Slide 2-1 2 CHAPTER 2 WHOLLY OWNED SUBSIDIARIES: POSTCREATION PERIODS

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Slide 2-1

2 CHAPTER 2

WHOLLY OWNED SUBSIDIARIES:

POSTCREATION PERIODS

Slide 2-2

2FOCUS OF CHAPTER 2

Ways to Value the Parent’s Investment Account in POSTCREATION Periods

Cost Method vs. Equity Method Driven Consolidation Procedures Income Statements Statements of Retained Earnings

Parent-Company-Only (PCO) Statements Articulation with Consolidated

Statements

Slide 2-3

2 The Cost Method:How It Works

It is cash basis driven: Record income at the parent level ONLY

when sub declares a dividend. Ignore sub’s earnings. Do NOT ignore sub’s losses. Write-down investment ONLY IF value

has been impaired. Write-downs result in a NEW cost basis.

Slide 2-4

2 The Cost Method: How It Works (cont.)

It is a one-way street!

The investment can be written down--but NEVER written up.

Slide 2-5

2 The Cost Method: Pros & Cons

Pros: Minimal G/L bookkeeping by parent. Simple consolidation procedures.

Cons: Overly conservative valuation. Parent can manipulate its reported

income. PCO statements--if used internally

or issued--may be of limited value.

Slide 2-6

2 The Cost Method: MAJOR Point of Interest

Although the parent CANmanipulate its OWNreported net income,

it can NEVER manipulate

CONSOLIDATED net income.

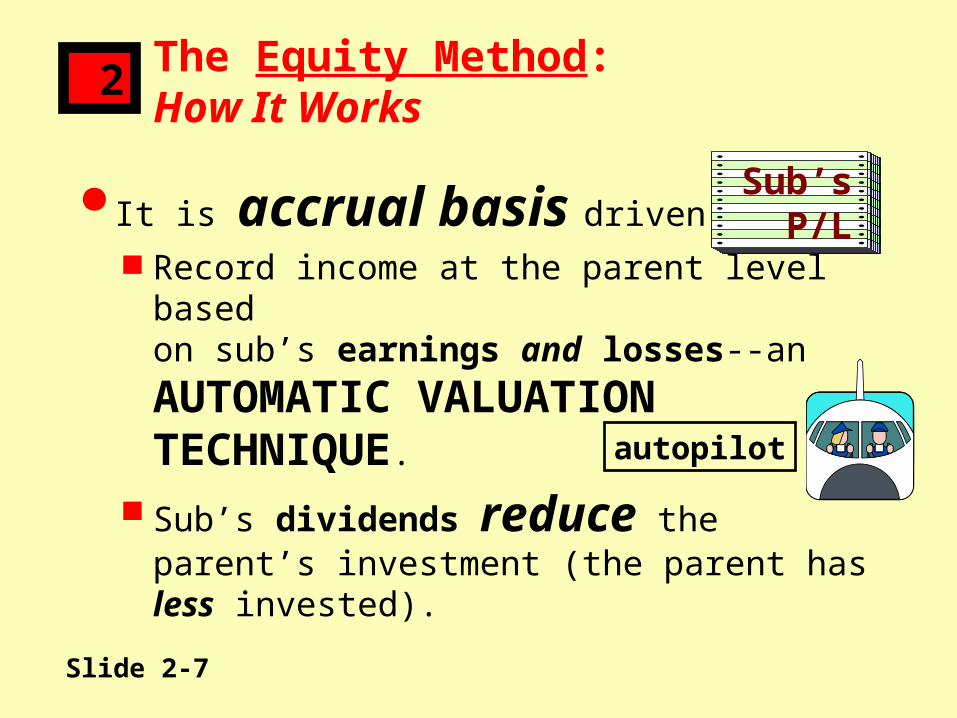

Slide 2-7

2 The Equity Method:How It Works

It is accrual basis driven: Record income at the parent level

based on sub’s earnings and losses--an

AUTOMATIC VALUATION TECHNIQUE.

Sub’s dividends reduce the parent’s investment (the parent has less invested).

Sub’s P/L

autopilot

Slide 2-8

2 The Equity Method: How It Works (cont.)

It is a two-way street!

The investment can be:(1) written down AND(2) written up.

Slide 2-9

2 The Equity Method:Pros and Cons

Pros: Based on economic activity--not the

parent-controlled dividend policy. Has 2 built-in checking figures.

Cons: Entails continual bookkeeping. Unnecessary work if PCO statements

are not used internally or issued to outsiders.

