Welcome to

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Welcome to

Chair’s Introduction to the Smart Cities UK Conference

Smart Cities UKRichard Rugg

MD, Carbon Trust Programmes

4th February 2016

Cities are key to achieving vital international climate goals

1. Over 50% of the global population now live in cities. They generate 80% of GDP and use 70% of the world’s energy

2. Municipalities hold key planning, housing, community engagement, taxation and education powers relevant to low carbon development

3. And power is being devolved to local governments around the world

Climate proof cities can realise significant co-benefits

1. Reduced fuel poverty

2. More diverse and resilient energy supply

3. Better water and flood risk management

4. Transport resilience

5. Resilient buildings

6. Improved air quality

7. Positive health impact

8. Enhanced city brand

9. Cost savings

10. Revenue generation opportunities

Smart Cities UK Sharing what we know, learning what we don’t…..

Foresighting – An Enabler

of Future Smart, Liveable

and Resilient Cities

Professor Chris Rogers

University of Birmingham

4th February 2016

What is the Purpose of Cities?

A place to trade (especially food)A place of safety

... with a source of clean water

An agglomeration of people... a place to live, work and play... an amalgam of residential, commercial, retail, industry, leisure, transport and open spaces, green spaces... a place of business, busyness and peaceful solitude... dynamic 24 hour city living... a place for biodiversity to flourish – trees, birds, bats

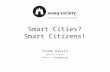

We (civil engineers) need to support all this by supply (water, electricity, gas, telecommunications , etc.), removal (wastewater, drainage, solid waste) and facilitation of movement (people, goods)… we need infrastructure systems… yet what is needed in the far future?… and where? Resilience Through Innovation

Critical Local Transport and Utility Infrastructure

What is the Purpose of Cities?

A place to trade (especially food)A place of safety

... with a source of clean water

An agglomeration of people... a place to live, work and play... an amalgam of residential, commercial, retail, industry, leisure, transport and open spaces, green spaces... a place of business, busyness and peaceful solitude... dynamic 24 hour city living... a place for biodiversity to flourish – trees, birds, bats

We (civil engineers) need to support all this by supply (water, electricity, gas, telecommunications , etc.), removal (wastewater, drainage, solid waste) and facilitation of movement (people, goods)… we need infrastructure systems… and our roads are congested

Resilience Through InnovationCritical Local Transport and Utility Infrastructure

27+

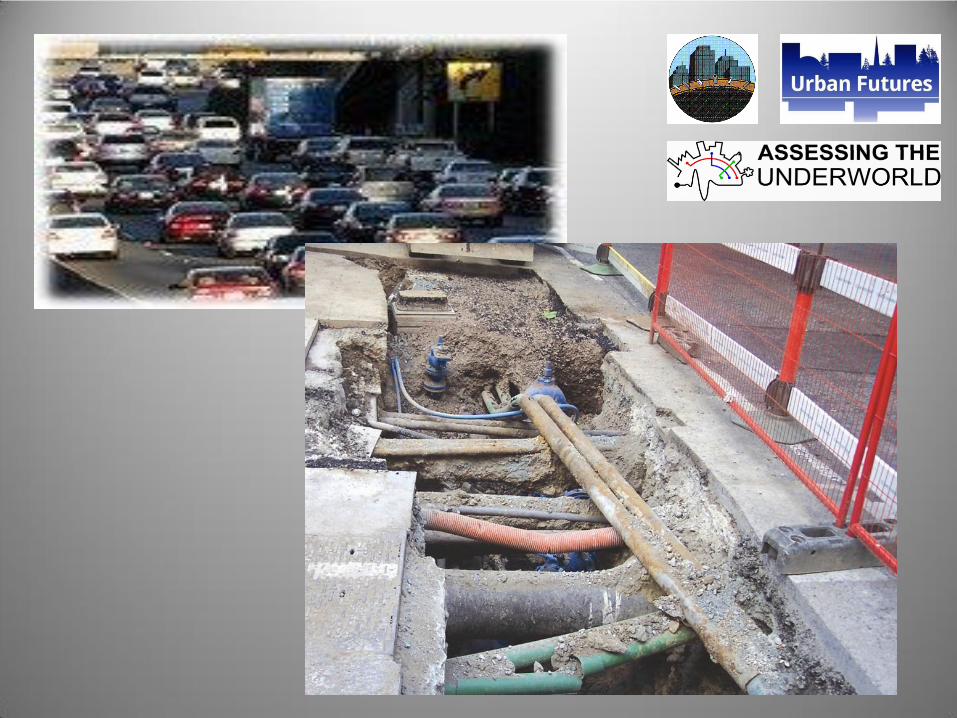

Current Infrastructure Systems

Tree Roots?

Current Infrastructure Systems

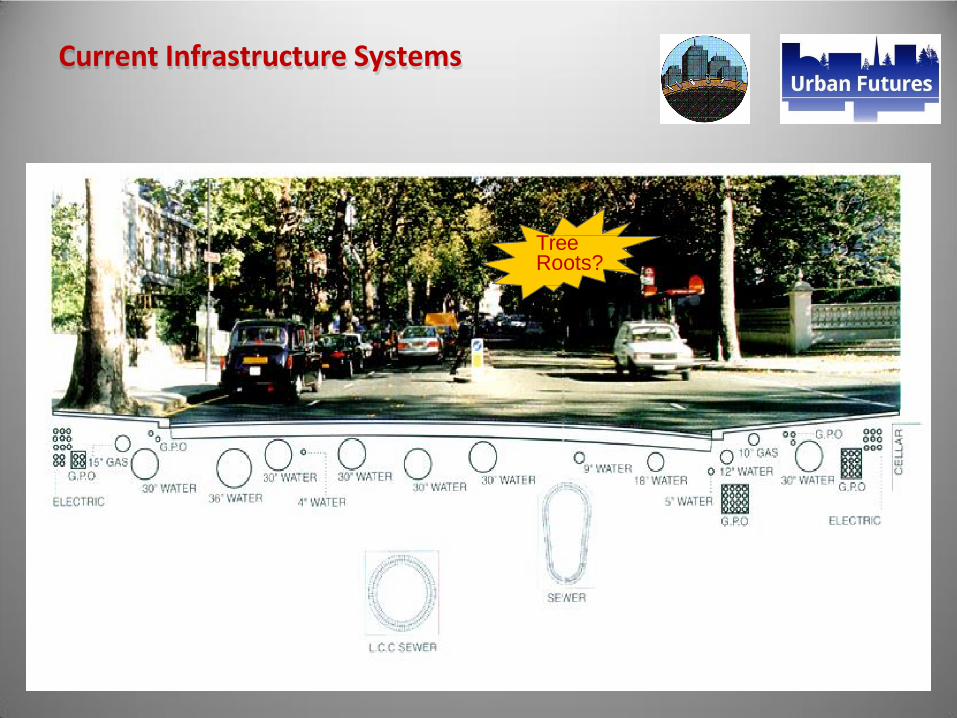

Alternative Infrastructure Systems

… enabling smarter streetworks?

District heating.

Electricity cables. Waste. Communications.

District cooling. Clean water. Sewage. Storm water. Gas.

‘cut and cover’ in Japan (2002) ‘DOT tunnelling’ in Japan (2002)

Foresight

Future of Cities

Introduction

Foresight Programme

“Helps make decisions today that are

resilient to the future”

Foresight’s major one to two-year

studies looking at key issues 10 - 100

years in the future where science and

technology are the main drivers for

change, or offer key solutions

MigrationComputer

TradingDisasters Identity

ObesityLand UseMental

CapitalGlobal Food

Infectious

Diseases

Intelligent

Infrastructure

Brain

Science

Cyber

TrustFlooding

2008

20132012

2010 2007

200620052004

20092011

Foresight Reports

Mental Capital

& Wellbeing

a :T

Fckling Obesities

uture Choices

Flooding &

Coastal Defence

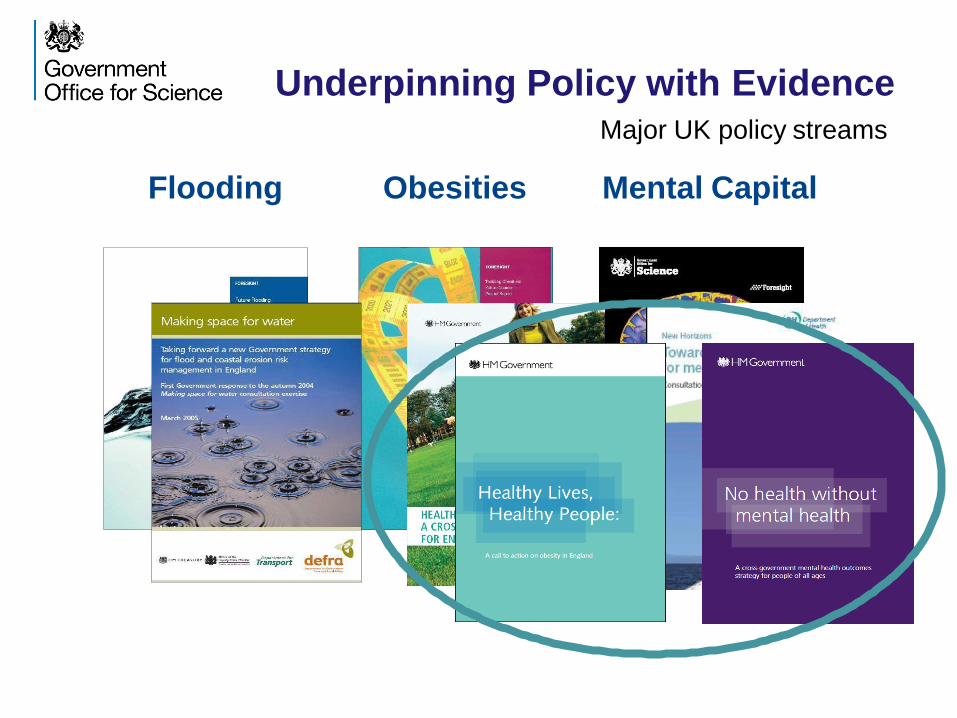

Major UK policy streams

Flooding Obesities Mental Capital

Underpinning Policy with Evidence

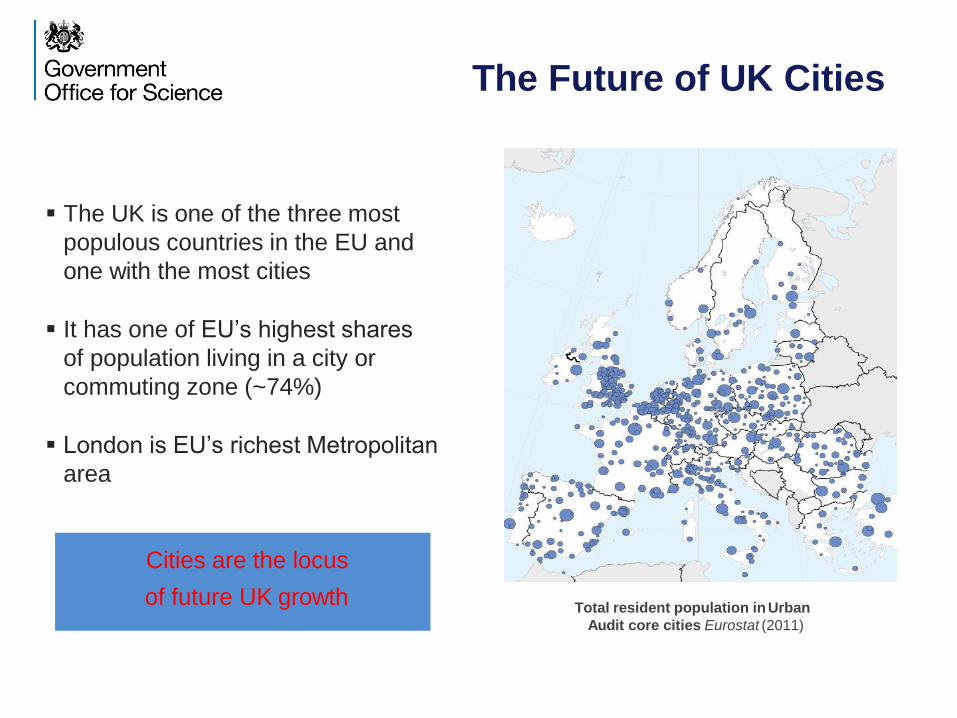

The Future of UK Cities

Cities are the locus

of future UK growth

The UK is one of the three most

populous countries in the EU and

one with the most cities

It has one of EU’s highest shares

of population living in a city or

commuting zone (~74%)

London is EU’s richest Metropolitan

area

Total resident population in Urban

Audit core cities Eurostat (2011)

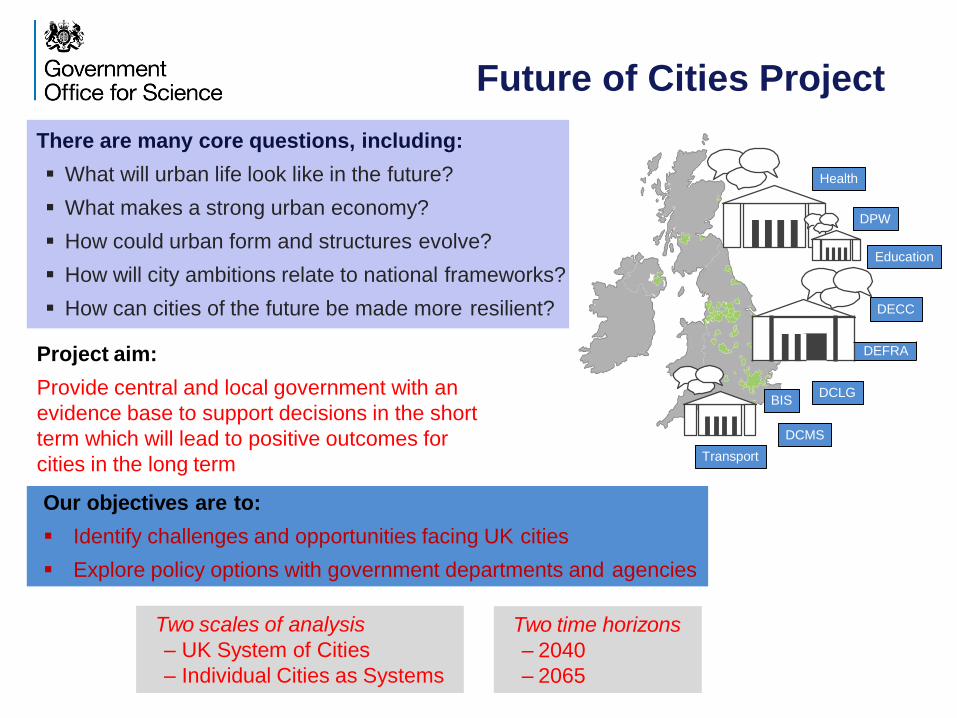

Future of Cities Project

There are many core questions, including:

What will urban life look like in the future?

What makes a strong urban economy?

How could urban form and structures evolve?

How will city ambitions relate to national frameworks?

How can cities of the future be made more resilient?

Our objectives are to:

Identify challenges and opportunities facing UK cities

Explore policy options with government departments and agencies

Project aim:

Provide central and local government with an

evidence base to support decisions in the short

term which will lead to positive outcomes for

cities in the long term

Education

DECC

DEFRA

DCLG

DPW

Health

BIS

Transport

DCMS

Two scales of analysis

– UK System of Cities

– Individual Cities as Systems

Two time horizons

– 2040

– 2065

Transitioning into a new

development cycle for UK cities

post-industrial citiesindustrial cities future cities

2000s1900s1800s

LondonmayorShift towards

Railway investment

Climate action

Devolution

Machine-based

technologies professional services

New towns

Digital technologies

Cotton trade

Canals

Mining

City Deals

OpenPolicy

Making

Brownfield

Foreign

investment

National

Grid

Welfare

state

Car-based

innovation

Motorways

Green belts

Public housing

schemes

Shopping &

business parks

RDAs

Shipbuilding

Municipal bonds

Legislation of local

government

Docklands

Imp

ort

an

ce

of

cit

ies

as

au

ton

om

ou

su

nit

s

… the rise, and fall, and rise again in the importance of cities

Transitioning into a new

development cycle for UK cities

post-industrial citiesindustrial cities future cities

1900s1800s 2000s

Greenbelts

Londonmayor

Climate action

New towns

Public housing

schemes

Open Policy Making

Car-based

innovation Digital technologiesRailway investment

Municipal bonds

Cotton trade

Canals

National

Grid

Motorways

Docklands

Mining

Brownfield development

Foreign

investment

Devolution

City Deals

RDAs

Shopping &

business parks

Shift towards

professional services

Welfare

state

Shipbuilding

Legislation of local

government

… add other contextual changes (demography, migration, …)

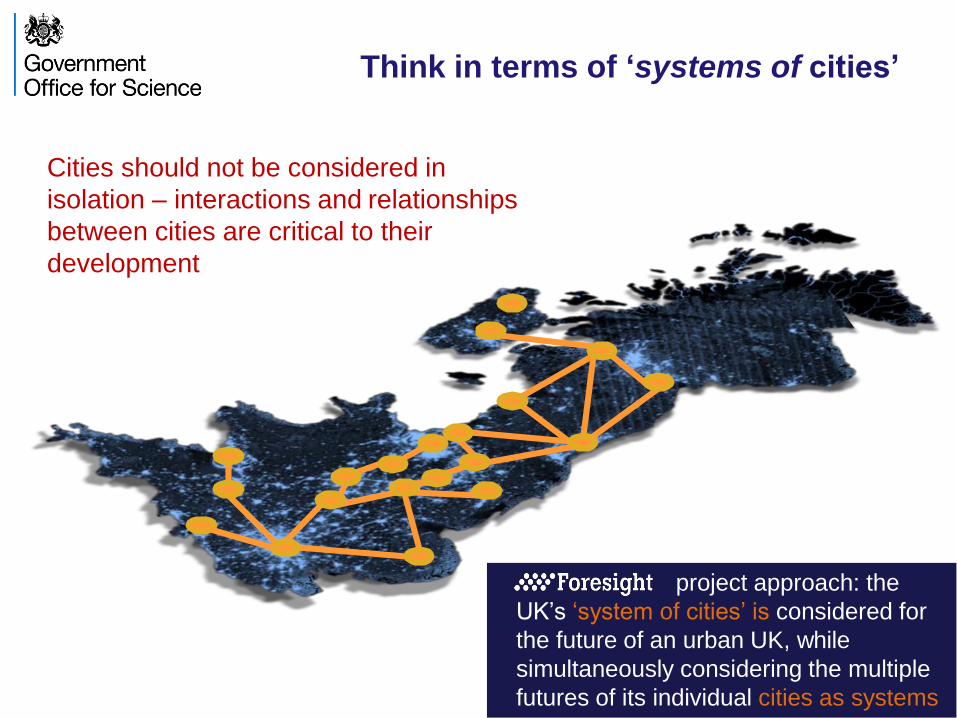

Think in terms of ‘systems of cities’

