Summer Internship Project Report On Working capital management At AKUMS DRUGS & PHARMACEUTICAL LTD HARIDWAR (Submitted For the Partial Fulfillment of the Requirement for the Degree of Master in Business Administration) Project Guide: Submitted By: MR. K.D SHARMA ANKITA NEGI FINANCE MANAGER &HR MANAGER 09720641 AKUMS, Hardwar

Summer Internship Project Report

Nov 23, 2014

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Summer Internship Project Report

On

Working capital management

At

AKUMS DRUGS & PHARMACEUTICAL LTD

HARIDWAR

(Submitted For the Partial Fulfillment of the Requirement for the Degree of Master in Business Administration)

Project Guide: Submitted By:

MR. K.D SHARMA ANKITA NEGI FINANCE MANAGER &HR MANAGER 09720641

AKUMS, Hardwar

UTTRAKHAND TECHNICAL UNIVERSITY,DEHRADUN

SESSION 2009-2011

DECLARATION

I hereby declare that the study entitled “WORKING CAPITAL MANGEMENT in the context of AKUMS DRUGS & PHARMACEUTICAL LTD SIDCUL, HARDWAR” being submitted by me in the partial fulfilment of the degree of “MASTERS IN BUSINESS ADMINISTRATION” is a record of my own work being a student of COER school of management affiliated to Uttarakhand technical university. The study was conducted at FINANCE Department, AKUMS DRUGS & PHARMACEUTICAL

The matter embodied in this project report has not been submitted anywhere else for any other degree/diploma. .

Place: Haridwar ANKITA NEGI

Date: 10-08-10 Roll No: 09720641

ACKNOWLEDGEMENT

I wish to express my sincere gratitude to Mr. K.D SHARMA, (Finance Manager AKUMS DRUGS & PHARMACEUTICAL Hardwar) for giving me the opportunity to do my summer training in his highly esteemed Organization.

I am grateful to Ms. LALIT ARORA (SENIOR ACCOUNT OFFICER), for his Valuable guidance, advice, suggestion and constant encouragement rendered to me at every stage.

I am extremely thankful to my Faculty Guide Mrs. JYOTSNA at College of Engineering Roorkee for her invaluable Guidance and Suggestions during my Training.

I am also thankful to all others who helped me directly or indirectly towards the completion of my works.

Ankita Negi

MBA

COER-SM

INDEX:-

COMPANY PROFILE

THEORITICAL BACKGROUND OF TOPIC

METHODOLOGY

FINDINGS

CONCLUSION

RECOMMENDATION

ANNEXURE

OBJECTIVES:

To analysis the working capital turnover ratio.

To analysis the current assets turnover ratio

To analysis the current liability turnover ratio

COMPANY PROFILE

INTRODUCTION:

Akums drugs & pharmaceutical ltd is situated in a excise free zone & well developed INDUSTRIAL AREA OF HARIDWAR (U.A), in INDIA was established & formed in the year 2004 by good efforts of MR. D.C. JAIN, MR. SANDEEP JAIN

Akums drugs is endeavoring to make a name in pharmaceutical industry.

Akums drugs has become the icon of INDIAN HEALTHCARE & A QUALITY PHARMA MANUFACTURER of the country, global vision AKUMS has been accredited with WHO-GMP,ISO 9001:2000 & ISO 14001:2004 CERTIFICATE.

Quality assurance:

Quality assurance is deals with all methods that individually & collectively influence the quality of products.

Hence q. a department looks after implementation of GMP, in all aspects of products manufacture & control .The Q.A. serve as countercheck for different departments like stores , production, engineering, personnel & administration, quality control etc. to ensure that all activities are performed as per respective SOP’S & records are maintained.

Besides the above mentioned, Q.A. performs additional tasks as under:-

Selection of approval of vendors.

Proving the details of storage conditions & monitoring of R.M & P.M

Checking of the active materials issued from the store department.

Independently monitoring & recording in process checks during manufacturing & packing.

Inspection of entire batches manufacturing & packing records for giving final approval for transfer to finished goods store.

