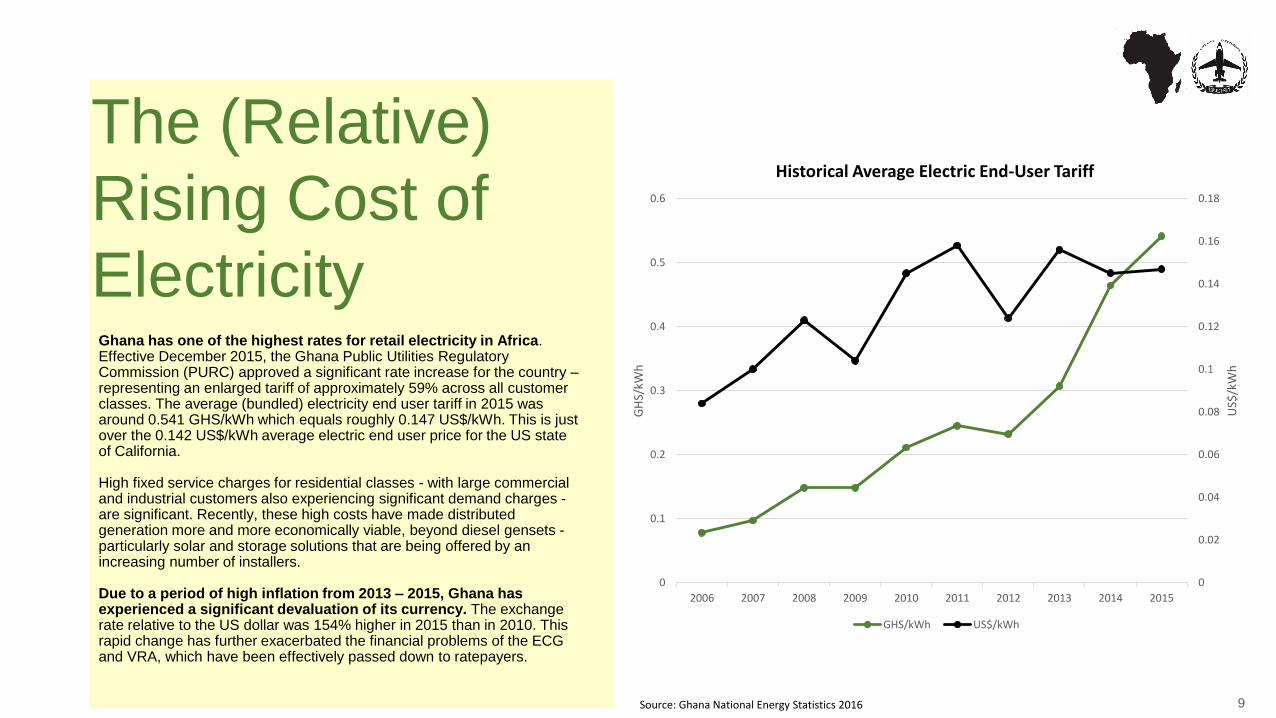

The (Relative)

Rising Cost of

ElectricityGhana has one of the highest rates for retail electricity in Africa. Effective December 2015, the Ghana Public Utilities Regulatory Commission (PURC) approved a significant rate increase for the country –representing an enlarged tariff of approximately 59% across all customer classes. The average (bundled) electricity end user tariff in 2015 was around 0.541 GHS/kWh which equals roughly 0.147 US$/kWh. This is just over the 0.142 US$/kWh average electric end user price for the US state of California.

High fixed service charges for residential classes - with large commercial and industrial customers also experiencing significant demand charges -are significant. Recently, these high costs have made distributed generation more and more economically viable, beyond diesel gensets -particularly solar and storage solutions that are being offered by an increasing number of installers.

Due to a period of high inflation from 2013 – 2015, Ghana has experienced a significant devaluation of its currency. The exchange rate relative to the US dollar was 154% higher in 2015 than in 2010. This rapid change has further exacerbated the financial problems of the ECG and VRA, which have been effectively passed down to ratepayers.

