Related Party Transactions – Disclosures & Regulatory Issues By Lee Leok Soon Head, Client Services Minority Shareholder Watchdog Group Smart Focus Business Solutions Seminar 17 November 2008 Hotel Maya Kuala Lumpur

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Related Party Transactions –Disclosures & Regulatory Issues

By

Lee Leok SoonHead, Client Services

Minority Shareholder Watchdog Group

Smart Focus Business Solutions Seminar

17 November 2008

Hotel Maya Kuala Lumpur

Let me begin as follows:

� IFRS 124 Disclosures & Listing Requirements� Definition and the Needs for regulations

� Determining Disclosures and Procedural Requirements

� Aggregation and principles

� Purposes for Disclosures and Percentage Ratios/Thresholds

� Main/Principal Advisers & Independent Advisers

� Managing Related Parties

� Corporate Liabilities of Directors

� Case Studies & Examples

Definition

� Definition of related parties under IFRS 124 is widely drawn.

� Related parties are considered in two groups:

� Those that are deemed to be related

� Those where a related party relationship is presumed.

� “Deemed” related party relationships cannot be rebutted. All material transactions with directors, group members, associates and joint ventures must normally be disclosed.

� “Presumed relationship” can be rebutted. Such transactions need not therefore be disclosed. The relevant party must prove no significant influence over the entity’s financial and operating policies.

� A related party can mean a director, major shareholder or person connected with such director or major shareholder.

� The question then arises ‘who is a related party?

� “Parties are considered to be related if at any time during the reporting period, one party has the ability to control the other party or exercise significant influence over the other party in making financial and operating decisions.”

Generally, deemed related parties include:

� Holding companies, subsidiaries and fellow subsidiaries

� Associates and joint ventures

� Individuals including their relatives having voting power giving them control or significant influence

� Key management personnel including their relatives

� Enterprises where controlling individual or key management personnel has significant influence

Definition

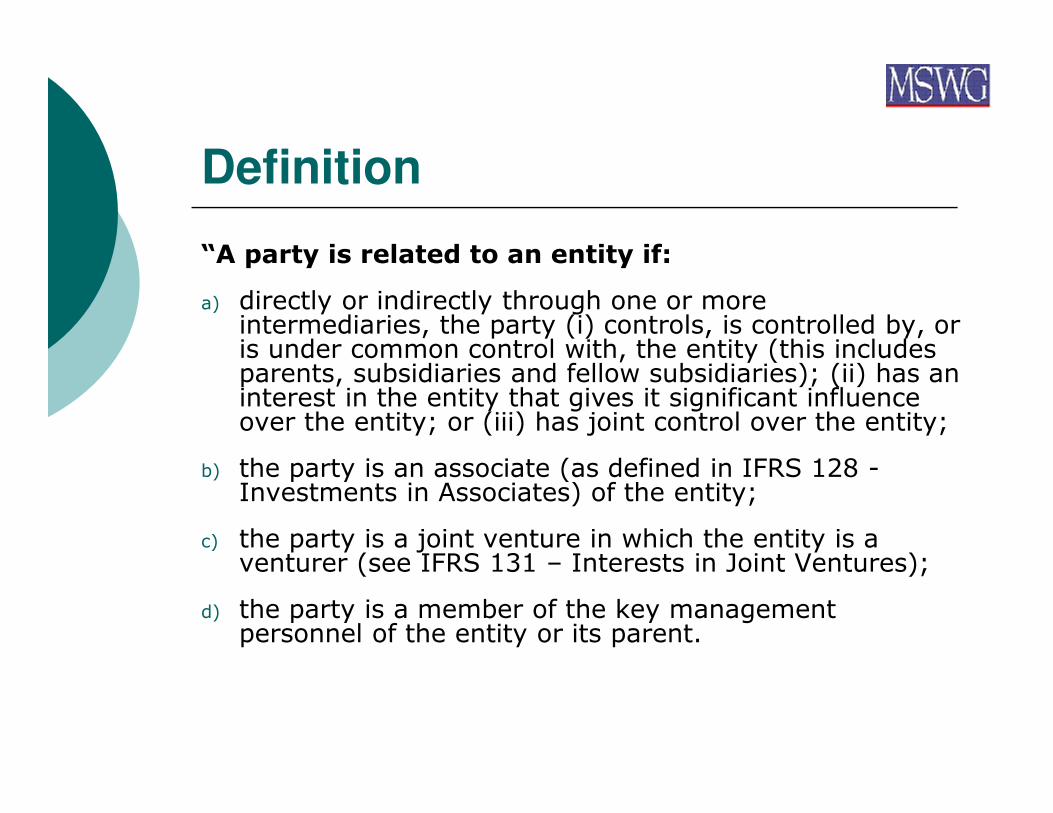

“A party is related to an entity if:

a) directly or indirectly through one or more intermediaries, the party (i) controls, is controlled by, or is under common control with, the entity (this includes parents, subsidiaries and fellow subsidiaries); (ii) has an interest in the entity that gives it significant influence over the entity; or (iii) has joint control over the entity;

b) the party is an associate (as defined in IFRS 128 -Investments in Associates) of the entity;

c) the party is a joint venture in which the entity is a venturer (see IFRS 131 – Interests in Joint Ventures);

d) the party is a member of the key management personnel of the entity or its parent.

� The party is a close member of the family of any individual referred to in (a) or (d);

� The party is an entity that is controlled, jointly controlled, or significantly influenced by or for which significant voting power in such entity resides with, directly or indirectly, any individual referred to in (d) or (e); or

� The party is a post-employment benefit plan for the benefit of employees of the entity, or of any entity that is a related party of the entity.

� Major shareholder - any person controlling 5 per cent or more of the voting rights in a listed issuer or in any of its subsidiaries. Past person who no longer has such voting rights but who did have them at any time within 6 months preceding the date of the transaction.

� Such person and connected person must abstain from all voting on the relevant resolutions, and disclose the nature and the extent of his/her interest.

