ICHIP 01/09/08 12:13 State of Illinois Comprehensive Health Insurance Plan Jim Edgar Governor 1992 Annu.al Report and Financial Summary Stephen F. Selcke Chairman, Board of Directors Roland W. Burris Attorney General Richard W. Carlson Executive Director

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

ICH

IP 0

1/09

/08

12:1

3

State of Illinois Comprehensive Health Insurance Plan

Jim Edgar Governor

1992 Annu.al Report and Financial Summary

Stephen F. Selcke Chairman, Board of Directors

Roland W. Burris Attorney General

Richard W. Carlson Executive Director

ICH

IP 0

1/09

/08

12:1

3

This Report is Dedicated to the Memory of

Lloyd M. Rice (February 23, 1929- November 5, 1992)

Among those who were in the forefront of establishing CHIP, Lloyd Rice holds a special place.

Lloyd, who from 1975 until his retirement in September of 1992 was head of the life, accident and health compliance section ofthe Department oflnsurance, served as a technical advisor during the early stages of CHIP. His contribution to the process in those early days is known all too well to those who worked with him.

Lloyd was a man with an infectious smile, a quick wit and a heart filled with compassion for those who knew suffering. During his years with the Department of Insurance, he was long a champion of those who suffered the effects of catastrophic illness or personal loss. He was instrumental in drafting a number of important legislative proposals and rules pertaining to life, accident and health insurance issues, including CHIP. He was well liked and respected by all who had the opportunity to work with him, consumers, providers, insurers and agents alike. This respect was not unspoken. Lloyd was given the Edward H. O'Connor Distinguished Service Award by the Chicago Association of Health Underwriters in April of 1992.

In addition to his work for CHIP, Lloyd served on Governor's Task Forces for long term care, Alzheimer's Disease and Project Heart for children without parents. He represented Illinois on various task forces and working groups of the National Association of Insurance Commissioners to address such issues as coordination ofbenefits, continuation rights and conversion policies, long term care, Medicare supplements and accelerated life insurance benefits. It is cruelly ironic that his own life should be cut short by cancer.

His contributions will be long remembered. His legacy will be the many important insurance laws and regulations which today protect the insurance consumers of Illinois. We are proud to dedicate this Annual Report to his memory.

ICH

IP 0

1/09

/08

12:1

3

State of Illinois Office of the Board of Directors

Comprehensive Health Insurance Plan

400 West Monroe Street, Suite 202 • Springfield, lllinois 62704-1823

Telephone: 217/782-6333 (Voice) • 217/782-6410 (TDD) • 217/782-6468 (FAX)

Consumer In formation: 1-800-962-8384 (Voice) • 1-800-545-2455 (TDD)

September 15, 1993

To the Honorable Members of the 88th General Assembly

It is my pleasure to present, on behalf of the Board of Directors of the Comprehensive Health Insurance Plan, the report for Calendar Year 1992.

This report is completed in accordance with the requirements of the Comprehensive Health Insurance Plan Act (215 ILCS 105/3) (from Ill. Rev. Stat. 1991. Ch. 73. par. 1303) and contains significant information concerning CHIP insureds, benefits, operations and cost containment activities.

Chairman of the Board of Directors

Printed on recycled paper

ICH

IP 0

1/09

/08

12:1

3State of Illinois

Office of the Board of Directors

Comprehensive Health Insurance Plan

The Honorable Jim Edgar Governor State of Illinois Room 207, State House Springfield, IL 62706

Dear Governor Edgar:

400 West Monroe Street, Suite 202 • Springfield, lllinois 62704-1823

Telephone: 217/782-6333 (Voice) • 2171782-6410 (IDD) • 217/782-6468 (FAX)

Consumer Information: 1-800-962-8384 (Voice) • J-800-545-2455 liD D)

September 15, 1993

On behalf of our Board of Directors, I am pleased to present the fourth Annual Report summarizing major activities of the Comprehensive Health Insurance Plan for Calendar Year 1992.

Through December 31, 1992, nearly 8,000 Illinois citizens had, at one time or another, availed themselves of coverage through CHIP. Many of these persons, who were ineligible for medical assistance and who found insurance otherwise impossible to obtain, have discovered they had very serious and economically devastating medical conditions. At year's end, al1 but three counties in I11inois had at least one CHIP enrollee. Yet, those covered by CHIP represent only a portion of the more than 12,000 who have applied for coverage since the Plan's inception; and there were nearly nine hundred on our waiting list at the end of 1992. Our experience through 1992 aJJows us to assure you, and the Members of the General Assembly, that CHIP has proven itself to be an essential and appropriate function of state government which is worthy of further investment and expansion as additional state revenues become available.

We hope that the proven track record of this important and successful state program will be kept in mind as you and other elected officials at both the state and federal levels consider various proposals for reforming our health care system. CHIP provides a solid foundation which can be built upon and developed to help meet the continuing needs of those among our eleven and one-half million residents who remain uninsured.

Executive Director

Printed on recycled paper

ICH

IP 0

1/09

/08

12:1

3 1992: Benefits Reach $75 Million At a time when speculation is rife about the future of health care in the United States, and when there is much debate about what will work and what will not, one thing is clear in Illinois.

CHIP is working. By the end of 1992 - three and one-half years after

CHIP began offering coverage to the uninsurable in Illinois- nearly 8,000 Illinois citizens had been provided coverage and more than $75 million in benefits had been paid out.

CHIP works because it serves a very real need. Numbers of people with serious health conditions who want and need health insurance coverage continue to find that commercial insurers will not provide it to them. At yearend, 900 applicants to CHIP were on the waiting list.

CHIP's Board of Directors plays a prominent role in planning and policy-making for the program, with particular involvement in the plan's financing, premium structure, grievance procedures and personnel matters.

Illinois Comprehensive Health Insurance Plan

In February of 1993, the CHIP board voted to increase the enrollment cap, which has been set at 4,500 since 1989, to 4,750. Enrollment caps are deemed necessary in order to ensure that premiums collected and appropriations from the Illinois general revenue fund are adequate to meet current and future claims and expenses. The board determined that the efficient operation of the plan warranted raising the enrollment cap, which will allow more uninsurable persons access to health insurance coverage.