Source: Ghana National Energy Statistics 2016

0

0.02

0.04

0.06

0.08

0.1

0.12

0.14

0.16

0.18

0

0.1

0.2

0.3

0.4

0.5

0.6

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

US$

/kW

h

GH

S/kW

h

Historical Average Electric End-User Tariff

GHS/kWh US$/kWh

10

ECG’s Uncertainty: Will

Privatization be it’s savior?The contentious issues of the Electric Company of Ghana’s privatization has come of the forefront of national news and political debates. The driving factor behind the privatization is the $498 million Millennium Challenge Corporation (MCC) Ghana Power Compact grant, which aims to create a financially viable power sector in Ghana to meet the needs of growing businesses and fight poverty across the country. A key element of the compact is the “Electricity Company of Ghana Financial and Operational Turnaround Project” which aims to bring in a private sector operator to improve the company’s operations while stimulating private sector investment. Under the MCC II, the government has committed to liquidate it’s share of the debts of the ECG over five years.

The process of charting the path forward for ECG has been especially tumultuous. Workers for the company have shown passionate concerns about their own future at the company. Members of the Public Utilities Workers Union (PUWU) has shown considerable resistance to ECG’s privatization through public demonstrations and other interventions. The Ghana Trades Union Congress (TUC) has also opposed the way the privatization process has been handled and called a bidder’s conference scheduled by the Millennium Development Authority (MiDA) for October 31st 2016 a “a betrayal of trust and demonstration of bad faith”. This is in turn led to the cancellation of the meeting, which to our knowledge has yet to be rescheduled.

Various groups have proposed creative paths for the ECG’s privatization. In September 2016, energy think tank Africa Centre for Energy Policy (ACEP) proposed a transfer of 51% of ECG’s equity so a strategic partner through a purchase of shares on the Ghana Stock Exchange (GSE). Another think tank, IMANI Centre for Policy and Education, has called for privatization of at least 80% of the distribution company.

Those interviewed have shown mixed reactions and recommendations to how the company should be privatized. Some have proposed a tiered approach of implementing best practices in high load urban areas, then a gradual conversion of these processes and procedures across the various regions of the ECG. Others recommended a traditional operations and maintenance (O&M) contract for five to ten years from a private sector consultancy to give an opportunity for improving performance and thus increasing the value of the assets and the operations prior to sale.

*It is also important to note, at the end of 2015 the government of Ghana owed the ECG an estimated $428 million USD.

11

National Rooftop

Solar Program

In 2016, the Energy Commission introduced a solar/battery storage

incentive program which intends to drive the installation of 15,000 customer

owned solar PV systems. This is would translate into approximately 25 – 30

MW of additional installed capacity (roughly 1.6% of the 2015 system peak).

The program reimburses the customer for the price of the solar panels

(up to 500 Watts) on the condition that they are responsible for the purchase of

all balance of system components (inverter, controller, battery system,

installation, etc.). This is roughly a 20% - 25% incentive, depending on the

apparatus that is installed. Specific requirements also include:

• Changing all household lightbulbs to LEDs

• Install all BoS components prior to the installation of program funded panels

• Install deep cycle batteries configured to be used be PV systems

• Use only solar installers licensed by the Energy Commission.

Although this program is a step in the right direction, there are significant

challenges for it to achieve its goal. Interviewees of this study cited multiple

obstacles to success. There is still a high initial capital cost for BoS

components that will likely deter many potential customers. Also, there is a lack

of customer education programs to help customer understand the benefits that

a PV system and battery can provide for both offsetting electricity costs and the

improving the reliability of electric supply.

