STUDY THE IMPACT OF COMPLIANCE AND BEST PRACTICES MANAGEMENT ON IT OUTSOURCING SPECIFIC TO LIFE SCIENCES – INFORMATION TECHNOLOGY INDUSTRIES IN INDIA Thesis Submitted to Padmashree Dr. D. Y. Patil University Department of Business Management in partial fulfillment of the requirements for the award of the Degree of DOCTOR OF PHILOSOPHY In BUSINESS MANAGEMENT Submitted by Mr. DAMODAR C RAO (Enrollment No. DYP-PhD 09005) Research Guide Dr. R. GOPAL DIRECTOR, DEAN & HEAD OF DEPARTMENT PADMASHREE DR. D.Y. PATIL UNIVERSITY DEPARTMENT OF BUSINESS MANAGEMENT Sector 4, Plot No. 10, CBD Belapur, Navi Mumbai – 400 614 August 2012

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

STUDY THE IMPACT OF COMPLIANCE AND BEST PRACTICES MANAGEMENT ON IT OUTSOURCING

SPECIFIC TO LIFE SCIENCES – INFORMATION TECHNOLOGY

INDUSTRIES IN INDIA

Thesis Submitted to Padmashree Dr. D. Y. Patil University Department of Business Management

in partial fulfillment of the requirements for the award of the Degree of

DOCTOR OF PHILOSOPHY

In BUSINESS MANAGEMENT

Submitted by

Mr. DAMODAR C RAO

(Enrollment No. DYP-PhD 09005)

Research Guide Dr. R. GOPAL

DIRECTOR, DEAN & HEAD OF DEPARTMENT

PADMASHREE DR. D.Y. PATIL UNIVERSITY DEPARTMENT OF BUSINESS MANAGEMENT

Sector 4, Plot No. 10, CBD Belapur, Navi Mumbai – 400 614

August 2012

i

DECLARATION

I hereby declare that the thesis entitled “Study the Impact of

Compliance and Best Practices Management on IT Outsourcing –

Specific Reference to Life Sciences – IT Industries in India”

submitted for the Award of Doctor of Philosophy in Business

Management at Padmashree Dr. D.Y. Patil University Department of

Business Management is my original work and the thesis has not

formed the basis for the award previously of any degree, associate

ship, fellowship or any other similar titles.

Place: Navi Mumbai

Date:

Signature of Guide Signature of Signature of Student

Head of Dept.

ii

CERTIFICATE

This is to certify that the thesis entitled “Study the Impact of Compliance

and Best Practices Management on IT Outsourcing – Specific

Reference to Life Sciences – IT Industries” and submitted by Mr.

Damodar C Rao is a bonafide research work for the award of the Doctor

of Philosophy in Business Management at Padmashree Dr. D. Y. Patil

University Department of Business Management in partial fulfillment of

the requirements for the award of the Degree of Doctor of Philosophy

in Business Management and that the thesis has not formed the basis

for the award previously of any degree, diploma, associate ship,

fellowship or any other similar title of any University or Institution.

Also it is certified that the thesis represents an independent work on the

part of the candidate.

Place: Navi Mumbai

Date:

Signature of the Signature of the Guide Head of Department

iii

ACKNOWLEDGEMENT

I am greatly indebted to Padmashree Dr. D.Y. Patil University,

Department of Business Management which has accepted me for the

Doctoral Program and provided me with an excellent opportunity to

carry out the present research work.

I am grateful to my guide, mentor, philosopher Dr. R. Gopal for having

guided me throughout the research span of time and for providing his

constructive criticism which made me bring my best. I would also like to

thank Sir for being approachable at any point of time without considering

his own precious personal time.

I thank Ms. Simpoo Singh for motivating me to pursue PhD and my

spouse Mrs. Sreedevi Rao (Devi) for her support in my research work. I

also thank my friends Giridhar Rao, Srihari Reddy and Venkat Reddy for

helping me reach industry contacts. I would be failing in my duty if I did not

thank IBM and my Managers for helping me throughout the research work.

Lastly, I thank all my near and dear ones who have been directly and

indirectly instrumental in the completion of my dissertation.

I convey many thanks to everyone who has been influential and

supportive in this research work.

Place: Mumbai Date: Signature of the student

iv

TABLE OF CONTENTS DECLARATION ............................................................................................................... i

CERTIFICATE................................................................................................................. ii

ACKNOWLEDGEMENT............................................................................................... iii

LIST OF TABLES.......................................................................................................... vii

LIST OF FIGURES....................................................................................................... viii

LIST OF ABBREVIATIONS ......................................................................................... ix

EXECUTIVE SUMMARY ........................................................................................... xiii

CHAPTER 1...................................................................................................................... 1

Introduction – Outsourcing Definitions and Practices.................................................. 1

1.1 Outsourcing – Origin of Concept.......................................................................... 3

1.2 Outsourcing and Offshoring – How Close and How Far?.................................... 7

1.3 Concepts of Outsourcing....................................................................................... 8

1.4 Outsourcing Evolution in India........................................................................... 11

1.5 Theories on Outsourcing..................................................................................... 12

1.6 Outsourcing Strategies ........................................................................................ 15

1.6.1 Size and Nature of Companies......................................................................... 15

1.6.2 Outsourcing Determinants ............................................................................... 17

1.6.3 What are Life Sciences Companies looking for?............................................. 25

1.6.4 How Life Sciences Companies are building up? ............................................. 27

1.6.5 India and China Contest................................................................................... 31

1.6.6 Gaps in Capabilities ......................................................................................... 35

1.7 Skills to Develop................................................................................................. 37

CHAPTER 2.................................................................................................................... 43

Review of Literature....................................................................................................... 43

2.1 Western Research on Outsourcing...................................................................... 51

2.2 India and China Research on Outsourcing.......................................................... 53

2.3 Studies on Life Sciences Companies Behavior .................................................. 63

2.4 Studies on Information Technology Companies Behavior................................. 65

v

2.5 Research Gap Analysis ....................................................................................... 67

CHAPTER 3.................................................................................................................... 69

Statement of the Problem and Research Methodology ............................................... 69

3.1 Statement of the Problem / Scope of the Study .................................................. 69

3.2 Objectives of the Study....................................................................................... 70

3.3 Hypothesis........................................................................................................... 71

3.4 Pre-study ............................................................................................................. 72

3.5 Primary and Secondary Data .............................................................................. 72

3.6 Instruments for Survey........................................................................................ 74

3.7 Selection of Samples........................................................................................... 75

3.8 Pre Testing Phase................................................................................................ 76

3.9 Tabulation and Statistical Analysis of Data........................................................ 76

3.10 Interpretation and Report Writing..................................................................... 77

3.11 Limitations of the Study.................................................................................... 77

3.12 Significance of the Study.................................................................................. 78

CHAPTER 4.................................................................................................................... 79

Data Interpretations and Findings................................................................................ 79

4.1 Data Analysis – Life Sciences (LS) Questionnaire Responses........................... 79

4.2 Data Analysis – Information Technology (IT) Questionnaire Responses ........ 113

CHAPTER 5.................................................................................................................. 138

Conclusion ..................................................................................................................... 138

CHAPTER 6.................................................................................................................. 149

Recommendations and Suggestions ............................................................................ 149

BIBLIOGRAPHY......................................................................................................... 160

REFERENCE SECTION............................................................................................. 181

Annex I – Objectives of the Study, Problem Statement, Research Gap, Hypothesis

and Survey Questions Mapping................................................................................... 182

Annex II – Offshore Outsourcing Destinations in India ........................................... 183

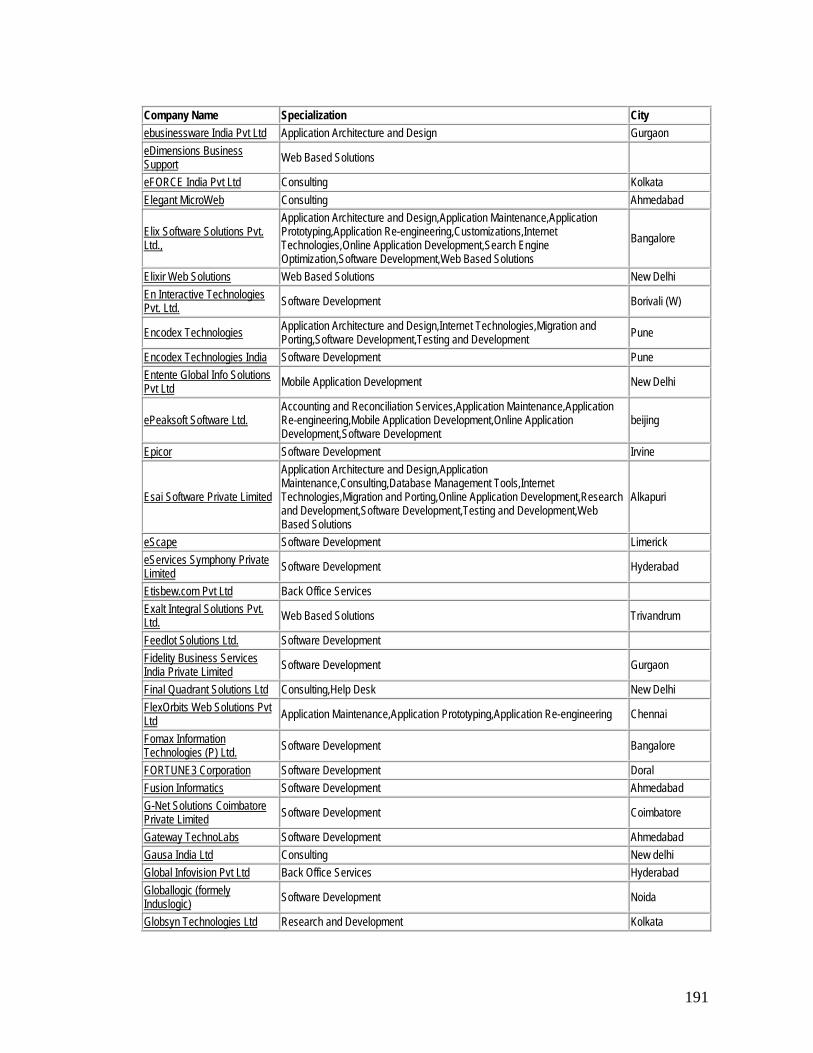

Annex III – List of Offshore Outsourcing Companies .............................................. 189

