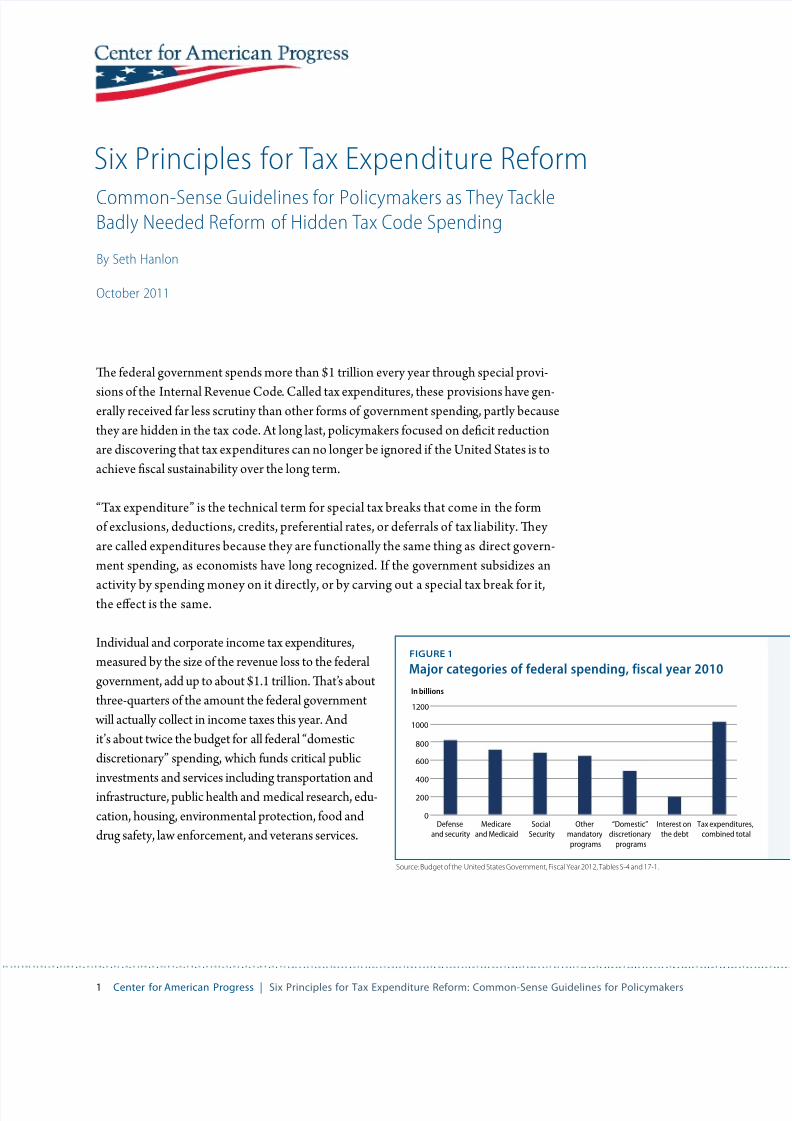

1 Center or American Progress | Six Principles or Tax Expenditure Reorm: Common-Sense Guidelines or Policymakers Six Principles for Tax Expen diture Reform Common-Sense Guidelines for Policymakers as They T ackle Badly Needed Reform of Hidden Tax Code Spending By Seth Hanlon October 2011 Te ederal governmen spends more han $1 rillion every year hrough special provi- sions o he Inernal Revenue Code . Called ax expendiures, hese provisions have gen- erally received ar less scruiny han oher orms o governmen spendin g, parly because hey are hidden in he ax code. A long las, policymakers ocused on deci reducion are discovering ha ax ex pendiures can no longer be ignored i he Unied Saes is o achieve scal susainabiliy over he long erm. “ ax expendiure” is he echnical erm or special ax breaks ha come in he orm o exclusions, deducions, credis, preeren ial raes, or deerrals o ax liabiliy. Tey are called expendiures because hey are uncionally he same hing as direc govern- men spending, as economiss have long recognized. I he governmen subsidizes an aciviy by spending money on i direcly, or by carving ou a special ax break or i, he eec is he same. Individual and corporae income ax expendiures, measured by he size o he revenue loss o he ederal governmen, add up o abou $1.1 ril lion. Ta’s abou hree-quarers o he amoun he ederal governmen will acually collec in income axes his year. And i’s abou wice he budge or all ederal “domesic discreionary” spending, which unds criical public invesmens and services including ransporaion and inrasrucure, public healh and medical research, edu- caion, housing, environmenal proecion, ood and drug saey, law enorcemen, and veerans services. Figure 1 Major categories o ederal spending, iscal year 2010 Source: Budget o the United States Government, Fiscal Year 2012, Tables S-4 and 17-1. 0 200 400 600 800 1000 1200 Defense and security Medicare and Medicaid Social Security Other mandatory programs “Domestic” discretionary programs Interest on the debt Tax expenditures, combined total In billions

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

8/3/2019 Six Principles for Tax Expenditure Reform

http://slidepdf.com/reader/full/six-principles-for-tax-expenditure-reform 1/11

1 Center or American Progress | Six Principles or Tax Expenditure Reorm: Common-Sense Guidelines or Policymakers

Six Principles for Tax Expenditure Reform

Common-Sense Guidelines for Policymakers as They TackleBadly Needed Reform of Hidden Tax Code Spending

By Seth Hanlon

October 2011

Te ederal governmen spends more han $1 rillion every year hrough special provi-

sions o he Inernal Revenue Code. Called ax expendiures, hese provisions have gen-erally received ar less scruiny han oher orms o governmen spending, parly because

hey are hidden in he ax code. A long las, policymakers ocused on deci reducion

are discovering ha ax expendiures can no longer be ignored i he Unied Saes is o

achieve scal susainabiliy over he long erm.

