Critical Perspectives on Accounting 17 (2006) 989–1005 Social investment: Subjectivism, sublation and the moral elevation of success Matthew Haigh University of Amsterdam Business School, University of Amsterdam, Roetersstraat 11, 1018GW Amsterdam, The Netherlands Received 1 June 2004; received in revised form 1 May 2005; accepted 1 August 2005 Abstract Investment products that deploy ethical values and social considerations in portfolio construction have persisted since the 1980s. Pitting Habermasian discourse ethics against Foucauldian power relations and radical institutionalism, the paper argues that socially directed mutual funds ascribe capital markets with validities of high moral magnitude, work up extant tendencies toward financial hegemony and stymie criticism of the political–economic order. Institutional pressures do not permit the exercise of an ethic stronger than an aesthetic care of the self. The balance struck between economic and social priorities is investigated by interviewing investment managers, reviewing archival material and surveying the attitudes of unit holders in retail social mutual funds. © 2005 Elsevier Ltd. All rights reserved. Keywords: Foucault; Habermas; Capital markets; Ethics; Mutual funds; Non-governmental organizations; Share- holder activism Investment managers claiming to deploy social considerations in mutual fund portfolios describe their practices variously as ‘ethical’, ‘green’, ‘mission-directed’, ‘sustainable’ and ‘socially responsible’. It is as convenient to use the term social funds. Social funds claim four objectives: to reform corporate behaviour by influencing corporations’ cost of capital, thus affecting their capital expenditure plans; to outperform mainstream investments by pre-empting the pricing of economic externalities (Abelson, 2002Abelson, 2002, p. 159) 1 ; E-mail address: [email protected]. 1 Abelson defines economic externalities as “any positive (beneficial) or negative (harmful) effect that market exchanges have on firms or individuals who do not participate directly in those exchanges”. Although social funds 1045-2354/$ – see front matter © 2005 Elsevier Ltd. All rights reserved. doi:10.1016/j.cpa.2005.08.012

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Critical Perspectives on Accounting 17 (2006) 989–1005

Social investment: Subjectivism, sublationand the moral elevation of success

Matthew HaighUniversity of Amsterdam Business School, University of Amsterdam, Roetersstraat 11,

1018GW Amsterdam, The Netherlands

Received 1 June 2004; received in revised form 1 May 2005; accepted 1 August 2005

Abstract

Investment products that deploy ethical values and social considerations in portfolio constructionhave persisted since the 1980s. Pitting Habermasian discourse ethics against Foucauldian powerrelations and radical institutionalism, the paper argues that socially directed mutual funds ascribecapital markets with validities of high moral magnitude, work up extant tendencies toward financialhegemony and stymie criticism of the political–economic order. Institutional pressures do not permitthe exercise of an ethic stronger than an aesthetic care of the self. The balance struck between economicand social priorities is investigated by interviewing investment managers, reviewing archival materialand surveying the attitudes of unit holders in retail social mutual funds.© 2005 Elsevier Ltd. All rights reserved.

Keywords: Foucault; Habermas; Capital markets; Ethics; Mutual funds; Non-governmental organizations; Share-holder activism

Investment managers claiming to deploy social considerations in mutual fund portfoliosdescribe their practices variously as ‘ethical’, ‘green’, ‘mission-directed’, ‘sustainable’ and‘socially responsible’. It is as convenient to use the term social funds. Social funds claimfour objectives: to reform corporate behaviour by influencing corporations’ cost of capital,thus affecting their capital expenditure plans; to outperform mainstream investments bypre-empting the pricing of economic externalities (Abelson, 2002Abelson, 2002, p. 159)1;

E-mail address: [email protected] Abelson defines economic externalities as “any positive (beneficial) or negative (harmful) effect that market

exchanges have on firms or individuals who do not participate directly in those exchanges”. Although social funds

1045-2354/$ – see front matter © 2005 Elsevier Ltd. All rights reserved.doi:10.1016/j.cpa.2005.08.012

990 M. Haigh / Critical Perspectives on Accounting 17 (2006) 989–1005

to supply evidence that practitioners can use to lobby for self-regulation; and, loudest of all,to provide a mechanism by which unit holders can connect financial objectives with moralprinciples (Haigh and Hazelton, 2004).

The latter objective demands an examination of the methods by which these mutualfunds select and apply social considerations, and in particular on the influence of institutionalpressures. The contribution of this paper is its investigation of moral and practical challengesencountered in this style of managed investment.

The paper divides into five sections. Section 1 outlines relevant literature and the distin-guishing characteristics of social funds. An ‘ideal’ social investment portfolio is described.Section 2, using radical institutional theory and Foucauldian power relations, argues thatsocial funds collectively prop up the political–economic status of financial institutions.

Section 3 examines institutional pressures that constrain the meaningful applicationof ethics in equity investment portfolios. The interplay between economic and socialconsiderations is investigated by analysing the discourses of social funds. Three discur-sive sources are used: semi-structured interviews with managers of selected Australiansocial funds, a survey of unit holders and interested consumers in North American,European and Australasian markets, and archival marketing material appearing in thosemarkets.

Section 4 identifies meta-ethical positions from which managers of social funds wouldselect and apply social considerations. The paper offers an alternate account of practicalmoral reasoning that, while impartial on ethical content, would require managers to justifyinvestment decisions on moral grounds. When prevailing institutional forces are considered,however, the model appears infeasible. Finally, Section 5 considers if social funds, despitetheir manifest inabilities to adopt strong forms of ethics, might be valuable to unit holdersfrom a subjectivist perspective.

1. Social investment research and practice

Empirical studies comparing the economic performance of social and mainstream mutualfunds dominate the literature on social investment. These studies find the economic perfor-mance, management styles and portfolio stocks of mainstream and social mutual funds to besimilar (Bauer et al., in press).2 Others examine methodological issues relating to portfolioconstruction (Kreander, 2001; Perks et al., 1992; Rockness and Williams, 1988). Althoughsome writers question the methods used by social funds to assess corporations (Schwartz,2003), the influence of institutional pressures on managers of social funds remains largelyunexamined. The unannounced launches of social investment products by most mainstreaminvestment banks over the period 1999–2003 would imply that communitarian frameworksas suggested by Kapur (1999) and Mackenzie (1997) do not inform current practice.

cannot predict that governments will recognise and price economic externalities, the claim is that investors standto reap an eventual benefit.

2 The results of these studies would suggest that social mutual funds investing in equities are an attractiveeconomic prospect, at least compared to other investments thought appropriate for social investors, such as ‘style-neutral’ government bonds and money market funds.