Cities should not be considered in

isolation – interactions and relationships

between cities are critical to their

development

project approach: the

UK’s ‘system of cities’ is considered for

the future of an urban UK, while

simultaneously considering the multiple

futures of its individual cities as systems

Derry/Londonder

ry

Belfast

Lancaster

Integrate intelligence from different places

integrated evidence

from over 20 individual cities with

city round tables and local projects

The richness and

uniqueness of context of

each city must be

harnessed for enhanced

overall prosperity and

wellbeing

Edinburgh

Newcastle

Glasgow

Bristol

CambridgeLondon

Cardiff

Leicester Milton Keynes

York

Birmingha

m

Mancheste

r

Rochdale

Sheffield

Leeds

Derby

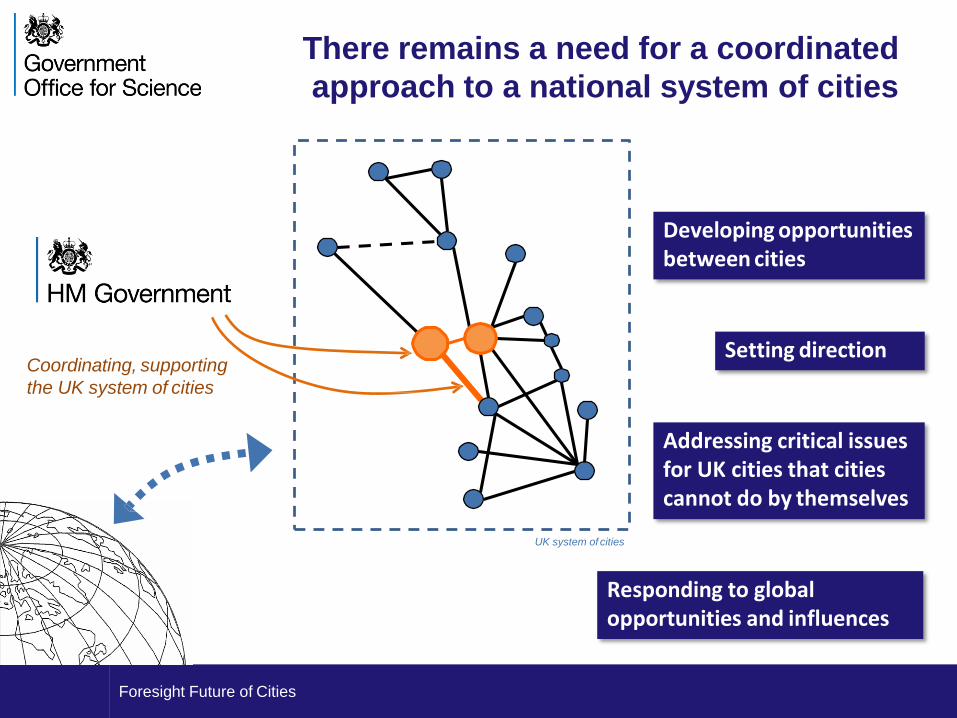

Foresight Future of Cities

There remains a need for a coordinated

approach to a national system of cities

Coordinating, supporting

the UK system of cities

Developing opportunities between cities

Setting direction

Responding to global opportunities and influences

Addressing critical issues for UK cities that cities cannot do by themselves

UK system of cities

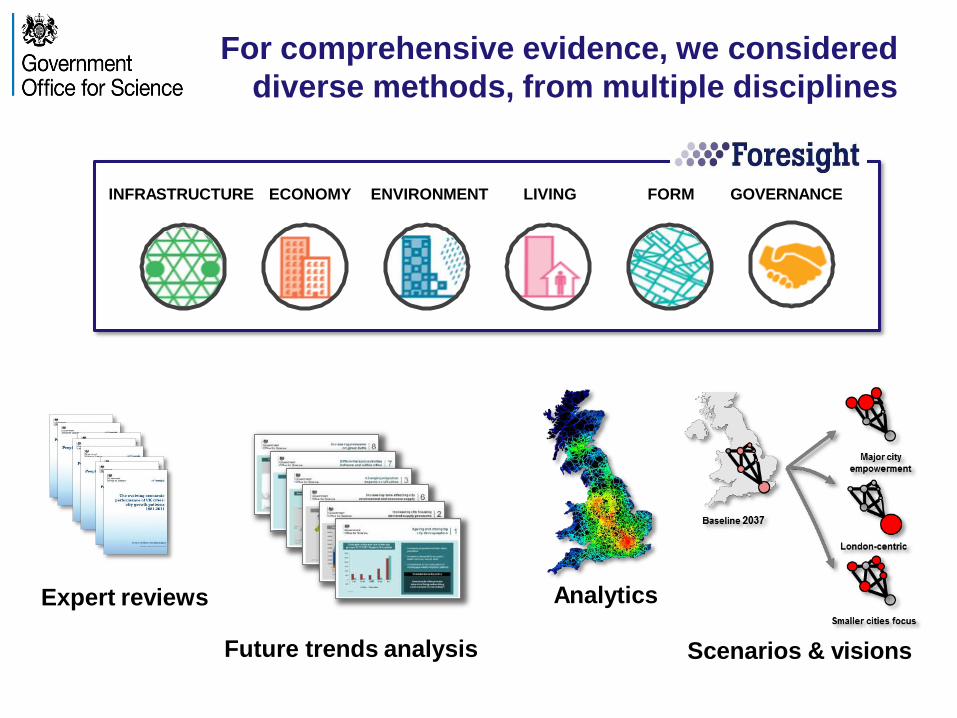

Foresight brings a comprehensive

co-created evidence base

City visits

Values, visions

Academic review papers

WorkshopsProjections

Trends analysis

Data analytics and modelling

Foresight Future of Cities

Foresight brings a comprehensive

co-created evidence base

City visits

Values, visions

Academic review papers

WorkshopsProjections

Trends analysis

Data analytics and modelling

Foresight Future of Cities

Expert reviews

Scenarios & visions

Analytics

Future trends analysis

LIVINGECONOMY ENVIRONMENT FORMINFRASTRUCTURE GOVERNANCE

For comprehensive evidence, we considered

diverse methods, from multiple disciplines

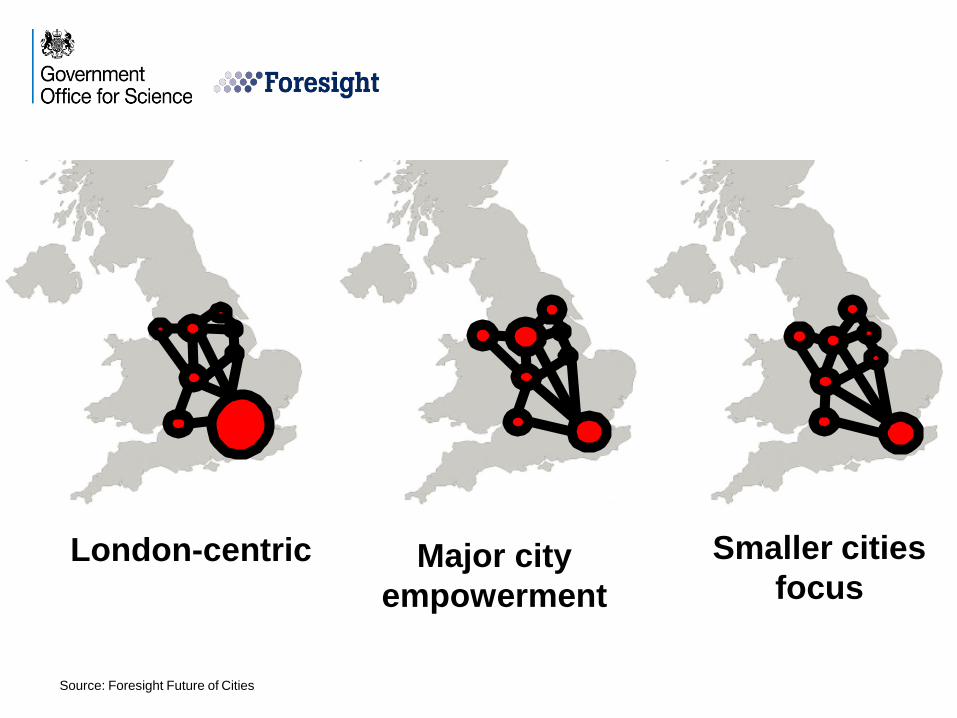

London-centric Smaller cities

focusMajor city

empowerment

Source: Foresight Future of Cities

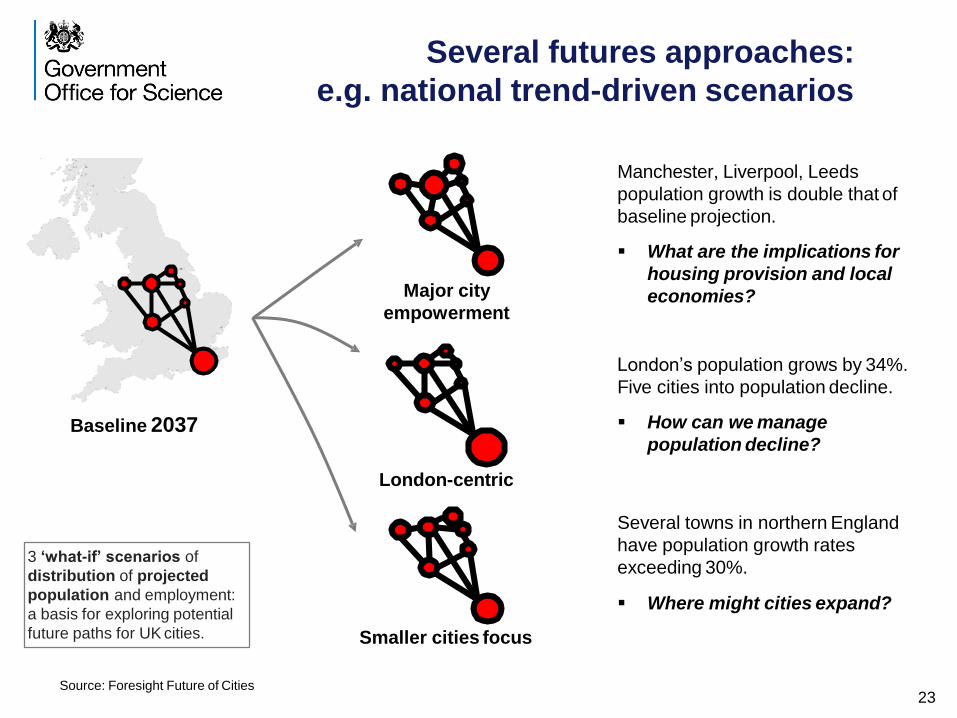

Several futures approaches:

e.g. national trend-driven scenarios

Major city

empowerment

London-centric

Smaller cities focus

Baseline 2037

3 ‘what-if’ scenarios of

distribution of projected

population and employment:

a basis for exploring potential

future paths for UK cities.

London’s population grows by 34%.

Five cities into population decline.

How can we manage

population decline?

Manchester, Liverpool, Leeds

population growth is double that of

baseline projection.

What are the implications for

housing provision and local

economies?

Several towns in northern England

have population growth rates

exceeding 30%.

Where might cities expand?

Source: Foresight Future of Cities23

Foresight Future of Cities

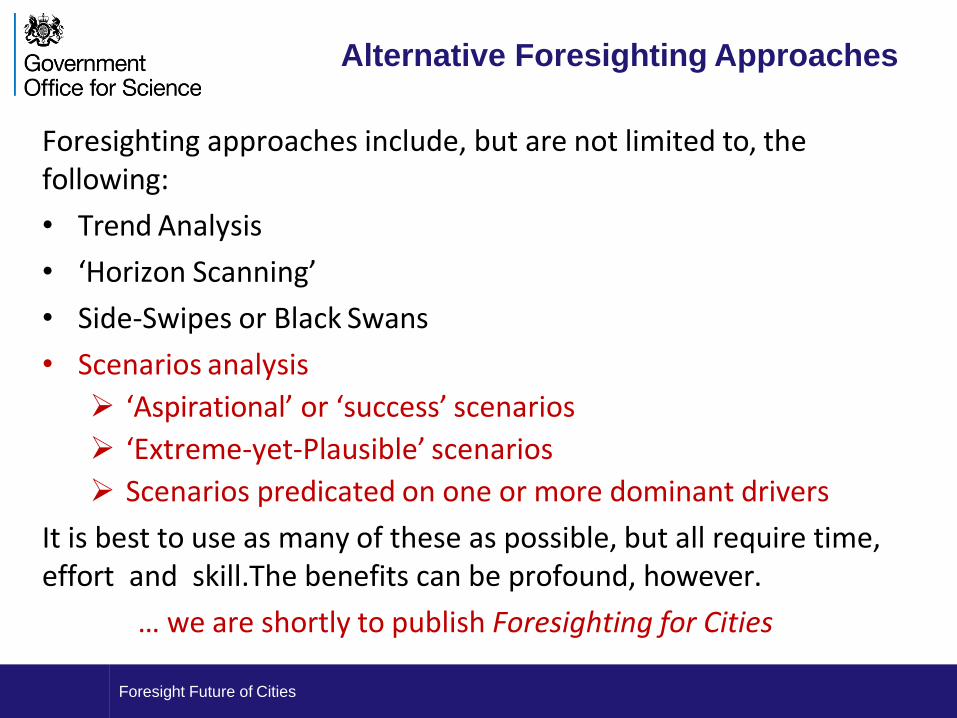

Alternative Foresighting Approaches

Foresighting approaches include, but are not limited to, the following:

• Trend Analysis

• ‘Horizon Scanning’

• Side-Swipes or Black Swans

• Scenarios analysis

‘Aspirational’ or ‘success’ scenarios

‘Extreme-yet-Plausible’ scenarios

Scenarios predicated on one or more dominant drivers

It is best to use as many of these as possible, but all require time, effort and skill.The benefits can be profound, however.

… we are shortly to publish Foresighting for Cities

Foresight – Aspirational Scenarios

We’re defining a set of principlesthat combine to describe the characteristics,or functions, of future cities we aspire to

• surveys of the aspirations of individuals from across society

• sector-focussed workshops (e.g. retail, environmental scientists, transport, heritage organisations, utility service providers, healthcare professionals, creative artists, etc.)

• Learning from the literature (five city typologies model)

Every city is unique, having developed as a result of its current andhistorical context, so to apply this thinking to cities

• we are establishing a city’s ‘aspirational principles’

• creating three extreme city scenarios around clustered visions

• exploring how cities might be re-engineered

… and hence what future infrastructures we should provide

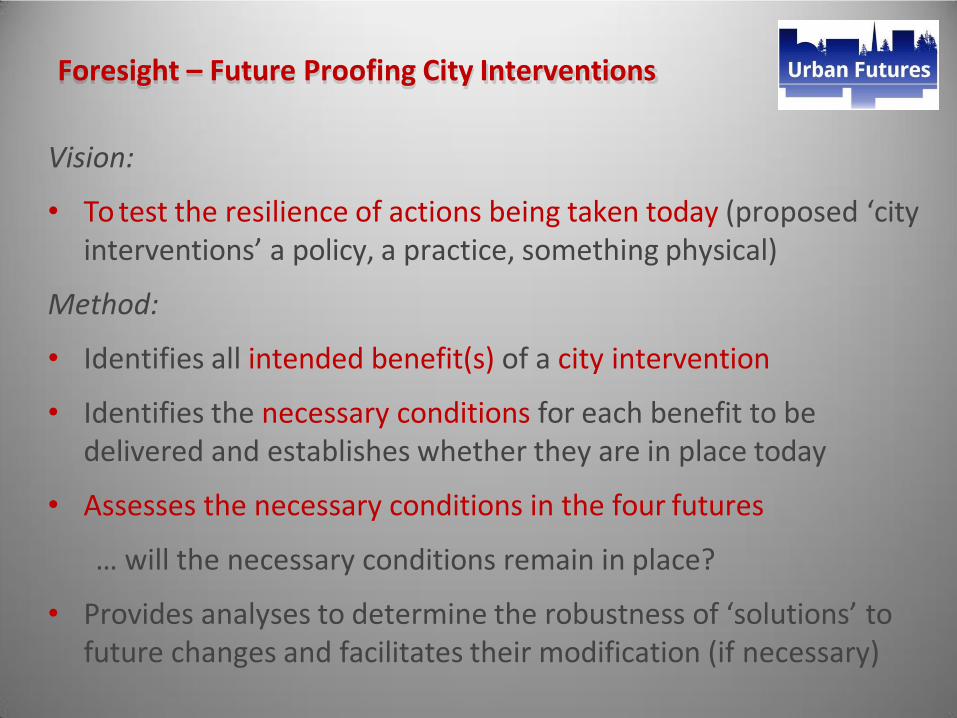

Foresight – Future Proofing City Interventions

Vision:

• To test the resilience of actions being taken today (proposed ‘cityinterventions’ a policy, a practice, something physical)

Method:

• Identifies all intended benefit(s) of a city intervention

• Identifies the necessary conditions for each benefit to be delivered and establishes whether they are in place today

• Assesses the necessary conditions in the four futures

… will the necessary conditions remain in place?

• Provides analyses to determine the robustness of ‘solutions’ tofuture changes and facilitates their modification (if necessary)

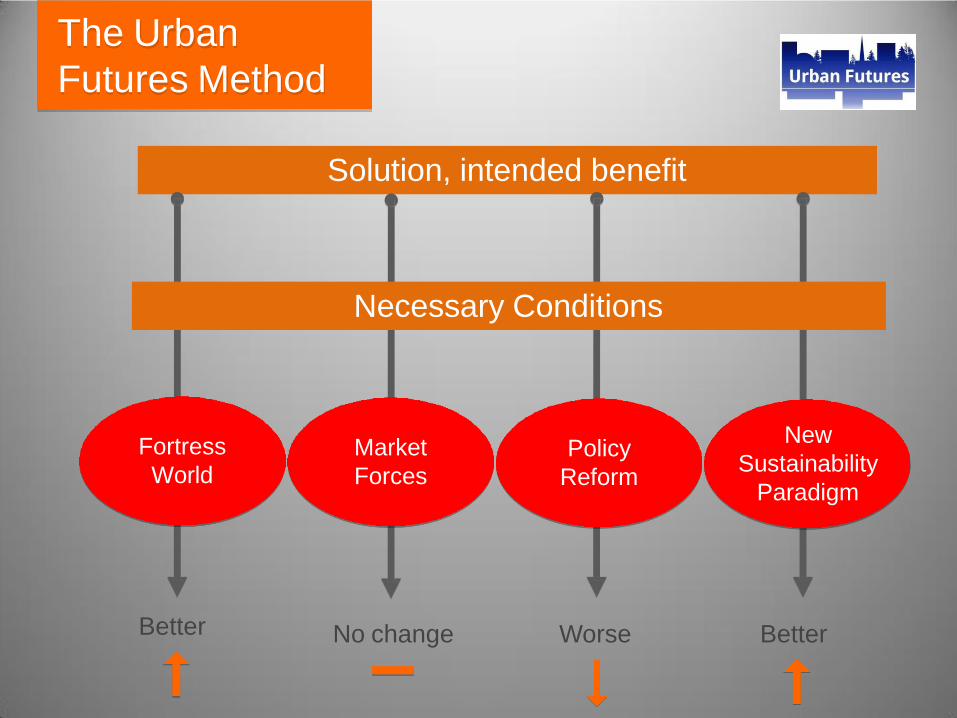

— In this scenario, powerful

actors organise themselves

into alliances in an effort to

safeguard their own

interests

— The UK divides into two

groups: an authoritarian

elite who live in

interconnected, protected

enclaves (‘gated

communities’) controlling

access to resources, and

an impoverished majority

outside

Fortress World

— In this scenario, current

demographic, economic,

environmental, and technological

trends unfold without major surprise,

with convergence toward today’s

structures

— Competitive, open markets drive UK

development. The self-correcting

logic of the market is expected to

cope with problems as they arise

— Sustainability issues are addressed

more through rhetoric than action

— Materialism and individualism spread

as core human values, whereas

social and environmental concerns

are secondary

Market Forces

Photo by lyzadanger, via Flickr

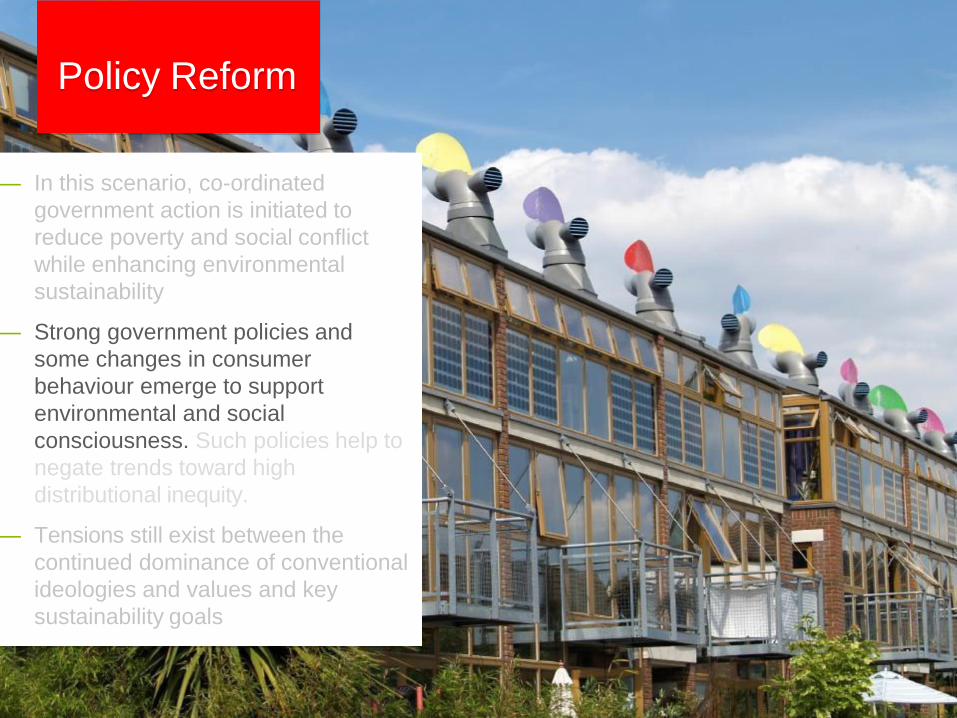

— In this scenario, co-ordinated

government action is initiated to

reduce poverty and social conflict

while enhancing environmental

sustainability

— Strong government policies and

some changes in consumer

behaviour emerge to support

environmental and social

consciousness. Such policies help to

negate trends toward high

distributional inequity.

— Tensions still exist between the

continued dominance of conventional

ideologies and values and key

sustainability goals

Policy Reform

— In this scenario, new socio-economic

arrangements and fundamental

alterations in societal values result in

changes to the character of UK urban

civilisation

— The notion of progress evolves and a

deeper basis for human happiness

and fulfilment is sought

— An ethos of ‘one planet living’

pervades, facilitating a shared vision

for a more sustained quality of life,

now and in the future

New Sustainability Paradigm

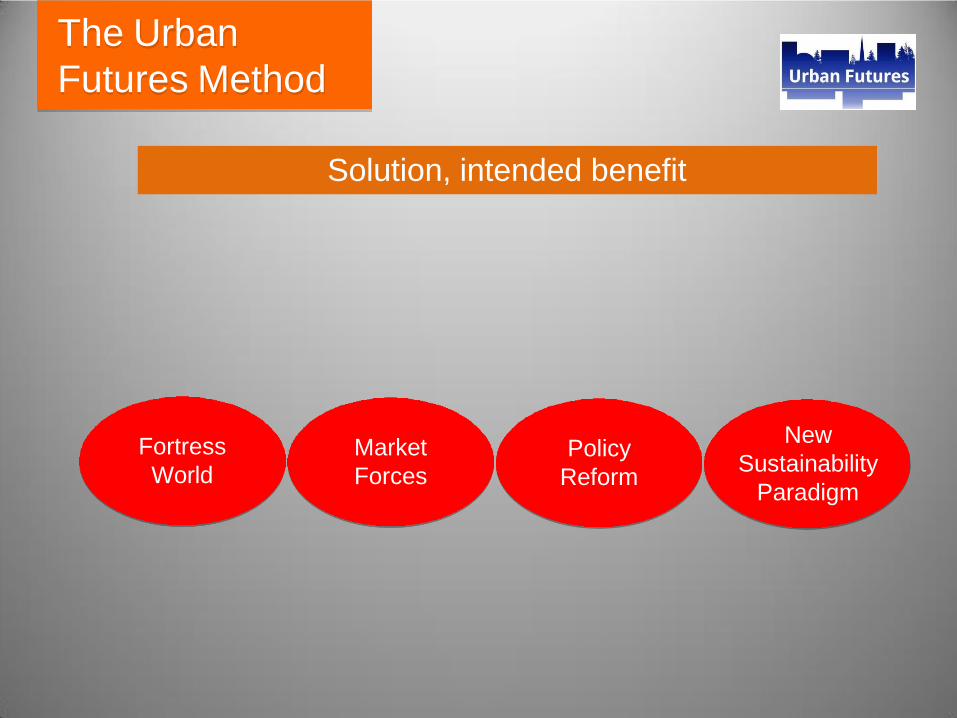

The Urban

Futures Method

Solution, intended benefit

Fortress

WorldMarket

ForcesPolicy

Reform

New

Sustainability

Paradigm

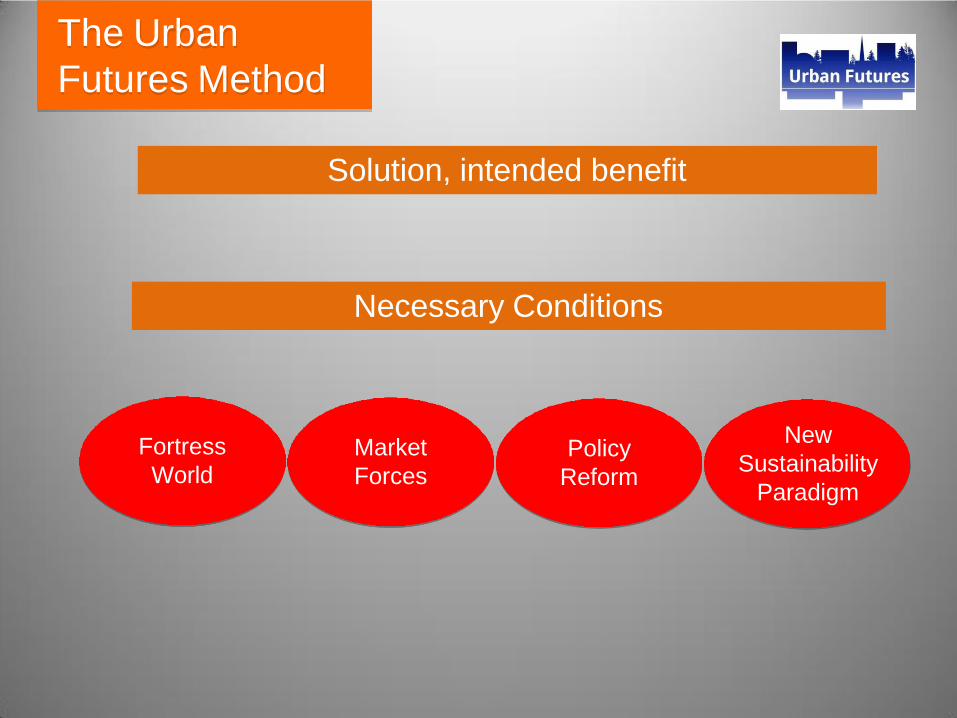

The Urban

Futures Method

Solution, intended benefit

Fortress

World

Necessary Conditions

Market

ForcesPolicy

Reform

New

Sustainability

Paradigm

The Urban

Futures Method

Solution, intended benefit

Fortress

World

Necessary Conditions

Market

ForcesPolicy

Reform

New

Sustainability

Paradigm

The Urban

Futures Method

Solution, intended benefit

Better No change Worse Better

Fortress

World

Necessary Conditions

Market

ForcesPolicy

Reform

New

Sustainability

Paradigm

Analysis

Methodology

Analysis in

Four

Scenarios

Solutions

and Intended

Benefits

Necessary

Conditions

Implement

Robust

Solutions

Implement

Vulnerable

Solutions

Adapt

Solutions

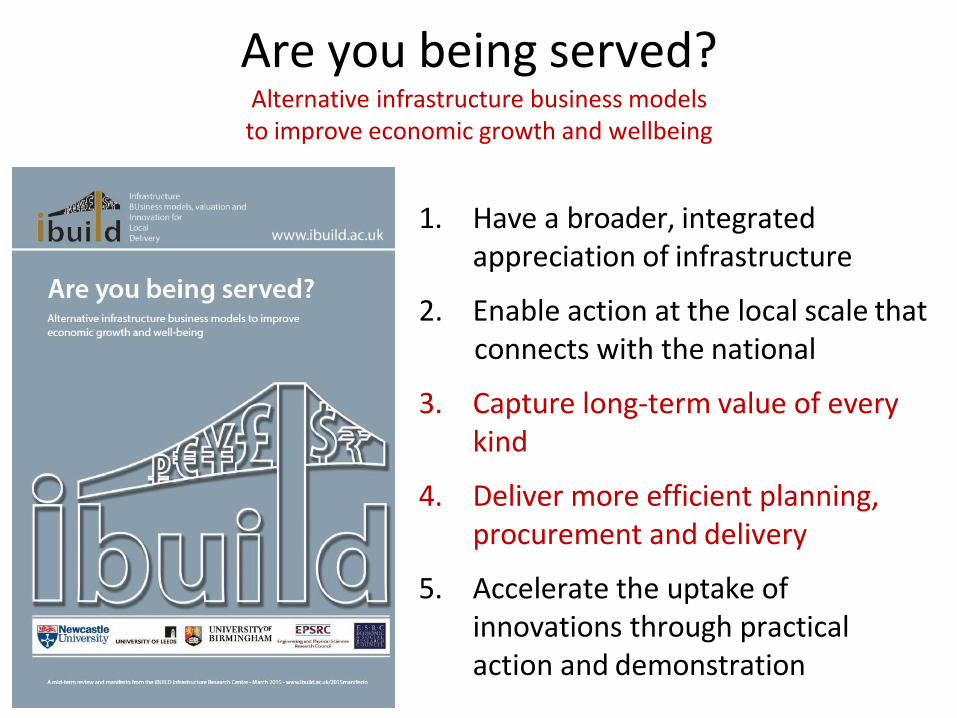

Infrastructure BUsiness models, valuation Innovation for Local Delivery

InfrastructureBUsiness models,valuationInnovationforLocal Delivery

www.ibuild.ac.uk

Are you being served?Alternative infrastructure business models to improve economic growth and wellbeing