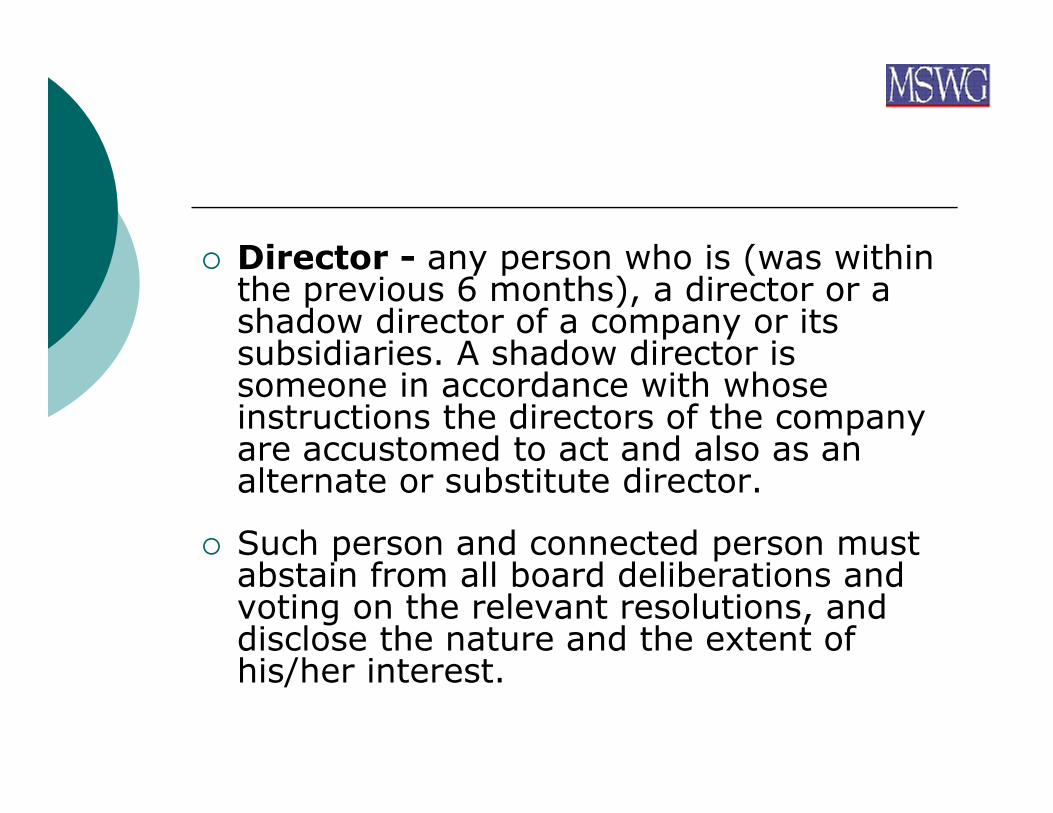

� Director - any person who is (was within the previous 6 months), a director or a shadow director of a company or its subsidiaries. A shadow director is someone in accordance with whose instructions the directors of the company are accustomed to act and also as an alternate or substitute director.

� Such person and connected person must abstain from all board deliberations and voting on the relevant resolutions, and disclose the nature and the extent of his/her interest.

� Associates - directors and substantial shareholders who are individuals, including their family (i.e. spouse or child). In case, the substantial shareholders are companies and associate includes a variety of associated companies within any subsidiary, holding company or fellow subsidiary of the holding company.

� IFRS 128 defines an associate as “an entity over which the entity has a significant influence and that is neither a subsidiary nor an interest in a joint venture”.

� Joint Venture - a contractual arrangement between two or more parties to undertake a specific business project subject to joint control in which parties meet costs of the project and receive a share of any resulting output.

� Connected Person - a member of that director or major shareholder’s family, a trustee of a trust (under which director or major shareholder or member of director’s or major shareholder’s family is sole beneficiary), a partner of that director or a partner of person connected to that director or major shareholder, a person or body corporate accustomed or obliged to act in accordance with the director or major shareholder or vice versa, a body corporate in which a director or major shareholder controls not less than 15 per cent of the votes, and a related body corporate.

� Family member includes spouse, parent, child including adopted child and step child, brother or sister and spouse of child and brother or sister.

� Such person and connected person must abstain from all deliberations or voting on the relevant resolutions, and disclose the nature and the extent of his/her interest.

� Interests can be categorized as direct or indirect. Both direct and indirect interests must be disclosed. A director has a direct interest when he/she is (i) a party to a transaction; (ii) a parent, child, adopted child or stepchild or spouse of a party to the transaction; and a director, officer or trustee of a party to the transaction.

� An indirect interest arises in a number of situations. For example, an indirect interest arises if a director has a material financial interest in another party to a transaction or in a party that will obtain a material financial benefit from the transaction.

� Partner - any person with whom director, major shareholder or person connected with director or major shareholder is in or proposes to enter into partnership with.

� A partnership is the relation which subsists between persons carrying on business in common with a view of profit. The relation between members of any company or association which is registered as a company under the Companies Act 1965 or as a co-operative society under any written law relating to co-operative societies or Section 3 of the Partnership Act 1961.

� IFRS 124 increases the disclosure requirement. It requires a listed issuer to disclose all material transactions with related parties, i.e. parties having a relationship (control or influence) that affects the independence of either the reporting entity or the other party and could have a significant effect on the financial position and operating results of the reporting entity.

The need for regulation: related party transactions?

� The general health of an entity is likely to be affected by those who make the decisions i.e. the directors of the company.

� The challenges to the regulators are therefore to ensure that the interests of all shareholders (majority and minority) are protected and that the directors maintain their duty in good faith and act in the best interest of the company.

“Related party transactions have been a feature of a number of financial scandals in recent years, many of which have had in common the dominance of the company by a powerful chief executive who was also involved with the related parties.”

Sir David Tweedie

Chairman

International Accounting Standards Board

United Kingdom

Case Example 1: Undisclosed Related Party Transactions

� Allegations of financial mismanagement have come to light in the hearings on the failed Principal Group in Canada.

� For example, the President of Principal Group, Donald Cormie, has claimed that he was unaware he had been signing authority for sales and purchases of real estate belonging to Principal Group’s two failed subsidiaries namely First Investors Corporation (FIC) and Associated Investors of Canada (AIC) respectively.

