MINISTRY OF LIVESTOCK DEVELOPMENT SMALLHOLDER DAIRY COMMERCIALIZATION PROGRAMME (SDCP) SMALLHOLDER FARMERS’ GUIDE TO DAIRY FARMING AS A BUSINESS Programme Coordination Unit Tel: +254-51-2210851 E-mail: [email protected] , [email protected] website www.sdcp.or.ke P.O. Box 12261-20100 Nakuru, Kenya.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

MINISTRY OF LIVESTOCK DEVELOPMENT

SMALLHOLDER DAIRY COMMERCIALIZATION PROGRAMME (SDCP)

SMALLHOLDER FARMERS’ GUIDE TO DAIRY FARMING AS A BUSINESS

Programme Coordination Unit Tel: +254-51-2210851 E-mail: [email protected] , [email protected] website www.sdcp.or.ke P.O. Box 12261-20100 Nakuru, Kenya.

SMALLHOLDER FARMERS’ GUIDE TO DAIRY FARMING AS A BUSINESS

PREFACE

Farming as a business is a relatively new concept for small-scale farmers who have

traditionally farmed as a way of life to provide for their subsistence needs. Commercial

farming was previously associated with industrial crops and large-scale farms. The

current approach involves a deliberate choice of farm enterprises with an aim of

maximizing on the benefits that farmers gain from their activities. It involves a change in

the way smallholder farming is perceived. This is because farming is a profitable venture

which provides gainful employment and a source of livelihood for many people.

SDCP has an overall objective of increasing the income of poor rural households that

depend substantially on production and trade of dairy products for their livelihood. This

is being achieved through the two programme purposes. First, improving the financial

returns of market oriented production and trade activities by small operators, through

improved information on market opportunities, increased productivity, cost reduction,

value addition and more reliable trade relations. Second, enabling more rural households

to create employment through, and benefit from expanded opportunities for market

oriented dairy activities, in particular because of strengthened farmer organizations.

This guide is intended to introduce smallholder farmers to the concept of farming as a

business and outlines some of the activities they can engage in to make their dairy

farming activities more profitable. It has been compiled by the Dairy Enterprise

Development Officer, SDCP. The contribution of Bernard Kimoro, the Dairy Production

Officer in providing livestock records and Jeff Otieno, the Assistant Monitoring and

Evaluation Officer in providing images and illustrations is acknowledged.

Lorna Mbatia

Dairy Enterprise Development Officer

Smallholder Dairy Commercialization Programme

June 2010

iii

TABLE OF CONTENTS

PREAMBLE ...................................................................................................................ii

TABLE OF CONTENTS .............................................................................................. iii

INTRODUCTION TO FARMING AS A BUSINESS ..................................................... 1

MY FARM BUSINESS................................................................................................... 5

FARM LEVEL DAIRY ENTERPRISE PLAN .......................................................... 10

RECORD KEEPING ..................................................................................................... 13

FINANCIAL MANAGEMENT .................................................................................... 16

MONEY .................................................................................................................... 16

SAVING ................................................................................................................... 17

INVESTMENT ......................................................................................................... 18

CREDIT .................................................................................................................... 18

APPENDICES ................................................................................................................. i

INDIVIDUAL COW RECORD ................................................................................... i

GENERAL HEALTH RECORD .................................................................................. i

VACCINATION RECORD ....................................................................................... iii

MILK PRODUCTION RECORD ............................................................................... iv

1

INTRODUCTION TO FARMING AS A BUSINESS

What is a business?

A business is an organization that buys or sells products or services for money. It can

also be defined as an activity in which a person earns a profit from providing a service or

from supplying goods.

A business involves buying and selling something. The buyer wants to meet a need. He

therefore pays some money for the goods or services he requires to meet that need. The

seller produces products or offers services that are needed by customers. He does this in

order to meet the needs of customers and earn profit in the process. Profit is the amount

left after subtracting the cost of giving a service or supplying goods from the amount paid

for the service or goods by the customer who buys them, i.e. Profit = Income – Expenses

Similarities between farming and other businesses

Farming is similar to other businesses that we are familiar with. In our local market there

are businesses like kiosks, furniture shops, tailoring and others. These businesses help us

to get what we need. They provide their owners with income and provide employment to

those who work there.

Dairy farmers on their part supply consumers with milk and milk products. They invest

in land, cows, capital, animal feeds and labour so that they can provide their families and

other consumers with milk. They must however earn profits from their activities if they

are going to operate as a successful business.

For farming to be carried out as a business the farmer must plan how he is going to sell

the milk so that he can get a good price and a reliable market. Like other businesses he

will need information about the price, availability of milk products, buyers, competitors,

input suppliers and other factors that affect his business. He will also carry out marketing

activities such as value addition, transporting milk to the collection point and selling.

2

Like other businesses farming is affected by seasonal patterns. Business like tailoring

and carpentry are also influenced by seasonal patterns such as demand for school uniform

and desks at the beginning of the year and demand for new clothes during the Christmas

season. Likewise a farmer must plan knowing that there are seasonal variations in

availability of feeds and other seasonal patterns such as high supply of milk in the wet

season. He may conserve feeds for the dry season to ensure that his cows have enough to

eat and produce milk throughout the year. He may also choose to have a contract with

those who buy from him so that the amount of milk sold and the price are determined

beforehand.

Importance of business

There are many benefits that businesses bring to a community and individuals. Some of

them are listed below.

1. A business is a source of employment for the business operator and his employees.

2. A business is a source of income. This helps in meeting the needs of the business

operator, his/her family and those who depend on the business.

3. A business helps in meeting the needs of the community through providing goods and

services close to where they are.

Tuiyo Mosop Multipurpose Group’s agro-vet shop in Kapsaret assists farmers to access inputs nearby

3

4. Businesses promote economic development and promote the welfare of the

community.

5. By creating employment, providing income generating opportunities and promoting

development in rural areas, businesses help in reducing rural-urban migration and the

accompanying problems such as mushrooming of slums.

