Smarter than beta Why factor investing? White Paper March 2015 Authored by: Alexander Davey, Director, Senior Equity Product Specialist Stephen Tong, Director, Senior Equity Product Specialist

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Smarter than beta

Why factor investing?

White Paper March 2015

Authored by:

Alexander Davey, Director, Senior Equity Product Specialist

Stephen Tong, Director, Senior Equity Product Specialist

2

Smarter than beta Why factor investing? What is factor investing? 3

Alternative weighting schemes 3

Investment considerations 5

Factor investing in practice 7

Implementation of factor strategies 7

Low volatility case study 8

Conclusion 11

Introduction

Factor investing offers the potential for excess

returns that are generally achieved through a rules-

based, transparent methodology. Many factors such

as Value, Quality, Momentum, and Low Volatility

have been shown to deliver excess returns with

persistency over the long term. Factors also offer a

language for understanding the sources of portfolio

returns. Together, factor exposures and portfolio

construction are key drivers of overall return patterns.

Therefore it is important for investors to understand

factors and evaluate factor strategies. In this paper,

we examine low volatility as a case study to show

factor investing in action.

3

What is factor investing? Alternative weighting schemes

Factor investing offers the potential for excess

returns and increases the transparency around the

sources of return.

The appeal of traditional cap-weighted investing is

based on the notion of efficient markets. Cap-

weighted investing is macro-consistent, high capacity

and cost effective, and it has served as a

performance reference for equity industry. Cap-

weighting never challenges the potential irrationality

of markets, yet it manages to produce better returns

over time than many active managers. The strength

of such passive investing highlights the importance of

a single factor – beta – in explaining equity returns,

and it sets the bar for any alternative strategy to

improve upon market returns.

Smart beta, including factor investing, categorizes a

host of techniques which aim to improve risk-

adjusted returns versus standard market indices.

They operate within the fundamental rules of asset

management, but may challenge and disrupt

common wisdom.

While cap-weighted index weights adjust according

to market prices, alternative weighting approaches

enable a systematic rebalancing discipline to add

value by taking advantage of excess volatility. By

removing the link with price, alternative weighting

strategies help protect investors from behavioral

biases and “irrational exuberances” that can escalate

or depress asset values. Some academic papers

have shown that many alternative weighting

strategies, regardless of criterion, have this powerful

effect. For example, research by Clare, Motson and

Thomas1 has shown that alternative weighting

strategies delivered better risk-adjusted returns than

the cap-weighted index (using data on the 1,000

largest US stocks every year from 1968 to the end of

2011).

Intuitively, such a rebalancing process may sound

mistaken. Cut winners to fund losers? The broad

answer is that stock markets can run away with

themselves (New York in the late 1920s; Japan in the

1980s; New York, again, in the late 1990s) only to

undergo substantial corrections. Alternative

weighting and rebalancing can be beneficial as a

primary strategic goal.

Portfolio returns can be driven by common

factors

Do hundreds of stocks in a portfolio represent

hundreds of individual contributory elements to the

portfolio? Certainly, each company will have

idiosyncratic elements, and, by extension,

concentrated portfolios might well exhibit more

unusual characteristics. But for portfolios with a

larger number of holdings, common factors may be

more telling, and many individual decisions can be

reinterpreted in aggregate as tilts towards a few

factor risk premiums. For Professor Ang, factors offer

a powerful, simplifying means of understanding the

most important sources of returns. This forms a basis

for factor investing.

“Thousands of correlated individual bets by

managers effectively become large bets on

factors. An equity manager going long 1,000

value-oriented stocks and underweighting 1,000

growth stocks does not have 1,000 separate

bets; he has one big bet on the value-growth

factor. A fixed income manager who squeezes

out the last bits of yield by finding 1,000

relatively illiquid bonds funded by short

positions in 1,000 liquid bonds (through the repo

market) has made one bet on an illiquidity

factor2.”

