Status of Nuclear Power Plants in the United States ASQ Energy and Environmental Conference August 28, 2006 Tom Mulford Managing Director Advanced Nuclear Technology Program EPRI

Status of Nuclear Power Plants in the United States ASQ Energy and Environmental Conference August 28, 2006 Tom Mulford Managing Director Advanced Nuclear.

Dec 31, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Status of Nuclear Power Plants in the United States

ASQ Energy and Environmental Conference

August 28, 2006

Tom MulfordManaging DirectorAdvanced Nuclear Technology ProgramEPRI

2© 2006 Electric Power Research Institute, Inc. All rights reserved.

Presentation Topics

• Current state of the U.S. nuclear energy industry

• Projected nuclear growth in the U.S.

• Current status of nuclear R&D within EPRI

• Priorities and assumptions for future nuclear industry

R&D

• Key technical and institutional challenges

3© 2006 Electric Power Research Institute, Inc. All rights reserved.

'82 '84 '86 '88 '90 '92 '94 '96 '98 '00 '02 '04

50%

60%

70%

80%

90%

100%

Ca

pa

cit

y F

ac

tor

(%)

Industry Performance Is Consistently Excellent

89.4% in 2001

90.3% in 2002

87.9% in 2003

90.1% in 2004

89.6% in 2005*

*Preliminary

Source: Energy Information Administration

4© 2006 Electric Power Research Institute, Inc. All rights reserved.

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0 Nuclear 1.72

Coal 2.21

Gas 7.51

Oil 8.09

Source: Global Energy Decisions

U.S. Electricity Production Costs(in 2005 cents/kWh) U.S. Electricity Production Costs(in 2005 cents/kWh)

5© 2006 Electric Power Research Institute, Inc. All rights reserved.

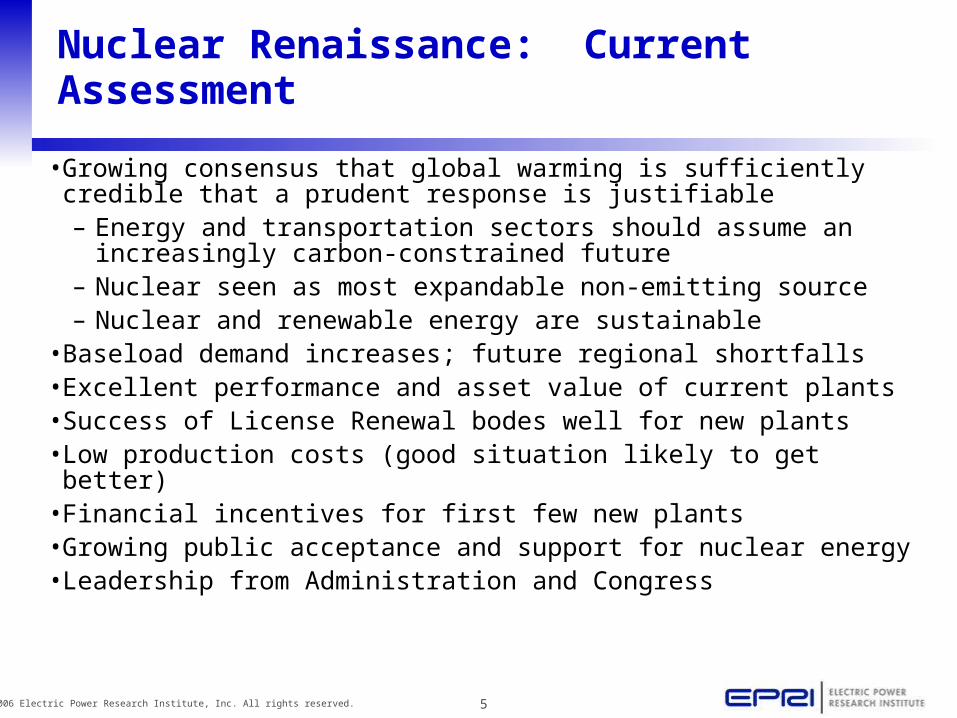

Nuclear Renaissance: Current Assessment

• Growing consensus that global warming is sufficiently credible that a prudent response is justifiable– Energy and transportation sectors should assume an

increasingly carbon-constrained future– Nuclear seen as most expandable non-emitting source– Nuclear and renewable energy are sustainable