Slide 2-10

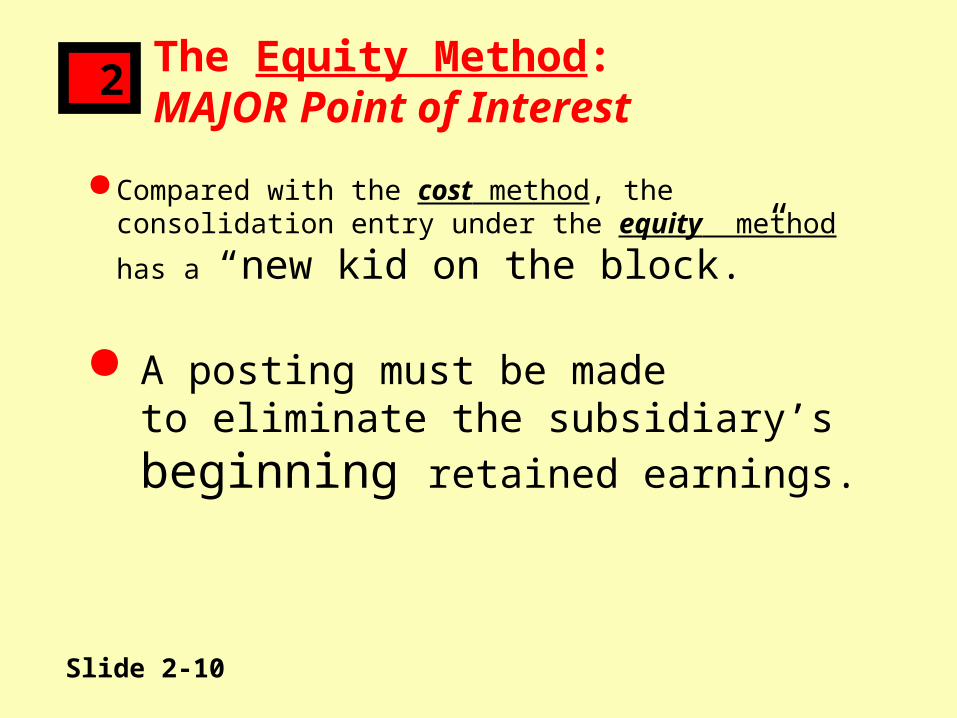

2 The Equity Method: MAJOR Point of Interest

Compared with the cost method, the consolidation entry under the equity method

has a “new kid on the block.”

A posting must be made to eliminate the subsidiary’s beginning retained earnings.

Slide 2-11

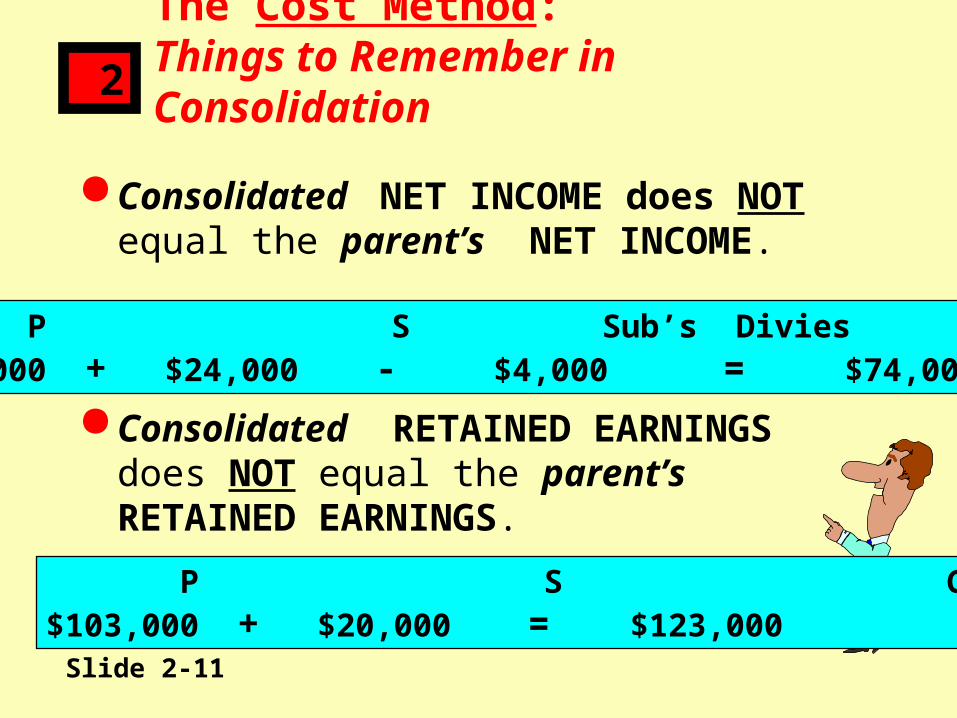

2 The Cost Method: Things to Remember in Consolidation

Consolidated NET INCOME does NOT equal the parent’s NET INCOME.

Consolidated RETAINED EARNINGSdoes NOT equal the parent’s RETAINED EARNINGS.

P S Sub’s Divies CON.$54,000 + $24,000 - $4,000 = $74,000

P S CON.$103,000 + $20,000 = $123,000

Slide 2-12

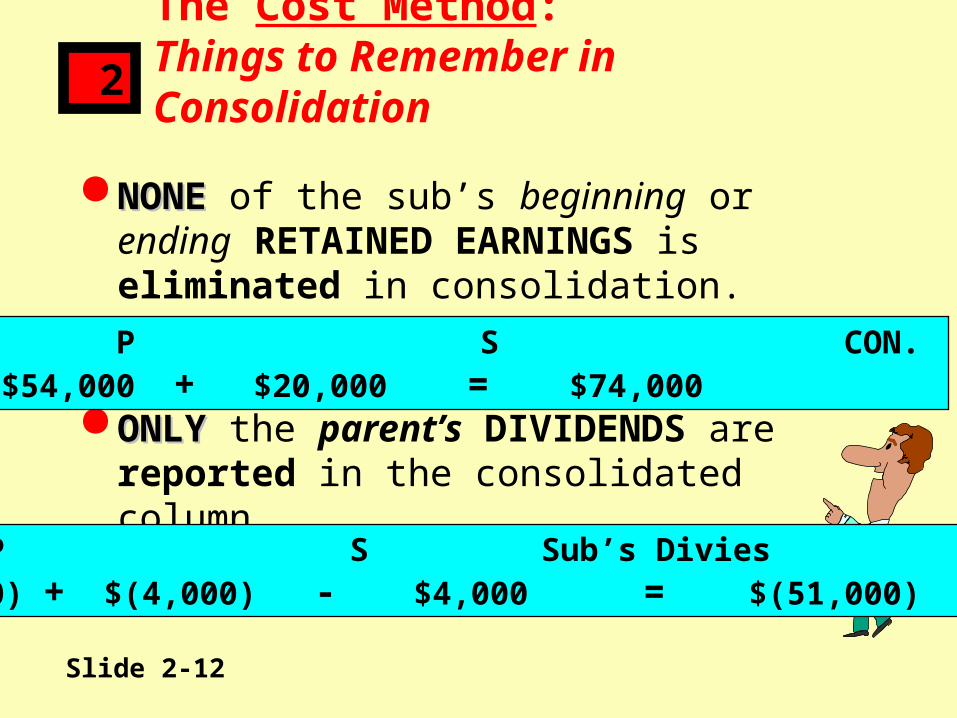

2 The Cost Method: Things to Remember in Consolidation

NONE NONE of the sub’s beginning or ending RETAINED EARNINGS is eliminated in consolidation.

