z Strategic and Financial Analysis of Auriga Industries A/S (Strategisk og finansiel analyse af Auriga Industries A/S) MSc Economics and Business Administration Master Thesis Written by: Michal Nielsen – MSc FIR Klaus Thøger Pedersen – MSc ASC Number of pages: 117 Number of characters: 272,626 Supervisor: Kristian Sørensen Hand-in date: 17.05.2016

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

z

Strategic and Financial Analysis of Auriga Industries A/S

(Strategisk og finansiel analyse af Auriga Industries A/S)

MSc Economics and Business

Administration

Master Thesis

Written by:

Michal Nielsen – MSc FIR

Klaus Thøger Pedersen – MSc ASC

Number of pages: 117

Number of characters: 272,626

Supervisor: Kristian Sørensen

Hand-in date: 17.05.2016

Executive Summary

The general purpose of this thesis is to investigate foundation-owned companies’ ability to maximize

shareholder value in highly innovative- and/or consolidation industries.

The paper adopts an inductive approach and narrows its focus on the agrochemical industry by applying

Auriga Industries A/S as case company with the purpose of conducting an in-depth external- and internal

analysis to uncover potential strategic dilemmas and implications influencing to the company’s ability to

maximize shareholder value. Auriga divested their operations to FMC in 2014 for a price of DKK 325.00 per

outstanding which will be the target to meet to optimize shareholder value.

The analysis identifies several strategic dilemmas that the Auriga Industries A/S needs to solve to be able to

maximize their strengths and opportunities as well as minimize their threats and weaknesses. The paper sets

up three different strategies, that the company can either adopt individually or as a combination.

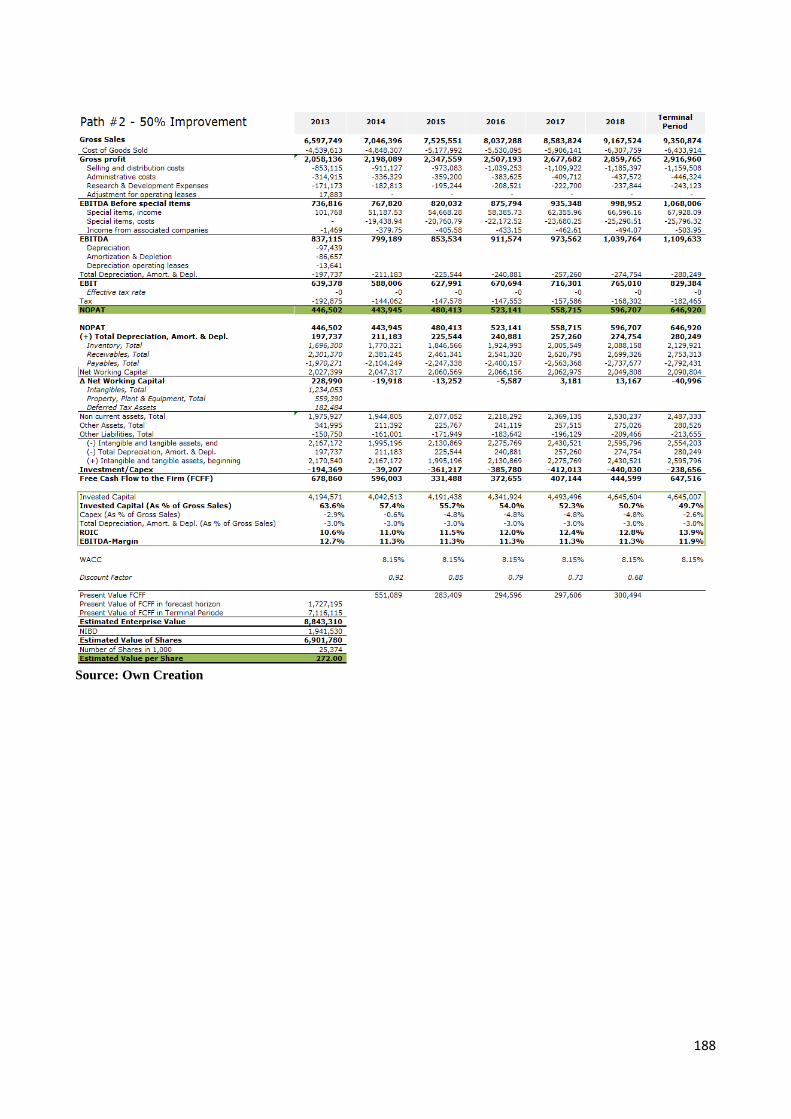

Path #1 mitigates production inefficiencies and result in an expected increase in the share price of DKK

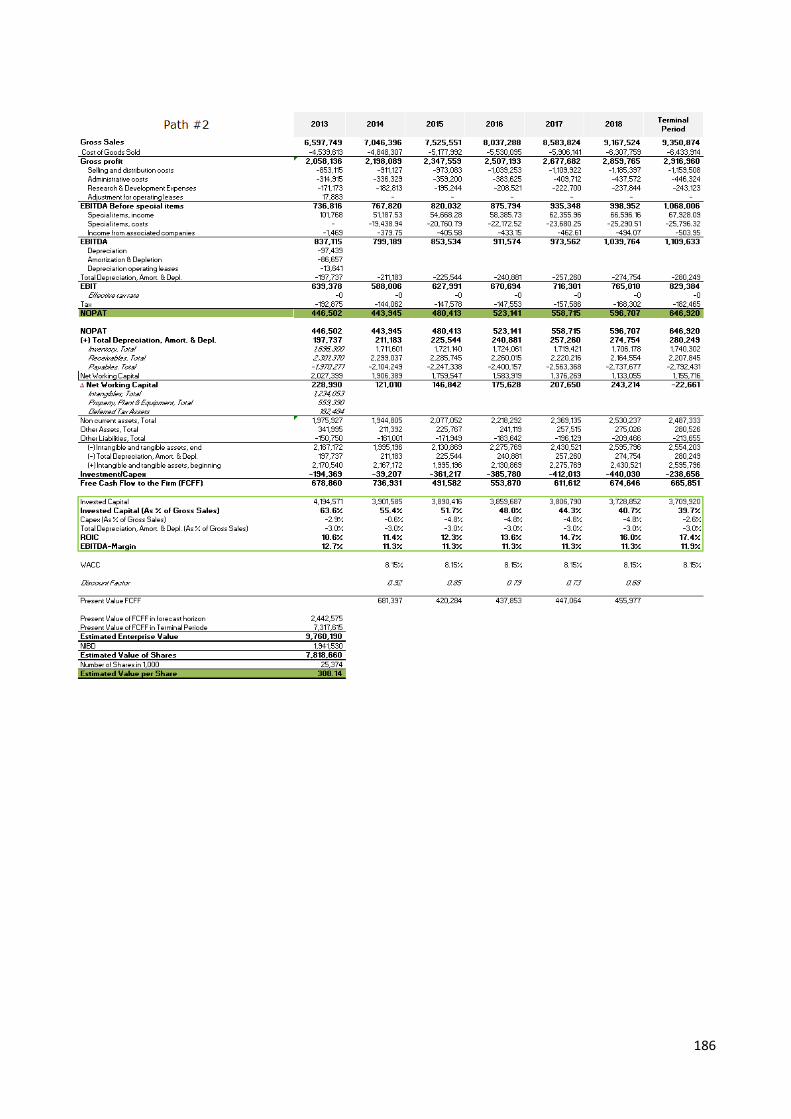

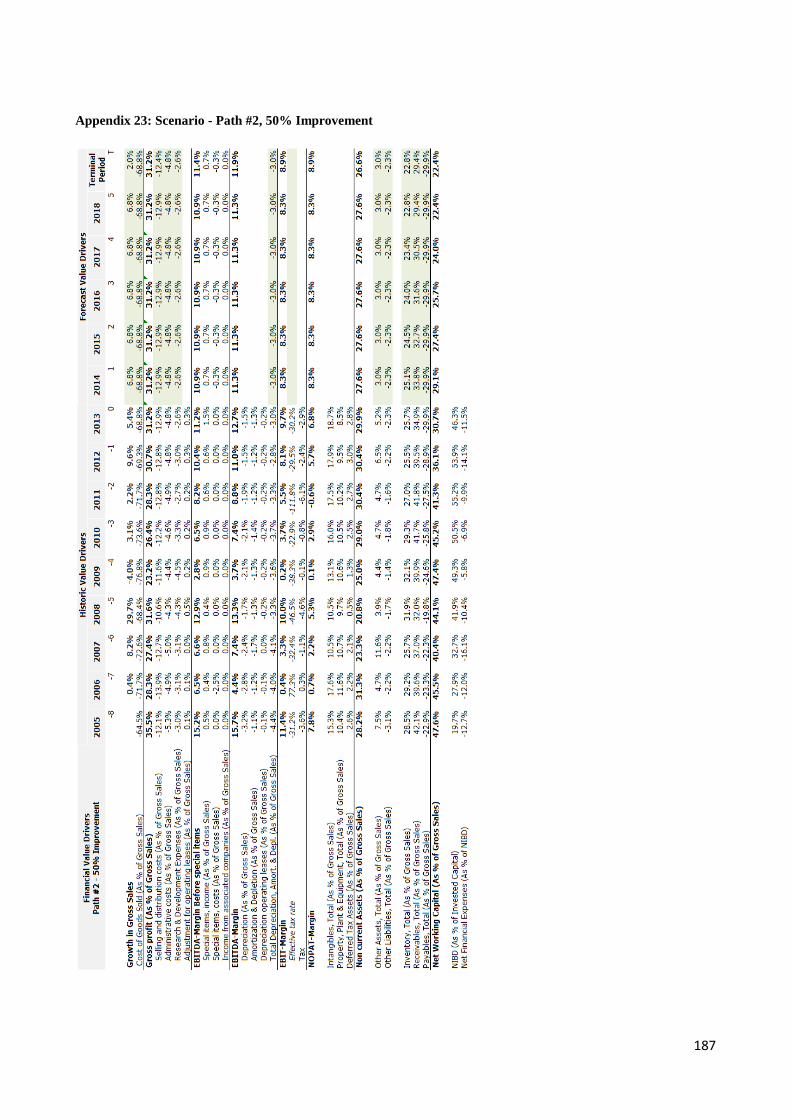

10.13 per outstanding share. Path #2 optimizes the company’s working capital processes which lead to an

expected increase in the share price of DKK 30.24. Path #3 strengthens the company’s innovative

capabilities and secures a better chance of penetrating the North American market which off-sets in an

expected increase in the share price of DKK 20.22 per outstanding share.

Because of the human, organizational and financial resources required, a simultaneously implementation of

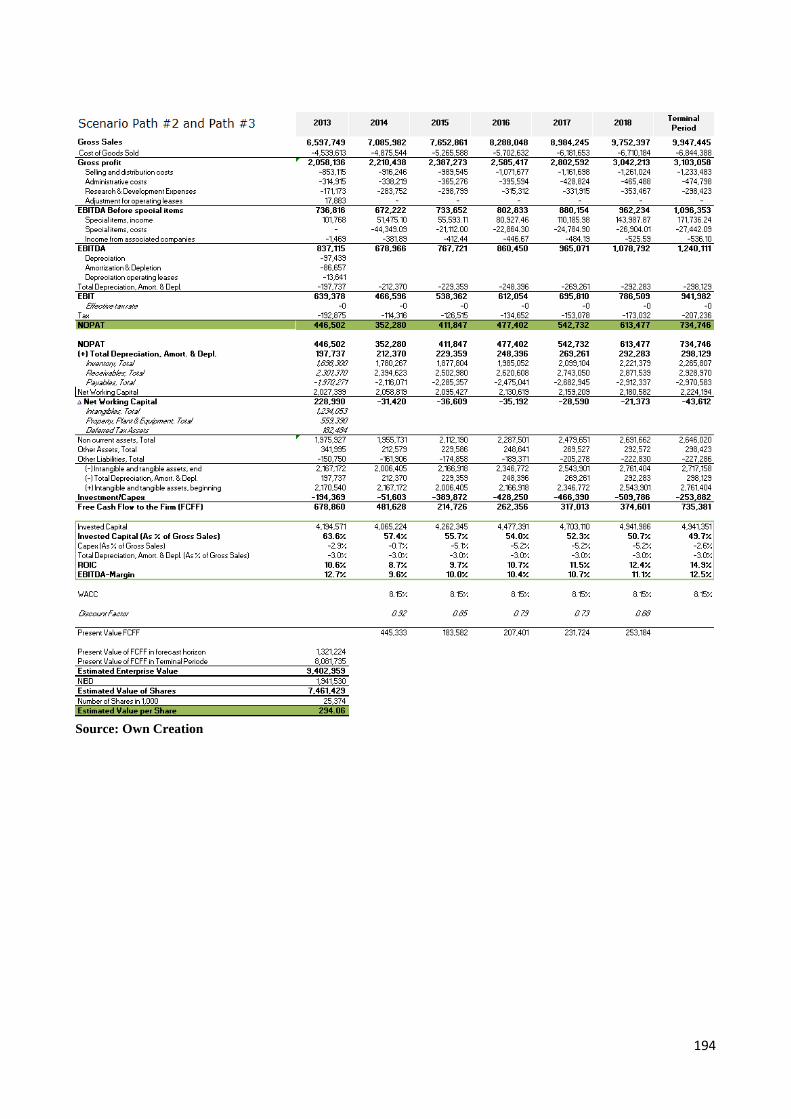

all three strategies are deemed unrealistic. Instead, the paper favors a joint initiation of path #2 and path #3

which would result in an expected increase in the share price of DKK 52.30 equaling a share price of DKK

294.06 per outstanding share.

As the expected value of implementing the two favored paths of DKK 294.06 per outstanding share does not

exceed the price of DKK 325.00 per outstanding share offered by FMC, it can be concluded that the offered

price from FMC optimizes shareholder value, and thus should be accepted.

General findings suggest that foundation charters potentially restrict consolidations, and as a possible result

the authorities have seemingly adopted a liberal stance towards accepting changes in foundation charters,

which have off-set a trend towards less restrictive charters – especially concerning divestments. The same

trend is observed with Auriga Industries A/S.

Managerial distance between a foundation and its operational company are positively correlated with

company performance. AURF and Auriga operate with high managerial distance, and should thus perform

well. This has not been the case with Auriga Industries A/S which has not been able to capture their share of

a growing market. A potential problem could be too much managerial distance, exemplified by the fact that

AURF as majority owner have tried to sell Auriga Industries A/S for the last fifteen years – they did just not

succeed until 2014. A possible effect of this unwanted marriage could be underinvestment causing

inefficiency and lack of responsiveness, resulting in low growth and thus affecting the ability to create

shareholder value.

As the internal and external analysis reveals Auriga Industries A/S have developed into a company, being in

a highly consolidating industry, where a divestment was the only right option to pursue in optimizing

shareholder value.

1. Introduction .................................................................................................. 1

1.1. Problem Statement & Research Questions .................................................... 2

1.1. Delimitations ..................................................................................................... 2

1.2. Conceptual Framework ................................................................................... 3

1.2.1. Data ................................................................................................................................ 4

1.2.2. Structure, Theories and Models – an Overview ............................................................. 6

2. Exposition .................................................................................................... 10

2.1.1. Industry Terminologies ................................................................................................10

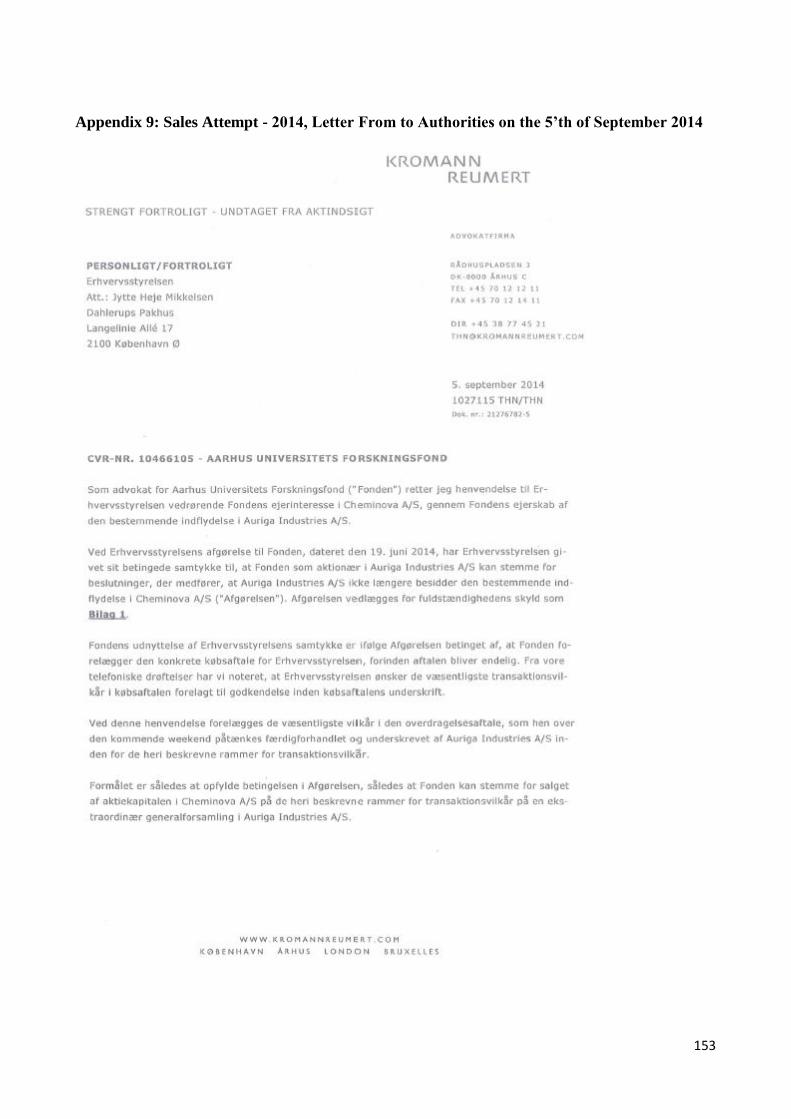

2.1.2. Auriga History .............................................................................................................11

2.1.3. Access to Documents Concerning the Sale Granted to Kurt Aabo ..............................12

2.1.4. Auriga in 2013 .............................................................................................................14

2.1.5. Stakeholders .................................................................................................................15

3. EXTERNAL ANALYSIS .......................................................................... 16

3.2. Exogenous Factors .......................................................................................... 19

3.2.1. PESTEL .......................................................................................................................19

3.2.1. Sub-conclusion – OT 1 ................................................................................................29

3.3. External Factors ............................................................................................. 30

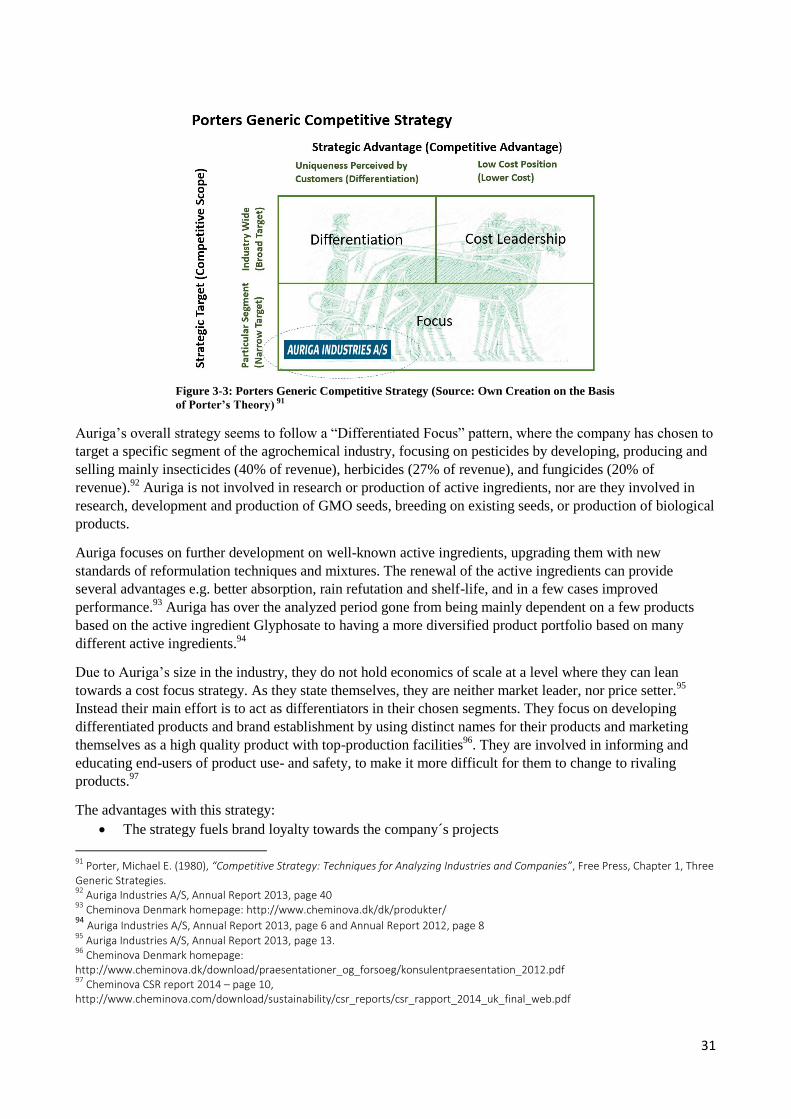

3.3.1. Generic Competitive Strategy ......................................................................................30

3.3.2. Porters Five Forces ......................................................................................................32

3.4. Benchmark Analysis – Financial Data ......................................................... 36

3.4.1. Sub-conclusion – OT 2 ................................................................................................39