Importance of farming as a business

Subsistence farming involves producing just enough for consumption by the farmer and

his family. Farming as a business on the other hand involves carrying out farming with

the aim of making profit. It involves planning and choosing farming enterprises that will

enable farmers to earn profit. It also involves having the market in mind when making

decisions about what and when to produce.

In order to engage in farming as a business the farmer invests so that he can make more

money. He may spend money to buy good quality animals, use A.I. services, provide

better feeds, engage in good husbandry practices and add value to what is produced

because these help him to earn more income.

Investing by providing enough quality feeds raises milk production and profit

4

Record keeping is an important business practice because it helps the businessman to

know how the business is performing. Farmers ought to keep records to help them assess

if they are making profit from their activities. The records also provide them with useful

information for decision making.

Besides farm records, the farmer will need to seek information on the opportunities

available and how best to carry out his business so that he can get more profit from his

farm. He can get information on how to improve on his farm business from extension

officers, field days, radio programmes, agricultural shows, magazines, brochures and

booklets.

5

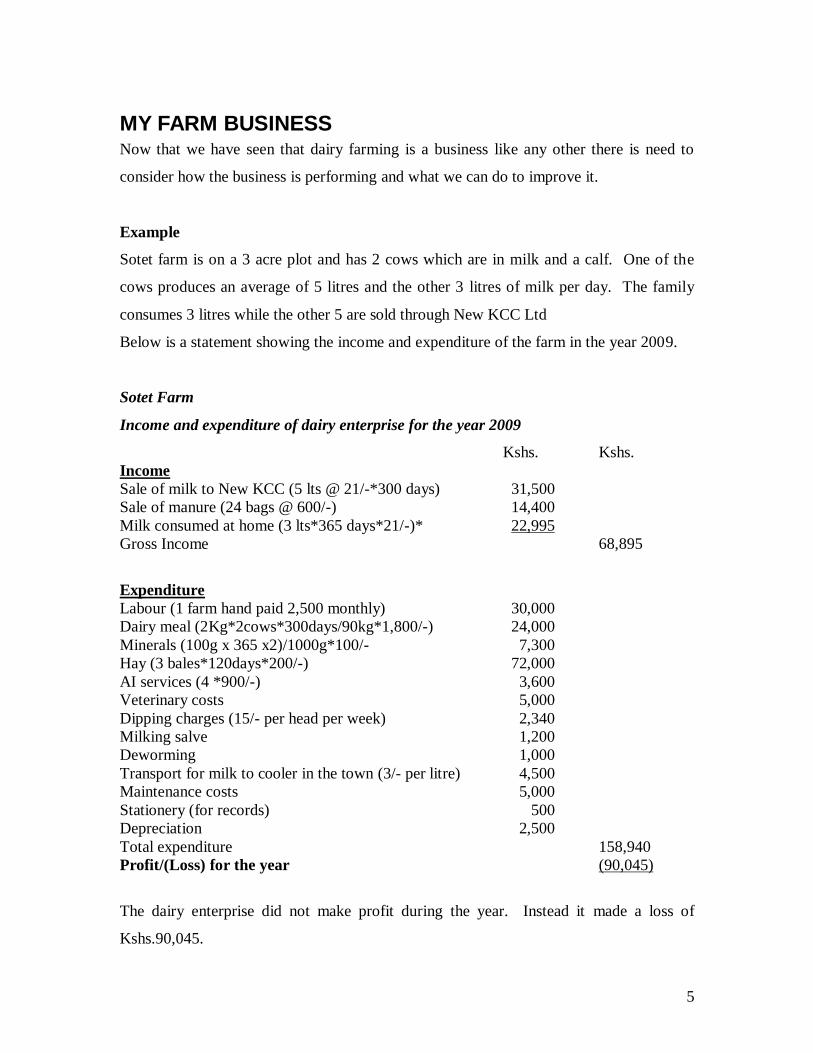

MY FARM BUSINESS Now that we have seen that dairy farming is a business like any other there is need to

consider how the business is performing and what we can do to improve it.

Example

Sotet farm is on a 3 acre plot and has 2 cows which are in milk and a calf. One of the

cows produces an average of 5 litres and the other 3 litres of milk per day. The family

consumes 3 litres while the other 5 are sold through New KCC Ltd

Below is a statement showing the income and expenditure of the farm in the year 2009.

Sotet Farm

Income and expenditure of dairy enterprise for the year 2009

Kshs. Kshs.

Income

Sale of milk to New KCC (5 lts @ 21/-*300 days) 31,500

Sale of manure (24 bags @ 600/-) 14,400

Milk consumed at home (3 lts*365 days*21/-)* 22,995

Gross Income 68,895

Expenditure

Labour (1 farm hand paid 2,500 monthly) 30,000

Dairy meal (2Kg*2cows*300days/90kg*1,800/-) 24,000

Minerals (100g x 365 x2)/1000g*100/- 7,300

Hay (3 bales*120days*200/-) 72,000

AI services (4 *900/-) 3,600

Veterinary costs 5,000

Dipping charges (15/- per head per week) 2,340

Milking salve 1,200

Deworming 1,000

Transport for milk to cooler in the town (3/- per litre) 4,500

Maintenance costs 5,000

Stationery (for records) 500

Depreciation 2,500

Total expenditure 158,940

Profit/(Loss) for the year (90,045)

The dairy enterprise did not make profit during the year. Instead it made a loss of

Kshs.90,045.

6

With a total expenditure of Kshs.158,940 the farmer would need to sell at least 7,569

litres of milk at 21/- to avoid making losses. This is an average of 21 litres per day

throughout the year. The amount at which the business does not make a profit or a loss is

referred to as the break even point. The farmer needs to operate above that level in

order to make a profit.

There are actions that the farmer can take to change this so that the dairy enterprise can

give him profit.

In order to increase profit he can

i. Increase income without raising costs by the same amount

ii. Maintain the same level of income while reducing the costs

iii. Increase income and reduce cost at the same time

Increasing income

A dairy farmer can increase income by

i. Increasing the amount of milk sold.

This involves increasing milk production and reducing milk losses. To increase milk

production he can feed his cows on better feeds and apply good management practices. If

the cows are of low genetic potential the farmer may replace them with cows that yield

more milk. The farmer can improve the quality of his herd by using artificial

insemination (AI) services and select the qualities that are desirable for the offspring.

