Short-term Investing for Corporations Idaho Association for Financial Professionals May 13, 2008 Rick Sabones, Director, Global Liquidity & Investments, Citi

Short-term Investing for Corporations Idaho Association for Financial Professionals May 13, 2008 Rick Sabones, Director, Global Liquidity & Investments,

Dec 25, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Short-term Investing for Corporations

Idaho Association for Financial ProfessionalsMay 13, 2008

Rick Sabones, Director, Global Liquidity & Investments, Citi

2

Overview & Agenda

Agenda:

Money Market Review

Corporate Investment Practices

Automation

Money Market Funds-Rule 2a-7 and “AAA” Ratings

Is it possible to achieve optimum returns given risk, liquidity and yield expectations in today’s current market?

Overview: First, with the financial and credit market turmoil that has persisted in the markets since August, the focus for cash investments has been on safety, preservation of capital and liquidity. The discussion will focus on maximizing the efficiency of your cash, the various investment options available and how current market conditions affect the decision process.

3

Money Market Review

4

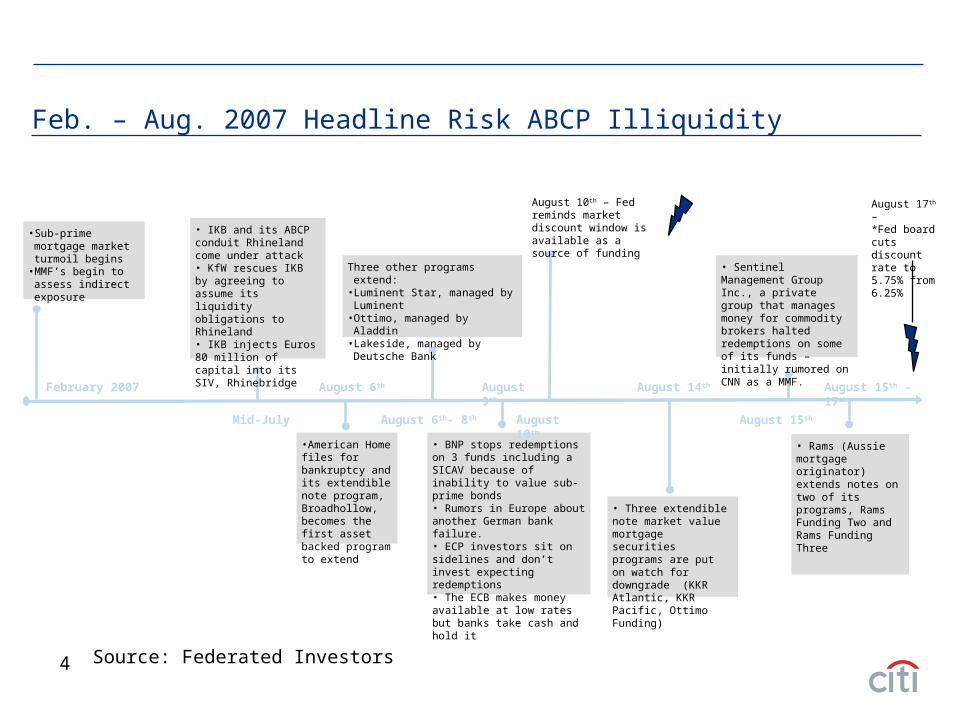

Feb. – Aug. 2007 Headline Risk ABCP Illiquidity

February 2007

Mid-July

August 9th

• Sub-prime mortgage market turmoil begins

• MMF’s begin to assess indirect exposure

• IKB and its ABCP conduit Rhineland come under attack • KfW rescues IKB by agreeing to assume its liquidity obligations to Rhineland• IKB injects Euros 80 million of capital into its SIV, Rhinebridge

August 6th- 8th

•American Home files for bankruptcy and its extendible note program, Broadhollow, becomes the first asset backed program to extend

August 6th

Three other programs extend:• Luminent Star, managed by

Luminent• Ottimo, managed by Aladdin• Lakeside, managed by Deutsche

Bank

• BNP stops redemptions on 3 funds including a SICAV because of inability to value sub-prime bonds• Rumors in Europe about another German bank failure.• ECP investors sit on sidelines and don’t invest expecting redemptions• The ECB makes money available at low rates but banks take cash and hold it

• Three extendible note market value mortgage securities programs are put on watch for downgrade (KKR Atlantic, KKR Pacific, Ottimo Funding)

• Rams (Aussie mortgage originator) extends notes on two of its programs, Rams Funding Two and Rams Funding Three

August 15th

August 14th August 15th – 17th

August 10th – Fed reminds market discount window is available as a source of funding

August 17th – *Fed board cuts discount rate to 5.75% from 6.25%

• Sentinel Management Group Inc., a private group that manages money for commodity brokers halted redemptions on some of its funds – initially rumored on CNN as a MMF.

August 10th

Source: Federated Investors

5

Aug. – Sept. 2007 ABCP Liquidity Facilities Drawn, SIV’s Downgraded

August 21st

Week of August 27th

• HBOS draws on ABCP liquidity facilities to repay maturing ABCP of Grampian Funding ($37 bn) and announces it will not return to the ABCP market until pricing improves

August 24th

• Certain non-bank sponsored Canadian ABCP programs have difficulty rolling ABCP and attempt to draw on their liquidity facilities • Banks refuse to fund liquidity facilities, claiming the condition to funding found in Canadian liquidity facilities--a “general market disruption”—did not occur• A syndicate of banks agreed to “the Montreal Proposal” to convert $40 bn of Canadian ABCP into longer term floating rate debt and repay ABCP investors

August 21st

• The SIV Cheyne Finance hits an enforcement trigger and enters into liquidation• S&P downgrades Cheyne ABCP to A-2 from A-1+, MTNs to A- from AAA and Mezzanine Notes to B- from A. • On August 29th, Moody’s places Cheyne’s subordinate notes on review for downgrade

August 24th – Fed advises market that bank affiliates’ ABCP may be financed through the discount window

September 5th

• Moody’s takes rating actions on several SIVs and revises its SIV methodology• Moody’s cites the deterioration of market value of certain portfolios and potential impact of crystallized losses following asset sales as the reason for the downgrades

• ANZ decides to finance A$2.5 bn of conduit assets on balance sheet and expects to move an additional A$2.1 bn over the next six weeks

