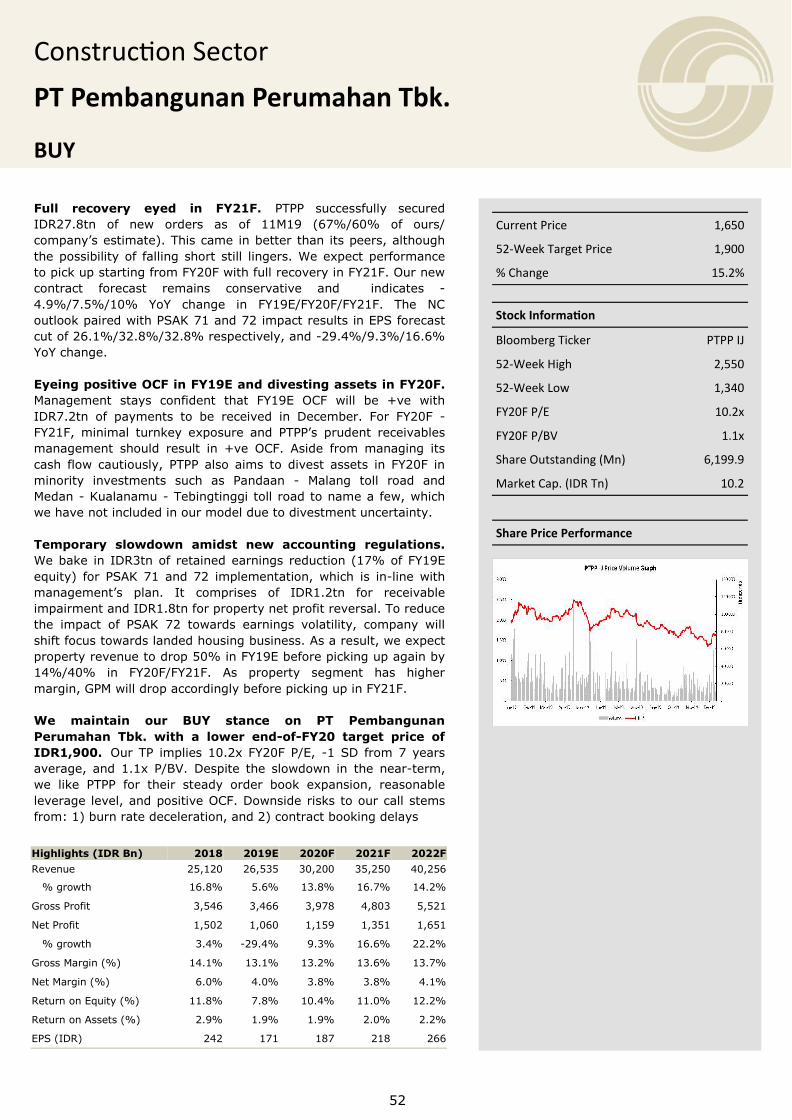

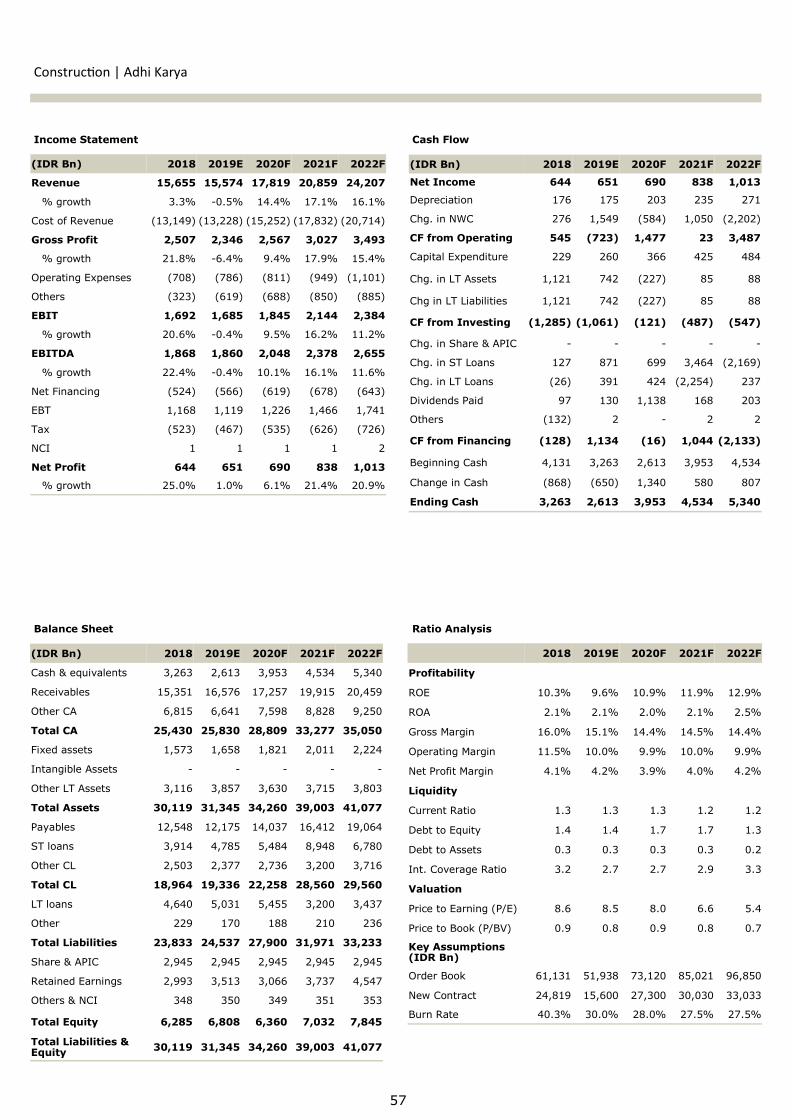

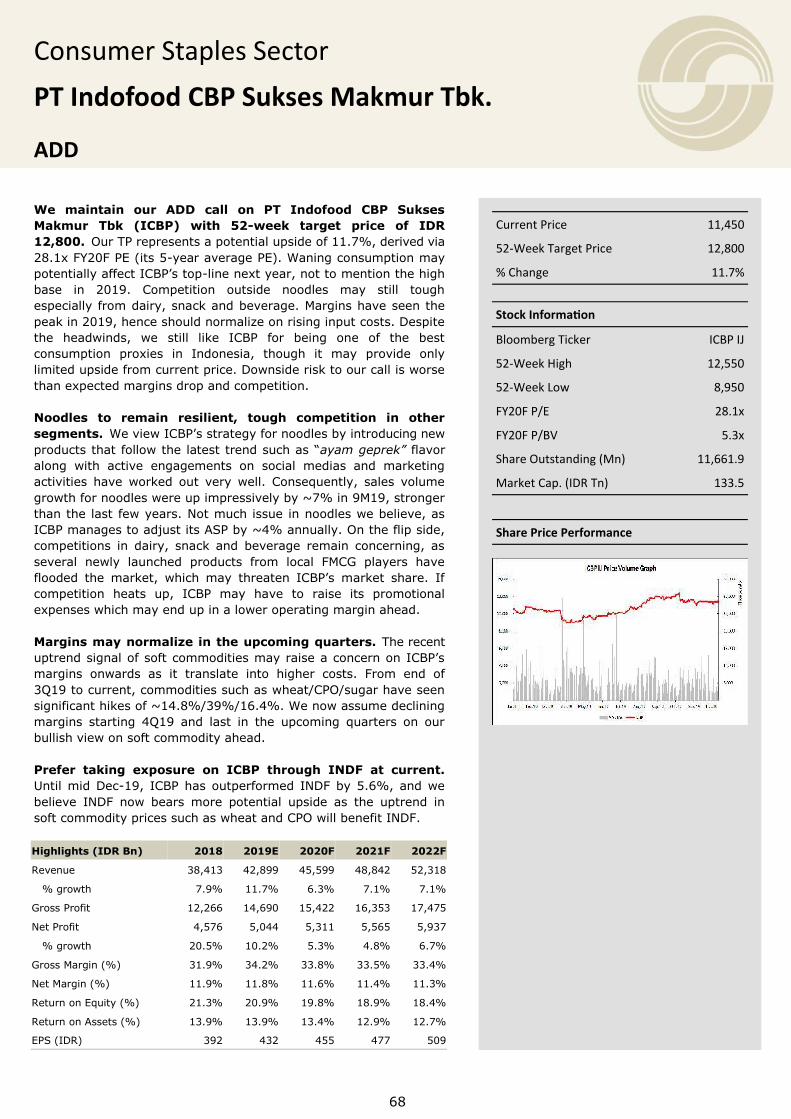

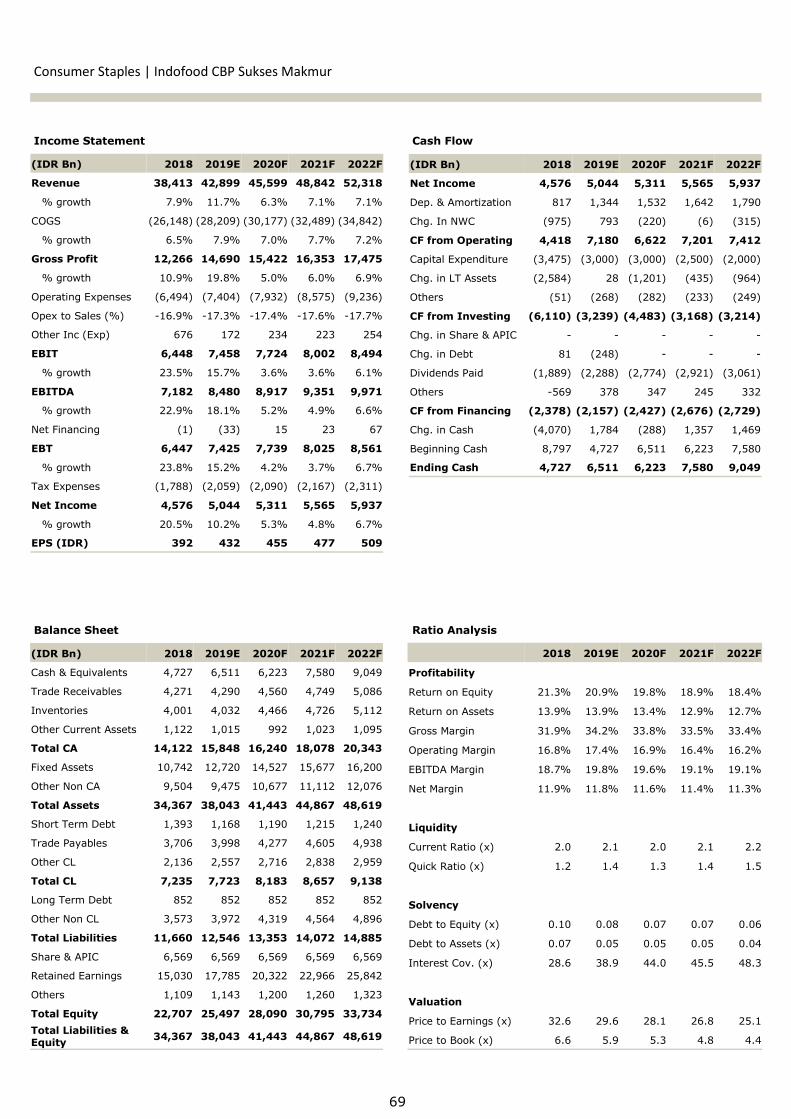

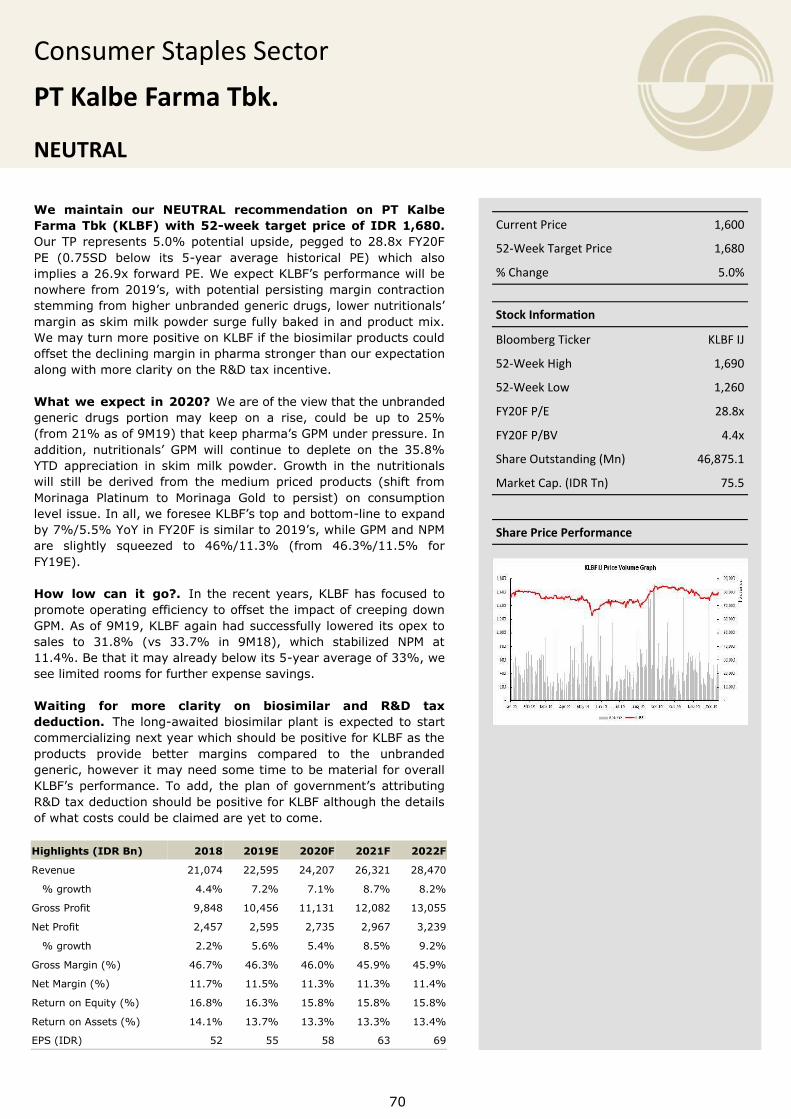

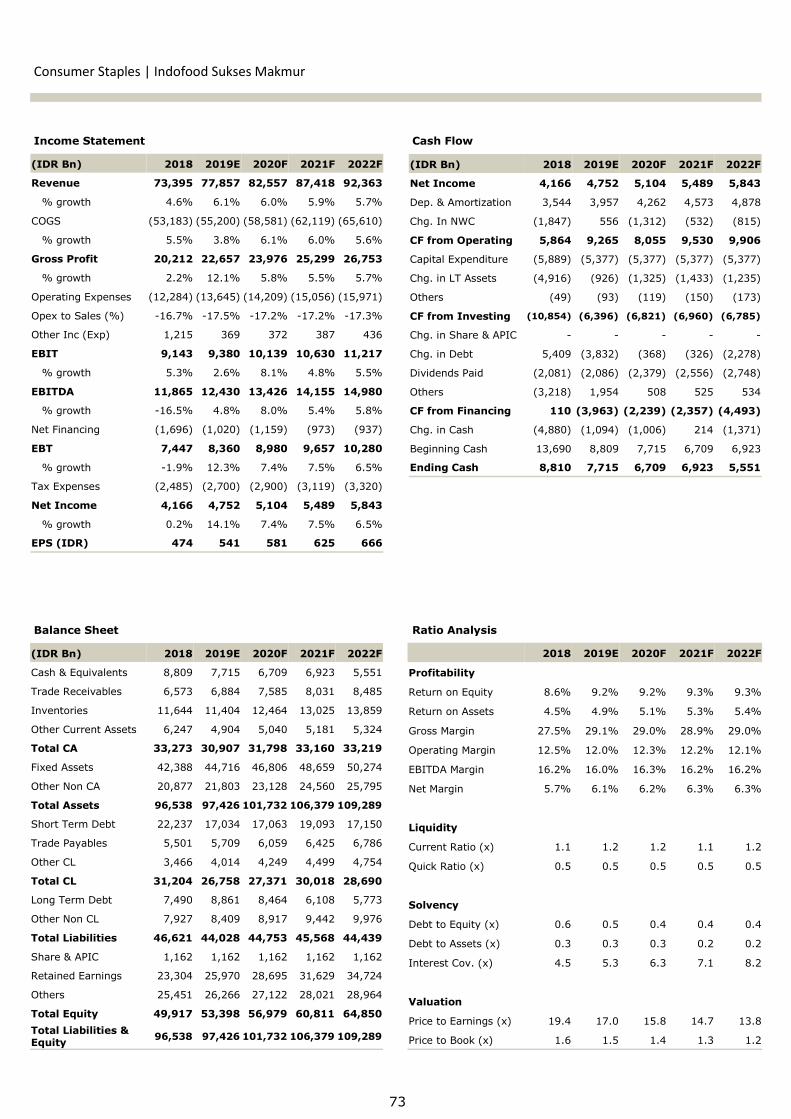

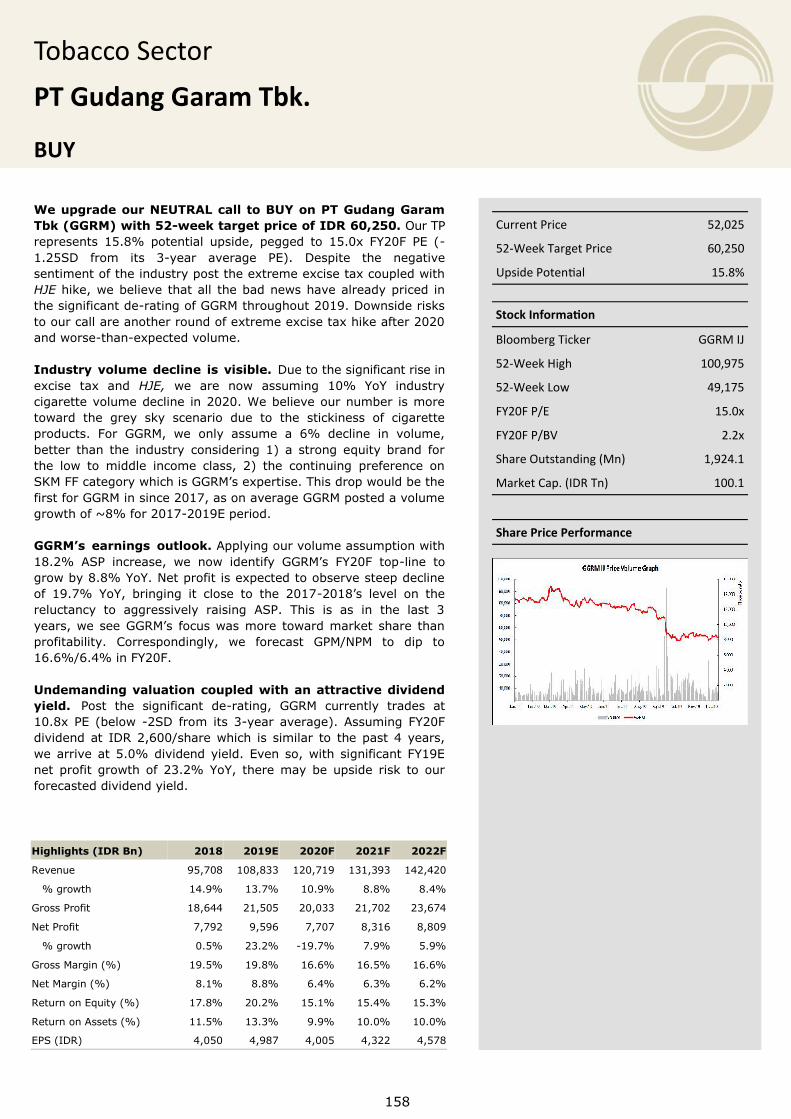

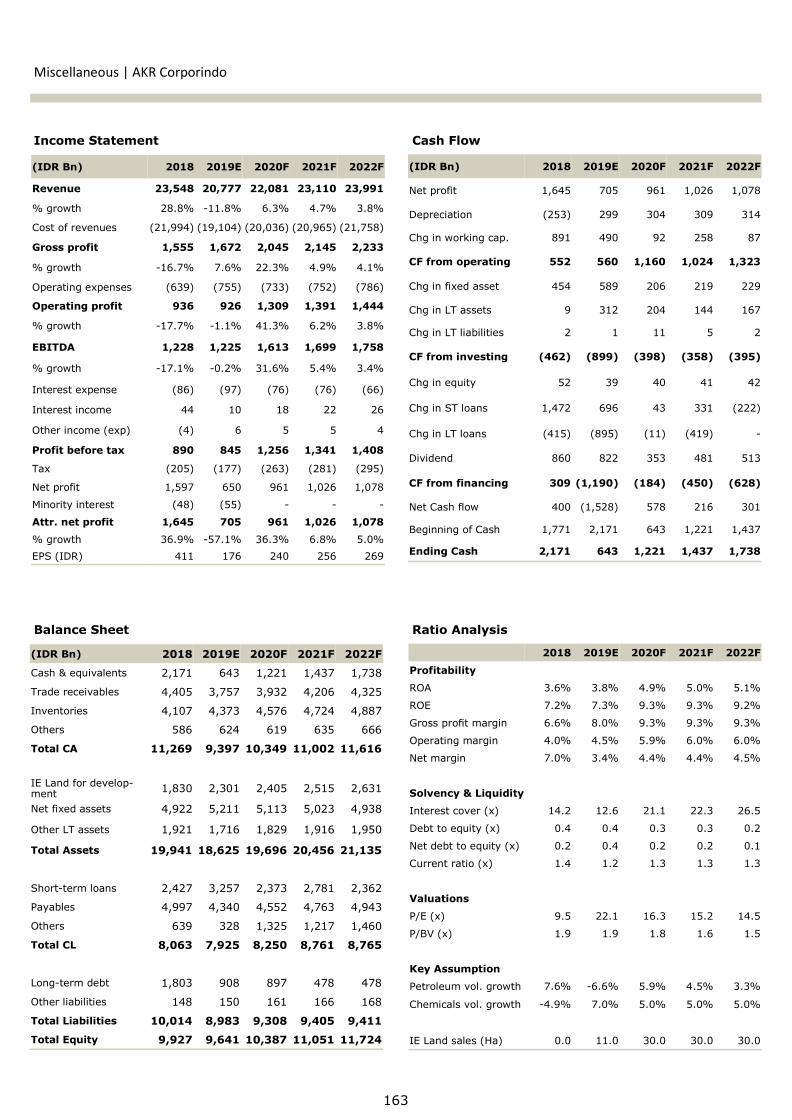

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

^ŝŶĂƌŵĂƐ^ĞŬƵƌŝƚĂƐŽŶƚĞŶƚƐ

&RQWHQWV 0DUNHW2XWORRN 6WDEOH%XOO<HDU

%DQNLQJ $XWRPRWLYH

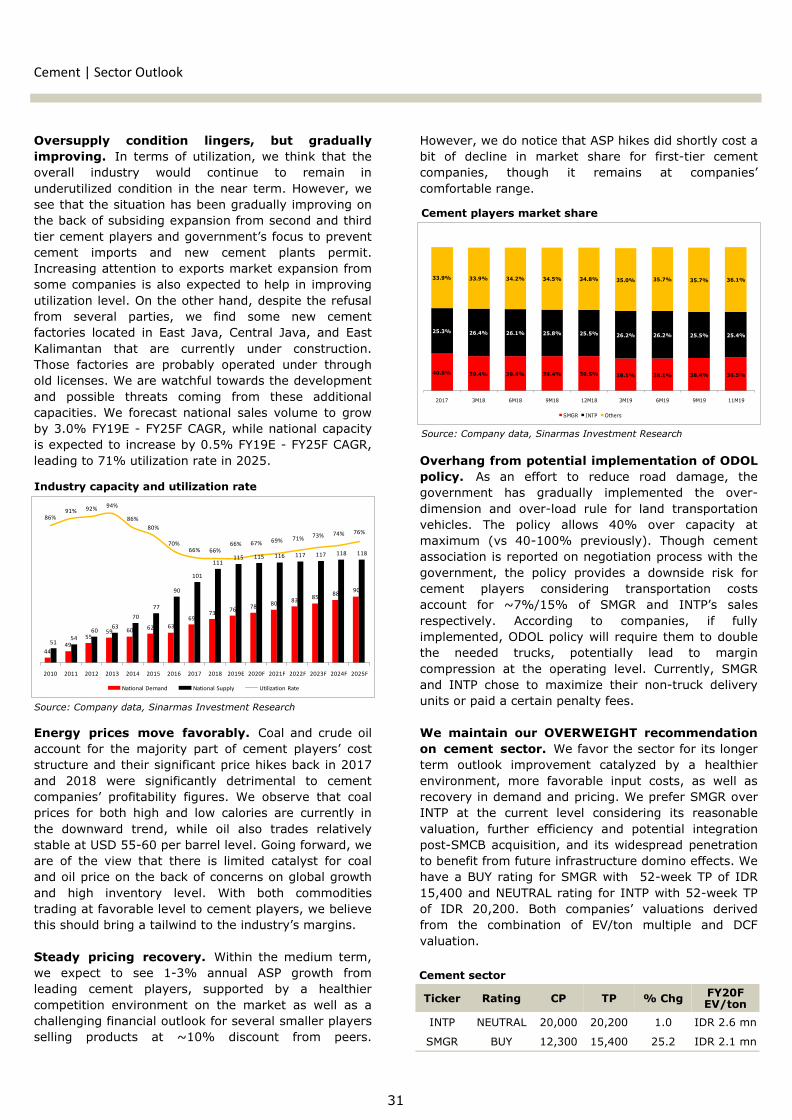

&HPHQW

&RDO0LQLQJ

&RQVXPHU &RQVWUXFWLRQ

,QGXVWULDO (VWDWH

0HGLD

0HWDO

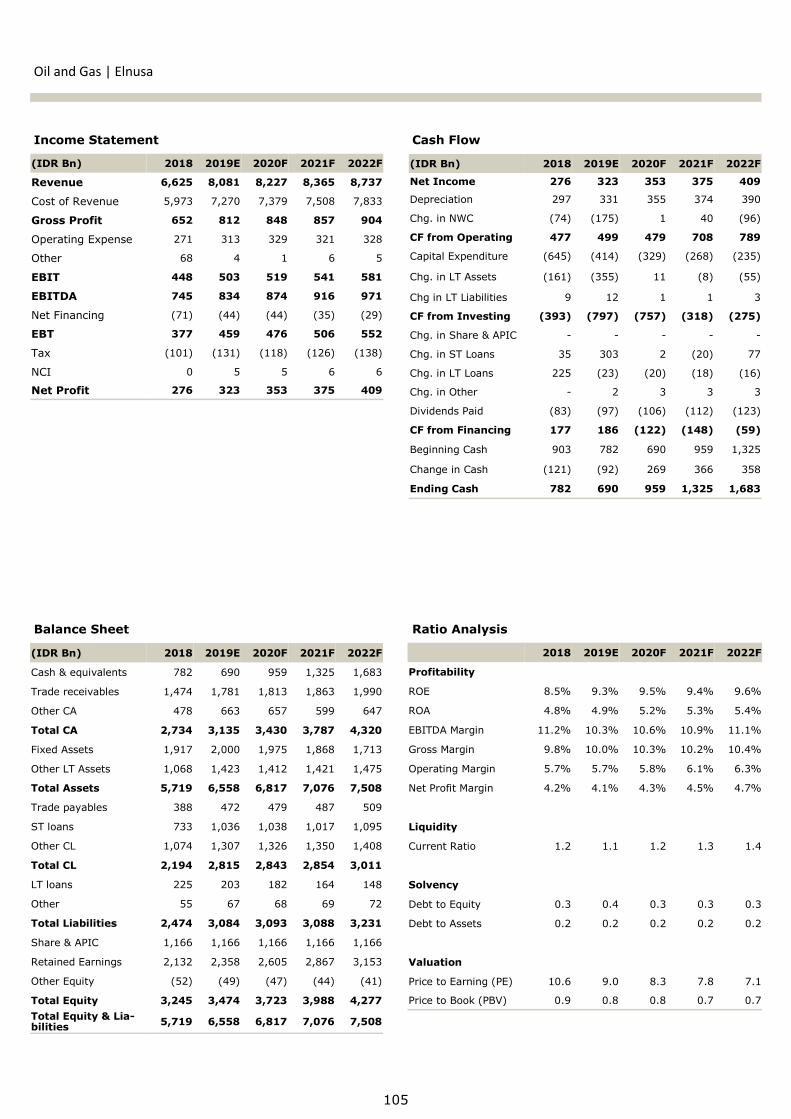

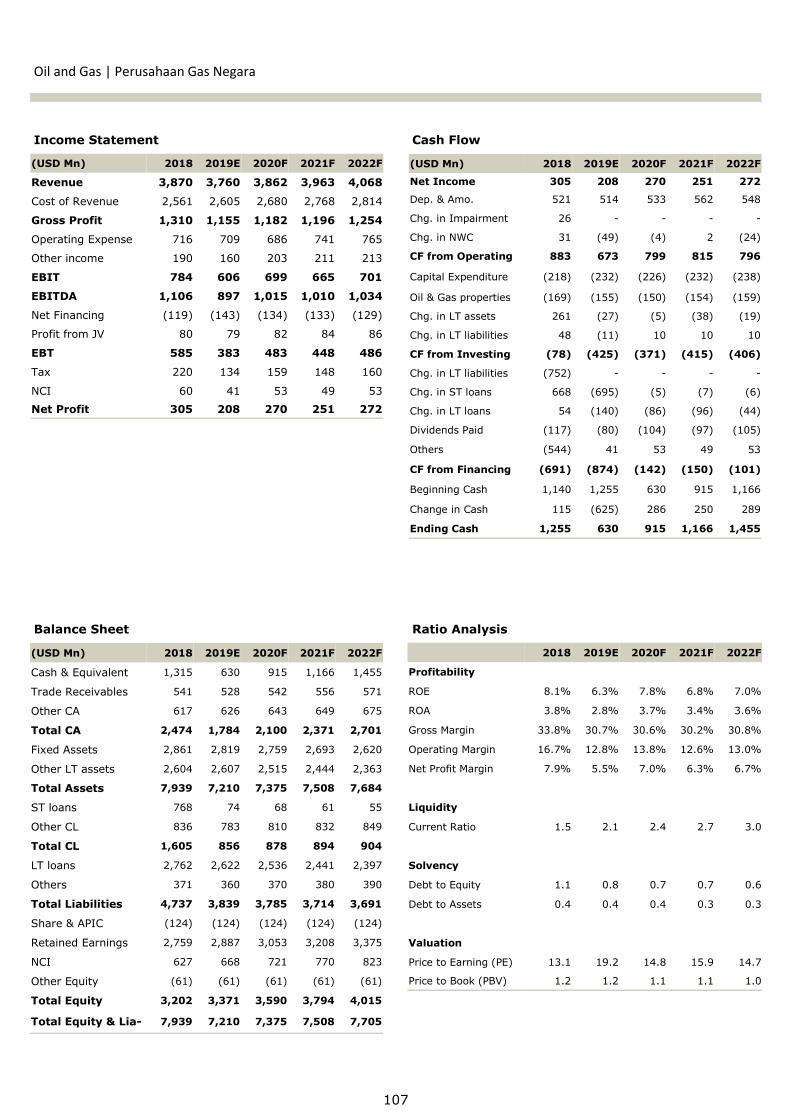

2LODQG*DV

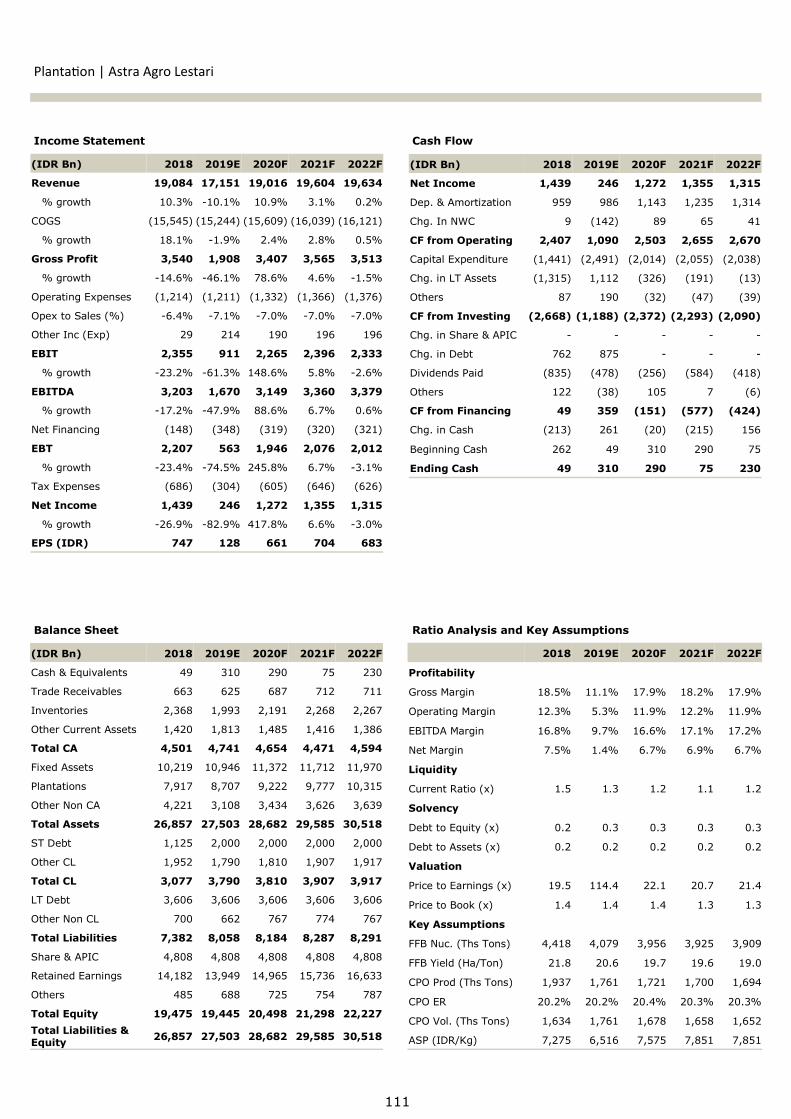

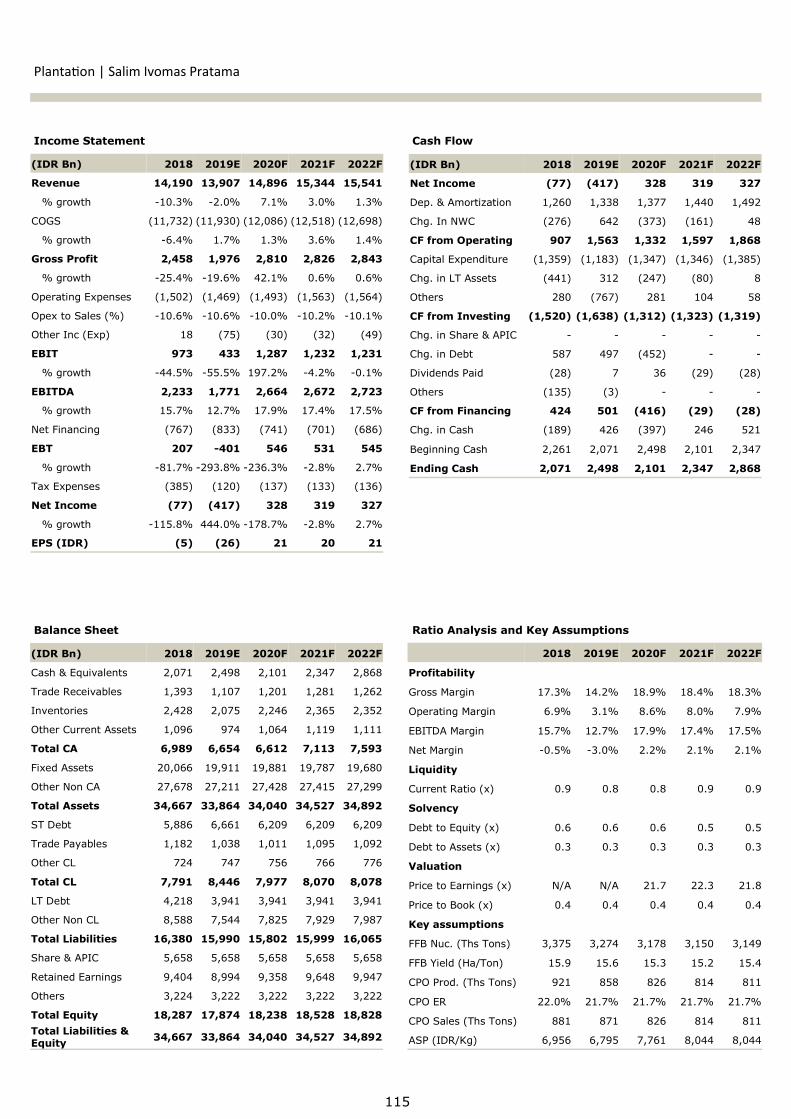

3ODQWDWLRQ

3XOS3DSHU

7HOFR

7REDFFR

5HWDLO

3URSHUW\

1

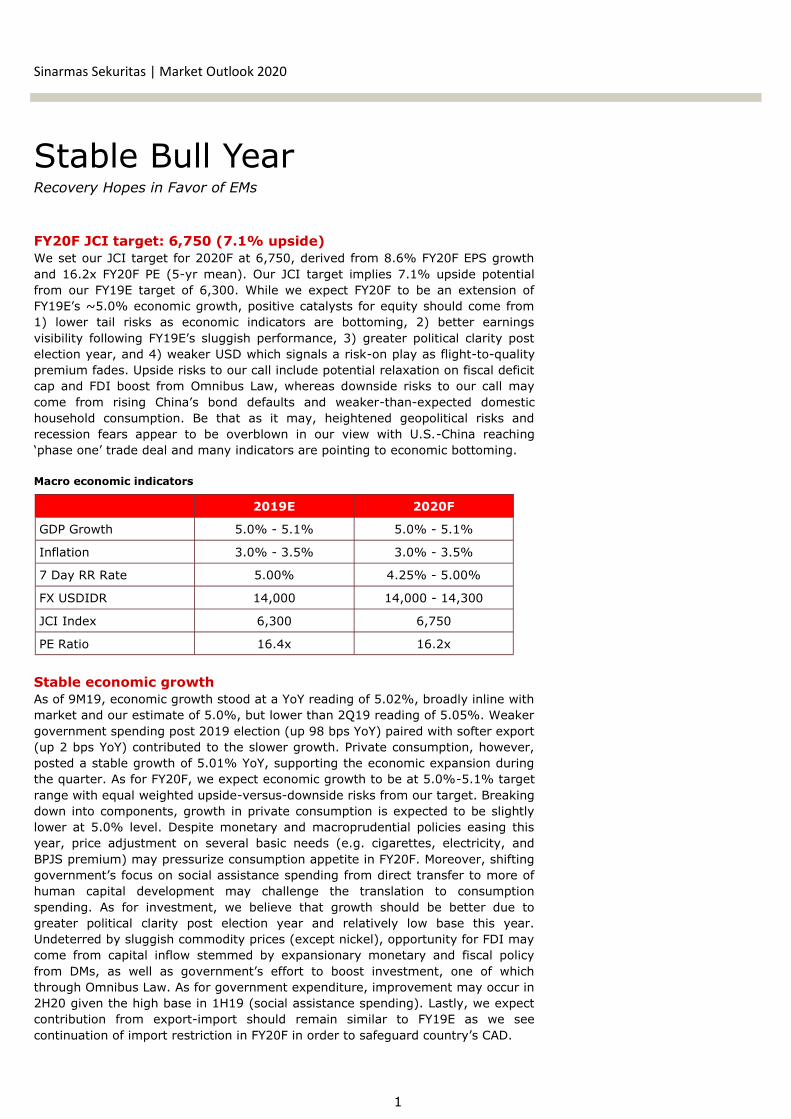

Stable Bull Year Recovery Hopes in Favor of EMs

FY20F JCI target: 6,750 (7.1% upside)

We set our JCI target for 2020F at 6,750, derived from 8.6% FY20F EPS growth

and 16.2x FY20F PE (5-yr mean). Our JCI target implies 7.1% upside potential

from our FY19E target of 6,300. While we expect FY20F to be an extension of

FY19E’s ~5.0% economic growth, positive catalysts for equity should come from

1) lower tail risks as economic indicators are bottoming, 2) better earnings

visibility following FY19E’s sluggish performance, 3) greater political clarity post

election year, and 4) weaker USD which signals a risk-on play as flight-to-quality

premium fades. Upside risks to our call include potential relaxation on fiscal deficit

cap and FDI boost from Omnibus Law, whereas downside risks to our call may

come from rising China’s bond defaults and weaker-than-expected domestic

household consumption. Be that as it may, heightened geopolitical risks and

recession fears appear to be overblown in our view with U.S.-China reaching