1. Have a broader, integrated appreciation of infrastructure

2. Enable action at the local scale thatconnects with the national

3. Capture long-term value of every kind

4. Deliver more efficient planning,procurement and delivery

5. Accelerate the uptake of innovations through practical action and demonstration

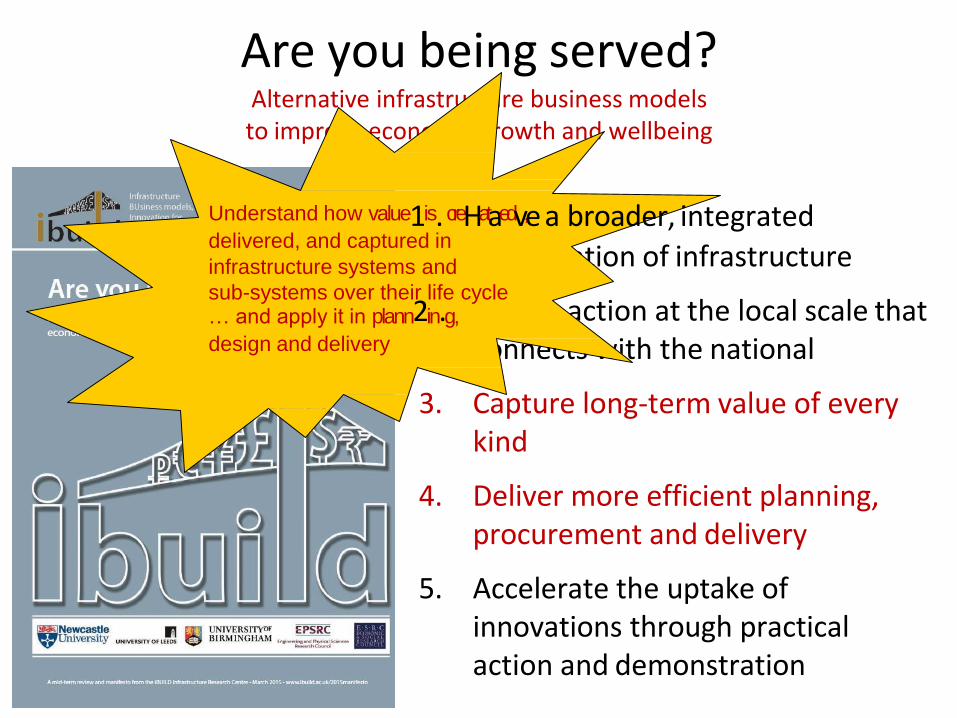

Are you being served?Alternative infrastructure business models to improve economic growth and wellbeing

appreciation of infrastructure

Enable action at the local scale thatconnects with the national

3. Capture long-term value of every kind

4. Deliver more efficient planning,procurement and delivery

5. Accelerate the uptake of innovations through practical action and demonstration

Understand how value1is. creHataedv,e a broader, integrateddelivered, and captured in

infrastructure systems and

sub-systems over their life cycle… and apply it in plann2in.g,

design and delivery

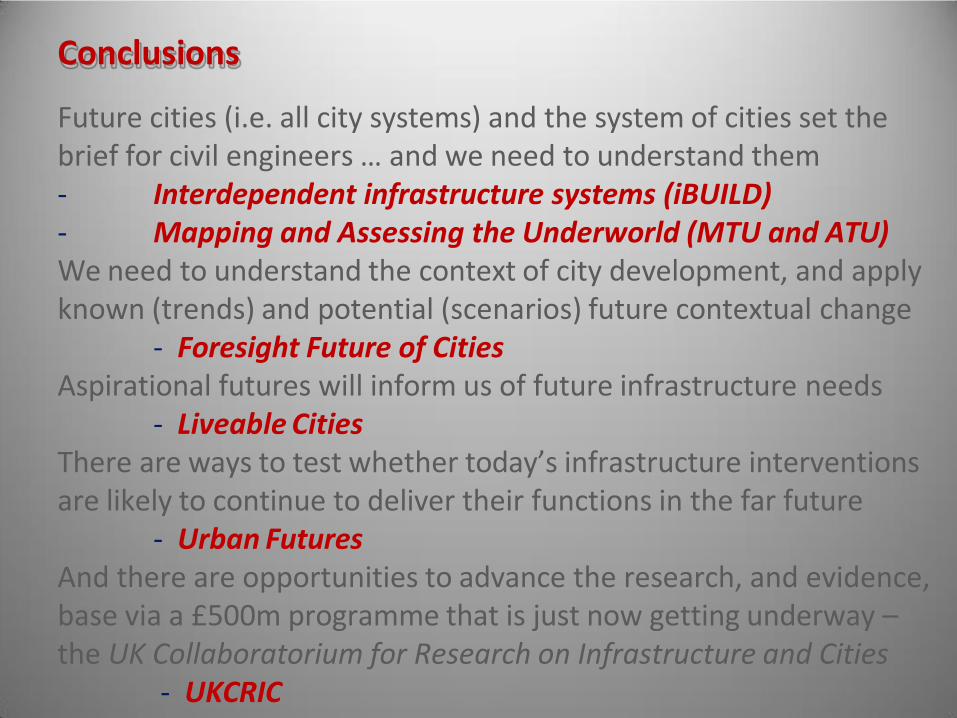

Conclusions

Future cities (i.e. all city systems) and the system of cities set the brief for civil engineers … and we need to understand them- Interdependent infrastructure systems (iBUILD)- Mapping and Assessing the Underworld (MTU and ATU) We need to understand the context of city development, and apply known (trends) and potential (scenarios) future contextual change

- Foresight Future of CitiesAspirational futures will inform us of future infrastructure needs

- Liveable CitiesThere are ways to test whether today’s infrastructure interventions are likely to continue to deliver their functions in the far future

- Urban FuturesAnd there are opportunities to advance the research, and evidence, base via a £500m programme that is just now getting underway –the UK Collaboratorium for Research on Infrastructure and Cities

- UKCRIC

If you have been …

Thank you for listening

Uudenmaan liitto // Nylands förbund // Helsinki-Uusimaa Regional CouncilUudenmaan liitto // Nylands förbund // Helsinki-Uusimaa Regional Council

RIS3 Reference site /

Helsinki Smart Region ///Johanna Juselius // Smart Cities UK 2016 Conference & Expo 4th Feb 2016

Uudenmaan liitto // Nylands förbund // Helsinki-Uusimaa Regional Council

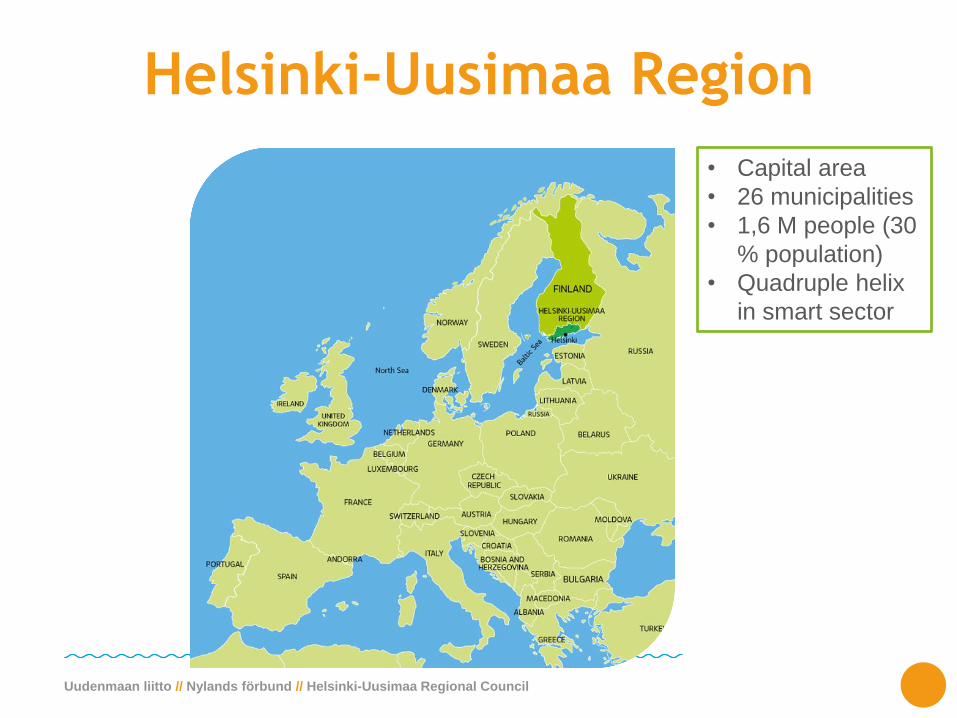

Helsinki-Uusimaa Region

• Capital area

• 26 municipalities

• 1,6 M people (30

% population)

• Quadruple helix

in smart sector

Uudenmaan liitto // Nylands förbund // Helsinki-Uusimaa Regional Council

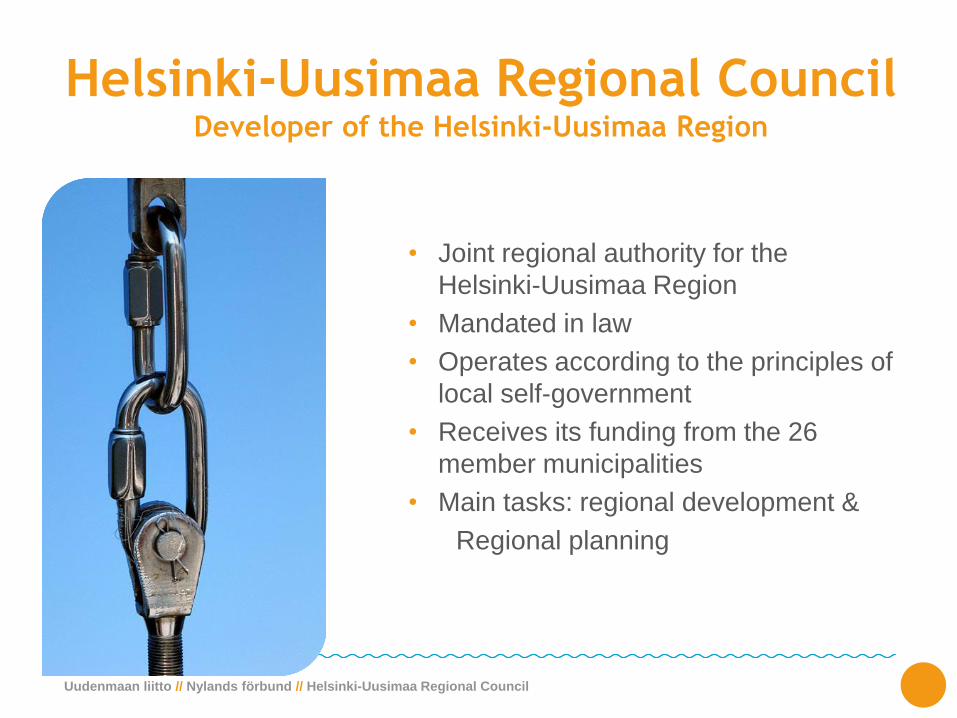

Helsinki-Uusimaa Regional CouncilDeveloper of the Helsinki-Uusimaa Region

• Joint regional authority for the

Helsinki-Uusimaa Region

• Mandated in law

• Operates according to the principles of

local self-government

• Receives its funding from the 26

member municipalities

• Main tasks: regional development &

Regional planning

Uudenmaan liitto // Nylands förbund // Helsinki-Uusimaa Regional Council

Smart Specialisation in Helsinki Region

Smart & Clean

RIS-reference site

Uudenmaan liitto // Nylands förbund // Helsinki-Uusimaa Regional Council

Starting point for the website project: If

you google ”Helsinki Smart Region”, you

get:

53

Uudenmaan liitto // Nylands förbund // Helsinki-Uusimaa Regional Council

Benchmarking:

What do others have?

> > >

54

Uudenmaan liitto // Nylands förbund // Helsinki-Uusimaa Regional Council 55

Smart City Wien

Uudenmaan liitto // Nylands förbund // Helsinki-Uusimaa Regional Council 56

Smart City Amsterdam

Uudenmaan liitto // Nylands förbund // Helsinki-Uusimaa Regional Council 57

Generalitat Valenciana

Uudenmaan liitto // Nylands förbund // Helsinki-Uusimaa Regional Council 58

Smart City

Stockholm

Uudenmaan liitto // Nylands förbund // Helsinki-Uusimaa Regional Council

The Conclusion:

Helsinki Region’s Smart

specialisation actors and initatives

are not presented consistently

anywhere.

59

Uudenmaan liitto // Nylands förbund // Helsinki-Uusimaa Regional Council

The Goal:

Smart Specialisation website for the Helsinki Region

The strategic starting point for the site is Smart

Specialisation S3 Platform

Content focus on emphasizing the streghts of the region: :

urban cleantech, human health tech, welfare city, smart citizen, digitalising industry

International target audience

60

Uudenmaan liitto // Nylands förbund // Helsinki-Uusimaa Regional Council

• Enables innovation on the

region.

Smart Specialisation

61

Boosting Europe’s profile in several sectors

• Is supporting the exisiting

strenghts of the region.

• EU-funding is give to projects

on line with the strategy .

• Helsinki Region has a strategy.This site tells

smartspecialisation

”as a story”

Uudenmaan liitto // Nylands förbund // Helsinki-Uusimaa Regional Council

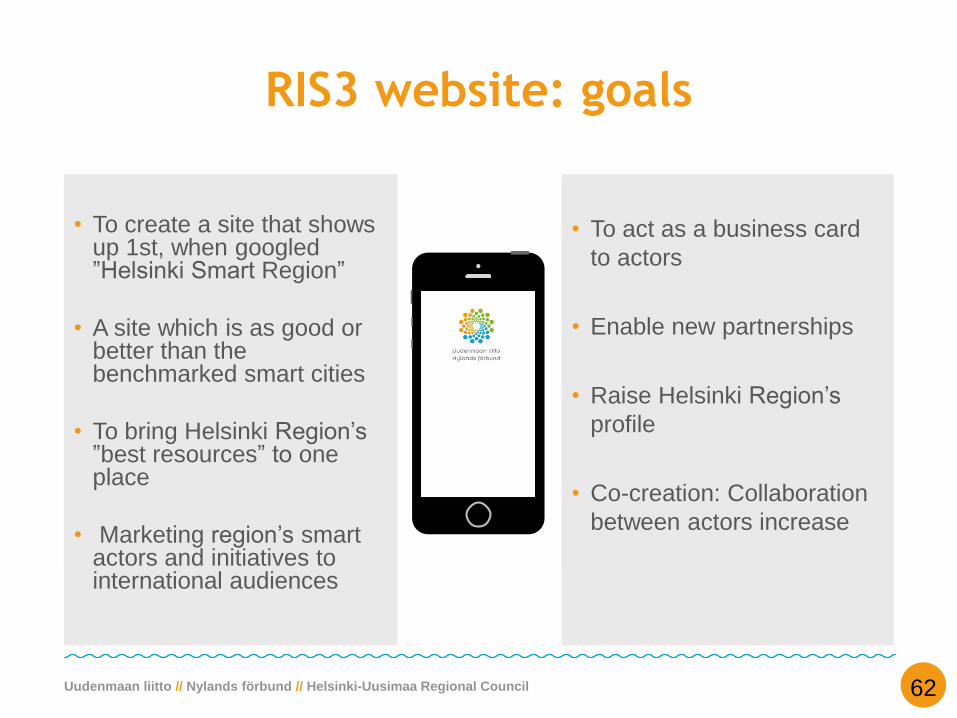

RIS3 website: goals

• To create a site that showsup 1st, when googled”Helsinki Smart Region”

• A site which is as good orbetter than thebenchmarked smart cities

• To bring Helsinki Region’s”best resources” to oneplace

• Marketing region’s smartactors and initiatives to international audiences

62

• To act as a business card

to actors

• Enable new partnerships

• Raise Helsinki Region’s

profile

• Co-creation: Collaboration

between actors increase

Uudenmaan liitto // Nylands förbund // Helsinki-Uusimaa Regional Council

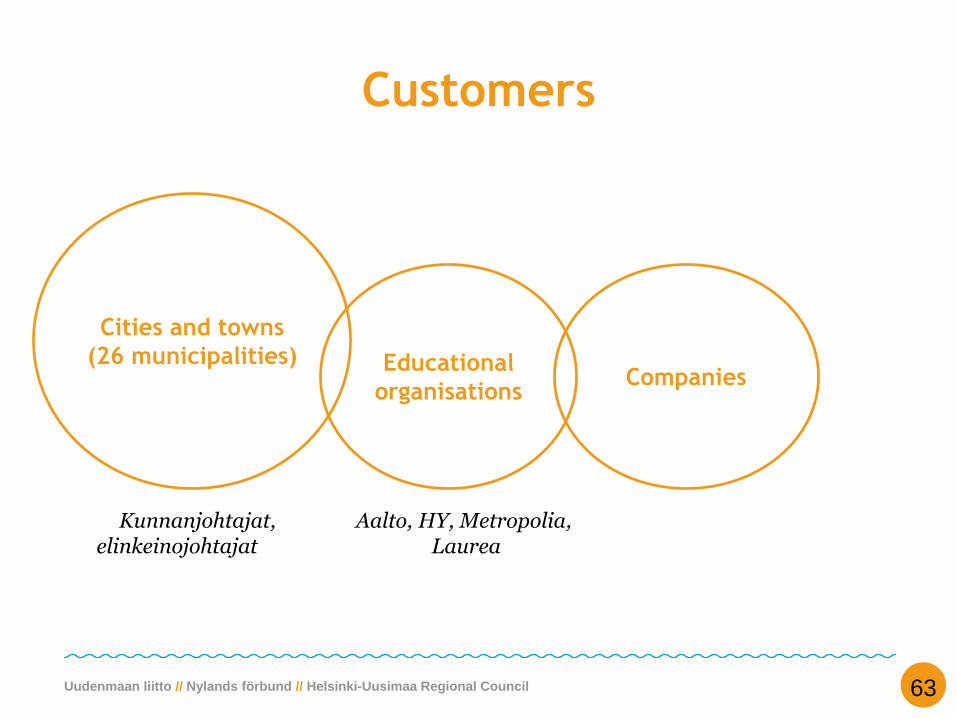

Customers

63

Cities and towns

(26 municipalities) Educational

organisations

Kunnanjohtajat, elinkeinojohtajat

Aalto, HY, Metropolia,Laurea

Companies

Uudenmaan liitto // Nylands förbund // Helsinki-Uusimaa Regional Council

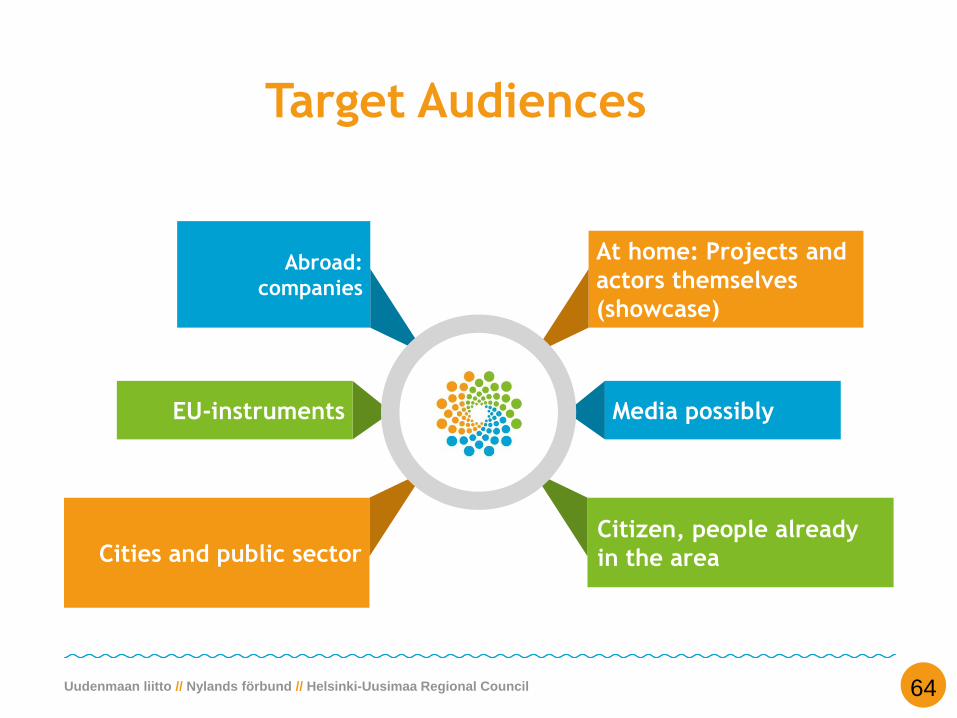

Target Audiences

64

At home: Projects and

actors themselves

(showcase)

Abroad:

companies

Citizen, people already

in the areaCities and public sector

Media possiblyEU-instruments

Uudenmaan liitto // Nylands förbund // Helsinki-Uusimaa Regional Council

The Content:

Helsinki SMART Region ”as a story”

65

How: Storyfying. We create and write Helsinki Region’s SMART ”story”.-Vision: Helsinki Region is a leader in the Baltic Sea region by 2040.

What is being said::

What kind of a Smart

Region –What makes

Helsinki Region unique

under this theme?

To whom?

Regional marketing

to target audiences,

business, future

Why Helsinki-

Uusimaa Regional

Council? A Neutral

actor, enabler, coach,

Main content:

SMART

spreadheads (Urban

Cleantech, Human

Health Tech, Smart

Citizen, Digitalizing

Industry, Welfare

City)

Esitystapa

Caseshttp://www.muo

toilutarinat.fi/en

/project/helsinki

-region-

infoshare/

Urban Cleantech: Key Actors

66

Universities

and

recearch

centers

Developers,

accelerators

enablers

BusinessPlatforms and

operational

environments

GHP (Helsinki Business

Hub)

GREENNET Finland

CLEEN Oy

Yritysverkosto

CLC ry

HSY (Hiilineutraalit asemanseudut, Ilmasto

Atlas)

SITRA

Helsinki-Uusimaa Regional Council

Helsinki (Kalasatama, Östersundom, Pasila,

Ilmastokatu, Tierkartta)

Vantaa (Kunkaankolmio, Kivistö,

Aviapolis,Vehkala)

Espoo (Länsimetron alue, Suurpelto,

Bioruukki)

Porvoo (Kilpilahti, Skaftskar)

Urban Cleantech

Brands and

marketing

Cities

and

Municipalities

Aalto University

Climate KIC

Material KIC

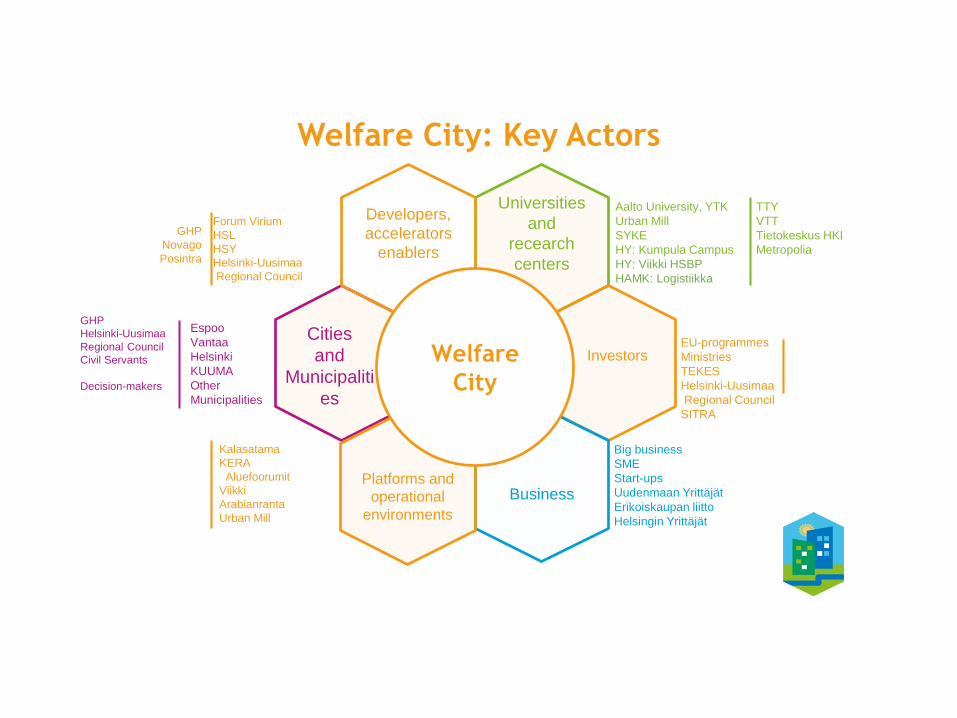

Welfare City: Key Actors

67

Universities

and

recearch

centers

Developers,

accelerators

enablers

BusinessPlatforms and

operational

environments

EU-programmes

Ministries

TEKES

Helsinki-Uusimaa

Regional Council

SITRA

Big business

SME

Start-ups

Uudenmaan Yrittäjät

Erikoiskaupan liitto

Helsingin Yrittäjät

Forum Virium

HSL

HSY

Helsinki-Uusimaa

Regional Council

Espoo

Vantaa

Helsinki

KUUMA

Other

Municipalities

Kalasatama

KERA

Aluefoorumit

Viikki

Arabianranta

Urban Mill

Welfare

City

Investors

Cities

and

Municipaliti

es

Aalto University, YTK

Urban Mill

SYKE

HY: Kumpula Campus

HY: Viikki HSBP

HAMK: Logistiikka

TTY

VTT

Tietokeskus HKI

Metropolia

GHP

Novago

Posintra

GHP

Helsinki-Uusimaa

Regional Council

Civil Servants

Decision-makers

Uudenmaan liitto // Nylands förbund // Helsinki-Uusimaa Regional Council

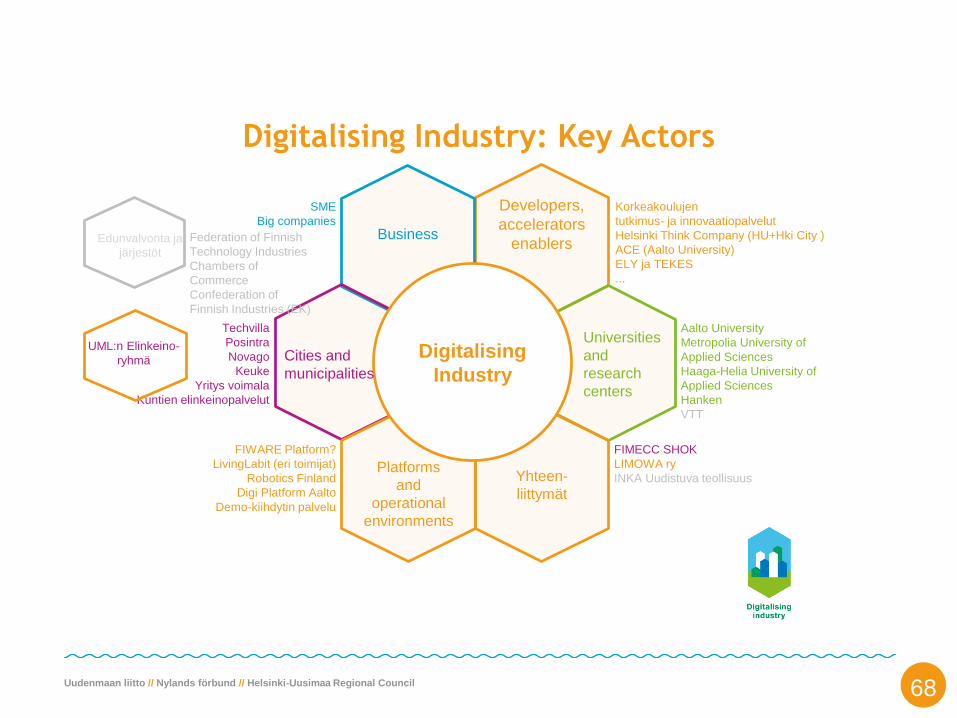

Digitalising Industry: Key Actors

68

Developers,

accelerators

enablersBusiness

Yhteen-

liittymät

Platforms

and

operational

environments

Korkeakoulujen

tutkimus- ja innovaatiopalvelut

Helsinki Think Company (HU+Hki City )

ACE (Aalto University)

ELY ja TEKES

...