M. Haigh / Critical Perspectives on Accounting 17 (2006) 989–1005 991

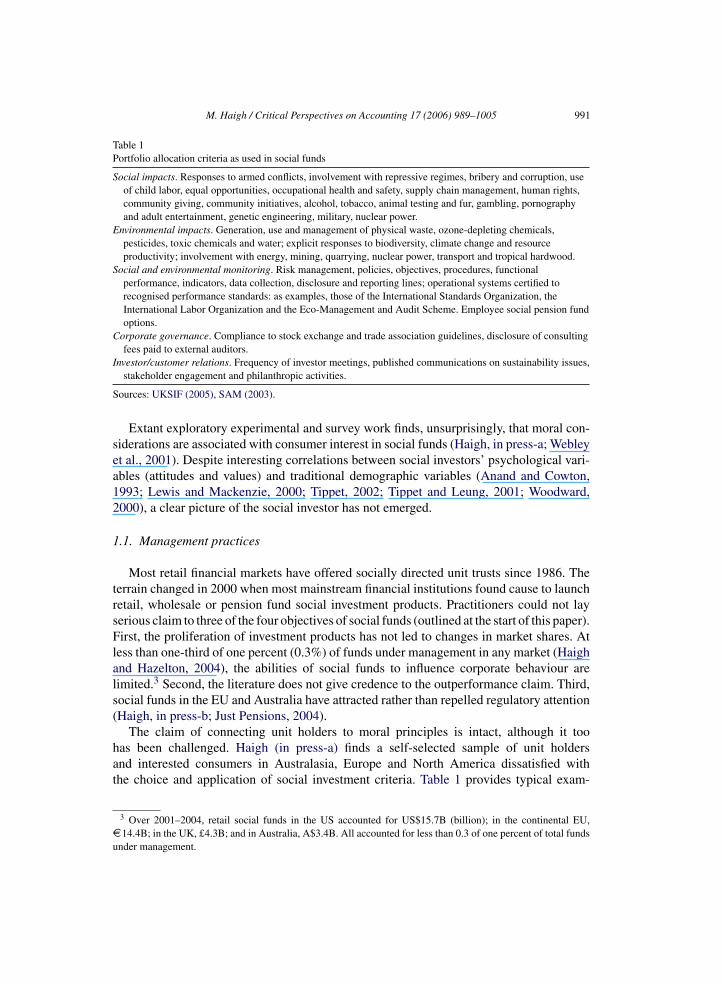

Table 1Portfolio allocation criteria as used in social funds

Social impacts. Responses to armed conflicts, involvement with repressive regimes, bribery and corruption, useof child labor, equal opportunities, occupational health and safety, supply chain management, human rights,community giving, community initiatives, alcohol, tobacco, animal testing and fur, gambling, pornographyand adult entertainment, genetic engineering, military, nuclear power.

Environmental impacts. Generation, use and management of physical waste, ozone-depleting chemicals,pesticides, toxic chemicals and water; explicit responses to biodiversity, climate change and resourceproductivity; involvement with energy, mining, quarrying, nuclear power, transport and tropical hardwood.

Social and environmental monitoring. Risk management, policies, objectives, procedures, functionalperformance, indicators, data collection, disclosure and reporting lines; operational systems certified torecognised performance standards: as examples, those of the International Standards Organization, theInternational Labor Organization and the Eco-Management and Audit Scheme. Employee social pension fundoptions.

Corporate governance. Compliance to stock exchange and trade association guidelines, disclosure of consultingfees paid to external auditors.

Investor/customer relations. Frequency of investor meetings, published communications on sustainability issues,stakeholder engagement and philanthropic activities.

Sources: UKSIF (2005), SAM (2003).

Extant exploratory experimental and survey work finds, unsurprisingly, that moral con-siderations are associated with consumer interest in social funds (Haigh, in press-a; Webleyet al., 2001). Despite interesting correlations between social investors’ psychological vari-ables (attitudes and values) and traditional demographic variables (Anand and Cowton,1993; Lewis and Mackenzie, 2000; Tippet, 2002; Tippet and Leung, 2001; Woodward,2000), a clear picture of the social investor has not emerged.

1.1. Management practices

Most retail financial markets have offered socially directed unit trusts since 1986. Theterrain changed in 2000 when most mainstream financial institutions found cause to launchretail, wholesale or pension fund social investment products. Practitioners could not layserious claim to three of the four objectives of social funds (outlined at the start of this paper).First, the proliferation of investment products has not led to changes in market shares. Atless than one-third of one percent (0.3%) of funds under management in any market (Haighand Hazelton, 2004), the abilities of social funds to influence corporate behaviour arelimited.3 Second, the literature does not give credence to the outperformance claim. Third,social funds in the EU and Australia have attracted rather than repelled regulatory attention(Haigh, in press-b; Just Pensions, 2004).

The claim of connecting unit holders to moral principles is intact, although it toohas been challenged. Haigh (in press-a) finds a self-selected sample of unit holdersand interested consumers in Australasia, Europe and North America dissatisfied withthe choice and application of social investment criteria. Table 1 provides typical exam-

3 Over 2001–2004, retail social funds in the US accounted for US$15.7B (billion); in the continental EU,D 14.4B; in the UK, £4.3B; and in Australia, A$3.4B. All accounted for less than 0.3 of one percent of total fundsunder management.

992 M. Haigh / Critical Perspectives on Accounting 17 (2006) 989–1005

ples of social investment criteria. The material is drawn from European and Australiansources.

Social funds use any or all of the material in Table 1. One can see that most of the listeditems relate to matters of community welfare, labour relations and ecological sustainability(Norton and Toman, 1997). Negative screening refers to a policy of avoiding stocks thatfall short on such criteria (light green). Positive screening refers to a policy of seeking outcorporations seen as leaders in terms of their ‘social performance’ (dark green). Best-of-sector and social overlay are variants of the latter in that they would allow investment inall industrial sectors. In addition to passive investment portfolios, some managers consultwith invested corporations and certain activist non-governmental organizations in areasin which they seek improvements. On occasion, managers have exercised (most often,threatened to exercise) their proxy voting rights to bring issues of concern to the attentionof boards.

