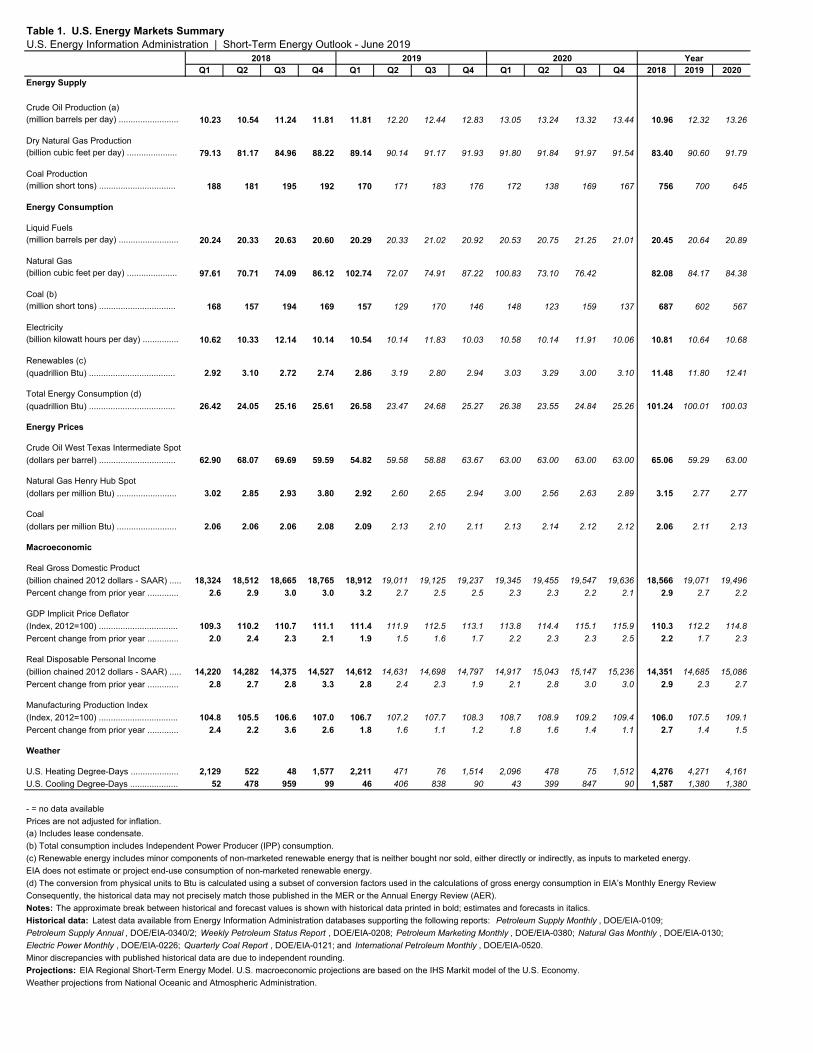

U.S. Energy Information Administration | Short-Term Energy Outlook June 2019 1 June 2019 Short-Term Energy Outlook (STEO) Forecast highlights Global liquid fuels • Brent crude oil spot prices averaged $71 per barrel (b) in May, largely unchanged from April 2019 and almost $6/b lower than the price in May of last year. However, Brent prices fell sharply in recent weeks, reaching $62/b on June 5. EIA forecasts Brent spot prices will average $67/b in 2019, $3/b lower than the forecast in last month’s STEO, and remain at $67/b in 2020. EIA’s lower 2019 Brent price path reflects rising uncertainty about global oil demand growth. • EIA forecasts global oil inventories will decline by 0.3 million barrels per day (b/d) in 2019 and then increase by 0.3 million b/d in 2020. Although global liquid fuels demand outpaces supply in 2019 in EIA’s forecast, global liquid fuels supply is forecast to rise by 2.0 million b/d in 2020, with 1.4 million of that growth coming from the United States. Global oil demand rises by 1.4 million b/d in 2020 in the forecast, up from expected growth of 1.2 million b/d in 2019. • Annual U.S. crude oil production reached a record 11.0 million b/d in 2018. EIA forecasts that U.S. production will increase by 1.4 million b/d in 2019 and by 0.9 million b/d in 2020, with 2020 production averaging 13.3 million b/d. Despite EIA’s expectation for slowing growth, the 2019 forecast would be the second-largest annual growth on record (following 1.6 million b/d in 2018), and the 2020 forecast would be the fifth-largest growth on record. • For the 2019 summer driving season, which runs from April through September, EIA forecasts that U.S. regular gasoline retail prices will average $2.76 per gallon (gal), down from an average of $2.85/gal last summer. The lower forecast gasoline prices primarily reflect EIA’s expectation of lower crude oil prices this summer. Natural gas • The Henry Hub natural gas spot price averaged $2.64/million British thermal units (MMBtu) in May, almost unchanged from April. EIA expects strong growth in U.S. natural gas production to put downward pressure on prices in 2019. EIA expects Henry Hub natural gas spot prices will average $2.77/MMBtu in 2019, down 38 cents/MMBtu from 2018. EIA expects natural gas prices in 2020 will again average $2.77/MMBtu.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

U.S. Energy Information Administration | Short-Term Energy Outlook June 2019 1

June 2019

Short-Term Energy Outlook (STEO)

Forecast highlights

Global liquid fuels

• Brent crude oil spot prices averaged $71 per barrel (b) in May, largely unchanged from April 2019 and almost $6/b lower than the price in May of last year. However, Brent prices fell sharply in recent weeks, reaching $62/b on June 5. EIA forecasts Brent spot prices will average $67/b in 2019, $3/b lower than the forecast in last month’s STEO, and remain at $67/b in 2020. EIA’s lower 2019 Brent price path reflects rising uncertainty about global oil demand growth.

• EIA forecasts global oil inventories will decline by 0.3 million barrels per day (b/d) in 2019 and then increase by 0.3 million b/d in 2020. Although global liquid fuels demand outpaces supply in 2019 in EIA’s forecast, global liquid fuels supply is forecast to rise by 2.0 million b/d in 2020, with 1.4 million of that growth coming from the United States. Global oil demand rises by 1.4 million b/d in 2020 in the forecast, up from expected growth of 1.2 million b/d in 2019.

• Annual U.S. crude oil production reached a record 11.0 million b/d in 2018. EIA forecasts that U.S. production will increase by 1.4 million b/d in 2019 and by 0.9 million b/d in 2020, with 2020 production averaging 13.3 million b/d. Despite EIA’s expectation for slowing growth, the 2019 forecast would be the second-largest annual growth on record (following 1.6 million b/d in 2018), and the 2020 forecast would be the fifth-largest growth on record.

• For the 2019 summer driving season, which runs from April through September, EIA forecasts that U.S. regular gasoline retail prices will average $2.76 per gallon (gal), down from an average of $2.85/gal last summer. The lower forecast gasoline prices primarily reflect EIA’s expectation of lower crude oil prices this summer.

Natural gas

• The Henry Hub natural gas spot price averaged $2.64/million British thermal units (MMBtu) in May, almost unchanged from April. EIA expects strong growth in U.S. natural gas production to put downward pressure on prices in 2019. EIA expects Henry Hub natural gas spot prices will average $2.77/MMBtu in 2019, down 38 cents/MMBtu from 2018. EIA expects natural gas prices in 2020 will again average $2.77/MMBtu.

U.S. Energy Information Administration | Short-Term Energy Outlook June 2019 2

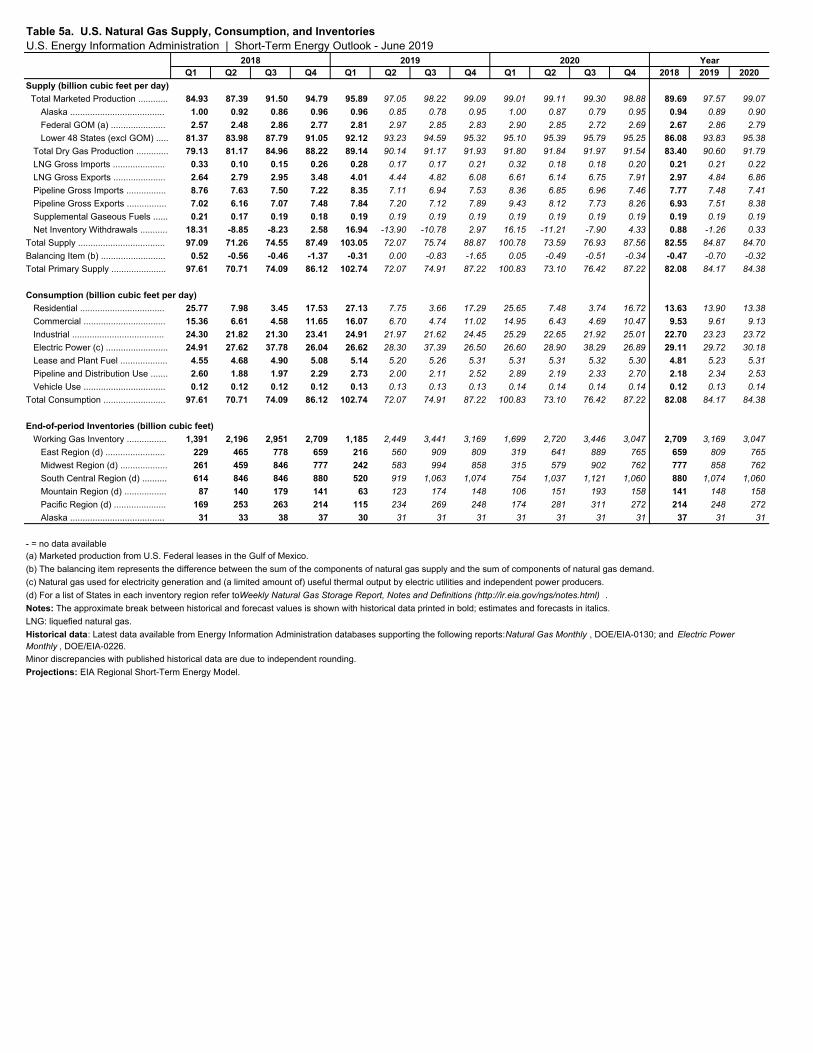

• EIA forecasts that U.S. dry natural gas production will average 90.6 billion cubic feet per day (Bcf/d) in 2019, up 7.2 Bcf/d from 2018. EIA expects natural gas production will continue to grow in 2020, albeit at a slower rate, averaging 91.8 Bcf/d next year.