~400

Installations

~2000

Applications

Source: Ghana Energy Commission Interview, November 2016

12

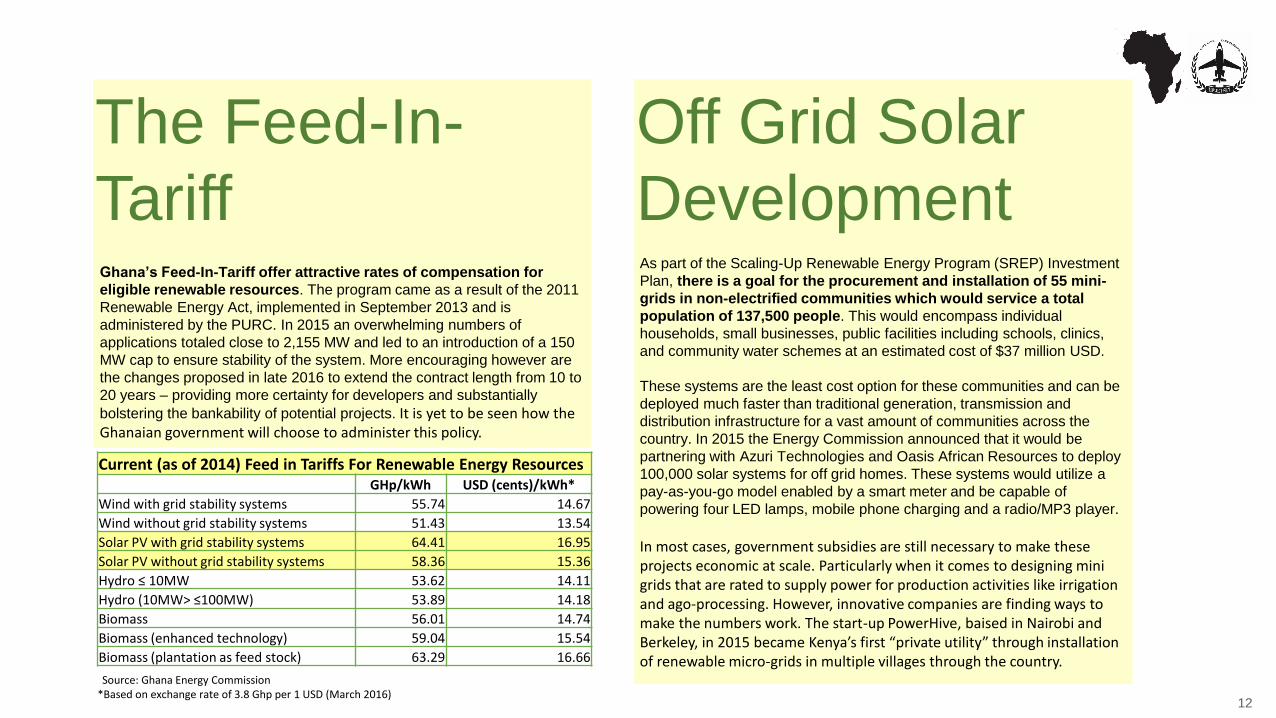

The Feed-In-

TariffGhana’s Feed-In-Tariff offer attractive rates of compensation for

eligible renewable resources. The program came as a result of the 2011

Renewable Energy Act, implemented in September 2013 and is

administered by the PURC. In 2015 an overwhelming numbers of

applications totaled close to 2,155 MW and led to an introduction of a 150

MW cap to ensure stability of the system. More encouraging however are

the changes proposed in late 2016 to extend the contract length from 10 to

20 years – providing more certainty for developers and substantially

bolstering the bankability of potential projects. It is yet to be seen how the Ghanaian government will choose to administer this policy.

Current (as of 2014) Feed in Tariffs For Renewable Energy ResourcesGHp/kWh USD (cents)/kWh*

Wind with grid stability systems 55.74 14.67

Wind without grid stability systems 51.43 13.54

Solar PV with grid stability systems 64.41 16.95

Solar PV without grid stability systems 58.36 15.36

Hydro ≤ 10MW 53.62 14.11

Hydro (10MW> ≤100MW) 53.89 14.18

Biomass 56.01 14.74

Biomass (enhanced technology) 59.04 15.54

Biomass (plantation as feed stock) 63.29 16.66

Source: Ghana Energy Commission*Based on exchange rate of 3.8 Ghp per 1 USD (March 2016)

Off Grid Solar

DevelopmentAs part of the Scaling-Up Renewable Energy Program (SREP) Investment

Plan, there is a goal for the procurement and installation of 55 mini-

grids in non-electrified communities which would service a total

population of 137,500 people. This would encompass individual

households, small businesses, public facilities including schools, clinics,

and community water schemes at an estimated cost of $37 million USD.

