Strategy Note Indonesia│June 19, 2018 IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT. IF THIS REPORT IS DISTRIBUTED IN THE UNITED STATES IT IS DISTRIBUTED BY CIMB SECURITIES (USA), INC. AND IS CONSIDERED THIRD-PARTY AFFILIATED RESEARCH. Powered by the EFA Platform Indonesia Strategy Democratic process and stock market ■ The past two decades of democratic process in Indonesia may provide neighbouring Malaysia with some constructive lessons, notwithstanding the differing circumstances. ■ The first five years after the historic general elections in 1999 saw systemic changes politically, such as media freedom, direct presidential elections and KPK's formation. ■ Economic reforms and growth took backseats initially though, as reflected in poor corporate earnings growth and equally anaemic stock market returns. ■ The next five years after that have been most rewarding to the capital market, so far to date, supported by the passing of investment laws and more economic reforms. Key difference between Indonesia and Malaysia's political systems Malaysia uses a UK style parliamentary system with a Prime Minister and party coalitions. Indonesia uses a hybrid multi-party presidential system. Indonesia has direct popular elections for President, and the President’s term is fixed, regardless of the breakdown of parties in the legislature, and limited to two terms. Both systems have multi parties with none having a simple majority. Coalitions of parties form the government and also the opposition. Both countries seem to have genuine democratic systems. Independence from Dutch to the ‘reformasi’ era Indonesia adopted parliamentary democracy after independence from the Netherlands and staged its first fair and free elections in 1955. Economic pressure amid anti- communist hysteria led to the change to presidential system in 1966, with Soeharto succeeding Soekarno as the country’s second President. Parliamentary elections were held every five years from 1973 and Soeharto ruled for 32 years until forced to step down in 1998, and conferred the presidency to his Vice President (VP), BJ Habibie. Post Soeharto era – more turmoil initially The Habibie administration started off with a key reform: press freedom. New electoral laws were introduced in 1999, which led to the first fair and free parliamentary election since 1955. PDI-Perjuangan, the party of an anti-Soeharto icon, won the most seats with 33% seats in a fragmented parliament. A coalition of parties formed the government consequently, with Gus Dur appointed as the country’s third president. He was ousted in 2001, and the parliament mandated his VP, Megawati, to be the nation's fourth president. Ushering in a new era, solidifying democratic process During the Megawati era, key reforms included formation of an independent Anti- Corruption Commission (KPK) and independent Judicial Commission; introduction of presidential term limits to two five-year terms; and an amendment from indirect elections via the People's Consultative Assembly (MPR) to direct popular presidential election. Indonesia ended the IMF relief programme in 2003 and embarked on an aggressive privatisation programme. 2004 marked the beginning of direct presidential elections. Political euphoria proven to be short-lived in the stock market In the past two decades since ‘reformasi’, stock market performance was at its best after the first four years or so of major political change. Susilo Bambang Yudhoyono's 1 st term was most rewarding to investors. The election of Jokowi as President in 2014 marked another significant change, which proved to be challenging to the stock market initially. 2019 shall see the parliamentary and presidential elections occurring concurrently. If history is a guide, the market may see more volatility ahead. Figure 1: JCI in US$ term since 1999 (shaded graphs represent times of election) SOURCES: CGS-CIMB RESEARCH, COMPANY REPORTS Indonesia Insert Analyst(s) Erwan TEGUH T (62) 21 3006 1720 E [email protected] Peter P. SUTEDJA T (62) 21 3006 1726 E [email protected] Namira LAHUDDIN T (62) 21 3006 1728 E [email protected] 0 200 400 600 800 1,000 1,200 JCI in US$ (1999 = 100)

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Strategy Note Indonesia│June 19, 2018

IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT. IF THIS REPORT IS DISTRIBUTED IN THE UNITED STATES IT IS DISTRIBUTED BY CIMB SECURITIES (USA), INC. AND IS CONSIDERED THIRD-PARTY AFFILIATED RESEARCH.

Powered by the EFA Platform

Indonesia Strategy Democratic process and stock market ■ The past two decades of democratic process in Indonesia may provide neighbouring

Malaysia with some constructive lessons, notwithstanding the differing circumstances. ■ The first five years after the historic general elections in 1999 saw systemic changes

politically, such as media freedom, direct presidential elections and KPK's formation. ■ Economic reforms and growth took backseats initially though, as reflected in poor

corporate earnings growth and equally anaemic stock market returns. ■ The next five years after that have been most rewarding to the capital market, so far

to date, supported by the passing of investment laws and more economic reforms.

Key difference between Indonesia and Malaysia's political systems Malaysia uses a UK style parliamentary system with a Prime Minister and party coalitions. Indonesia uses a hybrid multi-party presidential system. Indonesia has direct popular elections for President, and the President’s term is fixed, regardless of the breakdown of parties in the legislature, and limited to two terms. Both systems have multi parties with none having a simple majority. Coalitions of parties form the government and also the opposition. Both countries seem to have genuine democratic systems.

Independence from Dutch to the ‘reformasi’ era Indonesia adopted parliamentary democracy after independence from the Netherlands and staged its first fair and free elections in 1955. Economic pressure amid anti-communist hysteria led to the change to presidential system in 1966, with Soeharto succeeding Soekarno as the country’s second President. Parliamentary elections were held every five years from 1973 and Soeharto ruled for 32 years until forced to step down in 1998, and conferred the presidency to his Vice President (VP), BJ Habibie.

Post Soeharto era – more turmoil initially The Habibie administration started off with a key reform: press freedom. New electoral laws were introduced in 1999, which led to the first fair and free parliamentary election since 1955. PDI-Perjuangan, the party of an anti-Soeharto icon, won the most seats with 33% seats in a fragmented parliament. A coalition of parties formed the government consequently, with Gus Dur appointed as the country’s third president. He was ousted in 2001, and the parliament mandated his VP, Megawati, to be the nation's fourth president.

Ushering in a new era, solidifying democratic process During the Megawati era, key reforms included formation of an independent Anti-Corruption Commission (KPK) and independent Judicial Commission; introduction of presidential term limits to two five-year terms; and an amendment from indirect elections via the People's Consultative Assembly (MPR) to direct popular presidential election. Indonesia ended the IMF relief programme in 2003 and embarked on an aggressive privatisation programme. 2004 marked the beginning of direct presidential elections.

Political euphoria proven to be short-lived in the stock market In the past two decades since ‘reformasi’, stock market performance was at its best after the first four years or so of major political change. Susilo Bambang Yudhoyono's 1

st term

was most rewarding to investors. The election of Jokowi as President in 2014 marked another significant change, which proved to be challenging to the stock market initially. 2019 shall see the parliamentary and presidential elections occurring concurrently. If history is a guide, the market may see more volatility ahead.

Figure 1: JCI in US$ term since 1999 (shaded graphs represent times of election)

SOURCES: CGS-CIMB RESEARCH, COMPANY REPORTS

Indonesia

Insert

Analyst(s)

Erwan TEGUH

T (62) 21 3006 1720 E [email protected]

Peter P. SUTEDJA T (62) 21 3006 1726 E [email protected]

Namira LAHUDDIN T (62) 21 3006 1728 E [email protected]

0

200

400

600

800

1,000

1,200

JCI in US$ (1999 = 100)

2

Indonesia

Strategy Note│June 19, 2018

Indonesia democratic process: lessons for Malaysia?

BACKGROUND

A brief history of Indonesia’s democratic process

After gaining independence from the Netherlands, Indonesia adopted a parliamentary democracy. In 1955, free and fair elections took place. Thereafter, the People’s Consultative Assembly (MPR), which comprised parliament (or People's Representative Council, the DPR) and assorted appointed members, elected Soekarno as Indonesia's first president.

In 1966, amid anti-communist hysteria and economic challenges, Maj. Gen. Soeharto supplanted Soekarno, purged communists and elicited a presidential mandate from the MPR. Starting from 1973, parliamentary elections occurred every five years, though not widely perceived to be free or fair. Soeharto maintained the semblance of parliamentary democracy, securing a presidential mandate from MPR for seven consecutive terms.

In May 1998, a combination of factors pressured Soeharto: an economic cataclysm (due to the Asian Financial Crisis); machinates against him among ministers and generals; and a grassroots groundswell of nationwide demonstrations against ‘Corruption, Collusion and Nepotism’ (KKN). Indonesia was forced to receive aids from the International Monetary Fund (IMF) in 1998. Indonesia's GDP growth plunged more than 13% in 1998, leading to widespread poverty of over 24% of the population. Soeharto was forced to step down after 32 years in power, and took the constitutional step of conferring the presidency upon his Vice President, BJ Habibie.