• U.S. natural gas exports averaged 9.9 Bcf/d in 2018, and EIA forecasts that they will rise by 2.5 Bcf/d in 2019 and by 2.9 Bcf/d in 2020. Rising exports reflect increases in liquefied natural gas exports as new facilities come online. Rising natural gas exports are also the result of an expected increase in pipeline exports to Mexico.

• EIA estimates that natural gas inventories ended March at 1.2 trillion cubic feet (Tcf), 15% lower than levels from a year earlier and 28% lower than the five-year (2014–18) average. EIA forecasts that natural gas storage injections will outpace the previous five-year average during the 2019 April-through-October injection season and that inventories will reach almost 3.8 Tcf at the end of October, which would be 17% higher than October 2018 levels and about equal to the five-year average.

Electricity, coal, renewables, and emissions

• EIA expects the share of U.S. total utility-scale electricity generation from natural gas-fired power plants to rise from 35% in 2018 to 37% in 2019 and to 38% in 2020. EIA forecasts that the share of generation from coal will average 24% in 2019 and 23% in 2020, down from 27% in 2018. The forecast nuclear share of generation falls from 20% in 2019 to 19% in 2020, reflecting the retirement of some nuclear reactors. Hydropower averages a 7% share of total generation in the forecast for 2019 and 2020, similar to 2018. Wind, solar, and other nonhydropower renewables together provided 10% of U.S. generation in 2018. EIA expects they will provide 11% in 2019 and 13% in 2020.

• EIA forecasts that renewable fuels, including wind, solar, and hydropower, will collectively produce 18% of U.S. electricity in 2019 and almost 20% in 2020. EIA expects that annual generation from wind will surpass hydropower generation for the first time in 2019 to become the leading source of renewable electricity generation and maintain that position in 2020.

• EIA forecasts that U.S. coal consumption, which reached a 39-year low of 687 million short tons (MMst) in 2018, will fall to 602 MMst in 2019 and to 567 MMst in 2020. The falling consumption reflects lower demand for coal in the electric power sector.

• After rising by 2.7% in 2018, EIA forecasts that U.S. energy-related carbon dioxide (CO2) emissions will decline by 2.0% in 2019 and by 0.9% in 2020. EIA expects U.S. CO2 emissions will fall in 2019 and in 2020 because its forecast assumes that temperatures will return to near normal, and because the forecast share of electricity generated from natural gas and renewables increases while the forecast share generated from coal, which produces more CO2 emissions, decreases. Energy-related CO2 emissions are sensitive to weather, economic growth, energy prices, and fuel mix.

U.S. Energy Information Administration | Short-Term Energy Outlook June 2019 3

Petroleum and natural gas markets review Crude oil

Prices: The front-month futures price for Brent crude oil settled at $61.67 per barrel (b) on June 6, 2019, a decrease of $10.51/b from May 1. The front-month futures price for West Texas Intermediate (WTI) crude oil for delivery at Cushing, Oklahoma, decreased by $11.01/b during the same period, settling at $52.59/b on June 6 (Figure 1).

Crude oil price volatility increased in May after declining for four consecutive months and stayed at elevated levels into the first week of June. Demand-side concerns became the most salient issue during the past month and contributed to volatility and price declines for risk assets such as commodities and equities. Both China and the United States issued tariffs on each other, with the United States also announcing potential tariffs on Mexico near the end of May. In addition, expected industrial activity, as measured by the manufacturing Purchasing Managers’ Index (PMI), declined across several countries in May, and the U.S. manufacturing PMI fell to its lowest level since 2009. These developments are contributing to concerns that economic growth could be lower than market participants’ expectations, which would cause oil demand growth to also be lower than expected.

Declining crude oil production in Venezuela and Iran, as well as Saudi Arabian over-compliance with December 2018 Vienna agreement production cuts, pushed crude oil production among members of the Organization of the Petroleum Exporting Countries (OPEC) to 29.9 million barrels per day (b/d) in May, the lowest for any month since July 2014. In addition, production shut-ins in Russia related to contamination of the Druzhba crude oil pipeline have emerged, and the market effect of these reductions has been compounded by planned maintenance on crude oil production platforms in the North Sea, where crude oil grades are in many cases substitutable for the disrupted Russian barrels.

U.S. Energy Information Administration | Short-Term Energy Outlook June 2019 4

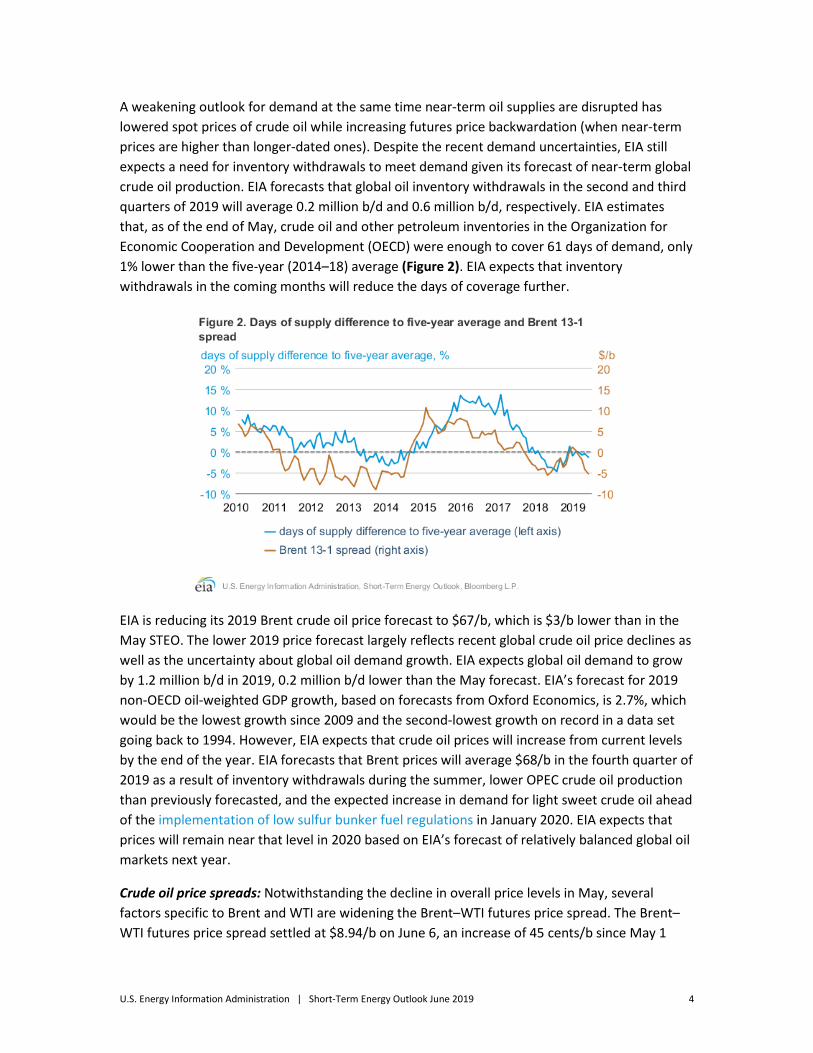

A weakening outlook for demand at the same time near-term oil supplies are disrupted has lowered spot prices of crude oil while increasing futures price backwardation (when near-term prices are higher than longer-dated ones). Despite the recent demand uncertainties, EIA still expects a need for inventory withdrawals to meet demand given its forecast of near-term global crude oil production. EIA forecasts that global oil inventory withdrawals in the second and third quarters of 2019 will average 0.2 million b/d and 0.6 million b/d, respectively. EIA estimates that, as of the end of May, crude oil and other petroleum inventories in the Organization for Economic Cooperation and Development (OECD) were enough to cover 61 days of demand, only 1% lower than the five-year (2014–18) average (Figure 2). EIA expects that inventory withdrawals in the coming months will reduce the days of coverage further.

EIA is reducing its 2019 Brent crude oil price forecast to $67/b, which is $3/b lower than in the May STEO. The lower 2019 price forecast largely reflects recent global crude oil price declines as well as the uncertainty about global oil demand growth. EIA expects global oil demand to grow by 1.2 million b/d in 2019, 0.2 million b/d lower than the May forecast. EIA’s forecast for 2019 non-OECD oil-weighted GDP growth, based on forecasts from Oxford Economics, is 2.7%, which would be the lowest growth since 2009 and the second-lowest growth on record in a data set going back to 1994. However, EIA expects that crude oil prices will increase from current levels by the end of the year. EIA forecasts that Brent prices will average $68/b in the fourth quarter of 2019 as a result of inventory withdrawals during the summer, lower OPEC crude oil production than previously forecasted, and the expected increase in demand for light sweet crude oil ahead of the implementation of low sulfur bunker fuel regulations in January 2020. EIA expects that prices will remain near that level in 2020 based on EIA’s forecast of relatively balanced global oil markets next year.

Crude oil price spreads: Notwithstanding the decline in overall price levels in May, several factors specific to Brent and WTI are widening the Brent–WTI futures price spread. The Brent–WTI futures price spread settled at $8.94/b on June 6, an increase of 45 cents/b since May 1

U.S. Energy Information Administration | Short-Term Energy Outlook June 2019 5

(Figure 3). In late April, flows on parts of the Druzhba pipeline, which supplies Russian Urals crude oil to Europe, were suspended because of contamination of the crude oil. This disruption limited availability of Urals for several refiners in Europe that are regular purchasers of the crude oil grade. By early June, some Druzhba pipeline flows had been restored, but other refineries were still waiting for the contaminated crude oil to be removed from the pipeline so that flows of uncontaminated crude oil could resume. The contaminated crude oil will have to be stored for several months and gradually blended with clean crude oil to dilute the contaminants so the oil can be refined. Certain North Sea crude oil streams can substitute for Urals, which likely contributed to some relative upward price pressure for Brent in May. In addition, planned maintenance at some North Sea fields is expected to reduce available deliveries for June, which may have also put upward price pressure on Brent prices relative to other crude oils.

