Copyright 2021 by P. Murali, Bakshi Ram, Puthira Prathap, K. Hari, and V. Venkatasubramanian. All rights reserved. Readers may make verbatim copies of this document for non-commercial purposes by any means, provided that this copyright notice appears on all such copies. Sugarcane Based Ethanol Production for Fuel Ethanol Blending Program in India by P. Murali, Bakshi Ram, Puthira Prathap, K. Hari, and V. Venkatasubramanian

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Copyright 2021 by P. Murali, Bakshi Ram, Puthira Prathap, K. Hari, and V. Venkatasubramanian. All rights reserved. Readers may make verbatim copies of this document for non-commercial purposes by any means, provided that this copyright notice appears on all such copies.

Sugarcane Based Ethanol Production for Fuel Ethanol Blending Program in India

by P. Murali, Bakshi Ram, Puthira Prathap, K. Hari, and V. Venkatasubramanian

1

Title: Sugarcane based Ethanol Production for Fuel Ethanol Blending Program in India

Authors: Dr. P. Murali1, Dr Bakshi Ram2 and D Puthira Prathap3, Dr.K. Hari4 and Dr. V. Venkatasubramanian5

Date: August 28 , 2021 at 12:30 p.m. –12:50 p.m.

Palanichamy Murali | Sugarcane Based Ethanol Production for Fuel Ethanol Blending Program in India

Abstract:

The energy strategy of India aims to chart the way forward to meet the Government’s

recent ambitious announcements in the energy domain such 175GW of renewable energy

capacity by 2022. Globally, biofuels assume importance due to growing energy demand and

environmental concerns. India aims 20 %blending of biofuel by 2030 to reduce the

commitment made in the Paris agreement. In India, bioethanol is mainly produced from

sugarcane. India has achieved 5 % blending of bio ethanol in 2019 ambitiously, awaiting to

achieve 20 %blending by 2030. The policy paper highlights sustainability issues related to

biofuel program in India encompassing the success story of ethanol blending program in

Brazil, production and feed-stock availability in India, potential of different feed-stocks for

ethanol production, role of sugarcane varieties in sustaining sugar & ethanol production, 2G

ethanol, price and procurement policy for ethanol and constraints in the EBP Program. Finally,

food security, energy security and climate change mitigation are critical to social, economic

and environmental sustainability. A successful resolution of these challenging issues requires

the goodwill and commitment of all nations. This policy paper will be immensely useful in

assessing the long-term sustainability of ethanol production and EBP in India.

Affiliations (usually as footnotes):

1Palanichamy Murali, senior scientist, Economics and statistics Section, ICAR-Sugarcane

Breeding Institute, Coimbatore, India,

2Bakshi Ram, Director, ICAR-Sugarcane Breeding Institute, Coimbatore, India

3Duraisamy Puthira Prathap, Principal scientist, Extension Section, ICAR-Sugarcane

Breeding Institute, Coimbatore, India

4K. Hari Principal scientist, Microbiology, Division of Crop production, ICAR-Sugarcane

Breeding Institute, Coimbatore, India and

5V. Venkatasubramanian, Director, ICAR- ATARI, Bengaluru, India

2

Sugarcane based Ethanol Production for Fuel Ethanol Blending Program in India

Dr. P. Murali, Dr Bakshi Ram and D Puthira Prathap

Abstract

The energy strategy of India aims to chart the way forward to meet the Government’s recent ambitious

announcements in the energy domain such 175 GW of renewable energy capacity by 2022. Globally,

biofuels assume importance due to growing energy demand and environmental concerns. India aims 20

% blending of biofuel by 2030 to reduce the commitment made in the Paris agreement. In India,

bioethanol is mainly produced from sugarcane. India has achieved 5 % blending of bio ethanol in 2019

ambitiously, awaiting to achieve 20 % blending by 2030. The policy paper highlights sustainability

issues related to biofuel program in India encompassing the success story of ethanol blending program

in Brazil, production and feed-stock availability in India, potential of different feed-stocks for

ethanol production, role of sugarcane varieties in sustaining sugar & ethanol production, 2G ethanol,

price and procurement policy for ethanol and constraints in the EBP Program. Finally, food security,

energy security and climate change mitigation are critical to social, economic and environmental

sustainability. A successful resolution of these challenging issues requires the goodwill and

commitment of all nations. This policy paper will be immensely useful in assessing the long-term

sustainability of ethanol production and EBP in India.

Ky words: Bio ethanol, sugarcane, ethanol blending program and policy options

3

1. INTRODUCTION

The energy strategy of India aims to chart the way forward to meet the Government’s recent

ambitious announcements in the energy domain such 175 GW of renewable energy capacity by 2022,

reduction in energy emissions intensity by 33%-35% by 2030 and share of non-fossil fuel-based

capacity in the electricity mix is aimed at above 40% by 2030. However, conventional or fossil fuel

resources are limited, non-renewable, polluting and therefore, need to be used prudently. On the other

hand, renewable energy resources are indigenous, eco-friendly and virtually inexhaustible.

The Paris Agreement is a landmark environmental accord that was adopted by nearly every

nation in 2015 to address climate change and its negative impacts. The deal aims to substantially reduce

global greenhouse gas emissions in an effort to limit the global temperature increase in this century to

2 degrees Celsius above preindustrial levels, while pursuing means to limit the increase to 1.5 degrees.

The agreement includes commitments from all major emitting countries to cut their climate-altering

pollution and to strengthen those commitments over time.

India is endowed with abundant renewable energy resources. Therefore, their use should be

encouraged in every possible way. Government of India has prepared a road map to reduce the import

dependency in Oil & Gas sector by adopting a five-pronged strategy which include, increasing domestic

production, adopting biofuels & renewables, energy efficiency norms, improvement in refinery

processes and demand substitution. This envisages a strategic role for biofuels in the Indian energy

basket.

Globally, biofuels assume importance due to growing energy demand and environmental

concerns. To encourage use of biofuels, several countries have put forth different policy options

mechanisms, incentives and subsidies suiting to their domestic requirements. As an effective tool for

rural development and generating employment, the primary approach for biofuels in India is to promote

indigenous feedstock production.

In India, bioethanol can be produced from multiple sources like sugar containing materials,

starch, celluloses and lignocelluloses. However, the present policy of Ethanol Blended Petrol (EBP)

Programme allows bioethanol to be produced from sugarcane juice, B-molasses and non-food feed

stock like molasses, cellulose and lignocellulosic materials including petrochemical route.

In the meanwhile, wonder sugarcane variety Co 0238 of ICAR- SBI has broken yield and

recovery barrier in the sub-tropical India. The yield has almost been doubled with progressive farmers

and average sugar recovery was improved more than 1.5 units (15%) which has resulted in significant

sugar surpluses in the country. Hence it needs to be diverted in a meaningful way for the production of

fuel ethanol and to sustain sugarcane production. It would help to reduce sugar surpluses as well as

significant quantity of fuel ethanol production to meet out blending target of EBP. All these existing

scenarios need to be addressed in a comprehensive way to provide solution to sugar surpluses, meeting

4

the demand of ethanol blending program and to bring a balance between food and fuel production with

a price stability leading to doubling income of the sugarcane farmers in the country.

Began in 2003 as a pilot project, the EBP programme has now been extended to the entire

country. It is implemented through a network of 186 depots of Oil Marketing Companies (OMCs),

drawing ethanol from 179 distilleries with an installed ethanol producing capacity of 305 crore litres.

National Policy on Biofuels will help the Indian sugar industry to (a) improve liquidity of

sugar mills by way of value addition to their revenues from supply of ethanol for EBP and reduce import

of fossil fuels (b) reduce sugar inventories and facilitate timely clearance of cane price dues of farmers

& improve their income (c) generate employment through setting up of new distilleries, including

expansion of existing distilleries (d) promote a cleaner and healthier environment, reducing greenhouse

gas emissions.

2. Sugarcane and sugar scenario

Sugarcane and sugar production in the country is fluctuating since start of the 21st century.