� When the subsidiaries had their licences revoked in June 1987, about 67,000 investors lost about $150.0 million. When the parent, Principal Group filed for bankruptcy in August, other investors lost about $60.0 million.

� Donald Cormie had built up a financial services conglomerate from the 1950s, eventually worth $1.2 billion.

� It is alleged that Donald Cormie used the company to bankroll an extravagant lifestyle for himself and his family using secret funds and a complex labyrinth of inter-connected companies.

� In his latest testimony, Donald Cormie has attempted to distance himself from the operation of the two key subsidiaries by saying that he did not realize he had signing rights on contracts issued by FIC and AIC respectively.

� It also transpired during the hearings that Donald Cormie’s daughter, Allison had been paid $120,000.00 in 1986 for “weather research”. Donald Cormie had a theory that economic cycles were linked to changes in climatic conditions.

� Allison described by her father as an archaeologist and expert in “isotope analysis and carbon dating techniques” received $120,000.00 in 1986 for research on weather records going back hundreds of years.

� When the research is completed, Donald Cormie said, he expects his daughter’s data on climate cycles will enable him to formulate more exact financial and economic predictions for the next 25 years.

� Some of the money from Donald Cormie’s empire also found its way to Estate Loan and Finance, a company owned by his wife, Eivor Cormie. By the time, Principal Group collapsed in August 1987, payments of $300,000.00 a month were being made to Estate Loan and Finance.

� Eivor Cormie, the court heard, was paid $270,000.00 in 1986 for developing a sales force for FIC including goodwill promotion, dances and parties staged for the company’s sales staff.

Source: Singapore Accountant, June 1988

“Joint ventures are often a means of sharing risks where the risks are particularly high. The amounts involved can be considerable and the effects of failure – spectacular”.

Geoffrey HolmesFormer Editor

Accountancy, ICAEW

IFRS 131 defines a joint venture “as a contractual arrangement whereby two or more parties undertake an economic activity which is subject to joint control”.

Any transactions that may involve the company in a number of important procedural formalities, most notably the obtaining of shareholders’ approval, are the transactions with related parties. It is not the size of the transactions but the relationship between the parties that is important to make the classification.

� A transaction with related parties is defined as “a transaction other than of a revenue nature in the ordinary course of business between a company (or any of its subsidiaries) and a related party; or any arrangement in which a company (or any of its subsidiaries) and a related party each invest in, or provide finance to, another undertaking or asset (a joint investment arrangement); or the entering into, amendment or termination of any contractual arrangement with a controlling shareholder”.

� A related party means a substantial shareholder, director or any of their associates or venturers.

Case Example 2: Unincorporated Joint Ventures

� A company participates in a number of unincorporated joint ventures which it proportionally consolidates in its group accounts. It has entered into transactions with the joint ventures.

� Does IFRS 124 –Related Party Disclosures require these transactions and the amounts due to or from the joint ventures at the balance sheet date, to be disclosed?

� Or can the exemption for transactions or balances between group entities that have been eliminated on consolidation be applied?

� IFRS 124 does require disclosure of the transactions and balances with the joint ventures and that the exemption for group entities does not apply. The joint ventures are not subsidiaries and the transactions and balances between the group and the joint ventures are not fully eliminated in the group accounts by proportional consolidation. The disclosure note could indicate the extent to which the transactions and balances have been eliminated by proportional consolidation but the gross details should be disclosed.

Source: Accountancy, July 1997

The usual recurrent related party transactions

The recurrent related party transactions are those with the frequency and regularity (made at least once in 3 years in the course of business). They are of revenue or trading nature necessary for the day to day operations of the business, contributing directly or indirectly to generation of revenue for the listed issuer.

A listed issuer having recurrent transactions of a revenue or trading nature for daily operations may seek shareholders’ mandate when (i) the transactions are in the ordinary course of business and terms are not more favourable than those generally available to the public. “In the ordinary course of business”only if reasonably expected to be carried out by relevant entity given the type of business; (ii) annual renewal for the shareholders’ mandate must be in order; (iii) disclosure in the annual report if the aggregate value of transactions conducted pursuant to mandate where consideration, value of the assets, capital outlay or costs of aggregate transactions is equal to or exceeds RM1.0 million or the percentage ratio of such recurrent transactions is equal to or exceeds 1 per cent whichever is the lower.

� Related party transactions that are exempt from issuing circular to shareholders or obtaining shareholders’ mandate or appointing main/principal adviser and independent adviser are covered in Bursa Securities Listing Requirements -Chapter 10: Transactions, Paragraph 10.08; and (v) interested parties must not vote. They include interested directors, major shareholder or interested persons connected with director or major shareholder.

� They must not vote where related party transactions involve their interests or the interested persons connected with them or major shareholder. Directors with any interest direct or indirect must abstain from board deliberations and voting on the relevant resolutions in respect of the related party transactions.

� Bursa Securities issued Practice Note No. 12/2001 to clarify on recurrent related party transactions of a revenue nature. Guidance Note No. 8/2006 is for MESDAQ companies

Procedural requirements

When the relevant transactions are those with related party, the following procedural requirements have to be observed, (i) make an announcement if required by Bursa Securities Listing Requirements; (ii) prepare to send an explanatory circular to shareholders, currently obtaining shareholders’ approval at the AGM; (iii) for the approval of its shareholders, where applicable, ensure that the related party abstains and takes all reasonable steps to ensure that its associates abstain from voting on the relevant transactions; and (iv) the relevant contracts if applicable must be supplied to Bursa Securities, i.e. the Stock Exchange, if requested.

� “A related party transaction is a transfer of resources, services or obligations between related parties, regardless of whether a price is charged”.

� Disclosures on related party transactions are (i) the amount of the transactions; (ii) the amount of outstanding balances, including terms and conditions and guarantees; (iii) provisions for doubtful debts related to the amount of outstanding balances; (iv) expense recognized during the period in respect of bad and doubtful debts due from related parties.

