ANALYSIS Social and private total Hicksian incomes of multiple use forests in Spain Pablo Campos * , Alejandro Caparro ´s 1 Instituto de Economı ´a y Geografı ´a (IEG), Consejo Superior de Investigaciones, Cientı ´ficas (CSIC), Pinar 25, 28006 Madrid, Spain Received 15 September 2004; received in revised form 1 May 2005; accepted 9 May 2005 Available online 5 July 2005 Abstract The present national accounting system for forests measures only the commercial flows of the production account and the consumption of durable goods produced by human intervention, and focuses particularly on final output, while ignoring any intermediate output not arising from harvested agricultural crops. Environmental goods and services, whether for public consumption or for the landowner’s private use (owner’s self-consumption), are ignored in conventional measurements of the net domestic product of forests. This paper presents and applies a forest accounting methodology that overcomes these limitations and allows for homogeneous aggregation of commercial and environmental values (using exchange values, and not welfare measurements, for the latter). We have applied the accounting system proposed here to two major types of multiple-use forest of the Iberian peninsula: Mediterranean forest (Monfragu ¨e cork oak dehesa) and conifer forest (Scottish pine in the Guadarrama mountain range). Our results show that non-commercial incomes are relatively more important in the pine forest under consideration, both in private and in social terms. Cork oak forest is notably more profitable in private terms than pine forest, however. Conventional national accounting measures only 24% and 77% of social total income in Guadarrama Scottish forest and Monfragu ¨e cork oak dehesa , respectively. D 2005 Elsevier B.V. All rights reserved. Keywords: Multiple use forests; Green national accounting; Hicksian income; Contingent valuation; Simulated exchange values 1. Introduction A growing interest in mitigating the deterioration and destruction of natural resources has led the public institutions in charge of national accounts and inter- national bodies to develop new methods to cover all flows of goods and services generated by forests and changes in the capital endowment of forests (ISWGNA, 1993; United Nations et al., 2003; Euro- stat, 2002; Nordhaus and Kokkelenberg, 1999). There is a general consensus that bproduction- based measures usually rely on Hicksian income, which is the standard definition of net domestic or national product used in the national income accounts 0921-8009/$ - see front matter D 2005 Elsevier B.V. All rights reserved. doi:10.1016/j.ecolecon.2005.05.005 * Corresponding author. Tel.: +34 91 411 10 98; fax: +34 91 562 55 67. E-mail addresses: [email protected] (P. Campos), [email protected] (A. Caparro ´s). 1 Tel.: +34 91 411 10 98; fax: +34 91 562 55 67. Ecological Economics 57 (2006) 545 – 557 www.elsevier.com/locate/ecolecon

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

www.elsevier.com/locate/ecolecon

Ecological Economics 5

ANALYSIS

Social and private total Hicksian incomes of

multiple use forests in Spain

Pablo Campos*, Alejandro Caparros 1

Instituto de Economıa y Geografıa (IEG), Consejo Superior de Investigaciones, Cientıficas (CSIC), Pinar 25, 28006 Madrid, Spain

Received 15 September 2004; received in revised form 1 May 2005; accepted 9 May 2005

Available online 5 July 2005

Abstract

The present national accounting system for forests measures only the commercial flows of the production account and the

consumption of durable goods produced by human intervention, and focuses particularly on final output, while ignoring any

intermediate output not arising from harvested agricultural crops. Environmental goods and services, whether for public

consumption or for the landowner’s private use (owner’s self-consumption), are ignored in conventional measurements of the

net domestic product of forests. This paper presents and applies a forest accounting methodology that overcomes these

limitations and allows for homogeneous aggregation of commercial and environmental values (using exchange values, and not

welfare measurements, for the latter). We have applied the accounting system proposed here to two major types of multiple-use

forest of the Iberian peninsula: Mediterranean forest (Monfrague cork oak dehesa) and conifer forest (Scottish pine in the

Guadarrama mountain range). Our results show that non-commercial incomes are relatively more important in the pine forest

under consideration, both in private and in social terms. Cork oak forest is notably more profitable in private terms than pine

forest, however. Conventional national accounting measures only 24% and 77% of social total income in Guadarrama Scottish

forest and Monfrague cork oak dehesa, respectively.

D 2005 Elsevier B.V. All rights reserved.

Keywords: Multiple use forests; Green national accounting; Hicksian income; Contingent valuation; Simulated exchange values

1. Introduction

A growing interest in mitigating the deterioration

and destruction of natural resources has led the public

0921-8009/$ - see front matter D 2005 Elsevier B.V. All rights reserved.

doi:10.1016/j.ecolecon.2005.05.005

* Corresponding author. Tel.: +34 91 411 10 98; fax: +34 91 562

55 67.

E-mail addresses: [email protected] (P. Campos),

[email protected] (A. Caparros).1 Tel.: +34 91 411 10 98; fax: +34 91 562 55 67.

institutions in charge of national accounts and inter-

national bodies to develop new methods to cover all

flows of goods and services generated by forests and

changes in the capital endowment of forests

(ISWGNA, 1993; United Nations et al., 2003; Euro-

stat, 2002; Nordhaus and Kokkelenberg, 1999).

There is a general consensus that bproduction-based measures usually rely on Hicksian income,

which is the standard definition of net domestic or

national product used in the national income accounts

7 (2006) 545–557

P. Campos, A. Caparros / Ecological Economics 57 (2006) 545–557546

[regulations] of virtually all nations todayQ (Nordhausand Kokkelenberg, 1999, p. 35). In the same line, the

Economic Account for Agriculture and Forest-

ry(EAA/EAF-97) system of the European Union

defines income as bthe maximum amount which the

beneficiary can consume over a given period without

reducing the volume of his/her assetsQ (Eurostat, 2000,p. 87).

Theoretical literature has also propounded the use

of net domestic product (NDP), which is closely

linked to the concept of Hicksian income2 (Hicks,

1946, pp. 172–173), as the most appropriate national

income measure given its welfare interpretation, under

a given set of ideal conditions. Weitzman (1976) laid

the theoretical foundations for such use, and later

research extended the concept to cover natural and

environmental resources (e.g., Dasgupta and Maler,

2000; Heal and Kristrom, 2001). Based on these pre-

cedents, Vincent (1999) proposed a theoretical model

of sustainable total income specific to forests; he

examined the issues of which items to include and

how to adjust for the dislocations of inter-sector

incomes in forests. However, the theoretical results

of these developments are far from showing a com-

plete and homogeneous integrated approach to mea-

sure total Hicksian income (Heal and Kristrom, 2001,

p. 74).

The definition of Hicksian income used in this

paper is as follows: the sustainable total income of

a forest is the flow (income) of money (real or imput-

ed) generated during an accounting period (one year)

which, being wholly consumed within that same ac-

counting period, leaves the forest with the same value

of economic wealth (capital) at the end of the period

as it had at the start in real terms, in the absence of

new discoveries of wealth and net transfers from

outside the forest. In this paper, we estimate that

item as conventional net domestic product (NDP)

extended to environmental goods and services, rather

than net national product (NNP), which refers to the

income produced in a given accounting period by the

nationals of a country.

