US Stats Petroleum Prices - 9-7-20 to 9-6-21 On-highway diesel +38.5% to $3.373/gallon Regular gasoline +43.6% to $3.176/gallon WTI crude oil +65.3% to $69.15/barrel Price Indices - August PPI +0.7% over July 2021 and +8.3% the past 12 months CPI +0.3% over July and +5.3% the past 12 months Leading Indicator of Remodeling Activity +8.5% in Q3 2021 and +7.6% in Q4 2021 LITHOGRAPHED BY SWIFT PRINT COMMUNICATIONS, INC., ST. LOUIS, CHICAGO, TETERBORO, CINCINNATI (PRINTED IN U.S.A.) September 24, 2021 VOLUME XCIX NUMBER 39 World Watch Canada Residential Building Permits - July Total +30.3% over July 2020 Single-family +35.7% over July 2020 Multifamily +26.3% over July 2020 Non-residential +5.5% over July 2020 Euro Area - Q2 2021 GDP +2.2% over Q1 2021 Employment +0.7% over Q1 2021 Vietnam - August Industrial production index -7.4% y-o-y Retail sales -33.7% y-o-y Exports -5.4% y-o-y Hardwood Market Report Lumber News Since 1922 For advertising sales: [email protected] For advertising: [email protected] | For subscriptions: [email protected] 780 Ridge Lake Blvd., Ste 102 Memphis, TN 38120-9426 Website: www.hmr.com Phone: 901-767-9126 Fax: 901-767-7534 Judd S. Johnson Editor [email protected] David Caldwell Assistant Editor [email protected] Andy Johnson Assistant Editor [email protected] Million Bd. Ft. 180 160 140 120 100 80 60 40 US Monthly Exports of Hardwood Lumber Jul-18 Aug-18 Sep-18 Oct-18 Nov-18 Dec-18 Jan-19 Feb-19 Mar-19 Apr-19 May-19 Jun-19 Jul-19 Aug-19 Sep-19 Oct-19 Nov-19 Dec-19 Jan-20 Feb-20 Mar-20 Apr-20 May-20 Jun-20 Jul-20 Aug-20 Sep-20 Oct-20 Nov-20 Dec-20 Jan-21 Feb-21 Mar-21 Apr-21 May-21 Jun-21 Jul-21 July -’18 138.4MM Bd. Ft. July -’21 114.1MM Bd. Ft. January through July 2021 hardwood lumber exports were 11.1% higher than the first seven months of 2020. Source: USDA Foreign Agricultural Service Graph: HMR

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

US StatsPetroleum Prices - 9-7-20 to 9-6-21On-highway diesel +38.5% to $3.373/gallonRegular gasoline +43.6% to $3.176/gallonWTI crude oil +65.3% to $69.15/barrel

Price Indices - AugustPPI +0.7% over July 2021and +8.3% the past 12 monthsCPI +0.3% over Julyand +5.3% the past 12 months

Leading Indicator of Remodeling Activity+8.5% in Q3 2021 and+7.6% in Q4 2021

LITHOGRAPHED BY SWIFT PRINT COMMUNICATIONS, INC., ST. LOUIS, CHICAGO, TETERBORO, CINCINNATI (PRINTED IN U.S.A.)

September 24, 2021

VOLUME XCIXNUMBER 39

World WatchCanada Residential Building Permits - July Total +30.3% over July 2020Single-family +35.7% over July 2020Multifamily +26.3% over July 2020Non-residential +5.5% over July 2020

Euro Area - Q2 2021 GDP +2.2% over Q1 2021Employment +0.7% over Q1 2021 Vietnam - AugustIndustrial production index -7.4% y-o-yRetail sales -33.7% y-o-yExports -5.4% y-o-y

Hardwood Market ReportLumber News Since 1922

For advertising sales: [email protected] advertising: [email protected] | For subscriptions: [email protected]

780 Ridge Lake Blvd., Ste 102Memphis, TN 38120-9426Website: www.hmr.comPhone: 901-767-9126Fax: 901-767-7534

Judd S. JohnsonEditor

David CaldwellAssistant [email protected]

Andy JohnsonAssistant [email protected]

Mill

ion

Bd

. Ft.

180

160

140

120

100

80

60

40

US Monthly Exports of Hardwood Lumber

Jul-

18A

ug

-18

Sep

-18

Oct

-18

No

v-18

Dec

-18

Jan

-19

Feb

-19

Mar

-19

Ap

r-19

May

-19

Jun

-19

Jul-

19A

ug

-19

Sep

-19

Oct

-19

No

v-19

Dec

-19

Jan

-20

Feb

-20

Mar

-20

Ap

r-20

May

-20

Jun

-20

Jul-

20A

ug

-20

Sep

-20

Oct

-20

No

v-20

Dec

-20

Jan

-21

Feb

-21

Mar

-21

Ap

r-21

May

-21

Jun

-21

Jul-

21

40

60

80

100

120

140

160

180

Jul-1

8Au

g-18

Sep-

18O

ct-1

8No

v-18

Dec-

18Ja

n-19

Feb-

19M

ar-1

9Ap

r-19

May

-19

Jun-

19Ju

l-19

Aug-

19Se

p-19

Oct

-19

Nov-

19De

c-19

Jan-

20Fe

b-20

Mar

-20

Apr-2

0M

ay-2

0Ju

n-20

Jul-2

0Au

g-20

Sep-

20O

ct-2

0No

v-20

Dec-

20Ja

n-21

Feb-

21M

ar-2

1Ap

r-21

May

-21

Jun-

21Ju

l-21

July -’18138.4MM

Bd. Ft.

July -’21114.1MM

Bd. Ft.

January through July 2021hardwood lumber exports

were 11.1% higher than the first seven months of 2020.

Source: USDA Foreign Agricultural Service Graph: HMR

SOUTHERN HARDWOODS2 9/24/21

PECAN & HICKORY FAS #1C #2A #2B 4/4 930 670 490 365 5/4 935 680 495 365 6/4 950 730 505 365 8/4 980 755 535 365

POPLAR FAS 1F #1C #2A #2B 4/4 1330 + 1320 + 800 550 430 5/4 1370 + 1360 + 810 560 430 6/4 1375 + 1365 + 815 570 430 8/4 1385 + 1375 + 825 580 435

SYCAMORE FAS #1C #2A 5/8 455 435 360 4/4 460 440 360 5/4 465 445 360 6/4 495 475 370 8/4 535 515 395

WILLOW FAS #1C #2A #2B 4/4 550 340 215 190 5/4 560 350 225 200 6/4 580 360 225 200 8/4 590 365 225 200

MIXED SOFT HARDWOODS FAS #1C #2A #2B

4/4 365 340 295 255 5/4 380 355 300 265 6/4 445 420 320 270 8/4 485 460 340 275

FRAMESTOCK - AIR DRIED4/4 OAK S2S (485-630)4/4 MIXED S2S (515-655)

CANTS - GREEN 560 (500-655)

TIES - 7x9 - GREENSOUTHERN - WEST - 9'CROSSTIES (34.50-39.00) Per Pc.

SOUTHERN - EAST - 8½'CROSSTIES (33.50-38.50) Per Pc.

