STATE STATE the of NSW Property Report

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

STATESTATEtheof

N S W P r o p e r t y R e p o r t

State of the State NSW Property Report p.1

Executive Summary

St.George Bank has commissioned RP Data to undertake an analysis of the New South Wales residential property market, specifically analysing the performance of houses and units. The analysis highlights the 12 Statistical Divisions (SD) throughout the state and looks at the market performance both recently and during the last decade.

The report looks at the broad national property market trends and then moves from this macro view into a more micro view within the specific markets of New South Wales.

During the past ten years, the national property market has seen a little bit of everything: strong growth, moderate growth, flat conditions and value declines. Nationally property values have increased at an average annual rate of 9.5 percent and in comparison, Sydney property values have underperformed recording growth of 6.4 percent annually. The relatively poor performance of Sydney is related to affordability pressures and the fact that it is a much more mature property market than most other Australian capital cities.

The national property market is moving out of a strong growth phase since the beginning of 2009 and Sydney has been one of the few capital city markets to still record growth in property values over the three months to August 2010. The expectation for the remainder of 2010 is that the rate of value growth will be quite flat in the capital cities and it is anticipated that this will result in flat growth for regional areas also. Sydney property values underperformed for five and a half years and only eclipsed their January 2004 peak in May 2009. As at August 2010, Sydney property values are 12.5 percent higher than the January 2004 peak.

Typically, the regional markets have recorded greater growth in prices than the Sydney market over the last decade, however, most have come from a much lower price base and in comparison to their counterparts in other states, they have under performed.

In many instances, the regional markets of New South Wales recorded a larger slump in prices during the Global Financial Crisis (GFC) than that recorded in Sydney. Subsequently, many regions have only recently witnessed median prices returning to their pre‐GFC peaks. Median prices of both houses and units have shown some easing in recent months suggesting that the slowdown in capital city markets coupled with a higher interest rate environment is impacting these regions.

In most instances, the average number of days it takes to sell a house (days on market) and the average level of vendor discount is at, or close to, historic low levels currently. With the property price growth now slowing, it is anticipated that these lead indicators will once again begin to increase.

The higher interest rate environment and fewer active buyers is likely to swing market conditions away from sellers and more in favour of the buyers. Buyers are likely to have more purchase options and less competition for stock, as a result they are likely to have greater scope for price negotiation.

Despite the slowing market conditions, New South Wales has a growing population and an insufficient supply of new dwellings to cater demand. Over time, unless this situation can be rectified there is likely to be intensifying upward pressure on property prices.

Although the next year is likely to be characterised as having fairly flat market conditions, certain areas and regions are likely to have stronger prospects for capital growth. In Sydney, well located properties close to the CBD and working nodes with quality amenities including: shops, schools, restaurants, major roads and public transport will likely have the strongest growth prospects. In regional areas, purchasers should look for similar features however, those regions closer to Sydney such as Hunter and Illawarra are likely to have the strongest potential for growth in median prices.

State of the State NSW Property Report

Contents

DISCLAIMERThe information provided in this publication is current as at the publication date only. In compiling this publication, rpdata.com has relied upon information supplied by a number of external sources. This publication is supplied on the basis that while rpdata.com believes all the information in it is deemed reliable at the publication date, it does not warrant its accuracy or completeness and to the full extent allowed by law excludes liability in contract, tort or otherwise, for any loss or damage sustained by subscribers, or by any other person or body corporate arising from or in connection with the supply or use of the whole or any part of the information in this publication through any cause whatsoever and limits any liability it may have to the amount paid to rpdata.com for the supply of such information.

RP Data recommends that individuals undertake their own research and seek independent financial advice before making any decisions.

© 2010 Copyright RP Data Ltd.

St.George Bank – A Division of Westpac Banking Corporation ABN 33 007 457 141 AFSL 233714 accepts no responsibility for the accuracy or completeness of this publication.