Post-Soeharto era

In the upheaval during the initial weeks of the Habibie administration, the press unilaterally exercised a newfound freedom from censors. Ministers later affirmed a policy of press freedom. The administration also conferred regional autonomy on provincial and district level regions, freed political prisoners, allowed new parties to form, and made preparations for the first free and fair elections since 1955. Habibie also stabilised the economy by forcing banks to merge. The state-owned Bank Mandiri, now the largest bank by asset, was born. He also oversaw the establishment of an independent central bank.

The administration, the outgoing parliament and various other prominent political actors agreed to commission a panel of esteemed experts to propose new electoral laws. This included rules on party eligibility and the formation of a General Election Commission (KPU) to administer the process. KPU rules required parties to demonstrate a nationwide network and presence, rather than being parochial entities that might engender inter regional rivalries or tensions. The KPU permitted the participation of Golkar (the Soeharto era ruling party and the party of Habibie).

In Nov 1999, a parliamentary election saw a plurality of votes go to PDI Perjuangan (PDI-P), the party of an anti Soeharto icon, Megawati (a daughter of Soekarno). Golkar finished second in a fragmented Parliament. However, PDI-P lacked a majority, and an alliance of other parties and MPR appointees chose the Nahdlatul Ulama (NU) cleric Abdurrahman Wahid (Gus Dur) for President, with Megawati as Vice President.

As a condition for his appointment, Gus Dur conferred a host of cabinet seats to representatives of parties in the legislature. Gus Dur oversaw the implementation of regional autonomy and fiscal decentralisation, as well as passing of a controversial labour law in 2000.

But Gus Dur’s eclectic and at times erratic style of governance led to an MPR majority ousting him in July 2001 and mandated Megawati to finish his five-year

3

Indonesia

Strategy Note│June 19, 2018

term. Megawati formed a new cabinet, again accommodating party representatives as ministers.

In a consequential development during the Megawati era, the MPR made several constitutional amendments, which originated from legislators elected in the pro-reform election of 1999. These included mandates for an independent Anti-Corruption Commission (KPK) and an independent Judicial Commission. They also included presidential term limits, a maximum of two five-year terms. Most importantly, an amendment changed the presidential election format: away from indirect elections via the MPR, in favour of direct popular election.

Megawati oversaw the end of IMF aids in Dec 2003, earlier than projected. As part of the fiscal reforms, major privatisations were implemented which led to the termination of the Indonesian Banking Restructuring Agency (IBRA) in 2004. GDP growth recovered to over 5% in 2004 and the poverty rate declined to less than 17%.

Direct presidential elections

The first direct presidential elections took place in 2004, featuring five contenders. These included a minister of Megawati’s, Lt. Gen. (ret) Susilo Bambang Yudhoyono (SBY), who formed a party at a late stage and announced his run. His vice presidential nominee was the Golkar business figure, Jusuf Kalla. In a second round run-off, they defeated the incumbent, who ran with the NU leader Hasyim Muzadi, by a narrow margin. The electorate clearly wanted a President that would demonstrate greater concern for the poor and greater resolve vis-à-vis corruption.

In yet another systemic change, in 2005, nearly 500 heads of provinces and district level governments nationwide became subject to direct popular election for the first time (from 1999-2004, regional legislatures had chosen them). These elections provided a mechanism for worthy local figures to rise upward through successive levels of executive leadership by winning popular elections, rather than rising through the conventional patronage-oriented routes, such as the career paths of civil servants, military personnel or party cadres.

In 2009, SBY paired with Bank Indonesia (BI) Governor Boediono to run for a second term. They again faced Megawati, who recruited Lt. Gen. (ret) Prabowo Subianto as her running mate. Kalla ran with former Military Chief Gen. (ret) Wiranto as his running mate. SBY campaigned on a clean governance platform and won a 60% majority in the first round.

During SBY’s 10-year tenure, Indonesia experienced both a commodity boom and a global financial crisis. Its GDP growth averaged 4-6%, peaking at 6.2% in 2010. Indonesia became part of the G20 club, the largest 20 economies in the world. However, fuel subsidies, averaging over c.2.2% of GDP, hampered development spending. Poverty rate improved dramatically to c.11%.

In 2012, the popular PDI-P mayor of Solo, Joko Widodo (Jokowi), dramatically won the election for Governor of Jakarta, defeating the Golkar-backed incumbent. His vice gubernatorial running mate, nominated by Prabowo’s Gerindra, was the former Golkar parliamentarian Basuki Tjahaja Purnama (‘Ahok’). Jokowi’s dramatic emergence rendered him a viable contender for president in 2014.

At a late stage in preparations for the 2014 election, Megawati conceded to the nomination of Widodo. The Jakarta Governor defeated his sole opponent, Lt Gen (ret) Prabowo Subianto, by six percentage points to become the country's seventh president.

Taking advantage of falling oil prices, Jokowi cut fuel subsidies and channelled the moneys into aggressive infrastructure spending. Over 2015-17, his administration spent some Rp990tr (c.7% of GDP) on infrastructure. He oversaw a tax amnesty programme in 2016-17 which raised c.Rp146tr for the government with some Rp4881tr (c.32% of GDP) of assets disclosed. GDP growth averaged c.5% while poverty rate improved slightly to 10.6% (2017), with unemployment rate improving to 5.3% (2017) from 5.7% (2014).

4

Indonesia

Strategy Note│June 19, 2018

Figure 2: Parliamentary seats allocation post Soerharto era – fragmented (shaded cells represent government coalition parties)

SOURCES: NEWS RESEARCH, KPU

Figure 3: Direct presidential election results

SOURCES: CGS-CIMB RESEARCH, COMPANY REPORTS

ASSESSING DEMOCRATISATION

Governance and politics

One of the key political manoeuvring and election campaigning points since ‘reformasi’ has been on how the President Candidate would treat the anti-corruption agency (or the “KPK”) if he/she were to be elected. The commission stands out as a rare example of an anti-corruption entity that has genuine independence, power and tenacity. KPK won exemptions from standard civil service hiring procedures. KPK also obtained powers to not only investigate but also to prosecute its own cases, with trials taking place in special Corrupt Crime Courts, in which a majority of judges are recruits from outside of the regular judiciary.

KPK has managed to persist because the selection of its five-person leadership, every four years, takes place through a process involving both the President and Parliament. No President has been willing to become notorious for appointing corrupt figures who would undermine the KPK.

The KPK has recorded a host of accomplishments. It successfully prosecuted hundreds of defendants, in cases where evidence of malfeasance is typically very clear cut. Over the years, it has targeted high ranking figures, including scores of parliamentarians, numerous party chairs, an in-law of President Yudhoyono (BI Deputy Governor Aulia Pohan), the speaker of Parliament (Setya Novanto), army and police generals, and hundreds of regional heads. The KPK has never lost a trial in court although in several cases, suspects have escaped

Party Seats % of vote Seats % of vote Seats % of vote Seats % of vote

Golkar 91 16% 107 19% 127 23% 120 26%

PDI-P 109 19% 95 17% 109 20% 153 33%

PKB 47 8% 27 5% 52 9% 51 11%

PPP 39 7% 37 7% 58 11% 58 13%

PD 61 11% 150 27% 56 10% 0%

PKS 40 7% 57 10% 45 8% 7 2%

PAN 48 9% 43 8% 53 10% 34 7%

PBB 0 0% - 0% 11 2% 13 3%

PBR 0 0% - 0% 14 3% 0%

PKPB 0% - 0% 2 0.4% 0%

PDS 0% - 0% 13 2% 0%

Gerindra 73 13% 26 5% 0% 0%

Hanura 16 3% 18 3% 0% 0%

Nasdem 36 6%

Others - 0% 10 2% 26 6%

Total 560 100% 560 100% 550 100% 462 100%

Government coalition 69% 75% 73% 25%

Opposition 31% 25% 27% 75%

100% 100% 100% 100%

2014 2009 2004 1999

First

round

Second

round

Joko Widodo - Jusuf Kalla 53.15% Susilo Bambang Yudhoyono - Boediono 60.80% Susilo Bambang Yudhoyono - Jusuf Kalla 33.57% 60.62%

Prabowo Subianto - Hatta Rajasa 46.85% Megawati Soekarnoputri - Prabowo Soebianto 26.79% Megawati Soekarnoputri - Hasyim Muzadi 26.61% 39.38%

Jusuf Kalla - Wiranto 12.41% Wiranto - Salahuddin Wahid 22.15%

Amien Rais - Siswono Yudohusodo 14.66%

Hamzah Haz - Agum Gumelar 3.01%

2004

20092014

5

Indonesia

Strategy Note│June 19, 2018

charges by filing pre-trial suits. The KPK has demonstrated that a public Indonesian institution can function professionally.

