Dave Ingram, MAAA, FSA, CERA, FRM, PRM Chair of IAA Enterprise & Financial Risk Committee November, 2011 Stress and Scenario Testing in a Risk-based Solvency Regime 1

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Dave Ingram, MAAA, FSA, CERA, FRM, PRM Chair of IAA Enterprise & Financial Risk Committee November, 2011

Stress and Scenario Testing in a Risk-based Solvency Regime

1

DISCLAIMER

• This presentation represents the opinions of the presenter, David Ingram. These are not necessarily the views of the International Actuarial Association or his employer, Willis Re.

• In the area of Risk Management it is always dangerous to rely on the opinions and analysis of a third party without verifying with your own research, thought, and analysis.

• This presentation is no exception to that rule.

2

A word from our lawyers • Willis Re Inc. is a reinsurance broker. Willis Re Inc. is not a law firm,

investment advisor or tax advisor. We do not give legal, investment or tax advice and nothing herein constitutes nor should be construed as such. Such ideas are offered for discussion purposes only and do not constitute advice of any kind. It is believed that the information used in creating this presentation is correct, but no representations are made as to its completeness or accuracy, nor are any warranties made as to its fitness for any purpose. You and your advisors must make an independent assessment regarding all such matters.

• Any comments or observations made herein are for academic purposes only and are not for the purposes of reliance. Any such comments do not reflect the views of Willis Re Inc. or its clients.

3

Humanity

“The real problem with humanity is the following: We have Paleolithic emotions; medieval institutions; and god like technology.”

2009 Dr. E.O. Wilson, Harvard University

Source: The Watchman’s Rattle, Thinking Our Way Out of Extinction, Rebecca D. Costa, 2009 Vanguard Press, Kindle Edition

4

Low frequency / High Severity Earthquake + Tsunami + Nuclear

5

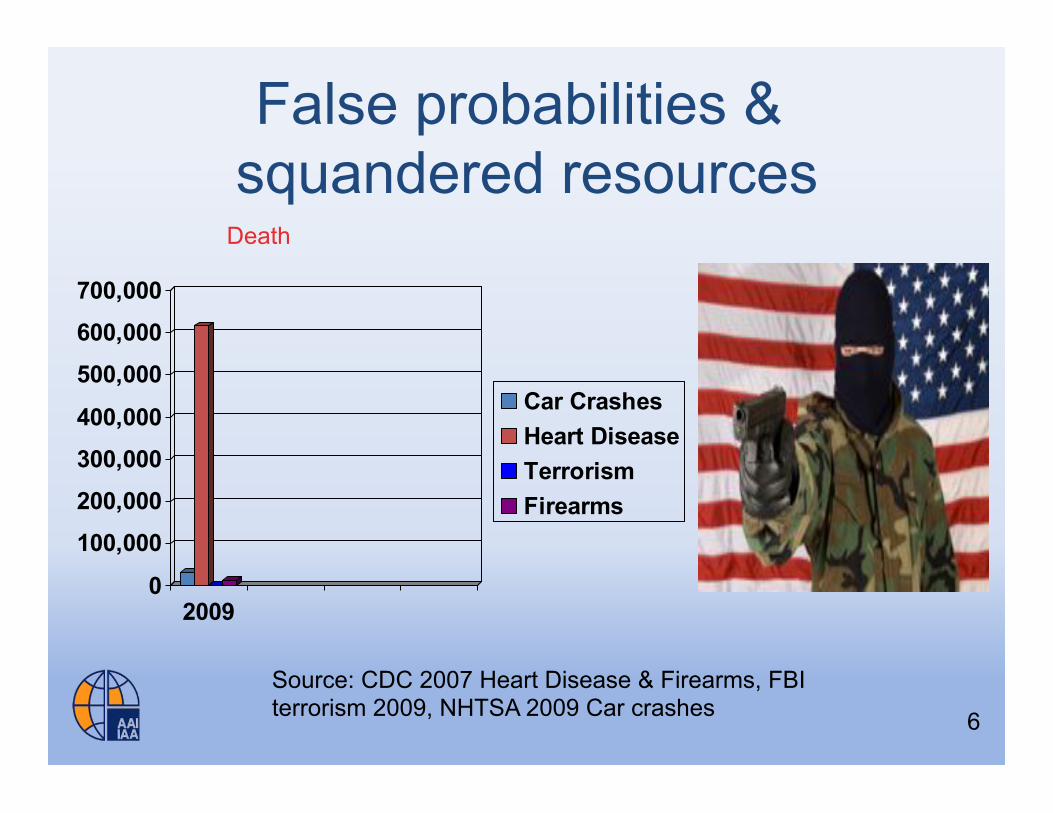

False probabilities & squandered resources

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

2009

Car CrashesHeart DiseaseTerrorismFirearms

Source: CDC 2007 Heart Disease & Firearms, FBI terrorism 2009, NHTSA 2009 Car crashes

Death

6

Decision Biases

Source: Wikipedia, Decision Making and behavioral biases

7

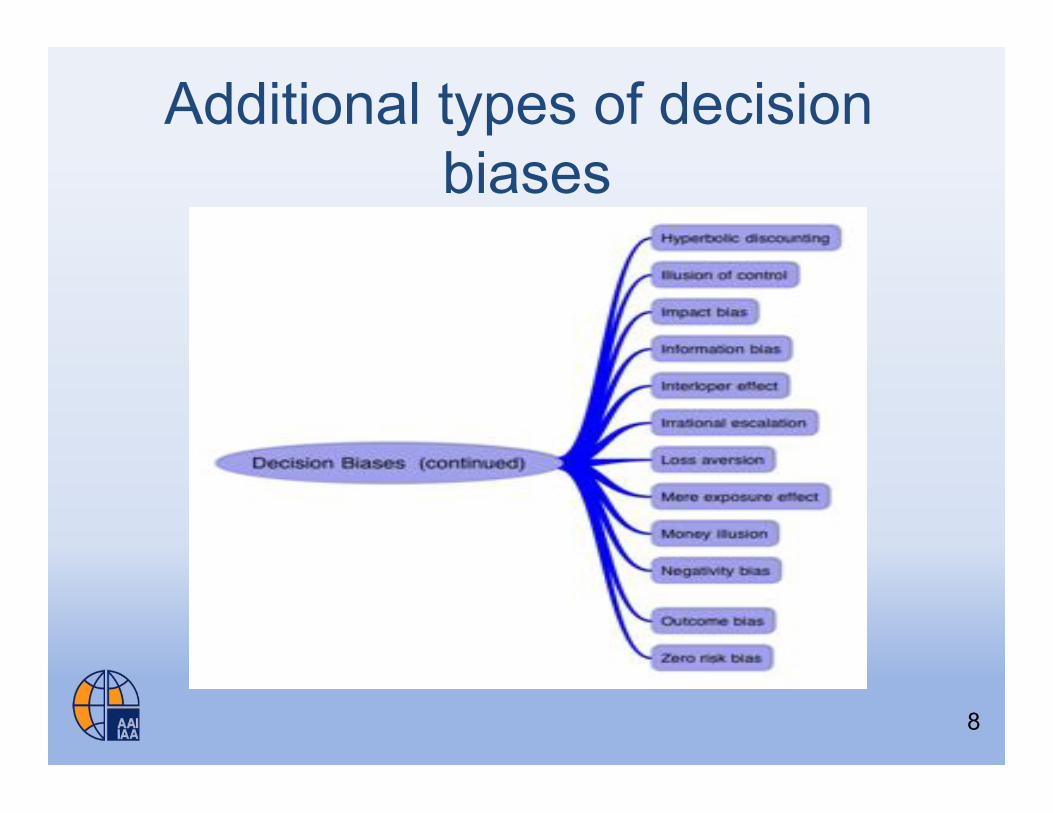

Additional types of decision biases

8

It is so darn frustrating • You note trends that reveal an

emerging uncertainty or you spot an emerging risk

• You can’t persuade anyone – Competitive market will not let you

condition the risk – The BOD is indifferent – The CFO’s vision is limited by the

needs of the quarter

9

As a consequence of the Financial Crisis

• Many different groups are coming to grips with this issue

• The only solution put forward so far is

10 10

Picture of a Stress Test

11 11

Stress Testing

With Stress Testing only one thing is different

IAJ November 2011 ERM NIRVANA 12

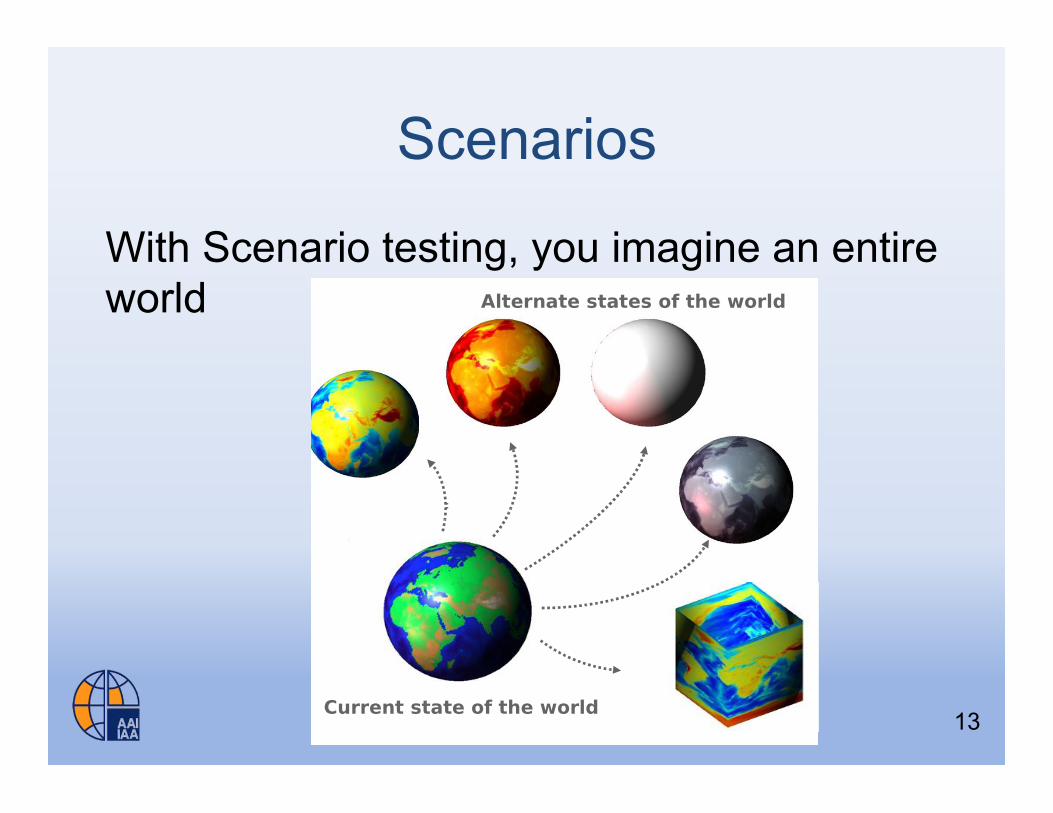

Scenarios

With Scenario testing, you imagine an entire world

!"#$%&'(() *"+,&-.$,/"#012!"#$%&3)4&'(()&

!"##$%&'(&)&$'*+'&,$'-*#./

0.&$#%)&$'(&)&$('*+'&,$'-*#./

!"#$%&'%#%()*+#,&-.

.$,/"#012&$"/&5,&2,,/&"2&6%17+%6&,89,#0:,/62&"5176&912205;,&<767#,&26"6,2&1<&6%,&=1#;>?&.$,/"#012&"#,&/16&<1#,$"2624&0/&6%"6&6%,@&/,,>&/16&9#,>0$6&6%,&<767#,&>,A,;19:,/64&576&#"6%,#&2%17;>&0;;7:0/"6,&912205;,&576&9,#%"92&,86#,:,&2067"601/2?&.$,/"#012&"#,&";21&>0<<,#,/6&<#1:&2,/2060A06@&"/";@202&=%,#,&6%,&0:9"$6&1<&"&B2:";;C&$%"/+,&1<&"&20/+;,&A"#0"5;,&02&,A";7"6,>?

()*+#,&-'%#,*%#+%*''*+$&#/%*/*0*+$%-1%,&'2%0#+#3*0*+$%#+4%,*35/#$-,6%,*75&,*0*+$'8%9"*6%#//-:%'*+&-,%0#+#3*0*+$%#+4%$"*%;-#,4%$-%0#2*%&+1-,0*4%4*)&'&-+'%#+4%#+%#+#/6'&'%-1%

