` Solvency Assessment and Management: Pillar III – Reporting & Disclosure Sub Committee SAM Communication Task Group Discussion Document 117 (v 3) A Comprehensive Glossary of SAM Terms 1. INTRODUCTION AND PURPOSE This glossary has been produced by the SAM Communication Task Group (CTG) in order to assist the user in gaining a better understanding of certain terms and definitions that have been developed within the Financial Services Boards (FSB) proposed Solvency Assessment and Management (SAM) regime. The terms and definitions contained within this document have been drawn from various sources and draft documents in circulation within the FSB‘s SAM Governance Structure, and as such are subject to further change and refinement. This document will be monitored and updated by the SAM CTG as and when deemed necessary and appropriate as the design of the new proposed SAM legislation approaches finality. This glossary contains proposed terms and definitions that have been exclusively derived for use within the FSB‘s SAM Governance Structure. A previous glossary document, Discussion Document 11, was also produced by the SAM CTG and was based primarily on terms, acronyms and definitions taken from the EU Solvency II Directive. (Please note that this document is still in draft and as such subject to further change and refinement leading up to the SAM implementation date of 1 January 2016)

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

`

Solvency Assessment and Management:

Pillar III – Reporting & Disclosure Sub Committee

SAM Communication Task Group

Discussion Document 117 (v 3)

A Comprehensive Glossary of SAM Terms

1. INTRODUCTION AND PURPOSE

This glossary has been produced by the SAM Communication Task Group (CTG) in order to assist

the user in gaining a better understanding of certain terms and definitions that have been developed

within the Financial Services Boards (FSB) proposed Solvency Assessment and Management (SAM)

regime.

The terms and definitions contained within this document have been drawn from various sources and

draft documents in circulation within the FSB‘s SAM Governance Structure, and as such are subject

to further change and refinement. This document will be monitored and updated by the SAM CTG as

and when deemed necessary and appropriate as the design of the new proposed SAM legislation

approaches finality.

This glossary contains proposed terms and definitions that have been exclusively derived for use

within the FSB‘s SAM Governance Structure.

A previous glossary document, Discussion Document 11, was also produced by the SAM CTG and

was based primarily on terms, acronyms and definitions taken from the EU Solvency II Directive.

(Please note that this document is still in draft and as such subject to further change and refinement leading up to the SAM implementation date of 1 January 2016)

Page | 2

2. SAM TERMS INCLUDED IN THE GLOSSARY

Absolute MCR (AMCR)

Accounting Consolidation

Act

Adjudicator

Adjustment for counterparty

default

Administrative action

committee

Administrative action

Administrative action procedure

Administrative penalty

Admissible assets

Ancillary own funds

Appellant

Application

Assessor

Associate

Auditing Profession Act

Auditor

Authorisation

Banks Act

Basic own funds (BOF)

Beneficial interest

Beneficiary

Best estimate (BEL)

Biometric risk factors

Board of directors

Boundaries of the contract

Branch of a foreign reinsurer

Branch of an insurer

Breach of the Solvency Capital Requirement

Business premises

Capital requirements

Captive Insurance Company

Captive insurer

Case record

Cash and cash equivalents

Cash-back and other loyalty provisions

Catastrophe risk

Cell

Cell Captive Insurer

Cell structure

Chair

Chief Executive Officer

Collective investment scheme

Commercial lines

Commissioner

Companies Act

Company

Competition Act

Complainant

Complaint

Complementary Identification Code (CIC) table

Conduct standard

Constitution

Consumer Protection Act

Contagion risk

Contingency Policy/Rent-a-captive

Contingent commission provisions

Contingent considerations

Contract Boundary

Contractual option

Contravention

Control function

Controlling company

Co-operatives Act

Cost-of-Capital

Council

Council for Medical Schemes

Council of Financial Regulators

Council standard

Court

Credit agreement

Currency risk

Current Tax Assets

Current Tax liabilities

Death event

Decision

Decision-maker

Deduction & Aggregation (D&A)

Deferred Tax Assets

Deferred Tax liabilities

Deputy Commissioner

Deputy Governor

Designated Authority

Director

Director-General

Disability

Disability event

Discretionary benefits

Discretionary participation features

Disqualified person

Document

Dual-regulated activity

Eligible financial institution

Eligible own funds

Employee Benefits and Termination Benefits

Page | 3

Encumber

Entitlement

Equity risk

Executive Committee

Executive Committee member

Expected Profits included in Future Cashflows (EPIFC)

Expected profits included in future premiums (EPIFP)

Expense risk

Finance Leases

Financial Advisory and Intermediary Services Act

Financial benchmark

Financial conglomerate

Financial crime

Financial crisis

Financial customer

Financial education

Financial guarantee

Financial inclusion

Financial institution

Financial institution representative

Financial Institutions (Protection of Funds) Act

Financial Intelligence Centre

Financial Intelligence Centre Act

Financial Liabilities

Financial Markets Act

Financial organ of state

Financial product

Financial product provider

Financial risk mitigation techniques

Financial Sector Conduct Authority

Financial sector law

Financial sector regulator

Financial service

Financial service provider

Financial Services Board Act

Financial Services Board

Financial Services Tribunal

Financial stability

Financial Stability Oversight Committee (FSOC)

Financial statements

Financial system

Financial year

First party cell

Fit and proper requirement

Foreign financial product

Foreign reinsurer

Friendly Societies Act

Fruitless and wasteful expenditure

Fully guaranteed

Fund

Fund member policy

Fungibility

Goodwill acquired

Governing body

Governor

Group Business

Grouped Individual Business

Grouped Individual policies

Group of companies

Group policy

Group undertaking

Head of a control function

Health event

Health insurance obligations

Holding company

Income protection and lump sum disability

Independent director

Individual policy

Inflation

Insourcing

Insurance business

Insurance group

Insurance obligations

Insurance policy

Insurance sub-group

Insured

Insurer

Intangible asset

Interest rate risk

Inter-group transaction

Inter-ministerial Council

Internal auditing

Inter-related

Inter-related person

Intra-group transaction

Inventories

Investigation

Investment value

Irregular expenditure

Joint rule

Joint standard

Key person

Lapse risk

Legislative instrument

Leniency agreement

Level of Basic Own Funds

Levies Act

Levy

LGD

Licence

Life Authorisation classes

Life event

Life insurance business

Page | 4

Life insurance policy

Life underwriting risk module

Linked

Linked business

Linked insurer

Linked Investment contracts

Listed

Lloyd‘s

Lloyd‘s underwriter

Longevity risk

Long-term Insurance Act

Look –through approach

Loss given default

Lump sum

Major business unit

Market Conduct Authority

Market infrastructure

Market-related

Market risk

Materiality

MCR

Medical expense insurance obligations

Member of the staff

Micro-insurance business

Micro-insurer

Minister

Mono-regulated activity

Morbidity

Morbidity or disability risk

Mortality risk

National Credit Act

National Credit Regulator

National Payment System Act

National Treasury

Net asset value

Nominee

Non-compliance

Non-Current Assets held for sale or discontinued operations

Non-equivalent jurisdictions

Non-executive director

Non-Life Authorisation classes

Non-life CAT Risk

Non-life insurance business

Non-life insurance policy

Non-life premium & reserve risk

Non-life underwriting risk

Non-life underwriting risk module

Non-operating holding company (NOHC)

Non-patrimonial loss

Non-regulated person

Non-SLT Health (Not Similar to Life Techniques) underwriting risk sub-module

Non-strategic participations

Official web site

Ombud

Ombud for Financial Services Providers

On-site inspection

Operating expenses

Operating levy

Operational risk

Organ of state

ORSA

Other contingent payment provisions

Other financial regulator

Outsourced

Outsourcing

Oversight Committee

Oversight Committee member

Own funds

Parent undertaking

Partially guaranteed

Participant

Participating undertaking

Payment system

Payment system operator

Payment system participant

Pension Funds Act

Person

Personal lines

Policy

Policyholder

Pooled fund

Premium

Prescribed

Probability distribution forecast

Promotion of Administrative Justice Act

Property Plant and Equipment

Property risk

Protection of Personal Information Act (POPI)

Provisions

Prudential Authority

Prudential standard

Public company

Public Finance Management Act

Pure discretionary benefit

Recognised scheme

Register

Registrar

Regulated activity

Page | 5

Regulated financial institution

Regulated person

Regulation

Regulator‘s directive

Regulatory action

Regulatory authority

Regulatory law

Regulatory strategy

Reinsurance business

Reinsurer

Related

Related party

Related person

Related undertaking

Remuneration

Reserve Bank

Reserve Bank Act

Resolution power

Respondent

Retrenchment risk

Return

Reverse Stress

Rider benefit

Ring-fenced funds

Risk concentration

Risk management system

Risk Margin

Risk mitigating action or management action

Rule

Scenario testing

Scheme

SCR

Section 25 memoranda of understanding

Section 77 memoranda of understanding

Securities

Senior management

Senior manager

Sensitivity testing

Settlement system

Shareholder value

Short-term Insurance Act

Significant influence

Significant owner

Special levy

Spread risk

Standard

Start of the policy

State-owned insurer

Statutory Ombud

Statutory scheme

Strategic participations

Stress testing

Submit

Subsidiary undertaking

Systemic

Systemically important financial institution (SIFI)

