1 INCEIF The Global University in Islamic finance Kuala Lumpur, Malaysia MIFP Title SHARIAH GOVERNANCE FRAMEWORK AND SHARIAH COMPLIANCE FOR ABC BANK Semester September 2014 Name: Hassan Mohamed Adan Matric No: 1400344 Date: 26/11/2014

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

INCEIF

The Global University in Islamic finance

Kuala Lumpur, Malaysia

MIFP

Title

SHARIAH GOVERNANCE FRAMEWORK AND SHARIAH

COMPLIANCE FOR ABC BANK

Semester September 2014

Name: Hassan Mohamed Adan

Matric No: 1400344

Date: 26/11/2014

2

ABSTRACT

This paper takes the structure of proposed shariah governance frame work SGF. The paper will be talk

about how to deal with the conflict of interest among difference organs of ABC bank according to the

proposed SGF. This essay contributes how the conflict of fatwa‟s between shariah committee of ABC

bank and shariah committee of the central bank is resolved. This study will also talk about what are the

management consequences if SGF is not complied with?

The concept of shariah governance framework set out the expectations on an Islamic financial

institution‟s ,shariah governance structures, processes and arrangements with the goal of ensuring that

all operations and business activities are consistent with Shariah principles at all times.(Bank Negara

Malaysia) BNM.

The paper attempts to explore the agency issues in the special context of ABC bank. According to the

proposed shariah governance frame work, the agency problems at Islamic financial institutions deserve

separate and widens the issue of separation of ownership and control underlying the agency theory

(Archer, Ahmed. and Al-Deehani, 1998).

The paper provides conflict of fatwa‟s between Central bank and ABC bank. In Shariah, a fatwa is the

guidance and instruction given by a Scholar (often called Mufti) who use the principles of Islamic

jurisprudence in order to derive rulings from various sources (Quran, Hadith etc).

Objectives of the research:

The following are the research objectives:

To understand how the structure of SGF for ABC bank.

To identify how the conflict of interest among the different organs of ABC bank is be tackled

according to the proposed SGF?

To identify how the conflict of fatwa‟s between shariah committee of ABC bank and shariah

committee of the central bank is resolved.

To identify what are the management consequences if SGF is not complied with?

Key terms of the research: Shariah governance frame work, conflict of interest, fatwa, shariah

governance.

3

Table of Contents

Cover Page----------------------------------------------------------------------------------------------------1

Abstract------------------------------------------------------------------------------------------------2

Research objectives----------------------------------------------------------------------------------2

Key terms of the research ---------------------------------------------------------------------------2

1.0 Introduction -------------------------------------------------------------------------------------4-5

2.0 Structure of the proposed SGF for ABC Bank-----------------------------------------------6

2.1 The importance of Shariah governance frame work---------------------------------------7-8

2.2 Objectives of shariah governance framework------------------------------------------------8

3.0 Conflict of interest among different organs of ABC bank --------------------------------8-9

4.0 Conflict of fatwa‟s between shariah committee of ABC bank and shariah committee

Of the central bank -------------------------------------------------------------------------------9-10

5.0 Management consequences if SGF is not complied with. -----------------------------------10

6.0 Conclusion and finding-------------------------------------------------------------------------10-11

4

1.0 Introduction

The Shariah governance system as defined by IFSB are guiding Principles on Shariah Governance

System in Institutions Offering Islamic Financial Services (IFSB-10) refers to a set of institutional and

organizational arrangements to oversee Shariah compliance aspects in Islamic Financial Institutions

(Zulkifli Hassan)1.

Shariah governance framework is a set of organizational arrangements through which Islamic financial

institutions ensure effective oversight, responsibility and accountability of the board of directors,

management and Shariah committee. The framework serves as a guide towards ensuring an operating

environment that is compliant with Shariah principles at all times. Shariah principles provide the

foundation for the practice of Islamic finance through the observance of the tenets, conditions and

principles propagated by Islam. Comprehensive compliance with Shariah principles would bring

confidence to the general public and the financial markets on the credibility of Islamic.

The paper attempts to explore the agency issues in the special context of ABC bank. According to the

proposed shariah governance frame work, the agency problems at Islamic financial institutions deserve

separate and widens the issue of separation of ownership and control underlying the agency theory.

The key sources of distinction arise from the observation that managers of Islamic banks and particular

examination for a number of reasons. The first is directly related to the nature of their operations,

which distinguishes them from conventional corporations. Finance operations are not only entrusted by

shareholders to maximize the value of their investments, but have a more compelling duty to achieve

these objectives in a Shariah-compliant manner (Archer, Ahmed. and Al-Deehani, 1998).