In contrast, Cushing WTI prices declined more than Brent prices in May because of logistical problems in the U.S. Midwest. Floods in the Midwest contributed to the temporary closure of several pipelines out of Cushing that provide feedstock to certain refiners. This disruption likely contributed to crude oil stocks in Cushing building by 4.8 million barrels from the first week in May to the last week in May, a month in which Cushing stocks typically draw by 2.1 million barrels, based on the five-year average stock change. Outside of the logistical issues in Cushing, U.S. commercial crude oil inventories increased in May. Total U.S. crude oil inventories increased by 15.7 million barrels in May, according to STEO estimates for the month, compared with a five-year average draw of 2.1 million barrels. If confirmed in monthly data, this year’s stock build would be the largest for the month of May since 1991.

Emerging market currencies: Some of the demand-side concerns affecting crude oil markets could also be reducing the value of emerging market currencies compared with the U.S. dollar. The Morgan Stanley Capital International (MSCI) Emerging Market Currency Index tracks a basket of emerging market currencies that declined 1% from May 1 through June 6 (Figure 4). A lower value of the index indicates emerging market currencies are depreciating against the U.S.

U.S. Energy Information Administration | Short-Term Energy Outlook June 2019 6

dollar. The recent decline in the MSCI Emerging Market Currency index could indicate a reduction in economic activity in countries such as China or South Korea, countries with relatively high weightings in the index. The Chinese manufacturing PMI for May declined to 49.4. Any reading lower than 50 indicates a contraction in manufacturing activity. In addition, total South Korean exports of all goods declined 9.4% from May 2018 to May 2019, the sixth consecutive month of year-over-year declines.

Petroleum products

Gasoline prices: The front-month futures price of reformulated blendstock for oxygenate blending (RBOB, the petroleum component of gasoline used in many parts of the country) settled at $1.71 per gallon (gal) on June 6, down 36 cents/gal since May 1 (Figure 5). The RBOB–Brent crack spread (the difference between the price of RBOB and the price of Brent crude oil) declined by 11 cents/gal to settle at 24 cents/gal during the same period.

After increasing in April, the gasoline crack spread again dropped lower than the five-year (2014–18) range in May, averaging 4 cents below the previous five-year low of 35 cents for that month in 2018. Factors contributing to the smaller crack spread could include gasoline stock builds and gasoline consumption that were lower than year-ago levels. EIA estimates that U.S. gasoline consumption averaged 9.39 million barrels per day (b/d) in May, a decrease of 0.16 million b/d from the same period last year. Gasoline stocks increased during the month, ending close to the five-year average after ending April 6% lower than year-ago levels.

Flooding in the Midwest reduced refinery operations in Oklahoma and limited crude oil and product deliveries to the region’s refineries, preventing crude and product movement from the Gulf Coast to the Midwest and contributing to regional disparities in U.S. gasoline stock levels. In addition, refinery issues on the West Coast normalized mid-month, contributing to a stock build in that area. EIA estimates gasoline stocks ended May 4% higher than the five-year average on

U.S. Energy Information Administration | Short-Term Energy Outlook June 2019 7

the Gulf Coast and 6% higher than the five-year average on the West Coast, while gasoline stocks in the Midwest were 7% lower than the five-year average.

Gasoline spot price differentials: In contrast to the United States, gasoline prices increased in Northwest Europe in May (Figure 6). Refinery shutdowns in the region, combined with the contamination of crude oil import pipelines from Russia, contributed to reduced refinery runs and gasoline production in Europe. Northwest Europe’s gasoline–Brent spot crack spread rose higher than the five-year low for the first time in 6 months and higher than the five-year average for the first time in 17 months. On May 20, these factors contributed to the lowest Gulf Coast gasoline spot price relative to Northwest Europe since November 2015. On May 31, they contributed to the lowest New York Harbor gasoline spot price relative to Northwest Europe since August 2011.

U.S. Energy Information Administration | Short-Term Energy Outlook June 2019 8

Ultra-low sulfur diesel prices: The ultra-low sulfur diesel (ULSD) front-month futures price decreased 31 cents/gal from May 1 to settle at $1.79/gal on June 6. The ULSD–Brent crack spread (the difference between the price of ULSD and the price of Brent crude oil) declined 6 cents/gal to settle at 32 cents/gal during the same period (Figure 7).

EIA estimates that U.S. distillate consumption in May was 3.9 million b/d, 380,000 b/d lower than in May 2018 and 40,000 b/d lower than the five-year average. However, some of the available transportation data are mixed. The truck tonnage data from the American Trucking Association for April (most recent available) show a 7.7% year-over-year increase, whereas the April 2019 Cass Freight Index report—reflecting the volume of freight shipments via all modes of domestic freight transportation, including rail, truck, and air—shows a 3.2% contraction for the month. Despite these and other economic indicators reflecting a potential slowdown in growth, EIA estimates distillate consumption will return to year-over-year growth through the third quarter of 2019. EIA’s forecast is based on the expectation of a 2.7% growth in U.S. GDP in 2019, indicating future growth in overall diesel demand.

U.S. Gulf Coast refinery margins: The recent increase in medium and heavy crude oil prices that peaked in November 2018 reversed somewhat in March, April, and the first half of May 2019, before increasing again in late May. Reductions in crude oil production from Venezuela are likely increasing the price of medium and heavy crude oils compared with light crude oils. The 5:3:2 crack spread—refining three barrels of gasoline and two barrels of distillate from five barrels of Mars crude oil, which exemplifies a complex U.S. Gulf Coast refinery margin—averaged $13.94 per barrel (b) in May, after reaching a 2019 high of $16.95/b (40 cents/gal) on April 10 (Figure 8). Comparatively stable distillate crack spreads have supported total refinery margins. Although U.S. Gulf Coast gasoline crack spreads have remained positive since February, weaker crack spreads in May put downward pressure on margins from the April highs.

U.S. Energy Information Administration | Short-Term Energy Outlook June 2019 9

Natural Gas

Prices: The front-month natural gas futures contract for delivery at the Henry Hub settled at $2.32/million British thermal units (MMBtu) on June 6, a decrease of 30 cents/MMBtu from May 1 (Figure 9). EIA estimates that U.S. natural gas production reached another record high in May. This persistent production growth contributed to injections of more than 100 billion cubic feet (Bcf) for five of the past six weeks, bringing U.S. working gas in underground storage levels closer to the five-year (2014–18) average, 9% higher than year-ago levels. Combined net injections into storage during April and May, in 2019, are estimated to be the largest on record for that two-month period at 831 Bcf (Figure 10), which helped to reduce futures prices even though inventories remain lower than the five-year average.

U.S. Energy Information Administration | Short-Term Energy Outlook June 2019 10

Money manager positions: The number of futures short positions money managers reported holding for NYMEX natural gas contracts rose above long positions on May 21, 2019, for the first time since December 26, 2017 (Figure 11). The money manager category of the Commitments of Traders report, published weekly by the Commodity Futures Trading Commission, include fund managers that conduct organized futures trading on behalf of clients, and they are not involved in physical oil trading as their business activity. A short position indicates expectations of lower prices while a long position indicates the opposite. On November 13, 2018, money managers’ net long positions reached a record high. Natural gas prices increased sharply in mid-November after colder-than-normal weather reduced natural gas inventories to about 700 Bcf lower than the five-year average. In April and May 2019, however, ongoing increases in natural gas production contributed to record injections into natural gas storage, which, combined with forecasts of below-normal temperatures for June, have lowered price expectations. The natural gas front-month futures price on June 6 of $2.32/MMBtu was the lowest since May 2016.

U.S. Energy Information Administration | Short-Term Energy Outlook June 2019 11

Notable forecast changes

• EIA forecasts Brent crude oil prices will average $67 per barrel (b) in 2019, down about $3/b from last month’s STEO forecast. The lower 2019 price forecast largely reflects recent price declines in global crude oil prices, which lowered the starting point for EIA’s forecast, and uncertainty about global oil demand growth. Forecast global liquid fuels supply and consumption were both lowered by about 0.2-0.3 million barrels per day (b/d) for 2019 and for 2020. The lower global supply growth forecast is mostly the result of lower crude oil production growth in the United States because of lower expected oil prices and an expectation of increasing crude oil production declines in Venezuela. The reduction in global demand growth reflects both a revision to historical data that carries through to the forecast and lower oil consumption growth in 2019 because of reduction in forecast 2019 oil-weighted GDP growth among countries not part of the Organization for Economic Cooperation and Development (OECD).

• For more information, see the detailed table of STEO forecast changes

• For ore information, see the detailed STEO table of forecast changes.

This report was prepared by the U.S. Energy Information Administration (EIA), the statistical and analytical agency within the U.S. Department of Energy. By law, EIA's data, analyses, and forecasts are independent of approval by any other officer or employee of the United States Government. The views in this report therefore should not be construed as representing those of the U.S. Department of Energy or other federal agencies.

Chart Gallery y for June e 2019

Shortr -rt-Term Energy Outlook

U.S. Energy Information Administration Independent Statistics & Analysis

0

20

40

60

80

100

120

2014 2015 2016 2017 2018 2019 2020

Sources: Short-Term Energy Outlook, June 2019, and CME Group

Note: Confidence interval derived from options market information for the five trading days ending Jun 6, 2019. Intervals not calculated for months with sparse trading in near -the-money options contracts.