August 28th

Source: Federated Investors

6

Sept. – Oct. 2007 Central Bank Intervention SIV Downgrades

September 18th September 6th

ECB injects $57.7 bn into the market; the Fed followed with three injections to the banking system totaling $31.25 bn in repos

September 12th - ECB injects £75 bn into market

September 18th - Fed eases Fed Funds rate by 50 bps to 4.75% and lowers discount rate by 50 bps

October 15th

• Several US Banks announce they are working on a proposal with the US Treasury called “M-LEC” (Master Liquidity Enhancement Conduit) to provide liquidity relief to SIVs via asset purchases • Details of plan still unclear, as market participants wait for more information to determine effectiveness of proposal

October 17th

• SIV Cheyne Finance’s receiver declares an insolvency of Cheyne, which halts payments and triggers an acceleration of all senior liabilities

• Moody’s downgrades Ottimo Funding’s ABCP to Not Prime

October 18th

• Ottimo begins to liquidate portfolio after failing to reach a resolution with creditors

• Rhinebridge’s manager declares an insolvency of Rhinebridge, which halts payments

October 19th

• Cheyne Finance’s senior notes are downgraded to “Default” by S&P

• Rhinebridge’s senior notes are downgraded to “Default” by S&P and Fitch

October 10th

• Fitch downgrades SIV Axon Financial Funding’s senior notes to F1/A from F1+/AAA

Source: Federated Investors

7

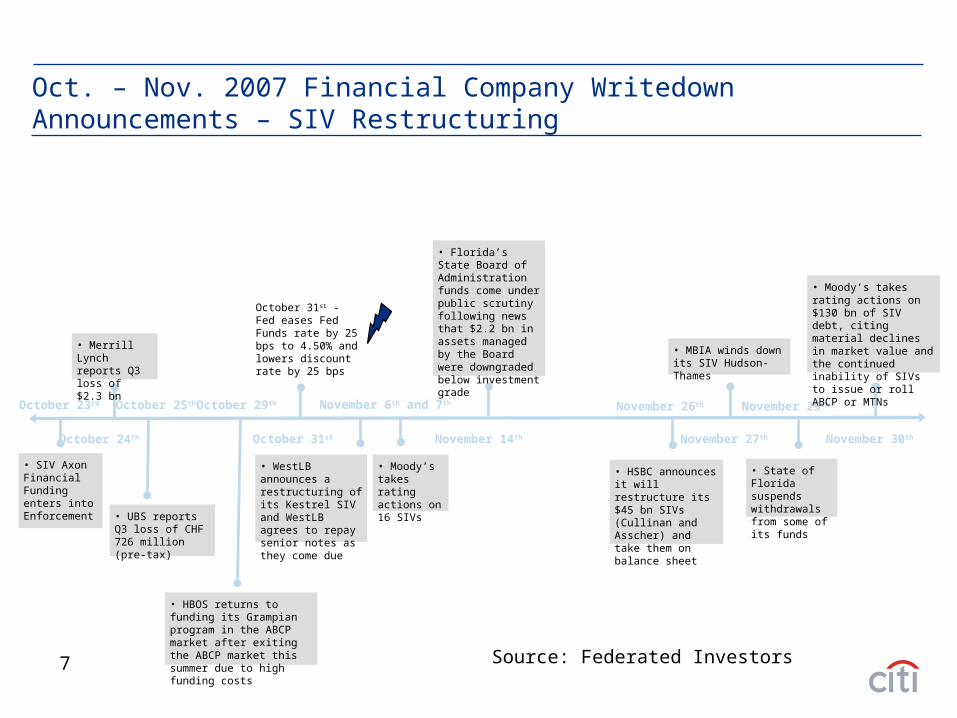

Oct. – Nov. 2007 Financial Company Writedown Announcements – SIV Restructuring

October 29th October 25th

October 31st

October 23rd

• SIV Axon Financial Funding enters into Enforcement

October 31st - Fed eases Fed Funds rate by 25 bps to 4.50% and lowers discount rate by 25 bps

• UBS reports Q3 loss of CHF 726 million (pre-tax)

• HBOS returns to funding its Grampian program in the ABCP market after exiting the ABCP market this summer due to high funding costs

November 6th and 7th

• Moody’s takes rating actions on 16 SIVs

November 14th

• Florida’s State Board of Administration funds come under public scrutiny following news that $2.2 bn in assets managed by the Board were downgraded below investment grade

November 26th

• HSBC announces it will restructure its $45 bn SIVs (Cullinan and Asscher) and take them on balance sheet

November 27th

• MBIA winds down its SIV Hudson-Thames

November 29th

• State of Florida suspends withdrawals from some of its funds

November 30th

• Moody’s takes rating actions on $130 bn of SIV debt, citing material declines in market value and the continued inability of SIVs to issue or roll ABCP or MTNs

• WestLB announces a restructuring of its Kestrel SIV and WestLB agrees to repay senior notes as they come due

