Strategy and Management Accounting for Intangible Assets Mikhail Davydov Anna Devyatova Alexander Shalamov Ksenia Shneyveys

Strategy and Management Accounting for Intangible Assets Mikhail Davydov Anna Devyatova Alexander Shalamov Ksenia Shneyveys.

Dec 16, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Strategy andManagement

Accounting for Intangible Assets

Mikhail DavydovAnna Devyatova

Alexander ShalamovKsenia Shneyveys

“Intangible asset management is the most important issue for top management at present…”Sumantra Ghoshal, Professor

London Business School

Intangible assets, % of market value

60

68

74

82

83

85

85

94

96

Chrysler

Honda

BP

GE

3M

ABB

Intel

Microsoft

Coca-Cola

Defining Intangible AssetsAssets having no material form that appear as a

result of (1) past events that has a (2) measurable effect and that presents a (3) future benefit . [Financial Accounting Standards Board (FASB)]

Assets arising as a result of past events and possess three main attributes: they are non physical in nature, they are capable of producing future economic net benefits, and they are protected legally or through a de facto right

[Bouteiller, 2002]

Defining Intangible Assets Non-physical sources of value (claims to future

benefits) generated by innovation (discovery), unique organizational designs, or human resource practices (B. Lev, 2003)

Any asset, belonging to a company or controlled by it, having no physical or financial (in case of financial investment) form, but capable of producing future economic benefits (D. Volkov, T. Garanina, 2007)

Defining Intangible Assets

Three terms are widely used: Intangible Assets — in accounting

literature, Knowledge Assets — by economists, Intellectual Capital — in management and

law literature; “and on the whole they come to the same: to the

future benefits that are not embodied materially”.

B.Lev, 2004

Defining Intangible AssetsINTANGIBLE ASSETS =

= INTELLECTUAL CAPITAL == KNOWLEDGE ASSETS =

= INTANGIBLES

Intangible Assets, recognized according to the accounting standards in accounting and bookkeeping records

Other Intangible Assets -- Intangible Assets non-recognized in accounting and bookkeeping records

Defining Intangible Assets

Composition and structure of intangible assets

INTELLECTUAL CAPITAL

HUMANCAPITAL

RELATIONSHIPCAPITAL

ORGANIZATIONAL (STRUCTURAL)CAPITAL

developed by International Federation of Accountants (IFAC, 1998)

Defining Intangible Assets HUMAN CAPITALDefinition capability of a

company to benefit from knowledge, skills and experience of employees, which immanently pertain to the latter.

For example: capability for

innovations creativity know-how and

experience ability to work in a team motivation learning capability educational and

professional level loyalty etc.

Defining Intangible Assets RELATIONSHIP CAPITALDefinition capability of a

company to benefit from resources connected with the company's external relations (with customer, suppliers, and other counteragents).

For example: brands suppliers loyalty of the

customers distribution channels business cooperation alliances and

partnerships licensing agreements franchising

agreementsetc.