The choice of such investment criteria depends on clients and founding members. UsingTable 1 as a guide, a manager would construct an ideal positive investment screen byseeking investments in corporations that might generate positive economic externalities(example, a mining corporation involved in developing renewable energy sources). Ideally,invested corporations would identify and consult relevant stakeholders as they address risksrelating to ecologies, communities, governmental regulations, business plans and corporatereputation. Corporations would disclose incentive payments and political contributions;employ ‘integrated’ risk management systems,4 link managers’ remuneration to risk-basedinitiatives, and adopt policies which promote fair hiring, fair promotion, high retention rates,flexible working arrangements and that recognise employees as capital. Such characteristicswould extend to subsidiaries, partly owned entities, suppliers, sub-contractors and businesscustomers. All such matters would be disclosed in investor communications and Internetcorporate websites.

A negative investment screen, in its ideal, would list industrial sectors thought to generatenegative economic externalities and prevent investments in corporations not conforming tothe criteria listed above.

In practice, managers of social funds are more prosaic. The best-of-sector index-huggingapproach is popular, as is using simple investment screens that exclude a few indus-tries. Most screens do not extend to subsidiaries and suppliers of invested corporations.Claims that portfolios are designed according to social investment screens are hard tojustify. Haigh (working paper) compares the 2003–2004 portfolios of a sample of Aus-tralian social funds with mainstream counterparts, noting close similarities and breachesof social funds’ negative investment screens. Moreover, information disclosures emanatingfrom social funds are generally poor in quality and not verified externally. Recent EU andAustralian laws mandating social reports from investment managers have been met withlacklustre responses, with few attempts to present audited information (Haigh, in press-b;Just Pensions, 2004).

4 Relevant criteria would differ between industries. In the resources sector, for example, ecological managementindicators would include monitoring greenhouse gas emissions according to protocol standards, monitoring wastegeneration, measuring biodiversity impacts from site rehabilitation and auditing tailing dams. Indirect indicatorswould include certifying to ISO 14001, EMAS and other schemes.

M. Haigh / Critical Perspectives on Accounting 17 (2006) 989–1005 993

2. Financial hegemony

This section argues that social funds constrain the objectives of non-governmental orga-nizations (NGOs) and legitimise those of capitalist institutions. The effect is likely to beunintentional, given the motivations of investment managers to maximise the economicperformance of their products, but nonetheless real. The constraining effect arises from thenature of power relations between financial institutions and social activist organizations(which on occasion advise social funds on asset allocation and other matters). Foucaultargues that power dominates by seeking resistance: “there are no relations of power withoutresistances . . . like power, resistance can be integrated in global strategies [of domination]”(Foucault, 1980Foucault, 1980, p. 142). The insight of Foucault central to this section isthat power-wielding ideologies are effective because they infiltrate social resistance.

Most of Foucault’s critics (there are many) gloss his work on institutional and interper-sonal relations (Armstrong, 1994; Neimark, 1994; others in Hoy, 1986, p. 7). Foucault usesextrinsic/intrinsic and explicit/implicit distinctions to explain how relations form and areconstituted. ‘Micro-power’ works at an implicit level by disguising itself as a form of domi-nation (Hoy, 2004, p. 76).5 Micro-power operates at two levels in social funds. This sectionaddresses micro-power at the level of managers and NGOs. The next section addresses theeffects of micro-power on the personal ethics of unit holders.

Social funds and NGOs can claim some common origins and, often, reciprocal member-ship. Collaborating would offer potential advantages to each. Investment managers oftenseek the advice of NGOs on portfolio allocation and shareholder actions.6 Some managerswhose governance policies extend to mounting extraordinary voting resolutions in investedcorporations have thought it necessary to form collaborations with NGOs such as Friends ofthe Earth (see, FOE, 2005). The US-based Calvert, the largest and most diverse social fund,usually withdraws resolutions after gaining access to management (Calvert, 2003). TheCalifornia Public Employees’ Retirement System, managing US$153 billion in December2003, also reports numerous voting resolutions.7

The 2002 conference of Australia’s Ethical Investment Association presented a rep-resentative of Friends of the Earth USA as a keynote speaker and hosted a panel dis-cussion between ecologist NGOs and managers of mutual funds. Such meetings have on

5 Foucault explains the familiar sovereign power of juridicial systems as extrinsically disseminated explicitpower. An intrinsic dimension operates by infiltrating public consciousness.

6 Shareholder activism colloquially describes the exercise of voting rights that attach to securities held byminority institutional and private shareholders. Extraordinary voting actions would describe the actions of minorityshareholders to requisition members to meet and vote on resolutions drafted by requisitioners. Routine votingactions relate to matters scheduled in regular corporation meetings of members. The broad objectives of shareholderactivists are described by a proponent (Viederman, 2005): “Shareholder activity is an effort on the part of . . .

shareholders to change the policies and/or the behavior of companies through a variety of means, includingmeetings with corporate officials, letter writing, proxy voting, co-filing of shareholder resolutions initiated byothers, and/or initiating a shareholder resolution. Initiation of a resolution is usually the end of an unsuccessfuleffort to obtain satisfaction from the corporation on issues raised through meetings and letter writing.”

7 Other advocates of voting actions are Innovest, based in New York City, and Friends Provident and Hermes,both based in the UK. The UK Pension Investment Research Consultants lobbies trustees to exercise their proxyvoting rights. Minority resolutions in Australia, to date, are limited to a few individuals and The WildernessSociety.

994 M. Haigh / Critical Perspectives on Accounting 17 (2006) 989–1005

occasion produced new NGOs. Examples are the Coalition for Environmentally Respon-sible Economies, the Interfaith Center on Corporate Responsibility and the ShareholderAction Network. The objectives of such groups are summarised by the following quotation:

A project of the Social Investment Forum and Co-op America, we seek to link insti-tutional investors and financial advisors with faith-based groups, and social justice,labour, and environmental organizations to encourage greater corporate responsibility.(Shareholder Action Network, 2005)

2.1. The drafting of NGOs into the operations of financial markets

Arguing the merits of ecological sustainability by co-opting scientific methods and eco-nomic parlance earns the admiration of Habermas (1981) and Foucault (1997, p. 275). Bothconsider organizations such as Friends of the Earth to represent a special case of effectiveresistance, important for creating social networks. Foucault did not witness their re-co-optation. By inverting the language of the ecological movement, financial institutions asserttheir political credentials and curtail the force of social activism.

Practitioners would no doubt protest. Of the tactics of power, Foucault states: “the logicis perfectly clear, the aims decipherable and yet it is often the case that no one is there to haveinvented them” (1978, p. 95). In relations between NGOs and mutual funds, outcomes arealways going to favour the objectives of capital investors (Honneth, 1991, p. 156). Radicalinstitutional theory provides three accounts of how this might happen. Radical institutional-ism explains how a dominant institution inculcates its values in other institutions that it seeksto control. Dugger (1989), who describes the colonising effect of the corporate form on suchas universities, families and public healthcare, develops radical institutional theory in termsof four processes: emulation, contamination, subordination and mystification. In terms ofthe claim of co-optation made above, contamination, subordination and mystification arerelevant.