However, despite its prosecutorial success, the KPK’s work has clearly not deterred officials from engaging in graft, bribery, mark-ups and kickbacks. Successive cases make clear that these habits remain widespread. The lack of impact perhaps reflects the neglect by the government of corruption prevention measures, especially institutional reforms.

Institutional reforms

Within months of the fall of Soeharto, Indonesia accomplished the liberalisation of its media and political parties, while conferring autonomy on regions and conducting genuinely free and fair legislative elections. Subsequent phases of democratisation strengthened these innovations. However, internal reforms of state institutions remained lacking. In effect, Indonesia accomplished the difficult aspects of democratisation (liberalising politics and instituting elections) but failed in the aspect that should, in theory, be simpler i.e. imposing internal reforms on the state apparatus.

In particular, there have been few meaningful reforms implemented for the state civil service, which Soeharto had long cultivated to function along the lines of a patronage-based machine. Civil servants often sought opportunities for generating economic rents, and promotions occurred based on personal loyalties, rather than professional merit.

Similarly, legal system institutions have been largely unreformed. The granting of complete independence to the judicial branch, without imposing any reforms to end Soeharto era habits of patronage, has not improved the public confidence on the legal system.

Figure 4: Key reforms since ‘reformasi’

SOURCES: CGS-CIMB RESEARCH, COMPANY REPORTS

STOCK MARKET IMPACT

Political euphoria usually short-lived in the stock market

From 1999 to present, the JCI has gained 939% cumulatively or some 13% CAGR, in IDR term. In USD term, the gains were 456% and 10% respectively. The first four years post Soeharto were the most challenging politically. While systemic political reforms were implemented, the stock market took a backseat. The political euphoria lasted less than three months (JCI surged 17%) and dwindled in the next 20 months or so. Similarly, in SBY’s 1

st term, the market

surged in the 1st three months, but dwindled over the following nine months.

SBY's re-election for a 2nd

term offered little surprises, hence no euphoria in the market as well. Jokowi’s election, coined by Time magazine as “A New Hope”, sparked a stock market rally which was also short-lived.

At the end, market gain sustainability has to be supported by corporate earnings. Corporate earnings in the 1

st five years post-Soeharto were lacklustre, further

roiled by poor political sentiment. SBY’s 1st term saw market earnings growth

doubling or some 15% CAGR, as the economy started to recover from AFC post banking restructuring, boosted by commodity boom in 2005-7. The commodity price reversal and GFC hurt earnings growth in SBY’s 2

nd term. Jokowi’s

administration saw the beginning of taper tantrum pains and monetary tightening mode. GDP hit bottom at some 4.7% in 2015, but has since rebounded, albeit

1999

Freeing of press, freeing of political prisoners, freeing of political parties, new electoral laws, regional

autonomy, removal of military from politics, imposition of presidential term limits

2000 Affirmation of human rights

2001 Special autonomy for Aceh and Papua, passage of Oil & Gas Law

2003 Formation of the KPK, passage of State Treasury Law

2004 Introduction of direct presidential elections

2005 Advent of direct elections for regional heads, settlement of Aceh conflict, formation of Constitutional Court

2007 Passage of Investment Law

2008 Revision of Negative Investment List (DNI)

6

Indonesia

Strategy Note│June 19, 2018

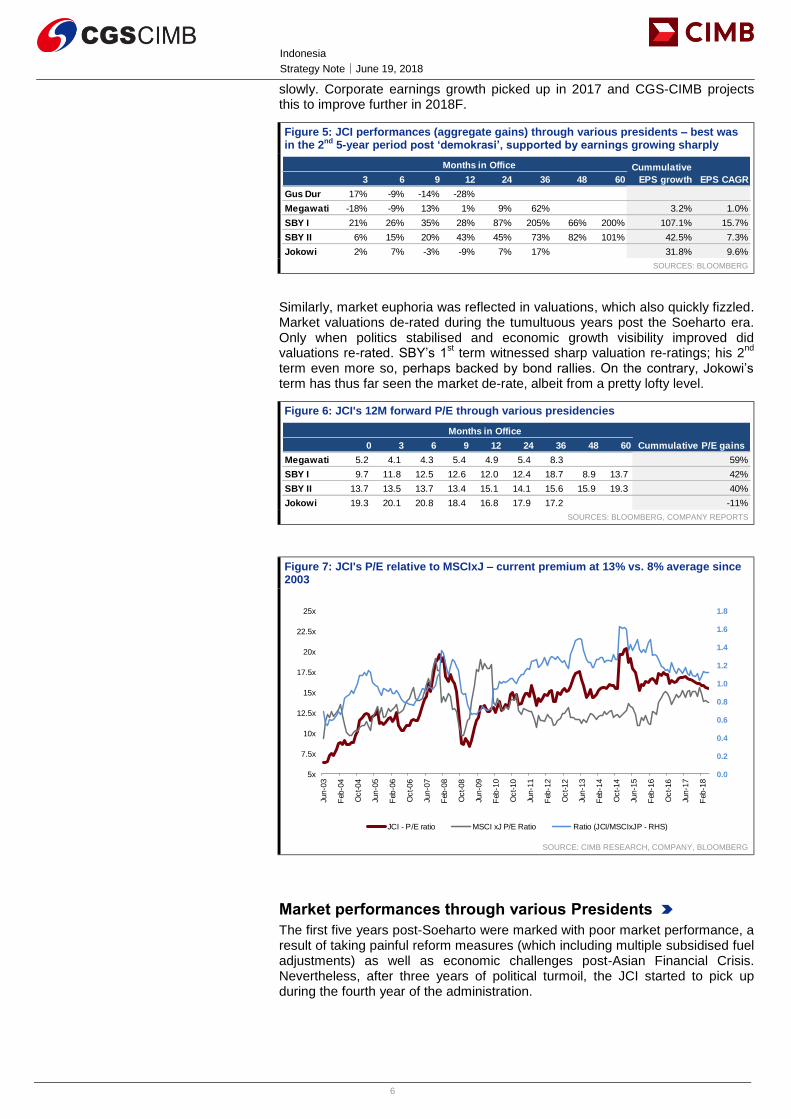

slowly. Corporate earnings growth picked up in 2017 and CGS-CIMB projects this to improve further in 2018F.

Figure 5: JCI performances (aggregate gains) through various presidents – best was in the 2nd 5-year period post ‘demokrasi’, supported by earnings growing sharply

SOURCES: BLOOMBERG

Similarly, market euphoria was reflected in valuations, which also quickly fizzled. Market valuations de-rated during the tumultuous years post the Soeharto era. Only when politics stabilised and economic growth visibility improved did valuations re-rated. SBY’s 1

st term witnessed sharp valuation re-ratings; his 2

nd

term even more so, perhaps backed by bond rallies. On the contrary, Jokowi’s term has thus far seen the market de-rate, albeit from a pretty lofty level.

Figure 6: JCI's 12M forward P/E through various presidencies

SOURCES: BLOOMBERG, COMPANY REPORTS

Figure 7: JCI's P/E relative to MSCIxJ – current premium at 13% vs. 8% average since 2003

SOURCE: CIMB RESEARCH, COMPANY, BLOOMBERG

Market performances through various Presidents

The first five years post-Soeharto were marked with poor market performance, a result of taking painful reform measures (which including multiple subsidised fuel adjustments) as well as economic challenges post-Asian Financial Crisis. Nevertheless, after three years of political turmoil, the JCI started to pick up during the fourth year of the administration.

3 6 9 12 24 36 48 60

Gus Dur 17% -9% -14% -28%

Megawati -18% -9% 13% 1% 9% 62% 3.2% 1.0%

SBY I 21% 26% 35% 28% 87% 205% 66% 200% 107.1% 15.7%

SBY II 6% 15% 20% 43% 45% 73% 82% 101% 42.5% 7.3%

Jokowi 2% 7% -3% -9% 7% 17% 31.8% 9.6%

Months in Office Cummulative

EPS growth EPS CAGR

0 3 6 9 12 24 36 48 60

Megawati 5.2 4.1 4.3 5.4 4.9 5.4 8.3 59%

SBY I 9.7 11.8 12.5 12.6 12.0 12.4 18.7 8.9 13.7 42%

SBY II 13.7 13.5 13.7 13.4 15.1 14.1 15.6 15.9 19.3 40%

Jokowi 19.3 20.1 20.8 18.4 16.8 17.9 17.2 -11%

Months in Office

Cummulative P/E gains

Title:

Source:

Please fill in the values above to have them entered in your report

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

5x

7.5x

10x

12.5x

15x

17.5x

20x

22.5x

25x

Jun-0

3

Feb

-04

Oct-04

Jun-0

5

Feb

-06

Oct-06

Jun-0

7

Feb

-08

Oct-08

Jun-0

9

Feb

-10

Oct-10

Jun-1

1

Feb

-12

Oct-12

Jun-1

3

Feb

-14

Oct-14

Jun-1

5

Feb

-16

Oct-16

Jun-1

7

Feb

-18

JCI - P/E ratio MSCI xJ P/E Ratio Ratio (JCI/MSCIxJP - RHS)

7

Indonesia

Strategy Note│June 19, 2018

Figure 8: The first five years post-Soeharto era – more downs than ups

SOURCES: BLOOMBERG, NEWS RESEARCH

SBY’s 10-year tenure (two successive terms) had less political noises, as the government coalitions were able to secure the majority in the legislative. As Indonesia’s economy started to pick up, boosted by commodity boom in 2004-2007 and followed by consumption and investment booms in 2010-12, the Indonesian stock market outperformed regional peers.