Hicksian income provides a substantial theoretical

advance with respect to the way income is now mea-

2 Similar concepts were put forward earlier by Fisher, in 1906,

and Lindahl, in 1933 (Aronsson et al., 1997).

sured by national accounting systems. To date, forest

income is not calculated fully in accordance with the

national accounts standard European System of

Accounts – ESA-95 – (Eurostat, 1996). Instead, the

satellite system EAA/EAF-97 (Eurostat, 2000) is in

use; this scheme fails to consider environmental

values and the capital balance. The Eurostat working

group that is now looking at how to incorporate

environmental values in the economic accounts of

European forests has proposed the pilot accounting

system The European Framework for Integrated En-

vironmental and Economic Accounting for Forests —

IEEAF — (Eurostat, 2002), which does take account

of the capital balance of a forest, as required by the

Regulation enacting ESA-95, although the integration

of environmental values is still out of the accounting

framework, since the integration of monetary environ-

mental values is bnot part of official statistical pro-

grammes [given that] the methods and assumptions

used in the valuation studies are not standardized, and

many theoretical and practical problems are still being

debatedQ (Eurostat, 2002, p. 45).In this paper we base our estimate of the sustain-

able total income (Hicksian income) of a forest on the

methodological proposal Agro-forestry Accounts Sys-

tem(AAS), as developed in recent articles (Campos,

1999; Caparros et al., 2001, 2003a). AAS presents a

method of calculation of Hicksian income which, in

line with the prescriptions of theory (Vincent, 1999;

Nordhaus and Kokkelenberg, 1999), estimates sus-

tainable total income within the applied national ac-

counting system (see also Lange (2004)). The

relationship of the AAS methodology with the recom-

mendations of the theoretical literature on green na-

tional accounting has been developed in Caparros et

al. (2003a).

The concept of Hicksian income may apply both to

estimation of social income and to calculation of pri-

vate income. Major differences may arise depending

on the significance of environmental services and

public expenditure, as shown in the applications pre-

sented in this paper. In particular, private income

includes private commercial goods and services and

environmental goods and services self-consumed by

the forest owner, while social total income includes the

private income of landowners and employees at mar-

ket prices plus environmental goods and services con-

sumed by free public visitors and by society as a whole

P. Campos, A. Caparros / Ecological Economics 57 (2006) 545–557 547

at simulated exchange prices. That is, as suggested in

Lange (2004), we include all forest goods and services,

both market and non-market in the flow accounts.

AAS was applied in Caparros et al. (2003a) to the

pine forests of the Guadarrama mountain range for

partial calculation of social income. Private capital

income from landowners’ self-consumption of envi-

ronmental services was not calculated, although, as

we shall show later, this item is significant in the

forests under study; the value of free mushroom-pick-

ing was not estimated, either, and this is also a sub-

stantial activity in pine forests. In this paper we extend

this application and compare it with another applica-

tion to Mediterranean forests. The two agro-forestry

systems considered are relevant systems of the Iberian

peninsula: (i) the pine forests of the Guadarrama

mountain range (representative of the mountain con-

ifers in Spain and similar to other coniferous forests in

northern-central Europe) and (ii) the cork oak forests

at Monfrague (representative of the dehesa-type Med-

iterranean forests of the southwestern Iberian penin-

sula). The applications presented here are interesting

in themselves, but their special role is to exemplify the

usefulness of AAS in comparing on a uniform basis

the commercial and non-commercial values generated

by two types of multiple-use forest.

The rest of the article is structured as follows.

Section two sets out our methodology, and is divided

into three sub-sections. The first sub-section describes

the simplified form of the AAS accounts system used.

The second provides a general analysis of the values

to be included in the system and the third briefly

outlines the two applications of AAS made for this

paper. Section three discusses the results of our com-

parison of the two accounting applications, and Sec-

tion four compares the results obtained applying the

AAS methodology to those that would be obtained

with current national accounting rules and with the

developments recently proposed. Finally, Section five

puts forth our main conclusions.

2. Methodology

2.1. The agro-forestry accounting system (AAS)

AAS divides data into three different accounts

(Campos, 1999; Caparros et al., 2003a). The produc-

tion account records the total cost incurred throughout

the accounting period by the activities giving rise to

the total output of the forest; the difference between

total cost and total output is the forest-owner’s oper-

ating benefit (margin) where all the work is done by

employees, as is the case in the two forests examined

here. Variations from initial and final values of capital

and inflows and outflows are reflected by two

accounts: the balance of production in progress and

the fixed capital balance. The first balance presents as

residual value the revalorisations of production in

progress at the end of the period, while the second

balance treats as residual value the revalorisations of

the durable finished goods involved in the economic

activities of the forests for more than one period (fixed

capital goods).

However, a uniform comparison of the two forests

cannot be made directly for any year in the cycle;

variation can be significant, according to the specific

time of the cycle at which measurements are taken.

Therefore, to compare the two forests, we have sim-

ulated a forest’s hypothetical steady state. This entails

that there are not capital gains other than those arising

from the effect of discounting production in progress,

and the AAS versus ESA/EAF comparison can be

made using only the simplified production account.

That is, in steady-state we can avoid considering

natural growth (GNG), production in progress used

(PPu) and capital balances (see Campos, 1999 and

Caparros et al., 2003a). The steady-state scenario

likewise implies that no income is associated with

increased carbon sequestration in the forest (Caparros

and Jacquemont, 2003; Caparros et al., 2003b).

The simplified production account under AAS

(Table 1) allows for the calculation of NVA (private

or social) using the following identities:

NVAX ¼ NOMX þ LCX; X ¼ P; Sð Þ

NOMX ¼ TOX � TCX; X ¼ P; Sð Þ;

where, NOM: net operating margin, TO: total output,

TC: total cost. LC: labour cost, and the subindex (P or

S) indicates private or social values.

The AAS methodology distinguishes between so-

cial income and private income. In steady-state, AAS

private total income (TIP) equals private net value

added at market prices (NVAP) from private commer-

cial goods (timber, cork, firewood, and grazing rent)

Table 1

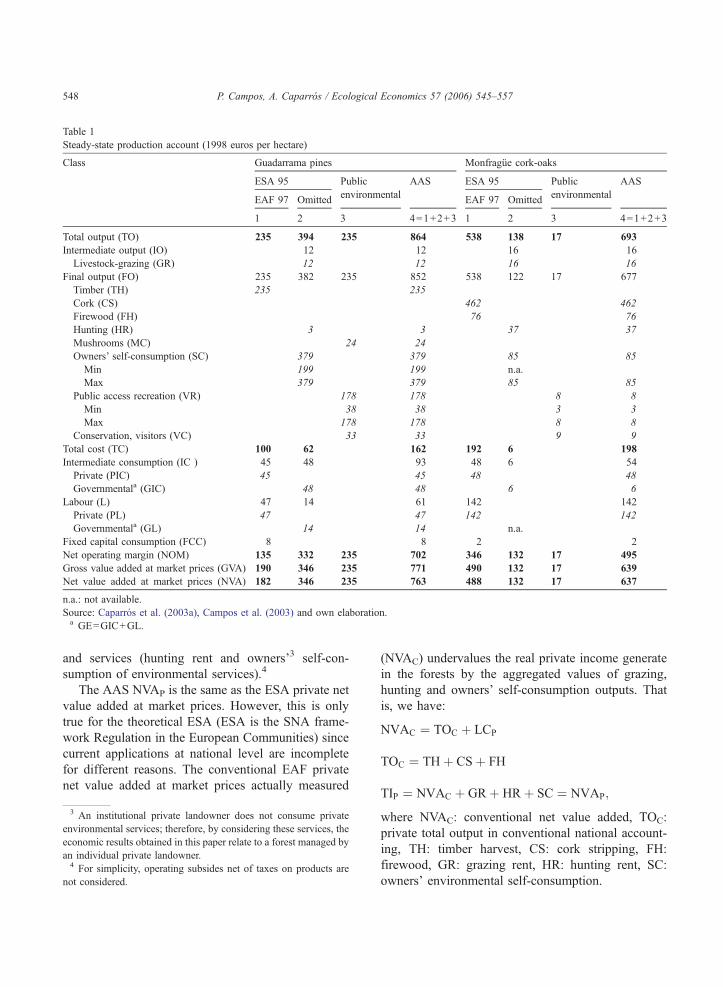

Steady-state production account (1998 euros per hectare)