The paper provides conflict of fatwa‟s between Central bank and ABC bank. In Shariah, a fatwa is the

guidance and instruction given by a Scholar (often called Mufti) who use the principles of Islamic

jurisprudence in order to derive rulings from various sources (Quran, Hadith etc).

A fatwa in the context of Islamic banking and finance is a religious opinion by a qualified Shariah

scholar on structure of an Islamic financial product, like a mortgage, the conduct of management, like

a fund manager, and operations of an Islamic financial institution, like an Islamic bank, determining

their compliance or otherwise with the Islamic law.

Fatwa, if issued by an individual scholar or jurist, is non-binding and therefore, its utility is rather

limited in this sense. However, if a collective body of scholars issues a fatwa under an enforcement

regime, like a government or another such authority, it could be made binding on the market

participants.

Legislation in Malaysia makes it compulsory, not only for all market players (Islamic banks and

Takaful companies) but also for the judges hearing the cases related with Islamic banks and finance in

1 PhD candidate, School of Government and International Affairs, Durham University, UK.

5

Malaysian courts, to abide by the fatwa‟s and Shariah rulings publically issued by the Shariah

Advisory Council of Bank Negara Malaysia, the central bank.In Pakistan, the Shariah Advisory Board

of the State Bank of Pakistan issues fatwa‟s to govern Islamic banking operations in the country. The

legal standing of such fatwa‟s has yet to be tested in a court of law2 .

Fatwa shopping is a threat to Islamic Finance Industry because it works against the harmonization of

fatwa‟s. Such harmonization is required in order to minimize complexities and execution difficulties

and to decrease the cost of structuring Islamic financial products thus providing more people with

access to such products (Lawai,1994).

Finally this paper discover management consequences if SGF not complied with.

Islamic financial institutions are required to operate in the Shariah compliant manner.( Zurina Shafii,

Supiah Salleh, Syahidawati Hj Shahwan)

SSB members are required to enable and assist the Licensee‟s management in by providing advice and

guidance regarding Shariah compliance. . (Curtis, Mallet-Prevost, Colt & Mosle LLP; University of

Pennsylvania Law School December 5, 2012)

2 ( Humayon Dar / Creative: Jamal Khurshid ,Published: September 8, 2013).

