SIMPOSIUM NASIONAL AKUNTANSI 9 PADANG Padang, 23-26 Agustus 2006 1 PROFITABILITY AND CORPORATE GOVERNANCE DISCLOSURE: AN INDONESIAN STUDY Dwi Novi Kusumawati Prasetya Mulya Business School Abstract This research aims to test empirically the relationship between profitability and the level of corporate governance voluntary disclosure. There are two streams of research regarding the direction of relationship between those two variables, making it interesting to be test statistically in the context of corporate governance disclosure. The GCG disclosure level is measured using 161 items recommended by GCG Codes which are developed by KNKCG (2001). Data are taken from annual reports 2002. The result shows that, after controlling the model by several variables usually used in the disclosure research, profitability are negatively correlated with GCG disclosure. In other words, companies tend to give more comprehensive GCG disclosure when facing a slowdown in profitability measurements. Therefore, market have to take cautious in considering the GCG disclosure given by public companies since it could be used by management to cover bad performance. Keywords : Corporate Governance, Voluntary Dislcosure, Profitability K-INT 14

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

8/14/2019 Simposium Nasional Akuntansi 9 Padang Profitability And

http://slidepdf.com/reader/full/simposium-nasional-akuntansi-9-padang-profitability-and 1/19

SIMPOSIUM NASIONAL AKUNTANSI 9 PADANG

Padang, 23-26 Agustus 2006 1

PROFITABILITY AND CORPORATE GOVERNANCE DISCLOSURE: AN

INDONESIAN STUDY

Dwi Novi KusumawatiPrasetya Mulya Business School

Abstract

This research aims to test empirically the relationship between profitability

and the level of corporate governance voluntary disclosure. There are two streams

of research regarding the direction of relationship between those two variables,

making it interesting to be test statistically in the context of corporate governance

disclosure. The GCG disclosure level is measured using 161 items recommended by

GCG Codes which are developed by KNKCG (2001). Data are taken from annual

reports 2002. The result shows that, after controlling the model by several variablesusually used in the disclosure research, profitability are negatively correlated with

GCG disclosure. In other words, companies tend to give more comprehensive GCG

disclosure when facing a slowdown in profitability measurements. Therefore, market

have to take cautious in considering the GCG disclosure given by public companies

since it could be used by management to cover bad performance.

Keywords: Corporate Governance, Voluntary Dislcosure, Profitability

K-INT 14

8/14/2019 Simposium Nasional Akuntansi 9 Padang Profitability And

http://slidepdf.com/reader/full/simposium-nasional-akuntansi-9-padang-profitability-and 2/19

SIMPOSIUM NASIONAL AKUNTANSI 9 PADANG

Padang, 23-26 Agustus 2006 2

1. INTRODUCTION

Disclosure management is one of strategic planning that has to be carefully

considered by management, especially for management of public companies. Any

information published to the market could create market perception which,

afterwards, could give an advantage or disadvantage for the company itself. Many

researches have been conducted in the field of disclosure. Those researches could be

divided into two categories. The first category is studies examining factors affecting

management disclosure decision, and the second one is studies examining effect of

disclosure to various evonomic events or market reaction to the disclosure.

Based on the type of disclosure, previous studies could also be divided into

studies examined disclosure in general, both mandatory and voluntary, and studies

examined certain type of disclosure, such as financial disclosure, social

responsibility disclosure, environmental disclosure, etc. This study investigates one

kind of disclosure that has not been researched much but getting more attention

recently, which is good corporate governance (GCG) disclosure.

Corporate governance, terms that is being concerned internationally since the

revelation of many international scandals such as Enron and WorldCom. Corporate

governance is not a new term or an innovation, but the public awareness of its

importance has just been built recently. This awareness has pushed standard setters

in many countries to develop and improve the corporate governance practices. In

Asia, corporate governance practices even has become the important element of

economic remodeling in overcoming economic crisis (FCGI, 2002).

Indonesia has also responded the market demand of good corporate

governance pratice by forming a committee in 1999 that is assigned to formulate and

recommend national codes on good corporate governance. This committee, Komite

Nasional tentang Kebijakan Corporate Governance (KNKCG), has published

corporate governance codes on 2001 as guidance for Indonesian companies in

implementing good corporate governance principles. The adoption of this copes is

voluntarily, except for several parts that has been obligated by national standard

setters such as Bapepam or JSX.

Labelle (2002) shows that the determinants of disclosure quality of corporate

governance practice may not be the same as the determinants of financial disclosuredecision aspects. Therefore, it is necessary to investigate whether the factors

K-INT 14

8/14/2019 Simposium Nasional Akuntansi 9 Padang Profitability And

http://slidepdf.com/reader/full/simposium-nasional-akuntansi-9-padang-profitability-and 3/19

SIMPOSIUM NASIONAL AKUNTANSI 9 PADANG

Padang, 23-26 Agustus 2006 3

affecting level of financial disclosure also become the factors affecting level of

corporate governance disclosure. Specifically, this study is aimed to test whether

profitability variable has the same direction of relationship with corporate

governance disclosure as with financial disclosure.

Kusumawati and Riyanto (2005) have attempted to test empirically the effect

of GCG disclosure to market value of the firm. The result suggested that market

respond the GCG disclosure positively. Market value of the firm was measured by

market to book ratio, one ratio that measure how much market, or the investors,

value one company compared to its book value. Therefore, it is interesting to test

whether the company, on the contrary, also gives something more back to investors.

