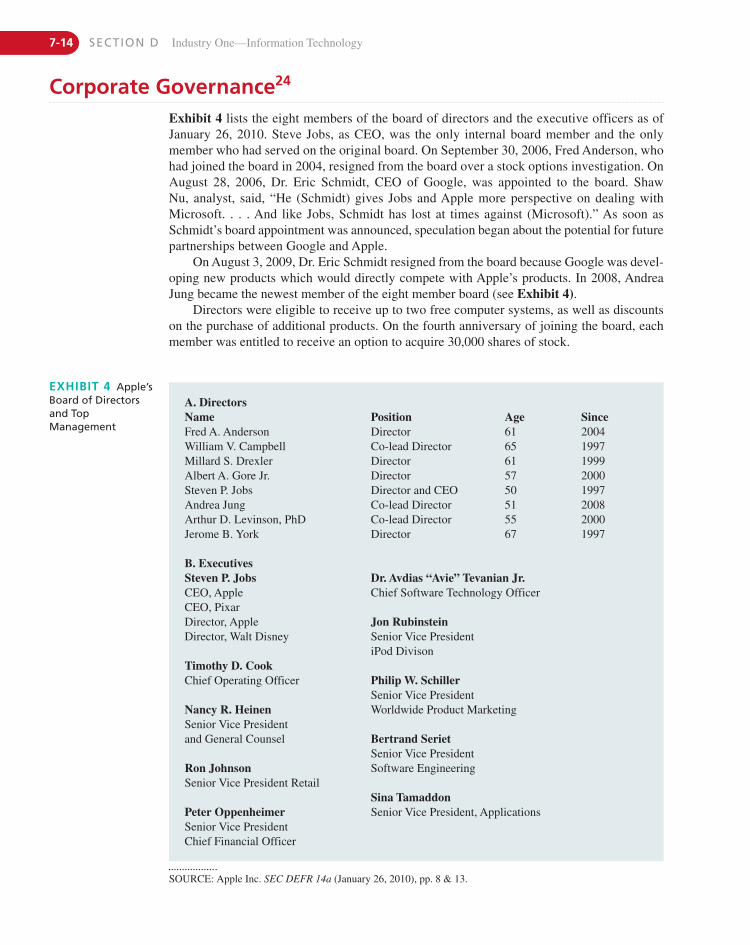

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

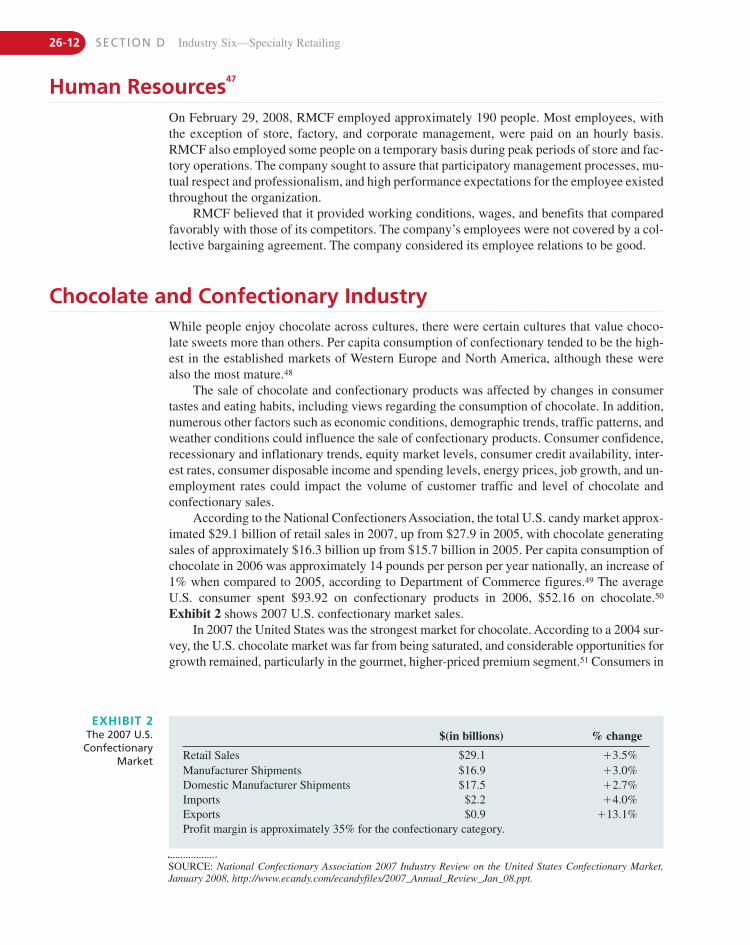

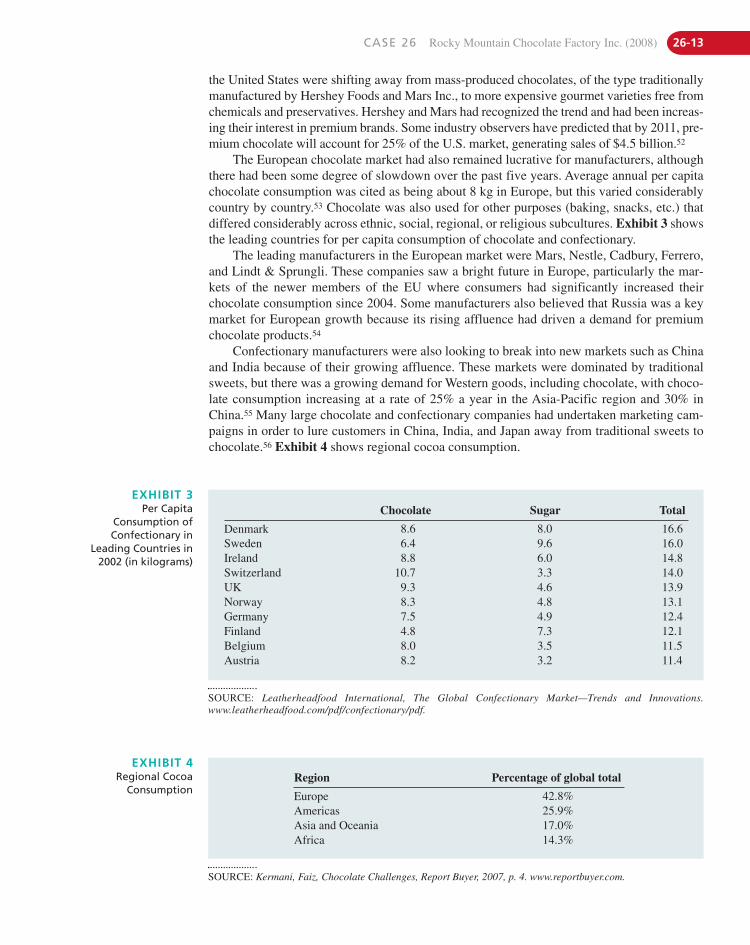

Transcript

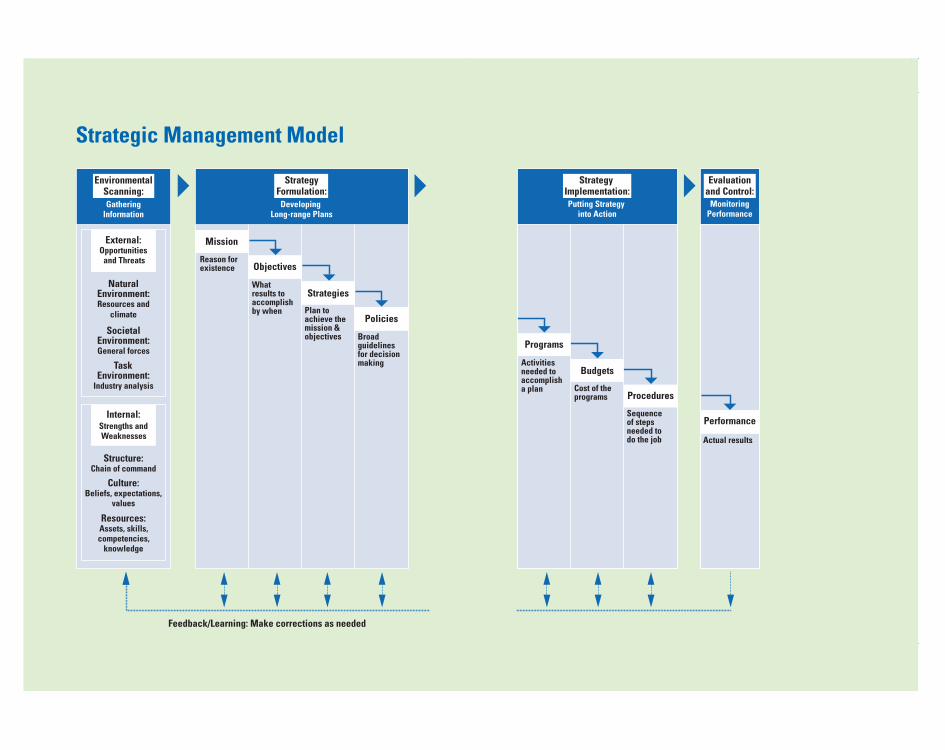

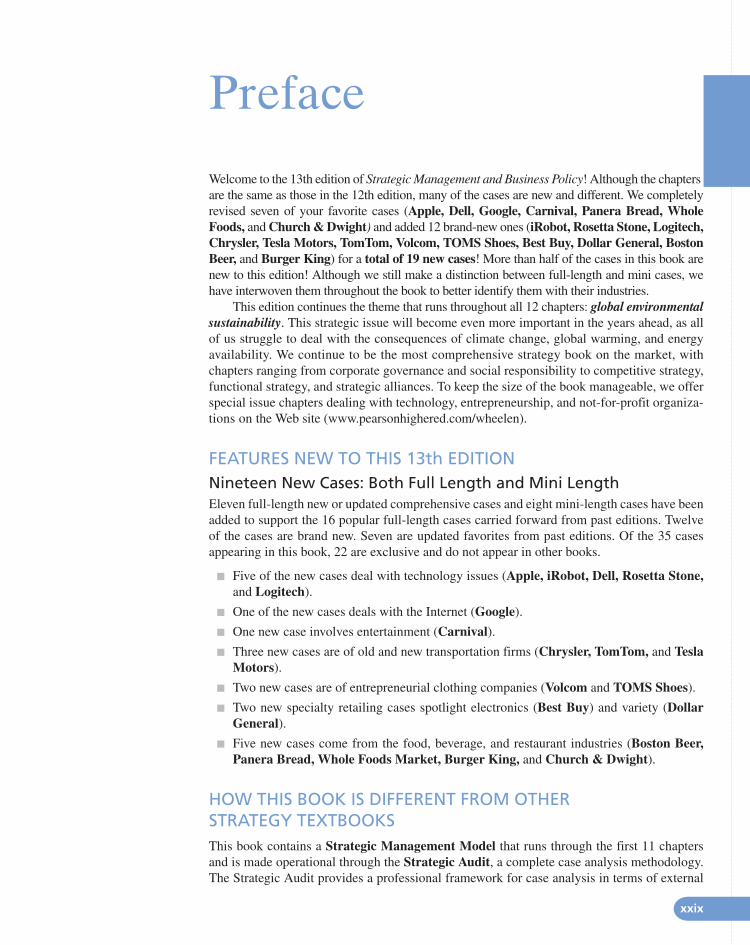

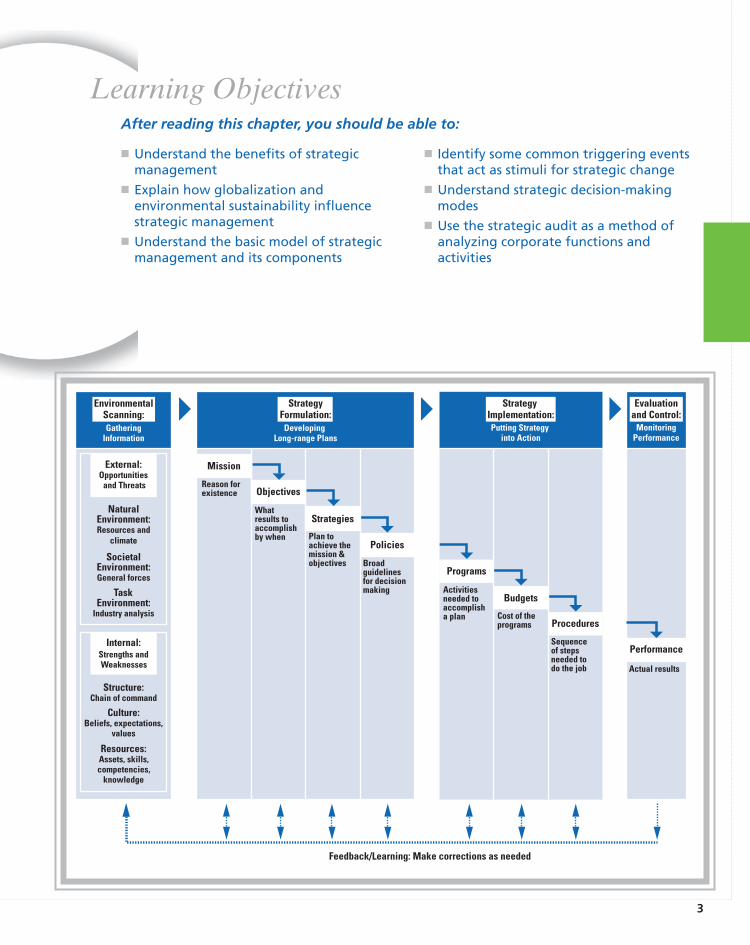

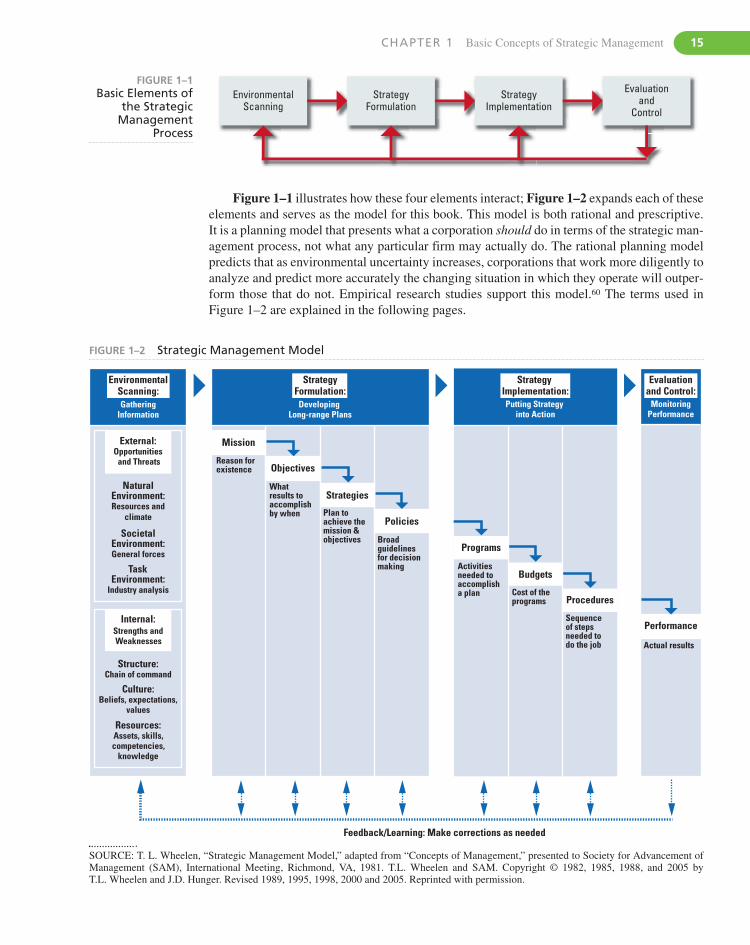

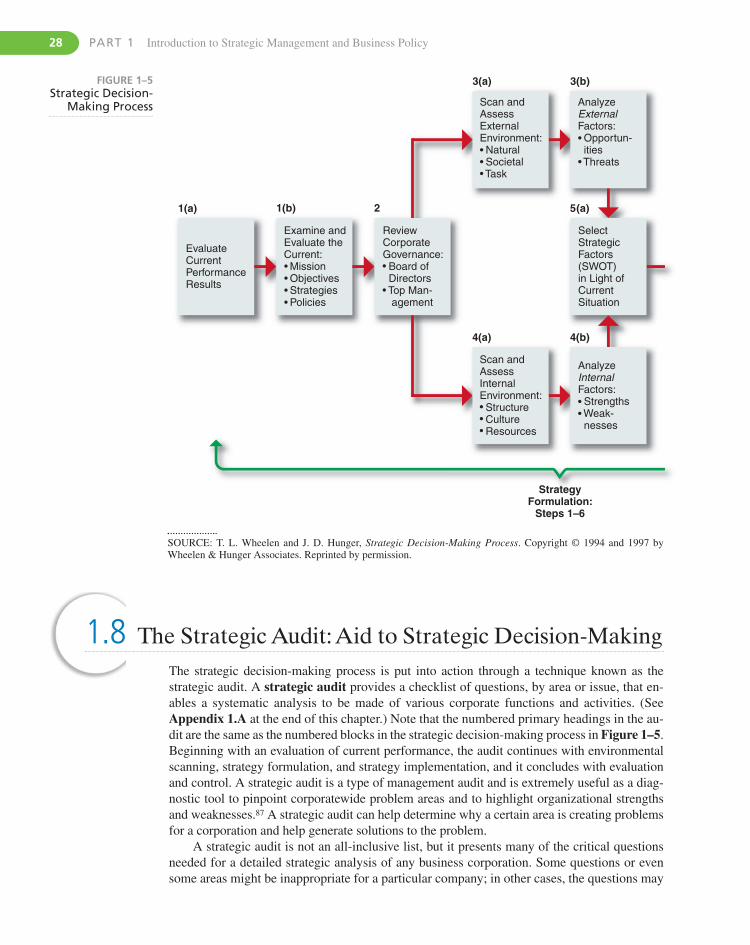

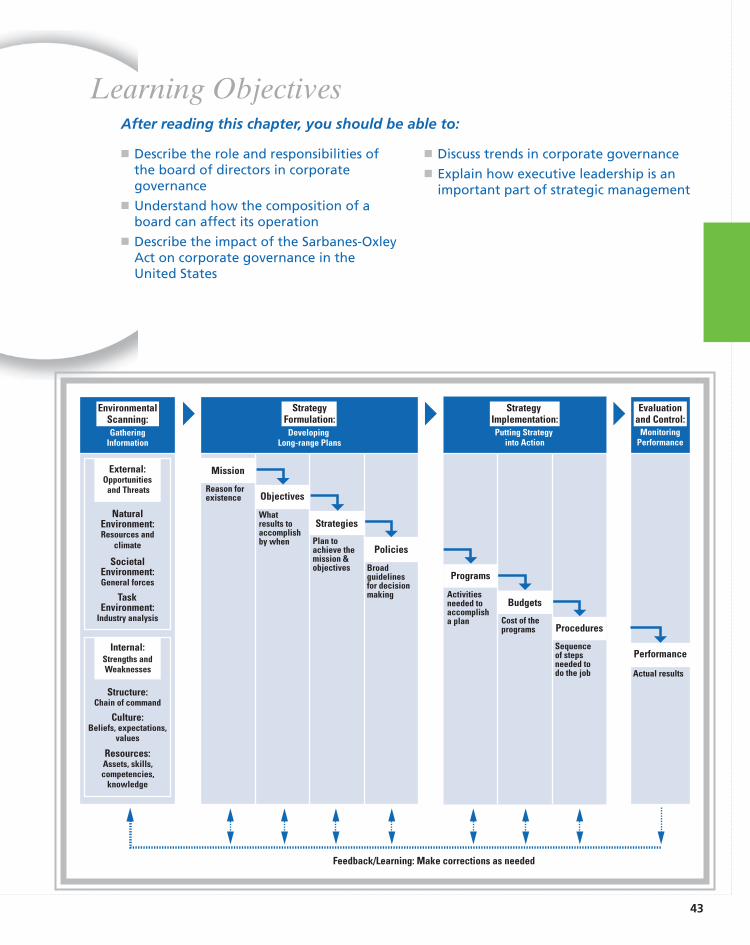

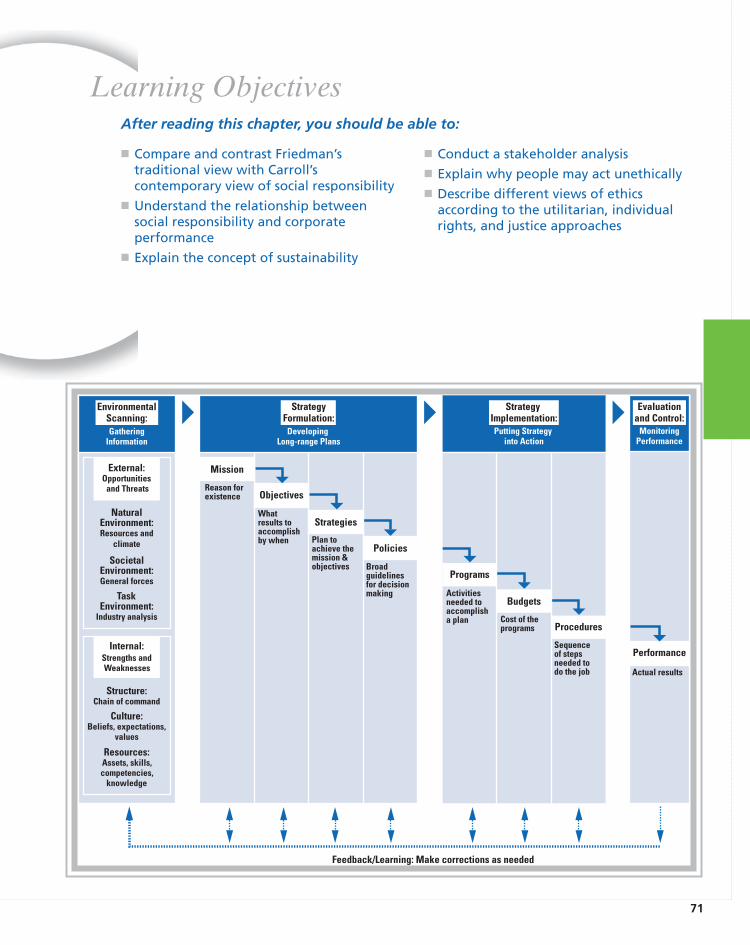

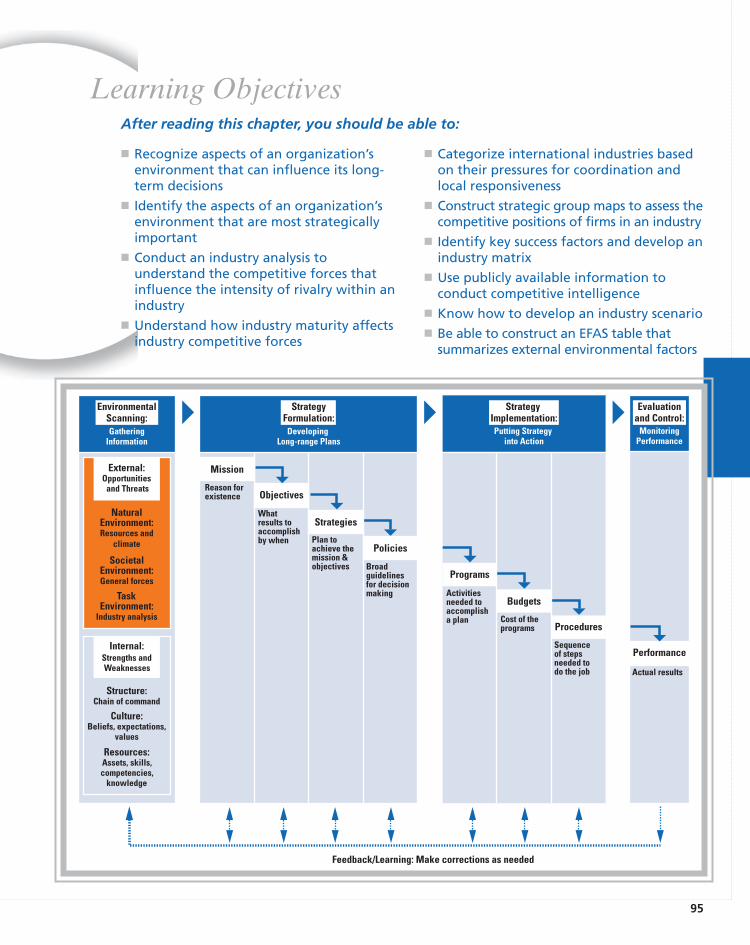

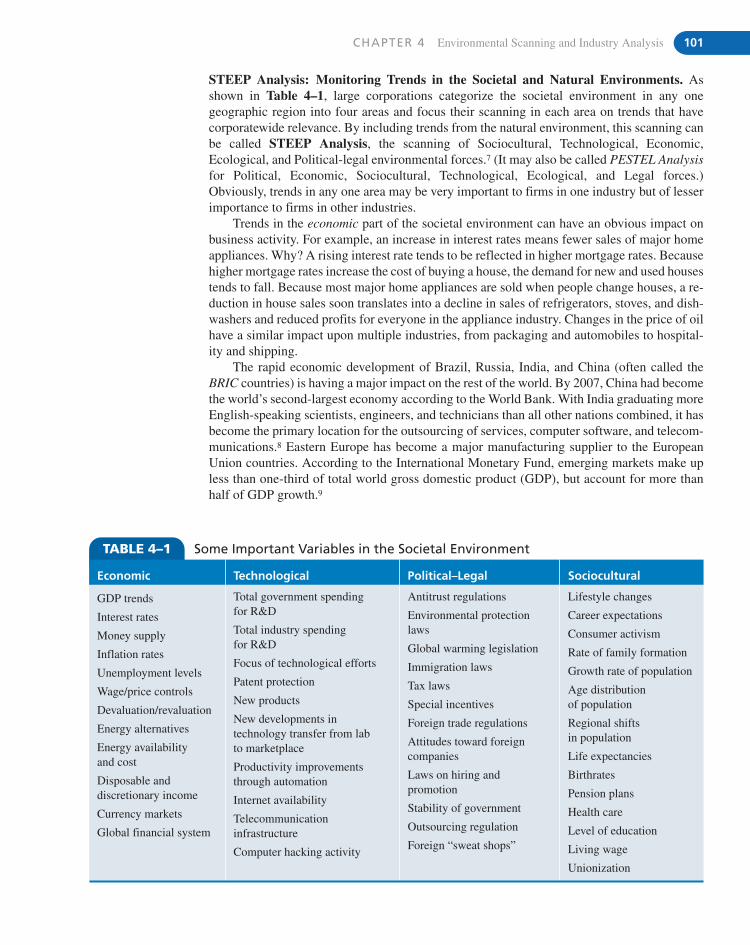

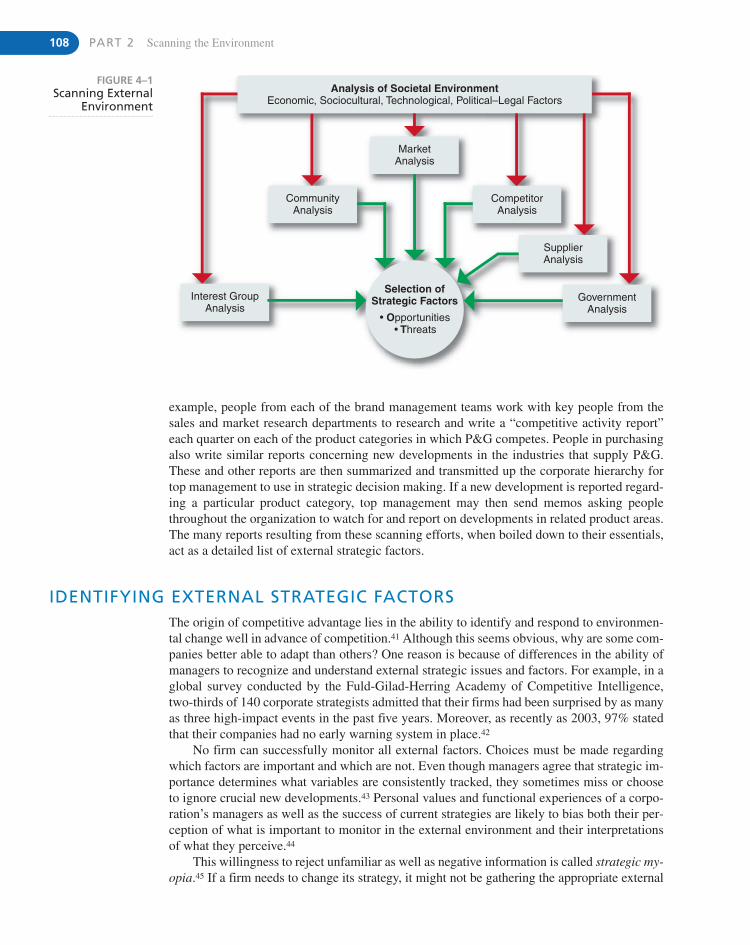

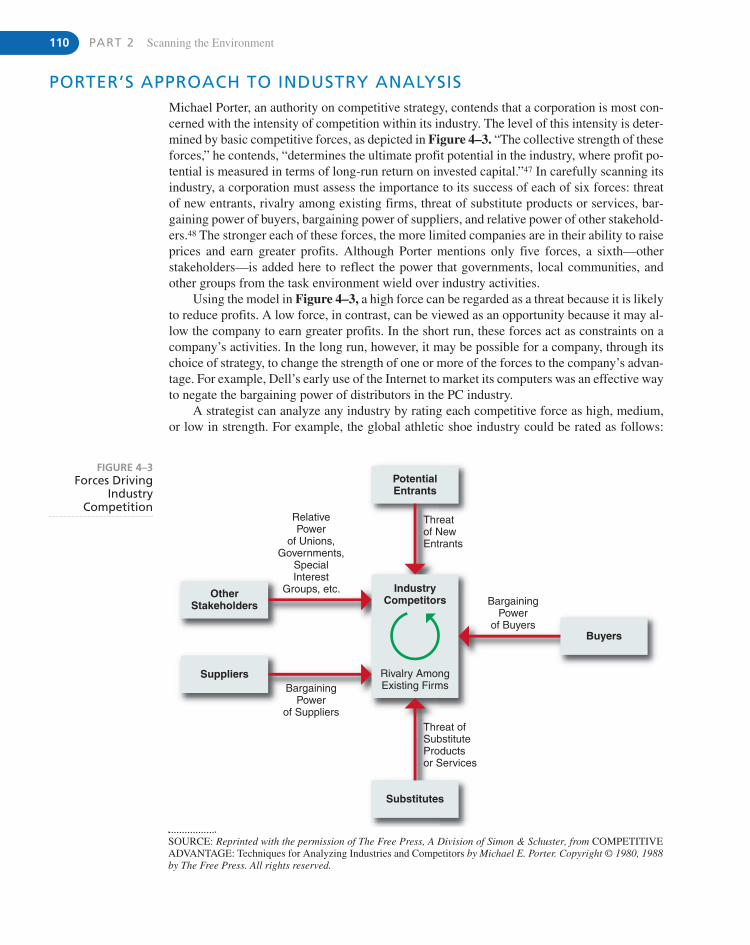

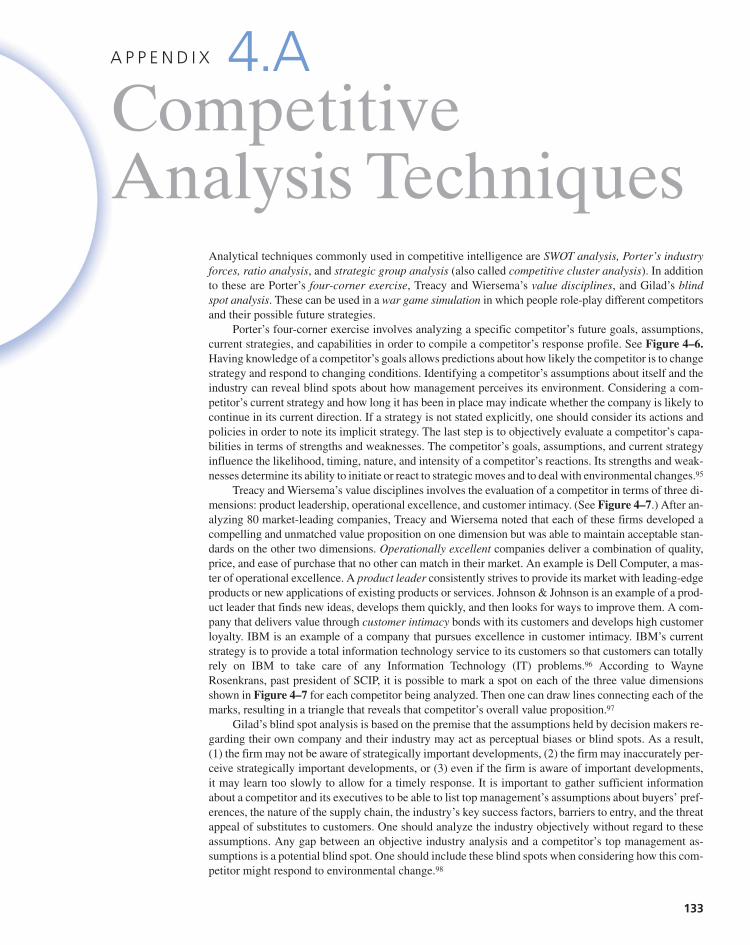

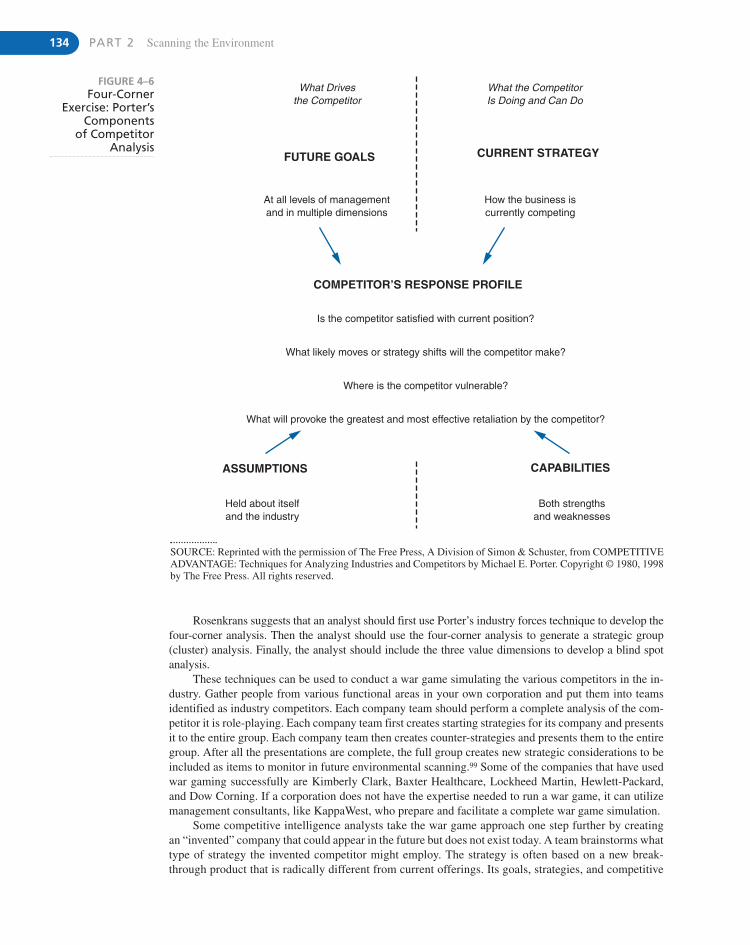

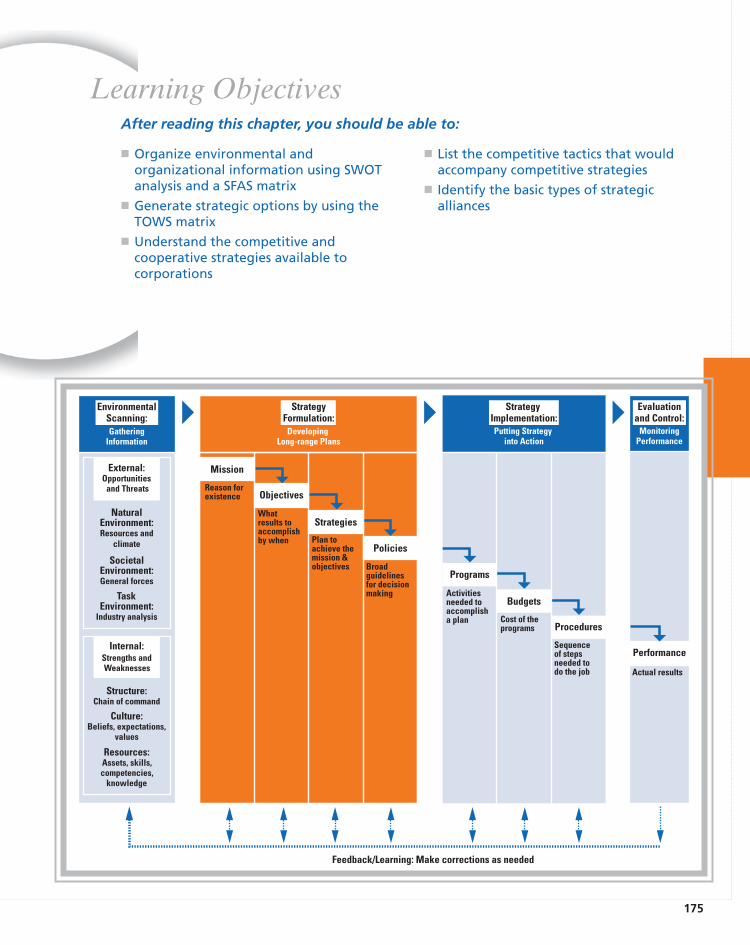