1 “We find that all of the alternative indices considered would have produced a better risk-adjusted performance than could have been achieved by having a passive exposure to a market capitalization-weighted index.” An evaluation of alternative equity indices, Cass Business School, Clare, A., Motson, N., Thomas, S., An evaluation of alternative equity indices, Cass Business School, 2013

2 Ang, A., Asset Management: a Systematic Approach to Factor Investing, Oxford University Press, 2014

4

Factor definitions

There are numbers of data points that can aid in the

understanding of listed companies, such as the

number of employees with relevant PhDs or the

enterprise’s industrial safety record. These data

points may even inform investors about potential

risks.

In explaining excess returns, only a small set of

factors seem to have a persistent risk premium

(Exhibit 1). This makes it worthwhile for investors to

recognize and exploit them. Factor investing entails

constructing a portfolio that has positive exposure to

a desired risk premium.

Factor investing – as many of its proponents will

agree – is not entirely new. Most investment

strategies have some degree of implicit factor bias,

and risk analytics and attribution have been

developed as the result of a desire to fully

understand and evaluate the sources of active

returns. We’ve seen active managers characterize

themselves as value managers or small cap

managers or quality managers. The nine-box style

matrix, dividing a general equity universe along style

and size dimensions, provided a structure to

categorize portfolio managers in an asset allocation

context.

Factor investing, as a more refined perspective on

risk premia, is a logical next step along this path.

Alternative weighting strategies can be characterized

in the context of factors. For example, equally-

weighted indices emphasize small cap stocks (i.e.,

the small size factor) relative to the cap-weighted

index, while Low Volatility strategies aim to capture

the Low Volatility factor. In a similar vein,

fundamental indexation – where stocks can be

weighted by one or more fundamental criterion (e.g.

value-added) that are believed to capture a stock's

intrinsic value – also focuses on a systematic

rebalancing “factor” in an attempt to take advantage

of excess volatility.

Key factors Risk rationale Behavioral rationale Assessment criteria examples

Value Uncertainty over future business

prospects

Fear, loss aversion

Book-to-price

Earnings-to-price

Small Size Illiquidity Inefficient information Market capitalization

Momentum Changing expectations Under-reaction to new information 12-month share price change

Low Volatility Leverage constraints favour

high-beta stocks

Investors prefer big winners or

“lottery” stocks

Return volatility (standard deviation)

Beta

Quality Potential for competitive

advantage to be eroded

Loss aversion

Return on Equity

Return on Capital Employed

Exhibit 1: Key factors

Source: HSBC Global Asset Management. For illustrative purposes only.

5

What is factor investing? Investment considerations

Factor investing is not as simple as building a portfolio

of stocks that rank highly on a specific factor. There is

fair debate over whether risk premiums are persistent.

In addition, the investment process – stock selection

(i.e., factor criteria) and portfolio construction

(weighting, rebalancing) – can have a significant

impact on investment outcomes.

Factor persistency

If factors have delivered excess returns on an

empirical basis, one naturally questions what can

drive persistency. Indeed, there are plausible

explanations put forward for individual factors that

suggest factor efficacy can be long-lasting. Financial

theory suggests investors earn higher returns for

bearing higher risk, so factors must be perceived, in

some way, as more risky for some market

participants. Behavioural finance may also highlight

investor actions that are unlikely to change.

Still, if cap-weighted indexation is the only macro-

consistent passive strategy, then investors may well

think of factor investing as a “more than passive”

strategy with potential capacity constraints. Risk

premia are susceptible to market erosion, through

arbitrage (i.e., popularity of the strategy and weight of

money) and the formation of a “crowded trade” which

can reduce potential returns. Some academics argue

that this is precisely what happened in the 1980s with

small caps3, following the Rolf Banz paper on the size

premium. Enough investors raised their allocations to

small caps – even at higher prices – to extinguish the

size premium. This interpretation remains a matter of

discussion, but it is a good reminder that factor risk

premiums are not immutable and remain part of the

organic, often surprising course of stock markets. On-

going analysis can evaluate how factor risk premiums

may change over time.

