CHAPTER 1: - INTRODUCTION 1.1HISTORY OF TEXTILE The history of textile is almost as old as that of human civilization and as time moves on the history of textile has further enriched itself. In the 6th and 7th century BC, the oldest recorded indication of using fiber comes with the invention of flax and wool fabric at the excavation of Swiss lake inhabitants. In India the culture of silk was introduced in 400AD, while spinning of cotton traces back to 3000BC. In China, the discovery and consequent development of sericulture and spin silk methods got initiated at 2640 BC while in Egypt the art of spinning linen and weaving developed in 3400 BC. The discovery of machines and their widespread application in processing natural fibers was a direct outcome of the industrial revolution of the 18th and 19th centuries. The discoveries of various synthetic fibers like nylon created a wider market for textile products and gradually led to the invention of new and improved sources of natural fiber. The development of transportation and communication facilities facilitated the path of transaction of localized skills and textile art among various countries. 1.1.1 TEXTILE HISTORY IN INDIA Indian textile enjoys a rich heritage and the origin of textiles in India traces back to the Indus valley Civilization where people used homespun cotton for weaving their clothes. Rig-Veda, 1 | Page

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

CHAPTER 1: - INTRODUCTION

1.1HISTORY OF TEXTILE

The history of textile is almost as old as that of human

civilization and as time moves on the history of textile has

further enriched itself. In the 6th and 7th century BC, the

oldest recorded indication of using fiber comes with the

invention of flax and wool fabric at the excavation of Swiss lake

inhabitants. In India the culture of silk was introduced in

400AD, while spinning of cotton traces back to 3000BC. In China,

the discovery and consequent development of sericulture and spin

silk methods got initiated at 2640 BC while in Egypt the art of

spinning linen and weaving developed in 3400 BC. The discovery of

machines and their widespread application in processing natural

fibers was a direct outcome of the industrial revolution of the

18th and 19th centuries. The discoveries of various synthetic

fibers like nylon created a wider market for textile products and

gradually led to the invention of new and improved sources of

natural fiber. The development of transportation and

communication facilities facilitated the path of transaction of

localized skills and textile art among various countries.

1.1.1 TEXTILE HISTORY IN INDIA

Indian textile enjoys a rich heritage and the origin of textiles

in India traces back to the Indus valley Civilization where

people used homespun cotton for weaving their clothes. Rig-Veda,

1 | P a g e

the earliest of the Veda contains the literary information about

textiles and it refers to weaving. Ramayana and Mahabharata, the

eminent Indian epics depict the existence of wide variety of

fabrics in ancient India. These epics refer both to rich and

stylized garment worn by the aristocrats and ordinary simple

clothes worn by the common people. The contemporary Indian

textile not only reflects the splendid past but also cater to the

requirements of the modern times.

Each and every region of India contributes in creating a myriad

of textile tradition. The hilly region of the country produces a

rich variety of woolen textiles. The pashmina and shahtoosh

shawls of Kashmir, shawls and woolen garments of Himachal Pradesh

and other north eastern states provides excellent examples of

world famous woolen Indian textiles. The barren and semi barren

regions like Rajasthan and Gujarat usually prefers embroidered

bright colored textiles. The coastal areas of the south eastern

regions prefer light colored fabrics and particularly cotton and

silk textiles are very popular over here. The home furnishing

utilitarian textile products like bedspreads and sheets, pillows

and cushions, linens and mats, curtains and napkins, carpets and

rugs and many such other items are produced by all parts of the

country.

Textiles are GUJARAT'S forte and one can find an immense variety

of textile traditions here that range from robust folk textiles

2 | P a g e

to fine brocades. In fact, the oldest known printed fabrics from

India were the resist dyed and printed cottons of Gujarat. These

printed fabric traditions are still going strong in Gujarat and

are considered an essential part of any fashionable Indian

woman's wardrobe. The ajrakh prints of the Kutch region and the

sodagiri prints of Paithapur are just two examples of Gujarat's

excellently printed textiles. The Matani-Pachedi print produced

by the Vaghari community priests in honor of the mother goddess

is another example of Gujarati skills in printing. Gujarat also

boasts of the patola, one of the finest hand woven textiles found

in Patan. In this process the warp and the weft are first tie-

dyed and then woven together, an act requiring highly specialized

skills.

One cannot ignore the intricate bandhej (tie-dyed fabric) of

Jamnagar, Mandavi, and Bhuj, which are used for wedding outfits

such as the gharchola odhni and saris. Brocades woven in

Jamnagar, Mehsana, Ahmedabad, and Surat with traditional patterns

of popat vel, (stylised parrot-flower borders) or asharfi

(circular gold coin) were once highly prized possessions.

Unfortunately, brocades are no longer produced, as they were

earlier. The only types available now are the brocade borders

woven on the power loom in Surat or simple patterns done in

Mehsana. Gujarat also has a vibrant mashru tradition, a fabric

with an interesting story behind its creation.

3 | P a g e

Mashru is woven with a combination of silk and cotton, the cotton

being the lower layer in touch with the skin. The fabric was

woven for Muslim men who were prohibited from wearing pure silk.

Though mashru is found all over India, Gujarati mashru has bold

patterns and colors that lend it an attractiveness of its own.

SURAT, the financial hub of the state of Gujarat, is known as the

textile city of Gujarat. And, the epithet is perfectly suited to

the city. The textile industry is one of the oldest and the most

widespread industries in Surat. A major part of the city's

population is associated with the textile industry. Surat is well

known for its synthetic products market. It is mainly engaged in

the production and trading of synthetic textile products.

Nearly 30 million metres of raw fabric and 25 million metres of

processed fabric are produced in Surat daily. The city has

several textile markets that exist since times immemorial. Zampa

Bazaar, Bombay Market, JJ Textile Market and Jash Market are

among them. Sachin, Kadodra and Pandesara are the areas of Surat

where manufacturing is mainly concentrated.

1.2 CONTRIBUTION OF TEXTILE INDUSRTY TO INDIAN ECONOMY

The textile industry is one of the leading sectors in the Indian

economy as it contributes nearly 14 percent to the total

industrial production. The textile industry in India is claimed

to be the biggest revenue earners in terms of foreign exchange

4 | P a g e

among all other industrial sectors in India. This industry

provides direct employment to around 35 million people, which has

made it one of the most advantageous industrial sectors in the

country. Some of the important benefits offered by the Indian

textile industry are as follows:

India covers 61 percent of the international textile market.

India covers 22 percent of the global market.

India is known to be the third largest manufacturer of cotton

across the globe.

India claims to be the second largest manufacturer as well as

provider of cotton yarn and textiles in the world.

India holds around 25 percent share in the cotton yarn

industry across the globe.

India contributes to around 12 percent of the world's

production of cotton yarn and textiles.

1.3 COMPANY DETAILS

COMPANY NAME: SHREE RAM DESIGNS PRIVATE LIMITED

5 | P a g e

FOUNDER/ DIRECTOR: Mr. Vijay Agrawal and Mr. Sushil Agrawal

COUNTRY/TERRITORY: India

YEAR OF ESTABLISHMENT: 2005

FUNCTIONS OF THE COMPANY: Dyeing of fancy sarees and dress

materials

ANNUAL SALES RANGE: Rs 25 crore (approx)

NO. OF EMPLOYEES: 300 employees

ADDRESS: Factory: Plot -7 Block 296/301

Tanthi -thaiya,

Kadodra,

Surat,

Gujarat

Office: 130, Reshamwala market,

Ring road,

Surat, Gujarat

WORKING HOURS: Three shifts each of 8 hours.

COMPANY GUIDE: Mr. Rishu Agrawal (Manager)

6 | P a g e

Contact No. 96240-51021

Shree Ram Designs Pvt. Ltd is a dyeing house, i.e. they provide

dyeing service to their customers who are actually business

organizations the wholesalers of sarees in Surat city textile

market. Their job is to dye the sarees as per the orders of the

customers.

1.4 HISTORY OF COMPANY

The company was established in the year 2005.The company was

started by MR. VIJAY AGARWAL & MR. SUSHIL AGRAWAL. As the company

is small scale private limited and recently developed, there is

no such big history or details regarding that. The owners started

the company after 10 years of experience in trading line in

Surat. In trading, the office of the firm was in Ashoka tower

with the name of Vijay silk mills.

1.5 BOND OF TRUST

Its bond of trust is consistent upon this remarkable notion given

below:

“We are proud to have some of the most reputable name in the

city. This has been achieved over time through the approach of

work fast and work smart. The bond of trust has been developed

because of our ability to fulfill our commitments to deliver the

7 | P a g e

right product at the right time. Check and balances are placed

from the initial stages to eliminate any possibility of error. “

1.6 VISION OF COMPANY

The company undertakes to apply the vision in letter and spirit

under the following guiding principles:

In time action

Clear understanding of customer’s instructions.

Clear communication with vendors

Clear instructions for production

Strict compliance with quality control system.

Total devotion maintains first class quality standard.

Absolute efforts for in time dispatch.

1.7 MISSION STATEMENT

Mission statement focused on its major commitments i.e. “QUALITY

WITH QUANTITY”

CORPORATE VALUES

Team work

Integrity

Excellence

Commitment to buyer.

8 | P a g e

Maintenance of consistent standard

GOALS

Continuous improvement.

Customer’s satisfaction.

Quality of product and system.

Company is also planning to starts its own trading unit which

will add to the profit margin of the company.

9 | P a g e

CHAPTER 2: - ORGANISATION STRUCTURE

The activities of Shree Ram Designs Pvt. Ltd can be grouped under

four departments, namely: - the Marketing Department, Production

Department, Financial Department and the Human Resource

Department.

The activities of Marketing Department and Production Market are

the responsibility of the Master and the activities of Financial

Department and Human Resource Department are the responsibility

of the Directors.

10 | P a g e

DIRECTORSALES PERSONASSISTANTSUPERVISORHEAD LABOURASSISTANTFINANCE HEADCOLLECTION MAN

2.1 MARKETING DEPARTMENT Thought there is no formal marketing department in the company

but the marketing activities are undertaken by the masters and

their sub-ordinates. Hence the marketing activities of the

masters and their sub-ordinates can be structured and categorized

under a separate Marketing Department.

2.1.1 ORGANIZATION STRUCTURE OF THE MARKETING DEPARTMENT

11 | P a g e

2.1.2 SALES VOLUME

Dress: 2,19,00,000 meters per year(approx)

Sarees:1,82,50,000 meters per year(approx)

Padding: approx 50% of dress material & 25% of sarees.

2.1.3 UNIQUE FEATURES OF THE PRODUCT

Strong color bonding

Color toning up to 92-100%

Less shrinkage

No color loss from the cloth even after repeated washes.

2.1.4 SEGMENTATION, TARGETING AND POSITIONING

12 | P a g e

First of all this is a business to business organization i.e.

they are a firm who firm who deals with saree wholesalers in the

Surat city. They are a Business to Business (B2B) organization.

The firm does not deal with final consumers.

Segmentation

Geographically - Northern India: - The Company has segmented

its market on geographical basis. It has segmented by

concentrating on those wholesalers who are trading with

retailers in North India. So it is making color ranges which

are more popular with trends of North Indian states.

Targeting

High end customer: - After geographically segmenting the

market, the company is targeting the high end customers, i.e.

to the big whole sellers who give bulk orders so that the

company never runs short of demand for its products.

Medium taste: - SHREE RAM DESIGNS is targeting the customers

who have medium taste clients. They are dyeing saris and dress

material which is worn by the middle and lower class women.

Positioning

Creating a brand image: - It has positioned itself by creating

a brand image in the market about its color ranges, good work,

on-time delivery and loyalty towards old customers.

13 | P a g e

2.1.5 MARKETING MIX

The marketing mix is probably the most famous phrase inmarketing. The elements are the marketing 'tactics'. Also knownas the 'four Ps', the marketing mix elements are price, place,product, and promotion.

The 4p’s of Shree Ram Designs are as follows:

PRODUCT

Product is defined as: “Good, idea, method, information, object,service, etc. that is the end result of a process and serves as aneed or want satisfier. It is usually a bundle of tangible andintangible attributes (benefits, features, functions, uses) thata seller offers to a buyer for purchase.”

The company ensures that the products are produced according tothe customer requirement and expectation. SRD is renowned in thelocal market for its excellent services, timely delivery ofquality finished products to their valued customers. SRDphilosophy of continuous improvement depends upon the way oftraining given to employees and regular meeting with parties fordiscussions, which emphasize the masters and assistants andultimately employees to understand that the company’s main aim

14 | P a g e

is to respond the customer’s ever changing needs in the mostefficient way.

They discover new color and designs by actively following thetrends of colors seen worn by actresses or popular ladies ontelevision daily soaps, which help them know which color may bepopularly accepted by all.

Since this is a dyeing unit, there are a variety of colors andquality of grey which are processed at Shree Ram Designs, but onein particular, the Russian quality of grey is the most popularorder received by this firm. Of all the orders received themajority orders received are of Russian quality.PRICE (PRICING POLICY)

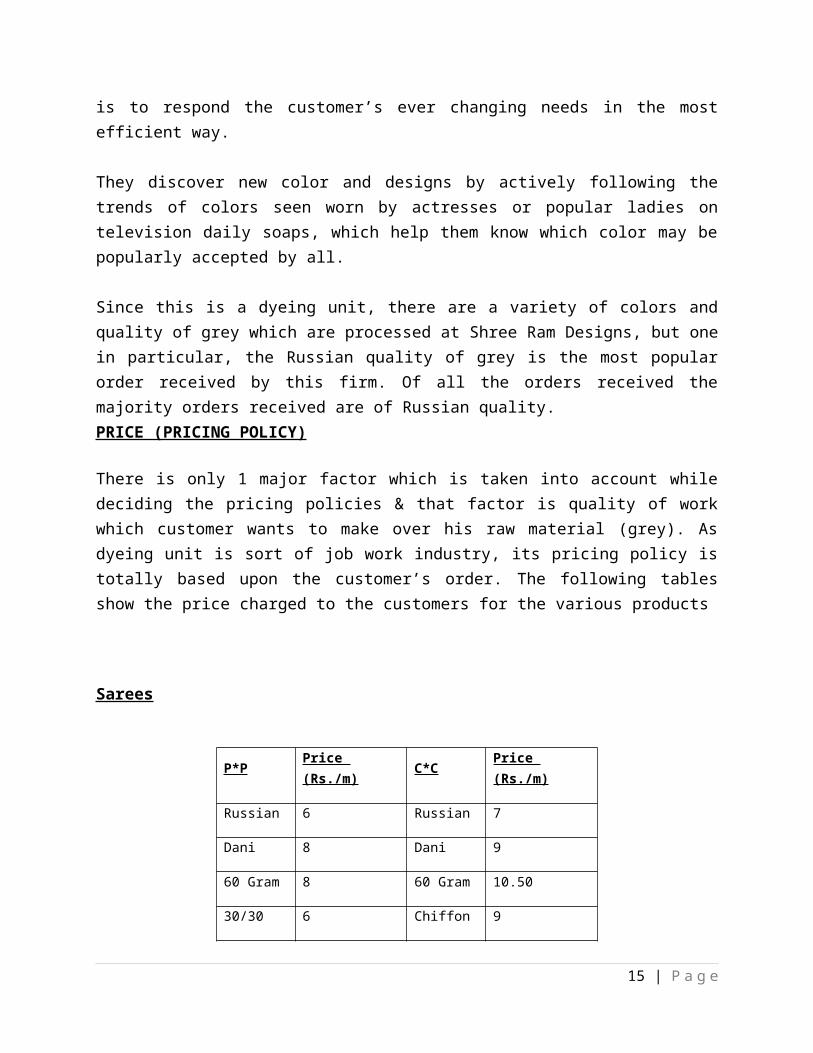

There is only 1 major factor which is taken into account whiledeciding the pricing policies & that factor is quality of workwhich customer wants to make over his raw material (grey). Asdyeing unit is sort of job work industry, its pricing policy istotally based upon the customer’s order. The following tablesshow the price charged to the customers for the various products

Sarees

P*P Price (Rs./m) C*C Price

(Rs./m)

Russian 6 Russian 7

Dani 8 Dani 9

60 Gram 8 60 Gram 10.50

30/30 6 Chiffon 9

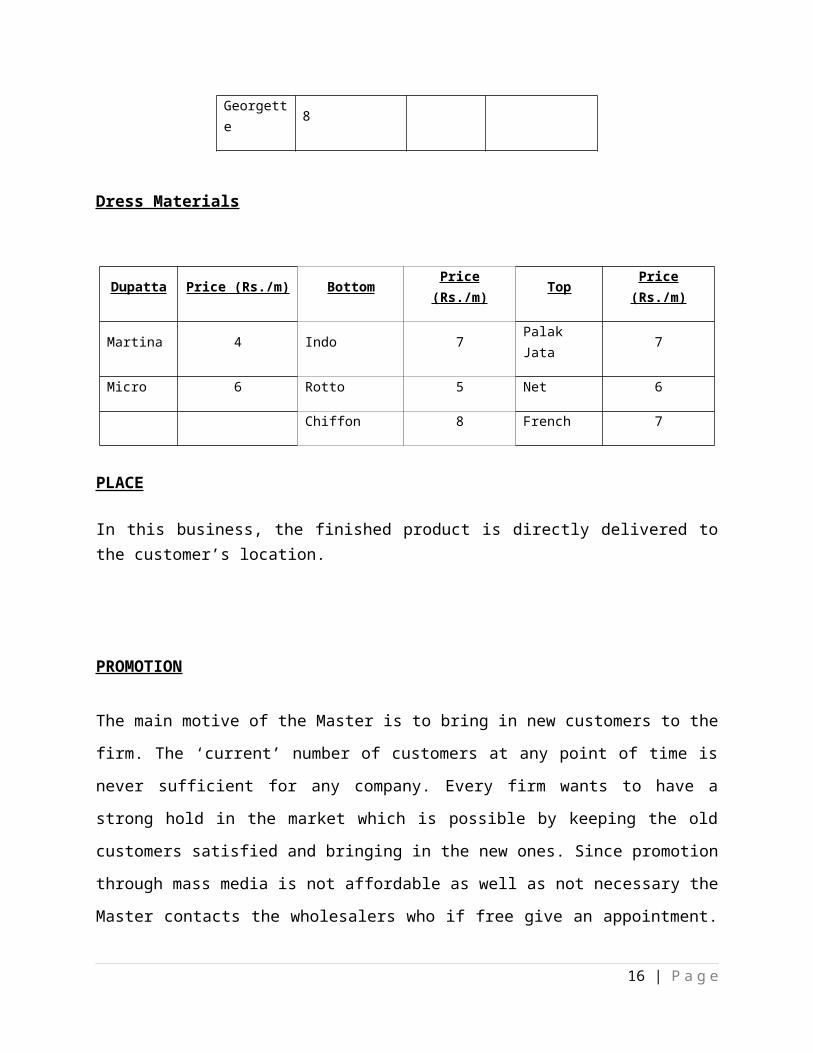

15 | P a g e

Georgette 8

Dress Materials

Dupatta Price (Rs./m) Bottom Price(Rs./m) Top Price

(Rs./m)

Martina 4 Indo 7 Palak Jata 7

Micro 6 Rotto 5 Net 6

Chiffon 8 French 7

PLACE

In this business, the finished product is directly delivered tothe customer’s location.