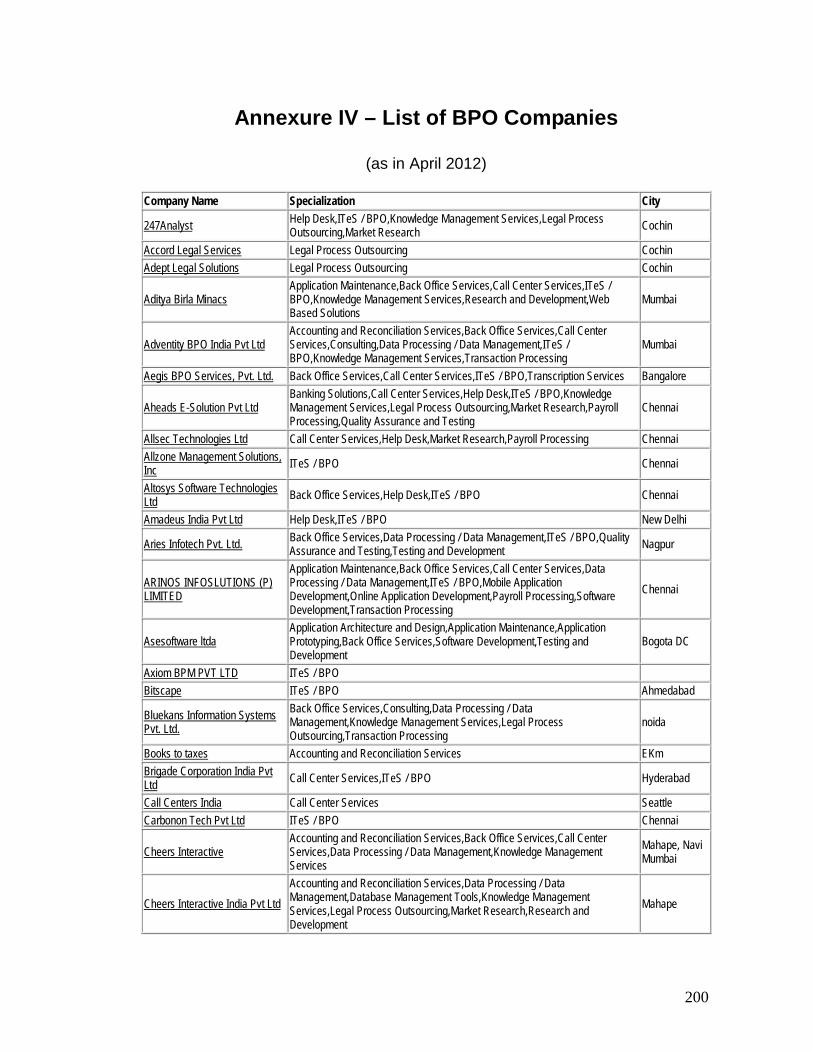

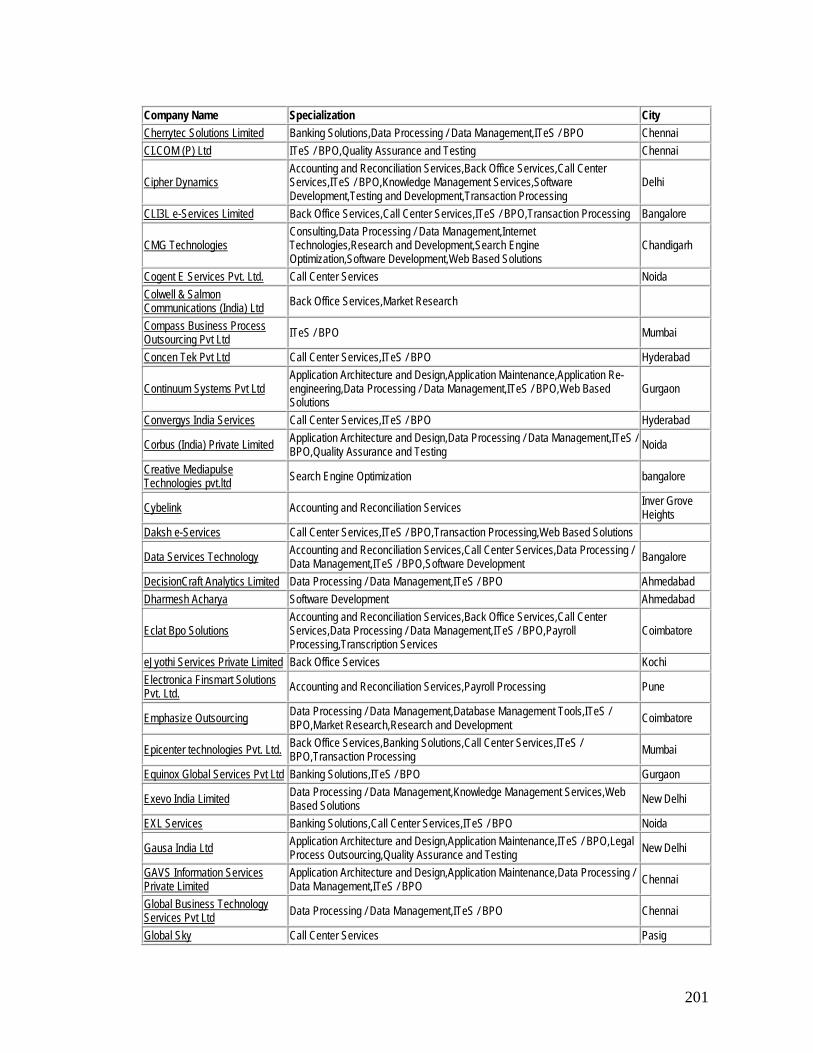

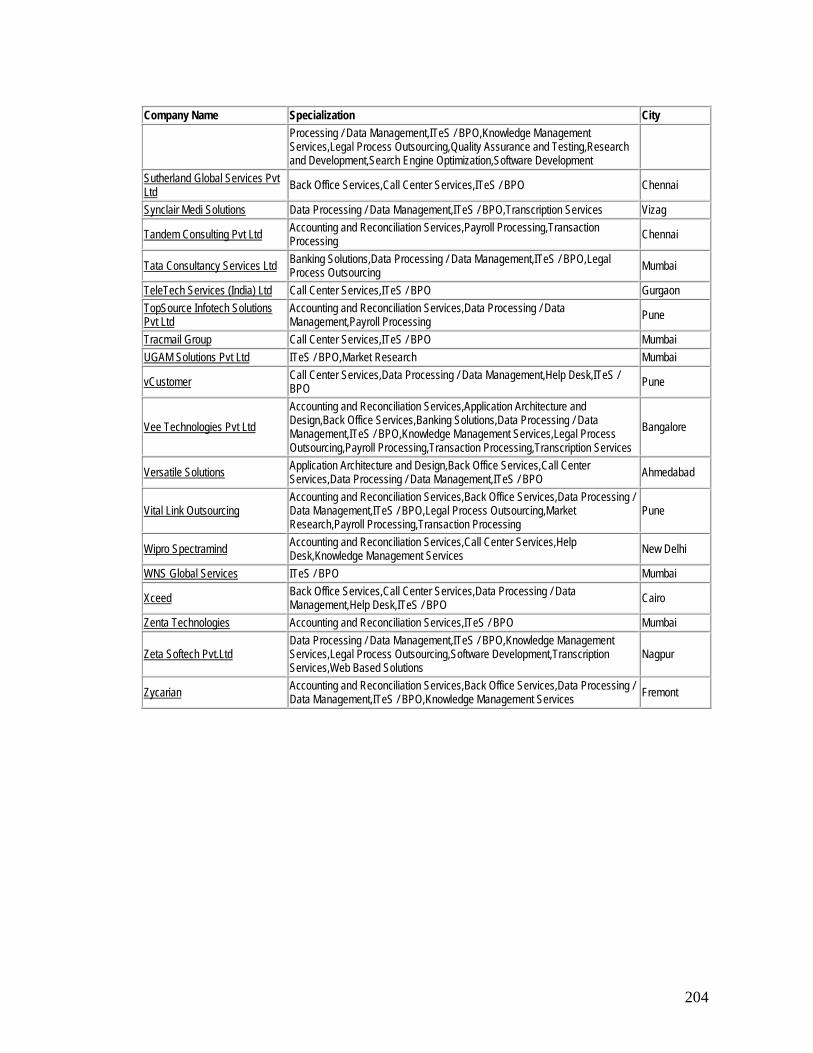

Annexure IV – List of BPO Companies...................................................................... 200

vi

Annex V – Companies Included in the Research....................................................... 205

Life Sciences Companies........................................................................................ 205

Information Technology Companies ...................................................................... 206

Annex VI – Research Questionnaires ......................................................................... 207

Life Sciences - IT Outsourcing (Survey-1)............................................................. 207

Life Sciences - IT Outsourcing (Survey-2)............................................................. 213

Annex VII – Statistical Tables of SPSS Analysis ....................................................... 219

vii

LIST OF TABLES

Section No.

Table No. Table Description Page

No.

1.6.2 1 Outsourcing Motivators and Models 20

1.6.2 2 Vendor Evaluation Parameters 21

1.6.2 3 Cultural Compatibility While Choosing Vendors 23

1.6.4 4 Parameters to Consider While Managing and Evaluating Contracts

24, 25

1.6.4 5 Ownership Structure in Companies 27

3.7 6 Selection of Samples 75

6.0 7 Matrix Analysis – Work Sheet 1 158

6.0 8 Matrix Analysis – Work Sheet 2 159

Annex I 9 Mapping of Objectives, Problem Statement, Research Gap, Hypothesis and Survey Questions

182

viii

LIST OF FIGURES

Section

No. Figure

No. Figure Description Page No.

1.1 1 List of Top 10 Pharmaceutical Companies 6

1.4 2 Outsourcing Evolution in India 11

1.5 3 Outsourcing Process 13

1.5 4 Leadership Thinking on Outsourcing Services 14

1.6.2 5 Outsourcing Profiles of Top 10 Life Sciences Companies 17

1.6.2 6 CIOs Perspectives on Blending Roles 18

1.6.4 7 Offshore Outsourcing Drivers 29

1.6.4 8 Priorities for European Companies Considering Offshoring 30

1.6.4 9 Savings Due to Offshore Outsourcing 31

1.6.5 10 IT Locations in India and Categorization 35

1.6.6 11 Gaps in Capabilities between Clients and Vendors – Demand 36

1.6.6 12 Gaps in Capabilities between Clients and Vendors - Supply 36

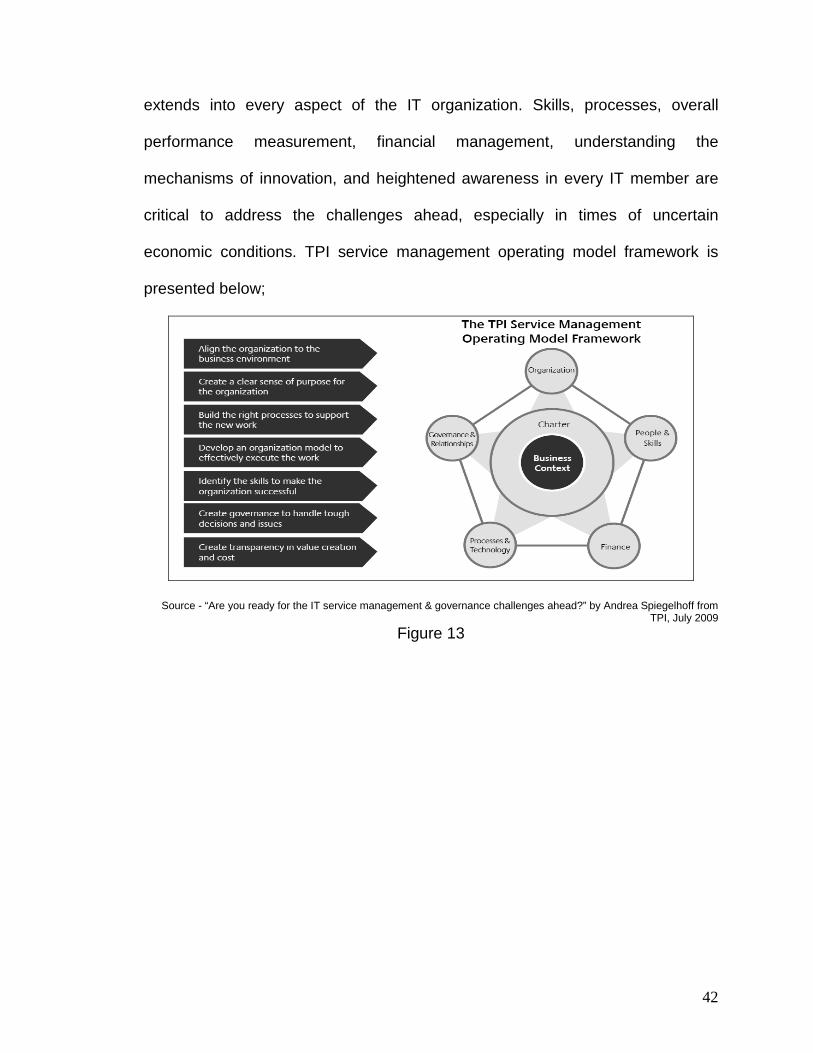

1.7 13 TPI Service Management Operating Model Framework 42

ix

LIST OF ABBREVIATIONS

AD - Application Development

AMS - Application Maintenance Services

APAC - Asia Pacific Region

BFSI - Banking, Financial Services and Insurance

BOT - Build-Operate-Transfer

BPO - Business Process Outsourcing

CDE - Center for Drug Evaluation, Taiwan

CDM - Clinical Data Management

CDSCO - Central Drugs Standard Control Organization, India

CEO - Chief Executive Officer

CHMP - Committee for Human Medicinal Products

CIO - Chief Information Officer

CMO - Contract Manufacturing Organizations

COBOL - Common Business Oriented Language

CRO - Clinical Research Organization

DAV - Drug Administration of Vietnam, Vietnam

EMA / EMEA - European Medicines Agency

EMR - Electronic Medical Record

ER - Electronic Record

ERP - Enterprise Resource Planning

ES - Electronic Signature

EU - European Union

x

FDA - Food and Drug Administration of United States of America

FP - Fixed Price

FSI - Floor Space Index

FTE - Full Time Equivalent

FY - Financial Year

GE - General Electric Company

GIE - Globally Integrated Enterprise

GSK - GlaxoSmithKline

GxP - Good Practices (where ‘x’ is a variable with C-Clinical, M-

Manufacturing, L-Laboratory, D-Distribution)