Figure 9: The 2nd 5-year period post-Soeharto (SBY’s 1st term) – the best stock market performance to date, unfazed by significant fuel price increases, but derailed by GFC

SOURCES: BLOOMBERG, NEWS RESEARCH

Title:

Source:

Please fill in the values above to have them entered in your report

6,000

7,000

8,000

9,000

10,000

11,000

12,000

13,000

300

400

500

600

700

800

900

Jan-9

9

Mar-

99

May-

99

Jul-99

Sep-9

9

Nov-

99

Jan-0

0

Mar-

00

May-

00

Jul-00

Sep-0

0

Nov-

00

Jan-0

1

Mar-

01

May-

01

Jul-01

Sep-0

1

Nov-

01

Jan-0

2

Mar-

02

May-

02

Jul-02

Sep-0

2

Nov-

02

Jan-0

3

Mar-

03

May-

03

Jul-03

Sep-0

3

Nov-

03

Jan-0

4

Mar-

04

May-

04

Jul-04

Sep-0

4

JCI IDR/US$

Indonesia's f irst legislative election since Reformasi era

Abdurrahman Wahid becomes the President

of Indonesia

The Upper House impeached President Abdurrahman Wahid

Megaw ati Soekarnoputri became President 2004 Legislative

Election

First ever Indonesia Presidential Election

Subsidised fuel price increase

Subsidised fuel priceincrease

Three consecutivemonths of subsidised

fuel price increase

Title:

Source:

Please fill in the values above to have them entered in your report

6,000

7,000

8,000

9,000

10,000

11,000

12,000

13,000

-

500

1,000

1,500

2,000

2,500

3,000

Jan-0

3

Apr-

03

Jul-03

Oct-03

Jan-0

4

Apr-

04

Jul-04

Oct-04

Jan-0

5

Apr-

05

Jul-05

Oct-05

Jan-0

6

Apr-

06

Jul-06

Oct-06

Jan-0

7

Apr-

07

Jul-07

Oct-07

Jan-0

8

Apr-

08

Jul-08

Oct-08

Jan-0

9

Apr-

09

Jul-09

Oct-09

JCI IDR/US$

SBY sw orn in asthe sixth President

of Indonesia

Subsidised fuel price increase

Subsidised fuel price increase

Subsidised fuel price cut

2009 LegislativeElection

2009 PresidentialElection

2004 LegislativeElection

2014 PresidentialElection (2 rounds)

8

Indonesia

Strategy Note│June 19, 2018

Figure 10: SBY’s 1st term – Indonesia government's IDR-denominated bond started to become a relevant asset class. Inflation spikes from fuel price adjustments aside, bond performed admirably

SOURCES: BLOOMBERG, NEWS RESEARCH

Figure 11: The 3rd 5-year period post-Soeharto (SBY’s 2nd term) – GDP growth peak in 2010, market boosted by QE. 2013 hit by taper tantrum, though political euphoria lifted market, briefly

SOURCES: BLOOMBERG, NEWS RESEARCH

Figure 12: SBY’s 2nd term – bond benefited from QE and also boosted by Indonesia attaining investment grade rating from Fitch in 2011. Politics seem to be of little consequences to bond performance

SOURCES: BLOOMBERG, NEWS RESEARCH

Title:

Source:

Please fill in the values above to have them entered in your report

6%

8%

10%

12%

14%

16%

18%

20%

22%

Jan-0

3

Apr-

03

Jul-03

Oct-03

Jan-0

4

Apr-

04

Jul-04

Oct-04

Jan-0

5

Apr-

05

Jul-05

Oct-05

Jan-0

6

Apr-

06

Jul-06

Oct-06

Jan-0

7

Apr-

07

Jul-07

Oct-07

Jan-0

8

Apr-

08

Jul-08

Oct-08

Jan-0

9

Apr-

09

Jul-09

Oct-09

10-yr bond yield

SBY sw orn in asthe sixth President

of Indonesia

Subsidised fuel price increase

Subsidised fuel price increase

Subsidised fuel price cut

2009 LegislativeElection

2009 PresidentialElection

2004 LegislativeElection

2014 PresidentialElection (2 rounds)

Title:

Source:

Please fill in the values above to have them entered in your report

8,000

9,000

10,000

11,000

12,000

13,000

-

1,000

2,000

3,000

4,000

5,000

6,000

Jan-0

8

Apr-

08

Jul-08

Oct-08

Jan-0

9

Apr-

09

Jul-09

Oct-09

Jan-1

0

Apr-

10

Jul-10

Oct-10

Jan-1

1

Apr-

11

Jul-11

Oct-11

Jan-1

2

Apr-

12

Jul-12

Oct-12

Jan-1

3

Apr-

13

Jul-13

Oct-13

Jan-1

4

Apr-

14

Jul-14

Oct-14

JCI IDR/US$

Subsidised fuel price increase

2014 LegislativeElection

2014 PresidentialElection

2009 LegislativeElection

2009 PresidentialElection

Title:

Source:

Please fill in the values above to have them entered in your report

5%

7%

9%

11%

13%

15%

17%

19%

21%

23%

Jan-0

8

Apr-

08

Jul-08

Oct-08

Jan-0

9

Apr-

09

Jul-09

Oct-09

Jan-1

0

Apr-

10

Jul-10

Oct-10

Jan-1

1

Apr-

11

Jul-11

Oct-11

Jan-1

2

Apr-

12

Jul-12

Oct-12

Jan-1

3

Apr-

13

Jul-13

Oct-13

Jan-1

4

Apr-

14

Jul-14

Oct-14

10-yr bond yield

Subsidised fuel price increase 2014 Legislative

Election2014 PresidentialElection

2009 LegislativeElection

2009 PresidentialElection

9

Indonesia

Strategy Note│June 19, 2018

The 2014 elections marked another significant change in Indonesia’s democracy journey, going by the transfer of power from one popularly elected President, SBY, to another, Joko Widodo, who represented an opposition party (PDI-P). Prolonged political noises, with uncertainties during the campaign and election periods, rattled confidence but the ensuing amicable election and concession by Prabowo in the intensely-run presidential elections restored confidence. The win by Jokowi, perceived to be a reformist, led to market euphoria.

That was short-lived, as market sentiment was hit by the concerns on whether Jokowi was able to push the reforms promised during the campaign given the government coalition (which at that time consisted of PDI-P, PKB, NasDem and Hanura) controlled only a minority fraction of c.37% in the parliament. The JCI corrected. Furthermore, China's sudden depreciation of the renminbi in 2015 led to EM sell-off. The market gained confidence when PPP and PAN joined the government coalition by 3Q15 (and later Golkar by 1Q16), and obtained majority of legislation seats.

Figure 13: Another political change (Jokowi’s era) – political euphoria lifted market initially; the ensuing economic reforms met by political challenges initially and commodity price collapsed in 2015 put pressure on market performance.

