C.I.B. (Challenge; Initiative; Benefit) Commerzbank (New York) Challenge: lack of returns generated from traditional banking products Initiative: Over a year: researched certain cash-based contracts approved by the S.E.C. as money-market equivalents (time-line of 90 days or less); investigated the intricate S.E.C. and insurance regulatory accounting standards; studied uses and flexibility of certain bank lending products; as well as, worked closely with best legal experts in insurance to test out possible product concept. Benefits: Including, but not limited to, the following: 1. developed regulatory structured arbitrage product; 2. enabled insurers issuing these contracts to invest in riskier assets maturing later than three months; 3. increased spread earned on these product by 300%; as well as, 4. pitched the product to five of the top ten issuers of cash-equivalent cash investment contracts.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

C.I.B. (Challenge; Initiative; Benefit)

Commerzbank (New York)

Challenge: lack of returns generated from traditional banking products Initiative: Over a year:

researched certain cash-based contracts approved by the S.E.C. as money-market equivalents (time-line of 90 days or less);

investigated the intricate S.E.C. and insurance regulatory accounting standards;

studied uses and flexibility of certain bank lending products; as well as,

worked closely with best legal experts in insurance to test out possible product concept.

Benefits: Including, but not limited to, the following:

1. developed regulatory structured arbitrage product; 2. enabled insurers issuing these contracts to invest in riskier assets

maturing later than three months; 3. increased spread earned on these product by 300%; as well as, 4. pitched the product to five of the top ten issuers of cash-equivalent

cash investment contracts.

Allstate Life Insurance Company 3075 Sanders Road North Allstate, Allstate 60062-7127

Attn Mr Steve Schaefer Re mmerzbank Insurance Liquidity Support Product for Allstate Life Insurance ("Allstate")

Dear Steve,

Thanks for calling me back today. In the previous ‘thank-you’ letter to Sarah Donahue, attached

hereto, we indicated our “loud-and-clear” understanding of Allstate’s liquidity support needs.

Since then, we have further modified the Insurance Liquidity Support Product (the “Facility”),

rendering its structure more flexible and linking pricing to your performance. Previously, we had

altered the proposed structure to extend the surrender notice period – or, the time-bucket – from

7-30 days to 364 days. Through these newer changes, the capital efficiency of the Facility’s credit

component reduces significantly the expected out-of-pocket cost of issuance for Allstate. Initially,

as a partner through a bi-lateral line, subsequently to be syndicated out to a group of highly rated

banks, we can accommodate directly, and simply, your specific appetite for issuing shorter-term

funding agreements. Thus can we work out the details of the Facility’s credit documents first.

The modified credit/funding agreement confers the following advantages upon Allstate:

1. Allstate positioned as a beneficiary of the flight-to-quality among funding agreement issuers;

2. ease of entry with a credit/funding agreement jointly issued by two double-A financial

institutions;

3. extended time-buckets require no change in your investment strategy or liability structure; and,

4. the support of the Bank’s capital markets team, the fifth best in euro-debt issuance, to allow, if

necessary, for a euro-medium term note issuance to take out the New Funding Agreement(s).

Borrower Allstate Life Insurance Company ("Allstate")

Lender The Bank or its commercial paper funding conduit, Four Winds Funding

Line Amount Up to U.S.$500,000,000 plus an incremental amount for accrued interest.

Term of Line 364-days, with a sixteen month term-out provision

Borrowing Length Up to sixteen months

Pricing Arranger’s Fee of 50 basis points, paid up-front; annual Facility Fee of 15 b.p.s;

and, interest margin of 35 b.p.s with a step-up in rates after 60 days

Covenants A few of which none are substantive

Conditions Precedent Receipt by the Bank of a ‘new’ funding agreement in its name and issued by

Allstate and containing the rolling-365-day surrender option

Defaults Fraud, bankruptcy, credit-event-upon-merger and a regulatory event

Default Remedy Accelerate the surrender period of the new funding agreement from one year to

one week

Funding Protocol If line undrawn on 364th day, no funding agreements are being surrrendered and

if the Bank does not consent to an extension, Allstate can draw under the line for

the full amount for sixteen months; the Bank reserves the right to accept either a

prommissory note or a new funding agreement with the rolling-365-day surrender

clause

In keeping with your potential time frame of early 2000 for serious discussions on this product,

we would like to set up a brief conference call among you, my counterparts on the capital markets

side and me to get a feel for what Allstate may be looking for in this Facility or, alternatively, in

upcoming euro-medium term note issues. We look forward to imminent contact with you.

DESCRIPTION of OPPORTUNITY for THE BANK This segment of the presentation reviews the realities (i.e., needs) in the life insurance market (i.e.,

the venue) for a new banking product – the “Insurance Liquidity Support Product” (the “Facility”).

The Need. In an effort to put idle surplus capacity to work, many life insurers have started to issue

funding agreements. These agreements are second generation guaranteed investment contracts

tailored for institutional investors other than pensions. Nevertheless, the eclipse of life insurers as

the money manager of choice by mutual funds or independent asset managers plus the cascade of

fixed income monies over to the equity side has left many insurers with strong general account

balance sheets and refined fixed income investment skills which currently languish. The Bank has

developed a means by which life carriers can put this under-deployed capacity back to work.

The Venue. Life insurers appear to have overlooked one large segment of the asset management

market -- the $1.1 TRILLION money market investment funds -- due to a perceived mismatch

between the insurers’ skills and investment horizon versus the requirements of these short-term

investors. Funding agreements issued by life insurers have penetrated only about 3-4% of this

market. This small share is not accidental but a consequence of the following constraints:

First, to meet federal regulatory standards, funding agreements must contain a surrender clause

allowing for immediate repayment of par value plus accrued interest to the investor.

Second, money market managers are constrained to buying double-A quality assets; the ratings

agencies place a clear analytical emphasis upon the ability of insurers to service a complete

run on their funding agreements.

Third, most funding agreement currently issued to money market investors are re-packaged as

short-term assets through a trust structure.

Influenced by the first and second requirements, insurers customarily purchase double-A rated,

easily tradable assets. These assets, yield significantly less than those traditionally held by life

carriers; the value-added of these insurers, measured in spread income, dissipates. The third

constraint narrows spreads further by imposing substantial -- at times prohibitive -- agency costs

upon the sponsoring insurer.

The Facility’s Concept. The Bank has devoted a year and employed several resources developing

a banking product which can enable companies like Allstate to issue funding agreements ‘their

way’ to money market funds. The Bank has tested the concept out on the two largest ratings

agencies for claims-paying ratings and worked closely with the premier law firm serving regulated

industries, like insurance. This outside counsel has researched the policies promulgated by the

Department of Insurance of the State of New York; New York’s standards are arguably the strictest

in the country. It has also cross-applied certain proprietary concepts involving similar products in

other regulated environments. At first glance, the Facility looks more like a crazy-quilt of detail.

Yet each of these apparently trivial parts of the product serves a specific interest of one of the five

key stakeholders: Allstate, the money market fund, state regulators, the ratings agencies and the

Bank.

Simply said, this Facility is a hybrid liquidity support and credit line issued from the Bank to

Allstate. The bank line employs the mechanics of a letter of credit but supports the life carrier on

the same level that ‘soft capital’ lines support monoline bond insurers. For a first-hand look at the

specifics, please refer to the attached “Summary of Indicative Terms and Conditions”. This hybrid

line blends the following features cited below.

An amount available to Allstate under the line sufficient to cover principal and accrued

interest;

Allstate’s freedom to invest in less liquid, better yielding assets for the amount of the bank

line;

Three years for Allstate to liquidate those assets or, more likely, to find a replacement money

market fund;

Direct payment to the investor by the Bank of the surrendered amount;

Few, if any, impediments to borrowing (even as an insurer is imminently to be seized by

regulators); and,

Minimum agency costs given the simplicity of the structure.

Tour of the Facility. The single draw, hybrid liquidity/credit line has the following terms:

Borrower Allstate U.S.A., Inc. (“Allstate”)

Bank Issuing Line the Bank AG; New York Branch (“the Bank”)

Lender The Bank or its commercial paper funding conduit.