BOARD ROAD - GREEN 560 (500-590)

F. O. B. MILLS - SOUTHERN AREAEstimate of FOB Southern mill point average market prices for well manufactured Southern hardwoods in truckload and greater quantities. Stocks are random widths and lengths, green, rough, and graded in accordance with NHLA rules. Prices in US dollars per M’. Prices published in Hardwood Market Report are presented only as a guide. See statement on back page. © 2021 Hardwood Market Report

ASH FAS 1F #1C #2A 4/4 1260 1250 790 510 5/4 1270 1260 810 530 6/4 1330 1320 845 570 8/4 1440 1430 910 600

BEECH FAS #1C #2A #3A 4/4 460 415 310 215 5/4 470 425 325 230 6/4 520 460 345 240

COTTONWOOD FAS #1C #2A #2B 4/4 780 575 260 215 5/4 770 565 280 230

SAP GUM FAS #1C #2A #2B

4/4 405 380 315 245 5/4 425 400 320 255 6/4 475 450 340 260 8/4 515 490 360 265

HACKBERRY FAS #1C #2A 4/4 530 480 295 5/4 555 505 320 6/4 595 545 340 8/4 640 590 350

SOFT MAPLE - WHAD FAS #1C #2A 4/4 925 600 350 5/4 950 710 410

SOFT MAPLE - WHND FAS #1C #2B

4/4 505 460 290 5/4 510 465 300 6/4 550 505 355 8/4 565 520 355

RED OAK FAS 1F #1C #2A #3A 4/4 1160 1150 915 845 780 5/4 1190 1180 920 850 785 6/4 1250 1240 925 860 790 8/4 1295 1285 930 - - - - - -FAS&1F ALONE 4/4 ADD $0 5/4 ADD $0 6/4 & 8/4 ADD $0

WHITE OAK FAS 1F #1C #2A #3A 4/4 2400 2390 1195 855 800 5/4 2690 2680 1285 860 805 6/4 2800 2790 1315 870 825 8/4 2885 2875 1335 - - - - - -FAS&1F ALONE 4/4 & 5/4 ADD $0 6/4 & 8/4 ADD $0

3KILN DRIED PRICES - SOUTHERN AREA9/24/21

Prices in this matrix are for kiln dried lumber measured before kiln drying. The first figure listed for each grade and thickness is the predominant index price; figures in parentheses are the prevailing range of index prices. Bold figures indicate change. Prices published in Hardwood Market Report are presented only as a guide. See statement on back page. © 2021 Hardwood Market Report

ASH 4/4 1870 (1815-2005) 1135 (1080-1210) 800 (735-850) 8/4 2300 (2215-2450) 1505 (1440-1560) 1095 (1030-1210) COTTONWOOD 4/4 975 (915-1030) 725 (670-800) - - - - - - - -

RED OAK 4/4 1715 [–25] (1645-1785) 1290 [–20] (1245-1400) 1135 (1070-1215) 5/4 2010 (1930-2120) 1510 (1430-1575) 1145 (1075-1235)

WHITE OAK 4/4 4370 (4220-4690) 2040 (1940-2150) 1360 (1285-1435) 5/4 4775 (4670-5065) 2240 (2155-2320) 1475 (1400-1600)

POPLAR 4/4 1995 (1910-2120) 1100 (1045-1160) 810 (765-860) 5/4 2025 (1955-2175) 1145 (1090-1220) 835 (780-895) 6/4 2045 (1975-2185) 1180 (1115-1225) - - - - - - - - 8/4 2100 (2015-2195) 1210 (1130-1265) - - - - - - -

Prices in this matrix are for kiln dried lumber measured after kiln drying ("net tally"). The first figure listed for each grade and thick-ness is the predominant index price; figures in parentheses are the prevailing range of index prices. Bold figures indicate change. Prices published in Hardwood Market Report are presented only as a guide. See statement on back page. © 2021 Hardwood Market Report

ASH 4/4 2010 (1950-2155) 1220 (1160-1300) 860 (790-915) 8/4 2470 (2380-2635) 1620 (1550-1680) 1175 (1105-1300)

COTTONWOOD 4/4 1050 (985-1105) 780 (720-860) - - - - - - - -

RED OAK 4/4 1850 [–25] (1775-1925) 1390 [–20] (1340-1510) 1220 (1150-1305) 5/4 2160 (2075-2275) 1620 (1535-1690) 1230 (1155-1330)

WHITE OAK 4/4 4700 (4530-5040) 2190 (2085-2310) 1460 (1380-1540) 5/4 5130 (5020-5440) 2405 (2315-2495) 1585 (1505-1720)

POPLAR 4/4 2140 (2055-2275) 1185 (1125-1250) 870 (825-925) 5/4 2175 (2100-2340) 1230 (1170-1310) 900 (840-960) 6/4 2200 (2125-2350) 1270 (1200-1320) - - - - - - - - 8/4 2255 (2165-2360) 1300 (1215-1360) - - - - - - - -

FAS #1 Common #2A Common

FAS (Net) #1 Common (Net) #2A Common (Net)

Southern Comments on page 14

APPALACHIAN HARDWOODS4 9/24/21

F. O. B. MILLS – APPALACHIAN AREAEstimate of FOB Appalachian mill point average market prices for well manufactured Appalachian hardwoods in truckload and greater quantities. Stocks are random widths and lengths, green, rough, and graded in accordance with NHLA rules. Prices in US dollars per M’. Prices published in Hardwood Market Report are presented only as a guide. See statement on back page. © 2021 Hardwood Market Report

HARD MAPLE - #1&2 WHITE FAS 1F #1C #2A

4/4 2500 + 2490 + 1635 + 1015 + 5/4 2600 2590 1645 + - - - 6/4 2635 2625 1645 + - - - 8/4 2725 2715 1645 + - - -

HARD MAPLE - UNSELECTED FAS 1F #1C #2A #3A

4/4 2240 + 2230 + 1465 + 825 + 625 + 5/4 2280 + 2270 + 1475 + 825 + 635 + 6/4 2310 + 2300 + 1475 + 830 + 670 + 8/4 2380 + 2370 + 1515 + 845 + 685 +

FAS&1F ALONE ADD $0

SOFT MAPLE - SAP&BTR FAS 1F #1C #2A

4/4 1845 + 1835 + 1150 + 695 5/4 1940 + 1930 + 1170 + 695 6/4 1955 + 1945 + 1210 + 705 8/4 1980 + 1970 + 1245 + 745

SOFT MAPLE - UNSELECTED FAS 1F #1C #2A

4/4 1750 + 1740 + 1030 + 600 5/4 1790 + 1780 + 1075 + 605 6/4 1815 + 1805 + 1100 + 610 8/4 1825 + 1815 + 1135 + 650

FAS&1F ALONE ADD $0

RED OAK FAS 1F #1C #2A #3A 4/4 1260 1250 1030 970 905 5/4 1310 1300 1035 970 905 6/4 1360 1350 1040 975 910 8/4 1405 1395 1040 980 920

FAS&1F ALONE #2A ALONE4/4 ADD $0 4/4 $970 5/4 ADD $0 6/4 & 8/4 ADD $0

WHITE OAK FAS 1F #1C #2A #3A 4/4 3180 + 3170 + 1500 975 915 5/4 3500 + 3490 + 1515 975 915 6/4 3590 + 3580 + 1525 995 935 8/4 3975 + 3965 + 1545 - - - - - -

FAS&1F ALONE 4/4 ADD $0 5/4 ADD $0 6/4 ADD $0 8/4 ADD $0

ASH FAS 1F #1C #2A

4/4 1260 1250 830 565 5/4 1285 1275 850 580 6/4 1400 1390 970 + 605 + 8/4 1505 1495 1045 + 650 +

BASSWOOD FAS 1F #1C #2A #2B

4/4 925 + 915 + 525 + 265 220 5/4 965 + 955 + 550 + 270 225 6/4 1000 + 990 + 585 + 275 235 8/4 1050 + 1040 + 625 + 290 245 9/4 1075 + 1065 + 665 + 295 260