West TexasIntermediate (WTI) spot price

95% NYMEX futures priceconfidence intervalupper bound

STEO forecastNYMEX futures price

95% NYMEX futures priceconfidence interval

West Texas Intermediate (WTI) crude oil price and NYMEX confidence intervalsdollars per barrel

0.27

0.31

-0.09

0.11

-0.50-0.40-0.30-0.20-0.100.000.100.200.300.400.50

2017 2018 2019 2020

Components of annual gasoline price changesdollars per gallon

Brent crude oil pricewholesale margin over crude

retail margin over wholesale

forecast

0.000.501.001.502.002.503.003.504.004.505.00

2016 2017 2018 2019 2020

monthly retail regular gasolineannual average gasolinemonthly Brent crude oilannual average Brent

U.S. gasoline and crude oil prices

dollars per gallon

forecast

Source: Short-Term Energy Outlook, June 2019

0.27

0.31

-0.09

0.11

-0.50

-0.40

-0.30

-0.20

-0.10

0.00

0.10

0.20

0.30

0.40

0.50

2017 2018 2019 2020

Components of annual gasoline price changesdollars per gallon

Brent crude oil pricewholesale margin over crude

retail margin over wholesale

net change

forecast

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

5.00

2016 2017 2018 2019 2020

monthly retail regular gasolineannual average gasolinemonthly Brent crude oilannual average Brent

U.S. gasoline and crude oil prices

dollars per gallon

forecast

Source: Short-Term Energy Outlook, June 2019

20

0.34

0.53

-0.08

0.18

-0.60

-0.40

-0.20

0.00

0.20

0.40

0.60

2017 2018 2019 2020

Components of annual dieselprices changesdollars per gallon

Brent crude oil pricewholesale marginover crude

retail marginover wholesale

net change

forecast

0.00

1.00

2.00

3.00

4.00

5.00

6.00

2016 2017 2018 2019 2020

monthly retail dieselannual average dieselmonthly Brent crude oilBrent annual average

U.S. diesel and crude oil prices

forecast

Source: Short-Term Energy Outlook, June 2019

0.34

0.53

-0.08

0.18

-0.60

-0.40

-0.20

0.00

0.20

0.40

0.60

2017 2018 2019 2020

Components of annual dieselprices changesdollars per gallon

Brent crude oil pricewholesale marginover crude

retail marginover wholesale

net change

forecast

0.00

1.00

2.00

3.00

4.00

5.00

6.00

2016 2017 2018 2019 2020

monthly retail dieselannual average dieselmonthly Brent crude oilBrent annual average

U.S. diesel and crude oil prices

dollars per gallon

forecast

Source: Short-Term Energy Outlook, June 2019

0123456789

2014 2015 2016 2017 2018 2019 2020

Henry Hub natural gas price and NYMEX confidence intervalsdollars per million Btu

Sources: Short-Term Energy Outlook, June 2019, and CME Group

Note: Confidence interval derived from options market information for the five trading days ending Jun 6, 2019. Intervals not calculated for months with sparse trading in near-the-money options contracts.

95% NYMEX futures priceconfidence intervalupper bound

STEO forecastNYMEX futures price

95% NYMEX futures priceconfidence intervallower bound

Henry Hub spot price

0

2

4

6

8

10

12

14

16

18

20

2015 2016 2017 2018 2019 2020

monthly residential priceannual average residentialmonthly Henry Hub spot priceHenry Hub annual average

U.S. natural gas pricesdollars per thousand cubic feet

forecast

Sources: Short-Term Energy Outlook, June 2019, and Refinitiv

-74

222

-173

39

-300

-200

-100

0

100

200

300

400

500

600

2017 2018 2019 2020

Components of annual changemillion kilowatthours per day

residential salesindustrial salescommercial and transportation salesdirect usenet change

forecast

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

2016 2017 2018 2019 2020

monthly history

monthly forecast

annual average

U.S. electricity consumptionmillion kilowatthours per day

Source: Short-Term Energy Outlook, June 2019

-74

222

-173

39

-300

-200

-100

0

100

200

300

400

500

600

2017 2018 2019 2020

Components of annual changemillion kilowatthours per day

residential salesindustrial salescommercial and transportation salesdirect usenet change

forecast

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

2016 2017 2018 2019 2020

monthly history

monthly forecast

annual average

U.S. electricity consumptionmillion kilowatthours per day

Source: Short-Term Energy Outlook, June 2019

0.85

0.40 0.26

0.66

forecast

-0.20

0.00

0.20

0.40

0.60

0.80

1.00

1.20

2017 2018 2019 2020

Components of annual changequadrillion British thermal units

net changesolar windhydropowerliquid biofuelsgeothermalwood biomasswaste biomass

forecast

0

2

4

6

8

10

12

14

2016 2017 2018 2019 2020

U.S. renewable energy supplyquadrillion British thermal units

Note: Hydropower excludes pumped storage generation. Liquid biofuels include ethanol and biodiesel. Other biomass includes municipal waste from biogenic sources, landfill gas, and other

Source: Short-Term Energy Outlook, June 2019

0.85

0.40 0.26

0.66

forecast

-0.20

0.00

0.20

0.40

0.60

0.80

1.00

1.20

2017 2018 2019 2020

Components of annual changequadrillion British thermal units

net changesolar windhydropowerliquid biofuelsgeothermalwood biomasswaste biomass

forecast

0

2

4

6

8

10

12

14

2016 2017 2018 2019 2020

U.S. renewable energy supplyquadrillion British thermal units

Note: Hydropower excludes pumped storage generation. Liquid biofuels include ethanol and biodiesel. Other biomass includes municipal waste from biogenic sources, landfill gas, and other non-wood waste.Source: Short-Term Energy Outlook, June 2019

-42

137

-104

-47

forecast

-200

-150

-100

-50

0

50

100

150

200

2017 2018 2019 2020

Components of annual changemillion metric tons

natural gaspetroleumcoalnet change

forecast

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

2016 2017 2018 2019 2020

total energy

petroleum

natural gas

U.S. annual carbon emissions by sourcemillion metric tons

Source: Short-Term Energy Outlook, June 2019

-42

137

-104

-47

forecast

-200

-150

-100

-50

0

50

100

150

200

2017 2018 2019 2020

Components of annual changemillion metric tons

natural gaspetroleumcoalnet change

forecast

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

2016 2017 2018 2019 2020

total energy

petroleum

natural gas

coal

U.S. annual carbon emissions by sourcemillion metric tons

Source: Short-Term Energy Outlook, June 2019

forecast

86889092949698

100102104106

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2014 2015 2016 2017 2018 2019 2020

World liquid fuels production and consumption balancemillion barrels per day

world production

world consumption

//0

-2-1012

Source: Short-Term Energy Outlook, June 2019

implied stock build

implied stock draw

forecast

86889092949698

100102104106

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2014 2015 2016 2017 2018 2019 2020

World liquid fuels production and consumption balancemillion barrels per day

world production

world consumption

//0

-2-1012

Source: Short-Term Energy Outlook, June 2019

implied stock build

implied stock draw

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Jan 2017 Jan 2018 Jan 2019

Estimated unplanned liquid fuels production outages million barrels per day

Source: Short-Term Energy Outlook, June 2019

non-OPECotherUnited StatesCanada

OPECVenezuelaSaudi ArabiaIranKuwaitIraqNigeriaLibya

1.61.4

1.21.4

0.0

0.5

1.0

1.5

2.0

2.5

3.0

2017 2018 2019 2020

Components of annual changemillion barrels per day

world changeOrganization of Economic Cooperation and Development (OECD)non-OECD

forecast

80

85

90

95

100

105

110

2017 2018 2019 2020

monthly historymonthly forecastannual average

World liquid fuels consumption million barrels per day

//0

Source: Short-Term Energy Outlook, June 2019

1.61.4

1.21.4

0.0

0.5

1.0

1.5

2.0

2.5

3.0

2017 2018 2019 2020

Components of annual changemillion barrels per day

world changeOrganization of Economic Cooperation and Development (OECD)non-OECD

forecast

80

85

90

95

100

105

110

2017 2018 2019 2020

monthly historymonthly forecastannual average

World liquid fuels consumption million barrels per day

//0

Source: Short-Term Energy Outlook, June 2019

1.6 1.4

1.21.4

-0.5

0.0

0.5

1.0

1.5

2.0

2017 2018 2019 2020

Annual change in world liquid fuels consumption million barrels per day

Source: Short-Term Energy Outlook, June 2019

forecast

worldother non-OECDMiddle EastIndiaChinaother OECDUnited States

0.6

2.5

0.2

2.0

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

2017 2018 2019 2020

Components of annual change million barrels per day

forecastOPEC countriesnon-OPEC

EurasiaNorth AmericaLatin Americaother non-OPEC

net change

60

70

80

90

100

110

120

130

140

2017 2018 2019 2020

monthly history

monthly forecast

annual average

World crude oil and liquid fuels production million barrels per day

//0

Source: Short-Term Energy Outlook, June 2019

0.6

2.5

0.2

2.0

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

2017 2018 2019 2020

Components of annual change million barrels per day

forecastOPEC countriesnon-OPEC

EurasiaNorth AmericaLatin Americaother non-OPEC

net change

60

70

80

90

100

110

120

130

140

2017 2018 2019 2020

monthly history

monthly forecast

annual average

World crude oil and liquid fuels production million barrels per day

//0

Source: Short-Term Energy Outlook, June 2019

0

20

40

60

80

100

120

2017 2018 2019 2020

World liquid fuels consumption million barrels per day

non-OECD

Organization for Economic Cooperation

forecast

0

20

40

60

80

100

120

2017 2018 2019 2020

World liquid fuels production million barrels per day

non-OPEC

Organization of the Petroleum Exporting

forecast

Source: Short-Term Energy Outlook, June 2019

forecast

0

20

40

60

80

100

120

2017 2018 2019 2020

World liquid fuels consumption million barrels per day

non-OECD

Organization for Economic Cooperationand Development (OECD)

forecast

0

20

40

60

80

100

120

2017 2018 2019 2020

World liquid fuels production million barrels per day

non-OPEC

Organization of the Petroleum ExportingCountries (OPEC)

forecast

Source: Short-Term Energy Outlook, June 2019

forecast

0.00.51.01.52.02.53.03.54.04.55.0

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Source: Short-Term Energy Outlook, June 2019