Term of Line Four years, with annual extensions beginning the sixth

month after closing, at the sole discretion of the Bank.

Maximum Borrowing Length Three years

Pricing Origination Fee; Commitment Fee; and, interest margin

(Please note that the commitment fee dissolves into the

margin upon a draw under the line.)

Covenants A few of which none are substantive

Conditions Precedent Proof of surrender by a designated money market fund and

receipt by the Bank of a ‘new’ funding agreement in its name

and issued by Allstate

Defaults Fraud, bankruptcy, credit-event-upon-merger and a

regulatory event

Default Remedy Accelerate the surrender period of the new funding

agreement from three years to one week

Funding Protocol Scheduled debt service of bank loan to be paid via the new

funding agreement

On opening day, Allstate sells a funding agreement to a money market fund with a market-

mandated seven day surrender period. Tthe Bank establishes the bank line in Allstate’s name for

an amount equal to par value plus reasonably projected accrued interest. The Bank also establishes

a ‘blocked’ deposit account in the name of Allstate. The blocked deposit account will contain funds

borrowed by Allstate but only be released with the consent of the Bank.

Time goes by and one day the money market fund surrenders its funding agreement upon seven

days notice. Upon receipt of the surrender notice and a copy of the surrendered funding agreement

from Allstate, the Bank places the required funds in Allstate’s blocked deposit account. Upon

receipt of the new funding agreement in its name from Allstate, the Bank releases the monies in the

blocked deposit account directly to the money market fund on behalf of Allstate.

The Credit Agreement and new funding agreement jointly stipulate that all payments of principal

and interest due under the loan will be paid to the Bank via the new funding agreement. The new

funding agreement also states that it is subject to the terms and condition within the Credit

Agreement. Other than these two provisions, the new funding agreement is identical with its

predecessor; that is, there is a seven day surrender period in favor of the Bank. The Credit

Agreement, however, states that the Bank agrees not to enforce the seven day surrender period for

the earliest of three years, regulatory seizure or bankruptcy.

This provision allows the Bank to surrender the new funding agreement immediately upon receipt.

The Credit Agreement effectively stretches the conventional one week surrender period out to

three years, all things being equal. This arrangement assures that the Bank will be a policyholder

with a standing claim to be honored within a week should state regulators take the life insurer into

receivership prior to its declaring bankruptcy.

the Bank essentially yields its contractual protections under the new funding and Credit

Agreement, as it would in a ‘soft capital’ line extended to a monoline financial guarantor. Like

those lines, the Facility would command premium pricing to compensate the bank for giving up

its controls. Nonetheless, under the simplified structure detailed above, the agency costs saved

would defray much of this incremental bank pricing. Furthermore, the enhanced yield earned on

those investments backing the bank-supported funding agreement would provide enough new

income to justify Allstate’s cost of re-deployment of its core investing skills. Pricing differentiated

over time will allow for an attractively low interest margin for thirty to ninety days, or the expected

time horizon of a liquidity facility. After the liquidity period has elapsed, the interest margin

increases noticeably to reflect the evolution of a liquidity line into credit support.

Appraisal of the Facility. So what does this bank line really do for Allstate? It avoids agency

costs and permits traditional insurance investing on contracts sold to short-term investors.

Fundamentally, Allstate pays “X” for the bank facility to earn “2 or 3X” of incremental spread.

Since the credit agreements underlying the designated funding agreements will comprise only 5%

(or less) of Allstate’s general account investments, the Bank will have repayment access to the

entire portfolio. The three year surrender period allows the insurer to sell relatively illiquid assets

at a pace which contains price concessions.

Should Allstate find that a secondary market of a particular asset class has evaporated, it would

also have sufficient time to sell an asset-backed security backed by the investments. Among the

Bank’s several specialized finance divisions, three of the strongest include real estate,

collateralized bond or loan obligations and structured finance for the packaging of the assets into

a security. the Bank would be available to aid Allstate in liquidating these illiquid assets through

the capital markets. Finally, the funding protocol of paying the loan via the new funding agreement

is structured to enable Allstate to book any borrowings under the line as a policyholder liability and

not debt. Of course, the Bank would enjoy the status of a policyholder in exchange for hassle-free

liquidity.

Conclusion. Life insurers need to protect their once dominant but now secondary market share in

asset management. Money market funds provide a large yet largely ignored market for life

insurance funding agreements.

Except that embedded in this opportunity is a mismatch of financial skills and investment horizons

that nullifies the potential gains.

The Bank can mend this apparent breach to produce a triple winner; that is, that Allstate, the Bank

and the fund all profit unmistakably. These three winners make this hybrid bank line a Facility.

PRODUCT REVIEW

Introduction. The Bank has recently developed a specialized product for selected, very highly

rated insurance companies. The product provides a specially designed liquidity support and credit

facility arrangement to an operating life insurance company (the “Insurer”), which will in turn

enable Insurer to sell medium term funding agreements to short-term money market investment

funds. Furthermore, the specially tailored provisions of the liquidity support and credit facility

will perm it considerably greater latitude than is now possible in the investment of the proceeds

from the funding agreement.

The Need. In an effort to put idle surplus capacity to work, many life insurers are selling funding

agreements. These agreements are second generation guaranteed investment contracts tailored for

institutional investors other than pension managers. Nevertheless, the eclipse by mutual funds of

life insurers as the money managers of choice plus the shift in recent years of fixed income monies

over to the equity side has left many insurers with strong general account balance sheets and

refined fixed income investment skills which currently languish. The Bank has developed a means

by which life insurers can put this underutilized capacity back to work.

The Opportunity. Life insurers appear to be underrepresented in one large segment of the asset

management market -- the $1.1 TRILLION of money market investment funds -- due to a perceived

mismatch between the insurers’ skills and investment horizons versus the requirements of these

short-term investors. Funding agreements issued by life insurers have penetrated only about 3-5%

of this market. This small share is not accidental but a consequence of the following constraints:

1. to meet federal regulatory standards, a funding agreement must contain a surrender clause

allowing for immediate repayment of par value plus accrued interest to the investor;

2. the ratings agencies place a clear analytical emphasis upon the ability of an insurer to service a

complete run on its funding agreements; and,

3. the typical funding agreement issued to a money market investor is re-packaged as a short-term

asset through a trust structure.

Influenced by the first and second hurdles, insurers customarily purchase double-A rated, easily

tradable assets with the proceeds of the funding agreements. These assets yield significantly less

than those traditionally held by life insurers which vitiates the value-added of the skilled fixed

income managers. The third constraint narrows spreads further by imposing substantial, at times

prohibitive, agency costs upon the sponsoring insurer.

Product Concept. The Bank has created a product which allows a selected Insurer to issue funding

agreements to money market funds. The Bank has built this product with the knowledge and

collaboration of the two largest ratings agencies for financial strength ratings (i.e., assessments of

life insurers’ abilities to pay their claims). The bank has worked closely with LeBoeuf, Lamb,

Greene & MacRae in developing the product. Each part of the product’s structure serves a specific

interest of five key stakeholders: Insurer, the money market fund, state regulators, the ratings

agencies and the Bank.

Simply said, this product is a back-up credit facility arranged by the Bank for the benefit of Insurer.

For a first-hand look at the specifics, please refer to the sections titled “Summary of Indicative

Terms and Conditions” and “Secondary Indicative Terms and Conditions”. To support Insurer’s

funding agreement, this arrangement blends the features cited below:

an amount available to Insurer under the line sufficient to cover principal and accrued interest

on the funding agreement;

Insurer’s freedom to invest in less liquid, better yielding assets for more than the amount of

the funding agreement being backed by the credit arrangement;

the ability by Insurer or a designated intermediary to remarket the funding agreement upon

the receipt of a surrender notice from the money market fund;

three years for Insurer to liquidate those assets or, more likely, to find a replacement money

market fund to take out the replacement funding agreement issued by Insurer to the Bank

(the “New Funding Agreement”);

direct payment to the money market fund by the Bank of the principal of, and interest accrued

upon, the funding agreement;

few, if any, impediments to borrowing even at times of stress for Insurer; and,

reduced agency costs with the absence of a trustee.

