COUNTRY PROFILE Sri Lanka Our quarterly Country Report on Sri Lanka analyses current trends. This annual Country Profile provides background economic and political information 1997-98 The Economist Intelligence Unit 15 Regent Street, London SW1Y 4LR United Kingdom

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

COUNTRY PROFILE

Sri LankaOur quarterly Country Report on Sri Lanka analyses currenttrends. This annual Country Profile provides backgroundeconomic and political information

1997-98The Economist Intelligence Unit15 Regent Street, London SW1Y 4LRUnited Kingdom

The Economist Intelligence Unit

The Economist Intelligence Unit is a specialist publisher serving companies establishing and managingoperations across national borders. For over 50 years it has been a source of information on businessdevelopments, economic and political trends, government regulations and corporate practice worldwide.

The EIU delivers its information in four ways: through subscription products ranging from newslettersto annual reference works; through specific research reports, whether for general release or for particularclients; through electronic publishing; and by organising conferences and roundtables. The firm is amember of The Economist Group.

London New York Hong KongThe Economist Intelligence Unit The Economist Intelligence Unit The Economist Intelligence Unit15 Regent Street The Economist Building 25/F, Dah Sing Financial CentreLondon 111 West 57th Street 108 Gloucester RoadSW1Y 4LR New York Wanchai United Kingdom NY 10019, USA Hong KongTel: (44.171) 830 1000 Tel: (1.212) 554 0600 Tel: (852) 2802 7288Fax: (44.171) 499 9767 Fax: (1.212) 586 1181/2 Fax: (852) 2802 7638e-mail: [email protected] e-mail: [email protected] e-mail: [email protected]

Website: http://www.eiu.com

Electronic deliveryEIU ElectronicNew York: Lou Celi or Lisa Hennessey Tel: (1.212) 554 0600 Fax: (1.212) 586 0248London: Moya Veitch Tel: (44.171) 830 1007 Fax: (44.171) 830 1023

This publication is available on the following electronic and other media:

Online databases CD-ROM Microfilm

FT Profile (UK) Knight-Ridder Information World Microfilms Publications (UK)Tel: (44.171) 825 8000 Inc (USA) Tel: (44.171) 266 2202

DIALOG (USA) SilverPlatter (USA) University Microfilms Inc (USA)Tel: (1.415) 254 7000 Tel: (1.800) 521 0600

LEXIS-NEXIS (USA)Tel: (1.800) 227 4908

Copyright© 1997 The Economist Intelligence Unit Limited. All rights reserved. Neither this publication nor any part of it may be reproduced, stored in a retrieval system, or transmitted in any form or by anymeans, electronic, mechanical, photocopying, recording or otherwise, without the prior permission of The Economist Intelligence Unit Limited.

All information in this report is verified to the best of the author’s and the publisher’s ability. However,the EIU does not accept responsibility for any loss arising from reliance on it.

Symbols for tables“n/a” means not available; “–” means not applicable

Printed and distributed by Redhouse Press Ltd, Unit 151, Dartford Trade Park, Dartford, Kent DA1 1QB, UK

ISSN 0269-5073

October 15, 1997 Contents

2 Basic data

3 Political background3 Historical background6 Constitution and institutions8 Political forces9 International relations and defence

10 The economy10 Economic structure11 Economic policy14 Economic performance16 Regional trends

17 Resources17 Population18 Education19 Health20 Natural resources and the environment

21 Economic infrastructure21 Transport and communications23 Energy provision24 Financial services28 Other services

29 Production29 Manufacturing30 Mining31 Agriculture33 Construction

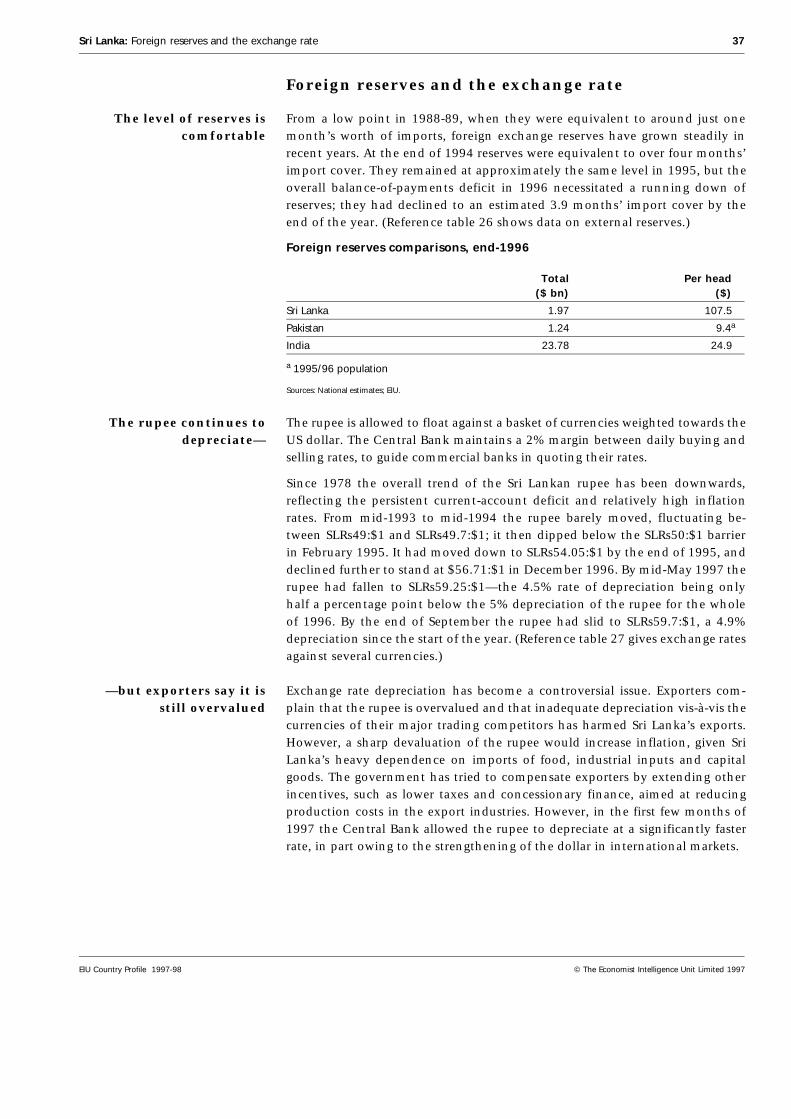

33 The external sector33 Merchandise trade35 Invisibles and the current account36 Capital flows and foreign debt37 Foreign reserves and the exchange rate

38 Appendices38 Sources of information39 Reference tables

1

EIU Country Profile 1997-98 © The Economist Intelligence Unit Limited 1997

Sri Lanka

Basic data

Land area 65,610 sq km

Population 18.3 million (mid-1996 estimate)

Main towns Population in ’000, 1990 estimates

Colombo 615 Jaffna 129Dehiwala-Mount Lavinia 193 Kandy 104Moratuwa 170 Galle 84

Climate Tropical

Weather in Colombo Hottest month, May, 26-31°C (average daily minimum); coldest month,December, 22-29°C; driest month, February, 69 mm average rainfall; wettestmonth, May, 371 mm average rainfall

Languages Sinhala, Tamil, English

Measures Metric system is displacing the UK (imperial) system. Local measure for copra:1 candy=254 kg; rice “measure”=2 lb

Currency Rupee (SLRs)=100 cents. Average exchange rate in 1996: SLRs55.27:$1.Exchange rate on October 15, 1997: SLRs59.53:$1.

Time 5 hours ahead of GMT

Fiscal year January-December

Public holidays in 1997 January 14 (Thai-pongal Day), January 23 (Duruthu Full Moon Poya), February 4(Sri Lanka National Day), February 9 (Ramadan Festival Day), February 21(Navam Full Moon Day), March 23 (Medin Full Moon Day), March 28 (GoodFriday), April 13 (Day before Sinhala & Tamil New Year Day), April 14 (Sinhala& Tamil New Year Day), April 22 (Bak Full Moon Day), May 1 (May Day),May 21 (Vesak Full Moon Day), May 22 (Day following Vesak Full Moon Day),June 20 (Poson Full Moon Day), July 18 (Holy Prophet’s Birth Day), July 19(Esala Full Moon Day), August 18 (Nikini Full Moon Day), September 16(Binara Full Moon Day), October 15 (Vap Full Moon Day), October 30(Deepavali Festival), November 14 (Il Full Moon Day), December 13 (UnduvapFull Moon Day), December 25 (Christmas Day)

2 Sri Lanka: Basic data

EIU Country Profile 1997-98 © The Economist Intelligence Unit Limited 1997

Political background

Historical background

History Sri Lanka was ruled by the Portuguese in the 16th century. In the 17th centurythe Dutch superseded the Portuguese, only to be ousted by the British at theend of the following century. Pressure for independence built up in the firsthalf of the 20th century. Sri Lanka (then known as Ceylon) became fullyindependent on February 4, 1948, although it remained a member of theCommonwealth.

The origins of the ethnicconflict lie in the colonial

period

The ethnic question has played a major role in Sri Lankan politics since inde-pendence. The immediate origins of the conflict lie in attempts by the majoritySinhalese to reverse what was seen as the excessive influence of Tamils beforeindependence. After the 1956 election, the Sinhalese-dominated government,seeking to overturn the previous dominance of English, made Sinhala theofficial language, which precipitated antagonism between Tamils andSinhalese. In 1958 the first intercommunal riots occurred. Tension between thetwo groups grew during the 1960s and 1970s; the Tamils sought to obtain afederal system of government and became alienated when this was refused bysuccessive governments.

Sinhalese extremistsemerged in the 1960s

In addition, economic policy, strongly influenced by socialist ideals and plan-ning, failed to provide adequate employment, particularly among educatedyouth. This led to the formation in the late 1960s of the People’s LiberationFront (Janatha Vimukthi Peramuna, JVP), which combined left-wing Marxistradicalism and Sinhalese extremism. In 1971 the first youth uprising occurred;although it was swiftly quelled, sporadic outbreaks of violence involvingextreme Tamils and the JVP erupted during the 1970s.

In the 1980s the LTTEturned to terrorism—

The failure of Tamil political parties to attain their aims by peaceful means ledto demands for an independent Tamil state, to be known as Eelam, and to theformation of terrorist groups dedicated to achieving this goal. Repressive actionby government troops only increased tension. Moderate Tamil parties began tolose influence as the situation deteriorated in the early 1980s. In 1983 a violentoutburst of intercommunal rioting occurred; as a result many Tamils fled thecountry and the more militant Tamil groups gained support. By 1987 the mainTamil terrorist group, the Liberation Tigers of Tamil Eelam (LTTE, or TamilTigers), led by Velupillai Prabhakaran, effectively controlled the northernpeninsula and the city of Jaffna.

—and India intervened— In May 1987 the army launched a full-scale offensive in the north. Underpolitical pressure from the Tamils in the southern Indian state of Tamil Nadu,India was drawn into Sri Lanka’s ethnic conflict and sent aid to the Tamilrebels. To avoid possible armed intervention by India, the Sri Lankan govern-ment held talks with the Indian prime minister at the time, Rajiv Gandhi. Theresulting Indo-Sri Lankan peace accord provided for the formation of provin-cial governments to which limited powers would be devolved. Sri Lanka’s

Sri Lanka: Historical background 3

EIU Country Profile 1997-98 © The Economist Intelligence Unit Limited 1997

Northern and Eastern provinces, corresponding to the Tamils’ desired Eelam,were provisionally united pending a referendum (which has yet to be held) todecide whether the union should be permanent.

