Sources of Sources of Government Revenue Government Revenue Chapter 9 Chapter 9

Sources of Government Revenue Chapter 9. Goals & Objectives 1.Economic impact of taxes. 2.3 criteria for effective taxation. 3.2 primary principles of.

Dec 24, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Sources of Government Sources of Government RevenueRevenue

Chapter 9Chapter 9

Goals & ObjectivesGoals & Objectives

1.1. Economic impact of taxes.Economic impact of taxes.

2.2. 3 criteria for effective taxation.3 criteria for effective taxation.

3.3. 2 primary principles of taxation.2 primary principles of taxation.

4.4. How taxes are classified.How taxes are classified.

5.5. Progressive nature of income taxes.Progressive nature of income taxes.

6.6. Sources of federal revenue.Sources of federal revenue.

7.7. State revenues.State revenues.

8.8. Local revenues.Local revenues.

9.9. Paycheck/payroll deductions.Paycheck/payroll deductions.

10.10. Tax Reforms. VAT & Flat taxes.Tax Reforms. VAT & Flat taxes.

2013 Tax Payers2013 Tax Payers

The Economics of TaxationThe Economics of Taxation

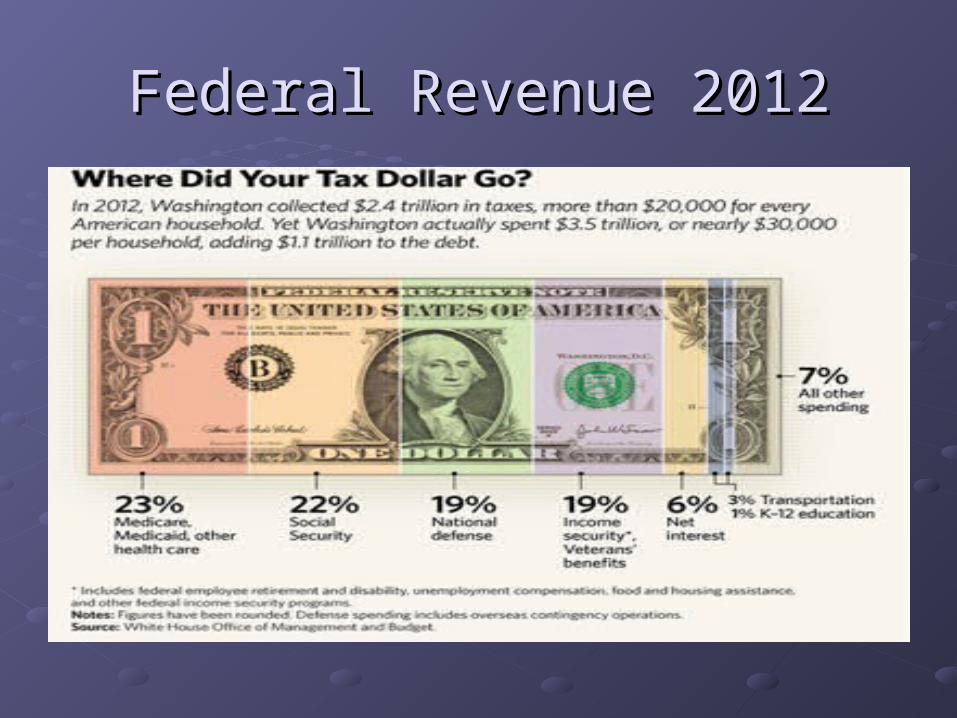

2012: 2012: Federal RevenueFederal Revenue: 2.4 Trillion: 2.4 Trillion

Rate of Government Growth Rate of Government Growth 1940-2013 an 1000 +% increase in 1940-2013 an 1000 +% increase in federal revenuesfederal revenues

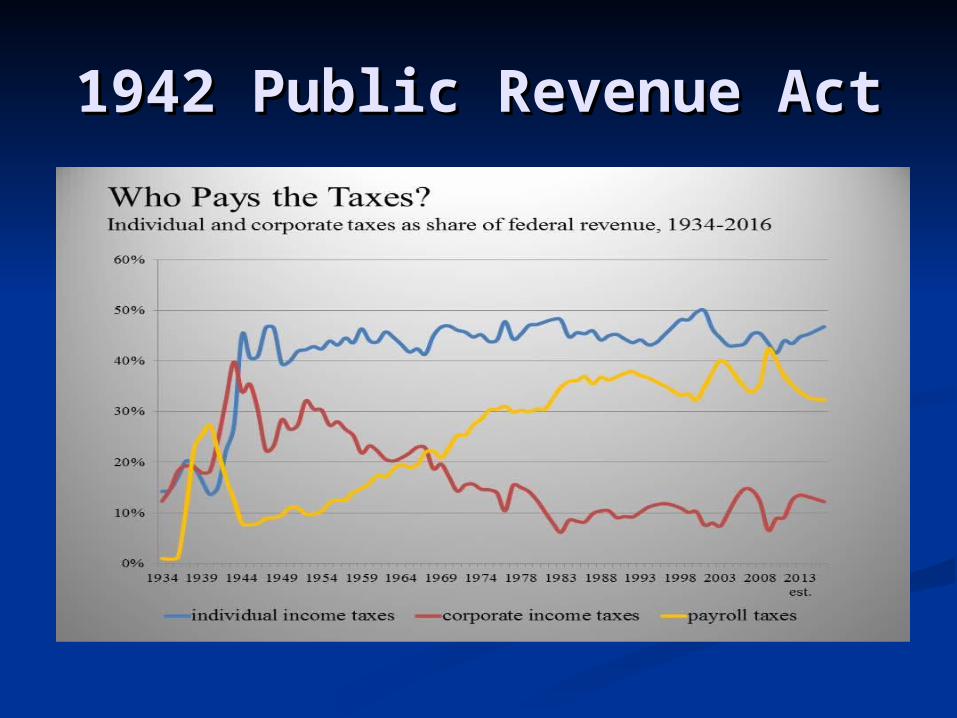

1942 Public Revenue Act?1942 Public Revenue Act?

Federal Revenue 2012Federal Revenue 2012

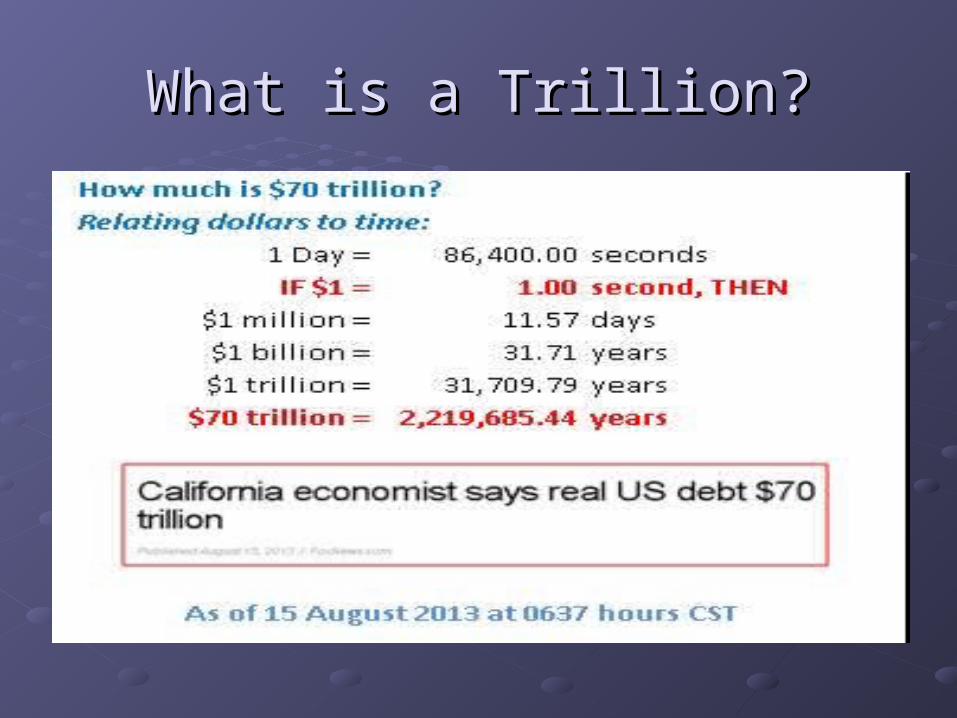

What is a Trillion?What is a Trillion?