Product Mechanics. Conceptually, the mechanics underlying this credit facility are simple.

Currently, ratings agency parameters for a funding agreement with a shorter surrender notice

period require an insurer to back it with at least twice the surrender value in near-cash investments.

These lower yielding assets eliminate the profitability historically enjoyed on medium term spread

products, making money market funds less desirable prospects.

In contrast, the Bank’s back-up facility – covering not only par value but also accrued interest –

inserts the Bank’s double-A $384 billion balance sheet between Insurer and the fund. The money

market fund may surrender its funding agreement with 7-30 days notice.

To honor the surrender of a funding agreement by a money market fund, Insurer borrows under

the facility and holds the borrowing on deposit with the Bank. Following the receipt of the New

Funding Agreement, which closely resembles the surrendered contract yet is subject to the terms

and conditions of the facility, the Bank releases directly to the money market fund the monies

already drawn by Insurer.

Funding agreement with 7-day surrender

interest paid every 6 months

Insurer’s

life

subsidiary

Money Market Fund

Par value of Funding Agreement paid

The Bank Blocked deposit account

the insurer

Money

Market

Fund Credit agreement

for par value AND 6 months interest

Insurer has up to three years to repay the borrowing. Finally, the facility establishes a repayment

protocol to allow Insurer to service the bank debt simultaneously through the repayment of the

New Funding Agreement. Each party -- the money market fund, the Bank and Insurer -- benefits

by the arrangement.

Product Benefits. By relinquishing most standard contractual controls, the Bank assures the

money market fund that it can surrender the funding agreement at will upon 7-30 days’ notice.

With three years to repay any drawings under the facility, Insurer can invest the proceeds of the

supported funding agreement in private placements and mortgages; it will have the time to sell off

these less liquid assets in an orderly manner to contain price concessions. Furthermore, the

transparency of the facility’s bilateral structure minimizes agency costs. In short, Insurer gets its

traditional spread back, while the money market fund suffers no compromise of liquidity. By

receiving the New Funding Agreement, the Bank has a policyholder claim against the general

account investments of Insurer which is senior to the claims of all general creditors. With the aid

of the repayment protocol, Insurer avoids taking debt onto its statutory balance sheet.

Once Insurer finds a buyer of a new agreement, it can redeem the New Funding Agreement from

the Bank from the proceeds; this policy redemption also extinguishes the bank debt under the

repayment protocol. Should Insurer find that a secondary market of a particular asset class has

evaporated, the three year loan maturity would give it sufficient time to sell an asset-backed

security backed by the investments. Among the Bank’s several specialized finance divisions, three

of the strongest include real estate, collateralized bond or loan obligations and structured finance

(for securitizing the assets into a tradable fixed income instrument). The Bank would be available

to aid Insurer in liquidating these static assets through the capital markets.

the

Bank

Replace-

ment fund

the

insurer replacement funding agt in the amount due

to the bank

amount due to bank

OR

the

insurer Bond dealers; asset-

backed market

invts sold or securitized

Money

Market

Fund

the insurer

the Bank

new funding agreement

Blocked deposit account

principal PLUS accrued

interest

the Bank

Repayment protocol defined in new

funding and credit agreements

the

insurer

New Funding Agreement

credit agreement New Funding Agreement

amount due to bank

amount due to bank

Conclusion. Money market funds provide a vast yet largely untapped market for life insurance

funding agreements. Life insurers need to access that market inexpensively and profitably. The

Bank can service this market with a product, which allows Insurer and the money market fund to

profit. By balancing the interests of Insurer and the money market fund, the bank facility leverages

resources taken for granted -- the ratings agencies and state regulators – to profit both the fund and

Insurer. Insurer earns higher investment yields with an increased spread, which is a multiple of

the facility’s cost. The money market fund retains the 5% historical return premium earned on

eligible funding agreements over conventional money market instruments.

Insurance Company Guaranteed Investment Contracts and Funding Agreements

OVERVIEW

Review of the current status of insurance deposit products. Life insurers have issued Guaranteed

Investment Contracts (“G.I.C.s”) for more than two decades. G.I.C.s were (and are) multi-year

bullet deposits backed by the balance sheets of large operating life insurance companies to compete

with similar products offered by leading banks; G.I.C. depositors were (and are) deemed to be

policyholders and senior to all creditors at all levels. As insurers evolved their G.I.C. products

consumers realized that traditional whole life policies were no longer economic.

As the retirement savings market matured, Funding Agreements (i.e., group or institutional deposit

products) have emerged as “second generation” G.I.C.s for other than pension-specific uses.

Funding Agreements have structured in clauses to enable rapid exit (i.e., 7-60 days) for short term

investors. Though eligible for purchase by money market managers, these structured Funding

Agreements are bilateral contracts which differ with each transaction to preclude secondary

trading.

The next step in the evolution of Funding Agreements. If they can be structured to meet S.E.C.

& O.C.C. approvals, Funding Agreements are attractive to money market funds, which require

maturities within 270 days. By making its double-A $384 billion balance sheet available to a select

few insurers with entrenched market positions and impeccable credit quality, the Bank can enhance

the comfort of life insurers in selling Funding Agreements since they can invest in less liquid assets

and still meet ratings agency liquidity concerns. The higher yields of Funding Agreements over

other money market instruments can induce short term investors to hold them. Such bank liquidity

support assures the availability of a swift exit from Funding Agreements required by money market

funds. Few Funding Agreements have been surrendered to date. Bank provided liquidity allows

the insurer enough time permit remarketing of the surrendered Funding Agreement. Any drawings

should not be outstanding for more than two months.

Assessment of the next step. The primary risk for a liquidity bank will be that of a long term draw

on the liquidity line for the following reasons:

1. deterioration of a particular credit 4. adverse rate shifts

2. loss of life insurers’ prestige

3. a sudden change in investor appetite

5. a spike in redemptions against a money

market manager

Transactional and market-based mitigants which assuage these concerns include:

1. availability to only half a dozen insurers

2. pricing to encourage remarketing of the

Funding Agreement

3. yield-based incentives for investors to hold

4. rating agency scrutiny and the impact of

those ratings upon market share

5. the Funding Agreements’ remarketability

to date; and,

6. the needed restructurings completed during

the lag times between the surrenders and

what would be the drawing dates under

liquidity lines

DISCUSSION IN DEPTH

Review of the current status of insurance deposit products. The Bank is developing a new money

management tool to bridge the disparity of a strong and growing demand for short term investments

within the regulated funds management sector and the excess supply of long term paper issued, in

this case, by insurance companies. A particularly rich possibility is the liquefaction of products –

like guaranteed investment contracts – which are long term but have no access to secondary markets

owing to their variety as each transaction is negotiated singly.

Life insurers have issued guaranteed investment

contracts for more than two

decades.

Guaranteed investment contracts (“G.I.C.”s) and their origins. G.I.C.s arrived in

the mid-1970s as an asset management product targeted toward pension funds and

other institutional money handlers who faced large, periodic and predictable cash

flows. With the influx of pension claimants (as the first generation of pensioners

began to retire), unstable interest rates and continual inflation, pension managers

sought out investments, the pay-outs of which would match closely the payment

obligations of the pension fund which could be calculated beforehand with

reasonable accuracy. As money managers to these pension funds in preceding

decades, life insurance companies suddenly confronted large group annuity

customers which needed to focus scheduled annuity payments into sporadically

timed and uneven cash flows. Such a requirement lent itself better to a series of

deposit payments, an open invitation for product substitutes to be offered to pension

funds by federally insured banks, to which the latter promptly responded.

G.I.C.s were

(and are) multi-year bullet

deposits backed by the balance sheets of large

operating life insurance

companies to compete with

similar products offered by

leading banks; G.I.C. depositors

were (and are) deemed to be policyholders

and senior to all creditors at all

levels.

