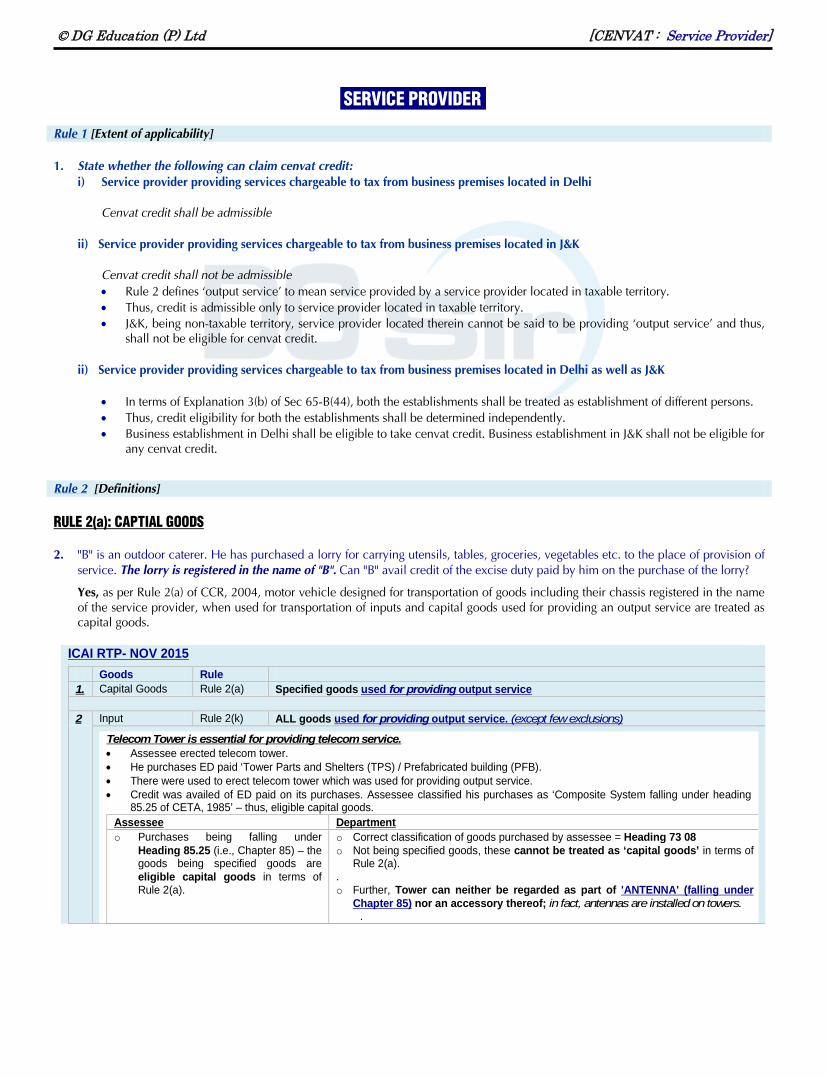

© DG Education (P) Ltd [CENVAT : Service Provider] SERVICE PROVIDER: Rule 1 [Extent of applicability] 1. State whether the following can claim cenvat credit: i) Service provider providing services chargeable to tax from business premises located in Delhi Cenvat credit shall be admissible ii) Service provider providing services chargeable to tax from business premises located in J&K Cenvat credit shall not be admissible • Rule 2 defines ‘output service’ to mean service provided by a service provider located in taxable territory. • Thus, credit is admissible only to service provider located in taxable territory. • J&K, being non-taxable territory, service provider located therein cannot be said to be providing ‘output service’ and thus, shall not be eligible for cenvat credit. ii) Service provider providing services chargeable to tax from business premises located in Delhi as well as J&K • In terms of Explanation 3(b) of Sec 65-B(44), both the establishments shall be treated as establishment of different persons. • Thus, credit eligibility for both the establishments shall be determined independently. • Business establishment in Delhi shall be eligible to take cenvat credit. Business establishment in J&K shall not be eligible for any cenvat credit. Rule 2 [Definitions] RULE 2(a): CAPTIAL GOODS 2. "B" is an outdoor caterer. He has purchased a lorry for carrying utensils, tables, groceries, vegetables etc. to the place of provision of service. The lorry is registered in the name of "B". Can "B" avail credit of the excise duty paid by him on the purchase of the lorry? Yes, as per Rule 2(a) of CCR, 2004, motor vehicle designed for transportation of goods including their chassis registered in the name of the service provider, when used for transportation of inputs and capital goods used for providing an output service are treated as capital goods. ICAI RTP- NOV 2015 . Goods Rule 1. Capital Goods Rule 2(a) Specified goods used for providing output service 2 Input Rule 2(k) ALL goods used for providing output service. (except few exclusions) Telecom Tower is essential for providing telecom service. • Assessee erected telecom tower. • He purchases ED paid ‘Tower Parts and Shelters (TPS) / Prefabricated building (PFB). • There were used to erect telecom tower which was used for providing output service. • Credit was availed of ED paid on its purchases. Assessee classified his purchases as ‘Composite System falling under heading 85.25 of CETA, 1985’ – thus, eligible capital goods. Assessee Department o Purchases being falling under Heading 85.25 (i.e., Chapter 85) – the goods being specified goods are eligible capital goods in terms of Rule 2(a). o Correct classification of goods purchased by assessee = Heading 73 08 o Not being specified goods, these cannot be treated as ‘capital goods’ in terms of Rule 2(a). . o Further, Tower can neither be regarded as part of 'ANTENNA' (falling under Chapter 85) nor an accessory thereof; in fact, antennas are installed on towers. .

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

© DG Education (P) Ltd [CENVAT : Service Provider]

SERVICE PROVIDER: Rule 1 [Extent of applicability] 1. State whether the following can claim cenvat credit:

i) Service provider providing services chargeable to tax from business premises located in Delhi Cenvat credit shall be admissible

ii) Service provider providing services chargeable to tax from business premises located in J&K

Cenvat credit shall not be admissible • Rule 2 defines ‘output service’ to mean service provided by a service provider located in taxable territory. • Thus, credit is admissible only to service provider located in taxable territory. • J&K, being non-taxable territory, service provider located therein cannot be said to be providing ‘output service’ and thus,

shall not be eligible for cenvat credit.

ii) Service provider providing services chargeable to tax from business premises located in Delhi as well as J&K • In terms of Explanation 3(b) of Sec 65-B(44), both the establishments shall be treated as establishment of different persons. • Thus, credit eligibility for both the establishments shall be determined independently. • Business establishment in Delhi shall be eligible to take cenvat credit. Business establishment in J&K shall not be eligible for

any cenvat credit.

Rule 2 [Definitions] RULE 2(a): CAPTIAL GOODS 2. "B" is an outdoor caterer. He has purchased a lorry for carrying utensils, tables, groceries, vegetables etc. to the place of provision of

service. The lorry is registered in the name of "B". Can "B" avail credit of the excise duty paid by him on the purchase of the lorry?

Yes, as per Rule 2(a) of CCR, 2004, motor vehicle designed for transportation of goods including their chassis registered in the name of the service provider, when used for transportation of inputs and capital goods used for providing an output service are treated as capital goods.

ICAI RTP- NOV 2015 .

Goods Rule 1. Capital Goods Rule 2(a) Specified goods used for providing output service 2 Input Rule 2(k) ALL goods used for providing output service. (except few exclusions)

Telecom Tower is essential for providing telecom service. • Assessee erected telecom tower. • He purchases ED paid ‘Tower Parts and Shelters (TPS) / Prefabricated building (PFB). • There were used to erect telecom tower which was used for providing output service. • Credit was availed of ED paid on its purchases. Assessee classified his purchases as ‘Composite System falling under heading

85.25 of CETA, 1985’ – thus, eligible capital goods. Assessee Department o Purchases being falling under

Heading 85.25 (i.e., Chapter 85) – the goods being specified goods are eligible capital goods in terms of Rule 2(a).

o Correct classification of goods purchased by assessee = Heading 73 08 o Not being specified goods, these cannot be treated as ‘capital goods’ in terms of

Rule 2(a). . o Further, Tower can neither be regarded as part of 'ANTENNA' (falling under

Chapter 85) nor an accessory thereof; in fact, antennas are installed on towers. .

