Slide 1 Solvency II – challenges and possibilities 7 th International Professional Meeting of Leaders of the Actuarial Profession and Actuarial Educators in Central & Eastern Europe Warsaw, 04 September 2006 Karel Van Hulle - European Commission

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Slide 1

Solvency II – challenges and possibilities

7th International Professional Meeting of Leadersof the Actuarial Profession and Actuarial Educators

in Central & Eastern Europe

Warsaw, 04 September 2006

Karel Van Hulle - European Commission

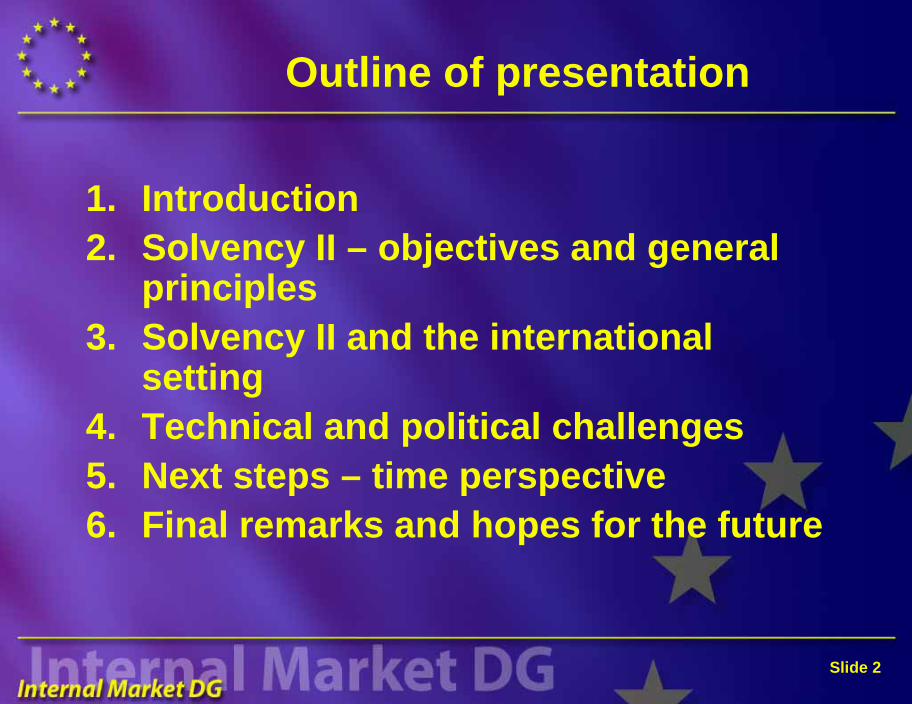

Slide 2

Outline of presentation

1. Introduction 2. Solvency II – objectives and general

principles3. Solvency II and the international

setting 4. Technical and political challenges5. Next steps – time perspective6. Final remarks and hopes for the future

Slide 3

1. Why Solvency II?

Müller report (1997) and Solvency IFundamental changes in insurance business and productsIncreased competition/pressure of shareholdersNow: fall of stock markets – low interest ratesConvergence between sectors – financial conglomeratesDevelopments of risk analysis methodsInternational developments (IAIS, IAA & IAS)

Slide 4

Solvency II: objectives

Fundamental review of EU insurance prudential frameworkCreate a prudential framework more appropriate to the risks facing insurance companiesTake into account the different needs for harmonisation (European level, international level, convergence of financial sectors)

Slide 5

Solvency II: objectives

Incentives for companies to know and manage own risksOpen and transparent project