Building factor exposure

While there is general agreement on the set of factors

that can drive excess returns, there is little consensus

on the criteria for creating exposure to a specific

factor, nor is there a common portfolio construction

methodology either for weighting or rebalancing. If

asset managers have different ranking criteria and

different portfolio construction approaches, risk and

return characteristics are likely to vary substantially

across factor strategies that share similar labels.

Investors should not presume there is homogeneity

across factor strategies.

As factor criteria and portfolio construction drive

portfolio factor exposures and ultimately return

patterns, they are critical components of investment

process design.

Each stock will have a unique factor profile

depending on the criteria used to determine

exposure to each factor. As a result, a stock ranking

highly on one factor may have positive or negative

exposures to other factors. How stocks are weighted

will determine the portfolio’s target factor exposure

and its residual exposure to other factors. A key

consideration of portfolio construction is how to

manage factor exposure versus residual exposures.

Attempting to maximize exposure to one factor may

drive higher residual exposures, while attempting to

minimize residual exposures could reduce the

exposure to the desired factor.

The portfolio factor profile has broad implications.

First and foremost, it provides the foundation for

portfolio returns. We know that factor returns can

vary with macroeconomic conditions and market

cycles. As well, the correlation of excess returns

between factors can vary over time. Together, these

elements drive the pattern of portfolio returns.

In terms of investment governance, inconsistent

factor exposures increases the difficulty in explaining

returns. In addition, competing factor exposures

could mask the impact of the target factor. For

example, in the recovery after the global financial

crisis, we saw that both Value and Momentum

factors delivered excess returns. Which factor could

we say was the main driver of returns? When factors

are coincident, risk frameworks are challenged.

Return attribution would be inconclusive as the

analysis would be dependent on the order in which

the factors were regressed.

3 See for example, Andrew Ang in Chapter 14 of Asset management: a systematic approach to factor investing. OUP, 2013

6

Multi-factor diversification

We also observe that factor returns are time-varying

and can have long return cycles, implying factor

strategies can outperform or underperform relative to

the market cap index over long periods.

Exhibit 2 shows that single factors have low or

negative correlation with other factors, which means

while one factor may experience a long period of

underperformance, another factor may

simultaneously outperform. While correlations

between factors may change over time, returns are

generally orthogonal, so it is unlikely that all factors

outperform or underperform at the same time.

Given the different return patterns and low

correlations across factors, it seems to be

straightforward that combining factors in a multi-

factor portfolio could help keep excess return

potential strong while the diversification could lower

tracking error. The power of factor combinations is

evident. Note that it is critical to combine highly

efficient or “pure” factor strategies to mitigate the

affects of residual exposures on the risk and return

characteristics of the combination.

We see dynamic factor allocation as the next frontier

in multi-factor strategies.

Qualitative and quantitative

Factor investing lends itself to quantitative

management. Stock selection and portfolio

construction, however, may not include parameters

that screen out unattractive investments. For

example, one might express the value factor by low

price to book ratio. However, a stock may have low

value because its business is at risk and the market

has rightly marked down its value. In some

situations, including an element of fundamental or

qualitative judgement could temper some of the

effects described above and bring additional value to

the investment process in assessing the investment

potential of individual names.

A step beyond quantitative management, indexation

through a systematic, rules-based approach can

create a transparent, liquid and cost-effective

investment solution, though rules transparency may

create an arbitrage opportunity for traders around

index changes.

Valu

e

Sm

all

Cap

Mo

men

tum

Lo

w

Vo

lati

lity

Qu

ali

ty

Value

Small Cap 0.4

Momentum 0.2 0.1

Low Volatility -0.2 0.3 0.0

Quality 0.3 0.1 0.1 -0.1

Exhibit 2: Factor correlations

Excess returns relative to MSCI World, from June 2001 to December 2014. Source: HSBC Global Asset Management Simulated data is shown for illustrative purposes only, and should not be relied on as an indication of future returns. Simulations are based on back testing assuming that the optimization models and rules in place today are applied to historical data. As with any mathematical model that calculates results from inputs, results may vary significantly according to the values applied. Prospective investors should understand the assumptions and evaluate these assumptions to determine if they are appropriate for their purposes. Some relevant events or conditions may not have been considered in the assumptions. Actual events or conditions may differ materially from assumptions. Past performance is indicative only and not a guarantee of future results.

