Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

SpringerBriefs in Business

For further volumes:http://www.springer.com/series/8860

Giorgio Gandellini • Alberto PezziDaniela Venanzi

Strategy for Action—I

The Logic and Contextof Strategic Management

123

Giorgio GandelliniDepartment of Business and LawUniversity of Rome IIIRome, Italy

Alberto PezziDepartment of Business and LawUniversity of Rome IIIRome, Italy

Daniela VenanziDepartment of Business and LawUniversity of Rome IIIRome, Italy

ISSN 2191-5482 e-ISSN 2191-5490ISBN 978-88-470-2486-1 e-ISBN 978-88-470-2487-8DOI 10.1007/978-88-470-2487-8Springer Milan Heidelberg New York Dordrecht London

Library of Congress Control Number: 2011942911

� The Author(s) 2012This work is subject to copyright. All rights are reserved by the Publisher, whether the whole or part ofthe material is concerned, specifically the rights of translation, reprinting, reuse of illustrations,recitation, broadcasting, reproduction on microfilms or in any other physical way, and transmission orinformation storage and retrieval, electronic adaptation, computer software, or by similar or dissimilarmethodology now known or hereafter developed. Exempted from this legal reservation are briefexcerpts in connection with reviews or scholarly analysis or material supplied specifically for thepurpose of being entered and executed on a computer system, for exclusive use by the purchaser of thework. Duplication of this publication or parts thereof is permitted only under the provisions ofthe Copyright Law of the Publisher’s location, in its current version, and permission for use must alwaysbe obtained from Springer. Permissions for use may be obtained through RightsLink at the CopyrightClearance Center. Violations are liable to prosecution under the respective Copyright Law.The use of general descriptive names, registered names, trademarks, service marks, etc. in thispublication does not imply, even in the absence of a specific statement, that such names are exemptfrom the relevant protective laws and regulations and therefore free for general use.While the advice and information in this book are believed to be true and accurate at the date ofpublication, neither the authors nor the editors nor the publisher can accept any legal responsibility forany errors or omissions that may be made. The publisher makes no warranty, express or implied, withrespect to the material contained herein.

Printed on acid-free paper

Springer is part of Springer Science+Business Media (www.springer.com)

To my daughters Eva and Maria, andstep-daughter Lucia,and to my grand-daughters Cristiana,Sofia, and Irma,and step-grand-son and daughtersLeonardo, Viola, and Ginevra

G. Gandellini

To my parentsA. Pezzi

To Paolo and AliceD. Venanzi

Contents

1 Defining and Understanding Strategic Management . . . . . . . . . . . 11.1 What is Strategy?. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11.2 The Source of the Company’s Wealth . . . . . . . . . . . . . . . . . . 21.3 The Importance of a Strategic Plan . . . . . . . . . . . . . . . . . . . . 31.4 The Usefulness of Modeling . . . . . . . . . . . . . . . . . . . . . . . . . 71.5 A Simplified Conceptual Model. . . . . . . . . . . . . . . . . . . . . . . 91.6 The S-Shaped Curve and the Opportunity Costs . . . . . . . . . . . 121.7 The Relationship Between Investments and Value:

Direct and Indirect Tools, and Professional Resources . . . . . . . 141.8 Highlights on Pricing Strategies. . . . . . . . . . . . . . . . . . . . . . . 161.9 Translation of the Above Concepts into Spreadsheet Models. . . 19

1.9.1 Relationships Among pcpV, Priceand Market Share. . . . . . . . . . . . . . . . . . . . . . . . . . . 20

1.9.2 Relationship Between Investments (‘‘Costs’’)and pcpV . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

1.9.3 Could We Do Better Than That, withthe Same Budget? . . . . . . . . . . . . . . . . . . . . . . . . . . 30

1.9.4 Closing the Circle Among Investments, pcpV,Value/Price Ratios, Market Share, Marketand Contribution . . . . . . . . . . . . . . . . . . . . . . . . . . . 31

1.9.5 Impact of the Professional Profiles on the Efficiencyin the Use of Resources . . . . . . . . . . . . . . . . . . . . . . 35

1.10 Strategic Management in Multiple Businessesand Related Models . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 381.10.1 Evaluating the Performance

of the Various Businesses . . . . . . . . . . . . . . . . . . . . . 391.10.2 How to Manage the ‘‘Portfolio’’ of Businesses . . . . . . 39

References . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43

vii

2 External and Internal Analysis of the Environment. . . . . . . . . . . . 452.1 Introduction. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 452.2 External Macro-Environment. . . . . . . . . . . . . . . . . . . . . . . . . 462.3 Industry and Competitive Environment. . . . . . . . . . . . . . . . . . 52

2.3.1 Structural Factors . . . . . . . . . . . . . . . . . . . . . . . . . . . 522.3.2 Extended Competition . . . . . . . . . . . . . . . . . . . . . . . 552.3.3 The Critical Role of Other Stakeholders . . . . . . . . . . . 602.3.4 Putting it all Together . . . . . . . . . . . . . . . . . . . . . . . 612.3.5 The Process of Scanning the Business Landscape . . . . 63

2.4 Internal Environment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 682.4.1 Resources . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 692.4.2 Capabilities and Competencies . . . . . . . . . . . . . . . . . 702.4.3 Resources, Capabilities and Competencies

to Gain a Competitive Advantage . . . . . . . . . . . . . . . 752.4.4 Strategy Selection and Gaps Identification . . . . . . . . . 77

2.5 SWOT Analysis: A Simple Framework for Assessingthe Firm’s Position Against the Environment . . . . . . . . . . . . . 782.5.1 The Importance of Distinguishing

Among Businesses . . . . . . . . . . . . . . . . . . . . . . . . . . 782.5.2 How to Identify Relevant Options

and Courses of Action . . . . . . . . . . . . . . . . . . . . . . . 82References . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 82

viii Contents

Overview of the Series

The innovative and unique feature of this short series on strategic management(two conceptually related, but independent volumes), which sets it apart from themyriad of books on the subject, is that it does not contain one single theoreticalconcept that cannot be translated into practice. Its aim is providing universitystudents and practitioners with a practical, decision-making, and action-orientedoverview, sometimes iconoclastic, of the strategic management process.

The objective is reached through the adoption, in most parts of this work, of aset of logical and judgmental models, which show the operational interrelation-ships among the relevant factors that have an impact on firms’ competitiveness andthat are or can be translated, where appropriate, into spreadsheet templates.

The model which introduces this first volume sets the stage for addressing theissue of value creation for the market, and the major phases of the strategicmanagement process: environmental analysis, strategy formulation and develop-ment, strategy evaluation and control. Its conceptual and operational structure isdescribed in the first part, together with a practically oriented definition of strategy,and a discussion of both the importance of strategic planning and of the logic andbenefits of the judgmental modeling approach to decision making.

The second part addresses the classical approaches to the analysis of theexternal and internal environmental factors, which have an impact on the‘‘functioning’’ of the basic model, i.e. the structural characteristics of the industrycontext, and the companies’ technical, organizational, financial, and humanresources, including the translation into operational models of otherwise rathertheoretical concepts.

The first part of the second volume expands the analysis of the strategicdecisions, emphasizing the importance of a sustainable competitive advantage, andproposing an integrated conceptual and operational framework (the ‘‘StratecoDashboard’’), that complements and significantly improves the recent and well-known Blue Ocean approach to strategy development.

ix

Finally, the second volume addresses the measurement of the performance ofstrategy in terms of value creation for the shareholders, highlighting differencesand similarities, as well as strengths and weaknesses, of the main metrics. Fur-thermore, it proposes a comprehensive and operational framework for theassessment of the financial feasibility of strategy, through the measurement of theimpact of the planned strategic moves on financial needs and the evaluation oftheir financial sustainability.

x Overview of the Series

Introduction to the First Volume

Contrary to the approach adopted by most textbooks on strategy, that start with thediscussion of strategic management in multiple businesses, suggesting variousconceptual models for managing the so-called ‘‘portfolio’’ of the firm’s activities,and devoting the largest part of their attention to these issues, the first part of thisfirst volume will be mainly focused on strategically managing a single business.