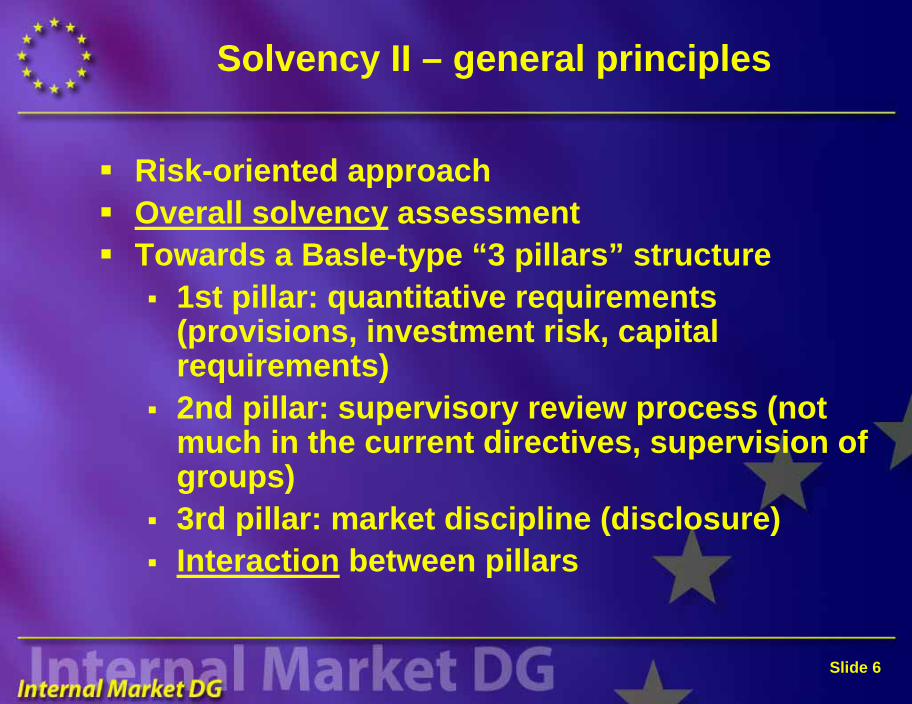

Slide 6

Solvency II – general principles

Risk-oriented approachOverall solvency assessmentTowards a Basle-type “3 pillars” structure

1st pillar: quantitative requirements (provisions, investment risk, capital requirements)2nd pillar: supervisory review process (not much in the current directives, supervision of groups)3rd pillar: market discipline (disclosure)Interaction between pillars

Slide 7

Solvency II – general principles

Consistency between sectors:- avoid arbitrage: identify the areas where quantitative standards must be similar- coordination with Basle rules- Financial Conglomerates Directive Quantitative impact studies (QIS)Address the procyclicality issueAnalyse the issue of regulatory reserveswith preferential tax treatment

Slide 8

Solvency II – Pillar I

Technical provisions (based on IASB)life:

risk free market rate for discountingadequate prudential margin/resilience testvaluing embedded options/guarantees

non-life:quantitative benchmark

Clarify the role of capital requirements:create a regulatory notion of "target capital" / economic capital / standard modeluse of internal models / partial models (incentives)safety net capital

Slide 9

Solvency II – Pillar 2

Internal control and risk managementdevelop internal control principlesdevelop principles for sound risk managementundertakings should draw up plans for:

investment policyasset-liability matchingreinsurance programmefair attitude to policyholders

