Soaring of the Gulf Falcons: Diversification in GCC Oil Exporters in Seven Propositions Reda Cherif and Fuad Hasanov International Monetary Fund 30 April 2014 DISCLAIMER: THE VIEWS EXPRESSED HEREIN ARE THOSE OF THE AUTHORS AND SHOULD NOT BE ATTRIBUTED TO THE IMF, ITS EXECUTIVE BOARD, OR ITS MANAGEMENT .

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Soaring of the Gulf Falcons: Diversification in GCC Oil Exporters

in Seven Propositions

Reda Cherif and Fuad Hasanov

International Monetary Fund

30 April 2014

DISCLAIMER: THE VIEWS EXPRESSED HEREIN ARE THOSE OF THE AUTHORS AND SHOULD NOT BE

ATTRIBUTED TO THE IMF, ITS EXECUTIVE BOARD, OR ITS MANAGEMENT.

Proposition 1

The prevailing growth model achieved a large improvement in human development indicators but also resulted in a decline in relative economic performance.

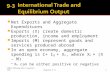

The current model relies heavily on oil

0

10

20

30

40

50

60

70

80

90

100

0

10

20

30

40

50

60

70

80

90

100

Average Oil Exports (% Exports)

1980s 1990s 2000s

1/ U.A.E. Goods and Services exports excludes re-exports.

Majority of nationals work in the government in most GCC

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Bahrain Kuwait Oman Qatar Saudi Arabia

Nationals: Public Nationals: Private Expats: Public Expats: Private

Composition of GCC Labor Market, 20121

1Kuwait data is 2011; U.A.E data unavailable for publication.

The GCC achieved huge improvements in HDI and living standards

55

60

65

70

75

80

55

60

65

70

75

80

1980 1990 2000 2012

GCC Life Expectancy, 1980–2012

(Years)

GCC

Bahrain

Kuwait

Oman

Qatar

Saudi Arabia

United Arab Emirates

But relative income declined

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

1970 1974 1978 1982 1986 1990 1994 1998 2002 2006 2010

Bahrain Kuwait

Oman Qatar

Saudi Arabia United Arab Emirates

GDP Per Worker (PPP $), 1970–2010

Proposition 2

A sustainable growth model requires a diversified tradable sector.

Non-oil GDP increased but productivity declined

Bahrain

KuwaitOman

Qatar

Saudi Arabia

United Arab Emirates

Indonesia

Norway

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

-6.0 -5.0 -4.0 -3.0 -2.0 -1.0 0.0 1.0 2.0

Avg TFP Growth 1980-2010 or available

Avg

No

n-o

il R

eal

GD

P G

row

th 1

98

0-2

010

or

avai

lab

le

Non-Oil GDP is misleading indicator

0

20

40

60

80

100

120

0

20

40

60

80

100

120

1990 1993 1996 1999 2002 2005 2008 2011

Agriculture Construction Transport

Trade Manufacturing Mining

Other

Bahrain - GDP by Sector, 1990–2011

(Share of total)

0

20

40

60

80

100

120

0

20

40

60

80

100

120

1990 1993 1996 1999 2002 2005 2008 2011

Agriculture Construction Transport

Trade Manufacturing Mining

Other

Singapore - GDP by Sector, 1990–2011

(Share of total)

It is all about export composition

79.1%

9.9%

6.2%1.5%

1.1% 0.8%1.3% Oil exports

Aluminum

Other Metals

Chemical

Food

Processing

Textiles

Other Light

Industry

Bahrain, Top 50 Exports of Goods, 2008

(Percent of total exports of goods)

24%

2%

1%

10%

11%

51%

1%

Singapore Exports by Sector, 2008

(Percent of total exports of goods)Oil

Food

Crude Materials

Chemical

products

Manufactured

Goods

Machinery &

Transport

EquipmentOthers

Yet GCC countries have attempted to diversify their economies

• Development of petrochemical and metal industries bear little linkages to the rest of the economy

• Promotion of services helped diversify economies but services may not be sufficient for sustainable growth – Focus on tourism, logistics, finance, etc.

• Recent attempts at creating clusters, technology parks, and manufacturing industries in free zones have yet to yield substantial results

Export sophistication has not improved in the GCC

4000

5000

6000

7000

8000

9000

10000

11000

12000

13000

14000

4000

5000

6000

7000

8000

9000

10000

11000

12000

13000

14000

1976 1979 1982 1985 1988 1991 1994 1997 2000 2003 2006

Co

nst

ant

$

Kuwait Oman

Saudi Arabia U.A.E.