‘phase one’ trade deal and many indicators are pointing to economic bottoming.

Macro economic indicators

Stable economic growth

As of 9M19, economic growth stood at a YoY reading of 5.02%, broadly inline with

market and our estimate of 5.0%, but lower than 2Q19 reading of 5.05%. Weaker

government spending post 2019 election (up 98 bps YoY) paired with softer export

(up 2 bps YoY) contributed to the slower growth. Private consumption, however,

posted a stable growth of 5.01% YoY, supporting the economic expansion during

the quarter. As for FY20F, we expect economic growth to be at 5.0%-5.1% target

range with equal weighted upside-versus-downside risks from our target. Breaking

down into components, growth in private consumption is expected to be slightly

lower at 5.0% level. Despite monetary and macroprudential policies easing this

year, price adjustment on several basic needs (e.g. cigarettes, electricity, and

BPJS premium) may pressurize consumption appetite in FY20F. Moreover, shifting

government’s focus on social assistance spending from direct transfer to more of

human capital development may challenge the translation to consumption

spending. As for investment, we believe that growth should be better due to

greater political clarity post election year and relatively low base this year.

Undeterred by sluggish commodity prices (except nickel), opportunity for FDI may

come from capital inflow stemmed by expansionary monetary and fiscal policy

from DMs, as well as government’s effort to boost investment, one of which

through Omnibus Law. As for government expenditure, improvement may occur in

2H20 given the high base in 1H19 (social assistance spending). Lastly, we expect

contribution from export-import should remain similar to FY19E as we see

continuation of import restriction in FY20F in order to safeguard country’s CAD.