• Baseload demand increases; future regional shortfalls• Excellent performance and asset value of current plants• Success of License Renewal bodes well for new plants• Low production costs (good situation likely to get better)• Financial incentives for first few new plants• Growing public acceptance and support for nuclear energy• Leadership from Administration and Congress

6© 2006 Electric Power Research Institute, Inc. All rights reserved.

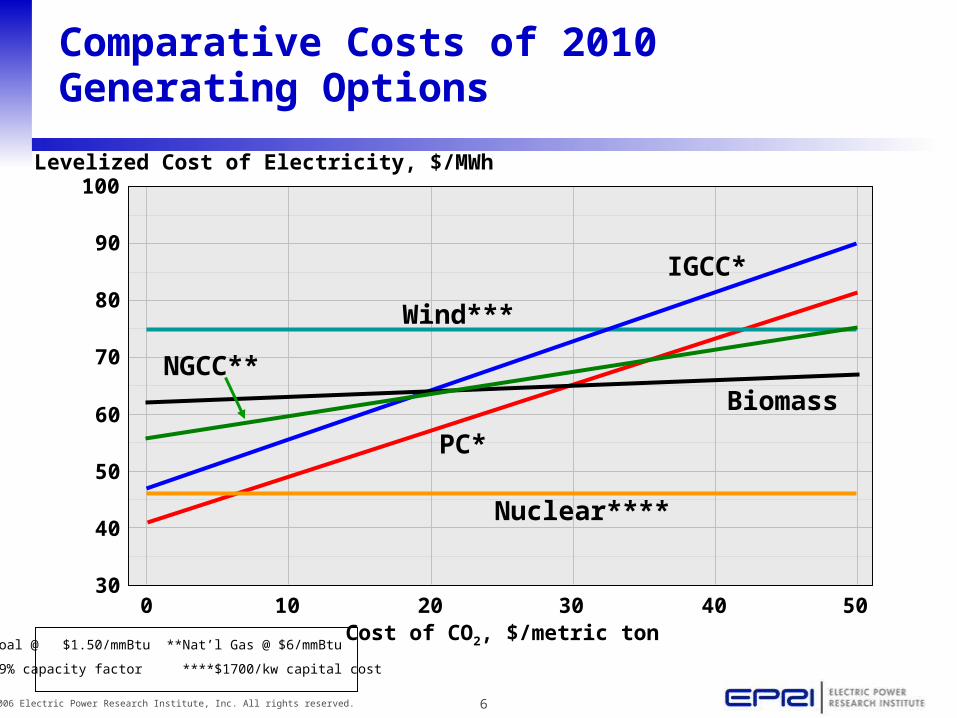

Comparative Costs of 2010 Generating Options

30

40

50

60

70

80

90

100

0 10 20 30 40 50Cost of CO2, $/metric ton

Levelized Cost of Electricity, $/MWh

Wind***

Nuclear****

PC*

IGCC*

BiomassNGCC**

*Coal @ $1.50/mmBtu **Nat’l Gas @ $6/mmBtu

***29% capacity factor ****$1700/kw capital cost

7© 2006 Electric Power Research Institute, Inc. All rights reserved.

Comparative Costs of 2020 Generating Options

30

40

50

60

70

80

90

100

0 10 20 30 40 50Cost of CO2, $/metric ton

Levelized Cost of Electricity, $/MWh

Nuclear****

Wind*** Biomass

IGCC* w/cap/t/sNGCC**

PC* w/cap/t/s

*Coal @ $1.50/mmBtu **Nat’l Gas @ $6/mmBtu

***29% capacity factor ****$1700/kw capital cost

8© 2006 Electric Power Research Institute, Inc. All rights reserved.