ONLY ONLY the parent’s DIVIDENDS arereported in the consolidated column.

P S CON. $54,000 + $20,000 = $74,000

P S Sub’s Divies CON.$(51,000) + $(4,000) - $4,000 = $(51,000)

Slide 2-13

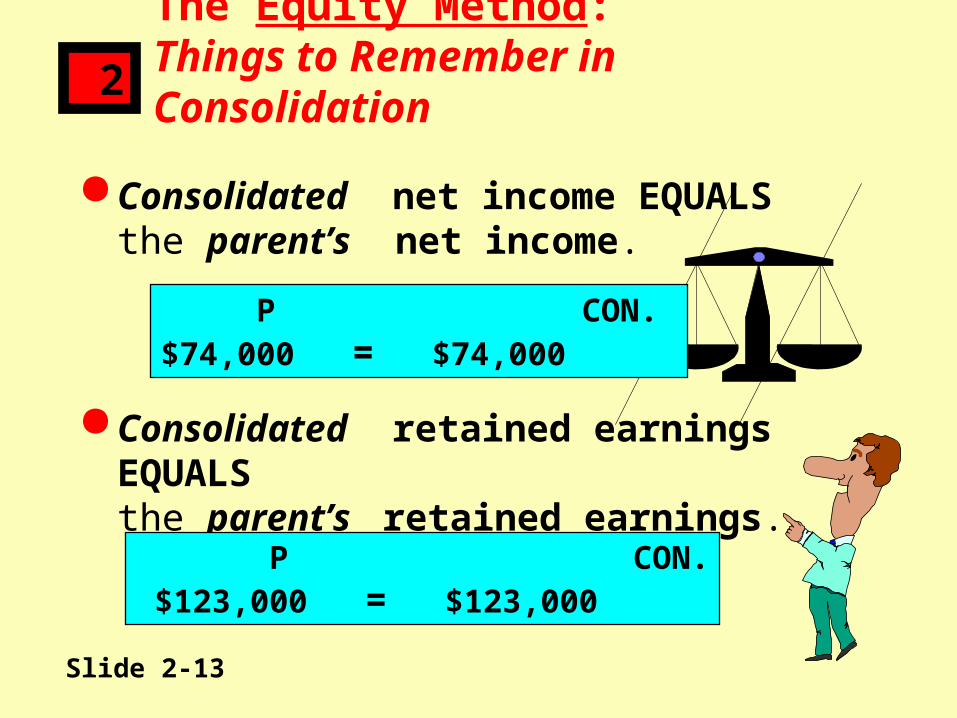

2 The Equity Method: Things to Remember in Consolidation

Consolidated net income EQUALSthe parent’s net income.

Consolidated retained earnings EQUALSthe parent’s retained earnings.

P CON. $74,000 = $74,000

P CON. $123,000 = $123,000

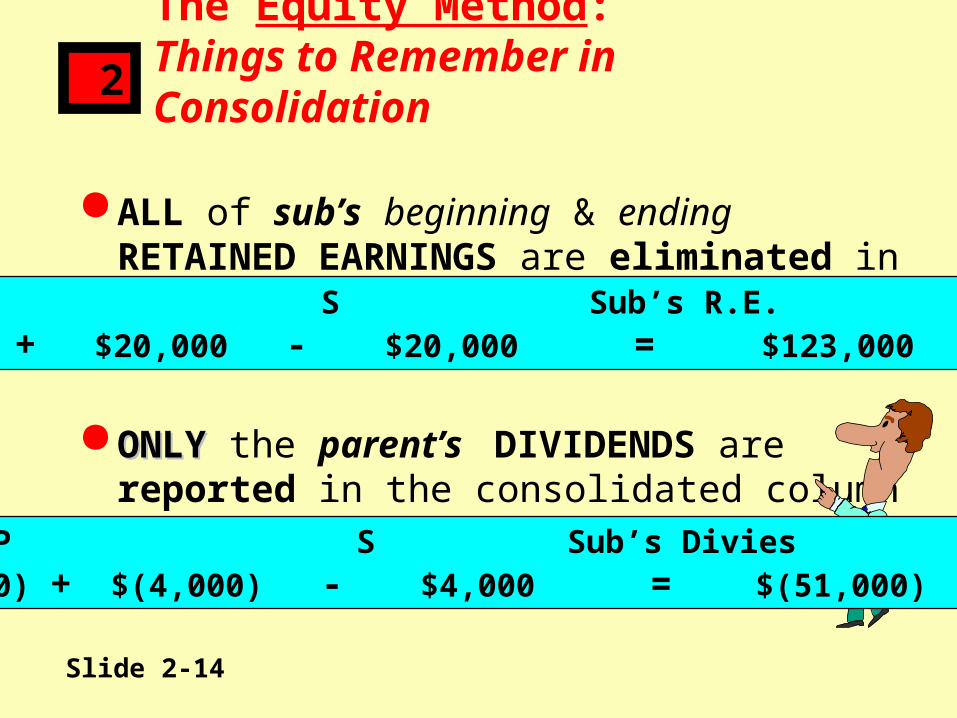

Slide 2-14

2 The Equity Method: Things to Remember in Consolidation

ALL of sub’s beginning & ending RETAINED EARNINGS are eliminated in consolidation.

ONLYONLY the parent’s DIVIDENDS arereported in the consolidated column(also occurs under the cost method). P S Sub’s Divies CON.