Methodology 3

National property market 4

Key economic and property data 7

Focus on Sydney 8

Focus on Hunter 14

Focus on Illawarra 20

Focus on Mid North Coast 26

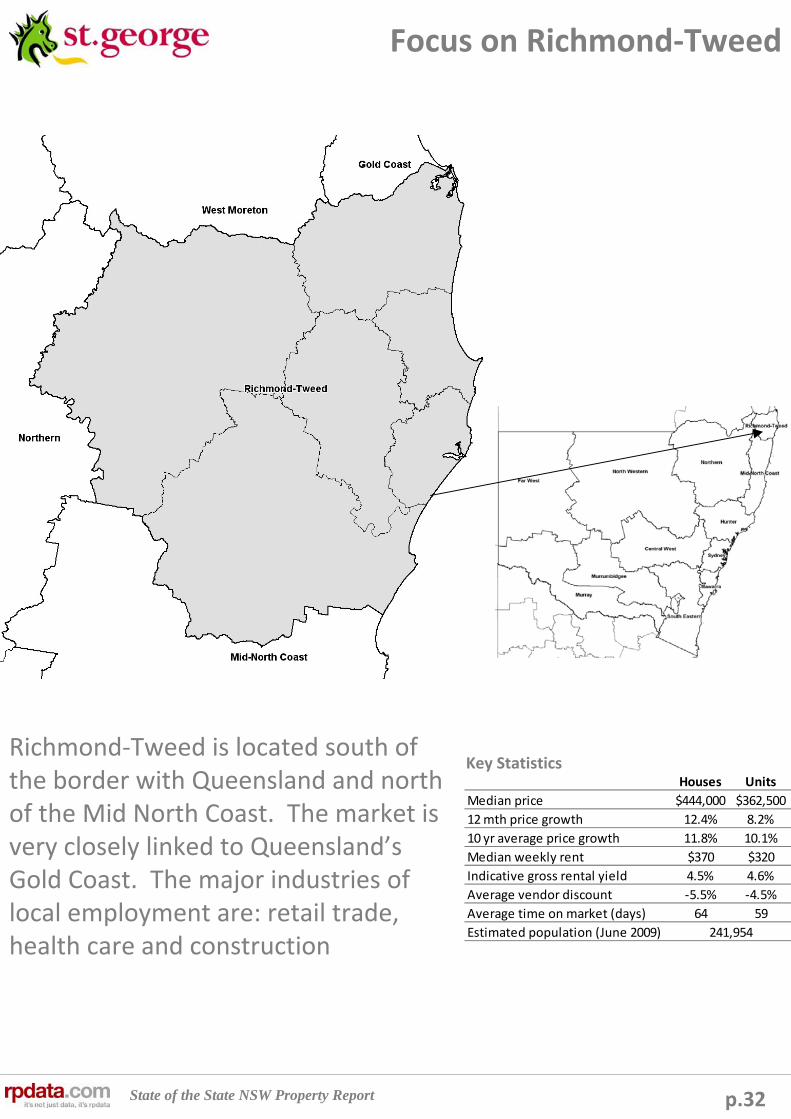

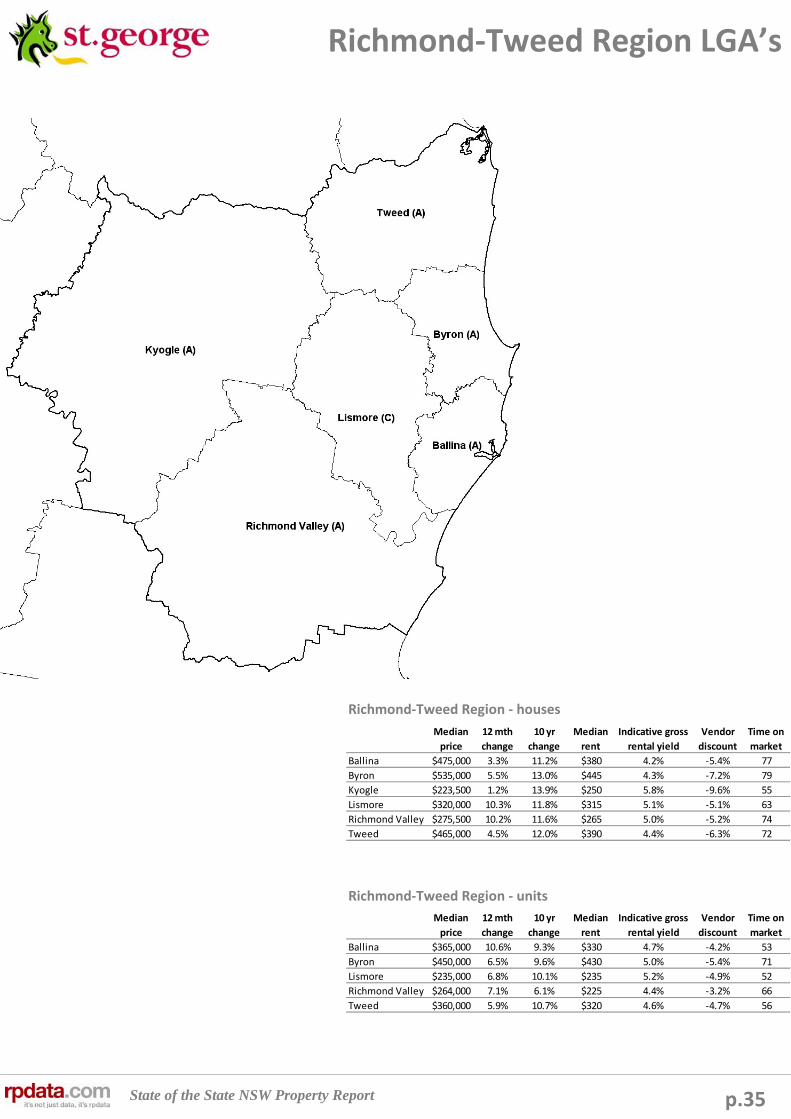

Focus on Richmond‐Tweed 32

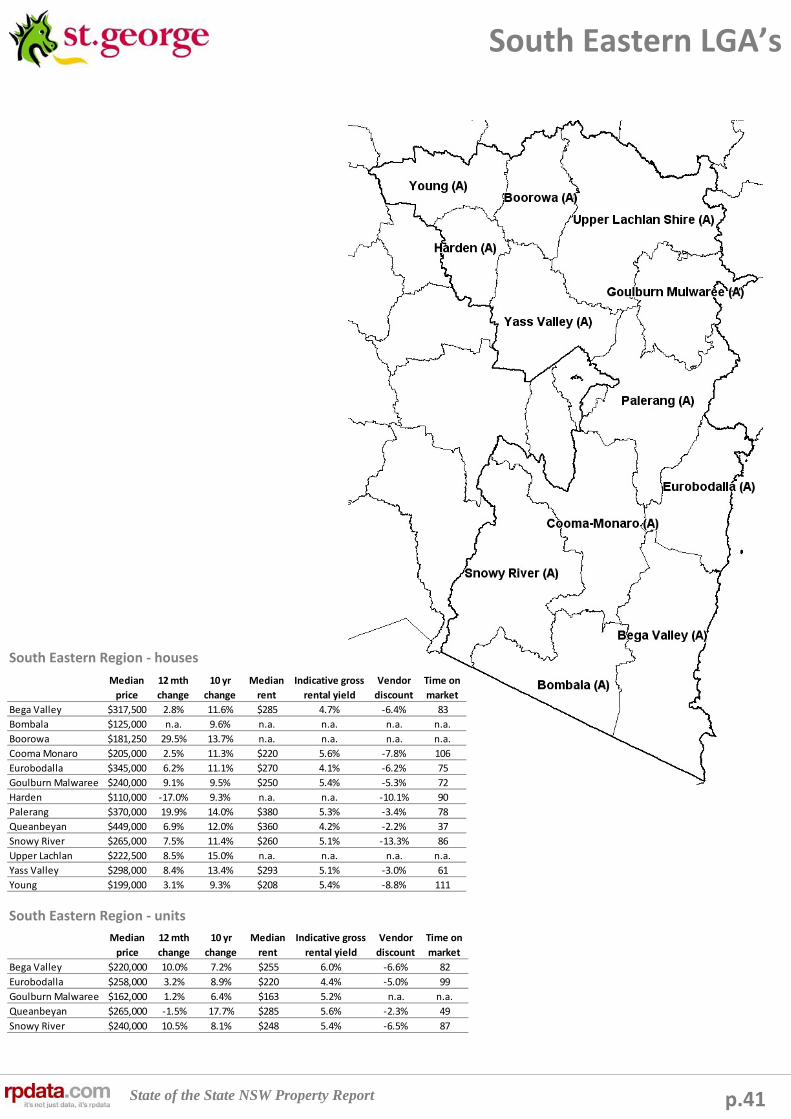

Focus on South Eastern 38

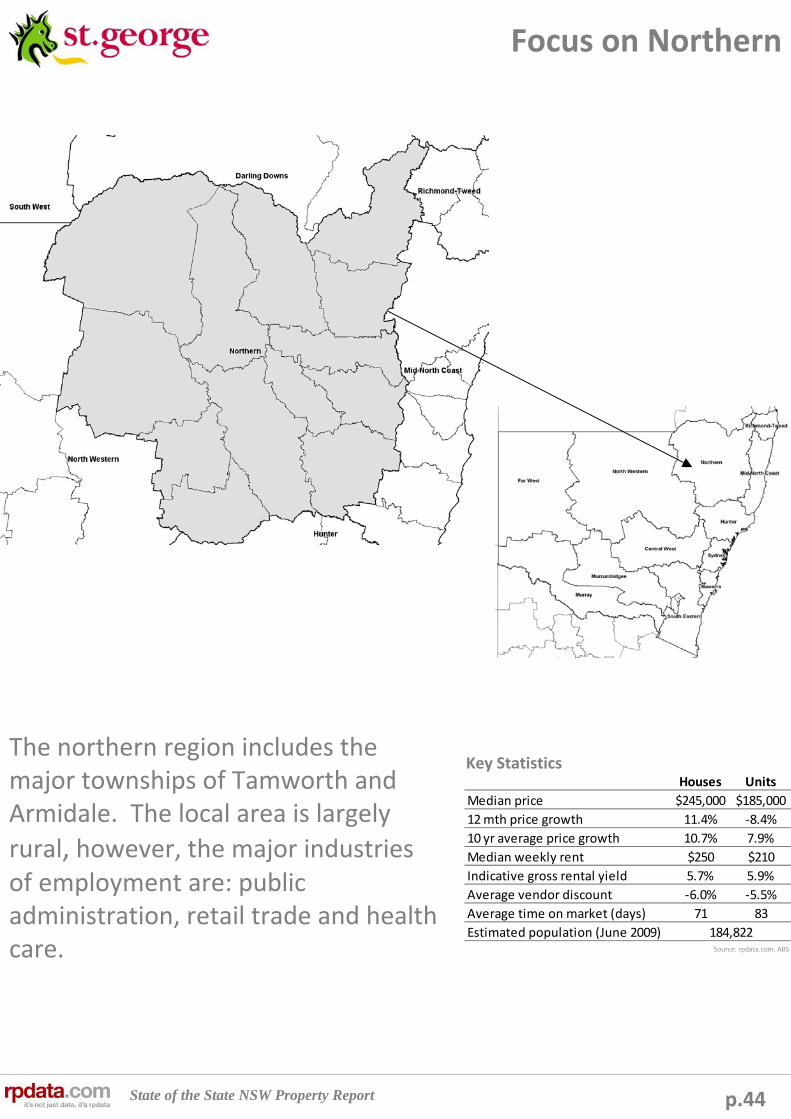

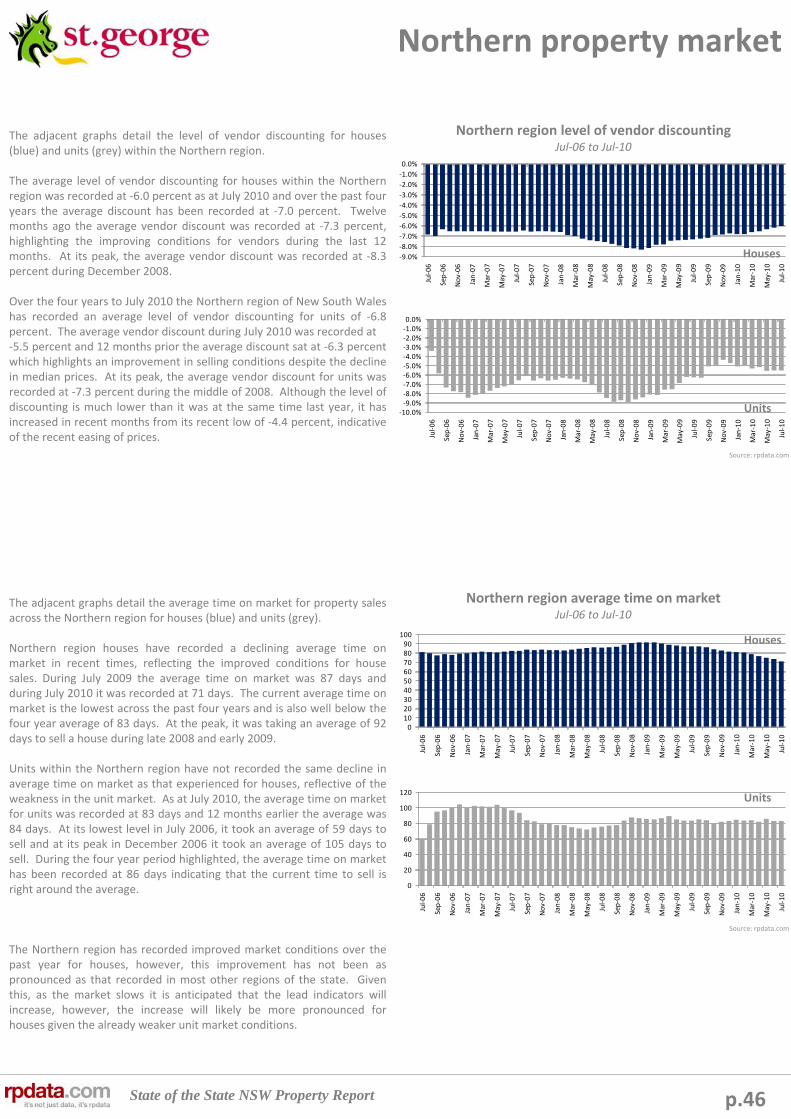

Focus on Northern 44

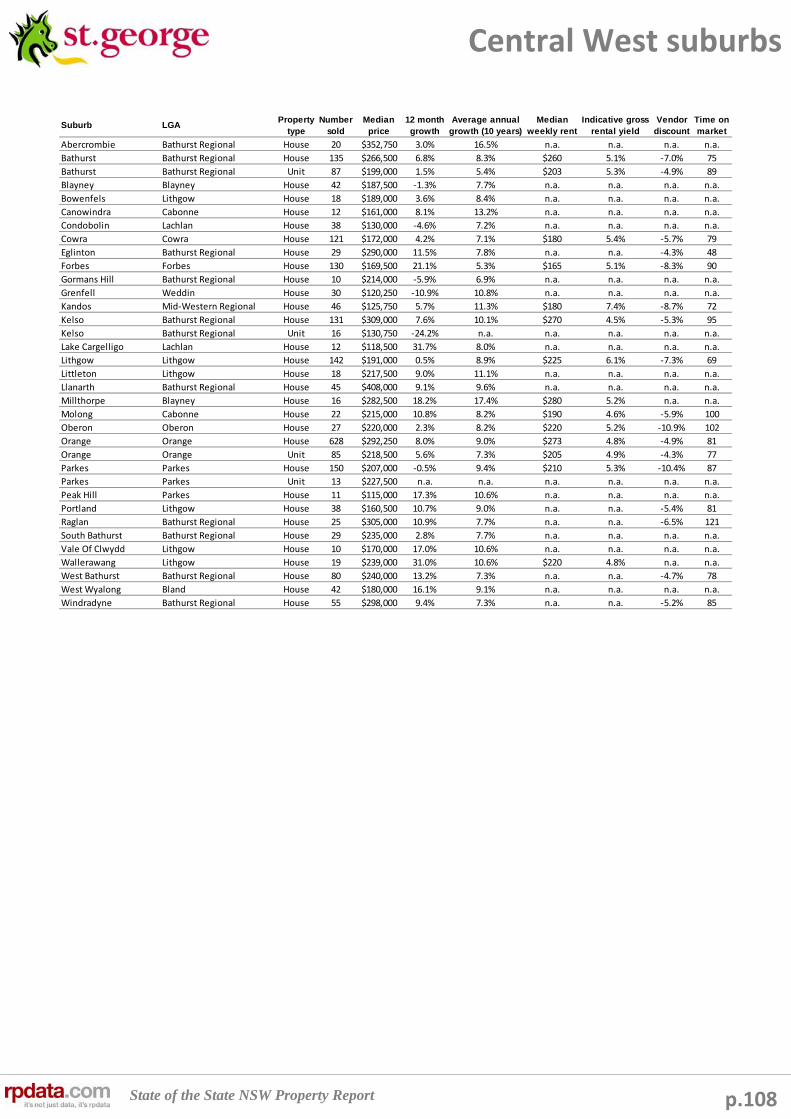

Focus on Central West 50

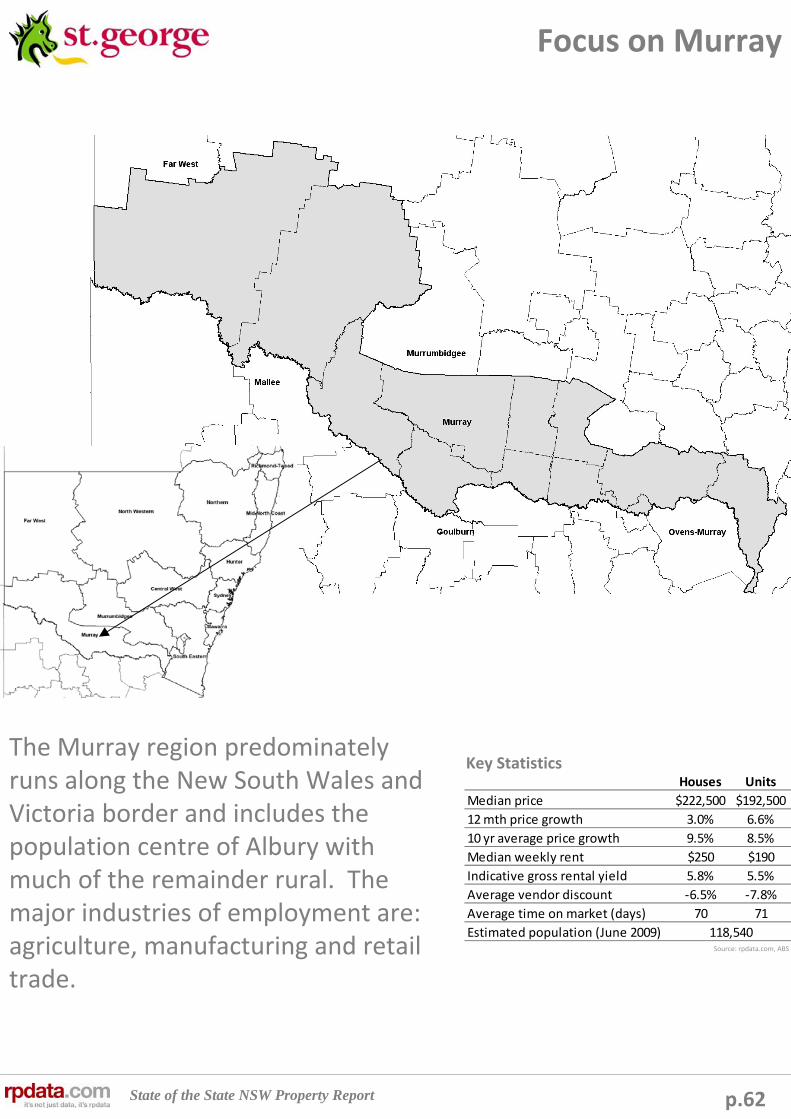

Focus on Murrumbidgee 56

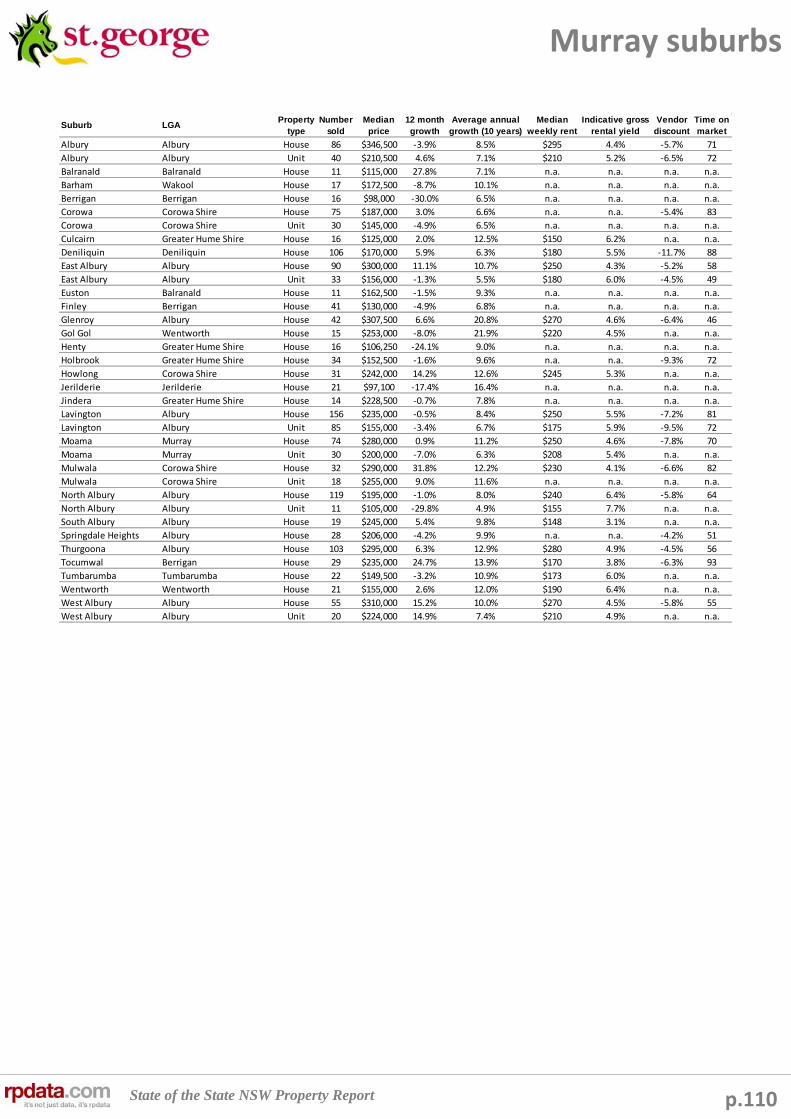

Focus on Murray 62

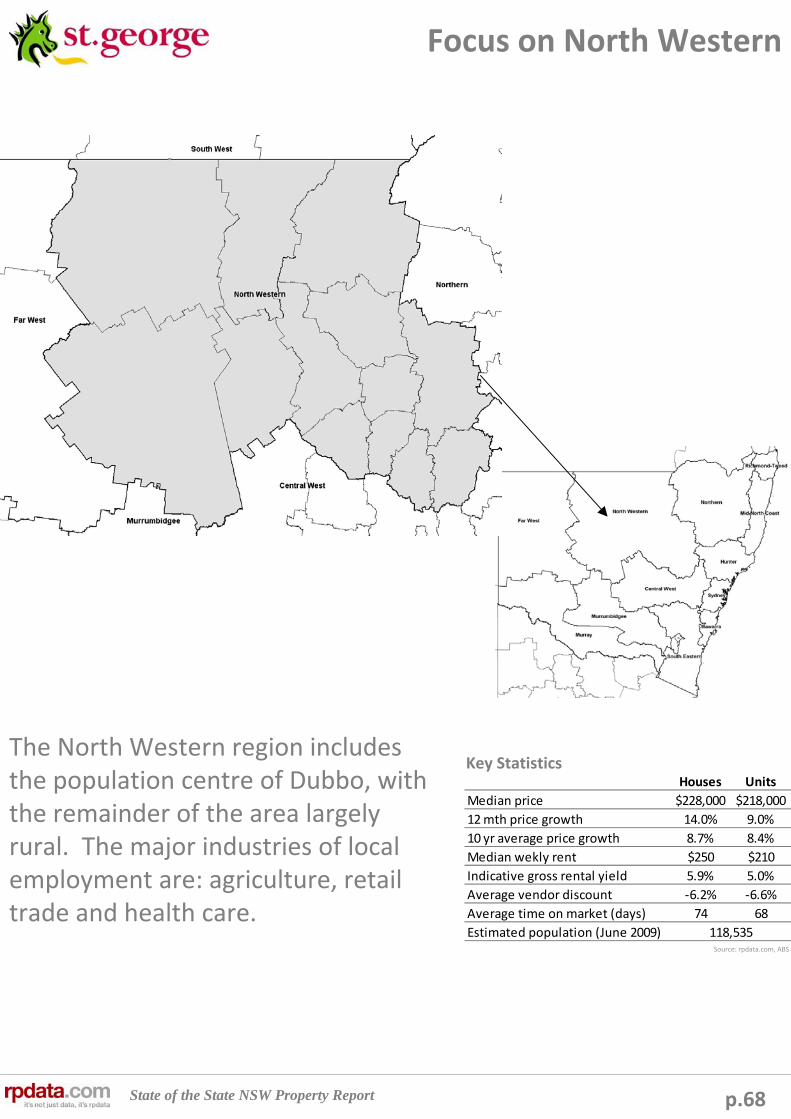

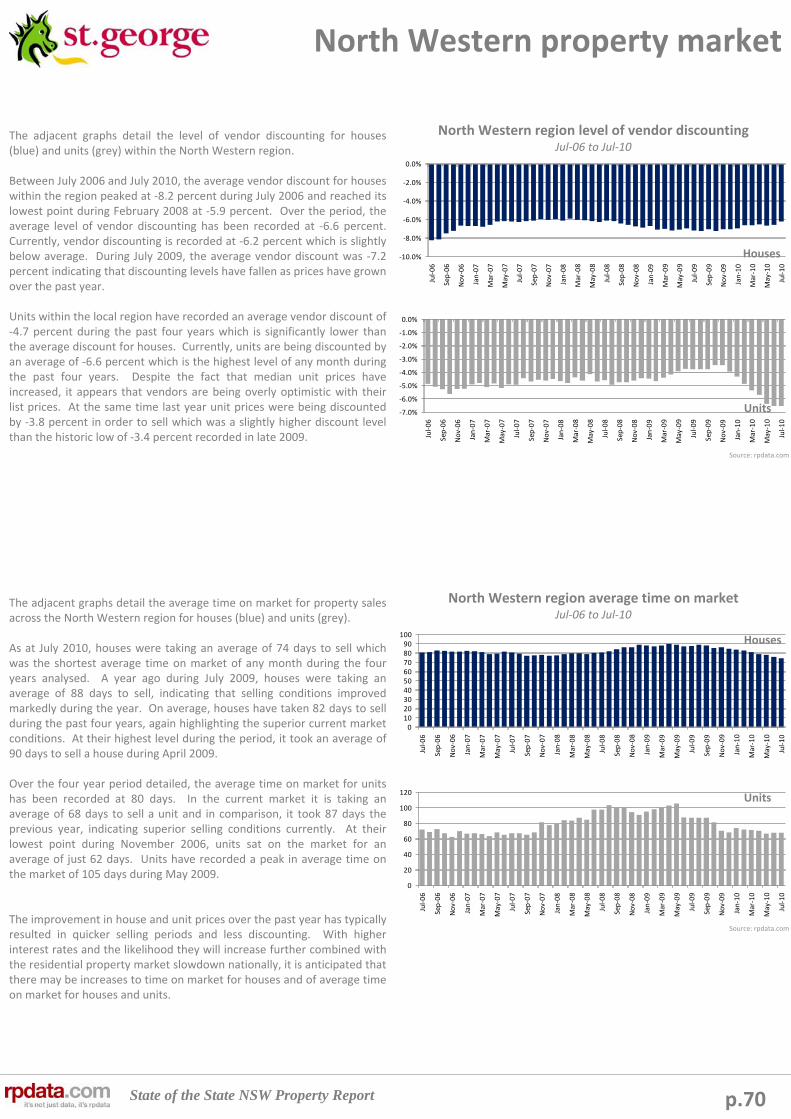

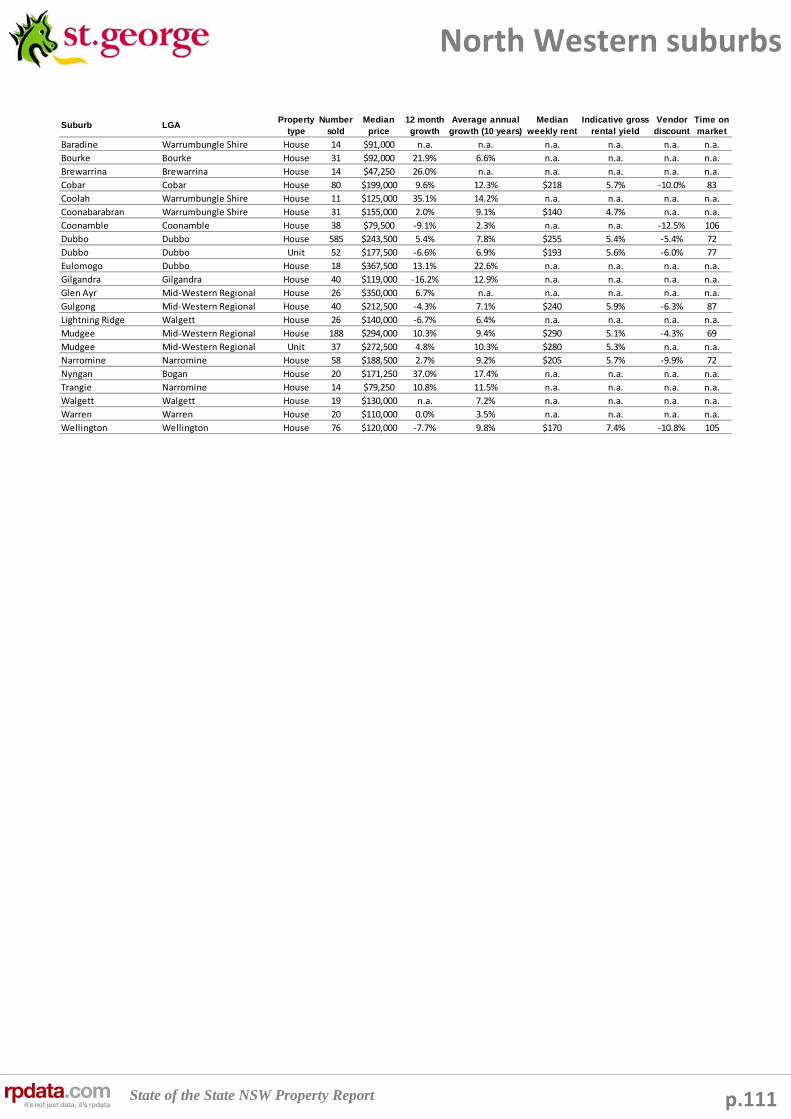

Focus on North Western 68

Focus on Far West 74

Findings / Conclusions 79

Appendix 1 80

Disclaimers 113

State of the State NSW Property Report p.3

Methodology

1. National data is based on the RP Data‐Rismark Home Value Index. Movements in property values, sales volumes, vendor discounting and time on market are calculated on a month‐by month basis. The national results are calculated across the combined capital cities of the country and are weighted based on the total stock within each of the capital cities.

2. Sydney data is based on the RP Data‐Rismark Home Value Index. Movements in property values, sales volumes, vendor discounting and time on market are calculated on a month‐by month basis.

3. All Statistical Division (SD) median prices and sales volumes are calculated on a three month rolling basis. Other calculations such as; time on market, vendor discounting, median weekly advertised rent and indicative gross rental yield are calculated on a rolling 12 month basis.

4. All Local Government Area (LGA) and suburb based data is calculated using a rolling 12 month calculation.

5. Where there are less than 10 results for any statistic during the calculation period, the statistic is deemed to be unreliable and is therefore not reported.

State of the State NSW Property Report

Source: rpdata.com, RP Data–Rismark Stratified Hedonic Home Value Index

p.4

National property market

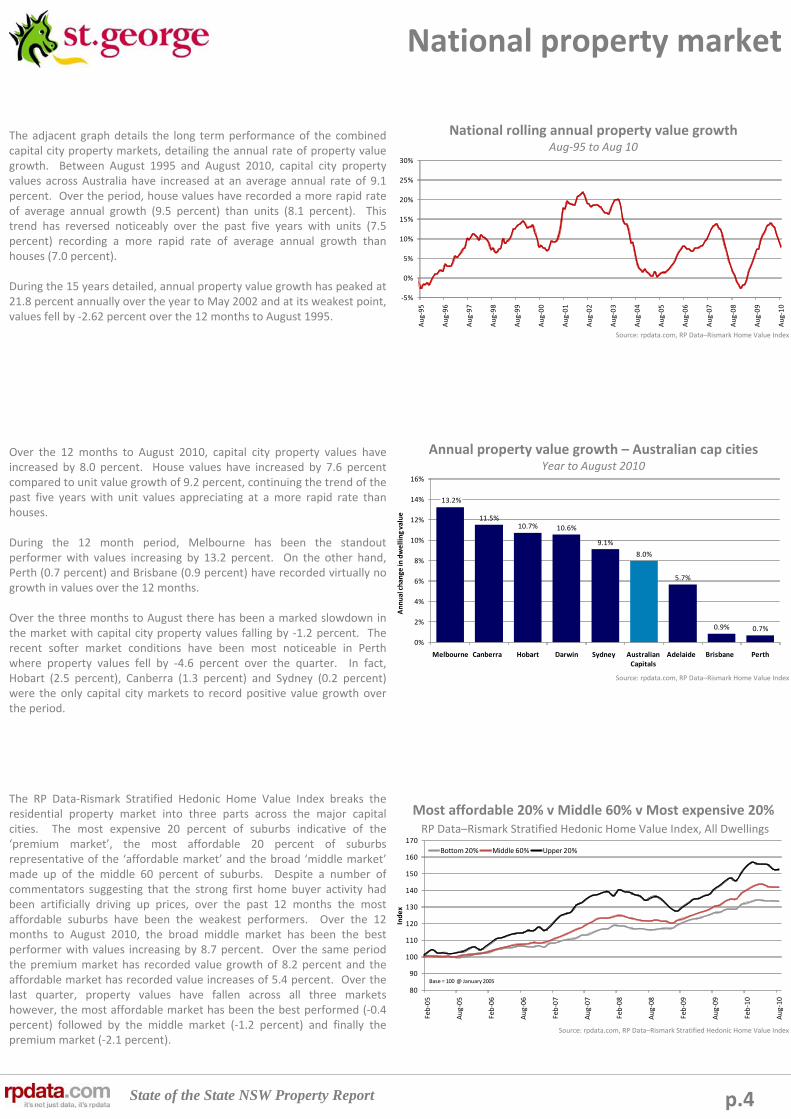

The adjacent graph details the long term performance of the combined capital city property markets, detailing the annual rate of property value growth. Between August 1995 and August 2010, capital city property values across Australia have increased at an average annual rate of 9.1 percent. Over the period, house values have recorded a more rapid rate of average annual growth (9.5 percent) than units (8.1 percent). This trend has reversed noticeably over the past five years with units (7.5 percent) recording a more rapid rate of average annual growth than houses (7.0 percent).

During the 15 years detailed, annual property value growth has peaked at 21.8 percent annually over the year to May 2002 and at its weakest point, values fell by ‐2.62 percent over the 12 months to August 1995.

Over the 12 months to August 2010, capital city property values have increased by 8.0 percent. House values have increased by 7.6 percent compared to unit value growth of 9.2 percent, continuing the trend of the past five years with unit values appreciating at a more rapid rate than houses.

During the 12 month period, Melbourne has been the standout performer with values increasing by 13.2 percent. On the other hand, Perth (0.7 percent) and Brisbane (0.9 percent) have recorded virtually no growth in values over the 12 months.

Over the three months to August there has been a marked slowdown in the market with capital city property values falling by ‐1.2 percent. The recent softer market conditions have been most noticeable in Perth where property values fell by ‐4.6 percent over the quarter. In fact, Hobart (2.5 percent), Canberra (1.3 percent) and Sydney (0.2 percent) were the only capital city markets to record positive value growth over the period.

The RP Data‐Rismark Stratified Hedonic Home Value Index breaks the residential property market into three parts across the major capital cities. The most expensive 20 percent of suburbs indicative of the ‘premium market’, the most affordable 20 percent of suburbs representative of the ‘affordable market’ and the broad ‘middle market’made up of the middle 60 percent of suburbs. Despite a number of commentators suggesting that the strong first home buyer activity had been artificially driving up prices, over the past 12 months the most affordable suburbs have been the weakest performers. Over the 12 months to August 2010, the broad middle market has been the bestperformer with values increasing by 8.7 percent. Over the same period the premium market has recorded value growth of 8.2 percent and the affordable market has recorded value increases of 5.4 percent. Over the last quarter, property values have fallen across all three markets however, the most affordable market has been the best performed (‐0.4 percent) followed by the middle market (‐1.2 percent) and finally the premium market (‐2.1 percent).

