Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

[1]

A G E N D A I T E M S

ITEM SUBJECT PAGE NO.

I CONFIRMATION OF THE MINUTES OF THE 51st SLBC MEETING HELD

ON THE 14th FEBRUARY 2015 2

II ACTION TAKEN REPORT ON THE 51st SLBC MEETING 3-4

KEY INDICATORS 5

III REVIEW OF PERFORMANCE UNDER ANNUAL CREDIT PLAN: 2014-15 6-7

LBS:STRENGTHENING OF MIS 7

IV BRANCH OPENING 2014-15 8

V EDUCATION LOAN 8

HOUSING LOAN 8

VI PM’S NEW 15 POINT PROGRAMME FOR THE WELFARE OF THE MINORITIES 9

VII PRADHAN MANTRI JAN-DHAN YOJNA 10

VIII

GOVERNMENT SPONSORED SCHEMES/ PROGRAMMES 11

(A) PRIME MINISTER’S EMPLOYMENT GENERATION PROGRAMME (PMEGP) 11

(B) NATIONAL URBAN LIVELIHOOD MISSION (NULM) 11

IX FINANCING TO SELF HELP GROUP 12

JOINT LIABILITY GROUP 12

X

XI

KISAN CREDIT CARD (KCC) 13-14

CROP INSURANCE SCHEME 14

DAIRY, FISHERY AND POULTRY 15

FARM MECHANISATION 15

ADVANCE GRANTED TO UNITS PROVIDING STORAGE FACILITY 15

AGRICULTURE TERM LOAN (ATL) 15

XII

CD RATIO 16

RECOVERY 17

NPA , WRITE-OFF AND CERTIFICATE CASES 17-18

PRIORITY SECTOR LENDING, AGRI CREDIT, DRI SCHEME & WEAKER SECTION 18-19

XIII OPENING OF NO FRILL ACCOUNTS AND TRANSACTIONS DONE BY BCAs 20

EXTENDING MOBILE BANKING AND INTERNET BANKING FACILITY 20

XIV IMPLEMENTATION OF FINANCIAL INCLUSION PLANS IN LWE AFFECTED DISTRICTS 21

XV INVESTIGATION OF CYBER FRAUD & COUNTERFEIT NOTES DETECTED BY BANKS 22

XVI FUNCTIONING OF RURAL SELF EMPLOYMENT TRAINING INSTITUTEs (RSETIs) 22-23

XVII FINANCIAL LITERACY INITIATIVES 24

XVIII

MEDIUM & SMALL ENTERPRISES 25

SMALL ROAD TRANSPORT OPERATORs (SRTOs) 25

ADVANCES GRANTED UNDER CGTMSE COVERAGE 25

MANUFACTURING SECTOR 25

XIX WEAVERS CREDIT CARD 26

FOOD PROCESSING UNITS 26

XX SECURITY RELATED CONCERN OF BANKS 27

XXI SPECIAL CENTRAL ASSISTANCE (SCA) TO SPECIAL COMPONENT PLAN (SCP)

FOR SCHEDULED CASTES 27

XXII MISCELLANEOUS

ISSUES

REGISTRATION OF SECURITY INTEREST WITH CERSAI 28

ESCALATION IN STAMP DUTY PAYABLE ON SECURITY DOCUMENTS

28

[2]

STATE LEVEL BANKERS’COMMITTEE

52ND REVIEW MEETING

NOTES ON AGENDA ITEMS

CONFIRMATION OF MINUTES OF THE

51ST STATE LEVEL BANKERS' COMMITTEE MEETING

HELD ON 14.02.2015

The House may please confirm the Minutes of the 51st State Level Bankers’ Committee

meeting held on the 14th February, 2015.

AGENDA-I

[3]

ACTION TAKEN REPORT ON THE ACTION POINTS OF 51ST SLBC MEETING HELD ON 14.02.2015 AT PATNA

[1] ACTION POINT Banks should put in concerted efforts to ensure achievement of 100% target set under ACP for 2014-15.

(Action: All Banks)

ACTION TAKEN: - Due to sincere efforts made by Banks in the State, ACP achievement during FY 2014-15, has been to the tune of 92.97% of the annual target as against

91.95% achieved during 2013-14. In absolute terms 21% increase in disbursement is observed in 2014-15 over previous year’s corresponding figure.

[2] ACTION POINT – Banks should give focus on issuance of new and renewal of KCC

and also increase financing in other Agri. Areas such as Dairy, Fishery and other allied activities in order to achieve the ACP target for Agri. Segment.

(Action: All Banks)

ACTION TAKEN: During the FY 2014-15, Banks in the State have extended credit to the tune of Rs.34680 Cr under Agriculture segment as compared to Rs. 28770 Cr provided during the same period last year, thus registering a growth of 21%. [3] ACTION POINT – Banks to ensure achievement of branch opening target under Financial Year 2014-15. Proposed centres for branch opening during March 2015 to be

provided to State Govt to sort out premises issues. (Action: All Banks)

ACTION TAKEN: -The Banks in the State have opened 389 branches during the FY 2014-15 out of which 181 has been opened in rural area.

[4] ACTION POINT – Private Banks to focus on education loans and housing loan in

order to achieve their current year annual target. (Action: Concerned Private Sector Banks)

ACTION TAKEN: - The private sector Banks in the State have sanctioned 95 education loan & 837 housing loans during the FY 2014-15 which is 22% & 44% respectively of their target .

[5] ACTION POINT – Banks to ensure issuance of acknowledgement on receipt of loan application form from borrowers. Checklist of documents required to process the loan

should also be enclosed with the application form. (Action: All Banks)

ACTION TAKEN: - Banks have started issuing acknowledgement of loan application. Checklist are also provided with the application form.

[6] ACTION POINT – Details of incentive mechanism for KCC recovery adopted by Uttar Pradesh Govt. to be obtained and put up for discussion.

(Action: State Government) ACTION TAKEN: - The State Govt. is requested to provide the Details of incentive

mechanism for KCC recovery adopted by Uttar Pradesh Govt.

AGENDA-II

[4]

[7] ACTION POINT – Rupay cards to be issued to all eligible farmers, while issuing and renewal of KCC.

(Action: All Banks)

ACTION TAKEN: -. The Banks have issued 749742 ATM cards to farmers up to March

2015. All Banks are requested to issue Rupay Cards to all the eligible KCC borrowers.

[8] ACTION POINT – Banks to achieve target under PMEGP and claim of margin money to be expedited. (Action: All Banks)

ACTION TAKEN: The Banks have sanctioned 3087 PMEGP loans during FY 2014-15.

[9] ACTION POINT - Banks to give more focus on advances under DRI schemes to achieve the benchmark of 1% of total aggregate advances during the previous year.

(Action: All Banks) ACTION TAKEN: During 2014-15 Rs. 49.86 Cr was disbursed by banks under DRI scheme which is 0.07 % of the total advances of Rs.66568.11Crore as on 31.03.2014.All

banks are requested to give adequate attention on this area and achieve the benchmark of 1% of total advances under DRI scheme.

[10] ACTION POINT – Notification on Waiver of Stamp duty on JLG loan Agreement to

be issued. (Action: State Government)

ACTION TAKEN: The matter is still unresolved. The State Govt. is requested to issue the notification on Waiver of Stamp duty on JLG loan Agreement.

[11] ACTION POINT – Workshop to be organised with Revenue Deptt, Govt of Bihar for speedy disposal of certificate cases in all districts.

(Action: State Government) ACTION TAKEN: Workshop organized, if any, has not been brought to the notice of

SLBC, Bihar. The State Govt. is requested to direct to concerned authorities to organise the workshop for speedy disposal of certificate cases in all districts.

[12] ACTION POINT – Banks to ensure updation of register 9 &10 related to certificate cases for faster disposal of certificate cases.

(Action: State Government)

ACTION TAKEN: Updation of register 9 & 10 is taking place. Banks are requested to

bring into notice of SLBC any difficulty faced by them in this regard.

