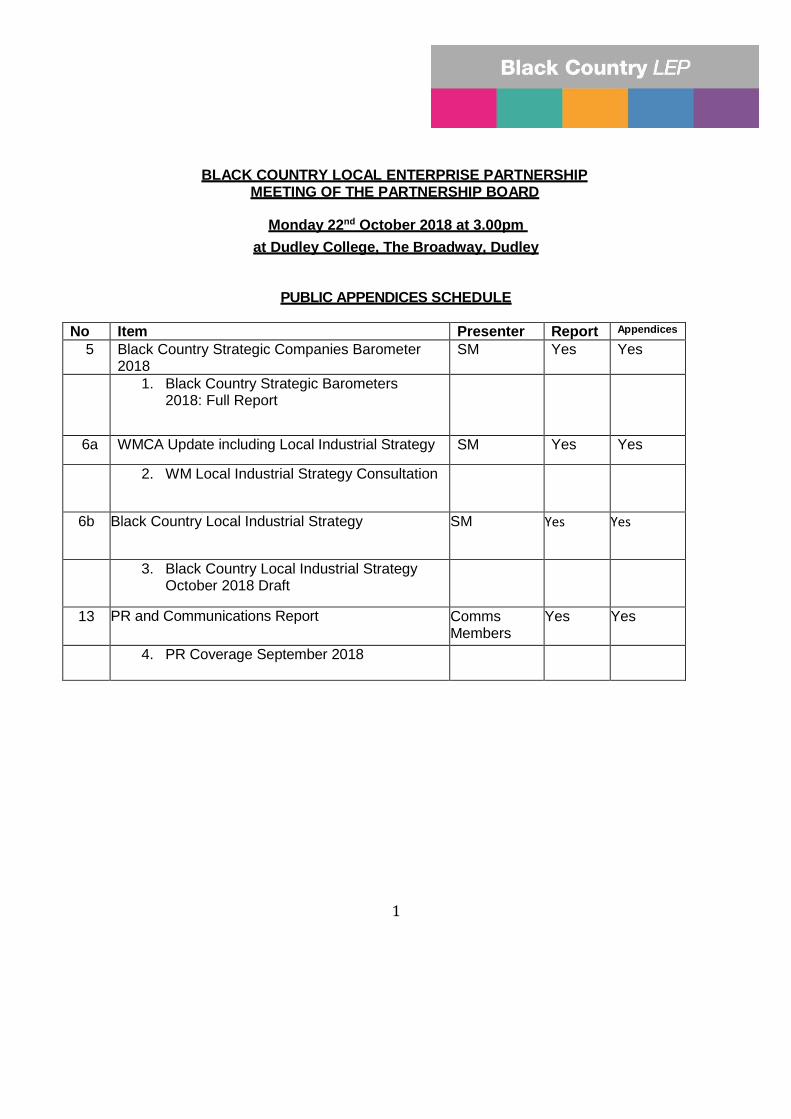

BLACK COUNTRY LOCAL ENTERPRISE PARTNERSHIP MEETING OF THE PARTNERSHIP BOARD Monday 22 nd October 2018 at 3.00pm at Dudley College, The Broadway, Dudley PUBLIC APPENDICES SCHEDULE No Item Presenter Report Appendices 5 Black Country Strategic Companies Barometer 2018 SM Yes Yes 1. Black Country Strategic Barometers 2018: Full Report 6a WMCA Update including Local Industrial Strategy SM Yes Yes 2. WM Local Industrial Strategy Consultation 6b Black Country Local Industrial Strategy SM Yes Yes 3. Black Country Local Industrial Strategy October 2018 Draft 13 PR and Communications Report Comms Members Yes Yes 4. PR Coverage September 2018 October 2018 DRAFT 1

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

BLACK COUNTRY LOCAL ENTERPRISE PARTNERSHIP

MEETING OF THE PARTNERSHIP BOARD

Monday 22nd October 2018 at 3.00pm

at Dudley College, The Broadway, Dudley

PUBLIC APPENDICES SCHEDULE

No Item Presenter Report Appendices

5 Black Country Strategic Companies Barometer 2018

SM Yes Yes

1. Black Country Strategic Barometers 2018: Full Report

6a WMCA Update including Local Industrial Strategy SM Yes Yes

2. WM Local Industrial Strategy Consultation

6b Black Country Local Industrial Strategy SM Yes Yes

3. Black Country Local Industrial Strategy October 2018 Draft

13 PR and Communications Report Comms Members

Yes Yes

4. PR Coverage September 2018

October 2018 DRAFT

1

0

Black Country Strategic Companies Barometer 2018

Strategic Companies Barometer

2018

Page 1

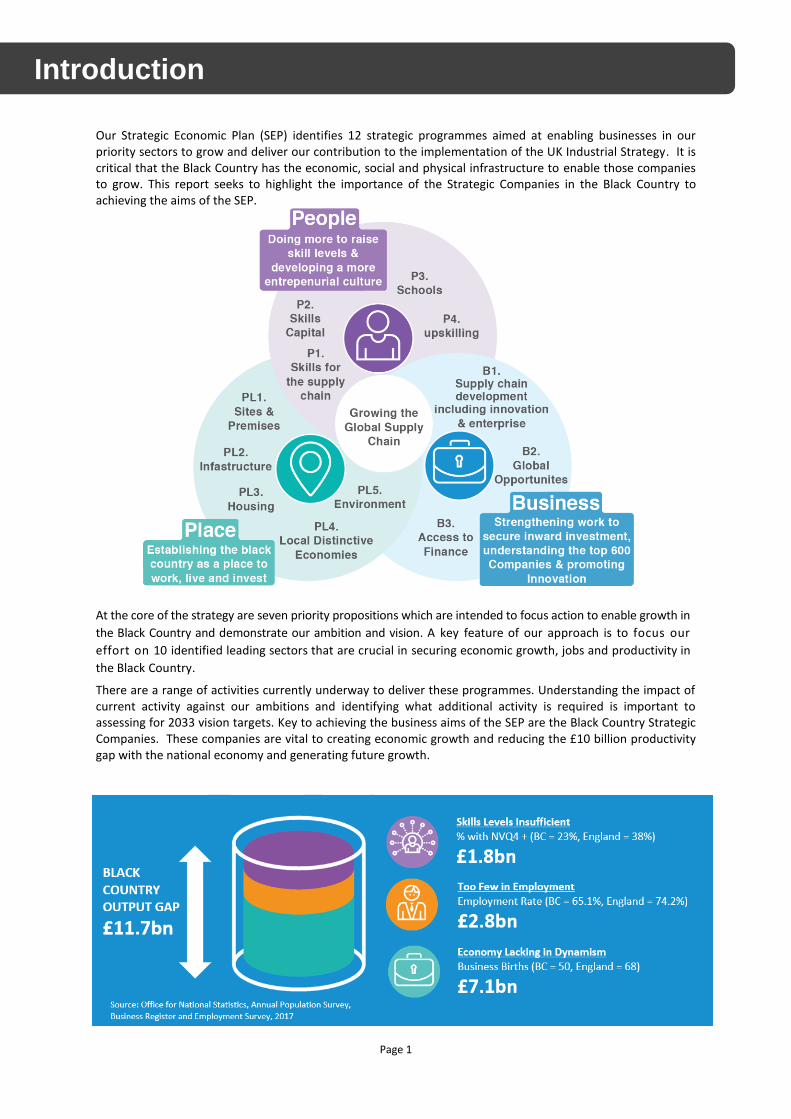

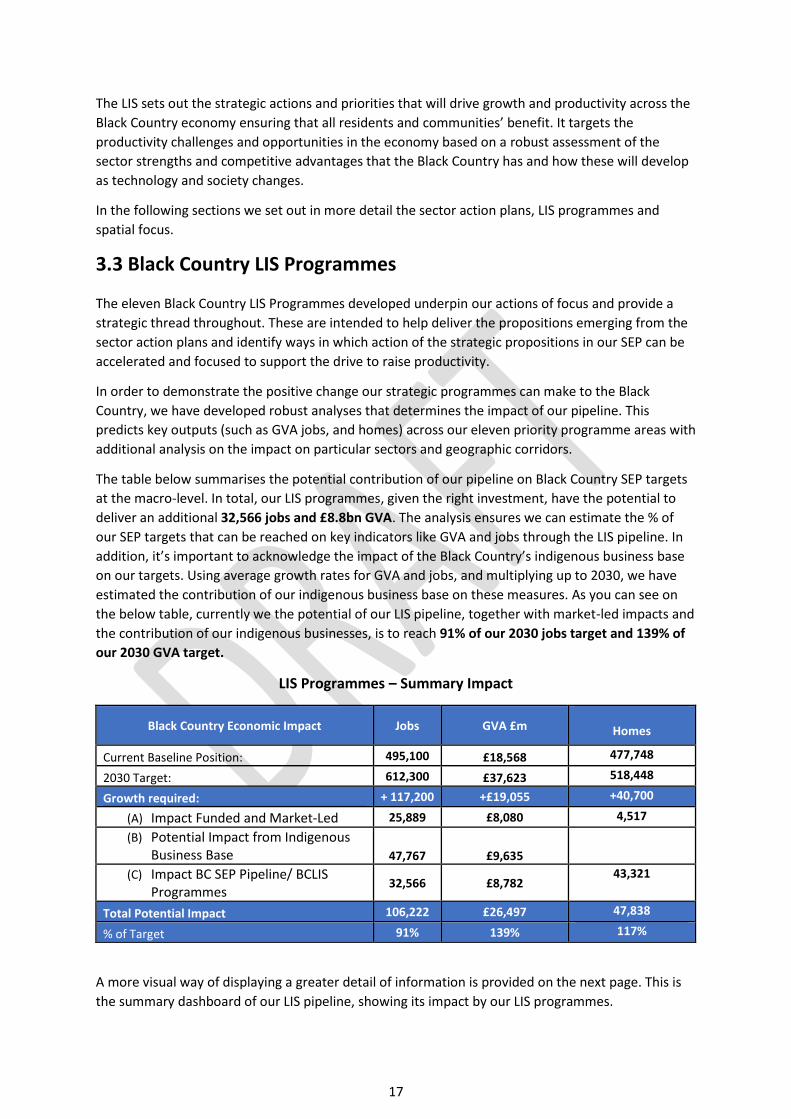

Our Strategic Economic Plan (SEP) identifies 12 strategic programmes aimed at enabling businesses in our priority sectors to grow and deliver our contribution to the implementation of the UK Industrial Strategy. It is critical that the Black Country has the economic, social and physical infrastructure to enable those companies to grow. This report seeks to highlight the importance of the Strategic Companies in the Black Country to achieving the aims of the SEP.

At the core of the strategy are seven priority propositions which are intended to focus action to enable growth in

the Black Country and demonstrate our ambition and vision. A key feature of our approach is to focus our

effort on 10 identified leading sectors that are crucial in securing economic growth, jobs and productivity in

the Black Country.

There are a range of activities currently underway to deliver these programmes. Understanding the impact of current activity against our ambitions and identifying what additional activity is required is important to assessing for 2033 vision targets. Key to achieving the business aims of the SEP are the Black Country Strategic Companies. These companies are vital to creating economic growth and reducing the £10 billion productivity gap with the national economy and generating future growth.

Introduction

Page 2

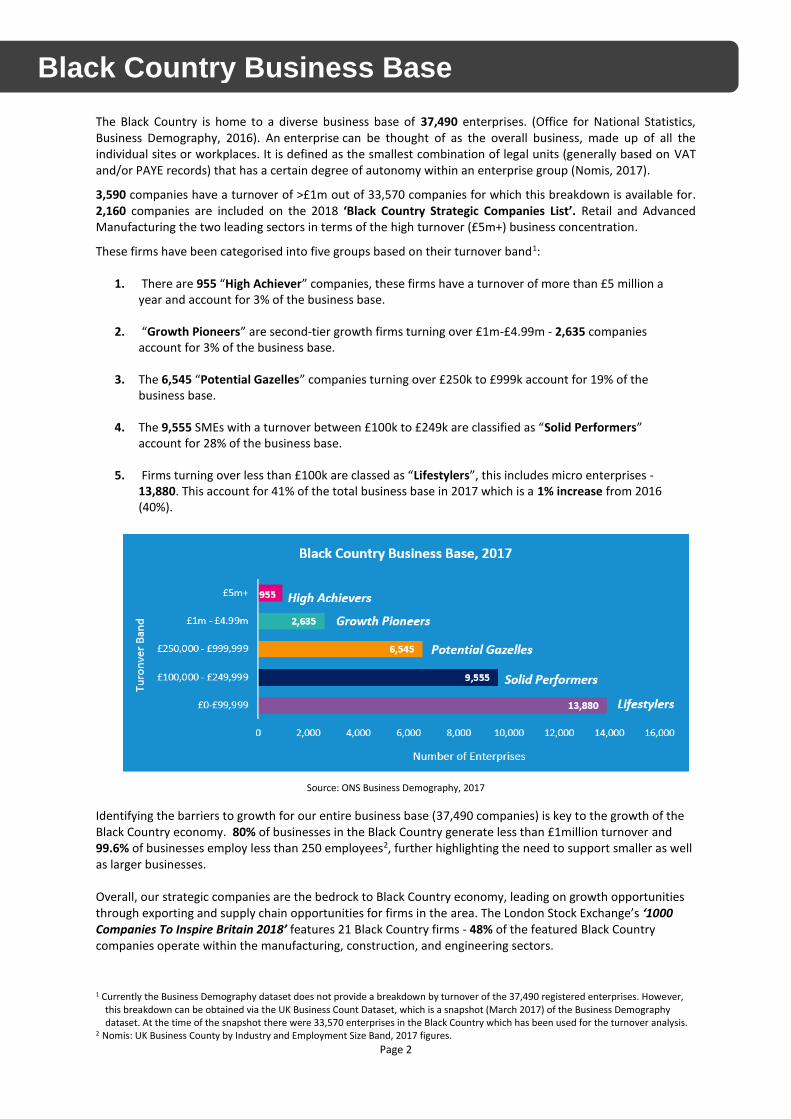

The Black Country is home to a diverse business base of 37,490 enterprises. (Office for National Statistics, Business Demography, 2016). An enterprise can be thought of as the overall business, made up of all the individual sites or workplaces. It is defined as the smallest combination of legal units (generally based on VAT and/or PAYE records) that has a certain degree of autonomy within an enterprise group (Nomis, 2017).

3,590 companies have a turnover of >£1m out of 33,570 companies for which this breakdown is available for. 2,160 companies are included on the 2018 ‘Black Country Strategic Companies List’. Retail and Advanced Manufacturing the two leading sectors in terms of the high turnover (£5m+) business concentration.

These firms have been categorised into five groups based on their turnover band1:

1. There are 955 “High Achiever” companies, these firms have a turnover of more than £5 million a year and account for 3% of the business base.

2. “Growth Pioneers” are second-tier growth firms turning over £1m-£4.99m - 2,635 companies

account for 3% of the business base. 3. The 6,545 “Potential Gazelles” companies turning over £250k to £999k account for 19% of the

business base. 4. The 9,555 SMEs with a turnover between £100k to £249k are classified as “Solid Performers”

account for 28% of the business base. 5. Firms turning over less than £100k are classed as “Lifestylers”, this includes micro enterprises -

13,880. This account for 41% of the total business base in 2017 which is a 1% increase from 2016 (40%).

Source: ONS Business Demography, 2017

Identifying the barriers to growth for our entire business base (37,490 companies) is key to the growth of the Black Country economy. 80% of businesses in the Black Country generate less than £1million turnover and 99.6% of businesses employ less than 250 employees2, further highlighting the need to support smaller as well as larger businesses. Overall, our strategic companies are the bedrock to Black Country economy, leading on growth opportunities through exporting and supply chain opportunities for firms in the area. The London Stock Exchange’s ‘1000 Companies To Inspire Britain 2018’ features 21 Black Country firms - 48% of the featured Black Country companies operate within the manufacturing, construction, and engineering sectors.