Validation of testing methods particularly non- pharmacopoeia methods.

Microbiological monitoring of purified WATER in manufacturing & filling areas etc.

Real time & accelerates stability testing as per WHO/ICH GUIDELINES.

Calibration of all laboratory equipments & instruments.

Monitoring residual quantity of medicaments after product charges are over.

Conduction quality monitoring tasks like manufacturing, cleaning validation, process validation, complaint. Product recall, training, self-inspection, quality audit, etc.

Approving SOP’S of all functional department & product master formula card.

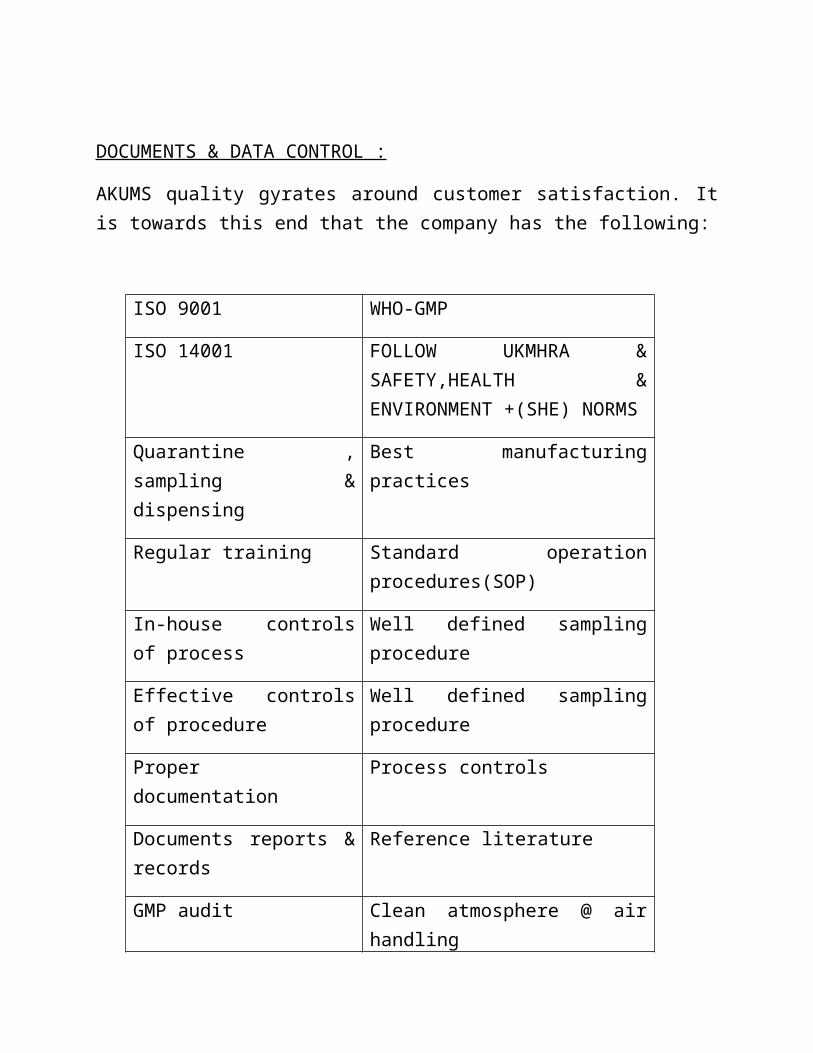

DOCUMENTS & DATA CONTROL :

AKUMS quality gyrates around customer satisfaction. It is towards this end that the company has the following:

ISO 9001 WHO-GMP

ISO 14001 FOLLOW UKMHRA & SAFETY,HEALTH & ENVIRONMENT +(SHE) NORMS

Quarantine , sampling & dispensing

Best manufacturing practices

Regular training Standard operation procedures(SOP)

In-house controls of process Well defined sampling procedure

Effective controls of procedure

Well defined sampling procedure

Proper documentation Process controls

Documents reports & records Reference literature

GMP audit Clean atmosphere @ air handling

Hygienic conditions Proper uniforms

Quality standards Own R&D

MANUFACTURING RANGE INCLUDES

ANTI-MALARIAL ANTIBIOTICS VITAMINS

Analgesics Anti-ulcerates Corticosteroids

Anti-diabetics Tranquilizers Sedatives

Gastri-intestinal Anti-bacterial Anti-ulcerates

Anti-allergic Anti-amoebic Antipyretics

Cough & cold preparation

Anti-diarrhea Food preparation

Ointments

(eye / ear/skin)

FINANCE DEPARTMENT OF AKUMS & PHARMACEUTICALS LTD.