$(51,000) + $(4,000) - $4,000 = $(51,000)

P S Sub’s R.E. CON.$123,000 + $20,000 - $20,000 = $123,000

Slide 2-15

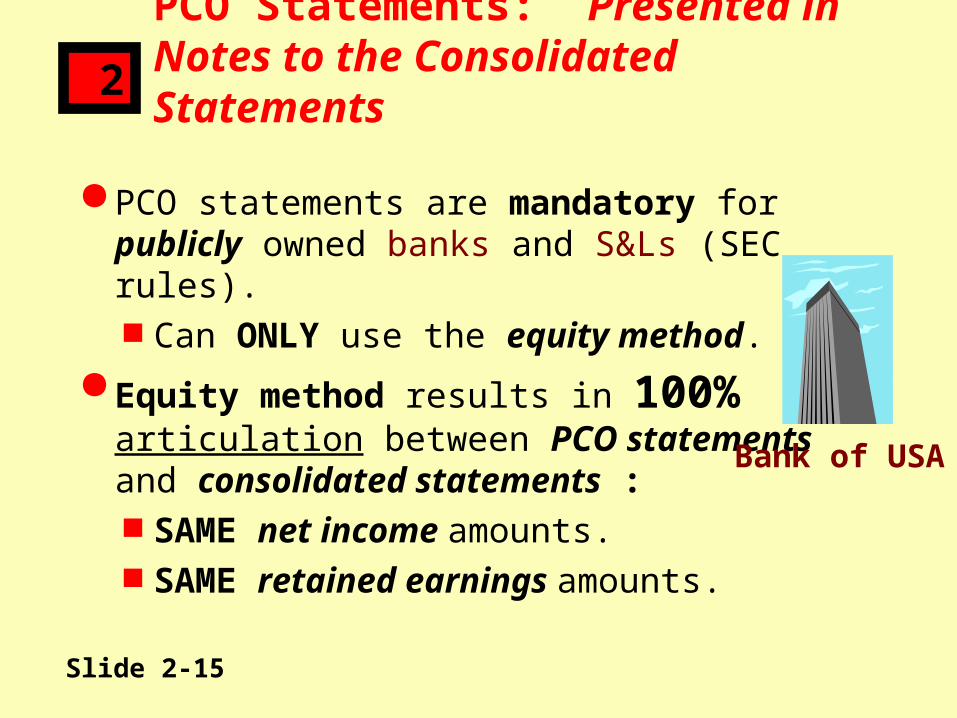

2 PCO Statements: Presented in Notes to the Consolidated Statements

PCO statements are mandatory for publicly owned banks and S&Ls (SEC rules). Can ONLY use the equity method.

Equity method results in 100%articulation between PCO statementsand consolidated statements : SAME net income amounts. SAME retained earnings amounts.

Bank of USA

Slide 2-16

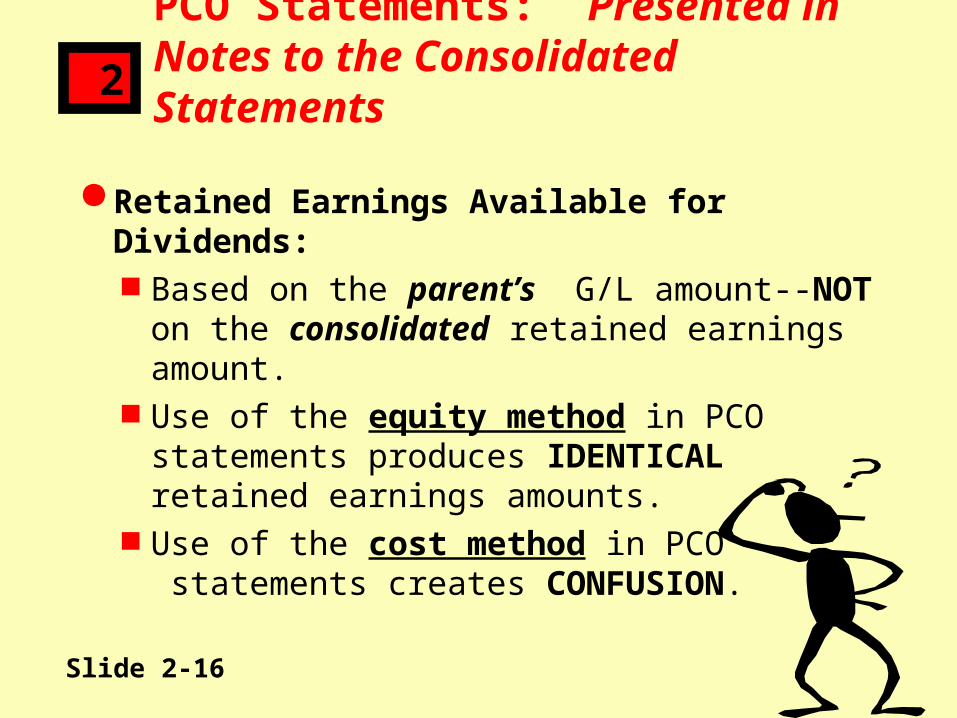

2 PCO Statements: Presented in Notes to the Consolidated Statements

Retained Earnings Available for Dividends: Based on the parent’s G/L amount--NOT

on the consolidated retained earnings amount.

Use of the equity method in PCO statements produces IDENTICALretained earnings amounts.

Use of the cost method in PCO statements creates CONFUSION.

Slide 2-17

2 Consolidation: The Most Important Point of All on Investment Basis

The consolidated statement

amounts are identical whether the parent usesthe cost method or the equity method--

this holds true for ALL 3 statements.

Slide 2-18

2 Total Investment Loss Situations: Equity Method Procedures

Parent Has GUARANTEED Sub’s Debt: NO interruption occurs in the application

of the equity method.

Parent can lose more than it has invested --parent is“on the hook.”

Slide 2-19

2 Total Investment Loss Situations: Equity Method Procedures (cont.)

Parent Has NOT GUARANTEED Sub’s Debt: Discontinue equity method when

sub’s equity reaches zero--resume ONLY WHEN sub’s equity becomes

positive.

Parent can NEVER lose more than it has invested.