SOURCES: BLOOMBERG, NEWS RESEARCH

Figure 14: Jokowi’s ongoing 1st term: further upgrades on sovereign ratings in 2017-18 helped to bolster confidence though FFR rate hikes challenged monetary policy. BI has since lifted rates 2x by 25bp

SOURCES: BLOOMBERG, NEWS RESEARCH

The general elections in 2019 shall mark another change in the election system whereby parliamentary and presidential elections would occur concurrently. Presidential nomination hence shall be brought forward, by Aug 2018. Market pundits suggest that if two pairs (of presidential candidates) are announced by

Title:

Source:

Please fill in the values above to have them entered in your report

9,000

10,000

11,000

12,000

13,000

14,000

15,000

3,500

4,000

4,500

5,000

5,500

6,000

6,500

7,000

Jan-1

3

Mar-

13

May-

13

Jul-13

Sep-1

3

Nov-

13

Jan-1

4

Mar-

14

May-

14

Jul-14

Sep-1

4

Nov-

14

Jan-1

5

Mar-

15

May-

15

Jul-15

Sep-1

5

Nov-

15

Jan-1

6

Mar-

16

May-

16

Jul-16

Sep-1

6

Nov-

16

Jan-1

7

Mar-

17

May-

17

Jul-17

Sep-1

7

Nov-

17

Jan-1

8

Mar-

18

May-

18

JCI IDR/US$

Subsidised fuel price increase

2014 LegislativeElection

2014 PresidentialElection

Title:

Source:

Please fill in the values above to have them entered in your report

5%

6%

6%

7%

7%

8%

8%

9%

9%

10%

10%

Jan-1

3

Mar-

13

May-

13

Jul-13

Sep-1

3

Nov-

13

Jan-1

4

Mar-

14

May-

14

Jul-14

Sep-1

4

Nov-

14

Jan-1

5

Mar-

15

May-

15

Jul-15

Sep-1

5

Nov-

15

Jan-1

6

Mar-

16

May-

16

Jul-16

Sep-1

6

Nov-

16

Jan-1

7

Mar-

17

May-

17

Jul-17

Sep-1

7

Nov-

17

Jan-1

8

Mar-

18

May-

18

10-yr bond yield

Subsidised fuel price increase

2014 LegislativeElection

2014 PresidentialElection

10

Indonesia

Strategy Note│June 19, 2018

Aug (one being Jokowi's), Jokowi’s chances to be reelected shall rise significantly. The stock market performance could perhaps be more like in SBY’s 2

nd term. If more than two pairs were announced, uncertainty may linger. The

stock market performance hence could be volatile, perhaps more like in 2014.

Figure 15: Top 10 outperforming and underperforming stocks during Abdurrahman Wahid's Presidency

SOURCES: CGS-CIMB RESEARCH, COMPANY REPORTS

Figure 16: Top 10 outperforming and underperforming stocks during Megawati's Presidency

SOURCES: CGS-CIMB RESEARCH, COMPANY REPORTS

Stock Sector

cummulative

stock gain (loss)

ULTJ IJ Equity Consumer Staples 315%

ASGR IJ Equity Industrials 217%

ADES IJ Equity Consumer Staples 185%

RMBA IJ Equity Consumer Staples 172%

UNVR IJ Equity Consumer Staples 156%

FASW IJ Equity Materials 152%

SMSM IJ Equity Consumer Discretionary 125%

ESTI IJ Equity Industrials 123%

HITS IJ Equity Energy 100%

MEDC IJ Equity Energy 92%

BBNI IJ Equity Financials -66%

PNBN IJ Equity Financials -68%

TINS IJ Equity Materials -68%

POLY IJ Equity Industrials -76%

ADMG IJ Equity Materials -78%

BNBR IJ Equity Diversified / Conglomerate -78%

BNII IJ Equity Financials -83%

BDMN IJ Equity Financials -84%

BNLI IJ Equity Financials -87%

INKP IJ Equity Materials -89%

Stock Sector cummulative stock gain (loss)

SMRA IJ Equity Real Estate 1022%

BUMI IJ Equity Energy 812%

TKIM IJ Equity Materials 645%

EPMT IJ Equity Health Care 568%

INCO IJ Equity Materials 524%

NISP IJ Equity Financials 455%

LPKR IJ Equity Real Estate 435%

BRPT IJ Equity Materials 416%

UNTR IJ Equity Industrials 403%

JRPT IJ Equity Real Estate 311%

KAEF IJ Equity Health Care -20%

BKSL IJ Equity Real Estate -21%

INDF IJ Equity Consumer Staples -22%

ULTJ IJ Equity Consumer Staples -23%

KIJA IJ Equity Real Estate -33%

BNBR IJ Equity Diversified / Conglomerate -36%

TRIM IJ Equity Financials -38%

BBNI IJ Equity Financials -39%

BCIC IJ Equity Financials -41%

BNGA IJ Equity Financials -54%

11

Indonesia

Strategy Note│June 19, 2018

Figure 17: Top 10 outperforming and underperforming stocks during SBY's first term as President

SOURCES: CGS-CIMB RESEARCH, COMPANY REPORTS

Figure 18: Top 10 outperforming and underperforming stocks during SBY's second term

SOURCES: CGS-CIMB RESEARCH, COMPANY REPORTS

Stock Sector

cummulative stock gain

(loss)

PTBA IJ Equity Energy 1550%

PGAS IJ Equity Utilities 1473%

CPIN IJ Equity Consumer Staples 1352%

MAYA IJ Equity Financials 1292%

TINS IJ Equity Materials 974%

UNTR IJ Equity Energy 929%

ANTM IJ Equity Materials 847%

DILD IJ Equity Real Estate 846%

IIKP IJ Equity Consumer Staples 800%

PWON IJ Equity Real Estate 750%

BHIT IJ Equity Diversified / Conglomerate -10%

PNIN IJ Equity Financials -13%

IMAS IJ Equity Consumer Discretionary -16%

KAEF IJ Equity Health Care -19%

GJTL IJ Equity Consumer Discretionary -20%

RALS IJ Equity Consumer Discretionary -31%

ENRG IJ Equity Energy -35%

BCIC IJ Equity Financials -44%

BNBR IJ Equity Diversified / conglomerate -66%

BKSL IJ Equity Real Estate -74%

Stock Sector

cummulative stock

gain (loss)

LPPF IJ Equity Consumer Discretionary 6150%

SCMA IJ Equity Media 2727%

ARNA IJ Equity Building Material 2518%

SMMT IJ Equity Energy 1981%

MAIN IJ Equity Consumer Staples 1625%

PBRX IJ Equity Industrial 1478%

MDRN IJ Equity Consumer Discretionary 1412%

AMRT IJ Equity Consumer Discretionary 1138%

MNCN IJ Equity Consumer Discretionary 1110%

MYOR IJ Equity Consumer Staples 1108%

BTEL IJ Equity Telecommunication Services -63%

ANTM IJ Equity Materials -63%

BLTA IJ Equity Industrials/shipping -69%

DEWA IJ Equity Industrials -72%

ENRG IJ Equity Energy -72%

INDY IJ Equity Energy -74%

BRPT IJ Equity Materials -83%

ELTY IJ Equity Real Estate -85%

DOID IJ Equity Industrials -88%

BUMI IJ Equity Energy -96%

12

Indonesia

Strategy Note│June 19, 2018

Figure 19: Top 10 outperforming and underperforming stocks during Jokowi's presidency

SOURCES: CGS-CIMB RESEARCH, COMPANY REPORTS

Stock Sector

cummulative stock gain

(loss)

INKP IJ Equity Materials 1732%

TPIA IJ Equity Materials 789%

INDY IJ Equity Energy 559%

FASW IJ Equity Materials 325%

DOID IJ Equity Industrial 303%

BFIN IJ Equity Financials 280%

SMMA IJ Equity Financials 216%

DNET IJ Equity Consumer Discretionary / Conglomerate 200%

BBTN IJ Equity Financials 164%

MYOR IJ Equity Consumer Staples 152%

BHIT IJ Equity Diversified / Conglomerate -65%

HERO IJ Equity Consumer Discretionary -66%

BMTR IJ Equity Media / Conglomerate -71%

LPCK IJ Equity Real Estate -73%

WINS IJ Equity Shipping -75%

SMCB IJ Equity Materials -75%

ENRG IJ Equity Energy -76%

MAIN IJ Equity Consumer Staples -77%

AISA IJ Equity Consumer Staples -79%

MPPA IJ Equity Consumer Discretionary -91%

13

Indonesia

Strategy Note│June 19, 2018

DISCLAIMER The content of this report (including the views and opinions expressed therein, and the information comprised therein) has been prepared by and belongs to CGS-CIMB or CIMB Investment Bank Berhad (“CIMB”), as the case may be. Reports relating to a specific geographical area are produced and distributed by the corresponding CGS-CIMB entity as listed in the table below. Reports relating to Malaysia are produced and distributed by CIMB.

This report is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

By accepting this report, the recipient hereof represents and warrants that he is entitled to receive such report in accordance with the restrictions set forth below and agrees to be bound by the limitations contained herein (including the “Restrictions on Distributions” set out below). Any failure to comply with these limitations may constitute a violation of law. This publication is being supplied to you strictly on the basis that it will remain confidential. No part of this report may be (i) copied, photocopied, duplicated, stored or reproduced in any form by any means or (ii) redistributed or passed on, directly or indirectly, to any other person in whole or in part, for any purpose without the prior written consent of CGS-CIMB or CIMB, as the case may be.