‐5%

0%

5%

10%

15%

20%

25%

30%

Aug‐95

Aug‐96

Aug‐97

Aug‐98

Aug‐99

Aug‐00

Aug‐01

Aug‐02

Aug‐03

Aug‐04

Aug‐05

Aug‐06

Aug‐07

Aug‐08

Aug‐09

Aug‐10

National rolling annual property value growthAug‐95 to Aug 10

13.2%

11.5%10.7% 10.6%

9.1%

8.0%

5.7%

0.9% 0.7%

0%

2%

4%

6%

8%

10%

12%

14%

16%

Melbourne Canberra Hobart Darwin Sydney Australian Capitals

Adelaide Brisbane Perth

Annual change

in dwelling value

Annual property value growth – Australian cap citiesYear to August 2010

80

90

100

110

120

130

140

150

160

170

Feb‐05

Aug‐05

Feb‐06

Aug‐06

Feb‐07

Aug‐07

Feb‐08

Aug‐08

Feb‐09

Aug‐09

Feb‐10

Aug‐10

Index

Bottom 20% Middle 60% Upper 20%

Base = 100 @ January 2005

Most affordable 20% v Middle 60% v Most expensive 20%RP Data–Rismark Stratified Hedonic Home Value Index, All Dwellings

Source: rpdata.com, RP Data–Rismark Home Value Index

Source: rpdata.com, RP Data–Rismark Home Value Index

State of the State NSW Property Report

0.0% 10.0% 20.0% 30.0% 40.0% 50.0%

Less than $300,000

$300,000 to $500,000

$500,000 to $700,000

$700,000 to $1m

Greater than $1mQ2 2010Q4 2008

‐10%

‐5%

0%

5%

10%

15%

20%

25%

30%

Aug‐95

Aug‐96

Aug‐97

Aug‐98

Aug‐99

Aug‐00

Aug‐01

Aug‐02

Aug‐03

Aug‐04

Aug‐05

Aug‐06

Aug‐07

Aug‐08

Aug‐09

Aug‐10

Houses Units

0

10,000

20,000

30,000

40,000

50,000

60,000

$0

$100,000

$200,000

$300,000

$400,000

$500,000

$600,000

Aug‐00

Feb‐01

Aug‐01

Feb‐02

Aug‐02

Feb‐03

Aug‐03

Feb‐04

Aug‐04

Feb‐05

Aug‐05

Feb‐06

Aug‐06

Feb‐07

Aug‐07

Feb‐08

Aug‐08

Feb‐09

Aug‐09

Feb‐10

Aug‐10

Volume of sales

RP Data‐Rismark Hedonic Index Rebased at Median Value

Month

Total sales volumes Houses Units

Note: The most recent five months worthof sales volumes are modelled based on historic levels of revision

p.5

National property market

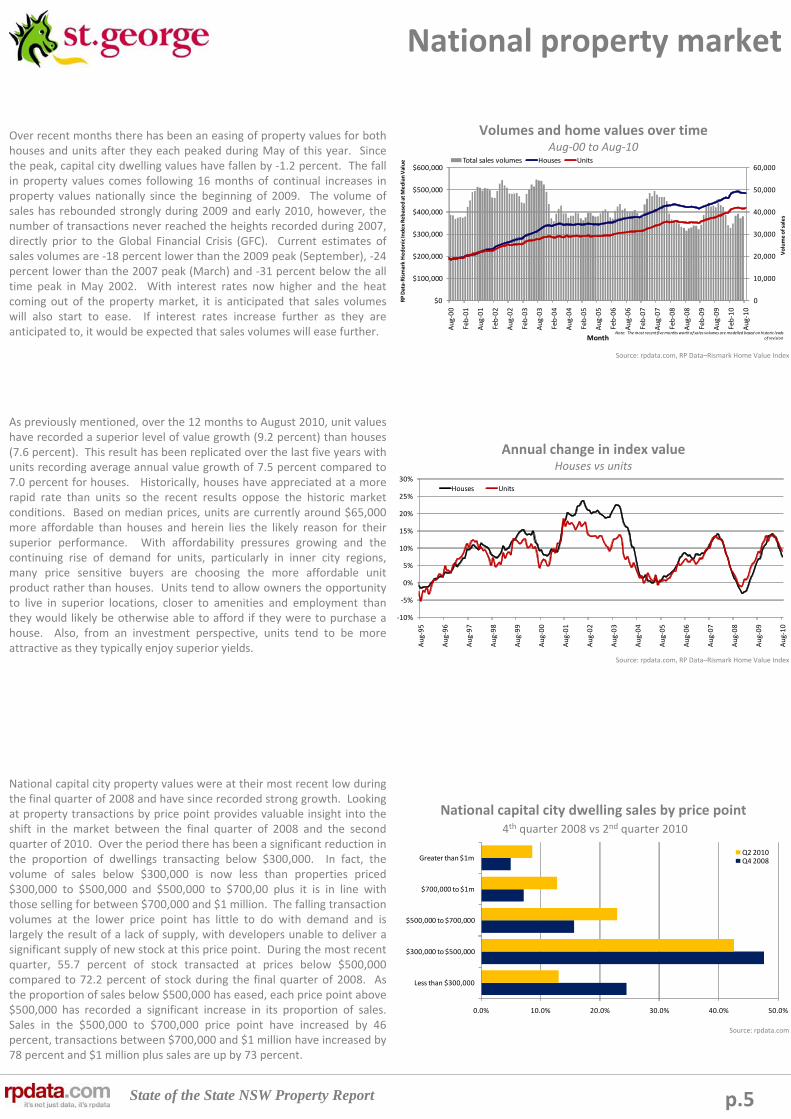

Over recent months there has been an easing of property values for both houses and units after they each peaked during May of this year. Since the peak, capital city dwelling values have fallen by ‐1.2 percent. The fall in property values comes following 16 months of continual increases in property values nationally since the beginning of 2009. The volume of sales has rebounded strongly during 2009 and early 2010, however, the number of transactions never reached the heights recorded during 2007, directly prior to the Global Financial Crisis (GFC). Current estimates of sales volumes are ‐18 percent lower than the 2009 peak (September), ‐24 percent lower than the 2007 peak (March) and ‐31 percent below the all time peak in May 2002. With interest rates now higher and the heat coming out of the property market, it is anticipated that sales volumes will also start to ease. If interest rates increase further as they are anticipated to, it would be expected that sales volumes will ease further.

As previously mentioned, over the 12 months to August 2010, unit values have recorded a superior level of value growth (9.2 percent) than houses (7.6 percent). This result has been replicated over the last five years with units recording average annual value growth of 7.5 percent compared to 7.0 percent for houses. Historically, houses have appreciated at a more rapid rate than units so the recent results oppose the historic market conditions. Based on median prices, units are currently around $65,000 more affordable than houses and herein lies the likely reason for their superior performance. With affordability pressures growing and the continuing rise of demand for units, particularly in inner city regions, many price sensitive buyers are choosing the more affordable unit product rather than houses. Units tend to allow owners the opportunity to live in superior locations, closer to amenities and employment than they would likely be otherwise able to afford if they were to purchase a house. Also, from an investment perspective, units tend to be more attractive as they typically enjoy superior yields.

National capital city property values were at their most recent low during the final quarter of 2008 and have since recorded strong growth. Looking at property transactions by price point provides valuable insight into the shift in the market between the final quarter of 2008 and the second quarter of 2010. Over the period there has been a significant reduction in the proportion of dwellings transacting below $300,000. In fact, the volume of sales below $300,000 is now less than properties priced $300,000 to $500,000 and $500,000 to $700,00 plus it is in line with those selling for between $700,000 and $1 million. The falling transaction volumes at the lower price point has little to do with demand and is largely the result of a lack of supply, with developers unable to deliver a significant supply of new stock at this price point. During the most recent quarter, 55.7 percent of stock transacted at prices below $500,000 compared to 72.2 percent of stock during the final quarter of 2008. As the proportion of sales below $500,000 has eased, each price point above $500,000 has recorded a significant increase in its proportion of sales. Sales in the $500,000 to $700,000 price point have increased by 46 percent, transactions between $700,000 and $1 million have increased by 78 percent and $1 million plus sales are up by 73 percent.

Volumes and home values over timeAug‐00 to Aug‐10

Annual change in index valueHouses vs units

National capital city dwelling sales by price point4th quarter 2008 vs 2nd quarter 2010

Source: rpdata.com

Source: rpdata.com, RP Data–Rismark Home Value Index

Source: rpdata.com, RP Data–Rismark Home Value Index

State of the State NSW Property Report

0

10

20

30

40

50

60

70

Aug‐05

Oct‐05

Dec‐05

Feb‐06

Apr‐06

Jun‐06

Aug‐06

Oct‐06

Dec‐06

Feb‐07

Apr‐07

Jun‐07

Aug‐07

Oct‐07

Dec‐07

Feb‐08

Apr‐08

Jun‐08

Aug‐08

Oct‐08

Dec‐08

Feb‐09

Apr‐09

Jun‐09

Aug‐09

Oct‐09

Dec‐09

Feb‐10

Apr‐10

Jun‐10

Aug‐10

‐8.0%

‐7.0%

‐6.0%

‐5.0%

‐4.0%

‐3.0%

‐2.0%

‐1.0%

0.0%

Aug‐05

Oct‐05

Dec‐05

Feb‐06

Apr‐06

Jun‐06

Aug‐06

Oct‐06

Dec‐06

Feb‐07

Apr‐07

Jun‐07

Aug‐07

Oct‐07

Dec‐07

Feb‐08

Apr‐08

Jun‐08

Aug‐08

Oct‐08

Dec‐08

Feb‐09

Apr‐09

Jun‐09

Aug‐09

Oct‐09

Dec‐09

Feb‐10

Apr‐10

Jun‐10

Aug‐10

3.5%

3.7%

3.9%

4.1%

4.3%

4.5%

4.7%

4.9%

5.1%

5.3%

5.5%

$260

$280

$300

$320

$340

$360

$380

$400

$420

$440

Aug‐05

Feb‐06

Aug‐06

Feb‐07

Aug‐07

Feb‐08

Aug‐08

Feb‐09

Aug‐09

Feb‐10

Aug‐10

Avg gross rental yield

Average rental rate ‐dwellings

Avg rental rate ‐ all dwellings

Avg gross yield ‐ Houses

Avg gross yield ‐ Units

p.6

National property market

Between August 2005 and December 2008, capital city median weekly rents have increased by $114/week. Since December 2008, just asproperty values once again began to increase, rental growth in the market has been virtually non existent. An extremely active first time buyer market thanks to Government incentives coupled with the lowest interest rates in almost 50 years, saw the first time buyer market record its greatest level of activity ever during 2009. As a result, upward pressure on rental rates eased and they fell or remained flat in most areas. Since September 2009 the First Home Owners Grant Boost has been rolled back and completely removed and official interest rates have been increased by 150 basis points, as a result the first home buyer market has slowed markedly. This slowdown is resulting in increasing levels of demand for rental properties and with the scepter of higher interest rates persisting, it will be even more difficult for those in the rental market to enter into home ownership. Given these prevailing market conditions it is expected that rental rates will increase over the coming 12 months.

The level of vendor discount measures the average difference between the price at which a property is initially listed and the ultimate price it sells for. Across the combined capital cities, the average vendor discount for houses is recorded at ‐5.6 percent currently and has been trending higher in recent months. The level of discounting for units has also been trending higher of late and is recorded at ‐5.5 percent. During the five years detailed, vendor discounting has been recorded at an average of ‐6.0 percent for houses and ‐5.6 percent for units. Discounting for houses has been as high as ‐7.1 percent and as low as ‐4.8 percent. For units, discounting levels peaked at ‐6.8 percent and have been as low as ‐4.1 percent. The recent increase in vendor discounting is in keeping with the slowdown in the residential property market. Typically, as the rate of value growth in the market slows, vendors take some time to adjust and vendor discounting will increase as a result. In comparison to the same time last year (when the property market was powering ahead) vendor discounting was recorded at ‐5.4 percent for houses and units. In the coming months as the market continues to slow, the level of vendor discounting may increase further.

The level of time on market measures the average period of time from when a property is first advertised for until a contract (which it ultimately sells for) is signed for that property. The figure provides a good benchmark and for potential sellers and purchasers if a property has been on the market significantly longer than these benchmarks, it may indicate that it is not appropriately priced. The average time on market is currently recorded at 45 days for houses and 38 days for units. During the five years detailed, the average time on market has been recorded at an average of 46 days for houses and 42 days for units. Over the period it has taken as much as an average of 59 days to sell a house and 53 days to sell a unit. Meanwhile, houses have sold in as short a timeframe as 39 days and 35 days for units. As with the vendor discounting figure, as the rate of property value growth in the market slows, time on market also tends to increase. Over the coming months we may also see the average time on market increase further as conditions transition. In comparison to the same time last year, the average time on market was recorded at 46 days for houses and 42 days for units.

National rental rates and gross yieldsAug‐05 to Aug‐10

Average vendor discount – capital city housesAug‐05 to Aug‐10

Average time on market – capital city housesAug‐05 to Aug‐10

Source: rpdata.com, RP Data–Rismark Home Value Index

Source: rpdata.com, RP Data–Rismark Home Value Index

Source: rpdata.com, RP Data–Rismark Home Value Index

State of the State NSW Property Report

0

5,000

10,000

15,000

20,000

25,000

Aug‐1976

Aug‐1977

Aug‐1978

Aug‐1979

Aug‐1980

Aug‐1981

Aug‐1982

Aug‐1983

Aug‐1984

Aug‐1985

Aug‐1986

Aug‐1987

Aug‐1988

Aug‐1989

Aug‐1990

Aug‐1991

Aug‐1992

Aug‐1993

Aug‐1994

Aug‐1995

Aug‐1996

Aug‐1997

Aug‐1998

Aug‐1999

Aug‐2000

Aug‐2001

Aug‐2002

Aug‐2003

Aug‐2004

Aug‐2005

Aug‐2006

Aug‐2007

Aug‐2008

Aug‐2009

Aug‐2010

Number of approvals

Total owner occupier finance commitments Rolling 6 month average

0

1,000

2,000

3,000

4,000

5,000

6,000

Aug‐1985

Jun‐1986

Apr‐1987

Feb‐1988

Dec‐1988

Oct‐1989

Aug‐1990

Jun‐1991

Apr‐1992

Feb‐1993

Dec‐1993

Oct‐1994

Aug‐1995

Jun‐1996

Apr‐1997

Feb‐1998

Dec‐1998

Oct‐1999

Aug‐2000

Jun‐2001

Apr‐2002

Feb‐2003

Dec‐2003

Oct‐2004

Aug‐2005

Jun‐2006

Apr‐2007

Feb‐2008

Dec‐2008

Oct‐2009

Aug‐2010

Total approvals

Total builing approvals Rolling 6 month average

‐5,000

0

5,000

10,000

15,000

20,000

Mar‐1982

Mar‐1983

Mar‐1984

Mar‐1985

Mar‐1986

Mar‐1987

Mar‐1988

Mar‐1989

Mar‐1990

Mar‐1991

Mar‐1992

Mar‐1993

Mar‐1994

Mar‐1995

Mar‐1996

Mar‐1997

Mar‐1998

Mar‐1999

Mar‐2000

Mar‐2001

Mar‐2002

Mar‐2003

Mar‐2004

Mar‐2005

Mar‐2006

Mar‐2007

Mar‐2008

Mar‐2009

Mar‐2010

Quarterly population growth

Natural Increase Total migration

p.7

Key economic and property data

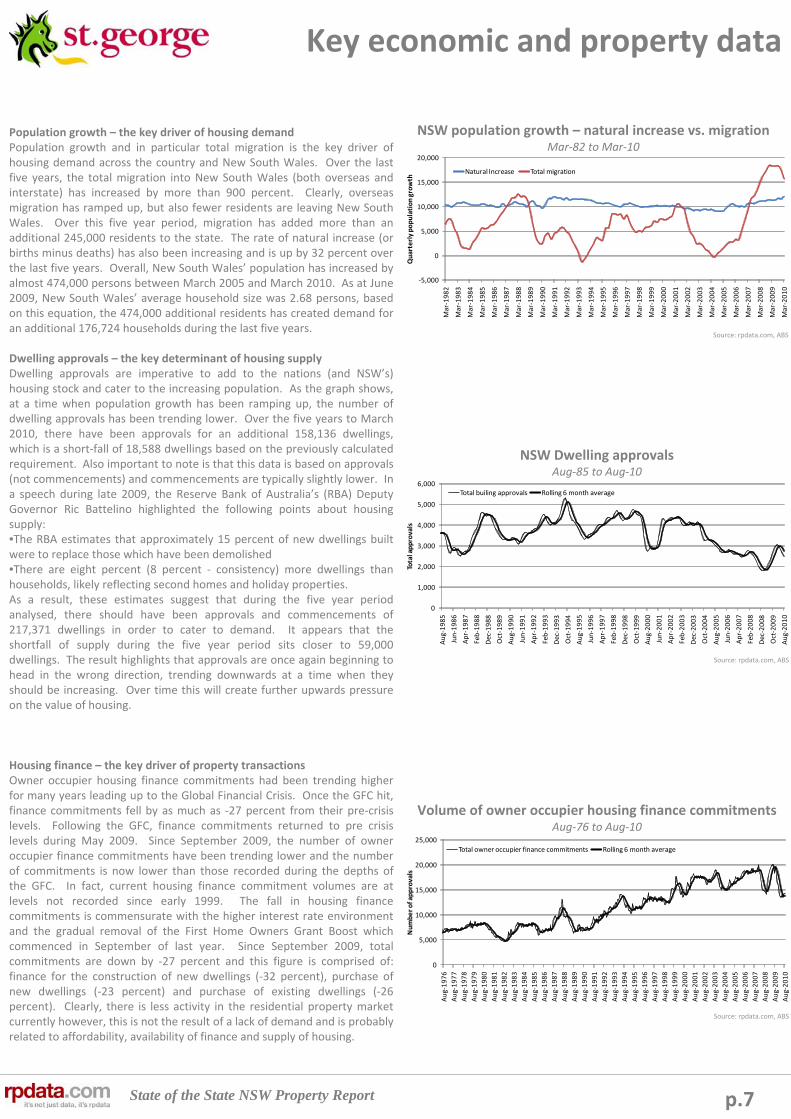

Population growth – the key driver of housing demandPopulation growth and in particular total migration is the key driver of housing demand across the country and New South Wales. Over the last five years, the total migration into New South Wales (both overseas and interstate) has increased by more than 900 percent. Clearly, overseas migration has ramped up, but also fewer residents are leaving New South Wales. Over this five year period, migration has added more than an additional 245,000 residents to the state. The rate of natural increase (or births minus deaths) has also been increasing and is up by 32 percent over the last five years. Overall, New South Wales’ population has increased by almost 474,000 persons between March 2005 and March 2010. As at June 2009, New South Wales’ average household size was 2.68 persons, based on this equation, the 474,000 additional residents has created demand for an additional 176,724 households during the last five years.

Dwelling approvals – the key determinant of housing supplyDwelling approvals are imperative to add to the nations (and NSW’s) housing stock and cater to the increasing population. As the graph shows, at a time when population growth has been ramping up, the number of dwelling approvals has been trending lower. Over the five years to March 2010, there have been approvals for an additional 158,136 dwellings, which is a short‐fall of 18,588 dwellings based on the previously calculated requirement. Also important to note is that this data is based on approvals (not commencements) and commencements are typically slightly lower. In a speech during late 2009, the Reserve Bank of Australia’s (RBA) Deputy Governor Ric Battelino highlighted the following points about housing supply:•The RBA estimates that approximately 15 percent of new dwellings built were to replace those which have been demolished •There are eight percent (8 percent ‐ consistency) more dwellings than households, likely reflecting second homes and holiday properties. As a result, these estimates suggest that during the five year periodanalysed, there should have been approvals and commencements of 217,371 dwellings in order to cater to demand. It appears that the shortfall of supply during the five year period sits closer to 59,000 dwellings. The result highlights that approvals are once again beginning to head in the wrong direction, trending downwards at a time when they should be increasing. Over time this will create further upwards pressure on the value of housing.

Housing finance – the key driver of property transactionsOwner occupier housing finance commitments had been trending higher for many years leading up to the Global Financial Crisis. Once the GFC hit, finance commitments fell by as much as ‐27 percent from their pre‐crisis levels. Following the GFC, finance commitments returned to pre crisis levels during May 2009. Since September 2009, the number of owner occupier finance commitments have been trending lower and the number of commitments is now lower than those recorded during the depths of the GFC. In fact, current housing finance commitment volumes are at levels not recorded since early 1999. The fall in housing finance commitments is commensurate with the higher interest rate environment and the gradual removal of the First Home Owners Grant Boost which commenced in September of last year. Since September 2009, total commitments are down by ‐27 percent and this figure is comprised of: finance for the construction of new dwellings (‐32 percent), purchase of new dwellings (‐23 percent) and purchase of existing dwellings (‐26 percent). Clearly, there is less activity in the residential property market currently however, this is not the result of a lack of demand and is probably related to affordability, availability of finance and supply of housing.