SECTION UNDER - AKUMS DRUGS & PHARMACEUTICALS LTD.

PURCHASE SECTION.

EMPLOYEE WELFARE SECTION.

PAY ROLL SECTION.

BANKS & MISCELLANEOUS.

1. PURCHASE DEPARTMENT:

IT INCLUDE THE FOLLOWING FUNCTION:

a) Deposists & advance payments to suppliers

b) Passing of bills for suppliers received

c) Pricing of goods receipt notes

d) Accounting of cash purchase made by materials department

e) Arrangement of cash purchase made by the material department

f) Arrangement for insurance of transit risk

g) Maintenance of books of accounts

2. EMPLOYEE WELFARE SECTION

The section is responsible to give the information to payroll section for payment and deduction of below mentioned benefits and incentives.

Other welfare schemes:-

Indian oil employees welfare co-operative society

LIC’s group saving linked insurance scheme

HBA mortgage redemption scheme

IOCL Employee group gratuity scheme

IOCL Superannuation benefit fund scheme

Personal claims and other payments

Leave travel concession

Reimbursement of medical expenses

Self leased accommodation

Travelling Allowance

Travelling allowance

Daily allowance

Local conveyance charges

TA for joining duty on first appointment

Transfeer benefits & settling time

Settling allowance

Displacement allowance

Transit allowance

Salary advance

Transportation of personal effects

Loading and unloading charges

Insurance charges

Excess baggage charges

Octroi charges

Packing charges

Travel expenses – for preparatory trip

Reimbursement of expenses for admission of school going children

Allowances on local transfer

Joining time

Facilities

Canteen services

Medical facilities

Housing facilities

Education facilities

Recreation clubs and centers

Social security

Provident fund

Group insurance scheme

Indian oil employees welfare co-operative scheme

Scheme for self insurance

Gratuity & compassionate gratuity

Other benefits

Membership of professional bodies

Children education assistance scheme

Incentive for acquiring higher qualification

Long service award

Issue of briefcase

Issue of calculators

Ex- gratia payment

Performances linked

Productivity linked incentive

3. PAY ROLL SECTION

Function of the section dealing with establishment can be broadly classified as follows:

Scrutiny and concurrence of proposal from personal department

Payment of salaries and allowances

Advances to employees

Deduction from pay bills

Statutory and statistical requirements.

Scrutiny and concurrence of proposal from personal department

Proposals requiring finance concurrence shall be received in the section and serutinized with reference to the rules applicable. Cases not covered by specific rules shall be referred to the appropriate authority for decision.

Payment of salaries and allowances

Pay and allowance shall be drawn by the finaces department on the basis of attendance particular which shall be send by the time office to finance giving details such as name of the employee.employee number, number of regular days, over time etc. under the mechanized system of pay roll accounting, the time cards are after filling in summary particulars through finance department to the data processing section. The data processing section shall prepare a statement, which is checked and confirmed by the time office subsequently. Pay and allowances are as mentioned below:

Scale of pay

Dearness allowance

City compensatory allowance

House rent allowance

Shift allowance

Washing allowance

Tea reimbursement

Special allowance

Patrolling allowance

Cash handling allowance

Tanker allowance

Conveyance allowance to blind

Reimbursement towards transport exptenses

Compensatory hill cum winter allowance

Non practicing allowance

Heavy equipment allowance

North Eastern Allowance

Special compensatory allowance

Professional updating expenses

Rationalization adjustment allowance

ADVANCE TO EMPLOYEE

Rules for various types of advances are prescribed in the personal manual on the basis of sanction and release order received from competent authority. The section dealing with advance shall prepare payment voucher debiting appropriate advance account and the same shall be passed on to cash section for payment. Recovery of advance shall be made in accordance with the installments given in the sanction order. Where the period of recovery is prescribed in the rule given in the relevant manuals. The same shall be done accordingly. All recoveries in respect of particular advance account shall be credited to the advance account. Loans and advances are mentioned below:

House building advance

Conveyance advance

Conveyance repair advance

Emergency advance

Funeral expenses

Festival advance

4. BANKS AND MISCELLANEOUS SECTION:-

This section shall be responsible for:

Receipts of cheques and bank drafts

Petty cash imprested by cheques and bank drafts

Payments

Safe custody of valuables and documents

Maintenance of special current accounts

Maintenance of bank cashbooks.

Reconciliation of bank account

THEORITICALBACKGROUND

MEANING OF WORKING CAPITAL

Working Capital is commonly defined as the difference between current assets and current liabilities. Efficient working capital management requires that firms should operate with some amount of working capital, the exact amount varying from firm to firm and depending, among other things on the nature of industry.

Capital required for a business can be classified in two main categories viz.

1) Fixed capital, and

2) Working capital.

Every business needs funds for two purposes-for establishments and to carry out its day-to-day operations. Long-term funds are required to create production facilities.

Through purchase of fixed assets such as plants and machinery, land, building, furniture, etc. An investment in these assets represents that part of firm’s capital which is blocked on permanent or fixed basis and is called fixed capital. Funds are also needed for short-term purpose for the purchase of raw material, payment of wages and other day-to-day expenses, etc. These funds are known working Capital. In simple words, working capital refers to that part of the firm’s capital, which is required for financing short-term or current assets such as cash, marketable securities, debtors and inventories. Funds thus invested in current assets keep revolving fast and are being constantly converted into cash and these cash flows out again in exchange for other current assets. Hence, it is also known as revolving or circulating capital or short-term capital.

CLASSIFICATION OF WORKING CAPITAL

Working Capital may be classified on two basis: -

a) On the basis of Concept: -

On the basis of concept, working capital can be classified as,

Gross Working Capital

Net Working Capital

b) On the basis of Time: -

On the basis of time, working capital can be classified as,

Permanent or Fixed Working Capital

Temporary or Variable Working Capital

Gross Working Capital: -

The Gross Working Capital is the Capital invested in the total current assets of the enterprises. Current assets are those assets, which can be converted into cash within a short period, normally an accounting year.

Gross Working Capital = Total Current Assets

Net Working Capital: -

The term Net Working Capital refers to the excess of current assets over current liabilities, or say,

Net Working Capital = Current Assets – Current Liabilities

Net Working Capital can be positive or negative. When the current assets exceed the current liabilities the working capital is positive and the negative working capital results when the current liabilities are more than the current assets. Current liabilities are those liabilities, which are intended to be paid in the ordinary course of business within a short period of normally one accounting year out of the current assets of the income of the business. The gross working capital concept is financial or going concern concept whereas net working capital is an accounting concept of working capital. Both the concepts have their own merits.

The gross concept is sometime preferred to the concept of working capital for the following reasons: -

It enables the enterprise to provide correct amount of working capital at correct time.

Every management is more interested in total current assets with which it has to operate then the sources from where it is made available.

It takes into consideration of the fact every increase in the funds of the enterprise would increase its working capital.

The concept is also useful in determining the rate of return on investments in working capital.

The net working capital concept, however, is also important for the following reasons:-

It is a qualitative concept, which indicates the firm’s ability to meet its operating expenses the short-term liabilities.

It indicates the margin of protection available to short term creditors.

It is an indicator of financial soundness of enterprise.

It suggests the need of financing a part of working capital requirement out of the permanent sources of funds.

Permanent or Fixed Working Capital: -

Permanent or fixed capital is the minimum amount, which is required to ensure effective utilization of fixed facilities and for maintaining the circulation of current assets. Every firm has to maintain a minimum level of current assets is called permanent or fixed working capital as this part of working capital is permanently blocked in current assets. As the business, grow the requirement of working capital also increases due to increase in current assets.

