Slides at: Greg Crabtree · PDF fileSlides at: Greg Crabtree [email protected] 256-704-0620

Mar 17, 2018

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

www.SimpleNumbers.me

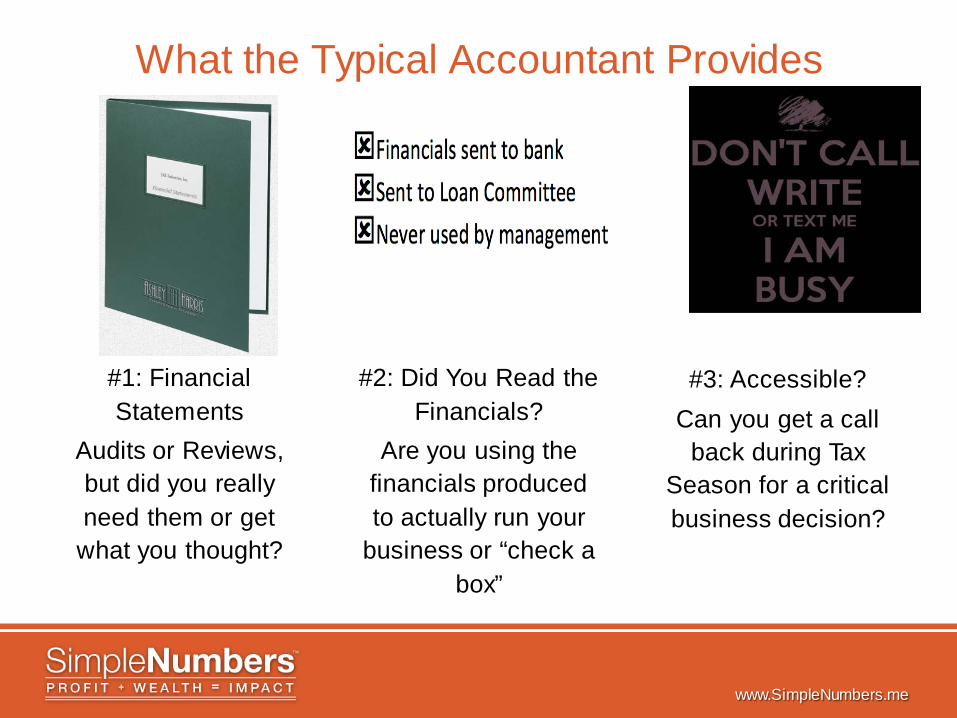

What the Typical Accountant Provides

#1: Financial Statements

Audits or Reviews, but did you really need them or get

what you thought?

#2: Did You Read the Financials?

Are you using the financials produced to actually run your

business or “check a box”

#3: Accessible? Can you get a call

back during Tax Season for a critical business decision?

www.SimpleNumbers.me

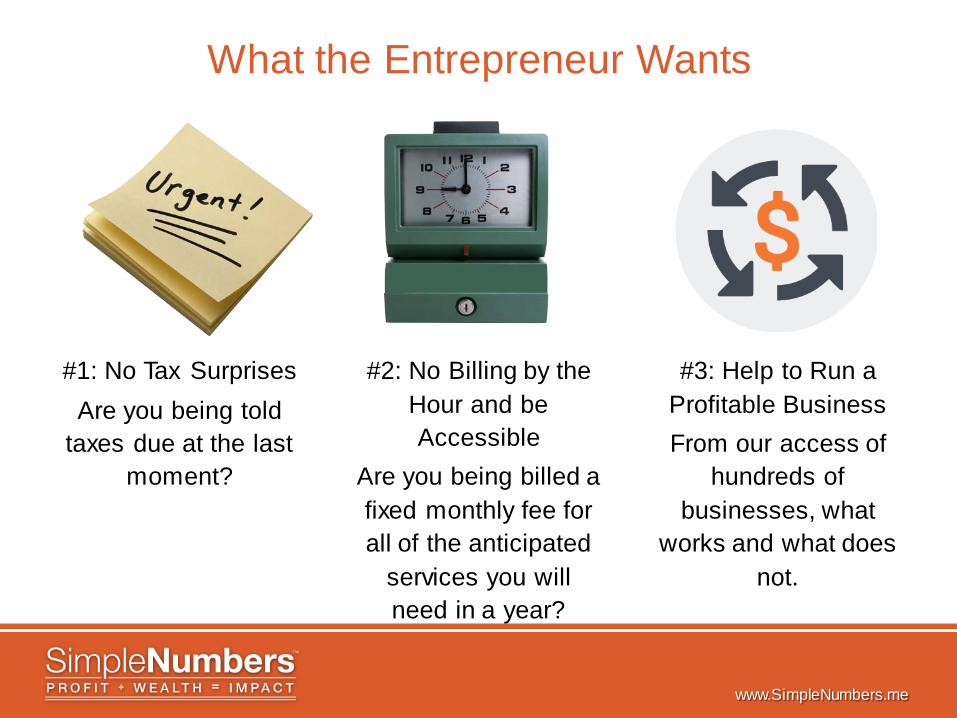

What the Entrepreneur Wants

#1: No Tax Surprises Are you being told

taxes due at the last moment?

#2: No Billing by the Hour and be Accessible

Are you being billed a fixed monthly fee for all of the anticipated

services you will need in a year?

#3: Help to Run a Profitable Business From our access of

hundreds of businesses, what

works and what does not.

www.SimpleNumbers.me

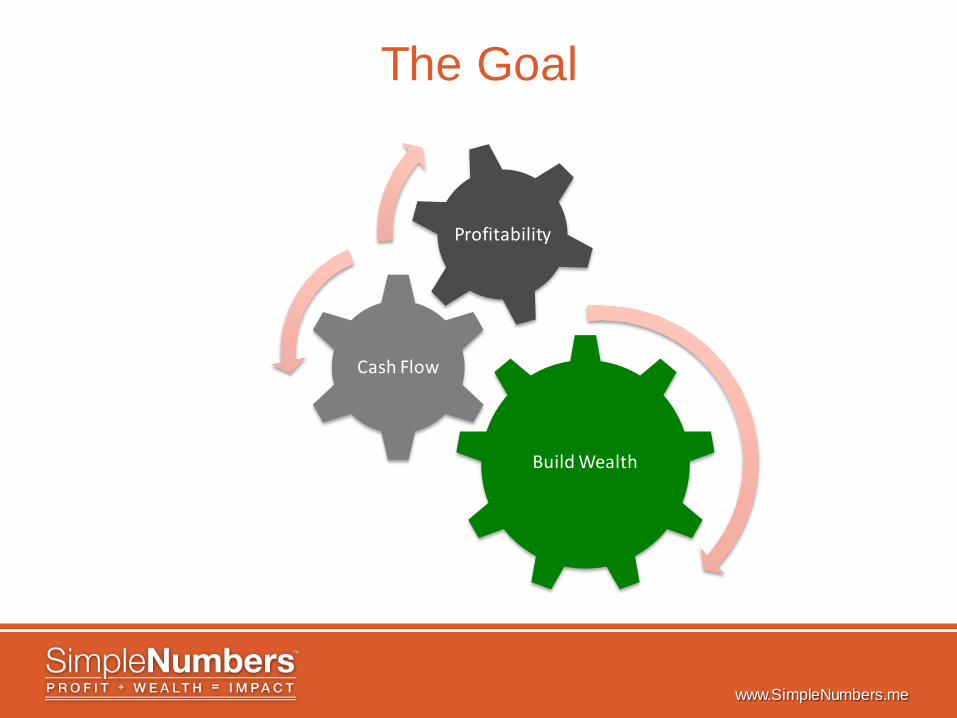

The Goal

Build Wealth

Cash Flow

Profitability

www.SimpleNumbers.me

The Solution: 3 Keys To Unlock Your Business Potential

#1: Remove Distortions

Are you looking at your ‘true’ numbers

and understand your ‘true’ targets?

#2: Labor Productivity

How are you measuring and

improving your labor productivity?

#3: Four Forces Of Cash Flow

Have you set your priorities right to build

a solid foundation?

www.SimpleNumbers.me

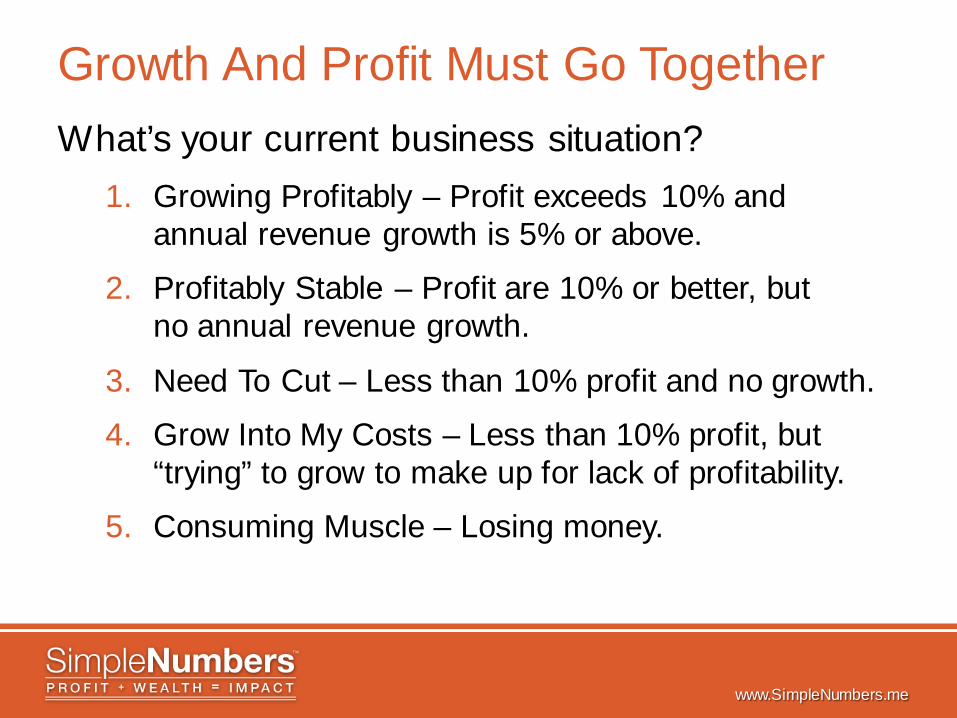

Growth And Profit Must Go Together What’s your current business situation?

1. Growing Profitably – Profit exceeds 10% and annual revenue growth is 5% or above.

2. Profitably Stable – Profit are 10% or better, but no annual revenue growth.

3. Need To Cut – Less than 10% profit and no growth.

4. Grow Into My Costs – Less than 10% profit, but “trying” to grow to make up for lack of profitability.

5. Consuming Muscle – Losing money.

www.SimpleNumbers.me

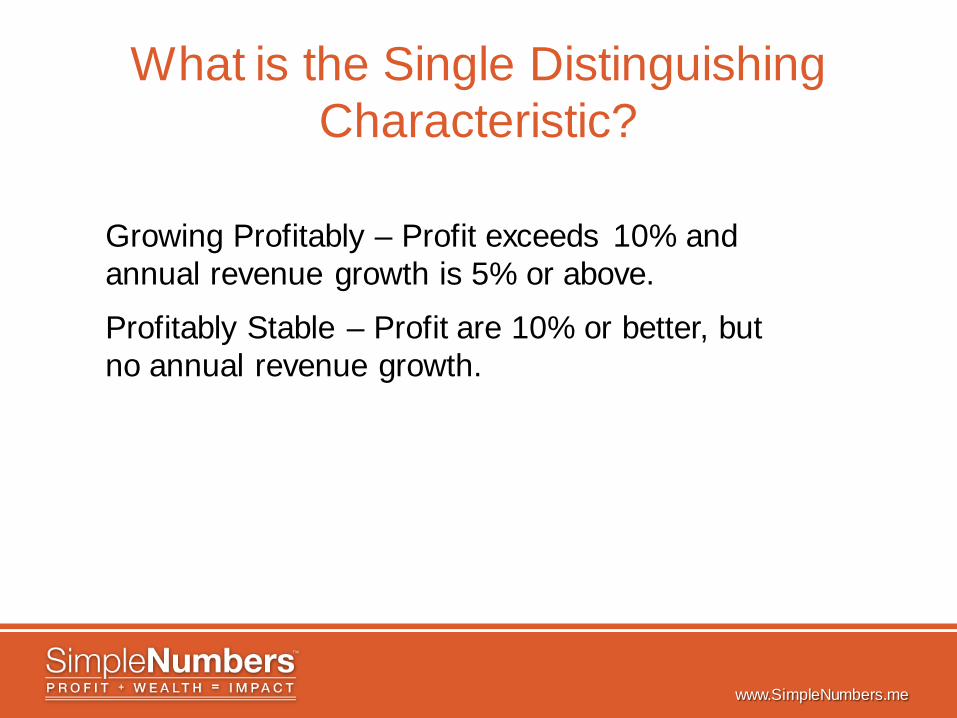

What is the Single Distinguishing Characteristic?

Growing Profitably – Profit exceeds 10% and annual revenue growth is 5% or above.

Profitably Stable – Profit are 10% or better, but no annual revenue growth.

www.SimpleNumbers.me

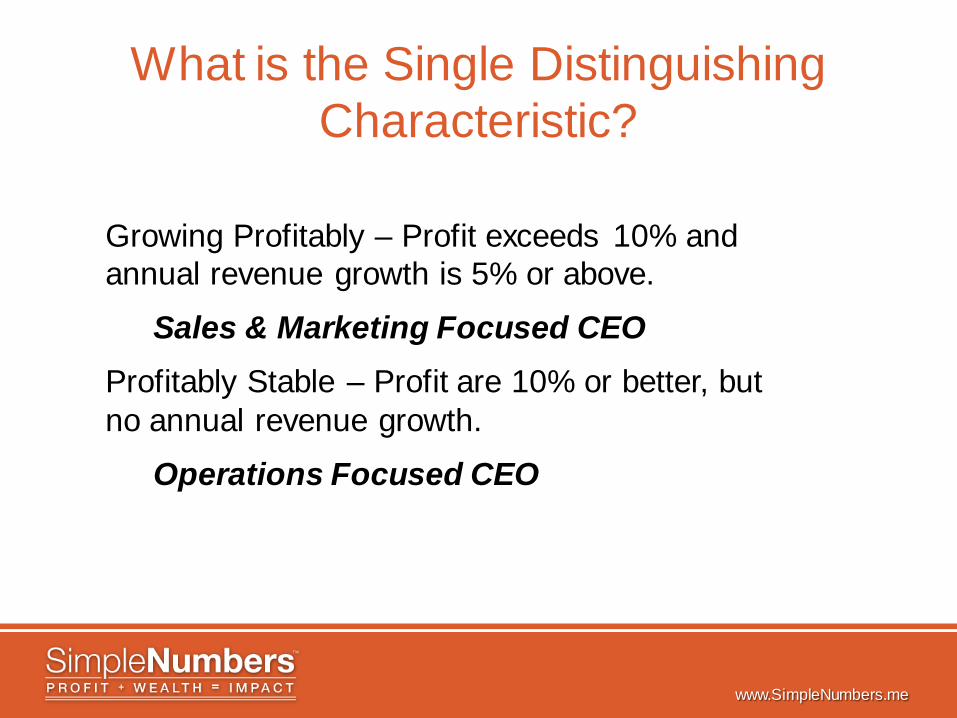

What is the Single Distinguishing Characteristic?

Growing Profitably – Profit exceeds 10% and annual revenue growth is 5% or above.

Sales & Marketing Focused CEO Profitably Stable – Profit are 10% or better, but no annual revenue growth.

Operations Focused CEO

www.SimpleNumbers.me

#1: Remove Distortions Are you looking at your ‘true’ numbers and understand your ‘true’ targets?