“ax expendiure” is he echnical erm or special ax breaks ha come in he orm

o exclusions, deducions, credis, preerenial raes, or deerrals o ax liabiliy. Tey

are called expendiures because hey are uncionally he same hing as direc govern-

men spending, as economiss have long recognized. I he governmen subsidizes an

aciviy by spending money on i direcly, or by carving ou a special ax break or i,he eec is he same.

Individual and corporae income ax expendiures,

measured by he size o he revenue loss o he ederal

governmen, add up o abou $1.1 rillion. Ta’s abou

hree-quarers o he amoun he ederal governmen

will acually collec in income axes his year. And

i’s abou wice he budge or all ederal “domesic

discreionary” spending, which unds criical public

invesmens and services including ransporaion and

inrasrucure, public healh and medical research, edu-

caion, housing, environmenal proecion, ood and

drug saey, law enorcemen, and veerans services.

Figure 1

Major categories o ederal spending, iscal year 2010

Source: Budget o the United States Government, Fiscal Year 2012, Tables S-4 and 17-1.

0

200

400

600

800

1000

1200

Defense

and security

Medicare

and Medicaid

Social

Security

Other

mandatory

programs

“Domestic”

discretionary

programs

Interest on

the debt

Tax expenditu

combined to

In billions

8/3/2019 Six Principles for Tax Expenditure Reform

http://slidepdf.com/reader/full/six-principles-for-tax-expenditure-reform 2/11

2 Center or American Progress | Six Principles or Tax Expenditure Reorm: Common-Sense Guidelines or Policymakers

Domesic discreionary spending has been hi hard by recen budge cus. Congress in

April chopped he budge auhoriy or his caegory by $39 billion in scal year 2011, a 7

percen cu rom las year’s levels. And in he recen agreemen ha ended his summer’s

deb limi crisis, Presiden Barack Obama and Congress cu nearly an addiional $1 rillion

rom discreionary spending over he nex 10 years, wih he heavies cus in he nonde-

ense caegory.

Under he so-called super commitee’s mandae, he nex round o deci reducion can

come rom any source. And so i is appropriae ha ax expendiures be on he able in

he super commitee’s deliberaions and in uure budge debaes. I’s jus as imporan

ha policymakers ge i righ when i comes o achieving deci reducion hrough ax

expendiure reorm. Tis issue brie oers six principles inended o guide hem:

• ax expendiures are spending.

• Like all orms o spending, ax expendiures should be assessed or cos eeciveness.

• “Upside-down” subsidies should be made more air and beter argeed.

• Eliminaing ax expendiures beneing seniors living on Social Securiy, working

amilies, and people wih very low incomes would be misguided.

• Te ax code should be scrubbed o ineecive business subsidies.

• Common-sense, scally responsible reorms o ax expendiures do no have o wai

or comprehensive ax reorm.

Tax expenditures are spending

Proposals o curail ax expendiures, including Presiden Obama’s, are oen widely

repored as “ax increases.” Bu economiss across he ideological specrum have long

recognized ha ax expendiures are really jus governmen spending ha happens o be

delivered hrough he ax code.

I he morgage ineres deducion, or example, were adminisered by he Deparmen

o Housing and Urban Developmen, and i operaed by sending homeowners checks

ha mach a porion o heir ineres paymens, i would be considered a spending pro-

gram. Bu because he morgage ineres deducion is acually adminisered by he IRS

and subsidizes homeownership hrough argeed ax benes, i is accouned or in he

ederal budge as a ax reducion.

Te disincion is mainly one o orm, no subsance, and i shouldn’ guide policymaking.

8/3/2019 Six Principles for Tax Expenditure Reform

http://slidepdf.com/reader/full/six-principles-for-tax-expenditure-reform 3/11

3 Center or American Progress | Six Principles or Tax Expenditure Reorm: Common-Sense Guidelines or Policymakers

Tis poin was underscored by a panel o prominen economiss and ax expers esiying

beore he Senae Finance Commitee on Sepember 13. As ormer Federal Reserve Board

Chairman Alan Greenspan old he senaors:

Cuts in tax expenditures can be alternatively structured, and viewed, as cuts in out-

lays rather than a reduction in revenues. Te deduction for interest on home mort-

gages, for example, could just as easily have been reconstituted as a subsidy payment to homeowners. Similarly, oil and gas depletion allowances could be restructured as

subsidies to producers.