Milk losses can be reduced through hygienic milk handling to prevent contamination and

Income Expenses

7

spoilage. Losses can also be reduced by using appropriate containers to avoid spillage

during transportation.

Investing in quality cows and good husbandry practices for increased profit

ii. Selling where prices are higher.

Farmers can identify alternative markets that can pay higher prices without them

incurring transport and other marketing costs that are equal to or in excess of additional

income to be earned at the alternative market. Through bulking milk farmers can collect

large volumes that give them bargaining power when negotiating for better prices.

iii. Preparing and selling high value products e.g. mursik, mala, cheese and yoghurt.

This enables farmers to earn more income after converting the milk into other forms that

are sold at a higher price. The demand for such products should be assessed and how they

will be marketed determined before starting such processes. There are additional costs

including licences, culture, flavour, packaging, energy, transport and labour. These costs

should not exceed the additional income earned if the business is to make profit.

8

iv. Selling by-products.

Farmers can sell manure and other farm by-products that other people require and are

willing to pay for. Farmers can produce surplus hay which they can sell during the dry

season when animal feed is in high demand and fetches high prices.

Reducing cost in order to increase profit

Another approach is to identify the respective costs and consider what can be done to

reduce them without reducing the level of milk production. In the previous example the

farmer can reduce costs by growing high quality feeds on the farm to reduce the

expenditure on dairy meal. He can also conserve feeds to avoid buying hay in the dry

season. Farmers who do not have sufficient land to plant fodder could buy hay when

there is plenty of feed because the prices are significantly lower and store it for the dry

season.

Timely heat detection can be used to reduce the number of repeats in AI service.

Similarly improved husbandry practices can lower the incidence of management diseases

and thus reduce the cost of veterinary services. Transport costs could be reduced by

bulking the milk with other farmers and using economies of scale as a means of reducing

the transport cost per litre of milk. Farmers can come together to purchase inputs in bulk

at a lower cost per unit in order to reduce the cost incurred.

9

Planning

The first step in running a successful business is to have a plan. Planning involves

identifying one’s goals and the necessary steps to achieve them. The farmer should plan

his farm to cater for the enterprises chosen in a way that will optimize the production.

The farmer will identify opportunities available based on market demand for various

products and consider the activities he will implement to take advantage of them. The

resources required to carry out the activities are then identified. The farmer plans for

how the resources will be availed and provide a timeframe for the implementation. A

plan is an important management tool because it guides what is to be done to achieve the

goals set and helps to monitor progress made.

10

Below is a sample farm plan

FARM LEVEL DAIRY ENTERPRISE PLAN

BACKGROUND INFORMATION

Name of farmer: Mfugaji Bora Gender: M

Date: May 15, 2010

District: Mashariki

Location: Katikati

Farm size: 3 acres

Description of general features of the farm:

Structures

Farmer’s house: Semi-permanent

Housing for cattle: None save for enclosure with barbed wire fence

Fencing: Barbed wire fence surrounding entire farm

Paddocks: None

Water harvesting and storage: None

Slope – gentle slope

Soils – loamy clay

Water availability: Water is fetched from a stream 500 metres from the farm

Current farm sketch

Existing enterprises

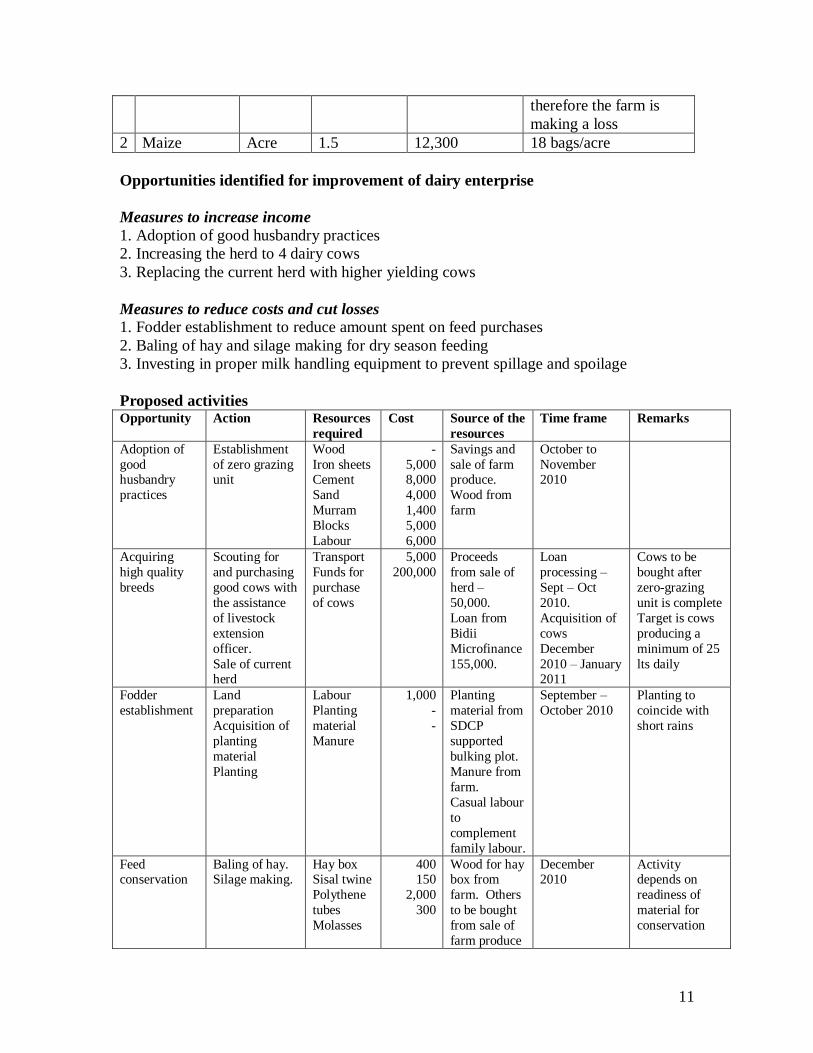

Enterprise Unit No. of units Gross margin Remarks

1 Dairy Cow 2 (90,045) 8 lts / per day. Costs

are more than income

11

therefore the farm is

making a loss

2 Maize Acre 1.5 12,300 18 bags/acre

Opportunities identified for improvement of dairy enterprise

Measures to increase income

1. Adoption of good husbandry practices

2. Increasing the herd to 4 dairy cows

3. Replacing the current herd with higher yielding cows

Measures to reduce costs and cut losses

1. Fodder establishment to reduce amount spent on feed purchases

2. Baling of hay and silage making for dry season feeding

3. Investing in proper milk handling equipment to prevent spillage and spoilage

Proposed activities Opportunity Action Resources

required

Cost Source of the

resources

Time frame Remarks

Adoption of

good husbandry

practices

Establishment

of zero grazing unit

Wood

Iron sheets Cement

Sand

Murram

Blocks

Labour

-

5,000 8,000

4,000

1,400

5,000

6,000

Savings and

sale of farm produce.

Wood from

farm

October to

November 2010

Acquiring

high quality

breeds

Scouting for

and purchasing

good cows with

the assistance

of livestock

extension

officer.

Sale of current herd

Transport

Funds for

purchase

of cows

5,000

200,000

Proceeds

from sale of

herd –

50,000.

Loan from

Bidii

Microfinance

155,000.

Loan

processing –

Sept – Oct

2010.

Acquisition of

cows

December

2010 – January 2011

Cows to be

bought after

zero-grazing

unit is complete

Target is cows

producing a

minimum of 25

lts daily

Fodder

establishment

Land

preparation

Acquisition of

planting

material

Planting

Labour

Planting

material

Manure

1,000

-

-

Planting

material from

SDCP

supported

bulking plot.

Manure from

farm.

Casual labour

to

complement

family labour.

September –

October 2010

Planting to

coincide with

short rains

Feed conservation

Baling of hay. Silage making.

Hay box Sisal twine

Polythene

tubes

Molasses

400 150

2,000

300

Wood for hay box from

farm. Others

to be bought

from sale of

farm produce

December 2010

Activity depends on

readiness of

material for

conservation

12

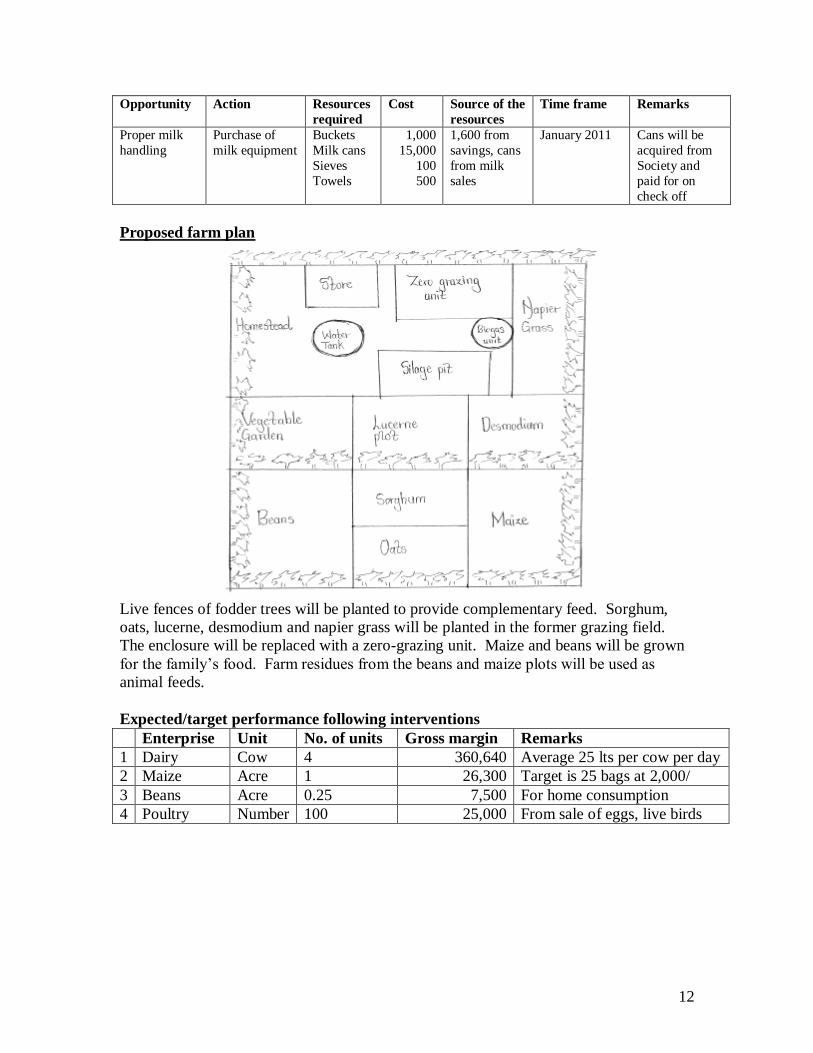

Opportunity Action Resources

required

Cost Source of the

resources

Time frame Remarks

Proper milk

handling

Purchase of

milk equipment

Buckets

Milk cans

Sieves

Towels

1,000

15,000

100

500

1,600 from

savings, cans

from milk

sales

January 2011 Cans will be

acquired from

Society and

paid for on

check off

Proposed farm plan

Live fences of fodder trees will be planted to provide complementary feed. Sorghum,

oats, lucerne, desmodium and napier grass will be planted in the former grazing field.

The enclosure will be replaced with a zero-grazing unit. Maize and beans will be grown

for the family’s food. Farm residues from the beans and maize plots will be used as

animal feeds.

Expected/target performance following interventions

Enterprise Unit No. of units Gross margin Remarks

1 Dairy Cow 4 360,640 Average 25 lts per cow per day

2 Maize Acre 1 26,300 Target is 25 bags at 2,000/

3 Beans Acre 0.25 7,500 For home consumption

4 Poultry Number 100 25,000 From sale of eggs, live birds

13

RECORD KEEPING

Introduction

Recording keeping is an important practice for any business.