7

Factor investing in practice Implementation of factor strategies

Accessing factor strategies

How can asset owners take advantage of factor

strategies? The key challenge for asset owners is

how best to incorporate these new strategies within

their investment portfolios.

Over time, factor strategies can deliver excess

returns versus cap-weighted indices. They introduce

tracking error versus the cap-weighted index. The

diversity in the behavior of various factors means that

combining factors is not merely a case of gluing

together boxes back into an original whole, as is the

case with the current style matrix. Investors can

select which factor or factor combination best suits

their investment beliefs and needs. We see factor

strategies as a complement to traditional active stock

selection strategies that aim to capture idiosyncratic

risk.

A factor perspective has advantages over a style

matrix perspective

If one picks an investment strategy from each style

matrix box, asset owners are obliged to evaluate the

contribution of market beta, factors, stock selection

and manager skill for each mandate. In the end, their

aggregate contribution may amount to little more

than the market itself. Of course, if a large-cap value

manager and a small-cap growth manager are

selected, there may be definite tilts to the pairing in

aggregate. But the investor may also acquire

elements of bias from each box which effectively

offset each other so that the investor ends up buying

the market, more or less. Manager style drift can also

negate asset allocation decisions. In contrast, factor

strategies do not sum to the market, so this outcome

is less likely.

Greater transparency of returns

Many asset owners familiar with traditional style

investing have attributed active returns to a

combination of style exposure and idiosyncratic risk,

or manager skill. Style manager returns are often

referenced against a relevant style index as well as a

broader standard market-cap index.

We see the prism of factors as providing additional

insight into active returns, in combination with

traditional attribution parameters. If active manager

returns are decomposed into factor exposures and

skill, it might be the case that returns once

considered driven by skill may now be the result of

factor exposure. As with style indices, traditional

active managers may be asked to outperform a

reference factor index rather than a cap-weighted

index, uncovering closet factor seekers. Active

managers will need to adapt, acknowledging the

power and pervasiveness of factors within their own

strategies.

8

Factor investing in practice Low volatility case study

We consider low volatility as a case study to show

factor investing in action.

Low volatility definition

The low volatility anomaly was first documented

academically by Haugen and Heins over forty years

ago4. They discovered that stocks with lower volatility

can deliver better returns than stocks with higher

volatility. Over twenty years ago, Nobel prize-winner

Fischer Black proposed that low beta stocks should

be considered a separate category, which would

enable asset owners to better understand how to

incorporate them into asset allocation – for example,

a split of 80% low beta stocks and 20% fixed income.

Over the past ten years, the low volatility anomaly

has been manifest in returns, as shown in Exhibit 3.

With the 2008 global financial crisis still fresh in the

minds of pension plan fiduciaries and their sponsors,

the ability to avoid precipitous depreciation is more

important for many than double-digit returns. Deficit

recovery plans and miserly yields in fixed income

mean that equity investing is still the first choice

‘engine’ for capital growth among retirement plans.

But given current conditions and goals, strategies

delivering improved risk-adjusted returns look more

attractive as part of the total mix.

Black’s perspective is finally being realized with the

tens of low volatility strategies available today.

Low Volatility persistency

Haugen and Heins’ findings are often presented as a

puzzle, because a so-called anomaly should be

arbitraged over time.

Two potential explanations suggest why the low

volatility anomaly could hold for some time. First,

efficient market theory assumes that investors can

use leverage and short-selling. In practice, however,

leverage is not at all common among long-term asset

owners such as pension plans. In addition, active

investors, constrained by guidelines against

employing leverage, may buy high-beta stocks to get

more ‘bang for their buck.’