[13] ACTION POINT – Notification to be issued by the State Govt. with regard to implementation of Interest Subvention scheme in the accounts of Self Help Groups, in

the 27 non-IAP districts, on the same line as in the 11 IAP districts. (Action: State Government)

ACTION TAKEN: Notification on the matter is still awaited from State Govt.

[14] ACTION POINT – Banks to ensure use of common format for account opening & 1st dose credit linkage of SHGs.

(Action: All Banks) ACTION TAKEN: Most banks have started using the common format but confirmation from all the banks is still awaited. All banks to confirm the use of common format for the

purpose.

[5]

STATE LEVEL BANKERS’ COMMITTEE, BIHAR KEY INDICATORS

(ALL BANKS)

(Rs. in Crore)

Sl.

No.

ITEMS MARCH’14 MARCH’15 Bench

-mark

1 DEPOSITS 183458.24 211302.05

2 ADVANCES 66687.77 79640.10

3

ADVANCES INCLUDING ADVANCES

GRANTED TO UNITS IN BIHAR BY

BRANCHES OPERATING OUTSIDE

BIHAR

74717.83 88459.61

4 ADVANCES INCLUDING RIDF 78678.00 93027.61

5 CD RATIO 42.89 44.03%

6 PRIORITY SECTOR ADVANCES 48005.69 55481.85

7 SHARE OF PSA IN TOTAL ADV

(SL.NO.2)(%) 71.99% 69.67% 40%

8 AGRICULTURAL ADV. 25379.65 30652.12

9 SHARE OF AGL. ADV IN TOTAL ADV

(SL.NO.2) (%) 38.06% 38.49% 18%

10 MSE ADV. 11042.33 13594.02

11 SHARE OF MSE ADV. IN PSA (%) 23.00% 24.50%

12 ADV. TO WEAKER SEC. 17510.92 20973.47

13 SHARE OF WEAKER SEC. IN PSA (%) 36.48 37.80% 25%

14 DRI ADV. 72.36 49.86

15 SHARE OF DRI ADV TOTAL ADV

(Sl.No.2) of March (%) 0.11% 0.06% 1%

16 ADV. TO WOMEN (DISBURSEMENT) 4444.90 5039.84

17 SHARE OF ADV. TO WOMEN IN

DISBURSEMENT (%) 7.79% 7.32% 5%

18 TOTAL NUMBER OF BRANCHES 5908 6297

A RURAL 3468 3649

B SEMI-URBAN 1362 1454

C URBAN 1078 1194

[6]

REVIEW OF PERFORMANCE UNDER ACP DURING THE

FINANCIAL YEAR 2014-15 UP TO MARCH’2015

The performance of Banks under the Annual Credit Plan 2014-15 up to March’2015, is as

under:- (Rs. in Crore)

Sector-wise break-up of targets and achievement: (Rs. in Crore)

Bank-wise and district-wise position is furnished on Page- 7A to 7D.

COMPARATIVE PERFORMANCE UNDER ACP

As on Mar’ 2014 vis-a-vis Mar’ 2015

(Rs. in Crore)

Banks

2014-15 2013-14 YOY

increase

in disb.

(%)

Target Ach. %

Ach Target Ach.

%

Ach

Comm 57166 52250 91.40 47938 43573 90.90 20%

Co-op 1003 362 36.07 802 310 38.64 17%

RRBs 15831 16185 102.24 13260 13124 98.98 23%

Total 74000 68797 92.97 62000 57007 91.95 21%

Banks Target Achievement % Ach.

Comm. Banks 57166 52250 91.40

Co-op. Banks 1003 362 36.07

RRBs 15831 16185 102.24

Total 74000 68797 92.97

Sector Target Achievement % Ach.

Agriculture 36000 34680 96.33

SME 8500 8875 104.40

OPS 7500 6484 86.45

TPS 52000 50038 96.23

NPS 22000 18759 85.27

Total 74000 68797 92.97

AGENDA-III

[7]

SECTOR-WISE PERFORMANCE:

(Rs. in Crore)

Sector

2014-15 2013-14 YOY

increase

in disb.

(%)

Target Ach. % Ach Target Ach. % Ach

Agl. 36000 34680 96.33 30286 28770 95.00 21%

MSE 8500 8875 104.40 4821 6238 129.40 42%

OPS 7500 6484 86.45 5723 4978 86.98 30%

TPS 52000 50038 96.23 40830 39986 97.93 25%

NPS 22000 18759 85.27 21170 17022 80.40 10%

Total 74000 68797 92.97 62000 57007 91.95 21%

The overall achievement of target during the period under review is 92.97%, as against

91.95% recorded during last year. In absolute terms, Banks have disbursed substantially

higher quantum of loan (68797 Cr. i.e 121% of last year) during the period under

review, than that of last year. It may be observed that the Commercial Banks & RRBs

have recorded impressive growth in their loan disbursements vis-a-vis their performance

over the same period last year. sector-wise performance growth in all segments except

NPS, has been quite healthy.

LEAD BANK SCHEME: STRENGTHENING OF MONITORING INFORMATION

SYSTEM (MIS)

In terms of RBI’s instructions in this regard, the LBS MIS- I, II & III of the state has

been prepared and is placed at page No. 7E to 7H of the Agenda Book for information of

the House.

LBS-IV and V which relates to financial inclusion, is also placed at page no. 7I to 7 P of

the Agenda Book.

The target for the current financial year has been fixed and circulated among all

concerned. A copy of target under LBS I,II & III for FY 2015-16 is placed at page no. 28G to 28AJ for information of the House.

ANNUAL CREDIT PLAN: 2015-16 TARGET 2015-16

The ACP of the state for FY 2015-16 has been decided to be Rs.84000 Crore which is 13.51% increase over last year’s target of Rs 74000 Cr.

On the basis of deliberations held during the meeting organised in this regard, the ACP

has been disaggregated and circulated among all concerned.

The Bank-wise and district-wise ACP of FY 2015-16 is placed at page No. 28A to

28F of the Agenda Book for information of the house.

[8]

PROPOSED BRANCH OPENING DURING FY 2014-15 Against the annual target of opening of 600 branches, in 2014-15 all Banks have opened

389 branches during the year.

The Bank-wise target and achievement during the FY 2014-15, is placed at page No. 8A for information of the House.

While opening the brick & mortar branches in rural areas during the current year all Banks are requested to give preference to unbanked villages having population of 10000

& above a detailed list of which has already been provided.

The Bank & District-wise information on Branch Network, ATM Network, ATM Card issued

and Point of Sale Terminals is placed at Page No. 8B & 8C for information.

The Minutes of the 24th Sub-committee meeting on Branch Opening and IT enabled financial inclusion held on 23.03.2015 is placed at page no. 8D to 8F for information of the House.

EDUCATION LOAN

Providing Education loan to the meritorious and needy students to enable them meet the

expenses of higher studies not only in the State but also outside the State in India and abroad is one of the priorities of the Banks in the state.

A copy of the Bank-wise target and achievement thereagainst is placed at page No. 8G

of the Agenda Book.

During the FY 2014-15, Education Loan amounting to Rs 870.56 Crores was sanctioned

to 25229 students and loan amounting to Rs. 805.30 Crore were disbursed among 25096 students. The achievement of all banks taken together is 50.46% of the targets

allocated. Controlling Head of all banks are requested to give focussed attention to financing under Education Loan in order to cover all the deserving student.

The bank-wise data on outstanding amount of Education loan as on 31.03.2015 is placed at page no.8H of Agenda Book.

Major Private Sector banks’ performance under education loan is below 5%.

The Bank-wise and district-wise target of FY 2015-16 has been fixed and circulated

among all concerned. A copy of target of FY 2015-16 is placed at page no. 28AG to 28AH for information of the House.

HOUSING LOAN

Loan amounting to Rs.2322.39 Crore was sanctioned to 14641 beneficiaries by Banks during the FY 2014-15, which shows an achievement of 61%of the target allocated. Out

of these, Housing Loan amounting to Rs. 2233.79 Cr has been disbursed among 14496 beneficiaries. The Bank-wise performance during the review period is placed at Page No. 8I.