NSW population growth – natural increase vs. migrationMar‐82 to Mar‐10

NSW Dwelling approvalsAug‐85 to Aug‐10

Volume of owner occupier housing finance commitments Aug‐76 to Aug‐10

Source: rpdata.com, ABS

Source: rpdata.com, ABS

Source: rpdata.com, ABS

State of the State NSW Property Report

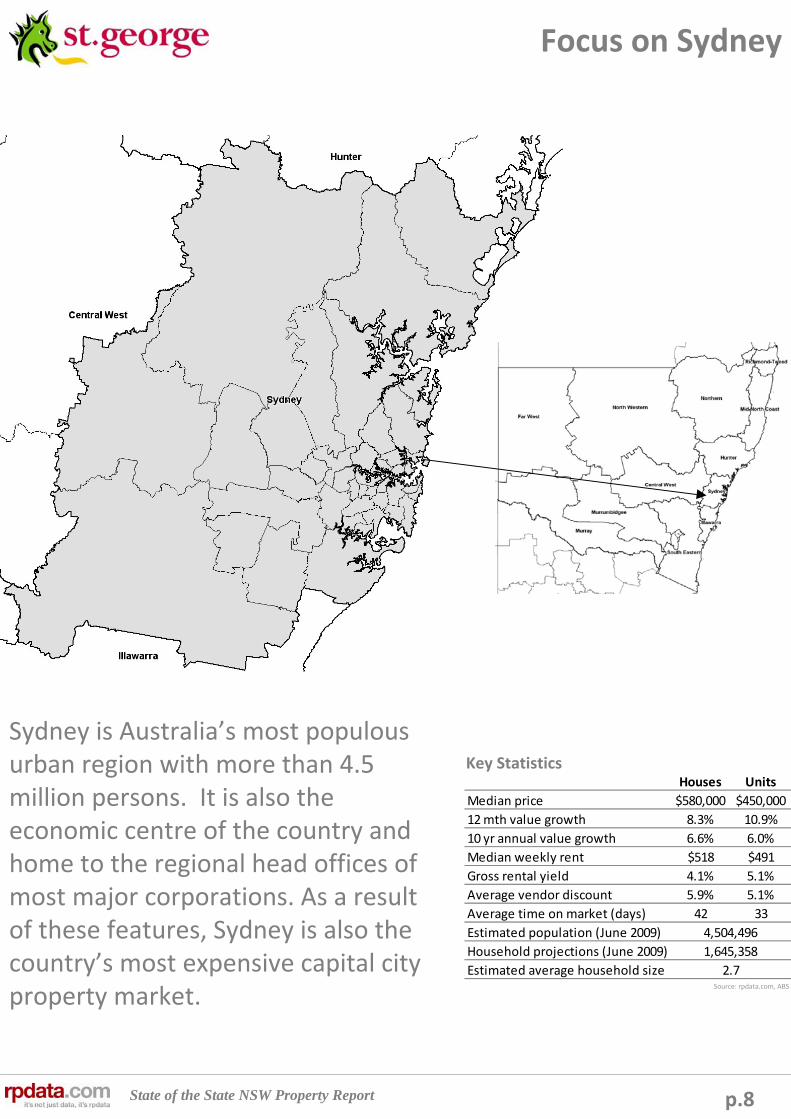

Houses Units

Median price $580,000 $450,000

12 mth value growth 8.3% 10.9%

10 yr annual value growth 6.6% 6.0%

Median weekly rent $518 $491

Gross rental yield 4.1% 5.1%

Average vendor discount 5.9% 5.1%

Average time on market (days) 42 33

Estimated population (June 2009)

Household projections (June 2009)

Estimated average household size

4,504,496

1,645,358

2.7

p.8

Focus on Sydney

Key Statistics

Sydney is Australia’s most populous urban region with more than 4.5 million persons. It is also the economic centre of the country and home to the regional head offices of most major corporations. As a result of these features, Sydney is also the country’s most expensive capital city property market.

Source: rpdata.com, ABS

State of the State NSW Property Report

80

90

100

110

120

130

140

Feb‐05

Aug‐05

Feb‐06

Aug‐06

Feb‐07

Aug‐07

Feb‐08

Aug‐08

Feb‐09

Aug‐09

Feb‐10

Aug‐10

Index

Bottom 20% Middle 60% Upper 20%

Base = 100 @ January 2005

‐10%

‐5%

0%

5%

10%

15%

20%

25%

30%

Aug‐95

Aug‐96

Aug‐97

Aug‐98

Aug‐99

Aug‐00

Aug‐01

Aug‐02

Aug‐03

Aug‐04

Aug‐05

Aug‐06

Aug‐07

Aug‐08

Aug‐09

Aug‐10

p.9

Sydney property market

The report previously detailed that the average annual rate of property value growth between August 1995 and August 2010 was 9.1 percentnationally. Sydney’s property market has underperformed the nation over that length of time, recording average annual value growth of 7.7 percent. It is important to recognise that the Sydney property market is much more mature than most of the other capital city markets. As a result, the level of value growth may not be as impressive as that of other cities where prices have typically moved from a much lower base.

Over the 15 year period highlighted, Sydney dwelling values recorded peak annual growth of 25.5 percent over the twelve months to May 2002. Meanwhile, property values fell by as much as ‐6.3 percent over the 12 months to February 2005.

Over the three months to August 2010, the rate of property value growth has shown a marked slowdown. Property values have increased by just 0.2 percent over the quarter. Putting this result in context, between the beginning of 2009 and August 2010, Sydney dwelling values have increased by a total of 18.4 percent. The result highlights that the upward pressure on property values in the market appears to be easing. This occurrence is not exclusive to Sydney, in fact, over the last quarter Sydney is one of just three capital city markets to have recorded growth in property values. The relatively strong performance of the Sydney market is due to the fact that for five and a half years there was no movement in Sydney property values and it wasn’t until mid 2009 that property values once again eclipsed their record high recorded in February 2004. From this February 2004 peak, property values fell by as much as ‐9.6 percent again highlighting the poor performance of the market between 2004 and 2009. Currently, Sydney property values are 12.5 percent higher than they were during the peak on 2004.

With value growth in all markets including Sydney slowing, it is interesting to look at the performance of individual sectors of the market. Over the 12 months to August 2010, the premium residential property market has been the best performed with values increasing by 11.3 percent. In comparison, values have increased by 10.0 percent in the middle market and by 4.8 percent in affordable suburbs. The results have been quite different over the last three months. During this period, the affordable and middle markets have recorded value growth of 0.3 percent whilst the premium market has recorded a softening in value growth of ‐0.2 percent. The premium market has tended to be a high risk high reward market over the years. For the remainder of 2010, the more affordable markets are likely to be the best performed. With the anticipation of higher interest rates next year, this will likely dampen growth at the more affordable end of the market.

Rolling annual property value growth – Sydney vs NationalAug‐95 to Aug 10

Rolling quarterly change in Sydney dwelling valuesAug‐05 to Aug‐10

‐4.0%

‐2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

Aug‐05

Oct‐05

Dec‐05

Feb‐06

Apr‐06

Jun‐06

Aug‐06

Oct‐06

Dec‐06

Feb‐07

Apr‐07

Jun‐07

Aug‐07

Oct‐07

Dec‐07

Feb‐08

Apr‐08

Jun‐08

Aug‐08

Oct‐08

Dec‐08

Feb‐09

Apr‐09

Jun‐09

Aug‐09

Oct‐09

Dec‐09

Feb‐10

Apr‐10

Jun‐10

Aug‐10

Most affordable 20% v Middle 60% v Most expensive 20%RP Data–Rismark Stratified Hedonic Home Value Index, All Dwellings

Source: rpdata.com, RP Data–Rismark Home Value Index

Source: rpdata.com, RP Data–Rismark Home Value Index

Source: rpdata.com, RP Data–Rismark Stratified Hedonic Home Value Index

State of the State NSW Property Report

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

$0

$100,000

$200,000

$300,000

$400,000

$500,000

$600,000

$700,000

Aug‐00

Feb‐01

Aug‐01

Feb‐02

Aug‐02

Feb‐03

Aug‐03

Feb‐04

Aug‐04

Feb‐05

Aug‐05

Feb‐06

Aug‐06

Feb‐07

Aug‐07

Feb‐08

Aug‐08

Feb‐09

Aug‐09

Feb‐10

Aug‐10

Volume of sales

RP Data‐Rismark Hedonic Index Rebased at Median Value

Month

Total sales volumes Houses Units

Note: The most recent five months worthof sales volumes are modelled based on historic levels of revision

0.0% 10.0% 20.0% 30.0% 40.0% 50.0%

Less than $300,000

$300,000 to $500,000

$500,000 to $700,000

$700,000 to $1m

Greater than $1mQ4 2008Q2 2010

‐10%

‐5%

0%

5%

10%

15%

20%

25%

30%

Aug‐95

Aug‐96

Aug‐97

Aug‐98

Aug‐99

Aug‐00

Aug‐01

Aug‐02

Aug‐03

Aug‐04

Aug‐05

Aug‐06

Aug‐07

Aug‐08

Aug‐09

Aug‐10

Houses Units

p.10

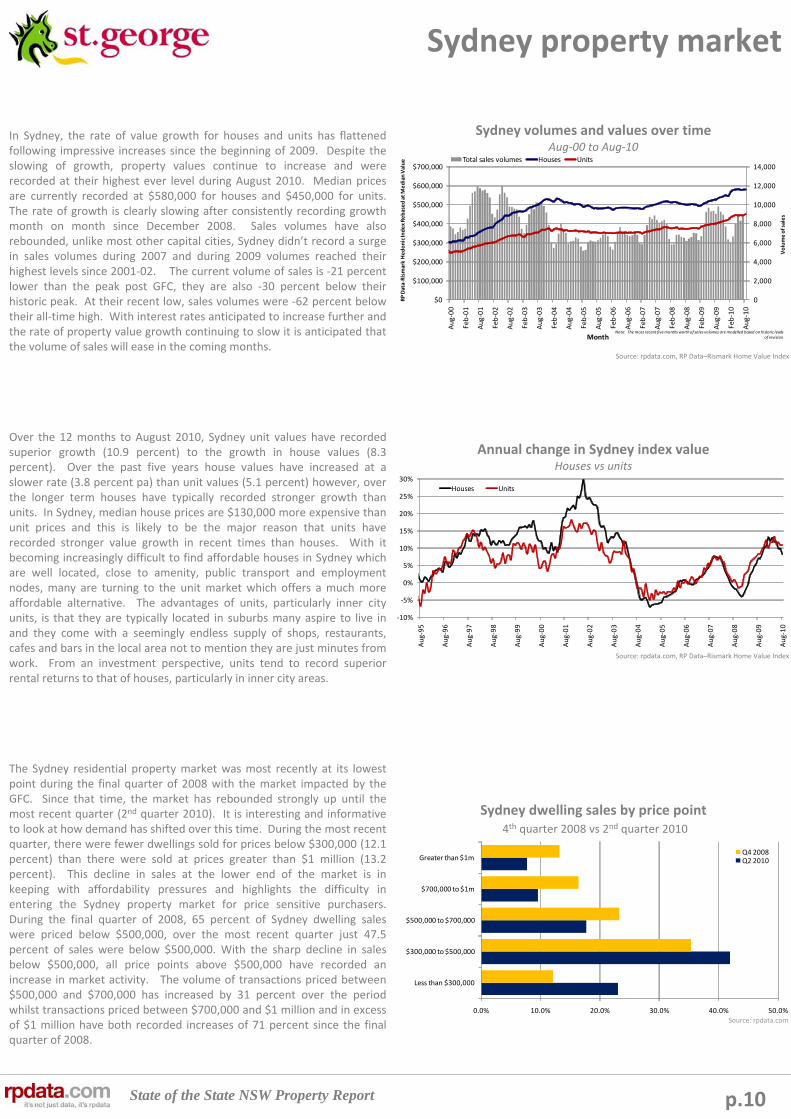

Sydney property market

In Sydney, the rate of value growth for houses and units has flattened following impressive increases since the beginning of 2009. Despite the slowing of growth, property values continue to increase and wererecorded at their highest ever level during August 2010. Median prices are currently recorded at $580,000 for houses and $450,000 for units. The rate of growth is clearly slowing after consistently recording growth month on month since December 2008. Sales volumes have also rebounded, unlike most other capital cities, Sydney didn’t record a surge in sales volumes during 2007 and during 2009 volumes reached their highest levels since 2001‐02. The current volume of sales is ‐21 percent lower than the peak post GFC, they are also ‐30 percent below their historic peak. At their recent low, sales volumes were ‐62 percent below their all‐time high. With interest rates anticipated to increase further and the rate of property value growth continuing to slow it is anticipated that the volume of sales will ease in the coming months.

Over the 12 months to August 2010, Sydney unit values have recorded superior growth (10.9 percent) to the growth in house values (8.3 percent). Over the past five years house values have increased at a slower rate (3.8 percent pa) than unit values (5.1 percent) however, over the longer term houses have typically recorded stronger growth than units. In Sydney, median house prices are $130,000 more expensive than unit prices and this is likely to be the major reason that units have recorded stronger value growth in recent times than houses. With it becoming increasingly difficult to find affordable houses in Sydney which are well located, close to amenity, public transport and employment nodes, many are turning to the unit market which offers a much more affordable alternative. The advantages of units, particularly inner city units, is that they are typically located in suburbs many aspire to live in and they come with a seemingly endless supply of shops, restaurants, cafes and bars in the local area not to mention they are just minutes from work. From an investment perspective, units tend to record superior rental returns to that of houses, particularly in inner city areas.

The Sydney residential property market was most recently at its lowest point during the final quarter of 2008 with the market impacted by the GFC. Since that time, the market has rebounded strongly up until the most recent quarter (2nd quarter 2010). It is interesting and informative to look at how demand has shifted over this time. During the most recent quarter, there were fewer dwellings sold for prices below $300,000 (12.1 percent) than there were sold at prices greater than $1 million (13.2 percent). This decline in sales at the lower end of the market is in keeping with affordability pressures and highlights the difficulty in entering the Sydney property market for price sensitive purchasers. During the final quarter of 2008, 65 percent of Sydney dwelling sales were priced below $500,000, over the most recent quarter just 47.5 percent of sales were below $500,000. With the sharp decline in sales below $500,000, all price points above $500,000 have recorded anincrease in market activity. The volume of transactions priced between $500,000 and $700,000 has increased by 31 percent over the period whilst transactions priced between $700,000 and $1 million and in excess of $1 million have both recorded increases of 71 percent since the final quarter of 2008.

Sydney volumes and values over timeAug‐00 to Aug‐10

Annual change in Sydney index valueHouses vs units

Sydney dwelling sales by price point4th quarter 2008 vs 2nd quarter 2010

Source: rpdata.com

Source: rpdata.com, RP Data–Rismark Home Value Index

Source: rpdata.com, RP Data–Rismark Home Value Index

State of the State NSW Property Report

0

10

20

30

40

50

60

70

Aug‐05

Oct‐05

Dec‐05

Feb‐06

Apr‐06

Jun‐06

Aug‐06

Oct‐06

Dec‐06

Feb‐07

Apr‐07

Jun‐07

Aug‐07

Oct‐07

Dec‐07

Feb‐08

Apr‐08

Jun‐08

Aug‐08

Oct‐08

Dec‐08

Feb‐09

Apr‐09

Jun‐09

Aug‐09

Oct‐09

Dec‐09

Feb‐10

Apr‐10

Jun‐10

Aug‐10

‐10.0%

‐9.0%

‐8.0%

‐7.0%

‐6.0%

‐5.0%

‐4.0%

‐3.0%

‐2.0%

‐1.0%

0.0%

Aug‐05

Oct‐05

Dec‐05

Feb‐06

Apr‐06

Jun‐06

Aug‐06

Oct‐06

Dec‐06

Feb‐07

Apr‐07

Jun‐07

Aug‐07

Oct‐07

Dec‐07

Feb‐08

Apr‐08

Jun‐08

Aug‐08

Oct‐08

Dec‐08

Feb‐09

Apr‐09

Jun‐09

Aug‐09

Oct‐09

Dec‐09

Feb‐10

Apr‐10

Jun‐10

Aug‐10

3.7%

4.2%

4.7%

5.2%

5.7%

6.2%

$350

$370

$390

$410

$430

$450

$470

$490

$510

$530

Aug‐05

Feb‐06

Aug‐06

Feb‐07

Aug‐07

Feb‐08

Aug‐08

Feb‐09

Aug‐09

Feb‐10

Aug‐10

Avg gross rental yield

Average rental rate ‐dwellings

Avg rental rate ‐ all dwellings

Avg gross yield ‐ Houses

Avg gross yield ‐ Units

p.11

Sydney property market

Between August 2005 and February 2009, Sydney’s median weekly rents increased by $143. Since rents reached $520/week in February 2010 they have not risen any higher and there have been some falls in rental rates. Similar to the national market, low interest rates, an active first home buyer market and property value falls during 2008 made property purchase quite attractive through 2009 with the greatest number of first home buyers in history. As a result, the upward pressure on rental rates eased. Now that official interest rates have increased by 150 basis points and are anticipated to increase further and the additional stimulus for first home buyers has been removed, the expectation is that there will be increased pressure on rental markets with fewer renters able to enter into home ownership. Given this, we expect to see increases in rental rates over the coming months which will be welcome news for landlords but not so for those in the rental market. With rental growth returning and property value growth flat, we expect to also see rental yields improve over the coming months after recording steep declines asproperty values have increased at a faster pace than rental markets in recent times.

Throughout Greater Sydney, the level of vendor discounting remains at levels well below the historic norm between 2005 and 2008, a time when the Sydney property market was well and truly underperforming in terms of value growth. Over recent months there has been a slight increase in the level of vendor discounting for houses, however, unit discounts have shown minimal change. Currently, the average level of vendor discounting for houses is recorded at ‐5.9 percent and units are at a much lower ‐5.1 percent. At the same time last year, the level of vendor discounting was recorded at ‐5.7 percent for houses and ‐4.9 percent for units. Over the five years analysed, vendor discounting has been recorded at an average of ‐6.8 percent for houses and ‐6.0 percent for units. With the market’s rate of property value growth slowing, albeit at not as significant a level in Sydney, the market will likely record some further increases to the level of vendor discounting, especially if interest rates are increased further.

Across Sydney, like vendor discounting levels, the average time on market is well below those levels typically recorded over the period between 2005 and 2008, indicating just how poorly the market was performing during this time. Also like vendor discounting, there has been a slight increase in the average time on market in recent month (for houses and units this time). The current average time on market for houses is recorded at 42 days for houses and 33 days for units. At the same time last year when the market was arguably stronger, the average time on market for houses was 45 days and for units it was 39 days. Over the period highlighted, time on market has recorded an average of 51 days for houses and 46 days for units. As with vendor discounting, with the heat coming out of the residential property market and expectations of higher interest rates, in coming months we anticipate that the average time on market will increase further.