Systemic event

Systemic risk

The Act

The Basic Solvency Capital Requirement (BSCR)

The life catastrophe sub-module

The life underwriting risk module

The value of technical provisions

Third party cell

This Act

Transferability

Tribunal

Underwritten on a group basis

Universal Life policies

Value-at-risk

Variable payment morbidity insurance obligations

Website

Winding-up

3. GLOSSARY OF SAM TERMS

Absolute MCR (AMCR) - The values of the absolute floor AMCR are the higher of: (a) ZAR 15 000 000 for non-life insurers, including captive insurers conducting non-life insurance business, (b) ZAR 15 000 000 for life insurers, including captive insurers conducting life insurance business, (c) 25% of the annualised operating expenses of the preceding 12 months. (Operating expenses as defined in Board Notice 169) (Source: SA QIS3 Technical Specifications)

Accounting Consolidation based on the standard formula - The standard formula for the calculation of the Solvency Capital Requirement (SCR) applied to the consolidated assets and liabilities. (Source: SA QIS3 Technical Specifications)

Page | 6

Act means the Short-term Insurance Act, 1998 (Act no. 53 of 1998), and a word or explanation, of which a meaning has been given in the Act, has that meaning; (Source: Board Notice 169 of 2011)

Adjudicator means the Pension Funds Adjudicator appointed in terms of section 181, and includes a Deputy Adjudicator and an Acting Adjudicator; (Source: Draft Twin Peaks Bill version 2)

Adjustment for counterparty default Therefore, the secondary legislation should include a definition as follows: The adjustment for counterparty default should approximate the loss given default of the counterparty, weighted with the probability of default of the counterparty. (Source: Final Position Paper 30)

Administrative action committee means a committee established in terms of section 150; (Source: Draft Twin Peaks Bill version 2)

Administrative action has the meaning defined in section 1 of the Promotion of Administrative Justice Act; (Source: Draft Twin Peaks Bill version 2)

Administrative action procedure means a procedure adopted in terms of section 149; (Source: Draft Twin Peaks Bill version 2)

Administrative penalty means a penalty imposed in terms of section 151; (Source: Draft Twin Peaks Bill version 2)

Admissible assets means the kinds of assets referred to in section 29 of the Act; (Source: Board Notice 169 of 2011)

Ancillary own funds - shall consist of items other than basic own funds which can be called up to absorb losses and that ―1 The amounts of ancillary own fund items to be taken into account when determining own funds shall be subject to prior supervisory approval. ‖Solvency II Level 1 Article 89 defines Ancillary own funds as―1. Ancillary own funds shall consist of items other than basic own funds which can be called up to absorb losses. Ancillary own funds may comprise the following items to the extent that they are not basic own fund items:(a) unpaid share capital or initial fund that has not been called up;(b) letters of credit and guarantees;(c) any other legally binding commitments received by insurance and reinsurance undertakings. In the case of a mutual or mutual-type association with variable contributions, ancillary own funds may also comprise any future claims which that association may have against its members by way of a call for supplementary contribution, within the following 12 months ICP 17 refers to contingent assets and capital interchangeably and defines them as ―contingent elements which are not considered as assets under the relevant accounting standards, where the likelihood of payment if needed is sufficiently high according to criteria specified by the supervisor (Source: Final Position Paper 25)

Ancillary own funds are items of capital other than basic own-funds which can be called up to absorb losses. They can comprise the following items to the extent they are not basic own-funds items: (a) Unpaid share capital or initial fund that has not been called up; (b) Letters of credit or guarantees; (c) Any other legally binding commitments received by insurers and reinsurers. (Source: SA QIS3 Technical Specifications)

Ancillary own funds consist of items, other than basic own funds, that may be called up by the insurer to absorb losses, and, to the extent that the items have not been called up or paid, may comprise of such items as may be prescribed. (Source: Draft Primary Legislation - Financial Soundness)

Appellant means a person who has lodged an appeal in terms of Part 3 of Chapter 6 against a decision of a regulatory authority; (Source: Draft Twin Peaks Bill)

Application, in relation to a regulatory law, means an application in terms of a regulatory law—(a) for the granting of an entitlement;(b) for the amendment or renewal of an entitlement;(c) for the amendment or withdrawal of any condition attached or other encumbrance applicable to an entitlement; or (d) in connection with any other matter provided for in a regulatory law; (Source: Draft Twin Peaks Bill)

Assessor means a person appointed as an assessor in terms of section 162(6); (Source: Draft Twin Peaks Bill version 2)

Page | 7

Associate has the meaning set out in the International Financial Reporting Standards issued by the International Accounting Standards Board or a successor body (Source: Draft Insurance Bill issued May 2015)

Auditing Profession Act means the Auditing Profession Act, 2005 (Act No. 26 of2005) (Source: Draft Insurance Bill issued May 2015)

Auditor means an auditor registered in terms of the Auditing Profession Act (Source: Draft Insurance Bill issued May 2015)

Authorisation means a license or registration or any other type of approval, permission or authorisation issued in terms of a regulatory law to carry out a regulated activity; (Source: Draft Twin Peaks Bill)

Banks Act means the Banks Act, 1990 (Act No. 94 of 1990); (Source: Draft Twin Peaks Bill version 2)

Basic own funds (BOF) is defined as the excess of assets over liabilities, valued in accordance with SAM rules, plus subordinated liabilities, less any exclusions listed below. Own funds is the sum of "BOF" and "ancillary own funds‖. (Source: SA QIS3 Technical Specifications)

Beneficial interest has the meaning set out in section 1 the Companies Act; (Source: Draft Primary Legislation - Governance Risk Management and Internal control)

Beneficiary means the person to whom an insurer undertakes to fulfil insurance obligations, which person may be or may not be the policyholder (Source: Draft Insurance Bill issued May 2015)

Best estimate (BEL) should correspond to the probability weighted average of future cash-flows taking account of the time value of money. Therefore, the best estimate calculation should allow for the uncertainty in the future cash-flows. The calculation should consider the variability of the cash flows in order to ensure that the best estimate represents the mean of the distribution of cash flow values. Allowance for uncertainty does not suggest that additional margins should be included within the best estimate. The best estimate is the average of the outcomes of all possible scenarios, weighted according to their respective probabilities. Although, in principle, all possible scenarios should be considered, it may not be necessary, or even possible, to explicitly incorporate all possible scenarios in the valuation of the liability, nor to develop explicit probability distributions in all cases, depending on the type of risks involved and the materiality of the expected financial effect of the scenarios under consideration. Moreover, it is sometimes possible to implicitly allow for all possible scenarios, for example in closed form solutions in life insurance or the chain-ladder technique in non-life insurance (Source: SA QIS3 Technical Specifications)

Biometric risk factors are underwriting risks covering any of the risks related to human life conditions, e.g.: (a) mortality/longevity rate; (b) morbidity rate; (c) disability rate. (Source: SA QIS3 Technical Specifications)

Board of directors means the board of directors of a public company or the controlling body of an association of persons formed under an Act of Parliament that performs similar roles and responsibilities as the board of directors of a public company; (Source: Draft Primary Legislation - Governance Risk Management and Internal control)

Board of directors means the—(a) board of directors of a company registered under the Companies Act;(b) board of directors of a co-operative registered under the Co-operatives Act; or (c) governing body of a member-based democratically controlled association of persons established by an Act of Parliament (Source: Draft Insurance Bill issued May 2015)

Boundaries of the contract - For the purpose of determining which insurance and reinsurance obligations arise in relation to an insurance or reinsurance contract, the boundaries of the contract shall be defined in the following manner: (a) Where the insurer or reinsurer has i. a unilateral right to terminate the contract; ii. a unilateral right to reject the premiums payable under the contract; or iii. a unilateral right to amend the premiums or the benefits payable under the contract at a future date in such a way that the premiums fully reflect the risks, then Any obligations which relate to insurance or reinsurance cover which might be provided by the insurance or reinsurer after that date do not belong to the existing contract, unless the insurers or reinsurer can compel the policyholder to pay the premium for those obligations. (b) Where the insurer or reinsurer has a unilateral right referred to in

Page | 8

point (a) that relates only to a part of the contract, the same principle as defined in point (a) above shall be applied to this part. (c) All other obligations relating to the contract, including obligations relating to unilateral rights of the insurer or reinsurer to renew and extend the scope of the contract, belong to the contract. (Source: SA QIS3 Technical Specifications)

Branch of a foreign reinsurer means an operating entity of a foreign reinsurer that is not a legal entity separate from the foreign reinsurer, and is part of a foreign reinsurer in terms of its organisation (Source: Draft Insurance Bill issued May 2015)