Class Guadarrama pines Monfrague cork-oaks

ESA 95 Public

environmental

AAS ESA 95 Public

environmental

AAS

EAF 97 Omitted EAF 97 Omitted

1 2 3 4=1+2+3 1 2 3 4=1+2+3

Total output (TO) 235 394 235 864 538 138 17 693

Intermediate output (IO) 12 12 16 16

Livestock-grazing (GR) 12 12 16 16

Final output (FO) 235 382 235 852 538 122 17 677

Timber (TH) 235 235

Cork (CS) 462 462

Firewood (FH) 76 76

Hunting (HR) 3 3 37 37

Mushrooms (MC) 24 24

Owners’ self-consumption (SC) 379 379 85 85

Min 199 199 n.a.

Max 379 379 85 85

Public access recreation (VR) 178 178 8 8

Min 38 38 3 3

Max 178 178 8 8

Conservation, visitors (VC) 33 33 9 9

Total cost (TC) 100 62 162 192 6 198

Intermediate consumption (IC ) 45 48 93 48 6 54

Private (PIC) 45 45 48 48

Governmentala (GIC) 48 48 6 6

Labour (L) 47 14 61 142 142

Private (PL) 47 47 142 142

Governmentala (GL) 14 14 n.a.

Fixed capital consumption (FCC) 8 8 2 2

Net operating margin (NOM) 135 332 235 702 346 132 17 495

Gross value added at market prices (GVA) 190 346 235 771 490 132 17 639

Net value added at market prices (NVA) 182 346 235 763 488 132 17 637

n.a.: not available.

Source: Caparros et al. (2003a), Campos et al. (2003) and own elaboration.a GE=GIC+GL.

P. Campos, A. Caparros / Ecological Economics 57 (2006) 545–557548

and services (hunting rent and owners’3 self-con-

sumption of environmental services).4

The AAS NVAP is the same as the ESA private net

value added at market prices. However, this is only

true for the theoretical ESA (ESA is the SNA frame-

work Regulation in the European Communities) since

current applications at national level are incomplete

for different reasons. The conventional EAF private

net value added at market prices actually measured

3 An institutional private landowner does not consume private

environmental services; therefore, by considering these services, the

economic results obtained in this paper relate to a forest managed by

an individual private landowner.4 For simplicity, operating subsides net of taxes on products are

not considered.

(NVAC) undervalues the real private income generate

in the forests by the aggregated values of grazing,

hunting and owners’ self-consumption outputs. That

is, we have:

NVAC ¼ TOC þ LCP

TOC ¼ THþ CSþ FH

TIP ¼ NVAC þ GRþ HRþ SC ¼ NVAP;

where NVAC: conventional net value added, TOC:

private total output in conventional national account-

ing, TH: timber harvest, CS: cork stripping, FH:

firewood, GR: grazing rent, HR: hunting rent, SC:

owners’ environmental self-consumption.

P. Campos, A. Caparros / Ecological Economics 57 (2006) 545–557 549

AAS social total income(TIS) includes private

income at market prices (NVAP), public environmen-

tal goods and services consumed by free public

visitors and governmental expenditures. That is, the

social total income item estimated aggregates the

different incomes generated by individual uses irre-

spective of the recipient, who may be the forest

landowner, workers, recreational visitors and hunters.

Thus:

TIS ¼ NVAP þMCþ VRþ VC� GIC ¼ NVAS;

where, MC: mushrooms collected, VR: public

visitors recreation, VC: public visitors conserva-

tion value and GIC: governmental intermediate

consumption.

The main differences with the EAF/EAA system is

that grazing resources, hunting and mushrooms gath-

ering are included in the agriculture production ac-

count (EAA), and not in EAF. However, hunting and

mushrooms are forest products and services and in-

come from grazing resources should be treated as an

intermediate output provided by the forest to livestock

activities. In addition, neither owner’s self-consump-

tion nor public recreation and conservation services

are taken into account in the presently applied EAA/

EAF framework.

The private or social capital profitability rate of

the steady state is obtained from the quotient of

capital income (NOM) and immobilised capital

(IMC): rX=NOMX/ IMCX (X=P, S). Immobilised

capital for the accounting period is intended to pro-

vide a standardised value of the average social or

private investment allocated during that period

to obtaining the social or private capital income of

the forest. Private immobilised capital is estimated as

follows (in the steady-state): IMCP=CiP+

0.5(TCP�FCC ), where CiP is the initial private

capital, essentially land (valued at market prices)

and FCC is fixed capital consumption. In the case

of social immobilized income (IMCS) we have added

to the IMCP the theoretical value associated to the

bsocialQ capital formed discounting the future value

of public uses at a given social discount rate (2.5%).

2.2. Values included in the production account

This sub-section sets out the values considered

under AAS so as to ensure that all relevant items

are included and to avoid double accounting. The

production account comprises production and costs

arising during a period, and provides the informa-

tion needed to calculate net value added at market

prices (termed dnet value addedT from now on). We

set out below the methods proposed for valuation

of goods and services by looking directly to the

market and by simulating specific markets.

2.2.1. Values drawn directly from the market

The production account places in order the income

and costs associated with each activity and arising

during the period. Prices for commercial goods and

services are offered objectively by the market and are

directly observable; hence estimating such prices is a

relatively simple – though laborious – process. This is

the case with the commercial values of wood, cork

and firewood.

2.2.2. Values obtained from simulated markets

Within a partial equilibrium framework, exchange

values (price times quantity) and not consumer sur-

plus values have been estimated (Vanoli, 1998, p.

363) for the goods and services which are not at

present explicitly and independently put up for sale.

This procedure is quite common in the central norma-

tive national accounts framework (ISWGNA, 1993),

where the use of prices from similar markets is pro-

posed as the first criterion for cases where no market

prices are observable. Hultkrantz (1992) uses this

method for the estimation of values for several non-

timber products only partially traded in markets in

Sweden (see also United Nations et al. (2003, chapter

8)), and so do we for hunting, grazing resources and

mushrooms gathering (using local market prices, see

below).

In the methodology followed here (Caparros et

al., 2001, 2003a), the procedure is extended to

include cases where no similar market prices exist

(e.g. public recreational services). In principle, noth-

ing distinguishes a service like public recreation

(presently outside of the market since access is

free, but which could be incorporated) from a

non-timber product like berries in Sweden (presently

outside of the market since picking is free, see

Hultkrantz (1992)). Nevertheless, since no market

for the recreational services of forests exists it is

necessary to simulate the market to determine what

P. Campos, A. Caparros / Ecological Economics 57 (2006) 545–557550

the price would be if the services were internalised.