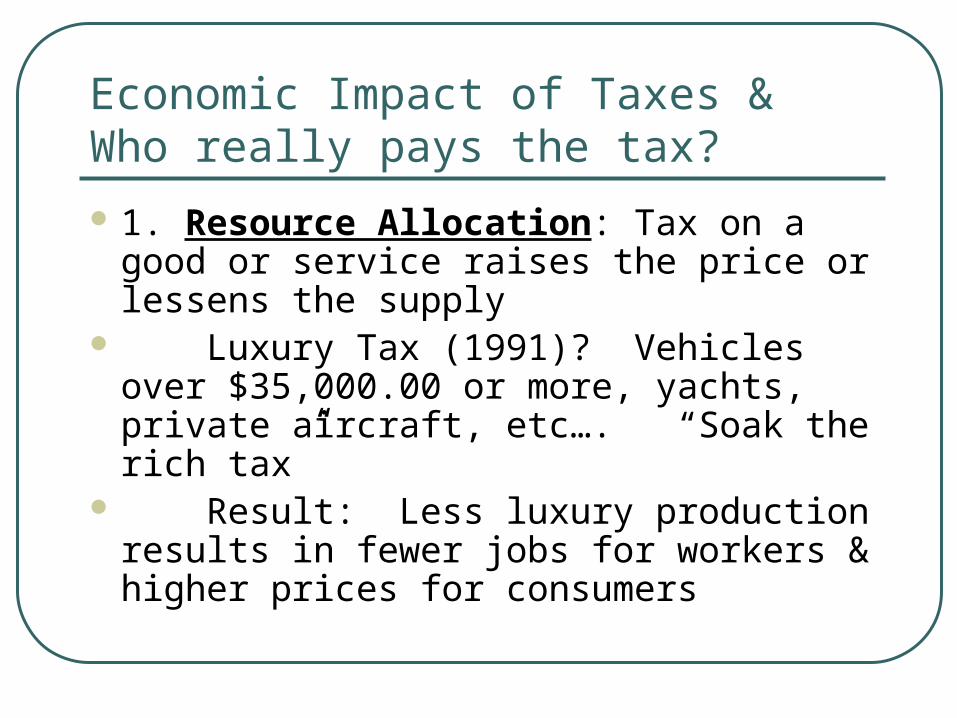

Economic Impact of Taxes & Who really pays the tax?

1. Resource Allocation: Tax on a good or service raises the price or lessens the supply

Luxury Tax (1991)? Vehicles over $35,000.00 or more, yachts, private aircraft, etc…. “Soak the rich tax”

Result: Less luxury production results in fewer jobs for workers & higher prices for consumers

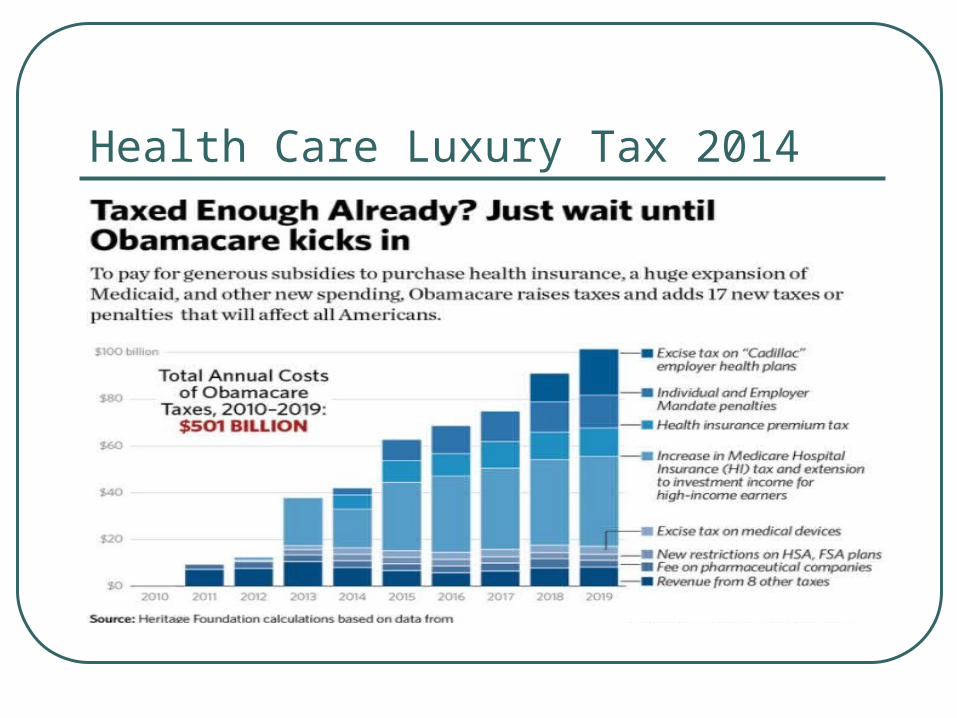

Health Care Luxury Tax 2014

Economic Impact of Taxes

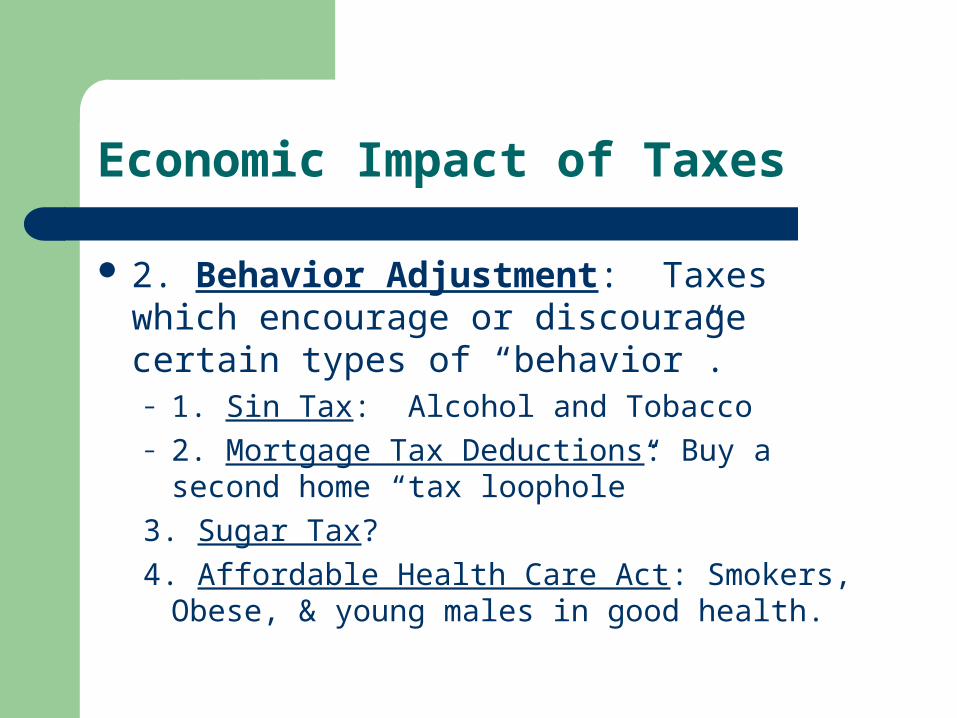

2. Behavior Adjustment: Taxes which encourage or discourage certain types of “behavior”.– 1. Sin Tax: Alcohol and Tobacco– 2. Mortgage Tax Deductions: Buy a second home

“tax loophole”