� The listed issuer must provide proof if it states that related party transactions were made on terms that are common in arm’s length transactions.

� Aggregation means that separate transactions may be aggregated and treated as one if agreed upon within 12 months.

� However, all material information, subject to certain exemptions, shall be disclosed either individually or in aggregate.

� Transactions which may be aggregated include (i) transactions entered into with the same party or parties connected with one another; (ii) acquisition or disposal of securities or interests in one particular company or asset; and (iii) acquisition or disposal of various parcels of land contiguous to each other.

The principles on aggregation are (i) transaction announced earlier pursuant to Chapter 10 shall not be aggregated with latest transaction when determining whether an announcement is required; (ii) transaction approved by shareholders or which was subject of aggregation with transaction approved by shareholders pursuant to Chapter 10 shall not be aggregated with latest transaction when determining whether any obligations are applicable; and (iii) if aggregation results in requirement for shareholders’ approval under Chapter 10, approval required only for latest transaction. Earlier transactions only require disclosure in circular.

� The rule of aggregation under Chapter 10, Paragraph 10.11 must be complied. In addition to making an immediate announcement for a related party transaction, Chapter 10, Paragraph 10,08(2) must be complied. However, a listed issuer is allowed to seek shareholders’ mandate in respect of recurrent related party transactions; (iv) circular to shareholders for shareholders’ approval. All the requirements set out under Chapter 10, Paragraph 10.09 must be complied.

� Annual report must disclose the aggregate value of recurrent transactions conducted pursuant to the mandate by types, names of related parties involved in each type and their relationship with the listed issuer.

“Related party transactions have been a feature of a number of financial scandals in recent years, many of which have had in common the dominance of the company by a powerful chief executive who was also involved with the related parties.”

Sir David Tweedie

Chairman

International Accounting Standards Board

United Kingdom

� The increasing emphasis on corporate governance makes it important for listed issuers to demonstrate transparency and accountability with proper compliance. One area of concern is related party transactions which are important for good corporate governance practice to improve investor confidence.

� The existence of control, joint control or influence can affect the terms on which the two parties transact. An understanding of the relationship and the terms on which two related parties have transacted is therefore important for understanding of a listed issuer’s financial statements.

� Listed issuers are required to disclose all transactions with related parties such as with directors, executives, associates and their family members under Bursa Securities Listing Requirements. While the great majority of related party transactions are perfectly normal, the special relationship between the involved related parties could create potential conflicts of interest which might result in transactions which benefit the people involved, detrimental to the shareholders.

� In the infamous Enron scandal, related party transactions with special purpose entities were used to help the company misreport their accounting numbers.

� The Maxwell affairs in the 1980s that caused the Accounting Standards Board (ASB) to re-consider the issue of related parties. The Maxwell affairs, it transpires, resulted in difficulties at MGN Group and Maxwell Communications, partly as a result of a number of related party transactions. Hence, the ASB revived the issue which subsequently developed it as FRS 8.

� The rationale for considering related parties is the reliability of accounting information that is involved with assurance in ensuring that accounting “tells it like it is”, something sometimes referred to as “faithful representation”. Thus, transactions are assumed to take place at arm’s length, i.e. on normal commercial terms.

� If that basic presumption (normally referred to as an accounting concept) is untrue, then the normal free market conditions do not exist and the results, cash flows and financial position may be manipulated in some way, possible to give investors the financial statements a view of things which normal market forces would not have given rise to.

� As FRS 8 points out, even though the parties involved may attempt to achieve arm’s length bargaining, the nature of the relationship may prevent this from happening.

“In the nature of things, the requirement to disclose related party transactions can never be a complete safeguard against deliberate dishonesty”.

Sir David Tweedie

Chairman

International Accounting Standards Board

United Kingdom

The Haw Par Affair – Related Party Transactions

In November 1979, the High Court of Singapore sentenced RichardTarling, a British and the former Chairman of Haw Par BrothersInternational Limited (or Haw Par Brothers) to six (6) months’imprisonment for failing to give a true and fair view of Haw ParBrothers’ profits for 1972. The decision was affirmed by the CriminalCourt of Appeal in January 1981.

The facts of the case

Slater Walker Securities Limited, U.K. in which Richard Tarling wasonce an executive, held major but not a majority interest in Haw ParBrothers, a company incorporated in Singapore. Haw Par Brothersrepresented Slater Walker’s interest in the Far East and waseffectively a director-controlled company through Richard Tarling.

Haw Par Brothers was mainly a holding company comprised of bothsubsidiary with a 50% or more ownership and associated corporationswith a less than 50% ownership. One of its wholly-owned subsidiaries inHong Kong, Grey Securities Limited (GSL) was used as a vehicle for HawPar Brothers Group to trade on stock markets in Hong Kong andSingapore respectively. GSL made phenomenal profits from its sharedealings and Haw Par Brothers management wanted to avoidconsolidating GSL’s profits with those of Haw Par Brothers Group.

The Haw Par Affair – Related Party Transactions (Cont’d)

To do this, a private unit trust, Melbourne Unit Trust (MUT) was set up on 27 June 1972 with all units of this trust effectively owned through nominees by Haw Par Brothers. On 28 June 1972, Haw Par Brothers then sold GSL to MUT at Haw Par Brothers’ original cost of HK$108 million. The market value of GSL’s underlying net assets was HK$60.3 million. Haw Par Brothers thus avoided consolidating GSL’s realised profits of HK$25.5 million since they now belonged to MUT. Since MUT was a unit trust as opposed to an incorporated company, its profits too were not consolidated in Haw Par Brothers Group’s profit and loss accounts for 1972.

As a result, Haw Par Brothers Group’s consolidated profits for the year ended 31 December 1972 were grossly understated, contrary to being consolidated in order to present a true and fair view of the Haw Par Group’s results and performance.

Source: The Haw Par Affair & The Reporting of Related Party Transactions in Asia Pacific Journal of Management, May 1984

by Sebastian ChongSenior Lecturer, School of Accountancy

National University of Singapore

Footnote comments: It is generally recognized that directors and managers are usually concerned with how transfer prices should be determined. IFRS 124 deals with this concern about how transactions between related parties should be reported in published financial statements. The mode of reporting and disclosures is also regulated by Bursa Securities Listing Requirements, Chapter 10 and the relevant PN 12/2001, PN 14/2002 and Guidance Note No. 8/2006 for companies listed on the stock exchange.