(i) Contamination replaces one set of meanings and motives in one institutional spherewith those originating in another sphere (Dugger, 1989, p. 144). By using social con-siderations as investment criteria, social funds contaminate the objectives of NGOs. Bydesign or not, when managers consult NGOs on portfolio policy and voting positions,issues of common interest will narrow to those which can be expressed in the discourseof capital investment.

Mintz and Schwartz (1990) examine capital markets’ dominating power over indus-trial corporations. In the signatory sense they describe (pp. 203–226), social fundsact as a type of ideological intermediary by according economic utility to resistancemovements. Issues such as repression of communities and the systemic destructionof large parts of ecological systems (if not entire: global warming), would be diffi-cult for social funds to translate into value propositions, and on most occasions areoverlooked.

(ii) Subordination describes processes whereby a dominant institution consolidates itsposition by linking to it the objectives of weakened institutions (Dugger, 1989, p.140). In NGO-social fund relations, subordination would describe the relegation ofNGOs’ objectives and the privileging of those of social funds. Social considerations

M. Haigh / Critical Perspectives on Accounting 17 (2006) 989–1005 995

accepted as valid are destined to operate within the “machinery of the establishedorder” (Marcuse, in Held, 1980, p. 161) and be subordinated to purposes that servecapital.

Contemporary societies interpolate and coordinate power using three controllingtechniques (Foucault, 1977, p. 68). Social funds exhibit them all. The declarativedistinction between social and mainstream investment, the market insignificance ofsocial funds, and the uncontested presentation of financial markets as a proper placefor social protest, all promote the capacity of the capital apparatus to control forcesthat might oppose it.

(iii) Mystification refers to processes by which a dominant organization or form of organiza-tion manipulates others by enlisting their support (Dugger, 1989, p. 46). Mystificationcoheres with Foucault’s account of micro-power. As investment managers turn to con-sider, as examples, matters of human rights and renewable energy, NGOs assist byfinding innovative ways to add economic value to investment portfolios. The disablingeffects of mystification echo Butler’s use of the psychoanalytic term foreclosure, a con-dition which refers to the predicament of a subjugated individual, such as a prisoner,who seeks her own subjection (Hoy, 2004, p. 97).

By contamination, subordination and mystification, social funds “solidify, intensify, opti-mise and incorporate” (Foucault, 1978, p. 42) the political–economic status of the fiscalorder. In Hegelian philosophy, to sublate is to supersede while retaining something of thenature of what is superseded. Social funds sublate ethics by valuing them instrumentally.Validities ascribed to economic success assume positions of high moral magnitude, dissentis ‘disciplined’ and transformed (Honneth, 1991, p. 166), and the choices of the best methodsto promote social welfare are implicitly delivered to capital markets. The outcome imputesthe expansion of capital with a ‘social imaginary’ (Laclau, 1990) which unfortunately leavesmost social problems unaddressed.

3. Balancing economic prudence with social considerations

This section examines social investment discourse to gauge priorities placed on eco-nomic and social considerations. The discourse was taken from three sources: interviewsof managers, marketing material and a survey of unit holders. The examination is followedby a reflection on implications for practised ethics.

The interviews were conducted in Sydney and Melbourne in October and Novemberof 2003. Thirteen practitioners were invited for interview; twelve accepted and anotherself-nominated. Interviewees included eight chief executive officers, principals and seniormanagers drawn from six social funds, which at the time of interview collectively rep-resented approximately 70 percent of the Australian social funds market. Remaininginterviewees were the principals of two financial planning practices, the principal of aninstitution that issued ‘green’ debentures to retail investors, an individual who investedin the stock market for the purpose of raising voting resolutions, and the chief policyofficer of an association representing Australian private sector pension funds. Four inter-viewees were female. The average duration of each interview was 90 minutes and most were

996 M. Haigh / Critical Perspectives on Accounting 17 (2006) 989–1005

tape-recorded in the head offices of represented organizations, confidentiality beingpromised as a condition of interview.8

Archival marketing material was taken from prospectuses and Internet websites of 19Australian, North American and UK social funds, and from the Internet websites of threesocial investment clubs in Asia, the US and the UK. Prospectuses examined were issued in2003 and 2004 by pioneer social funds (circa 1986) and mainstream investment banks. Pro-prietary sources are not named. The investment clubs are named below where appropriate.

As expected, managers accorded priorities to economic considerations. One interviewee,a company secretary, reflected on pressures to meet financial targets:

“At the end of the day we are a mainstream fund manager, competing against othermainstream funds.”

In the same interview, the fund’s chief executive officer underlined the operating focus:

“We live and die by our investment returns . . . I would assess that ten percent ofour unit holders are here because of the SRI overlay. SRI is a nice addition but is ofsecondary importance because we are at the light green end of the spectrum with ournegative screen.” (emphasis added)

The general manager of a ‘dark green’ fund deemed that to survive in an economicallycompetitive market, social funds needed to

“. . . soften the edges of rigid ethical stances. They have to go out and demonstrate ahard, sound quality investment rationale or you will never get past the asset consultantsand researchers out there.”9

The shareholder activist interviewed for this paper had gained access to senior manage-ment in a number of Australian corporations engaged in forestry operations. Avoidinga confrontational approach, she advocated a “business case model based on educatingmanagement” of economic and public relations benefits generated by improving wastemanagement and developing alternate markets.

The archival material (websites and prospectuses) echoed the economically instrumentalimportance of social considerations.

“The objective . . . is to incorporate investors’ values into their long-term investmentobjectives without compromising investment returns.”

“A careful consideration of environmental and social factors adds value to existingfinancial analysis.” (ASRIA, 2005)

“Responding to social concerns should not only avoid the liability that may be incurredwhen a product or service is determined to have a negative social impact . . . but . . .

better position [a corporation] to develop opportunities . . .”

8 Notes, tape recordings and a copy of the general form of the questions asked are available on request from theauthor.

9 On reflection, interviewees’ responses were probably tainted. For various reasons, it is thought that intervieweesimagined the interviewer would be impressed with economic performance.

M. Haigh / Critical Perspectives on Accounting 17 (2006) 989–1005 997

“By screening companies . . . by standards of social responsibility, [the manager]challenges companies to reach for a higher ‘bottom line’ and offers investors theopportunity to do good while doing well.”