HAS - Health Sciences Authority, Singapore

HCL - Fast Growing India’s IT Services Company

IBM - World’s Leading IT Services Company

ICH - International Conference on Harmonization

ICT - Information and Communication Technologies Regulation

IP - Intellectual Property

ISO - International Standards Organization

IT - Information Technology

ITeS / ITES - Information Technology Enabled Services

ITO - Information Technology Outsourcing

JV - Joint Venture

KPI - Key Performance Indicator

KPMG - Consulting and Research Oriented Company

xi

KPO - Knowledge Process Outsourcing

LS - Life Sciences

M&A - Merger and Acquisition

MedDRA - Medical Directory for Regulatory Activities

MedSafe - Medicine and Medical Devices Safety Authority, New

Zealand

MSA - Master Services Agreement

NASSCOM - National Association of Software and Services Companies

NCE - New Chemical Entity

NCI - National Cancer Institute

NCR - National Capital Region

NEC - Consulting Services Company

NPCB - National Life Sciences Control Bureau, Malaysia

NTT Data - Consulting Services Company

ODC - Offshore Delivery Center

PAT - Process Analytical Technology

PC - Personal Computer

PDMA - Life Sciences and Medical Devices Agency, Japan

PMO - Project Management Office

POC / PoC - Proof Of Concept

PWC - Price Waterhouse Coopers

QbD - Quality by Design

QC/QA - Quality Control and Quality Assurance

xii

R&D - Research and Development

ROI - Return On Investment

SCM - Supply Chain Management

SEI CMM - Software Engineering Institute - Capability Maturity Model

SEZ - Special Economic Zone

SFDA - State Food and Drug Administration, China

SLA - Service Level Agreement

SM&G - Service Management and Governance

SMB - Small and Medium Business

SME - Subject Matter Expert

SOW - Statement of Work

TARP - Troubled Asset Relief Program

T&M - Time and Material

TCS - Indian based IT Services Company

TCV - Total Contract Value

TGA - Therapeutic Drug Administration, Australia

TPI - Strategic Consulting Services Company

UK - United Kingdom

UNCTAD - United Nations Conference on Trade and Development

US - United States of America

USD - United States Dollar

VMT - Vendor Management Team

Y-o-Y - Year-on-Year

xiii

EXECUTIVE SUMMARY

The advent of Information Technology (IT) has slowly spread into the Life

Sciences (LS) industry and India has been playing a vital role in this

metamorphosis. It is still believed, there is a lot of head-room for Life Sciences

companies to consider more and more offshore outsourcing of their business

functions. However, Life Sciences companies happen to be late starters in

outsourcing world. The primary reasons for this sluggish phenomenon can be

attributed to the ‘highly regulated industry’ and thereby the ‘conservative

behavior of key decision makers’, besides some of the ‘data privacy

implications’. This study is conducted to understand and explore these ‘more’

options and alternatives that both Life Sciences and Information Technology

companies could adopt and develop respectively and leverage benefits in the

tough world of patent expiries, reducing profit margins and lack of depth in the

product pipeline. Not to forget the dearth of the block buster drugs.

Life Sciences industry, until early 1990’s, was considered to be hesitant in

adopting cutting-edge solutions and technologies due to its intrinsic

conservative nature. Reasons such as failure in regulatory compliance and

audits, loss of intellectual property, problems in training, leakage of sensitive

information, made even large companies skeptical for adopting and using

contemporary systems. But the situation has changed considerably at present,

xiv

and there is a heavy focus on innovative operational models along with some

risk-based approaches.

Today, there is hardly any aspect of Supply Chain Management (SCM) left

untouched by IT, which collectively reduces the time-to-discover and time-to-

market of a drug. Given the thrust from regulatory agencies to adopt innovative

technologies, some of the global companies have already reached certain

scales of maturity and excellence. Areas where IT is being deployed extensively

are;

§ Pre-clinical (Drug Discovery & Development), Clinical Trials Research

and Development

§ Manufacturing Planning, Execution and Intelligence

§ Quality Assurance and Quality Control

§ Material and Demand Management

§ Warehouse, Distribution and

§ Global Trade Management

Increased application of IT in the Life Sciences industry has propelled lead

agencies to work on developing new guidance and regulations based on the

latest science of risk management and quality assurance using automation

techniques.

xv

Fuel-to-fire

It is a critical time, rewarding and exciting time, to be in a Life Sciences-IT

environment. Following are the elements enforcing this situation;

• First, the challenges facing in promoting and protecting the public health

are greater than ever with stringent regulatory focus.

• Second, with the advent of new technologies, the opportunities to

provide significant benefits to the public have never been greater. New

standards are being designed to encourage cost-reduction and

precision-enhancing innovation in manufacturing processes and

technology.

• With the increasing number of generic drug approvals, its becoming

extremely difficult for innovator companies to maintain their Research &

Development (R&D) spend Year-on-Year (Y-o-Y) and produce block-

buster drugs anymore.

Under the above mentioned circumstances, it is important to study the impact of

compliance and best practices adopted by Information Technology companies.

As part of the literature review, 250 research publications, articles, news letters,

and other thought process documents were reviewed. The primary sources of

the information were internet with public domain access and University

Journals. From the literature review, it is observed that several researches have

been conducted on role of Information Technology in Life Sciences, and IT

xvi

playing as a catalyst in Life Sciences processes. However, literature review did

not reveal the impact of regulations on the overall offshore outsourcing strategy.

The above mentioned gaps in literature review influenced the type and nature of

questions for this research study. The research questions were inclined towards

following parameters;

ü General Information about Respondent

ü Information related to Type of Company

ü Information related to Organizational Structure

ü Information related to Regulatory Compliance Adherence

ü Information related to Best Practices Adopted

ü Information related to Risks & Strategy

ü Information related to Operational Principles / Delivery Excellence

ü Information related to Growth Initiatives

ü Information related to Training and Knowledge Building

ü Information related to Geographical Reach

ü Information related to Organizational Perception towards Outsourcing

ü Information related to Organizational Perception towards Services

This study includes – new processes and operations that could be considered

for offshore outsourcing, highlighting regulatory implications and over all cost

xvii

maintenance and of course benefits. Based on the research questions, the

following were the research objectives;

1. To understand dynamic compliance and best practices adopted by

organizations in IT outsourcing

2. To analyze the impact of compliance and best practices management on

IT outsourcing strategy

3. Identify other bottlenecks in IT outsourcing business management

4. To explore future avenues in IT outsourcing

5. To provide recommendations to both Life Sciences and Information

Technology companies on smarter compliant offshore outsourcing

Methodology Adopted

The study concentrated both on primary and secondary data. The secondary

data provided information on the state of affairs in the Life Sciences –

Information Technology offshore outsourcing world. The primary survey was a

critical component of the study, as it yielded crucial data on the impact of

compliance on outsourcing and kind of services provided.

The local of study was India, China, Denmark and USA and employees from 33

Life Sciences companies and 27 Information Technology companies were

selected using stratified random sampling and 755 employees in various roles

and departments were interviewed.

xviii

FINDINGS OF THE STUDY

Size of Organization:

1. From the study it was found that big Life Sciences companies proactively

engage IT service providers in supporting business operations.

2. Also, it was found from the study that the age and maturity of the Life

Sciences companies will have a dependency on choosing whether or not to

engage an IT service provider.

3. Life Sciences companies that run on heavy automation are more likely to

engage IT service provider for support.

Outsourcing Strategy:

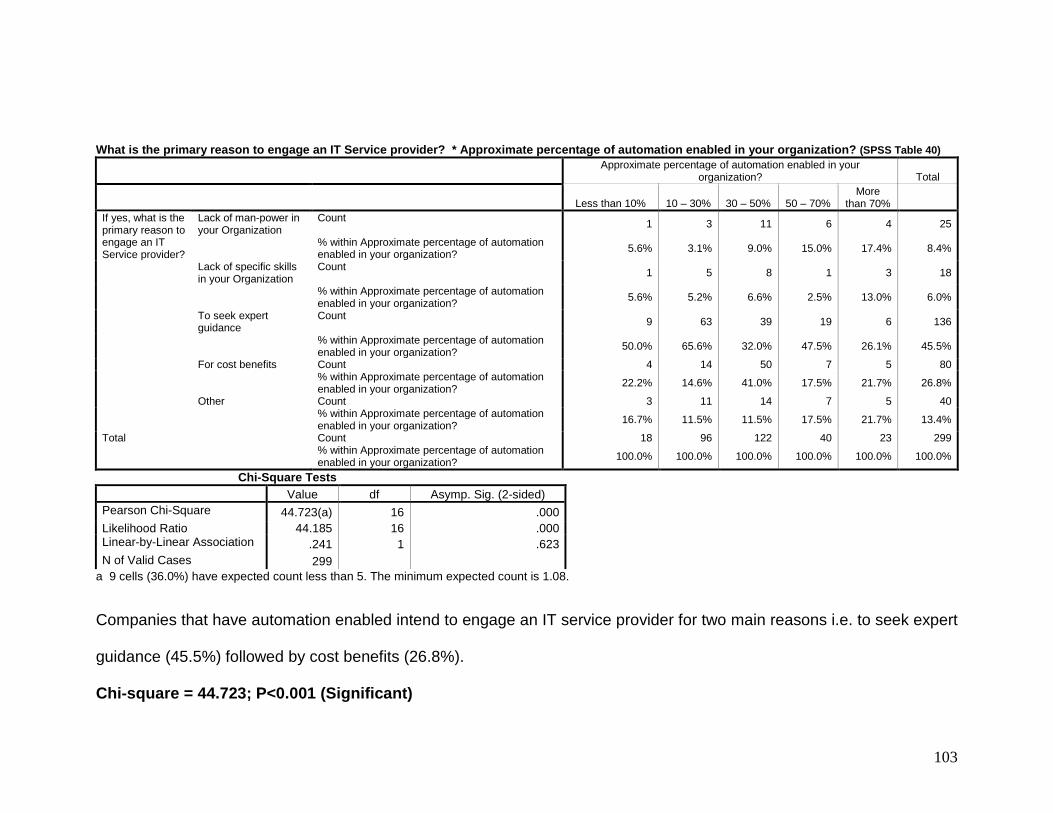

1. The primary reasons to engage service provider were - To seek expert

guidance and Cost benefits.

2. IT companies have started building specific industry capabilities to align and

get closer to Life Sciences industry value chain. The various methods that

are leveraged are - To hire industry professionals, Internal workshops /

training and Understand client pain-points and prepare suitable solutions.

3. Organizations do hire and retain core Subject Matter Experts (SMEs) while

catering to Life Sciences clients.

4. Interestingly, the requirements from Life Sciences companies like need for

Innovative business models, Streamlining IT enables operations, and

Managing IT regulatory compliance better is driving these companies to

reach out to IT companies.

xix

5. It was found that Cost barriers could be one of the reasons for not going the

outsourcing way.

6. Life Sciences companies that are running since more than 30 years are

more willing to embrace the FDA newer technologies initiatives and

outsource their processes.