Temporary or Variable Working Capital: -

Temporary or variable working capital is the amount of working capital, which is required to meet the seasonal demands and some special exigencies. Variable working capital can further be classified as seasonal working capital and special working capital. The capital required to meet the seasonal need of the enterprise is called the seasonal working capital. Special working capital is that part of working capital which is required to meet special exigencies such as launching of extensive marketing campaign for conducting research etc.

Temporary working capital differ from permanent working capital in the sense that it is required for short periods and cannot be permanently employed gainfully in business

CALCULATE CURRENT ASSETS TO FIXED ASSET RATIO

A firm needs current and fixed assets to support a particular level of output. However, to support the same level of output the firm can have different levels of current assets. As the firm’s output and sales increases, the need for current asset increases. Generally the current assets do not increase in direct proportion to output; current assets may increase at a decreasing rate with input. This relationship is based upon the notion that it takes a greater proportional investment in current assets when only a few units of output are produced than it does later on when the firm can use its current assets more efficiently.

The level of the current assets can be measured by relating current assets to fixed assets.

There are three policies:-

CONSERVATIVE current assets policy:

CA/FA is higher. It implies greater liquidity and lower risk.

AGGRESSIVE current assets policy:

CA/FA is lower. It implies higher risk and poor liquidity.

MODERATE current assets policy:

CA/FA ratio falls in the middle of conservative and aggressive policies.

NEEDS AND OBJECTIVES FOR WORKING CAPITAL

Every business needs some amount of working capital. The needs for working capital, arises due to time gap between production and realization of cash from sales. There is an operating cycle involved in sales and realization of cash. There are time gaps in purchase of raw material and production, production and sales, and realization of cash.

Thus, working capital is needed for the following purposes: -

For the purchase of raw material, component and spares.

To pay wages and salaries.

To incur day- to- day expenses and overhead costs such as fuel, power and office expenses etc.

To meet the selling costs such as packing, advertising etc.

To provide credit facilities to the customers.

To maintain the inventories of raw material, work in progress, store, spares, and finished stock

For studying the need of working capital in a business, one has to study the business under varying circumstances such as new concern, as a growing and one, which has attained maturity. A new concern requires a lot of funds to meets its initial requirement such as promotion and formation etc. These expenses are called preliminary expenses and are capitalized. The amount needed for working capital depends upon the size of the company and the ambition of its promoters. Greater the size of the business unit, generally will be the requirement of the

working capital. The requirement of the working capital goes on increasing with the growth and expansion of the business until its gains

maturity. At maturity, the amount of working capital required is called normal working capital.

IMPORTANCE OF WORKING CAPITAL

1. Time devoted to working capital management:-

The largest portion of financial manager’s time is devoted to day to day internal operation the firm. This may be appropriately sum up under the heading "WORKING CAPITAL MANAGEMENT".

2. Investment in current assets: -

current assets represent more than half of the total assets of a business firm. Because they represent largest investment and because this investment tends to relatively volatile, current assets are worthy for the financial manager's careful attention.

3. Importance for small firm:-

current assets are similarly important for the financial manager's of small firm. Further small firm are relatively limited access to the long term markets, it must necessarily rely on the trade credit and short term bank loan , both of net effect on net working capital by increased current liabilities.