Note: Black line represents 2009-2018 average (2.3 million barrels per day).

forecast

2009-2018 average

Organization of the Petroleum Exporting Countries (OPEC) surplus crude oil production capacitymillion barrels per day

forecast

40

45

50

55

60

65

70

75

80

Jan 2014 Jan 2015 Jan 2016 Jan 2017 Jan 2018 Jan 2019 Jan 2020

Source: Short-Term Energy Outlook, June 2019

Organization for Economic Cooperation and Development (OECD)commercial inventories of crude oil and other liquidsdays of supply

monthly range from January 2014 - December 2018//

0

0.52

1.611.36

0.94

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

2017 2018 2019 2020

Components of annual changemillion barrels per day

Federal Gulf of Mexico (GOM)

Lower 48 excluding GOMAlaska

forecast

0

2

4

6

8

10

12

14

16

2017 2018 2019 2020

monthly history

monthly forecast

annual average

U.S. crude oil production million barrels per day

Source: Short-Term Energy Outlook, June 2019

0.52

1.611.36

0.94

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

2017 2018 2019 2020

Components of annual changemillion barrels per day

Federal Gulf of Mexico (GOM)

Lower 48 excluding GOMAlaskanet change

forecast

0

2

4

6

8

10

12

14

16

2017 2018 2019 2020

monthly history

monthly forecast

annual average

U.S. crude oil production million barrels per day

Source: Short-Term Energy Outlook, June 2019

20

forecast

275300325350375400425450475500525550575600

Jan 2014 Jan 2015 Jan 2016 Jan 2017 Jan 2018 Jan 2019 Jan 2020

Source: Short-Term Energy Outlook, June 2019

U.S. commercial crude oil inventoriesmillion barrels

//

monthly range from January 2014 - December 2018

0.8

2.22.0

1.3

0.0

1.0

2.0

3.0

4.0

5.0

2017 2018 2019 2020

Components of annual changemillion barrels per day

ethanol and biodieselnatural gas plant liquidscrude oilnet change

forecast

0

5

10

15

20

25

2017 2018 2019 2020

total monthly production

forecast

annual average

U.S. crude oil and liquid fuels productionmillion barrels per day

Source: Short-Term Energy Outlook, June 2019

0.8

2.22.0

1.3

0.0

1.0

2.0

3.0

4.0

5.0

2017 2018 2019 2020

Components of annual changemillion barrels per day

ethanol and biodieselnatural gas plant liquidscrude oilnet change

forecast

0

5

10

15

20

25

2017 2018 2019 2020

total monthly production

forecast

annual average

U.S. crude oil and liquid fuels productionmillion barrels per day

Source: Short-Term Energy Outlook, June 2019

0.3

0.5

0.2 0.2

-0.25

0.00

0.25

0.50

0.75

1.00

2017 2018 2019 2020

Components of annual change

motor gasolinedistillate fueljet fuelhydrocarbon gas liquidsother fuelsnet change

forecast

0

5

10

15

20

25

2017 2018 2019 2020

monthly history

monthly forecast

annual average

U.S. liquid fuels product supplied(consumption) million barrels per day

Source: Short-Term Energy Outlook, June 2019

0.3

0.5

0.2 0.2

-0.25

0.00

0.25

0.50

0.75

1.00

2017 2018 2019 2020

Components of annual change

million barrels per day

motor gasolinedistillate fueljet fuelhydrocarbon gas liquidsother fuelsnet change

forecast

0

5

10

15

20

25

2017 2018 2019 2020

monthly history

monthly forecast

annual average

U.S. liquid fuels product supplied(consumption) million barrels per day

Source: Short-Term Energy Outlook, June 2019

020

forecast

6080

100120140160180200220240260280

Jan 2014 Jan 2015 Jan 2016 Jan 2017 Jan 2018 Jan 2019 Jan 2020

U.S. gasoline and distillate inventoriesmillion barrels

Source: Short-Term Energy Outlook, June 2019

monthly range from January 2014 - December 2018

total motor gasoline inventory

total distillate fuel inventory

forecast

-8

-6

-4

-2

0

2

4

6

8

10

Jan 2013 Jan 2014 Jan 2015 Jan 2016 Jan 2017 Jan 2018 Jan 2019 Jan 2020

Note: Liquids fuels include: gasoline, distillate fuels, hydrocarbon gas liquids, jet fuel, residual fuel oil, unfinished oils, other hydrocarbons/oxygenates, and other oils.Source: Short-Term Energy Outlook, June 2019

U.S. net imports of crude oil and liquid fuelsmillion barrels per day

crude oil net imports

totalnet imports

liquid fuelsnet imports

0.3

0.60.6

0.4

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

2017 2018 2019 2020

Components of annual changemillion barrels per day

net changenatural gasolinebutanespropaneethane

forecast

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

2017 2018 2019 2020

monthly production

monthly forecast

annual average

U.S. natural gas plant liquids productionmillion barrels per day

Source: Short-Term Energy Outlook, June 2019

0.3

0.60.6

0.4

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

2017 2018 2019 2020

Components of annual changemillion barrels per day

net changenatural gasolinebutanespropaneethane

forecast

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

2017 2018 2019 2020

monthly production

monthly forecast

annual average

U.S. natural gas plant liquids productionmillion barrels per day

Source: Short-Term Energy Outlook, June 2019

20

0.11

0.340.23

0.14

-0.25

0.00

0.25

0.50

2017 2018 2019 2020

Components of annual change

million barrels per day

net changenatural gasolineethanepropanebutanes

forecast

0

1

2

3

4

5

2017 2018 2019 2020

monthly history

monthly forecast

annual average

U.S. hydrocarbon gas liquids product supplied (consumption)million barrels per day

Source: Short-Term Energy Outlook, June 2019

0.11

0.340.23

0.14

-0.25

0.00

0.25

0.50

2017 2018 2019 2020

Components of annual change

million barrels per day

net changenatural gasolineethanepropanebutanes

forecast

0

1

2

3

4

5

2017 2018 2019 2020

monthly history

monthly forecast

annual average

U.S. hydrocarbon gas liquids product supplied (consumption)million barrels per day

Source: Short-Term Energy Outlook, June 2019

-2.5

-2.0

-1.5

-1.0

-0.5

0.0

0.5

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

U.S. net trade of hydrocarbon gas liquids (HGL) million barrels per day

net tradepropaneethanenatural gasolinebutanes

forecast

Source: Short-Term Energy Outlook, June 2019

net importsnet exports

forecast

0

25

50

75

100

125

Jan 2014 Jan 2015 Jan 2016 Jan 2017 Jan 2018 Jan 2019 Jan 2020

monthly range from January 2014 - December 2018

Source: Short-Term Energy Outlook, June 2019

U.S. commercial propane inventoriesmillion barrels

2.4

9.7

7.9

1.5

-4

0

4

8

12

16

2017 2018 2019 2020

Components of annual changebillion cubic feet per day

U.S. non-Gulf of Mexico U.S. Gulf of Mexiconet change

forecast

0

25

50

75

100

125

2017 2018 2019 2020

monthly history

monthly forecast

annual average

U.S. marketed natural gas production billion cubic feet per day

Source: Short-Term Energy Outlook, June 2019

2.4

9.7

7.9

1.5

-4

0

4

8

12

16

2017 2018 2019 2020

Components of annual changebillion cubic feet per day

U.S. non-Gulf of Mexico U.S. Gulf of Mexiconet change

forecast

0

25

50

75

100

125

2017 2018 2019 2020

monthly history

monthly forecast

annual average

U.S. marketed natural gas production billion cubic feet per day

Source: Short-Term Energy Outlook, June 2019

-0.7

7.8

2.10.2

-9.0

-7.0

-5.0

-3.0

-1.0

1.0

3.0

5.0

7.0

9.0

2017 2018 2019 2020

Components of annual changebillion cubic feet per day

net changeindustrialelectric powerresidential and commercialother

forecast

0

20

40

60

80

100

120

140

160

180

2017 2018 2019 2020

monthly historymonthly forecastannual average

U.S. natural gas consumption billion cubic feet per day

Source: Short-Term Energy Outlook, June 2019

-0.7

7.8

2.10.2

-9.0

-7.0

-5.0

-3.0

-1.0

1.0

3.0

5.0

7.0

9.0

2017 2018 2019 2020

Components of annual changebillion cubic feet per day

net changeindustrialelectric powerresidential and commercialother

forecast

0

20

40

60

80

100

120

140

160

180

2017 2018 2019 2020

monthly historymonthly forecastannual average

U.S. natural gas consumption billion cubic feet per day

Source: Short-Term Energy Outlook, June 2019

20

forecast

-50

-25

0

25

50 net storage builds

Source: Short-Term Energy Outlook, June 2019

forecast

-25

0

25

50

75

100

125

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2014 2015 2016 2017 2018 2019 2020

U.S. natural gas production, consumption, and net importsbillion cubic feet per day

consumption

production

net trade (imports minus exports)

forecast

-50

-25

0

25

50 net storage builds

net storage withdrawals

Source: Short-Term Energy Outlook, June 2019

forecast

-25

0

25

50

75

100

125

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2014 2015 2016 2017 2018 2019 2020

U.S. natural gas production, consumption, and net importsbillion cubic feet per day

consumption

production

net trade (imports minus exports)