$"*%&+'5,*,<'%,&'2%)-+)*+$,#$&-+'13

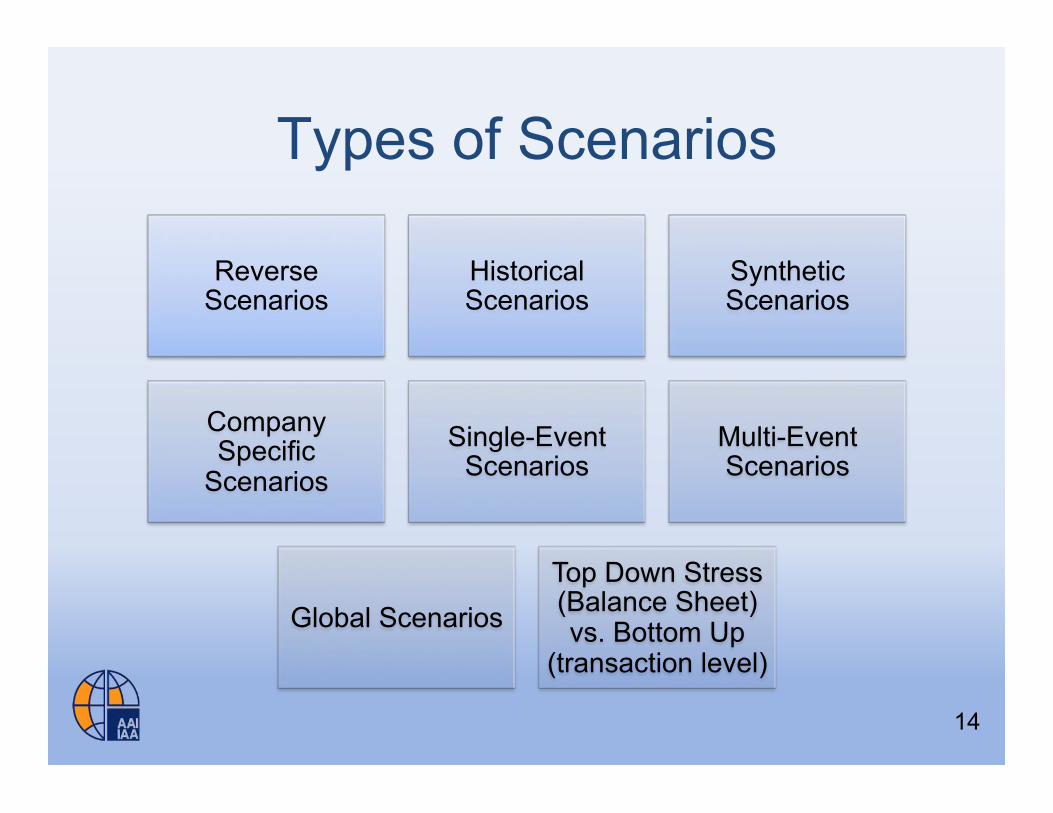

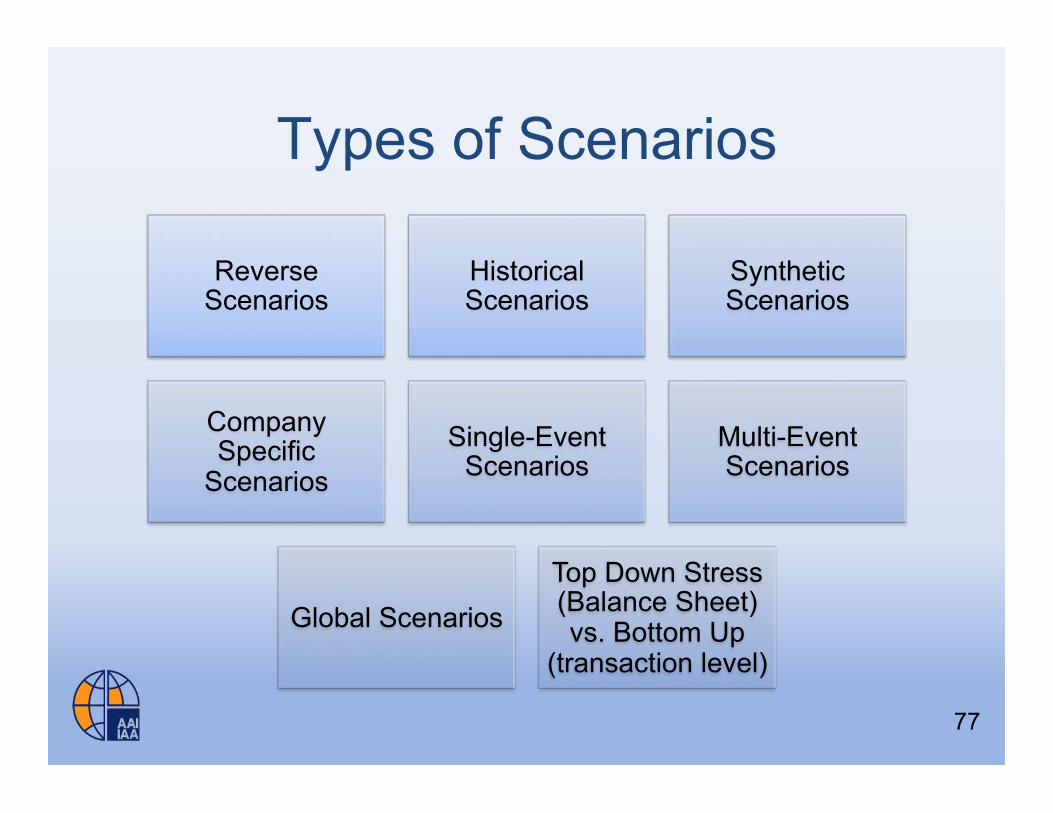

Types of Scenarios

Reverse Scenarios

Historical Scenarios

Synthetic Scenarios

Company Specific

Scenarios Single-Event

Scenarios Multi-Event Scenarios

Global Scenarios Top Down Stress (Balance Sheet) vs. Bottom Up

(transaction level)

14

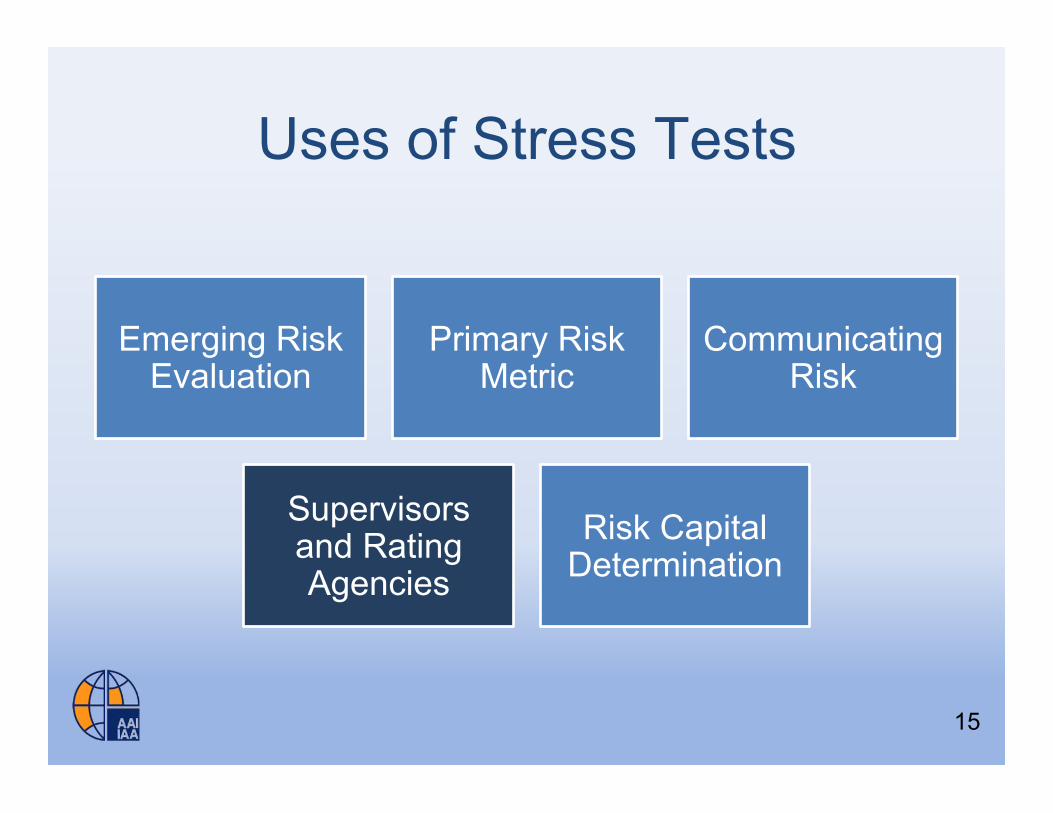

Uses of Stress Tests

Emerging Risk Evaluation

Primary Risk Metric

Communicating Risk

Supervisors and Rating Agencies

Risk Capital Determination

15

STRESS TESTING AND EMERGING RISKS

16

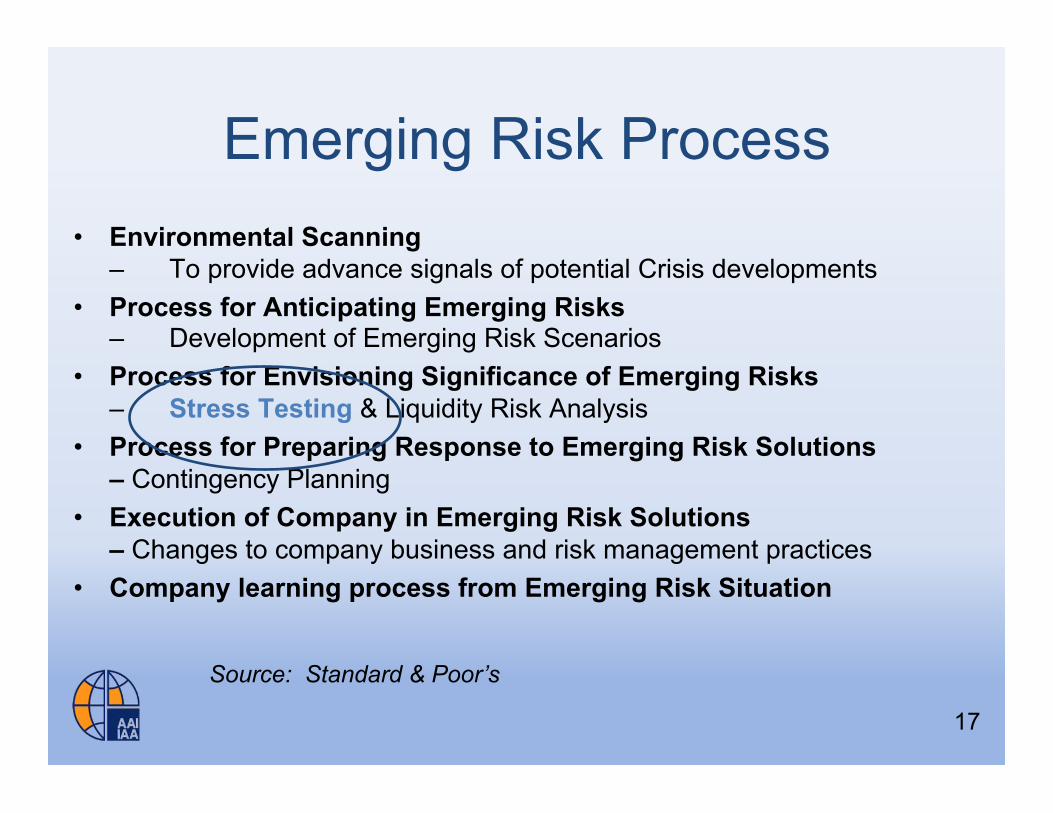

Emerging Risk Process • Environmental Scanning

– To provide advance signals of potential Crisis developments • Process for Anticipating Emerging Risks

– Development of Emerging Risk Scenarios • Process for Envisioning Significance of Emerging Risks

– Stress Testing & Liquidity Risk Analysis • Process for Preparing Response to Emerging Risk Solutions

– Contingency Planning • Execution of Company in Emerging Risk Solutions

– Changes to company business and risk management practices • Company learning process from Emerging Risk Situation

Source: Standard & Poor’s

17

World Economic Forum Emerging Risks Scenarios

• Oil price shock • Fall in value of US$ • Chinese economic hard

landing • Demographic shift • Blow up in asset prices

Economic Environmental • Climate change • Freshwater loss • Tropical storms • Earthquakes • Inland flooding

18 18

World Economic Forum Emerging Risk Scenarios

• International terrorism • Weapons of mass

destruction • Interstate/civil wars • Failed states • Transnational crime • Globalization fallback • Regional instability

Geopolitical Societal • Pandemics • Infectious diseases • Chronic diseases • Liability regimes

Technological • Critical information

infrastructure • Nanotechnology

19 19

Emerging Risks Survey

Source: Society of Actuaries

20

!"#$%&' !()*+

• !,&-. /001

– 234 5-. ,&-#6 '$%#7

– 804 9.-:);6 #$)"<6

– 804 =.%( >, -" )''6;,&-#6'

• ?6#6:@6& /0A0

– 8B4 C).. -" D).>6 %EFGH

– 8I4 J";6&");-%").;6&&%&-':

– 8A4 9$-"6'6 6#%"%:-#$)&K .)"K-"<

– 804 5-. ,&-#6 '$%#7

B

20

Other Emerging Risks • Depression • Sovereign Default • Hyperinflation • Currency Crisis • Break up of the Euro

• Solar Weather

21

Emerging Risks Types of Tests

Types of Tests – Stress Tests – Reverse Scenarios – Macro Scenarios – Historical Scenarios – Synthetic Scenarios – Company Specific Scenarios – Narrowly Specified Scenarios – Broadly Specified Scenarios

22

More on Emerging Risks Process

• May want to consider setting action triggers depending upon future changes in stress test results – As well as on indicators of immanence

23

STRESS TESTS AS A PRIMARY RISK METRIC

24

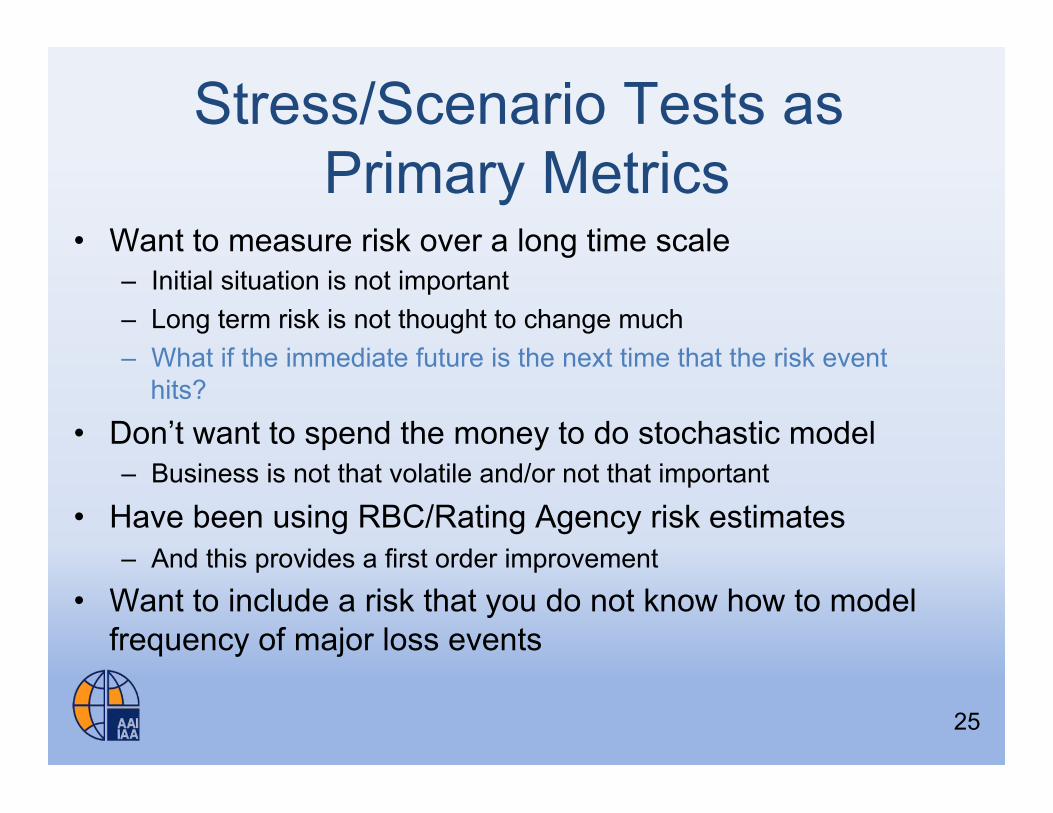

Stress/Scenario Tests as Primary Metrics

• Want to measure risk over a long time scale – Initial situation is not important – Long term risk is not thought to change much – What if the immediate future is the next time that the risk event

hits?