4. COMPANY ANALYSIS – THE INTERNAL FACTORS ..................... 41

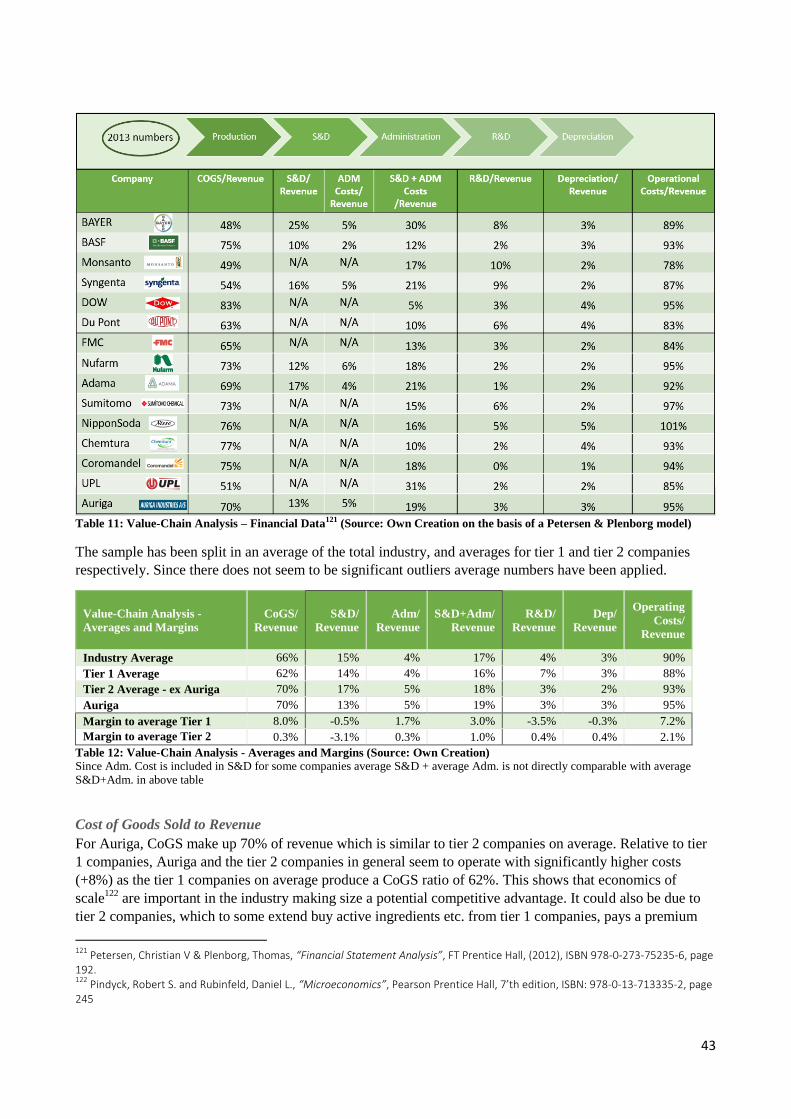

4.1. Value-Chain Analysis – Financial Data........................................................ 41

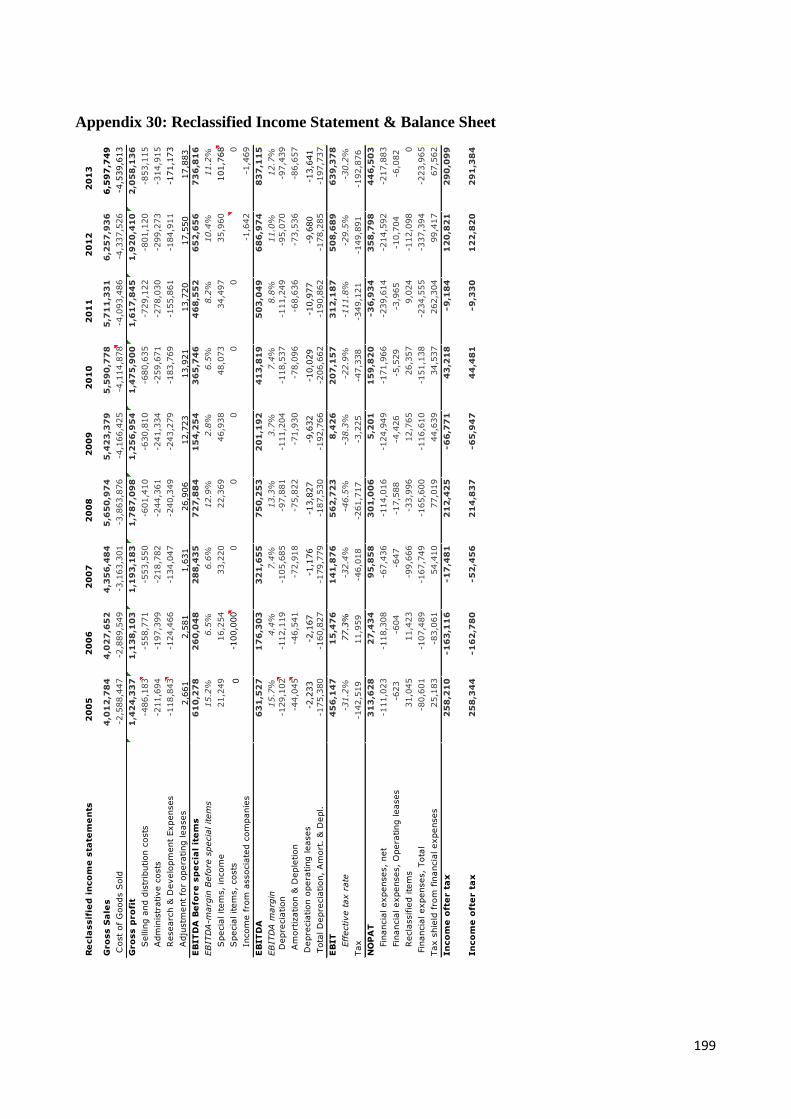

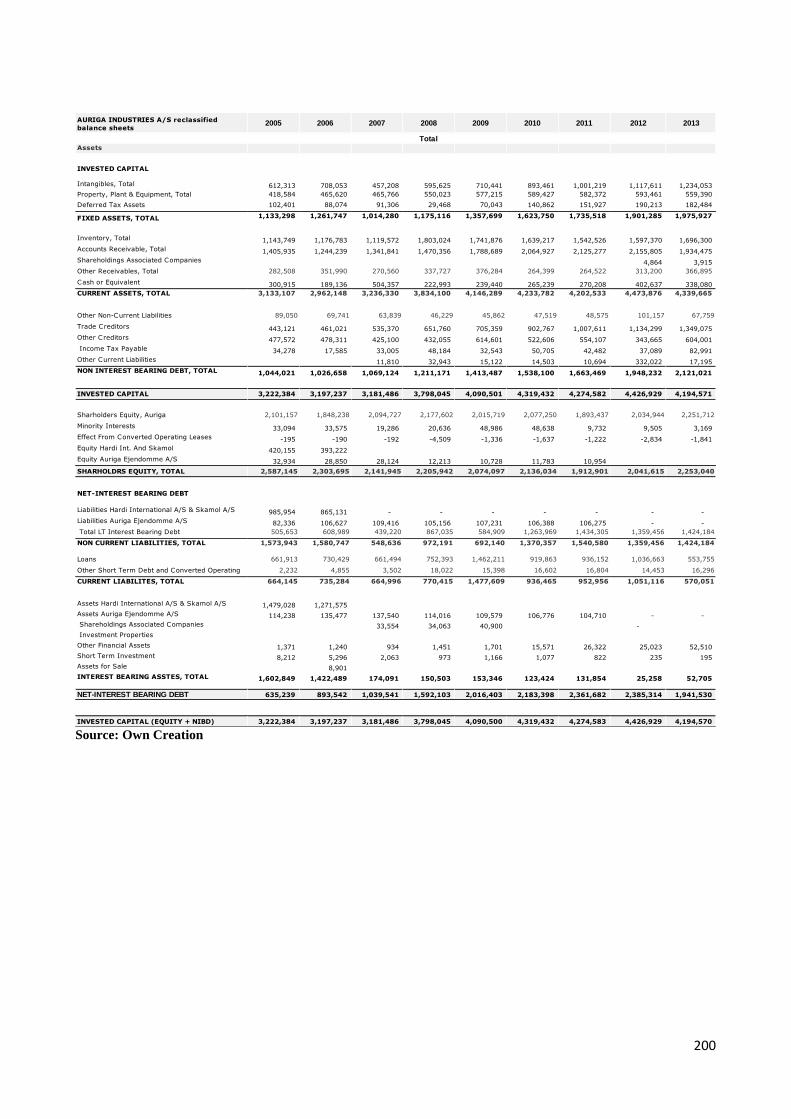

4.2. Financial Analysis ........................................................................................... 44

4.2.1. Accounting quality .......................................................................................................45

4.2.2. Re-classifying the Financial Statements ......................................................................46

4.2.3. Reclassification ............................................................................................................48

4.2.4. Tax ...............................................................................................................................50

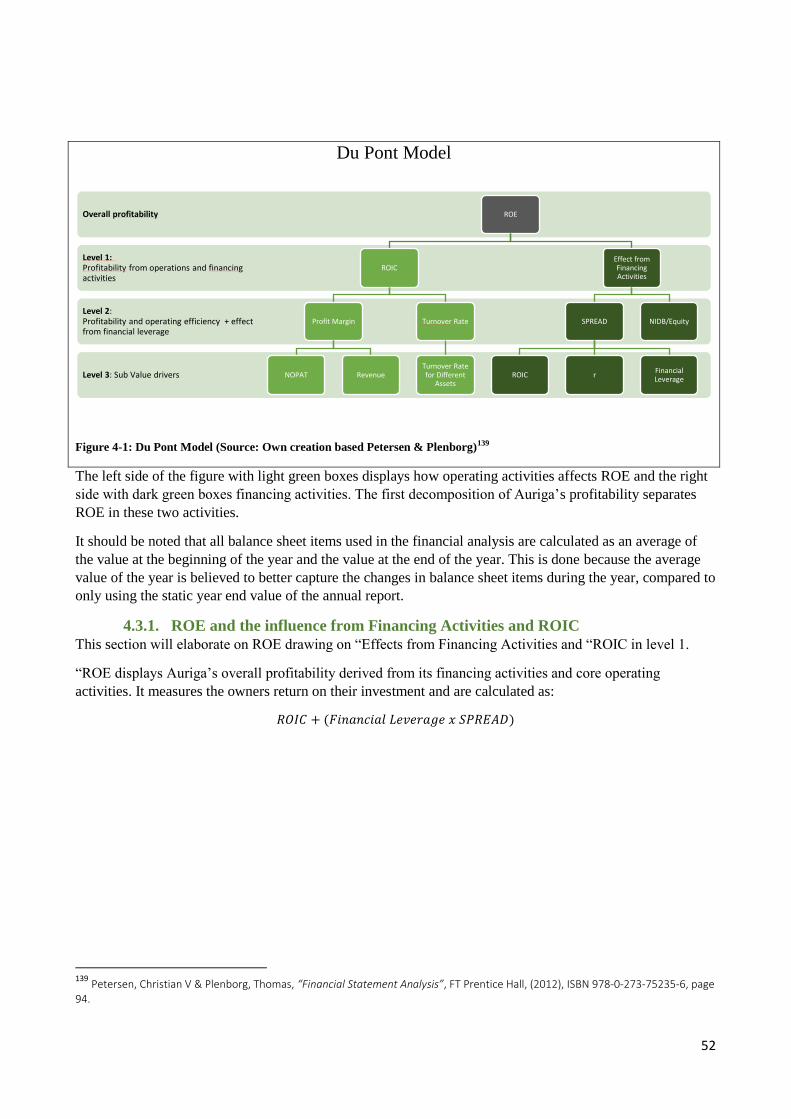

4.3. Profitability analysis ....................................................................................... 51

4.3.1. ROE and the influence from Financing Activities and ROIC .....................................52

4.3.2. Effect from financing activities ...................................................................................53

4.3.3. Effect from operating activities ...................................................................................54

4.3.4. Trend Analysis and Common Size Analysis of Profit Statement ................................56

4.3.5. Common Size and Days on Hand Analysis .................................................................57

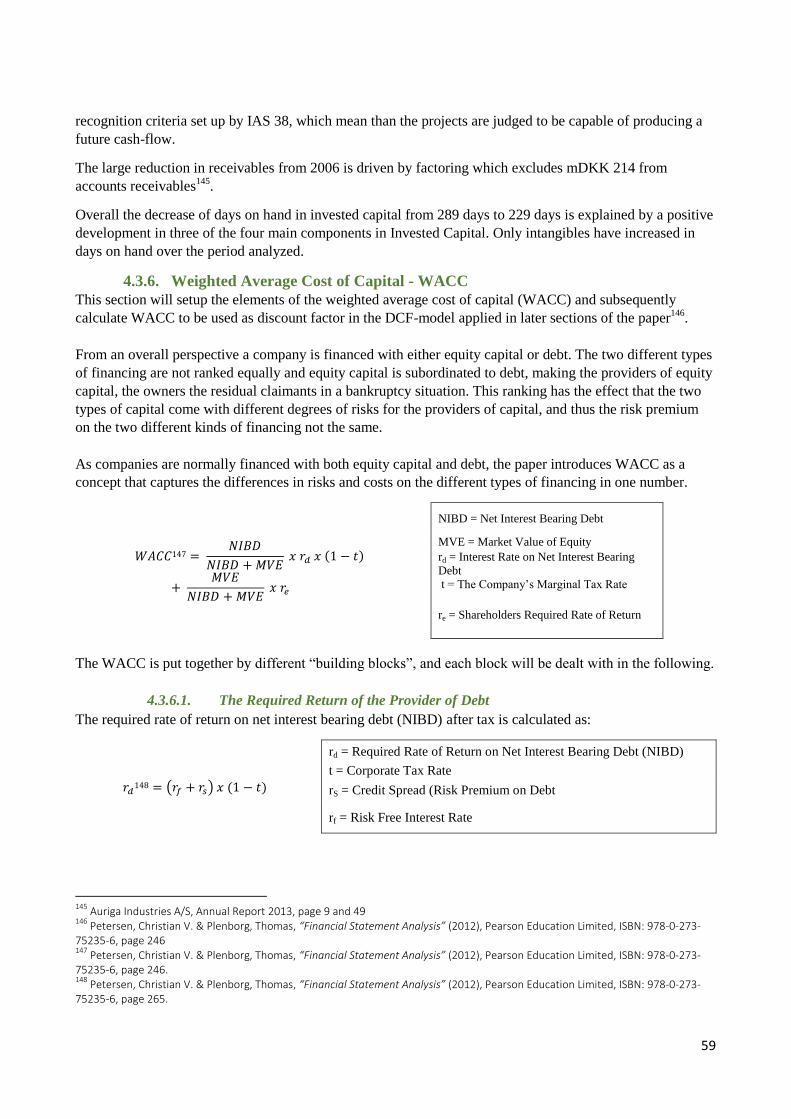

4.3.6. Weighted Average Cost of Capital - WACC ...............................................................59

4.4. Stakeholder and Corporate Governance Analysis ...................................... 62

4.4.1. Corporate Governance setup at Auriga ........................................................................62

4.4.2. Corporate Governance and Stakeholder analysis ........................................................66

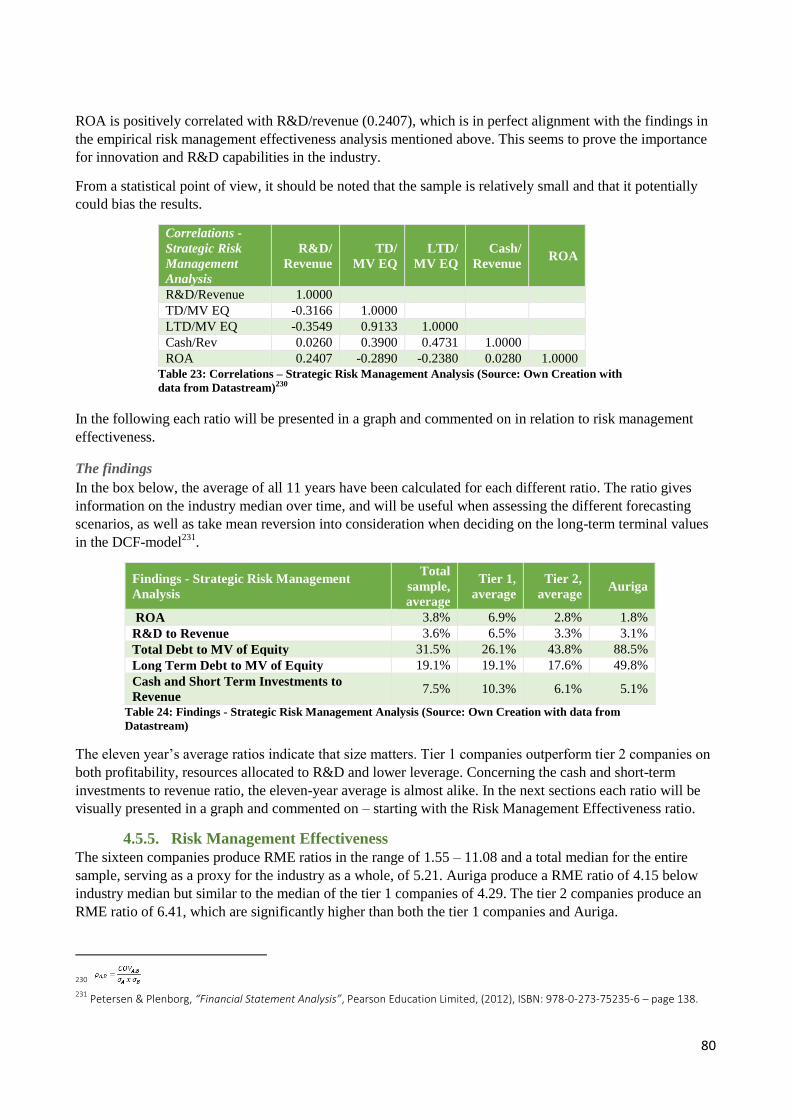

4.5. Risk Management Analysis ........................................................................... 73

4.5.1. Theoretical Terms and Aspects on Risk ......................................................................73

4.5.2. Risk in a Corporate Setting ..........................................................................................74

4.5.3. General Risks in Auriga ...............................................................................................77

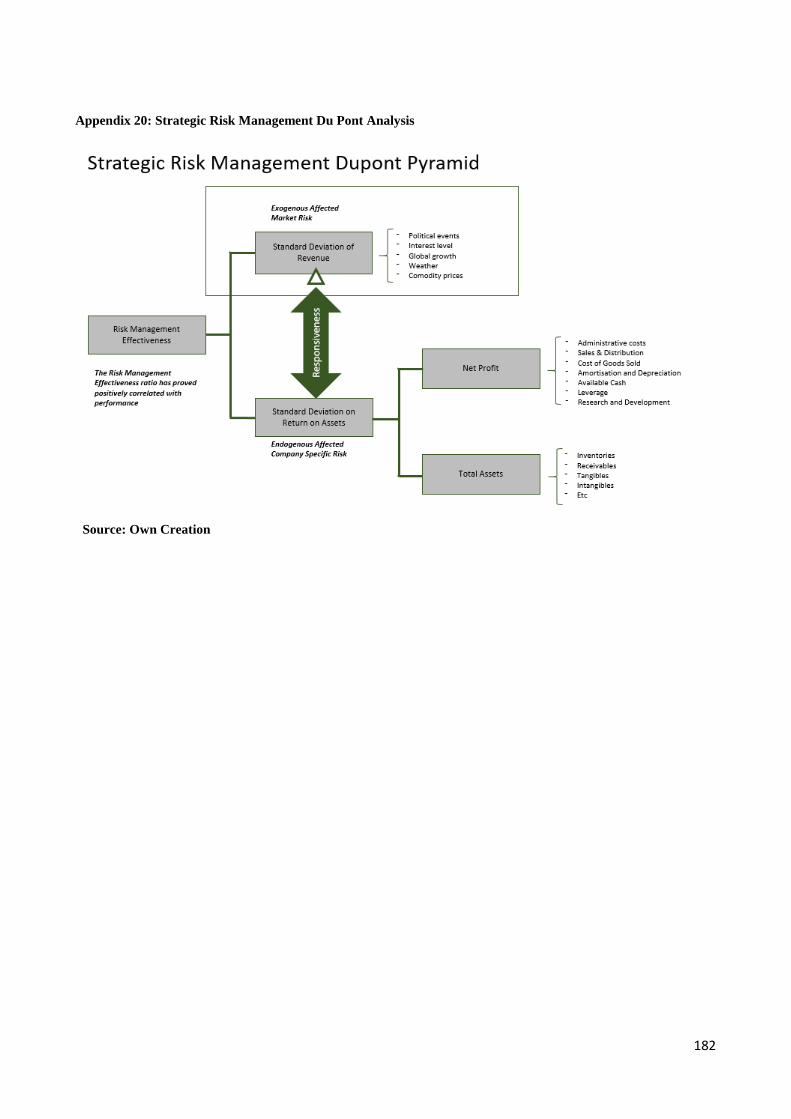

4.5.4. Strategic Risks Management Analysis.........................................................................79

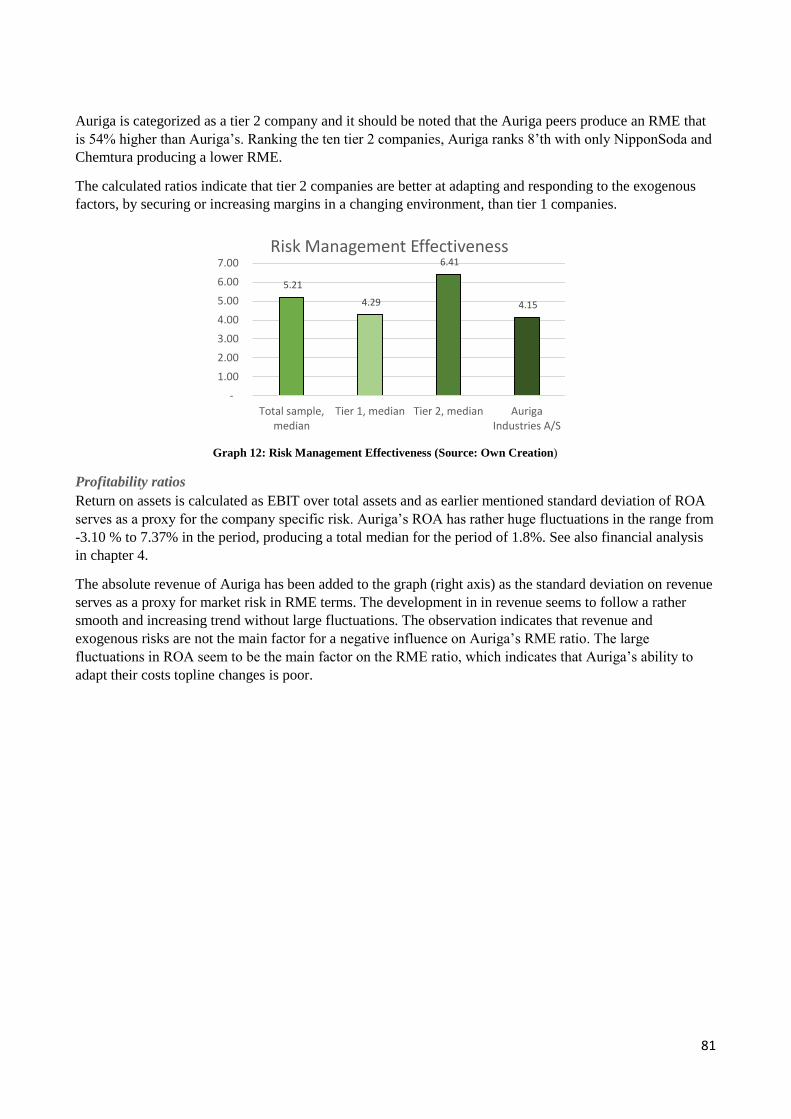

4.5.5. Risk Management Effectiveness ..................................................................................80

4.6. Sub-conclusion – Internal Factors (SW) ...................................................... 85

5. STRATEGIC ASSESSMENT ................................................................... 88

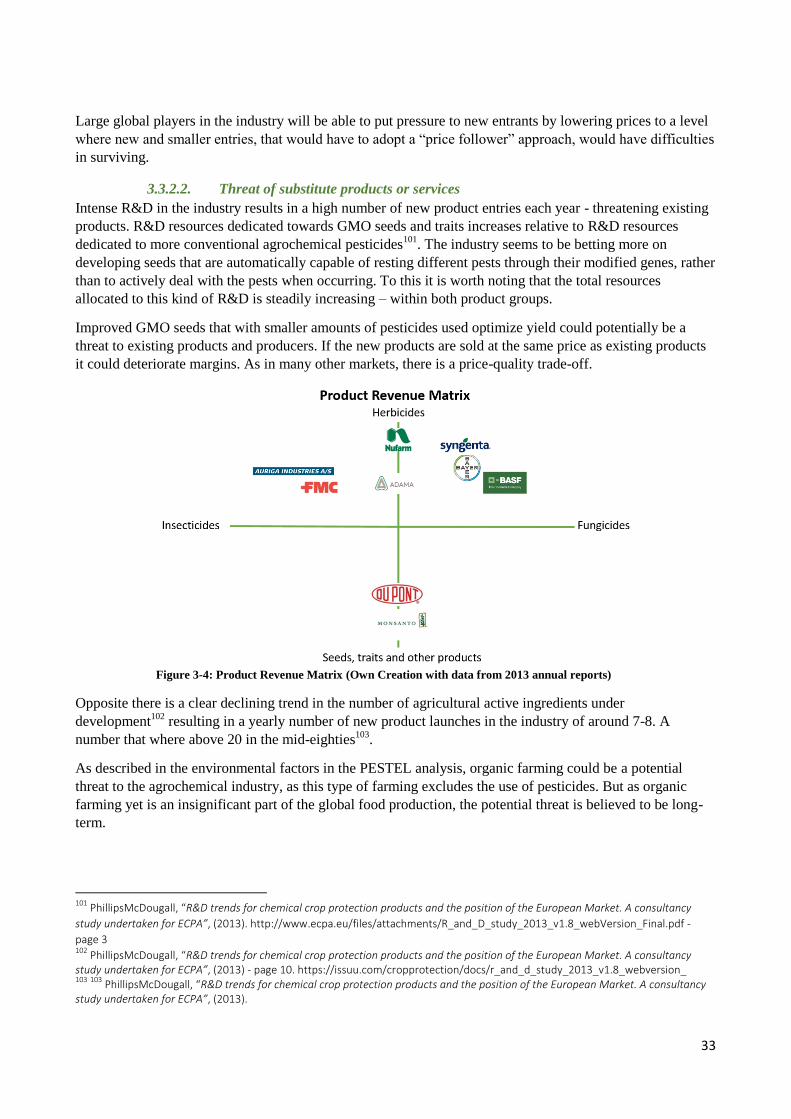

5.1. SWOT .............................................................................................................. 88

5.1.1. Opportunities ...............................................................................................................88

5.1.2. Threats .........................................................................................................................89

5.1.1. Strengths ......................................................................................................................89

5.1.2. Weaknesses ..................................................................................................................90