BEECH FAS 1F #1C #2A #3A 4/4 730 720 570 435 370 5/4 740 730 590 455 375 6/4 755 745 640 470 385 8/4 770 760 655 475 400

BIRCH FAS 1F #1C #2A

4/4 1140 1130 800 510 5/4 1185 1175 850 555 6/4 1230 1220 900 590 8/4 1255 1245 925 605

FAS&1F ALONE ADD $85

CHERRY FAS 1F #1C #2A #3A 4/4 1490 1480 840 480 375 5/4 1520 1510 840 480 385 6/4 1595 1585 870 480 405 8/4 1650 1640 890 500 415

CHERRY - NORTH CENTRAL FAS 1F #1C #2A #3A

4/4 1580 1570 860 480 385 5/4 1640 1630 865 480 385 6/4 1700 1690 890 490 425 8/4 1795 1785 935 505 430

HICKORY FAS 1F #1C #2A #2B

4/4 1140 1130 850 740 545 5/4 1310 1300 915 745 545 6/4 1495 1485 995 760 555 8/4 1535 1525 1020 790 555

APPALACHIAN HARDWOODS 59/24/21

WHITE OAK - WHND FAS 1F #1C SW 4/4 1425 1415 1000 680 5/4 1455 1445 1050 710

POPLAR FAS 1F #1C #2A #2B 4/4 1450 1440 870 665 465 5/4 1470 1460 880 675 480 6/4 1475 1465 885 700 490 8/4 1490 1480 900 705 495 10/4 1540 1530 925 730 510 12/4 1575 1565 945 745 520 16/4 1615 1605 975 760 525

WALNUT FAS 1F #1C #2A 4/4 3990 3890 2430 1330 5/4 4070 3970 2465 1350 6/4 4195 4095 2500 1355 8/4 4470 4370 2515 1365

FRAMESTOCK - AIR DRIED

4/4 OAK S2S (530-650)

4/4 MIXED S2S (550-670)

CANTS - GREEN 685 (580-800)

TIES - 7x9 - GREEN

SOUTHERN APPALACHIAN - 8½'CROSSTIES (34.75-39.75) Per Pc.

NORTHERN APPALACHIAN - 8½'CROSSTIES (34.50-39.00) Per Pc.

BOARD ROAD - GREEN 595 (555-655)

© 2021 Hardwood Market Report

I t is likely remodeling stimulates a higher percent-age of domestic consumption of grade hardwood

However, with supplies relatively low, pricing in most reported activity remains clustered around the listings or contained within the ranges. Green #2A&Btr Ash is moving at a steady pace to concentration yards and end users. Reported prices lift the 6/4 and 8/4 #1C and #2A listings $15 but leave all the other listings in place.

HARD MAPLE: Sawmills have solid order files for green #1&2 White and Unselected Hard Maple. Mill operators state that 4/4 Fas&1f and 4/4 #1C are moving best, though most items are highly salable. Prices are not advancing as quickly as in the summer, but they are edging up. Accordingly, the listings climb $20 for #1&2 White 4/4 Fas&1f, Unselected 4/4 through 8/4 Fas&1f, and 4/4 through 8/4 #1C in both color designations. Ad-ditionally, the #2A and #3A figures rise $15 in all pub-lished thicknesses. Market circumstances are similar for kiln dried Hard Maple, although most reported prices have plateaued for now, keeping the listings and ranges in check.

SOFT MAPLE: In the last 30 to 45 days, market inten-sity for this species has increased from an already good baseline. Demand for 4/4 #2A&Btr is vibrant from the cabinet industry and decent from wood furniture plants. As such, mills are concentrating production in the 4/4 thickness, and thicker items are in low supply. Green

lumber than new home construction. Spending on residential repairs and remodeling has been in record territory all year, far surpassing historical levels. This trend has been highly favorable for manufacturers of wood cabinets, flooring, residential moulding, and wood and upholstered furniture. Most manufacturers of these products have increased finished goods pro-duction this year, substantially in some cases, although labor and raw material supply constraints have capped growth. Amid these circumstances, domestic demand for a broad range of grade hardwood lumber items has been and remains good. Hardwood sawmill production has gradually increased this year, but supplies of most items are not overwhelming markets. Exports have also been a net positive, despite downturns in China and, more recently, Vietnam. During the first seven months of 2021, US exports of hardwood lumber to China were 53.6 MMBF lower than during the same period in 2020. However, combined shipments to all other destinations increased 136.5 MMBF, for a net gain of 82.9 MMBF.

ASH: Sales contacts report a slight decline in kiln dried Ash business, stemming mostly from sagging Chinese and Vietnamese demand. Most other domestic and in-ternational markets are performing more consistently. Prices have transitioned from firm to steady, though certain thick stock items are showing some softness. (Continued on Page 7)

6

ASH 4/4 1885 (1800-2000) 1210 (1155-1305) 860 (815-955) 5/4 2080 (1975-2195) 1335 (1280-1445) 1000 (930-1070) 6/4 2265 (2140-2420) 1535 (1470-1625) 1175 (1095-1255) 8/4 2415 (2270-2555) 1650 (1585-1750) 1280 (1210-1395) BASSWOOD 4/4 1440 [+25] (1350-1530) 895 (820-955) 575 (535-645) 5/4 1505 [+25] (1420-1560) 900 (860-955) - - - - - - - - 9/4 1515 [+20] (1460-1590) 965 (920-1030) - - - - - - - -

CHERRY 4/4 2160 (2045-2275) 1345 (1280-1425) 810 (750-885) 5/4 2295 (2210-2425) 1395 (1340-1480) 875 (820-915) 6/4 2370 (2260-2525) 1540 (1465-1635) - - - - - - - - 8/4 2475 (2360-2635) 1620 (1530-1695) - - - - - - - -

CHERRY 4/4 2190 (2045-2280) 1420 (1300-1485) 895 (820-955)North Central 5/4 2325 (2210-2420) 1450 (1355-1525) 895 (820-955) 6/4 2415 (2260-2520) 1585 (1490-1680) - - - - - - - - 8/4 2500 (2370-2675) 1670 (1570-1775) - - - - - - - -

HICKORY 4/4 1745 (1655-1860) 1410 [+25] (1340-1515) 1220 (1150-1280) HARD MAPLE 4/4 3290 (3120-3475) 2140 (2020-2275) 1485 (1395-1570)#1&2 White 5/4 3535 (3365-3765) 2190 (2060-2300) 1470 (1395-1570) 6/4 3550 (3355-3770) 2195 (2060-2300) - - - - - - - - 8/4 3625 (3415-3765) 2215 (2050-2325) - - - - - - - -

HARD MAPLE 4/4 2960 (2830-3065) 1870 (1790-1935) 1135 (1070-1220)Unselected 5/4 3200 (3055-3305) 1915 (1840-2005) 1160 (1100-1245) 6/4 3375 (3245-3560) 1980 (1895-2060) - - - - - - - - 8/4 3460 (3295-3685) 2045 (1935-2120) - - - - - - - -

SOFT MAPLE 4/4 2720 (2535-2860) 1665 [+20] (1555-1735) 1090 (1025-1165)Sap&Btr 5/4 2815 (2695-2995) 1675 [+20] (1615-1770) 1065 (1005-1145) 6/4 2835 (2700-3005) 1725 [+20] (1660-1815) 1075 (1025-1135) 8/4 2940 (2800-3150) 1770 [+20] (1705-1875) 1095 (1030-1170)