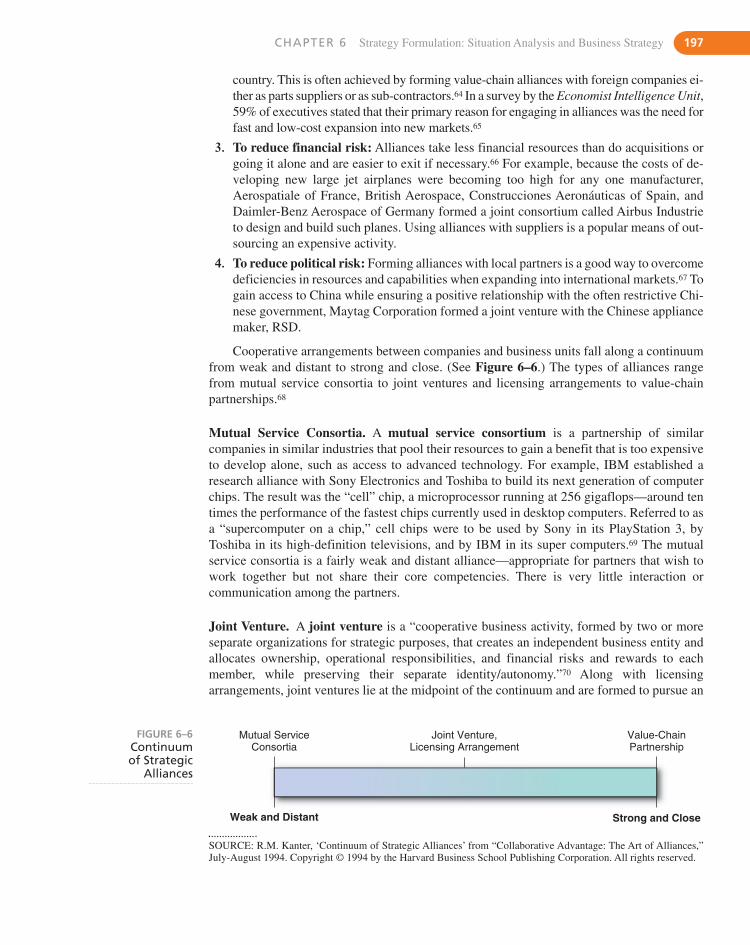

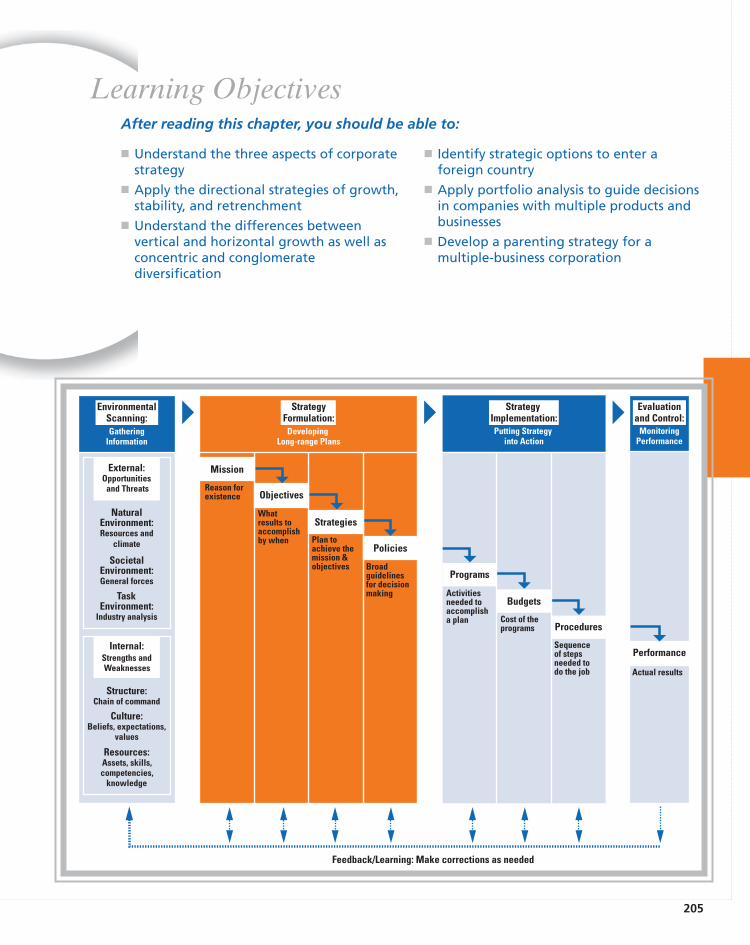

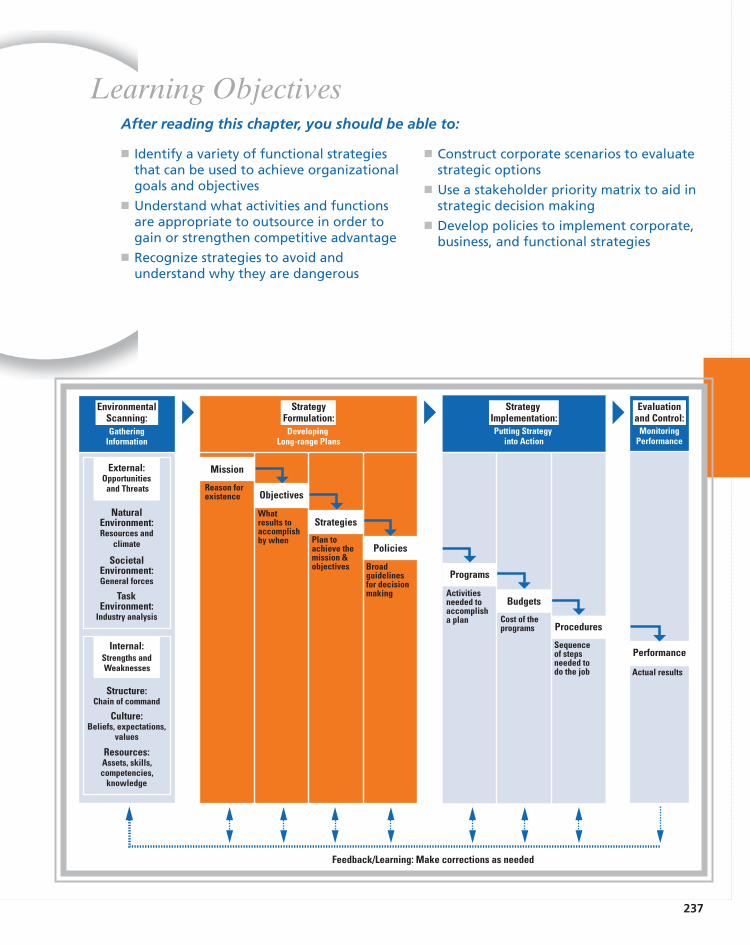

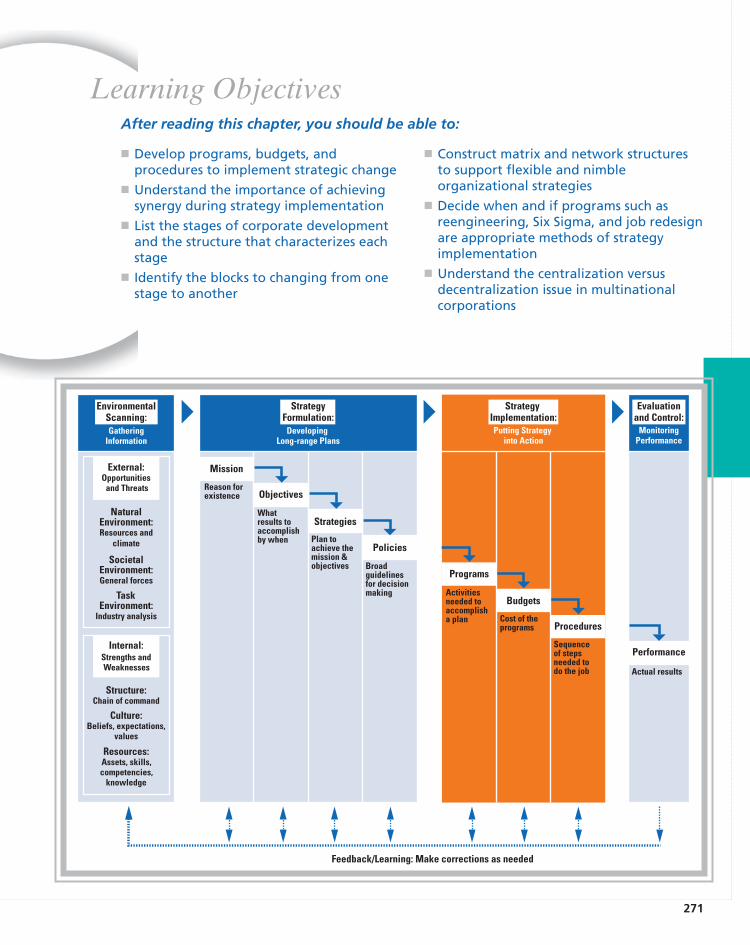

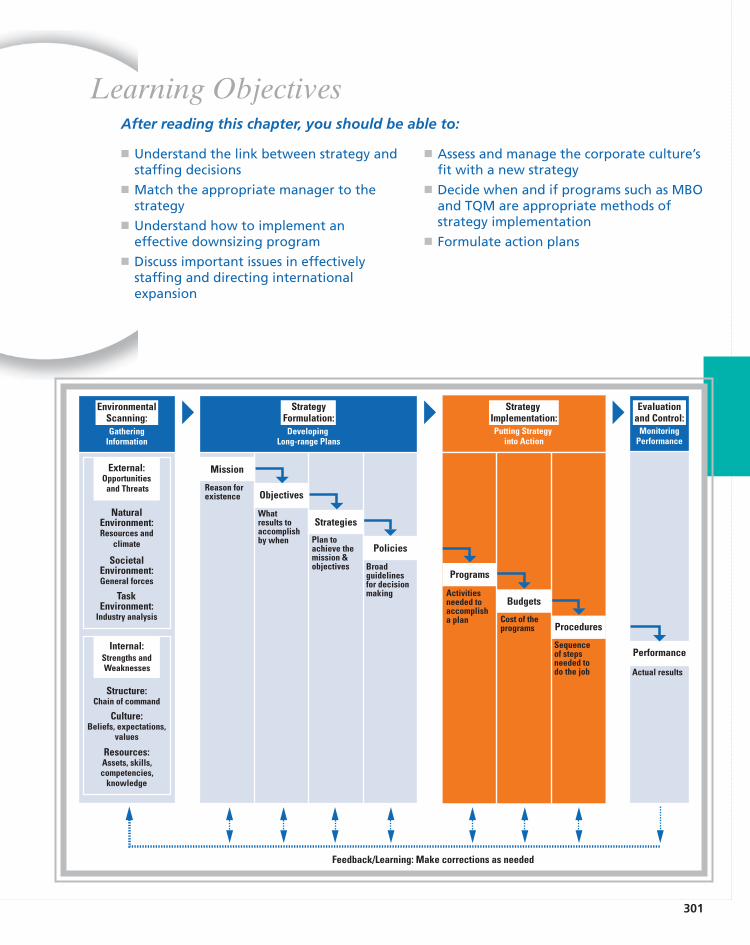

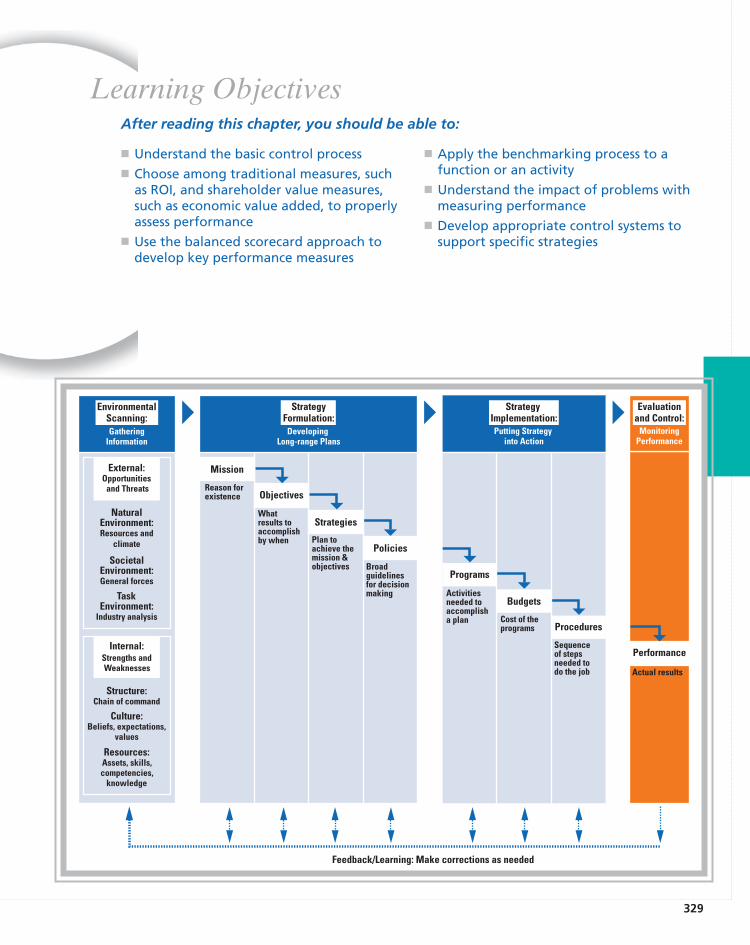

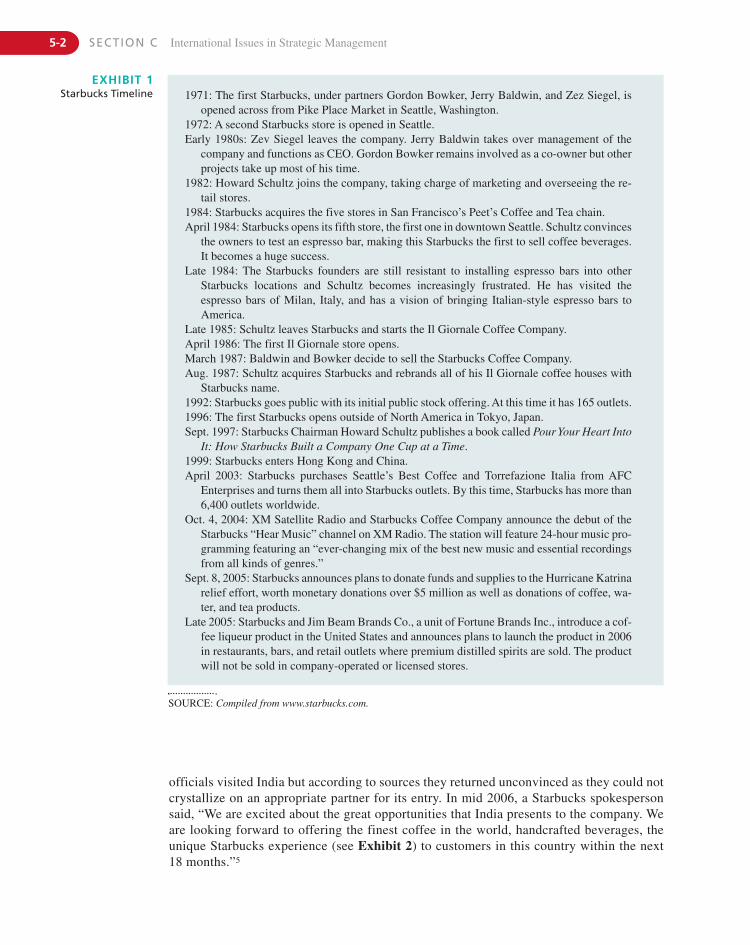

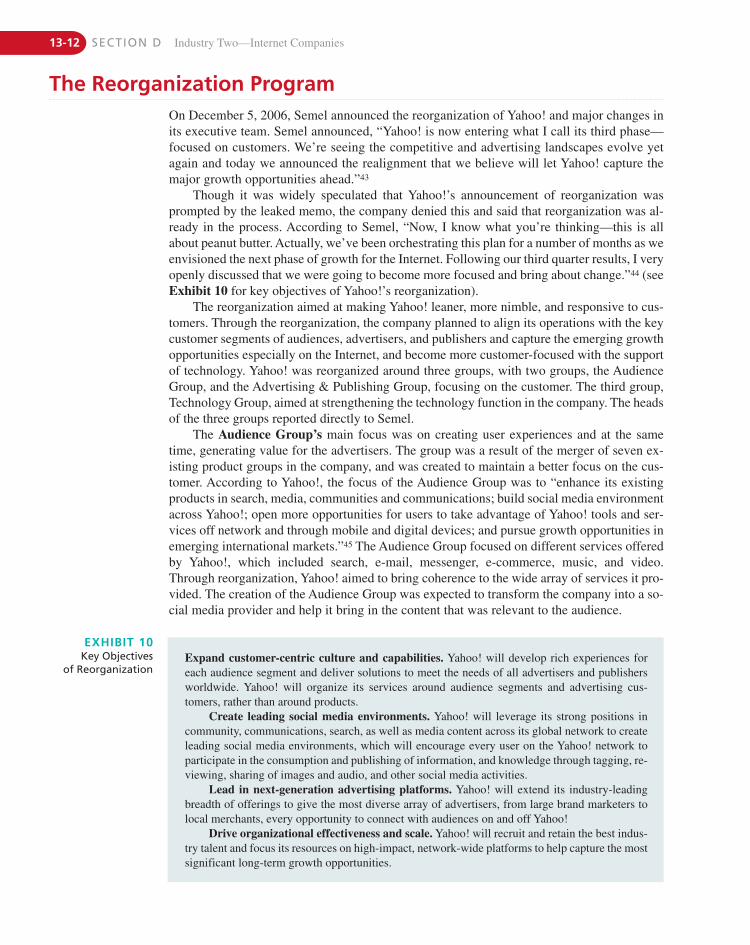

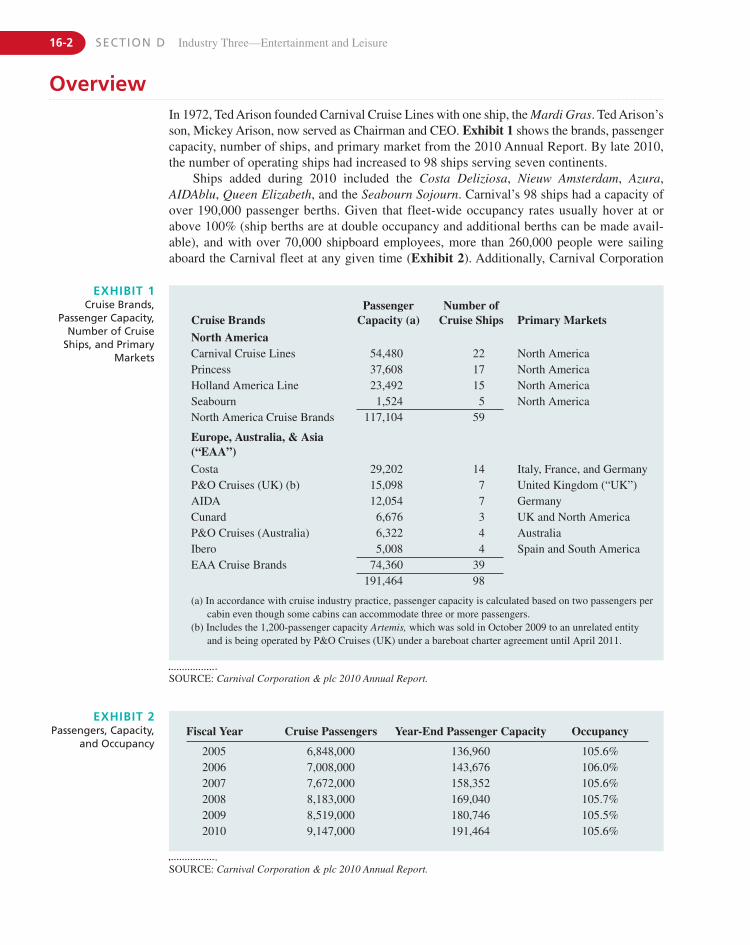

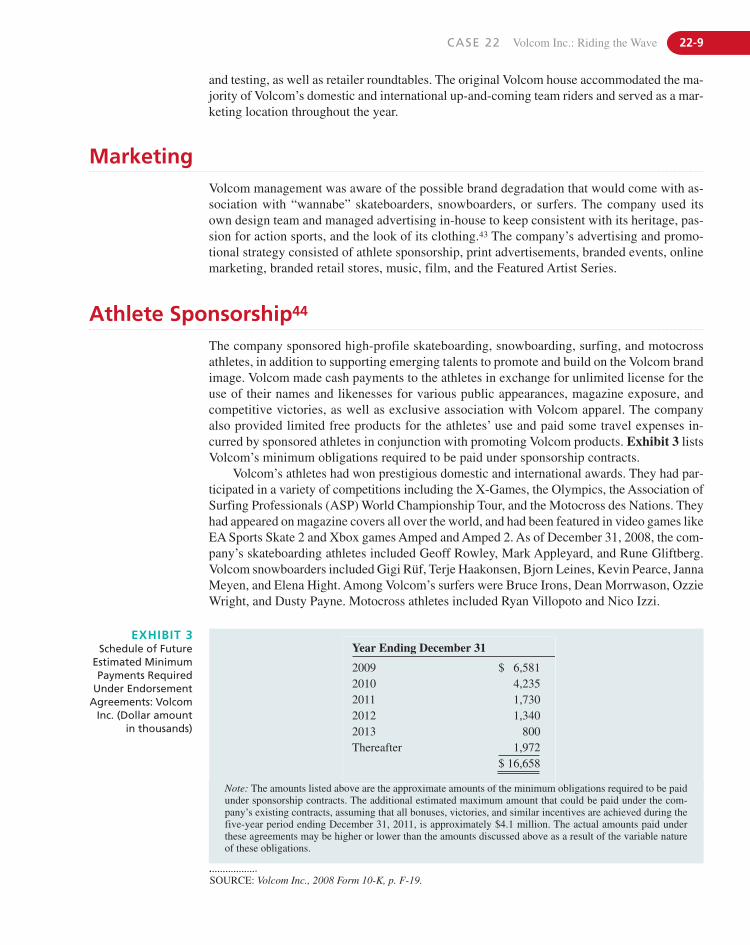

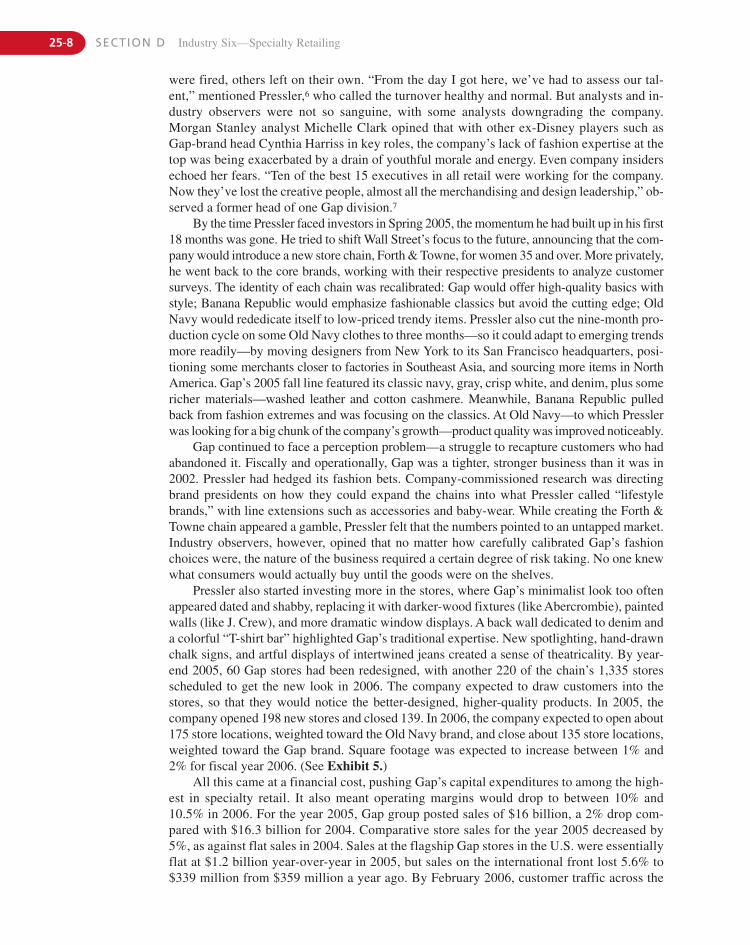

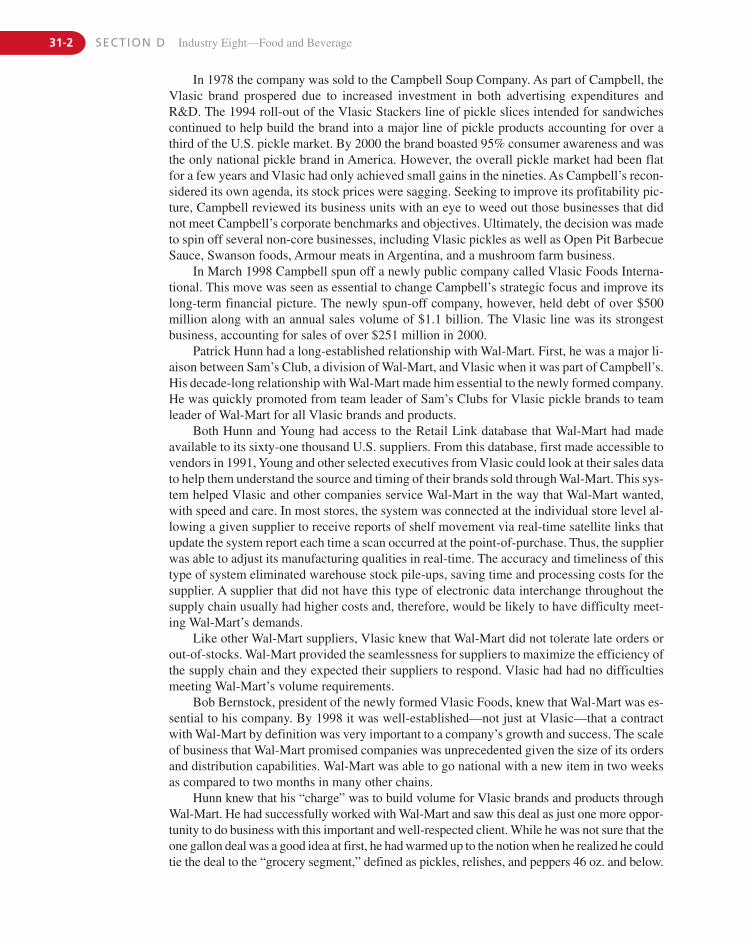

Strategic Management Model

GatheringInformation

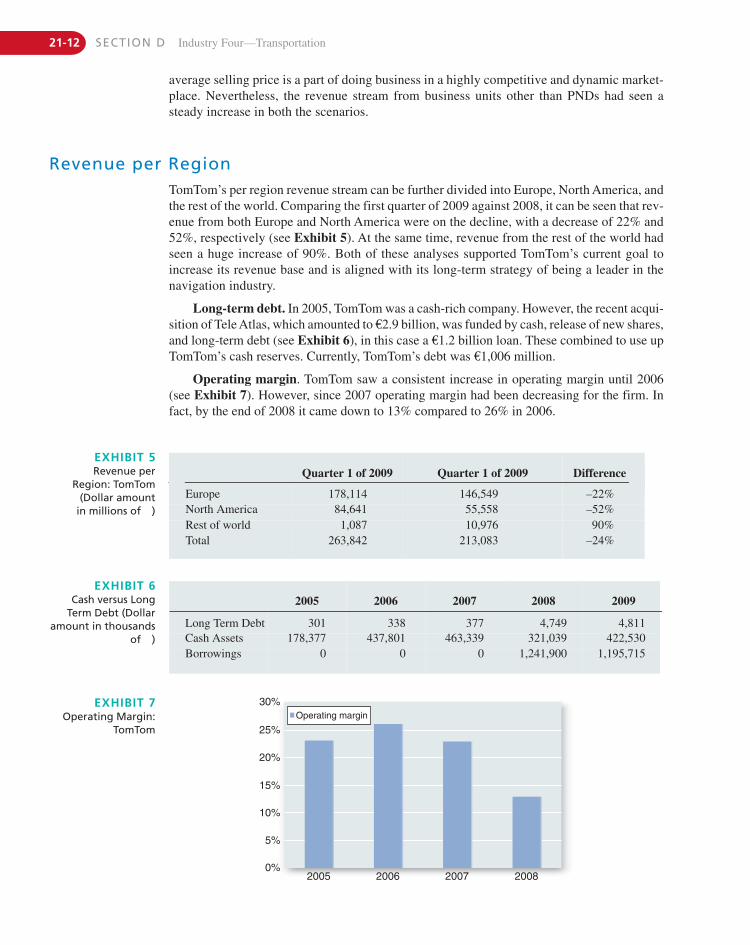

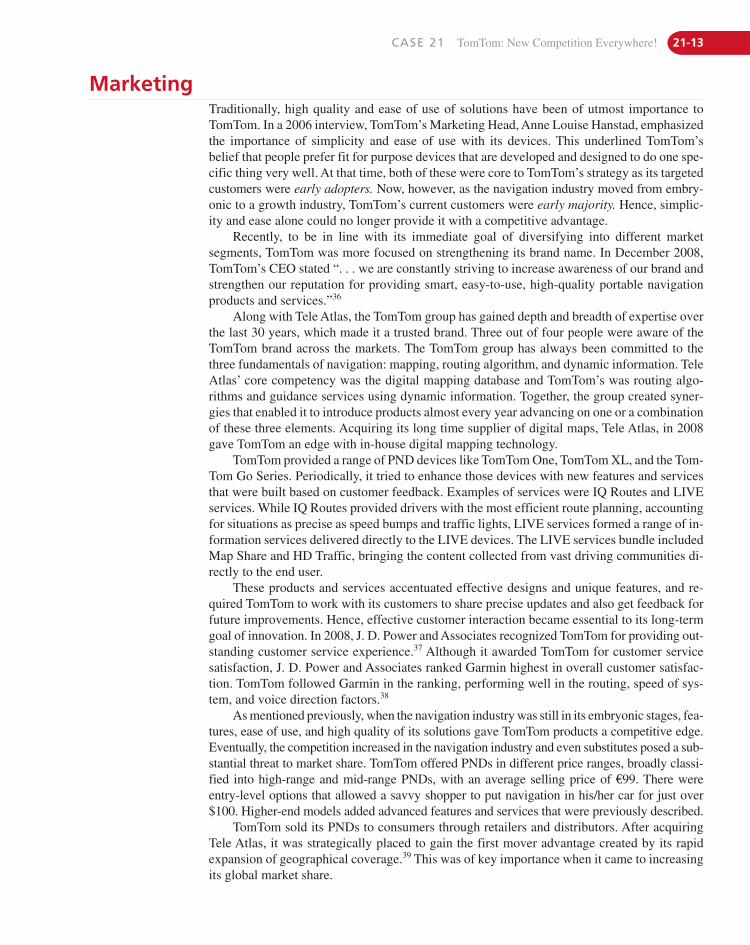

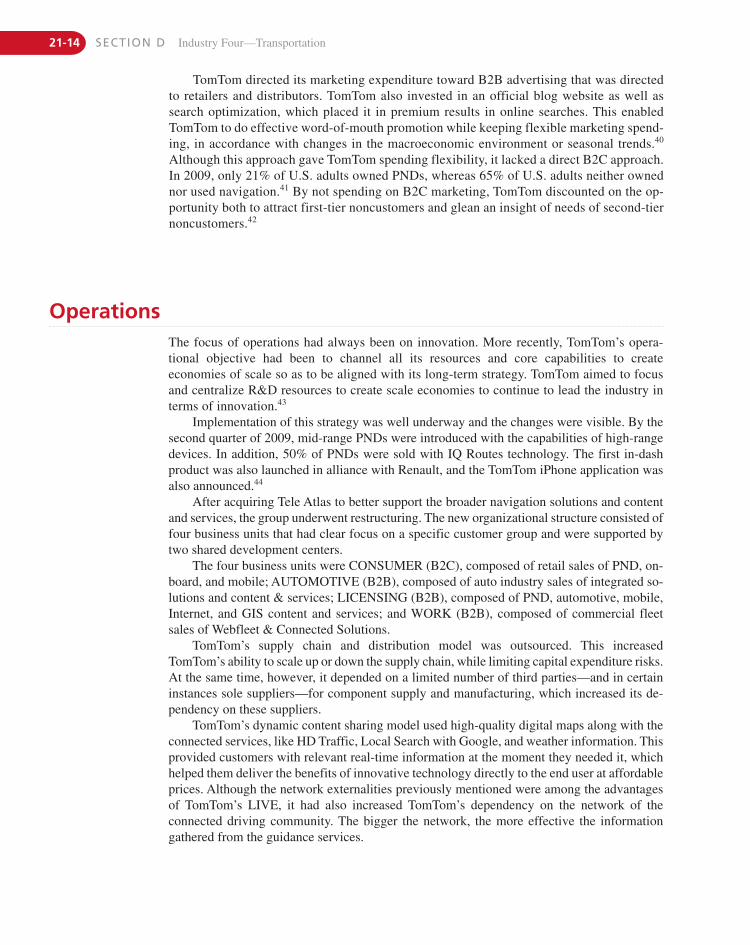

SocietalEnvironment:General forces

NaturalEnvironment:Resources and

climate

TaskEnvironment:

Industry analysis

Internal:Strengths andWeaknesses

Structure:Chain of command

Culture:Beliefs, expectations,

values

Resources:Assets, skills,competencies,

knowledge

External:Opportunities

and Threats

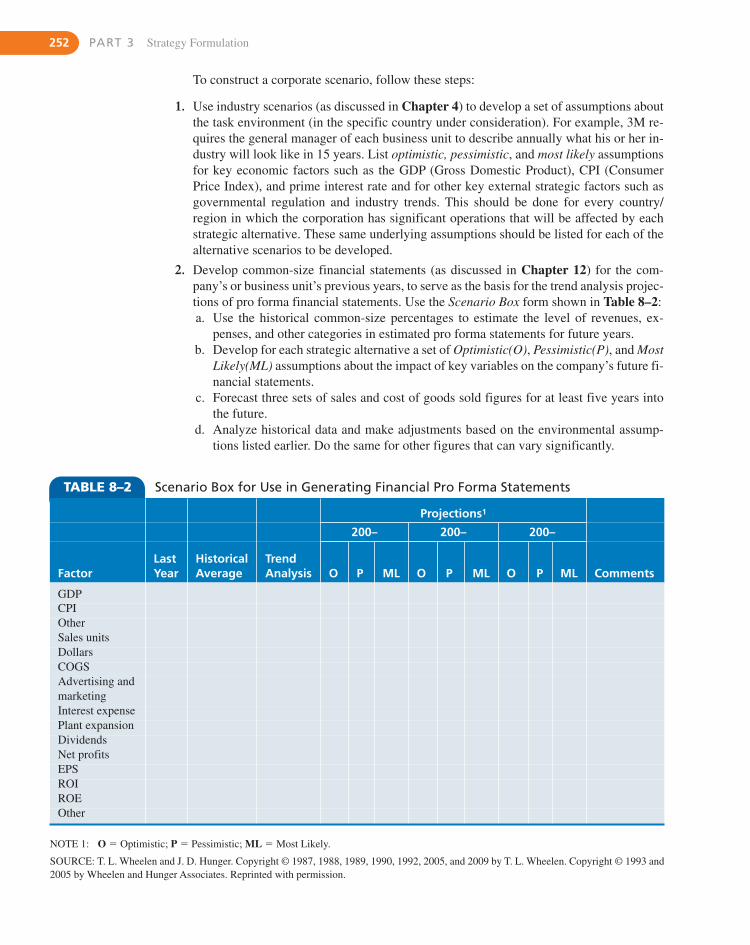

Developing Long-range Plans

Mission

Reason forexistence Objectives

Whatresults to accomplishby when

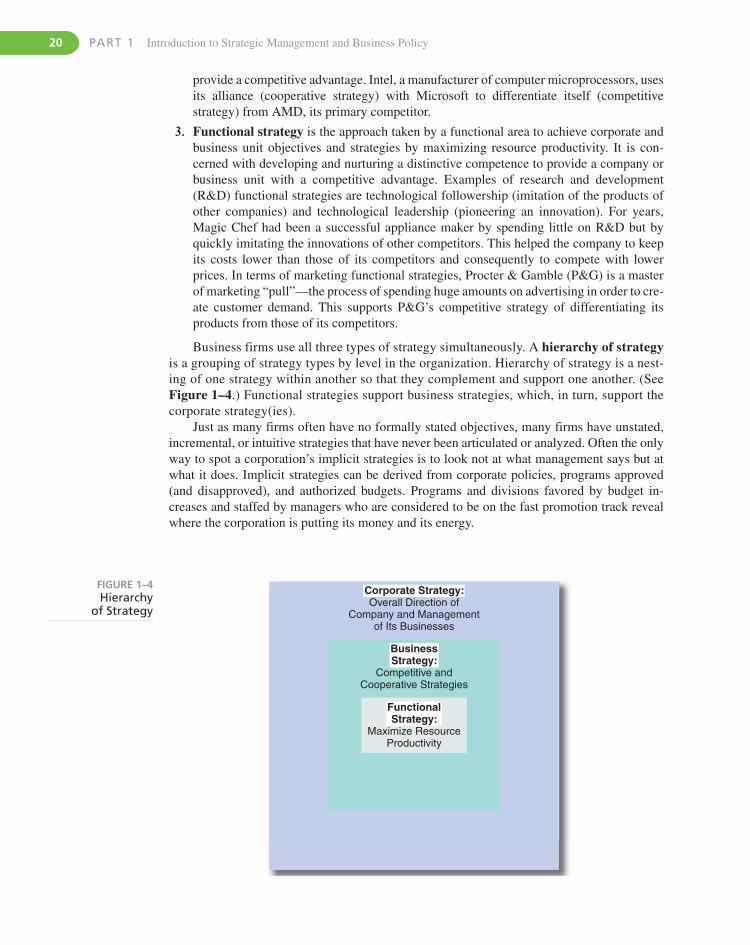

Strategies

Plan toachieve themission &objectives

Policies

Broadguidelinesfor decisionmaking

EnvironmentalScanning:

StrategyFormulation:

Feedback/Learning: Make corrections as needed

Putting Strategy into Action

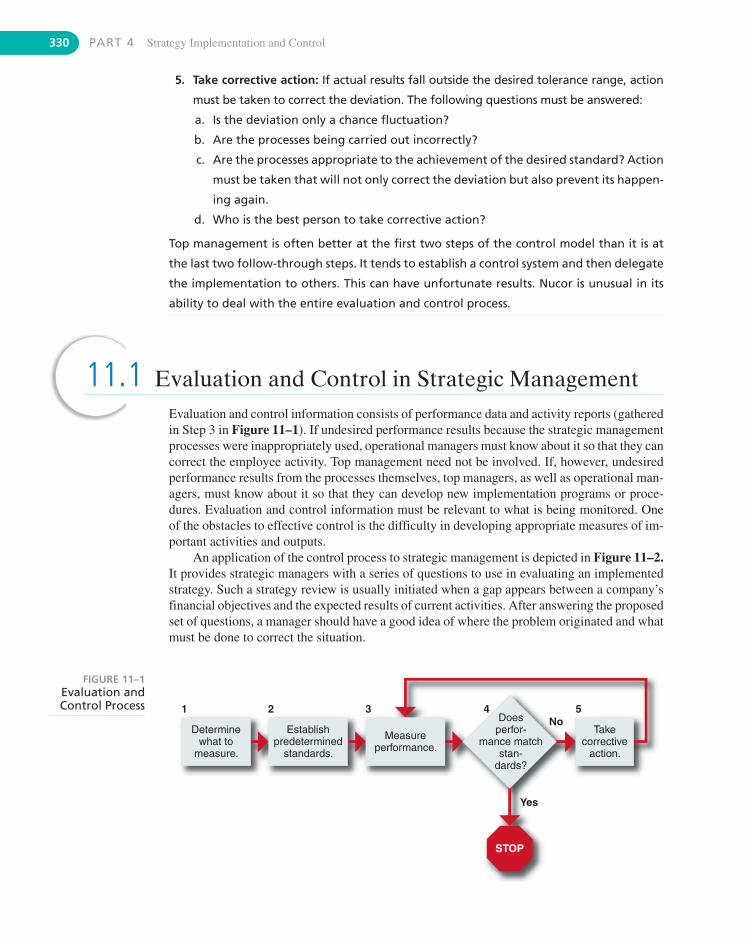

MonitoringPerformance

Programs

Activitiesneeded to accomplisha plan

Budgets

Cost of theprograms Procedures

Sequenceof stepsneeded to do the job

Performance

Actual results

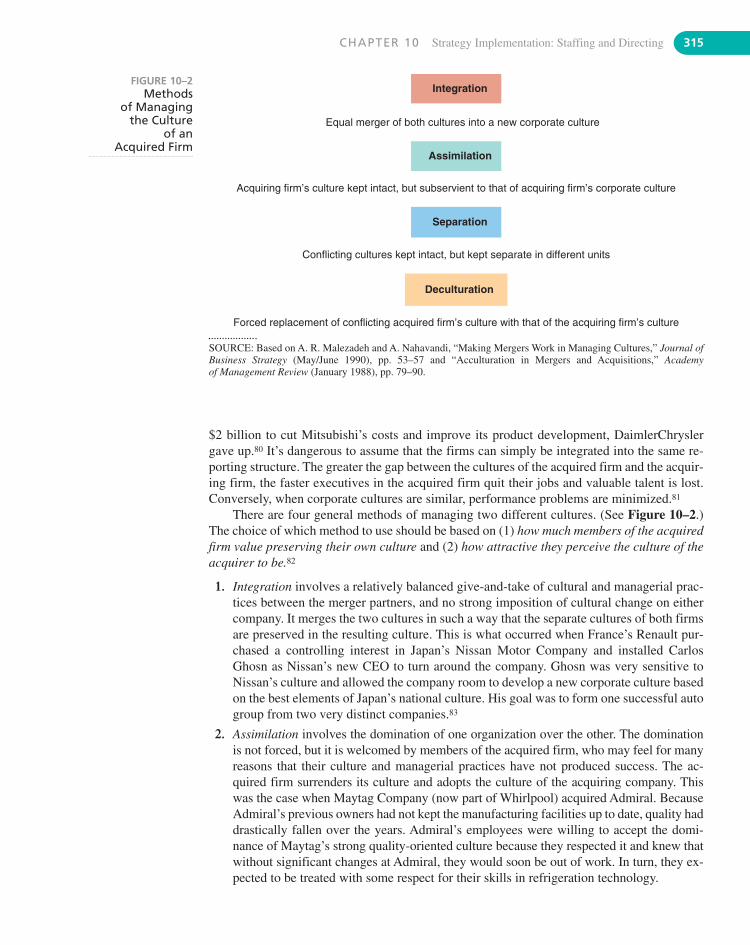

Strategy Implementation:

Evaluationand Control:

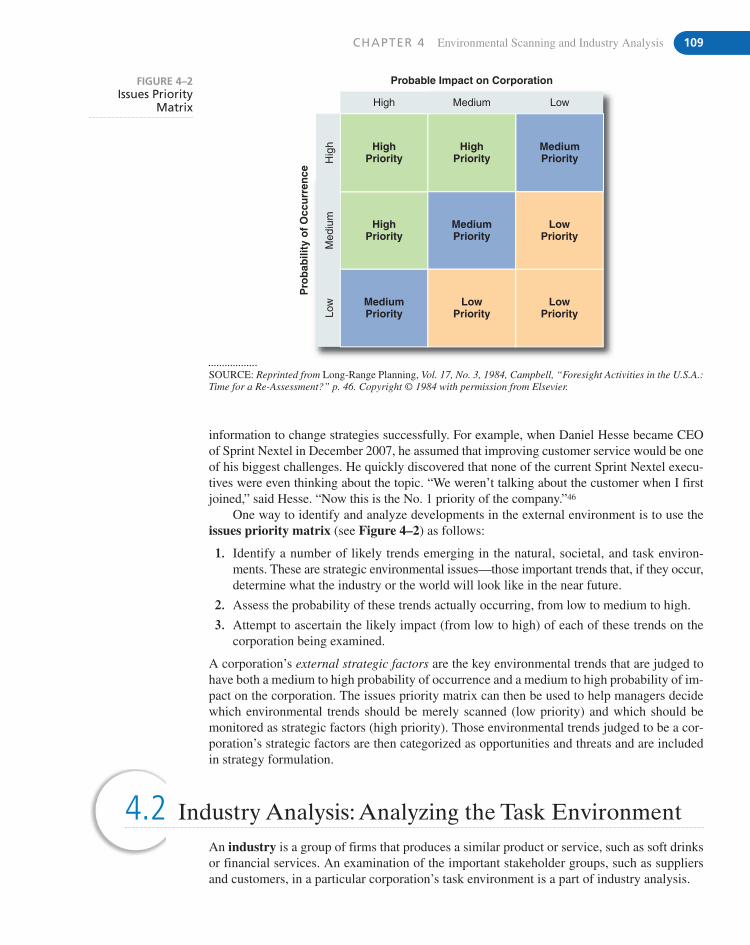

THIRTEENTH EDITION

StrategicManagement

and BusinessPolicy

TOWARD GLOBAL SUSTAINABILITY

This page intentionally left blank

THIRTEENTH EDITION

Thomas L. WheelenFormerly with University of VirginiaTrinity College, Dublin, Ireland

J. David HungerIowa State University St. John’s University

StrategicManagement

and BusinessPolicy

TOWARD GLOBAL SUSTAINABILITY

with major contributions by

Kathryn E. Wheelen

Alan N. HoffmanBentley University

Boston Columbus Indianapolis New York San Francisco Upper Saddle RiverAmsterdam Cape Town Dubai London Madrid Milan Munich Paris Montreal

Toronto Delhi Mexico City Sa~o Paulo Sydney Hong Kong Seoul Singapore Taipei Tokyo

Editorial Director: Sally YaganEditor in Chief: Eric SvendsenSenior Acquisitions Editor: Kim NorbutaEditorial Project Manager: Claudia FernandesEditorial Assistant: Carter AndersonDirector of Marketing: Patrice Lumumba JonesSenior Marketing Manager: Nikki Ayana JonesMarketing Assistant: Ian GoldSenior Managing Editor: Judy LealeProduction Project Manager: Becca GrovesSenior Operations Supervisor: Arnold VilaOperations Specialist: Cathleen PetersenCreative Director: Blair Brown

Credits and acknowledgments borrowed from other sources and reproduced, with permission, in this textbookappear on the appropriate page within text.

Copyright © 2012, 2010, 2008, 2006, 2004 by Pearson Education, Inc., publishing as Prentice Hall. Allrights reserved. Manufactured in the United States of America. This publication is protected by Copyright, andpermission should be obtained from the publisher prior to any prohibited reproduction, storage in a retrievalsystem, or transmission in any form or by any means, electronic, mechanical, photocopying, recording, orlikewise. To obtain permission(s) to use material from this work, please submit a written request to PearsonEducation, Inc., Permissions Department, One Lake Street, Upper Saddle River, New Jersey 07458, or you mayfax your request to 201-236-3290.

Many of the designations by manufacturers and sellers to distinguish their products are claimed as trademarks.Where those designations appear in this book, and the publisher was aware of a trademark claim, the designationshave been printed in initial caps or all caps.

Library of Congress Cataloging-in-Publication DataWheelen, Thomas L.

Strategic management and business policy : toward global sustainability / Thomas L. Wheelen, J. David Hunger. — 13th ed.

p. cm.Includes bibliographical references and index.ISBN-13: 978-0-13-215322-5ISBN-10: 0-13-215322-X

1. Strategic planning. 2. Strategic planning—Case studies.3. Sustainability. I. Hunger, J. David, II. Title.

HD30.28.W43 2012658.4'012—dc22

2011013549

Senior Art Director/Supervisor: Janet SlowikCover Designer: Liz HarasymcukCover Photo: Courtesy of NASA/Shutterstock Interior Designer: Maureen EideMedia Project Manager, Editorial: Denise VaughnMedia Project Manager, Production: Lisa RinaldiFull-Service Project Management: Emily Bush,S4Carlisle Publishing ServicesComposition: S4Carlisle Publishing ServicesPrinter/Binder: Courier/KendalvilleCover Printer: Lehigh-Phoenix Color/HagerstownText Font: 10/12 Times Roman

10 9 8 7 6 5 4 3 2 1ISBN 10: 0-13-215322-XISBN 13: 978-0-13-215322-5

Dedicated to

KATHY, RICHARD, AND TOM BETTY, KARI AND JEFF, MADDIE ANDMEGAN, SUZI AND NICK, SUMMER ANDKACEY, LORI, MERRY AND DYLAN, AND WOOFIE (ARF!).

SPECIAL DEDICATION TO KATHRYN WHEELEN:

Kathryn has worked on every phase of the case section of this book. Until this edition, she also managedthe construction of the Case Instructor’s Manual. She has done every job with a high level of dedication

and concern for both the case authors and the readers of this book.

NOLA AKALA

DAVID ALEVY

TARA ALGEO

DAVID ARMSTRONG

MIKE ASKEW

LAURA BAILEY

NICK BAKER

ALICIA BARNES

ASHLEY BARNES

ALICE BARR

SHERRY BARTEL

KENDRA BASSI

JAY BECKENSTEIN

JOSH BECKENSTEIN

NICOLE BELL

CATHY BENNETT

KATIE BOLLIN

SCOTT BORDEN

JENNIFER BOYLE

AUNDREA BRIDGES

SUZANNE BROWN

ALEXANDRA BUEHLER

KYLE BURDETTE

WHITNEY CAMERON

RUTH CARDIFF

AMY CAREY

MEGAN CARRICO

MARTI CARTER

ANDREA CATULLO-LINN

MEREDITH CHANDLER

LUKE CLAEYS

KAYLEE CLAYMORE

BRIAN COBB

JENNIFER COLE

TARYLL CONNOLLY

THAYNE CONRAD

DONNA CONROY

CAITLIN COUTHEN

MEGAN JOY COWART

CYNDI CRIMMINS

KASEY CROCKETT

DAN CURRIER

KELLY DAN

MICHLENE DAOUD HEALY

STACY DAVIS

FRANK DEL CASTILLO

MEREDITH DELA ROSA

CHRIS DELANEY

GEORGE DEVENNEY

DANA DODGE (Frick)

KATE DOLDER

BARBARA DONLON

HEIDI DRESSLER

TRACY DYBALSKI

BRIAN DYK

KIM ECK

TRISH EICHHOLD

KRISTIN ELBER

KELSEY ELLIOTT

KATIE EYNON

GENEVA FARROW

MARIA FELIBERTY

MIKE FINER

MICHELLE FINNERTY

CANDAS FLETCHER

ROBERT FLORY

MARCIA FLYNN

BRAD FORRESTER

MARGARET FRENCH

STEPHANIE FRITSON

MARK GAFFNEY

MICHELLE GARCIA-JUCHTER

SYBIL GERAUD

AMBER GOECKE

CAROLYN GOGOLIN

ADAM GOLDSTEIN

BETH GRUNFELD

MICAELA HAIDLE

GREG HAITH

DEMETRIUS HALL

BRIDGET HANNENBERG

BRYAN HARRELL

TARA HARTLEY

KENNY HARVEY

ALISON HASKINS

CAROL HAWKS

JENNIFER HEILBRUNN

CHRISTINE HENRY

LYNN HICKS

JULIE HILDEBRAND

DAUNNE HINGLE

WENDI HOLLAND

CHRISTY HUMENIUK

GENE HUMENIUK

ANDREA IORIO

SUSAN JACKSON

PAM JEFFRIES

BRITTANY JUCHNOWSKI

ANJALI JUSTUS

CHERYL KABB

LAURA KAPPES

GIA KAUL

JULIE KESTENBAUM

KARTAPURKH KHALSA

KIM KIEHLER

AMANDA KILLEEN

WALT KIRBY

MARY-JO KOVACH

ROBYN KOVAR

GREG KRAMP

DANIEL KRAUSS

MICHAEL KRISANDA

GINA LaMANTIA

CHAFIKA LANDERS

DOROTHY LANDRY

DUSTIN LANGE

ALIX LaSCOLA

JOE LEE

APRIL LEMONS

KIMBERLY LENAGHAN

This book is also dedicated to the following Prentice Hall/Pearson salesrepresentatives who work so hard to promote this book:

vi

TRICIA LISCIO

BETH LUDWIG

CARY LUNA

JEMINA MACHARRY

KATIE MAHAN

LAURA MANN

PATRICIA MARTINEZ

CHRISTINA MASTROGIOVANNI

SONNY MATHARU

TONY MATHIAS

BROOK MATTHEWS

GEORGIA MAY

ALICIA MCAULIFFE

MASON McCARTNEY

KAREN McFADYEN

BRIAN McGARRY

MICHELLE McGOVERN

IRENE McGUINNESS

RYAN McHENRY

CRISTIN McMICHAEL

KEVIN MEASELLE

RAY MEDINA

KELLY MEIERHOFER

MOLLY MEINERS

MATT MESAROS

SHALON MILLER

JAMI MINARD

WILLIAM MINERICH

EMILY MITCHELL

JILINE MIX

JULIE MOREL

RAFAEL MORENO

TRACY MORSE

OLIVIA MOUG

DOLLY MUNIZ

TRICIA MURPHY

LAUREN MURROW

AMBER MYLLION (Parks)

LINDA NELSON

LYNNE NICLAIR

BOB NISBET

BETSY NIXON

TOM NIXON

LAURA NOAH

COLLEEN O’DELL

DEBBIE OGILIVE

SARI ORLANSKY

DAVE OSTROW

DARCEY PALMER

KRISTINA PARKER

TONI PAYNE

JULIANNE PETERSON

MELISSA PFISTNER

CANDACE PINATARO

BELEN POLTORAK

ELIZABETH POPIELARZ

MEGAN PRENDERGAST

NICOLE PRICE

JILL PROMESSO

LENNY ANN RAPER

JOSH RASMUSSEN

AMANDA RAY

SONYA REED

RICHARD RESCH

MARY RHODES

BRAD RITTER

DAN ROBERTSON

MATT ROBINSON

JENNIFER ROSEN

DOROTHY ROSENE

KELLEEN ROWE

RICH ROWE

PEYTON ROYTEK

SENG SAECHAO

STEVE SARTORI

LYNDA SAX

BOB SCANLON

MARCUS SCHERER

KIMBERLY SCHEYVING

HEIDI SCHICK (Miller)

BRAD SCHICK

CHRIS SCHMIDT

DEBORAH SCHMIDT

MOLLY SCHMIDT

CORRINA SCHULTZ

WHITNEY SEAGO

CHRISTIANA SERLE

MARTHA SERNAS

MARY SHAPIRO

BARBARA SHERRY

KEN SHIPBAUGH

DAVE SHULER

JESSICA SIEMINSKI

LEA SILVERMAN

AUTUMN SLAUGHTER

KRISTA SLAVICEK

SCOTT SMITH

ADRIENNE SNOW

LEE SOLOMONIDES

BEN STEPHEN

DAN SULLIVAN

JOHN SULLIVAN

LORI SULLIVAN

STEPHANIE SURFUS

AMANDA SVEC

CHRISTINA TATE

SARAH THOMAS

ABBY THORNBLADH

KATY TOWNLEY

ELIZABETH TREPKOWSKI

TARA TRIPP

CAROLYN TWIST

JOE VIRZI

AMANDA VOLZ

BRITNEY WALKER

MADELEINE WATSON

BEN WEBER

DANIEL WELLS

MARK WHEELER

LIZ WILDES

MICHELLE WILES

BRIAN WILLIAMS

ERIN WILLIAMS

CINDY WILLIAMSON

RACHEL WILLIS

SIMON WONG

KIMBERLY WOODS

JACKIE WRIGHT

HEATHER WRUBLESKY

GEORGE YOUNG

MARY ZIMMERMANN

KACIE ZIN

DEDICATION vii

This page intentionally left blank

Brief Contents

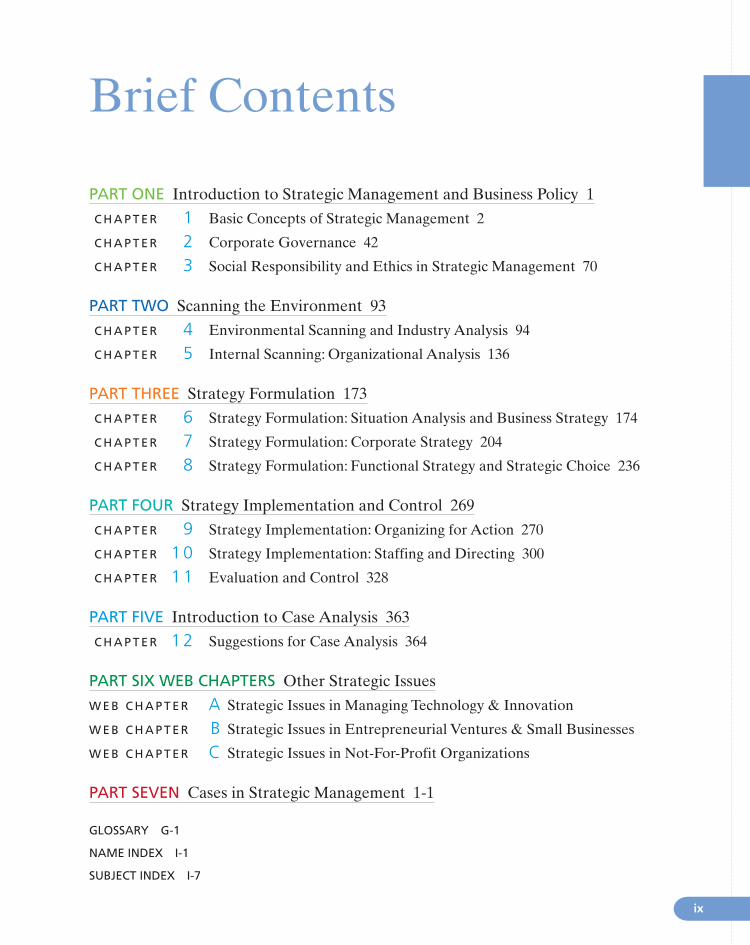

PART ONE Introduction to Strategic Management and Business Policy 1

C H A P T E R 1 Basic Concepts of Strategic Management 2

C H A P T E R 2 Corporate Governance 42

C H A P T E R 3 Social Responsibility and Ethics in Strategic Management 70

PART TWO Scanning the Environment 93

C H A P T E R 4 Environmental Scanning and Industry Analysis 94

C H A P T E R 5 Internal Scanning: Organizational Analysis 136

PART THREE Strategy Formulation 173

C H A P T E R 6 Strategy Formulation: Situation Analysis and Business Strategy 174

C H A P T E R 7 Strategy Formulation: Corporate Strategy 204

C H A P T E R 8 Strategy Formulation: Functional Strategy and Strategic Choice 236

PART FOUR Strategy Implementation and Control 269

C H A P T E R 9 Strategy Implementation: Organizing for Action 270

C H A P T E R 1 0 Strategy Implementation: Staffing and Directing 300

C H A P T E R 1 1 Evaluation and Control 328

PART FIVE Introduction to Case Analysis 363

C H A P T E R 1 2 Suggestions for Case Analysis 364

PART SIX WEB CHAPTERS Other Strategic Issues

W E B C H A P T E R A Strategic Issues in Managing Technology & Innovation

W E B C H A P T E R B Strategic Issues in Entrepreneurial Ventures & Small Businesses

W E B C H A P T E R C Strategic Issues in Not-For-Profit Organizations

PART SEVEN Cases in Strategic Management 1-1

GLOSSARY G-1

NAME INDEX I-1

SUBJECT INDEX I-7

ix

This page intentionally left blank

Contents

Preface xxix

PART ONE Introduction to Strategic Management and Business Policy 1

C H A P T E R 1 Basic Concepts of Strategic Management 2

1.1 The Study of Strategic Management 5

Phases of Strategic Management 5

Benefits of Strategic Management 6

1.2 Globalization and Environmental Sustainability: Challenges to Strategic Management 7

Impact of Globalization 8

Impact of Environmental Sustainability 8

Global Issue: REGIONAL TRADE ASSOCIATIONS REPLACE NATIONAL TRADE BARRIERS 9

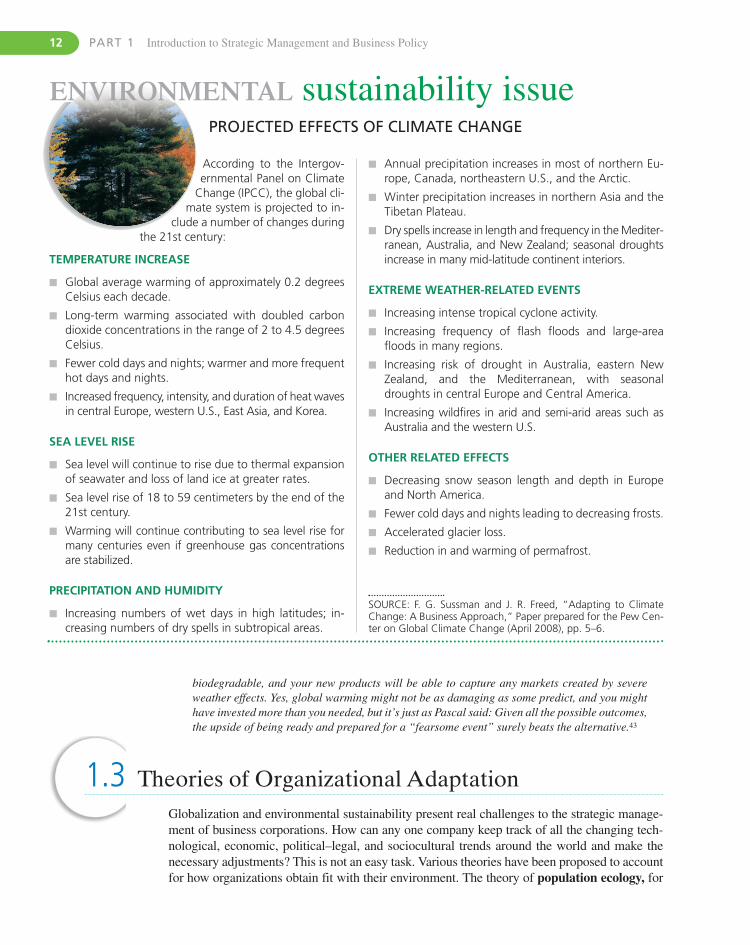

Environmental Sustainability Issue: PROJECTED EFFECTS OF CLIMATE CHANGE 12

1.3 Theories of Organizational Adaptation 12

1.4 Creating a Learning Organization 13

1.5 Basic Model of Strategic Management 14

Environmental Scanning 16

Strategy Formulation 17

Strategy Highlight 1.1: DO YOU HAVE A GOOD MISSION STATEMENT? 18

Strategy Implementation 21

Evaluation and Control 22

Feedback/Learning Process 23

1.6 Initiation of Strategy: Triggering Events 23

Strategy Highlight 1.2: TRIGGERING EVENT AT UNILEVER 24

1.7 Strategic Decision Making 25

What Makes a Decision Strategic 25

Mintzberg’s Modes of Strategic Decision Making 25

Strategic Decision-Making Process: Aid to Better Decisions 27

1.8 The Strategic Audit: Aid to Strategic Decision-Making 28

1.9 End of Chapter Summary 29

APPENDIX 1.A Strategic Audit of a Corporation 34

xi

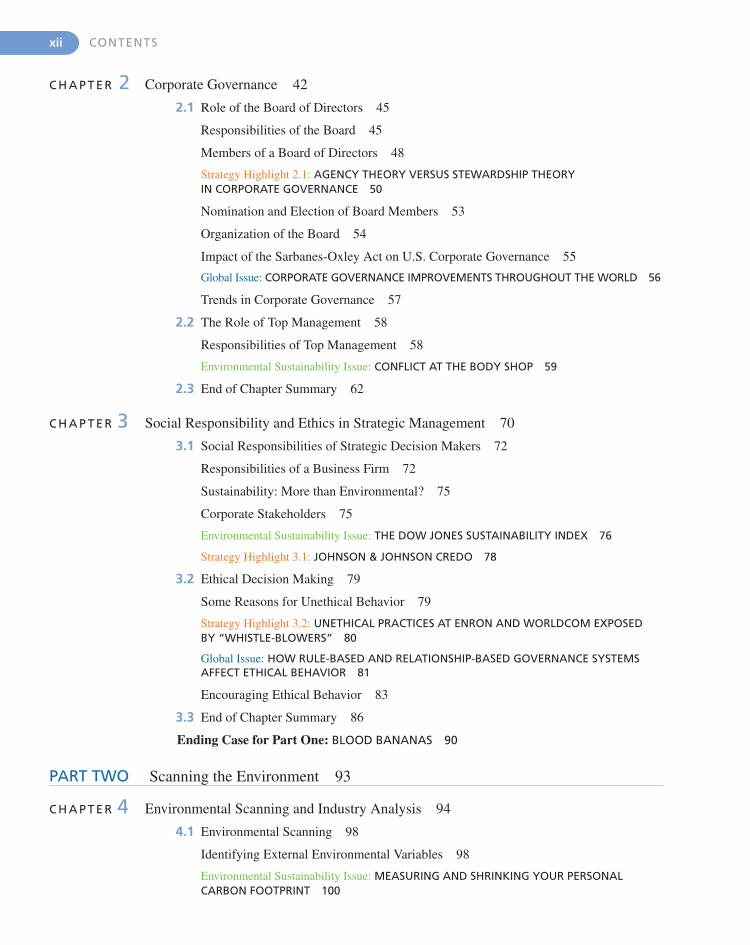

C H A P T E R 2 Corporate Governance 42

2.1 Role of the Board of Directors 45

Responsibilities of the Board 45

Members of a Board of Directors 48

Strategy Highlight 2.1: AGENCY THEORY VERSUS STEWARDSHIP THEORY IN CORPORATE GOVERNANCE 50