6. STRATEGIC DILEMMAS ....................................................................... 91

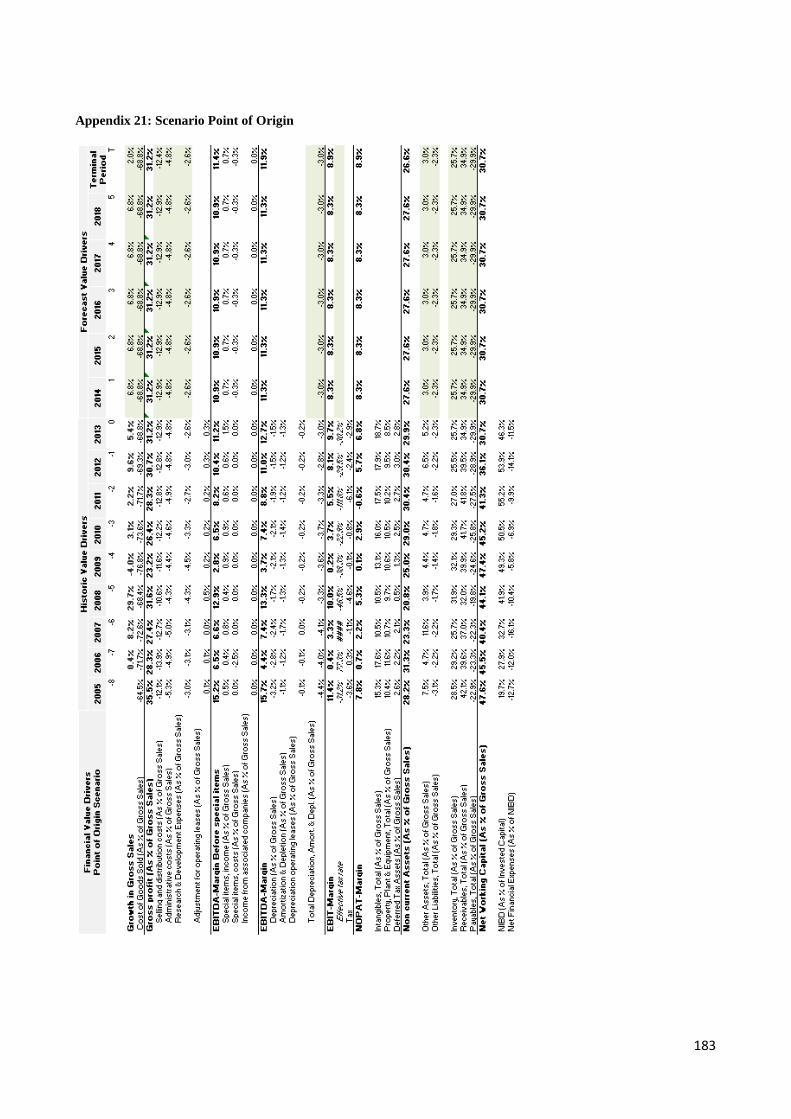

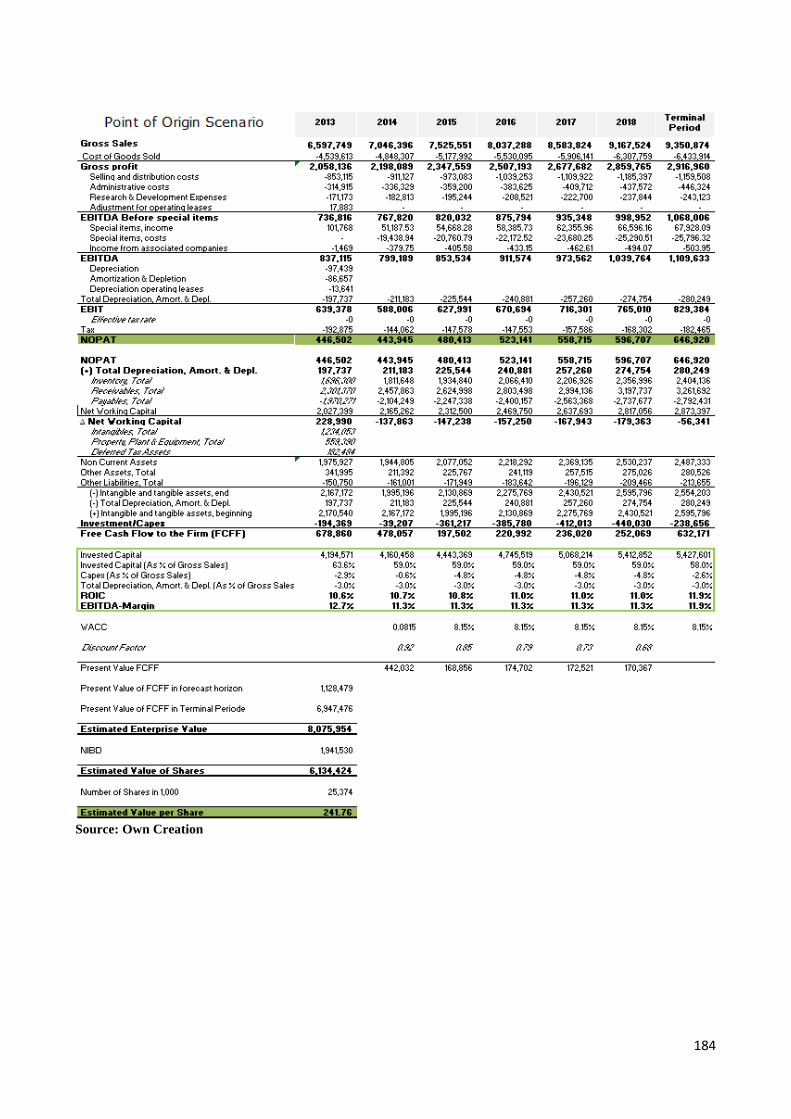

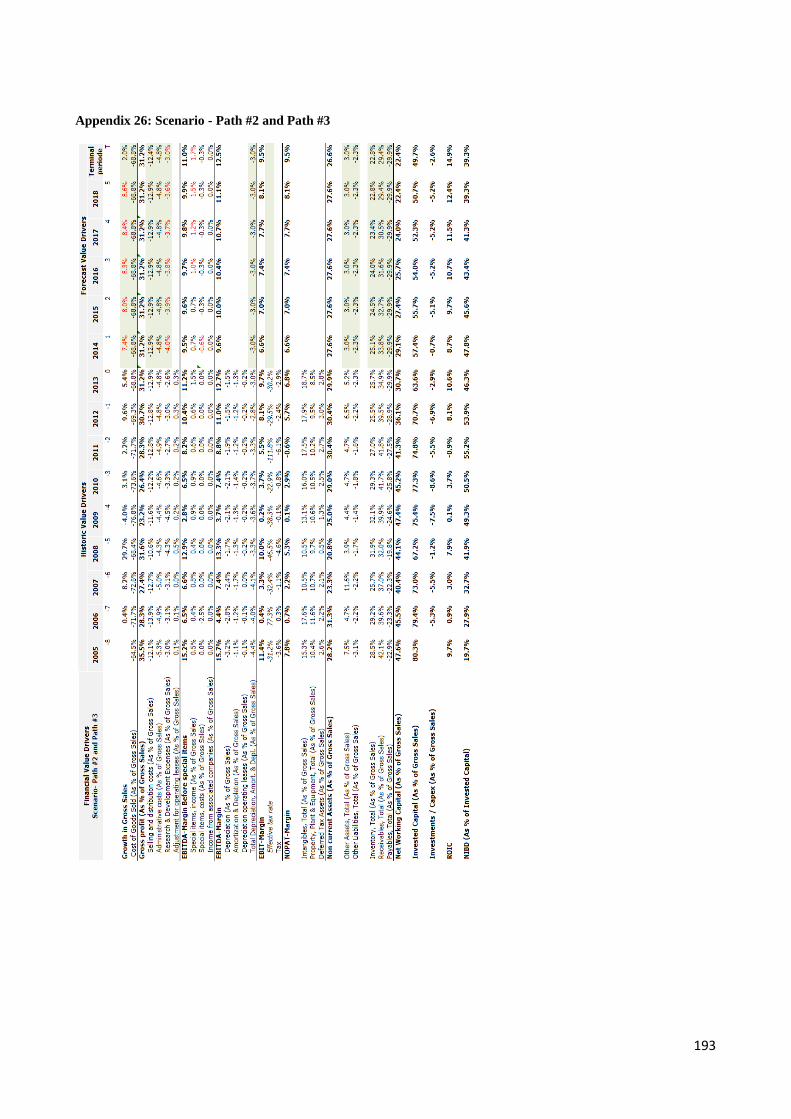

6.1. Setting Value Drivers ..................................................................................... 91

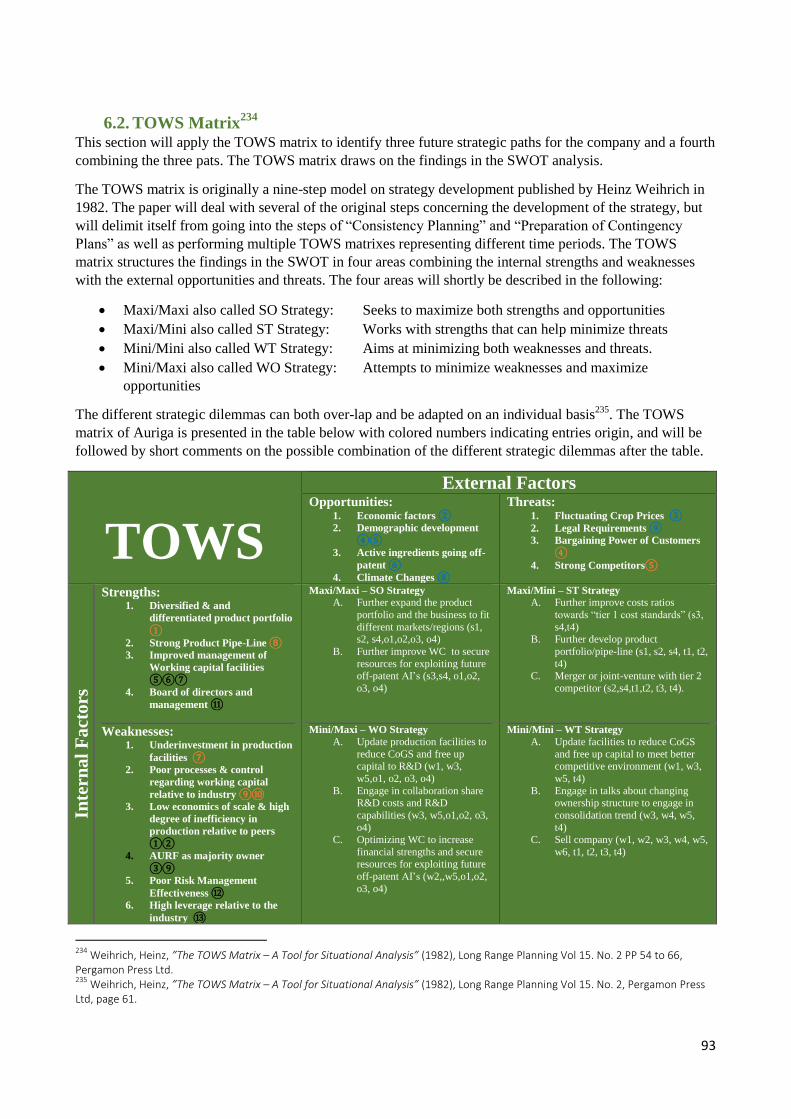

6.2. TOWS Matrix ................................................................................................. 93

7. FORECASTING & SCENARIO ANALYSIS ........................................ 95

7.1. Setting Up the Strategic Paths ....................................................................... 95

7.1.1. Free cash flow (FCFF/FCFE) ......................................................................................95

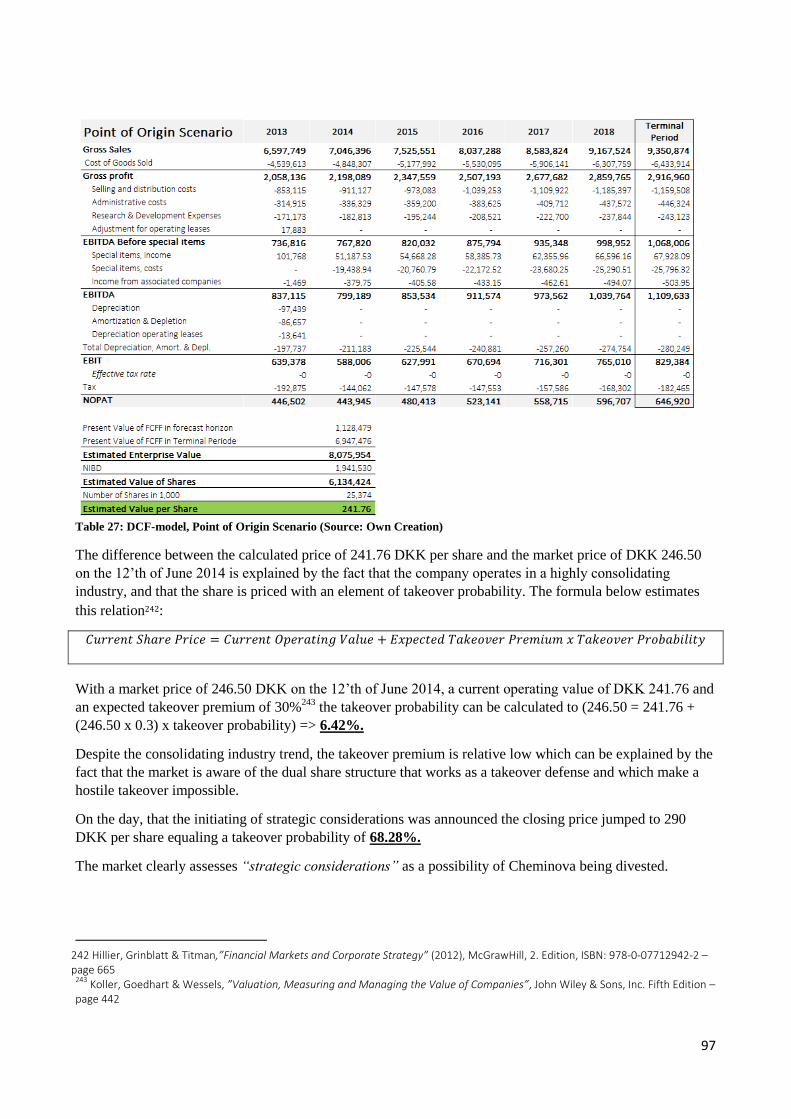

7.1.2. DCF-model – Point of Origin Scenario .......................................................................96

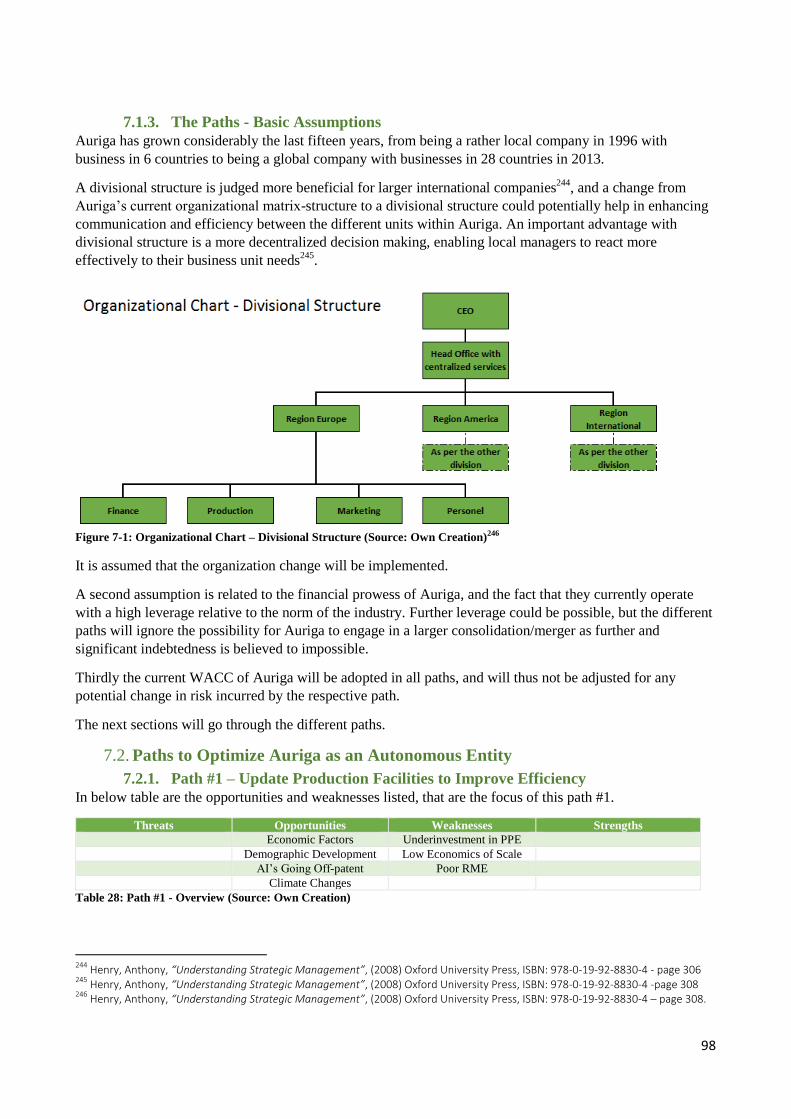

7.1.3. The Paths - Basic Assumptions ...................................................................................98

7.2. Paths to Optimize Auriga as an Autonomous Entity .................................. 98

7.2.1. Path #1 – Update Production Facilities to Improve Efficiency ...................................98

7.2.2. Path #2 – Initiate Projects to Optimize Working Capital Management .....................101

7.2.3. Path #3 – Joint Venture/Collaboration with US Based Chemtura .............................104

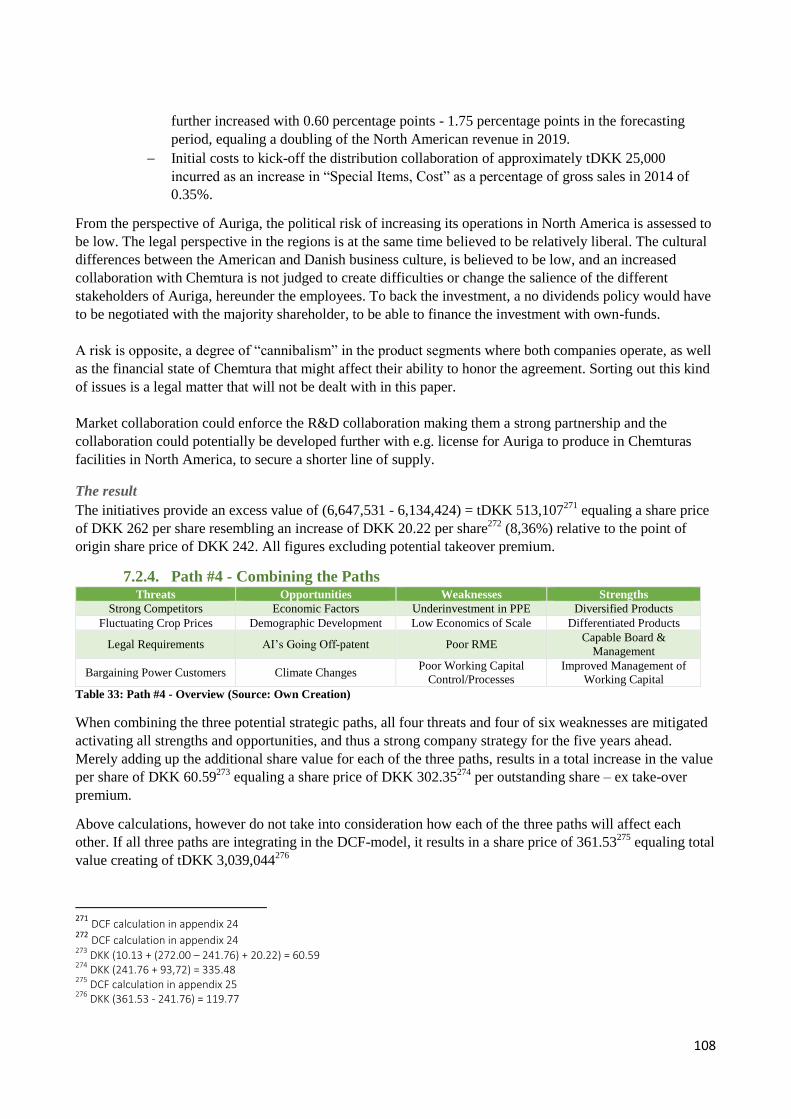

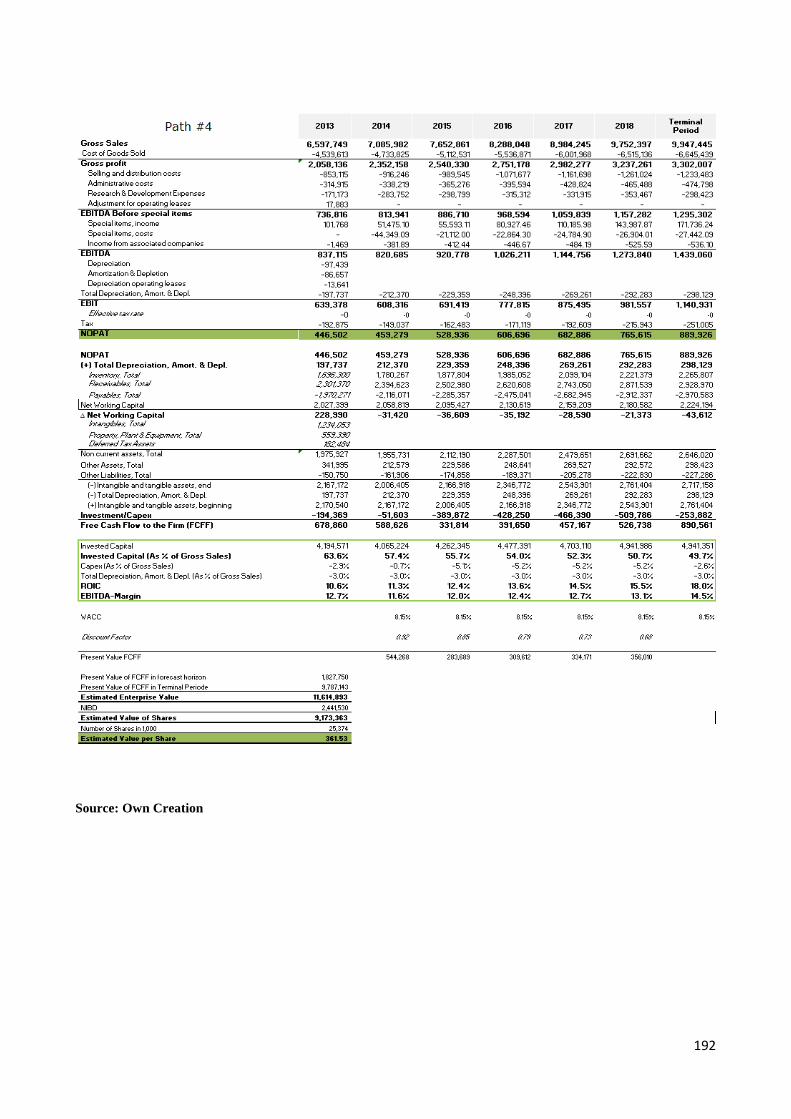

7.2.4. Path #4 - Combining the Paths ..................................................................................108