The first temptation is to use consumer surplus

measurements (or any other welfare measure) pro-

vided by contingent valuation studies (see United

Nations et al. (2003, chapter 9) or Skanberg

(2001)). However, this implies assuming that all

the visitors pay their maximum willingness to pay

(WTP) and this is too strong an assumption if the

objective is to simulate a real market. Therefore,

this paper assumes that the owner can only choose

one price for the recreational access and that his/her

revenues will be given according to demand. This

paper further assumes that the forest-owner will set

the price for access to his/her property in order to

maximise his/her revenues (assuming a linear de-

mand function, this maximisation will occur for the

median, for the price half of the population is ready

to pay). This provides an upper limit for the market

revenue of the recreational services provided by the

forests (costs still need to be deducted). A lower

limit will be given by the costs of the services,

assuming that the owner sets the price in order to

cover the costs5 with no margin (or with a given

dstandardT margin). The former option implies a mo-

nopolistic solution assuming that no variable costs

exist (the monopolist would maximise his/her benefit

and with no variable costs this implies maximisation

of the revenues) and the latter option is a perfect

market solution. The real market price would be in

between, and in the particular case studies considered,

probably close to the monopoly solution since the

areas studied are relatively unique in their respective

regions. Thus, we use the value of the monopoly

solution for aggregation.

The issue of the number of units consumed

remains. The conventional procedure (Hultkrantz,

1992; Skanberg, 2001) consists in multiplying the

simulated market price by all the units consumed

outside the market; thus, assuming that the setting of

a price would not reduce consumption. This assump-

tion is acceptable if the influence on the overall results

is small (see mushrooms above). Nevertheless, estab-

lishing a price would obviously reduce the number of

units consumed. Concretely, if the price for the recre-

5 Since costs are assumed to be constant, marginal and average

costs are equal.

ational service were set equal to the median of the

WTP, only 50% of current visitors would be ready to

pay it (Caparros et al., 2003a).

A similar criterion is supported by the Eurostat

Task Force on Forest Environmental and Economic

Accounting: bFor a service with a zero price, the

consumer surplus represents the area under a stated

demand curve, and often the valuation studies allow

deriving the shape of this demand curve. This can

then be used to determine a dquasi-marketT value of

the service. If the demand curves are linear, it can be

shown that the maximum hypothetical dquasi-market

valueT [price] of output would be 50 % of the

consumer surplus. Analyses of the forms of demand

curves derived from contingent valuation method

(CVM) studies show that they tend to be convex

rather than linear, which implies that the dquasi-marketT value will be less than 50% of consumer

surplus (Eurostat, 2002, p. 48).QA value for bconservationQ has also been included,

although the integration of this value in national ac-

counting is probably arguable, since it is a passive-use

value. We have included the total value that visitors

declared to be ready to pay for this concept to a fund,

since under this assumption each agent could pay a

different amount, his/her maximum willingness to pay

(Caparros et al., 2003a). Conservation is a concept

that could be estimated, theoretically, for society as a

whole, but due to data limitations, we have focused

solely on visitors.

In addition to the public access environmental

services described above, this paper also estimates

the environmental services (in a large sense) that the

owner of the farm consumes himself (Martin and

Jefferies, 1966; Samuel and Thomas, 1999). These

environmental services include private recreational

services, the possibility to invite friends, the

bcountry way of lifeQ, etc. As stated above, owner’s

self-consumption is valued in the central national

accounting framework with market prices (and in

the SEEA (United Nations et al., 2003)). Unfortu-

nately, market prices for these services are not

available. The value of these services should be

capitalised in the price of the land, since owners

are willing to pay for these private uses when they

decide the price to pay for a piece of land. Thus, a

hedonic price approach could give us the part of the

land price that corresponds to this use. Nevertheless,

P. Campos, A. Caparros / Ecological Economics 57 (2006) 545–557 551

this approach has two main drawbacks, one that

applies generally and one that is more particular

to our case studies. The general problem is that

our approach is actually more interested in flow

values6 (production and value added) and these

values could only be obtained from a capital value

once the discount rate is fixed (an always extremely

delicate task). The particular drawback comes from

the low number of transactions in the areas what

makes the application of a hedonic approach a dif-

ficult task. Therefore, we followed an alternative

option.

In purely financial terms, owners may be losing

money by keeping their properties, since they might

obtain higher revenues in alternative investments.

The difference between the capital income in an

alternative investment and their present market cap-

ital income is what they are actually bpayingQ for

the environmental services that they enjoy7 (Campos

and Riera, 1996, p. 89). Nevertheless, this is only a

lower bound for the price that the market of land-

owners is ready to pay for this environmental service.

To find the upper bound we asked landowners about

their maximum willingness to pay for the private

environmental services that they enjoy (the question

was framed in terms of the maximum amount that

they were ready to lose before selling their property).

This is the upper bound for the market price of these

environmental services, because if they had found

somebody ready to pay more than this amount they

would have sold their property bto other investors

who have similar feelings for the land (Pope and

Goodwind, 1984, p. 750).Q The real market price is

somewhere in between these two bounds. Neverthe-

less, if the interviewed landowners (a representative

sample of the current landowners) are representative

of all the landowners-market-agents, the price would

be close to the value expressed by them as the min-

imum level in order to sell (otherwise transactions

would never take place). Thus, we use again the

upper limit for aggregation purposes.

6 Kallio (1999) estimates owners’ WTP for self-consumption of

environmental goods and services as a flow, although in terms of

utility.7 To do this calculation we need to know the appropriate interest

rate, what is easier to obtain than the discount rate, since they do not

always coincide.

2.3. Description of accounting applications

The pine forests (Pinus silvestris, L.) of the Gua-

darrama range (PGs) and the cork oak (Quercus

suber, L.) dehesas of Monfrague (DMs) are set

apart in social terms and by considerable differences

in altitude and climate. Monfrague shire is near the

Sierra de Gredos range in Caceres province, about 250

km from Madrid. A relatively flat area, it registers

average annual rainfall of 550 mm and has a Medi-

terranean climate. Visitors are relatively few, at an

estimated two visits per hectare per annum. The Gua-

darrama pine forests are in a high mountain area and

have a Mediterranean-Continental climate, with annu-

al rainfall in excess of 800 mm. Visiting rates are high,

at 29 visits per hectare per annum, due to its proximity

to Madrid: only 60 km away at the nearest point. Sole-

boundary forest properties in Monfrague and Guadar-

rama are frequently large estates, often in excess of

1000 ha. Private landowners therefore tend to use

employees when they take direct charge of the private

agricultural, forestry and livestock uses of their prop-

erty. In the Guadarrama pinewoods, public land-

owners abound, as do private properties held in

common by residents’ associations; but the great ma-

jority of dehesasin Monfrague are owned by private

individuals.

For pines in Guadarrama, we accepted the artificial

regeneration cycle of 110 years, which is usual in the

study area, reiterating indefinitely. For commercial

data, we examined the accounts of a large private

property (1966 ha) over a five-year period (this prop-

erty is currently in a steady-state from an economic

point of view). This data where completed with data

from other two large properties and with in-depth

interviews with the various economic agents involved,

such as silviculture firms. See Caparros et al. (2003a)

for a more detailed presentation.