—deploying its troopsagainst the Tigers—

The Sri Lankan army was to withdraw and the Tamil groups were to laydown their arms, and the Indian Peace Keeping Force (IPKF) was established toguarantee the end of the fighting. The Tigers, however, accepted the accord onlyreluctantly, and soon resumed their offensive. The IPKF was then deployedagainst the Tigers and took their stronghold of Jaffna, relegating the LTTEtemporarily to a guerrilla role.

—until Mr Premadasaordered them out and

negotiated with the LTTE

The presidential election in December 1988 brought the former prime minister,Ranasinghe Premadasa, to power. This was followed by a parliamentary electionin February 1989. The new president, openly critical of the peace accord,ordered the IPKF to withdraw and embarked on direct negotiations with theTigers. As the IPKF carried out a staged withdrawal, finally leaving in March1990, the Tigers reclaimed effective power in the Jaffna peninsula.

The second JVP uprisingparalysed the country

In 1989 the country was gripped by another, more serious wave of terror andviolence inspired this time by the JVP. Aided by unofficial vigilante groups, thesecurity forces reacted ruthlessly, imposing their own brand of terror. AmnestyInternational estimated that around 60,000 people lost their lives in extra-judicial killings, committed either by the JVP or by the security forces. Thecampaign was finally brought to an end in November 1989 by the capture andexecution of most of the JVP leaders.

The Tigers resumed theiroffensive in 1990

Uneasy negotiations with the Tigers continued throughout the first half of1990, but fighting broke out again in June. In the Eastern province the armywas able to gain control of the towns relatively quickly. In the north the Tigersproved to be more difficult to overcome, although the army had some successin containing their activities.

In 1993 Mr Premadasa wasassassinated—

In 1993 the country was rocked by a double assassination. First, LalithAthulathmudali, the leader of one of the main opposition groups, was shot andkilled. One week later Mr Premadasa was killed by a Tiger suicide bomber. Afterthe assassination the prime minister, Dingiri Banda Wijetunga, served aspresident for the remainder of Mr Premadasa’s term of office. RanilWickremasinghe was appointed prime minister, and his United National Party(UNP) government began cautious constitutional reform.

—and a year later the PAwas voted into power

After suffering political reverses, the UNP government decided to bring forwardthe general election to August 1994, having first announced a generous newwelfare programme. The UNP lost the election. The incoming People’s Alliance(PA) administration, however, is one seat short of an overall majority in parlia-ment and depends on two ethnic minority parties, one Tamil and one Muslim,to remain in power. Chandrika Kumaratunga, the daughter of two formerprime ministers, Solomon and Sirimavo Bandaranaike, and the deputy leaderof the largest party in the PA, the Sri Lanka Freedom Party (SLFP), was ap-pointed prime minister.

4 Sri Lanka: Historical background

EIU Country Profile 1997-98 © The Economist Intelligence Unit Limited 1997

The general election, Aug 16, 1994

Party Seats won % of seats

People’s Alliance 105 46.7

United National Party 94 41.8

Eelam People’s Democratic Party 9 4.0

Sri Lanka Muslim Congress 7 3.1

Tamil United Liberation Front 5 2.2

Democratic People’s Liberation Front 3 1.3

Sri Lanka Progressive Front 1 0.4

Nuwara Eliya independent group 1 0.4

Total 225 100.0Source: Press reports.

After being votedpresident in 1994—

In October 1994 political violence again shook the country. The leader of the UNPopposition and his party’s candidate in the forthcoming presidential election,Gamini Dissanayake, was killed by a suicide bomber at an election rally togetherwith 50 others. In the November 9 election Mrs Kumaratunga scored a landslidevictory over Mr Dissanayake’s widow, Sirima Dissanayake. Mrs Kumaratungastood down as prime minister and her mother, Mrs Bandaranaike, was sworn inas prime minister for the third time.

—Mrs Kumaratungaopened peace talks

Shortly after coming to power Mrs Kumaratunga’s government opened peacenegotiations with the Tigers. The talks led to a cessation of hostilities inJanuary 1995. The government’s genuine efforts to resolve the ethnic conflictwon the country international sympathy, while the Tigers, who unilaterallycalled off the truce in April 1995, lost much goodwill, even in the Indian stateof Tamil Nadu.

Jaffna fell to the securityforces in December 1995—

The military conflict then intensified. In December 1995 the security forcestook the former Tiger stronghold of Jaffna, dealing a major psychological blowto the militants. The Jaffna peninsula was brought under army control by April1996 and, although civilian life has been restored largely to normal, the LTTEhas demonstrated, by sporadic hit and run attacks, that it is still capable ofinflicting high military and civilian casualties.

—and high-level conflictcontinued in 1996

The euphoria over the capture of Jaffna evaporated in January 1996 whenTamil suicide bombers blew up the Central Bank in the heart of the financialdistrict of the capital, Colombo. This was followed by a massive attack on anarmy camp in Mullaitivu in which some 1,200 soldiers lost their lives. Govern-ment forces struck back, and in October captured Kilinochchi, the jungle townto which the Tigers had moved their headquarters following the loss of Jaffna.

The government ispursuing both military

and political options

The government is combining military and political methods in its efforts toend the ethnic conflict. Two major offensives were launched in 1997 aimed atcompleting the security forces’ domination of the Northern province. OperationBrave Force, launched in February 1997, succeeded in establishing a supplyroute between Vavuniya and the town of Mannar on the northwestern coast.This was followed in May 1997 by Operation Sure Victory, intended to reopenthe road between Vavuniya and the Jaffna peninsula (although by the end of

Sri Lanka: Historical background 5

EIU Country Profile 1997-98 © The Economist Intelligence Unit Limited 1997

September only the first 25 km of the 65-km route had been brought undergovernment control). Despite these efforts, the Tigers remain capable of launch-ing attacks throughout the country—as they proved on October 15, when abomb and fighting in the financial district of Colombo left 18 dead and over 100injured, including several foreign businessmen and tourists.

Meanwhile, the government is pursuing its objective of reaching a politicalsettlement to the ethnic problem through constitutional change, by devolvingmore power to Sri Lanka’s troubled provinces. At local government electionsheld in March 1997, the PA won control of 194 of the 238 assemblies, butreceived only 48.9% of the vote, not the level of popular support which wouldhave enabled it to push these constitutional reforms through parliament on itsown. In April hopes for a political settlement received a boost when an under-standing, brokered by the UK government, was reached between the PA andthe UNP, with both parties agreeing not to undermine the peace effort forpolitical gain. The proposals for constitutional reform and the granting oflimited autonomy to Tamils were to be presented to parliament by November1997. However, by the end of September, cross-party support for the proposalswas waning, and delays seemed probable.

Important recent events

1989: JVP uprising in the south.1990: Phased withdrawal of the Indian Peace Keeping Force begins. Tamil Tigersbreak off peace negotiations in June. 1993: Mr Premadasa is assassinated by a Tamil suicide bomber in May. 1994: The PA is voted into power in parliamentary elections. In October theopposition presidential candidate is assassinated; in November Mrs Kumaratungascores a landslide victory in the presidential election. 1995: Cessation of hostilities in January but Tamil Tigers unilaterally resume fightingin April. Fighting intensifies and Jaffna falls to the security forces in December. 1996: The Central Bank is bombed in January and the Tigers overrun an army campkilling 1,200 soldiers. The army retaliates by intensifying its operations in the east,defeating the Tigers in Kilinochchi.1997: The PA and the UNP agree a bipartisan approach to forging a politicalsettlement to the ethnic conflict. The PA scores a victory at local governmentelections. Two major offensives are launched against the Tigers, one in February andone in May. On October 15 a bomb exploded in the central business district.

Constitution and institutions

Democracy has lastedsince independence

Despite its problems, Sri Lanka has managed to maintain an unbroken recordof democracy since independence. Elections have been held regularly and,although abuses have occurred, these elections have in general been freely andfairly contested. The country passes the critical test of democracy in that elec-tions have on several occasions resulted in a peaceful change of government.

Following independence, the country had a Westminster-style constitutionwith the British monarch as head of state, executive power in the hands of aprime minister governing in cabinet, and a bicameral legislature. In 1972 the

6 Sri Lanka: Constitution and institutions

EIU Country Profile 1997-98 © The Economist Intelligence Unit Limited 1997

country became a republic, although remaining within the Commonwealth.Its name was changed from Ceylon to Sri Lanka and the legislature becameunicameral. Although it had a president as head of state, executive powerremained vested in the prime minister and cabinet.

In 1978 the countryswitched to a presidential

system—

Sweeping changes were made in 1978 after J R Jayewardene became primeminister in 1977. The new constitution introduced a presidential system ofgovernment, with the president combining the roles of head of state, head ofgovernment and head of the armed forces, as well as head of the governingparty. The powers of the prime minister and the cabinet were drastically re-duced. The previous first-past-the-post system of voting was replaced by asystem of modified proportional representation. Mr Jayewardene became thefirst president under the 1978 constitution and held the position for two terms,until the end of 1988. In addition to the national legislature, there are twofurther tiers of government, local and provincial. Provincial governments wereestablished as a result of the Indo-Sri Lankan accord of 1987.

—which the presentgovernment has promised

to abolish

Disenchantment with the powerful executive presidency mounted during theauthoritarian rule of Mr Premadasa and after his assassination there was strongpressure for a return to the non-presidential system of government. In late1994 Mrs Kumaratunga pledged herself to abolish the executive presidencyby July 1995. Draft proposals to end the presidential system and return toWestminster-style rule were tabled in mid-January 1995. These proposals havenot yet been put into action (see The presidency, below).

The presidency

Saddled with a flimsy majority in parliament and self-serving coalition partners,Mrs Kumaratunga can thank the powerful executive presidency she inherited for thesurvival of her government. The power of the presidency has come in useful onseveral occasions when Mrs Kumaratunga has intervened to settle controversialdisputes through executive decisions. Ironically, one of the key election pledges thatswept her party into power was the abolition of the presidency, but practicalconsiderations have delayed its implementation. The government has linked theconstitutional amendment required for this with the more contentious amendmentsbeing considered for greater Tamil autonomy. Should the government fail to receivea mandate to implement the devolution package (which must be approved by atwo-thirds vote of parliament), it has a convenient excuse for its failure to abolish thepresidency.

There are 28 ministries and several other governmental departments andagencies. Sri Lanka has approximately 200 public enterprises encompassing avariety of organisational forms, including commercial enterprises, boards,bureaux, authorities, corporations, agencies and institutes.

The judiciary is independent. The Supreme Court has sole jurisdiction overinterpretation of the constitution and also has the final say in adjudicatingupon charges against the president.

Sri Lanka: Constitution and institutions 7

EIU Country Profile 1997-98 © The Economist Intelligence Unit Limited 1997

Political forces

There are many political parties. The three major parties, all Sinhalese-dominated, are the United National Party (UNP), the Sri Lanka Freedom Party(SLFP) and the Democratic United National Lalith Front (DUNLF). Alliancesbetween these parties and a number of minor parties with leftist leanings arecommon for electoral purposes.

The UNP is facing internaldivisions—

The UNP was in power from independence to 1956, from 1965 to 1970 andfrom 1977 to 1994, when it became the first party to embrace free-marketeconomics. Banished to the opposition benches after 17 consecutive years inoffice, the UNP leadership under the command of Mr Wickremasinghe is seek-ing to infuse new life into the party by recruiting young professionals andtechnocrats. However, internal divisions have debilitated the UNP, which hasmounted little challenge to the PA.