October 24th

• Merrill Lynch reports Q3 loss of $2.3 bn

Source: Federated Investors

8

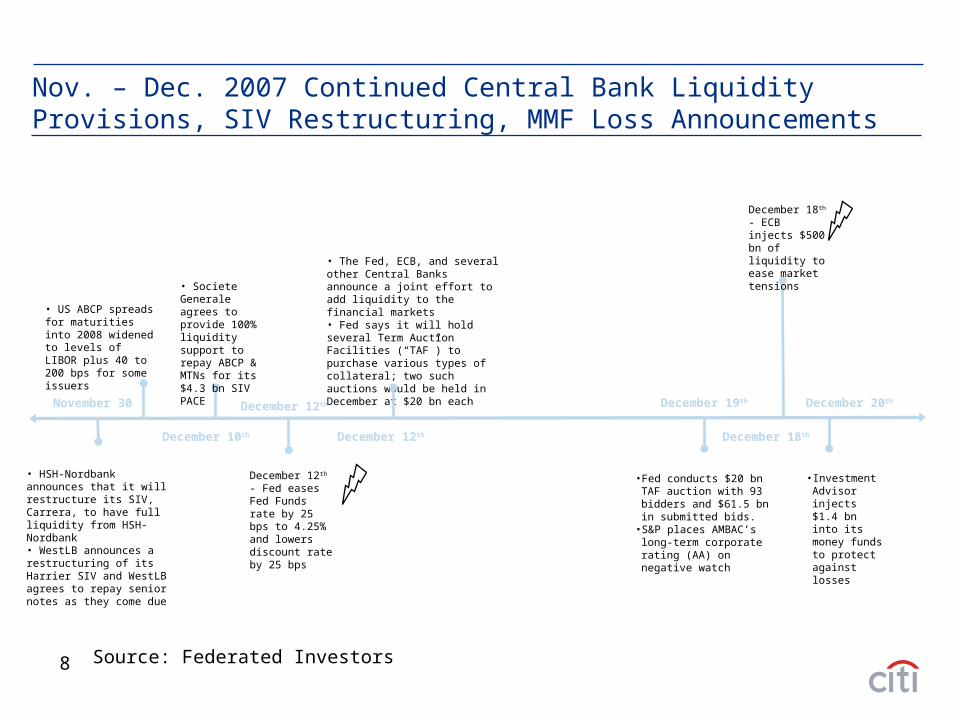

Nov. – Dec. 2007 Continued Central Bank Liquidity Provisions, SIV Restructuring, MMF Loss Announcements

December 10th

November 30

• HSH-Nordbank announces that it will restructure its SIV, Carrera, to have full liquidity from HSH-Nordbank• WestLB announces a restructuring of its Harrier SIV and WestLB agrees to repay senior notes as they come due

December 12th December 19th

• Fed conducts $20 bn TAF auction with 93 bidders and $61.5 bn in submitted bids.

• S&P places AMBAC’s long-term corporate rating (AA) on negative watch

December 12th

• The Fed, ECB, and several other Central Banks announce a joint effort to add liquidity to the financial markets• Fed says it will hold several Term Auction Facilities (“TAF”) to purchase various types of collateral; two such auctions would be held in December at $20 bn each

• Societe Generale agrees to provide 100% liquidity support to repay ABCP & MTNs for its $4.3 bn SIV PACE

December 12th - Fed eases Fed Funds rate by 25 bps to 4.25% and lowers discount rate by 25 bps

December 18th - ECB injects $500 bn of liquidity to ease market tensions

December 20th

• Investment Advisor injects $1.4 bn into its money funds to protect against losses

• US ABCP spreads for maturities into 2008 widened to levels of LIBOR plus 40 to 200 bps for some issuers

December 18th

Source: Federated Investors

9

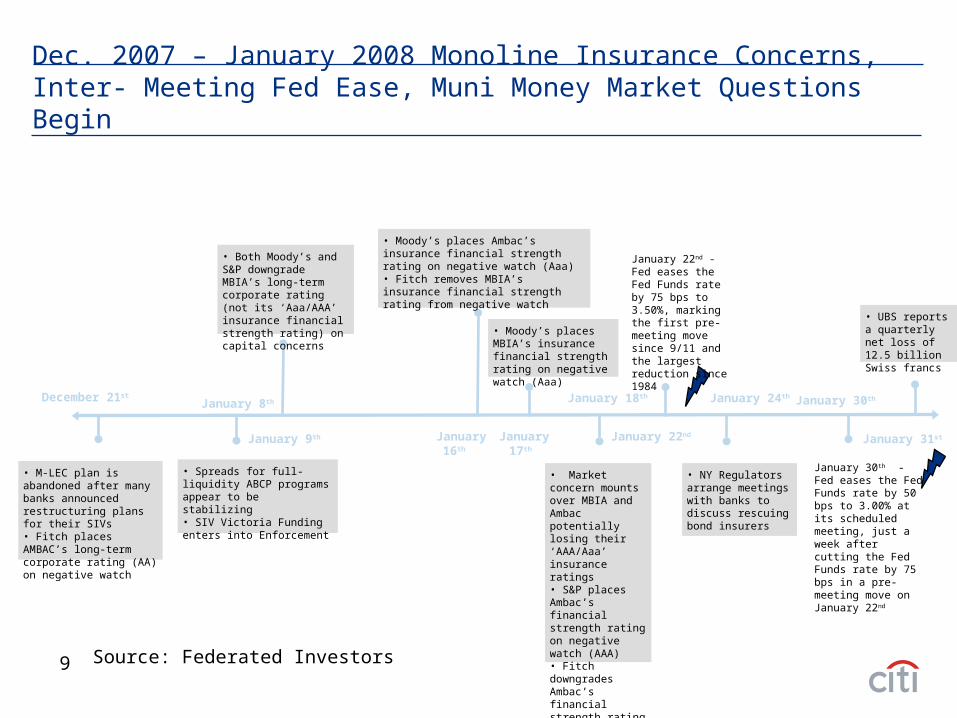

Dec. 2007 – January 2008 Monoline Insurance Concerns, Inter- Meeting Fed Ease, Muni Money Market Questions Begin

December 21st January 8th

• Spreads for full-liquidity ABCP programs appear to be stabilizing • SIV Victoria Funding enters into Enforcement

• M-LEC plan is abandoned after many banks announced restructuring plans for their SIVs• Fitch places AMBAC’s long-term corporate rating (AA) on negative watch

• Both Moody’s and S&P downgrade MBIA’s long-term corporate rating (not its ‘Aaa/AAA’ insurance financial strength rating) on capital concerns

January 9th January 22nd

January 22nd - Fed eases the Fed Funds rate by 75 bps to 3.50%, marking the first pre-meeting move since 9/11 and the largest reduction since 1984

• NY Regulators arrange meetings with banks to discuss rescuing bond insurers

January 24th

• Moody’s places Ambac’s insurance financial strength rating on negative watch (Aaa) • Fitch removes MBIA’s insurance financial strength rating from negative watch

January 16th

• Market concern mounts over MBIA and Ambac potentially losing their ‘AAA/Aaa’ insurance ratings• S&P places Ambac’s financial strength rating on negative watch (AAA)• Fitch downgrades Ambac’s financial strength rating to AA

January 18th

• Moody’s places MBIA’s insurance financial strength rating on negative watch (Aaa)

January 17th

January 30th

January 31st

• UBS reports a quarterly net loss of 12.5 billion Swiss francs

January 30th - Fed eases the Fed Funds rate by 50 bps to 3.00% at its scheduled meeting, just a week after cutting the Fed Funds rate by 75 bps in a pre-meeting move on January 22nd

Source: Federated Investors

10

Feb. 2008 – March 2008 Muni Money Market Questions Continue, Counterparty Risk Becomes a Crisis

Municipal money market funds

exercise puts due

to concerns

over bond

insurer ratings

Fannie Mae posts

a $3.55 billion 4Q

loss; Freddie

Mac posts a $2.5 billion loss.