Presiden Ronald Reagan’s chie economic advisor, Marin Feldsein, likewise esied ha

when ax expendiures are reduced, “he economic eec is he same as any oher reduc-

ion in governmen oulays.” And Edward Kleinbard, ormer direcor o Congress’s Join

Commitee on axaion, explained ha “deliberae Congressional subsidy programs baked

ino he ax code…are a orm o governmen spending, no ax reducions.”1

Once you recognize ha ax expendiures are simply a hidden orm o spending, i makes nosense o slash ederal programs and enilemens while leaving ax expendiures o he able.

Tis is especially rue because he Budge Conrol Ac, enaced in Augus, subjecs oher

crucially imporan ederal programs o signican cus in he coming years. Caps imposed

by he Budge Conrol Ac will cu discreionary spending by nearly $1 rillion over he

nex 10 years. Te resul is ha discreionary spending would decline rom 9 percen o

gross domesic produc, or GDP, o abou 6.2 percen by 2021, which, as Congressional

Budge Oce Direcor Douglas Elmendor noes, is “ well below he 8.7 percen average

over he pas 40 years.”2 Wih discreionary spending already subjec o hese caps, uure

deci reducion mus be balanced across he ederal budge, including on he revenue sideo he ledger. o be sure, he bes and mos sraighorward way o raise signican revenue

migh simply be o allow he Bush ax rae cus or op income earners expire on schedule

a he end o 2012. Bu even hose who are adaman abou keeping all ax raes where hey

are now should be open o reducing hidden ax code spending.

Ta doesn’ mean ax expendiure reorms need o happen now. Te op prioriy oday

should be job creaion, no deci reducion. And overly severe cus o ax expendi-

ures, like all scal conracion, should be avoided in he near erm while he economy

sruggles o recover. Bu lawmakers should pursue an approach ha gradually reorms or

phases ou ineecive ax expendiures.

8/3/2019 Six Principles for Tax Expenditure Reform

http://slidepdf.com/reader/full/six-principles-for-tax-expenditure-reform 4/11

4 Center or American Progress | Six Principles or Tax Expenditure Reorm: Common-Sense Guidelines or Policymakers

Like all forms of s pending, tax expenditures should be assessed for cost

effectiveness

When he governmen delivers ax preerences o cerain axpayers, i increases he

burden on all oher axpayers (or, given oday’s decis, on uure axpayers). Congress

mus hereore exercise jus as much diligence wih ax expendiures as i does wih

ederal programs ha spend money direcly.

Ta means ha each ax expendiure should be evaluaed or cos eeciveness. As

wih direc governmen spending programs, some ax expendiures are more eecive

han ohers. Some are vially imporan and some are waseul or poorly designed.

Some help low-income amilies work heir way ou o povery, while ohers pad he

pros o he larges companies in he world. We mus disinguish meriorious ax

expendiures rom waseul ones.

And ye he $1 ril lion in annual ax expendiure spending is rarely reviewed or eec-

iveness. Mos ax expendiures are permanen xures o he ax code, and some havelong oulased heir original purpose. Even ax expendiures ha have expiraion daes

are ypically renewed every year by Congress in he so-called “exenders” package wih

much less scruiny han is given o direc spending in he appropriaions process.

In CAP’s 2010 repor “Governmen Spending Undercover ,” Lily Bachelder and Eric

oder deailed a ramework or evaluaing ax expendiures. Tey suggesed our

undamenal quesions ha policymakers should consider in deciding which “IRS-

adminisered spending programs” o keep and which ones o cu:

•

Wha goals does he program poenially seek o achieve, i any?• Do hese goals remain worhy o axpayer suppor and i so, how much?• Wihin his budge consrain is he program srucured as eecively as i could be in

order o achieve is objecives?• I no, how could i be resrucured o maximize is eeciveness?

I Congress regularly sough answers o hese quesions, he ax expendiure budge

could be made much more ecien, reducing he deci by billions.

“Upside-down” subsidies should be made more fair and better targeted

Tough each ax expendiure should be evaluaed on is own meris, a large number o

ax expendiures share a common design faw ha reduces heir cos eeciveness. ax

expendiures ha aim o provide incenives hrough ax exclusions or deducions are

oen poorly argeed because o he so-called “upside-down” eec. Ta is, hey end o

provide he larges governmen subsidies o hose who need hem he leas while pro-

viding litle or no bene o hose who could use hem he mos. Tis happens because

deducions and exclusions are more valuable o hose in higher ax brackes.

8/3/2019 Six Principles for Tax Expenditure Reform

http://slidepdf.com/reader/full/six-principles-for-tax-expenditure-reform 5/11

5 Center or American Progress | Six Principles or Tax Expenditure Reorm: Common-Sense Guidelines or Policymakers

A prooypical example is he morgage ineres deduc-

ion. Tis $100 billion ax expendiure, whose purpose is

promoing homeownership, is undermined by is unair

and inecien design.

Consider: I a amily in he 15 percen ax bracke (wih

axable income beween $17,000 and $69,000) claimshe deducion, he governmen essenially maches 15

cens or every dollar in morgage ineres paid. Tus, a

amily wih $65,000 in income and $10,000 in morgage

ineres would derive $1,500 in savings rom he mor-

gage ineres deducion.