For the cork oaks of Monfrague we assumed a

natural regeneration cycle of 144 years, also reiter-

ating indefinitely (Campos et al., 2003). In this case

no property in the area is at the steady-state, so that

data could not be obtained from one particular prop-

erty. However, data from different properties and in-

depth interviews with several silvicultural firms

working in the region permitted us to simulate the

revenues and cost that would be obtained in a hy-

pothetical steady-state.

P. Campos, A. Caparros / Ecological Economics 57 (2006) 545–557552

Hunting and grazing resources have been value

at forest gate local imputed market prices (Rodrı-

guez et al., 2004, p. 89), and mushroom gathered

have been valued at forest gate market prices (only

in Guadarrama), taking into account mushroom pro-

ductivity from a similar area 150 km far from

Guadarrama, the Pinar Grande in Soria (Martınez,

2003).

For our study of Guadarrama, environmental ser-

vices to free public visitors, which comprise recrea-

tional use and the conservation value of a registered

habitat, were valued using a dichotomous contingent

valuation survey on 520 respondents. The output of

the recreational service was valued as outlined in the

preceding section, while the conservation value was

valued as the total annual contribution to a fund as

stated by visitors (Caparros et al., 2003a; Caparros

and Campos, 2002). Landowners’ self-consumption

was valued using an open contingent valuation survey

on 21 individuals.8 The sample is representative,

given the small number of large private landowners

in the area (Campos and Martınez, 2004).

For the cork oak dehesasof Monfrague, we includ-

ed three environmental services. Recreational services

and habitat conservation services for free public visi-

tors were valued by multiplying the average9 WTP

obtained from the two questions posed in the contin-

gent valuation survey (Campos, 1998) by 50% of

estimated visits10. This survey comprised 419 inter-

views. Landowners’ environmental self-consumption

was valued using a contingent valuation survey on 19

individuals (Campos and Mariscal, 2003).

8 The value attributed to environmental self-consumption was the

average for the three main steady-state pine forests of the sample, as

these are the only ones representing the case-study.9 The contingent valuation survey for Guadarrama was dichoto-

mous, using a censored logit model for estimates; hence the mean

and the median were the same. To avoid that the use of the median

in the case of Monfrague (where the contingent valuation survey

was open) increases the difference between the two case studies due

to different ways of estimating willingness to pay, we chose to use

the mean for Monfrague (which was higher than the median). Even

so, the results made for a far lower value for free public recreation in

DMs (Table 1).10 It was assumed that the value of habitat conservation would be

included in a single entry price in conjunction with the recreational

value, unlike the Guadarrama survey, where it was estimated by

visitors’ estimated contribution to an annual habitat-conservation

fund.

3. Comparison of applied results

3.1. Total output

The main commercial output of each forest is

wood, for pine, and cork, for cork oak. Private total

output is higher in the dehesas of Monfrague

(DMs), although this is particularly true for com-

mercial total output, given the high value of cork

production. On the contrary, social total output is

higher in the PG. The reason is that DMs output is

chiefly commercial, whereas the greater part of total

PG income is environmental, both private and so-

cial (Table 1)11. Since the currently applied EAF

system focuses on commercial values (timber or

cork), current national accounts capture a higher per-

centage of the total output in the cases of the dehesas

in Monfrague.

The two methods used to estimate public access

recreation and owners self-consumption of environ-

mental services have yield high differences. This is

especially true in the case of the Guadarrama pines,

although both methods have shown that the two

values under consideration are relevant in this sys-

tem. In the case of the dehesas of Monfrague, only

one method could be applied to the estimation of

owners self-consumption (since commercial private

profitability is above market low risk interest rates,

see below). In regard to public access recreational

services, both methods applied have yielded low

values in the dehesas.

Timber contributes 27% of the social total output

(TOS) of PGs and 37% of the private total output.

Consumption of environmental services by the public

accounts for 25% of TOS and landowners’ environ-

mental self-consumption contributes 60% of private

total output (TOP), using upper bounds for aggrega-

tion (Tables 2 and 3).

Social and private total outputs are very similar

for DMs, given the small number of visitors per

hectare per annum. TOP accounts for the lions

share of the total output of DMs, insofar as public

environmental output is barely 2%. The main part of

11 The difference in the WTP for recreational use is partly

explained by the payment vehicle: an entry fee at Monfrague and

increased travel cost in Guadarrama.

Table 2

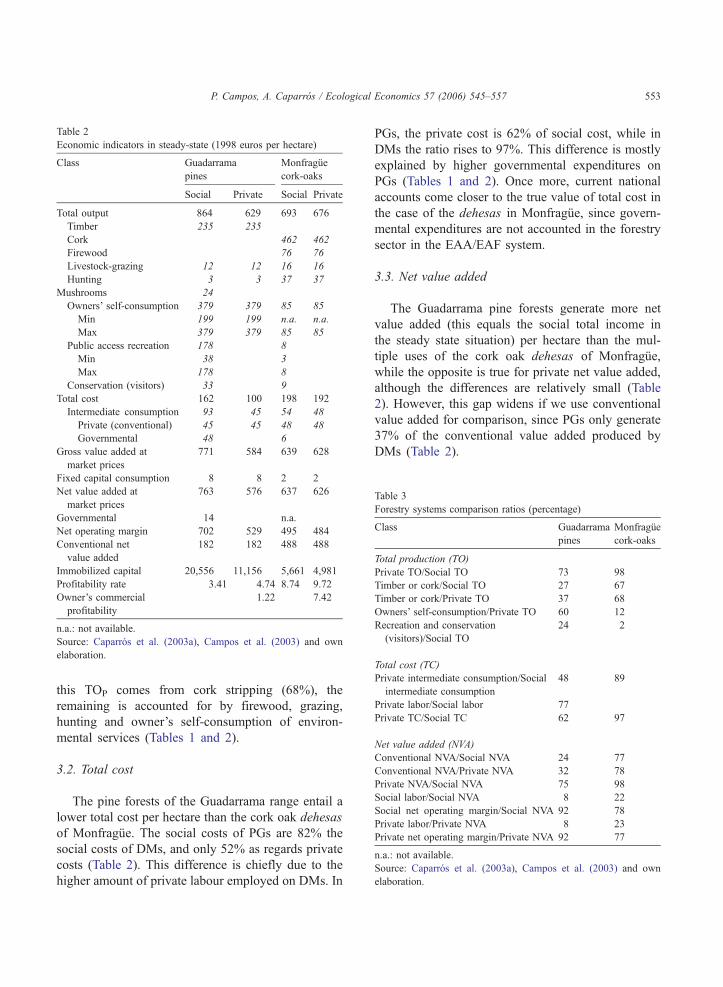

Economic indicators in steady-state (1998 euros per hectare)

Class Guadarrama

pines

Monfrague

cork-oaks

Social Private Social Private

Total output 864 629 693 676

Timber 235 235

Cork 462 462

Firewood 76 76

Livestock-grazing 12 12 16 16

Hunting 3 3 37 37

Mushrooms 24

Owners’ self-consumption 379 379 85 85

Min 199 199 n.a. n.a.

Max 379 379 85 85

Public access recreation 178 8

Min 38 3

Max 178 8

Conservation (visitors) 33 9

Total cost 162 100 198 192

Intermediate consumption 93 45 54 48

Private (conventional) 45 45 48 48

Governmental 48 6

Gross value added at

market prices

771 584 639 628

Fixed capital consumption 8 8 2 2

Net value added at

market prices

763 576 637 626

Governmental 14 n.a.