1 Currently the Business Demography dataset does not provide a breakdown by turnover of the 37,490 registered enterprises. However,

this breakdown can be obtained via the UK Business Count Dataset, which is a snapshot (March 2017) of the Business Demography dataset. At the time of the snapshot there were 33,570 enterprises in the Black Country which has been used for the turnover analysis.

2 Nomis: UK Business County by Industry and Employment Size Band, 2017 figures.

Black Country Business Base

Page 3

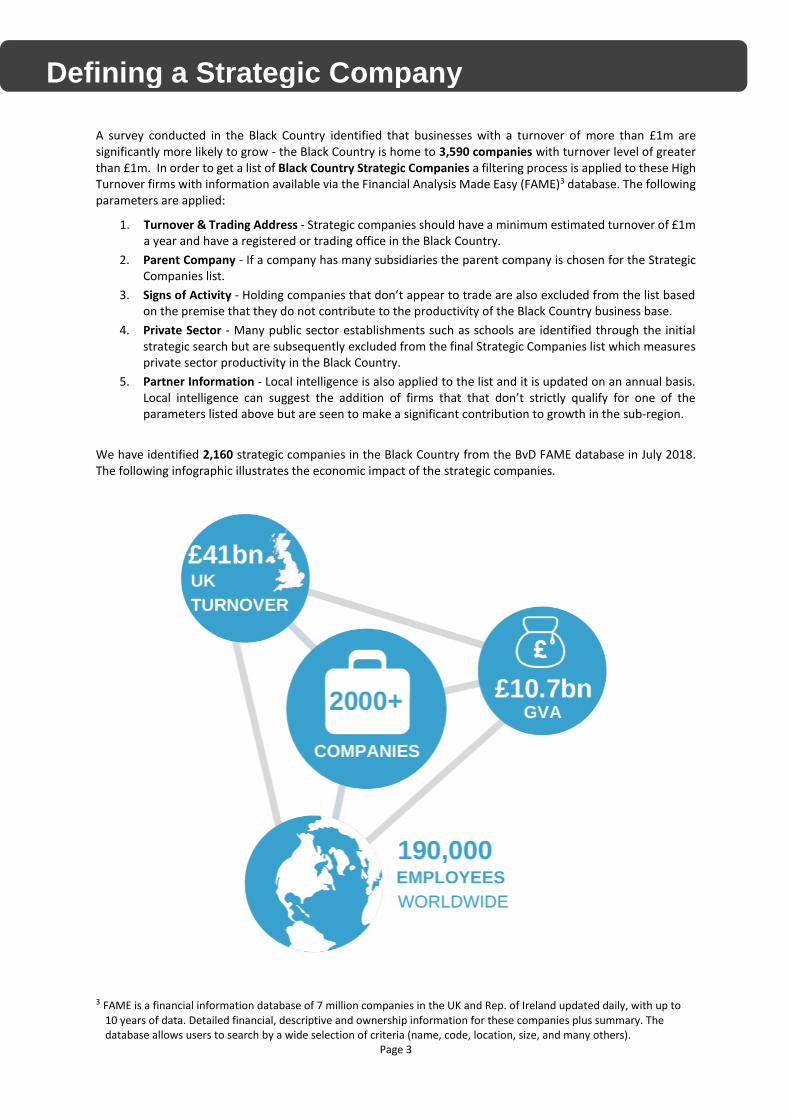

A survey conducted in the Black Country identified that businesses with a turnover of more than £1m are significantly more likely to grow - the Black Country is home to 3,590 companies with turnover level of greater than £1m. In order to get a list of Black Country Strategic Companies a filtering process is applied to these High Turnover firms with information available via the Financial Analysis Made Easy (FAME)3 database. The following parameters are applied:

1. Turnover & Trading Address - Strategic companies should have a minimum estimated turnover of £1m a year and have a registered or trading office in the Black Country.

2. Parent Company - If a company has many subsidiaries the parent company is chosen for the Strategic Companies list.

3. Signs of Activity - Holding companies that don’t appear to trade are also excluded from the list based on the premise that they do not contribute to the productivity of the Black Country business base.

4. Private Sector - Many public sector establishments such as schools are identified through the initial strategic search but are subsequently excluded from the final Strategic Companies list which measures private sector productivity in the Black Country.

5. Partner Information - Local intelligence is also applied to the list and it is updated on an annual basis. Local intelligence can suggest the addition of firms that that don’t strictly qualify for one of the parameters listed above but are seen to make a significant contribution to growth in the sub-region.

We have identified 2,160 strategic companies in the Black Country from the BvD FAME database in July 2018. The following infographic illustrates the economic impact of the strategic companies.

3 FAME is a financial information database of 7 million companies in the UK and Rep. of Ireland updated daily, with up to

10 years of data. Detailed financial, descriptive and ownership information for these companies plus summary. The database allows users to search by a wide selection of criteria (name, code, location, size, and many others).

Defining a Strategic Company

Page 4

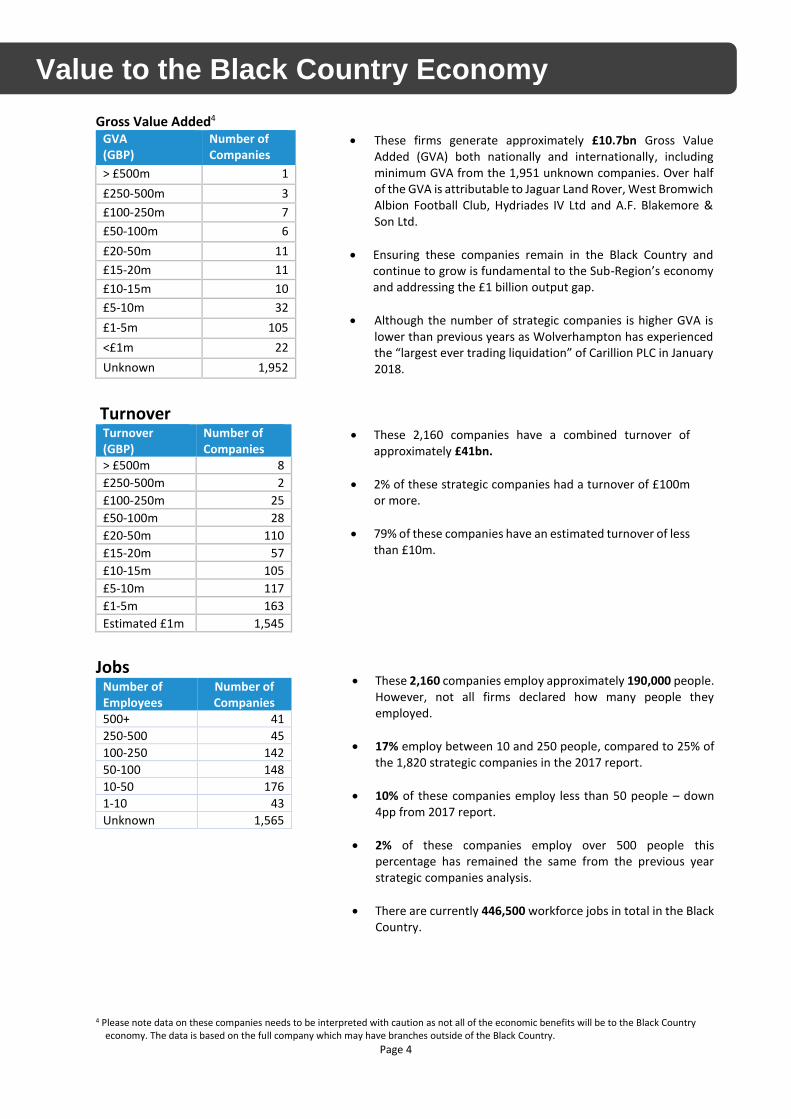

Gross Value Added4

GVA (GBP)

Number of Companies

> £500m 1

£250-500m 3

£100-250m 7

£50-100m 6

£20-50m 11

£15-20m 11

£10-15m 10

£5-10m 32

£1-5m 105

<£1m 22

Unknown 1,952

Turnover

Turnover (GBP)

Number of Companies

> £500m 8

£250-500m 2

£100-250m 25

£50-100m 28

£20-50m 110

£15-20m 57

£10-15m 105

£5-10m 117

£1-5m 163

Estimated £1m 1,545

Jobs

Number of Employees

Number of Companies

500+ 41

250-500 45

100-250 142

50-100 148

10-50 176

1-10 43

Unknown 1,565

4 Please note data on these companies needs to be interpreted with caution as not all of the economic benefits will be to the Black Country

economy. The data is based on the full company which may have branches outside of the Black Country.

• These 2,160 companies employ approximately 190,000 people. However, not all firms declared how many people they employed.

• 17% employ between 10 and 250 people, compared to 25% of the 1,820 strategic companies in the 2017 report.

• 10% of these companies employ less than 50 people – down 4pp from 2017 report.

• 2% of these companies employ over 500 people this percentage has remained the same from the previous year strategic companies analysis.

• There are currently 446,500 workforce jobs in total in the Black Country.

• These 2,160 companies have a combined turnover of approximately £41bn.

• 2% of these strategic companies had a turnover of £100m or more.

• 79% of these companies have an estimated turnover of less than £10m.

• These firms generate approximately £10.7bn Gross Value Added (GVA) both nationally and internationally, including minimum GVA from the 1,951 unknown companies. Over half of the GVA is attributable to Jaguar Land Rover, West Bromwich Albion Football Club, Hydriades IV Ltd and A.F. Blakemore & Son Ltd.

• Ensuring these companies remain in the Black Country and continue to grow is fundamental to the Sub-Region’s economy and addressing the £1 billion output gap.

• Although the number of strategic companies is higher GVA is lower than previous years as Wolverhampton has experienced the “largest ever trading liquidation” of Carillion PLC in January 2018.