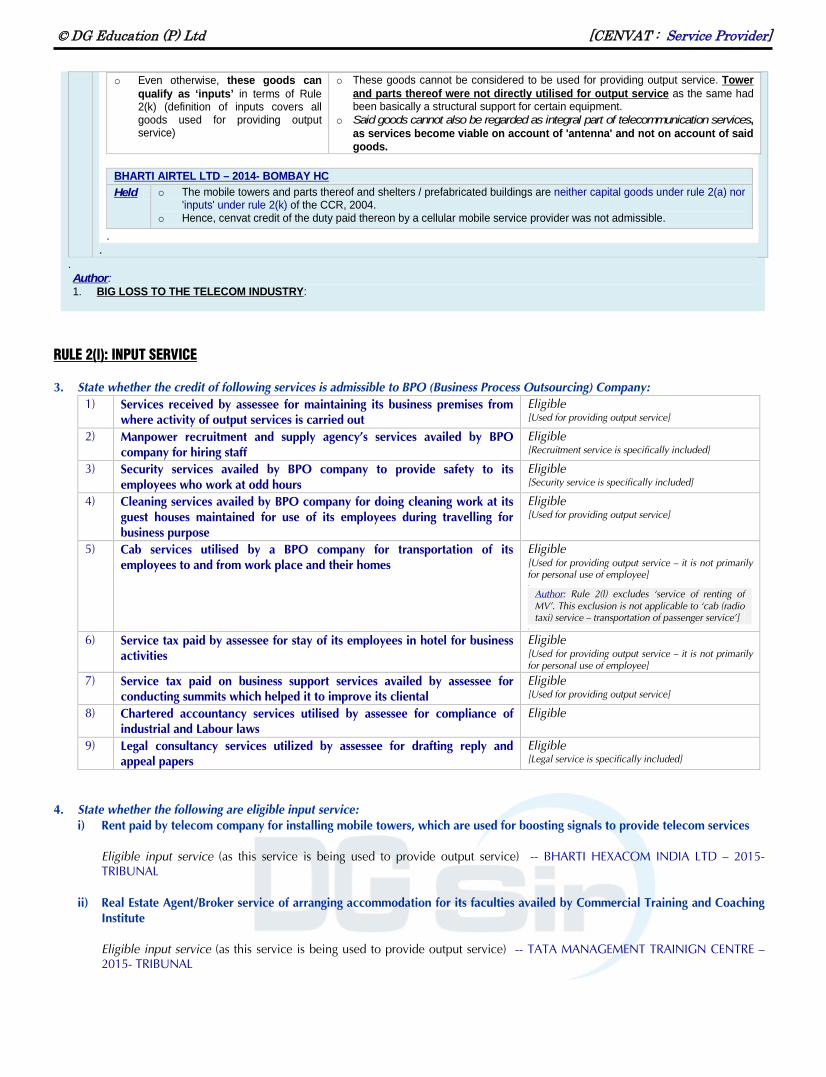

© DG Education (P) Ltd [CENVAT : Service Provider]

o Even otherwise, these goods can qualify as ‘inputs’ in terms of Rule 2(k) (definition of inputs covers all goods used for providing output service)

o These goods cannot be considered to be used for providing output service. Tower and parts thereof were not directly utilised for output service as the same had been basically a structural support for certain equipment.

o Said goods cannot also be regarded as integral part of telecommunication services, as services become viable on account of 'antenna' and not on account of said goods.

BHARTI AIRTEL LTD – 2014- BOMBAY HC Held o The mobile towers and parts thereof and shelters / prefabricated buildings are neither capital goods under rule 2(a) nor

'inputs' under rule 2(k) of the CCR, 2004. o Hence, cenvat credit of the duty paid thereon by a cellular mobile service provider was not admissible.

. .

. Author: 1. BIG LOSS TO THE TELECOM INDUSTRY:

RULE 2(l): INPUT SERVICE 3. State whether the credit of following services is admissible to BPO (Business Process Outsourcing) Company:

1) Services received by assessee for maintaining its business premises from where activity of output services is carried out

Eligible [Used for providing output service]

2) Manpower recruitment and supply agency’s services availed by BPO company for hiring staff

Eligible [Recruitment service is specifically included]

3) Security services availed by BPO company to provide safety to its employees who work at odd hours

Eligible [Security service is specifically included]

4) Cleaning services availed by BPO company for doing cleaning work at its guest houses maintained for use of its employees during travelling for business purpose

Eligible [Used for providing output service]

5) Cab services utilised by a BPO company for transportation of its employees to and from work place and their homes

Eligible [Used for providing output service – it is not primarily for personal use of employee] .

Author: Rule 2(l) excludes ‘service of renting of MV’. This exclusion is not applicable to ‘cab (radio taxi) service – transportation of passenger service’]

.

6) Service tax paid by assessee for stay of its employees in hotel for business activities

Eligible [Used for providing output service – it is not primarily for personal use of employee]

7) Service tax paid on business support services availed by assessee for conducting summits which helped it to improve its cliental

Eligible [Used for providing output service]

8) Chartered accountancy services utilised by assessee for compliance of industrial and Labour laws

Eligible

9) Legal consultancy services utilized by assessee for drafting reply and appeal papers

Eligible [Legal service is specifically included]

4. State whether the following are eligible input service:

i) Rent paid by telecom company for installing mobile towers, which are used for boosting signals to provide telecom services Eligible input service (as this service is being used to provide output service) -- BHARTI HEXACOM INDIA LTD – 2015- TRIBUNAL

ii) Real Estate Agent/Broker service of arranging accommodation for its faculties availed by Commercial Training and Coaching

Institute Eligible input service (as this service is being used to provide output service) -- TATA MANAGEMENT TRAINIGN CENTRE – 2015- TRIBUNAL

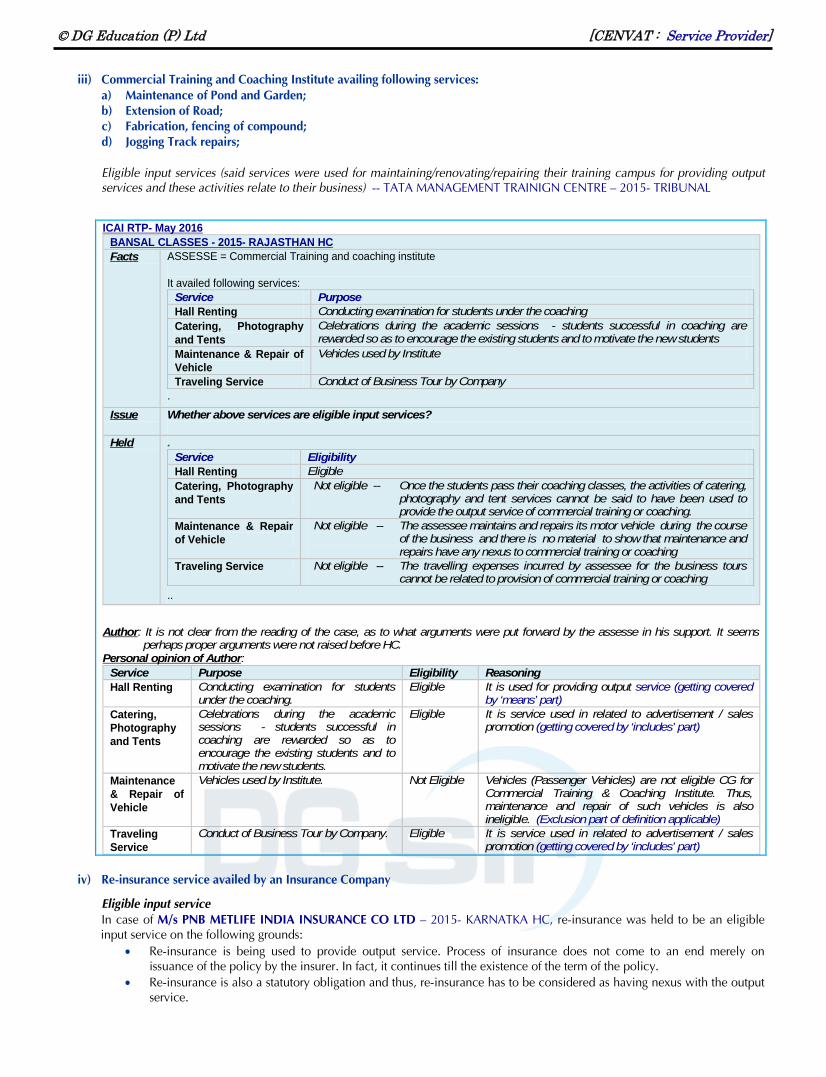

© DG Education (P) Ltd [CENVAT : Service Provider]

iii) Commercial Training and Coaching Institute availing following services: a) Maintenance of Pond and Garden; b) Extension of Road; c) Fabrication, fencing of compound; d) Jogging Track repairs; Eligible input services (said services were used for maintaining/renovating/repairing their training campus for providing output services and these activities relate to their business) -- TATA MANAGEMENT TRAINIGN CENTRE – 2015- TRIBUNAL

