R. Venkatakrishnan & Associates Chartered Accountants Offices at Chennai, Bangalore, Hyderabad & Salem Service Tax For Hospitality Industry - R. Mohan B.com, FCA

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Service Tax

For

Hospitality Industry

- R. Mohan B.com, FCA

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

DISCLAIMERDISCLAIMERDISCLAIMERDISCLAIMER

The opinions and views expressed by the author are of his personal views and are subject to differ from that of the Statutory

Authority.

The author is not responsible for any action taken based on this publication.

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

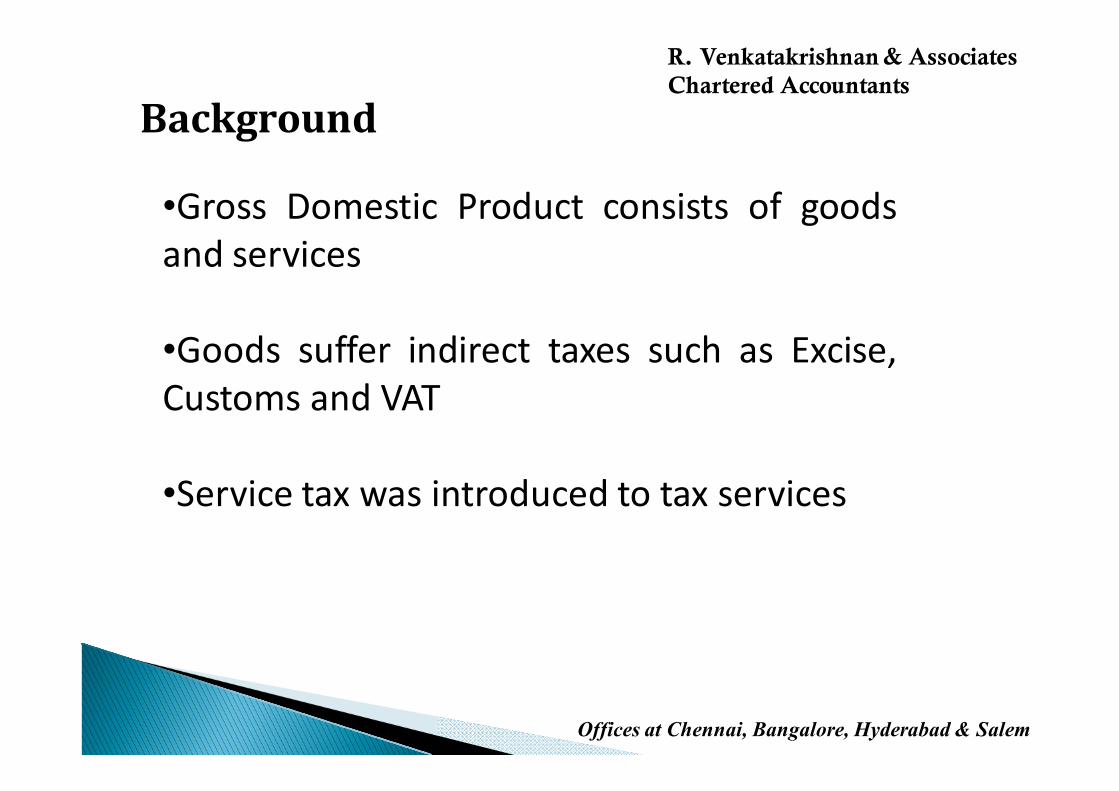

Background

•Gross Domestic Product consists of goods

and services

•Goods suffer indirect taxes such as Excise,

Customs and VAT

•Service tax was introduced to tax services

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Whether levy of service tax is

constitutional?

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Vide Entry 97 of Schedule VII of the

Constitution of India, the Central

Government levies Service Tax

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Which is the Regulatory

Authority for Service Tax

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Central Board of Excise and Customs (CBEC) is

the regulatory Authority

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Which is the Governing Law for

Service Tax

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

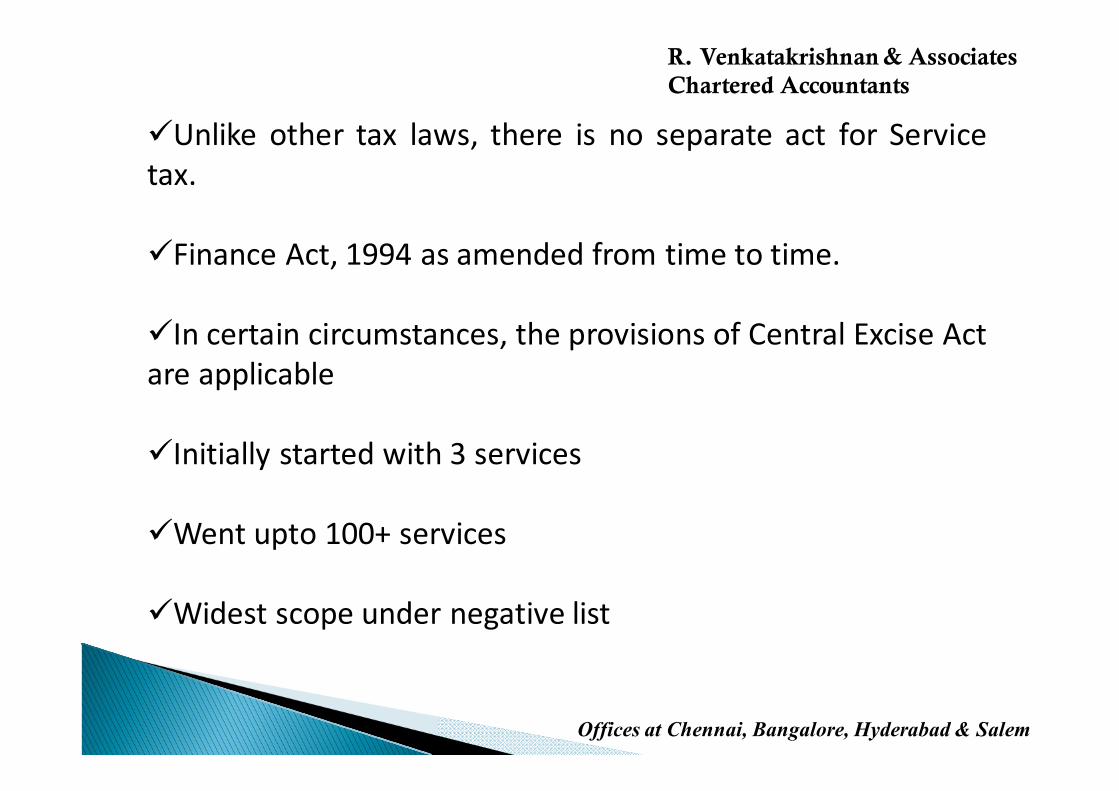

�Unlike other tax laws, there is no separate act for Service

tax.

�Finance Act, 1994 as amended from time to time.

�In certain circumstances, the provisions of Central Excise Act

are applicable

�Initially started with 3 services

�Went upto 100+ services

�Widest scope under negative list

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

�Service Tax Rules, 1994

�CENVAT Credit Rules, 2004

�Point of Taxation Rules, 2011

�Service Tax (Determination of Value) Rules, 2006

�Place of Provision of Services Rules, 2012

�Service tax Voluntary Compliance Encourage Scheme / Rules,

2013

�Taxation of services : CBEC’s Education Guide

Important Rules / Guidelines

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Why is Finance Act of 2012

significant?

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

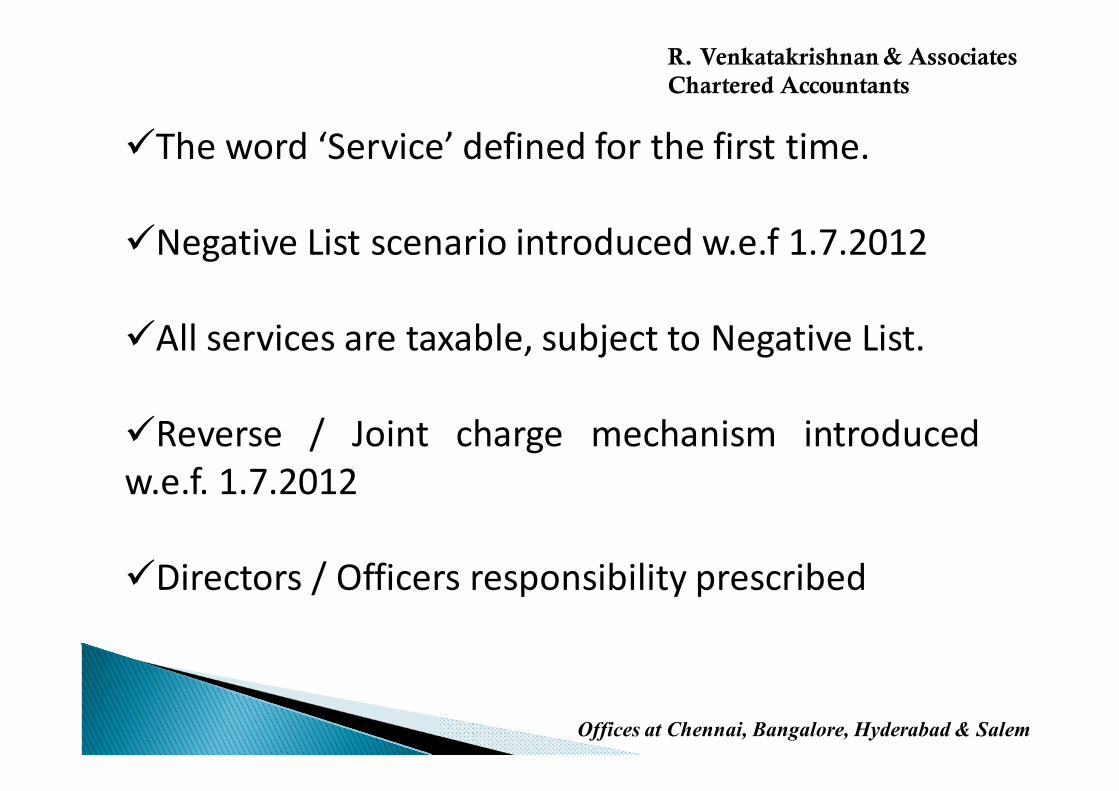

�The word ‘Service’ defined for the first time.

�Negative List scenario introduced w.e.f 1.7.2012

�All services are taxable, subject to Negative List.

�Reverse / Joint charge mechanism introduced

w.e.f. 1.7.2012

�Directors / Officers responsibility prescribed

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

What is Service? – Sec 65B(44)

Any activity carried out by a person for another for

consideration, and includes a declared service,

but shall not include…..

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

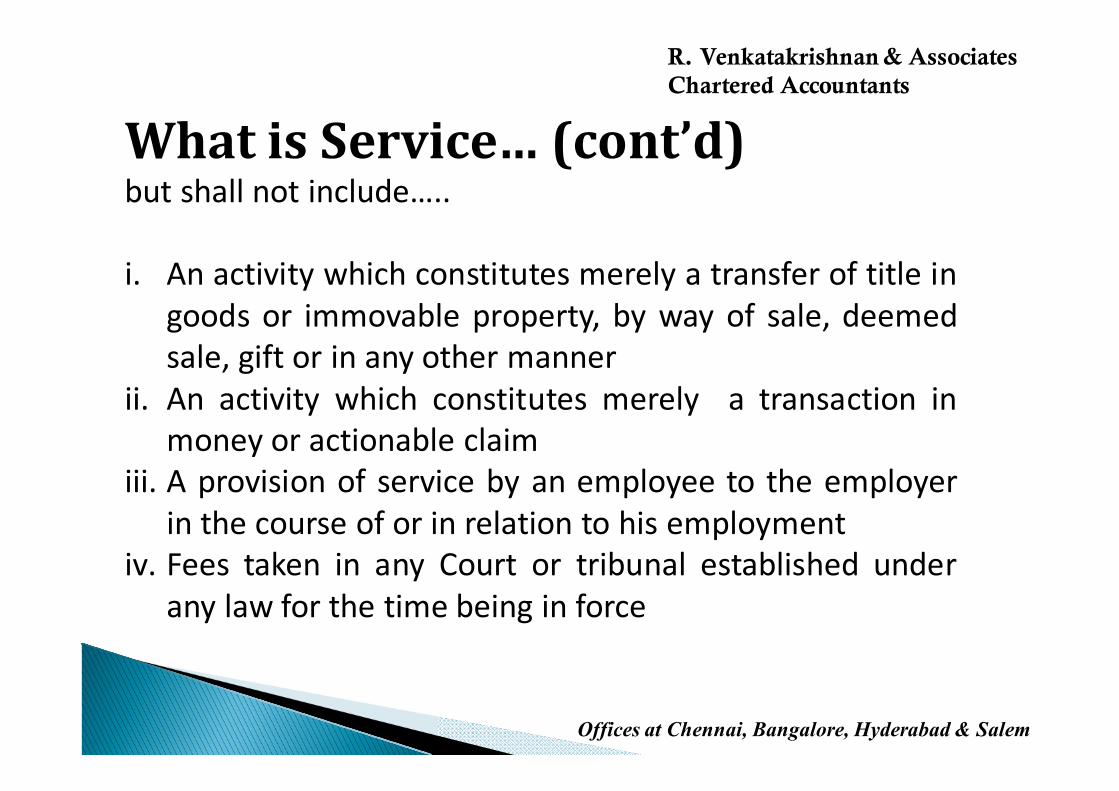

What is Service… (cont’d)but shall not include…..