UBS liquidates $24 billion

in MBS, Carlyle

Group hit with margin

calls

Bear Stearns

forced to borrow

from Fed through

JP Chase

On a Sunday, Fed announces

deal between

Bear and JP Chase; also creation of

Primary Dealer Credit

Facility

Fed announces

Term Securities Lending Facililty;

first auction on Mar 27th

Mar 18th – Fed eases monetary

policy by 75 bps,

bringing the Fed Funds target to

2.25%. The move was less than what was

expected by the market.

Mar 4-6 Mar 11

Mar 14

Rumors of Bear

Stearns liquidity

crisis grip market

Mar 12

Mar 16

Mar 18

Mar 19 – Mar 27

Flight to quality to Treasury

market; yields on Treasury

bills and Treasury repo driven below

1%

OFHEO, Fannie Mae, and Freddie Mac announce major

initiative to increase liquidity to agency MBS market (up to

$200 billion).

FHFBAnnounces new MBS limit for FHLBs

February

Feb 27 & 28

Source: Federated Investors

11

2.25% FF Target75 bp ease Mar 18

4.75% FF Target50 bp ease Sep 18

4.5% FF Target25 bp ease Oct 31

4.25% FF Target25 bp ease Dec 11

3.5% FF Target75 bp intermeeting ease

Jan 22

3% FF Target50 bp ease Jan 30

5.25% FF Target

Mid-August

Fed encourages

discount window

borrowing

Dec 12

Term Auction Facility (TAF)

Mar 7

Expanded TAF

Mar 11

Term Securities Lending Facility

Mar 16

Primary Dealer

Lending Facility

Summary of Major Federal Reserve ActionsAugust 2007 – March 2008

Source: Federated Investors

12

Losses and foreclosures on specific mortgages have caused the housing market to spiral downward, deflating housing prices

Opacity in mortgage instruments caused a crisis in investor confidence

Global economic prospects for 2008 rest partially on the US outlook.

The US economy is likely to either

– Return to moderate growth in the second half of 2008, or

– Remain in slowdown/recession

Citi economists currently anticipate modest growth in US GDP for 2008, with inflation remaining elevated

The US housing contraction is expected to continue through 2008 and possibly 2009

Exports are expected to hold up, due to strong demand from the rest of the world and a weaker US Dollar

An Uncertain Economic Backdrop

Citi Economists currently forecast global growth of 2.9% in 2008, led by the Emerging Markets.

GDP Growth Inflation Current Acct/GDP2007F 2008F 2009F 2007F 2008F 2009F 2007F 2008F 2009F

World 3.9 2.9 2.8 3.1 4.3 3.0 0.3 0.0 (0.2)US 2.2 1.3 1.6 2.9 4.0 2.1 (5.3) (5.3) (4.7)Euro Area 2.6 1.4 1.2 2.1 3.0 1.8 0.2 0.0 (0.1)Emerging Markets 7.2 6.1 5.9 5.3 7.0 5.6 4.5 3.4 2.2

Source: Citi EMA, “Global Economic Outlook & Strategy,” April 24, 2008.

Sub-prime mortgage delinquencies and defaults in the US have led to significant turmoil in credit and equity markets, and are now affecting the broader US economy.

13

$5.00$5.40 $5.25

$4.70

$0.0

$1.0

$2.0

$3.0

$4.0

$5.0

$6.0

2004 2005 2006 2007

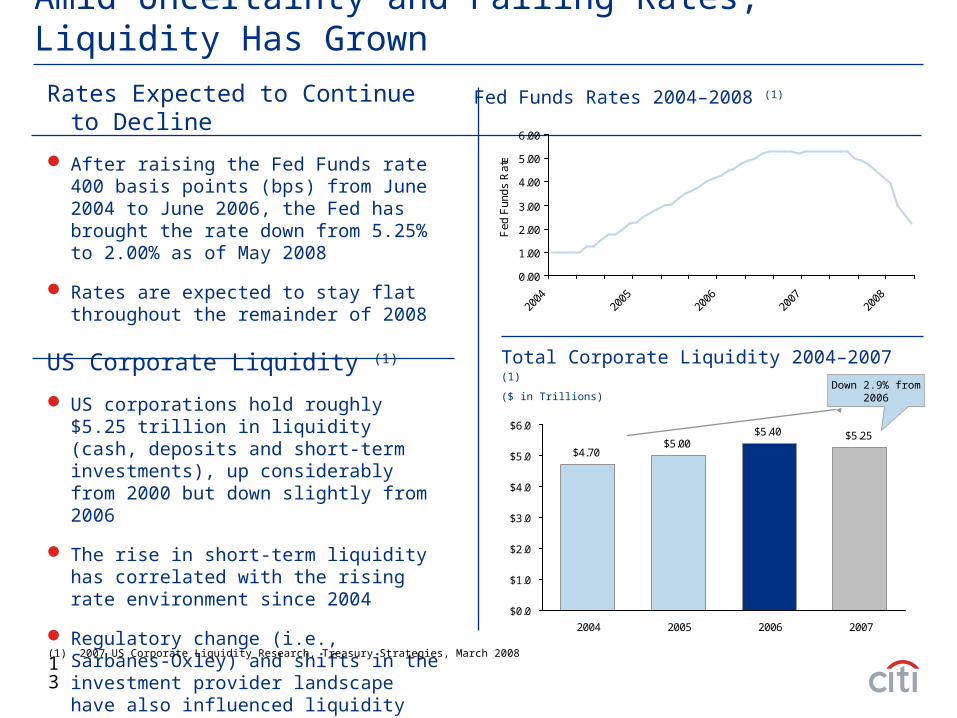

Amid Uncertainty and Falling Rates, Liquidity Has Grown

Rates Expected to Continue to Decline

After raising the Fed Funds rate 400 basis points (bps) from June 2004 to June 2006, the Fed has brought the rate down from 5.25% to 2.00% as of May 2008

Rates are expected to stay flat throughout the remainder of 2008

US Corporate Liquidity (1)

US corporations hold roughly $5.25 trillion in liquidity (cash, deposits and short-term investments), up considerably from 2000 but down slightly from 2006

The rise in short-term liquidity has correlated with the rising rate environment since 2004

Regulatory change (i.e., Sarbanes-Oxley) and shifts in the investment provider landscape have also influenced liquidity management practices

0.00

1.00

2.00

3.00

4.00

5.00

6.00

2004

2005

2006

2007

2008

Fed

Fun

ds R

ate

Fed Funds Rates 2004–2008 (1)

Total Corporate Liquidity 2004–2007 (1)

($ in Trillions) Down 2.9% from

2006

(1) 2007 US Corporate Liquidity Research, Treasury Strategies, March 2008

14

Corporate Investment Practices

15

Types of Cash

.