Aalto University

Metropolia University of

Applied Sciences

Haaga-Helia University of

Applied Sciences

Hanken

VTT

FIMECC SHOK

LIMOWA ry

INKA Uudistuva teollisuus

SME

Big companies

Techvilla

Posintra

Novago

Keuke

Yritys voimala

Kuntien elinkeinopalvelut

FIWARE Platform?

LivingLabit (eri toimijat)

Robotics Finland

Digi Platform Aalto

Demo-kiihdytin palvelu

Digitalising

Industry

Universities

and

research

centers

Cities and

municipalities

UML:n Elinkeino-

ryhmä

Edunvalvonta ja

järjestöt

Federation of Finnish

Technology Industries

Chambers of

Commerce

Confederation of

Finnish Industries (EK)

Uudenmaan liitto // Nylands förbund // Helsinki-Uusimaa Regional Council

Smart Citizen: Key Actors

69

Smart

Citizen

Universities

and

recearch

centers

3rd sector

Developers,

accelerators

enablers

Cities

and

Municipalitie

s

Business

Platforms

and

operational

environments

Helsinki University

Kuluttajatutkimuskeskus

FGI Paikkatietokeskus

Aalto University

Metropolia University of

Applied Sciences

Laurea University of

Applied Sciences

VTT

TTL

HUMAK

DIAK

Arcada

Haaga-Helia

COSS ry

Helka ry

Marja-Verkko

Open Knowledge Finland

TIEKE, Tietoyhteiskunnan

kehittämiskeskus

Lapinlahden Lähde

SME

Start-ups

Big business

Helsinki-Uusimaa

Regional Council

Statistics Finland

Helsinki Region

Ingoshare

Forum Virium

HSY

Helsinki

Espoo

Vantaa

23 other municipalities

6Aika

DIGILE

INKA: Älykäs kaupunki

HRI

Fiksu Kalasatama

Tekes

ELY

HSL

Smart

Citizen

Uudenmaan liitto // Nylands förbund // Helsinki-Uusimaa Regional Council

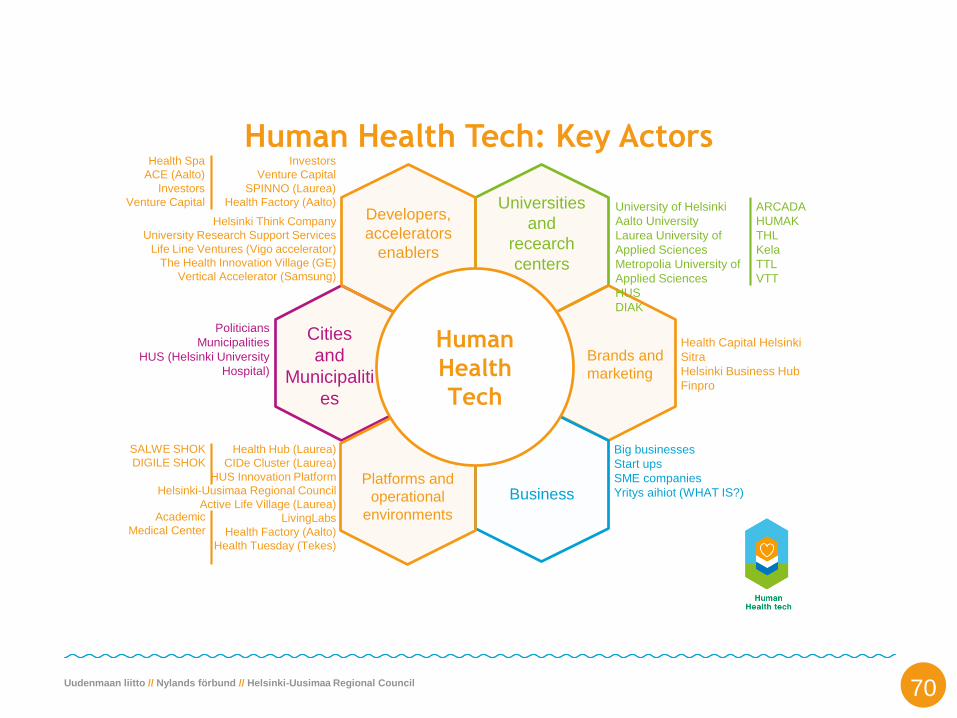

Human Health Tech: Key Actors

70

Universities

and

recearch

centers

Developers,

accelerators

enablers

BusinessPlatforms and

operational

environments

Health Capital Helsinki

Sitra

Helsinki Business Hub

Finpro

Big businesses

Start ups

SME companies

Yritys aihiot (WHAT IS?)

Helsinki Think Company

University Research Support Services

Life Line Ventures (Vigo accelerator)

The Health Innovation Village (GE)

Vertical Accelerator (Samsung)

Politicians

Municipalities

HUS (Helsinki University

Hospital)

Health Hub (Laurea)

CIDe Cluster (Laurea)

HUS Innovation Platform

Helsinki-Uusimaa Regional Council

Active Life Village (Laurea)

LivingLabs

Health Factory (Aalto)

Health Tuesday (Tekes)

Human

Health

Tech

Brands and

marketing

Cities

and

Municipaliti

es

University of Helsinki

Aalto University

Laurea University of

Applied Sciences

Metropolia University of

Applied Sciences

HUS

DIAK

ARCADA

HUMAK

THL

Kela

TTL

VTT

Investors

Venture Capital

SPINNO (Laurea)

Health Factory (Aalto)

Health Spa

ACE (Aalto)

Investors

Venture Capital

SALWE SHOK

DIGILE SHOK

Academic

Medical Center

Uudenmaan liitto // Nylands förbund // Helsinki-Uusimaa Regional Council

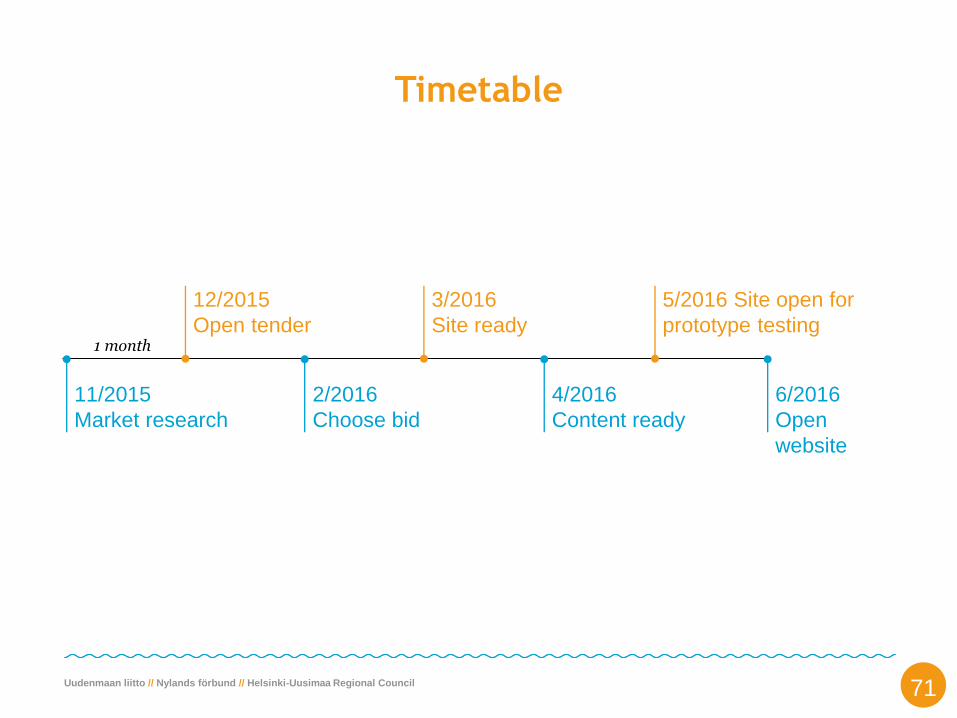

Timetable

71

1 month

11/2015

Market research

12/2015

Open tender

2/2016

Choose bid

4/2016

Content ready

3/2016

Site ready

5/2016 Site open for

prototype testing

6/2016

Open

website

Uudenmaan liitto // Nylands förbund // Helsinki-Uusimaa Regional Council

UUDENMAANLIITTO.FI

PRESENTATION STRUCTURE

What is a smart city?

What is needed to deliver a

smart city?

How can smart

technology help?

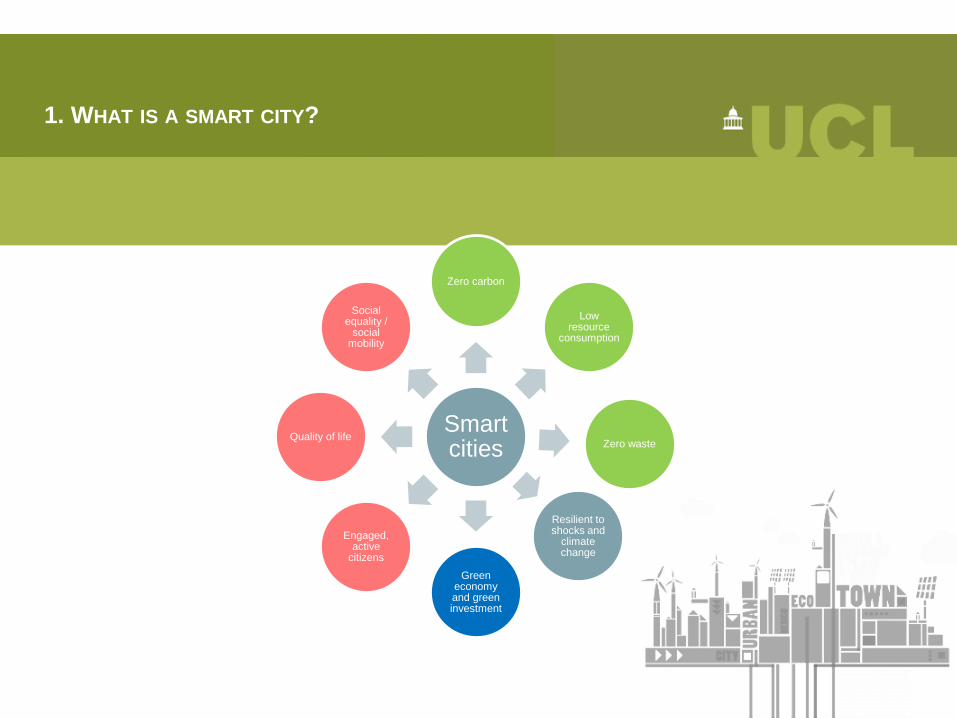

1. WHAT IS A SMART CITY?

Smart cities

Zero carbon

Low resource

consumption

Resilient to shocks and

climate change

Zero waste

Green economy and green investment

Engaged, active

citizens

Quality of life

Social equality /

social mobility

DONGTAN

Type New

Stage Construction (halted)

Scale 70,000

Implementation Technological innovation

Flagship project

Zero energy, GHG neutral, water circular

Natural capital for economic growth

Traditional Chinese small town urban form

Cosmopolitan orientation

MASDAR (UAE)

“Zero-carbon, zero-waste”

Traditional Arab architecture + hi-tech

Solar powered PRT and desalination

PV, CSP energy, waste incineration

Renewable energy R&D living lab

“Carbon neutral, not zero carbon”

Feels like a non-place

Type New

Stage Construction

Scale 40,000

Implementation Technological innovation

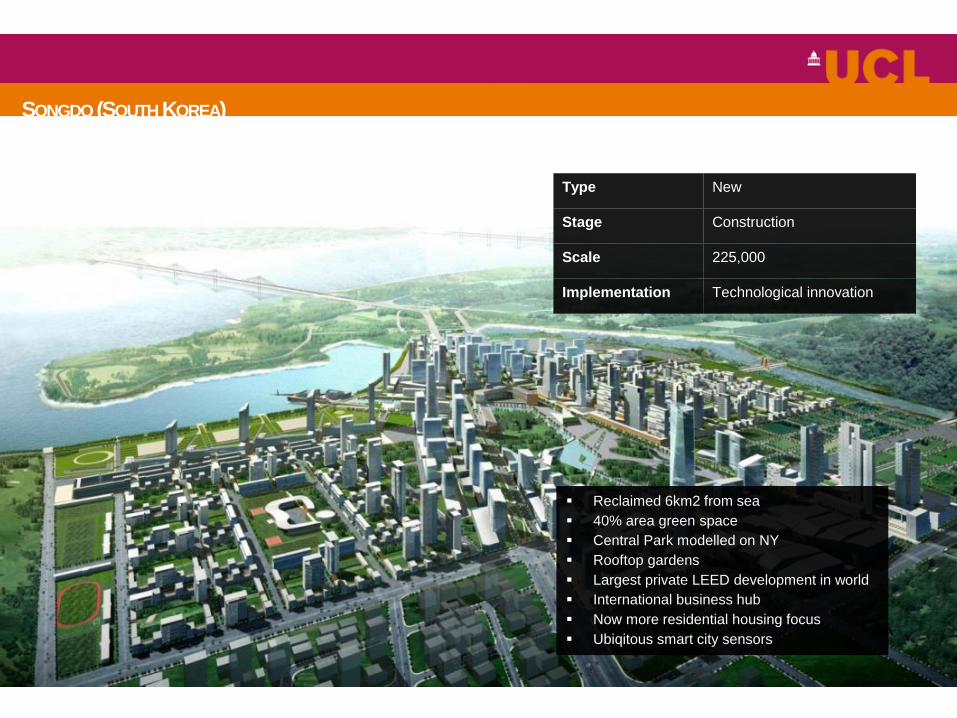

SONGDO (SOUTH KOREA)

Type New

Stage Construction

Scale 225,000

Implementation Technological innovation

Reclaimed 6km2 from sea

40% area green space

Central Park modelled on NY

Rooftop gardens

Largest private LEED development in world

International business hub

Now more residential housing focus

Ubiqitous smart city sensors

TIANJIN ECO-CITY (CHINA)

Type Extension

Stage Construction

Scale 350,000

Implementation Technological innovation

Built with expertise from Singapore

Energy from waste

High EE buildings standards, cold climate

90% public transport, cycling, walking mode

split

Wetlands

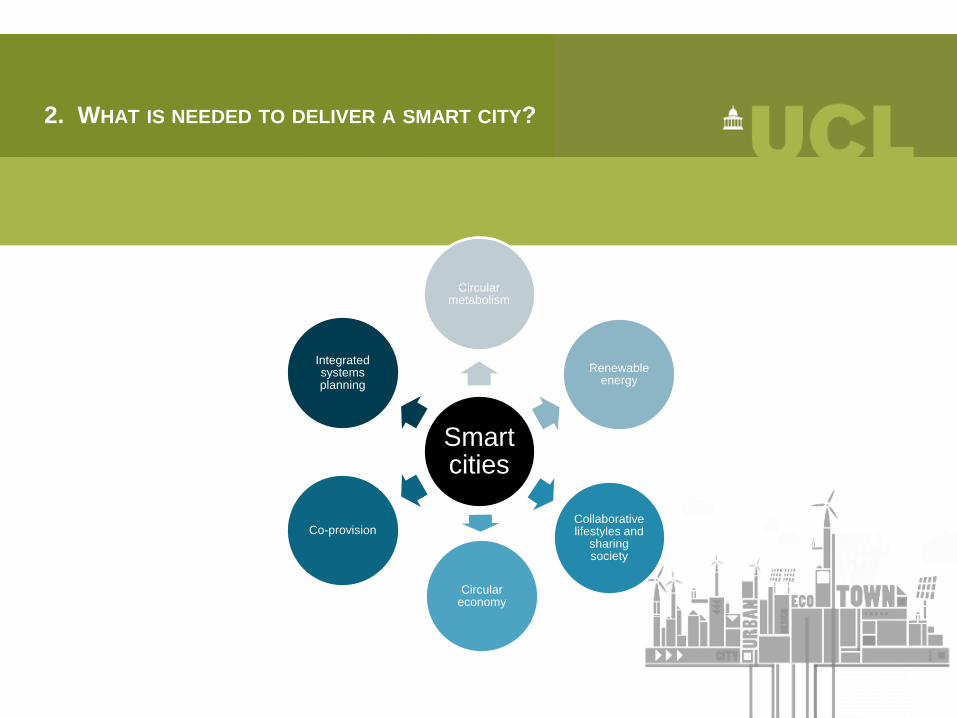

2. WHAT IS NEEDED TO DELIVER A SMART CITY?

Smart cities

Circular metabolism

Renewable energy

Circular economy

Collaborative lifestyles and

sharing society

Co-provision

Integrated systems planning

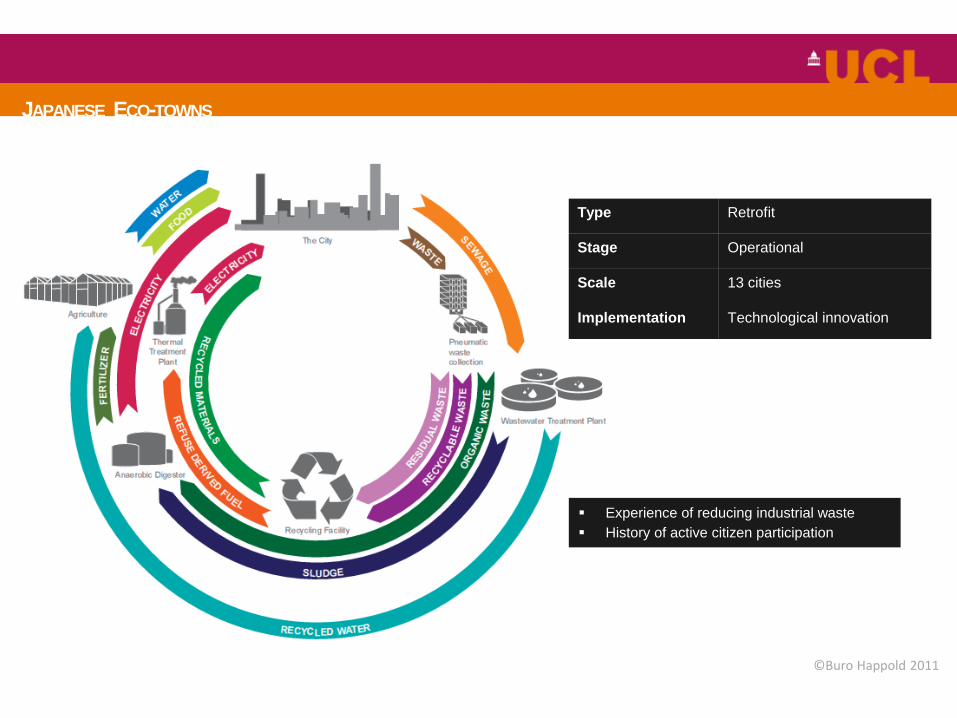

JAPANESE ECO-TOWNS

©Buro Happold 2011

Type Retrofit

Stage Operational

Scale 13 cities

Implementation Technological innovation

Experience of reducing industrial waste

History of active citizen participation

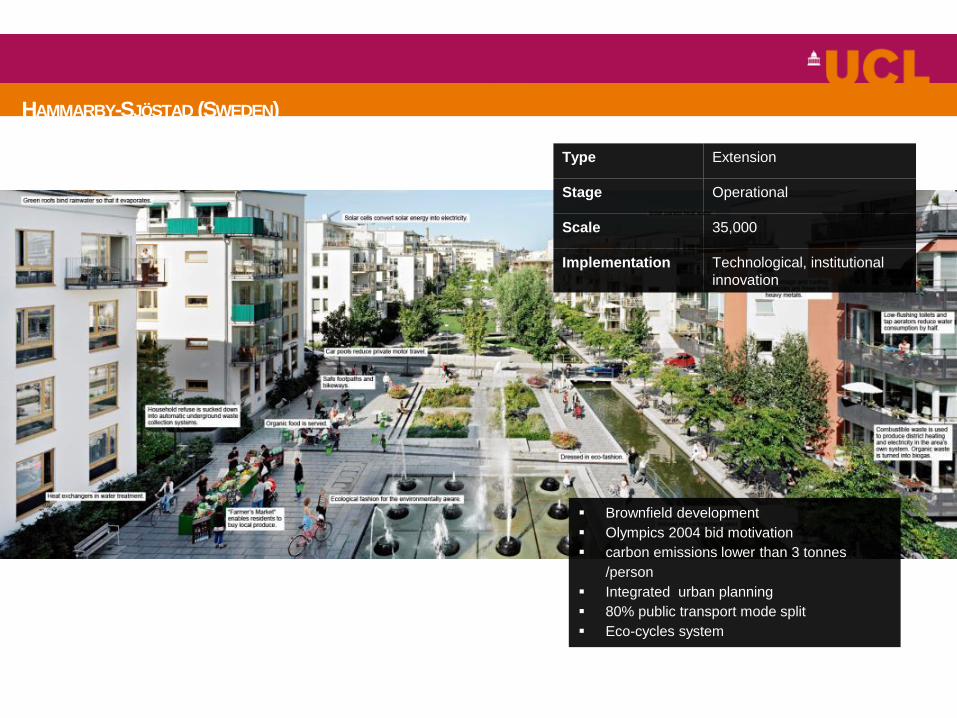

HAMMARBY-SJÖSTAD (SWEDEN)

Brownfield development

Olympics 2004 bid motivation

carbon emissions lower than 3 tonnes

/person

Integrated urban planning

80% public transport mode split

Eco-cycles system

Type Extension

Stage Operational

Scale 35,000

Implementation Technological, institutional

innovation

STOCKHOLM ROYAL SEAPORT (SWEDEN)

Brownfield development

10,000 new apartments, 30,000 new places

to work and 600,000m² of commercial space

Integrated urban planning

Fossil fuel free 2030

By 2020, carbon emissions lower than 1.5

tonnes /person

Smart technology – smart grid, ev’s, lifestyle

apps

Eco-cycles system

Type Extension

Stage Construction

Scale 40,000

Implementation Technological, institutional

innovation

VAUBAN (FREIBURG, GERMANY)

Type Extension

Stage Operational

Scale 5,000

Implementation Cultural, institutional and

technical innovation

Energy plus, passive houses ultra-low energy

standard

Co-provision – baugruppen, community energy coops

Collaborative planning

Collaborative lifestyles – car-share, housing coops,

cohousing.

Affordable housing

3. HOW CAN SMART TECHNOLOGY HELP?

Smart Technologies

Strategic monitoring

resource flows and performance

Personal / lifestyle monitoring –

promote sustainable

lifestyles

Educational apps for raising

awareness and changing behaviour

Enabling renewable

technologies –smart grid

Creating social networking

platforms for sharing resources and collaboration

Creating platforms for collaborative institutions and

processes–community energy coops; co-building,

collaborative planning, etc

Enabling integrated systems planning

// Linked projects:

1. Zero Carbon Urban Realties

2. Lost in translation – translation of eco-urban

planning models to new contexts

3. Circular Cities Research Hub

If you would like to hear more contact:

BUILDING THE FUTURE TOGETHER

Justin AndersonChairman & CEO Flexeye. Founder & Director HyperCat.

THE INTERNET OF THINGS &

THE ROLE FOR SMART CITIES

CASE STUDY: BUILDING THE SMART STRATEGY FOR THE UK'S LARGEST REGENERATION PROJECT

Justin Anderson Executive Chairman Flexeye @jpeanderson

Old Oak & Park Royal Development Corp

THE UK’S

BIGGEST REGENERATION SCHEME

66%

90%Old Oak & Park Royal Development Corp

COLLABORATIVE

INNOVATION

SMART VISION & STRATEGY

ACCESS TO DATA

CLEAN & GREEN

PEOPLE CENTRIC

SAFE & SMART TECHNOLOGY

SMART UTILITIES INFASTRUCTURE

SMART ENERGY

5.0 RECOMMENDATIONS:

TRANSPORT & PUBLIC REALM

UTILITIES INFRASTRUCTURE

SMART SUSTAINABILITY

CROSS CUTTING

5.1 TRANSPORT & PUBLIC REALM

• Dynamic street marking

• Smart city technology

• Virtual modeling

• Digital and fixed signage

• Waste management

• Last-mile delivery

• Freight consolidation & sharing

• Free flow (360) station

• Safety & security

5.2 UTILITIES INFRASTRUCTURE

• Digital communication

infrastructure

• Innovation

• Energy harvesting

• Detailed asset modeling

• Storing information

• Information management

& digital platforms

• Safety & security

5.3 SMART SUSTAINABILITY

• Smarter building management

• Local energy production and

storage

• Flexible energy demand

• Sustainable construction

• Air quality

• Vehicle movement

• Climate resilience

• Energy strategy targets

5.4 CROSS CUTTING

• Interoperability across data

and systems

• Scalability & flexibility

• Resilient & dependence

• Best practice

• Data privacy

• Incentive structures

“DO YOU WANT

WHEELS WITH YOUR IPAD

SIR?”