As insurers evolved their

G.I.C. products, consumers

realized that traditional whole life policies were

no longer economic.

As the retirement savings market

matured, Funding

Agreements (i.e., group or

institutional deposit

products) have emerged as

“second generation”

G.I.C.s for other than pension-specific uses.

Insurance companies sought to defend their traditional market by issuing their own

deposit products, which they called G.I.C.s. The insurers involved deemed these

‘non-bank’ certificates of deposit as “group” annuities, often with only one payment

(instead of several over time). Through this definition of these time deposits as

‘bullet’ annuities, pension managers investing in G.I.C.s enjoyed the status of

policyholders with claims senior to all creditors at all levels in the event of an

insurer’s insolvency. In addition, in lieu of deposit insurance sponsored by the

federal government, state guaranty funds, typically financed through a 2% or so

premium tax, would frequently provide secondary support to these G.I.C.

depositors-as-policyholders. Subsequently, state insurance regulators often agreed

with insurers and considered these contracts to be group annuities since they relied

upon the insurers’ statutory balance sheets; that is, G.I.C.s would be “guaranteed”

by the insurance investments owned by the issuers on behalf of all of their

policyholders. Excess assets built up over years of writing life policies gave many

life insurers stronger and liquid balance sheets to substantiate these guaranties.

On another front, during the 1970s, insurers had to defend against incursions into

their traditional markets by investment funds. Whole life policies and traditional

individual life insurance annuities tended to have asset accumulation rates (i.e.,

assumed investment returns credited to the policyholders) set by state regulators at

unrealistically low levels. Mutual Funds, however, credited to their investors’

respective accounts the total returns earned on investments net of management and

administration fees. These portfolio returns tended to be higher than those

structured into individual life insurance products or annuities. Consumers quickly

realized that it made more sense to purchase inexpensive limited term insurance

(e.g., for the next five years) and invest in mutual funds the premium monies saved.

Such limited term life products were not particularly profitable for insurers.

Consequently, insurers developed less profitable interest sensitive life policies

which granted higher accumulation rates. To enable insurers to compete directly

with mutual funds, G.I.C.s also represented a new generation of pooled savings

products when mutual funds began to displace individual life insurance annuities as

the retirement savings vehicles of choice during the 1970s.

Explanation of Funding Agreements. In the late 1980s, frequently with the aid of

intermediaries, life insurers developed Funding Agreements to expand their product

mixes and target markets. The original and maturing G.I.C. portfolios were either

treading water or contracting due to a secular decline in interest rates and the

widespread conversion from ‘defined benefit’ to ‘defined contribution’ plans.

(Defined contribution plans fix the amount of the employers’ yearly contributions –

usually pegged to percentages of their profits – into the pension pools whereas the

defined benefit plans specified the periodic pension payments the future retirees

would receive.) These original Funding Agreements resemble G.I.C.s in the timing

of their cash flows but were designed for a wider market.

With a wider field of competition than it has been used to, the life insurance

industry has been targeting new buyers of its deposit products and found

Funding Agreements are

beginning to structure in clauses to

enable rapid exit (i.e., 7-30 days)

for short term investors.

Though eligible for purchase by money market

managers, these Funding

Agreements are bilateral

contracts which differ in each

transaction to preclude

secondary trading.

If structured to meet S.E.C. &

O.C.C. approvals,

Funding Agreements are

attractive to money market

funds, which require

maturities within 270 days.

The bank liquidity support

enhances the comfort of life

insurers in selling Funding

Agreements since they can

invest in less liquid assets and still meet ratings agency liquidity

concerns.

many which have historically been by-passed by life insurers: short term and money

market investment funds. Funding Agreements structure in liberal surrender clauses

previously seen only for contracts issued by companies carrying unquestioned

liquidity. Surrender provisions explicitly spell out the terms under which investors

can surrender their agreements back to the issuing insurers. Most recently, upon

federal regulatory approvals, these embedded – and unconditional –surrenders

within Funding Agreements have started to fill a chronic funding gap within the

capital markets by turning these long term spread products into synthetic short term

instruments. Since these agreements are bilateral contracts, negotiated on a

customer-by-customer basis, they do not enjoy the liquidity of a secondary market

which requires standardized, easily divisible securities.

From a regulatory standpoint, for example, a five year Funding Agreement

embedded with an unconditional surrender with a 30 day settlement qualifies as a

30 day investment. If a money manager holds that agreement until expiry in five

years, it will technically hold a 30-day asset which it rolls over 61 times. Standby

bank support can take the underlying product concept of the flexible Funding

Agreements one step further to assure this liquidity as well as to standardize and to

catalyze the formation of a secondary market. While these liquid markets manage

in excess of $1 TRILLION of assets, the face amount of Funding Agreements held by

money market funds comprises less than 2% of this prospective market.

The next step in the evolution of Funding Agreements. Modified Funding

Agreements, then, are designed to qualify as eligible short term investments for the

Securities & Exchange Commission and the Office of the Controller of the Currency

for inclusion in money market and short term investment funds. The S.E.C. and

O.C.C. already accept the current bilateral Funding Agreements, with their

surrender provisions, as synthetic short term investments. These bank supported

agreements have been reviewed by the two leading ratings agencies and tailored to

the specific concerns of the agencies:

1. Surrender periods – the time interval from the initial notification by the money

market fund to the insurer of its intent to surrender its contract to the actual

release of funds to the fund manager – to be in the 7-30 day range;

2. A period of time sufficient to allow the life insurers to re-sell the assets backing

the liquefied Funding Agreements;

3. No substantive conditions to lending short of fraud;

4. Few financial covenants or technical defaults;

5. Restrictions of the amount of lines available to a modest percentage of general

account assets;

6. Reliance upon highly rated banks to provide the liquidity; and,

7. No specific inclusion of named remarketing intermediaries.

The bank supported Funding Agreements are expected to enjoy the support of state

insurance regulators since large banks – with their access to instantaneous and

inexpensive funding – will assure the liquidity of this market.

The higher

yields of Funding Agreements over

other money market

instruments can induce short

term investors to hold them.

Structured properly, a Funding Agreement allows an insurance company to lock in

an attractive spread through relatively low funding costs (i.e., the guaranteed

payment rate under a G.I.C.). For the short term fund manager, it confers 7-22 basis

points of additional return which creates ample incentive for that investor to hold

the Funding Agreement through its many implicit roll-overs. Should these spreads

disappear for more than a moment, the money market manager can simply surrender

the policy to the insurer, which would draw on the liquidity line to purchase the

agreement at the end of the 7-30 day contractually stated settlement period. In

theory, the life insurer – or its designated intermediary – would have the time

afforded by the settlement period to find a replacement buyer of the Funding

Agreement on behalf of the insurer. Such bank

support assures the availability of a swift exit from

Funding Agreements required by

money market funds.

Any drawings should not be

outstanding for more than two

months.

The liquidity supports an insurer in honoring the surrender clause under the Funding

Agreement. This liquidity support liquefies the Funding Agreement to make it an

eligible money market investment. For example, were a contract surrendered with

a 30 day settlement, the insurer, or its designated intermediary, would have a month

to recruit another buyer of the Funding Agreement to prevent the draw on the

committed bank line to fund the insurer's purchase of the agreement. If an alternate

buyer could not be found, the bank would hold the asset for up to three years.

Historical experience indicates that a bank’s interim holding period between the

funding of the surrender when it is executed and the subsequent resale of the

Funding Agreement would be 30-60 days with two month holds occurring for

situations requiring a restructuring of the contract to render it marketable.

Few Funding Agreements

surrendered to date.

Specifically, of the $6 billion of bilateral Funding Agreements sold to money market

funds to date, only 5-6% have been surrendered back to the insurance company.