Bu or a amily in he highes 35 percen ax bracke

(wih axable income o $379,150 or above), he gov-

ernmen maches 35 cens or every dollar in morgage

ineres. So a amily wih $500,000 in income and$40,000 in morgage ineres derives $14,000 in ax sav-

ings—nearly 10 imes as much in dollar erms, and more

han wice as much as a percenage o each household’s

morgage ineres expense. (see able above)

Tis is a simplied example,3 bu i illusraes he

“upside-down” dynamic ha conribues o he morgage

ineres deducion being 10 imes more valuable in dollar

erms or he average high-income amily han he aver-

age middle-income amily.4

A similar eec happens wihoher ax expendiures, including reiremen and educaion savings

incenives and he chariable deducion. (see gure 2 a righ)

Besides being unair, upside-down ax expendiures are also inecien. Tey give he

bigges subsidies o he people who would mos likely ake he desired acion—buy a

house, save disposable income—even wihou he incenive.5

Tere are wo ways o addressing he upside-down eec, one incremenal and one more

comprehensive. Le’s ake hem in urn.

Te incremenal approach is o cap deducions a a cerain amoun, or example a 28

percen, as Presiden Obama has proposed in his annual budges and he American Jobs

Ac proposed in Sepember. Te 28 percen proposal reduces he upside-down eec

o he morgage ineres deducion and oher ax code subsidies by limiing he value o

he bene o wha axpayers in he 28 percen ax bracke receive.6 I wouldn’ aec he

middle-income amily in he example above—in ac, he proposal expressly exemps all

households wih adjused gross income under $200,000 ($250,000 or couples), very

The upside-down efect o the mortgage interest dedu

Middle-income

household

High-incom

household

Income $65,000 $500,000

Tax bracket 15 percent 35 percent

Mortgage interest paid $10,000 $40,000

Current value o subsidy or

mortgage interest

$1,500 (15 percent o

interest paid)

$14,000 (35 perc

interest paid

Value o subsidy or mortgage

interest under Obama proposal

on itemized deductions

$1,500 (15 percent) $11,200 (28 per

Figure 2

The upside-down eect o itemized deductions

Percent increase in ater-tax income rom itemized deductions

Source: http://www.urban.org/UploadedPDF/1001234_tax_expenditures.pd (table 2, with interactive ef

0

0.5

1

1.5

2

2.5

3

3.5

In percent

Bottom 20% Second 20% Middle 20% Fourth20% Top 20% Top 1%

8/3/2019 Six Principles for Tax Expenditure Reform

http://slidepdf.com/reader/full/six-principles-for-tax-expenditure-reform 6/11

6 Center or American Progress | Six Principles or Tax Expenditure Reorm: Common-Sense Guidelines or Policymakers

ew o whom are in ax brackes higher han 28 percen in any even. Te wealhier amily

in our example above would sill be eniled o a large morgage ineres deducion, bu he

value o ha deducion would be limied o 28 percen o he $40,000 i pays in morgage

ineres, or $11,200.7 Ta’s sill a much bigger housing subsidy han he middle-income

amily receives, even measured per dollar o morgageineres. Ye he 28 percen proposal

would be much airer han exising law and raise signican revenue.8

O course, 28 is no a magic number. Congress could raise revenue even by simply

keeping he maximum value o iemized deducions a he curren 35 percen while

allowing he op ax rae o rever o he Clinon-era 39.6 percen, as i is scheduled

o do in 2013. Ta opion would keep he marginal incenive provided by iemized

deducions or op-bracke axpayers (including or morgage ineres and chariable

giving) exacly where hey are now.

Te more comprehensive way o improve he airness and cos eciency o ax expen-

diures is o ransorm hem ino fa credis. Credis are beter argeed because hey

give he same bene, per dollar o expense, o axpayers in all brackes. Te Cener or American Progress, in is recen long-erm balanced budge plan, “Budgeing or Growh

and Prosperiy ,” proposed o ransorm deducions or morgage ineres, chariable deduc-

ions, and reiremen savings ino fa credis over ime.

Te repor o he co-chairs o he presiden’s deci commission (known as “Bowles-

Simpson”) likewise proposed o urn iemized deducions ino 12 percen ax credis,

maching he botom-bracke ax rae under he co-chairs’ “illusraive” plan.9 Ta is, i you

pay $1,000 in morgage ineres, you could reduce your ax bill by $120, regardless o your

ax bracke. Tis would give he same ax bene o amilies in he lowes ax bracke as o

all oher amilies. Te Biparisan Policy Cener’s Deb Reducion ask Force would simi-larly replace iemized deducions wih 15 percen reundable ax credis. (A “reundable”

credi means i can also bene people wih no ederal income ax liabiliy.)

• Eliminaing ax expendiures beneing seniors living on Social Securiy, working

amilies, and people wih very low incomes would be misguided.

Sirred up by he pernicious myh ha many Americans have no “skin in he game”

because hey don’ pay axes, some have suggesed ha a cenral goal o ax code reorm

should be increasing he number o households ha have ederal income ax liabiliy in any

given year. (see box on page 8)

Presidenial candidae Jon Hunsman, or example, recenly proposed o sweep away all ax

expendiures on he heory ha “he ax burden is carried by oo ew.” Tis conuses he

desirable goal o broadening he income ax base wih he misguided noion ha everyone,

every year, should owe ederal income axes in addiion o he axes hey already pay.