As CHIP enters its fifth year of service to the people of Illinois, the pieces of the health care delivery puzzle are as yet unassembled. Yet CHIP has given us a look at one important piece - insurance for the uninsurable - and has allowed us to see how something can work for the benefit of the public, and work well. CHIP- and the State of Illinois- are in a better position now, with the experience we have had, to meet the health care challenges that will come tomorrow.

"Insurance for the Uninsurable" _ 1 _

ICH

IP 0

1/09

/08

12:1

3 Funding and Administration Program Funding

CHIP is funded partly by premiums paid by enrollees and, to the extent that premiums do not meet anticipated expenses, partly by an appropriation from the state's General Revenue Fund.

Illinois law requires that the premium charged be 135 percent of the rates charged individuals for comparable coverage by five or more insurance companies having the highest volume of individual health insurance premium in Illinois. Premiums paid by persons insured under CHIP averaged approximately $3,900 per year in 1992.

Premiums paid by insureds covered slightly more than 50 percent of the program's total cost during 1992, and an appropriation from the state's General Assembly was needed to fund the balance. Such annual appropriations have been necessary since the program began, due in large part to the serious health problems and medical conditions that are characteristic of CHIP enrollees.

Illinois Comprehensive Health Insurance Plan "Insurance for the Uninsurable" -2-

ICH

IP 0

1/09

/08

12:1

3

Administration

CHIP is governed by a seventeen-member board of directors, which includes the Director of Insurance as Chairman, the Attorney General, the Chairperson of the Health Care Cost Containment Council, ten public members appointed by the Governor, and four legislative members.

The administration of the program-underwriting, premium billing, claims and customer service-is done pursuant to a contract with an administrative carrier. Since January 1, 1992, Health Care Service Corporation, which does business as Blue Cross and Blue Shield of Illinois, has served in this capacity.

The board's activities are supported and managed by a small staff based in Springfield, headed by its Executive Director, Richard W. Carlson. Mr. Carlson formerly served as Assistant Director of the Illinois Department of Insurance (1981-1989) and as Superintendent ofthe Illinois State Lottery (1977-1981). Mr. Carlson is the co-author of An Introduction to the Illinois General Assembly and was on the legislative staff for the Illinois State Senate from 1969 to 1977. He was named as a Charter Member of the Samuel K. Gove Legislative Staff Intern Hall of Fame for outstanding public service by Illinois Issues magazine.

The independent accounting firm ofKPMG Peat Marwick serve as the board's independent auditor and has,

Illinois Comprehensive Health Insurance Plan

since the inception of the program, annually audited the plan's financial statements.

Robert E. Wagner, an attorney and president ofRobert E. Wagner and Associates, serves the Board as its outside legal counsel. He is a former Assistant Attorney General, and continues to serve as Special Assistant Attorney General for the Department of Insurance and the CHIP Board. He is a member of the Federation of Regulatory Counsel and maintains an active private practice in insurance regulatory law.

Ronald M. Wolf serves the board as its outside consulting actuary and is a Vice President and Principal ofTillinghast, a Towers Perrin Company, in St. Louis. He is a Fellow of the Society of Actuaries, a Member of the American Academy of Actuaries, and a Fellow of the Conference of Actuaries in Public Practice.

The board also receives substantial actuarial support from an Actuarial Advisory Committee comprised of six of the leading life and health actuaries in this state (See

Page 5). 1,his committee meets periodically to review with Mr. Wolf and members of the board's Finance Committee the results ofhis work and any recommendations he plans on making on rate adjustments or other actuarial matters prior to their submission to the board. Their contribution has been very generous and helpful in assuring the longterm financial stability and success of CHIP.

"Insurance for the Uninsurable" -3-

ICH

IP 0

1/09

/08

12:1

3

atiiiJ.JtiiUUWC.&tJ!#IQQQIUJ#I!iiitWW!i\ltili&III!UJI .. I&MII~Mii&.wllillilil!lll'\iiiWiiiiit» t#i£h)i hiA$ ,$ $

$tephen.J!/Sel~k;, Sprit1gfield; Chair. Director oflnsu'rant:&; f(j)jner. Director of ~gislativ~·Afftiirs, Office of the Governor; fonn~r.DirectorofthE! Department ofProfes• si(i.nal Regulation~ · ·

Holt~l'able Rola~d W. Burris, Chicago, li}lec~d AttorneyG~tteral of the State of llli· n()is irt l999;<p:Mvi6tl~tv served three ~~r:rris ·. as ~h~ ~1~~~4 Sta~ @o'nlptroller from 11)7~ . .~•·19~1;fortlletl)irt'1cto:t ()fthe Dlinois IJe;;.·• Ptlttment o(Ger~er£ll ServiCes. Juris Docror, Howard University J#lw School ..

J~h~ni"!JltUil~, Ro¢kfocd. Chair, ~linois H~a}th Ctire Cpst Conf,ainment Council; ·.•· President> H~alth Care •• C()nsultarit~,Inc;} President, Rockford Council for Affordable Health Care.

PUBLIC MEMBERS

Robert L. Adler, Chicago. Co-Chair, Pen;onnel Committee. Insurance Consultant; retired President & C.E.O., Associated Agencies, Inc., Chicago; past Board Chairman of Jewish Federation of Chicago; graduate of University of lllinois, DHL, Hebrew Union College.

Russell Alberding, Lake Bluff. Chair, Communications Committee. Consultant on benefit plan communication and pre-retirement planning. Retired principal, Wm. M. Mercer, Inc. Former Trustee and President, local Board of Education and Community CoHege.

CHIP Board Members

Howard J. Bolnick, F.S.A, Chicago. Chair, Finance Committee. President, Celtic Life Insurance Company; former partner, Coopers & Lybrand, specializing in actuarial consulting; Vice President, American Academy of Actuaries; Fellow of the Society of Actuaries; M.B.A. from the University of Chicago.

Raymond J. DeFilippo, R.H.U., Bloomington. Chair, Underwriting & Carrier Oversight Committee. Retired Director of Group & Health Insurance for Country Life Insurance Company; Member, Technical Advisory Panel of the Senate Select Committee on Hospital Cost Containment when original CHIP legislation was debated. Registered Health Insurance Underwriter.