Regulatory Impact:

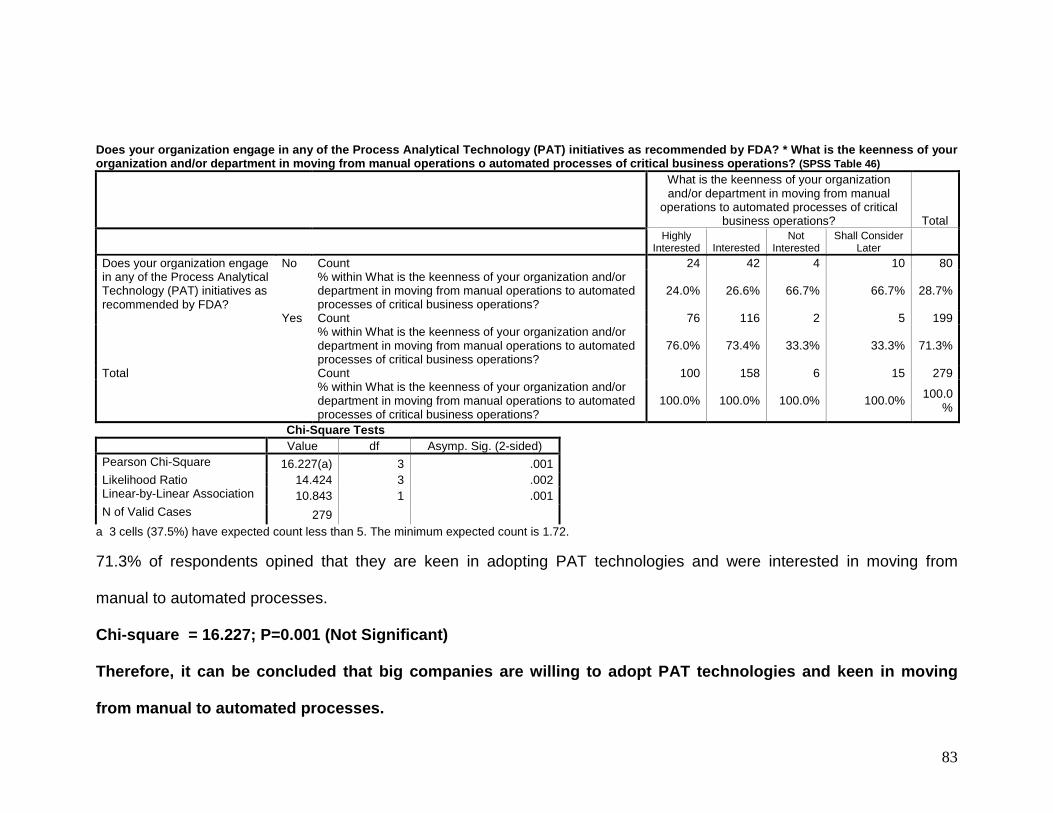

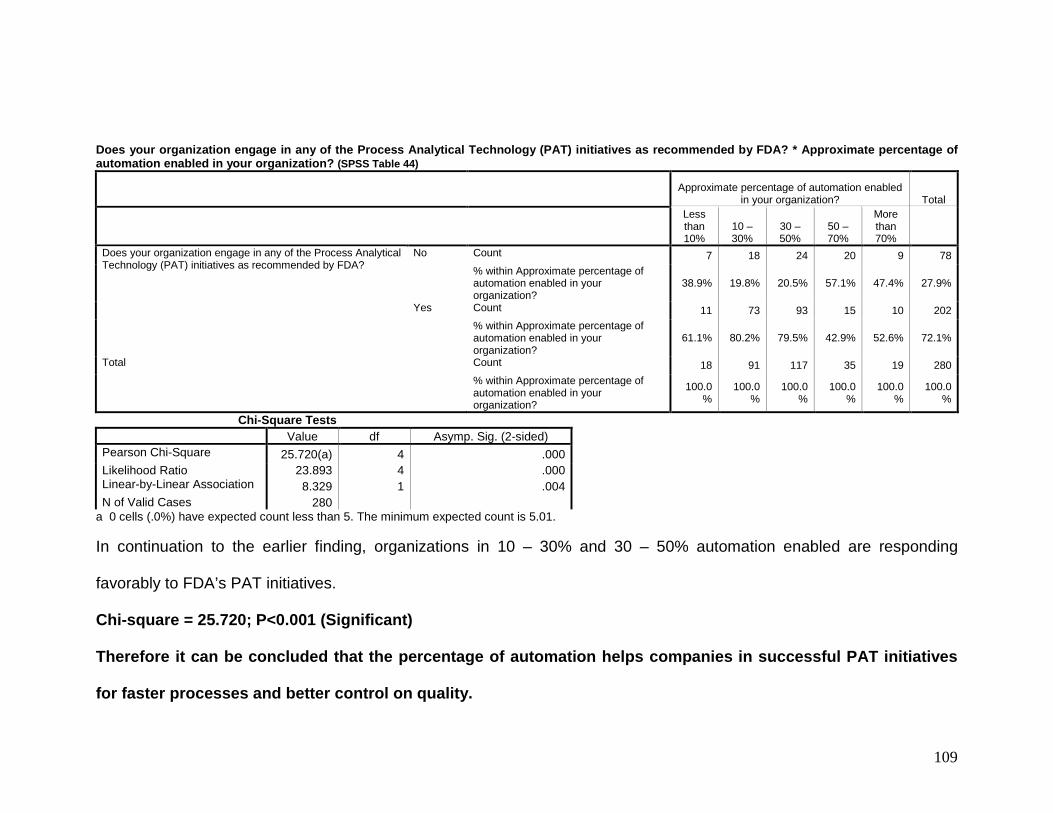

1. From the study it was found that a majority of the manufacturing companies

engage in Process Analytical Technology (PAT) initiatives as recommended

by FDA.

2. It was found that IT companies who have the expertise to support the Life

Sciences companies during regulatory audits and inspections have an edge

over other service providers

3. From the study it was found that manufacturing departments with less than

70% automated processes within Life Sciences companies are front runners

in adopting newer technologies recommended by Food & Drug

Administration (FDA). In the same companies, where there is more than

70.0% of automation enabled, Quality Control & Quality Assurance (QC/QA)

functions have shown much keenness in embracing newer technologies.

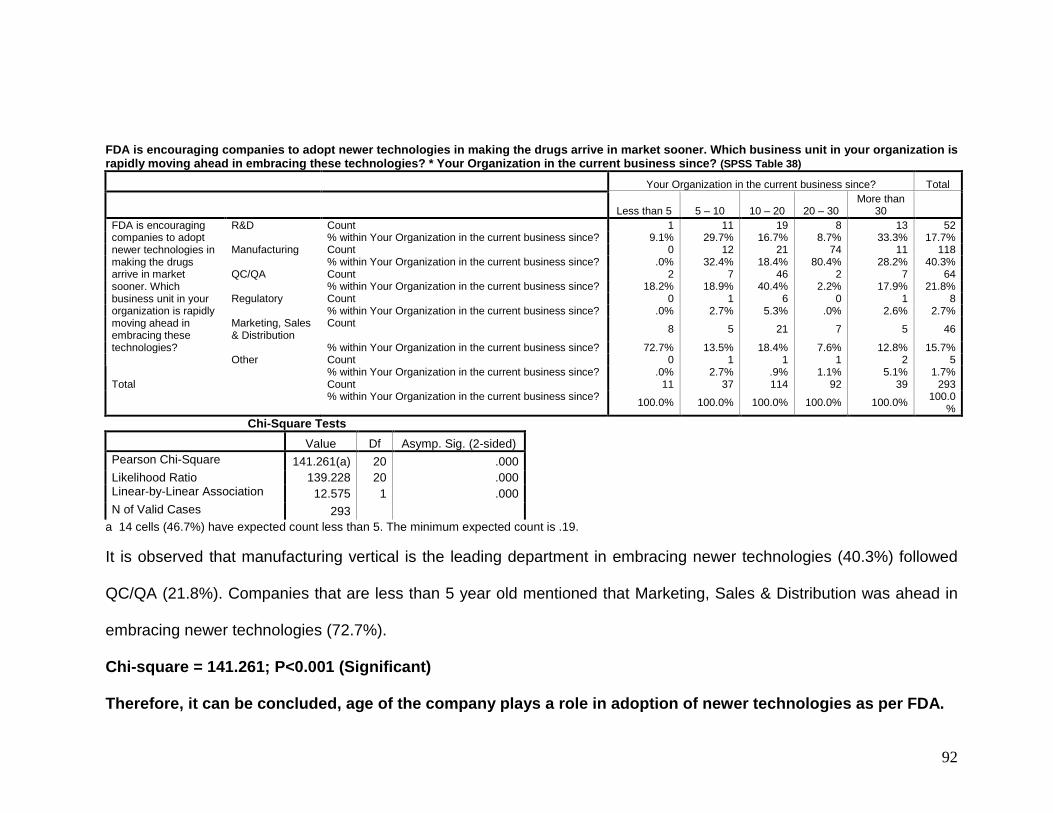

4. Life Sciences companies that are less than 20 years old with strong

regulatory expertise are ahead in adopting newer technologies

recommended by FDA.

xx

5. It was found that a majority of Life Sciences companies were strongly

confident in adopting IT enabled processes and comply to impending

regulations and clearing audits smoothly.

Smarter Outsourcing:

1. From the study it was found that Life Sciences companies with 30 – 50%

automation, struggle with Cost barriers and are reluctant to engage an

external service provider. It is found that these companies have limited

allotted budgets for automation. Hence, they prefer to manage with

internally available knowledge and expertise to a larger extent.

2. Indian based Life Sciences companies which did not have multinational

sites, were managing IT themselves.

3. It was found from the study that more the automation levels in a

company, the company has shown higher interest levels in embracing

newer technologies recommended by FDA like the PAT.

4. It was found that manufacturing and QC/QA verticals are amongst the

leading departments in moving from manual to automated processes.

5. Companies that have operations in more than one country are more

likely to automate their processes.

6. Amongst the Life Sciences companies that host’s central IT infrastructure

in India, there is high interest in moving from manual to automated

processes.

xxi

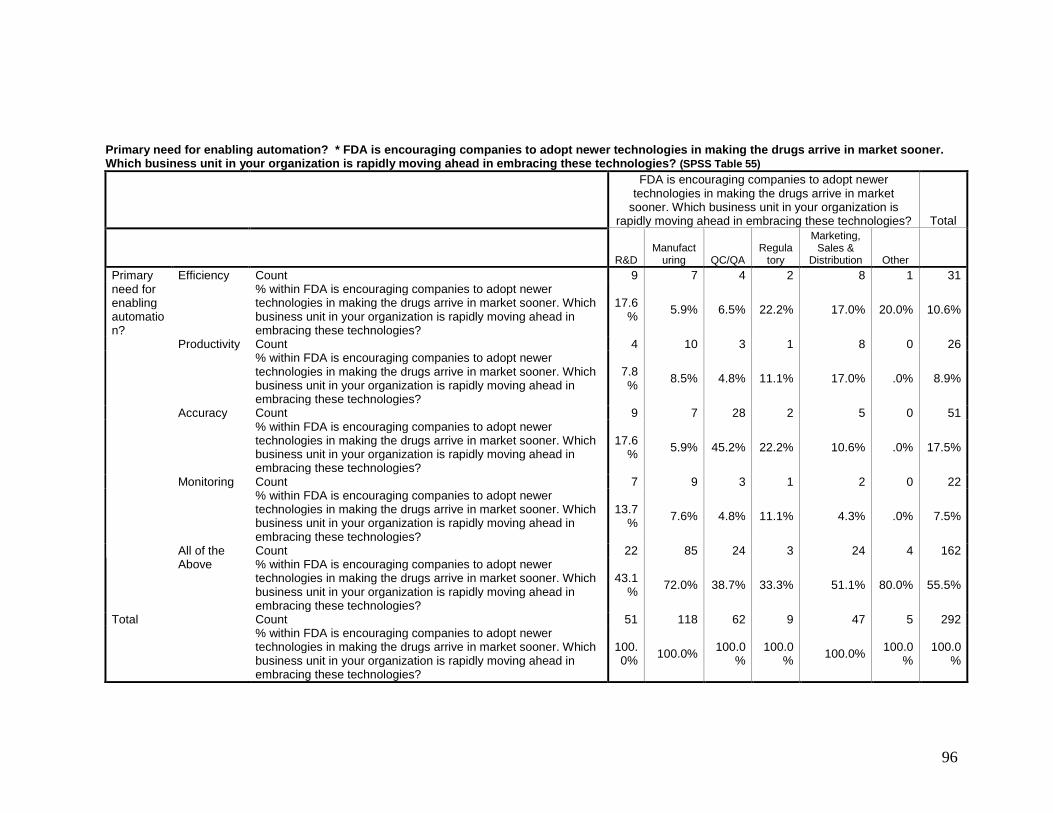

7. It was found that there was a same level of response on primary need for

automation from respondents from various departments. They opine

Efficiency, Productivity, Accuracy and Monitoring are the primary drivers

for outsourcing.

8. It was found that IT service providers when they were engaged in Clinical

research followed by R&D, Manufacturing and QC/QA functions were

able to engage in higher percentage with Life Sciences companies. And

primary reason that was driving Life Sciences companies towards

service providers was – Requirement of Innovative business models.

Recommendations

1. Life Sciences (LS) companies need to consider the globalization path and

effectively adopt the IT integration path.

2. LS companies can start off with outsourcing some of their no-core, non-

critical operations, and gradually consider other core and critical operations

for outsourcing. This will allow them to develop and get familiarized with the

process of outsourcing and understand risks better.