PROMOTION

The main motive of the Master is to bring in new customers to the

firm. The ‘current’ number of customers at any point of time is

never sufficient for any company. Every firm wants to have a

strong hold in the market which is possible by keeping the old

customers satisfied and bringing in the new ones. Since promotion

through mass media is not affordable as well as not necessary the

Master contacts the wholesalers who if free give an appointment.

16 | P a g e

So to learn the way to rope in new customers, I alongwith Mr.

Chetan Gupta a Master in the firm, went to visit some prospective

wholesalers in the market. Some of them were: -

M/s Shree Shyam Sarees: - We offered them Russian sarees with a

yellow dyeing. They were already having their orders processed at

Shree Vasudev mills, so the Mr. Chetan knew about the pricing of

the Vasudev so he offered him a price of 2.95 rs/ metre

guaranteeing a flawless dyeing and on-time delivery. And next day

a grey lot of 50 takas(1taka = 100 metre), form M/s Shree Shyam

Sarees was supplied to the factory.

M/s Orange Sarees: - Situated in Millenium Textile Market, they

are challenging suppliers in the market. They were asking for

different colors. They wanted a certain shade in orange; they did

not bargain much in price, they were getting what they exactly

needed, so they placed an order of 36 takas.

M/s Khaitan Slk Mills: - They are big time wholesalers, judging

by the size and number of shops. They demanded quicker delivery,

while the standard time is 7 to 9 days. They were demanding the

delivery to be completed in 5 days, no discounts in price. They

offered if the delivery is made in 5 days, as this was not

possible so Chetan Master charged them a higher price by charging

them 10p/m extra.

17 | P a g e

M/s Varun Prints: - These are also resellers in the market. They

wanted to have 20000 meters processed in 3 day’s time, which was

not possible, so the master offered him completion of definite

produce within 1 week. They were in urgency so the time was

negotiated to 4 days.

M/s Anshi Silk Mills: - A person visited the factory from their

firm, they were looking for a new color to sell. They got what

they were looking for, some kind of shade in Green. They were

offered a price which was acceptable. Now this was not the

exactly marketing part, because the person was by himself out in

the field to explore, and though being a new customer himself he

was treated well. He was not treated as if forced to do so. The

Master was polite and even being busy gave him sufficient

attention.

2.1.6 THREATS TO THE COMPANY

Industry competitors (segment rivalry): - There is very internal

segment rivalry. There is high amount of competition existing in

the textile industry. There is a very large no. of textile

processing mills in Surat.

Threat of buyers’ growing bargaining power: - As mentioned above

that there is heavy segment rivalry among the dyeing and printing

units, so the customer bargaining power is quite high here.

Moreover there is nothing like customer loyalty existing in this

18 | P a g e

industry. Regular customer of one firm if offered similar quality

at another firm will switch off immediately. Only quality or

product differentiation plays very less role in retaining of the

customer.

Threat of suppliers’ growing bargaining power: - The suppliers in

this industry are suppliers of coal, dyes, chemicals, Bagasse,

lignite, etc. now in this for lignite there is quota system for

every dyeing and printing units, and that they get from

government so there is no quota system as such but for the rest

of the commodities the bargaining power is quite high because

there is large availability for these goods. Here the company

gets equitation from different suppliers and then it orders goods

as per rates, payment conditions, etc.

Threat of substitute products: - The Company does not need to

fear about the substitute products, because there is no

substitute available for dyeing in sarees or dress materials in

the market. As it’s a dyeing mill value addition which is in

recent boom also do not affect.

Threat of new entrants: - This threat always remains with a

growing industry. Outsiders are lured by the profits of the

existing business firms. Surat textile industry is a growing

industry. Here the entry barrier is also not quite high as

compared to the profits so many new firms are coming these days.

Therefore there is a high threat of new entrants in this

industry.

19 | P a g e

2.1.7 DIFFERENT REPORTS GENERATED IN MARKETING DEPARTMENT

The following reports are not exactly termed as reports as they

are just records which the Masters and their respective teams

which need to be maintained the Master regularly.

DAILY REPORT

SALES REPORT: - This report shows nothing but the total dispatch

made by the firm on a particular day. It is made on basis of no.

of grey dispatched after finishing from the unit. The main aim

for preparing this is to check whether the production capacity is

increasing, decreasing or remaining same.

MARKET FEEDBACK: - This report shows whether the customers got

their lots fully or not. And second thing prepared by this is

that whether the tone and finishing of the color and chemical are

set as per order or not. The main aim for preparing this is to

check whether the party getting their order on time or not and

whether it is up to their standard defined or not.

WEEKLY

QUALITY RELATED ISSUE REPORT: - These reports are prepared on

weekly basis to check out whether all the parties have got their

tone and finishing of their fabric as per their requirement or

not. Moreover, it is analyzed that for a particular tone only

problem or whether there is overall problem in tone which may be

20 | P a g e

possible due to problem in machinery. This is prepared and

actions are taken for machines if overall there is disturbance in

Color-tone setting or else masters are asked and recheck if the

problem occurs in any particular tone only.

COMPETITORS’ PRICE REPORT: - To check out the changes in the

prices charged by the competitors (increasing or decreasing) and

finding out reasons behind that. If the competitors’ prices are

increasing, it is well and good for the profit of the firm but in

case of decrease in price, the firm also has to reduce the rates

which may decrease the firm’s profits. This job is not done only

by the Master, but the Directors also keep a track of the

competitor’s prices and they keep on passing the necessary

information to the Master.

MONTHLY

PAYMENT RECOVERY AND OUTSTANDING REPORTS: - The payment recovery

and payment outstanding repots are prepared to know what amount

of a particular party is recovered and what amount is still

pending. As in processing system of Surat, there is payment

period of 90 days. In spite of paying fully at the end of 3

months, party’s use to pay part payments on regular period. This

report maintains amount pending and recovered in that particular

month of all the party’s of the firm.

2.1.8 DETAILS OF CUSTOMERS

21 | P a g e

Since it is a Job Based firm. That is the work is based totally

on the job as ordered by the client. So it is not a fixed list,

but some of the clients whose orders are regularly processed at

Shree Ram Designs are:

Divya textiles

Gopi silk mills

Lifestyle Sarees Private Ltd.

Oswal Sarees

Monica textiles

Sarita enterprise

Samiksha Sarees Ltd.

Shripal enterprise

Sonu fashion

Shorya fashion

Tanvi desigers

Veer vijay silk mills

Vaibhav silks

Neer international

Mansi fabrics

Ritu fabrics

Sumit sarees

Supriya sarees

2.1.10 TYPES AND CLASSIFICATION OF THE PRODUCT

22 | P a g e

DRESS MATERIALS

In Shree Ram dyeing mills, we can find out the best quality in

this segment (range). The qualities in the dress section majorly

produced in this firm are salwar, dupatta and Kurta. The major

production is of dress materials every day due to increasing

demand. Every day nearby 60,000 meters are dyed of dress

division. The Company is well known for best settling down the

roughness of grey in its range.

SAREES

23 | P a g e

In sarees section, only two types of qualities are produced in

this firm. They are catonic by catonic (C*C) and polyester by

polyester (P*P). The per day production of sarees are nearby

40000 to 50000mts per day. Generally one stenter is allotted to

sarees master and remaining two are given to the dress master.

Production of sarees fabric takes shorter time span than one

batch of dress materials products.

24 | P a g e

2.2 PRODUCTION DEPARTMENT

2.2.1 ORGANIZATION STRUCTURE OF PRODUCTION DEPARTMENT

25 | P a g e

26 | P a g e

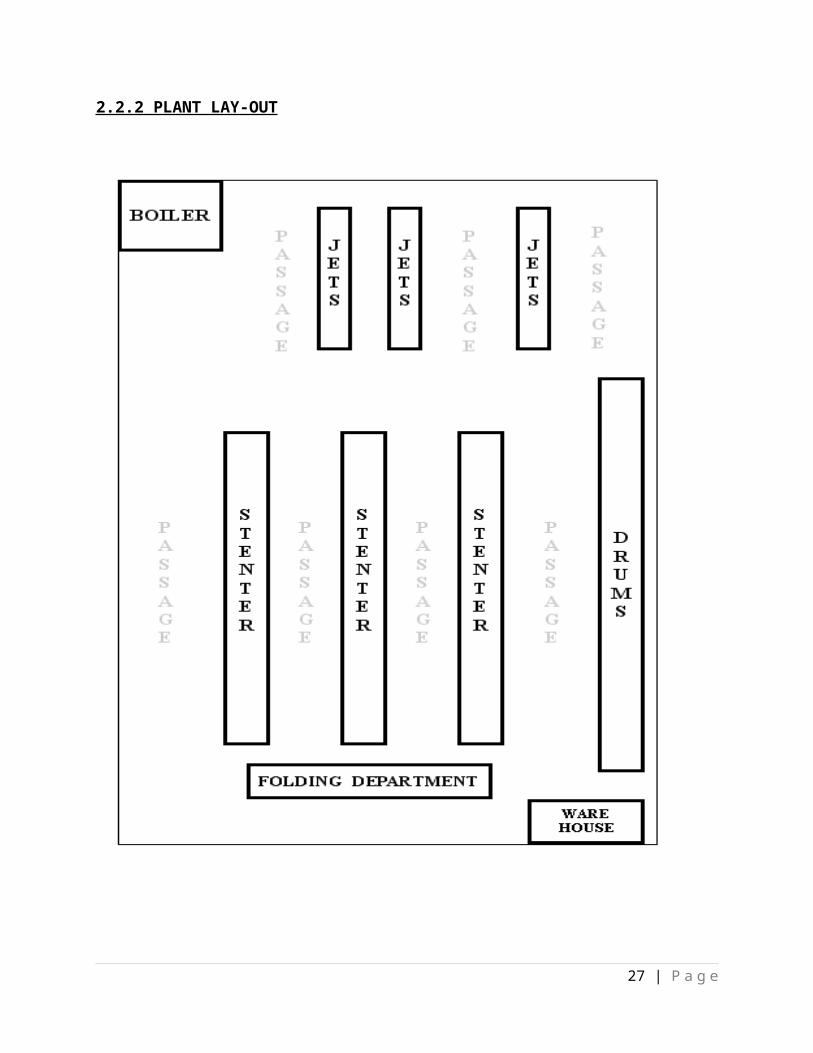

2.2.2 PLANT LAY-OUT

27 | P a g e

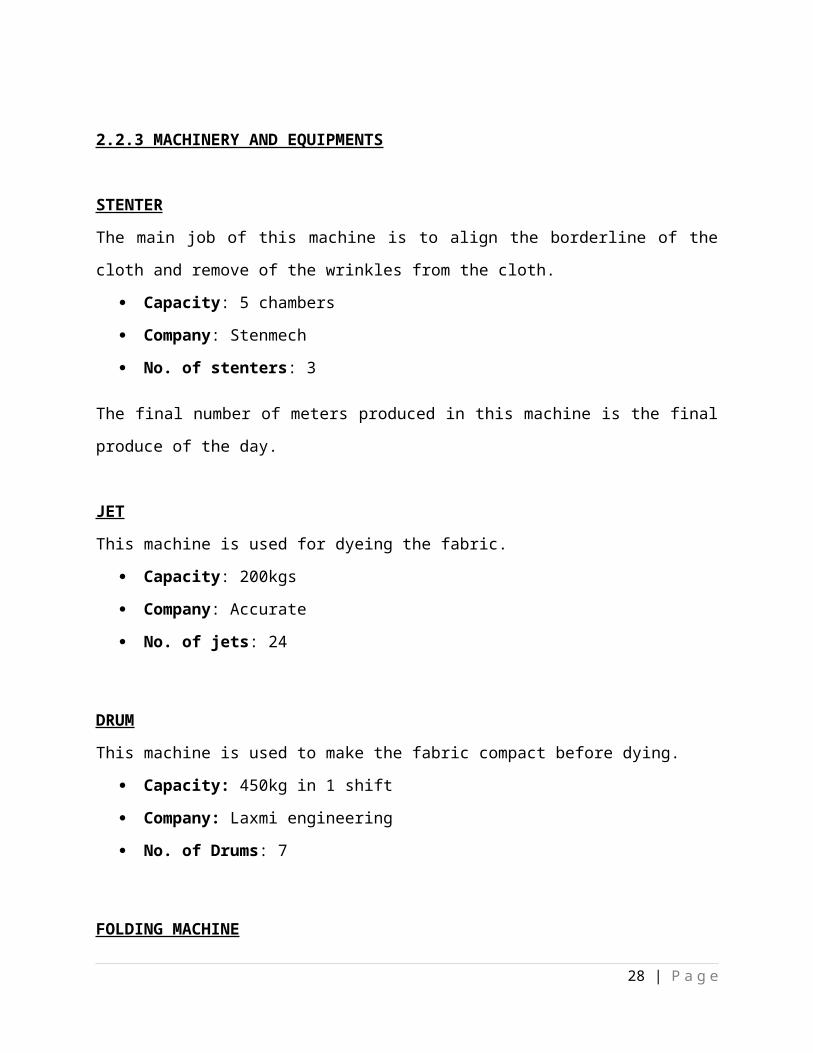

2.2.3 MACHINERY AND EQUIPMENTS

STENTER

The main job of this machine is to align the borderline of the

cloth and remove of the wrinkles from the cloth.

Capacity: 5 chambers

Company: Stenmech

No. of stenters: 3

The final number of meters produced in this machine is the final

produce of the day.

JET

This machine is used for dyeing the fabric.

Capacity: 200kgs

Company: Accurate

No. of jets: 24

DRUM

This machine is used to make the fabric compact before dying.

Capacity: 450kg in 1 shift

Company: Laxmi engineering

No. of Drums: 7

FOLDING MACHINE

28 | P a g e

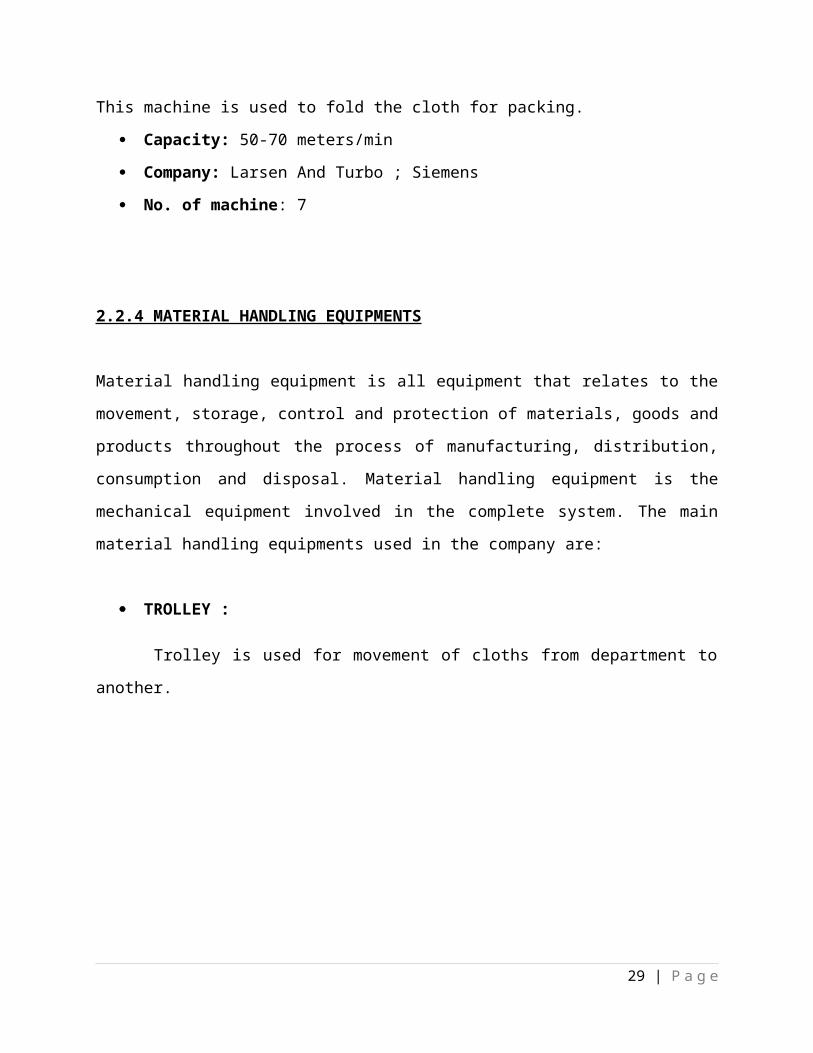

This machine is used to fold the cloth for packing.

Capacity: 50-70 meters/min

Company: Larsen And Turbo ; Siemens

No. of machine: 7

2.2.4 MATERIAL HANDLING EQUIPMENTS

Material handling equipment is all equipment that relates to the

movement, storage, control and protection of materials, goods and

products throughout the process of manufacturing, distribution,

consumption and disposal. Material handling equipment is the

mechanical equipment involved in the complete system. The main

material handling equipments used in the company are:

TROLLEY :

Trolley is used for movement of cloths from department to

another.

29 | P a g e

PIPES:

Pipes are used for movement of gases, steam and various

chemicals.

30 | P a g e

31 | P a g e

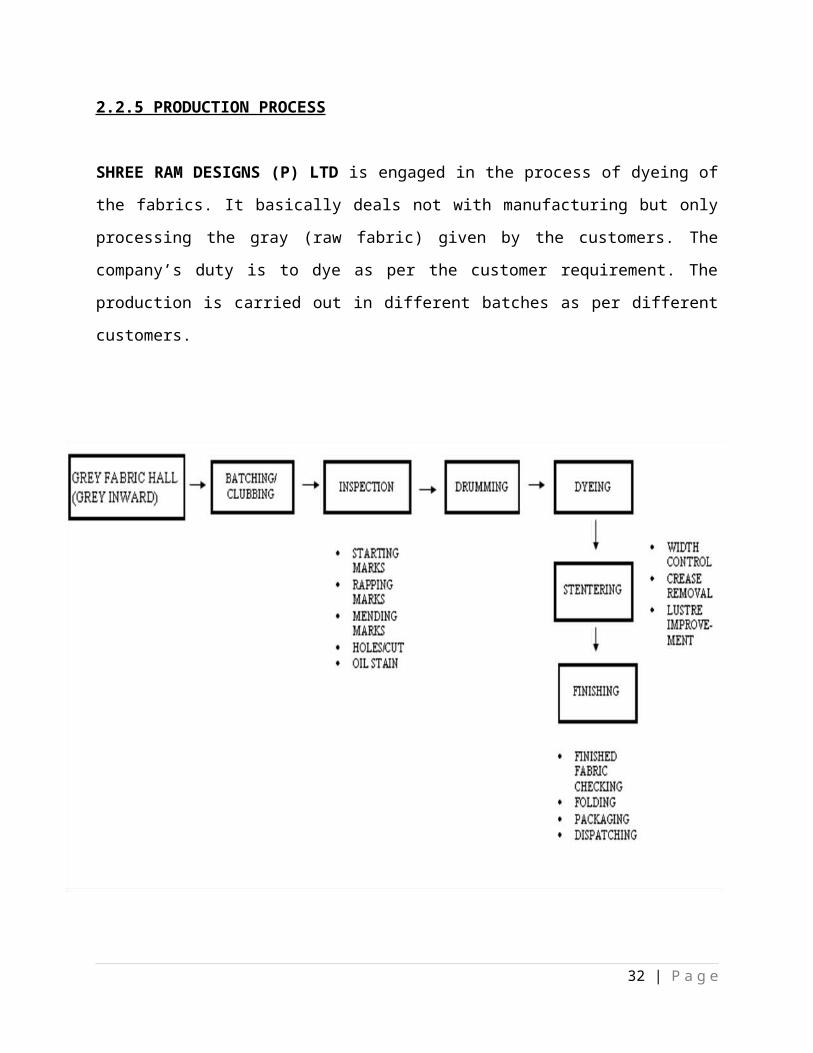

2.2.5 PRODUCTION PROCESS

SHREE RAM DESIGNS (P) LTD is engaged in the process of dyeing of

the fabrics. It basically deals not with manufacturing but only

processing the gray (raw fabric) given by the customers. The

company’s duty is to dye as per the customer requirement. The

production is carried out in different batches as per different

customers.