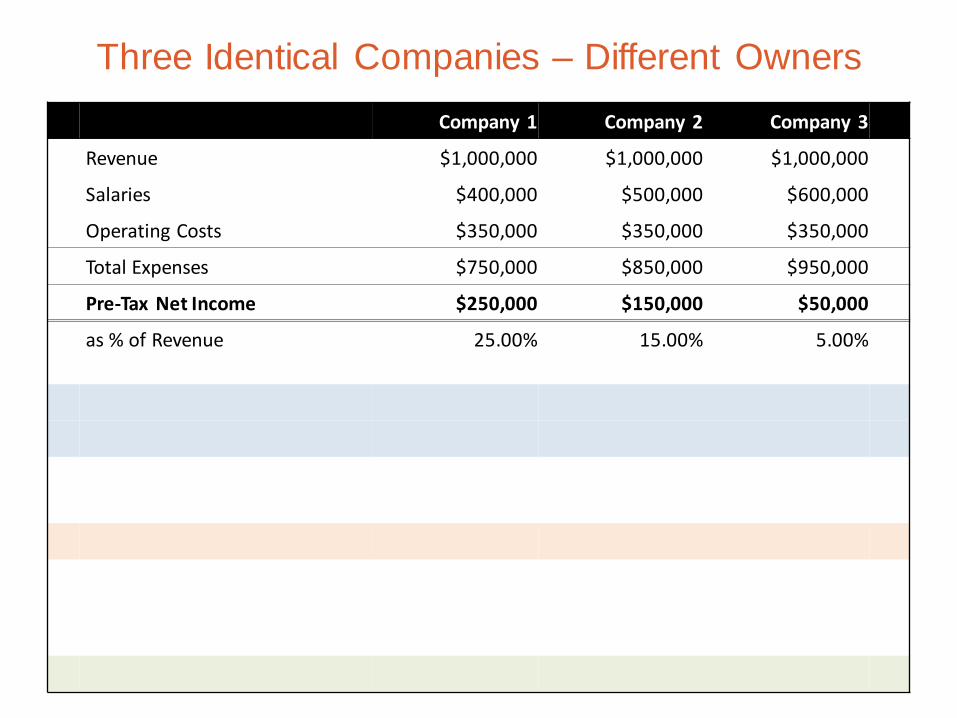

Three Identical Companies – Different Owners Company 1 Company 2 Company 3

Revenue $1,000,000 $1,000,000 $1,000,000

Salaries $400,000 $500,000 $600,000

Operating Costs $350,000 $350,000 $350,000

Total Expenses $750,000 $850,000 $950,000

Pre-Tax Net Income $250,000 $150,000 $50,000

as % of Revenue 25.00% 15.00% 5.00%

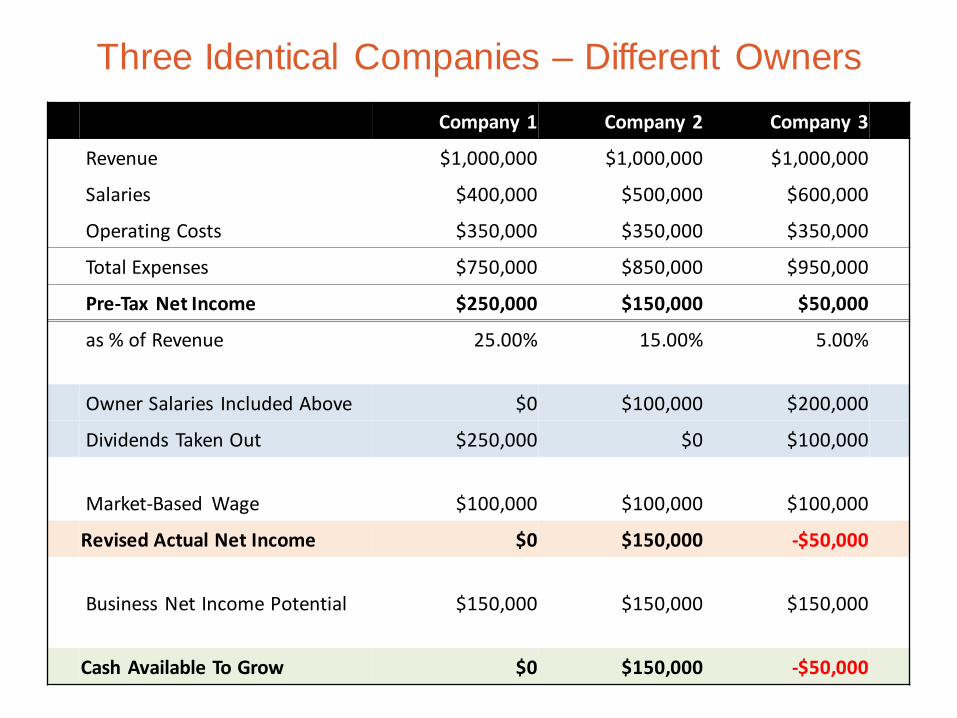

Three Identical Companies – Different Owners Company 1 Company 2 Company 3

Revenue $1,000,000 $1,000,000 $1,000,000

Salaries $400,000 $500,000 $600,000

Operating Costs $350,000 $350,000 $350,000

Total Expenses $750,000 $850,000 $950,000

Pre-Tax Net Income $250,000 $150,000 $50,000

as % of Revenue 25.00% 15.00% 5.00%

Owner Salaries Included Above $0 $100,000 $200,000

Dividends Taken Out $250,000 $0 $100,000

Market-Based Wage $100,000 $100,000 $100,000

Revised Actual Net Income $0 $150,000 -$50,000

Business Net Income Potential $150,000 $150,000 $150,000

Cash Available To Grow $0 $150,000 -$50,000

www.SimpleNumbers.me

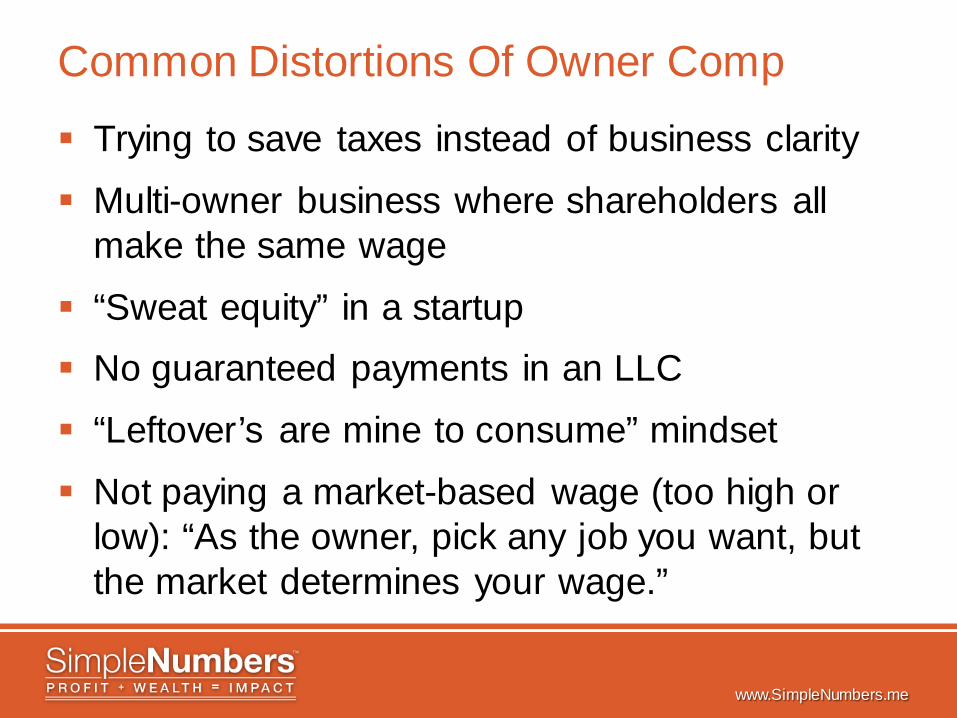

Common Distortions Of Owner Comp

Trying to save taxes instead of business clarity

Multi-owner business where shareholders all make the same wage

“Sweat equity” in a startup No guaranteed payments in an LLC

“Leftover’s are mine to consume” mindset

Not paying a market-based wage (too high or low): “As the owner, pick any job you want, but the market determines your wage.”

REVENUE

Watch Your Language – Words Matter

EBITDA Earnings before: Interest, Taxes,

Depreciation & Amortization

PRE-TAX PROFITS

GROSS MARGIN Revenue less direct costs,

excluding labor

CONTRIBUTION

MARGIN Gross Margin less direct labor cost

Busin

ess E

ngin

e Bu

sines

s Cha

ssis

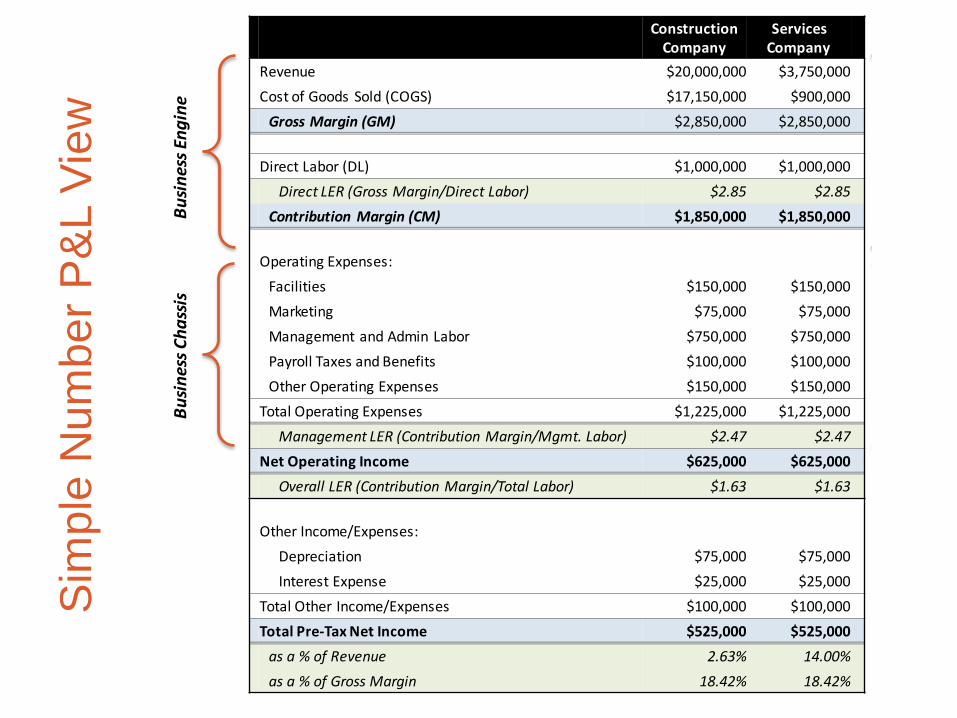

Construction Company

Services Company

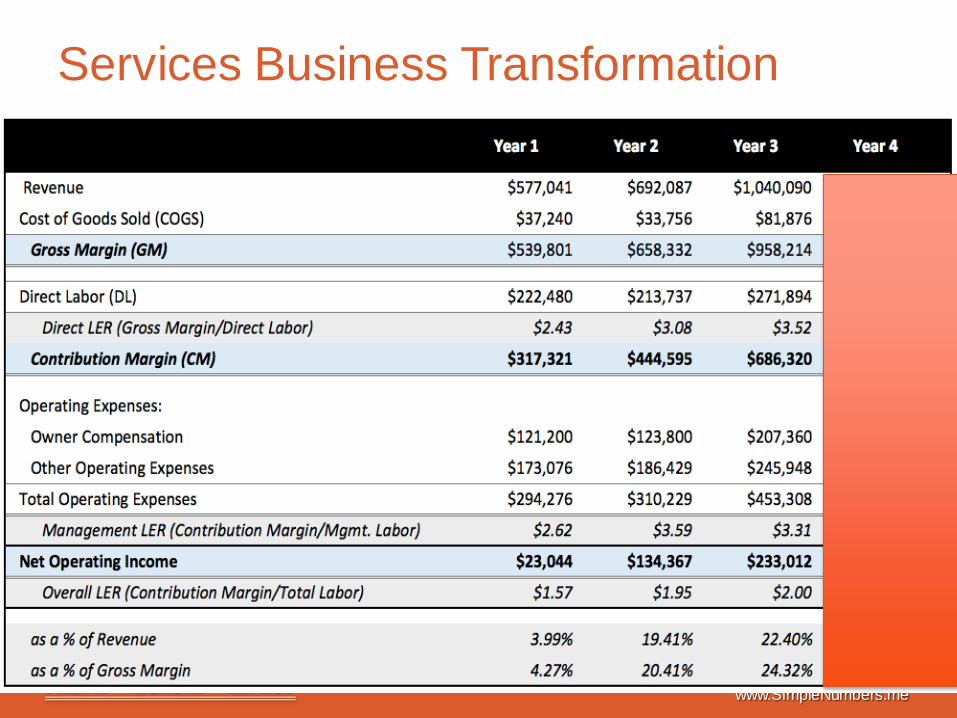

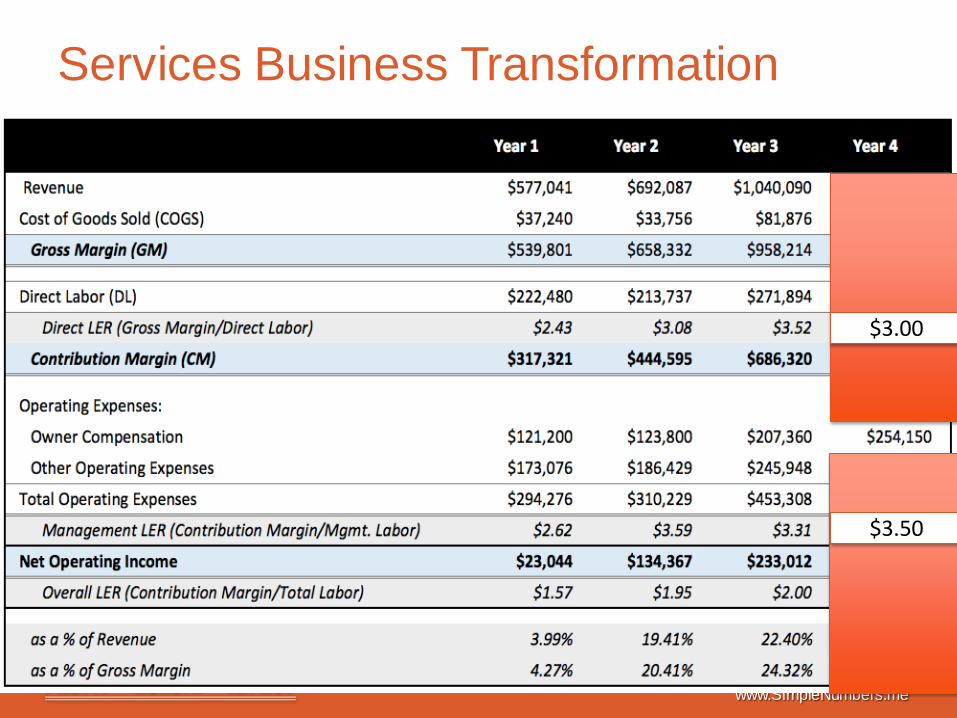

Revenue $20,000,000 $3,750,000 Cost of Goods Sold (COGS) $17,150,000 $900,000 Gross Margin (GM) $2,850,000 $2,850,000 Direct Labor (DL) $1,000,000 $1,000,000 Direct LER (Gross Margin/Direct Labor) $2.85 $2.85 Contribution Margin (CM) $1,850,000 $1,850,000

Operating Expenses: Facilities $150,000 $150,000 Marketing $75,000 $75,000 Management and Admin Labor $750,000 $750,000 Payroll Taxes and Benefits $100,000 $100,000 Other Operating Expenses $150,000 $150,000 Total Operating Expenses $1,225,000 $1,225,000 Management LER (Contribution Margin/Mgmt. Labor) $2.47 $2.47 Net Operating Income $625,000 $625,000 Overall LER (Contribution Margin/Total Labor) $1.63 $1.63

Other Income/Expenses: Depreciation $75,000 $75,000 Interest Expense $25,000 $25,000 Total Other Income/Expenses $100,000 $100,000 Total Pre-Tax Net Income $525,000 $525,000 as a % of Revenue 2.63% 14.00% as a % of Gross Margin 18.42% 18.42%

Sim

ple

Num

ber P

&L

View

www.SimpleNumbers.me

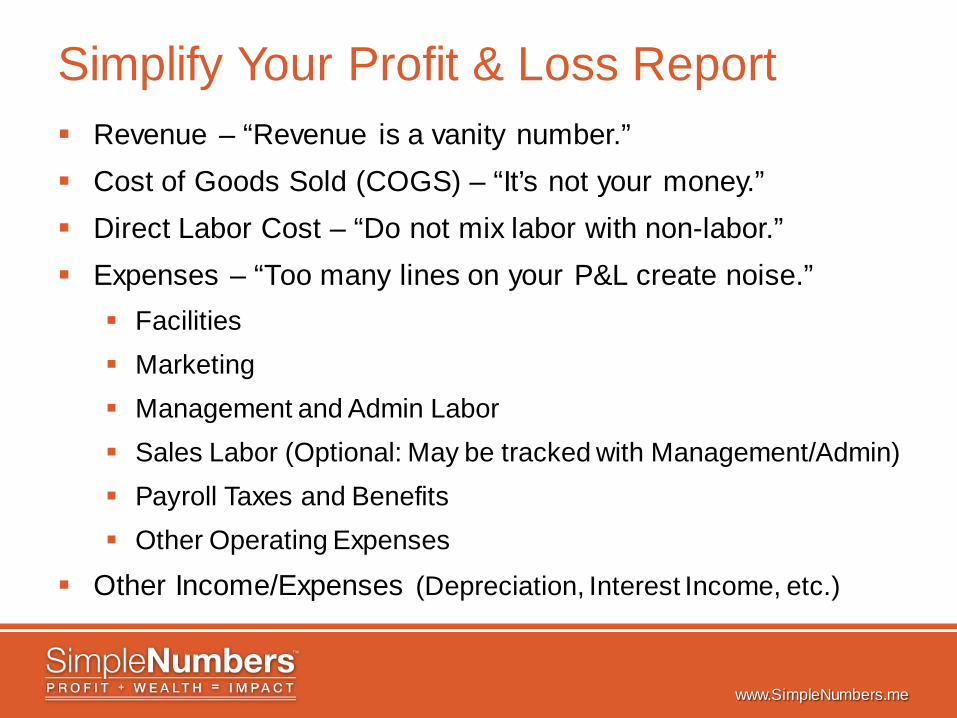

Simplify Your Profit & Loss Report Revenue – “Revenue is a vanity number.” Cost of Goods Sold (COGS) – “It’s not your money.” Direct Labor Cost – “Do not mix labor with non-labor.” Expenses – “Too many lines on your P&L create noise.” Facilities Marketing Management and Admin Labor Sales Labor (Optional: May be tracked with Management/Admin) Payroll Taxes and Benefits Other Operating Expenses

Other Income/Expenses (Depreciation, Interest Income, etc.)

www.SimpleNumbers.me

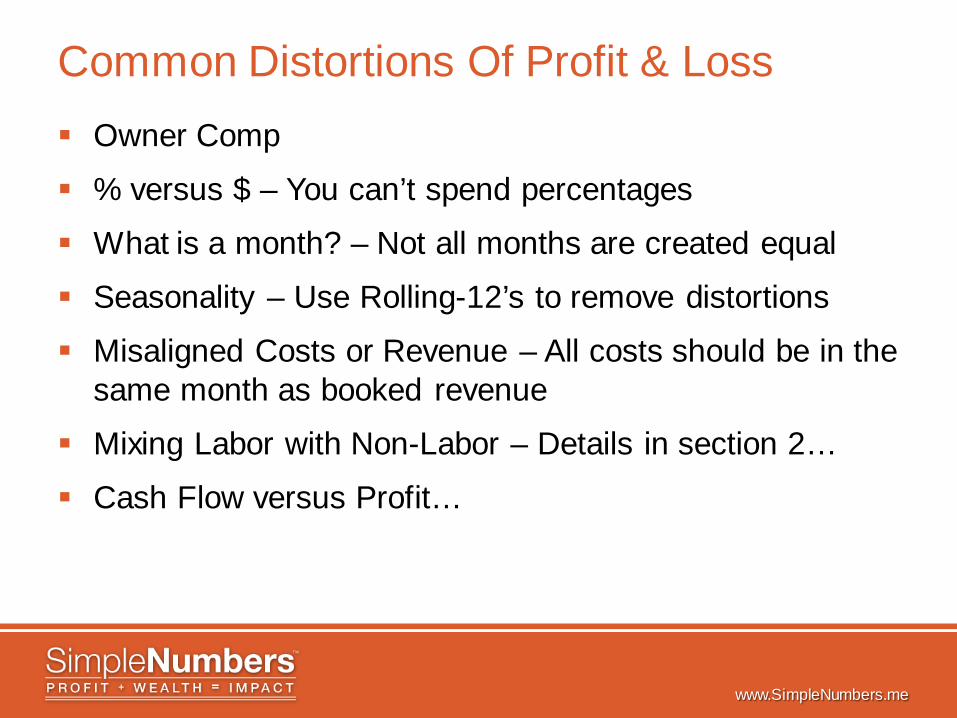

Common Distortions Of Profit & Loss Owner Comp

% versus $ – You can’t spend percentages

What is a month? – Not all months are created equal

Seasonality – Use Rolling-12’s to remove distortions

Misaligned Costs or Revenue – All costs should be in the same month as booked revenue

Mixing Labor with Non-Labor – Details in section 2…

Cash Flow versus Profit…

www.SimpleNumbers.me

#1: Remove Distortions – Action Items

Simplify your P&L

Accurately report Owner Compensation

Focus on the “true” numbers: Gross Margin

Contribution Margin

The right pre-tax Profit Margin

View financials in Rolling-12’s

Understand what “paying taxes” really means

www.SimpleNumbers.me

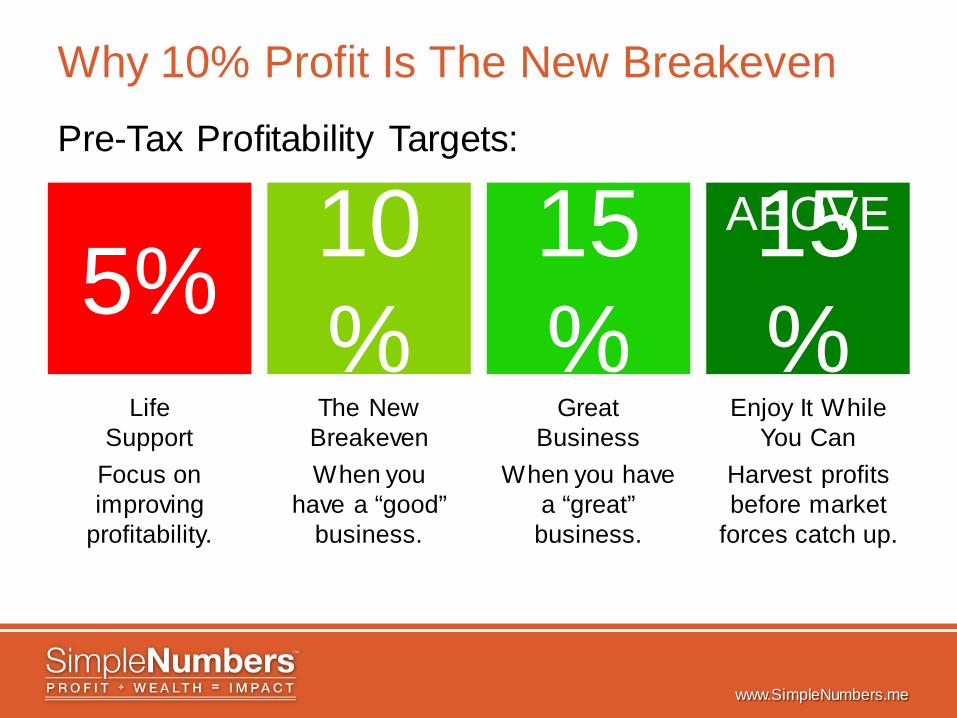

Why 10% Profit Is The New Breakeven Pre-Tax Profitability Targets:

Life Support

Focus on improving

profitability.