—while the SLFP leads theruling coalition—

The SLFP was founded in 1951 by Solomon Bandaranaike and won the 1956general election. It has its roots in Sinhalese nationalism. Mr Bandaranaike wasassassinated in 1959, and was succeeded in 1960 by his widow, Sirimavo, who

Main political figures

Chandrika Kumaratunga: The president’s genuine effortsto resolve the ethnic crisis and accelerate economic reformshave been thwarted by the intransigence of the Tigers andlack of support for her economic policies among her coalitionpartners. Her popularity among Colombo’s elite and theinvestor community has waned, although she still largelyretains the support of the rural population.

Velupillai Prabhakaran: The LTTE leader’s influencewaned significantly after the government took control of theJaffna peninsula, but Mr Prabhakaran is still a key figure.Should the rebel leader opt for negotiations or—lesslikely—accept a political solution, the impact on the countryin general and on the economy would be instantaneous.

Ranil Wickremasinghe: Head of the opposition UNP. Theonly obvious alternative national leader to Mrs Kumaratunga,he appears in no hurry to dislodge her or her government. Heis concentrating on rebuilding the UNP before making a bid forpower. He also favours giving the present regime more time tomake military progress against the LTTE.

Anuruddha Ratwatte: The deputy defence minister, andgenerally credited with having given the security forces thepolitical backing and motivation that made their campaign inthe north successful, he is one of the most powerfulindividuals in the cabinet, and is said to be one of thecontenders for the premiership.

Sirimavo Bandaranaike: Although physically feeble, thegrand old lady of Sri Lankan politics is a steadying influencein the inexperienced and impetuous PA coalition. The primeminister’s position is especially significant in the executivepresidential system; if the president dies, the prime minister isthe immediate successor.

M H M Ashraff: The ports minister and SLMC leader, andan important member of the PA coalition, he has on morethan one occasion quarrelled with the president andthreatened to quit the coalition. As the leader of a minorityparty, Mr Ashraff’s concerns are communal and regional anddo not always coincide with the priorities of the alliance ingeneral. But, if his party were to quit the alliance, the PAwould be hard-pressed to stay in power.

S Thondaman: The livestock minister and CWC leader, hisobscure portfolio in the cabinet disguises the fact that, likeMr Ashraff, Mr Thondaman is a power broker in the alliance.He also controls the largest trade union in the plantationsector, and is in a position to pressure the government forconcessions.

Srimani Athulathmudali: The leader of the DUNLF, she isanother key coalition partner who can make life difficult forthe alliance. She represents a group of alliance members whoinsist on the abolition of the presidency and who wieldsignificant bargaining power.

8 Sri Lanka: Political forces

EIU Country Profile 1997-98 © The Economist Intelligence Unit Limited 1997

became the world’s first woman prime minister. After being defeated in 1965,the SLFP returned to power from 1970 to 1977, still with Mrs Bandaranaike atits head. Its left-wing economic policies included a far-reaching programme ofnationalisation which sapped much of the economy’s dynamism.

Mrs Kumaratunga has succeeded her mother both as leader of the SLFP and thePeople’s Alliance (PA). She is the widow of Vijaya Kumaratunga, a popular filmstar, who was a leading figure in the United Socialist Alliance (USA), a left-wingamalgam of five small parties. In its current term in office the SLFP, as the coreof the PA, has pursued policies of economic reform, including privatisation andfinancial reforms.

—and the DUNLF is aspent force

The DUNLF was formed in 1991, following the failure of a campaign to im-peach Mr Premadasa and the subsequent expulsion from the UNP of eight ofthe campaign’s leaders. It generally supports the UNP’s economic line, butseeks to curb presidential power. After Mr Athulathmudali’s assassination in1993 the leadership passed to Mr Dissanayake, but in the following months theparty split. Mr Dissanayake and other leaders rejoined the UNP. Some othermembers followed Srimani Athulathmudali, the widow of the murdered leader,into the PA.

Smaller parties largelyrepresent ethnic groupings

There are a number of Tamil parties and groups which remain within the main-stream political system (although none has sufficient support yet to speak forthe Sri Lankan Tamil people as a whole). The largest is the Eelam People’sDemocratic Party (EPDP), which has nine seats in parliament, while the trad-itionally moderate Tamil United Liberation Front (TULF) has five and theDemocratic People’s Liberation Front (DPLF), a former guerrilla group, has three.

The Ceylon Workers’ Congress (CWC) is effectively the party of the IndianTamils. Its leader, S Thondaman, has normally worked with the parties inpower and usually holds a cabinet post.

The Sri Lanka Muslim Congress (SLMC) was formed in 1980, and has operatedas a political party since 1986, to promote the interests of Sri Lankan Muslims.In August 1994 it won seven seats in parliament, enabling it to hold thebalance of power along with other small parties.

While the LTTE can be regarded as an extremist Tamil movement, Sinhaleseextremists have found a home in the Janatha Vimukthi Peramuna (JVP). Itsmost durable base has been among the unemployed youth in the south of theisland. After the killing of its leaders at the end of 1989, the JVP lost much ofits force. Elements of the radical movement still exist and there is concern thatserious discontent could again see the JVP grow in influence.

International relations and defence

Relations with Westerngovernments have

fluctuated

Sri Lanka became strongly pro-Western after 1977 when the economy was liber-alised and substantial quantities of aid flowed into the country. Between 1988and 1993 relations with the West deteriorated owing to the government’s poorrecord on human rights; aid was often linked to this issue. Some governments,such as that of the UK, even imposed an embargo on arms sales to Sri Lanka.

Sri Lanka: International relations and defence 9

EIU Country Profile 1997-98 © The Economist Intelligence Unit Limited 1997

Since 1994 Mrs Kumaratunga’s genuine efforts to resolve the ethnic conflicthave won favour with Western governments and restored international sympa-thy for the country’s fight against the Tamil Tigers; inflows of foreign aid haveagain increased.

Relations with India haveimproved in the 1990s

Relations with the dominant regional power, India, have always been of criticalimportance. Indo-Sri Lankan relations were excellent for over three decades,before the eruption of racial conflict in Sri Lanka in the early 1980s and theemergence of what was perceived as Sri Lanka’s pro-Western foreign policy. Theagreement to permit Voice of America to set up a transmitting station on the is-land and the lease of the Trincomalee Oil Farm to a US-led consortium wereviewed with suspicion by India. Relations between the two countries remaineduneasy after the signing of the Indo-Sri Lankan peace accord in 1987, deteriorat-ing to an all-time low during the presidency of Mr Premadasa, who ordered thewithdrawal of the Indian Peace Keeping Force, starting in 1990. India’s disas-trous military involvement in Sri Lanka’s civil war, and the assass-ination of itsprime minister, Rajiv Gandhi, by the LTTE, led it to adopt a less aggressivestance in Sri Lanka’s ethnic conflict. Relations with India have been restored totheir former cordial levels by the present government, and both countries arenow united against the LTTE.

Defence spending is high Despite the civil war and high defence expenditure, the total size of the armedforces is modest, at 110,000-115,000. This includes a navy of 10,300 men, andan air force of 10,000 (according to the Institute of Strategic Studies). Service isvoluntary. The two operations mounted against the Tigers in 1997 causedheavy losses of men and equipment.

The economy

Economic structure

Agriculture remainsimportant—

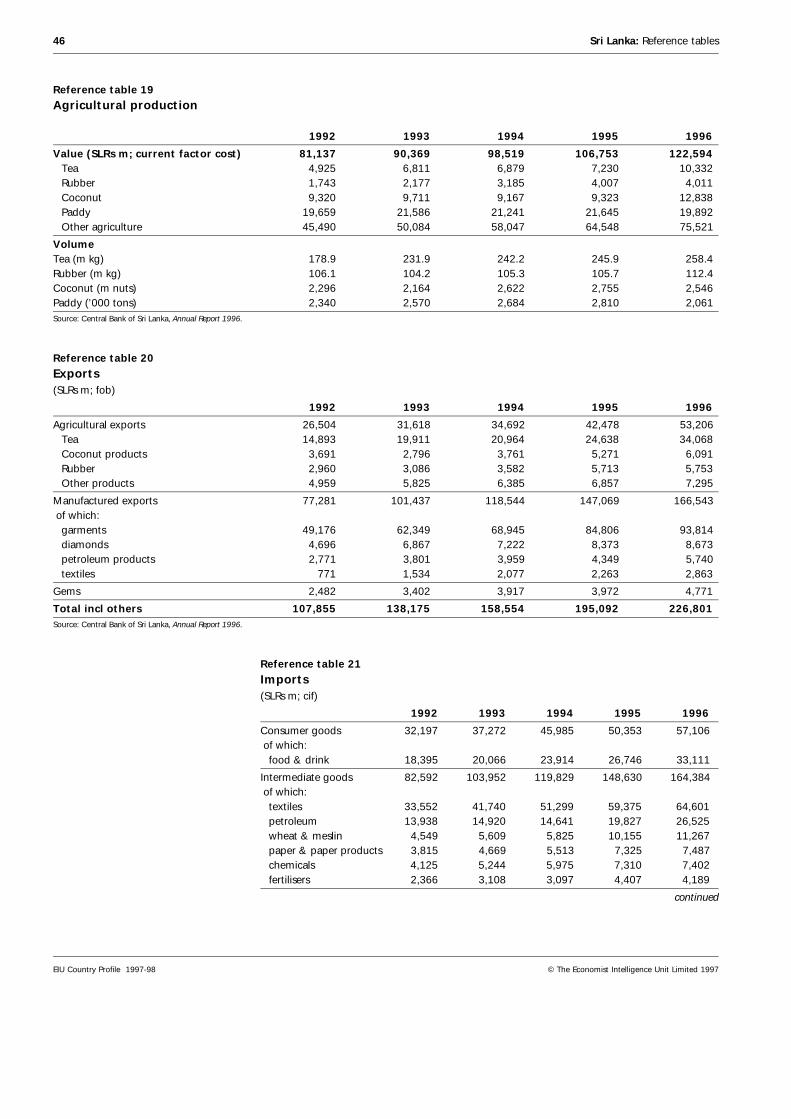

Sri Lanka’s economy is still largely agricultural; just under 20% of real GDP isgenerated by this sector (including forestry and fishing), and almost 40% of theisland’s labour force is employed in it. The agriculture sector is dominated bythree export crops—tea, rubber and coconut—and by paddy rice (mostly fordomestic consumption), which together account for over half of agriculturalproduction in value terms.

Main economic indicators, 1996

Real GDP growth (%) 3.8

Consumer price inflation (%) 15.9

Current-account balance ($ m) 653.0

Exchange rate (SLRs:$) 55.27

Population (m) 18.3Sources: Central Bank of Sri Lanka, Annual Report 1996; EIU.