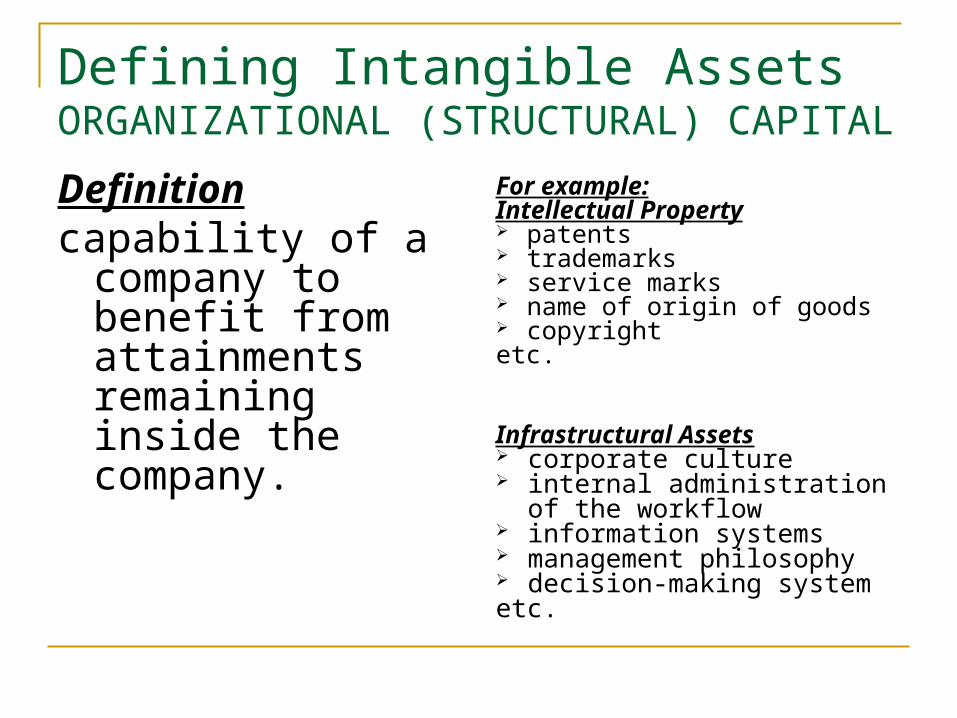

Defining Intangible Assets ORGANIZATIONAL (STRUCTURAL) CAPITALDefinitioncapability of a

company to benefit from attainments remaining inside the company.

For example:Intellectual Property patents trademarks service marks name of origin of goods copyrightetc.

Infrastructural Assets corporate culture internal administration

of the work flow information systems management philosophy decision-making systemetc.

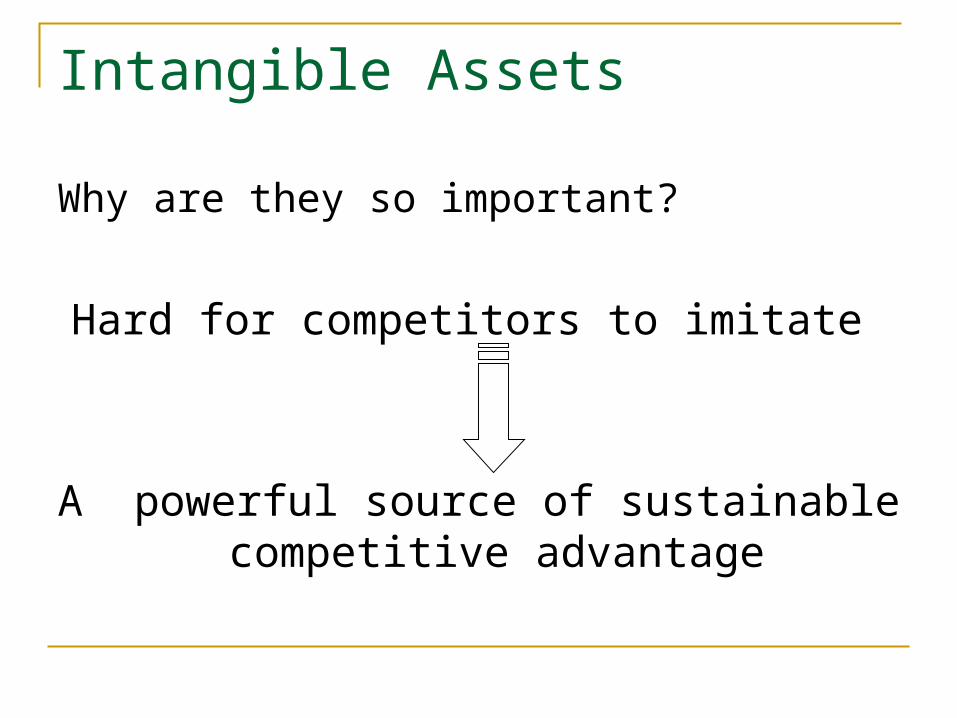

Intangible Assets

Why are they so important?

Hard for competitors to imitate

A powerful source of sustainable competitive advantage

Measuring Intangible Assets

If you can’t measure it, you can’t manage it.

George O. Odiorne

Measuring the value of intangible assets is the holy grail of accounting.