The New Breakeven When you

have a “good” business.

Great Business

When you have a “great”

business.

Enjoy It While You Can

Harvest profits before market

forces catch up.

5% 10%

15%

15%

ABOVE

www.SimpleNumbers.me

Cash Flow Versus Profit Chart Chart is based on the following assumptions: Profit levels shown: 5%, 10%, and 15%

Revenue at $100,000 per month

Tax Rate 40%

A service-based business that bills at the end of the month and gets paid in an average of 45 days

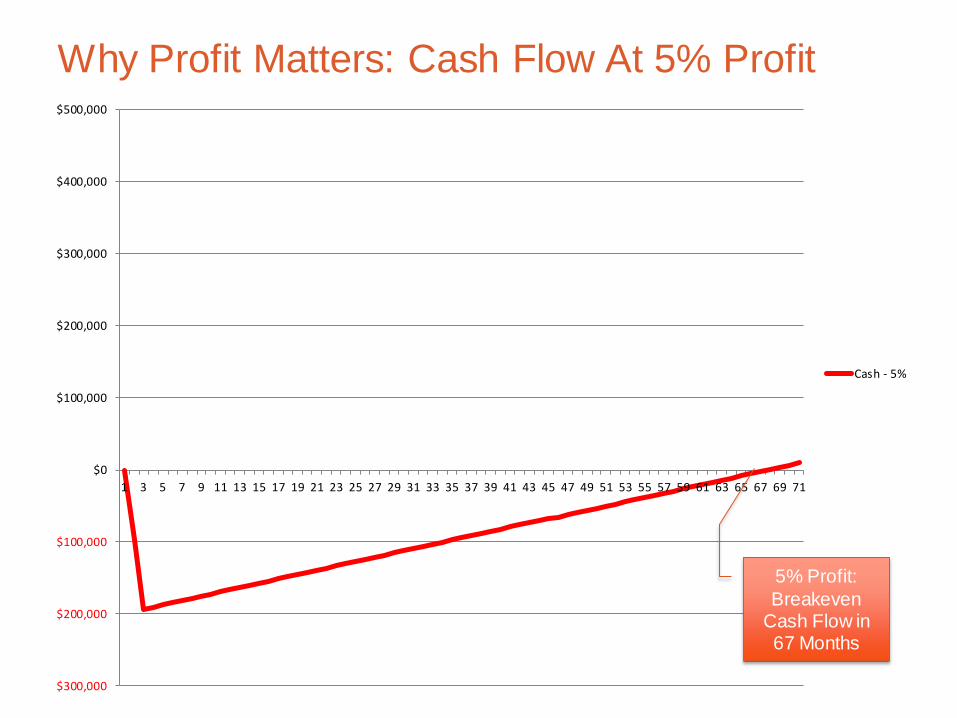

Why Profit Matters: Cash Flow At 5% Profit

$300,000

$200,000

$100,000

$0

$100,000

$200,000

$300,000

$400,000

$500,000

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29 31 33 35 37 39 41 43 45 47 49 51 53 55 57 59 61 63 65 67 69 71

Cash - 5%

Cash - 10%

Cash - 15%

5% Profit: Breakeven

Cash Flow in 67 Months

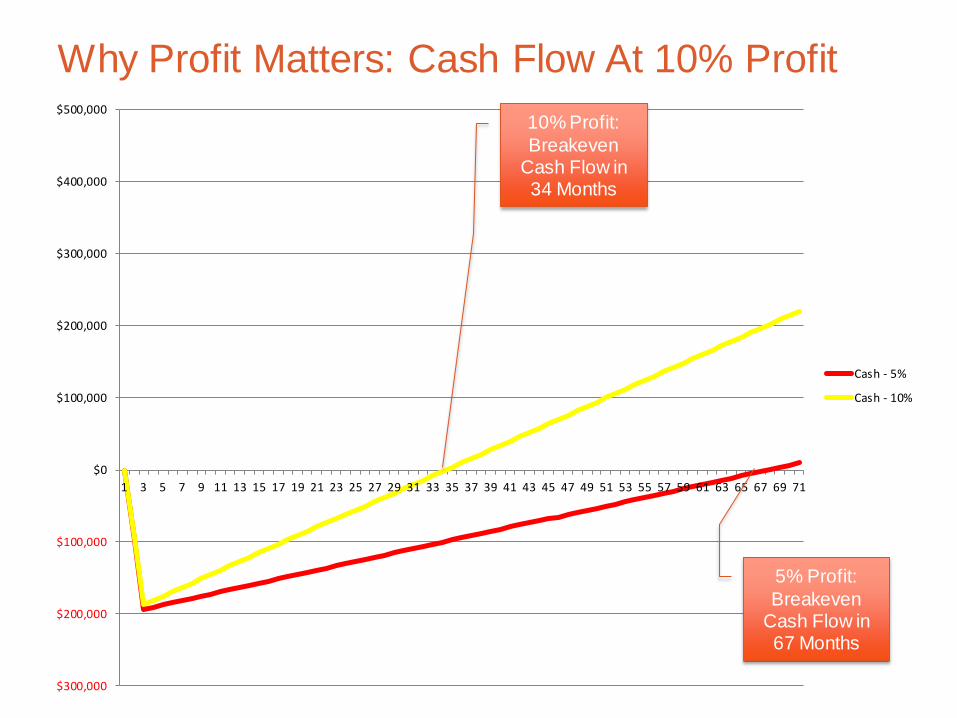

Why Profit Matters: Cash Flow At 10% Profit

$300,000

$200,000

$100,000

$0

$100,000

$200,000

$300,000

$400,000

$500,000

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29 31 33 35 37 39 41 43 45 47 49 51 53 55 57 59 61 63 65 67 69 71

Cash - 5%

Cash - 10%

Cash - 15%

5% Profit: Breakeven

Cash Flow in 67 Months

10% Profit: Breakeven

Cash Flow in 34 Months

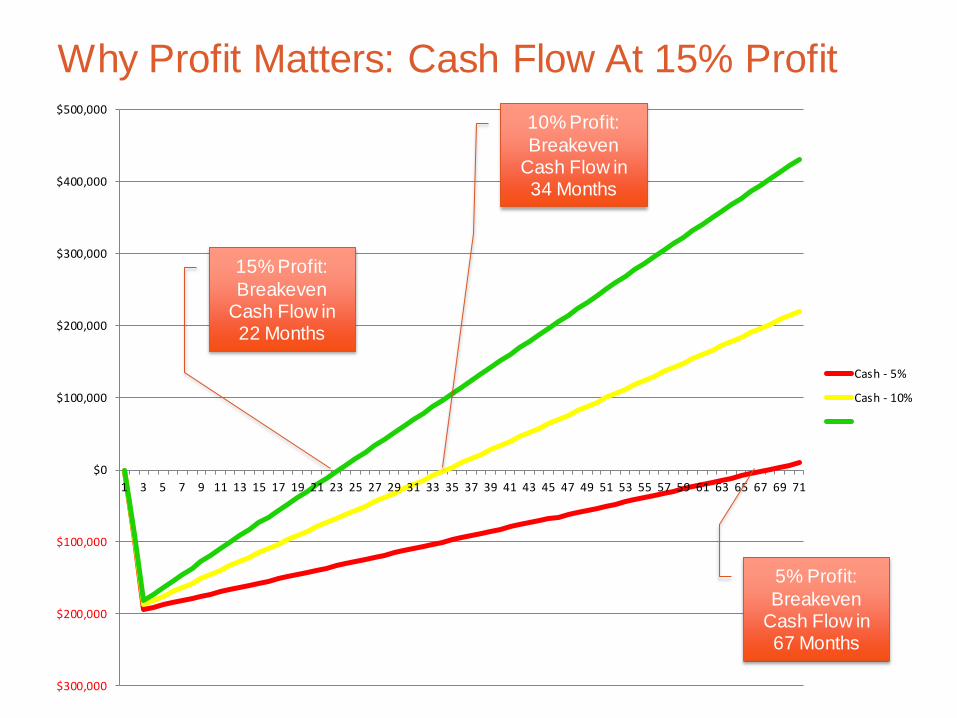

Why Profit Matters: Cash Flow At 15% Profit

$300,000

$200,000

$100,000

$0

$100,000

$200,000

$300,000

$400,000

$500,000

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29 31 33 35 37 39 41 43 45 47 49 51 53 55 57 59 61 63 65 67 69 71

Cash - 5%

Cash - 10%

Cash - 15%

5% Profit: Breakeven

Cash Flow in 67 Months

10% Profit: Breakeven

Cash Flow in 34 Months

15% Profit: Breakeven

Cash Flow in 22 Months

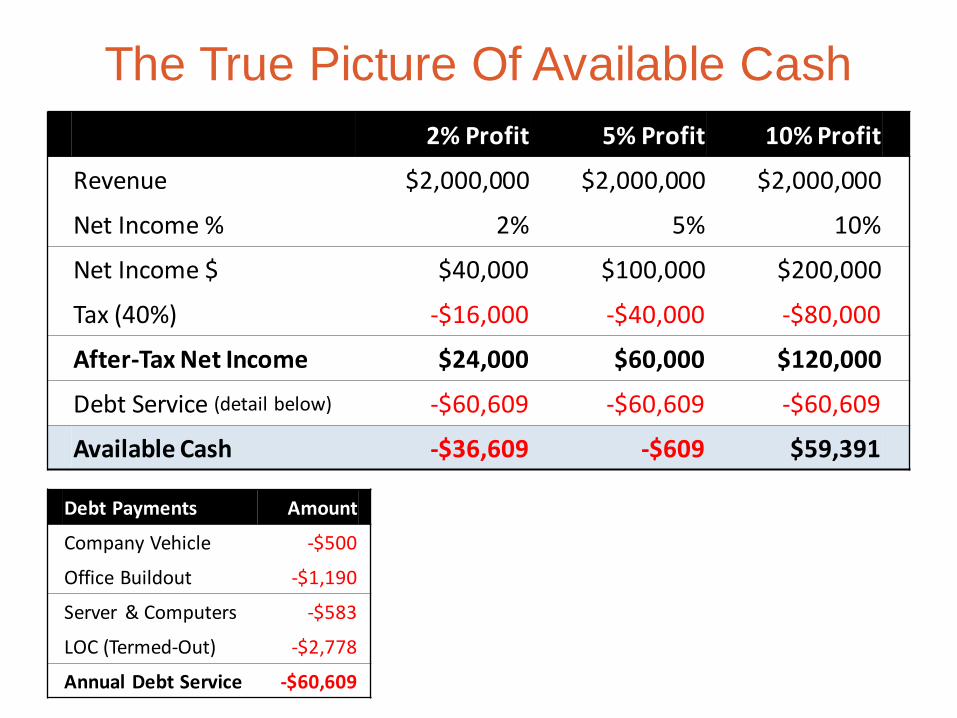

The True Picture Of Available Cash 2% Profit 5% Profit 10% Profit

Revenue $2,000,000 $2,000,000 $2,000,000

Net Income % 2% 5% 10%

Net Income $ $40,000 $100,000 $200,000

Tax (40%) -$16,000 -$40,000 -$80,000

After-Tax Net Income $24,000 $60,000 $120,000

Debt Service (detail below) -$60,609 -$60,609 -$60,609

Available Cash -$36,609 -$609 $59,391

Debt Payments Amount

Company Vehicle -$500

Office Buildout -$1,190

Server & Computers -$583

LOC (Termed-Out) -$2,778

Annual Debt Service -$60,609

www.SimpleNumbers.me

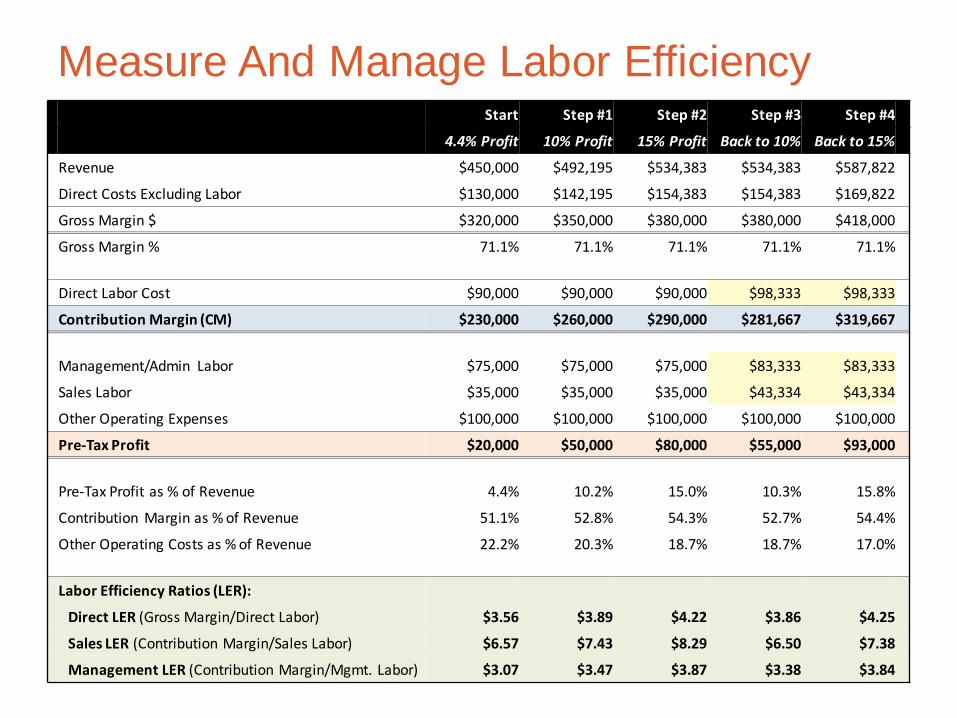

Getting To 15% Pre-Tax Profit Know your current capacity

Being profitable and maintaining market share can be better than growth

Remember that 10% is the new breakeven Use the “baffle” concept to grow to 15% profit

before increasing labor cost

Start Step #1 Step #2 Step #3 Step #4

4.4% Profit 10% Profit 15% Profit Back to 10% Back to 15%

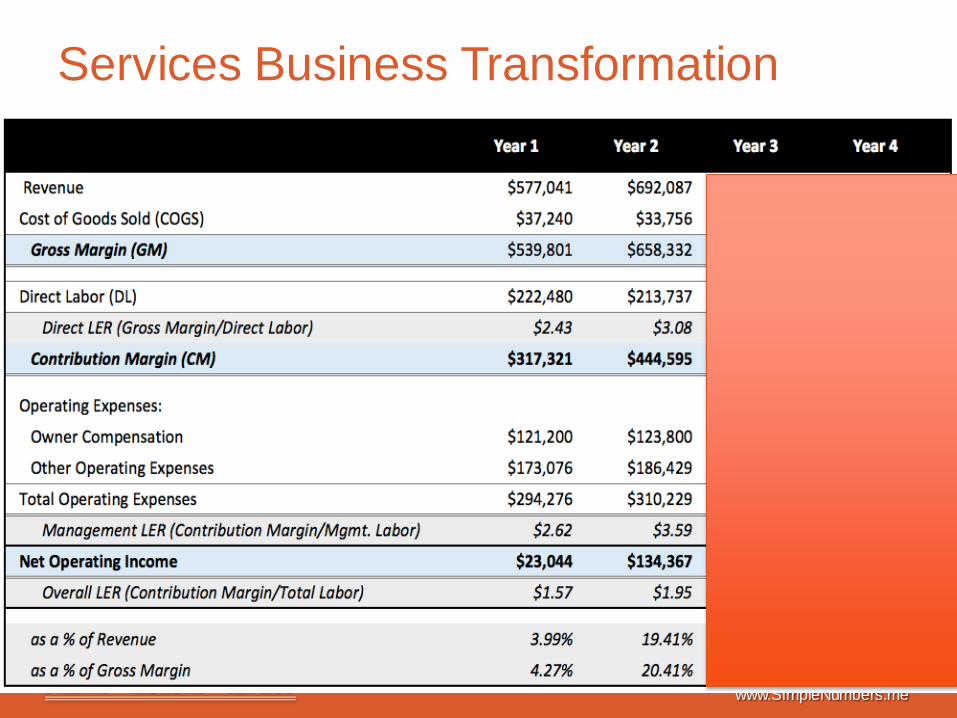

Revenue $450,000 $492,195 $534,383 $534,383 $587,822

Direct Costs Excluding Labor $130,000 $142,195 $154,383 $154,383 $169,822

Gross Margin $ $320,000 $350,000 $380,000 $380,000 $418,000

Gross Margin % 71.1% 71.1% 71.1% 71.1% 71.1% Direct Labor Cost $90,000 $90,000 $90,000 $98,333 $98,333

Contribution Margin (CM) $230,000 $260,000 $290,000 $281,667 $319,667 Management/Admin Labor $75,000 $75,000 $75,000 $83,333 $83,333

Sales Labor $35,000 $35,000 $35,000 $43,334 $43,334

Other Operating Expenses $100,000 $100,000 $100,000 $100,000 $100,000

Pre-Tax Profit $20,000 $50,000 $80,000 $55,000 $93,000 Pre-Tax Profit as % of Revenue 4.4% 10.2% 15.0% 10.3% 15.8%

Contribution Margin as % of Revenue 51.1% 52.8% 54.3% 52.7% 54.4%

Other Operating Costs as % of Revenue 22.2% 20.3% 18.7% 18.7% 17.0% Labor Efficiency Ratios (LER):

Direct LER (Gross Margin/Direct Labor) $3.56 $3.89 $4.22 $3.86 $4.25

Sales LER (Contribution Margin/Sales Labor) $6.57 $7.43 $8.29 $6.50 $7.38

Management LER (Contribution Margin/Mgmt. Labor) $3.07 $3.47 $3.87 $3.38 $3.84

Measure And Manage Labor Efficiency

www.SimpleNumbers.me

#2: Labor Productivity How are you measuring and improving your labor productivity?

www.SimpleNumbers.me

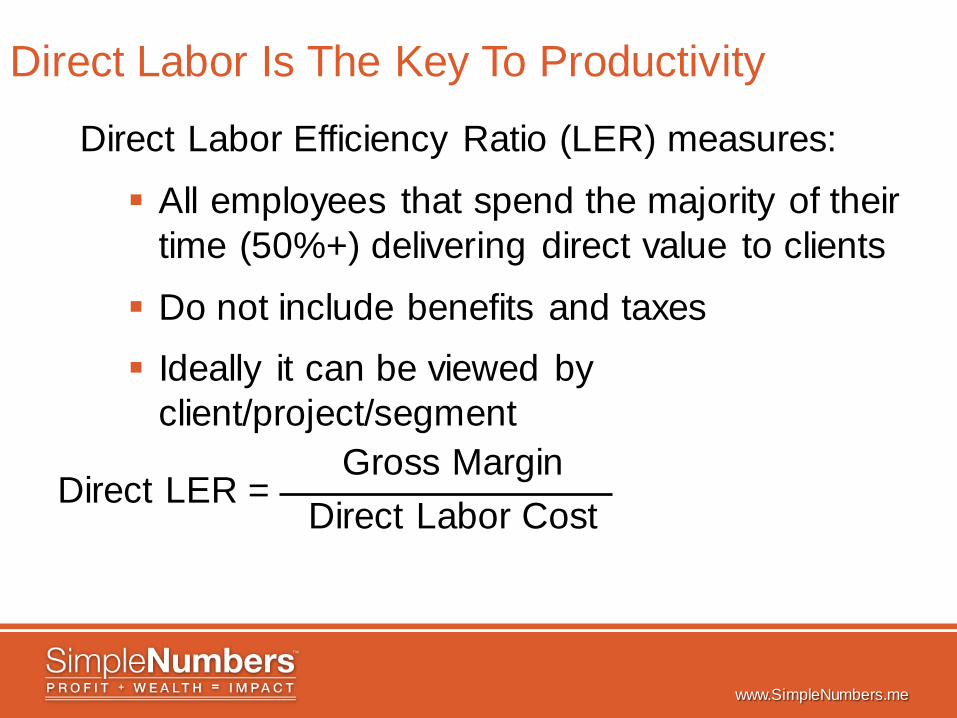

Direct Labor Is The Key To Productivity

Direct Labor Efficiency Ratio (LER) measures:

All employees that spend the majority of their time (50%+) delivering direct value to clients

Do not include benefits and taxes Ideally it can be viewed by

client/project/segment Gross Margin

Direct Labor Cost

Direct LER =

www.SimpleNumbers.me

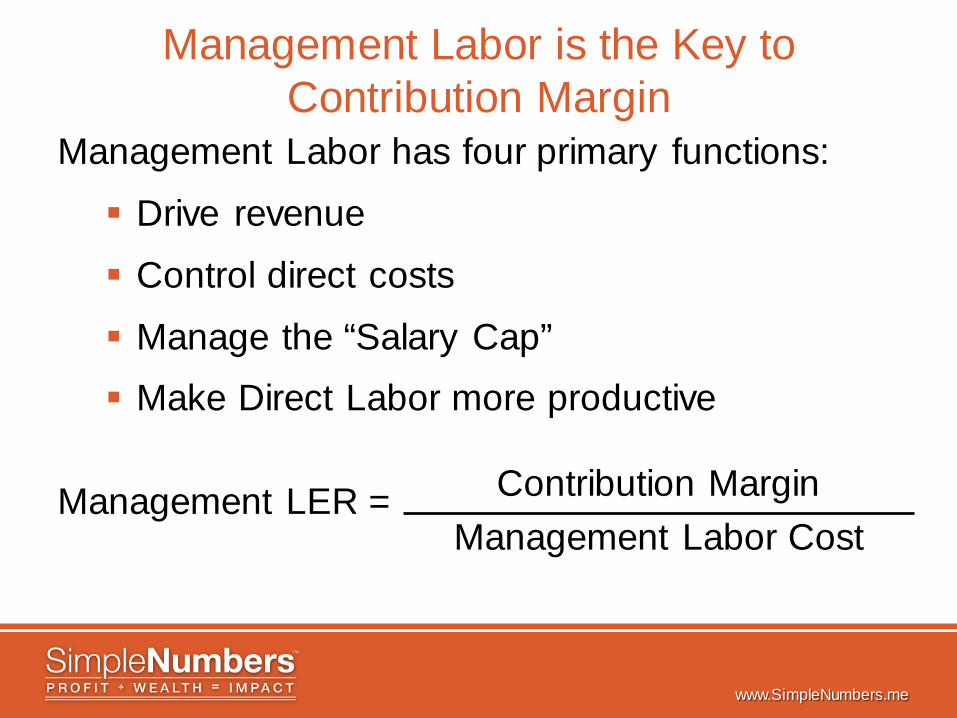

Management Labor is the Key to Contribution Margin

Management Labor has four primary functions:

Drive revenue

Control direct costs

Manage the “Salary Cap” Make Direct Labor more productive

Contribution Margin Management Labor Cost

Management LER =

www.SimpleNumbers.me

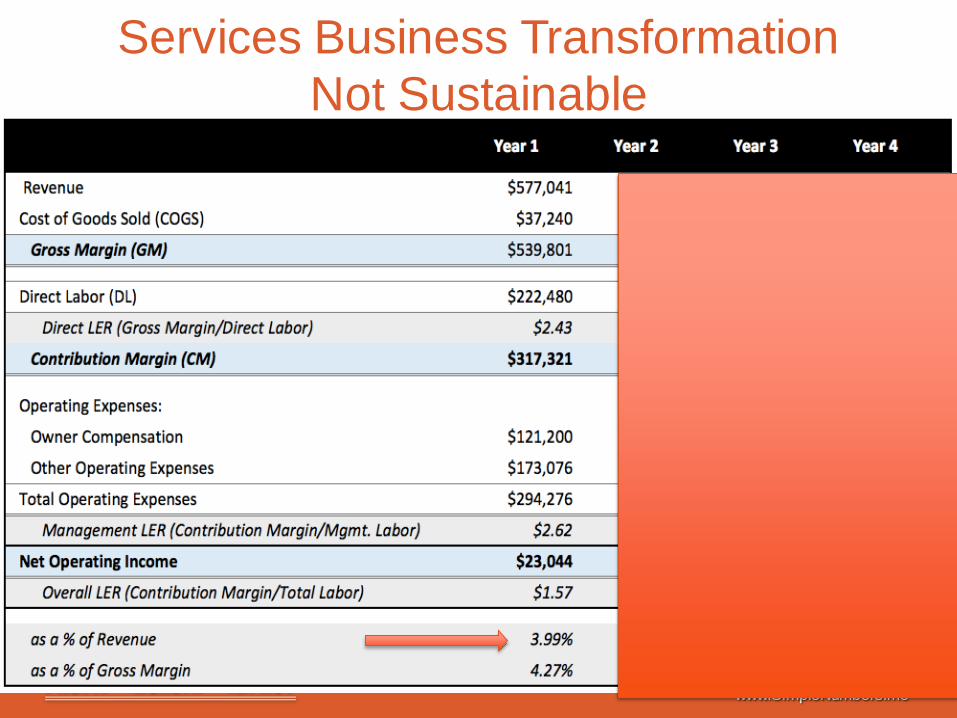

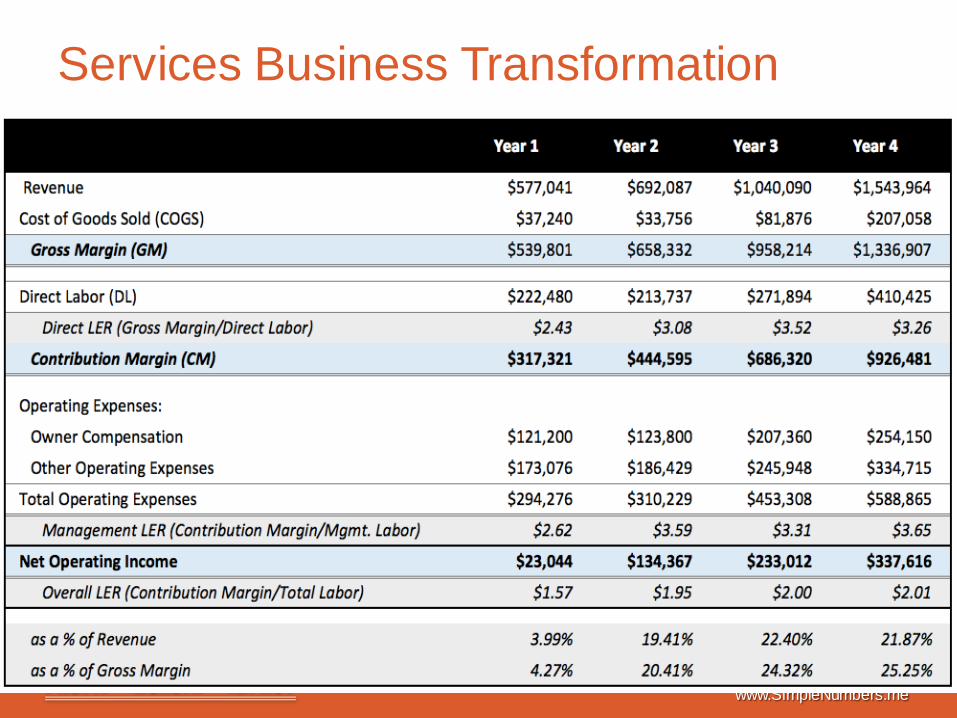

Services Business Transformation Not Sustainable

www.SimpleNumbers.me

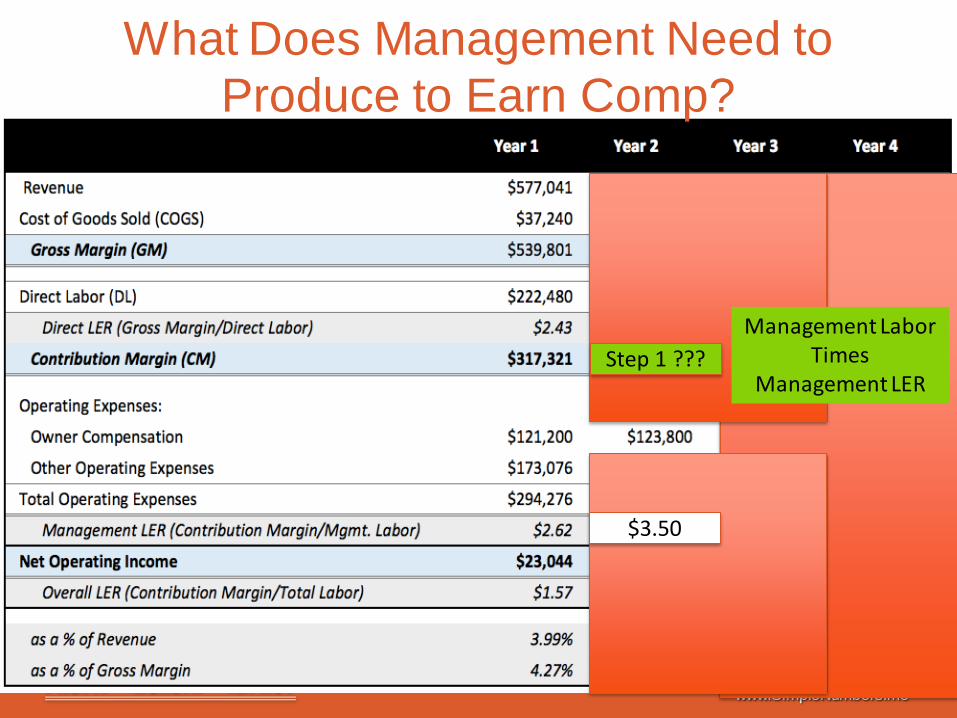

What Does Management Need to Produce to Earn Comp?

$3.50

Step 1 ??? Management Labor

Times Management LER

www.SimpleNumbers.me

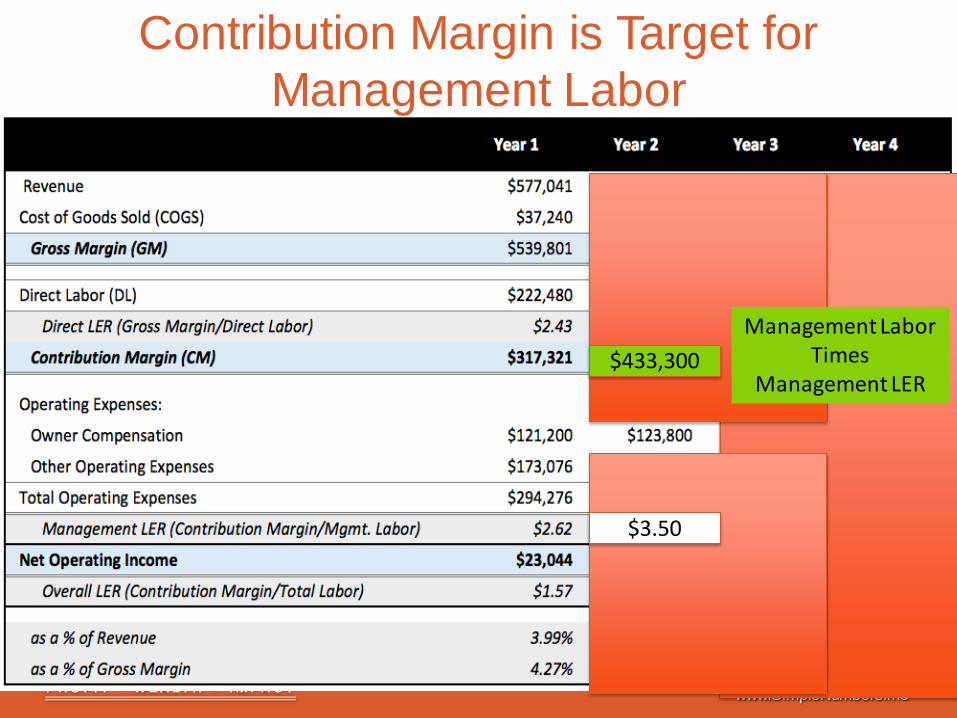

Contribution Margin is Target for Management Labor

$3.50

Management Labor Times

Management LER $433,300

www.SimpleNumbers.me

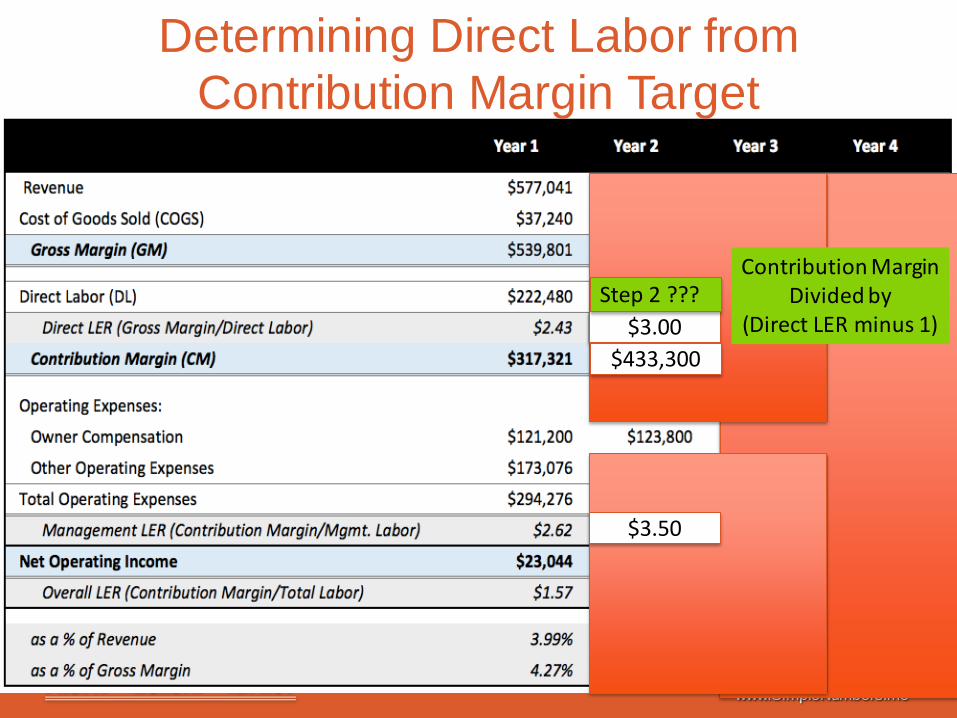

Determining Direct Labor from Contribution Margin Target

$3.50

$3.00 Step 2 ???

$433,300

Contribution Margin Divided by

(Direct LER minus 1)

www.SimpleNumbers.me

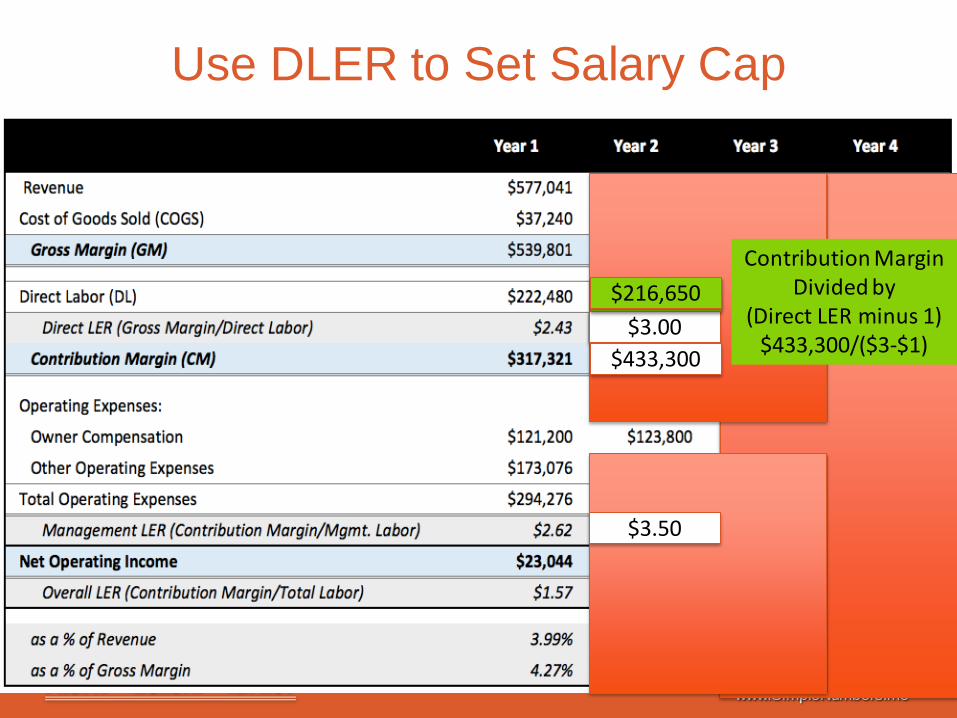

Use DLER to Set Salary Cap

$3.50

$3.00 Step 2 ???

$433,300

Contribution Margin Divided by

(Direct LER minus 1) $433,300/($3-$1)