32 | P a g e

The process goes as: -

Deposition of grey

Batching/clubbing

Inspection

Drumming

Dyeing or printing or both

Stentering

Folding

Packing

Dispatching

The gray cloth, which belongs to the customer, is being deposited

by the customer in the company. As and when the company receives

the material from the customer lot no. along with the customer

code is been provided for safety purpose, so that the gray cloth

of different customers and of same or different quality do not

get mixed. Now lots of grey are batched according to master

production plan. The lots which have to undergo same process are

33 | P a g e

clubbed together. Then the fabric is inspected .the following

faults may appear:

Starting marks

Rapping marks

Mending marks

Holes/cut

Oil stain

The next step is to remove impurities and protruding fibers from

the fabric in the machine called DRUM. While drumming, the fabric

is being washed to remove the dirt, dust and impurities from the

cloth. This is done, because the color does not fix properly on

dirty fabric. After washing of the cloth, some chemical and steam

is given to set the grains to the fabric and to whiten the

fabric. The drumming process takes around 5-6 hours

approximately, depending upon the quality of the fabric.

34 | P a g e

Now the stage comes to dye the fabric in JET. The fabric in jet

undergoes three processes consuming around 6 hours. First two

hours are for weight reduction of the cloth, next 2 hours dyes

the cloth in desired color and the last 2 hours are for washing

of the cloth to remove the chemical and extra color from the

cloth.

35 | P a g e

DRUM

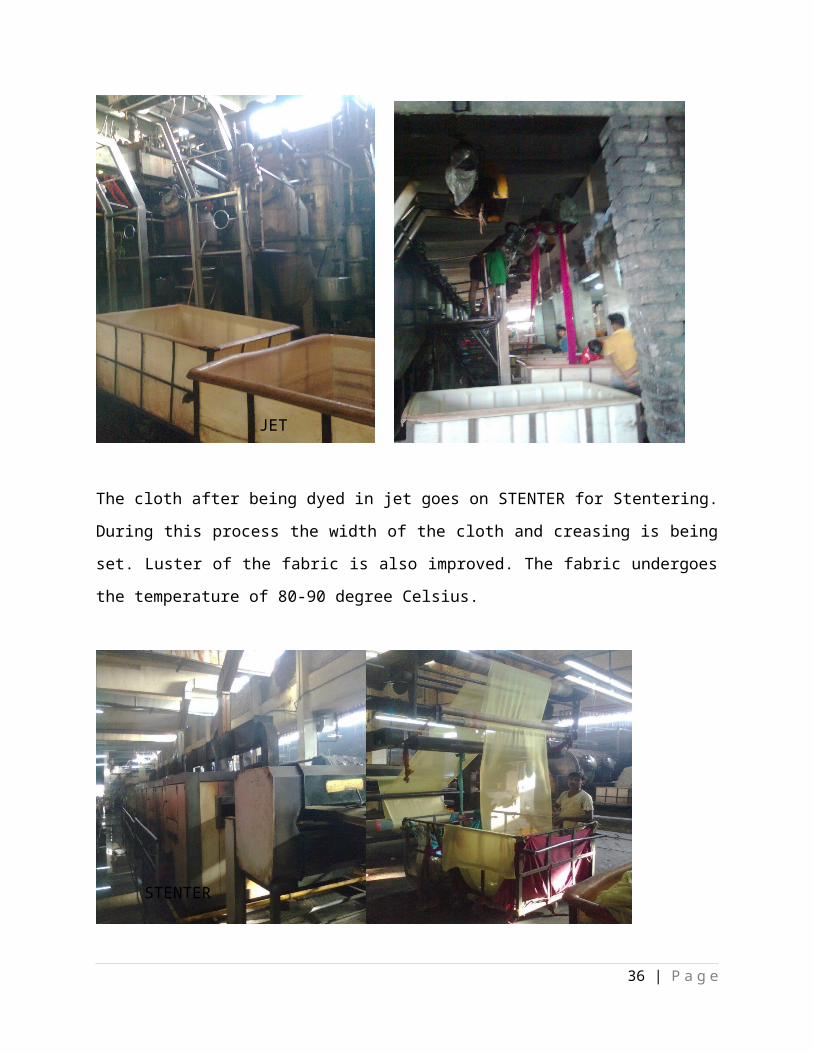

The cloth after being dyed in jet goes on STENTER for Stentering.

During this process the width of the cloth and creasing is being

set. Luster of the fabric is also improved. The fabric undergoes

the temperature of 80-90 degree Celsius.

36 | P a g e

JET

STENTER

This finished fabric is then inspected. After inspection it goes

to FOLDING machine and thereby packing and finally it is

dispatched.

37 | P a g e

FOLDING MACHINE

38 | P a g e

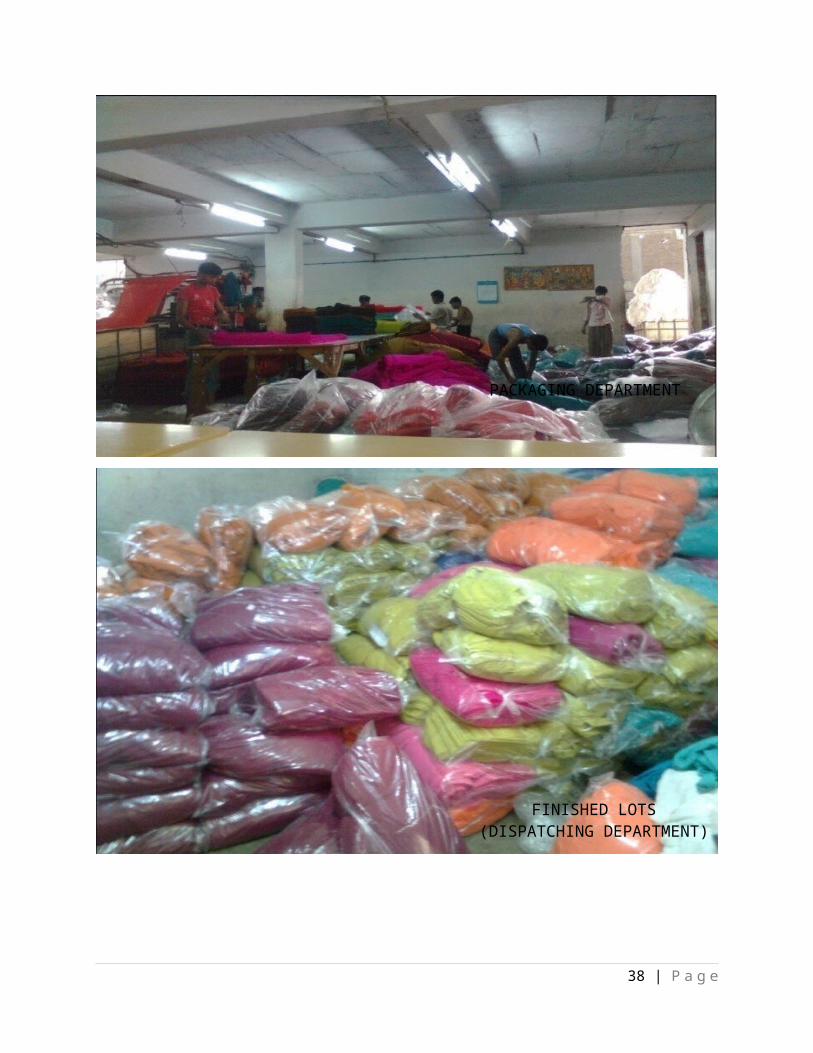

PACKAGING DEPARTMENT

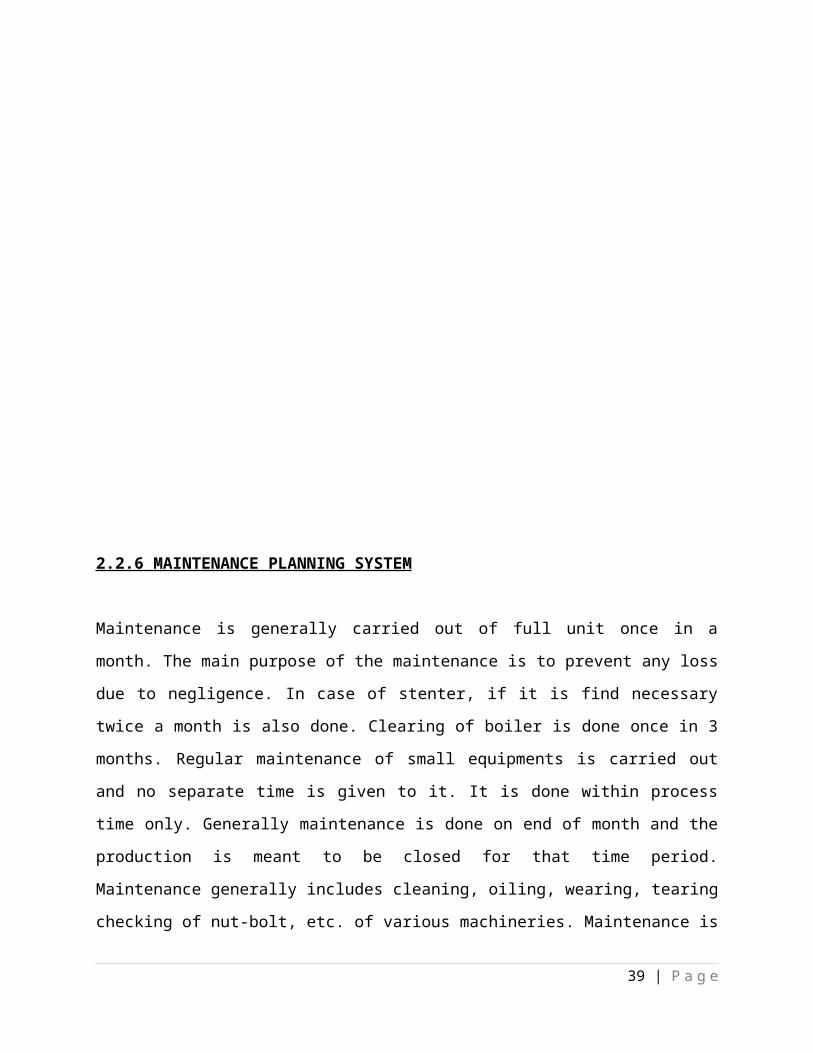

FINISHED LOTS(DISPATCHING DEPARTMENT)

2.2.6 MAINTENANCE PLANNING SYSTEM

Maintenance is generally carried out of full unit once in a

month. The main purpose of the maintenance is to prevent any loss

due to negligence. In case of stenter, if it is find necessary

twice a month is also done. Clearing of boiler is done once in 3

months. Regular maintenance of small equipments is carried out

and no separate time is given to it. It is done within process

time only. Generally maintenance is done on end of month and the

production is meant to be closed for that time period.

Maintenance generally includes cleaning, oiling, wearing, tearing

checking of nut-bolt, etc. of various machineries. Maintenance is

39 | P a g e

carried out to check for any wear and tear in machine parts. Also

it is carried out as to check whether all the equipments are

working properly and to prevent any accidents or faulty

production.

2.2.7 WASTE MANAGEMENT

Waste management is very important from all points of view. In

this company, ETP (EFFLUENT TREATMENT PLANT) had been constructed

at the time of its inception. The process is fully automated. All

the liquid and solid wastes of colors, chemicals and fuel are

passed into this treatment plant through well constructed

pipelines within the firm. After making it safe to release,

wastes are dump to nearby drainage System through pipelines.

Recently, a CETP (COMMON EFFLUENT TREATMENT PLANT) has been

developed by government for waste management in every industrial

area. The best part of this is that the management of CETP is

taken care by government and owners of the dyeing units have are

liable only to pay for the service they receive from this

treatment plant developed by government. All the old mils, which

had already developed their own ETP, have not been the part of

CETP but new units which are developing do not miss this

opportunity of becoming its member and getting burden free

totally from management of mill waste.

40 | P a g e

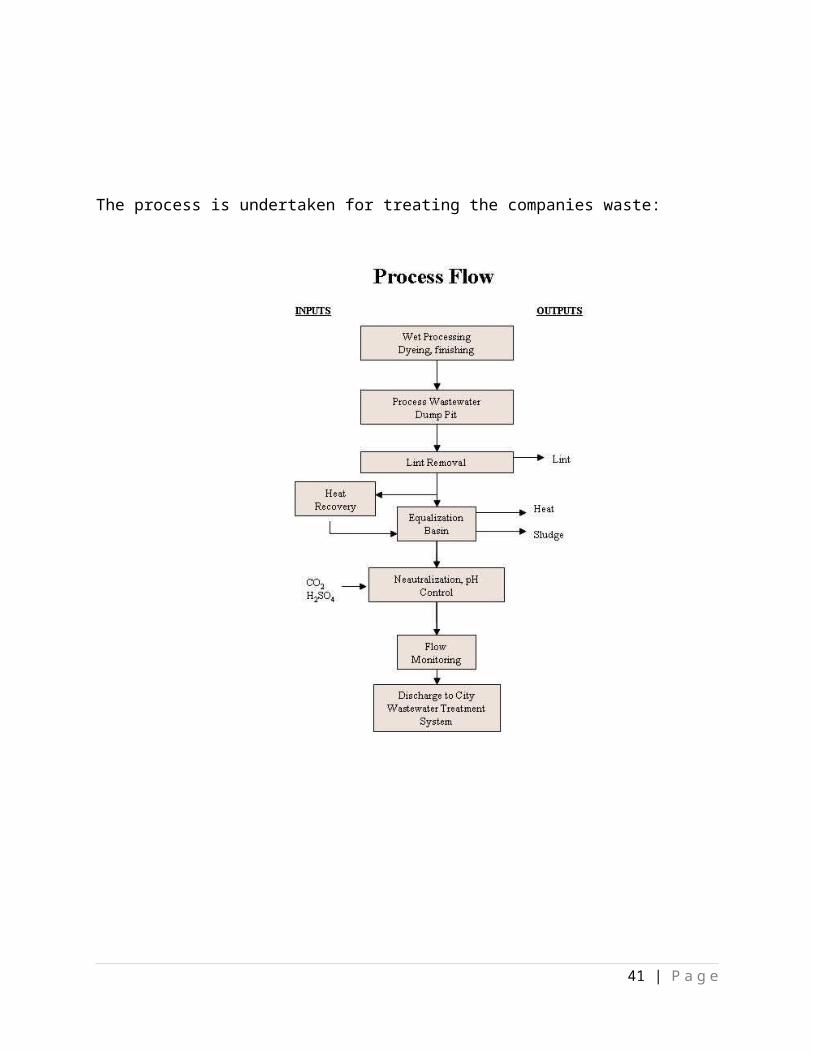

The process is undertaken for treating the companies waste:

41 | P a g e

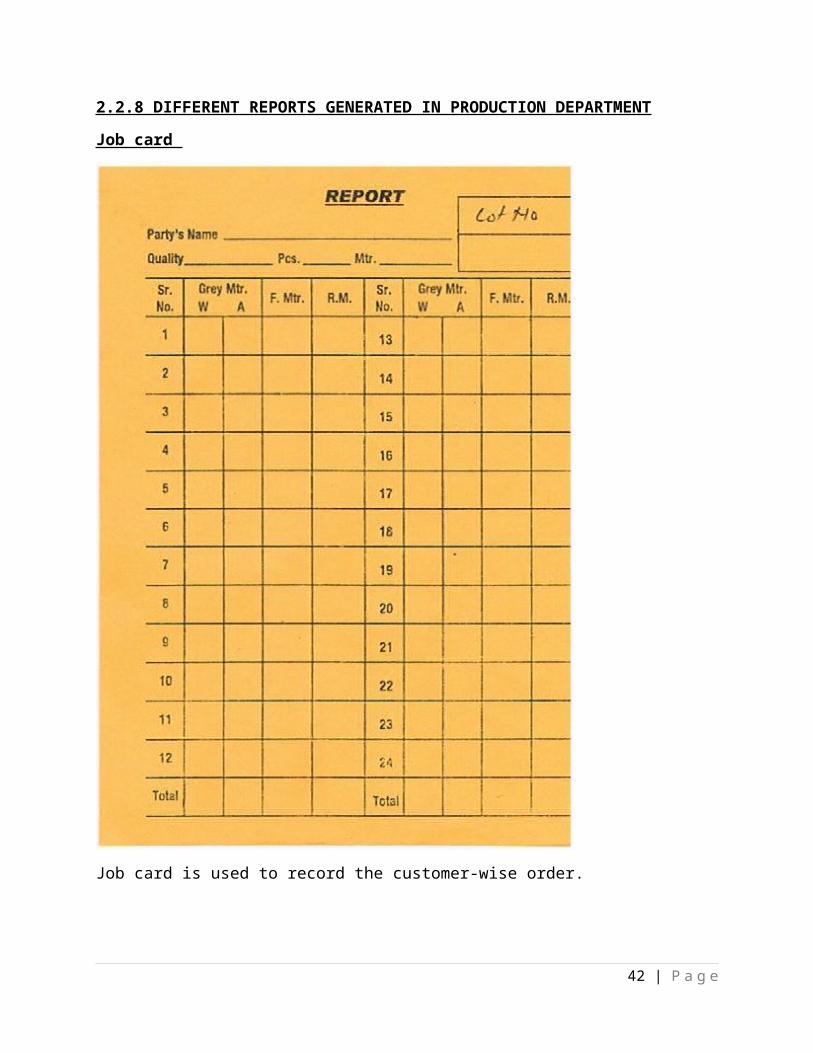

2.2.8 DIFFERENT REPORTS GENERATED IN PRODUCTION DEPARTMENT

Job card

Job card is used to record the customer-wise order.

