Article Value Chain Analysis in interfirm relationships – Henri C.Dekker Mariyanti Abdul Majid (809135) Syaratul Ain abdul aziz (807462) Teo Chai Lie (809173) 30 Jun 2012

Sma Article Jun 2012

Oct 26, 2014

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Article

Value Chain Analysis in interfirm relationships –

Henri C.Dekker

Mariyanti Abdul Majid (809135)Syaratul Ain abdul aziz (807462)

Teo Chai Lie (809173)

30 Jun 2012

Interfirm Relationships• New challenge for management accounting(MA)• Is the provision of information for the coordination

and optimization of activities across firms in a value chain

• Value Chain Analysis(VCA) useful tool• Few empirical evidence recorded in written form• Case study on the use of Activity-Based

Costing(ABC) Model to support Supply Chain Management(SCM) in practice between J.Sainsbury and a group of suppliers

• ABC model was based on the principle of VCA and integrated cost information across the supply chain

• The findings explained using organizational theory and transaction cost economics

Intoduction • In the Past, very little attention on Interfirm

relationships on the agenda of MA researchers and only recently more attention given for the accounting literature

• Why? Due to the implication for organizational design and management control within and between organizations based on decision making– Make-or-buy decision and outsourcing activities– Inter-organizational cost management– Supply chain relationships– Alliances and business networks– VCA

Cont.• Focus – the use of VCA in buyer-supplier

relationships for coordinating supply chain interdependence (J.Sainsbury and its suppliers)

• Porter – VCA is to analyze the value chain for strategic improvement

• Shank & Govindarajan – core idea of CVA is to break up “the chain activities that runs from basic raw materials to end-user customers into strategically relevant segments in order to understand the behavior of costs and the sources of differentiation”

• Lord – criticism on the relevance of the concept for practice

• Mainly from an intrafirm perspective• Little empirical evidence of its use

Cont.• Case analysis – How J.Sainsbury used VCA to manage the

supply chain in cooperative relationships with suppliers• Sainsbury has developed an ABC model to support its SCM

practices with a group of suppliers – no empirical evidence published– In-depth of description of interfirm cost management

practices is provided and key features of Sainsbury’s VCA practices are identified

– Case observation based on organizational theory and transaction cost economics

– The role of management accounting in interfirm relationships

– The concept of VCA in interfirm relationships– How Sainsbury uses principles of the VCA concept to

support its SCM with suppliers– Finding and conclusion

Part 1

• Management accounting in interfirm relationships

• Value chain analysis as a coordination mechanism in interfirm relationships

• Managing interdependence in the CV• Accounting information for VCA• Performing a VCA• The hazards of VCA in interfirm relationships• Empirical evidence on CVA

Management accounting in interfirm relationships

• Seal et al.(1999) – important roles of MA in interfirm relationships

• To make-or-buy decision that can lead to the initiation of a partnership

• The use of management accounting in the actual management of a partnership

• The partners’ responsibilities to each other, which creates a role for performance measurement

• Tomkins(2001) – the use of information in interfirm relationships

• The mastery of events – the management of tasks to be performed in the relationship in the pursuit of value creation

• The development of trust – reflect the need to gain confidence in each other’s behavior

Cont.• Gulati and Singh(1998) – purposes of

governance in interfirm relationshipsi. The coordination of interdependent tasks

(organization theory – Thompson 1967)• The need for coordination varies with to the degree of

interdependence and the uncertainty of tasks performed within the interfirm relationship -Thompson, 1967

• Creation of value by interfirm coordination• The greater the task interdependence and uncertainty,

the more coordination is required -Thompson, 1967• Interfirm coordination takes place between independent

firms, which situation lacks the use of formal authority relationships

• Tomkins(2001) – interfirm coordination based on “Type 2 information” enables entities ‘ to plan and make decisions on collaborative futures’ and ‘to make judgements on strategies, investments and on-going operations’

Cont.ii. The management of appropriation

concerns (transaction cost economics – Williamson 1985)

• Partners in interfirm relationships need to safeguard their interests against the potentially opportunistic behavior of the others

• Manage it in related to the charecteristics of the transaction taking place and characteristics of human being

• Trust in the other’s goodwill is an important informal control mechanism that adds the partner’s level of confidence that opportunism will not occur, and thus influences the level of formal control required

• Information required to warrant trust as ‘Type 1 information’ (Tomkins 2001)

Cont.