The Bank-wise and district-wise target of FY 2015-16 has been fixed and circulated among all concerned. A copy of target of FY 2015-16 is placed at page no. 28AI to 28AJ

for information of the House.

AGENDA-V

AGENDA-IV

[9]

PM’S NEW 15-POINT PROGRAMME FOR WELFARE OF MINORITY COMMUNITY

In accordance with the guidelines issued by the Government of India in this regard,

Banks have to ensure that within the overall target for Priority Sector lending (PSA),

15% of PSA is provided to Minority Communities.

With this objective in view, 121 minority concentrated districts in the country have been

identified exclusively for monitoring the credit flow to minority communities. In Bihar,

the following seven districts are identified for the purpose :-(i) Kishanganj (ii) Araria

(iii) Purnea (iv) Katihar (v) Sitamarhi (vi) Darbhanga and (vii) West Champaran .

In these identified districts, total priority sector loans (PSA) outstanding as on

31.03.2015 was Rs 8060.03 Crore (No. of borrowers: 959831) out of which loans

amounting to Rs.3790.36 Crore (47% of PSA) were provided to 419653 (44%of PSA)

borrowers belonging to minority communities. The amount provided to minority

communities by banks in the above mentioned districts ranges from 31 to 77%. Thus, all

the districts have achieved the target of providing more than 15% of their priority sector

loans to persons belonging to minority communities.

District-wise performance regarding loans extended to minority communities in the

identified districts is furnished below.

LENDING TO MINORITY COMMUNITIES

AS ON 31st March’2015 (Amt. in Lacs)

SL. No.

Minority

Concentrated Districts in

Bihar

Priority Sector Advance

Out of (A) Total Advances to Minority

%age Share of Minority

Advance ( B to A ) (A) (B)

No. Amt. No. Amt. No. Amt.

1 ARARIA 76760 77170 59022 47073 74 61

2 PURNEA 145535 144726 62580 62232 43 43

3 KATIHAR 208615 112226 60498 47135 29 42

4 KISHANGANJ 77165 60325 57873 46450 75 77

5 DARBHANGA 212065 176224 93308 88112 44 50

6 SITAMARHI 89365 98225 23235 30449 26 31

7 W CHAMPARAN 150326 137107 63137 57585 42 42

TOTAL 959831 806003 419653 379036 44 47

AGENDA-VI

[10]

PRADHAN MANTRI JAN-DHAN YOJANA

Three Social Security Schemes were launched by the Hon’ble Prime Minister on

09.05.2015 as a second phase of PMJDY.

PRADHAN MANTRI SURAKSHA BIMA YOJNA Under the scheme, persons having savings bank account and aged between 18 to 70 yrs

can be insured for a sum of Rs.2.00 lacs against accidental death on a payment of small premium of Rs.12/-per year. The coverage is available also in case of complete or partial

disability. The premium is to be debited automatically from the SB A/C on the basis of authorisation by the customer. The insurance is effective from 1st June to 31st May each year and is renewable.

PRADHAN MANTRI JIVAN JYOTI BIMA YOJNA

This scheme also provides an insurance coverage at very low premium. Under the scheme any saving bank account holder aged between 18 to 50yrs can be insured for a

sum of Rs.2.00 lacs against death on a payment of yearly premium of Rs.330/-.The premium is to debited from his saving account. The insurance will be valid from 1st June

to 31St May each year and is renewable. ATAL PENSION YOJNA

Persons aged between 18 to 40yrs not having any social security coverage are eligible

under this scheme. The scheme is mainly targetted to workers of unorganised sector.After attaining the age of 60yrs the contributor will get a pension between 1000 to 5000 P.M. depending upon his monthly contribution.After the death of pensioner and

his spouse their nominee will be paid a lump-sum amount.

EXTENSION OF BANKING SERVICES TO ALL THE REMAINING UNBANKED VILLAGES IRRESPECTIVE OF POPULATION CRITERIA BY MARCH, 2016:

Reserve Bank of India has instructed for providing banking facilities in all the remaining unbanked villages irrespective of population criteria i.e. all villages with population below

2000 by August’2015 instead of earlier guidelines to cover by March’2016. All Banks have submitted their Roadmap for providing banking services in villages with population

below 2000. The total No. of such identified villages is 27343. Till March’2015 25620 such villages as against the target of 20018 villages were covered by the Banks. Bank-wise allotment and progress as on 31.03.2015 is placed at Page No10A for

information of the House.

AGENDA-VII

[11]

GOVT. SPONSORED SCHEMES/ PROGRAMMES

(A) PRIME MINISTER’S EMPLOYMENT GENERATION PROGRAMME (PMEGP)

Against the physical target of 7648 projects for FY 2014-15, Banks have sanctioned

3087 projects amounting to Rs. 201.18 Cr, which is 40% of the target. The information

regarding loan sanctioned & disbursed by Banks is provided on Page No. 11A of the

Agenda Book for information of the House.

Banks in the state could not debit the margin money to the tune of Rs. 32.27 Cr before

30.04.2015(the extended timeline for debiting margin money) for 1231 projects

sanctioned till 30.03.2015 for want of fund. KVIC has advised vide their letter no.

DB/PMEGP/Target Allocation/2015-16/592 dated: 05.05.2015 (placed at 11B) that the

margin money of these 1231 projects is to be adjusted from the fund allotted to the

state for the year 2015-16.

The Bank-wise and district-wise target of FY 2015-16 has been fixed and circulated

among all concerned. As Rs. 32.27 crores is to be adjusted for the 1231 proposals

sanctioned & disbursed by the banks in 2014-15, from Rs. 90.72 crores of

margin money allocated for the state for 2015-16, the remaining Rs. 58.44

crores has been distributed among banks/districts against the state target of

4245 for the year 2015-16. A copy of target of FY 2015-16 is placed at page no. 28AK

to 28AL for information of the House.

(B) NATIONAL URBAN LIVELIHOOD MISSION (NULM)-SELF EMPLOYMENT

PROGRAMME

Urban SHGs are to be provided financial support under the National Urban Livelihood

Mission (NULM) and the target in this regard has been given to the state by Govt. of

India. In 42 Urban Local Bodies (ULBs) the state has been given target for financing

under Self Employment Program (SEP), Social Mobilization & Institution Development

(SM&ID) and Support to Urban Street Vendors (SUSV).

As allocation of wards has been done among the banks, the applications pertaining to a

specific ward should be disposed by the bank/bank branch which has responsibility of

the ward.

AGENDA-VIII

[12]

FINANCE TO SELF HELP GROUPS (SHGs)

SHGs play a very crucial and effective role in providing timely and adequate credit and other

financial services to the vulnerable and weaker sections resulting in overall economic

development of the society and Banks play a facilitating role through credit linkages to them.

Banks have opened savings bank account of 116952 SHGs and have credit-linked 51403

SHGs during the financial year 2014-15, with total Bank-finance of Rs. 283.52 Crore. Bank

wise SHG savings and credit-linkage during 2014-15 is furnished on Page 12A.

The Reserve Bank of India has already advised the detailed guidelines for

operationalisation of the Interest Subvention Scheme under NRLM for SHG credit. All

Banks are requested to provide the stipulated interest- subvention to all eligible SHG

accounts.

The Minutes of the 24th Sub-committee meeting on SHGs and RSETI held on 23.03.2015

is placed at page no. 12C to 12E for information of the House.

The Bank-wise and district-wise target of FY 2015-16 has been fixed and circulated

among all concerned. A copy of target of FY 2015-16 is placed at page no. 28AM to

28AN for information of the House.

JOINT LIABILITY GROUP

Against the yearly target of 50,000 units, Banks have sanctioned 50296 number of JLGs

amounting to Rs. 562.93 Crores which is 100% of the annual target during F.Y. 2014-

15. The RRBs have performed much better than the Commercial Banks with regard to

credit linkage of JLGs & SHGs. As SHG & JLG are important tools to reach the so far

financially excluded rural people, all Banks are requested to reach out of the weaker

sections of the society through these two routes during 2015-16.

The Bank-wise performance under JLG is placed at Page No 12B for information of the

House.

