1 AMI-Partners Source: AMI-Partners (www.ami-partners.com) SMB Trends & Direction 2011 It’s Time to Restart Your Engines AMI-Partners New York, Houston, Los Angeles, Singapore, Shanghai, Bangalore, Kolkata, London, Tokyo (ALL CONTENT IN THIS DOCUMENT REPRESENTS AMI-PARTNERS’ INTELLECTUAL PROPERTY AND CANNOT BE REPRODUCED WITHOUT WRITTEN CONSENT FROM AMI-PARTNERS)

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1 AMI-PartnersSource: AMI-Partners (www.ami-partners.com)

SMB Trends & Direction 2011

It’s Time to Restart Your Engines

AMI-PartnersNew York, Houston, Los Angeles, Singapore, Shanghai,

Bangalore, Kolkata, London, Tokyo

(ALL CONTENT IN THIS DOCUMENT REPRESENTS AMI-PARTNERS’ INTELLECTUAL PROPERTY AND CANNOT BE REPRODUCED WITHOUT WRITTEN CONSENT FROM AMI-PARTNERS)

2 AMI-PartnersSource: AMI-Partners (www.ami-partners.com)

Agenda

1

2

3

4

ICT Market Trends

Top Challenges & Opportunities for SMBs

SMB Drivers & Trends

Key Takeaways

3 AMI-PartnersSource: AMI-Partners (www.ami-partners.com)

SMB Expectations About Upcoming Business Conditions in the Next 3-6 Months

13%4%

13%

5%

37%

36%

37%

55%

SB MB

Get better

Stay the same

Get worse

Not sure

• Market sentiment seems to be stabilizing and SMBs are increasingly optimistic about their prospects for 2011. This optimism is expected to encourage companies to focus on key business drivers like customer acquisition, customer satisfaction, employee efficiency/productivity.

4 AMI-PartnersSource: AMI-Partners (www.ami-partners.com)

SMB Actions Being Considered to Increase Revenues

84%

70%

52%

43%

92%

57%

46%

36%

Improve existing customer experiences and retention

Invest in new customer acquisition activities & methods

Improve processes or invest in training to increase employee

productivity

Expand into other markets/opportunities

MBs

SBs

•How can specific solutions be positioned to assist SMBs?

• SMBs will be keen to invest in ICT solutions that are closely aligned to the key business drivers above. But companies are also keen to work the right technology and able partner that will ensure that the ICT solution will address the business needs

5 AMI-PartnersSource: AMI-Partners (www.ami-partners.com)

AMI View of Waves of Adoption By Country Economic Stage

MM NIM EM

Desktop PCs1 99% 100% 97%

Notebook PCs 83% 54% 36%

High-Speed/ Internet 88% 94% 59%

Anti-Virus 83% 94% 71%

Basic Web site 60% 31% 36%

Productivity Suites1 82% 95% 93%

Accounting SW1, 2 54% 42% 25%

MM NIM EM

LAN/Server 38% 19% 10%

e-Comm Web Site 25% 13% 11%

WLAN 23% 11% 4%

Network Firewall 31% 14% 8%

Intrusion Detection 10% 4% 2%

Doc & Content Mgt.1 15% 16% 12%

Business Intel Apps1 15% 32% 6%

Hosted Apps (SaaS) 21% 16% 6%

Hosted IP Tel/ IP Centrex1 2% 1% 0.4%

MM NIM EM

Intranet 14% 4% 3%

WAN 10% 7% 3%

VPN 28% 9% 7%

IP SAN 2% 1% 1%

Fibre Channel SAN 1% 1% 1%

CRM3 2% 1% 0.5%

ERP/SCM 6% 4% 3%

IP PBX 4% 1% 1%

MM (Mature Markets) = US, CA, UK, GE, FR, JP, AU, DE, FI, IT, NZ, NO, SD, Rest of W EuropeNIM (Newly Industrialized Markets) = HK, TW, SING, MA, KREM (Emerging Markets) = CH, IN, INDO, PH, TH, VT, RU, CZ, PO BR, MX, RO AP, RO EEMEA, RO LATAM