$216,650

www.SimpleNumbers.me

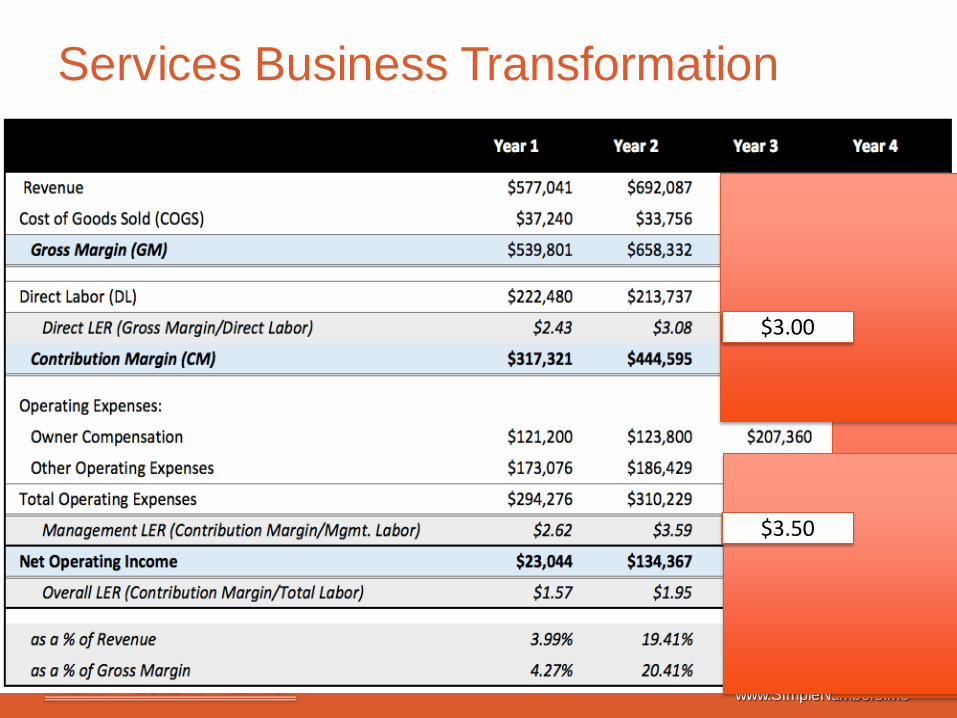

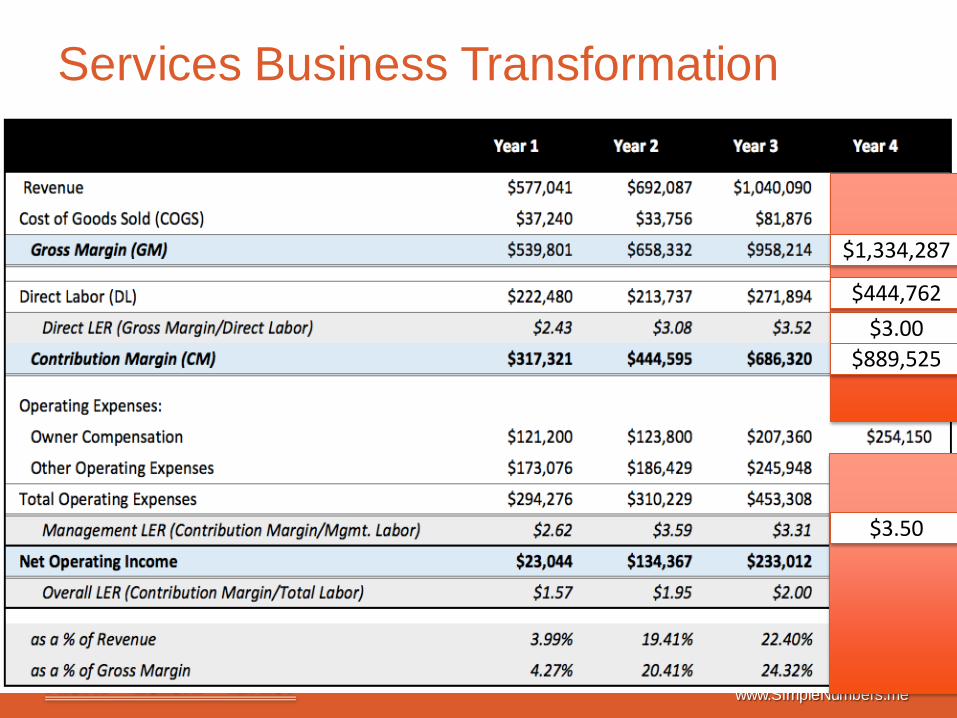

Services Business Transformation

$3.50

$3.00

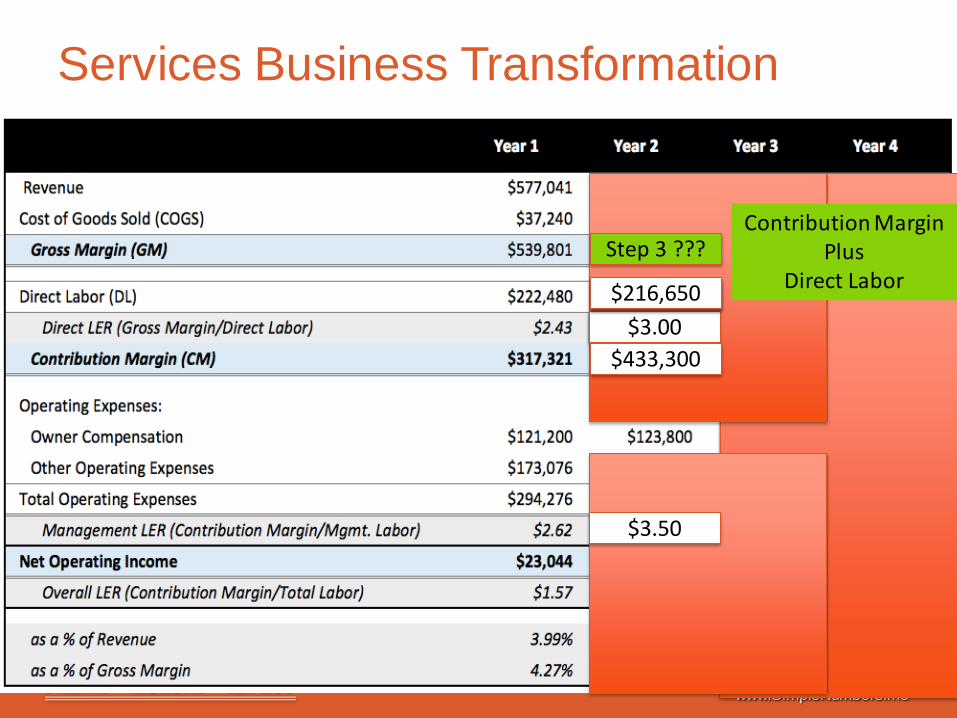

Step 3 ???

$433,300

$216,650 $216,650

Contribution Margin Plus

Direct Labor

www.SimpleNumbers.me

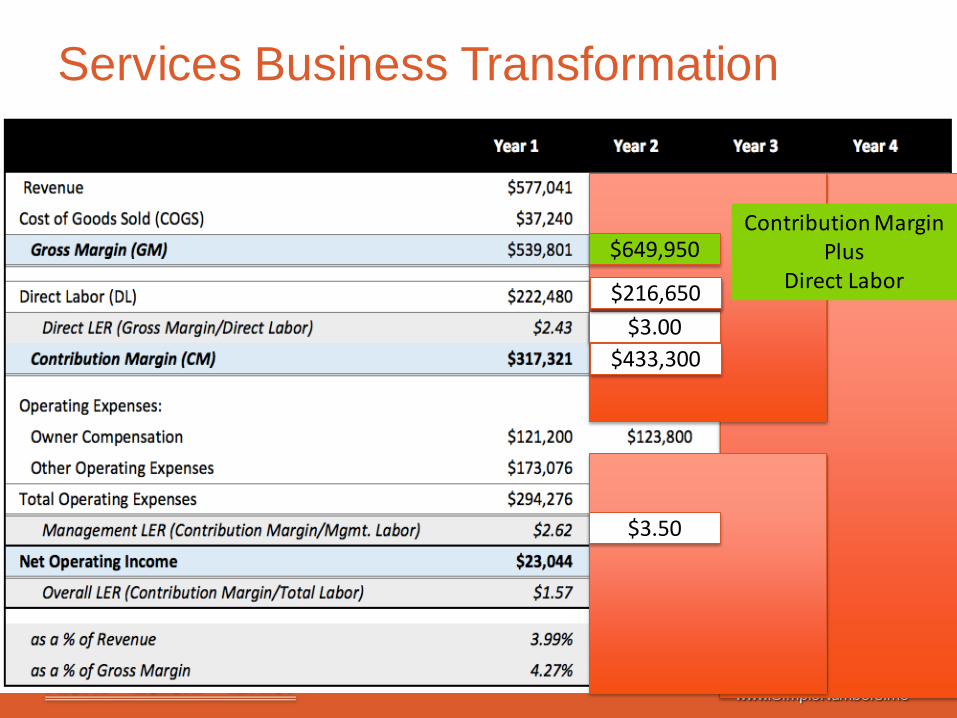

Services Business Transformation

$3.50

$3.00 $433,300

$216,650 $216,650

Contribution Margin Plus

Direct Labor $649,950

www.SimpleNumbers.me

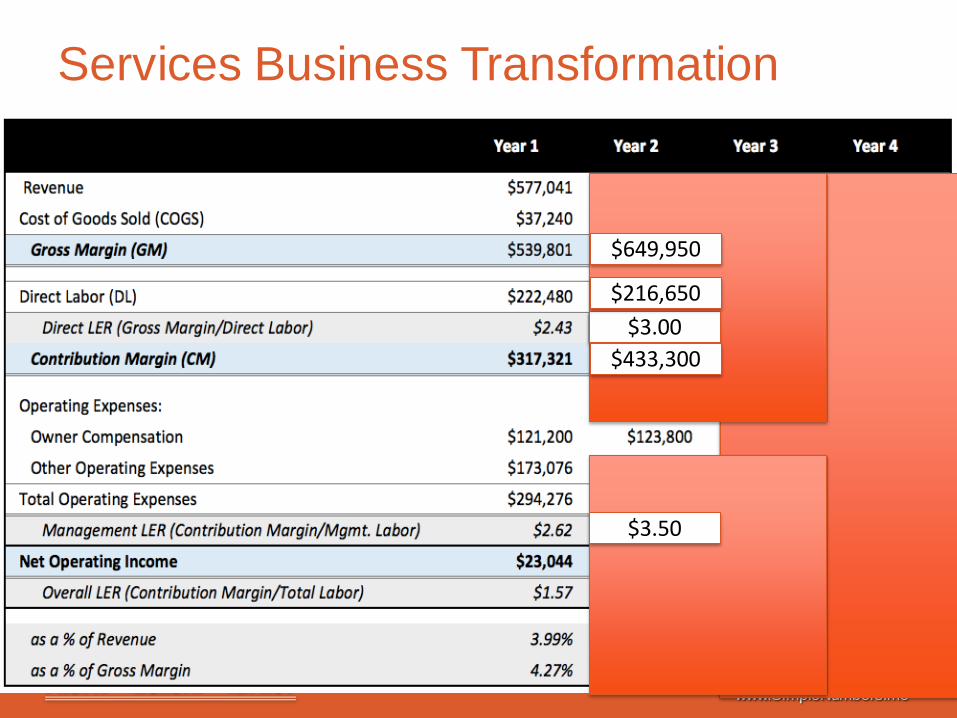

Services Business Transformation

$3.50

$3.00

$649,950

$433,300

$216,650

www.SimpleNumbers.me

Services Business Transformation

www.SimpleNumbers.me

Services Business Transformation

$3.50

$3.00

www.SimpleNumbers.me

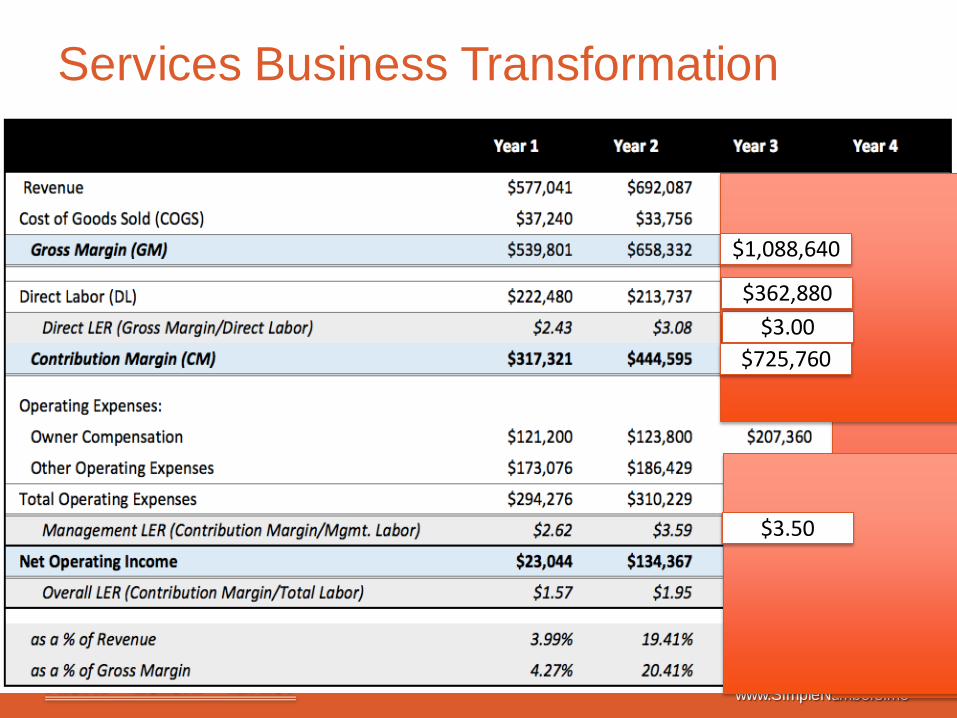

Services Business Transformation

$3.50

$3.00

$1,088,640

$725,760

$362,880

www.SimpleNumbers.me

Services Business Transformation

www.SimpleNumbers.me

Services Business Transformation

$3.50

$3.00

www.SimpleNumbers.me

Services Business Transformation

$3.50

$3.00

$1,334,287

$889,525

$444,762

www.SimpleNumbers.me

Services Business Transformation

www.SimpleNumbers.me

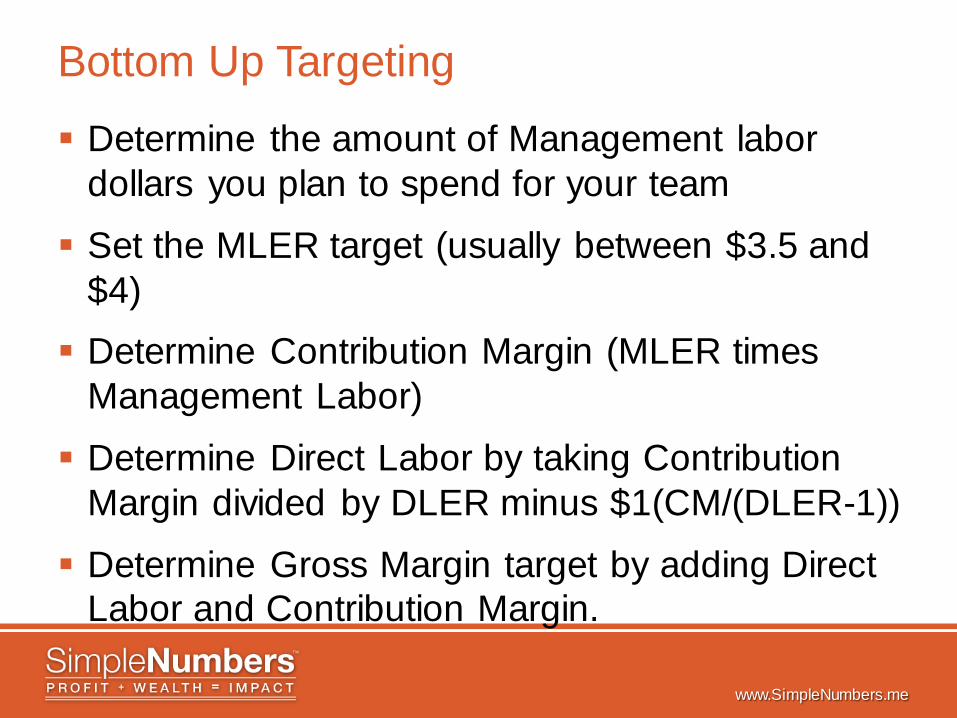

Bottom Up Targeting

Determine the amount of Management labor dollars you plan to spend for your team

Set the MLER target (usually between $3.5 and $4) Determine Contribution Margin (MLER times

Management Labor)

Determine Direct Labor by taking Contribution Margin divided by DLER minus $1(CM/(DLER-1))

Determine Gross Margin target by adding Direct Labor and Contribution Margin.

www.SimpleNumbers.me

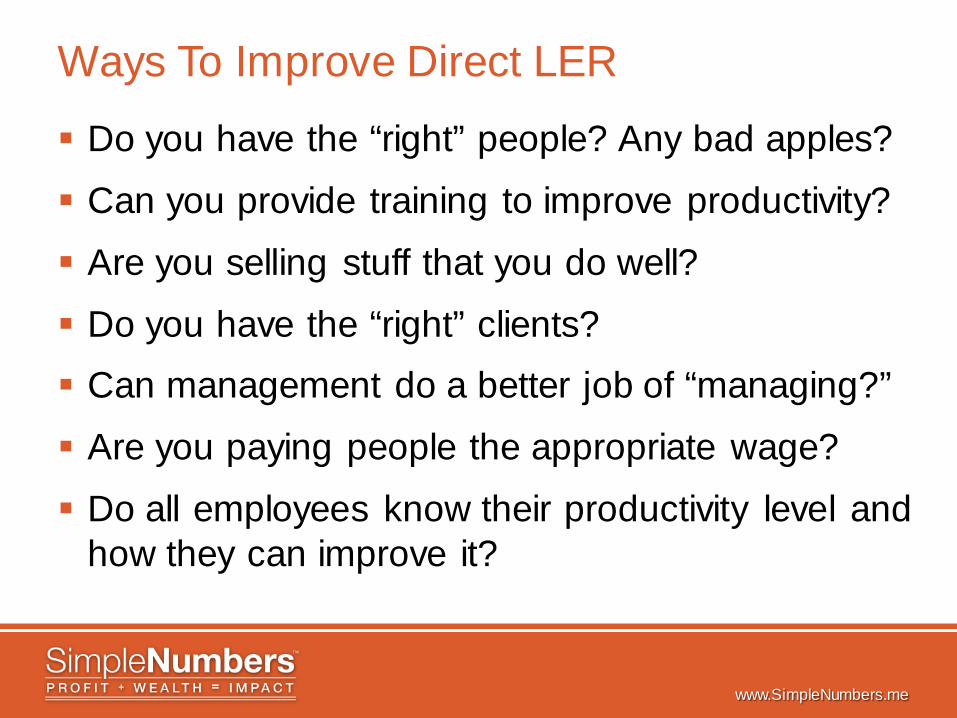

Ways To Improve Direct LER

Do you have the “right” people? Any bad apples?

Can you provide training to improve productivity?

Are you selling stuff that you do well?

Do you have the “right” clients? Can management do a better job of “managing?”

Are you paying people the appropriate wage?

Do all employees know their productivity level and how they can improve it?

www.SimpleNumbers.me

Ways To Improve Management LER

Communicate the Contribution Margin target that justifies Management Team comp.

No “Cousin Eddie” roles

Build Management Team one key hire at a time Evaluate “blended roles” so that management is