Branch of an insurer means an operating entity of an insurer that is part of the insurer in terms of its organisation and is not a legal entity separate from the insurer, but is established outside of the Republic (Source: Draft Insurance Bill issued May 2015)

Breach of the Solvency Capital Requirement (A significant breach) is defined as the earlier of the following events: (a) Own funds are equal to or less than 75% of the Solvency Capital Requirement. (b) A breach of the Solvency Capital Requirement is not resolved within a two month period (Source: SA QIS3 Technical Specifications)

Business premises means a building or a part of a building that is used in connection with the carrying on of a business of providing a financial product or financial service; (Source: Draft Twin Peaks Bill version 2)

Capital requirements means - collectively the solvency capital requirement and minimum capital requirement; (Source: Draft Primary Legislation - Governance Risk Management and Internal control)

Captive Insurance Company: A ―captive insurance company‖ means – an insurance or reinsurance juristic party created and owned by one or several industrial, commercial or financial entities, other than an insurance or reinsurance group entity. The purpose of which is to provide insurance or reinsurance cover for the entity‘s risks or entities to which it belongs, and only a small part, if any, of its risk exposure is related to providing insurance or reinsurance to other related parties where the other related parties are limited to the employees of the entity or entities to which it belongs. (Source: SA QIS3 Technical Specifications)

Captive insurer means an insurer that only insures its own operational risks, the operational risks of its holding company or subsidiaries of its holding company; (Source: Draft Insurance Bill issued May 2015)

Case record, in relation to an administrative appeal lodged or to be lodged in terms of Part 3 of Chapter 6, means—(a) any documentation and any written or electronic evidence, recommendations or other factual information which was before there regulatory authority when it took the decision appealed or to be appealed against; and (b) the reasons for the decision; (Source: Draft Twin Peaks Bill)

Cash and cash equivalents - Cash comprises cash on hand and demand deposits (Source: SA QIS3 Technical Specifications)

Cash-back and other loyalty provisions: The total technical provisions per line of business for insurance policy benefits that entitle a policyholder to predetermined benefits on the expiry of a specified period and under specified circumstances. This includes loyalty benefits that depend only on whether or not the policyholder lapses but not on whether or not the policyholder has claimed during a specified period. (Source: SA QIS3 Technical Specifications)

Cash-back bonus means a benefit provided for in a policy document that entitles a policyholder to a predetermined benefit on the expiry of a specified period and under specified circumstances; (Source: Board Notice 169 of 2011)

Catastrophe risk Under the non-life underwriting risk module, catastrophe risk is defined in the Solvency II Framework Directive (Directive 2009/138/EC) as: ―the risk of loss, or of adverse change in the value of insurance liabilities, resulting from significant uncertainty of pricing and provisioning assumptions related to extreme or exceptional events (Source: SA QIS3 Technical Specifications) CAT risks stem from extreme or irregular events that are not sufficiently captured by the capital requirements for premium and reserve risk. The catastrophe risk capital requirement is calibrated at the 99.5% VaR (annual view) (Source: SA QIS3 Technical Specifications)

Page | 9

Cell Captive insurer means an insurer that only conducts insurance business through cell structures (Source: Draft Insurance Bill issued May 2015)

Cell Captive Insurer: A ―cell captive insurer‖ (referred to as the „cell provider‟ or „promoter‟) is an insurance company which rents its insurance license to other organisations under onerous terms. The license may be used strictly for an organisations own assets risk, which is referred to as first party cell or for the organisations clients, which is referred to as third party cell. The conditions extended upon the organisation renting under the third party basis are express and onerous and the organisation seeking the license will have to comply with all applicable legislation and capitalisation requirements before the application will be granted by the cell captive insurer. (Source: SA QIS3 Technical Specifications)

Cell means an equity participation in a specific class of shares of an insurer, which equity participation is administered and accounted for separately from other classes of shares; (Source: Board Notice 169 of 2011)

Cell: A ―cell‖ means an equity participation in a specific class of shares of an insurer. This equity participation is administered and accounted for separately from other classes of shares. (Source: SA QIS3 Technical Specifications)

Cell structure means an arrangement under which an entity (cell owner)—(a) holds an equity participation in a specific class or type of shares of an insurer, which equity participation is administered and accounted for separately from other classes or types of shares; and(b) is entitled to a share of the profits and liable for a share of the losses as a result of the equity participation linked to profits or losses generated by the insurance business referred to in paragraph (c); and(c) places insurance business with the insurer referred to in paragraph (a), which business is ring-fenced on a going concern basis from the other insurance business of that insurer (Source: Draft Insurance Bill issued May 2015)

Chair means the person holding the office of the Chair of the Tribunal in terms of section 155(4); (Source: Draft Twin Peaks Bill version 2)

Chief Executive Officer means the Chief Executive Officer of the Prudential Authority appointed in terms of section 31(1), or a person acting as the Chief Executive Officer; (Source: Draft Twin Peaks Bill version 2)

Collective investment scheme has the meaning defined in section 1 of the Collective Investments Schemes Control Act, 2002 (Act No. 45 of 2002); (Source: Draft Twin Peaks Bill version 2)

Commercial lines means non-life insurance business other than in respect of personal lines; (Source: Discussion Document 29: Authorisation and Reporting Classes of Business under SAM)

Commissioner means the Commissioner of the Financial Sector Conduct Authority appointed in terms of section 57(1), or a person acting as the Commissioner; (Source: Draft Twin Peaks Bill version 2)

Commissioner means the Commissioner of the Market Conduct Authority appointed in terms of section 21(1), or a person acting as Commissioner designated in terms of section 21(6); (Source: Draft Twin Peaks Bill)

Companies Act means the Companies Act, 2008 (Act No. 71 of 2008) (Source: Draft Insurance Bill issued May 2015)

Companies Act means the Companies Act, 2008 (Act No. 71 of 2008); (Source: Draft Primary Legislation - Governance Risk Management and Internal control)

Companies Act means the Companies Act, 2008 (Act No. 71 of 2008); (Source: Draft Twin Peaks Bill version 2)

Company has the meaning defined in section 1 of the Companies Act; (Source: Draft Twin Peaks Bill version 2)

Competition Act means the Competition Act, 1998 (Act No. 89 of 1998); (Source: Draft Twin Peaks Bill version 2)

Page | 10

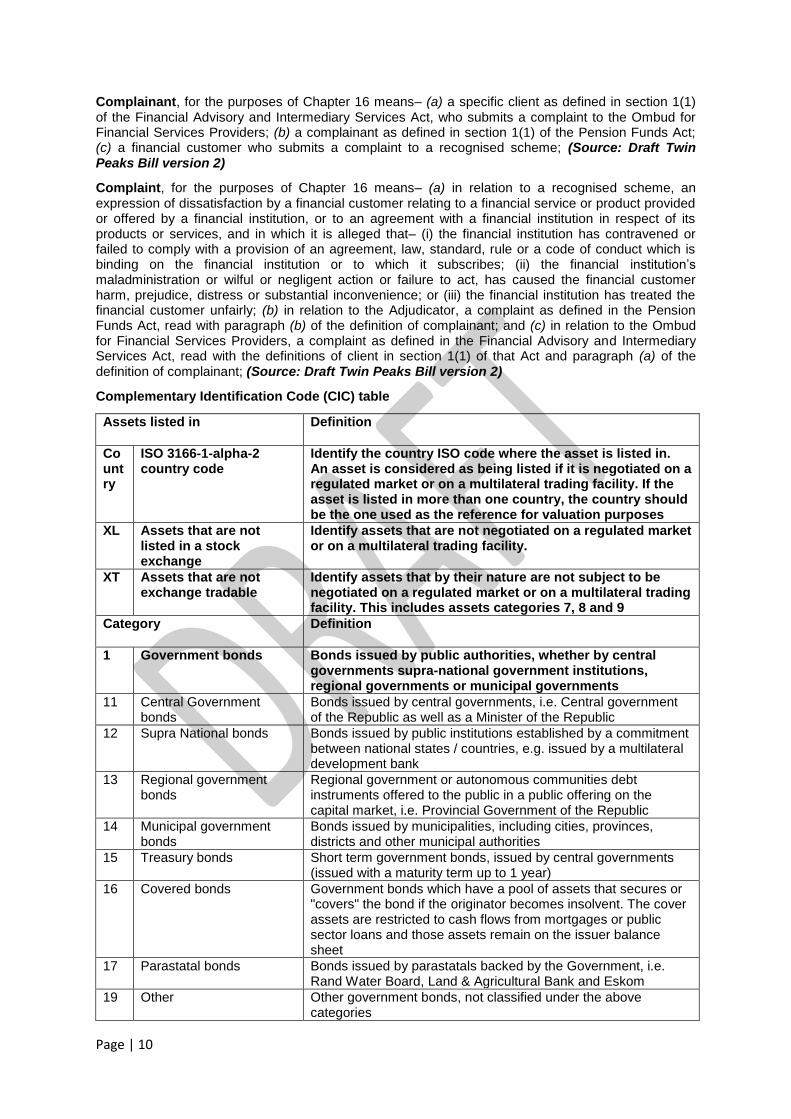

Complainant, for the purposes of Chapter 16 means– (a) a specific client as defined in section 1(1) of the Financial Advisory and Intermediary Services Act, who submits a complaint to the Ombud for Financial Services Providers; (b) a complainant as defined in section 1(1) of the Pension Funds Act; (c) a financial customer who submits a complaint to a recognised scheme; (Source: Draft Twin Peaks Bill version 2)