Sinarmas Sekuritas | Market Outlook 2020

2019E 2020F

GDP Growth 5.0% - 5.1% 5.0% - 5.1%

Inflation 3.0% - 3.5% 3.0% - 3.5%

7 Day RR Rate 5.00% 4.25% - 5.00%

FX USDIDR 14,000 14,000 - 14,300

JCI Index 6,300 6,750

PE Ratio 16.4x 16.2x

2

Lower tail risks

Many global economic indicators that we monitor (global manufacturing PMI,

China credit impulse, Japan machine tool orders, and global semiconductor sales)

have shown apparent recovery in 2H19 following the downturn in 1H19. For the

most parts, we view these improvements are the products of central banks

easing, expansive fiscal policies, and improving trade war development. While the

bears are still cautious toward the yield curve, upticks in most of these indicators

signal a continuation of cyclical recovery for global trades and industrial activities

in the near-to-medium term. Taking all into account, we do not expect the global

economy to turn 180 degrees, nevertheless, the possibility of a sharp downturn in

FY20F should be minimal in our view. As such, reduced tail risks will bring positive

catalysts for stock prices which we believe favor EM equities relative to DMs.

Sinarmas Sekuritas | Market Outlook 2020

GDP contribution as of 9M19

Source: BPS, Sinarmas Investment Research

GDP component %YoY growth

Source: BPS, Sinarmas Investment Research

Global PMI started to rebound in Aug-19

Source: Bloomberg, Sinarmas Investment Research

China credit impulse vs US ISM

Source: Bloomberg, Sinarmas Investment Research

Japan machine tool orders vs MSCI World EPS

Source: Bloomberg, Sinarmas Investment Research

Semiconductor sales vs MSCI World EPS

Source: Bloomberg, Sinarmas Investment Research

45.0

46.0

47.0

48.0

49.0

50.0

51.0

52.0

53.0

54.0

55.0

2012 2013 2014 2015 2016 2017 2018 2019

Global PMI

-100.00%

-50.00%

0.00%

50.00%

100.00%

150.00%

200.00%

-150

-100

-50

0

50

100

150

200

250

300

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

Japan Machine Tool Orders YoY - LHS MSCI World Index Trailing 12M EPS YoY Change - RHS

-100.00%

-50.00%

0.00%

50.00%

100.00%

150.00%

200.00%

-60.00%

-40.00%

-20.00%

0.00%

20.00%

40.00%

60.00%

80.00%

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

Global Semiconductor Sales - LHS MSCI World Index Trailing 12M EPS - RHS

-10%

-5%

0%

5%

10%

15%

20%

HH Consumption Govt Spending Investment Export Import

56.6%

1.5%

9.6%

32.3%

-0.1%

HH Consumption Inventory Changes Govt Spending Investment Net Export (Import)

49

50

51

52

53

54

55

21

23

25

27

29

31

33

35

2012 2013 2014 2015 2016 2017 2018 2019

China Credit Impulse - LHS Global PMI

3

Better earnings visibility

We see better earnings visibility in FY20F with JCI EPS rising 8.6% YoY versus a

lackluster growth of 2.7% YoY in FY19E. We turn more constructive on earnings

quality as we see positive turnaround in numerous sectors. Firstly, better earnings

quality should come from Banking sector (which contributes a large proportion of

index EPS) following this year’s mid-single digit growth and spurred by better

liquidity condition from easing policies as well as escalating government capex

spending post election year. Meanwhile, the IFRS 9 adoption should bring FY20F

EPS higher due to potentially lower credit cost. Similarly, we also see a number of

sectors which will experience a turnaround in earnings such as Automotive (Astra

International), Cement, Consumer Staples, Nickel, Oil & Gas, Plantation, and Pulp

& Paper. We regard the underperformance in FY19 has led to JCI’s sluggish

performance versus regional indices. As earnings recover, we expect some of the

capital outflow to return.

Sector EPS projection under our coverage

Sinarmas Sekuritas | Market Outlook 2020

US 2Y/10Y continued to rise since Aug-19

-0.4

-0.3

-0.2

-0.1

0

0.1

0.2

0.3

2016 2017 2018 2019

JAPAN 10Y YIELD

Japan 10Y yield breached 0% first time since Mar-19

Sector FY19E EPS Growth FY20F EPS Growth

Automotive -2.6% 9.6%

Banking 6.2% 15.7%

Cement -9.2% 37.2%

Coal Mining 4.7% -9.2%

Construction -20.9% -4.1%

Consumer Staples -2.1% 4.9%

Industrial Estate 44.0% 11.6%

Media 14.1% 3.5%

Nickel -20.6% 67.4%

Oil and Gas -28.6% 27.1%

Plantation* -79.4% 365.0%

Property 10.5% -24.1%

Pulp and Paper -37.0% 21.3%

Retail 2.9% 12.4%

Telecommunication 64.7% 14.5%

Tobacco 12.4% -14.9%

JCI 2.7% 8.6%

*Figures on the table exclude SIMP due to negative PAT

Source: Bloomberg, Sinarmas Investment Research Source: Bloomberg, Sinarmas Investment Research

-50

0

50

100

150

200

2014 2015 2016 2017 2018

US 2Y/10Y spread

4

Greater certainty post 2019 election

Being a political year, 2019 was colored with uncertainties. Thereupon, this

resulted in lower investment and business confidence across the board. Despite

rising inquiries for industrial lands leading to and following 2019 presidential

election, business activities and consumption spending were postponed as many

decided to take wait-and-see stance. As political overhang clears, pent-up demand

from both foreign and local investors now has a better chance to materialize. This,

we expect, may be further strengthened by Omnibus Law, which we will discuss

below.

Risk-on sentiment from weaker USD

There are few factors that may contribute to weaker USD in FY20F. First, as Fed’s

‘QE’ continues, the value of U.S. Dollar is expected to weaken due to rising

liquidity. While Chairman Powell has denied Fed’s balance sheet expansion for

reserve management purposes as a form of QE, the treasury purchases will add

the Dollar supply and increase liquidity. Second, lower volatility reading (VIX) on

the back of improving global backdrop from trade front and PMIs are expected to

further pressurize U.S. Dollar’s value as a safe-haven as well. Lastly, subdued

inflation in the U.S. has diminished Fed’s ability to raise rates in the near future.

This keeps a cap on Dollar’s strength. All of these factors pointing to weaker USD

should improve the risk-on sentiment on EMs as currency exchange risks have

always overshadowed EM equities.

Sinarmas Sekuritas | Market Outlook 2020

6.9%

2.7%

8.6%8.8%

9.4%

FY18 FY19E FY20F FY21F FY22F

JCI EPS growth (%YoY)

Consolidated coverage EPS growth

Fed’s balance sheet

Source: Bloomberg, Sinarmas Investment Research

3.5

3.7

3.9

4.1

4.3

4.5

4.7

2015 2016 2017 2018 2019

Fed Balance Sheet (in USD Mn)

0

5

10

15

20

25

30

35

2015 2016 2017 2018 2019

VIX

Cboe volatility index (VIX) is near all time low

Source: Bloomberg, Sinarmas Investment Research

Source: Sinarmas Investment Research

5

Rupiah to remain stable in FY20F

To date, Rupiah has appreciated against USD by 3 ppt, outperforming a handful

majority in EM currencies basket and despite 100 bps rate cuts in 2H19 (vs 75 bps

FFR cuts). In addition to the massive foreign inflow of IDR 171.9tn to the bond

market (SBN), Bank Indonesia continued to be supportive toward Rupiah

exchange rates via bond and FX markets in order to maintain economic stability.

Onwards, we expect USDIDR to be within 14,000-14,300 range. While we see

rooms for more policy easing (50-75 bps), weaker USD outlook should provide

cushion to Rupiah in FY20F. Downside risk to our call is worse-than-expected

global turmoil fueled by rising China’s bond defaults.

Sinarmas Sekuritas | Market Outlook 2020

FOMC dot plots

Source: Bloomberg

USDIDR real spread vs IDR (%YoY, Inverted)

Source: Bloomberg, OJK, Sinarmas Investment Research

EM currencies performance vs USD

Source: Bloomberg

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%-1.00

0.00

1.00

2.00

3.00

4.00

5.00

6.00

2012 2013 2014 2015 2016 2017 2018 2019

Real Spread IDR (% YoY) [RHS]

7DRRR vs CPI

Source: Bank Indonesia, Sinarmas Investment Research

3.25 3.183.4 3.41

3.23 3.12 3.18 3.2

2.883.16 3.23 3.13

2.822.57 2.48

2.83

3.32 3.28 3.323.49 3.39

3.133.00

4.25 4.25 4.25 4.25

4.75

5.25 5.255.50

5.75 5.756.00 6.00 6.00 6.00 6.00 6.00 6.00 6.00

5.755.50

5.255.00 5.00

0

1

2

3

4

5

6

7

Jan-18 Feb-18 Mar-18 Apr-18 May-18 Jun-18 Jul-18 Aug-18 Sep-18 Oct-18 Nov-18 Dec-18 Jan-19 Feb-19 Mar-19 Apr-19 May-19 Jun-19 Jul-19 Aug-19 Sep-19 Oct-19 Nov-19

Inflation (%YoY) 7DRRR

6

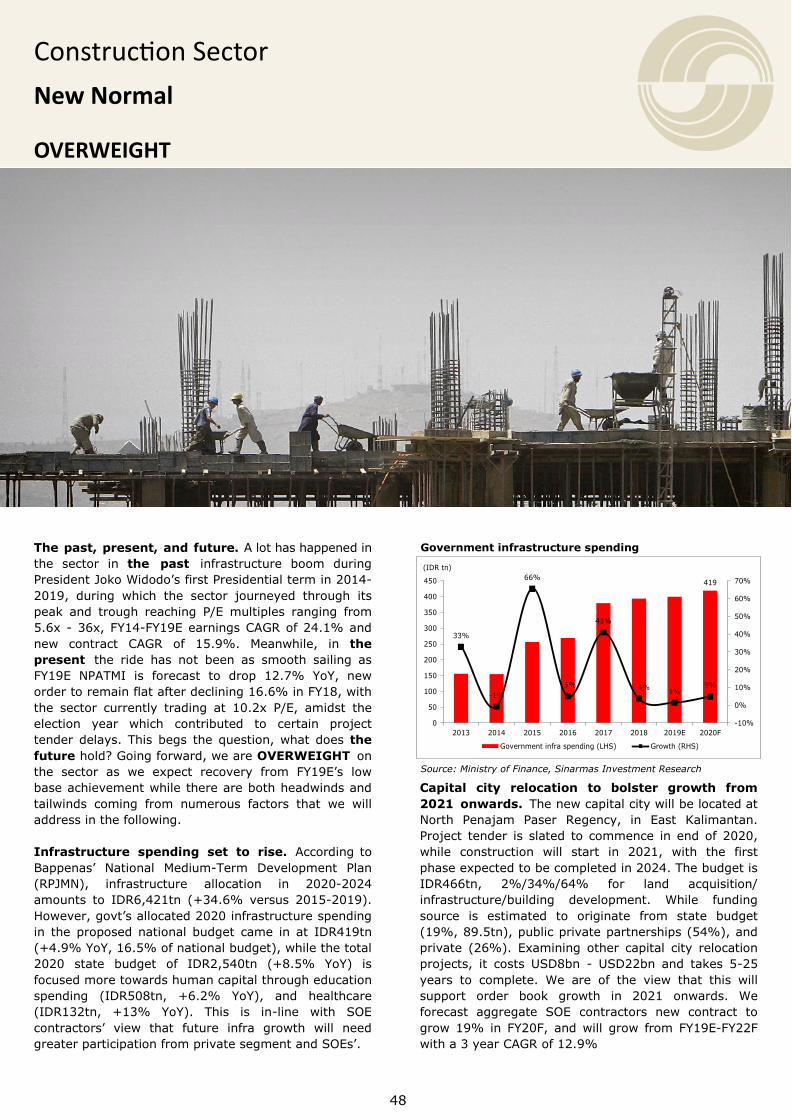

Upside risk from Omnibus Law

As we have mentioned briefly in the paragraph above, the introduction of Omnibus

Law can be a key catalyst for investment and business confidence. One of the

structural issues in Indonesian economy has been the lack of FDI. Aside from the

lengthy paperwork and numerous permits/regulations required, the complexity of

layers in Indonesian bureaucracy has become a major pushback. The proposed

Omnibus Law will simplify a wide range of areas (labor laws, investment

requirements, land acquisition rules, and many others) and act as a replacement

to the current existing and overlapping laws. Moreover, MoF is also pushing for a

lower corporate tax and the removal of dividend tax to be included in the Omnibus

Bill in order to further improve the country’s attractiveness. This, however, will be

done in stages to safeguard the fiscal impacts. As for corporate tax, tax rate will

be reduced gradually from current 25% to 22% in FY21/22, and to 20% in FY23.

Furthermore, companies that go public in FY21-23 will get to enjoy an additional

benefit of 3 ppt income tax (PPh) reduction from 22% in FY21/22 and 20% in

FY23 to 19%/17% respectively. While timeline and details are still under

discussion, passing rate for the bill is expected to be high as, in terms of political

support, political parties from President Widodo’s coalition control more than 70%

of the parliament. Meanwhile, the execution of the bill will provide upside risks to

the JCI.

Downside risk from China’s bond defaults

While we are guiding for a brighter global economic picture, downside risk to our

call may come from China’s bond market. Following a record default in China’s

domestic bonds this year, there are USD 8.6bn offshore bonds that will be due

next year. Admittedly, these bonds have at least 15% yields as they are classified

as stressed. Accounted for almost 40% of the total outstanding corporate dollar

bonds, with policymakers continue limiting leverage, these bonds may stem risks

to EMs from many perspectives; tighter liquidity, FX volatility, and shift from

equities to save-haven assets.

U.S.-China: Prisoner’s Dilemma

Using the prisoner’s dilemma analogy in game theory, the U.S.-China trade talk

may have appeared to have thin chances of success at the beginning. Aside from

being the two largest economies in the world, the two countries have eloquent

ways of expressing differences. On one hand, U.S. taunted China with trade tariffs

on a wide range of Chinese products. On the contrary, China intimidated U.S. with

their ‘self-destructive nuclear option’ by selling U.S. treasuries. After months of

negotiation, however, the two countries finally managed to reach the ‘phase one’

trade deal just before the year ended. Though the tangible impact from this is not

enough to exempt both countries from heading into an economic slowdown, it

shows that neither country wants to continue a standoff due to respective

personal interests from both presidents: 2020 U.S. presidential election (Trump)

and political stability (Xi). To note, the state of the economy, normally portrayed

in the capital market performance, is a crucial determinant to the incumbent’s

electability to win the election votes. With the next U.S. presidential election is

approaching, this trade negotiation is very important for Trump’s political career.

Hence, it is Trump’s best interest to close this deal and use it for his 2020 re-

election campaign. On the flip side, while it is too early to assume what the final

outcome may be, ‘phase one’ trade deal has eliminated the worst possible

outcome for both countries.

Sinarmas Sekuritas | Market Outlook 2020

7

What to buy?

In all, we believe FY20F to be a year of stability as many indicators are signaling a

continuation of cyclical recovery for global trades and industrial activities. As such,

reduced tail risks should bring positive catalysts for stock prices primarily for EMs.

In addition, better earnings visibility and weaker USD are also the key factors to

our positive stance toward JCI. Lastly, from the domestic perspective, we see a

brighter macroeconomic picture for Indonesia given the less uncertainty in political

overhang as well as the proposed Omnibus Law, which will be a tailwind to JCI’s

performance in FY20F. With that being said, our top picks for this year are: BMRI

(BUY, FY20 TP: 8,650), BBNI (BUY, FY20 TP: 9,150), SMGR (BUY, FY20

TP: 15,400), WIKA (BUY, FY20 TP: 2,510), BSDE (BUY, FY20 TP: 1,500),

SMRA (BUY, FY20 TP: 1,300), MAPI (BUY, FY20 TP: 1,300), and TLKM

(BUY, FY20 TP: 4,950). From the commodity sector, we like LSIP (BUY, FY20

TP: 1,720) as we see recent rally in CPO price to sustain in FY20F. As for small-to

-mid cap, we continue to like WEGE (BUY, FY20 TP: 480) due to its

undemanding valuation, favorable sector outlook, and expansion in modular

segment. Still from small-to-mid cap, we also like DMAS (BUY, FY20 TP: 360)

as it captures the improving investment outlook in Indonesia. Lastly, we also see

defensive name such as INDF (BUY, FY20 TP: 9,200) is attractive supported by

its commodity-related business and cheap valuation.

Sinarmas Sekuritas | Market Outlook 2020

S&P 500 performance during previous presidential terms

Source: Bloomberg, Sinarmas Investment Research

0

500

1000

1500

2000

2500

3000

3500

1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

George H. W. Bush

Start, Total Index

Return 51%

Bill Clinton Start,

Total Index Return

210%

George W. Bush Start,

Total Index Return -

40%

Barack Obama Start,

Total Index Return

182%

Donald Trump Start,

Total Index Return 38%

8

Our view on commodities:

CPO: the arrival of long-awaited positive breeze

Although it might be a bit delayed, however CPO prices have started a rally since

end of 1H19 and currently still stands strong at MYR 2,850/ton on several reasons

such as supportive MPOB data, drop in CPO output, better demand from China

and India along with positive effect on phase one trade deal between US-China.

We expect the output drop in 2019 is only the beginning and will extend to 2020

onwards, on limited new plantings from the previous years plus more aggressive

replanting program undertaken by big CPO players. Meanwhile in the near-term,

production will also under pressure due to the cutback in fertilizer application and

recent drought and haze that may pose knock-on effect on production yield in

2020. Coupled with the expected strong incremental demand backed by the B30

implementation in Indonesia starting early 2020, we reiterate our bullish stance

on the industry and expect CPO price to trade at average of MYR 2,500 per ton in

FY20F.

Pulp and Paper: pulp price conundrum

2019 is a sloppy year for pulp and paper industry following pulp price slump since

end of FY18 and remains low at current moment. The bearish pulp price outlook

mainly came from weakening pulp demand that resulted in high inventories both

in China and European ports (two biggest users for pulp). We believe further

observation on pulp demand along with the inventory level is important to see

where price will be going on from current level. Overall, we expect pulp price to

recover in 2020, although only at moderate magnitude and will occur by fastest in

2H20. We are now seeing benchmark pulp price at USD 650/ton in FY20F.

Sinarmas Sekuritas | Market Outlook 2020

Inventory almost fall to its 5-years average level

Source: Bloomberg, Sinarmas Investment Research

-

500

1,000

1,500

2,000

2,500

3,000

3,500

Jun-18 Aug-18 Oct-18 Dec-18 Feb-19 Apr-19 Jun-19 Aug-19 Oct-19

MPOB Production MPOB Export MPOB Inventory 5Y Avg Inventory

9

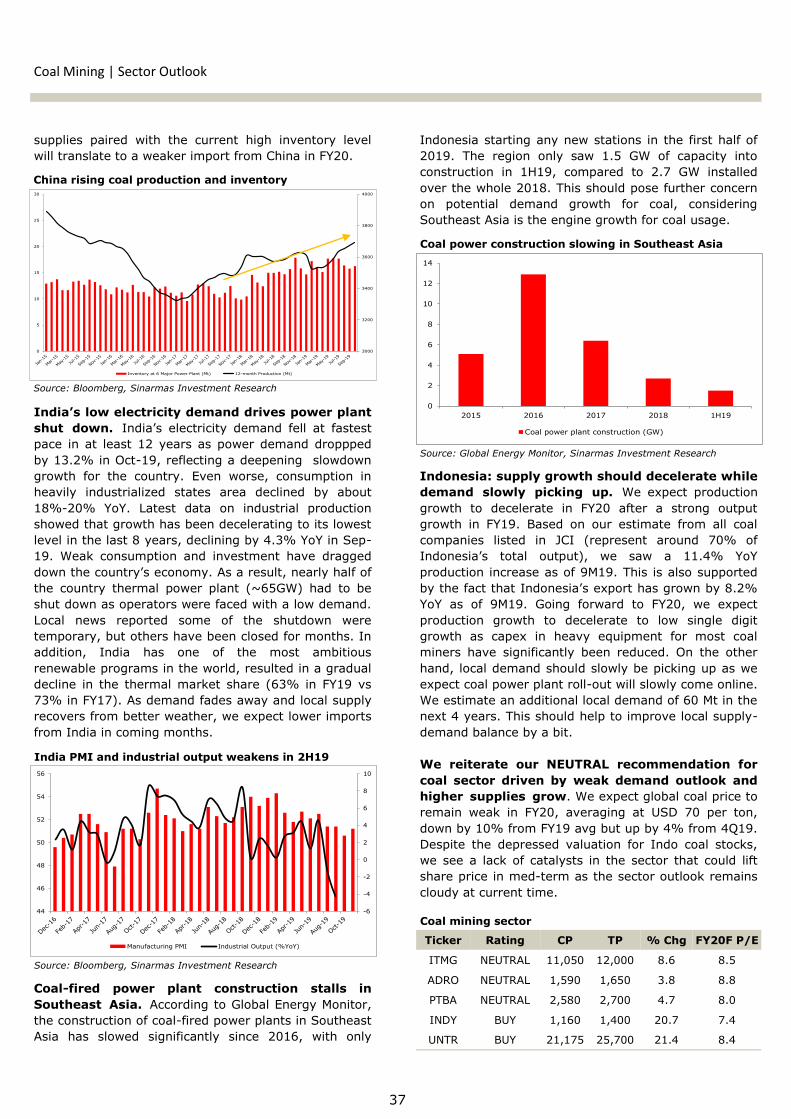

Coal: weakness persists as demand fades

Global economy slowdown, fueled from US-China trade war, has impacted energy

demand, especially for China and India (two biggest consumers for coal). As a

result, coal price has moved in a continuous negative direction during 2019,

closing in at USD 67.9 per ton (Newcastle 6,322) as of Nov-19, or down by

33.5% compared to a year ago. Going forward to FY20, we believe that global coal

price could keep dimming as we see demand to remain weak while supplies grow.