i. An activity which constitutes merely a transfer of title in

goods or immovable property, by way of sale, deemed

sale, gift or in any other manner

ii. An activity which constitutes merely a transaction in

money or actionable claim

iii. A provision of service by an employee to the employer

in the course of or in relation to his employment

iv. Fees taken in any Court or tribunal established under

any law for the time being in force

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Declared Service – Sec 66E

�List specified in the section

�Any change is by amending the section

�Borderline items included here

�Restricted definition

�Refer handout for the list

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

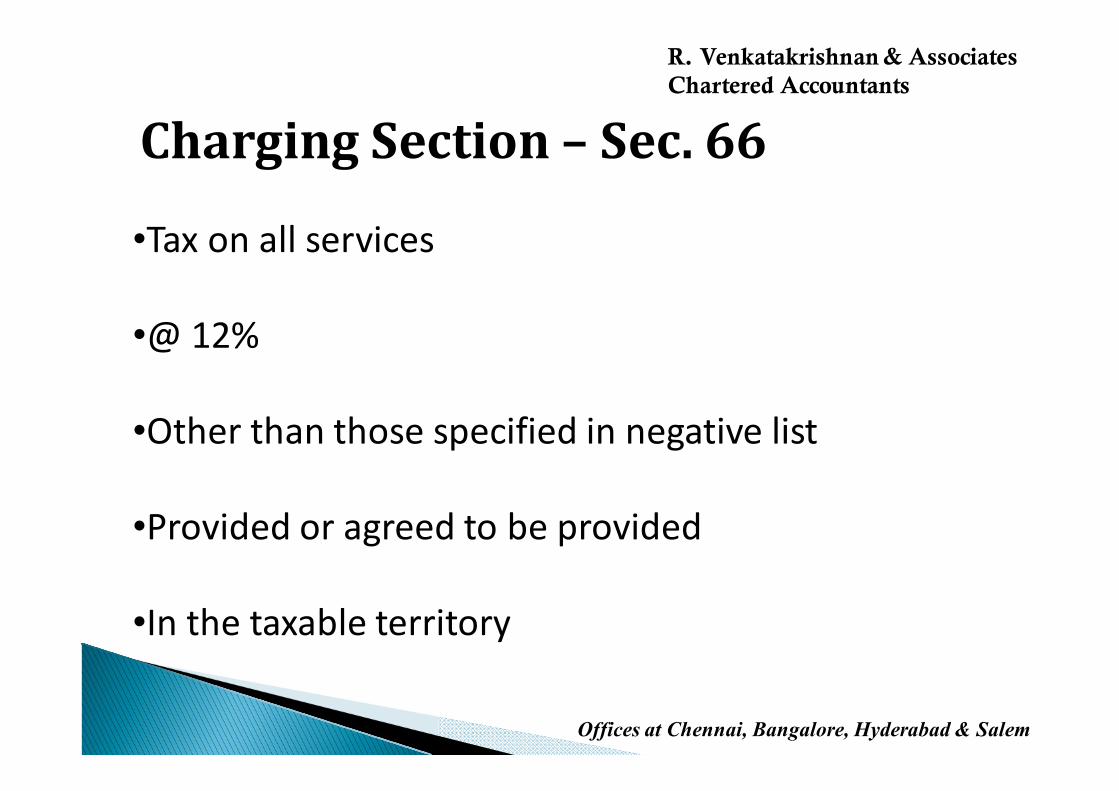

Charging Section – Sec. 66

•Tax on all services

•@ 12%

•Other than those specified in negative list

•Provided or agreed to be provided

•In the taxable territory

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

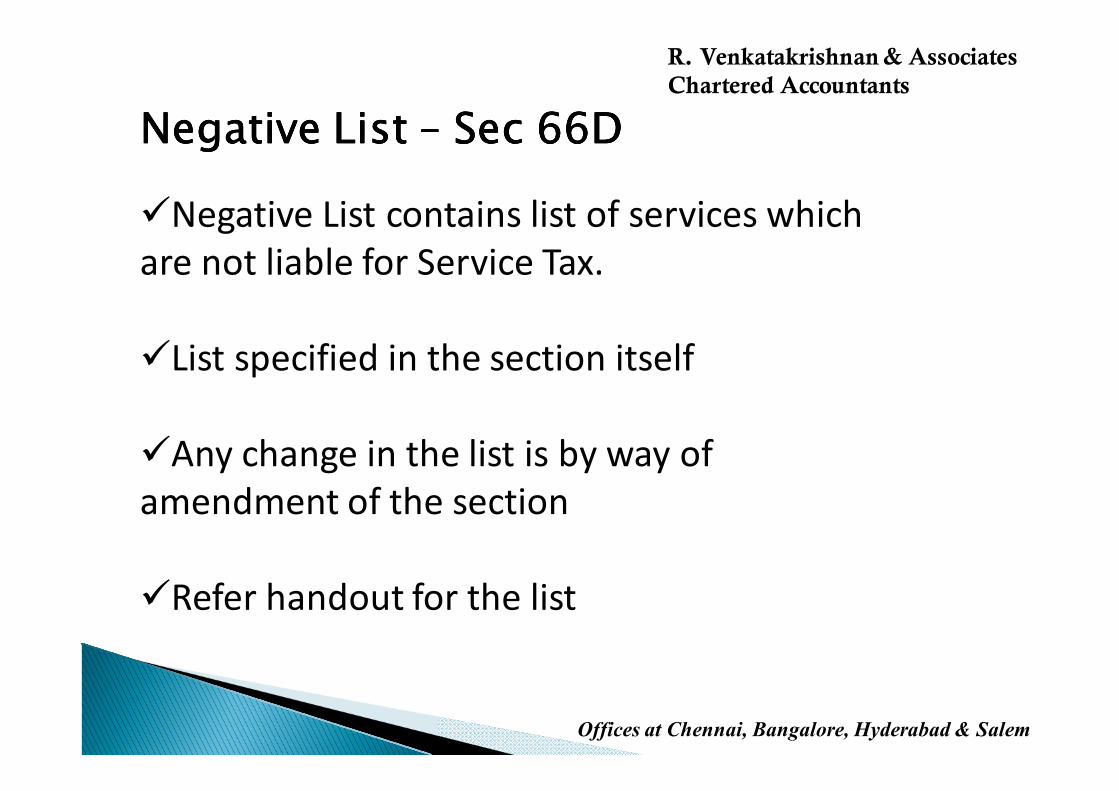

Negative List Negative List Negative List Negative List –––– Sec 66DSec 66DSec 66DSec 66D

�Negative List contains list of services which

are not liable for Service Tax.

�List specified in the section itself

�Any change in the list is by way of

amendment of the section

�Refer handout for the list

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Mega ExemptionMega ExemptionMega ExemptionMega Exemption

�Section 93(1) – empowers

�Many exemptions provided on adhoc basis

�Mega exemption under Negative List

�These are taxable services otherwise

�Refer handout for list

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

What is an Exempted What is an Exempted What is an Exempted What is an Exempted Service?Service?Service?Service?

�CCR – Rule 2(e)

�Exempted services means taxable services which are

exempt from the whole of service tax

�Negative list of services

�Abated value of the services subjected to abatement

�But not export of service

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

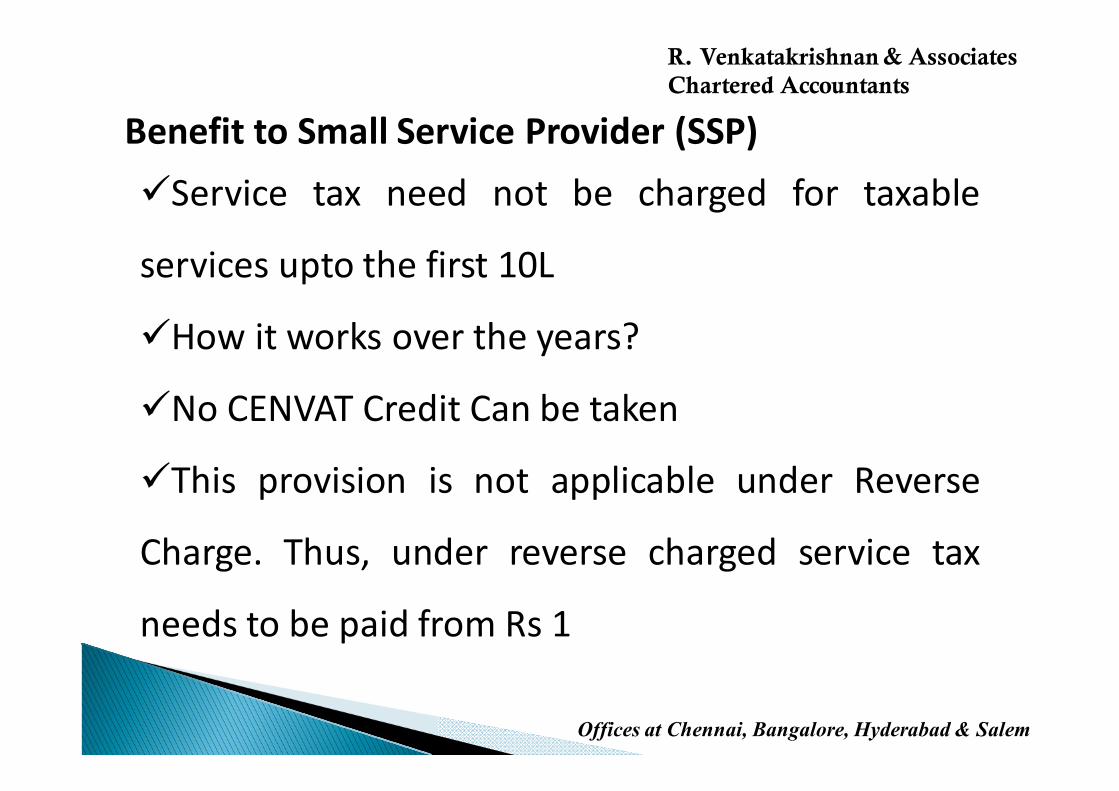

Benefit to Small Service Provider (SSP)

�Service tax need not be charged for taxable

services upto the first 10L

�How it works over the years?

�No CENVAT Credit Can be taken

�This provision is not applicable under Reverse

Charge. Thus, under reverse charged service tax

needs to be paid from Rs 1

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Applicability Test Applicability Test Applicability Test Applicability Test –––– How it works?How it works?How it works?How it works?

�Excluded nature of activities – Section 65B(44) –

Not service – Not taxable

�Negative list of services – Section 66D – Not

taxable

�Mega exemption services – Notification 25/2012

– Not taxable

�Declared services – Section 66E – Specifically

taxable

�Specific exemptions – As per notifications

�All other services – Generally taxable

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Whether Free service is liable

to Service tax?

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

As there is no Consideration, services

carried out free of cost is not

chargeable to service tax

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

What is What is What is What is Bundled Service?Bundled Service?Bundled Service?Bundled Service?

Bundled Services means a bundle of provision of

more than one service, wherein an element of

provision of one service is combined with element

of provision of another services or services

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Taxation of Bundled ServiceTaxation of Bundled ServiceTaxation of Bundled ServiceTaxation of Bundled Service

i. When two or more services are naturally bundled in ordinary

course of business

Taxation - It will be treated as a single services based on the

service which gives essential character to the bundle.

ii. When two or more services are not naturally bundled in

ordinary course of business

Taxation - It will be treated as a single services based on the

service which results in the highest liability of service tax

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Rates of Service

�Service Tax rate is 12% plus education cess and

SHE Cess.

�In specific cases Abatement is Provided

�Egs: For Sale of Food in Restaurant 60%

abatement is provided i.e., charged on at 40%

�No Service Tax on actual expenses charged on

‘Pure Agent’ basis.

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Rates of Service… cont’d

�Under Reverse charge service tax is charged at

12.36%. However, the liability to pay tax shifts to the

recipient of service either fully or partially

�Cum duty principle can be followed (12.36/112.36)

Note: Service Tax, Education Cess and SHE Cess

should be separately shown in the invoice.

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

LETS HAVE

EXERCISE – 1

Which are Taxable Services?

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Q.Q.Q.Q. M/s. ABC Enterprises manages the

entire marriage of Mr. X and charges

Rs.100 per visitor?

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Q.Q.Q.Q. Mr. Shastry carries our pooja in a

temple premises and gets a monthly

retainer fees paid. In addition to this,

he also carries out religious functions

for many individual families.

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Q.Q.Q.Q. Bangalore Education Trust is running a

school and charges its students tuition

fees, laboratory fees and few other charges

on periodical basis.

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Q.Q.Q.Q. Karunya Trust is a animal care

organization. It takes care of pets of

general public for any limited period and

charges them a per day charge.

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Q.Q.Q.Q. Mr. Y is a don in the making. He

carries out smuggling, killing and many

other illegal activities for a ransom or a

fee.

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Q.Q.Q.Q. Sony Entertainment Pvt. Ltd. starts a

training Institute to promote singing

for kids between 5-15 years

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Q.Q.Q.Q. Mr. X provides cheque discounting

facility, wherein cheques of more than

10,000 are discounted for a service fee of

Rs. 30

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Q.Q.Q.Q. Mr Z supplies labour to Tumkur Flower

Association, wherein on a daily basis they

are required to prepare bouquets which

are sent to Bangalore

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Q.Q.Q.Q. Rohit shetty was paid Rs. 10 cr by Actor

Surya for not producing the Hindi Version of

Singam 2

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

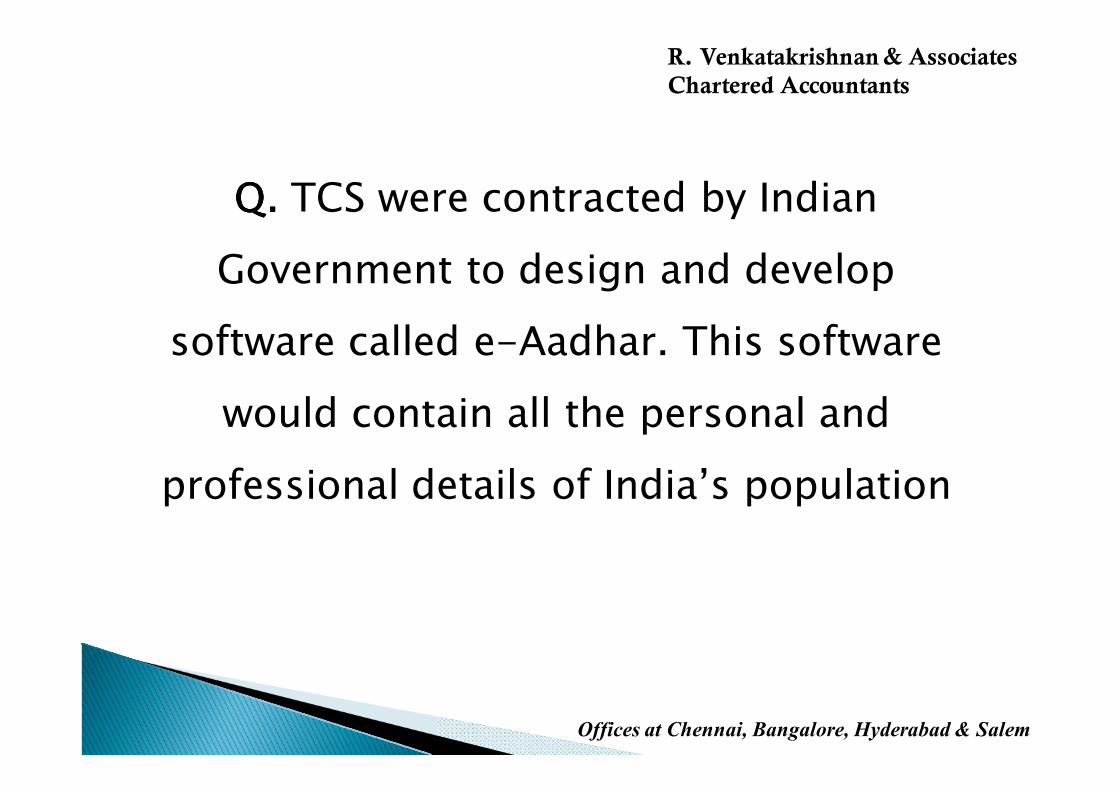

Q.Q.Q.Q. TCS were contracted by Indian

Government to design and develop

software called e-Aadhar. This software

would contain all the personal and

professional details of India’s population

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Q. Q. Q. Q. X, a Bangalorean residing in Mumbai

died because of a road accident in

Mumbai. For his final rites his body was

sent to Bangalore from Mumbai via

Air India

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

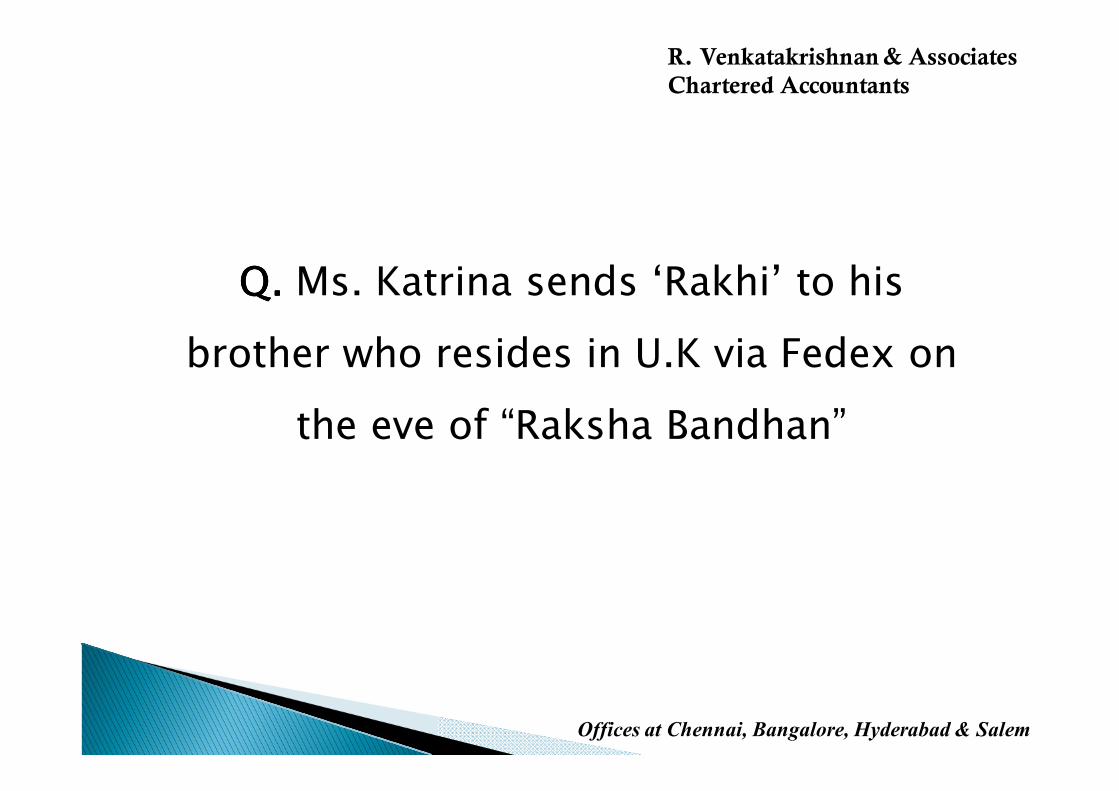

Q.Q.Q.Q. Ms. Katrina sends ‘Rakhi’ to his

brother who resides in U.K via Fedex on

the eve of “Raksha Bandhan”