• Don’t want to spend the money to do stochastic model – Business is not that volatile and/or not that important

• Have been using RBC/Rating Agency risk estimates – And this provides a first order improvement

• Want to include a risk that you do not know how to model frequency of major loss events

25

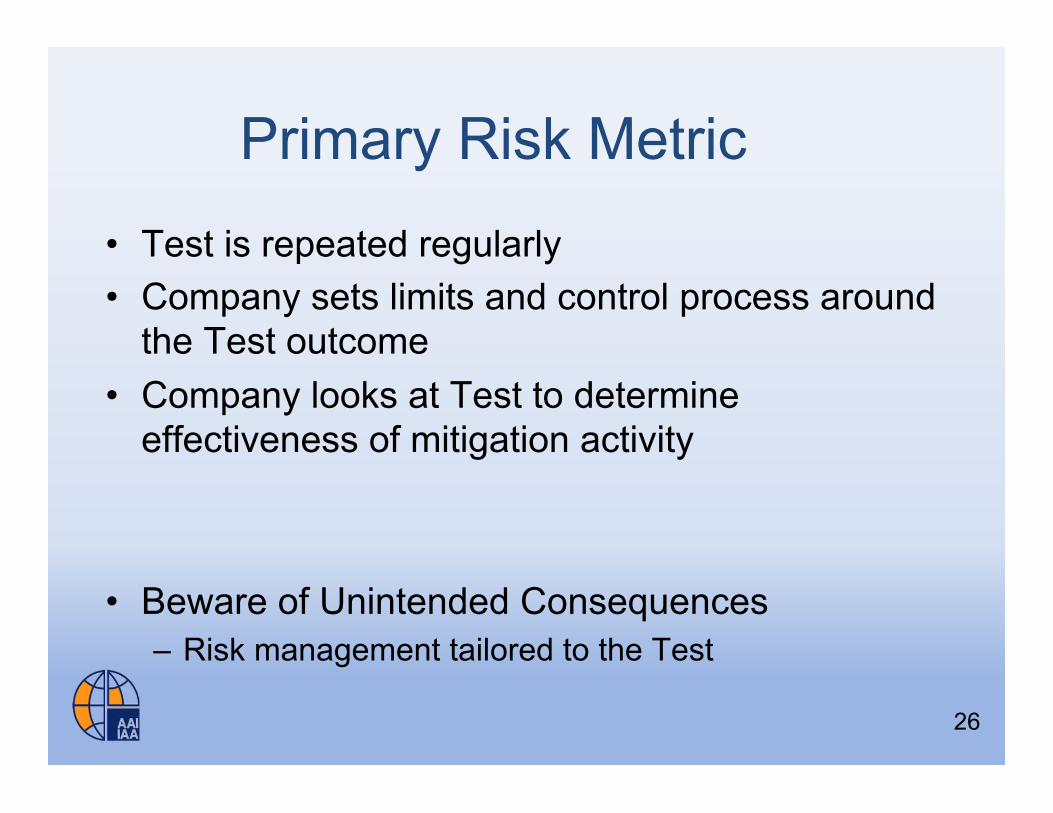

Primary Risk Metric

• Test is repeated regularly • Company sets limits and control process around

the Test outcome • Company looks at Test to determine

effectiveness of mitigation activity

• Beware of Unintended Consequences – Risk management tailored to the Test

26

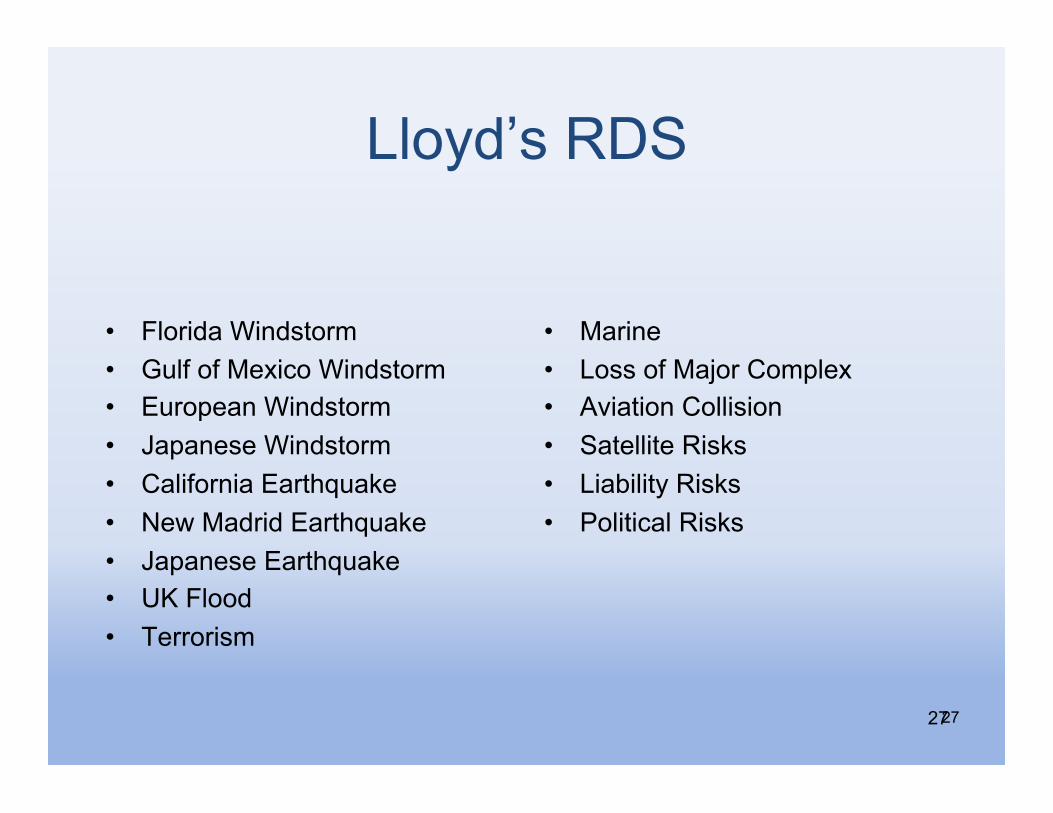

Lloyd’s RDS

• Florida Windstorm • Gulf of Mexico Windstorm • European Windstorm • Japanese Windstorm • California Earthquake • New Madrid Earthquake • Japanese Earthquake • UK Flood • Terrorism

• Marine • Loss of Major Complex • Aviation Collision • Satellite Risks • Liability Risks • Political Risks

27 27

Lloyd’s RDS Terrorism Scenario

28 28

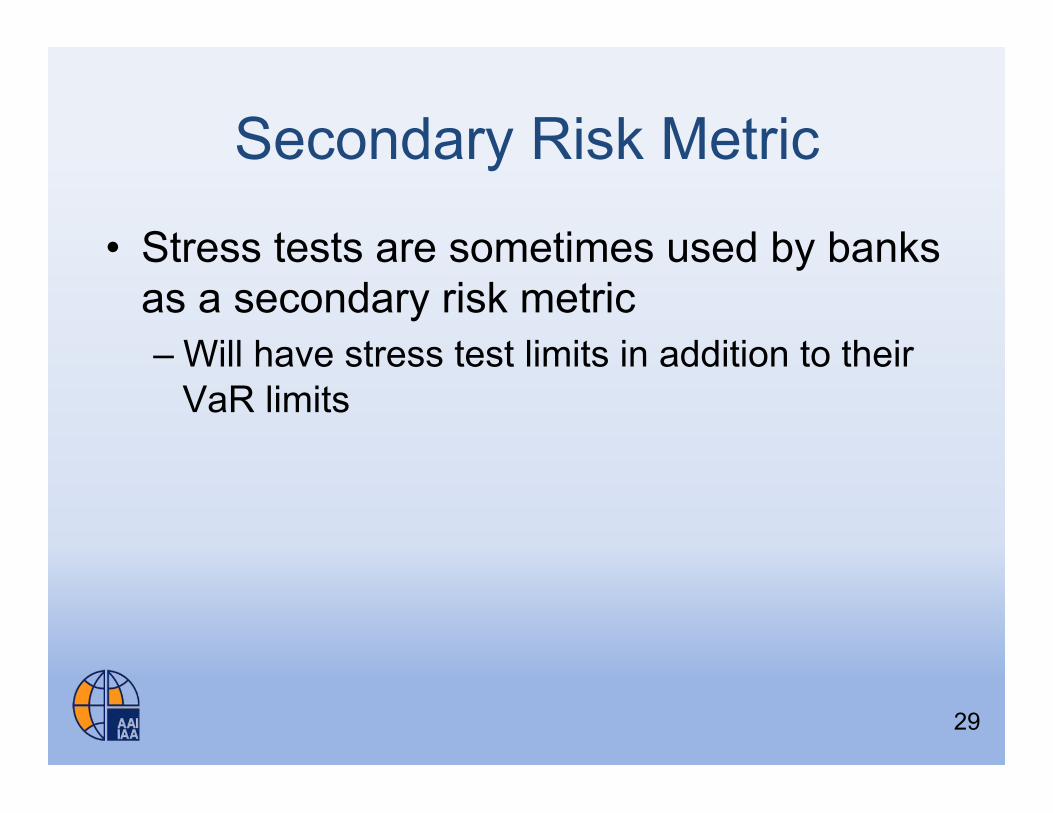

Secondary Risk Metric

• Stress tests are sometimes used by banks as a secondary risk metric – Will have stress test limits in addition to their

VaR limits

29

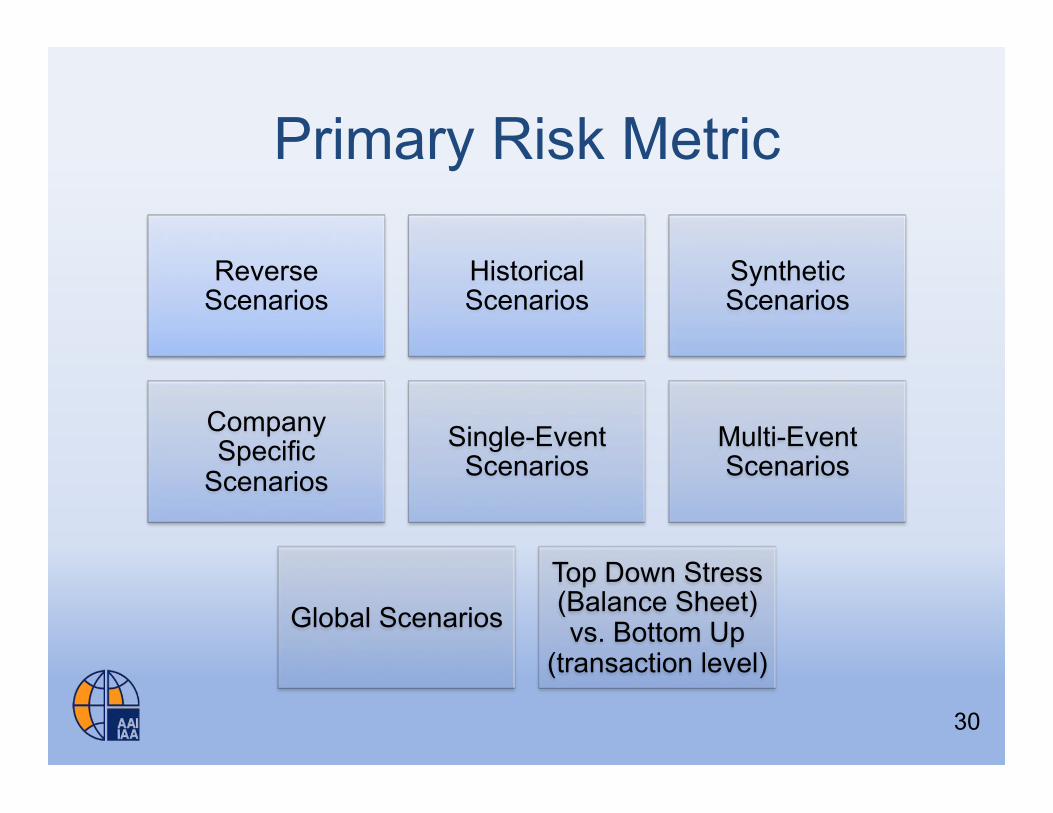

Primary Risk Metric

Reverse Scenarios

Historical Scenarios

Synthetic Scenarios

Company Specific

Scenarios Single-Event

Scenarios Multi-Event Scenarios

Global Scenarios Top Down Stress (Balance Sheet) vs. Bottom Up

(transaction level)

30

STRESS TESTS FOR COMMUNICATING WITH SENIOR MANAGEMENT AND BOARD

31

Problem with Statistical Approach

• Many people are not conversant with statistics “The average loss for stochastic scenarios with likelihood less than

1%”

– is just not something that resonates

• Stress Tests and especially Scenario Tests are stories – People all relate to stories

32

Stories

• Might include: – Reason for the choice of scenario

• Relevance of Scenario to the company

– Back story on the scenario – Description of the scenario – Description of Post event happenings – Other assumptions

Story must be believable!

33

Historical Scenarios

34

!"#$"##%

$%

&'()*+,-%./%0,1-234256%(17%08,1(92.%:1(+6-2-%

!"#$%&'()*$%+,-'-).'-/(&'"%+%-8,1(92.-%%;,<=<%05.8>%)(9>,5%89(-?%./%#!@AB%0,*5,)C,9%##5?%

DEE#B%FG+/%H(9B%DEEA"DEE@%0GC*92),%89,725%892-,-B<<<I%

.,0(/1#2"%+%-8,1(92.-%;7,4,+.*),15%./%*.5,13(+%-8,1(92.-%5?(5%8.G+7%

.88G9%%-G8?%(-%(%*(17,)28%I%

.,3&'4)-8,1(92.-%;?6*.5?,38(+%-8,1(92.-%21/.9),7%C6%?2-5.928(+%)(9>,5%

).4,-",4,15-%CG5%1.5%1,8,--(92+6%+21>,7%5.%(%-*,82J8%892-2-<I%

!#$-'25'/,)%$%+,-'-)K2,+7%LG94,%0?2M-%;,<=<%N"O%#"DP"PE"#EEC*I%

059,--%Q(5928,-%R%-2)G+5(1,.G-%).4,%21%92->%/(85.9%*928,"9(5,-%(17%

4.+(3+23,-%%

S(9=,%TG85G(3.1-%21%,'8?(1=,%9(5,-%

5

U%

Example: Most historical scenarios run by banks by type of assets (BCBS, 2005) BCBS= Basel Committee on Banking Supervision Asset type Historical scenarios Interest rates 1994 – bond market sell-off 1997 – Asian financial crisis 1998 – Combined Russian debt default and LTCM failure 2001 – 9/11 terrorist attacks in the U.S. 2003 – bond market sell-off Equities 1987 – October Black Monday

1997 – Asian financial crisis 2000 – bursting of the IT bubble 2001 - 9/11 terrorist attacks in the U.S.

FX 1992 – EMS (European Monetary System) crisis

1997 – Asian financial crisis 1998 - Russian debt default

Commodities 1973-1974 – Oil crisis Credit 1997 – Asian financial crisis

1998 – Combined Russian debt default and LTCM failure 2001 - 9/11 terrorist attacks in the U.S.

34

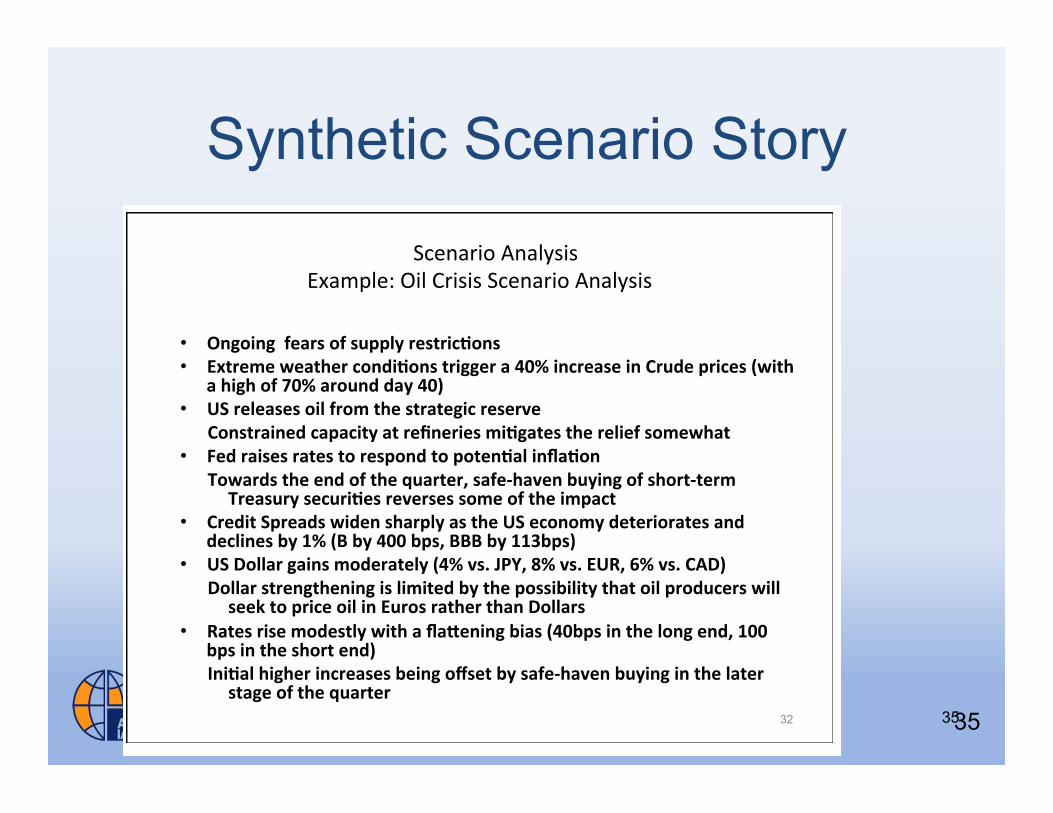

Synthetic Scenario Story

35

!"#$"##%

#&%

'()*+,(-(./0%12,%3%4225%6/,(00%67(.3,+2%

• '(8(93.7(%! :;(%0/,(00%07(.3,+2%0;2*85%<(%,(8(93./%/2%3.38=>(%/;(%7*,,(./%?20+@2.%+.%/;(%A,-B0%?2,C28+2%(D3-?8(%

• '(38+0@7%! :;(%0/,(00%07(.3,+2%0;2*85%<(%72.0+0/(./%E+/;%/;(%7*,,(./%(72.2-+7%(.9+,2.-(./F%

• G./(,.38%H2.0+0/(.7=%! :;(,(%0;2*85%<(%.2%+.72.0+0/(.7+(0%+.%/(,-0%21%/;(%-3,I(/%,+0I%0;27I0%+.%/;(%0/,(00%/(0/%J(F4F%.(43@9(%9283@8+@(0%2,%+./(,(0/%,3/(0KF%%