ICAI RTP- May 2016 BANSAL CLASSES - 2015- RAJASTHAN HC Facts ASSESSE = Commercial Training and coaching institute

It availed following services:

Service Purpose Hall Renting Conducting examination for students under the coaching Catering, Photography and Tents

Celebrations during the academic sessions - students successful in coaching are rewarded so as to encourage the existing students and to motivate the new students

Maintenance & Repair of Vehicle

Vehicles used by Institute

Traveling Service Conduct of Business Tour by Company .

Issue Whether above services are eligible input services?

Held . Service Eligibility Hall Renting Eligible Catering, Photography and Tents

Not eligible -- Once the students pass their coaching classes, the activities of catering, photography and tent services cannot be said to have been used to provide the output service of commercial training or coaching.

Maintenance & Repair of Vehicle

Not eligible -- The assessee maintains and repairs its motor vehicle during the course of the business and there is no material to show that maintenance and repairs have any nexus to commercial training or coaching

Traveling Service Not eligible -- The travelling expenses incurred by assessee for the business tours cannot be related to provision of commercial training or coaching

..

Author: It is not clear from the reading of the case, as to what arguments were put forward by the assesse in his support. It seems perhaps proper arguments were not raised before HC.

Personal opinion of Author: Service Purpose Eligibility Reasoning Hall Renting Conducting examination for students

under the coaching. Eligible It is used for providing output service (getting covered

by ‘means’ part) Catering, Photography and Tents

Celebrations during the academic sessions - students successful in coaching are rewarded so as to encourage the existing students and to motivate the new students.

Eligible It is service used in related to advertisement / sales promotion (getting covered by ‘includes’ part)

Maintenance & Repair of Vehicle

Vehicles used by Institute. Not Eligible Vehicles (Passenger Vehicles) are not eligible CG for Commercial Training & Coaching Institute. Thus, maintenance and repair of such vehicles is also ineligible. (Exclusion part of definition applicable)

Traveling Service

Conduct of Business Tour by Company. Eligible It is service used in related to advertisement / sales promotion (getting covered by ‘includes’ part)

iv) Re-insurance service availed by an Insurance Company

Eligible input service In case of M/s PNB METLIFE INDIA INSURANCE CO LTD – 2015- KARNATKA HC, re-insurance was held to be an eligible input service on the following grounds:

• Re-insurance is being used to provide output service. Process of insurance does not come to an end merely on issuance of the policy by the insurer. In fact, it continues till the existence of the term of the policy.

• Re-insurance is also a statutory obligation and thus, re-insurance has to be considered as having nexus with the output service.

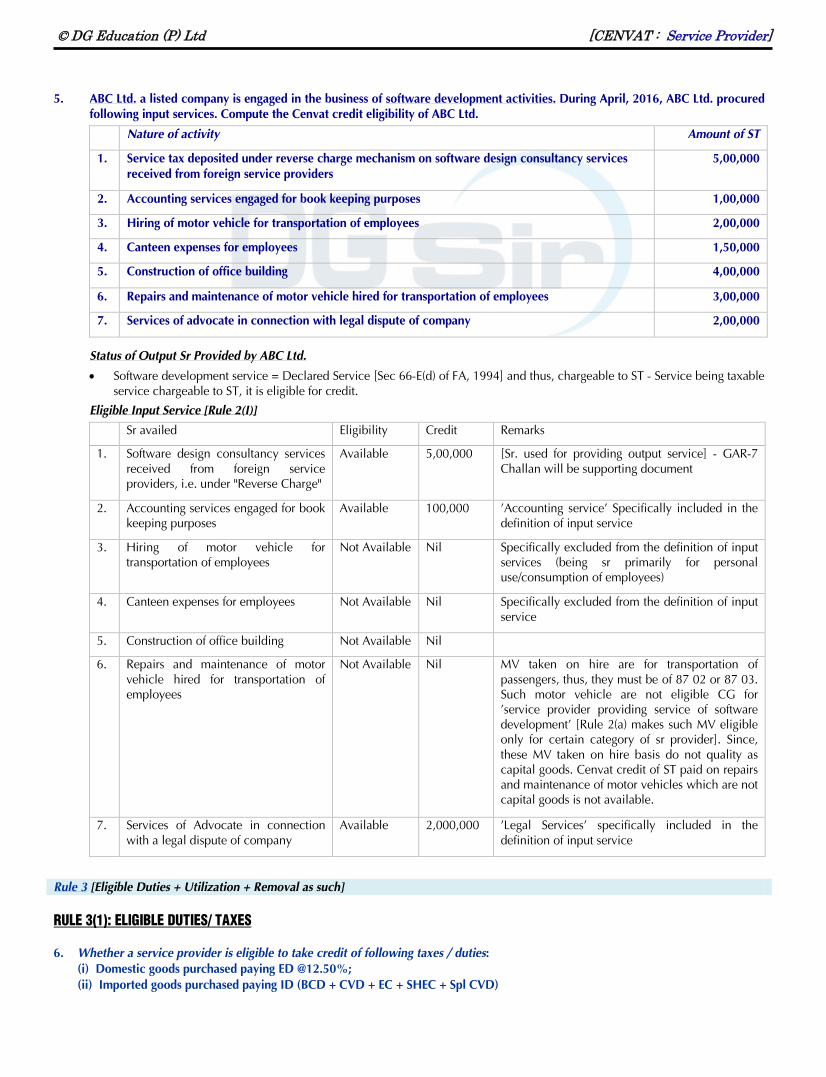

© DG Education (P) Ltd [CENVAT : Service Provider]

5. ABC Ltd. a listed company is engaged in the business of software development activities. During April, 2016, ABC Ltd. procured following input services. Compute the Cenvat credit eligibility of ABC Ltd.

Nature of activity Amount of ST

1. Service tax deposited under reverse charge mechanism on software design consultancy services received from foreign service providers

5,00,000

2. Accounting services engaged for book keeping purposes 1,00,000

3. Hiring of motor vehicle for transportation of employees 2,00,000

4. Canteen expenses for employees 1,50,000

5. Construction of office building 4,00,000

6. Repairs and maintenance of motor vehicle hired for transportation of employees 3,00,000

7. Services of advocate in connection with legal dispute of company 2,00,000

Status of Output Sr Provided by ABC Ltd.

• Software development service = Declared Service [Sec 66-E(d) of FA, 1994] and thus, chargeable to ST - Service being taxable service chargeable to ST, it is eligible for credit.