Value to the Black Country Economy

Page 5

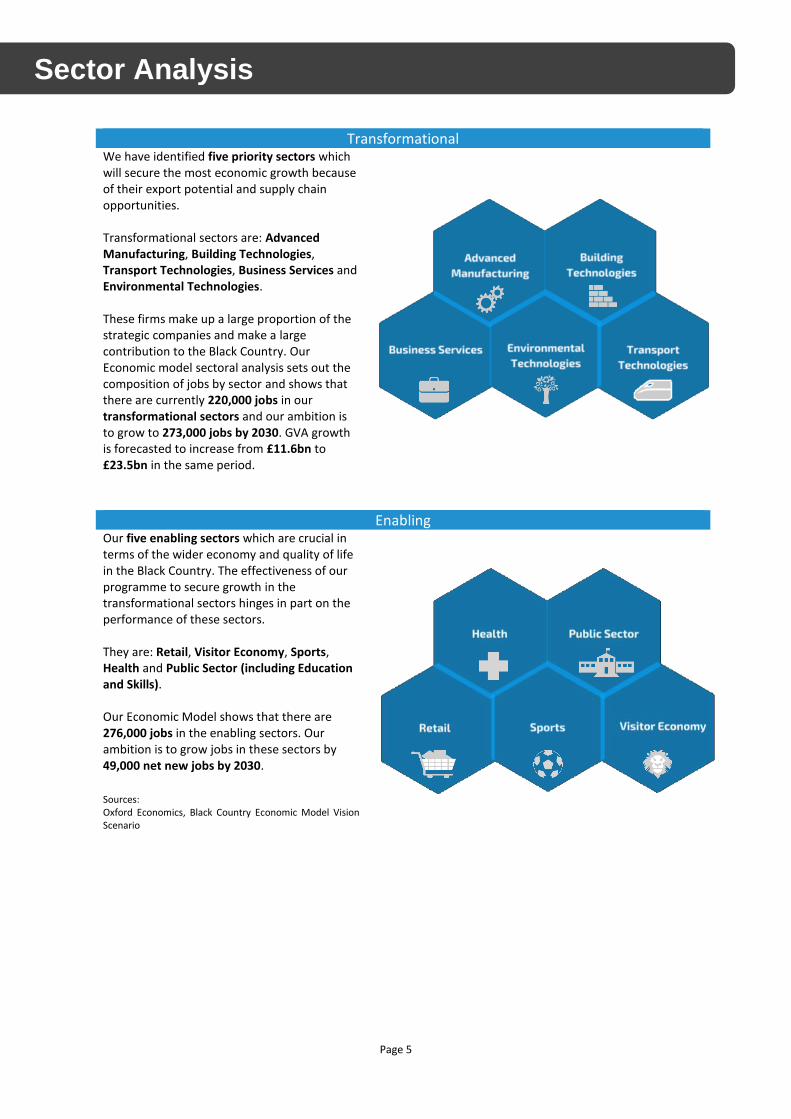

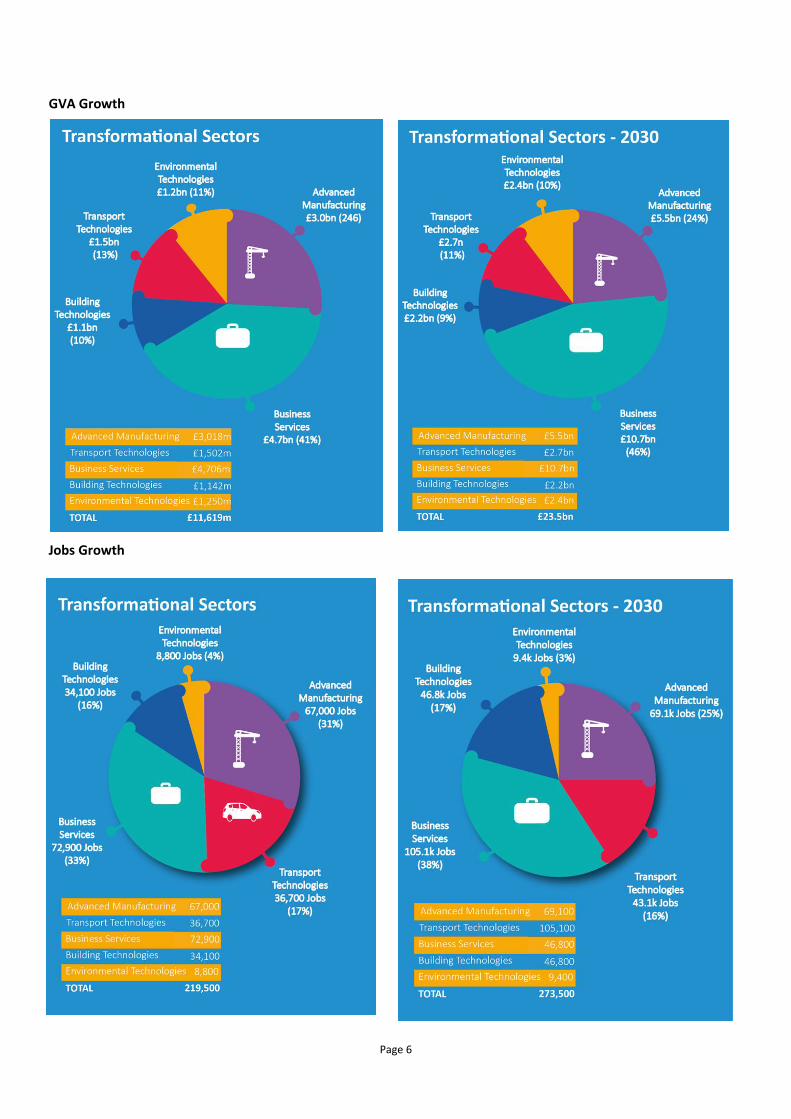

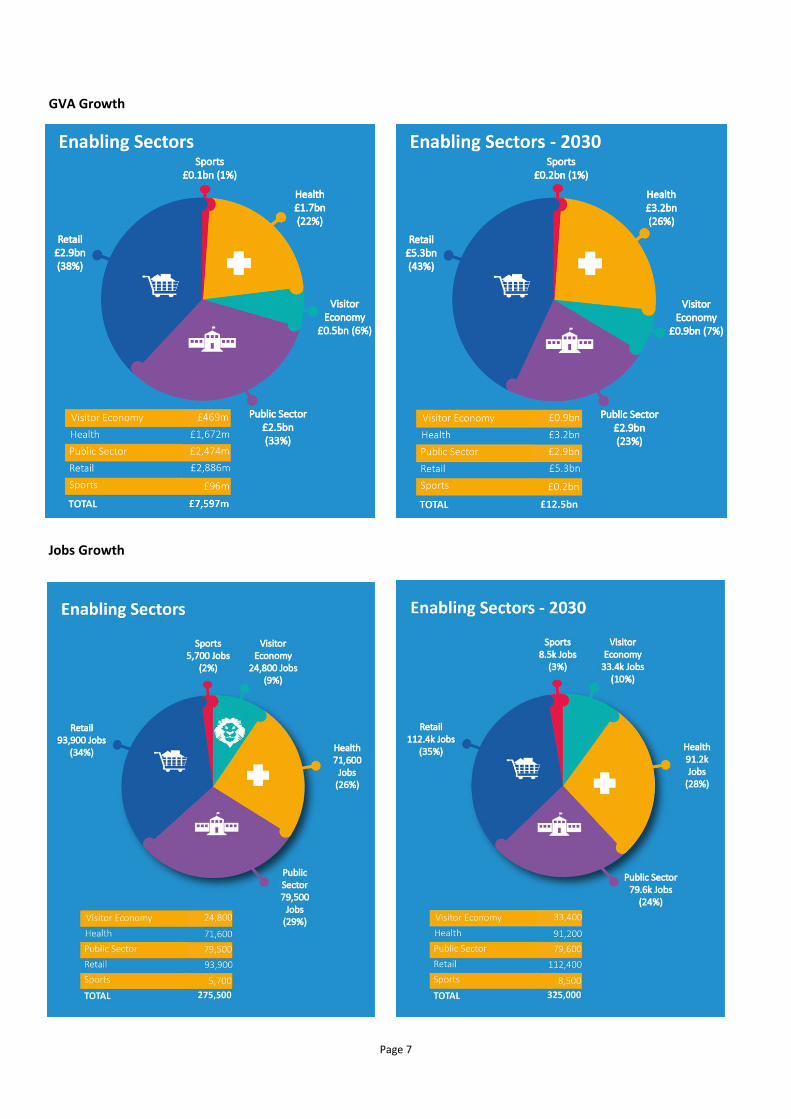

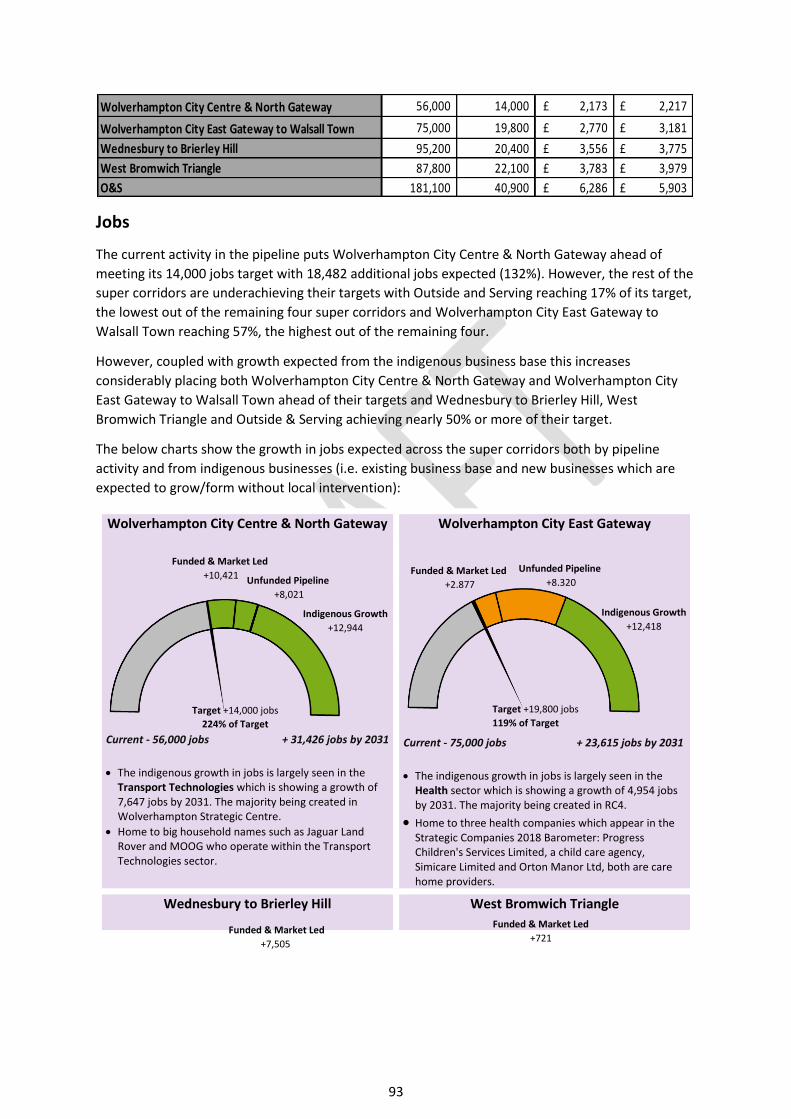

Transformational We have identified five priority sectors which will secure the most economic growth because of their export potential and supply chain opportunities. Transformational sectors are: Advanced Manufacturing, Building Technologies, Transport Technologies, Business Services and Environmental Technologies. These firms make up a large proportion of the strategic companies and make a large contribution to the Black Country. Our Economic model sectoral analysis sets out the composition of jobs by sector and shows that there are currently 220,000 jobs in our transformational sectors and our ambition is to grow to 273,000 jobs by 2030. GVA growth is forecasted to increase from £11.6bn to £23.5bn in the same period.

Enabling Our five enabling sectors which are crucial in terms of the wider economy and quality of life in the Black Country. The effectiveness of our programme to secure growth in the transformational sectors hinges in part on the performance of these sectors. They are: Retail, Visitor Economy, Sports, Health and Public Sector (including Education and Skills). Our Economic Model shows that there are 276,000 jobs in the enabling sectors. Our ambition is to grow jobs in these sectors by 49,000 net new jobs by 2030. Sources: Oxford Economics, Black Country Economic Model Vision Scenario

Sector Analysis

Page 6

GVA Growth

Jobs Growth

Page 7

GVA Growth

Jobs Growth

Page 8

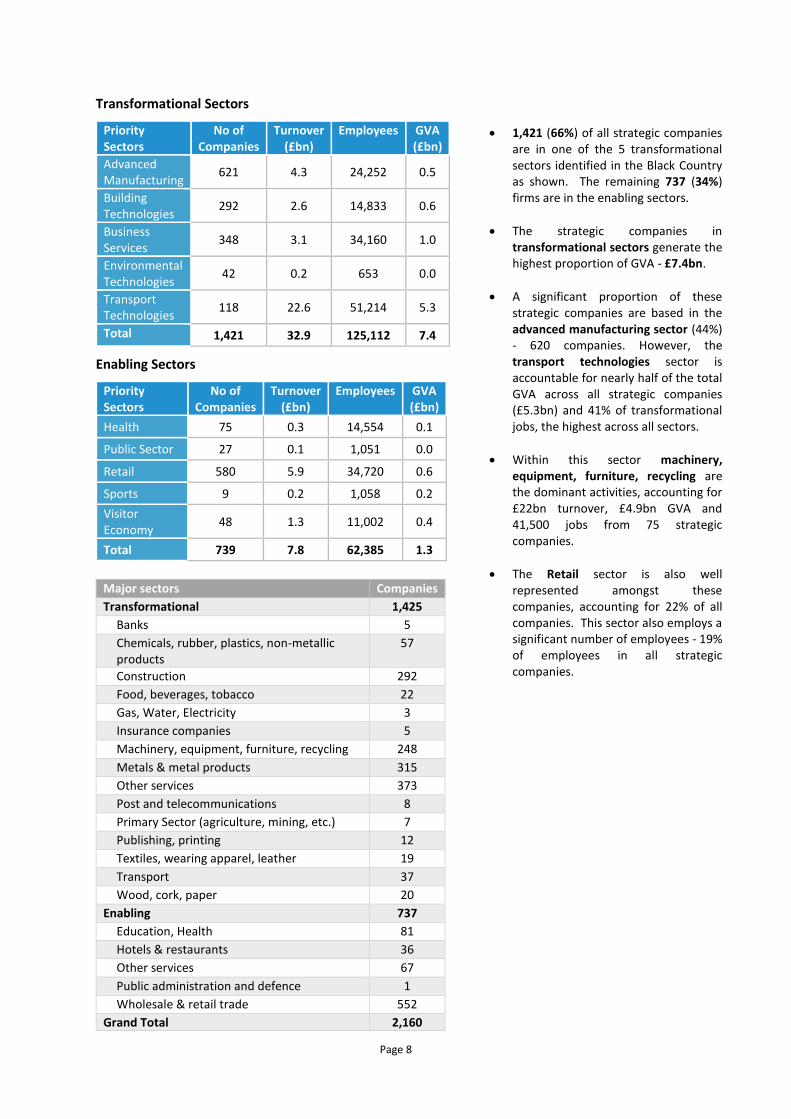

Transformational Sectors

Priority Sectors

No of Companies

Turnover (£bn)

Employees GVA (£bn)

Advanced Manufacturing

621 4.3 24,252 0.5

Building Technologies

292 2.6 14,833 0.6

Business Services

348 3.1 34,160 1.0

Environmental Technologies

42 0.2 653 0.0

Transport Technologies

118 22.6 51,214 5.3

Total 1,421 32.9 125,112 7.4

Enabling Sectors

Priority Sectors

No of Companies

Turnover (£bn)

Employees GVA (£bn)

Health 75 0.3 14,554 0.1

Public Sector 27 0.1 1,051 0.0

Retail 580 5.9 34,720 0.6

Sports 9 0.2 1,058 0.2

Visitor Economy

48 1.3 11,002 0.4

Total 739 7.8 62,385 1.3

Major sectors Companies

Transformational 1,425

Banks 5

Chemicals, rubber, plastics, non-metallic products

57

Construction 292

Food, beverages, tobacco 22

Gas, Water, Electricity 3

Insurance companies 5

Machinery, equipment, furniture, recycling 248

Metals & metal products 315

Other services 373

Post and telecommunications 8

Primary Sector (agriculture, mining, etc.) 7

Publishing, printing 12

Textiles, wearing apparel, leather 19

Transport 37

Wood, cork, paper 20

Enabling 737

Education, Health 81

Hotels & restaurants 36

Other services 67

Public administration and defence 1

Wholesale & retail trade 552

Grand Total 2,160

• 1,421 (66%) of all strategic companies are in one of the 5 transformational sectors identified in the Black Country as shown. The remaining 737 (34%) firms are in the enabling sectors.

• The strategic companies in transformational sectors generate the highest proportion of GVA - £7.4bn.

• A significant proportion of these strategic companies are based in the advanced manufacturing sector (44%) - 620 companies. However, the transport technologies sector is accountable for nearly half of the total GVA across all strategic companies (£5.3bn) and 41% of transformational jobs, the highest across all sectors.

• Within this sector machinery, equipment, furniture, recycling are the dominant activities, accounting for £22bn turnover, £4.9bn GVA and 41,500 jobs from 75 strategic companies.

• The Retail sector is also well represented amongst these companies, accounting for 22% of all companies. This sector also employs a significant number of employees - 19% of employees in all strategic companies.

Page 9

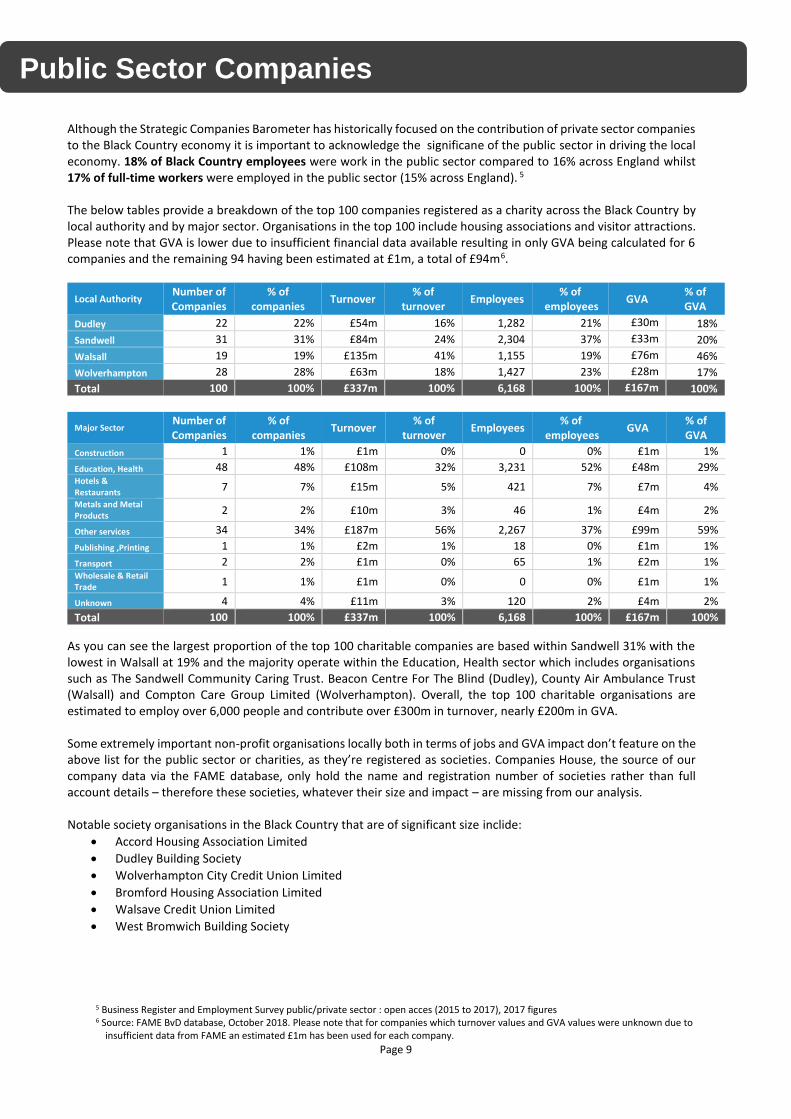

Although the Strategic Companies Barometer has historically focused on the contribution of private sector companies to the Black Country economy it is important to acknowledge the significane of the public sector in driving the local economy. 18% of Black Country employees were work in the public sector compared to 16% across England whilst 17% of full-time workers were employed in the public sector (15% across England). 5 The below tables provide a breakdown of the top 100 companies registered as a charity across the Black Country by local authority and by major sector. Organisations in the top 100 include housing associations and visitor attractions. Please note that GVA is lower due to insufficient financial data available resulting in only GVA being calculated for 6 companies and the remaining 94 having been estimated at £1m, a total of £94m6.

Local Authority Number of Companies

% of companies

Turnover % of

turnover Employees

% of employees

GVA % of GVA

Dudley 22 22% £54m 16% 1,282 21% £30m 18%

Sandwell 31 31% £84m 24% 2,304 37% £33m 20%

Walsall 19 19% £135m 41% 1,155 19% £76m 46%

Wolverhampton 28 28% £63m 18% 1,427 23% £28m 17%

Total 100 100% £337m 100% 6,168 100% £167m 100%

Major Sector Number of Companies

% of companies

Turnover % of

turnover Employees

% of employees

GVA % of GVA

Construction 1 1% £1m 0% 0 0% £1m 1%

Education, Health 48 48% £108m 32% 3,231 52% £48m 29% Hotels & Restaurants

7 7% £15m 5% 421 7% £7m 4%

Metals and Metal Products 2 2% £10m 3% 46 1% £4m 2%

Other services 34 34% £187m 56% 2,267 37% £99m 59%

Publishing ,Printing 1 1% £2m 1% 18 0% £1m 1%

Transport 2 2% £1m 0% 65 1% £2m 1% Wholesale & Retail Trade 1 1% £1m 0% 0 0% £1m 1%

Unknown 4 4% £11m 3% 120 2% £4m 2%

Total 100 100% £337m 100% 6,168 100% £167m 100%

As you can see the largest proportion of the top 100 charitable companies are based within Sandwell 31% with the lowest in Walsall at 19% and the majority operate within the Education, Health sector which includes organisations such as The Sandwell Community Caring Trust. Beacon Centre For The Blind (Dudley), County Air Ambulance Trust (Walsall) and Compton Care Group Limited (Wolverhampton). Overall, the top 100 charitable organisations are estimated to employ over 6,000 people and contribute over £300m in turnover, nearly £200m in GVA. Some extremely important non-profit organisations locally both in terms of jobs and GVA impact don’t feature on the above list for the public sector or charities, as they’re registered as societies. Companies House, the source of our company data via the FAME database, only hold the name and registration number of societies rather than full account details – therefore these societies, whatever their size and impact – are missing from our analysis. Notable society organisations in the Black Country that are of significant size inclide:

• Accord Housing Association Limited

• Dudley Building Society

• Wolverhampton City Credit Union Limited

• Bromford Housing Association Limited

• Walsave Credit Union Limited

• West Bromwich Building Society

5 Business Register and Employment Survey public/private sector : open acces (2015 to 2017), 2017 figures 6 Source: FAME BvD database, October 2018. Please note that for companies which turnover values and GVA values were unknown due to

insufficient data from FAME an estimated £1m has been used for each company.