One of the returns that is expected could enhace shareholders’ value is profitability.

Profitability is one variable that is extensively being researched in many

disclosure studies. Most of the studies conducted in financial disclosure proved

positive relationship between profitability and financial disclosure level (Shinghvi

and Desai, 1971; Lang and Lundholm, 1993; Ahmed and Courtis, 1999; Haniffa and

Cooke, 2002; Miller, 2002). Studies conducted on other type of disclosure, such as

social and environmental disclosure gives mixed result though most studies recently

gives negative correlation between those two variables.

Study examined the relationship between corporate performance and

corporate governance disclosure has been conducted by Bujaki and McConomy

(2002) in Canada. Using revenue as measurement, the study suggested that firms

facing a slowdown in revenues tend to increase their disclosure of coporate

governance practices, consistent with an effort to reassure investors and relieve

share price preassure (Beneish, 1997 in Bujaki and McConomy, 2002). Moreover,

the study also revealed that firms manage corporate governance disclosuresubsequent to an apparent failure, to ensure that thay have more comprehensive

corporate governance disclosures thereafter.

Based on previous studies described before, it is interesting to examine the

relationship between profitability and GCG disclosure level. Moreover, it is

interesting to test the direction of that relationship since the research in corporate

governance disclosure has not been conducted much. Therefore, the research

question of this study is whether profitability affects the level of corporate

governance voluntary disclosure in Indonesia.

K-INT 14

8/14/2019 Simposium Nasional Akuntansi 9 Padang Profitability And

http://slidepdf.com/reader/full/simposium-nasional-akuntansi-9-padang-profitability-and 4/19

SIMPOSIUM NASIONAL AKUNTANSI 9 PADANG

Padang, 23-26 Agustus 2006 4

2. LITERATURE REVIEW AND HYPOTHESIS

2.1. Profitability and GCG Disclosure

Voluntary disclosure has been researched in many studies. There are many

factors hypothesized as the influencing factors in disclosure decision making of

management. Most of the literature investigates firms’ specific characteristics as

primary variables affecting the level of voluntary disclosure (Singhvi and Desai,

1971; Chow and Wong-Baren, 1987; lang and Lundholm, 1993; Meek et al., 1995;

Craig and Diga, 1998, etc). Haniffa and Cooke (2002) divide firms’ specific

characteristics into 3 parts, which are corporate structure, corporate performance,

and market-related firms’ specific characteristics. This study will focus on corporate

performance characteristic, as measured by profitability, while the other

characteristics will be used as control variables.

The effect of corporate performance on disclosure level could be positive,

negative, or constant (Lang and Landholm, 1993). The positive relationship is based

on assumption that company will disclose more when it has good or extraordinary

performance. This relationship is supported with adverse selection theory which

predicts that with certain disclosure cost, high-performed companies will give

disclosure while companies below the expectation will not disclose.

Well performed companies also being motivated to differentiate themselves

from other companies in order to enhance their capital with the best-achievable

terms. In this case, they are aimed to reduce their own cost of capital by giving more

disclosure to the market. Therefore, well performed companies are expected to

disclose more information about their performance (Meek et al., 1995).

Certain types of negative information, especially earnings, could also beingdisclosed voluntarily by the firms in order to reduce litigation cost. This hypothesis

supports negative correlation between performance and disclosure level. Disclosure

is also hypothesized that it could reduce cost of capital through the reduction of

information gathering cost by investors. This cost reduction could enhance the

amount of investors willing to invest on the company, thereafter could enhance

liquidity and decrease the cost of capital. In this point of view, then, company

performance will not affect disclosure level.

K-INT 14

8/14/2019 Simposium Nasional Akuntansi 9 Padang Profitability And

http://slidepdf.com/reader/full/simposium-nasional-akuntansi-9-padang-profitability-and 5/19

SIMPOSIUM NASIONAL AKUNTANSI 9 PADANG

Padang, 23-26 Agustus 2006 5

2.2. Pimary Hypothesis

Most of the studies previously discussed support the positive relationship

between corporate performance (profitability) and disclosure level in annual report.

Study conducted by Ahmed and Courtis (1999) which combined 12 profitability

studies suggests that profitability, in general, having positive and significant

relationship with voluntary disclosure level. However, this relationship is not found,

or insignificant, in the disclosure study combined mandatory and voluntary

disclosure.

Studies mentioned before are conducted on financial disclosure. Study in the

specific type of disclosure, corporate governance disclosure, has been conducted by

Bujaki and McConomy (2002). The study reveals that firm facing a slowdown in

revenues tends to increase their disclosure of corporate governance practices.

Moreover, firms suffering serious corporate governance gailures tend to provide

extensive disclosure of governance guidelines implemented in the period after such

failures.

Jackson and Carter (1995) stated that the contemporary interest in corporate

governance is, in significant part, activated because of the revelation of many

scandals in the world of business. The interests intended to be served by such

monitoring are those of shareholders. The favoured approached to improving

corporate governance is to increase the light cast on corporate practice. The favorite

metaphor is that of transparency, making the invisible visible. But, by illuminating

some things, other things inevitably become cast in shadow.

Corporate governance can be seen as intended to throw light upon aspects of

corporate practice, by means of transaparency or disclosure. But, if the light to be

cast is selective, it becomes appropriate to ask, on what grounds is selection made,and who are to be the arbiters of what should be disclosed (Jackson and Carter,

1995). This management of light and shadow (chiaroscuro in art) makes some issues

visible and conceals others. Thus, in the case of corporate governance disclosure, do

companies experiencing bad performance use this light-and-shadow management in

making decision of corporate governance disclosure?