10 Sri Lanka: Economic structure

EIU Country Profile 1997-98 © The Economist Intelligence Unit Limited 1997

—but manufacturing’sshare of GDP is larger—

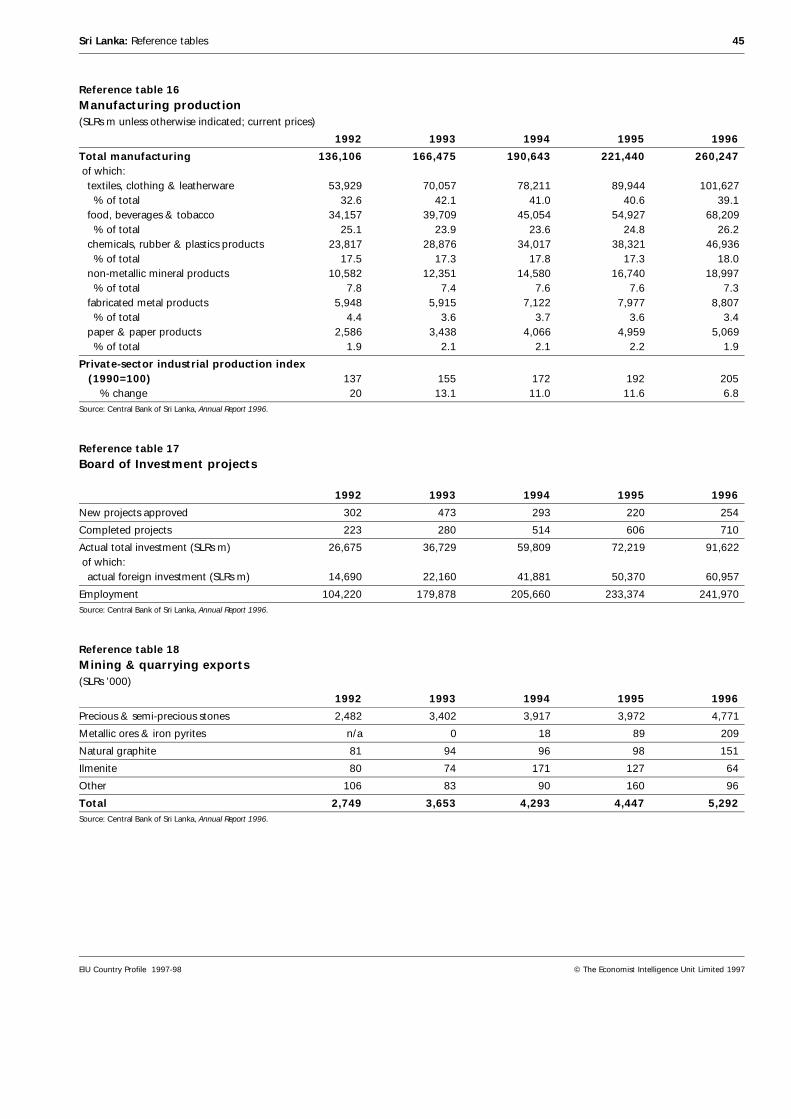

The manufacturing sector has grown rapidly, boosting its share of GDP from18.5% in 1992 to 21% in 1996. Since 1995 manufacturing’s share of GDP hasexceeded that of agriculture. In 1992-96 manufacturing has also emerged as thelead sector underpinning economic growth. Although the country’s manufac-turing base is still dominated by the garment industry (41% of total exports in1996), in recent years the share of other industrial exports, notably jewellery,machinery, and electrical and chemical products, has grown rapidly, from 26%in 1992 to 32% in 1996. Progressive privatisation of state enterprises has en-abled the private sector to dominate manufacturing. Small and medium enter-prises account for nearly 90% of private industrial units.

—and services’ share isgreater still

The services sector accounted for 49.8% of GDP in 1996, and is principallycomposed of wholesale and retail trade, financial services, transport and com-munications, public administration and defence and tourism. The tourismsector remains vulnerable to racial tension on the island.

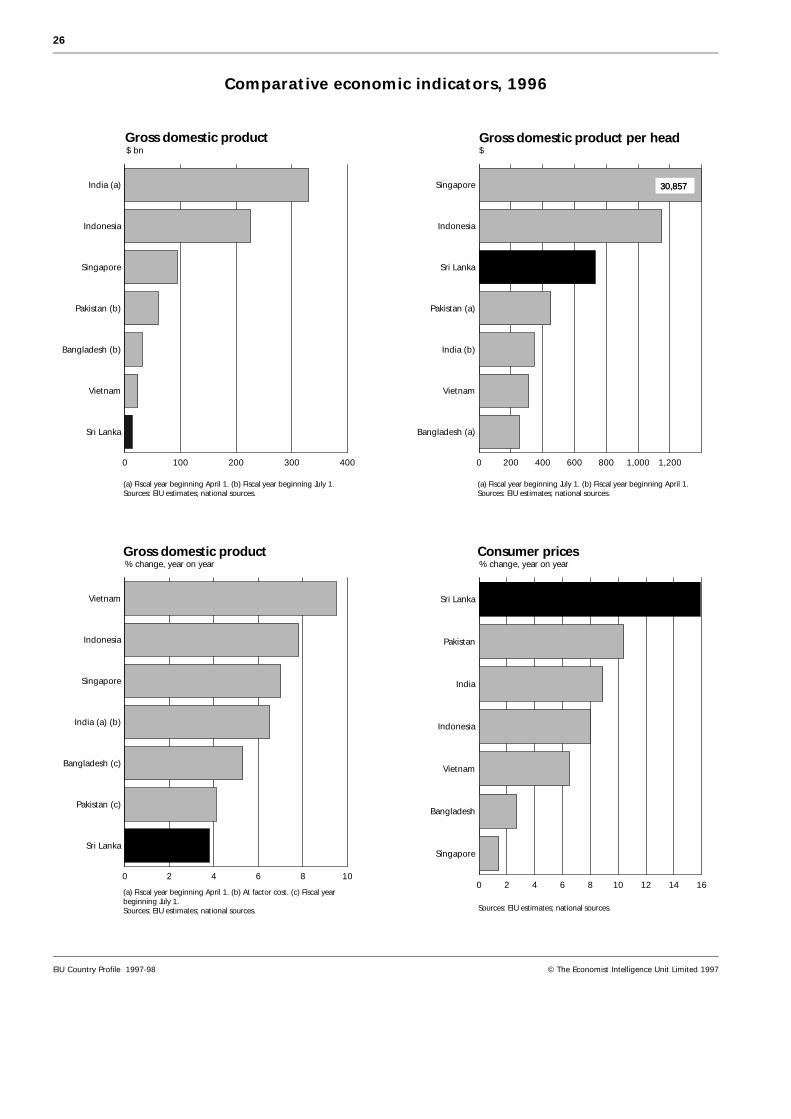

Comparative economic indicators, 1996

Sri Lanka India Pakistan

GDP ($ bn) 14.4 331.7 64.2

GDP per head ($) 790 350 480

Consumer price inflation (%) 15.9 8.9 10.4

Current-account balance ($ bn) –0.7 –5.5 –4.0

Exports of goods & services fob ($ bn) 4.1 35.5 8.6

Imports of goods & services fob ($ bn) 4.9 42.7 12.0Sources: National sources; EIU; IMF, International Financial Statistics.

Economic policy

Liberalisation after 1977boosted growth—

In the past two decades, economic policy has been marked by two distinctwaves of economic liberalisation. In 1977 the government of J R Jayewardene,reversing the socialist policies of its predecessor, introduced a liberal, openeconomic policy aimed at creating conditions for sustained economic growth,higher employment and a shift of resources from consumption to investment.Early measures included the abolition of import restrictions, the easing of pricecontrols, a cutback in food subsidies, the opening up to the private sector ofareas previously reserved for the public sector, and active encouragement offoreign investment. These measures were coupled with a massive increase inpublic investment, the centrepiece of which was the Accelerated MahaweliDevelopment Programme, a huge combined power, irrigation, agriculturaldevelopment and settlement programme. The result was an acceleration inGDP growth to an average annual rate of 6% in 1978-83, more than double the2.9% achieved in 1971-77.

—but failed to reform thepublic sector

This rate of growth could not be sustained, however, mainly because the 1977reforms did not address the fundamental problem of a large and inefficientpublic sector. Around 50% of industry remained in the public sector and govern-ment and semi-government institutions accounted for over one-fifth of totalemployment. Low returns on public investment further exacerbated the situ-ation, while export competitiveness was eroded by the government’s reluctance

Sri Lanka: Economic policy 11

EIU Country Profile 1997-98 © The Economist Intelligence Unit Limited 1997

to adjust the exchange rate. With the escalation in the civil conflict in the northfrom 1983 and the Janatha Vimukthi Peramuna (JVP) terrorist insurgency in thesouth in 1988-89, real annual GDP growth slowed to a mere 2% in 1987-89 andthe country was on the verge of a balance-of-payments crisis.

Further reform in 1989-93paid dividends—

In 1989 a second and more rigorous liberalisation programme was introducedby Ranasinghe Premadasa’s United National Party government. The economicreform programme was supported by an IMF Enhanced Structural AdjustmentFacility (ESAF). Stabilisation measures included a devaluation of the rupee andthe abolition of major subsidies. These were complemented by an ambitiousprivatisation drive. Tax, tariff and trade reforms were also begun, and thecurrent account was freed of exchange controls. GDP growth rose from 2.3% in1989 to 6.9% in 1993.

—but momentum was lostunder the PA

government—

The People’s Alliance (PA) government, elected in 1994, pledged to continuewith the economic reform programme. However, being a coalition of fractiouspolitical parties with differing economic ideologies, the economic policy envi-ronment during the first two years of PA rule was characterised by inconsistentpolicy statements that were not matched by action. For over a year after it cameto power no new privatisations were undertaken. Wheat, flour and fertilisersubsidies were reintroduced which, together with soaring defence expenditure,imposed a severe strain on the budget. Labour unrest reached unprecedentedlevels in early 1995, undermining business confidence. Increased governmentborrowing fuelled a rise in interest rates and inflation climbed to double digitsby the end of 1995. The country’s growth was further crippled by a severedrought and a power crisis in the first half of 1996.

—although there is now astronger effort to

accelerate reforms

In the second half of 1996, the government reinvigorated its policy reforms.The privatisation programme was revived with the sale of six regional plant-ation companies, the steel corporation and two salt companies to privateinvestors. The sale of the remaining plantation companies was to be completedby the end of 1997. In August Japan’s Nippon Telephone and Telegraph boughta 35% stake and full management control of Sri Lanka Telecom. In its budgetfor 1997 the government introduced a comprehensive package of incentivesand regulatory reforms designed to revive investor confidence. Unproductivesubsidies were phased out and efforts to expand infrastructural facilities werestepped up.

Persistently high fiscaldeficits—

The reduction of the fiscal deficit has emerged as the most serious challengefacing policy-makers. Unsustainably high fiscal deficits are the primary causeof macroeconomic instability, since they raise inflation and interest rates. Therecord of successive governments in fiscal management has been poor. In 1994a sharp escalation in defence spending raised the deficit, excluding grants, toaround 10% of GDP. In 1996 the deficit was contained at 8.9% of GDP partlyowing to a reduction in capital spending. Although escalating defence expend-iture has been primarily responsible for the increase in recurrent expenditure,increased spending on subsidies and mounting interest and wage bills havealso played a part. (Reference table 1 gives a breakdown of government revenueand expenditure.)

12 Sri Lanka: Economic policy

EIU Country Profile 1997-98 © The Economist Intelligence Unit Limited 1997

—will be difficult toreduce

The medium-term objective is to reduce the fiscal deficit to 7.5% of GDPin 1997 and 4.5% by 1999. Much government expenditure, such as security/defence costs and interest payments, are difficult to compress, although thegovernment used privatisation proceeds to retire SLRs10bn of public debt inAugust 1997. Most of the reduction will be made by cutting the civil servicewages and pension bill through administrative reforms and by trimming sub-sidies and social transfers. Such measures require considerable political courageand have been avoided by successive governments. Instead, capital expend-iture has been sacrificed to cover increased recurrent expenditure, and as aconsequence public investment has suffered. Nevertheless, in its 1997 budgetthe government made an attempt to prune expenditure. A 20% across-the-board cut in all recurrent expenditure and a 25% reduction in overtime pay-ments is to be effected. The abolition of the wheat subsidy (most of it wasremoved in August 1996, with another reduction in August 1997) will effec-tively reduce welfare payments by 10%.