Richard F. Kotz, Glencoe. Associate Corporate General Counsel & Assistant Secretary, Sears, Roebuck and Co.; Board of Directors and Executive Vice President, Mental Health Association of Greater Chicago; consultant to National Institute of Mental Health; former Glencoe Village Trustee; former President of Midwest regional group of the American Society of Corporate Secretaries and former National Board Member of the Society; graduate of Wharton School of Finance and Commerce and University of Pennsylvania Law School; M.B.A. from the American University.

Saul J. Morse, Springfield. Treasurer and Consumer Member; Chair, Grievance Committee. Vice President and General Counsel, lllinois State Medical Society; 1985 Disabled Advocate of the Year, lllinois Department of Rehabilitation Services.

Illinois COmprehensive Health Insurance Plan

Deborah Oughton, Springfield. Secretary and Consumer Member. Vice President, Keck Company, Vice President, Nevada Corporation, Legislative and Marketing Consultant, formerly Vice President, illinois Head Injury Association; Director of State Mandates Office; Deputy Director of House Republican Staff.

Bryan W. Swank, C.L.U., Waukegan. CoChair, Personnel Committee. Vice President, Swank Insurance Agency, Inc.; Senior Vice President, Statewide Insurance Company; Past-President, Independent Insurance Agents of Lake County; holds Chartered Life Underwriter. Graduate of Northern Illinois University.

(Two Public Member Vacancies)

Honorilblt! HoWiird c.-rroll, State SenatOr, Chicago. Member; SeMte Committees on Appropriatic:m; Financial Institutions; and St;ate 99v~l'flmeii~. Op~rations and Exec1.1tive Appointtrientl; .. M~mbertlllinois ~gislative Inf<>:nna1;io~ Sy~tem. Prtt<:~icing Att<Jl'tle)'; Juri$ I>()¢tl:)r, DePc8ul Univerl3ity College .()f Law.·········· ... · · · · ········· · ··· ·····

. H6n61'8bte ;rank il\fa~titlo, State Itep• resentative, Spring Valley. Member, House Committees on Aging; Agriculture and Con" servation; f\.pproprilttions "":·Public Safety; Elen'lentary B:nd. Secondary Education; andinsut• ance,B.S; lllinois State University.

Bo~toJ'tlble M&rgaret R; ParceUs, State R,ePresentative, Gl~fl.yiew. MinoritySpoke~pe:rs<>n, H()use InsuranCE! Qo'rtUrl:ittee; M:emher, ijous~. Q9l'nmittf!es on.Q<>naumer··•· f!ott!Ction;.·.

. F}xe¢q'l;iY~.; a,n~ Fit1aitcl~}lt1stitutipns; 'g,A.

l.Jni)~~~ty of~~a. / < > .••••••..• •••·•·· •• > • · ••(()pe :t<J~±PID~() ~wl:)eryacancy)

"Insurance for the Uninsurable" -4-

ICH

IP 0

1/09

/08

12:1

3

Actuarial Advisory Committee

Charles J. Sherfey, Chairman, is a past-President of the Chicago Actuarial Association. Mr. Sherfey is a Fellow of the Society of Actuaries, a Fellow of the Canadian Institute of Actuaries, a Member of the American Academy of Actuaries and a Chartered Life Underwriter. He has a Bachelor of Arts degree in Economics from the University of Nebraska and is a member of the Board of Pensions of the Presbyterian Church (USA).

MichaelS. Ahroe is a principal in the Chicago office of Milliman & Robertson, Inc., and is a Fellow of the Society of Actuaries and a member of the American Academy of Actuaries. His area of expertise is health insurance. He has assisted a variety of clients with administration and management, strategic planning and acquisitions, as well as marketing and pricing. Mr. Abroe has advised many types of organizations, such as hospitals, insurance companies, Blues Plans, HMOs and PPOs. Before joining Milliman & Robertson, Mr. Abroe was Vice President and Health Actuary at Bankers Life and Casualty where he was responsible for all actuarial aspects concerning their individual and small group health lines of business.

Paul W. Janus is Senior Vice President and Chief Actuary for Bankers Life and Casualty Company. He is a Fellow of the Society of Actuaries and a member of the American Academy of Actuaries. He has served as President of the Chicago Actuarial Association and as Chairman of the Health Insurance Association of America's Individual Insurance Committee. He is a 1961 graduate of Knox College, Galesburg, Illinois.

...

Illinois Comprehensive Health Insurance Plan

Carl F. Ricciardelli has been Vice President and Chief Actuary at Blue Cross and Blue Shield of Illinois for the past nine years. His career spans more than 35 years in management and actuarial work with a number of life and health insurers as well as in the consulting field. He is an Associate of the Society of Actuaries, a Member of the American Academy of Actuaries, and Enrolled Actuary, and a Fellow of the Life Management Institute.

Richard J. Ruppel is Vice President and Actuary for the Golden Rule Insurance Company, a position he has held since 1967. He is a member of the Society of Actuaries and the American Academy of Actuaries. He is a 1959 graduate of St. Meinrad College, St. Meinrad, Indiana and holds a Master of Science degree from Butler University, Indianapolis, Indiana.

Norman J. Zwitter is an actuary for the CNA Insurance Companies. He is a Fellow of the Society of Actuaries, Member, Academy of Actuaries, and Member of American Academy of Actuaries Health Committee. Mr. Zwitter received his Bachelor of Arts degree in Mathematics from the University ofWisconsin-Milwaukee in 1970 and is a Chartered Life Underwriter and a Fellow of the Life Management Institute .