Records are written information about what has been done, bought, sold, etc

Importance of records

They help us to stay in control of resources.

They help us in decision making.

They help in monitoring performance.

They communicate about the farm business to other parties. When we are dealing

with other parties they may require information and evidence from records kept e.g.

when seeking business development assistance or when we approach financial

institutions for a loan.

Our minds cannot store all the important information which we may need to refer to later.

We may also not remember all the important information instantly as and when required

even if we have a good memory. It is therefore necessary to document information for

reference by the farmer and other parties who work with him.

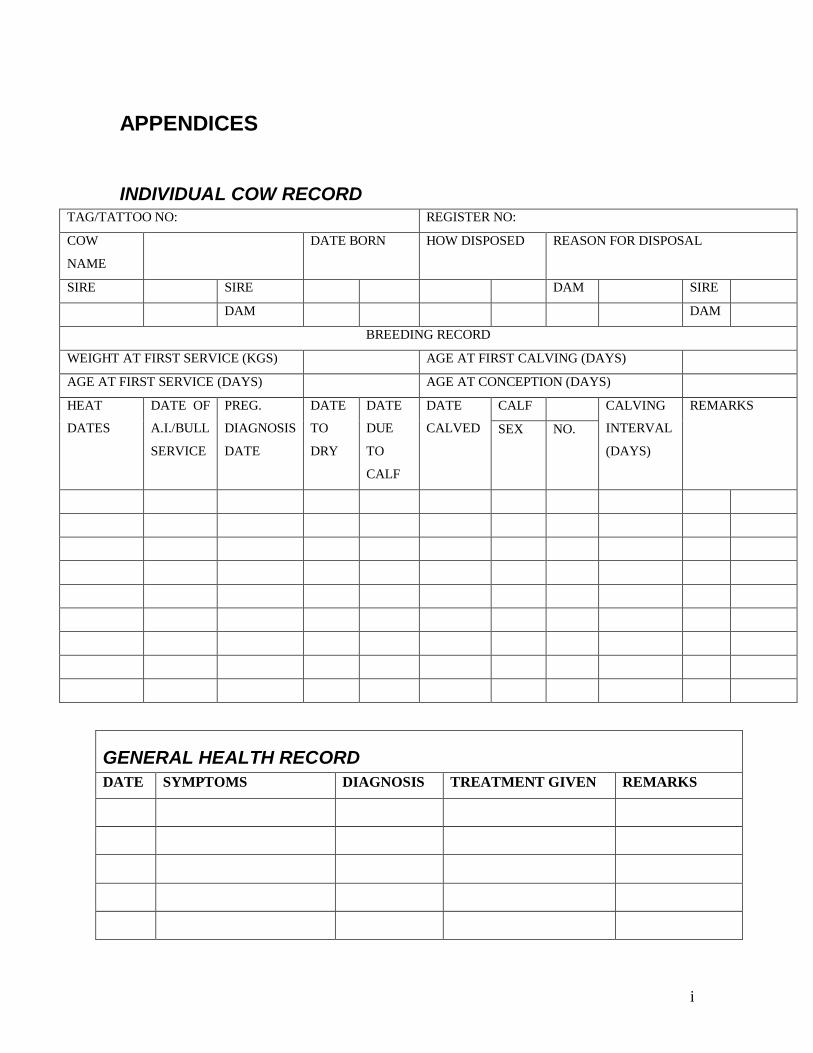

3. What records should the farmer keep? Below are some records kept by dairy farmers.

There are other samples in the annex.

a. Farm plan showing homestead, partitions for various enterprises, other developments,

pathways and unused land.

b. Milk production records

Date Morning Evening Total Calf

consumption

Home

consumption

Sales Price Value

14

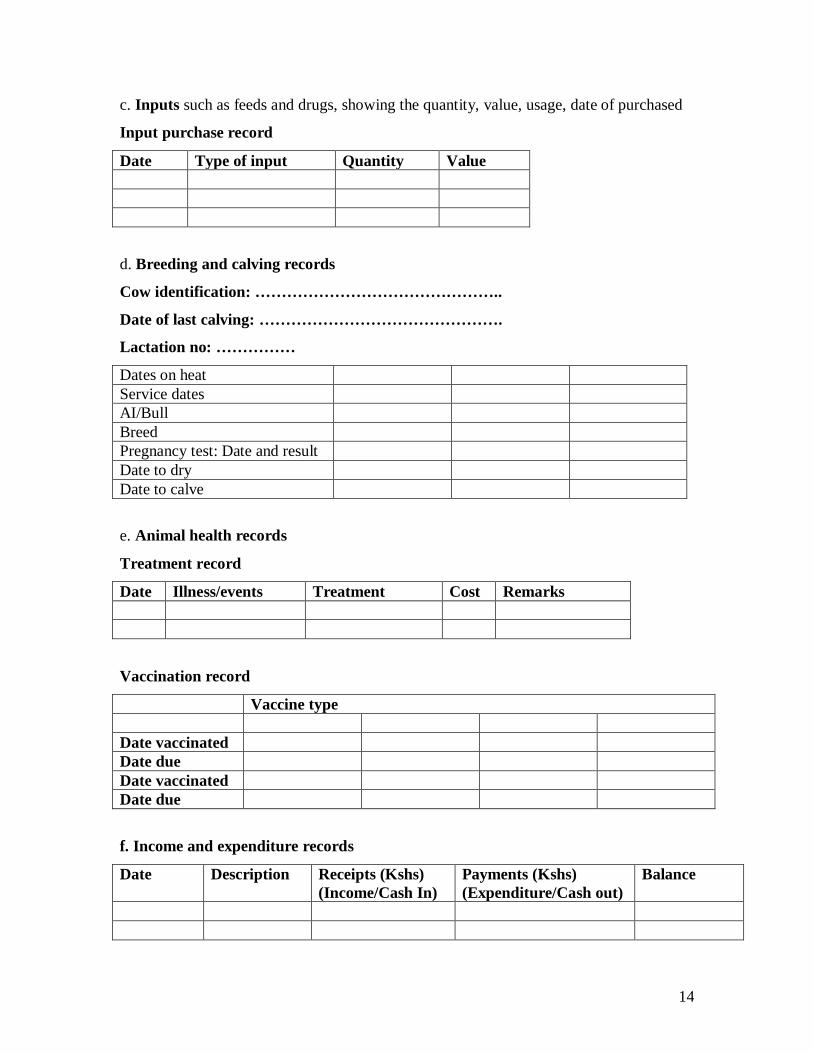

c. Inputs such as feeds and drugs, showing the quantity, value, usage, date of purchased

Input purchase record

Date Type of input Quantity Value

d. Breeding and calving records

Cow identification: ………………………………………..