Only one was surrendered to the insurer for credit reasons when the claims-paying

ratings of the life carrier involved, the U.S.-based operations of the failing

Confederated Life of Canada, fell precipitately from single-A to triple-B. For these

same reasons, as well as the unpleasant surprise to the capital markets of the

management of the Canadian parent to petition its government for regulatory

rehabilitation, neither the leading remarketer of these modified Funding Agreements

nor Confederated Life could locate a new buyer for the Funding Agreement. The

insurer then repurchased the contract. During the subsequent receivership under

U.S. law (and separated from Canadian law), the former owner of the agreement did

not face U.S. bankruptcy preference exposure. Bank provided

liquidity allows the insurer

enough time permit

remarketing of the surrendered

Funding Agreement.

In each of the other cases, a leading intermediary for these agreements, which the

Bank would recommend, negotiated a reduction in pricing for the issuing insurers

due to strong demand among money market managers. The continued ability to

remarket a surrendered contract will be vital to the product’s success for the Bank.

Assessment of the next step. The primary risk for a liquidity bank will be that of a long term draw

on the liquidity line for the following reasons:

deterioration of a particular

credit

A decline of an insurer’s credit profile. This would occur for two reasons. For life

issuers of Funding Agreements, the market would come to believe that its asset

quality has deteriorated to the point that its ability to honor claims is open to doubt.

In essence, short term fund managers and other investors would conclude that there

are not enough good assets to go around. Adverse changes in the insurer’s claims-

paying ratings over time would confirm this declining credit profile.

loss of life insurers’ prestige

Industry risk. Insurers have lost some of their credibility in the capital markets over

the past decade. In the early 1990s, with the collapse of four large players, the life

insurance industry lost its luster among most investors. The recent investment fraud

perpetrated by Martin Frankel and the widespread market practice scandals have not

cast the life insurance industry or its regulators in a positive light. These cases have

precipitated flights to quality in the past which benefitted the strongest and largest

companies in each sector, among which were the prime issuers of Funding

Agreements. Should recent events lead to another flight to quality, Allstate should

benefit directly.

a spike in redemptions

against a money market manager

Liquidity. The money market portfolio manager himself could have liquidity

difficulties attendant to a sudden and unexpected increase in redemptions (i.e.,

surrenders by money market investors to their asset managers), requiring the rapid

raising of cash by the manager. Under such market conditions, the money market

manager may well be inclined to surrender his Funding Agreement now rather than

run the risk of liquidity complications later should the redemptions continue.

adverse interest rate shifts

Spreads over LIBOR widen for subsequently issued Funding Agreements. This

rate arbitrage would induce the agreement holder to surrender – or ‘trade-in’ – his

lower paying agreement for a richer paying agreement carrying the same credit risk.

At this juncture, the insurer would have to make a choice: begin paying the market

rate on the Funding Agreement or close it out by honoring an almost certain

surrender.

a sudden change in

investor appetite

One money market fund is merged into another which lacks the appetite for

Funding Agreements. This phenomenon has, in fact, explained roughly 60% of

the cases where the bilateral contracts originally placed by a leading intermediary

have been surrendered back to the insurer.

Several mitigants reduce the likelihood of any of these five event occurring. Structural – i.e.,

transaction specific – mitigants will be negotiated into the body of the Funding Agreements and

corresponding bank documents. Market mitigants involve market practices among issuers of

Funding Agreements or economic factors confronted by all money market managers.

availability to only half a

dozen insurers

Eligibility criteria based upon a superior credit profile and leading market

position. The usefulness of this mitigant would be to avoid less credit worthy

issuers in the first place. The universe of larger life insurance companies has

an average S&P financial strength rating (i.e., the assessment of the ability to

honor claims) of double-A. Beyond this simple ratings-based criterion,

eligible companies for this product must demonstrate market leadership and

expertise in Funding Agreements.

yield-based incentives for

investors to hold

The money manager’s economic motive for holding the Funding

Agreement. Short term investment managers compete in a highly competitive

market. The top performers outshine their mediocre counterparts by only a

few basis points. These managers are explicitly accountable, much of the

time, to their investors; that is, they have a fiduciary responsibility to

maximize portfolio return. Thus while, on its own, a Funding Agreement may

not seem like a prudent investment legally, it is permissible under

professional and S.E.C. investment standards when embedded within a larger,

highly diversified portfolio. The regulatory eligibility of these higher yielding

synthetic money market instruments, allows the money market fund manager

to buy and hold (or, technically, roll over) the contract. As discussed earlier,

unless circumstances are extreme, the portfolio manager will be

understandably averse toward divesting a value-adding asset.

pricing to encourage the remarketing of

the Funding Agreement

Pricing to render uneconomic for the insurer the long term ownership by the bank

of the Funding Agreement. Pricing is above the insurer’s corresponding level of

bank liquidity pricing for two reasons. First, higher pricing would provide a direct

incentive to the insurer to remarket the Funding Agreement. (‘Remarket’ means

either the resale of the existing agreement or the issuing of a new contract to replace

the old.) Should the bank end up holding the contract for several years, it would be

a credit provider and earn the additional income as would be expected.

rating agency scrutiny and the impact of those

ratings upon market share

Use of inadequately tapped resources to enable banks to forego traditional

contractual controls. The liquidity line is somewhat like a soft capital line provided

to monoline bond insurers in that banks are compensated for relinquishing their

traditional controls. The bank line contemplated by this transaction satisfies the

concerns of the two largest national credit rating agencies ranked by market share

for insurance financial strength ratings. This unconditional liquidity will be

available for three years, targeted toward only those few insurers most likely to

maintain superior balance sheets over time, and limited to a small percentage of

general account assets. The rating agencies will monitor this activity to make sure

that lines will not be excessive while regulators will hold companies accountable

under statutory accounting for compromising the integrity of their asset quality.

Further, market share for institutional deposit accounts is sensitive to rating agency

changes. Thus will the rating agencies and, secondarily, the insurance regulators

provide the oversight and control functions for the banks.

the Funding Agreements’

remarketability to date

The Funding Agreement’s remarketability. Actual experience, over the past six or

seven years, bears out that there is ample demand for a previously surrendered

Funding Agreement which allowed for 7-30 day surrenders but had no liquidity

support. This mitigant redresses best those cases where the money market fund

endures a spate of redemptions or merges into a larger fund which shuns such

synthetic instruments.

the needed restructurings

completed during the lag-times between the surrenders and drawings under liquidity

lines

The incentive for the issuer to restructure the agreement during the settlement

period. Actual experience also indicates that restructured Funding Agreements often

command lower rates than had been the case prior to surrenders. The issuing insurer

has every incentive to get the agreement back to market before its name-in-the-

market suffers even if that means increasing the return to the investor of the Funding

Agreement. The prospect of uneconomic bank financing together with possible

losses realized upon the sale of assets and the certain trading expenses entailed in

disposing of those assets would likely overcome the reluctance of an insurer to reset

its pricing.

SUMMARY OF INDICATIVE TERMS AND CONDITIONS December 1999

The following terms and conditions are not necessarily the final ones to be submitted by

Commerzbank AG, New York Branch (“the Bank”) to an operating insurance company of Allstate

Life Insurance Company licensed and domiciled in the State of Allstate (“Allstate”). This summary

is intended to frame the discussion of a proposed transaction among Allstate, qualifying money

market or stable value asset funds (the “Fund”) and the Bank, as Arranger and Agent for a

syndicate of banks rated AA- or better by S&P (the “Bank Group”), involving the execution and

delivery of a credit agreement and a funding agreement or simultaneously issued and identical

funding agreements in the aggregate value of up to $500,000,000 between Allstate and Fund

(collectively, the “Funding Agreement”). Please note that these indicative terms and conditions

do not represent a commitment to lend, or to make lending capacity available to, Allstate.

Arranger and Agent: Commerzbank AG; New York Branch (“the Bank”)

Facility Amount: Up to $500,000,000 plus an increment for the maximum

possible accrued interest on the Funding Agreement.

Lenders: Financial institutions rated AA- or better by S&P or sponsored

funding conduits (in each case, a “Lender”).

Borrower: Allstate.

Funding Agreement: The Funding Agreement must have a floating rate of interest

and a maturity date not to exceed seven (7) years. Delivery of a

substitute Funding Agreement to the Agent for the benefit of

the Lenders (the “New Funding Agreement”) with the

conditions set forth in the Secondary Indicative Terms and

Conditions, shall be one of the preconditions for funding the

loan under the Credit Agreement.