SOFT MAPLE 4/4 2410 (2305-2520) 1430 (1350-1490) 890 (840-965)Unselected 5/4 2570 (2480-2705) 1495 (1415-1555) 900 (850-965) 6/4 2690 (2580-2840) 1575 (1515-1675) 970 (930-1040) 8/4 2855 (2745-3000) 1600 (1535-1720) 1025 (975-1090)

RED OAK 4/4 1755 [–20] (1625-1890) 1335 [–15] (1235-1410) 1185 (1115-1255) 5/4 2005 [–20] (1845-2140) 1505 (1395-1580) 1250 (1165-1305) 6/4 2110 (2020-2255) 1635 (1535-1745) 1285 (1205-1375) 8/4 2165 (2050-2300) 1705 (1630-1815) 1370 (1280-1465)

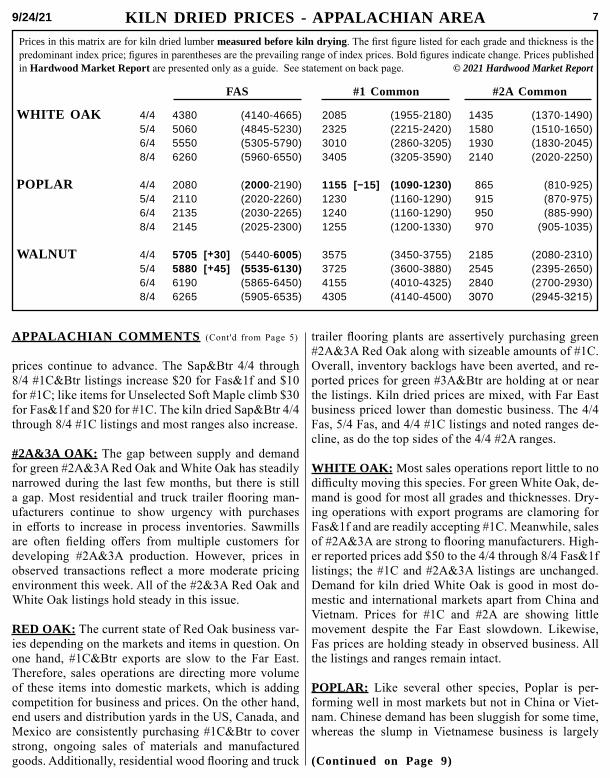

KILN DRIED PRICES - APPALACHIAN AREA 9/24/21

FAS #1 Common #2A Common

Prices in this matrix are for kiln dried lumber measured before kiln drying. The first figure listed for each grade and thickness is the predominant index price; figures in parentheses are the prevailing range of index prices. Bold figures indicate change. Prices published in Hardwood Market Report are presented only as a guide. See statement on back page. © 2021 Hardwood Market Report

KILN DRIED PRICES - APPALACHIAN AREA 79/24/21

FAS #1 Common #2A Common

Prices in this matrix are for kiln dried lumber measured before kiln drying. The first figure listed for each grade and thickness is the predominant index price; figures in parentheses are the prevailing range of index prices. Bold figures indicate change. Prices published in Hardwood Market Report are presented only as a guide. See statement on back page. © 2021 Hardwood Market Report

WHITE OAK 4/4 4380 (4140-4665) 2085 (1955-2180) 1435 (1370-1490) 5/4 5060 (4845-5230) 2325 (2215-2420) 1580 (1510-1650) 6/4 5550 (5305-5790) 3010 (2860-3205) 1930 (1830-2045) 8/4 6260 (5960-6550) 3405 (3205-3590) 2140 (2020-2250)

POPLAR 4/4 2080 (2000-2190) 1155 [–15] (1090-1230) 865 (810-925) 5/4 2110 (2020-2260) 1230 (1160-1290) 915 (870-975) 6/4 2135 (2030-2265) 1240 (1160-1290) 950 (885-990) 8/4 2145 (2025-2300) 1255 (1200-1330) 970 (905-1035)

WALNUT 4/4 5705 [+30] (5440-6005) 3575 (3450-3755) 2185 (2080-2310) 5/4 5880 [+45] (5535-6130) 3725 (3600-3880) 2545 (2395-2650) 6/4 6190 (5865-6450) 4155 (4010-4325) 2840 (2700-2930) 8/4 6265 (5905-6535) 4305 (4140-4500) 3070 (2945-3215)

trailer flooring plants are assertively purchasing green #2A&3A Red Oak along with sizeable amounts of #1C. Overall, inventory backlogs have been averted, and re-ported prices for green #3A&Btr are holding at or near the listings. Kiln dried prices are mixed, with Far East business priced lower than domestic business. The 4/4 Fas, 5/4 Fas, and 4/4 #1C listings and noted ranges de-cline, as do the top sides of the 4/4 #2A ranges.

WHITE OAK: Most sales operations report little to no difficulty moving this species. For green White Oak, de-mand is good for most all grades and thicknesses. Dry-ing operations with export programs are clamoring for Fas&1f and are readily accepting #1C. Meanwhile, sales of #2A&3A are strong to flooring manufacturers. High-er reported prices add $50 to the 4/4 through 8/4 Fas&1f listings; the #1C and #2A&3A listings are unchanged. Demand for kiln dried White Oak is good in most do-mestic and international markets apart from China and Vietnam. Prices for #1C and #2A are showing little movement despite the Far East slowdown. Likewise, Fas prices are holding steady in observed business. All the listings and ranges remain intact.

POPLAR: Like several other species, Poplar is per-forming well in most markets but not in China or Viet-nam. Chinese demand has been sluggish for some time, whereas the slump in Vietnamese business is largely

prices continue to advance. The Sap&Btr 4/4 through 8/4 #1C&Btr listings increase $20 for Fas&1f and $10 for #1C; like items for Unselected Soft Maple climb $30 for Fas&1f and $20 for #1C. The kiln dried Sap&Btr 4/4 through 8/4 #1C listings and most ranges also increase.

#2A&3A OAK: The gap between supply and demand for green #2A&3A Red Oak and White Oak has steadily narrowed during the last few months, but there is still a gap. Most residential and truck trailer flooring man-ufacturers continue to show urgency with purchases in efforts to increase in process inventories. Sawmills are often fielding offers from multiple customers for developing #2A&3A production. However, prices in observed transactions reflect a more moderate pricing environment this week. All of the #2&3A Red Oak and White Oak listings hold steady in this issue.

RED OAK: The current state of Red Oak business var-ies depending on the markets and items in question. On one hand, #1C&Btr exports are slow to the Far East. Therefore, sales operations are directing more volume of these items into domestic markets, which is adding competition for business and prices. On the other hand, end users and distribution yards in the US, Canada, and Mexico are consistently purchasing #1C&Btr to cover strong, ongoing sales of materials and manufactured goods. Additionally, residential wood flooring and truck

APPALACHIAN COMMENTS (Cont'd from Page 5)

(Continued on Page 9)

ASH 4/4 2025 (1935-2150) 1300 (1240-1400) 925 (875-1025) 5/4 2235 (2125-2360) 1435 (1375-1550) 1075 (1000-1150) 6/4 2435 (2300-2600) 1650 (1580-1745) 1265 (1175-1350) 8/4 2595 (2440-2750) 1770 (1700-1880) 1375 (1300-1500) BASSWOOD 4/4 1545 [+25] (1450-1645) 960 (880-1025) 620 (575-695) 5/4 1615 [+25] (1525-1675) 970 (925-1025) - - - - - - - - 9/4 1630 [+25] (1570-1710) 1040 (990-1110) - - - - - - - -