The Bank-wise and district-wise target of FY 2015-16 has been fixed and circulated

among all concerned. A copy of target of FY 2015-16 is placed at page no. 28AO for

information of the House.

AGENDA-IX

[13]

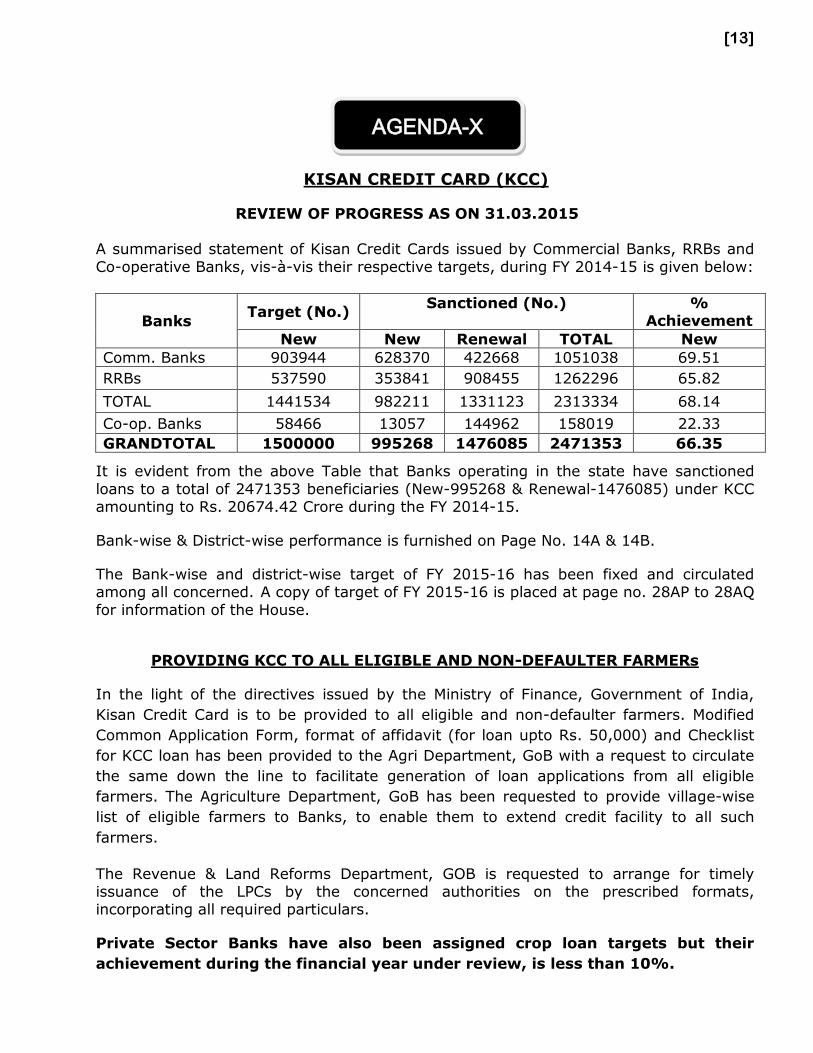

KISAN CREDIT CARD (KCC)

REVIEW OF PROGRESS AS ON 31.03.2015

A summarised statement of Kisan Credit Cards issued by Commercial Banks, RRBs and

Co-operative Banks, vis-à-vis their respective targets, during FY 2014-15 is given below:

Banks Target (No.)

Sanctioned (No.) % Achievement

New New Renewal TOTAL New

Comm. Banks 903944 628370 422668 1051038 69.51

RRBs 537590 353841 908455 1262296 65.82

TOTAL 1441534 982211 1331123 2313334 68.14

Co-op. Banks 58466 13057 144962 158019 22.33

GRANDTOTAL 1500000 995268 1476085 2471353 66.35

It is evident from the above Table that Banks operating in the state have sanctioned

loans to a total of 2471353 beneficiaries (New-995268 & Renewal-1476085) under KCC amounting to Rs. 20674.42 Crore during the FY 2014-15.

Bank-wise & District-wise performance is furnished on Page No. 14A & 14B.

The Bank-wise and district-wise target of FY 2015-16 has been fixed and circulated among all concerned. A copy of target of FY 2015-16 is placed at page no. 28AP to 28AQ

for information of the House.

PROVIDING KCC TO ALL ELIGIBLE AND NON-DEFAULTER FARMERs

In the light of the directives issued by the Ministry of Finance, Government of India,

Kisan Credit Card is to be provided to all eligible and non-defaulter farmers. Modified

Common Application Form, format of affidavit (for loan upto Rs. 50,000) and Checklist

for KCC loan has been provided to the Agri Department, GoB with a request to circulate

the same down the line to facilitate generation of loan applications from all eligible

farmers. The Agriculture Department, GoB has been requested to provide village-wise

list of eligible farmers to Banks, to enable them to extend credit facility to all such

farmers.

The Revenue & Land Reforms Department, GOB is requested to arrange for timely issuance of the LPCs by the concerned authorities on the prescribed formats, incorporating all required particulars.

Private Sector Banks have also been assigned crop loan targets but their

achievement during the financial year under review, is less than 10%.

AGENDA-X

[14]

ISSUANCE OF ATM CARDS TO KCC HOLDERS

As per RBI instructions, all KCC borrowers are to be issued ATM cum Debit Cards. The

Bank-wise information on ATM Cards issued to KCC borrowers is placed at Page No 14C of the Agenda Book for information of the House. All Banks are requested to ensure that

ATM cards are issued to all eligible KCC borrowers both at the time of new sanction as well as at the time of renewal.

CROP INSURANCE SCHEME

As per information received from Patna Regional Office of Agriculture Insurance

Company of India Ltd, 889497 farmers have been covered under WBCIS Kharif 2014,

391249 farmers have been extended the benefit of crop insurance coverage under

MNAIS Kharif 2014 and 888111 farmers have been covered under NAIS RABI 2014-15.

Thus, a total of 2168857 farmers have been provided the crop insurance cover, the sum

insured being Rs. 5339.07 Crores and the area covered being 2654527.60 hectares by

Agriculture Insurance Company of India Ltd. The information on crop insurance received

from three insurance companies are as under:

NAME OF

THE INSURANCE COMPANY

NO. OF FARMERS

WHOSE CROPS

INSURED

AREA

(IN HA.)

SUM

INSURED

(IN CR)

Agriculture Insurance Company Of

India Ltd 2168857 2654527.60 5339.07

Chola Mandalam 346759 53227.57 39.25

SBI General Insurance 96145 76917 173.06

TOTAL 2611761 2707755.17 5551.38

Thus, as per information received from the above said 3 insurance companies, a total of

2611761 farmers have been provided crop insurance cover, the sum insured being Rs.

5551.38 Crores and the area covered being 2707755.17 hectares.

Controlling Head of all banks operating in the State have been requested to instruct their

operating functionaries to ensure to cover all the crop loans under crop insurance and

the claims of agriculture crop insurance should be credited into the beneficiary’s account

within 15 days of receipt of claim and no interest should be charged in the loan account

of borrowers on the claim amount, for the period beyond 15 days of receipt of claim till

the date of credit. In case of interest being applied on the claim amount credited with

delay beyond 15 days, it should be refunded to the beneficiaries. Controlling Head of all

banks operating in the State have also been requested to instruct their operating

functionaries to ensure submission of statement of crop insurance at monthly intervals

to the Insurance Companies. It should also be ensured that the statement so submitted

is complete in all respects.

The position of insurance as advised by Agriculture Insurance Company of India Ltd is

furnished on Page- 14D.

[15]

DAIRY, FISHERY & POULTRY

Banks have sanctioned loans amounting to Rs 438.04 Crore to 23814 beneficiaries under various Dairy schemes, Rs. 48.75 Crore to 2139 beneficiaries under Fishery schemes

and Rs. 96.08 Crore to 1492 beneficiaries under Poultry schemes during the FY 2014-15. Bank wise performance is furnished on page no. 15A to 15C.

Frequent changes in the policy & implementation mechanism has adversely impacted the performance of banks under Dairy.