The effects on the financial statements can be seen in two-fold:

� First, the amount of business might vary -a controlling party may determine exactly how much business is done.

� Second, the terms of the transactions, i.e. credit terms, the prices, may be different. Goods or services may be transferred in exchange for assets, the price of which is difficult or impossible to determine. The question is, how should all these transactions be communicated to investors so as to facilitate their understanding of the situation?

� Financial reporting is essentially just about two things - how to measure and what to disclose.

� The first possibility is that the accounts are restated to give the picture which would have been shown had the transactions taken place on normal commercial terms, i.e. on terms which would have been transacted with an external unrelated party.

� First, the transactions do not represent what actually happened and indeed, to pretend that the transactions took place with an external party is simply untrue.

� Second, it may lead to inflating profits and assets, thus conflicting with the concept of prudence.

� Third, it may be difficult to estimate what normal commercial terms might have been.

� The second possibility is to disclose what has happened in the notes to the accounts.

� Disclosures are often thought to be useful in showing a true and fair view because it enables investors to appreciate fully what has happened and to make their own adjustments.

� A concern about increasing disclosure requirements would put the onus on what to do about an accounting issue of the investors rather than on the preparer. It should be borne in mind that the increased disclosures and the amount of detail in them are perhaps, becoming somewhat excessive.

� Not only are related parties potentially numerous, the required disclosures are also lengthy (i) names of the transacting related parties; (ii) description of the relationship and the transactions; (iii) the amounts involved; (iii) balances with the related parties at the balance sheet date, including provisions made and amounts written off such balances; and (iv) any other elements necessary for an understanding of the financial statements.

� Just how useful disclosures about related parties are to the average investor remains to be seen, (i) they are often extremely complicated; (ii) their significance is difficult to assess; and (iii) nevertheless, they largely remove the excuse “if only I had known, otherwise I would not have bought the company’s shares”.

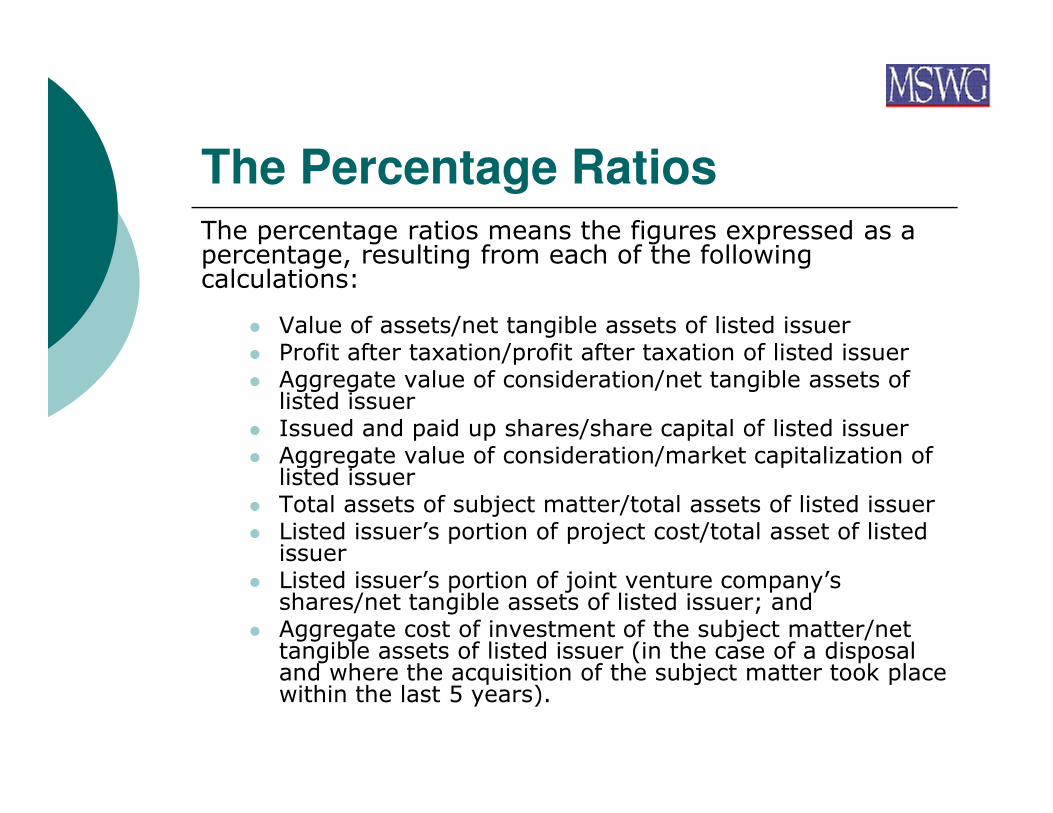

The Percentage RatiosThe percentage ratios means the figures expressed as a percentage, resulting from each of the following calculations:

� Value of assets/net tangible assets of listed issuer� Profit after taxation/profit after taxation of listed issuer� Aggregate value of consideration/net tangible assets of

listed issuer� Issued and paid up shares/share capital of listed issuer� Aggregate value of consideration/market capitalization of

listed issuer� Total assets of subject matter/total assets of listed issuer� Listed issuer’s portion of project cost/total asset of listed

issuer� Listed issuer’s portion of joint venture company’s

shares/net tangible assets of listed issuer; and� Aggregate cost of investment of the subject matter/net

tangible assets of listed issuer (in the case of a disposal and where the acquisition of the subject matter took place within the last 5 years).