not staying “busy” with low value roles to avoid the high value tasks

Invest in training, daily huddles and feedback processes

www.SimpleNumbers.me

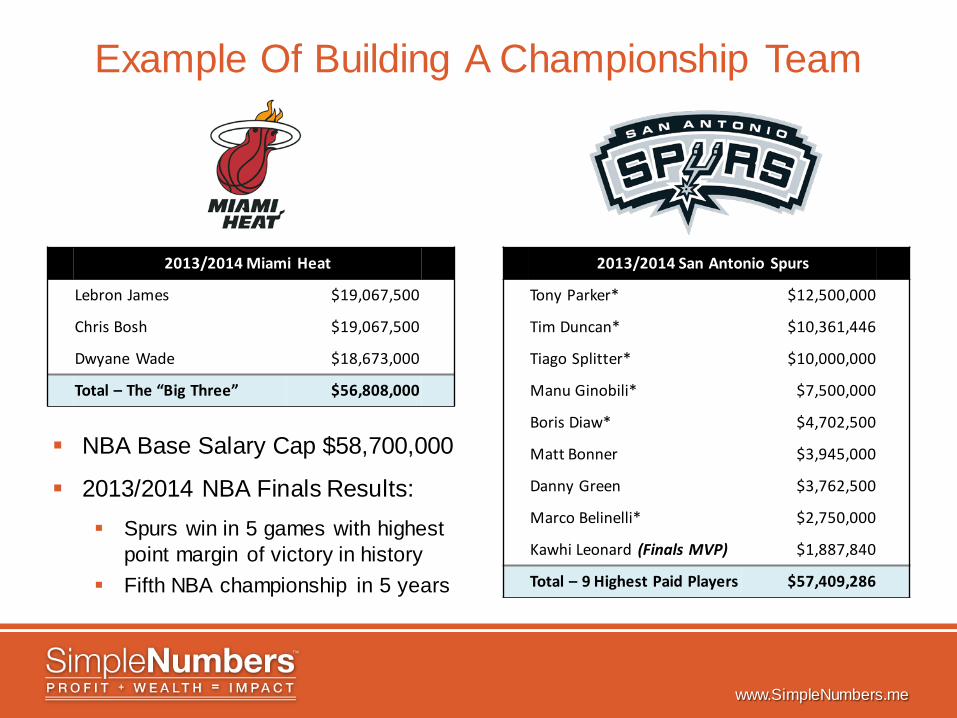

Example Of Building A Championship Team

NBA Base Salary Cap $58,700,000

2013/2014 NBA Finals Results: Spurs win in 5 games with highest

point margin of victory in history Fifth NBA championship in 5 years

2013/2014 Miami Heat

Lebron James $19,067,500

Chris Bosh $19,067,500

Dwyane Wade $18,673,000

Total – The “Big Three” $56,808,000

2013/2014 San Antonio Spurs

Tony Parker* $12,500,000

Tim Duncan* $10,361,446

Tiago Splitter* $10,000,000

Manu Ginobili* $7,500,000

Boris Diaw* $4,702,500

Matt Bonner $3,945,000

Danny Green $3,762,500

Marco Belinelli* $2,750,000

Kawhi Leonard (Finals MVP) $1,887,840

Total – 9 Highest Paid Players $57,409,286

www.SimpleNumbers.me

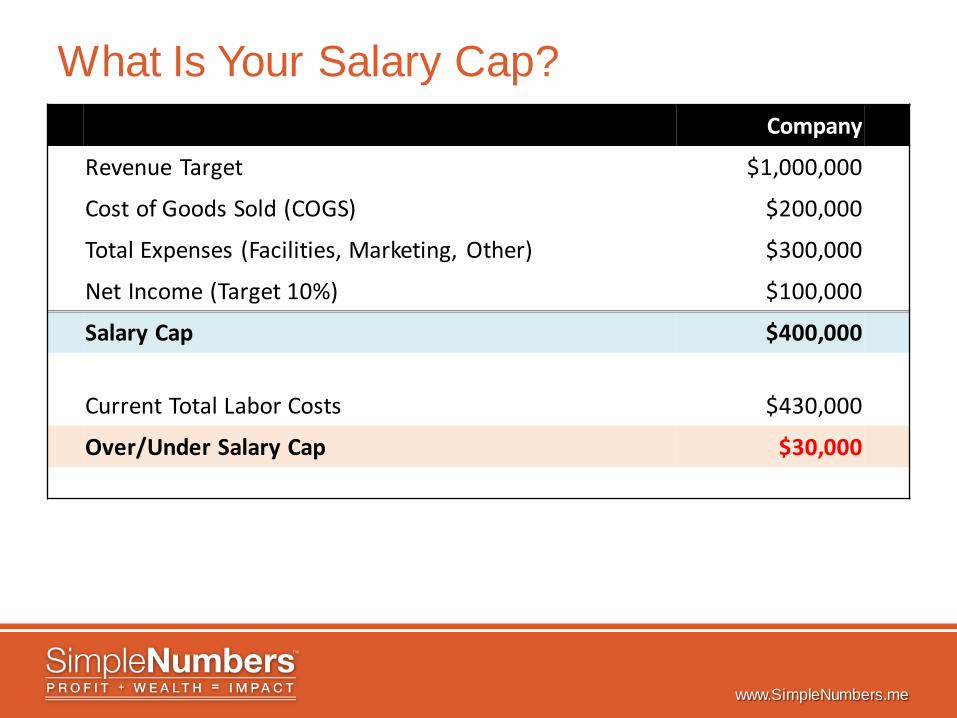

What Is Your Salary Cap? Company

Revenue Target $1,000,000

Cost of Goods Sold (COGS) $200,000

Total Expenses (Facilities, Marketing, Other) $300,000

Net Income (Target 10%) $100,000

Salary Cap $400,000 Current Total Labor Costs $430,000

Over/Under Salary Cap $30,000

www.SimpleNumbers.me

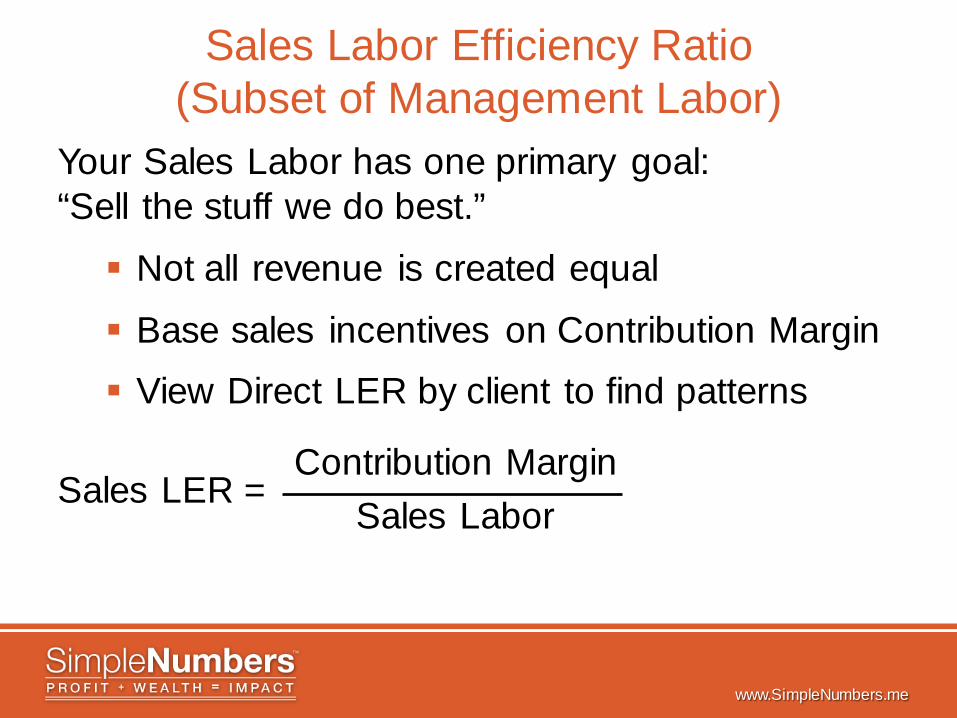

Sales Labor Efficiency Ratio (Subset of Management Labor)

Your Sales Labor has one primary goal: “Sell the stuff we do best.”

Not all revenue is created equal

Base sales incentives on Contribution Margin View Direct LER by client to find patterns

Contribution Margin Sales Labor

Sales LER =

www.SimpleNumbers.me

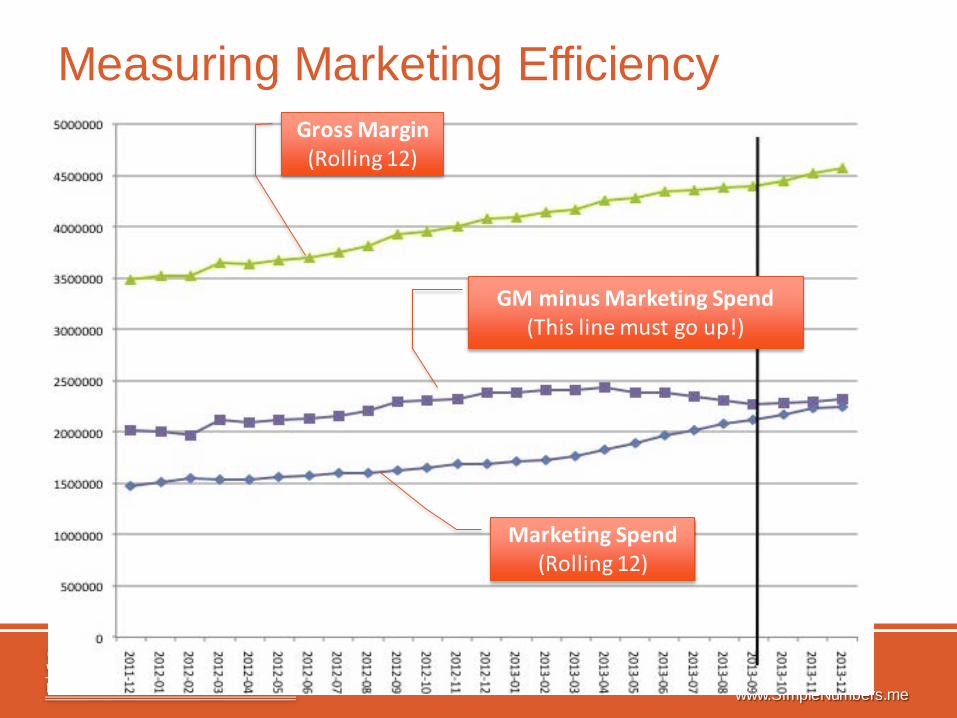

Measuring Marketing Efficiency Gross Margin

(Rolling 12)

Marketing Spend (Rolling 12)

GM minus Marketing Spend (This line must go up!)

www.SimpleNumbers.me

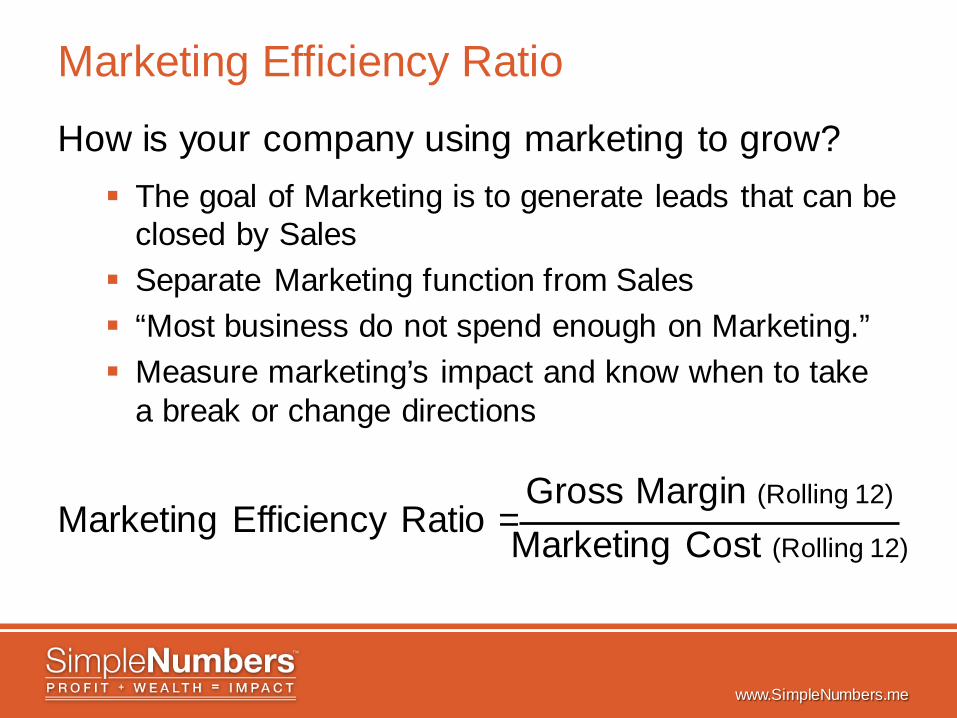

Marketing Efficiency Ratio

How is your company using marketing to grow? The goal of Marketing is to generate leads that can be

closed by Sales Separate Marketing function from Sales “Most business do not spend enough on Marketing.” Measure marketing’s impact and know when to take

a break or change directions

Gross Margin (Rolling 12)

Marketing Cost (Rolling 12)

Marketing Efficiency Ratio =

www.SimpleNumbers.me

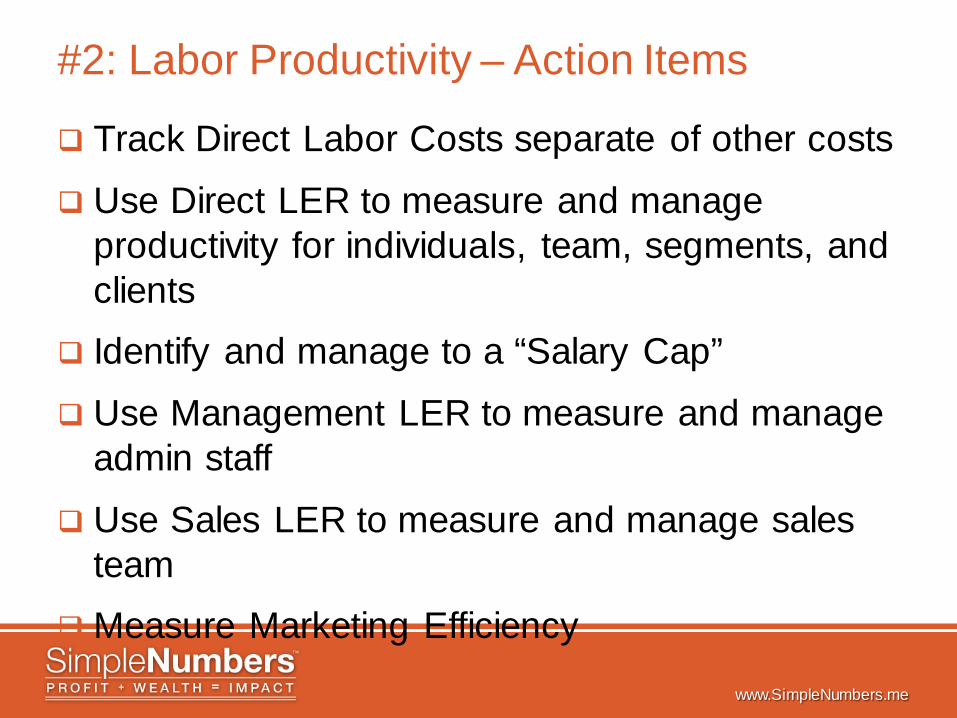

#2: Labor Productivity – Action Items

Track Direct Labor Costs separate of other costs

Use Direct LER to measure and manage productivity for individuals, team, segments, and clients

Identify and manage to a “Salary Cap”

Use Management LER to measure and manage admin staff

Use Sales LER to measure and manage sales team

Measure Marketing Efficiency

www.SimpleNumbers.me

3 Year Planning Template Start with the Big Picture Before Getting Bogged Down in the Details

www.SimpleNumbers.me

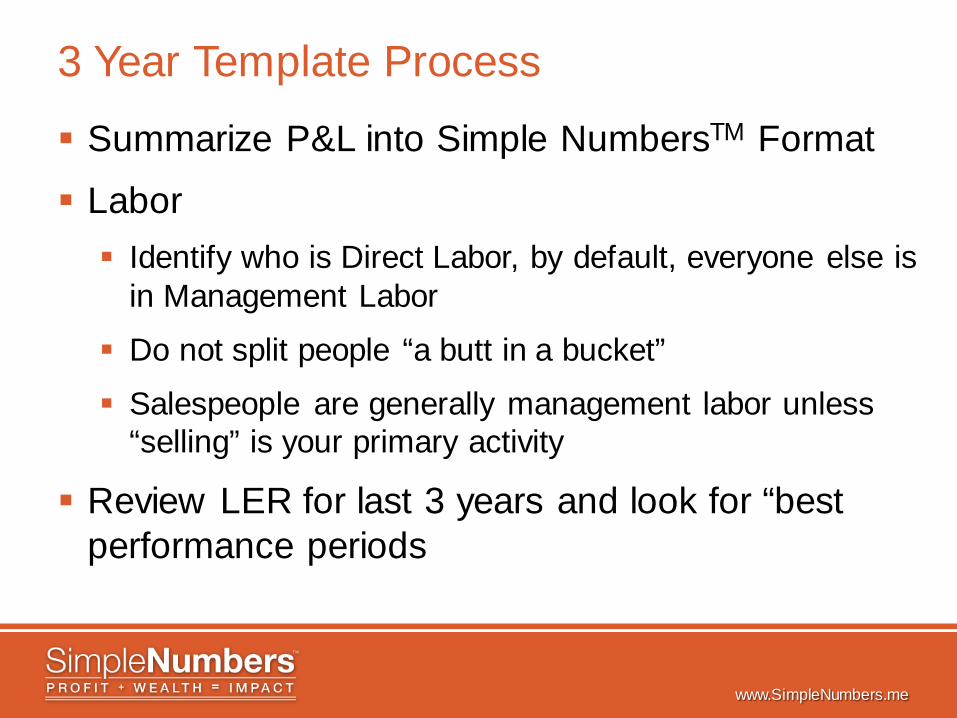

3 Year Template Process

Summarize P&L into Simple NumbersTM Format

Labor Identify who is Direct Labor, by default, everyone else is

in Management Labor

Do not split people “a butt in a bucket”

Salespeople are generally management labor unless “selling” is your primary activity

Review LER for last 3 years and look for “best performance periods

www.SimpleNumbers.me

3 Year Template Process- Continued

Forecast P&L Top Down Method Set Revenue, GM targets

Set DLER & MLER targets to then determine salary cap for both labor buckets

Bottom Up Method Set Management Labor $

Determine Contribution Margin $ Target

Set Direct LER at rate needed to cover current Direct Labor levels

www.SimpleNumbers.me

3 Year Template Process- Continued

Forecast Operating Expenses Facilities – input from historical. Typically includes rent,

utilities, repairs, telecommunications, IT

Marketing – control as a % of sales (below P&L in highlighted area

Payroll taxes and benefits – avoid combining with Labor, control as a % of all labor in highlighted area

Other Operating Expenses – the “Great Catchall” – all the noise but little you can really do about it. Forecast it as a % of Contribution Margin based on history.

www.SimpleNumbers.me

3 Year Template Process- Continued

Balance Sheet Limited to the items that really matter

Inventory – put in Other Assets if you have Inventory

Forecast A/R DSO – input days sales outstanding to drive A/R balances

Profit Distributions – only include the distributions that are not for tax coverage

Taxes – Taxes have been accounted for as “Tax Distributions”. If you pay taxes inside the company, it should represent a similar amount.

www.SimpleNumbers.me

Power of One Template From Scaling Up by Verne Harnish (original concept developed by Alan Miltz)

www.SimpleNumbers.me

Power of One Template

Gary’s Furniture Example Review the data from the Gary’s Furniture tab in relation

to the discussion in Scaling Up by Verne Harnish. This will give you a good understanding on how to use the template

LER – I have added the LER component to the original work that Alan Miltz did for Scaling Up so that you can match to the Simple Numbers P&L

Template Tab is an example of a smaller business without inventory as comparison

Blank tab is for you to input your own data

www.SimpleNumbers.me

Communicating Compensation How talk about compensation drives what you get.

www.SimpleNumbers.me

What drives performance?

Teams with unequal pay won fewer games when pay differences were not connected to performance. But they won more games when differences in pay were based on players’ contributions. Equity matters more than equality. Differences in pay aren’t a problem as long as they’re fair. When players are paid less than teammates who aren’t performing any better, jealousy, resentful, and discouragement often follow. When they’re paid less than teammates who deliver more value, they understand. Source: Adam Grant is a Wharton professor and the bestselling author of Give and Take. Sign up for his free newsletter at www.giveandtake.com

www.SimpleNumbers.me

Principles of Market Wages

Create your own “market wage scale” Compare productivity by team member if possible Evaluate teams in total performance Adjust wage scale before adjusting individual

wages No “cost of living wage adjustments” Raises based on moving up a level or scale

increase

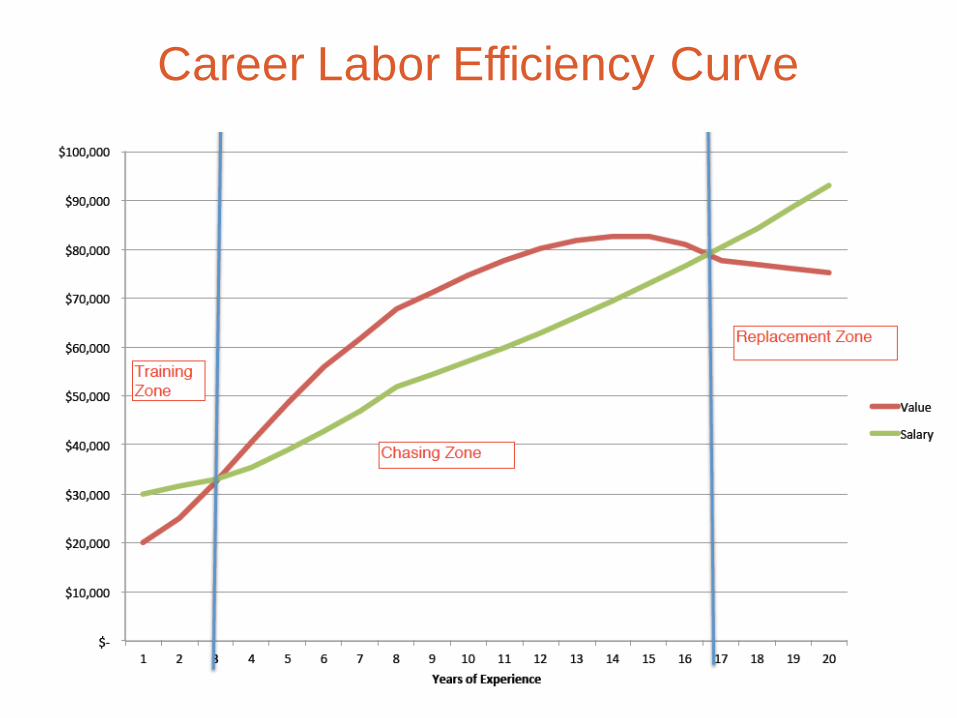

Career Labor Efficiency Curve

www.SimpleNumbers.me

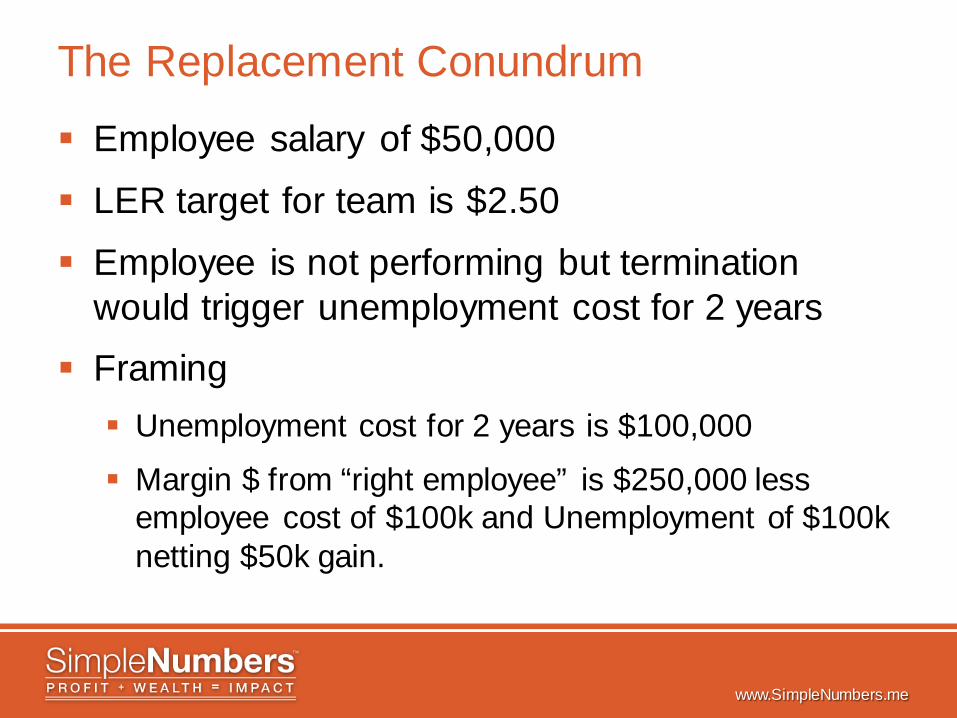

The Replacement Conundrum

Employee salary of $50,000

LER target for team is $2.50

Employee is not performing but termination would trigger unemployment cost for 2 years