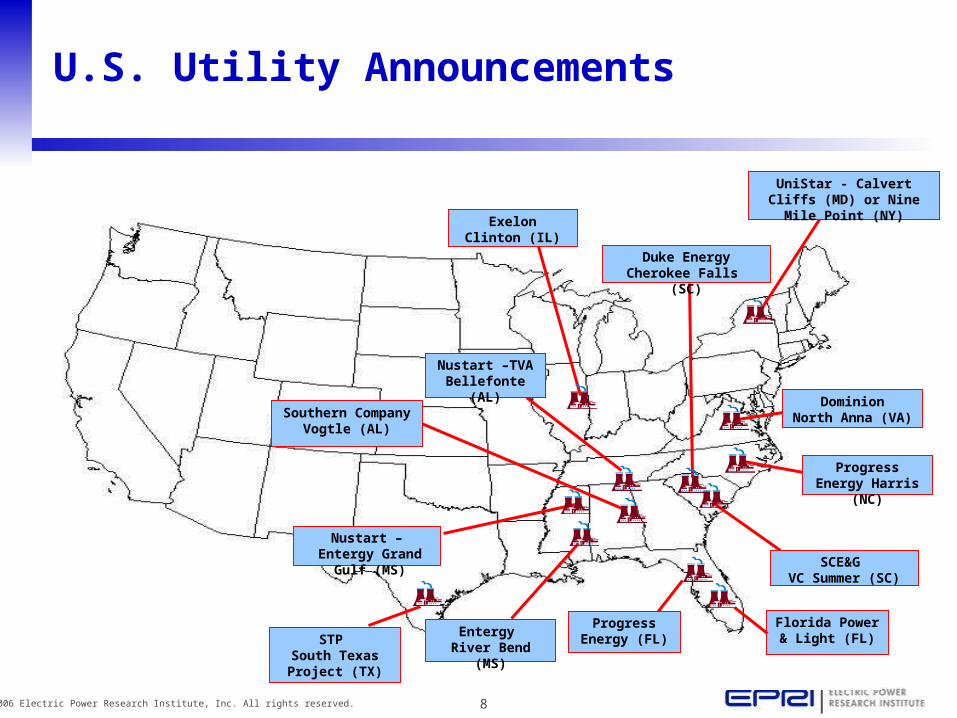

U.S. Utility Announcements

ExelonClinton (IL)

Entergy River Bend (MS)

Progress Energy (FL)

UniStar - Calvert Cliffs (MD) or Nine Mile Point (NY)

DominionNorth Anna (VA)

Duke EnergyCherokee Falls (SC)

Southern Company Vogtle (AL)

Nustart – Entergy Grand Gulf (MS)

SCE&G VC Summer (SC)

Progress Energy Harris (NC)

Nustart –TVA Bellefonte (AL)

Florida Power & Light (FL)STP

South Texas Project (TX)

9© 2006 Electric Power Research Institute, Inc. All rights reserved.

Summary Estimate of New Nuclear Power PlantsBased on the Design Centered Approach

(as of 7/2/06)

2619Total

--------------------

33Unspecified

42ABWR

55EPR

33ESBWR

116AP 1000

UnitsCOLs

Number of Reference COLs: 4Number of Environmental Reviews: 19+

Source: NRC

10© 2006 Electric Power Research Institute, Inc. All rights reserved.

Nuclear power remains in the generation portfolio mix

only if the current fleet meets/exceeds expectations

EPRI Nuclear R&D Strategy: Existing Plant Optimization

• Over 85% of our work

• Safe, reliable, economic operations

• Effective spent fuel management

• Equipment reliability

• Materials and fuel

• Workforce and infrastructure

11© 2006 Electric Power Research Institute, Inc. All rights reserved.