The Percentage Thresholds

If a listed issuer (or any of its subsidiaries) has entered or proposes to enter into a transaction (whether by way if cash or otherwise) with a related party (whether directly or indirectly), then the said listed issuer should take the following measures:

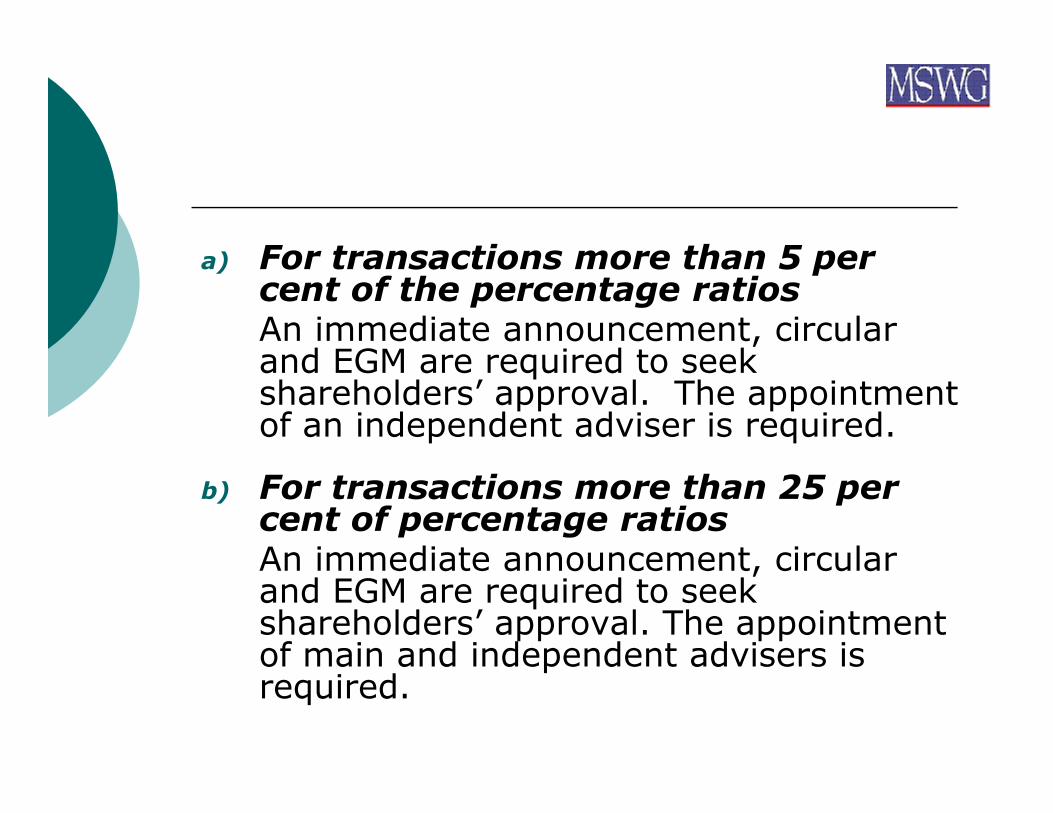

a) For transactions more than 5 per cent of the percentage ratiosAn immediate announcement, circular and EGM are required to seek shareholders’ approval. The appointment of an independent adviser is required.

b) For transactions more than 25 per cent of percentage ratiosAn immediate announcement, circular and EGM are required to seek shareholders’ approval. The appointment of main and independent advisers is required.

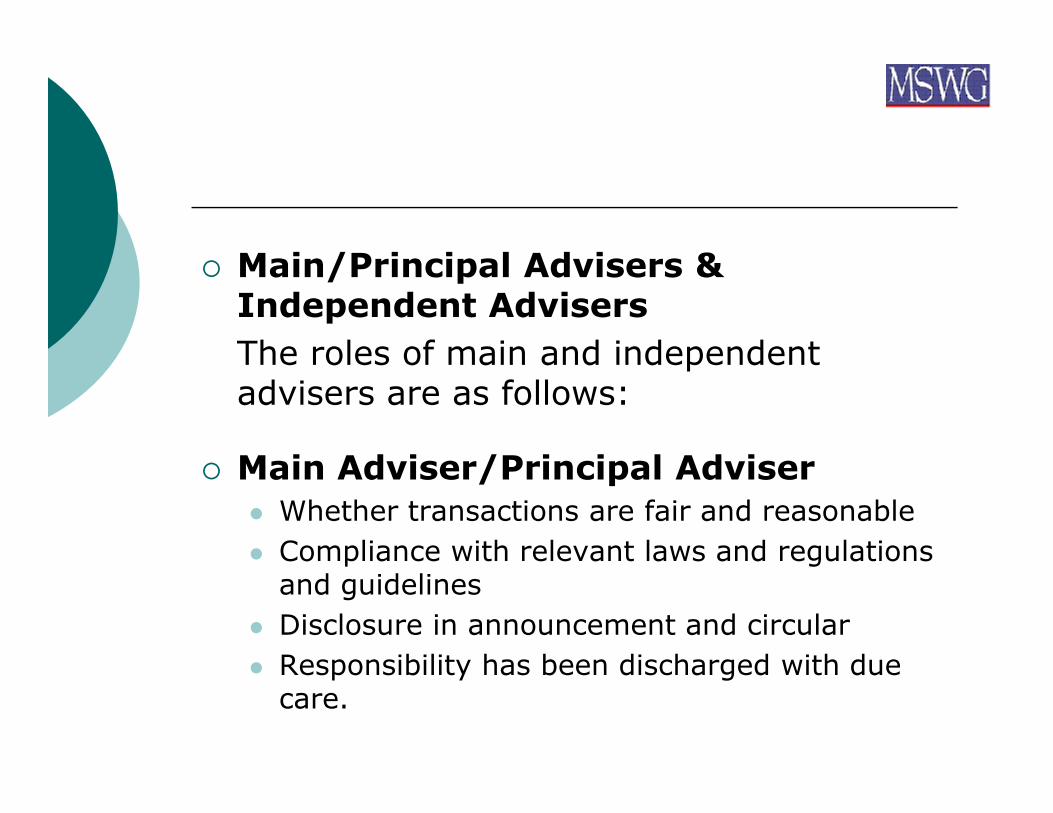

� Main/Principal Advisers & Independent Advisers

The roles of main and independent advisers are as follows:

� Main Adviser/Principal Adviser

� Whether transactions are fair and reasonable

� Compliance with relevant laws and regulations and guidelines

� Disclosure in announcement and circular

� Responsibility has been discharged with due care.