The information contained in this research report is prepared from data believed to be correct and reliable at the time of issue of this report. CGS-CIMB or CIMB, as the case may be, may or may not issue regular reports on the subject matter of this report at any frequency and may cease to do so or change the periodicity of reports at any time. Neither CGS-CIMB nor CIMB has an obligation to update this report in the event of a material change to the information contained in this report. Neither CGS-CIMB nor CIMB accepts any, obligation to (i) check or ensure that the contents of this report remain current, reliable or relevant, (ii) ensure that the content of this report constitutes all the information a prospective investor may require, (iii) ensure the adequacy, accuracy, completeness, reliability or fairness of any views, opinions and information, and accordingly, CGS-CIMB and CIMB, their respective affiliates and related persons including China Galaxy International Financial Holdings Limited (“CGIFHL”) and CIMB Group Sdn. Bhd. (“CIMBG”) and their respective related corporations (and their respective directors, associates, connected persons and/or employees) shall not be liable in any manner whatsoever for any consequences (including but not limited to any direct, indirect or consequential losses, loss of profits and damages) of any reliance thereon or usage thereof. In particular, CGS-CIMB and CIMB disclaim all responsibility and liability for the views and opinions set out in this report.

Unless otherwise specified, this report is based upon sources which CGS-CIMB or CIMB, as the case may be, considers to be reasonable. Such sources will, unless otherwise specified, for market data, be market data and prices available from the main stock exchange or market where the relevant security is listed, or, where appropriate, any other market. Information on the accounts and business of company(ies) will generally be based on published statements of the company(ies), information disseminated by regulatory information services, other publicly available information and information resulting from our research.

Whilst every effort is made to ensure that statements of facts made in this report are accurate, all estimates, projections, forecasts, expressions of opinion and other subjective judgments contained in this report are based on assumptions considered to be reasonable as of the date of the document in which they are contained and must not be construed as a representation that the matters referred to therein will occur. Past performance is not a reliable indicator of future performance. The value of investments may go down as well as up and those investing may, depending on the investments in question, lose more than the initial investment. No report shall constitute an offer or an invitation by or on behalf of CGS-CIMB or CIMB, as the case may be, or any of their respective affiliates (including CGIFHL, CIMBG and their respective related corporations) to any person to buy or sell any investments.

CGS-CIMB, CIMB, their respective affiliates and related corporations (including CGIFHL, CIMBG and their respective related corporations) and/or their respective directors, associates, connected parties and/or employees may own or have positions in securities of the company(ies) covered in this research report or any securities related thereto and may from time to time add to or dispose of, or may be materially interested in, any such securities. Further, CGS-CIMB, CIMB, their respective affiliates and their respective related corporations (including CGIFHL, CIMBG and their respective related corporations) do and seek to do business with the company(ies) covered in this research report and may from time to time act as market maker or have assumed an underwriting commitment in securities of such company(ies), may sell them to or buy them from customers on a principal basis and may also perform or seek to perform significant investment banking, advisory, underwriting or placement services for or relating to such company(ies) as well as solicit such investment, advisory or other services from any entity mentioned in this report.

CGS-CIMB, CIMB or their respective affiliates (including CGIFHL, CIMBG and their respective related corporations) may enter into an agreement with the company(ies) covered in this report relating to the production of research reports. CGS-CIMB or CIMB, as the case may be, may disclose the contents of this report to the company(ies) covered by it and may have amended the contents of this report following such disclosure.

The analyst responsible for the production of this report hereby certifies that the views expressed herein accurately and exclusively reflect his or her personal views and opinions about any and all of the issuers or securities analysed in this report and were prepared independently and autonomously. No part of the compensation of the analyst(s) was, is, or will be directly or indirectly related to the inclusion of specific recommendations(s) or view(s) in this report. The analyst(s) who prepared this research report is prohibited from receiving any compensation, incentive or bonus based on specific investment banking transactions or for providing a specific recommendation for, or view of, a particular company. Information barriers and other arrangements may be established where necessary to prevent conflicts of interests arising. However, the analyst(s) may receive compensation that is based on his/their coverage of company(ies) in the performance of his/their duties or the performance of his/their recommendations and the research personnel involved in the preparation of this report may also participate in the solicitation of the businesses as described above. In reviewing this research report, an investor should be aware that any or all of the foregoing, among other things, may give rise to real or potential conflicts of interest. Additional information is, subject to the duties of confidentiality, available on request.

Reports relating to a specific geographical area are produced by the corresponding CGS-CIMB entity as listed in the table below. The term “CGS-CIMB” shall denote, where appropriate, the relevant entity distributing or disseminating the report in the particular jurisdiction referenced below, or, in every other case except as otherwise stated herein, CGS-CIMB Securities International Pte. Ltd. and its affiliates, subsidiaries and related corporations.

14

Indonesia

Strategy Note│June 19, 2018

Country CGS-CIMB Entity Regulated by

Hong Kong CGS-CIMB Securities (Hong Kong) Limited Securities and Futures Commission Hong Kong

India CGS-CIMB Securities (India) Private Limited Securities and Exchange Board of India (SEBI)

Indonesia PT CGS-CIMB Sekuritas Indonesia Financial Services Authority of Indonesia

Singapore CGS-CIMB Research Pte. Ltd. Monetary Authority of Singapore

South Korea CGS-CIMB Securities (Hong Kong) Limited, Korea Branch Financial Services Commission and Financial Supervisory Service

Thailand CGS-CIMB Securities (Thailand) Co. Ltd. Securities and Exchange Commission Thailand

Reports relating to Malaysia are produced by CIMB as listed in the table below:

Country CIMB Entity Regulated by

Malaysia CIMB Investment Bank Berhad Securities Commission Malaysia

Other Significant Financial Interests:

(i) As of June 18, 2018 CIMB has a proprietary position in the securities (which may include but not limited to shares, warrants, call warrants and/or any other derivatives) in the following company or companies covered or recommended in this report:

(a) -

(ii) Analyst Disclosure: As of June 19, 2018, the analyst(s) who prepared this report, and the associate(s), has / have an interest in the securities (which may include but not limited to shares, warrants, call warrants and/or any other derivatives) in the following company or companies covered or recommended in this report:

(a) -

This report does not purport to contain all the information that a prospective investor may require. Neither CGS-CIMB or CIMB, as the case may be, nor any of their respective affiliates (including CGIFHL, CIMBG and their related corporations) make any guarantee, representation or warranty, express or implied, as to the adequacy, accuracy, completeness, reliability or fairness of any such information and opinion contained in this report. Neither CGS-CIMB or CIMB, as the case may be, nor any of their respective affiliates nor their related persons (including CGIFHL, CIMBG and their related corporations) shall be liable in any manner whatsoever for any consequences (including but not limited to any direct, indirect or consequential losses, loss of profits and damages) of any reliance thereon or usage thereof.

This report is general in nature and has been prepared for information purposes only. It is intended for circulation amongst CGS-CIMB’s or CIMB’s (as the case may be) clients generally and does not have regard to the specific investment objectives, financial situation and the particular needs of any specific person who may receive this report. The information and opinions in this report are not and should not be construed or considered as an offer, recommendation or solicitation to buy or sell the subject securities, related investments or other financial instruments or any derivative instrument, or any rights pertaining thereto.

Investors are advised to make their own independent evaluation of the information contained in this research report, consider their own individual investment objectives, financial situation and particular needs and consult their own professional and financial advisers as to the legal, business, financial, tax and other aspects before participating in any transaction in respect of the securities of company(ies) covered in this research report.

The securities of such company(ies) may not be eligible for sale in all jurisdictions or to all categories of investors.

Australia: Despite anything in this report to the contrary, this research is provided in Australia by CGS-CIMB Securities (Singapore) Pte. Ltd. and CGS-CIMB Securities (Hong Kong) Limited. This research is only available in Australia to persons who are “wholesale clients” (within the meaning of the Corporations Act 2001 (Cth) and is supplied solely for the use of such wholesale clients and shall not be distributed or passed on to any other person. You represent and warrant that if you are in Australia, you are a “wholesale client”. This research is of a general nature only and has been prepared without taking into account the objectives, financial situation or needs of the individual recipient. CGS-CIMB Securities (Singapore) Pte. Ltd. and CGS-CIMB Securities (Hong Kong) Limited do not hold, and are not required to hold an Australian financial services license. CGS-CIMB Securities (Singapore) Pte. Ltd. and CGS-CIMB Securities (Hong Kong) Limited rely on “passporting” exemptions for entities appropriately licensed by the Monetary Authority of Singapore (under ASIC Class Order 03/1102) and the Securities and Futures Commission in Hong Kong (under ASIC Class Order 03/1103).