Actually, the firm’s competitive success and wealth are the result of a sum ofindividual transactions with the market, and the logic and profitability of eachtransaction depend on the type of relationship between the firm and an individualcustomer, within the context of a well defined and very specific ‘‘strategic businessunit’’ (SBU) or product/market combination: how can we address the issue ofmanaging strategically the firm’s presence in multiple SBUs, discussed at the endof the first part, if we do not understand in depth, first of all, the logic of the mono-business interaction that represents the basic ‘‘brick’’ of the entire firm’sconstruction?

Obviously, doing business will also imply a number of interactions with manyother players and stakeholders, and will be affected by numerous factors, bothexternal and internal: however, most of these aspects, discussed in the second partof this volume, will inevitably be seen from the perspective of a relativelyhomogeneous industry and company context.

xi

Chapter 1Defining and Understanding StrategicManagement

Abstract After a short ‘‘operational’’ definition of strategy, we will focus ourattention on the mechanism that creates a company’s wealth, and on the criticalrelevance of a market orientation, including the creation of value for thecustomers, for triggering this mechanism. We will then emphasize the importanceof formalizing the strategic decisions into an explicit strategic plan, and supportingthe plan with appropriate conceptual and operational decision models. We willtherefore discuss the basic concepts and models that link together the firm’s marketand economic performance, including an overview of pricing strategies, andprovide a concrete translation of these models into several spreadsheet templates.Finally, we will extend the modeling approach to the issue of strategic managingmultiple businesses, providing a number of conceptual frameworks that could betranslated into operational decision support systems.

Keywords Strategic management � Strategic planning � Strategic business unit �Marketing strategy � Market share � Pricing strategy � Value/price ratio � Criticalmass � Demand curve � Judgmental modeling � Decision support systems �Portfolio analysis

1.1 What is Strategy?

Among the various definitions found in the literature, we think that, from thepractical and managerial perspective that inspires this book, the following com-bination of concepts best conveys the nature and purpose of strategy:

• set of decisions;• related to the allocation of resources;• over the medium-long term;• to one or more product/market combinations;

G. Gandellini et al., Strategy for Action—I, SpringerBriefs in Business,DOI: 10.1007/978-88-470-2487-8_1, � The Author(s) 2012

1

• in view of specific objectives;• considering external opportunities and threats;• and internal capabilities and constraints;• definition of the related action plans.

This definition is applicable to any business context. For the sake of simplicityand conciseness, we will focus our attention on profit-oriented organizations, forwhich the ability to create wealth is, by definition, one of the major objectives.However, most of the concepts discussed here can be applied also to non-profitorganizations, which institutionally have other objectives, but could not surviveand prosper without funding.

In the following pages, after having reminded an obvious and basic concept(which is, unfortunately, frequently forgotten), emphasized the essentiality of astrategic plan (which is rarely mentioned in most textbooks), and highlighted theusefulness of judgmental modeling (which is totally neglected by most authors),we propose a simple conceptual and operational model that briefly describes therelationships between the resource allocation decisions and the profitabilityobjectives within an hypothetical business (i.e. a specific product/market combi-nation), postponing to the subsequent chapters a more in-depth discussion of themajor phases of the strategic planning process: environmental analysis, strategyformulation and development, strategy evaluation and control.

1.2 The Source of the Company’s Wealth

Everybody understands that the only true source of wealth for any profit-orientedorganization is the market, which purchases the company’s products or services:without sales, the company would not produce any revenues, and all the otherpotential providers of funds and resources (shareholders, banks, suppliers) would,sooner or later (probably, sooner) stop feeding it.

At the heart of any business strategy and plan we therefore need to have asound marketing strategy and plan: all the other company’s functional areas(R&D, manufacturing, HR, finance, logistics) are just ‘‘ancillary’’ to the marketingfunction, and would not survive without the company’s ability to profitably satisfythe market (see McKenna 1991).

If we agree on these interrelated objectives, i.e. reaching profitability throughmarket satisfaction, we should also agree on the need for estimating, measuringand controlling their achievement, and understanding their relationships, in orderto make strategic decisions that could positively influence their behavior over time.

The synthetic and elementary indicators we are suggesting for measuring thesetwo factors are, respectively, the following:

1. contribution margins, which represent the most appropriate variable forassessing the actual contribution (revenues less variable and direct fixed costs)of a given and specific business to the overall company’s profitability,

2 1 Defining and Understanding Strategic Management

particularly if the company operates in more than one business unit, which isthe most frequent case:

– it would be totally senseless to relate profitability to market share withoutreferring to a specific market and competitive context;

– the overall firm’s profitability (profit or loss) will therefore be the net result ofcombining the contributions of various business units, and paying with thesecontributions the costs that are not the direct responsibility of any of theseunits (for example, the CEO’s salary or the headquarters’ rent).

2. market share, which represents the portion of the market’s purchases satisfiedby a given company, with reference to a specific and well defined industrysector or segment, within a given time horizon:

– this indicator is critical also for small and medium enterprises (SMEs), pro-vided that the market in which they compete is correctly identified anddelimited (the so-called ‘‘pertinent’’ or reachable market);

– again, it would be senseless to measure the market share, i.e. the company’sability to compete, in relation to a market (defined, for example, in geo-graphical terms) that the company is not ‘‘physically’’ able to reach.

As far as this last point is concerned, a totally different indicator is the ratiobetween the market that the company is ‘‘able’’ to reach and the market that it‘‘could’’ possibly reach (the ‘‘actual’’ market, a subset of the so-called ‘‘theoretical’’and ‘‘available’’ market, normally defined in geographical terms) with a largermarketing organization: this indicator, that is even more important from aninternational perspective, just measures the relative size of the company, not itsability to satisfy the market better than the competitors.

More will be said below about the relationships between these factors and,specifically, their relative importance: however, saying that ‘‘market share is notanymore fashionable …’’ as some authors do in the attempt of being perceived as‘‘original’’ (Simon et al. 2006), is either trivial (if they mean that market shareshould not be pursued at the expense of profitability) or a nonsense (if they meanthat market share is unimportant): without a market position (precisely, ‘‘some’’market share) it would be impossible to generate any profit.

1.3 The Importance of a Strategic Plan

Coherently with the action-oriented approach of this book, we already said that animportant and final point to address in the development of strategic choices is thedefinition of an action plan, i.e. which specific actions must be performed,by whom, within which deadlines, and at which costs, in order to reach the chosenobjectives. This definition is essential also for assessing the practical feasibility ofthe strategic choices.

1.2 The Source of the Company’s Wealth 3

An obvious prerequisite of the action plan is therefore a description of thereasoning behind these choices in the so-called strategic plan, that shouldexplicitly address, more or less in depth, depending on the complexity of thecontext in which the firm operates, and on the size and complexity of the firm’sorganization, the following major points:

• clear definition of the business(es) in which the firm operates or wants tooperate: products and/or services addressed to specific target users, product/market segmentation;

• environmental and industry analysis (external environment, market, infra-structures, channels, competition, suppliers) within this or these businesses, inrelation both to the past and to the estimated future trends: in particular, explicitprojection of the market potentials in the businesses and segments of interest,opportunities that could be exploited and threats that should be faced;

• company profile (organizational structure, resources and skills), past behaviorand strategic choices, and obtained results (if applicable), interpretation of thereasons of these results, identification of strengths and weaknesses in relation tothe environmental and industry opportunities and threats;

• identification of specific objectives (market position, profitability, etc., overalland by segment) and definition of the most relevant strategic choices, i.e. typeand amount of resources to be allocated to specific businesses and overall,in order to reach the objectives;

• definition of the organizational setting that will be needed for implementingthe strategies: structure and major assets, human resources, roles and respon-sibilities, management systems;

• projection of the economic and financial results that will depend on theimplementation of the above choices.