Net operating margin 702 529 495 484

Conventional net

value added

182 182 488 488

Immobilized capital 20,556 11,156 5,661 4,981

Profitability rate 3.41 4.74 8.74 9.72

Owner’s commercial

profitability

1.22 7.42

n.a.: not available.

Source: Caparros et al. (2003a), Campos et al. (2003) and own

elaboration.

Table 3

Forestry systems comparison ratios (percentage)

Class Guadarrama

pines

Monfrague

cork-oaks

Total production (TO)

Private TO/Social TO 73 98

Timber or cork/Social TO 27 67

Timber or cork/Private TO 37 68

Owners’ self-consumption/Private TO 60 12

Recreation and conservation

(visitors)/Social TO

24 2

Total cost (TC)

Private intermediate consumption/Social

intermediate consumption

48 89

Private labor/Social labor 77

Private TC/Social TC 62 97

Net value added (NVA)

Conventional NVA/Social NVA 24 77

Conventional NVA/Private NVA 32 78

Private NVA/Social NVA 75 98

Social labor/Social NVA 8 22

Social net operating margin/Social NVA 92 78

Private labor/Private NVA 8 23

Private net operating margin/Private NVA 92 77

n.a.: not available.

Source: Caparros et al. (2003a), Campos et al. (2003) and own

elaboration.

P. Campos, A. Caparros / Ecological Economics 57 (2006) 545–557 553

this TOP comes from cork stripping (68%), the

remaining is accounted for by firewood, grazing,

hunting and owner’s self-consumption of environ-

mental services (Tables 1 and 2).

3.2. Total cost

The pine forests of the Guadarrama range entail a

lower total cost per hectare than the cork oak dehesas

of Monfrague. The social costs of PGs are 82% the

social costs of DMs, and only 52% as regards private

costs (Table 2). This difference is chiefly due to the

higher amount of private labour employed on DMs. In

PGs, the private cost is 62% of social cost, while in

DMs the ratio rises to 97%. This difference is mostly

explained by higher governmental expenditures on

PGs (Tables 1 and 2). Once more, current national

accounts come closer to the true value of total cost in

the case of the dehesas in Monfrague, since govern-

mental expenditures are not accounted in the forestry

sector in the EAA/EAF system.

3.3. Net value added

The Guadarrama pine forests generate more net

value added (this equals the social total income in

the steady state situation) per hectare than the mul-

tiple uses of the cork oak dehesas of Monfrague,

while the opposite is true for private net value added,

although the differences are relatively small (Table

2). However, this gap widens if we use conventional

value added for comparison, since PGs only generate

37% of the conventional value added produced by

DMs (Table 2).

P. Campos, A. Caparros / Ecological Economics 57 (2006) 545–557554

In DMs, similar magnitudes are obtained for social

and private total income, unlike PGs, where private

total income accounts for 75% of social total income

(Table 3). The distribution of total income between

labour and capital income also differs for PGs and

DMs, since labour is relatively more important in

Monfrague.

In the case of PGs, conventional net value added

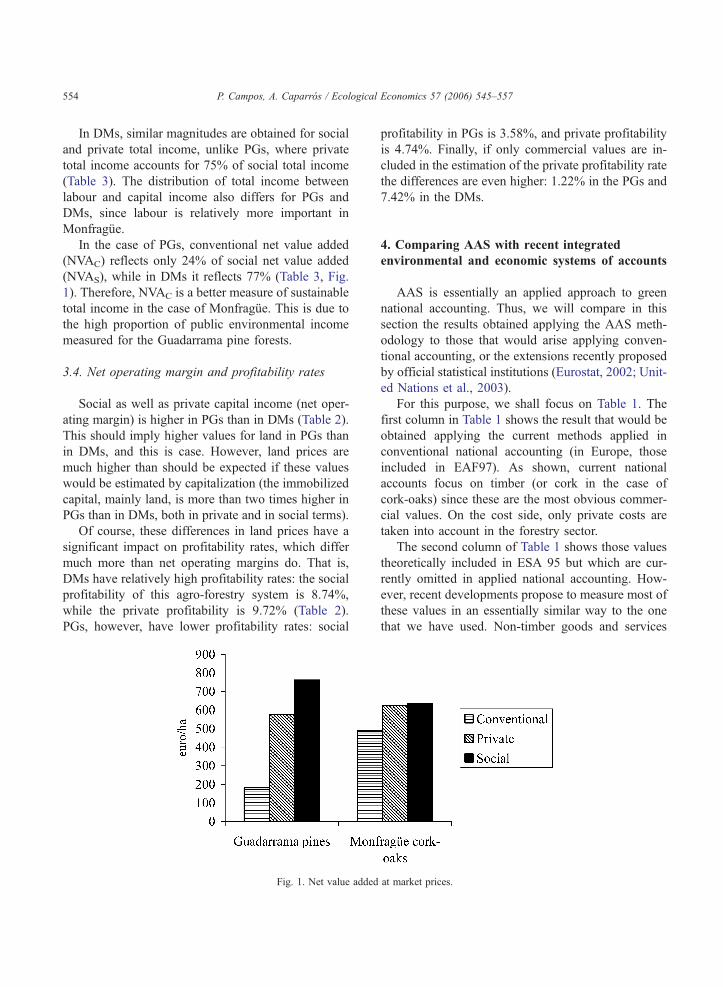

(NVAC) reflects only 24% of social net value added

(NVAS), while in DMs it reflects 77% (Table 3, Fig.

1). Therefore, NVAC is a better measure of sustainable

total income in the case of Monfrague. This is due to

the high proportion of public environmental income

measured for the Guadarrama pine forests.

3.4. Net operating margin and profitability rates

Social as well as private capital income (net oper-

ating margin) is higher in PGs than in DMs (Table 2).

This should imply higher values for land in PGs than

in DMs, and this is case. However, land prices are

much higher than should be expected if these values

would be estimated by capitalization (the immobilized

capital, mainly land, is more than two times higher in

PGs than in DMs, both in private and in social terms).

Of course, these differences in land prices have a

significant impact on profitability rates, which differ

much more than net operating margins do. That is,

DMs have relatively high profitability rates: the social

profitability of this agro-forestry system is 8.74%,

while the private profitability is 9.72% (Table 2).

PGs, however, have lower profitability rates: social

Fig. 1. Net value added

profitability in PGs is 3.58%, and private profitability

is 4.74%. Finally, if only commercial values are in-

cluded in the estimation of the private profitability rate

the differences are even higher: 1.22% in the PGs and

7.42% in the DMs.

4. Comparing AAS with recent integrated

environmental and economic systems of accounts

AAS is essentially an applied approach to green

national accounting. Thus, we will compare in this

section the results obtained applying the AAS meth-

odology to those that would arise applying conven-

tional accounting, or the extensions recently proposed

by official statistical institutions (Eurostat, 2002; Unit-

ed Nations et al., 2003).

For this purpose, we shall focus on Table 1. The

first column in Table 1 shows the result that would be

obtained applying the current methods applied in

conventional national accounting (in Europe, those

included in EAF97). As shown, current national

accounts focus on timber (or cork in the case of

cork-oaks) since these are the most obvious commer-

cial values. On the cost side, only private costs are

taken into account in the forestry sector.