• Require the use of control mechanisms and can have significant implications for the role of management accounting in interfirm relationships

• SMA – the VCA is a technique that can play an important role in the management of supply chain relationships (based on the concept of VC)

• Dekker, a VCA is used to analyze, coordinate and optimize linkages between activities in the VC by focusing on the interdependence between these activities

VCA as a coordination mechanism in interfirm

relationships•Managing interdependence in the VC•Porter (1985) – strategic cost analysis, to better manage linkages between buyers and suppliers in VCA

•Type of relationships in VCa) Relationships between activitiesb) Relationships between Business Units of the firmc) Relationships between firm and its buyers and suppliers (vertical linkages)

•Can reduce costs and to enhance differentiation

•Thompson (1967) – interdependence needs to be managed by coordination mechanisms, in order to achieve efficient and effective outcomes•VCA is a structured methods to analyze the effects of strategically important activities on the costs or differentiation of the VC•CVA is a mechanism that facilitates the optimization and coordination of interdependent activities in the VC, which may cross organizational boundaries

Cont.• Accounting information for VCA

Porter, 1985 – traditional accounting systems unable to adequately support VCA

Shank, 1989 – fundamental problem of the value added concept is that it “ start too late and it stop too soon”.

Hergert and Morris, 1989 – deficiencies of traditional accounting systems

i. Do not focus on critical activitiesii. Do not account for interdependence between activitiesiii. Offer poor reflection of the economics of performing an activity

ABC and Strategic Cost Management(SCM)ABC – regarding the problem of performing an internal VCASCM – accounting information is used for developing and

supporting a firm’s strategies ( now as SMA)Lord, 1996 – SMA is about analyses of different strategic

dimensions of the firm such as competitor analyses, strategic positioning analyses and analysis of the VC in which the firm operates.

Cont. • Performing a VCA

– Interdependence between activities of buyers and suppliers – To analyze the behavior of costs and the sources of

differentiation– Develop and maintain competitive advantage – use the

outcomes of the analysis to control cost drivers better than competitors do or to reconfigure the VC

• Shank and Govindarajan – either by reducing cost while keeping value constant, or by increasing value while keeping costs constant

– ABC analysis as a basis to perform VCA and solve the problems of accounting systems

• The hazards of VCA in interfirm relationships– Transaction hazards (appropriate design of governance

structures in interfirm relationships)• The exchange of sensitive information• A fair division of cost and benefits• The appropriation of investment to be made in specific assets

Cont.

• Empirical evidence on VCA– Limited and ambiguous – “a frigment of academic imagination”

(Lord 1996)– Survey evidence on SMA and VCA

practices, but the adoption rates are based on global descriptions of the VCA methods, no insight is gained into what these practices actually consists of

– Internally oriented VCA not an analysis of activites across the wider VC involving more firms.

Part 2• The use of VCA by J.Sainsbury

• Research design• SCM at Sainsbury• A cost model for VCA

– The initiation and goal of the model– The design of the model– The content of the model– The use of the model– An example of a supply chain analysis– Decision making and negotiations

Part 2• The use of VCA by J.Sainsbury

• Research design• SCM at Sainsbury• A cost model for VCA

– The initiation and goal of the model– The design of the model– The content of the model– The use of the model– An example of a supply chain analysis– Decision making and negotiations

Research Design

• An interview in three different topics– Company information– The management relationships with suppliers &