Nomination and Election of Board Members 53

Organization of the Board 54

Impact of the Sarbanes-Oxley Act on U.S. Corporate Governance 55

Global Issue: CORPORATE GOVERNANCE IMPROVEMENTS THROUGHOUT THE WORLD 56

Trends in Corporate Governance 57

2.2 The Role of Top Management 58

Responsibilities of Top Management 58

Environmental Sustainability Issue: CONFLICT AT THE BODY SHOP 59

2.3 End of Chapter Summary 62

C H A P T E R 3 Social Responsibility and Ethics in Strategic Management 70

3.1 Social Responsibilities of Strategic Decision Makers 72

Responsibilities of a Business Firm 72

Sustainability: More than Environmental? 75

Corporate Stakeholders 75

Environmental Sustainability Issue: THE DOW JONES SUSTAINABILITY INDEX 76

Strategy Highlight 3.1: JOHNSON & JOHNSON CREDO 78

3.2 Ethical Decision Making 79

Some Reasons for Unethical Behavior 79

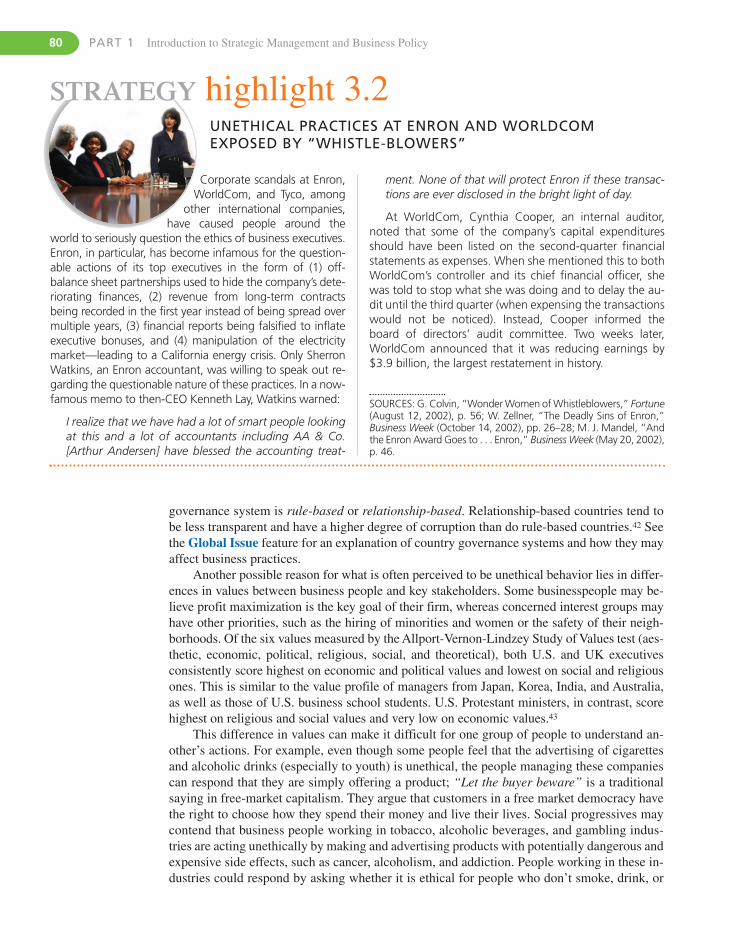

Strategy Highlight 3.2: UNETHICAL PRACTICES AT ENRON AND WORLDCOM EXPOSED BY “WHISTLE-BLOWERS” 80

Global Issue: HOW RULE-BASED AND RELATIONSHIP-BASED GOVERNANCE SYSTEMSAFFECT ETHICAL BEHAVIOR 81

Encouraging Ethical Behavior 83

3.3 End of Chapter Summary 86

Ending Case for Part One: BLOOD BANANAS 90

PART TWO Scanning the Environment 93

C H A P T E R 4 Environmental Scanning and Industry Analysis 94

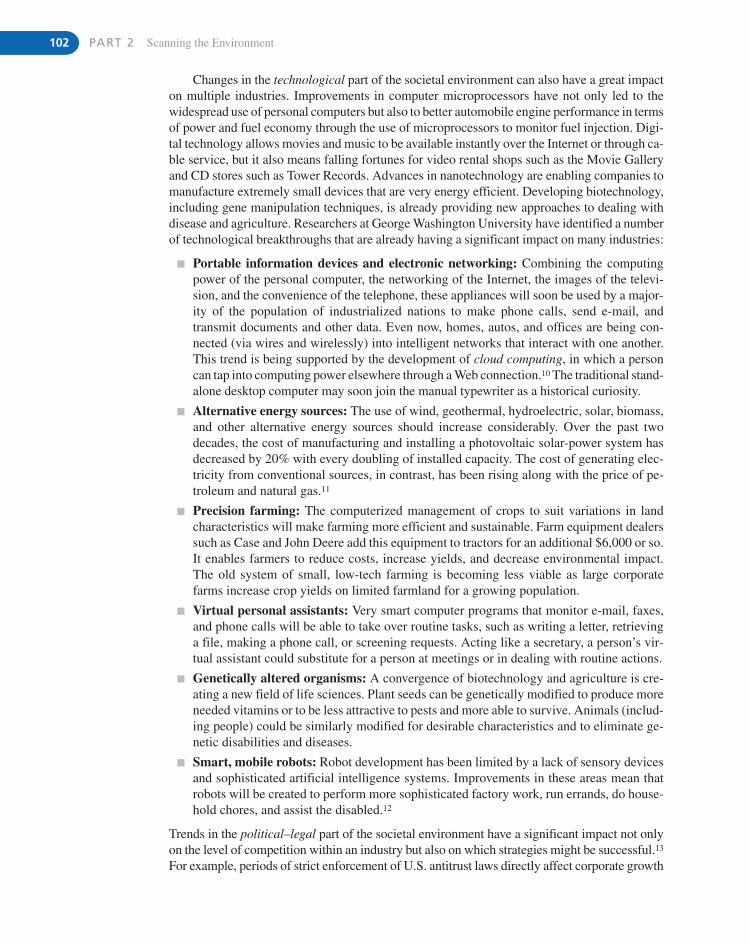

4.1 Environmental Scanning 98

Identifying External Environmental Variables 98

Environmental Sustainability Issue: MEASURING AND SHRINKING YOUR PERSONALCARBON FOOTPRINT 100

xii CONTENTS

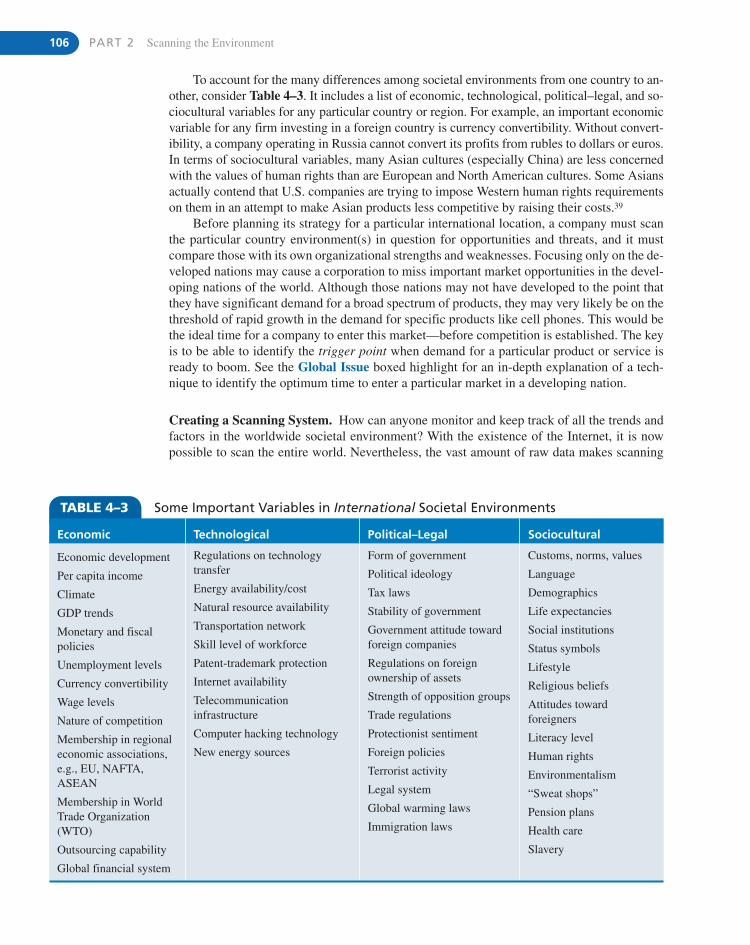

Global Issue: IDENTIFYING POTENTIAL MARKETS IN DEVELOPING NATIONS 107

Identifying External Strategic Factors 108

4.2 Industry Analysis: Analyzing the Task Environment 109

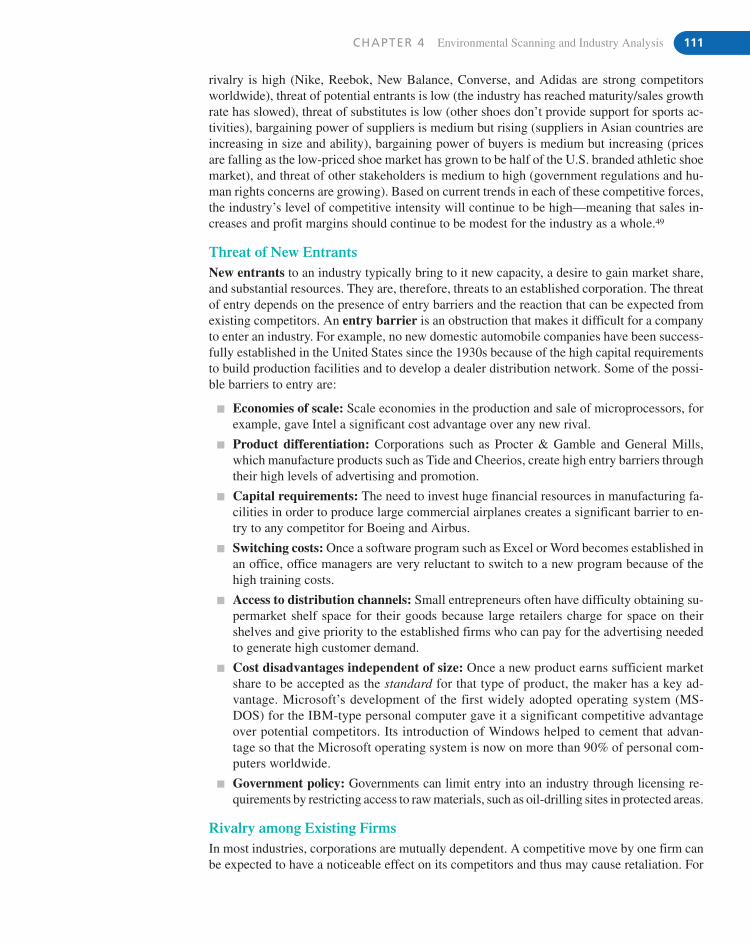

Porter’s Approach to Industry Analysis 110

Industry Evolution 114

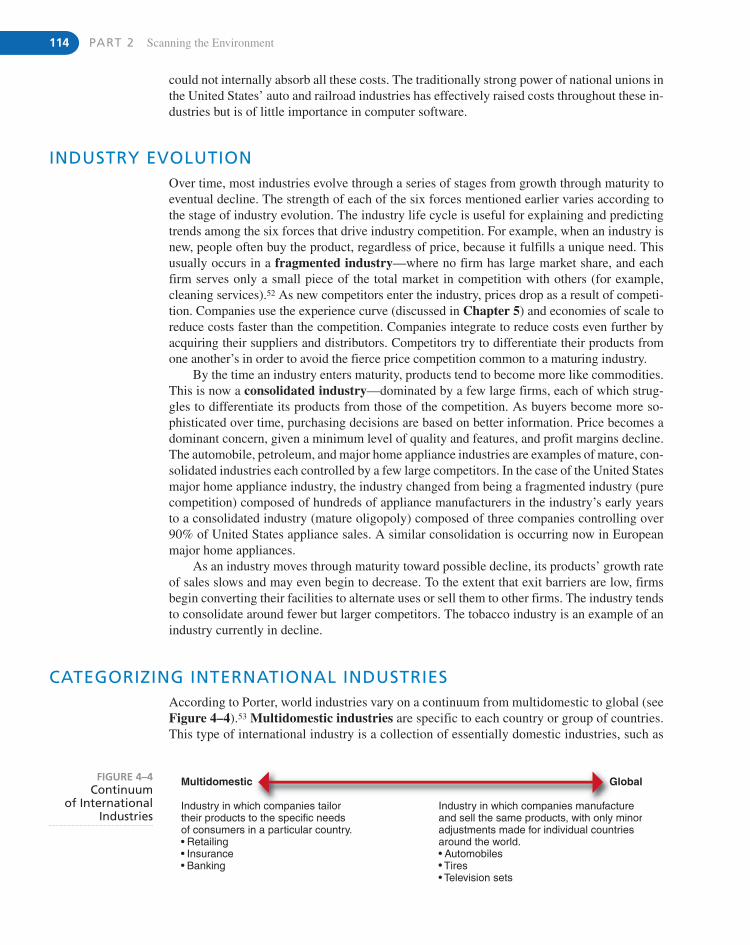

Categorizing International Industries 114

International Risk Assessment 115

Strategic Groups 115

Strategic Types 117

Hypercompetition 117

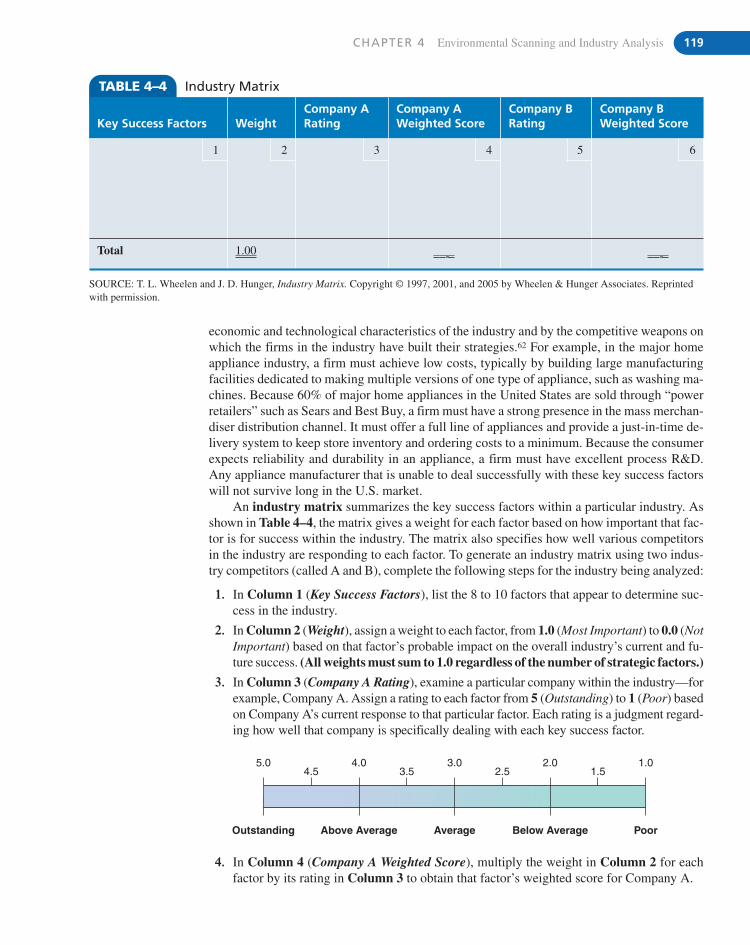

Using Key Success Factors to Create an Industry Matrix 118

Strategy Highlight 4.1: MICROSOFT IN A HYPERCOMPETITIVE INDUSTRY 118

4.3 Competitive Intelligence 120

Sources of Competitive Intelligence 121

Strategy Highlight 4.2: EVALUATING COMPETITIVE INTELLIGENCE 122

Monitoring Competitors for Strategic Planning 122

4.4 Forecasting 123

Danger of Assumptions 123

Useful Forecasting Techniques 124

4.5 The Strategic Audit: A Checklist for Environmental Scanning 125

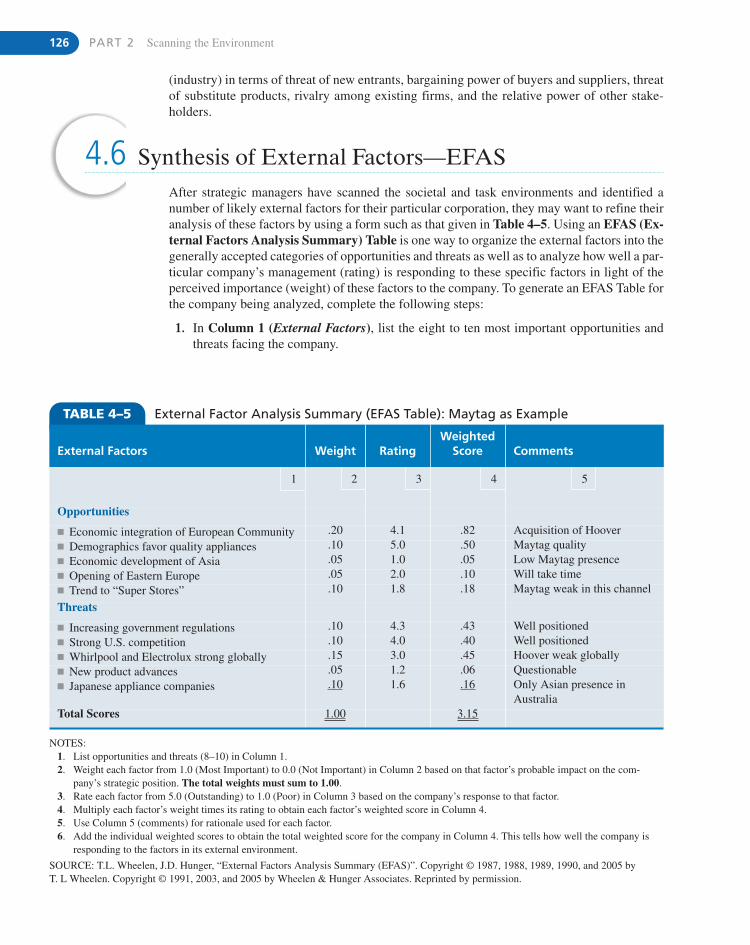

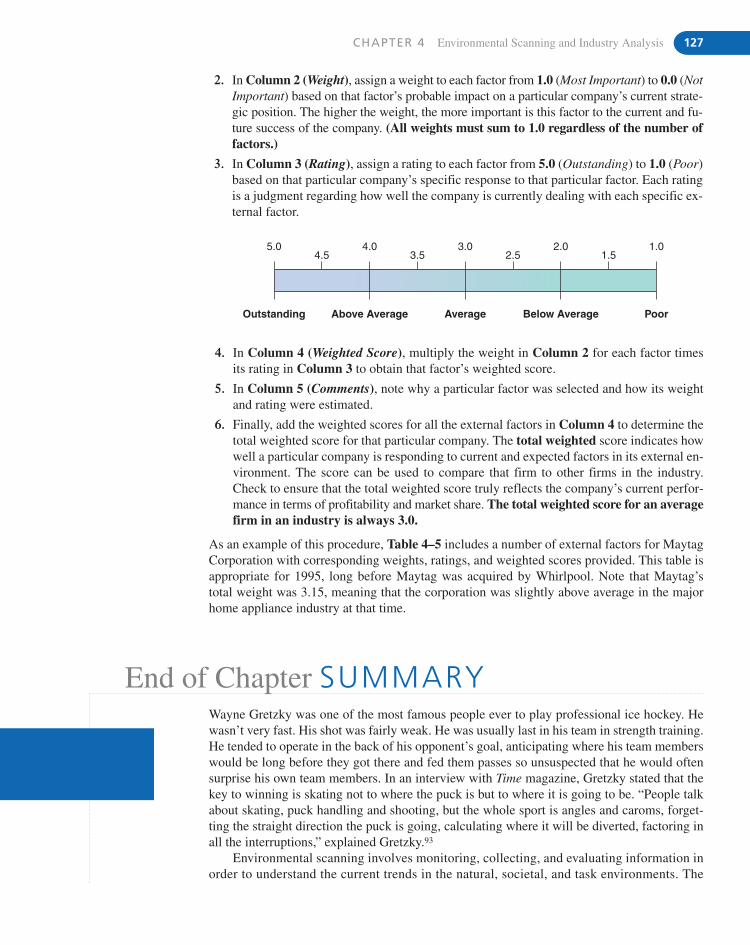

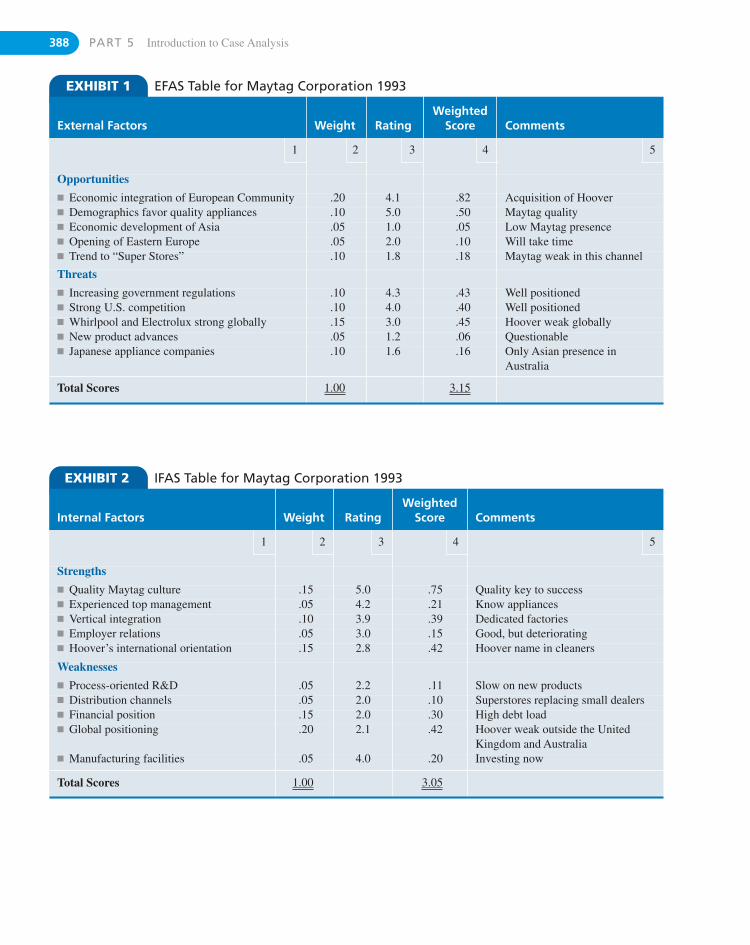

4.6 Synthesis of External Factors—EFAS 126

4.7 End of Chapter Summary 127

APPENDIX 4.A Competitive Analysis Techniques 133

C H A P T E R 5 Internal Scanning: Organizational Analysis 136

5.1 A Resource-Based Approach to Organizational Analysis 138

Core and Distinctive Competencies 138

Using Resources to Gain Competitive Advantage 139

Determining the Sustainability of an Advantage 140

5.2 Business Models 142

5.3 Value-Chain Analysis 143

Strategy Highlight 5.1: A NEW BUSINESS MODEL AT SMARTYPIG 144

Industry Value-Chain Analysis 145

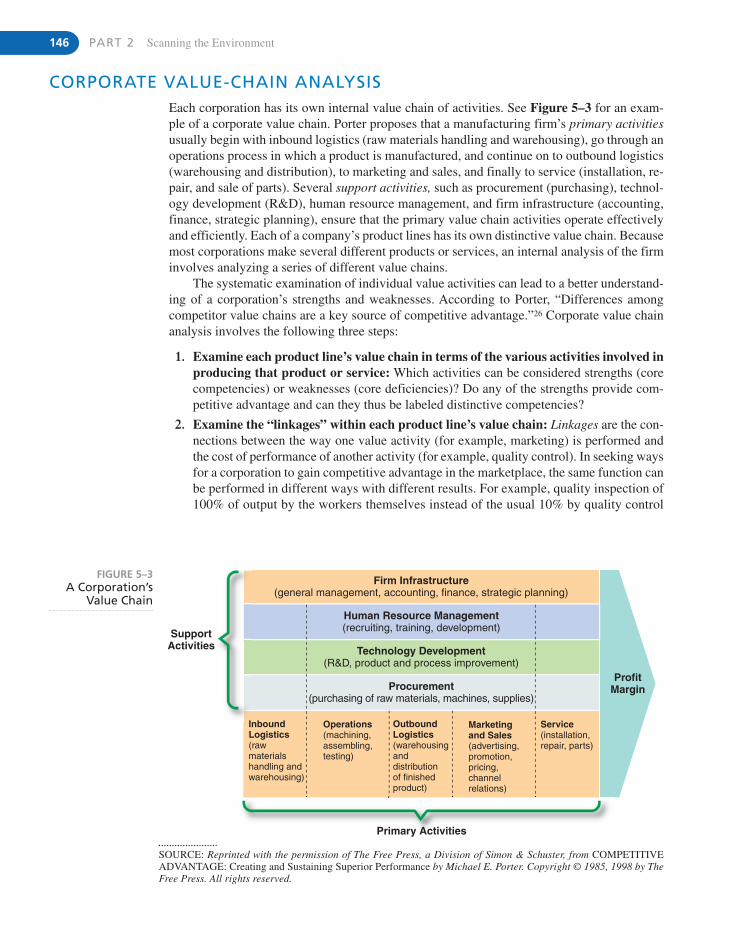

Corporate Value-Chain Analysis 146

5.4 Scanning Functional Resources and Capabilities 147

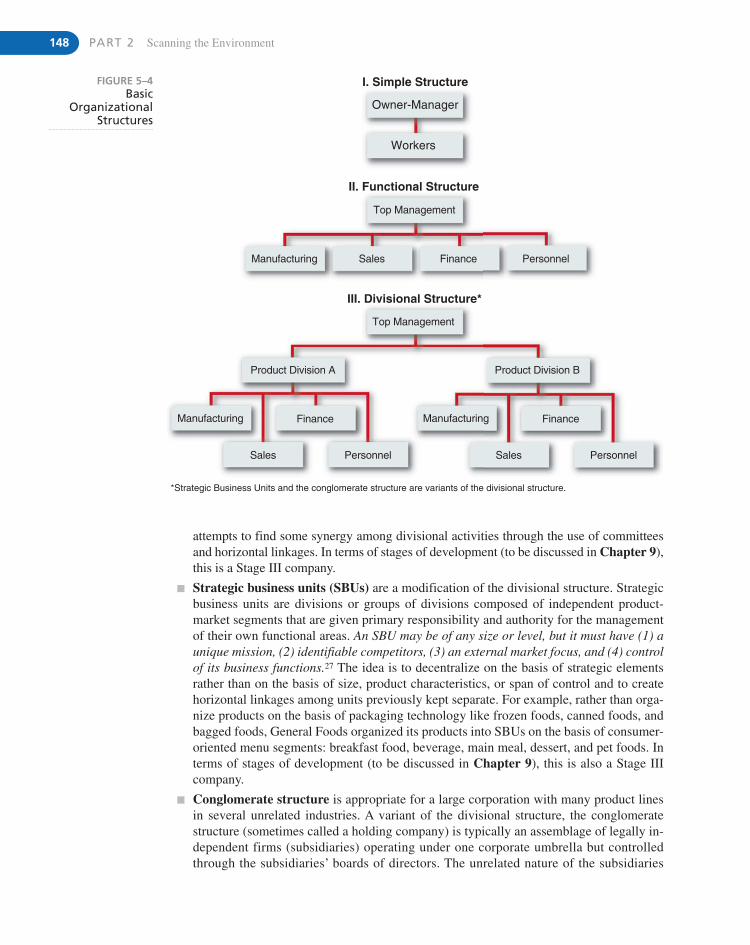

Basic Organizational Structures 147

Corporate Culture: The Company Way 149

CONTENTS xiii

Global Issue: MANAGING CORPORATE CULTURE FOR GLOBAL COMPETITIVEADVANTAGE: ABB VERSUS MATSUSHITA 150

Strategic Marketing Issues 151

Strategic Financial Issues 153

Strategic Research and Development (R&D) Issues 154

Strategic Operations Issues 156

Strategic Human Resource (HRM) Issues 158

Environmental Sustainability Issue: USING ENERGY EFFICIENCY FOR COMPETITIVEADVANTAGE AND QUALITY OF WORK LIFE 161