Slide 2-20

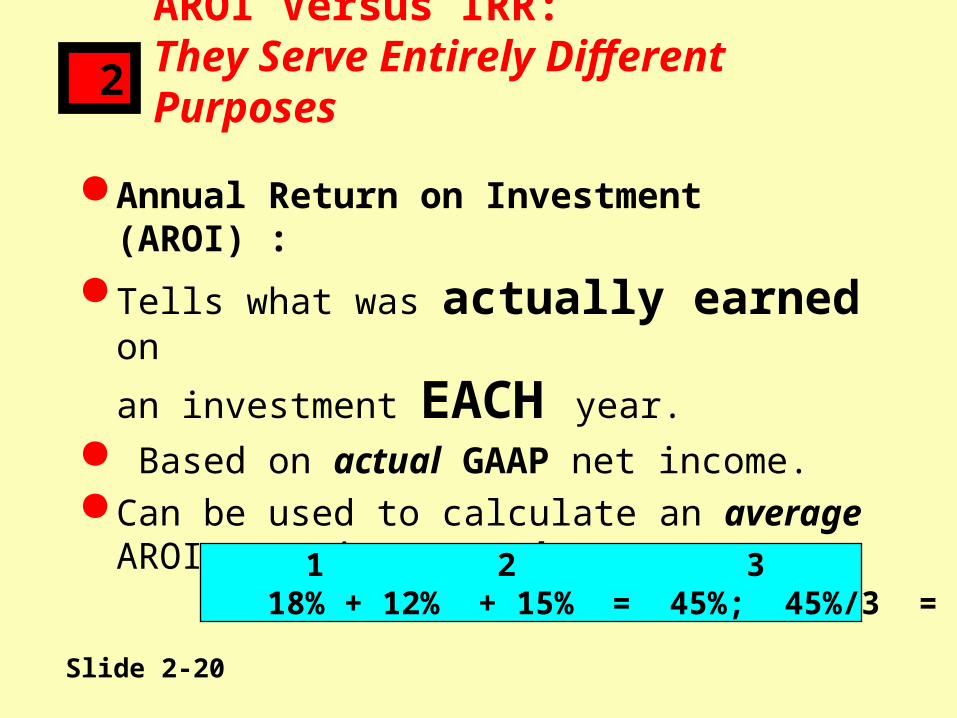

2 AROI Versus IRR: They Serve Entirely Different Purposes

Annual Return on Investment (AROI) :

Tells what was actually earned on

an investment EACH year. Based on actual GAAP net income. Can be used to calculate an average

AROI covering several years. 1 2 3 AVG. 18% + 12% + 15% = 45%; 45%/3 = 15%

Slide 2-21

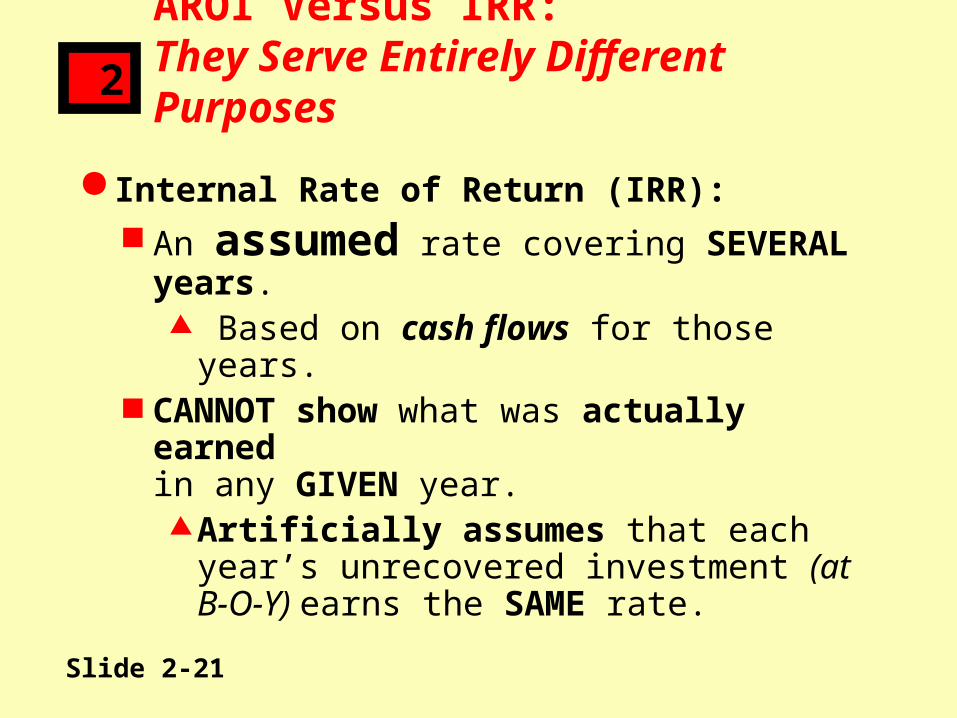

2 AROI Versus IRR: They Serve Entirely Different Purposes

Internal Rate of Return (IRR): An assumed rate covering

SEVERAL years. Based on cash flows for those

years. CANNOT show what was actually

earnedin any GIVEN year.Artificially assumes that each

year’s unrecovered investment (at B-O-Y) earns the SAME rate.