Severe drought in 2003 and 2004 have reduced sugarcane and sugar production necessitate import of

sugar for domestic consumption and has stalled the ambitious bioethanol program in the country.

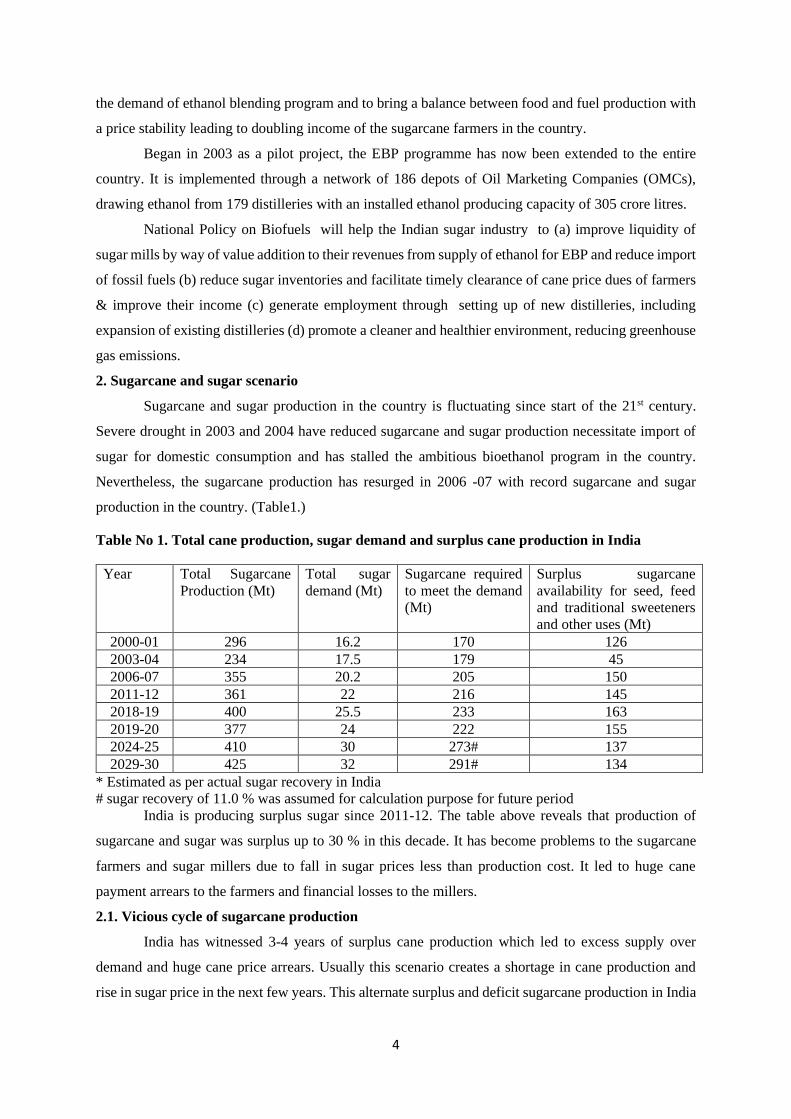

Nevertheless, the sugarcane production has resurged in 2006 -07 with record sugarcane and sugar

production in the country. (Table1.)

Table No 1. Total cane production, sugar demand and surplus cane production in India

Year Total Sugarcane

Production (Mt)

Total sugar

demand (Mt)

Sugarcane required

to meet the demand

(Mt)

Surplus sugarcane

availability for seed, feed

and traditional sweeteners

and other uses (Mt)

2000-01 296 16.2 170 126

2003-04 234 17.5 179 45

2006-07 355 20.2 205 150

2011-12 361 22 216 145

2018-19 400 25.5 233 163

2019-20 377 24 222 155

2024-25 410 30 273# 137

2029-30 425 32 291# 134

* Estimated as per actual sugar recovery in India

# sugar recovery of 11.0 % was assumed for calculation purpose for future period

India is producing surplus sugar since 2011-12. The table above reveals that production of

sugarcane and sugar was surplus up to 30 % in this decade. It has become problems to the sugarcane

farmers and sugar millers due to fall in sugar prices less than production cost. It led to huge cane

payment arrears to the farmers and financial losses to the millers.

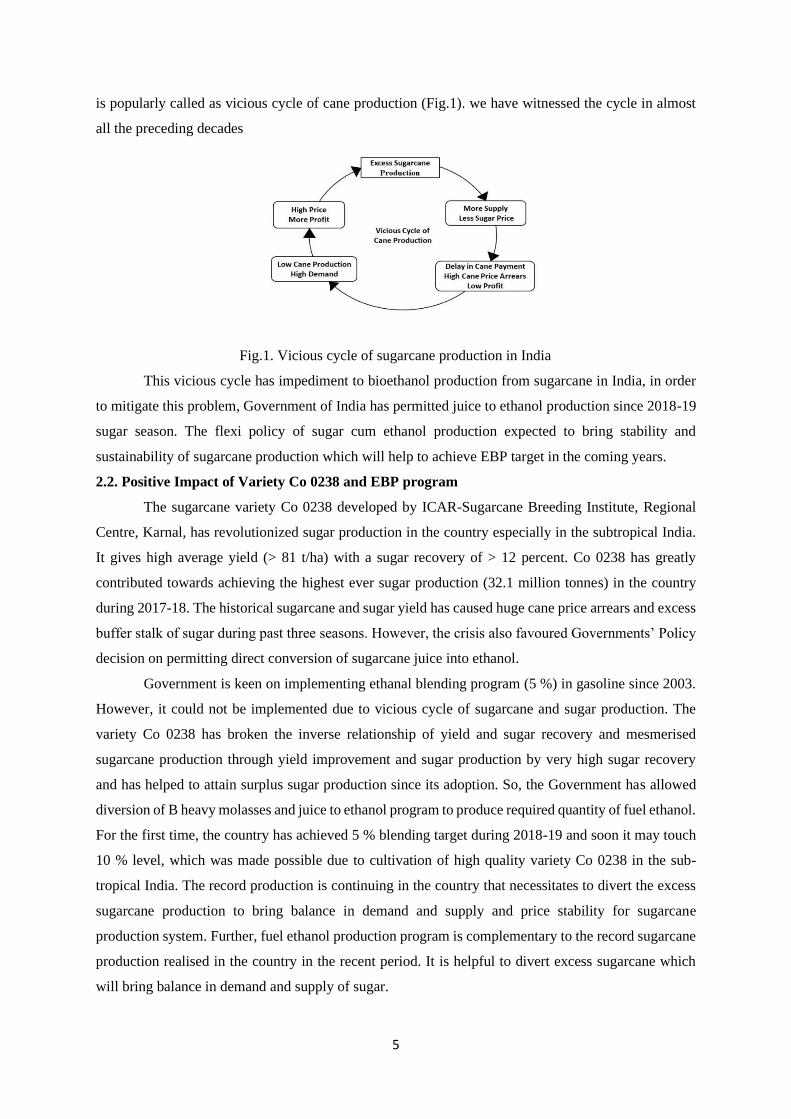

2.1. Vicious cycle of sugarcane production

India has witnessed 3-4 years of surplus cane production which led to excess supply over

demand and huge cane price arrears. Usually this scenario creates a shortage in cane production and

rise in sugar price in the next few years. This alternate surplus and deficit sugarcane production in India

5

is popularly called as vicious cycle of cane production (Fig.1). we have witnessed the cycle in almost

all the preceding decades

Fig.1. Vicious cycle of sugarcane production in India

This vicious cycle has impediment to bioethanol production from sugarcane in India, in order

to mitigate this problem, Government of India has permitted juice to ethanol production since 2018-19

sugar season. The flexi policy of sugar cum ethanol production expected to bring stability and

sustainability of sugarcane production which will help to achieve EBP target in the coming years.

2.2. Positive Impact of Variety Co 0238 and EBP program

The sugarcane variety Co 0238 developed by ICAR-Sugarcane Breeding Institute, Regional

Centre, Karnal, has revolutionized sugar production in the country especially in the subtropical India.