Type: Committed non-revolving line of credit (the “Facility”).

Use of Proceeds: Liquidity support for the Funding Agreement.

Documentation: Documentation shall include, but not be limited to, the

surrendered Funding Agreement, the New Funding Agreement,

the credit agreement among Allstate, the Lenders and the Agent

(the “Credit Agreement”), the commercial paper, policyholder

deposit or promissory notes, by Allstate in favor of each Lender

(the “Notes” and – together with the Funding Agreement, the

New Funding Agreement, and the Credit Agreement – the

“Transaction Documents”).

Commitment Termination Date:

364 days from the closing date. The Commitment Termination

Date may be extended at the discretion of the Required Banks.

If the Commitment Termination Date is extended but less than

all of the Banks consent to such extension, to the extent that

such Banks are not replaced by other qualified institutions, each

non-consenting Bank (a “Non-Extending Bank”) shall fund its

unused Commitment Amount into a blocked deposit account at

the Agent (subject to prior delivery by the Borrower of a New

Funding Agreement for the benefit of the Non-Extending Bank

in the amount of the deposit held by the Agent) which may be

used to make future Advances up to the then applicable Final

Maturity Date defined below. Amounts funded by a Bank as

described in the preceding sentence shall bear interest at the

normal rate applicable to the Notes and such Bank shall also be

entitled to receive the Facility Fee applicable to such amounts.

Borrowing Periods: Up to sixteen months from the date of borrowing with

borrowing under the Facility permitted on any day during the

life of the commitment up to, and including, the Commitment

Termination Date. The maturity of the borrowing of up to

sixteen months shall be the “Final Maturity Date”.

‘Best Efforts’ Arranger’s Fee: 50.0 basis points on the Facility amount.

Facility Fee: 15.0 basis points per annum on the Facility amount, payable on

the closing date and on each Anniversary Date of the closing

date when the Commitment Termination Date, as defined

above, has been extended at the sole discretion of the Lender(s)

for an additional 364 days.

Participation Fee: To be determined by market pricing and to be paid directly to

each Lender on the closing date.

Interest Rate: LIBOR + 35.0 basis points per annum. After sixty (60) days,

the interest rate for the Facility shall be stepped-up to LIBOR +

85.0 basis points per annum.

Default Rate: Prime + 200 basis points per annum.

Collateral: Any borrowing under the Facility shall be secured by the

issuance of the New Funding Agreement by Allstate to the

Agent for the benefit of the Lenders with a principal amount

equal to the Surrender Amount of the surrendered Funding

Agreement. Such New Funding Agreement shall include and

preserve all of the Fund’s rights under the Funding Agreement.

If a Non-Extending Bank deposits funds into a blocked-deposit

account for up to the Final Maturity Date (for the account of

Allstate), its deposit account shall be secured by a New Funding

Agreement. Please refer to the Secondary Indicative Terms and

Conditions for the New Funding Agreement attached hereto.

Surrender Amount: The principal amount of the Funding Agreement plus accrued

interest, the total amount of which shall not exceed the amount

of the total commitments under the Facility.

Surrender Notice: Notification to Allstate by the Fund, with a copy telefaxxed to

the Agent, of its intent to surrender the Funding Agreement.

Borrowing Event: Aside from cases, which involve Non-Extending Banks, a

Borrowing Event occurs upon a failure of the Borrower or a

nationally recognized intermediary acting on behalf of the

Borrower to remarket the Funding Agreement within seven (7)

days of the date of the Surrender Notice. Upon the occurrence

of such Borrowing Event, (1) Allstate will execute and deliver

a Borrowing Notice to the Agent requesting a loan in an amount

equal to the Surrender Amount; (2) Allstate will telefax a copy

of the Fund’s Surrender Notice to the Agent; (3) Allstate will

send a copy of the Funding Agreement, together with evidence

that the Funding Agreement has been cancelled, to the Agent;

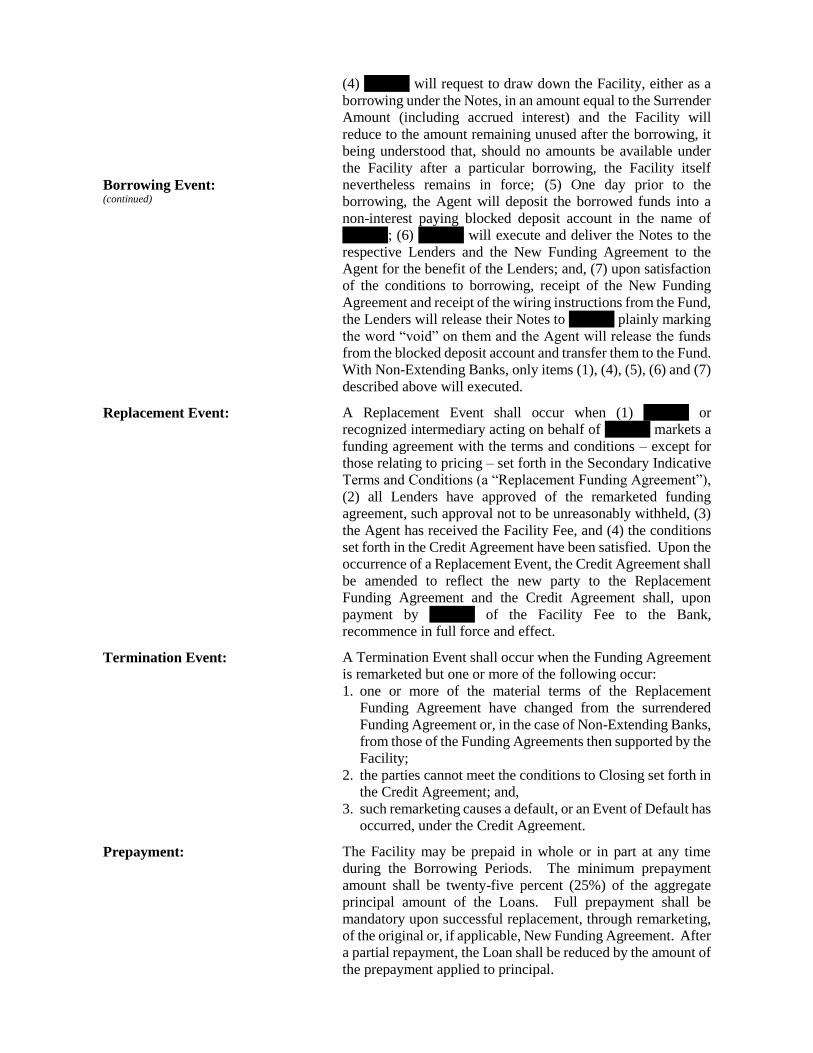

Borrowing Event: (continued)

(4) Allstate will request to draw down the Facility, either as a

borrowing under the Notes, in an amount equal to the Surrender

Amount (including accrued interest) and the Facility will

reduce to the amount remaining unused after the borrowing, it

being understood that, should no amounts be available under

the Facility after a particular borrowing, the Facility itself

nevertheless remains in force; x(5) One day prior to the

borrowing, the Agent will deposit the borrowed funds into a

non-interest paying blocked deposit account in the name of

Allstate; (6) Allstate will execute and deliver the Notes to the

respective Lenders and the New Funding Agreement to the

Agent for the benefit of the Lenders; and, (7) upon satisfaction

of the conditions to borrowing, receipt of the New Funding

Agreement and receipt of the wiring instructions from the Fund,

the Lenders will release their Notes to Allstate plainly marking

the word “void” on them and the Agent will release the funds

from the blocked deposit account and transfer them to the Fund.

With Non-Extending Banks, only items (1), (4), (5), (6) and (7)

described above will executed.