Since the studies supporting positive relationship between profitability and

disclosure are conducted in financial disclosure field, the hypothesis of this study

will be in the form of negative relationship. It is also consistent with previous

K-INT 14

8/14/2019 Simposium Nasional Akuntansi 9 Padang Profitability And

http://slidepdf.com/reader/full/simposium-nasional-akuntansi-9-padang-profitability-and 6/19

SIMPOSIUM NASIONAL AKUNTANSI 9 PADANG

Padang, 23-26 Agustus 2006 6

research and arguments in the corporate governance disclosure field. Thus, the

primary hypothesis could be stated as follows.

H 1: Profitability negatively affects the GCG disclosure level in annual report.

2.3. Controlling Variables Hypotheses

As stated previously, there are many studies have been conducted in the

disclosure studies. Firm specific characteristics are the primary variables found to be

affecting disclosure level. Therefore, there are several control variables that have to

be included in the model to better understand the effect of primary variable, which is

profitability. The control variables used in this study are size, listing status, auditor

status, industry, and dispersed owndership level. Those variables are taken from

disclosure literature whose arguments are considered to be relevant in the corporate

governance disclosure case.

Size. One assumption that supports the relationship between size and

disclosure level is that the disclosure cost will decrease along with the increase of

disclosure level (Lang and Lundholm, 1993). Besides the disclosure cost, the size

hypothesis is also supported with information spreading cost theory, competitive

disadvantage theory, transaction cost theory, and agency theory.

H 2: Size positively affects the GCG disclosure level in annual report.

Listing status. It is defined as whether the company is listed in other

countries or not. Corporate governance has been practiced abroad for quiet long

time, especially in America and Europe, while in Indonesia (or Asia) corporate

governance is still a relatively new issue and is just debated since the economic

crisis. Therefore, it is expected that companies listed in foreign stock exchange will

tend to practice and disclose GCG information as a result of the force given by

international investors and standard setters.

H 3: Listing status positively affets the GCG disclosure level in annual report.

Auditor status. The auditor used by companies also has positive relationship

with the level of disclosure (Haniffa and Cooke 2002). Big-Four accounting firms

are said to have the power to insist companies to reveal more information because

they have more skills and experience to audit the information, and because they have

K-INT 14

8/14/2019 Simposium Nasional Akuntansi 9 Padang Profitability And

http://slidepdf.com/reader/full/simposium-nasional-akuntansi-9-padang-profitability-and 7/19

SIMPOSIUM NASIONAL AKUNTANSI 9 PADANG

Padang, 23-26 Agustus 2006 7

to retain their reputation. Therefore, auditor could act as a border of management

opportunistic behavior (Watts and Zimmerman, 1986).

This research do not use auditor status defined as the Big-Four firms, instead

it defined as whether the company is audited by accounting firm affiliated with

foreign accounting firms or not. The argument used is because it is assumed that

foreign accounting firms have already had more experience and knowledge on

corporate governance issues compared to local accounting firms.

H 4 : Auditor status positively affects the level of GCG dislcosure in annual report.

Industry. The variation of disclosure level is more being influenced by the

sensitivity of one industry to political costs (Craig and Diga, 1998). Companies that

are more sensitive will be forced to give more information than other companies in

other industries. Disclosure could also vary and will be higher in certain industries

that is regulated and monitored by government. Studies about the difference of

disclosure level based on industry have been conducted by Meek et al. (1995), Craig

and Diga (1998), Haniffa and Cooke (2002), Rahman and Hamdan, and Bujaki and

McConomy (2002). All of those studies, in the financial voluntary disclosure, give a

significant result.

H 5 : Industry type affects the GCG disclosure level in annual report.

Dispersed ownership level. The agency theory states that disclosure will be

higher for companies which have more dispersed ownership (Haniffa and Cooke

2002). It happen because with dispersed ownership, the owner will demand more

disclosure to monitor management opportunistic behavior compared to companies

that have more centralized ownership.

This variable has also being investigated by Labelle (2002) specifically inthe case of corporate governance disclosure. Labelle (2002) posits that managers of

management-controlled (diffused ownership) company could use their control of

information disclosed to public in the most favorable and defensible manner. This

argument shows that companies with more dispersed ownership have bigger interest

in providing more qualified information compared to owner-controlled companies.

H 6 : Dispersed ownership level positively affects the GCG disclosure level in

annual report.

K-INT 14

8/14/2019 Simposium Nasional Akuntansi 9 Padang Profitability And

http://slidepdf.com/reader/full/simposium-nasional-akuntansi-9-padang-profitability-and 8/19

SIMPOSIUM NASIONAL AKUNTANSI 9 PADANG

Padang, 23-26 Agustus 2006 8

3. RESEARCH METHODS

3.1. Research Model

The problem examined in this study is whether profitability affects voluntaryGCG disclosure level. The relationship is controlled with other firm characteristics

variables, which are size, listing status, auditor status, industry and dispersed

ownership level. Those control variables are used because they have been

empirically tested as having effect on disclosure level in many studies. The research

model could be described in Figure 1.

INSERT FIGURE 1 HERE.