Strategic Information Systems/Technology Issues 162

5.5 The Strategic Audit: A Checklist for Organizational Analysis 163

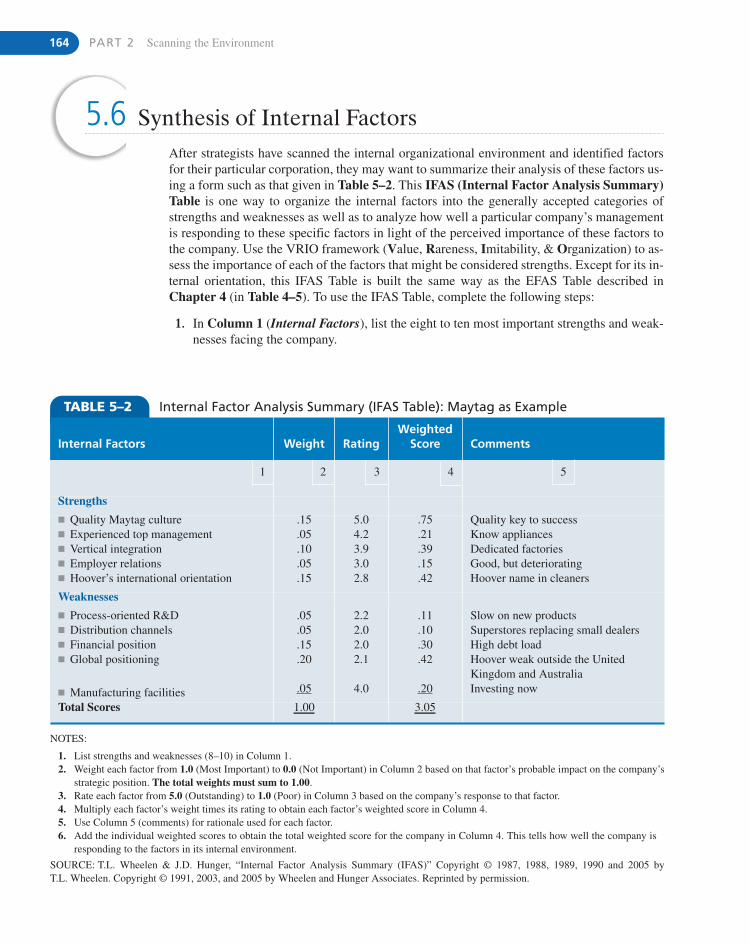

5.6 Synthesis of Internal Factors 164

5.7 End of Chapter Summary 165

Ending Case for Part Two: BOEING BETS THE COMPANY 170

PART THREE Strategy Formulation 173

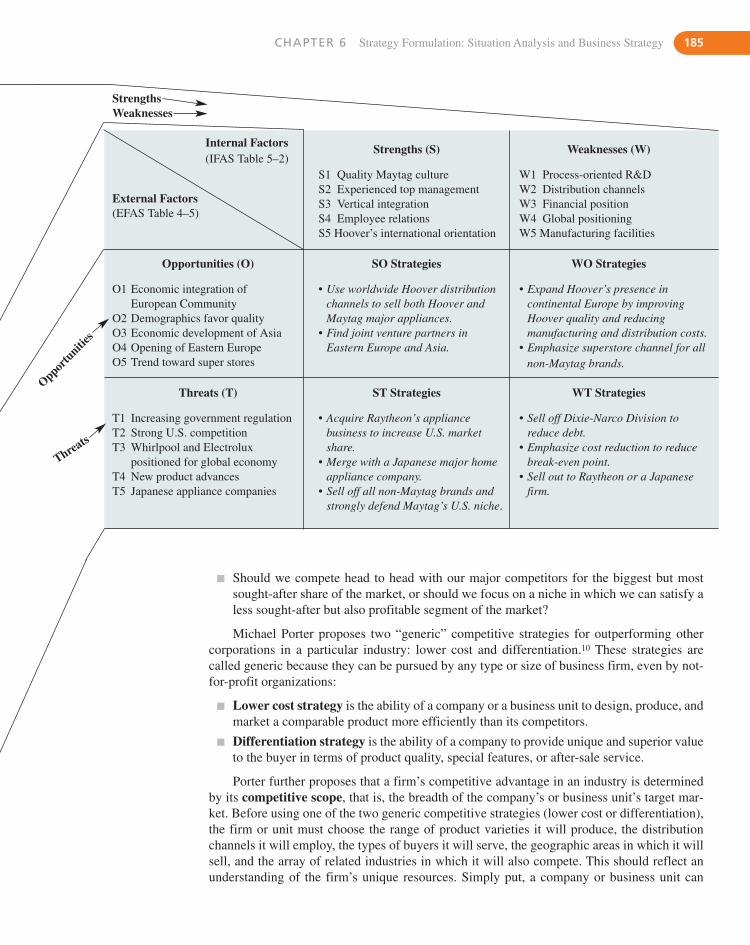

C H A P T E R 6 Strategy Formulation: Situation Analysis and Business Strategy 174

6.1 Situation Analysis: SWOT Analysis 176

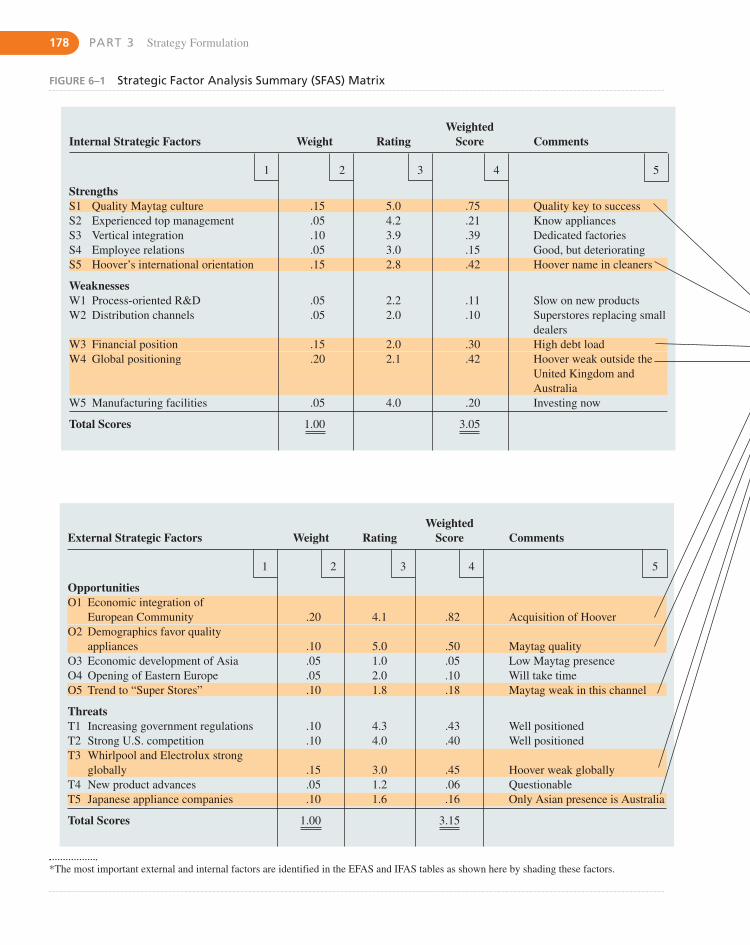

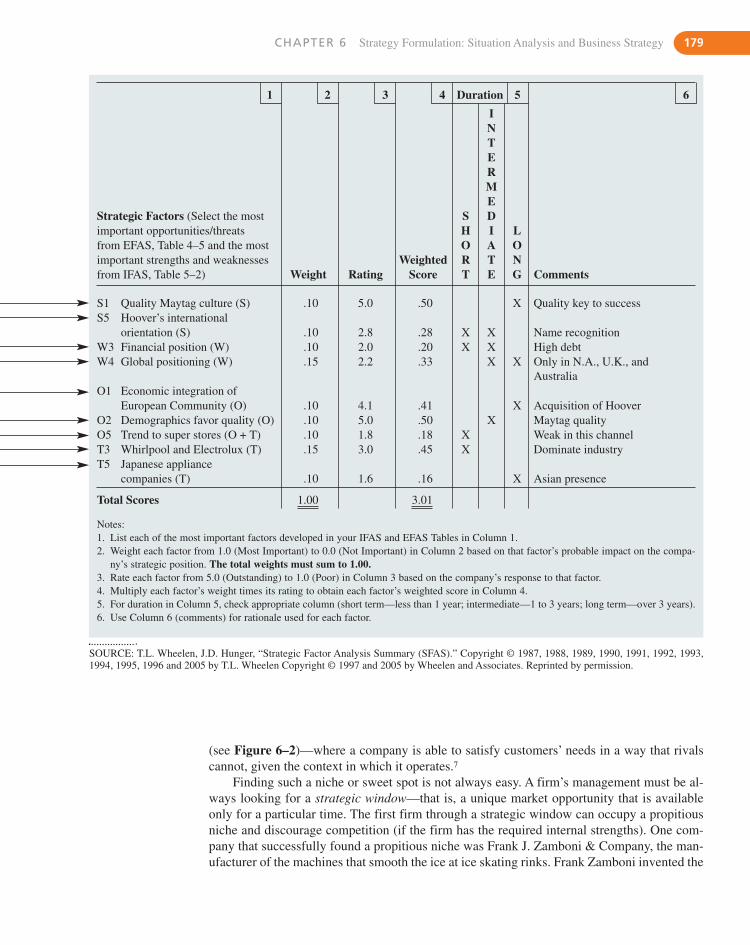

Generating a Strategic Factors Analysis Summary (SFAS) Matrix 176

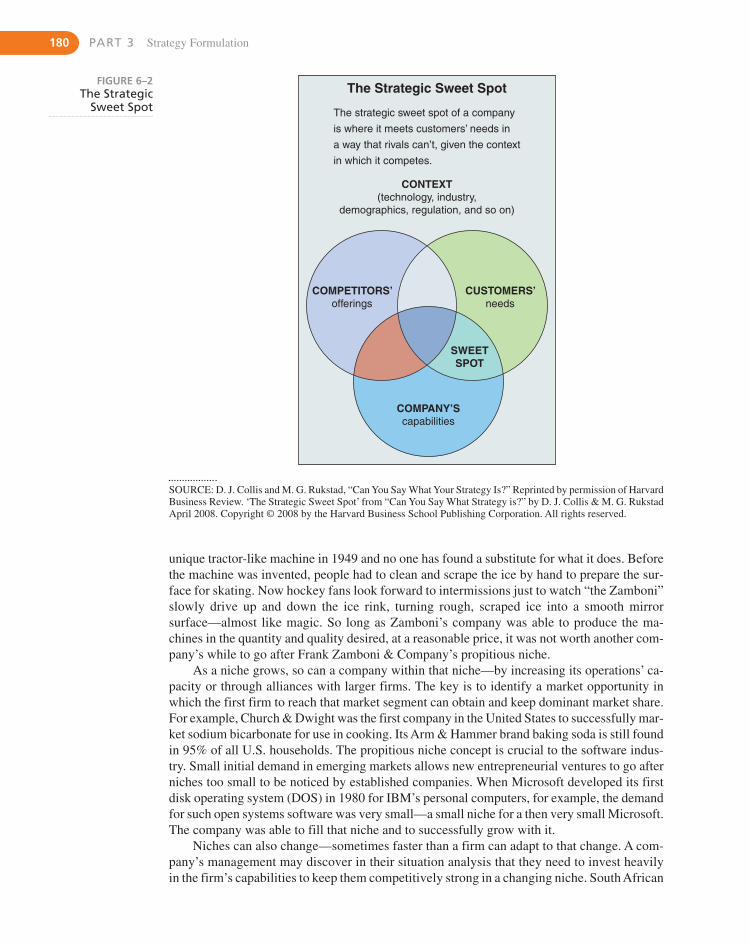

Finding a Propitious Niche 177

Global Issue: SAB DEFENDS ITS PROPITIOUS NICHE 181

6.2 Review of Mission and Objectives 181

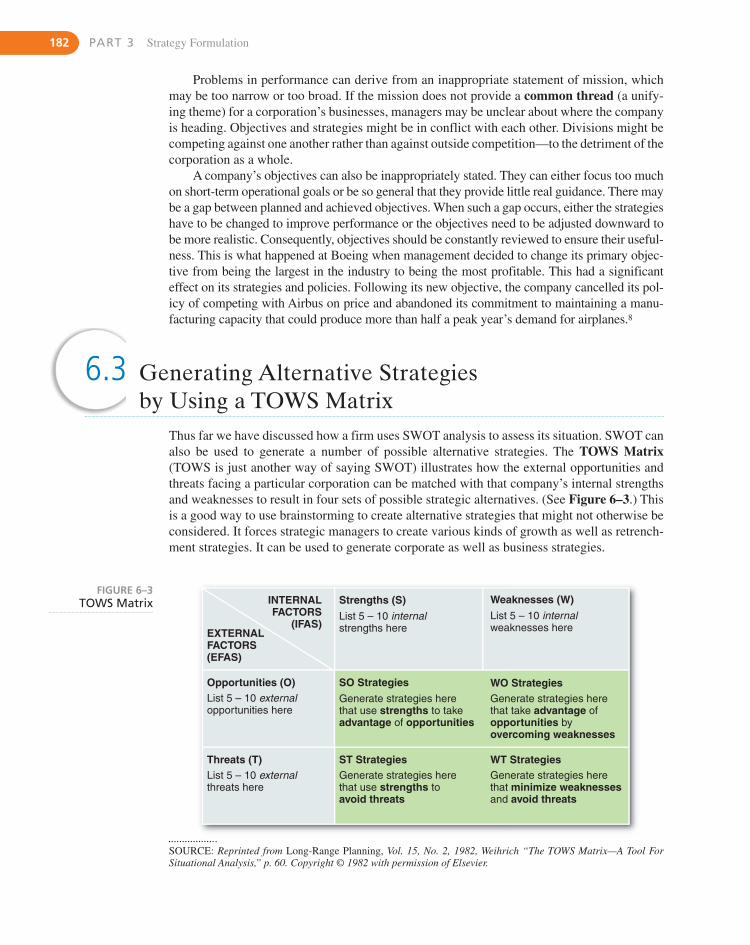

6.3 Generating Alternative Strategies by Using a TOWS Matrix 182

6.4 Business Strategies 183

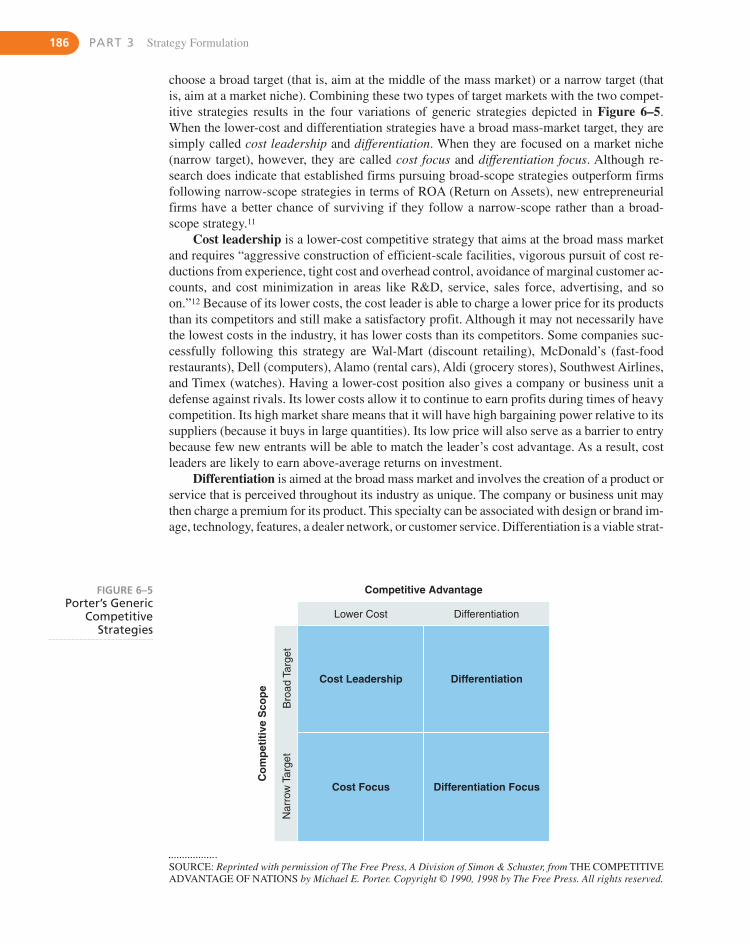

Porter’s Competitive Strategies 183

Environmental Sustainability Issue: PATAGONIA USES SUSTAINABILITY AS DIFFERENTIATION COMPETITIVE STRATEGY 187

Cooperative Strategies 195

6.5 End of Chapter Summary 199

C H A P T E R 7 Strategy Formulation: Corporate Strategy 204

7.1 Corporate Strategy 206

7.2 Directional Strategy 206

Growth Strategies 207

Strategy Highlight 7.1: TRANSACTION COST ECONOMICS ANALYZES VERTICAL GROWTH STRATEGY 210

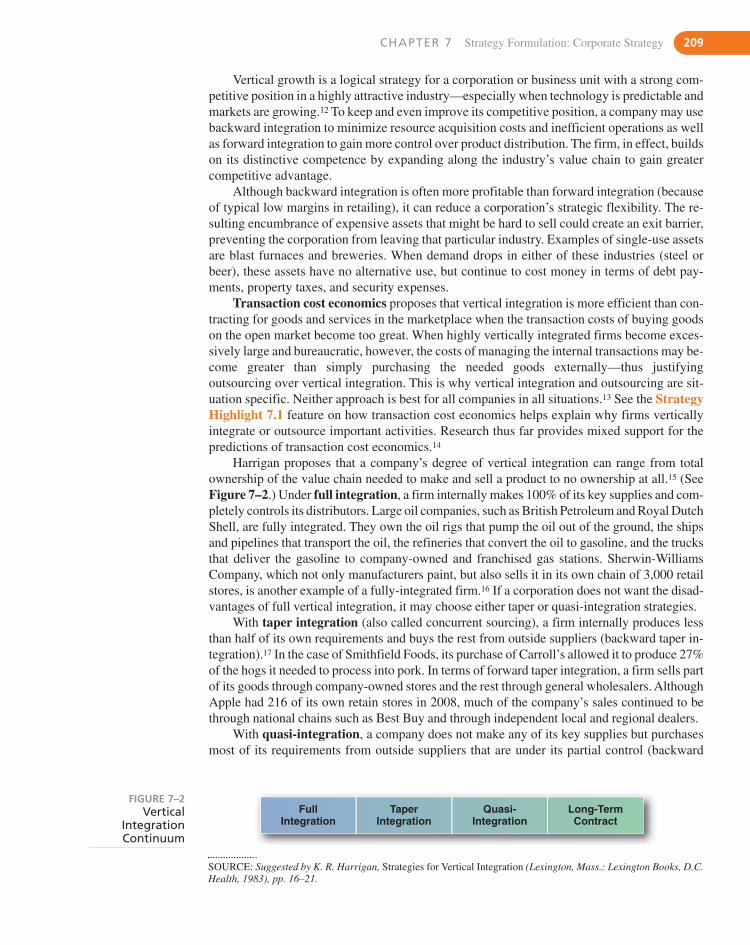

xiv CONTENTS

Global Issue: COMPANIES LOOK TO INTERNATIONAL MARKETS FOR HORIZONTAL GROWTH 212

Strategy Highlight 7.2: SCREENING CRITERIA FOR CONCENTRIC DIVERSIFICATION 215

Controversies in Directional Growth Strategies 216

Stability Strategies 217

Retrenchment Strategies 218

7.3 Portfolio Analysis 220

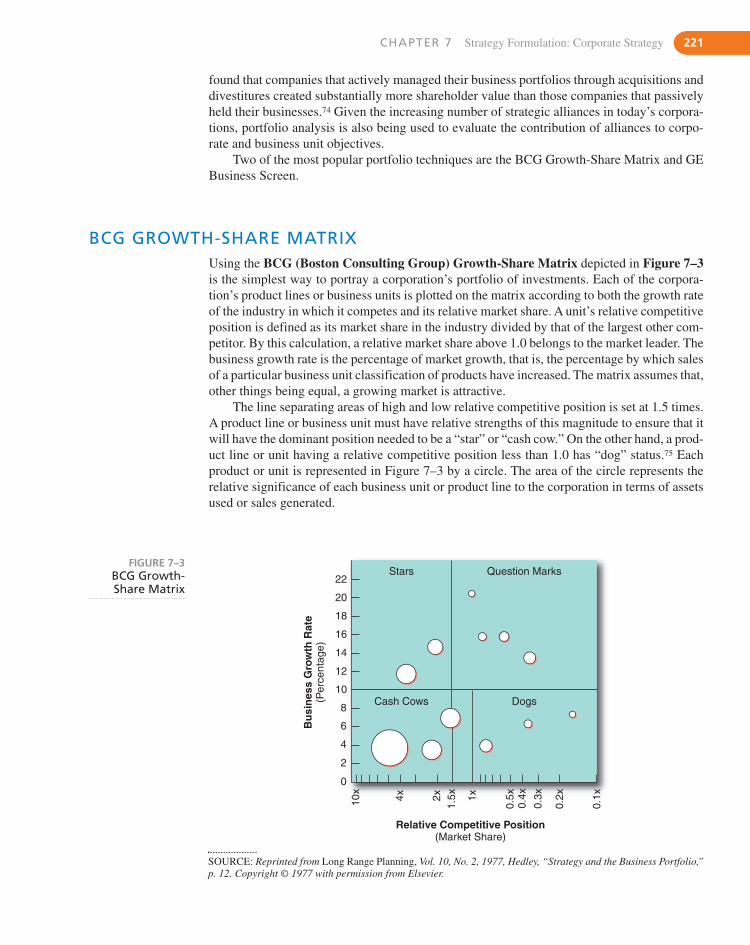

BCG Growth-Share Matrix 221

Environmental Sustainability Issue: GENERAL MOTORS AND THE ELECTRIC CAR 222

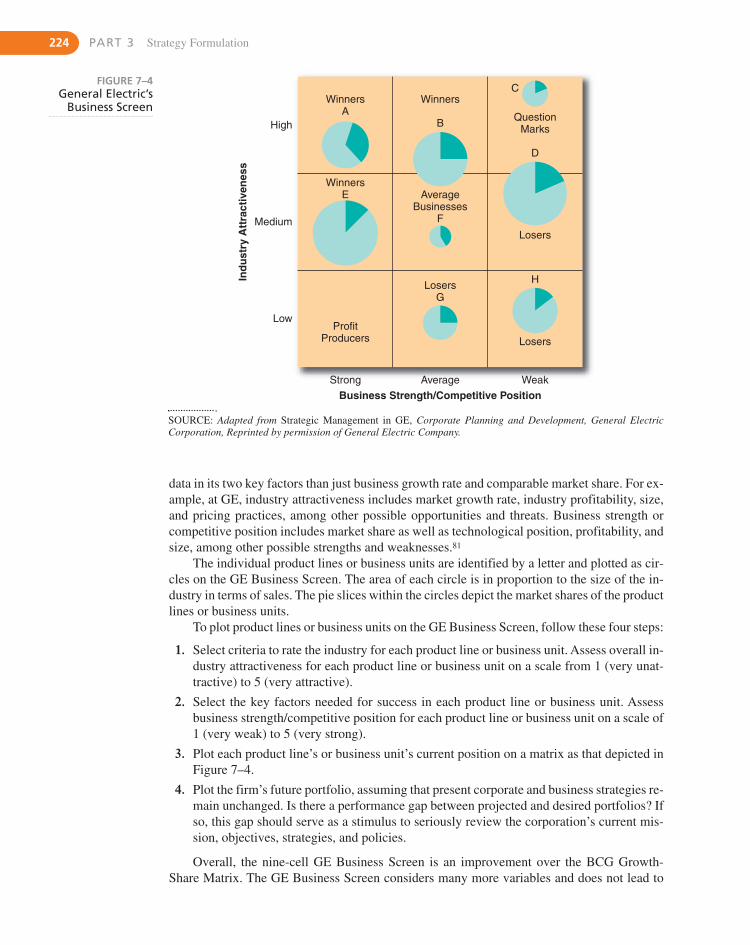

GE Business Screen 223

Advantages and Limitations of Portfolio Analysis 225

Managing a Strategic Alliance Portfolio 225

7.4 Corporate Parenting 226

Developing a Corporate Parenting Strategy 227

Horizontal Strategy and Multipoint Competition 228

7.5 End of Chapter Summary 229

C H A P T E R 8 Strategy Formulation: Functional Strategy and Strategic Choice 236

8.1 Functional Strategy 238

Marketing Strategy 238

Financial Strategy 239

Research and Development (R&D) Strategy 241

Operations Strategy 242

Global Issue: INTERNATIONAL DIFFERENCES ALTER WHIRLPOOL’S OPERATIONS STRATEGY 243

Purchasing Strategy 244

Environmental Sustainability Issue: OPERATIONS NEED FRESH WATER AND LOTS OF IT! 245