7.3. Assessment of divestment relative to Auriga’s strategic opportunities ... 109

8. Discussion .................................................................................................. 112

9. Conclusion ................................................................................................. 116

10. List of Litterature: ................................................................................... 118

10.1. Books, Articles and Scientific Research Papers ........................................ 118

10.2. Annual Reports: ........................................................................................... 122

10.3. Homepages .................................................................................................... 123

11. List of Tables, Figures and Graphs ........................................................ 126

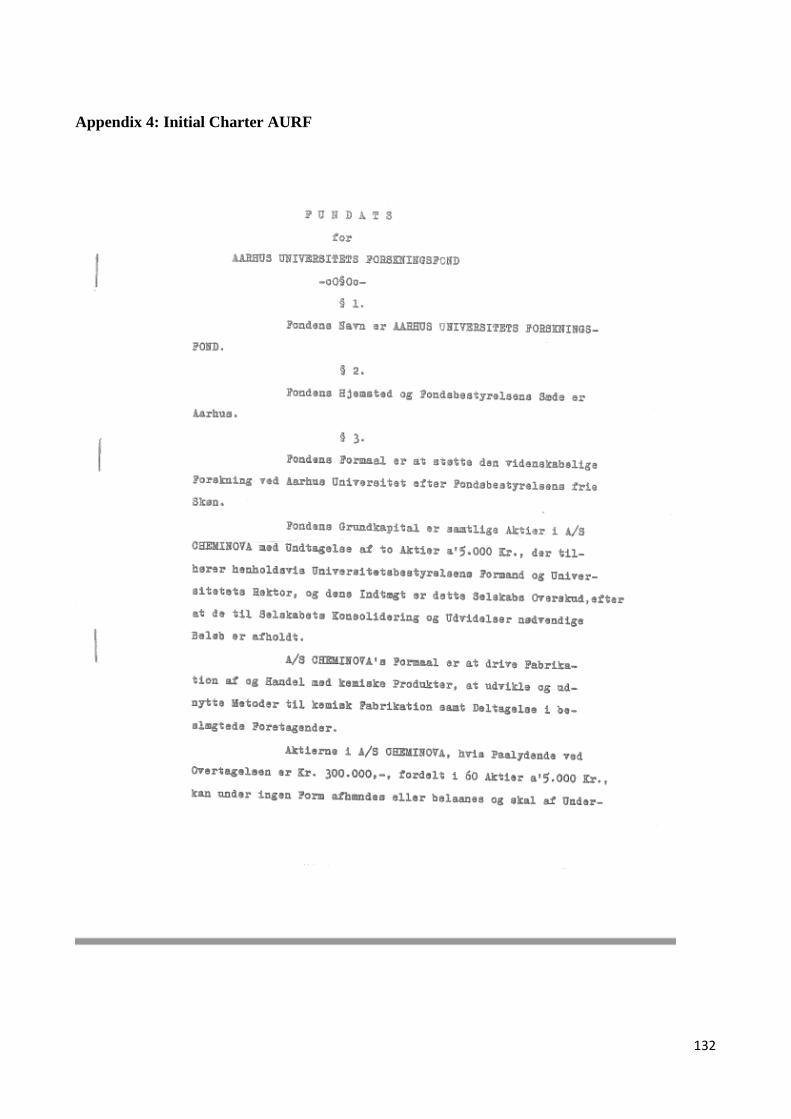

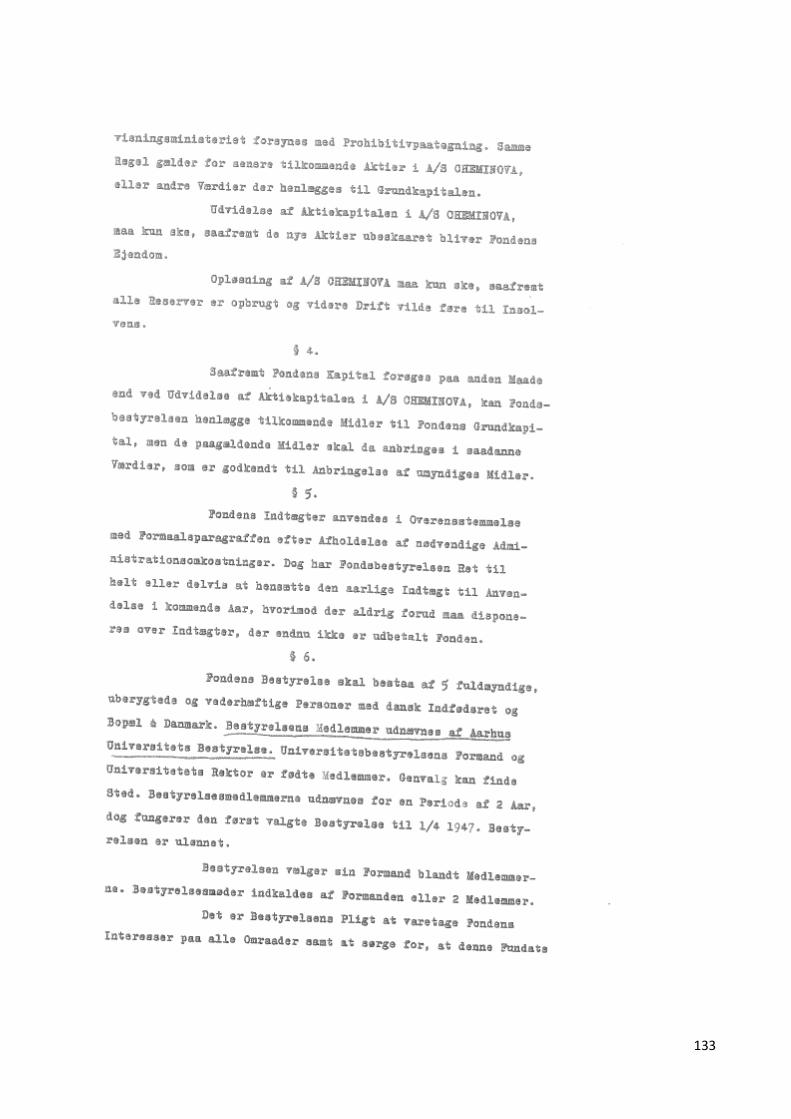

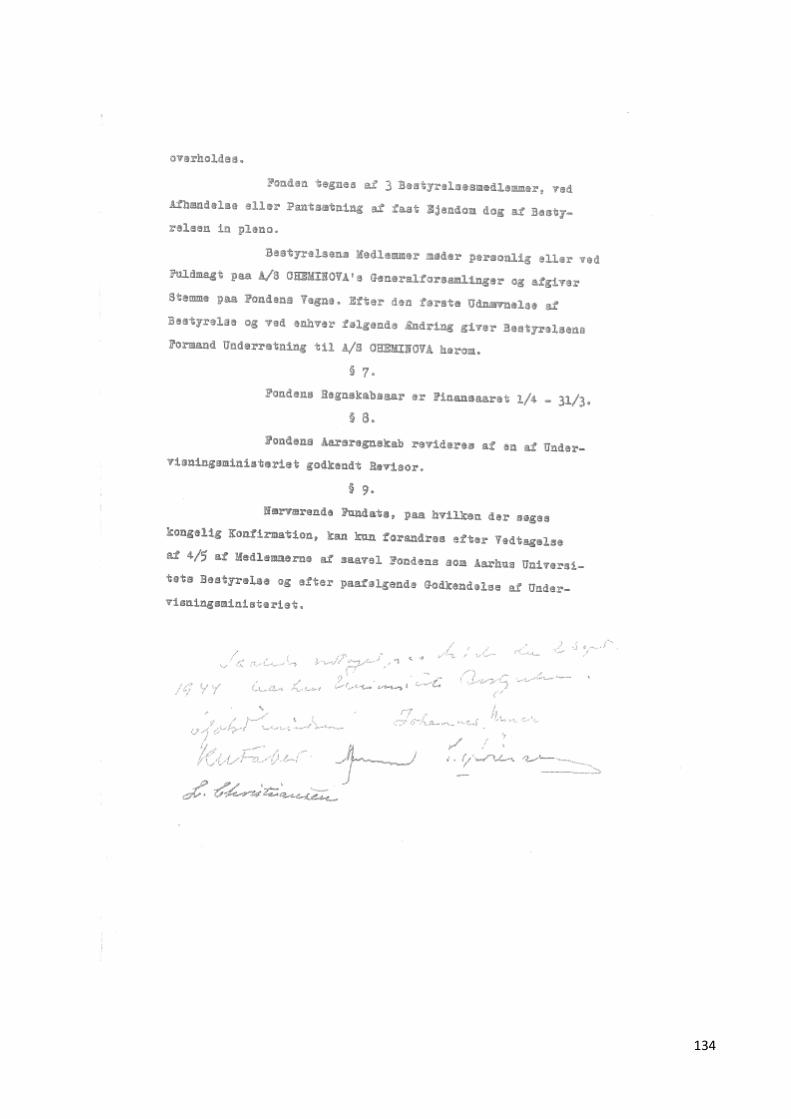

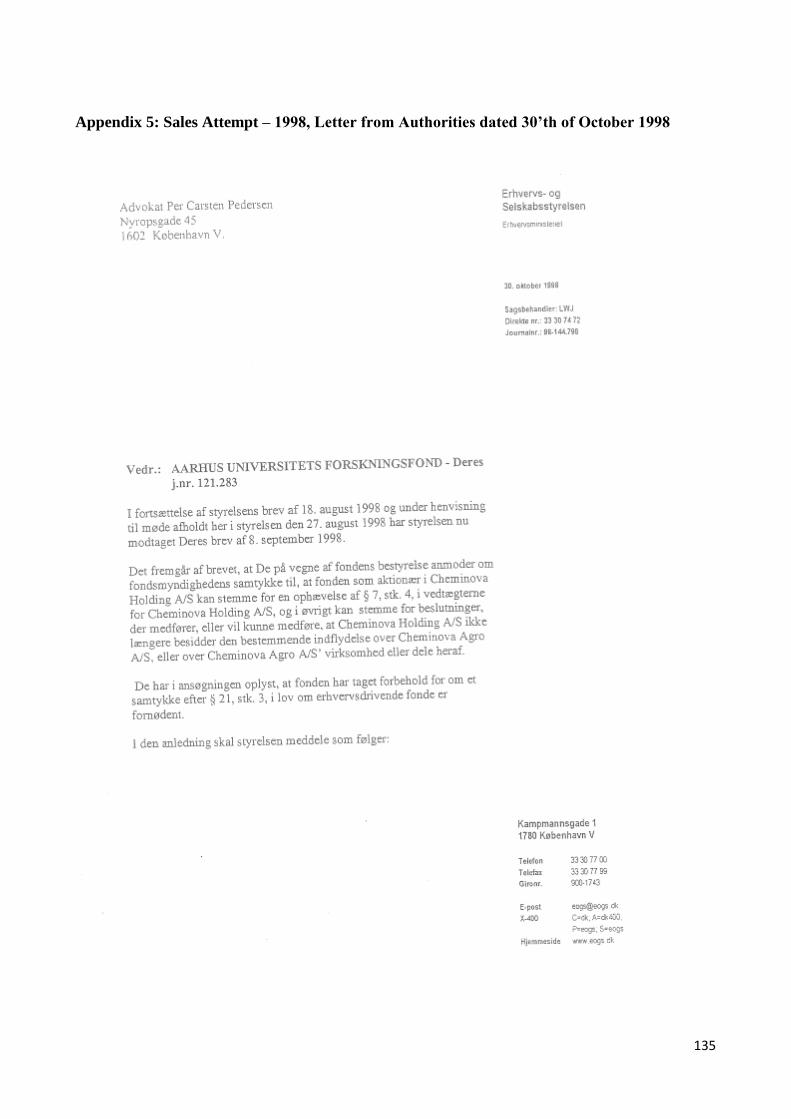

12. Appendix ................................................................................................... 128

1

Figure 1-1: Introductionary Triangle (Source: Own creation)

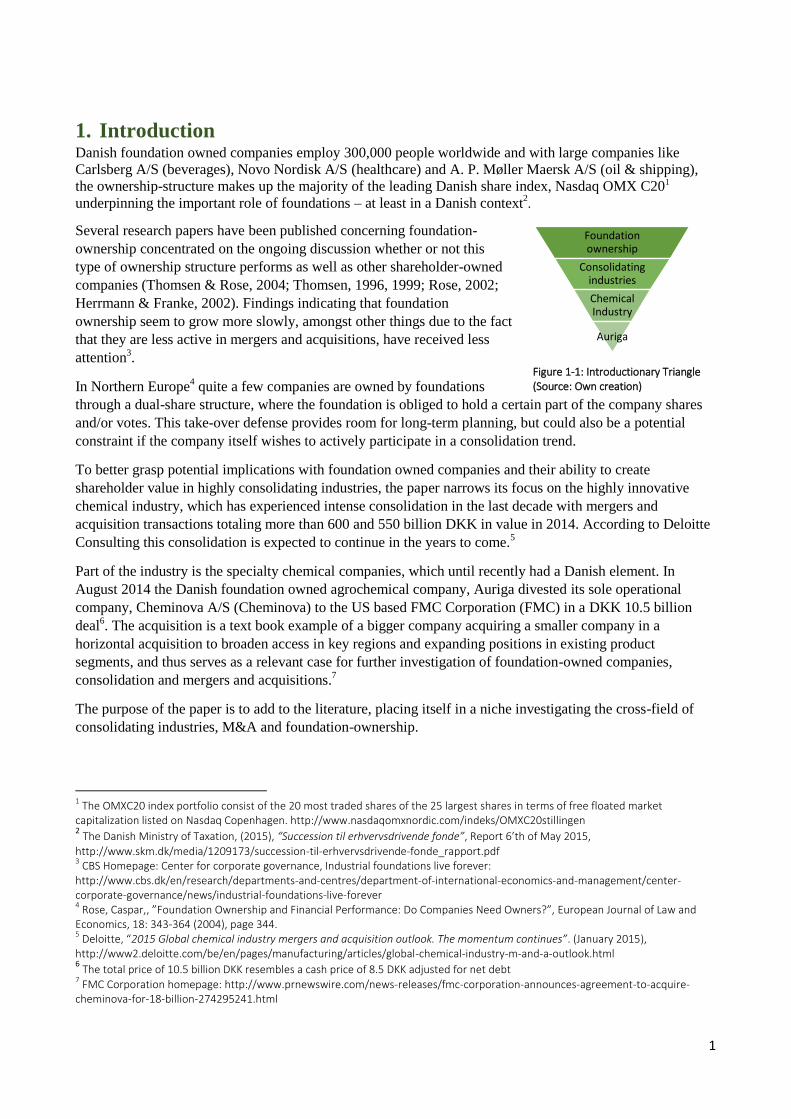

1. Introduction Danish foundation owned companies employ 300,000 people worldwide and with large companies like

Carlsberg A/S (beverages), Novo Nordisk A/S (healthcare) and A. P. Møller Maersk A/S (oil & shipping),

the ownership-structure makes up the majority of the leading Danish share index, Nasdaq OMX C201

underpinning the important role of foundations – at least in a Danish context2.

Several research papers have been published concerning foundation-

ownership concentrated on the ongoing discussion whether or not this

type of ownership structure performs as well as other shareholder-owned

companies (Thomsen & Rose, 2004; Thomsen, 1996, 1999; Rose, 2002;

Herrmann & Franke, 2002). Findings indicating that foundation

ownership seem to grow more slowly, amongst other things due to the fact

that they are less active in mergers and acquisitions, have received less

attention3.

In Northern Europe4 quite a few companies are owned by foundations

through a dual-share structure, where the foundation is obliged to hold a certain part of the company shares

and/or votes. This take-over defense provides room for long-term planning, but could also be a potential

constraint if the company itself wishes to actively participate in a consolidation trend.

To better grasp potential implications with foundation owned companies and their ability to create

shareholder value in highly consolidating industries, the paper narrows its focus on the highly innovative

chemical industry, which has experienced intense consolidation in the last decade with mergers and

acquisition transactions totaling more than 600 and 550 billion DKK in value in 2014. According to Deloitte

Consulting this consolidation is expected to continue in the years to come.5

Part of the industry is the specialty chemical companies, which until recently had a Danish element. In

August 2014 the Danish foundation owned agrochemical company, Auriga divested its sole operational

company, Cheminova A/S (Cheminova) to the US based FMC Corporation (FMC) in a DKK 10.5 billion

deal6. The acquisition is a text book example of a bigger company acquiring a smaller company in a

horizontal acquisition to broaden access in key regions and expanding positions in existing product

segments, and thus serves as a relevant case for further investigation of foundation-owned companies,

consolidation and mergers and acquisitions.7

The purpose of the paper is to add to the literature, placing itself in a niche investigating the cross-field of

consolidating industries, M&A and foundation-ownership.

1 The OMXC20 index portfolio consist of the 20 most traded shares of the 25 largest shares in terms of free floated market

capitalization listed on Nasdaq Copenhagen. http://www.nasdaqomxnordic.com/indeks/OMXC20stillingen 2 The Danish Ministry of Taxation, (2015), “Succession til erhvervsdrivende fonde”, Report 6’th of May 2015,

http://www.skm.dk/media/1209173/succession-til-erhvervsdrivende-fonde_rapport.pdf 3 CBS Homepage: Center for corporate governance, Industrial foundations live forever:

http://www.cbs.dk/en/research/departments-and-centres/department-of-international-economics-and-management/center-corporate-governance/news/industrial-foundations-live-forever 4 Rose, Caspar,, ”Foundation Ownership and Financial Performance: Do Companies Need Owners?”, European Journal of Law and

Economics, 18: 343-364 (2004), page 344. 5 Deloitte, “2015 Global chemical industry mergers and acquisition outlook. The momentum continues”. (January 2015),

http://www2.deloitte.com/be/en/pages/manufacturing/articles/global-chemical-industry-m-and-a-outlook.html 6 The total price of 10.5 billion DKK resembles a cash price of 8.5 DKK adjusted for net debt

7 FMC Corporation homepage: http://www.prnewswire.com/news-releases/fmc-corporation-announces-agreement-to-acquire-

cheminova-for-18-billion-274295241.html

Foundation ownership

Consolidating industries

Chemical Industry

Auriga

2

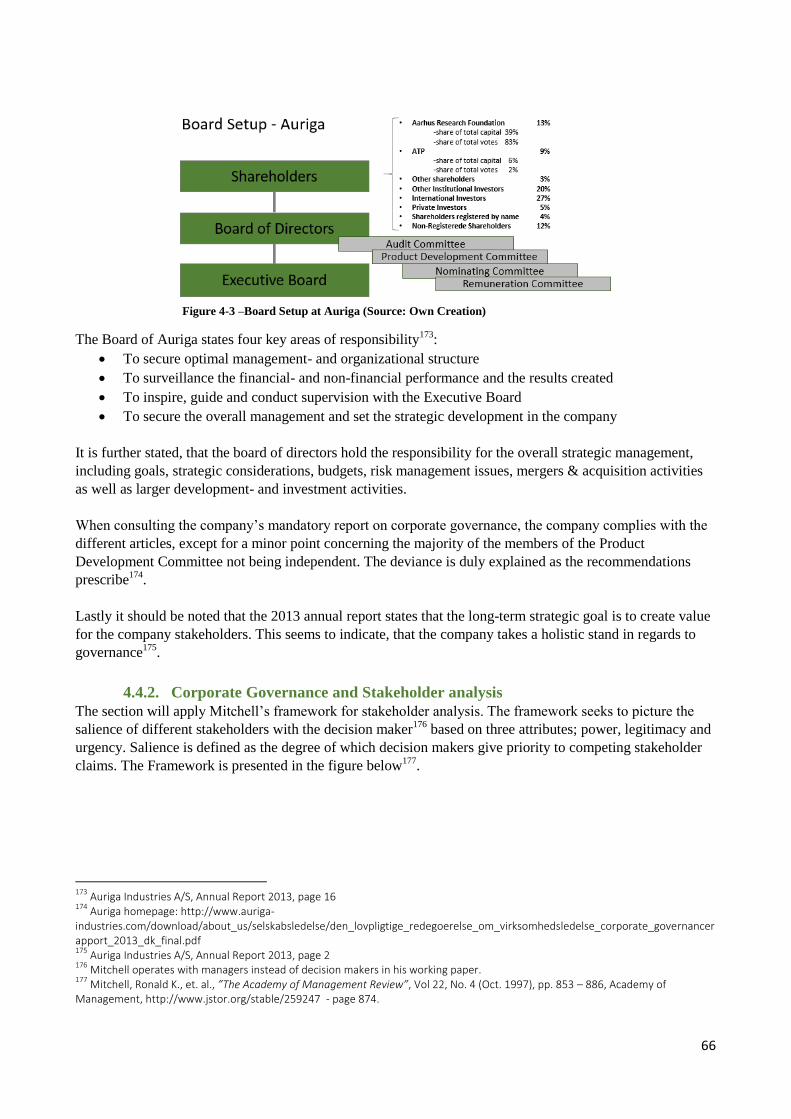

1.1. Problem Statement & Research Questions8

With the stage set in the introduction the paper will investigate foundation-owned companies’ ability to

maximize shareholder value in highly innovative- and/or consolidating industries.

To structure the investigation, the paper will answer the following research questions:

I. Based on exogenous, external and internal factors assess which strategic dilemmas are facing Auriga

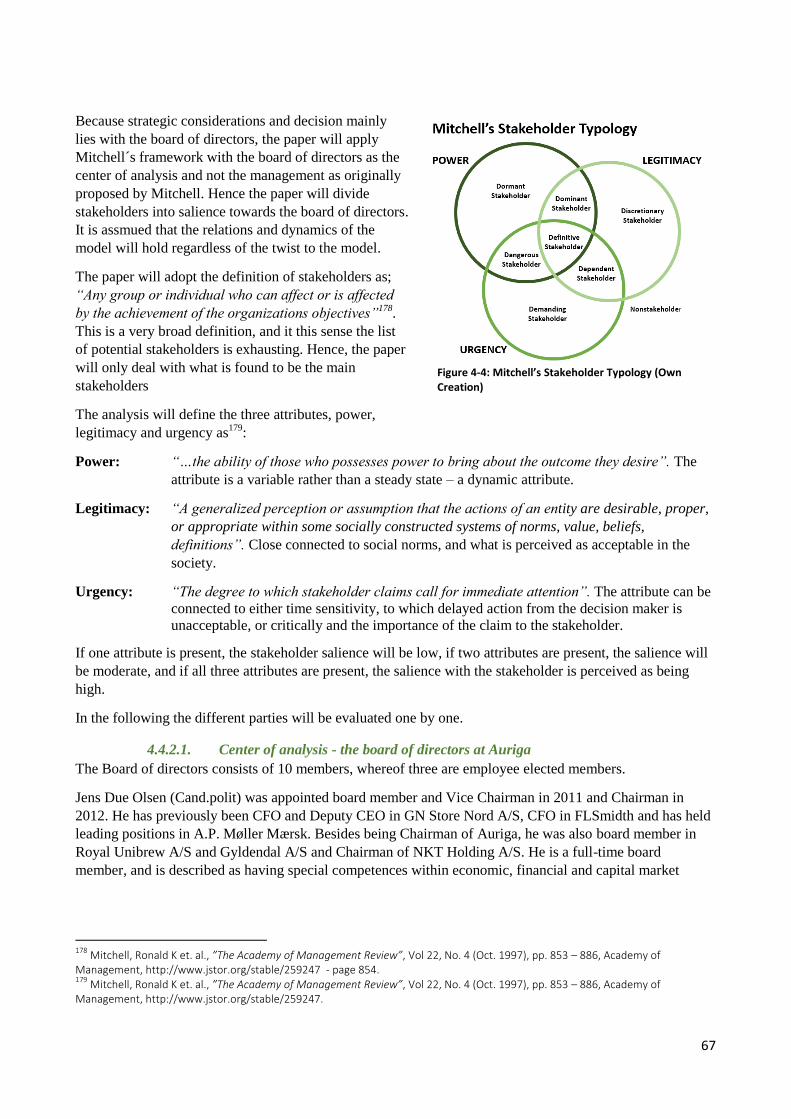

and thus alternative strategic options for the company?

II. Investigate if the divestment maximized shareholder value after the takeover?

III. Deduce possible structural changes and governance implications which can be learned from the

horizontal acquisition of a foundation owned company?

1.1. Delimitations This section will explain the boundaries of the paper.

The focal point of the paper will be on issues relating to the target less so deal with internal issues with the

acquirer.

Because Auriga is a foundation owned company, touching upon governance issues is key, and this topic will

therefore be an important part of the paper. Issues related to the legal acceptance of the change in the

foundational object of clause will not be addressed as this subject is more suitable for a paper focusing on

legal issues rather than this paper focusing on economic, financial and governance issues.

Figure 1-2: Focus of the Paper (Source: Own creation)

The environmental and competitive environment analyses will only cover key points concerning the different

markets and regions. Auriga operates in more than 25 countries divided into 4 regions and a detailed

description of each country/region is not possible, both due to information not publicly disclosed and the

formal- and time constraints regarding the paper.

Production methods and products are not described in detail – both since information is not disclosed and

because of the industry being rather complex which would involve specialized knowledge with both authors

and readers.

Some of the material and references used is originally published in Danish. Texts and citations have been

translated to the best of our ability, and if any details, contrary to expectations has been lost in translation

process it is the Danish text which is applicable.

The time period for most analyses in this paper is 8 to 10 years, as it provides a reasonable period for

analyzing trends. Expanding the ex-post period analyzed is not believed to provide further value to the ex-

ante projections that will be conducted later in the paper.

8 Ankersborg, Vibeke & Watt, Merete, “Tænk selv! Videnskabsteori og undersøgelsesdesign i samfundsvidenskab” (2007), Forlaget

Politiske Studier, page 9. Model used for developing the problem.

3

The last full-year Auriga owned Cheminova was 2013, why this is also the “cut-off year” of the paper. This

means that the paper to a high degree uses historical information, and that information and events since then

could potentially have influenced/motivated the description, analysis and conclusions of this paper.

It could be argued that the paper should be written in past-tense but it is written in present-time, as 2013 is

the “cut-off year” in all instances.