Eligible Input Service [Rule 2(I)]

Sr availed Eligibility Credit Remarks

1. Software design consultancy services received from foreign service providers, i.e. under "Reverse Charge"

Available 5,00,000 [Sr. used for providing output service] - GAR-7 Challan will be supporting document

2. Accounting services engaged for book keeping purposes

Available 100,000 'Accounting service' Specifically included in the definition of input service

3. Hiring of motor vehicle for transportation of employees

Not Available Nil Specifically excluded from the definition of input services (being sr primarily for personal use/consumption of employees)

4. Canteen expenses for employees Not Available Nil Specifically excluded from the definition of input service

5. Construction of office building Not Available Nil

6. Repairs and maintenance of motor vehicle hired for transportation of employees

Not Available Nil MV taken on hire are for transportation of passengers, thus, they must be of 87 02 or 87 03. Such motor vehicle are not eligible CG for 'service provider providing service of software development' [Rule 2(a) makes such MV eligible only for certain category of sr provider]. Since, these MV taken on hire basis do not quality as capital goods. Cenvat credit of ST paid on repairs and maintenance of motor vehicles which are not capital goods is not available.

7. Services of Advocate in connection with a legal dispute of company

Available 2,000,000 'Legal Services' specifically included in the definition of input service

Rule 3 [Eligible Duties + Utilization + Removal as such] RULE 3(1): ELIGIBLE DUTIES/ TAXES 6. Whether a service provider is eligible to take credit of following taxes / duties:

(i) Domestic goods purchased paying ED @12.50%; (ii) Imported goods purchased paying ID (BCD + CVD + EC + SHEC + Spl CVD)

© DG Education (P) Ltd [CENVAT : Service Provider]

(iii) Input services availing paying ST@14% (2 marks)

Rule 3(1) of CCR, 2004 states duties/taxes eligible for credit. In terms of Rule 3, (i) ED @12.50% is eligible for credit; (ii) CVD is eligible for credit, but not other import duties (iii) ST@14% is eligible for credit

RULE 3(4): UTILIZATION OF CREDIT 7. Whether cenvat credit availed on input services during the period May 1, 2016 to May 6, 2016 can be utilized for the payment of

service tax on the output services provided for the month ended April 2015, which is due for payment of May 6, 2016. (2 marks)

As per provisions of Rule 3(4) of Cenvat Credit Rules, 2004, while paying service tax for a particular month, cenvat credit as available upto the last day of the month can only be utilized for payment of service tax liability of that particular month. Therefore, while paying service tax for month of April, cenvat credit as available upto the last day of April, 2015 can only be utilized. The credit availed during the period of 1st May to 6th May, 2015 can’t be utilized for paying service tax liability of the April month.

Rule 4 [Availment of Credit: Timing and Extent] Rule 5 [Refund of Credit to exporter] 8. Discuss in brief provisions relation to refund of credit to service exporter under Rule 5 of CCR, 2004.

In terms of Rule 5 of CCR, 2004, a service provider who provides an output service which is exported as per Rule 6-A of STR, 1994, can claim refund of cenvat credit. Maximum admissible refund shall be determined as per following formulae: = [Net Cenvat credit of (input and input service) * Export Turnover (of the quarter) / Total Quarter (of the quarter)] Where,

Net Cenvat credit = Total Credit of input and input service as availed in quarter

Exported Turnover of services (accrual basis)

= Value of the export service calculated in the following manner: .

Payments received during the quarter for export services Add Export services whose provision has been completed for which payment had been

received in advance in any period prior to the quarter Less: advances received for services for which the provision of service has not been

completed during the quarter .

Total Turnover of services (accrual basis)

= Sum total of the value of following

Export turnover of services (as computed on accrual basis as per above) and (+) Value of all other services, during the relevant period

(+) all inputs removed as such under Rule 3(5), during the relevant period .

Such refund shall be admissible subject to conditions, safeguards and procedure specified by CBEC. As per specified procedure [N/N 27/2012],

… Such refund can be claimed on ‘quarterly basis’ … Refund claim [Form-A] shall be submitted to the AC/DC. … Refund shall be filed before the expiry of period specified in Sec 11-B (i.e., within 1 year from DATE OF EXPORT*) … Refund claimed shall not be more than the amount lying in the balance at the end of the quarter for which refund claim

is being made or at the time of filing of refund claim, whichever is less.

© DG Education (P) Ltd [CENVAT : Service Provider]

SERVICE EXPORTER : Time limit for filing claim for refund of Cenvat Credit:

1. Refund shall be claimed as per conditions, limitation and procedure specified by notification issued by CBEC: N/N 27/2012 has been issued by CBEC which, inter alia, provides that Refund shall be filed on QUARTERLY BASIS. ‘The application in Form A along with the proof of due exportation and the relevant extracts of the records maintained under the

said rules, in original are lodged with the AC/DC before the expiry of the period specified in Sec 11-B of CEA, 1944’.

As discussed in context of manufacturer exporter, • Recently, MADRAS HC in case of CELEBRITY DESIGN INDIA (P) LTD. -2015 has held that time limit shall be considered strictly as per

wordings of N/N 27/2012, i.e., from date of export only (and not from last date of concerned quarter). Special issue from view point of service exporter is that .

What shall be taken as ‘DATE OF EXPORT OF SERVICE’? .

UNDER EXCISE, date of export of goods is well defined under Sec 11-B. Sec 11-B has been made applicable to ST. but, then its determination has been an issue in dispute.

Date of export of service shall be? (a) date of export of service; or (b) date of export invoice; or (c) date of receipt of foreign exchange; or (d) date when both services have been exported and consideration received (whichever is later)' .

• Recently, AP HC in case of HYUNDAI MOTOR INDIA LTD. -2015 has held that o for claiming refund under Rule 5 of CCR, 2004, output is required to be exported in accordance with RULE 6-A OF STR, 1994. o Once service is exported refund claim can be filed subject to limitation as prescribed u/Sec 11B of the Act. o In the instant case export of service is complete only when foreign exchange is received in India as per Rule 6-A. o In case of export of Services, export is complete only when foreign exchange is received in India. Therefore relevant date of export of

services is date of receipt of foreign exchange. o Refund claims filed within 1 year from the date of receipt of foreign exchange shall be treated as filed in time and cannot be held as

time barred. o [Author:: In above case, service was provided first and proceeds were realized later. What will happen if proceeds/advances are realized first and services are provided later. Thus, issue is not free for dispute (some contrary opinions are also existing). ]

.

9. Ascertain whether the refund of Service tax paid on input services can be claimed in the following cases- Total credit of Service tax on input services Rs. 6,000. Total turnover of output service Rs 30,000. Output service exported Rs. 20,000

[Nov, 2009 - 3 Marks] Rule 5 of the Cenvat Credit Rules, 2004 provides for refund to output service provider who exports service without payment of

service tax. The refundable amount shall be calculated as per the following formulae: = Cenvat credit (of Input + Input Service) * Export Turnover / Total Turnover

Thus, admissible refund in given situation is = [6,000 * 20,000/30000] = 4,000 Rule 5-B [Refund of Credit to SP provider providing service under partial reverse charge] 10. Discuss the admissible refund under Rule 5-B under the following situations:

Case-A Case-B Sr under full reverse charge Sr under partial reverse charge

ST Liability on Output Sr in hands of SP Nil 50% of total ST of 1,00,000 Duty/Tax paid on

(a) Capital Goods (b) Input (c) Input Service

1,00,000 2,00,000 2,50,000

1,00,000 2,00,000 2,50,000

Case-A: Where full reverse charge is applicable on the service, then such service is not considered as ‘output service’ within the

meaning of Rule 2(p) of CCR, 2004, and hence, provider of service is not eligible to avail any credit at all. Thus, no question

© DG Education (P) Ltd [CENVAT : Service Provider]

of refund arises in this situation.

Case-B: Where partial reverse charge is applicable on the service, then such service is ‘output service’ within the meaning of Rule 2(p) of CCR, 2004. Hence, provider of such service is eligible for credit. Further, though ST liability is partial, credit is admissible in full. Any surplus credit of input and input service can be claimed as refund u/Rule 5-B of CCR, 2004. In given example, full ST liability of 25,000 can be paid through credit of capital goods. Thus, entire unutilized credit of input and input services (2,00,000 + 2,50,000) can be claimed as refund.

11. Explain the conditions safeguards and limitations subject to which refund of cenvat Credit shall be allowed to service providers

providing services taxed on partial reverse charge basis.