Logistics Strategy 246

Human Resource Management (HRM) Strategy 246

Information Technology Strategy 247

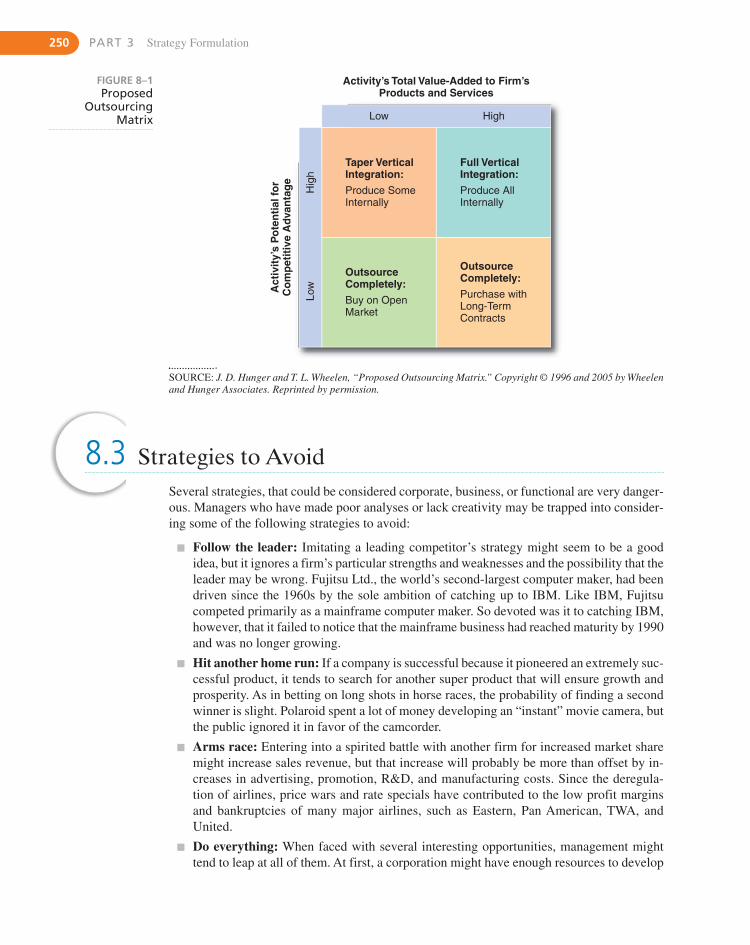

8.2 The Sourcing Decision: Location of Functions 247

8.3 Strategies to Avoid 250

8.4 Strategic Choice: Selecting the Best Strategy 251

Constructing Corporate Scenarios 251

Process of Strategic Choice 257

CONTENTS xv

8.5 Developing Policies 258

8.6 End of Chapter Summary 259

Ending Case for Part Three: KMART AND SEARS: STILL STUCK IN THE MIDDLE? 266

PART FOUR Strategy Implementation and Control 269

C H A P T E R 9 Strategy Implementation: Organizing for Action 270

9.1 Strategy Implementation 272

9.2 Who Implements Strategy? 273

9.3 What Must Be Done? 273

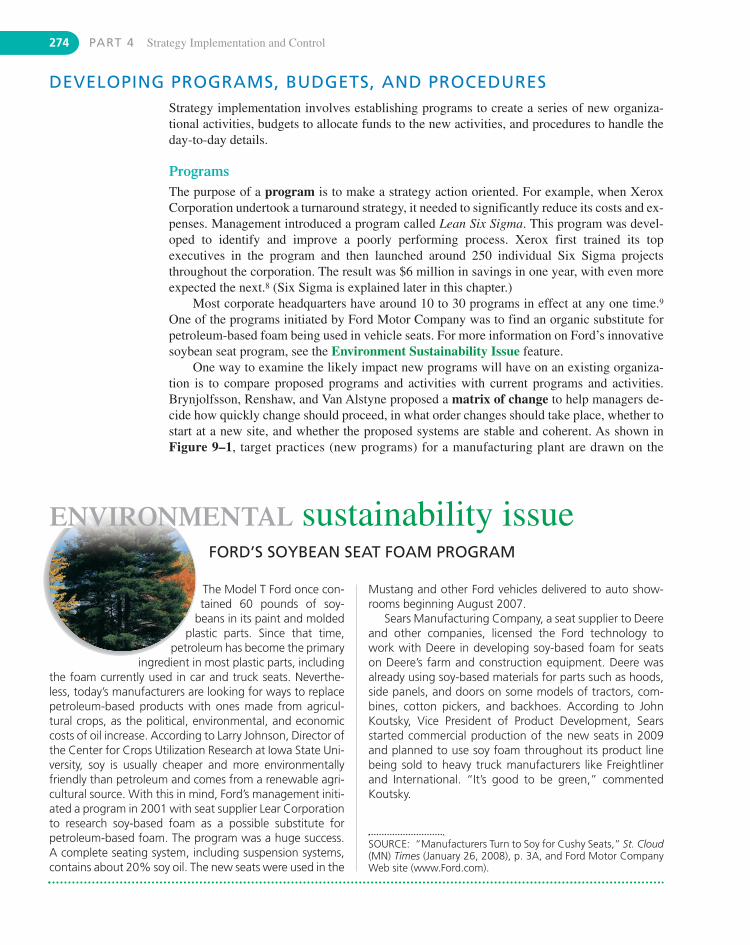

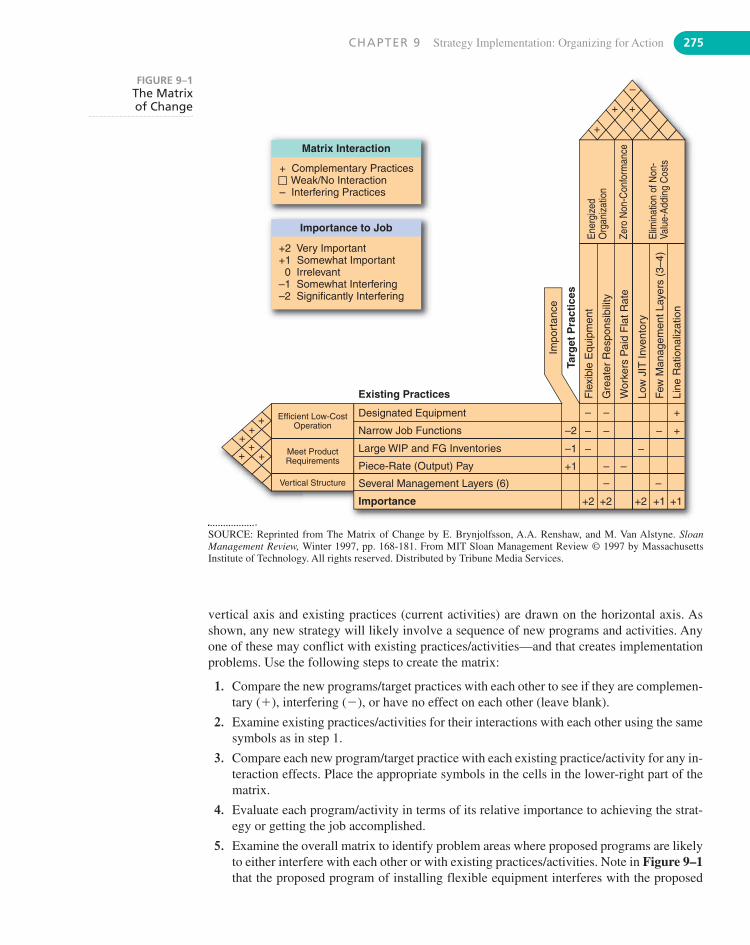

Developing Programs, Budgets, and Procedures 274

Environmental Sustainability Issue: FORD’S SOYBEAN SEAT FOAM PROGRAM 274

Strategy Highlight 9.1: THE TOP TEN EXCUSES FOR BAD SERVICE 277

Achieving Synergy 278

9.4 How Is Strategy to Be Implemented? Organizing for Action 278

Structure Follows Strategy 279

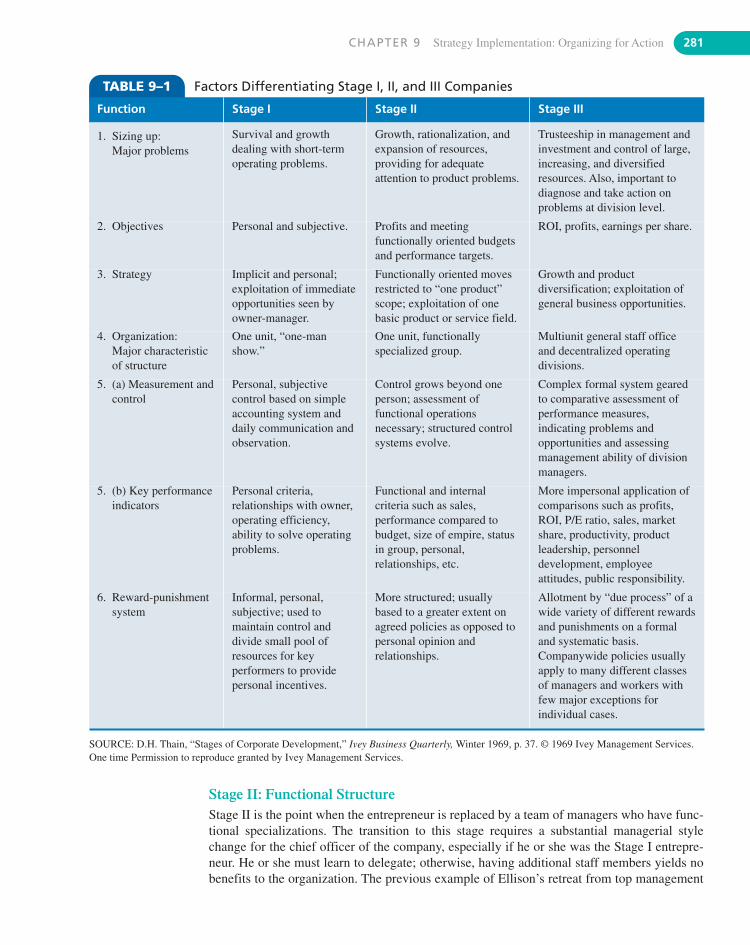

Stages of Corporate Development 280

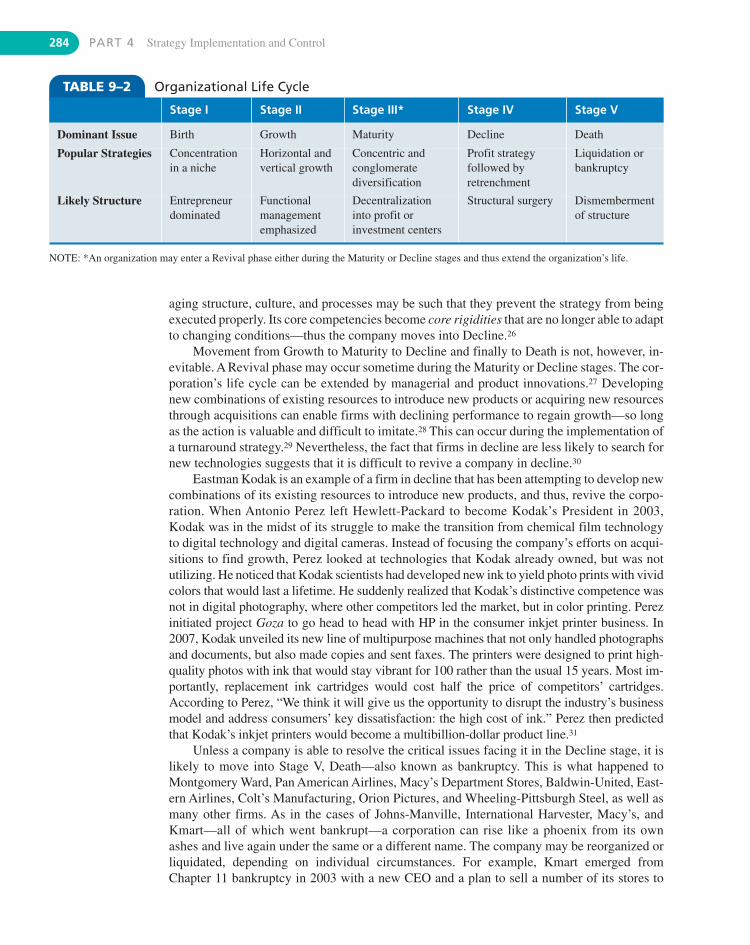

Organizational Life Cycle 283

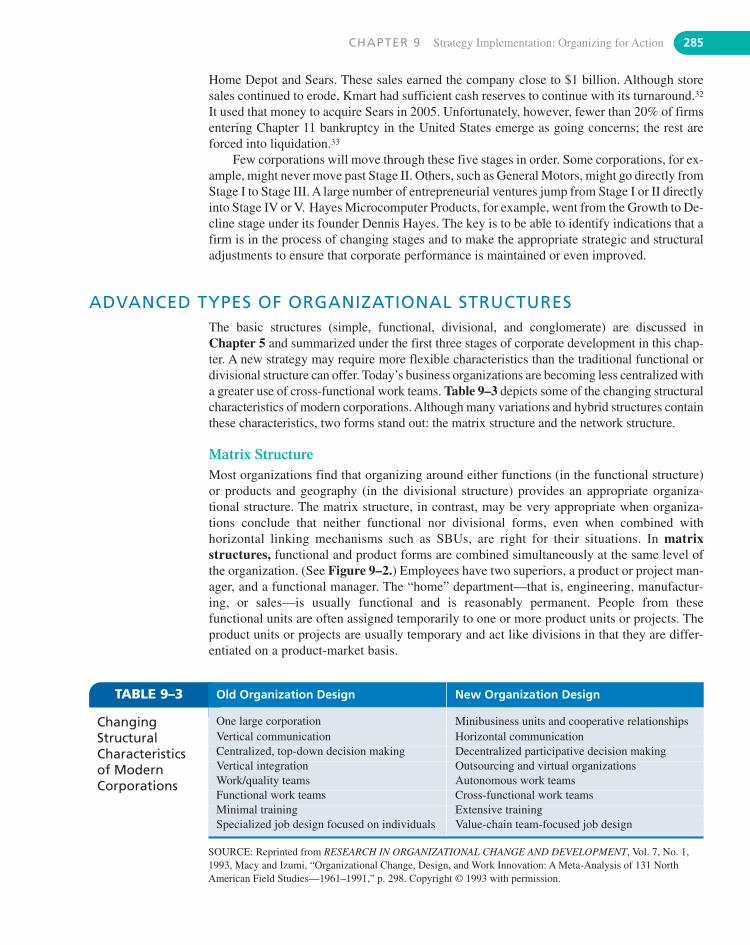

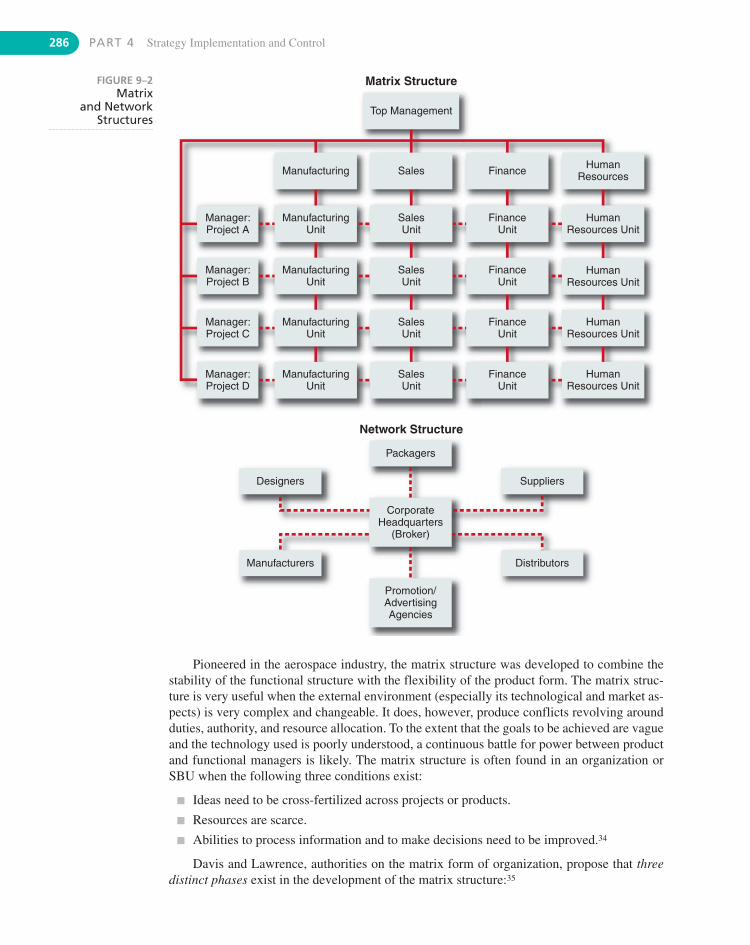

Advanced Types of Organizational Structures 285

Reengineering and Strategy Implementation 288

Six Sigma 289

Designing Jobs to Implement Strategy 290

Strategy Highlight 9.2: DESIGNING JOBS WITH THE JOB CHARACTERISTICS MODEL 291

9.5 International Issues in Strategy Implementation 291

International Strategic Alliances 292

Stages of International Development 293

Global Issue: MULTIPLE HEADQUARTERS: A SIXTH STAGE OF INTERNATIONAL DEVELOPMENT? 294

Centralization Versus Decentralization 294

9.6 End of Chapter Summary 296

C H A P T E R 1 0 Strategy Implementation: Staffing and Directing 300

10.1 Staffing 302

Staffing Follows Strategy 303

Selection and Management Development 305

Strategy Highlight 10.1: HOW HEWLETT-PACKARD IDENTIFIES POTENTIAL EXECUTIVES 306

Problems in Retrenchment 308

International Issues in Staffing 309

xvi CONTENTS

10.2 Leading 311

Managing Corporate Culture 311

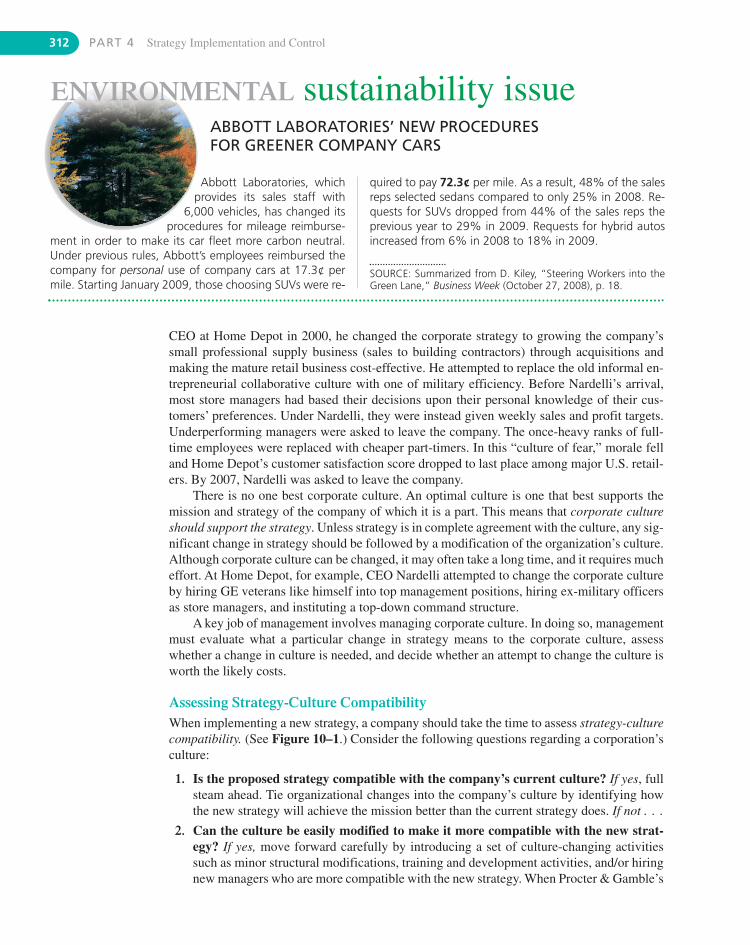

Environmental Sustainability Issue: ABBOTT LABORATORIES’ NEW PROCEDURES FOR GREENER COMPANY CARS 312

Action Planning 316

Management by Objectives 318

Total Quality Management 318

International Considerations in Leading 319

Global Issue: CULTURAL DIFFERENCES CREATE IMPLEMENTATION PROBLEMS IN MERGER 321

10.3 End of Chapter Summary 322

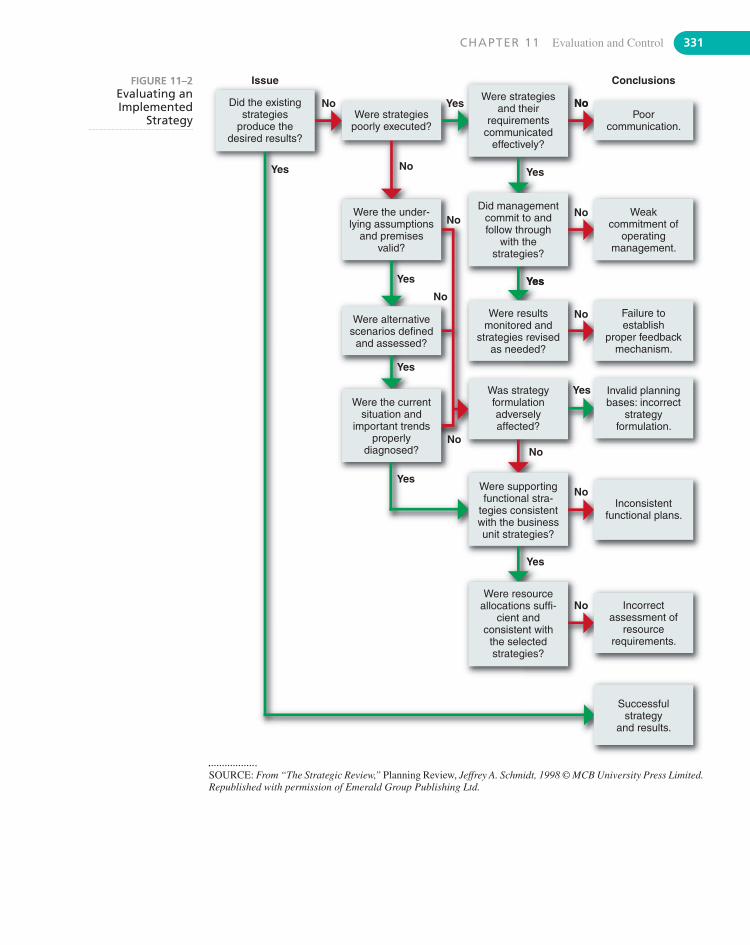

C H A P T E R 1 1 Evaluation and Control 328

11.1 Evaluation and Control in Strategic Management 330

11.2 Measuring Performance 332

Appropriate Measures 332

Types of Controls 332

Activity-Based Costing 334

Enterprise Risk Management 335

Primary Measures of Corporate Performance 335

Environmental Sustainability Issue: HOW GLOBAL WARMING COULD AFFECT CORPORATE VALUATION 340

Primary Measures of Divisional and Functional Performance 342

International Measurement Issues 344

Global Issue: COUNTERFEIT GOODS AND PIRATED SOFTWARE: A GLOBAL PROBLEM 346

11.3 Strategic Information Systems 347

Enterprise Resource Planning (ERP) 347

Radio Frequency Identification (RFID) 348

Divisional and Functional IS Support 348

11.4 Problems in Measuring Performance 348

Short-Term Orientation 349

Goal Displacement 350

11.5 Guidelines for Proper Control 351

Strategy Highlight 11.1: SOME RULES OF THUMB IN STRATEGY 351

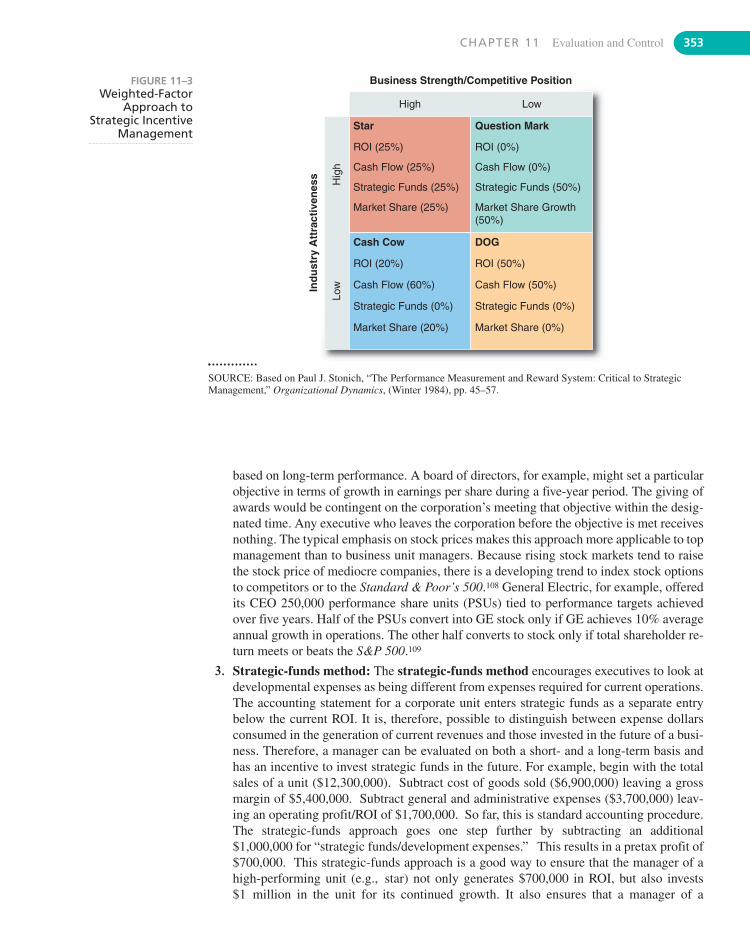

11.6 Strategic Incentive Management 352

11.7 End of Chapter Summary 354

Ending Case for Part Four: HEWLETT-PACKARD BUYS EDS 360

CONTENTS xvii

PART FIVE Introduction to Case Analysis 363

C H A P T E R 1 2 Suggestions for Case Analysis 364

12.1 The Case Method 365

12.2 Researching the Case Situation 366

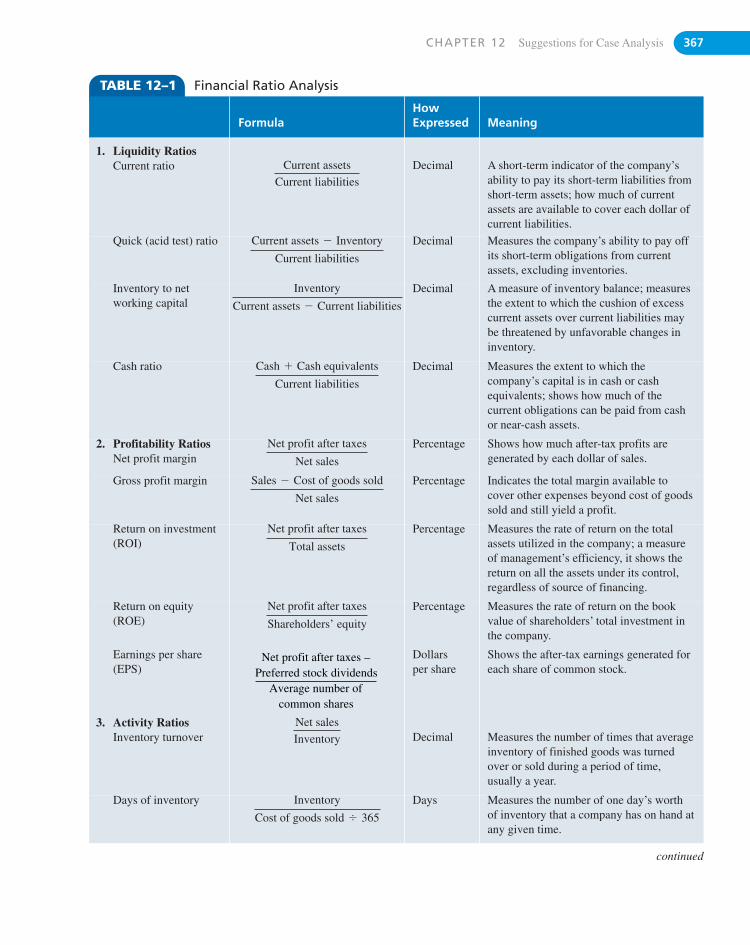

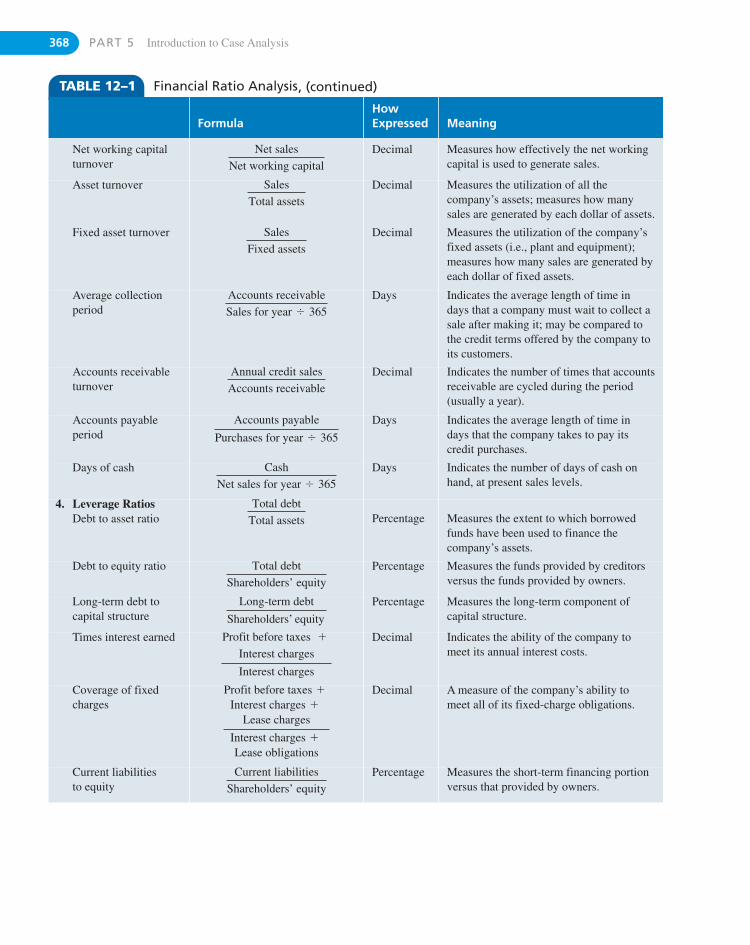

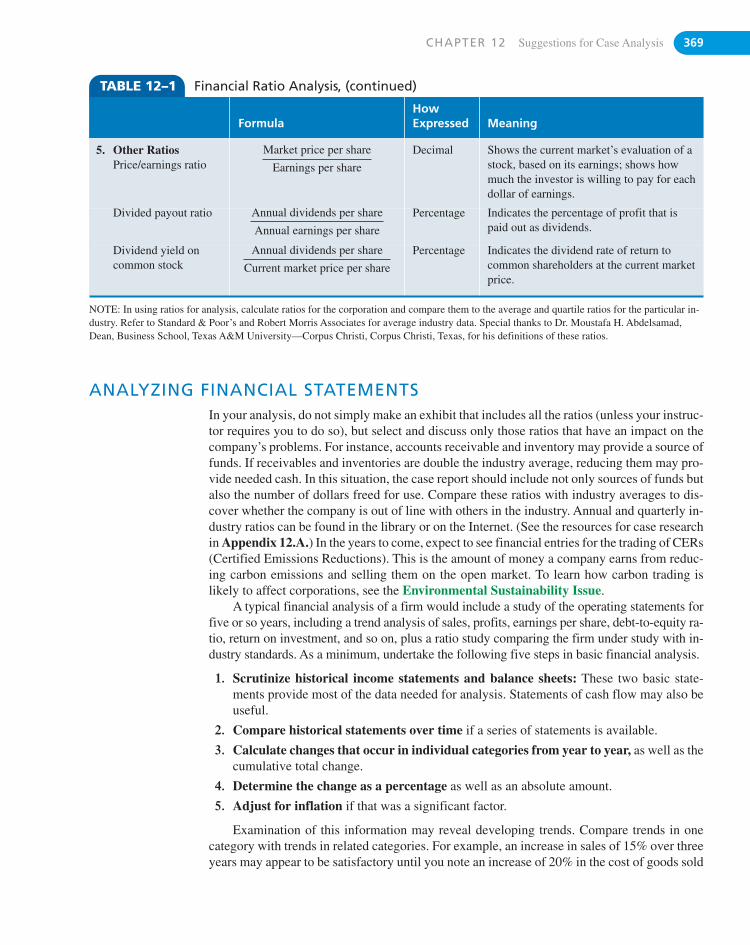

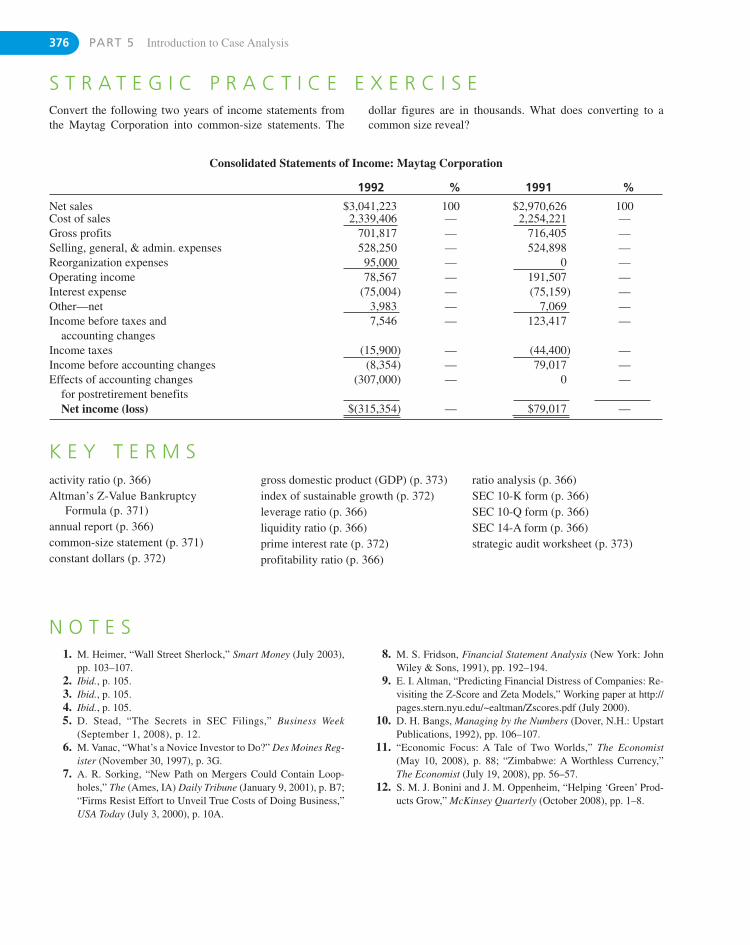

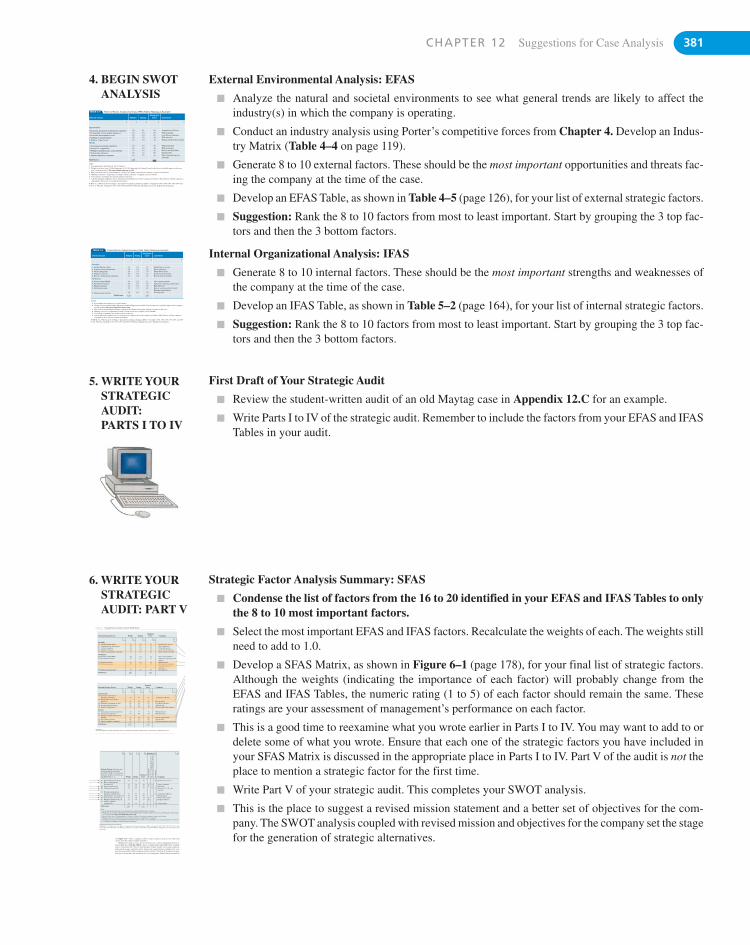

12.3 Financial Analysis: A Place to Begin 366

Analyzing Financial Statements 369

Environmental Sustainability Issue: IMPACT OF CARBON TRADING 370

Global Issue: FINANCIAL STATEMENTS OF MULTINATIONAL CORPORATIONS: NOT ALWAYS WHAT THEY SEEM 371

Common-Size Statements 371

Z-value and Index of Sustainable Growth 371

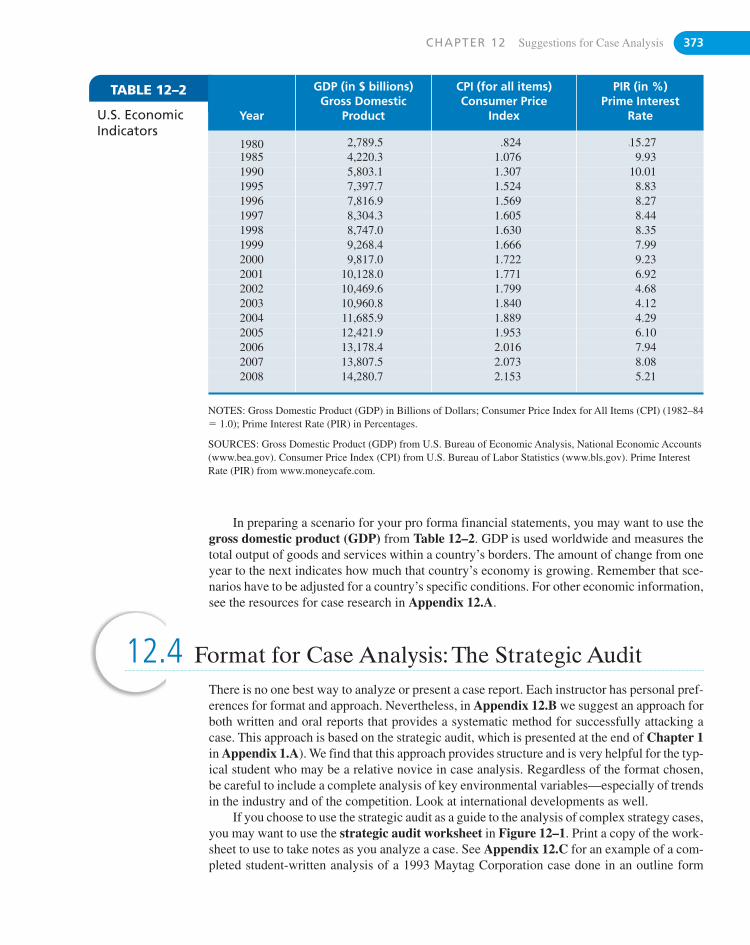

Useful Economic Measures 372

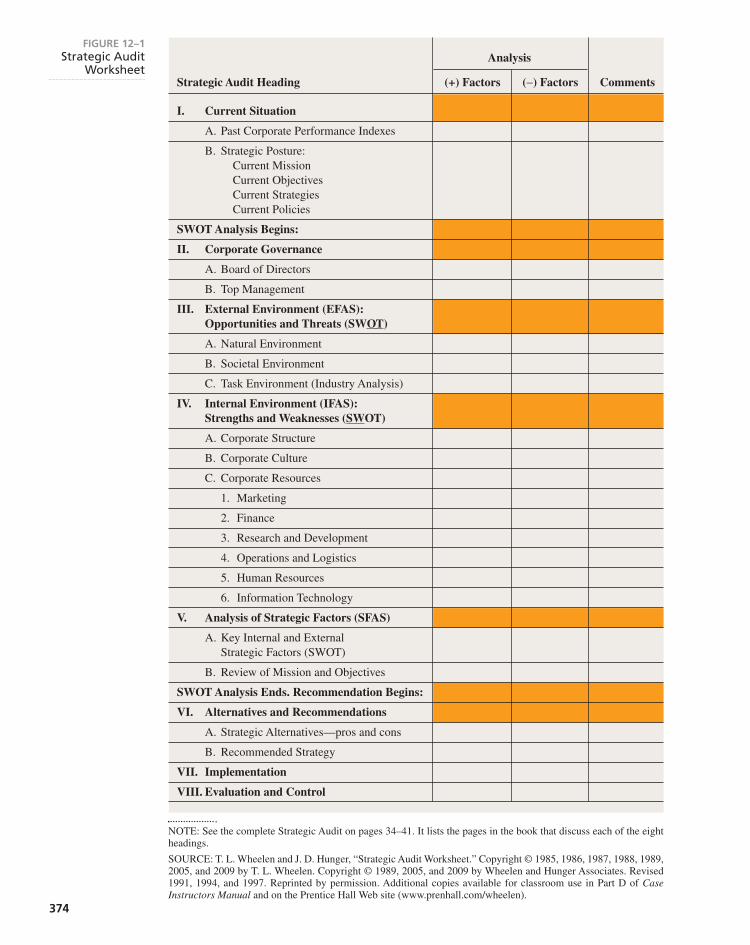

12.4 Format for Case Analysis: The Strategic Audit 373

12.5 End of Chapter Summary 375

APPENDIX 12.A Resources for Case Research 377

APPENDIX 12.B Suggested Case Analysis Methodology Using the Strategic Audit 380

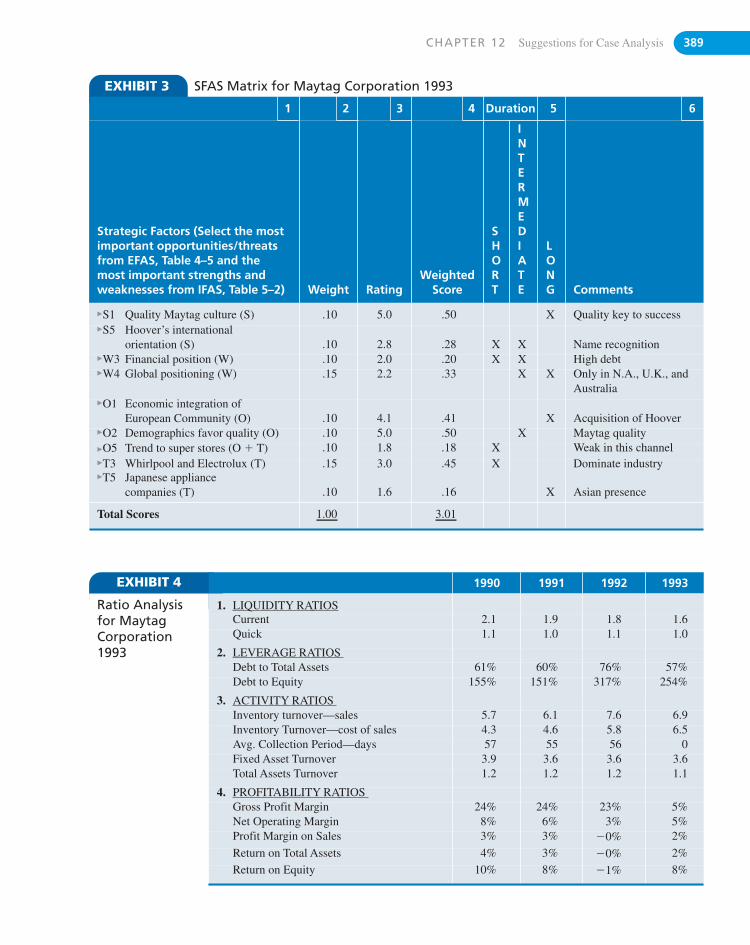

APPENDIX 12.C Example of a Student-Written Strategic Audit 383

Ending Case for Part Five: IN THE GARDEN 391

GLOSSARY G-1

NAME INDEX I-1

SUBJECT INDEX I-1

PART SIX WEB CHAPTERS Other Strategic Issues

W E B C H A P T E R A Strategic Issues in Managing Technology and Innovation

1 The Role of Management

Strategy Highlight 1: EXAMPLES OF INNOVATION EMPHASIS IN MISSION STATEMENTS

2 Environmental Scanning

External Scanning

Internal Scanning

3 Strategy Formulation

Product vs. Process R&D

Technology Sourcing

Global Issue: USE OF INTELLECTUAL PROPERTY AT HUAWEI TECHNOLOGIES

Importance of Technological Competence

Categories of Innovation

Product Portfolio

xviii CONTENTS

4 Strategy Implementation

Developing an Innovative Entrepreneurial Culture

Organizing for Innovation: Corporate Entrepreneurship

Strategy Highlight 2: HOW NOT TO DEVELOP AN INNOVATIVE ORGANIZATION

5 Evaluation and Control

Evaluation and Control Techniques

Evaluation and Control Measures

6 End of Chapter Summary

W E B C H A P T E R B Strategic Issues in Entrepreneurial Ventures and Small Businesses

1 Importance of Small Business and Entrepreneurial Ventures

Global Issue: ENTREPRENEURSHIP: SOME COUNTRIES ARE MORE SUPPORTIVE THAN OTHERS

Definition of Small-Business Firms and Entrepreneurial Ventures

The Entrepreneur as Strategist

2 Use of Strategic Planning and Strategic Management

Degree of Formality

Usefulness of the Strategic Management Model

Usefulness of the Strategic Decision-Making Process

3 Issues in Corporate Governance

Boards of Directors and Advisory Boards

Impact of the Sarbanes-Oxley Act

4 Issues in Environmental Scanning and Strategy Formulation

Sources of Innovation

Factors Affecting a New Venture’s Success

Strategy Highlight 1: SUGGESTIONS FOR LOCATING AN OPPORTUNITY AND FORMULATING A BUSINESS STRATEGY

5 Issues in Strategy Implementation

Substages of Small Business Development

Transfer of Power and Wealth in Family Businesses

6 Issues in Evaluation and Control

7 End of Chapter Summary

W E B C H A P T E R C Strategic Issues in Not-for-Profit Organizations

1 Why Not-for-Profit?

Global Issue: WHICH IS BEST FOR SOCIETY: BUSINESS OR NOT-FOR-PROFIT?