1.2. Conceptual Framework A global company is a complex entity and

creating a holistic picture, incorporating the

external business environment as well as the

company’s internal state, framework and

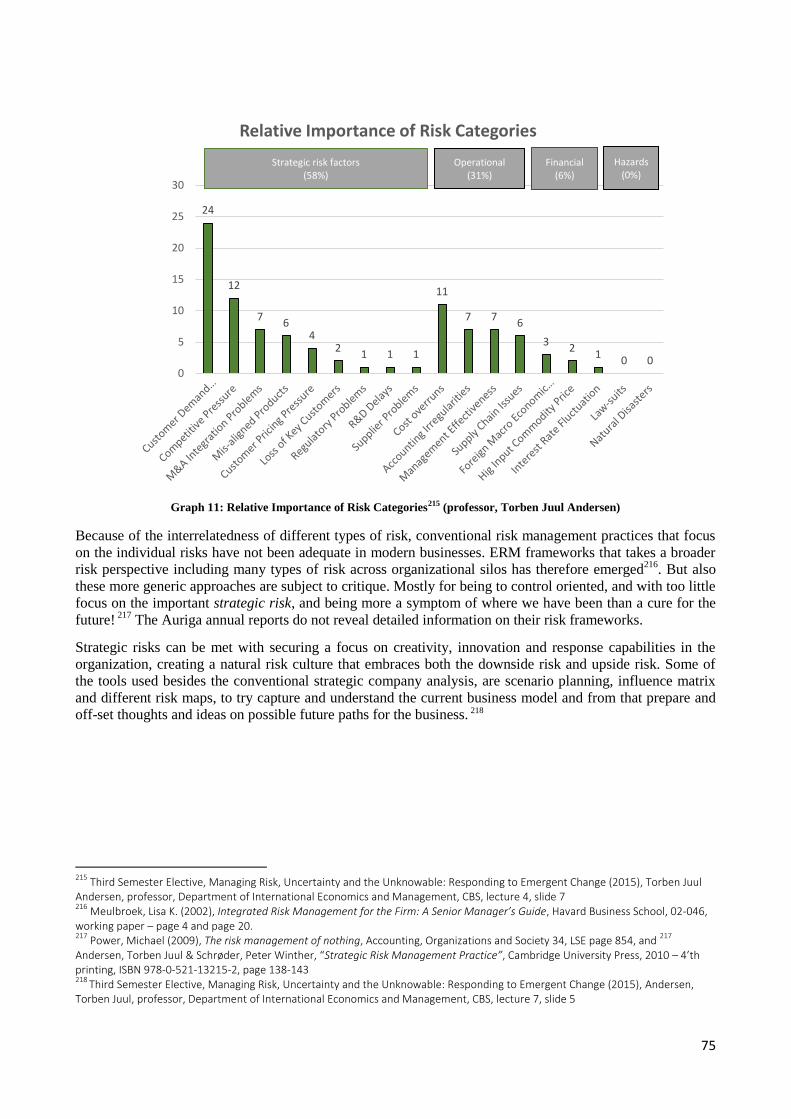

processes is a coherent process, bridging from

market and industry understanding to

organizational setup and internal financial

analysis. As a result, the paper is compelled to

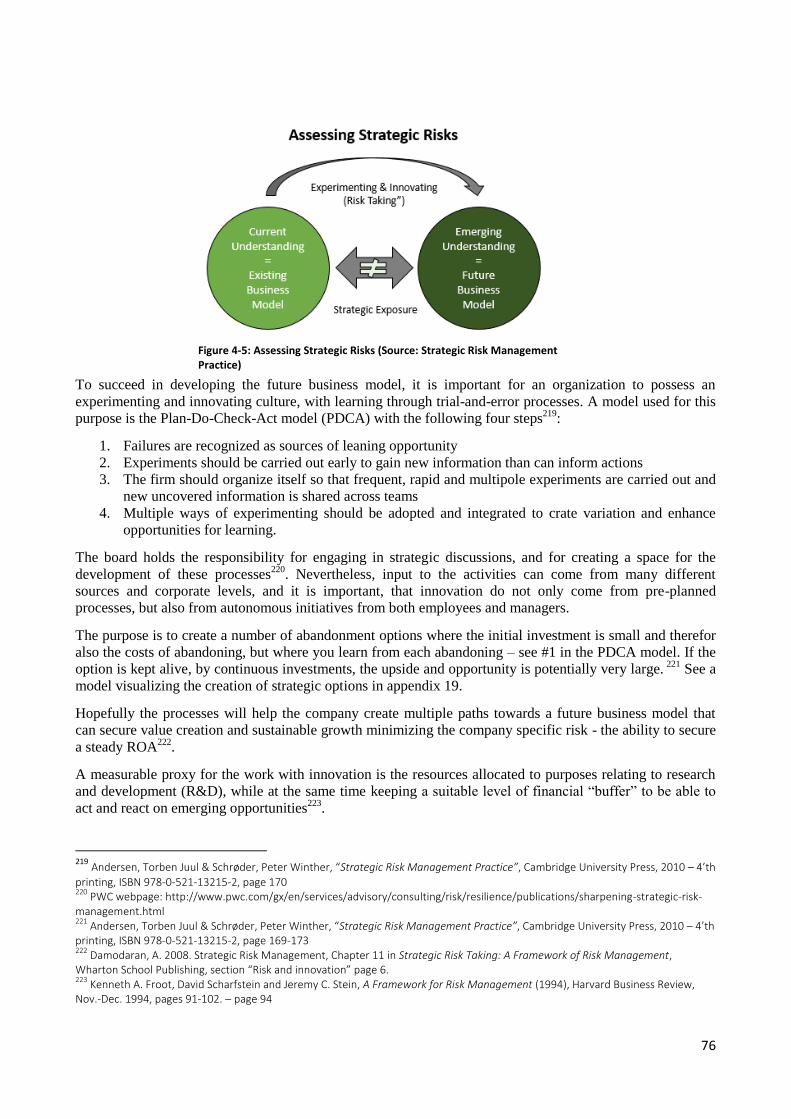

draw on and make use of a wide variety of

models and theoretical approaches of

structural, managerial and financial origin.

Together, the different elements create the

focal point that enables the paper to answer

the problem.

The paper will adopt an inductive and

positivistic mindset as the aim of the paper is

to use a case company for as a reference for

potential general implications with foundation-owned companies operating in highly innovative- and/or

consolidating sectors. This is done mainly through observable and quantifiable findings.

The use of a case-company enables the paper to center the analysis in the framework where the value-

creation takes place, and provides the opportunity to conduct a qualitative and quantitative in-depth study

with the purpose of uncovering internal processes and implications that potentially could affect a company’s

ability to create shareholder value.

The methodology will be dynamic and explorative, with a time-frame that mainly covers the ex-post period

from 2003 – 2013, though later sections of the paper also conducts ex-ante projections beyond 2013.

The paper will take the overall perspective of all shareholders, and answer the research questions from the

viewpoint of this particular group of stakeholders.

It is important to note, that the case company as a specific entity has unique features, but also that there could

be other potential case companies, which just as well could have served the same purpose – both in regards

to a specific industry as well as a specific company.

Auriga has been chosen as case-company because it exists in an industry which is both highly R&D focused

and that experiences a high degree of consolidation. Both are elements that put pressure on cash flow and

liquidity which can be contradictory with charters and capabilities of foundations.

Another reason for choosing Auriga as case-company is that the board of directors and the shareholders have

deemed the divestment to FMC as the transaction that maximizes shareholder value and conversely that

Auriga did not have the relevant potential to continue as an independent company.

Figure 1-3: Model and Theories Applied to Create Focal

Point (Source: Own creation)

4

The external approach – hereunder the use of a large industry sample, will be used to develop a quantitative

perspective on the agrochemical industry in which the case-company operates.

The paper applies both quantitative and qualitative measures and thus constructs a framework of a

combination perspective. Data and findings will continuously be visualized by the use of graphs, tables and

figures, and presented for the reader in the sections where the information is most relevant.

Put together, the scope of the paper is to combine theories and methods that best fit the constraint of the

paper and the information and data available. To avoid an endless discloser of models and theories applied at

this point, each relevant theory and model is described in the chapter where it is applied.

The structure is visualized in figure 1.4.

To clarify the conceptual framework used in the problem statement a brief description the three main

concepts is listed below.

Maximizing shareholder value: Creating the highest possible risk adjusted return in monetary value to

individuals or organizations possessing part of the company. On a more operational level shareholder value

can be defined as Market Value Added (MVA), Total Value ex Total Capital, Net Present Value or Present

Value of Future EVA9. This paper will adopt a less restrictive definition and define shareholder value as the

present value of free cash flows to the firm, deducted net interest bearing debt, equaling estimated value of

outstanding shares or the value per share when deducting the number of outstanding shares.

Highly innovative industries: The conceptual framework of highly innovative industries can be measured

in many different ways. The paper adopts the wide OECD definition on innovation: “An innovation is the

implementation of a new or significantly improved product (good or service), or process, a new marketing

method, or a new organizational method in business practices, workplace organization or external

relations”10

.

The main criterion in this paper is that a large amount of resources in the form of monetary value is required

to maintain or increase a company’s position in the industry. How this monetary value is specifically

distributed or used is not addressed. When e.g. measuring innovative capabilities in the peer analysis, R&D

spending is solely used as a reference point for the degree of resources allocated to the matter.

Highly consolidating industries: The main criterion when defining a consolidating industry is that the

industry is characterized by an ongoing transition from many small companies to a few larger companies.

This change forces companies within the industry to either find a niche, be the acquirer or be targeted for

acquisitions. In highly consolidating industries, economics of scale11

is of importance, and mergers and

acquisitions are therefore a necessity for the long-term survival.

1.2.1. Data

The data used in the paper is primarily of quantitative character, and can be divided into two overall groups –

detailed accounting data on Auriga, and more wide-spread financial data on the agrochemical industry as a

whole. Each group of data will be commented on in the following – both in regards to gathering and

processing the data as well as checking for validity and reliability.

9 Stuart III, G. Bennet, “EVA, Fact and Fantasy”, Stern Stewart & Co., BankAmerica – Journal of Applied Corporate Finance, page 72

and 74(Materialesamling efterår 2014 – Køb og salg af virksomheder, Cand. Merc. R80, Bind 1, Academic books page 130 and 132 10

OECD, “Guidelines for Collecting and Interpreting Innovation Data”, (2005) OECD Publishing, third edition - page 46. http://www.oecd-ilibrary.org/docserver/download/9205111e.pdf?expires=1462037616&id=id&accname=guest&checksum=20B46D37F9B2E326BA64F4C45ACD178B 11

Brealey, Myers & Allen, “Principles of Corporate Finance”, Global Edition, McGraw Hill Irwin, ISBN:978-0-07-131417-6 – page.823.

5

1.2.1.1. Specific Auriga Data

The detailed accounting data on Auriga where extracted from Orbis International which is a database on 200

million companies across the globe powered by Bureau van Dijk12

. Setting up the data for further analysis,

the data was spot checked against annual reports downloaded from the Auriga company website. As the

sample was short of several items, these items were found in the annual reports and added to the sample

manually.

The data was subsequently processed in Excel by the use of financial analysis, trend analysis, common size

analysis etc. to uncover the company’s financial and operational abilities.

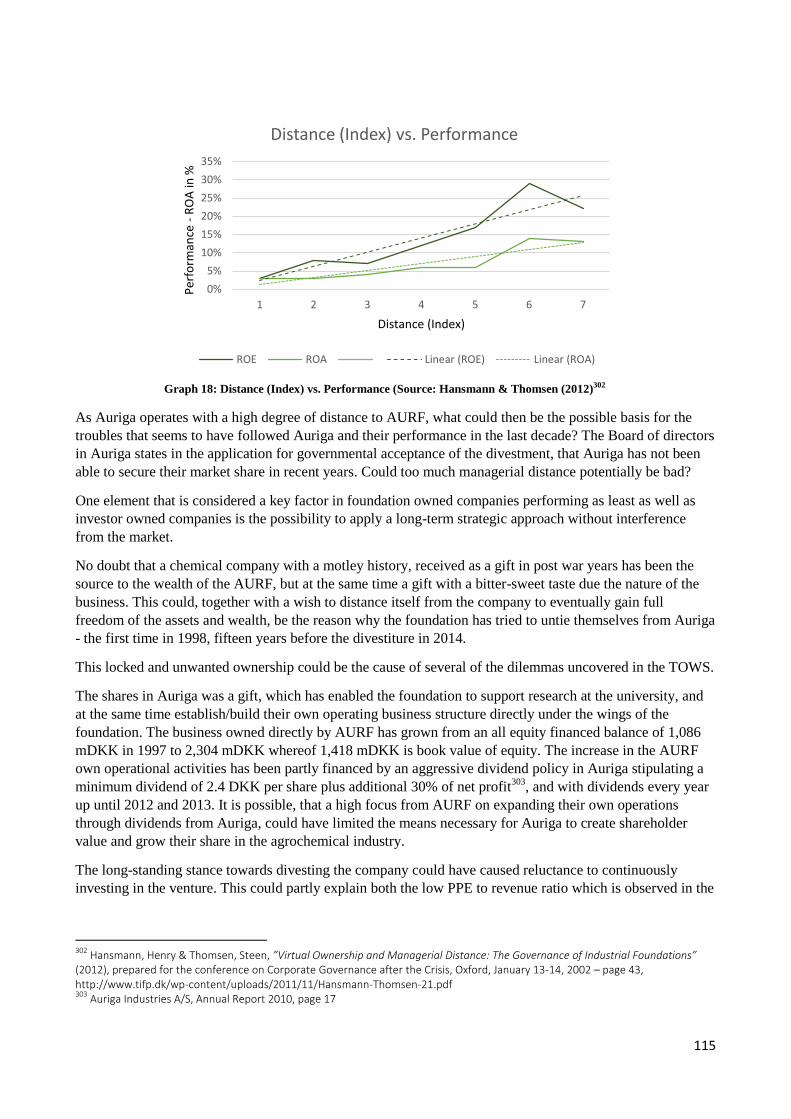

It is acknowledged that e.g. annual reports come with a certain degree of subjectivity, and that companies to

some degree uses “fabrication”13

in order to produce a certain picture of the company. But as the rules

regulating financial statements from listed companies are rather fierce, it is believed that the data in general

are of high quality, providing a “true and fair view” of the current state.

It is believed that the data is of as high quality as possible, and that the results produced from the data is

reliable, and valid as another paper applying the same data would reach similar results.

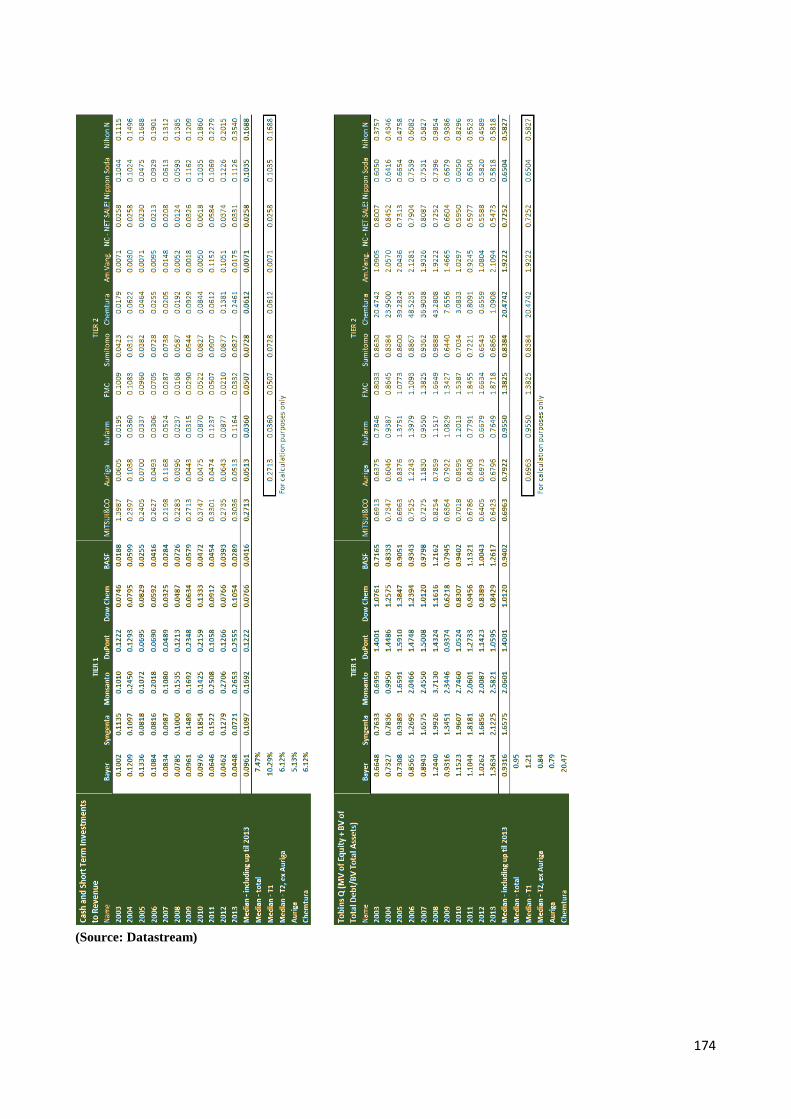

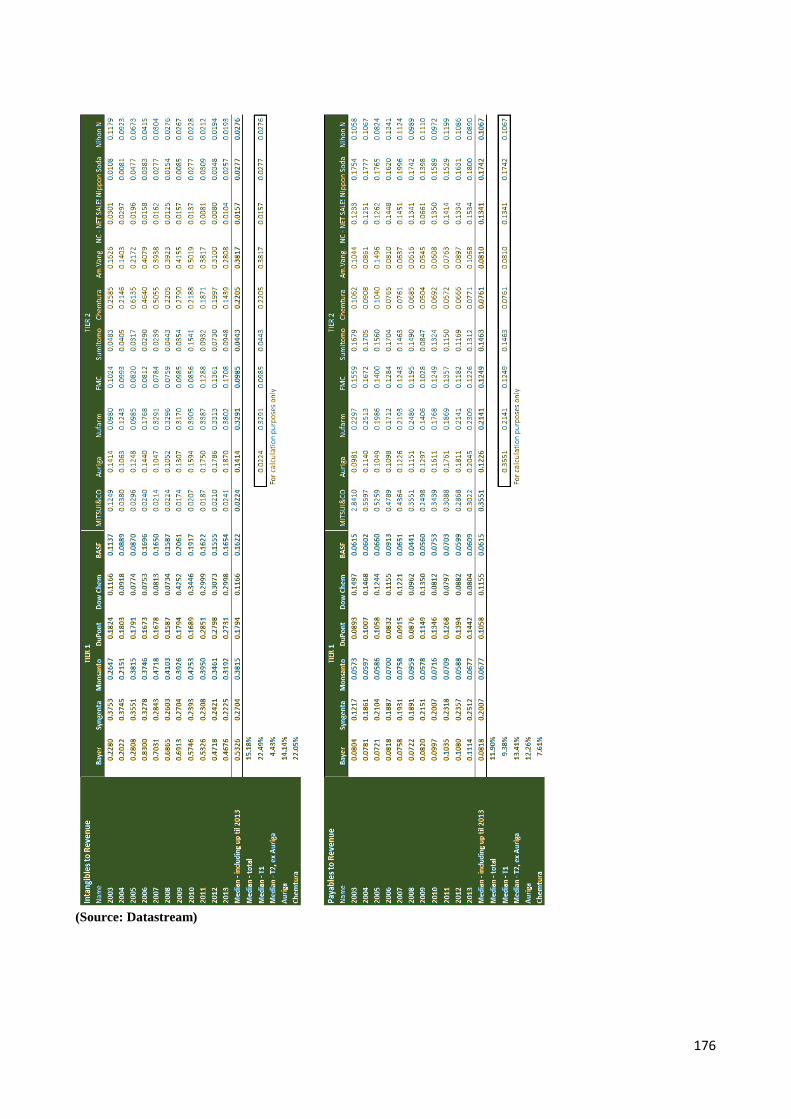

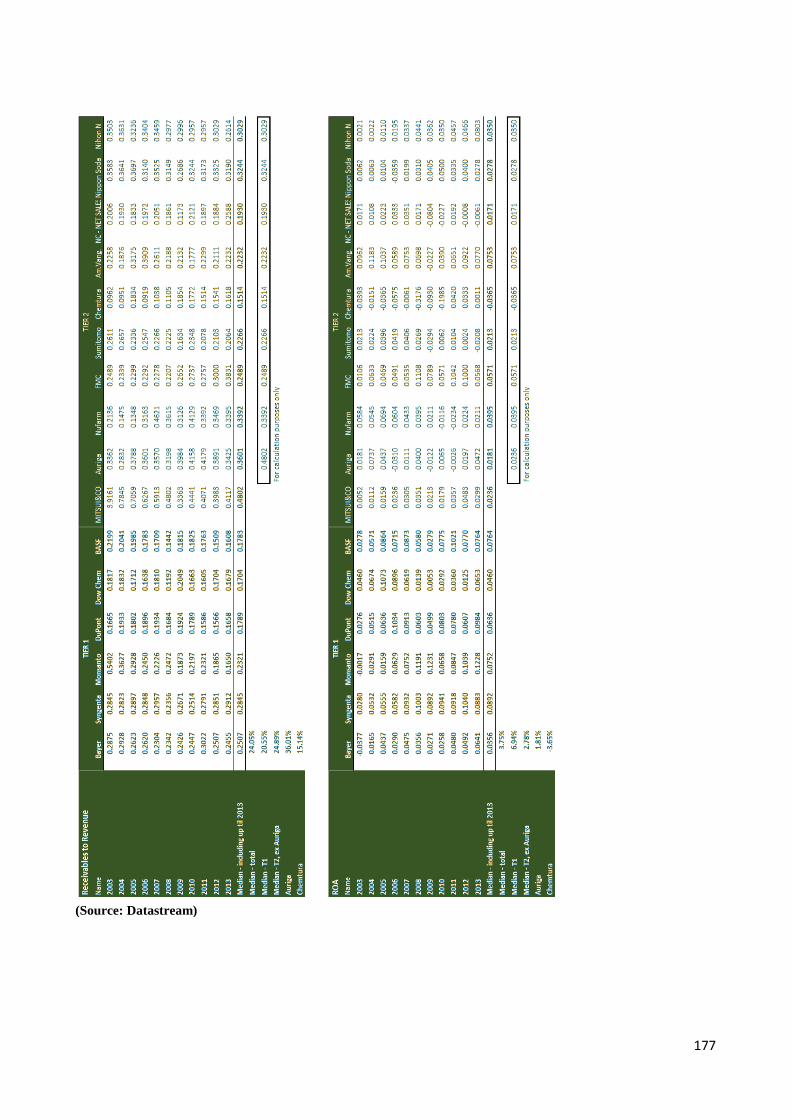

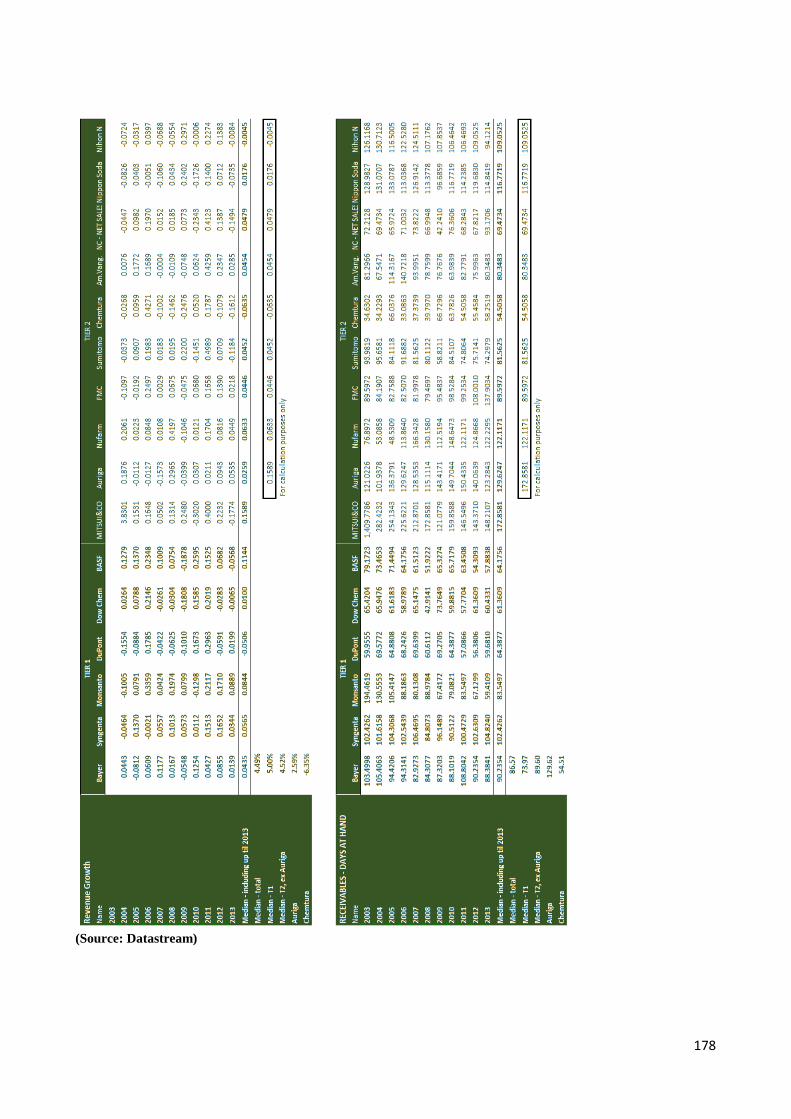

1.2.1.2. Industry Data

The industry data sample was extracted from Reuters Datastream Professional14

for the purpose of

establishing a picture of the characteristics and levels of the different financial ratios in the agrochemical

industry

The initial sample consisted of a total of 54 companies within the agrochemical industry. To secure a high

degree of consistency, companies where Datastream was not able to provide a complete set of data, both in

regards to the time period and the different items, where excluded from the sample. A total of 27 companies

where deducted as there were no financial data available at all – mostly because companies being either

privately or state owned. Another 11 companies were deducted due to incomplete financial data, resulting in

a net sample of a total of 16 companies. Of the 16 companies 6 are categorized as tier 1 companies, and 10 as

tier 2 companies – the latter including Auriga.