We should re-emphasize that the heart of a good strategic plan is themarketing plan, that supports the major and most difficult part of any plan, i.e. theprojection of revenues, based on an assessment of the market potentials, and onestimates of the reachable market shares, depending on both the planned strategiesand the expected competitive profiles and behavior.

In turn, the strategic plan is the heart of the so-called business plan, thatcomplements the strategic projections with additional details about the ownership,governance, financial, and organizational aspects.

The usefulness of a plan and of an explicit and formalized description of thefirm’s intentions and activities, over an appropriate period of time (at least 3years), looks obvious if we consider the following:

• the firm’s investments (whichever they are) normally have an impact that isdiluted over time: the outcomes of these investments do not happen instantly,and it is therefore important to estimate their evolution in order to keep it undercontrol;

• once a resource has been allocated, it is rarely easy to backtrack: it is thereforebetter to estimate in advance and as explicitly as possible the impact of that

4 1 Defining and Understanding Strategic Management

allocation against possible alternatives, especially considering the significantopportunity costs that are intrinsic to any decision, systematically neglected inthe business practice;

• the environmental and market system (including the company within it)evolves over time, and it therefore makes sense to prevent unexpected events:it is clear that not everything can be anticipated, but a serious forecasting effortcan greatly reduce the level of uncertainty and the risks;

• the customers’ behavior is significantly affected by previous experiences, andthe market positions gained by the competitors can represent importantstrengths: it is therefore critical to interpret the market scenario from a dynamicperspective, with the forward-looking view that can only be developed by agood planning practice.

All this is even more true in case of new ventures or significant changes in thefirm’s life, and in the absence of appropriate information about the likely evolutionof the industry.

The major and numerous benefits provided by a good strategic plan should bequite obvious, but it is worth listing them, classified in the following categories:

1. analysis, interpretation and information management:

– a plan forces the identification and description of the industry characteristics,and of the related opportunities and threats;

– consequently, it allows the identification of the firm’s potential strengthsand weaknesses in relation to these characteristics;

– it therefore facilitates the identification of the information needs, and a checkof completeness of the analysis;

– over time, it allows the creation, development, and consolidation of aninvaluable knowledge base and a hardly copyable know-how, that are easilyaccessible anytime and by anybody (qualified and interested in contributing tothem), instead of being randomly stored and dispersed in the brains of fewpeople, with all the attached risks of being lost;

– not to mention the often neglected fact that a plan facilitates planning, i.e.helps at developing, over time, the ability to capitalize experiences and know-how, to look forward, and to formulate realistic and quantifiable projections,based on explicit, systematic, and thoughtful assumptions.

2. guidance, direction and control:

– a plan forces the definition of specific and measurable objectives: withoutthese, we would just have generic statements of intent, hardly translatable intoconcrete guidelines for action;

– in view of these objectives, it requires the development of medium and long-term forecasts and projections;

– especially if the projections are supported by simple software tools such as anelectronic spreadsheet, it will be easy to conduct sensitivity analyses of the

1.3 The Importance of a Strategic Plan 5

estimated results, based on changes in the assumptions, and compare therelative attractiveness of alternative courses of action;

– in practice, the plan represents an explicit guide to action, i.e. a sort ofcompass that allows an easier identification of the route to be followed forreaching the objectives;

– thanks to this compass, it will therefore be easier to focus the firm’s efforts,improving the effectiveness of the planned moves;

– it will also be easier to translate the strategic guidelines into operationalplans, with the identification of roles, responsibilities, activities, deadlinesand the possibility of controlling both the attainment of the stated objectivesand the correct implementation of the planned activities.

3. consistency and resources:

– with a written plan, it is much easier to assess the soundness and coherenceof both the decisions and the underlying estimates;

– in particular, it is easier to check the coherence between the stated objectivesand the necessary financial, technological, and human resources forreaching them;

– not to mention the fact that a good and credible plan facilitates the access tofinancial resources and/or better conditions in using them, irrespective oftheir source (banks, shareholders, private investors, venture capitalists);

– furthermore, the plan facilitates an integrated and balanced view of thefirm’s portfolio of activities allowing the identification of the appropriateresponsibilities and the assignment of specific objectives to the various levelsof the corporate structure and facilitating the reconciliation of potentiallyconflicting objectives among the various functional areas (e.g. sales vs.manufacturing or finance).

4. savings and risk management:

– thanks also to the above advantages, a plan allows a reduction of theuncertainty, and a corresponding abatement of risks;

– a better focalization of the efforts reduces waste and, therefore, increases theoperational efficiency;

– not to mention that the savings can be diverted into more promising uses,facilitating the attainment of the critical mass that is necessary to compete inthe various market contexts.

5. communication and motivation:

– strictly connected to the accessibility of the know-how crystallized in theplan, is the possibility of communicating its contents and logic to all thepeople that, within the company or systematically in contact with it (forexample, sales agents), could or should contribute to its implementation intheir respective areas of competence;

6 1 Defining and Understanding Strategic Management

– communicating facilitates a better understanding and sharing, not just of theinformation, but also of the firm’s objectives and constraints, which furtherreinforces their reconciliation with the individual expectations;

– communicating and sharing are the best ingredients of motivation, since theygive everybody an explicit sense of mission and belonging;

– stimulating also a better awareness of the need for a coherent integration ofeverybody’s efforts towards common goals, and of the importance ofteamwork;

– obviously, the existence of an explicit plan also allows a better communi-cation with the outside world, facilitating, for example and with all thenecessary precautions for protecting confidentiality, the development ofalliances with other firms and potential partners;

– not to mention the possibility of supporting and improving, with appropriatelyselected information on an ongoing basis, the relationships with the pressand the development of public relations initiatives;

– finally, the availability of a good strategic plan, if correctly communicated, isa good symptom of advanced managerial culture, and this could more easilyattract key professional resources, which could otherwise be reluctant toembark on a boat without any compass.

Considering all the above advantages of an appropriate strategic planningactivity, it is rather incredible to see that a large majority of companies (especiallysmall firms, but not just them) does not have a real strategic or marketing plan.

An explanation of this apparently strange phenomenon, in addition to the lackof managerial culture in most countries, is that planning is not easy, strains thebrain, takes a lot of time, and, sometimes, a lot of money.

One of the few ways of reducing the impact of these constraints and facilitatingat least an embryonic planning activity, is that of simplifying and automating(although with some inevitable initial investment, especially in terms of time), thestrategic planning process: this is exactly the purpose of the judgmental modelingapproach that will be discussed and exemplified in the following pages.

1.4 The Usefulness of Modeling

The industry and market phenomena that need to be taken into consideration inorder to estimate the indicators suggested under Sect. 1.2, present—in relation, forexample, to those typical of manufacturing—a series of interrelated characteristicsthat make the estimates particularly difficult and complex:

• non linearity, such as the relationship between investments and results (seeSect. 1.6 under Fig. 1.2 ‘‘The S-shaped curve’’);

• carry-over and lags: the response to this period’s investments will occur in futureperiods (lag) and could depend on a cumulative effect of the same investments overtime (carryover): for example, the investments in communication can produce

1.3 The Importance of a Strategic Plan 7

results that are rarely immediate, and, on the other hand, the market’s reactions in 1year could be triggered both by the investments in that year and by the ‘‘memory’’of the previous investments in the mind of the consumers;

• decay of the responses with time in the absence of further stimulation: even verywell-known brands like Coke would lose sales without continuous and signifi-cant communication investments;

• multiplicity of causal factors: for example, sales will depend on the combinedeffects of a series of investments (R&D that improves the quality of products,advertising, sales force, distribution channels, etc.);

• interactivity of these factors: for example, brand image strongly depends on thecompany’s performance on the ‘‘key success factors’’, but could also affect theperception of such performance (e.g. reducing the demand’s sensitivity to price);

• variability and instability of market reactions and competitors’ moves: forexample, an economic crisis could significantly reduce the overall sales ofexpensive products, but, at the same time, contribute to the expansion of acompany’s market share in the same industry, due to the bankruptcy of othercompetitors;

• multiplicity of casual factors, that could strongly contribute to the variabilityof market’s and competitors’ behavior: for example, a totally unexpected eco-logical disaster in a country could destroy, at least for a while, the production ofspecific fresh foods;

• specificity and diversity of the various industry and geographic contexts, thatmake particularly difficult, if not impossible, the generalization of specificstrategic or organizational solutions: let us just consider, for example, the majordifferences, from industry to industry, in terms of sensitivity to price or ratiobetween fixed and variable costs;

• qualitative culture of most managers, who are more comfortable with verbaland debatable analyses and assessments than with systematic and rigorousquantitative approaches.