These systems are the least cost option for these communities and can be

deployed much faster than traditional generation, transmission and

distribution infrastructure for a vast amount of communities across the

country. In 2015 the Energy Commission announced that it would be

partnering with Azuri Technologies and Oasis African Resources to deploy

100,000 solar systems for off grid homes. These systems would utilize a

pay-as-you-go model enabled by a smart meter and be capable of

powering four LED lamps, mobile phone charging and a radio/MP3 player.

In most cases, government subsidies are still necessary to make these projects economic at scale. Particularly when it comes to designing mini grids that are rated to supply power for production activities like irrigation and ago-processing. However, innovative companies are finding ways to make the numbers work. The start-up PowerHive, baised in Nairobi and Berkeley, in 2015 became Kenya’s first “private utility” through installation of renewable micro-grids in multiple villages through the country.

13

Breaking Down Barriers and Seizing OpportunitiesSignificant challenges exist towards the adoption of distributed solar throughout Ghana. Like many African countries, it is difficult to secure financing

for such projects and high initial capital costs are cost prohibitive for the majority of businesses and residential customers. However, there are

pathways that can be taken by the stakeholders that have the power to address these issues. Namely, regulators should continue instituting

progressive policies and enabling their success through collaboration with the ECG. There is considerable interest from foreign investors into the

country’s energy sector yet it is not realized due to regulatory hurdles and contracting issues that these companies must face when dealing with the

government. It is imperative to streamline this process to achieve the potential that solar energy offers both businesses and residential communities.

Off-grid developments are also a huge opportunity, with a growing amount of financing available through foreign aide funds and innovative start-ups

growing their presence throughout Africa. Particularly with the transfer of political power as a result of the December 2016 election, there are huge

opportunities to break down barriers and empower further solar adoption across Ghana.

03

1 4

• Lack of financial data to

analyze creditworthiness of

businesses and residents

• Quality of main potential

off-taker (ECG) is

perceived as low

• Regulatory lag has

potential to kill projects in

various stages of

development

Threat

Ghana Solar

SWOT

Analysis

• High levels of solar

irradiance across the

country lead to high

capacity factors for solar

installations

• Solar + storage systems

and micro grids offer

considerable value in

enhancing reliability and

electrifying communities

Opportunity

• Challenges in securing project financing, very high commercial bank interest rates (25% and higher)

• Regulatory hurdles due to entrenched practices and corruption, other African markets perceived to be more amiable

• High VAT on imported solar system components

Weakness

• Stable political environment

in comparison to other

African countries

• Targeted regulatory policies

to promote solar

development

• Substantial forecasted load

growth (up to 8% annually)

and fast growing economy

Strength

15

A real estate development boom

has been evident in Ghana,

particularly in the urban center of

Accra. Some developers have

incorporated solar systems

individually or as part of a micro

grid in new subdivision type

residential communities. This

subsequently increases the

properties value and avoids the

issue of sunk cost from diesel

generators previously installed.

New Construction

The Ghana Energy Commission

offers an attractive Feed-In-Tariff

for qualifying resources. Recently,

the terms have been made even

more economically attractive with

a proposal to extend the contract

period from 10 to 20 years. For

qualifying solar resources, the

compensation rate currently

stands at close to $0.15 - $0.17

USD per kWh. There are currently

an overwhelmingly high level of

applications.

Feed-In-Tariff

Since 2007 the Ghana Energy

Development and Access Project

(GEDAP) has helped provide over

16,000 rural households with

electricity. This has proved out a

viable model for project financing

and deployment. Furthermore,

studies have proven that there is a

surprisingly high willingness to pay

for energy services from rural

citizens.

Rural Mini-Grids

Mobile payments have

revolutionized many of Africa’s

developing economies. This option

to finance small scale systems has

significant potential across Ghana,

moving beyond just phone

charging and light to power LED

TVs and other energy efficient

home appliances. Smart metering

technology and cellular control

allows for assurance of cash flows

and monitoring of system health by

the developer.