1.8

-0.3 -1.9

-4.7-7.6

-20

-15

-10

-5

0

5

10

2016 2017 2018 2019 2020

Annual natural gas tradebillion cubic feet per day

gross importsas liquefiednatural gasby pipeline

net trade

gross exportsby pipelineas liquefied natural gas

forecast

Source: Short-Term Energy Outlook, June 2019

forecast

-50%-25%

0%25%50%

Source: Short-Term Energy Outlook, June 2019

Percent deviation from 2014 - 2018 average

0

1,000

2,000

3,000

4,000

5,000

Jan 2014 Jan 2015 Jan 2016 Jan 2017 Jan 2018 Jan 2019 Jan 2020

U.S. working natural gas in storagebillion cubic feet

storage level forecast

monthly range from January 2014 - December 2018

forecast

-50%-25%

0%25%50%

Source: Short-Term Energy Outlook, June 2019

Percent deviation from 2014 - 2018 average

0

1,000

2,000

3,000

4,000

5,000

Jan 2014 Jan 2015 Jan 2016 Jan 2017 Jan 2018 Jan 2019 Jan 2020

U.S. working natural gas in storagebillion cubic feet

storage level forecast

monthly range from January 2014 - December 2018

2.1%

3.2%

1.1%

-0.8%

2.7%

0.0%

1.3% 1.2%

-2%

0%

2%

4%

6%

2013 2014 2015 2016 2017 2018 2019 2020

Annual growth in residential electricity pricespercent

forecast

0

5

10

15

20

2013 2014 2015 2016 2017 2018 2019 2020

U.S. monthly residential electricity pricecents per kilowatthour

historyforecast

Source: Short-Term Energy Outlook, June 2019

2.1%

3.2%

1.1%

-0.8%

2.7%

0.0%

1.3% 1.2%

-2%

0%

2%

4%

6%

2013 2014 2015 2016 2017 2018 2019 2020

Annual growth in residential electricity pricespercent

forecast

0

5

10

15

20

2013 2014 2015 2016 2017 2018 2019 2020

U.S. monthly residential electricity pricecents per kilowatthour

historyforecast

Source: Short-Term Energy Outlook, June 2019

0%

20%

40%

60%

80%

100%

2013 2014 2015 2016 2017 2018 2019 2020

percent share

forecast

28% 28% 33% 34% 32% 35% 37% 38%

39% 39% 33% 30% 30%27% 24% 23%

0.0

2.5

5.0

7.5

10.0

12.5

20132014201520162017201820192020

U.S. electricity generation by fuel, all sectorsmillion megawatthours per day

forecast

coal

natural gas

nuclearnon-hydro renewableshydropowerother

Note: Labels show percentage share of total generation provided by coal and natural gas.Source: Short-Term Energy Outlook, June 2019

0%

20%

40%

60%

80%

100%percent share

forecast

28% 28% 33% 34% 32% 35% 37% 38%

39% 39% 33% 30% 30%27% 24% 23%

0.0

2.5

5.0

7.5

10.0

12.5

U.S. electricity generation by fuel, all sectorsmillion megawatthours per day

forecast

coal

natural gas

nuclearnon-hydro renewableshydropowerother

Note: Labels show percentage share of total generation provided by coal and natural gas.Source: Short-Term Energy Outlook, June 2019

46

-19

-56 -54

-80

-60

-40

-20

0

20

40

60

2017 2018 2019 2020

Components of annual changemillion short tons

Western region

Appalachian region

Interior regionnet change

forecast

0

15

30

45

60

75

90

2016 2017 2018 2019 2020

monthly history

monthly forecast

annual average

U.S. coal production million short tons

Source: Short-Term Energy Outlook, June 2019

46

-19

-56 -54

-80

-60

-40

-20

0

20

40

60

2017 2018 2019 2020

Components of annual changemillion short tons

Western region

Appalachian region

Interior regionnet change

forecast

0

15

30

45

60

75

90

2016 2017 2018 2019 2020

monthly history

monthly forecast

annual average

U.S. coal production million short tons

Source: Short-Term Energy Outlook, June 2019

-14

-30

-86

-35

-100

-80

-60

-40

-20

0

20

2017 2018 2019 2020

Components of annual changemillion short tons

electric powerretail and other industrycoke plantsnet change

forecast

0

20

40

60

80

100

120

2016 2017 2018 2019 2020

monthly historymonthly forecastannual average

U.S. coal consumption million short tons

Source: Short-Term Energy Outlook, June 2019

-14

-30

-86

-35

-100

-80

-60

-40

-20

0

20

2017 2018 2019 2020

Components of annual changemillion short tons

electric powerretail and other industrycoke plantsnet change

forecast

0

20

40

60

80

100

120

2016 2017 2018 2019 2020

monthly historymonthly forecastannual average

U.S. coal consumption million short tons

Source: Short-Term Energy Outlook, June 2019

forecast

0255075

100125150175200225250

Jan 2014 Jan 2015 Jan 2016 Jan 2017 Jan 2018 Jan 2019 Jan 2020

Source: Short-Term Energy Outlook, February 2019

U.S. electric power coal inventoriesmillion short tons

monthly range from January 2014 - December 2018

0%

2%

4%

6%

8%

10%

12%

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

U.S. annual energy expendituresshare of gross domestic product

Source: Short-Term Energy Outlook, June 2019

forecast

0

200

400

600

800

1,000

1,200

1,400

1,600

total summer0

50

100

150

200

250

300

350

400

April May June July August September

U.S. summer cooling degree dayspopulation-weighted

20172018201920202009-2018 average

warmer

cooler

Note: EIA calculations based on National Oceanic and Atmospheric Administration (NOAA) data. Projections reflect NOAA's 14-16 month outlook.Source: Short-Term Energy Outlook, June 2019

0

200

400

600

800

1,000

1,200

1,400

1,600

totalsummer

0

50

100

150

200

250

300

350

400

April May June July August September

U.S. summer cooling degree dayspopulation-weighted

20172018201920202009-2018 average

warmer

cooler

Note: EIA calculations based on National Oceanic and Atmospheric Administration (NOAA) data. Projections reflect NOAA's 14-16 month outlook.Source: Short-Term Energy Outlook, June 2019

0

1,000

2,000

3,000

4,000

total winter0

250

500

750

1,000

October November December January February March

2016/172017/182018/192019/202008-2018 average

U.S. winter heating degree dayspopulation-weighted

cooler

warmer

Note: EIA calculations based on National Oceanic and Atmospheric Administration (NOAA)

Source: Short-Term Energy Outlook, June 2019

0

1,000

2,000

3,000

4,000

total winter0

250

500

750

1,000

October November December January February March

2016/172017/182018/192019/202008-2018 average

U.S. winter heating degree dayspopulation-weighted

cooler

warmer

Note: EIA calculations based on National Oceanic and Atmospheric Administration (NOAA) data. Projections reflect NOAA's 14-16 month outlook.

Source: Short-Term Energy Outlook, June 2019

CA

NV

OR

WA

AZ

OK

KS

NE

SD

MN

IA

MO

IL

WI

MI

OHIN

KY

TN

ND

UT

ID

CO

WY

MT

NM

AR

AL

LA

MS

TX

FL

GA

SC

NC

VAWV

PA NJ

DEMD

NY

NH

ME

VT

MACT RI

AK

HI

NortheastWest

South

Midwest

East SouthCentraldivision

West SouthCentraldivision

PacificContiguous

division

Mountaindivision

West North Centraldivision

East North Centraldivision

SouthAtlanticdivision

PacificNoncontiguous

division

MiddleAtlanticdivision

NewEnglanddivision

U.S. Census regions and divisions

Source: U.S. Energy Information Administration, Short-Term Energy Outlook

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 2018 2019 2020

Energy Supply

Crude Oil Production (a)(million barrels per day) ......................... 10.23 10.54 11.24 11.81 11.81 12.20 12.44 12.83 13.05 13.24 13.32 13.44 10.96 12.32 13.26

Dry Natural Gas Production(billion cubic feet per day) ..................... 79.13 81.17 84.96 88.22 89.14 90.14 91.17 91.93 91.80 91.84 91.97 91.54 83.40 90.60 91.79

Coal Production(million short tons) ................................ 188 181 195 192 170 171 183 176 172 138 169 167 756 700 645

Energy Consumption

Liquid Fuels(million barrels per day) ......................... 20.24 20.33 20.63 20.60 20.29 20.33 21.02 20.92 20.53 20.75 21.25 21.01 20.45 20.64 20.89

Natural Gas(billion cubic feet per day) ..................... 97.61 70.71 74.09 86.12 102.74 72.07 74.91 87.22 100.83 73.10 76.42 82.08 84.17 84.38

Coal (b)(million short tons) ................................ 168 157 194 169 157 129 170 146 148 123 159 137 687 602 567

Electricity(billion kilowatt hours per day) ............... 10.62 10.33 12.14 10.14 10.54 10.14 11.83 10.03 10.58 10.14 11.91 10.06 10.81 10.64 10.68

Renewables (c)

(quadrillion Btu) .................................... 2.92 3.10 2.72 2.74 2.86 3.19 2.80 2.94 3.03 3.29 3.00 3.10 11.48 11.80 12.41

Total Energy Consumption (d)

(quadrillion Btu) .................................... 26.42 24.05 25.16 25.61 26.58 23.47 24.68 25.27 26.38 23.55 24.84 25.26 101.24 100.01 100.03

Energy Prices

Crude Oil West Texas Intermediate Spot

(dollars per barrel) ................................ 62.90 68.07 69.69 59.59 54.82 59.58 58.88 63.67 63.00 63.00 63.00 63.00 65.06 59.29 63.00

Natural Gas Henry Hub Spot

(dollars per million Btu) ......................... 3.02 2.85 2.93 3.80 2.92 2.60 2.65 2.94 3.00 2.56 2.63 2.89 3.15 2.77 2.77

Coal

(dollars per million Btu) ......................... 2.06 2.06 2.06 2.08 2.09 2.13 2.10 2.11 2.13 2.14 2.12 2.12 2.06 2.11 2.13

Macroeconomic

Real Gross Domestic Product

(billion chained 2012 dollars - SAAR) ..... 18,324 18,512 18,665 18,765 18,912 19,011 19,125 19,237 19,345 19,455 19,547 19,636 18,566 19,071 19,496

