Strategic Considerations for Video Services

Strategic Considerations for Video Services. DRAFT page 1 SVOD and AVOD: Strategic Considerations (1 of 2) Previous discussions have evaluated the launch.

Dec 13, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Strategic Considerations for Video Services

DRAFT

page 2

SVOD and AVOD: Strategic Considerations (1 of 2)

• Previous discussions have evaluated the launch of a programmed video service as a standalone profit driver, key considerations include:

– Investment in content and programming required to compete with leading services

– Number of customers likely to be acquired

– Revenue per customer

– Ongoing relationship with customers

• If a service is intended to be a standalone profit driver, the SVOD vs. AVOD decision depends partly on appetite for investment and risk

– SVOD can be a high risk, high reward proposition

• Significant investment in content required given heavy investment by many competitors

• Harder to secure customers for paid service

• But SVOD offers the potential for higher revenue per customer (e.g. ~ $10/month of subscription revenue) and an ongoing relationship

– AVOD can be a lower risk model, but with lower revenue per customer

• Success is possible at a lower level of investment; despite numerous competitors, investment in exclusive content for AVOD services has been more modest

• Easier to secure customers for AVOD services

• But revenue per customer is lower (e.g., ~$0.03 of ad revenue per view), and programming expertise is required to keep customers coming back

DRAFT

page 3

SVOD and AVOD: Strategic Considerations (2 of 2)

• Sony’s existing revenue-generating services and connected device footprint give us the opportunity to evaluate the SVOD vs. AVOD decision differently

• If a programmed video service is viewed as a customer acquisition tool for other revenue generating services and hardware sales, strategic considerations change

– Strategic considerations include:

– Creating a compelling and competitive content offering with a reasonable investment

– Acquiring the greatest number of customers for the service

– Providing those customers with a reason to return on a regular basis

– Monetize by cross-selling these customers on paid services (i.e., Music Unlimited, Video Unlimited, PlayStation Plus) and hardware

– AVOD’s characteristics better satisfy these strategic considerations:

– Lower investment in content is required to be competitive

– Free-to-consumer positioning makes it easier to acquire customers

– A well-programmed service provides a reason for customers to return on a regular basis

– Service can be deeply integrated into other paid offerings, encouraging cross-selling and co-promotion