Unit holders were repeatedly reminded of the economic benefits that could be expectedfrom government-assisted market pricing of negative and positive economic externalities.

“The best long term, stable returns will come from the support of sustainable busi-nesses [because] society will require business to meet the full ecological costs ofproduction and will . . . pay for those goods . . . which have lower ecological costs.”

“Long term rewards will come from those organizations whose products, servicesand methods enhance the human condition and the traditional American values ofindividual initiative, equality of opportunity and cooperative effort.”

Guarantees of eventual economic outperformance were described in general terms.

“Companies taking a lead in [sustainable] development will gain a competitive edgeand outperform their industry peers . . . The best long term, stable returns will comefrom the support of sustainable businesses because society will require business tomeet the full ecological costs of production and will pay for those goods which havelower ecological costs.”

“Relative outperformance comes from investing in quality companies [that] will bere-rated to their true valuation at a later date.”

“Reducing negative externalities are seen as consistent with long term profit maximi-sation . . . environmental efficiency attracts a return premium.”

An interview with a manager of a US social fund appeared on the Internet website of SRIWorld Group (2004). An opinion given in the interview summarises the material above:

“Corporate governance reform is a secondary objective, a means of achieving theprimary objective . . . to earn money for its investors.”

The importance of normative concerns to social investors is already known (Webley et al.,2001) as is their reluctance to direct more than a small portion of their discretionary wealthto social funds (Lewis and Mackenzie, 2000). However, some recent evidence suggeststhat unit holders would not prioritise economic and social considerations any differentlyto the statements given above. An Internet questionnaire conducted by Haigh (in press-a)examined the relative pull of economic and social considerations in retail social funds.The survey attracted approximately 400 respondents from North America, Australasia andEurope. As expected, most respondents accorded high priority to economic performance.One in two respondents had considered social funds but not invested due, in part, to socialfunds’ mixed economic performance.

Respondents who had invested in social funds held most of their discretionary wealth inmainstream investments. However, this group sought to reflect their ethical values in theirinvestment choices. Typical responses to a question on motivations to invest were:

998 M. Haigh / Critical Perspectives on Accounting 17 (2006) 989–1005

“[I prefer] to invest in individual companies that reflect my values, rather than investin managed funds that have a lowest common denominator ethical rating.”

“It’s difficult to find a fund that applies the same screen that I would like.”

“Ethical Funds offer a ‘like it or leave it’ choice. I screen the companies I invest inmyself.”

3.1. The possibilities of ethics in social funds

The material given above provides some evidence that unit holders expect social fundmanagers to carefully choose, apply and report social considerations.10 Such expectationscollectively present a problem to managers accustomed to assuring clients that social fundsneed not mean that economic performance will be compromised.

Institutional pressures impoverish the other-directedness that social funds might practicein three ways. One, possibilities for free-willed debate are negated when ethics are restrictedto those that reify the institution of investing. Debate between affected parties forms thecornerstone of most recognised moral decision-making models. In practice, debate is oftenthe first casualty. Habermas (1990) recognises the danger when distinguishing betweenstrategic and communicative actions:

“(I)n strategic action one actor seeks to influence the behaviour of another by means ofthe threat of sanctions or the prospect of gratification in order to cause the interactionto continue as the first actor desires.” (Habermas, 1990, p. 58, original emphasis)

The absence of argumentation in social funds is typical of strategic action. Managers donot make it a rule to debate with clients and corporations how they should select and applysocial considerations. Any suggestion from a client is accepted providing it is economicallyfeasible and within the law.

Two, by conflating finance capital with social responsibilities, social funds present thepursuit of economic return on capital as a universal interest. Such an instrumentalist con-struction of social responsibility excludes all those who for one reason or another do notown property. Disguising fractional interests as universal reflects the dominance of ideologymore than it recognises normative obligations.

Three, a commitment to generating economic wealth effectively restricts managers’strongest ethic to upholding fiduciary obligations. The virtue of self-interest cannot becountenanced as representing a plausible model of ethics. The possibilities of ethics (andreligions and social protest) erode when they are bracketed within structures that makepossible commodity production, as ethics are converted into matters of discretion.

4. A meta-ethical critique

This section examines the struggle between economic and other-directed moral prin-ciples, as introduced in the previous section, by identifying the meta-ethical positions of

10 As expected, statistically significant associations appeared between respondents’ purchase/hold intentions andtheir attitudes towards managers’ investment methods (Haigh, in press-a).

M. Haigh / Critical Perspectives on Accounting 17 (2006) 989–1005 999

managers of social funds. Meta-ethics describes the assumptions a moral actor would rely onto determine the acceptability of moral norms (Williams, 1985, p. 73). Different meta-ethicalstances would suggest different approaches to choosing and applying investment criteria,which in turn would lead to different portfolio decisions. Managers’ meta-ethical positionsare gauged from the interviews and archival marketing material described in the previoussection. Section 4.1 considers the possibilities for an alternate meta-ethical position.

Social funds are yet to articulate the normative bases of their choice of investment cri-teria, and where relevant, their voting actions. Mackenzie (1997), grappling to identify themoral principles used in a UK social fund, refers to ‘deliberative’ and ‘investor-led’ socialfunds. The former refer to the ethical values or articulated social missions of founding orga-nizations. Most social funds are ‘investor-led’ in that their investment criteria are informedby members’ suggestions. The meta-ethical stances of investor-led social funds are thoughtto be egoism and subjectivism. Egoism is likely to direct the use of subjectively chosennon-economic investment criteria: the following justifies the argument.

4.1. Egoism

An egoist stance describes an approach to ethics motivated by arbitrary self-interest.Its doctrine holds that all human actions when properly understood are, and should be,motivated by selfish desires (Feinberg, 1995, p. 70). A counter-example is the observedwillingness of some human beings to sacrifice their selfish concerns to live in accordancewith other-directed moral principles. The egoist’s response would be that prudence moti-vated these individuals (Mackie, 1977, p. 190).11 Markets, competitors and peers remindmanagers that prudence is the dominant ethical value. What are morally relevant, Rawlsreminds us, are gains and losses made on types of interests such as wealth and prestige(Reed, 1999, p. 464).

As an egoist cannot prove that providing for private desires is more objectively desirablethan doing the same for others, an egoist’s moral norms will always be subjective (Mackie,1977, p. 143).