CONTENTS xix

2 Importance of Revenue Source

Sources of Not-for-Profit Revenue

Patterns of Influence on Strategic Decision Making

Usefulness of Strategic Management Concepts and Techniques

3 Impact of Constraints on Strategic Management

Impact on Strategy Formulation

Impact on Strategy Implementation

Impact on Evaluation and Control

4 Not-for-Profit Strategies

Strategic Piggybacking

Strategy Highlight 1: RESOURCES NEEDED FOR SUCCESSFUL STRATEGIC PIGGYBACKING

Mergers

Strategic Alliances

5 End of Chapter Summary

PART SEVEN Cases in Strategic Management 1-1

S E C T I O N A Corporate Governance and Social Responsibility: Executive Leadership

CASE 1 The Recalcitrant Director at Byte Products Inc.: Corporate Legality versusCorporate Responsibility 1-7(Contributors: Dan R. Dalton, Richard A. Cosier, and Cathy A. Enz)A plant location decision forces a confrontation between the board of directors and the CEO regardingan issue in social responsibility and ethics.

CASE 2 The Wallace Group 2-1(Contributor: Laurence J. Stybel)Managers question the company’s strategic direction and how it is being managed by its founderand CEO. Company growth has resulted not only in disorganization and confusion amongemployees, but in poor overall performance. How should the board deal with the company’sfounder?

S E C T I O N B Business Ethics

CASE 3 Everyone Does It 3-1(Contributors: Steven M. Cox and Shawana P. Johnson)When Jim Willis, Marketing VP, learns that the launch date for the company’s new satellite willbe late by at least a year, he is told by the company’s president to continue using the earlierpublished date for the launch. When Jim protests that the use of an incorrect date to marketcontracts is unethical, he is told that spacecraft are never launched on time and that it is commonindustry practice to list unrealistic launch dates. If a realistic date was used, no one would contractwith the company.

xx CONTENTS

CASE 4 The Audit 4-1(Contributors: John A. Kilpatrick, Gamewell D. Gantt, and George A. Johnson)A questionable accounting practice by the company being audited puts a new CPA in a difficultposition. Although the practice is clearly wrong, she is being pressured by her manager to ignore itbecause it is common in the industry.

S E C T I O N C International Issues in Strategic Management

CASE 5 Starbucks’ Coffee Company: The Indian Dilemma 5-1(Contributors: Ruchi Mankad and Joel Sarosh Thadamalla)Starbucks is the world’s largest coffee retailer with over 11,000 stores in 36 countries and over10,000 employees. The case focuses on India as a potential market for the coffee retailer, presentinginformation on India’s societal environment and beverage industry. Profiles are provided for variousexisting coffee shop chains in India. The key issue in the case revolves around the question: Arecircumstances right for Starbucks to enter India?

CASE 6 Guajilote Cooperativo Forestal: Honduras 6-1(Contributors: Nathan Nebbe and J. David Hunger)This forestry cooperative has the right to harvest, transport, and sell fallen mahogany trees in La Muralla National Park of Honduras. Although the cooperative has been successful thus far, it isfacing some serious issues: low prices for its product, illegal logging, deforestation by poor farmers,and possible world trade restrictions on the sale of mahogany.

S E C T I O N D General Issues in Strategic Management

I N D U S T RY O N E : Information Technology CASE 7 Apple Inc.: Performance in a Zero-Sum World Economy 7-1

(Contributors: Kathryn E. Wheelen, Thomas L. Wheelen II, Richard D. Wheelen, Moustafa H.Abdelsamad, Bernard A. Morin, Lawrence C. Pettit, David B. Croll, and Thomas L. Wheelen)Apple, the first company to mass-market a personal computer, had become a minor player in anindustry dominated by Microsoft. After being expelled from the company in 1985, founder Steve Jobsreturned as CEO in 1997 to reenergize the firm. The introduction of the iPod in 2001, followed by theiPad, catapulted Apple back into the spotlight. However, in 2011 Jobs was forced to take his thirdmedical leave, leading to questions regarding his ability to lead Apple. How can Apple continue itssuccess? How dependent is the company on Steve Jobs?

CASE 8 iRobot: Finding the Right Market Mix? 8-1(Contributor: Alan N. Hoffman)Founded in 1990, iRobot was among the first companies to introduce robotic technology into theconsumer market. Employing over 500 robotic professionals, the firm planned to lead the roboticsindustry. Unfortunately, its largest revenue source, home care robots, are a luxury good and vulnerableto recessions. Many of iRobot’s patents are due to expire by 2019. The firm is highly dependent uponsuppliers to make its consumer products and the U.S. government for military sales. What is the beststrategy for its future success?

CASE 9 Dell Inc.: Changing the Business Model (Mini Case) 9-1(Contributor: J. David Hunger)Dell, once the largest PC vendor in the world, is now battling with Acer for second place in the global PCmarket. Its chief advantages—direct marketing and power over suppliers—no longer provided acompetitive advantage. The industry’s focus has shifted from desktop PCs to mobile computing, software,and technology services, areas of relative weakness for Dell. Is it time for Dell to change its strategy?

exclusive

newexclusive

newexclusive

newexclusive

CONTENTS xxi

CASE 10 Rosetta Stone Inc.: Changing the Way People Learn Languages 10-1(Contributors: Christine B. Buenafe and Joyce P. Vincelette)Rosetta Stone’s mission was to change the way people learn languages. The company blendedlanguage learning with technology at a time when globalization connected more and more individualsand institutions to each other. How should the company move forward? Would it be appropriate forRosetta Stone to offer products like audio books or services in order to increase market share? Whichinternational markets could provide the company with a successful future?

CASE 11 Logitech (Mini Case) 11-1(Contributor: Alan N. Hoffman)Logitech, the world’s leading provider of computer peripherals, was on the forefront of mouse,keyboard, and video conferencing technology. By 2010, however, Logitech’s products were threatenedby new technologies, such as touch pads, that could replace both the mouse and keyboard. As theperipherals market begins to disintegrate, Logitech is considering a change in strategy.

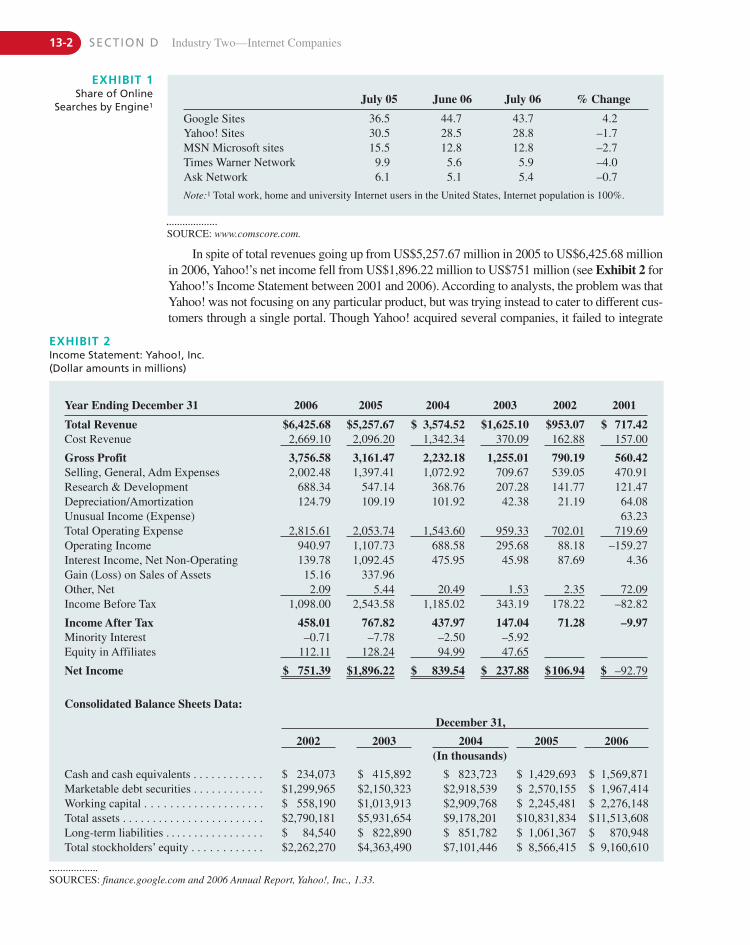

I N D U S T RY T W O : INTERNET COMPANIES

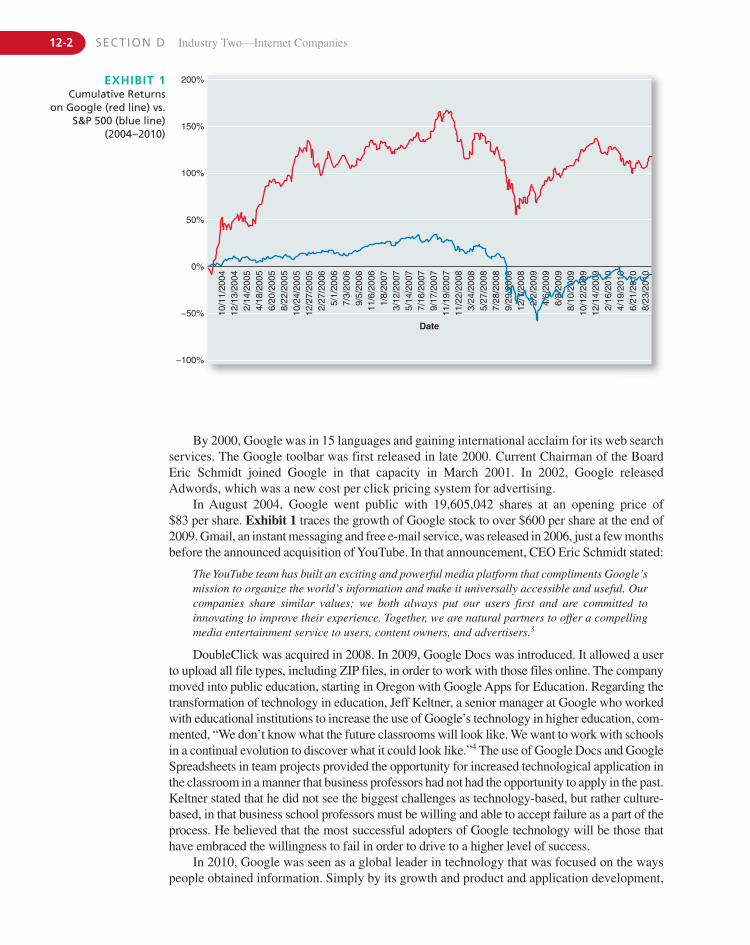

CASE 12 Google Inc. (2010): The Future of the Internet Search Engine 12-1(Contributor: Patricia A. Ryan)Google, an online company that provides a reliable Internet search engine, was founded in 1998 and soonreplaced Yahoo as the market leader in Internet search engines. By 2010, Google was one of the strongestbrands in the world. Nevertheless, its growth by acquisition strategy was showing signs of weakness. Its2006 acquisition of YouTube had thus far not generated significant revenue growth. Groupon, a shoppingWeb site, rebuffed Google’s acquisition attempt in 2010. Is it time for a strategic change?

CASE 13 Reorganizing Yahoo! 13-1(Contributors: P. Indu and Vivek Gupta)Yahoo! created the first successful Internet search engine, but by 2004 it was losing its identity. Was ita search engine, a portal, or a media company? On December 5, 2006, Yahoo’s CEO announced areorganization of the company into three groups. It was hoped that a new mission statement and a newstructure would make Yahoo leaner and more responsive to customers. Would this be enough to turnaround the company?

I N D U S T RY T H R E E : ENTERTAINMENT AND LEISURE

CASE 14 TiVo Inc.: TiVo vs. Cable and Satellite DVR: Can TiVo survive? 14-1(Contributors: Alan N. Hoffman, Randy Halim, Rangki Son, and Suzanne Wong)TiVo was founded to create a device capable of recording digitized video on a computer hard drive fortelevision viewing. Even though revenues had jumped from $96 million in 2003 to $259 million in2007, the company had never earned a profit. Despite many alliances, TiVo faced increasingcompetition from generic DVRs offered by satellite and cable companies. How long can the companycontinue to sell TiVo DVRs when the competition sells generic DVRs at a lower price or gives themaway for free?

CASE 15 Marvel Entertainment Inc. 15-1(Contributors: Ellie A. Fogarty and Joyce P. Vincelette)Marvel Entertainment was known for its comic book characters Captain America, Spider Man, the Fantastic Four, the Incredible Hulk, the Avengers, and the X-Men. With its 2008 self-producedfilms, Iron Man and The Incredible Hulk, Marvel had expanded out of comic books to become aleader in the entertainment industry. The company was no longer competing against other comicbook publishers like DC Comics, but was now competing against entertainment giants like WaltDisney and NBC Universal. What should Marvel’s management do to ensure the company’s futuresuccess?

newexclusive

newexclusive

newexclusive

exclusive

xxii CONTENTS

CASE 16 Carnival Corporation and plc (2010) 16-1(Contributors: Michael J. Keeffe, John K. Ross III, Sherry K. Ross, Bill J. Middlebrook, and Thomas L. Wheelen)With its “fun ship,” Carnival Cruises changed the way people think of ocean cruises. The cruisebecame more important than the destination. Through acquisition, Carnival expanded its product lineto encompass an entire range of industry offerings. How can Carnival continue to grow in the industryit now dominates?

I N D U S T RY F O U R : TRANSPORTATION

CASE 17 Chrysler in Trouble 17-1(Contributors: Barnali Chakraborty and Vivek Gupta)On April 30, 2009, Chrysler Motors, the third-largest auto manufacturer in the United States, filedfor bankruptcy protection along with its 24 wholly owned U.S. subsidiaries. As a condition of theU.S. federal government’s loan of more than $8 billion, Fiat was given 20% of the new ChryslerCorporation with the option of increasing its stake to 51% by 2016 after the new company hadrepaid the federal government’s loan. What does Chrysler need to do to ensure the success of itspartnership with Fiat?

CASE 18 Tesla Motors Inc. (Mini Case) 18-1(Contributor: J. David Hunger)Tesla Motors was founded in 2004 to produce electric automobiles. Its first car, the Tesla Roadster,sold for $101,000. It could accelerate from zero to 60 mph in 3.9 seconds and cruise for 236 miles on asingle charge. In contrast to existing automakers, Tesla sold and serviced its cars through the Internetand its own Tesla stores. With the goal of building a full line of electric vehicles, Tesla Motors facedincreasing competition from established automakers. How could Tesla Motors succeed in an industrydominated by giant global competitors?

CASE 19 Harley-Davidson Inc. 2008: Thriving through a Recession 19-1(Contributors: Patricia A. Ryan and Thomas Wheelen)Harley-Davidson 2008: Thriving Through Recession is a modern success story of a motorcyclecompany that turned itself around by emphasizing quality manufacturing and image marketing. Afterconsistently growing through the 1990s, sales were showing signs of slowing as the baby boomerscontinued to age. Safety was also becoming an issue. For the first time in recent history, sales andprofits declined in 2007 from 2006. Analysts wondered how the company would be affected in arecession. How does Harley-Davidson continue to grow at its past rate?

CASE 20 JetBlue Airways: Growing Pains? 20-1(Contributors: Shirisha Regani and S. S. George)JetBlue Airways had been founded as a “value player” in the niche between full service airlines andlow-cost carriers. Competition had recently intensified and several airlines were taking advantage ofbankruptcy protection to recapture market share through price cuts. JetBlue’s operating costs wererising as a result of increasing fuel costs, aircraft maintenance expenses, and service costs. HasJetBlue been growing too fast and was growth no longer sustainable?

CASE 21 TomTom: New Competition Everywhere! 21-1(Contributor: Alan N. Hoffman)TomTom, an Amsterdam-based company that provided navigation services and devices, led thenavigation systems market in Europe and was second in popularity in the United States. However, thecompany was facing increasing competition from other platforms using GPS technology like cellphones and Smartphones with a built-in navigation function. As its primary markets in the UnitedStates and Europe mature, how can the company ensure its future growth and success?

newexclusive

exclusive

new

newexclusive

CONTENTS xxiii

newexclusive

I N D U S T RY F I V E : CLOTHING

CASE 22 Volcom Inc.: Riding the Wave 22-1(Contributors: Christine B. Buenafe and Joyce P. Vincelette)Volcom was formed south of Los Angeles in 1991 as a clothing company rooted in the action sports ofskateboarding, surfing, and snowboarding. By 2008, Volcom-branded products were sold throughoutthe United States and in over 40 countries. It did not own any manufacturing facilities, but insteadworked with foreign contract manufacturers. As a primary competitor in the boardsports community,Volcom was committed to maintaining its brand, position, and lifestyle and needed to reassess itsstrategy.

CASE 23 TOMS Shoes (Mini Case) 23-1(Contributor: J. David Hunger)Founded in 2006 by Blake Mycoskie, TOMS Shoes is an American footwear company based in SantaMonica, California. Although TOMS Shoes is a for-profit business, its mission is more like that of anot-for-profit organization. The firm’s reason for existence is to donate to children in need one newpair of shoes for every pair of shoes sold. By 2010, the company had sold over one million pairs ofshoes. How should the company plan its future growth?

I N D U S T RY S I X : SPECIALTY RETAILING

CASE 24 Best Buy Co. Inc.: Sustainable Customer Centricity Model? 24-1(Contributor: Alan N. Hoffman)Best Buy, the largest consumer electronics retailer in the United States, operates 4,000 stores in NorthAmerica, China, and Turkey. Best Buy distinguishes itself from competitors by deploying adifferentiation strategy based on superior service rather than low price. The recent recession hasstressed its finances and the quality of its customer service. How can Best Buy continue to haveinnovative products, top-notch employees, and superior customer service while facing increasedcompetition, operational costs, and financial stress?

CASE 25 The Future of Gap Inc. 25-1(Contributor: Mridu Verma)Gap Inc. offered clothing, accessories, and personal care products under the Gap, Banana Republic,and Old Navy brands. After a new CEO introduced a turnaround strategy, sales increased briefly, thenfell. Tired of declining sales, the board of directors hired Goldman Sachs to explore strategies toimprove, ranging from the sale of its stores to spinning off a single division.

CASE 26 Rocky Mountain Chocolate Factory Inc. (2008) 26-1(Contributors: Annie Phan and Joyce P. Vincelette)Rocky Mountain Chocolate Factory had five company-owned and 329 franchised stores in 38 states,Canada, and the United Arab Emirates. Even though revenues and net income had increased from2005 through 2008, they had been increasing at a decreasing rate. Candy purchased from the factoryby the stores had actually dropped 9% in 2008 from 2007. Was the bloom off the rose at RockyMountain Chocolate?

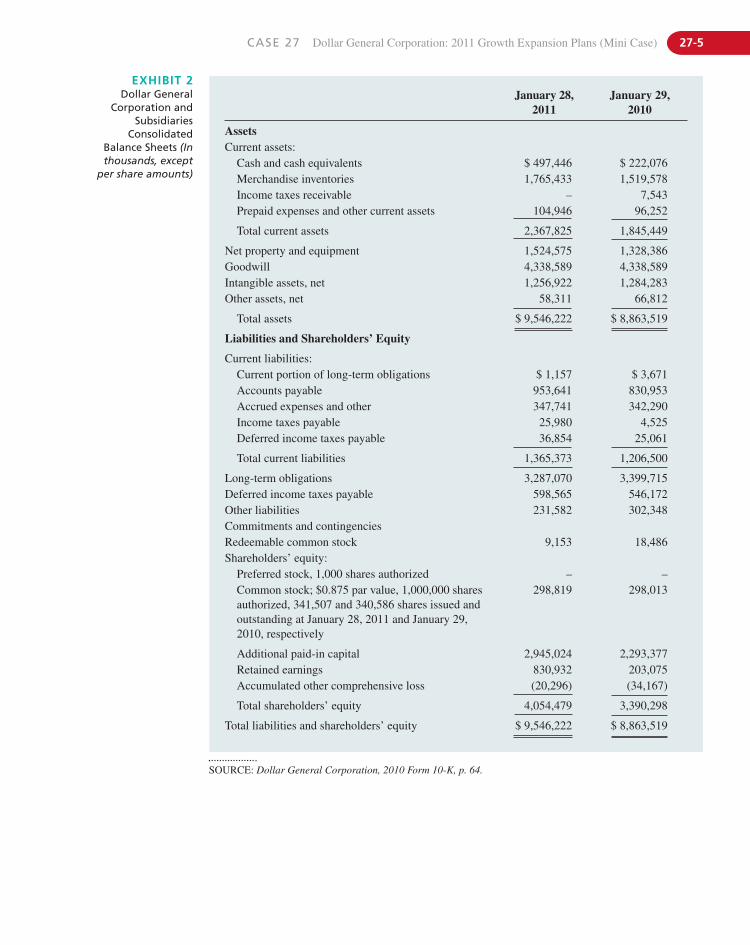

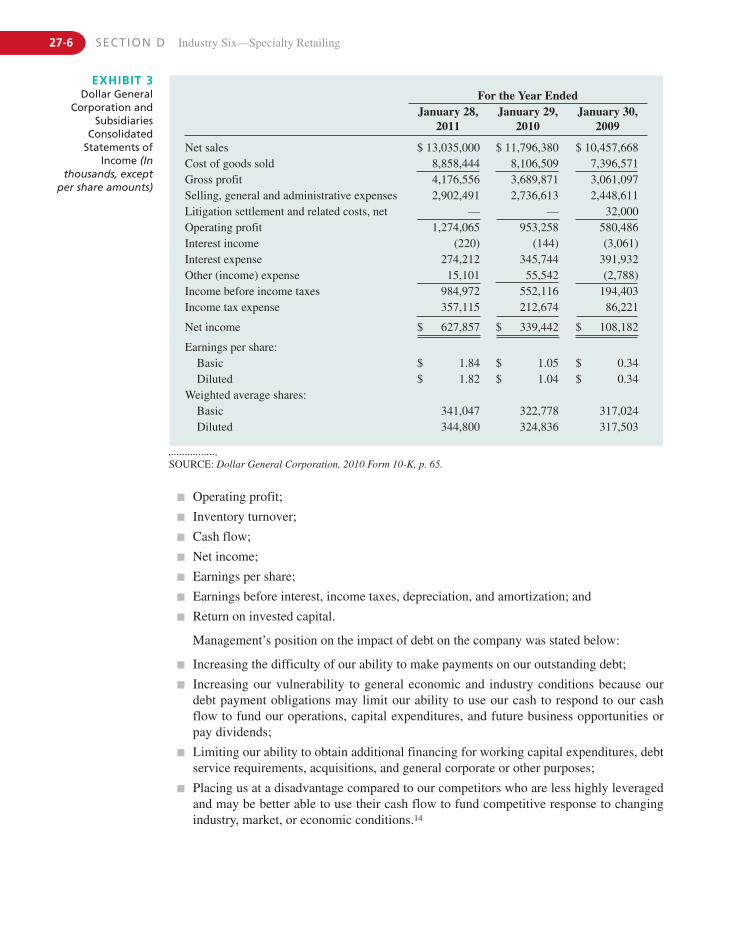

CASE 27 Dollar General Corporation (Mini Case) 27-1(Contributor: Kathryn E. Wheelen)With annual revenues of $12.7 billion and 9,200 stores in 35 states, Dollar General is the largest of thediscount “dollar stores” in the United States. Although far smaller than its “big brothers” Wal-Martand Target, Dollar General has done very well during the recent economic recession. In 2011, it plansto open 625 new stores in three new states. Given that the company has substantial long-term debt, isthis the right time to expand the company’s operations?

newexclusive

newexclusive

exclusive

newexclusive

xxiv CONTENTS

newexclusive

I N D U S T RY S E V E N : MANUFACTURING

CASE 28 Inner-City Paint Corporation (Revised) 28-1(Contributors: Donald F. Kuratko and Norman J. Gierlasinski)Inner-City Paint makes paint for sale to contractors in the Chicago area. However, the founder’s lackof management knowledge is creating difficulties for the firm, and the company is in financialdifficulty. Unless something is done soon, it may go out of business.

CASE 29 The Carey Plant 29-1(Contributors: Thomas L. Wheelen and J. David Hunger)The Carey Plant was a profitable manufacturer of quality machine parts until it was acquired by theGardner Company. Since its acquisition, the plant has been plagued by labor problems, increasingcosts, leveling sales, and decreasing profits. Gardner Company’s top management is attempting toimprove the plant’s performance and better integrate its activities with those of the corporation byselecting a new person to manage the plant.

I N D U S T RY E I G H T: FOOD AND BEVERAGE

CASE 30 The Boston Beer Company: Brewers of Samuel Adams Boston Lager (Mini Case) 30-1(Contributor: Alan N. Hoffman)The Boston Beer Company was founded in 1984 by Jim Koch, viewed as the pioneer of the Americancraft beer revolution. Brewing over 1 million barrels of 25 different styles of beer, Boston Beer is thesixth-largest brewer in the United States. Even though overall domestic beer sales declined 1.2% in2010, sales of craft beer have increased 20% since 2002, with Boston Beer’s increasing 22% from2007 to 2009. How can the company continue its rapid growth in a mature industry?

CASE 31 Wal-Mart and Vlasic Pickles 31-1(Contributor: Karen A. Berger)A manager of Vlasic Foods International closed a deal with Wal-Mart that resulted in selling morepickles than Vlasic had ever sold to any one account. The expected profit of one to two cents per jarwas not sustainable, however, due to unplanned expenses. Vlasic’s net income plummeted and thecompany faced bankruptcy. Given that Wal-Mart was Vlasic’s largest customer, what action shouldmanagement take?

CASE 32 Panera Bread Company (2010): Still Rising Fortunes? 32-1(Contributors: Joyce Vincelette and Ellie A. Fogarty)Panera Bread is a successful bakery-café known for its quality soups and sandwiches. Even thoughPanera’s revenues and net earnings have been rising rapidly, new unit expansion throughout NorthAmerica has fueled this growth. Will revenue growth stop once expansion slows? The retirement ofCEO Ronald Shaich, the master baker who created the “starter” for the company’s phenomenalgrowth, is an opportunity to rethink Panera’s growth strategy.

CASE 33 Whole Foods Market (2010): How to Grow in an Increasingly Competitive Market?(Mini Case) 33-1(Contributors: Patricia Harasta and Alan N. Hoffman)Whole Foods Market is the world’s leading retailer of natural and organic foods. The companydifferentiates itself from competitors by focusing on innovation, quality, and service excellence,allowing it to charge premium prices. Although the company dominates the natural/organic foodscategory in North America, it is facing increasing competition from larger food retailers, such as Wal-Mart, who are adding natural/organic foods to their offerings.

exclusive

newexclusive

newexclusive

newexclusive

CONTENTS xxv

CASE 34 Burger King (Mini Case) 34-1(Contributor: J. David Hunger)Founded in Florida in 1953, Burger King has always trailed behind McDonald’s as the second-largestfast-food hamburger chain in the world. Although its total revenues dropped only slightly from 2009,its 2010 profits dropped significantly, due to high expenses. Burger King’s purchase by an investmentgroup in 2010 was an opportunity to rethink the firm’s strategy.

CASE 35 Church & Dwight: Time to Rethink the Portfolio? 35-1(Contributor: Roy A. Cook)Church & Dwight, the maker of ARM & HAMMER Baking Soda, has used brand extension tosuccessfully market multiple consumer products based on sodium bicarbonate. Searching for a newgrowth strategy, the firm turned to acquisitions. Can management successfully achieve a balancing actbased on finding growth through expanded uses of sodium bicarbonate while assimilating a divergentgroup of consumer products into an expanding international footprint?

S E C T I O N E Web Mini CasesAdditional Mini Cases Available on the Companion Web Site at www.pearsonhighered.com/wheelen.

W E B C A S E 1 Eli Lily & Company(Contributor: Maryanne M. Rouse)A leading pharmaceutical company, Eli Lilly produces a wide variety of ethical drugs and animalhealth products. Despite an array of new products, the company’s profits declined after the firm lostpatent protection for Prozac. In addition, the FDA found quality problems at several of the company’smanufacturing sites, resulting in a delay of new product approvals. How should Lily position itself ina very complex industry?

W E B C A S E 2 Tech Data Corporation(Contributor: Maryanne M. Rouse)Tech Data, a distributor of information technology and logistics management, has rapidly grown through acquisition to become the second-largest global IT distributor. Sales and profitshave been declining, however, since 2001. As computers become more like a commodity, theincreasing emphasis on direct distribution by manufacturers threaten wholesale distributors likeTech Data.

W E B C A S E 3 Stryker Corporation(Contributor: Maryanne M. Rouse)Stryker is a leading maker of specialty medical and surgical products, a market expected to showstrong sales growth. Stryker markets its products directly to hospitals and physicians in the UnitedStates and 100 other countries. Given the decline in the number of hospitals due to consolidationand cost containment efforts by government programs and health care insurers, the industryexpects continued downward pressure on prices. How can Stryker effectively deal with thesedevelopments?

W E B C A S E 4 Sykes Enterprises(Contributor: Maryanne M. Rouse)Sykes provides outsourced customer relationship management services worldwide in a highlycompetitive, fragmented industry. Like its customers, Sykes has recently been closing its callcenters in America and moving to Asia in order to reduce costs. Small towns felt betrayed by thefirm’s decision to leave—especially after providing financial incentives to attract the firm.Nevertheless, declining revenue and net income has caused the company’s stock to drop to an all-time low.

xxvi CONTENTS

newexclusive

new

W E B C A S E 5 Pfizer Inc.(Contributor: Maryanne M. Rouse)With its acquisition in 2000 of rival pharmaceutical firm Warner-Lambert for its Lipitor prescriptiondrug, Pfizer has become the world’s largest ethical pharmaceutical company in terms of sales. Alreadythe leading company in the United States, Pfizer’s purchase of Pharmacia in 2002 moved Pfizer fromfourth to first place in Europe. Will large size hurt or help the company’s future growth andprofitability in an industry facing increasing scrutiny?

W E B C A S E 6 Williams-Sonoma(Contributor: Maryanne M. Rouse)Williams-Sonoma is a specialty retailer of home products. Following a related diversificationgrowth strategy, the company operates 415 Williams-Sonoma, Pottery Barn, and Hold Everythingretail stores throughout North America. Its direct sales segment includes six retail catalogues andthree e-commerce sites. The company must deal with increasing competition in this fragmentedindustry characterized by low entry barriers.

W E B C A S E 7 Tyson Foods Inc.(Contributor: Maryanne M. Rouse)Tyson produces and distributes beef, chicken, and pork products in the United States. It acquired IBP, amajor competitor, but has been the subject of lawsuits by its employees and the EPA. How shouldmanagement deal with its poor public relations and position the company to gain and sustain competitiveadvantage in an industry characterized by increasing consolidation and intense competition?

W E B C A S E 8 Southwest Airlines Company(Contributor: Maryanne M. Rouse)The fourth-largest U.S. airline in terms of passengers carried and second-largest in scheduled domesticdepartures, Southwest was the only domestic airline to remain profitable in 2001. Emphasizing high-frequency, short-haul, point-to-point, and low-fare service, the airline has the lowest cost per availableseat mile flown of any U.S. major passenger carrier. Can Southwest continue to be successful ascompetitors increasingly imitate its competitive strategy?

W E B C A S E 9 Outback Steakhouse Inc.(Contributor: Maryanne M. Rouse)With 1,185 restaurants in 50 states and 21 foreign countries, Outback (OSI) is one of the largest casualdining restaurant companies in the world. In addition to Outback Steakhouse, the company iscomposed of Carrabba’s Italian Grill, Fleming’s Prime Steakhouse & Wine Bar, Bonefish Grill, Roy’s,Lee Roy Selmon’s, Cheeseburger in Paradise, and Paul Lee’s Kitchen. Analysts wonder how long OSIcan continue to grow by adding new types of restaurants to its portfolio.