It gives high average yield (> 81 t/ha) with a sugar recovery of > 12 percent. Co 0238 has greatly

contributed towards achieving the highest ever sugar production (32.1 million tonnes) in the country

during 2017-18. The historical sugarcane and sugar yield has caused huge cane price arrears and excess

buffer stalk of sugar during past three seasons. However, the crisis also favoured Governments’ Policy

decision on permitting direct conversion of sugarcane juice into ethanol.

Government is keen on implementing ethanal blending program (5 %) in gasoline since 2003.

However, it could not be implemented due to vicious cycle of sugarcane and sugar production. The

variety Co 0238 has broken the inverse relationship of yield and sugar recovery and mesmerised

sugarcane production through yield improvement and sugar production by very high sugar recovery

and has helped to attain surplus sugar production since its adoption. So, the Government has allowed

diversion of B heavy molasses and juice to ethanol program to produce required quantity of fuel ethanol.

For the first time, the country has achieved 5 % blending target during 2018-19 and soon it may touch

10 % level, which was made possible due to cultivation of high quality variety Co 0238 in the sub-

tropical India. The record production is continuing in the country that necessitates to divert the excess

sugarcane production to bring balance in demand and supply and price stability for sugarcane

production system. Further, fuel ethanol production program is complementary to the record sugarcane

production realised in the country in the recent period. It is helpful to divert excess sugarcane which

will bring balance in demand and supply of sugar.

6

It is approximately estimated that one tonne sugarcane will yield 600-700 litres of cane juice,

similarly, one tonne of sugarcane will yield 65–70 litres of ethanol under normal production scenario.

For Eg. One Kilo Litres Per Day (KLPD) ethanol distillery unit require 10.5 lakh kilo litre of cane juice

for production of ethanol on daily basis. Alternatively, one 100 KLPD needs about 1500 tonne of

sugarcane on daily basis and need about 4 lakh tonnes annually for its operation. Hence, 100 such

distilleries could divert about 40 million tonnes of surplus sugarcane during bumper production. It will

help to reduce about 4 to 4.5 million tonnes of surplus sugar production subject to sugar recovery in the

country. On other hand, operation of 500 plus sugar mills may also produce ethanol, in addition to sugar

production by establishing juice to ethanol distillery unit. These sugar cum ethanol production could

also be used to regulate the optimum sugar and ethanol production in the country.

2.3. Trade and Excess sugar production

Globally, Brazil leads the export market of sugar followed by Thailand and EU countries.

Though India is a leading producer of sugarcane and sugar, it doesn’t have competitive edge for

exporting sugar. Exporting of sugar heavily demanded policy support from government which may not

be a sustainable solution for sugar sector. Huge stock of sugar erodes profitability of the sugar mills

which leads to cane payment arrears to the farmers. On the other hand, demand for petrol is ever growing

in the country also widens the current account deficit in the trade account. So, implementing ethanol

blending program would be helpful to solve the twin problems of excess sugar production by diverting

excess juice to fuel ethanol production and reducing current account deficit by reducing our oil imports.

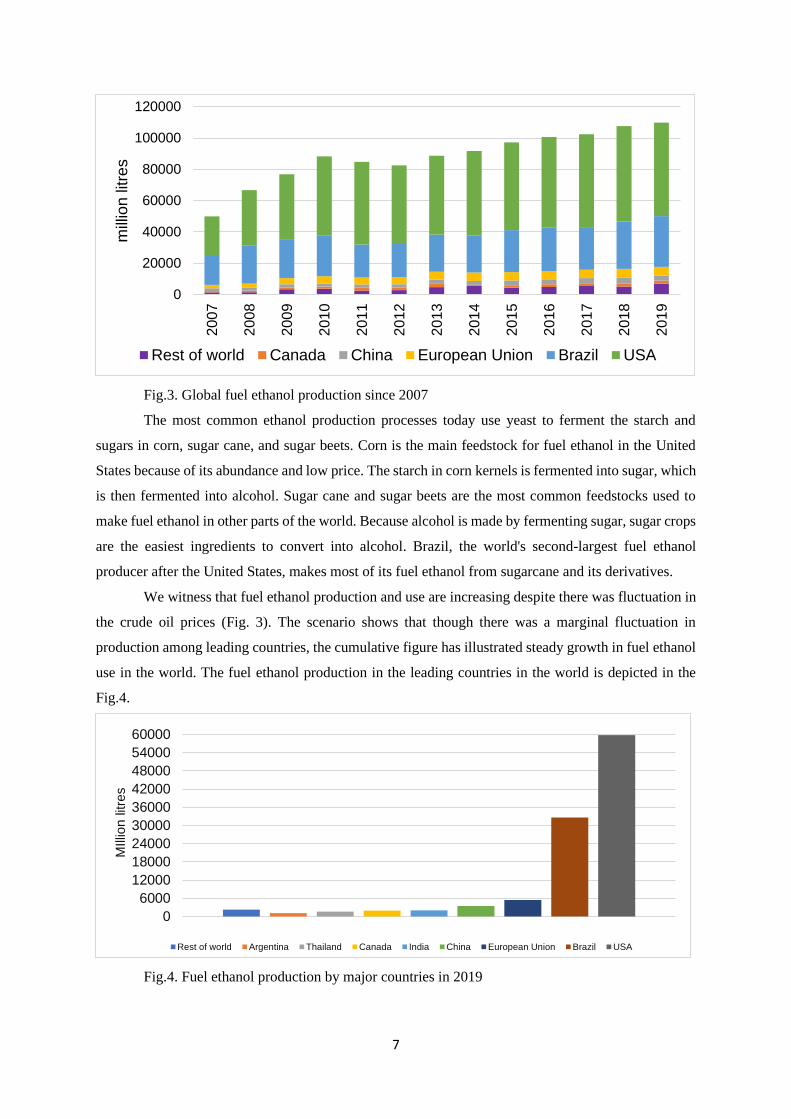

2.4. Global fuel ethanol production

The global ethanol production by a country or region, from 2007 to 2019 is depicted in the

Fig.3. Global production continues to increase to the market demand. Globally, The United States is the

largest producer of fuel ethanol since 2007 followed by Brazil. Together, the United States and Brazil

account for 84% of the world's ethanol production. European Union, China and Canada are the other

leading fuel ethanol producers and the category of other countries also progressing in fuel ethanol use

is visible in the global statistics.

7

Fig.3. Global fuel ethanol production since 2007

The most common ethanol production processes today use yeast to ferment the starch and

sugars in corn, sugar cane, and sugar beets. Corn is the main feedstock for fuel ethanol in the United

States because of its abundance and low price. The starch in corn kernels is fermented into sugar, which

is then fermented into alcohol. Sugar cane and sugar beets are the most common feedstocks used to

make fuel ethanol in other parts of the world. Because alcohol is made by fermenting sugar, sugar crops

are the easiest ingredients to convert into alcohol. Brazil, the world's second-largest fuel ethanol

producer after the United States, makes most of its fuel ethanol from sugarcane and its derivatives.