Sydney rental rates and gross yieldsAug‐05 to Aug‐10

Average vendor discount – Sydney housesAug‐05 to Aug‐10

Average time on market – Sydney housesAug‐05 to Aug‐10

Source: rpdata.com, RP Data–Rismark Home Value Index

Source: rpdata.com, RP Data–Rismark Home Value Index

Source: rpdata.com, RP Data–Rismark Home Value Index

State of the State NSW Property Report

Suburb Median price Median rent Rental yield

North St Marys $273,000 $350 6.7%

Warragamba $249,000 $318 6.6%

Willmot $220,000 $280 6.6%

Miller $275,000 $350 6.6%

Chain Valley Bay $269,000 $340 6.6%

Lethbridge Park $225,000 $283 6.5%

Tregear $225,000 $280 6.5%

Bidwill $241,250 $300 6.5%

Tuggerawong $286,000 $355 6.5%

Whalan $242,000 $300 6.4%

Suburb Number sold Median price 12 month growth

Willmot 35 $220,000 9.5%

Tregear 46 $225,000 7.1%

Lethbridge Park 55 $225,000 4.7%

Emerton 23 $234,000 7.1%

Blackett 38 $239,500 8.9%

Bidwill 26 $241,250 0.5%

Whalan 68 $242,000 10.0%

Warragamba 38 $249,000 ‐0.4%

San Remo 87 $260,000 11.8%

Gorokan 168 $260,000 6.1%

Suburb Number sold Median price 12 month growth

Woolwich 12 $4,230,000 0.0%

Bellevue Hill 84 $3,910,000 25.2%

Vaucluse 97 $3,800,000 16.3%

Dover Heights 42 $2,650,000 9.4%

Tamarama 12 $2,575,000 17.0%

Palm Beach 50 $2,550,000 8.5%

Rose Bay 65 $2,400,000 49.5%

Clontarf 30 $2,312,500 ‐5.6%

Double Bay 32 $2,300,000 ‐12.9%

Kangaroo Point 12 $2,297,500 0.0%

Suburb Number sold Median price 12 month growth

Rose Bay 65 $2,400,000 49.5%

Kensington 52 $1,715,000 42.9%

Malabar 45 $1,290,000 36.5%

Bondi Junction 85 $1,226,000 36.2%

South Coogee 42 $1,695,000 35.6%

Darlington 41 $735,000 35.6%

Balmain 181 $1,180,000 34.4%

Queens Park 52 $1,750,000 33.6%

Woolloomooloo 13 $814,000 33.4%

Wollstonecraft 13 $1,800,000 33.3%

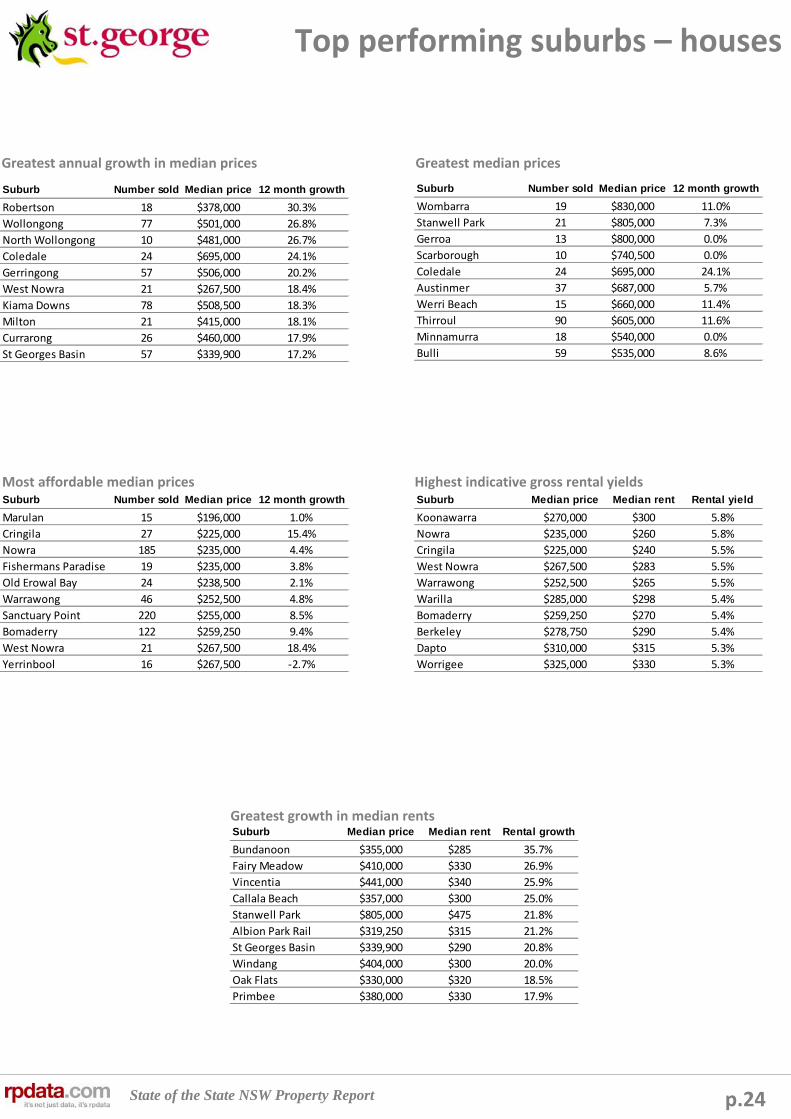

p.12

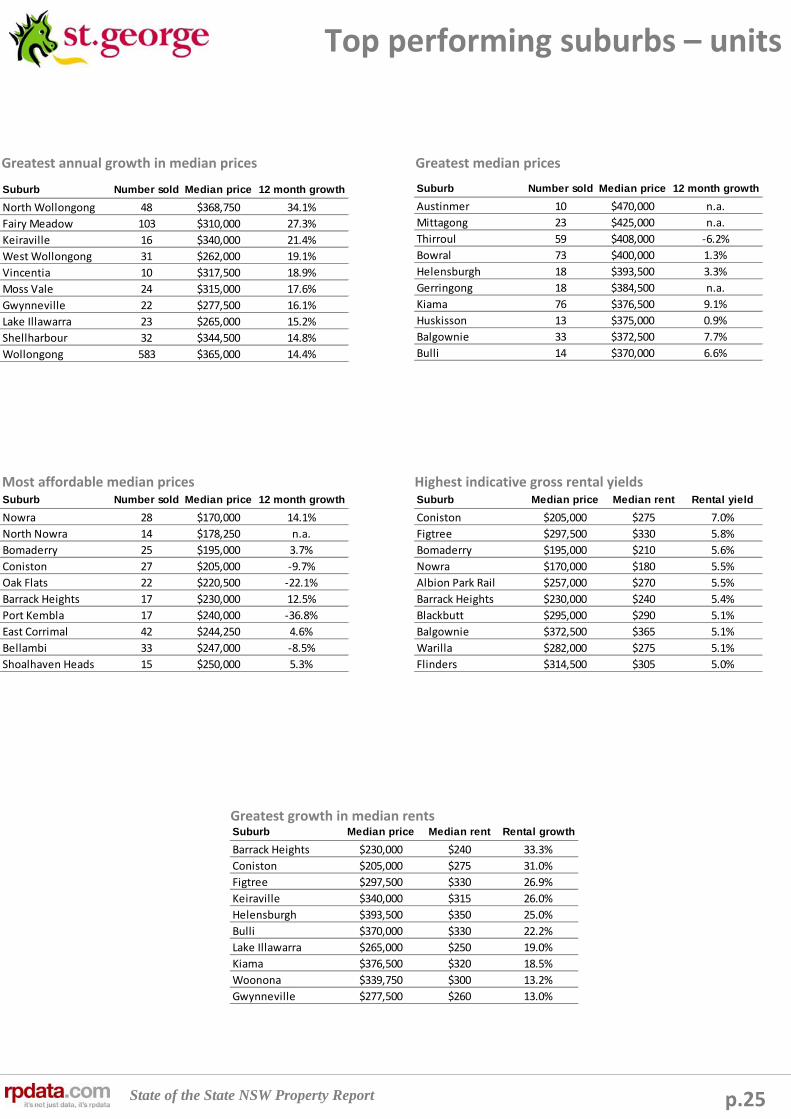

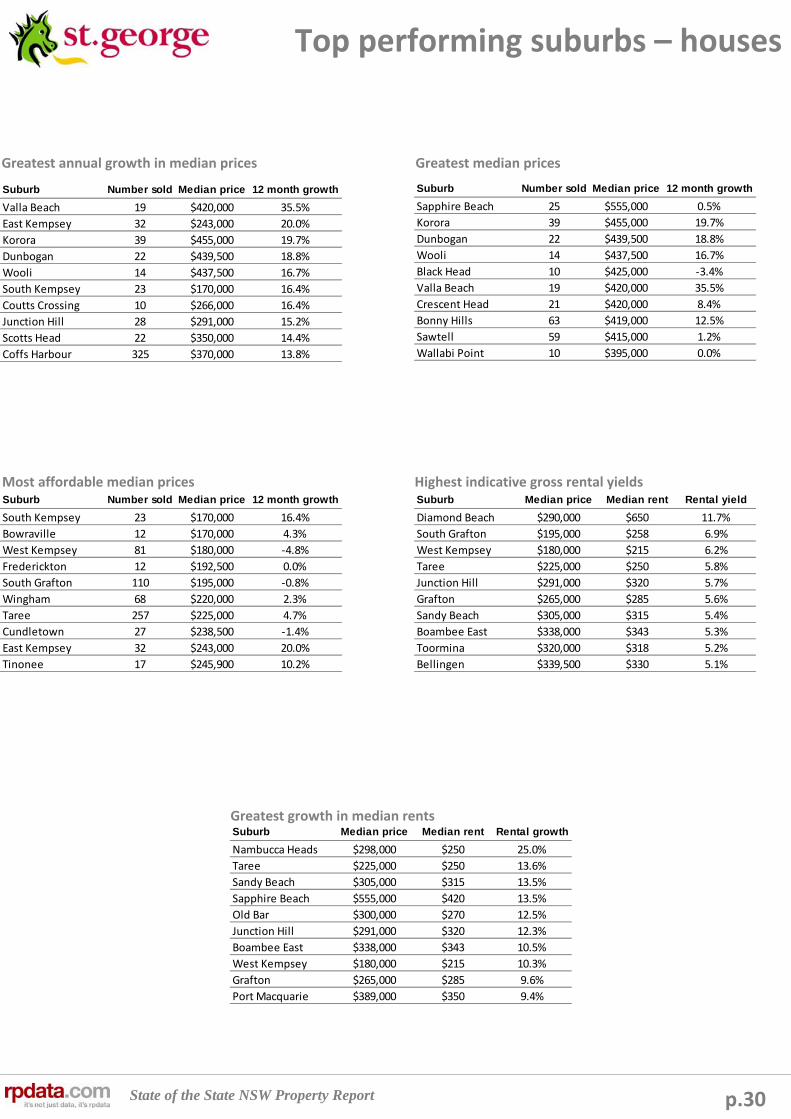

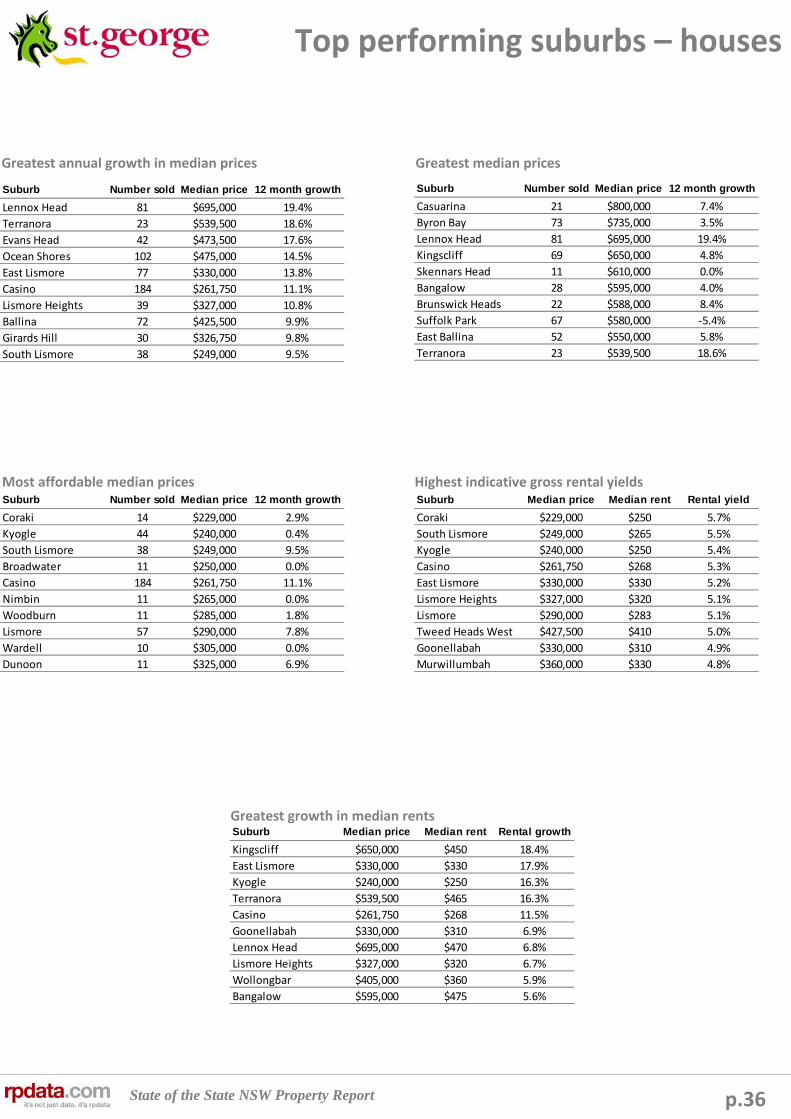

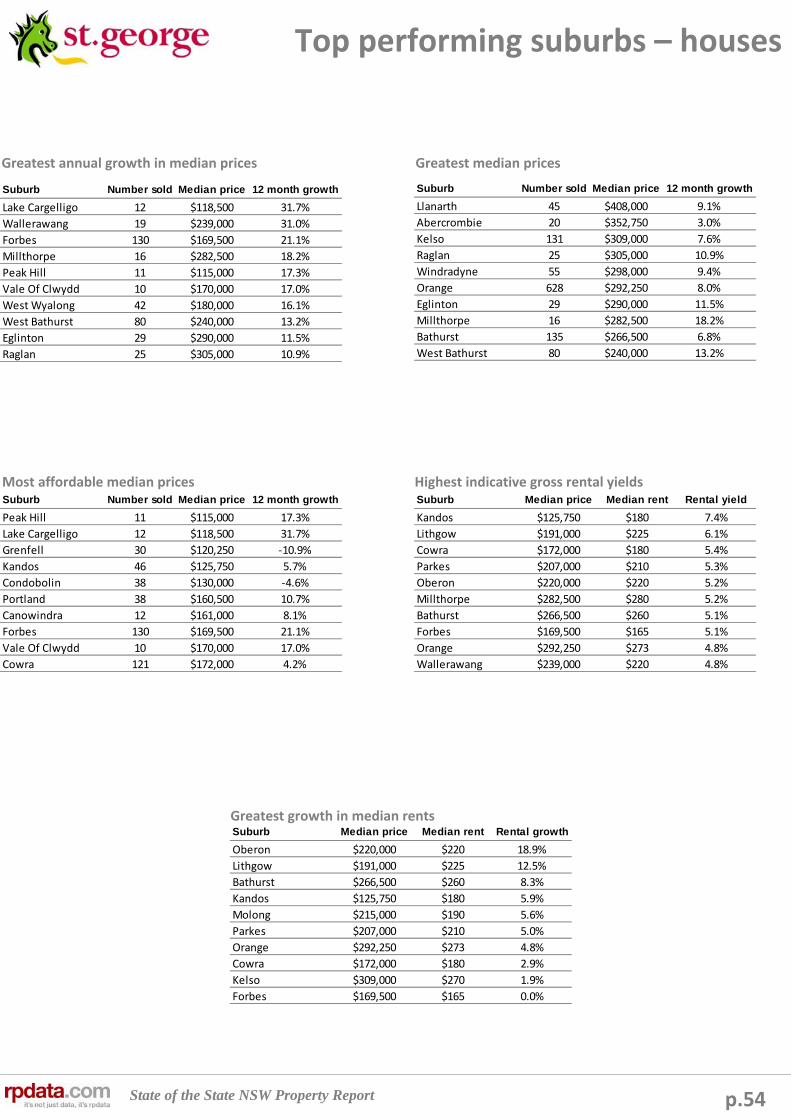

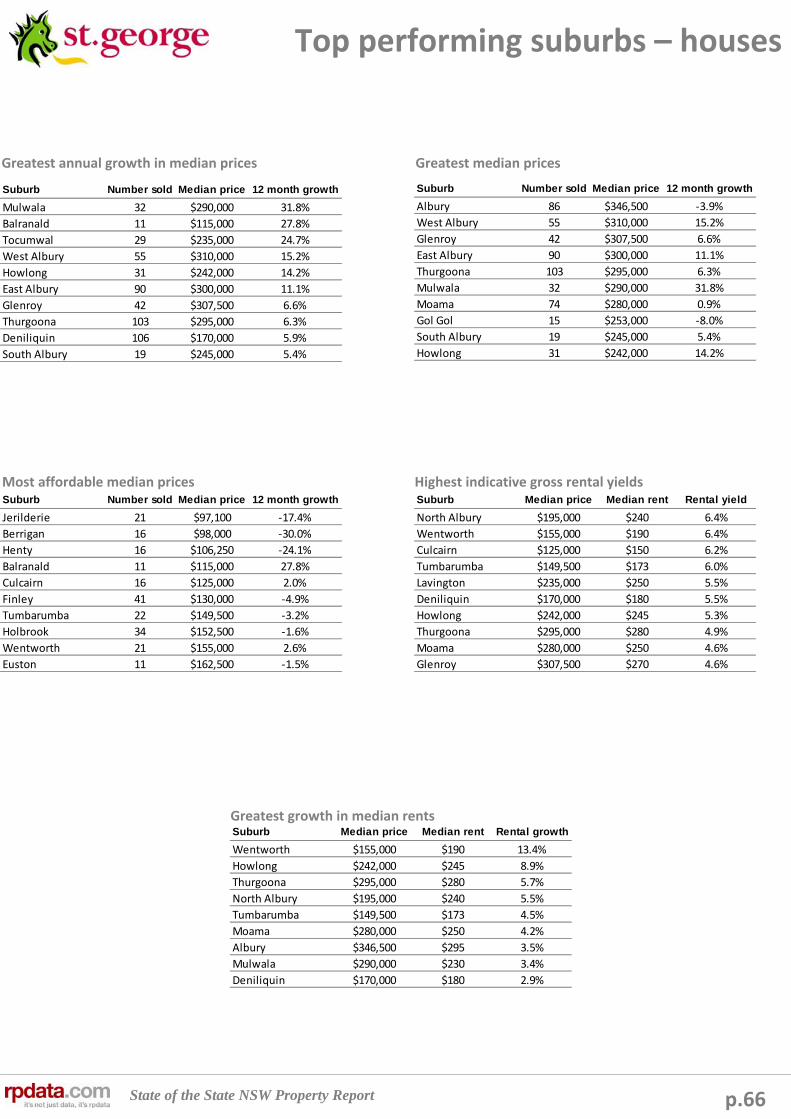

Top performing suburbs ‐ houses

Suburb Median Price Median Rent Rental Growth

St Huberts Island $745,000 $528 50.7%

Middle Cove $1,142,000 $1,050 50.0%

Yowie Bay $946,500 $860 43.3%

Waverton $1,610,000 $975 42.3%

Wyongah $300,000 $300 39.5%

Tuggerawong $286,000 $355 36.5%

Macmasters Beach $600,000 $435 35.9%

Bullaburra $315,000 $310 34.8%

Potts Point $784,000 $575 32.2%

Charmhaven $308,000 $290 31.8%

Greatest annual growth in median prices Greatest median prices

Most affordable median prices Highest indicative gross rental yields

Greatest growth in median rents

State of the State NSW Property Report

Suburb Median price Median rent Rental growth

Condell Park $385,000 $435 52.6%

Glenfield $238,500 $295 40.5%

Dural $455,000 $450 36.4%

Carramar $197,000 $260 30.0%

West Pennant Hills $585,000 $450 28.6%

Beecroft $525,000 $460 24.3%

Lavender Bay $600,000 $588 23.7%

Moorebank $325,000 $370 23.3%

Cambridge Park $275,500 $340 21.4%

Glenmore Park $365,000 $375 21.0%

Suburb Median price Median rent Rental yield

Ultimo $302,500 $468 8.0%

Bradbury $202,250 $273 7.0%

Carramar $197,000 $260 6.9%

Lakemba $228,250 $300 6.8%

Punchbowl $245,000 $320 6.8%

Wetherill Park $302,500 $390 6.7%

Mount Druitt $225,000 $290 6.7%

Werrington $225,000 $290 6.7%

Fairfield $245,000 $310 6.6%

The Entrance North $245,100 $310 6.6%

Suburb Number sold Median price 12 month growth

Vineyard 14 $136,500 n.a.

Carramar 53 $197,000 23.1%

Berkeley Vale 41 $198,000 ‐10.0%

Bradbury 28 $202,250 ‐23.5%

Warwick Farm 114 $210,000 18.6%

Minto 37 $210,000 1.9%

Leumeah 59 $210,000 ‐22.2%

Gorokan 31 $211,000 3.9%

Cabramatta 253 $220,000 14.6%

Ambarvale 22 $220,000 12.8%

Suburb Number sold Median price 12 month growth

Dawes Point 17 $1,750,000 29.6%

Point Piper 24 $1,640,000 n.a.

Milsons Point 72 $1,217,500 n.a.