Global economy slowdown will continue to weigh down on thermal demand,

particularly from China and India. On the other hand, current high inventories

level and additional local supplies from China’s new and more efficient mine this

year will likely drive up supplies, lowering their need of imports. Hence, we expect

global coal price to remain weak in FY20, averaging at USD 70 per ton, down by

10% from FY19 avg but up by 4% from 4Q19. Indonesia’s low coal price,

however, should be more resilient as we see improvement in demand/supply

balance driven by decelerating production growth and new power plant roll out.

Nickel: improving balance

After recent outperformance in 3Q19 boosted by the changes in Indonesia ore

export ban regulation, nickel stocks dived in recent months as nickel price pulled

back to USD 13,000 per ton from its highest level at USD 18,050 in Sep-19.

Recent nickel fallout was driven by weakness in the stainless steel and EV sales

department, as well as ramp-up ore export coming from Indonesia prior to the

ban deadline (Jan-20). Despite recent weakness, we forecast nickel price to

rebound in FY20 as we see the current inventory remains low while demand will

still grow modestly paired with a moderate supply growth as higher refined output

will be strained by lower ore availability from Indonesia’s ore export ban. Wood

Mackenzie forecasts demand to grow by 3.8% YoY in FY20, slowing down from

6.3% in FY19. Stainless steel and EV batteries remain to be the engine drivers for

nickel consumption growth. On the other hand, refined nickel output is forecasted

to grow by 5.3% in FY20, declining from 8.3% in FY19. Nickel mined production,

however, is expected to drop by 3% YoY. These should level out the demand/

supply balance in FY20, after posting a supply deficit in the past 4 years. We

forecast nickel price to average at USD 15,000 per ton in FY20, rising from USD

14,000 per ton average in FY19.

Sinarmas Sekuritas | Market Outlook 2020

China rising coal production and inventory

Source: Bloomberg, Sinarmas Investment Research

3000

3200

3400

3600

3800

4000

0

5

10

15

20

25

30

Inventory at 6 Major Power Plant (Mt) 12-month Production (Mt)

10

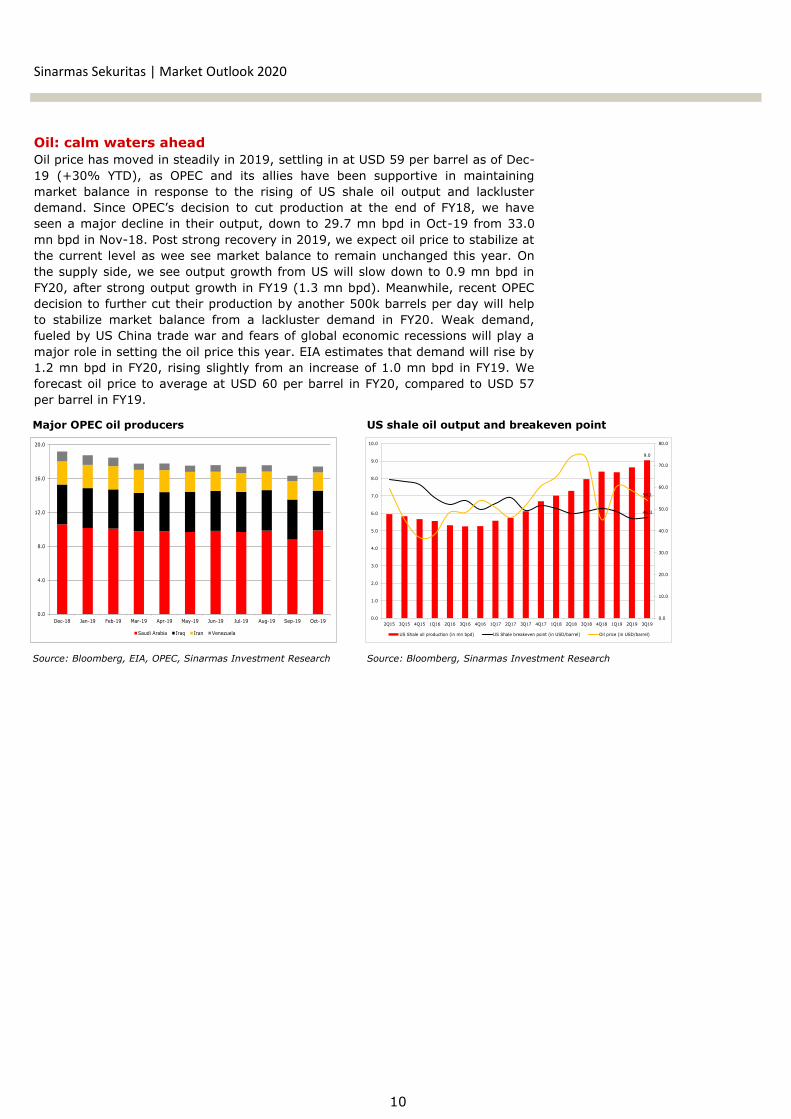

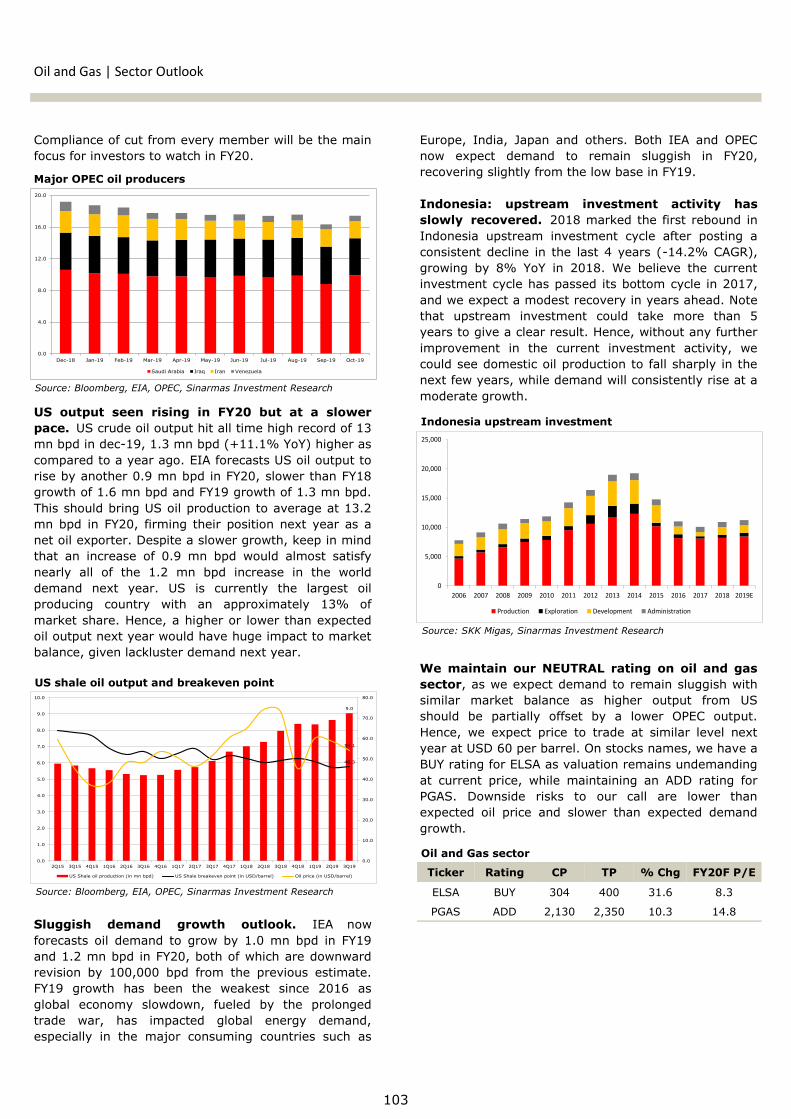

Oil: calm waters ahead

Oil price has moved in steadily in 2019, settling in at USD 59 per barrel as of Dec-

19 (+30% YTD), as OPEC and its allies have been supportive in maintaining

market balance in response to the rising of US shale oil output and lackluster

demand. Since OPEC’s decision to cut production at the end of FY18, we have

seen a major decline in their output, down to 29.7 mn bpd in Oct-19 from 33.0

mn bpd in Nov-18. Post strong recovery in 2019, we expect oil price to stabilize at

the current level as wee see market balance to remain unchanged this year. On

the supply side, we see output growth from US will slow down to 0.9 mn bpd in

FY20, after strong output growth in FY19 (1.3 mn bpd). Meanwhile, recent OPEC

decision to further cut their production by another 500k barrels per day will help

to stabilize market balance from a lackluster demand in FY20. Weak demand,

fueled by US China trade war and fears of global economic recessions will play a

major role in setting the oil price this year. EIA estimates that demand will rise by

1.2 mn bpd in FY20, rising slightly from an increase of 1.0 mn bpd in FY19. We

forecast oil price to average at USD 60 per barrel in FY20, compared to USD 57

per barrel in FY19.

Sinarmas Sekuritas | Market Outlook 2020

Major OPEC oil producers

Source: Bloomberg, EIA, OPEC, Sinarmas Investment Research

US shale oil output and breakeven point

0.0

4.0

8.0

12.0

16.0

20.0

Dec-18 Jan-19 Feb-19 Mar-19 Apr-19 May-19 Jun-19 Jul-19 Aug-19 Sep-19 Oct-19

Saudi Arabia Iraq Iran Venezuela

Source: Bloomberg, Sinarmas Investment Research

9.0

46.3

54.1

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

2Q15 3Q15 4Q15 1Q16 2Q16 3Q16 4Q16 1Q17 2Q17 3Q17 4Q17 1Q18 2Q18 3Q18 4Q18 1Q19 2Q19 3Q19

US Shale oil production (in mn bpd) US Shale breakeven point (in USD/barrel) Oil price (in USD/barrel)

11

Sinarmas Sekuritas | Rating Summary

2019E 2020F 2019E 2020F 2019E 2020F IDR Bn USD Mn

Automotive

1 ASII ADD 6,850 7,800 13.9% -1.1 10.4 14.7 13.4 2.1 1.9 277,312.3 19,776.9

Banking

2 BMRI BUY 7,375 8,650 17.3% 14.1 15.8 13.7 11.8 2.0 2.0 344,166.7 24,544.8

3 BBRI NEUTRAL 4,280 4,540 6.1% 5.3 8.7 16.4 15.1 2.8 2.6 527,920.1 37,649.4

4 BBCA ADD 31,800 35,675 12.2% 10.1 16.9 30.9 26.4 5.1 4.6 784,029.3 55,914.2

5 BBNI BUY 7,650 9,150 19.6% 0.7 20.1 11.2 9.4 1.4 1.4 142,662.2 10,174.2

6 BBTN NEUTRAL 2,170 2,300 6.0% -58.4 126.7 20.8 10.8 1.0 1.3 22,980.3 1,638.9

Cement

7 INTP NEUTRAL 20,000 20,200 1.0% 44.0 8.3 44.6 41.2 3.1 3.1 73,624.6 5,250.7

8 SMGR BUY 12,300 15,400 25.2% -28.9 58.2 41.6 26.3 2.6 2.5 72,957.7 5,203.1

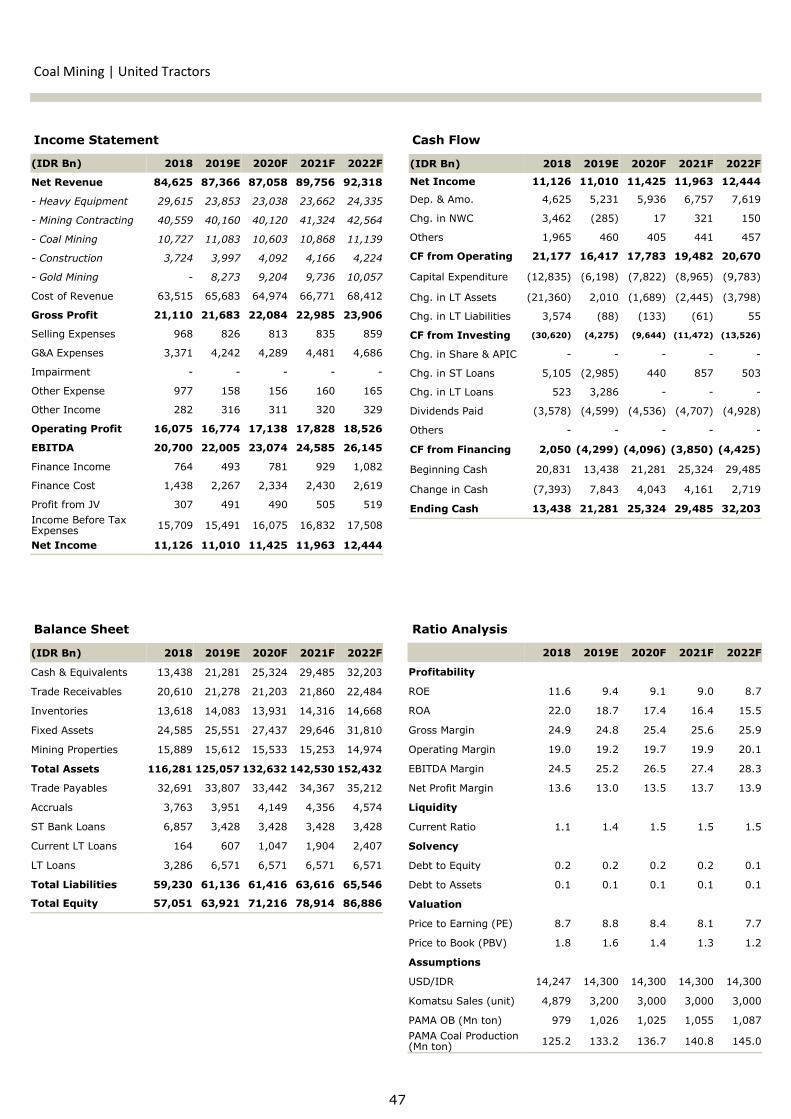

Coal Mining

9 ITMG NEUTRAL 11,050 12,000 8.6% -48.5 -15.7 7.1 8.5 1.0 1.1 12,485.7 890.4

10 ADRO NEUTRAL 1,590 1,650 3.8% 17.8 -14.9 7.5 8.8 0.8 0.8 50,857.7 3,627.0

11 PTBA NEUTRAL 2,580 2,700 4.7% -19.5 -4.4 7.7 8.0 1.5 1.4 29,723.3 2,119.8

12 INDY BUY 1,160 1,400 20.7% -51.8 -14.8 6.4 7.4 0.4 0.4 6,043.8 431.0

13 UNTR BUY 21,175 25,700 21.4% -1.0 3.8 8.8 8.4 1.6 1.4 78,985.6 5,633.0

Construction

14 WIKA BUY 2,050 2,510 22.4% 19.3 5.1 10.9 10.4 1.4 1.4 18,388.4 1,311.4

15 PTPP BUY 1,650 1,900 15.2% -29.4 9.3 11.1 10.2 0.9 1.1 10,229.8 729.6

16 ADHI BUY 1,225 1,550 26.5% 1.0 6.1 8.5 8.0 0.8 0.9 4,362.0 311.1

17 WSKT NEUTRAL 1,445 1,570 8.7% -47.5 -48.5 10.2 19.9 1.1 1.1 19,614.4 1,398.8

18 WTON BUY 440 570 29.5% 7.0 9.1 9.6 8.8 1.4 1.3 3,834.8 273.5

19 WSBP NEUTRAL 324 350 8.0% -26.1 13.8 11.1 9.8 1.1 1.0 8,541.0 609.1

20 WEGE BUY 296 480 62.2% 3.8 14.2 10.0 8.8 1.9 1.8 2,833.3 202.1

Consumer Staples

21 UNVR NEUTRAL 41,225 43,900 6.5% -20.6 1.0 46.3 45.8 47.9 47.1 314,546.8 22,432.4

22 ICBP ADD 11,450 12,800 11.8% 10.2 5.3 29.6 28.1 5.9 5.3 133,528.8 9,522.8

23 KLBF NEUTRAL 1,600 1,680 5.0% 5.6 5.4 30.3 28.8 4.7 4.4 75,000.2 5,348.8

24 INDF BUY 7,750 9,200 18.7% 14.1 7.4 17.0 15.8 1.5 1.4 68,048.3 4,853.0

25 MYOR NEUTRAL 2,020 2,160 6.9% -2.3 7.9 28.8 26.7 5.0 4.5 45,164.6 3,221.0

26 SIDO ADD 1,275 1,400 9.8% 19.8 6.2 26.2 24.7 6.6 6.2 19,125.0 1,363.9

27 ROTI BUY 1,305 1,540 18.0% 61.0 20.5 34.3 30.2 2.6 2.8 8,073.4 575.8

28 UCID** BUY 1,500 1,900 26.7% 65.6 47.6 26.4 17.8 1.4 1.3 6,234.9 444.7

Industrial Estate

29 DMAS BUY 302 360 19.2% 84.0 12.9 19.0 16.8 2.4 2.4 14,555.8 1,038.1

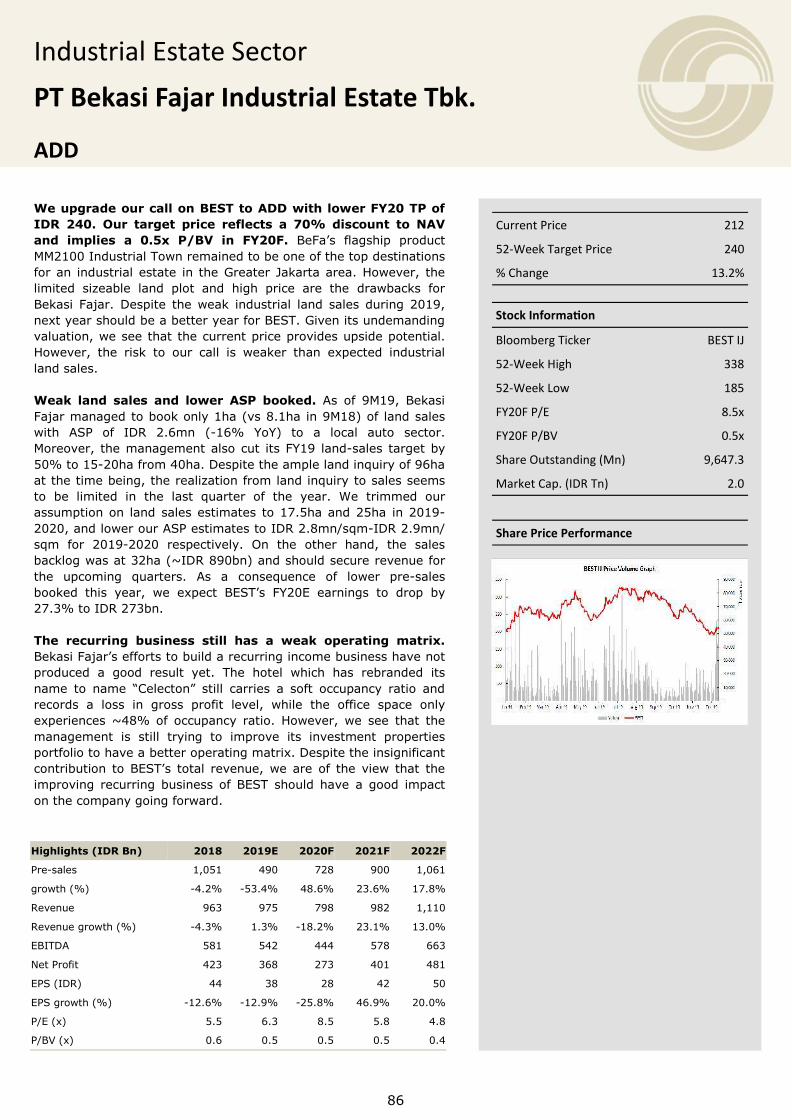

30 BEST ADD 212 240 13.2% 12.9 25.8 6.3 8.5 0.5 0.5 2,045.2 145.9

31 SSIA NEUTRAL 700 700 0.0% 156.5 141.5 34.1 14.1 0.8 0.8 3,293.7 234.9

Media

32 SCMA ADD 1,445 1,650 14.2% -2.9 4.5 16.7 16.0 4.8 4.4 21,340.9 1,522.0

33 MNCN NEUTRAL 1,590 1,650 3.8% 30.5 2.8 11.8 11.5 1.9 1.7 22,699.0 1,618.8

No Ticker Rating Current Price* Target Price % ChgEPS Growth (%) PER (x) PBV (x) Market Capitalization