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Q. Q. Q. Q. Mr. K has started foreign money

exchange service wherein on request from

the clients he will arrange for conversion

of foreign exchange from Reserve Bank of

India for a commission of 2%

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

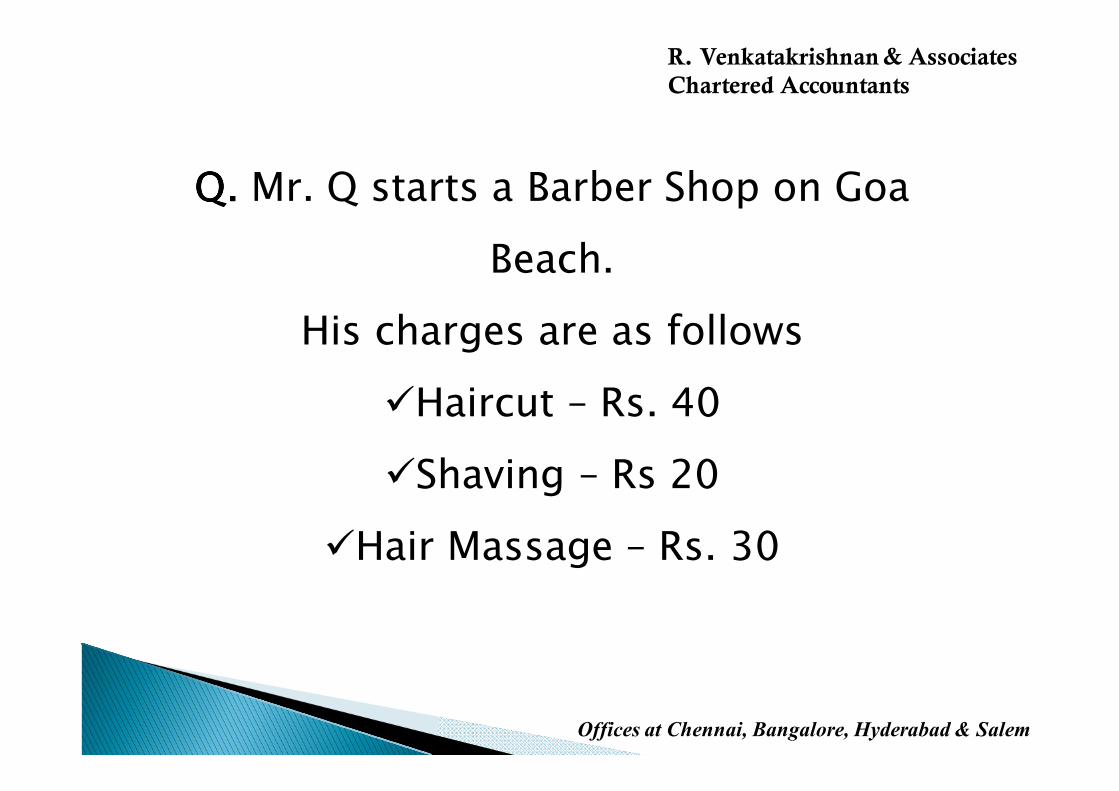

Q. Q. Q. Q. Mr. Q starts a Barber Shop on Goa

Beach.

His charges are as follows

�Haircut – Rs. 40

�Shaving – Rs 20

�Hair Massage – Rs. 30

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

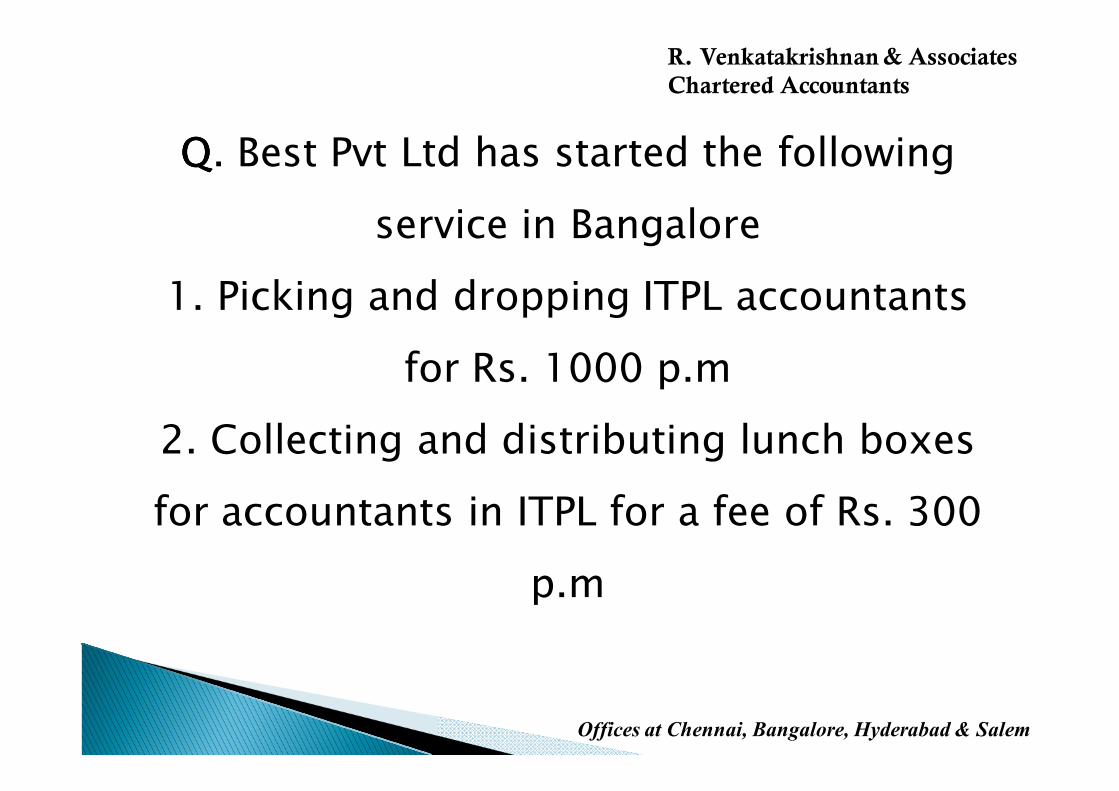

QQQQ. Best Pvt Ltd has started the following

service in Bangalore

1. Picking and dropping ITPL accountants

for Rs. 1000 p.m

2. Collecting and distributing lunch boxes

for accountants in ITPL for a fee of Rs. 300

p.m

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

QQQQ. Wonderla has opened a resort cum

amusement park in Whitefield. Entry

fee for 2 Day & 1 Night is Rs. 1,999

per person. Charges for resort and

amusement park is clearly demarked

on the entrance tickets

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Mr. A, an individual, is running a trading

organization under the name and style of

A & Associates. He also runs another

business of A1 Taxi Services. For his

trading organization he uses the taxi

services of A1 taxis.

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

PROCEDURESPROCEDURESPROCEDURESPROCEDURES

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Procedures Procedures Procedures Procedures ---- RegistrationRegistrationRegistrationRegistration

�To be registered within 30 days

�Decentralized registration is possible

�Application in ST – 1 – No registration fee

�PAN must

�PAN based STC (Service Tax Code) No.

�Documents required for registration –

Address Proof, Charter of the entity

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Procedures Procedures Procedures Procedures ---- ContractingContractingContractingContracting

�Check up the applicability before contracting

�Provide in the contract – “Service tax as

applicable, presently @ 12.36%”

�“Service tax not applicable” / “Service tax

inclusive”

�Mention the ST registration number

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Procedures Procedures Procedures Procedures ---- BillingBillingBillingBilling

�Mention separately – Even though it is an

‘Inclusive of ST’ contract.

�Mention ST registration number in the invoice

�No special invoice format.

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Procedures Procedures Procedures Procedures ---- AccountingAccountingAccountingAccounting

�ST billed to be accounted separately

�ST account to tally with the returns – Monthly

reconciliation

�Total turnover for the financial year as per Service

tax returns should tally with the signed financials

�Check whether your accounting software is

enabled for service tax

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Procedures Procedures Procedures Procedures ---- Due date for PaymentDue date for PaymentDue date for PaymentDue date for Payment

�ST is payable on Accrual basis

Category of AssesseeCategory of AssesseeCategory of AssesseeCategory of Assessee

Periodicity Periodicity Periodicity Periodicity

of Paymentof Paymentof Paymentof Payment

Payment through Payment through Payment through Payment through

Internet BankingInternet BankingInternet BankingInternet BankingOthersOthersOthersOthers

Individuals/ Proprietary firms and partnership firms whose aggregate value of taxable turnover is less than 50L

Every calendar quarter

6th of the month immediately following the said quarter

5th of the month immediately following the said quarter

Individuals or Proprietary firms and partnership firms whose aggregate value of taxable turnover is more than 50L

Every calendar month

6th of the month immediately following the said month

5th of the month immediately following the said month

Others Every calendar month

6th of the month

immediately

following the said

month

5th of the month immediately following the said month

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Procedures Procedures Procedures Procedures ---- Mode of payment Mode of payment Mode of payment Mode of payment

�Payable on 31st March for the month of March�Payment to be paid through GAR 7 challan�If the assessee has paid service tax of Rs 10L ormore in the preceding F.Y then service tax needs tobe paid Online

Note: Service tax along with Education and SHE cess

should be separately shown while making the

payment . Interest also to be shown separately.

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Procedures Procedures Procedures Procedures ---- Head of PaymentHead of PaymentHead of PaymentHead of Payment

�From 1st July, 2012, instructions were issued tomake all the payments under new code known as‘Not in Negative List’.

�These instructions were later changed andassessee were asked to make payment under theold code itself.

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Procedures Procedures Procedures Procedures ---- DocumentationDocumentationDocumentationDocumentation

�No special documents or registers

�Only regular invoice, books of accounts sufficient with

separate account for ST

�Cenvat Credit Register – Rule 9(5) of CCR

�Copies of original purchase bills for claiming of credit to be

retained safely

�Preserve records for 5 years

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Procedures Procedures Procedures Procedures ---- ReturnsReturnsReturnsReturns

�ST-3 Returns to be filed. �Compulsory E- return�Return for all types of services�Half yearly return by 25th of the month following the particular half-year (25th April and 25th October)�Only one Revised Return is possible�Revised return needs to be filed within 90 days of the date of filling

Note: Service tax returns for the period Oct’12 – Mar’13

needs to be filled by 31st August 2013. Excel utility for the

same is yet to be made available by the department

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Procedures - Payment of Interest & Penalty

�Interest for delay in payment of service tax –18% p.a.�Interest calculations are on daily basis�Penalty @ 2% per month or Rs.200 per day whichever is higher, subject to the max. of ST

�Penalty for late filling of service tax returns –Max of Rs. 20,000 irrespective of the tax amount (except NIL returns)

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Procedures - Payment of Interest

& Penalty... Cont’dPeriod Of Delay Late Fee

15 days from the date prescribed

for submission of the return

Rs. 500

Beyond 15 days but not later than

30 days from the date prescribed

for submission of the return

Rs. 1,000

Beyond 30 days from the date

prescribed for submission of the

return

An amount of Rs.1000 plus Rs.100

for every day from the 31st day till

the date of furnishing the said

return, subject to a maximum of

Rs.20,000/-

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

CENVAT CREDITCENVAT CREDITCENVAT CREDITCENVAT CREDIT

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Credits Under Credits Under Credits Under Credits Under Service Tax Service Tax Service Tax Service Tax –––– General ProvisionsGeneral ProvisionsGeneral ProvisionsGeneral Provisions

�Available as per CENVAT Rules.