Robert S. Kaplan, David P. Norton

Measuring Intangible Assets

34 methods for measuring intangible assets (1950’s – 2004)

Probably, the list is not closed!

4 approaches for measuring intangibles

1) Direct Intellectual Capital methods (DIC)2) Market Capitalization Methods (MCM)3) Return on Assets methods (ROA) 4) Scorecard Methods (SC)

1) Direct Intellectual Capital methods (DIC)

Estimate the $-value of intangible assets by identifying its various components. Once these components are identified, they can be directly evaluated, either individually or as an aggregated coefficient.

Example: Technology broker (TB)

Measuring Intangible Assets

(Annie Brooking, 1996)Assess the value of the IC of a firm based on diagnostic

analysis of a firm’s response to 20 questions covering four major components of IC: market assets, human-centered assets, intellectual property, infrastructure assets.

Questionnaire indicators.3 methods of calculating dollar value for IC: The cost approach: based on assessment of

replacement cost of the asset; The market approach: uses market comparables to

assess value; The income approach: assess the income-providing

capability of the asset.

Measuring Intangible Assets1)DIC Technology broker (TB)

Calculate the difference between a company's market capitalization and its stockholders' equity as the value of its intellectual capital.

Example: Market measure of company’s IC

IC=market capitalization-stockholders’s equity

Market value = $ 12.77 billionStockholder equity = $ 1.47 billion IC = $ 11.3 billion

Measuring Intangible Assets2) Market Capitalization Methods (MCM)

Step 1 : determine the “realized IC” Market value = $ 12.77 billion

Stockholder equity = $ 1.47 billion “realized IC” = $ 11.3 billion

Measuring Intangible AssetsDIC/MCM: FiMIAM methodology

Measuring Intangible AssetsDIC/MCM: FiMIAM methodology

Step 2 : identifying the relevant components of IC

Step 3 : assigning relative weights to IC components

Step 4: assigning value organizational learning 0.04 * $11,3 billion = $ 452

million knowledge product0.08 * $11,3 billion = $ 904

million patents0.07 * $11,3 billion = $ 791

million

Measuring Intangible Assets3) Return on Assets methods (ROA)Tangible assets and the annual financial

growth figures are compared to the industry average. Above average earnings are then utilized to estimate the value of intangible assets.

Example: Economic Value Added (EVATM)Calculated by adjusting the company’s

disclosed profit with charges to intangibles. Changes in EVA provide an indication of whether the firm’s intellectual capital is productive or not.

The various components of intangible assets or intellectual capital are identified as indicators and indices are generated and reported in scorecards or as graphs.

Measuring Intangible Assets4) Scorecard Methods (SC)