Tamarama 23 $1,000,000 46.5%

Darling Point 71 $985,000 ‐33.2%

Cremorne Point 48 $960,000 34.7%

Little Bay 24 $949,500 31.9%

Millers Point 69 $875,000 11.1%

Huntleys Cove 35 $870,000 38.6%

Cabarita 19 $870,000 10.4%

Suburb Number sold Median price 12 month growth

Enmore 21 $445,000 48.3%

Tamarama 23 $1,000,000 46.5%

Huntleys Cove 35 $870,000 38.6%

Rushcutters Bay 109 $487,000 38.2%

Ramsgate Beach 33 $490,000 36.5%

Bateau Bay 22 $300,000 36.4%

Cremorne Point 48 $960,000 34.7%

Bondi Junction 171 $615,000 32.3%

Little Bay 24 $949,500 31.9%

Darlington 12 $427,500 31.0%

p.13

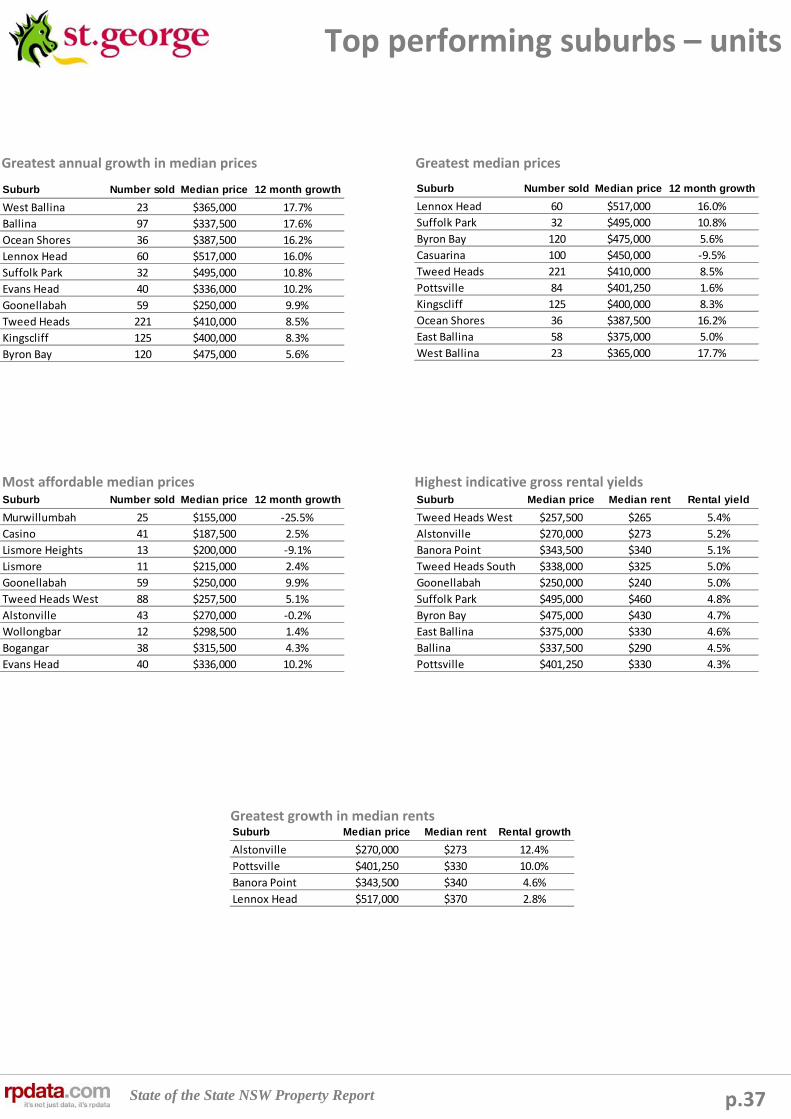

Top performing suburbs – units

Greatest annual growth in median prices Greatest median prices

Most affordable median prices Highest indicative gross rental yields

Greatest growth in median rents

State of the State NSW Property Report

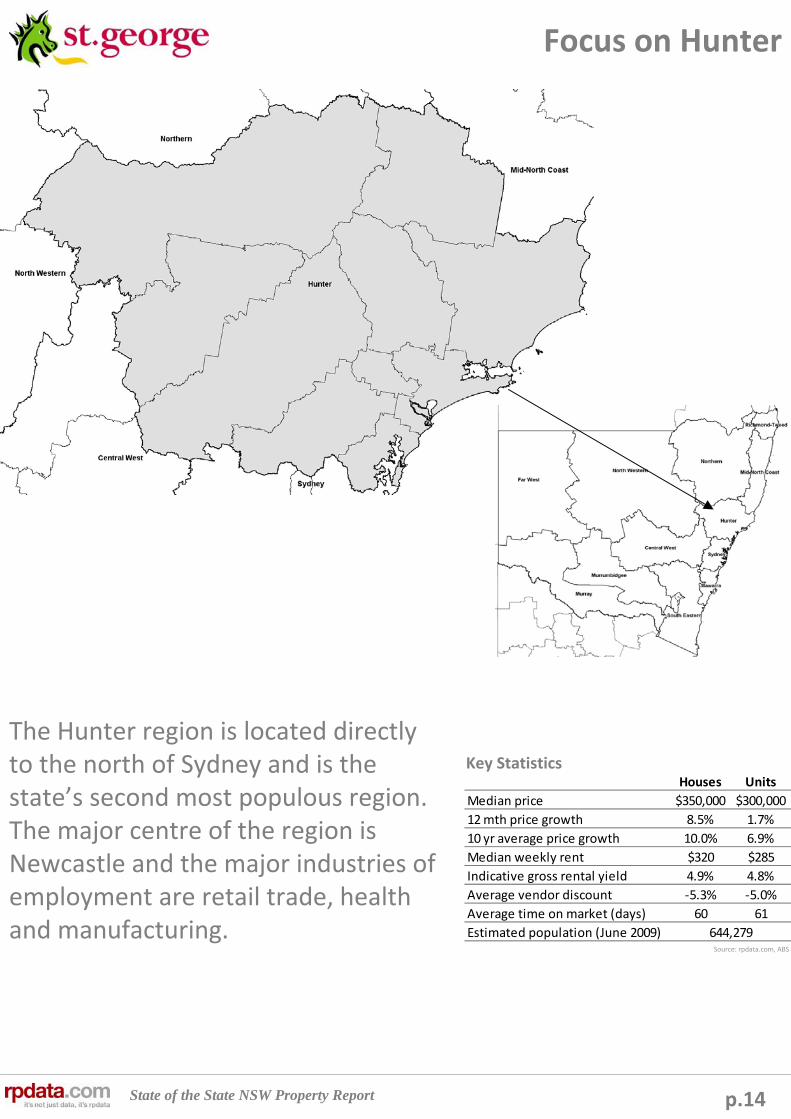

Houses Units

Median price $350,000 $300,000

12 mth price growth 8.5% 1.7%

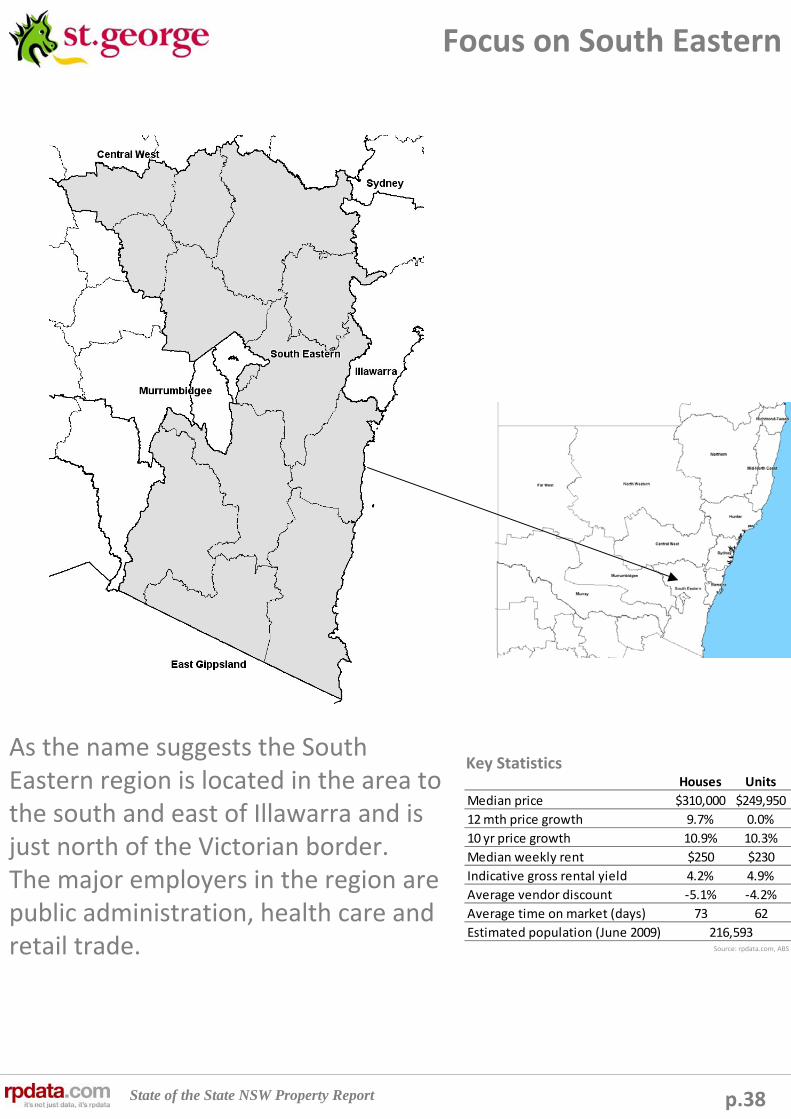

10 yr average price growth 10.0% 6.9%

Median weekly rent $320 $285

Indicative gross rental yield 4.9% 4.8%

Average vendor discount ‐5.3% ‐5.0%

Average time on market (days) 60 61

Estimated population (June 2009) 644,279

p.14

Focus on Hunter

Key Statistics

The Hunter region is located directly to the north of Sydney and is the state’s second most populous region. The major centre of the region is Newcastle and the major industries of employment are retail trade, health and manufacturing.

Source: rpdata.com, ABS

State of the State NSW Property Report

3.5%

3.7%

3.9%

4.1%

4.3%

4.5%

4.7%

4.9%

5.1%

Sep‐05

Nov‐05

Jan‐06

Mar‐06

May‐06

Jul‐06

Sep‐06

Nov‐06

Jan‐07

Mar‐07

May‐07

Jul‐07

Sep‐07

Nov‐07

Jan‐08

Mar‐08

May‐08

Jul‐08

Sep‐08

Nov‐08

Jan‐09

Mar‐09

May‐09

Jul‐09

Sep‐09

Nov‐09

Jan‐10

Mar‐10

May‐10

Jul‐10

Houses Units

0

1,000

2,000

3,000

4,000

5,000

6,000

$0

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

$350,000

$400,000

Jul‐00

Jan‐01

Jul‐01

Jan‐02

Jul‐02

Jan‐03

Jul‐03

Jan‐04

Jul‐04

Jan‐05

Jul‐05

Jan‐06

Jul‐06

Jan‐07

Jul‐07

Jan‐08

Jul‐08

Jan‐09

Jul‐09

Jan‐10

Jul‐10

Rolling quarterly volume of sales

Median price

Quarterly volume of sales Houses Units

p.15

Hunter property market

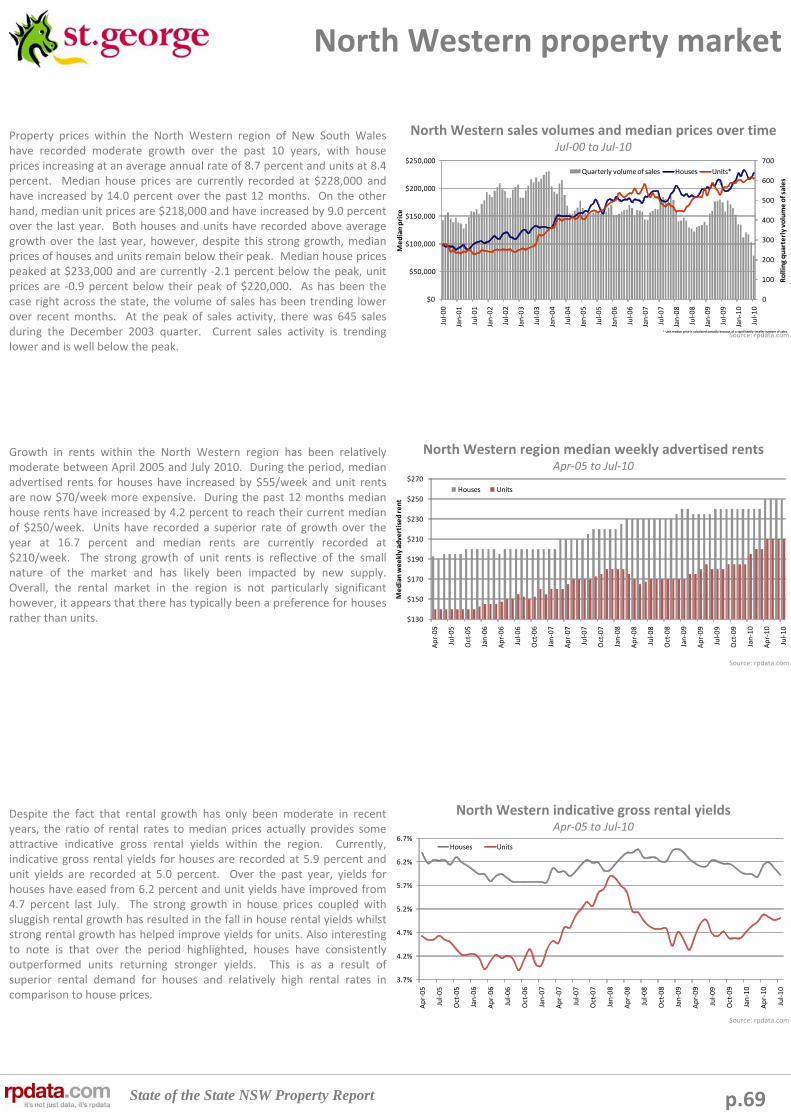

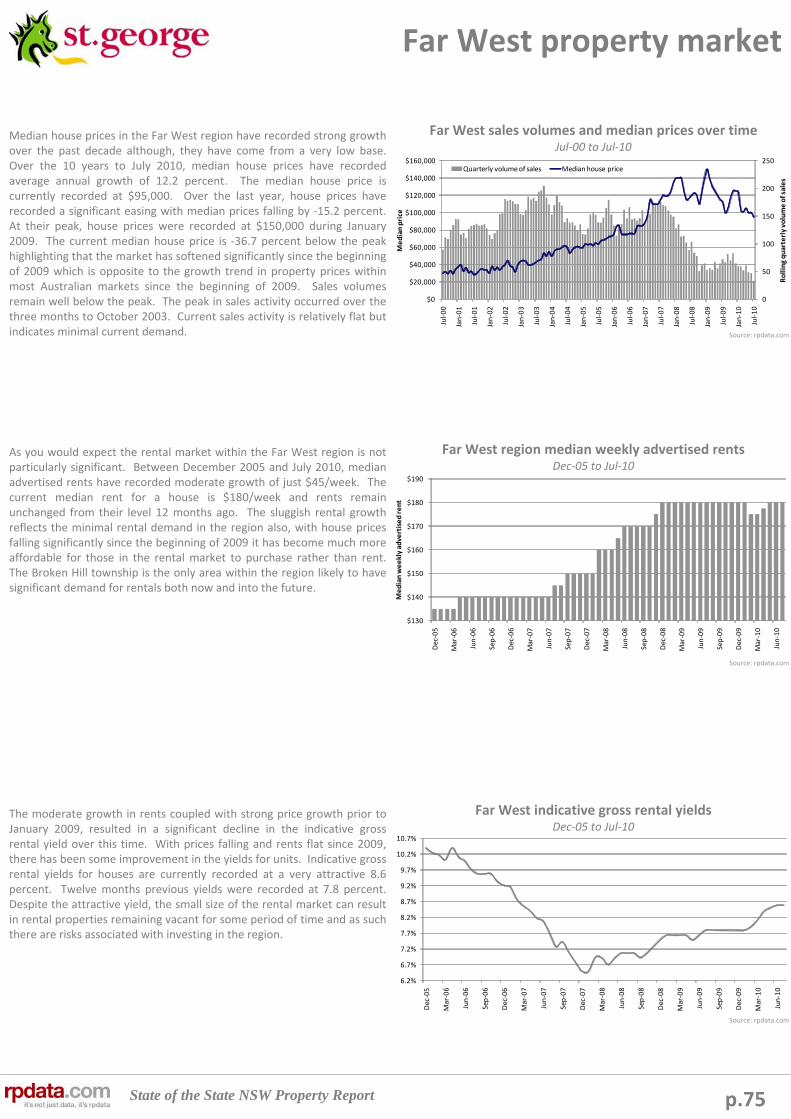

Throughout the Hunter region, house prices have increased at an average annual rate of 10.0 percent during the last decade compared with unit growth of 6.9 percent annually. During the last 12 months, median price growth has been at below average levels with houses increasing by 8.5 percent and units by just 1.7 percent. The current median house price throughout the region is recorded at $350,000 and the median unit price is recorded at $300,000. Median house prices are currently at their historic high whilst median unit prices are ‐6.3 percent below their peak of $320,000. Sales volumes across the Hunter region have been below their all‐time peak since mid 2002, however, there was an improvement during 2009. Evidence suggests that sales volumes are softening once more and we expect that the easing will continue for the remainder of the year. Like most regional areas of the country, the Hunter region’s rebound out of the GFC has not been as strong as that recorded in the capital city markets with property price growth improving, it is still lagging that of Sydney.

Unlike most regions across Australia, median weekly rents in the Hunter region have continued to increase since the post GFC recovery. Between September 2005 and July 2010, median weekly rents have increased by a total of $100 for houses and $75 for units. Currently, median weekly rents are recorded at $320 for houses and $285 for units. Over the last 12 months, median weekly rents have increased by 8.5 percent forhouses and 5.6 percent for units indicating that rental demand is still quite strong within the region. The Hunter region takes in quite a vast area and includes coastal tourism areas, mining and resource regions and farming and agricultural. Across the region, rents have continued to increase but this doesn’t necessarily reflect the performance within individual markets. Moving forward, major regional centres such as Newcastle and mining regions are likely to be best positioned for further increases to rental rates.

With the rate of property price growth across the region quite sluggish over the past year, indicative gross rental yields have been flat over the period. Indicative gross rental yields are recorded at 4.9 percent for houses and 4.8 percent for units. At the same time last year, yields were at the same levels for houses and units. The indicative gross rental yield for houses is quite high potentially making investment attractive whereas unit yields sit below that of houses. Over the last couple of months, yields have been improving at a time when there has been minimalgrowth in property prices. Over the next year, the best prospects for a quality investment return are likely to be those properties in mining areas of the region or those well located, close to the centre of major population centres such as Newcastle. Also look to areas which attract strong rental demand due to their location close to working nodes or close to universities.

Hunter sales volumes and median prices over timeJul‐00 to Jul‐10

Hunter region median weekly advertised rentsSep‐05 to Jul‐10

Hunter indicative gross rental yieldsSep‐05 to Jul‐10

$200

$220

$240

$260

$280

$300

$320

$340

Sep‐05

Nov‐05

Jan‐06

Mar‐06

May‐06

Jul‐06

Sep‐06

Nov‐06

Jan‐07

Mar‐07

May‐07

Jul‐07

Sep‐07

Nov‐07

Jan‐08

Mar‐08

May‐08

Jul‐08

Sep‐08

Nov‐08

Jan‐09

Mar‐09

May‐09

Jul‐09

Sep‐09

Nov‐09

Jan‐10

Mar‐10

May‐10

Jul‐10

Median weekly advertised rent

Houses Units

Source: rpdata.com

Source: rpdata.com

Source: rpdata.com

State of the State NSW Property Report

‐9.0%

‐8.0%

‐7.0%

‐6.0%

‐5.0%

‐4.0%

‐3.0%

‐2.0%

‐1.0%

0.0%

Jul‐04

Oct‐04

Jan‐05

Apr‐05

Jul‐05

Oct‐05

Jan‐06

Apr‐06

Jul‐06

Oct‐06

Jan‐07

Apr‐07

Jul‐07

Oct‐07

Jan‐08

Apr‐08

Jul‐08

Oct‐08

Jan‐09

Apr‐09

Jul‐09

Oct‐09

Jan‐10

Apr‐10

Jul‐10

‐9.0%

‐8.0%

‐7.0%

‐6.0%

‐5.0%

‐4.0%

‐3.0%

‐2.0%

‐1.0%

0.0%

Jul‐04

Oct‐04

Jan‐05

Apr‐05

Jul‐05

Oct‐05

Jan‐06

Apr‐06

Jul‐06

Oct‐06

Jan‐07

Apr‐07

Jul‐07

Oct‐07

Jan‐08

Apr‐08

Jul‐08

Oct‐08

Jan‐09

Apr‐09

Jul‐09

Oct‐09

Jan‐10

Apr‐10

Jul‐10

0102030405060708090

100

Jul‐04

Oct‐04

Jan‐05

Apr‐05

Jul‐05

Oct‐05

Jan‐06

Apr‐06

Jul‐06

Oct‐06

Jan‐07

Apr‐07

Jul‐07

Oct‐07

Jan‐08

Apr‐08

Jul‐08

Oct‐08

Jan‐09

Apr‐09

Jul‐09

Oct‐09

Jan‐10

Apr‐10

Jul‐10

0

10

20

30

40

50

60

70

80

90

Jul‐04

Oct‐04

Jan‐05

Apr‐05

Jul‐05

Oct‐05

Jan‐06

Apr‐06

Jul‐06

Oct‐06

Jan‐07

Apr‐07

Jul‐07

Oct‐07

Jan‐08

Apr‐08

Jul‐08

Oct‐08

Jan‐09

Apr‐09

Jul‐09

Oct‐09

Jan‐10

Apr‐10

Jul‐10

p.16

Hunter property market

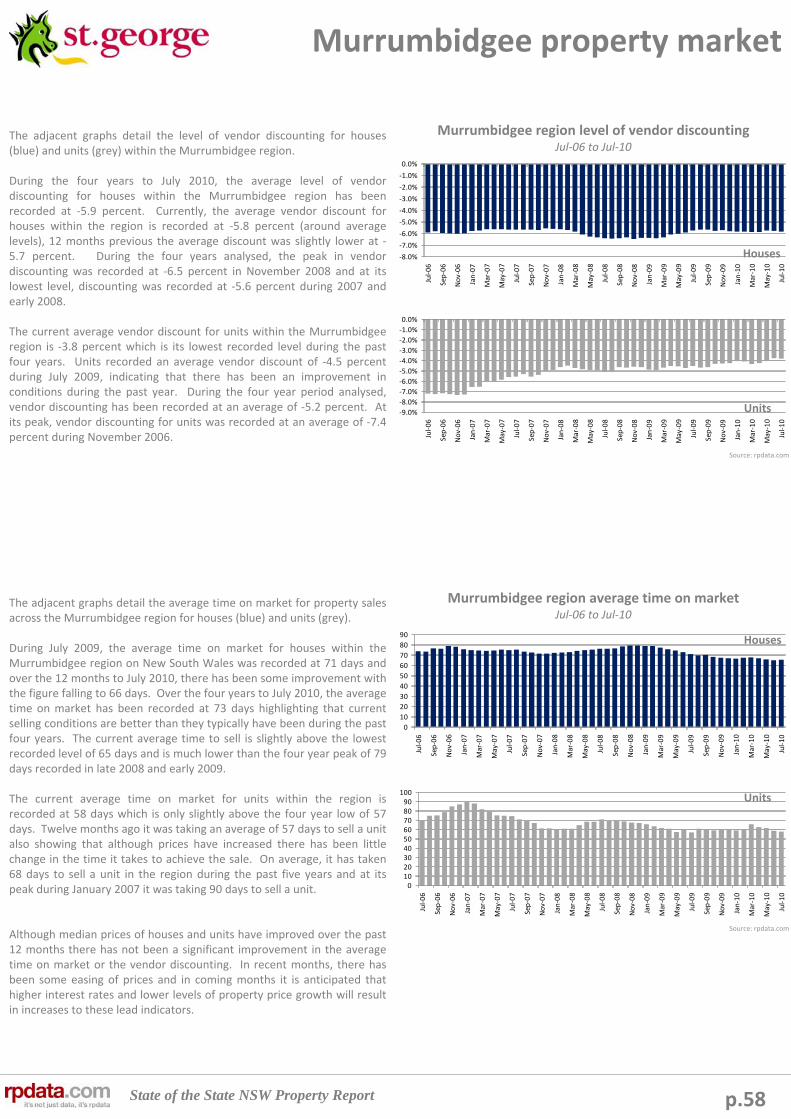

The adjacent graphs detail the level of vendor discounting across the Hunter region for houses (blue) and units (grey).