�Definition of ‘input service’-Rule 2(l)

�Includes – All input services

�Office repairs & renovation, advertisement,

sales promotion, market research, storage,

accounting, auditing, finance, recruitment,

coaching and training, business exhibition, legal

services, inward and outward transportation…

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Credits Under Credits Under Credits Under Credits Under Service Tax Service Tax Service Tax Service Tax –––– General ProvisionsGeneral ProvisionsGeneral ProvisionsGeneral Provisions

× Excludes – Specified services

× Works contract for construction of building or

civil structure

× Rent a cab service

× Repair & Maintenance of vehicles

× Insurance of vehicles

× Services in relation to personal use or

consumption by employees

× Outward transportation beyond the place of

removal

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Credits Under Credits Under Credits Under Credits Under Service Tax Service Tax Service Tax Service Tax –––– ConditionsConditionsConditionsConditions

�Provisions of CCR

�Credit can be claimed on accrual basis

x Exception – Credit on reverse charge

�If not paid to service provider within 90 days,

Credit to be reversed

�Documents to be preserved

�Cenvat credit register to be maintained

�Input credit documents to be without any defect

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Credits Under Credits Under Credits Under Credits Under Service Tax Service Tax Service Tax Service Tax –––– Partial creditPartial creditPartial creditPartial credit

�Rule 6(3) of CCR

�Three types of service providers

1. Providing only exempted services

2. Providing only taxable services

3. Providing taxable and exempted services

�Type 1 – No cenvat credit

�Type 2 – Cenvat credit for all allowable inputs

�Type 3 – Partial credit mechanism

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Partial credit mechanismPartial credit mechanismPartial credit mechanismPartial credit mechanism

�Available for Type 3 service providers

�Emphasis on relativity / utilisation of input services

to / for output services

�Input services can be used for three purposes

�(i) Utilised wholly for taxable services

�(ii) Utilised wholly for exempted services

�(iii) Utilised partly for taxable and partly for

exempted services (Common inputs)

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

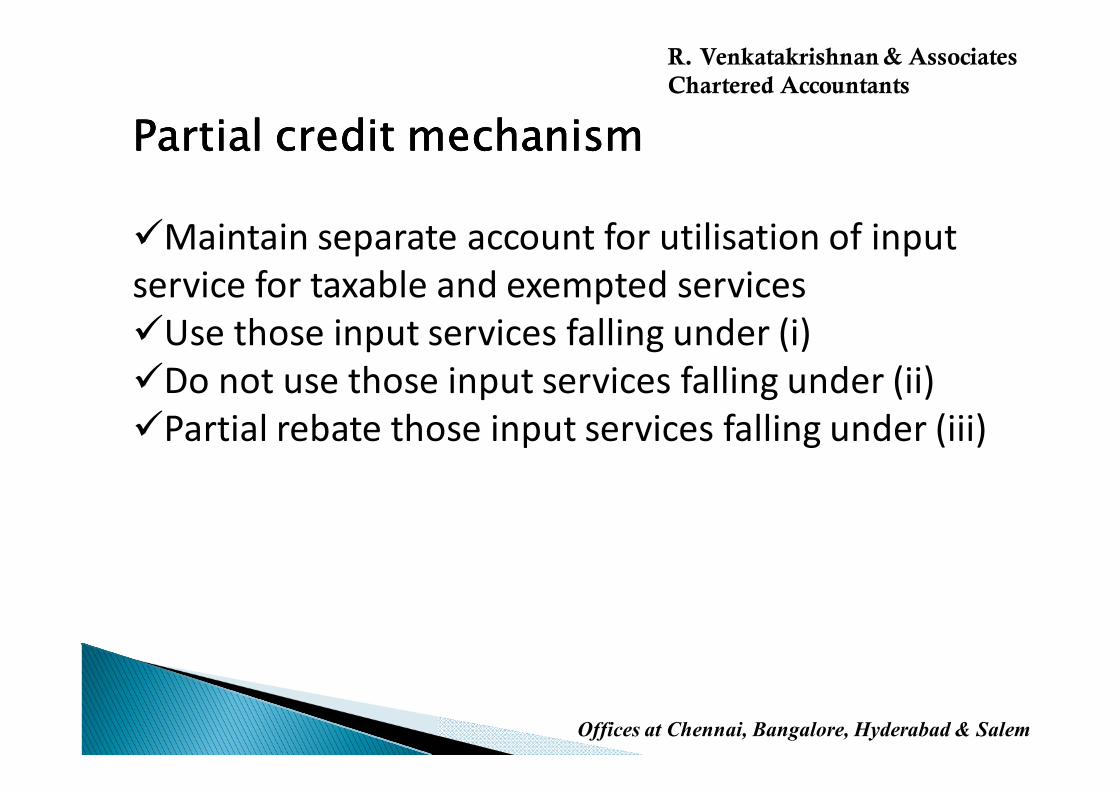

Partial credit mechanismPartial credit mechanismPartial credit mechanismPartial credit mechanism

�Maintain separate account for utilisation of input

service for taxable and exempted services

�Use those input services falling under (i)

�Do not use those input services falling under (ii)

�Partial rebate those input services falling under (iii)

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

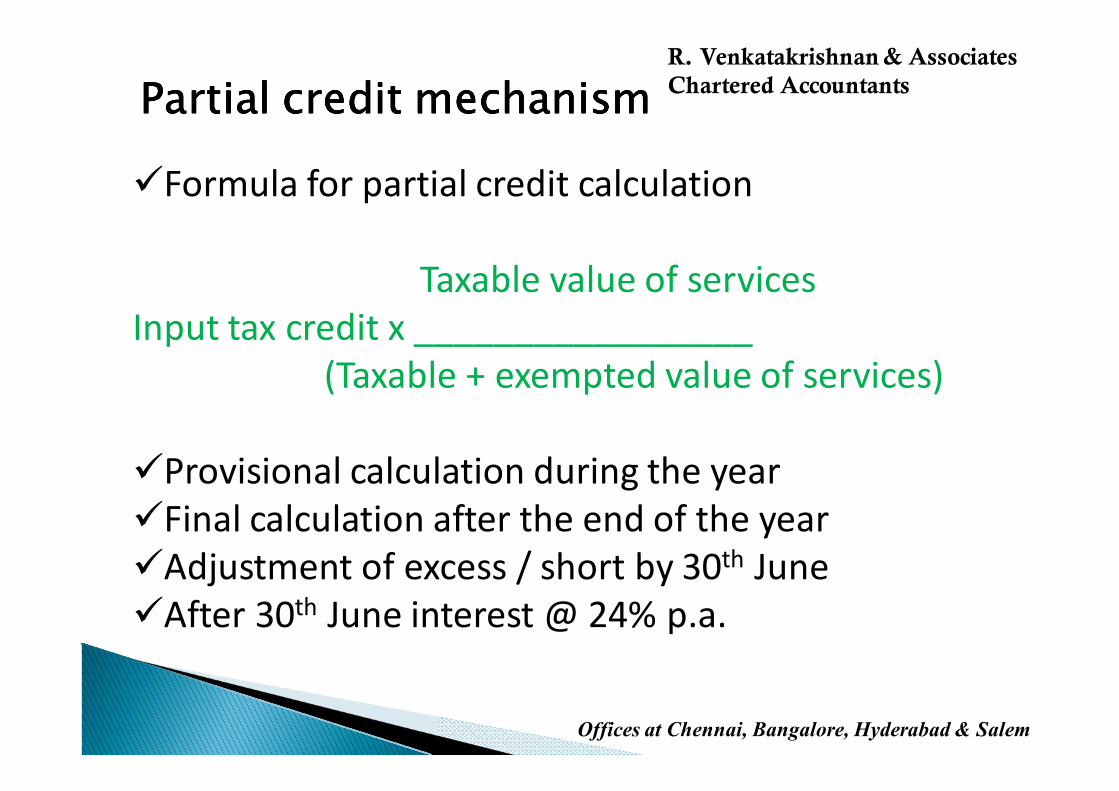

Partial credit mechanismPartial credit mechanismPartial credit mechanismPartial credit mechanism

�Formula for partial credit calculation

Taxable value of services

Input tax credit x _________________

(Taxable + exempted value of services)

�Provisional calculation during the year

�Final calculation after the end of the year

�Adjustment of excess / short by 30th June

�After 30th June interest @ 24% p.a.

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

LETS HAVE

EXERCISE – 2

Simulation for CENVAT Credit

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Q.Q.Q.Q. Holiday Hotels Limited, buys groceries,

fruits and commodities which are used in

the preparation of food. For the

transportation of these inputs, the

company pays transportation charges to

the transporter who charges service tax.

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Q.Q.Q.Q. XYZ Limited is a legal consulting

company and uses courier services to

send many couriers to its clients. There

is a service tax charge charged by the

courier agency on the courier charges.

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Q.Q.Q.Q. Karnataka Government has started a

project called “TechKannada”. Through this

project, IT training will be provided to MLA’s

and other government officials on a regular

basis. For this project the Government has

hired services of various free -lancers. These

professionals are charging service tax for

providing their services.

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Q.Q.Q.Q. TTD hotels has decided it diversify their

business by venturing into Amusement Parks.

They have contracted Shobha Builders for

planning and constructing the layout. Shobha

Developers are providing the required

material and services for carrying out the

construction. The total contract value agreed

is Rs. 10 cr exclusive of VAT and Service tax.

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Q.Q.Q.Q. Mr. Tiny, a consultant whose turnover is 5L

until December’13. In the month of January,

he obtained an unexpected new contract for

which he received an advance of Rs. 20L. In

the month of January he received the bill for

his December training cost on which service

tax is charged. Whether Input credit can be

claimed on the same.

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

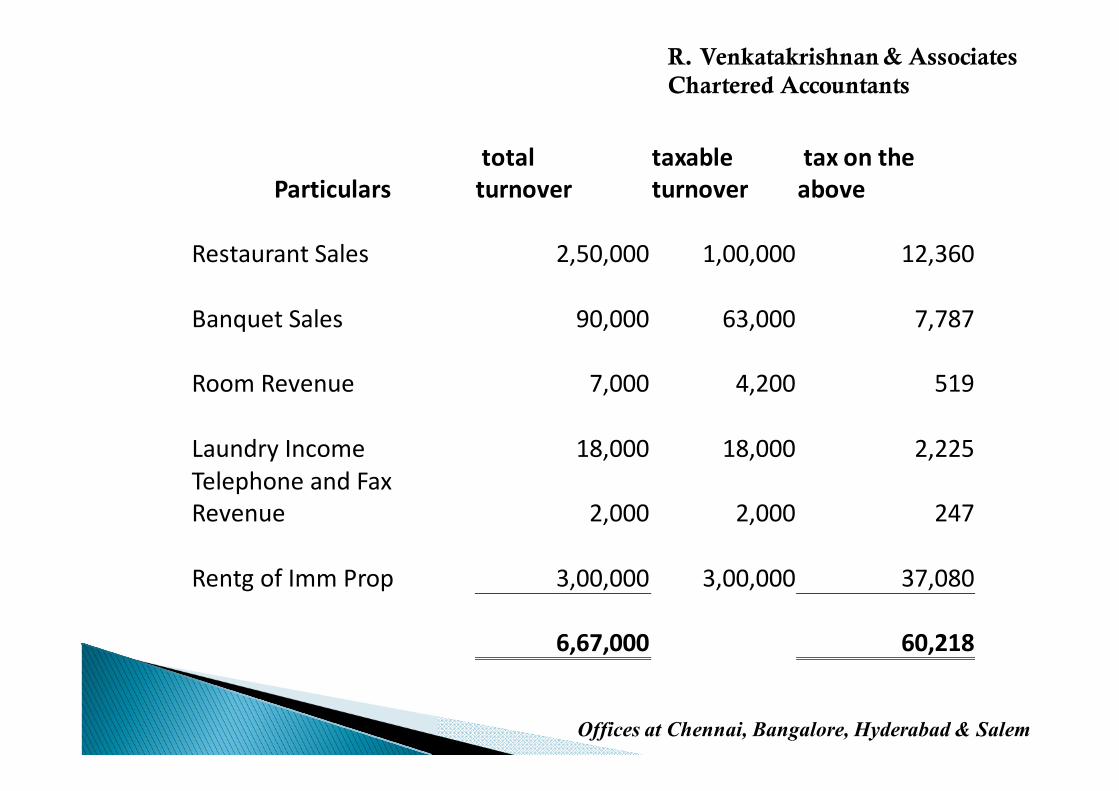

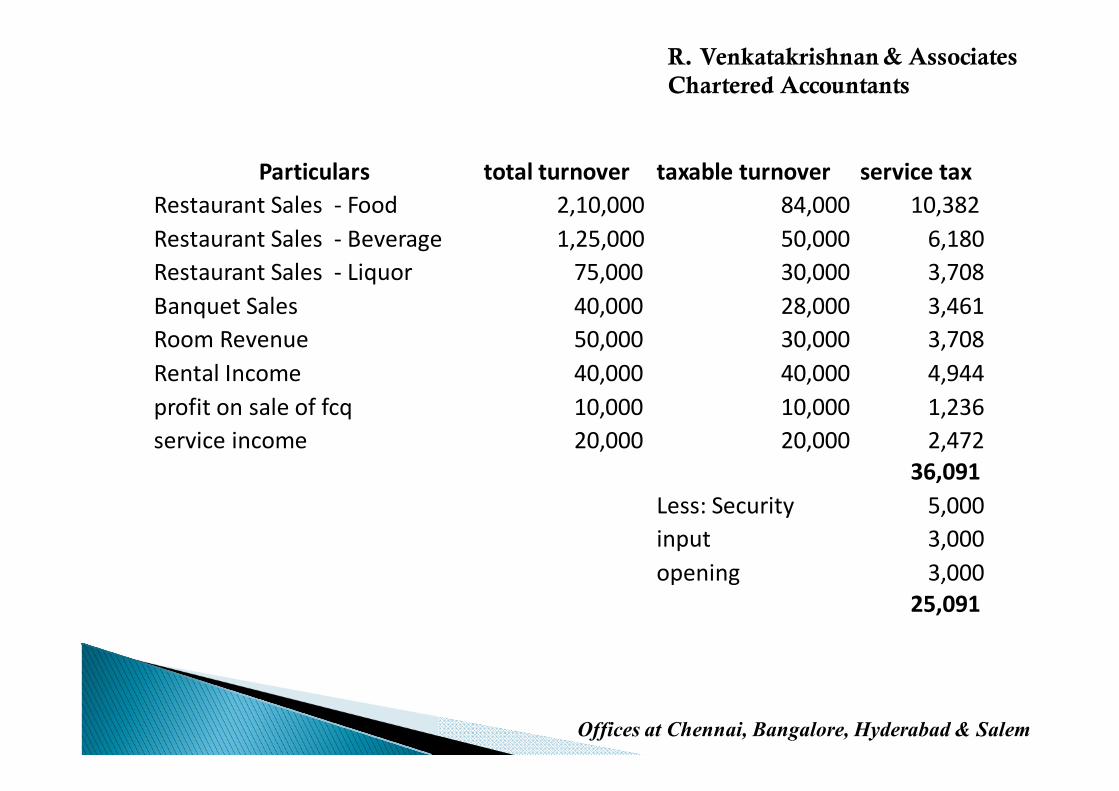

Q.Q.Q.Q. Compute the Service Tax output Liability for July’2013

Income details for July 2013Income details for July 2013Income details for July 2013Income details for July 2013

Restaurant Sales – Rs. 2,50,000Banquet Sales – Rs. 90,000Room Revenue – Rs. 7,000Laundry Income – Rs 18,000Telephone and Fax Revenue – 2,000Renting of immovable property – Rs. 3,00,000.