Complaint, for the purposes of Chapter 16 means– (a) in relation to a recognised scheme, an expression of dissatisfaction by a financial customer relating to a financial service or product provided or offered by a financial institution, or to an agreement with a financial institution in respect of its products or services, and in which it is alleged that– (i) the financial institution has contravened or failed to comply with a provision of an agreement, law, standard, rule or a code of conduct which is binding on the financial institution or to which it subscribes; (ii) the financial institution‘s maladministration or wilful or negligent action or failure to act, has caused the financial customer harm, prejudice, distress or substantial inconvenience; or (iii) the financial institution has treated the financial customer unfairly; (b) in relation to the Adjudicator, a complaint as defined in the Pension Funds Act, read with paragraph (b) of the definition of complainant; and (c) in relation to the Ombud for Financial Services Providers, a complaint as defined in the Financial Advisory and Intermediary Services Act, read with the definitions of client in section 1(1) of that Act and paragraph (a) of the definition of complainant; (Source: Draft Twin Peaks Bill version 2)

Complementary Identification Code (CIC) table

Assets listed in Definition

Country

ISO 3166-1-alpha-2 country code

Identify the country ISO code where the asset is listed in. An asset is considered as being listed if it is negotiated on a regulated market or on a multilateral trading facility. If the asset is listed in more than one country, the country should be the one used as the reference for valuation purposes

XL Assets that are not listed in a stock exchange

Identify assets that are not negotiated on a regulated market or on a multilateral trading facility.

XT Assets that are not exchange tradable

Identify assets that by their nature are not subject to be negotiated on a regulated market or on a multilateral trading facility. This includes assets categories 7, 8 and 9

Category Definition

1 Government bonds Bonds issued by public authorities, whether by central governments supra-national government institutions, regional governments or municipal governments

11 Central Government bonds

Bonds issued by central governments, i.e. Central government of the Republic as well as a Minister of the Republic

12 Supra National bonds Bonds issued by public institutions established by a commitment between national states / countries, e.g. issued by a multilateral development bank

13 Regional government bonds

Regional government or autonomous communities debt instruments offered to the public in a public offering on the capital market, i.e. Provincial Government of the Republic

14 Municipal government bonds

Bonds issued by municipalities, including cities, provinces, districts and other municipal authorities

15 Treasury bonds Short term government bonds, issued by central governments (issued with a maturity term up to 1 year)

16 Covered bonds Government bonds which have a pool of assets that secures or "covers" the bond if the originator becomes insolvent. The cover assets are restricted to cash flows from mortgages or public sector loans and those assets remain on the issuer balance sheet

17 Parastatal bonds Bonds issued by parastatals backed by the Government, i.e. Rand Water Board, Land & Agricultural Bank and Eskom

19 Other Other government bonds, not classified under the above categories

Page | 11

2 Corporate bonds (including fixed and variable interest bonds)

Bonds issued by corporations

21 Conventional bonds Bonds issued by corporations, that don't fall into the categories identified below. Subordinated bonds to be included in this category.

22 Convertible bonds Corporate bonds that the holder can convert into shares of common stock in the issuing company or cash of equal value, having debt and equity-like features

23 Commercial paper Corporate bonds classifiable as money market securities, with original maturity lesser than 270 days; i.e. promissory notes

24 Money market instruments

Short term debt securities (original maturity lesser than 1 year), e.g. certificate of deposit, bankers' acceptances and other highly liquid instruments

25 Hybrid bonds Corporate bonds that have debt and equity-like features, but are not convertible.

26 Common covered bonds Corporate bonds which have a pool of assets that secures or "covers" the bond if the originator becomes insolvent. The cover assets are restricted to cash flows from mortgages or public sector loans and those assets remain on the issuer balance sheet

27 Parastatal bonds Bonds issued by parastatals not backed by the Government

28 Preference shares Preference shares redeemable at a future date.

29 Other Other corporate bonds, not classified under the above categories

3 Equity Shares representing corporations' capital, i.e., representing ownership in a corporation

31 Common equity Equity that represent basic property rights on corporations

32 Equity of real estate related corporation

Equity representing capital from real estate related corporations

33 Equity rights Rights to subscribe to additional shares of equity at a set price, i.e. share options

34 Convertible and other preference shares

Preference shares convertible to common equity (ordinary shares) as well as other preference shares, i.e. perpetual preference shares.

39 Other Other equity, not classified under the above categories

4 Investment funds Undertakings the sole purpose of which is the collective investment in transferrable securities and/or in other financial assets

41 Equity funds Investment funds mainly invested in equity relative to the total portfolio

42 Debt funds Investment funds mainly invested in bonds relative to the total portfolio

43 Money market funds Investment funds mainly invested in money market instruments relative to the total portfolio

44 Asset allocation funds Fund which invests its assets pursuing a specific asset allocation objective, e.g. primarily investing in the securities of companies in countries with nascent stock markets or small economies, specific sectors or group of sectors, specific countries of other specific investment objective; i.e. Forex balance funds

45 Real estate funds Investment funds mainly invested in real estate relative to the total portfolio

46 Alternative funds Funds whose investment strategies include such as hedging, event driven, fixed income directional and relative value, managed futures, commodities etc.

47 Private Equity Funds Investment funds used for making investments in equity securities following strategies associated with private equities.

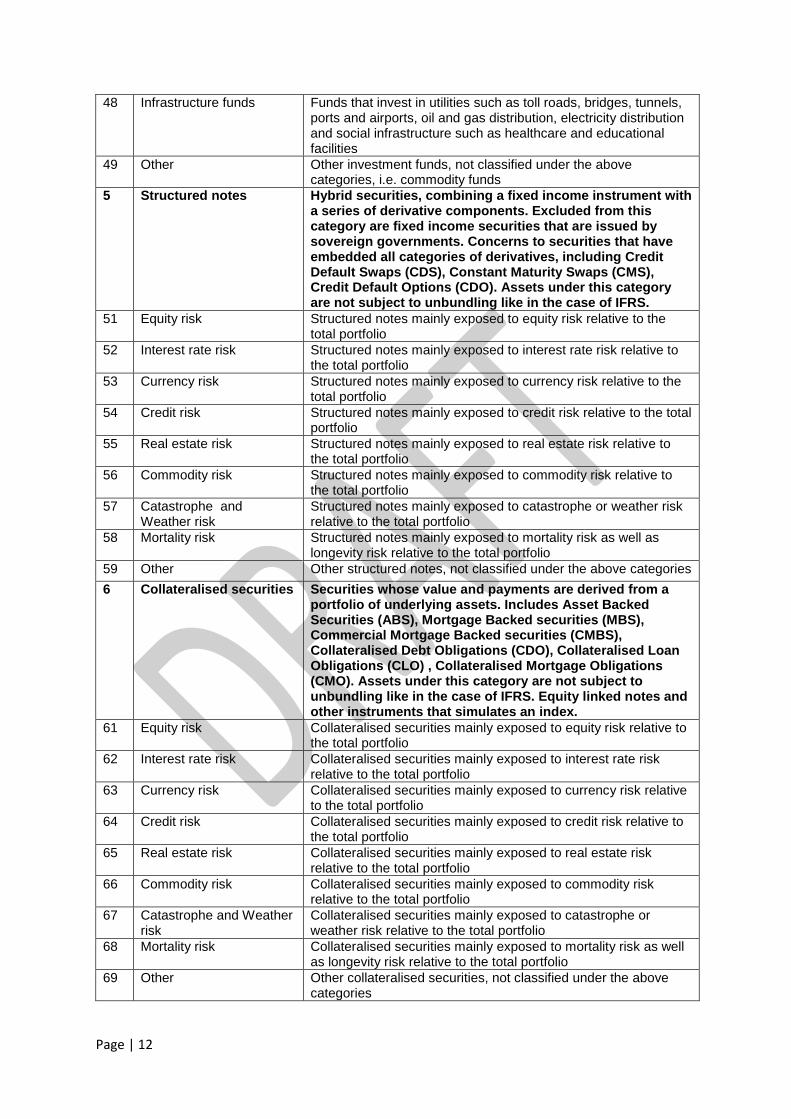

Page | 12

48 Infrastructure funds Funds that invest in utilities such as toll roads, bridges, tunnels, ports and airports, oil and gas distribution, electricity distribution and social infrastructure such as healthcare and educational facilities

49 Other Other investment funds, not classified under the above categories, i.e. commodity funds

5 Structured notes Hybrid securities, combining a fixed income instrument with a series of derivative components. Excluded from this category are fixed income securities that are issued by sovereign governments. Concerns to securities that have embedded all categories of derivatives, including Credit Default Swaps (CDS), Constant Maturity Swaps (CMS), Credit Default Options (CDO). Assets under this category are not subject to unbundling like in the case of IFRS.