3.2. Sample

Sample is taken from annual reports 2002 published by public companies

listed on Jakarta Stock Exchange. Annual report is used disclosure medium since

previous research has found that the disclosure level in the annual report is

positively correlated with disclosure level in other medium (Lang and Lundholm,

1993). Campbell (2000) also notes that annual reports are the most widely

distributed of all publicly produced documents of an organization (Bujaki and

McConomy, 2002). All companies are treated the same, regardless their industry,

since it will be controlled by controlling variables.

3.3. Operational Definitions and Measurements of Variables

The measurement of GCG voluntary disclosure level variable is based on

items in the GCG Codes recommended by KNKCG 2001. Explicitly, KNKCG

(2001) stated that the Codes are developed using method that is enabling companies

to enhance and adopt GCG standards which are more contructive and flexible, and

not using the regulation that could force companies to implement them. Thus, the

adoption of the Codes is voluntary in nature for public companies, except for several

parts of the Codes that has been obligated by Bapepam or JSX, such as the

regulation about independent commissionaire, audit committee, and corporate

secretary. Therefore, all items that have been regulated by other standard setters

have been excluded from GCG disclosure level measurement.

For each items recommended by the Codes (the most detail items), a

company will be given one point if it disclose certain item and zero if it doesn’t give

K-INT 14

8/14/2019 Simposium Nasional Akuntansi 9 Padang Profitability And

http://slidepdf.com/reader/full/simposium-nasional-akuntansi-9-padang-profitability-and 9/19

SIMPOSIUM NASIONAL AKUNTANSI 9 PADANG

Padang, 23-26 Agustus 2006 9

any disclosure concerning that item. The total items being used as benchmark are

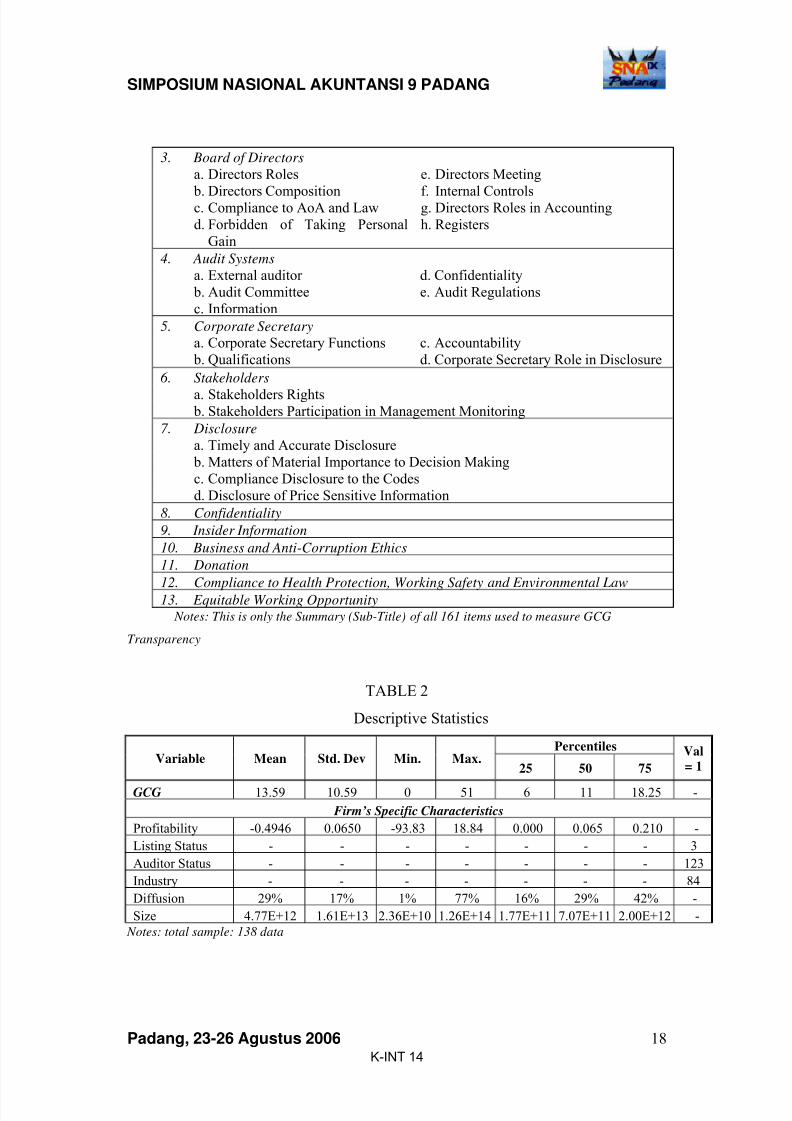

161 items. In summary, the transparency items could be described in Table 1.

INSERT TABLE 1 HERE

The definition of disclosure level in this study is the amount of GCG

information disclosed in annual report both directly and indirectly. It means that the

point given to company stated GCG information explicitly in the corporate

governance chapter of the annual report will be the same as the company stated that

information implicitly in the other chapters of annual report such as notes to

financial statement, management report, etc. The total points given to certain annual

report becomes the proxy of GCG disclosure level of a company.

The profitability contruct are being measured by return on equity (ROE)

ratio. The selection of this ratio is based on the argument that the primary interest

intended to be served by corporate governance are those of shareholders (Jackson

and Carter, 1995). This focus of shareholders has also being explicitly stated by

KNKCG (2001), which said that the objective of GCG Codes are “…..to maximize

firm value and firm value for shareholders…..”. Therefore, this study will use ROE

since this ratio measure the rate of return earned by shareholders.