The second column of Table 1 shows those values

theoretically included in ESA 95 but which are cur-

rently omitted in applied national accounting. How-

ever, recent developments propose to measure most of

these values in an essentially similar way to the one

that we have used. Non-timber goods and services

at market prices.

P. Campos, A. Caparros / Ecological Economics 57 (2006) 545–557 555

(e.g. hunting or mushrooms) are supposed to be in-

cluded in future national accounting systems accord-

ing to Eurostat (2002) or United Nations et al. (2003).

Owners’ self-consumption of environmental ser-

vices is conceptually an ESA 95 value, since the

market incorporates it in the value of land. However,

the difficulties to estimate a flow value imply that

even recent developments (Eurostat, 2002; United

Nations et al., 2003) do not consider to include this

value. The AAS proposes to include these values, but

the difficulties to obtain an accurate flow value are

recognised (we therefore show two values, a lower

bound and an upper bound, expecting the real value to

be somewhere in between).

The value of the grazing resource rent is currently

incorporated indirectly in conventional accounts in the

agricultural sector, although it would be more appro-

priate to include it as an intermediate production of

the forestry sector (Vincent and Hartwick, 1997, p.

25). Grazing resources have been valued using market

prices for renting pastures, and not using market

prices of artificial feeding, as has been proposed in

other applications (Skanberg, 2001, p. 51). In Mon-

frague, market prices for a forage unit (FU) from

grazing rented is about 50% cheaper than the same

FU obtained from commercial hay at farm gate

(Rodrıguez et al., 2004, p. 89).

On the costs side, the main contribution of the

AAS system is to incorporate governmental expendi-

tures (GE) in the forest under consideration. In the

SNA bGovernment administration is a non-market

service with no identifiable product sold in markets,

so it is valued in national accounts at its cost of

production (Lange, 2004, p. 83).Q However, includinggovernment expenditures in the output side has a

strong risk of double counting if the services produced

have already been valued; e.g., fire fighting efforts

(the lion’s share of public expenditures in Spain) have

a direct impact on commercial timber output. Thus,

we have included governmental expenditures only in

the cost side.

The third column of Table 1 presents public envi-

ronmental values. These values are the most contro-

versial ones and current proposals (Eurostat, 2002;

United Nations et al., 2003) do not expect them to

be included in national accounts in the near future.

The main reason is the lack of homogeneity between

the exchange values considered in conventional na-

tional accounting and the welfare measurements (in

terms of consumer surplus or any of the Hicksian

welfare measurements) yielded by environmental val-

uation techniques. To overcome this difficulty we

have tried to estimate exchange values for these public

environmental values (mainly free access recreation).

That is, we have tried to measure the output that could

be produced in the forest if public access would have

a price (a single price for all visitors, not their max-

imum willingness to pay). That is, we have used

environmental valuations techniques to know the de-

mand function (assuming no wealth effect) and have

assumed that the owner will set a single price. Once

more, the uncertainty surrounding this hypothetical

marketing of environmental services advised to give

an interval for the result.

Nevertheless, assuming the existence of markets

that actually do not exist implies counting money in

the forestry sector that was actually spent somewhere

else. That is, visitors would have paid the price as-

sumed (according to the information provided by the

contingent valuation studies), but they actually did not

and thus spend it somewhere else. That is, bthe chal-

lenge is to utilize non-market values in the forest

sector, which are estimated in the macroeconomic or

general equilibrium context of analysis. The value

must be consistent and comparable with market values

in the large system (FAO, 1998, p. 4).Q However, thisproblem applies as well to the imputed owner’s con-

sumption of real estate property rent in conventional

national accounting (SNA/ESA). That is, as happens

already in conventional accounting, if the method

proposed in this paper would be followed nationwide

a part of national income would not be brealQ money,

and the same part of national consumption would also

not be paid with brealQ money. But, in any case,

homogeneity with real exchange values would be

pushed as far as possible, and homogeneity with the

solution proposed in current national accounts for

values such as the rent of your own house would be

almost complete (at least in the case of owner’s self-

consumption of environmental values). In other

words, there are other exceptions in conventional

national accounting that depart from observable mar-

ket prices in the SNA framework, and ba rigorous

restriction of the SNA to market transactions would

seriously limit its analytical power (Bartelmus, 1998,

p. 269).Q

P. Campos, A. Caparros / Ecological Economics 57 (2006) 545–557556

5. Conclusions

This paper has presented and applied a methodol-

ogy that allows for uniform comparison of private and

social incomes generated by multiple-use forests. We

have made commercial and non-commercial measure-

ments, both for cork oak forests of Monfrague shire

and pine forests of the Guadarrama mountain range.

For non-commercial goods and services, we measured

four environmental values in each region, three by the

contingent valuation technique (public access recrea-

tion, conservation and owners self-consumption of

environmental services) and one by applying on-site

market prices (mushrooms).

The results show that public environmental bene-

fits make a very substantial contribution to social

total income in the case of the Guadarrama pine

forests. Public non-commercial benefits are relatively

less important, however, in the case of the Monfra-

gue cork oak dehesas. In both cases, environmental

self-consumption by landowners is high, especially

in the case of Guadarrama, and explains a substantial

part of the market price of the forests; hence the

estimation of these benefits should be a priority for

future research.

Concerning the green national accounting debate,

the main conclusion to be drawn from these applica-

tions is that incorporating environmental values (es-

pecially free access recreational values and owner’s

self-consumption of environmental services) can be

done in an applied framework using information

from non-market valuation techniques and adapting

rules currently under use in conventional national

accounting.

As expected, when the relative importance of the

environmental values is low, as compared to commer-

cial values, conventional national accounting approx-

imates good the true total income generated in the

forest, while the opposite is true if environmental

values are important. The exchange values for these

environmental goods and services, obtained simulat-

ing markets, have proven to be relatively very impor-

tant (as compared to commercial values) in one of the

case-studies under consideration (Guadarrama) and

not so important in the other case (the dehesas).

These results probably do not match a priori percep-

tions in Spain, especially concerning the relative im-

portance of commercial values in dehesas, so that a

systematic application of these kinds of methodolo-

gies can prove to be very useful for rigorous public

forestry policy making.

Acknowledgements

The preparation of this paper has benefited from

the projects CICYT-AMB99-1161 and F096-040,

funded by the Comision Interministerial de Ciencia

y Tecnologıa. We have also received support under the

Convenio entre el CSIC y la Sociedad Anonima Belga

de los Pinares de El Paular.We thank the useful

comments from anonymous referees to the first ver-

sion of this article. The authors are solely responsible

for the information and analysis presented.

References

Aronsson, T., Johansson, P.-O., Lofgren, K.-G., 1997. Welfare

Measurement, Sustainability and Green National Accounting:

A Growth Theoretical Approach. Edward Elgar, Cheltenham.

175 pp.

Bartelmus, P., 1998. The value of nature: valuation and evaluation

in environmental accounting. In: Uno, K., Bartelmus, P. (Eds.),

Environmental Accounting in Theory and Practice. Kluwer

Academic Publishers, London, pp. 263–307.

Campos, P., 1998. Contribucion de los visitantes a la con-

servacion de Monfrague. Bienes publicos, mercado y ges-

tion de los recursos naturales. In: Hernandez, C.G. (Ed.), La

Dehesa: Aprovechamiento Sostenible de los Recursos Natur-

ales. Fundacion Pedro Arce-Editorial Agrıcola Espanola,

Madrid, pp. 241–263.