SCM practices– The cost model

SCM at Sainsbury

• Founded or came to UK in 1869• Sainsbury is the 2nd ranked in supermarket chain

in UK after Tesco• Market share 16.1 in London Stock Exchange• Over 23,000 products and 4,000 suppliers• Around 1993;

– develop cooperative relationship with suppliers– introduced new IS in supply chain– Less contact with suppliers

• In 1998;– Comprehensive MIS-system called SID-to

coordinate activity with suppliers– SCM supported by Logistics Department– 3 types of suppliers:

• Core suppliers-major impact, SID to exchange info• Middle-large suppliers-’cross-docking’• Small-suppliers-little impact,small products,EDI(web

based)

SCM at Sainsbury

A cost model for VCA

• The initiation and goal of the model– Until 1996, cost of supply chain were based on the yearly

distribution costs (lack of control, hi cost, little information, interdependent xtvt very low)

– Sainsbury senior management requested Logistic Department to develop ABC

– For greater u/standing of total supply chain process to improve decision making and deliver clear u/standing of inter-relationship of costs and xtvts

– And to analyze cost xtvts in supply chain with suppliers(reduce costs, better controls)

• The design of the model– Included are all xtvts involved from end supplier

production line to supermarket shelf– Costs of both parties were allocated to xtvts– This model considered the costs of xtvts in the

supply chain– Analyze costs from different perspective(eg:

supplier network, geographical region,store category)

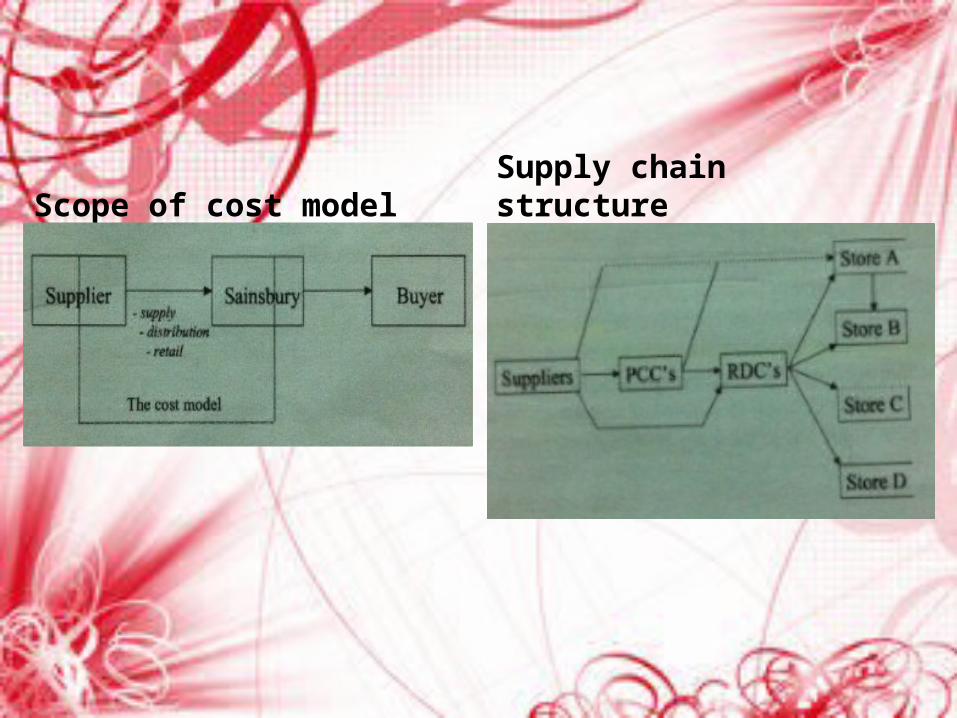

A cost model for VCA

Scope of cost model Supply chain structure

• The content of the model– 36 participate suppliers are were mainly core

suppliers because of the large volume and leads to large benefits.