POWER FROM

THIN AIR

GET WELL SOON

MEETBIGSISTER

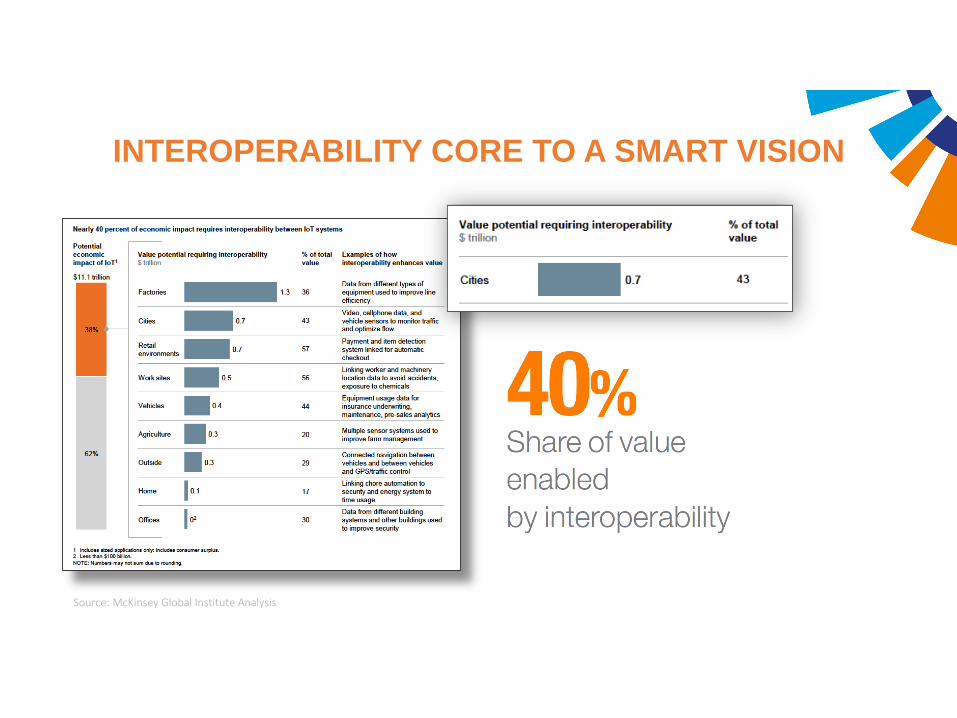

INTEROPERABILITY CORE TO A SMART VISION

Source: McKinsey Global Institute Analysis

USING HYPERCAT

Rear-camera

Tyre pressure GPS Temperature Messaging Panic button

Service & fuel Tachograph Driver behaviour Engine codes Front-camera

Job dispatching

Capacity sensors

Light

ADD INTEROPERABLE SYSTEMS

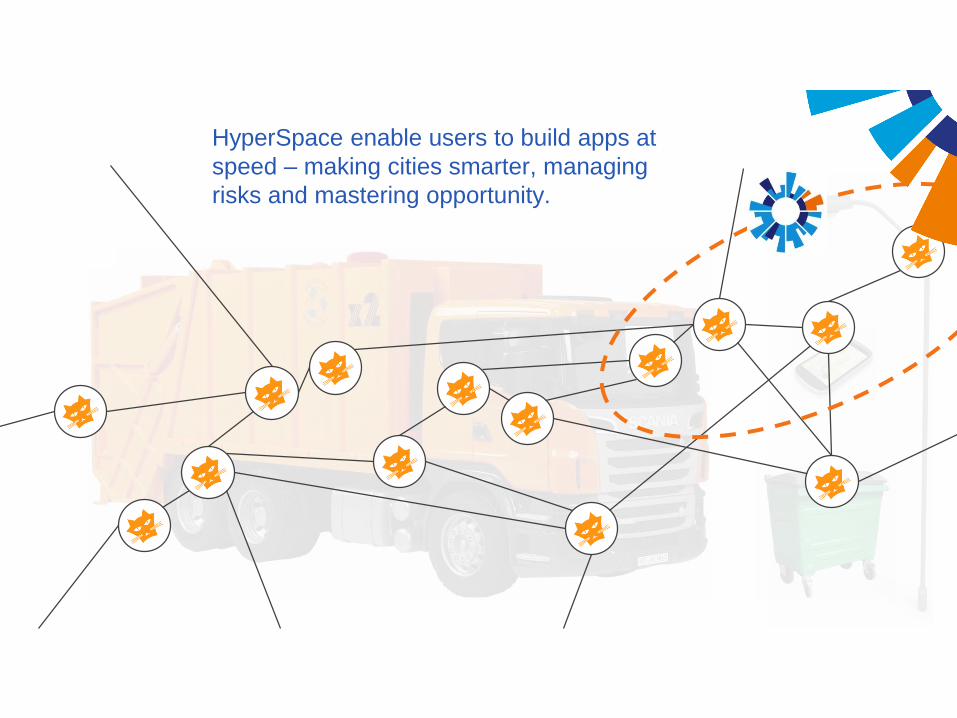

DRIVING VALUE WEB INNOVATION

HyperSpace enable users to build apps at

speed – making cities smarter, managing

risks and mastering opportunity.

Smart Logistics

Smart Parking

Smart Water

Smart Buildings

Smart Highways

Smart Facilities

SmartFoodSafety

My Guardian Smart EnergyFleet Fault Diagnosis

Smart Lighting

++

HYPERCAT SPEARHEADS / HYPERSPACE

The Leading Enabler of Smart Cities

February 2016

About CityFibre

• Builder, operator & owner of citywide

fibre optic network infrastructure

• Wholesale shared infrastructure model

• Significant presence in 36 UK cities

• Over 40 service provider relationships

• Over 3,000 customer premises served

• Citywide fibre deployment enabling

transformational digital opportunities

A Builder of UK Gigabit Cities

A Gigabit City is a Smarter City

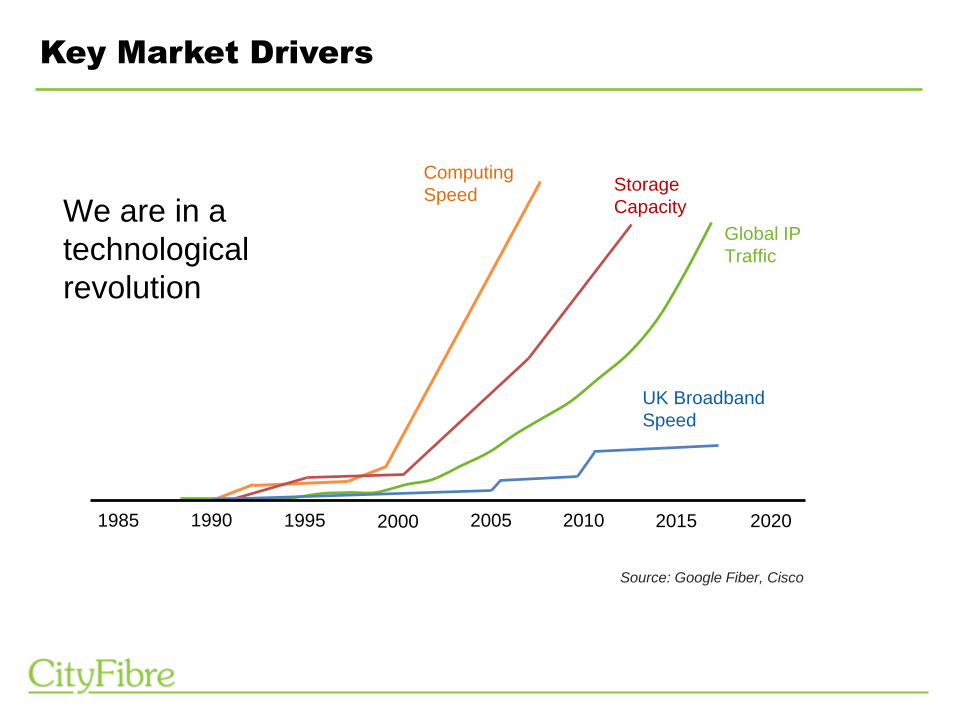

Key Market Drivers

Computing

SpeedStorage

Capacity

Global IP

Traffic

UK Broadband

Speed

1985 1990 20051995 2000 2010 2015 2020

Source: Google Fiber, Cisco

We are in a

technological

revolution

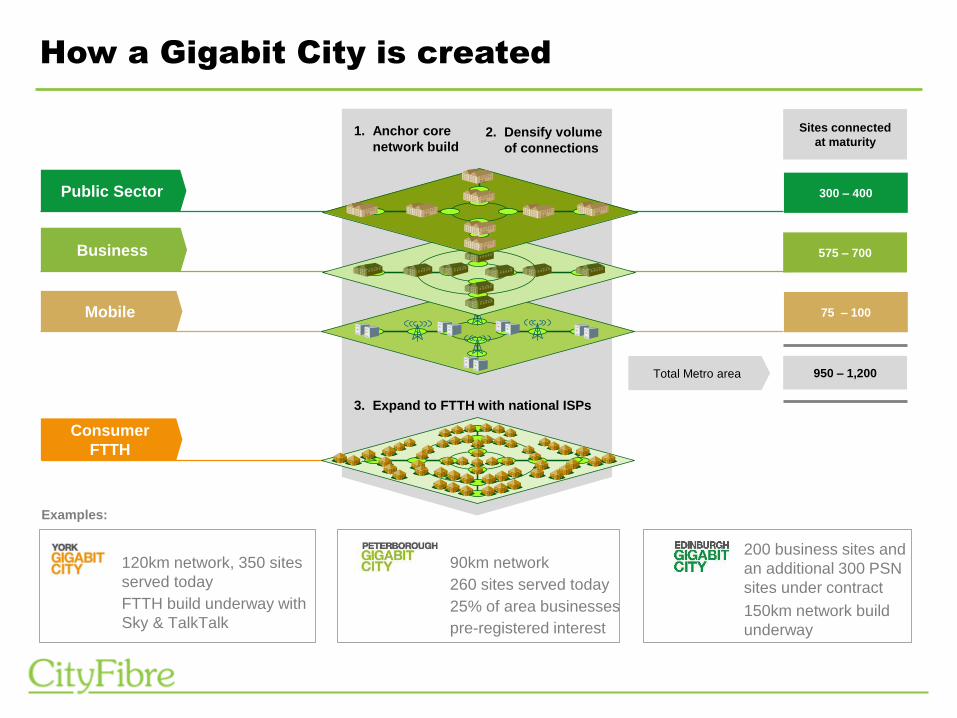

How a Gigabit City is created

Consumer

FTTHConsumers with 100Mbps+symmetrical internet access

Sites connected

at maturity

950 – 1,200

Mobile

Total Metro area

75 – 1003G, LTE, 4G backhaul,data centres

Business 575 – 700SME with Gbps site to siteand internet services

Public Sector 300 – 400Core network, Public Sector anchor client, schools, colleges, universities, public health

1. Anchor core

network build2. Densify volume

of connections

3. Expand to FTTH with national ISPs

120km network, 350 sites

served today

FTTH build underway with

Sky & TalkTalk

90km network

260 sites served today

25% of area businesses

pre-registered interest

200 business sites and

an additional 300 PSN

sites under contract

150km network build

underway

Examples:

CityFibre: Edinburgh Metro Network

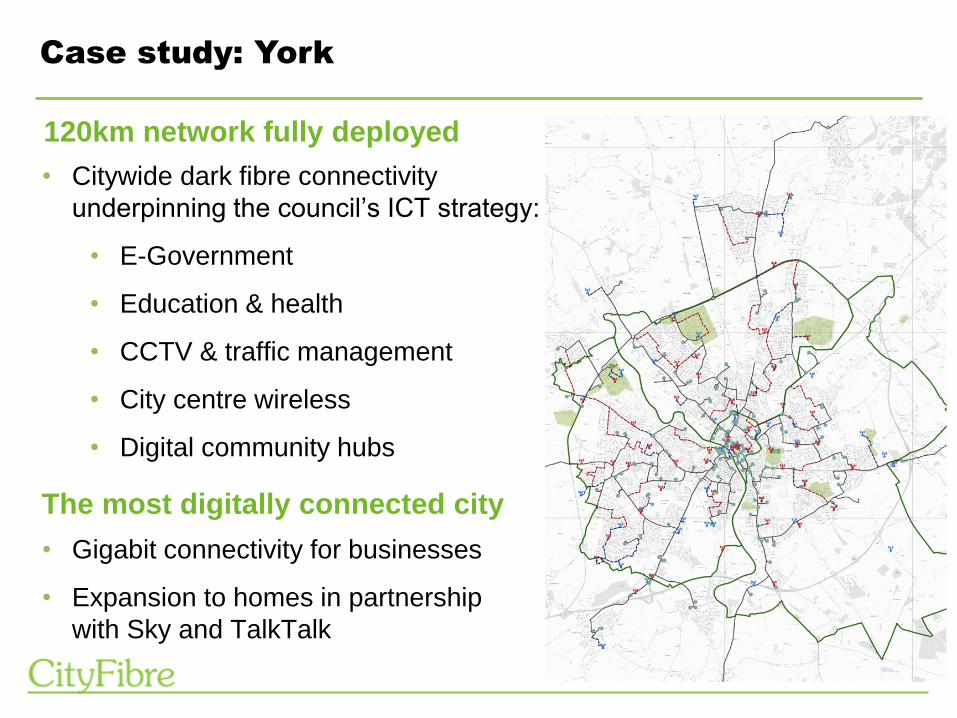

Case study: York

• Citywide dark fibre connectivity

underpinning the council’s ICT strategy:

• E-Government

• Education & health

• CCTV & traffic management

• City centre wireless

• Digital community hubs

• Gigabit connectivity for businesses

• Expansion to homes in partnership

with Sky and TalkTalk

120km network fully deployed

The most digitally connected city

Peterborough: The little city that could, and did

Peterborough trumps Moscow,

Dubai and Buenos

Aires to win 2015 World Smart City

Award!!!

“This Gigabit City deal is the most

important development for

Peterborough since the railways.

It is future proof.”

- Marco Cereste, Leader

of Peterborough City Council

(Nov. ‘14)

November 2015

Long term benefits of ubiquitous fibre

• €1.8bn return on €600m investment:

• €900m in increased employment

• €200m increase in property values

• €16m annual ICT savings for Government

• €8.5m annual savings for businesses

Stockholm – 22 years of investment

Fibre to everything

• 700 service providers

• 4 LTE networks

• 90% of residential premises on net

The Smart City

Smart Local Government

Smart Education

Smart Business

Smart Living &

Communities

Smart Mobility

Smart Utilities &

Environment

Digital

Government

Digital

Economy

Digital

Communities

Digital

Environment

Fibre is at the core of the Smart City

Question and Answers

Refreshments and Networking

SMART CITIES PRESENTATIONFebruary 2016

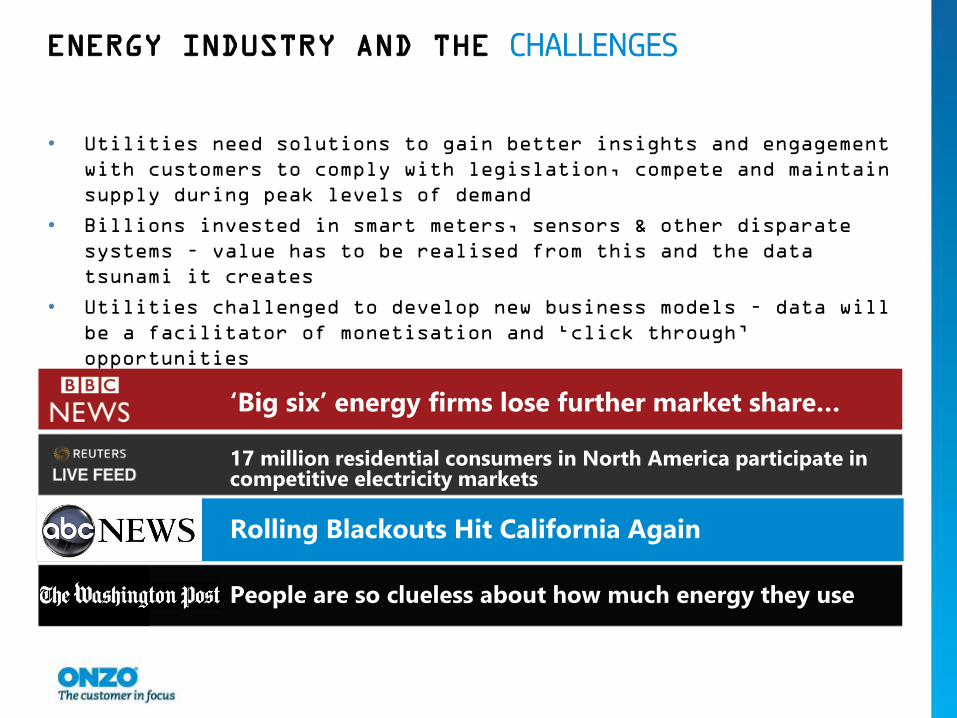

ENERGY INDUSTRY AND THE CHALLENGES

• Utilities need solutions to gain better insights and engagement

with customers to comply with legislation, compete and maintain

supply during peak levels of demand

• Billions invested in smart meters, sensors & other disparate

systems – value has to be realised from this and the data

tsunami it creates

• Utilities challenged to develop new business models – data will

be a facilitator of monetisation and ‘click through’

opportunities

‘Big six’ energy firms lose further market share…

17 million residential consumers in North America participate in competitive electricity markets

Small rivals hurt energy’s Big Six

People are so clueless about how much energy they use

Rolling Blackouts Hit California Again

ENERGY INDUSTRY IS PRIMED FOR TRANSFORMATION

Telco

• New services

• More

differentiatio

n in price &

service

Banking

• Instant access

to data

• Increase in

self service

Retail

• Meaningful

recommendations

• Consumer

profiles

• Improved

logistics on

delivery

Utilities

• Billing relationship only

• Lack of insight for usage

Personalised and Digitised

• Informed competition

inhibited

• Lack of differentiation on

services

No digital transformation

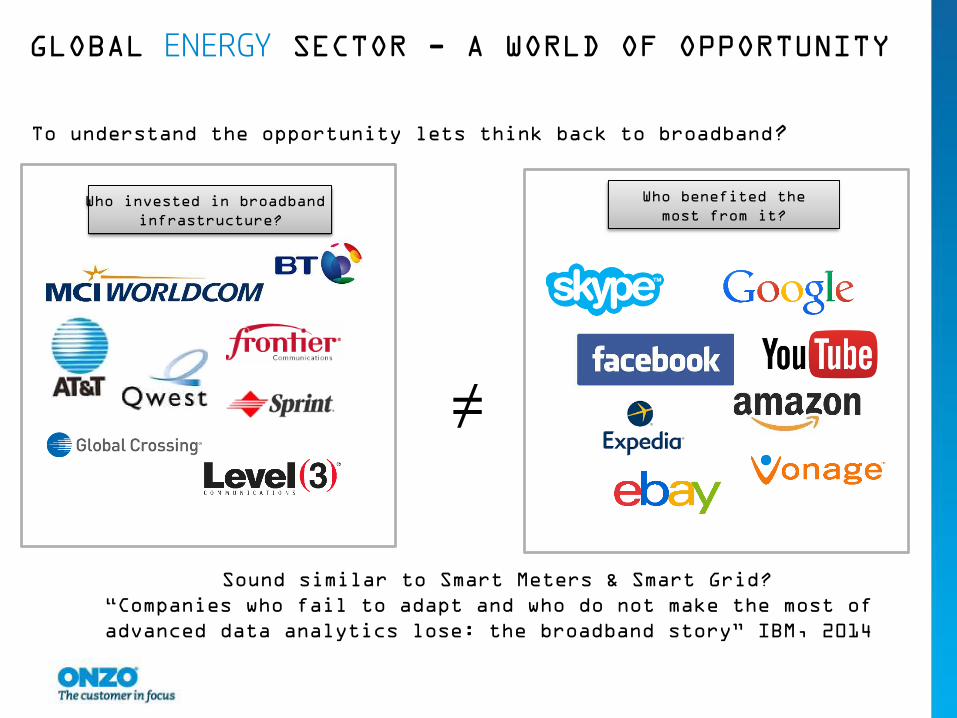

GLOBAL ENERGY SECTOR - A WORLD OF OPPORTUNITY

To understand the opportunity lets think back to broadband?

Who invested in broadband

infrastructure?

Who benefited the

most from it?

Sound similar to Smart Meters & Smart Grid?

“Companies who fail to adapt and who do not make the most of

advanced data analytics lose: the broadband story” IBM, 2014

≠

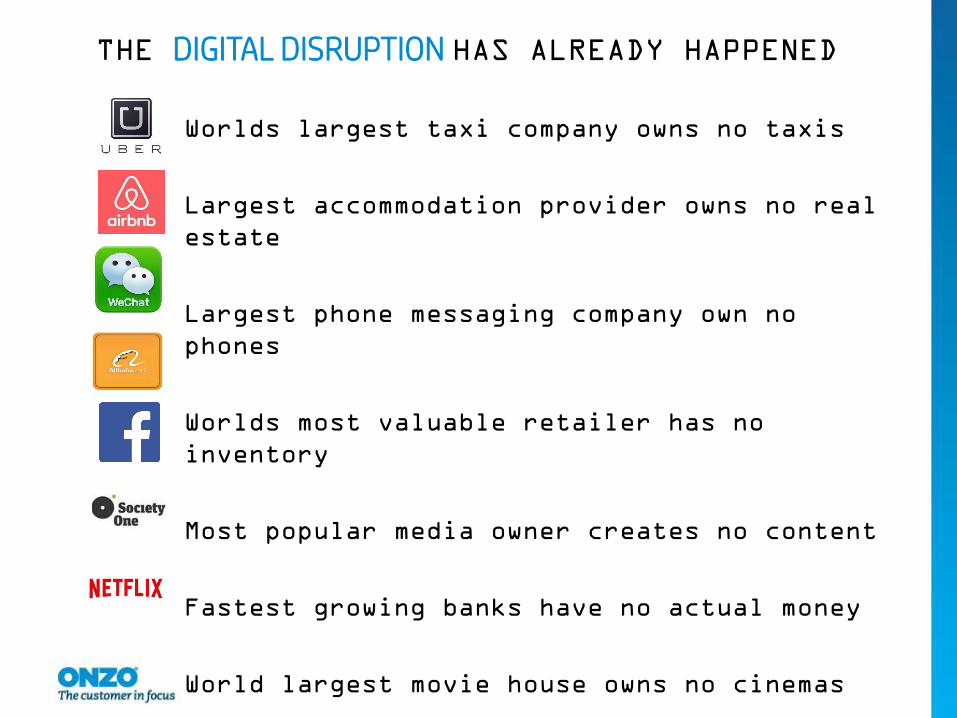

THE DIGITAL DISRUPTION HAS ALREADY HAPPENED

Worlds largest taxi company owns no taxis

Largest accommodation provider owns no real

estate

Largest phone messaging company own no

phones

Worlds most valuable retailer has no

inventory

Most popular media owner creates no content

Fastest growing banks have no actual money

World largest movie house owns no cinemas

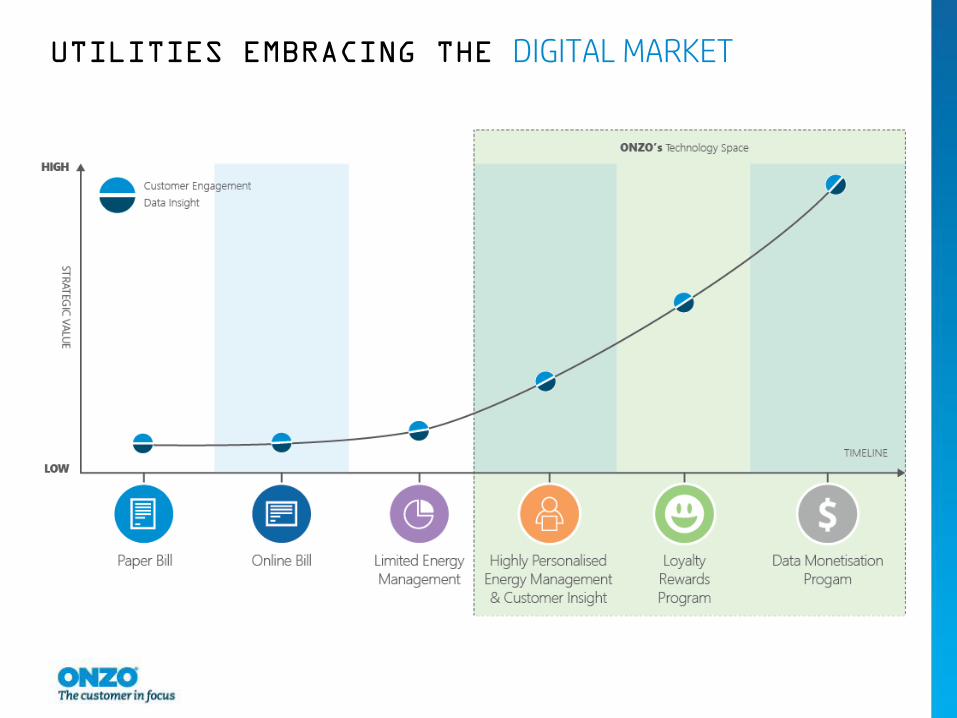

UTILITIES EMBRACING THE DIGITAL MARKET

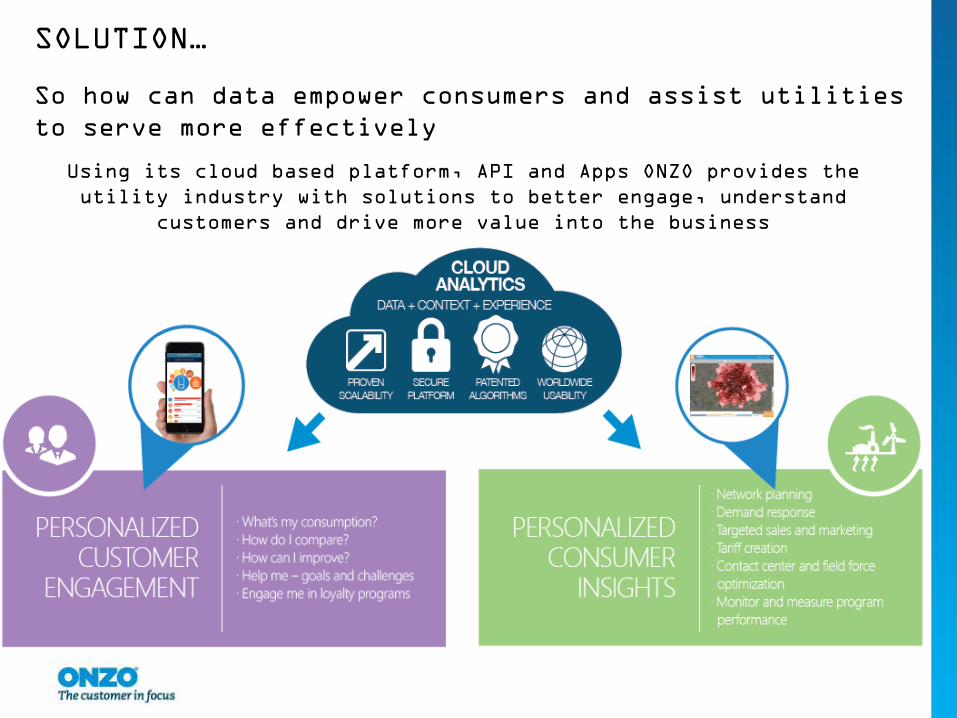

SOLUTION…

So how can data empower consumers and assist utilities

to serve more effectively

Using its cloud based platform, API and Apps ONZO provides the

utility industry with solutions to better engage, understand

customers and drive more value into the business

SO WHAT DOES THIS MEAN FOR SMART CITIES….