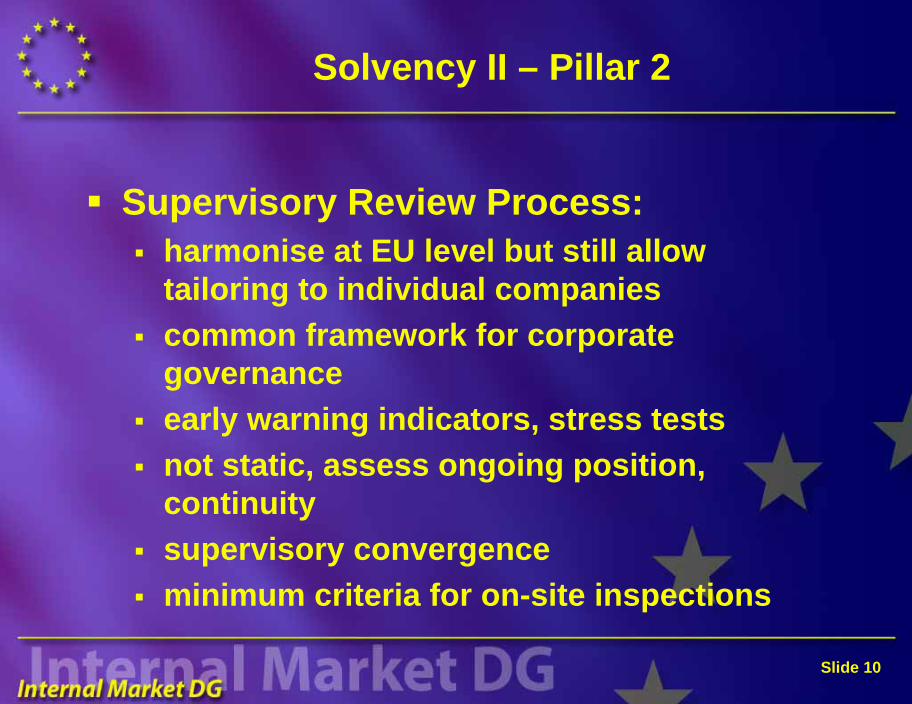

Slide 10

Solvency II – Pillar 2

Supervisory Review Process:harmonise at EU level but still allow tailoring to individual companiescommon framework for corporate governanceearly warning indicators, stress testsnot static, assess ongoing position, continuitysupervisory convergenceminimum criteria for on-site inspections

Slide 11

Solvency II – Pillar 2

coordinated supervisory action in times of crisis (dangers of forced selling, pro-cyclicality)intervention powers and responsibilities definedtransparent supervisory action (criteria publicly disclosed)peer review process

Slide 12

Solvency II – Pillar 3

disclosure reinforces market mechanisms and risk-based supervisioncoordinate reporting burden (ECOFIN wish to reduce administrative burden)

BUTdifficultdisclosure can aggravate problem

Slide 13

3. Solvency II and the international setting

SOLVENCY II

IASB accounting

OECD developments

US/NAIC work

IAIS Solvency

Canadian, Australian projects

IAA ActuarialGuidance

MemberStates' projects

Basle II project

Slide 14

4. Solvency II – technical and politicalchallenges

4.1 Organisational and technical complexity - timing constraints- Lamfalussy- ”sufficiently high level of harmonisation”

4.2 Accounting environment- IASB phase II uncertainty- towards different sets of accounts

4.3 Cutting edge of actuarial and financial techniques- prudential levels- establishment of technical provisions- solvency requirement; ”target” and ”minimum”- use of internal models

Slide 15

Solvency II – technical and politicalchallenges (cont.)

4.4 Capital levels and calculation complexity: acceptance or complaints from industry?

4.5 International inspiration- IAIS- IAA- Basel II (Capital Requirements Directive)

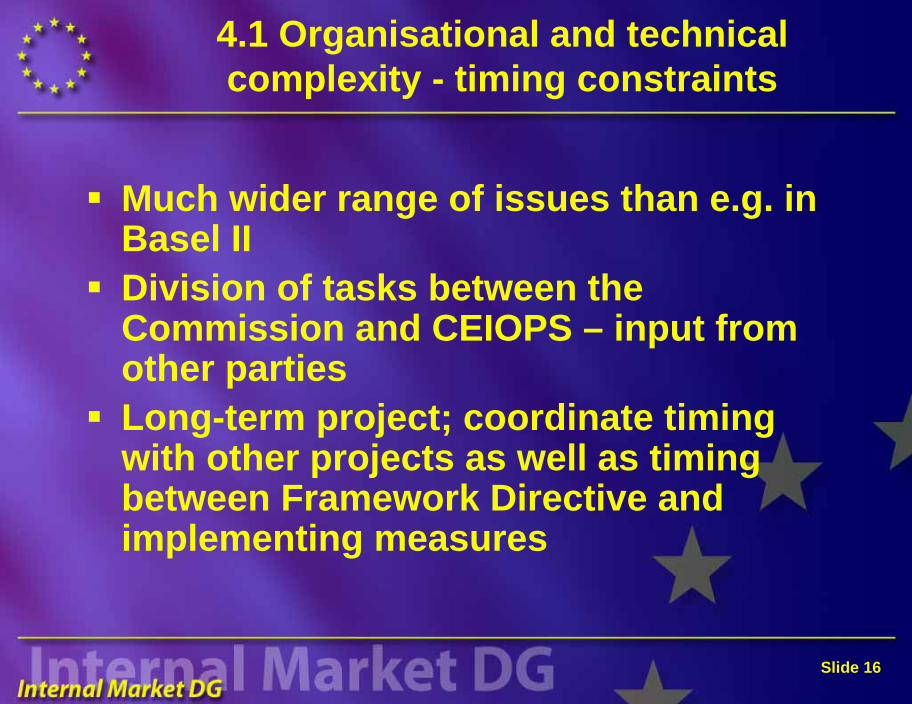

Slide 16

4.1 Organisational and technicalcomplexity - timing constraints

Much wider range of issues than e.g. in Basel IIDivision of tasks between the Commission and CEIOPS – input from other partiesLong-term project; coordinate timing with other projects as well as timing between Framework Directive and implementing measures