3. Sugar Tax?

4. Affordable Health Care Act: Smokers, Obese, & young males in good health.

Excise Tax & Tanning Booth Behavior Adjustment

Economic Impact of Taxes

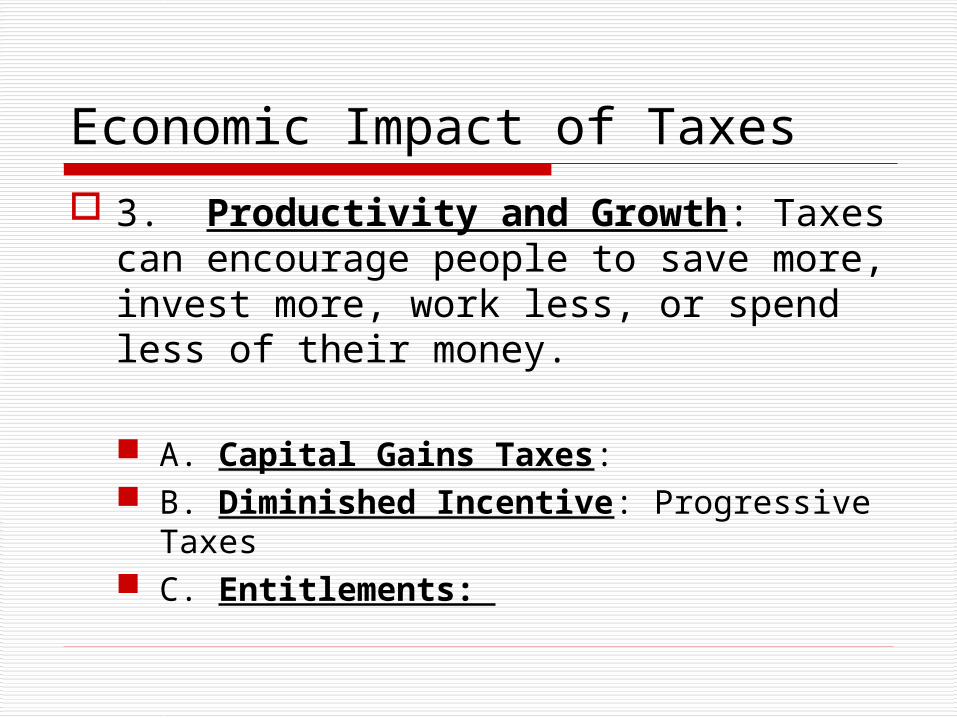

3. Productivity and Growth: Taxes can encourage people to save more, invest more, work less, or spend less of their money.

A. Capital Gains Taxes: B. Diminished Incentive: Progressive

Taxes C. Entitlements:

Taxes & Productivity

Economic Impact of Taxes

4. The Incidence of a Tax: Who really pays taxes?

“The party being taxed is not always the one that bears the burden of taxes?”

A. Property Taxes? B. Sales Taxes? C. Corporate Taxes? D. Utility Taxes, Severance Taxes

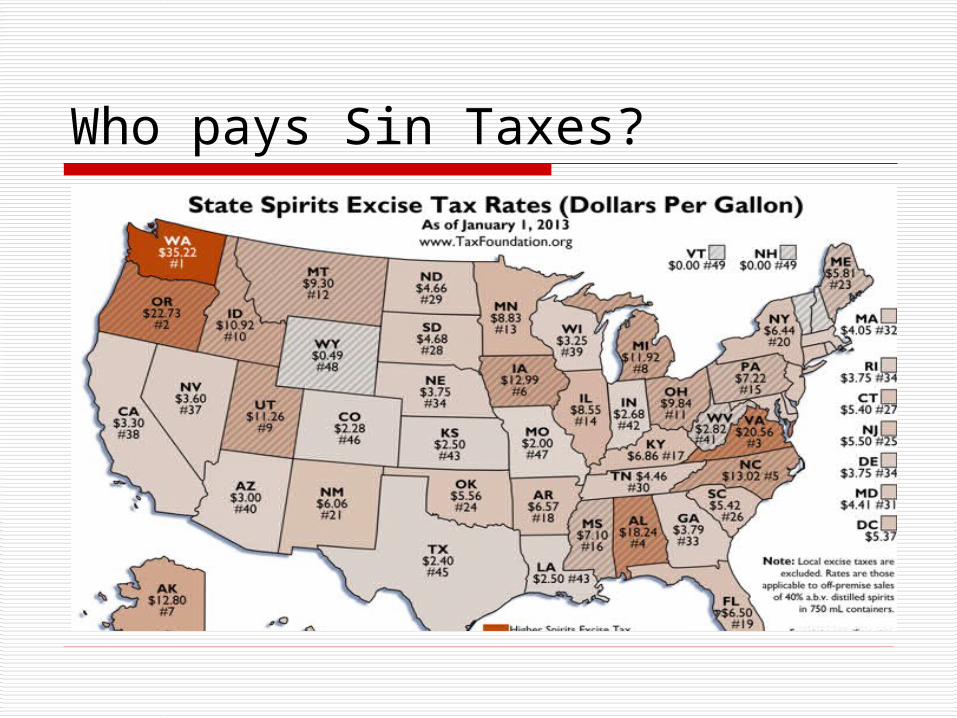

Who pays Sin Taxes?

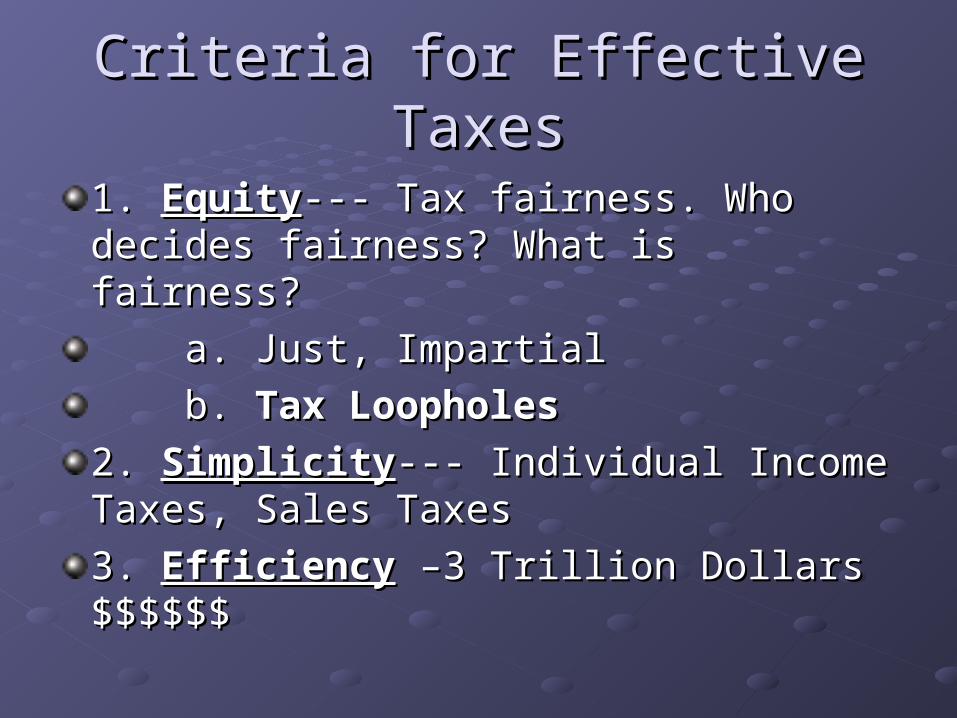

Criteria for Effective TaxesCriteria for Effective Taxes

1. 1. EquityEquity--- Tax fairness. Who decides --- Tax fairness. Who decides fairness? What is fairness?fairness? What is fairness?

a. Just, Impartiala. Just, Impartial

b. b. Tax LoopholesTax Loopholes

2. 2. SimplicitySimplicity--- Individual Income Taxes, --- Individual Income Taxes, Sales TaxesSales Taxes