• L,3.*83,+/=%! :;(%0/,(00%07(.3,+2%0;2*85%<(%72.5*7/(5%E+/;%0*M7+(./%5(/3+8%/2%?,29+5(%-(3.+.41*8%,(0*8/0%3/%93,+2*0%0*<N?2,C28+2%8(9(80F%

31

%%%%%%67(.3,+2%O.38=0+0%%PD3-?8(Q%R+8%H,+0+0%67(.3,+2%O.38=0+0%%

• !"#$%"#&&'()*+&$'&+,--./&*(+0*%12$"+&

• 340*(5(&6()07(*&1$"8%2$"+&0*%##(*&)&9:;&%"1*()+(&%"&<*,8(&-*%1(+&=6%07&

)&7%#7&$'&>:;&)*$,"8&8)/&9:?&

• @A&*(.()+(+&$%.&'*$5&07(&+0*)0(#%1&*(+(*B(&

<$"+0*)%"(8&1)-)1%0/&)0&*(C"(*%(+&5%2#)0(+&07(&*(.%('&+$5(67)0&

• D(8&*)%+(+&*)0(+&0$&*(+-$"8&0$&-$0("2).&%"E)2$"&

F$6)*8+&07(&("8&$'&07(&G,)*0(*H&+)'(I7)B("&J,/%"#&$'&+7$*0I0(*5&

F*()+,*/&+(1,*%2(+&*(B(*+(+&+$5(&$'&07(&%5-)10&

• <*(8%0&A-*()8+&6%8("&+7)*-./&)+&07(&@A&(1$"$5/&8(0(*%$*)0(+&)"8&

8(1.%"(+&J/&K;&=L&J/&9::&J-+H&LLL&J/&KKMJ-+?&

• @A&N$..)*&#)%"+&5$8(*)0(./&=9;&B+O&PQRH&S;&B+O&3@TH&U;&B+O&<VN?&

N$..)*&+0*("#07("%"#&%+&.%5%0(8&J/&07(&-$++%J%.%0/&07)0&$%.&-*$8,1(*+&6%..&

+((W&0$&-*%1(&$%.&%"&3,*$+&*)07(*&07)"&N$..)*+&

• T)0(+&*%+(&5$8(+0./&6%07&)&E)X("%"#&J%)+&=9:J-+&%"&07(&.$"#&("8H&K::&

J-+&%"&07(&+7$*0&("8?&

Y"%2).&7%#7(*&%"1*()+(+&J(%"#&$Z+(0&J/&+)'(I7)B("&J,/%"#&%"&07(&.)0(*&

+0)#(&$'&07(&G,)*0(*&

32 35

Soverign Default Story

36

4

Scenario: Narrative

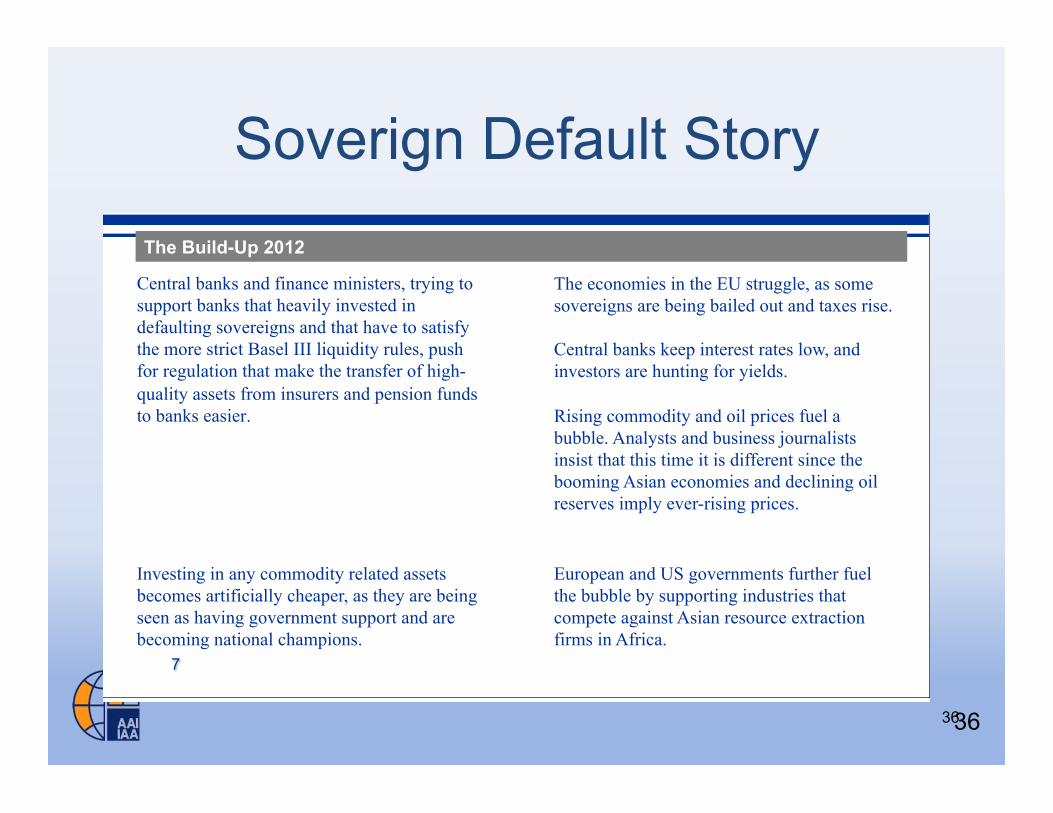

Central banks and finance ministers, trying to support banks that heavily invested in defaulting sovereigns and that have to satisfy the more strict Basel III liquidity rules, push for regulation that make the transfer of high-quality assets from insurers and pension funds to banks easier.

The economies in the EU struggle, as some sovereigns are being bailed out and taxes rise. Central banks keep interest rates low, and investors are hunting for yields. Rising commodity and oil prices fuel a bubble. Analysts and business journalists insist that this time it is different since the booming Asian economies and declining oil reserves imply ever-rising prices.

The Build-Up 2012

European and US governments further fuel the bubble by supporting industries that compete against Asian resource extraction firms in Africa.

Investing in any commodity related assets becomes artificially cheaper, as they are being seen as having government support and are becoming national champions. 7

Scenario: Narrative

8

A number of banks default that were heavily exposed to speculative investments, impacting directly those insurers that lent liquid bonds against illiquid collateral

Insurers holding illiquid assets are savagely punished, since the market does not know the value of their portfolios and their share prices collapse..

In 2015, the commodity bubble bursts, the Asian and African economies which propped up the financial markets go into recession and a flight to safety results.

The Crash 2015

Speculators and day traders go into commodities, throwing further gasoline into the bubble. Africa is becoming the new China and is taking up the slack of Asia, that sees growth declining.

The Mania 2013-2014 Some insurers are buying up long-dated bonds issued by start-ups that try to benefit from the commodities bubble. They outperform their more conservative competitors. The CEOs of the underperforming insurers are replaced and exposures to the speculative bubble in the insurance market increases

36

Soverign Default Story

37

4

Scenario: Narrative

Central banks and finance ministers, trying to support banks that heavily invested in defaulting sovereigns and that have to satisfy the more strict Basel III liquidity rules, push for regulation that make the transfer of high-quality assets from insurers and pension funds to banks easier.

The economies in the EU struggle, as some sovereigns are being bailed out and taxes rise. Central banks keep interest rates low, and investors are hunting for yields. Rising commodity and oil prices fuel a bubble. Analysts and business journalists insist that this time it is different since the booming Asian economies and declining oil reserves imply ever-rising prices.

The Build-Up 2012

European and US governments further fuel the bubble by supporting industries that compete against Asian resource extraction firms in Africa.

Investing in any commodity related assets becomes artificially cheaper, as they are being seen as having government support and are becoming national champions. 7

Scenario: Narrative

8

A number of banks default that were heavily exposed to speculative investments, impacting directly those insurers that lent liquid bonds against illiquid collateral

Insurers holding illiquid assets are savagely punished, since the market does not know the value of their portfolios and their share prices collapse..

In 2015, the commodity bubble bursts, the Asian and African economies which propped up the financial markets go into recession and a flight to safety results.

The Crash 2015

Speculators and day traders go into commodities, throwing further gasoline into the bubble. Africa is becoming the new China and is taking up the slack of Asia, that sees growth declining.

The Mania 2013-2014 Some insurers are buying up long-dated bonds issued by start-ups that try to benefit from the commodities bubble. They outperform their more conservative competitors. The CEOs of the underperforming insurers are replaced and exposures to the speculative bubble in the insurance market increases

37

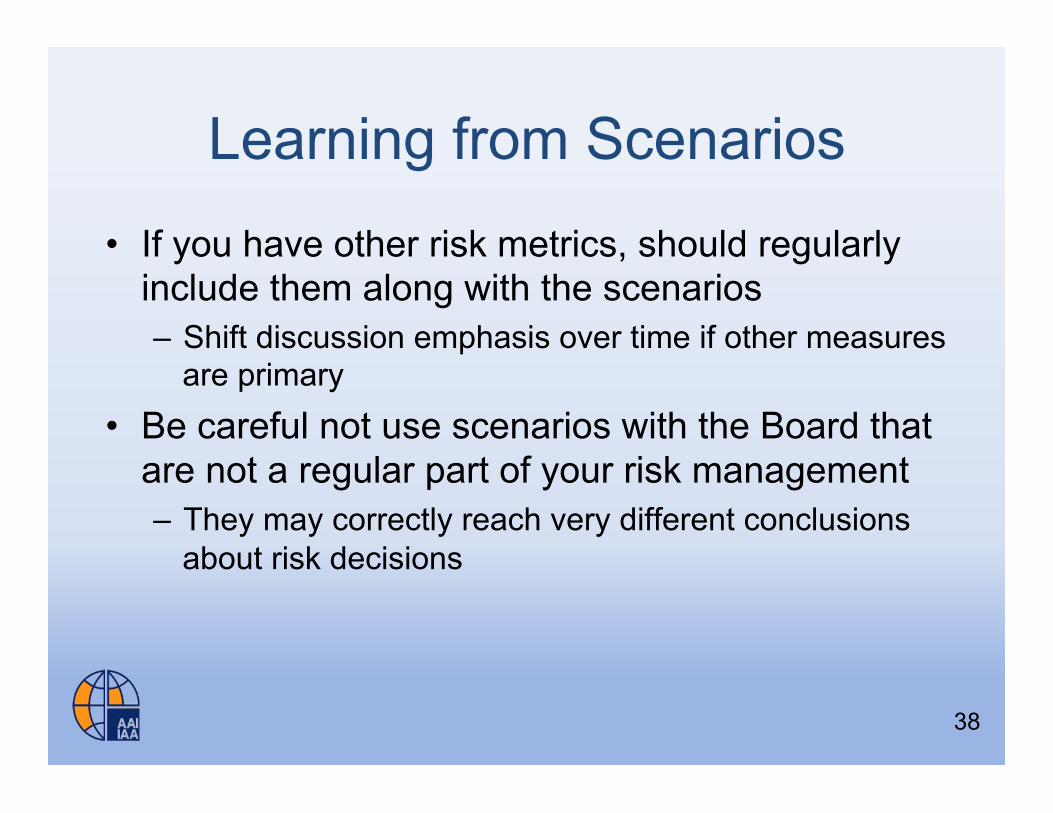

Learning from Scenarios

• If you have other risk metrics, should regularly include them along with the scenarios – Shift discussion emphasis over time if other measures

are primary

• Be careful not use scenarios with the Board that are not a regular part of your risk management – They may correctly reach very different conclusions

about risk decisions

38

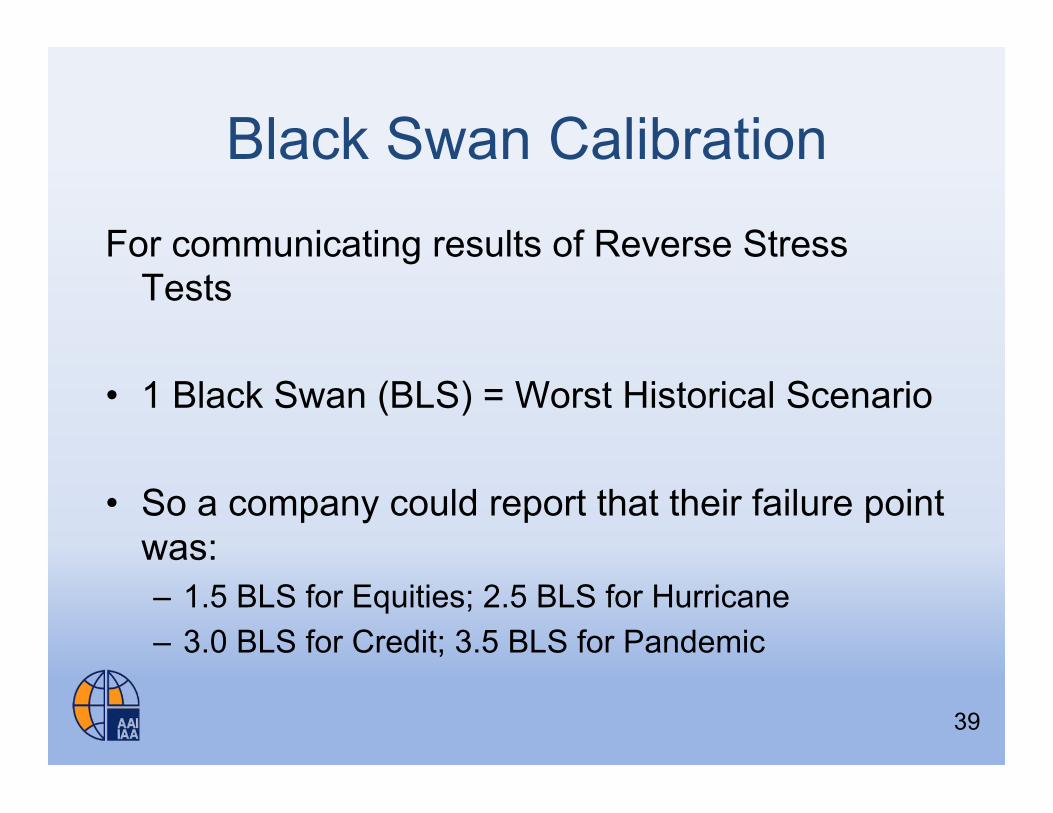

Black Swan Calibration

For communicating results of Reverse Stress Tests

• 1 Black Swan (BLS) = Worst Historical Scenario

• So a company could report that their failure point was: – 1.5 BLS for Equities; 2.5 BLS for Hurricane – 3.0 BLS for Credit; 3.5 BLS for Pandemic