The Bank-wise and district-wise target of FY 2015-16 has been fixed and circulated

among all concerned. A copy of target of FY 2015-16 is placed at page no. 28AR to 28AT for information of the House.

FARM MECHANISATION

Against the financial target of Rs.2221.87 Crore for the year 2014-15, Banks have sanctioned loans amounting to Rs. 671.52 Crore to 26210 farmers for purchasing farm

equipments. While during the same period last year Banks could sanction loans amounting to Rs 611.51 Crore to 14120 farmers, registering Y-o-Y growth of 09% in terms of amount sanctioned and 86% in term of no. of beneficiaries. Bank-wise target

and performance is furnished on Page no. 15D for information.

Controlling head of all Banks are requested to advise their branches to initiate requisite measures to increase lending under the scheme.

The Bank-wise and district-wise target of FY 2015-16 has been fixed and circulated

among all concerned. A copy of target of FY 2015-16 is placed at page no. 28AV for information of the House.

ADVANCES GRANTED TO UNITS PROVIDING STORAGE FACILITY

Banks have sanctioned loans amounting to Rs. 90.01 Crore to 1232 farmers for storage facility during the financial year 2014-15. All banks are requested to pay more attention

towards financing under the scheme as there is a huge demand for storage facility.

Bank- wise target and performance is furnished on Page No. 15E for information.

The Bank-wise and district-wise target of FY 2015-16 has been fixed and circulated among all concerned. A copy of target of FY 2015-16 is placed at page no. 28AU for information of the House.

AGRICULTURE TERM LOAN (ATL)

Against the financial target of Rs.10343.96 Crore for the year 2014-15, Banks have sanctioned loans amounting to Rs. 14572.83 Crore to 727168 farmers.

Bank-wise target and performance is furnished on Page no. 15F for information.

The Bank-wise and district-wise target of FY 2015-16 has been fixed and circulated

among all concerned. A copy of target of FY 2015-16 is placed at page no. 28AW for information of the House.

AGENDA-XI

[16]

CD RATIO (As on 31.03.2015)

(Rs. in Crore)

Bank Deposits Advances CD ratio

Comm. Banks 187478 75407 40.22

Co-op. Banks 2265 1211 53.49

RRBs 21560 11841 54.92

Total 211302 88460 41.86

RIDF ------- 4567 -----

Total (Advances +RIDF) 211302 93027 44.03

Investment ------- 7234 --------

Grand Total (Adv.+RIDF+Inv.) 211302 100261 47.45

As at the end of March’2015, CD Ratio of the state stood at 44.03% which shows an

increase of 114 basis points as compared to March’2014. If write-off to the tune of

Rs.550.44 Crores had not taken place during the period, the CD ratio of the State would

have increased by another 26 bps. The CD ratio of the State would have improved

further by 245 basis points, had the State Government utilised the total amount of

Rs.9756.08 Crore (as on 31.03.2015), sanctioned under RIDF. As on 31st March, 2015

only 47% of the amount sanctioned under RIDF was utilised by the Government of

Bihar.

Bank-wise and district-wise details are furnished on Page no. 19A to 19D.

A positive feature of the CD Ratio of the districts is that no district is having a CD Ratio of

less than 25%. This has happened for the first time in the state.

It is pertinent to mention here that an amount of Rs.8819.51 Crores have been financed

to units functioning in Bihar by SBI, PNB, Allahabad Bank, Corporation Bank, Indian

Overseas Bank, Punjab & Sind Bank, IDBI bank, State Bank of Bikaner & Jaipur, Federal

Bank and Axis Bank by their branches operating outside the State and the amount has

been taken into account for calculating the CD ratio as per guidelines issued by the

Reserve Bank of India vide their circular No.-RPCD.LBS.BC.No.47/02.13.03/2005-06

dated 9th November 2005.

AGENDA-XII

[17]

RECOVERY

A summary of the recovery data (as on 31.03.2015) is given below. (Rs.in Crore)

Bank Demand raised Amount recovered Recovery %

Comm. Banks 21270 11794 55.45

Co-op. Banks 701 234 33.39

RRBs 6096 5287 86.73

Total 28067 17315 61.69

Recovery percentage is at 61.69% of the total demand raised by Banks as on 31st March, 2015. The recovery position needs improvement in order to drive the financing

by Banks in the State. While the Banks are following up with the borrowers for recovery of their dues, the State government is requested to help the Banks in their efforts. A better recovery culture will act as an incentive for Banks to lend more.

Bank-wise position of recovery as on 31.03.2015 is furnished on Page No. 19E.

With regard to disposal of top ten certificate cases of the districts, the progress has not

been very encouraging. The State Government is requested to sensitize the functionaries at district level to give adequate attention towards disposal of certificate cases, execution of Possession Notice under SARFAESI Act and action against big

defaulters of the district so that Banks may recover their dues from the defaulters. In the first Sub-Committee meeting of SLBC on Industries held on 30.10.2013, it was

decided that monthly meeting should be conducted by SDC (Banking) in each district on Recovery & Certificate Case related issues of Banks. In the 51st SLBC meeting held on

21.02.2015, top 10 certificate cases of each district was incorporated in the agenda book for recovering the dues from the defaulters. The State Govt. is requested to suitably instruct the concerned district authorities to hold the said meeting in all Districts on

regular basis for discussing all recovery related issues of Banks.

NPAs & WRITE-OFF

As on 31.03.2015, overall position of NPAs and the amount of loans written off is as

under:

(Rs. in Crore)

Banks Total

Adv.

Total

NPA

% of

NPA

Amt.

written-off

Comm. Banks 66368 4018 6.05 474

Co-op. Banks 1211 299 24.66 0

RRBs 11841 268 2.26 76

Total 79420 4585 5.77 550

NPA of Banks at 5.77% is a matter of great concern. All steps should be taken for

bringing the NPA level below 3%.

Amount Written off and Segment-wise details of NPA amount is furnished on Page No.

19F for discussion and review by the House.

[18]

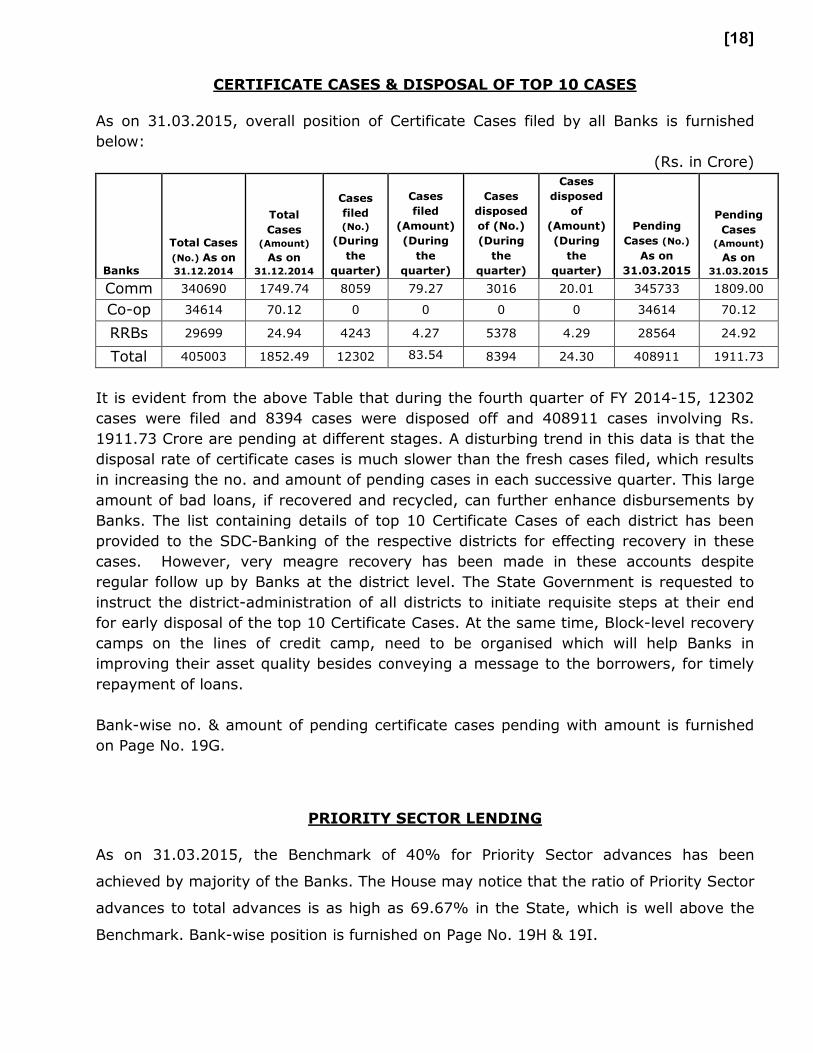

CERTIFICATE CASES & DISPOSAL OF TOP 10 CASES

As on 31.03.2015, overall position of Certificate Cases filed by all Banks is furnished

below:

(Rs. in Crore)

Banks

Total Cases

(No.) As on

31.12.2014

Total

Cases

(Amount)

As on

31.12.2014

Cases

filed

(No.)