We witness that fuel ethanol production and use are increasing despite there was fluctuation in

the crude oil prices (Fig. 3). The scenario shows that though there was a marginal fluctuation in

production among leading countries, the cumulative figure has illustrated steady growth in fuel ethanol

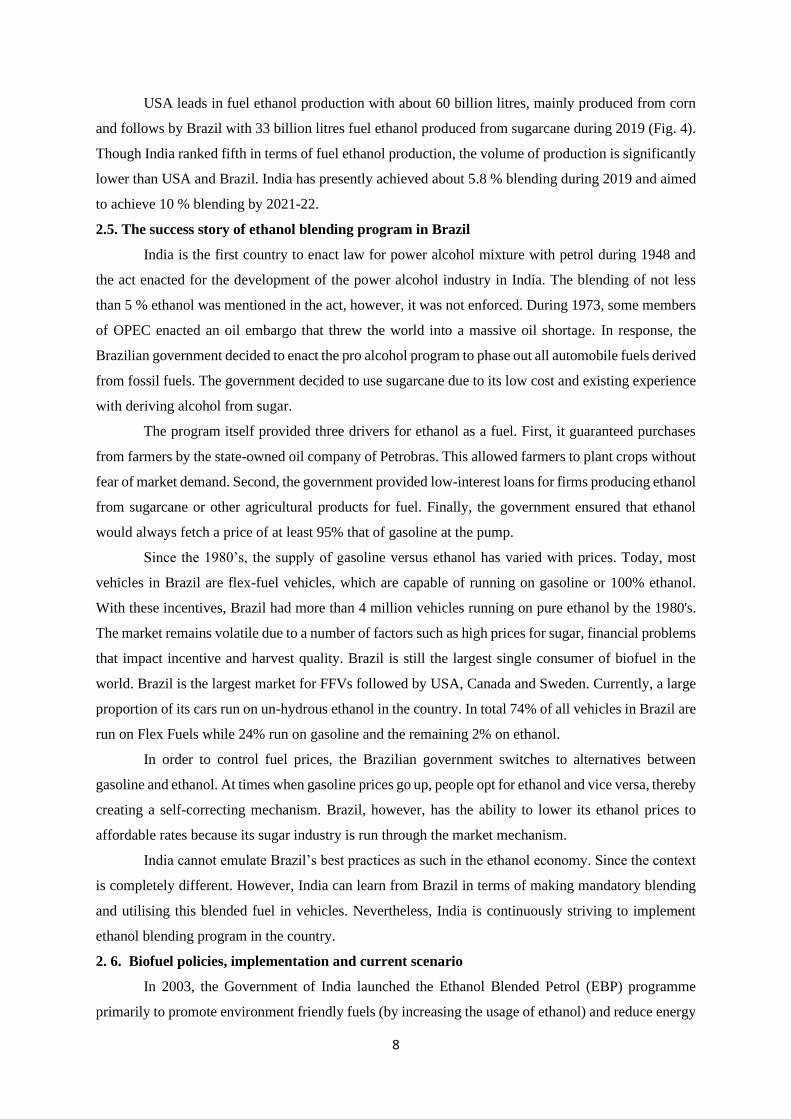

use in the world. The fuel ethanol production in the leading countries in the world is depicted in the

Fig.4.

Fig.4. Fuel ethanol production by major countries in 2019

0

20000

40000

60000

80000

100000

120000

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

mill

ion

litre

s

Rest of world Canada China European Union Brazil USA

0

6000

12000

18000

24000

30000

36000

42000

48000

54000

60000

MIllio

n litre

s

Rest of world Argentina Thailand Canada India China European Union Brazil USA

8

USA leads in fuel ethanol production with about 60 billion litres, mainly produced from corn

and follows by Brazil with 33 billion litres fuel ethanol produced from sugarcane during 2019 (Fig. 4).

Though India ranked fifth in terms of fuel ethanol production, the volume of production is significantly

lower than USA and Brazil. India has presently achieved about 5.8 % blending during 2019 and aimed

to achieve 10 % blending by 2021-22.

2.5. The success story of ethanol blending program in Brazil

India is the first country to enact law for power alcohol mixture with petrol during 1948 and

the act enacted for the development of the power alcohol industry in India. The blending of not less

than 5 % ethanol was mentioned in the act, however, it was not enforced. During 1973, some members

of OPEC enacted an oil embargo that threw the world into a massive oil shortage. In response, the

Brazilian government decided to enact the pro alcohol program to phase out all automobile fuels derived

from fossil fuels. The government decided to use sugarcane due to its low cost and existing experience

with deriving alcohol from sugar.

The program itself provided three drivers for ethanol as a fuel. First, it guaranteed purchases

from farmers by the state-owned oil company of Petrobras. This allowed farmers to plant crops without

fear of market demand. Second, the government provided low-interest loans for firms producing ethanol

from sugarcane or other agricultural products for fuel. Finally, the government ensured that ethanol

would always fetch a price of at least 95% that of gasoline at the pump.

Since the 1980’s, the supply of gasoline versus ethanol has varied with prices. Today, most

vehicles in Brazil are flex-fuel vehicles, which are capable of running on gasoline or 100% ethanol.

With these incentives, Brazil had more than 4 million vehicles running on pure ethanol by the 1980's.

The market remains volatile due to a number of factors such as high prices for sugar, financial problems

that impact incentive and harvest quality. Brazil is still the largest single consumer of biofuel in the

world. Brazil is the largest market for FFVs followed by USA, Canada and Sweden. Currently, a large

proportion of its cars run on un-hydrous ethanol in the country. In total 74% of all vehicles in Brazil are

run on Flex Fuels while 24% run on gasoline and the remaining 2% on ethanol.

In order to control fuel prices, the Brazilian government switches to alternatives between

gasoline and ethanol. At times when gasoline prices go up, people opt for ethanol and vice versa, thereby

creating a self-correcting mechanism. Brazil, however, has the ability to lower its ethanol prices to

affordable rates because its sugar industry is run through the market mechanism.

India cannot emulate Brazil’s best practices as such in the ethanol economy. Since the context

is completely different. However, India can learn from Brazil in terms of making mandatory blending

and utilising this blended fuel in vehicles. Nevertheless, India is continuously striving to implement

ethanol blending program in the country.

2. 6. Biofuel policies, implementation and current scenario

In 2003, the Government of India launched the Ethanol Blended Petrol (EBP) programme

primarily to promote environment friendly fuels (by increasing the usage of ethanol) and reduce energy

9

imports. The programme, in general, was conceptualised with multiple objectives in mind. By

increasing the usage of biofuels, it aimed to reduce carbon emissions while also saving foreign exchange

and reducing import dependency. More specifically, the EBP programme injects liquidity into the sugar

sector by providing a sustained demand for ethanol. Thus, it armed in the reduction of accumulated

arrears and permits timely payments for cane farmers.

The commercial production and marketing of ethanol blended gasoline had started in January

2003, the first phase of the ethanol blended petrol (EBP) programme that mandated blending of 5 %

ethanol in gasoline in 9 states and 4 union territories. In August 2005, the government completed an

agreement between the sugar industry and petroleum companies to enable the purchase of ethanol and

the ethanol programme was restarted in a limited number of designated states and union territories.

With a strong resurgence in sugarcane/sugar production in 2006-07, the GOI announced the second

phase of the EBP programme in September 2006 that mandated 5% blending of ethanol with petrol

(gasoline) subject to commercial viability in 20 states and 8 union territories.

The GOI had initially planned to launch the third stage of the EBP from October 1, 2008

wherein (i) the ethanol blend ratio was to be raised from 5% to 10 % and (ii) 5% blending was to be

made mandatory across the country in all the states.

The erstwhile National Policy on Biofuels (2009) permitted the procurement of non-food

feedstock like molasses, celluloses and lignocelluloses. However, due to the short supply of sugarcane

and sugar molasses in 2008-09 and forecast of short supplies in 2009 -10, the government has deferred

the proposed implementation of the third phase of the EBP. Since 2013, the GOI has mandated of 5 %

blending of ethanol in petrol for the fuel use in the country. Nevertheless, until 2017–18 ethanol for

EBP programme came from molasses, allowing utilisation of a by-product of the sugar industry. The

present output of molasses allows for the production of approximately 3 billion litres of alcohol/ethanol,

which is targeted at 10% blending.

Thus, India has different phases of ethanol blending policies and program since 2003, the

meaningful blending of ethanol with petrol was started after ten years of biofuel policy formulation.

With the available fuel ethanol production, ethanol blending was achieved only 0.67% in 2012-13 and

4.22% in 2017-18 (Table. 2).