The use of logical models, i.e. of synthetic, abstract and simplified represen-tations of the reality, could significantly reduce the complexity of the analysis viaan explicit identification of the most relevant variables that could have an impacton the company’s results, their behavior and interrelationships.

Obviously, the more simplified are the models, the less accurate is theirinterpretative and predictive power. However, even a very simple model, if welldesigned, could offer a series of important benefits:

• it helps at clarifying managers’ ideas about the behavior of the reality and thenature of problems, promoting a systematic and structured reasoning, even ifexhaustive and reliable data are not easily available;

• it is explicit and ‘‘transparent’’ (especially if developed on an electronicspreadsheet), and can be shared, discussed and negotiated, in view of potentialadaptations and improvements;

• in particular, when translated into mathematical functions (in an electronicspreadsheet), it allows to conduct easy sensitivity analyses and ‘‘what-if’’

8 1 Defining and Understanding Strategic Management

simulations, in order to see the extent to which the results projected by themodel can be positively or negatively affected by different inputs (values of theendogenous or exogenous variables);

• it represents a permanent and accessible knowledge base, that can be movedover time and space, instead of being confined in the brains of few experts;

• it does not get ‘‘sick’’, nor it suffers managers’ psychological or emotionalproblems;

• it allows the identification and control of aspects and variables that require morein-depth analyses, for example pointing out the need for more specific andcritical data;

• it provides a logical basis for quantifying and measuring industry and marketphenomena;

• it is an almost unique tool for comparing the actual outcomes of the managerialdecisions to the expected results, for designing appropriate decision supportsystems, and for a continuous updating of the logic behind the decisions;

• if used consistently and systematically, it allows a continuous enrichment, overtime, of the knowledge base, the production of statistics, the identification oftrends, benchmarks and best practices;

• finally, if combined and integrated with other connected models, it can consti-tute the backbone of a planning system, that, once designed, just needs to befed over time with new inputs, with limited additional efforts.

Overall, the adoption of models and estimates makes the decision making,forecasting, and planning processes more systematic and explicit, usefully com-plementing managers’ intuition, feelings and experience.

1.5 A Simplified Conceptual Model

The simplified conceptual model depicted in Fig. 1.1 (Gandellini et al. 2005)represents the type of relationship between contribution margins and market share,and identifies the major factors that positively or negatively affect the com-pany’s ability to produce wealth:

• some of these factors (market size and behavior, and competitors’ moves) arerelatively outside the company’s control and must be estimated;

• others (the strategic decisions) can be managed in order to optimize the balancebetween market position and profitability.

We should emphasize, at this point, that all the relationships described in thefigure are meaningful only if they are viewed within the context of a specificproduct/market combination or ‘‘strategic business unit’’ (SBU: a homoge-neous area of business in terms of user characteristics and needs that can besatisfied by a specific type of product or service): otherwise, it would be totallysenseless to relate the firm’s market performance to its economic results.

1.4 The Usefulness of Modeling 9

The model only represents ‘‘actual’’, objective and causal relationships amongthe relevant factors, and does not take into consideration other possible relation-ships that could only depend on subjective managerial decisions: for example, adirect connection (in a dynamic perspective) between contribution and investments(costs) or the frequent (and totally absurd) connection between costs and price.

The top part of the figure represents relationships that are obvious by definition:

• the contribution is the difference between revenues and direct costs;• the revenues are the product of the unit price times the quantities sold.

It should also be obvious that the quantities sold are the product of the marketsize times the market share (i.e. the company’s ability to satisfy a portion of themarket and ‘‘win’’ a number of individual purchases against the competitors), butthis evident relationship is often neglected and misunderstood, probably due to theingrained use, borrowed from the economists, of directly relating quantities toprices, without the intermediation of the variables that actually and directly affectvolumes (market size and market share), in the ‘‘infamous’’ demand curve (seealso Sect. 1.8 about pricing strategies).

We should also say that the frequent practice of measuring market shares inmonetary terms, often justified by the heterogeneity of the goods sold in terms ofquality and price, is not very useful from a strategic standpoint, unless it iscomplemented by an estimate of the corresponding indicator in terms of quantities:

• first of all, the SBU or product/market segment within which the share is beingmeasured must be as homogeneous as possible, otherwise we would incur therisk of comparing apples to oranges, and the entire notion of ‘‘share’’ would bemeaningless;

• secondly, the market needs are satisfied with the purchase of individual units ofconcrete goods or services (i.e. quantities), the prices paid (the money) beingjust the compensation of the suppliers that, having been chosen by the market

Fig. 1.1 The ‘‘engine’’ of an organization’s wealth

10 1 Defining and Understanding Strategic Management

and having gained their share of it, deliver these goods or services: in otherwords, people buy a ‘‘real thing’’, not a monetary value, and the market size ismade of a sum of real things.

In conclusion, if we really want to understand how profits are generated, weneed to identify the causal relationships among the relevant factors that affectthem: from the perspective of an individual company, causally relating prices andquantities is rather misleading, since the actual causal relationship is betweenmarket share and company’s sales (quantities), in the context of a givenmarket demand, no matter how this demand is generated.

From the figure, it should also be evident that, other things equal, there is adirect and positive relationship between market share and profitability, interme-diated by quantities sold and revenues.

The problem is that ‘‘things’’ are rarely ‘‘equal’’, since, in order to generatemarket share, we need to consider the factors that affect it:

1. price, which is inversely correlated to market share (broken arrow in the fig-ure): always other things equal, the lower the price the higher the share, that iswhy the acquisition of market share via reductions in prices could be costly,since the additional quantities sold could not necessarily make up, in terms oftotal contribution, for the loss in unit margins;

2. the ‘‘perceived [by the market] competitive profile [of the company] in termsof value’’ (pcpV); this critical factor, directly correlated to market share,represents the (perceived) value that the company is able to offer to the marketat a given price:

– this overall value is the result of the company’s competitive performance inrelation to the criteria adopted by the market in making the purchasedecision (the so-called ‘‘key success factors’’ in a strict sense, e.g.: brand,quality, customization, service, etc.), and obviously depends on the relativeimportance assigned by the market to these criteria;

– it should be noted that even a high price level could contribute, at least tosome extent and with varying degrees depending on the type business(especially, but not only, with ‘‘status symbol’’ products or services), to theperception of value (arrow price?value in the figure): that is why it could berather difficult to manage the contradictory effects of price (it reduces thewillingness to buy while raising the perception of value);

– furthermore, in a dynamic perspective, also the acquired market positioncould reinforce the perception of value and positively or negatively affect thecompany’s performance in relation to the ‘‘brand’’ factor (for the sake of sim-plicity, this potential ‘‘recursive’’ relationship is not depicted in the figure).

The company’s value/price ratio, more or less explicitly and consciouslycompared (by the market) to analogous ratios proposed by other competing sup-pliers, is what determines the customer’s willingness to buy from a company oranother.

1.5 A Simplified Conceptual Model 11

It is obvious that, in order to improve this ratio via an improvement of theperception of value by the market (and not only via price reductions), thecompany must invest resources (arrow costs?value in the figure), and theinvestment could not necessarily be ‘‘paid’’ by the additional contribution gener-ated by a larger market share.