(During

the

quarter)

Cases

filed

(Amount)

(During

the

quarter)

Cases

disposed

of (No.)

(During

the

quarter)

Cases

disposed

of

(Amount)

(During

the

quarter)

Pending

Cases (No.)

As on

31.03.2015

Pending

Cases

(Amount)

As on

31.03.2015

Comm 340690 1749.74 8059 79.27 3016 20.01 345733 1809.00

Co-op 34614 70.12 0 0 0 0 34614 70.12

RRBs 29699 24.94 4243 4.27 5378 4.29 28564 24.92

Total 405003 1852.49 12302 83.54 8394 24.30 408911 1911.73

It is evident from the above Table that during the fourth quarter of FY 2014-15, 12302

cases were filed and 8394 cases were disposed off and 408911 cases involving Rs.

1911.73 Crore are pending at different stages. A disturbing trend in this data is that the

disposal rate of certificate cases is much slower than the fresh cases filed, which results

in increasing the no. and amount of pending cases in each successive quarter. This large

amount of bad loans, if recovered and recycled, can further enhance disbursements by

Banks. The list containing details of top 10 Certificate Cases of each district has been

provided to the SDC-Banking of the respective districts for effecting recovery in these

cases. However, very meagre recovery has been made in these accounts despite

regular follow up by Banks at the district level. The State Government is requested to

instruct the district-administration of all districts to initiate requisite steps at their end

for early disposal of the top 10 Certificate Cases. At the same time, Block-level recovery

camps on the lines of credit camp, need to be organised which will help Banks in

improving their asset quality besides conveying a message to the borrowers, for timely

repayment of loans.

Bank-wise no. & amount of pending certificate cases pending with amount is furnished

on Page No. 19G.

PRIORITY SECTOR LENDING

As on 31.03.2015, the Benchmark of 40% for Priority Sector advances has been

achieved by majority of the Banks. The House may notice that the ratio of Priority Sector

advances to total advances is as high as 69.67% in the State, which is well above the

Benchmark. Bank-wise position is furnished on Page No. 19H & 19I.

[19]

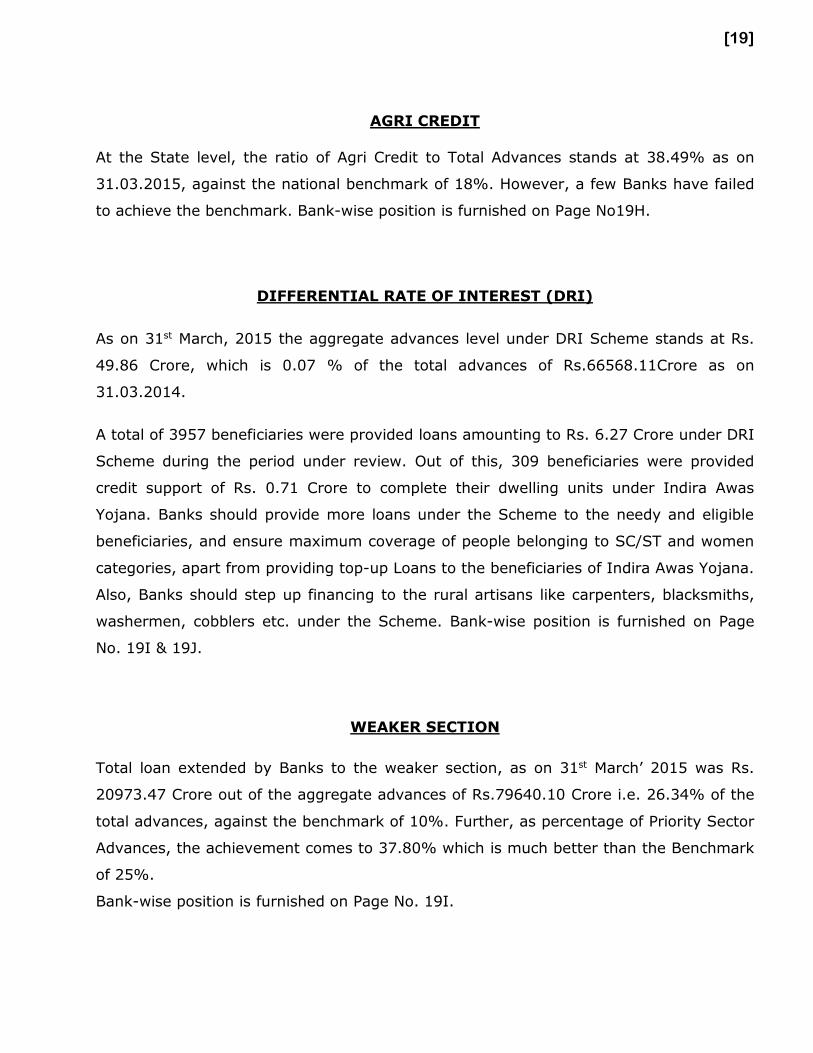

AGRI CREDIT

At the State level, the ratio of Agri Credit to Total Advances stands at 38.49% as on

31.03.2015, against the national benchmark of 18%. However, a few Banks have failed

to achieve the benchmark. Bank-wise position is furnished on Page No19H.

DIFFERENTIAL RATE OF INTEREST (DRI)

As on 31st March, 2015 the aggregate advances level under DRI Scheme stands at Rs.

49.86 Crore, which is 0.07 % of the total advances of Rs.66568.11Crore as on

31.03.2014.

A total of 3957 beneficiaries were provided loans amounting to Rs. 6.27 Crore under DRI

Scheme during the period under review. Out of this, 309 beneficiaries were provided

credit support of Rs. 0.71 Crore to complete their dwelling units under Indira Awas

Yojana. Banks should provide more loans under the Scheme to the needy and eligible

beneficiaries, and ensure maximum coverage of people belonging to SC/ST and women

categories, apart from providing top-up Loans to the beneficiaries of Indira Awas Yojana.

Also, Banks should step up financing to the rural artisans like carpenters, blacksmiths,

washermen, cobblers etc. under the Scheme. Bank-wise position is furnished on Page

No. 19I & 19J.

WEAKER SECTION

Total loan extended by Banks to the weaker section, as on 31st March’ 2015 was Rs.

20973.47 Crore out of the aggregate advances of Rs.79640.10 Crore i.e. 26.34% of the

total advances, against the benchmark of 10%. Further, as percentage of Priority Sector

Advances, the achievement comes to 37.80% which is much better than the Benchmark

of 25%.

Bank-wise position is furnished on Page No. 19I.

[20]

OPENING OF NO-FRILL ACCOUNTs AND TRANSACTIONS DONE BY BCAs

As per information received from Banks, a total of 13648111 No-Frill accounts were

opened during FY 2014-15. Thus, a total of 27407774 No-frill accounts have been

opened till 31st March, 2015 cumulatively. Out of these, 21975270 accounts are

operational.

Bank & District-wise details with respect to No Frill accounts opened and transactions

carried out by BCAs is furnished on Page No. 20A to 20D.