3. It is found from the research, that LS companies which have strong

regulatory departments are front-runners in outsourcing. So companies can

focus on improving their expertise levels in regulatory departments and

consider outsourcing for a strategic advantage.

xxii

4. Information Technology (IT) companies need to understand the complexity

and regulatory governance of the LS industry and accordingly provide

business specific solutions.

5. For new initiatives, IT companies could consider prototype or Proof-of-

Concepts (POC) before actually working on the large business operations.

This will allow both client and service provider to understand the challenges

/ risks and accordingly prepare corrective actions and remediation plans for

the big play. (Details on POC model are provided in Chapter 8,

Recommendations and Suggestions).

6. IT companies could train their staff and hire industry experts who can work

with their LS clients and provide business specific solutions which are

regulatory compliant and consistently meets quality attributes.

In addition to the above points and based on wide industry experience,

worksheets were tabulated using Matrix Analysis and are presented in the

Conclusion section of this study.

1

CHAPTER 1

Introduction – Outsourcing Definitions and Practices

The industry trend is that more and more Life Sciences companies are exploring

opportunities to offshore or outsource their processes. This trend is fast catching

up for obvious benefits that can be achieved by deploying such a model. This

research study relates to the integration of technological and managerial

considerations from both Life Sciences and Information Technology into

exploring further opportunities in the likelihood of outsourcing and offshoring

critical processes and activities in the life sciences industry.

Dearth of block buster drugs is forcing Life Sciences companies to explore ‘more’

options and alternatives that can be adopted and leverage benefits in the tough

world of patent expiries, reducing profit margins and lack of depth in the product

pipeline. Life Sciences industry needs to catch up with developments in

information technology. It has been lagging behind. It is not that a company hates

outsourcing Information Technology, but people don’t like outsourcing, when they

have to suffer. What does this mean? This means, a company would love

outsourcing, if it is a pleasant experience for them.

Outsourcing in today’s world is considered to be more of a strategic initiative and

a key management option rather than considering it as a mere cost cutting

2

operation. It has proven to the companies in achieving their business objectives

through operational excellence and better market positioning. Most, if not all,

major Life Sciences companies have been outsourcing, or are evaluating the

benefits of outsourcing, one or more of their noncore business functions to a

third-party service provider. Over the last seven years, Life Sciences companies

have been primarily outsourcing all or part of their back-office Information

Technology (IT) infrastructure, such as the mainframe, mid-range, desktop, or

application maintenance functions. Recently, Life Sciences companies have

become more and more innovative in the types of business functions that they

consider ripe for outsourcing. Functions that are being considered include human

resources (operations or payroll), financial transaction processing (particularly

accounts payable), procurement, distribution, logistics and clinical data

management.

The Pharma industry – buffeted by the possibility of price controls, declining drug-development productivity (higher costs, fewer drugs), stricter regulatory scrutiny, and competition from a growing number of “me-too” drugs-is, in a state of turbulence. This instability is putting financial pressure on all the industry players, not just the weaker ones; earnings of the sector‘s top companies have fallen by 25 percent since 2002. Meanwhile, companies must rethink core business processes (such as drug development and commercialization) and seek new ways to increase their yield and productivity.

Source – Adapted from McKinsey Report, January 2006

Definition of Offshoring – Offshoring describes the relocation of a business

process by a company from one country to another—typically an operational

process, such as manufacturing, or supporting processes, such as accounting.

The term used in several distinct but closely related ways. It is sometimes used

broadly to include substitution of a service from any foreign source for a service

3

formerly produced internally to the firm. In other cases, only imported services

from subsidiaries or other closely related suppliers are included. A further

complication is that intermediate goods, such as partially completed computers,

are not consistently included in the scope of the term. Offshoring can be seen in

the context of either production offshoring or services offshoring. In this study,

focus is on services offshoring and outsourcing.

Though the concept of offshoring is on the rise in the Life Sciences industry,

there is a tremendous pressure on companies towards innovating more effective

and swift processes and also reduce the overall costs in R&D, manufacturing,

supply chain and regulatory compliance.

Life Sciences Industry comprises of three main categories i.e. Pharmaceutical,

Medical Devices and Biologics. In this research, there is more focus and deep

dive on the Pharmaceutical Industry but referred to as Life Sciences.

1.1 Outsourcing – Origin of Concept

Outsourcing could be defined as the shifting or delegating a company's day to

day operations or business process to an external service provider, done in

anticipation of a better quality, lower rates and in a sense of getting an edge over

one's competitors. When a company's operations or business processes are

outsourced to firms in foreign countries, often to take advantage of cheap skilled

4

labor, it is referred to as Offshore outsourcing or Offshoring. In this arrangement,

functions previously performed by an organization are supplied under contract

from a third party. While outsourcing is not exactly a new innovation, the shifts

that have occurred recently in this space are worth noting.

Some Other Definitions of Outsourcing;

§ The concept of taking internal company functions and paying an outside firm

to handle them is called Outsourcing. Outsourcing is done to save money,

improve quality, or free company resources for other activities. Outsourcing

was first done in the data-processing industry and has spread to areas,

including tele-messaging and call centers.

§ A long-term, results-oriented relationship with an external service provider for

activities traditionally performed within the company. Outsourcing usually

applies to a complete business process. It implies a degree of managerial

control and risk on the part of the provider.

§ The transfer of components or large segments of an organization's internal IT

infrastructure, staff, processes or applications to an external resource such as

an Application Service Provider

Advantages of Outsourcing

Proponents of outsourcing cite a variety of reasons for "letting others do it".

Some of the notable advantages in outsourcing are listed in the following page;

5

Cost savings - By outsourcing functions that were previously performed in house,

companies are often able to reduce their employee levels and related costs, such

as recruitment, supervision, salary and benefits. By outsourcing a capital

intensive function, a company can also reduce the costs of equipment

obsolescence and depreciation. A portion of company’s cost savings will go to

the outsourcer, but outsourcing vendors have a tighter control of fringe benefits

and run leaner overhead structures.

Quality of service - Because the company is the outsourcer's customer, teams

are more likely to experience a "can-do attitude," which may not always be

exhibited by an in-house staff.

More capital funds - Outsourcing reduces the need to invest capital in non-core

business functions, thereby freeing capital to invest in profit-making aspects of

the business.

State-of-the-art technology - Outsourcers have to spend time and money on the

most current equipment and on employee training to remain competitive. By

outsourcing certain areas, you are assured of receiving the most efficient

services and the latest technological advances within that particular function.

Price stability - By signing a contract to outsource, you will likely be able to obtain

stable pricing, eliminating the future need to shop around. Stable pricing allows

the company to budget operating expenses and capital purchases more

accurately, while potentially preventing the likelihood of surprise expenses.

6

New business partners - Outsourcers clearly wish to be viewed as business

partner. And as a business partner, they share in the desire to keep service

provider operating at its maximum potential. Through this business partner

arrangement, outsourcers are eager to introduce service provider to other

outsourcers to assist in that goal.

More time to focus on core business activities – This is another intangible benefit

of outsourcing. If a company is to be successful and profitable, management is

needed to spend time planning and directing the company's business strategies

and not wasting time worrying about managing certain administrative or ancillary

functions.

List of Top 10 Pharmaceutical Companies as per May 2010 report is provided

below;

2010 Rank (2009 rank)

Company & Headquarters

2009 Rx Sales (millions in USD)

2009 R&D Spend (millions in USD)

2009 Top Selling Drugs

1 (1) Pfizer $ 45.4 $ 7845 Lipitor, Lyrica, Celebrex

2 (3) Sanofi-Aventis $ 42.0 $ 6567 Lantus, Lovonox, Plavix

3 (4) Novartis $ 38.4 $ 6308 Dionov, Gleevec, Zemeta

4 (2) GlaxoSmithKline $ 37.8 $ 6286 Seretide/Advair, Valtex

5 (8) Roche $ 37.6 $ 8570 Avastin, Rituxan, Herceptin

6 (6) AstraZeneca $ 32.8 $ 4409 Nexium, Seroquel, Crestor

7 (7) Merck $ 25.2 $ 5845 Singulair, Hyzaar, Januvla

8 (6) Johnson & Johnson $ 22.5 $ 4591 Remicade, Eprex, Floxin

9 (9) Eli Lilly $ 21.2 $ 4300 Zyprexa, Cymbalta, Humalog

10 (11) Bristol-Myers Squibb $ 18.8 $ 3647 Plavix, Abilify, Reyataz

Source – Adapted from The Pharma Exec 50, May 2010, www.pharmaexec.com

Figure 1

7

1.2 Outsourcing and Offshoring – How Close and How Far?

Outsourcing is – to put it plain and simply – subcontracting. The phrase “IT

Outsourcing services,” refers to merely subcontracting IT work to a third party or

Service Provider. Outsourcing, contrary to popular belief, does not necessarily

refer to sending work overseas. A company in New Jersey could “outsource”

work to a company in Indianapolis. One of the most common examples of

outsourcing is telephone sales and call center services. While many companies

used to employ their own in-house call centers, these services are now usually

subcontracted through a third party company.

Offshoring – merely refers to any company, service, or client that is based

overseas. Offshore outsourcing means that you are subcontracting work to

overseas companies. If a company based in Texas has subcontracted a

company in India to develop their website or provide their call center services,

that Texas company has outsourced offshore. Offshore outsourcing does not,

however, refer to hiring employees from overseas to work at your company in-

house.

Benefits of outsourcing within the same Country versus Outsourcing

overseas

Outsourcing Offshore – Outsourcing offshore or offshore outsourcing is one of

the best strategies for a company to get work done without breaking the bank; as

8

in, offshore outsourcing allows companies to accomplish necessary tasks (such

as creating efficient websites or call centers) without having to hire new talent in-

house for things like IT application development, product development and rich

internet application development. Offshore outsourcing also allows companies to

access an entirely new talent pool, and allows access to brilliant new technology.

Outsourcing Domestically – Domestic outsourcing usually happens for two

reasons: Either a company is subcontracting another company for work they

cannot do in-house, or, a company is seeking cheap call center services.

Typically, outsourcing offshore is more lucrative. Not only is it usually far more

cost efficient, but it also allows companies to access quality professionals and

technologies that are not widely found in a particular host country.

1.3 Concepts of Outsourcing

Offshore outsourcing services can be mainly divided into Technology Services

Outsourcing, Business Process Outsourcing (BPO), Software R&D and

Knowledge Process Outsourcing (KPO).

Technology Services Outsourcing

Companies that utilize technology require sophisticated, quick-responding

computer systems and software that are flexible enough to respond to the

increasing capabilities of technology and the rapid changes in business models.

9

Selecting the right technology partner is an integral part of many successful

ventures. Following are the specific types of technology services.

· Electronic Commerce (eCommerce)

· Infrastructure (Networks)

· Software (Applications)

· Telecommunications

· Website Development & Hosting

Business Process Outsourcing (BPO)

With globalization, enterprises have been challenged to find the niches where

they add the greatest economic value to the world's economy. As a result,

enterprises have looked for ways to avoid making investments in employees and

infrastructures that do not have a high yield. As service providers witnessed this

development, they began to create whole enterprises based on narrow business

processes. The term "BPO" (Business Process Outsourcing") was coined in

about 1995 and became popular a few years later, accelerated by the explosion

of Internet business in the field of;

· Customer Contact (Customer Relations Management)

· Equipment

· Finance / Accounting

· Human Resources

· Logistics

10

· Procurement / Supply Chain Management

· Security

Software R&D

Offshore Software R&D is a provision of software development services by an

external supplier positioned in a country that is geographically remote from the

client enterprise; a type of offshore outsourcing. In this context, it refers to the

offshore development phase of software. The main reason behind the companies

to use offshore software development services is the higher development cost of

the local service providers. The global software R&D services market as

contrasted to Information Technology Outsourcing (ITO) and BPO is rather

young and currently is at early stages of its development. Apparently, India is

leading the world in this field.

Knowledge Process Outsourcing (KPO)

Knowledge Process Outsourcing (KPO) describes the outsourcing of core

business activities, which often are competitively important or form an integral

part of a company's value chain. Therefore KPO requires advanced analytical

and technical skills as well as a high degree of proprietary domain expertise.

Reasons behind KPO include an increase in specialized knowledge and

expertise, additional value creation, the potential for cost reductions, and a

shortage of skilled labor.