The sample has been processed in Excel to calculate a wide variety of financial ratios covering both the

individual year as well as median numbers for both Auriga, tier 1 companies, tier 2 companies and the

industry as a whole. The Median has been applied to meet skewness and outliers in the data. When

processing the data, cross-references have been performed to avoid mistakes in calculating the different

ratios.

Assessing the size of the sample, it is believed to be large enough, to be able to show relevant industry trends

relative to Auriga, and the scrupulous work processing the data secures a high validity measuring what the

data is supposed to measure.

The sample is also subject to the calculation of both descriptive statistics and correlations. From a statistical

point of view, the paper could have wished for a larger sample, as a sample of 11 data points on each

company and a total of 176 data points for the entire industry, a degree of bias cannot be excluded.

12

Bureau Van Dijk homepage: http://www.bvdinfo.com/en-gb/home 13

Skærbæk, Peter, (2005) “Annual Reports as Interaction Devices: The Hidden Construction of Mediated Communication”, Financial Accountability & Management, 21 (4), November 2005, 0267-4424. 14

Thomson Reuters Datastream Professional is a powerful tool that integrates economic research and strategy with cross assets analysis to seamlessly bring together top down and bottom up in one single integrated application, https://forms.thomsonreuters.com/datastream/

6

Other sources of information are written literature on different economic subjects - e.g. books and working

papers published in well reputed financial journals. Also homepages will be applied, but it goes for both

sources of data that a sound source of criticism will be applied, to secure reliable conclusions. The use of

newspaper articles will be minimized, but cannot be completely avoided.

The next section will provide an overview of the further developments and structure of the paper.

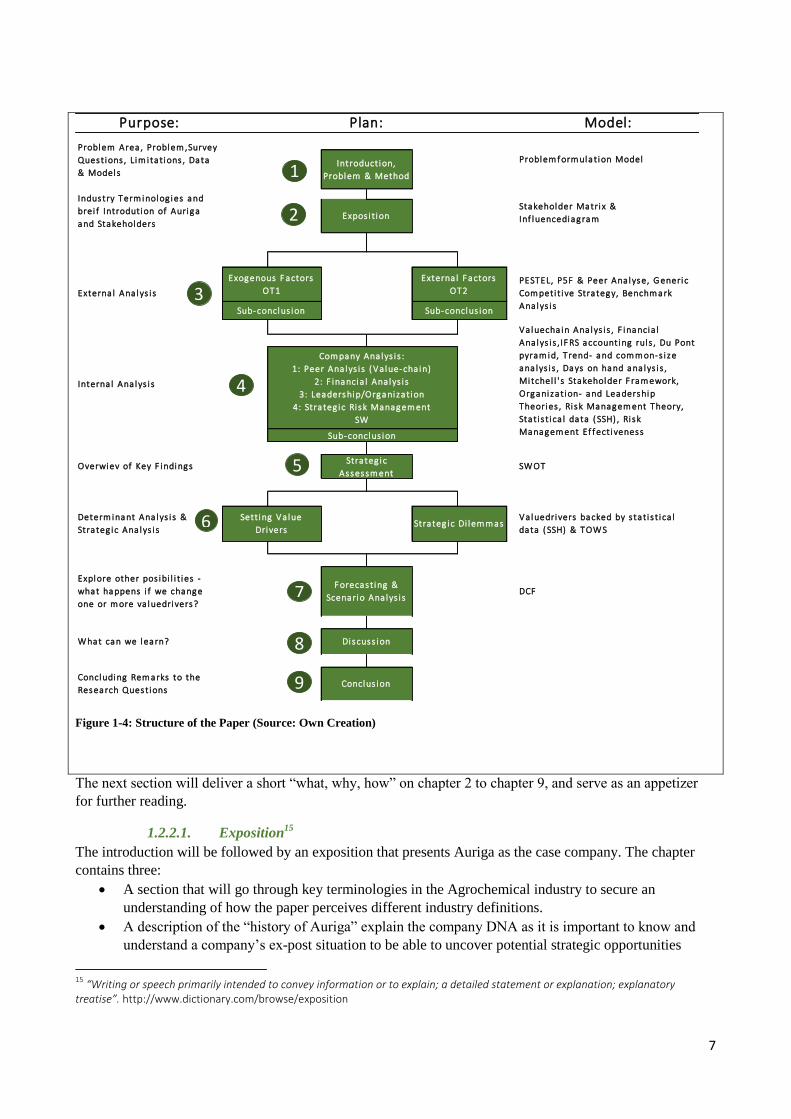

1.2.2. Structure, Theories and Models – an Overview

The paper consists of nine chapters with one or more sub-sections plus chapter 10 to chapter 12 with

formalia, and makes use of a top down approach where the environment analyzed continuously narrows in.

The left-side of the model explains the purpose of each chapter, the mid-section visualized the plan/structure

of the chapter, and the right-side lists the tools used for solving the purpose of the specific chapter.

7

Figure 1-4: Structure of the Paper (Source: Own Creation)

The next section will deliver a short “what, why, how” on chapter 2 to chapter 9, and serve as an appetizer

for further reading.

1.2.2.1. Exposition15

The introduction will be followed by an exposition that presents Auriga as the case company. The chapter

contains three:

A section that will go through key terminologies in the Agrochemical industry to secure an

understanding of how the paper perceives different industry definitions.

A description of the “history of Auriga” explain the company DNA as it is important to know and

understand a company’s ex-post situation to be able to uncover potential strategic opportunities

15

“Writing or speech primarily intended to convey information or to explain; a detailed statement or explanation; explanatory treatise”. http://www.dictionary.com/browse/exposition

Expos i t ionStakeholder Matri x &

Inf luencediagram

Purpose: Plan: Model:

Introduction,

Problem & Method

Problem Area , Problem ,Survey

Questions , Lim i tations , Data

& Models

Industry Term inolog ies and

brei f Introdution of Auriga

and Stakeholders

Problem f orm ulation Model

Conclus ion

Va luedrivers backed by s ta ti s t i ca l

data ( SSH) & TOW S

DCF

Strateg ic

Assessm entSW OT

Strateg ic Di lem m as

F orecasting &

Scenario Ana lys i s

Di scuss ion

Sub-conclus ion

PESTEL, P5F & Peer Ana lyse, G eneric

Com peti t i ve Strategy, Benchm ark

Ana lys i s

Exogenous F actors

OT1

Externa l F actors

OT2

Sub-conclus ion

Com pany Ana lys i s :

1: Peer Ana lys i s ( Va lue-cha in)

2: F inancia l Ana lys i s

3: Leadership/Organization

4: Stra teg ic Ri sk Managem ent

SW

Valuecha in Ana lys i s , F inancia l

Ana lys i s , IF RS accounting rul s , Du Pont

pyram id, Trend- and com m on-s i ze

ana lys i s , Days on hand ana lys i s ,

Mi tchel l ' s Stakeholder F ram ework,

Organization- and Leadership

Theories , Ri sk Managem ent Theory,

Sta ti s t i ca l data ( SSH) , Ri sk

Managem ent Ef f ecti veness

Concluding Rem arks to the

Research Questions

Externa l Ana lys i s

Sub-conclus ion

Interna l Ana lys i s

Overwiev of Key F indings

Determ inant Ana lys i s &

Strateg ic Ana lys i s

Sett ing Va lue

Drivers

Explore other pos ibi l i t ies -

what happens i f we change

one or m ore va luedrivers?

W hat can we learn?

1

2

3

4

5

6

7

8

9

8

An overview of the “2013 Auriga” at the time for the divestment including a stakeholder overview,

to provide basic information on the company and the gallery of characters involved.

External Analysis – Exogenous and External factors

The idea of this chapter is to define the different factors affecting the company. The section will start out

with a description of the different markets in which Auriga operates, subsequently followed by an analysis of

bot exogenous and external factors, by the use of the following theories and models:

PESTEL analysis, to uncover exogenous elements affecting the industry as a whole. As there are

many macro factors influencing a global company, the PESTEL framework will categorize and

identify key strategic elements to take into consideration in later stages of the paper when identifying

trends that will make its way into the competitive environment16

.

Porters Generic strategy to identify Auriga’s current strategic path

The Porters Five Forces (P5F) framework has been chosen because it uncovers the competitive

environment and the degree of attractiveness of being part of the agrochemical industry. Besides the

apparent benefit of casting light on the competitive environment, it is stated that at least parts of the

framework are present in every business analysis, as well as the competitive environment is believed

to have great impact on a company’s performance.17

The P5F will be complemented with an industry peer-analysis on financial ratios that will be

calculated as averages over an eleven-year period and at the same time divided into the two main

tiers in the industry – tier 1 and tier 2. The purpose is to uncover at what levels the different piers

operate and to cast light on potential differences, if any. This information will be helpful in

evaluating key figures in later chapters of the paper.

Each of the two sections will be rounded off with a sub-conclusion named OT 1 and OT 2 resembling the

Opportunities and Threats in the SWOT analysis which will be described in a later section.

Company Analysis – Internal Factors

This chapter will set out with a financial value-chain analysis on Auriga and its peers, produced on 2013-

data. The value-chain will contain the following building blocks; production, Sale & distribution (S&D),

Administration, R&D and depreciation. The point is to recap the newest financial information at the time for

the divestment, to assess where in the value-chain Auriga is superior to its competitors, and where Auriga

has room for improvement.

The Value-chain analysis will be followed by a complete in-depth financial analysis with a full scale

reformulation of profit statement and balance sheet to bring forth a true picture of the company´s core

profitability and cash-flow generating capabilities18

. Profitability will be analyzed using the “Du Pont

pyramid”19

combined with trend-, common-size- and peer-analysis20

.

16

Henry, Anthony, “Understanding Strategic Management” (2008), Oxford University Press, ISBN: 978-0-19-928830-4, page 51. 17

Henry, Anthony, “Understanding Strategic Management” (2008), Oxford University Press, ISBN: 978-0-19-928830-4, page 61 og 68. 18

Christian V. Petersen & Thomas Plenborg “Financial Statement Analysis” FT Prentice Hall Financial Times, ISBN: 978-273-75235-6,

Page 68. 19

Christian V. Petersen & Thomas Plenborg “Financial Statement Analysis” FT Prentice Hall Financial Times, ISBN: 978-273-75235-6, Page 94 and 120. 20

20 Christian V. Petersen & Thomas Plenborg “Financial Statement Analysis” FT Prentice Hall Financial Times, ISBN: 978-273-75235-

6, Page 111.

9

The next section will describe the overall governance structure of Auriga and perform an analysis of the key

stakeholders identified in the exposition. Mitchell’s Stakeholder Typology framework21

will be applied to

assess the salience of different stakeholders on the basis of three attributes: power, legitimacy and urgency in

relation to the divestment and the possible future strategic opportunities. When assessing different

stakeholders, it is natural at the same time to also touch upon the organizational structure and different

corporate governance issues that potentially could affect the company, its operations and its future strategy.

The section will furthermore draw on different leadership and organizational theories.

Innovation is a key factor in securing the strategic options that are to be the basis for future growth. The

strategic risk management section will describe and analyze different risk measures - among these the risk

management effectiveness relative to industry peers. The section will be based on the findings of Torben

Juul Andersen, Professor at the Department of International Economics and Management, and his article

from 2009; “Effective risk management outcomes: exploring effects of innovation and capital structure”.

The section will be rounded off with a sub-conclusion named SW resembling the Strengths and Weaknesses

in the SWOT analysis which will be put together in the following chapter.

Strategic Assessment

The essentials from both external sub-conclusions and the internal sub-conclusion will be listed in a SWOT

analysis framework, in the well-known internal strengths and weaknesses and the external opportunities and

threats. The section joins the forces of both the financial analysis and the strategic analysis, and rounds-up

the ex-post parts of the paper. Blue numbers will identify operational value drivers extracted from the

exogenous analysis, red numbers operational value drivers from the external analysis and black numbers

operational value drivers from the internal analysis. Each entry will be accompanied by an impact

assessment and a short description of which financial items it effects.

Setting the Value Drivers

This chapter kicks-off the ex-ante looking part of the paper and will identify key financial value drivers

which define the underling fundamental development of Auriga. Each financial value driver will be

connected to relevant operational value drivers identified in the exogenous, external and internal analysis.

Each entry will contain the same numbers and colors used in the sub conclusions and the SWOT analysis,

thus making it easy to recognize its origin. The financial value drivers recognized will later be applied in a

DCF model to calculate three different strategic scenarios and a fourth combining all three scenarios.

Strategic Dilemmas

Drawing on elements defined in the SWOT, this section will assess and combine strengths, weaknesses,

opportunities and threats, by applying the TOWS-matrix to structure forward looking strategic dilemmas.

Each entry can be traced back to the SWOT analysis and the three sub conclusions by number and color.

Forecasting & Scenario Analysis

This section starts with a brief description of models applied and next, on the basis on the strategic and

financial analysis, investigates three different strategic opportunities/paths for Auriga to follow. The three

paths are subsequently combined in a fourth path, hereby investigating Auriga’s full potential as a stand-

alone entity. Lastly an analysis of the divestment relative to Auriga’s different strategic options/paths is

executed. Sensitivity analysis to supplement DCF calculations and the offered price from FMC could have

proven useful but due to the limitations of the paper it has been discarded.

21

Ronald K. Mitchell et. al.,, ”The Academy of Management Review”, Vol 22, No. 4 (Oct. 1997), pp. 853 – 886, Academy of Management, http://www.jstor.org/stable/259247 - page 874

10

Discussion and Conclusion

Lastly the findings in the analysis and the chosen path will be discussed and put into perspective for future

situations and improvements in similar cases.

2. Exposition22 The exposition provides an introduction of Auriga and thus creates a foundation for moving on to the

external analysis in chapter 3 and the internal analysis chapter 4.

2.1.1. Industry Terminologies

This initial section will provide brief description of the most important terminologies in the agrochemical

industry.

Agrochemical is the term for a range of products, used for the purpose of enhancing or securing yields in the

agricultural industry. Agrochemicals can be divided into two main categories; pesticides and fertilizers.23

According to the European Commission a pesticide is; “…something that prevents, destroys, or controls a

harmful organism ('pest') or disease, or protects plants or plant products during production, storage and

transport”24

. The term includes; herbicides, fungicides, insecticides as the most commonly used pesticides in

the agricultural industry. Herbicides are used to kill or inhibit unwanted plants (weeds) that compete with the

wanted plants (crops) for light, water and nutrition25

. Herbicides can be non-selective with the same effect on

all plants, or selective by which the herbicide only affects certain weeds26

. A Fungicide kills or prevents

growth of fungi’s or fungal spores and an insecticide kills, harm, repel or mitigate pests that might attack and

harm crops27

.

The main product segments within the Agrochemical industry are described below:

Crop

protection

Production of different kind of pesticides a described above

Seed treatment Development of crop protection products which are applied directly on the seed before it

is sown.

Hybrid seed Development of new and better seeds by crossing two different, but related plants in a

controlled environment - Almost the same as cross-pollination of two related plants -

only done much faster. A big advantage/disadvantage with hybrid seeds are that seeds

from the crops planted do not have the same characteristic as the seed planted and

therefore are not suitable for use.

GMO Seed28

Often referred to as traits. The two main groups within this segment are:

Development of new crops which are genetically modified to resist specific pesticide

products so that the spraying of the pesticide does not harm the crop. E.g. Monsanto have

22

Gyldendal, Den Store Danske homepage: http://denstoredanske.dk/Natur_og_milj%C3%B8/Milj%C3%B8_og_forurening/Vandmilj%C3%B8,_spildevand_og_olieforurening/Cheminova & Cheminova homepage, http://www.cheminova.dk/dk/om_os/historie/ & Danmarkshistorien .dk by Aarhus Universitet - http://danmarkshistorien.dk/leksikon-og-kilder/vis/materiale/cheminova-auriga-1938-2014/?no_cache=1 and webpage of Auriga. 23

P. Hough, “The Trading and Use of Agrochemicals”, Department of Law, Middlesex University London, Springer Science, page 2, http://www.springer.com/gp/book/9789400774537?wt_mc=ThirdParty.SpringerLink.3.EPR653.About_eBook#aboutBook 24

European Commission homepage on Pesticides: http://ec.europa.eu/food/plant/pesticides/index_en.htm 25

The Essential Chemical Industry – online homepage: (18th March 2013) Crop Protection Chemicals, CIEC Promoting Science at the University of York, http://www.essentialchemicalindustry.org/materials-and-applications/crop-protection-chemicals.html 26

Auriga Industries A/S annual report 2011, page 12. 27

The Essential Chemical Industry – online homepage: (18th March 2013) Crop Protection Chemicals, CIEC Promoting Science at the University of York, http://www.essentialchemicalindustry.org/materials-and-applications/crop-protection-chemicals.html 28

GMO = Genetically Modified Organism

11

developed crops that can tolerate Rond-Up and other type of Glyphosate products29

.

Development of new crops which are capable of protecting themselves against pests and

fungi and which have improved nutrient uptake30

. Seeds from crops grown with patented

GMO seeds are often not allowed to be planted, as this violates the manufacturing

companies’ right to the seeds31

.

To understand the dynamics of the industry it is important to distinguish between tier 1 companies and tier 2

companies:

Tier 1 companies are defined by possessing the capabilities and the resources to research and

discover new active ingredients and by having a global market presence. Tier 1 companies are large

corporations often with divisions outside the agrochemical industry.

Tier 2 companies are defined by capabilities to produce/synthesize off-patented active ingredients,

develop new products based on off-patented active ingredients, and a global market presence. Auriga

is considered to be a tier 2 company.

Active ingredients are the main substance in pesticides and many pesticide products contain more than one

active ingredient. In order to produce pesticide products, active ingredients are mixed with different inert

ingredients which among other things can help increase shelf-life, attract pests or helps spread the product

more evenly on surfaces.32

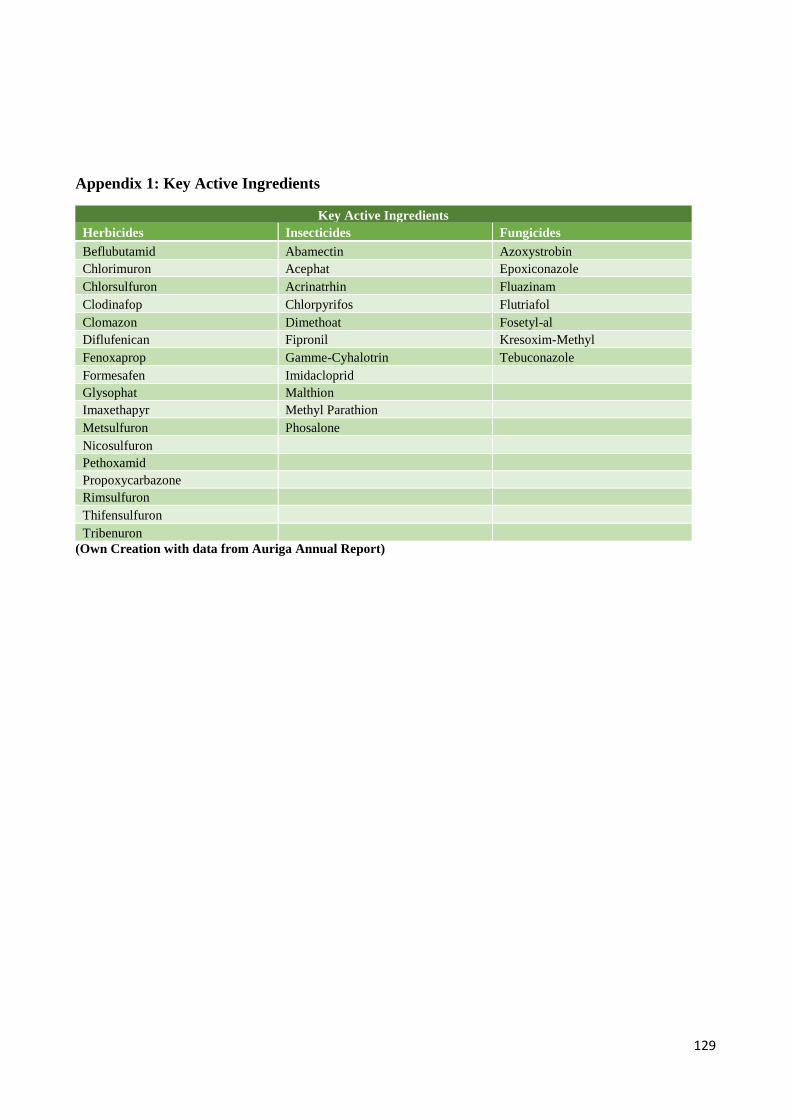

The different key active ingredients used in the industry can be seen in appendix

1.

Tier 1 companies have the capital and knowhow to research and develop new active ingredients that can be

used in new pesticides. E.g. in the 1970s, US company Monsanto patented the active ingredient Glyphosate

which was used in their Herbicide block-buster Roundup. Today their patent has expired, making is possible

for other players to produce and mix their own Glyphosate products. Today Glyphosate is still the most

widely used active ingredient in the agrochemical industry33

.

Formulation is a process wherein active ingredients produced by the company or bought from third parties

are mixed with other chemicals and additives to produce pesticide products designed for various uses in the

agriculture industry.

2.1.2. Auriga History

This section will briefly describe the origin of Auriga and the path the company has traveled to become the

company it was up until the divestment to FMC in 2014. The purpose is to create a basic understanding of

the company and its history which will prove useful in later chapters. The description will briefly touch upon

the 2013 key figures of the company. For a complete history of Auriga – including “The early days” see

appendix 2 and appendix 12 for an overview of Auriga’s stock price development

2.1.2.1.1. Recent history

In the 1990s competition was fierce and in search for new ways to increase topline growth and mitigate risk

Cheminova aimed to diversify their business into new markets. This change of strategy had already started in

1987 with the acquisition of the Fur based Skamol A/S which manufactures and markets thermal insulating

29

Monsanto, Annual Report 2015 – page 4 30

Monsanto, Annual Report 2015 – page 4 31

Monsanto homepage: http://www.monsanto.com/newsviews/pages/why-does-monsanto-sue-farmers-who-save-seeds.aspx 32

National Pesticide Information Center homepage: http://npic.orst.edu/ingred/ 33

Ecochem homepage: http://www.ecochem.com/ENN_glyphosate.html

12

materials for a wide range of heat intensive industries. Not a line of business with a fit to the current value

chain.

Ten years later in 1997, Cheminova closed two other significant acquisitions when acquiring the last 70% of

the share capital in Hardi International A/S and Indian Lupin Agrochemicals. Hardi International A/S

produced sprayers for the agriculture industry. Before the acquisition Hardi International A/S performed at

an acceptable level, but after the change of ownership the performance decreased and on serval occasions

Auriga had to inject additional capital. Acquisition of Indian Lupin Agrochemicals gave access to new

production facilities in India and helped penetrate the Indian growth market.

A few years later the company changed the name of the holding company to Auriga.

In 2006 the company decided on a major strategic change with the public announcement of initiating process

towards divesting both Skamol A/S and Hardi International A/S, ending a diversification strategy that started

20 years earlier. The realization was that keeping a continuous strong position in the agrochemical market

would demand a full focus on this key area34

.

The divestment was effectuated in 2007 with Skamol A/S being sold with an acceptable profit and Hardi

International A/S with a loss. The divestments had a total negative effect on the 2007 annual report35

.