Behaviorally, investors are so keen to meet relative

performance targets versus benchmark indices that

high beta stocks prove too much of a temptation.

Institutional investment consultancies such as

Russell have been vocal on the excessive volatility

that active managers in aggregate can bring to

pension fund portfolios5. Equally, investors can make

poor decisions in the light of heavy losses, effectively

selling at or near the lowest value of their assets.

Mathematically, it can be more rewarding to

participate in much of a bull run and lose less on the

downside than it is to experience the full ups and

downs of equity markets. This is a facet of the power

of compounding and could be a part of the rationale

for low volatility investing.

4 Haugen, R., Heins, A.J., On the Evidence Supporting the Existence of Risk Premiums in the Capital Market, 1972, http://papers.ssrn.com/sol3/papers.cfm?abstract_id=1783797

5 Maton, B., Blurring the lines, IPE, March 2014: www.ipe.com/reports/smart-beta/blurring-the-lines/10001291.article

MSCI ACWI

MSCI ACWI

Minimum Volatility

Number of stocks 2471 349

Beta 1.0 0.62

Tracking error (%) - 8.05

Return

10-year annualized (%) 6.37 8.40

Volatility

10-year annualized (%) 16.57 11.01

Sharpe Ratio

10-year 0.35 0.63

Max drawdown

31 Oct 07 – 9 Mar 09 58.38 43.41

Exhibit 3: Characteristics of a low volatility strategy

Source: MSCI, net USD returns as of 27 February 2015. For illustrative purposes only. Past performance is indicative only and not a guarantee of future results.

9

Building low volatility exposure

Three low volatility indices demonstrate differences

between strategies aimed at expressing the same

factor. The MSCI ACWI Minimum Volatility Index

applies an optimization process to deliver the lowest

return variance, with a maximum limit of ±5% on its

sector weights relative to the cap-weighted index.

The MSCI ACWI Volatility Tilt Index reweights the

cap-weighted index by the inverse of security price

variance. In contrast, the S&P Low Volatility Indices

screen for the least volatile stocks, have no such

sector constraints and their constituents are weighted

relative to the inverse of their volatility.

Exhibit 4 shows the return and volatility for the three

indices and the underlying cap-weighted index. Each

of the Low Volatility indices showed attractive

performance characteristics relative to the underlying

index, but the performance of the two MSCI volatility

strategies shows how a difference in investment

process can drive different outcomes.

Low volatility stock selection and portfolio

construction approaches also result in residual

exposures that might be helpful for investors to

understand. For example, the MSCI ACWI Minimum

Volatility Index has a lower exposure to value and a

higher exposure to small size than MSCI ACWI.

Many of the unglamorous stocks in low volatility

investing can be fixed income-like in their

characteristics, which can make them more

susceptible to interest rate changes. Observe the

relative performance of the MSCI ACWI Minimum

Volatility Index in comparison to its respective cap-

weighted index in 2013 as the Federal Reserve

began to discuss tapering of their quantitative easing

program and expectations of US interest rate hikes

grew.

Exhibit 4: Comparison of low volatility indices

Ten years annualized through 27 February 2015. Volatility tilt figures are gross Source: MSCI, S&P For illustrative purposes only Past performance is indicative only and not a guarantee of future results.

Index

MSCI

ACWI

Minimum

Volatility

MSCI

ACWI

Volatility

Tilt

MSCI

ACWI

S&P 500

Low

Volatility

S&P

500

Return 8.40 7.34 6.37 8.37 7.31

Volatility 11.01 14.10 16.57 10.55 14.76

Sharpe ratio 0.63 0.45 0.35 - -

Tracking error 8.05 3.54 - - -

Note: The shaded area represents ±1 standard deviation exposure tilt versus the MSCI ACWI. Exposures outside this area are deemed significant. Source: HSBC Global Asset Management, Style Research, December 2014. For illustrative purposes only. Past performance is indicative only and not a guarantee of future results.