Public Sector Companies

Page 10

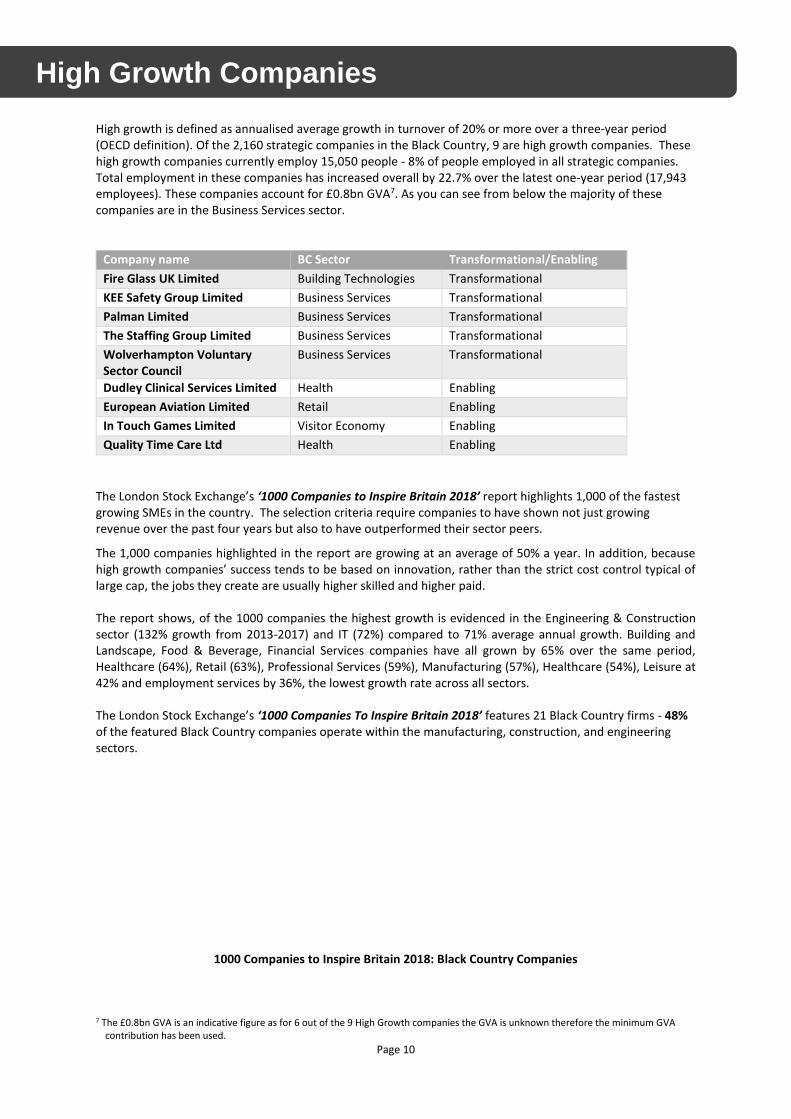

High growth is defined as annualised average growth in turnover of 20% or more over a three-year period (OECD definition). Of the 2,160 strategic companies in the Black Country, 9 are high growth companies. These high growth companies currently employ 15,050 people - 8% of people employed in all strategic companies. Total employment in these companies has increased overall by 22.7% over the latest one-year period (17,943 employees). These companies account for £0.8bn GVA7. As you can see from below the majority of these companies are in the Business Services sector.

Company name BC Sector Transformational/Enabling

Fire Glass UK Limited Building Technologies Transformational

KEE Safety Group Limited Business Services Transformational

Palman Limited Business Services Transformational

The Staffing Group Limited Business Services Transformational

Wolverhampton Voluntary Sector Council

Business Services Transformational

Dudley Clinical Services Limited Health Enabling

European Aviation Limited Retail Enabling

In Touch Games Limited Visitor Economy Enabling

Quality Time Care Ltd Health Enabling

The London Stock Exchange’s ‘1000 Companies to Inspire Britain 2018’ report highlights 1,000 of the fastest growing SMEs in the country. The selection criteria require companies to have shown not just growing revenue over the past four years but also to have outperformed their sector peers.

The 1,000 companies highlighted in the report are growing at an average of 50% a year. In addition, because high growth companies’ success tends to be based on innovation, rather than the strict cost control typical of large cap, the jobs they create are usually higher skilled and higher paid. The report shows, of the 1000 companies the highest growth is evidenced in the Engineering & Construction sector (132% growth from 2013-2017) and IT (72%) compared to 71% average annual growth. Building and Landscape, Food & Beverage, Financial Services companies have all grown by 65% over the same period, Healthcare (64%), Retail (63%), Professional Services (59%), Manufacturing (57%), Healthcare (54%), Leisure at 42% and employment services by 36%, the lowest growth rate across all sectors. The London Stock Exchange’s ‘1000 Companies To Inspire Britain 2018’ features 21 Black Country firms - 48% of the featured Black Country companies operate within the manufacturing, construction, and engineering sectors.

1000 Companies to Inspire Britain 2018: Black Country Companies

7 The £0.8bn GVA is an indicative figure as for 6 out of the 9 High Growth companies the GVA is unknown therefore the minimum GVA

contribution has been used.

High Growth Companies

Page 11

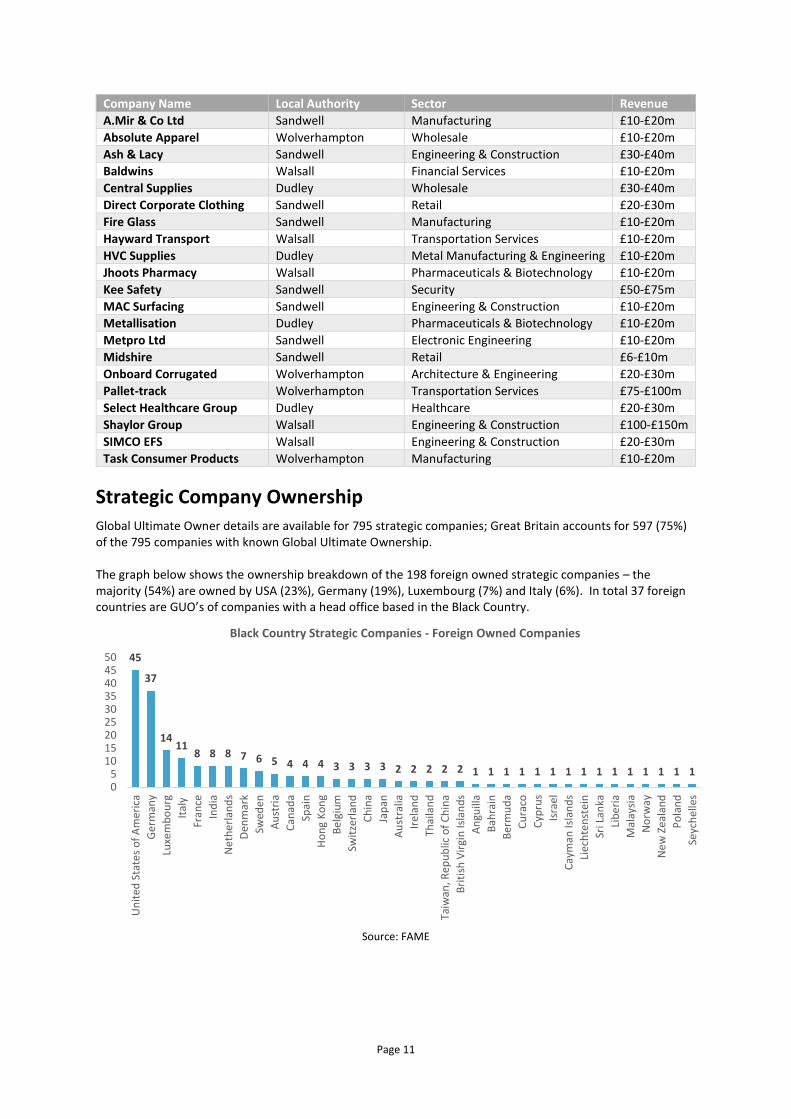

Company Name Local Authority Sector Revenue

A.Mir & Co Ltd Sandwell Manufacturing £10-£20m

Absolute Apparel Wolverhampton Wholesale £10-£20m

Ash & Lacy Sandwell Engineering & Construction £30-£40m

Baldwins Walsall Financial Services £10-£20m

Central Supplies Dudley Wholesale £30-£40m

Direct Corporate Clothing Sandwell Retail £20-£30m

Fire Glass Sandwell Manufacturing £10-£20m

Hayward Transport Walsall Transportation Services £10-£20m

HVC Supplies Dudley Metal Manufacturing & Engineering £10-£20m

Jhoots Pharmacy Walsall Pharmaceuticals & Biotechnology £10-£20m

Kee Safety Sandwell Security £50-£75m

MAC Surfacing Sandwell Engineering & Construction £10-£20m

Metallisation Dudley Pharmaceuticals & Biotechnology £10-£20m

Metpro Ltd Sandwell Electronic Engineering £10-£20m

Midshire Sandwell Retail £6-£10m

Onboard Corrugated Wolverhampton Architecture & Engineering £20-£30m

Pallet-track Wolverhampton Transportation Services £75-£100m

Select Healthcare Group Dudley Healthcare £20-£30m

Shaylor Group Walsall Engineering & Construction £100-£150m

SIMCO EFS Walsall Engineering & Construction £20-£30m

Task Consumer Products Wolverhampton Manufacturing £10-£20m

Strategic Company Ownership

Global Ultimate Owner details are available for 795 strategic companies; Great Britain accounts for 597 (75%) of the 795 companies with known Global Ultimate Ownership. The graph below shows the ownership breakdown of the 198 foreign owned strategic companies – the majority (54%) are owned by USA (23%), Germany (19%), Luxembourg (7%) and Italy (6%). In total 37 foreign countries are GUO’s of companies with a head office based in the Black Country.

Source: FAME

45

37

1411

8 8 8 7 6 5 4 4 4 3 3 3 3 2 2 2 2 2 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

05

101520253035404550

Un

ited

Sta

tes

of

Am

eric

a

Ge

rman

y

Luxe

mb

ou

rg

Ital

y

Fran

ce

Ind

ia

Ne

the

rlan

ds

Den

mar

k

Swed

en

Au

stri

a

Can

ada

Spai

n

Ho

ng

Ko

ng

Bel

giu

m

Swit

zerl

and

Ch

ina

Jap

an

Au

stra

lia

Irel

and

Thai

lan

d

Taiw

an, R

epu

blic

of

Ch

ina

Bri

tish

Vir

gin

Isla

nd

s

An

guill

a

Bah

rain

Ber

mu

da

Cu

raco

Cyp

rus

Isra

el

Cay

man

Isla

nd

s

Liec

hte

nst

ein

Sri L

anka

Lib

eri

a

Mal

aysi

a

No

rway

Ne

w Z

eal

and

Po

lan

d

Seyc

hel

les

Black Country Strategic Companies - Foreign Owned Companies

0

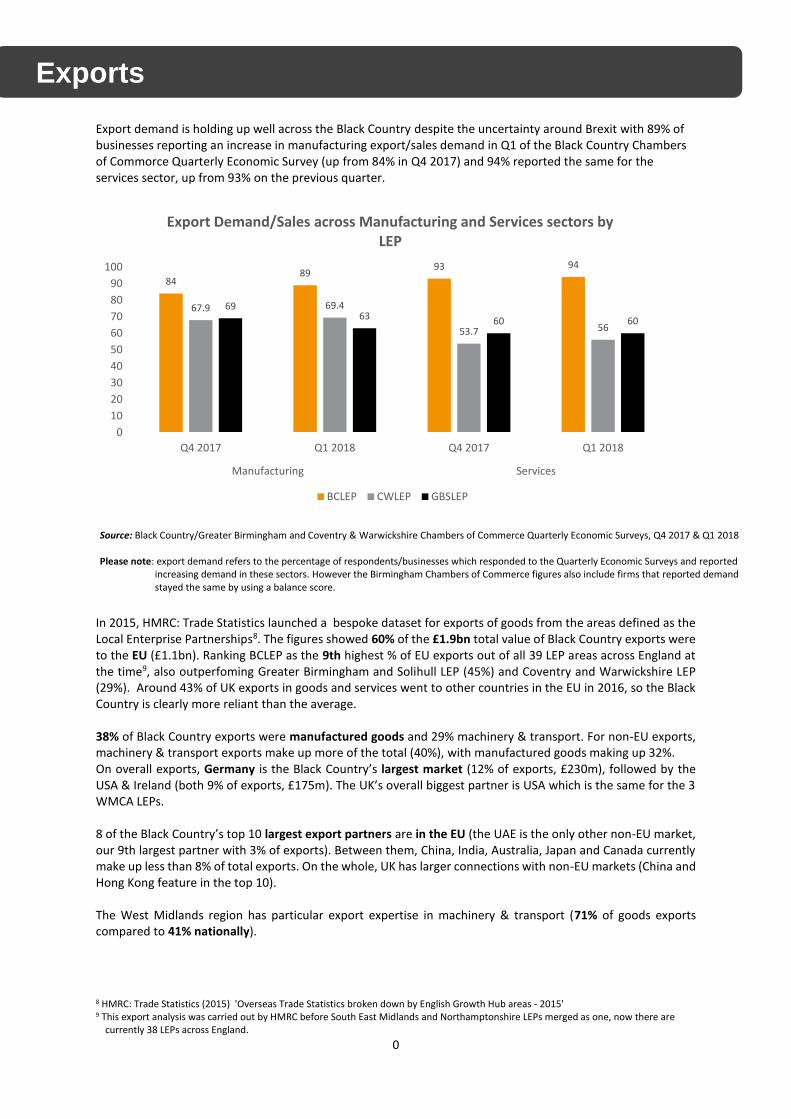

Export demand is holding up well across the Black Country despite the uncertainty around Brexit with 89% of businesses reporting an increase in manufacturing export/sales demand in Q1 of the Black Country Chambers of Commorce Quarterly Economic Survey (up from 84% in Q4 2017) and 94% reported the same for the services sector, up from 93% on the previous quarter.

In 2015, HMRC: Trade Statistics launched a bespoke dataset for exports of goods from the areas defined as the Local Enterprise Partnerships8. The figures showed 60% of the £1.9bn total value of Black Country exports were to the EU (£1.1bn). Ranking BCLEP as the 9th highest % of EU exports out of all 39 LEP areas across England at the time9, also outperfoming Greater Birmingham and Solihull LEP (45%) and Coventry and Warwickshire LEP (29%). Around 43% of UK exports in goods and services went to other countries in the EU in 2016, so the Black Country is clearly more reliant than the average. 38% of Black Country exports were manufactured goods and 29% machinery & transport. For non-EU exports, machinery & transport exports make up more of the total (40%), with manufactured goods making up 32%. On overall exports, Germany is the Black Country’s largest market (12% of exports, £230m), followed by the USA & Ireland (both 9% of exports, £175m). The UK’s overall biggest partner is USA which is the same for the 3 WMCA LEPs. 8 of the Black Country’s top 10 largest export partners are in the EU (the UAE is the only other non-EU market, our 9th largest partner with 3% of exports). Between them, China, India, Australia, Japan and Canada currently make up less than 8% of total exports. On the whole, UK has larger connections with non-EU markets (China and Hong Kong feature in the top 10). The West Midlands region has particular export expertise in machinery & transport (71% of goods exports compared to 41% nationally).