The level of vendor discounting for houses within the Hunter region is currently recorded at it’s lowest level between July 2004 and July 2010. Vendor discounting is recorded at ‐5.2 percent and in comparison to 12 months previous when discounting was recorded at ‐6.4 percent, the level of negotiation required by those selling houses has declined markedly over the last 12 months. Vendor discounting for housesreached its highest level of ‐8.4 percent during early 2005. Over the six year period vendor discounting has been recorded at an average of ‐7.0 percent.

Unit discounting levels are also recorded at their lowest level over the period analysed. Currently, the average level of vendor discounting sits at ‐4.5 percent and 12 months ago it was recorded at ‐6.0 percent, again indicating that the level of price negotiation has declined during the last year as market conditions have improved. At its peak, the level of vendor discounting for units was recorded at ‐8.1 percent during late 2005. The average vendor discounting during the last six years has been recorded at ‐6.4 percent, much lower than the long‐term average for houses.

The adjacent graphs detail the average time on market for property sales across the Hunter region for houses (blue) and units (grey).

The average time on market for houses across the Hunter region has recorded a noticeable easing in recent times and is currently recorded at its historic low level. Currently, it takes an average of 60 days to sell a house across the region and in comparison, it took an average of 73 days to sell just 12 months ago. The average time on market was recorded at as much as 85 days back in 2005, in recent times the average time on market was as high as 83 days in November of 2008. Over the period houses have taken an average of 77 days to sell.

Throughout the Hunter region the unit market has recorded a similar decline in the average time on market over recent times to that of houses. Units are selling quicker than any other time throughout the period. Units are currently selling after an average of 61 days and at the same time last year it was taking 78 days. At their peak, units took an average of 90 days to sell in June 2006 more recently, the average time on market for units reached as high as 85 days during late 2008. Units have recorded an average time on market of 81 days over the six year period.

The results for vendor discounting and time on market indicate that the residential property market’s performance has been improving which is confirmed by the growth in property prices over the past year. With capital city property value growth slowing in recent months and the likelihood of higher interest rates over the coming months we would expect that there is likely to be an increase in both lead indicators over the coming months.

Hunter region level of vendor discountingJul‐04 to Jul‐10

Hunter region average time on marketJul‐04 to Jul‐10

Source: rpdata.com

Source: rpdata.com

Houses

Units

Houses

Units

State of the State NSW Property Report p.17

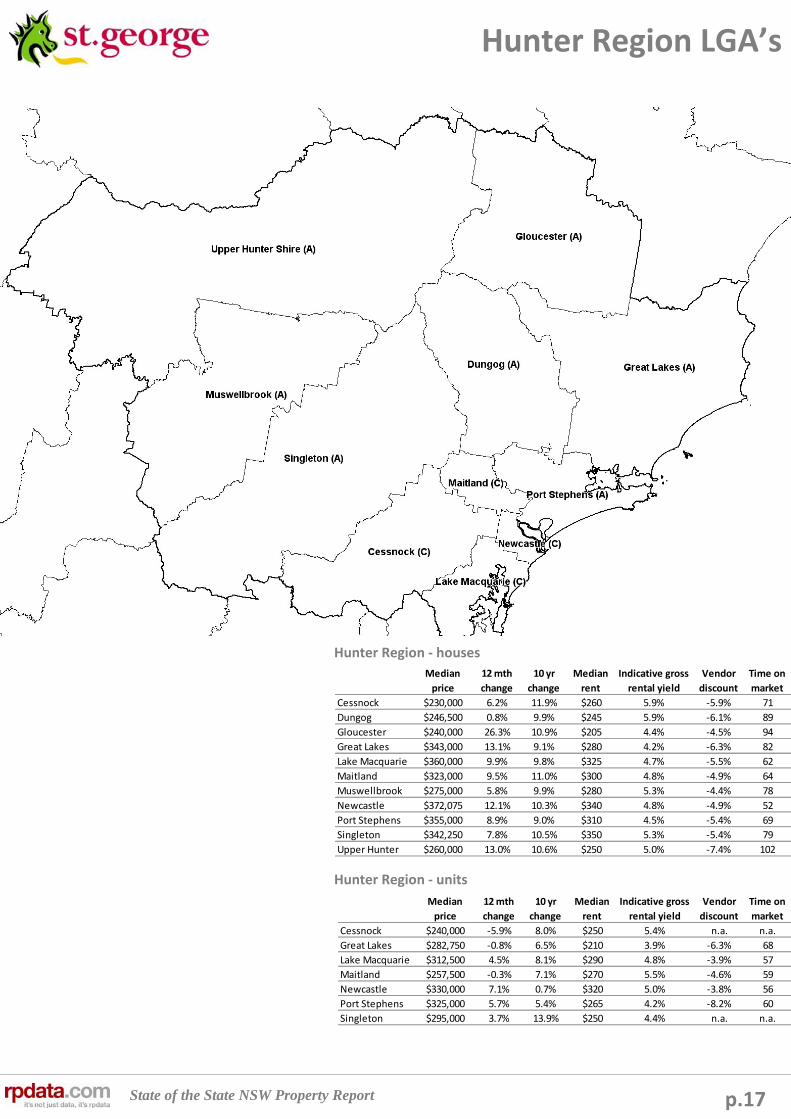

Hunter Region LGA’s

Median

price

12 mth

change

10 yr

change

Median

rent

Indicative gross

rental yield

Vendor

discount

Time on

market

Cessnock $240,000 ‐5.9% 8.0% $250 5.4% n.a. n.a.

Great Lakes $282,750 ‐0.8% 6.5% $210 3.9% ‐6.3% 68

Lake Macquarie $312,500 4.5% 8.1% $290 4.8% ‐3.9% 57

Maitland $257,500 ‐0.3% 7.1% $270 5.5% ‐4.6% 59

Newcastle $330,000 7.1% 0.7% $320 5.0% ‐3.8% 56

Port Stephens $325,000 5.7% 5.4% $265 4.2% ‐8.2% 60

Singleton $295,000 3.7% 13.9% $250 4.4% n.a. n.a.

Hunter Region ‐ houses

Hunter Region ‐ units

Median

price

12 mth

change

10 yr

change

Median

rent

Indicative gross

rental yield

Vendor

discount

Time on

market

Cessnock $230,000 6.2% 11.9% $260 5.9% ‐5.9% 71

Dungog $246,500 0.8% 9.9% $245 5.9% ‐6.1% 89

Gloucester $240,000 26.3% 10.9% $205 4.4% ‐4.5% 94

Great Lakes $343,000 13.1% 9.1% $280 4.2% ‐6.3% 82

Lake Macquarie $360,000 9.9% 9.8% $325 4.7% ‐5.5% 62

Maitland $323,000 9.5% 11.0% $300 4.8% ‐4.9% 64

Muswellbrook $275,000 5.8% 9.9% $280 5.3% ‐4.4% 78

Newcastle $372,075 12.1% 10.3% $340 4.8% ‐4.9% 52

Port Stephens $355,000 8.9% 9.0% $310 4.5% ‐5.4% 69

Singleton $342,250 7.8% 10.5% $350 5.3% ‐5.4% 79

Upper Hunter $260,000 13.0% 10.6% $250 5.0% ‐7.4% 102

State of the State NSW Property Report

Suburb Median price Median rent Rental growth

Denman $271,500 $350 37.3%

Abermain $195,000 $250 35.1%

The Junction $565,000 $418 30.5%

Greta $266,000 $330 26.9%

Mallabula $299,000 $330 26.9%

Hamilton North $350,000 $380 24.6%

Lorn $487,500 $368 24.6%

Shortland $277,500 $305 22.0%

Warabrook $440,000 $365 21.7%

Bellbird $220,000 $268 21.6%

Suburb Median price Median rent Rental yield

Windale $210,500 $285 7.0%

Denman $271,500 $350 6.7%

Abermain $195,000 $250 6.7%

Branxton $270,000 $345 6.6%

Greta $266,000 $330 6.5%

Kurri Kurri $220,000 $270 6.4%

Bellbird $220,000 $268 6.3%

West Wallsend $268,000 $310 6.0%

Cessnock $217,000 $250 6.0%

Weston $225,000 $258 6.0%

Suburb Number sold Median price 12 month growth

Murrurundi 11 $130,000 ‐7.8%

Coomba Park 14 $170,500 ‐14.5%

Merriwa 17 $177,000 14.2%

Stanford Merthyr 11 $190,000 0.0%

Abermain 34 $195,000 ‐7.1%

Bulahdelah 17 $210,000 5.0%

Windale 40 $210,500 13.8%

Kearsley 12 $212,500 13.3%

Cessnock 235 $217,000 0.9%

Kurri Kurri 92 $220,000 3.8%

Suburb Number sold Median price 12 month growth

Bar Beach 13 $1,250,000 0.0%

The Hill 14 $880,750 1.7%

Newcastle East 10 $725,000 0.0%

Hamilton East 17 $720,000 12.1%

Merewether 202 $681,186 6.2%

Rothbury 12 $646,000 0.0%

Hamilton South 45 $632,000 18.7%

Newcastle 14 $600,000 3.6%

Redhead 45 $580,000 6.7%

Merewether Heights 22 $578,750 16.3%

Suburb Number sold Median price 12 month growth

Lorn 18 $487,500 43.4%

Dudley 26 $527,500 36.3%

Maitland 37 $300,000 33.3%

Morpeth 22 $400,000 32.5%

Mallabula 15 $299,000 32.3%

Karuah 22 $288,750 31.3%

Morisset Park 25 $458,000 30.3%

Millfield 11 $225,000 28.6%

Garden Suburb 33 $510,000 27.5%

Balmoral 17 $378,000 26.4%

p.18

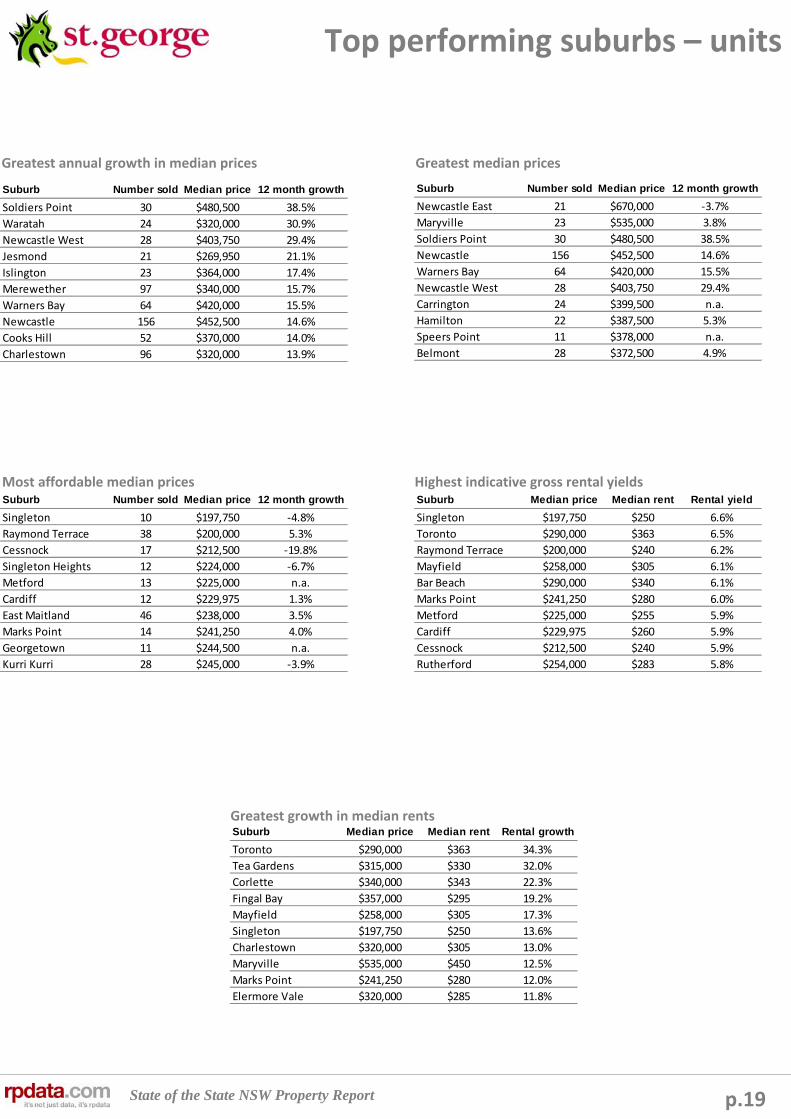

Top performing suburbs – houses

Greatest annual growth in median prices Greatest median prices

Most affordable median prices Highest indicative gross rental yields

Greatest growth in median rents

State of the State NSW Property Report

Suburb Median price Median rent Rental growth

Toronto $290,000 $363 34.3%

Tea Gardens $315,000 $330 32.0%

Corlette $340,000 $343 22.3%

Fingal Bay $357,000 $295 19.2%

Mayfield $258,000 $305 17.3%

Singleton $197,750 $250 13.6%

Charlestown $320,000 $305 13.0%

Maryville $535,000 $450 12.5%

Marks Point $241,250 $280 12.0%

Elermore Vale $320,000 $285 11.8%

Suburb Median price Median rent Rental yield

Singleton $197,750 $250 6.6%

Toronto $290,000 $363 6.5%

Raymond Terrace $200,000 $240 6.2%

Mayfield $258,000 $305 6.1%

Bar Beach $290,000 $340 6.1%

Marks Point $241,250 $280 6.0%

Metford $225,000 $255 5.9%

Cardiff $229,975 $260 5.9%

Cessnock $212,500 $240 5.9%

Rutherford $254,000 $283 5.8%

Suburb Number sold Median price 12 month growth

Singleton 10 $197,750 ‐4.8%

Raymond Terrace 38 $200,000 5.3%

Cessnock 17 $212,500 ‐19.8%

Singleton Heights 12 $224,000 ‐6.7%

Metford 13 $225,000 n.a.

Cardiff 12 $229,975 1.3%

East Maitland 46 $238,000 3.5%

Marks Point 14 $241,250 4.0%

Georgetown 11 $244,500 n.a.

Kurri Kurri 28 $245,000 ‐3.9%

Suburb Number sold Median price 12 month growth

Newcastle East 21 $670,000 ‐3.7%

Maryville 23 $535,000 3.8%

Soldiers Point 30 $480,500 38.5%

Newcastle 156 $452,500 14.6%

Warners Bay 64 $420,000 15.5%

Newcastle West 28 $403,750 29.4%

Carrington 24 $399,500 n.a.

Hamilton 22 $387,500 5.3%

Speers Point 11 $378,000 n.a.

Belmont 28 $372,500 4.9%

Suburb Number sold Median price 12 month growth

Soldiers Point 30 $480,500 38.5%

Waratah 24 $320,000 30.9%

Newcastle West 28 $403,750 29.4%

Jesmond 21 $269,950 21.1%

Islington 23 $364,000 17.4%

Merewether 97 $340,000 15.7%

Warners Bay 64 $420,000 15.5%

Newcastle 156 $452,500 14.6%

Cooks Hill 52 $370,000 14.0%

Charlestown 96 $320,000 13.9%

p.19

Top performing suburbs – units

Greatest annual growth in median prices Greatest median prices

Most affordable median prices Highest indicative gross rental yields

Greatest growth in median rents

State of the State NSW Property Report

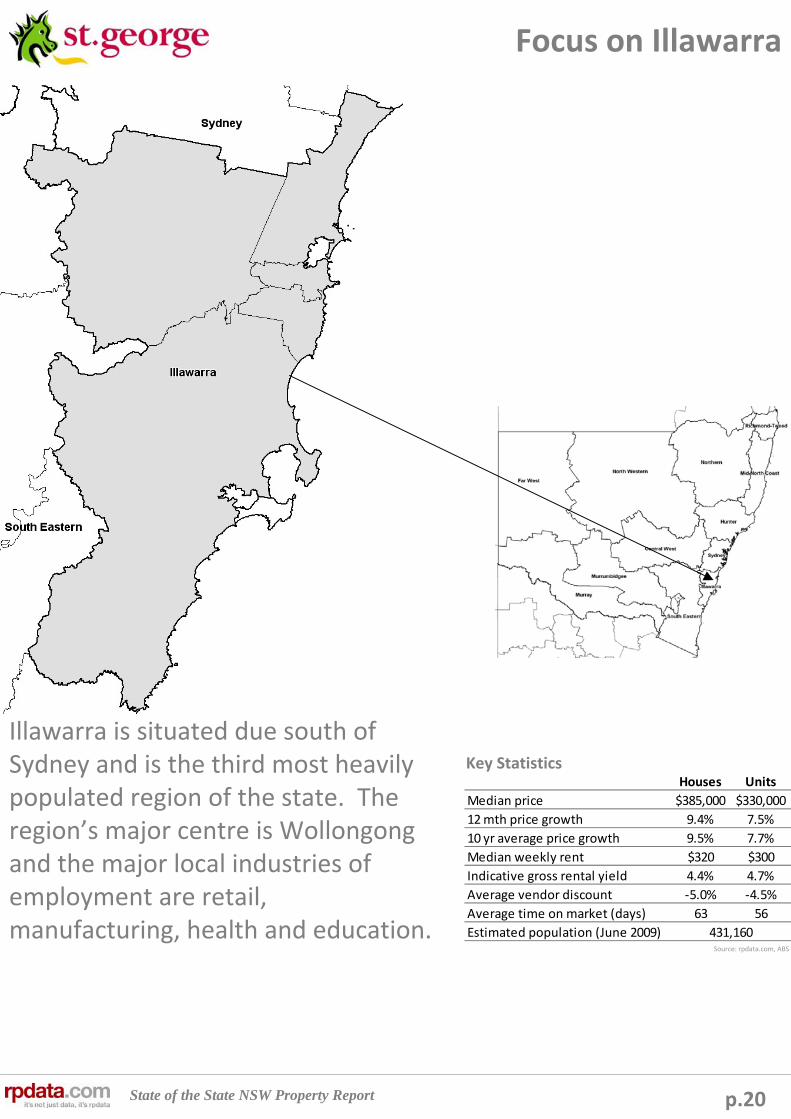

Houses Units

Median price $385,000 $330,000

12 mth price growth 9.4% 7.5%

10 yr average price growth 9.5% 7.7%

Median weekly rent $320 $300

Indicative gross rental yield 4.4% 4.7%

Average vendor discount ‐5.0% ‐4.5%

Average time on market (days) 63 56

Estimated population (June 2009) 431,160

p.20

Focus on Illawarra

Key Statistics

Illawarra is situated due south of Sydney and is the third most heavily populated region of the state. The region’s major centre is Wollongong and the major local industries of employment are retail, manufacturing, health and education.