Post the strategy change Auriga continued developing and expanding their markets with the acquisitions of

Uruguayan Abielux S.A. and German Stähler, opening of representation offices in Thailand, Kenya, Croatia

and Romania and partnering up with Libanese AgriNova, granting them distribution rights to the Cheminova

product portfolio in the Middel East, Turkey, North Africa and the Gulf area36

.

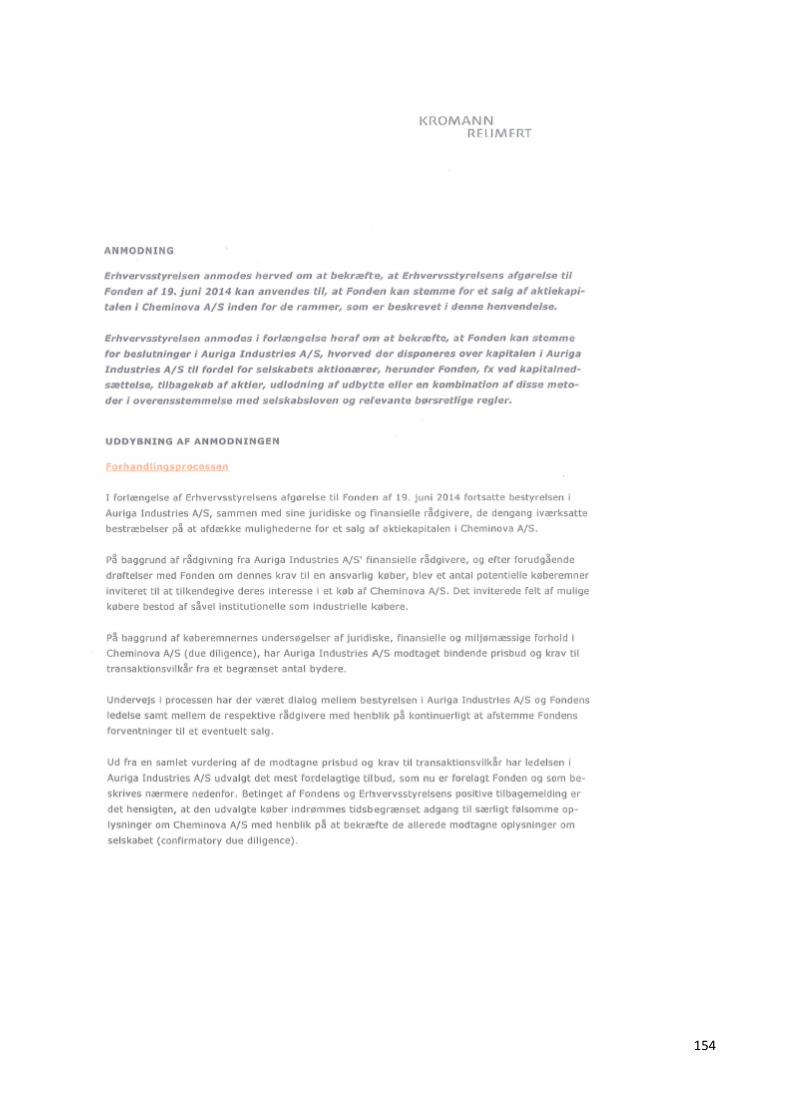

2.1.3. Access to Documents Concerning the Sale Granted to Kurt Aabo

I order for Auriga to divest Cheminova to FMC Corporate, AURF had to change the instrument of

foundation, to be allowed to deviate from the clause of being the sole owner of A-shares. A change of the

clause has to be accepted by the Danish Business Authority – confer the Law on Foundations clause 21

section 3.37

Former Information Manager with Auriga38

, Kurt Aabo39

has been granted access to documents concerning

the acceptance of changing the instrument of foundation. To see documents provide by Kurt Aabo see

appendix 3.

The key points and documents will be described in the following sections.

2.1.3.1. First Application for Changing the Instrument of Foundation

On the 8’th of September 1998 the law firm; “Pedersen & Jantzen” applied, on behalf of the Aarhus

Research Foundation, for the Danish Business Authority’s approval of a change in the instrument of

foundations article 7 section 4 which stipulates that the foundation at all time is to possess at least 51% of the

total voting rights in Cheminova Holding A/S. The argument for changing the instrument of foundation is

34

Auriga Industries A/S, Annual Report 2006, page 1 35

Auriga Industries A/S, Annual Report 2007, page 1 36

AgriNova homepage: http://www.agrinova-sal.com/profile.html 37

Retsinformation homepage: https://www.retsinformation.dk/forms/r0710.aspx?id=163656. Please note that a change to the law has been proposed and enacted by parliment on the 3’rd of June 2014. 38

Sperling, Anna von “Cheminova skal stå skoleret for ministeren”, Information on the 16’th of November 2008 https://www.information.dk/2007/07/cheminova-staa-skoleret-ministeren & Kamstrup, Lars, ”Aktionær: Ejer har et ansvar ved salg af Cheminova”, Dagbladet Holstedbro-Struer on the 30’th of August 2014, http://m.dagbladet-holstebro-struer.dk/lemvig/aktionaer-ejer-har-et-ansvar-ved-salg-af-cheminova 39

Aabo, Kurt, Søndervej 5, 6280 Højer, telephone number: 40569930, email: [email protected]

13

that the industry is experiencing a consolidating trend, which results in several challenges for the company

as:

Large competitors have advantage in economics of scale enforcing them to develop their own

patented products.

The Large competitors have a broader product palette with products supplementing each other

The large competitors dominate the net of distributers

Large competitors are able to carry out a price policy that could be a problem for the company

It is expected that the industry will move towards having five dominant players, and that it in these market

conditions would be beneficial to be able to enter a strategic alliance to secure own economics of scale. Such

an alliance would make it difficult to be able to continue as the majority shareholder.

The Danish Business Authority approves the application in a letter dated 30’th of October 2008, with a

notion that if a deal is made, the foundation has to account for its current status, and account for how the deal

will affect the foundations object of clause.

Negotiations concerning the sale was conducted, but without a fruitful result.

See the original documents in appendix 5

2.1.3.2. Second Application Clarifying the Earlier Approval

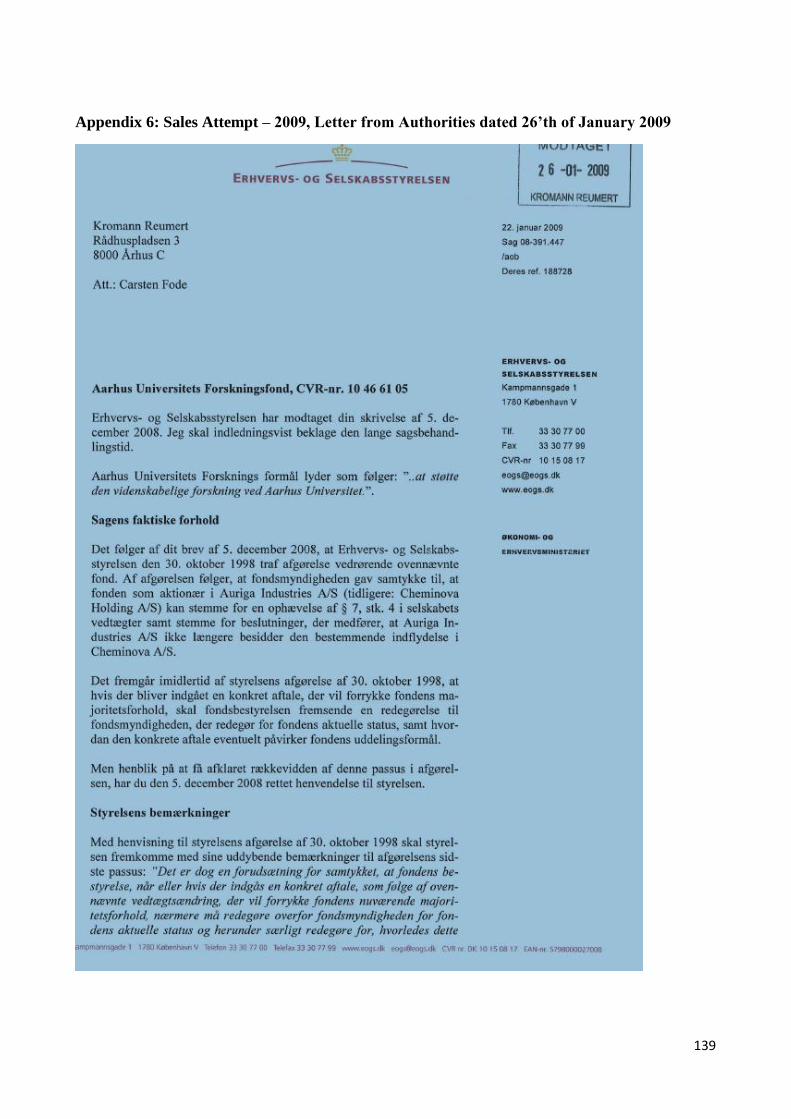

On the 5’th of December 2008, the law firm “Kromann Reumert” made an application with the Danish

Business Authority as a continuation of the approval from the 30’th of October 2008, to clarify the notion

concerning the two issues that was to be accounted for in the case of a sale, and confirm that the notion does

not influence the approval of the possible change in the object of clause.

The application is answered on the 22’nd of January 2009, where the Danish Business authority confirms,

that the last notion does not influence the essence of the approval to change the instrument of foundations

article 7, section 4.

Considerations concerning the sale were terminated due to the development of the financial crisis.

See the original documents in appendix 6

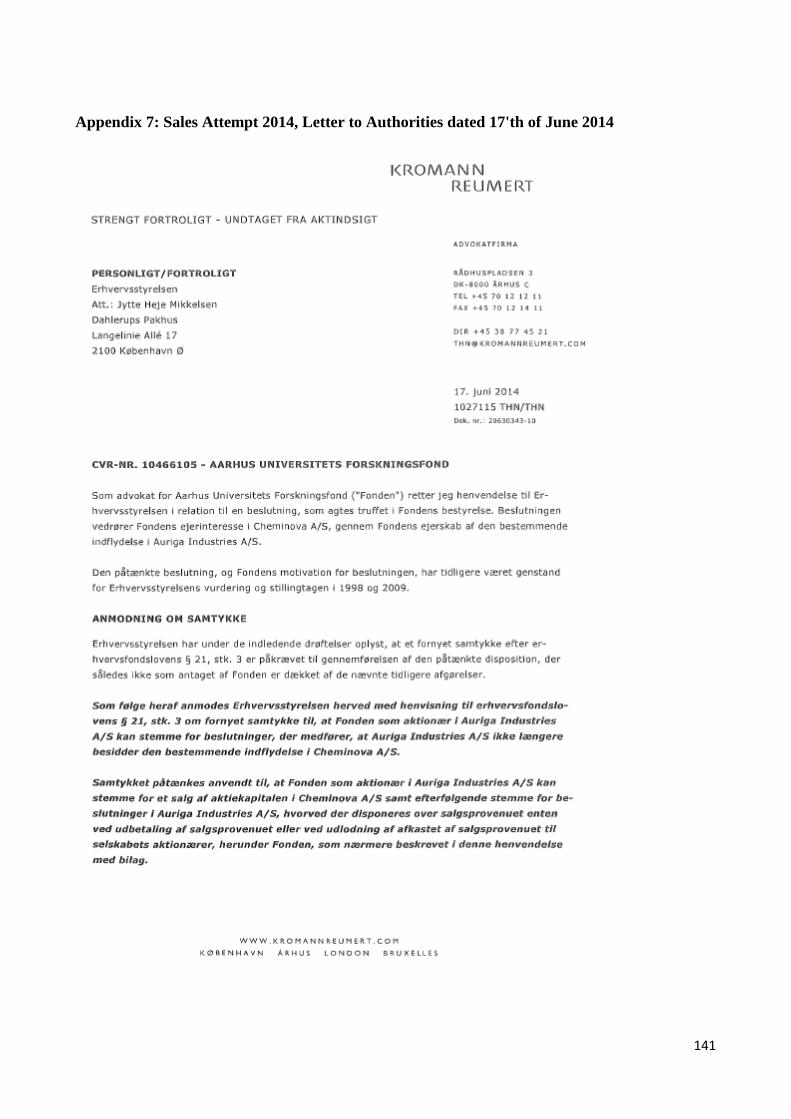

2.1.3.3. Renewal of Earlier Approvals

In a letter dated 17’th of June 2014, the law firm “Kromann Reumert” applies for renewal of earlier

approvals concerning changing the instrument of foundations article 7, section 4.

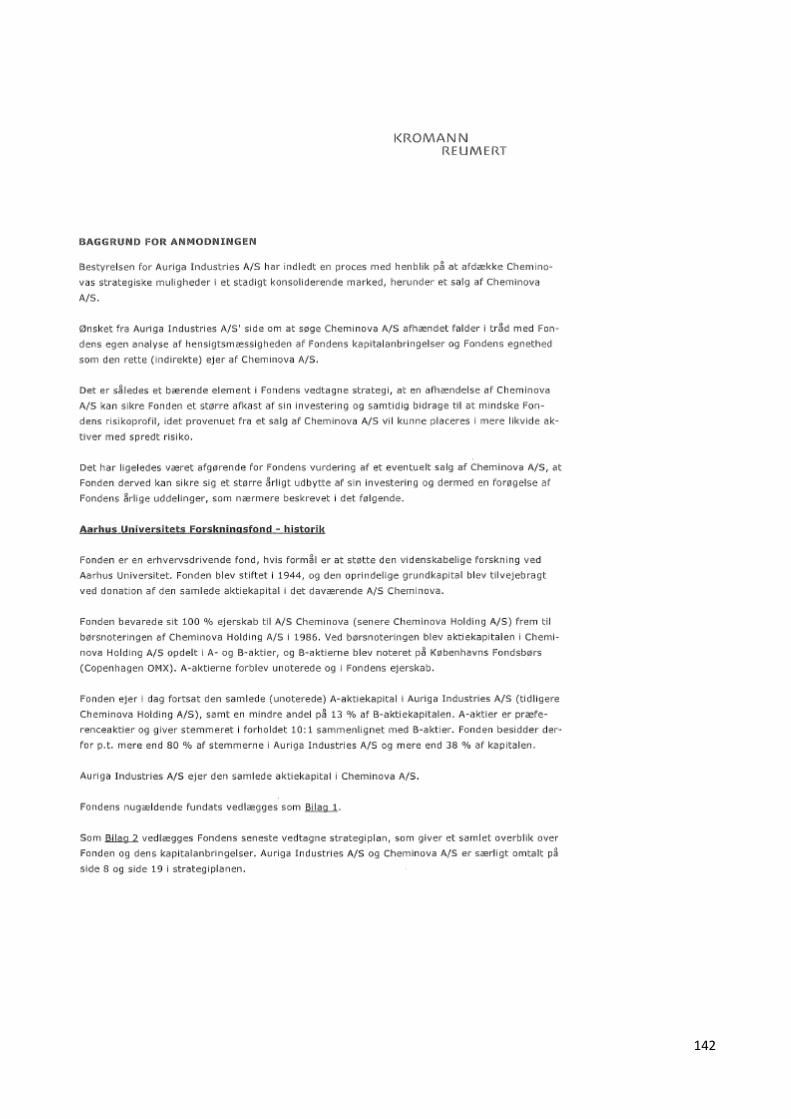

The background to the application is that the board of directors with Auriga has initiated a process to

uncover strategic opportunities in a consolidating market – including the possibility of a sale.

It is stated, that the wish from the board of directors to divest Cheminova is in line with the foundations own

analysis concerning the asset structure of the foundation, and the foundation being a suitable owner for

Cheminova.

The foundations argument for renewal of earlier applications is that a divestment of Cheminova could

provide the foundation with a better return on its investments, minimize its total risk, and secure or even

increase the basis for endowments.

The foundation concludes the following:

The risk of having a large share of its asset base tied up in a single stock is not optimal

The agrochemical industry is experiencing intense consolidation trends which make economics of

scale even more important in the future.

14

If you as a company is not an active player in the consolidation in the industry, you are at risk to be

bought

The foundation does not have the resources to support a future consolidation of Cheminova, which

does not make the foundation the right owner of Cheminova.

The application is enclosed in a memorandum produced by the board of directors of Cheminova dated 14’th

of May, which argues, that Cheminova currently is in a strong position to proactively lead discussion on

value creating consolidation, and that the company will risk marginalization over time and loose its

competitive advantage, if it does not use this momentum.

The application is further backed by a memorandum also dated the 14’th of May produced by the accountant

of the foundation, “PwC” that also concludes the Cheminova has gone through a positive development in the

last two years, and that the timing of a sale of Cheminova in 2014 to secure the endowments are good.

The Danish Business Authority approves the request, to change the Instrument of Foundation article 7,

section 4, on the 19’th of June 2014 with the notion, that they are to be presented of the sales agreement

before a sale is final. See the original documents in appendix 7,8,9,10 and 11.

The conditional sale to FMC mentioned in the introduction is announced in a company announcement dated

the 8’th of September 2014, and announced final

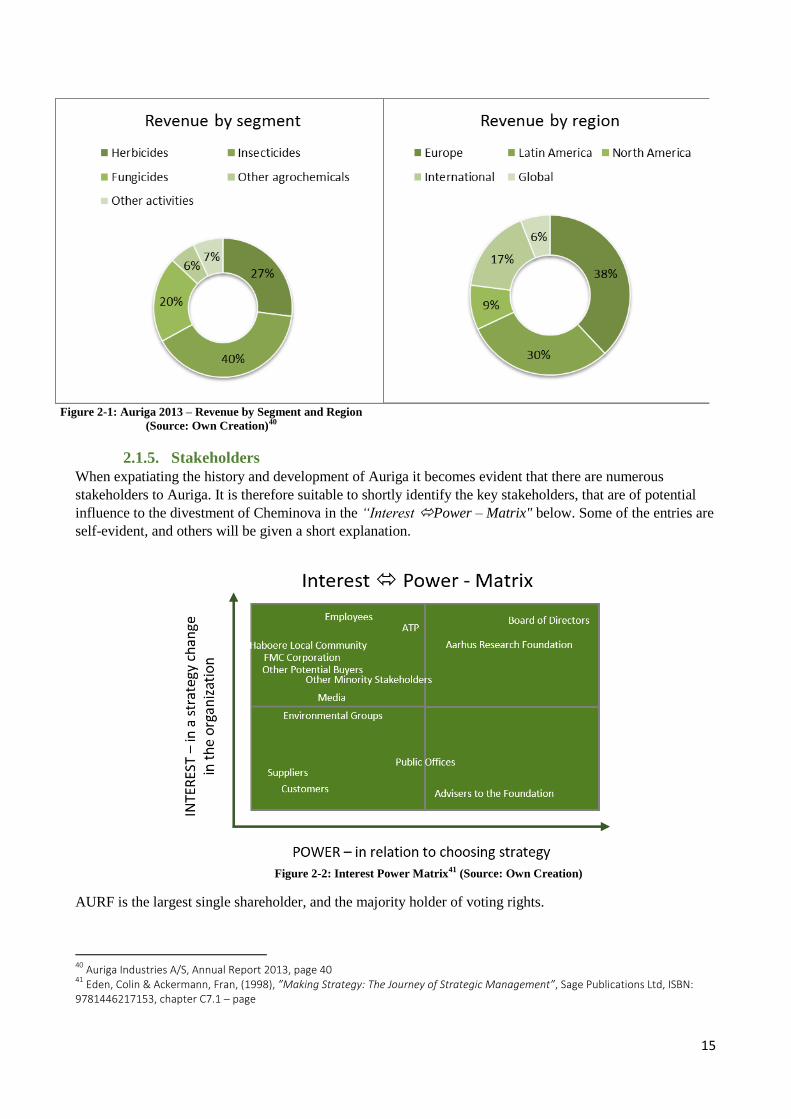

2.1.4. Auriga in 2013

In 2013 Auriga is a global enterprise with a large palate of products within herbicides, fungicides and

insecticides mainly distributed to countries in Europa and the Americas.

The company slogan “Helping you grow” has a two-fold meaning. Firstly Auriga wants to produce new and

innovative solutions within crop protection to secure the yield of farmers. Secondly Auriga wants to create

value for all stakeholders – being economically, professionally or humanitarian.

The company employs 2,200 people whereas 850 are employed in Denmark, mainly at the headquarters in

Harboøre.

In 2013 Auriga’s revenue summed close to DKK 6.6 billion producing a net income of DKK 290 million.

The company had subsidiaries in 24 countries, representation offices in another 4 countries, production

facilities in Denmark and India and formulation sites in UK, Germany Australia and Italy. For an overview

of Auriga’s global business units from 1996 to 2013 see appendix 13.

15

2.1.5. Stakeholders

When expatiating the history and development of Auriga it becomes evident that there are numerous

stakeholders to Auriga. It is therefore suitable to shortly identify the key stakeholders, that are of potential

influence to the divestment of Cheminova in the “Interest Power – Matrix" below. Some of the entries are

self-evident, and others will be given a short explanation.

Figure 2-2: Interest Power Matrix41 (Source: Own Creation)

AURF is the largest single shareholder, and the majority holder of voting rights.

40

Auriga Industries A/S, Annual Report 2013, page 40 41

Eden, Colin & Ackermann, Fran, (1998), ”Making Strategy: The Journey of Strategic Management”, Sage Publications Ltd, ISBN: 9781446217153, chapter C7.1 – page

Figure 2-1: Auriga 2013 – Revenue by Segment and Region

(Source: Own Creation)40

16

ATP as the second largest shareholder and because of their size and expertise believed to be a weighty

partner in the companies they choose to invest in.

Advisers to the foundation are professional consultancy houses and law firms that are hired as advisers on

different matters concerning the future strategic considerations.

Environmental groups are believed to have an interest of the future of a chemical company.

FMC as the acquirer of Cheminova.

3. EXTERNAL ANALYSIS

This chapter will conduct an analysis of the external and endogenous factors, by applying a PESTEL

analysis, a Porters Five Forces analysis, and a peer-analysis based on industry numbers.

But first and foremost the different markets where Auriga is present will shortly be described in the

following.

3.1.1.1.1. Global overview

Auriga operates its global activities from their head office in Harboøre, Denmark.

The company produces active ingredients at production facilities in Denmark and India and micro nutrition

formulations are produced in Headland, Great Britain. The company furthermore has formulation and

packaging plants with subsidiaries in India, Australia, Germany, Italy and Great Britain.

The next sections will go through the main characteristics of the different regions defined by Auriga42

.

42

Auriga Industries A/S, Annual Report 2010, page 12-13

17

Figure 3-1: Global Overview – Auriga Industries A/S

(Source: Own Creation with data from Auriga Industries A/S Annual Report 2013, pages 39 and 62)

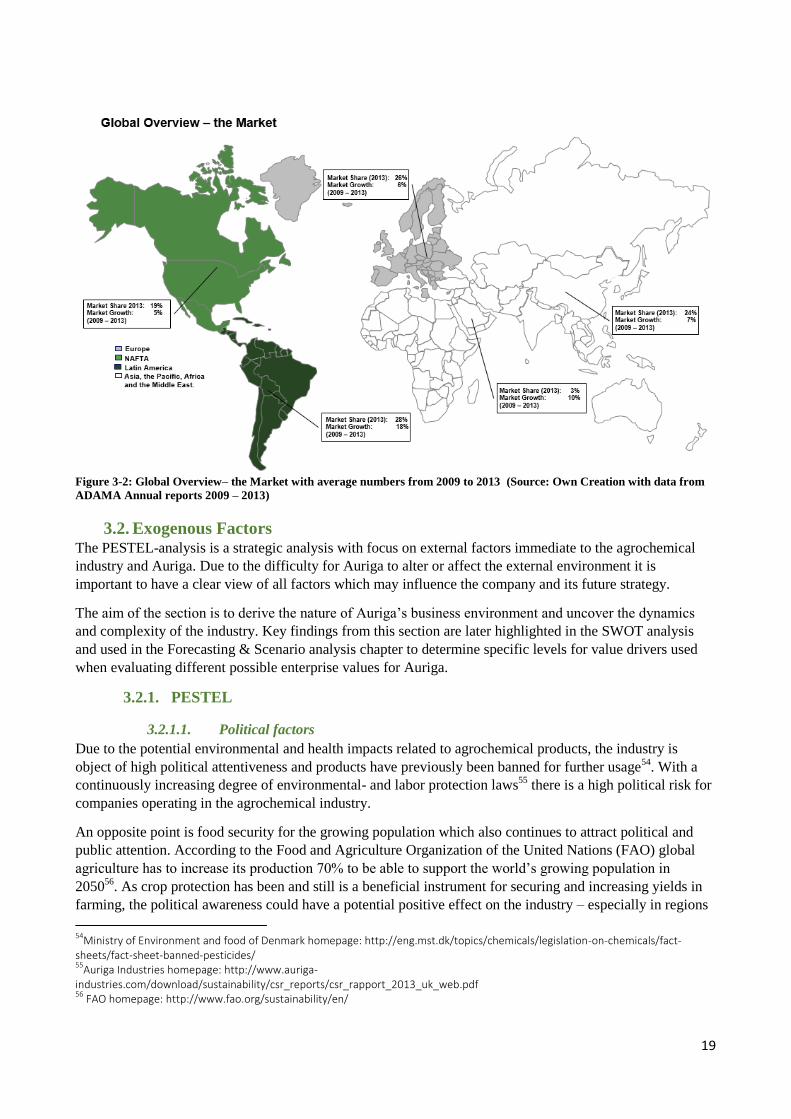

3.1.1.1.2. Europe

The European market makes up around 26%43

of the world market of pesticides and approximately 38%44

of

Auriga’s revenue. The crop structure of Europe is rather dispersed with both the big corn crops but also

wine, fruits and vegetables. The region is strictly regulated concerning the use of GMO crops – see the

PESTEL analysis in chapter 3. A typical farm in Nord and Central Europe is between 50-80 hectares in size

concentrated on few crops, while a farm in south Europe typical has 5-30 hectares with many different crops.