The 1997 budget The 1997 budget attempted to revive business confidence by introducingseveral measures designed to boost the domestic and export manufacturingsectors. The measures included:

• 100% exemption from duty and taxes on capital and intermediate goods forproducers who export 50% of output, and 50% exemption for producers whoexport 25-49% of output;

• extending offshore borrowing facilities to all exporters;

• lowering the minimum investment requirement for duty-exempt imports fornew investments in “advanced technology” industries from SLRs10m ($169,492) toSLRs4m;

• an investment tax allowance of 75-100% of the cost of new plant to beavailable as a deduction against specified assessable undertakings;

• increased depreciation allowances on plant, machinery and equipment;

• a progressive reduction in corporate and personal taxes from 35% to 25% byApril 1999;

• the national security levy on capital goods reduced from 2% to 0.5%; and

• the planned introduction of a goods and services tax in 1997.

Summary of government finances, 1996a

SLRs m % of GDP

Total revenue & grants 154,779 20.1 Tax revenue 130,202 16.9 of which: income taxes 20,751 2.7 taxes on property 5,279 0.7 taxes on treasury bills 1,604 0.2 general sales & turnover tax 37,361 4.9 excise tax 22,067 2.9 defence levy 16,441 2.1 taxes on international trade 25,463 3.3 Non-tax revenue 16,077 2.1 Grants 8,500 1.1

continued

Sri Lanka: Economic policy 13

EIU Country Profile 1997-98 © The Economist Intelligence Unit Limited 1997

SLRs m % of GDP

Expenditure & lending excl repayments 214,710 27.9 Current expenditure 170,629 22.2 of which: wages, goods & services 78,666 10.2 interest payments 46,021 6.0 transfers & subsidies 46,813 6.1 Capital expenditure 40,034 5.2 Lending excl repayments 4,047 0.5

Memorandum itemsBudget deficit (before grants) 68,431 8.9Budget deficit (after grants) 59,931 7.8

a Provisional.

Source: Central Bank of Sri Lanka, Annual Report 1996.

A tight monetary policy— In recent years, monetary policy has focused principally on controlling infla-tion, with the Central Bank of Sri Lanka relying on indirect policy instruments,including open market operations, to influence the growth of money supply. In1992-93 monetary growth was fuelled by a large increase in foreign capitalinflows and an expansion in private-sector credit; this led to the operation of atight monetary policy. In 1993-95 an even stronger emphasis on controllinginflation led to a tightening of monetary policy to compensate for a wideningfiscal deficit caused by high defence spending. This stance precipitated a severeliquidity crisis at the end of 1995 and led to a brief relaxation of monetary policyin the first half of 1996. By the end of 1996 a sharp decline in the growth ofprivate-sector credit, as investment and economic growth slowed perceptibly,led to a significant deceleration in the growth of the broad money supply; thisfell from 19.2% in December 1995 to 10.8% in December 1996.

—has now been relaxed tostimulate growth

Following a difficult year in 1996 the Central Bank is now attempting to usemonetary policy to stimulate economic growth. By mid-1997 several measuresaimed at increasing liquidity and reducing interest rates had been introduced.The reserve ratio on rupee deposits was cut from 15% to 12%, and that onforeign currency deposits was waived. Two- and four-year Treasury bonds wereintroduced, marking the first step towards developing a market for longer-termdebt securities while simultaneously establishing a benchmark for the directionof long-term interest rates. Heavy intervention by the Central Bank in theshort-term Treasury-bill market also led to a reduction in short-term rates.(Reference table 2 includes monetary aggregates, and Reference table 3 showsinterest rates.)

Economic performance

Manufacturing is themain engine of growth—

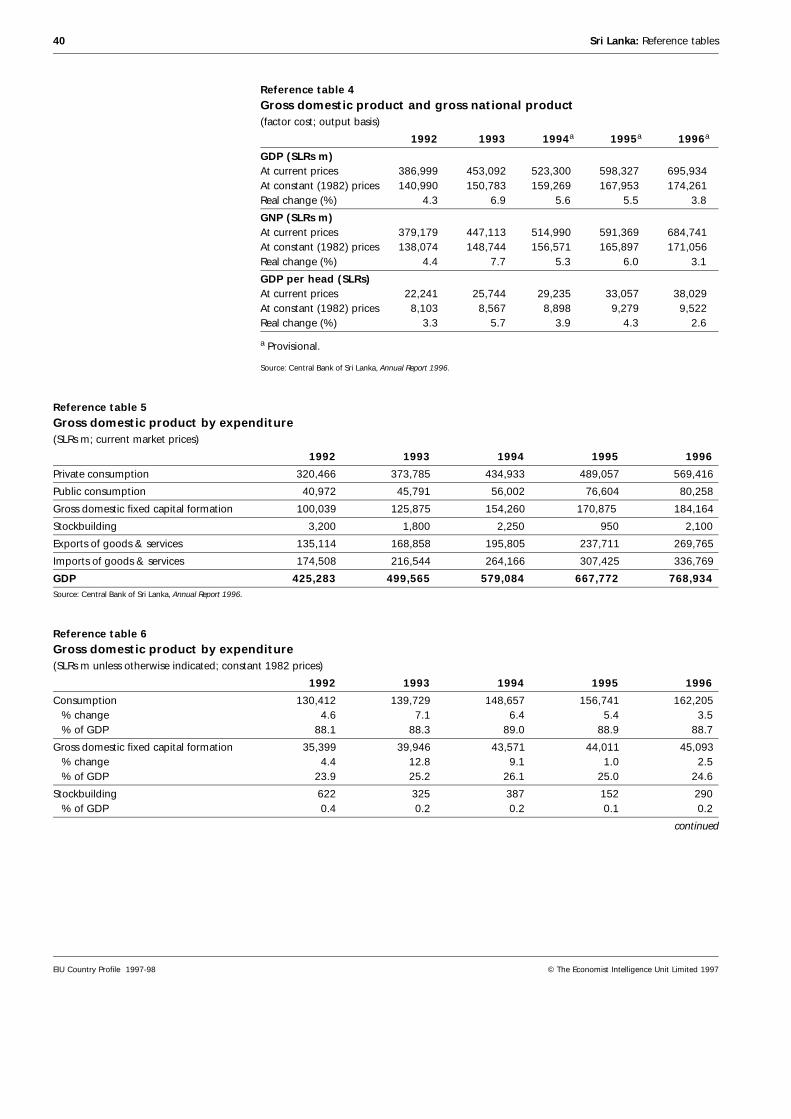

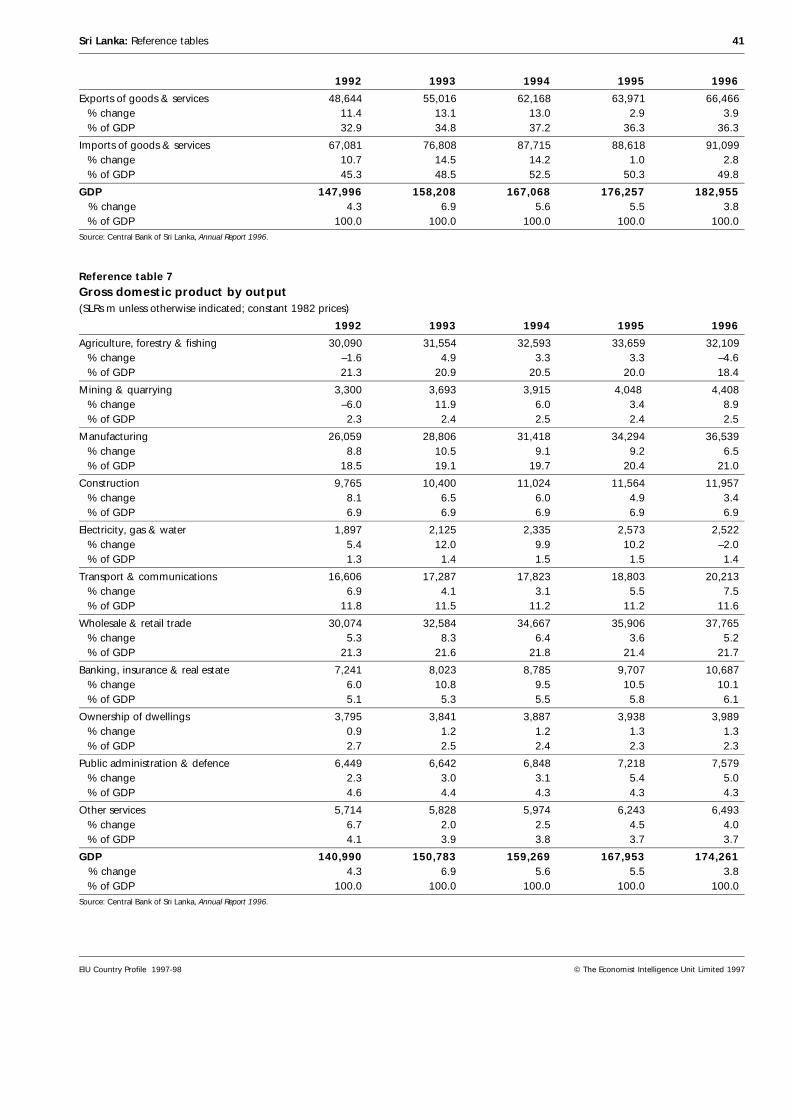

Real annual GDP growth averaged 5.2% in 1992-96. The manufacturing sectoremerged as the main engine of growth, expanding at an annual average rate of8.8% per year in 1992-96, offsetting a lacklustre agriculture performance. In1992-96 agricultural growth averaged a mere 1%. In 1996 agricultural outputdeclined by 4.6% (the worst performance since 1987), but a 6.5% expansion inmanufacturing helped GDP growth to reach 3.8%. (Reference tables 4-7 pro-vide various measures of GDP.)

14 Sri Lanka: Economic performance

EIU Country Profile 1997-98 © The Economist Intelligence Unit Limited 1997

Manufacturing growth has become more impressive as the relative size of thesluggish public sector has declined, enabling private industry to predominate.In 1996 the private sector contributed 90% of total value added in manufac-turing. The clothing industry, whose predominant position in manufacturingremains unchallenged, and the food-processing industry together accountfor nearly two-thirds of industrial production, followed by chemicals, rubber,petroleum and plastics products.

—although the servicesector has also expanded

sharply

The service sector has benefited from economic liberalisation; it grew at anaverage annual rate of 5.7% in 1992-96. Financial services and communications,which have direct links to manufacturing, have been the most dynamic sectors,followed by wholesale and retail trade. In 1990-94 growth in tourism and alliedservices made a significant contribution to overall growth in services.

Gross domestic product(% real change; 1982 factor cost)

Annualaverage

1996 1992-96

GDP 3.8 5.2 Agriculture –4.6 1.0 Mining & quarrying 8.9 4.7 Manufacturing 6.5 8.8 Construction 3.4 5.8 Services 5.8 5.7Source: Central Bank of Sri Lanka, Annual Report 1996.

Expenditure data revealslackening investment

and exports

Data on real growth in expenditure are subject to periodic revisions. Generaltrends indicate that GDP growth since 1990 has been driven primarily by anexpansion in exports and to a lesser extent by an increase in private domesticand foreign investment. Exports of goods and services grew in real terms at anannual average rate of 8.8% per year in 1992-96, while annual fixed investmentgrowth averaged 5.9%. In 1995 and 1996, however, fixed capital investmentgrew by an average of only 1.7% annually, due to a dramatic slowdown inforeign and domestic investment, prompted by heightened political uncer-tainty, an unfavourable policy environment and labour unrest. The drought in1996, which hit agricultural output, also slowed exports of goods and services.