In a short-term perspective, depending on the competitive situation, it istherefore normal that the acquisition of market shares could be more costlythan profitable: however, if resources are correctly allocated to the appropriatetools and the levels of investment tend to increase, over time, less than propor-tionally in relation to the increase in market share, a ‘‘virtuous’’ cycle can takeplace: appropriate investments produce an increase in market share, that triggersmore revenues and contribution, and part of this contribution could be used to feedadditional investments, and so on. In any event, it is clear that, in a medium-longterm perspective, and other things equal, a larger market share should bepositively correlated to a better financial performance, due to several obviousfactors: better market knowledge and experience, due to more extensive (and,probably, longer) presence, better visibility, better ability to exploit economies ofscale, more bargaining power with the suppliers and lower unit costs, etc.

By the way, the positive correlation between market share and profitability(ROI) was empirically tested and documented by Buzzell and Bradley (1987), withhis famous ‘‘PIMS’’ Project (see an update in Farris and Moore 2006).

It should be noted that the company’s investments could also positivelycontribute to the market expansion (arrow costs?market in the figure), via theacquisition of new users that formerly were not part of the target market: thispossibility (i.e. increase in company’s sales without a corresponding reduction incompetitors’ sales) is particularly relevant in growing businesses, but does notundermine the concept of market share acquisition, since the company‘‘occupies’’ the position with the new users to the detriment of potential intrusionsby any competitor.

Finally, the broken line that divides the figure into two parts separates what wecall ‘‘the visibility area’’ from the rest: companies normally ‘‘see’’ very well allthe variables above the line (including, evidently, the two factors which summa-rize their strategic decisions), but rarely control those below the line, which,unfortunately, directly affect the economic and financial performance. In partic-ular, they do not even attempt to estimate the critical ‘‘pcpV’’, nor they bother toassess their market position.

1.6 The S-Shaped Curve and the Opportunity Costs

With the above comments, we are not necessarily saying that ‘‘the higher theshare the better’’: any conclusion mostly depends on the specific competitivesituation in the business, since it is obvious that, beyond a certain point andespecially in mature and low-growth industries, further increases in market share

12 1 Defining and Understanding Strategic Management

will imply the reduction of the competitors’ shares, and it is very likely that thesecompetitors will retaliate (for example, with significant price reductions) in orderto maintain and protect their market position. The end result, via reciprocalretaliations, will probably be that all the competitors in the industry will make lessmoney and, therefore, also the investments of the company that initiated themarket escalation will not be any more profitable as before.

The most important guideline, from a strategic perspective, will therefore bethat of reaching a good balance, or an acceptable compromise, among thefollowing factors:

• relative market position (share);• type and size of the investments needed to produce and maintain that market

position;• amount of contribution or ‘‘return’’ generated by that market position.

The typical relationship between investments (in this case, marketing invest-ments) and results (in this case, market share) is depicted in Fig. 1.2.

This curve, called also ‘‘logistic curve’’, describes the relationship betweeninvestments in specific resources and specific results obtainable with theseinvestments, a critical concept in strategic planning, which can be applied to anytype of resource able to produce some results (e.g.: exposure produced byadvertising investments, orders produced by the sales force, quality improvementsproduced by R&D, etc.):

• up to a certain ‘‘minimum level’’ of investment (normally called ‘‘threshold’’ or‘‘critical mass’’), results do not show significant increases and, therefore, thecompany does not obtain visible and significant results;

• beyond this level, results grow at an exponential rate up to another point(a reasonably ‘‘maximum’’ level of investment called ‘‘ceiling’’);

• beyond this ceiling, results could continue growing, but at a diminishing rate,and therefore additional investments would not be convenient.

Obviously, the ‘‘critical mass’’ necessary to compete, and the correspondingshape and width of the S-shaped curve, vary greatly, depending on the specificbusiness, the type of resources and results taken into consideration, and the marketand competitive context.

Fig. 1.2 The S-shaped curve

1.6 The S-Shaped Curve and the Opportunity Costs 13

As a concluding remark, we should point out that a ‘‘single’’ version of theabove mentioned model, that synthesizes a given strategy in a given businesscontext (investments and price), can only take into explicit consideration ‘‘out-of-pocket’’ costs: however, in a real life situation, it would also be important tocompare multiple and alternative strategies, in order to estimate the opportunitycosts that could depend on the choice of one of them in relation to the others.

This is something that managers rarely do, totally underestimating the risks andthreats of using scarce resources in just a specific direction, without consideringalternative, and potentially more promising, uses of the same resources.

1.7 The Relationship Between Investments and Value: Directand Indirect Tools, and Professional Resources

In addition to the critical relationship between value and price, which has a directimpact on the firm’s market position, within a specific business and market context,the most relevant relationship from a strategic standpoint (i.e. from a resource allo-cation perspective) is that between investments (all translatable into costs) and value.

In fact, this is the relationship that, together with the choices about price,summarizes the actual ‘‘strategy’’ of the firm: as far as the value/price ratio isconcerned, while price is an independent variable, since it is determined exoge-nously in relation to the above model (see also below, under Sect. 1.8), the valueperceived by the market is directly affected by the decisions about the use of thefirm’s resources, that, in the above model, are summarized under the label ‘‘costs’’.

Assuming, for the sake of simplicity, that the value perceived by the market isthe result of a combination of just three aspects (brand, quality, and service), therelationship is exemplified in the right part of Fig. 1.3.

In the headings of the three columns we can see the hypothetical components ofvalue, i.e. the criteria adopted by the market in making a choice among alternativesuppliers or ‘‘Key competitive Success Factors’’.

In the rows are listed several tools or resources in which the company can invest inorder to satisfy the market’s expectations: we call these tools ‘‘direct’’, since they canhave an immediate impact on the perceived firm’s performance in relation to thecomponents of value. As we can see from the highlighted intersections in the matrix:

• on the one side, the same tool can affect multiple components of value;• on the other side, the same component of value can be affected by multiple tools.

Obviously, the relative importance of each tool for the affected component ofvalue will vary depending on the specific business of interest. This aspect will beconcretely exemplified under Sect. 1.9 (in particular, Fig. 1.9).

In the upper left part of the figure we listed other resources or tools that we call‘‘indirect’’, since their impact on the components of value cannot be perceived bythe market, being, in a certain sense, ‘‘behind the scene’’. However, these tools can

14 1 Defining and Understanding Strategic Management

significantly affect the way in which the direct tools are managed, i.e. the man-agement’s ability to perform their tasks.

The reasoning is that, the better is the management’s professional profile (thanksalso to appropriate investments in the ‘‘indirect’’ tools), the more effective andefficient will be the investment in the managed ‘‘direct’’ tools: for example, and otherthings equal, a given investment in R&D could be partially wasted if the professionalprofile of the manager in charge of managing it is not sufficiently good. This lastaspect will be concretely exemplified under Sect. 1.9 (in particular, Fig. 1.18).

Conceptually, the idea of distinguishing between direct and indirect tools issimilar to that of distinguishing between primary and support activities in the‘‘value chain’’ (Porter 1985) that will be discussed in the second chapter: however,we think that the first approach is more suitable for translating the concept into aspreadsheet model.

Simplifying, we can now summarize, in the Fig. 1.4, the logic of the conceptualmodel that relates the company’s decisions to its market and competitiveperformance.

Starting from the bottom left corner of the figure, we can see the logicalconnections among the various parts of the model, which replicates, although in asimplified way, what happens in a real-life situation:

1. the investments in the so-called ‘‘indirect tools’’ can have a positive impact onthe managers’ professional profiles;

2. thanks to an improvement in their professional profiles, managers can bettercontrol the tools and resources which have a direct impact on the company’scompetitiveness;

3. thanks to the improved control, all the investments made in these ‘‘direct’’ toolsor resources can be much more effective in terms of impact on the componentsof the value perceived by the market, and therefore on the company’s perceivedcompetitive profile and, finally, on the Value/Price ratio.