EPRI Nuclear Materials Degradation and Aging

• Materials Corrosion– Environment-related degradation

mechanisms• PWR Steam Generator Management

– Tubing materials degradation issues• BWR Materials Management

– Reactor pressure vessel, piping and internals

• PWR Materials Management– Alloy 600 stress corrosion cracking– Vessel, piping and internals

• Water Chemistry Control– Water chemistry-based degradation

mitigation• Non Destructive Evaluation

12© 2006 Electric Power Research Institute, Inc. All rights reserved.

Time

Cu

mu

lative Degrad

ation

1970s 1980s 1990s 2000s0

BWR Pipe

PWR Steam Generators

PWR Heater sleeves and instrument nozzles

RPV Head BWR Internals

Erosion-Corrosion

Alloy 600 Welds

Materials Issues Have Been, Are and Will Remain Challenging… 40 years and beyond

?

13© 2006 Electric Power Research Institute, Inc. All rights reserved.

EPRI Nuclear Fuel Reliability Program

• Characterize and mitigate corrosion and excessive crud deposition

• Quantify and address impacts of water chemistry changes—develop guidelines

• Interface with NRC to establish accident and burn up extension licensing criteria

• Monitor and assess margins

• Investigate fuel failure root causes and identify corrective actions

• Develop and apply ultrasonic fuel cleaning technology at PWRs and BWRs

14© 2006 Electric Power Research Institute, Inc. All rights reserved.

EPRI Nuclear HLW & Spent Fuel Management

• Spent fuel storage and transportation

– DOE/EPRI/NRC cooperation on fission product burnup credit data – huge implications

– EPRI transportation risk studies

• Yucca Mountain (YM)

– Input to EPA on YM standard

– Work to achieve YM licensing

– Support industry input to the new DOE spent fuel handling approach

15© 2006 Electric Power Research Institute, Inc. All rights reserved.

EPRI Nuclear R&D Strategy:New Plant Deployment

• Consensus utility requirements; standardization

• Cost sharing with DOE

• Support of NEI and new plant consortia

– Demonstrate the new licensing process

– Address generic technical issues

• Environmental contributions

Initiate construction of ALWRs by 2010 to assure

nuclear’s place in future generation portfolio

16© 2006 Electric Power Research Institute, Inc. All rights reserved.