Replacement Event: A Replacement Event shall occur when (1) Allstate or

recognized intermediary acting on behalf of Allstate markets a

funding agreement with the terms and conditions – except for

those relating to pricing – set forth in the Secondary Indicative

Terms and Conditions (a “Replacement Funding Agreement”),

(2) all Lenders have approved of the remarketed funding

agreement, such approval not to be unreasonably withheld, (3)

the Agent has received the Facility Fee, and (4) the conditions

set forth in the Credit Agreement have been satisfied. Upon the

occurrence of a Replacement Event, the Credit Agreement shall

be amended to reflect the new party to the Replacement

Funding Agreement and the Credit Agreement shall, upon

payment by Allstate of the Facility Fee to the Bank,

recommence in full force and effect.

Termination Event: A Termination Event shall occur when the Funding Agreement

is remarketed but one or more of the following occur:

1. one or more of the material terms of the Replacement

Funding Agreement have changed from the surrendered

Funding Agreement or, in the case of Non-Extending Banks,

from those of the Funding Agreements then supported by the

Facility;

2. the parties cannot meet the conditions to Closing set forth in

the Credit Agreement; and,

3. such remarketing causes a default, or an Event of Default has

occurred, under the Credit Agreement.

Prepayment: The Facility may be prepaid in whole or in part at any time

during the Borrowing Periods. The minimum prepayment

amount shall be twenty-five percent (25%) of the aggregate

principal amount of the Loans. Full prepayment shall be

mandatory upon successful replacement, through remarketing,

of the original or, if applicable, New Funding Agreement. After

a partial repayment, the Loan shall be reduced by the amount of

the prepayment applied to principal.

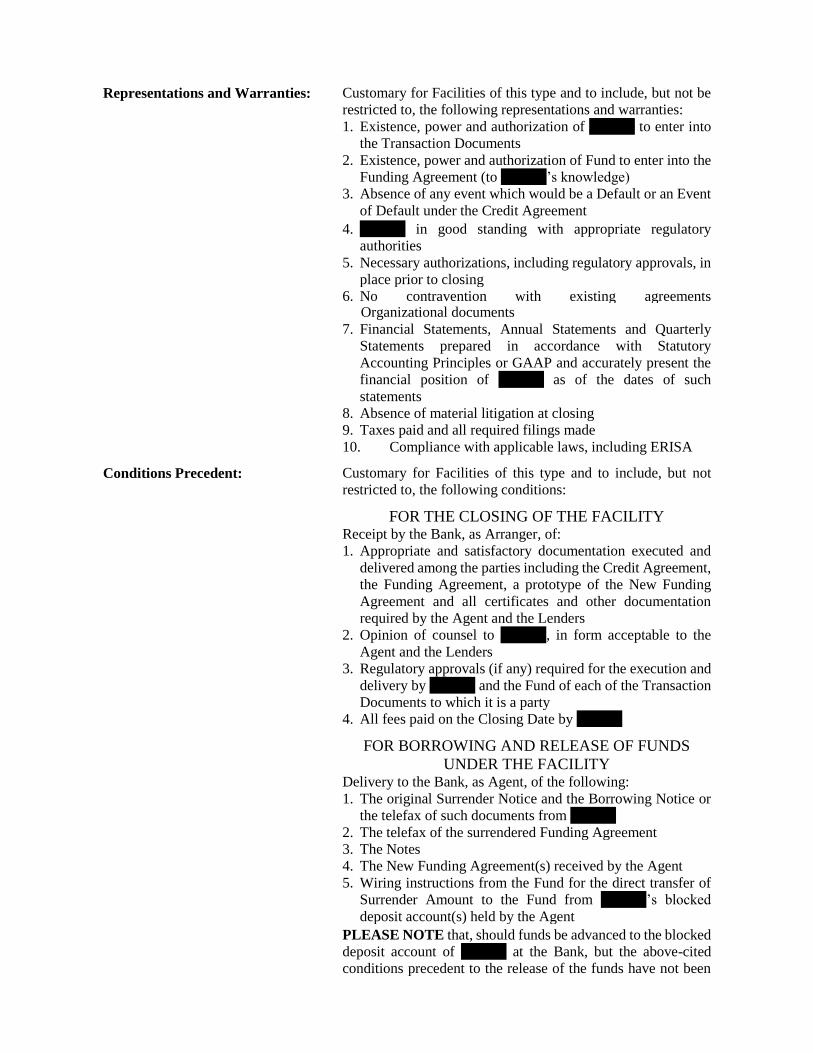

Representations and Warranties: Customary for Facilities of this type and to include, but not be

restricted to, the following representations and warranties:

1. Existence, power and authorization of Allstate to enter into

the Transaction Documents

2. Existence, power and authorization of Fund to enter into the

Funding Agreement (to Allstate’s knowledge)

3. Absence of any event which would be a Default or an Event

of Default under the Credit Agreement

4. Allstate in good standing with appropriate regulatory

authorities

5. Necessary authorizations, including regulatory approvals, in

place prior to closing

6. No contravention with existing agreements

orxxxxxxxxxxxxxx Organizational documents

7. Financial Statements, Annual Statements and Quarterly

Statements prepared in accordance with Statutory

Accounting Principles or GAAP and accurately present the

financial position of Allstate as of the dates of such

statements

8. Absence of material litigation at closing

9. Taxes paid and all required filings made

10. Compliance with applicable laws, including ERISA

Conditions Precedent: Customary for Facilities of this type and to include, but not

restricted to, the following conditions:

FOR THE CLOSING OF THE FACILITY Receipt by the Bank, as Arranger, of:

1. Appropriate and satisfactory documentation executed and

delivered among the parties including the Credit Agreement,

the Funding Agreement, a prototype of the New Funding

Agreement and all certificates and other documentation

required by the Agent and the Lenders

2. Opinion of counsel to Allstate, in form acceptable to the

Agent and the Lenders

3. Regulatory approvals (if any) required for the execution and

delivery by Allstate and the Fund of each of the Transaction

Documents to which it is a party

4. All fees paid on the Closing Date by Allstate

FOR BORROWING AND RELEASE OF FUNDS

UNDER THE FACILITY Delivery to the Bank, as Agent, of the following:

1. The original Surrender Notice and the Borrowing Notice or

the telefax of such documents from Allstate

2. The telefax of the surrendered Funding Agreement

3. The Notes

4. The New Funding Agreement(s) received by the Agent

5. Wiring instructions from the Fund for the direct transfer of

Surrender Amount to the Fund from Allstate’s blocked

deposit account(s) held by the Agent

PLEASE NOTE that, should funds be advanced to the blocked

deposit account of Allstate at the Bank, but the above-cited

conditions precedent to the release of the funds have not been

met or an event of default occurs when a borrowing is

outstanding, the Bank, on behalf of the Lenders, will have full

recourse to those funds for the re-payment of said borrowing.

Covenants: Customary for Facilities of this type and to include, but not be

restricted to, the following covenants:

1. Submission of the annual and quarterly statutory and, if

available, GAAP financial statements of Allstate and the

Fund.

2. The New Funding Agreement to rank pari passu with those

of other policyholders of Allstate.

3. Compliance with laws, maintenance of existence, limitations

on mergers, consolidations, sale of assets, additional debt

and additional liens.

Events of Default: Customary for Facilities of this type and to include, but not be

restricted to, the following events:

1. Payment default by Allstate

2. Credit event upon merger/change of ownership or control of

Allstate with credit consequences

3. Insolvency or bankruptcy of Allstate or seizure, placement

into receivership, rehabilitation of, or other intervention by

any regulators into, Allstate

4. Invalidity or unenforceability of, or default under, or

material change in any provision of, the Funding Agreement

or the New Funding Agreement

5. Cross default to other material debt, including surplus

debentures or surplus notes, of the Borrower

6. Refusal by Allstate to honor the Agent’s request to issue a

New Funding Agreement to Agent per the terms of the

Secondary Indicative Terms and Conditions

Required Banks: Lenders holding 51% or more of the commitments (or if

terminated, of the loans) for amendments and waivers, 100%

for money terms.

Governing Law: The State of New York.

Indemnifications: Indemnification of the Agent and the Lenders in the event of

changes in laws with respect to capital adequacy or reserves.