Fig. 1.3 Relationship between investments (resources employed = costs) and value

1.7 The Relationship Between Investments and Value 15

1.8 Highlights on Pricing Strategies

If we agree about the logic summarized in Fig. 1.1 above, we can hardly challengethe view that setting the price is a major and ‘‘central’’ (not just in graphical terms)strategic choice, since it directly affects the relative value/price ratio perceivedby the market (compared to alternative value/price ratios offered by the competi-tors), and, therefore, the market’s willingness to buy from a supplier or another.

Since this ‘‘willingness to buy’’ is nothing less than the major trigger of anycompany’s wealth, it is therefore quite strange to see that the issue of pricing islargely ignored by most writers on strategy (luckily, not by all of them), probablybecause they assume that this topic should only be addressed in marketing books(evidently forgetting that marketing is at the heart of any successful businessstrategy) and/or that discussing such an issue is too ‘‘prosaic’’ for a book onstrategy.

Being among those who firmly believe that the pricing strategy is a major issuein strategic management, we will therefore address at least its most relevant aspects.

The findings of a survey conducted by a major Italian business school (Guerini2002) show that about 70% of the interviewed companies decide their prices, as apolicy, and at least initially (i.e. before realizing that the policy doesn’t work),based on the unit full cost of their products, therefore adding to the variable costthe so-called unit fixed cost (total fixed costs divided by the number of unitsproduced), which is obviously an entity that does not exist in real terms, since itdepends on a ratio between an actual figure (fixed costs) and a largely uncorrelated(or arbitrarily set) denominator (units produced or planned).

Fig. 1.4 The logic of the firms’ strategic behavior (investments in the available tools)

16 1 Defining and Understanding Strategic Management

As a matter of fact, the unit full cost could just represent a conventional indicatorof a firm’s ‘‘efficiency’’ compared to its competitors (i.e. ability to produce morewith lower overall costs), but it is totally wrong to use it as a benchmark for settingprices, at least in 99.999% of the cases, since it is very likely that this approachwill produce either a loss of sales or reduced margins: unfortunately, a majorconsulting firm became famous for having endorsed and rationalized this practice,despite its applicability by only 0.001% of the companies (Henderson 1984).

We will not spend additional words on the absurdity of the cost-plus approach,which can be easily dismantled by any good marketing book, but we willemphasize, instead, the logical and practical method for setting a strategicallyappropriate price.

Other things equal, given a specific product/market combination, specificcompetitive profiles (i.e. the firm’s perceived profile in terms of value offered tothe market in relation to other offers), and within a given range of variability ofprice (which will be determined considering several factors, including the com-petitors’ current and expected behavior, the managers’ and salesmen’s opinions,an estimate of the potentially positive impact of price on the perception of value,and, if possible, appropriate market surveys), the market’s willingness to buyfrom a specific company (i.e. to award to it a ‘‘slice’’ of the overall market ‘‘pie’’)is inversely related to its prices.

This type of relationship is normally summarized in the famous ‘‘demandcurve’’ described in Fig. 1.5.

As you can see, in a normal competitive context (we are not talking aboutcommodities), the price is the independent variable that has an impact on thedependent variable (see the right-angle broken arrow in the figure). However,contrary to what the economists say, in a real life situation the actual ‘‘directrelationship’’ is not between price and quantities, but between price and share thatthe company is able to gain, given a certain market size (see also what we saidunder Sect. 1.5). If we really want to understand what is going on in the market, wemust realize that the relationship between price and quantities is just indirect(i.e. intermediated), since quantities are affected by the product of market sizetimes market share, no matter how the market size was generated.

As you can also see, the ‘‘wall’’ that prevents the curve from moving up, meansthat the demand’s behavior is something objective, absolutely real, and concrete,against which we incur the risk of breaking our head if we are not able to see it:

• the market ‘‘sees’’ our price (given a certain perceived value and the competingvalue/price offerings): other things equal, if we lower it, our share will increase,if we increase it, our share will diminish, unless price is a major component ofthe perceived value (in this case, we should consider, and choose from, multipledemand curves, depending on different price ranges);

• the market could not care less about our costs: that is why considering our costsfor setting prices could be totally misleading; obviously, the lower limit will berepresented by the unit variable cost, unless we want to lose money and/or get

1.8 Highlights on Pricing Strategies 17

rid of some competitors with a lower staying power than ours from a financialstandpoint.

Having said that, and assuming that the estimate of the demand behavior israther accurate, and that the curve is constantly bent downwards as in the abovefigure, setting the price is a totally straightforward operation, depending on thefirm’s specific objectives. We can hypothesize at least two different situations:

• if our objective is covering as quickly as possible the largest part of the targetmarket, we will obviously select the lowest price;

• if our objective is optimizing either the revenues or the contribution, we willneed to figure out the demand function (preferably, using a polynomial form),and use a linear programming routine (specifying the objective and the pricerange constraints): both operations can easily and immediately be performedwith any good electronic spreadsheet.

Summing up, we can represent in Fig. 1.6 the major logical steps that should beundertaken for correctly setting appropriate prices.

As you can see, we are not suggesting a specific starting point, since this shouldbe a sort of ‘‘iterative’’ activity, depending on possible changes, either in theindustry environment or in the firm’s overall strategy. Furthermore, we do notpresent specific approaches for estimating the possible competitive reactions to thecompany’s decision (middle-bottom part of the figure): you can better study thisissue in any good book on pricing.

Fig. 1.5 The demand curve of a company

18 1 Defining and Understanding Strategic Management

1.9 Translation of the Above Conceptsinto Spreadsheet Models

Managerial decisions (including strategic decisions) are made by individuals, andindividuals often base their choices on experience, contingent opportunities, intu-ition and feelings, instead of looking for the appropriate information, and/orcomplementing the poor quality of the available information (in terms of relevance,specificity, reliability, precision, exhaustiveness, and timeliness) with adequateassumptions and estimates.

What is even worse, they do not make explicit their decision making process: itis therefore difficult, if not impossible, to capitalize on previous decisions, nor is itpossible to share, discuss and improve their underlying logic.

The spreadsheet models discussed here do not have a ‘‘scientific’’ foundation:they only have the purpose of supporting, and making explicit and systematic,the logical process adopted by the decision maker in analyzing a given industrycontext and making the related decisions.

No matter how bad are the available data in a real life situation, the importanceof a systematic process in addressing a managerial problem remains intact:the lack of appropriate data that could ‘‘feed’’ the process will be complementedby reasonable assumptions and estimates, subject to verification and improve-ments based on future experience of the actual outcomes of the decisions.

Particularly for this reason, most of the inputs suggested for the followingspreadsheet models, basically represent estimates or reasonable ‘‘guesses’’,unless the decision maker can count on specific and appropriate data based onaccurate industry and market research (something that rarely happens in the real life).

However, even in this last case, the estimates will be replaced by the researchfindings only if the purpose of the analysis is to interpret the current or past

Fig. 1.6 A logical approach to price setting

1.9 Translation of the Above Concepts into Spreadsheet Models 19

industry or market behavior. Otherwise, if the findings describe an ‘‘expected’’future behavior, in view of a strategic or tactical decision, they will inevitablyremain ‘‘estimates’’: decisions are made for the future, and precise and reliabledata about the future do not exist by definition, especially in business. In fact, itshould be noted that, even in more ‘‘scientific’’ domains, such as mechanics andelectronics, the future behaviour of an object (e.g. the horsepower actually sup-plied by a Formula 1 engine) cannot be projected with total certainty.

1.9.1 Relationships Among pcpV, Price and Market Share

This first part of the model is more ‘‘descriptive’’ than ‘‘prescriptive’’, since itattempts a ‘‘snapshot’’ of a current or past market situation: however, it could beused for ‘‘predicting’’ a future situation, assuming significant changes in the inputvariables.

Let us look at the bottom right part of Fig. 1.1 above: we see that market shareis affected by the pcpV (a direct and positive relationship) and by price (inverserelationship), and that, at the same time, price could also positively affect the pcpV.