Building The

Basic Infrastructure

Wave I

Connecting The Enterprise

Wave II

Extending The Enterprise

(Leveraging the Network)

Wave III

1 = Countries included in this calculation are: US ,CA ,FR ,GE UK ,RU ,PO ,JP ,AU ,CH ,IN ,KR ,BR ,MX

2 = Acctg SW = Bkkpg/Acctg SW Pkgs. + Online Svcs.3 = ”True” CRM

% of PC SMBs

Evolving Distribution, Ecosystem Partners, Business Processes, Security and Service/Support Needs(Data Above Shows Penetration Among PC Firms)

6 AMI-PartnersSource: AMI-Partners (www.ami-partners.com)

Growth to be Fueled More by Emerging Market Ratherthan Mature Ones

Sales of Smartphones

Value-added services

Mobile telephony

Web 2.0

Communication collaboration

• Markets (countries/industries) are increasingly looking at ICT solutions as a way to leapfrog the competition.

• ICT Solutions are being considered as a tool to overcome their weakness/limitations

• The border between consumer technology and commercial technology/solutions have vanished

• The borders on location of work are starting to be re-written and companies are forced to constantly look at ICT solutions that will give business benefits

7 AMI-PartnersSource: AMI-Partners (www.ami-partners.com)

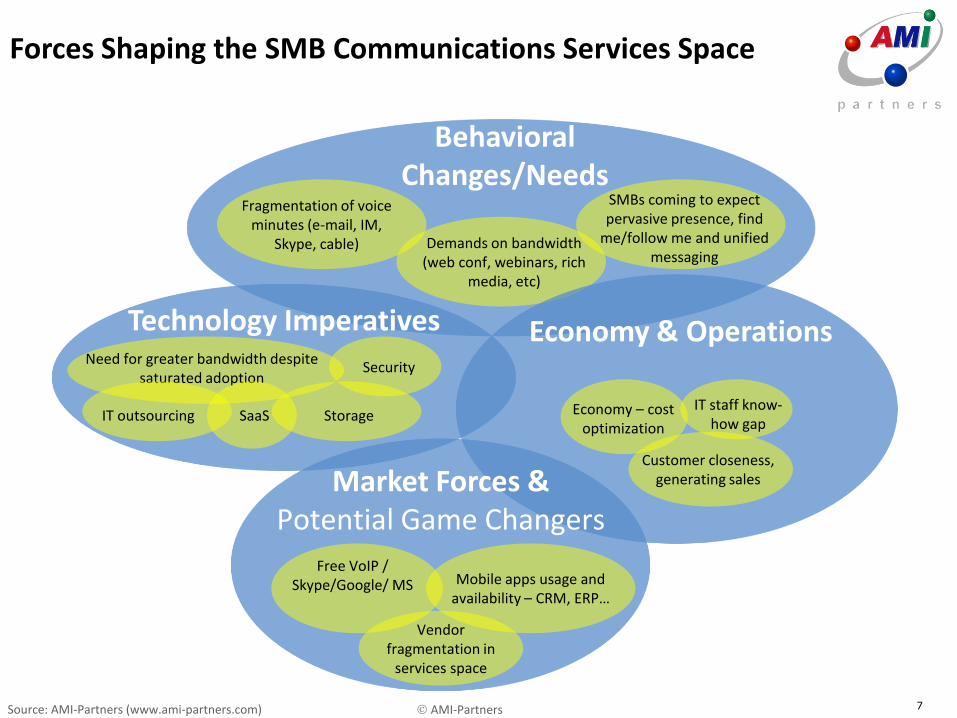

Forces Shaping the SMB Communications Services Space

Behavioral Changes/Needs

Fragmentation of voice minutes (e-mail, IM,

Skype, cable) Demands on bandwidth (web conf, webinars, rich

media, etc)

SMBs coming to expect pervasive presence, find

me/follow me and unified messaging

Economy & Operations

Economy – cost optimization

Customer closeness, generating sales

IT staff know-how gap

Technology ImperativesNeed for greater bandwidth despite

saturated adoption

SaaS

Security

StorageIT outsourcing

Market Forces &Potential Game Changers

Free VoIP / Skype/Google/ MS

Vendor fragmentation in

services space

Mobile apps usage and availability – CRM, ERP…

8 AMI-PartnersSource: AMI-Partners (www.ami-partners.com)

What is Cloud Services?