6

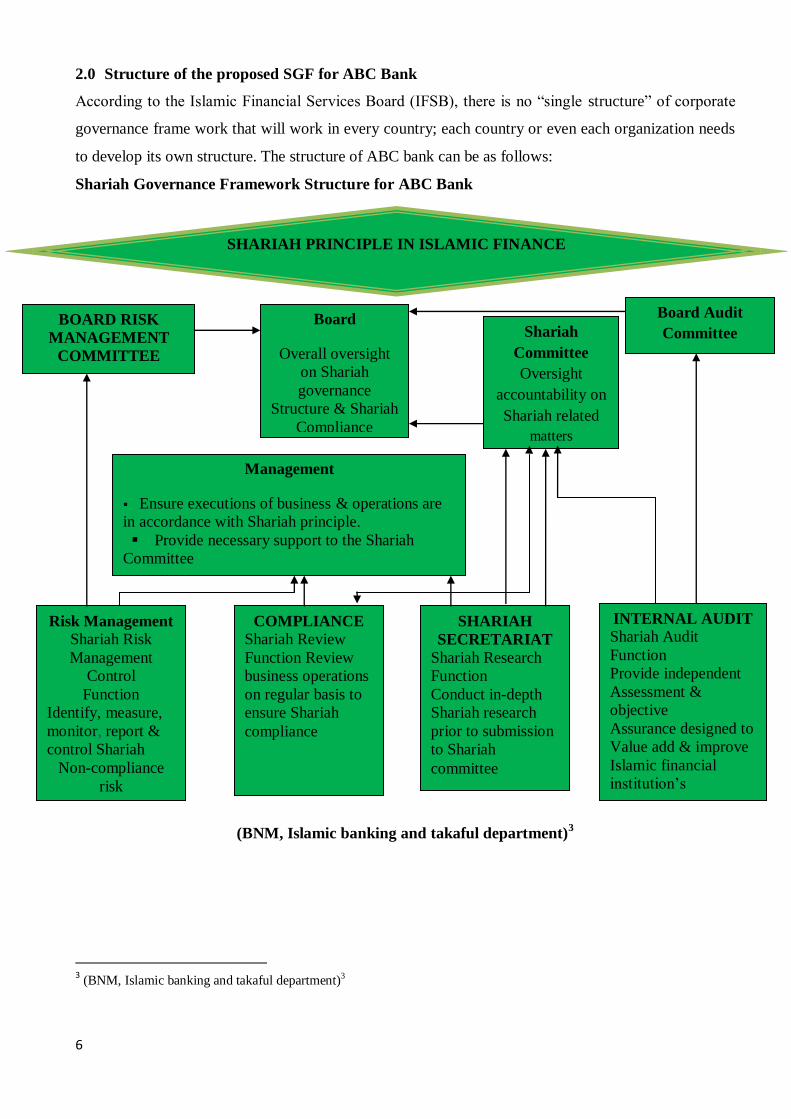

2.0 Structure of the proposed SGF for ABC Bank

According to the Islamic Financial Services Board (IFSB), there is no “single structure” of corporate

governance frame work that will work in every country; each country or even each organization needs

to develop its own structure. The structure of ABC bank can be as follows:

Shariah Governance Framework Structure for ABC Bank

(BNM, Islamic banking and takaful department)3

3 (BNM, Islamic banking and takaful department)

3

Shariah

Committee

Oversight

accountability on

Shariah related

matters

SHARIAH PRINCIPLE IN ISLAMIC FINANCE

BOARD RISK

MANAGEMENT

COMMITTEE

Board

Overall oversight

on Shariah

governance

Structure & Shariah

Compliance

Board Audit

Committee

Management

Ensure executions of business & operations are

in accordance with Shariah principle.

Provide necessary support to the Shariah

Committee

Risk Management

Shariah Risk

Management

Control

Function

Identify, measure,

monitor, report &

control Shariah

Non-compliance

risk

COMPLIANCE

Shariah Review

Function Review

business operations

on regular basis to

ensure Shariah

compliance

SHARIAH

SECRETARIAT

Shariah Research

Function

Conduct in-depth

Shariah research

prior to submission

to Shariah

committee

INTERNAL AUDIT

Shariah Audit

Function

Provide independent

Assessment &

objective

Assurance designed to

Value add & improve

Islamic financial

institution‟s

compliance with

Shariah

7

2.1 The importance of Shariah governance frame work

The principles of Islamic finance place great emphasis on strong corporate governance values and

structure, transparency, disclosure of information and exacting adherence to Shariah principles.

The framework serves as a guide towards ensuring an operating environment that is compliant with

Shariah principles at all times.

The framework aims essentially to strengthen the Shariah governance process, decision making,

accountability and independence. To reinforce the Shariah compliance functions, internal Shariah

review and audit requirements will be introduced, supported by an appropriate risk management

process and research capability. It is envisaged that the implementation of the framework will

contribute towards evolving a more robust and sound Shariah governance framework within Islamic

financial institutions which, in turn, will promote Shariah compliance throughout the organization.

Under the framework, the board will be responsible for the overall Shariah oversight of Islamic

financial institutions and the effective functioning of the Shariah governance structure, policies and

processes.

However, the board must recognize the independence of the Shariah committee and uphold the

committee‟s decisions on Shariah aspects of the institution‟s business operations. While the framework

does not specifically require an Islamic financial institution to appoint a Shariah expert among its

board members, the board is encouraged to consider co-opting members on the board who have strong

Shariah knowledge in order to serve as a „bridge‟ between the board and the Shariah committee. The

board shall also reasonably remunerate the Shariah committee members, to commensurate and reflect

the accountability, duties and responsibilities of the Shariah committee.

The role and function of the Shariah committee has been expanded further from merely advisory in

nature to assume a higher degree of accountability. The Shariah committee will now be accountable

for the implementation of decisions and opinions throughout the Islamic financial institution.

Consistent with its stature, the Shariah committee shall have direct access to the board. The Shariah

committee shall also report directly to the Bank where the committee believes that non-compliances on

Shariah matters in the Islamic financial institution have not been effectively and adequately addressed

by the Islamic financial institution.

In supporting the board and the Shariah committee, the senior management of an Islamic financial

institution is responsible to promote a strong culture of Shariah awareness and compliance within the

organization, including implementing best practices in Shariah governance in all aspects of the

institution‟s operations. The senior management is also responsible for ensuring that all submissions to

the Shariah committee are adequately researched and supported by a thorough study on the Shariah

issues, product structuring and documentation. This would entail the development of internal Shariah

8

research capabilities which are supported by adequate knowledge and resources to provide and

undertake research effectively.