Table 2: Details of Ethanol Supplied and Blending Percentages

Ethanol Supply

Year

Tendered Qty

by OMC’s*

(crore Lit)

Qty Allocated

(crore Lit)

Qty Supplied

(crore Lit)

Blending %age

PSU OMCs

2012-13 103.0 32.0 15.4 0.67

2013-14 115.0 70.4 38.0 1.53

2014-15 128.0 86.5 67.4 2.33

2015–16 266.0 130.5 111.4 3.51

2016–17 280.0 80.7 66.5 2.07

2017–18 313.0 161.04 150.5 4.22

10

2018–19 329.0 225.0 190.0 5.80

*Oil marketing companies (OMCs)

In the past, various measures have been undertaken by the GOI encourage the domestic

production of ethanol. These include amendments to the Industries (Development and Regulation) Act,

1951, to legislate exclusive Central control over denatured alcohol, reduction of the Goods and Services

Tax (GST) levied on ethanol for EBP to 5%, reintroduction of the administered price mechanism,

expansion of the programme and opening up alternate production routes. The government has also

adopted different pricing methods to boost the supplies of ethanol for the EBP programme. However,

the level of ethanol blending has remained low.

It has clearly indicated that 5 % of EBP was not achieved despite there was policy support and

surplus sugarcane and sugar production since 2012-13 in the country. As is evident from the Table 2

above, the quantity of ethanol supplied has been significantly lower than the tendered quantity. This is

largely due to supply-side constraints, which include limited distillation capacity and availability of

molasses. Finally, India has achieved five percent blending during 2019 due to new policy directives

coupled with fair pricing of fuel ethanol for blending EBP program.

2.7. Bioethanol demand in India

Recently, the country made sincere efforts in implementing bioethanol blending program to

achieve 10 % blending by 2021-22 and 20 % blending by 2030. The petrol demand also ever increasing

and future requirement of fuel ethanol is estimated based on petrol demand. The projected demand for

petrol and the amount of ethanol required for 5, 10 and 20 % blending for different time periods is given

in the Table 3.

Table: 3. Future petrol demand and ethanol requirement in India

Year Petrol demand

Million litres (M.L)

Ethanol blending requirements

Million litres (M.L)

5 % 10 % 20 %

2017-18 36015 1621 3241 6483

2024-25 49482 2227 4453 8907

2029-30 60203 2709 5418 10836

The above demands were worked out based on lag linear demand function fitted for petrol. The

bioethanol requirement was estimated by fitting a simple function of petrol demand. The ethanol

demand for 5%, 10% and 20% of the requirement would be 2709, 5418 and 10836 million litres in the

year 2030. Nevertheless, the country had already demonstrated potential alcohol production of 3200

Million litres in 2006-07 which was good enough to fulfil the 5 % blending requirement of the country.

The additional quantity required for fuel ethanol and other uses will be met through capacity building

with diversified feedstocks and new generation technologies.

2.8. National Policy on Biofuels – 2018

The poor implementation of ethanol blending program had its own impediments and

bottlenecks over a period of time. It has necessitated to bring out comprehensive policy capsule with

11

production support measures for sustainable fuel ethanol production blending program to achieve 10 %

blending during 2021-22 and 20 % by 2030 in the country. Hence, GOI, has brought out policy on

biofuel-2018 and it is being implemented since May 2018 in the country. The 2018 National Policy on

Biofuels broadens the scope for the raw material procurement for ethanol production.

The key points of the policy are following:

Funding: Policy would fund Rs. 5000 cr to 2G ethanol bio refineries over 6 years in addition to

tax incentives, higher purchase price compared to 1G fuels. (Note – These steps are similar to those

taken by Brazilian government to support the growth of ethanol as a bio-fuel market)

Forex Savings: 1 crore litres of E10 would save Rs.28 cr of forex. So, with the supply of about

150 crore litres of ethanol during 2017-18, has saved about Rs. 4000 crores of forex.

OMC Capex: 100 KLPD bio refinery would cost about Rs. 800 crores investment. Currently,

OMCs are in the process of setting up 12 2G bio refineries with a total investment of Rs. 10,000 crores.

This should lead to additional capacity of about 1200 KLPD annually.

As per new biofuel policy, The Cabinet Committee on Economic Affairs (CCEA) raised the

procurement price of ethanol derived from 100 per cent sugarcane juice to Rs 62.65 per litre from the

current rate of Rs 59.40. The price for ethanol produced from B-heavy molasses (intermediary

molasses) was hiked to Rs 57.61 a litre from the current Rs 52.43 but that for ethanol produced from

C-heavy molasses was increased to Rs 45.69 from Rs 43.70.

Conventionally, sugar is extracted in 3 stages, with very little sugar left to be extracted after the

3rd stage. Left over after the 3rd stage is the molasses (C -molasses), which has very low sugar content

(non recoverable sugars) and traditionally this molasses is processed in a distillery for ethanol

production. Going forward, ethanol should be produced from B-heavy molasses, which contains

considerably more sugar to augment ethanol production. However, if the mills cut back on the sugar

output, they will have to be compensated with a competitive price for ethanol. Ethanol also can be

extracted via B Heavy molasses route to get higher yield of ethanol per tonne of sugarcane.

The 2018 National Policy on Biofuels seeks to address these issues.

Under the new biofuel policy, a national Biofuel Coordination Committee has been set up in

2018. It envisages to resolve the lack of raw material availability by expanding the base of raw materials

to include B molasses, sugarcane juice and damaged food grains unfit for human consumption. This

measure aims to help OMCs achieve higher blending targets. Presently, the Ministry of Petroleum and

Natural Gas (MoP&NG) is undertaking the EBP programme to achieve 10% ethanol blending

percentage in petrol by 2021–22.

Attempts to incentivise ethanol production have been made via an interest subvention scheme,

namely: the scheme for augmenting and enhancing ethanol production capacity. The scheme is jointly

monitored by MoP&NG and the Department of Food and Public Distribution (DFPD). So far, the DFPD

has approved (in-principle) 114 proposals for a maximum loan amount of ₹6,139.08 crore, for granting

interest subvention. The Government of India has also allocated additional funds for the scheme. These

12

proposals are estimated to add another 2000 million litres of ethanol production capacity. The

procurement of ethanol from grain surplus projected by the Ministry of Agriculture and Farmers’

Welfare has also been approved.

The amendment of the IDR Act also aims to smoothen inter- and intra-state movement of

ethanol by giving the central Government exclusive control over it. The possibility of higher blending,

beyond 10%, in ethanol-surplus states of Uttar Pradesh and Maharashtra is also being explored to avoid

the movement of ethanol across the country. For this, the Bureau of Indian Standards has already

notified E-20 Standards.

Public sector OMCs follow an order of priority for ethanol procurement: from 100% sugarcane

juice, B heavy molasses/ partial sugarcane juice, C heavy molasses, and damaged food grains. The task

force feels there is significant scope to enhance allocation of ethanol produced through 100% sugarcane

juice route.

The Indian approach to biofuels is based solely on non-food feed stocks to be raised on

degraded or wastelands which are not suited to farming, thus avoiding a possible conflict of fuel vs.

food security. An estimated 55.3 million hectares are considered wasteland in India which could be

brought into productive use by raising bio-fuel crops (Maheswari et al. 2007). Minimum Purchase Price

(MPP) for purchase of bioethanol would be announced with periodic revision. Major thrust will be

given to research, development and demonstration with focus on plantations, processing and production

of biofuels, including second generation biofuels. Financial incentives, including subsidies and grants

will be provided for second generation biofuels.

3. Supply side initiatives for bio ethanol production

Potential of different feedstocks for ethanol production

Developed and developing countries are aspiring to increase the production of biofuels in order

to reduce dependence on crude oil, improve energy security, and adopt biofuel technologies to support

rural development. The focus of this study was to identify the available feedstocks and their quantities

for bioethanol production that can support this policy. The potential energy crops identified were sweet

sorghum, maize, sugar beet and broken grains of cereals was identified to be the most suitable feedstock

for bioethanol production since an average of less than 50% of their domestic supply is consumed as

food. The potential crop and ethanol yield per ha are given in the Table.4.

