Slide 15-1 Copyright © 2003 Pearson Education, Inc. The Law of One Price • Identical goods sold in different countries must sell for the same price when their prices are expressed in terms of the same currency. – Example : If the dollar/pound exchange rate is $1.50 per pound, a sweater that sells for $45 in New York must sell for £30 in London. – The $ price of good i is the same wherever it is sold: P i US = (E $/€ ) x (P i E ) P i US is the $ price of good i in the U.S. P i E is the corresponding euro price in Europe E $/€ is the dollar/euro exchange rate

Slide 15-1Copyright © 2003 Pearson Education, Inc. The Law of One Price Identical goods sold in different countries must sell for the same price when their.

Dec 17, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Slide 15-1

Copyright © 2003 Pearson Education, Inc.

The Law of One Price

• Identical goods sold in different countries must sell for the same price when their prices are expressed in terms of the same currency.

– Example: If the dollar/pound exchange rate is $1.50 per pound, a sweater that sells for $45 in New York must sell for £30 in London.

– The $ price of good i is the same wherever it is sold:

PiUS = (E$/€) x (Pi

E)

PiUS is the $ price of good i in the U.S.

PiE is the corresponding euro price in Europe

E$/€ is the dollar/euro exchange rate

Slide 15-2

Copyright © 2003 Pearson Education, Inc.

Purchasing Power Parity

Theory of Purchasing Power Parity (PPP)• The exchange rate between two counties’ currencies

equals the ratio of the counties’ price levels.

• It compares average prices across countries.

• It predicts a dollar/euro exchange rate of:

• E$/€ = PUS/PE

PUS is the dollar price of a reference commodity

basket sold in the United States

PE is the euro price of the same basket in Europe

• In practice, US and eurozone price indexes are based on different baskets price statistics won’t bear out absolute PPP

Slide 15-3

Copyright © 2003 Pearson Education, Inc.

Absolute PPP and Relative PPPAbsolute PPP: exchange rates equal relative price levels.

Relative PPP: the percentage change in the exchange rate over any period equals the difference between the percentage changes in national price levels (the difference in inflation rates).

– Relative PPP between the United States and Europe would be:

(E$/€,t - E$/€, t –1)/E$/€, t –1 = US, t - E, t

where:

t = inflation rate

Purchasing Power Parity

Slide 15-4

Copyright © 2003 Pearson Education, Inc.

Monetary approach to the exchange rate: express price

levels in terms of domestic money demand and supplies: – In the US: PUS = Ms

US/L (R$, YUS)

– In Europe: PE = MsE/L (R€, YE)

From Absolute PPP: E$/€ = PUS/PE

E$/€ = [MsUS/L (R$, YUS)]÷[Ms

E/L (R€, YE)]

Predictions:– An increase in the U.S. (European) money supply causes a proportional

long-run depreciation (appreciation) of the dollar against the euro.

– A rise in the interest rate on dollar (euro) denominated assets causes a depreciation (appreciation) of the dollar against the euro ???

– A rise in U.S. (European) output causes an appreciation (depreciation) of the dollar against the euro.

A Long-Run Exchange Rate Model Based on PPP

Slide 15-5

Copyright © 2003 Pearson Education, Inc.

Ongoing Inflation, Interest Parity, and PPP

• Money supply growth at a constant rate eventually results in ongoing inflation at the same rate.

• The Fisher Effect: A rise (fall) in a country’s expected inflation rate eventually causes an equal rise (fall) in its interest rate

• The international interest rate difference is the difference between expected national inflation rates:

R$ - R€ = eUS - e

E

Interest Rates and the Long Run Exchange Rate: the Monetary Model

Slide 15-6

Copyright © 2003 Pearson Education, Inc.

2

R$2 = R$

1 + E2$/€

The Fisher Effect, the Interest Rate, and the Exchange Rate Under

the Flexible-Price Monetary Approach

How a Rise in U.S. Monetary Growth Affects When Goods Prices are Flexible

1

R$1

Money demand,L(R$, YUS)

1'E1$/€

45° line

Dollar/euro exchange rate, E$/€

Rates of return(in dollar terms)

U.S. real money holdings

Dollar/euroexchangerate, E$/€

Initial expected return on euro deposits

Expected return on euro deposits after rise in expected dollar depreciation

E1$/€

M1US

P2US

E2$/€ 2'

M1US

P1US

PPP relation

Slide 15-7

Copyright © 2003 Pearson Education, Inc.