3. 3. EfficiencyEfficiency –3 Trillion Dollars $$$$$$ –3 Trillion Dollars $$$$$$

Tax Loopholes Tax Loopholes

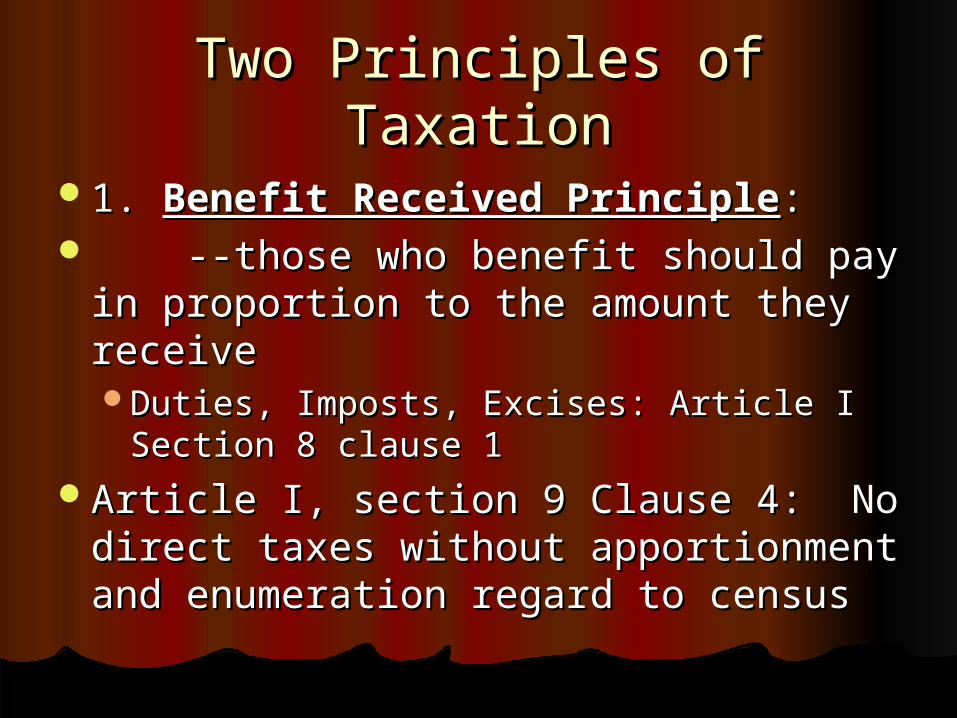

Two Principles of TaxationTwo Principles of Taxation

1. 1. Benefit Received PrincipleBenefit Received Principle:: --those who benefit should pay in --those who benefit should pay in

proportion to the amount they proportion to the amount they receivereceiveDuties, Imposts, Excises: Article I Duties, Imposts, Excises: Article I

Section 8 clause 1Section 8 clause 1Article I, section 9 Clause 4: No Article I, section 9 Clause 4: No

direct taxes without apportionment direct taxes without apportionment and enumeration regard to censusand enumeration regard to census

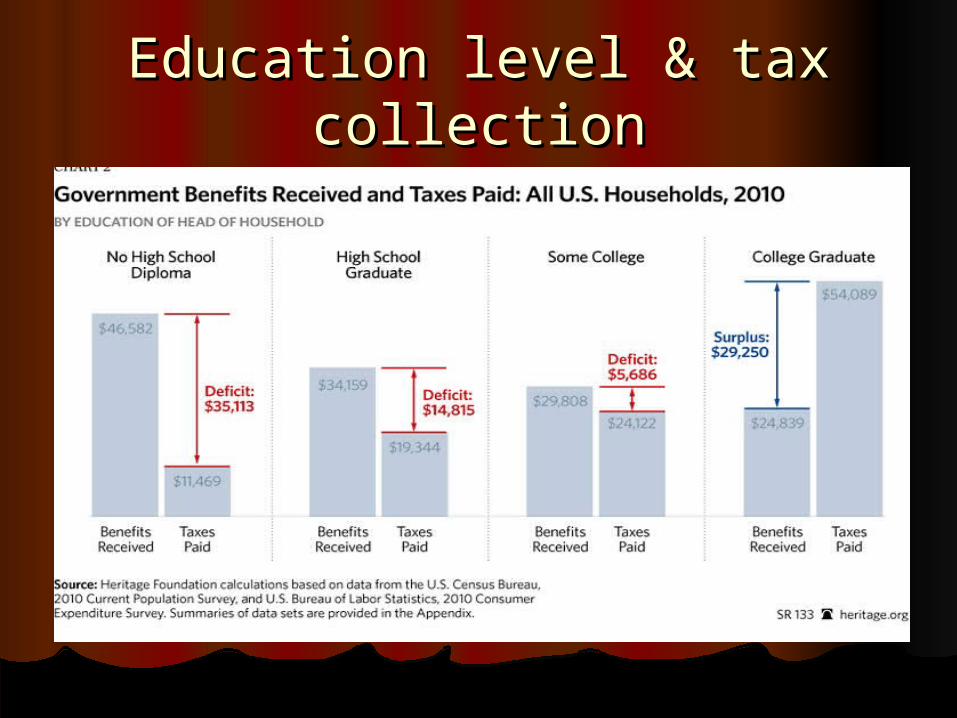

Education level & tax Education level & tax collectioncollection

Two Principles of TaxationTwo Principles of Taxation

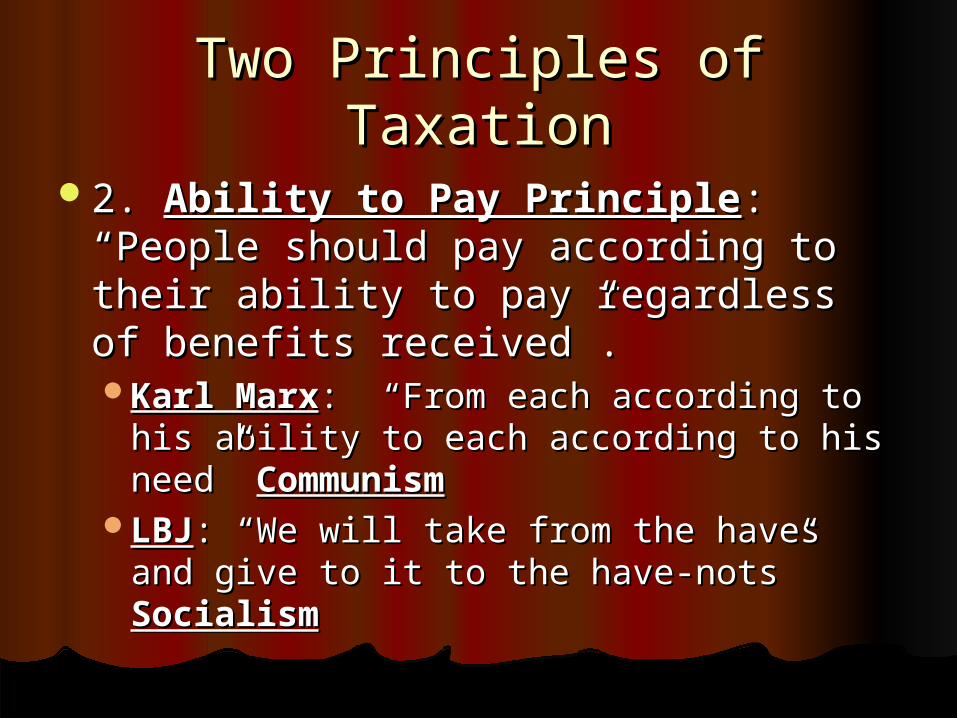

2. 2. Ability to Pay PrincipleAbility to Pay Principle: : ““People People should pay according to their ability should pay according to their ability to pay regardless of benefits receiveto pay regardless of benefits receivedd ””..Karl MarxKarl Marx: : ““From each according to his From each according to his

ability to each according to his needability to each according to his need”” CommunismCommunism

LBJLBJ: : ““We will take from the haves and We will take from the haves and give to it to the have-notsgive to it to the have-nots”” SocialismSocialism