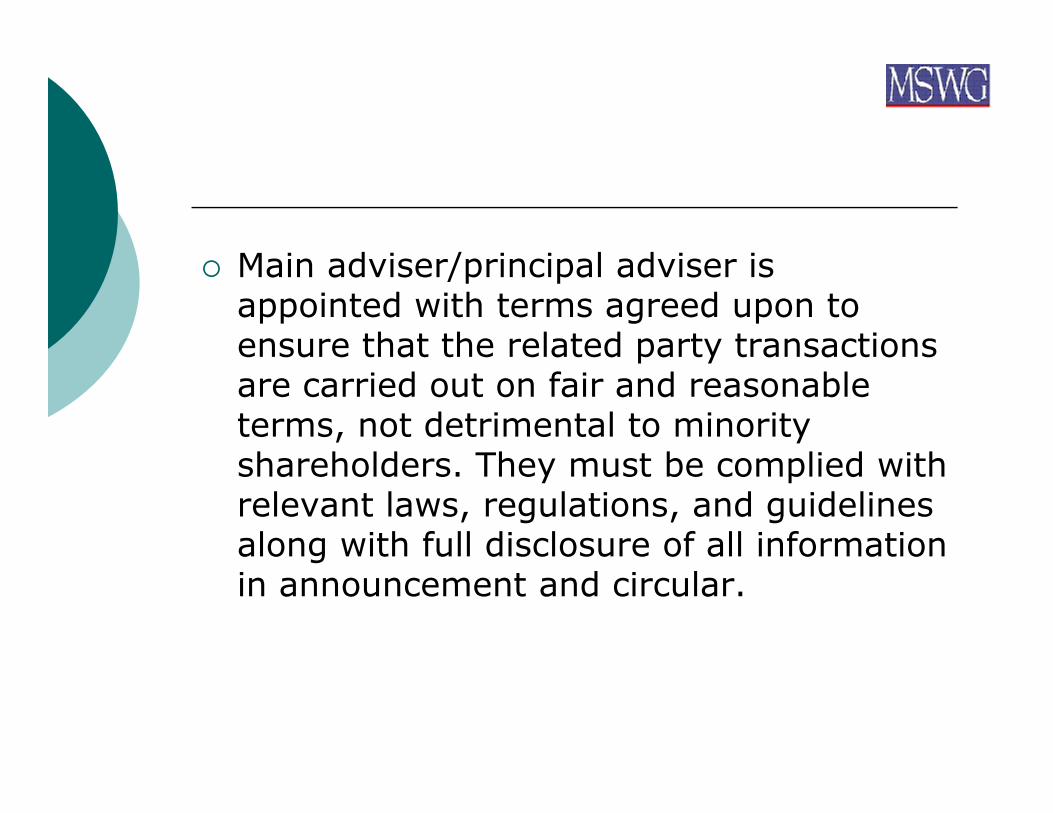

� Main adviser/principal adviser is appointed with terms agreed upon to ensure that the related party transactions are carried out on fair and reasonable terms, not detrimental to minority shareholders. They must be complied with relevant laws, regulations, and guidelines along with full disclosure of all information in announcement and circular.

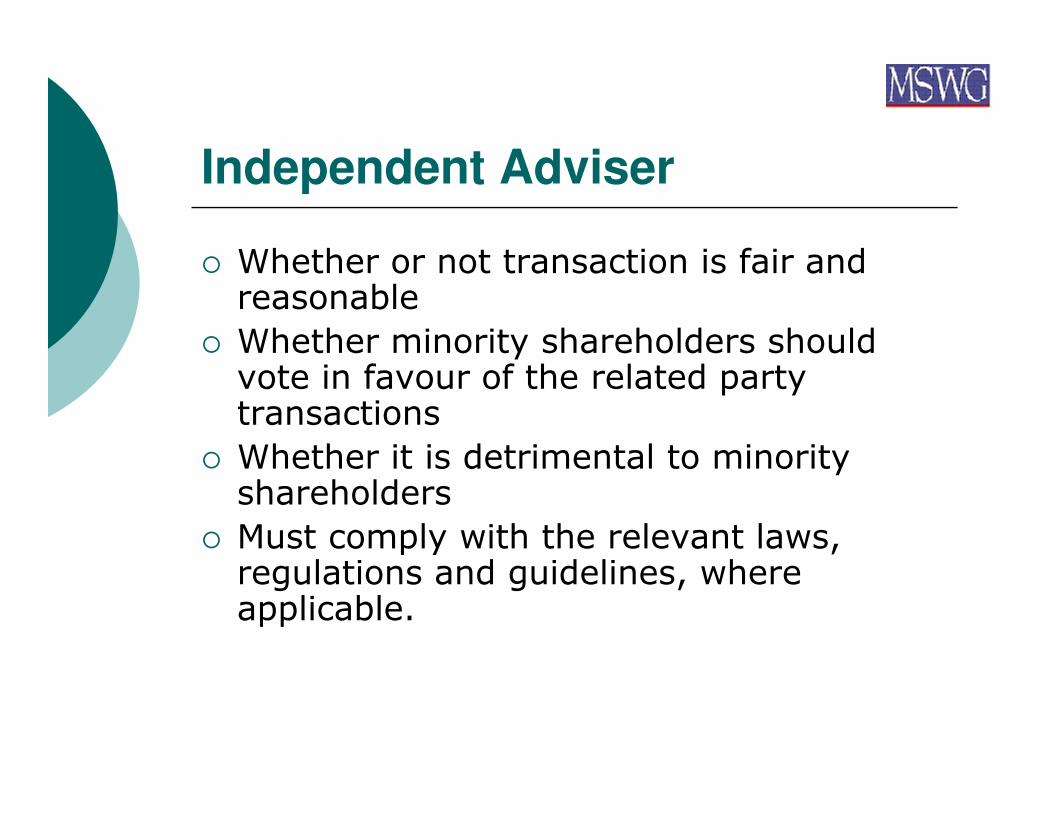

Independent Adviser

� Whether or not transaction is fair and reasonable

� Whether minority shareholders should vote in favour of the related party transactions

� Whether it is detrimental to minority shareholders

� Must comply with the relevant laws, regulations and guidelines, where applicable.