The conditions, safeguards and limitations subject to which refund of cenvat Credit shall be allowed to service providers providing services taxed on partial reverse charge basis has been notified vide Notification No. 12/2014. The relevant provisions are as under: 1) Services eligible for refund: The refund shall be claimed of unutilised cenvat credit taken on inputs and input services during

the half year for which refund is claimed, for providing following output services namely : i. Renting of a motor vehicle designed to carry passengers on non abated value, to any person who is not engaged in a similar

business; ii. Service portion in the execution for a works contract;

Author Services of supply or manpower or Security Service: • Upto 31st March, 2015, partial reverse charge was applicable to these services (SP -25% and SR-75%). Thus, refund upto 31st

March, 2015 period can be claimed u/Rule 5-B of CCR, 2004. • However, on/from 1st April, 2015, partial reverse charge has been made applicable to such services and now such services are

subject to full reverse charge. At present, SP shall not be liable to pay any ST. Further, he shall not be entitled to claim any credit in relation of such service. Thus, there will not be any question of refund of credit in relation to such services.

2) Refund of unutilised Cenvat Credit : Refund that would be admissible to service provider shall be lower of the following

amounts — i. Amount equivalent to the amount of ST liability paid or payable by the recipient of service with respect to the partial

reverse charge services. ii. Amount as per the formula = (A) – (B)

Where,

A = Cenvat credit taken on inputs and input services during the half year ×

Turnover of output service under partial reverse charge during the half year Total turnover during the half year

B = Service Tax paid by the service provider for such partial reverse charge services during the half year;

However, the maximum amount of refund which shall be admissible shall be credit lying untilized with the assessee at the end of half-year.

3) Refund claim after filing return: The refund claim shall be filed after filing of service tax return as prescribed under rule 7 of the Service Tax Rules for the period for which refund is claimed.

4) Refund amount to be debited to cenvat A/c: The amount claimed as refund shall be debited by the claimant from his cenvat credit account at the time of making the claim. However, if refund is sanctioned of lower amount, then it shall be eligible for re-credit.

Example: • Of refund of Rs 5 lakh is claimed, then Rs 5 lakh shall be debited to cenvat account. • However, if only Rs 4 lakh is allowed as refund, then balance Rs 1 lakh can be taken as re-credit.

[Expected] 12. Mr A has provided the following services during half-year ending on 31st March, 2016. Determine the admissible refund under

rule 5-B of CCR, 2004, in view of the following particulars: (a) Value of ‘Service of Renting of Passenger Vehicle’ provided to ABC Ltd= 2,00,000 (b) Value of other services (taxable) provided= 10,00,000 (c) Total amount of cenvat credit taken on inputs during the half-year = 80,000 (d) Total amount of cenvat credit taken on input services during half year= 1,40,000

© DG Education (P) Ltd [CENVAT : Service Provider]

Half year = (1st Oct, 2015- 31st March, 2016) Unutilized credit at the end of half-year = 84,040 (as computed below) = Maximum refund which is possible.

Particulars Amount in Rs. Total credit of half year (input and input service) = (80,000 + 1,40,000) 2,20,000 Service tax payable by X

• ST under partial reverse charge liability [Rs. 2,00,000 × 14% × 50%] = 14,000 • ST under normal charge liability [10,00,000 *14%] = 1,40,000

1,54,000

Unutilized credit at the end of half-year 66,000 Presuming that this balance was in cenvat register as on the date of filing refund claim under Rule 5-B, it is the maximum possible refund which can be claimed.

However, admissible refund shall be lower of following 2:

i. ST liability paid/payable by the recipient of service with respect to the partial reverse charge services : = [Rs. 2,00,000 × 14% × 50%] = Rs. 14,000

ii. Amount as per the formula as prescribed in the Notification No. 12/2014:

Amount of Refund = (A) - (B) = Rs. 36,667- Rs. 14,000

= Rs. 22,667

A = Cenvat credit taken on inputs and input services during the half year ×

Turnover of output service under partial reverse charge during the half year Total turnover during the half year

= Rs. 2,20,000 ×

Rs. 2,00,000 Rs. 12,00,000

= Rs. 36,667

B = Service Tax paid by the service provider for such partial reverse charge services during the half year; = [Rs. 2,00,000 × 14% × 50%] = Rs. 14,000

Thus, refund to be claimed by Mr. X will be of Rs. 14,000. Rule 6 [Provisioning of Exempted Services] 13. Briefly explain : Exempted Services (Nov 2013 - 3 Marks)

Exempted service: Rule 2(e) of CCR, 2004 defines ‘exempted service’ As per that definition, ‘exempted service’ shall cover following: 1) Service on which no ST is leviable u/s 66B of the Finance Act, 1994; 2) Taxable service which is fully exempt from ST;

3) Taxable service whose part of value is exempted on the condition that no credit of inputs and input services, used for providing

such taxable service, shall be taken; However, if a service can be said to be ‘exported service’ in terms of Rule 6A of STR, 1994, then such service shall not be treated as

‘exempted service’ even though such service does not attract any ST levy u/s 66-B of FA, 1994.

Author: EXEMPTED SERVICES • In case of service tax, which is a tax on rendering of services, in a normal course exempted services are those services which are exempt

from whole of the service tax leviable thereon under a notification issued u/Sec 93 of the Finance Act, 1994. • However for the limited purpose of CCR, 2004, services on which no service tax is leviable u/Sec 66-B of the Finance Act 1994 and also

those taxable services whose part of value is exempted on the condition that no cenvat credit of inputs and input services used for providing such taxable services has been taken, are also considered as exempted services.

14. If a service provider exports his service for which payment is to be received later on, then whether such service is treated as

‘exempted service’ for purpose of Rule 6?

© DG Education (P) Ltd [CENVAT : Service Provider]

Rule 2(e) excludes service exported in terms of Rule 6A of Service Tax Rules, 1994, from the definition of 'exempted service'. However, one of the conditions of Rule 6A is that payment of exported service is received in convertible foreign exchange. Hence, if payment is not so received, the service becomes an 'exempted service' under Rule 2(e). To avoid applicability of Rule 6 in this situation, a provision has been made by way of Rule 6(8) that during a period of 6 months or extended period allowed by RBI, the service would not be regarded as 'exempted service' for the purposes of Rule 6 of the Cenvat Credit Rules, 2004. However, after expiry of time permitted by RBI, the service would become 'exempted service' and Cenvat reversal would be required as per Rule 6(3). As Per Rule 6(8)(b), Cenvat Credit already reversed owing to non-realization of export proceeds of services can be re-taken suo-motu on pro rata basis to the extent of payment realized on the basis of documentary evidence of realization.