11

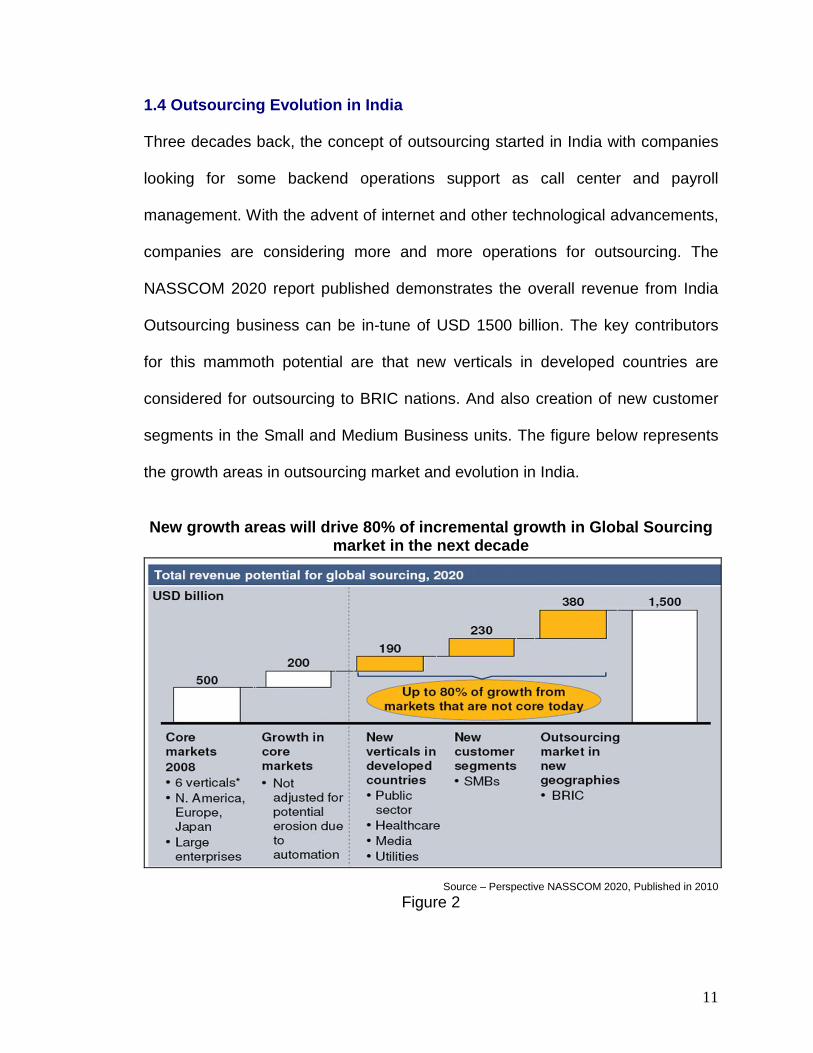

1.4 Outsourcing Evolution in India

Three decades back, the concept of outsourcing started in India with companies

looking for some backend operations support as call center and payroll

management. With the advent of internet and other technological advancements,

companies are considering more and more operations for outsourcing. The

NASSCOM 2020 report published demonstrates the overall revenue from India

Outsourcing business can be in-tune of USD 1500 billion. The key contributors

for this mammoth potential are that new verticals in developed countries are

considered for outsourcing to BRIC nations. And also creation of new customer

segments in the Small and Medium Business units. The figure below represents

the growth areas in outsourcing market and evolution in India.

New growth areas will drive 80% of incremental growth in Global Sourcing

market in the next decade

Source – Perspective NASSCOM 2020, Published in 2010

Figure 2

12

1.5 Theories on Outsourcing

The government agencies in the USA define outsourcing as “the movement of

work that was formerly conducted in-house by employees directly paid by a

company to a different company” (Brown and Siegel, 2005). The company

outsourcee might be located in the country (onshore outsourcing) or in another

country (offshore outsourcing) (Brown and Siegel, 2005). The notion of in-

sourcing is implied if the company carries out the activity independently in the

country of its origin (Gião et al., 2008). It is clear from the definitions that the

major difference between outsourcing and in-sourcing is who carries the

responsibility about the activity.

John (2006) describes four categories of outsourcing:

1. “Commodity-like”. It is a cost-driven type with no innovation required.

2. “Customized-activities”. The outsourcer demands the outsourcee is being

involved in internal processes deeper.

3. “Business Process Outsourcing”. Outsourcee has to work in close

cooperation with outsourcer and to be well aware about its strategy.

4. “Strategic outsourcing”. The degree of integration between parties is very

high as it includes outsourcing of the core competency. Responsibility is

shared between parties. Innovation is a requirement. Outsourcing of R&D

falls down into this category.

13

Theories Driving Outsourcing

Economies of Scale and Scope – Odagiri (2003) applies this theory because the

firm cannot achieve high utilization rate of equipment and decrease costs

associated with a product if it does not produce high volume. Hence, he

proposes to outsource that activity.

The Transaction-Cost Theory – Jonson et al. (2008) argue that the activity should

be remained in-house if the firm’s transaction costs in its control are lower than

relying on transactions in the market. Odagiri (2003) describes intellectual right

for the invention as an appropriate transaction cost for R&D.

The Capability Theory – Developing of the capability is a time-consuming

process.

Source – Outsourcing Process, Adapted, Kumar et al. (2007)

Figure 3

14

Therefore, it might be quicker and cheaper to find a partner who already has

certain capability (Odagiri, 2003). Odagiri (2003) provides an example of

collaboration with universities and creating alliances with specialist firms in R&D.

Key Benefits of offshoring

So far the key drivers for the majority of offshore engagements have been the

desire to reduce costs and improve the service quality. Using offshore locations

with a lower cost base is clearly an attractive option in the search for cost

reductions. As per IBM CEO Study 2010, CEOs across the industries need to

think differently and avoiding complexity is not an option, instead the choice

comes in how they respond to it.

Source – Leadership Thinking from IBM CEO Study, January 2010

Figure 4

15

1.6 Outsourcing Strategies

1.6.1 Size and Nature of Companies

In the Life Sciences industry, adoption of outsourcing and offshoring their

processes has come more as a compulsion to meet the growing cost and

expansion of business across countries. This is unlike in other industries.

Companies in other industries want to consider outsourcing to stay ahead of

competition by providing faster, easier and efficient products to the consumers.

Same phenomenon is applicable to the service industry too.

Big Life Sciences companies cannot stay away from outsourcing for long due to

the diversification of the business channels and geographical spread. To add to

this is the challenge of growing staff and increasing number of products and

pipeline. Also to manage and harmonize the processes, product lines, and

distribution channels consistently across countries with varied time zones and

then deliver in a standard manner is challenging. Also, when the staff is absorbed

onto company’s rolls, provident fund, medical benefits and insurance, and other

compensatory benefits have to be arranged as per country labour laws. If a

company intends to overcome this challenge and set-up teams to operate in

various time zones, the overheads will be blowing up the costs phenomenally.

Though these big companies have significant number of IT staff on board, the

muscle power needed to perform global implementations and ensuring 24x7

16

support in a long run is difficult to achieve. Apparently, outsourcing for these big

companies becomes more of a necessity rather than an option.

On the other hand, small and medium sized companies can afford to consider

outsourcing as an option, rather than a necessity. They are in an advantageous

position due to the lesser complexities in their supply chain, manufacturing

verticals and managing staff. Usually these companies have staff located in few

locations in a specific country or one more country outside base. The factors like

time zone difference, 24x7 availability and diversified product lines do not arise.

So the smaller companies opt to outsourcing model in smaller steps by

considering only small portions of business processes to be outsourced at a time.

They do not opt for a big-bang approach. These companies set-up their own IT

teams who can work and turn-around the IT pieces as and when needed. Due to

lesser volume of tasks and type of work, these are manageable internally.

There are some companies which are relatively much smaller in the industry and

manufacturing certain niche products in low volume that yield high value. These

companies are going away from the trend, show much keenness in moving with

the growing technology and consider outsourcing options easily. Such

companies are few and tend to have a competitive advantage over other players

in the same league.

17

1.6.2 Outsourcing Determinants

Further to explanation provided in the earlier section on how size and nature of

the company is driving the outsourcing decisions, it is further understood that

there are some determinants which serve as driving points in making outsourcing

decisions. The figure below demonstrates the outsourcing profiles of ten of the

top twenty pharmaceutical companies. It shows the pervasive use of managed

services in Infrastructure and AMS, regardless of which service provider has

been providing the service.

Across Life Sciences, most companies have outsourcing services positions

Source – IBM CIO Study, 2009, www.ibm.com

Figure 5

18

A successful outsourcing project is only possible if the outsourcing decision has

taken into consideration all known costs and benefits associated with the project.

It is also important that the contract be effectively negotiated and managed in a

manner it will be beneficial and keep the stakeholders satisfied with the decision

made.

Successful CIOs blend three pairs of roles that seem contradictory, but are actually complementary

Source – IBM CIO Study, October 2009, www.ibm.com

Figure 6

Though there are some standard outsourcing determinants, it is not possible to

provide a simple criteria template for an outsourcing versus insourcing cost-

benefit analysis. Each organization must determine its priorities, criteria, and

weight for each project depending on its individual capabilities. Though an option

might seem quantifiably more expensive, it could be the most effective choice for

meeting the company's needs. A successful project would require constant

19

information, true cost and benefit estimates and should also have specific goals

to achieve.

Moving Outsourcing Relationships Up the Value Chain

Many outsourcing relationships begin with optimism and mutual amiability. Both

sides profess the need for the client to focus on its core-competencies while the

outsourcer's commitment should be in leveraging its technical expertise to deliver

strategic value. Outsourcing alliances are generally based on certain key

business drivers, as exhibited in the following table that details a comparative-

grid that should be used while deciding on outsourcing strategy. While

transactional-alliances are dictated with outsourcing motivators for building

strategic alliances, a four-step model is detailed in the following paragraphs.

An outsourcing alliance begins with the outsourcer exhibiting its specialized

qualities. At the time the contract is signed, the outsourcer projects excellent

performance capabilities. Due to lack of quality and delivery excellence,

problems arise very soon. Subsequent problems arise during periodic

performance reviews and assessments. The client's objectives of becoming more

focused are hindered. Cost reductions and efficiency enhancements are not up

to the mark. The outsourcer struggles to address the clients’ obscure business

objectives, meet aggressive performance targets and also focus on its own profit

margins.

20

Business Driver Outsourcing Motivators Suggested Outsourcing Model /Strategy to be pursued

Reduce and Control Operating Costs

Free up capacity Reduce Cost Capture benefits quickly

Outsource large sustenance assignments that consume a large proportion of resources. Capitalize on vendors economies of scale to do the job more cost effectively

Lack of employee resources

Increased capacity Speedy ramp up of resources Building knowledge repository

Outsource specific skills (such as systems maintenance which are resource-demanding) that are less critical to future development and value creation Refocus on strategic core-competencies

Technology Expertise

Access to world-class capabilities, best practices, new technology tools etc Shrink product’s time-to-market

Outsource major development efforts demanding state-of-the-art technology expertise. Outsource to a vendor specializing in the requisite technology domain, ensuring the availability of ‘ready-resources’ and capitalizing on ‘first-mover’ advantage

Share Risk Share risks in terms of technology transitioning or launching new products

Outsource technology assignments that do not conform to explicitly defined scope, specification and implementation plans. Go in for a time and material execution model for such projects that are difficult to complete in time.