Islamic financial institutions are also expected to establish three functions that provide a system of

checks and balances within the organization, which include the following:

A shariah risk management control function that is able to identify all possible risk of Shariah

noncompliance and, where appropriate, remedial measures to manage this risk.

A shariah review function that continuously assesses Shariah compliance of all activities and

operations. Where instances of non-compliances are identified, the institution is expected to

take prompt rectification measures and put in place the necessary mechanisms to avoid such

recurrences.

A shariah audit function that performs annual audits to provide an independent assessment of

the adequacy and compliance of the Islamic financial institution with established policies and

procedures, and the adequacy of the Shariah governance process. (Bank Negara Malaysia).

2.2 Objectives of shariah governance frame work

The Shariah Governance Framework for the Islamic Financial Institutions (the Framework) is designed

to meet the following objectives:

(i) Sets out the expectations of the Bank on an IFI‟s Shariah governance structures, processes and

arrangements to ensure that all its operations and business activities are in accordance with Shariah;

(ii) Provides a comprehensive guidance to the board, Shariah Committee and management of the IFI in

discharging its duties in matters relating to Shariah; and

(iii) Outlines the functions relating to Shariah review, Shariah audit, Shariah risk management and

Shariah research4.

3.0 Conflict of interest among different organs of ABC bank

The conflict of interest among different organs of Islamic bank involves much more than mere

disagreement about details of the model.( Omar Nayeem, Mohamed Shiliwala and Wasim Shiliwala).

The most important variations stem from the need to comply with Shariah and the contractual

characteristics separating the cash flow and control rights for a class of investors – the IAH (Sarker,

2000; IFQ, 2007). According to Islamic financial service board(IFSB) principle six An IIFS shall

recognize the conflicts of interest between it and its clients that arise from the type of products it

offers, and either avoid them, or disclose and manage them, bearing in mind its fiduciary duties to

investment account holders as well as shareholders. In IIFS, conflicts of duty may occur since their

management is required to act in the best interests of two categories of stakeholders who may have

differing interests, such as shareholders and IAH, or shareholders and Takaful participants. Hence,

4 (Bank Negara Malaysia) BNM

9

conflicts of interest between two categories of stakeholders are translated into conflicts of duty for the

board of directors and management of the IIFS. In this connection, the fiduciary duties of an IIFS to

stakeholders, including IAH or Takaful participants, are crucial. The conflicts of interest may be

managed, and that proper management to ensure fair treatment of stakeholders may require disclosure,

internal rules of confidentiality, or other appropriate methods or combinations of methods. (IFSB,

principle six).

The Board is required to undertake annual checks on the independence and conflicts of interest of SSB

members as well as their annual performance and report the results to the Central Bank of Oman. The

SSB members are made solely and personally responsible for their own work as members of the SSB.

Notably, the SSB members are admonished to “appreciate the diversity of opinions among various

mainstream schools of thought and differences in expertise among the fellow members” of the SSB.

In the event of an actual or potential issue of independence impairment, SSB members are obligated to

document the issue, review and address the issue with the SSB, and, if the issue is unresolved, resign

from the SSB and take the issue to the with the issue to the Licensee‟s General Assembly. This is yet

another step toward a strong professional conduct and responsibility framework. How it will be

implemented is yet to be determined.( Curtis, Mallet-Prevost, Colt & Mosle LLP; University of

Pennsylvania Law School December 5, 2012)

4.0 Conflict of fatwa’s between shariah committee of ABC bank and shariah committee of the

central bank.

Fatwa is a religious ruling, issued or given by a scholar on the matters of Islamic laws (Ali, 2005).

Fatwa is required on matters where there is no clear and straightforward guidance from Quran and

Sunnah. Fatwa shopping refers to seeking opinion and rulings by Islamic Scholars on matters where

there is ambiguity that a certain product or banking activity is in line with Shariah or not. Fatwa

resolves controversies and addresses key challenges faced by Islamic Financial Industry.( Muhammad

Shaukat Malik, Ali Malik and Waqas Mustafa).

Fatwa shopping is being increasingly used by some stakeholders (Mohammad ayub)5

The decisions and fatwa of the SB are binding on the IBI. However in case of difference of opinion

between the SB and the IBI‟s management on any Shariah related matter, the fatwa/opinion of the SB

etc, the issue shall be referred to the SBP Shariah Board for decision.