42 | P a g e

43 | P a g e

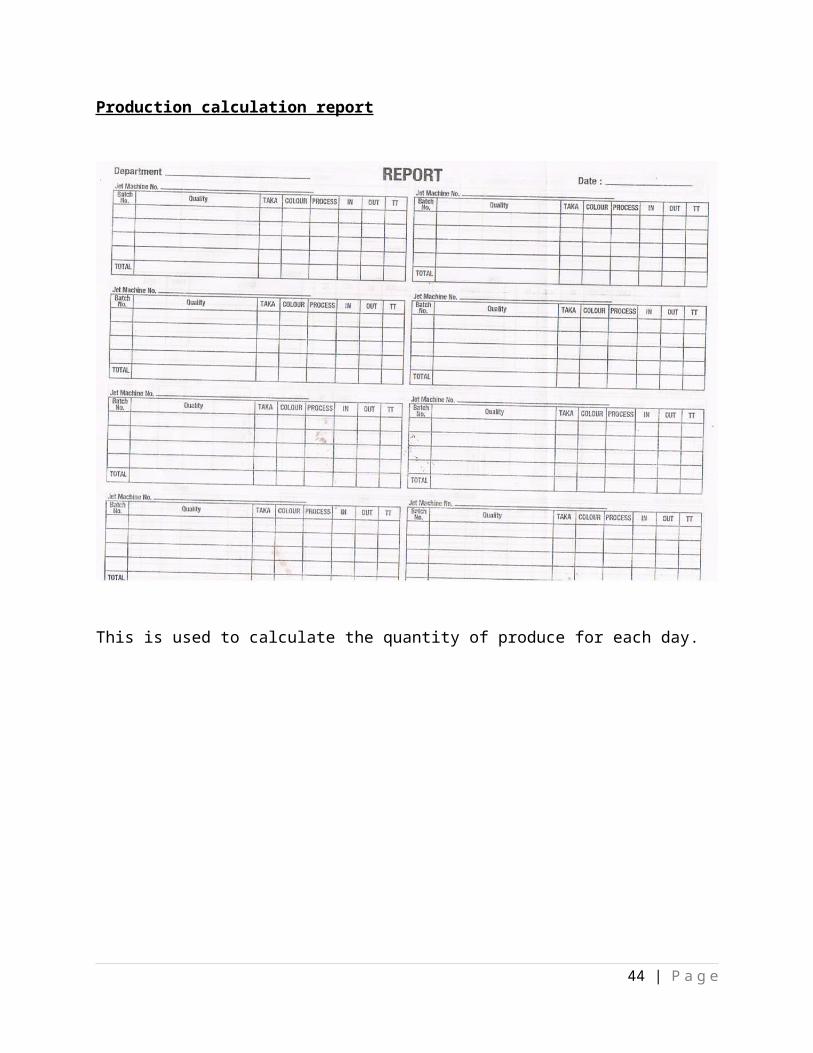

Production calculation report

This is used to calculate the quantity of produce for each day.

44 | P a g e

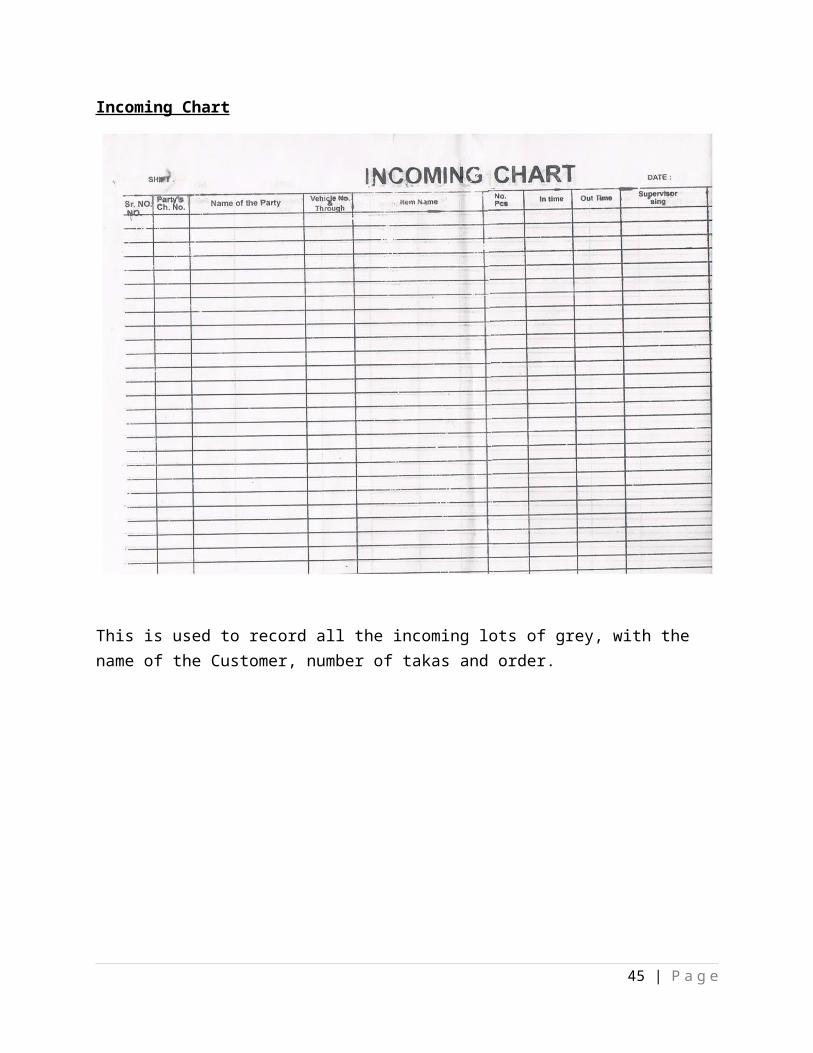

Incoming Chart

This is used to record all the incoming lots of grey, with the name of the Customer, number of takas and order.

45 | P a g e

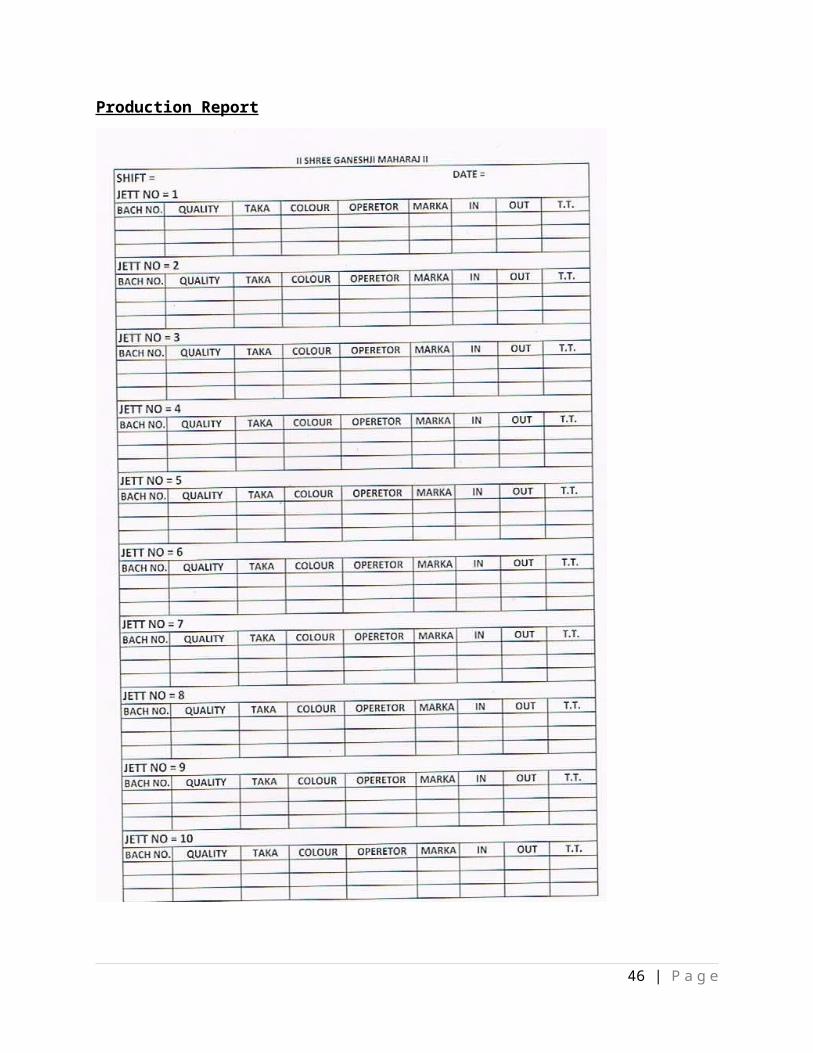

Production Report

46 | P a g e

This report is used to direct the operator about the quantity and

the quality to be processed with the name of the colour.

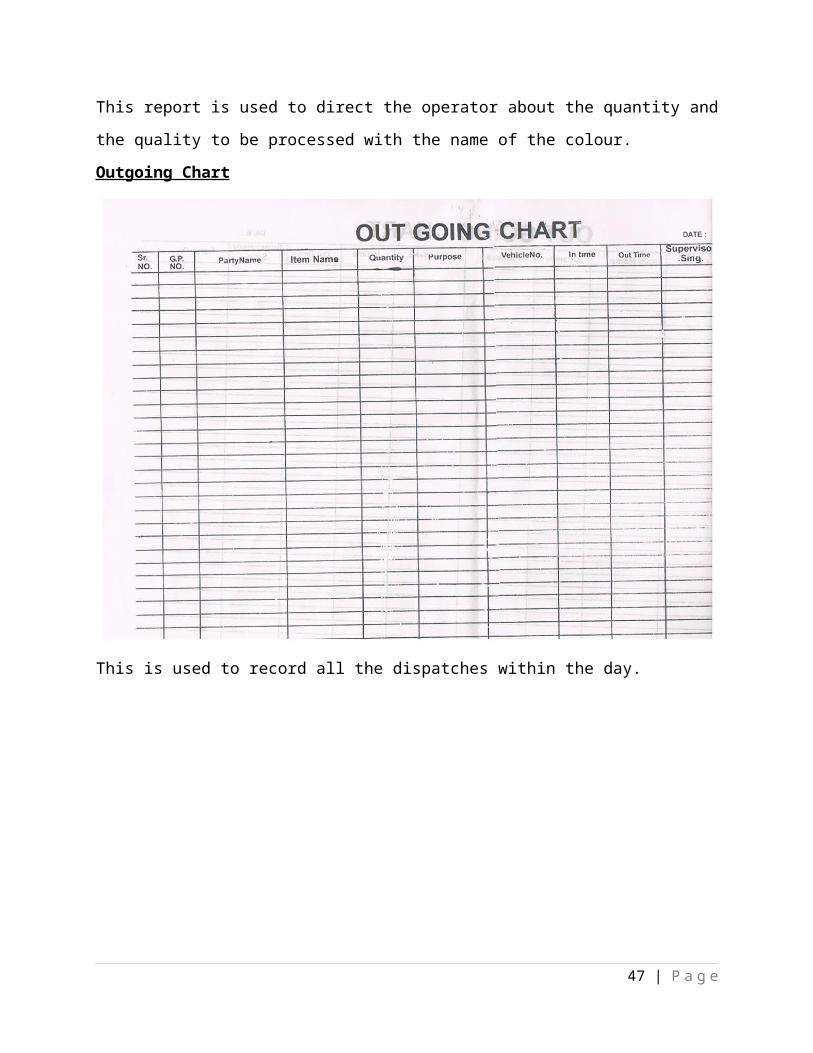

Outgoing Chart

This is used to record all the dispatches within the day.

47 | P a g e

2.2.9 PRODUCTION PLANNING AND CONTROL

Production Planning and Control (PPC) is the nervous system of

the organization and its basic task is to receive information

from the customer and link it to the production. It involves the

Pre-Production Analysis to ensure quality and reproducibility.

PPC has two further branches:

A) Material Resource Planning

B) Production Planning and Monitoring

Material Resource Planning: - Material Resource Planning is done

for the material procurement, like dyes, fuels, etc. It is

basically done to analyze that how much is needed, what is

needed, when is needed, what is the cost of the material and how

to acquire the resources. Generally, the stock is maintained for

a month and new supply is ordered just before the end of every

month

Production Planning: - It includes the planning like the Dyeing

Plan (we can also call it as the Master Plan). Back Ward

Production Planning is done and this Production Time Line

involves when’s and what’s of the production. Date Wise Plans are

made from work order to delivery.

Monitoring: - It is the different entity. Monitoring is done for

the whole production process and in this we check out the

48 | P a g e

planning implementation. If the planning is failed, re-planning

is done for that. Off- the- track and on-the- track planning is

also done by the PPC.

Documents Generated In PPC

Store Plan: - It involves all the documentation about the

sundries being used in the production of the order. It also

involves the information about Fuel, etc .Store Plan is basically

a Quantity Plan.

Dyeing Plan: - It is related with the Dyeing of the fabric that

how much dyes and chemicals are required. For the procurement of

the materials, PPC goes for the purchase department.

The Production Planning and Control is the nervous system of our

organization and undoubtedly it is our key success factor. The

nucleus of Shree Ram Design’s remarkable success has been its

impeccable system. PPC conducts detailed pre- production analysis

to ensure quality and reproducibility.

2.2.10 MATERIAL CODIFICATION SYSTEM

It is necessary that the raw materials from two customers should

not get mixed or exchanged .for this purpose, the following

coding practice is followed in the company:

Every customer of the company is given a unique identity code.

For example, the code of the “Radhe Silk Mills “is RSM. Only Top

Management is aware about what this code stands for. The entire

49 | P a g e

process in the factory now goes on the basis of work of ‘RSM’.

After the customer code, lot number is given according to the

number of grey lots received by the company i.e. 1, 2, 3, 4, etc.

Many a time’s all lots are not supposed to undergo the same

process. Suppose 50 lot of a RSM are received and of which 40

are for drumming (whitening) and remaining are of regular dyeing

procedure. Then the allotment is made in the following way:

CUSTOMER’S CODE, GREY NO., and PROCESS NAME.”RSM-1-D” which means

Radhe silk mill lot no. 1 is for drumming. RSM-41-N” which means

Radhe silk mill lot no. 41 is for normal dyeing. Then the grey

collection cards are sent to the respective Dyeing Masters of the

customers. the whole procedure of dyeing goes on as per the

master program given to the operators of different machines.

Finally the dispatching of finished dyed grey lots is made

according to the identity code and the priorities to the various

customers.

2.2.11 MATERIALS INWARD PROCESS

Material inward procedure generally begins with the gate entry

made by the security guard on the no. of grey lot entered into

the firm and at what time with the no. of tempo. Then the gate

entry pass is given to the grey checking section supervisor. The

details of gate pass are cross checked, and then the grey lots

are separated according to the parties. Then every grey lots of a

particular party are given with a unique identity code. The job

50 | P a g e

card of every party’s grey lot is prepared. Then the grey lots

are sent for the process as per the program made by the

respective master.

2.2.12 ANALYSIS OF PLANT LOCATION

The location of the plant has a crucial effect on the

profitability of a project, and the scope for future expansion.

Many factors must be considered while selecting a suitable site.

The following are the factors which have made the owners select

the site:

Industrial Area: - Tanti Thaiya is an area under G.I.D.C., so it

is an area assigned for Industrial development. This area is also

situated very far from residential areas, so no harm to common

man due to Industrial pollution.

Situated near the Textile Market: - Kadodra is the industrial

area nearest to Ring Road, the Business hub for the textile

industry in Surat. So, all the suppliers and buyers may first

visit the companies in this area when on a search for new

processor.

Easy availability of colors and chemicals: - Colors and chemicals

are the major essentials for dyeing process and the suppliers for

these products are also located in Sachin and Pandesara which are

near to Tanti Thaiya.

Availability of Labor: - Labor is easily available in this area.

51 | P a g e

Other factors are:

Availability of Utilities: Water, Fuel, Power.

Availability of Suitable Land.

Environmental Impact, And Effluent Disposal.

Local Community Considerations.

Climate.

Political Strategic Considerations.

52 | P a g e

2.2.13 INVENTORY CONTROL

Inventory control is the delicate balance of the costs versus

profits associated with having stock on hand.

Inventory control means keeping the overall costs associated with

having inventory as low as possible without creating problems.

This is also sometimes called stock control. It is an important

part of any business that must have a stock of products or items

on hand. Correctly managing inventory control is a delicate

balance at all times between having too much and too little in

order to maximize profits. The costs associated with holding

stock, running out of stock, and placing orders must all be

looked at and compared in order to find the right formula for a

particular business.

The raw materials, work-in-process

goods and completely finished goods that are considered to be the

portion of a business's assets those are ready or will be

ready for sale. Inventory represents one of the most important

assets that most businesses possess, because the turnover of

inventory represents one of the primary sources

of revenue generation and subsequent earnings for the company's

shareholders/owners

Being a process house, the company’s inventory constitutes of:

Dyes

Chemicals

Fuel

53 | P a g e

Dyes can be bifurcated into two types:

a. Reactive dyes: These types of dyes are used especially for

cotton cloth. For example; Golden Yellow HER, Orange H2ER,

etc.

b. Disperse Dyes: These types of dyes are utilized for the

polyester cloth. For Example: Rubine B-Red 167, Dark Red 2B,

etc.

Chemicals, also known as intermediaries are used at almost all

the stages. For example: - during washing, drumming, dyeing and

finishing.

The chemicals which company uses are:

Acetic Acid Caustic Soda

Citric Acid Common Salt

DyeAux FinAux

KSD Levecol NID

Manali T.K.P. Ran-SC

Sandosoft CWS Sodium-Hydro-Sulphite

Tangoline UDA Powder

Fuel, in the process house consists of:

(a) Coal

(b) Bagasse

(c) Wood

54 | P a g e

(d) Electricity

The objectives of inventory control are:

Quality – products need to be maintained in as good a condition

as possible while they are being stored. For perishable products

this means not storing them for very long.

Speed – inventories must be in the right place to ensure fast

response to customer requests.

Dependability – the right stock must be in the right place at the

right time to satisfy customer demand. There is no point having

the wrong products in stock.

Flexibility – stock should be managed to allow the operation to

be flexible. For example, that may mean keeping sufficient stock

to allow the operations processes to switch to producing

something else and yet being able to satisfy customers during

that period from existing stock levels.

Cost – if possible the total cost of managing stock levels should

be minimized.