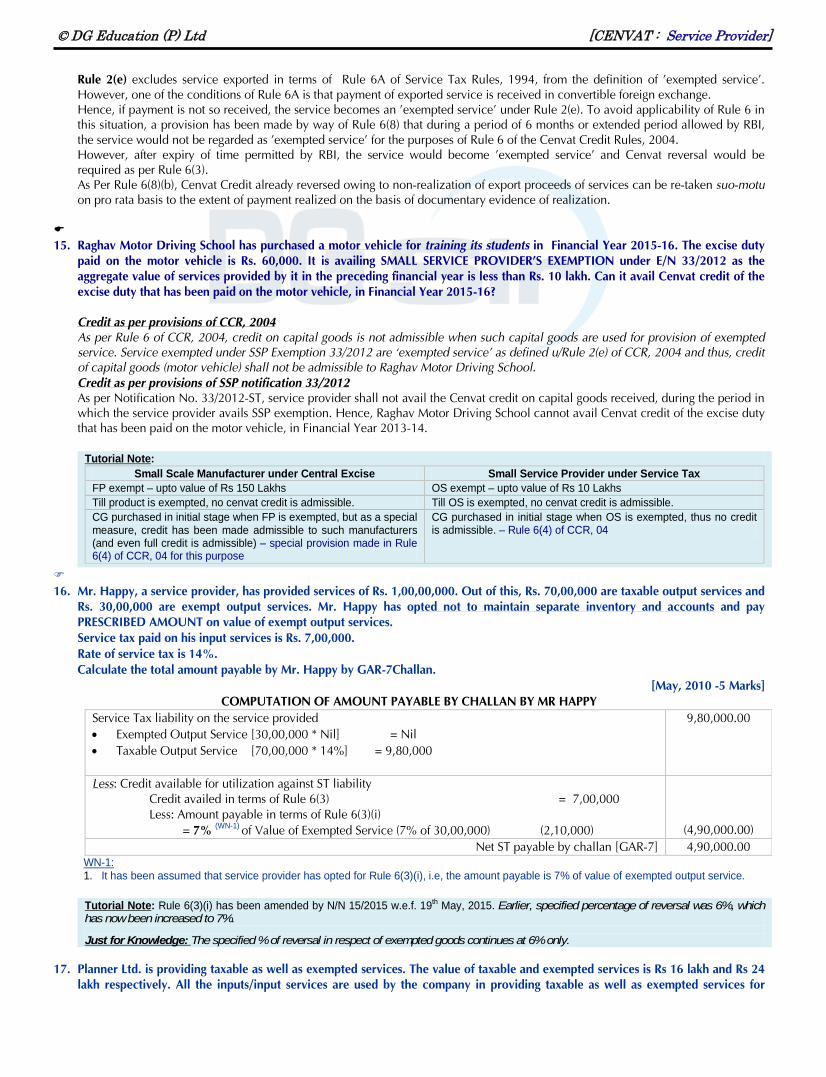

15. Raghav Motor Driving School has purchased a motor vehicle for training its students in Financial Year 2015-16. The excise duty

paid on the motor vehicle is Rs. 60,000. It is availing SMALL SERVICE PROVIDER'S EXEMPTION under E/N 33/2012 as the aggregate value of services provided by it in the preceding financial year is less than Rs. 10 lakh. Can it avail Cenvat credit of the excise duty that has been paid on the motor vehicle, in Financial Year 2015-16?

Credit as per provisions of CCR, 2004 As per Rule 6 of CCR, 2004, credit on capital goods is not admissible when such capital goods are used for provision of exempted service. Service exempted under SSP Exemption 33/2012 are ‘exempted service’ as defined u/Rule 2(e) of CCR, 2004 and thus, credit of capital goods (motor vehicle) shall not be admissible to Raghav Motor Driving School. Credit as per provisions of SSP notification 33/2012 As per Notification No. 33/2012-ST, service provider shall not avail the Cenvat credit on capital goods received, during the period in which the service provider avails SSP exemption. Hence, Raghav Motor Driving School cannot avail Cenvat credit of the excise duty that has been paid on the motor vehicle, in Financial Year 2013-14.

Tutorial Note:

Small Scale Manufacturer under Central Excise Small Service Provider under Service Tax FP exempt – upto value of Rs 150 Lakhs OS exempt – upto value of Rs 10 Lakhs Till product is exempted, no cenvat credit is admissible. Till OS is exempted, no cenvat credit is admissible. CG purchased in initial stage when FP is exempted, but as a special measure, credit has been made admissible to such manufacturers (and even full credit is admissible) – special provision made in Rule 6(4) of CCR, 04 for this purpose

CG purchased in initial stage when OS is exempted, thus no credit is admissible. – Rule 6(4) of CCR, 04

.

16. Mr. Happy, a service provider, has provided services of Rs. 1,00,00,000. Out of this, Rs. 70,00,000 are taxable output services and

Rs. 30,00,000 are exempt output services. Mr. Happy has opted not to maintain separate inventory and accounts and pay PRESCRIBED AMOUNT on value of exempt output services.

Service tax paid on his input services is Rs. 7,00,000. Rate of service tax is 14%. Calculate the total amount payable by Mr. Happy by GAR-7Challan.

[May, 2010 -5 Marks] COMPUTATION OF AMOUNT PAYABLE BY CHALLAN BY MR HAPPY

Service Tax liability on the service provided • Exempted Output Service [30,00,000 * Nil] = Nil • Taxable Output Service [70,00,000 * 14%] = 9,80,000

9,80,000.00

Less: Credit available for utilization against ST liability Credit availed in terms of Rule 6(3) = 7,00,000 Less: Amount payable in terms of Rule 6(3)(i) = 7% (WN-1) of Value of Exempted Service (7% of 30,00,000) (2,10,000)

(4,90,000.00) Net ST payable by challan [GAR-7] 4,90,000.00

WN-1: 1. It has been assumed that service provider has opted for Rule 6(3)(i), i.e, the amount payable is 7% of value of exempted output service.

Tutorial Note: Rule 6(3)(i) has been amended by N/N 15/2015 w.e.f. 19th May, 2015. Earlier, specified percentage of reversal was 6%, which has now been increased to 7%.

Just for Knowledge: The specified % of reversal in respect of exempted goods continues at 6% only.

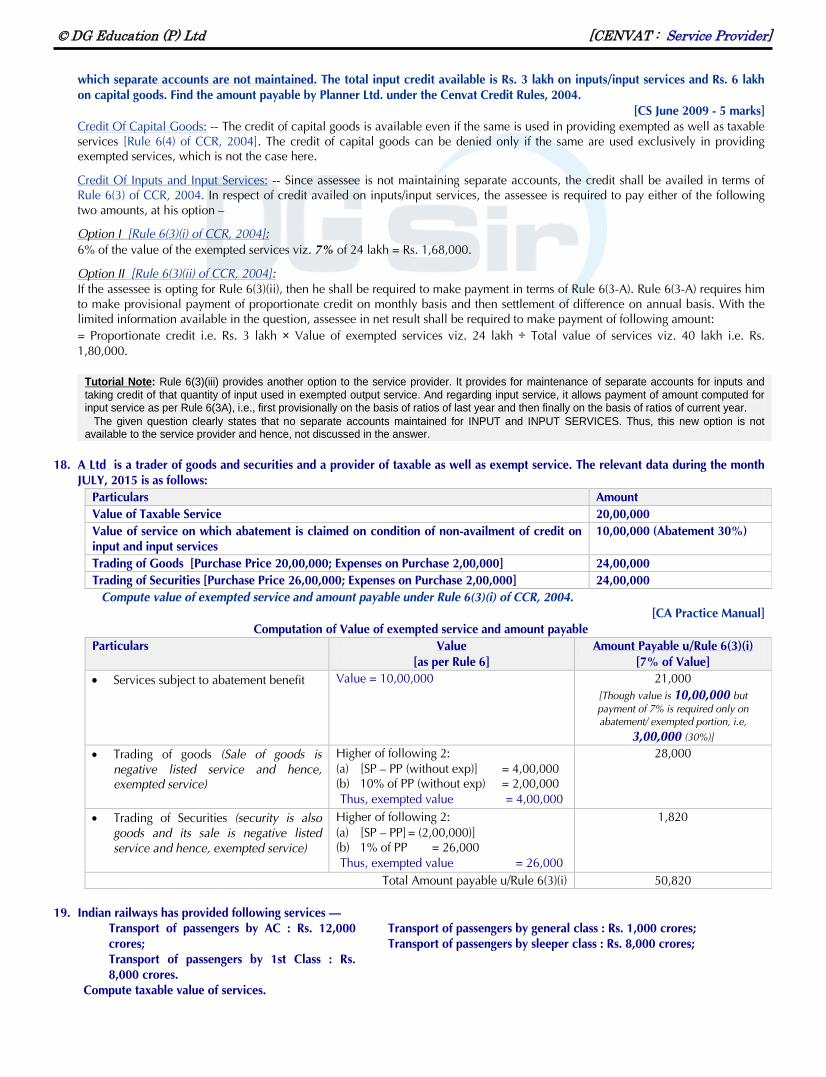

17. Planner Ltd. is providing taxable as well as exempted services. The value of taxable and exempted services is Rs 16 lakh and Rs 24 lakh respectively. All the inputs/input services are used by the company in providing taxable as well as exempted services for

© DG Education (P) Ltd [CENVAT : Service Provider]

which separate accounts are not maintained. The total input credit available is Rs. 3 lakh on inputs/input services and Rs. 6 lakh on capital goods. Find the amount payable by Planner Ltd. under the Cenvat Credit Rules, 2004.