Allstate to pay all reasonable out-of-pocket costs associated

with the preparation, execution, administration and

enforcement of the Facility document (including fees for the

Bank’s counsel). The Bank, as Arranger, to be held harmless

or indemnified by Allstate against all losses, claims or damages

related to the Facility except in cases attendant to the Bank’s

own gross negligence or willful misconduct.

Increased Costs: The Credit Agreement shall include customary provisions

relating to yield protection, availability and default rate. Such

increased cost protection shall be applicable to the blocked

deposits – for the account of Allstate – established by the Agent

on behalf of each Non-Extending Bank.

Confidentiality: This term sheet shall remain confidential for Allstate

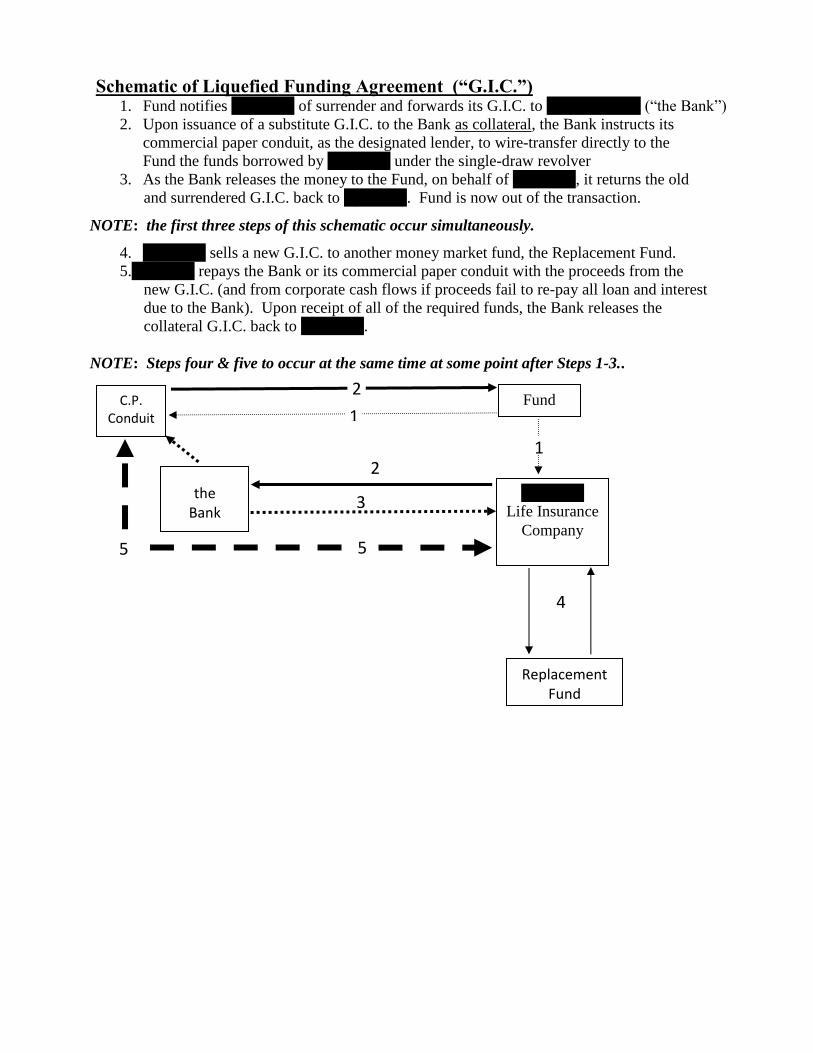

Schematic of Liquefied Funding Agreement (“G.I.C.”) 1. Fund notifies Specimen of surrender and forwards its G.I.C. to Commerzbank (“the Bank”)

2. Upon issuance of a substitute G.I.C. to the Bank as collateral, the Bank instructs its

commercial paper conduit, as the designated lender, to wire-transfer directly to the

Fund the funds borrowed by Specimen under the single-draw revolver

3. As the Bank releases the money to the Fund, on behalf of Specimen, it returns the old

and surrendered G.I.C. back to Specimen. Fund is now out of the transaction.

NOTE: the first three steps of this schematic occur simultaneously.

4. Specimen sells a new G.I.C. to another money market fund, the Replacement Fund.

5.Specimen repays the Bank or its commercial paper conduit with the proceeds from the

new G.I.C. (and from corporate cash flows if proceeds fail to re-pay all loan and interest

due to the Bank). Upon receipt of all of the required funds, the Bank releases the

collateral G.I.C. back to Specimen.

NOTE: Steps four & five to occur at the same time at some point after Steps 1-3..

C.P. Conduit

the Bank

Fund

Specimen

Life Insurance

Company

Replacement Fund

1

1

2

2

3

4

5 5

SECONDARY INDICATIVE TERMS & CONDITIONS OF NEW FUNDING AGREEMENT

December 1999

The following terms and conditions are not necessarily the final ones to be submitted by

Commerzbank AG, New York Branch (“the Bank”) to an eligible operating insurance subsidiary

of Allstate Life Insurance Company, licensed and domiciled in the State of Allstate (“Allstate”).

This summary is intended to frame the discussion of the New Funding Agreement referenced in

the SUMMARY OF INDICATIVE TERMS AND CONDITIONS (the “Term Sheet”)

immediately preceding this Secondary Indicative Terms and Conditions (the “Supporting Terms”).

All terms defined in the Term Sheet shall apply to these Supporting Terms. Please note that these

indicative terms and conditions do not represent a commitment by the Bank to lend, or to make

lending capacity available, to Allstate.

Issuer: Allstate.

Beneficiary: The Bank or its commercial paper conduit (the “Agent” on

behalf of the Lenders and as Collateral Agent on behalf of Non-

Extending Banks).

New Funding Agreement: A Funding Agreement, or several Funding Agreements, in the

name of the Bank as Agent and as Collateral Agent (the “New

Funding Agreement”), each with the same terms as those of the

surrendered Funding Agreement; any exceptions to be specified

contractually.

Amount: The Surrender Amount (i.e., the amount stated on the

underlying Funding Agreement as well as the New Funding

Agreements previously issued to the Agent for the Non-

Extending Banks plus any interest contractually accrued

thereunder).

Maturity: The same as that stated in the surrendered Funding Agreement,

in any event, not longer than seven (7) years.

Documentation: Documents issued by Allstate in its ordinary practice.

Surrender Eligibility: Immediate.

The Bank Surrender Amount: The principal amount of the New Funding Agreement(s) and

any interest due on the New Funding Agreement(s) on the day

Allstate honors the surrender.

Surrender Notice Period: A period of time not to exceed the earlier of the maturity date

of the borrowing under the Facility – or up to sixteen months –

and the maturity date of the New Funding Agreement(s). If a

Surrender Acceleration Event (as defined below) occurs, the

Surrender Notice Period becomes seven (7) days.

Surrender Acceleration Event: If one (or more) of the following events occur, the Surrender

Notice Period accelerates to seven (7) days:

1. a default under the Credit Agreement which involves the

payments due under that agreement;

2. bankruptcy protection filed by or against Allstate;

3. the seizure – or intervention into the affairs – of Allstate by

regulatory authorities; or,

4. another default under the Credit Agreement, which is not

remedied for ninety (90) days.

Interest Rates: A floating rate of interest equal to that rate which would be

concurrently applicable under the Credit Agreement.

Assignment: The Agent shall have the authority to assign the New Funding

Agreement(s) to a new Fund upon the remarketing of the New

Funding Agreement(s).

Representations and Warranties: The same as those applicable to the Facility with particular note

of the following:

1. Necessary authorizations, including regulatoryapprovals, in

place prior to issuance

2. No contravention with existing agreements or organ-

izational documents

Covenants & Other Terms: Customary for Funding Agreements.

Governing Law: State of New York.

Indemnifications: Identical with those applicable to the Facility.

Confidentiality: Allstate shall execute a Confidentiality Agreement with respect

to the transactions set forth herein and the documentation to be

provided in connection with such transactions.

Related Documents