2.2.14 INVENTORY VALUATION METHOD

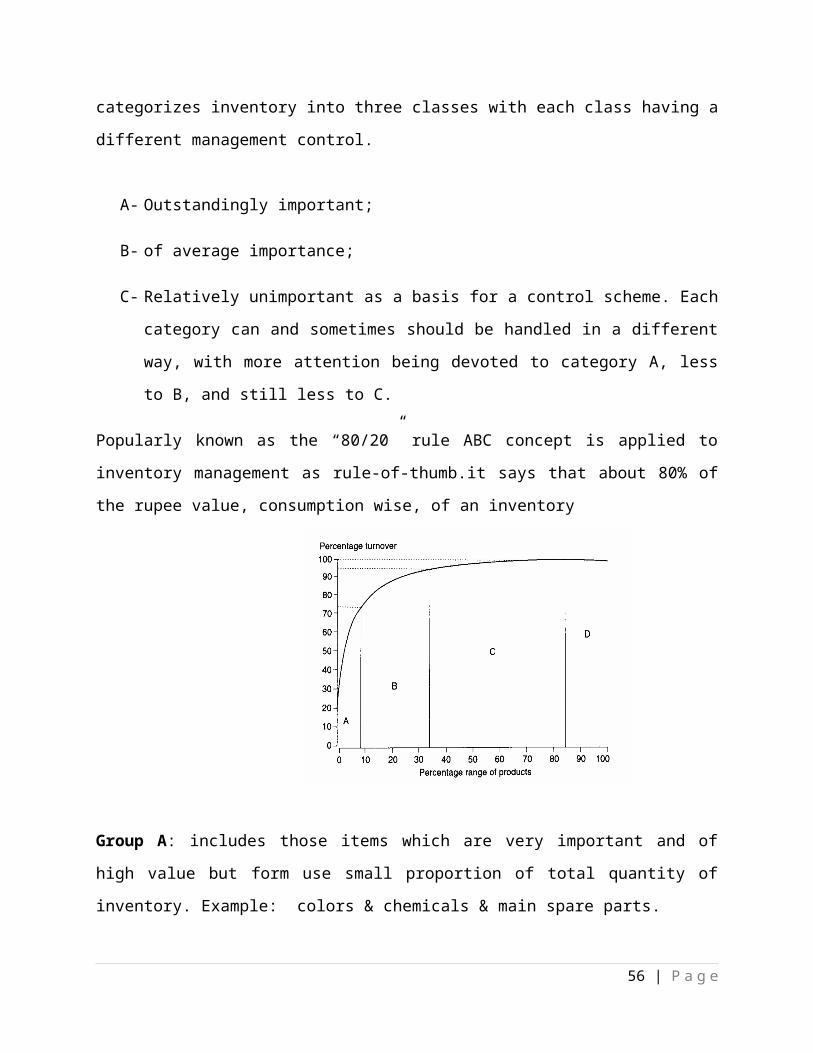

ABC analysis

The ABC classification process is an analysis of a range of

objects, such as finished products, items lying in Inventory or

customers into three categories. It’s a system of categorization,

with similarities to Pareto analysis, and the method usually

55 | P a g e

categorizes inventory into three classes with each class having a

different management control.

A- Outstandingly important;

B- of average importance;

C- Relatively unimportant as a basis for a control scheme. Each

category can and sometimes should be handled in a different

way, with more attention being devoted to category A, less

to B, and still less to C.

Popularly known as the “80/20” rule ABC concept is applied to

inventory management as rule-of-thumb.it says that about 80% of

the rupee value, consumption wise, of an inventory

Group A: includes those items which are very important and of

high value but form use small proportion of total quantity of

inventory. Example: colors & chemicals & main spare parts.

56 | P a g e

Group B: includes those items which are less important and of

low value but form use large proportion of items they group A.

Example: Bagasse & other fuels

Group C: the remaining items must be placed in category C.

VED analysis

As per VED classification, items can be divided in three groups:

Vital items

Essential items

Desirable items

VITAL ITEMS:

They are those items without which production will stop

instantly. All raw materials are vital items. For example:

colors, chemicals, grey, etc

ESSENTIAL ITEMS: - They are those items without which production

may not stop instantly but there can be problems like slow-down

of production. Example: Coal, bagasse.etc

DESIRABLE ITEMS: - They are those items without which production

may not stop instantly nor it will slow down but there may be

some inconvenience in manufacturing. For example: trolleys.

2.2.15 INVENTORY MANAGEMENT

57 | P a g e

The inventory plays an important role in the capital investment

and balance sheet of the business. Shree Ram Designs (P) ltd.

being a process house constitutes more than 200 items in its

inventory. As inventory management policy, the company implies

nothing scientifically. It is the trend that they manage it on

the basis of their experience. The below is the record of EOQ and

Re-Order Level of few inventories. The production department

intimates his daily requisition to the store manager and thereby

to the purchase department and order is being placed for the

same, after going through the last purchases done.

CHEMICALS

The chemicals which company uses are:

Acetic Acid Caustic Soda

Citric Acid Common Salt

DyeAux FinAux

KSD Levecol NID

Manali T.K.P. Ran-SC

Sandosoft CWS Sodium-Hydro-Sulphite

Tangoline UDA Powder

It can be seen that the EOQ and ROL for the chemicals are more in

most cases than actual practice. Therefore, it can be appreciated

that the co., without being stock-out blocks only needed amount

of working capital.

FUELS

58 | P a g e

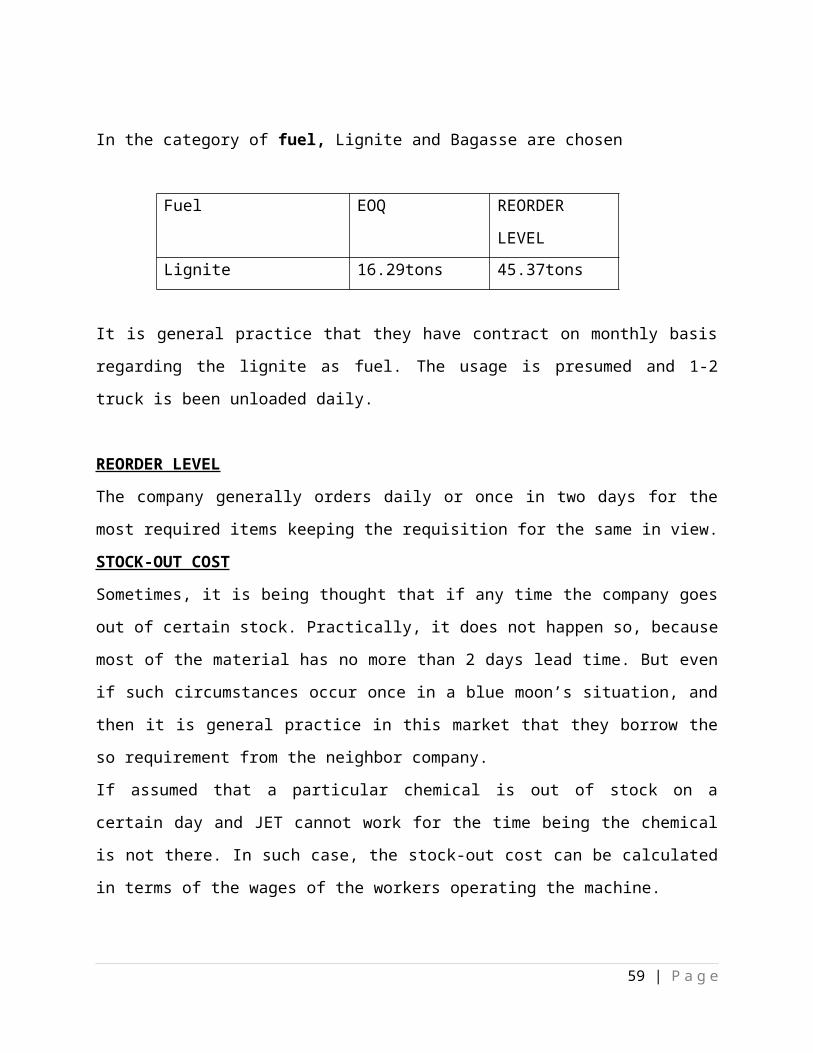

In the category of fuel, Lignite and Bagasse are chosen

Fuel EOQ REORDER

LEVELLignite 16.29tons 45.37tons

It is general practice that they have contract on monthly basis

regarding the lignite as fuel. The usage is presumed and 1-2

truck is been unloaded daily.

REORDER LEVEL

The company generally orders daily or once in two days for the

most required items keeping the requisition for the same in view.

STOCK-OUT COST

Sometimes, it is being thought that if any time the company goes

out of certain stock. Practically, it does not happen so, because

most of the material has no more than 2 days lead time. But even

if such circumstances occur once in a blue moon’s situation, and

then it is general practice in this market that they borrow the

so requirement from the neighbor company.

If assumed that a particular chemical is out of stock on a

certain day and JET cannot work for the time being the chemical

is not there. In such case, the stock-out cost can be calculated

in terms of the wages of the workers operating the machine.

59 | P a g e

MAJOR SUPPLIERS OF THE INVENTORY

1. DYES: - Color-Tex (P) Ltd., Anubha Polyweaves (P) Ltd.; an

agency of Spectrum, Tanmay Traders, etc.

2. CHEMICALS: - Manali Gum Industries (P) Ltd., United Organic,

Dye cells India, etc.

3. FUEL: - Parth Traders, G.M.D.C. for lignite and Gujarat

Electricity Board for Electricity.

2.2.16 PURCHASE DEPARTMENT

Every aspect of organization for the manufacturing of the product

like sundries,

stationary, parts of machineries that can be available locally,

chemicals and dyes etc. have to be purchase locally from the

local markets. These are usually the general items, involve local

purchase. For the purchase of machines, machinery that is not

available in the local market, import department involves in such

purchases. This whole import department is concerned with the

high involvement machinery. Things are purchased according the

buyer demand. No buying is done without the order. As such no

inventory level is maintained for such goods as these goods are

utilized immediately and plan is made for the minimum for the

week.

Three most important documents used in the purchase department

are:

60 | P a g e

Store Plan: - Store plan comes from the purchase & store

requisition. a level of all the colors & chemicals are

maintained in the storage dept. colors & chemicals which are

very commonly used are kept in good quantity & rare used are

kept with minimum fixed level. Purchase is made prior to 4-5

days before when it will be required and it is not available

in stock.

MPR: Material Procurement Recognition: - Every department

issues this then the purchase department is responsible for

procurement.

MRP: Material Requirement and Planning: - This document is

used within factory for issuing the material.

61 | P a g e

2.2.17 QUALITY CONTROL SYSTEM

Quality Control refers to setting certain standards for

production and matching production with those standards.

Management of every company is specially committed to the good

quality both in production and end results. The Management of SRM

has been successful in creating and maintaining the quality

culture in the organization. Daily quality report is sent to the

manager.

Quality Control Process

The process of quality control starts from the suppliers and ends

at customer. They start quality control right from the receiving

of grey to purchase of chemicals, dyes and other materials. For

this purpose, inspection is made to see whether the purchased

material is up to required quality standard or not. If not, it is

rejected. If accepted, Dyes and chemicals are also examined for

their brands, proper combinations, quality, colors and other

characteristics.

Inspection for quality standards is made throughout the step by

step manufacturing process, especially during grey inspection for

weight, width and blend ratio.

Some of the important tests carried out are:

Weight check and measure

Quality check and measure

62 | P a g e

Construction check and measure

Blend ratio check and measure

Size % check and measure

Absorbency check and measure

Whitener check and measure

pH check and measure

Washing fastness check and measure

Light check and measure

Shrinkage check and measure

Staring check and measure

2.2.18 CHEMICALS USED:

ACETIC ACID: - This chemical is used during the process of

dyeing. It helps to maintain basic ‘pH’ level, thereby helps

for better leveling of the dyes. After being purchased, Acetic

Acid is sent for Lab Testing, where it is observed that if its

freezing point is -4 degree Celsius and it constitutes 98% of

Glacial Acetic Acid. The lead time for this chemical is 1

week.

CAUSTIC SODA: - Caustic Soda is used during Drumming of the

cloth. It acts as a swelling agent. It helps in opening up all

the pores of the yarn and thereby discarding the impurities.

It also helps in better penetration of the dyes in the cloth.

Caustic Soda Flakes constitutes 90% of Common Salt. Its lead

time is 3 days.

63 | P a g e

CITRIC ACID: - Citric Acid helps to retain the brightness of

the dyes during the finish process Citric Acid is also used as

a substitute of Acetic Acid at some crucial stages, where the

latter turns to be volatile. Its lead time is 2 days. During

heat setting, sometimes Acetic Acid loses its strength after

drying, in such case Citric Acid is used in place of Acetic

Acid.

COMMON SALT: - It is a cheap substitute of Caustic Soda. It is

seasonal item, not available in rainy season. Its lead time is

4 days. The co. purchases it from Bhuj in Gujarat.

DYEAUX: - The DyeAux is used at the stage of dyeing of the

cloth. It is a Dyeing Auxiliary, helps in increasing the

fastness of the color. Its lead time is 2 days.

FINAUX: - This is a chemical used at the time of giving finish

to the fabric. It is used for better smoothening of the cloth.

Its lead time is 2 days.

KSD: - This chemical is being used at almost all stages. It is

deforming agent, prevents the formation of foam during the

process; be it; washing, dyeing, bleaching, Stentering,

printing or padding. Its lead time is 5-6 hours.

LEVECOL NID: - It is a cleaning agent, used while washing and

bleaching the cloth. It helps in removing stains and dirt. Its

lead time is 2 days.

MANALI T.K.P.: - This is a type of gum, acts as major

constituent in printing paste. It is 100% natural product made

64 | P a g e

out of ‘Gawar seeds’. It is seasonal item and is scarce in

rainy season. Its lead time is 1 week.

RAN-SC: - This chemical is used during finish. It acts a major

thickening agent, helps in filling up the fibers of the

fabric. Its lead time is 14 days. The co. purchases this item

from Nagpur.

SANDOSOFT CWS: - Sandosoft CWS is used during finish stage on

stenter. It is used to get better lusture feel of the fabric.

Its lead time is 2 days.

SODIUM-HYDRO-SULPHITE: - It is used during bleaching and

washing after printing. It removes all the impurities

including extra chemicals and dyes present in the fabric

during the process. Its lead time is 5 days.

The above chemicals constitute upto 34% of the total cost of the

entire process. There is no fixed cost of an individual

chemical. The contribution to cost of each and evcery chemical

varies as per the requirement of the quality and colour of the

order.

65 | P a g e

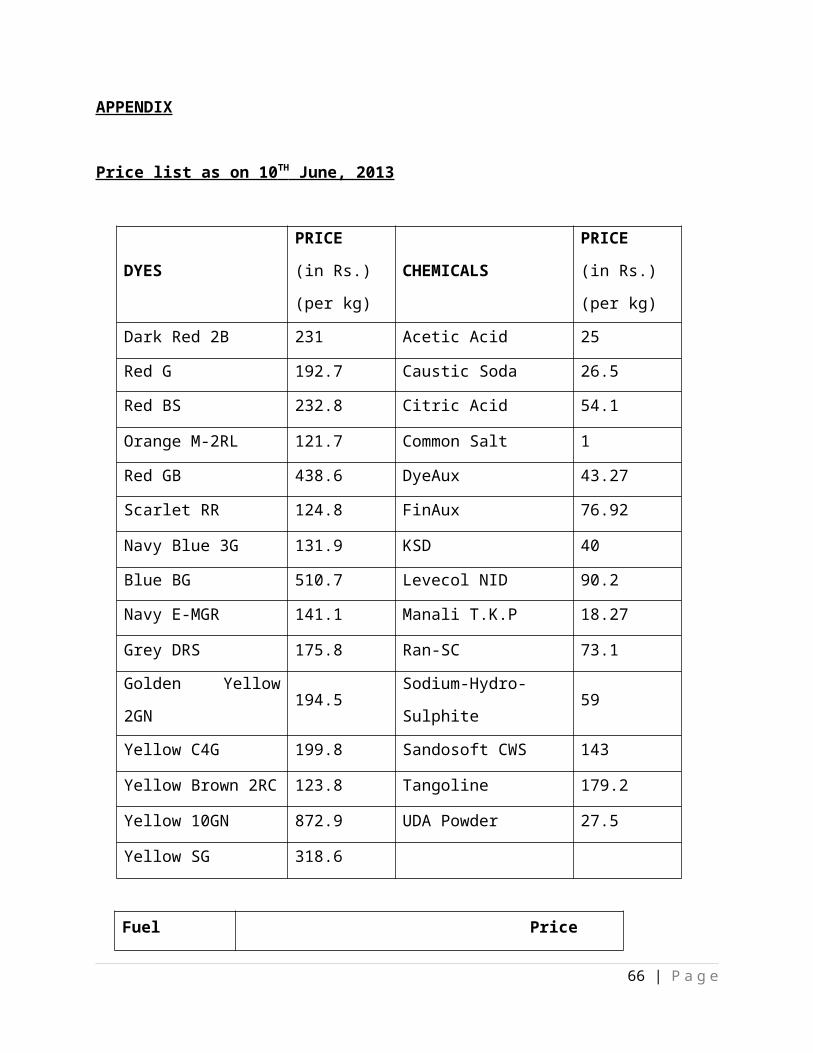

APPENDIX

Price list as on 10 TH June, 2013

DYES

PRICE

(in Rs.)

(per kg)

CHEMICALS

PRICE

(in Rs.)

(per kg)

Dark Red 2B 231 Acetic Acid 25

Red G 192.7 Caustic Soda 26.5

Red BS 232.8 Citric Acid 54.1

Orange M-2RL 121.7 Common Salt 1

Red GB 438.6 DyeAux 43.27

Scarlet RR 124.8 FinAux 76.92

Navy Blue 3G 131.9 KSD 40

Blue BG 510.7 Levecol NID 90.2

Navy E-MGR 141.1 Manali T.K.P 18.27

Grey DRS 175.8 Ran-SC 73.1

Golden Yellow

2GN194.5

Sodium-Hydro-

Sulphite59

Yellow C4G 199.8 Sandosoft CWS 143

Yellow Brown 2RC 123.8 Tangoline 179.2

Yellow 10GN 872.9 UDA Powder 27.5

Yellow SG 318.6

Fuel Price

66 | P a g e

(in Rs./ton)

Lignite 1940

2.3 FINANCIAL MANAGEMENT

2.3.1 ORGANISATION STRUCTURE OF FINANCE DEPARTMENT

2.3.2 REVENUE BUDGETING

Company has decided revenue budgeting in following ways:

Production cost: 20% contract base

(Daily wages)

80% monthly base

All other cost: Totally monthly base

67 | P a g e

DirectorBankingInsuranceTime Keeper

2.3.3 COSTING METHOD

Cost is calculated on the basis of batch.