CHERRY 4/4 2325 (2200-2450) 1445 (1375-1530) 870 (805-950) 5/4 2470 (2375-2605) 1500 (1440-1590) 940 (880-985) 6/4 2550 (2430-2715) 1655 (1575-1755) - - - - - - - - 8/4 2665 (2540-2835) 1745 (1645-1825) - - - - - - - -

CHERRY 4/4 2350 (2200-2450) 1530 (1400-1600) 960 (880-1025)North Central 5/4 2500 (2375-2600) 1560 (1460-1640) 960 (880-1025) 6/4 2600 (2435-2715) 1705 (1600-1805) - - - - - - - - 8/4 2690 (2550-2875) 1800 (1690-1910) - - - - - - - -

HICKORY 4/4 1875 (1780-2000) 1515 [+25] (1440-1625) 1310 (1235-1375)

HARD MAPLE 4/4 3530 (3350-3730) 2300 (2170-2445) 1595 (1500-1685)#1&2 White 5/4 3800 (3615-4045) 2350 (2210-2470) 1580 (1500-1685) 6/4 3810 (3600-4050) 2355 (2210-2470) - - - - - - - - 8/4 3890 (3675-4050) 2380 (2200-2500) - - - - - - - -

HARD MAPLE 4/4 3180 (3040-3290) 2010 (1925-2080) 1220 (1150-1310)Unselected 5/4 3435 (3280-3545) 2055 (1975-2150) 1245 (1180-1335) 6/4 3620 (3480-3820) 2125 (2035-2210) - - - - - - - - 8/4 3715 (3535-3960) 2195 (2080-2275) - - - - - - - -

SOFT MAPLE 4/4 2920 (2725-3075) 1790 [+20] (1670-1865) 1170 (1100-1250)Sap&Btr 5/4 3020 (2900-3220) 1800 [+20] (1735-1900) 1145 (1080-1230) 6/4 3045 (2900-3225) 1850 [+20] (1780-1950) 1155 (1100-1220) 8/4 3155 (3005-3380) 1900 [+20] (1830-2015) 1175 (1105-1255)

SOFT MAPLE 4/4 2590 (2480-2705) 1535 (1450-1600) 955 (905-1035)Unselected 5/4 2765 (2665-2905) 1605 (1520-1670) 965 (915-1040) 6/4 2890 (2770-3050) 1690 (1625-1800) 1045 (1000-1120) 8/4 3070 (2950-3220) 1720 (1650-1850) 1100 (1050-1170)

RED OAK 4/4 1890 [–20] (1750-2030) 1435 [–15] (1330-1515) 1275 (1200-1350) 5/4 2155 [–20] (1985-2300) 1620 (1500-1700) 1345 (1250-1400) 6/4 2270 (2170-2420) 1760 (1650-1875) 1380 (1295-1475) 8/4 2330 (2200-2470) 1835 (1750-1950) 1470 (1375-1575)

KILN DRIED PRICES - APPALACHIAN AREA 9/24/218

Prices in this matrix are for kiln dried lumber measured after kiln drying ("net tally"). The first figure listed for each grade and thick-ness is the predominant index price; figures in parentheses are the prevailing range of index prices. Bold figures indicate change. Prices published in Hardwood Market Report are presented only as a guide. See statement on back page. © 2021 Hardwood Market Report

FAS (Net) #1 Common (Net) #2A Common (Net)

KILN DRIED PRICES - APPALACHIAN AREA 99/24/21

WHITE OAK 4/4 4710 (4450-5010) 2240 (2100-2340) 1540 (1470-1600) 5/4 5435 (5200-5615) 2500 (2380-2600) 1700 (1625-1775) 6/4 5965 (5700-6220) 3230 (3075-3450) 2075 (1970-2200) 8/4 6735 (6400-7035) 3665 (3450-3865) 2300 (2170-2420)

POPLAR 4/4 2235 (2150-2355) 1240 [–20] (1170-1320) 930 (870-995) 5/4 2270 (2170-2430) 1320 (1245-1385) 985 (935-1050) 6/4 2295 (2180-2435) 1330 (1245-1385) 1020 (950-1065) 8/4 2305 (2175-2470) 1350 (1290-1430) 1045 (970-1110) WALNUT 4/4 6135 [+30] (5850-6450) 3840 (3700-4030) 2345 (2235-2480) 5/4 6315 [+50] (5950-6580) 4000 (3870-4175) 2735 (2575-2850) 6/4 6640 (6300-6925) 4470 (4310-4650) 3050 (2900-3155) 8/4 6740 (6345-7025) 4620 (4450-4830) 3295 (3160-3450)

Prices in this matrix are for kiln dried lumber measured after kiln drying ("net tally"). The first figure listed for each grade and thick-ness is the predominant index price; figures in parentheses are the prevailing range of index prices. Bold figures indicate change. Prices published in Hardwood Market Report are presented only as a guide. See statement on back page. © 2021 Hardwood Market Report

FAS (Net) #1 Common (Net) #2A Common (Net)

attributable to the recent resurgence of COVID in that country. Since both markets consume primarily #1C and #2A, kiln dried prices for those grades are showing evi-dence of softening. However, at this time, only the kiln dried 4/4 #1C listings and ranges warrant decreases. De-mand for upper grade Poplar is vibrant in North Amer-ica and decent in several international markets. All the green Fas&1f and most of the kiln dried Fas figures re-main intact, although the low sides of the kiln dried 4/4 Fas ranges advance.

WALNUT: **NOTICE: An error was discovered this week in the price matrix on page 7 for kiln dried 5/4 Fas. The listing was shown as 5550 beginning in the September 3rd issue, when no change had oc-curred in our database from the August 27th issue showing 5835. The error has been corrected, and the price published in this issue includes an increase from 5835.** Sawmills are readily moving developing green #2A&Btr Walnut. However, several point out higher demand for 4/4 and 5/4 than for thicker stocks. Reported prices have not meaningfully changed during the last few weeks, allowing the listings to stand. Mills and yards that offer kiln dried Walnut are pleased with market conditions. Shipments are slow to China and Vietnam but brisk to other destinations. The 4/4 and 5/4 Fas listings and noted ranges climb on higher reported

prices. All the other published figures hold steady.

FRAMESTOCK, CANTS, TIES, & BOARD ROAD: Business is good for producers and resellers of solid hardwood framestock. Upholstered furniture factories are busy and need steady streams of raw materials for frames. Last week’s increases have the Oak and Mixed Species framestock ranges in order.

Wood pallet manufacturers continue to show strong interest in available pallet cants and lumber. For most, business is limited more by labor supply than by de-mand. Raw materials supplies also remain an issue for some. Reported cant prices vary widely across the re-gion but are largely unchanged from a week ago.

According to the Railway Tie Association, 7x9 crosstie inventories declined from March through June (the most recent data). In order to bulk up inventories, treating op-erations are being assertive with purchase volumes and prices. To better reflect observed prices, both ends of the Southern Appalachian 7x9 crosstie range are raised $0.75, with $0.50 increases made to both ends of the Northern Appalachian range.

Demand for board road has trended slightly higher this year. Supplies are thin due to heavy competition from tie and #2A&3A Oak markets. The board road listing and range accurately reflect current prices in the marketplace.