"Insurance for the Uninsurable" -5-

ICH

IP 0

1/09

/08

12:1

3

, , I ,

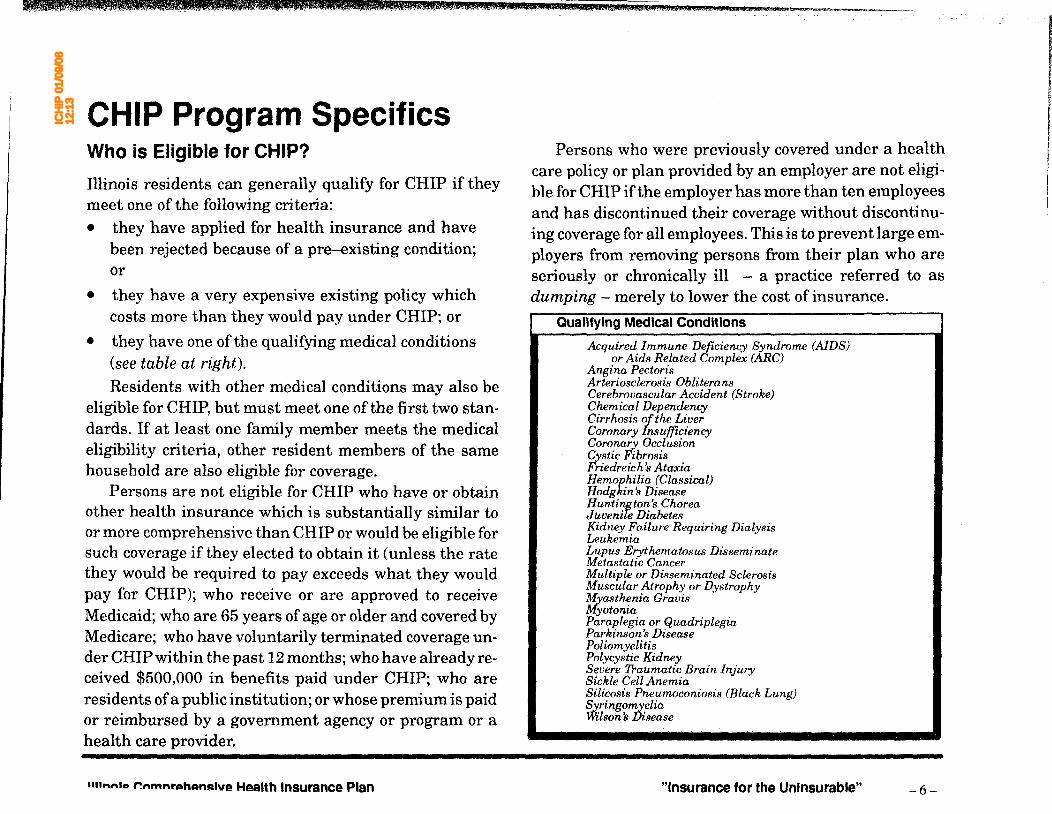

CHIP Program Specifics Who is Eligible for CHIP?

Illinois residents can generally qualify for CHIP if they meet one of the following criteria: • they have applied for health insurance and have

been rejected because of a pre-existing condition; or

• they have a very expensive existing policy which costs more than they would pay under CHIP; or

• they have one of the qualifying medical conditions (see table at right). Residents with other medical conditions may also be

eligible for CHIP, but must meet one of the first two standards. If at least one family member meets the medical eligibility criteria, other resident members of the same household are also eligible for coverage.

Persons are not eligible for CHIP who have or obtain other health insurance which is substantially similar to or more comprehensive than CHIP or would be eligible for such coverage if they elected to obtain it (unless the rate they would be required to pay exceeds what they would pay for CHIP); who receive or are approved to receive Medicaid; who are 65 years of age or older and covered by Medicare; who have voluntarily terminated coverage under CHIP within the past 12 months; who have already received $500,000 in benefits paid under CHIP; who are residents of a public institution; or whose premium is paid or reimbursed by a government agency or program or a health care provider.

am .. nlco ~nmnr~~~ohAn.!itlvA HAalth Insurance Plan

Persons who were previously covered under a health care policy or plan provided by an employer are not eligible for CHIP if the employer has more than ten employees and has discontinued their coverage without discontinuing coverage for all employees. This is to prevent large employers from removing persons from their plan who are seriously or chronically ill - a practice referred to as dumping - merely to lower the cost of insurance.

Qualifying Medical Conditions

Acquired Immune Deficiency Syndrome (AIDS) or Aids Related Complex (ARC)

Angina Pectoris Arteriosclero.'lis Obliterans Cerebrovascular Accident (Stroke) Chemical Dependency Cirrho.'lis of the Liver Coronary Insufficiency Coronary Occlusion Qystic Fibrosis Friedreich 8 Ataxia Hemophilia (Classical) Hodgkin's Disease Huntington's Chorea Juvenile Diabetes Kidney Failure Requiring Dialysis Leukemia Lupus Erythematosus Disseminate Metastatic Cancer Multiple or Disseminated Sclerosis Muscular Atrophy or Dystrophy l!fyastht:nia Gravis Myotoma Paraplegia or Quadriplegia Parkinson's Disease Poliomyelitis Polycystic Kidney Severe Traumatic Brain Injury Sickle Cell Anemia Silicosis Pneumoconiosis (Black Lung) Syringomyelia llilson 's Disease