• Migration of software application, Infrastructure (Servers, Storage, etc.) into a shared/3rd party location where they are managed and supported to meet a specific SLA

9 AMI-PartnersSource: AMI-Partners (www.ami-partners.com)

Infrastructure to Support Accelerated Cloud Growth

0%

10%

20%

30%

40%

50%

60%

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Pe

net

rati

on

-%

of

MB

s W

W

SaaS Smartphones Broadband Hosted VoIP RMITS* Netbooks

1990s 2000s

•Enterprise class apps –

Siebel, etc.

•Predominantly 1:1

•Expensive

•No bandwidth

•Effective broadband

•SLAs and QoS

•SOA, Web 2.0

•Multitenant/PaaS

•Lightweight/MB apps

2010+

•Super

Broadband

•MB mindset

•Economy

•Smartphones

•Netbooks/

tablets

•Telcos as a

channel

*Remotely Managed IT services

Recession Economic Shock

10 AMI-PartnersSource: AMI-Partners (www.ami-partners.com)

Cloud Has Strong Momentum in the SMB Market

25%

33%

55%

45%

60% 60%

70%65%

NA EMEA APAC LATAM

Q1 '09 Q1 '10

SMBs WILLINGNESS TO INVEST IN 3rd PARTY SOLUTIONS WITH FLEXIBLE, MONTHLY, PER USER PAYMENT STRUCTURE (% OF PC SMBs)

11 AMI-PartnersSource: AMI-Partners (www.ami-partners.com)

Key SMB Cloud Drivers for 2011

1) Infrastructure

in place to support

accelerated cloud growth

2) Economic environment accentuating

cloud benefits

3) Proliferation of mobility and

ubiquitous data access

mindset

4) Cloud value proposition

alignment with core MB needs

5) Remote Managed IT

Services (RMITS) entering

mainstream MB

6) Demand for integrated “As

a Service” solutions

12 AMI-PartnersSource: AMI-Partners (www.ami-partners.com)

SMB Growth Opportunities - Collaborative and IP-based

Solutions are Driving the Bulk of Growth in APAC Telecom Market

Broadband

Dial-Up

IP Trunking

Smartphone Equip

Cell Phone Service

IP/PBX

Pure TDM-PBX

WAN

Audio Conferencing

Video Conferencing

Web Conferencing

Website HostingHosted VoIP

Managed Security

SaaS

Applications Hosting

CAGR

HighLow

High

Sp

en

d

<0% 20% 30% 40% 50+%

13 AMI-PartnersSource: AMI-Partners (www.ami-partners.com)

SMB Cloud Services Usage Snapshot (Singapore)

19%

13%

7%

4%

4%

4%

2%

26%

Acctg/fin

CRM

Proj mgt

HR

BI

Payroll

ERP

ANY SaaS

SaaS

53%

28%

25%

16%

15%

12%

5%

5%

4%

76%

Instant messaging

Hosted productivity suites

Security

Servers

Web conferencing

Data storage/back-up

Document collaboration

Video conferencing

Audio conferencing

ANY Infrastructure

Infrastructure

• Applications (Software or Infrastructure) are the key to the adoptionof Cloud services. Companies should develop a detailed roadmap to understand which applications are best suited to be moved to the Cloud

14 AMI-PartnersSource: AMI-Partners (www.ami-partners.com)

n = 116

Q15. What are the reasons that would make you consider taking up or continue using online hosted software, i.e. SaaS? Q16. For the options you have selected, please rank them in order of priority.