3.4. Data Analysis Methods

The statistic method being used is multiple regressions analysis. The

regression equation developed empirically test the relationship between firm’s

specific characteristics and disclosure level. The primary characteristic being

focused is profitability while the other characteristics will be considered as control

variables. The regression equation could be notated as follows.

e DISPb INDUSTRY b AUDIT b LISTINGbSIZE bPROFIT baGCG +++++++= 654321

GCG : GCG disclosure level in annual report

PROFIT : profitability, measured by ROE

SIZE : company’s size, measured by total assets at period end

LISTING : foreign listing status (dummy, 1 if listed in foreign

company)

AUDIT : external auditors’ affiliation status (dummy, 1 if affiliated)

K-INT 14

8/14/2019 Simposium Nasional Akuntansi 9 Padang Profitability And

http://slidepdf.com/reader/full/simposium-nasional-akuntansi-9-padang-profitability-and 10/19

SIMPOSIUM NASIONAL AKUNTANSI 9 PADANG

Padang, 23-26 Agustus 2006 10

INDUSTRY : industry codes (dummy, 1 if financial, trading, service or

investment, infrastructure, utility and transportation

industry)

DISP : dispersed ownership level (ratio of total shares owned by

shareholder who own ≤ 5% of shares to the total extending

shares)

4. RESULT AND ANALYSIS

4.1. Descriptive Statistics

Descriptive statistics of all variables could be found in Table 2. GCG

disclosure level used in this research is the same GCG level used in Kusumawati and

Riyanto (2005). From the table, it seems that the company gives GCG information

about 13-14 items in annual report (mean=13.59) from all 161 items that could be

disclosed regarding the KNKCG codes (8.44%). The highest score is 51 points while

the lowest one is 0 points which shows that there is no indication of GCG practices

or voluntary GCG disclosure.

Most companies were just giving minimal GCG disclosure in annual report

since 50% of the samples have GCG level below the average and only 25% of the

samples have GCG level of 18.25 points. The low level of GCG transparency could

be caused by several reasons. It could be describe the real condition of low GCG

practice in Indonesia, or it could be because management doesn’t perceive the

annual report as the right media to disclose GCG practice. The other possibility is

that GCG codes were established using the ideal picture of GCG practice in detail

and it may be too costly for the company to disclose GCG practices in detail in the

annual report.INSERT TABLE 2 HERE

4.2. Regression Analysis

The initial equation doesn’t meet heteroscedasticity assumption of multiple

regression as tested using K-B test (p-value = 0.022). Therefore, the dependent

variable is then being transformed using log transformation. After excluded several

outlier data (absolute standardize residuals > 1.96), the total sample used in the

analysis is 134 data. The final equation then has met normality (Kolmogorov-

K-INT 14

8/14/2019 Simposium Nasional Akuntansi 9 Padang Profitability And

http://slidepdf.com/reader/full/simposium-nasional-akuntansi-9-padang-profitability-and 11/19

SIMPOSIUM NASIONAL AKUNTANSI 9 PADANG

Padang, 23-26 Agustus 2006 11

Smirnov test), heteroscedasticity (KB test) and multicolinearity (VIF and tolerance

value). The result of regression assumption test is presented in Table 3 and Figure 2.

INSERT TABLE 3 HERE

INSERT FIGURE 2 HERE

The result of multiple regression analysis is presented in Table 4.

INSERT TABLE 4 HERE

As shown in table 4, profitability is marginally significant (10% significance

level) regarding its relationship with GCG disclosure level (p-value = 0.065). The

control variables that having very significant result (1% significance level) are

company’s size (p-value = 0.000) and auditor’s status (p-value = 0.009). The other 2

control variables, listing status and dispersed ownership level, are marginally

significant (p-value = 0.076 and 0.063). On the contrary, industry type is

insignificant.

Profitability (H1) is empirically affects GCG disclosure negatively. This

result is consistent with the research conducted by Bujaki and McConomy (2002)

stated that firms facing a slow-down in revenue will tend to disclose more about

their corporate governance practices in annual report. This result also consistent with

the “light-and-shadow management” theory argued by Jackson and Carter (1995)

implying that management will try to shed light to corporate governance practices

disclosure in order to put the bad performance in shadow.

Size (H2) affects GCG positively, as predicted in hypothesis and positive

theory. This result is consistent with previous corporate governance disclosure

studies (Labelle, 2002; Bujaki and McConomy, 2002) and also consistent with

previous disclosure studies in general, both abroad (Shinghvi and Desai, 1971;

Chow and Wong-Boren, 1987; Lang and Lundholm, 1993; Meek et al., 1995; Craigand Diga, 1998; Ahmed and Courtis, 1999; Haniffa and Cooke, 2002; Chou and

Gray, 2002; Rahman and Hamdan) and in Indonesia (Sabeni, 2002; Fitriany, 2001;

Marwata, 2001; Hadi and Sabeni, 2002; Gunawan, 2000).

The other firm’s specific characteristic which also has a very significant

result is auditors’ status (H4). The positive coefficient of these variables implies that

companies using internationally affiliated public accounting firms give higher GCG

transparency compared to the unaffiliated one. Therefore, H4 is supported, which is

consistent with most of previous studies in the area of disclosure in general (Singhvi

K-INT 14

8/14/2019 Simposium Nasional Akuntansi 9 Padang Profitability And

http://slidepdf.com/reader/full/simposium-nasional-akuntansi-9-padang-profitability-and 12/19

SIMPOSIUM NASIONAL AKUNTANSI 9 PADANG

Padang, 23-26 Agustus 2006 12

and Desai, 1971; Ahmed and Courtis, 1999; Haniffa and Cooke, 2002; Fitriany,

2001).