APPALACHIAN COMMENTS (Cont'd from Page 7)

NORTHERN HARDWOODS10

ASH FAS SEL #1C #2A

4/4 1235 1225 765 + 490 + 5/4 1290 1280 785 + 500 + 6/4 1360 1350 830 + 515 + 8/4 1430 1420 860 + 530 +

ASPEN FAS SEL #1C #2A #2B

4/4 850 840 510 300 220

BASSWOOD FAS SEL #1C #2A #2B

4/4 1070 1055 605 300 240 5/4 1075 1060 615 310 240 6/4 1085 1070 630 320 250 8/4 1100 1085 650 330 255 9/4 1145 1130 690 345 - - -

BEECH FAS SEL #1C #2A #3A

4/4 695 675 535 325 260 5/4 705 685 545 335 270 6/4 725 705 605 360 300 8/4 745 725 620 365 300 FAS&SEL ALONE ADD $90

BIRCH FAS SEL #1C #2A #3A

4/4 1530 1510 950 625 430 5/4 1555 1535 960 640 445 6/4 1605 1585 1025 650 455 8/4 1630 1610 1050 670 470

Red Birch Add . . . . . . . . . . . . . . .$ 305 Sap Birch Add. . . . . . . . . . . . . . .$ 140 FAS&SEL ALONE ADD $0

NORTHERN SOFT GREY ELM FAS SEL #1C #2A #2B 4/4 670 655 420 290 265

HARD MAPLE - #1&2 WHITE FAS SEL #1C #2A

4/4 2625 2605 1660 1040 5/4 2645 2625 1675 - - - 6/4 2710 + 2690 + 1700 - - - 8/4 2780 + 2760 + 1740 - - -

HARD MAPLE - UNSELECTED FAS SEL #1C #2A #3A 4/4 2370 2350 1485 835 685 5/4 2450 2430 1525 840 690 6/4 2495 + 2475 + 1550 875 690 8/4 2530 + 2510 + 1580 900 - - -

Sap 1-Face in cuttings Add . . . . . . .$100 FAS&SEL ALONE ADD $0

CANTS - GREEN 595 (500-755)

PALLET LBR - GREEN4/4 x RW 440 (400-505)5/4 x RW 465 (415-515)6/4 x RW 490 (440-530)

4/4 x SW 485 (445-535)5/4 x SW 495 (445-555) 6/4 x SW 525 (475-570)

TIES - 7x9 - GREENNORTHERN - 8½’CROSSTIES (30.25-35.00) Per Pc.

BOARD ROAD - GREEN 540 (480-565)

9/24/21

F. O. B. MILLS - NORTHERN AREAEstimate of FOB Northern mill point average market prices for well manufactured Northern hardwoods in truckload and greater quanti-ties. Stocks are random widths and lengths, green, rough, and graded in accordance with NHLA rules. Prices in US dollars per M’. Prices published in Hardwood Market Report are presented only as a guide. See statement on back page. © 2021 Hardwood Market Report

SOFT MAPLE - SAP&BTR FAS SEL #1C #2A 4/4 1930 1910 1260 735 5/4 1965 1945 1260 745 6/4 2000 1980 1280 760 8/4 2060 2040 1320 780

SOFT MAPLE - UNSELECTED FAS SEL #1C #2A #2B

4/4 1755 + 1735 + 1105 + 595 380 5/4 1790 + 1770 + 1105 + 625 380 6/4 1840 + 1820 + 1120 + 650 385 8/4 1880 + 1860 + 1165 + 675 390 FAS&SEL ALONE ADD $0

RED OAK FAS SEL #1C #2A #3A

4/4 1305 1285 920 700 610 5/4 1330 1310 925 705 615 6/4 1370 1350 930 725 620 8/4 1415 1395 950 - - - - - -

FAS&SEL ALONE #2A ALONE4/4 & 5/4 ADD $0 4/4 $700 6/4 & 8/4 ADD $0

WHITE OAK FAS SEL #1C #2A #3A 4/4 2620 + 2600 + 1250 780 660 5/4 2845 + 2825 + 1295 790 675 6/4 2925 + 2905 + 1370 - - - - - -FAS&SEL ALONE 4/4 ADD $0 5/4 ADD $0 6/4 ADD $0

SOUTHERN HARDWOODS

P

KILN DRIED PRICES - NORTHERN AREA 119/24/21

Prices in this matrix are for kiln dried lumber measured before kiln drying. The first figure listed for each grade and thickness is the predominant index price; figures in parentheses are the prevailing range of index prices. Bold figures indicate change. Prices published in Hardwood Market Report are presented only as a guide. See statement on back page. © 2021 Hardwood Market Report

FAS #1 Common #2A Common

ASH 4/4 1645 (1580-1770) 1100 (1045-1210) 805 (740-885)

ASPEN 4/4 1315 (1210-1370) 790 (700-875) 505 (450-575)

BASSWOOD 4/4 1510 (1400-1585) 860 (795-915) 505 (450-550) 5/4 1520 (1390-1595) 885 (820-925) 520 (475-560) 8/4 1525 (1430-1600) 950 (890-1005) 575 (525-610) 9/4 1535 (1450-1605) 1015 (945-1060) 595 (550-630)

YELLOW BIRCH 4/4 2110 [+25] (2020-2215) 1380 [+15] (1305-1465) 875 (805-960)

HARD MAPLE 4/4 3505 (3385-3585) 2210 (2150-2285) 1585 (1520-1725)#1&2 White 5/4 3585 (3505-3700) 2235 (2165-2330) - - - - - - - - 6/4 3625 (3555-3715) 2265 (2195-2345) - - - - - - - - 8/4 3690 (3630-3770) 2305 (2230-2370) - - - - - - - -

HARD MAPLE 4/4 3195 (3135-3260) 1940 (1875-1995) 1305 (1260-1360)Unselected 5/4 3265 (3185-3325) 1970 (1920-2035) 1315 (1270-1370)

SOFT MAPLE 4/4 2795 (2700-2915) 1625 (1575-1775) 1040 (980-1120)Sap&Btr 5/4 2810 (2735-2895) 1635 (1585-1770) 1050 (1000-1125) 6/4 2855 (2790-2910) 1650 (1600-1790) 1055 (1005-1130) 8/4 2900 (2845-2985) 1715 (1660-1820) 1075 (1020-1135)

SOFT MAPLE 4/4 2565 (2505-2650) 1460 (1410-1555) 900 (850-965)Unselected

RED OAK 4/4 1880 [–25] (1805-2020) 1445 (1385-1540) 1090 (1035-1145) 5/4 1995 (1930-2095) 1455 (1405-1545) 1095 (1045-1155) 6/4 2025 (1950-2120) 1460 (1405-1550) - - - - - - - -

WHITE OAK 4/4 4125 (3975-4385) 1965 (1900-2120) 1280 (1175-1390)

rices have reached record highs for a number of grade lumber items in key Northern species. Kiln

dried #1&2 White Hard Maple 4/4 Fas is one such item; prices have more than doubled from January 3, 2020 to this issue. Sap&Btr 4/4 Fas Soft Maple pricing is almost 60% higher than the first of 2020. Kiln dried 4/4 Fas Birch prices have risen over 56% the past 20 months. Kiln dried 4/4 Fas Ash and White Oak prices are at re-cord levels, with Ash gaining 42% and White Oak up 89% from January of last year through September 24, 2021. The reasons for the sharp increases in hardwood

lumber and even industrial product prices are well doc-umented. Production has been slow to recover from the COVID-19 lockdowns last year because of lack of la-bor. The entire supply stream has been set back and pos-sibly damaged. However, many mills indicate log decks have improved this summer, and most end users state that in process lumber inventories have increased. The before mentioned record high prices are causing some buyers to be more cautious with purchases. Neither dis-

(Continued on Page 12)

12 9/24/21

NORTHERN COMMENTS (Cont'd from Page 11)

tributors, yards, nor secondary manufacturers want to be caught with high cost raw materials should prices retreat. While there are some moderately lower prices reported, information shows contraction has been mod-erate and species, grade, and thickness specific.