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Particulars

total

turnover

taxable

turnover

tax on the

above

Restaurant Sales 2,50,000 1,00,000 12,360

Banquet Sales 90,000 63,000 7,787

Room Revenue 7,000 4,200 519

Laundry Income 18,000 18,000 2,225

Telephone and Fax

Revenue 2,000 2,000 247

Rentg of Imm Prop 3,00,000 3,00,000 37,080

6,67,000 60,218

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

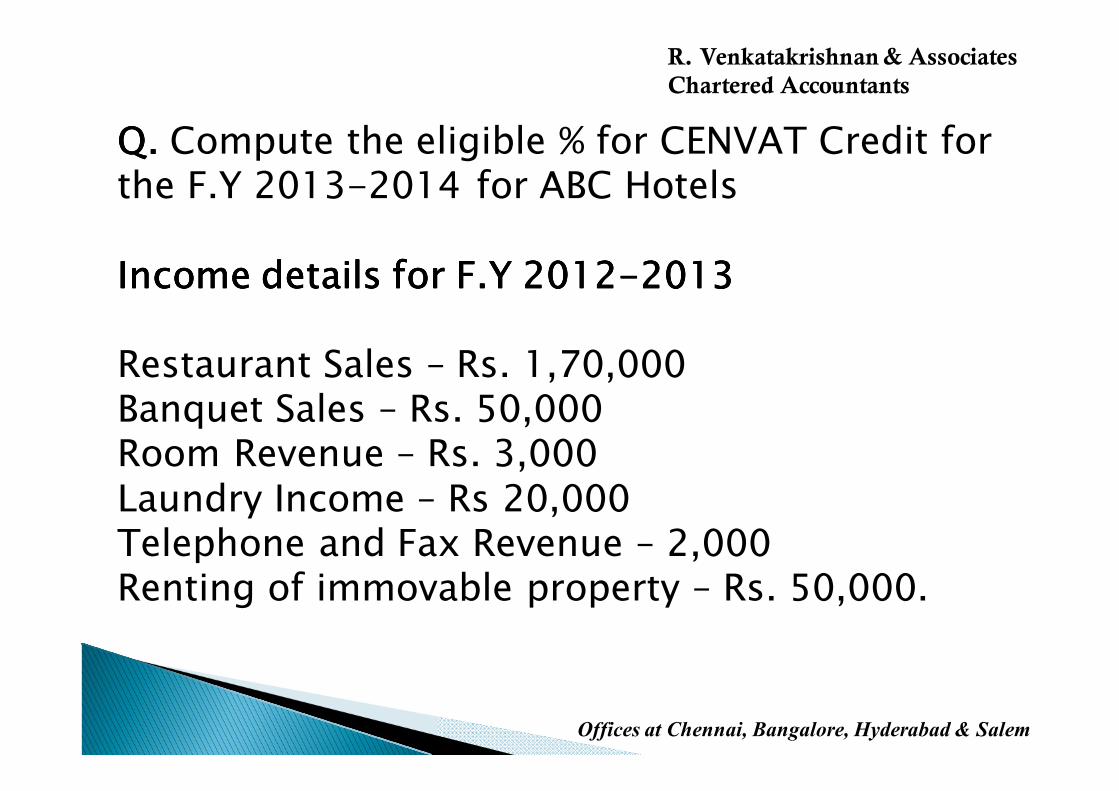

Q.Q.Q.Q. Compute the eligible % for CENVAT Credit for the F.Y 2013-2014 for ABC Hotels

Income details for F.Y 2012Income details for F.Y 2012Income details for F.Y 2012Income details for F.Y 2012----2013201320132013

Restaurant Sales – Rs. 1,70,000Banquet Sales – Rs. 50,000Room Revenue – Rs. 3,000Laundry Income – Rs 20,000Telephone and Fax Revenue – 2,000Renting of immovable property – Rs. 50,000.

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

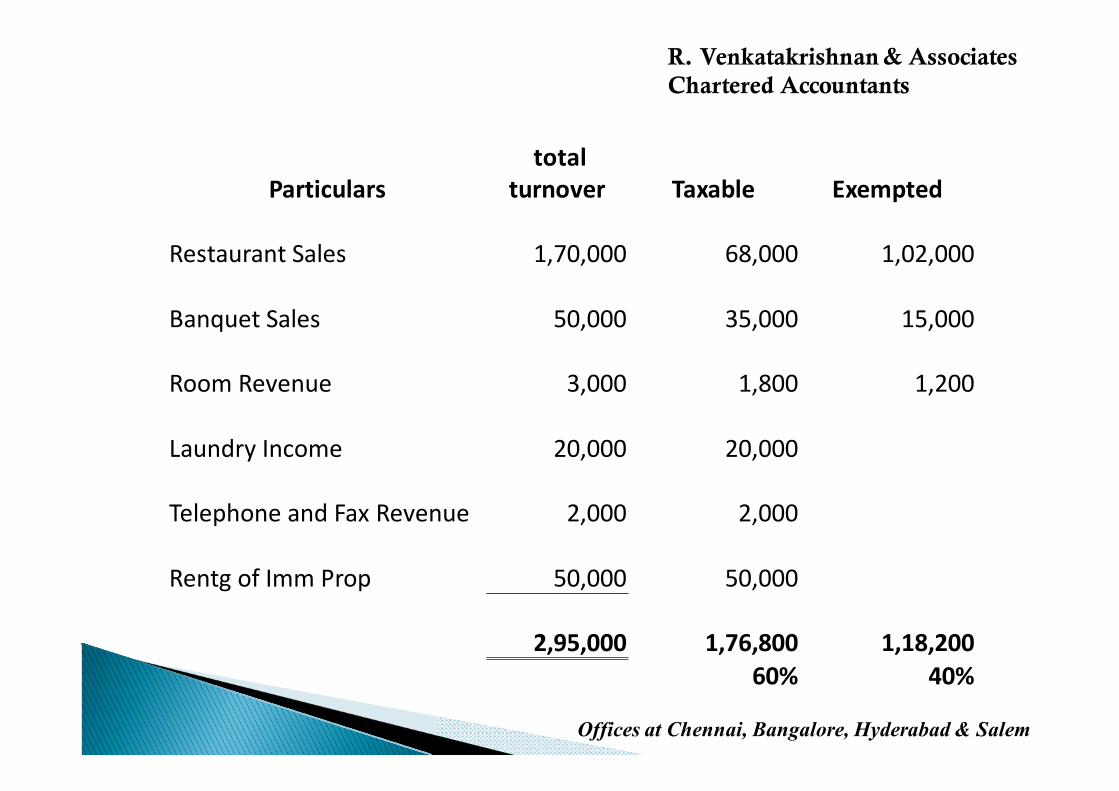

Particulars

total

turnover Taxable Exempted

Restaurant Sales 1,70,000 68,000 1,02,000

Banquet Sales 50,000 35,000 15,000

Room Revenue 3,000 1,800 1,200

Laundry Income 20,000 20,000

Telephone and Fax Revenue 2,000 2,000

Rentg of Imm Prop 50,000 50,000

2,95,000 1,76,800 1,18,200

60% 40%

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

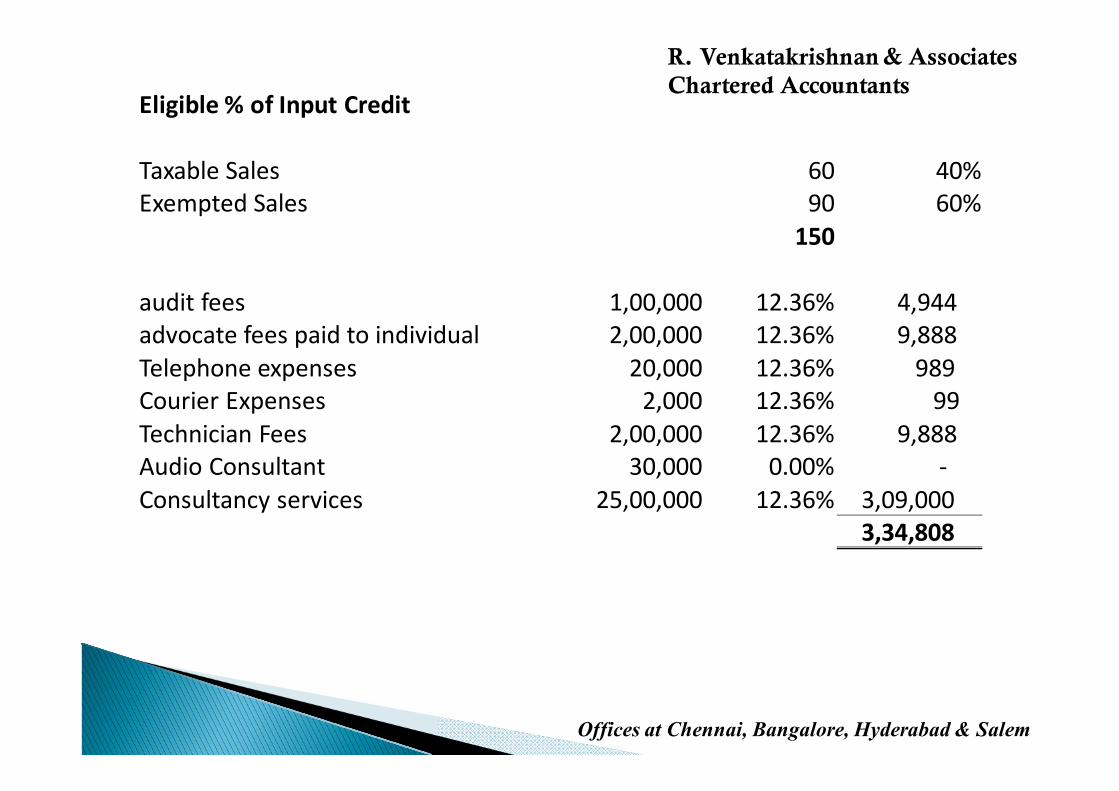

Q.Q.Q.Q. Toys Audio Pvt Ltd is into manufacturing and servicing of Audio Systems, Speakers, etc.

During the F.Y 12-13 the total turnover was Rs. 150L.Local Sales - 60L Interstate Sales – 30LTaxable services – 60L

For For For For the F.Y the F.Y the F.Y the F.Y 13131313----14 14 14 14 the following the following the following the following are are are are expensesexpensesexpensesexpensesStatutory Audit Fees – 1L Advocate Fees paid to Individual – 2LTelephone expenses - 20,000Courier expense – 2,000Technician Fees – 2LAudio Consultant (Small Service Provider) – 30,000Consultancy services incurred against taxable output services – 25L

Which are the services for which input credit can be claimed and to what Which are the services for which input credit can be claimed and to what Which are the services for which input credit can be claimed and to what Which are the services for which input credit can be claimed and to what extentextentextentextent

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Eligible % of Input Credit

Taxable Sales 60 40%

Exempted Sales 90 60%

150

audit fees 1,00,000 12.36% 4,944

advocate fees paid to individual 2,00,000 12.36% 9,888

Telephone expenses 20,000 12.36% 989

Courier Expenses 2,000 12.36% 99

Technician Fees 2,00,000 12.36% 9,888

Audio Consultant 30,000 0.00% -

Consultancy services 25,00,000 12.36% 3,09,000

3,34,808

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Q.Q.Q.Q. Compute the Service Tax payable for July’2013

Eligible % of Input Credit for 2012-2013 – 60%

Income details for July 2013Income details for July 2013Income details for July 2013Income details for July 2013

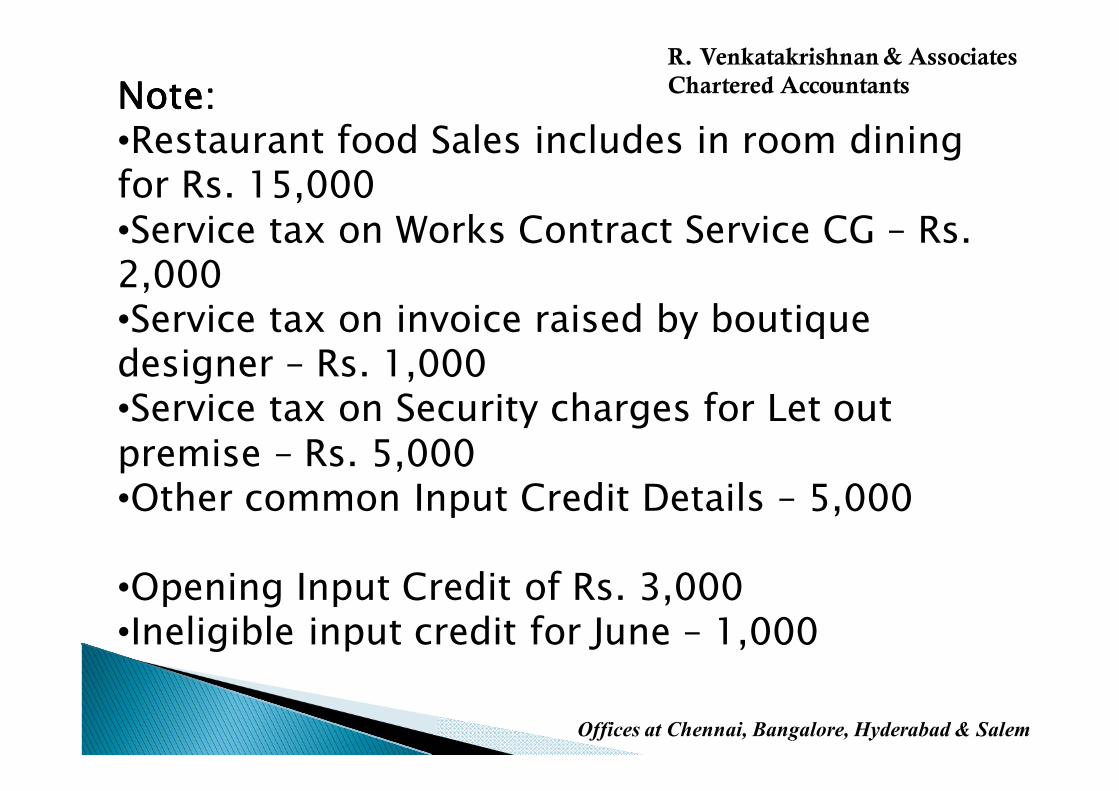

�Restaurant Sales for Food – Rs. 2,25,000�Restaurant Sales for Beverage – Rs. 1,25,000�Restaurant Sales for Liquor – Rs. 75,000�Banquet Sales – Rs. 40,000�Room Revenue – Rs. 50,000�Rental Income – Rs. 40,000�Profit on Sale of Foreign Currency –10,000�Scrap Sales – Rs. 5,000�Boutique sales – Rs 10,000�Service Income from hire of Accessories - 20,000 cont’dcont’dcont’dcont’d

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Note:Note:Note:Note:•Restaurant food Sales includes in room dining for Rs. 15,000•Service tax on Works Contract Service CG – Rs. 2,000•Service tax on invoice raised by boutique designer – Rs. 1,000•Service tax on Security charges for Let out premise – Rs. 5,000•Other common Input Credit Details – 5,000

•Opening Input Credit of Rs. 3,000•Ineligible input credit for June – 1,000

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Particulars total turnover taxable turnover service tax

Restaurant Sales - Food 2,10,000 84,000 10,382

Restaurant Sales - Beverage 1,25,000 50,000 6,180

Restaurant Sales - Liquor 75,000 30,000 3,708

Banquet Sales 40,000 28,000 3,461

Room Revenue 50,000 30,000 3,708

Rental Income 40,000 40,000 4,944

profit on sale of fcq 10,000 10,000 1,236

service income 20,000 20,000 2,472

36,091

Less: Security 5,000

input 3,000

opening 3,000

25,091

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Point of Taxation

Rules, 2011

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

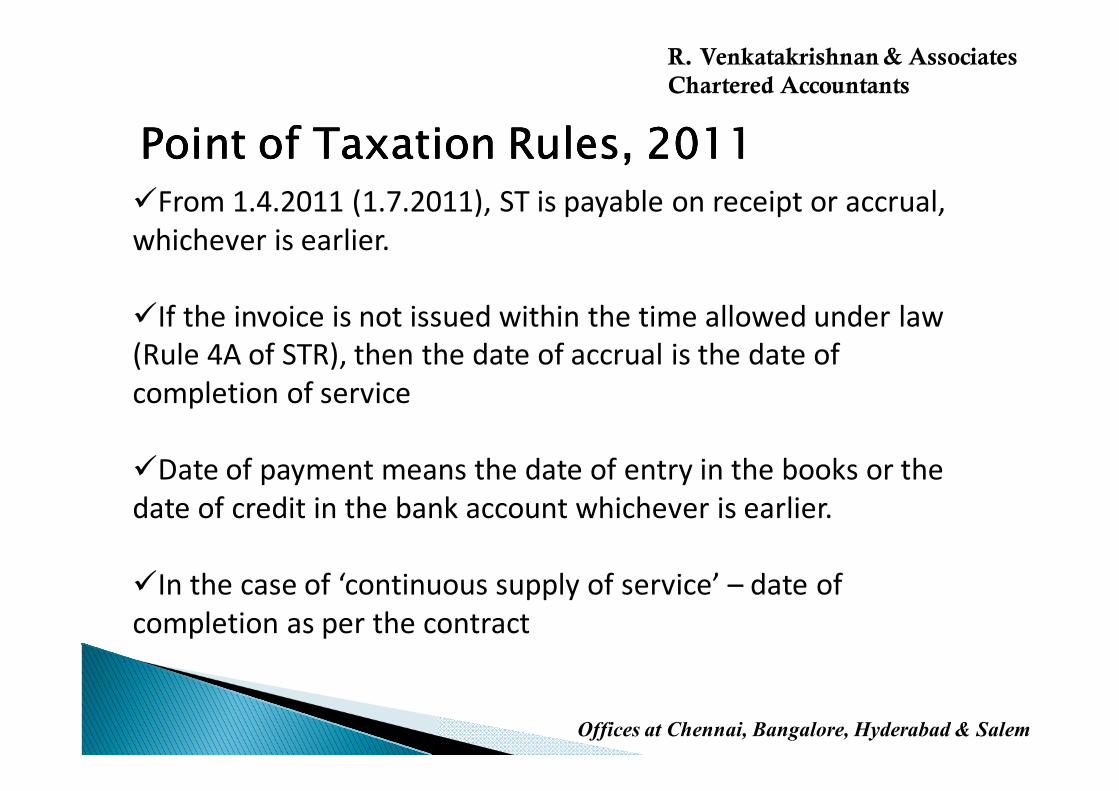

Point of Taxation Rules, 2011Point of Taxation Rules, 2011Point of Taxation Rules, 2011Point of Taxation Rules, 2011

�From 1.4.2011 (1.7.2011), ST is payable on receipt or accrual,

whichever is earlier.