8/3/2019 Six Principles for Tax Expenditure Reform

http://slidepdf.com/reader/full/six-principles-for-tax-expenditure-reform 7/11

7 Center or American Progress | Six Principles or Tax Expenditure Reorm: Common-Sense Guidelines or Policymakers

In ac, he kinds o people who have ederal income ax liabiliy in any paricular year

end o be seniors living on Social Securiy, working amilies wih children, and people

wih very low incomes (including he unemployed, disabled, and ull-ime sudens).

Tese people are among he leas able o aord o pay more in axes. Bu i you sar

wih he misdiagnosis ha hey don’ pay enough in axes, hen your misguided remedy

would be o arge ax expendiures ha bene hem. Tese include, mos prominenly:

• Tax exclusion of Social Security benefits. Mos Social Securiy benes are excluded

rom ederal income axes, and his reamen is considered a ax expendiure. For

example, a reired couple receiving he average annual Social Securiy bene o

$22,884 would currenly owe no ederal income axes unless hey had a subsanial

amoun o oher income (which mos seniors do no).10 A ull 93 percen o he ben-

e o he nonaxaion o Social Securiy benes accrues o households wih incomes

under $75,000. Te larges bene, as a share o income, goes o households earning

beween $20,000 and $50,000 in income.11 Tese households would be hi hardes i

his ax expendiure were eliminaed.

• Earned income tax credit. Te EIC is a reundable ax credi or low-income working

individuals and amilies. I is designed o encourage work while oseting he impac

o income, payroll, and oher axes as well as he cos o child care. I is one o he ed-

eral governmen’s mos successul iniiaives o enable low-income workers o join he

workorce and reduce welare reliance, which is why i has hisorically enjoyed very

broad biparisan suppor. Presiden Reagan called i he “bes ani-povery, he bes

pro-amily, he bes job creaion measure o come ou o Congress.” Te EIC lied

5.4 million people ou o povery in 2010, including 3 million children.

• Child tax credit. Enaced under Presiden Clinon and expanded under Presidens

George W. Bush and Obama, he child ax credi lowers he ax burden or amilies

raising children. I provides a parially reundable ax credi or low- and middle-

income amilies o up o $1,000 per child. In recognizing ha amilies wih more

mouhs o eed have greaer nancial burdens, he child ax credi urhers he ideal

o a ax sysem ha is based on abiliy o pay. Te reundable aspec o he child ax

credi enables low-income amilies o bene while also encouraging work; because is

benes are phased in wih earned income, you have o work o claim i.

Slashing hese ax expendiures would creae enormous hardship or seniors and work-

ing amilies. While hey have he eec o pushing some people o he ederal income

ax rolls (people who would owe only a litle income ax anyway), i’s criical o remem-

ber ha on he whole, ax expendiures provide much bigger benes o high-income

households, boh in absolue dollar erms and relaive o heir incomes, largely because

o he upside-down problem discussed above.12 Reducing or eliminaing broad-based

ax expendiures beneing low- and moderae-income amilies would make he ax

code less air, no more.

8/3/2019 Six Principles for Tax Expenditure Reform

http://slidepdf.com/reader/full/six-principles-for-tax-expenditure-reform 8/11

8 Center or American Progress | Six Principles or Tax Expenditure Reorm: Common-Sense Guidelines or Policymakers

Fact No. 1: All Americans pay taxes

The ederal income tax is only one part o an overall tax system supporting

government services at ederal, state, and local levels. The ederal income

tax raises only about 30 percent o all tax revenue, and only 45 percent

o ederal tax revenue. The idea that some households pay “no taxes” is

simply alse because it ignores all other taxes, including payroll, sales,

corporate income, property, and excise taxes.

Taking these taxes into account, all households pay taxes. Everyone

has “skin in the game.” Even the poorest one-th o Americans, withincomes averaging $12,500 per year, paid about one-sixth o their ex-

tremely modest incomes in taxes in 2010, on average. The next-poorest

group, with incomes averaging $25,300, paid more than one-th o

their income in taxes. And no one is getting skinned. The most ortunate

1 percent, with average incomes o $1.25 million, pay 30 percent o their

income in taxes—not much more than the 25.1 percent paid by those in

the middle.13

Fact No. 2: The ederal income tax was never supposed to be paid by every

American every year

Though all households pay a signicant amount in taxes every year, not

every household pays every kind o tax every year. The ederal income

tax is not intended to be a per-person “head tax.” It raises revenue based

on ability to pay. By the very nature o an income tax, people tend to pay

it during their prime income-earning years—not in years when they are

in school, out o work, or retired. And because people with low levels o

income have the least ability to pay ederal income taxes, they generally

aren’t required to do so. This is by design, and it is not an “injustice.” In

act, while many conservatives today seem to want to shit more o the tax

burden down the income ladder, both President Ronald Reagan and Presi-

dent George W. Bush trumpeted the importance o removing the working

poor rom the income tax rolls.14

In a typical year, about 35 percent to 40 percent o households will not

owe ederal income tax.15 That gure is higher at times o high unemplo

ment, which is why it has risen to an estimated 46 percent this year.16

Further, two-thirds o the households who do not owe ederal income

taxes will pay ederal payroll taxes. Only 18 percent o households, the

majority o them occupied by the elderly, will owe neither ederal incom

nor payroll taxes.17

Fact No. 3: People who don’t pay ederal income tax in a typical year tend

be seniors living on Social Security, people with very low levels o income

including the unemployed, and working amilies with children

A recent analysis by the nonpartisan Tax Policy Center provides a clear p

ture o why some households will not have ederal income tax liability th

year. All policymakers who have expressed concern that too ew people

owe ederal income taxes should read it.