Slope = +

Slope = +

t0

MUS, t0

Slope =

(a) U.S. money supply, MUS

Time

Slope = Slope =

t0

Slope = +

t0

t0

R$2 = R$

1 +

R$1

Long-Run Time Paths of U.S. Economic Variables after a Permanent Increase in the Growth Rate of the U.S. Money Supply

(d) Dollar/euro exchange rate, E$/€

Time

(b) Dollar interest rate, R$

Time(c) U.S. price level, PUS

Time

A Long-Run Exchange Rate Model Based on PPP

Slide 15-8

Copyright © 2003 Pearson Education, Inc.

Inflation and Interest Rates in Switzerland, the United States, and Italy, 1970-2000

Slide 15-9

Copyright © 2003 Pearson Education, Inc.

Empirical Evidence on PPP and the Law of One Price: Weak Support … If Any

The Dollar/DM Exchange Rate and Relative U.S./German Price Levels, 1964-2000

Slide 15-10

Copyright © 2003 Pearson Education, Inc.

Trade barriers and nontradables. Transport costs and governmental trade restrictions make trade expensive and in some cases create nontradable goods.

Departures from free competition. e. g., pricing to market

International differences in price level measurement:

-- People living in different counties spend their incomes in different ways.

Explaining the Problems with PPP

Slide 15-11

Copyright © 2003 Pearson Education, Inc.

Explaining the Problems with PPP: Lower productivity in tradable goods sector lower wages, lower costs and prices of nontradables in poor countries

Price Levels and Real Incomes, 1992

Slide 15-12

Copyright © 2003 Pearson Education, Inc.

The Real Exchange Rate (q$/€): a summary measure of prices in one country relative to prices in another country.

q$/€ = (E$/€ x PE)/PUS

– Example: If the European reference commodity basket costs €100, the U.S. basket costs $120, and the nominal exchange rate is $1.20 per euro, then the real dollar/euro exchange rate is 1 U.S. basket per European basket

q$/€ UP Real depreciation of the $

– Either E$/€ UP: gotta pay more for euros

– or PE UP: gotta pay more for their stuff with E$/€ unchanged

– or PUS down: they pay less for our stuff with E$/€ unchanged

Beyond Purchasing Power Parity: A General Model of Long-Run Exchange Rates

Slide 15-13

Copyright © 2003 Pearson Education, Inc.

• In a world where PPP does not hold, the long-run values of real exchange rates depend on demand and supply conditions. The real exchange rate changes in response to:

– A change in world relative demand for American products

– A change in relative output supply

• Nominal and Real Exchange Rates in Long-Run Equilibrium

E $/€ = q$/€ x (PUS/PE)– From relative PPP, changes in national money supplies

and demands proportional long-run movements in nominal exchange rates and international price level ratios

– Changes in the long-run real exchange rate, however, also affect the long-run nominal exchange rate.

Beyond Purchasing Power Parity: A General Model of Long-Run Exchange Rates

Slide 15-14

Copyright © 2003 Pearson Education, Inc.

The most important determinants of long-run swings in nominal exchange rates (assuming that all variables start out at their long-run levels):• A shift in relative money supply levels

• A shift in relative money supply growth rates

• A change in relative output demand

• A change in relative output supply– When all disturbances are monetary in nature, exchange rates

obey relative PPP in the long run.

– When disturbances occur in output markets, the exchange rate is unlikely to obey relative PPP, even in the long run.

Beyond Purchasing Power Parity: A General Model of Long-Run Exchange Rates

Slide 15-15

Copyright © 2003 Pearson Education, Inc.

Beyond Purchasing Power Parity: A General Model of Long-Run Exchange Rates

Effects of Money Market and Output Market Changes on the Long-Run Nominal Dollar/Euro Exchange Rate, E$/€

Slide 15-16

Copyright © 2003 Pearson Education, Inc.

Beyond Purchasing Power Parity: A General Model of Long-Run Exchange Rates

Figure 15-5: The Real Dollar/Yen Exchange Rate, 1950-2000

Slide 15-17

Copyright © 2003 Pearson Education, Inc.