�If the invoice is not issued within the time allowed under law

(Rule 4A of STR), then the date of accrual is the date of

completion of service

�Date of payment means the date of entry in the books or the

date of credit in the bank account whichever is earlier.

�In the case of ‘continuous supply of service’ – date of

completion as per the contract

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

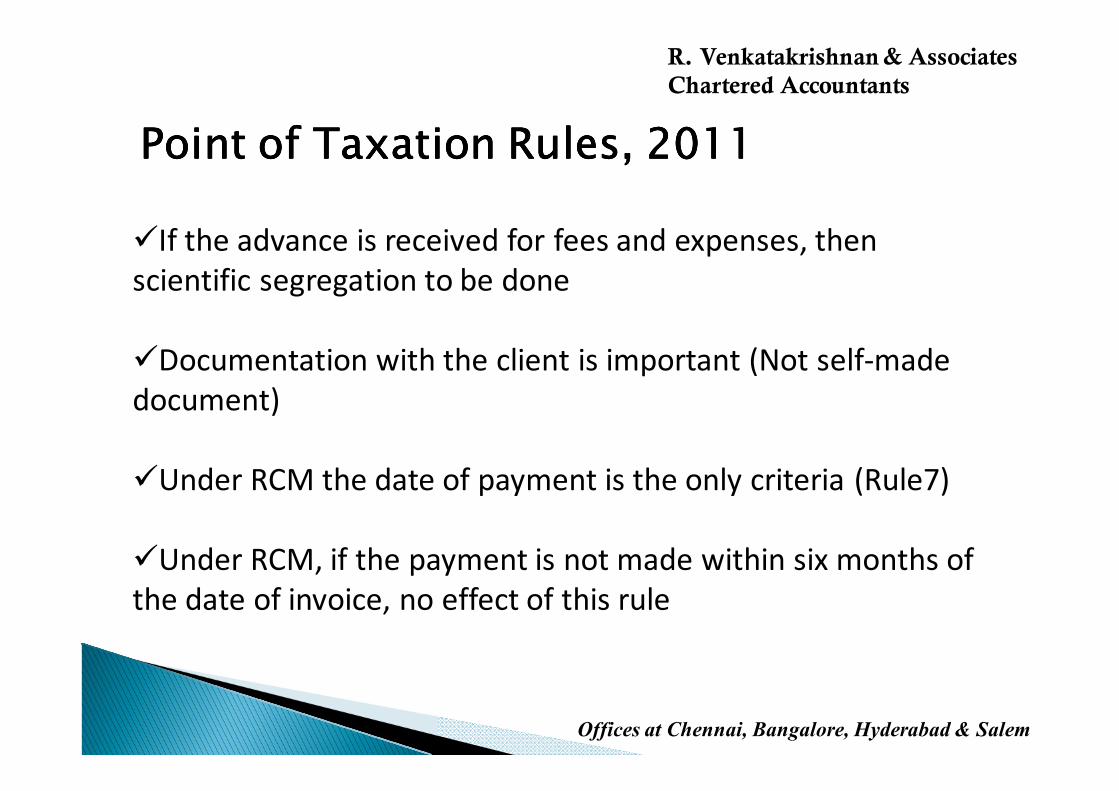

Point of Taxation Rules, 2011Point of Taxation Rules, 2011Point of Taxation Rules, 2011Point of Taxation Rules, 2011

�If the advance is received for fees and expenses, then

scientific segregation to be done

�Documentation with the client is important (Not self-made

document)

�Under RCM the date of payment is the only criteria (Rule7)

�Under RCM, if the payment is not made within six months of

the date of invoice, no effect of this rule

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Point of Taxation Rules, 2011Point of Taxation Rules, 2011Point of Taxation Rules, 2011Point of Taxation Rules, 2011

�In the case of IPR, at the time of payment or invoice,

whichever is earlier.

�Best judgment of CEO

�Invoice raised prior to 1.4.2012 / 1.4.2011 (10.3%) and

payment received after 1.4.2012 (12.36%) – Delhi CA

Society’s case.

�Rate of exchange – Section 67A

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Place of Provision

of Services

Rules, 2012

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Place of Provision of Service Rules, 2012Place of Provision of Service Rules, 2012Place of Provision of Service Rules, 2012Place of Provision of Service Rules, 2012

�Replaces Import and Export Rules

�Default Rule 3 – Location of the service receiver

�Rule 4 – Related to goods – Place of performance of the

service

�Rule 4 – Physical presence of the service receiver – Place of

performance of the service

�Rule 5 – Immovable property – Location of the property

(Present or future)

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Place of Provision of Service Rules, 2012Place of Provision of Service Rules, 2012Place of Provision of Service Rules, 2012Place of Provision of Service Rules, 2012

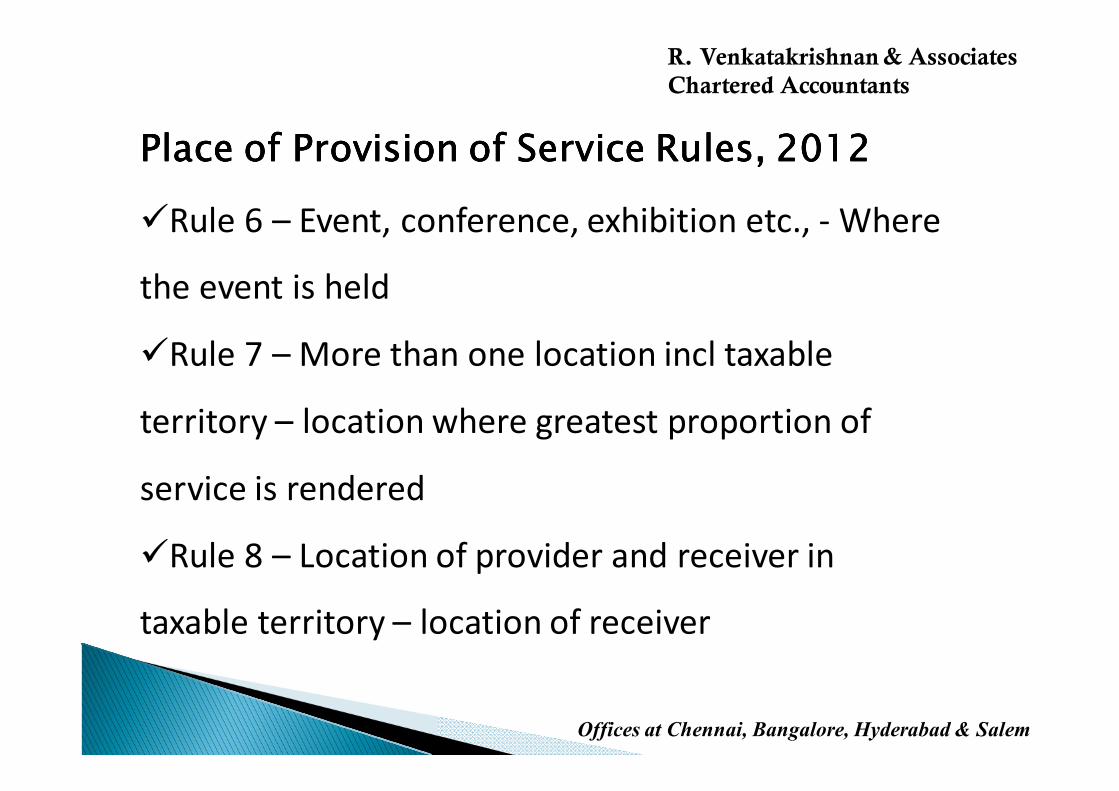

�Rule 6 – Event, conference, exhibition etc., - Where

the event is held

�Rule 7 – More than one location incl taxable

territory – location where greatest proportion of

service is rendered

�Rule 8 – Location of provider and receiver in

taxable territory – location of receiver

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Place of Provision of Service Rules, 2012Place of Provision of Service Rules, 2012Place of Provision of Service Rules, 2012Place of Provision of Service Rules, 2012

�Rule 9 – Location of service provider in the case of –

Banking, financial, NBFC, Online information, Intermediary

services, hiring of transport upto one month

�Rule 10 – Transportation of goods – destination of goods

– exception GTA

�Rule 11 – Passenger transportation – Place of embarking

�Rule 12 – On Board conveyance – First point of departure

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Reverse Charge

Mechanism

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

LEGAL PROVISIONSLEGAL PROVISIONSLEGAL PROVISIONSLEGAL PROVISIONS

�Proviso to Section 68(2) inserted w.e.f. 1.7.2012

�Rule 2(1)(d) – Person liable for paying service tax

�Notification No.30/2012 & 45/2012

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

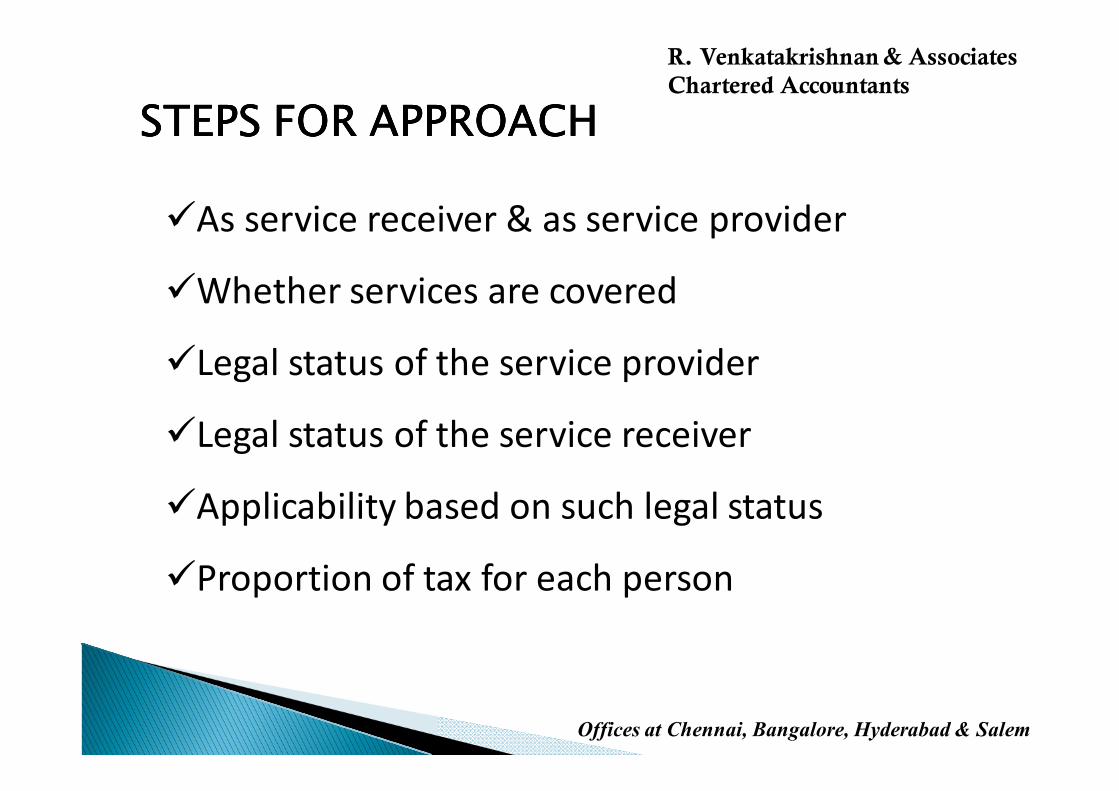

STEPS FOR APPROACHSTEPS FOR APPROACHSTEPS FOR APPROACHSTEPS FOR APPROACH

�As service receiver & as service provider

�Whether services are covered

�Legal status of the service provider

�Legal status of the service receiver

�Applicability based on such legal status

�Proportion of tax for each person

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

AS A SERVICE RECEIVERAS A SERVICE RECEIVERAS A SERVICE RECEIVERAS A SERVICE RECEIVER

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

AS A SERVICE PROVIDERAS A SERVICE PROVIDERAS A SERVICE PROVIDERAS A SERVICE PROVIDER

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

CERTAIN REFLECTIONSCERTAIN REFLECTIONSCERTAIN REFLECTIONSCERTAIN REFLECTIONS

�No threshold exemption

�Different valuation method for works contract

�Wider definition of security services

�Confusion on manpower supply services

�Services by directors

�Exemptions for metered taxis, radio taxis and

auto rickshaws

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

CERTAIN REFLECTIONSCERTAIN REFLECTIONSCERTAIN REFLECTIONSCERTAIN REFLECTIONS

�Accounting through sub-ledgers

�Non eligibility of CENVAT credit for payment

�Due based on date of payment and not date of

invoice / accounting

�CENVAT credit only after payment

�Correct proportion of tax

�Effect of excess charge – for both persons

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

CERTAIN REFLECTIONSCERTAIN REFLECTIONSCERTAIN REFLECTIONSCERTAIN REFLECTIONS

�Failure to deduct by Service receiver

�Failure by service provider to pay his proportion

of tax

�Individual Vs Business entity

�Body corporate Vs Company

�Firm and LLP

�Amendment of registration certificate

�Accounting code in Challan

�Does not apply to services rendered prior to

1.7.2012

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Exercise 3

Simulation for

Reverse Charge

Mechanism

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Q. HolidayQ Pvt Ltd. Intends to file a suit against

‘Radio Two’, a popular English Radio channel in

Bangalore for defaming the hotel service on Air. To

know whether they can file such suit, HolidayQ

approaches ABC & Co, a firm of consultants. For this

service, ABC & Co charges Rs. 10,000

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Q. Lakeview Hotel Pvt Ltd. Had filed an appeal

with the Commissioner of Service tax in relation

to a earlier years refund case. The appeal was

rejected by the Commissioner. To challenge this,

the hotel approached M/s PQR, Chartered

Accountants, wherein Mr. Q, the partner will

represent the hotel at the CESTAT. For one

appearance the fee is Rs. 40,000

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Q. XYZ Hotels Pvt Ltd., approached ICICI

Bank for a loan of Rs. 50 Cr. ICICI agreed to

give the loan only on the condition that Mr.