8 HMRC: Trade Statistics (2015) 'Overseas Trade Statistics broken down by English Growth Hub areas - 2015' 9 This export analysis was carried out by HMRC before South East Midlands and Northamptonshire LEPs merged as one, now there are

currently 38 LEPs across England.

8489

93 94

67.9 69.4

53.7 56

6963 60 60

0

10

20

30

40

50

60

70

80

90

100

Q4 2017 Q1 2018 Q4 2017 Q1 2018

Manufacturing Services

Export Demand/Sales across Manufacturing and Services sectors by LEP

BCLEP CWLEP GBSLEP

Exports

Source: Black Country/Greater Birmingham and Coventry & Warwickshire Chambers of Commerce Quarterly Economic Surveys, Q4 2017 & Q1 2018 Please note: export demand refers to the percentage of respondents/businesses which responded to the Quarterly Economic Surveys and reported

increasing demand in these sectors. However the Birmingham Chambers of Commerce figures also include firms that reported demand stayed the same by using a balance score.

Page 1

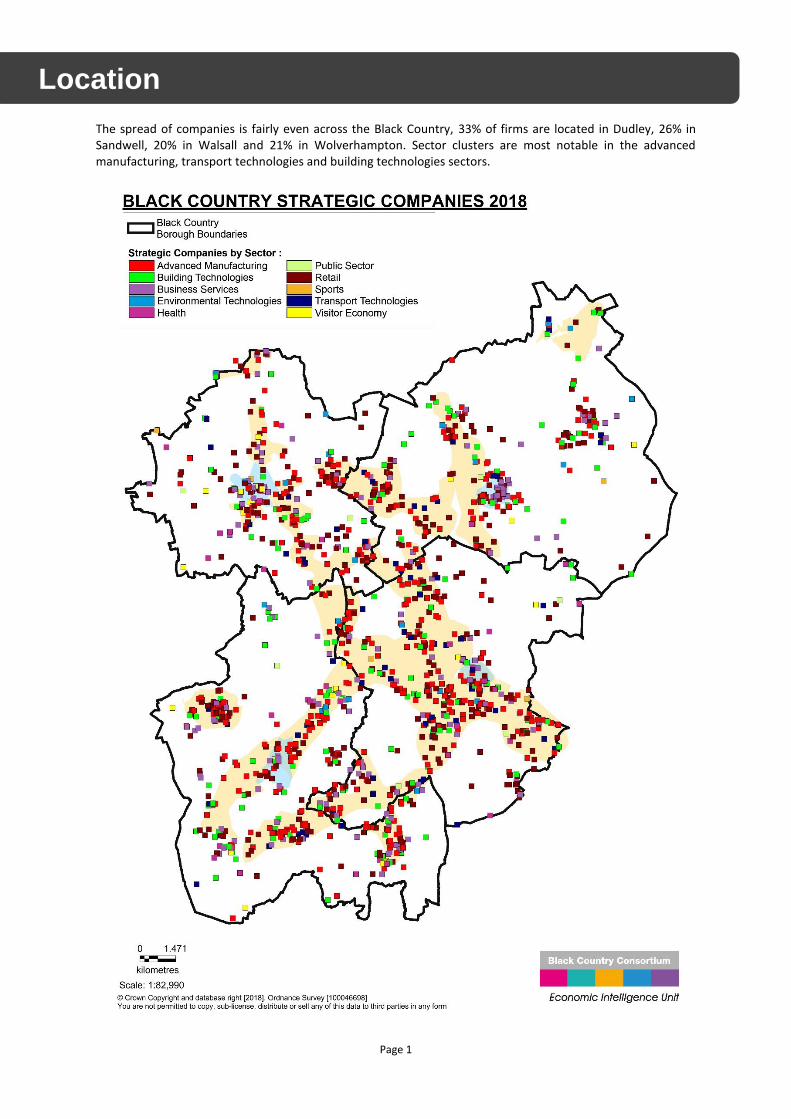

The spread of companies is fairly even across the Black Country, 33% of firms are located in Dudley, 26% in Sandwell, 20% in Walsall and 21% in Wolverhampton. Sector clusters are most notable in the advanced manufacturing, transport technologies and building technologies sectors.

Location

Page 2

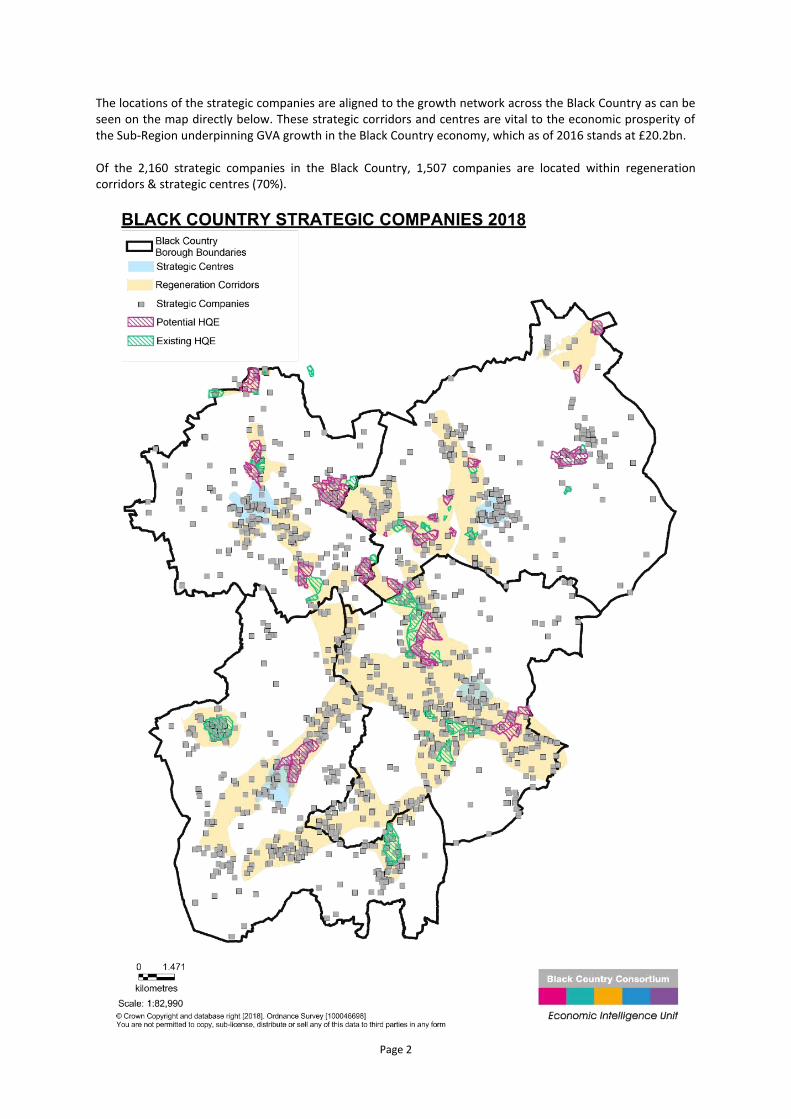

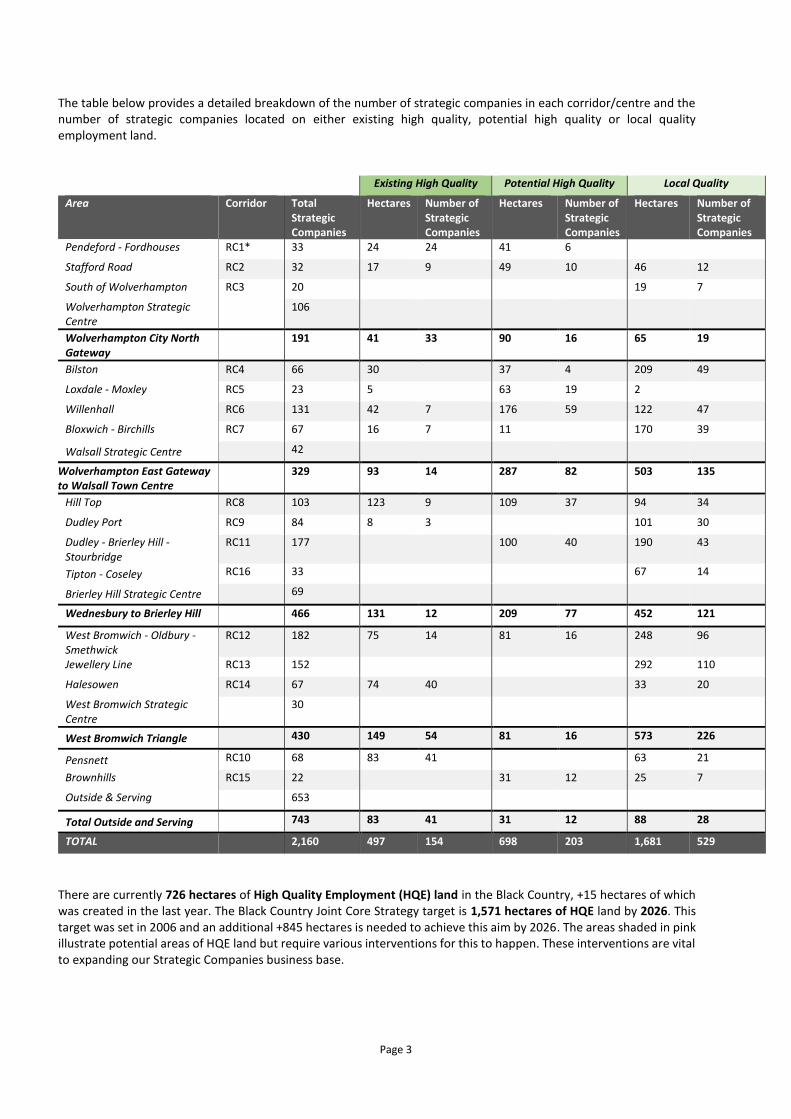

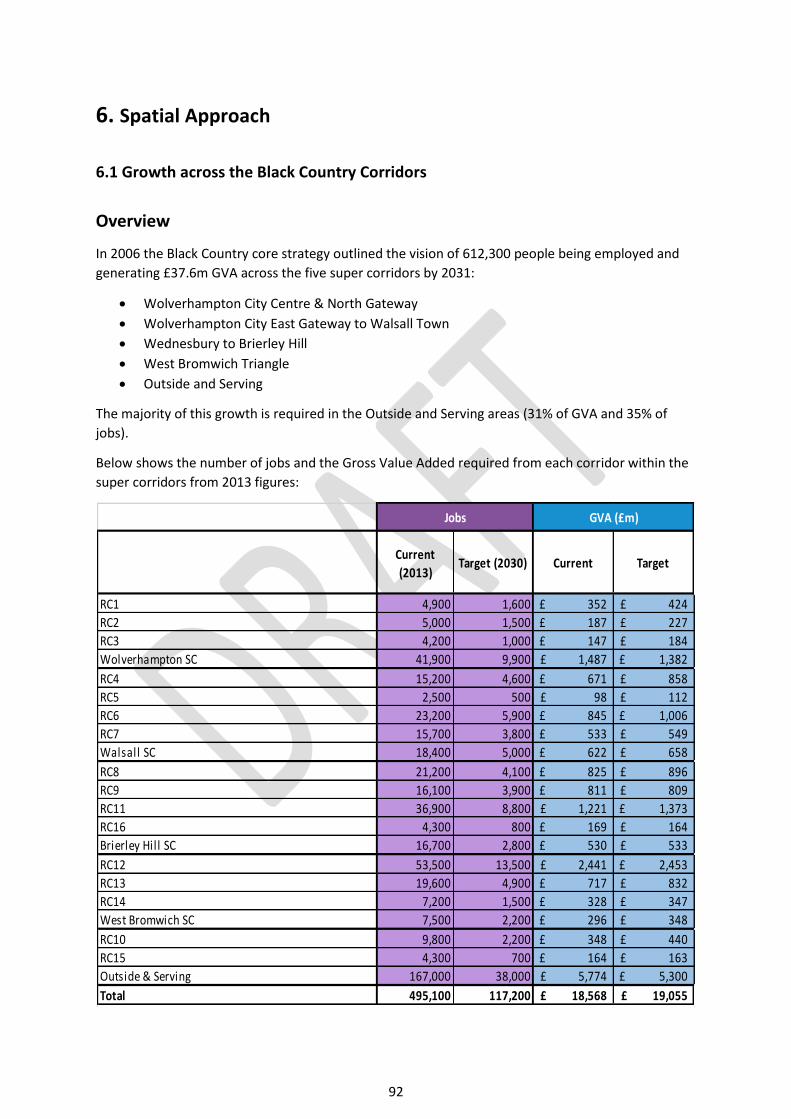

The locations of the strategic companies are aligned to the growth network across the Black Country as can be seen on the map directly below. These strategic corridors and centres are vital to the economic prosperity of the Sub-Region underpinning GVA growth in the Black Country economy, which as of 2016 stands at £20.2bn. Of the 2,160 strategic companies in the Black Country, 1,507 companies are located within regeneration corridors & strategic centres (70%).

Page 3

The table below provides a detailed breakdown of the number of strategic companies in each corridor/centre and the number of strategic companies located on either existing high quality, potential high quality or local quality employment land.

Existing High Quality Potential High Quality Local Quality

Area Corridor Total Strategic Companies

Hectares Number of Strategic Companies

Hectares Number of Strategic Companies

Hectares Number of Strategic Companies

Pendeford - Fordhouses RC1* 33 24 24 41 6

Stafford Road RC2 32 17 9 49 10 46 12

South of Wolverhampton RC3 20 19 7

Wolverhampton Strategic Centre

106

Wolverhampton City North Gateway

191 41 33 90 16 65 19

Bilston RC4 66 30 37 4 209 49

Loxdale - Moxley RC5 23 5 63 19 2

Willenhall RC6 131 42 7 176 59 122 47

Bloxwich - Birchills RC7 67 16 7 11 170 39

Walsall Strategic Centre 42

Wolverhampton East Gateway to Walsall Town Centre

329 93 14 287 82 503 135

Hill Top RC8 103 123 9 109 37 94 34

Dudley Port RC9 84 8 3 101 30

Dudley - Brierley Hill - Stourbridge

RC11 177 100 40 190 43

Tipton - Coseley RC16 33 67 14

Brierley Hill Strategic Centre 69

Wednesbury to Brierley Hill 466 131 12 209 77 452 121

West Bromwich - Oldbury - Smethwick

RC12 182 75 14 81 16 248 96

Jewellery Line RC13 152 292 110

Halesowen RC14 67 74 40 33 20

West Bromwich Strategic Centre

30

West Bromwich Triangle 430 149 54 81 16 573 226

Pensnett RC10 68 83 41 63 21

Brownhills RC15 22 31 12 25 7

Outside & Serving 653

Total Outside and Serving 743 83 41 31 12 88 28

TOTAL 2,160 497 154 698 203 1,681 529

There are currently 726 hectares of High Quality Employment (HQE) land in the Black Country, +15 hectares of which was created in the last year. The Black Country Joint Core Strategy target is 1,571 hectares of HQE land by 2026. This target was set in 2006 and an additional +845 hectares is needed to achieve this aim by 2026. The areas shaded in pink illustrate potential areas of HQE land but require various interventions for this to happen. These interventions are vital to expanding our Strategic Companies business base.

Page 4

All mapping in this document is subject to the following statement: © Crown Copyright and database right [2018]. Ordnance Survey [100046698] You are not permitted to copy, sub-license, distribute or sell any of this data to third parties in any form.