O the taxpayers who do not owe ederal income taxes because o tax ex

penditures, the largest group (44 percent) are seniors. Most elderly tax

ers do not owe ederal income tax, primarily because most Social Securit

benets are exempt rom taxation.18 The next-largest group is low-incom

working amilies with children. That’s because the United States supportworking amilies through the earned income tax credit and child tax

credit. These credits are vitally important to millions o amilies and have

traditionally enjoyed broad bipartisan support.

The Tax Policy Center’s report ound that the biggest reason some house

holds do not owe ederal income taxes in any given year is that they hav

very little income (including laid-of workers, students, the disabled, and

retirees). A third o those with no ederal income tax liability have less th

$10,000 in cash income and 62 percent have less than $20,000 (includin

Social Security and other government benets).19 The basic structure o

the income tax “exempts subsistence levels o income,” as the Tax Policy

Center’s Roberton Williams explains.20

Debunking the myth o the “nontaxpayer”

8/3/2019 Six Principles for Tax Expenditure Reform

http://slidepdf.com/reader/full/six-principles-for-tax-expenditure-reform 9/11

9 Center or American Progress | Six Principles or Tax Expenditure Reorm: Common-Sense Guidelines or Policymakers

And because he earned income ax credi and child ax credi are broad-based provi-

sions ha enable and encourage work, reducing or eliminaing hem would be eco-

nomically inecien. In his respec, i is imporan ha hey be disinguished rom he

narrow and inecien ax expendiures like he myriad subsidies or specic indusries.

The tax code should be scrubbed of ineffective business subsidies

Te ax code is sued wih abou $130 billion in annual ax expendiures beneing

businesses or indusries.21 Te approximaely $100 billion in annual corporae ax

expendiures represens a signican share (one-quarer o one-hal) o al l corporae

ax revenues. Indeed, ax expendiures help explain why he Unied Saes collecs

relaively litle revenue rom corporae income axes by inernaional sandards, even

hough our sauory corporae ax rae is relaively high.

Some business ax subsidies are paricularly indeensible. Te oil indusry is he

beneciary o more han $4 billion in annual ax code spending. wo o he majorsubsidies in he ax code—expensing o inangible drilling coss and “percenage

depleion”—were enaced in 1916 and 1926, respecively, a a ime when oil explora-

ion was a fedgling indusry. oday, he oil and gas indusry is a maure, exremely

proable indusry enjoying record pros rom high gas prices. I does no need

axpayer incenives o do wha i already does.

Anoher egregious example is he “carried ineres” loophole.22 By exploiing ha loop-

hole, hedge und and privae equiy und managers—some o he riches people on he

plane—can cu he ax rae on much o heir compensaion rom he op ordinary ax

rae o 35 percen o he preerenial capial gains rae o 15 percen. Tere’s no reason osubsidize nancial proessions ha are already among he mos lucraive.

Te ax code includes innumerable smaller subsidies ha disor he choices made by

businesses. A now-inamous example is he ax reamen o corporae jes. Companies

can wrie o he coss o hese purchases over ve years, even hough passenger jes

mus be depreciaed over seven years—and he planes acually las or decades.23

Corporae je wrie-os are no he larges ax subsidy. Tey are esimaed o cos he

governmen “only” $4.7 billion over 10 years.24 Bu hey have become symbolic o he

way he ax code plays avories. Similarly subsidized oher indusries include horse

breeding, lm and elevision producion, and racerack consrucion.25

Te criical quesion is no wheher he secors ha receive special ax breaks suppor

jobs or economic aciviy—o course hey do—bu wheher here is a srong enough

public policy reason o give hem axpayer subsidies no available o oher businesses. A

useul ramework or evaluaing special ax provisions is wheher, i hey were srucured

as direc spending programs, hey would make economic sense or represen he bes

8/3/2019 Six Principles for Tax Expenditure Reform

http://slidepdf.com/reader/full/six-principles-for-tax-expenditure-reform 10/11

10 Center or American Progress | Six Principles or Tax Expenditure Reorm: Common-Sense Guidelines or Policymakers

use o axpayer dollars. For example, i i does no make sense or he governmen o pay

companies direcly o drill or explore or oil, hen he governmen shouldn’ be doing he

economic equivalen hrough he ax code.

Common-sense, fiscally responsible reforms to tax expenditures do not

have to wait for comprehensive tax reform

Deenders o waseul or inecien ax expendiures oen asser ha any changes should

only be considered in he conex o overall ax reorm. Invoking he prospec o a uure

ax code overhaul les everyone bene rom he saus quo while appearing pro-reorm.