Slide 2-22

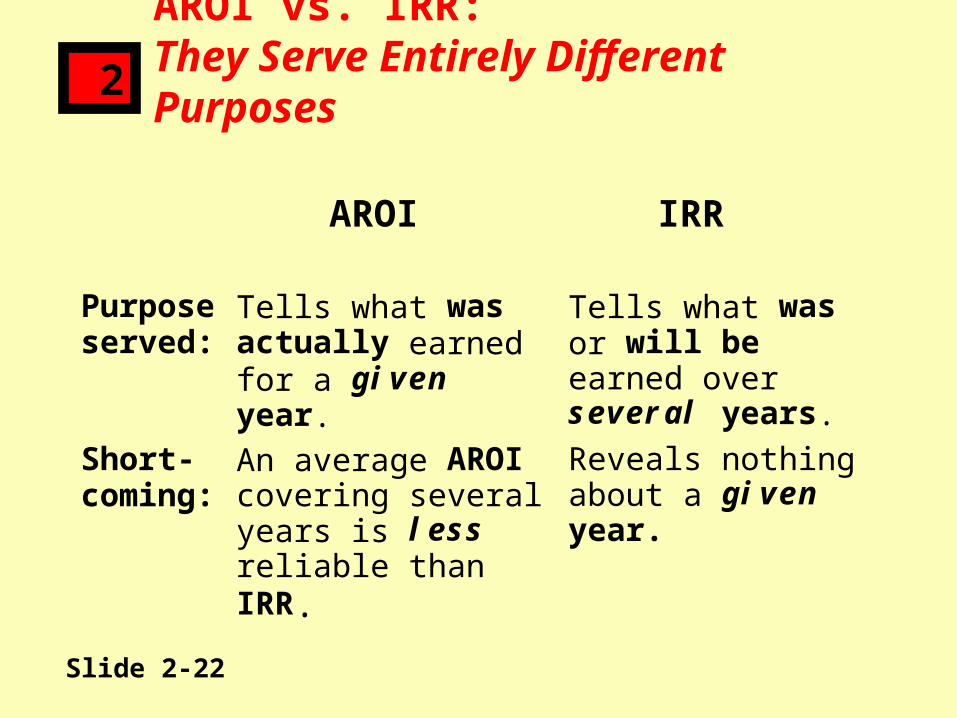

2 AROI vs. IRR: They Serve Entirely Different Purposes

AROI IRR

Purpose served:

Tells what was actually earned for a given year.

Tells what was or will be earned over several years.

Short-coming:

An average AROI covering several years is less reliable than IRR.

Reveals nothing about a given year.

Slide 2-23

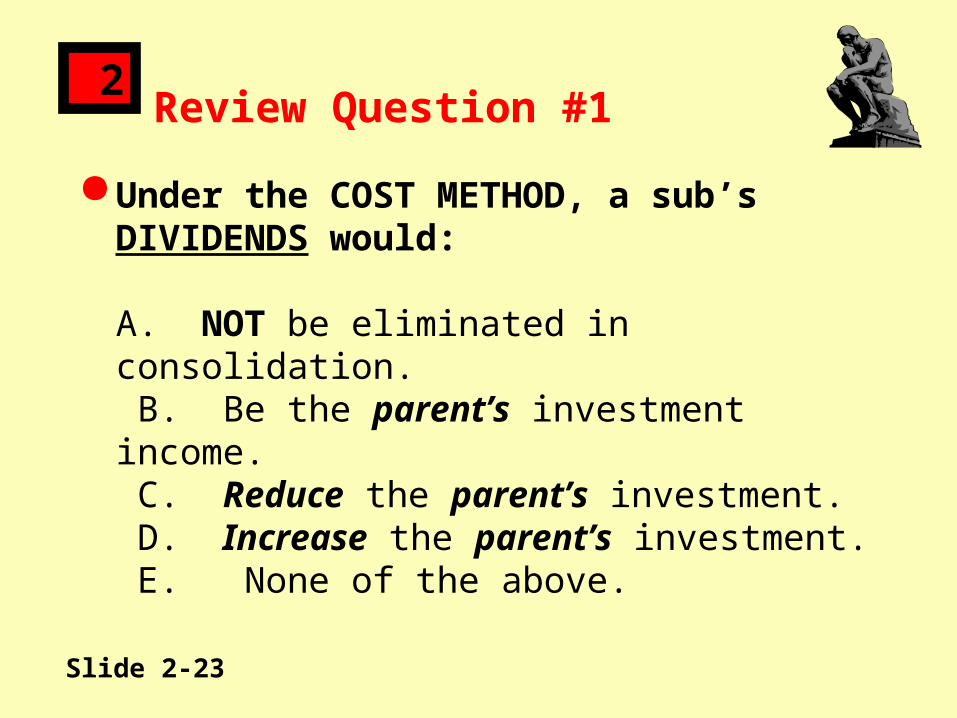

2Review Question #1

Under the COST METHOD, a sub’s DIVIDENDS would:

A. NOT be eliminated in consolidation. B. Be the parent’s investment income. C. Reduce the parent’s investment. D. Increase the parent’s investment. E. None of the above.

Slide 2-24

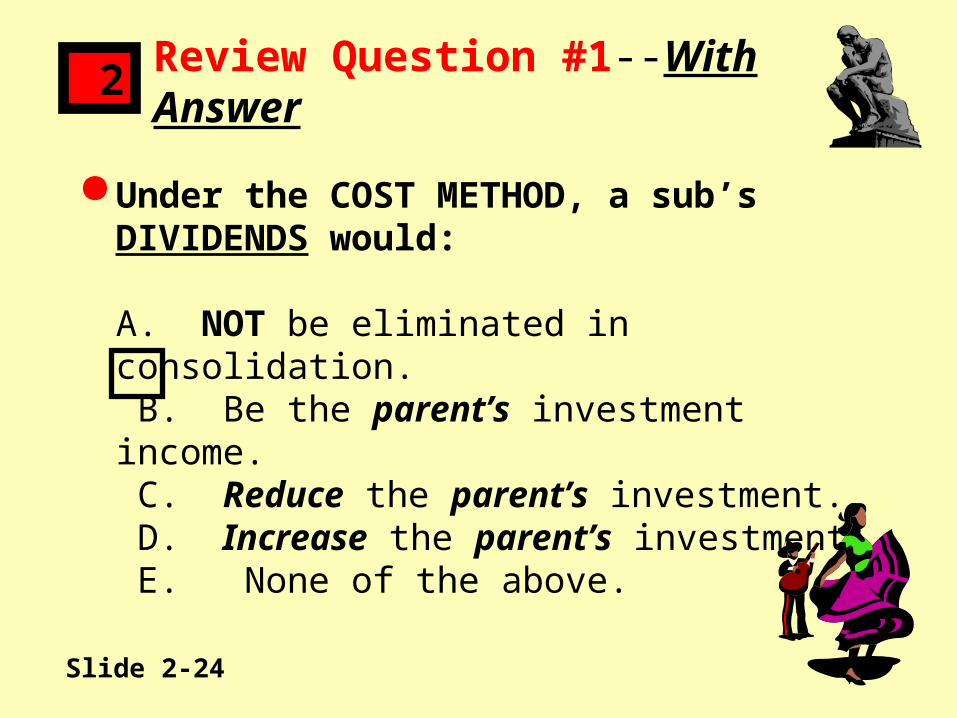

2Review Question #1--With Answer

Under the COST METHOD, a sub’s DIVIDENDS would:

A. NOT be eliminated in consolidation. B. Be the parent’s investment income. C. Reduce the parent’s investment. D. Increase the parent’s investment. E. None of the above.