Factors affecting the cost:

Labor

Raw material

Machinery

Maintenance

Electricity

Transportation

Dyes

Chemical

Gas

The total cost of

Classification of Cost in Different Categories

In order to make the job more easily, cost are classified into

different categories. The classification is as follows:

Fuel:

Coal and Lignite

Gas

68 | P a g e

Electricity

Diesel

Oil

Salary:

Salary

Labor (to contractor)

Wages

Color/ Chemical

Administrative expense

Other Expenses

Interest

Octroi

Packing

Store

Thread

Water

Other expense

2.3.4 COST STRUCTURE

Cost is anything incurred for producing a particular product or

service which is valuable in terms of money. And costing is

defined as a “technique & process of ascertaining cost.” Cost structure is

a statement showing all the cost incurred in the firm while

production process is taken place. The cost structure of this

firm is as follows:-

69 | P a g e

Direct Expenses: -

a) Colour

b) Chemical

c) Coal

d) Carriage/ Transport Expenses for bringing Grey

e) Labour Wages

Indirect Expenses

Factory Expenses: -

a) Electricity

b) Salary to Operators

c) Raw Material Testing

d) Stores

e) Maintenance of Machinery

f) Depreciation of Machinery

70 | P a g e

Administrative Expenses:-

a) Salary to Directors

b) Salary to Master

c) Salary to Supervisors

d) Salary to other Staff members

Selling Expenses:-

a) Packing

b) Transportation Cost

c) Sampling for Display

d) Collection

Other Expenses:-

a) Water Treatment

b) Sewage and Waste Treatment Plant

c) Printing

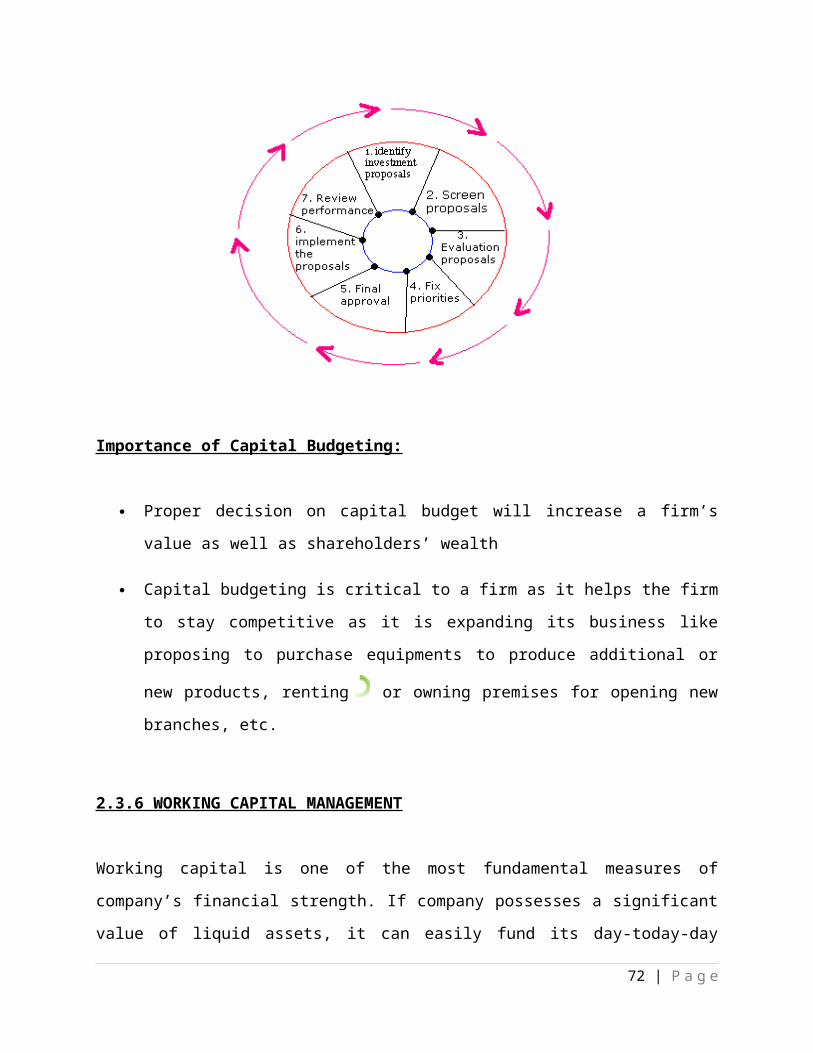

2.3.5 CAPITAL BUDGETING

Capital budgeting is a process of planning expenditures incurred

on assets whose cash flow is expected to range beyond one year.

In other words, it is defined as a process that requires planning

for setting up budgets on projects expected to have long-term

implications. It can be used for processes such as the purchase

of new equipment or launching of a new product in the market.

Businesses prefer to intricately study a project before taking it

on, as it has a great impact on the Company’s Financial

Performance.

71 | P a g e

Importance of Capital Budgeting:

Proper decision on capital budget will increase a firm’s

value as well as shareholders’ wealth

Capital budgeting is critical to a firm as it helps the firm

to stay competitive as it is expanding its business like

proposing to purchase equipments to produce additional or

new products, renting or owning premises for opening new

branches, etc.

2.3.6 WORKING CAPITAL MANAGEMENT

Working capital is one of the most fundamental measures of

company’s financial strength. If company possesses a significant

value of liquid assets, it can easily fund its day-today-day

72 | P a g e

business obligation. Working capital also provides insight on how

efficiency a company’s management able to oversee the company

operation. The speed at which the company is able to manage its

short term assets and short term liabilities are also crucial to

its business success. Keeping working capital level to minimum

required for efficient operation keeps cost down. This means

controlling buying, handling, storing, and managing stock

property.

In simple terms, working capital refers to the cash a company

requires in order to finance its day to day business operation or

In other words, working capital refers to the amount of capital

which is already available to an organization. The term working

capital is more an accounting term a management concept. There

are two concept of working capital for the purpose of definition-

Gross concept and Net concept. Gross concept refers to firm’s

current assets. The firm’s total current assets are termed as

gross working capital .net concept refers to current assets less

current liabilities. That means, working capital is difference

between resources in cash or readily convertible into cash will

soon be required.

Working Capital= Current Assets – Current Liabilities

The total working capital of the company is Rs.3, 63, 53,612.

Statement Showing Flow Of Funds (in ‘000 Rs)Sources of Funds Amt Application of Funds Amt

73 | P a g e

(Rs.)

(Rs.)Paid Up Capital 19580 Purchase of New Fixed

Assets

12769

Reserves & Surplus 07590 Investments 01634Secured Loans 10491 Increase in Working

Capital

33654

Unsecured Loans 11133 Deferred Tax Asset 00112Loss from operation

activities

00625

Total 48794 Total 48794

2.3.7 INTERNAL AUDIT POLICY

Internal audit is essential for companies. It is a review of

operations and record under taken within a business by special

assigned staff. The companies audit is carried out by its

accountant. The following checks are undertaken by him:

Taxation compliance

Supporting venture

Return materials

Inward-outward bills

Outdoor materials

Employee turnover

2.3.8 FINANCIAL CONTROL SYSTEMS

Basic Color and chemical costing are daily calculated.

74 | P a g e

Stock and debtors are daily reporting in marketing department

Sales or profit are monthly and quarterly reporting

Expenses are yearly reporting

2.3.9 ACCOUNTING POLICIES

Basis of preparation of financial statements: - The financial

statements are prepared under the historical cost convention,

on and comply with of accounting standards referred to in

section 211(3C) of the companies act, 1956.

Fixed assets: - Fixed assets (expected land) are stated at

costs and include incidental and installation expenses

incurred in putting the assets to use and less depreciation.

Depreciation: - Depreciation on Fixed Assets has been provided

on Written down Value Method at the rate specified in the

Schedule XIV of the Companies Act, 1956.

Investment: - Investments are stated at cost of acquisition.

Inventories: - Items include Color & Chemicals, Packing

Materials, Coal & Lignite, Fuel, and Consumable Stores &

Spares are valued at Cost. Work in Process includes materials,

labor cost and other relative overheads.

Revenue Recognition: - Revenue is recognized on its accrual,

sales is accounted when goods are supplied and recorded net of

trade discount and rebates but including excise duty and value

added tax. Late payment charges/ discounts are recognized on

the ground of prudence as and when recovered.

75 | P a g e

Retirement Benefits: - Estimated liability for gratuity on the

Balance Sheet date has not been quantified, the same is

accounted for on actual payment basis.

Borrowing Cost: - Borrowing costs that are directly

attributable to the acquisition, construction or production of

qualifying assets are capitalized as part of the cost of the

asset. Other borrowing costs are recognized as an expense in

the period in which they are incurred.

Segment Accounting: - The company has identified only one

segment viz. TEXTILES, and commission income credited is also

identified to be relating to textile segment exclusively.

Deferred Taxation: - In accordance with the accounting

standard 22, accounting for taxes on income, issued by the

institute of chartered accountants of India (‘ICAI’), the

company has provided for deferred tax at 31st march, 2013.

Deferred tax resulting from timing differences between boo k

and tax profits is accounted for, at the current rate of tax,

to extent that the timing differences are expected to

crystallize.

Deferred tax on account of unabsorbed depreciation and other

provisions are recognized only when there is a virtual certainty

supported by convincing evidence that such assets will be

realized.

2.3.10 INVENTORY VALUATION METHOD

76 | P a g e

Raw Materials - At Identified Cost

Raw Materials obsolete - At Lower of Identified Cost

Process Stock - At Average Cost

Finished goods - At Lower of Cost or Net Realizable Value

Parts, Consumable & Spares - At Weighted Average Cost

77 | P a g e

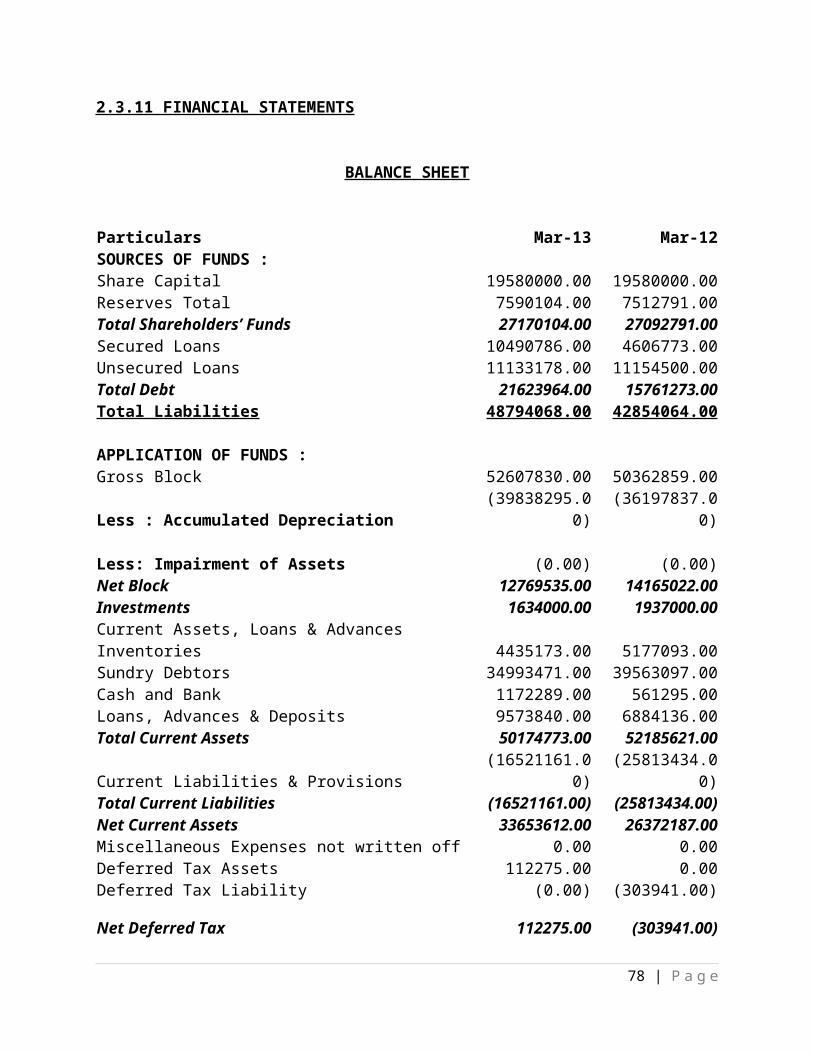

2.3.11 FINANCIAL STATEMENTS

BALANCE SHEET

Particulars Mar-13 Mar-12SOURCES OF FUNDS :Share Capital 19580000.00 19580000.00Reserves Total 7590104.00 7512791.00Total Shareholders’ Funds 27170104.00 27092791.00Secured Loans 10490786.00 4606773.00Unsecured Loans 11133178.00 11154500.00Total Debt 21623964.00 15761273.00Total Liabilities 48794068.00 42854064.00

APPLICATION OF FUNDS :Gross Block 52607830.00 50362859.00

Less : Accumulated Depreciation(39838295.0

0)(36197837.0

0)

Less: Impairment of Assets (0.00) (0.00)Net Block 12769535.00 14165022.00Investments 1634000.00 1937000.00Current Assets, Loans & AdvancesInventories 4435173.00 5177093.00Sundry Debtors 34993471.00 39563097.00Cash and Bank 1172289.00 561295.00Loans, Advances & Deposits 9573840.00 6884136.00Total Current Assets 50174773.00 52185621.00

Current Liabilities & Provisions(16521161.0

0)(25813434.0

0)Total Current Liabilities (16521161.00) (25813434.00)Net Current Assets 33653612.00 26372187.00Miscellaneous Expenses not written off 0.00 0.00Deferred Tax Assets 112275.00 0.00Deferred Tax Liability (0.00) (303941.00)

Net Deferred Tax 112275.00 (303941.00)

78 | P a g e

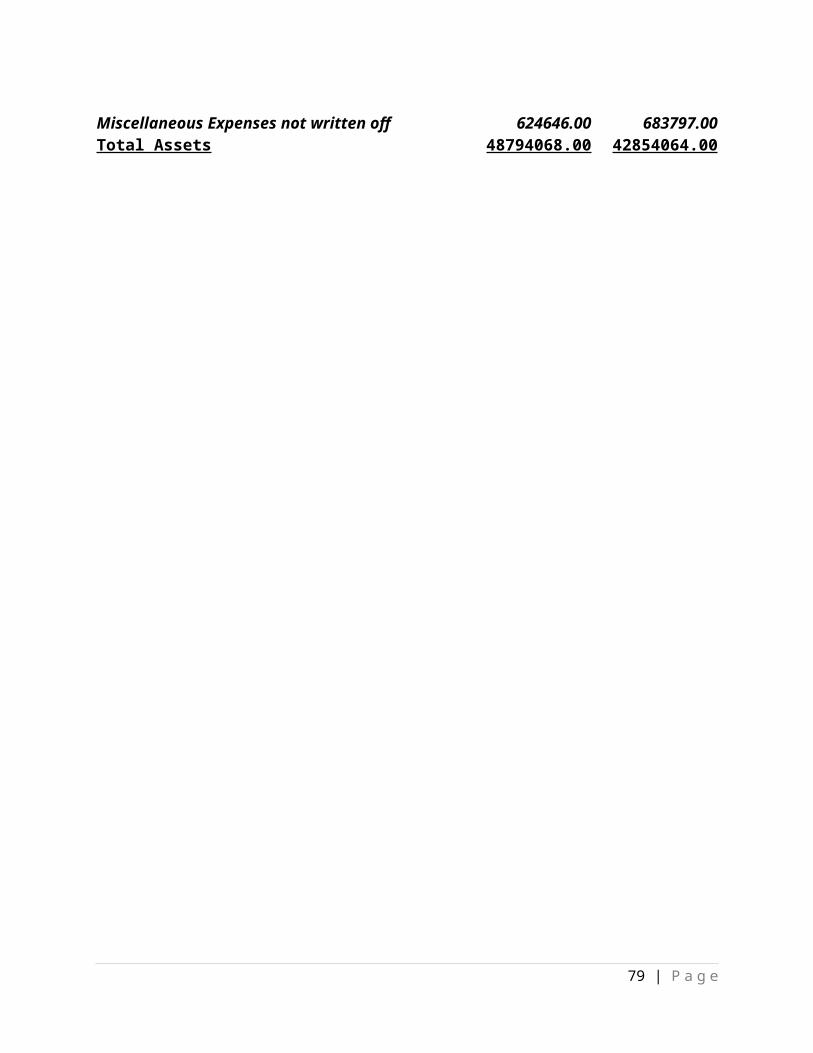

Miscellaneous Expenses not written off 624646.00 683797.00Total Assets 48794068.00 42854064.00

79 | P a g e

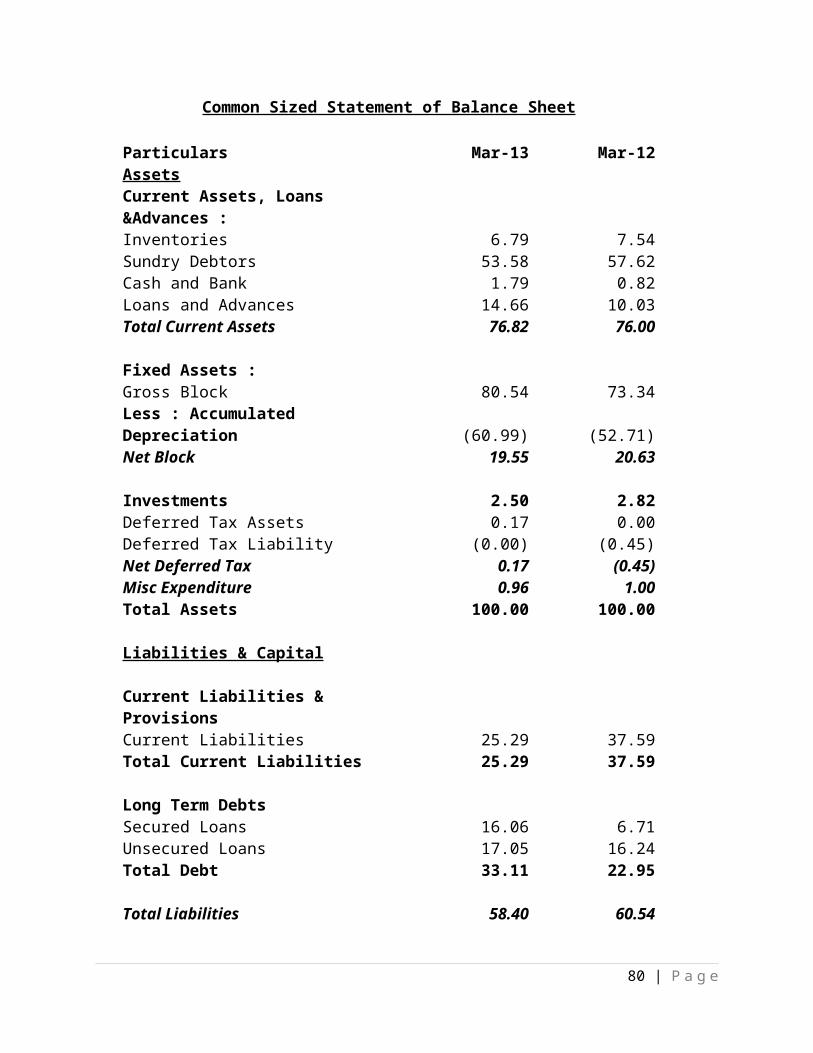

Common Sized Statement of Balance Sheet

Particulars Mar-13 Mar-12AssetsCurrent Assets, Loans &Advances :Inventories 6.79 7.54Sundry Debtors 53.58 57.62Cash and Bank 1.79 0.82Loans and Advances 14.66 10.03Total Current Assets 76.82 76.00

Fixed Assets :Gross Block 80.54 73.34Less : Accumulated Depreciation (60.99) (52.71)Net Block 19.55 20.63

Investments 2.50 2.82Deferred Tax Assets 0.17 0.00Deferred Tax Liability (0.00) (0.45)Net Deferred Tax 0.17 (0.45)Misc Expenditure 0.96 1.00Total Assets 100.00 100.00

Liabilities & Capital

Current Liabilities & ProvisionsCurrent Liabilities 25.29 37.59Total Current Liabilities 25.29 37.59

Long Term DebtsSecured Loans 16.06 6.71Unsecured Loans 17.05 16.24Total Debt 33.11 22.95