Indonesia Malaysia

Mexico

Goods Export Sophistication: 1976–2006

Sustainable growth requires diversified exports

• Empirically, export sophistication is an important determinant of long-run growth – Hausmann, Hwang, and Rodrik (2007), Spatafora and Papageorgiou (2013), and Cherif and Hasanov (2014)

• Theoretically, continuous introduction of new goods and tasks and moving up the “quality ladder” lead to sustained productivity gains – Lucas (1993) and Aghion and Howitt (1992)

Proposition 3

Both the initial technological gap and the size of oil revenues determine the chances of success or failure at diversification in oil-exporting countries, while policies adopted magnify or mitigate this effect.

The GCC faced high oil revenues at low levels of technology

Kuwait

Norway

OmanQatarSaudi Arabia

U.A.E.

Bahrain

0

100

200

300

400

500

600

700

0 2000 4000 6000 8000 10000 12000

Re

al M

ach

ine

ry e

xp

ort

s p

er

ca

pit

a, 1

97

0

Real oil exports per capita, 1970-2012 average

Machinery Real Exports per Capita (1970) vs. Oil Revenues

(1970-2012 Average)

US level in 1970

Low Dutch Disease

Moderate Dutch

Disease

Acute Dutch Disease

Moderate to High Dutch Disease

Low Dutch Disease

Acute Dutch Disease

Moderate to High

Dutch Disease

Canada

The technological upgrading that followed was minimal

0

500

1000

1500

2000

2500

3000

0 1000 2000 3000 4000 5000 6000 7000 8000 9000 10000

Ma

ch

ine

ry r

ea

l e

xp

ort

s p

er

ca

pit

a

Real oil exports per capita, 1970-2000 average

Machinery Real Exports per Capita (1970 vs. 2000) vs. Oil Revenues (1970-2000)

Machinery real exports per capita,

2000

Machinery real exports per capita,

1970

US level in 2000

US level in 1970

Canada

Oman

Norway

U.A.E.

Kuwait Qatar

Bahrain Saudi

Arabia

Malaysia

Mexico

Indonesia

Norway: Falling prey to the Dutch Disease

• In 2012, manufacturing hourly wages were the highest in the world and about double that of the US or Japan

• Unit labor costs increased by 50 percent in the 2000s, whereas they declined in Germany and Sweden

• Annual average hours per worker declined by 600 hours since 1960 to about 1400 hours in 2012, third lowest in OECD

The Norwegian Disease: Norway experienced decline in export sophistication

4000

6000

8000

10000

12000

14000

16000

4000

6000

8000

10000

12000

14000

16000

1970 1974 1978 1982 1986 1990 1994 1998 2002 2006 2010

Canada Denmark Malaysia Norway

Goods Export Sophistication, 1976-2006

A few relative successes: Importance of policies

• Indonesia, Malaysia, and Mexico did better than other oil exporters and prepared the ground before the oil revenues started falling

• Import substitution strategy created mostly inefficient firms because they were not encouraged to compete on international markets

• The policy mix of Malaysia involved investment in higher value added comparative advantage industries (e.g. natural resource-related manufacturing) and going beyond comparative advantage (e.g. electronics)

• Indonesia and Mexico show that relying mostly on low wages and labor intensive manufacturing would eventually lead to limited productivity gains

• These countries’ experience suggests that a focus on competing on international markets and an emphasis on technological upgrade and climbing the value added ladder is crucial

Export sophistication improved amid dwindling oil revenues

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

10000

-600

-400

-200

0

200

400

600

800

1000

1200

1970

19

73

19

76

1979

1982

19

85

19

88

1991

1994

19

97

20

00

2003

2006

20

09

20

12

Indonesia

0

2000

4000

6000

8000

10000

12000

14000

-1000

-500

0

500

1000

1500

2000

2500

3000

1970

1973

1976

1979

1982

1985

1988

1991

1994

1997

2000

2003

2006

2009

2012

Malaysia

Net oil exports deflated by US CPI per capita Exports Sophistication (RHS)

Proposition 4

Exports diversification must start now.

It takes decades

• The experience of oil exporters and other countries suggests that it take a long time to develop industries

• It took Malaysia 20-30 years to increase export sophistication

• What if oil prices fell again as in the 1980s-90s?

Avoiding another large and lasting decline in welfare

0

5

10

15

20

25

30

35

40

45

50

75

80

85

90

95

100

105

110

115

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010

Co

nst

ant (

19

82

-84

) $/b

arre

l

Ind

ex (1

98

0=

100

)

Real Consumption per capita and Real Oil Price, 1980–2010

Real Consumption Per Capita (PPP) Real Oil Price (RHS)

Average NFA/GDP: 3 percent in 1980 vs. 54 percent in 2006

Proposition 5

The standard policy advice—implementing structural reforms, improving institutions and business environment, investing in infrastructure, and reducing regulations—may not be sufficient to spur tradable production because of market failures.