39

Communicating Risk

Reverse Scenarios

Historical Scenarios

Synthetic Scenarios

Company Specific

Scenarios Single-Event

Scenarios Multi-Event Scenarios

Global Scenarios Top Down Stress (Balance Sheet) vs. Bottom Up

(transaction level)

40

STRESS TESTS FOR REGULATORS AND RATING AGENCIES

41

Recent Developments

• US and European Bank Stress Tests • European Insurer Stress Tests • IMF / IAA Stress Testing Workshop • AM Best SRQ

42

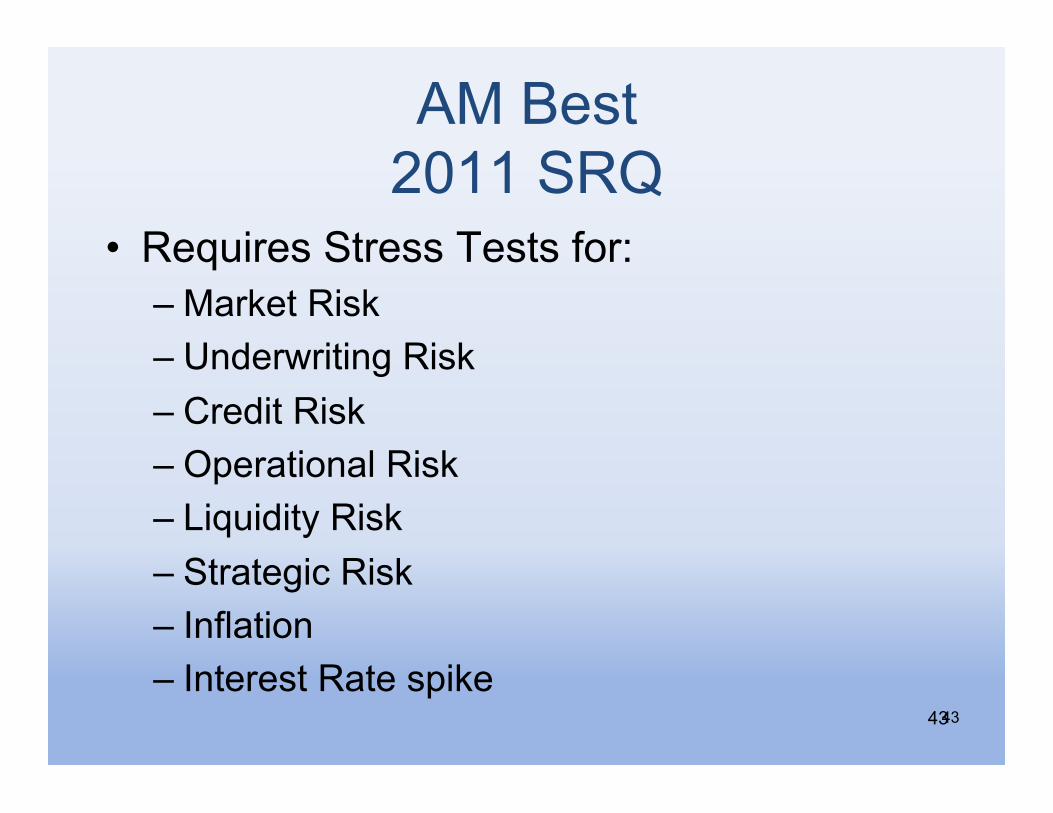

AM Best 2011 SRQ

• Requires Stress Tests for: – Market Risk – Underwriting Risk – Credit Risk – Operational Risk – Liquidity Risk – Strategic Risk – Inflation – Interest Rate spike

43 43

44 44

Outcome of EIOPA Stress Tests

45

!!"

#$$%&$'(&")&*+,(*""

"" !""#$"%&$'()*"+#$,

( *-(./0(1*22*3- *-(4 (

-,.$./,&"0'1.(',"/&23%&"*(%&** 455 " (

6.7.8+8")&9+.%&:";'1.(',"<6;)="/&23%&"*(%&** !4>

" (

?3,@&70A"?+%1,+*" B>4

" (

6;)"03@&%'$&"%'(.3"" "

CDEF (

6;)"03@&%'$&"%'(.3".7"/'*&,.7&"*0&7'%.3 " C>EF (

6;)"03@&%'$&"%'(.3".7"':@&%*&"*0&7'%.3 " >D!F (

6;)"03@&%'$&"%'(.3".7".72,'(.37"*0&7'%.3 " CB>F (

567%8&(3-($2*"*12$((8%7*&%2( *-(./0(1*22*3-( %,(%(7$#8$-&%"$(39($2*"*12$(8%7*&%2

:32;$-8<('$9*8*&(39(+-'$#&%=*-",((-3&(6$$&*-"(

&>$(?@0((A*-(./0(1*22*3-B

G'*&,.7&"*0&7'%.3 H> !4IH >IJ

#:@&%*&"*0&7'%.3 !4E >JIE BIB

K72,'(.37"*0&7'%.3 4D !EIE >I4

?3@&%&.$7"?(%&**"?0&7'%.3 CC 4IJ CIB

Capital

45

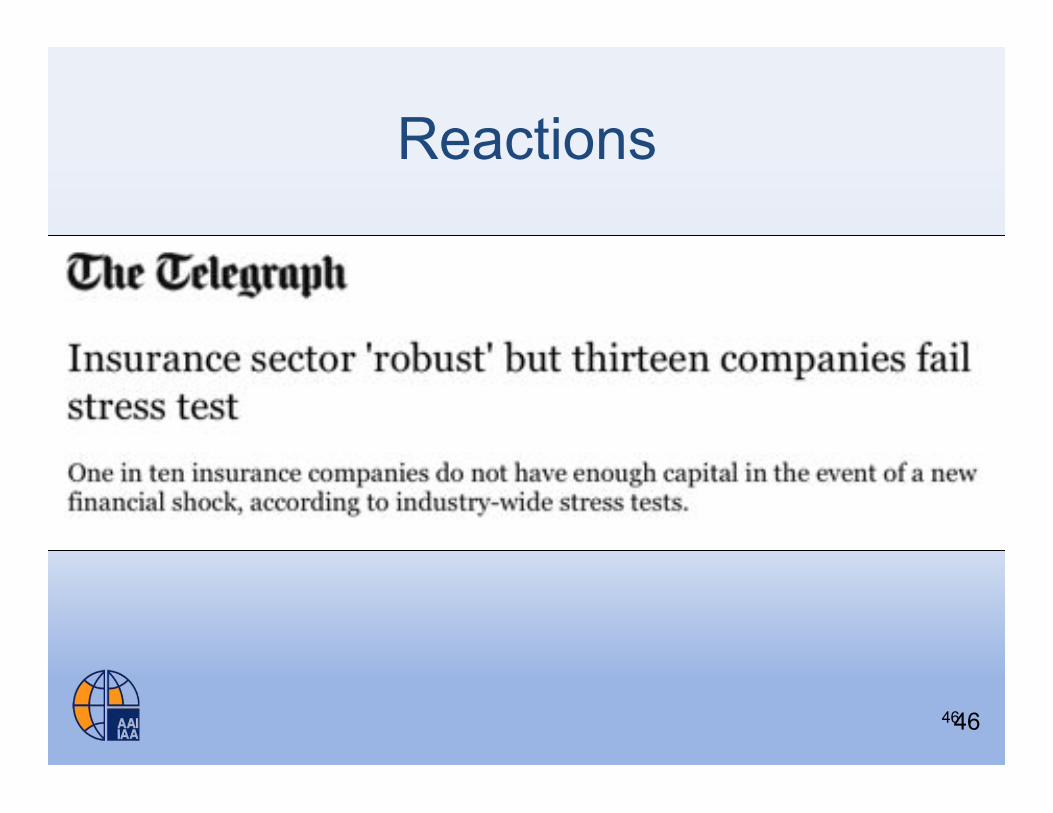

Reactions

46 46

Another Reaction

47 47

NAIC on Stress Tests • Utilizing the extensive NAIC database, the NAIC can perform stress

tests on both micro and macro levels. At present, insurance companies in the U.S. are not required to perform nor report stress test results to the regulators.

• The G20 has stated, “We commit to conduct robust, transparent stress tests as needed.”

• IAIS Insurance Core Principles, upon which supervisory regimes are assessed in the Financial Sector Assessment Program (FSAP), state, “The supervisory authority requires insurers to recognise the range of risks that they face and assess and manage them effectively.” There is also the following advanced criteria: “The supervisory authority requires that insurers undertake regular stress testing for a range of adverse scenarios in order to assess the adequacy of capital resources in case technical provisions have to be increased.”

48 48

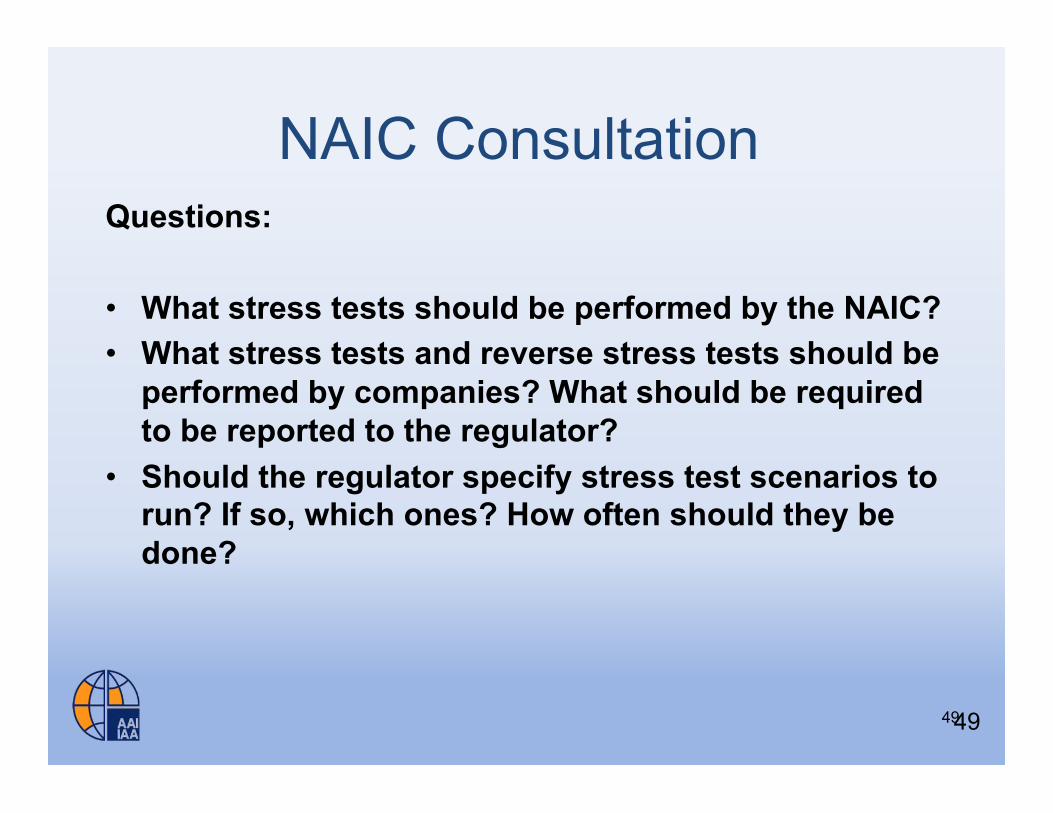

NAIC Consultation Questions:

• What stress tests should be performed by the NAIC? • What stress tests and reverse stress tests should be

performed by companies? What should be required to be reported to the regulator?

• Should the regulator specify stress test scenarios to run? If so, which ones? How often should they be done?

49 49

International Monetary Fund

50

!"#$%&&'()*!"#'#+,-+.)#/,$,0.1#1"/,(2"&1"34#'%3+2(,3,1$4#,"#"115#26#(17%3'3,2"'.#022$34#'77.)#$3(1$$#31$3$#32#$13#8'7,3'.#(19%,(1&1"3$4#(1$3(',","-#3+1#%$1#26#$3(1$$#31$3,"-#'$#'#/%."1('0,.,3,1$#$%(/1,..'"81#322.:!"$%('"81#,"5%$3()#,$#2/1(;+1.&15#;,3+#"1;#'"5#$2&13,&1$#%"822(5,"'315#$3(1$$#31$3#(19%,(1&1"3$:#<+1#$)$31&,8#'"5#8(2$$02(51(#,$$%1$#'"5#,&7.,8'3,2"$#26#3+1#$2.%3,2"$#62%"5#62(#3+1#0'"=,"-#$1832(#+'/1#'#31"51"8)#32#01#3('"$61((15#32#3+1#,"$%('"81#$1832(#;,3+2%3#5%1#(1-'(5#26#5,661(1"3,'3,2"#%"51(#+,-+#3,&1#7(1$$%(1:

>1'51($+,7#(2.1#,"#'55(1$$,"-#$)$31&,8#'"5#8(2$$02(51(#,$$%1$#,"#3+1#0'"=,"-#$1832(:<+1(1#,$#'"#1?7183'3,2"#32#$11#3+1#!@A#1?7'"5,"-#3+,$#.1'51($+,7#32#3+1#,"$%('"81#'"5#23+1(#6,"'"8,'.#$1832($:B1/1.27#&'8(2182"2&,8#322.$#32#'55(1$$#$)$31&,8#(,$=#,"#3+1#;+2.1#6,"'"8,'.#$1832(4#,"8.%5,"-#,"$%('"81:C2,"3#2%3##72$$,0.1#62(&$#26#(1-%.'32()#'(0,3('-1:

50

IMF Proposal

51

!"#"$%&'(')*+"))'*")*',%+'-$%.($'(/*0#"'01)2+(1/"'-+%2&)'()'('*%%$'*%'())"))'+"-2$(*%+3'()'4"$$'()'%&"+(*0%1($'()&"/*)'%,'/+%)).%+5"+'01)2+(1/"'(/*0#0*3'

40*6'*6"'2$*07(*"'"8&"/*"5'%2*/%7"*%'07&+%#"')2+#"0$$(1/"'%,'01*"+1(*0%1($'(/*0#"'$(+-"'01)2+"+)'(15'+"01)2+"+)(#%0501-'52&$0/(*0%1'(15'(&&$301-'*6"'+0-6*'$"#"$'%,'+"-2$(*0%1'(15')2&"+#0)0%19

:6"')*+"))'*")*'40$$'."'2)"5'*%;<))"))'*6"'07&(/*'%,'/(&0*($'7%.0$0*3'01'*07")'%,',01(1/0($')*+"))<))"))7"1*'%,'-+%2&)= 01*"+1($'7%5"$)'(15'>2($0*3'%,'+0)?'7(1(-"7"1*@%1*+0.2*"'*%'*6"'(1($3)0)'%,'/%1*(-0%1'40*601'(15'(7%1-'-+%2&)A1*"+'*6"'1""5"5'B%C

51

IMF Proposal

52

!"#"$%&'(')*+"))'*")*',%+'-$%.($'(/*0#"'01)2+(1/"'-+%2&)'()'('*%%$'*%'())"))'+"-2$(*%+3'()'4"$$'()'%&"+(*0%1($'()&"/*)'%,'/+%)).%+5"+'01)2+(1/"'(/*0#0*3'

40*6'*6"'2$*07(*"'"8&"/*"5'%2*/%7"*%'07&+%#"')2+#"0$$(1/"'%,'01*"+1(*0%1($'(/*0#"'$(+-"'01)2+"+)'(15'+"01)2+"+)(#%0501-'52&$0/(*0%1'(15'(&&$301-'*6"'+0-6*'$"#"$'%,'+"-2$(*0%1'(15')2&"+#0)0%19