Total Liabilities 58.40 60.54

80 | P a g e

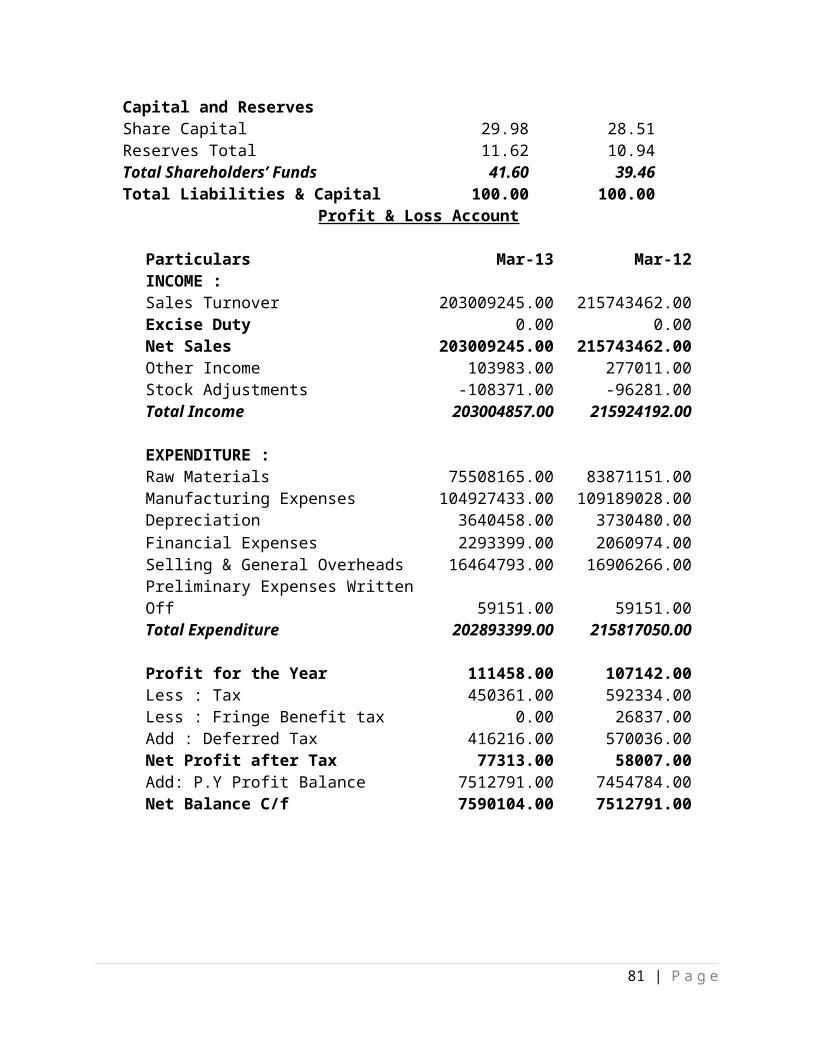

Capital and ReservesShare Capital 29.98 28.51Reserves Total 11.62 10.94Total Shareholders’ Funds 41.60 39.46Total Liabilities & Capital 100.00 100.00

Profit & Loss Account

Particulars Mar-13 Mar-12INCOME :Sales Turnover 203009245.00 215743462.00Excise Duty 0.00 0.00Net Sales 203009245.00 215743462.00Other Income 103983.00 277011.00Stock Adjustments -108371.00 -96281.00Total Income 203004857.00 215924192.00

EXPENDITURE :Raw Materials 75508165.00 83871151.00Manufacturing Expenses 104927433.00 109189028.00Depreciation 3640458.00 3730480.00Financial Expenses 2293399.00 2060974.00Selling & General Overheads 16464793.00 16906266.00Preliminary Expenses WrittenOff 59151.00 59151.00Total Expenditure 202893399.00 215817050.00

Profit for the Year 111458.00 107142.00Less : Tax 450361.00 592334.00Less : Fringe Benefit tax 0.00 26837.00Add : Deferred Tax 416216.00 570036.00Net Profit after Tax 77313.00 58007.00Add: P.Y Profit Balance 7512791.00 7454784.00Net Balance C/f 7590104.00 7512791.00

81 | P a g e

82 | P a g e

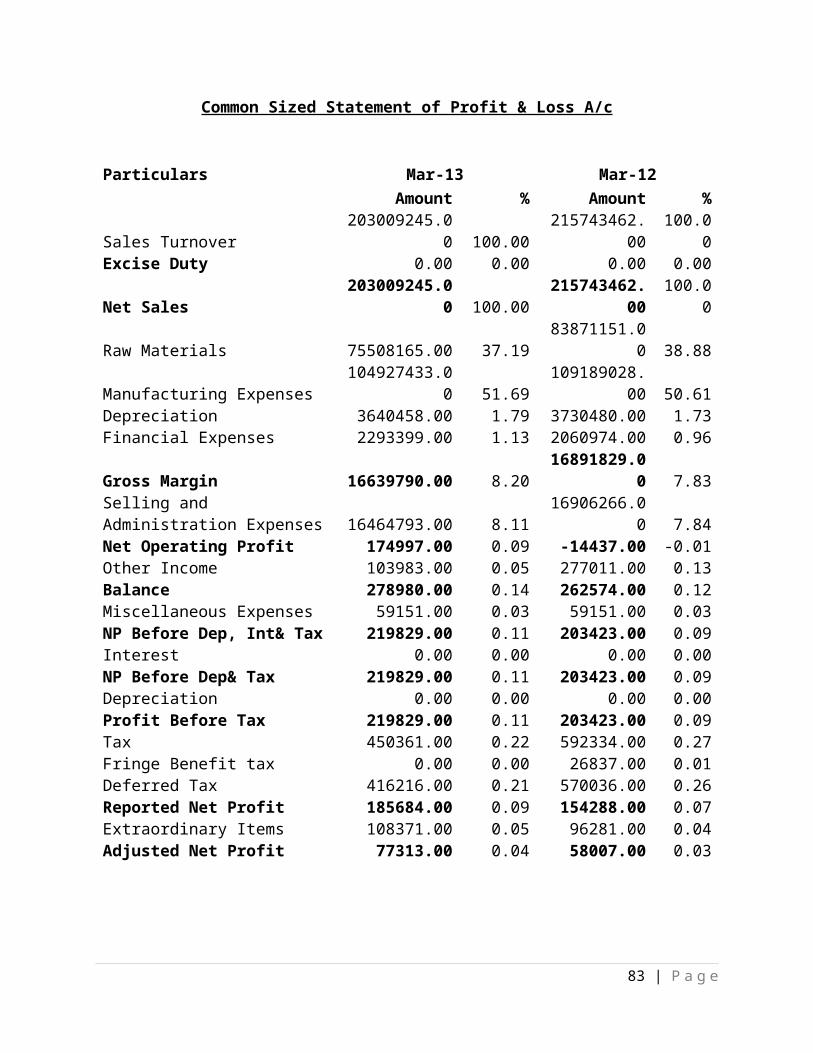

Common Sized Statement of Profit & Loss A/c

Particulars Mar-13 Mar-12Amount % Amount %

Sales Turnover203009245.0

0 100.00215743462.

00100.0

0Excise Duty 0.00 0.00 0.00 0.00

Net Sales203009245.0

0 100.00215743462.

00100.0

0

Raw Materials 75508165.00 37.1983871151.0

0 38.88

Manufacturing Expenses 104927433.0

0 51.69109189028.

00 50.61Depreciation 3640458.00 1.79 3730480.00 1.73Financial Expenses 2293399.00 1.13 2060974.00 0.96

Gross Margin 16639790.00 8.2016891829.0

0 7.83Selling and Administration Expenses 16464793.00 8.11

16906266.00 7.84

Net Operating Profit 174997.00 0.09 -14437.00 -0.01Other Income 103983.00 0.05 277011.00 0.13Balance 278980.00 0.14 262574.00 0.12Miscellaneous Expenses 59151.00 0.03 59151.00 0.03NP Before Dep, Int& Tax 219829.00 0.11 203423.00 0.09Interest 0.00 0.00 0.00 0.00NP Before Dep& Tax 219829.00 0.11 203423.00 0.09Depreciation 0.00 0.00 0.00 0.00Profit Before Tax 219829.00 0.11 203423.00 0.09Tax 450361.00 0.22 592334.00 0.27Fringe Benefit tax 0.00 0.00 26837.00 0.01Deferred Tax 416216.00 0.21 570036.00 0.26Reported Net Profit 185684.00 0.09 154288.00 0.07Extraordinary Items 108371.00 0.05 96281.00 0.04Adjusted Net Profit 77313.00 0.04 58007.00 0.03

83 | P a g e

84 | P a g e

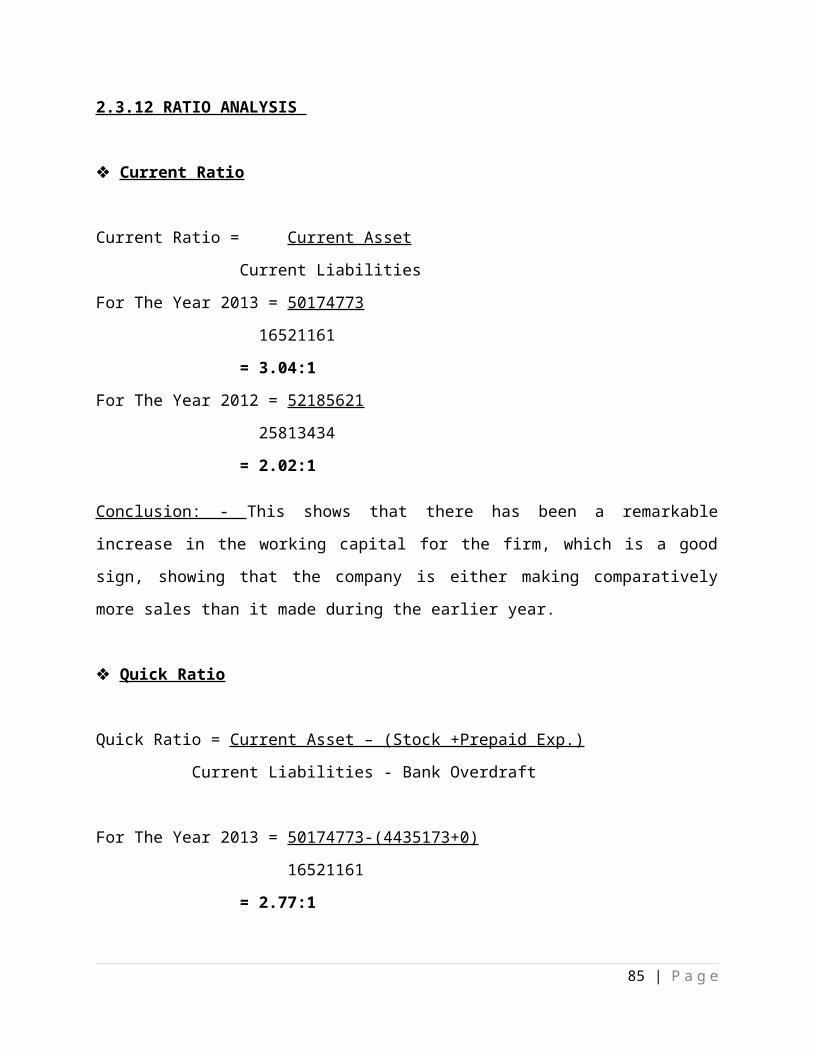

2.3.12 RATIO ANALYSIS

Current Ratio

Current Ratio = Current Asset

Current Liabilities

For The Year 2013 = 50174773

16521161

= 3.04:1

For The Year 2012 = 52185621

25813434

= 2.02:1

Conclusion: - This shows that there has been a remarkable

increase in the working capital for the firm, which is a good

sign, showing that the company is either making comparatively

more sales than it made during the earlier year.

Quick Ratio

Quick Ratio = Current Asset – (Stock +Prepaid Exp.)

Current Liabilities - Bank Overdraft

For The Year 2013 = 50174773-(4435173+0)

16521161

= 2.77:1

85 | P a g e

For The Year 2012 = 52185621-(5177093+0)

25813434

= 1.82:1

Conclusion: -It can be clearly observed that the increase in the

ratio of current assets is due to increase in the proportion of

such assets which can be easily converted into cash.

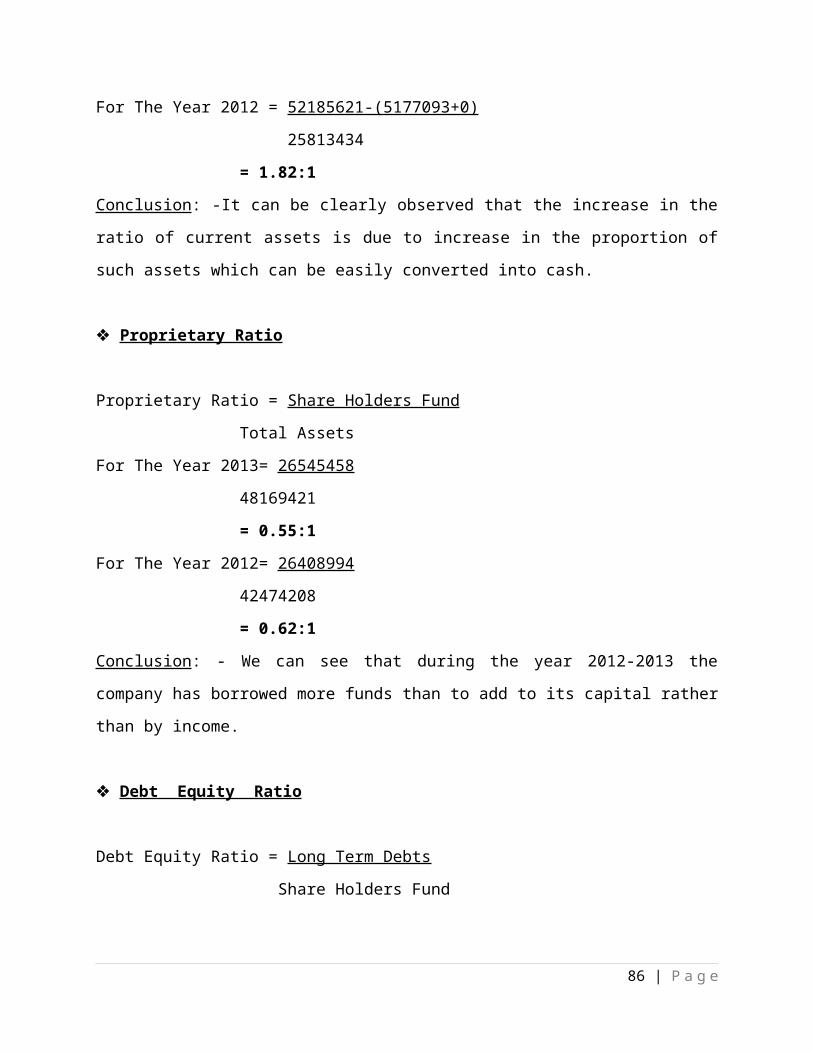

Proprietary Ratio

Proprietary Ratio = Share Holders Fund

Total Assets

For The Year 2013= 26545458

48169421

= 0.55:1

For The Year 2012= 26408994

42474208

= 0.62:1

Conclusion: - We can see that during the year 2012-2013 the

company has borrowed more funds than to add to its capital rather

than by income.

Debt Equity Ratio

Debt Equity Ratio = Long Term Debts

Share Holders Fund

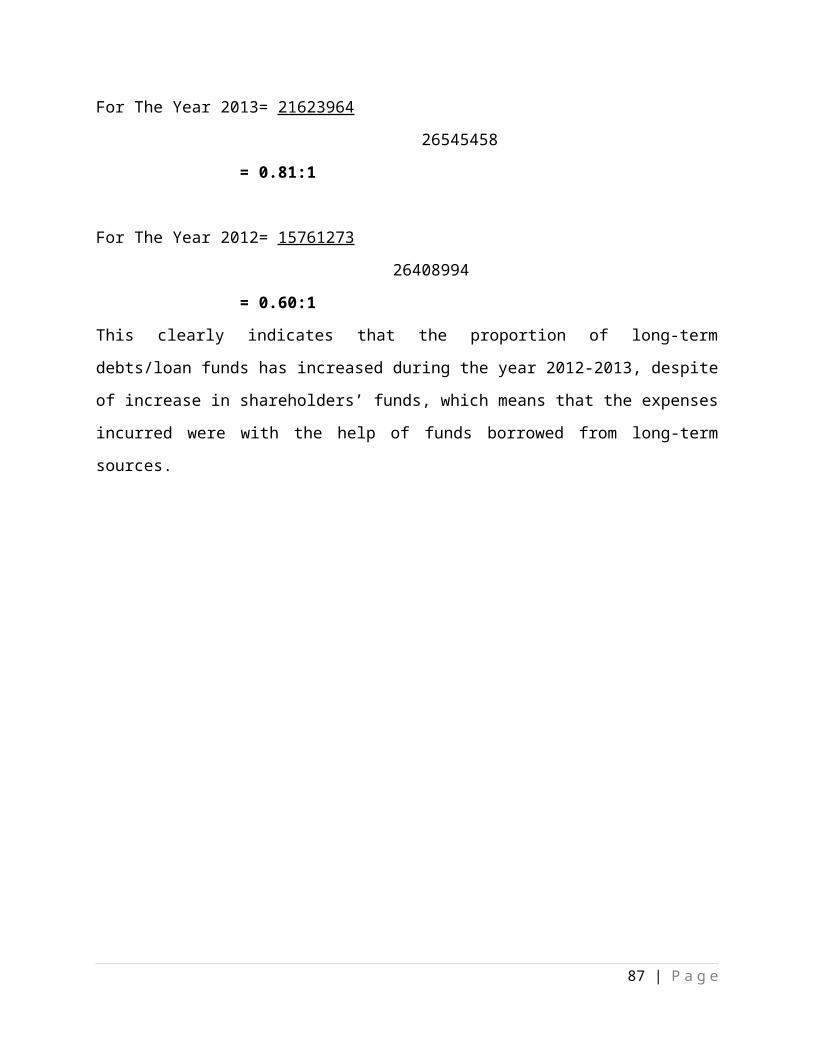

86 | P a g e

For The Year 2013= 21623964

26545458

= 0.81:1

For The Year 2012= 15761273

26408994

= 0.60:1

This clearly indicates that the proportion of long-term

debts/loan funds has increased during the year 2012-2013, despite

of increase in shareholders’ funds, which means that the expenses

incurred were with the help of funds borrowed from long-term

sources.