Canada: This research report has not been prepared in accordance with the disclosure requirements of Dealer Member Rule 3400 – Research Restrictions and Disclosure Requirements of the Investment Industry Regulatory Organization of Canada. For any research report distributed by CIBC, further disclosures related to CIBC conflicts of interest can be found at https://researchcentral.cibcwm.com .

China: For the purpose of this report, the People’s Republic of China (“PRC”) does not include the Hong Kong Special Administrative Region, the Macau Special Administrative Region or Taiwan. The distributor of this report has not been approved or licensed by the China Securities Regulatory Commission or any other relevant regulatory authority or governmental agency in the PRC. This report contains only marketing information. The distribution of this report is not an offer to buy or sell to any person within or outside PRC or a solicitation to any person within or outside of PRC to buy or sell any instruments described herein. This report is being issued outside the PRC to a limited number of institutional investors and may not be provided to any person other than the original recipient and may not be reproduced or used for any other purpose.

France: Only qualified investors within the meaning of French law shall have access to this report. This report shall not be considered as an offer to subscribe to, or used in connection with, any offer for subscription or sale or marketing or direct or indirect distribution of financial instruments and it is not intended as a solicitation for the purchase of any financial instrument.

Germany: This report is only directed at persons who are professional investors as defined in sec 31a(2) of the German Securities Trading Act (WpHG). This publication constitutes research of a non-binding nature on the market situation and the investment instruments cited here at the time of the publication of the information.

The current prices/yields in this issue are based upon closing prices from Bloomberg as of the day preceding publication. Please note that neither the German Federal Financial Supervisory Agency (BaFin), nor any other supervisory authority exercises any control over the content of this report.

Hong Kong: This report is issued and distributed in Hong Kong by CGS-CIMB Securities (Hong Kong) Limited (“CHK”) which is licensed in Hong Kong by the Securities and Futures Commission for Type 1 (dealing in securities), Type 4 (advising on securities) and Type 6 (advising on corporate finance) activities. Any investors wishing to purchase or otherwise deal in the securities covered in this report should contact the Head of Sales at

15

Indonesia

Strategy Note│June 19, 2018

CGS-CIMB Securities (Hong Kong) Limited. The views and opinions in this research report are our own as of the date hereof and are subject to change. If the Financial Services and Markets Act of the United Kingdom or the rules of the Financial Conduct Authority apply to a recipient, our obligations owed to such recipient therein are unaffected. CHK has no obligation to update its opinion or the information in this research report.

This publication is strictly confidential and is for private circulation only to clients of CHK.

CHK does not make a market on other securities mentioned in the report.

India: This report is issued and distributed in India by CGS-CIMB Securities (India) Private Limited (“CGS-CIMB India”) which is registered with the National Stock Exchange of India Limited and BSE Limited as a trading and clearing member under the Securities and Exchange Board of India (Stock Brokers and Sub-Brokers) Regulations, 1992. In accordance with the provisions of Regulation 4(g) of the Securities and Exchange Board of India (Investment Advisers) Regulations, 2013, CGS-CIMB India is not required to seek registration with the Securities and Exchange Board of India (“SEBI”) as an Investment Adviser. CGS-CIMB India is registered with SEBI as a Research Analyst pursuant to the SEBI (Research Analysts) Regulations, 2014 ("Regulations").

This report does not take into account the particular investment objectives, financial situations, or needs of the recipients. It is not intended for and does not deal with prohibitions on investment due to law/jurisdiction issues etc. which may exist for certain persons/entities. Recipients should rely on their own investigations and take their own professional advice before investment.

The report is not a “prospectus” as defined under Indian Law, including the Companies Act, 2013, and is not, and shall not be, approved by, or filed or registered with, any Indian regulator, including any Registrar of Companies in India, SEBI, any Indian stock exchange, or the Reserve Bank of India. No offer, or invitation to offer, or solicitation of subscription with respect to any such securities listed or proposed to be listed in India is being made, or intended to be made, to the public, or to any member or section of the public in India, through or pursuant to this report.

The research analysts, strategists or economists principally responsible for the preparation of this research report are segregated from the other activities of CGS-CIMB India and they have received compensation based upon various factors, including quality, accuracy and value of research, firm profitability or revenues, client feedback and competitive factors. Research analysts', strategists' or economists' compensation is not linked to investment banking or capital markets transactions performed or proposed to be performed by CGS-CIMB India or its affiliates.

CCGS-CIMB India has not received any investment banking related compensation from the companies mentioned in the report in the past 12 months.

CGS-CIMB India has not received any compensation from the companies mentioned in the report in the past 12 months.

Indonesia: This report is issued and distributed by PT CGS-CIMB Sekuritas Indonesia (“CGS-CIMB Indonesia”). The views and opinions in this research report are our own as of the date hereof and are subject to change. CGS-CIMB Indonesia has no obligation to update its opinion or the information in this research report. Neither this report nor any copy hereof may be distributed in Indonesia or to any Indonesian citizens wherever they are domiciled or to Indonesian residents except in compliance with applicable Indonesian capital market laws and regulations.

This research report is not an offer of securities in Indonesia. The securities referred to in this research report have not been registered with the Financial Services Authority (Otoritas Jasa Keuangan) pursuant to relevant capital market laws and regulations, and may not be offered or sold within the territory of the Republic of Indonesia or to Indonesian citizens through a public offering or in circumstances which constitute an offer within the meaning of the Indonesian capital market law and regulations.

Ireland: CGS-CIMB is not an investment firm authorised in the Republic of Ireland and no part of this document should be construed as CGS-CIMB acting as, or otherwise claiming or representing to be, an investment firm authorised in the Republic of Ireland.

Malaysia: This report is distributed by CIMB solely for the benefit of and for the exclusive use of our clients. CIMB has no obligation to update, revise or reaffirm its opinion or the information in this research reports after the date of this report.

New Zealand: In New Zealand, this report is for distribution only to persons who are wholesale clients pursuant to section 5C of the Financial Advisers Act 2008.

Singapore: This report is issued and distributed by CGS-CIMB Research Pte Ltd (“CGS-CIMBR”). CGS-CIMBR is a financial adviser licensed under the Financial Advisers Act, Cap 110 (“FAA”) for advising on investment products, by issuing or promulgating research analyses or research reports, whether in electronic, print or other form. Accordingly CGS-CIMBR is a subject to the applicable rules under the FAA unless it is able to avail itself to any prescribed exemptions.

Recipients of this report are to contact CGS-CIMB Research Pte Ltd, 50 Raffles Place, #16-02 Singapore Land Tower, Singapore in respect of any matters arising from, or in connection with this report. CGS-CIMBR has no obligation to update its opinion or the information in this research report. This publication is strictly confidential and is for private circulation only. If you have not been sent this report by CGS-CIMBR directly, you may not rely, use or disclose to anyone else this report or its contents.

If the recipient of this research report is not an accredited investor, expert investor or institutional investor, CGS-CIMBR accepts legal responsibility for the contents of the report without any disclaimer limiting or otherwise curtailing such legal responsibility. If the recipient is an accredited investor, expert investor or institutional investor, the recipient is deemed to acknowledge that CGS-CIMBR is exempt from certain requirements under the FAA and its attendant regulations, and as such, is exempt from complying with the following : (a) Section 25 of the FAA (obligation to disclose product information); (b) Section 27 (duty not to make recommendation with respect to any investment product without having a reasonable basis where you may be reasonably expected to rely on the recommendation) of the FAA; (c) MAS Notice on Information to Clients and Product Information Disclosure [Notice No. FAA-N03]; (d) MAS Notice on Recommendation on Investment Products [Notice No. FAA-N16]; (e) Section 36 (obligation on disclosure of interest in securities), and (f) any other laws, regulations, notices, directive, guidelines, circulars and practice notes which are relates to the above, to the extent permitted by applicable laws, as may be amended from time to time, and any other laws, regulations, notices, directive, guidelines, circulars, and practice notes as we may notify you from time to time. In addition, the recipient who is an accredited investor, expert investor or institutional investor acknowledges that a CGS-CIMBR is exempt from Section 27 of the FAA, the recipient will also not be able to file a civil claim against CGS-CIMBR for any loss or damage arising from the recipient’s reliance on any recommendation made by CGS-CIMBR which would otherwise be a right that is available to the recipient under Section 27 of the FAA, the recipient will also not be able to file a civil claim against CGS-CIMBR for any loss or damage arising from the recipient’s reliance on any recommendation made by CGS-CIMBR which would otherwise be a right that is available to the recipient under

16

Indonesia

Strategy Note│June 19, 2018

Section 27 of the FAA.