[CS June 2009 - 5 marks] Credit Of Capital Goods: -- The credit of capital goods is available even if the same is used in providing exempted as well as taxable

services [Rule 6(4) of CCR, 2004]. The credit of capital goods can be denied only if the same are used exclusively in providing exempted services, which is not the case here.

Credit Of Inputs and Input Services: -- Since assessee is not maintaining separate accounts, the credit shall be availed in terms of Rule 6(3) of CCR, 2004. In respect of credit availed on inputs/input services, the assessee is required to pay either of the following two amounts, at his option –

Option I [Rule 6(3)(i) of CCR, 2004]: 6% of the value of the exempted services viz. 7% of 24 lakh = Rs. 1,68,000.

Option II [Rule 6(3)(ii) of CCR, 2004]: If the assessee is opting for Rule 6(3)(ii), then he shall be required to make payment in terms of Rule 6(3-A). Rule 6(3-A) requires him

to make provisional payment of proportionate credit on monthly basis and then settlement of difference on annual basis. With the limited information available in the question, assessee in net result shall be required to make payment of following amount:

= Proportionate credit i.e. Rs. 3 lakh × Value of exempted services viz. 24 lakh ÷ Total value of services viz. 40 lakh i.e. Rs. 1,80,000.

Tutorial Note: Rule 6(3)(iii) provides another option to the service provider. It provides for maintenance of separate accounts for inputs and taking credit of that quantity of input used in exempted output service. And regarding input service, it allows payment of amount computed for input service as per Rule 6(3A), i.e., first provisionally on the basis of ratios of last year and then finally on the basis of ratios of current year. The given question clearly states that no separate accounts maintained for INPUT and INPUT SERVICES. Thus, this new option is not available to the service provider and hence, not discussed in the answer.

18. A Ltd is a trader of goods and securities and a provider of taxable as well as exempt service. The relevant data during the month

JULY, 2015 is as follows: Particulars Amount Value of Taxable Service 20,00,000 Value of service on which abatement is claimed on condition of non-availment of credit on input and input services

10,00,000 (Abatement 30%)

Trading of Goods [Purchase Price 20,00,000; Expenses on Purchase 2,00,000] 24,00,000 Trading of Securities [Purchase Price 26,00,000; Expenses on Purchase 2,00,000] 24,00,000

Compute value of exempted service and amount payable under Rule 6(3)(i) of CCR, 2004. [CA Practice Manual]

Computation of Value of exempted service and amount payable Particulars Value

[as per Rule 6] Amount Payable u/Rule 6(3)(i)

[7% of Value] • Services subject to abatement benefit Value = 10,00,000

21,000

[Though value is 10,00,000 but payment of 7% is required only on abatement/ exempted portion, i.e,

3,00,000 (30%)]

• Trading of goods (Sale of goods is negative listed service and hence, exempted service)

Higher of following 2: (a) [SP – PP (without exp)] = 4,00,000 (b) 10% of PP (without exp) = 2,00,000 Thus, exempted value = 4,00,000

28,000

• Trading of Securities (security is also goods and its sale is negative listed service and hence, exempted service)

Higher of following 2: (a) [SP – PP] = (2,00,000)] (b) 1% of PP = 26,000 Thus, exempted value = 26,000

1,820

Total Amount payable u/Rule 6(3)(i) 50,820 19. Indian railways has provided following services —

Transport of passengers by AC : Rs. 12,000 crores;

Transport of passengers by 1st Class : Rs. 8,000 crores.

Transport of passengers by general class : Rs. 1,000 crores; Transport of passengers by sleeper class : Rs. 8,000 crores;

Compute taxable value of services.

© DG Education (P) Ltd [CENVAT : Service Provider]

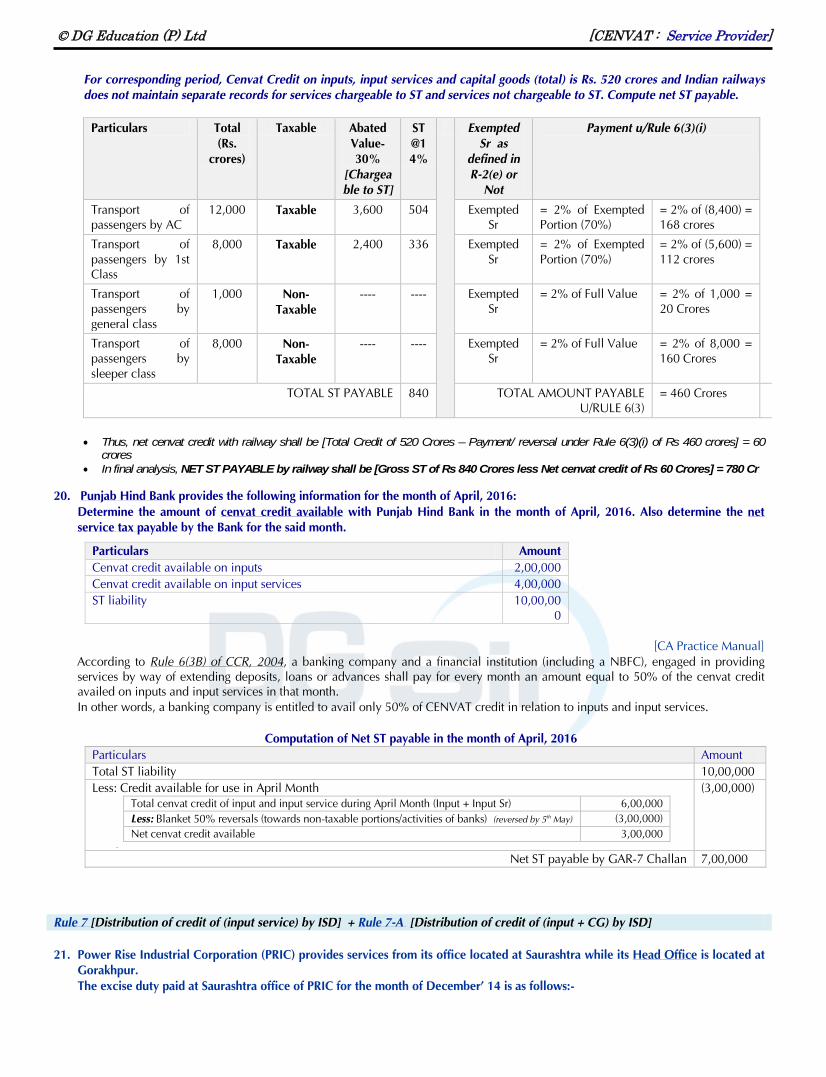

For corresponding period, Cenvat Credit on inputs, input services and capital goods (total) is Rs. 520 crores and Indian railways does not maintain separate records for services chargeable to ST and services not chargeable to ST. Compute net ST payable.

Particulars Total

(Rs. crores)

Taxable Abated Value- 30%

[Chargeable to ST]

ST@14%

Exempted Sr as

defined in R-2(e) or

Not

Payment u/Rule 6(3)(i)

Transport of passengers by AC

12,000 Taxable 3,600 504 Exempted Sr

= 2% of Exempted Portion (70%)

= 2% of (8,400) = 168 crores

Transport of passengers by 1st Class

8,000 Taxable 2,400 336 Exempted Sr

= 2% of Exempted Portion (70%)

= 2% of (5,600) = 112 crores

Transport of passengers by general class

1,000 Non-Taxable

---- ---- Exempted Sr

= 2% of Full Value = 2% of 1,000 = 20 Crores

Transport of passengers by sleeper class

8,000 Non-Taxable

---- ---- Exempted Sr

= 2% of Full Value = 2% of 8,000 = 160 Crores

TOTAL ST PAYABLE 840 TOTAL AMOUNT PAYABLE U/RULE 6(3)

= 460 Crores

. • Thus, net cenvat credit with railway shall be [Total Credit of 520 Crores – Payment/ reversal under Rule 6(3)(i) of Rs 460 crores] = 60

crores • In final analysis, NET ST PAYABLE by railway shall be [Gross ST of Rs 840 Crores less Net cenvat credit of Rs 60 Crores] = 780 Cr

20. Punjab Hind Bank provides the following information for the month of April, 2016: Determine the amount of cenvat credit available with Punjab Hind Bank in the month of April, 2016. Also determine the net

service tax payable by the Bank for the said month.