EXTENDING MOBILE BANKING AND INTERNET BANKING FACILITY

All Banks should extend mobile Banking and internet Banking facility to customers as

these are not only cost-effective but also adds to customer-convenience. As per

information received by SLBC, Banks have provided Mobile Banking facility to 2793248

customers whereas the facility of Internet Banking has been provided to 1866926

customers. Controlling Head of all Banks operating in the State are requested to bestow

their attention and initiate requisite steps for extending these facilities further as it

would facilitate the service delivery of Banks.

Bank-wise information regarding Mobile Banking and Internet Banking facility provided,

is furnished on Page 20E.

AGENDA-XIII

[21]

IMPLEMENTATION OF FINANCIAL INCLUSION PLANS IN LWE AFFECTED

DISTRICTS

The Government of India is regularly reviewing the progress made in implementing

Financial Inclusion in Left Wing Extremist (LWE) affected districts in the State of Bihar

with a focus on development of Infrastructure, Credit availability, Advocacy, Livelihood

development etc. There are 15 LWE affected districts in Bihar.

Banks operating in these districts are implementing financial inclusion plans on a priority basis for extending Banking facilities to these LWE affected areas. Credit extension by

Banks during the financial year 2014 - 2015 in these districts is furnished below, which shows improvement in all the districts, over the same period during the last Financial Year:

:SL.

No.

District

Disbursement under ACP during

the quarter ended March’15

Disbursement under ACP during

the quarter ended March’14

Growth

(%)

(Rs. in Lakh) (Rs. in Lakh)

1 Arwal 38764 31783 21.96 2 Aurangabad 155992 141335 10.37 3 Bhojpur 188770 167029 13.02

4 East Champaran 270860 200762 34.92 5 Gaya 234588 203553 15.25 6 Jamui 84870 67376 25.96 7 Jehanabad 62735 48791 28.58 8 Kaimur 155226 118489 31.00 9 Munger 96487 75595 27.64 10 Nalanda 152713 130259 17.24 11 Nawada 83764 70380 19.02 12 Patna 1184625 1034628 14.50 13 Rohtas 232535 190596 22.00 14 Sitamarhi 133358 110235 20.98 15 West Champaran 257201 208457 23.38 TOTAL 3332488 2799268 19.05

It is evident from the above that Banks have extended higher quantum of credit as

compared to last year in the LWE affected districts.

AGENDA-XIV

[22]

INVESTIGATION OF CYBER FRAUD & COUNTERFEIT NOTES

DETECTED BY BANKS

As per the suggestion of DFS, Govt. of India, investigation of cyber frauds and other

related issues is a regular agenda item of all SLBCs across the country. Controlling Head

of all Banks operating in the State are requested to bring to the notice of the State

Government occurrences of cyber fraud and detection of counterfeit notes so that

appropriate steps may be initiated by the Government in this regard. At the State Head

Quarter a separate wing has been established for speedy investigation and disposal of

cases related to cyber crime.

FUNCTIONING OF RURAL SELF EMPLOYMENT TRAINING INSTITUTEs (RSETIs)

RSETIs are functional in all the 38 districts of the State. They are engaged in skill

development of the unemployed youth for undertaking self employment venture/ wage

employment. Up to the quarter ending MArch’2015 of the financial year, 759 training

programmes have been organised and 20819 youth were imparted training by the

RSETIs. Altogether 90818 persons have been trained by the RSETIs in the State by

organizing 3272 programmes since inception. The detailed information pertaining to

RSETIs in the State is placed on Page No. 23A for information.

Controlling Head of all Banks operating in the State have been requested to arrange to

issue instructions to all their branches to sponsor at least 5 trainees in a financial year to

the RSETI functioning in the district and also to provide credit-linkage to at least 5

RSETI trained persons in a financial year. This will help the trained youth to start their

own venture and also improve the grading of RSETIs as settlement of trainees is a key

parameter for grading by GoI.

Under the PMEGP Scheme, the beneficiaries are to be provided training before loan is

disbursed to them. The KVIC, KVIB & DIC are requested to utilise the Training facilities

available at the RSETIs for PMEGP beneficiaries.

AGENDA-XVI

AGENDA-XV

[23]

LAND ALLOTMENT AT RSETIs

Allotment of land in two districts is pending in Nawada and Patna in connection with

construction of RSETI building. The state government has already advised the District

Magistrates of these districts to make available land at the earliest so that building of

RSETI may be constructed thereat. The encroachment in the allotted land for RSETI at

Jamui has come in the way of construction of building. State Govt. is requested to help

resolve the issue to enable RSETI Jamui complete construction. All Banks which have

been provided with land and fund, are requested to complete construction of RSETI

building at the earliest. MoRD, Govt. of India has now issued specific instructions for

withdrawal of fund from the banks where construction work does not commence on or

before 01.07.2015.

REIMBURSEMENT OF EXPENSES

The State Govt. has directed the District Magistrates of all districts for payment of

training expenses to concerned RSETIs. However there are still many instances of bills

pending with distt. authorities. The Deputy Secretary, MoRD, GoI, New Delhi has

advised that MoRD would be reimbursing the cost of training BPL candidate in RSETIs

which are graded A/B/AA/AB/BA/BB through the State Rural Livelihood Mission.

The modalities for reimbursement of training expenses of RSETI has been provided by

MoRD. Modalities for reimbursement of training cost of RSETIs for 2013-14, 2014-15 has

been advised to all banks having RSETI responsibilities. Banks are requested to submit

reimbursement claim for 2013-14 onwards to SRLM, Govt. of Bihar at the earliest for

settlement.

[24]

FINANCIAL LITERACY INITIATIVES Financial Literacy Centers (FLCs) are functional in all the districts in the State. 152977

persons participated in 2029 camps organised by the FLCs during the fourth quarter of

FY 2014-15. The information pertaining to FLCs in the State is placed at Page No. 24A

for information.

As per instructions received from the GoI, all rural branches are to conduct at least one

financial literacy camp in each month and Financial Literacy Guide, Diary & Poster,

designed by RBI, is to be used by the branches in the camp to explain the basic financial

issues. The data of Financial Literacy Camps organised by rural branches in the districts

is placed at page no. 24B.

The Financial Literacy materials, as per requirement of Banks has been printed and

distributed by SLBC among Banks in the state. All Banks are requested to ensure that

their rural branches undertake Financial Literacy activities using the standard Financial

Literacy materials at the required intervals.

AGENDA-XVII

[25]

MICRO, SMALL & MEDIUM ENTERPRISES

The Reserve Bank of India’s instructions to the scheduled commercial banks, as advised vide

MSME Development Institute, Patna letter No. SLBC/MSME-DI/2011/1306 dated 14th March,

2012 regarding enhancing credit flow to Micro, Small & Medium Enterprises (MSMEs), is as under:-

1. Achieve a 20% year-on-year growth in credit to Micro & Small Enterprises to ensure enhanced credit flow.

2. Allocation of 60% of the MSE advances to the Micro Enterprises is to be achieved in stages viz. 50% in the year 2010-11, 55% in the year 2011-12 and 60% in the year 2012-13 and

3. Achieve a 10% annual growth in number of Micro Enterprises accounts.

The performance of Banks in this regard as on 31.03.2015 is placed at page no. 25A of the Agenda Book.

SMALL ROAD TRANSPORT OPERATORS (SRTOs)

Against the target of financing 22000 units, Banks in the state have sanctioned loan

amounting to Rs. 593.06 Crore for purchasing 14619 vehicles by SRTOs during the FY 2014-15 which is 66% of the annual target. Bank-wise performance is furnished on Page

No. 25B.

The Bank-wise and district-wise target of FY 2015-16 has been fixed and circulated among all concerned. A copy of target of FY 2015-16 is placed at page no. 28AX for

information of the House.

ADVANCES GRANTED UNDER CGTMSE COVERAGE

A total of 46259 units were financed by Banks involving Rs.1629.65 Crore with CGTMSE

cover, up to March’2015 during the FY under review. Further, loans amounting to Rs. 1614.96 Crore were disbursed to 46211 units under CGTMSE cover. Considering the

wide scope available for coverage of loans under CGTMSE, controlling Head of all Banks in the state are requested to instruct their operating functionaries to cover all the eligible units under CGTMSE.