12

Sinarmas Sekuritas | Rating Summary

2019E 2020F 2019E 2020F 2019E 2020F IDR Bn USD Mn

Metal

34 INCO NEUTRAL 3,490 3,700 6.0% -34.2 135.1 67.1 28.5 1.4 1.3 34,677.8 2,473.1

35 ANTM ADD 850 970 14.1% -10.7 21.2 29.8 24.6 1.2 1.2 20,426.2 1,456.7

Oil and Gas

36 ELSA BUY 304 400 31.6% 17.0 9.1 9.0 8.3 0.8 0.8 2,218.7 158.2

37 PGAS ADD 2,130 2,350 10.3% -31.6 29.7 19.2 14.8 1.2 1.1 51,634.4 3,682.4

Plantation

38 AALI NEUTRAL 13,425 14,600 8.8% -82.9 417.8 114.4 22.1 1..4 1.4 25,838.9 1,842.7

39 LSIP BUY 1,420 1,720 21.1% -64.0 256.4 98.2 27.6 1.4 1.3 9,688.5 690.9

40 SIMP BUY 390 450 15.4% N/A N/A N/A 21.7 0.4 0.4 6,168.4 439.9

Property

41 BSDE BUY 1,255 1,500 19.5% 115.7 -43.9 10.3 18.4 0.9 0.8 24,154.6 1,722.6

42 SMRA BUY 1,030 1,300 26.2% 6.9 14.1 39.4 34.3 1.9 1.8 14,859.6 1,059.7

43 ASRI ADD 242 280 15.7% -63.3 15.3 15.4 13.4 0.6 0.5 4,755.2 339.1

44 PWON ADD 570 640 12.3% 5.7 -18.1 11.5 14.0 1.8 1.7 27,451.0 1,957.7

45 CTRA ADD 1,060 1,170 10.4% -24.9 -13.3 24.4 28.1 1.2 1.2 19,673.9 1,403.1

Pulp and Paper

46 INKP BUY 7,875 10,400 32.1% -45.1 17.9 12.4 10.5 1.0 0.9 43,084.0 3,072.6

47 TKIM NEUTRAL 11,300 12,350 9.3% -17.8 26.7 13.3 10.5 1.9 1.6 35,179.4 2,508.9

Retail

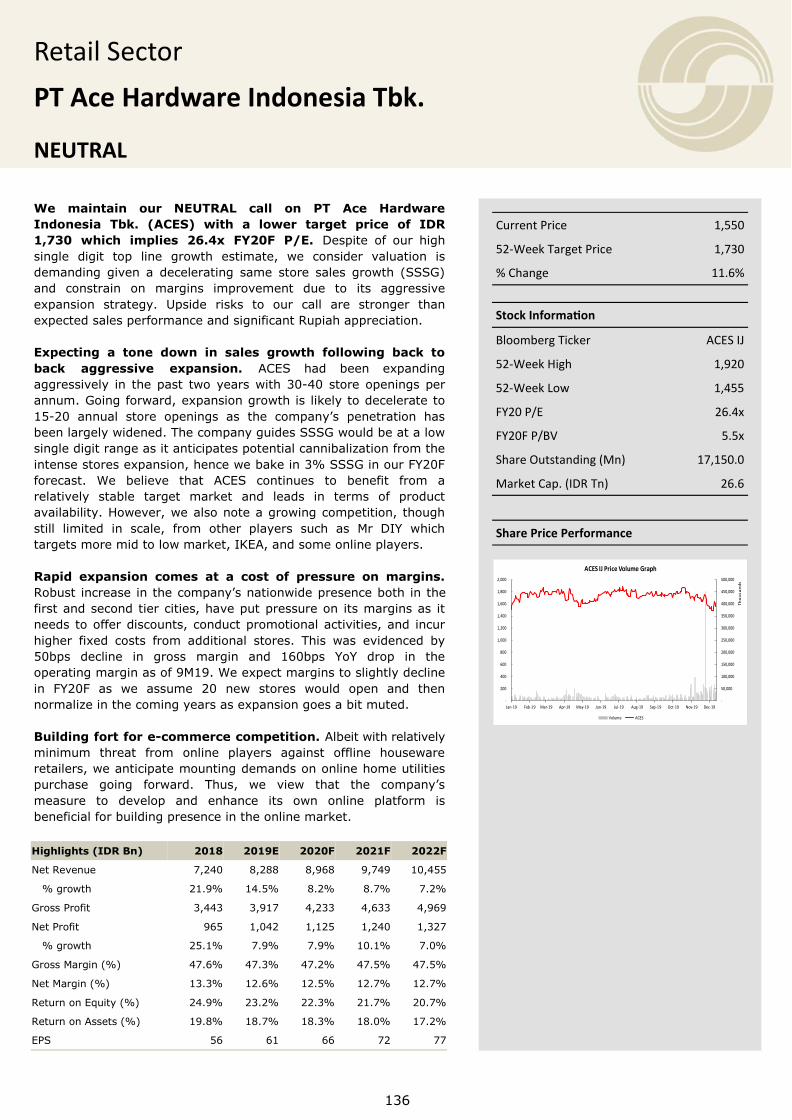

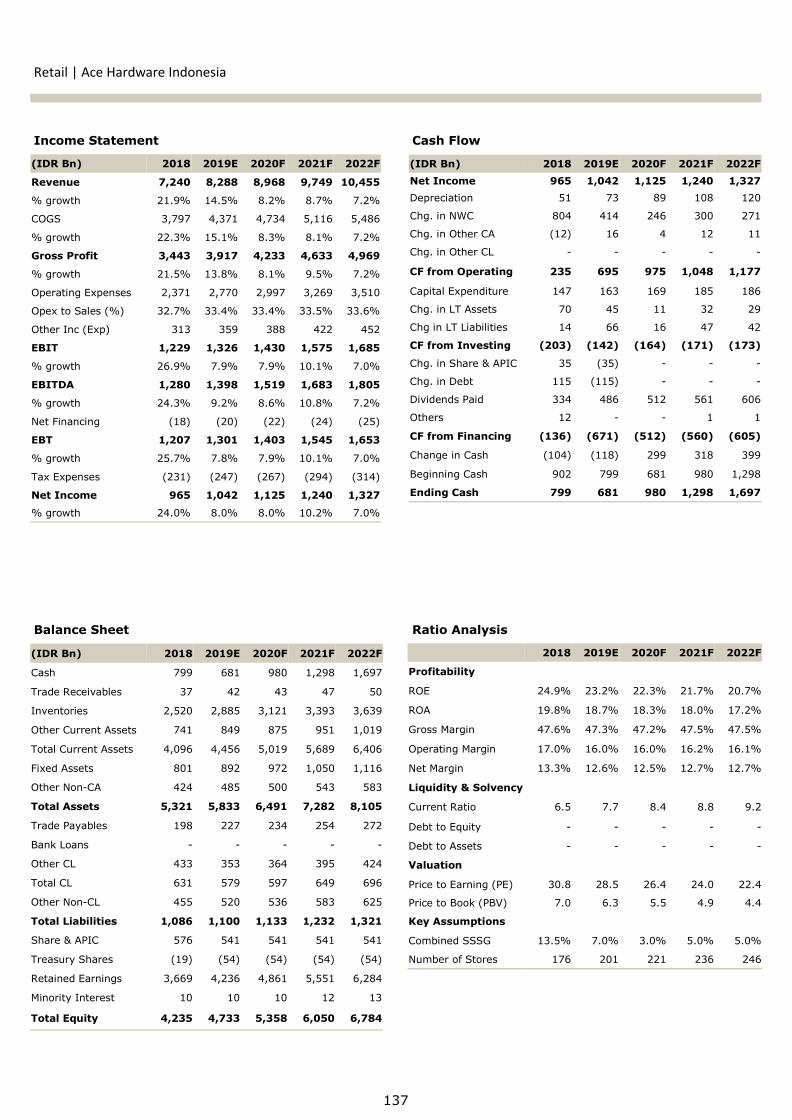

48 ACES NEUTRAL 1,550 1,730 11.6% 7.9 7.9 28.5 26.4 6.3 5.5 26,582.5 1,895.8

49 ERAA ADD 1,625 1,870 15.1% -68.8 89.1 22.5 11.9 1.2 1.1 5,183.8 369.7

50 LPPF NEUTRAL 3,700 4,030 8.9% 27.6 -0.4 8.4 8.4 4.9 4.3 10,378.1 740.1

51 MAPI BUY 1,030 1,300 26.2% 21.7 20.0 24.1 20.1 2.9 2.6 17,098.0 1,219.4

52 RALS NEUTRAL 1,035 1,140 10.1% 8.3 2.2 12.7 12.4 2.1 2.1 7,344.4 523.8

Telecommunication

53 TLKM BUY 3,990 4,950 24.1% 12.7 15.2 24.1 20.9 4.8 4.5 395,258.2 28,188.4

54 EXCL ADD 3,240 3,650 12.7% 3.3 4.5 45.6 31.4 2.0 1.9 34,629.0 2,469.6

55 ISAT ADD 3,120 3,600 15.4% N/A N/A N/A N/A 0.9 1.0 16,953.9 1,209.1

Tobacco

56 HMSP BUY 2,060 2,500 21.4% 6.2 -11.7 20.2 22.9 8.1 8.4 239,615.2 17,088.5

57 GGRM BUY 52,025 60,250 15.8% 23.2 -19.7 12.1 15.0 2.2 2.1 100,100.7 7,138.8

Miscellaneous

58 AKRA NEUTRAL 3,840 3,900 1.6% -1.4 37.0 22.1 16.3 1.9 1.8 15,416.4 1,099.4

59 BIRD BUY 2,890 3,500 21.1% -28.9 23.6 27.2 22.0 1.3 1.3 7,231.1 515.7

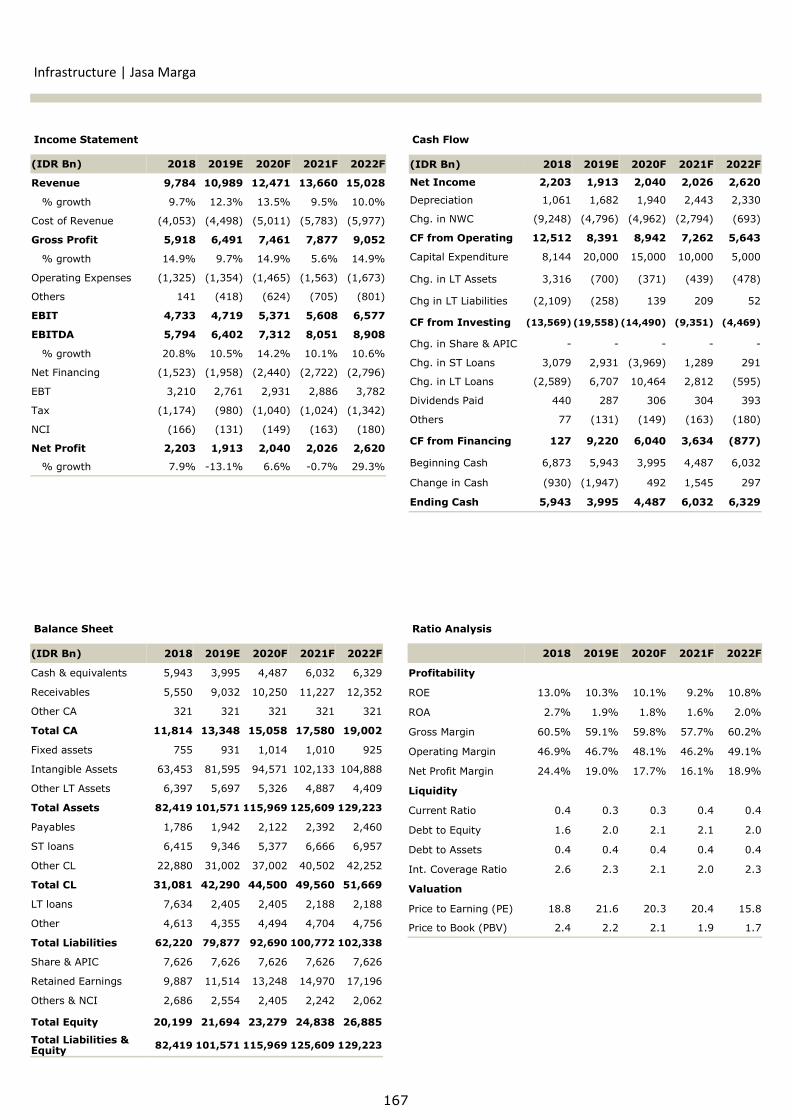

60 JSMR NEUTRAL 5,225 5,700 9.1% -13.1 6.6 21.6 20.3 2.2 2.1 37,922.4 2,704.5

* As of market closing on December 13,2019

** IPO price at IDR 1,500 per share

% ChgNo Ticker Rating Current Price* Target PriceEPS Growth (%) PER (x) PBV (x) Market Capitalization

13

This page is intentionally left blank

ƵƚŽŵŽƟǀĞ^ĞĐƚŽƌ ^ŚŝŌƚŽ>ŽǁĞƌ'ĞĂƌ

KsZt/',d

)<)7KHDGMXVWPHQWSHULRG0RYLQJLQWRWKH\HDUZHVHHWKDWWKHDXWRPRWLYHVHFWRUZLOOEHKDYLQJDQ DGMXVWPHQW SHULRG WR WKH QHZ UHJXODWLRQ FKDQJHVWKDW ZHUH VHW LQ QDPHO\ 33 7KLVUHJXODWLRQFKDQJHVWKHWD[VWUXFWXUHRQDYHKLFOHIURPHQJLQH-VL]HG-EDVHG WR FDUERQ-EDVHG 7KLV UHJXODWLRQZLOOEHHIIHFWLYHVWDUWLQJ2FWREHU:HVHHWKDWWKH*RYHUQPHQW RI ,QGRQHVLD LQWHQGV WR SURPRWH WKHDGRSWLRQRIHOHFWULFYHKLFOHV(9DQGHQKDQFHWKHIDVW-JURZLQJ ORFDO DXWR PDQXIDFWXULQJ EDVH IRU H[SRUWRULHQWDWLRQ:LWKWKDWEHLQJVDLGZHEHOLHYHWKDWDXWRPDQXIDFWXUHUV ZLOO SUHSDUH WR SXUVXH ORZHU FDUERQHPLVVLRQHQJLQHVDQGSRVVLEO\(9HOHFWULFYHKLFOHOLQH-XSVZKLOHFRQVXPHUVPLJKWSRVWSRQHEX\LQJQHZFDUVHVSHFLDOO\ZKHQWKHUHDUHQRWPDQ\QHZPRGHOVEHLQJODXQFKHGGXULQJWKH\HDU

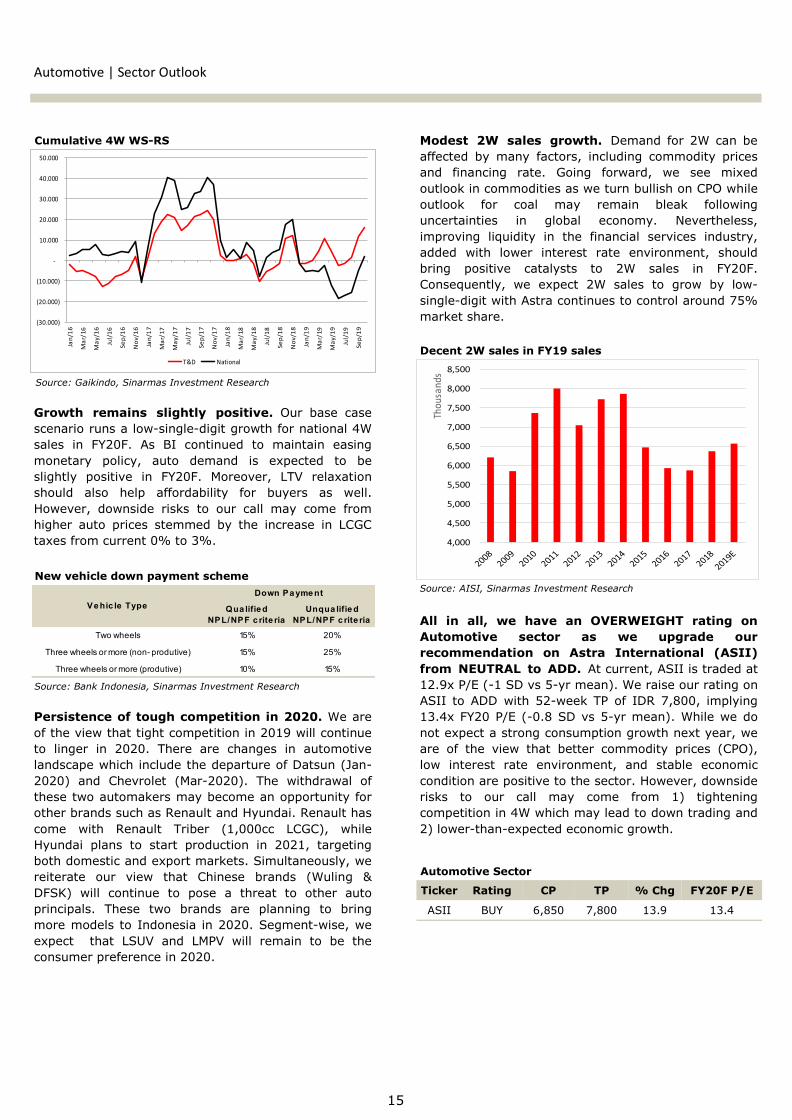

)< ZHDN GHPDQG LQ WKH RYHUDOO VHFWRU $VRI0QDWLRQDO:VDOHVSRVWHGVOXJJLVKSHUIRUPDQFHDV LW ZHQW GRZQ E\ <R< DV XQLW VDOHV ZHUHUHFRUGHGDWN0HDQZKLOHGRPHVWLF:VDOHVDOVRUHFRUGHGDZHDNJURZWKRI<R<ZLWKPQXQLWVVROG GXULQJ WKH SHULRG 7KURXJKRXW WKH \HDU GHPDQGZDVZHDNLQZKLFKZHEHOLHYHZDVSDUWO\DWWULEXWDEOHWRWKH VRIW *'3 H[SDQVLRQ GHFOLQLQJ FRPPRGLW\ SULFHVDQG D QXPEHU RI SROLWLFDO HYHQWV :RUVHQHG E\ WKHLQWHQVH FRPSHWLWLRQ PRVW RI WKH DXWRPRWLYH EUDQGVH[SHULHQFHGDQHJDWLYHJURZWK LQ)<H[FHSW:XOLQJ<R<PDUNHWVKDUH')6.PDUNHWVKDUHDQGRWKHUDXWRPDNHUVZKLFKKDYHQLFKHPDUNHWVXFKDV1LVVDQ%0:DQG0,1,,QRXURSLQLRQSRVLWLYH<R<SHUIRUPDQFHIURP:XOLQJDQG')6.ZHUHDWWULEXWDEOHWRWKHPRUHIOH[LEOHSULFLQJVWUDWHJ\ZKLFKLVPRUHDIIRUGDEOHFRPSDUHGWRWKH-DSDQHVHEUDQGVLQDGGLWLRQ WR WKH ORZ EDVH LQ WKH SUHYLRXV \HDU $V IRU1LVVDQ $OO-1HZ /LYLQD ODXQFKLQJ KDG KHOSHG WKHEUDQG¶VVDOHVDV LW UHFRUGHGVLPLODUSHUIRUPDQFH WR LWVWZLQ 0LWVXELVKL ([SDQGHU 0HDQZKLOH WKH WRS-DXWRPDNHUV LQ ,QGRQHVLDQ PDUNHW ZKLFK DUH 7R\RWD'DLKDWVX +RQGD 0LWVXELVKL DQG 6X]XNL SRVWHG DQHJDWLYH \HDUO\ JURZWK RI UHVSHFWLYHO\ /RRNLQJ DW $VWUD¶VSHUIRUPDQFHFRPSDQ\PDQDJHGWRPDLQWDLQLWVPDUNHWVKDUHDWLQ0EHWWHUWKDQWKHVDPHSHULRGODVW \HDU 0 7KLV ZDV VXSSRUWHG E\7R\RWD-'DLKDWVXDVWKH\RXWSHUIRUPHGWKHLUSHHUV