"Insurance for the Uninsurable" -6-

ICH

IP 0

1/09

/08

12:1

3

Options for Coverage Under CHIP

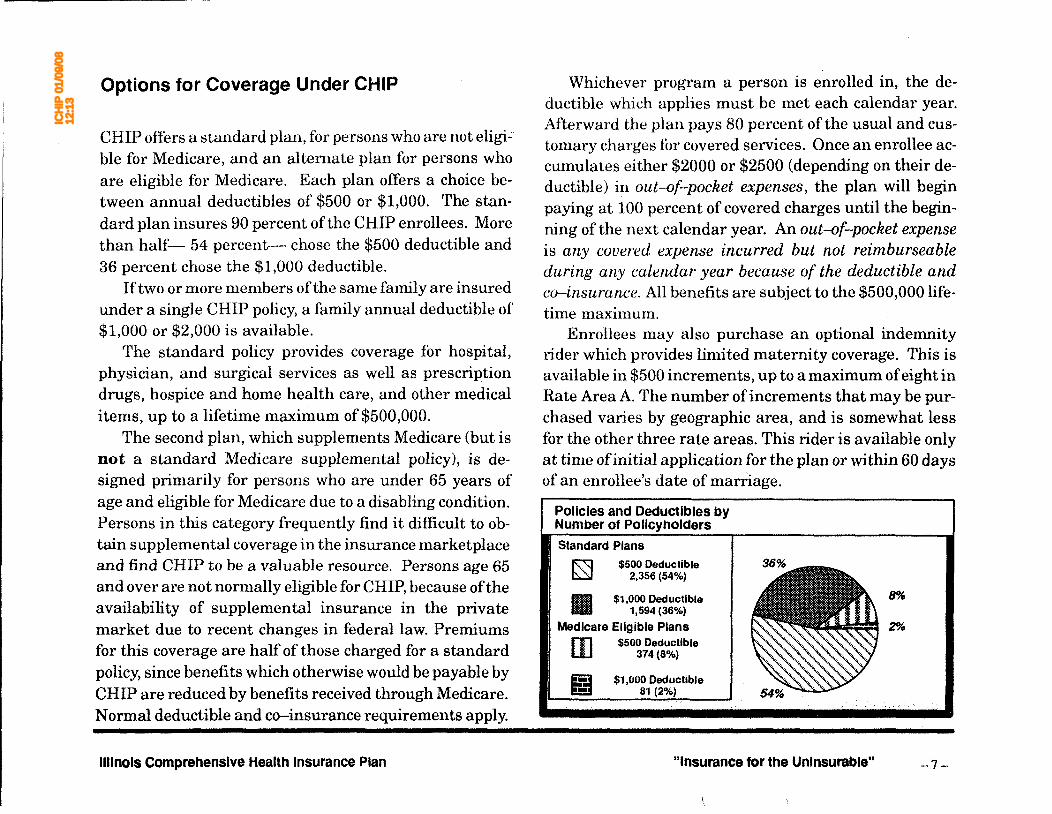

CHIP offers a standard plan, for persons who are not eligi..: ble for Medicare, and an alternate plan for persons who are eligible for Medicare. Each plan offers a choice between annual deductibles of $500 or $1,000. The standard plan insures 90 percent of the CHIP enrollees. More than half- 54 percent- chose the $500 deductible and 36 percent chose the $1,000 deductible.

If two or more members of the same family are insured under a single CHIP policy, a family annual deductible of $1,000 or $2,000 is available.

The standard policy provides coverage for hospital, physician, and surgical services as well as prescription drugs, hospice and home health care, and other medical items, up to a lifetime maximum of$500,000.

The second plan, which supplements Medicare (but is not a standard Medicare supplemental policy), is designed primarily for persons who are under 65 years of age and eligible for Medicare due to a disabling condition. Persons in this category frequently find it difficult to obtain supplemental coverage in the insurance marketplace and find CHIP to be a valuable resource. Persons age 65 and over are not normally eligible for CHIP, because of the availability of supplemental insurance in the private market due to recent changes in federal law. Premiums for this coverage are half of those charged for a standard policy, since benefits which otherwise would be payable by CHIP are reduced by benefits received through Medicare. Normal deductible and co-insurance requirements apply.

Illinois Comprehensive Health Insurance Plan

Whichever program a person is enrolled in, the deductible which applies must be met each calendar year. Afterward the plan pays 80 percent of the usual and customary charges for covered services. Once an enrollee accumulates either $2000 or $2500 (depending on their deductible) in out-of-pocket expenses, the plan will begin paying at 100 percent of covered charges until the beginning of the next calendar year. An out-of-pocket expense is any covered expense incurred but not reimburseable during any calendar year because of the deductible and co-insurance. All benefits are subject to the $500,000 lifetime maximum.

Enrollees may also purchase an optional indemnity rider which provides limited maternity coverage. This is available in $500 increments, up to a maximum of eight in Rate Area A. The number of increments that may be purchased varies by geographic area, and is somewhat less for the other three rate areas. This rider is available only at time of initial application for the plan or within 60 days of an enrollee's date of marriage.

Policies and Deductlbles by Number of Policyholders

Standard Plans

r:;::'q $500 Deductible ~ 2,356 (54%)

lllllll $1,000 Deductible - 1,594 (36%)

Medicare Eligible Plans

rn $500 Deductible 374 (8%)

E:Ef $1,000 Deductible 81 (2%)

"Insurance for the Uninsurable" -7-

ICH

IP 0

1/09

/08

12:1

3 Pre-Existing Medical Conditions

In most cases, benefits are not payable under a policy issued by CHIP for care received by an enrollee during the first six months of coverage for any condition or illness which was either manifest or for which an enrollee received medical advice or attention during the six month period prior to the effective date of coverage. After a policy has been in force for six months, conditions that preexisted the policy effective date are treated the same as any other illness.

At the inception of CHIP, any enrollee whose policy became effective during the first year of the plan's operation (May 1, 1989 to May 1, 1990) could pay a permanent 10 percent surcharge on their premiums and reduce the sixmonth waiting period to two months. The coverage that was given, however, excluded any charges for treatment of a pre-existing condition directly or indirectly related to surgery for the full six months. This option expired pursuant to Illinois law on May 1, 1990 and by that time 982 enrollees had availed themselves of it.

Another option that Illinois law permitted at plan inception was a complete waiver of the six-month exclusionary period. To qualify, applicants had to demonstrate that they had previously satisfied a similar waiting period on pre-existing conditions under another policy and that they were involuntarily terminated from their previous coverage. This option remains available in a limited number of cases. Due to a change in Illinois law, however, applicants must now also

Illinois Comprehensive Health Insurance Plan

• apply for coverage no later then 30 days following the date of their involuntary termination;

• be ineligible for continuation or conversion rights to substantially similar coverage following termination; and

• pay a permanent surcharge of up to 10 percent.

Seven new waivers were put into effect during 1992.

Self-Reported Diagnoses of Enrollees with Pre-Existing Condition Waivers

Category of Disease/Condition Number Percent

Heart Conditions 359 20% Cancer 285 16% Brain/Nervous System Conditions 182 10% Diabetes 174 10% Mental Conditions, Dependencies, etc. 120 7"k Muscular-skeletal System 117 7% Digestive System, Kidneys, Liver, etc. 101 6% Circulatory Blood Diseases 80 5% Unknown 57 3% Respiratory System Disorders 48 3% AIDS or AIDS Related Conditions 41 2% Lupus 30 2% Congenital Disorders 28 2% Other Conditions 138 7"/o

TOTAL 1,760 100.00%

"Insurance for the Uninsurable" --8-

ICH

IP 0

1/09

/08

12:1

3

How Much Does CHIP Coverage Cost?

Compliance with the 135 percent statutory requirement· is monitored through periodic review and recommendations from Tillinghast, the board's outside consulting actuary. rro develop premiums in accordance with the statutory requirement, CHIP's consulting actuaries begin by averaging the premiums charged by the five largest insurers offering individual comprehensive major medical policies in Illinois, adjusting for differences in coverage. Their recommendations are then reviewed by actuaries from the Illinois Department of Insurance and the Actuarial Advisory Committee before being presented to the board's Finance Committee and, later, to the board for final approval. Based on such reviews, rates for the CHIP program were raised once during 1992. Premiums paid by CHIP enrollees, like premiums paid to insurance companies, vary dependent upon one's age, sex, where he or she lives within the state, the type of policy and the deductible amount.