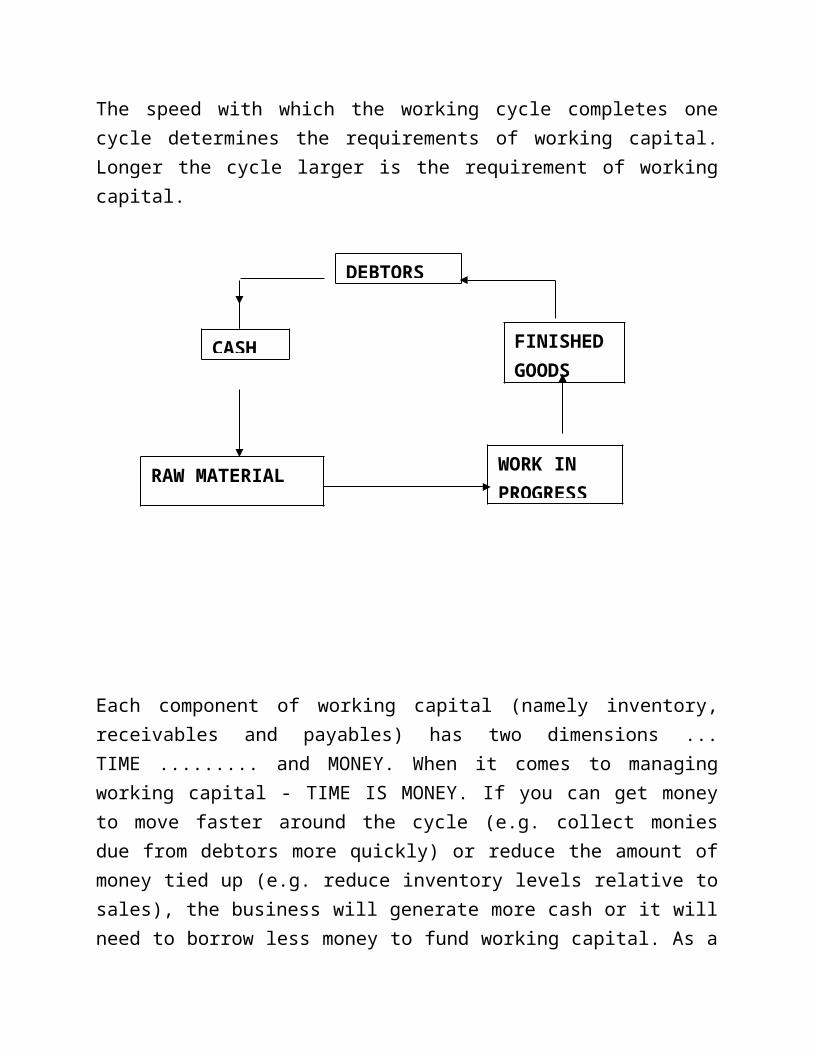

WORKING CAPITAL CYCLE: -

The speed with which the working cycle completes one cycle determines the requirements of working capital. Longer the cycle larger is the requirement of working capital.

Each component of working capital (namely inventory, receivables and payables) has two dimensions ... TIME ......... and MONEY. When it comes to managing working capital - TIME IS MONEY. If you can get money to move faster around the cycle (e.g. collect monies due from debtors more quickly) or reduce the amount of money tied up (e.g. reduce inventory levels relative to sales), the business will generate more cash or it will need to borrow less money to fund working capital. As a consequence, you could reduce the cost of bank interest or you'll have additional free money available to support additional sales growth or investment.

DEBTORS

FINISHED GOODS

CASH

RAW MATERIALWORK IN PROGRESS

METHODOLOGY

THE FOLLOWING DATA WHICH I TAKE HERE IS AN SECONDARY DATA BECAUSE IT IS FROM THE BALANCE SHEET & P&L ACCOUNT OF THE COMPANY. From The Website.

FINDINGS & ANALYSIS

PARTICULARS Mar’06 Mar’07 Mar’08 MAR’09 MAR’10

CURRENT

ASSEST

2292.28 2834.68 3743.98 4419.57 5483.42

CURRENT LIABLITIES

1006.15 1053.91 1396.86 1568.71 2524.77

NET WORKING CAPITAL

1286.10 1780.77 2347.12 2850.86 2958.65

TURNOVER 2981.35 3561.99 4203.29 5234.29 5605.69

TABLE IN CRORE

GRAPHICAL REPRESENTATION OF WORKING CAPITAL:-

Interpretation: -

If we see from the above table, it can be clearly seen that net working capital has continuously rise up from MAR’06 TO MAR’10. It is good for the company because its turnover is also increased

WORKING CAPITAL TURNOVER RATIO:-

This ratio helps to measure the efficiency of the utilization of the working capital. It signifies that for an amount of sales, a relative amount of working capital is needed. This ratio shows the direct relationship between the sales and working capital.