6RXUFH*DLNLQGR6LQDUPDV,QYHVWPHQW5HVHDUFK

$XWRPRWLYHEUDQG0ZKROHVDOHV

Ra nk Bra nd Ma rke t Sha re YoY Growth

1 TOYOTA 32.4% - 6.2%

2 DAIHATSU 17.7% - 10.7%

3 HONDA 13.2% - 16.1%

4 MITSUBISHI MOTORS 11.8% - 19.0%

5 SUZUKI 9.4% - 19.5%

6 MITSUBISHI FUSO 4.3% - 18.0%

7 HINO 3.0% - 21.0%

8 ISUZU 2.4% - 5.0%

9 WULING 1.9% 17.8%

10 NISSAN 1.3% 98.0%

ƵƚŽŵŽƟǀĞ^ĞĐƚŽƌKƵƚůŽŽŬ

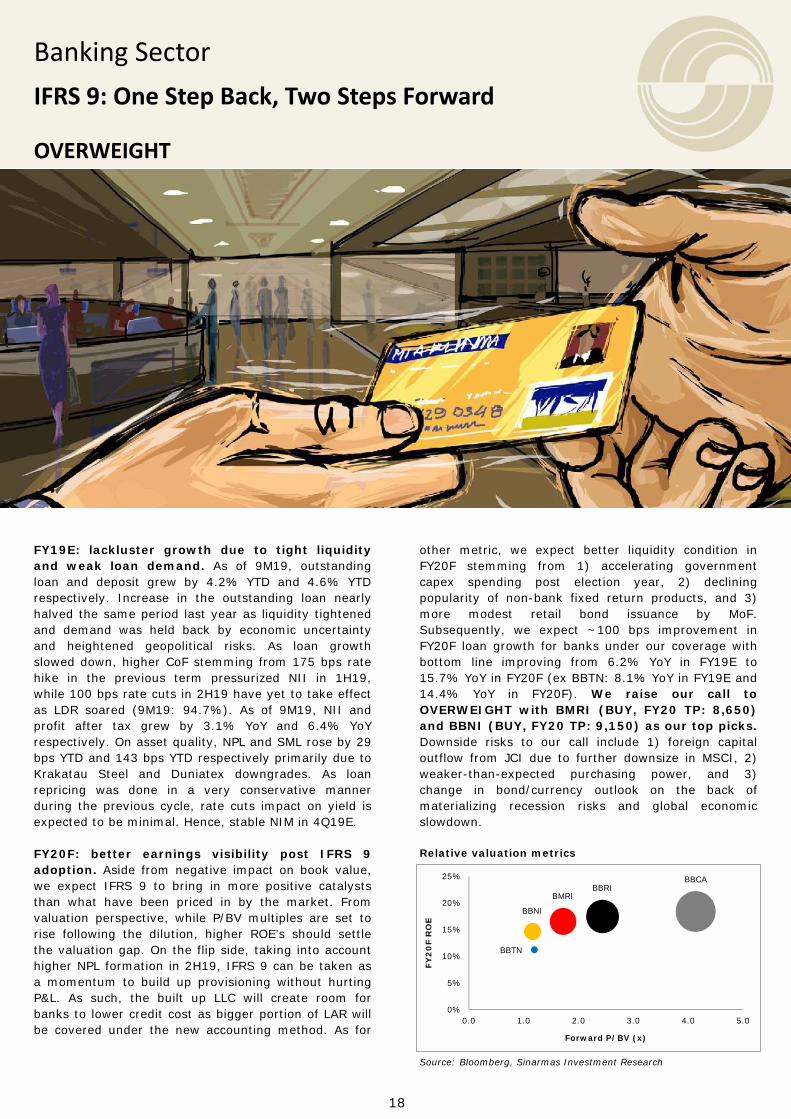

0RGHVW : VDOHV JURZWK 'HPDQG IRU : FDQ EHDIIHFWHG E\PDQ\ IDFWRUV LQFOXGLQJ FRPPRGLW\ SULFHVDQG ILQDQFLQJ UDWH *RLQJ IRUZDUG ZH VHH PL[HGRXWORRNLQFRPPRGLWLHVDVZHWXUQEXOOLVKRQ&32ZKLOHRXWORRN IRU FRDO PD\ UHPDLQ EOHDN IROORZLQJXQFHUWDLQWLHV LQ JOREDO HFRQRP\ 1HYHUWKHOHVVLPSURYLQJ OLTXLGLW\ LQ WKH ILQDQFLDO VHUYLFHV LQGXVWU\DGGHG ZLWK ORZHU LQWHUHVW UDWH HQYLURQPHQW VKRXOGEULQJ SRVLWLYH FDWDO\VWV WR : VDOHV LQ )<)&RQVHTXHQWO\ ZH H[SHFW : VDOHV WR JURZ E\ ORZ-VLQJOH-GLJLWZLWK$VWUDFRQWLQXHVWRFRQWURODURXQGPDUNHWVKDUH

$OO LQ DOO ZH KDYH DQ 29(5:(,*+7 UDWLQJ RQ$XWRPRWLYH VHFWRU DV ZH XSJUDGH RXUUHFRPPHQGDWLRQ RQ $VWUD ,QWHUQDWLRQDO $6,,IURP 1(875$/ WR $'' $WFXUUHQW$6,,LVWUDGHGDW[3(-6'YV-\UPHDQ:HUDLVHRXUUDWLQJRQ$6,, WR $''ZLWK -ZHHN 73 RI ,'5 LPSO\LQJ[)<3( -6'YV-\UPHDQ:KLOHZHGRQRWH[SHFWDVWURQJFRQVXPSWLRQJURZWKQH[W\HDUZHDUH RI WKH YLHZ WKDW EHWWHU FRPPRGLW\ SULFHV &32ORZ LQWHUHVW UDWH HQYLURQPHQW DQG VWDEOH HFRQRPLFFRQGLWLRQDUHSRVLWLYHWRWKHVHFWRU+RZHYHUGRZQVLGHULVNV WR RXU FDOO PD\ FRPH IURP WLJKWHQLQJFRPSHWLWLRQLQ:ZKLFKPD\OHDGWRGRZQWUDGLQJDQGORZHU-WKDQ-H[SHFWHGHFRQRPLFJURZWK

*URZWK UHPDLQV VOLJKWO\ SRVLWLYH 2XU EDVH FDVHVFHQDULRUXQVDORZ-VLQJOH-GLJLWJURZWKIRUQDWLRQDO:VDOHV LQ )<) $V %, FRQWLQXHG WR PDLQWDLQ HDVLQJPRQHWDU\ SROLF\ DXWR GHPDQG LV H[SHFWHG WR EHVOLJKWO\ SRVLWLYH LQ )<) 0RUHRYHU /79 UHOD[DWLRQVKRXOG DOVR KHOS DIIRUGDELOLW\ IRU EX\HUV DV ZHOO+RZHYHU GRZQVLGH ULVNV WR RXU FDOO PD\ FRPH IURPKLJKHU DXWR SULFHV VWHPPHG E\ WKH LQFUHDVH LQ /&*&WD[HVIURPFXUUHQWWR

3HUVLVWHQFHRIWRXJKFRPSHWLWLRQLQ:HDUHRIWKHYLHZWKDWWLJKWFRPSHWLWLRQLQZLOOFRQWLQXHWR OLQJHU LQ 7KHUH DUH FKDQJHV LQ DXWRPRWLYHODQGVFDSHZKLFKLQFOXGHWKHGHSDUWXUHRI'DWVXQ-DQ- DQG &KHYUROHW 0DU- 7KH ZLWKGUDZDO RIWKHVHWZRDXWRPDNHUVPD\EHFRPHDQRSSRUWXQLW\IRURWKHUEUDQGVVXFKDV5HQDXOWDQG+\XQGDL5HQDXOWKDVFRPH ZLWK 5HQDXOW 7ULEHU FF /&*& ZKLOH+\XQGDL SODQV WR VWDUW SURGXFWLRQ LQ WDUJHWLQJERWKGRPHVWLFDQGH[SRUWPDUNHWV6LPXOWDQHRXVO\ZHUHLWHUDWH RXU YLHZ WKDW &KLQHVH EUDQGV :XOLQJ ')6. ZLOO FRQWLQXH WR SRVH D WKUHDW WR RWKHU DXWRSULQFLSDOV 7KHVH WZR EUDQGV DUH SODQQLQJ WR EULQJPRUHPRGHOVWR ,QGRQHVLD LQ6HJPHQW-ZLVHZHH[SHFW WKDW /689 DQG /039 ZLOO UHPDLQ WR EH WKHFRQVXPHUSUHIHUHQFHLQ

6RXUFH$,6,6LQDUPDV,QYHVWPHQW5HVHDUFK

'HFHQW:VDOHVLQ)<VDOHV

7LFNHU 5DWLQJ &3 73 &KJ )<)3(

$6,, %8<

$XWRPRWLYH6HFWRU

6RXUFH*DLNLQGR6LQDUPDV,QYHVWPHQW5HVHDUFK

&XPXODWLYH::6-56

6RXUFH%DQN,QGRQHVLD6LQDUPDV,QYHVWPHQW5HVHDUFK

1HZYHKLFOHGRZQSD\PHQWVFKHPH

Qua lifie d NPL/NPF c rite ria

Unqua lifie d NPL/NPF c rite ria

Two wheels 15% 20%

Three wheels or more (non- produtive) 15% 25%

Three wheels or more (produtive) 10% 15%

Down Pa yme nt

Ve hic le Type

4,000

4,500

5,000

5,500

6,000

6,500

7,000

7,500

8,000

8,500

Thou

sand

s

(30.000)

(20.000)

(10.000)

-

10.000

20.000

30.000

40.000

50.000

Jan/

16

Mar

/16

May

/16

Jul/

16

Sep/

16

Nov

/16

Jan/

17

Mar

/17

May

/17

Jul/

17

Sep/

17

Nov

/17

Jan/

18

Mar

/18

May

/18

Jul/

18

Sep/

18

Nov

/18

Jan/

19

Mar

/19

May

/19

Jul/

19

Sep/

19T&D National

:H UDLVH RXU UDWLQJ RQ 37 $VWUD ,QWHUQDWLRQDO 7EN $6,,IURP1(875$/WR$''ZLWK)<73RI,'52XWWDUJHWSULFH LV GHULYHG IURP 6273 YDOXDWLRQ ZLWK LPSOLHG FRQVROLGDWHG)<) 3( DQG 3%9 RI [ DQG [ UHVSHFWLYHO\ 2YHUDOO ZHEHOLHYH$6,,WRKDYHDPRUHIDYRUDEOHRXWORRNLQGHVSLWHWKHFKDOOHQJLQJ FRPSHWLWLRQ ODQGVFDSH $PDLQWDLQHGPDUNHW VKDUH LQDXWREXVLQHVVLPSURYLQJ&32SULFHVDQG%DQN3HUPDWDGLYHVWPHQWVKRXOG EH WKH UHWDLQLQJ SRVLWLYH FDWDO\VWV IRU $6,, +RZHYHU WKHULVNV WR RXU FDOO DUH ZRUVH-WKDQ-H[SHFWHG FRPSHWLWLRQ LQ :EXVLQHVV IXUWKHU GHWHULRUDWLRQ LQ FRPPRGLW\ SULFHV DQG VORZHU-WKDQ-H[SHFWHGHFRQRPLFJURZWK 0RGHVW JURZWK LQ $XWRPRWLYH EXVLQHVV $V IRU )<) ZHH[SHFWQDWLRQDODXWRVDOHV WRJURZPRGHUDWHO\DWZLWK$VWUD¶VVKDUHEHLQJPDLQWDLQHGDW)URP:VHJPHQWZHIRUHFDVWWKHQDWLRQDO : VDOHV WR JURZ DW ORZ-VLQJOH-GLJLW UDWH 'HVSLWH WKHFKDOOHQJLQJ ODQGVFDSH VKRZQ LQ ZH UHPDLQ FDXWLRXVO\RSWLPLVWLF WRZDUG WKH RYHUDOO RXWORRN $GGLWLRQDOO\ ZH DUH PRUHFRQVWUXFWLYHRQ&32SULFHVGULYHQE\OLPLWHG&32SURGXFWLRQJURZWKZLWK LPSURYLQJ RYHUDOO GHPDQG VXSSRUWHG E\ % SURJUDP0RUHRYHU HDVLQJ PRQHWDU\ DQG PDFURSUXGHQWLDO SROLFLHV IURP %,VKRXOGDOVRKHOSVWLPXODWHFRQVXPHUV¶DSSHWLWHIRUDXWRVHFWRU 0DUJLQ LPSURYHPHQW$VRI4ZHVHHPDUJLQ LPSURYHPHQWDFURVV $VWUD¶V VXEVLGLDULHV $XWRPRWLYH PDQXIDFWXULQJ PDUJLQ'DLKDWVX VDZ DQ LPSURYHPHQW DVPDUJLQ UHFRYHUHG WR LQ4YVLQ+:HH[SHFWDXWRPDQXIDFWXULQJPDUJLQWRVWDELOL]H DW WKLV OHYHO LQ WKH QHDU-WR-PHGLXP WHUP 2Q WKH RWKHUKDQG8175¶VHDUQLQJVVKRXOGUHPDLQUHVLOLHQW&$*5)<(-)<)GHVSLWHWKHZHDNLQGXVWU\RXWORRNIURPPLQLQJVHFWRU:HH[SHFW0DUWDEHWRSRVWHDUQLQJVJURZWKLQ)<VXSSRUWHGE\KLJKHU $63 H[SLULQJ KHGJH SRVLWLRQZKLFKZLOO OLIW WKH JROG SULFHDVVXPSWLRQWR86'0HDQZKLOHZHH[SHFW$&67HDUQLQJVWRWXUQSRVLWLYHLQ)<DIWHUERRNLQJDORVVWKLV\HDU2QWRSRIWKDWZH H[SHFW &32SULFH WR VWDELOL]H DW 50WRQ LQ ZKLFKZLOOUHGXFHSUHVVXUHRQ$$/,¶VERWWRPOLQH

^ƚŽĐŬ/ŶĨŽƌŵĂƟŽŶ

ůŽŽŵďĞƌŐdŝĐŬĞƌ ^///:

ϱϮ-tĞĞŬ,ŝŐŚ ϴϱϱϬ

ϱϮ-tĞĞŬ>Žǁ ϲϮϱϬ

&zϮϬ&W ϭϯϰdž

&zϮϬ&Ws ϭϵdž

^ŚĂƌĞKƵƚƐƚĂŶĚŝŶŐ;DŶͿ ϰϬϰϴϯϲ

DĂƌŬĞƚĂƉ;/ZdŶͿ Ϯϳϳϯ

^ŚĂƌĞWƌŝĐĞWĞƌĨŽƌŵĂŶĐĞ

ƵƌƌĞŶƚWƌŝĐĞ ϲϴϱϬ

ϱϮ-tĞĞŬdĂƌŐĞƚWƌŝĐĞ ϳϴϬϬ

йŚĂŶŐĞ ϭϯϵй

ƵƚŽŵŽƟǀĞ^ĞĐƚŽƌ

WdƐƚƌĂ/ŶƚĞƌŶĂƟŽŶĂůdďŬ

+LJKOLJKWV,'5%Q ( ) ) )

5HYHQXH

*URVV3URILW

(%,7'$

JURZWK -

1HW3URILW

JURZWK -

(%,7'$0DUJLQ

1HW0DUJLQ

5HWXUQRQ$VVHW

5HWXUQRQ(TXLW\

ƵƚŽŵŽƟǀĞƐƚƌĂ/ŶƚĞƌŶĂƟŽŶĂů

,QFRPH6WDWHPHQW .H\$VVXPSWLRQV

%DODQFH6KHHW 5DWLR$QDO\VLV

( ) ) )

86','5

:6DOHV7KV8QLW

:6DOHV7KV8QLW

:0DUNHW6KDUH

:0DUNHW6KDUH

&RDO3ULFH0W

$YJ&RDO3ULFH0W

.RPDWVX6DOHV8QLW

3$0$3URG0Q7RQV

3$0$2%0Q7RQV

7703URG0Q7RQV

1HZ&RQWUDFW%Q

%XUQ5DWH

))%3URG7KV7RQV

))%<LHOG7RQV+D

&323URG7KV7RQV

([WUDFWLRQ5DWH

&326DOHV7KV7RQV

&32$63,'5NJ

,'57Q ( ) ) )

1HW5HYHQXH

-$XWRPRWLYH

-)LQDQFLDO -+HDY\(TXLSPHQW0LQLQJ&RQWUDFWLQJ

-$JULEXVLQHVV

&RVWRI5HYHQXH

-$XWRPRWLYH

-)LQDQFLDO -+HDY\(TXLSPHQW0LQLQJ&RQWUDFWLQJ

-$JULEXVLQHVV

*URVV3URILW

6HOOLQJ([SHQVHV

*$([SHQVHV

2SHUDWLQJ3URILW

(%,7'$

)LQDQFH,QFRPH

)LQDQFH&RVW 6KDUHRI3URILWRI$VVRFLDWHV

,QFRPH%HIRUH7D[([SHQVHV

1HW,QFRPH

( ) ) )

3URILWDELOLW\ 5HWXUQRQ$VVHW

5HWXUQRQ(TXLW\

*URVV0DUJLQ

2SHUDWLQJ0DUJLQ

(%,7'$0DUJLQ

1HW0DUJLQ

/LTXLGLW\ &XUUHQW5DWLR;

4XLFN5DWLR;

6ROYHQF\ 'HEW(TXLW\;

'HEW$VVHWV;

9DOXDWLRQV 3(;

3%9;

,'57Q ( ) ) )

&DVKDQG(TXLYDOHQWV

7UDGH5HFHLYDEOHV

)LQDQFLQJ5HFHLYDEOHV

2WKHU5HFHLYDEOHV

,QYHQWRULHV

7RWDO&$

1&5HFHLYDEOHV

,QYHVWPHQWV

3ODQWDWLRQV

0LQLQJ3URSHUWLHV

&RQFHVVLRQV

)L[HG$VVHWV

7RWDO$VVHWV

67%RUURZLQJV

/7%RUURZLQJV

$FFRXQW3D\DEOHV

7RWDO/LDELOLWLHV

7RWDO(TXLW\

other metric, we expect better liquidity condition in FY20F stemming from 1) accelerating government capex spending post election year, 2) declining popularity of non-bank fixed return products, and 3) more modest retail bond issuance by MoF. Subsequently, we expect ~100 bps improvement in FY20F loan growth for banks under our coverage with bottom line improving from 6.2% YoY in FY19E to 15.7% YoY in FY20F (ex BBTN: 8.1% YoY in FY19E and 14.4% YoY in FY20F). We raise our call to OVERWEIGHT with BMRI (BUY, FY20 TP: 8,650) and BBNI (BUY, FY20 TP: 9,150) as our top picks. Downside risks to our call include 1) foreign capital outflow from JCI due to further downsize in MSCI, 2) weaker-than-expected purchasing power, and 3) change in bond/currency outlook on the back of materializing recession risks and global economic slowdown. Relative valuation metrics

FY19E: lackluster growth due to tight liquidity and weak loan demand. As of 9M19, outstanding loan and deposit grew by 4.2% YTD and 4.6% YTD respectively. Increase in the outstanding loan nearly halved the same period last year as liquidity tightened and demand was held back by economic uncertainty and heightened geopolitical risks. As loan growth slowed down, higher CoF stemming from 175 bps rate hike in the previous term pressurized NII in 1H19, while 100 bps rate cuts in 2H19 have yet to take effect as LDR soared (9M19: 94.7%). As of 9M19, NII and profit after tax grew by 3.1% YoY and 6.4% YoY respectively. On asset quality, NPL and SML rose by 29 bps YTD and 143 bps YTD respectively primarily due to Krakatau Steel and Duniatex downgrades. As loan repricing was done in a very conservative manner during the previous cycle, rate cuts impact on yield is expected to be minimal. Hence, stable NIM in 4Q19E. FY20F: better earnings visibility post IFRS 9 adoption. Aside from negative impact on book value, we expect IFRS 9 to bring in more positive catalysts than what have been priced in by the market. From valuation perspective, while P/BV multiples are set to rise following the dilution, higher ROE’s should settle the valuation gap. On the flip side, taking into account higher NPL formation in 2H19, IFRS 9 can be taken as a momentum to build up provisioning without hurting P&L. As such, the built up LLC will create room for banks to lower credit cost as bigger portion of LAR will be covered under the new accounting method. As for

18

Banking Sector

IFRS 9: One Step Back, Two Steps Forward

OVERWEIGHT

Source: Bloomberg, Sinarmas Investment Research

BMRIBBRI

BBCA

BBNI

BBTN

0%

5%

10%

15%

20%

25%

0.0 1.0 2.0 3.0 4.0 5.0

FY2

0F

RO

E

Forward P/BV (x)

Banking | Sector Outlook

Percentage of loans being financed by low cost deposits

BMRI (BUY, FY20 TP: 8,650) and BBNI (BUY, FY20 TP: 9,150) as our top picks. As we look beyond FY19, we find BMRI and BBNI to be good stock picks going into 2020 given the risk-reward associated with each bank. Aside from discounted valuations of 0.5 SD and 1.0 SD respectively, BMRI and BBNI offer clear earning visibility with comforting margin of error. Post IFRS 9, we expect CoC to decline by 50 bps YoY for BMRI (~15% of FY19E NPAT) and 37 bps YoY for BBNI (~15% of FY19E NPAT). Meanwhile, NII and NIM are likely to remain stable with mid-to-high single digit growth in FY20F supported by better loan demand as impact from monetary easing materializes and improving liquidity condition as competition from non-bank loosen.

Impact of IFRS 9 adoption

Minimal upside on NIM despite 100 bps 7DRRR cuts in 2H19. While OTC rates have been lowered by up to 50 bps for shorter tenor TD’s (1-6M), longer TD’s (12M), however, sees a little to no change across BUKU I-IV banks as liquidity has yet to ease. This paired with bigger third-party-fund contribution from institutions constrained banks’ ability to lower CoF. Thus, we expect 4Q19 NIM to give a better color for short- to medium-term NIM outlook as asset/liability growth consolidates in the quarter. In the meantime, we expect loan and deposit to grow at similar pace given that LDR and LFR are at the upper end of the spectrum. As for banks under our coverage, our model shows stable NIM outlook for BMRI, BBNI, and BBTN, while BBRI and BBCA may see slight margin deterioration (~20 bps vs our FY19E) on the back of new KUR scheme for BBRI and historical margin trend for BBCA during easing cycles. TD rate changes QoQ (bps)

Normalizing interest expense as liquidity eases. Banking interest expense in 9M19 soared by 24.9% YoY, much higher than the past 3-yr (FY16-18) average rise of 4.7% YoY. This was primarily caused by two things, 1) Big-4 banks grabbing TD market share aggressively from BUKU I-III to accommodate incoming loan demand, which is illustrated from the chart below as % of loans funded by CASA continued to drop as Big-4 banks dominate TD. 2) Pressure on CoF was amplified by the 175 bps 7DRRR hikes, which caused banks to raise TD rates even further. Onwards, we expect the trend to change course as tight liquidity calls for a more balanced growth between loan and deposit. Our model suggests interest expense to rise by 6.0%-8.8% in FY20F versus 16.5%-22.4% in FY19E for banks under our coverage.