:6"')*+"))'*")*'40$$'."'2)"5'*%;<))"))'*6"'07&(/*'%,'/(&0*($'7%.0$0*3'01'*07")'%,',01(1/0($')*+"))<))"))7"1*'%,'-+%2&)= 01*"+1($'7%5"$)'(15'>2($0*3'%,'+0)?'7(1(-"7"1*@%1*+0.2*"'*%'*6"'(1($3)0)'%,'/%1*(-0%1'40*601'(15'(7%1-'-+%2&)A1*"+'*6"'1""5"5'B%C

52

IMF Next Steps

53

!"#$%&'()'*)$()&(*'"+$,)-"'./)'*)#0/#"%1)2#3#,'/)%4#)+#%4'5','-6)%4$%)&1)$//,&7$8,#)%')1%"#11)%#1%&(-)-,'8$,)-"'./19($8,#)$(5)/"'+'%#)%4#).1#)'*)%4#)1%"#11)%#1%1)*'")-,'8$,)-"'./1)$%)%4#)1./#"3&1'"6)7',,#$-.#1),#3#,:'(&%'")%4#)/"'/#").1#)$(5)7'(1%$(%)./5$%&(-)'*)%4#)%'',1;

53

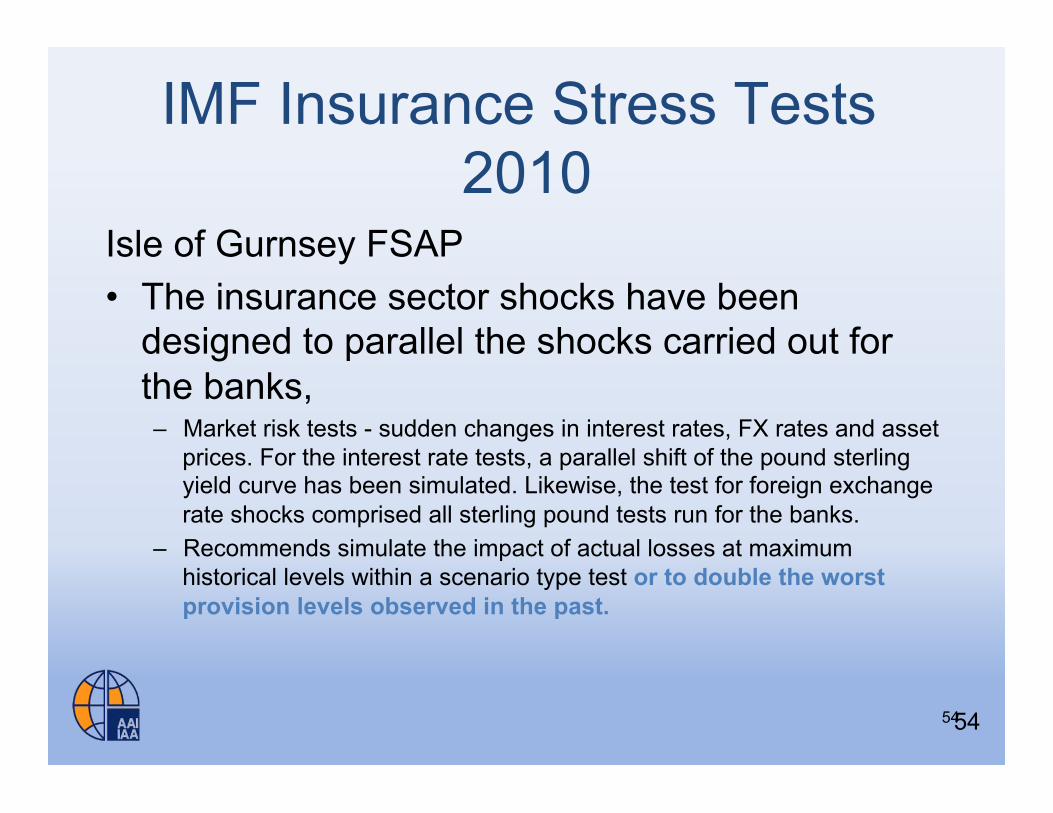

IMF Insurance Stress Tests 2010

Isle of Gurnsey FSAP • The insurance sector shocks have been

designed to parallel the shocks carried out for the banks, – Market risk tests - sudden changes in interest rates, FX rates and asset

prices. For the interest rate tests, a parallel shift of the pound sterling yield curve has been simulated. Likewise, the test for foreign exchange rate shocks comprised all sterling pound tests run for the banks.

– Recommends simulate the impact of actual losses at maximum historical levels within a scenario type test or to double the worst provision levels observed in the past.

54 54

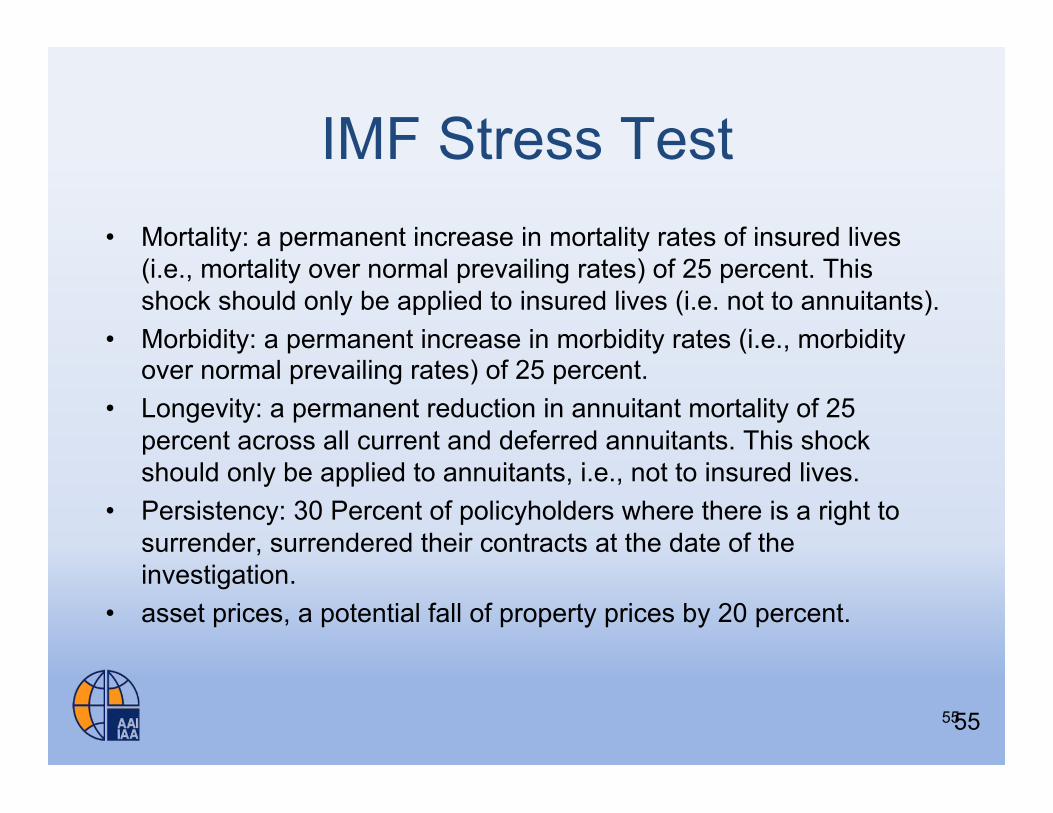

IMF Stress Test • Mortality: a permanent increase in mortality rates of insured lives

(i.e., mortality over normal prevailing rates) of 25 percent. This shock should only be applied to insured lives (i.e. not to annuitants).

• Morbidity: a permanent increase in morbidity rates (i.e., morbidity over normal prevailing rates) of 25 percent.

• Longevity: a permanent reduction in annuitant mortality of 25 percent across all current and deferred annuitants. This shock should only be applied to annuitants, i.e., not to insured lives.

• Persistency: 30 Percent of policyholders where there is a right to surrender, surrendered their contracts at the date of the investigation.

• asset prices, a potential fall of property prices by 20 percent.

55 55

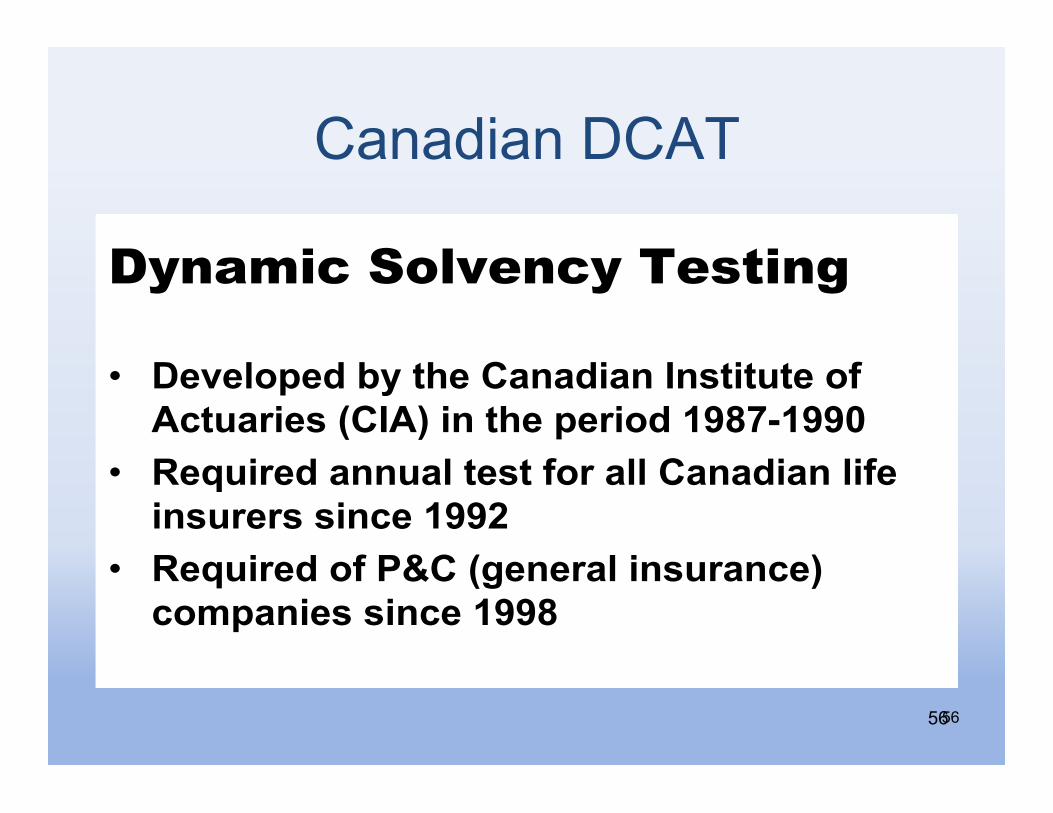

Canadian DCAT

!

!"#$%&'()*+,-#'"(.-/0

" !"#"$%&"'()*(+,"(-./.'0./(1/2+0+3+"(%4(56+3.70"2(8-159(0/(+,"(&"70%'(:;<=>:;;?

" @"A307"'(.//3.$(+"2+(4%7(.$$(-./.'0./($04"(0/237"72(20/6"(:;;B

" @"A307"'(%4(CD-(8E"/"7.$(0/237./6"9(6%F&./0"2(20/6"(:;;<

56 56

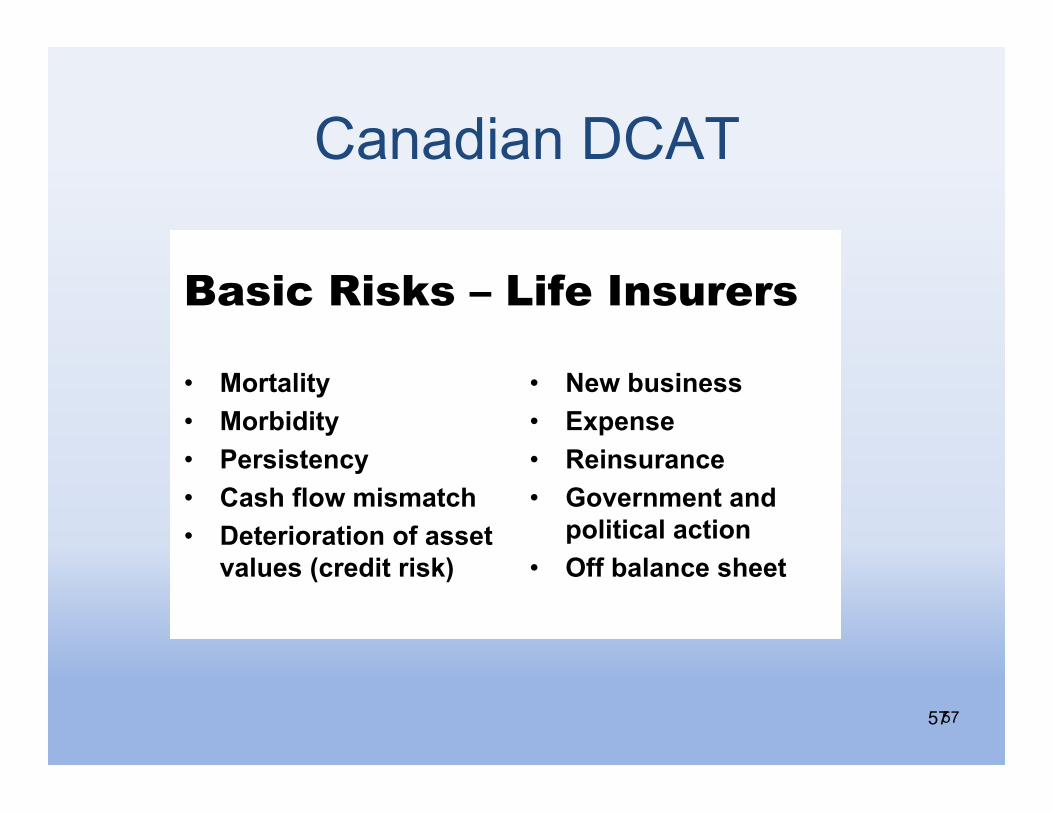

Canadian DCAT

57

!"

!"#$%&'$#(#&) *$+,&-.#/0,0#

# !"#$%&'$(# !"#)'*'$(# +,#-'-$,./(# 0%-123&"425'-5%$/1# 6,$,#'"#%$'".2"32%--,$27%&8,-29/#,*'$2#'-:;

# <,42)8-'.,--# =>?,.-,# @,'.-8#%./,# A"7,#.5,.$2%.*2?"&'$'/%&2%/$'".

# B332)%&%./,2-1,,$

57

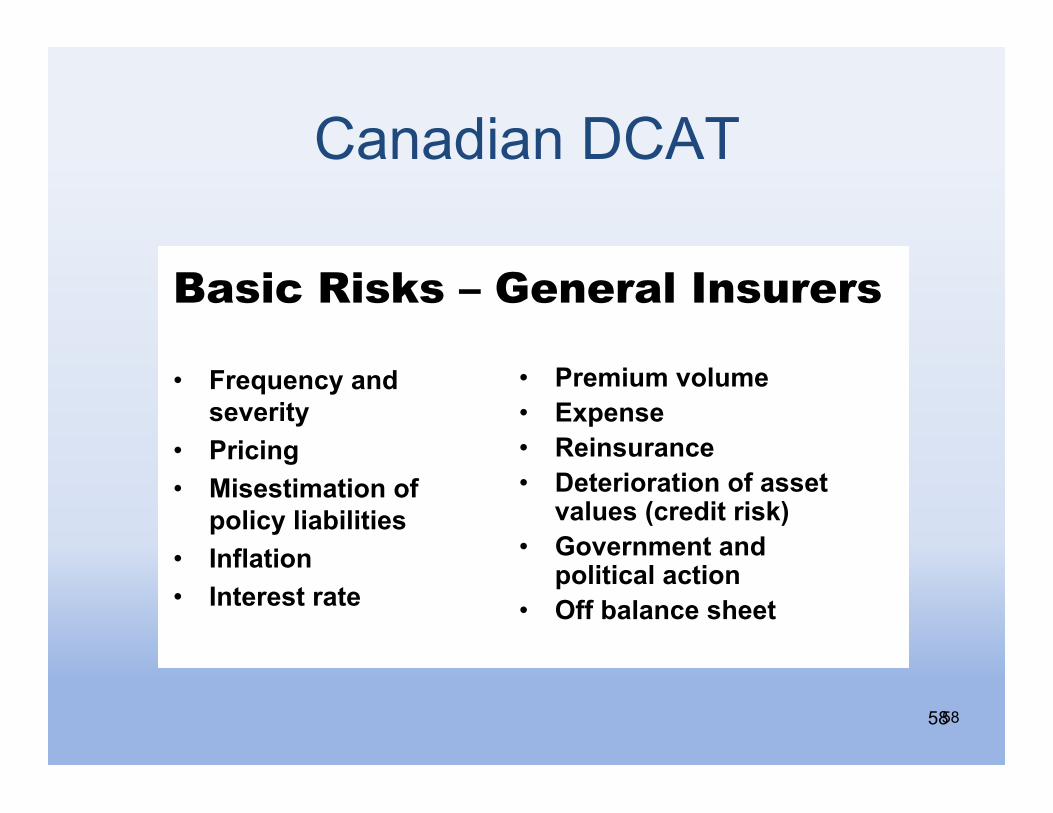

Canadian DCAT

58

!"