Percent change from prior year ............. 2.6 2.9 3.0 3.0 3.2 2.7 2.5 2.5 2.3 2.3 2.2 2.1 2.9 2.7 2.2

GDP Implicit Price Deflator

(Index, 2012=100) ................................. 109.3 110.2 110.7 111.1 111.4 111.9 112.5 113.1 113.8 114.4 115.1 115.9 110.3 112.2 114.8

Percent change from prior year ............. 2.0 2.4 2.3 2.1 1.9 1.5 1.6 1.7 2.2 2.3 2.3 2.5 2.2 1.7 2.3

Real Disposable Personal Income

(billion chained 2012 dollars - SAAR) ..... 14,220 14,282 14,375 14,527 14,612 14,631 14,698 14,797 14,917 15,043 15,147 15,236 14,351 14,685 15,086

Percent change from prior year ............. 2.8 2.7 2.8 3.3 2.8 2.4 2.3 1.9 2.1 2.8 3.0 3.0 2.9 2.3 2.7

Manufacturing Production Index

(Index, 2012=100) ................................. 104.8 105.5 106.6 107.0 106.7 107.2 107.7 108.3 108.7 108.9 109.2 109.4 106.0 107.5 109.1

Percent change from prior year ............. 2.4 2.2 3.6 2.6 1.8 1.6 1.1 1.2 1.8 1.6 1.4 1.1 2.7 1.4 1.5

Weather

U.S. Heating Degree-Days .................... 2,129 522 48 1,577 2,211 471 76 1,514 2,096 478 75 1,512 4,276 4,271 4,161

U.S. Cooling Degree-Days .................... 52 478 959 99 46 406 838 90 43 399 847 90 1,587 1,380 1,380

EIA does not estimate or project end-use consumption of non-marketed renewable energy.

Table 1. U.S. Energy Markets Summary U.S. Energy Information Administration | Short-Term Energy Outlook - June 2019

2018 2019 2020 Year

- = no data available

Prices are not adjusted for inflation.

(a) Includes lease condensate.

(b) Total consumption includes Independent Power Producer (IPP) consumption.

(c) Renewable energy includes minor components of non-marketed renewable energy that is neither bought nor sold, either directly or indirectly, as inputs to marketed energy.

Minor discrepancies with published historical data are due to independent rounding.

Projections: EIA Regional Short-Term Energy Model. U.S. macroeconomic projections are based on the IHS Markit model of the U.S. Economy.

Weather projections from National Oceanic and Atmospheric Administration.

(d) The conversion from physical units to Btu is calculated using a subset of conversion factors used in the calculations of gross energy consumption in EIA’s Monthly Energy Review

Consequently, the historical data may not precisely match those published in the MER or the Annual Energy Review (AER).

Notes: The approximate break between historical and forecast values is shown with historical data printed in bold; estimates and forecasts in italics.

Historical data: Latest data available from Energy Information Administration databases supporting the following reports: Petroleum Supply Monthly , DOE/EIA-0109;

Petroleum Supply Annual , DOE/EIA-0340/2; Weekly Petroleum Status Report , DOE/EIA-0208; Petroleum Marketing Monthly , DOE/EIA-0380; Natural Gas Monthly , DOE/EIA-0130;

Electric Power Monthly , DOE/EIA-0226; Quarterly Coal Report , DOE/EIA-0121; and International Petroleum Monthly , DOE/EIA-0520.

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 2018 2019 2020Crude Oil (dollars per barrel)

West Texas Intermediate Spot Average .............................. 62.90 68.07 69.69 59.59 54.82 59.58 58.88 63.67 63.00 63.00 63.00 63.00 65.06 59.29 63.00

Brent Spot Average ............................................................. 66.84 74.53 75.02 68.29 63.14 68.84 66.94 67.67 67.00 67.00 67.00 67.00 71.19 66.69 67.00

U.S. Imported Average ........................................................ 58.08 64.67 66.20 55.33 54.25 59.19 56.89 59.37 57.56 57.56 57.56 57.56 61.35 57.44 57.56

U.S. Refiner Average Acquisition Cost ............................... 61.89 67.29 69.03 59.39 55.71 57.83 57.29 61.48 60.36 60.36 60.36 60.36 64.45 58.12 60.36U.S. Liquid Fuels (cents per gallon)

Refiner Prices for Resale

Gasoline ........................................................................... 186 213 213 178 167 203 197 185 194 206 202 187 198 188 197

Diesel Fuel ....................................................................... 199 219 222 212 192 204 210 218 221 228 227 227 213 206 226

Heating Oil ....................................................................... 193 205 214 201 189 194 201 210 217 217 218 219 200 199 217

Refiner Prices to End Users

Jet Fuel ............................................................................ 197 217 220 212 193 201 207 215 219 224 223 222 212 204 222

No. 6 Residual Fuel Oil (a) ............................................... 149 162 176 175 153 146 139 138 113 116 118 117 166 143 116

Retail Prices Including Taxes

Gasoline Regular Grade (b) ............................................. 258 285 284 262 236 280 273 264 267 283 281 267 273 264 275

Gasoline All Grades (b) .................................................... 270 294 292 271 245 288 284 276 279 295 294 279 282 274 287

On-highway Diesel Fuel ................................................... 302 320 324 327 302 310 309 321 323 329 329 331 318 311 328

Heating Oil ....................................................................... 287 298 325 316 300 305 294 305 315 307 307 315 301 302 313Natural Gas

Henry Hub Spot (dollars per thousand cubic feet) .............. 3.13 2.96 3.04 3.94 3.02 2.69 2.74 3.05 3.11 2.66 2.72 3.00 3.27 2.88 2.87

Henry Hub Spot (dollars per million Btu) ............................ 3.02 2.85 2.93 3.80 2.92 2.60 2.65 2.94 3.00 2.56 2.63 2.89 3.15 2.77 2.77 U.S. Retail Prices (dollars per thousand cubic feet)

Industrial Sector ............................................................... 4.44 3.83 3.73 4.71 4.68 3.74 3.61 4.15 4.54 3.66 3.60 4.10 4.20 4.06 4.00

Commercial Sector .......................................................... 7.64 8.08 8.77 7.61 7.62 8.00 8.35 7.68 7.68 8.09 8.42 7.68 7.82 7.78 7.83

Residential Sector ............................................................ 9.37 11.93 17.93 9.97 9.46 11.80 16.39 10.61 9.82 12.24 16.71 10.70 10.49 10.60 10.92

U.S. Electricity Power Generation Fuel Costs (dollars per million Btu)

Coal .................................................................................. 2.06 2.06 2.06 2.08 2.09 2.13 2.10 2.11 2.13 2.14 2.12 2.12 2.06 2.11 2.13

Natural Gas ..................................................................... 3.96 3.09 3.23 4.05 3.70 2.77 2.71 3.28 3.48 2.71 2.66 3.21 3.54 3.07 2.98

Residual Fuel Oil (c) ......................................................... 11.47 13.02 14.02 14.49 11.93 13.79 12.91 12.73 12.98 13.72 13.02 12.79 12.95 12.82 13.10

Distillate Fuel Oil .............................................................. 15.77 16.61 16.82 16.01 14.92 15.87 16.05 16.88 17.13 17.58 17.49 17.57 16.13 15.94 17.42 Retail Prices (cents per kilowatthour)

Industrial Sector ............................................................... 6.81 6.87 7.22 6.82 6.66 6.88 7.20 6.78 6.70 6.93 7.26 6.83 6.93 6.89 6.94

Commercial Sector .......................................................... 10.54 10.60 10.89 10.55 10.41 10.71 10.97 10.59 10.42 10.74 11.02 10.67 10.66 10.68 10.73

Residential Sector ............................................................ 12.59 13.03 13.15 12.75 12.66 13.29 13.35 12.93 12.75 13.49 13.50 13.12 12.89 13.06 13.22

(c) Includes fuel oils No. 4, No. 5, No. 6, and topped crude.

Table 2. Energy PricesU.S. Energy Information Administration | Short-Term Energy Outlook - June 2019

2018 2019 2020 Year

- = no data available

Prices are not adjusted for inflation.

(a) Average for all sulfur contents.

(b) Average self-service cash price.

Projections: EIA Regional Short-Term Energy Model.

Notes: The approximate break between historical and forecast values is shown with historical data printed in bold; estimates and forecasts in italics.

Prices exclude taxes unless otherwise noted.

Historical data: Latest data available from Energy Information Administration databases supporting the following reports: Petroleum Marketing Monthly , DOE/EIA-0380;

Weekly Petroleum Status Report , DOE/EIA-0208; Natural Gas Monthly , DOE/EIA-0130; Electric Power Monthly , DOE/EIA-0226; and Monthly Energy Review , DOE/EIA-0035.

WTI and Brent crude oils, and Henry Hub natural gas spot prices from Reuter's News Service (http://www.reuters.com).

Minor discrepancies with published historical data are due to independent rounding.