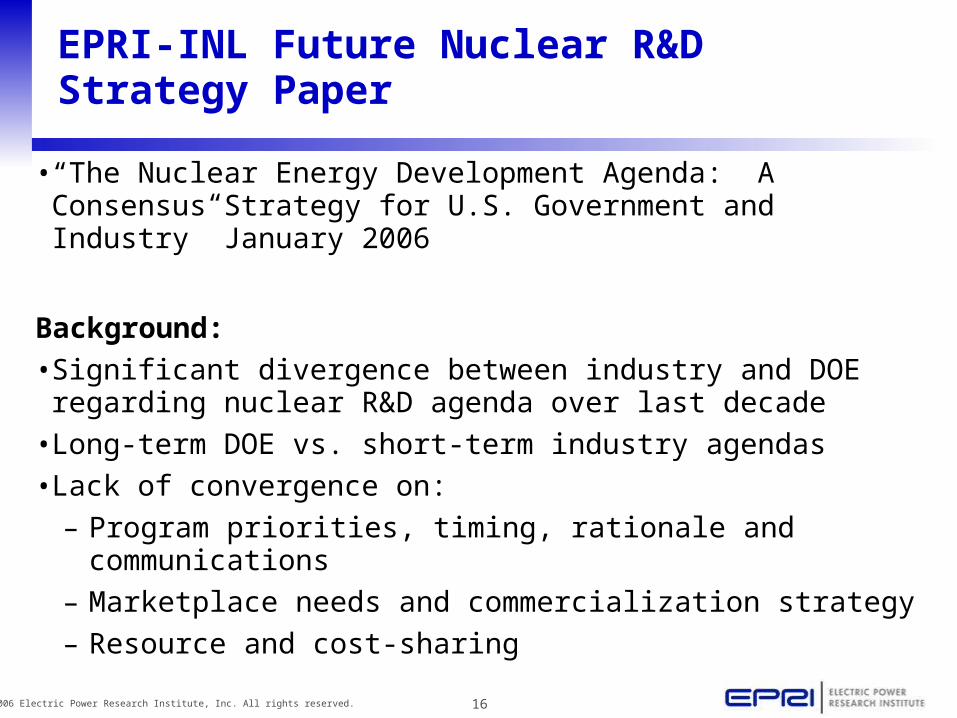

EPRI-INL Future Nuclear R&D Strategy Paper

• “The Nuclear Energy Development Agenda: A Consensus Strategy for U.S. Government and Industry” January 2006

Background:

• Significant divergence between industry and DOE regarding nuclear R&D agenda over last decade

• Long-term DOE vs. short-term industry agendas

• Lack of convergence on:

– Program priorities, timing, rationale and communications

– Marketplace needs and commercialization strategy

– Resource and cost-sharing

17© 2006 Electric Power Research Institute, Inc. All rights reserved.

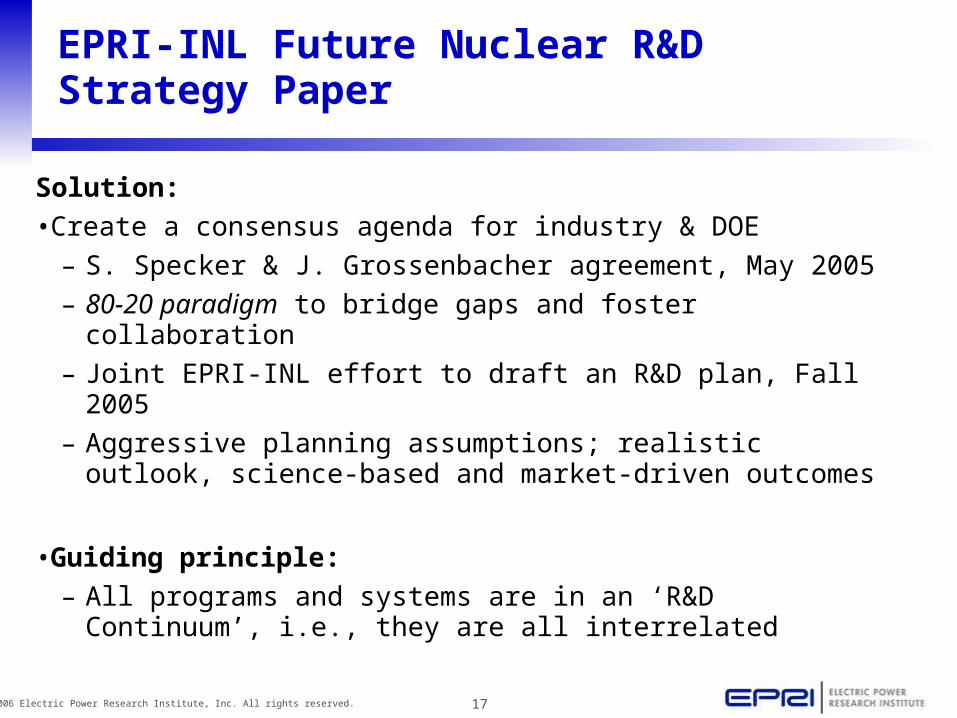

EPRI-INL Future Nuclear R&D Strategy Paper

Solution:

• Create a consensus agenda for industry & DOE

– S. Specker & J. Grossenbacher agreement, May 2005

– 80-20 paradigm to bridge gaps and foster collaboration

– Joint EPRI-INL effort to draft an R&D plan, Fall 2005

– Aggressive planning assumptions; realistic outlook, science-based and market-driven outcomes

• Guiding principle:

– All programs and systems are in an ‘R&D Continuum’, i.e., they are all interrelated

18© 2006 Electric Power Research Institute, Inc. All rights reserved.