Listing status (H3) shows a marginally significant result. This result implies

that foreign listed companies give higher GCG transparency than companies which

are only listed in JSX. However, the conclusion derived from this hypothesis should

be interpreted carefully considering there are only 3 companies in the sample listed

abroad, which make the data less representative.

The last hypothesis that is also marginally significant is the dispersed

ownership level hypothesis (H6). However, the coefficient of this variable is not

consistent with the prediction. H6 argues that dispersed ownership positively affects

GCG transparency, while the regression analysis gives a negative relationship. This

result is not consistent with Labelle (2002) though in that study the positive and

significant result could only applied in 1 from 2 periods.

The only variable that is not significant is industry type (H5, p-value 0,452).

This is consistent with Labelle (2002) which posits that corporate governance

disclosure is not sensitive to industry since the corporate governance itself is a

general accepted practice. Previous Indonesian studies on disclosure in general also

give insignificant result (Gunawan, 2000; Fitriany, 2001).

5. CONCLUSIONS

This study is aimed to test empirically whether profitability affects GCG

voluntary disclosure level in annual reports. If it does, then in what direction is the

relationship? This research question is very interesting to be tested empirically since

there has not been many research conducted in corporate governance disclosure

level yet. Most of previous disclosure studies are aimed to explore financial

disclosure and environmental or social disclosure. While the financial disclosure

stream proved that profitability affects disclosure level positively, the environmental

and social disclosure proved other direction of the relationship.

This study finds that profitability affects GCG voluntary disclosure level

negatively. It implies that when companies are facing decline in profitability, they

will tend to give more disclosure about corporate governance practices in order to

relieve the market preassure. The result is consistent with other research on GCG

voluntary disclosure conducted in Canada by Bujaki and McConomy (2002). The

K-INT 14

8/14/2019 Simposium Nasional Akuntansi 9 Padang Profitability And

http://slidepdf.com/reader/full/simposium-nasional-akuntansi-9-padang-profitability-and 13/19

SIMPOSIUM NASIONAL AKUNTANSI 9 PADANG

Padang, 23-26 Agustus 2006 13

result also supports the “light-and-shadow management” argued by Jackson and

Carter (1995).

Interestingly, research conducted by Kusumawati and Riyanto (2005) using

the same GCG disclosure index has proved that GCG disclosure, along with other

corporate governance variables, is valued by investors. In other words, investors are

willing to pay higher premium for companies that practice and disclose GCG

information in the annual report. Therefore, investors or shareholders should take

cautious against companies’ disclosure comprehensively since the disclosure itself

could be used by management to shed light on something and to shadow the other

things.

This study has several limitations. First, as stated by Healy and Palepu

(2001), the measurement of transparency used in this study has several limitations.

This method involves the judgment of researcher in the measurement process so that

it will be very difficult to be replicated. Besides, this method usually could only be

applied in one media of disclosure, such as annual report.

Second, the GCG codes developed by KNKCG (2001) are the ideal picture

of good corporate governance that can be implemented by companies. This study

could only make comparison between the ideal pictures with the practices disclosed

by management. If the corporate governance practices stated in annual report are not

the picture of actual implementation of corporate governance in the company, then

the GCG score in this research will not represent the actual condition of corporate

governance practices. Future research could use self-assessment checklist to

measure actual GCG score and compare it with GCG score developed in this study

to get better picture of the corporate governance practice in Indonesia.

K-INT 14

8/14/2019 Simposium Nasional Akuntansi 9 Padang Profitability And

http://slidepdf.com/reader/full/simposium-nasional-akuntansi-9-padang-profitability-and 14/19

SIMPOSIUM NASIONAL AKUNTANSI 9 PADANG

Padang, 23-26 Agustus 2006 14

REFERENCES

Ahmed,K. and J. K. Courtis. 1999. Association between Corporate Characteristicsand Disclosure Levels in Annual Reports: A Meta-Analysis. British

Accounting Review 31: 35-61.

Arifin, H. Haron, and D. N. Ibrahim. Consensus Between Users and Preparers on the

Importance of Voluntary Disclosure Items in Annual Reports: An

Indonesian Study.

Botosan, C. A. 1997. Disclosure Level and the Cost of Equity Capital. The

Accounting Review (July): 323-349.

Botosan, C. A., and M. A. Plumlee. 2002. A Re-examination of Disclosure Leveland the Expected Cost of Equity Capital. Journal of Accounting Research

(March): 21-40.

Bujaki, M. and B. J. McConomy. 2002. Corporate governance: Factors Influencing

Voluntary Disclosure by Publicly Traded Canadian Firms. Canadian

Accounting Perspectives 1: 105-139.

Chau, G. K., and S. J. Gray. 2002. Ownership Structure and Corporate Voluntary

Disclosure in Hong Kong and Singapore. The International Journal of

Accounting 37: 247-265.

Chow, C. W., and A. Wong-Boren. 1987. Voluntary Financial Disclosure by

Mexican Corporations. The Accounting Review (July): 533-541.

Craig, R., and J. Diga. 1998. Corporate Accounting Disclosure in ASEAN. Journal

of International Financial Management and Accounting 3: 246-274.