Four distinct types of corporate cash. Each type has unique characteristics and objectives.

– Operating Cash is the daily transactional buffer of a corporation, for the “payroll to payroll” cycle. Must be 100% convertible into cash at zero risk and immediate liquidity.

– Reserve Cash is the cushion to sustain a corporation through the seasonal / business cycle. There is little need to convert this entire amount to cash on a daily basis.

– Accumulation Cash is cash in excess of operating and reserve balances, set aside for strategic purposes or a major financial event.

– Required Cash represents funds that must be set aside for specific activities, usually with restrictions. This includes escrows, performance deposits, sinking funds, etc.

16

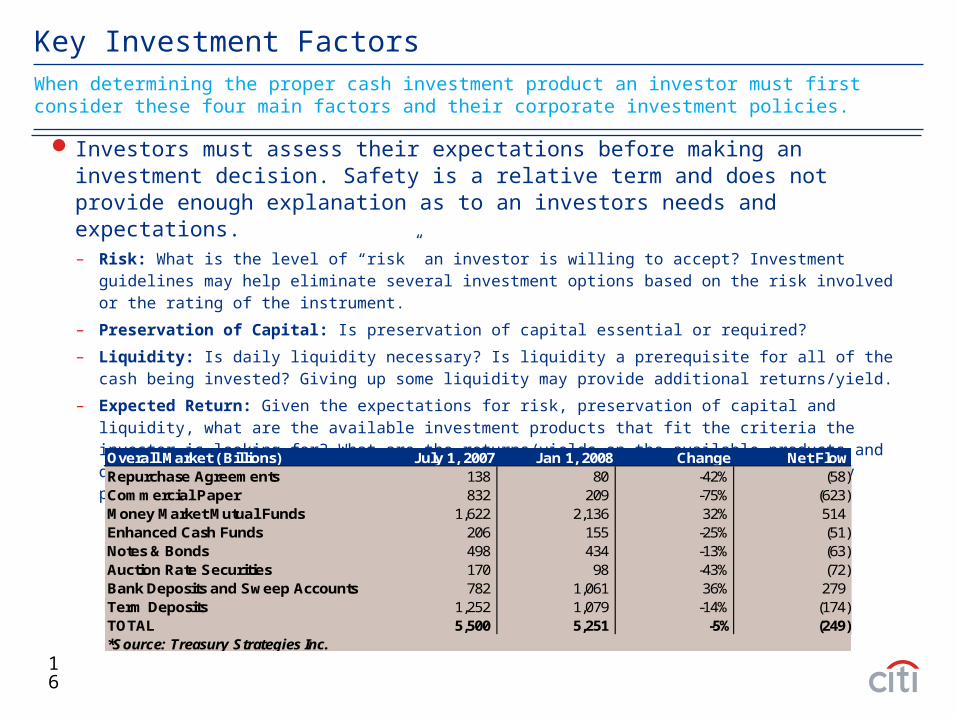

Key Investment Factors

Investors must assess their expectations before making an investment decision. Safety is a relative term and does not provide enough explanation as to an investors needs and expectations.– Risk: What is the level of “risk” an investor is willing to accept? Investment guidelines may help eliminate several

investment options based on the risk involved or the rating of the instrument.

– Preservation of Capital: Is preservation of capital essential or required?

– Liquidity: Is daily liquidity necessary? Is liquidity a prerequisite for all of the cash being invested? Giving up some liquidity may provide additional returns/yield.

– Expected Return: Given the expectations for risk, preservation of capital and liquidity, what are the available investment products that fit the criteria the investor is looking for? What are the returns/yields on the available products and do they provide a return that the investor is expecting? Different products may provide a wide spectrum of returns given the current market turmoil.

When determining the proper cash investment product an investor must first consider these four main factors and their corporate investment policies.

Overall Market ( Billions) July 1, 2007 Jan 1, 2008 Change Net FlowRepurchase Agreements 138 80 -42% (58)Commercial Paper 832 209 -75% (623)Money Market Mutual Funds 1,622 2,136 32% 514Enhanced Cash Funds 206 155 -25% (51)Notes & Bonds 498 434 -13% (63)Auction Rate Securities 170 98 -43% (72)Bank Deposits and Sweep Accounts 782 1,061 36% 279Term Deposits 1,252 1,079 -14% (174)TOTAL 5,500 5,251 -5% (249)*Source: Treasury Strategies Inc.

17

Corporate Liquidity Portfolios – Money Fund Usage

Falling market interest rates – short term “lag effect” & lower opportunity costs of using MMFs vs. direct investments

Greater risk aversion – shift away from direct investments

Downturn in economic cycle – treasuries may seek to remain more liquid in uncertain times

U.S. Domestic Money Funds

Historical & 2008 YTDKey Reasons

MMF assets have increased by $892

billion, or 34.2%, in the past 8 months

Money Fund Assets ($B) & Returns (%)

3,506

3,126

2,057

2,2852,385

1,6131,845

2,272

2,052 1,913 2.75

5.014.77

2.93

1.070.88

1.56

3.984.93

6.18

1,000

1,500

2,000

2,500

3,000

3,500

4,000

99 00 01 02 03 04 05 06 07 08ytd

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

Source: Crane Data, ICI.

Institutional Money Funds assets rose dramatically in H2 2007 and are expected to continue rising in 2008, with corporate investment behavior as one key driver.