Huge opportunity in energy to complement the smart city and

its communities

1. Technology is evolving and services are becoming more

personalised

2. People engagement is now an opportunity

3. Community Support - Fuel poverty support and support of pre-

paid

4. Consumer Insights - will help manage energy network better and

use resources effectively

5. Distributed Energy Resources - can be dynamically managed and

planned from the outset.

6. Energy demand is increasing with more devices and applications

such electric vehicles

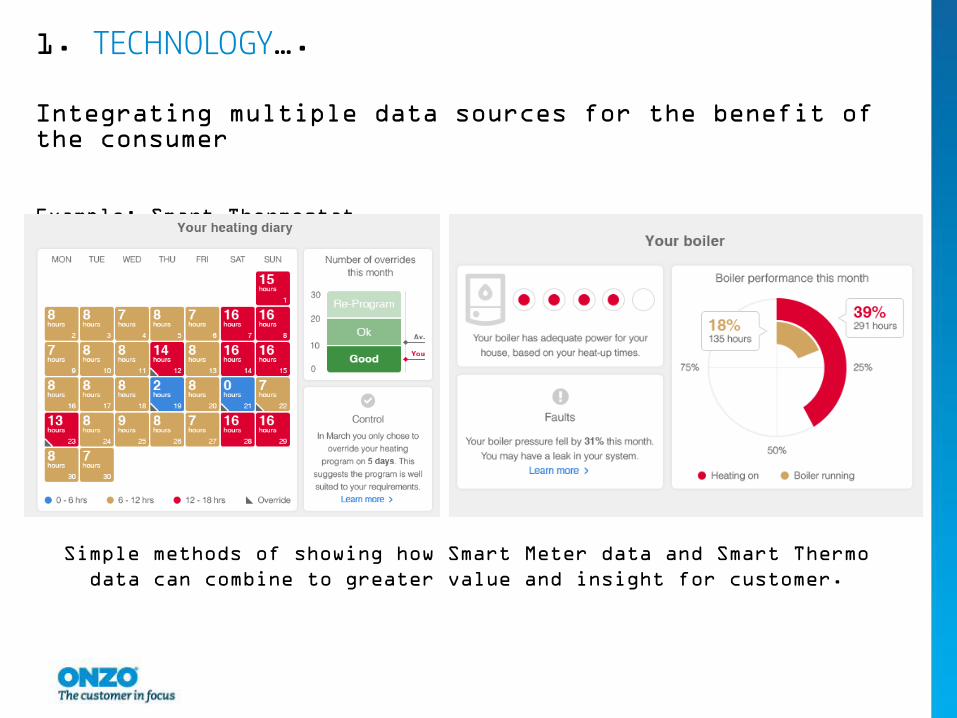

1. TECHNOLOGY….

Integrating multiple data sources for the benefit of the consumer

Example: Smart Thermostat

Simple methods of showing how Smart Meter data and Smart Thermo

data can combine to greater value and insight for customer.

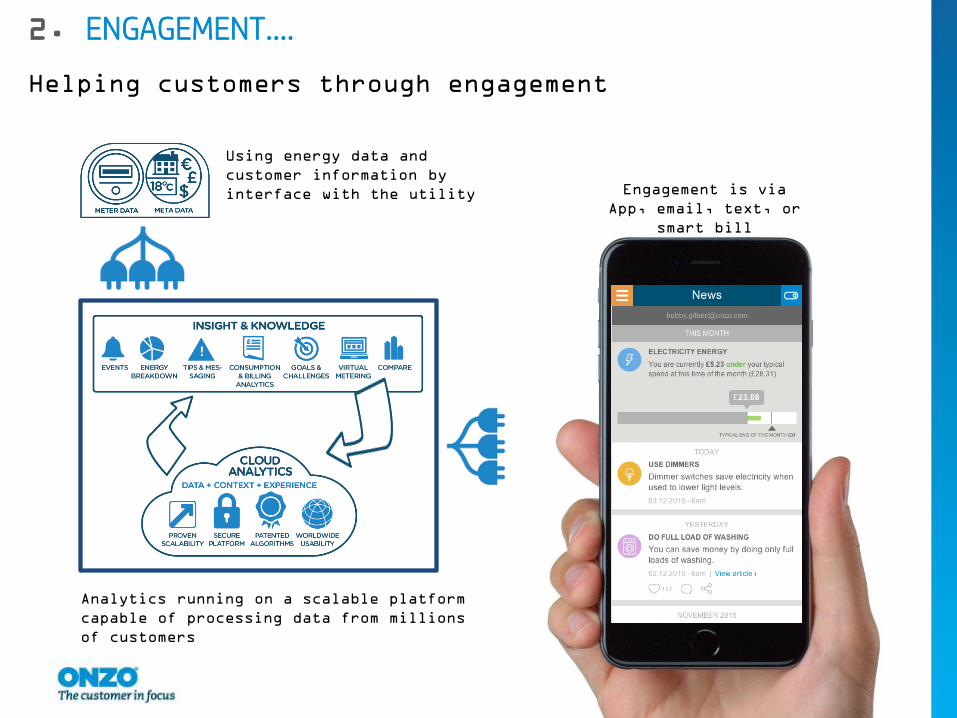

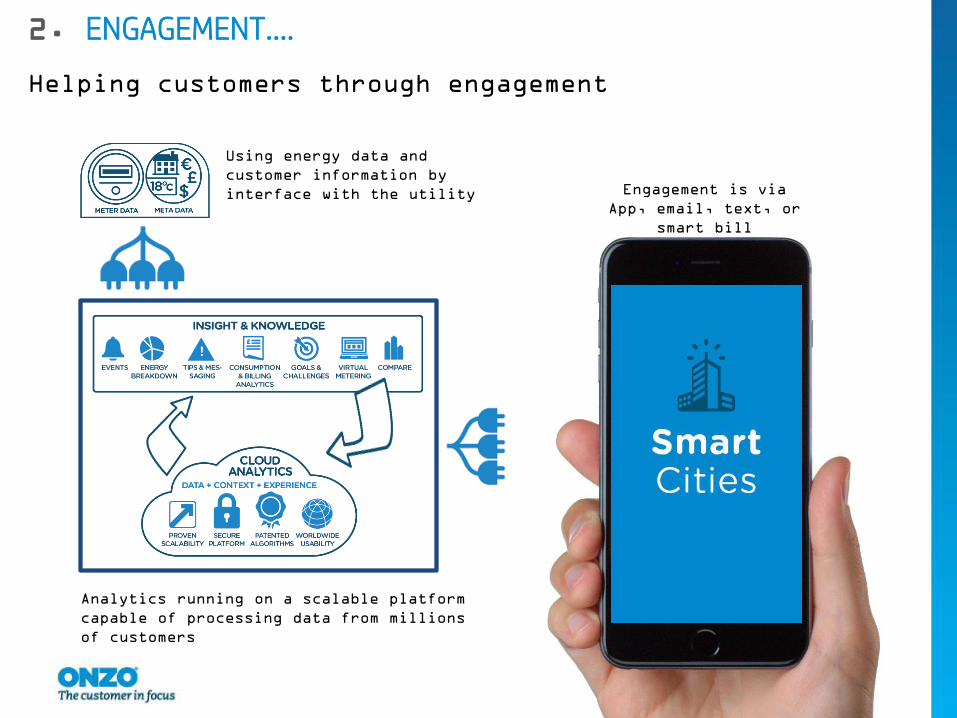

2. ENGAGEMENT….

Helping customers through engagement

Analytics running on a scalable platform

capable of processing data from millions

of customers

Using energy data and

customer information by

interface with the utility Engagement is via

App, email, text, or

smart bill

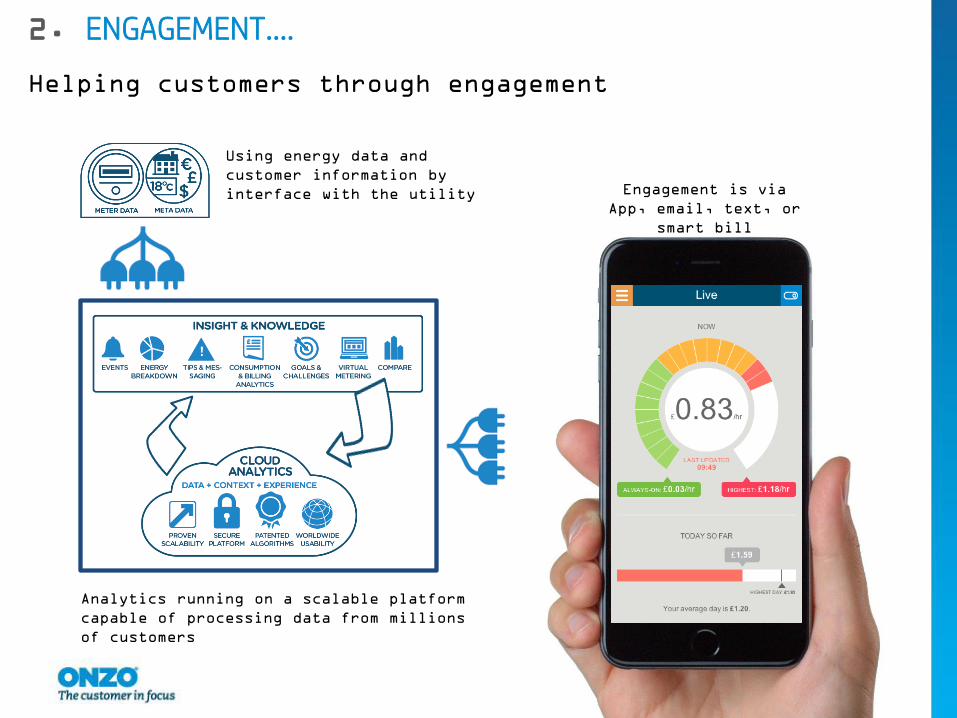

2. ENGAGEMENT….

Helping customers through engagement

Engagement is via

App, email, text, or

smart bill

Using energy data and

customer information by

interface with the utility

Analytics running on a scalable platform

capable of processing data from millions

of customers

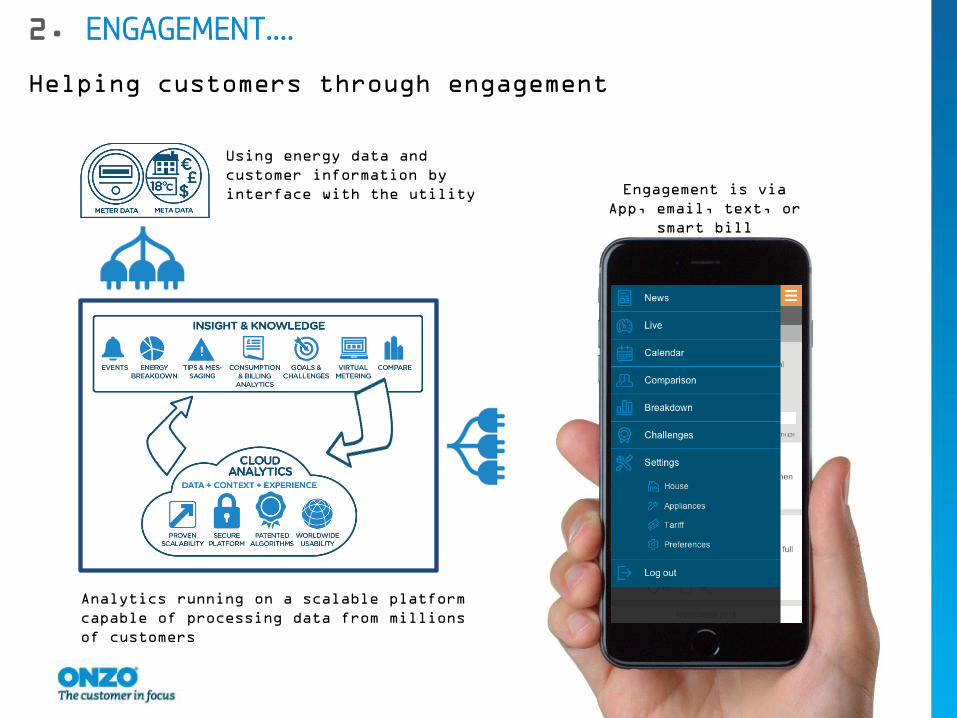

2. ENGAGEMENT….

Helping customers through engagement

Engagement is via

App, email, text, or

smart bill

Using energy data and

customer information by

interface with the utility

Analytics running on a scalable platform

capable of processing data from millions

of customers

2. ENGAGEMENT….

Helping customers through engagement

Engagement is via

App, email, text, or

smart bill

Using energy data and

customer information by

interface with the utility

Analytics running on a scalable platform

capable of processing data from millions

of customers

2. ENGAGEMENT….

Helping customers through engagement

Engagement is via

App, email, text, or

smart bill

Using energy data and

customer information by

interface with the utility

Analytics running on a scalable platform

capable of processing data from millions

of customers

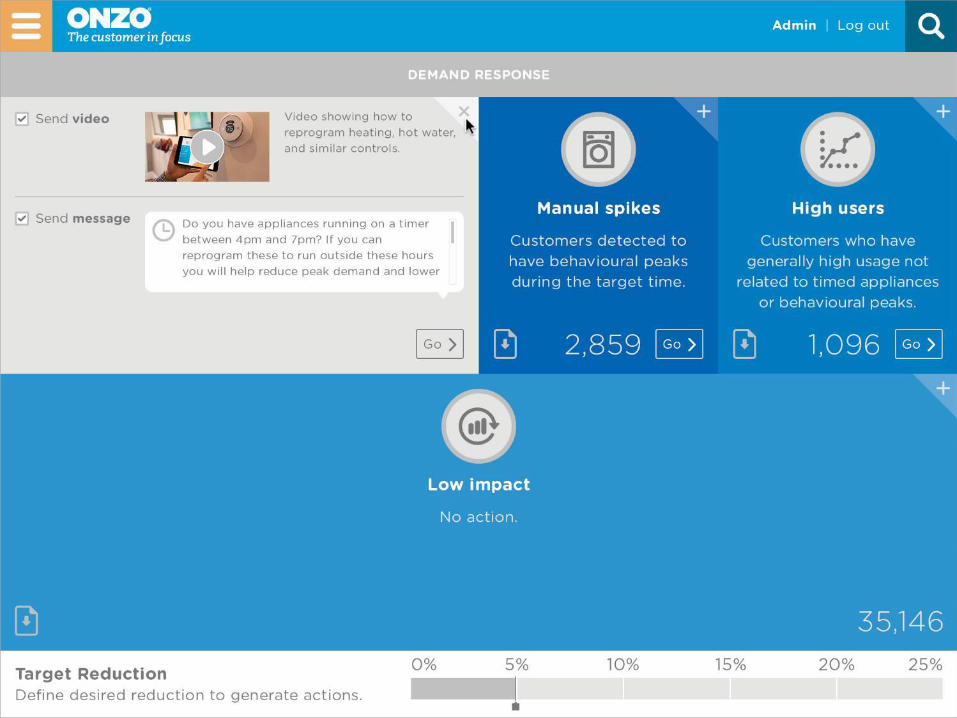

3. COMMUNITY SUPPORT

Providing support for the vulnerable and those in fuel poverty

Weather & Meter Data

House 1

House 2

• Tracking usage

and managing

pre-payment

expenditure

• Identifying

vulnerable

customers not

heating their

home

• Identifying

vulnerable

customers using

electric

heaters not

central heating

• Data analytics provides a wealth of information about

every customer

• Enabling segmentation and focus for utilities to be more

effective towards customers

• Targeted and relevant actions and messages to help with

the management of their energy use

• Highly relevant messaging for demand response management,

product campaigns, energy tips and even tariff

optimisation.

Energy provider can become the trusted advisor

4. INSIGHT

Helping the Utility understand customers better

139

140

141

142

143

144

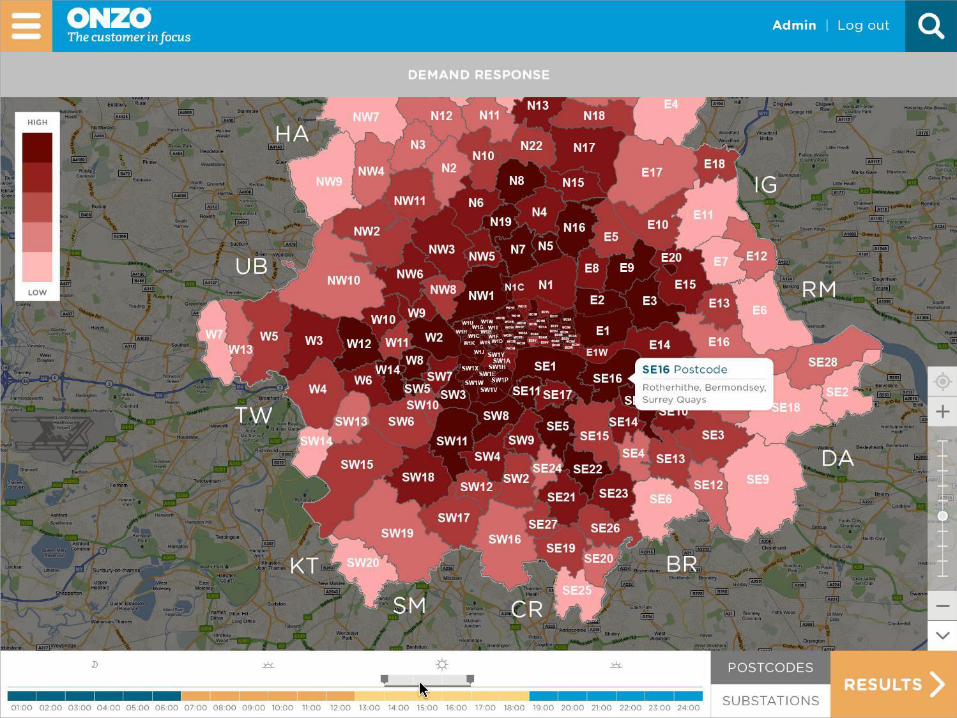

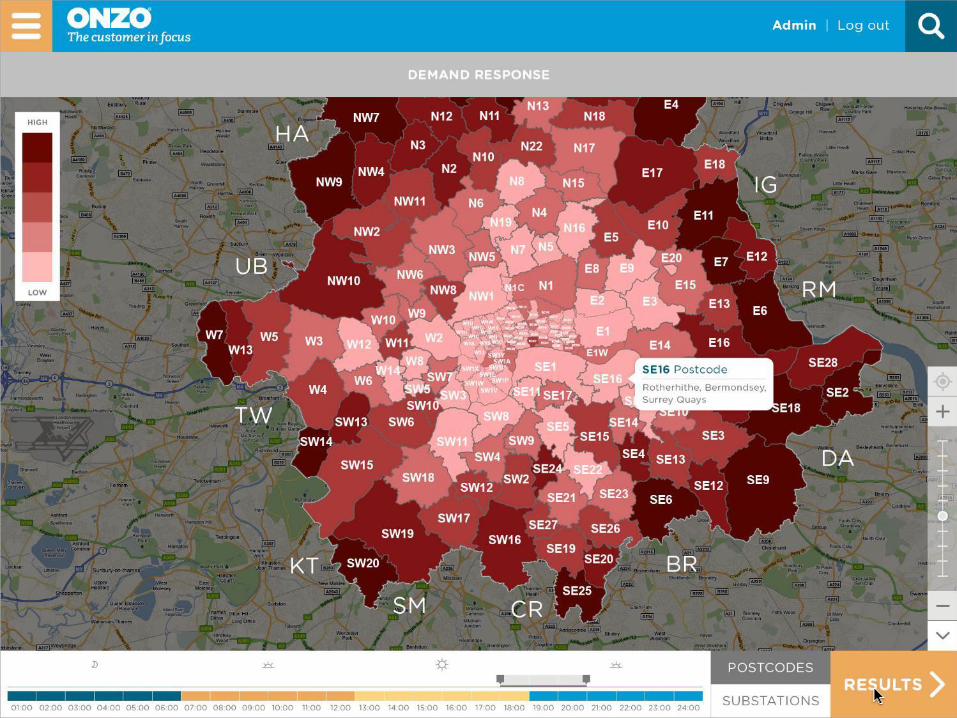

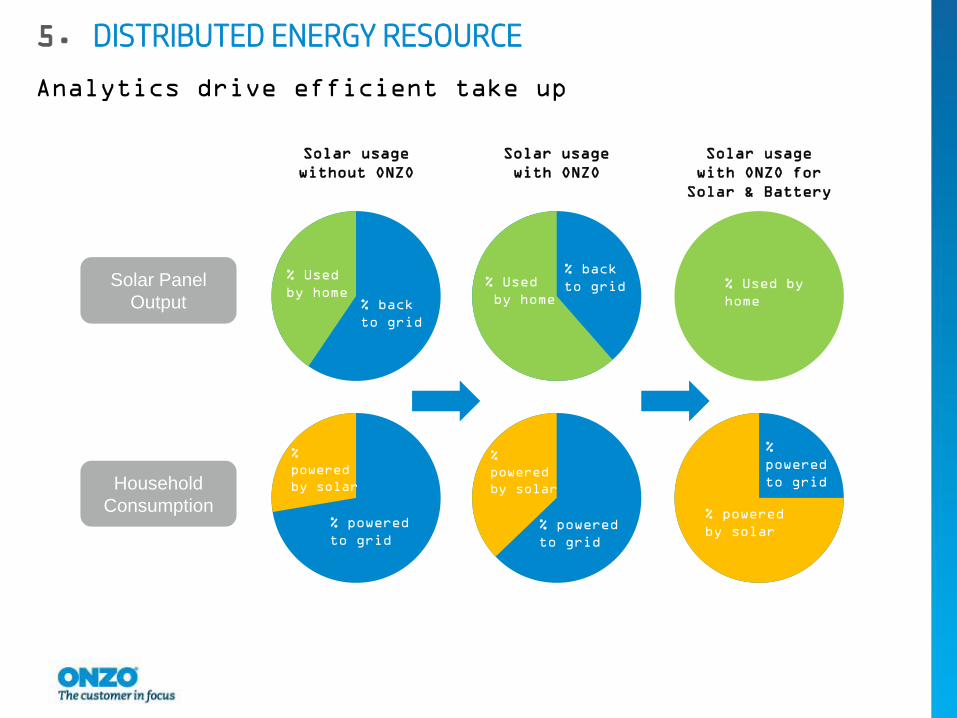

5. DISTRIBUTED ENERGY RESOURCE

Analytics drive efficient take up

Solar usage

without ONZO

Solar usage

with ONZO

Solar usage

with ONZO for

Solar & Battery

Solar Panel

Output

Household

Consumption

% Used

by home% Used

by home

% Used by

home% back

to grid

% back

to grid

% powered

to grid

% powered

to grid

%

powered

to grid

% powered

by solar

%

powered

by solar

%

powered

by solar

• Identify owners of electric vehicles from meter data, without

the need to survey your customers

• Profile customers’ usage and evaluate the possible effect of

demand response programs.