A, manager at ICICI, should be appointed as

a Nominee director at XYZ Hotel.

Subsequently Mr. A is appointed as a

Director and is paid sitting fees of Rs.

10,000 for every meeting

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Q. Mr. T, director of the company travels to

Australia for a Business Trip. As per the company

policy Mr. T will be paid a per diem of $100

everyday during his stay in Australia. Mr. T

spends on an average $70 per day and the rest is

shown as an Income in his income tax returns

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Q. Mr. R, non executive director of UV Hotels Pvt

Ltd, arranges a business meet for foreign

investors at KP Restaurant. The meet is followed

with dinner, expenses for the same is paid by

Mr. R. The food bill was raised on Mr. R’s name.

Mr. R in turn gets the expenses reimbursed from

the company.

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Q. Mr. KT, a prominent engineer of BDA was

provided a Guest house facility by the authority.

For this guest house, “MAC security agency” is

providing security services. On a monthly basis,

an invoice for Rs. 15,000 in the favour of BDA is

raised by MAC and payment for the same is

made by BDA

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Q. Mr. I, an insurance agent from GIC, arranges for

fire insurance policy for ST Hotels Pvt. Ltd. Mr. I is

also practicing as an insurance consultant after

office hours. For suggesting a good fire insurance

policies to ST Hotels, Mr. I charges Rs. 5,000 as an

insurance consultant fee

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Q. Mr. Sidda after being elected as the chief

ministers decides to provide all its minsters with

a BMW Car. This car is rented out from a local

dealer for a period of 5 years. Rental invoice for

the same is raised on a monthly basis.

What if the driver for the same is also provided

by the local dealer?

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Q. Auditors of TRK hotels have commenced the

statutory audit for the F.Y 2012-2013. For travelling to

the hotel for audit, the auditors have arranged for a

cab facility. The total transportation cost is initially

paid by the auditor and then reimbursed from the

hotel after is audit is over.

Whether there will be any change in provisions if the

above cost is included in the audit bill as out of pocket

expenses.

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Q. ‘Vget’ Hotel Pvt Ltd. has decided to revamp

its operations by shifting from a Normal Hotel

to a Business Hotel. To execute this they have

incurred heavy expenses for changing the room

set up to a Business Centre/Conference room

set up. Also they have applied for conversion of

their company to LLP.

For the revamping, they are incurring various

civil work costs.

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Q. M/s JTFS, Chartered Accountants have been

requested by its Client JTR Hotels for either of the

below arrangements.

1. Mr. K an employee of CA firm will visit the JTR hotels

twice in a week and review their accounts and issue a

report containing his observations; or

2. Mr. K will be placed full time at JTR and report to the

Manager (Accounts). In addition to reviewing the

accounts and issuing observations, he will also attend

to other work given to him by the Manager (Accounts)

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Q. Mr. TKT, a travel agent in Malaysia has

entered into an agreement with ‘KLF Hotel Pvt

Ltd’ in India. As per the agreement, the agent

will promote the hotel in Malaysia and would

book rooms for Visitors who are travelling to

India. For these services, the agent is charging

5% commission on a monthly basis based on the

number of rooms booked by him.

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Certain new

provisions

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

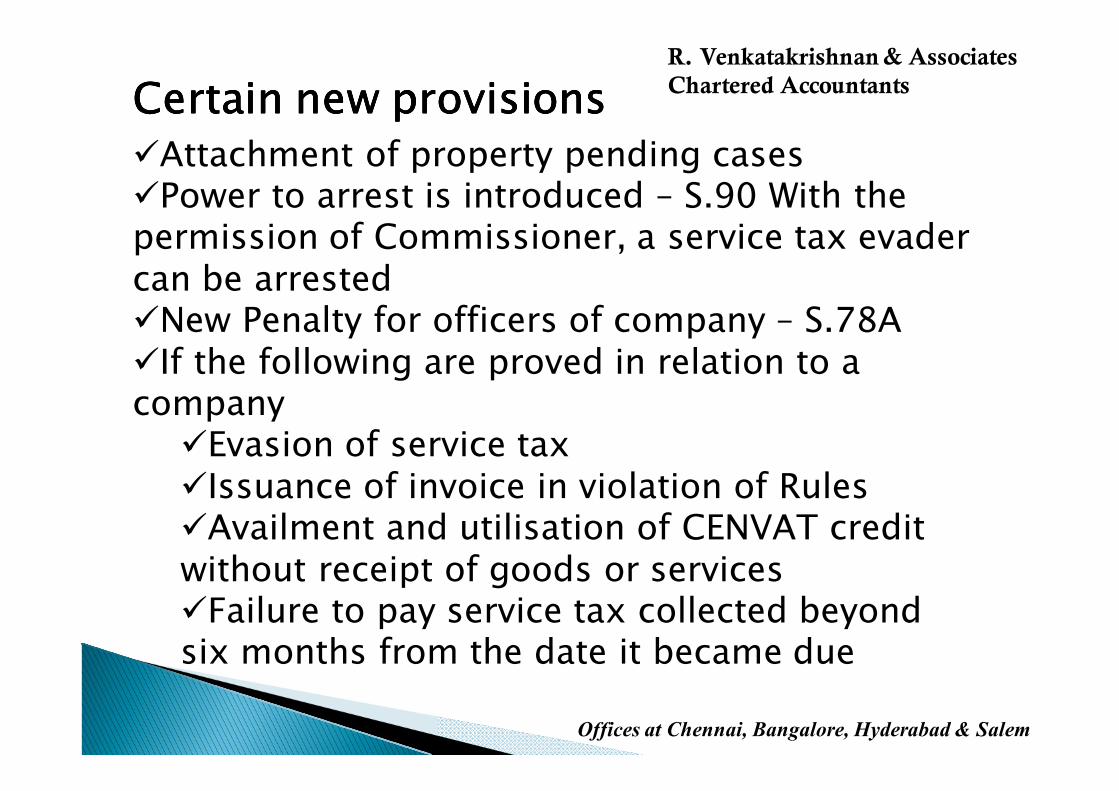

Certain new provisionsCertain new provisionsCertain new provisionsCertain new provisions

�Attachment of property pending cases�Power to arrest is introduced – S.90 With the permission of Commissioner, a service tax evader can be arrested�New Penalty for officers of company – S.78A�If the following are proved in relation to a company

�Evasion of service tax�Issuance of invoice in violation of Rules�Availment and utilisation of CENVAT credit without receipt of goods or services�Failure to pay service tax collected beyond six months from the date it became due

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Certain new provisions Certain new provisions Certain new provisions Certain new provisions –––– Cont’d.,Cont’d.,Cont’d.,Cont’d.,

�Then the following officers are liable for penalty

�Any director

�Manager

�Secretary

�Other officer of the company,

�Who was responsible at the time of

contravention

�Was knowingly concerned about the

contravention

�Penalty upto a maximum of Rs.1 Lakh

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

SERVICE TAX FOR

HOSPITALITY INDUSTRY

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Various Category of output ServicesVarious Category of output ServicesVarious Category of output ServicesVarious Category of output Services

�Renting of rooms for a period less than 3

months with a daily rent in excess of

Rs.1,000/- Taxed at 60%

�Restaurant Services– Taxed at 40%

�Banquets – Taxed @ 70%

�Taxi Services – Taxed @ 40%

�Other services – Taxed fully

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Renting of Hotel, Inn, Guest Renting of Hotel, Inn, Guest Renting of Hotel, Inn, Guest Renting of Hotel, Inn, Guest HouseHouseHouseHouse

& & & &

Restaurant Services Restaurant Services Restaurant Services Restaurant Services

& & & &

Banquet ServicesBanquet ServicesBanquet ServicesBanquet Services

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

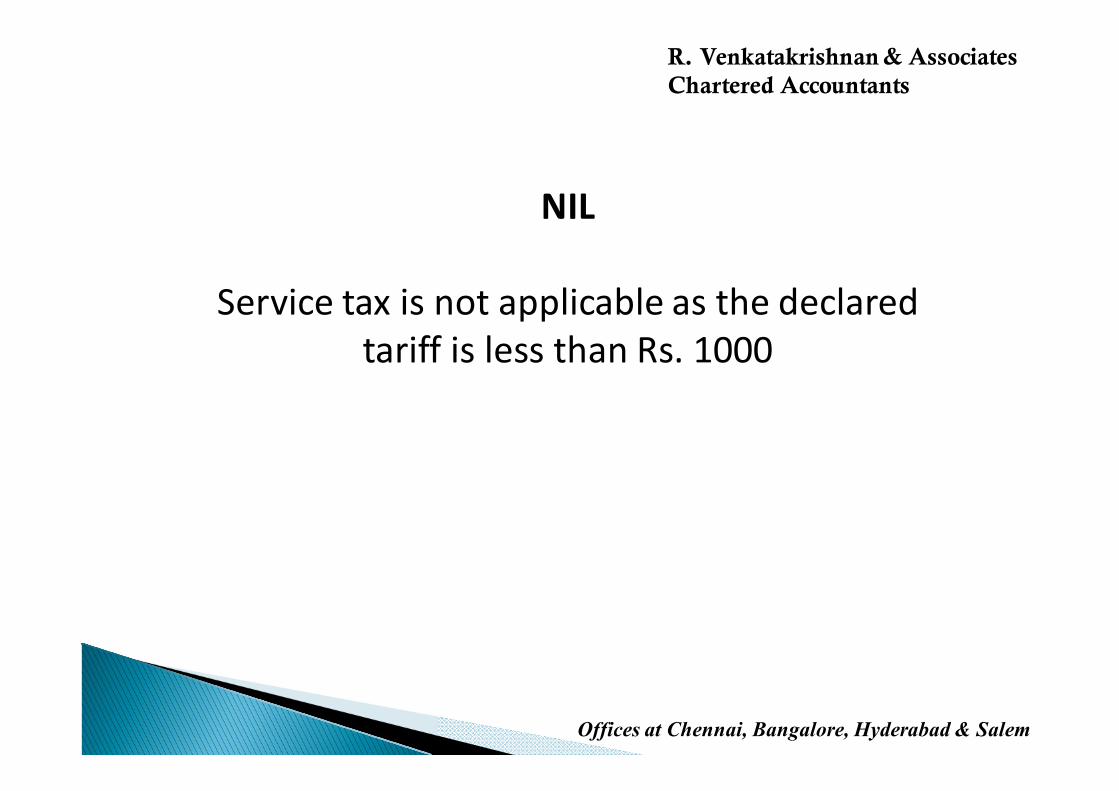

Q. On what rate, service tax is charged?

Case 1: Case 1: Case 1: Case 1:

Declared tariff – 900

Actual room rent charged – 800

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

NIL

Service tax is not applicable as the declared

tariff is less than Rs. 1000

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Q. On what rate, service tax is charged?

Case 2: Case 2: Case 2: Case 2:

Declared tariff – 1,200

Actual room rent charged – 1,100

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Rs 1,100

As the actual amount charged is Rs. 1,100

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

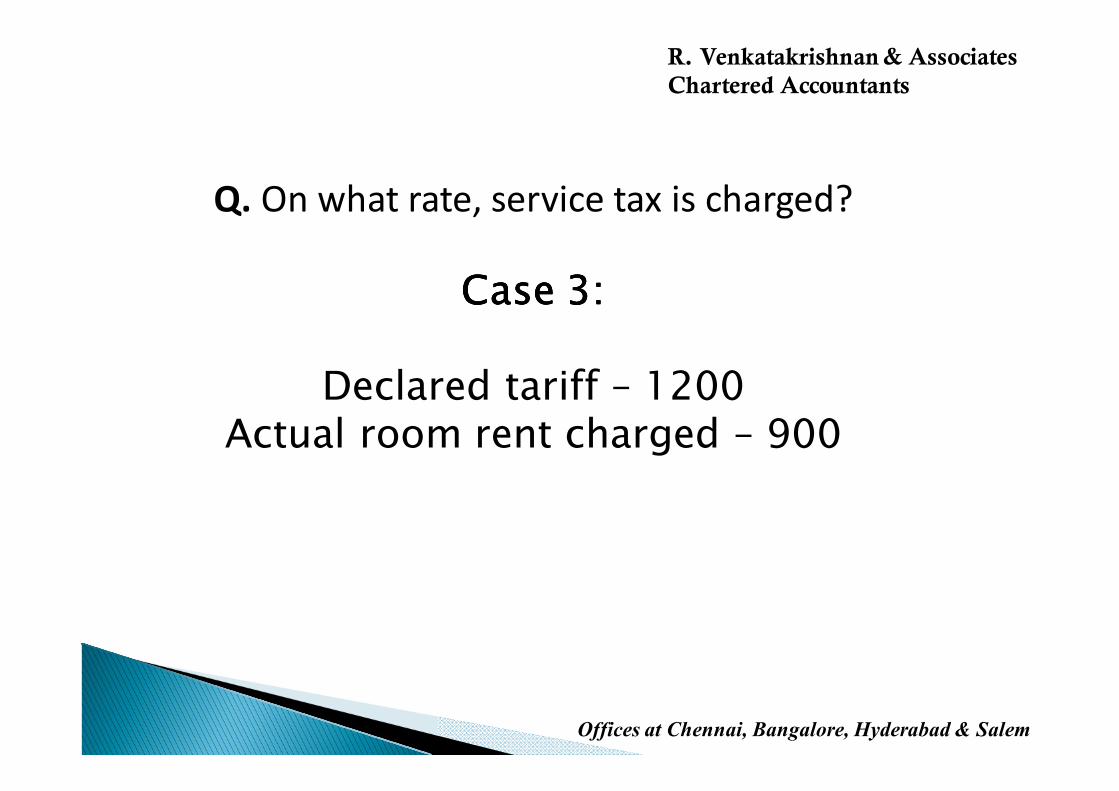

Q. On what rate, service tax is charged?

Case 3: Case 3: Case 3: Case 3:

Declared tariff – 1200Actual room rent charged – 900

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

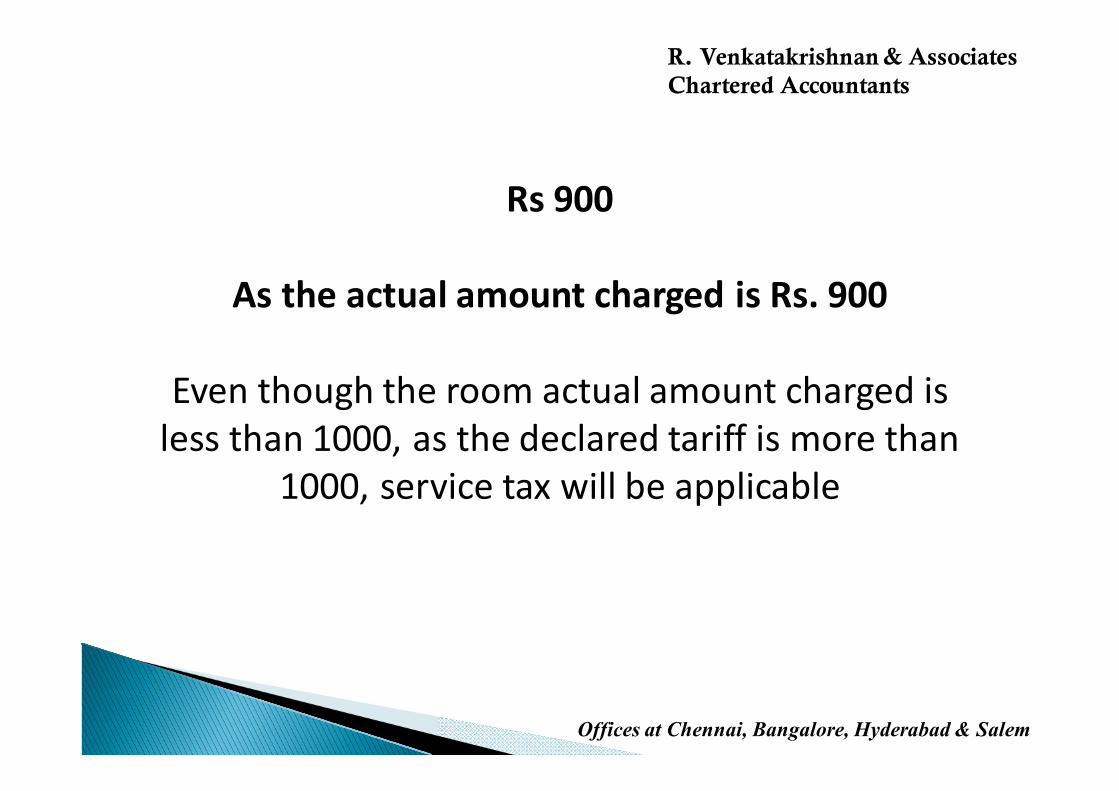

Rs 900

As the actual amount charged is Rs. 900

Even though the room actual amount charged is

less than 1000, as the declared tariff is more than

1000, service tax will be applicable

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Bundled Service Bundled Service Bundled Service Bundled Service –––– Ex.1Ex.1Ex.1Ex.1

Complimentary breakfast or lunch provided with

the Room Stay. What is the rate of Service Tax?