Balanced Scorecard Method

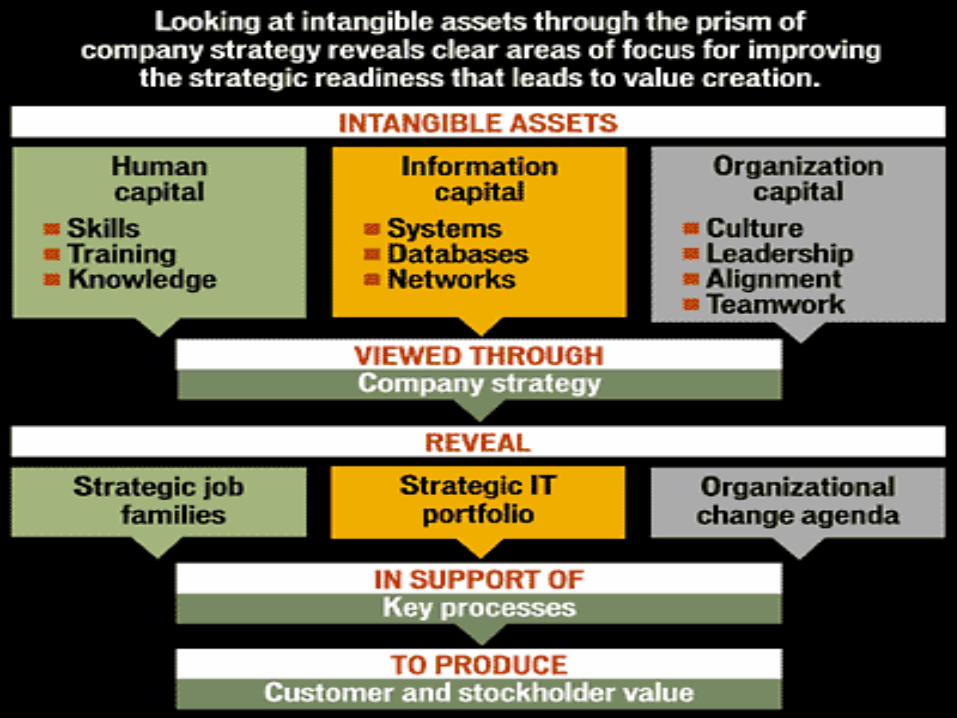

A way to systematically measure the alignment of company’s human, information and organization capital to the company’s strategy (by D. Norton and R. Kaplan)

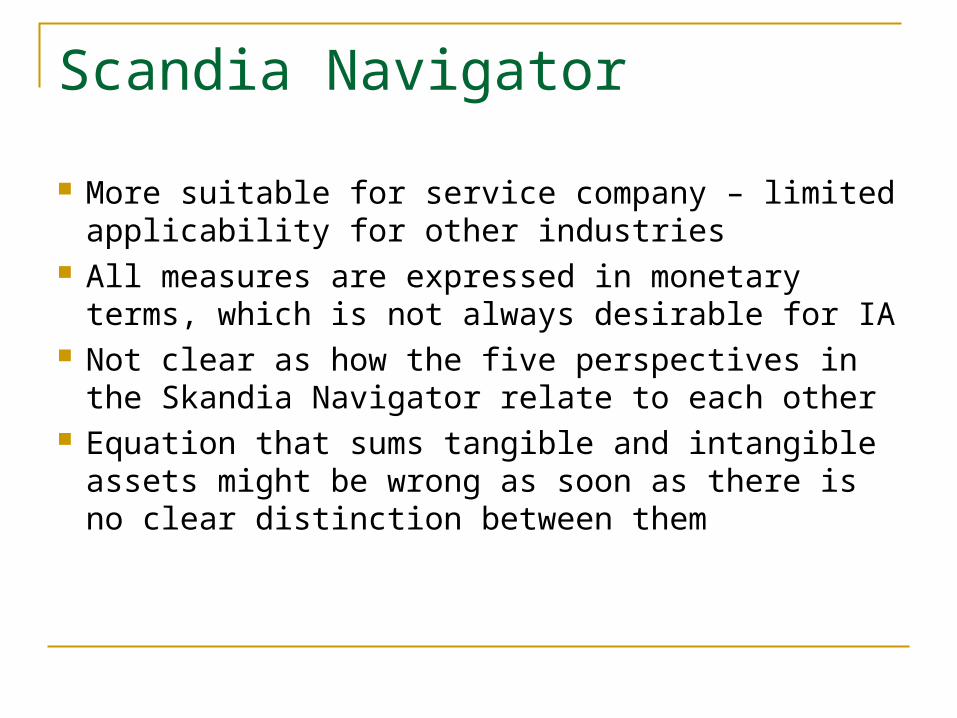

Scandia Navigator

Developed by Scandia (1994) IA are divided into: human

capital, customer capital, process capital and innovation capital

Focuses on: the financial focus, the customer perspective (customer focus), the process perspective (process focus), the human perspective (human focus), and the renewal and development perspective (innovation focus)

200 indicators

Scandia Navigator

More suitable for service company – limited applicability for other industries

All measures are expressed in monetary terms, which is not always desirable for IA

Not clear as how the five perspectives in the Skandia Navigator relate to each other

Equation that sums tangible and intangible assets might be wrong as soon as there is no clear distinction between them

IC Index Approach

Splits IA into human capital and structural capital, separating “thinking” and “non-thinking” assets, then dividing them into subgroups