18

CP/Repo/CD

27%

Other35%

MM Mut Funds20%

Notes/Bonds18%

CP/Repo/CD

45%

Other32%

Notes/Bonds13%

MM Mut Funds10%

1999Corporate Liquidity

by Instrument

CP/Repo/CD

15%

Other28%

MM Mut Funds36%

Notes/Bonds21%

2004Corporate Liquidity

by Instrument

CP/Repo/CD

24%

Other26%

MM Mut Funds21%

Notes/Bonds29%

CP/Repo/CD

25%

Other25%

MM Mut Funds27%

Notes/Bonds23%

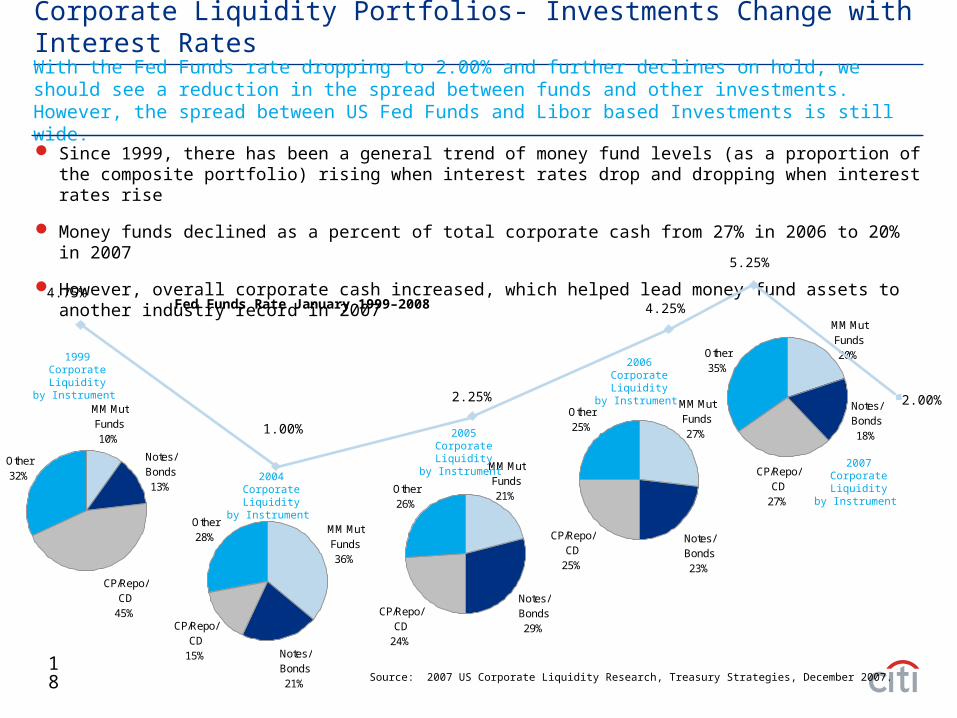

Corporate Liquidity Portfolios- Investments Change with Interest Rates

Since 1999, there has been a general trend of money fund levels (as a proportion of the composite portfolio) rising when interest rates drop and dropping when interest rates rise

Money funds declined as a percent of total corporate cash from 27% in 2006 to 20% in 2007

However, overall corporate cash increased, which helped lead money fund assets to another industry record in 2007

4.75%Fed Funds Rate January 1999–2008 4.25%

1.00%

2.25%

5.25%

Source: 2007 US Corporate Liquidity Research, Treasury Strategies, December 2007.

2005Corporate Liquidity

by Instrument

2006Corporate Liquidity

by Instrument

2007Corporate Liquidity

by Instrument

2.00%

With the Fed Funds rate dropping to 2.00% and further declines on hold, we should see a reduction in the spread between funds and other investments. However, the spread between US Fed Funds and Libor based Investments is still wide.

19

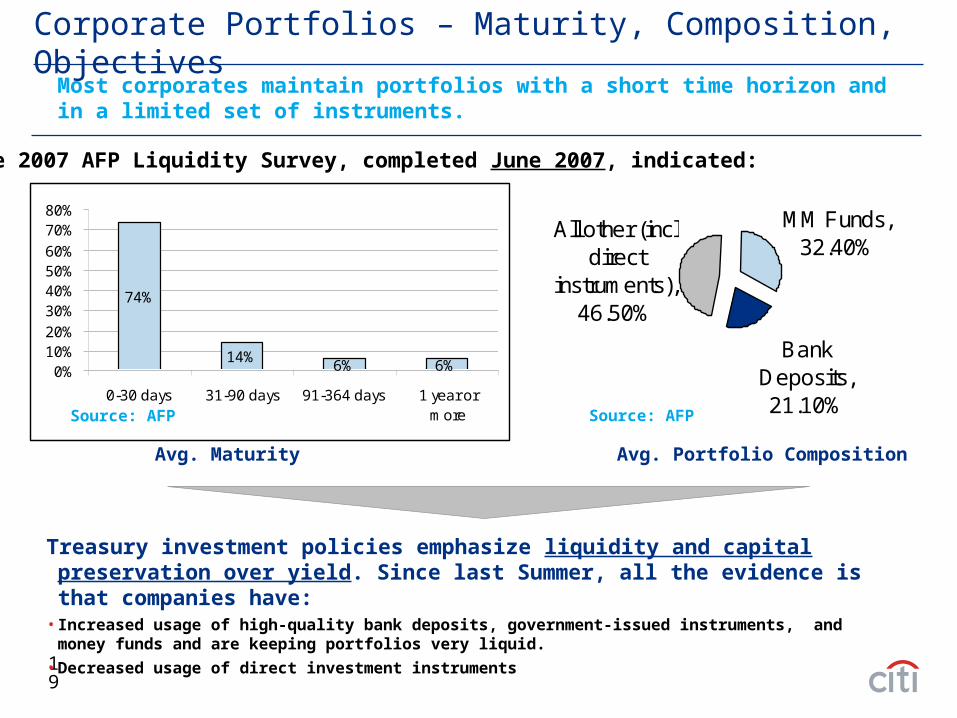

Corporate Portfolios – Maturity, Composition, ObjectivesMost corporates maintain portfolios with a short time horizon and in a limited set of instruments.

74%

14%6% 6%0%

10%20%

30%40%50%60%

70%80%

0-30 days 31-90 days 91-364 days 1 year ormore

Avg. Maturity Avg. Portfolio Composition

Treasury investment policies emphasize liquidity and capital preservation over yield. Since last Summer, all the evidence is that companies have:

• Increased usage of high-quality bank deposits, government-issued instruments, and money funds and are keeping portfolios very liquid.

• Decreased usage of direct investment instruments

The 2007 AFP Liquidity Survey, completed June 2007, indicated:

MM Funds, 32.40%

Bank Deposits, 21.10%

All other (incl direct

instruments), 46.50%

Source: AFP Source: AFP

20

In the drive for greater control and oversight over global portfolios, the need for automation has become more pressing...