For the purpose of establishing rates, the state is divided into four geographical rate areas that reflect the differences in the cost of medical care in those areas. To be consistent with the rating practices of the insurers whose premiums are used to develop the CHIP rates, these areas were- through 1992- defined using Post Office zip codes.

During 1992, the CHIP board adopted a revised area basis for rating based on counties. The area definitions described here were in effect through 1992. The revised rate areas took effect in February of 1993.

Illinois Comprehensive Health Insurance Plan

• Rate Area A: Zip code 606. The City of Chicago and some adjacent suburbs. This is the area where health care costs and, in consequence, premiums are the highest.

• Rate Area B: Zip codes 600, 601, 602, 603, 604, 607. Suburban Cook and neighboring counties.

• Rate Area C: Zip codes 605, 611, 616, 627. Urbanized downstate areas-such as Rockford, Peoria and Springfield.

• Rate Area D: Rest of State. The remaining downstate areas of Illinois, including its rural areas. This rate area has the lowest premiums.

Annu~.l Premiums for Standard Polley With ~soo Deductible for Rate Area B

$Dollars$ 14000r-----------------------------~

D Male 12000

10000 II Female

8000 Average Premium

. 6000 v_ 4000~····• • I• io

-

2000

1 1 0 W-I~~.J_ A B C D E F G H J K

"Insurance for the Uninsurable"

AGE GROUPS

A .:30

8 30-34

c 35-39

0 41J-44

E 45-49

f50-54

G 55-511

H606-f

ltiS-4;9

J 70-74

K~ 75

-9-

ICH

IP 0

1/09

/08

12:1

3 CHIP Population Characteristics Enrollment

By statute, each year the Board of Directors is required to estimate the number of new policies it believes it has the financial capacity to issue during the year. The board must then take the necessary steps to assure that plan enrollment does not exceed the number of illinois residents which it has estimated can be insured at any one time. Accordingly, enrollment has been limited to 4,500 since 1989, a limit that was first met in February of 1990. In 1993, the CHIP board increased this cap to 4, 7 50. Persons who apply for coverage, who would otherwise qualify except for the limitation on enrollment, are placed on a waiting list. As existing insureds drop or terminate their CHIP coverage, these openings are filled with those who are at the top of this waiting list.

Since CHIP became operative in May, 1989, the cumulative enrollment through 1992 was 7,777(see chart at right). Enrollment at the end of 1992 stood at 4,405.

Applications during 1992 totaled 2,208 -an average of 184 per month and an increase of21 percent over the 1991 total of 1,832. At year-end, 877 persons were on the waiting list.

Illinois Comprehensive Health Insurance Plan

During 1992, 916 CHIP policyholders terminated or had their coverage terminated. The largest percentage of terminations is due to non-payment, as in past years. In these cases, the policies lapsed because the premiums were not paid.

Cancellations notwithstanding, persistency of policies issued by CHIP is strong, with 93 percent of policies issued in 1992 still in force at the end of the year.

Cumulative Plan Enrollment 1989-1992

Veat As of the end of 1992, nearly 8,000 Illinois citizens had at one time or another been covered by CHIP

0 1000 2000 3000 4000 5000 6000 7000 8000 9000

"Insurance for the Uninsurable" -10-

ICH

IP 0

1/09

/08

12:1

3

Enrollment Activity and Terminations

Enrollment Activity by Policy Type January 1, 1992- December 31, 1992

Slllndard $500

Applications Received 1398

Applications Approved 791 Applications Rejected 55 Applications Withdrawn 124 Applications Pended 410 Applications Incomplete 18

NUMBER INSURED AT YEAR'S END NUMBER WAIT-LISTED AT YEAR'S END

Reasons for Termination by Policyholders

Non-payment Policyholder's Request Other Coverage Death NSF Check Medicare (Under 65) Non-resident Reached Age 65 Medicaid Maximum Benefit 1G-Day Free Look Maximum Age for a Dependent

Standard $1000

695

445 21 62

161 6

518 167 108 87 13 9 5 4 2 1 1 1

916

Illinois Comprehensive Health Insurance Plan

Afed Supp MedSupp TOTALS $500 $1000

93 22 2208 57 9 1302 .· ..

4 1 81 7 2 195

24 10 605 1 25

4405 877

57% 18% 0 Non-payment 12%

125% I 9% IIIII Policyholder's Requeal 1% 1%

lSJ All-other Reaaona 1% 1% 0% 0% 0% .0%

100%

"Insurance for the Uninsurable" -11-

ICH

IP 0

1/09

/08

12:1

3 Persistency of Policies Issued

Policy per&lstency for CHIP Is worthy of note. More than 2,000 per~ 1991

Issued In-Force sons who were entoll.ed during .the plan's first year of operation

January 99 76 n% were st111 covered and 93 percent of those who became covered during 1992 were still.enrolled attbe.end of the year. Such persls· February 87 58 67% tency Is quite good by insurance Industry standards. March 125 89 71%

April 61 37 61% May 47 39 83%

1989 June 68 49 72% Issued In-Force July 88 64 73%

May 1779 863 49% August 110 86 78% June 395 187 47% September 111 89 80% July 365 170 47% October 87 75 86% August 347 149 43% November 71 56 79% September 541 250 46% December 54 48 89% October 366 162 44% November 328 147 45% TOTAL 1991 1,008 766 76% December 382 162 42%

TOTAL 1989 4,503 2,090 46% 1992 Issued In-Force

January 68 53 78%

1990 February 46 40 87% Issued In-Force March 71 64 90%

January 433 207 48% April 58 51 88%

February 139 64 46% May 57 52 91%

March 64 20 31% June 74 67 91% April 79 38 48% July 83 n 93% May 41 28 68% August 66 62 94%

June n 40 52% September 113 110 97%

July 70 38 54% October 114 111 97% August 52 32 62% November 126 125 99% September 94 44 47% December 44 44 100% October 91 51 56% I TOTAL 1992 November 82 50 61% 920 856 93%

December 124 81 65%

TOTAL 1990 1,346 693 51% I CUMULA17VE ?,r/7 4.405 51% TO.TAL

Illinois Comprehensive Health Insurance Plan "Insurance for the Uninsurable" -12-

ICH

IP 0

1/09

/08

12:1

3

Age, Sex and Geography

Age-Sex Distribution: Thirty three percent of CHIP enrollees at the end of 1992 were between the ages of 55 and 64 (see pie chart, at right). The next largest age groups into which enrollees fell are: ages 45 to 54 (21 percent); ages 35 to 44 (17 percent); ages 0 to 25 (15 percent); and ages 25 to 34 (13 percent). Only about 1 percent of CHIP enrollees are age 65 or older. Many of those in the under age 25 category are children who have serious medical conditions, many of whom require constant care, and who have been unable to obtain insurance coverage elsewhere. As for the age 65 and older category, there are now ample choices in the open market for supplemental coverage when persons become eligible for Medicare. CHIP is only appropriate at this age if a person is ineligible for Medicare.