In Nord and Central Europe wholesale and retail is often merged where in south Europe distribution is more

fragmented with many small distributors and retailers45

.

Despite the sometimes difficult weather situations and a pressured market for glyphosate Auriga has

experienced growth in the years up till 2014. The growth is primarily driven by launching new products,

better market penetration with new subsidiaries in Austria and Serbia and opening of representation offices

in Romania and Croatia.

Besides their headquarters and production facilities in Denmark Auriga holds a wide network of subsidiaries,

representation offices and formulation plants throughout the region.

3.1.1.1.3. Latin America

The region includes Brazil, Argentina, Colombia, Mexico and the rest of Central- and South America, with

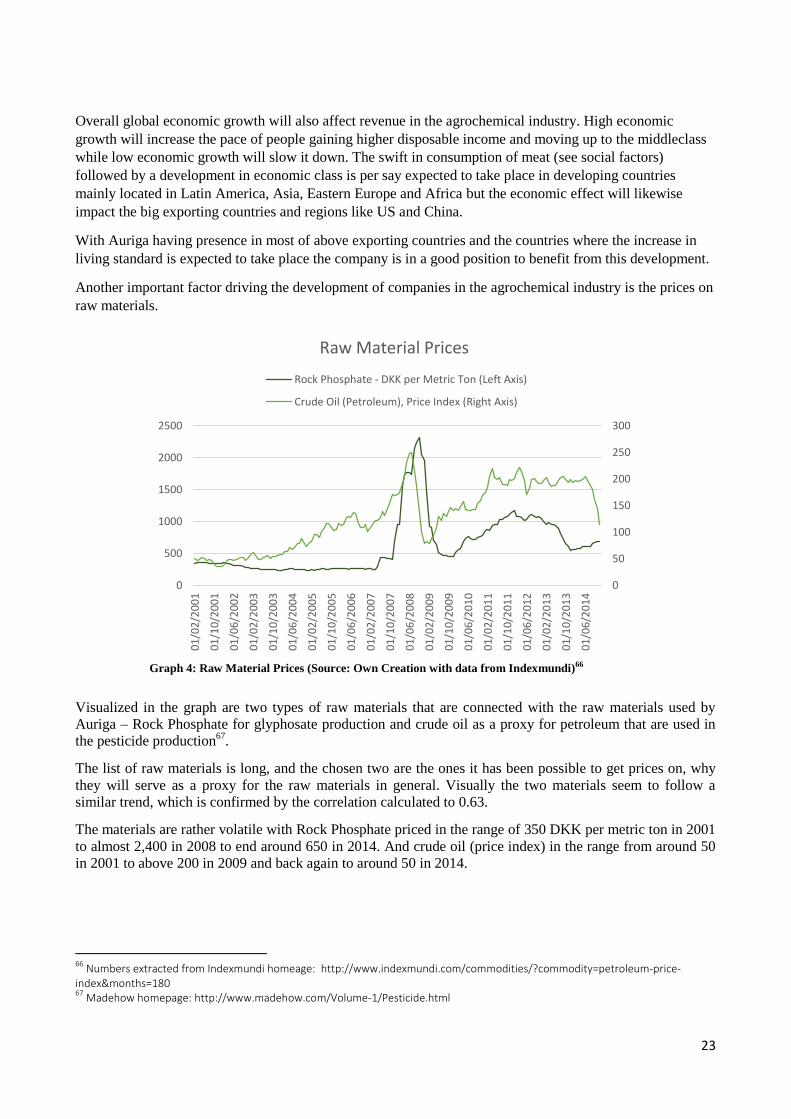

Brazil and Argentina accounting for 80% of the regions market-value. Latin American makes up around

28%46

of the world market of pesticides and approximately 30%47

of Auriga’s revenue in 2013. The most

43

ADAMA, Annual Report 2013, page 25 44

Auriga Industries A/S, Annual Report 2013, page 39 (2,522,089/6,597,749) 45

Auriga Industries A/S, Annual Report 2012, page 12 46

ADAMA, Annual Report 2013, page 25 47

Auriga Industries A/S, Annual Report 2013, page 39 (1,984,867/6,597,749)

18

used crops are corn, maize and soybean. Auriga holds subsidiaries in Columbia, Argentina, Uruguay and in

the main market of Brazil. A typical farm in North Brazil if often more the 50,000 hectares and equipped

with high technical devises enabling farmers to be highly effective. Distribution is done directly to big farms

and cooperatives and through wholesale and retailers.

Auriga has experienced growth in revenue in Latin America in the years leading up to 2014. The main

reasons are better direct present with products being sold directly to both big farms in Brazil and Argentina

and small farmers in Mexico, launch of new differentiated products, increase of farmed areas and good

weather conditions.

The region is characterized by long payment terms which affected Auriga’s revenue negatively in 2009 when

they implemented a stricter credit policy48

. The region is also characterized by a general decline in sale of

glyphosate products.

3.1.1.1.4. North America

The region includes US and Canada. North American makes up around 19%49

of the world market but only

approximately 9%50

of Auriga’s revenue in 2013. Major crops in the region are corn, maize and soybeans.

Auriga has subsidiaries in both US and Canada. A typical farm is between 500 – 2,000 hectares and highly

effective. Distribution is much alike in North and Central Europe, just much bigger. Wholesale and retail is

characterized by a few big companies with a large amount of shops.

North America has experienced increased glyphosate resistance and therefor new differentiated products,

especially to crops like soy and cotton51

are considered key elements in raising revenue.

Auriga experienced difficult years in 2009-2011 due to declining sale of glyphosate products, poor inventory

management and difficult weather conditions in Texas. Opposite in 2012-2013 Auriga experienced two-digit

growth figures due to registration and launch of new differentiated products - amongst others based on the

active ingredients flutriafol and gamma-cyhalotrhin.

3.1.1.1.5. International

The region includes India, Australia, Asia, the Middle East and Africa. Asia accounts for 24%52

of the world

market and approximately 17%53

of Auriga’s revenue in 2013. Auriga holds subsidiaries in China, Taiwan,

Russia and India. Auriga has a production plant in India, an associated company in Lebanon and

representation offices in Kenya and Ukraine. In Australia, Auriga has a formulation and packaging plant and

the company states that they hold good relations with established distributers. In India, which is the main

market for Auriga in this region, a typical farm is 1.2 hectares in size and family owned. Distribution is

characterized by a large amount of independent wholesalers’ and larger farmers buying pesticides in the

cities and selling to smaller farmers in their local village.

This high growth region presents a highly volatile development from year to year due to a tricky monsoon in

Asia and political instability in especially the Middle East.

Market share and market growth in the different geographical areas are stated in the figure below:

48

Auriga Industries A/S, Annual Report 2009, page 8 49

ADAMA, Annual Report 2013, page 25 50

Auriga Industries A/S, Annual Report 2013, page 39 (604,927/6,597,749) 51

Auriga Industries A/S, Annual Report 2009, page 13 52

ADAMA, Annual Report 2013, page 25 53

Auriga Industries A/S, Annual Report 2013, page 39 (1,095,902/6,597,749)

19

Figure 3-2: Global Overview– the Market with average numbers from 2009 to 2013 (Source: Own Creation with data from

ADAMA Annual reports 2009 – 2013)

3.2. Exogenous Factors The PESTEL-analysis is a strategic analysis with focus on external factors immediate to the agrochemical

industry and Auriga. Due to the difficulty for Auriga to alter or affect the external environment it is

important to have a clear view of all factors which may influence the company and its future strategy.

The aim of the section is to derive the nature of Auriga’s business environment and uncover the dynamics

and complexity of the industry. Key findings from this section are later highlighted in the SWOT analysis

and used in the Forecasting & Scenario analysis chapter to determine specific levels for value drivers used

when evaluating different possible enterprise values for Auriga.

3.2.1. PESTEL

3.2.1.1. Political factors

Due to the potential environmental and health impacts related to agrochemical products, the industry is

object of high political attentiveness and products have previously been banned for further usage54

. With a

continuously increasing degree of environmental- and labor protection laws55

there is a high political risk for

companies operating in the agrochemical industry.

An opposite point is food security for the growing population which also continues to attract political and

public attention. According to the Food and Agriculture Organization of the United Nations (FAO) global

agriculture has to increase its production 70% to be able to support the world’s growing population in

205056

. As crop protection has been and still is a beneficial instrument for securing and increasing yields in

farming, the political awareness could have a potential positive effect on the industry – especially in regions

54

Ministry of Environment and food of Denmark homepage: http://eng.mst.dk/topics/chemicals/legislation-on-chemicals/fact-sheets/fact-sheet-banned-pesticides/ 55

Auriga Industries homepage: http://www.auriga-industries.com/download/sustainability/csr_reports/csr_rapport_2013_uk_web.pdf 56

FAO homepage: http://www.fao.org/sustainability/en/

20

like the Americas, Africa and Asia with high population growth. Changes in agricultural subsidies and tax on

both crops and pesticides can also affect the industry for agrochemicals.

The industry is also influenced by grass-root- and non-government organizations (NGO) like Greenpeace

and WWF. These organizations lobby for their diametrical cause by providing information on potential

hazards related to the production and use of pesticides and GMO techniques, herby influencing the

governmental apparatus.57

The political environment of Auriga’s main regions; Europe and Latin America will be expanded in the

following.

Europe is a region of industrialized countries with developed democracies, strong governments and high

public awareness concerning health and environmental issues. Successively the political environment for the

agrochemical industry is assessed stricter compared to other parts of the world. Likewise, the expected

demographic development of the region with a declining population does not raise high political concerns

regarding food scarcity. In Europe, the interest organization of ECPA represents the agrochemical industry

with 21 companies, 32 national associations and 26,000 people employed in the industry.

In Latin America and region International where several countries are undergoing rapid transformation

shifting from developing- to industrialized countries, and where most democracies still are young and fragile,

the political awareness is primarily focused on increasing farm productivity and to a lesser extent on health

and environmental issues. The political focus on farm productivity is to a large extent driven by a great part

of the populations living in poverty which makes it necessary for politicians, to focus on keeping food prices

at an affordable level58

. The political environments in these countries are assessed to be friendlier for the

agrochemical industry compared to e.g. Europe and the US.

3.2.1.2. Economic factors

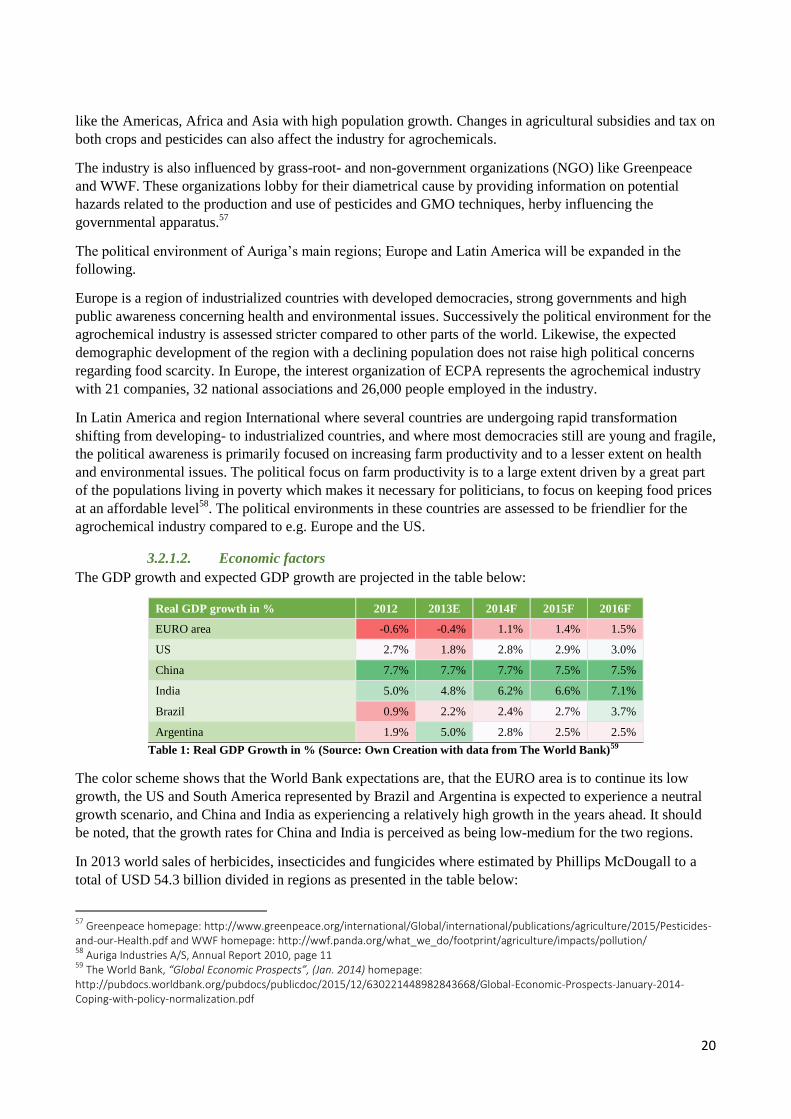

The GDP growth and expected GDP growth are projected in the table below:

Real GDP growth in % 2012 2013E 2014F 2015F 2016F

EURO area -0.6% -0.4% 1.1% 1.4% 1.5%

US 2.7% 1.8% 2.8% 2.9% 3.0%

China 7.7% 7.7% 7.7% 7.5% 7.5%

India 5.0% 4.8% 6.2% 6.6% 7.1%

Brazil 0.9% 2.2% 2.4% 2.7% 3.7%

Argentina 1.9% 5.0% 2.8% 2.5% 2.5%

Table 1: Real GDP Growth in % (Source: Own Creation with data from The World Bank)59

The color scheme shows that the World Bank expectations are, that the EURO area is to continue its low

growth, the US and South America represented by Brazil and Argentina is expected to experience a neutral

growth scenario, and China and India as experiencing a relatively high growth in the years ahead. It should

be noted, that the growth rates for China and India is perceived as being low-medium for the two regions.

In 2013 world sales of herbicides, insecticides and fungicides where estimated by Phillips McDougall to a

total of USD 54.3 billion divided in regions as presented in the table below:

57

Greenpeace homepage: http://www.greenpeace.org/international/Global/international/publications/agriculture/2015/Pesticides-and-our-Health.pdf and WWF homepage: http://wwf.panda.org/what_we_do/footprint/agriculture/impacts/pollution/ 58

Auriga Industries A/S, Annual Report 2010, page 11 59

The World Bank, “Global Economic Prospects”, (Jan. 2014) homepage: http://pubdocs.worldbank.org/pubdocs/publicdoc/2015/12/630221448982843668/Global-Economic-Prospects-January-2014-Coping-with-policy-normalization.pdf

21

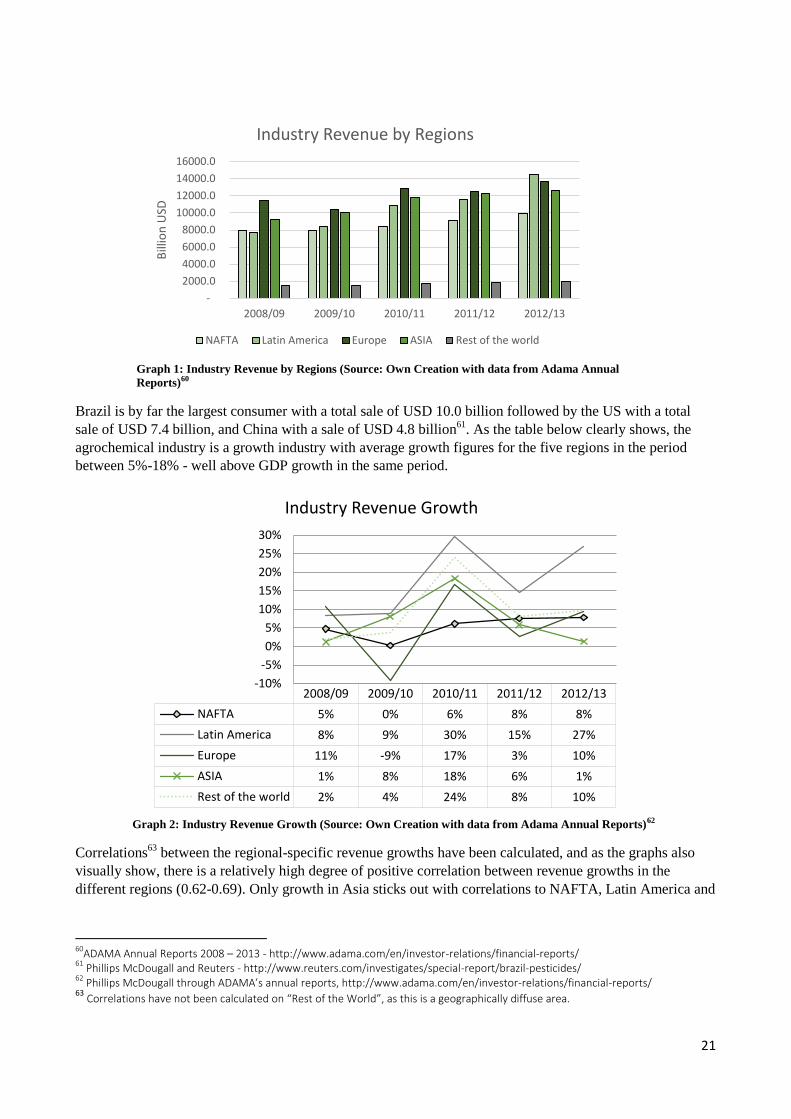

Graph 1: Industry Revenue by Regions (Source: Own Creation with data from Adama Annual

Reports)60

Brazil is by far the largest consumer with a total sale of USD 10.0 billion followed by the US with a total

sale of USD 7.4 billion, and China with a sale of USD 4.8 billion61

. As the table below clearly shows, the

agrochemical industry is a growth industry with average growth figures for the five regions in the period

between 5%-18% - well above GDP growth in the same period.

Graph 2: Industry Revenue Growth (Source: Own Creation with data from Adama Annual Reports)62

Correlations63

between the regional-specific revenue growths have been calculated, and as the graphs also

visually show, there is a relatively high degree of positive correlation between revenue growths in the

different regions (0.62-0.69). Only growth in Asia sticks out with correlations to NAFTA, Latin America and

60

ADAMA Annual Reports 2008 – 2013 - http://www.adama.com/en/investor-relations/financial-reports/ 61

Phillips McDougall and Reuters - http://www.reuters.com/investigates/special-report/brazil-pesticides/ 62

Phillips McDougall through ADAMA’s annual reports, http://www.adama.com/en/investor-relations/financial-reports/ 63

Correlations have not been calculated on “Rest of the World”, as this is a geographically diffuse area.

-

2000.0

4000.0

6000.0

8000.0

10000.0

12000.0

14000.0

16000.0

2008/09 2009/10 2010/11 2011/12 2012/13

Bill

ion

USD

Industry Revenue by Regions

NAFTA Latin America Europe ASIA Rest of the world

2008/09 2009/10 2010/11 2011/12 2012/13

NAFTA 5% 0% 6% 8% 8%

Latin America 8% 9% 30% 15% 27%

Europe 11% -9% 17% 3% 10%

ASIA 1% 8% 18% 6% 1%

Rest of the world 2% 4% 24% 8% 10%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

Industry Revenue Growth

22

Europe of 0.12, 0.47 and 0.22 respectively. Thus, seeking diversified revenue across different regions would

eventually have to involve the Asian region.

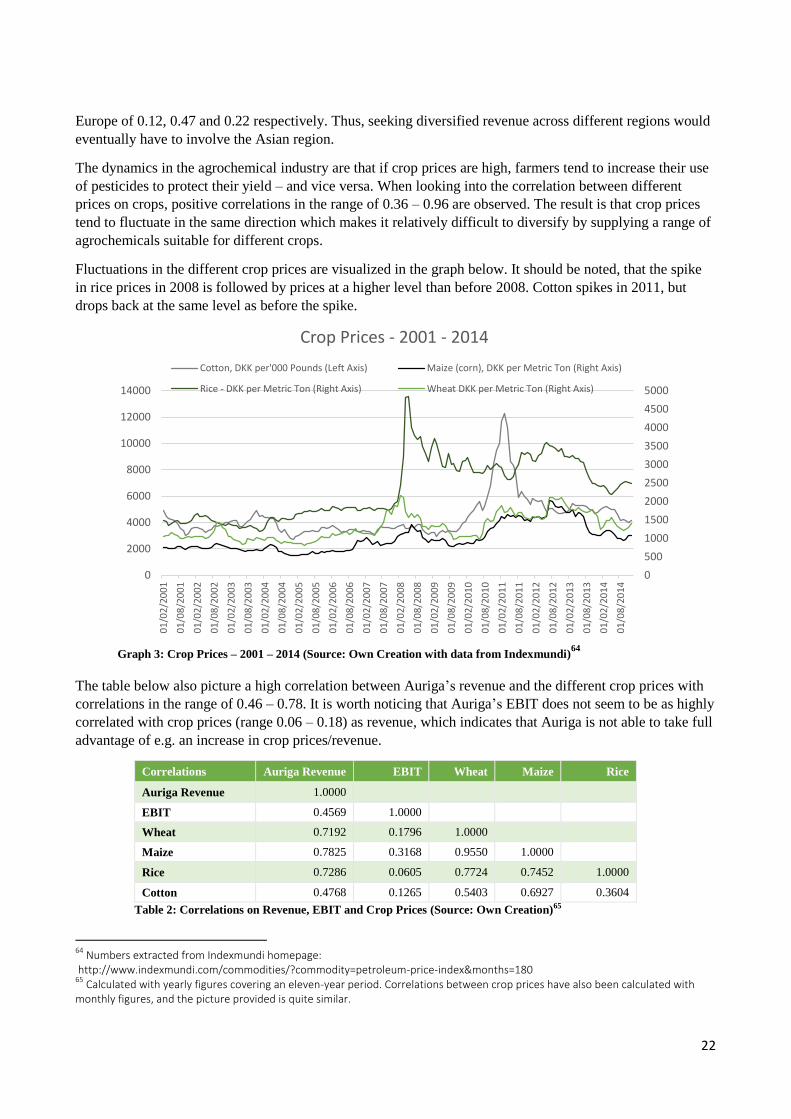

The dynamics in the agrochemical industry are that if crop prices are high, farmers tend to increase their use

of pesticides to protect their yield – and vice versa. When looking into the correlation between different

prices on crops, positive correlations in the range of 0.36 – 0.96 are observed. The result is that crop prices

tend to fluctuate in the same direction which makes it relatively difficult to diversify by supplying a range of

agrochemicals suitable for different crops.

Fluctuations in the different crop prices are visualized in the graph below. It should be noted, that the spike

in rice prices in 2008 is followed by prices at a higher level than before 2008. Cotton spikes in 2011, but

drops back at the same level as before the spike.

Graph 3: Crop Prices – 2001 – 2014 (Source: Own Creation with data from Indexmundi)

64

The table below also picture a high correlation between Auriga’s revenue and the different crop prices with

correlations in the range of 0.46 – 0.78. It is worth noticing that Auriga’s EBIT does not seem to be as highly

correlated with crop prices (range 0.06 – 0.18) as revenue, which indicates that Auriga is not able to take full

advantage of e.g. an increase in crop prices/revenue.

Correlations Auriga Revenue EBIT Wheat Maize Rice

Auriga Revenue 1.0000

EBIT 0.4569 1.0000

Wheat 0.7192 0.1796 1.0000

Maize 0.7825 0.3168 0.9550 1.0000