Dubiel, S. Corporate Goverrnance: Terus Melangkah Sambil Mencari Cara Terbaik,

dalam The Essense of Corporate governance

Fitriany. 2001. Signifikansi Perbedaan Tingkat Kelengkapan Pengungkapan Wajib

dan Sukarela pada Laporan Keuangan Perusahaan Publik yang Terdaftar diBEJ. Simposium Nasional Akuntansi IV.

Forum for Corporate governance in Indonesia (FCGI). 2002. Tata Kelola

Perusahaan (Corporate governance). The Essence of Good Corporate

governance: Konsep dan Implementasi Perusahaan Publik dan Korporasi

Indonesia. Jakarta: Yayasan Pendidikan Pasar Modal Indonesia dan Sinergy

Communication.

Foster, G. 1986. Financial Statement Analysis. .Second Edition. USA: Prentice Hall.

K-INT 14

8/14/2019 Simposium Nasional Akuntansi 9 Padang Profitability And

http://slidepdf.com/reader/full/simposium-nasional-akuntansi-9-padang-profitability-and 15/19

SIMPOSIUM NASIONAL AKUNTANSI 9 PADANG

Padang, 23-26 Agustus 2006 15

Frost, C. A., and W. R. Kinney, Jr. 1996. Disclosure Choices of Foreign Registrants

in the United States. Journal of Accounting Research 34: 67-84.

Gunawan, Y. 2002. Analisis Pengungkapan Informasi Laporan Tahunan pada

Perusahaan yang Terdaftar di BEJ. Simposium Nasional Akuntansi III .

Hadi, N., and A. Sabeni. 2002. Analisa Faktor-faktor yang Mempengaruhi Luas

Pengungkapan Sukarela dalam Laporan Tahunan Perusahaan Go-Public di

BEJ. MAKSI (Agustus): 90-104.

Haniffa, R. M., and T. F. Cooke. 2002. Culture, Corporate governance and

Disclosure in Malaysian Corporations. ABACUS 38: 317-349.

Healy, P. M., and K. G. Palepu. 2001. A Review of the Empirical Disclosure

Literature. Journal of Accounting Economics 31.

Jackson N., and Carter P. 1995. Organizational Chiaroscuro: Throwing Light on the

Concept of Corporate Governance. Human Relations 48: 875 – 889.

Khomsiyah. 2003. Hubungan Corporate governance dan Pengungkapan Informasi:

Pengujian Simultan. Simposium Nasional Akuntansi VI .

Komite Nasional Kebijakan Corporate governance (KNKCG). 2001. Pedoman

Good Corporate governance: Ref. 4. 0.

Kusumawati, D.N., and Riyanto B. 2005. Corporate Governance dan Kinerja:

Analisis Pengaruh Compliance Reporting dan Struktur Dewan terhadap

Kinerja. Simposium Nasional Akuntansi VIII.

Lang, M., and R. Lundholm. 1993. Cross-Sectional Determinants of Analyst Ratings

of Corporate Disclosures. Journal of Accounting Research 31: 246-271.

Marwata. 2001. Hubungan antara Karakteristik Perusahaan dan Kualitas Ungkapan

Sukarela dalam Laporan Tahunan Perusahaan Publik di Indonesia.

Simposium Nasional Akuntansi IV .

Meek, G. K., C. B. Roberts, and S. J. Gray. 1995. Factors Influencing VoluntaryAnnual Report Disclosures by U.S., U.K., and Continental European

Multinational Corporations. Journal of International Business Studies 26.

Miller, G. S. 2002. Earnings Performance and Discretionary Disclosure. Journal of

Accounting Research (March): 173-204.

Patel, S. A., A. Balic, and I. Bwakira. 2002. Measuring Transparency and Disclosure

at Firm-level in Emerging Markets. Emerging Markets Reviews 2: 325-337.

Rahman, A. A., and M. D. Hamdan. Voluntary Disclosure Using Graphical

Information in Annual Reports of Malaysian Companies.

K-INT 14

8/14/2019 Simposium Nasional Akuntansi 9 Padang Profitability And

http://slidepdf.com/reader/full/simposium-nasional-akuntansi-9-padang-profitability-and 16/19

SIMPOSIUM NASIONAL AKUNTANSI 9 PADANG

Padang, 23-26 Agustus 2006 16

Rahman, A. R. 2002. Incomplete Financial Contracting, Disclosure, Corporate

governance and Firm Value. Working Paper (November).

Sabeni, A. 2002. An Empirical Analysis of the Relation between the BOD

Composition and the Level of Voluntary Disclosure. Simposium Nasional Akuntansi V.

Singhvi, S. S., and H. B. Desai. 1971. An Empirical Analysis of the Quality of

Corporate Financial Disclosure. The Accounting Review (January): 129-138

Singleton, W. R., and S. Globerman. 2002. The Changing Nature of Financial

Disclosure in Japan. The International Journal of Accounting 37: 95-111.

Team C Siaga Project. 2002. Indonesian Financial Disclosure Checklist Based on

Indonesian Capital Market Supervisory Agency Rules and Statements of

Financial Accounting Standards.

Watts, R. L., and J. L. Zimmerman. 1986. Positive Accounting Theory. USA:

Prentice Hall.

Young, M. N., D. Ahlstrom, G. D. Bruton, and E. S. Chan. 2001. The Resource

Dependence, Service and Control Functions of Boards of Directors in Hong

Kong and Taiwanese Firms. Asia Pacific Journal of Management 18: 223-

244.