Exhibit 5: Risk exposures of the MSCI ACWI Minimum

Volatility Index relative to the parent index, MSCI ACWI

(2.6)

1.3

(2.6) (2.5) (1.9) (2.3)

(0.5) (0.2)

0.6 0.1

1.1

(0.5)

1.1 0.2

(2.0)

1.1

(4.3)

(9.4)

2.0

(2.0)

(5.6)

(10)

(8)

(6)

(4)

(2)

0

2

Bo

ok t

o P

rice p

er

Sha

re

Div

ide

nd

Yie

ld

Ea

rnin

gs Y

ield

Cash

flo

w Y

ield

Sa

les t

o P

rice

EB

ITD

A to

Pri

ce

Retu

rn o

n E

quity

Ea

rnin

gs G

row

th

Incom

e/S

ale

s

Sa

les G

row

th

IBE

S 1

2M

th G

r

IBE

S 1

Yr

Rev

Mark

et

Cap

Mark

et

Be

ta

Mom

en

tum

Sh

ort

Te

rm

Mom

en

tum

Med

ium

Te

rm

Deb

t/E

quity

Fore

ign

Sa

les

Va

lue

Forw

ard

Gro

wth

His

tori

c G

row

th

Gro

wth

Sources: HSBC Global Asset Management, Bloomberg, as of 31 December 2014. For illustrative purposes only. Past performance is indicative only and not a guarantee of future results.