A company needs to identify key IA indicators

They need to be ranked according to their importance

Indicators chosen must be weighted and summarized into a single index

IC Index Approach

Allows organizations to measure how changes in the market or changes in other performance indicators correlate with the changes in the IC Index

BUT Using aggregates makes it difficult to identify the

key business drivers Weightings for each of the different measures is

done subjectively which can be dangerous if managers get it wrong

IA Monitor

Three categories are taken into account: 1. intangibles represented by competence of

employees 2. intangibles related to the internal structure of the

organization

3. those related to the external structure including brand names, image, and relationships with suppliers and most importantly relationships with customers

Three measurement groups: growth and

renewal, efficiency, stability

IA Monitor

Emphasises the internal perspective

Not a valuation approach

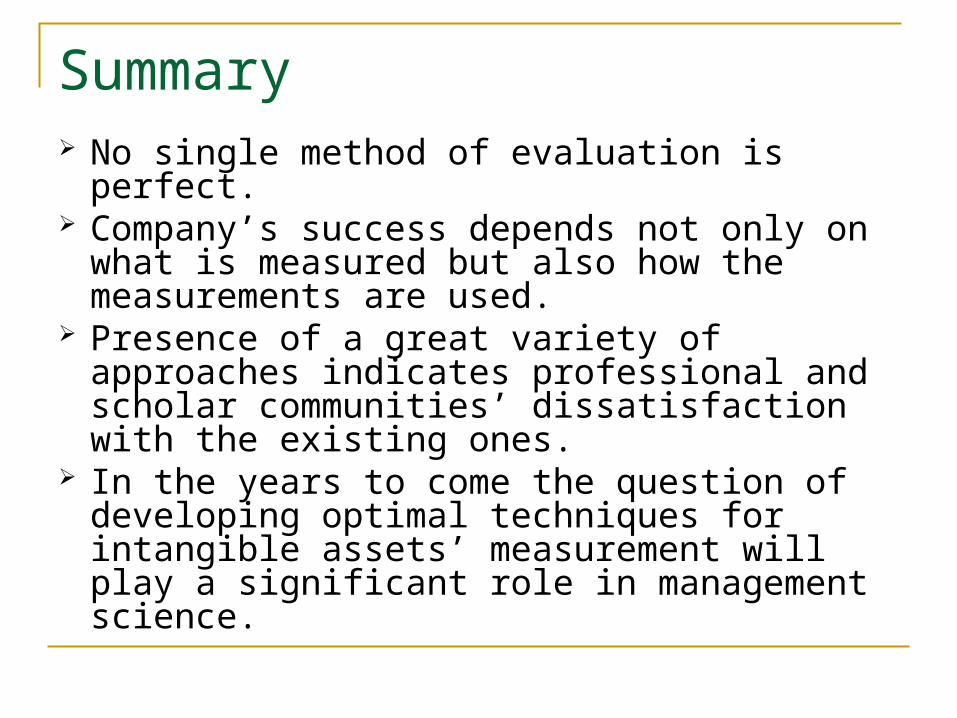

Summary No single method of evaluation is perfect. Company’s success depends not only on

what is measured but also how the measurements are used.

Presence of a great variety of approaches indicates professional and scholar communities’ dissatisfaction with the existing ones.

In the years to come the question of developing optimal techniques for intangible assets’ measurement will play a significant role in management science.

Practical approach: Brand Valuation PricewaterhouseCoopers(1)Develop key performance indicators

(KPI) to monitor the performance of the intangible

(2) Conduct a yearly assessment of the brand value

(3) Allocating a value to the brand on a regular basis and tracking it over time.