Standard policy advice for growth may not be sufficient

• Standard policy prescription includes macroeconomic stability, minimum state intervention and an enabling environment conducive to investment in both physical and human capital

• It consists in tackling “government failures” (Rodrik 2005)

• The GCC has improved in most of these dimensions but relative economic improvement did not follow

Tackling “Government Failures” I

0

20

40

60

80

100

120

140

160

180

200

020406080100120140

Ease

of

Do

ing

Bu

sin

ess

(Ran

kin

g a

mo

ng

18

3 c

ou

ntr

ies)

Global Competitiveness Index

(Ranking among 134 countries)

Doing Business vs. Global Competitiveness Index, 2013Singapore

U.A.E

Kuwait

Bahrain Oman

Saudi Arabia

Qatar

Tackling “Government Failures” II

1

2

3

4

5

6

7

$500 $5,000 $50,000

Sco

re

GDP per capita

Kuwait

Bahrain

Saudi

Arabia

Qatar

U.A.E.

Quality of Infrastructure, 2013

(Score of 7 "meets the highest standards in the world")

USA

Tackling “Government Failures” III

-20

20

60

100

140

180

-20

20

60

100

140

180

Bahrain Kuwait Oman Qatar Saudi

Arabia

U.A.E. Chile Malaysia Mexico Indonesia Norway

Local competition intensity Prevalence of trade barriers

Sources: The World Economic Forum's Global Competitiveness Indicators (2013-14).

Monopoly Related Indicators (Rank 1 - 142, the lower rank the better)

Tackling “Government Failures” IV

0

10

20

30

40

50

60

70

80

90

100

0

10

20

30

40

50

60

70

80

90

100

Bahrain Kuwait Oman Qatar Saudi

Arabia

U.A.E. Chile Malaysia Mexico Indonesia Norway

Source: The World Economic Forum's Global Competitiveness Indicators

(2013-14).

Burden of customs procedures

“Market failures” are the binding constraint

• High scores in infrastructure quality and other business quality indicators in the GCC and much better than in successful oil exporters

• Norway could not escape the Dutch disease although government failures are basically nonexistent there, in particular in comparison with other oil exporters

• The diversification in successful oil exporters began when oil revenues were dwindling or about to start declining. Were it due to solving the government failures, this would have been a very unlikely coincidence

• Firms choose to produce non-tradables over tradables because of risk-return trade-off largely favoring non-tradables

• The “market failures” necessitate government intervention

Proposition 6

The government needs to change the prevailing incentive structure in the society.

Current incentive structure is not conducive for sustainable growth

• Public sector is the “employer of first resort”

• Generous pensions, early retirement age (below 60), high consumer subsidies (10-20 percent of GDP) and transfers

• The current system is not conducive to investment in human capital, employment in the private sector, and entrepreneurship

Changing incentives

• Setting firm limits on public employment and wages, substituted with social safety nets and minimal income and training vouchers

• Improving education quality through – Early childhood education programs (Heckman 2008) – Teacher quality enhancement programs

• Changing social attitudes through “Saemaul Undong”-type social development program – Encouraging communities to undertake small scale projects to improve

their surrounding environment, followed by the investment in income-generating projects

– The Saemaul Undong “…was in a sense, a movement for spiritual reform of Korean people, and has achieved a lot in this respect. It changed people’s attitude from laziness to diligence, from dependence to self-reliance, and from individual selfishness to cooperation with others.” (Choe 2005)

Proposition 7

The state could act as a venture capitalist and foster public-private collaboration to design and implement strategies that go beyond the comparative advantage sectors and target high value-added sectors with large potential spillovers and productivity gains.

The state as a venture capitalist

Experiences in other countries suggest: • Policy mix in vertical and horizontal diversification

• Vertical approach:

– Creating clusters around comparative advantage sectors in oil and gas, e.g. Norway in the 1970s

– Building domestic capabilities and climbing the “quality ladder” with the emphasis on technological transfer and upgrade

• Horizontal approach: – Endeavoring beyond comparative advantage sectors – Pursuing high value added manufacturing and services such as IT – Venturing into innovation sectors

Policies for diversification in other countries

• Taxing non-tradable sectors and using subsidies to support exporters

• Using development banks, venture capital funds, and export promotion agencies

• Creating clusters with links to universities and investing in specific-purpose skills and infrastructure

• Coordinating regionally on strategies

3 key elements of success

• Clarity: The main policy objective should be the development of domestic exporters in high value added products stated in clear terms and measurable objectives

• Discipline: There must be a high level of government commitment to the objectives in social and industrial development with a comprehensive and credible accountability framework

• Trust: A high level of cooperation and trust is required for policies to succeed. Without tackling simultaneously social incentives, the strategies proposed would fail

Concluding remarks

• International experience of successful oil exporters suggest that the GCC countries have been trying some of the policies cited (e.g. horizontal and vertical diversification, clusters, investment funds)

• However, the main challenge is to fix the incentives for both firms and workers

• An emphasis on competing in international markets, technological upgrading, climbing the value added ladder, and enforcing market discipline and accountability is needed

Related Documents