Pay As You Go

Emerging Business Models

16

Making the

Business Case

Cost effective project financing is difficult to attain in Ghana, with commercial

banks offering upwards of 25% annual interest rates and microfinance

institutions still very steep as well. This creates substantial financing

challenges for both developers and off-takers in the region. Local solar

energy dealers and installers need to have education and access to trade

finance and working capital to be able to maintain business operations.

There needs to be better facilitation by the government to capital providers –

including international development grants, impact investment funds, and

other private sector investors.

Identify Cost-Effective Project Financing

The “price to beat” for distributed solar assets depends on: 1) The retail rate

of electricity delivered by ECG and 2) the cost of operating existing diesel

generators. The economics can certainly pencil out, but are contingent on a

wide array of factors. The uncertainty of future retail rate movements and

price of diesel create risks when evaluating a long term investment into a

solar system. Rigorous analysis by project developers, off-takers, and capital

providers is pivotal to lowering risks and adding certainty to forecasted cash

flows from investments into solar.

Quantify the “Price to Beat”

17

Engaging the

Customer

Building a skilled local installer network is very difficult in Ghana’s business

conditions. It is critical for developers to establish these sales and operational

channels to reach desired levels of scale. The Ministry of Power and Energy

Commission have a certification process in place to qualify installers – this

should be leveraged as a channel to provide support and resources to these

suppliers. Additionally, clear expectations need to be established for warranty

and repair/maintenance activity.

Improve Last Mile Distribution

Specific industries can benefit significantly from solar, yet there is a lack of

customer education targeted towards businesses and entrepreneurs.

Manufacturers and distributors should investigate products designed for specific

industry applications – from large scale manufacturing to agriculture and small

scale retail. Opportunities in incorporating solar into new residential and

commercial developments should be explored by solar services providers.

Marketing material presenting payback periods considering proxy loads for

specific businesses may prove compelling to owners.

Deliver Targeted Industry Education

18

Navigating the Regulatory Environment

Although there is a formal NEM policy in place, the ECG does not currently

compensate customers for excess energy that they put back onto the grid. To

ensure value for both stakeholders, the policy should be amended to

compensate customers at a value of solar (not retail) and set size limits on

systems, as well as a potential cap on the amount of capacity. This would give

certainty for customers making long term investment decisions and provide

value to the ECG. Also, the Feed-In Tariff cap should be revisited and

compensation numbers should be reset to remain competitive but not such

that it is oversubscribed.

Fix Net Energy Metering / Feed-In Tariff Policies

Multiple interview participants noted significant regulatory challenges when

responding to and negotiating government issued tenders. The Put Call Option

Agreement (PCOA) was cited as a contracting structure that has been critical

in the success of multiple solar projects in Nigeria. A standard procurement

process and independent oversight would also help streamline and ensure the

integrity of solicitations and administration of government funding.

Rework Government Contracting

19

- Interview Respondent

Dealing with regulators in Ghana requires that you be patient, polite,

and persistent.

20

About The AuthorAbout The SponsorAlexander Pischalnikov is an energy sector consultant providing strategic advisory services to utilities, financial investors, independent power producers, policy makers and solutions providers across North America and Europe. Mr. Pischalnikov is an expert on distributed energy resource (DER) economics and regulatory policy and helps clients evaluate investments and strategic initiatives in smart grid technology and DERs in light of uncertain economic, operational and regulatory conditions.

Mr. Pischalnikov is a Principal Consultant in the Energy & Utilities practice at PA Consulting Group, an international management consulting, technology and innovation firm based in London. He also serves as a strategic advisor to Sunpowerd. Alexander resides in Los Angeles, California

Contact: www.sunpowerd.com Contact: [email protected]

Sunpowerd is an innovative renewable energy technology company based in New York, NY and Accra, Ghana. The company manufacturers and distributes an all-in-one portable, lightweight and inflatable solar lamp that is fit for lighting up Africa! This eco-friendly rechargeable solar lamp provides 6 – 12 hours of light when it is needed most.

Sunpowerd also works with government entities, financial investors, businesses and renewable energy product developers to facilitate the deployment of capital towards both off-grid and grid-connected solar energy systems across Africa. Sunpowerd strives to make an impact on the social and economic development of the African continent through clean and reliable renewable energy.

Related Documents