• Offer specific time of use tariffs to manage network demand.

• Only target electric vehicle users to save on marketing costs.

6. ENERGY DEMAND

Managing increasing energy demand EV will become the focus

Example: Electric vehicle ownership in California

• Huge opportunity for Smart Cities to embrace the change

happening in the utility industry and the use of data

• Smart Cities will be able to progress engagement to empower

consumers and gain trust

• Use Insights to understand consumer behaviour, influence it

and focus the offering of specific services and tailor the

delivery of energy efficiently

• Offer specific, relevant and tailored services

• Enable energy saving to those who needed it

• Data will be the source and the power to enable Smart Cities

to engage and involve consumers

CONCLUSION

Smart Cities are sitting on a GOLDMINE of data and consumers and technological capability

DAN HUBERT - CEO APPYPARKING

PARKING CONFUSION

PARKING

PARKING IS A COMMODITY

THE PARKING PLATFORM™

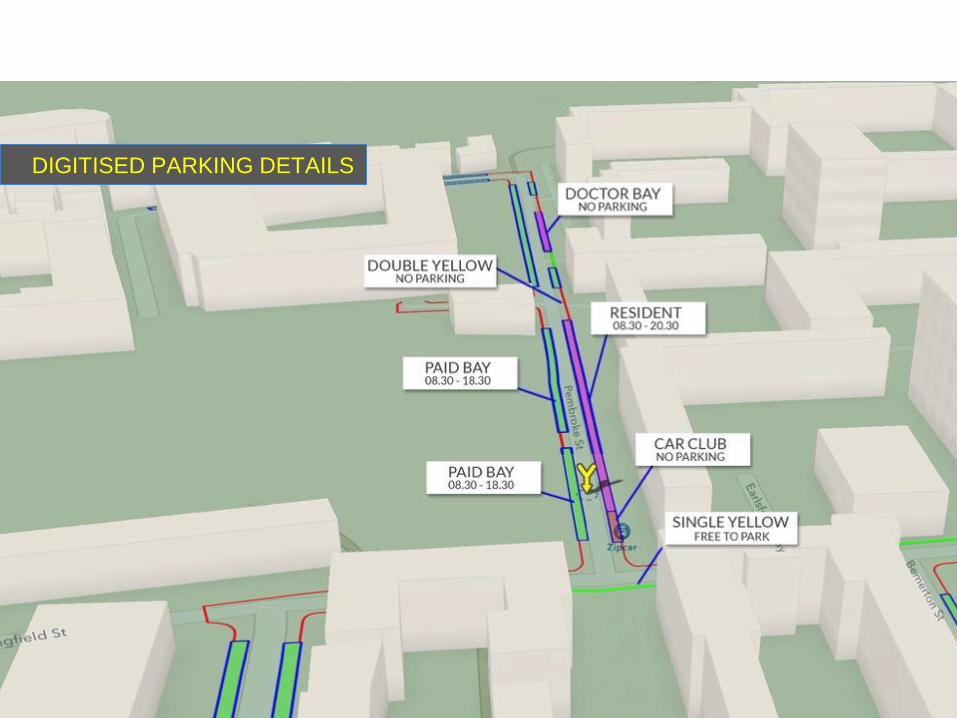

DIGITISED PARKING DETAILS

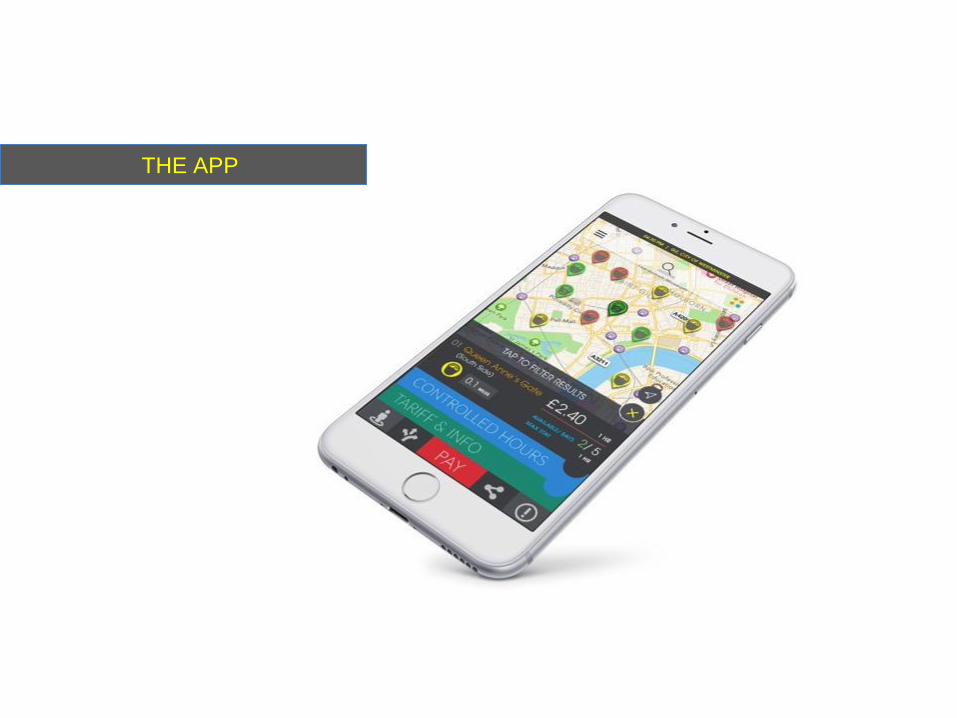

THE APP

THE WEBSITE

SENSOR PARTNER

• Low Power Radio Technology

• One base station covers 3km urban radius

• 1000’s of sensors connect one base station.

• 5 years battery life.

REAL TIME BAY SENSORS

Sparkit SensorNwave Base

StationReal time bay

availability

Application Server

NWAVE Sensors

Base Station

Application Server

Real Time

‘ONE CLICK’ PARKING

5 Tips & Tools to improve collaboration - I use them all!Daniel O’Connor

CEO Warp It

Linkedin: Daniel Bede O’Connor

Head of Customer Happiness

Twitter: @Warp It_

Aim

Take home tips you can use today/ tomorrow

To bring smart cities about quicker easier through collab

Why?

Improvement

Development

Pace of change

Collab

Nothing new

Reinvented

Internet/mobile

Resource pressure

1 tips

To collab you need rapport

Understand objectives

Align objectives

2 tipsListen

2 ears one mouth

2 tips

3 tools>Objectives

Governance-understanding

Projects- aligning

Surplus capacity

Crowd

The Wisdom of Crowds: Why the Many Are Smarter Than the Few

James Surowiecki

Crowd

Getting stuff done together

Making

Improving

Changing

Developing

Asana/ Basecamp/ Trello

Vision

Aim

Objectives

Milestones

Tasks

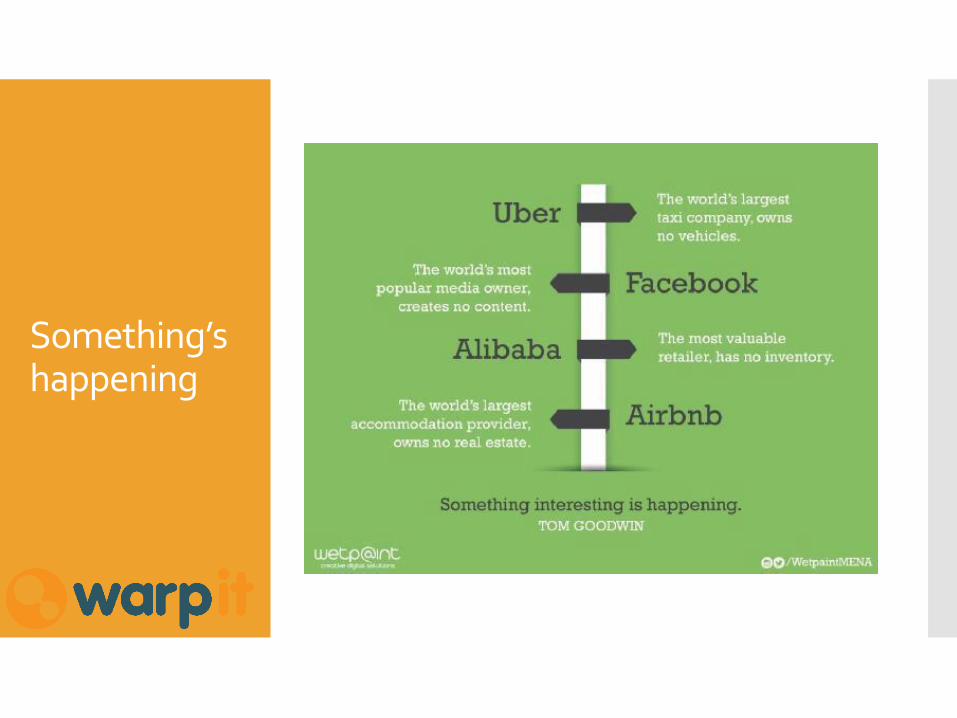

Something’s happening

Something’s happening

Something’s happening

Something’s happening

Something’s happening? 20 years?

Something’s happening

Something’s happening

Dating service

Waste Manager

Cilla Black versus Tinder

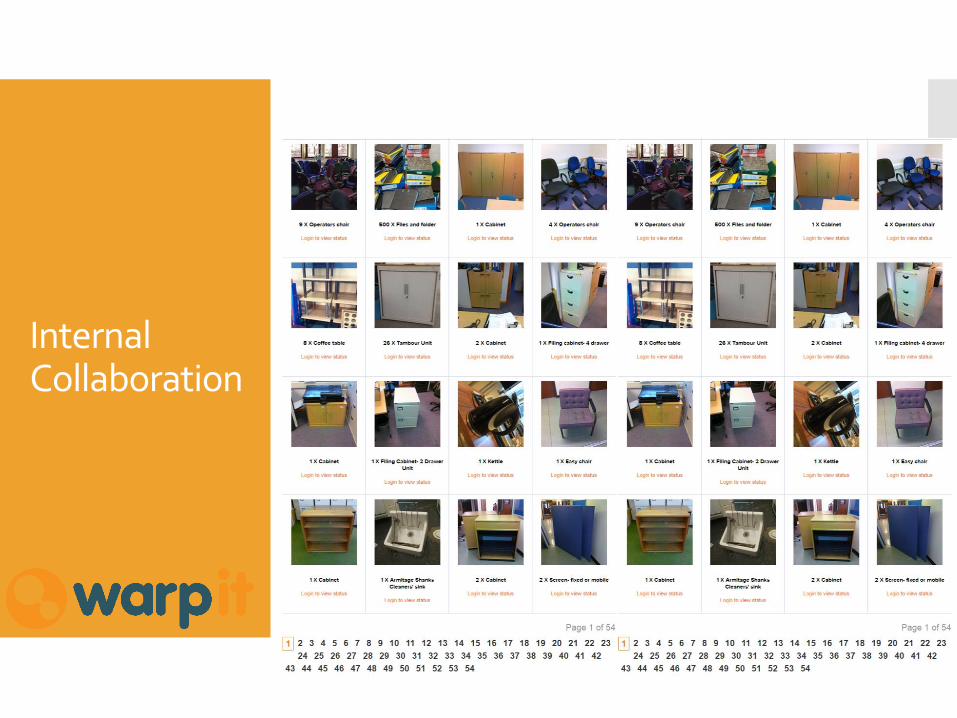

Internal Collaboration

Internal Collaboration

Internal Collaboration

Internal Collaboration

Internal Collaboration

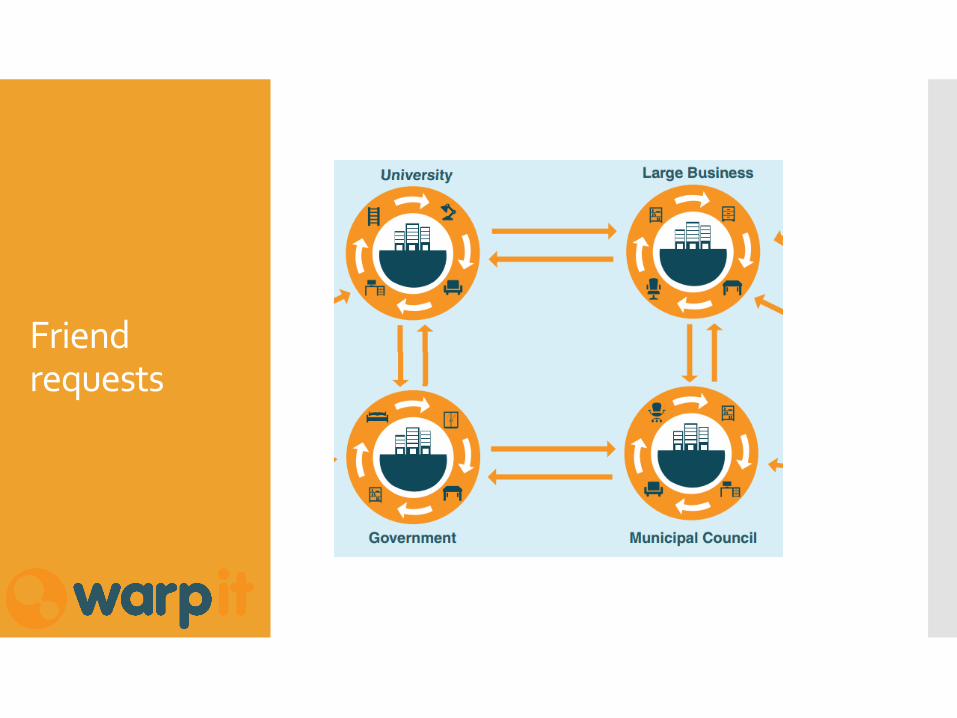

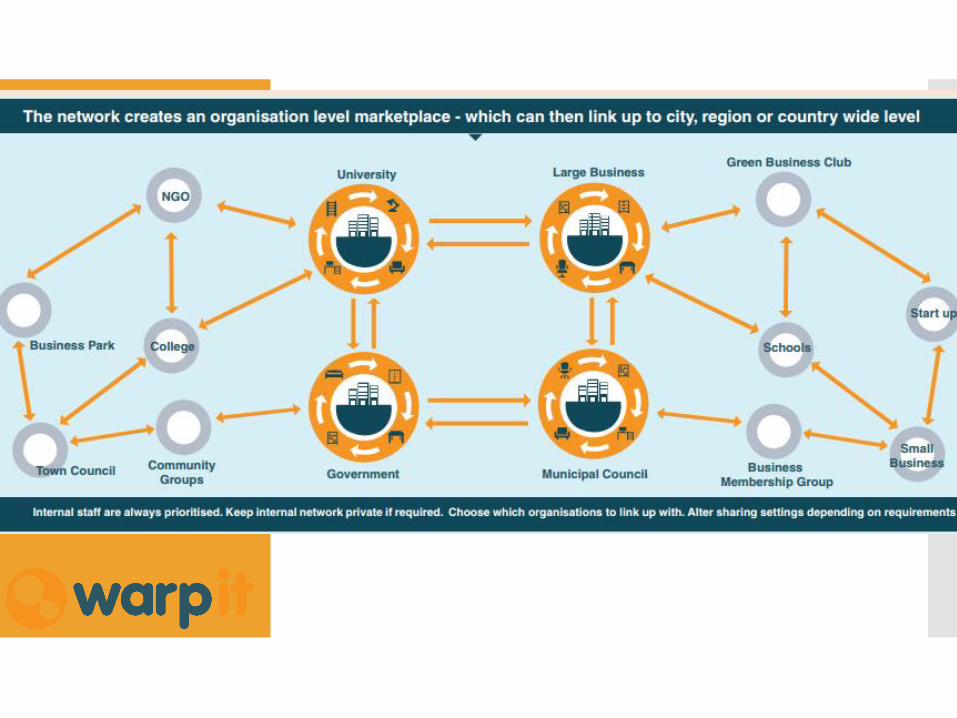

Friend requests

External Collaboration

Collab

Summary

Rapport

Understand-Loomio

Align- Asana

Surplus assets eg

Communicate better!

Linkedin: Daniel Bede O’Connor

Go to www.GetWarpIt.com

fill in call back request

© 2015 Silver Spring Networks. All rights reserved.

Brian Mcguigan

Commercial Director, Europe, Smart City Services

Silver Spring Networks

February 2016

WHAT LESSONS SHOULD

SMART CITY INITIATIVES LEARN

FROM THE SMART GRID?

© 2015 Silver Spring Networks. All rights reserved.

Questions &

Discussion

Key lessons

for cities

Evolution of

the Smart

Grid – key

lessons

Introduction

Comparison

of Smart grid

and Smart

City markets

Smart Grids to Smart Cities…..

© 2015 Silver Spring Networks. All rights reserved. 201

20

1

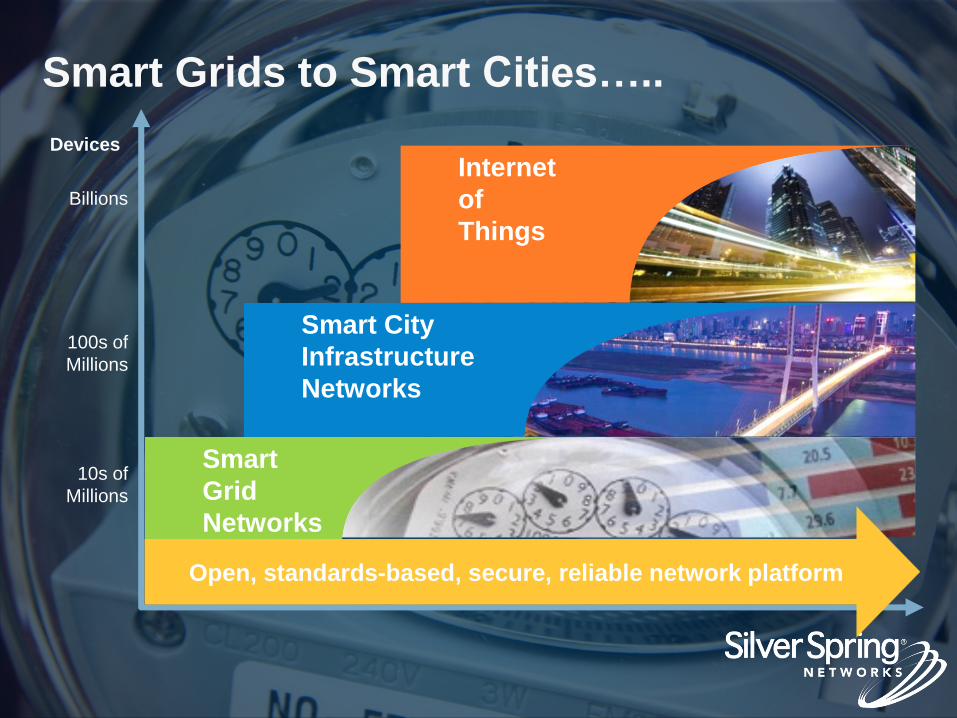

UTILITY SMART GRID JOURNEY

A platform for ongoing

innovation…

© 2013 Silver Spring Networks. All rights reserved.

202

Smart Grids to Smart Cities…..

Time

100s of

Millions

Billions

10s of

Millions

Smart

Grid

Networks

Smart City

Infrastructure

Networks

Internet

of

Things

Devices

Open, standards-based, secure, reliable network platform

© 2015 Silver Spring Networks. All rights reserved. 203

20

3

HOW DO CITIES COMPARE?

Similar to Utilities in some ways….

Some important differences…..

© 2015 Silver Spring Networks. All rights reserved. 204

DRIVERS FOR CONNECTED CITIES

Local Energy EfficiencyBudgetaryEnvironmental SecurityNew Demands

Operational Efficiency Reduce Costs & Carbon New Revenue Streams

© 2015 Silver Spring Networks. All rights reserved. 205

INCREASED MOBILITY DRIVES COMPETITON

• COMPETITIVE PRESSURES

- Business investment

- Skilled workers

- Quality of life

• ENVIRONMENTAL IMPERATIVES

- Community health

- Carbon emission reduction

• CITIZEN DEMANDS

- Community services

- Effective use of resources and budget

- Improve Quality of Life

© 2015 Silver Spring Networks. All rights reserved. 206

20

6

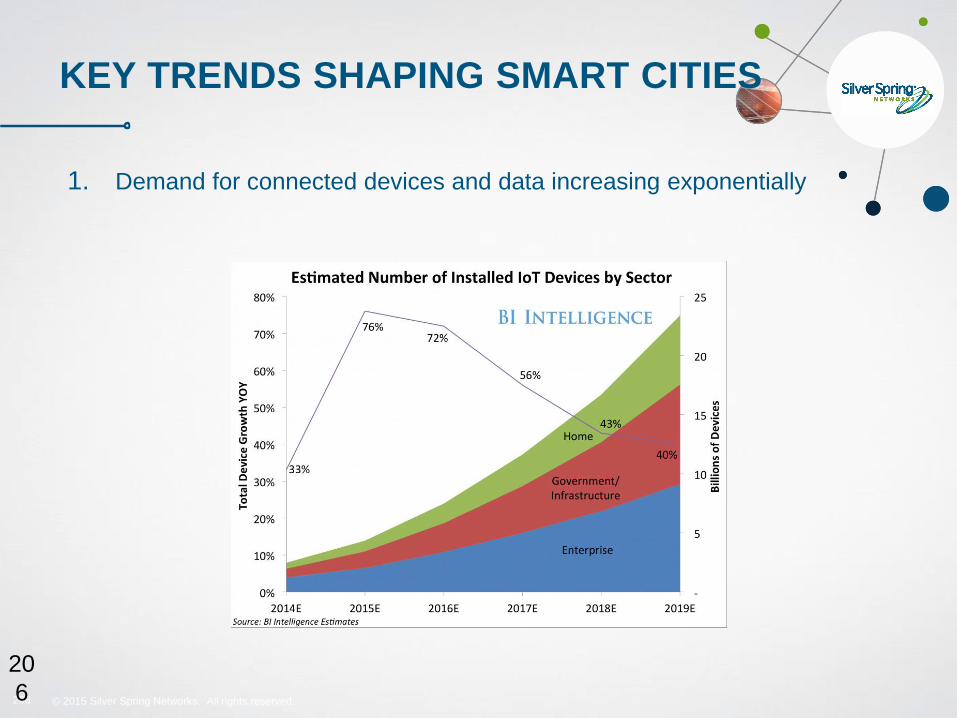

KEY TRENDS SHAPING SMART CITIES

1. Demand for connected devices and data increasing exponentially

© 2015 Silver Spring Networks. All rights reserved. 207

20

7

SMART CITY – WHAT DEVICES?POTENTIAL IOT APPLICATIONS

© 2015 Silver Spring Networks. All rights reserved. 208

20

8

KEY TRENDS SHAPING SMART CITIES

1. Demand for connected devices and data increasing exponentially

2. Cities looking for flexible building blocks

© 2015 Silver Spring Networks. All rights reserved. 209

PARIS – A SHARED HIGHWAY MANAGEMENT PLATFORM

Traffic Signal

Control

Lighting control

and fault

monitoring

City

Advertising

Panels

EV Charging

Infrastructure

Bike rental

management

+

© 2015 Silver Spring Networks. All rights reserved. 210

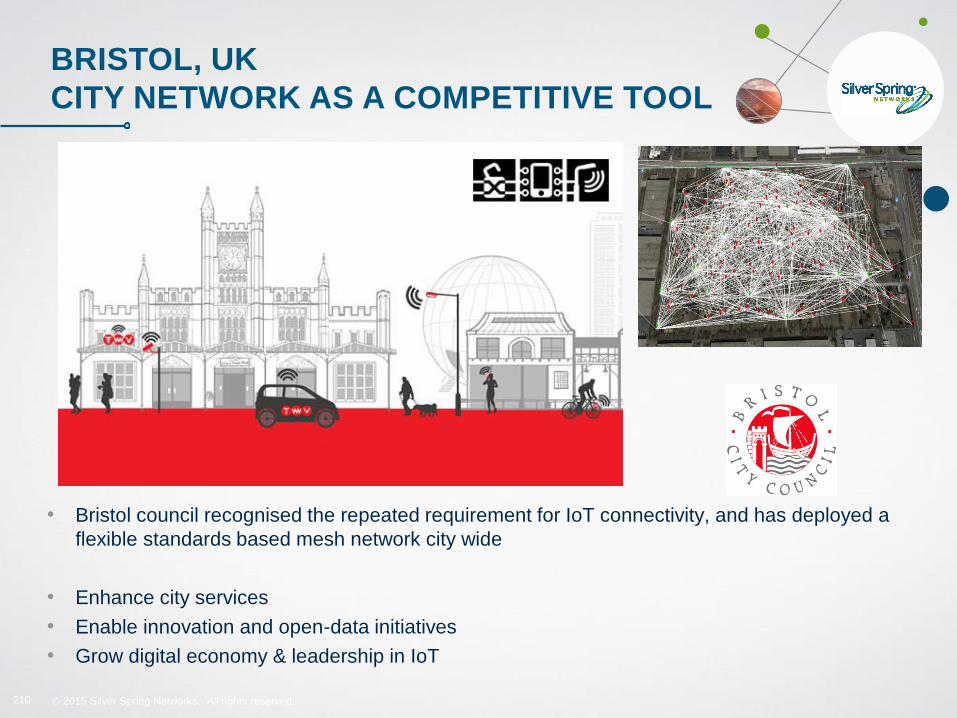

BRISTOL, UK

CITY NETWORK AS A COMPETITIVE TOOL

• Bristol council recognised the repeated requirement for IoT connectivity, and has deployed a

flexible standards based mesh network city wide

• Enhance city services

• Enable innovation and open-data initiatives

• Grow digital economy & leadership in IoT

© 2015 Silver Spring Networks. All rights reserved. 211

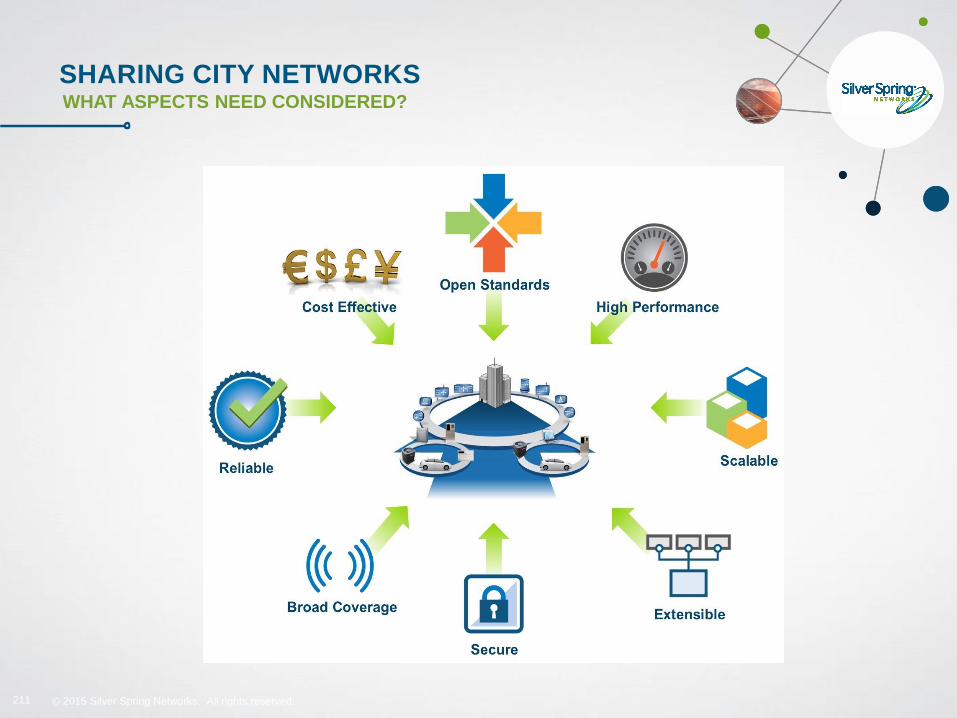

SHARING CITY NETWORKSWHAT ASPECTS NEED CONSIDERED?