The share of private consumption in GDP fell from 75% in 1992 to 74% in1996. Public consumption, which averaged 9.5% of GDP in 1992-94, rose to anaverage of 11% in 1995-96 as a result of the increases in defence and welfarespending.

Persistent high inflation— High inflation has been a persistent problem in Sri Lanka over the past decade.Cost-push factors such as wage adjustments, increases in indirect taxes, highinterest rates and exchange rate depreciation have contributed to increases inprices. Seasonal scarcities of agricultural commodities and inefficient agricul-tural production are also inflationary factors, owing to the heavy weighting(69.3%) accorded to food and beverages in the consumer price index. In 1996increases in food prices accounted for 83% of the increase in the overall con-sumer price index. In recent years the principal causes of demand-induced

Sri Lanka: Economic performance 15

EIU Country Profile 1997-98 © The Economist Intelligence Unit Limited 1997

inflationary pressures have been the high level of government spending andthe rapid rate of monetary expansion.

The suppression of inflation—by a combination of subsidies and reductions inkey administered prices—resulted in single-figure inflation in 1994 and 1995.With the lifting of the subsidies, hikes in administered prices, continued depre-ciation of the exchange rate and a sharp increase in public spending, inflationrose sharply at the end of 1995 and averaged 15.9% in 1996. Assisted by a morebuoyant agricultural sector, inflationary pressures are beginning to abate.Although the rate of inflation between January and April 1997 averaged 14.5%,it was declining.

Persistently high inflation has prevented any increase in real incomes, sincewage increases have generally not kept pace with the rise in prices. There are noreliable statistics for income distribution, but anecdotal evidence suggests amarked widening in income disparities. Rising food prices have also preventedany significant rise in discretionary spending, since the bulk of incomesare spent on basic necessities. (Reference table 8 includes data on prices andwages trends.)

—has eroded exportcompetitiveness

As the rate of inflation in Sri Lanka has tended to be higher than those of itscompetitors, the country’s price competitiveness has suffered. This problemhas been exacerbated by high interest rates and the lack of concessionaryfinancing to the export sector. Since exchange rate depreciation also fuelsinflation, the government has been reluctant to devalue the currency to theextent exporters demand. The 1997 budget, acknowledging the difficultiesfaced by exporters, announced several measures designed to provide relief tothe export sector.

Prices(% change)

Annualaverage

1996 1992-96

Consumer prices 15.9 11.0

Wholesale prices 20.5 10.0Sources: Central Bank of Sri Lanka, Annual Report 1996; EIU.

Regional trends

A regional developmentplan for the south—

Regional development became a priority only after the uprising by JVPSinhalese militants in the south in 1988-89. This galvanised the UnitedNational Party government to draw up a southern area development plan.However, apart from establishing a third investment promotion zone in theprovince (where only a handful of industries are located), other projects todevelop the south made little progress. The present government has accordedsimilar priority to the development of the south, but has made more progressin implementing its plans. In 1996 a Southern Development Authority (SDA)was established, charged with the implementation of a development plan; byMarch 1997 the SDA had formally launched the first of its projects—a $19.3mcaustic soda manufacturing plant. The SDA then released a blueprint for the

16 Sri Lanka: Regional trends

EIU Country Profile 1997-98 © The Economist Intelligence Unit Limited 1997

development of the Southern province into the next century. The $3.4bnproject envisages the creation of a new city, Ruhunapura, with a port, inter-national airport and high speed highway connecting it to Colombo.

—and others are suggested The Asian Development Bank (ADB) has provided technical assistance for thepreparation of a development master plan for the North-Central province.While projects to develop the Northern and Eastern provinces have been inexistence since the late 1980s the civil war has prevented their implementation.

Integrated RuralDevelopment Programmes

Regional development has been primarily effected, albeit on a small scale,through Integrated Rural Development Programmes. These presently cover 17of the island’s 26 districts. These projects, which are primarily foreign-funded(usually by grants) and initially focused on the development of infrastructure,now concentrate on the creation of income-generating projects and the devel-opment of skills in rural areas. Development funds (known as criteria-basedgrants) are released by central government to the provincial councils to allowthem to undertake development projects. The funding that each provincereceives is determined by criteria that take into account the population of eachprovince and selected indicators of social and economic differences betweenprovinces. However, the annual allocation of SLRs1bn ($17.6m) between nineprovinces has not been increased in recent years and is insufficient to make anyreal contribution to development.

Resources

Population

Sri Lanka prides itself on being a multiracial and multifaith society. TheSinhalese, who comprise nearly three-quarters of the population, speak Sinhala,one of the oldest Aryan languages, and are mainly Buddhists.

The population ispredominantly rural

Sri Lanka’s population was estimated at 18.3 million in mid-1996. About 70%of the people live in the island’s south-western area (the so-called wet zone),which accounts for about three-quarters of the cultivated land and most of thecountry’s industry. In 1996 only 22% of the population was urban, a propor-tion little changed from 15 years earlier.

Population growth isbeing controlled—

Sri Lanka’s demographic achievements are commendable for a low-incomecountry. Declining fertility rates, a consequence of improved education amongwomen and the relatively high use of contraceptives, have enabled the countryto move to an advanced stage of demographic transition, with populationgrowth expected to approach replacement level before the turn of the century.(See Reference table 9 for data on population growth rates.) Falling birth ratesand increased life expectancy are also changing the age profile of the popul-ation. The number of old people is expected to rise by the turn of the century,exerting more pressure on tertiary health facilities.

Sri Lanka: Population 17

EIU Country Profile 1997-98 © The Economist Intelligence Unit Limited 1997

—but unemploymentremains high

Unemployment has become a pressing political and social issue. The unemploy-ment rate was 11.6% in 1996, little changed from 12.1% in 1994 and 12.0%in 1995. It has been estimated that the economy needs to generate at least158,000 new jobs annually if the unemployment rate is to be halved by 2001.

The profile of the unemployed is also of concern. About two-thirds are 24 yearsof age or under, and are relatively well-educated. While the high proportion ofeducated youth among the unemployed is partly explained by the historicaltendency of many young people to remain unemployed for long periods of timein expectation of government jobs, it is also due to a mismatch between theskills imparted by the education system and those demanded in the job market.(Reference table 10 includes data on the labour force and unemployment.)

The role of the Tamils The Sri Lankan Tamils account for 12.7% of the population (1981 census). Themajority are Hindu, but there is a substantial Christian minority. The Tamils aretraditionally concentrated in the north and east of the island. Before inde-pendence the Tamils played an important role in political life and accounted fora disproportionately large share of government employees and of the educatedpopulation; this fuelled resentment among the Sinhalese community.

So-called upcountry, or “Indian”, Tamils form 5-6% of the population. Descen-dants of people brought from India by the British to work on tea plantations,many were denied citizenship after independence. Some returned to India inthe late 1960s under an agreement with the Indian government. However,many remained and all who did so were granted citizenship in 1988.

Muslims and others Muslims constitute around 7% of the population and are concentrated in theEastern province and in Colombo. They are largely traders and, althoughTamil-speaking, remain apart from the Tamil community. Finally, there aresmall groups of “Burghers” (Eurasians of mixed descent), Malays and a smallnumber of highly respected Veddas, descendants of the original inhabitants ofthe island before Sinhalese settlement; together, these groups make up about1% of the total population.

Population by age group, 1996

’000 % of total

0-14 years 6,477 35.2

15-54 years 10,137 55.3

55 & over 1,731 9.5Source: Central Bank of Sri Lanka, Annual Report 1996.

Education

Impressive educationindicators—

The education system, targeted as a high priority by the government after inde-pendence, is advanced by developing country standards. Participation rates arehigh, which is borne out by the high literacy rate of 90%. The pupil/teacherratio is low at 22 students per teacher in 1994 (average male and female rate),although there are significant regional disparities in the availability of teachers.

18 Sri Lanka: Education

EIU Country Profile 1997-98 © The Economist Intelligence Unit Limited 1997

—conceal problemswith quality

It is now widely accepted that the quality of Sri Lanka’s education system,particularly at secondary and tertiary levels, needs to be upgraded to keep pacewith the changing needs of the economy. At the secondary level, the profi-ciency of students in mathematics and science is disappointing. Examinationresults are poor and dropout rates at secondary and tertiary levels are high.

The inability to raise the quality of education has less to do with inadequatefunding (government spending on education averaged 2.8% of GDP in 1992-96)than with efficient utilisation. Three-quarters of recurrent expenditure on educ-ation is on salaries, at the expense of quality-enhancing expenditures such asinstruction materials and maintenance of facilities. There is also a severe short-age of experienced and trained teachers. Many trained teachers opted for anearly retirement scheme in the early 1990s, and were replaced by a mass ofuntrained graduates. Low teacher morale (largely because of low pay) andabsenteeism are other problems. There is also a marked disparity betweenfacilities in urban and rural schools.

University education lacksan industrial orientation

In the past two decades, the tertiary education system has failed to adapt to thechanging economic structure. The university curriculum remains rooted intraditional non-vocational courses. There is a lack of industrial orientationamong graduates, who possess neither relevant practical skills nor an adequatecommand of the English language. This has led to a paradoxical situation inwhich on the one hand there are a growing number of “educated unemployed”and on the other a growing shortage of labour to fill middle level and juniormanagerial positions in the private sector. The government is attempting totackle this problem through the establishment of a Skills Development Fund.The programme, a joint venture between the government and the country’sfour chambers of commerce, was formally launched in February 1997 and aimsto train and finally absorb graduates into the private sector. Several technicaland vocational training institutions and schemes have been in operation overthe past decade but they have tended not to be demand-oriented and hencehave not proved effective in meeting the demands of the employment market.

Sri Lanka’s rapidly deteriorating education standards have prompted thegovernment to declare education reform a priority. A task force to revamp theeducational system was appointed in 1996. Some of the policy changes it hasrecommended include greater emphasis on the teaching of English, significantchanges in the curriculum and the use of modern technology in the classroom.

Health

High standards ofhealthcare—

Thanks to the emphasis placed on health by successive governments, Sri Lankahas an extensive system of public health services. These, like education, areprovided by the state free of charge. The country’s health indicators are impres-sive. Between 1985 and 1995 life expectancy increased from 67 to 70 years formen and from 71 to 74 years for women, according to the Asian DevelopmentBank (ADB). There has also been a sustained decline in infant mortality.

—are declining In recent years the demand for health services has grown, owing to increasedpublic awareness of health matters, the relative ageing of the population and the

Sri Lanka: Health 19

EIU Country Profile 1997-98 © The Economist Intelligence Unit Limited 1997

large number of casualties of the civil war. But limited financial resources haveprevented a similar increase in supply, leading to a progressive deterioration inthe standard of health care. The underuse of health facilities at the rural leveland the overcrowding of health centres and hospitals are also a major problem,compounded by insufficient facilities and a shortage of drugs in rural clinics.

Malaria and infantmalnutrition are

increasing—

An increase in child malnutrition and the resurgence of malaria are two areasof concern. One-third of children under three years old are underweight fortheir age. Malaria, eradicated in the 1960s, reached epidemic proportions in theearly 1990s. A malaria control programme organised by the World HealthOrganisation (WHO) led to a decline in the incidence of malaria in 1994 and1995. But the lack of preventive measures in war-affected areas and refugeecamps led to a resurgence of the disease in 1996, with the number of casesrising from 140,000 in 1995 to 184,000 in 1996.