Exhibit 6: Relative performance of the MSCI ACWI

Minimum Volatility Index versus MSCI ACWI

0.90

0.95

1.00

1.05

1.10

Dec/12 Jun/13 Dec/13 Jun/14 Dec/14

Fed tapering discussion

Defensives

outperform

Rela

tive p

erf

orm

an

ce o

f M

SC

I A

CW

I

Min

imu

m V

ola

tility

vers

us M

SC

I A

CW

I

10

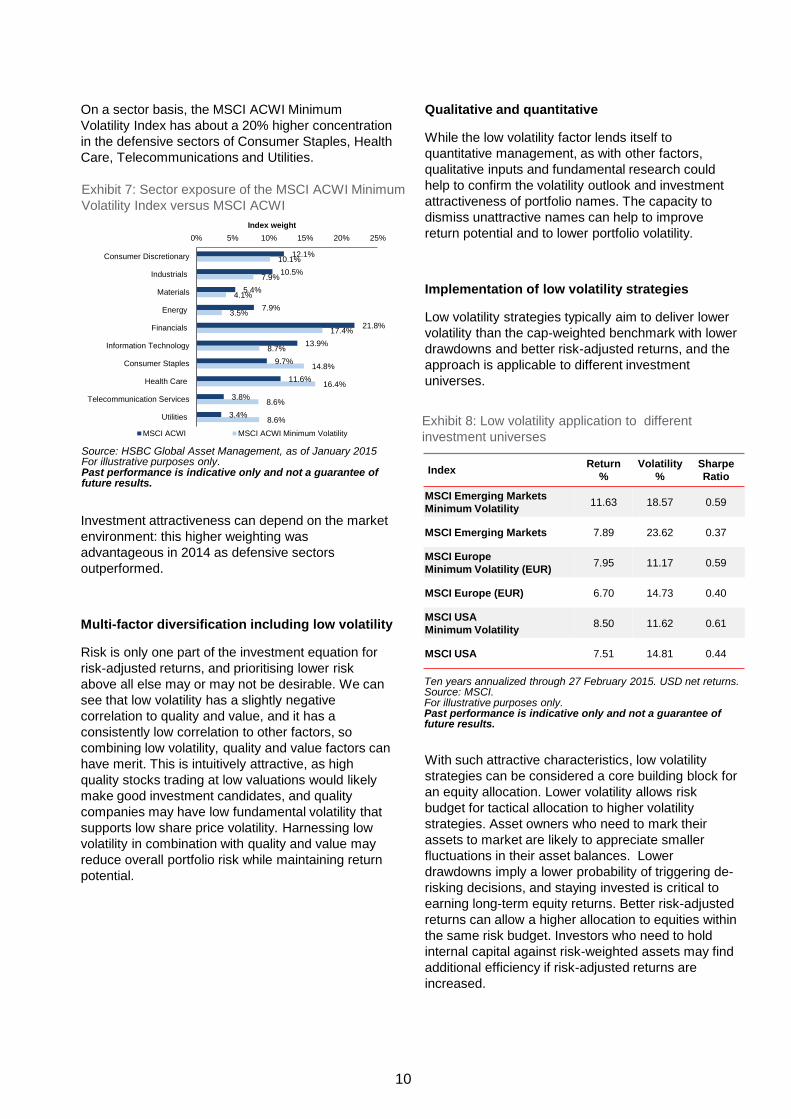

On a sector basis, the MSCI ACWI Minimum

Volatility Index has about a 20% higher concentration

in the defensive sectors of Consumer Staples, Health

Care, Telecommunications and Utilities.

Investment attractiveness can depend on the market

environment: this higher weighting was

advantageous in 2014 as defensive sectors

outperformed.

Multi-factor diversification including low volatility

Risk is only one part of the investment equation for

risk-adjusted returns, and prioritising lower risk

above all else may or may not be desirable. We can

see that low volatility has a slightly negative

correlation to quality and value, and it has a

consistently low correlation to other factors, so

combining low volatility, quality and value factors can

have merit. This is intuitively attractive, as high

quality stocks trading at low valuations would likely

make good investment candidates, and quality

companies may have low fundamental volatility that

supports low share price volatility. Harnessing low

volatility in combination with quality and value may

reduce overall portfolio risk while maintaining return

potential.

Qualitative and quantitative

While the low volatility factor lends itself to

quantitative management, as with other factors,

qualitative inputs and fundamental research could

help to confirm the volatility outlook and investment

attractiveness of portfolio names. The capacity to

dismiss unattractive names can help to improve

return potential and to lower portfolio volatility.

Implementation of low volatility strategies

Low volatility strategies typically aim to deliver lower

volatility than the cap-weighted benchmark with lower

drawdowns and better risk-adjusted returns, and the

approach is applicable to different investment

universes.

With such attractive characteristics, low volatility

strategies can be considered a core building block for

an equity allocation. Lower volatility allows risk

budget for tactical allocation to higher volatility

strategies. Asset owners who need to mark their

assets to market are likely to appreciate smaller

fluctuations in their asset balances. Lower

drawdowns imply a lower probability of triggering de-

risking decisions, and staying invested is critical to

earning long-term equity returns. Better risk-adjusted

returns can allow a higher allocation to equities within

the same risk budget. Investors who need to hold

internal capital against risk-weighted assets may find

additional efficiency if risk-adjusted returns are

increased.

Source: HSBC Global Asset Management, as of January 2015 For illustrative purposes only. Past performance is indicative only and not a guarantee of future results.

Exhibit 7: Sector exposure of the MSCI ACWI Minimum

Volatility Index versus MSCI ACWI

12.1%

10.5%

5.4%

7.9%

21.8%

13.9%

9.7%

11.6%

3.8%

3.4%

10.1%

7.9%

4.1%

3.5%

17.4%

8.7%

14.8%

16.4%

8.6%

8.6%

0% 5% 10% 15% 20% 25%

Consumer Discretionary

Industrials

Materials

Energy

Financials

Information Technology

Consumer Staples

Health Care

Telecommunication Services

Utilities

Index weight

MSCI ACWI MSCI ACWI Minimum Volatility

Index Return

%

Volatility

%

Sharpe

Ratio

MSCI Emerging Markets

Minimum Volatility 11.63 18.57 0.59

MSCI Emerging Markets 7.89 23.62 0.37

MSCI Europe

Minimum Volatility (EUR) 7.95 11.17 0.59

MSCI Europe (EUR) 6.70 14.73 0.40

MSCI USA

Minimum Volatility 8.50 11.62 0.61

MSCI USA 7.51 14.81 0.44

Exhibit 8: Low volatility application to different

investment universes

Ten years annualized through 27 February 2015. USD net returns. Source: MSCI. For illustrative purposes only. Past performance is indicative only and not a guarantee of future results.