Date of last calving: ……………………………………….

Lactation no: ……………

Dates on heat

Service dates

AI/Bull

Breed

Pregnancy test: Date and result

Date to dry

Date to calve

e. Animal health records

Treatment record

Date Illness/events Treatment Cost Remarks

Vaccination record

Vaccine type

Date vaccinated

Date due

Date vaccinated

Date due

f. Income and expenditure records

Date Description Receipts (Kshs)

(Income/Cash In)

Payments (Kshs)

(Expenditure/Cash out)

Balance

15

g. Activity record

Activity Start date Completion date Resources used Cost Remarks

There are other records which a farmer can keep to aid him in obtaining information

about his business, making decisions, assessing performance and obtaining external

assistance. These records provide information which is used to generate financial

statements such as profit and loss account and balance sheet.

16

FINANCIAL MANAGEMENT

MONEY

Money is a medium of exchange. Before money was used for exchange there was barter

trade where parties exchanged the commodities they needed. Money is preferred as a

medium of exchange for several reasons:

1. It is widely acceptable.

2. It can be held in various denominations making it divisible.

3. It is easy to carry.

4. It facilitates trade in different areas and commodities.

Importance of money

Money is important because it enables us to pay for the things that we need such as: food,

clothes, shelter, school fees, medicine, utilities such as telephone and other necessities of

life. Money is used for investment e.g. plots of land, poultry, sheep, goats, dairy cows,

shares, equipment, business and rental houses. People also save money to meet future

needs and leave inheritance for their children.

Sources of money

Money is acquired through different ways. Some of them are: sale of farm produce, sale

of assets, trading, employment, dividends, interest income and loans.

The loans can be given to individuals or groups by merry-go-rounds, village savings and

loan associations, cooperative societies, banks, microfinance institutions and some

government programmes among others. Njaa Marufuku Kenya a programme under the

Ministry of Agriculture, CDF, Youth Enterprise Fund and Women Enterprise Fund are

some of the government programmes that can be approached for funds by groups.

17

SAVING

A clay money ‘bank’ used for keeping savings

Purpose of saving

1. Daily financial management: to manage and deal with day-to day expenses and

occurrences as well as emergencies.

2. Consumption smoothing: dealing with seasonality by holding over income from one

period to another.

3. Accumulation: building up savings to meet large future expenses such as purchase

of land, equipment, payment of school fees, etc.

4. Insurance: building up savings to deal with irregular events such as illness, burials,

marriage, ceremonies, etc

Savings may be in the form of money or in kind e.g. livestock, foodstuff in granary, etc.

There are advantages and disadvantages of savings in the different forms. For some

people saving in the form of money may tempt them to use it for other purposes. Where

the savings are held in kind there are risks such as disease outbreaks which can affect

livestock making it disadvantageous to the owner. On the other hand there is the

likelihood that the livestock will have offspring and the value of the herd will increase.

The farmer should choose the form that is appropriate to his circumstances such as

18

income patterns and the purpose for which he is saving. The circumstances of the farmer

will also determine how frequently he saves.

When deciding on where to keep savings there is need to consider safety, ease of

withdrawal when there is need to access money, closeness to avoid high travelling costs,

high interest rates on savings and simplicity of procedures.

INVESTMENT

Investment is putting aside money in something that will increase in value or increase the

ability to earn additional income in future. People invest for various reasons. Some of

them are:

To increase income so that one is able to meet future needs and aspirations.

Wealth and employment creation.

Security for old age and to create a reserve for use in times of emergencies.

Leaving inheritance for children.

There is need to consider the feasibility of an investment. One should not put money in a

venture which will not generate sufficient returns just because someone else has invested

in the same. Get-rich-quick ventures such as the pyramid schemes result in losses and

should therefore be avoided.

CREDIT

This is one of the sources of money. It is money given by one party to another for a time

with the understanding that the party which has received it will pay it back at a later date

according to the terms agreed on.

People take loans for different purposes some of which are listed below.

Investment e.g. in business, plots of land, livestock, etc

Consumption purposes e.g. to buy food or household items, pay school fees, etc

Attending to emergencies e.g. illness

19

Sources of loan funds

There are various places where people can obtain loans. The availability of loans varies

from place to place as well as with the circumstances of the person seeking the loan.

1. Groups which have merry-go-round where members can save and also get loans

based on their level of savings.

2. Savings and credit cooperative societies (SACCO) which give loans to members.

3. Banks. Some of the banks have specialized products to meet the needs of clients.

E.g. Cooperative bank (maziwa loan) and Equity bank (mifugo loan) for livestock

farmers.

4. Agricultural Finance Corporation (AFC).

5. Micro Finance Institutions (MFI) e.g. K-REP, Faulu Kenya, Kenya Women

Finance Trust (KWFT), SMEP, SISDO, KADET, etc.

6. Youth Enterprise Fund.

7. Women Enterprise Fund.

8. Traders who give goods and services on credit.

The different sources have advantages and disadvantages. The farmer should therefore

choose the source that meets his needs and is convenient to his circumstances.

Features of a loan

Principal: This is the amount of money borrowed

Interest: refers to the cost of the loan which is calculated as a percentage of the

principal. Interest may be charged on a fixed amount or on a reducing balance. This

will affect the total amount paid on the loan.

Grace period: This is the duration between the time a loan is disbursed and the time

that repayment begins.

Repayment period: refers to the time given for the loan and interest to be paid in full.