Slide 2-25

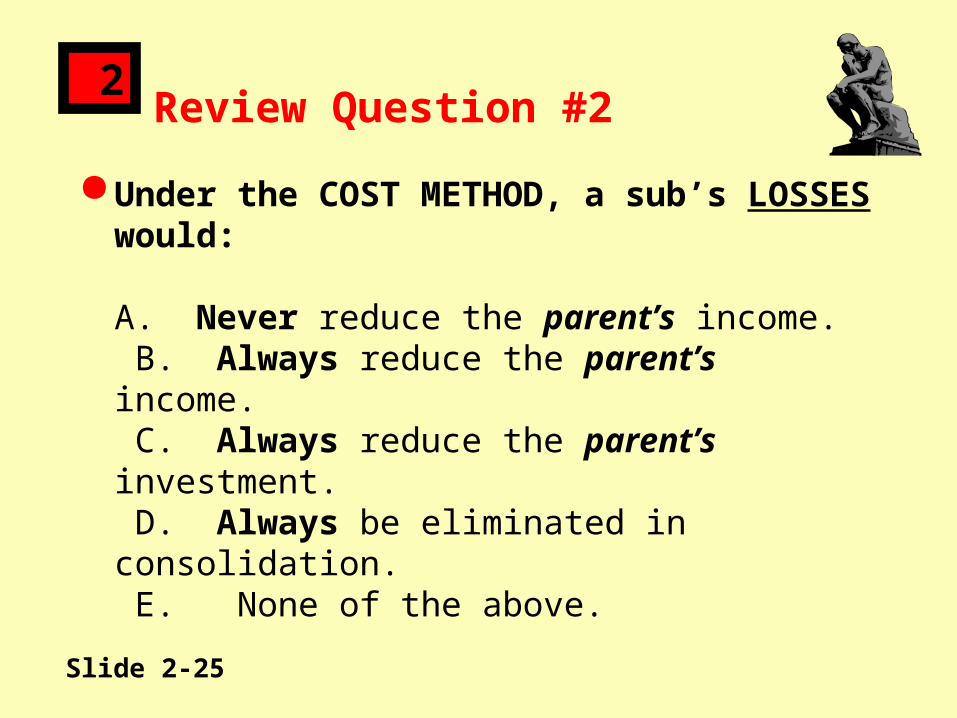

2Review Question #2

Under the COST METHOD, a sub’s LOSSES would:

A. Never reduce the parent’s income. B. Always reduce the parent’s income. C. Always reduce the parent’s investment. D. Always be eliminated in consolidation. E. None of the above.

Slide 2-26

2Review Question #2--With Answer

Under the COST METHOD, a sub’s LOSSES would:

A. Never reduce the parent’s income. B. Always reduce the parent’s income. C. Always reduce the parent’s investment. D. Always be eliminated in consolidation. E. None of the above.

Slide 2-27

2Review Question #3

Under the EQUITY METHOD, a sub’s DIVIDENDS would:

A. NOT be eliminated in consolidation. B. Be the parent’s investment income. C. Reduce the parent’s investment. D. Increase the parent’s investment. E. None of the above.

Slide 2-28

2Review Question #3--With Answer

Under the EQUITY METHOD, a sub’s DIVIDENDS would:

A. NOT be eliminated in consolidation. B. Be the parent’s investment income. C. Reduce the parent’s investment. D. Increase the parent’s investment. E. None of the above.

Slide 2-29

2Review Question #4

Under the EQUITY METHOD, a sub’s LOSSES would:

A. Never reduce the parent’s income. B. Normally reduce the parent’s income. C. Always reduce the parent’s investment. D. Always be eliminated in consolidation. E. None of the above.

Slide 2-30

2Review Question #4--With Answer

Under the EQUITY METHOD, a sub’s LOSSES would:

A. Never reduce the parent’s income. B. Normally reduce the parent’s income. C. Always reduce the parent’s investment. D. Always be eliminated in consolidation. E. None of the above.