Spending vs Taxes PaidSpending vs Taxes Paid

3 Types of Taxes

1. Proportional: Everyone pays the same percentage regardless on income. Benefits received principle----Flat Taxes:

no loopholes, no subsidies, no entitlements

3 Types of Taxes

2. Progressive Taxes: Higher taxes are placed on higher incomes

“The more you make the more they take” Karl Marx: “the redistribution of wealth” The more able, smarter, productive you are,

the more taxes you must pay….diminished incentive

3 Types of Taxes

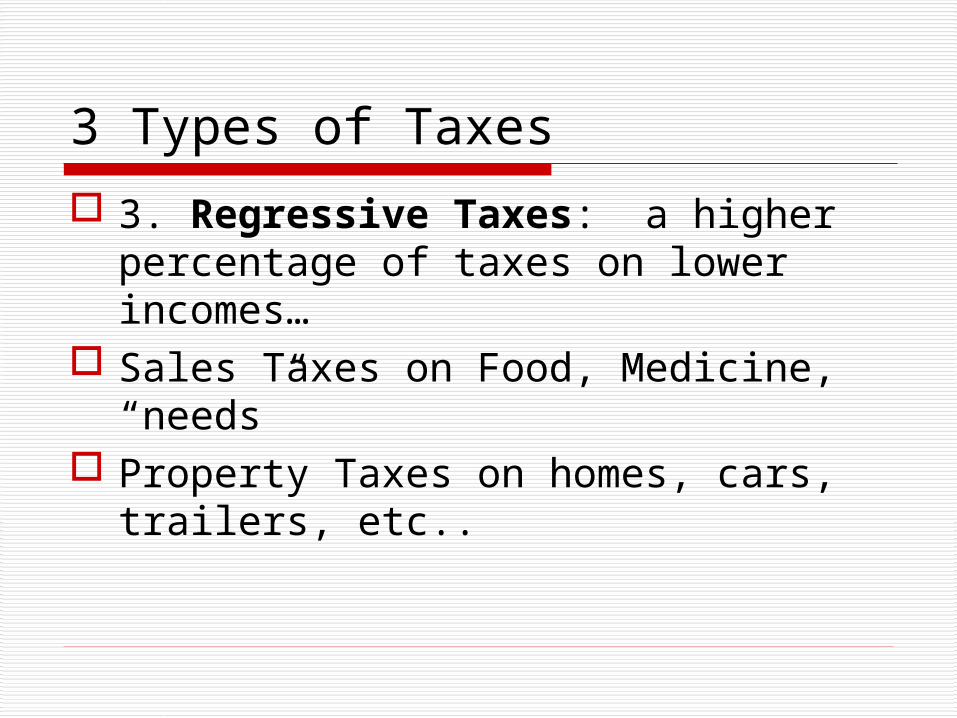

3. Regressive Taxes: a higher percentage of taxes on lower incomes…

Sales Taxes on Food, Medicine, “needs”

Property Taxes on homes, cars, trailers, etc..

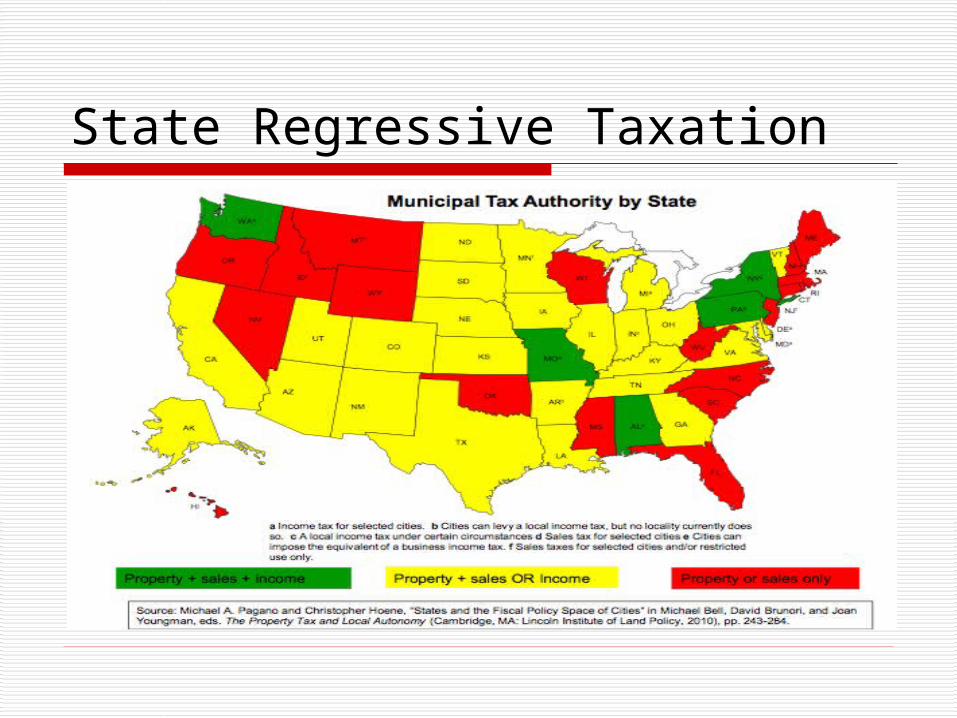

State Regressive Taxation

The Federal Tax SystemThe Federal Tax System 1. 1. Individual Income TaxesIndividual Income Taxes: 1913---16: 1913---16thth

amendment:amendment: 1787-1913… Business Foreign and 1787-1913… Business Foreign and

Domestic paid 89% of taxes see pie chartDomestic paid 89% of taxes see pie chart 1913-1942…Top 10% of workers earning 1913-1942…Top 10% of workers earning

over $500,000 a year or more paid income over $500,000 a year or more paid income taxestaxes

1935: Public Salary Tax (Social Security) 1935: Public Salary Tax (Social Security) 1942-2007…Public Revenue Act… 800% 1942-2007…Public Revenue Act… 800%

tax increasetax increase

1942 Public Revenue Act1942 Public Revenue Act

Individual Income TaxesIndividual Income Taxes

1. 1. Payroll withholding systemPayroll withholding system: : automatic deduction: Federal Income, automatic deduction: Federal Income, Social Security, Medicare, State Income, Social Security, Medicare, State Income, Local IncomeLocal Income IRS—Internal Revenue Tax: Private Business IRS—Internal Revenue Tax: Private Business

contracted by the Federal Treasury Department to contracted by the Federal Treasury Department to collect income taxes. Why a private company?collect income taxes. Why a private company?

Example: US Military Rules vs. Blackwater USA Example: US Military Rules vs. Blackwater USA

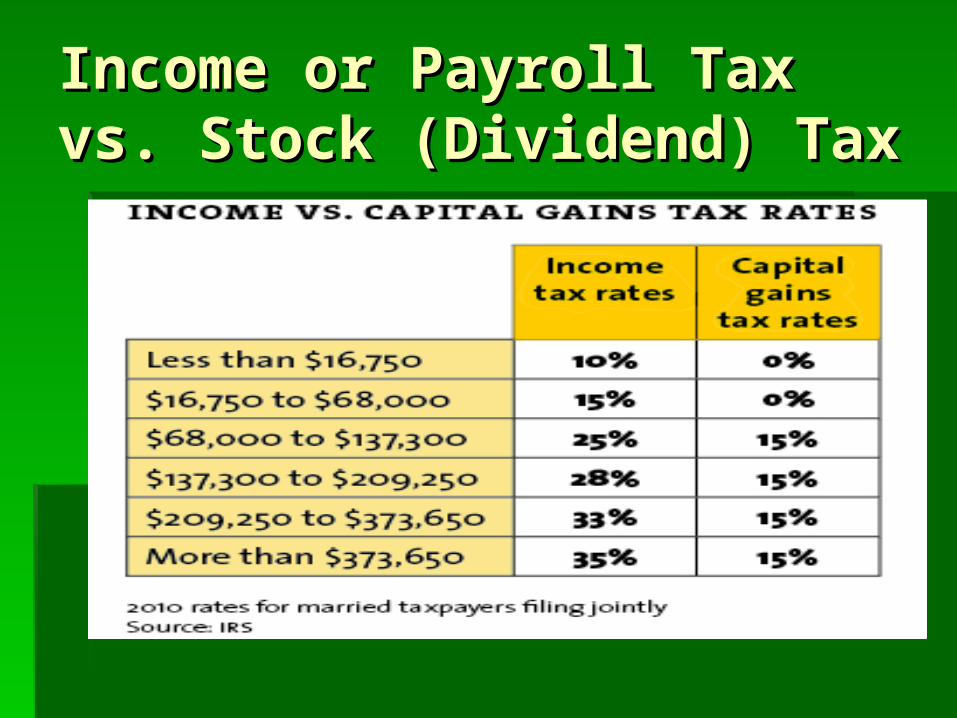

Income or Payroll Tax vs. Income or Payroll Tax vs. Stock (Dividend) TaxStock (Dividend) Tax