!"#$%&'$#(#&) *+,+-".&/,#0-+-#

# !"#$%#&'()*&+),#-#"./(

# 0".'.&1# 2.,#,/.3*/.4& 45)647.'()7.*8.7./.#,

# 9&57*/.4&# 9&/#"#,/)"*/#

# 0"#3.%3)-47%3## :;6#&,## <#.&,%"*&'## =#/#".4"*/.4&)45)*,,#/)-*7%#,)>'"#+./)".,?@

# A4-#"&3#&/)*&+)647./.'*7)*'/.4&

# B55)8*7*&'#),C##/

58

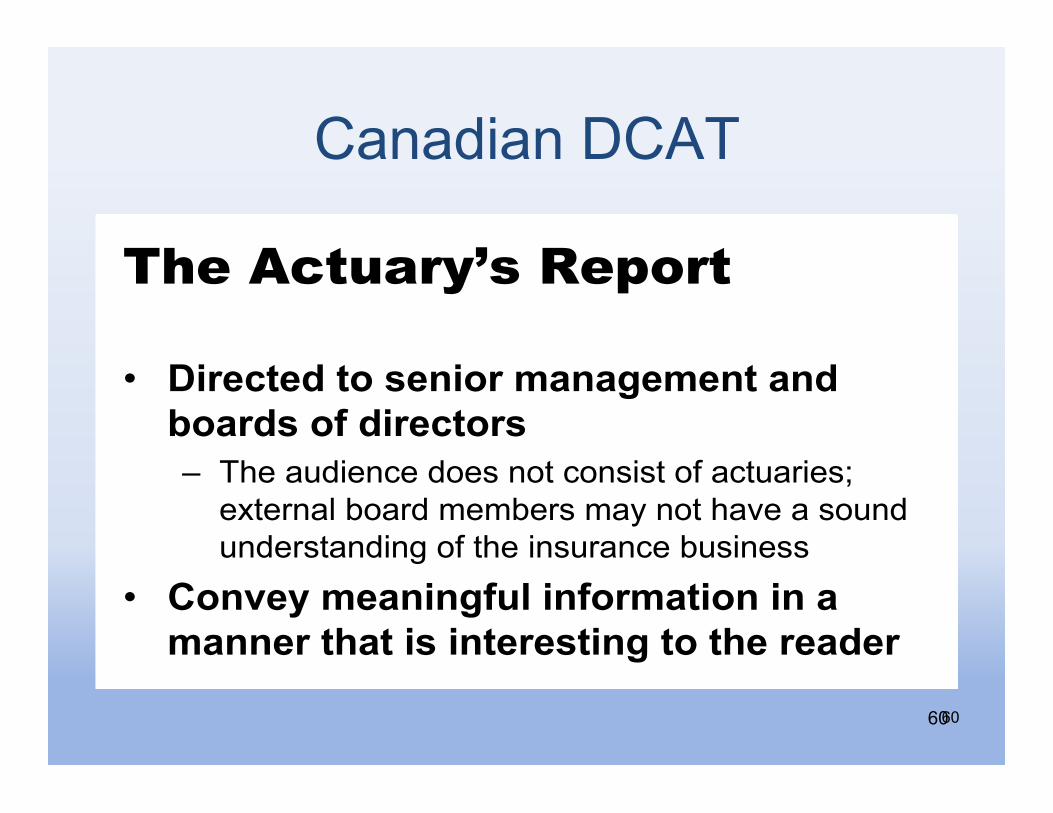

Canadian DCAT

59

!"

!"#"$%&'()*$"'+,&-*

# !"#$%#&$'"()*%+#+",,-%.$()/$.%0(*1%23$%)'#+($(4#%5+#)'$##%6,"'%7 6(*/).$#%"%#2"'."(.%*0%&*16"()#*'

# 8*.$,%1"'"9$1$'2%($"&2)*'%2*%&3"'9$#%)'%$:6$()$'&$$ %&'(&)*+,-+.')/01-'-2+,

# ;*'#).$(%($9+,"2*(-%($"&2)*'

59

Canadian DCAT

!"

!"#$%&'()*+,-$.#/0*'

# !"#$%&$'(&)(*$+")#(,-+-.$,$+&(-+'(/)-#'*()0('"#$%&)#*$ %&'()*+,'-.'(+/'0(-/1(./-0,01(/2().1*)3,'04('51'3-)6(7/)3+(8'87'30(8)9(-/1(&):'()(0/*-+(*-+'301)-+,-;(/2(1&'(,-0*3)-.'(7*0,-'00

# 1)+2$3(,$-+"+.045("+0)#,-&")+("+(-(,-++$#(&6-&("*("+&$#$*&"+.(&)(&6$(#$-'$#

60 60

Canadian DCAT Example: Recession and Stagflation scenario

• Driven by rapid rise in price of oil caused by industrialization of India and China

• US$ falls 25% over five years due to budget and trade deficits

• Inflation driven upwards 300 points in one year by lower dollar and oil price

• Interest rates follow suit

From 2006 DCAT Report 61

62

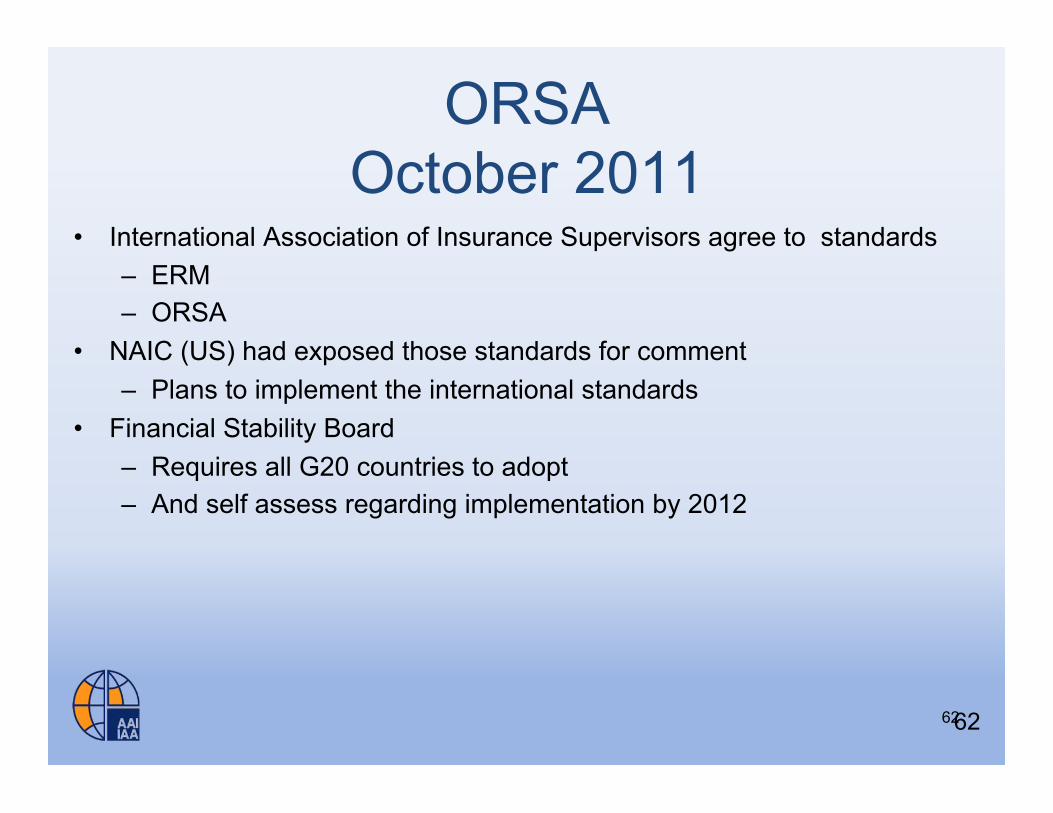

ORSA October 2011

• International Association of Insurance Supervisors agree to standards – ERM – ORSA

• NAIC (US) had exposed those standards for comment – Plans to implement the international standards

• Financial Stability Board – Requires all G20 countries to adopt – And self assess regarding implementation by 2012

62

63

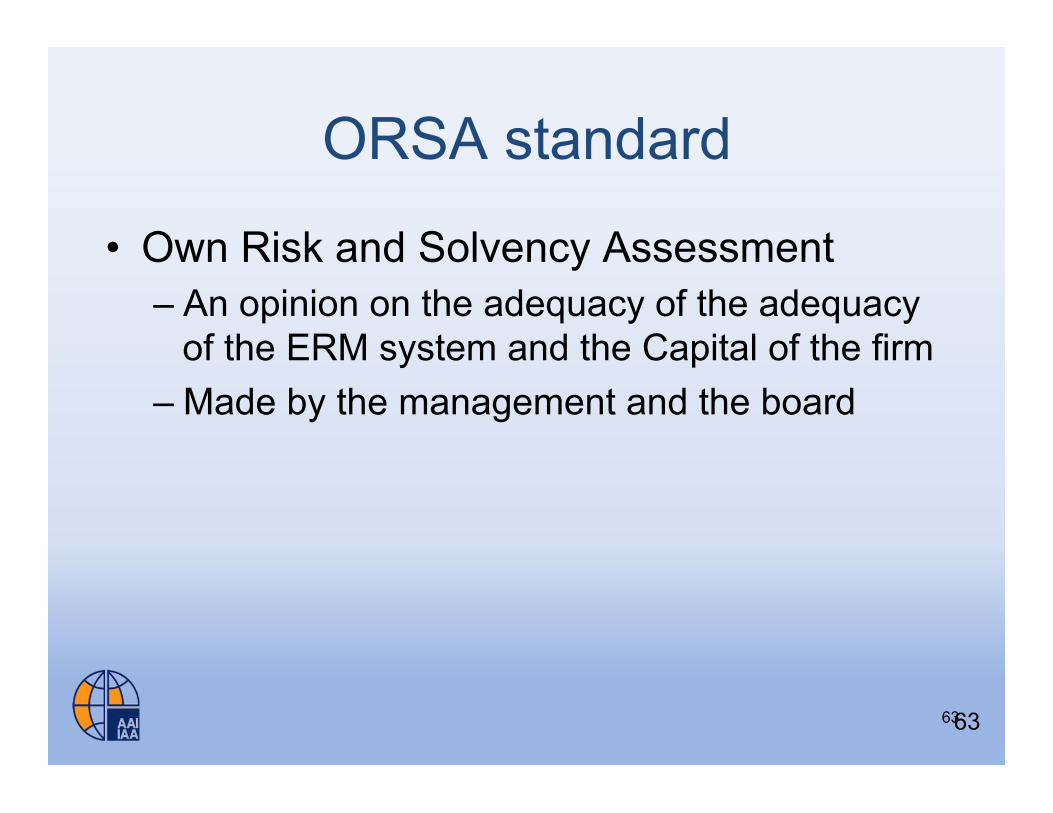

ORSA standard

• Own Risk and Solvency Assessment – An opinion on the adequacy of the adequacy

of the ERM system and the Capital of the firm – Made by the management and the board