Table 4. The Potential crops for biofuel production in India

Crop Ethanol yield

(Iitres/tonne)

Crop/stalk yield

(t/ha)

Ethanol production

(litres/ha)

Sugarcane 70 80 5600

Sugar beet 100 50.6 5060

Maize 360 5.9 2133

Sweet Sorghum* 26.3 38.5 1013

Source: FAO production yearbook 1979 and 2018 * Fresh stalk yield

13

Today, nearly all ethanol produced in the world is derived from starch and sugar-based

feedstocks. The sugars in these feedstocks are easy to extract and ferment, making large-scale ethanol

production at affordable cost. The sugar based different feedstocks are being used for fuel ethanol

production depend on geography, cost of cultivation and food and alternative uses in the respective

countries in the world. The technically feasible alternative feedstocks in the country are discussed

below.

3.1. Energy canes

Indian sugar and by-product industries are transforming into multiproduct manufacturing sugar

complexes to utilize every part of canes supplied to the mill and to improve the financial viability of

the industry. The sugar mills are looking for other options to improve the profitability. Most of the sugar

mills have now converted into sugar complexes with the combined production of sugar, ethanol,

cogeneration, bio-compost etc. Policy on biofuel, 2018 broaden the scope for production of bioethanol

from all forms ligno cellulose, it has opened up new avenue for energy cane cultivation.

ICAR-SBI has developed clones with mean harvestable biomass yield under limited irrigation

condition was 241.47 t/ha while under normal irrigation condition the yield was 289.08 t/ha. This clone

can be ratooned for at least 7-8 years hence replanting can be avoided every year. This promising clone

is identified as an ideal energy canes due to more biomass yield per unit area and requires low input,

low production cost and low nutrient requirement which are the characteristics of energy canes. This

type of energy canes can be harvested as whole canes with trash and tops and directly fed into the boilers

to produce electricity.

3.2. Maize

Maize is the leading crop and serves as the feedstock for most domestic ethanol production in

the USA. Corn ethanol meets the renewable fuel category of the Renewable Fuel Standard (RFS). This

ensures there are enough feedstocks to meet demand in livestock feed, human food, and export markets.

Maize is the third most important cereal crop after rice and wheat for India. Globally it is highly valued

for its multifarious use as food, feed, fodder and raw material for large number of industrial products.

Currently maize production in India meets the domestic requirement especially for feed industry.

Additional maize production has to be strategically planned for biofuel production. In India, maize is

considered as important alternate feedstock for sugarcane since, the cost of maize production is

equivalent to the price of b heavy molasses. To meet the biofuel industry in the country, further research

efforts are to be taken up to utilize maize stalks and cobs to utilize them as feedstock.

3.3. Sugar Beet

Contrary to cereals, pulses and root crops, the main component of sugar crops is not starch but

simple monosaccharides (glucose and fructose) and particularly disaccharides (sucrose or saccha-rose).

The chemical composition of sugar beet roots makes this raw material, an attractive feedstock for

ethanol fermentation. In the manufacture of sugar from sugar beet, various intermediates, by-products

and wastes are generated, which can be used for the production of energy and other value-added

14

products including biofuel. Sugar is the prime component that gives value to the sugar beet crop and

the by-products generated in its extraction (pulp and molasses) give a benefit up to 10% of the value of

the sugar. The sugar content in sugar beet can vary from 12% to 20%. In order to obtain the highest

yield from sugar beet, several factors must be considered, such as varieties, the location and

management practices. The knowledge of the interdependence of those factors is decisive in the

cultivation of sugar beet varieties for ethanol production and can provide a basis for directing the crop

for this sector of the economy.

3.4. Sweet sorghum

The National Policy on Biofuels 2018 has identified sweet sorghum as one of the candidate

crops for augmenting biofuel production in the country. Sugar industries are exploring the possibilities

of complementing their existing molasses-based ethanol production with alternative raw material to fill-

in the lean period of sugarcane crushing for year-round operations. In addition, sweet sorghum is ideal

feedstock for second generation bio ethanol production. The major impediment of converting biomass

to biofuels is high pre-treatment costs for removal of lignin besides high cost of enzymes used for

saccharification. In view of the current remunerative price for ethanol, the use of sweet sorghum as

biofuel feedstock in existing sugar mills is going to be a win-win situation for both industry and resource

poor, dry land farmers. Sweet sorghum being a promising alternative feedstock for sustainable ethanol

production can also provide a wide range of environmental, economic and employment benefits under

rainfed conditions.

3.5. Broken and surplus rice and wheat grains

The National Biofuel Coordination Committee (NBCC) took the decision to utilize broken &

surplus rice and wheat grain which will lead to utilisation of part of a huge stockpile of 30.57 million

tonnes (MT) of rice which is almost 128% more than the buffer stock and strategic requirement norms.

At present, the Food Corporation of India (FCI) has huge rice stock from previous years lying with

millers on behalf of FCI. In India, the total capacity of grain-based distilleries is close to 2 billion litres,

of which around 38% (750 million litres) is lying unused. Using surplus rice for ethanol will address

the concern of about 750 million litres of grain-based distillery capacities that are lying idle, due to the

lack of feedstock. Similarly, broken and surplus grains can also be used for grain-based fuel ethanol

production. Effective utilization of these raw materials needs effective coordination of different

ministries and there is clear possibility of using them as biofuel feedstock in the country.

3.6. Second Generation Biofuels

Cellulosic Ethanol Feedstocks

Cellulosic feedstocks are non-food based and include crop residues, wood residues, dedicated

energy crops and industrial and other wastes. These feedstocks are composed of cellulose,

hemicellulose and lignin. Lignin is usually separated out and converted to heat and electricity for the

15

conversion process. It's more challenging to release the sugars in these feedstocks for conversion to

ethanol. Second-generation biofuel feedstock is the nonedible byproduct of food crops. For example,

rice, wheat straw and corn husks are second-generation feedstocks. There are advantages to use the

inevitable byproduct of the agricultural industry for biofuel production; no additional fertilizer, water,

or land are required to grow this feedstock. Industry does use some of this nonedible byproduct to

produce animal feed, however there is a substantial amount that could also be used for biofuel

production.

4. Demand side initiatives for fuel ethanol blending program

4.1. Fuel ethanol filling stations

Ethanol blending has become mandatory in the country since 2013 and India is pursuing the

objective of 20 % blending by 2030. Apart from blending, Flexi vehicles are operating in Brazil USA

and EU countries. Its requisite ethanol filling bunks in the existing fuel station in a phased manner. It

encourages commuters to buy flexi vehicles in the coming years. In addition, there are demands to run

eco vehicles, farm implements and vehicles at metro cities with ethanol to reduce pollution. It will

accelerate the ethanol demand and ensure value chain for fuel ethanol production.

4.2. Flexi fuel vehicles

As ethanol FFVs became commercially available during the late 1990s, the common use of the

term "flexible-fuel vehicle" became synonymous with ethanol FFVs. In the United States flex-fuel

vehicles are also known as "E85 vehicles". In Brazil, the FFVs are popularly known as "total flex" or

simply "flex" cars. In Europe, FFVs are also known as "flexifuel" vehicles.

The most common commercially available FFV in the world market is the ethanol flexible-fuel

vehicle, with about 60 million automobiles, motorcycles and light duty trucks manufactured and sold

worldwide by March 2018 and concentrated in four markets, Brazil (30.5 million light-duty vehicles

and over 6 million motorcycles), the United States (21 million by the end of 2017), Canada (1.6 million

by 2014) and Europe, led by Sweden (243,100). In addition to flex-fuel vehicles running with ethanol,

in Europe and the US, mainly in California, there have been successful test programs with methanol

flex-fuel vehicles, known as M85 flex-fuel vehicles.

The rapid success of flex vehicles was made possible by the existence of 33,000 filling stations

with at least one ethanol pump available by 2006, a heritage of the early Pro-alcohol ethanol program

in Brazil. These facts, together with the mandatory use of E25 blend of gasoline throughout the country,

allowed Brazil in 2008 to achieve more than 50% of fuel consumption in the gasoline market from

sugarcane-based ethanol.