51 Equity risk Structured notes mainly exposed to equity risk relative to the total portfolio

52 Interest rate risk Structured notes mainly exposed to interest rate risk relative to the total portfolio

53 Currency risk Structured notes mainly exposed to currency risk relative to the total portfolio

54 Credit risk Structured notes mainly exposed to credit risk relative to the total portfolio

55 Real estate risk Structured notes mainly exposed to real estate risk relative to the total portfolio

56 Commodity risk Structured notes mainly exposed to commodity risk relative to the total portfolio

57 Catastrophe and Weather risk

Structured notes mainly exposed to catastrophe or weather risk relative to the total portfolio

58 Mortality risk Structured notes mainly exposed to mortality risk as well as longevity risk relative to the total portfolio

59 Other Other structured notes, not classified under the above categories

6 Collateralised securities Securities whose value and payments are derived from a portfolio of underlying assets. Includes Asset Backed Securities (ABS), Mortgage Backed securities (MBS), Commercial Mortgage Backed securities (CMBS), Collateralised Debt Obligations (CDO), Collateralised Loan Obligations (CLO) , Collateralised Mortgage Obligations (CMO). Assets under this category are not subject to unbundling like in the case of IFRS. Equity linked notes and other instruments that simulates an index.

61 Equity risk Collateralised securities mainly exposed to equity risk relative to the total portfolio

62 Interest rate risk Collateralised securities mainly exposed to interest rate risk relative to the total portfolio

63 Currency risk Collateralised securities mainly exposed to currency risk relative to the total portfolio

64 Credit risk Collateralised securities mainly exposed to credit risk relative to the total portfolio

65 Real estate risk Collateralised securities mainly exposed to real estate risk relative to the total portfolio

66 Commodity risk Collateralised securities mainly exposed to commodity risk relative to the total portfolio

67 Catastrophe and Weather risk

Collateralised securities mainly exposed to catastrophe or weather risk relative to the total portfolio

68 Mortality risk Collateralised securities mainly exposed to mortality risk as well as longevity risk relative to the total portfolio

69 Other Other collateralised securities, not classified under the above categories

Page | 13

7 Cash and equivalents (issued by registered Banking institutions)

Money in the physical form, bank deposits and other money deposits

71 Cash Notes and coins in circulation that are commonly used to make payments

72 Transferable deposits (cash equivalents)

Deposits exchangeable for currency on demand at par and which are directly usable for making payments by cheque, draft, giro order, direct debit/credit, or other direct payment facility, without penalty or restriction including call deposits, current accounts, fixed deposits, bankers‘ acceptance and negotiable certificate of deposit

73 Other deposits short term (less than one year)

Deposits other than transferable deposits, with initial maturity inferior to 1 year, that cannot be used to make payments at any time and that are not exchangeable for currency or transferable deposits without any kind of significant restriction or penalty

74 Other deposits with term longer than one year

Deposits other than transferable deposits, with initial maturity superior to 1 year, that cannot be used to make payments at any time and that are not exchangeable for currency or transferable deposits without any kind of significant restriction or penalty

75 Cash deposits to cedents Cash deposits relating to reinsurance accepted

79 Other Other cash and equivalents, not classified under the above categories

8 Mortgages and loans Financial assets created when creditors lend funds to debtors, with collateral or not, including cash pools.

81 Uncollateralized loans made

Loans made without collateral, i.e. debentures

82 Loans made collateralized with securities

Loans made with collateral in the form of financial securities, i.e. policyholder loans and claims against LT insurers ito a policy

84 Mortgages Loans made with collateral in the form real estate

85 Other collateralized loans made

Loans made with collateral in any other form

89 Other Other mortgages and loans, not classified under the above categories

9 Property Buildings, land, other constructions that are immovable and equipment

91 Property (office and commercial)

Office and commercial building used for investment

92 Property (residential) Residential buildings used for investment

94 Property (under construction)

Real estate that is under construction, for future own usage or future usage as investment

99 Other Other real estate, not classified under the above categories

A Futures Standardised contract between two parties to buy or sell a specified asset of standardised quantity and quality at a specified future date at a price agreed today

A1 Equity and index futures Futures with equity or stock exchange indices as underlying

A2 Interest rate futures Futures with bonds or other interest rate dependent security as underlying

A3 Currency futures Futures with currencies or other currencies dependent security as underlying

A5 Commodity futures Futures with commodities or other commodities dependent security as underlying

A7 Catastrophe and Weather risk

Futures mainly exposed to catastrophe or weather risk

A8 Mortality risk Futures mainly exposed to mortality risk as well as longevity risk

A9 Other Other futures, not classified under the above categories

Page | 14

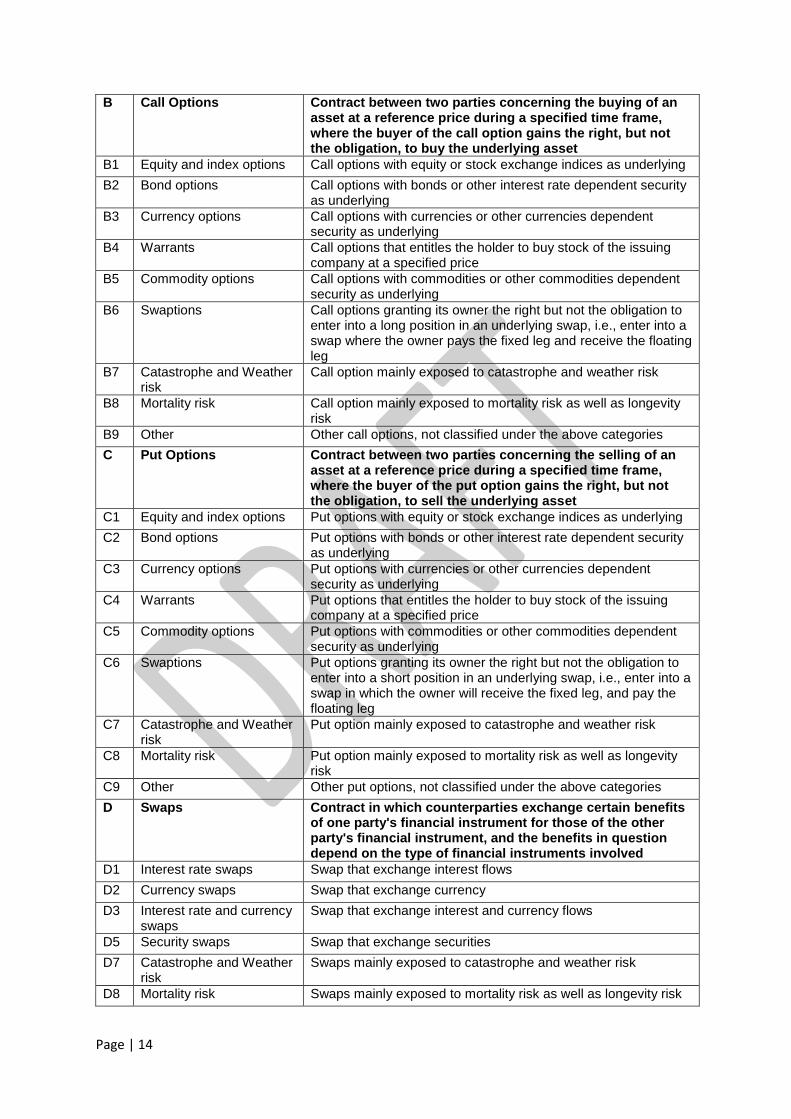

B Call Options Contract between two parties concerning the buying of an asset at a reference price during a specified time frame, where the buyer of the call option gains the right, but not the obligation, to buy the underlying asset

B1 Equity and index options Call options with equity or stock exchange indices as underlying

B2 Bond options Call options with bonds or other interest rate dependent security as underlying

B3 Currency options Call options with currencies or other currencies dependent security as underlying

B4 Warrants Call options that entitles the holder to buy stock of the issuing company at a specified price

B5 Commodity options Call options with commodities or other commodities dependent security as underlying

B6 Swaptions Call options granting its owner the right but not the obligation to enter into a long position in an underlying swap, i.e., enter into a swap where the owner pays the fixed leg and receive the floating leg

B7 Catastrophe and Weather risk

Call option mainly exposed to catastrophe and weather risk

B8 Mortality risk Call option mainly exposed to mortality risk as well as longevity risk

B9 Other Other call options, not classified under the above categories

C Put Options Contract between two parties concerning the selling of an asset at a reference price during a specified time frame, where the buyer of the put option gains the right, but not the obligation, to sell the underlying asset