4.2. Subjectivism

Ethical subjectivists would maintain that the feeling or emotion one has towards anyaction is sufficient to judge its rightness or wrongness. A statement such as ‘It is wrong toinvest in industries of type XYZ’ would be viewed as an expression of moral intuition morethan as a statement supplied by moral reason. Radical subjectivism, also known as decision-ism, expresses a belief that any normative position is impossible. In radical subjectivist mod-els, “[w]hat is important is that one simply decide, since the normative basis of the decisioncan only be arbitrary” (Wolin, 1985, p. 75, original emphasis). Moral debate is meaninglessas only private individual preferences can adjudicate between competing values.

The discourse of social investment suggests a radical subjectivist ethic. The findings ofthe interviews conducted for this paper support Schwartz, who concludes that investment

11 Prudence, or enlightened self-interest, refers to a doctrine that the welfare of others is best promoted bypreserving one’s own interests: ‘If you want X, do Y’.

1000 M. Haigh / Critical Perspectives on Accounting 17 (2006) 989–1005

“methods of social funds . . . reflect investors’ particular social, religious, or politicalattitudes or beliefs and nothing more” (2003, p. 212). In interviews, managers justifiedtheir use of social considerations by referring to religious principles, ad hoc suggestionsreceived from clients or to prevailing social norms. None believed it was his/her properrole to adjudicate on clients’ ethical values.

One interviewee, the principal of a social research firm engaged by several Australiansocial funds, was reluctant to define the ethics that social funds have adopted or should adopt:“You tell me what ethical is. Ethical means something different to everybody.” The EthicalInvestment Association (2002), subscribed to by most Australian social fund managers andby many Australian financial planners, states in a government submission that it “has noposition on what ethics should be or what issues should be considered ethical . . . the marketwill drive the scope and nature of ethical considerations”.

Managers do not apprise investors of the meta-ethical bases by which they choose invest-ment criteria. Prospectuses list negative and positive screens as another piece of informationfor consideration alongside management expense ratios and other economic information.The meta-ethical basis that would allow a fund manager to assess the ‘social performance’of another organization is overlooked.

The 2004 prospectus of one social fund baldly stated the basis of its investment approach.

ANALYTICAL APPROACH AND ETHICAL POLICY. In simple terms, research isdirected at discovering ‘good’ shares in ‘good’ companies which own ‘good’ busi-nesses.

Another prospectus explicitly denied the manager’s ability to adjudicate on ethical valuesand moral principles.

INVESTMENT APPROACH. [The manager] will assess potential investments basedon their potential environmental impact, social benefit, ethical considerations or labourstandards to the extent that they are consistent with our . . . values. We do not havea predetermined view about what constitutes these factors or impose predeterminedscreens or weightings to these factors. We also do not set fixed levels for holdings ofparticular investments based on these criteria.

4.3. Implications

The discursive examples given above reveal a common belief that a subjectivist approachis a sufficient basis from which to select one’s ethical values and make moral decisions.The assumption emerges as much in what is not said; managers will not dispute an ethicalvalue or moral principle for fear of losing a client’s account. In various forums, investmentorganizations have raised questions over the legality of such an approach, expressing doubtsthat an ad hoc investment policy would be legally sufficient to acquit managers’ fiduciaryresponsibilities. In the words of an interviewee working in a pension funds association:

“The process [portfolio construction] is reactionary, not coherent or systematic. Theprocess is based on fads, there’s no reasoning. And where’s the investment focus inthat too?”

M. Haigh / Critical Perspectives on Accounting 17 (2006) 989–1005 1001

The practical effect is that a subjectivist approach does not promote sound decision-making. Some examples illustrate. Several of the managers interviewed had issued prospec-tuses claiming they avoided investments in the tobacco industry. Those managers werequeried as to their investments in a certain large publicly listed Australian corporation thatsold packaging materials to tobacco manufacturers. None of the interviewees consideredthat a moral question arose. Questioned further, managers appealed to their clients’ con-cerns, claiming they would extend only to corporations ‘directly involved’ in producingtobacco products.12

Some managers did recognise their moral accountability. One social fund held its largestinvestment in November 2003 in a corporation whose primary product was soap. Ani-mal fats are used as a production material in most commercially available soap. The‘Ethical Policy’ attached to that fund’s 2003 and 2004 prospectuses stated that the man-ager would avoid investments in corporations seen as “harmful to people, animals or theenvironment [and] involved in activities such as . . . cruelty to animals”. The fund’s chiefexecutive officer was interviewed and asked what the term ‘involvement’ meant in practice.He replied:

“Effectively, a sort of a second derivative is acceptable. So for example, we have avery successful investment in a company that makes soap. So we sort of deem that tobe a bit of a second derivative.”

Questioned further, the officer admitted that this arbitrary choice did not justify thedecision on moral grounds, but that, pragmatically, he “had to draw the line somewhere”.

The lasting consequence of subjectivism, and perhaps providing reason for its adoptionin social funds, is that it disallows standards “by which one could possible judge one answerto be better than another” (Singer, 1994, p. 7). Consequently, prudence loads the ‘bottomline’, as it were, and dominates decision-making (Williams, 1972, p. 37).

4.4. Towards robust moral decision-making

If corporations are to be assessed using moral criteria, those who conduct such assess-ments are as equally assessable (Graham, 2001).13 To wit, moral responsibilities arise whenmanagers advertise that they use social considerations as investment criteria. Accordingly,an onus falls on managers to debate investment criteria with directly affected parties; namely,with clients and invested corporations.

Three characteristics of moral judgments might provide a reasonable foundation to judgethe acceptability of corporate actions (Reed, 1999). Adapted to suit social funds, managersshould be able to

12 Most interviewees admitted that they had not asked their clients if the particular investment would be of moralconcern.13 The moral realm applies to a collective entity (such as a mutual fund and corporation) on account of what it

does or on account of what happens to it. Graham’s concern is not with whether a collective entity can be heldmorally responsible for what it does – that status is generally accepted – but considers moral status on account ofactions brought on an entity.

1002 M. Haigh / Critical Perspectives on Accounting 17 (2006) 989–1005

(i) describe and justify the bases of normative obligations and judgments;(ii) clarify their responsibilities and those of their investments and clients;

(iii) establish and justify priority rules capable of resolving conflicting valid claims.

In a search for a mechanism that would empower social funds with such abilities, a neo-Kantian model is considered. The choice is made to accommodate investment managers’manifest aversion to deliberating on moral norms. A Kantian model would not stipulate,for example, how social funds should best answer matters of an applied nature (such asdetermining the permissible extent of investment in an industry listed in a negative invest-ment screen). Instead of stipulating ethical content and moral principles, Kantian modelscall attention to processes used to select and apply moral norms. What becomes at issue iswhether or not moral norms deserve to be recognised.