4.3. Long term Price and procurement policy for ethanol

The Brazilian Government switches to alternatives between gasoline and ethanol in order to

control fuel prices. At times when gasoline prices go up, people opt for ethanol and vice versa, thereby

creating a self-correcting mechanism. Brazil has the ability to lower its ethanol prices to affordable rates

16

because its sugarcane industry is run through the market mechanism. This means that there is no

minimum price at which sugarcane has to be purchased. In India’s case, the Government cannot reduce

ethanol prices, because sugarcane has an FRP, which is reasonably priced high. In this case, the price

of ethanol has to cover the cost by ex-mills in purchasing the sugarcane from farmers.

Industry has been demanding a long-term pricing formula for ethanol to encourage setting up or

capacity enhancement of fuel ethanol production. It is recommended that the Ministry of Petroleum and

Natural Gas examine the suggestion in a holistic manner keeping in view the need for providing some

indication for the pricing formula for ethanol so as to reduce uncertainties of return on the investments

being made for bioethanol production. Similarly, the production and purchase support measures for the

period of minimum ten years is expected to sustain the fuel ethanol demand for averting the risks and

uncertainty in the upcoming ethanol market.

5. Constraints in the EBP Program

The future viability of the Indian sugar industry will depend on value-addition and

diversification through ethanol and cogeneration. Diversification will allow the mills to exploit scale

economies and improve economic efficiency and profitability in the industry. In order to tap full

potential, molasses need to be fully available for fuel ethanol program apart from other uses.

6. Impact of Biofuel Feedstock on Food/Price/Livelihood

India does not produce any ethanol from cereal grains (maize, etc.) thus, there has been no

impact of the ethanol programme on the domestic market for food, feed and trade of cereal grains and

byproducts. Fortunately, India’s sugar demand increasing and necessitated sugar production would be

30 million tonnes in 2025. So, sugarcane cultivation is inevitable and has to be increased substantially

to satisfy domestic demand. Increase in cane cultivation is helpful for more ethanol production through

by product (molasses). The only hitch is sugarcane pricing. Price should be increased substantially to

sustain the sugarcane farmers in sugarcane cultivation. Then, the sugar industry will not be lacking in

meeting the requirement of fuel ethanol in the country. Potentially India became a sugar surplus country

for the past 5 seasons, that led to huge cane price arrears to the farmers and liquidity crisis in the

industry. In the current season nearly 14 MT of accumulated sugar stocks leading to further losses.

Hence diversion of juice to ethanol will substantially reduce the glut in sugar, increased sugar price and

probably a viable sugar complex. Further with the improved sugarcane varieties and production

technologies, India can easily achieve the growing demand for sugar and alcohol in the coming years.

7. Way forward

The government, since 2016, has been putting in place policies (including the 2018 National

Policy on Biofuels) to achieve the EBP targets by stipulated time frame. It has offered better price for

ethanol, ensured oil companies blend, addressed supply issues and removed restrictions imposed by tha

State governments. In 2018-19 (December-November period), The blending rate was more than 5 per

cent for the first time in the country.

17

For India’s ethanol blending programme to deliver, three critical factors of policy consistency,

stability in price and flexibility are essential. It must be made clear that ethanol blending with petrol

will continue irrespective of oil prices and such unequivocal statement will prepare the stakeholders to

make necessary investment.

Sugar mills need to make substantial investment in bioethanol distilleries. Appreciations to the

government’s subsidised loan scheme, as many as 114 mills are expanding their capacities, which

should in the next 24 months add 900 million litres of ethanol capacity. Capacity for another 1000

million litres needs to be created. If the government sticks to its plan of increasing the blending rate to

20 per cent by 2030, automotive players will have to study if engines need to be modified. These

investments will not materialise without policy consistency.

Ethanol has competing users and for OMCs to get their share for blending should pay a

remunerative price. The government has ensured this for 2017-18 and 2018-19. It is anybody’s guess

that what would be the price next year as crude prices soften. For ensuring price stability, ethanol pricing

should be delinked from crude prices. Even if crude falls, ethanol price for blending should remain

remunerative considering the overall benefits. Also, the government should handhold the programme

till it stabilises. Brazil did just that. It’s ethanol programme started in the 1970s and for over 25 years

the government fixed the price and shielded it from market fluctuations. Brazil’s average blending rate

of 40-45 per cent would not have been possible without such grand support from the government.

Flexibility is another important virtue. In India, ethanol is produced after distilling molasses, a

by-product of sugar. As against the domestic consumption of 26 million tonnes, sugar output in 2017-

18 was 32.2 million tonnes and 2018-19 season (33.13 million tonnes) was also another bumper year

for cane production. This glut could have been avoided if mills were allowed to produce ethanol directly

from cane juice or by converting B heavy molasses earlier in the process instead of producing sugar.

This would put an end to the sugar cycle (non-climate triggered) and the debilitating cane arrears.

Fortunately, the new bio-fuel policy allows this. It also permits damaged/broken food grains apart from

agri-waste to be converted into ethanol. It should be nurtured to become market player to EBP program.

A consistent and flexible policy is the only way to derive many advantages of the gasohol

programme which offers the benefits of blending ethanol with petrol for fuelling vehicles. It is

environment-friendly. It also helps to reduce India’s dependence on oil imports. Our country is the third

largest consumer of crude oil after China and US and importing as much as 82 per cent of its needs.

Lower imports reduce the current account deficit which in turn eases the pressure on the rupee, leading

to lower inflation and interest rates and thereby, fuelling economic growth.

A mission mode programme involving relevant ministries and departments is needed to develop

indigenous second-generation biofuels technologies including cocktail enzymes is inevitable. The

patented and protected imported technologies are costly and may not suitable for our country.

18

Though India is progressing in EBP program in last couple of years, there is a risk and

uncertainty on availability of feedstock from sugarcane alone. It is due to two reasons. The first and

foremost is production and price fluctuation in the sugarcane and sugar production system and 20 %

blending target needs minimum of 10000 million litres which may not be possible due to non

availability of the raw materials round the year and other necessitated demand for potable and chemical

industries. Hence, suggested potential raw materials for ethanol production need to be produced in a

most efficient way for sustainability.

By 2040, it is estimated that India will become the largest consumer of crude oil. Importing

bulk of that requirement will leave us vulnerable economically and strategically. Ethanol blending is a

possible way to avoid the grim situation. It should become a national policy that is supported by all

stakeholders irrespective of the Government.

8. Conclusion

A huge opportunity lies in promoting the adoption of ethanol for meeting domestic fuel

requirements and country the has already achieved 5% blending during 2019 due to new policy

directives coupled with fair pricing of fuel ethanol for blending EBP program. The potential of the sugar

sector, seen from this perspective is immense and there are many facets of this industry, not fully

explored. The momentum is picking up globally, whereby the sugar plants are being seen as multi

product industrial complexes which manufacture not only sugar but also industrial / potable alcohol,

fuel ethanol as equally valuable activity. While, production of industrial / potable alcohol and electricity

is now a well established activity in the sugar mills in India, the end use related to fuel ethanol is

gradually picking up due to recent Government incentives. In the last few years, a number of integrated

sugar plants have come up with process flexibilities of shift between sugar and ethanol.

However, a long-term viable pricing formula for sugarcane-sugar-ethanol had to be worked out

so as to reduce uncertainties of return on the investments being made for bio ethanol production. The

future viability of the Indian sugar industry will depend on value-addition and diversification through

ethanol and cogeneration. India with the huge captive consumption base for not only sugar but also for

alcohol-based by-products of sugar industry paradoxically faces issues of sugar surplus and idling

industrial capacities. Diversification of bio-based products will allow the mills to exploit scale

economies and improve economic efficiency and profitability in the sugar industry. Inclusion of tropical

sugar beet in the program will have additional advantage.