We also know that the pcpV, i.e. the suppliers’ competitive profile perceived bythe market, is the overall result of their performance on the so-called ‘‘key successfactors’’ (KSFs), that, in practice, are the criteria adopted by buyers in choosingamong suppliers and making the purchase decision: these criteria could obviouslyvary, in terms of both content and relative importance, depending on businessesand industry sectors.

In this (very) simplified spreadsheet model (Fig. 1.7), we translate these conceptsand relationships (with the only addition of the variable ‘‘elasticity indicator’’) intoconcrete and ‘‘operational’’ mathematical functions, assuming that we are in thebusiness of ‘‘small wheels for special applications in the office furniture industry’’.

This model (the yellow or light-shaded cells contain numerical inputs) attemptsto show how the performance of three hypothetical competitors (A, B, and C) inthis business, in relation to the criteria adopted by the market in making thepurchase decision, can affect their ‘‘probability’’ of gaining a share of a givenmarket (we should note that this is a ‘‘static’’ model, since it does not take intoconsideration the potential impact on future market shares of the market positionsor competitive profiles acquired in the past: however, this limitation could easilybe removed with the inclusion of ‘‘past market shares’’ or ‘‘past competitiveprofiles’’ as components of value, and linking together multiple models, each onerepresenting the results obtained at the end of a given planning period):

• in the top left part of the figure we see the list of the KSFs, and their estimatedrelative importance for the buyers; another simplifying assumption is that allthese KSFs are independent from each other: this means that potential synergiesamong the various factors do not exist, and that a competitor’s performance onone of them does not affect its performance on another factor; this is not

20 1 Defining and Understanding Strategic Management

necessarily true in a real life situation (for example, a good level of servicecould positively affect the company’s brand image), but this restriction could beremoved in a relatively more sophisticated model; ‘‘price’’ is included in this listas a positive contributor to the value perceived by the market;

• the matrix in the top right part of the figure contains a numerical assessment, on ascale from 0 to 10, of the competitors’ performance on these factors: as we can see,all the figures are entered as inputs, except for the performance on ‘‘price’’ (as apositive contributor to the perceived value), which is the result of a standardiza-tion, always on a scale from 0 to 10, of the actual prices ($) charged by thecompetitors and listed in the second row below the matrix; the standardization isnecessary, in order to calculate an overall weighted ‘‘perceived value’’ that couldinclude price as a component: for this purpose, the actual price levels must beexpressed with the same unit of measurement adopted for the other components ofvalue: the ‘‘trick’’ is comparing the actual price levels of the competitors to theprice range found in the business (bottom right rows in the figure), and making theminimum price equal to 0 and the maximum price equal to 10; a more detailedexplanation of the standardization procedure is presented below;

• based on these assessments (KSFs’ weight and competitors’ performance) wecan calculate the overall perceived value (pcpV) of each competitor (see thesecond row below the matrix), which is just the weighted average of its per-formance on the various factors:

pcpV ¼½ f 1 � w1ð Þ þ f 2 � w2ð Þ þ � � � þ fn � wnð Þ�=ðw1þ w2

þ � � � þ wnÞ þ � � � þ wnÞ

Fig. 1.7 Relationship between value/price ratio and market share (neutral ‘‘elasticity’’ to price)

1.9 Translation of the Above Concepts into Spreadsheet Models 21

where the symbols f1, f2, fn…, fn represent the scores of each competitor on thevarious factors, and w1, w2,…, wn the weights of the same factors (in thisspecific case, the division by the sum of the weights is redundant, since theseweights are expressed in percentages, but it could be necessary when their sumis different from 100);

• based on the (reasonable) assumption that the market chooses a supplier basedon a comparison among the value/price ratios offered by the available andreachable suppliers, we then calculate this ratio for the three competitors (seethe first row in the bottom part of the figure: the ratio is multiplied by 100 inorder to get rid of the decimals): in practice, the meaning of this ratio can beinterpreted as ‘‘the amount of value offered by each supplier for one dollar’’;

• it could therefore be reasonable to assume that the proportion between the value/price ratio offered by any supplier and the sum of the price/value ratios offered byall the suppliers in the business would represent the probability, for any supplier, ofgaining a corresponding share of the market demand (second row in the bottompart of the figure): had the market ‘‘perfect information’’ about the availableofferings, its rational choice would obviously be that of selecting only the best one(supplier C, in our case), assuming also comparable transaction costs for reachingthe suppliers: however, these conditions (perfect information, rationality, andcomparability or absence of transaction costs) do not apply in a real life situation.

However, this reasoning implicitly assumes that the market is equally sensitive to valueand price (an increase in price could be compensated by a ‘‘proportional’’ increase in value,and vice versa), but this could not be the case in most market situations:

• in ‘‘cost conscious’’ industry sectors, the market could not be willing to pay ahigh price, even if the value offered is proportionally adequate;

• in ‘‘status symbol’’ or luxury industry sectors, the market could not be willing toaccept a low value, even if the price is very competitive.

In order to take care of this problem, we therefore include, in the value/priceratio, the consideration of a sort of ‘‘price elasticity indicator’’, just adding, for thesake of simplicity, this indicator (e) to the denominator of the ratio, as a power ofprice (in this way, an indicator higher than 1 will more than proportionally increasethe value of the denominator and decrease the V/P ratio):

V

Pe

It is well known that a true indicator of ‘‘demand elasticity to price’’ could varyacross competitors and depending on the initial price levels considered. However,in order to show that price could be more or less important than value in specificmarket contexts, and that some competitors could profit from (or be penalized by)this aspect, we think that the use of this simple indicator could make the point,without too many analytical sophistications.

In Fig. 1.7, e is equal to 1 (neutral indicator), and we implicitly assume that themarket is equally sensitive to value and price.

22 1 Defining and Understanding Strategic Management

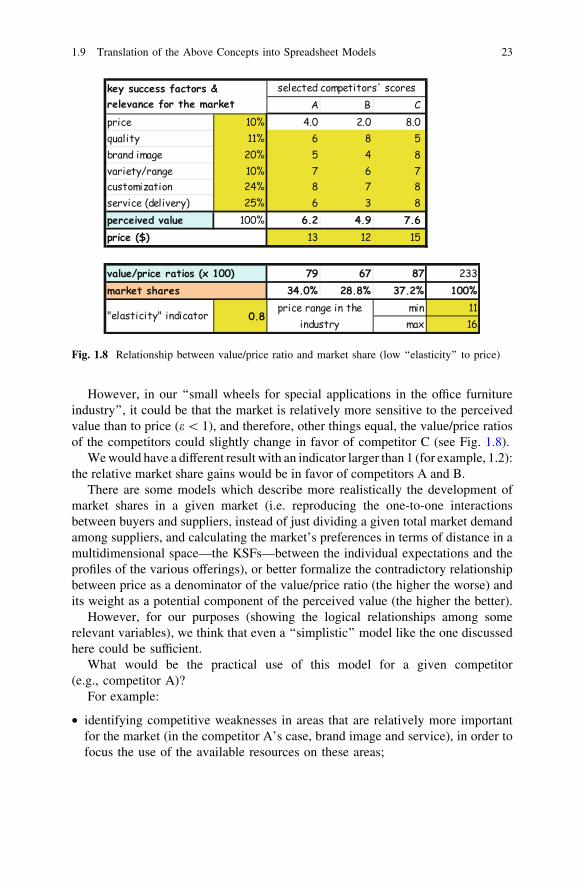

However, in our ‘‘small wheels for special applications in the office furnitureindustry’’, it could be that the market is relatively more sensitive to the perceivedvalue than to price (e\ 1), and therefore, other things equal, the value/price ratiosof the competitors could slightly change in favor of competitor C (see Fig. 1.8).

We would have a different result with an indicator larger than 1 (for example, 1.2):the relative market share gains would be in favor of competitors A and B.