© 2015 Silver Spring Networks. All rights reserved. 212

21

2

KEY TRENDS SHAPING SMART CITIES

1. Demand for connected devices and data increasing exponentially

2. Cities looking for flexible building blocks

3. Open standards and interoperability becoming key

© 2015 Silver Spring Networks. All rights reserved. 213

21

3

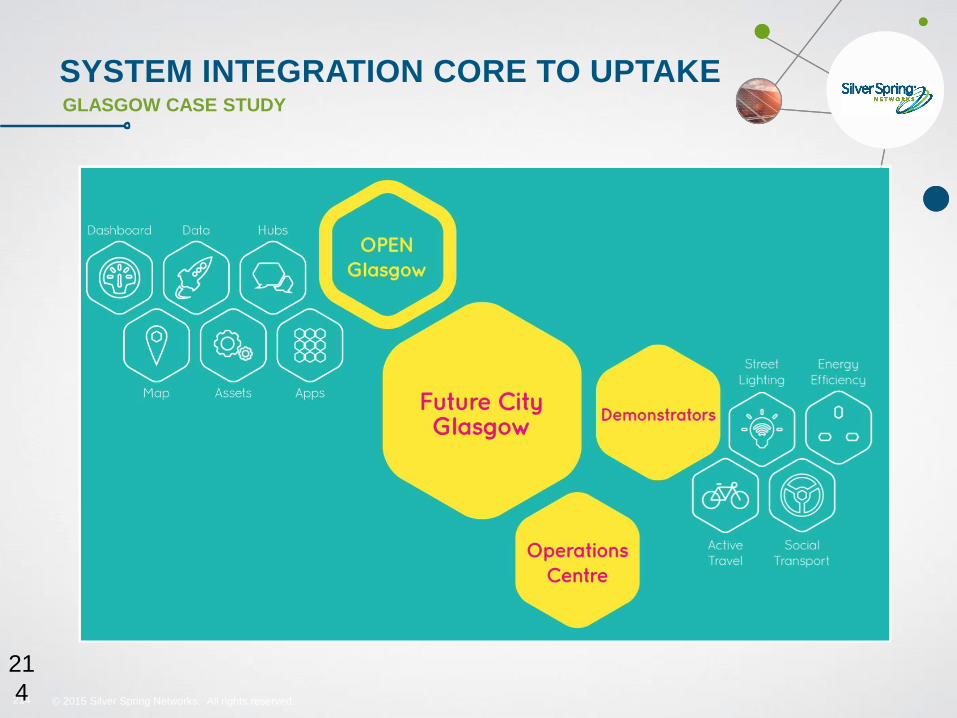

SYSTEM INTEGRATION CORE TO UPTAKEGLASGOW CASE STUDY

© 2015 Silver Spring Networks. All rights reserved. 214

21

4

SYSTEM INTEGRATION CORE TO UPTAKEGLASGOW CASE STUDY

© 2015 Silver Spring Networks. All rights reserved. 215

21

5

KEY TRENDS SHAPING SMART CITIES

1. Demand for connected devices and data increasing exponentially

2. Cities looking for flexible building blocks

3. Open standards and interoperability becoming key

4. Intelligence moving to the edge

© 2015 Silver Spring Networks. All rights reserved. 216

ITS for better safety for Cyclists

Intelligent street light – extra light on accident black spots

© 2015 Silver Spring Networks. All rights reserved. 217

21

7

KEY TRENDS SHAPING SMART CITIES

1. Demand for connected devices and data increasing exponentially

2. Cities looking for flexible building blocks

3. Open standards and interoperability becoming key

4. Intelligence moving to the edge

5. Security and privacy strategies emerging

© 2015 Silver Spring Networks. All rights reserved. 218218

21

8

SECURITY

“ALL IT TAKES IS ONE INCIDENT”

© 2015 Silver Spring Networks. All rights reserved. 219219

21

9

© 2015 Silver Spring Networks. All rights reserved. 220

22

0

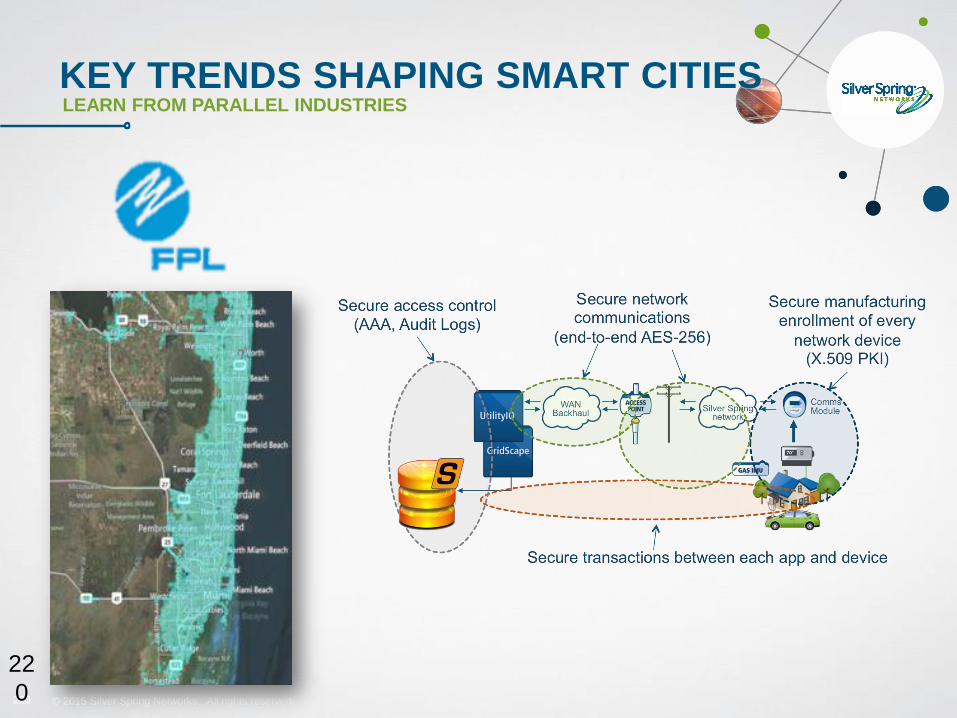

KEY TRENDS SHAPING SMART CITIESLEARN FROM PARALLEL INDUSTRIES

© 2015 Silver Spring Networks. All rights reserved. 221

22

1

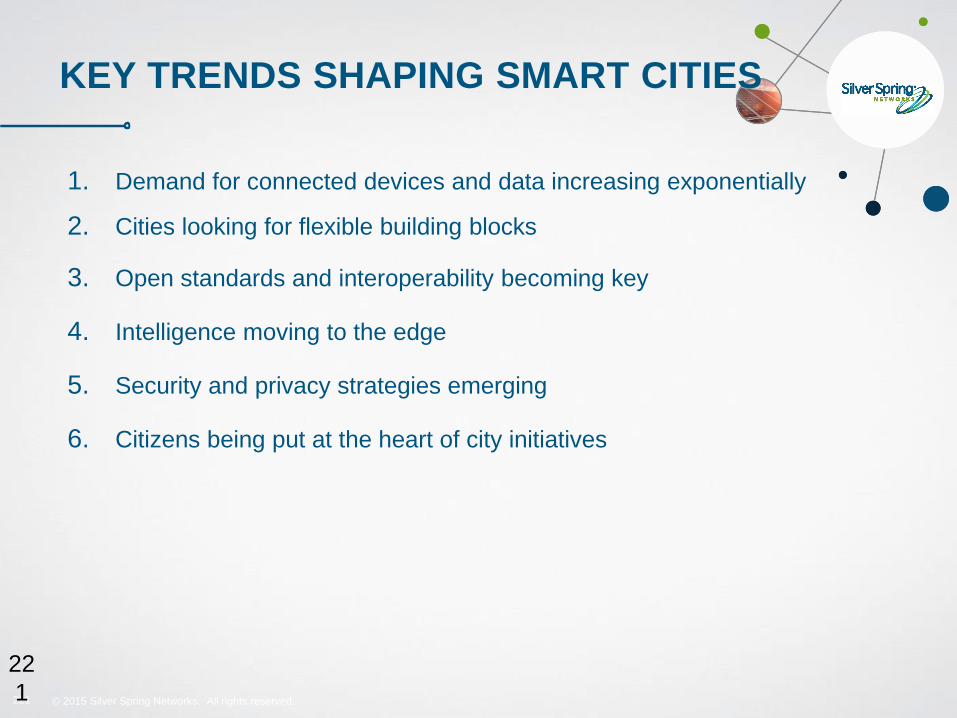

KEY TRENDS SHAPING SMART CITIES

1. Demand for connected devices and data increasing exponentially

2. Cities looking for flexible building blocks

3. Open standards and interoperability becoming key

4. Intelligence moving to the edge

5. Security and privacy strategies emerging

6. Citizens being put at the heart of city initiatives

© 2015 Silver Spring Networks. All rights reserved. 222

22

2

COMMUNITY IMPACTCITIZENS BEING PUT AT THE HEART OF CITY INITIATIVES

© 2015 Silver Spring Networks. All rights reserved. 223

22

3

NEW INTERACTIONSCITIZENS BEING PUT AT THE HEART OF CITY INITIATIVES

© 2015 Silver Spring Networks. All rights reserved. 224

Glasgow Case Study – Open by default

© 2015 Silver Spring Networks. All rights reserved. 225

Focus on Citizen empowerment

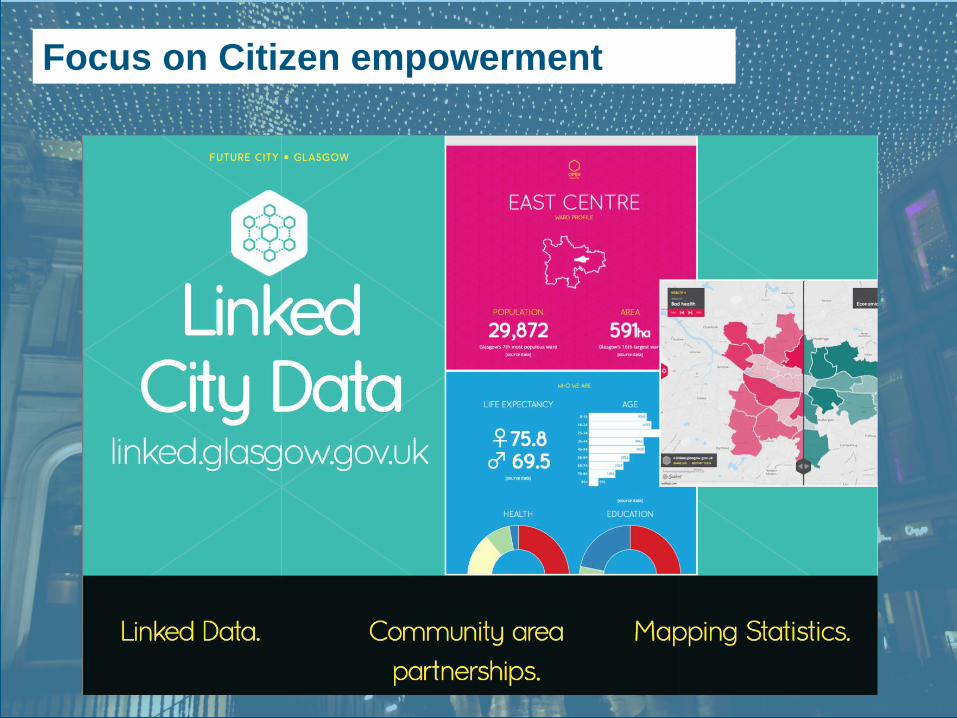

© 2015 Silver Spring Networks. All rights reserved. 226

22

6

MAKING CITIES FUN IS IMPORTANT TOO…

© 2015 Silver Spring Networks. All rights reserved. 227

THANK YOU, QUESTIONS?

Contact welcome to discuss opportunities in IoT &

smart city initiatives

e-mail: [email protected]

Mobile: +44 (0) 7859 068 695

Lunch & Networking

The Carbon TrustSupporting city leadership on carbon reduction

Smart Cities UKRichard Rugg, MD, Programmes

› Created in 2001 by the UK government with the mission to accelerate the move to a sustainable, low carbon economy

› Fully independent not-for-dividend private company, with all surpluses from commercial activities reinvested in our mission

230

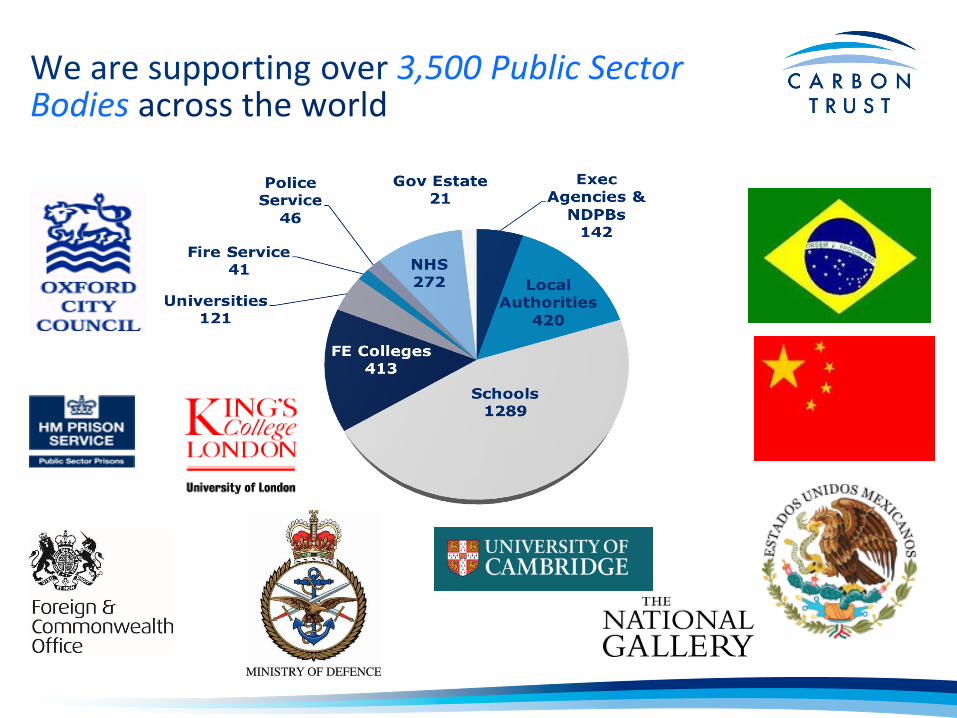

We are supporting over 3,500 Public Sector Bodies across the world

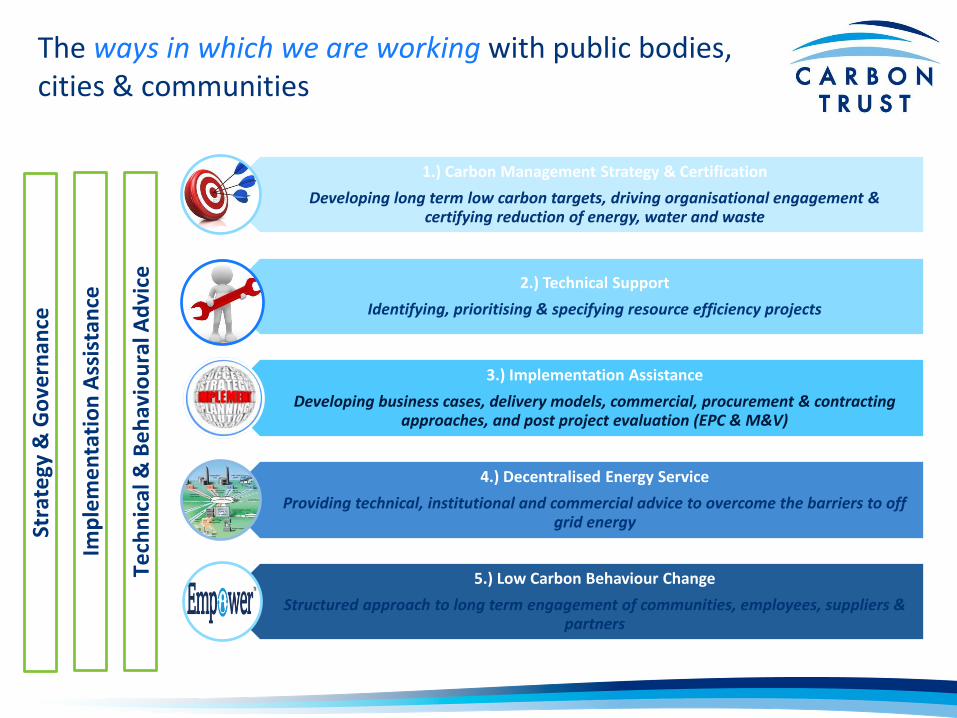

1.) Carbon Management Strategy & Certification

Developing long term low carbon targets, driving organisational engagement & certifying reduction of energy, water and waste

2.) Technical Support

Identifying, prioritising & specifying resource efficiency projects

3.) Implementation Assistance

Developing business cases, delivery models, commercial, procurement & contracting approaches, and post project evaluation (EPC & M&V)

4.) Decentralised Energy Service

Providing technical, institutional and commercial advice to overcome the barriers to off grid energy

5.) Low Carbon Behaviour Change

Structured approach to long term engagement of communities, employees, suppliers & partners

The ways in which we are working with public bodies, cities & communities

Stra

tegy

& G

ove

rnan

ce

Imp

lem

en

tati

on

Ass

ista

nce

Tech

nic

al &

Be

hav

iou

ral A

dvi

ce

Cities are key to achieving international climate goals

1. Over 50% of the global population now live in cities – and they consume 70% of the world’s energy

2. Municipalities hold key planning, housing, community engagement, taxation and education powers relevant to low carbon development

3. And power is being devolved to local governments around the world

Carbon Trust is working with the UN, the World Bank & the UK’s FCO to support cities in developing city-wide carbon reduction strategies

We are helping our customers to save £2.6bn

Mobilise stakeholders

Gather inventory

Identify opportunities

Develop strategy

Implement and review

1 2 3 4 5

Low Carbon Cities MalaysiaCity-wide inventory & 25% savings

Low Carbon States MexicoImplementing energy efficiency

Low Carbon Cities Panama City leadership on sustainable schools

Low Carbon Cities UK City-wide targets, city-wide projects

Low Carbon Cities UKPlanning locally sourced energy

Carbon Trust Cities Outlook

› We’re launching an independent Cities Outlook to showcase the progress & potential for global cities to assess, mitigate & adapt to climate change and associated risks.

› We’ll be assessing cities across four areas:

› current sustainability and carbon emissions

› current risk

› mitigation potential

› adaptation potential

› Data will be used to:

› enact change on a local level and help to improve a City’s sustainability and preparation for climate change

› Facilitate a compare and contrast assessment to identify common strengths, weaknesses and holistic challenges

› Our vision is to ensure that the City Outlook become an established resource, achieving engagement with government leaders, media and other community stakeholders, enabling positive change on a global scale

› The Carbon Trust are exploring partner collaborations 239

Our mission is to accelerate the move to a sustainable, low carbon economy

Keep in touch!

0207 832 4614

•

•

•

•

• POSITIONING

• CAMERA TYPE

• ENROLMENT

Having the right technology in place can prevent

events like this from happening in the future

GOVERNMENT

RETAIL

CASINOS

ESTATE MANAGEMENT SERVICES

PRIVATE SECURITY COMPANIES

CORPORATE

HOTEL & HOSPITALITY

STADIUMS & PUBLIC VENUES

In Motion Identification (IMID) technology includes facial recognition and behavioural analytics to swiftly identify those with access authorization, while preventing entry of unauthorized visitors.

ACCESS CONTROL

CONTACTLESS

The most secure biometric technology on the market

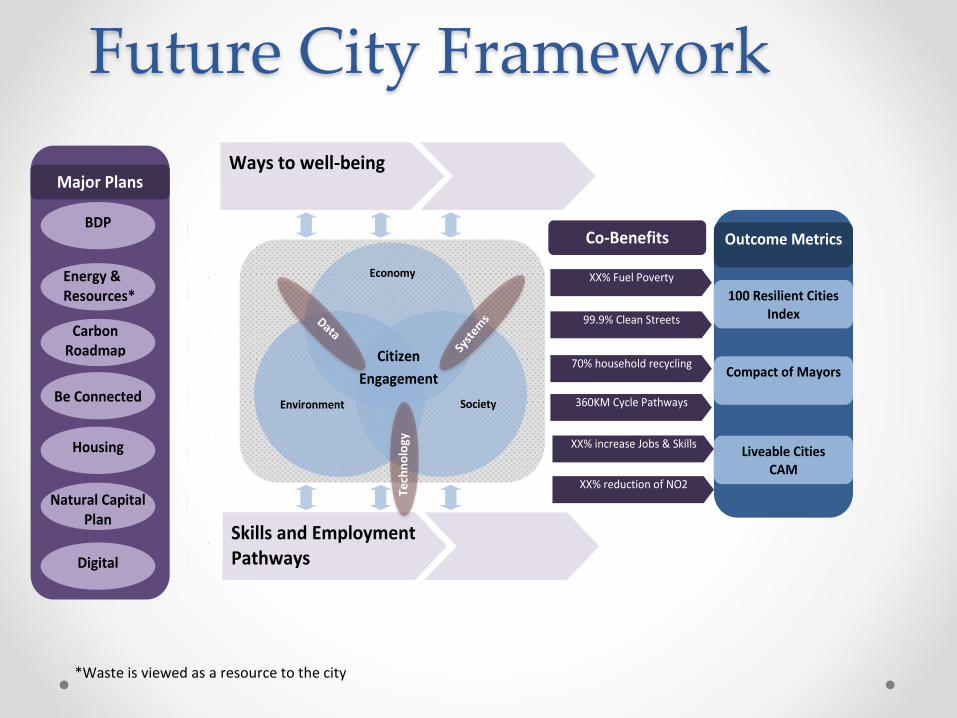

Cllr. Lisa Trickett

Cabinet Member for Sustainability

Film clip

Future City Framework

BDP

Housing

Major Plans

XX% Fuel Poverty

Economy

Environment Society

Citizen

Engagement

99.9% Clean Streets

70% household recycling

360KM Cycle Pathways

Outcome Metrics

Compact of Mayors

XX% increase Jobs & Skills

XX% reduction of NO2

Co-Benefits

Energy & Resources*

Be Connected

100 Resilient Cities Index

Liveable Cities CAM

Skills and Employment Pathways

Ways to well-being

Digital

Natural Capital Plan

Carbon Roadmap

Tech

no

logy

*Waste is viewed as a resource to the city

A great place to live, work and play

Chair’s Closing Comments

Richard Rugg, Managing Director,

Programmes, The Carbon Trust

Related Documents