Page 5

Appendix - Strategic Company List

Company name Local Authority BC Sector

00261074 Dudley Advanced Manufacturing

02229539 PLC Dudley Business Services

1ST Access Group Limited Walsall Advanced Manufacturing

21stcentury Drinks Limited Walsall Retail

360 - DMG Ltd Walsall Environmental Technologies

4 Oak Limited Dudley Retail

65bit Software Limited Dudley Business Services

77 GLB Limited Walsall Business Services

8p.M. Chemist Limited Walsall Retail

A & A Walters Limited Dudley Business Services

A & D Joinery & Interiors Limited Dudley Advanced Manufacturing

A & J Mucklow Group P L C Dudley Business Services

A & M EDM Limited Sandwell Advanced Manufacturing

A & T Enclosures Limited Dudley Advanced Manufacturing

A C Steels Ltd Walsall Advanced Manufacturing

A J S Metals Limited Walsall Advanced Manufacturing

A P B Painting Services Limited Dudley Building Technologies

A S K Property Construction Limited Walsall Building Technologies

A Thompson Motor Bodies Limited Sandwell Retail

A&H Construction & Developments (Holdings) Limited Dudley Building Technologies

A&T Chatha Ltd. Walsall Building Technologies

A. & P.J. Steels Limited Dudley Advanced Manufacturing

A. B. Construction (West Midlands) Limited Wolverhampton Building Technologies

A. Hingley Transport (Brierley Hill) Limited Dudley Transport Technologies

A. MIR & CO. Limited Sandwell Retail

A. S. K. Developments Limited Wolverhampton Business Services

A. T. Sheds & Fencing Limited Dudley Advanced Manufacturing

A. W. Baxter Limited Wolverhampton Transport Technologies

A.B.A Cranes Limited Dudley Business Services

A.B.R. (Specialist Welding) Limited Sandwell Advanced Manufacturing

A.B.S. (Burton) Limited Walsall Retail

A.Clarke & Co.(Smethwick)Limited Sandwell Transport Technologies

A.E.Chapman & Co.,(Old Hill)Limited Sandwell Retail

A.E.Poxon & Sons Limited Walsall Retail

A.F.Blakemore And Son Limited Walsall Retail

A.J. Baker (Grinding) Limited Walsall Advanced Manufacturing

A.J. Metal Products Limited Dudley Advanced Manufacturing

A.K. International (Imports & Exports) Limited Dudley Retail

A.K.Hughes Limited Dudley Advanced Manufacturing

A.P.D. Truck Mixer Repairs Ltd Walsall Advanced Manufacturing

A.S. Rubber & Plastics Limited Sandwell Advanced Manufacturing

A.S.H. Plastics (Wolverhampton) Limited Wolverhampton Advanced Manufacturing

A.T.B. Systems Limited Dudley Advanced Manufacturing

A2Z Wholesale Fashion Jewellery Limited Dudley Retail

ABA Crane Hire Limited Dudley Business Services

Abacus Builders Merchants (Walsall) Limited Walsall Retail

Abbey Spuncast Limited Walsall Advanced Manufacturing

Page 6

ABC Early Learning & Childcare Centre UK Limited Wolverhampton Business Services

ABI Facilities Engineering Ltd Walsall Building Technologies

Able Recruitment Services Limited Wolverhampton Business Services

Absolute Apparel Limited Wolverhampton Retail

Accumix Concrete Limited Dudley Advanced Manufacturing

Accurate Laser Cutting Limited Sandwell Advanced Manufacturing

Accurate Section Benders Limited Dudley Advanced Manufacturing

Acerinox (U.K.) Limited Walsall Retail

ACL (2002) Limited Sandwell Advanced Manufacturing

Acme Spring CO. Limited(The) Sandwell Advanced Manufacturing

Acorn To Oaks Advisory And Consultancy Services Limited Wolverhampton Business Services