Bank-wise performance data is furnished on Page No. 25C for information of the House.

ADVANCES GRANTED UNDER MANUFACTURING SECTOR

Against the financial target of Rs.850 Crore for the year 2014-15, up to March’2015, during the FY under review loan amounting to Rs 1165.62 Crores were sanctioned to

14637 units and out of that Rs. 1132.07 Crores were disbursed among 14634 units under Manufacturing Sector. The achievement of all banks taken together is 137.13% of

the targets allocated.

Bank-wise performance data is furnished on Page No. 25D for information of the House.

The Bank-wise and district-wise target of FY 2015-16 has been fixed and circulated

among all concerned. A copy of target of FY 2015-16 is placed at page no. 28AY for information of the House.

AGENDA-XVIII

[26]

WEAVERS CREDIT CARD

Weavers Credit Card (WCC) scheme aims at providing adequate and timely assistance

from the Banks to the Weavers to meet their credit requirements i.e. the investment

needs as well as the working capital needs of weavers in a flexible and cost effective

manner. The Scheme is valid for both rural and urban areas. Controlling Head of all

Banks of the State are requested to initiate requisite steps for proper implementation of

the Scheme in the State.

Against the target of 5000, only 1543 applications for loans amounting to Rs. 14.22

Crore have been sanctioned by Banks during the period under review. The Bank-wise

achievement as on 31.03.2015 is furnished on Page No. 26A.

FOOD PROCESSING UNITS

In the 44th SLBC meeting Food Processing industry was identified as focus area for the

State

Banks have sanctioned loans amounting to Rs.409.59 Crore to 1421 Food Processing

Units during financial year 2014-15. Controlling Head of all Banks are requested to

instruct their operating functionaries to intensify efforts for increasing finance to such

units.

Bank- wise performance is furnished on Page No. 26B for information.

The Minutes of the 24th Sub-committee meeting on Branch Opening and IT enabled

financial inclusion held on 23.03.2015 is placed at page no. 25E to 25H for information

of the House

AGENDA-XIX

[27]

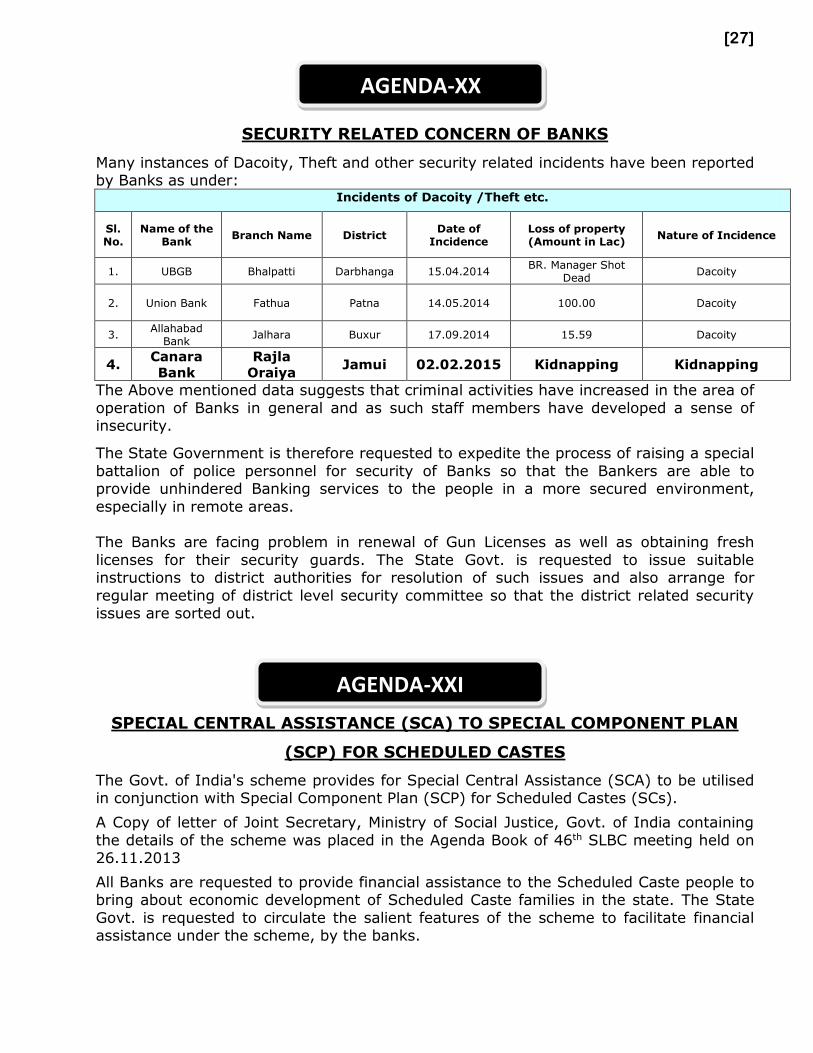

SECURITY RELATED CONCERN OF BANKS

Many instances of Dacoity, Theft and other security related incidents have been reported by Banks as under:

Incidents of Dacoity /Theft etc.

Sl. No.

Name of the Bank

Branch Name District Date of

Incidence Loss of property (Amount in Lac)

Nature of Incidence

1. UBGB Bhalpatti Darbhanga 15.04.2014 BR. Manager Shot

Dead Dacoity

2. Union Bank Fathua Patna 14.05.2014 100.00 Dacoity

3. Allahabad

Bank Jalhara Buxur 17.09.2014 15.59 Dacoity

4. Canara

Bank

Rajla

Oraiya Jamui 02.02.2015 Kidnapping Kidnapping

The Above mentioned data suggests that criminal activities have increased in the area of

operation of Banks in general and as such staff members have developed a sense of insecurity.

The State Government is therefore requested to expedite the process of raising a special

battalion of police personnel for security of Banks so that the Bankers are able to provide unhindered Banking services to the people in a more secured environment,

especially in remote areas. The Banks are facing problem in renewal of Gun Licenses as well as obtaining fresh

licenses for their security guards. The State Govt. is requested to issue suitable instructions to district authorities for resolution of such issues and also arrange for

regular meeting of district level security committee so that the district related security issues are sorted out.

SPECIAL CENTRAL ASSISTANCE (SCA) TO SPECIAL COMPONENT PLAN

(SCP) FOR SCHEDULED CASTES

The Govt. of India's scheme provides for Special Central Assistance (SCA) to be utilised in conjunction with Special Component Plan (SCP) for Scheduled Castes (SCs).

A Copy of letter of Joint Secretary, Ministry of Social Justice, Govt. of India containing

the details of the scheme was placed in the Agenda Book of 46th SLBC meeting held on 26.11.2013

All Banks are requested to provide financial assistance to the Scheduled Caste people to bring about economic development of Scheduled Caste families in the state. The State

Govt. is requested to circulate the salient features of the scheme to facilitate financial assistance under the scheme, by the banks.

AGENDA-XX

AGENDA-XXI

[28]

MISCELLANEOUS ISSUES

REGISTRATION OF SECURITY INTEREST WITH CENTRAL ELECTRONIC

REGISTRY (CERSAI)

MEMBERSHIP FOR CERSAI IN SLBC MEETINGS

Central Registry of Securitisation Asset Reconstruction and Security Interest of India

(CERSAI) is a Government Company which provides the platform for filing registrations

of transactions of securitisation, asset reconstruction and security interest by the banks

and financial institutions to avoid multiple loaning on the same security. The Banks are

requested to register their transaction on CERSAI portal for avoiding multiple loaning on

security which will help in reduction of NPA.

ESCALATION IN STAMP DUTY PAYABLE ON SECURITY DOCUMENTS

The escalation in stamp duty payable on security documents pertaining to non-Agri

loans from Rs. 100/- to Rs. 1000/- is acting as a hurdle in credit dispensation to small

borrowers, particularly under retail lending, DRI, WCC etc. The State Government is

earnestly requested to look into the matter so that the credit growth, particularly under

small loan segment, is not adversely affected.

AGENDA-XXII

Related Documents