2%

2%

3%

3%

3%

3%

4%

8%

20%

53%

3%

1%

2%

5%

2%

3%

1%

3%

8%

6%

22%

15%

3%

2%

1%

4%

3%

9%

8%

9%

1%

2%

1%

1%

1%

3%

2%

5%

1%

1%

1%

Save on manpower resources (eg. no need for IT person)

Access to next-generation application functionality not available in traditional software

Improve internal and external collaboration

Enable focus on core competencies

No need to worry about upgrades and patches and upgrading due to technology advancement

Covert fixed IT costs to variable costs

Improve service levels

Reduce risk

Faster implementation

Reduce capital and/or operating costs

Simpler software management

Mobility (customers can access documents, emails, records etc. anytime, anywhere)

Ranked 1 Ranked 2 Ranked 3 Ranked 4 Ranked 5

% of SBs who answered 5, “Very Likely” + 4, “Likely“ + 3, “Maybe” in Q14

SaaS Opportunity Analysis

Important Factors for Considering or Continuing SaaSsoftware management and costs reduction are the main drivers for SBs to consider or continue SaaS.

15 AMI-PartnersSource: AMI-Partners (www.ami-partners.com)

Key Takeaways

• Technology is enabling SMB mobility and driving need for ubiquitous data access

• SMB ICT needs continue to rise, while internal IT support is being downsized

• More smart devices, each consuming more in 2011

• SMBs are looking for communicated value proposition which has tighter relevancy with their business issues and goals

• Mindset is shifting towards managing cash flow via service based models

– Hosted VPN, Software as a Service, Hosted infrastructure

• SMB employees want "Anytime, anywhere, always" functionality from their business applications just like any larger enterprise mobile workers.

• Infrastructure for accelerated cloud adoption is in place; Availability of compelling offerings, bundles and pricing options is key to uptake

16 AMI-PartnersSource: AMI-Partners (www.ami-partners.com)

Venu ReddyVP, Asia Pacific

[email protected]: (65) 6220 5535 ext 125

AMI-Partners78 Shenton Way, #27-01A

Singapore 079120

Thank You

17 AMI-PartnersSource: AMI-Partners (www.ami-partners.com)

Contact Information

For Client Inquiries or to purchase other similar reports please email us at [email protected] or contact one of our offices directly at :

United States

546 Fifth AvenueNew York , New York 10036

T: 212-944-5100 F: 212 944 2288

London, England

BCM Box 2299London, England WC1N3XX

T: +44 2089872756 F: +44 7789 551606

703 Central Plaza2/6 Sarat Bose Road

Kolkata – 700020

T: +33 4003 3093 F: +33 4003 3097

Kolkata, India

Bangalore, India

Gopal Towers146 Ramaiah Street, Off Airport Road

Kodihalli, Bangalore – 560008

T: +80 6451 5732 F: +80 4148 2612

78 Shenton Way #27-01A Singapore 079120

T: +65 6220 5535 F: +65 6220 5536

Singapore

Unit 2203, Hong Kong Plaza 283 Huai Hai Central Road

Shanghai, PR China, 200021

T: +86 21 6390 6298 F: +86 21 6390 6128

Shanghai, PR China

Related Documents

![[MS-SMB]: Server Message Block (SMB) ProtocolMS-SMB...2 / 180 [MS-SMB] - v20160714 Server Message Block (SMB) Protocol Copyright © 2016 Microsoft Corporation Release: July 14, 2016](https://static.cupdf.com/doc/110x72/5eca5802c38f4e40c93e9ef9/ms-smb-server-message-block-smb-protocol-ms-smb-2-180-ms-smb-v20160714.jpg)

![[MS-SMB]: Server Message Block (SMB) Protocol Specificationdocshare01.docshare.tips/files/5883/58834888.pdf2 / 179 [MS-SMB] — v20110610 Server Message Block (SMB) Protocol Specification](https://static.cupdf.com/doc/110x72/5eca5807c38f4e40c93e9f01/ms-smb-server-message-block-smb-protocol-spe-2-179-ms-smb-a-v20110610.jpg)