11

Conclusion ?

Factor strategies have attractive investment

characteristics that should naturally drive

adoption by asset owners, and the breadth and

growth of factor investing has been astonishing.

Assets in smart beta strategies have grown 170%

over the past five years to over $540 billion

globally, according to Morningstar. Fiduciaries

that acknowledge the benefits of factor investing

have reshaped their investment strategies

accordingly.

It is clear that the investment process—factor

criteria and portfolio construction—can have a

direct impact on outcomes, and provide more

transparency into what is being delivered,

thereby helping to increase asset owner

confidence. For asset managers, we believe that

having conceptual clarity is key to advancing

beyond the current thinking and to deliver even

more robust factor strategies.

12

Authors ?

Stephen joined HSBC in 2014 as a Senior Equity

Product Specialist supporting global, European, UK

and thematic equities. Previously he worked on

sustainable solutions as Head of Emerging Markets

Portfolio Management at Bank Vontobel. Prior, he

was at AllianceBernstein for twelve years in

Singapore, Tokyo and London.

Stephen holds a Master of Business Administration

from Stanford University, an M.S. Food Science from

the University of California at Davis, and a B.S.

Mechanical Engineering and Nuclear Engineering

with High Honors from the University of California at

Berkeley. Stephen is a CFA charterholder.

Stephen Tong

Director, Senior Equity Product

Specialist

HSBC Global Asset Management

(UK)

Alexander Davey is the Director of Alternative Beta

Strategies with HSBC Global Asset Management

(UK) Ltd., joining the firm in 2014. He has 17 years

industry experience having held both sales and

investment focused roles with Barclay Global

Investors, Morgan Stanley Investment Management

and most recently Barclays Wealth and Investment

Management.

Alexander has a BA Honours in History from the

University of York and is a full Member of the

Chartered Securities Institute.

Alexander Davey

Director, Senior Equity Product

Specialist

HSBC Global Asset Management

(UK)

13

For financial professionals only. Not for further distribution

This document is for information only and does not constitute investment advice, a solicitation or a

recommendation to buy, sell or subscribe to any investments.

HSBC Global Asset Management has based this document on information obtained from sources it believes to

be reliable but which it has not independently verified. HSBC Global Asset Management and HSBC Group

accept no responsibility as to its accuracy or completeness.

The views expressed above were held at the time of preparation and are subject to change without notice.

Forecasts, projections or targets where provided are indicative only and are not guaranteed in any way. HSBC

Global Asset Management accepts no liability for any failure to meet such forecasts, projections or targets.

The value of any investments and any income from them can go down as well as up and investors may not get

back the amount originally invested. Where overseas investments are held the currency exchange may also

cause the value of such investments to fluctuate.

Past performance is indicative only and is no guarantee of future results. It is important to understand that

alternative beta indices do not outperform capitalization weighted indices at all times. In certain cases they can

underperform cap-weighted indices over considerable time periods.

US persons (both entities and individuals) are subject to US taxation on their worldwide income and may be

subject to tax and other filing obligations with respect to their US and non-US accounts. The Foreign Account

Tax Compliance Act (FATCA) is a US law designed to prevent the use of non-US accounts or non-US entities

to avoid US taxation of income and assets. To meet this objective, FATCA imposes on US and non-US entities

certain documentation, due diligence, withholding and reporting requirements with respect to accounts and

certain payments. Investors should consult their independent tax advisors about investment tax implications.

HSBC Global Asset Management is the brand name for the asset management businesses of HSBC Group.

HSBC Global Asset Management (USA) Inc. is an investment adviser registered in the US with the Securities

and Exchange Commission.

The contents of this document are confidential and may not be reproduced or further distributed to any person

or entity, whether in whole or in part, for any purpose.

© Copyright 2015 HSBC Global Asset Management. All rights reserved. CA# 20150320 - 111328

Important information ?

Related Documents