63

64

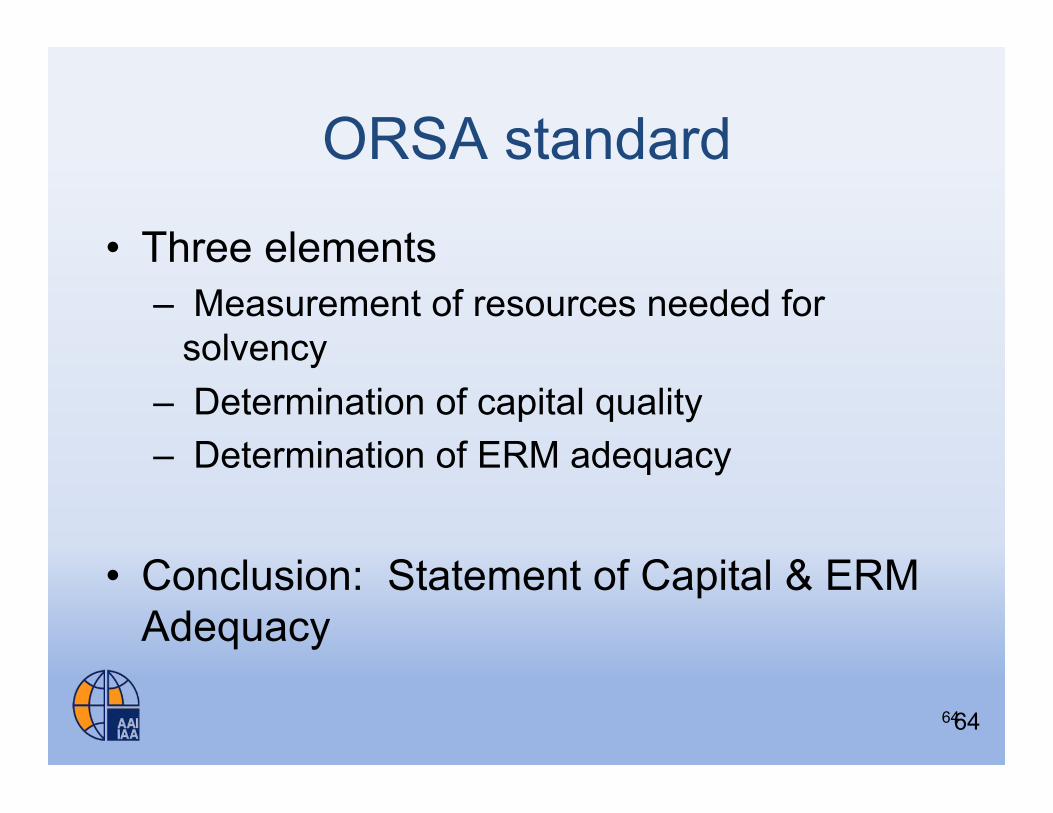

ORSA standard

• Three elements – Measurement of resources needed for

solvency – Determination of capital quality – Determination of ERM adequacy

• Conclusion: Statement of Capital & ERM Adequacy

64

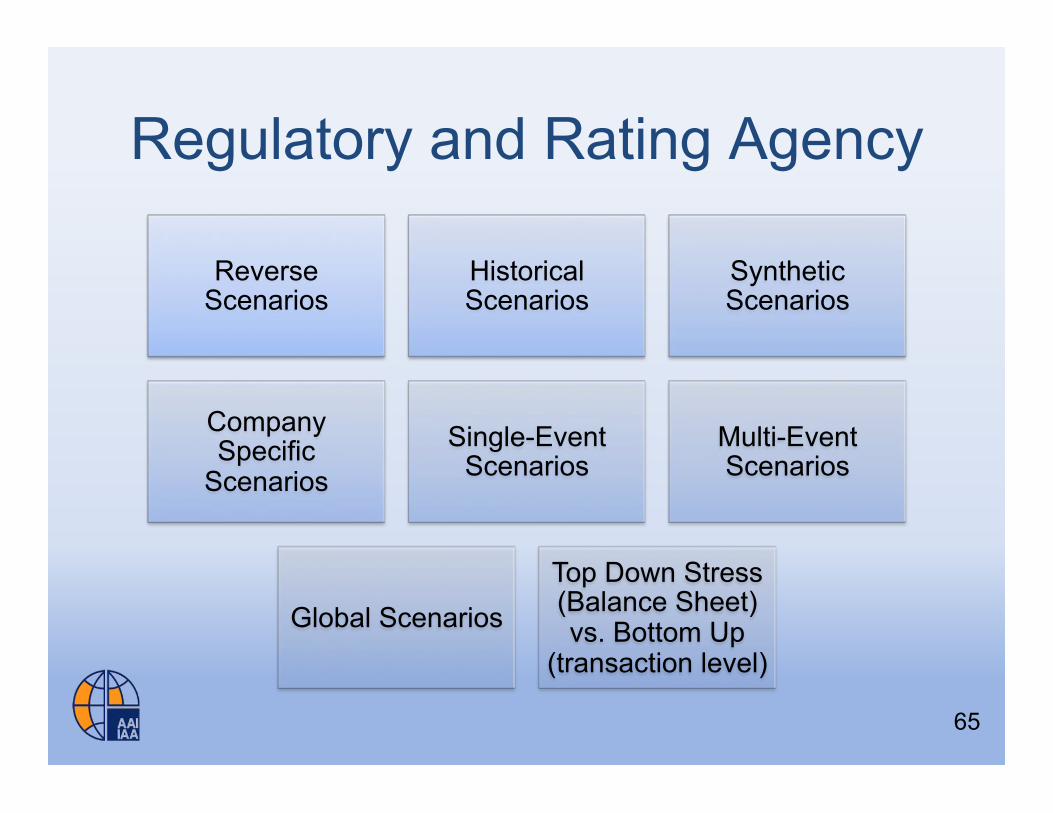

Regulatory and Rating Agency

Reverse Scenarios

Historical Scenarios

Synthetic Scenarios

Company Specific

Scenarios Single-Event

Scenarios Multi-Event Scenarios

Global Scenarios Top Down Stress (Balance Sheet) vs. Bottom Up

(transaction level)

65

Developing Stress Tests

9/13/11

3

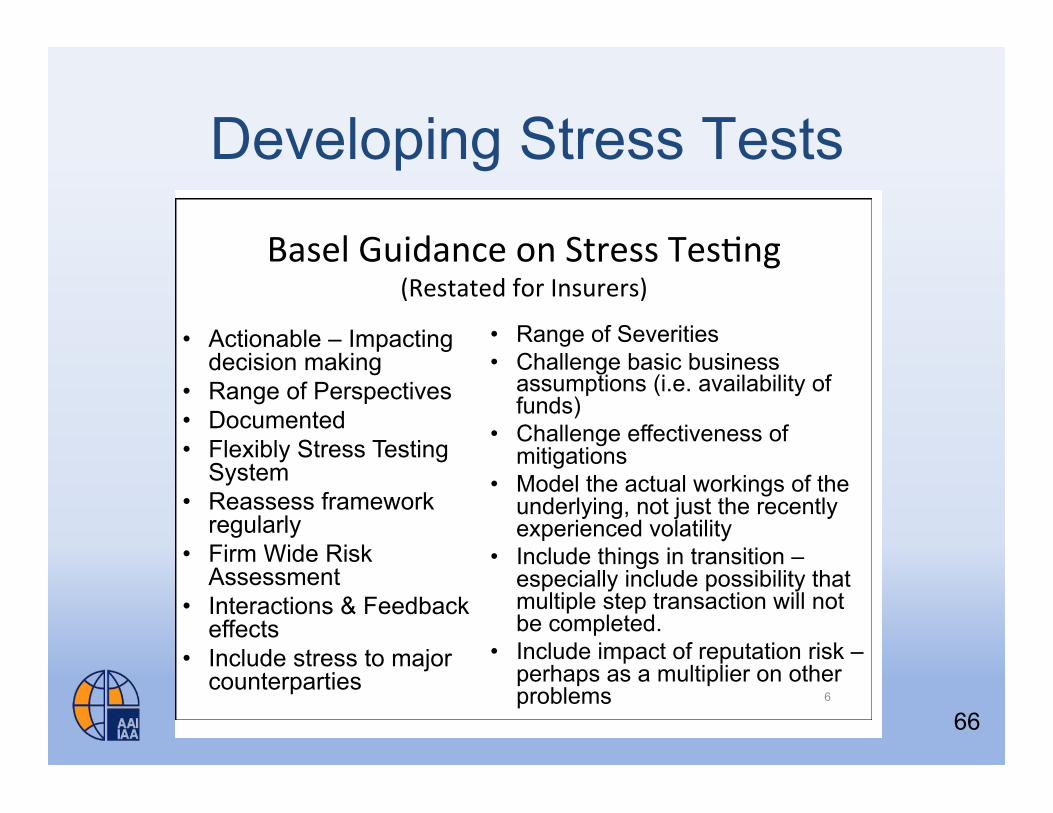

!"#$!%%&'()*++&,*+-./&01.234&53(*+&

• 61.7+&23&"1(8)9(:&,)1.+;3)41-3.&<&*8=>*49+4&;3)&2)1+-?&28)1-3.&49+41(?>&&

– !+&(>1(&1&@1A&3)&1&;*1(8)*&3;&B1.7+&

• 5**2&(3&23&+948C(1.*38+&+()*++&(*+-./&<&1CC&3;&(>*&?34=1.9*+&1(&3.?*&– %CC3A+&?34=1)9+3.&3.&(>*&+14*&B1+9+&<&+14*&=39.(&9.&-4*D&

• 5*E(&41)7*(&)*=3)(&;)34&(>*&!%!'&A9CC&9.?C82*&+()*++&(*+(&9.;3)41-3.&• 6*+(&+()*++&(*+(&A38C2&B*&+?*.1)93+&3;&B3(>&1++*(&1.2&C91B9C9(:&+()*++*+&(>1(&

A*)*&?33)29.1(*2&A9(>&*1?>&3(>*)&• !.+8)1.?*&/)38=+&23&B8+9.*++&(>1(&?1.&B*&F(&9.(3&G&B8?7*(+H&

– ,)129-3.1C&9.+8)1.?*&I.2*)A)9-./&– 53.J,)129-3.1C&I.2*)A)9-./&– '*49&,)129-3.1C&8.2*)A)9-./&&

– 53.&!.+8)1.?*&

• !(&9+&=3++9BC*&(>1(&(>*&.3.J()129-3.1C&1.2&.3.J9.+8)1.?*&1?-K9-*+&1)*&+:+(*49?1CC:&94=3)(1.(&L1+&(>*:&B*?14*&;3)&%!MN&

5

• Traditional Investment • Non-Traditional Investment • Semi-Traditional Investment

61+*C&M8921.?*&3.&'()*++&,*+-./&L0*+(1(*2&;3)&!.+8)*)+N&

• Actionable – Impacting decision making

• Range of Perspectives • Documented • Flexibly Stress Testing

System • Reassess framework

regularly • Firm Wide Risk

Assessment • Interactions & Feedback

effects • Include stress to major

counterparties

• Range of Severities • Challenge basic business

assumptions (i.e. availability of funds)

• Challenge effectiveness of mitigations

• Model the actual workings of the underlying, not just the recently experienced volatility

• Include things in transition – especially include possibility that multiple step transaction will not be completed.

• Include impact of reputation risk – perhaps as a multiplier on other problems

6

66

S&P – Example of Stress Calibration

67 67

Concern with Supervisor use of Stress Tests from Insurers

• Move towards publicly disclosed stress tests – They become bright line – May overwhelm all other uses of stress tests

• At least under that name

68 68

USING STRESS TESTS FOR COMPANY DETERMINATION OF RISK CAPITAL NEEDED

69

70

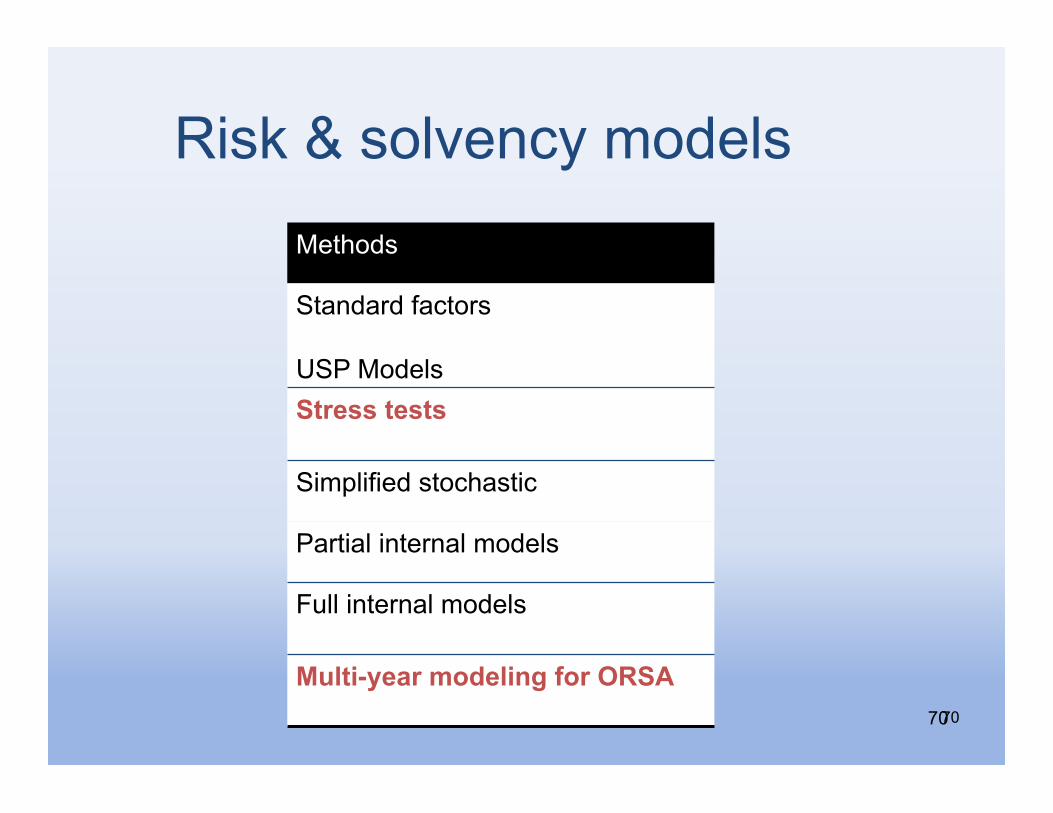

Risk & solvency models

Methods

Standard factors USP Models Stress tests Simplified stochastic

Partial internal models

Full internal models

Multi-year modeling for ORSA 70

Using Stress Tests For Risk Capital

• Allows company to include detailed information about the retained risks – That standard factors do not capture

• Much easier to validate than stochastic model

• Much easier to communicate than stochastic model

71

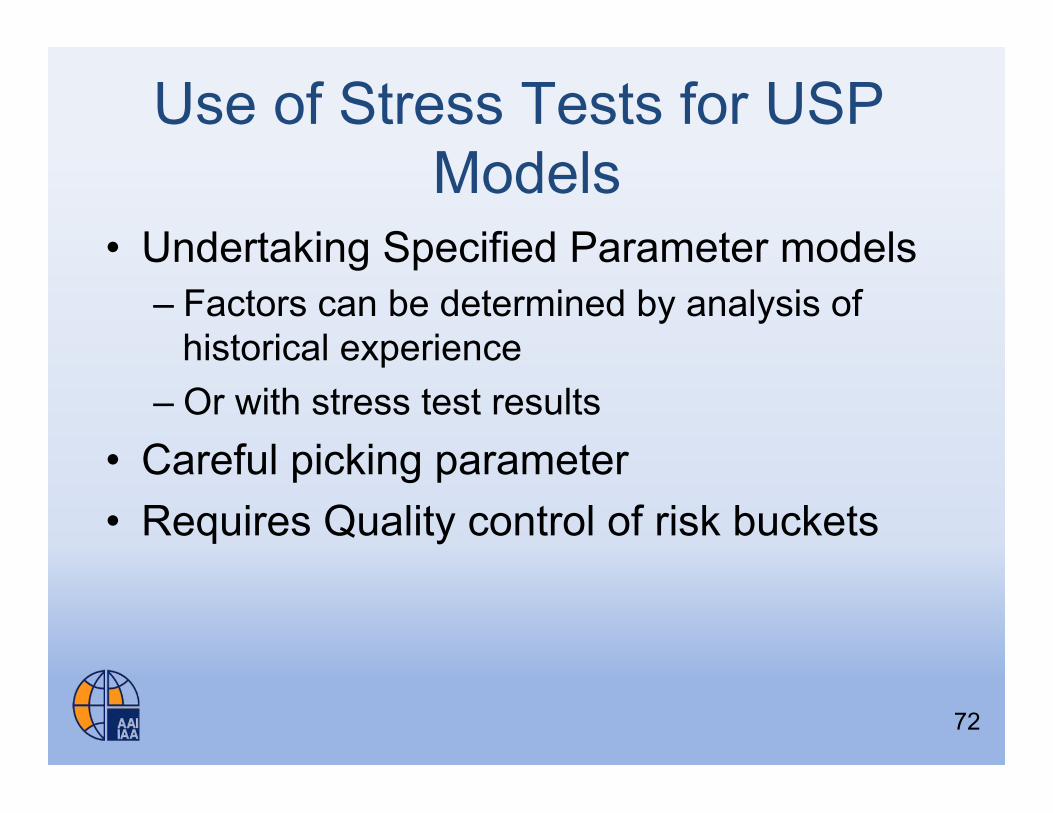

Use of Stress Tests for USP Models

• Undertaking Specified Parameter models – Factors can be determined by analysis of

historical experience – Or with stress test results

• Careful picking parameter • Requires Quality control of risk buckets

72

Use of Stress Tests with Stochastic Models

• Calibration and validation of stochastic models – Generally involves looking at the likelihood of the loss from a scenario

test compared to • Actual historical frequency • Perceived likelihood

– As a “sense check” • Does it make sense that the equity model says that a 2009 result

(historical scenario) is a 1 in 300 year scenario? • Develop Historical Scenarios to show losses with current exposures

to compare with stochastic model

– Determine likelihood estimates from the stochastic model of the losses from a set of scenario tests

• Every time there is a change in the stochastic model or model parameters

– Provides a test of how much the model is changing

73

Risk Capital

Reverse Scenarios

Historical Scenarios

Synthetic Scenarios

Company Specific

Scenarios Single-Event

Scenarios Multi-Event Scenarios

Global Scenarios Top Down Stress (Balance Sheet) vs. Bottom Up

(transaction level)

74

Conclusions

• Stress and Scenario Tests have many valuable uses

• Supervisors can leverage all of these – Care must be taken not to overuse

75

Types of Scenarios

Reverse Scenarios

Historical Scenarios

Synthetic Scenarios

Company Specific

Scenarios Single-Event

Scenarios Multi-Event Scenarios

Global Scenarios Top Down Stress (Balance Sheet) vs. Bottom Up

(transaction level)

77

Sources

1. IAA Solvency Committee Draft Paper on Stress Testing (In process by Philipp Keller and Alan Brender)

78

Related Documents