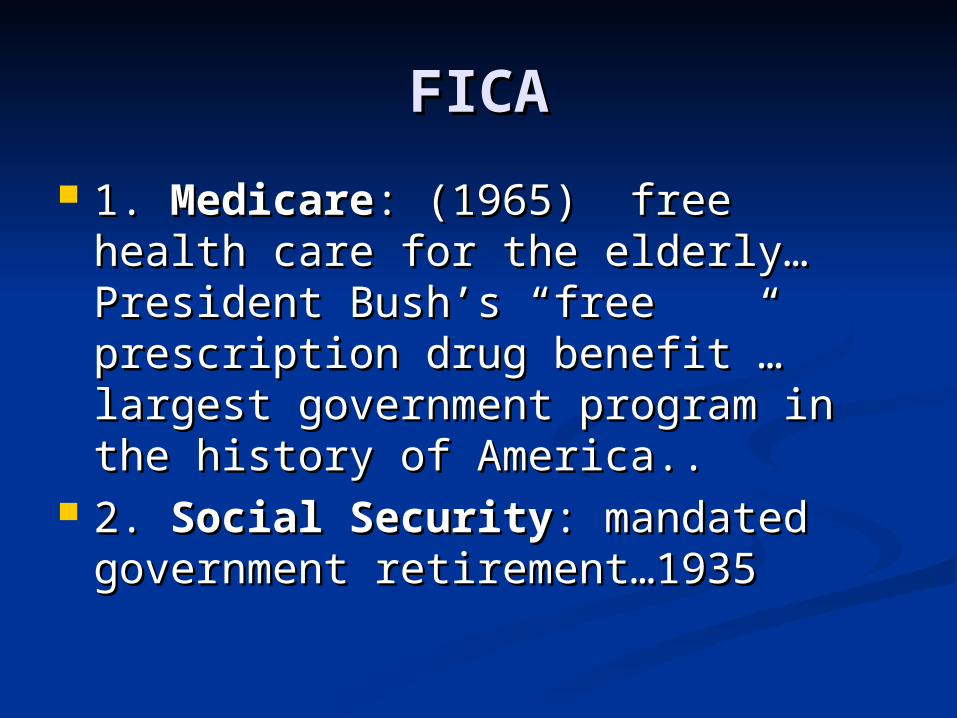

FICAFICA

1. 1. MedicareMedicare: (1965) free health : (1965) free health care for the elderly…President care for the elderly…President BushBush’’s s ““free prescription drug free prescription drug benefitbenefit””…largest government …largest government program in the history of America..program in the history of America..

2. 2. Social SecuritySocial Security: mandated : mandated government retirement…1935government retirement…1935

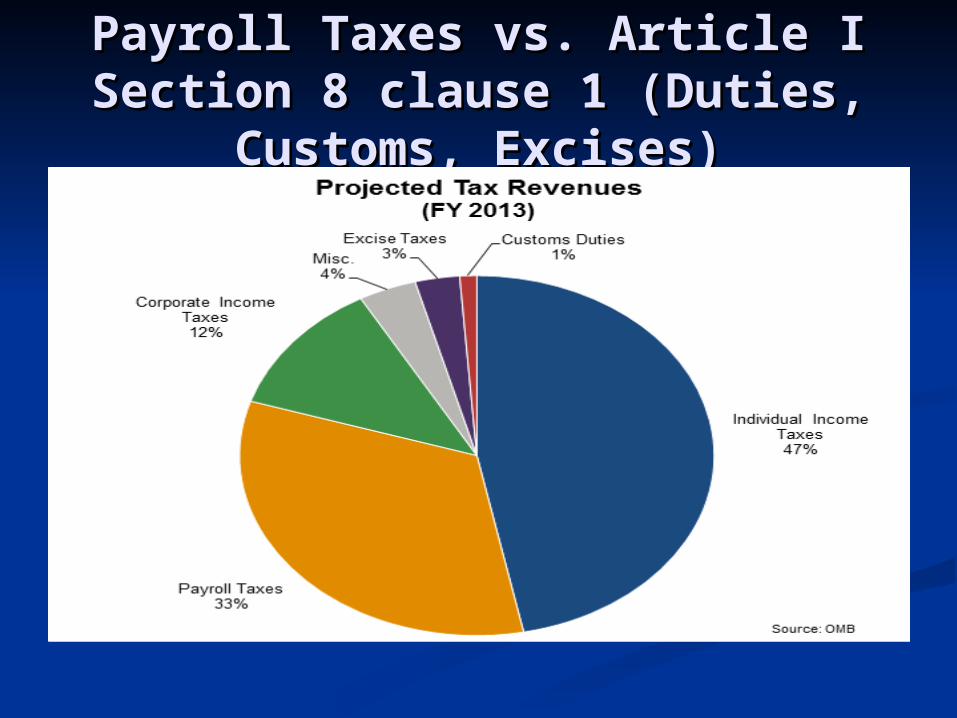

Payroll Taxes vs. Article I Payroll Taxes vs. Article I Section 8 clause 1 (Duties, Section 8 clause 1 (Duties,

Customs, Excises)Customs, Excises)

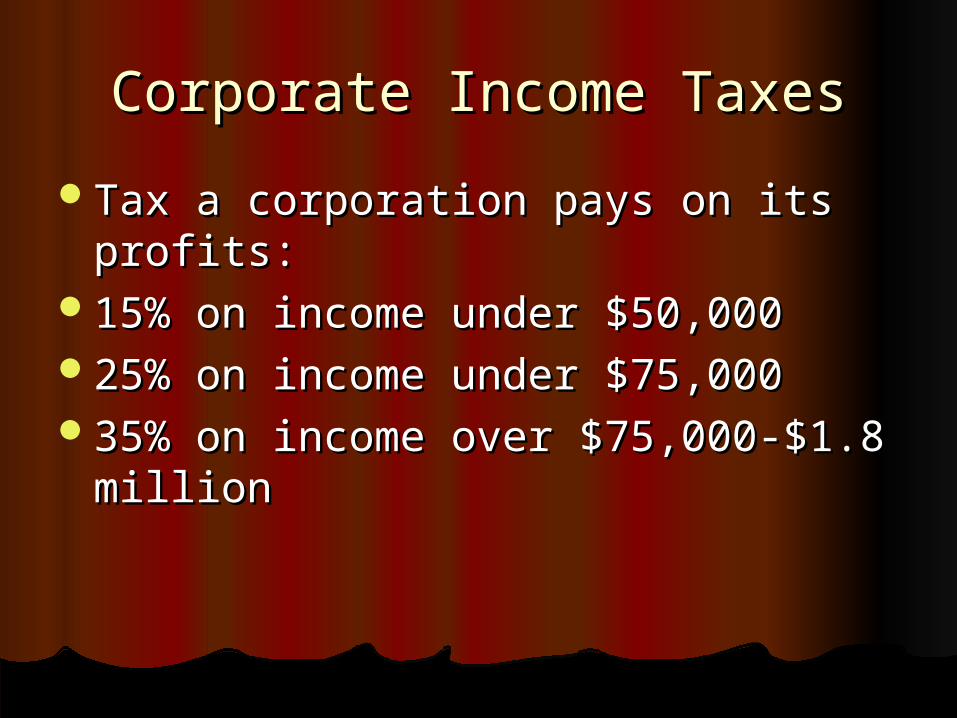

Corporate Income TaxesCorporate Income Taxes

Tax a corporation pays on its profits: Tax a corporation pays on its profits: 15% on income under $50,00015% on income under $50,00025% on income under $75,00025% on income under $75,00035% on income over $75,000-$1.8 35% on income over $75,000-$1.8

millionmillion

1932 Corporate Taxes1932 Corporate Taxes

Other Federal Taxes

1. Excise Taxes: tax on a business that is handed down in the form of higher prices to the consumers, “Hidden Tax” “Theft Tax”