C1 Equity and index options Put options with equity or stock exchange indices as underlying

C2 Bond options Put options with bonds or other interest rate dependent security as underlying

C3 Currency options Put options with currencies or other currencies dependent security as underlying

C4 Warrants Put options that entitles the holder to buy stock of the issuing company at a specified price

C5 Commodity options Put options with commodities or other commodities dependent security as underlying

C6 Swaptions Put options granting its owner the right but not the obligation to enter into a short position in an underlying swap, i.e., enter into a swap in which the owner will receive the fixed leg, and pay the floating leg

C7 Catastrophe and Weather risk

Put option mainly exposed to catastrophe and weather risk

C8 Mortality risk Put option mainly exposed to mortality risk as well as longevity risk

C9 Other Other put options, not classified under the above categories

D Swaps Contract in which counterparties exchange certain benefits of one party's financial instrument for those of the other party's financial instrument, and the benefits in question depend on the type of financial instruments involved

D1 Interest rate swaps Swap that exchange interest flows

D2 Currency swaps Swap that exchange currency

D3 Interest rate and currency swaps

Swap that exchange interest and currency flows

D5 Security swaps Swap that exchange securities

D7 Catastrophe and Weather risk

Swaps mainly exposed to catastrophe and weather risk

D8 Mortality risk Swaps mainly exposed to mortality risk as well as longevity risk

Page | 15

D9 Other Other swaps, not classified under the above categories

E Forwards Non-standardised contract between two parties to buy or sell an asset at a specified future time at a price agreed today

E1 Forward interest rate agreement

Forward contract in which one party pays a fixed interest rate, and receives a floating interest rate equal to a underlying rate, at the predefined forward date

E2 Forward exchange rate agreement

Forward contract in which one party pays an amount in one currency, and receives an equivalent amount in a different currency resulting from the conversion using the contractual exchange rate, at the predefined forward date

E7 Catastrophe and Weather risk

Forwards mainly exposed to catastrophe and weather risk

E8 Mortality risk Forwards mainly exposed to mortality risk as well as longevity risk

E9 Other Other forwards, not classified under the above categories

F Credit derivatives Derivative whose value is derived from the credit risk on an underlying bond, loan or any other financial asset

F1 Credit default swap Credit derivative transaction in which two parties enter into an agreement whereby one party pays the other a fixed periodic coupon for the specified life on the agreement and the other party makes no payments unless a credit event relating to a predetermined reference asset occurs

F2 Credit spread option Credit derivative that will generate cash flows if a given credit spread between two specific assets or benchmarks changes from its current level

F3 Credit spread swap A swap in which one party makes a fixed payment to the other on the swap's settlement date and the second party pays the first an amount based on the actual credit spread

F4 Total return swap A swap in which the non-floating rate side is based on the total return of an equity or fixed income instrument with the life longer that the swap

F9 Other Other credit derivatives, not classified under the above categories

(Source: Light Parallel Run CIC Table and definitions)

Conduct standard means a standard made in terms of section 95; (Source: Draft Twin Peaks Bill version 2)

Constitution means the Constitution of the Republic of South Africa, 1996; (Source: Draft Twin Peaks Bill)

Consumer Protection Act means the Consumer Protection Act, 2008 (Act No. 68 of 2008); (Source: Draft Twin Peaks Bill version 2)

Contagion risk is taken from the IAIS glossary as follows: ―As part of a group or conglomerate, and aside from intragroup exposures of a financial nature, there may be a risk that the support of the insurer by internal or external parties may suffer if there is a concern about another part of the group of which it is a part (Source: Final Position Paper 85)

Contingency Policy/Rent-a-captive: A ―contingency policy‖ is an insurance policy typically used to provide for the primary layers of an insurance programme or for ―difficult to insure‖ risks.. A contingency policy may insure multiple risks and is typically written for a one year period. A contingency policy may be issued as a standalone policy or may form part of a reinsurance arrangement, whereby reinsurance is structured above the protection provided by the contingency policy. At renewal or cancellation a performance bonus may be declared to the insured, based on claims experience. (Source: SA QIS3 Technical Specifications)

Contingent commission provisions: The total technical provisions per line of business for contingent commissions payable by a reinsurer to a cedant under a reinsurance agreement where these contingent commissions depend on the profitability of the total business ceded. From the

Page | 16

cedant‟s perspective this will be typically a negative technical provision (i.e. technical asset). From the reinsurer‘s perspective this will be typically a positive technical provision (i.e. technical liability). e.g. profit-share, sliding scale and other contingent commissions. (Source: SA QIS3 Technical Specifications)

Contingent considerations - A contingent consideration is either:(a) a possible obligation that arises from past events and whose existence will be confirmed only by the occurrence or non-occurrence of one or more uncertain future events not wholly within the control of the entity; or (b) a present obligation that arises from past events but is not recognised because: (i) it is not probable that an outflow of resources embodying economic benefits will be required to settle the obligation; or (ii) the amount of the obligation cannot be measured with sufficient reliability. (Source: SA QIS3 Technical Specifications)

Contract Boundary - For the purpose of determining which insurance and reinsurance obligations arise in relation to an insurance or reinsurance contract, the boundaries of the contract shall be defined in the following manner:(a) Where the insurer or reinsurer has i. a unilateral right to terminate the contract; ii. a unilateral right to reject the premiums payable under the contract; or iii. a unilateral right to amend the premiums or the benefits payable under the contract at a future date in such a way that the premiums fully reflect the risks, then Any obligations which relate to insurance or reinsurance cover which might be provided by the insurance or reinsurer after that date do not belong to the existing contract, unless the insurers or reinsurer can compel the policyholder to pay the premium for those obligations.(b) Where the insurer or reinsurer has a unilateral right referred to in point (a) that relates only to a part of the contract, the same principle as defined in point (a) above shall be applied to this part. (c) All other obligations relating to the contract, including obligations relating to unilateral rights of the insurer or reinsurer to renew and extend the scope of the contract, belong to the contract. (Source: SA QIS3 Technical Specifications)

Contractual option is defined as a right to change the benefits, to be taken at the choice of its holder (generally the policyholder), on terms that are established in advance. Thus, in order to trigger an option, a deliberate decision of its holder is necessary. Some (non-exhaustive) examples of contractual options which are pre-determined in contract and do not require again the consent of the parties to renew or modify the contract include the following: (a) Surrender value option, where the policyholder has the right to fully or partially surrender the policy and receive a pre-defined lump sum amount;(b) Paid-up policy option, where the policyholder has the right to stop paying premiums and change the policy to a paid-up status;(c) Annuity conversion option, where the policyholder has the right to convert a lump survival benefit into an annuity at a pre-defined minimum rate of conversion;(d) Policy conversion option, where the policyholder has the right to convert from one policy to another at pre-specific terms and conditions; and(e) Extended coverage option, where the policyholder has the right to extend the coverage period at the expiry of the original contract without producing further evidence of health. (Source: SA QIS3 Technical Specifications)

Contravention includes a non-compliance with a financial sector law, and an offence in terms of a financial sector law; (Source: Draft Twin Peaks Bill version 2)

Control function means -(a) the risk management function;(b) the compliance function;(c) internal audit function;(d) in the case of a long-term insurer, the actuarial function; or(e) all of these functions; (Source: Board Notice 158 of 2014)

Control function within a governance framework, means – (a) the risk management function; (b) the compliance function; (c) the actuarial control function;(d) internal audit function;(e) all of these functions; or(f) any combination of these functions; (Source: Draft Primary Legislation - Governance Risk Management and Internal control)

Control function within a governance framework, means the risk management function, the compliance function, the actuarial control function and internal audit function;‘‘; (Source: Draft ILAB version 2 - Non-Life)

Control function within a governance framework, means the risk management function, the compliance function, the actuarial control function and internal audit function;‘‘; (Source: Draft ILAB version 2 - Life)

Control functions means the dedicated functions (whether in the form of a unit or department) of an insurer responsible for supporting the board in the fulfilment of its oversight responsibilities in respect

Page | 17

of risk management, compliance, actuarial control, internal audit and any other function prescribed (Source: Draft Insurance Bill issued May 2015)

Controlling company means a holding company of an insurance group that is a public company whose only business is the acquiring, holding and managing of another company or other companies (Source: Draft Insurance Bill issued May 2015)

Controlling company means a non-operating holding company of an insurance group that is subject to this Act; (Source: Draft Primary Legislation – Solo and Group requirements)

Controlling company means a non-operating holding company of an insurance group that is subject to this Part; (Source: Draft ILAB version 2 - Life)

Controlling company means a non-operating holding company of an insurance group that is subject to this Part; (Source: Draft ILAB version 2 - Non-Life)

Controlling company means a non-operating holding company of an insurance group that is subject to this Chapter; (Source: Final Position Paper 27)

Controlling company means the non-operating holding company of a financial conglomerate that is subject to Chapter 11; (Source: Draft Twin Peaks Bill version 2)