87 | P a g e

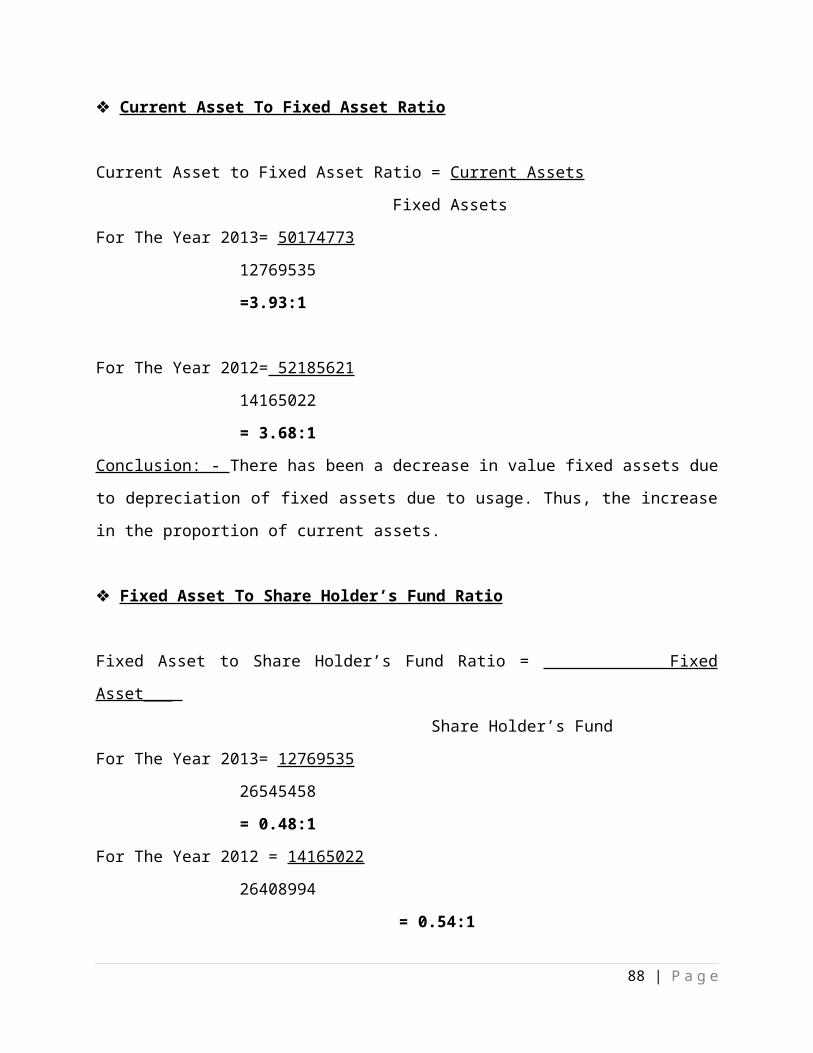

Current Asset To Fixed Asset Ratio

Current Asset to Fixed Asset Ratio = Current Assets

Fixed Assets

For The Year 2013= 50174773

12769535

=3.93:1

For The Year 2012= 52185621

14165022

= 3.68:1

Conclusion: - There has been a decrease in value fixed assets due

to depreciation of fixed assets due to usage. Thus, the increase

in the proportion of current assets.

Fixed Asset To Share Holder’s Fund Ratio

Fixed Asset to Share Holder’s Fund Ratio = Fixed

Asset___

Share Holder’s Fund

For The Year 2013= 12769535

26545458

= 0.48:1

For The Year 2012 = 14165022

26408994

= 0.54:1

88 | P a g e

Conclusion: - The decrease in the proportion of fixed assets to

the shareholders’ funds partly due to depreciation and we can

also see that there has been a slight increase in the value of

shareholders’ funds.

89 | P a g e

Current Asset To Proprietary Ratio

Current Asset to Proprietary Ratio = Current Asset__

Proprietor’s Fund

For The Year 2013= 50174773

26545458

=1.89:1

For The Year 2012=52185621

26408994

= 1.98:1

Conclusion: -The slight decrease in the proportion of current

assets to the proprietor’s funds is mainly due to increase in

proprietor funds.

Gross Profit Ratio

Gross Profit Ratio = Gross Profit × _100

Net Sales

For The Year 2013= 22573647 x 100

203009245

= 11.12%

For The Year 2012= 22683283 × 100

215743462

= 10.51%

Conclusion: - The increase in gross profit ratio is due to the

decrease in basic direct expenses of wages. The wages decreased

90 | P a g e

due to the modernization of machines in printing machines, which

resulted in less labor.

Operating Ratio

Operating Ratio = (Operating Exp. + Cogs) × _100

Net Sales

For The Year 2013= ( 22398650 +180443598) × 100

203009245

= 202884248 × 100

203009245

= 99.94%

For The Year 2012 = ( 22697720 +193060179) × 100

215743462

= 215757899 × 100

215743462

= 100.01%

Conclusion: - We can see that the company incurs a very high

amount of operating expenses and sells them just merely above the

cost price, due to which the operating ratio is very high. Even

91 | P a g e

the small decrease in the operating ratio was due to

improvisation in the production techniques.

Operating Profit Ratio

Operating Profit Ratio = 100 – Operating Ratio

For The Year 2013 = 100 – 99.94 %

= 0.06%

For The Year 2012 = 100 – 100.01 %

= -0.01 %

Conclusion: - The Company made some operating profit during the

last year because of last year because of better techniques.

92 | P a g e

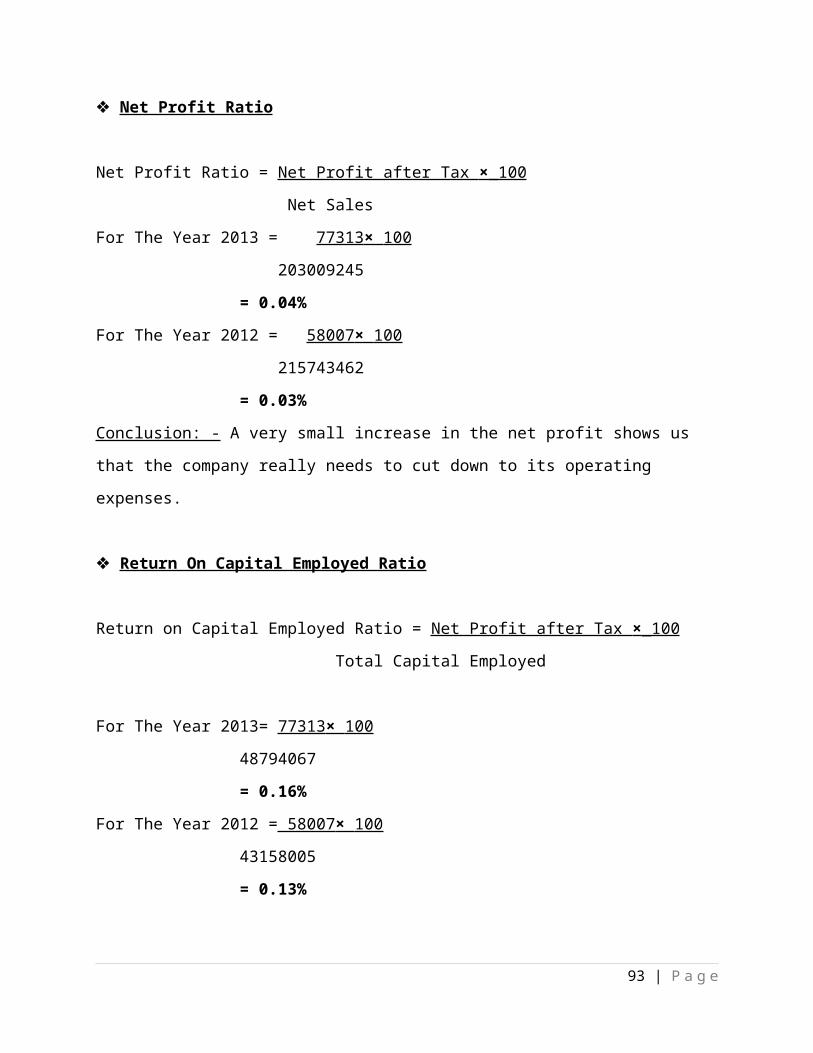

Net Profit Ratio

Net Profit Ratio = Net Profit after Tax × _100

Net Sales

For The Year 2013 = 77313 × 100

203009245

= 0.04%

For The Year 2012 = 58007 × 100

215743462

= 0.03%

Conclusion: - A very small increase in the net profit shows us

that the company really needs to cut down to its operating

expenses.

Return On Capital Employed Ratio

Return on Capital Employed Ratio = Net Profit after Tax × _100

Total Capital Employed

For The Year 2013= 77313 × 100

48794067

= 0.16%

For The Year 2012 = 58007 × 100

43158005

= 0.13%

93 | P a g e

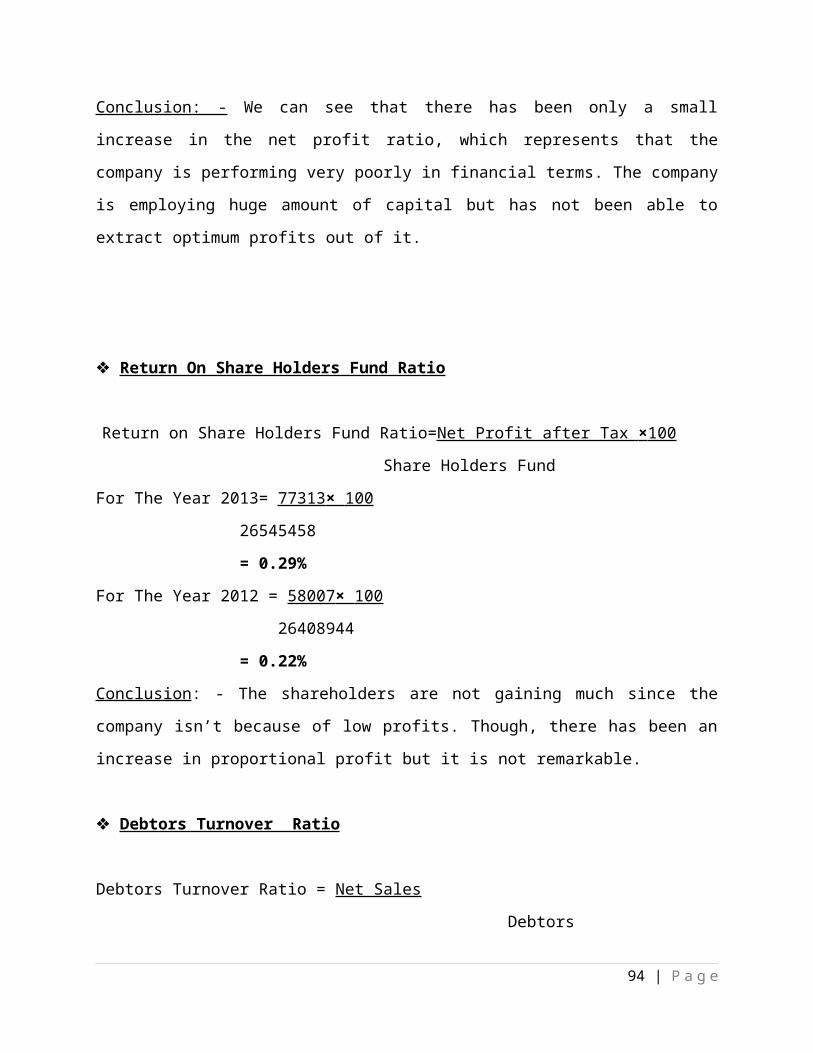

Conclusion: - We can see that there has been only a small

increase in the net profit ratio, which represents that the

company is performing very poorly in financial terms. The company

is employing huge amount of capital but has not been able to

extract optimum profits out of it.

Return On Share Holders Fund Ratio

Return on Share Holders Fund Ratio=Net Profit after Tax × 100

Share Holders Fund

For The Year 2013= 77313 × 100

26545458

= 0.29%

For The Year 2012 = 58007 × 100

26408944

= 0.22%

Conclusion: - The shareholders are not gaining much since the

company isn’t because of low profits. Though, there has been an

increase in proportional profit but it is not remarkable.

Debtors Turnover Ratio

Debtors Turnover Ratio = Net Sales

Debtors

94 | P a g e

For The Year 2013 = 203009245

34993471

=5.80

For The Year 2012 = 215743462

39563097

=5.45

Average Collection Period = ____ 12 Months______

Debtors Turnover Ratio

For The Year 2013= 360_

5.80

= 62 days

For The Year 2012 = 360

5.45

= 66 days

Conclusion: -The increase in the Debtors Turnover Ratio and the

decrease in the Average Collection Period is a good sign as the

company is now receiving payments quicker than during the

previous year.

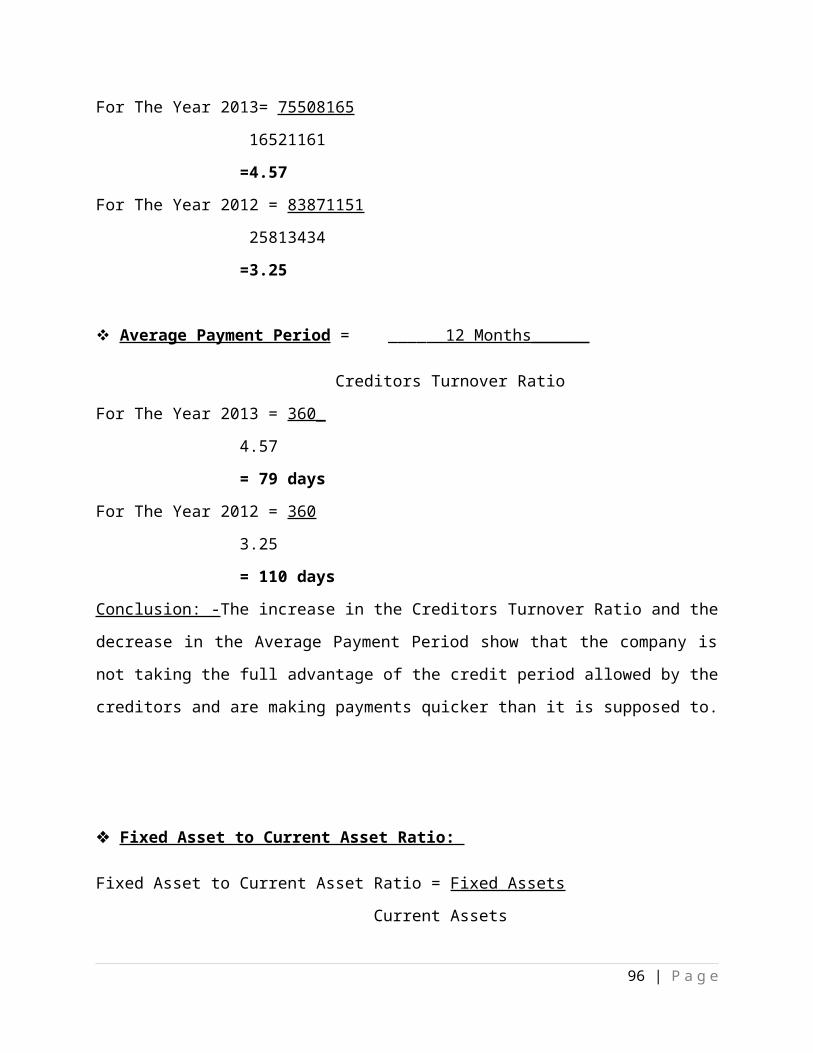

Creditors Turnover Ratio

Creditors Turnover Ratio = Net Purchases

Creditors

95 | P a g e

For The Year 2013= 75508165

16521161

=4.57

For The Year 2012 = 83871151

25813434

=3.25

Average Payment Period = ____ 12 Months______

Creditors Turnover Ratio

For The Year 2013 = 360_

4.57

= 79 days

For The Year 2012 = 360

3.25

= 110 days

Conclusion: -The increase in the Creditors Turnover Ratio and the

decrease in the Average Payment Period show that the company is

not taking the full advantage of the credit period allowed by the

creditors and are making payments quicker than it is supposed to.

Fixed Asset to Current Asset Ratio:

Fixed Asset to Current Asset Ratio = Fixed Assets

Current Assets

96 | P a g e

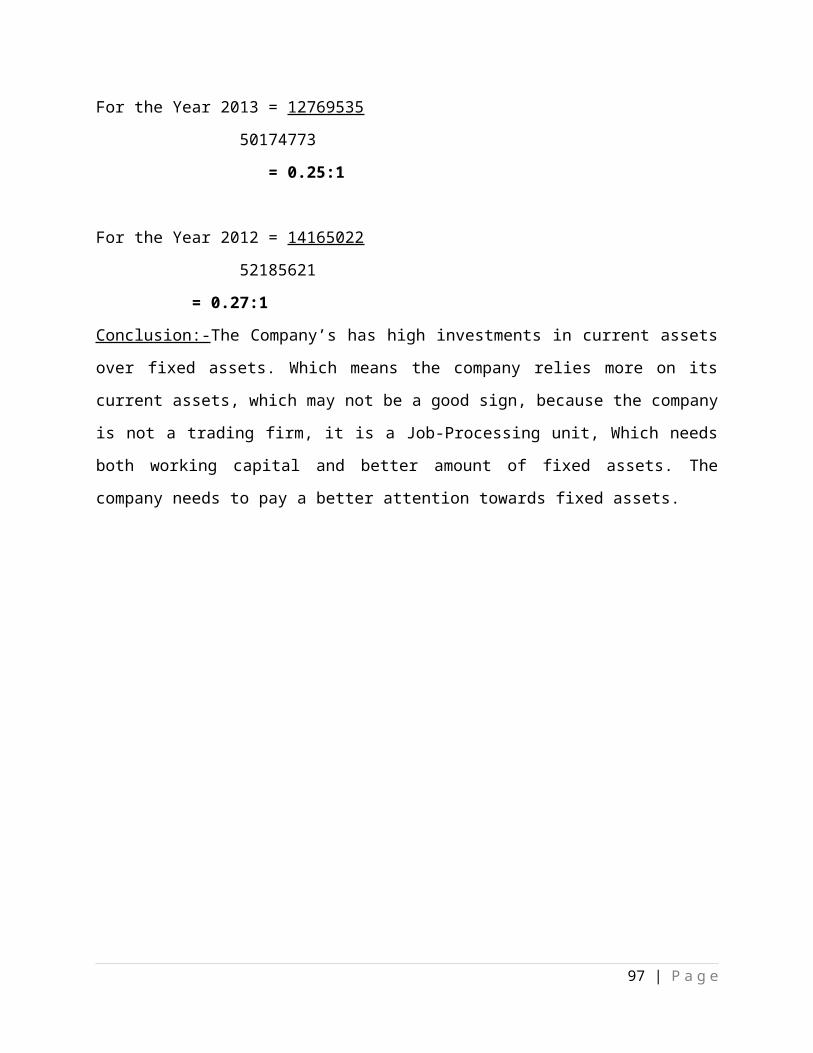

For the Year 2013 = 12769535

50174773

= 0.25:1

For the Year 2012 = 14165022

52185621

= 0.27:1

Conclusion:-The Company’s has high investments in current assets

over fixed assets. Which means the company relies more on its

current assets, which may not be a good sign, because the company

is not a trading firm, it is a Job-Processing unit, Which needs

both working capital and better amount of fixed assets. The

company needs to pay a better attention towards fixed assets.

97 | P a g e

2.4 HUMAN RESOURCE MANAGEMENT

2.4.1 ORGANIZATION STRUCTURE OF HUMAN RESOURCE DEPARTMENT

98 | P a g e

2.4.2 ORGANIZATIONAL CULTURE

Shree Ram considers its employees to be its biggest assets.

Adequate facilities exist and are constantly upgraded to improve

the social environment.

The organization has following statement for their social

culture:

‘We strictly, under all cost, forbid child labor and forced

labor’

2.4.3 HUMAN RESOURCE PLANNING PROCESS

Shree Ram designs have no scientific human resource planning

process. They have to determine and assuming that the company

will have an adequate number of qualified persons, available at

the proper times, performing jobs which meet the need of company

and which provide satisfaction for the company and individuals.

2.4.4 RECRUITMENT, TRAINING, COMPENSATION AND LAYING-OFF

Human resource department is responsible for

Recruiting

99 | P a g e

Training

Compensation

Performance appraisal

Laying-off

Recruiting

In Shree ram for management hiring three interviews are conducted

if they are

experienced. If they fresh graduate then first oral test is done

after this interview

interview. If he is passed, he is kept for work on 1 month trial

basis. If he is fonnd suitable, then he is appointed and all

terms & conditions are decided. This process is done for

management Trainees.

Training