2. Death Taxes: Estate and Gift Taxes18-50% of valued assets.Estate salesGift Taxes: 40% of valued asset

Death Tax by State

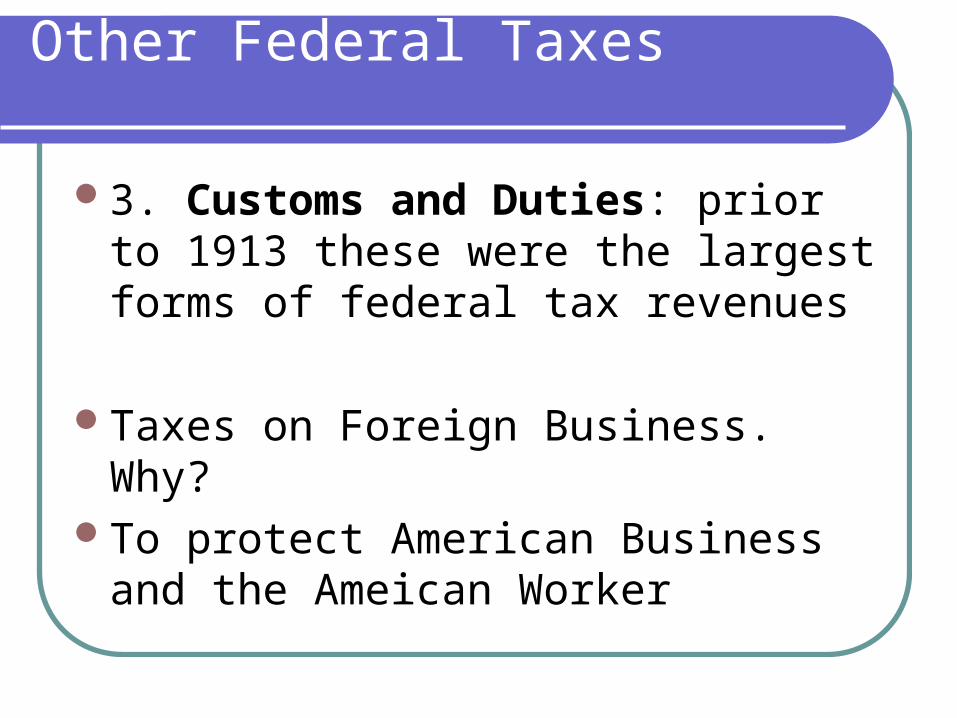

Other Federal Taxes

3. Customs and Duties: prior to 1913 these were the largest forms of federal tax revenues

Taxes on Foreign Business. Why?To protect American Business and the

Ameican Worker

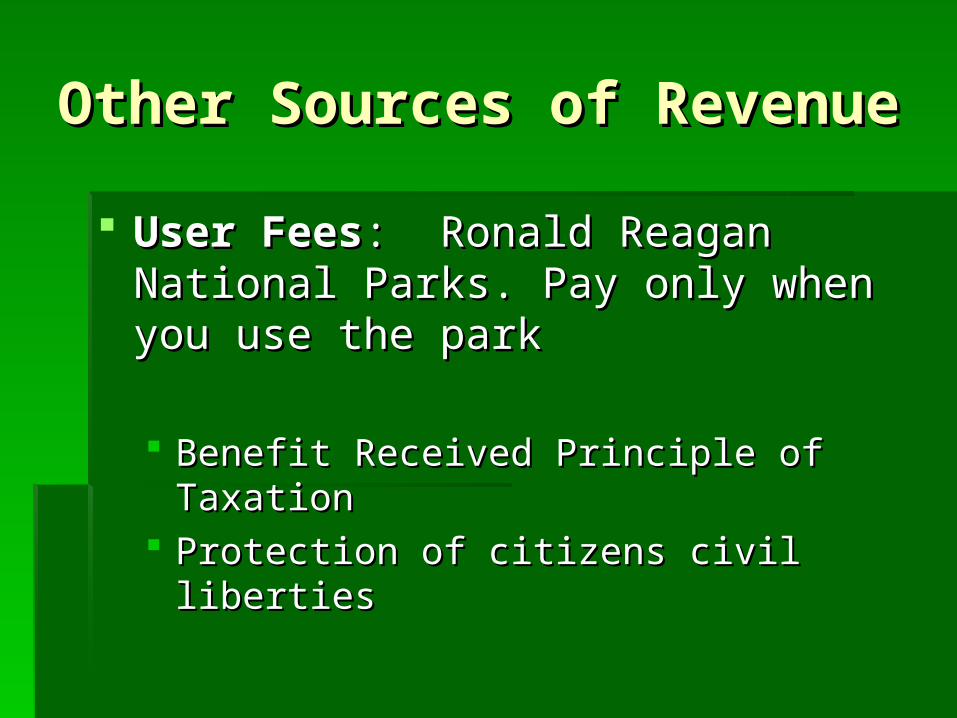

Other Sources of Other Sources of RevenueRevenue

User FeesUser Fees: Ronald Reagan National : Ronald Reagan National Parks. Pay only when you use the parkParks. Pay only when you use the park

Benefit Received Principle of TaxationBenefit Received Principle of Taxation Protection of citizens civil libertiesProtection of citizens civil liberties

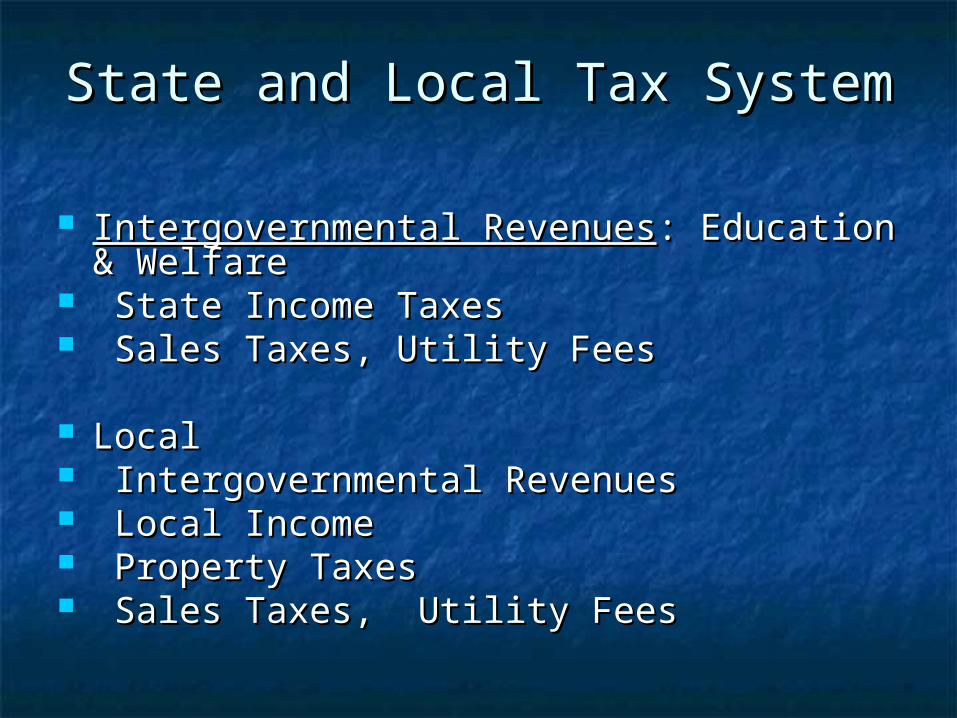

State and Local Tax SystemState and Local Tax System

Intergovernmental RevenuesIntergovernmental Revenues: Education & : Education & WelfareWelfare

State Income TaxesState Income Taxes Sales Taxes, Utility FeesSales Taxes, Utility Fees

LocalLocal Intergovernmental RevenuesIntergovernmental Revenues Local IncomeLocal Income Property TaxesProperty Taxes Sales Taxes, Utility FeesSales Taxes, Utility Fees