Framing Unemployment cost for 2 years is $100,000

Margin $ from “right employee” is $250,000 less employee cost of $100k and Unemployment of $100k netting $50k gain.

www.SimpleNumbers.me

Incentive Compensation Incentive pay will never get you out of management and leadership of your team. Make sure your incentives are grounded in principles and ties to company output in a win/win.

www.SimpleNumbers.me

Principles of Incentives

Outcome must produce a win/win scenario Needs to be relatively simple to calculate and is

based on a true “driver” metric that can be significantly influenced by the recipient (we like contribution margin)

Establish Minimum, Target and Stretch and reset scale each year

Base Target as a % of Base pay Payout Quarterly but back end load

www.SimpleNumbers.me

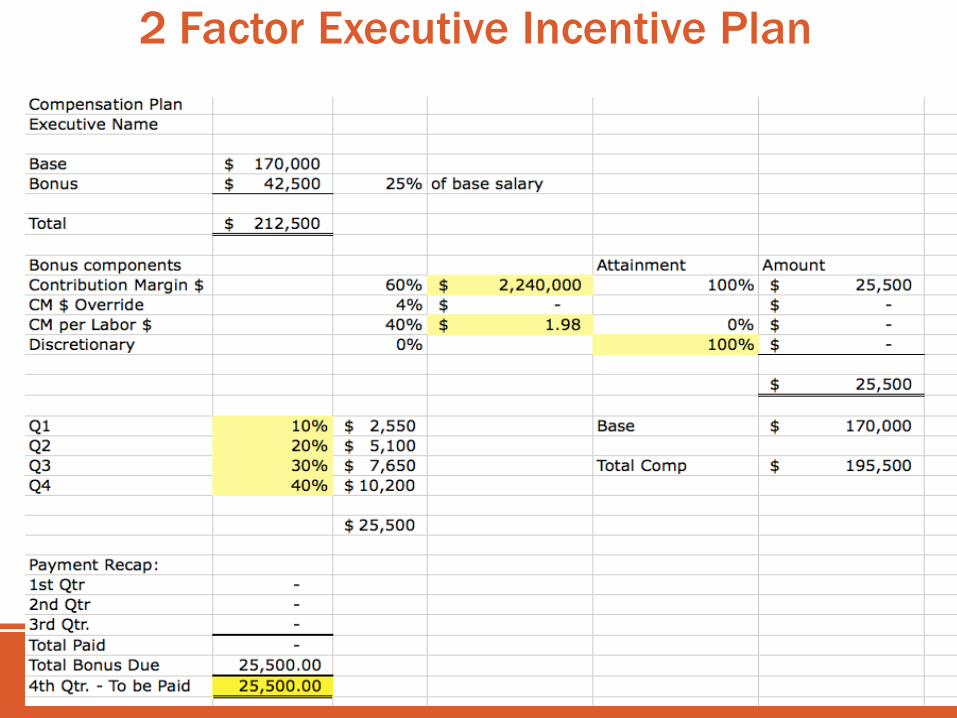

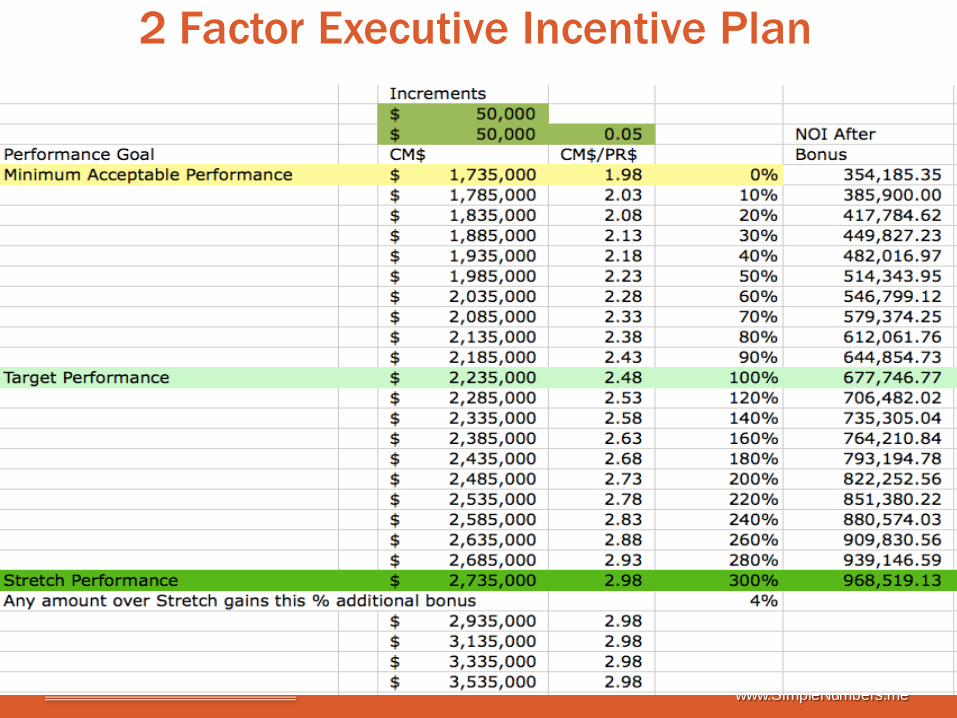

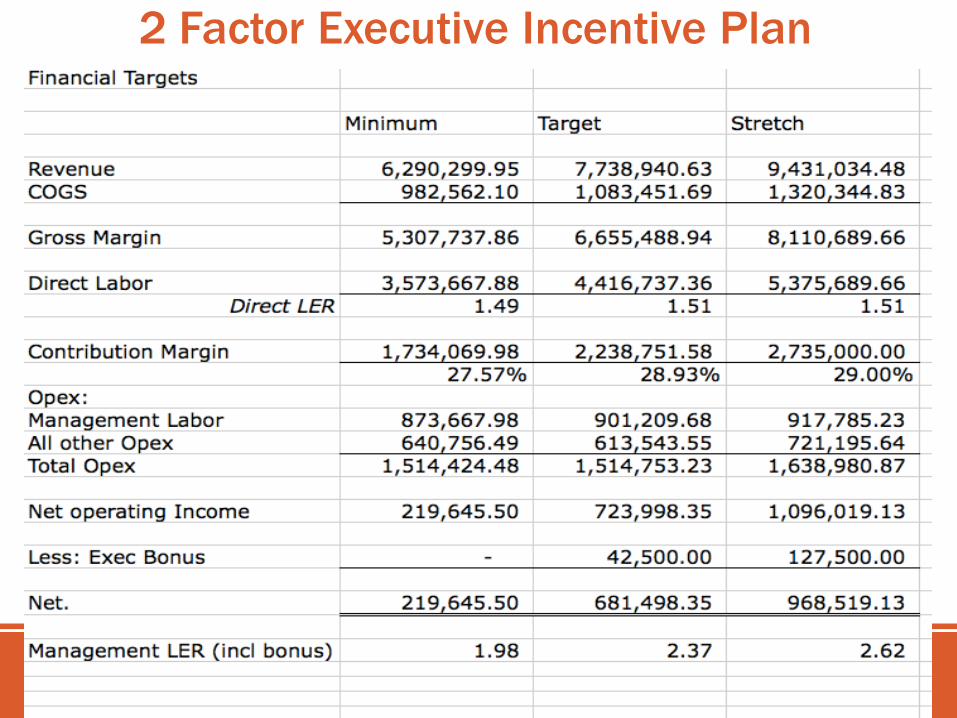

2 Factor Executive Incentive Plan

www.SimpleNumbers.me

2 Factor Executive Incentive Plan

www.SimpleNumbers.me

2 Factor Executive Incentive Plan

www.SimpleNumbers.me

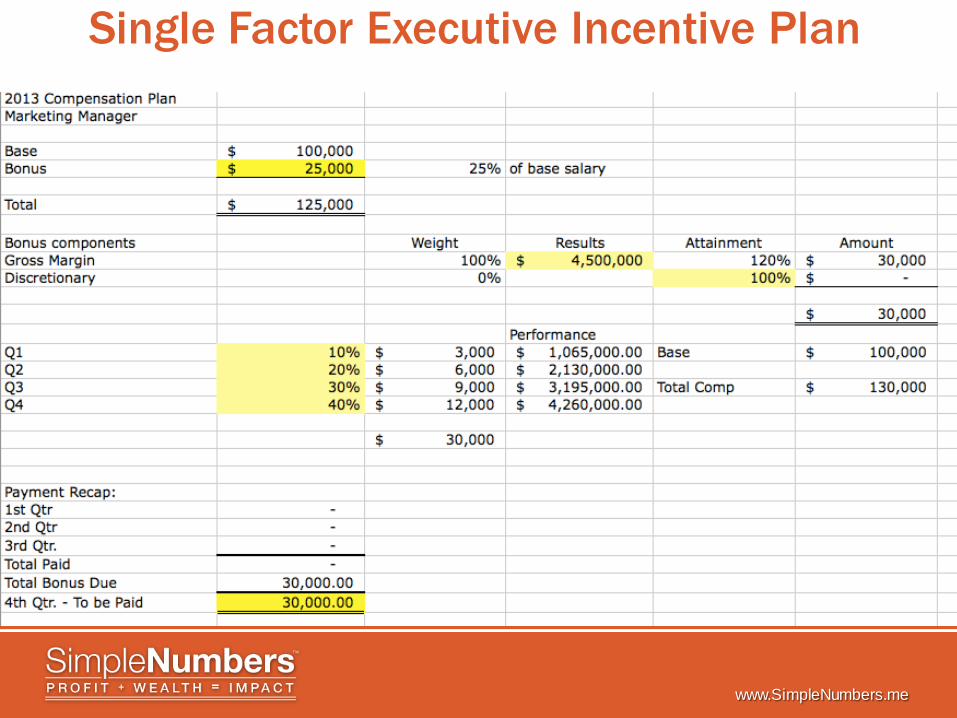

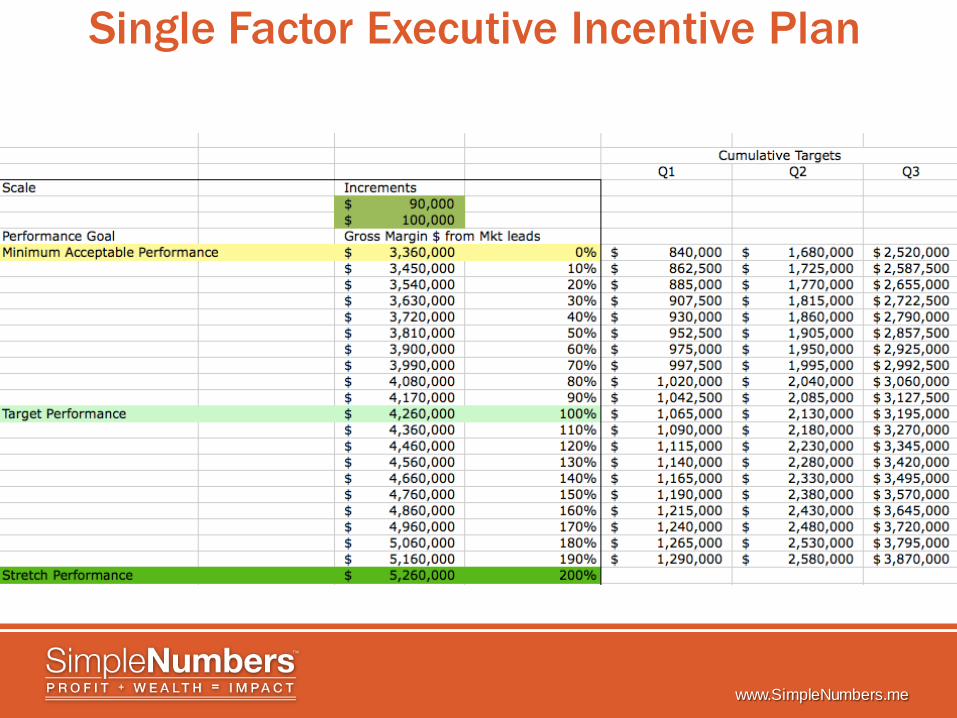

Single Factor Executive Incentive Plan

www.SimpleNumbers.me

Single Factor Executive Incentive Plan

www.SimpleNumbers.me

Owner Participation

1. Owners should only participate in incentive plans when

1. There are multiple owners that work in the business that each have different roles

2. There are outside investors who do not work in the business

3. You want to participate with other executive team members who are not owners

2. Don’t do an incentive thinking it will change your performance.

www.SimpleNumbers.me

#3: Four Forces of Cash Flow Have you set your priorities right to build a solid foundation?

www.SimpleNumbers.me

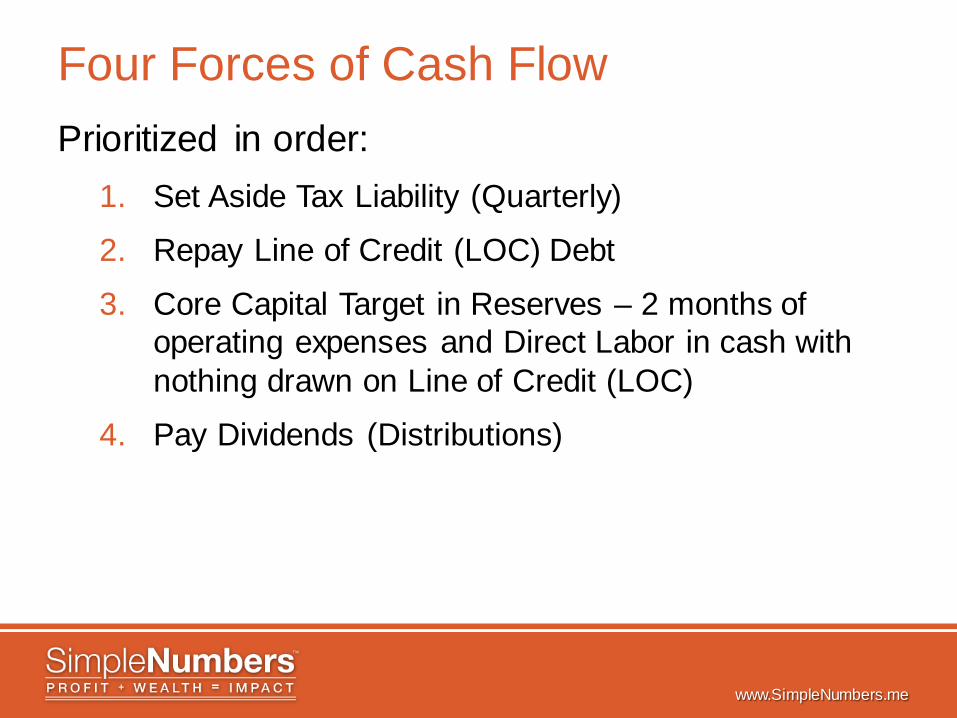

Four Forces of Cash Flow Prioritized in order:

1. Set Aside Tax Liability (Quarterly)

2. Repay Line of Credit (LOC) Debt

3. Core Capital Target in Reserves – 2 months of operating expenses and Direct Labor in cash with nothing drawn on Line of Credit (LOC)

4. Pay Dividends (Distributions)

www.SimpleNumbers.me

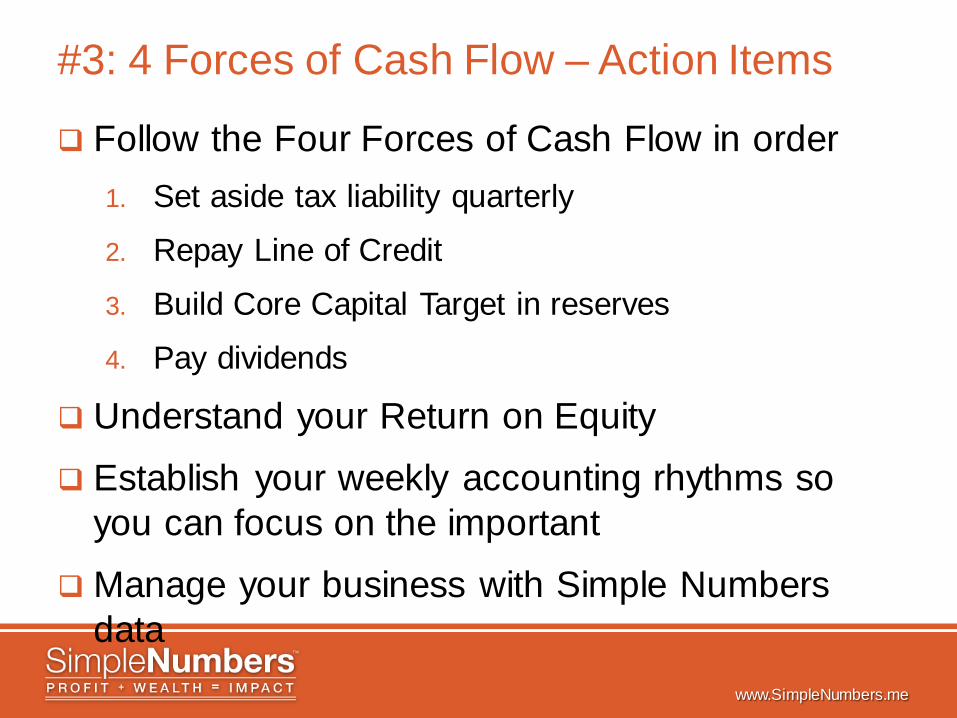

#3: 4 Forces of Cash Flow – Action Items

Follow the Four Forces of Cash Flow in order 1. Set aside tax liability quarterly