Acotis Enterprise Limited Wolverhampton Retail

Acousta Foam Limited Dudley Building Technologies

Acoustaproducts Limited Dudley Building Technologies

Acquire The Best Limited Dudley Advanced Manufacturing

Active 8 Care Ltd Dudley Health

Acton Banks Limited Wolverhampton Business Services

Actuant Acquisitions Finance Limited Walsall Business Services

Actuant Global Financing Limited Walsall Business Services

Adam Jones Investments Limited Dudley Transport Technologies

Adams Enclosures Limited Walsall Advanced Manufacturing

Adastra Access Limited Walsall Building Technologies

ADI Treatments Limited Sandwell Advanced Manufacturing

Admiral Self Storage Ltd Walsall Business Services

Adroit Accessories Limited Walsall Retail

Advanced Chemical Etching Limited Wolverhampton Advanced Manufacturing

Advanced Delivery Services Limited Dudley Transport Technologies

Advanced Direct Mail Limited Dudley Business Services

Advanced Seals And Gaskets Limited Dudley Advanced Manufacturing

Advancel Limited Dudley Transport Technologies

Adwin Spring Company Limited Sandwell Advanced Manufacturing

Aeroplas (U.K.) Limited Sandwell Advanced Manufacturing

Aerotech Inspection & NDT Limited Sandwell Business Services

AGS Accountants And Business Advisors Limited Dudley Business Services

AIB Foods Limited Wolverhampton Retail

Air Seating (Holdings) Limited Dudley Advanced Manufacturing

Air Seating Limited Dudley Advanced Manufacturing

Airline Component Services Limited Walsall Transport Technologies

Airport Travel Limited Sandwell Business Services

AJS Profiles Limited Sandwell Business Services

AJT Supplies Limited Sandwell Advanced Manufacturing

Akaal Plastics Ltd Sandwell Advanced Manufacturing

Alamgeer Foods Limited Walsall Retail

Alan Warwick Limited Walsall Retail

Alanto Limited Walsall Advanced Manufacturing

Albany Finance Co.Limited(The) Dudley Business Services

Albert Jagger Holdings Limited Walsall Retail

Albion Developments (Midlands) Limited Sandwell Building Technologies

Albion Leasing (West Midlands) Limited Dudley Business Services

Albion Sections Limited Sandwell Advanced Manufacturing

Alca Fasteners Limited Walsall Advanced Manufacturing

Page 7

Alcomet Limited Dudley Retail

Aldridge Accident & Repair Centre Limited Walsall Retail

Aldridge Trimming Limited Wolverhampton Retail

Alexander And James Limited Dudley Retail

Alexandra House Care Services Limited Dudley Business Services

Alexara Limited Sandwell Retail

Alissa Jebal Alab Joint Venture Company Limited Sandwell Health

All Alloy Slitting Services Limited Sandwell Advanced Manufacturing

All Clear Services Limited Walsall Environmental Technologies

All Seasons Contracting CO. Limited Dudley Building Technologies

Allens Crankshafts Ltd Wolverhampton Advanced Manufacturing

Alliance In Partnership Limited Dudley Visitor Economy

Alliance Optical CO. (Harborne) Limited Walsall Retail

Allied International Trading Limited Sandwell Health

Allied Machine & Engineering CO. (Europe) Ltd. Dudley Retail

ALM Distribution Limited Dudley Retail

Alpha Designs Upholstery Limited Wolverhampton Advanced Manufacturing

Alphamation Limited Dudley Transport Technologies

Alpharm Ltd Wolverhampton Retail

Alpha-Rowen Limited Sandwell Advanced Manufacturing

Alphaside Limited Sandwell Retail

Alphonsus Homes Limited Dudley Business Services

Alphonsus Services Limited Dudley Business Services

Alstain Metal Services Limited Dudley Retail

Alternative Trading 2014 Ltd Walsall Environmental Technologies

Altrad Beaver 84 Limited Sandwell Retail

Alucast Limited Walsall Advanced Manufacturing

Aluminium Special Products Limited Dudley Advanced Manufacturing

Alwin Limited Sandwell Environmental Technologies

Amber Shearing Limited Sandwell Advanced Manufacturing

Ambertex Limited Sandwell Retail

Ames Group Limited Dudley Public Sector

Amlin Motors Limited Dudley Retail

Amojess Limited Sandwell Retail

Amphion Construction Limited Dudley Building Technologies

Ample Fabrics Limited Wolverhampton Retail

Ample Limited Wolverhampton Advanced Manufacturing

Amtella Limited Walsall Building Technologies

AMX Design Limited Dudley Retail

Ancol Pet Products Limited Walsall Advanced Manufacturing

Andrew Wommack Ministries - Europe Walsall Business Services

Andrews Sykes Group PLC Wolverhampton Business Services

Andyfreight Holdings Limited Dudley Transport Technologies

Angel Springs Holdings Limited Wolverhampton Visitor Economy

Angle Ring Holdings Limited Sandwell Advanced Manufacturing

Anocote Limited Wolverhampton Advanced Manufacturing

Ansaldo Nuclear Limited Wolverhampton Transport Technologies

Ansell Jones Limited Walsall Transport Technologies

Anthony C. Rickards Limited Walsall Retail

Anvil Steels (Sandwell) Limited Sandwell Advanced Manufacturing

AP Lifting Gear Company Ltd. Dudley Retail

Page 8

Apex Machining Services Limited Sandwell Advanced Manufacturing

APG UK Limited Dudley Business Services

Apic UK Limited Sandwell Advanced Manufacturing

Apollo Chemicals Group Limited Dudley Business Services

Apollo Flow Measurement Limited Walsall Transport Technologies

Applied Coating Technologies Limited Sandwell Business Services

Apton Partitioning Limited Dudley Advanced Manufacturing

Aqua Holdings Limited Sandwell Advanced Manufacturing

Arabis Building Limited Walsall Building Technologies

Arc Alloys Limited Dudley Advanced Manufacturing

Arc Specialist Engineering Limited Wolverhampton Business Services

Arcare (West Midlands) Limited Wolverhampton Business Services

Arcc Communications Limited Sandwell Building Technologies

Arcelor SSC UK Barking Limited Wolverhampton Advanced Manufacturing

Arcelormittal Distribution Solutions UK Limited Wolverhampton Retail

Arcelormittal Tailored Blanks Birmingham Limited Sandwell Transport Technologies

Ardel OEM Limited Wolverhampton Retail

Arford Steel Profiles Limited Dudley Advanced Manufacturing

Argus Fire Protection Company Limited Dudley Building Technologies

ARK Aurora Ltd Sandwell Business Services

Arlec Fabrications Limited Sandwell Advanced Manufacturing

Arlec Management Limited Sandwell Advanced Manufacturing

Armoloy (U.K.) Limited Wolverhampton Advanced Manufacturing

Armon Limited Sandwell Advanced Manufacturing

Art Industrial Limited Wolverhampton Building Technologies

Asbestos Abatement Services Limited Walsall Building Technologies

Ascon Industrial Roofing Limited Dudley Building Technologies

Ash & Lacy Automotive Limited Sandwell Advanced Manufacturing

Ash & Lacy Pressings Limited Sandwell Advanced Manufacturing

Ashdale Care Homes Limited Dudley Business Services

Ashley Manor Upholstery Limited Dudley Advanced Manufacturing

Ashmore Properties Limited Sandwell Business Services

Ashmores Press Brake Tooling Limited Sandwell Advanced Manufacturing

Ashwood Nurseries Limited Dudley Retail

Ashworth Europe Limited Dudley Transport Technologies

Assa Abloy Limited Walsall Advanced Manufacturing

Asset Alliance Leasing Limited Wolverhampton Business Services

Assured Safety Recruitment Limited Walsall Business Services

A-Stat Office Technology Limited Wolverhampton Advanced Manufacturing

Astec Europe Limited Dudley Retail

ATB Special Products Limited Sandwell Advanced Manufacturing

ATE Truck & Trailer Sales Limited Wolverhampton Retail

Atlas Ball And Bearing CO. Limited Walsall Retail

Atticrose Limited Walsall Transport Technologies

Attley Cladding Limited Dudley Building Technologies

Attleys Roofing Limited Dudley Building Technologies

ATU Investments Limited Walsall Business Services

AUM Healthcare Limited Walsall Retail

AUM Supply Chain Ltd Wolverhampton Retail

Aurubis UK Ltd Sandwell Advanced Manufacturing

Auto Styling Truckman Group Limited Dudley Retail

Page 9

Autobitz International Ltd Walsall Retail

Autoguard Alarms Limited Dudley Building Technologies

Autosales Limited Wolverhampton Retail

Autoshop Limited Walsall Retail

Avanti West Midlands Limited Dudley Business Services

Axalta Coating Systems West Bromwich UK Limited Sandwell Advanced Manufacturing

Axiom Building Solutions Limited Wolverhampton Environmental Technologies

B & J Distribution Limited Walsall Retail

B C S Associates Limited Dudley Health

B D Healthcare Limited Walsall Retail

B G Building & Contracting Ltd Wolverhampton Business Services

B. & G. Transport (Dudley) Limited Dudley Transport Technologies

B. E. Barker Limited Wolverhampton Building Technologies

B. Shakespeare & Company Limited Dudley Retail

B.& G.Lock & Tool Co.Limited Walsall Advanced Manufacturing

B.B. Price Limited Dudley Advanced Manufacturing

B.E. Wedge Holdings Limited Walsall Advanced Manufacturing

B.E.S. Limited Wolverhampton Retail

B.G.N. Boards Company Limited Sandwell Retail

B.M.I. Engineering Limited Dudley Advanced Manufacturing

B.S.T. Supplies & CO Ltd Wolverhampton Advanced Manufacturing

B.T.C. Activewear Limited Sandwell Retail

Baby Travel Ltd Wolverhampton Retail

Bache Brown & CO. Limited Dudley Business Services

Bache Pallets Limited Dudley Advanced Manufacturing

Baddlesmere Limited Sandwell Building Technologies

Bahia Superstores Limited Walsall Retail

Bains Supersave Ltd Wolverhampton Retail

Baker Boys Limited Sandwell Advanced Manufacturing

Baldwins (Dursley) Limited Walsall Business Services

Banelec Limited Dudley Building Technologies

Banners Lane Engineering Company Limited Dudley Advanced Manufacturing

Bannisteel Limited Sandwell Advanced Manufacturing

Barhale Limited Walsall Building Technologies

Barlow Motors Limited Wolverhampton Retail

Barnfather Holdings Limited Walsall Advanced Manufacturing

Baydonian Limited Walsall Retail

Baylis Automotive (Smethwick) Limited Sandwell Advanced Manufacturing

Bayliss Trust Limited(The) Wolverhampton Business Services

BBS Technology Limited Dudley Business Services

BCR Restaurants Limited Wolverhampton Retail

BD Profiles Limited Dudley Advanced Manufacturing

Beacon Centre For The Blind Dudley Health

Beaconsfield Products (Halesowen) Limited Sandwell Advanced Manufacturing

Bearwood Builders Supply CO. (Smethwick) Limited Sandwell Retail

Beauimel Floors Limited Walsall Building Technologies

Beck Prosper Limited Dudley Advanced Manufacturing

Beckett Abrasives Limited Walsall Retail

Beck's Butchers Limited Walsall Retail

Bedford Canning Company Limited Wolverhampton Advanced Manufacturing

Beesley Fuel Services Limited Sandwell Retail

Page 10

Beeswift Limited Sandwell Retail

Beltrami UK Limited Dudley Retail

Benbow Steels Limited Sandwell Advanced Manufacturing

Bentley House Limited Sandwell Health

Berck Limited Sandwell Advanced Manufacturing

Bernstein Ltd Walsall Retail

Bertrandt UK Limited Sandwell Business Services

Bespoke Global Resourcing Ltd Wolverhampton Business Services

Beswick Resources Ltd Dudley Health

Beta Heat Treatment Limited Sandwell Advanced Manufacturing

Bevan Group Ltd Sandwell Transport Technologies

Beverley Parks (Paignton) Limited Dudley Visitor Economy

Biasi UK Limited Walsall Retail

BIG Bear Plastic Products Limited Wolverhampton Advanced Manufacturing

BIG Time Soft Drinks Limited Wolverhampton Advanced Manufacturing

Billingham & Kite Limited Dudley Building Technologies

Bills Group Limited Dudley Transport Technologies

Bilston Properties Limited Sandwell Business Services

Biokil Crown Limited Dudley Building Technologies

BIP (Oldbury) Limited Sandwell Advanced Manufacturing

Birchfield Engineering Limited Dudley Advanced Manufacturing

Birchills Automotive (Presswork) Limited Walsall Advanced Manufacturing

Birford Cable & Harness Limited Wolverhampton Advanced Manufacturing

Birmingham Garage & Industrial Doors Limited Sandwell Building Technologies

Birmingham Plating Company Ltd. Sandwell Building Technologies

Birmingham Roofing Supplies Limited Dudley Building Technologies

Birmingham Seals Company Limited Walsall Retail

Bishoprise Limited Wolverhampton Advanced Manufacturing

BJ Cheese Packaging Ltd Sandwell Retail

BJS Distribution Storage And Couriers Limited Walsall Transport Technologies

BKB Media Limited Walsall Business Services

Black Country Chamber of Commerce & Industry Wolverhampton Business Services

Black Country Commercials Ltd Dudley Retail

Black Country Consortium Limited Dudley Public Sector

Black Country Pallets Limited Sandwell Business Services

Black Country Pressings Limited Walsall Advanced Manufacturing

Black Country Properties Limited Wolverhampton Building Technologies

Black Country Scaffold Limited Dudley Building Technologies

Black Country Together C.I.C. Sandwell Business Services

Black Country Women's Aid Sandwell Visitor Economy

Blackacres Developments Limited Dudley Building Technologies

Blackbrook Estates Limited Dudley Building Technologies

Blackbrook Valley Developments (Dudley) Limited Dudley Building Technologies

Blackheath Group Limited Dudley Business Services

Blackprint Limited Dudley Advanced Manufacturing

Blacks Vets Limited Dudley Health

Blakeshall Developments Limited Dudley Building Technologies

Blitz Recycling Limited Wolverhampton Environmental Technologies

Bloomfield Packaging Limited Dudley Advanced Manufacturing

Bloom's (Wolverhampton) Limited Wolverhampton Retail

Blue SKY Commercial Limited Dudley Business Services

Page 11

Bluecross Pharmacy Limited Dudley Retail

Bluesky Products Limited Wolverhampton Retail

BOB Richardson Tools & Fasteners Limited Dudley Retail

Bodykraft (Dudley) Limited Dudley Advanced Manufacturing

Bollhoff Fastenings Limited Walsall Retail

Boltfast Limited Walsall Retail

Boltight Limited Walsall Advanced Manufacturing

Bordesley Green Garage (Bilston) Limited Sandwell Retail

Boro Foundry Limited(The) Dudley Advanced Manufacturing

Boseco Limited Dudley Advanced Manufacturing

Boswell & CO. (Steels) Limited Dudley Retail

Boswell Holdings Limited Dudley Retail

Bowman Stor Limited Walsall Advanced Manufacturing

Bowyer Green Limited Dudley Business Services

Bradcray Limited Sandwell Advanced Manufacturing

Bradley Environmental Consultants Limited Dudley Building Technologies

Brambles Property Services Ltd Walsall Business Services

Branded Housewares Limited Wolverhampton Retail

Brandenburg Holdings Limited Dudley Advanced Manufacturing

Brave GB Limited Walsall Retail

Breeze Recruitment Driveforce Limited Wolverhampton Business Services

Brierley Lifting Tackle Company Limited Dudley Retail

Briggs Amasco Limited Sandwell Building Technologies

Brighton One Limited Wolverhampton Visitor Economy

Brighton-Best International, (UK) Limited Sandwell Retail

Bri-Mac Engineering Limited Dudley Advanced Manufacturing

Brinbirch Limited Dudley Business Services

Brindley Asphalt Limited Wolverhampton Building Technologies

Bristol Forklifts Ltd. Walsall Retail

British Youth For Christ Dudley Business Services

Britmet Tileform Limited Dudley Building Technologies

Broadgate Partners Limited Wolverhampton Business Services

Broadhurst Industries PLC Dudley Advanced Manufacturing

Broadway Kitchens & Bedrooms (Midlands) Limited Walsall Advanced Manufacturing

Broadwood Educational Services Limited Dudley Health

Broadwood Residential Limited Dudley Health

Brockhouse Group Limited Sandwell Advanced Manufacturing

Brockmoor Foundry Company Limited(The) Dudley Advanced Manufacturing

Broen-Lab Ltd. Dudley Retail

Bromford Iron And Steel Company Limited Sandwell Advanced Manufacturing

Bronx Engineering Limited Dudley Transport Technologies

Brooks England Limited Sandwell Advanced Manufacturing

Brooks Forgings Limited Sandwell Advanced Manufacturing

Brownhills Investments Limited Walsall Business Services

Broyce Control Limited Wolverhampton Advanced Manufacturing

Brushware (U.K.) Limited Dudley Advanced Manufacturing

Bryant Electrical (Midlands) Limited Sandwell Building Technologies

Bryland Fire Protection Limited Dudley Retail

BSB Auto Parts PTY Ltd Sandwell Retail

BSC Diecasting & Finishing Ltd Walsall Advanced Manufacturing

BTI Studios Ltd Sandwell Business Services

Page 12

Bucknall Management Services Limited Walsall Business Services

Bull Construction Limited Dudley Building Technologies

Burcas Limited Sandwell Advanced Manufacturing

Burke Bros Recovery Limited Wolverhampton Retail

Burrows Group Limited Wolverhampton Public Sector

Buse Gases Limited Sandwell Business Services

Business Supplies Limited Walsall Retail

Butterfly Embroidery Limited Sandwell Advanced Manufacturing

C & A Flooring Ltd Wolverhampton Building Technologies

C & S Electrical Installations Ltd. Sandwell Building Technologies

C & W Commercials Limited Sandwell Retail

C Brown Services Limited Dudley Advanced Manufacturing

C J Tool And Mouldings Limited Dudley Transport Technologies

C R F Sections Limited Dudley Advanced Manufacturing

C S Labels Limited Walsall Advanced Manufacturing

C&F Group Holdings Limited Walsall Advanced Manufacturing

C. Adams & Sons (Midlands) Limited Sandwell Retail

C. Fullard (Metals) Limited Walsall Retail

C. Hearn & Sons (Darlaston) Limited Walsall Retail

C.& S.Steels(Wolverhampton)Limited Wolverhampton Advanced Manufacturing

C.A.B. Joinery Services Limited Sandwell Building Technologies

C.A.Clemson & Sons Limited Dudley Retail

C.A.S. (Mount Farm) Limited Wolverhampton Building Technologies

C.Beech & Sons (Netherton) Limited Dudley Retail

C.C. Contracting Limited Dudley Building Technologies

C.E. Gilbert & Son (Developments) Limited Dudley Building Technologies

C.G.Murray & Son Limited Dudley Retail

C.M. Electrical Wholesalers Limited Sandwell Retail

CAB Automotive Ltd. Sandwell Transport Technologies

Cable & Alloys (Willenhall) Limited Walsall Retail

Cables Britain Limited Sandwell Retail

CAD Duct Solutions Ltd Dudley Building Technologies

Cadmore Lodge Limited Dudley Health

Camcraft Limited Sandwell Advanced Manufacturing

Canberra Wells Limited Dudley Retail

Cannon Tools Limited Sandwell Retail

Capital Appliance Centre Limited Wolverhampton Retail

Capital Outsourcing Group Limited Walsall Business Services

Caprillo Ltd Walsall Retail

Car Parts Industries UK Limited Sandwell Transport Technologies

Caram (ABR) Limited Wolverhampton Visitor Economy

Careerlink Limited Walsall Business Services

Carjan Properties Limited Dudley Building Technologies

Carlton Care Homes Ltd Dudley Health

Carlyle Limited Sandwell Business Services

Carrs Tool Steels Limited Sandwell Retail

Carsharlton (North ST) Limited Dudley Building Technologies

Carver (Wolverhampton) Limited Wolverhampton Building Technologies

Carver Group Limited Walsall Transport Technologies

Casino 36 Limited Wolverhampton Visitor Economy

Casper Stores Limited Wolverhampton Retail

Page 13

Cassel Hotels Limited Wolverhampton Visitor Economy

Castings Public Limited Company Walsall Advanced Manufacturing

Castle Carbide Limited Dudley Retail

Castlehill Crafts Ltd Dudley Business Services

Castlemore Group Holdings Limited Dudley Building Technologies

Caterfish Limited Walsall Retail

CDS (Midlands) Limited Wolverhampton Health

Cemineral Limited Dudley Retail

Ceney (Developments) Limited Dudley Building Technologies

Central Access Hire And Sales Ltd Walsall Building Technologies

Central Patternmaking Limited Walsall Advanced Manufacturing

Central Plate Services Limited Walsall Advanced Manufacturing

Central Plumbing & Heating Services Limited Dudley Building Technologies

Central RPL Limited Sandwell Building Technologies

Central Steel Pickling Limited Sandwell Business Services

Central Supplies (Brierley Hill) Ltd Dudley Retail

Central Waste Oil Collections Limited Walsall Environmental Technologies

Challenge Power Transmission Limited Wolverhampton Advanced Manufacturing

Chamberlin PLC Walsall Advanced Manufacturing

Chanco (Garages) Limited Sandwell Retail

Chapel Ascote Farms Limited Sandwell Advanced Manufacturing

Chapel Tyres Limited Sandwell Retail

Chapel Windows Limited Dudley Building Technologies

Charles Clark Motors Limited Wolverhampton Retail

Charles Fellows Supplies Limited Dudley Retail

Charlie Brown Limited Sandwell Retail

Charnat Care Limited Sandwell Business Services

Charter Castings Limited Sandwell Advanced Manufacturing

Charter Court Financial Services Group PLC Wolverhampton Business Services

Charterbridge Properties Limited Wolverhampton Business Services

Chartway Industrial Services Limited Dudley Business Services

Chase Plant Hire Limited Walsall Business Services

Chatsworth UK Limited Sandwell Advanced Manufacturing

Chemex International Limited Sandwell Retail

Chemique UK Limited Walsall Advanced Manufacturing

Chemviron Carbon Limited Dudley Advanced Manufacturing

Cherry Garden Properties Limited Sandwell Building Technologies