19

Source: Bank Indonesia, Sinarmas Investment Research

Ticker Rating CP TP % Chg FY20F P/BV

BMRI BUY 7,375 8,650 17.3 2.0

BBRI NEUTRAL 4,280 4,540 6.1 2.6

BBCA ADD 31,800 35,675 12.2 4.6

BBNI BUY 7,650 9,150 19.6 1.4

BBTN NEUTRAL 2,170 2,300 6.0 1.3

Banking Sector

Ticker Equity (IDR Tn) BV Dilution (%)

BMRI 29.0 14.2

BBRI 8.0 3.9

BBCA 6.0 3.5

BBNI 12.5 10.3

BBTN 4.5 18.3

Source: Sinarmas Investment Research

IDR Time Deposit 1Q19 2Q19 3Q19

1 Month -13 -9 -38

3 Month +6 -9 -24

6 Month +30 -8 -15

12 Months +25 +16 +2

Source: Bank Indonesia, Sinarmas Investment Research

74 77 78 7874

72

46 4446

4745 46

58 5861 61

59 58

40

50

60

70

80

90

2015 2016 2017 2018 2019

Big-4 ex-Big-4 Industry

20

Share Price Performance

Current Price 7,375

52‐Week Target Price 8,650

% Change 17.3%

Banking Sector

PT Bank Mandiri Tbk.

Stock Informa on

Bloomberg Ticker BMRI IJ

52‐Week High 8,175

52‐Week Low 6,275

FY20F P/E 11.8x

FY20F P/BV 2.0x

Share Outstanding (Mn) 46,666.7

Market Cap. (IDR Tn) 344.2

FY19E: stable earnings growth backed by healthy NIM and prudent CoC. As of 10M19, total loan grew by 4.6% YoY (up 1.3% YTD), while customer deposit grew by 6.1% YoY (up 5.8% YTD). From liquidity perspective, LDR came down to 93.1% in 10M19 (dn 415 bps YTD, dn 131 bps YoY). To add, BMRI still has sizeable variable rate government bonds (yield: 5.8%) that will mature gradually until Jul-20 as liquidity buffer and can be used to support asset growth. As bank tries to avoid TD price war through other types of funding outside customer deposit, NIM is relatively stable compared to its peers. In the meantime, we expect no major downgrades in 4Q19 and credit cost should remain within management guidance of 1.5%-1.7% for FY19E (10M19: 1.4%). FY20F: an extension of FY19 with bottom line improvement stemming from lower credit cost. We expect FY20F growth rate to be similar to FY19E for BMRI with ~100 bps improvement driven by corporate segment. As for deposit collection, we expect stable CoF from FY19 as competition in TD pricing should further soften in FY20F catalyzed by 1) 100 bps 7DRRR cuts in 2H19 and 2) less competition from non-bank fixed return products as well as retail bonds. On profitability front, as NPL formation deteriorates and bank allocates required amount of provision to comply with IFRS 9, FY20F earning is expected to grow above industry rate benefiting from lower credit cost. Thus, we think the risk-reward for Bank Mandiri is attractive given the earning visibility and discounted valuation (-0.5 SD) at current market price. We reiterate our BUY rating on PT Bank Mandiri (Persero) Tbk (BMRI) with 52-week TP of IDR 8,650, implying 2.0x FY20F P/BV (17.3% upside potential). As for FY20F, we estimate BMRI’s NPAT at IDR 33.1tn (up 15.8% from our FY19E) with NIM, NPL, and credit cost at 538 bps (dn 5 bps YoY), 262 bps (dn 8 bps YoY), and 120 bps YoY (dn 50 bps YoY) respectively. Impact on equity from IFRS 9 adoption is estimated at IDR 29.0tn or equivalent to 14% BV dilution. Post IFRS 9, we expect credit cost to normalize at 120 bps baking in 1% new NPL formation and 120% coverage ratio.

Highlights (IDR Tn) 2018 2019E 2020F 2021F 2022F

Total Loans 799.6 855.5 941.1 1,032.6 1,133.1

Total Customer Deposits 840.9 894.5 988.0 1,095.2 1,208.8

Net Interest Income 54.6 59.1 62.7 67.2 73.8

Pre-provision Op. Profit 48.3 51.4 53.9 58.2 64.5

Net Income 25.0 28.5 33.1 35.6 39.5

Net Interest Margin (%) 5.4 5.4 5.4 5.4 5.4

Gross NPL (%) 2.8 2.7 2.6 2.5 2.5

Credit Cost (%) 1.9 1.7 1.2 1.2 1.2

Return on Equity (%) 14.6 15.0 16.5 16.9 16.6

Return on Assets (%) 2.2 2.4 2.6 2.5 2.6

BUY

‐

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

‐

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

Jan‐19 Feb‐19 Mar‐19 Apr‐19 May‐19 Jun‐19 Jul‐19 Aug‐19 Sep‐19 Oct‐19 Nov‐19 Dec‐19

Thousands

BMRI IJ Price Volume Graph

Volume BMRI

21

Income Statement Financial Ratios

Balance Sheet Loan Portfolio and NPL

Banking | Bank Mandiri

(IDR Tn) 2018 2019E 2020F 2021F 2022F

Interest Income 81.0 90.5 96.9 104.8 115.2

% change 11.8% 7.0% 8.2% 10.0%

Interest Expense 26.4 31.4 34.2 37.6 41.4

% change 19.2% 8.8% 10.0% 10.1%

Net Int. Income 54.6 59.1 62.7 67.2 73.8

% change 8.2% 6.0% 7.2% 9.9%

Other Op. Income 31.2 31.7 32.6 34.5 36.3

% change 1.4% 3.0% 5.7% 5.3%

Operating Expense 52.0 53.5 52.2 55.3 58.6

% change 3.0% -2.5% 6.0% 6.0%

PPOP 48.3 51.4 53.9 58.2 64.5

% change 6.3% 5.0% 8.0% 10.8%

Net Op. Income 33.9 37.3 43.1 46.4 51.5

% change 10.0% 15.7% 7.5% 11.1%

Pre-tax Income 33.9 37.2 43.1 46.4 51.5

% change 9.7% 15.8% 7.5% 11.1%

Net Income 25.0 28.5 33.1 35.6 39.5

% change 14.1% 15.8% 7.5% 11.1%

(IDR Tn) 2018 2019E 2020F 2021F 2022F

Cash 27.3 22.4 27.7 28.7 24.4

CA w/ Central Bank 59.9 52.1 51.0 53.6 56.3

CA w/ Other Banks 14.8 14.9 15.7 17.4 19.0

Interbank Placement 22.5 37.6 37.6 38.6 40.5

Total Loans - Net 767.8 822.1 875.3 963.2 1,059.8

Marketable Sec. 65.9 62.3 66.5 73.3 80.8

Government Bonds 114.3 142.4 152.0 167.6 184.8

Fixed Assets 38.4 40.4 42.2 43.9 45.4

Total Assets 1,202.3 1,290.5 1,379.7 1,517.3 1,666.3

Demand Deposits 200.5 213.5 239.2 267.9 294.6

Saving Deposits 338.6 350.5 382.0 420.2 462.2

Time Deposits 301.8 330.5 366.8 407.2 452.0

Total Deposits 840.9 894.5 988.0 1,095.2 1,208.8

Deposit from Others 16.9 18.4 19.5 21.4 23.5

Marketable Sec. 19.1 32.5 34.4 37.7 41.3

Fund Borrowings 51.7 54.1 56.7 59.4 62.3

Sub. Debts 0.7 0.7 0.7 0.7 0.7

Total Liabilities 1,017.3 1,082.1 1,175.2 1,285.9 1,404.8

Total Equity 185.0 208.4 204.5 231.4 261.6

(%) 2018 2019E 2020F 2021F 2022F

LDR 95.1 95.6 95.3 94.3 93.7

LFR 86.0 85.5 85.6 85.0 84.8

CASA 64.1 63.1 62.9 62.8 62.6

NIM 5.4 5.4 5.4 5.4 5.4

Avg. Loan Yield 9.5 9.5 9.4 9.4 9.4

Avg. CoF 2.6 2.9 2.8 2.8 2.8

Gross NPL 2.8 2.7 2.6 2.5 2.5

Credit Cost 1.9 1.7 1.2 1.2 1.2

Coverage Ratio 144.6 144.8 266.5 268.1 258.2

Cost to Income 69.8 69.5 66.7 66.7 66.0

Cost Efficiency 60.5 58.9 54.8 54.4 53.2

Return on Assets 2.2 2.4 2.6 2.5 2.6

Return on Equity 14.6 15.0 16.5 16.9 16.6

Profit Margin 31.9 32.6 35.3 35.1 35.4

Asset Turnover 7.0 7.3 7.3 7.2 7.2

Equity Multiplier (x) 6.6 6.3 6.5 6.6 6.5

PBV (x) 2.2 2.0 2.0 1.8 1.6

PE (x) 15.6 13.7 11.8 11.0 9.9

(%) 2018 2019E 2020F 2021F 2022F

Small 6.9 7.0 7.0 7.0 7.0

% NPL 2.8 1.9 1.9 1.9 1.9

Micro 12.5 13.9 13.9 13.9 13.9

% NPL 0.9 0.9 0.9 0.9 0.9

Consumer 10.7 10.5 11.3 11.3 11.3

% NPL 2.2 2.5 2.2 2.2 2.2

Commercial 17.4 16.6 15.7 15.7 15.7

% NPL 10.5 10.9 10.5 10.0 10.0

Corporate 39.7 39.2 39.2 39.2 39.2

% NPL 0.2 0.1 0.3 0.2 0.2

International 0.5 0.5 0.5 0.5 0.5

% NPL - - - - -

Subsidiaries 12.3 12.3 12.3 12.3 12.3

% NPL 2.5 2.9 2.9 2.9 2.9

Collectability 1 93.3 92.6 92.7 92.8 92.8

Collectability 2 3.9 4.7 4.7 4.7 4.7

Collectability 3-5 2.8 2.7 2.6 2.5 2.5

22

Share Price Performance

Current Price 4,280

52‐Week Target Price 4,540

% Change 6.1%

Banking Sector

PT Bank Rakyat Indonesia Tbk.

Stock Informa on

Bloomberg Ticker BBRI IJ

52‐Week High 4,730

52‐Week Low 3,520

FY20F P/E 15.1x

FY20F P/BV 2.6x

Share Outstanding (Mn) 123,345.8

Market Cap. (IDR Tn) 527.9

FY19E: inline performance though 4Q19 should see slower asset growth. As of 10M19, total loan portfolio grew by 8.7% YoY (up 5.8% YTD), whereas deposit grew by 6.1% YoY (up 50 bps YTD), causing LDR to rise to 94.3% (up 2.2% YoY, up 4.7% YTD). From micro segment, while deposit grew above industry rate (9.8% YoY vs 7.5% YoY), LDR rose to 107.0% in 9M19 as micro loans grew by 13.2% YoY during the period. Micro loans, however, are expected to slow down in 4Q19 as bank has fulfilled 95% of FY19 KUR quota by Oct-19. From asset quality perspective, we expect NPL to improve by 30 bps to 2.8% in 4Q19 following Krakatau Steel and Duniatex downgrades (63% and 100% LLC respectively). New KUR scheme may serve as headwinds for Micro and NIM. Government has decided to lower KUR lending rate for FY20 by 100 bps to 6%, while keeping interest subsidy unchanged at 10.5%/5.5%/14% for Micro/Retail/TKI KUR. Moreover, maximum ticket size for Micro KUR will be increased from IDR 25mn to IDR 50mn starting 2020. Higher credit limit for Micro KUR may pose a risk of cannibalization. The new asset yield from Micro KUR is at 6%+10.5%, whereas Kupedes’ asset yield is at 20%-22%. From ticket size perspective, while maximum credit limit for Kupedes is at IDR 250mn, average ticket size still stands at IDR 55mn, relatively close to Micro KUR maximum credit limit. Therefore, loan growth and NIM may get affected given the likelihood of shifting borrowers from Kupedes to KUR as it has 15% rate difference from borrowers’ point of view. We downgrade PT Bank Rakyat Indonesia (Persero) Tbk (BBRI) from ADD to NEUTRAL with 52-week TP of IDR 4,540, implying 2.6x FY20F P/BV (6.1% upside potential). As for FY20F, we forecast BBRI’s NPAT at IDR 37.0tn (up 8.7% from our FY19E) with NIM, NPL, and credit cost at 659 bps (dn 20 bps YoY), 278 bps (dn 2 bps YoY), and 180 bps (dn 50 bps YoY) respectively. Impact on equity from IFRS 9 adoption is estimated at IDR 8.0tn or equivalent to 4% BV dilution. Meanwhile, we expect credit cost to normalize at 180 bps post IFRS 9 taking into account new NPL formation and additional provisioning for secondary reserves and undisbursed loans.

NEUTRAL

Highlights (IDR Tn) 2018 2019E 2020F 2021F 2022F

Total Loans 840.2 932.6 1,035.2 1,158.0 1,296.5

Total Customer Deposits 944.3 999.3 1,118.4 1,266.5 1,424.7

Net Interest Income 77.7 81.0 83.7 91.1 100.4

Pre-provision Op. Profit 59.5 63.2 64.2 69.9 76.9

Net Income 32.4 34.1 37.0 40.0 43.7

Net Interest Margin (%) 7.1 6.8 6.6 6.6 6.6

Gross NPL (%) 2.1 2.8 2.8 2.7 2.6

Credit Cost (%) 2.3 2.3 1.8 1.8 1.8

Return on Equity (%) 18.4 17.5 17.5 17.3 17.1

Return on Assets (%) 2.7 2.6 2.6 2.6 2.5

‐

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

‐

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

Jan‐19 Feb‐19 Mar‐19 Apr‐19 May‐19 Jun‐19 Jul‐19 Aug‐19 Sep‐19 Oct‐19 Nov‐19 Dec‐19

Thousands

BBRI IJ Price Volume Graph

Volume BBRI

23

Banking | Bank Rakyat Indonesia

Income Statement Financial Ratios

Balance Sheet Loan Portfolio and NPL

(IDR Tn) 2018 2019E 2020F 2021F 2022F

Interest Income 111.6 120.5 126.5 138.2 152.4

% change 8.0% 5.0% 9.3% 10.3%

Interest Expense 33.9 39.5 42.7 47.1 52.0

% change 16.5% 8.2% 10.1% 10.4%

Net Int. Income 77.7 81.0 83.7 91.1 100.4

% change 4.2% 3.4% 8.8% 10.2%

Other Op. Income 24.4 26.8 28.5 30.5 32.2

% change 10.0% 6.2% 7.0% 5.7%

Operating Expense 60.3 65.0 65.7 71.5 77.8

% change 7.8% 1.1% 8.7% 8.9%

PPOP 59.5 63.2 64.2 69.9 76.9

% change 6.1% 1.6% 8.9% 10.0%

Net Op. Income 41.7 42.8 46.5 50.1 54.8

% change 2.5% 8.6% 7.9% 9.3%

Pre-tax Income 41.8 42.8 46.5 50.1 54.8

% change 2.4% 8.7% 7.9% 9.3%

Net Income 32.4 34.1 37.0 40.0 43.7

% change 5.3% 8.7% 7.9% 9.3%

(IDR Tn) 2018 2019E 2020F 2021F 2022F

Cash 27.4 13.1 28.5 42.3 48.1

CA w/ Central Bank 71.2 70.4 72.7 77.8 83.7

CA w/ Other Banks 12.7 15.0 15.8 16.6 17.4

Interbank Placement 87.0 74.0 77.7 81.5 85.6

Total Loans - Net 804.7 888.9 978.7 1,095.7 1,227.7

Marketable Sec. 184.3 175.1 170.7 170.7 170.7

Government Bonds 1.5 1.1 1.2 1.2 1.3

Fixed Assets 26.9 28.3 29.7 31.2 32.7

Total Assets 1,296.9 1,352.3 1,476.7 1,643.0 1,825.4

Demand Deposits 180.7 180.7 202.5 224.8 249.8

Saving Deposits 387.2 417.8 464.9 523.0 578.5

Time Deposits 376.4 400.9 451.0 518.6 596.4

Total Deposits 944.3 999.3 1,118.4 1,266.5 1,424.7

Deposit from Others 9.1 17.3 18.8 20.7 22.7

Marketable Sec. 37.4 19.9 22.3 24.0 25.8

Fund Borrowings 40.5 40.5 41.5 41.5 41.5

Sub. Debts 1.5 1.5 1.5 1.6 1.6

Total Liabilities 1,111.6 1,146.9 1,257.4 1,400.1 1,556.4

Total Equity 185.3 205.5 219.3 242.9 269.0

(%) 2018 2019E 2020F 2021F 2022F

LDR 89.0 93.3 92.6 91.4 91.0

LFR 81.4 86.5 86.1 85.5 85.5

CASA 60.1 59.9 59.7 59.0 58.1

NIM 7.1 6.8 6.6 6.6 6.6

Avg. Loan Yield 13.1 12.7 12.2 12.1 12.0

Avg. CoF 2.8 3.0 2.9 2.9 2.9

Gross NPL 2.1 2.8 2.8 2.7 2.6

Credit Cost 2.3 2.3 1.8 1.8 1.8

Coverage Ratio 197.3 159.9 188.6 193.0 198.6

Cost to Income 69.3 71.0 70.0 70.3 70.3

Cost Efficiency 59.1 60.3 58.6 58.8 58.7

Return on Assets 2.7 2.6 2.6 2.6 2.5

Return on Equity 18.4 17.5 17.5 17.3 17.1

Profit Margin 29.1 28.3 29.3 29.0 28.7

Asset Turnover 9.2 9.1 8.9 8.9 8.8

Equity Multiplier (x) 6.9 6.8 6.7 6.7 6.8

PBV (x) 3.1 2.8 2.6 2.3 2.1

PE (x) 17.3 16.4 15.1 14.0 12.8

(%) 2018 2019E 2020F 2021F 2022F

Micro 34.1 35.2 36.8 38.4 40.0

% NPL 1.0 1.3 1.3 1.3 1.3

Consumer 16.3 16.0 15.6 15.2 14.8

% NPL 1.0 1.4 1.4 1.4 1.4

Small Commercial 22.8 22.6 22.0 21.4 20.8

% NPL 3.1 3.7 4.0 4.0 4.0

Medium 2.3 2.6 2.5 2.5 2.4

% NPL 6.8 5.3 5.3 5.3 5.3

SOE 13.3 12.6 11.7 10.9 10.0

% NPL 1.1 1.0 1.5 1.5 1.5

Corporate Non-SOE 11.3 11.0 11.3 11.7 12.0

% NPL 5.5 10.5 9.5 8.5 7.5

Collectability 1 95.3 93.8 93.8 94.0 94.2

Collectability 2 2.5 3.4 3.4 3.3 3.2

Collectability 3-5 2.1 2.8 2.8 2.7 2.6

24

Share Price Performance

Current Price 31,800

52‐Week Target Price 35,675

% Change 12.2%

Banking Sector

PT Bank Central Asia Tbk.

Stock Informa on

Bloomberg Ticker BBCA IJ

52‐Week High 32,125

52‐Week Low 24,900

FY20F P/E 26.4x

FY20F P/BV 4.6x

Share Outstanding (Mn) 24,655.0

Market Cap. (IDR Tn) 784.0

FY19E: stellar performance supported by strong top line growth. As of 10M19, total loan portfolio grew by 8.4% YoY (up 5.3% YTD), whereas customer deposit grew by 10.2% YoY (up 7.8% YTD). Subsequently, LDR stood at 83.4% as of 10M19 (dn 1.4% YoY, dn 2.0% YTD) with healthy CASA ratio of 75.8%. Profitability wise, NII and profit after tax grew by 13.7% YoY and 13.9% YoY respectively. While asset quality remained robust with an NPL ratio of 1.6% (vs 2.7% industry) as of 3Q19, management raised bank-only credit cost from 101 bps in FY18 to 124 bps in 10M19 as they built provision for downgraded debtors that are previously in category 2 loans and have been in the watch list for awhile. NIM is expected to soften amid easing cycle. Margin-wise, BBCA is known to be one of the most resilient banks when it comes to key rate changes supported by ample liquidity and healthy CASA ratio. During easing cycle, however, NIM tends to soften due to bank’s asset and liability profile. Baking in 100 bps 7DRRR cuts in 2H19, we expect minor drop in NIM (~10 bps) in FY20F. Nonetheless, margin compression should remain minimal as we expect better loan demand in FY20F stemming from easing domestic political uncertainty and pick up in working capital as well as consumption loans. As for bank’s core performance, we expect similar trend in FY19E to be carried out in FY20F. We raise PT Bank Central Asia Tbk (BBCA) from NEUTRAL to ADD with 52-week TP of IDR 35,675, implying 4.6x FY20F P/BV (12.2% upside potential). As for FY20F, we forecast BBCA’s NPAT at IDR 33.3tn (up 16.9% YoY from our FY19E) with NIM, NPL, and credit cost at 657 bps (dn 12 bps YoY), 149 bps (dn 13 bps YoY), and 80 bps (dn 40 bps YoY) respectively. Impact on equity from IFRS 9 adoption is estimated at IDR 6.0tn or equivalent to 3% BV dilution. Simultaneously, we expect credit cost to normalize at 80 bps after the adjustment. While bank is traded at +2.0 SD, strong earning visibility with >18.0% ROE makes BBCA continuously attractive especially under low rate environment. Downside risk to our estimate includes IFRS 9 adjustment on non-loan earning assets and undisbursed loans.