Automation – A Pressing Need

Companies realizing that many of time-intensive processes can be automated, releasing greater efficiency and allowing better control

• 28% of respondents to TSI’s 2007 survey said they spend over two hours a day managing their investment portfolio

• Respondents spent the most time on the daily cash positioning process (gathering balance reports, determining dollar amount to invest, and cash forecasting).

• Timely policy compliance checking, portfolio reporting and benchmarking is getting much more focus due to the events in the market

3%

2%

2%

4%

4%

7%

9%

20%

24%

Workstation

30%

45%

42%

44%

42%

18%

14%

31%

85%

Automated*SpreadsheetOnlineE-MailFaxPhone

Benchmark Performance

Confirm Trades

Execute Trades

Compare Investment Yields

Compare Investment Instruments

Determine Desired Maturities

Cash Forecasting

Determine Dollar Amount to Invest

Gather Balance Reports

38%27%3%0%1%

0%43%23%14%25%

40%13%9%45%

15%40%8%4%17%

15%38%6%3%19%

48%11%4%6%3%

76%5%4%0%1%

64%11%6%0%2%

15%61%7%3%2%

3%

2%

2%

4%

4%

7%

9%

20%

24%

Workstation

30%

45%

42%

44%

42%

18%

14%

31%

85%

Automated*SpreadsheetOnlineE-MailFaxPhone

Benchmark Performance

Confirm Trades

Execute Trades

Compare Investment Yields

Compare Investment Instruments

Determine Desired Maturities

Cash Forecasting

Determine Dollar Amount to Invest

Gather Balance Reports

38%27%3%0%1%

0%43%23%14%25%

40%13%9%45%

15%40%8%4%17%

15%38%6%3%19%

48%11%4%6%3%

76%5%4%0%1%

64%11%6%0%2%

15%61%7%3%2%

Tools Utilized for Liquidity Management Processes (% Respondents)

* Online + WorkstationSource: Treasury Strategies

21

Automation – PortalsAs corporations strive for greater control and oversight over global portfolios, the need for automation has become more pressing...creating the opportunity for investment portals

Organizations that use Investment Portals

Do NotUse71%

Use29%

Portal usage is increasing - Just under a third of investors in the U.S. use investment portals. Usage in North America and Europe continues to increase

Helping the inflow to MMFs - Portal users tend to use money funds more heavily. 67% of portal users invest in money funds

Portal Use - Money Market Fund Usage

Over half of port. In MFs

38%

Do not use MFs33%

Under half of port. In MFs

29%

Source: Treasury Strategies

22

Visualization: A Window into Cash

Aggregation

Integration

Analytics

Global banks are racing to provide enterprise-wide visibility across global cash (accounts, debt and investments, cash pools)

Corporates should integrate this visibility with TWS, ERP systems

Banking portals will increasingly incorporate online transaction tools for intercompany treasury-related processes (e.g. CF)

Corporations should demand their bank to provide customizable analytics to further support these decision tools

Information Reporting• Data Aggregation &

Integration Service• Portal Service

Information Reporting• Data Aggregation &

Integration Service• Portal Service

MeasureForecastDecision

SupportAct

23

Access to the portfolio's compliance status

Automatically e-mails compliance violations to specified individuals

Configurable compliance guidelines can be set to meet the needs of individual investment policies

Compliance

Automation-Analytics

Compares the performance of daily portfolio and index total returns

Illustrates the main factors affecting the performance of the portfolio through portfolio-level performance attribution

Assesses multi – manager performance by providing you with a view of each portfolio and its index

Accounting

Performance

Provides assurance that the accounting numbers are accurate, complete, and easily verifiable

Daily, independent accounting information, including a balance sheet, income statement, statement of cash flows, impairment, cash flow forecasting, and more

Reporting on both aggregate and individual portfolios

24

Custodians

ERP/TWS Systems

Clearwater

Decision Analytics

Providers

Automation-Analytics

25

Money Market Funds –

Rule 2a-7 and “AAA” Ratings

26

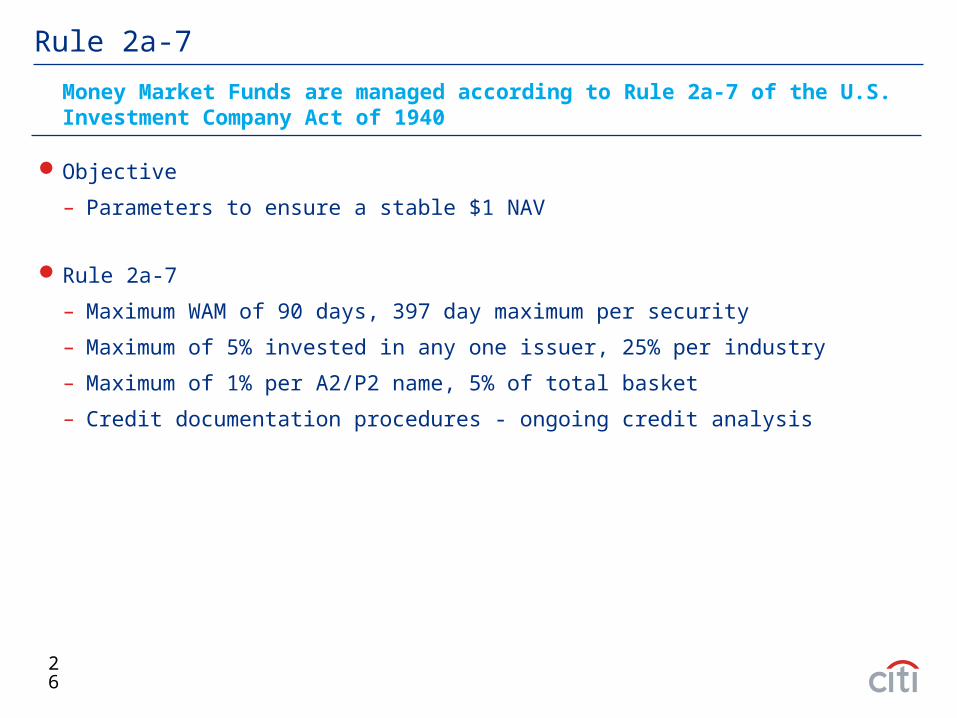

Rule 2a-7

Objective

– Parameters to ensure a stable $1 NAV

Rule 2a-7

– Maximum WAM of 90 days, 397 day maximum per security

– Maximum of 5% invested in any one issuer, 25% per industry

– Maximum of 1% per A2/P2 name, 5% of total basket

– Credit documentation procedures - ongoing credit analysis

Money Market Funds are managed according to Rule 2a-7 of the U.S. Investment Company Act of 1940