Source: rpdata.com, ABS

State of the State NSW Property Report

3.5%

3.7%

3.9%

4.1%

4.3%

4.5%

4.7%

4.9%

5.1%

Sep‐05

Nov‐05

Jan‐06

Mar‐06

May‐06

Jul‐06

Sep‐06

Nov‐06

Jan‐07

Mar‐07

May‐07

Jul‐07

Sep‐07

Nov‐07

Jan‐08

Mar‐08

May‐08

Jul‐08

Sep‐08

Nov‐08

Jan‐09

Mar‐09

May‐09

Jul‐09

Sep‐09

Nov‐09

Jan‐10

Mar‐10

May‐10

Jul‐10

Houses Units

$200

$220

$240

$260

$280

$300

$320

$340

Sep‐05

Nov‐05

Jan‐06

Mar‐06

May‐06

Jul‐06

Sep‐06

Nov‐06

Jan‐07

Mar‐07

May‐07

Jul‐07

Sep‐07

Nov‐07

Jan‐08

Mar‐08

May‐08

Jul‐08

Sep‐08

Nov‐08

Jan‐09

Mar‐09

May‐09

Jul‐09

Sep‐09

Nov‐09

Jan‐10

Mar‐10

May‐10

Jul‐10

Median weekly advertised rent

Houses Units

0

500

1,000

1,500

2,000

2,500

3,000

3,500

$0

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

$350,000

$400,000

$450,000

Jul‐00

Jan‐01

Jul‐01

Jan‐02

Jul‐02

Jan‐03

Jul‐03

Jan‐04

Jul‐04

Jan‐05

Jul‐05

Jan‐06

Jul‐06

Jan‐07

Jul‐07

Jan‐08

Jul‐08

Jan‐09

Jul‐09

Jan‐10

Jul‐10

Rolling quarterly volume of sales

Median price

Quarterly volume of sales Houses Units

p.21

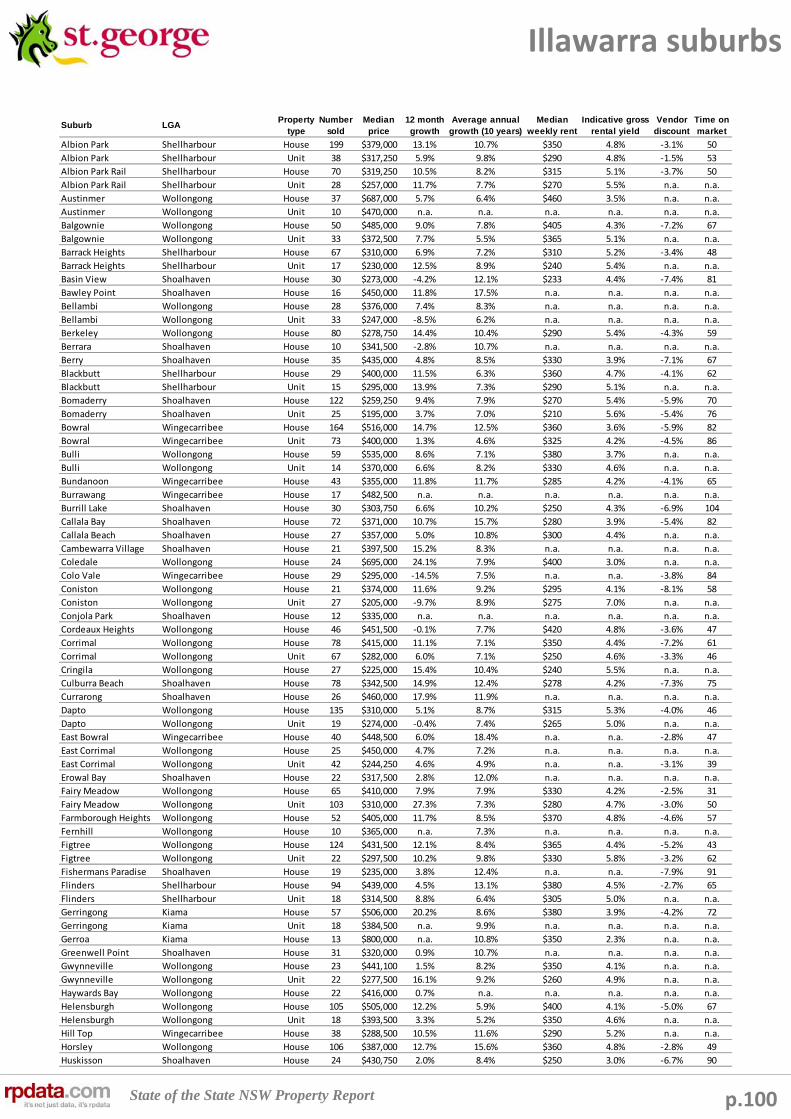

Illawarra property market

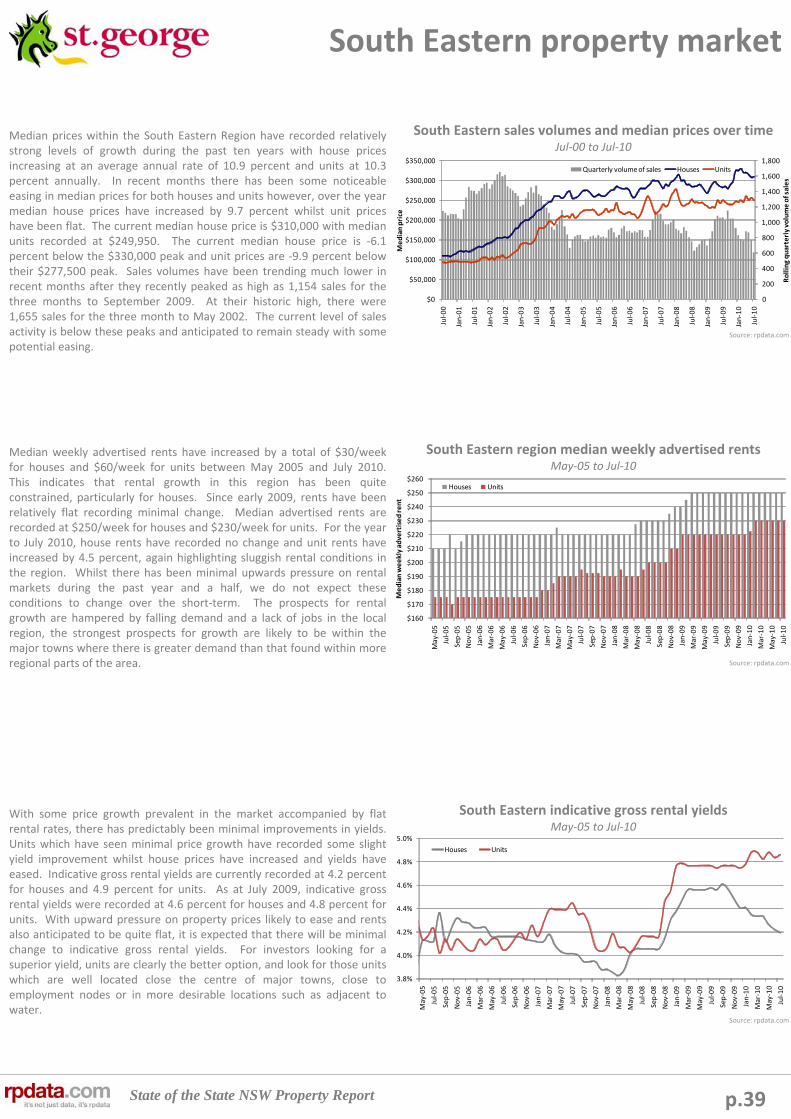

The Illawarra region has recorded average annual house price growth of 9.5 percent over the last decade and units have recorded average growth levels of 7.7 percent during the same period. During the last year, median prices have increased at rates in line with the 10 year average with house prices up by 9.4 percent and unit prices increasing 7.5 percent. Across the Illawarra region, the median house price was recorded at $385,000 over the three months to July 2010 and the median unit price sat at $330,000. Both house and unit prices are slightly below their peaks which were recorded at $389,000 for houses and $345,000 for units. Sales volumes across the region reached their historic highs during the three months to May 2002. Since that time, volumes have typically been well below the peak, however, there was a strong resurgence in market activity during early 2009. Current sales volumes are relatively flat but with the slower market conditions we expect some tapering of volumes during the remainder of 2010.

Illawarra median rents have continued to increase steadily over recent times whereas many regional and capital city regions have seen minimal growth in rents. Over the period highlighted, median house rents in the region have increased by a total of $80/week and unit rents haveincreased by $70/week which is a moderate level of growth compared with other regions. Median advertised rents for the region are currently recorded at $320/week for houses and $300/week for units indicating little difference in price between renting a house or unit. During the last 12 months, median rents have increased by 10.3 percent and unit rents have increased by 11.1 percent. The growth in rents over the past 12 months has been quite impressive and highlights that there is ongoing demand for housing within this region of the state. With price growth anticipated to be fairly minimal over the next year, the prospect for strong rental growth is more subdued, however, well located properties in major areas of the region will likely have the best prospect for further rental rate growth.

With rental rates and property prices increasing during the last 12 months, there has been a softening of rental yields recorded across the region. Indicative gross rental yields for houses are recorded at 4.4 percent and units at 4.7 percent. During July 2009 indicative gross rental yields were recorded at 4.4 percent for houses and 4.8 percent for units, however, they have been at higher levels during the year. In recent months yields have eased, however more recently there has been a slight improvement in house yields whilst unit yields have been quite flat. During the next 12 months it is anticipated that there will be minimal overall change to rental yields due to the expectation of softer capital growth and rental growth conditions during the period. Stronger rental yields are likely to be afforded to those properties with superior locations in areas which are most attractive to renters – close to water, close to town centres and close to education and working nodes.

Illawarra sales volumes and median prices over timeJul‐00 to Jul‐10

Illawarra region median weekly advertised rentsSep‐05 to Jul‐10

Illawarra indicative gross rental yieldsSep‐05 to Jul‐10

Source: rpdata.com

Source: rpdata.com

Source: rpdata.com

State of the State NSW Property Report

‐9.0%

‐8.0%

‐7.0%

‐6.0%

‐5.0%

‐4.0%

‐3.0%

‐2.0%

‐1.0%

0.0%

Jul‐04

Oct‐04

Jan‐05

Apr‐05

Jul‐05

Oct‐05

Jan‐06

Apr‐06

Jul‐06

Oct‐06

Jan‐07

Apr‐07

Jul‐07

Oct‐07

Jan‐08

Apr‐08

Jul‐08

Oct‐08

Jan‐09

Apr‐09

Jul‐09

Oct‐09

Jan‐10

Apr‐10

Jul‐10

‐9.0%

‐8.0%

‐7.0%

‐6.0%

‐5.0%

‐4.0%

‐3.0%

‐2.0%

‐1.0%

0.0%

Jul‐04

Oct‐04

Jan‐05

Apr‐05

Jul‐05

Oct‐05

Jan‐06

Apr‐06

Jul‐06

Oct‐06

Jan‐07

Apr‐07

Jul‐07

Oct‐07

Jan‐08

Apr‐08

Jul‐08

Oct‐08

Jan‐09

Apr‐09

Jul‐09

Oct‐09

Jan‐10

Apr‐10

Jul‐10

0102030405060708090

100

Jul‐04

Oct‐04

Jan‐05

Apr‐05

Jul‐05

Oct‐05

Jan‐06

Apr‐06

Jul‐06

Oct‐06

Jan‐07

Apr‐07

Jul‐07

Oct‐07

Jan‐08

Apr‐08

Jul‐08

Oct‐08

Jan‐09

Apr‐09

Jul‐09

Oct‐09

Jan‐10

Apr‐10

Jul‐10

0102030405060708090

100

Jul‐04

Oct‐04

Jan‐05

Apr‐05

Jul‐05

Oct‐05

Jan‐06

Apr‐06

Jul‐06

Oct‐06

Jan‐07

Apr‐07

Jul‐07

Oct‐07

Jan‐08

Apr‐08

Jul‐08

Oct‐08

Jan‐09

Apr‐09

Jul‐09

Oct‐09

Jan‐10

Apr‐10

Jul‐10

p.22

Illawarra property market

The adjacent graphs detail the level of vendor discounting across theIllawarra region for houses (blue) and units (grey).

Average levels of vendor discounting throughout the Illawarra region are currently at their lowest ever level for houses. The current level of vendor discounting for houses is recorded at ‐5.0 percent. At the same time last year, the average level of vendor discounting was recorded at ‐6.3 percent indicating that over the last 12 months conditions for sellers have improved markedly. At their highest level, vendor discounting was recorded at ‐8.2 percent during April 2005. Over the six years highlighted, the average vendor discount has been recorded at ‐7.1 percent.

Unit discounting levels are currently recorded at levels above their historic low of ‐3.9 percent and have increased in recent months. Average vendor discount levels are recorded at ‐4.5 percent. Over the last 12 months, the average vendor discount has actually increased having been recorded at ‐4.4 percent during July 2009. At its highest level during 2005, the average vendor discount was recorded at ‐7.7 percent. Over the last six years, discounting levels for units have typically been lower than that for houses, recorded at an average of ‐6.3 percent.

The adjacent graphs detail the average time on market for property sales across the Illawarra region for houses (blue) and units (grey).

On average, houses throughout the Illawarra region have recorded a decline in the time it takes to sell and are currently at their lowest level during the last six years. On average it took 63 days to sell a house within the region during July 2010 in comparison, 12 months prior it was taking an average of 75 days to sell a house. The average selling time recorded its historic high level of 88 days in late 2005 / early 2006 and for much of the last six years it has taken more than 80 days to sell a house in the region.

Units within the Illawarra region of the state have seen a similar decline in the average time it takes to sell a property as has been recorded for houses and are at their lowest level of any time during the last six years. Currently, units are taking an average of 56 days to sell and at the same time last July, units were taking an average of 71 days to sell. The average time to sell across the region peaked at 88 days in 2005 and typically, the average time on market has been longer than 70 days over the six year period.

The results for vendor discounting and time on market indicate that the residential property markets performance has been improving and is arguably in the best condition for some time, as a result properties have been selling quicker and have been recording lower discount levels. Although conditions have improved, higher interest rates and fewer buyers are likely to result in some increase to these lead indicators during the coming months.

Illawarra region level of vendor discountingJul‐04 to Jul‐10

Illawarra region average time on marketJan‐04 to Jul‐10

Source: rpdata.com

Source: rpdata.com

Houses

Units

Houses

Units

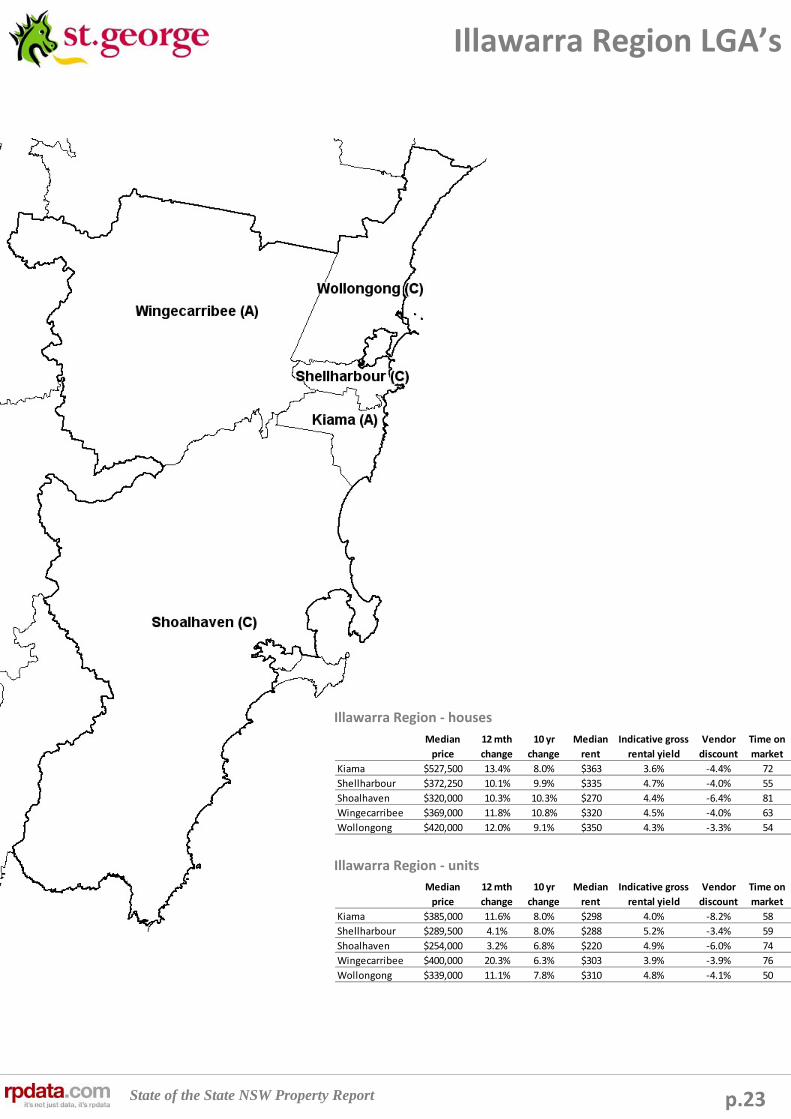

State of the State NSW Property Report p.23

Illawarra Region LGA’s

Illawarra Region ‐ houses

Illawarra Region ‐ units

Median

price

12 mth

change

10 yr

change

Median

rent

Indicative gross

rental yield

Vendor

discount

Time on

market

Kiama $527,500 13.4% 8.0% $363 3.6% ‐4.4% 72

Shellharbour $372,250 10.1% 9.9% $335 4.7% ‐4.0% 55

Shoalhaven $320,000 10.3% 10.3% $270 4.4% ‐6.4% 81

Wingcarribee $369,000 11.8% 10.8% $320 4.5% ‐4.0% 63

Wollongong $420,000 12.0% 9.1% $350 4.3% ‐3.3% 54

Median

price

12 mth

change

10 yr

change

Median

rent

Indicative gross

rental yield

Vendor

discount

Time on

market

Kiama $385,000 11.6% 8.0% $298 4.0% ‐8.2% 58

Shellharbour $289,500 4.1% 8.0% $288 5.2% ‐3.4% 59

Shoalhaven $254,000 3.2% 6.8% $220 4.9% ‐6.0% 74

Wingcarribee $400,000 20.3% 6.3% $303 3.9% ‐3.9% 76

Wollongong $339,000 11.1% 7.8% $310 4.8% ‐4.1% 50

Median

price

12 mth

change

10 yr

change

Median

rent

Indicative gross

rental yield

Vendor

discount

Time on

market

Kiama $527,500 13.4% 8.0% $363 3.6% ‐4.4% 72

Shellharbour $372,250 10.1% 9.9% $335 4.7% ‐4.0% 55

Shoalhaven $320,000 10.3% 10.3% $270 4.4% ‐6.4% 81

Wingecarribee $369,000 11.8% 10.8% $320 4.5% ‐4.0% 63

Wollongong $420,000 12.0% 9.1% $350 4.3% ‐3.3% 54

Median

price

12 mth

change

10 yr

change

Median

rent

Indicative gross

rental yield

Vendor

discount

Time on

market

Kiama $385,000 11.6% 8.0% $298 4.0% ‐8.2% 58

Shellharbour $289,500 4.1% 8.0% $288 5.2% ‐3.4% 59

Shoalhaven $254,000 3.2% 6.8% $220 4.9% ‐6.0% 74

Wingecarribee $400,000 20.3% 6.3% $303 3.9% ‐3.9% 76

Wollongong $339,000 11.1% 7.8% $310 4.8% ‐4.1% 50

State of the State NSW Property Report

Suburb Median price Median rent Rental growth

Bundanoon $355,000 $285 35.7%

Fairy Meadow $410,000 $330 26.9%

Vincentia $441,000 $340 25.9%

Callala Beach $357,000 $300 25.0%

Stanwell Park $805,000 $475 21.8%

Albion Park Rail $319,250 $315 21.2%

St Georges Basin $339,900 $290 20.8%

Windang $404,000 $300 20.0%

Oak Flats $330,000 $320 18.5%

Primbee $380,000 $330 17.9%

Suburb Median price Median rent Rental yield

Koonawarra $270,000 $300 5.8%

Nowra $235,000 $260 5.8%

Cringila $225,000 $240 5.5%

West Nowra $267,500 $283 5.5%

Warrawong $252,500 $265 5.5%

Warilla $285,000 $298 5.4%

Bomaderry $259,250 $270 5.4%