The model chosen for consideration here is Habermas’ discourse ethics. Habermasshares with the Kantian tradition a premise that ethical ideals differ to such an extentthat ethics cannot normatively recommend particular values at all, but can only providea specific procedure of conflict resolution. In Moral Consciousness and Communica-tive Action, Habermas (1990) assumes that individuals can reach advanced stages ofpractical reasoning by using processes of discursive argumentation, which, is argued,represent the best possible method for resolving moral questions (Habermas, 1990, p.144). Discourse ethics uses Kant’s injunction (1997, p. 31) that an action is permittedonly as far as all affected by the action would be willing for it to happen. AdvancingKant, discourse ethics presents argumentation as the single criterion for moral, principleddecision-making.

However, such arguments must follow some ground rules. Habermas describes threelevels of possible participation in argumentation: the speaker, the listener and the watcher(see, Kant, 1994, p. 12314). In an ‘ideal speech situation’, individuals adopt all three per-spectives. The model overcomes subjectivity by addressing and resolving conflict, whereeveryone’s interests are preserved without compromise (Habermas, 1990, p. 12), at leastin theory. It is an open question whether managers could operationalise discourse ethics orany reasonably sophisticated moral decision-making model. Habermas acknowledges thecontext-bound application of his model (1993, p. 14). In a competitive market environment,discursive rules of reversible position-taking and non-coercion would be almost impossibleto apply. In a legal environment where fiduciary interests are interpreted as financial benefits(Whincop, 2003), moral principles are destined to remain secondary.

In summary, a subjectivist approach to assessing investments on social grounds is highon rhetoric and low on maintenance, which would not be significant if there were no con-sequences. A subjectivist basis for decision making, set against prudence, threatens tocompromise the motivation for the decision (Mackie, 1977, p. 34). In the case of socialfunds, that motivation is, surely, a concern for the welfare of others. Social considerationsare informed by clients’ suggestions, media attention paid to matters of corporate malfea-sance and little else. Such ‘methods’ permit economic interests as the single value worthyof sustained commitment. Institutional pressures to demonstrate economically justifiableoutcomes reify that ethic.

14 Habermas sources the structure from the Kantian device of the ‘rational impartial observer’.

M. Haigh / Critical Perspectives on Accounting 17 (2006) 989–1005 1003

5. A subjectivist ethic

This paper does not deny the inventiveness of social funds. Compared to other forms ofsocial protest, the allocative power of finance capital lends productivity and organising force,at least in the abstract, to designing solutions to social problems. Without agreed methods ofarriving at common, basic moral principles, however, social investment is unlikely to offerany real alternative to the current economic and social order. The conundrum between eco-nomic and social considerations discussed above justifies a call for work on initiatives thatwould promote the meaningful exercise of social considerations in capital markets. Lobby-ing governments for structural changes, industry sectoral reviews (see, UKSIF, 2005) andmounting voting resolutions with parent and other institutions are examples of institutionalactions that might more successfully lead to observable social improvements.

When considering the claimed objectives of social investment, it is difficult to ignorethe cynicism of McGoun et al. (2003) and Roberts (2003) towards the uneasy marriageof institutional social activism and profitable business enterprise. Yet, the material abovesuggests that at least some managers and unit holders of social investment funds experiencefrustration that their funds do not exercise ethical values more strongly. In an institutionalsetting where the single universally binding norm is prudence, an aesthetically derivedmoral awareness might have some currency.

Nietzsche’s concept of ressentiment refers to “a resentment of oneself that arises becauseone is not powerful enough . . . to generate one’s own values” (Hoy, 2004, p. 3). Foucault isthinking of this when he describes individuals’ capacities to exercise ethical relations withthemselves. Drawing from the aesthetics of the Stoics, Foucault’s reading of ressentiment isan individual’s search for a meaningful life in contemporary materialist societies (Foucault,1997, p. 282).

The social investors in Haighin (press-a) and Webley et al. (2001) had directed the bulk oftheir discretionary assets to mainstream investments. Even so, respondents’ attitudes, com-ments and the fact that they had self-selected for the studies all indicate that they consideredsocial funds important. ‘Connecting’ personal moral principles and financial objectivesappears an aesthetic one, in the sense of a proper relation to oneself and one’s capacities(Patton, 1994). Even respondents who had considered but not purchased social funds valuedsocial investment for allowing them to link their awareness of the need to consider socialwelfare when making economic decisions. Knowing that managers used social considera-tions to select portfolio stocks had become significant in itself (ressentiment), independentof personal investment decisions. Some responses in Haigh (press-a) illustrate this attitude.

“[Social funds] bring an added ‘moral’ dividend.”

“I wanted peace of mind. I am passionate on environmental issues. . . . Socially respon-sible investing is simply the right thing to do.”

“We need to try to educate more [financial intermediaries] . . . to realize that investorscan care about our environment . . .”

From this lens, it would be of little moral significance to social investors if social funds donot defend their methods and voting policies. For social investors, what becomes morally sig-

1004 M. Haigh / Critical Perspectives on Accounting 17 (2006) 989–1005

nificant is the opportunity to express ethical values and ‘be ethical’ (Cordwell, 2004). Socialfunds then become significant for promoting a weak, ascetic “ethical self-transformation”(Osborne, 1999, p. 52) in which self-interest appears other-directed.

Acknowledgements

The author appreciates the constructive comments of anonymous reviewers and thesubmissions editor of this journal, helpful comments of discussants and participants atthe Critical Perspectives on Accounting 2005 Conference, City University of New York,and comments of participants at the Australian Centre for Continental Philosophy 2004Conference, Macquarie University.

References

Abelson P. Lectures in public economics. 4th ed. Sydney: Applied Economics; 2002.Anand P, Cowton CJ. The ethical investor: dimensions of investment behavior. Journal of Economic Psychology

1993;14:377–85.Armstrong P. The influence of Michel Foucault on accounting research. Critical Perspectives on Accounting

1994;5:25–55.ASRIA. The association for sustainable and responsible investment in Asia (Available), www.asria.org/sri (January

2005).Bauer R, Koedijk K, Otten R. International evidence on ethical managed fund performance and investment style.