Planwide, the split between the sexes is nearly even, with 51 percent percent female and 49 percent male.

Participation by females is lower in the younger years, evens up in the middle-aged category, and then outstrips males in the older age groups. Females comprise only 43 percent, versus 57 percent for males, of the under 25 age group. Then they even up at 50 percent with males in the 35-44 age group, and they are 58 percent of the 55-64 age category.

Illinois Comprehensive Health Insurance Plan

Age Composition and Age-Sex Distribution

CHIP Age Composition at Year-End

Age Composition By Sex at Year's End

900

800 0 Female

700 Ill Mala

600

500

400

300

200

100

0 \ 25 25-34 35-44 45-04 55-64 \65

"Insurance for the Uninsurable" -13-

ICH

IP 0

1/09

/08

12:1

3

111!~,_!1"1\l"l!l a;!_! ... ijiii!~ ! .. f!.!.!~~,! ... !. !u:!! .. ,tlli!\1111!11 p!;;: :;;!, !.s;;;;l"! ... ! .. !,!_!.ll!!~""rl"!,(I<»MJ~MI!Jf'i':fl!.&m:!i.iil ! .. !w.,.!!¥1i+A!i 4!< !, =;;;a:z .. !:; Q='l':""f\\1:, =~ +~~-=~ 14=( -========·=; ==· ;:IJ ::::::41#:;;:; :;;M 4Z;;;#lbi;;;;;;ill¥;;;U;;;;;IMI!I'I;.... __ ... _ ... ,._, -Oi---~~~~~~-ilf--l!lll_, ---;o ~-.,__.,--,...,_~~~ --

Distribution by Rate Area: Chicago and the suburban or "collar" counties (areas A and B, respectively) are home to 62 percent of the people enrolled in CHIP. The next largest group lives in downstate, rural Illinois (area D). This area accounts for 24 percent of the people enrolled in CHIP at the end of 1992

As the map at right clearly shows, CHIP is serving persons throughout Illinois. At least one person in all but three counties in Illinois was enrolled in CHIP at yearend 1992.

Distribution by Rate Area

D Area A 9.5%

Ill Area B 52.8%

~ AreaC 13.6%

sa Area 0 24.1%

Illinois Comprehensive Health Insurance Plan

Distribution by County

As of 12/31192, all but three Illinois counties had residents enrolled in CHIP.

D 400-450

CJ 300-400

rzJ 100-150

~ 50-100

[I 11-50

CJ 10 or less

• NONE

"Insurance for the Uninsurable" -14-

ICH

IP 0

1/09

/08

12:1

3 Benefits Paid to Policyholders A health insurance plan experiences a lag between the_ time an insured receives medical services and the time bills for these services are submitted by providers and finally processed for payment. For this reason, the claims that are paid by the end of any given month do not represent all of the claims which were incurred prior to the end of that month and will eventually be paid. In recognition of claims that have been incurred but not reported, a reserve is established.

During calendar year 1992, benefits totaled $26,287,468. In anticipation of claims that were not submitted by year-end, a reserve of $9.2 million was established.

The summary which appears on the next page is of paid claims only. It details how much was charged and paid by category of service.

In order to provide some insight into the nature of conditions for which treatments were received, the last table in this section provides charge and utilization information by highest utilization category for both inpatient and outpatient claims processed during 1992.

Illinois Comprehensive Health Insurance Plan "Insurance fOr the Uninsurable" -15-

ICH

IP 0

1/09

/08

12:1

3

Wiiii!NijiJQJ$@Qi£i4¥.4113 ,QiQ$Q($PkS44&J,_S;p .. ;; .. ¢; ;itiiA!\¥iiJ 4Qt;;¥4M\#¥li)IQ\.SU 4; JU ¥¥J4Z

Summary of Charges and Payments 1992

I Distribution by Benefit Category

Category

Inpatient Physician Major Medical Outpatient Coordinated Home Care Loose Bills Extended CarefSkilled Nursing Medicare Deductlbles Other/ Medical Professional

Total

4 1AWJQUW44M # 411 Ml4iiliiU.U

Benefits Paid %Benefits

$12,0!J8,186 46% 6,184,151 23% 4,108,385 160k 2,792,390 10%

722,198 3% 430,017 2%

31;131 0% 20;823 0% 682.68 0%

$26,388,56:'1* 100%

• Total does not reflect adjustments of prior claims or other subsequent adjustments and thus will differ from the financial statement at the end of this report.

Payments of 26.3 million to CHIP insureds during 1992 brought the total of payments since 1989 to $75,628,613.

Illinois Comprehensive Health Insurance Plan

Ill

• D

ml

Inpatient

Physician

M~or Me leal

Ou~atlent/ ther

Where were they treated?

ER

Fifty-six percent of charges incurred in 1992 were for services rendered in an inpatient setting.