Slide 2-31

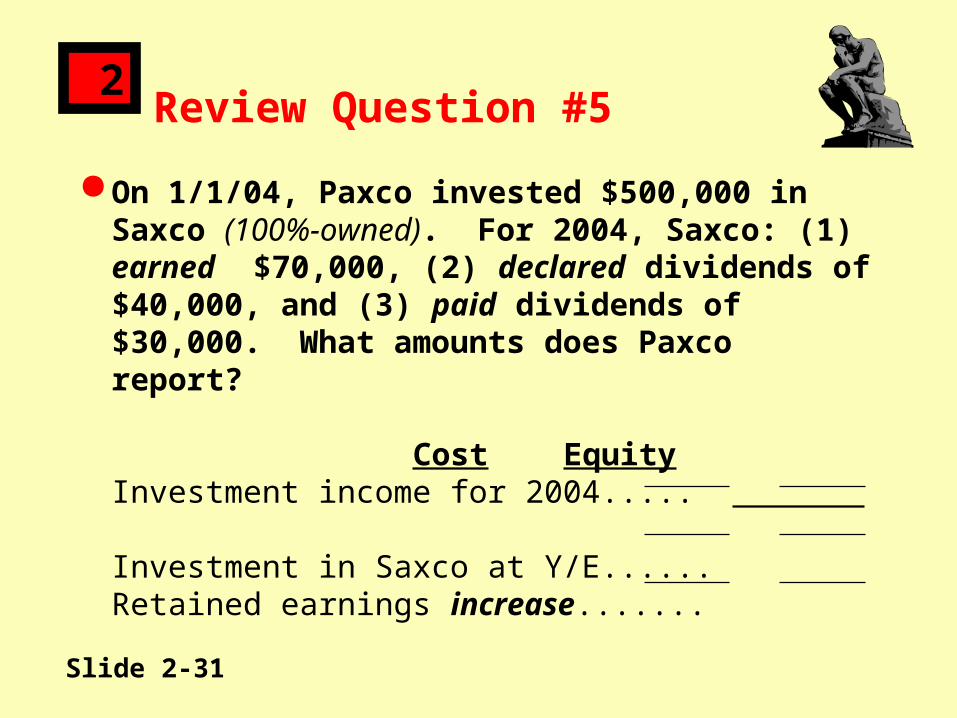

2Review Question #5

On 1/1/04, Paxco invested $500,000 in Saxco (100%-owned). For 2004, Saxco: (1) earned $70,000, (2) declared dividends of $40,000, and (3) paid dividends of $30,000. What amounts does Paxco report? Cost EquityInvestment income for 2004..... Investment in Saxco at Y/E......Retained earnings increase.......

Slide 2-32

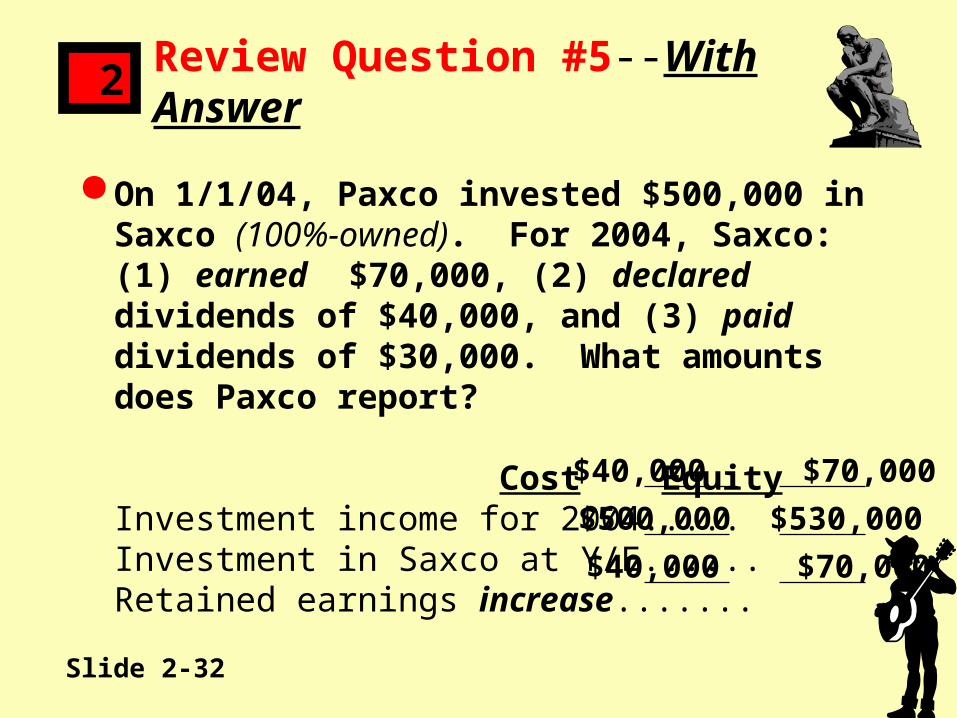

2Review Question #5--With Answer

On 1/1/04, Paxco invested $500,000 in Saxco (100%-owned). For 2004, Saxco: (1) earned $70,000, (2) declared dividends of $40,000, and (3) paid dividends of $30,000. What amounts does Paxco report? Cost EquityInvestment income for 2004..... Investment in Saxco at Y/E......Retained earnings increase.......

$40,000 $70,000

$500,000 $530,000

$40,000 $70,000

Slide 2-33

2Review Question #6

A parent can lose MORE THAN than it has invested:

A. Only under the cost method. B. Only under the equity method. C. Under either the cost or equity methods. D. Only if the subsidiary is not consolidated. E. None of the above.

Slide 2-34

2Review Question #6--With Answer

A parent can lose MORE THAN than it has invested:

A. Only under the cost method. B. Only under the equity method. C. Under either the cost or equity methods. D. Only if the subsidiary is not consolidated. E. None of the above.

Slide 2-35

2Review Question #7

Parent-company-only (PCO) statements are usually presented in notes only when:

A. The parent uses the cost method. B. The parent uses the equity method. C. The subsidiary is not consolidated. D. The SEC’s rules require them. E. None of the above.

Slide 2-36

2Review Question #7--With Answer

Parent-company-only (PCO) statements are usually presented in notes only when:

A. The parent uses the cost method. B. The parent uses the equity method. C. The subsidiary is not consolidated. D. The SEC’s rules require them. E. None of the above.

Slide 2-37

2Review Question #8

When a parent-sub relationship exists, STATE LAWS require dividends to be based on the:

A. Parent’s retained earnings. B. Sub’s retained earnings. C. Consolidated retained earnings. D. The lower of the parent’s OR the consolidated retained earnings. E. None of the above.

Slide 2-38

2Review Question #8--With Answer

When a parent-sub relationship exists, STATE LAWS require dividends to be based on the:

A. Parent’s retained earnings. B. Sub’s retained earnings. C. Consolidated retained earnings. D. The lower of the parent’s OR the consolidated retained earnings. E. None of the above.

Slide 2-39

2End of Chapter 2

Time to Clear Things Up--Any Questions?

Related Documents