K-INT 14

8/14/2019 Simposium Nasional Akuntansi 9 Padang Profitability And

http://slidepdf.com/reader/full/simposium-nasional-akuntansi-9-padang-profitability-and 17/19

SIMPOSIUM NASIONAL AKUNTANSI 9 PADANG

Padang, 23-26 Agustus 2006 17

APPENDIX

FIGURE 1Research Model

Primary Variable

Profitability

Control Variables

Size

Listing status

Auditor status

Dispersed Ownership

Voluntary GCG

Disclosure Level

TABLE 1

Summary of GCG Dislcoure Items1. Shareholders

a. Shareholder Rights

b. General Meetings of Shareholders

c. Equitable Treatment of Shareholders

d. Shareholders Accountability

e. Appointment and Remuneration System of the Board

2. Board of Commissionaires

a. Commissionaires Functions

b. Commissionaires Composition

c. Compliance to Articles of Association (AoA) and Law

d. Meetings of Commissionairese. Information for Commissionaires

f. Other Business Relationship between Commissionaires and/or Directors and

the Company

g. Forbidden of Taking Personal Gain

h. Appointment, Remuneration and Performance Evaluation of non-Directors

Executives

i. Commitee Established by Commissionaires

K-INT 14

8/14/2019 Simposium Nasional Akuntansi 9 Padang Profitability And

http://slidepdf.com/reader/full/simposium-nasional-akuntansi-9-padang-profitability-and 18/19

SIMPOSIUM NASIONAL AKUNTANSI 9 PADANG

Padang, 23-26 Agustus 2006 18

3. Board of Directors

a. Directors Roles

b. Directors Compositionc. Compliance to AoA and Law

d. Forbidden of Taking Personal

Gain

e. Directors Meeting

f. Internal Controlsg. Directors Roles in Accounting

h. Registers

4. Audit Systems

a. External auditor

b. Audit Committee

c. Information

d. Confidentiality

e. Audit Regulations

5. Corporate Secretary

a. Corporate Secretary Functions

b. Qualifications

c. Accountability

d. Corporate Secretary Role in Disclosure

6. Stakeholders

a. Stakeholders Rights b. Stakeholders Participation in Management Monitoring

7. Disclosure

a. Timely and Accurate Disclosure

b. Matters of Material Importance to Decision Making

c. Compliance Disclosure to the Codes

d. Disclosure of Price Sensitive Information

8. Confidentiality

9. Insider Information

10. Business and Anti-Corruption Ethics

11. Donation

12. Compliance to Health Protection, Working Safety and Environmental Law13. Equitable Working Opportunity Notes: This is only the Summary (Sub-Title) of all 161 items used to measure GCG

Transparency

TABLE 2

Descriptive Statistics

PercentilesVariable Mean Std. Dev Min. Max.

25 50 75

Val

= 1

GCG 13.59 10.59 0 51 6 11 18.25 -

Firm’s Specific Characteristics

Profitability -0.4946 0.0650 -93.83 18.84 0.000 0.065 0.210 -

Listing Status - - - - - - - 3

Auditor Status - - - - - - - 123

Industry - - - - - - - 84

Diffusion 29% 17% 1% 77% 16% 29% 42% -

Size 4.77E+12 1.61E+13 2.36E+10 1.26E+14 1.77E+11 7.07E+11 2.00E+12 -

Notes: total sample: 138 data

K-INT 14

8/14/2019 Simposium Nasional Akuntansi 9 Padang Profitability And

http://slidepdf.com/reader/full/simposium-nasional-akuntansi-9-padang-profitability-and 19/19

SIMPOSIUM NASIONAL AKUNTANSI 9 PADANG

Padang, 23-26 Agustus 2006 19

TABLE 3

Multicolinearity and Heteroscedasticity Test

Variables Tolerance VIF

Profitability 0.988 1.013

Listing status 0.919 1.089

Auditor status 0.944 1.059

Industry 0.948 1.055

Diffusion 0.964 1.037

Log Size 0.864 1.157

p-value Koenker-Bassett(KB) test = 0.123

FIGURE 2

Normality Test

Notes: p-value Kolmogorov-Smirnov = 0.200

Regression Standardized Residual

2 , 0 0 1 , 7 5

1 , 5 0 1 , 2 5

1 , 0 0 , 7 5

, 5 0 , 2 5

0 , 0 0 - , 2 5

- , 5 0 - , 7 5

- 1 , 0 0

- 1 , 2 5

- 1 , 5 0

- 1 , 7 5

- 2 , 0 0

- 2 , 2 5

Histogram

Dependent Variable: GCG (log)

F r e q u e n

c y

20

10

0

Std. Dev = ,98

Mean = 0,00

N = 134,00

Normal P-P Plot of Regression

Dependent Variable: GCG (log)

Observed Cum Prob

1,0,8,5,30,0

E x p e c t e d C u m P

r o b

1,0

,8

,5

,3

0,0

TABLE 4

Regression Analysis

VariabelIndependen

UnstandardizedCoefficient

StandardizedCoefficient

t Sig(1-tailed)

Constant -0.948 - -2.147 0.017

Profitability -0.005 -0.118 -1.523 0.065

Listing status 0.282 0.116 1.443 0.076

Auditor status 0.216 0.189 2.387 0.009

Industry 0.059 0.082 1.037 0.151

Diffusion -0.253 -0.121 -1.545 0.063

Log Size 0.152 0.333 4.004 0.000

Uji ANOVA

Adjusted R 2

Variabel dependen

: F = 6.979 ( p-value 0,000)

: 0,212

: GCG disclosure level

Related Documents