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Bundled Service Bundled Service Bundled Service Bundled Service –––– Ex.1Ex.1Ex.1Ex.1

As the Essential character is accommodation

service. Thus, this will be taxed under

accommodation service at 60%

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Bundled Service – Ex 2

ABC Hotels provides a 4D/3N package with

the facility of breakfast. What is the nature of

Service

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Bundled Service – Ex 2

This is the case of natural bundling of service

in the ordinary course of Business wherein

hotel accommodation gives the bundle the

essential character and therefore will be taxed

under accommodation service

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Bundled Service – Ex 3

KPM Hotels undertakes a booking for a

conference of 100 delegates on a lump sum

package with the following facilities

�Accommodation for the delegates

�Breakfast for the delegates

�Tea and Coffee during conference

�Access to fitness room for the delegates

�Availability of conference room

�Business Centre

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Bundled Service – Ex 3

�The above services are chargeable to different tax

rates

�None of them are able to provide the essential

character of service.

�However, the above service can be described as

convention centre and to be taxed at full rate

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Q. Q. Q. Q. Whether Service Tax is applicable on no-show

charges, retention charges, penalties etc charged

to the customer

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

�No show, retention charges, penalties etc are

charged for non – fulfillment of the commitment of

the guest.

�Service tax will be applicable as It is a forfeited

deposits.

�Represent consideration for the agreement that

was entered into for provision of service.

�No abatement

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Q. Whether Service Tax is applicable on

damages recovered on account of

damage to property by the customer

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

�Valuation rule exclude amount received in the

nature of accidental damages due to unforeseen

action not relatable to the provision of service

�Thus such amount recovered will not attract tax

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Guest House facilities to employeesGuest House facilities to employeesGuest House facilities to employeesGuest House facilities to employees

It’s a transaction between employer and employee in

the course of employment. Hence, no taxable services

are rendered by the company concerned

Further, it is a Perk which is part of salary hence

excluded from the definition of service.

If a branch / division is charged for the facilities used

by the employees of the branch / division, then there

is no tax on self-service.

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Q. Whether Guest House facilities provided

to

Non-employees is Taxable?

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

�Employees of various group companies stay in the said

guest house and bills are raised on the group companies.

�Taxable service of short term accommodation is

provided by one person to another person.

�Tax is payable even if the amount recovered is on cost

basis.

�If it is provided free of cost, there is no monetary

consideration and hence no service / service tax.

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Guest House / Rooms provided free

of cost to selected people

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

�Services are provided free of cost for commercial

purposes

�There is no monetary consideration

�There is no service tax

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Group discount / Quantity discountGroup discount / Quantity discountGroup discount / Quantity discountGroup discount / Quantity discount

�In case of quantity discounts given for providing

high volume business, service tax will be payable

only on the amount received by hotel on such short

term accommodation.

�If a credit note is issued at the end of the year for

volume, then Service tax credit can also be

extended.

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Whether Service Tax is to be

charged on Room Service

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Under the erstwhile regime, services provided by a restaurant

with an air-conditioned facility and a license to serve liquor on

its premises (and not in a hotel’s rooms) attracted Service Tax.

Furthermore, it was clarified in Circular 139/8/2011 – TRU dated

10 May 2011 that food served in a room would not be liable to

Service Tax under “accommodation services” or “restaurant

services.”

From 1 July 2012, the list of declared services includes a “service

portion in an activity wherein goods, being food or any other

article of human consumption or any drink (whether or not

intoxicating) is supplied in any manner as a part of the activity.”

Hence, under the Negative List regime, dining in a hotel room

should qualify as a taxable service.

cont’d

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Rule 2C of the Valuation Rules stipulates that the value of a service portion in any activity involving

supply of food, drink, etc., in a restaurant is 40% of the total amount charged.

Whether the valuation mechanism under Rule 2C can be applied to food and beverages provided in room, or whether in-room dining could attract Service Tax on full value (since identification of actual value of

service may be difficult)

We are of the view that service tax needs to be charged at full rate for food & beverage supplied in

room service. In other words, “no abatement”

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Whether Service tax is to be

charged on take away or parcel

services

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Circular dated 28.02.2011 clarified that on mere sale

of food by way of pick – up or home delivery, no

service tax would be attracted.

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Whether Service tax is to be Whether Service tax is to be Whether Service tax is to be Whether Service tax is to be

charged on Service Chargescharged on Service Chargescharged on Service Chargescharged on Service Charges

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

�No service tax is not to be charged on service

charges as the amount received doesn’t constitute

any consideration for the hotel.

�However, if any % of amount is retained by the

hotel and balance is distributed to the waiters then

service tax needs to be charged on service charges

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

If service tax on service charge is

applicable then at what % will it

be charged?

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

If service tax is applicable on service charges, then service tax will be charged at

12.36%

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Whether Luxury Tax should Included

for the purpose of determining the

room rent

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

For the purpose of service tax luxury tax has

to be excluded from the taxable value

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Whether recovery of electricity,

water charges, maintenance will

form part of value of taxable

services?

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Recovery of Electricity, Water charges will form

part of value of taxable services on or after 1st July,

2012. However, it was held in Econ Hinjewadi

Infrstructure(P) Ltd v/s CCE (Mum – CESTAT) that

electricity is goods, thus service tax will should not

be charged on the same

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Whether the service provider

can claim the benefit of

Property Tax paid on the

Immovable property

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Yes, the service provider can reduce the

amount of property tax paid from the

taxable value of service and charge tax only

on the balance portion of tax

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Rent a cab Services/Renting of Motor

Vehicle to a person not engaged in

similar line of business

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Ex. for Renting of Motor Vehicle

Mr. X and Firm Y are both engaged in the business

of renting of motor vehicle. Mr. X does not own

any motor vehicle, but Firm Y owns 5 cars. Mr. X

takes 2 cars from Firm Y on hire, and then rents it

out to Mr. Z. In this case, both Mr X and Firm Y

will be treated as a provider of renting of motor

vehicle service

Note: Ownership of vehicle is not a requirement

for renting out motor Vehicle

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Is it compulsory that the service

provider should be in the business of

renting of Motor Vehicle

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

No, there is not stipulation that the service

provider shall be engaged in business of

renting of motor vehicle.

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Whether the purpose of Renting out is

Relevant?

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

No, the purpose of renting out is not relevant

as it can be rented out for any purpose

ranging from private journeys or for

commercial trips

R. Venkatakrishnan & Associates

Chartered Accountants

Amnesty Scheme

2013

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

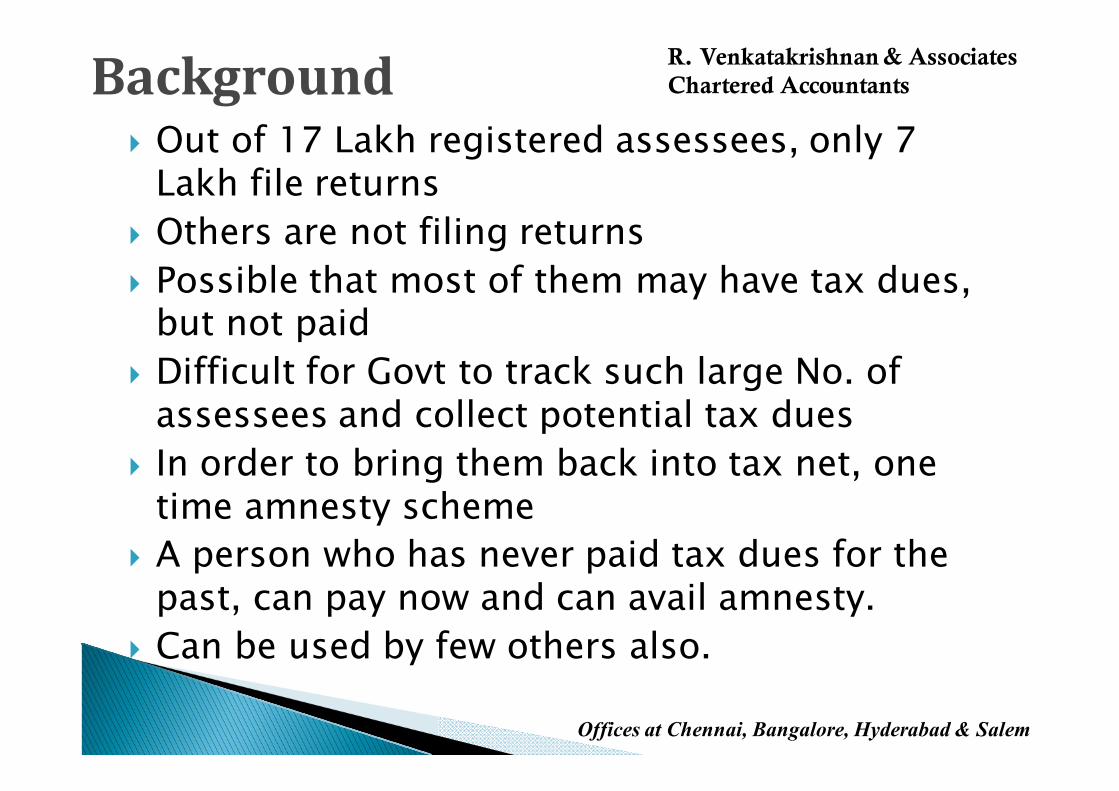

� Out of 17 Lakh registered assessees, only 7 Lakh file returns

� Others are not filing returns

� Possible that most of them may have tax dues, but not paid

� Difficult for Govt to track such large No. of assessees and collect potential tax dues

� In order to bring them back into tax net, one time amnesty scheme

� A person who has never paid tax dues for the past, can pay now and can avail amnesty.

� Can be used by few others also.

Background

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

� Name – Service tax voluntary compliance encouragement scheme, 2013 (SVCES 2013)

� Introduced for the first time in service tax history

� Current special scheme for slashing of penalty to 25% is continuing and is independent of this scheme.

Features

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

� Applicable to all types of persons who are◦ Unregistered and not paid tax at all

◦ Registered but not declared tax at all

◦ Registered but not declared tax partly

Applicability

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

� Will also cover instances where there was short payment due to◦ Difference in valuation of service◦ Clerical error◦ Excess / wrong CENVAT credit availed due to any reason◦ Due to interpretation issues◦ Audit etc., completed by the Department in the past, but has not found out the non payment◦ Non payment of tax on import of services◦ Non payment of tax under new reverse charge w.e.f. 1.7.2012

Scope of Applicable

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

� Covers tax dues for the period from 1.10.2007 to 31.12.2012

� Immunity from interest, penalty and other proceedings, once the declared taxes are paid.

APPLICABILITY – Time & Extent

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

Default of payment is notnotnotnot found out by the Dept till 31.1.2013. – It means � No Show cause notice has been issued

� No search has been conducted

� No communication seeking any type of information has been sent

� No investigation procedure has been conducted

� No order has been issued determining the tax payable

� No audit is under process

Exclusions

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

� Where return was already filed declaring the tax payable, but tax remains unpaid.

� Where the Department has already detected a non payment on a specific issue, for some part of the period, this scheme cannot be used for the balance period for the same issue.

� For any taxes due from 1.1.2013 for the same issues.

Ineligibility

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

� Prepare the calculations, get it verified and check the applicability of the scheme

� Assessee to make an application

� Last date for making application – 31.12.13

� 50% of the declared tax should be paid before 31.12.13

� Without payment of this 50% also, declaration can be filed earlier to 31.12.13. But the tax should be subsequently paid before 31.12.13

� Balance 50% to be paid on or before 30.6.14

Procedure

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

� It is also possible to pay the balance 50% tax by 31.12.14, along with interest of 18% p.a.

� Interest is applicable from 1.7.14 only.

� It is possible to make payment on various dates in installments, but the entire payments should be made within the specific dates.

� After payment of all the taxes, the Department will issue a certificate of discharge.

Remittance of Taxes

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

� No refund shall be issued for any taxes paid under this scheme.

� When the declared taxes are not paid, it is recoverable along with interest. But penalty is not applicable.

� When the declaration is substantiallysubstantiallysubstantiallysubstantially false, a show cause notice will be issued and declaration can be rejected by the Department.

� In such a case, penalty proceedings will be applicable

� But the show cause notice should be issued within one year from the date of filing the declaration.

Other Issues

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

� If any other show cause notice etc., is issued, between March 1st & December 31st - whether an assessee can avail this option?

� Status if the Department rejects the application of the assessee, for reasons other than false declaration? Whether penalty is not applicable, because it is a voluntary declaration?

� Whether the scheme is available to a person, who is registered, paid all the taxes, but not filed returns, either for some period or all periods? (To save penalty for non filing of returns).

Scheme Requires Clarity

On..

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

� Amendment to declaration - After making the declaration, whether a person can increase or decrease the declaration amount?

� Withdrawal - After making the declaration, whether a person can withdraw the declaration for genuine reasons?

Clarifications Required on..

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

� After declaring, if the Department rejects the application, what happens?◦ Tax is definitely payable.

◦ Interest will also become payable

◦ The Department will also levy penalty stating that it is not a voluntary disclosure, but for this scheme and may levy penalty under various sections

◦ But all these can be challenged by the assessee.

Issues – Rejection of Application

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

� No time limit specified for the Department to reject the application.

� However, such rejection cannot happen after the certificate of discharge is issued.

Closure

R. Venkatakrishnan & Associates

Chartered Accountants

Offices at Chennai, Bangalore, Hyderabad & Salem

� The Government is being approached with queries for seeking clarifications on this scheme

� Will have to wait and watch

Clarifications in pipeline

R. Venkatakrishnan & Associates

Chartered Accountants

Chennai

+91 44 24618778 / 24618740

Bangalore

+91 80 23418753

Hyderabad

+91 40 66620039 / 27611565

Salem

+91 42 74554458

http://www.rvkassociates.comhttp://www.rvkassociates.comhttp://www.rvkassociates.comhttp://www.rvkassociates.com

Related Documents