The policy paper highlights sustainability issues related to biofuel program in India

encompassing the success story of ethanol blending program in Brazil, production and feed-stock

availability in India, potential of different feed-stocks for ethanol production, role of sugarcane varieties

in sustaining sugar & ethanol production, 2G ethanol, price and procurement policy for ethanol and

constraints in the EBP Program. All aspects of EBP have been discussed in detail, especially the recent

initiatives taken by the GOI.

19

Finally, food security, energy security and climate change mitigation are critical to social,

economic and environmental sustainability, not only at the national level but also globally. A successful

resolution of these challenging issues requires the goodwill and commitment of all nations to work

together. This policy paper will be immensely useful in assessing the long-term sustainability of ethanol

production and EBP in India.

References

Alternative Fuels Data Center: Flexible Fuel Vehicles". Alternative Fuels and Advanced Vehicles Data

Center. U.S. Department of Energy. Retrieved 2020-05-23.

An introduction to biofuels, foods, livestock, and the environment Yaser Dahman, Ahmad Chaudhry,

in Biomass, Biopolymer-Based Materials, and Bioenergy, 2019.

BAFF (January 2015). "Bought ethanol cars". Bio Alcohol Fuel Foundation. Archived from the original

on 2011-07-21. Retrieved 2015-08-26.

Bio-energy and agriculture: promises and challenges (2006). International Food Policy Research

Institute.

Carpita NC (1996) Structure and biogenesis of the cell walls of grasses. Annu Rev Plant Physiol Plant

Mol Biol 47(1):445–476. doi: 10.1146/annurev.arplant.47.1.445.

Cheng Lei, Jian Zhang, Lin Xiao and Jie Bao (2014). An alternative feedstock of corn meal for industrial

fuel ethanol production: Delignified corncob residue. Bioresource Technology. Volume 167,

September 2014, Pages 555-559.

Curcio, Mário (2018-03-23). "Carro flex chega aos 15 anos com 30,5 milhões de unidades" [Flex car

arrives at 15 with 30.5 million units]. Automotive Business (in Portuguese). Retrieved 2018-

12-15.

Doblin MS, Pettolino F, Bacic A (2010) Plant cell walls: the skeleton of the plant world. Funct Plant

Biol 37(5):357–381.

Ethanol Guide (2005). Pro Cana Information and Events. Sao Paulo.

FAO (2005) OECD-FAO Agricultural Outlook 2005/2014. Edit FAO, Rome.

Grabber JH (2005) How do lignin composition, structure, and cross-linking affect degradability? A

review of cell wall model studies. Crop Sci 45(3):820–831. doi:10.2135/cropsci2004.0191

Grabber JH, Ralph J, Lapierre C, Barrière Y (2004) Genetic and molecular basis of grass cell-wall

degradability. I. Lignin–cell wall matrix interactions. C R Biol 327(5):455–465. doi:

10.1016/j.crvi. 2004.02.009.

Harris PJ, Stone BA (2008) Chemistry and Molecular Organization of Plant Cell Walls. In: Himmel

ME (ed) Biomass Recalcitrance. Blackwell Publishing Ltd., Oxford, UK, pp 61–93

Himmel ME, Picataggio SK (2008) Our challenge is to acquire deeper understanding of biomass

recalcitrance and conversion. In: Himmel ME (ed) Biomass Recalcitrance. Blackwell

Publishing Ltd., Oxford, UK, pp 1–6

http://petroleum.nic.in/petstat.pdf

20

http://petroleum.nic.in/sites/default/files/biofuelpolicy2018_1.pdf

http://www.svlele.com/biofuture.html

https://afdc.energy.gov/fuels/ethanol_feedstocks.html

https://niti.gov.in/node/1287

J.L. Ramos, M. Valdivia, F. Garcia-Lorente, A. Segura Benefits and perspectives on the use of biofuels.

Microb Biotechnol, 9 (4) (2016), pp. 436-440.

Jørgensen H, Kristensen JB, Felby C (2007) Enzymatic conversion of lignocellulose into fermentable

sugars: challenges and opportunities. Biofuels Bioprod Biorefin 1(2):119–134.

doi:10.1002/bbb.4.

Murali, P., Hari, K. & Puthira Prathap, D. An Economic Analysis of Biofuel Production and Food

Security in India. Sugar Tech 18, 447–456 (2016). https://doi.org/10.1007/s12355-015-0412-z.

Murali, P. K Hari. (2011). Bio-fuel market scenario in India. Sugar Tech 13 (4), 394-398.

M.M.S. Moretti, D.A. Bocchini-Martins, R. Silva, A. Rodrigues, L.D. Sette, E. Gomes Selection of

thermophilic and thermotolerant fungi for the production of cellulases and xylanases under

solid-state fermentation. Braz J Microbiol, 43 (3) (2012), pp. 1062-1071.

M.P. Vásquez, J.N. da Silva, M.B. de Souza Jr., N. Pereira Jr. Enzymatic hydrolysis optimization to

ethanol production by simultaneous saccharification and fermentation. Appl Biochem

Biotechnol, 137–140 (1–12) (2007), pp. 141-153.

Mitchell D (2005) Sugar policies: Opportunity for change. Int. Sug. J. 107: 1273.

NAAS 2015. Bio-fuels to Power Indian Agriculture. Policy Paper No. 76, National Academy of

Agricultural Sciences, New Delhi: 24 p

Nigam, R. B. and P. K. Agrawal (2004). Ethanol manufacture from cane juice and molasses.

International Conference on Bio-fuels, New Delhi.

OECD–FAO (2008). Agricultural Outlook 2008–2017, Paris, Rome.

Pradeep Agrawal., 2012. India's Petroleum Demand: Empirical Estimations and Projections for the

Future. IEG Working Paper No. 319.

R. Silva, E.S. Lago, C.W. Merheb, M.M. Macchione, Y.K. Park, E. Gomes. Production of xylanase and

cmcase on solid state fermentation in different residues by Thermoascus aurantiacus Miehe.

Braz J Microbiol, 36 (2005), pp. 235-241.

Report of the Committee on Development of Bio-fuel. Planning Commission, Government of India.

Report of the Working Group, Tenth Plan.

Rose JKC (2003) The plant cell wall. Annual Plant Reviews, vol 8. CRC Press and Wiley Blackwell,

Oxford.

Ryan, Lisa; Turton, Hal (2007). Sustainable Automobile Transport. Edward Elgar Publishing Ltd,

England. pp. 40–41. ISBN 978-1-84720-451-6.

21

Santos, C.R., Costa, P.A.C.R., Vieira, P.S. et al. Structural insights into β-1,3-glucancleavage by a

glycoside hydrolase family. Nat Chem Biol 16, 920–929 (2020).

https://doi.org/10.1038/s41589-020-0554-5.

S.M. Scully, J. Orlygsson (2015) Recent advances in second generation ethanol production by

thermophilic bacteria. Energies, 8, pp. 1-30.

Sugar Report (2003). Ministry of Food and Agriculture, Government of India.

Trostle R. (2008). Global Agricultural Supply and Demand: Factors Contributing to the Recent Increase

in Food Commodity Prices. ERS/USDA.

V. Ferreira, M.O. Faber, S.S. Mesquita, N. Pereira Jr. (2010) Simultaneous saccharification and

fermentation process of different cellulosic substrates using a recombinant Saccharomyces

cerevisiae harbouring the β-glucosidase gene. Electron J Biotechnol, 13 (2) 10.2225/vol13-

issue2-fulltext-1.

www.iea.org/

www.mnre.gov.in.

Y. You, S. Yang, L. Bu, J. Jiang, D. (2016) Sun Comparative study of simultaneous saccharification

and fermentation byproducts from sugarcane bagasse using steam explosion, alkaline hydrogen

peroxide and organosolv pretreatments. RSC Adv, 6, pp. 13723-13729

Zhao X, Zhang L, Liu D (2012) Biomass recalcitrance. Part I: the chemical compositions and physical

structures affecting the enzymatic hydrolysis of lignocellulose. Biofuels Bioprod Biorefin 6(4):

465–482. doi:10.1002/bbb.1331.

Related Documents