Campos, P., 1999. Hacia la medicion de la renta de bienestar del uso

multiple de un bosque. Investigacion Agraria: Sistemas y Recur-

sos Forestales 8 (2), 407–422.

Campos, P., Mariscal, P., 2003. Preferencias de los propietarios e

intervencion publica: el caso de las dehesas de la comarca de

Monfrague. Investigacion Agraria: Sistemas y Recursos Fore-

stales 12 (3), 407–422.

Campos, P., Martınez, M., 2004. Multiple use of pinus sylvestrisand

quercus pyrenaicaforests in the Spanish central system. In:

Schnabel, S., Ferreira, A. (Eds.), Sustainability of Agro-Silvo-

Pastoral Systems — Dehesas, Montados, Advances in GeoEcol-

ogy, vol. 37. Catena-Verlag, Reiskirchen, pp. 71–84.

Campos, P., Riera, P., 1996. Rentabilidad social de los bosques.

Analisis aplicado a las dehesas y los montados ibericos. Infor-

macion Comercial Espanola 751, 47–62.

Campos, P., Martın, D., Montero, G., 2003. Economıas de la

reforestacion del alcornoque y la regeneracion natural del alcor-

nocal. In: Pulido, F., Campos, P., Montero, G. (Eds.), La Gestion

Forestal de la Dehesa: Historia, Ecologıa, Selvicultura y Econ-

omıa. IPROCOR, Merida, pp. 107–164.

P. Campos, A. Caparros / Ecological Economics 57 (2006) 545–557 557

Caparros, A., Campos, P., 2002. Economıa del uso recreativo en los

pinares de la sierra de Guadarrama. Revista Espanola de Estu-

dios Agrosociales y Pesqueros 195, 121–146.

Caparros, A., Jacquemont, F., 2003. Carbon offset programs and

biodiversity: an economic and legal analysis. Ecological Eco-

nomics 46, 143–157.

Caparros, A., Campos, P., Montero, G., 2001. Applied multiple use

forest accounting in the Guadarrama pinewoods (Spain). Inves-

tigacion Agraria: Sistemas y Recursos Forestales 1, 93–110

(Special issue).

Caparros, A., Campos, P., Montero, G., 2003a. An operative frame-

work for total Hicksian income measurement: application to a

multiple use forest. Environmental and Resource Economics 26,

173–198.

Caparros, A., Campos, P., Martın, D., 2003b. Influence of carbon

dioxide abatement and recreational services on optimal forest

rotation. International Journal of Sustainable Development 6 (3),

345–358.

Dasgupta, P., Maler, K.-G., 2000. Net national product, wealth, and

social well-being. Environment and Development Economics 5

(1 & 2), 69–93.

Eurostat, 1996. European System of Accounts — ESA-95. ECSC-

EC-EAEC, Luxembourg. 383 pp.

Eurostat, 2000. Manual on Economic Accounts for Agriculture and

Forestry – EAA/EAF – 97 (Rev.1.1). European Communities,

Luxembourg. 181 pp.

Eurostat, 2002. The European Framework for Integrated Environ-

mental and Economic Accounting for Forests—IEEAF. Euro-

pean Communities, Luxembourg. 106 pp.

Food and Agriculture Organization (FAO), 1998. Economic and

Environmental Accounting for Forestry: Status and Current

Efforts. Planning and Statistics Branch/Policy and Planning

Division/Forestry Department, Rome. www.fao.org. 03/16/

2005.

Heal, G., Kristrom, B., 2001. National Income and the Environ-

ment. http://papersssm.com/sol3/delivery.cfm/SSRN-ID279112-

CODE011118600.pdf. 01/10/2003.

Hicks, J., 1946. Value and Capital, 2nd edition. Oxford University

Press, Oxford. 340 pp.

Hultkrantz, L., 1992. National account of timber and forest envi-

ronmental services in Sweden. Environmental and Resource

Economics 2, 283–305.

Inter-Secretariat Working Group on National Accounts (ISWGNA),

1993. System of National Account 1993. EC-IMF-OECD-UN-

WB, Luxembourg-New York-Paris-Washington. 711 pp.

Kallio, T., 1999. Non-market benefits and forest owners’ total utility

in profitability calculations. In: Roper, C.S., Park, A. (Eds.), The

Living Forest. Non-Market Benefits of Forestry. Forestry Com-

mission, London, pp. 196–202.

Lange, G.M., 2004. Manual for environmental and economic

accounts for forestry: a tool for cross-sectoral policy analysis.

FAO Working Paper. FAO, Rome. 120 pp.

Martin, W.E., Jefferies, G.L., 1966. Relating ranch prices and

grazing permit values to ranch productivity. Journal of Farm

Economics 48 (2), 233–242.

Martınez, F., 2003. Produccion y Aprovechamiento de boletus

edulis bull. Fr. En un Bosque de pinus sylvestris L. Junta de

Castilla y Leon. 134 pp.

Nordhaus, W., Kokkelenberg, E.C. (Eds.), 1999. Nature’s Numbers:

Expanding the National Economic Accounts to Include the

Environment. National Academic Press, Washington. 250 pp.

Pope III, C.A., Goodwind Jr., H.L., 1984. Impacts of consumptive

demand on rural land values. American Journal of Agricultural

Economics 66 (5), 750–754.

Rodrıguez, Y., Campos, P., Ovando, P., 2004. Commercial economy

in a public Dehesa in Monfrague Shire. In: Schnabel, S., Fer-

reira, A. (Eds.), Sustainability of Agro-Silvo-Pastoral Systems

— Dehesas, Montados, Advances in GeoEcology, vol. 37.

Catena-Verlag, Reiskirchen, pp. 85–96.

Samuel, J., Thomas, T., 1999. The valuation of unpriced forest

products by private woodland owners in Wales. In: Roper,

C.S., Park, A. (Eds.), The Living Forest. Non-Market Benefits

of Forestry. Forestry Commission, London, pp. 203–212.

Skanberg, K., 2001. Monetary forest accounts for timber and other

forest related goods and services for Sweden 1987–99. Envi-

ronmental Accounts for Forest. Test of a Proposal Framework

for Non-ESA/SNA Functions. Statistics Sweden/National Insti-

tute of Economic Research: 46–76. epp.eurostat.cec.eu.int (03/

16/2005).

United Nations, Commission of the European Communities, Inter-

national Monetary Fund, Organisation for Economic Coopera-

tion, Development and World Bank, 2003. Handbook of

National Accounting. Integrated Environmental and Economic

Accounting 2003. http://unstats.un.org/unsd/envAccounting/

seea2003.pdf. 24/08/2004.

Vanoli, A., 1998. Modelling and accounting work in national and

environmental accounts. In: Uno, K., Bartelmus, P. (Eds.),

Environmental Accounting in Theory and in Practice. Kluwer

Academic Publishers, Dordrecht, pp. 355–373.

Vincent, J.R., 1999. A framework for forest accounting. Forest

Science 45 (4), 552–561.

Vincent, J.R., Hartwick, J.M., 1997. Accounting for the Benefits of

Forest Resources: Concepts and Experience. FAO/Forestry De-

partment, Rome.

Weitzman, M.L., 1976. On the welfare significance of national

product in a dynamic economy. Quarterly Journal of Economics

90, 156–162.

Related Documents