—but communicablediseases are under control

The shift in emphasis from curative to preventive health in recent years hashelped to control the spread of other communicable diseases, such as AIDS,other sexually transmitted diseases and water-borne diseases. The incidence ofvaccine-preventable diseases has also fallen.

A shift to a private healthsystem is considered

The government’s strategy is to improve peripheral health services, give greateraccess to healthcare to the poor and reduce rural-urban disparities in healthcareprovision. One of the main problems facing policy-makers is finding themoney to meet the rising demand for health services. One option suggested byinternational lending agencies is to introduce user fees in the public sector.

There is a growing consensus that the development of a broader private-sectorhealth system is the most feasible alternative. Since 1990 participation by theprivate sector in the health sector has been expanding. The private sector pro-vides around 50% of primary healthcare, while the bulk of hospital care isstill provided by state-run facilities. As the cost of health facilities providedby the private sector is high, they still remain largely inaccessible to lowerincome groups.

Natural resources and the environment

Natural resources arebeing depleted—

Sri Lanka is richly endowed with forests and water resources. But in recent yearsland degradation has become a major environmental problem. Forest cover hasbeen depleted from an estimated 28% of the total land area in 1975 to 20% in1992 (although estimates vary, and some show an increase in forest coverduring this time); at the present rate of deforestation, forest cover is projectedto shrink to only 10% by 2000. According to the ADB, the rate of deforestationin Sri Lanka is 3.5% of the total forest area per year—the second fastest rate inAsia (beaten only by Nepal).

With a mean rainfall of 2,000 mm per year, Sri Lanka is rich in freshwaterresources, but there has also been a rapid rise in the demand for water forirrigation, power generation, and domestic and industrial use. In the coastalzone, erosion and mining of coral reefs to obtain lime for the constructionindustry has become a major environmental hazard.

20 Sri Lanka: Natural resources and the environment

EIU Country Profile 1997-98 © The Economist Intelligence Unit Limited 1997

—and pollution is onthe rise—

Even though the level of industrialisation in Sri Lanka is relatively low byinternational standards, water pollution is rising. A 1989 survey on industrialpollution revealed that, of 7,610 industrial enterprises, 291 had high pollutingpotential, and 1,900 had medium polluting potential. The major sources of airpollution are the burning of fuel wood, industrial emissions and power plants.Although air pollution in Colombo has not reached the levels in cities such asNew Delhi and Bangkok, the increase in vehicles on the roads has alreadypushed it to unacceptable levels. Solid-waste management is another growingenvironmental problem.

—prompting someenvironmental measures—

In keeping with international trends, Sri Lanka is placing increased emphasis onenvironmental management, and in recent years increased resources have beenallocated by central government to environment protection. Some recent meas-ures include the creation of a cabinet-rank minister for the environment,strengthening the Central Environmental Authority and technical support tocreate environmental awareness in development-oriented ministries and bodies.

—but enforcement needsto be improved

The National Environment Act was introduced in 1980. In 1988 amendmentsto the act introduced environmental standards for industry, and environ-mental impact assessments for development projects were made mandatory.However, in spite of a well-articulated environmental policy, inadequate finan-cial resources and the lack of technical expertise in regulatory and advisoryservices have prevented effective enforcement and monitoring of environ-mental regulations. Little attention has been paid to the development ofeconomic incentives for encouraging environment-friendly technologies inindustry, and virtually no penalties are imposed for pollution.

Economic infrastructure

Transport and communications

Roads are inadequatelymaintained—

Sri Lanka has a road network of approximately 100,000 km, of which 11,079 kmare either A or B class roads, maintained by the Road Development Authority.Over the past decade fiscal constraints have hampered the maintenance,rehabilitation and new construction of roads. The failure to develop the roadnetwork, coupled with the increased demand for movement of passengers andgoods, has resulted in severe traffic congestion on the main national highways.Since 1986 only 1,000 km of national highways have been rehabilitated, withdonor assistance. The lack of a well-developed road network has been one ofthe principal factors inhibiting the regional dispersal of industry. In 1996 pre-paratory work was initiated on the construction of two national highways.Private investment on a build-operate-transfer (BOT) basis is being solicited forthe Colombo-Katunayake Expressway which will link the capital to the airport.The Asian Development Bank (ADB) has shown interest in financing the con-struction of the Colombo-Matara highway, which will link Colombo to theSouthern province.

Sri Lanka: Transport and communications 21

EIU Country Profile 1997-98 © The Economist Intelligence Unit Limited 1997

—bus services areinefficient—

Public passenger road services were provided until recently by the Sri LankaTransport Board (SLTB). In 1990, in view of the SLTB’s losses, the governmentbegan privatising the SLTB; by the end of 1994, 93 privatised companies werein operation.

The number of small-scale private bus operators has grown in recent years, andin 1996 the private bus sector accounted for over 60% of road transport serv-ices. Nearly 95% of private operators are single bus owners. Over the next threeyears the government plans to restrict the issue of licenses to those operatorswith a minimum fleet of 50 buses.

—and investment in theindustry is stifled by

regulated prices

Both public and private services suffer from considerable overcrowding andinefficiency. Although the current bus fleet numbers 21,000 (12,000 in theprivate sector, 9,000 in the privatised sector), around 40% of these are eitherobsolete or in urgent need of repair. The regulation of prices in the transportsector has inhibited investment. Political considerations have resulted in pricesbeing fixed at levels well below the market price, so there is little incentive foroperators to maintain or invest in new buses. In 1996 the government permit-ted a 15% rise in bus fares, but this was well below the 20-40% increase recom-mended by the Transport Fare Committee.

The rail network isrun-down

Sri Lanka Railways (SLR) has 1,982 km of track. For well over a decade therailway has run at a loss and has been a major drain on public resources.Inefficient management and lack of investment in rail infrastructure has re-sulted in a sustained decline in the quality of services, leading to reducedpublic use. In 1995 a project, funded by the Japanese government’s OverseasEconomic Cooperation Fund (OECF), was started to rehabilitate railway tracks,locomotives and workshops. The conversion of Sri Lanka Railways into a profit-oriented venture is probable. Foreign investment to electrify the suburbanrailway network on a BOT basis is being sought.

Telecommunications areexpanding rapidly—

Since 1991, when Sri Lanka Telecom was converted into a commercial corpor-ation and the sector was opened to private operators, the telecommunicationsindustry has displayed lively growth. The number of telephone lines has risenfrom 180,724 in 1994 to an estimated 254,000 in 1996. Telephone density hasrisen from 0.73 per 100 persons in 1994 to 1.4 per 100 persons in 1996.International facilities were augmented with the commissioning of a 2,000-lineexchange and the installation of a digital satellite station. Private-sector invest-ment in the sector grew even faster. By the end of 1996 there were four mobile-phone operators (the number of cellular phone subscribers increased from29,182 to 71,228 between 1994 and 1996), six Internet service providers, fiveprivate paging companies and four privately operated payphone networks.

—and privatisation willimprove service quality

In spite of the expansion in the communications industry, service quality isbelow standard. There exists a huge gap between demand for and supply oftelephone facilities. In 1996 demand for telephones reached 510,500, of which256,000 were officially on the waiting list—but only 50,150 new telephoneconnections were made. In 1996 the government gave up its monopoly, andtwo joint ventures, Lanka Bell (now a joint venture with Korea Telecom)and Suntel (led by Telia of Sweden), were granted approval to set up parallel

22 Sri Lanka: Transport and communications

EIU Country Profile 1997-98 © The Economist Intelligence Unit Limited 1997

networks. These two networks, which became operational at the end of 1996,will provide 200,000 new connections over the next two years. In August 1997a 35% stake and management control of Sri Lanka Telecom was bought byJapan’s Nippon Telegraph and Telephone (NTT) for $225m.

Ports are being expanded Sri Lanka has three ports that can accommodate deep-sea vessels—Colombo,Trincomalee and Galle. The largest of these is Colombo, which has been out-standingly successful in recent years, becoming a major transhipment port andranking in the world’s top 30 in terms of tonnage handled. Colombo’s successhas caused problems of congestion, and tariffs are relatively high. To relievecongestion, the port’s capacity of 1.4m twenty-foot equivalent units (TEUs)was expanded by an additional 700,000 TEUs with the commissioning of twonew terminals in 1995 and 1996. Contracts for the expansion of the main quayand the construction of a new container terminal on a BOT basis have beenawarded to P&O of Australia. Work on the project, which involves investmentof $950m, is expected to begin in 1998 and will expand the port’s handlingcapacity by a further 750,000 TEUs. In 1997 a new oil terminal was commis-sioned at Colombo port.

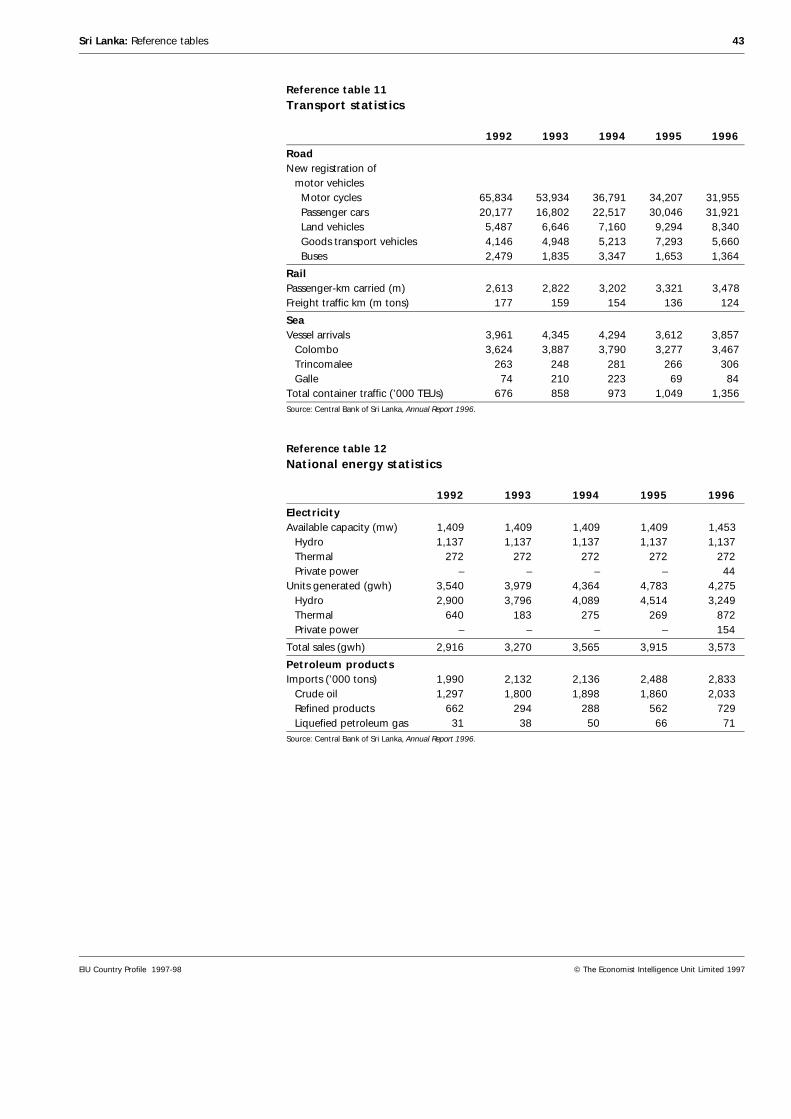

Plans to develop Galle port may be abandoned in view of the proposal in 1997to develop a port in Hambantota as part of the southern area developmentmaster plan. (Reference table 11 includes data on road, rail and sea transport.)