Source – Adapted from Outsourcing: A Decision of Trust, April 2002, Hughes Software Systems

Table 1

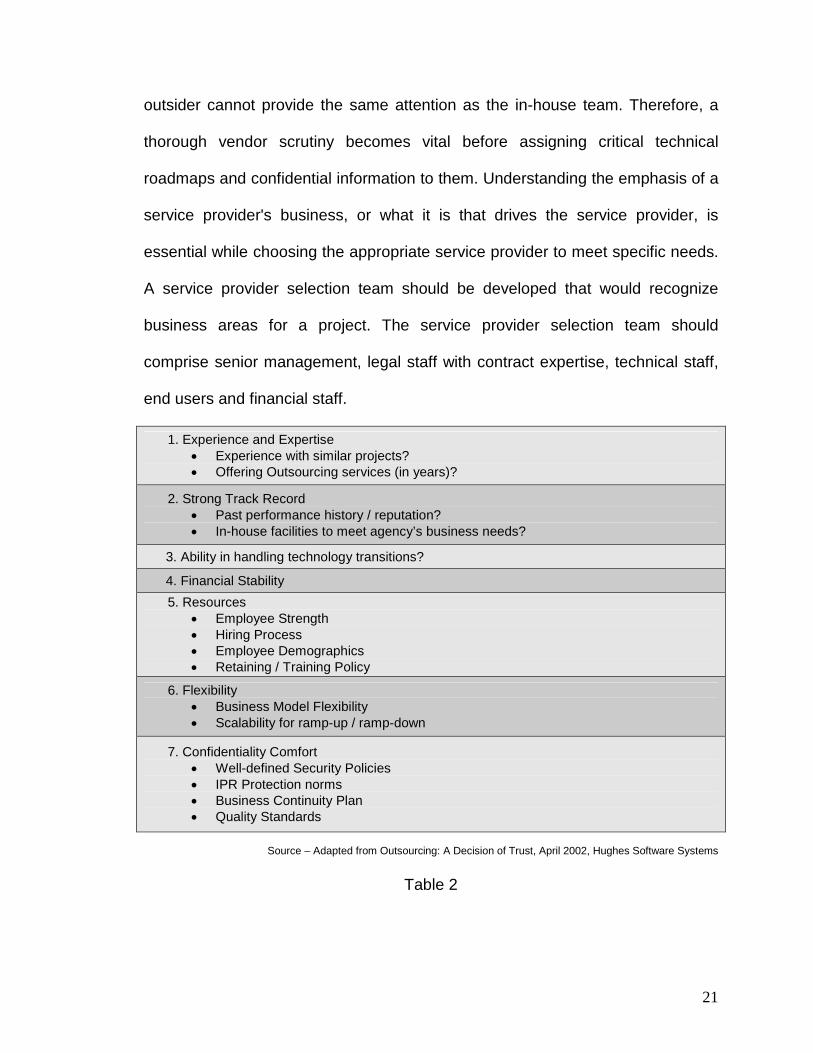

Selecting the Vendor

Every Life Sciences company will have a Vendor Selection Process with well

defined criteria based on the type of the services procured from the vendor /

service provider. Depending on the complexity and criticality of the project, the

prospective service provider has to be classified accordingly and evaluated

against the set parameters. Some outsourcing companies believe that an

21

outsider cannot provide the same attention as the in-house team. Therefore, a

thorough vendor scrutiny becomes vital before assigning critical technical

roadmaps and confidential information to them. Understanding the emphasis of a

service provider's business, or what it is that drives the service provider, is

essential while choosing the appropriate service provider to meet specific needs.

A service provider selection team should be developed that would recognize

business areas for a project. The service provider selection team should

comprise senior management, legal staff with contract expertise, technical staff,

end users and financial staff.

1. Experience and Expertise · Experience with similar projects? · Offering Outsourcing services (in years)?

2. Strong Track Record · Past performance history / reputation? · In-house facilities to meet agency’s business needs?

3. Ability in handling technology transitions?

4. Financial Stability

5. Resources · Employee Strength · Hiring Process · Employee Demographics · Retaining / Training Policy

6. Flexibility · Business Model Flexibility · Scalability for ramp-up / ramp-down

7. Confidentiality Comfort · Well-defined Security Policies · IPR Protection norms · Business Continuity Plan · Quality Standards

Source – Adapted from Outsourcing: A Decision of Trust, April 2002, Hughes Software Systems

Table 2

22

It should be acknowledged that somewhere the external service providers would

be making money on the outsourcing agreement otherwise they would not be

willing to enter into an agreement. Signing a contract in haste could lead to

working with a service provider who is not responsive to company's needs and

who sticks precisely to the contract letter, charging the agency for any additional

services provided.

Cultural Compatibility

Besides the maturity of companies and thought process on Outsourcing, the

impact of Culture influences some of the decisions made. For an outsourcer, it

becomes imperative to look at this cultural dimension as well to develop a

synergized relationship with prospective service providers. Each company is

culturally different and every company has a need to have their cultural fitment

identification methods. Here are some of the standard questions that can be

considered while evaluating the cultural fitment of service providers.

23

Source – Forrester Research, Inc. October 2008

Table 3

It should be borne in mind that a service provider's business goals are always

different from those of the client. The client and the service provider must be

prepared to identify and resolve the differences that might arise. History suggests

relationships which did not have good cultural fit do not last for long. This

resulted despite the client and the service provider being mature with good

delivery capabilities.

24

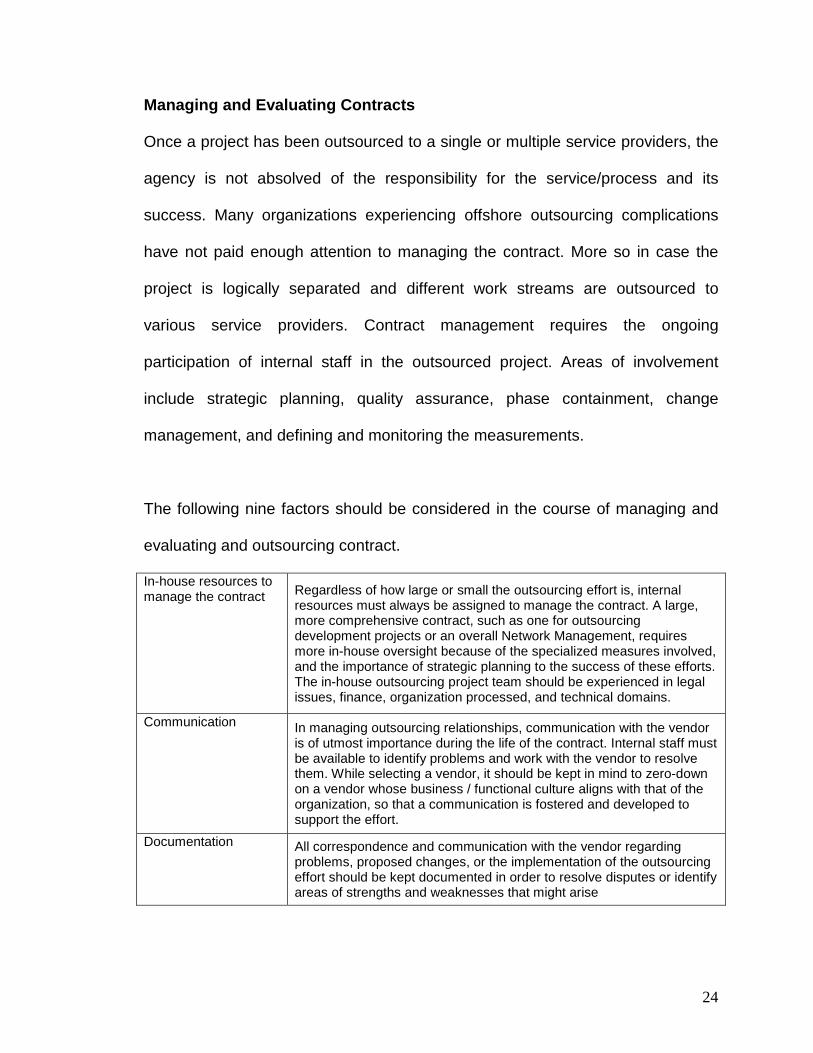

Managing and Evaluating Contracts

Once a project has been outsourced to a single or multiple service providers, the

agency is not absolved of the responsibility for the service/process and its

success. Many organizations experiencing offshore outsourcing complications

have not paid enough attention to managing the contract. More so in case the

project is logically separated and different work streams are outsourced to

various service providers. Contract management requires the ongoing

participation of internal staff in the outsourced project. Areas of involvement

include strategic planning, quality assurance, phase containment, change

management, and defining and monitoring the measurements.

The following nine factors should be considered in the course of managing and

evaluating and outsourcing contract.

In-house resources to manage the contract Regardless of how large or small the outsourcing effort is, internal

resources must always be assigned to manage the contract. A large, more comprehensive contract, such as one for outsourcing development projects or an overall Network Management, requires more in-house oversight because of the specialized measures involved, and the importance of strategic planning to the success of these efforts. The in-house outsourcing project team should be experienced in legal issues, finance, organization processed, and technical domains.

Communication In managing outsourcing relationships, communication with the vendor is of utmost importance during the life of the contract. Internal staff must be available to identify problems and work with the vendor to resolve them. While selecting a vendor, it should be kept in mind to zero-down on a vendor whose business / functional culture aligns with that of the organization, so that a communication is fostered and developed to support the effort.

Documentation All correspondence and communication with the vendor regarding problems, proposed changes, or the implementation of the outsourcing effort should be kept documented in order to resolve disputes or identify areas of strengths and weaknesses that might arise

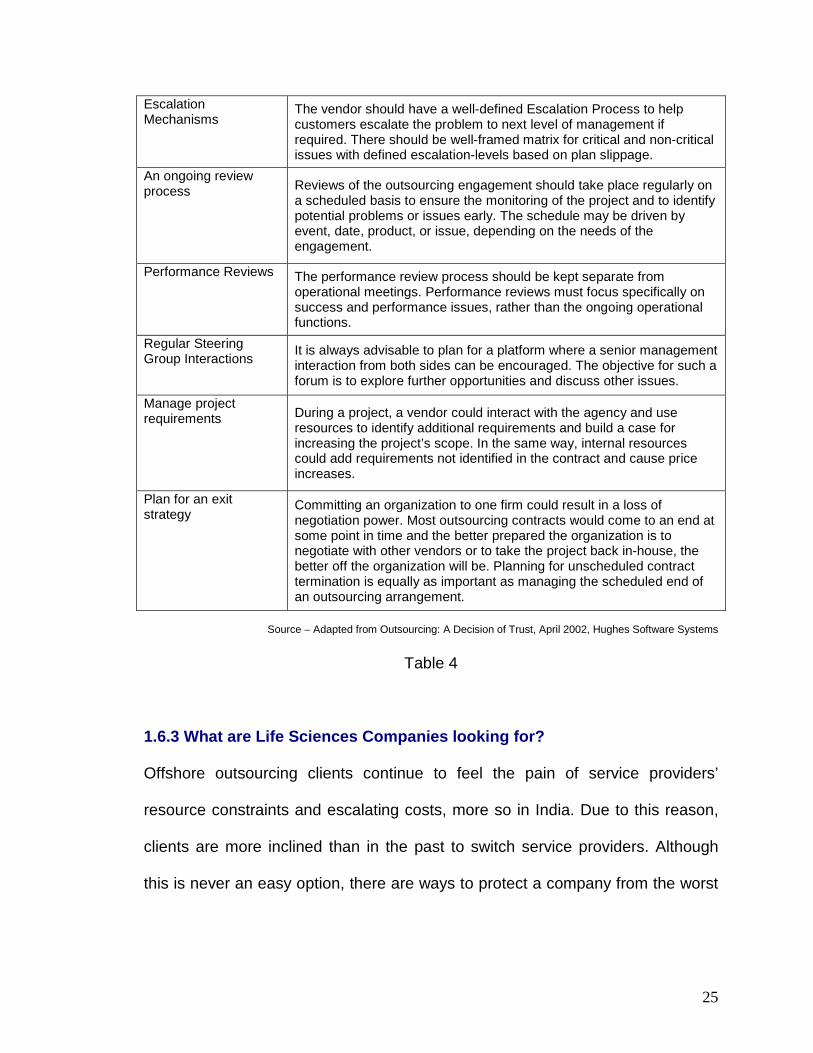

25

Escalation Mechanisms

The vendor should have a well-defined Escalation Process to help customers escalate the problem to next level of management if required. There should be well-framed matrix for critical and non-critical issues with defined escalation-levels based on plan slippage.

An ongoing review process Reviews of the outsourcing engagement should take place regularly on

a scheduled basis to ensure the monitoring of the project and to identify potential problems or issues early. The schedule may be driven by event, date, product, or issue, depending on the needs of the engagement.

Performance Reviews The performance review process should be kept separate from operational meetings. Performance reviews must focus specifically on success and performance issues, rather than the ongoing operational functions.

Regular Steering Group Interactions

It is always advisable to plan for a platform where a senior management interaction from both sides can be encouraged. The objective for such a forum is to explore further opportunities and discuss other issues.

Manage project requirements During a project, a vendor could interact with the agency and use

resources to identify additional requirements and build a case for increasing the project’s scope. In the same way, internal resources could add requirements not identified in the contract and cause price increases.

Plan for an exit strategy

Committing an organization to one firm could result in a loss of negotiation power. Most outsourcing contracts would come to an end at some point in time and the better prepared the organization is to negotiate with other vendors or to take the project back in-house, the better off the organization will be. Planning for unscheduled contract termination is equally as important as managing the scheduled end of an outsourcing arrangement.