Slide 17

4.2 Accounting environment

IASB developments should be taken into account; difficultiesHow other solvency projects addressedthe accounting linkage (incl. IAIS)IASB phase 2 is a reference pointCompatibility with the expectedoutcome of IASB projectAdjustments and additions for supervisory purposesCurrent accounting solutions?

Slide 18

4.3 Cutting edge of actuarial and financial techniques

Uniform level of prudence across the EUOverall prudence (target capital level)Defined prudence in the technicalprovisions

Total balance sheet approach

Slide 19

4.3 Cutting edge of actuarial and financial techniques (cont.)

Technical provisions: Best estimate plus risk margin (percentileapproach ”75%” or cost of capitalapproach?QIS 1 and QIS 2Links between pillar 1 and pillar 2

Slide 20

4.3 Cutting edge of actuarial and financial techniques (cont.)

Solvency requirements:”Target” and ”minimum” levels: now called SCR (Solvency Capital Requirement) and MCR (Minimum Capital Requirement)SCR, MCR: Purpose and calculation methods, risks to includeSolvency control levels

Internal models:State of developmentAustralian experienceBanking experience of partial models

Slide 21

4.4 Capital levels and calculation complexity: acceptance or complaints from industry?

Likely higher solvency requirements(the current ones are too low)Calibration of the solvency formulas

Complexity of methods: costs for companies, particularly SME insurers(an advanced industry calls for advanced supervisory tools, howeveravoid unnecessary complications)

Slide 22

4.5 International inspiration – Use of IAIS standards and IAA material

The Solvency II system should be compatible with IAIS principles, standards and guidanceFurthermore, the wording of the Framework Directive could be inspiredby IAIS Cornerstones Document and Structure PaperOpenness to use IAA standards and material

Slide 23

4.5 International inspiration (cont.) – Challenges

Will the IAIS develop into an international standard-setter?Use of IAA material: however, IAA normally writes professional guidanceto actuaries, not e.g. general specifications to IASB accounting rulesBasel II (CRD): What parts can be usedfor inspiration? What can the bankers learn from Solvency II?

Slide 24

5. Next steps – time perspective

Three waves of calls for advice addressed to CEIOPS based upon Framework for ConsultationDrafting of a Framework Directive (Lamfalussy approach)Recast of existing Insurance DirectivesImpact Assessement with public hearing on 21 June 2006 If all goes well, a new principles directiveproposal could be ready towards July 2007

Slide 25

6. Final remarks and hopes for the future

(quote) ”Solvency II – curse or blessing?”LIKELY CONSEQUENCES FOR COMPANIES

Changes in supervisory, solvency and accounting regimes will influence insurancecompanies’ business models

Focus on risk management in generalRisk management of balance sheet risks in particular:

ALM-based approachInternal models (market consistency)Pricing of products (financial products in particular)Risk mitigation (reinsurance, hedging..)

Slide 26

6. Final remarks and hopes for the future(cont.)

HOPES FOR THE FUTUREA system catering for the interest of policyholders as well as assuring the efficiency of the insurance industryParadigm shift in supervisory methods and reportingIASB must prepare high quality standards, theoreticallyfounded as well as practicableProactive stance from industry and actuaries absolutelyessentialA successful Solvency II will have great impact on the international insurance standard-settingCEIOPS Solvency II work will ensure not only common rules, but also common application

Slide 27

Karel Van Hulle, Head of UnitInsurance and Pensions UnitInternal Market DGEuropean Commission (C107 1/28)B-1049 Brussels, Belgium

+32-2-295.79.54Fax +32-2-299.30.75E-mail [email protected] Market DG / Insurance website:http://ec.europa.eu/internal_market/insurance/index_en.htm

Related Documents