Co-operatives Act means the Co-operatives Act, 2005 (Act No. 14 of 2005) (Source: Draft Insurance Bill issued May 2015)

Cost-of-Capital rate is the annual rate to be applied to the capital requirement in each period. Because the assets covering the capital requirement themselves are assumed to be held in marketable securities, this rate does not account for the total return but merely for the spread over and above the risk free rate. (Source: SA QIS3 Technical Specifications)

Council for Medical Schemes means the Council for Medical Schemes established in terms of section 3 of the Medical Schemes Act, 1998 (Act No. 131 of 1998); (Source: Draft Twin Peaks Bill version 2)

Council means the Financial Services Ombud Schemes Council referred to in section 168; (Source: Draft Twin Peaks Bill version 2)

Council of Financial Regulators means the Council established in terms of section 79; (Source: Draft Twin Peaks Bill version 2)

Council standard means a standard made by the Council, after having followed a procedure substantially similar to that required in terms of part 2 of Chapter 7; (Source: Draft Twin Peaks Bill version 2)

Court means a Superior Court as defined in section 1 of the Superior Courts Act, 2013 (Act No. 10 of 2013); (Source: Draft Twin Peaks Bill version 2)

Credit agreement includes, but is not limited to, a credit agreement referred to in section 1 of the National Credit Act; (Source: Draft Twin Peaks Bill version 2)

Currency risk arises from changes in the level or volatility of currency exchange rates. (Source: SA QIS3 Technical Specifications)

Current Tax Assets - Income taxes include all domestic and foreign taxes based on taxable profits and withholding taxes payable by a group entity (Source: SA QIS3 Technical Specifications)

Current Tax liabilities - Income taxes include all domestic and foreign taxes based on taxable profits and withholding taxes payable by a group entity. (Source: SA QIS3 Technical Specifications)

Death event means the event of the life of a person or an unborn having ended; (Source: Discussion Document 29: Authorisation and Reporting Classes of Business under SAM)

Death event means the event of the life of a person or an unborn having ended (Source: Draft Insurance Bill issued May 2015)

Decision, in relation to an administrative action, means a decision taken in relation to a specific person affecting the rights of that person; (Source: Draft Twin Peaks Bill)

Page | 18

Decision-maker means– (a) a financial sector regulator;(b) any other person who has made a decision in terms of a power conferred or a duty imposed on that person by or in terms of a financial sector law, and that financial sector law grants a right of appeal to the Tribunal to any person aggrieved by a decision of that person; (c) a statutory ombud (Source: Draft Twin Peaks Bill version 2)

Deduction & Aggregation (D&A) - The sum of the standard formula solo SCR and solo own funds of the participating insurance undertaking (adjusted to remove the treatment of intragroup transactions from the solo SCR and own funds) and the proportional share of each related insurance undertaking in the group. Under this method, group solvency is assessed through the sum of the adjusted solo solvency capital requirements and own funds of the participating undertakings and of the proportional48 share of its related undertakings. The treatment of participations in particular types of entities at solo level will be reflected in the aggregated group SCR. For participations in non-financial entities, the equity risk charge as described in section SCR.2. in the solo SCR of the participating entity should be applied to ensure a consistent approach with the other methods (Source: SA QIS3 Technical Specifications)

Deferred Tax Assets - Deferred tax assets are the amounts of income taxes recoverable in future periods in respect of: (a) deductible temporary differences; (b) the carry forward of unused tax losses; and (c) the carry forward of unused tax credits. (Source: SA QIS3 Technical Specifications)

Deferred Tax liabilities - Income taxes include all domestic and foreign taxes based on taxable profits and withholding taxes payable by a group entity. (Source: SA QIS3 Technical Specifications)

Deputy Commissioner means a person appointed as a Deputy Commissioner in terms of section 57(3), or a person acting as a Deputy Commissioner; (Source: Draft Twin Peaks Bill version 2)

Deputy Governor means a person appointed in terms of section 4 or 6(1)(a) of the Reserve Bank Act as a Deputy Governor of the Reserve Bank; (Source: Draft Twin Peaks Bill version 2)

Designated authority, for the purposes of Part 1 of Chapter 17, means–(a) an organ of state responsible for the regulation, supervision or enforcement of legislation regulating the financial sector, taxation, the administration of justice, and law enforcement; (b) a body similar to an organ of state referred to in paragraph (a), that is designated in terms of the laws of a foreign country as being responsible for the regulation, supervision or enforcement of legislation regulating the financial sector, taxation, the administration of justice, and law enforcement; (c) a market infrastructure that is responsible for the supervision of persons authorised by that infrastructure in terms of the Financial Markets Act; or (d) an Ombud established in terms of a financial sector law or a recognised scheme, including a scheme that was recognised in terms of the Financial Services Ombud Schemes Act, 2004 (Act No. 37 of 2004); (e) a payment system management body as recognised and established in terms of section 3(3) of the National Payment System Act; (Source: Draft Twin Peaks Bill version 2)

Director means a member of a board of directors (Source: Draft Insurance Bill issued May 2015)

Director means a member or an alternate member of a governing body; (Source: Draft Twin Peaks Bill version 2)

Director-General means the Director-General of the National Treasury, or a person acting as the Director-General; (Source: Draft Twin Peaks Bill version 2)

Disability event means the event of a person becoming temporarily or permanently disabled so that the person is unable to— (a) continue his or her occupation or employment;(b) participate in any occupation or employment that is reasonably suitable for that person given, amongst other matters, his or her education, experience and age; or (c) carry on the functions required for normal activities of life (Source: Draft Insurance Bill issued May 2015)

Disability event means the event of the –(a) occupational ability of the mind or body of a person becoming so temporarily or permanently impaired that the person is unable to –(i) continue his or her occupation or employment or; or(ii) participate in any occupation or employment that is reasonably suitable for that person given, amongst others, his or her education, experience and age; or(b) the functional ability of the mind or body of a person becoming so temporarily or permanently impaired

Page | 19

that the a person is fully or partially unable to carry on normal activities of life; (Source: Discussion Document 29: Authorisation and Reporting Classes of Business under SAM)

Disability refers to the inability of the life assured - due to sickness, injury, disease, illness or infirmity - to engage in his/her own occupation, or any other occupation for which he is suited in terms of training, education and experience. (Source: SA QIS3 Technical Specifications)

Discretionary benefits correspond to the sum of the ―conditional discretionary benefit‖ and ―pure discretionary benefit‖ items. The definitions of ―conditional discretionary benefit‖ and ―pure discretionary benefit‖ should not be understood as requirement that they should be valued separately. Only a distinction between guaranteed benefits and discretionary benefits should be required (Source: Final Position Paper 32)

Discretionary participation features are defined as additional benefits that are contractually based on: a) the performance of a specified pool of contracts or a specified type of contract or a single contract b) realised and/or unrealised investment return on a specified pool of assets held by the issuer; orc) the profit or loss of the company, fund or other entity that issues the contract (Source: Final Position Paper 32)

Discretionary participation features means where the insurance obligations under a policy are supplemented with additional insurance obligations -(a) that are likely to be a significant portion of the total insurance obligations under the policy;(b) the amount or timing of which are contractually at the discretion of the insurer; and(c) that are contractually based on -(i) the performance of a specified pool of policies or a specified type of policy;(ii) realised and/or unrealised investment returns on a specified pool of assets held by the insurer; or(iii) the profit or loss of the insurer that issues the policy (Source: Discussion Document 29: Authorisation and Reporting Classes of Business under SAM)

Disqualified person means a person who– (a) is engaged in the business of a financial institution, or has a direct material financial interest in a financial institution, except as a financial customer; (b) is a Member of the Cabinet referred to in section 91 of the Constitution, a Member of the Executive Council of a Province referred to in section 215 of the Constitution, a member of Parliament, a member of a provincial legislature, or a mayor or councillor of a municipal council; (c) is an office-bearer of, or is in a remunerated leadership position in, a political party; (d) has at any time been removed from an office of trust; (e) is or has been subject to disbarment; (f) is or has at any time been sanctioned for contravening a law relating to the regulation or supervision of financial institutions, or the provision of financial products or financial services; (g) is or has at any time been convicted of– (i) theft, fraud, forgery, uttering of a forged document, perjury or an offence involving dishonesty, whether in the Republic or elsewhere; or(ii) an offence in terms of the Prevention of Corruption Act, 1958 (Act No. 6 of 1958), the Corruption Act, 1992 (Act No. 94 of 1992) or Parts 1 to 4, or sections 17, 20 or 21, of the Prevention and Combating of Corrupt Activities Act, 2004 (Act No. 12 of 2004), or a similar offence in terms of the law of a foreign country; (h) who is or has been convicted of any other offence committed after the Constitution of the Republic of South Africa, 1993, came into operation, where the penalty imposed for the offence is or was imprisonment without the option of a fine; (i) is subject to a provisional sequestration order or is an unrehabilitated insolvent; (j) is disqualified from acting as a director or executive officer of a financial institution in terms of legislation; or (k) is declared by the High Court to be of unsound mind or mentally disordered, or is detained in terms of the Mental Health Act, 1973 (Act No. 18 of 1973); (Source: Draft Twin Peaks Bill version 2)