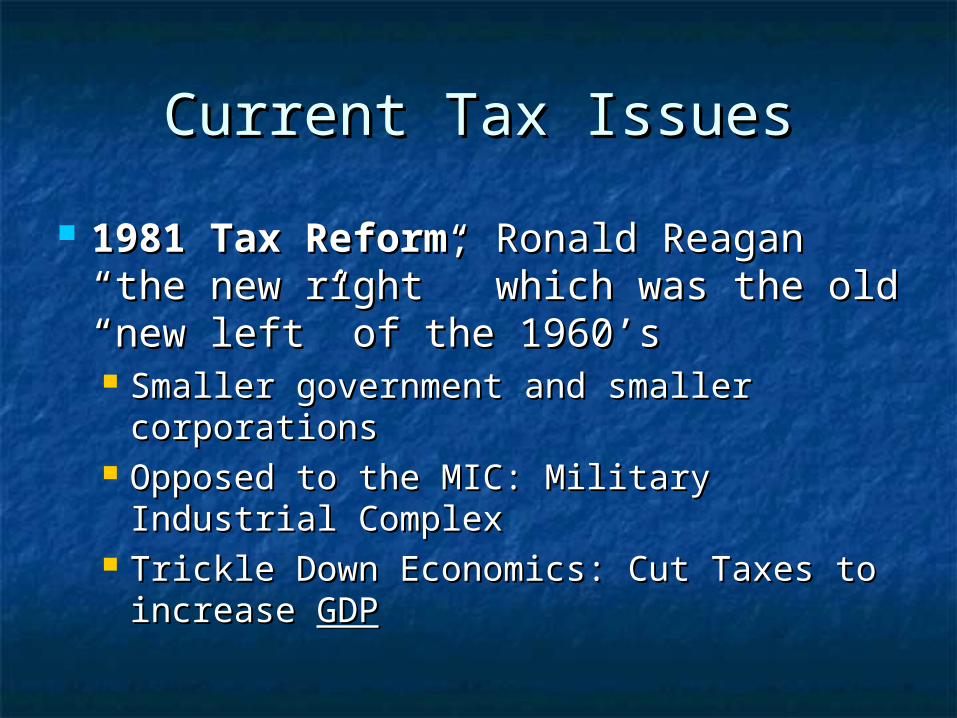

Current Tax IssuesCurrent Tax Issues

1981 Tax Reform1981 Tax Reform; Ronald Reagan ; Ronald Reagan ““the new rightthe new right”” which was the old which was the old ““new leftnew left”” of the 1960 of the 1960’’ss Smaller government and smaller Smaller government and smaller

corporationscorporations Opposed to the MIC: Military Industrial Opposed to the MIC: Military Industrial

ComplexComplex Trickle Down Economics: Cut Taxes to Trickle Down Economics: Cut Taxes to

increase increase GDPGDP

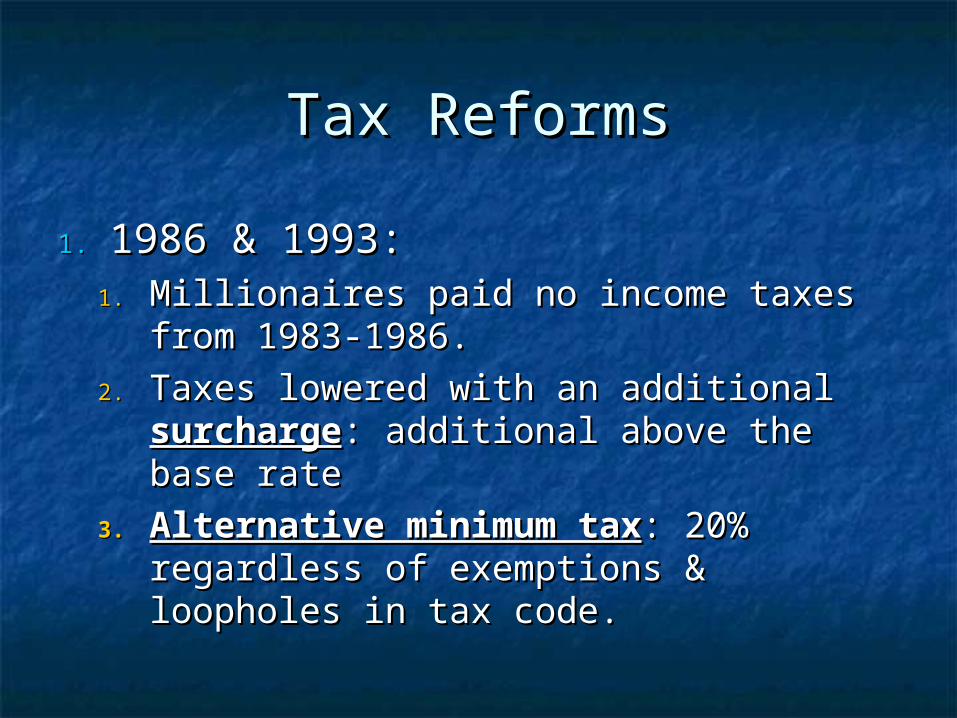

Tax ReformsTax Reforms

1.1. 1986 & 1993: 1986 & 1993: 1.1. Millionaires paid no income taxes from Millionaires paid no income taxes from

1983-1986. 1983-1986.

2.2. Taxes lowered with an additional Taxes lowered with an additional surchargesurcharge: additional above the base : additional above the base raterate

3.3. Alternative minimum taxAlternative minimum tax: 20% : 20% regardless of exemptions & loopholes in regardless of exemptions & loopholes in tax code.tax code.

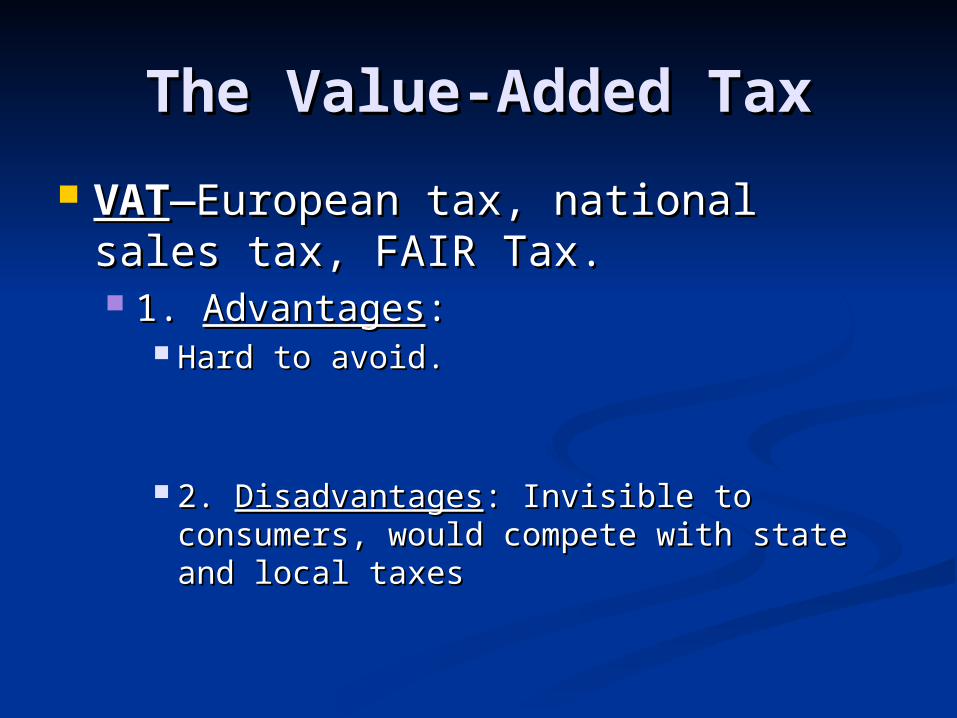

The Value-Added TaxThe Value-Added Tax

VATVAT—European tax, national sales —European tax, national sales tax, FAIR Tax.tax, FAIR Tax. 1. 1. AdvantagesAdvantages: :

Hard to avoid.Hard to avoid.

2. 2. DisadvantagesDisadvantages: Invisible to consumers, : Invisible to consumers, would compete with state and local taxeswould compete with state and local taxes

Value Added Tax StepsValue Added Tax Steps

National Sales Tax: Obama-National Sales Tax: Obama-phonesphones

The Flat TaxThe Flat Tax

1. 1. AdvantagesAdvantages: : What groups support the flat tax What groups support the flat tax system?system?2. 2. DisadvantagesDisadvantages: : What interest groups oppose the flat What interest groups oppose the flat tax system and Why?tax system and Why?

Flat Tax Closes LoopholesFlat Tax Closes Loopholes

Related Documents