27

Rule 2a-7 – A Brief History

28

“AAA” Rated Funds

Funds may be “AAA” rated by:

– Moody’s

– S&P

– Fitch IBCA

Rating agencies impose further investment restrictions and monitoring beyond Rule 2a-7

– WAM: 60 days

– Non-rated funds can buy A2/P2 paper

– Non-rated funds are not monitored on a regular basis by a third party, rated funds are continually reviewed on a weekly basis

A rated fund provides added layers of protection and comprehensive on-going due diligence mandated by the rating agencies

29

Rated * Non-Rated

WAM

Max Fund WAM 60 days 90 days

Max maturity per security 397 days 397 days

Diversification

Max per Security 5% 5%

Max per Industry 25% 25%

Max Illiquid basket allocation 10% 10%

Rating Criteria

Minimum A1+/P1 allocation 50% N/A

Maximum A2/P2 allocation 0% 5%

*Rated funds must also undergo weekly monitoring by each agency that rates the portfolio

“AAA” Rated vs. Non-rated Money Market Funds

30

Summary

Concerns about credit quality and liquidity have forced investors to move cash to “safe”, high quality instruments

Global corporations are increasingly centralizing their global cash and investing processes and oversight

Money market funds have weathered the credit & liquidity storm and remain an attractive cash investment option

Money market funds and high quality bank time deposits are the most common “active” investments, with usage of the former growing especially rapidly

Usage of automation / investment portals is increasingly common, with the fastest growth now occurring internationally

31

Q & A

32

33

Mutual Fund Disclosures

An investment in a money market portfolio is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. Although a money market portfolio seeks to preserve the value of an investment at $1.00 per share, it is possible to lose money by investing in a money market portfolio.

Investors should consider a fund's objectives, risks, and charges and expenses, and read the prospectus carefully before investing or sending money. The prospectus contains this and other information about the Funds.

34

IRS Circular 230 Disclosure: Citigroup Inc. and its affiliates do not provide tax or legal advice. Any discussion of tax matters in these materials (i) is not intended or written to be used, and cannot beused or relied upon, by you for the purpose of avoiding any tax penalties and (ii) may have been written in connection with the "promotion or marketing" of any transaction contemplated hereby("Transaction"). Accordingly, you should seek advice based on your particular circumstances from an independent tax advisor.

Any terms set forth herein are intended for discussionpurposes only and are subject to the final terms as set forth in separate definitive written agreements. This presentation is not a commitment to lend, syndicate afinancing, underwrite or purchase securities,or commit capital nor does it obligate us to enter into such a commitment, nor are we acting as a fiduciary to you. By accepting this presentation, subject to applicable lawor regulation, you agree to keep confidential the existence of and proposed terms for any Transaction.

Prior to entering into any Transaction, you should determine, without reliance upon us or our affiliates, the economic risks and merits (and independently determine that you are able to assume these risks)as well asthe legal, tax and accounting characterizationsand consequencesof any such Transaction. In this regard, by accepting this presentation, you acknowledge that (a) we are not in the business of providing (and you arenot relying on us for) legal, tax or accounting advice, (b) there may be legal, tax or accounting risks associatedwith any Transaction, (c) you should receive (and rely on) separate and qualified legal, tax and accountingadvice and (d) you should apprise senior management in your organization as to such legal, tax and accounting advice (and any risks associated with any Transaction) and our disclaimer as to these matters. Byacceptanceof these materials, you and we hereby agree that from the commencement of discussions with respect to any Transaction, and notwithstanding any other provision in this presentation, we hereby confirmthat no participant in any Transaction shall be limited from disclosing the U.S. tax treatment or U.S. tax structure of such Transaction.

We are required to obtain, verify and record certain information that identifies each entity that enters into a formal business relationship with us. We will ask for your complete name, street address, and taxpayer IDnumber. We may also request corporate formation documents, or other forms of identification, to verify information provided.

Any prices or levels contained herein are preliminary and indicative only and do not represent bids or offers. These indications are provided solely for your information and consideration, are subject to change at anytime without notice and are not intended as a solicitation with respect to the purchaseor sale of any instrument. The information contained in this presentation may include results of analyses from a quantitative modelwhich represent potential future events that may or may not be realized, and is not a complete analysis of every material fact representing any product. Any estimates included herein constitute our judgment as of thedate hereof and are subject to change without any notice. We and/or our affiliates may make a market in these instruments for our customersand for our own account. Accordingly, we may have a position in any suchinstrument at any time.

Although this material may contain publicly available information about Citi corporate bond research, fixed income strategy or economic and market analysis, Citi policy (i) prohibits employees from offering, directly orindirectly, a favorable or negative researchopinion or offering to change an opinion as consideration or inducement for the receipt of business or for compensation; and (ii) prohibits analysts from being compensated forspecific recommendations or views contained in research reports. So as to reduce the potential for conflicts of interest, as well as to reduce any appearance of conflicts of interest, Citi has enacted policies andprocedures designed to limit communications between its investment banking and research personnel to specifically prescribed circumstances.

[TRADEMARK SIGNOFF: add the appropriate signoff for the relevant legal vehicle]

© 2007 Citigroup Global Markets Inc. Member SIPC. All rights reserved. Citi and Citi and Arc Design are trademarks and service marks of Citigroup Inc. or its affiliates and are used and registered throughout the world.

© 2007 Citigroup Global Markets Limited. Authorized and regulated by the Financial Services Authority. All rights reserved. Citi and Citi and Arc Design are trademarks and service marks of Citigroup Inc. or its affiliates and are used and registered throughout the world.

© 2007 Citibank, N.A. All rights reserved. Citi and Citi and Arc Design are trademarks and service marks of Citigroup Inc. or its affiliates and are used and registered throughout the world.

© 2007 Citigroup Inc. All rights reserved. Citi and Citi and Arc Design are trademarks and service marks of Citigroup Inc. or its affiliates and are used and registered throughout the world.

© 2007 [Name of Legal Vehicle] [Name of regulatory body.] All rights reserved. Citi and Citi and Arc Design are trademarks and service marks of Citigroup Inc. or its affiliates and are used and registered throughout the world.

Related Documents