ASH: In the Upper Midwest, the number of timber tracts with live Ash trees has dwindled. Some sawmill oper-ators are not processing this species any longer, which is contributing to green lumber shortfalls. Concentra-tion yards and secondary manufacturers are readily absorbing developing green #2A&Btr production. Last week’s changes have the upper grade figures in order, but the 4/4 through 8/4 #1C and #2A listings are raised $20 and $15, respectively. North American demand for kiln dried Ash is good and is keeping inventories thin for most grades and thicknesses. Transactions point out some additional price inflation, though adjustments are occurring within the #2A&Btr ranges.

ASPEN: While interest in this species is solid, lack of production has driven price inflation more than a rise in demand. Mills that produce Aspen on a regular basis are still processing this species. But, sawmill operators that intermittently saw Aspen are focused on higher valued species, such as Hard and Soft Maple, limiting Aspen availability. Reported prices for green #2B&Btr have trended up, but past increases have the published fig-ures in order. Likewise, information holds the kiln dried listings and ranges intact.

BASSWOOD: Most area mills report decent log decks for this time of year. High valued whitewoods, such as Hard and Soft Maple, are taking priority over Basswood production. Nonetheless, Basswood logs are being sawn. Markets are readily absorbing developing supplies and want more. Reported prices for green #2B&Btr have trended higher, though past increases have the published listings in order for now. Kiln dried demand is strong, with some end users substituting Basswood where they can to bring down total raw material costs. New business combined with regular business has depleted kiln dried inventories. Transactions point out sufficiently higher numbers to raise the low sides of the 4/4 Fas ranges.

HARD MAPLE: Over time, US hardwoods have lost market share to imported species and finished goods. But, the supply pipeline for these items has been dis-

rupted by COVID-19 lockdowns in countries supplying the US with such products. Hard Maple has benefitted from these circumstances, as have most other domestic species. Demand is strong and is keeping developing supplies shipped at record high prices. In this issue, the green 6/4 and 8/4 Fas&Sel listings are raised $25 for both color classifications. Most area mills indicate log decks have grown, and green lumber output has been up long enough to increase kiln dried availability. In cas-es, sales companies are exerting more effort to sell kiln dried stocks. Upward price pressures have eased, allow-ing the kiln dried Unselected and #1&2 White #2A&Btr figures to stand this week.

SOFT MAPLE: While Soft Maple prices have risen sharply, Hard Maple prices are even higher, which has boosted demand for Soft Maple. Markets are readily ab-sorbing developing green supplies. The gap between re-ported Sap&Btr and Unselected prices has narrowed. In-formation holds the Sap&Btr #2A&Btr listings in check but raises the Unselected 4/4 through 8/4 #1C&Btr fig-ures $25 for Fas&Sel and $15 for #1C. Meanwhile, sales companies indicate order files are solid for kiln dried stocks, and transactions point out firm to higher pricing. However, any noted price gains are within the Unselected and Sap&Btr #2A&Btr ranges.

RED OAK: Data show sawmill production has edged up the past four months. However, Red Oak output in the Northern region has not increased significantly. Most sawmill operators are processing whitewoods to avoid stain damage. However, green Red Oak out-put is meeting the market’s needs. Supply and demand are closely aligned, and reported prices are stable. No changes are required to the #3A&Btr listings. Markets for kiln dried Red Oak have cooled to a degree. Inven-tories are sufficient for short term needs, with some ex-cess upper grade available. Transactions point out low-er pricing for 4/4 Fas that reduces the listings and low sides of the ranges.

WHITE OAK: Sawmill production of White Oak has not significantly improved. While green common grade supplies are meeting buyers’ needs, Fas&Sel output is falling short of demand. The 4/4 through 6/4 Fas&Sel listings climb $25. Markets for kiln dried White Oak are mixed, but inventories are not particularly high for any grade/thickness combination. Transactions point out prices in line with last week, allowing the #2A&Btr figures to stand.

PALLET LUMBER, CANTS, TIES, & BOARD ROAD: The strong US economic recovery has fueled growing demand for pallets and containers.Manufacturers are working to fill deep order files. Raw material supplies, including cants and lumber, have improved the past several weeks. Yet, buyers indicate they would like to build on hand supplies. Reported prices for cants are up, lifting the top side of the range $15. No changes are warranted to the random or selected width pallet lumber figures.

Projections for tie purchases have changed little. Busi-ness for the remainder of 2021 and 2022 is expected to

Prices in this matrix are for kiln dried lumber measured after kiln drying (“net tally”). The first figure listed for each grade and thick-ness is the predominant index price; figures in parentheses are the prevailing range of index prices. Bold figures indicate change. Prices published in Hardwood Market Report are presented only as a guide. See statement on back page. © 2021 Hardwood Market Report

ASH 4/4 1770 (1700-1905) 1180 (1125-1300) 865 (795-950)

ASPEN 4/4 1415 (1300-1470) 850 (750-940) 545 (485-620)

BASSWOOD 4/4 1625 (1505-1700) 925 (855-985) 545 (485-590) 5/4 1630 (1495-1710) 950 (880-995) 560 (510-600) 8/4 1635 (1535-1715) 1020 (955-1080) 620 (565-655) 9/4 1645 (1555-1720) 1090 (1015-1140) 640 (590-680)

YELLOW BIRCH 4/4 2265 [+25] (2170-2380) 1485 [+20] (1405-1575) 940 (865-1030)

HARD MAPLE 4/4 3765 (3635-3850) 2375 (2310-2455) 1700 (1630-1850)#1&2 White 5/4 3850 (3765-3975) 2400 (2325-2500) - - - - - - - - 6/4 3890 (3815-3990) 2430 (2355-2515) - - - - - - - - 8/4 3960 (3895-4045) 2475 (2395-2545) - - - - - - - -

HARD MAPLE 4/4 3430 (3365-3500) 2085 (2015-2145) 1405 (1355-1465)Unselected 5/4 3505 (3420-3570) 2120 (2065-2190) 1415 (1365-1475)

SOFT MAPLE 4/4 3000 (2900-3130) 1745 (1690-1905) 1120 (1055-1205)Sap&Btr 5/4 3015 (2935-3110) 1755 (1700-1900) 1125 (1075-1205) 6/4 3065 (2995-3125) 1775 (1720-1925) 1130 (1080-1215) 8/4 3110 (3050-3200) 1845 (1785-1955) 1155 (1095-1220)

SOFT MAPLE 4/4 2755 (2690-2845) 1570 (1515-1670) 965 (915-1035)Unselected

RED OAK 4/4 2025 [–25] (1945-2175) 1550 (1485-1655) 91170 (1110-1230) 5/4 2145 (2075-2250) 1560 (1510-1660) 1175 (1125-1240) 6/4 2175 (2095-2275) 1570 (1510-1665) - - - - - - - -

WHITE OAK 4/4 4430 (4270-4710) 2115 (2045-2280) 1375 (1265-1495)

#2A Common (Net)

KILN DRIED PRICES - NORTHERN AREA 139/24/21

FAS (Net) #1 Common (Net)

be decent for the tie industry. However, treaters have struggled to source enough ties to meet inventory ob-jectives. Hardwood sawmill production has been slow to rise, and Northern mills are focusing output on high valued whitewoods, which is limiting tie production all the more. Reported prices are firm to higher, but any price changes are within the range.

Demand for board road is decent and is expected to be good through the remainder of the year. Regular pro-ducers are processing board road, though supplies are marginally adequate to satisfy total needs. Reported prices are firm and in line with the listing and range.