DRAFT

page 4

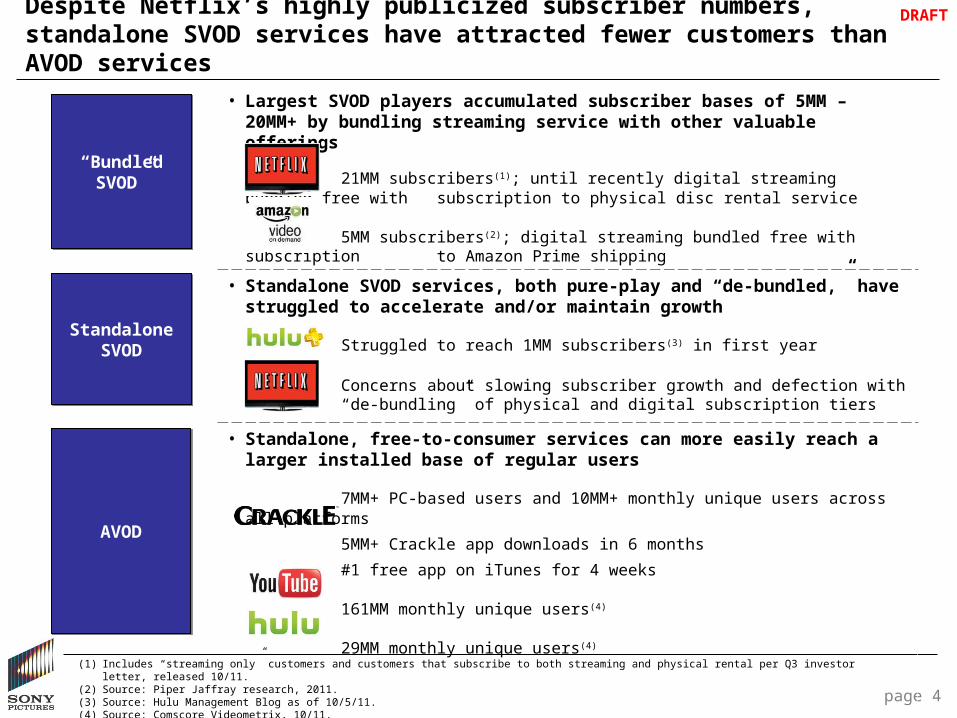

Despite Netflix’s highly publicized subscriber numbers, standalone SVOD services have attracted fewer customers than AVOD services

• Largest SVOD players accumulated subscriber bases of 5MM – 20MM+ by bundling streaming service with other valuable offerings

21MM subscribers(1); until recently digital streaming bundled free with subscription to physical disc rental service

5MM subscribers(2); digital streaming bundled free with subscription to Amazon Prime shipping

• Standalone SVOD services, both pure-play and “de-bundled,” have struggled to accelerate and/or maintain growth

Struggled to reach 1MM subscribers(3) in first year

Concerns about slowing subscriber growth and defection with recent “de-bundling” of physical and digital subscription tiers

• Standalone, free-to-consumer services can more easily reach a larger installed base of regular users

7MM+ PC-based users and 10MM+ monthly unique users across all platforms

5MM+ Crackle app downloads in 6 months

#1 free app on iTunes for 4 weeks

161MM monthly unique users(4)

29MM monthly unique users(4)

“Bundled SVOD”

“Bundled SVOD”

Standalone SVOD

Standalone SVOD

AVODAVOD

(1) Includes “streaming only” customers and customers that subscribe to both streaming and physical rental per Q3 investor letter, released 10/11.(2) Source: Piper Jaffray research, 2011.(3) Source: Hulu Management Blog as of 10/5/11.(4) Source: Comscore Videometrix, 10/11.

DRAFT

page 5

And Competition for SVOD Services is Increasing…

…but similar lessons are playing out again

• Gaining traction, but offering is bundled with a full linear channel that customers have already paid for; no incremental charge

– 4MM+ app downloads(1) with participating distribution partners including Fios, Uverse, Google TV, Cox, Comcast, DirecTV, Dish, Suddenlink and Charter

• Apps getting traction and buzz, but like HBO Go, they are bundled as an add-on to a full fledged service after authentication

• Despite content from 3 studios, has had limited success securing distribution and customers for a ~$10 per month service

• Poor customer acquisition on cable has limited it’s ability to drive growth of the digital offering

– Linear pay TV network is available to 30MM+ subscribers through its current distribution relationships but has only managed to accumulate ~9MM(2) actual subscribers to date

TV EverywhereTV Everywhere

(1) Source: Time Warner Q2 earnings call as of 8/3/11.(2) Source: Industry reports as of 8/12/11.

DRAFT

• Historically licensed under rev-share only

• Currently investing up to $100MM to producers as an enticement to launch original content channels, but still less than the SVOD services

• Currently expects to pay content providers $300MM(3) in CY2011

page 6

SVOD and AVOD: Content Investment

• While the ability to attract customers to standalone SVOD services at $10 per month is still being tested, the required content investment in these services remains high:

• Invested $1.2B in content in calendar 2010(1) with increases expected going forward

• Estimated that Amazon paid $200-300MM for Lovefilm(2)

– Lovefilm investing heavily in rights acquisitions

• Although values not disclosed, continue to announce high profile content deals with major content providers (e.g., ABC, CBS, Fox, NBC, PBS)

• Value of network content contributed by owners not disclosed but assumed to be a multiple of Hulu Classic

– Media owners include NBCU, News Corp. and Disney

(1) Source: company filings dated 2/18/11.(2) Source: company filings and press releases. Note: Specific valuation for Lovefilm not publicly disclosed.(3) Source: Hulu Management Blog as of 4/4/11.

• By contrast, AVOD services initially drove significant viewership with little to no content cost. Investment is increasing, but still well below investment in SVOD

SVOD

AVOD

Related Documents