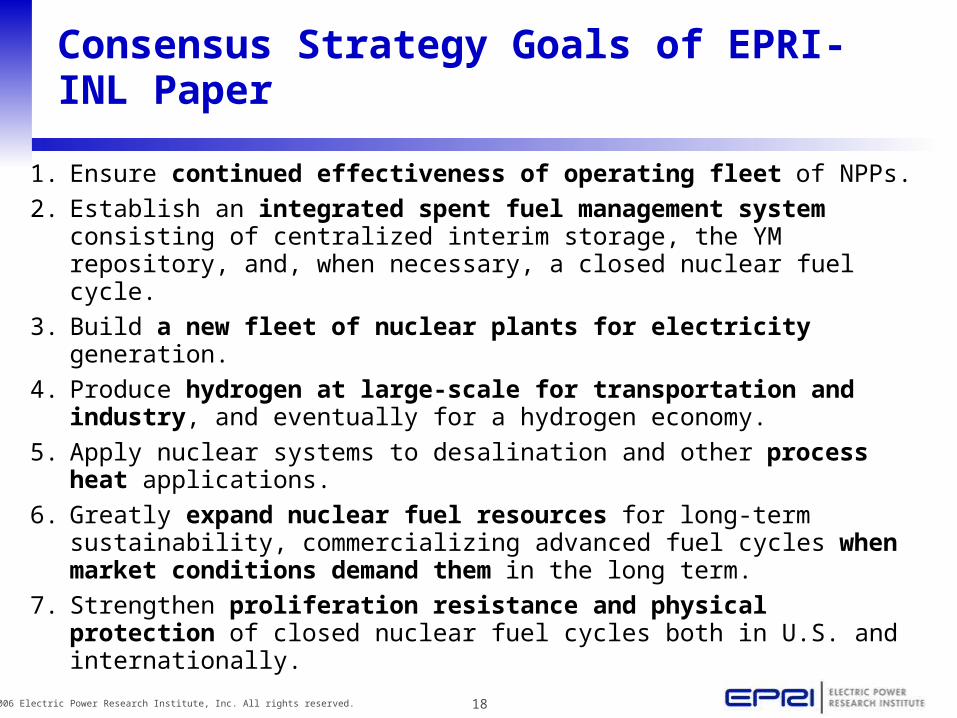

Consensus Strategy Goals of EPRI-INL Paper

1. Ensure continued effectiveness of operating fleet of NPPs.

2. Establish an integrated spent fuel management system consisting of centralized interim storage, the YM repository, and, when necessary, a closed nuclear fuel cycle.

3. Build a new fleet of nuclear plants for electricity generation.

4. Produce hydrogen at large-scale for transportation and industry, and eventually for a hydrogen economy.

5. Apply nuclear systems to desalination and other process heat applications.

6. Greatly expand nuclear fuel resources for long-term sustainability, commercializing advanced fuel cycles when market conditions demand them in the long term.

7. Strengthen proliferation resistance and physical protection of closed nuclear fuel cycles both in U.S. and internationally.

19© 2006 Electric Power Research Institute, Inc. All rights reserved.