In case any difference of opinion between an IBI and the SBP inspection team regarding Shariah

conformity of IBI‟s products/ services/ transactions, the matter shall be referred to SBP Shariah Board

for decision. Similarly in case of difference of opinion between the Islamic Banking Department of

5 The editor of the JIBM and director research and training at the riphah centre of Islamic business, Islamabad

10

SBP and IBI on Shariah conformity of any existing or proposed new product or service of the IBI, the

structure, process flows, underlying agreements etc of such products shall be referred to SBP Shariah

Board for decision on the Shariah permissibility or otherwise of such products. The SB may also refer

Shariah issues to SBP for consideration of SBP Shariah Board. The case shall be sent to SBP along

with its arguments based on Shariah. The SBP Shariah Board shall provide guidance in such cases at

its earliest convenience.(Islamic banking department state bank of Pakistan April 2014).

5.0 Management consequences if SGF is not complied with.

Islamic financial institutions are required to operate in the Shariah compliant manner.( Zurina Shafii,

Supiah Salleh, Syahidawati Hj Shahwan)

SSB members are required to enable and assist the Licensee‟s management in by providing advice and

guidance regarding Shariah compliance. Management, on the other hand, is responsible for observing

and implementing SSB fatawa, rulings and decisions and making them available to those have

implementation responsibilities and to other stakeholders. It is obligated, on a timely basis, to disclose

information and provide necessary informational access to the SSB through the Internal Shariah

Reviewer (or risk Board penalties). Management is obligated to allocate adequate resources (including

people, systems and processes) to support the Shariah governance framework.

In instances of non-compliance with the Shariah requirements, the management is obligated to take

remedial action, including notification of the Internal Shariah Reviewer and the SSB, cessation of new

business relating to the non-compliance, and acting on the remedial and preventative advice of the

Internal Shariah Reviewer and/or the SSB. These are commendable steps toward a strong professional

conduct and professional responsibility system, but these steps leave a broad range of unaddressed

questions. (Curtis, Mallet-Prevost, Colt & Mosle LLP; University of Pennsylvania Law School

December 5, 2012)

6.0 Conclusion and finding

The previous discussion shows shariah governance framework of ABC Bank which means set of

organizational arrangements through which Islamic financial institutions ensure effective oversight,

responsibility and accountability of the board of directors, management and Shariah committee.

The conflicts of interest may be managed, and that proper management to ensure fair treatment of

stakeholders may require disclosure, internal rules of confidentiality, or other appropriate methods or

combinations of methods.

Fatwa is a religious ruling, issued or given by a scholar on the matters of Islamic laws

Fatwa shopping is being increasingly used by some stakeholders (Mohammad ayub)6

6 The editor of the JIBM and director research and training at the riphah centre of Islamic business, Islamabad

11

The decisions and fatwa of the SB are binding on the IBI. However in case of difference of opinion

between the SB and the IBI‟s management on any Shariah related matter, the fatwa/opinion of the SB

etc, the issue shall be referred to the SBP Shariah Board for decision

Islamic financial institutions are required to operate in the Shariah compliant manner.

In instances of non-compliance with the Shariah requirements, the management is obligated to take

remedial action, including notification of the Internal Shariah Reviewer and the SSB, cessation of new

business relating to the non-compliance, and acting on the remedial and preventative advice of the

Internal Shariah Reviewer and/or the SSB.

12

References

1. (Bank Negara Malaysia) BNM.

2. (Archer, Ahmed. and Al-Deehani, 1998).

3. Islamic Financial Service Board (IFSB)

4. (Zulkifli Hassan).

5. (Lawai,1994).

6. (Curtis, Mallet-Prevost, Colt & Mosle LLP; University of Pennsylvania Law School December

5, 2012)

7. .( Omar Nayeem, Mohamed Shiliwala and Wasim Shiliwala).

8. (Sarker, 2000; IFQ, 2007).

9. (Ali, 2005).

10. ( Muhammad Shaukat Malik, Ali Malik and Waqas Mustafa).

11. (Mohammad ayub)

12. .(Islamic banking department state bank of Pakistan April 2014).

13. .( Zurina Shafii, Supiah Salleh, Syahidawati Hj Shahwan)

Related Documents

![[final] SHARIAH COMPLIANCE FUNCTION IN MALAYSIAN …](https://static.cupdf.com/doc/110x72/6194591ac3d08e0aef6e9869/final-shariah-compliance-function-in-malaysian-.jpg)