Instalment: Payments are divided into amounts to be paid periodically. The amounts

comprise a portion of the principal and interest.

Security/collateral: Usually the lender requires an asset that can be sold in event of

the borrower’s failure to repay the loan. The type and value of the security depends

on the loan amount and the policy of the lender. Land title deeds, motor vehicle

20

logbooks, equipment, warehouse receipts and group guarantee are some of the forms

of security which are commonly used.

Preliminary expenses e.g. application fees, agreement fees.

When taking a loan it is important to understand the terms and conditions. It is also

important to know various costs that will be charged e.g. application fees, agreement

fees, management fees and the amount of principal and interest that are due each month.

When one takes a loan he should realize that it is not free money. It is money that comes

at a cost and which must be repaid at a future date. Failure to repay may have legally

enforceable consequences resulting in loss to the borrower.

Borrowing money as a group

There are various loans available for different purposes such as development, school fees,

purchase of shares, household items, dairy cows, farm equipment and construction of

farm structures. Loans are available to individuals and groups. A group may have a

proposed investment project but may lack sufficient funds to implement it. They may opt

to finance the project using a loan. Members are responsible for repaying the loan.

Group guarantee is one of the ways of securing money advanced to group members.

Under this method members commit themselves to repay funds owed to the lender when

the borrower defaults. The method is increasingly popular because borrowers who lack

title deeds, motor vehicle log books or other forms of security can take loans.

Managing default

When a borrower fails to pay money owed on the specified date as agreed with the lender

he is said to have defaulted. The reasons for failure to repay on time are diverse. In

event of failure to repay on time there are consequences.

1. The lender may sell the asset pledged as security resulting in loss to the borrower.

2. The borrower may be sued.

3. Where members of the group have committed themselves as guarantors they will

put pressure on the defaulter to force him to repay. In the event that he still does

not repay they may take his possessions so that they are sold and money obtained

to cover the outstanding amount.

21

4. The defaulter may lose credibility depending on the reasons for default. The

guarantors may not want to guarantee him in future while to the lender the credit

rating will be negative making it difficult to access a loan in future

When borrowing one should remember that the money belongs to someone else. The

borrower should therefore be a good steward and use it for productive purposes and repay

it as agreed with the lender. If it becomes difficult to raise the instalments as agreed, the

borrower can consider the options available to him including negotiating with the lender

to accept lower instalments or extending the loan period.

With the many possible sources of credit a borrower may find himself over-burdened

with loans. The borrower should therefore protect himself by making sure that he is not

over-exposed.

When taking a loan

1. Make sure that you borrow an amount that you are able to repay

2. Consider the cost of the loan. The investment being funded by borrowed funds

should give profit that is more than the amount paid for borrowing in the form of

interest, application fees, processing fees and other costs associated with using

borrowed funds.

3. Consider the expected cash-flows and whether they will meet the requirements for

payment of instalments and leave a surplus that justifies taking the loan.

4. Know the terms and conditions of the loan. Are you ready to abide by them?

22

MARKETING

Farming as a business involves production with the market in mind. It is driven by what

is being demanded by consumers. The farmer should therefore identify his market so that

he can know what to produce, when to produce and how much of it. Marketing is

important to farming as a business because it involves the processes that move products

from the farm to the consumer and translates it into income. Four key components of

marketing should be considered when making decisions. These are: product; price;

place; and promotion.

Product

The product to be sold will be determined by the customers’ needs, tastes and

preferences. The dairy farmer has the option of selling fresh milk or milk products if

there is a market for them and they can be produced and sold at a profit. The products

should be well packaged and labelled for them to be attractive to customers.

Price

The price of the product will be influenced by production costs, the price being offered

by the buyers, the level of supply and demand, the price of similar products or substitutes,

desired profit margin and the bargaining power of the farmer among other factors.

Place

This involves decisions on how the product will reach the consumer. There different

ways of reaching consumers depending on the people involved in the marketing chain.

The farmer may take milk to a collection centre or engage a transporter to carry the milk

for him, sell it direct to consumers or sell through middlemen. The decision of how the

product will reach the consumer will depend on the distance, costs involved, presence of

middlemen, transporters, processors and collection centres among other considerations.

Promotion

This involves creating awareness about a product for example through advertising and

making samples available for tasting. It is essential to the success of the business because

customers must become aware of the products so that they can buy. This is particularly

important for new products and new brands which are being introduced in the market.

Conclusion

The farmer who is engaging in dairy farming as a business should be prepared to invest in

good quality cows, proper housing, good management practices and feeding. He should

plan his business and focus on the market, what the customers want and are willing to

pay for. Like other businesses dairy farming is a profitable business if the business

farmer invests and makes the right decisions regarding his enterprise.

i

APPENDICES

INDIVIDUAL COW RECORD TAG/TATTOO NO: REGISTER NO:

COW

NAME

DATE BORN HOW DISPOSED REASON FOR DISPOSAL

SIRE SIRE DAM SIRE

DAM DAM

BREEDING RECORD

WEIGHT AT FIRST SERVICE (KGS) AGE AT FIRST CALVING (DAYS)

AGE AT FIRST SERVICE (DAYS) AGE AT CONCEPTION (DAYS)

HEAT

DATES

DATE OF

A.I./BULL

SERVICE

PREG.

DIAGNOSIS

DATE

DATE

TO

DRY

DATE

DUE

TO

CALF

DATE

CALVED

CALF CALVING

INTERVAL

(DAYS)

REMARKS

SEX NO.