Source – Adapted from Outsourcing: A Decision of Trust, April 2002, Hughes Software Systems

Table 4

1.6.3 What are Life Sciences Companies looking for?

Offshore outsourcing clients continue to feel the pain of service providers’

resource constraints and escalating costs, more so in India. Due to this reason,

clients are more inclined than in the past to switch service providers. Although

this is never an easy option, there are ways to protect a company from the worst

26

ravages of engagement failures. Some of the best practices are provided below

safely disengaging an underperforming provider.

Previously Minor performances Have Become More Significant

In the past, when Indian providers failed to perform, the impact was minimal for

most companies. Today, however, failures are more expensive and more

commonplace for the following reasons:

Providers are working on more critical projects - In large part due to their prior

successes with Indian service providers, clients are asking their offshore firms to

take on more critical projects than they did in the 1990s. Failures in these

projects can be painful and embarrassing to stakeholders and potentially can

have a significant financial impact on the business.

Failure or underperformance is now more prevalent - As resource constraints

and skyrocketing growth handicap service providers, the quality of resources

deployed to projects and the quality of account and project management is

bound to suffer. The result is that more projects seem to be failing or

“underperforming.” And there seems to be a perception in clients that the service

providers appear less concerned about these failures than they did in the past.

Costs have gone up - Hourly rates have increased; overhead costs have gone

up; and the dollar has been volatile against the rupee. Adding to this, the service

providers sometimes are paid for rework now and are charging for every single

hour of staff work, even if it’s to redo something that wasn’t done properly the first

27

time. Previously, clients were willing to deal with substandard work because the

labor rate and free rework made it acceptable, but as offshore rates and other

costs climb, client tolerance for poor work has dropped dramatically.

1.6.4 How Life Sciences Companies are building up?

In order to remain competitive, it is crucial for a firm to articulate its offshoring

strategy around the usual competitiveness drivers: costs, quality, and risk

management, that is, proper management control of offshored operations. A 2x2

matrix presented in the following page, captures the different management

possibilities, with the ownership structure on the horizontal axis and the

localization on the vertical axis.

The focus is on the bottom cells, as globalization, liberalization and new

Information and Communication Technologies (ICT) affect management

possibilities and allow a real choice of management structure. Clearly, the matrix

is overly simplified as other forms of ownership with different levels of

management control are possible.

Ownership Internalized (Activities performed

In-house Externalized (External Suppliers)

Outsourcing

At Home Company performs the activities at home Suppliers in home country

Foreign Countries Own subsidiary in foreign country (intra-firm [captive] offshoring)

Suppliers in foreign countries (offshore outsourcing)

Source: Pyndt and Pedersen (2006), p.12

Table 5

28

COST REDUCTION

Service businesses are influenced significantly by the cost factor when deciding

to offshore some of their activities. As mentioned previously, competitive

pressures to reduce costs and improve productivity force many companies to

restructure and reorganize the way they perform their activities. Offshoring

appears to be a good alternative for many service activities as developing

nations now offer comparable services at lower cost.

The cost-influenced move to offshore some activities is first motivated by the

disparity between salaries and wages. The workforce in developing nations such

as India now offers a vast variety of services that is quite comparable in quality to

those available in industrialized countries but at a much lower cost. Thus,

offshoring can give companies a major competitive advantage in terms of cost

effectiveness.

Two surveys confirm that cost reduction is the main motive for offshore

outsourcing. The first survey, conducted jointly by Duke University and Archstone

Consulting, draws its results from 102 mostly American corporations of different

sizes.

29

Source – Duke University CIBER/Archstone Consulting (2005) White Paper

Figure 7

The reason why cost is the top priority is that cost may be a convenient metric

when comparing locations or providers, especially when savings can be high.

Increased competition, both at local and global levels, forces a firm to reduce

costs and offshore outsourcing allows the firm to achieve this goal.

The competitive pressures may be so high that one firm proceeding with

offshoring is enough to drag all the others in a given industry (domino effect).

Moreover, surveys may not capture the fact that companies evolving in a

competitive market often tend to follow the leader and are thus more disposed to

proceed to offshore operations if the leader or leaders proceed with such a

strategy. Managers are thus constrained to either make better use of

technologies and/or to proceed with re-engineering the labour force, two

30

concepts that can be complementary and simultaneously feasible when the firm

opts for an offshoring strategy; a possible result can be higher-quality goods and

services at lower costs.

European companies have similar priorities as the survey conducted jointly by

United Nations Conference on Trade and Development (UNCTAD) and Roland

Berger Strategic Consultants shown below. Since services are typically labour

intensive, this study makes a distinction between two types of costs, where

labour costs should be defined as the ratio of wage over productivity.

Source – Roland Berger Strategic Consultants (2004) White Paper

Figure 8

The different categories of cost may be more relevant for a company establishing

a new internal offshore operation, for instance, a captive call centre (insourcing).

As for offshore outsourcing, some of these costs may already be incurred by the

provider and included in the price charged. There are other types of costs, such

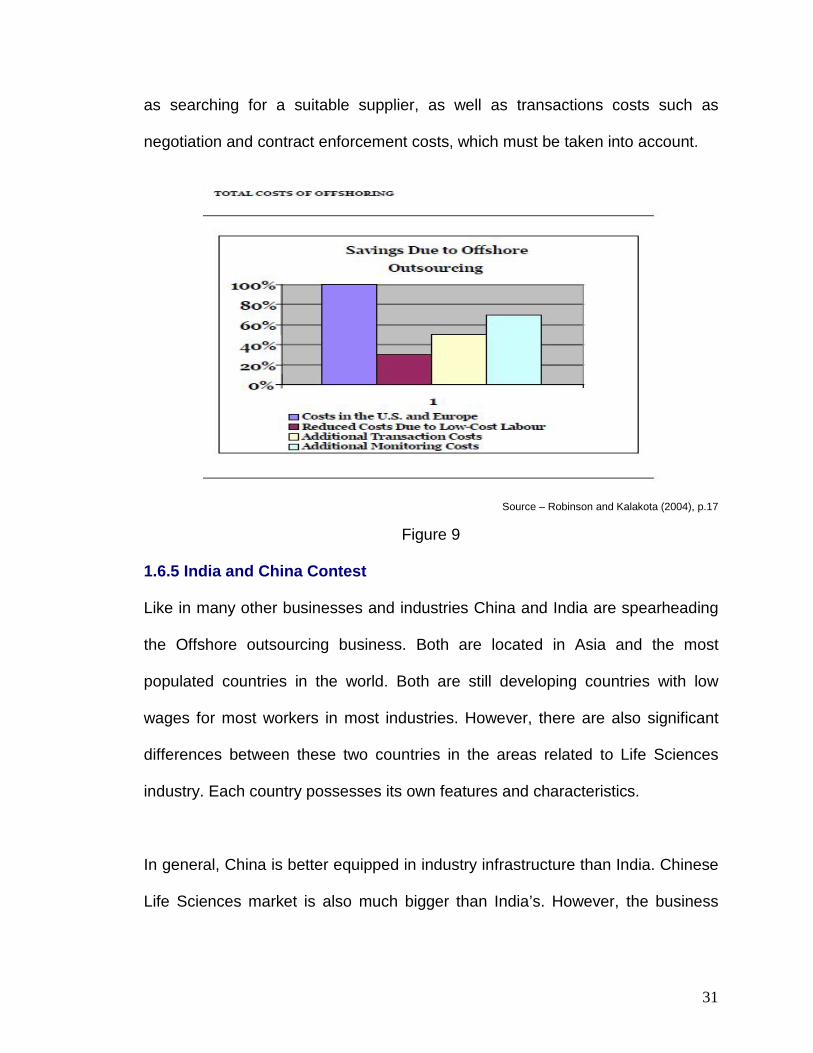

31

as searching for a suitable supplier, as well as transactions costs such as

negotiation and contract enforcement costs, which must be taken into account.

Source – Robinson and Kalakota (2004), p.17

Figure 9

1.6.5 India and China Contest

Like in many other businesses and industries China and India are spearheading

the Offshore outsourcing business. Both are located in Asia and the most

populated countries in the world. Both are still developing countries with low

wages for most workers in most industries. However, there are also significant

differences between these two countries in the areas related to Life Sciences

industry. Each country possesses its own features and characteristics.

In general, China is better equipped in industry infrastructure than India. Chinese

Life Sciences market is also much bigger than India’s. However, the business

32

operation style and philosophy in Indian companies are closer to the Westerner

than in Chinese companies. Indian companies are also more familiar with the

Western regulations than Chinese companies. They also have broader global

presence than Chinese companies. China is better in education of biology than

India. The biotechnology industry in China is also more advanced than in India.

However, Indian Life Sciences companies have invested more in R&D and have

a much broader product scope than Chinese companies.

In traditional Life Sciences sector, Chinese companies are still limited to

manufacturing of traditional products which are marketed in limited number of

Countries. But, in the biotech sector, Chinese companies possess much stronger

capabilities in R&D and manufacturing of macro compounds than Indian

companies. In professional outsourcing service, the two countries provide close

service scopes and possess close service capabilities. However, there are still

differences in each service sector between these two countries. In discovery

service, Chinese companies and Indian companies possess close skills and offer

similar services and qualities.

However, in target identification and validation as well as those related areas

such as research in genomics and proteomics, Chinese companies possess

stronger service capabilities than Indian companies; whereas in small molecule

drug R&D, Indian companies are more capable than Chinese companies.

33

In preclinical research service, Chinese CROs possess better service capabilities

than Indian CROs; whereas in clinical research service, it is just opposite. In

process R&D and scale-up synthesis, both countries possess similar capabilities.

However, Indian companies possess better skills and capabilities than Chinese

companies in formulation, manufacturing and marketing of generic drugs. Major

pharma and biotech companies play different strategies in these two countries. In

India, they tend to form more close collaborations such as risk-sharing

outsourcing with an Indian company to co-develop drug candidates, but very few

of them are willing to permanently set up a decent size of R&D center or

manufacturing facility in the country. In stark contrast, almost all major pharma

and biotech companies have invested hundreds of millions of dollars in China to

establish their wholly owned R&D centers and large scale manufacturing and

marketing facilities. Many of their China R&D centers have already reached

decent sizes and gained strong capabilities. They are ready to conduct full-scale

research independently.

At present, India is better than China in small molecule drug R&D and

manufacturing. But China is superior over India in biotechnologies including the

R&D and manufacturing of macro compounds. India offers better product quality

but China has more cost reduction advantage. In terms of investment

opportunities, China seems to present more attractions than India as its industry

infrastructure and biotechnologies are more advanced. The mature life sciences

34

markets in the United States, Europe and Japan are expected to grow in low

single digits for the foreseeable future. In addition, we see life sciences

companies established within the emerging markets focusing their growth plans

on these mature markets, which will put the existing players under even more

pressure. While mature markets still represent the bulk of the profits, there is

general agreement that growth will come from the emerging markets. It is less

clear how best to capture that growth and create a sustainable global model that

could potentially benefit both mature and emerging markets.

In India, almost 3 decades ago, Bangalore was considered as the hub for any IT

company for both Indian companies as well as the foreign based multi-nationals

who were planning to invest in India. After Bangalore, companies have started

moving to other cities like Hyderabad and Pune. Over the years and with benefits

from state and central governments, many other cities have come up as IT hubs

in India.

India started its growth path by providing basic level of IT support functions in the

Banking and Finance sector and then gradually moving onto other industries.

With growing availability of more skilled personnel in IT knowledge both on

technical, functional and consulting, companies have started to explore other

niche areas of business that could be offshored. Based on the stage of

35

development for IT-BPO, the locations can be categorized into four groups, viz,

Leader, Challenger, Follower and Aspirants as represented in the following page.

Source – NASSCOM Report, Jun 2009, www.nasscom.in

Figure 10

1.6.6 Gaps in Capabilities

To be successful in new evolving market, IT Organizations and Suppliers need to

be more agile, innovative and move up the Global value chain and need to

develop wider ‘Global Capability Leadership and Talent Pool’.

The Life Sciences industry has tended to be skeptical about the value of large

scale spending on computing. But in November 2010, 250 or more senior

executives from many of the sector's largest companies have travelled to the

36

World Pharma IT Congress in London to find out what their peers - heads of IT,

knowledge management, informatics, e-business are doing to remain competitive

in the market. Louisa Carson, conference organiser for Oxford International, said