There are some models which describe more realistically the development ofmarket shares in a given market (i.e. reproducing the one-to-one interactionsbetween buyers and suppliers, instead of just dividing a given total market demandamong suppliers, and calculating the market’s preferences in terms of distance in amultidimensional space—the KSFs—between the individual expectations and theprofiles of the various offerings), or better formalize the contradictory relationshipbetween price as a denominator of the value/price ratio (the higher the worse) andits weight as a potential component of the perceived value (the higher the better).

However, for our purposes (showing the logical relationships among somerelevant variables), we think that even a ‘‘simplistic’’ model like the one discussedhere could be sufficient.

What would be the practical use of this model for a given competitor(e.g., competitor A)?

For example:

• identifying competitive weaknesses in areas that are relatively more importantfor the market (in the competitor A’s case, brand image and service), in order tofocus the use of the available resources on these areas;

Fig. 1.8 Relationship between value/price ratio and market share (low ‘‘elasticity’’ to price)

1.9 Translation of the Above Concepts into Spreadsheet Models 23

• assessing the extent to which an improvement of the company’s scores in theseareas could improve the overall competitive performance.

This will be the subject of the following discussion.

1.9.2 Relationship Between Investments (‘‘Costs’’) and pcpV

In the above pages we described the relationships among pcpV, price and marketshare, entering the ‘‘scores’’ of three hypothetical competitors’ on the KSFs,together with their price levels, as an input to the model (the intermediate outputbeing the pcpV, and the final output the market share).

Let us look now at a possible way of describing how the scores and, therefore,the pcpV of a given competitor ‘‘A’’ can be affected by its strategic decisions interms of investments (identified as ‘‘costs’’ in Fig. 1.1 above): in this case, theinputs will be represented by estimates and investment decisions, and thecompetitor’s ‘‘scores’’ in relation to the various KSFs and overall (the pcpV) willbe the output.

The objective of this part of the model is therefore more ‘‘prescriptive’’ than‘‘descriptive’’, since it attempts to identify alternative investment choices, in orderto support the selection of the best alternative.

Logically speaking, the investment decisions (level and distribution ofresources) should be made in order to reach a given objective (in our case, a givenlevel of pcpV): however, our main purpose here is to address specifically the‘‘allocation’’ issue, i.e. how to best allocate a given amount of limited resourcesamong various tools in order to maximize the pcpV objective.

Once understood the reasoning and criteria behind the allocation decision,nothing will prevent us from addressing the problem the other way around,i.e. setting an overall objective (a given level of pcpV) and deciding both theamount and the distribution of resources accordingly.

1st stepLet us assume, for the sake of simplicity, that:

• the only components of the pcpV, contrary to what discussed in the previous partof the model, are ‘‘quality, image, and service’’, and their relative importance is,respectively, 20, 35 and 45%: these weights are an input to the model(estimates), already considered (even though in relation to a different mix ofKSFs) in the first part of the model;

• the only available tools for improving the company’s performance on theseKSFs are those listed in Fig. 1.9: R&D, advertising, sales force, raw materialsand components, logistics and channels’ margins;

• both the KSFs and the tools are ‘‘independent’’ variables, i.e. they are notinfluencing each other, and synergistic effects among them do not exist.

24 1 Defining and Understanding Strategic Management

The first two restrictions could easily be removed just adding other KSFs andtools, the third one could be removed with a relatively simple integration of themodel, but the basic criteria and methodology for addressing the resource allo-cation problem would not change.

Other simplifying restrictions will be introduced later.We think that, again in the absence of objective data, it is reasonable to expect

that a manager could (and should) make an explicit assessment of the relativeimpact of the various tools listed in the figure on each KSF: the percentageweights entered in the columns on the right part of the figure therefore representnew inputs to the model (estimates), and, for each column, their sum is 100%since, by definition, we do not have other tools available.

We can easily see that, as in a real life situation, an individual tool can have animpact on multiple KSFs, and, at the same time, an individual KSF can bemanaged with (or affected by) multiple tools. It is also obvious that, for a giventool, the same amount of investment can affect, at the same time, multiple KSFs (i.e.it is not necessary to ‘‘multiply’’ the investment by the number of KSFs affected).

In the simplified example provided here, we see that quality and image are bothaffected by two different tools, while service is affected by four different tools (twoof them are also affecting image).

Once again, we emphasize the fact that this type of models does not have a‘‘scientific’’ foundation: it only has the purpose of supporting, and making explicitand systematic, the logical process adopted by the decision maker in analyzing agiven industry context and making the related decisions.

2nd stepBefore deciding the amount of resources that ‘‘should’’ be allocated to each

different tool in order to maximize the company’s competitive profile on quality,image, and service, given certain constraints in terms of resource availability, weneed to identify, at least in principle, how many resources ‘‘could’’ be assignedto each tool.

Fig. 1.9 Estimated relevance of various tools for managing the components of value

1.9 Translation of the Above Concepts into Spreadsheet Models 25

Our suggestion is to identify, for each tool (e.g. R&D), the ‘‘critical mass’’ orthreshold below which we would not attain significant and ‘‘visible’’ results (e.g. interms of quality), and the ‘‘ceiling’’ beyond which results would improve at adiminishing rate (see the S-shaped curve).

Here, again, we think that knowledgeable managers should be able to make thistype of assessment, based on their experience in managing the tools, theirknowledge of the business and the competition, and just plain common sense.

The assessments made by a hypothetical manager in our ‘‘industrial compo-nents’’ case, about the minimum and maximum ‘‘reasonable investments’’ (from astrategic perspective, we call the amount of resources assigned to these tools‘‘investments’’, even though they actually represent ‘‘costs’’ for the period) in thebusiness, are presented in the right part of Fig. 1.10: these are the last inputs tothis part of the model that represent estimates made by the decision maker.

We can see that these ‘‘investments’’ can be grouped into two categories:

• variable and ‘‘virtual’’ (or ‘‘opportunity’’) costs, which will obviously be paidby sales: the % commissions paid to the sales force, the raw materials andcomponents ($ per kilogram: for the sake of simplicity, we assume that theproduct variable costs are limited to raw material and components, butobviously this is not true in the real life), and the % margins granted to thedistribution channels on the end-user price (these are, in fact, opportunity costs,since they are not subtracted from the revenues, but only reduce the amount ofrevenues that could have been realized with direct sales to the end-users, i.e. theso-called ‘‘virtual revenues’’);

• fixed costs (thousands of dollars: K$), which will be paid upfront or during theyear, no matter how much will be sold, by a given budget (always for sim-plicity, we assume that also these costs will be paid, by the budget, during theplanning period, e.g. the year, so that we will not need to bother about depre-ciation of assets: however, the logic underlying the resource allocation decisionsdoes not change): R&D (e.g., maintenance, upgrading, and salaries), advertising(fairs and exhibitions, trade magazines, catalogs and technical literature, andlogistics (rent of warehouses, salaries, maintenance of trucks).

3rd stepNow we need to decide how much to ‘‘spend’’ in each different tool in order to

maximize the company’s competitive profile on quality, image, and service (and,therefore, on its overall pcpV), given the analysis conducted above and a specificconstraint in terms of budget.

It is easier to address this issue if we focus the allocation problem on the fixedcosts paid by the budget, assuming that we could spend the maximum amount ofmoney (repaid by sales) in the variable costs. These restrictions will be easilyremoved later.

Furthermore, in order to make the reasoning more clear, let us assume, for now,that the only component of the perceived value for the market is quality: from theabove figures we know that the only available tools for improving quality are R&D(weighting 60%), and raw materials and components (weighting 40%).

26 1 Defining and Understanding Strategic Management

Having assumed that we could spend the maximum amount in raw materials andcomponents (the variable cost), we just need to decide how much to spend in R&D.

What will be the impact of our decision on our performance on quality?Obviously, if we could spend the maximum amount of money also in R&D, our

performance would be the highest, based on our own assumptions about theeffectiveness of these tools and given the assumed availability of just these toolsfor improving quality.

However, how to estimate the combined impact on quality of raw material andcomponents, and R&D, if, for budget reasons, we could not spend the maximum inR&D (we will easily see that this problem is significant when we consider all theother KSFs and tools)?