W E B C A S E 10 Intel Corporation(Contributor: J. David Hunger)Although more than 80% of the world’s personal computers and servers use its microprocessors, Intelis facing strong competition from AMD in a maturing market. Sales growth is slowing. Profits areexpected to rise only 5% in 2006 compared to 40% annual growth previously. The new CEO decides toreinvent Intel to avoid a fate of eventual decline.

W E B C A S E 11 AirTran Holdings Inc.(Contributor: Maryanne M. Rouse)AirTran (known as ValuJet before a disastrous crash in the Everglades) is the second-largest low-fare scheduled airline (after Southwest) in the United States in terms of departures and, along withSouthwest, the only U.S. airline to post a profit in 2004. The company’s labor costs as a percentageof sales are the lowest in the industry. Will AirTran continue to be successful in this highlycompetitive industry?

CONTENTS xxvii

W E B C A S E 12 Boise Cascade/Office Max(Contributor: Maryanne M. Rouse)Boise Cascade, an integrated manufacturer and distributor of paper, packaging, and wood products,purchased OfficeMax, the third-largest office supplies catalogue retailer (after Staples and OfficeDepot), in 2003. Soon thereafter, Boise announced that it was selling its land, plants, headquarterslocation, and even its name to an equity investment firm. Upon completion of the sale in 2004, thecompany assumed the name of OfficeMax. Can this manufacturer become a successful retailer?

W E B C A S E 13 H. J. Heinz Company(Contributor: Maryanne M. Rouse)Heinz, a manufacturer and marketer of processed food products, pursued global growth via marketpenetration and acquisitions. Unfortunately, its modest sales growth was primarily from itsacquisitions. Now that the firm has divested a number of lines of businesses and brands to Del MonteFoods, analysts wonder how a 20% smaller Heinz will grow its sales and profits in this verycompetitive industry.

W E B C A S E 14 Nike Inc.(Contributor: Maryanne M. Rouse)Nike is the largest maker of athletic footwear and apparel in the world with a U.S. market shareexceeding 40%. Since almost all its products are manufactured by 700 independent contractors(99% of which are in Southeast Asia), Nike is a target of activists opposing manufacturing practicesin developing nations. Although industry sales growth in athletic footwear is slowing, Nike refusedto change its product mix in 2002 to suit Foot Locker, the dominant global footwear retailer. Is ittime for Nike to change its strategy and practices?

W E B C A S E 15 Six Flags Inc.: The 2006 Business Turnaround(Contributor: Patricia A. Ryan)Known for its fast roller coasters and adventure rides, Six Flags has successfully built a group ofregional theme and water parks in the United States. Nevertheless, the company has not turned aprofit since 1998. Long-term debt had increased to 61% of total assets by 2005. New management isimplementing a retrenchment strategy, but industry analysts are unsure if this will be enough to savethe company.

W E B C A S E 16 Lowe’s Companies Inc.(Contributor: Maryanne M. Rouse)As the second-largest U.S. “big box” home improvement retailer (behind Home Depot), Lowe’scompetes in a highly fragmented industry. The company has grown with the increase in homeownership and has no plans to expand internationally. With more than 1,000 stores in 2004, Lowe’sintended to increase its U.S. presence with 150 store openings per year in 2005 and 2006. Are therelimits to Lowe’s current growth strategy?

W E B C A S E 17 Movie Gallery Inc.(Contributor: J. David Hunger)Movie Gallery is the second-largest North American video retail rental company, specializing in therental and sale of movies and video games through its Movie Gallery and Hollywood Entertainmentstores. Growing through acquisitions, the company is heavily in debt. The recent rise of online videorental services, such as Netflix, is cutting into retail store revenues and reducing the company’s cashflow. With just $135 million in cash at the end of 2005, Movie Gallery’s management finds itself facingpossible bankruptcy.

xxviii CONTENTS

Preface

Welcome to the 13th edition of Strategic Management and Business Policy! Although the chaptersare the same as those in the 12th edition, many of the cases are new and different. We completelyrevised seven of your favorite cases (Apple, Dell, Google, Carnival, Panera Bread, WholeFoods, and Church & Dwight) and added 12 brand-new ones (iRobot, Rosetta Stone, Logitech,Chrysler, Tesla Motors, TomTom, Volcom, TOMS Shoes, Best Buy, Dollar General, BostonBeer, and Burger King) for a total of 19 new cases! More than half of the cases in this book arenew to this edition! Although we still make a distinction between full-length and mini cases, wehave interwoven them throughout the book to better identify them with their industries.

This edition continues the theme that runs throughout all 12 chapters: global environmentalsustainability. This strategic issue will become even more important in the years ahead, as allof us struggle to deal with the consequences of climate change, global warming, and energyavailability. We continue to be the most comprehensive strategy book on the market, withchapters ranging from corporate governance and social responsibility to competitive strategy,functional strategy, and strategic alliances. To keep the size of the book manageable, we offerspecial issue chapters dealing with technology, entrepreneurship, and not-for-profit organiza-tions on the Web site (www.pearsonhighered.com/wheelen).

FEATURES NEW TO THIS 13th EDITIONNineteen New Cases: Both Full Length and Mini LengthEleven full-length new or updated comprehensive cases and eight mini-length cases have beenadded to support the 16 popular full-length cases carried forward from past editions. Twelveof the cases are brand new. Seven are updated favorites from past editions. Of the 35 casesappearing in this book, 22 are exclusive and do not appear in other books.

� Five of the new cases deal with technology issues (Apple, iRobot, Dell, Rosetta Stone,and Logitech).

� One of the new cases deals with the Internet (Google).

� One new case involves entertainment (Carnival).� Three new cases are of old and new transportation firms (Chrysler, TomTom, and Tesla

Motors).

� Two new cases are of entrepreneurial clothing companies (Volcom and TOMS Shoes).

� Two new specialty retailing cases spotlight electronics (Best Buy) and variety (DollarGeneral).

� Five new cases come from the food, beverage, and restaurant industries (Boston Beer,Panera Bread, Whole Foods Market, Burger King, and Church & Dwight).

HOW THIS BOOK IS DIFFERENT FROM OTHER STRATEGY TEXTBOOKSThis book contains a Strategic Management Model that runs through the first 11 chaptersand is made operational through the Strategic Audit, a complete case analysis methodology.The Strategic Audit provides a professional framework for case analysis in terms of external

xxix

and internal factors and takes the student through the generation of strategic alternatives andimplementation programs.

To help the student synthesize the many factors in a complex strategy case, we developedthree useful techniques:

� External Factor Analysis (EFAS) Table in Chapter 4This reduces the external Opportunities and Threats to the 8 to 10 most important exter-nal factors facing management.

� Internal Factor Analysis (IFAS) Table in Chapter 5This reduces the internal Strengths and Weaknesses to the 8 to 10 most important internalfactors facing management.

� Strategic Factor Analysis Summary (SFAS) Matrix in Chapter 6This condenses the 16 to 20 factors generated in the EFAS and IFAS Tables into the 8 to 10most important (strategic) factors facing the company. These strategic factors become thebasis for generating alternatives and a recommendation for the company’s future direction.

Suggestions for Case Analysis are provided in Appendix 12.B (end of Chapter 12) andcontain step-by-step procedures for how to use the Strategic Audit in analyzing a case. Thisappendix includes an example of a student-written Strategic Audit. Thousands of studentsaround the world have applied this methodology to case analysis with great success. TheCase Instructor’s Manual contains examples of student-written Strategic Audits for each ofthe full-length comprehensive strategy cases.

FEATURES FOCUSED ON ENVIRONMENTAL SUSTAINABILITY� Each chapter contains a boxed insert dealing with an issue in environmental sustainability.

� Each chapter ends with Eco Bits, interesting tidbits of ecological information, such as thenumber of plastic bags added to landfills each year.

� Special sections on sustainability are found in Chapters 1 and 3.

� A section on the natural environment is included in the societal and task environments inChapter 4.

TIME-TESTED FEATURESThis edition contains many of the same features andcontent that helped make previous editions success-ful. Some of the features are the following:

xxx PREFACE

� A Strategic Management Model runs through-out the first 11 chapters as a unifying concept.(Explained in Chapter 1)

� The Strategic Audit, a way to operationalize the strategic decision-making process, serves as a checklist in case analysis. (Chapter 1)

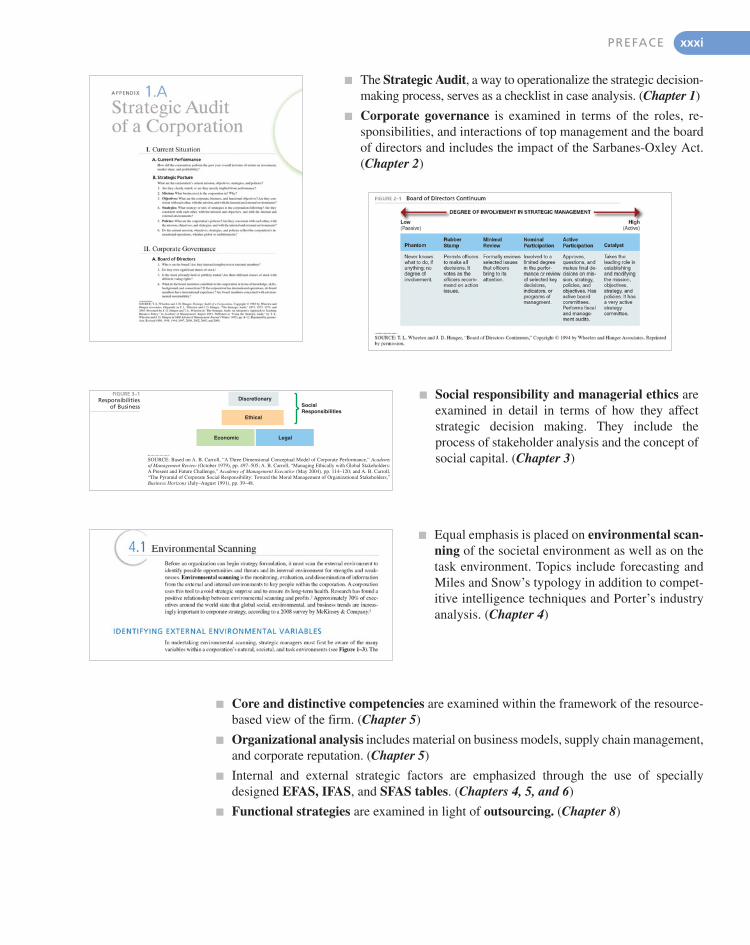

� Corporate governance is examined in terms of the roles, re-sponsibilities, and interactions of top management and the boardof directors and includes the impact of the Sarbanes-Oxley Act.(Chapter 2)

� Social responsibility and managerial ethics areexamined in detail in terms of how they affectstrategic decision making. They include theprocess of stakeholder analysis and the concept ofsocial capital. (Chapter 3)

� Equal emphasis is placed on environmental scan-ning of the societal environment as well as on thetask environment. Topics include forecasting andMiles and Snow’s typology in addition to compet-itive intelligence techniques and Porter’s industryanalysis. (Chapter 4)

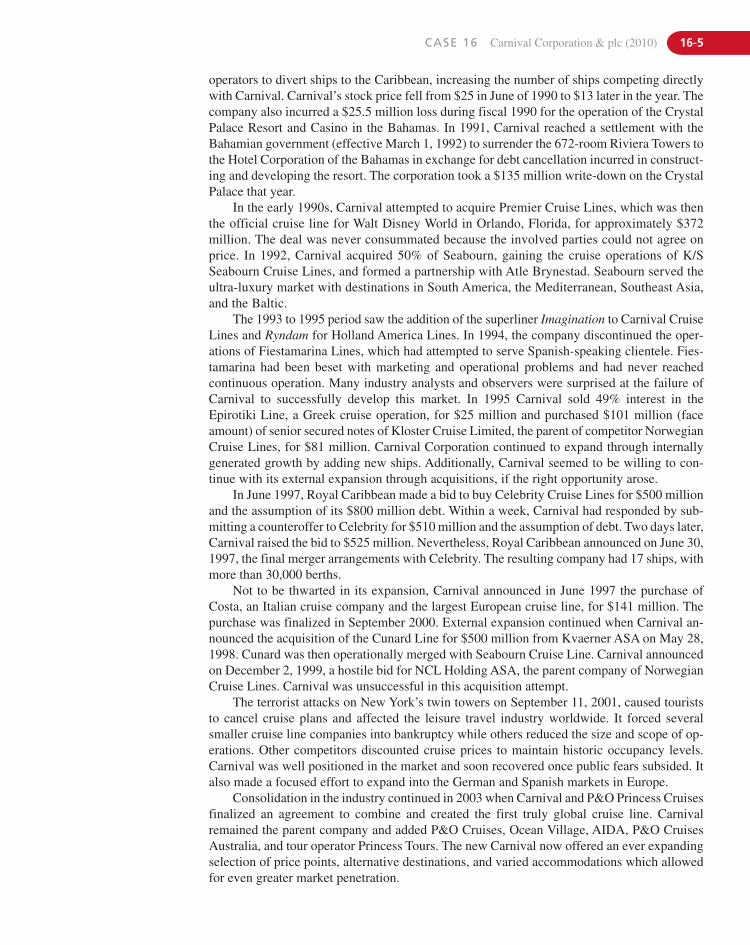

Discretionary

Ethical

LegalEconomic

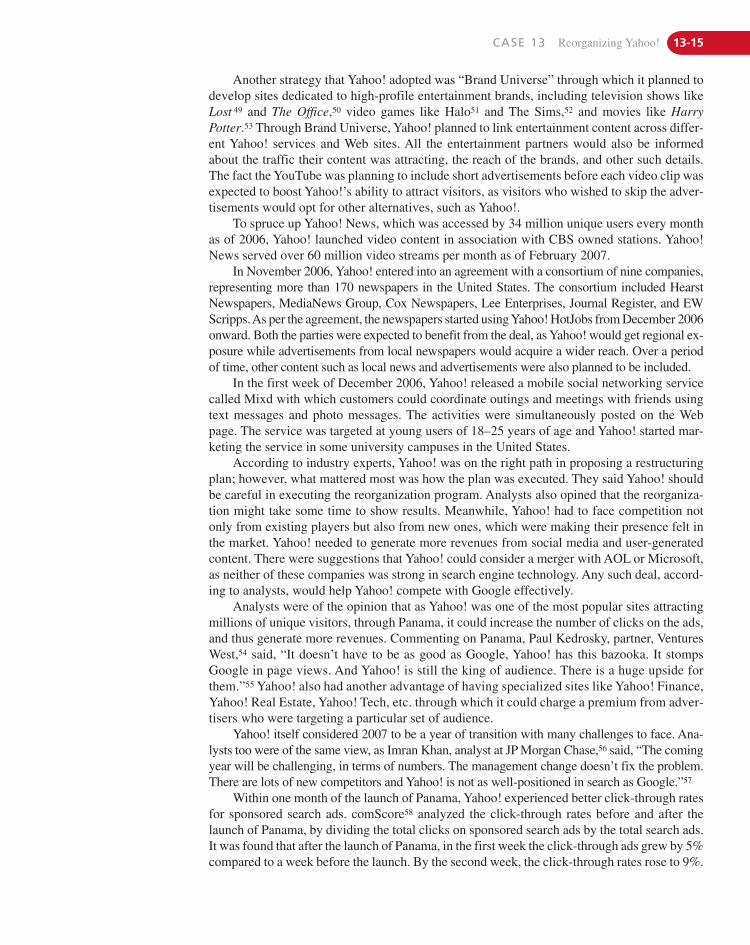

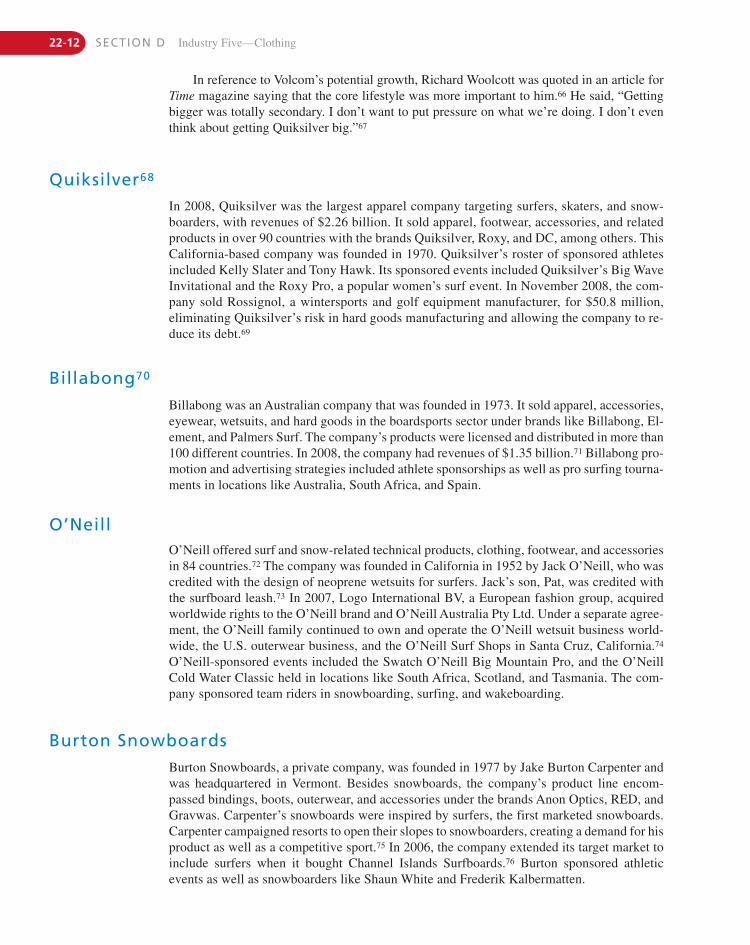

SocialResponsibilities

FIGURE 3–1Responsibilities

of Business

SOURCE: Based on A. B. Carroll, “A Three Dimensional Conceptual Model of Corporate Performance,” Academyof Management Review (October 1979), pp. 497–505; A. B. Carroll, “Managing Ethically with Global Stakeholders: A Present and Future Challenge,” Academy of Management Executive (May 2004), pp. 114–120; and A. B. Carroll,“The Pyramid of Corporate Social Responsibility: Toward the Moral Management of Organizational Stakeholders,”Business Horizons (July–August 1991), pp. 39–48.

� Core and distinctive competencies are examined within the framework of the resource-based view of the firm. (Chapter 5)

� Organizational analysis includes material on business models, supply chain management,and corporate reputation. (Chapter 5)

� Internal and external strategic factors are emphasized through the use of speciallydesigned EFAS, IFAS, and SFAS tables. (Chapters 4, 5, and 6)

� Functional strategies are examined in light of outsourcing. (Chapter 8)

PREFACE xxxi

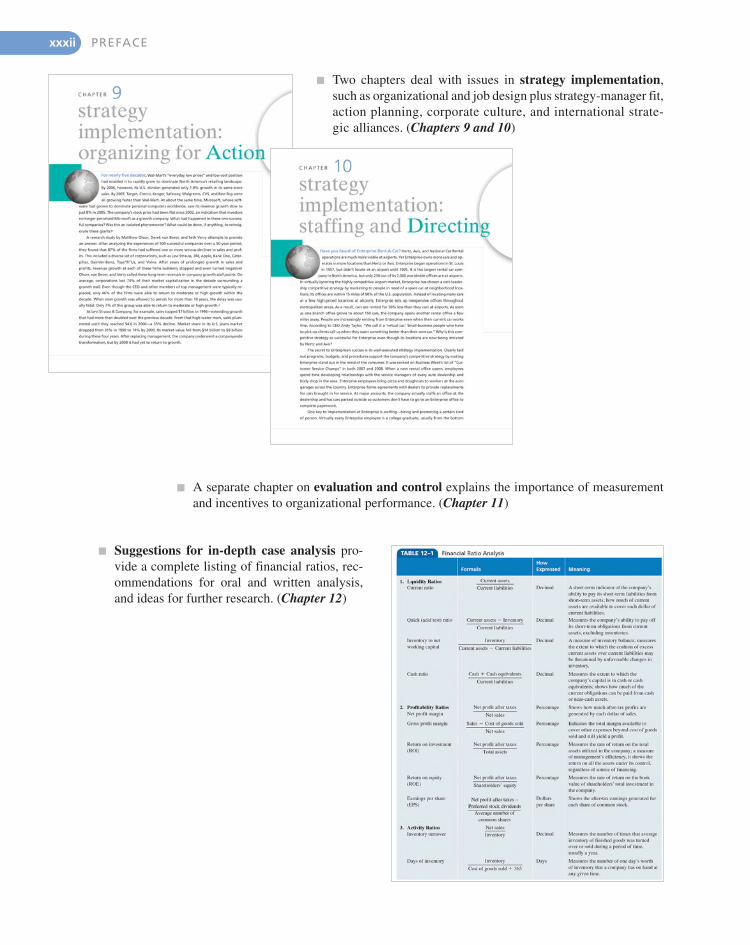

� Two chapters deal with issues in strategy implementation,such as organizational and job design plus strategy-manager fit,action planning, corporate culture, and international strate-gic alliances. (Chapters 9 and 10)

� A separate chapter on evaluation and control explains the importance of measurementand incentives to organizational performance. (Chapter 11)

� Suggestions for in-depth case analysis pro-vide a complete listing of financial ratios, rec-ommendations for oral and written analysis,and ideas for further research. (Chapter 12)

xxxii PREFACE

� The Strategic Audit Worksheet is based on the time-testedStrategic Audit and is designed to help students organize andstructure daily case preparation in a brief period of time. Theworksheet works exceedingly well for checking the level ofdaily student case preparation—especially for open class dis-cussions of cases. (Chapter 12)

� Special chapters deal with strategic issues in managingtechnology and innovation, entrepreneurial ventures andsmall businesses, and not-for-profit organizations. (WebChapters A, B, and C, respectively) These issues are oftenignored by other strategy textbooks, but are available on thisbook’s Web site at www.pearsonhighered.com/wheelen.

� An experiential exercise focusing on thematerial covered in each chapter helps thereader to apply strategic concepts to an actualsituation.

� A list of key terms and the pages in which they are discussed enable the reader to keeptrack of important concepts as they are introduced in each chapter.

� Learning objectives begin each chapter.

� Each Part ends with a short case that acts to integrate the material discussed withinthe previous chapters.

� Timely, well-researched, and class-tested cases deal with interesting companies andindustries. Many of the cases are about well-known, publicly held corporations—idealsubjects for further research by students wishing to “update” the cases.

Both the text and the cases have been class-tested in strategy courses and revised based onfeedback from students and instructors. The first 11 chapters are organized around a StrategicManagement Model that begins each chapter and provides a structure for both content andcase analysis. We emphasize those concepts that have proven to be most useful in under-standing strategic decision making and in conducting case analysis. Our goal was to make thetext as comprehensive as possible without getting bogged down in any one area. Endnotereferences are provided for those who wish to learn more about any particular topic. All casesare about actual organizations. The firms range in size from large, established multinationalsto small, entrepreneurial ventures, and cover a broad variety of issues. As an aid to caseanalysis, we propose the Strategic Audit as an analytical technique.

PREFACE xxxiii

SUPPLEMENTSInstructor Resource CenterAt www.pearsonhighered.com/irc, instructors can access teaching resources available withthis text in downloadable, digital format. Registration is simple and gives you immediate ac-cess to new titles and new editions. As a registered faculty member, you can download re-source files and receive immediate access and instructions for installing course managementcontent on your campus server. In case you ever need assistance, our dedicated technical sup-port team is ready to assist instructors with questions about the media supplements that ac-company this text. Visit http://247.pearsoned.com/ for answers to frequently asked questionsand toll-free user support phone numbers. The Instructor Resource Center provides the fol-lowing electronic resources.

Instructor’s ManualsTwo comprehensive Instructor’s Manuals have been carefully constructed to accompany thisbook. The first one accompanies the concepts chapters; the second one accompanies the cases.

Concepts Instructor’s ManualTo aid in discussing the 12 strategy chapters as well as the three web special issue chapters,the Concepts Instructor’s Manual includes:

� Suggestions for Teaching Strategic Management: These include various teachingmethods and suggested course syllabi.

� Chapter Notes: These include summaries of each chapter, suggested answers to discus-sion questions, and suggestions for using end-of-chapter cases/exercises and part-endingcases, plus additional discussion questions (with answers) and lecture modules.

Case Instructor’s ManualTo aid in case method teaching, the Case Instructor’s Manual includes detailed suggestionsfor use, teaching objectives, and examples of student analyses for each of the full-length com-prehensive cases. This is the most comprehensive Instructor’s Manual available in strategicmanagement. A standardized format is provided for each case:

1. Case Abstract

2. Case Issues and Subjects

3. Steps Covered in the Strategic Decision-Making Process

4. Case Objectives

5. Suggested Classroom Approaches

6. Discussion Questions

7. Case Author’s Teaching Note

8. Student-Written Strategic Audit, if appropriate

9. EFAS, IFAS, and SFAS Exhibits

10. Financial Analysis—ratios and common-size income statements, if appropriate

PowerPoint SlidesPowerPoint slides, provided in a comprehensive package of text outlines and figures corre-sponding to the text, are designed to aid the educator and supplement in-class lectures.

xxxiv PREFACE

Test Item FileThis Test Item File contains over 1,200 questions, including multiple-choice, true/false, andessay questions. Each question is followed by the correct answer, page reference, AACSBcategory, and difficulty rating.

TestGenTestGen software is preloaded with all of the Test Item File questions. It allows instructors tomanually or randomly view test questions, and to add, delete, or modify test-bank questionsas needed to create multiple tests.

Videos on DVDExciting and high-quality video clips help deliver engaging topics to the classroom to helpstudents better understand the concepts explained in the textbook. Please contact your localrepresentative to receive a copy of the DVD.

CourseSmartCourseSmart eTextbooks were developed for students looking to save on required or recom-mended textbooks. Students simply select their eText by title or author and purchase immedi-ate access to the content for the duration of the course using any major credit card. With aCourseSmart eText, students can search for specific keywords or page numbers, take notesonline, print out reading assignments that incorporate lecture notes, and bookmark importantpassages for later review. For more information or to purchase a CourseSmart eTextbook, visitwww.coursesmart.com.

AcknowledgmentsWe thank the many people at Prentice Hall/Pearson who helped to make this edition possi-ble. We thank our editor, Kim Norbuta. We are especially grateful to Kim’s project manager,Claudia Fernandes, who managed to keep everything on an even keel. We also thank Becca Groves and Emily Bush, who took the book through the production process.

We are very thankful to Jeanne McNett, Assumption College; Bob McNeal, AlabamaState University; Don Wicker, Brazosport College; Dan Kipley, Azusa Pacific University;Roxanna Wright, Plymouth State University; Kristl Davison, University of Mississippi;Francis Fabian, University of Memphis; Susan Fox-Wolfgramm, Hawaii Pacific University;Conrad Francis, Nova Southeastern University; and Gene Simko, Monmouth University fortheir constructive criticism of the 12th edition cases. They helped us to decide which of ourfavorite cases to keep and which to delete or update.

We are very grateful to Kathy Wheelen for her first-rate administrative support of thecases and to Alan N. Hoffman for helping us with the Case Instructor’s Manual. We areespecially thankful to the many students who tried out the cases we chose to include in thisbook. Their comments helped us find any flaws in the cases before the book went to theprinter.

In addition, we express our appreciation to Wendy Klepetar, Management DepartmentChair of Saint John’s University and the College of Saint Benedict, for her support andprovision of the resources so helpful to revise a textbook. Both of us acknowledge our debt to

PREFACE xxxv

Dr. William Shenkir and Dr. Frank S. Kaulback, former Deans of the McIntire School ofCommerce of the University of Virginia, for the provision of a work climate most supportiveto the original development of this book.

We offer a special thanks to the hundreds of case authors who have provided us withexcellent cases for the 13 editions of this book. We consider many of these case authors to beour friends. A special thanks to you!! The adage is true: The path to greatness is through others.

Lastly, to the many strategy instructors and students who have moaned to us about theirproblems with the strategy course: We have tried to respond to your problems and concerns asbest we could by providing a comprehensive yet usable text coupled with recent and complexcases. To you, the people who work hard in the strategy trenches, we acknowledge our debt.This book is yours.

T. L. W.Saint Petersburg, Florida

J. D. H.St. Joseph, Minnesota

xxxvi PREFACE

About the Contributors

MOUSTAFA H. ABDELSAMAD, DBA (George Washington University), is Dean of the Collegeof Business at Texas A&M University–Corpus Christi. He previously served as Dean of theCollege of Business and Industry at University of Massachusetts–Dartmouth and as Professorof Finance and Associate Dean of Graduate Studies in Business at Virginia CommonwealthUniversity. He is Editor–in-Chief of SAM Advanced Management Journal and InternationalPresident of the Society of Advancement of Management. He is author of A Guide to CapitalExpenditure Analysis and two chapters in the Dow Jones–Irwin Capital Budgeting Handbook.He is the author and coauthor of numerous articles in various publications.

Hitesh (John) P. Adhia, CPA, MS and BA (University of South Florida), is the President andChief Investment Officer of Adhia Investment Advisors, Inc. (the “Firm”). Mr. Adhia is a CPAand has been in the finace industry since 1982. Mr Adhia is the founder and Investment Man-ager for the Adhia Twenty Fund, and the Adhia Health Care Fund, the Adhia Short Term Ad-vantage Fund, the Adhia Arbitrage Fund, and the Adhia Derivative Fund. Prior to formingAdhia Investment Advisors, Mr. Adhia owned a Tampa-based public accounting practice andalso served as Acting CFO and Independent Advisor to the Well Care Group of Companies. Mr.Adhia has over twenty years experience in managing fixed income strategies.

KAREN A. BERGER, PhD (M. Phil and New York University), MBA (University of Connecticut),MA (Columbia University), and BA (S.U.N.Y. at Buffalo), is Chairperson of the MarketingDepartment and Associate Professor of Marketing at Pace University. She previously held aca-demic positions with New York University, Stern School of Business, and Mercy College. Bergerhas published literature in the field of Marketing and has won several teaching awards.

CHRISTINE B. BUENAFE, student of The College of New Jersey, co-author with JoyceVincelette of the Rosetta Stone and Volcom cases in this edition.

BARNALI CHAKRABORTY, is a faculty member at the ICFAI Center for Management Research(ICMR).

RICHARD A. COISER, PhD (University of Iowa), is Dean and Leeds Professor of Managementat Purdue University. He formerly was Dean and Fred B. Brown Chair at the University ofOklahoma and was Associate Dean for Academics and Professor of Business Administrationat Indiana University. He served as Chairperson of the Department of Management at IndianaUniversity. For seven years prior to assuming his current position, he was a Planning Engineerwith Western Electric Company and Instructor of Management and Quantitative Methods atthe University of Notre Dame. Dr. Coiser is interested in researching the managerial decision-making process, organization responses to external forces, and participative management. Hehas published in Behavior Science, Academy of Management Journal, Academy of Manage-ment Review, Organizational Behavior and Human Performance, Management Science,Strategic Management Journal, Business Horizons, Decision Sciences, Personnel Psychology,Journal of Creative Behavior, International Journal of Management, The Business Quarterly,Public Administration Quarterly, Human Relations, and other journals. In addition, Dr. Coiserhas presented numerous papers at professional meetings and has coauthored a management

xxxvii

text. He has been active in many executive development programs and has acted as management-education consultant for several organizations. Dr. Coiser is the recipient of Teaching Excellence Awards in the MBA Program at Indiana and a Richard D. Irwin Fellowship. He be-longs to the Institute of Management, Sigma Iota Epsilon, and the Decision Sciences Institute.

ROY A. COOK, DBA (Mississippi State University), is past Associate Dean of the School of Business Administration and previously a Professor at Fort Lewis College, Durango, Col-orado. He has written a best-selling textbook, Tourism: The Business of Travel, now in its2nd edition, and has two forthcoming textbooks: Cases and Experiential Exercises in Hu-man Resource Management and Guide to Business Etiquette. He has authored numerous ar-ticles, cases, and papers based on his extensive experience in the hospitality industry andresearch interests in the areas of strategy, small business management, human resource man-agement, and communication. Dr. Cook has served as the Director of Colorado’s Center forTourism Research® and Editor of The Annual Advances in Business Cases, and also on theeditorial boards of the Business Case Journal, the Journal of Business Strategies, and theJournal of Teaching and Tourism. He is a member of the Academy of Management, Societyfor Case Research (past President), and the International Society of Travel and Tourism Ed-ucators. Dr. Cook teaches courses in Strategic Management, Small Business Management,Tourism and Resort Management, and Human Resource Management.

STEVEN M. COX, PhD (University of Nebraska), is an Associate Professor of Marketing,McColl School of Business, Queens University of Charlotte. He has a 25-year career in execu-tive level marketing and sales positions with AT&T, GE, and several satellite imaging compa-nies. He owns and manages LSI, a geographic information system company. He currently servesas a case reviewer for the Business Case Journal and the Southeast Case Research Journal.

DAVID B. CROLL, PhD (Pennsylvania State University), is Professor Emeritus of Accountingat the McIntire School of Commerce, the University of Virginia. He was Visiting Associate Pro-fessor at the Graduate Business School, the University of Michigan. He is on the editorial boardof SAM Advanced Management Journal. He has published in the Accounting Review and theCase Research Journal. His cases appear in 12 accounting and management textbooks.

DAN R. DALTON, PhD (University of California, Irvine), is the Dean of the Graduate School ofBusiness, Indiana University, and Harold A. Polipl Chair of Strategic Management. He was for-merly with General Telephone & Electronics for 13 years. Widely published in business andpsychology periodicals, his articles have appeared in the Academy of Management Journal,Journal of Applied Psychology, Personnel Psychology, Academy of Management Review, andStrategic Management Journal.