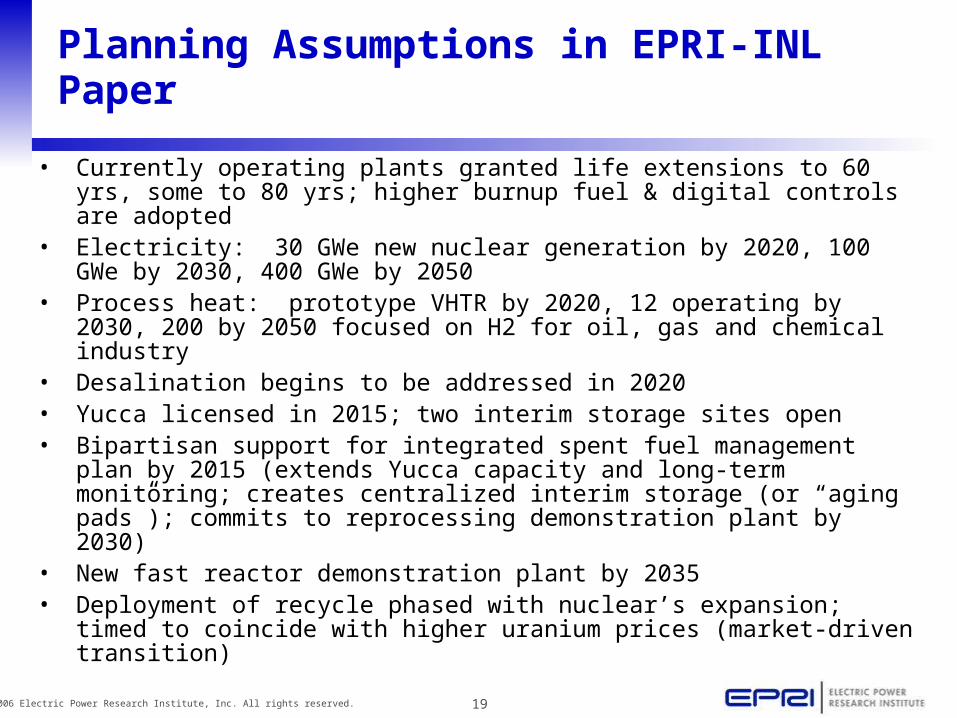

Planning Assumptions in EPRI-INL Paper

• Currently operating plants granted life extensions to 60 yrs, some to 80 yrs; higher burnup fuel & digital controls are adopted

• Electricity: 30 GWe new nuclear generation by 2020, 100 GWe by 2030, 400 GWe by 2050

• Process heat: prototype VHTR by 2020, 12 operating by 2030, 200 by 2050 focused on H2 for oil, gas and chemical industry

• Desalination begins to be addressed in 2020• Yucca licensed in 2015; two interim storage sites open• Bipartisan support for integrated spent fuel management plan by

2015 (extends Yucca capacity and long-term monitoring; creates centralized interim storage (or “aging pads”); commits to reprocessing demonstration plant by 2030)

• New fast reactor demonstration plant by 2035• Deployment of recycle phased with nuclear’s expansion; timed

to coincide with higher uranium prices (market-driven transition)

20© 2006 Electric Power Research Institute, Inc. All rights reserved.

Conclusions of the EPRI-INL Paper

• Nuclear energy development in the U.S. requires a consensus of industry and government

• Significant LWR research is needed (e.g., HBU fuel)• Nuclear’s contribution to process heat is an important priority• A proliferation-resistant closed nuclear fuel cycle should be

ready for deployment by mid-century– Primary driver: energy/environmental sustainability– ‘Full actinide recycle’ important to integrated, cost-

effective spent fuel management – Existing reprocessing technology not adequate to

accomplish global non-proliferation and domestic spent fuel management objectives

• Strategy for rebuilding U.S. nuclear infrastructure is needed

21© 2006 Electric Power Research Institute, Inc. All rights reserved.