Practical approach: Brand Valuation PricewaterhouseCoopers

Year ended March 31 2003 2002 2001

PBIT 1 158.93

943.39 696.03

Less: non-brand income 89.65 59.77 53.43

Adjusted profit 1 069.28

883.62 642.60

Inflation compound factor at 6% 1.000 1.064 1.132

Present value of profits for the brand 1 069.28

940.02 727.25

Weightage factor 3 2 1

Three-year average weighted profits 969.19

Remuneration of capital (5% of average capital employed)

123.52

Brand-related profits 845.67

Tax at 36.75% 310.78

Brand earnings 534.88

Multiple-applied 14.00

Brand value 7 488.00

In Rs Crore

Practical approach: Brand Valuation PricewaterhouseCoopers

The methodology followed for valuing the brand is given below:(1) Determine brand earnings• Determine brand profits by elimination of non-brand profits from

the total profits of the company• Restate the historical profits at present-day values• Provide for the remuneration of capital to used for purposes

other than promotion of the brand• Adjust for taxes(2) Determine the brand-strength or brand-earnings multipleBrand-strength multiple is a function of a multitude of factors such

as leadership, stability, market, internationality, trend, support and

protection. These factors have been evaluated on a scale of 1 to 100 internally by the Infosys management, based on the information

available within the company.(3) Compute the brand value by multiplying the brand earnings

with the multiple derived in step 2 above.

Practical approach: Brand Valuation PricewaterhouseCoopersINFOSYS Brand value,

Rs Crore

Market capitalization,

Rs Crore%

2001 5 376 26 926 20%

2002 7 257 24 654 29%

2003 7 488 26 847 28%

… … … …

2006 22 915 82 154 28%

2007 31 617 115 307 27%

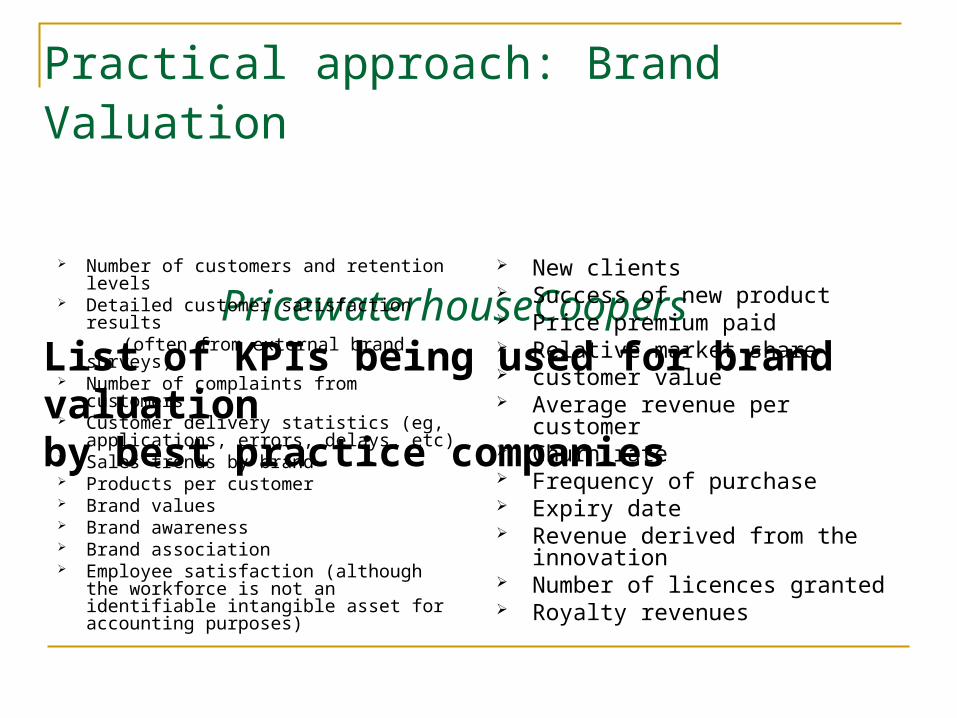

Practical approach: Brand Valuation PricewaterhouseCoopersList of KPIs being used for brand valuationby best practice companies

Number of customers and retention levels

Detailed customer satisfaction results

(often from external brand surveys) Number of complaints from

customers Customer delivery statistics (eg,

applications, errors, delays, etc) Sales trends by brand Products per customer Brand values Brand awareness Brand association Employee satisfaction (although the

workforce is not an identifiable intangible asset for accounting purposes)

New clients Success of new product Price premium paid Relative market share customer value Average revenue per customer Churn rate Frequency of purchase Expiry date Revenue derived from the

innovation Number of licences granted Royalty revenues

Thank you!

Related Documents