– Suppliers have to provide a reliable cost data and cost driver quantities

A cost model for VCA

• The use of the model– After data updated, cost analyses can be perfomed– Suppliers-received part of the analyses (incl. own xtvt

costs, Sainsbury xtvts costs related to them, average xtvt costs of supplier network)

– Discussions(Sainsbury & suppliers)-three types of analyses:

• Benchmark analyses-compare supplier vs network• Strategic what-if analyses-effects of changes in supply chain-

improving supply chain• Trend analyses-monitor and intervene supply chain

A cost model for VCA

• An example of a supply chain analyses– Plastic crates for chilled products– Sainsbury & large suppliers discussed about the use

to improvise efficiency of product handling xtvts– The model were used to calculate cost consequences

of adopting or not– Benchmark analyses shows differences and cost adv

for adopting suppliers– Strategic what-if analyses analyze changes for

adopting and calculate supply chain costs could be reduced

A cost model for VCA

Identify idea and improvemen

t

Sainsbur

y and supplier

agreed

Investment proposal

Management

accounts-rate of

return

Further negotiation

s

A cost model for VCA

• Decision making and negotiations

• Need to assess & improve current supply chain performance

• Exchange of sensitive cost information• Sharing of costs, benefits & investments

that resulted from supply chain changes

Managing Interdependence and

Appropriation Concerns

• Supply chain analyses performed were benchmarking between suppliers, regions and store types to identify opportunities for improvement, strategic what-if analyses to quantify the cost consequences of supply chain changes and monitoring of supply chain cost development over time.

• Demonstrates the central role that accounting can play as a coordination mechanism in SCM

The Coordination of Supply Chain

Activities

Discussion

• Supplying cost information to buyer can be detrimental for suppliers as it increases their vulnerability to opportunistic behavior.

• The use of the information, reputation effects in the supplier network and the suppliers’ trust will to be powerful mechanisms to manage these concerns.

The Exchange of Cost Information

• How a supplier was not willing to invest in specific crate handling technology due to concerns about the cost consequences and the investment to be made

• Firms are only willing to participate in a joint project when the investment earns an adequate rate of return for the risks associated, and when the partners have the prospect of receiving a fair share of the benefits (Tomkins: 2001)

The Division of Benefits, Cost and

Investment

Discussion

• Increased the interaction between the parties

• Suppliers perceived less risk of ending u with negative outcomes

• Suppliers would come with new ideas for supply chain improvement

The Effects on Relationships with

Suppliers

• Compared to the conceptualization of VCA in the literature

• Cope with Hergest and Morris’ (1989) critique on traditional accounting systems for supporting a VCA

• Able to manage the efficiency of the larger supplier network by “negotiated adjustments”

A Comparison with the Literature

Discussion

•How a firm solve the problems when they are planning to perform a VCA•To investigate how focusing on a broader segment of the value chain and on activities characterized by higher levels of interdependence influence the use of VCA in interfirm relationships.•Focus on how such a complex structure of coordination mechanisms fulfills firms’ needs to manage their interfirm interdependence in the wider value chain.

Some Directions for Further Research

Discussion

Conclusion• How firms attempt to manage interdependence in the

value chain using cost information and which obstacles they may encounter in the efforts.

• Integrated cost date was used for 3 specific purposes– To analyze the cost performance of supply chain activities– To calculate the cost consequences of changing supply chain

operations– To periodically monitor the development of supply chain

costs over time• To manage coordination requirements and appropriation

concerns in interfirm relationships, organizational theory and transaction cost economics were found useful

Related Documents

![INVENTION PROMOTION ACT - KIPO · 2018-01-16 · [This Article Newly Inserted by Act No. 10357, Jun. 8, 2010] Article 9 Deleted. Article 9-2](https://static.cupdf.com/doc/110x72/5e2d24412ae9f828f6447897/invention-promotion-act-kipo-2018-01-16-this-article-newly-inserted-by-act.jpg)