Particulars Amount Cenvat credit available on inputs 2,00,000 Cenvat credit available on input services 4,00,000 ST liability 10,00,00

0

[CA Practice Manual] According to Rule 6(3B) of CCR, 2004, a banking company and a financial institution (including a NBFC), engaged in providing

services by way of extending deposits, loans or advances shall pay for every month an amount equal to 50% of the cenvat credit availed on inputs and input services in that month. In other words, a banking company is entitled to avail only 50% of CENVAT credit in relation to inputs and input services.

Computation of Net ST payable in the month of April, 2016

Particulars Amount Total ST liability 10,00,000 Less: Credit available for use in April Month

Total cenvat credit of input and input service during April Month (Input + Input Sr) 6,00,000 Less: Blanket 50% reversals (towards non-taxable portions/activities of banks) (reversed by 5th May) (3,00,000) Net cenvat credit available 3,00,000

.

(3,00,000)

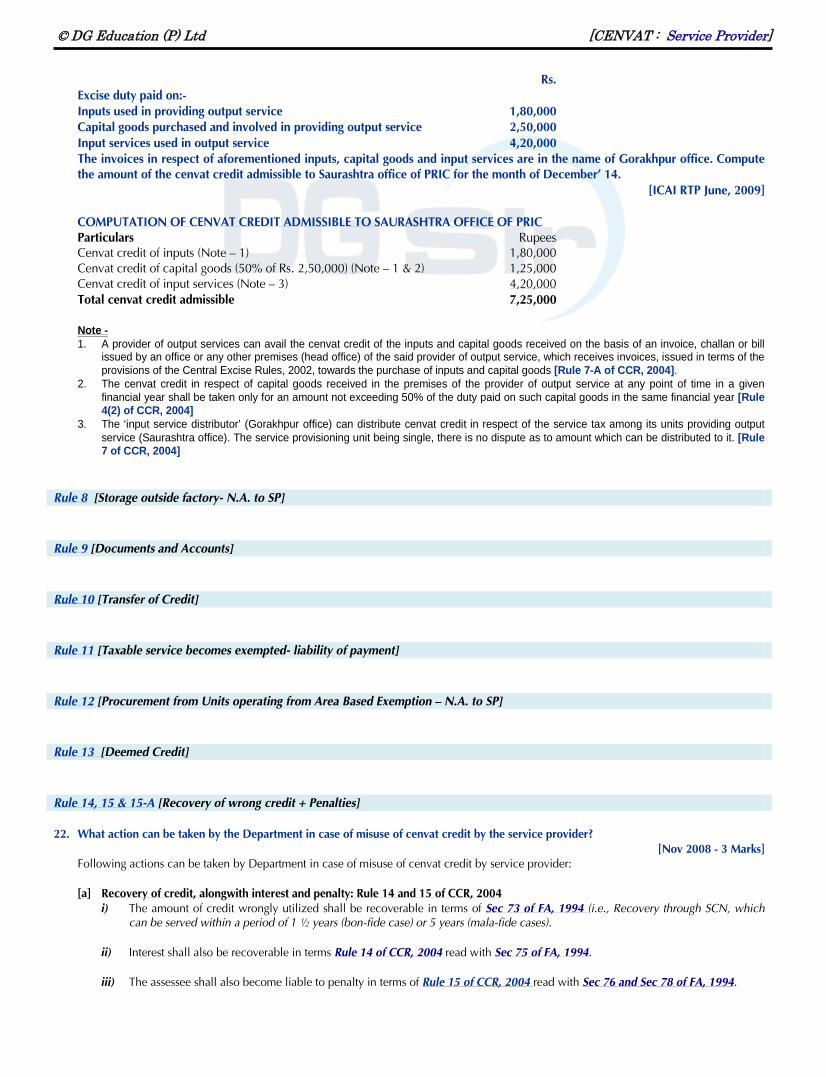

Net ST payable by GAR-7 Challan 7,00,000 Rule 7 [Distribution of credit of (input service) by ISD] + Rule 7-A [Distribution of credit of (input + CG) by ISD] 21. Power Rise Industrial Corporation (PRIC) provides services from its office located at Saurashtra while its Head Office is located at

Gorakhpur. The excise duty paid at Saurashtra office of PRIC for the month of December’ 14 is as follows:-

© DG Education (P) Ltd [CENVAT : Service Provider]

Rs. Excise duty paid on:- Inputs used in providing output service 1,80,000 Capital goods purchased and involved in providing output service 2,50,000 Input services used in output service 4,20,000 The invoices in respect of aforementioned inputs, capital goods and input services are in the name of Gorakhpur office. Compute

the amount of the cenvat credit admissible to Saurashtra office of PRIC for the month of December’ 14. [ICAI RTP June, 2009]

COMPUTATION OF CENVAT CREDIT ADMISSIBLE TO SAURASHTRA OFFICE OF PRIC Particulars Rupees Cenvat credit of inputs (Note – 1) 1,80,000 Cenvat credit of capital goods (50% of Rs. 2,50,000) (Note – 1 & 2) 1,25,000 Cenvat credit of input services (Note – 3) 4,20,000 Total cenvat credit admissible 7,25,000 Note -

1. A provider of output services can avail the cenvat credit of the inputs and capital goods received on the basis of an invoice, challan or bill issued by an office or any other premises (head office) of the said provider of output service, which receives invoices, issued in terms of the provisions of the Central Excise Rules, 2002, towards the purchase of inputs and capital goods [Rule 7-A of CCR, 2004].

2. The cenvat credit in respect of capital goods received in the premises of the provider of output service at any point of time in a given financial year shall be taken only for an amount not exceeding 50% of the duty paid on such capital goods in the same financial year [Rule 4(2) of CCR, 2004]

3. The ‘input service distributor’ (Gorakhpur office) can distribute cenvat credit in respect of the service tax among its units providing output service (Saurashtra office). The service provisioning unit being single, there is no dispute as to amount which can be distributed to it. [Rule 7 of CCR, 2004]

Rule 8 [Storage outside factory- N.A. to SP] Rule 9 [Documents and Accounts] Rule 10 [Transfer of Credit] Rule 11 [Taxable service becomes exempted- liability of payment] Rule 12 [Procurement from Units operating from Area Based Exemption – N.A. to SP] Rule 13 [Deemed Credit] Rule 14, 15 & 15-A [Recovery of wrong credit + Penalties] 22. What action can be taken by the Department in case of misuse of cenvat credit by the service provider?

[Nov 2008 - 3 Marks] Following actions can be taken by Department in case of misuse of cenvat credit by service provider:

[a] Recovery of credit, alongwith interest and penalty: Rule 14 and 15 of CCR, 2004 i) The amount of credit wrongly utilized shall be recoverable in terms of Sec 73 of FA, 1994 (i.e., Recovery through SCN, which

can be served within a period of 1 ½ years (bon-fide case) or 5 years (mala-fide cases). ii) Interest shall also be recoverable in terms Rule 14 of CCR, 2004 read with Sec 75 of FA, 1994.

iii) The assessee shall also become liable to penalty in terms of Rule 15 of CCR, 2004 read with Sec 76 and Sec 78 of FA, 1994.

© DG Education (P) Ltd [CENVAT : Service Provider]

[b] Criminal proceedings can also be initiated against the service provider

In terms of Sec 89 of FA, 1994, availment and utilization of credit of tax/duty without actual receipt of taxable service or excisable goods in violation of CCR, 2004 is an offence, which is punishable with imprisonment. … If amount involved exceeds 50 lakhs, then imprisonment can be for a period upto 3 years. … If amount involved is equal to or less than Rs 50 lakhs, then imprisonment can be for a period upto 1 year. However, this offence is non-cognizable and bailable. Author: • Arrest prior to imprisonment: As per revised guidelines (issued in 2015), no arrest shall be made where the amount involved in offence

does not exceed Rs 100 Lakhs (i.e., Rs 1 crore)

Related Documents