2. Repay Line of Credit

3. Build Core Capital Target in reserves

4. Pay dividends

Understand your Return on Equity

Establish your weekly accounting rhythms so you can focus on the important

Manage your business with Simple Numbers data

www.SimpleNumbers.me

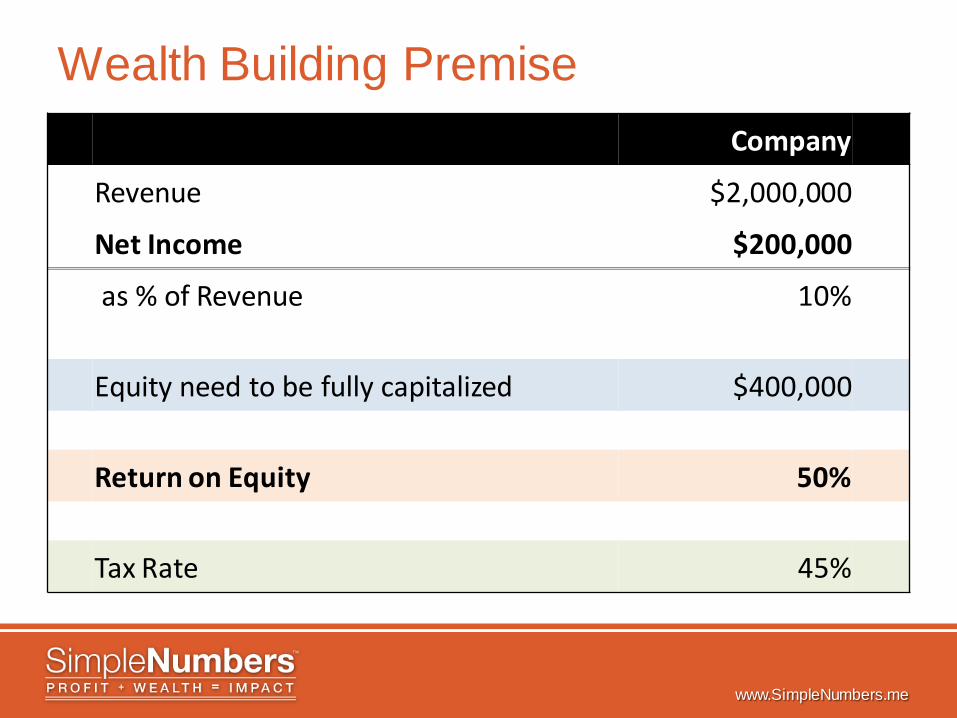

Wealth Building Premise Company

Revenue $2,000,000

Net Income $200,000

as % of Revenue 10%

Equity need to be fully capitalized $400,000

Return on Equity 50%

Tax Rate 45%

www.SimpleNumbers.me

Weekly Accounting Rhythm Deposits: Take to the bank daily

Separate duties if possible

Use remote deposit

Log into online account to record ACH payments

Daily email to management on bank balance and who paid

www.SimpleNumbers.me

Weekly Accounting Rhythm Invoices: Invoice weekly, if possible

Have the invoicing done by those closest to the customer

Break monthly billing into 4 cycles

If invoicing is in a separate system, reconcile weekly

www.SimpleNumbers.me

Weekly Accounting Rhythm Bill Payments: Only pay bills once a week on the same day

Use the “bill” process in QuickBooks to get the right date on the expense

2-week Cash Flow forecast report each week

Turn off automatic sweep on LOC

www.SimpleNumbers.me

Weekly Accounting Rhythm Online Banking: Check bank activity online daily

Use a two monitor environment

Do a “soft” reconciliation daily

Make your accounting system be the authoritative bank balance, not the bank’s

Use online bank alerts

www.SimpleNumbers.me

Weekly Accounting Rhythm Credit Cards: Input charge detail into your records

Download activity if at all possible

Update once a week on the same day

www.SimpleNumbers.me

Weekly Accounting Rhythm Payroll: If a QuickBooks user, we like QuickBooks Assisted

Payroll the best, all data is held within your records

Use one of the major players (ADP, Insperity, Paychex, etc) if you want it separate. Try to automate the entry back into your books

Do not do it yourself! The #1 possibility of fraud

Update Labor Efficiency Ration (LER) reports after every payroll

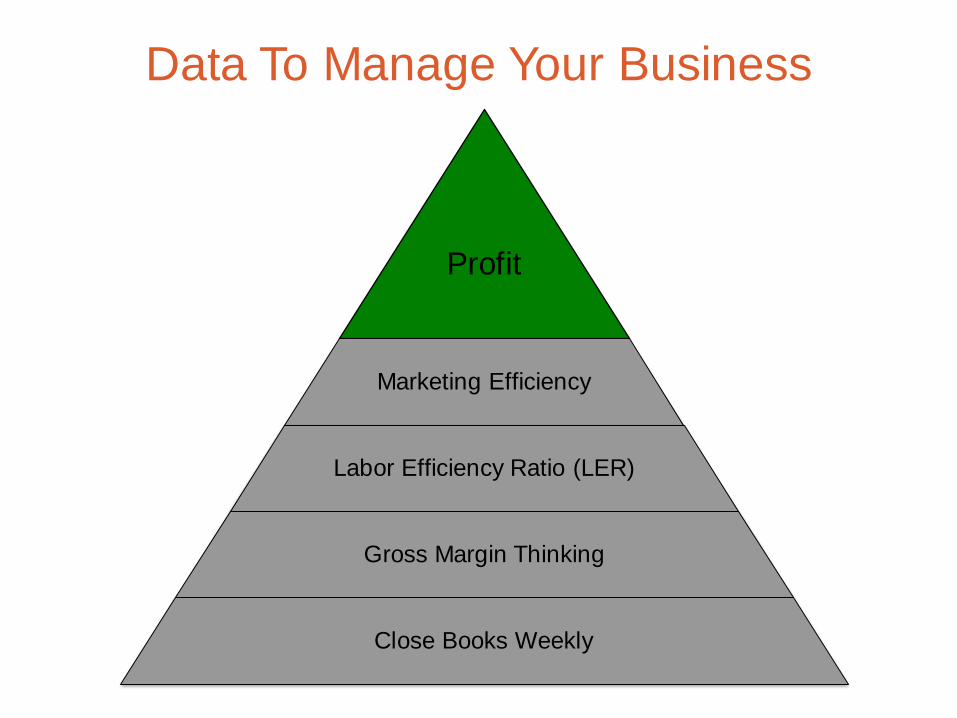

Profit

Marketing Efficiency

Labor Efficiency Ratio (LER)

Gross Margin Thinking

Close Books Weekly

Data To Manage Your Business

www.SimpleNumbers.me

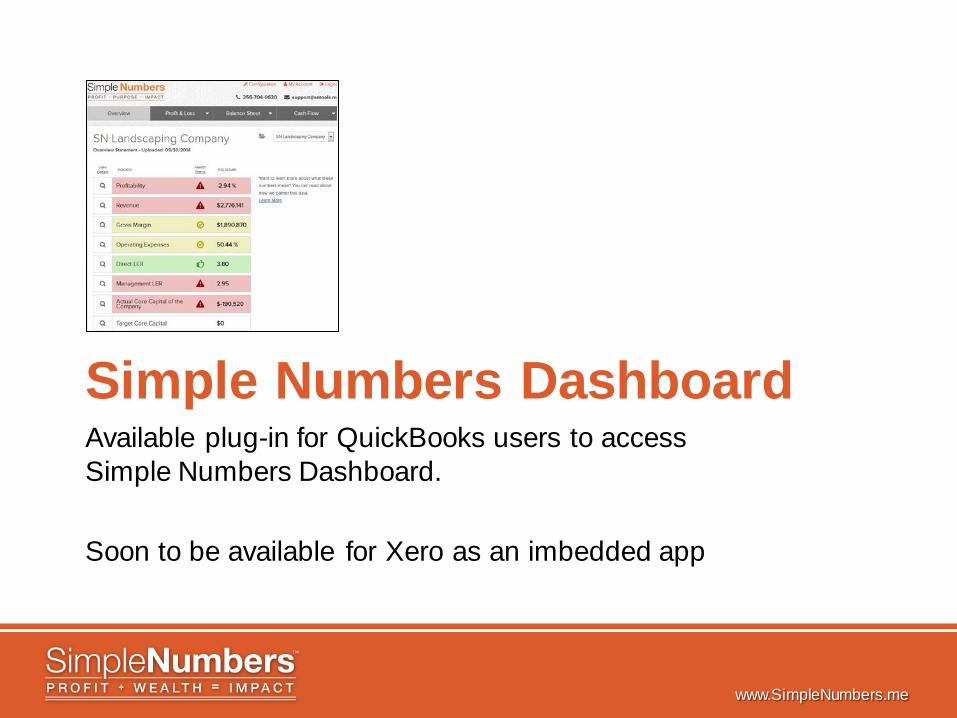

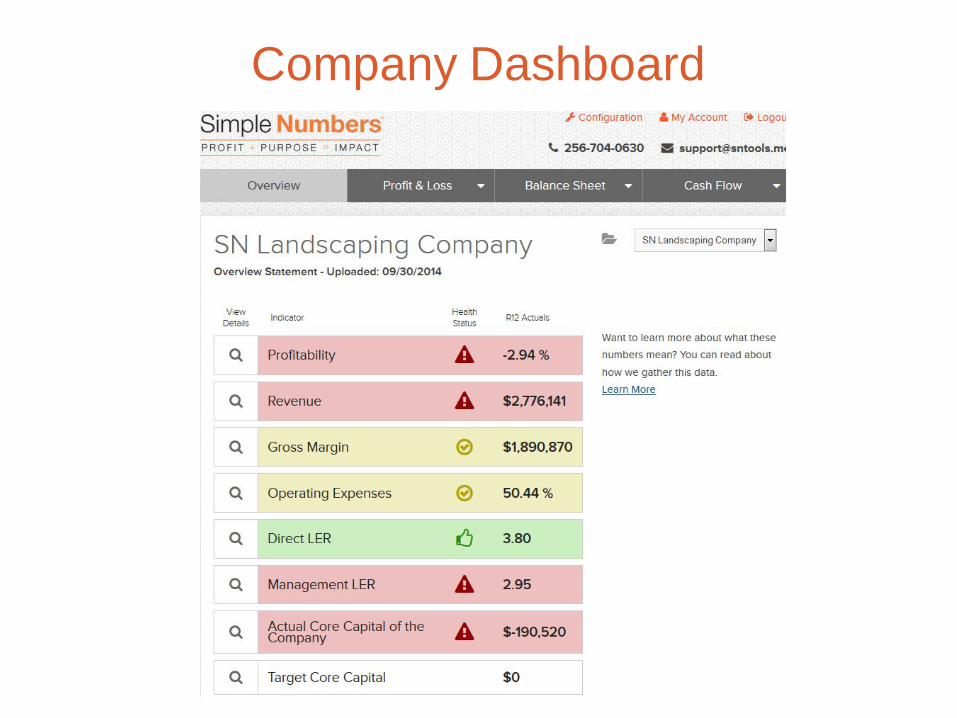

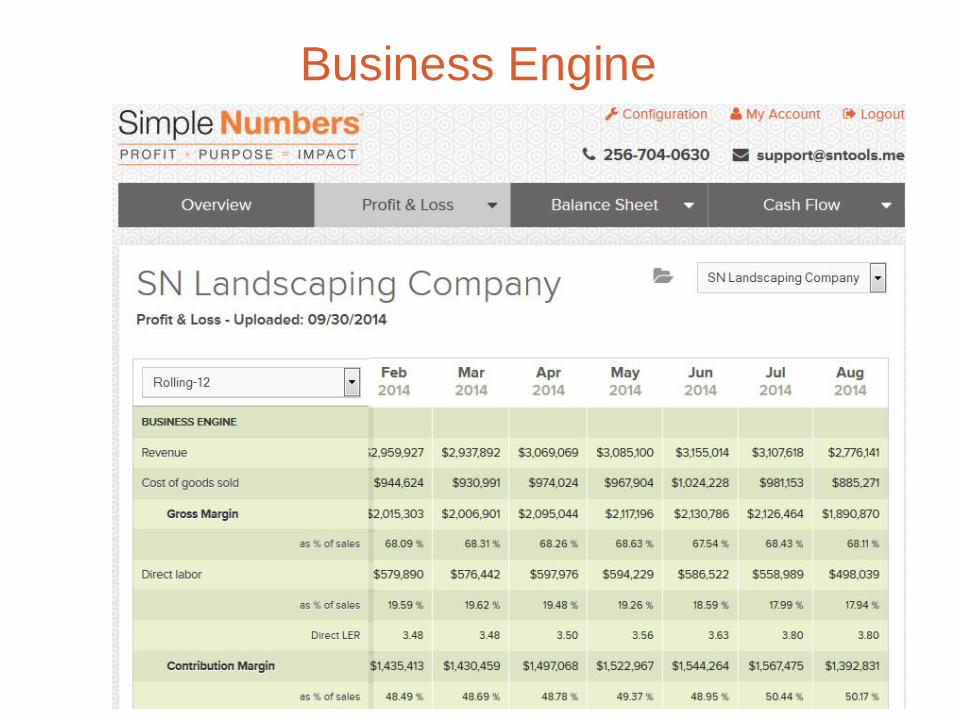

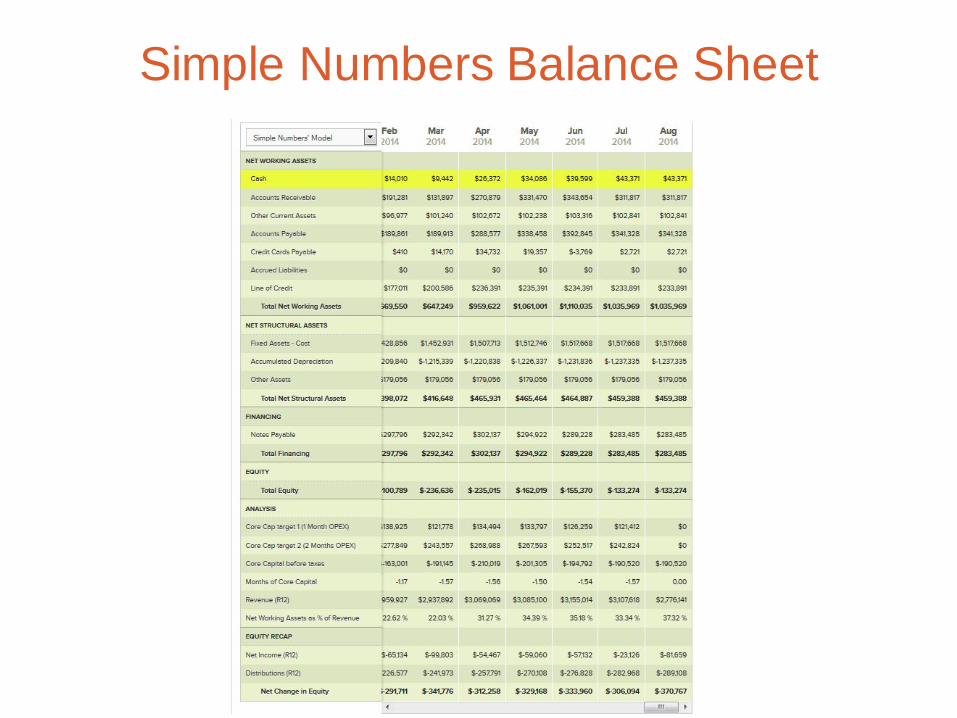

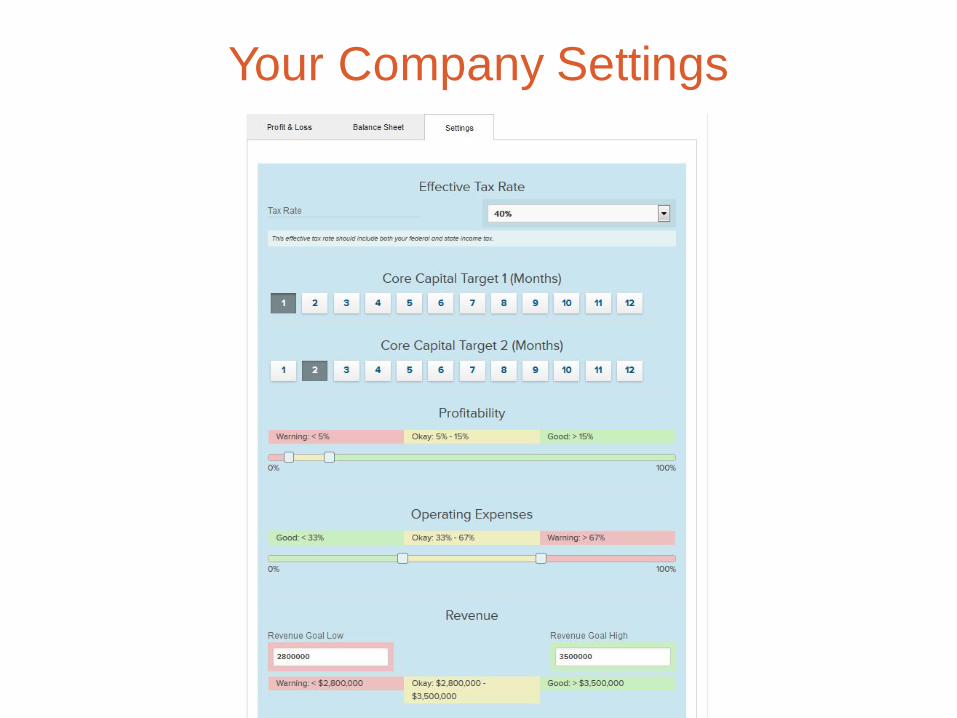

Simple Numbers Dashboard Available plug-in for QuickBooks users to access Simple Numbers Dashboard. Soon to be available for Xero as an imbedded app

Company Dashboard

Business Engine

Simple Numbers Balance Sheet

Your Company Settings

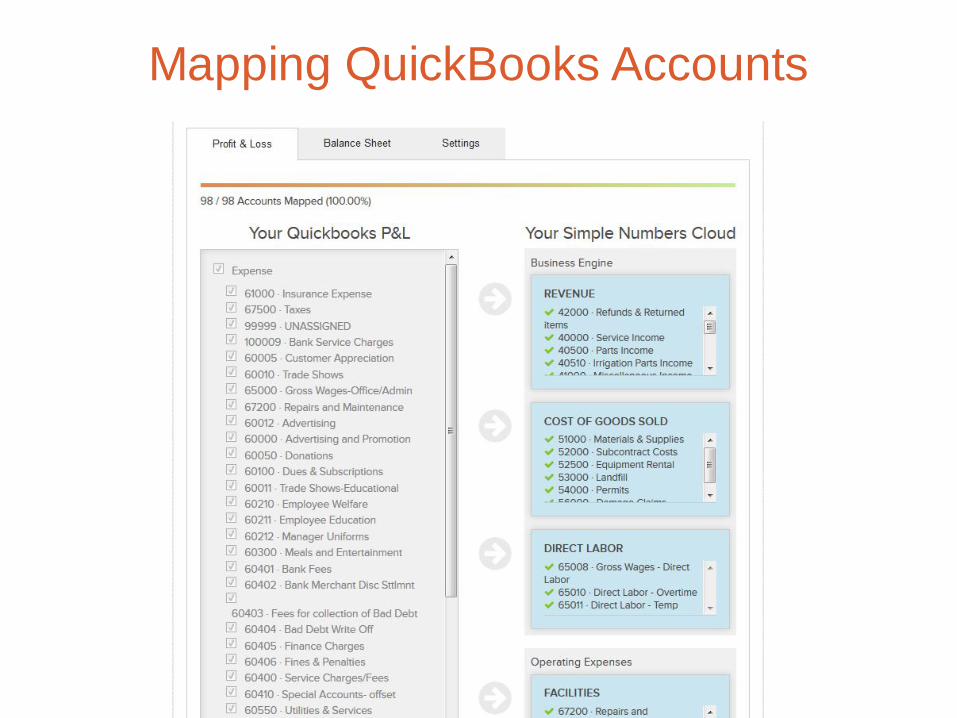

Mapping QuickBooks Accounts

www.SimpleNumbers.me

SimpleNumbers Profit Tool

Works with QuickBooks desktop versions

Soon to be released for Xero

Mapping and consulting packages available

Go to www.simplenumbers.me for pricing and to subscribe

Related Documents