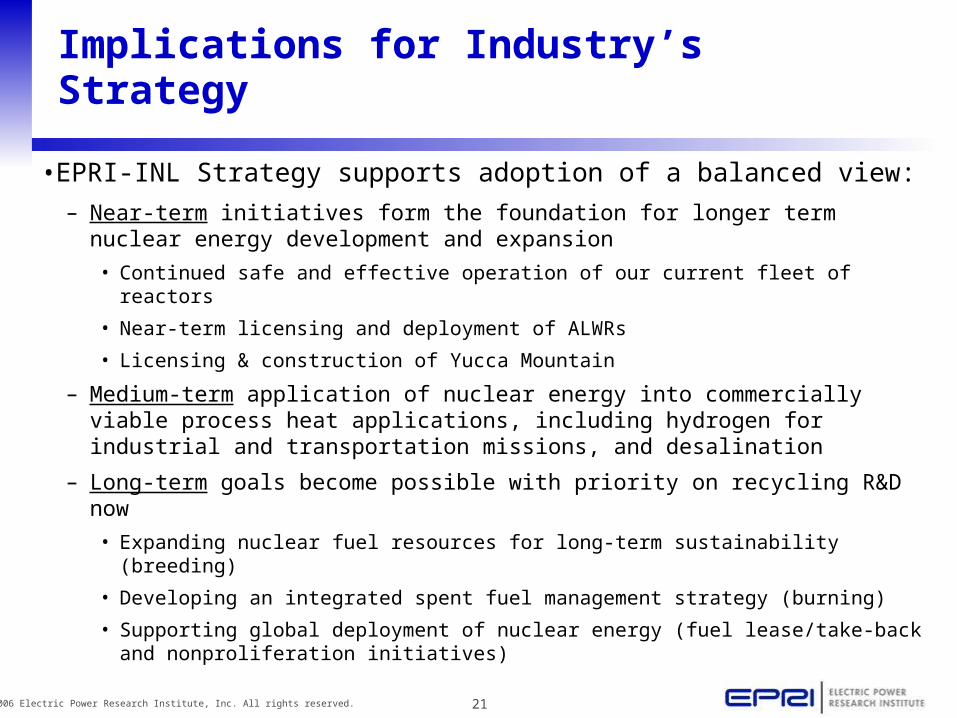

Implications for Industry’s Strategy

• EPRI-INL Strategy supports adoption of a balanced view:

– Near-term initiatives form the foundation for longer term nuclear energy development and expansion

• Continued safe and effective operation of our current fleet of reactors

• Near-term licensing and deployment of ALWRs

• Licensing & construction of Yucca Mountain

– Medium-term application of nuclear energy into commercially viable process heat applications, including hydrogen for industrial and transportation missions, and desalination

– Long-term goals become possible with priority on recycling R&D now

• Expanding nuclear fuel resources for long-term sustainability (breeding)

• Developing an integrated spent fuel management strategy (burning)

• Supporting global deployment of nuclear energy (fuel lease/take-back and nonproliferation initiatives)

22© 2006 Electric Power Research Institute, Inc. All rights reserved.

Implications for DOE’s Fuel Cycle Strategy

• EPRI-INL Paper: U.S. can embark on major new plant deployment and not have to build a second repository, even if closed fuel cycle deployment not achieved until 2050.

• EPRI-INL conclusion contingent on establishing an integrated, cost-effective spent fuel management strategy:– Allowing for expansion of the YM site to its full technical capacity

– Reducing the rate of spent fuel generation via development of high performance LWR fuel (factor of two achievable)

– Maintaining engineered cooling of YM for 50+ years prior to closure

– Providing for interim centralized storage or “aging pads”

– Deploying multi-purpose canisters approved by NRC

– Implementing an effective spent fuel transportation system

– Eventual recycling of spent fuel to reduce volume and heat rate, thus making much more effective use of repository space.

23© 2006 Electric Power Research Institute, Inc. All rights reserved.

Nuclear Renaissance: Near-Term Challenges

• High capital cost (mitigated by standardization, incentives)

• New Plant Licensing:

– Uncertainty in regulatory process

– Process duration; implications to time-to-market

– Up-front licensing resource demands

• Confidence in spent fuel management solutions

• Infrastructure, especially in rapid expansion scenarios:

– Fabrication and manufacturing capacity

– Engineering capability

– Skilled construction trades

– QA, NDE, HP, O&M personnel

Related Documents