ADD

Highlights (IDR Tn) 2018 2019E 2020F 2021F 2022F

Total Loans 543.0 597.3 657.0 735.1 821.3

Total Customer Deposits 635.0 695.4 763.5 845.6 939.4

Net Interest Income 45.3 50.6 54.3 60.1 67.2

Pre-provision Op. Profit 35.4 42.7 46.9 52.8 60.4

Net Income 25.9 28.5 33.3 37.5 43.0

Net Interest Margin (%) 6.5 6.7 6.6 6.6 6.6

Gross NPL (%) 1.4 1.6 1.5 1.5 1.5

Credit Cost (%) 0.5 1.2 0.8 0.8 0.8

Return on Equity (%) 18.3 17.6 18.4 18.5 18.6

Return on Assets (%) 3.3 3.3 3.5 3.6 3.7

‐

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

‐

5,000

10,000

15,000

20,000

25,000

30,000

35,000

Jan‐19 Feb‐19 Mar‐19 Apr‐19 May‐19 Jun‐19 Jul‐19 Aug‐19 Sep‐19 Oct‐19 Nov‐19 Dec‐19

Thousands

BBCA IJ Price Volume Graph

Volume bbca

25

Banking | Bank Central Asia

Income Statement Financial Ratios

Balance Sheet Loan Portfolio and NPL

(IDR Tn) 2018 2019E 2020F 2021F 2022F

Interest Income 56.8 64.1 68.9 76.2 85.0

% change 12.9% 7.5% 10.5% 11.6%

Interest Expense 11.5 13.4 14.6 16.1 17.8

% change 17.2% 8.5% 10.3% 10.9%

Net Int. Income 45.3 50.6 54.3 60.1 67.2

% change 11.8% 7.3% 10.6% 11.8%

Other Op. Income 17.7 21.9 24.9 27.6 30.7

% change 23.6% 13.4% 10.8% 11.4%

Operating Expense 30.3 36.8 37.3 40.4 43.7

% change 21.2% 1.5% 8.2% 8.1%

PPOP 35.4 42.7 46.9 52.8 60.4

% change 20.6% 9.9% 12.6% 14.4%

Net Op. Income 32.7 35.8 41.9 47.2 54.2

% change 9.5% 16.9% 12.8% 14.7%

Pre-tax Income 32.7 35.8 41.9 47.2 54.2

% change 9.5% 16.9% 12.8% 14.7%

Net Income 25.9 28.5 33.3 37.5 43.0

% change 10.1% 16.9% 12.8% 14.7%

(IDR Tn) 2018 2019E 2020F 2021F 2022F

Cash 21.7 29.1 32.7 35.3 41.7

CA w/ Central Bank 43.5 46.3 48.8 51.0 53.1

CA w/ Other Banks 8.5 11.0 11.6 12.2 12.7

Interbank Placement 31.7 34.4 36.1 38.5 40.8

Total Loans - Net 529.4 581.5 633.6 709.6 793.5

Marketable Sec. 109.1 118.0 132.8 146.5 163.2

Government Bonds - - - - -

Fixed Assets 19.3 20.3 21.3 22.4 23.5

Total Assets 824.8 908.9 996.1 1,105.4 1,231.0

Demand Deposits 166.8 182.3 204.3 230.7 260.3

Saving Deposits 316.8 339.0 367.7 404.2 443.2

Time Deposits 151.4 174.1 191.5 210.7 236.0

Total Deposits 635.0 695.4 763.5 845.6 939.4

Deposit from Others 6.5 8.5 9.8 11.1 12.7

Marketable Sec. 0.2 0.0 0.0 0.0 0.0

Fund Borrowings 2.1 3.0 3.1 3.3 3.5

Sub. Debts - - - - -

Total Liabilities 673.0 737.1 806.3 889.2 984.1

Total Equity 151.8 171.8 189.7 216.3 247.0

(%) 2018 2019E 2020F 2021F 2022F

LDR 85.5 85.9 86.1 86.9 87.4

LFR 84.3 84.5 84.6 85.5 86.0

CASA 76.2 75.0 74.9 75.1 74.9

NIM 6.5 6.7 6.5 6.5 6.5

Avg. Loan Yield 8.9 9.1 8.9 8.9 8.9

Avg. CoF 1.6 1.7 1.6 1.6 1.6

Gross NPL 1.4 1.6 1.5 1.5 1.5

Credit Cost 0.5 1.2 0.8 0.8 0.8

Coverage Ratio 178.7 163.6 239.5 232.9 227.1

Cost to Income 56.1 58.4 55.4 54.5 53.2

Cost Efficiency 48.1 50.7 47.1 46.1 44.6

Return on Assets 3.3 3.3 3.5 3.6 3.7

Return on Equity 18.3 17.6 18.4 18.5 18.6

Profit Margin 45.5 44.4 48.3 49.3 50.6

Asset Turnover 7.2 7.4 7.2 7.2 7.3

Equity Multiplier (x) 5.6 5.4 5.3 5.2 5.0

PBV (x) 5.8 5.1 4.6 4.1 3.6

PE (x) 34.0 30.9 26.4 23.4 20.4

(%) 2018 2019E 2020F 2021F 2022F

Corporate 39.7 41.0 41.0 41.0 41.0

% NPL 1.3 1.5 1.4 1.4 1.4

Commercial & SME 34.2 34.1 34.1 34.1 34.1

% NPL 1.6 1.9 1.6 1.6 1.6

Consumer 26.2 24.9 24.9 24.9 24.9

% NPL 1.2 1.5 1.5 1.5 1.5

Mortgage 16.3 16.1 16.1 16.1 16.1

Vehicle 7.4 6.5 6.5 6.5 6.5

Credit Card 2.4 2.3 2.3 2.3 2.3

Collectability 1 96.8 96.0 96.4 96.6 96.6

Collectability 2 1.8 2.3 2.1 1.9 1.9

Collectability 3-5 1.4 1.6 1.5 1.5 1.5

26

Share Price Performance

Current Price 7,650

52‐Week Target Price 9,150

% Change 19.6%

Banking Sector

PT Bank Negara Indonesia Tbk.

Stock Informa on

Bloomberg Ticker BBNI IJ

52‐Week High 10,250

52‐Week Low 6,650

FY20F P/E 9.4x

FY20F P/BV 1.4x

Share Outstanding (Mn) 18,648.7

Market Cap. (IDR Tn) 142.7

FY19E: slower growth capped by liquidity. As of 10M19, total outstanding loan grew by 12.5% YoY (up 7.9% YTD), while customer deposit increased by 3.2% YoY (up 1.7% YTD). Major drag on deposit collection came from saving deposit, which as of 10M19 dropped by 8.5% YTD (up 2.0% YoY) for the bank-only portion. Demand deposit, on the other hand, grew nicely at 4.2% YTD (up 12.4% YoY), keeping CASA ratio at 64.3% (up 222 bps YoY, dn 97 bps YTD). To date, LDR surged to 96.9% (up 800 bps YoY, up 811 bps YTD) as growth gap between loan and deposit widened. From asset quality perspective, we expect NPL to stay below 200 bps in 4Q19 following Krakatau Steel and Duniatex downgrades (26% LLC for both debtors). FY20F: better earning visibility on the back of stabilizing NIM and lower credit cost. Previously, management’s growth focus tilted more toward asset growth (lending) than it did to deposit, causing customer profile to be less sticky and price sensitive. Going forward, management aims to introduce more retail banking products in an effort to grow CASA deposit. Meanwhile, as one of the largest payroll banks, management believes that BBNI needs to work on retaining payrolls from fleeing to other transactional banks. On profitability front, as NPL formation deteriorates and higher LLC is allocated amid IFRS 9 adoption, we view FY20F earning to grow above industry level stemmed by stable and lower credit cost. With that being said, we think BBNI should outperform its peers given the earning visibility and discounted valuation (-1.0 SD). We raise our rating for PT Bank Negara Indonesia (Persero) Tbk (BBNI) from ADD to BUY with 52-week TP of IDR 9,150, implying 1.4x FY20F P/BV (19.6% upside potential). As for FY20F, we forecast BBNI’s NPAT at IDR 18.2tn (up 20.1% YoY from our FY19E) with NIM, NPL, and credit cost at 507 bps (up 13 bps YoY), 207 bps (up 21 bps YoY), and 120 bps (dn 37 bps YoY) respectively. Impact on equity from IFRS 9 adoption is estimated at IDR 12.5tn or equivalent to 10% BV dilution. Post IFRS 9, we expect credit cost to normalize at 120 bps baking in 1% new NPL formation and 120% coverage ratio.

BUY

Highlights (IDR Tn) 2018 2019E 2020F 2021F 2022F

Total Loans 512.8 569.2 637.5 719.3 812.7

Total Customer Deposits 578.8 594.6 661.4 751.1 853.1

Net Interest Income 35.4 35.6 38.8 42.9 48.7

Pre-provision Op. Profit 27.0 27.5 30.1 33.9 39.0

Net Income 15.0 15.1 18.2 20.5 23.7

Net Interest Margin (%) 5.3 4.9 5.1 5.1 5.2

Gross NPL (%) 2.0 1.9 2.1 2.0 2.0

Credit Cost (%) 1.5 1.6 1.2 1.2 1.2

Return on Equity (%) 14.3 13.0 14.7 15.4 15.8

Return on Assets (%) 2.0 1.8 2.1 2.2 2.2

‐

20,000

40,000

60,000

80,000

100,000

120,000

‐

2,000

4,000

6,000

8,000

10,000

12,000

Jan‐19 Feb‐19 Mar‐19 Apr‐19 May‐19 Jun‐19 Jul‐19 Aug‐19 Sep‐19 Oct‐19 Nov‐19 Dec‐19

Thousands

BBNI IJ Price Volume Graph

Volume BBNI

27

Banking | Bank Negara Indonesia

Income Statement Financial Ratios

Balance Sheet Loan Portfolio and NPL

(IDR Tn) 2018 2019E 2020F 2021F 2022F

Interest Income 54.1 57.6 62.7 68.7 76.9

% change 6.4% 8.9% 9.5% 11.9%

Interest Expense 18.7 22.0 23.9 25.8 28.2

% change 17.8% 8.5% 8.2% 9.0%

Net Int. Income 35.4 35.6 38.8 42.9 48.7

% change 0.3% 9.2% 10.3% 13.6%

Other Op. Income 17.6 18.9 20.4 22.4 24.6

% change 7.2% 8.2% 9.9% 9.8%

Operating Expense 33.5 35.4 36.5 39.6 43.5

% change 5.8% 3.0% 8.6% 9.9%

PPOP 27.0 27.5 30.1 33.9 39.0

% change 2.0% 9.1% 12.7% 15.2%

Net Op. Income 19.6 19.1 22.8 25.7 29.8

% change -2.8% 19.7% 12.7% 15.9%

Pre-tax Income 19.8 19.0 22.8 25.7 29.8

% change -4.2% 20.1% 12.7% 15.9%

Net Income 15.0 15.1 18.2 20.5 23.7

% change 0.7% 20.1% 12.7% 15.9%

(IDR Tn) 2018 2019E 2020F 2021F 2022F

Cash 14.0 8.9 12.2 17.0 25.9

CA w/ Central Bank 35.6 35.6 36.9 38.8 40.4

CA w/ Other Banks 13.1 13.1 13.6 14.3 14.9

Interbank Placement 39.3 23.6 24.7 26.4 28.1

Total Loans - Net 497.9 552.9 606.7 686.2 777.0

Marketable Sec. 32.0 28.8 28.8 28.8 28.8

Government Bonds 86.8 82.5 86.5 92.1 98.2

Fixed Assets 26.1 26.1 26.1 27.4 28.8

Total Assets 808.6 837.1 904.6 1,008.4 1,130.3

Demand Deposits 169.3 189.2 212.8 244.3 279.2

Saving Deposits 206.1 206.1 229.0 254.3 286.1

Time Deposits 203.4 199.4 219.6 252.5 287.9

Total Deposits 578.8 594.6 661.4 751.1 853.1

Deposit from Others 14.2 14.9 16.2 17.9 19.7

Marketable Sec. 3.0 3.0 3.0 3.0 3.0

Fund Borrowings 52.0 46.8 50.8 55.9 61.6

Sub. Debts - - - - -

Total Liabilities 698.2 713.5 779.1 866.6 969.6

Total Equity 110.4 123.6 125.5 141.8 160.8

(%) 2018 2019E 2020F 2021F 2022F

LDR 88.6 95.7 96.4 95.8 95.3

LFR 79.1 86.3 87.2 86.9 86.7

CASA 64.8 66.5 66.8 66.4 66.3

NIM 5.3 4.9 5.1 5.1 5.2

Avg. Loan Yield 10.1 9.7 9.7 9.7 9.7

Avg. CoF 2.7 3.1 3.2 3.1 3.0

Gross NPL 2.0 1.9 2.1 2.0 2.0

Credit Cost 1.5 1.6 1.2 1.2 1.2

Coverage Ratio 148.3 153.7 233.3 227.2 221.7

Cost to Income 72.7 75.1 72.6 71.8 70.6

Cost Efficiency 63.1 65.0 61.5 60.6 59.3

Return on Assets 2.0 1.8 2.1 2.2 2.2

Return on Equity 14.3 13.0 14.7 15.4 15.8

Profit Margin 27.9 26.4 29.1 29.9 31.0

Asset Turnover 7.1 7.0 7.2 7.2 7.2

Equity Multiplier (x) 7.2 7.0 7.0 7.2 7.1

PBV (x) 1.6 1.4 1.4 1.2 1.1

PE (x) 11.3 11.2 9.4 8.3 7.2

(%) 2018 2019E 2020F 2021F 2022F

Corporate 29.6 32.4 32.1 31.8 31.5

% NPL 1.7 1.4 1.6 1.5 1.4

SOE 21.6 19.8 19.0 18.2 17.4

% NPL 0.0 0.0 0.0 0.0 0.0

Medium 14.6 13.4 13.4 13.4 13.4

% NPL 2.6 3.9 4.4 4.4 4.4

Small 12.9 13.4 14.0 14.6 15.2

% NPL 1.6 2.2 2.4 2.4 2.4

Consumer 15.5 15.0 15.5 16.0 16.5

% NPL 2.1 2.1 2.1 2.1 2.1

Subsidiaries 5.8 6.0 6.0 6.0 6.0

% NPL - - - - -

Collectability 1 94.1 94.0 94.0 94.2 94.2

Collectability 2 3.9 4.1 3.9 3.8 3.8

Collectability 3-5 2.0 1.9 2.1 2.0 2.0

28

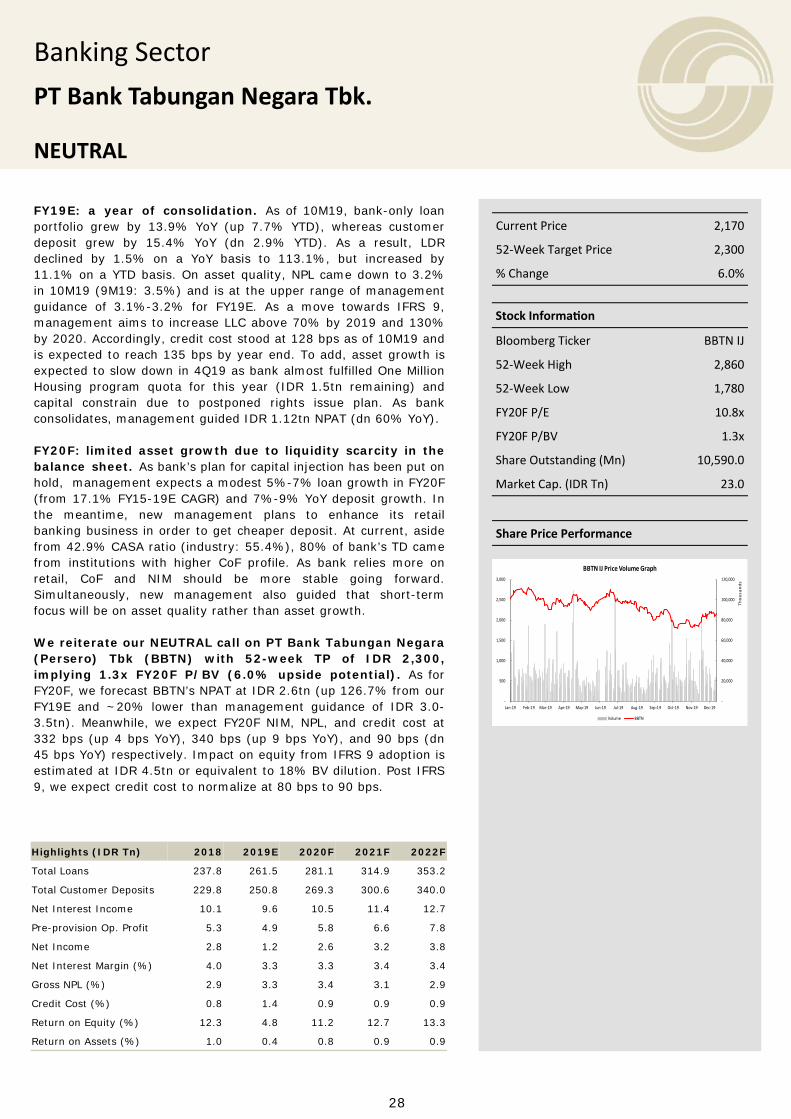

Share Price Performance

Current Price 2,170

52‐Week Target Price 2,300

% Change 6.0%

Banking Sector

PT Bank Tabungan Negara Tbk.

Stock Informa on

Bloomberg Ticker BBTN IJ

52‐Week High 2,860

52‐Week Low 1,780

FY20F P/E 10.8x

FY20F P/BV 1.3x

Share Outstanding (Mn) 10,590.0

Market Cap. (IDR Tn) 23.0

FY19E: a year of consolidation. As of 10M19, bank-only loan portfolio grew by 13.9% YoY (up 7.7% YTD), whereas customer deposit grew by 15.4% YoY (dn 2.9% YTD). As a result, LDR declined by 1.5% on a YoY basis to 113.1%, but increased by 11.1% on a YTD basis. On asset quality, NPL came down to 3.2% in 10M19 (9M19: 3.5%) and is at the upper range of management guidance of 3.1%-3.2% for FY19E. As a move towards IFRS 9, management aims to increase LLC above 70% by 2019 and 130% by 2020. Accordingly, credit cost stood at 128 bps as of 10M19 and is expected to reach 135 bps by year end. To add, asset growth is expected to slow down in 4Q19 as bank almost fulfilled One Million Housing program quota for this year (IDR 1.5tn remaining) and capital constrain due to postponed rights issue plan. As bank consolidates, management guided IDR 1.12tn NPAT (dn 60% YoY). FY20F: limited asset growth due to liquidity scarcity in the balance sheet. As bank’s plan for capital injection has been put on hold, management expects a modest 5%-7% loan growth in FY20F (from 17.1% FY15-19E CAGR) and 7%-9% YoY deposit growth. In the meantime, new management plans to enhance its retail banking business in order to get cheaper deposit. At current, aside from 42.9% CASA ratio (industry: 55.4%), 80% of bank’s TD came from institutions with higher CoF profile. As bank relies more on retail, CoF and NIM should be more stable going forward. Simultaneously, new management also guided that short-term focus will be on asset quality rather than asset growth. We reiterate our NEUTRAL call on PT Bank Tabungan Negara (Persero) Tbk (BBTN) with 52-week TP of IDR 2,300, implying 1.3x FY20F P/BV (6.0% upside potential). As for FY20F, we forecast BBTN’s NPAT at IDR 2.6tn (up 126.7% from our FY19E and ~20% lower than management guidance of IDR 3.0-3.5tn). Meanwhile, we expect FY20F NIM, NPL, and credit cost at 332 bps (up 4 bps YoY), 340 bps (up 9 bps YoY), and 90 bps (dn 45 bps YoY) respectively. Impact on equity from IFRS 9 adoption is estimated at IDR 4.5tn or equivalent to 18% BV dilution. Post IFRS 9, we expect credit cost to normalize at 80 bps to 90 bps.

NEUTRAL

Highlights (IDR Tn) 2018 2019E 2020F 2021F 2022F

Total Loans 237.8 261.5 281.1 314.9 353.2

Total Customer Deposits 229.8 250.8 269.3 300.6 340.0

Net Interest Income 10.1 9.6 10.5 11.4 12.7

Pre-provision Op. Profit 5.3 4.9 5.8 6.6 7.8

Net Income 2.8 1.2 2.6 3.2 3.8

Net Interest Margin (%) 4.0 3.3 3.3 3.4 3.4

Gross NPL (%) 2.9 3.3 3.4 3.1 2.9

Credit Cost (%) 0.8 1.4 0.9 0.9 0.9

Return on Equity (%) 12.3 4.8 11.2 12.7 13.3

Return on Assets (%) 1.0 0.4 0.8 0.9 0.9

‐

20,000

40,000

60,000

80,000

100,000

120,000

‐

500

1,000

1,500

2,000

2,500

3,000