CGS-CIMBR, its affiliates and related corporations, their directors, associates, connected parties and/or employees may own or have positions in securities of the company(ies) covered in this research report or any securities related thereto and may from time to time add to or dispose of, or may be materially interested in, any such securities. Further, CGS-CIMBR, its affiliates and its related corporations do and seek to do business with the company(ies) covered in this research report and may from time to time act as market maker or have assumed an underwriting commitment in securities of such company(ies), may sell them to or buy them from customers on a principal basis and may also perform or seek to perform significant investment banking, advisory, underwriting or placement services for or relating to such company(ies) as well as solicit such investment, advisory or other services from any entity mentioned in this report.

As of June 18, 2018, CGS-CIMBR does not have a proprietary position in the recommended securities in this report.

CGS-CIMBR does not make a market on other securities mentioned in the report.

South Korea: This report is issued and distributed in South Korea by CGS-CIMB Securities (Hong Kong) Limited, Korea Branch (“CGS-CIMB Korea”) which is licensed as a cash equity broker, and regulated by the Financial Services Commission and Financial Supervisory Service of Korea. In South Korea, this report is for distribution only to professional investors under Article 9(5) of the Financial Investment Services and Capital Market Act of Korea (“FSCMA”).

Spain: This document is a research report and it is addressed to institutional investors only. The research report is of a general nature and not personalised and does not constitute investment advice so, as the case may be, the recipient must seek proper advice before adopting any investment decision. This document does not constitute a public offering of securities.

CGS-CIMB is not registered with the Spanish Comision Nacional del Mercado de Valores to provide investment services.

Sweden: This report contains only marketing information and has not been approved by the Swedish Financial Supervisory Authority. The distribution of this report is not an offer to sell to any person in Sweden or a solicitation to any person in Sweden to buy any instruments described herein and may not be forwarded to the public in Sweden.

Switzerland: This report has not been prepared in accordance with the recognized self-regulatory minimal standards for research reports of banks issued by the Swiss Bankers’ Association (Directives on the Independence of Financial Research).

Thailand: This report is issued and distributed by CGS-CIMB Securities (Thailand) Co. Ltd. (“CGS-CIMB Thailand”) based upon sources believed to be reliable (but their accuracy, completeness or correctness is not guaranteed). The statements or expressions of opinion herein were arrived at after due and careful consideration for use as information for investment. Such opinions are subject to change without notice and CGS-CIMB Thailand has no obligation to update its opinion or the information in this research report.

CGS-CIMB Thailand may act or acts as Market Maker, and issuer and offerer of Derivative Warrants and Structured Note which may have the following securities as its underlying securities. Investors should carefully read and study the details of the derivative warrants in the prospectus before making investment decisions.

AAV, ADVANC, AMATA, ANAN, AOT, AP, BA, BANPU, BBL, BCH, BCP, BCPG, BDMS, BEAUTY, BEC, BEM, BJC, BH, BIG, BLA, BLAND, BPP, BTS, CBG, CENTEL, CHG, CK, CKP, COM7, CPALL, CPF, CPN, DELTA, DTAC, EA, EGCO, EPG, GFPT, GLOBAL, GLOW, GPSC, GUNKUL, HMPRO, INTUCH, IRPC, ITD, IVL, KBANK, KCE, KKP, KTB, KTC, LH, LHBANK, LPN, MAJOR, MALEE, MEGA, MINT, MONO, MTLS, PLANB, PSH, PTL, PTG, PTT, PTTEP, PTTGC, QH, RATCH, ROBINS, S, SAWAD, SCB, SCC, SCCC, SIRI, SPALI, SPRC, STEC, STPI, SUPER, TASCO, TCAP, THAI, THANI, THCOM, TISCO, TKN, TMB, TOP, TPIPL, TRUE, TTA, TU, TVO, UNIQ, VGI, WHA, WORK.

Corporate Governance Report:

The disclosure of the survey result of the Thai Institute of Directors Association (“IOD”) regarding corporate governance is made pursuant to the policy of the Office of the Securities and Exchange Commission. The survey of the IOD is based on the information of a company listed on the Stock Exchange of Thailand and the Market for Alternative Investment disclosed to the public and able to be accessed by a general public investor. The result, therefore, is from the perspective of a third party. It is not an evaluation of operation and is not based on inside information.

The survey result is as of the date appearing in the Corporate Governance Report of Thai Listed Companies. As a result, the survey result may be changed after that date. CGS-CIMB Thailand does not confirm nor certify the accuracy of such survey result.

Score Range: 90 - 100 80 – 89 70 - 79 Below 70 or No Survey Result

Description: Excellent Very Good Good N/A

United Arab Emirates: The distributor of this report has not been approved or licensed by the UAE Central Bank or any other relevant licensing authorities or governmental agencies in the United Arab Emirates. This report is strictly private and confidential and has not been reviewed by, deposited or registered with UAE Central Bank or any other licensing authority or governmental agencies in the United Arab Emirates. This report is being issued outside the United Arab Emirates to a limited number of institutional investors and must not be provided to any person other than the original recipient and may not be reproduced or used for any other purpose. Further, the information contained in this report is not intended to lead to the sale of investments under any subscription agreement or the conclusion of any other contract of whatsoever nature within the territory of the United Arab Emirates.

United Kingdom and European Economic Area (EEA): In the United Kingdom and European Economic Area, this material is also being distributed by CGS-CIMB Securities (UK) Limited (“CGS-CIMB UK”). CGS-CIMB UK is authorized and regulated by the Financial Conduct Authority and its registered office is at 27 Knightsbridge, London, SW1X7YB. The material distributed by CGS-CIMB UK has been prepared in accordance with CGS-CIMB’s policies for managing conflicts of interest arising as a result of publication and distribution of this material. This material is for distribution only to, and is solely directed at, selected persons on the basis that those persons: (a) are eligible counterparties and professional clients of CGS-CIMB UK; (b) have professional experience in matters relating to investments falling within Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (as amended, the “Order”), (c) fall within Article 49(2)(a) to (d) (“high net worth companies, unincorporated associations etc”) of the Order; (d) are outside the United Kingdom subject to relevant regulation in each jur isdiction, material(all such persons together being referred to as “relevant persons”). This material is directed only at relevant persons and must not be acted on or relied on by persons who are not relevant persons. Any investment or investment activity to which this material relates is available only to relevant persons and will be engaged in only with relevant persons.

17

Indonesia

Strategy Note│June 19, 2018

Where this material is labelled as non-independent, it does not provide an impartial or objective assessment of the subject matter and does not constitute independent “research” (cannot remove research from here under the applicable rules of the Financial Conduct Authority in the UK. Consequently, any such non-independent material will not have been prepared in accordance with legal requirements designed to promote the independence of research (cannot remove research from here) and will not subject to any prohibition on dealing ahead of the dissemination of research. Any such non-independent material must be considered as a marketing communication.

United States: This research report is distributed in the United States of America by CGS-CIMB Securities (USA) Inc, a U.S. registered broker-dealer and a related company of CGS-CIMB Research Pte Ltd, PT CGS-CIMB Sekuritas Indonesia, CGS-CIMB Securities (Thailand) Co. Ltd, CGS-CIMB Securities (Hong Kong) Limited, CGS-CIMB Securities (India) Private Limited, and is distributed solely to persons who qualify as “U.S. Institutional Investors” as defined in Rule 15a-6 under the Securities and Exchange Act of 1934. This communication is only for Institutional Investors whose ordinary business activities involve investing in shares, bonds, and associated securities and/or derivative securities and who have professional experience in such investments. Any person who is not a U.S. Institutional Investor or Major Institutional Investor must not rely on this communication. The delivery of this research report to any person in the United States of America is not a recommendation to effect any transactions in the securities discussed herein, or an endorsement of any opinion expressed herein. CGS-CIMB Securities (USA) Inc, is a FINRA/SIPC member and takes responsibility for the content of this report. For further information or to place an order in any of the above-mentioned securities please contact a registered representative of CGS-CIMB Securities (USA) Inc.

CIMB Securities (USA) Inc. does not make a market on other securities mentioned in the report.

CGS-CIMB Securities (USA) Inc. has not managed or co-managed a public offering of any of the securities mentioned in the past 12 months.

CGS-CIMB Securities (USA) Inc. has not received compensation for investment banking services from any of the company mentioned in the past 12 months.

CGS-CIMB Securities (USA) Inc. neither expects to receive nor intends to seek compensation for investment banking services from any of the company mentioned within the next 3 months.

Other jurisdictions: In any other jurisdictions, except if otherwise restricted by laws or regulations, this report is only for distribution to professional, institutional or sophisticated investors as defined in the laws and regulations of such jurisdictions.

Corporate Governance Report of Thai Listed Companies (CGR). CG Rating by the Thai Institute of Directors Association (Thai IOD) in 2017, Anti-Corruption 2017