Chicken Joes Limited Walsall Advanced Manufacturing

China Industries Limited Wolverhampton Advanced Manufacturing

Chord Properties Limited Walsall Building Technologies

Chrysalis Key2key Limited Sandwell Business Services

Churchbridge Estates Limited Sandwell Building Technologies

Citizens Advice Sandwell Ltd Sandwell Health

CK Special Gases Limited Sandwell Retail

Clamason Industries Limited Dudley Advanced Manufacturing

Clark Brookes Turner Cary Limited Sandwell Business Services

Clarkwood Engineering Limited Wolverhampton Advanced Manufacturing

Classic Enterprises (UK) Limited Dudley Retail

Claverley Group Limited Wolverhampton Business Services

Clean Image (UK) Limited Dudley Public Sector

Clinpharm Plus Ltd Dudley Retail

Page 14

CMK (Treatments) Limited Sandwell Building Technologies

CMS (Tipton) Limited Sandwell Business Services

CMS Hire Limited Wolverhampton Business Services

CMS Motors Limited Dudley Retail

CMT Engineering Limited Sandwell Advanced Manufacturing

Cobco 840 Limited Walsall Business Services

Cognitive Network Solutions Limited Dudley Business Services

Coil Processing Supplies Limited Sandwell Retail

Coin-A-Drink Limited Walsall Visitor Economy

Colin Pardoe Limited Dudley Advanced Manufacturing

Colter Steels Limited Walsall Business Services

Coltham Developments Limited Wolverhampton Business Services

Comar Engineering Services Limited Wolverhampton Transport Technologies

Comfort Beds Company Limited Walsall Retail

Commercial Trade Vehicles (UK) Limited Wolverhampton Retail

Complete Washroom Solutions Limited Dudley Environmental Technologies

Complex Cold Forming Limited Sandwell Transport Technologies

Component Supplies Limited Dudley Advanced Manufacturing

Compton Care Group Limited Wolverhampton Public Sector

Concept Stainless Limited Sandwell Retail

Concorde Commercial Maintenance Limited Walsall Advanced Manufacturing

Connect Advertising & Marketing LLP Wolverhampton Business Services

Connectwise Ltd Dudley Business Services

Connolley Metals Limited Wolverhampton Retail

Consolidated Steel Products Ltd. Dudley Advanced Manufacturing

Construction Fastener Techniques Limited Dudley Business Services

Contract Flooring Solutions Limited Dudley Building Technologies

Controlled Heat Treatments Limited Dudley Transport Technologies

Cooper & Jackson Limited Dudley Advanced Manufacturing

Cooper Coated Coil Limited Wolverhampton Advanced Manufacturing

Cooper Mobile Services Limited Wolverhampton Retail

Co-Ordsport Limited Dudley Retail

Cope Technology Limited Dudley Advanced Manufacturing

Copper & Automotive Washer Company Limited Walsall Advanced Manufacturing

Corbetts Dudley Ltd Dudley Retail

Corbetts Support Systems Limited Sandwell Retail

Cordwell Estates Limited Dudley Building Technologies

Cornvalley Limited Wolverhampton Business Services

Cornwall Holdings Limited Sandwell Advanced Manufacturing

Cornwallis Limited Sandwell Advanced Manufacturing

Cosmetics R Us 1 Limited Wolverhampton Retail

Cosmic Jeans Limited Sandwell Retail

Cotdean Nursing Homes Limited Dudley Health

Cottam & Preedy.Limited Sandwell Building Technologies

Cotterell Partnership Limited Wolverhampton Business Services

Cougar Monitoring Ltd. Sandwell Public Sector

Counterplas Limited Sandwell Advanced Manufacturing

Countrywide Industrial Cleaning Services Ltd Wolverhampton Public Sector

County Saddlery Limited Walsall Advanced Manufacturing

County Stationery Limited Sandwell Retail

Coupes And Convertibles Limited Dudley Retail

Page 15

Cousins Furniture Stores Limited Sandwell Retail

Coventry Leasing Limited Wolverhampton Business Services

Cox & CO (Dudley) Limited Dudley Business Services

Cox & CO Limited Dudley Business Services

Cox & Plant Ltd Wolverhampton Advanced Manufacturing

Cox Hire Limited Dudley Business Services

Craddock Holdings Limited Walsall Advanced Manufacturing

Cradley Heath Motor Co.Ltd Sandwell Retail

Craig & Derricott Limited Walsall Advanced Manufacturing

Crane Rail Installations (U.K.) Limited Sandwell Building Technologies

CRE (W.Mids) Limited Sandwell Business Services

Croft Architectural Hardware Limited Walsall Advanced Manufacturing

Crombies Accountants Limited Wolverhampton Business Services

Crosby Management Training Ltd Wolverhampton Business Services

Crosland Cutters Limited Dudley Advanced Manufacturing

Crossways Care Ltd Dudley Health

Crown Polishing And Plating Company Limited Wolverhampton Advanced Manufacturing

Crown Screw Limited Sandwell Retail

Crown Technologies Limited Wolverhampton Advanced Manufacturing

CST Holdings (UK) Limited Walsall Retail

CTS Investments Worcester Limited Walsall Retail

Cube Precision Engineering Limited Sandwell Advanced Manufacturing

Cure Leukaemia Sandwell Health

Currall Lewis & Martin (Construction) Limited Sandwell Building Technologies

Custom Technology Solutions Limited Dudley Public Sector

Customark Limited Dudley Advanced Manufacturing

Cuxson Gerrard & Company Limited Sandwell Advanced Manufacturing

D & M Meats Limited Wolverhampton Retail

D & M Plating Limited Wolverhampton Business Services

D & R Contract Services Limited Walsall Building Technologies

D Kumar Ltd Dudley Health

D.& J.Bailey(Flooring)Limited Walsall Building Technologies

D.E. Siviter (Motors) Limited Wolverhampton Retail

D.G.S. (Grinding Wheels & Machines) Limited Wolverhampton Advanced Manufacturing

D.K. Rewinds Limited Sandwell Transport Technologies

D.P. Forrest Limited Sandwell Retail

D.S. Willetts (Stainless) Limited Wolverhampton Advanced Manufacturing

Daily Irish Services Limited Sandwell Transport Technologies

Dakro Environmental Limited Sandwell Public Sector

Dale Structural Engineers Limited Sandwell Advanced Manufacturing

Dalvie Storage Systems Limited Wolverhampton Building Technologies

Dancing Leopard Clothing Limited Walsall Advanced Manufacturing

Daneways Limited Dudley Building Technologies

Daniel Batham & Son Limited Dudley Advanced Manufacturing

Dartmouth Global Trading CO. Limited Dudley Business Services

Data Modul Limited Walsall Retail

Davicon Mezzanine Floors Limited Dudley Advanced Manufacturing

David Manners Limited Sandwell Retail

Davies Woven Wire Limited Dudley Advanced Manufacturing

Davis-Standard Ltd Dudley Transport Technologies

Davroy Contracts Limited Walsall Building Technologies

Page 16

Dawson Bros.(Timber)Limited Dudley Advanced Manufacturing

Dawson Bros.(Timber)Limited Dudley Advanced Manufacturing

Deal Pot Limited Wolverhampton Retail

Deepdale Engineering CO. Limited Dudley Advanced Manufacturing

Delight Bite Limited Sandwell Visitor Economy

Deligo Limited Dudley Retail

Dell Factor Limited Wolverhampton Retail

De-Met Limited Dudley Advanced Manufacturing

Dent & Partners Limited Wolverhampton Building Technologies

Denwire Limited Dudley Retail

Dessa Limited Sandwell Building Technologies

Devilbiss Healthcare Limited Sandwell Retail

Dewsbury & Proud Limited Wolverhampton Building Technologies

Diamond Box Limited Sandwell Advanced Manufacturing

Diamond Coatings Limited Dudley Advanced Manufacturing

Diesel Technic UK & Ireland Ltd. Dudley Retail

Digby Trading Limited Dudley Retail

Digital Office Limited Dudley Business Services

Ding Dang Do Limited Sandwell Business Services

Dinsmores Limited Walsall Advanced Manufacturing

Direct Channel Support Systems Limited Dudley Retail

Direct Corporate Clothing PLC Sandwell Retail

Direct Healthcare Limited Sandwell Retail

Direct Personnel Midlands Limited Sandwell Business Services

Direct Security Systems (Midlands) Limited Walsall Building Technologies

Discount Cars (Dudley) Limited Dudley Retail

DLF Developments Ltd Walsall Building Technologies

DMG Wholesale Limited Walsall Retail

Doal International Limited Sandwell Advanced Manufacturing

Dom-Uk Ltd Sandwell Advanced Manufacturing

Donghua Limited Wolverhampton Retail

Doocey Holdings Limited Sandwell Building Technologies

Dormer Tools (UK) Limited Dudley Retail

Dpdgroup UK Ltd Sandwell Transport Technologies

Drillcore (Wednesbury) Limited Sandwell Building Technologies

Druids Heath Golf Club Limited Walsall Business Services

Drywall Steel Sections Limited Sandwell Advanced Manufacturing

Drywite Limited Dudley Retail

DSP (UK) Limited Sandwell Retail

Ducati Wolverhampton Limited Dudley Retail

Ducatt Heating Company Limited(The) Dudley Building Technologies

Ductmann Limited Dudley Environmental Technologies

Dudley And West Midlands Zoological Society Limited Dudley Visitor Economy

Dudley Clinical Services Limited Dudley Health

Dudley Council For Voluntary Service(The) Dudley Health

Dudley District Citizens Advice Bureaux Dudley Business Services

Dudley Waste Services Limited Wolverhampton Business Services

Dukehill Limited Sandwell Business Services

Dukehill Services Limited Sandwell Business Services

Dunns Waste Management Limited Dudley Environmental Technologies

Duright Engineering Limited Sandwell Advanced Manufacturing

Page 17

E & S Motors Limited Walsall Retail

E Plan Energy Limited Dudley Building Technologies

E R Grove & CO Limited Dudley Business Services

E W Turner And Company Limited Walsall Advanced Manufacturing

E. Hulme & Son Limited Walsall Advanced Manufacturing

E.B.C. Group (U.K.) Limited Dudley Advanced Manufacturing

E.J. Bowman Holdings Limited Wolverhampton Advanced Manufacturing

E.O'Neill & Son Painting And Decorating Ltd Wolverhampton Building Technologies

Eagle Generators Ltd Sandwell Retail

Earnest Machine Products Company Ltd Wolverhampton Retail

Easiflo Investments Limited Dudley Advanced Manufacturing

Easington Associates Limited Sandwell Business Services

East End Foods Limited Sandwell Retail

East Street Homes (South East) Limited Sandwell Building Technologies

Eastern Leisure Limited Walsall Visitor Economy

Easygates Limited Dudley Advanced Manufacturing

Eccles (UK Foundries FE) Limited Walsall Advanced Manufacturing

Ecigruk Ltd Walsall Retail

Eclipse Plumbing & Heating CO. Limited Wolverhampton Building Technologies

Eclipse Sprayers Limited Sandwell Advanced Manufacturing

Eco-1 Electrical Solutions Ltd Walsall Building Technologies

Edge Careers Ltd Dudley Business Services

Edge Freelance Ltd Dudley Business Services

Edmund Howdle (Butchers) Limited Walsall Retail

Edwards Accountants (Midlands) Limited Walsall Business Services

Edwin Holden's Bottling Company Limited Dudley Business Services

EFB Holdings Limited Walsall Retail

EFD Induction Limited Wolverhampton Advanced Manufacturing

Ehrco Limited Dudley Retail

Electrixs Installations Limited Wolverhampton Building Technologies

Electro Discharge Limited Dudley Advanced Manufacturing

Electrolytic Plating Company Limited(The) Walsall Advanced Manufacturing

Elegant Dickens Heath Village Limited Dudley Building Technologies

Elite Aluminium Systems Limited Walsall Advanced Manufacturing

Elite Fasteners Limited Walsall Advanced Manufacturing

Elite Systems (UK) Limited Dudley Building Technologies

Eliza Tinsley Limited Sandwell Retail

Elta Fans Limited Dudley Transport Technologies

Elta Group Limited Dudley Advanced Manufacturing

Emerald Vehicle Sales Ltd Walsall Retail

Empire Sheds Limited Dudley Advanced Manufacturing

Empire Star Limited Sandwell Retail

Enablelink Limited Dudley Environmental Technologies

Endersleigh Limited Sandwell Retail

Energy Insurance Services Limited Walsall Business Services

Energy Saving Glass Ltd Dudley Advanced Manufacturing

Energy Tubes Limited Dudley Advanced Manufacturing

Enfield High Street (Agg19) Limited Walsall Business Services

English Plastics Limited Walsall Advanced Manufacturing

Ensco 535 Limited Sandwell Retail

Ensen Limited Dudley Retail

Page 18

Environmental Contracts Limited Dudley Environmental Technologies

Environmental Integrated Solutions Limited Dudley Business Services

Environmental Resource Group Limited Walsall Environmental Technologies

Envirotreat Technologies Limited Dudley Environmental Technologies

Epharmit Limited Dudley Business Services

Erodex Graphite Systems Limited Dudley Business Services

Erollingbikes Ltd Sandwell Retail

Ervin Amasteel Sandwell Advanced Manufacturing

Esprit Group UK Limited Sandwell Advanced Manufacturing

Essentia Protein Solutions Limited Sandwell Advanced Manufacturing

Essential Supply Products Limited Dudley Business Services

Estil Limited Dudley Building Technologies

Estilo Electrical Services Limited Dudley Building Technologies

Estilo Interiors Limited Dudley Building Technologies

Euro Architectural Hardware Limited Walsall Retail

Euro Products Limited Dudley Advanced Manufacturing

Euro Stock Traders Limited Wolverhampton Retail

Eurocraft Technologies Limited Dudley Advanced Manufacturing

Eurofins Food Testing UK Limited South Staffordshire Advanced Manufacturing

Eurohire Vehicle Rentals (Oldbury) Limited Sandwell Business Services

Eurolec Components (Midlands) Limited Dudley Retail

European African Trading CO. Ltd Sandwell Business Services

European Aviation Limited Dudley Retail

European Electrical Laminations Limited Dudley Advanced Manufacturing

European Handling Equipment Limited Dudley Retail

European Industrial Group Limited Walsall Advanced Manufacturing

European Mezzanine Systems Limited Dudley Building Technologies

European Minardi Team Limited Dudley Sports

European Skybus Limited Dudley Transport Technologies

European Truck Parts Limited Sandwell Retail

Eurowire Containers Limited Dudley Advanced Manufacturing

Eurstyle Limited Walsall Advanced Manufacturing

Eutectic Alloy Castings (Wolverhampton) Limited Wolverhampton Advanced Manufacturing

Evoca UK Limited Wolverhampton Retail

Exallot Limited Sandwell Advanced Manufacturing

Excel 2000 Windows Limited Dudley Building Technologies

Excel Print Limited Walsall Advanced Manufacturing

Excelsior Panelling Systems Ltd Dudley Advanced Manufacturing

Exclusive Collections Ltd Wolverhampton Retail

Express Bonding Services Limited Sandwell Advanced Manufacturing

F & J Exports Limited Dudley Retail

F. Martin And Son Limited Walsall Advanced Manufacturing

F.A.Gill.Limited Wolverhampton Advanced Manufacturing

F.P. Gaunt & Sons Limited Sandwell Business Services

Fablink Limited Wolverhampton Advanced Manufacturing

Fabory UK Limited Sandwell Retail

Fabwell Ltd Dudley Transport Technologies

Facepunch Group Limited Walsall Business Services

Factory Plant Projects Limited Dudley Retail

Fairfax Saddles Limited Walsall Advanced Manufacturing

Fairlawns Hotel Limited(The) Walsall Visitor Economy

Page 19

Faraday Electrical Installations Ltd. Dudley Building Technologies

Farcroft Restorations Ltd Walsall Business Services

Farrellys Metal Polishers Limited Walsall Advanced Manufacturing

Fastauto Limited Dudley Retail

Fastener Network Holdings Limited Dudley Advanced Manufacturing

Fastline Steel Services UK Ltd Wolverhampton Advanced Manufacturing

FBC Manby Bowdler LLP Wolverhampton Business Services

Fellows & Fullwood Limited Dudley Retail

Ferdotti Motor Services Limited Sandwell Retail

Feridax Group Limited Dudley Retail

Fern Manufacturing Group Limited Wolverhampton Business Services

Fern Plastic Products Limited Wolverhampton Advanced Manufacturing

Fine Mesh Metals Limited Dudley Advanced Manufacturing

Finesse Coaches Ltd Sandwell Transport Technologies

Finesse Windows Limited Dudley Building Technologies

Finn TEC Commercials Limited Wolverhampton Retail

Fire & Acoustic Seals Limited Sandwell Retail

Fire Glass UK Limited Sandwell Building Technologies

Firecracker Limited Sandwell Retail

Fireguard Safety Equipment Company Limited Walsall Retail

Firestop Manufacturing Limited Sandwell Retail

First Care Services Limited Wolverhampton Health

First Choice Assembly Limited Dudley Building Technologies

First Components Limited Dudley Advanced Manufacturing

First For Education Limited Dudley Business Services

First National Vehicles Limited Dudley Retail

Firstmark Consultancy Limited Sandwell Advanced Manufacturing

Fisher Alvin Limited Sandwell Advanced Manufacturing

Five Star Motors Limited Dudley Retail

Fives Bronx Limited Dudley Transport Technologies

Flatworldworks Limited Wolverhampton Business Services

Fleet Express & Logistics Limited Walsall Transport Technologies

Fleetline Tyre Services Limited Sandwell Retail

Flight Club Darts Limited Dudley Sports

Flint & Partners Eyecare Limited Wolverhampton Retail

Flint CPS Inks UK Ltd Wolverhampton Advanced Manufacturing

Floors 4 You Ltd Dudley Retail

Floris Books Trust Limited Dudley Business Services

Foley Steels Limited Wolverhampton Retail

Folkes Forgings Acquisition Limited Dudley Business Services

Folkes Properties Limited Dudley Building Technologies

Fontana Fasteners UK Limited Sandwell Retail

Fontus Health Ltd Walsall Advanced Manufacturing

Foresight Recruitment Solutions Limited Walsall Business Services

Forgeco Ltd Wolverhampton Advanced Manufacturing

Forging Developments UK Limited Sandwell Transport Technologies

Formbend Limited Sandwell Advanced Manufacturing

Formit Limited Dudley Transport Technologies

Formrite Precision Limited Walsall Transport Technologies

Forsyth James Ltd Dudley Business Services

Fort Jason Limited Dudley Transport Technologies

Page 20

Fortel Construction Group Limited Walsall Business Services

Fortify Limited Walsall Business Services

Forton Supplies Limited Wolverhampton Retail

Fortress Interlocks Limited Wolverhampton Transport Technologies

Four Seasons Air Conditioning Supplies Limited Dudley Building Technologies

Foxborough Developments Limited Sandwell Building Technologies

Francis Catering (Holdings) Limited Dudley Retail

Freeflow Pipesystems Ltd Sandwell Advanced Manufacturing

Freemans Confectionery Supplies Limited Walsall Retail

French Ludlam & CO Limited Dudley Business Services

Friars 702 Limited Dudley Visitor Economy

Friends Jewellers Ltd Sandwell Retail

Frontline Exhibitions Limited Dudley Business Services

Fuhr UK Ltd Wolverhampton Retail

Full Fat Things Limited Wolverhampton Business Services

Fun & Fries Ltd Dudley Visitor Economy

Fundamental Fashions Limited Dudley Retail

Futura Design Limited Sandwell Advanced Manufacturing

G & D Supplies Limited Sandwell Retail

G B Springs Limited Wolverhampton Retail

G B Tyres (UK) Ltd Sandwell Retail

G F Laser Limited Dudley Advanced Manufacturing

G F S A Limited Dudley Advanced Manufacturing

G J F Fabrications Limited Walsall Advanced Manufacturing

G L Mastics Limited Dudley Building Technologies

G M Treble Holdings Limited Wolverhampton Retail

G P Salads Limited Wolverhampton Retail

G. John Power Limited Dudley Advanced Manufacturing

G. Stow PLC Walsall Building Technologies

G.B.G. Fences Limited Walsall Building Technologies

G.C. Rickards (Investments) Limited Walsall Building Technologies

G.C. Rickards Limited Walsall Retail

G.E. Starr Limited Wolverhampton Advanced Manufacturing

G.H.Stafford & Son Limited Walsall Retail

G.J.N. Supplies Limited Dudley Retail

G.K.C.C. Limited Dudley Retail

G.N. Grosvenor Limited Wolverhampton Retail

Garanday Limited Wolverhampton Visitor Economy

Gardeco Limited Dudley Retail

Garland Products Limited Dudley Retail

Garratts Wolverhampton Limited Wolverhampton Business Services

GAS & Industrial FAN Services Limited Dudley Advanced Manufacturing

Gatc Biotech Limited South Staffordshire Advanced Manufacturing

Gaugemaster Company Limited Wolverhampton Advanced Manufacturing

Geetee Investments Limited Dudley Building Technologies

Geldbach (UK) Limited Sandwell Retail

Genee World Limited Wolverhampton Retail

Generic Punching Systems Limited Dudley Advanced Manufacturing

Genie Solutions Limited Wolverhampton Business Services

Genius Facades Ltd Wolverhampton Advanced Manufacturing

Geo. Johnson (Metals) Limited Dudley Retail

Page 21

Geoff Perry Associates Limited Walsall Advanced Manufacturing

George Brothers Investments Limited Sandwell Business Services

George Griffiths (Springs) Limited Sandwell Advanced Manufacturing

George Perry (Wholesale Fruit & Vegetables) Limited Wolverhampton Retail

George Taylor & CO. Lifting Gear (Europe) Limited Walsall Business Services

Georisk Management Ltd Sandwell Building Technologies

GHR Holdings Limited Walsall Advanced Manufacturing

Giffords Equipment Limited Sandwell Business Services

Giffords Property Limited Sandwell Advanced Manufacturing

Giles Evans Limited Wolverhampton Retail

Gilmore Building Supplies Limited Walsall Retail

Giomani Designs Ltd Walsall Retail

Glassworks Equipment Limited Dudley Advanced Manufacturing

Glaze Auto Parts Limited Wolverhampton Retail

Glendale Architectural Metalwork (UK) Ltd Sandwell Advanced Manufacturing