W.C. turnover ratio = sales /working capital

YEAR CALCULATION RATIOMAR’06 2981.35/1286.13 2.318MAR’07 3561.99/1780.77 2.002MAR’08 4203.29/2347.12 1.791MAR,09 5234.29/2850.86 1.836MAR’10 5605.69/2958.65 1.895

GRAPH

INTERPRETATION: By observing the above ratio we find that the organization was using its working capital in the best possible manner in mar’06, this ratio is 2.318 but in the year 2007-09 this ratio has rapidly come down from 2.002 to 1.836 & in the year 2010 this ratio is increase to 1.895 . This increase was becausethe sales do increase in the same ratio so it shows that working capital management is in a proper manner and in accordance to sales.

CURRENT ASSETS TURNOVER RATIO :-

This ratio indicates the efficiency with which current assets turn into sales. A higher current assets turn over rate or a lower current assets turnover period is better. It indicates the efficient use of the funds and the reverse case indicates reduced lock-up of funds in current assets. C.A.turnover ratio = sales / current assetsYEAR CALCULATION RATIOMAR’06 2981.35/1286.13 2.3180MAR’07 3561.99/1780.77 2.002MAR’08 4203.29/2347.12 1.791MAR’09 5234.29/2850.86 1.836MAR’10 5605.69/2958.65 1.895

GRAPH

Interpretation:- By observing the above ratio we find that current assets turnover rate increased in MAR’06. Then after there was a decline from MAR’07-09 but very soon the company improved its current assets position from 1.836 to 1.895 in MAr’10. This increment shows that the current asset management is improving.

CURRENT LIABLITIES TURN OVER RATIO:-

CURRENT LIABLITIES TURN OVER RATIO=SALES/LIABLITIES

YEAR CALCULATION RATIO

MAR’06 2981.35/1006.15 2.963

MAR’07 3561.99/1053.91 3.380

MAR’08 4203.29/1396.86 3.009

MAR’09 5234.29/1568.71 3.337

MAR’10 5605.69/2524.77 2.339

GRAPH:-

INTERPRETATION: From the graph we can see the fluctuation in the current liabilities. In the mar’09 it is 3.337 which was going down in mar’10 by 2.339.

SUMMARY OF FINDINGS

The company is able to reduce its working capital from in a span of FIVE years without affecting the sales of the company which means that company is sincerely utilizing its funds and has reduced the locking of funds.

The latest working capital ratio indicates the efficiency of utilization of net working capital is increased

The current assets turnover ratio has increased which indicates that current assets is efficiently turning into sales.

The current liabilities shows fluctuation ,in mar’10 the C.L reduces which means company maintained its working capital in well manner.

CONCLUSION & RECOMMENDATION

CONCLUSION

By observing the ratio come under working capital management we can say that the company doing good & also improving their sale year by year.

The company also doing well by reducing current liability,& improving their current assets & working capital . So we can say that the company manage w.c management in good way.

RECOMMENDATION

The current assets turnover has decreased from mar’07-09 by 2 to 1.836 , so the company should try to improve this ratio through increase in sales or reduce the un-necessary lock up of funds in current assets.

There is a increase in current liabilities which is not good for the credit of company so the organization should try to reduce the current liabilities through speedy payment to creditors and reduce the un-necessary provisions.

There is a big fluctuation in working capital turnover ratio This was because the sales did not increase in the same ratio as working capital increased. So the company should manage the working capital and should properly estimate for an amount of sales how much working is needed so that the un-necessary lock up of funds in working capital may not occur.

ANNEXURE

BIBLOGRAPHY

FINANCIAL MANAGEMENT - I.M. PANDAY

WORKING CAPITAL MANAGEMENT- J.D. AGGARWAL

FINANCIAL MANAGEMENT- SASHI K. GUPTA

AKUMS DRUGS & PHARMACEUTICAL PVT. LTD- BALANCE SHEET& P&L ACCOUNT

Related Documents