GENERAL HEALTH RECORD

DATE SYMPTOMS DIAGNOSIS TREATMENT GIVEN REMARKS

ii

iii

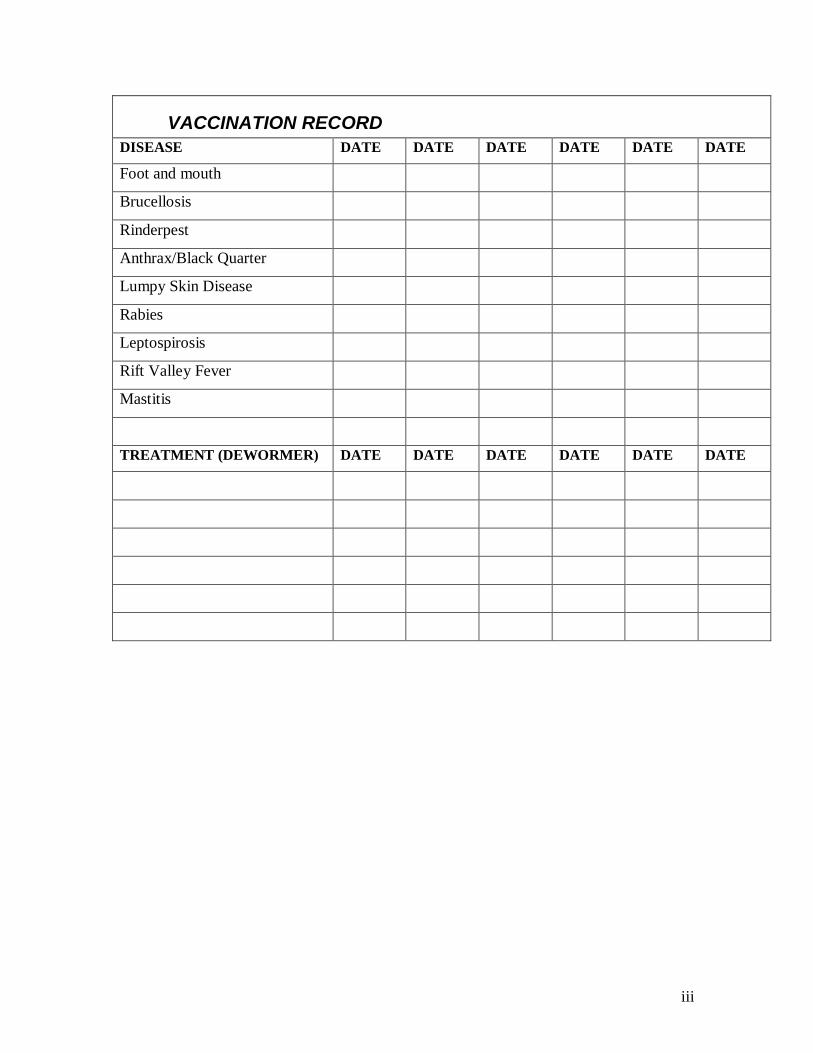

VACCINATION RECORD

DISEASE DATE DATE DATE DATE DATE DATE

Foot and mouth

Brucellosis

Rinderpest

Anthrax/Black Quarter

Lumpy Skin Disease

Rabies

Leptospirosis

Rift Valley Fever

Mastitis

TREATMENT (DEWORMER) DATE DATE DATE DATE DATE DATE

iv

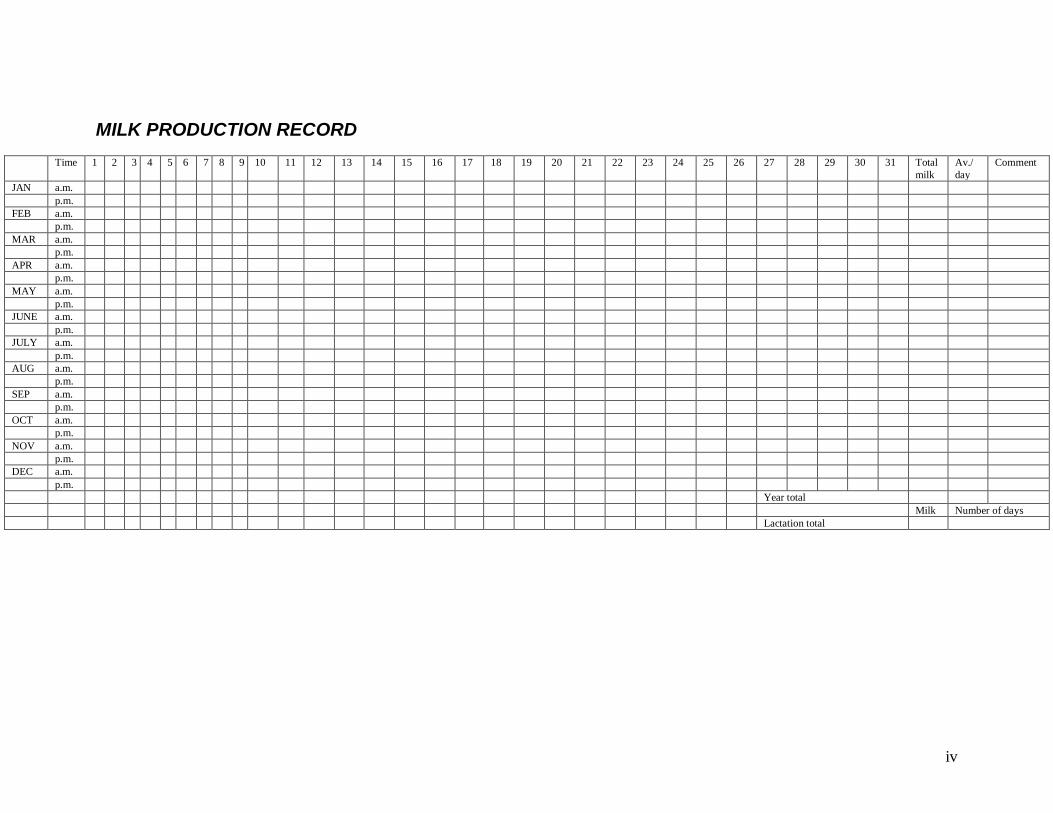

MILK PRODUCTION RECORD

Time 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 Total

milk

Av./

day

Comment

JAN a.m.

p.m.

FEB a.m.

p.m.

MAR a.m.

p.m.

APR a.m.

p.m.

MAY a.m.

p.m.

JUNE a.m.

p.m.

JULY a.m.

p.m.

AUG a.m.

p.m.

SEP a.m.

p.m.

OCT a.m.

p.m.

NOV a.m.

p.m.

DEC a.m.

p.m.

Year total

Milk Number of days

Lactation total

Related Documents