"Insurance for the Uninsurable" -16-

ICH

IP 0

1/09

/08

12:1

3 Twenty-Five Top Diagnoses by Utilization Rate Inpatient Claims Processed in 1992

Admits Daya per per Average Provider

Primarl£ Diaanoaia Admits 1,000 D•X! lo!&!! ~Q.li Cbergea

Coronary Atherosclerosis 47 10.5 204 45.5 4.3 590,814 Chest Pain Unspecified 44 9.8 80 17.8 1.8 152,569 Congestive Heart Failure or Disease 38 8.5 232 51.7 6.1 399,569 Acute Pancreatitis Abcess of Pancreas 31 6.9 246 54.9 7.9 492,924 Pneumonia Organism Unspecified 29 6.5 100 22.3 3.4 207,278 Diabetes w/ Unspecified Complications 28 6.2 67 14.9 2.4 6S,91'2 Coronary Insufficiency Syndrome 27 6.0 72 16.1 2.7 207,327 Pneumocystosls 27 6.0 108 24.1 4.0 242,729 Fracture of Unspecified Bones Clo~ 25 5.6 45 10.0 1.8 124;483 Abdominal Epigastric Umbilical Pain 24 5.4 51 11.4 2.1 74,732 Depressive Disorder Recurrent ~isode 24 5.4 177 39.5 7.4 170,139 Involutional Melancholia Single pisode 24 5.4 205 45.7 8.5 160,804 Liver Cirrhosis Portal Cirrhosis 24 5.4 45 10.0 1.9 263,373 Chemotherap~ Session 23 5.1 83 18.5 3.6 141,845 H~povolemia luid of Plasma Depletion 22 4.9 56 12.5 2.5 94,868 Idiopathic Thrombocythemia Panm~etoais 17 3.8 29 6,5 1.7 101,282 Urina~ Tract Infection Site Unspecified 17 3.8 106 23.6 6.2 212,437 Acute yocardlallnfarct Anterior Wall · 16 3.6 70 15.6 4.4 193,714 Syncope Falnlln~ Vasovagal Atteck 16 3.6 32 7.1 2.0 63,052 Cystic Fibroais 0 Meconium Ileus 15 3.3 84 18.7 5.6 121,425 Diabetic Acidosis WO Coma Juvenile Type 15 3.3 41 9.1 2.7 71,882 Regional Enteritis Chrons Dis Unap Site 15 3.3 47 10.5 3.1 63,332 Cerebral Infarction Unspecified 14 3.1 48 10.7 3.4 77,063 Convulsions Convulsive Seizure Disorders 14 3.1 12 2.7 .9 24,818 Displaced Lumbar Intervertebral Disc 14 3.1 59 13.2 4.2 89,516

Fifteen Top Diagnoses by Utilization Rate Outpatient Claims Processed In 1992

Admits per Provider

Primarx Diasnoaia Admits '•!!l!! ~blt5ill

Chronic Kidney Failure Chronic Uremia 307 68.5 734,574 Malignancy Female Breast Unsp SUe 213 47.5 127,027 Abdomina Epigastric Umbilical Pain 168 37.5 72,231 Other Physical Therapy Remedial Exercise 151 33.7 29,905 Diabetes Mellitus Adult Onset 140 31.2 16,333 ConviJisi<ma Convulsiv• Seizur• Disorder• 133 29.7 ' 30,483 Cheat Pain Unspecified 130 29.0 58,907 Kidney Tr!lnaplant Recipient 129 28.8 65,077 L•ul«nnil! Ba•QphUic EQS!no~~hillc Chronic 123 27.4 26;672 Coronaa; Atherosclerosis A HD 122 27.2 82,756 Follow p Exam Aft•r s:rwy 115 25.6 58,529 Heart Disease Un•pecifl 95 21.2 23,172 Anemia NEC NOS 92 20.5 41,816 Leukemia Chronic LymGhatlc Ly,mphocytlc 88 19.6 39,187 Backache Unspecified ack Pa n 78 17.4 27,303

Illinois COmprehensive Health Insurance Plan "Insurance for the Uninsurable" -17-

ICH

IP 0

1/09

/08

12:1

3 Cost Containment Illinois law permits CHIP to implement cost containment measures, which are especially critical for state subsidized health care programs since they serve to minimize the need for deficit funding.

The administrative agreement entered between CHIP and Blue Cross and Blue Shield of illinois provides for fixed administrative fees per insured and also allows CHIP to receive a discount on all claims paid by this administrator.

CHIP enrollees are all issued CHIP Blue Cross and Blue Shield identification cards. This facilitates quick admission for them to hospitals under contract with Blue Cross, and allows- in many cases- for hospital bills to be submitted electronically to the plan administrator. It also has allowed several CHIP enrollees with recurrent breast cancer, who have met specific medical criteria on a case-by-case basis, to participate in a clinical trials program of the National Cancer Institute involving autologous bone marrow transplantation (ABMT). While this procedure is currently not a covered expense under a CHIP policy, the plan administrator, Blue Cross and Blue Shield oflllinois, is providing financial assistance for this particular medical research program. In connection with this program, Blue Cross and Blue Shield of Illinois has made sizeable contributions from its corporate funds on behalf of several CHIP enrollees. These were not insurance benefits, and were not paid out of any CHIP or State of illinois funds.

Illinois Comprehensive Health Insurance Plan

CHIP requires pre-admission review of all hospital and skilled nursing facility confinements and medical management of all large cases. Penalties for non-<:ompliance with pre-admission review requirement are spelled out in the CHIP policy, and may involve benefit reductions or, in some cases, denial of payment for hospital charges.

Admission pre-certification is conducted for CHIP by the plan administrator, Blue Cross and Blue Shield of Illinois. Reports from the Medical Services Advisory Program for 1992 show that a reduction of the number of hospital days by 203 resulted in a savings of$108,733.

CHIP also requires prior approval for benefits payable for certain durable medical equipment, hospice and home health care services and specified organ transplants.

"Insurance for the Uninsurable" -18-

ICH

IP 0

1/09

/08

12:1

3 Summary of Operations

Illinois Comprehensive Health Insurance Plan Year Ended December 31,1992

Plan Income: Net Written Premiums Less: Unearned Premiums Net Earned Premiums Investment Income

Total Plan Income

Plan Expenses: Paid Losses Incurred But Not Reported Total Incurred Losses

Agent Referral Fees Administrator Expenses CffiP Board Office Expenses Total Administration Expenses

Total Plan Expenses

$15,723,361 (464,271)

23,224,932 2,000,000

18,900 968,011

1,004,721

Plan Deficit January 1, 1992 -December 31, 1992

Illinois Comprehensive Health Insurance Plan

$15,259,090 1,717,722

$16,976,812

$25,224,932

$1,991,632

$27,216,564

$(10.239.752)

"Insurance for the Uninsurable" -19-

ICH

IP 0

1/09

/08

12:1

3

Printed by Authority of the State of illinois lOC 9/93 '

Related Documents