Beneciaries sugges a willingness o give up heir ax breaks i everyone else does, and

poliicians can pose as ax reormers wihou having o ideniy whose ax breaks hey’d

close.26 Te resul is ha ough choices on ax expendiures are avoided, while direc gov-

ernmen spending programs ace he budge ax.

Comprehensive ax reorm is a desirable goal. Te ax code is badly in need o an overhaulo broaden he ax base. Bu sweeping ax reorm may no happen or many years. Te las

comprehensive ax code overhaul was a quarer-cenury ago, in he ax Reorm Ac o

1986. Ta legislaion was enaced only aer several years o wiss and urns and is now

viewed as a singularly rare accomplishmen.27

Policymakers oday universally agree on he need or “ax reorm,” bu here is enormous

disagreemen over such undamenal quesions as wheher ax reorm should raise, hold

consan, or lower revenues (o say nohing o which revenue benchmarks o use) and

wheher he overall ax burden should be made more or less progressive han i is now.28

Given hese realiies, here is no good reason o exemp ax expendiures rom ongoing

eors o reduce long-erm decis. Jus because a waseul subsidy is echnically a ax

break does no mean ha i can only be deal wih hrough overarching ax reorm. Tere

are many ways o reorm ax expendiures o reduce heir budge cos or eliminae he

leas jusiable ones. None o hese opions would preclude a laer, more undamenal ax

reorm. And eliminaing he mos waseul ax expendiures could make undamenal ax

reorm more likely by reducing he number o indusries wih vesed ineress o proec.

Many policymakers have over he las year come o recognize ha any credible and bal-

anced approach o addressing he Unied Saes’ long-erm scal challenges mus include

signican ax expendiure reorms. By adhering o he principles oulined in his issue

brie, policymakers can increase he airness and cos eciency o ax expendiures while

balancing our shor-erm economic challenges and long-erm scal challenges.

Seth Hanlon is Director of Fiscal Reform for the Doing What Works project at American Progress.

8/3/2019 Six Principles for Tax Expenditure Reform

http://slidepdf.com/reader/full/six-principles-for-tax-expenditure-reform 11/11

11 Center or American Progress | Six Principles or Tax Expenditure Reorm: Common Sense Guidelines or Policymakers

Endnotes

1 “Examining Whether There is a Role or Tax Reorm in Comprehensive Decit Reduction and U.S. Fiscal Policy,” Senate Finance Committee Hearing, Sep-tember 13, 2011, available at http://nance.senate.gov/hearings/hearing/?id=a6c20c-5056-a032-521e-b4d151014e97.

2 “Discretionary Spending Under the Budget Control Act o 2011,” Congressional Budget Oce, Director’s Blog, (August 8, 2011), available at http://cbob-log.cbo.gov/?p=2597.

3 These gures do not take into account the “Pease” limitation on itemized deductions, which is currently repealed but is scheduled to go back into efectin 2013 under current law, or the separate calculation required under the Alternative Minimum Tax. It also assumes that both households itemize theirdeductions.

4 The skewed distribution o the mortgage interest deduction also results rom the act that upper-income households tend to have larger mortgagepayments, and interest is deductible on up to $1.1 million in mortgage debt. Households with incomes between $200,000 and $500,000 derive an aver-age benet o $3,572, while households with incomes between $50,000 and $75,000 derive an average benet o $364, according to estimates in: “TaxBenets o the Mortgage Interest Deduction, Basel ine: Current Law; Distribution o Federal Tax Change by Cash Income Level, 2011,” available at http://www.taxpolicycenter.org/numbers/displayatab.cm?Docid=3146&DocTypeID=1. These are roughly consistent with other estimates. See: Seth Hanlon,“Tax Expenditure o the Week: The Mortgage Interest Deduction,” Center or American Progress, January 26, 2011.

5 For more detailed discussions o the ineciency o upside-down tax expenditures, see: Lily L. Batchelder, Fred T. Goldberg, Jr., and Peter R. Orszag,“Reorming Tax Incentives into Uniorm Reundable Tax Credits,” (Washington: Brookings Institution, 2006), availabl e at http://www.brookings.edu/papers/2006/08taxes_orszag.aspx; Lily Batchelder and Eric Toder, “Government Spending Undercover” (Washington: Center or American Progress, 2010),available at http://www.americanprogress.org/issues/2010/04/pd/govspendingundercover.pd .

6 The proposal applies to itemized deductions as well as certain other tax expenditures that take the orm o “above-the-line” deductions and exclusions,including exclusions or employer-sponsored health insurance, municipal bond interest, and oreign-earned income and certain other business, healthcare, and education-related deductions.

7 Or 39.6 percent, as would be the case in 2013 under current law, under which the high-income Bush tax cuts are scheduled to expire.

8 I applied only to itemized deductions, it is estimated to raise $321 billion; applied to a broader set o deductions and exclusions (as President Obama hasproposed in the American Jobs Act), it would raise $405 billion.