Exceptions

A number of exceptions to the usual requirements are available where the related party disclosures do not apply. Among these exceptions are: (i) the issue of securities for cash pursuant to an opportunity which is made available to all shareholders on the same terms. This would cover, for example, the case of a related party benefitting from a rights issue; (ii) the issue of new securities in accordance with the exercise of conversion or subscription rights attached to listed securities or previously approved by the shareholders. For example, the act of conversion of listed convertible loan stock would not trigger the related party provisions. For example, payment of dividend, bonus issue, share splits, issue of securities for cash on a pro-rata basis;

(iii) Transactions between a listed issuer or any of its subsidiaries and an investee company where the related party has no interest in the investee; (iv) common directorship but with no shareholdings; (v) acquisition or disposal whereby the related party holds less than 5 per cent in the third party company; (vi) provision of financial assistance or services by licensed financial institutions upon normal commercial terms and in ordinary

(viii) where the terms and circumstances of a joint investment arrangement are, in the opinion of an independent adviser, no less favourable to the company than for related party; (ix) in relation to a listed issuer with an issued and paid up capital of RM60.0 million and above, the consideration, value of the assets, capital outlay or costs of the recurrent transaction under Bursa Securities Listing Requirements is equal to or exceeds RM1.0 million or the percentage ratio of such recurrent transaction is equal to or exceeds 1 per cent whichever is the higher;

(x) in relation to a listed issuer with an issued and paid up capital of less than RM60.0 million, the consideration, value of the assets, capital outlay or costs of the transaction is equal to or exceeds RM1.0 million or the percentage ratio of such transaction is equal to or exceeds 1 per cent, whichever is the lower; and (xi) the rule of aggregation under Bursa Securities Listing Requirements - Chapter 10: Transactions, Paragraph 10.11 - Aggregation of Transactions.

Managing related parties and relationships

� It is one of the most difficult aspects in financial reporting.

� “It is a common practice of companies in organizing their businesses through the medium of other companies in the group, associated undertakings and other related entities that have caused transactions between related parties to become a routine and necessary part of the operations of many business enterprises. Related parties may nevertheless enter into transactions that unrelated parties would either not undertake or would undertake only on different terms. Reporting control relationships and related party transactions draws the attention of users of financial statements to the possibility that those statements may have been affected by the relationships”.

Charles Gubbins, BSc, CAManaging Director

Practical Training DivisionATC (Eastern) Ltd, U.K.

� Related party transactions are one of the most important elements because (i) IFRS 124 and Bursa Securities Listing Requirements require disclosures of all material related party transactions and certain control relationships; (ii) in the absence of adequate disclosures, financial statements may be distorted or misleading; (iii) the instances of fraudulent financial reporting and misappropriation of assets that have been facilitated by the use of undisclosed related party.

� In addition, related parties and related party transactions are also difficult to audit for several reasons – (i) transactions with related parties are not always easily identifiable; (ii) even though auditors are thorough in their audit procedures, they rely on directors and management to identify related parties and related party transactions; (iii) such transactions may not be easily tracked by internal control system and risk management;

� Related party transactions are complex, requiring proper accounting and auditing through sound knowledge and careful analysis.

Managing related party relationships requires directors and management to properly define the following terms used.

� Control

� Significant influence

� Joint control

� Key management personnel

� Close members of family and of individuals

� Willing seller-willing buyer principle

� Arm’s length price

“Fundamental to financial reporting is the assumption that financial statements reflect the results of arm’s length bargaining between independent parties. The presence of transactions between related parties inevitably raises questions as to the meaningfulness of the resulting information”.

Mike Metcalf, BSc, FCA

Head of Technical Department

Arthur Young McClelland Moores & Co (Chartered Accountants), U.K.

Related party transactions - Why a standard is needed?

Accountancy, May 1979

Corporate Liabilities of Directors

� To act honestly and use reasonable diligence

� Improper use of any information

� Breach of any of the provisions to make profits for oneself

� Conflicts of interest in dealing with the company

� Use of company information

Role and responsibilities of audit committee

� Failure to identify related parties and related party transactions

� Inadequate examination of related party transactions

� Improper disclosures of related party transactions

� Internal auditors, external auditors and audit committee must see that related party confirmation letters are prepared and dispatched to related parties concerned for confirmation to be obtained.

� They must also see that related party questionnaire be prepared and responded to by related parties concerned.

� The primary objectives of related party confirmation letters and questionnaire are to (i) determine the existence of related parties; (ii) to identify all material transactions with related parties; (iii) to examine identified related party transactions; and (iv) to determine the adequacy of disclosures.

“Recent business events reflect the increasing use of complex business structures that include off-balance sheet entities. Because some of these entities may be related parties, the proper accounting and auditing of such transactions require sound understanding and extremely careful analysis”.

Chuck Landes

Director of Audit & Attest Standards,

AICPA, U.S.A

Case Study

“Beyond salary and stock options, some executives and board members find other ways to earn money from their companies. For example, consider two board members at Foamex International Inc had consulting contracts worth up to US$150,000 last year, and the wife of Chief Executive Officer of Channell Commercial Corporation got US$72,000 for offering advice on the company’s insurance needs.

Such arrangements are not unusual, and they are not illegal. All companies have to do is disclose them in the annual reports. But such business deals between a listed issuer and a side business are connected to its

related parties”.

Source: Steve Toloken

Related party transactions attracting attention

Case Studies and Case Examples

� Discussions and Participation

� Related Party Transactions in Annual Reports

Thank You

Join MSWG Subscriber Services

Minority Shareholder Watchdog Group

Tkt 11, Bangunan KWSP,

No. 3, Changkat Raja Chulan,

Off Jalan Raja Chulan

50200 Kuala Lumpur

www.mswg.org.my

Email: [email protected]/[email protected]

Tel: 2070 9090

Fax: 2070 9107

Related Documents