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 2018 2019 2020

Supply (million barrels per day) (a)

OECD ................................................. 29.13 29.31 30.46 31.20 30.61 31.21 31.85 32.75 33.13 33.49 33.66 34.18 30.03 31.61 33.62

U.S. (50 States) .............................. 16.77 17.39 18.40 18.96 18.91 19.63 20.06 20.70 20.87 21.22 21.40 21.61 17.89 19.83 21.28

Canada ........................................... 5.32 5.10 5.33 5.42 5.01 4.86 5.17 5.21 5.36 5.36 5.40 5.46 5.30 5.06 5.40

Mexico ............................................. 2.17 2.13 2.09 1.95 1.92 2.08 2.06 2.03 2.01 1.99 1.97 1.95 2.08 2.02 1.98

Other OECD ................................... 4.88 4.68 4.64 4.86 4.77 4.64 4.57 4.80 4.89 4.92 4.88 5.17 4.76 4.69 4.96

Non-OECD ......................................... 70.14 70.47 70.96 70.95 69.20 69.05 69.45 69.27 68.29 69.43 69.82 69.28 70.63 69.24 69.21

OPEC .............................................. 37.46 37.07 37.34 37.29 35.86 35.17 35.19 35.10 34.66 34.74 34.89 34.65 37.29 35.33 34.73

Crude Oil Portion ......................... 32.10 31.78 32.02 31.94 30.47 29.89 30.19 30.08 29.66 29.72 29.87 29.60 31.96 30.15 29.71

Other Liquids (b) .......................... 5.36 5.29 5.33 5.36 5.39 5.28 5.00 5.02 5.01 5.01 5.02 5.05 5.33 5.17 5.02

Eurasia ............................................ 14.44 14.44 14.63 14.89 14.83 14.48 14.67 14.87 14.95 15.02 15.04 15.11 14.60 14.72 15.03

China ............................................... 4.79 4.84 4.78 4.86 4.92 4.89 4.87 4.91 4.89 4.92 4.92 4.97 4.82 4.90 4.93

Other Non-OECD ........................... 13.45 14.12 14.20 13.90 13.59 14.51 14.72 14.38 13.80 14.75 14.97 14.55 13.92 14.30 14.52

Total World Supply ............................ 99.27 99.78 101.42 102.14 99.81 100.26 101.30 102.01 101.42 102.92 103.47 103.46 100.66 100.85 102.82

Non-OPEC Supply ............................. 61.81 62.71 64.08 64.85 63.95 65.09 66.11 66.91 66.76 68.18 68.59 68.81 63.37 65.53 68.09

Consumption (million barrels per day) (c)

OECD ................................................. 47.62 46.99 47.93 47.52 47.39 46.69 48.09 48.17 47.56 47.07 48.30 48.23 47.52 47.59 47.79

U.S. (50 States) .............................. 20.24 20.33 20.63 20.60 20.29 20.33 21.02 20.92 20.53 20.75 21.25 21.01 20.45 20.64 20.89

U.S. Territories ................................ 0.10 0.08 0.09 0.11 0.12 0.11 0.12 0.13 0.12 0.11 0.12 0.13 0.10 0.12 0.12

Canada ........................................... 2.32 2.34 2.56 2.49 2.33 2.37 2.48 2.45 2.41 2.35 2.45 2.43 2.43 2.41 2.41

Europe ............................................. 14.09 14.23 14.69 14.12 14.02 14.14 14.64 14.34 13.99 14.19 14.70 14.40 14.28 14.28 14.32

Japan .............................................. 4.27 3.43 3.53 3.89 4.11 3.37 3.44 3.76 3.98 3.26 3.34 3.67 3.78 3.67 3.56

Other OECD ................................... 6.60 6.57 6.42 6.32 6.53 6.38 6.41 6.56 6.54 6.41 6.44 6.59 6.48 6.47 6.50

Non-OECD ......................................... 51.54 52.59 52.56 52.89 52.78 53.78 53.79 53.84 53.91 54.96 54.98 55.19 52.40 53.55 54.76

Eurasia ............................................ 4.78 4.83 5.11 4.98 4.80 4.87 5.24 5.09 4.90 4.99 5.37 5.27 4.93 5.00 5.13

Europe ............................................. 0.75 0.74 0.76 0.76 0.75 0.75 0.77 0.77 0.76 0.76 0.78 0.78 0.75 0.76 0.77

China ............................................... 13.80 14.00 13.73 13.95 14.28 14.47 14.20 14.41 14.76 14.95 14.67 14.90 13.87 14.34 14.82

Other Asia ....................................... 13.77 14.02 13.60 14.00 14.16 14.30 13.93 14.28 14.46 14.62 14.19 14.55 13.85 14.17 14.46

Other Non-OECD ........................... 18.44 19.00 19.36 19.20 18.78 19.38 19.66 19.29 19.04 19.63 19.97 19.70 19.00 19.28 19.58

Total World Consumption .................. 99.16 99.58 100.49 100.42 100.17 100.47 101.89 102.01 101.48 102.03 103.28 103.43 99.92 101.14 102.56

Total Crude Oil and Other Liquids Inventory Net Withdrawals (million barrels per day)

U.S. (50 States) ................................. 0.36 -0.06 -0.70 0.22 0.15 -0.63 -0.16 0.27 0.05 -0.37 -0.10 0.32 -0.05 -0.09 -0.03

Other OECD ...................................... -0.01 0.12 0.18 -0.08 -0.14 0.28 0.25 -0.09 0.00 -0.17 -0.03 -0.12 0.05 0.07 -0.08

Other Stock Draws and Balance ....... -0.46 -0.25 -0.41 -1.87 0.35 0.57 0.49 -0.18 0.00 -0.35 -0.06 -0.24 -0.75 0.31 -0.16

Total Stock Draw ............................ -0.11 -0.19 -0.93 -1.73 0.36 0.21 0.58 -0.01 0.05 -0.89 -0.19 -0.04 -0.74 0.29 -0.27

End-of-period Commercial Crude Oil and Other Liquids Inventories (million barrels)

U.S. Commercial Inventory ............... 1,196 1,207 1,272 1,262 1,249 1,310 1,325 1,304 1,303 1,340 1,351 1,324 1,262 1,304 1,324

OECD Commercial Inventory ............ 2,804 2,804 2,857 2,861 2,856 2,892 2,884 2,871 2,870 2,922 2,936 2,920 2,861 2,871 2,920

the United Arab Emirates, Venezuela.

Table 3a. International Petroleum and Other Liquids Production, Consumption, and InventoriesU.S. Energy Information Administration | Short-Term Energy Outlook - June 2019

2018 2019 2020 Year

- = no data availableOECD = Organization for Economic Cooperation and Development: Australia, Austria, Belgium, Canada, Chile, the Czech Republic, Denmark, Estonia, Finland,

France, Germany, Greece, Hungary, Iceland, Ireland, Israel, Italy, Japan, Latvia, Luxembourg, Mexico, the Netherlands, New Zealand, Norway, Poland, Portugal,

Slovakia, Slovenia, South Korea, Spain, Sweden, Switzerland, Turkey, the United Kingdom, the United States.

OPEC = Organization of the Petroleum Exporting Countries: Algeria, Angola, Congo (Brazzaville), Ecuador, Equatorial Guinea, Gabon, Iran, Iraq, Kuwait, Libya, Nigeria, Saudi Arabia,

Minor discrepancies with published historical data are due to independent rounding.

Projections: EIA Regional Short-Term Energy Model.

(a) Supply includes production of crude oil (including lease condensates), natural gas plant liquids, biofuels, other liquids, and refinery processing gains.

(b) Includes lease condensate, natural gas plant liquids, other liquids, and refinery processing gain. Includes other unaccounted-for liquids.

(c) Consumption of petroleum by the OECD countries is synonymous with "petroleum product supplied," defined in the glossary of the EIA Petroleum Supply Monthly ,

DOE/EIA-0109. Consumption of petroleum by the non-OECD countries is "apparent consumption," which includes internal consumption, refinery fuel and loss, and bunkering.

Notes: The approximate break between historical and forecast values is shown with historical data printed in bold; estimates and forecasts in italics.

Historical data: Latest data available from Energy Information Administration international energy statistics.

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 2018 2019 2020

North America ........................................................... 24.25 24.63 25.82 26.33 25.84 26.57 27.28 27.95 28.24 28.57 28.78 29.02 25.27 26.92 28.65

Canada ........................................................................ 5.32 5.10 5.33 5.42 5.01 4.86 5.17 5.21 5.36 5.36 5.40 5.46 5.30 5.06 5.40

Mexico .......................................................................... 2.17 2.13 2.09 1.95 1.92 2.08 2.06 2.03 2.01 1.99 1.97 1.95 2.08 2.02 1.98

United States ............................................................... 16.77 17.39 18.40 18.96 18.91 19.63 20.06 20.70 20.87 21.22 21.40 21.61 17.89 19.83 21.28

Central and South America .................................... 4.90 5.65 5.72 5.37 5.00 5.88 6.14 5.75 5.18 6.16 6.40 6.00 5.41 5.70 5.94

Argentina ...................................................................... 0.67 0.69 0.68 0.68 0.68 0.68 0.67 0.67 0.69 0.69 0.69 0.69 0.68 0.68 0.69

Brazil ............................................................................ 2.95 3.64 3.75 3.36 2.99 3.91 4.19 3.77 3.18 4.18 4.44 4.01 3.43 3.72 3.96

Colombia ...................................................................... 0.86 0.89 0.89 0.91 0.92 0.89 0.89 0.90 0.91 0.88 0.88 0.90 0.89 0.90 0.89

Other Central and S. America ..................................... 0.42 0.43 0.40 0.41 0.42 0.41 0.39 0.40 0.40 0.40 0.39 0.40 0.41 0.40 0.40

Europe ........................................................................ 4.37 4.20 4.12 4.32 4.26 4.16 4.06 4.27 4.33 4.35 4.30 4.59 4.25 4.18 4.39

Norway ......................................................................... 1.97 1.80 1.81 1.87 1.79 1.68 1.70 1.74 1.80 1.83 1.89 2.07 1.86 1.73 1.90

United Kingdom ........................................................... 1.16 1.17 1.10 1.22 1.25 1.28 1.17 1.29 1.31 1.31 1.20 1.29 1.16 1.25 1.28

Eurasia ........................................................................ 14.44 14.44 14.63 14.89 14.83 14.48 14.67 14.87 14.95 15.02 15.04 15.11 14.60 14.72 15.03

Azerbaijan .................................................................... 0.81 0.81 0.80 0.81 0.82 0.79 0.76 0.78 0.76 0.76 0.75 0.75 0.81 0.79 0.76

Kazakhstan .................................................................. 1.98 1.96 1.90 2.00 2.04 1.88 1.99 2.13 2.15 2.08 2.08 2.13 1.96 2.01 2.11

Russia .......................................................................... 11.20 11.24 11.50 11.66 11.57 11.40 11.50 11.55 11.64 11.79 11.82 11.85 11.40 11.51 11.78