Document includes books, records, securities or accounts, and any information, including information stored or recorded electronically, digitally, photographically, magnetically or optically, and any device by means of which information is recorded or stored; (Source: Draft Twin Peaks Bill version 2)

Dual-regulated activity means business of the nature contemplated in Part 2 of Schedule 2; (Source: Draft Twin Peaks Bill)

Eligible financial institution means any of the following: (a) a financial institution licensed or required to be licensed as a bank in terms of the Banks Act; (b) a financial institution licensed or required to be licensed as a long-term insurer in terms of the Long-term Insurance Act or a short-term insurer in terms of the Short-term Insurance Act; (c) a market infrastructure; (d) a financial institution prescribed in Regulations;1 (Source: Draft Twin Peaks Bill version 2)

Eligible own funds comprise the sum of basic own funds and ancillary own funds adjusted in accordance with the prescribed tiering restrictions; ―basic own funds‖ consist of -(a) the excess of

Page | 20

assets over liabilities valued in accordance with sections 41, 42 and 43 of this Act; and(b) subordinated liabilities; (Source: Draft Primary Legislation - Financial Soundness)

Employee Benefits and Termination Benefits - As defined in IAS 19(Source: SA QIS3 Technical Specifications)

Encumber means any limitation on or qualification in respect of the exercise of a contractual right, including, but not limited to, any contractual obligation that must be fulfilled before that contractual right may be exercised (Source: Draft Insurance Bill issued May 2015)

Entitlement means—(a) an authorisation, as defined in this Act; (b) any exemption or exclusion issued in terms of a regulatory law from a requirement of a regulatory law or imposed in terms of a regulatory law; or(c) any other benefit or privilege issued in terms of a regulatory law; (Source: Draft Twin Peaks Bill)

Equity risk arises from the level or volatility of market prices for equities. Exposure to equity risk refers to all assets and liabilities whose value is sensitive to changes in equity prices. (Source: SA QIS3 Technical Specifications)

Executive Committee means the Committee established in terms of section 56; (Source: Draft Twin Peaks Bill version 2)

Executive Committee member means the Commissioner or a Deputy Commissioner of the Financial Sector Conduct Authority; (Source: Draft Twin Peaks Bill version 2)

Expected Profits included in Future Cashflows (EPIFC) result from the recognition of profits yet to be earned, emanating from the cash flows from existing (in-force) business that are expected to be received in the future. EPIFC is also known as the surrender value gap (SVG), and both terms can be used interchangeably. (Source: SA QIS3 Technical Specifications)

Expected profits included in future premiums (EPIFP) result from the recognition of profits yet to be earned, emanating from the premiums from existing (in-force) business that are expected to be received in the future. (Source: SA QIS3 Technical Specifications)

Expense risk arises from the variation in the expenses incurred in servicing insurance and reinsurance contracts. This includes the risk arising from the variation in the growth of expenses over and above that of inflation. (Source: SA QIS3 Technical Specifications)

Finance Leases - Classification of leases is based on the extent to which risks and rewards incidental to ownership of a leased asset lie with the lessor or the lessee. (Source: SA QIS3 Technical Specifications)

Financial Advisory and Intermediary Services Act means the Financial Advisory and Intermediary Services Act, 2002 (Act No. 37 of 2002); (Source: Draft Twin Peaks Bill version 2)

Financial benchmark means an analysis by which the performance of an investment is assessed; (Source: Draft Twin Peaks Bill version 2)

Financial conglomerate means a group of companies that comprises – (a) one or more eligible financial institutions; (b) the holding companies, including any controlling companies, of an eligible financial institution; (c) their related persons or inter-related persons, including persons located or incorporated outside of the Republic; and (d) their associates as identified in the International Financial Reporting Standards issued by the International Accounting Standards Board or a successor body, but excludes any holding company or similar entity that is incorporated outside of the Republic; (Source: Draft Twin Peaks Bill version 2)

Financial conglomerate means an insurance group that includes -(a) at least one person subject to registration under this Act; and(b) at least one person subject to registration, licensing or approval under –(i) the laws, other than this Act, referred to in the definition of ―financial institution‖ in section 1 of the Financial Institutions (Protection of Funds) Act, 2001 (Act 28 of 2001);(ii) the Banks Act, 1990 (Act No. 94 of 1990), the Mutual Banks Act, 1993 (Act No. 124 of 1993) or the Co-operative Banks Act, 2007 (Act No. 40 of 2007); or(iii) the National Credit Act, 2005 (Act No. 34 of 2005); or(c) at least one non-regulated person; and(d) their related and inter-related persons; (Source: Draft Primary Legislation – Solo and Group requirements)

Page | 21

Financial conglomerate means an insurance group that includes -(a) At least one person subject to registration under this Act; and(b) At least one person subject to registration, licensing or approval under The laws, other than this Act, referred to in the definition of ―financial institution‖ in section 1 of the Financial Institutions (Protection of Funds) Act, 2001 (Act 28 of 2001),(ii) The Banks Act, 1990 (Act No. 94 of 1990), the Mutual Banks Act, 1993 (Act No. 124 of 1993) or the Co-operative Banks Act, 2007 (Act No. 40 of 2007); or (iii) The National Credit Act, 2005 (Act No. 34 of 2005); or(c) At least one person that issues a financial product as defined in the Financial Advisory and Intermediary Services Act, 2002 (Act No. 37 of 2002) or furnishes advise or renders intermediary services in respect of a financial product as defined in the Financial Advisory and Intermediary Services Act, 2002, and the issuing of that financial product is not subject to registration, licensing or approval under any Act of Parliament; and (d) Their related and inter-related persons. (Source: Final Position Paper 27)

Financial conglomerate means an insurance group that includes at least one person subject to registration, licensing or approval under— (a) the laws, other than this Act, referred to in the definition of "financial institution" in section 1 of the Financial Institutions (Protection of Funds) Act;(b) the Banks Act, 1990 (Act No. 94 of 1990), the Mutual Banks Act, 1993 (Act No. 124 of 1993) or the Co-operative Banks Act, 2007 (Act No. 40 of 2007); or (c) the National Credit Act, 2005 (Act No. 34 of 2005) (Source: Draft Insurance Bill issued May 2015)

Financial conglomerate means an insurance group that includes—(a) at least one person subject to registration under this Act; and(b) at least one person subject to registration, licensing or approval under—(i) the laws, other than this Act, referred to in the definition of‗ ‗financial institution‘‘ in section 1 of the Financial Institutions(Protection of Funds) Act, 2001 (Act No. 28 of 2001);(ii) the Banks Act, 1990 (Act No. 94 of 1990), the Mutual Banks Act, 1993 (Act No. 124 of 1993) or the Co-operative Banks Act, 2007 (Act No. 40 of 2007); or(iii) the National Credit Act, 2005 (Act No. 34 of 2005); or(c) at least one person that provides a financial product as defined in the Financial Advisory and Intermediary Services Act, 2002 (Act No. 37of 2002), and the activity of providing that financial product is not subject to registration, licensing or approval under another Act of Parliament; and(d) their related and inter-related persons; (Source: Draft ILAB version 2 - Life)

Financial conglomerate means an insurance group that includes—(a) at least one person subject to registration under this Act; and(b) at least one person subject to registration, licensing or approval under—(i) the laws, other than this Act, referred to in the definition of ‗financial institution‘ in section 1 of the Financial Institutions(Protection of Funds) Act, 2001 (Act No. 28 of 2001);(ii) the Banks Act, 1990 (Act No. 94 of 1990), the Mutual Banks Act, 1993 (Act No. 124 of 1993), or the Co-operative Banks Act, 2007 (Act No. 40 of 2007); or(iii) the National Credit Act, 2005 (Act No. 34 of 2005); or(c) at least one person that provides a financial product as defined in the Financial Advisory and Intermediary Services Act, 2002 (Act No. 37of 2002), and the activity of providing that financial product is not subject to registration, licensing or approval under another Act of Parliament; and(d) their related and inter-related persons; (Source: Draft ILAB version 2 - Non-Life)

Financial crime means each of the following:(a) an offence in terms of a financial sector law; (b) an offence in connection with the provision of a financial product or a financial service; (c) an offence related to the handling of the proceeds of crime; (d) an offence in terms of the Financial Intelligence Centre Act; (Source: Draft Twin Peaks Bill version 2)

Financial crisis means a crisis in the financial system caused by a systemic risk, weakness or disruption in the financial system; (Source: Draft Twin Peaks Bill)

Financial customer means a person to or for whom a financial product or a financial service is offered or provided, irrespective of the capacity in which the person is offered or receives the product or service, and includes the– (a) successor in title of the person; and (b) beneficiary of the product or service; (Source: Draft Twin Peaks Bill version 2)