9 National Commission on Fiscal Responsibility and Reorm, “The Moment o Truth” (2010), available at http://www.scalcommission.gov/news/moment-truth-report-national-commission-scal-responsibility-and-reorm.

10 Social Security benets are entirely exempt or households with “provisional income” below $25,000. Provisional income includes adjusted gross income plusone-hal o Social Security benets plus some otherwise tax-exempt income. See: Internal Revenue Service, “Social Security and Equivalent Railroad Retire-ment Benets” (2010), available at http://www.irs.gov/pub/irs-pd/p915.pd .

11 “Tax Benets o Partial Exclusion or Social Security Benets, Baseline: Current Law; Distribution o Federal Tax Change by Cash Income Level, 2011,” avail-able at http://www.taxpolicycenter.org/numbers/displayatab.cm?Docid=3140&DocTypeID=1.

12 Leonard Burman, Eric Toder, and Christopher Geissler, “How Big Are Total Individual Tax Expenditures, and Who Benets rom Them” (Washington: TaxPolicy Center, 2008), p. 10–13.

13 Figures are based on the Institute on Taxation and Economic Policy Tax Model, which includes all ederal, state, and local taxes (personal and corporateincome, payroll, property, sa les, excise, estate, etc.). See: Citizens or Tax Justice, “America’s Tax System Is Not as Progressive as You Think” (2011), availableat http://www.ctj.org/pd/taxday2011.pd . Even taking only ederal income taxes into account, the poorest 20 p ercent o households pay 4 percent o their incomes in taxes according to the Congressional Budget Oce. See: Congressional Budget O ce tables, available at http://cbo.gov/publications/collections/tax/2010/all_tables.pd .

14 President Ronald Reagan, “Letter to Members o the House o Representatives Urging Support or Tax Reorm Legislation,” December 9, 1985; PresidentGeorge W. Bush, Address to Congress, February 27, 2001.

15 Chuck Marr and Brian Highsmith, “Misconceptions and Realities About Who Pays Taxes” (Washington: Center on Budget and Policy Priorities, 2011); “TaxUnits with Zero or Negative Tax Liabilit y, 2004-2008,” available at http://www.taxpolicycenter.org/numbers/Content/PDF/T09-0412.pd; “Tax Units withZero or Negative Tax Liabili ty, 2012-2022,” available at http://www.taxpolicycenter.org/numbers/displayatab.cm?Docid=3055&DocTypeID=7.

16 Rachel Johnson and others, “Why Some Tax Units Pay No Income Tax” (Washington: Urban-Brookings Tax Policy Center, 2011).

17 “Who Doesn’t Pay Federal Taxes?”, available at http://www.taxpolicycenter.org/taxtopics/ederal-taxes-households.cm.

18 “Percentage o Tax Units that Pay No Individual I ncome Tax by Filing Status and Cash Income Level, Current Law, 2011-2013,” available at http://www.taxpolicycenter.org/numbers/displayatab.cm?Docid=3106&DocTypeID=1.

19 Johnson and others, “Why Some Tax Units Pay No Income Tax.” The Tax Policy Center’s denition o cash income can be ound here: “The Numbers,” avail-able at http://www.taxpolicycenter.org/numbers/displayatab.cm?DocID=574.

20 The sum o the personal exemption and standard deduction means that an individual’s rst $9,500 in income, and a couple’s rst $19,000, are not subjectto ederal income taxes (though they are subject to payroll taxes). See: Ro berton Williams, “Why Do People Pay No Federal Income Tax?”, TaxVox, July 27,2011, available at http://taxvox.taxpolicycenter.org/2011/07/27/why-do-people-pay-no-ederal-income-tax-2/.

21 President’s Economic Recovery Advisory Board, “The Report on Tax Reorm Options: Simplication, Compliance, and Corporate Taxation” (2010).

22 The carried interest loophole is a component o the larger tax expenditure that provides preerential tax rates on capital gains.

23 Richard Rubin and Andrew Zajac, “Corporate Jet Tax Gets Six Obama Mentions, Nicks Decit,” Bloomberg, June 30, 2011.

24 Oce o Management and Budget, “Living Within Our Means and Investing in the Future” (2011).

25 IRC sections 168(e)(3)(A), 168(e)(3)(C)(ii), 181, 199(c)(6).

26 John M. Broder, “Oil Executives, Deending Tax Breaks, Say They’d Cede Them i Everyone Did,” The New York Times, May 12, 2011, available at http://www.nytimes.com/2011/05/13/business/13oil.html; Eric Toder, “Ryan’s Tax Plan is not 1986-Style Reorm,” TaxVox, April 12, 2011, available at http://taxvox.taxpolicycenter.org/2011/04/12/ryan%E2%80%99s-tax-plan-is-not-1986-style-reorm/.

27 Jefrey H. Birnbaum and Alan S. Murray, Showdown at Gucci Gulch: Lawmakers, Lobbyists, and the Unlikely Triumph of Tax Reform (1987).

28 For a discussion o the daunting obstacles to 1986-style tax reorm in the present context, see: Daniel N Shaviro, “1986-Style Tax Reorm: A Good IdeaWhose Time H as Passed,”Tax Notes, May 23, 2011.

Related Documents