Energy provision

Overdependence onhydropower—

Some 64% of the island’s total energy demand is met by firewood, most of it forhousehold use. The only other indigenous energy source, hydropower,accounted for 13% of energy use in 1991, according to the Central Bank ofSri Lanka. Imported oil, much of which is refined domestically, is the largestsource of commercial energy. The Ceylon Petroleum Corporation (CPC) is thestate oil company responsible for importing, refining and distributing all petro-leum products except liquefied petroleum gas (LPG); the latter is marketed byShell, which bought the Colombo Gas Company in 1995. The transmission anddistribution of electricity are handled by the Ceylon Electricity Board (CEB).Projects to improve the country’s transmission and distribution network havehad limited success in reducing system losses, which in 1996 were equivalent totwo months of electricity consumption. An attempt in 1996 to privatise thedistribution network had to be abandoned because of stiff union resistance.

—precipitated a powercrisis in 1996—

Sri Lanka’s generation system is predominantly hydro-based, leaving it vulner-able to seasonal rainfall fluctuations. Since 1992 there have been no additionsto the national grid, since projects to augment the country’s thermal generat-ing capacity were subject to bureaucratic delays, political interference and en-vironmental considerations. In early 1996 the rains failed, which precipitateda severe power shortage and forced the government to adopt emergency meas-ures, such as subsidising the import of private generators and buying thermalpower from private operators. These measures imposed a heavy financial bur-den on the CEB.

Sri Lanka: Energy provision 23

EIU Country Profile 1997-98 © The Economist Intelligence Unit Limited 1997

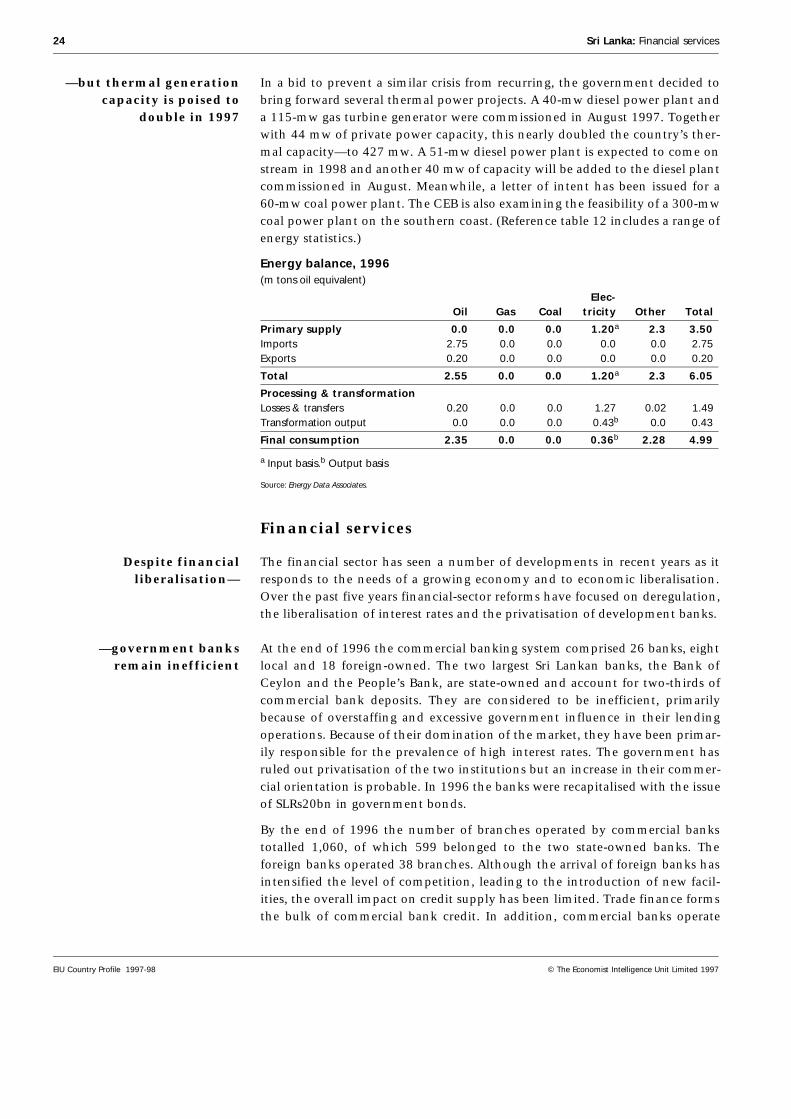

—but thermal generationcapacity is poised to

double in 1997

In a bid to prevent a similar crisis from recurring, the government decided tobring forward several thermal power projects. A 40-mw diesel power plant anda 115-mw gas turbine generator were commissioned in August 1997. Togetherwith 44 mw of private power capacity, this nearly doubled the country’s ther-mal capacity—to 427 mw. A 51-mw diesel power plant is expected to come onstream in 1998 and another 40 mw of capacity will be added to the diesel plantcommissioned in August. Meanwhile, a letter of intent has been issued for a60-mw coal power plant. The CEB is also examining the feasibility of a 300-mwcoal power plant on the southern coast. (Reference table 12 includes a range ofenergy statistics.)

Energy balance, 1996(m tons oil equivalent)

Elec- Oil Gas Coal tricity Other Total

Primary supply 0.0 0.0 0.0 1.20a 2.3 3.50Imports 2.75 0.0 0.0 0.0 0.0 2.75Exports 0.20 0.0 0.0 0.0 0.0 0.20

Total 2.55 0.0 0.0 1.20a 2.3 6.05

Processing & transformationLosses & transfers 0.20 0.0 0.0 1.27 0.02 1.49Transformation output 0.0 0.0 0.0 0.43b 0.0 0.43

Final consumption 2.35 0.0 0.0 0.36b 2.28 4.99

a Input basis.b Output basis

Source: Energy Data Associates.

Financial services

Despite financialliberalisation—

The financial sector has seen a number of developments in recent years as itresponds to the needs of a growing economy and to economic liberalisation.Over the past five years financial-sector reforms have focused on deregulation,the liberalisation of interest rates and the privatisation of development banks.

—government banksremain inefficient

At the end of 1996 the commercial banking system comprised 26 banks, eightlocal and 18 foreign-owned. The two largest Sri Lankan banks, the Bank ofCeylon and the People’s Bank, are state-owned and account for two-thirds ofcommercial bank deposits. They are considered to be inefficient, primarilybecause of overstaffing and excessive government influence in their lendingoperations. Because of their domination of the market, they have been primar-ily responsible for the prevalence of high interest rates. The government hasruled out privatisation of the two institutions but an increase in their commer-cial orientation is probable. In 1996 the banks were recapitalised with the issueof SLRs20bn in government bonds.

By the end of 1996 the number of branches operated by commercial bankstotalled 1,060, of which 599 belonged to the two state-owned banks. Theforeign banks operated 38 branches. Although the arrival of foreign banks hasintensified the level of competition, leading to the introduction of new facil-ities, the overall impact on credit supply has been limited. Trade finance formsthe bulk of commercial bank credit. In addition, commercial banks operate

24 Sri Lanka: Financial services

EIU Country Profile 1997-98 © The Economist Intelligence Unit Limited 1997

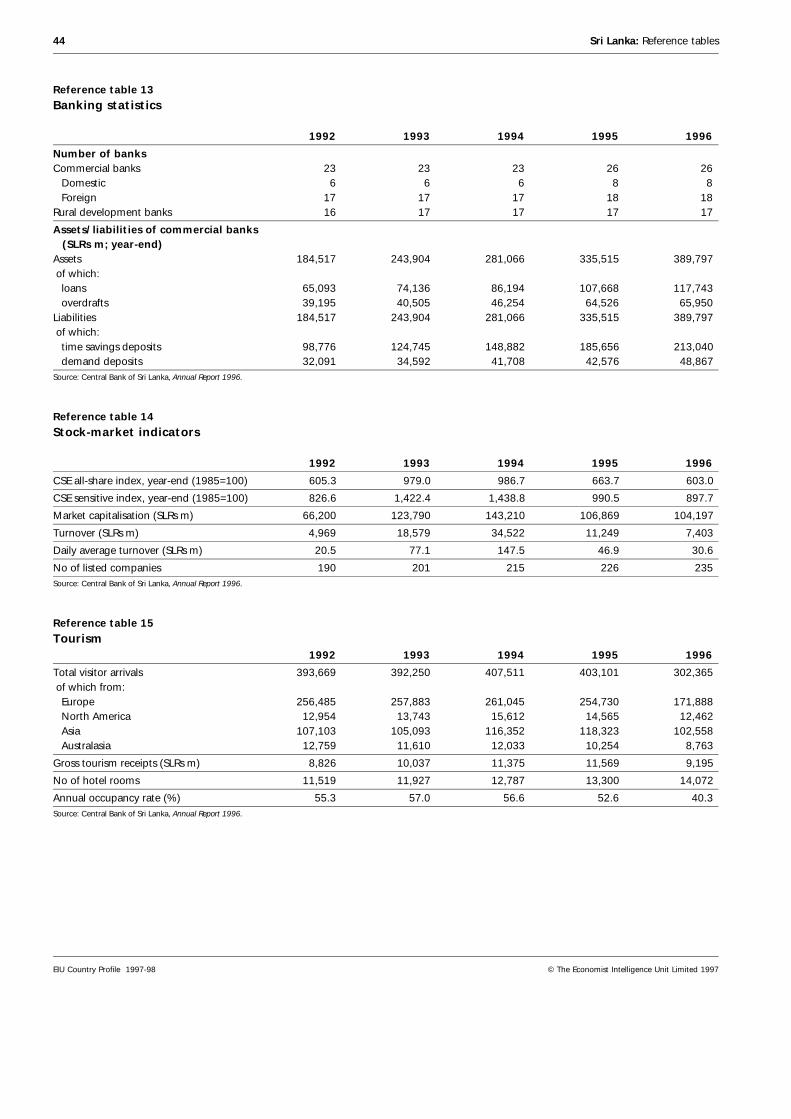

Foreign Currency Banking Units (FCBUs), which channel credit primarily tocompanies operating in the export processing zones. In 1996 the facility wasextended to all exporters. Credit to the rural sector and small firms is chan-nelled mainly through the two state banks and the cooperative institutions.(Reference table 13 includes statistics on commercial banking.)

Other banking andfinancial institutions

Other principal banking and financial institutions include the two main devel-opment banks, the National Development Bank (NDB) and the DevelopmentFinance Corporation of Ceylon (DFCC); they channel long-term funds, primar-ily from international lending agencies, and also provide equity financing,mainly in the industrial, tourism and financial sectors. Other long-term financeinstitutions are the Housing Development Finance Corporation (HDFC), theNational Housing Development Authority (NHDA), the State Mortgage andInvestment Bank (SMIB) and the National Savings Bank (NSB).

There are a number of finance companies. Following some insolvencies andpoor administration, supervision of these was tightened at the end of the1980s. The number of companies shrank from 60 at the end of 1989 to 25 atend-1996.

Sri Lanka also has seven merchant banks, whose activities are concentrated ondiscounting trade bills, lease financing and investment in Treasury bills andthe stock market. At the end of 1996 there were six venture capital companies,providing start-up financing to small and medium-sized companies, and threeregistered leasing companies.

Six insurance companies, two of which are state-owned, together with the NSBand two pension funds, the Employee’s Provident Fund and the Employee’sTrust Fund, predominate in the mobilisation of long-term resources. The fundsof the NSB and pension funds are almost entirely pre-empted by the govern-ment to finance its deficit.