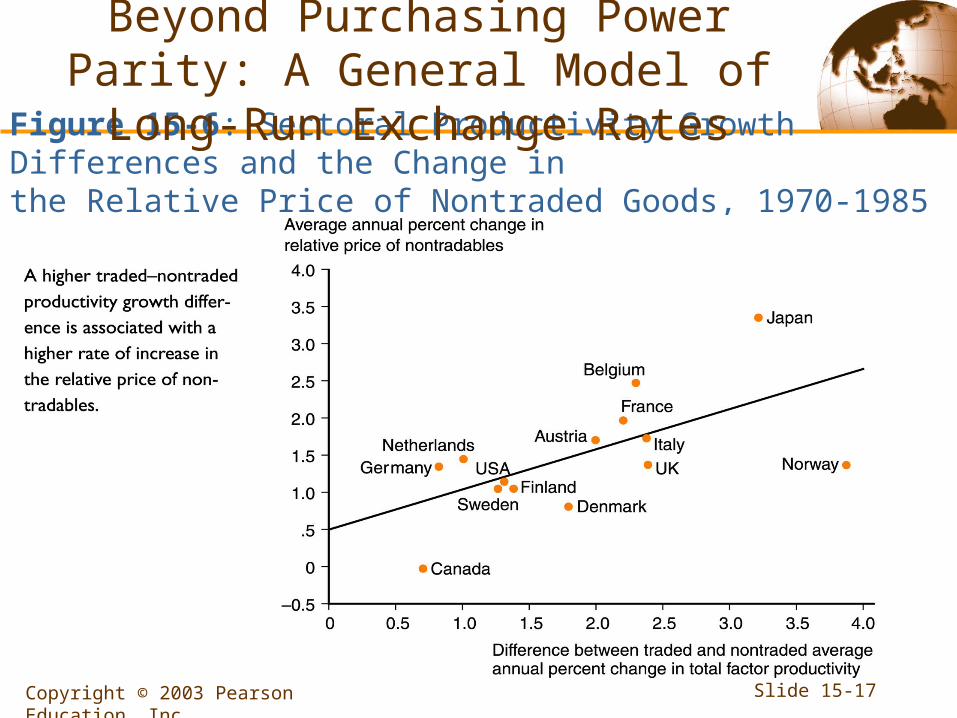

Figure 15-6: Sectoral Productivity Growth Differences and the Change in the Relative Price of Nontraded Goods, 1970-1985

Beyond Purchasing Power Parity: A General Model of Long-Run Exchange Rates

Slide 15-18

Copyright © 2003 Pearson Education, Inc.

The expected change in the real exchange rate, the expected change in the nominal rate, and expected inflation are related as follows. From q$/€ = (E$/€ x PE)/PUS

(qe$/€ - q$/€)/q$/€ = [(Ee

$/€ - E$/€)/E$/€] – (eUS - e

E)

From uncovered interest rate parity,

R$ - R€ = [(Ee$/€ - E$/€)/E$/€] = (qe

$/€ - q$/€)/q$/€ + (eUS - e

E)

• When the market expects relative PPP to prevail (no change in the real exchange rate) the dollar-euro interest difference is just the expected inflation difference between U.S. and Europe.

International Interest Rate Differences and the Real Exchange Rate

Slide 15-19

Copyright © 2003 Pearson Education, Inc.

Real Interest Parity

Expected real interest rate (re) = the nominal interest rate (R) less expected inflation rate (e).

The difference in expected real interest rates between the U.S. and Europe is:

reUS – re

E = (R$ - eUS) - (R € - e

E)

Since R$ - R€ = (qe$/€ - q$/€)/q$/€ + (e

US - eE)

(R$ - eUS) - (R € - e

E) = reUS – re

E = (qe$/€ - q$/€)/q$/€

Real Interest Parity: A real interest rate differential compensates for any expected real depreciation.

Slide 15-20

Copyright © 2003 Pearson Education, Inc.

Real Interest Parity: re

US – reE = (qe

$/€ - q$/€)/q$/€

Expected movements in real exchange rates differences in real interest rates

Real interest rates in different countries need not be equal, even in the long run, if continuing change in output markets is expected.

Slide 15-21

Copyright © 2003 Pearson Education, Inc.

Summary

Absolute PPP states that the purchasing power of any currency is the same in any country and implies relative PPP.

Relative PPP predicts that percentage changes in exchange rates equal differences in national inflation rates.

The law of one price is a building block of the PPP theory.• It states that under free competition and in the absence

of trade impediments, a good must sell for a single price regardless of where in the world it is sold.

Slide 15-22

Copyright © 2003 Pearson Education, Inc.

Summary

The monetary approach to the exchange rate uses PPP to explain long-term exchange rate behavior exclusively in terms of money supply and demand.• The Fisher effect predicts that long-run international

interest differentials result from different national rates of ongoing inflation.

The empirical support for PPP and the law of one price is weak in recent data.• The failure of these propositions in the real world is

related to trade barriers, departure from free competition and international differences in price level measurement.

Slide 15-23

Copyright © 2003 Pearson Education, Inc.

Summary

Deviations from relative PPP can be viewed as changes in a country’s real exchange rate.

A stepwise increase in a country’s money stock leads to a proportional increase in its price level and a proportional fall in its currency’s foreign exchange value.

The (real) interest parity condition equates international differences in nominal (real) interest rates to the expected percentage change in the nominal (real) exchange rate.

Related Documents