J Banking Finance, in press.Calvert. Resolution filing history (Available), www.calvert.com/sri 2766.html (August 2003b).Cordwell C. Foucault and ethical universality. Inquiry 2004;47:580–96.Dugger WM. Corporate hegemony. New York: Greenwood Press; 1989.Ethical Investment Association. The financial services reform bill submission to the parliamentary joint statutory

committee on corporations and securities. Sydney: Ethical Investment Association; 2002.Feinberg J. Psychological egoism. In: Pojman LP, editor. Ethical theory: classical and contemporary readings. 2nd

ed. Belmont, CA: Wadsworth Pub; 1995.Foucault M. On the genealogy of ethics: an overview of work in progress. In: Rabinow P, editor. Ethics: subjectivity

and truth volume one [Hurley R, et al., Trans.]. Harmondsworth: Penguin Books; 1997. p. 253–80.Foucault M. In: Gordon C, editor. Power/knowledge selected interviews and other writings 1972–1977 [Gordon

C, Trans.]. New York: Pantheon Books; 1980.Foucault M. History of sexuality. Vol. 1: An introduction [Hurley R, Trans.]. New York: Pantheon Books; 1978.Foucault M. Discipline and punish: the birth of the prison [Sheridan A, Trans.]. New York: Pantheon Books; 1977.FOE [Friends of the Earth]. The potential and limitations of shareholder activism, (Available), http://www.foe.

org/international/shareholder/potential.html (January 2005).Graham K. The moral significance of collective entities. Inquiry 2001;44:21–42.Habermas J. Justification and application: remarks on discourse ethics. UK: Polity Press; 1993.Habermas J. Moral consciousness and communicative action. Cambridge: Basil Blackwell; 1990.Habermas J. New social movements. Telos 1981;49:33–7.Haigh M. What counts in social investment: international survey evidence. Adv Public Interest Acc, in press-a.Haigh M. Managed investments, managed disclosures: financial services reform in practice. Acc Audit Acc J, in

press-b.Haigh M, Hazelton J. Financial markets: a tool for social responsibility? Journal of Business Ethics

2004;52(1):59–71.Held D. Introduction to critical theory. Berkeley: University of California Press; 1980.Honneth A. The critique of power: reflective stages in a critical social theory [Baynes K, Trans.]. Cambridge, MA:

MIT Press; 1991.

M. Haigh / Critical Perspectives on Accounting 17 (2006) 989–1005 1005

Hoy DC. Critical resistance: from poststructuralism to post-critique. Cambridge, MA: MIT Press; 2004.Hoy DC, editor. Foucault: a critical reader. Oxford: Basil Blackwell; 1986.Just Pensions. Will UK pension funds become more responsible? London: Just Pensions; 2004.Kant I. Gregor M, editor. Groundwork of the metaphysics of morals. Cambridge: Cambridge University Press;

1997.Kant I. Pure practical reason and the moral law. In: Singer P, editor. Ethics. Oxford: Oxford University Press;

1994. p. 123–31.Kapur BK. Harmonization between communitarian ethics and market economics. J Markets Morality

1999;2(1):35–52.Kreander N. An analysis of european ethical funds (Occasional Research Paper No. 33). London: Certified Accoun-

tants Educational Trust; 2001.Laclau E. New reflections on the revolution of our time. London: Verso Books; 1990.Lewis A, Mackenzie C. Support for investor activism among UK Ethical Investors. J Business Ethics

2000;24(3):215–22.Mackenzie C. Ethical investment and the challenge of corporate reform. Unpublished doctoral thesis, University

of Bath; 1997.Mackie JL. Ethics: inventing right and wrong. London: Penguin Books; 1977.McGoun EG, Dunkak MS, Bettner MS, Allen DE. Walt’s Street and Wall Street: theming, theater and experience

in finance. Crit Perspect Acc 2003;14(6):647–62.Mintz B, Schwartz M. Capital flows and the process of financial hegemony. In: Zukin S, DiMaggio P, editors.

Structures of capital. Cambridge: Cambridge University Press; 1990. p. 203–26.Neimark MK. Regicide revisited: Marx, Foucault and accounting. Crit Perspect Acc 1994;5(1):87–108.Norton B, Toman MA. Sustainability: ecological and economic perspectives. Land Economics 1997;73(4):97–111.Osborne T. Critical spirituality: on ethics and politics in the later Foucault. In: Ashenden S, Owen D, editors.

Foucault contra Habermas. London: Sage Publications; 1999. p. 45–59.Patton P. Foucault’s subject of power. Political Theor Newslett 1994;6(1):60–71.Perks RW, Rawlinson DH, Ingram L. An exploration of ethical investment in the UK. Br Acc Rev 1992;24:43–65.Reed D. Stakeholder management theory: a critical theory perspective. Business Ethics Quart 1999;9(3):453–83.Roberts J. The manufacture of corporate social responsibility: constructing corporate sensibility. Organization

2003;10(2):249–58.Rockness J, Williams PF. A descriptive study of social responsibility mutual funds. Acc Organ Soc 1988;

13(4):397–411.SAM. Sustainable Asset Management Research Inc. (Available), www.sam.com.au (November 2003).Schwartz MS. The ‘Ethics’ of ethical investing. J Business Ethics 2003;43:195–213.Shareholder Action Network. (Available) www.shareholderaction.org (January 2005).Singer P. Introduction, Ethics. Oxford: Oxford University Press; 1994. p. 1–13.SRI World Group, Inc. Watchdog fund established to take a bite out of corporate governance malfeasance”

(Available), www.socialfunds.com/news/paper.cgi/paper1290.html (April 2004).Tippet J. Investors’ perceptions of the relative importance of investment issues. Acc Forum 2002;24(3):278–95.Tippet J, Leung P. Defining ethical investment and its demography in Australia. Aust Acc Rev 2001;11(3):44–55.UKSIF. UK Social Investment Forum. (Available) www.uksif.org (January 2005).Viederman S. Essay from Jessie Smith Noyes Foundation 1997 Annual Report, (Available) www.foe.org/

international/shareholder/uscampaigns.html (January 2005).Webley P, Lewis A, Mackenzie C. Commitment among ethical investors: an experimental approach. J Econ Psychol

2001;22(1):27–42.Whincop MJ. The role of the shareholder in corporate governance: a theoretical approach, (Available)

www.austlii.edu.au (February 2003).Williams B. Ethics and the limits of philosophy. London: Fontana Paperbacks and William Collins; 1985.Williams B. Interlude: relativism, from “Morality”. An introduction to ethics. London: Cambridge University

Press; 1972. p. 34–9.Wolin R. Foucault’s aesthetic decisionism. Telos 1985;67:71–86.Woodward T. The profile of individual ethical investors and their choice of investment criteria. Bournemouth

University: Occasional Paper; 2000.

Related Documents