T

14 9/24/21

he US economy is booming, but supply snags have decreased activity for a number of industries. For

WHITE OAK: White Oak log decks have been slow to increase, but production has risen slightly. Markets are readily absorbing all grades and thicknesses, but report-ed prices have stabilized. Transactions point out numbers centered on the #3A&Btr listings. Demand for kiln dried Fas White Oak remains strong. On the other hand, inter-est in #1C and #2A is softer, especially from Vietnam. The kiln dried #2A&Btr listings and ranges are reflective of activity, allowing the published figures to stand.

POPLAR: A number of US distributors indicate lumber inventories have grown and are reaching desired levels, including Poplar. Too, secondary manufacturers have added to kiln dried raw material supplies. Sales com-panies are exerting more effort to sell developing kiln dried Poplar. Reported prices are steady for the upper grades and somewhat softer for #1C and #2A. But, the #2A&Btr listings and ranges are in order. Markets for green Fas&1f remain strong, while common grade de-mand has eased. Reported prices vary accordingly, with $20 added to all published thicknesses of Fas&1f, and the #1C, #2A, and #2B figures holding steady.

FRAMESTOCK, CANTS, TIES, & BOARD ROAD: Despite decent summer time drying conditions, well air dried framestock inventories are low relative to demand. Limited mill output earlier this year is contributing to shortfalls now. Reported prices have trended higher, though past adjustments have the Oak and Mixed Spe-cies ranges in order for now.

Cant production has edged up the past few weeks, though most wooden pallet and container manufacturers would like to have more supply. Too, the volume of pine used in pallets is climbing, due to better availability and declining prices. Information holds the hardwood cant listing and range in check this week.

Most treaters state that tie receipts remain low for this time of year. High #2A&3A Oak prices and the slow rise in total mill output are credited with limiting tie production. Prices for 7x9 crossties continue to trend higher, but changes are confined to the ranges.

Mills that regularly process board road are having no difficulty shipping developing supplies. Most buyers would like to increase board road purchases. Reported prices are firm and hold the listing and range in check.

SOUTHERN AREA

example, home builders were unable to source adequate framing material earlier this year, and pricing for almost all homebuilding products soared. The higher costs and limited supplies of such materials impacted new home construction, which has had a slight impact on domestic demand for hardwood lumber and finished goods more recently. However, hardwood lumber production has not risen sharply, which has prevented major overruns. Yet, pricing has either stabilized or softened for most items.

ASH: Active North American markets have been the primary reason kiln dried Ash supplies are down at this point in 2021. Coupled with that has been low sawmill output for much of the year. Reported prices for kiln dried #2A&Btr are in line with last week. Green Ash production remains controlled, as sawmill operators fo-cus on Red Oak and White Oak. Transactions point out some upward price movement for high grade Ash, but no changes are warranted to any of the #2A&Btr listings.

#2A&3A OAK: Hardwood sawmill production has slowly edged up after falling to the lowest level ever recorded in May of last year. Through August 2021, mill output averaged just over 6.5 billion board feet. At the same time, solid wood flooring plants have added shifts and hours to work schedules, increasing the vol-ume of lumber needed. However, some end users have made headway in adding to raw material supplies. In cases, higher grades of green and kiln dried lumber are filling voids in #2A&3A shortfalls. Current data show prices are firm but have stabilized, allowing the green #2A&3A Red and White Oak listings to stand.

RED OAK: Optimal drying conditions for lumber and a rise in sawmill production have increased kiln dried Red Oak inventories. Better availability has made buy-ers more cautious with purchases. The effect is softer pricing for 4/4 #1C&Btr. Information reduces the 4/4 #1C&Btr listings and noted range figures. Markets for 4/4 #2A are steady, driven by the solid wood flooring industry. Prices for thicker stocks of Red Oak are sta-ble, allowing the published figures to stand. Mills and resellers are having little difficulty finding outlets for green Red Oak, though interest in #2A&3A is better than for #1C&Btr. The #3A&Btr listings are representa-tive of reported prices.

OAK STRIP FLOORINGFigures in the Appalachian and Southern area columns are estimates of manufacturers’ predominant prices for unfinished Oak strip flooring; prices in the other column are estimates of prevailing industry ranges of manufacturers’ prices. Variations in prices are due, in part, to differ-ences in freight, the nature of markets, volumes ordered and shipped, etc. Prices are for truckload quantities graded in accordance with rules or comparable standards set forth by NOFMA. Prices are in US Dollars per square foot (SF) and are net of dealer discount fees and commis-sions. Figures in bold print signify price changes. Prices in Hardwood Market Report are presented only as a guide. See statement on back page. © 2021 Hardwood Market Report

159/24/21

3/4 x 2-1/4" APPALACHIAN SOUTHERN PREVAILING RANGESEL&BTR WHITE OAK 4.20 4.20 4.10-4.35 (+.10/+.05)

SEL&BTR RED OAK 4.08 (+.03) 4.05 (+.05) 3.90-4.15 (NC/+.05)

No. 1 COM WHITE OAK 3.60 3.60 3.52-3.70 (+.04/NC)

No. 1 COM RED OAK 3.50 3.50 3.35-3.60

No. 2 COM WHITE OAK 2.20 2.20 2.10-2.30 (+.03/NC)

No. 2 COM RED OAK 2.15 2.15 2.00-2.25 (+.05/NC)

3/4 x 3-1/4" APPALACHIAN SOUTHERN PREVAILING RANGESEL&BTR WHITE OAK 4.25 (+.03) 4.25 (+.03) 4.10-4.35 (NC/+.05)

SEL&BTR RED OAK 4.08 (+.03) 4.07 (+.02) 3.90-4.15 (NC/+.05)

No. 1 COM WHITE OAK 3.70 3.70 3.57-3.80

No. 1 COM RED OAK 3.55 3.55 3.37-3.60

No. 2 COM WHITE OAK 2.55 (+.05) 2.55 (+.05) 2.40-2.60 (NC/+.05)

No. 2 COM RED OAK 2.40 2.35 (+.03) 2.28-2.50 (+.03/NC)

M anufacturers report increases in finished goods inventory available for sale. The changeover

from being grossly oversold to having stock on hand is a huge transformation psychologically. The seller is not saying “no” to customers as much and, in cases, might even be the one initiating phone calls to make sales.

The shift in manufacturers’ inventory to sales ratio is profound. However, the scope of finished goods inven-tory – the volume and items included – is far from over-whelming. Manufacturers are still struggling to fulfill customers’ orders promptly and without substituting items to complete loads.

Furthermore, the improved inventory status should be no surprise. Manufacturers have worked diligently to build back their labor force and increase raw material inventories specifically to boost finished goods output.

There are other influences changing the Oak strip floor-ing inventory/sales makeup. The rate of new single family housing completions is much slower than the rate of housing starts. Inadequate supplies of all types

of building materials, components, interior fittings, and even appliances are contributing factors. So are record high prices for the aforementioned materials and goods. Importantly, higher prices always invite greater compe-tition, and it is very likely supplies of other floor cover-ing materials have also improved. Census data show more single family housing units were completed than started in the same month only three times between January 2020 and July 2021. The differential of completions to sales was substantially greater in the March through July 2021 period. There is a lot of single family housing units under construc-tion that will eventually be completed. But, where those units are within the construction process is uncertain. Are these in process housing inventories accumulating before or after hardwood flooring is installed?

The rate of price increases for Oak strip flooring slowed this week. While adjustments are warranted to the noted listings and ranges, strained budgets have consumers, installers, and builders looking toward lower grades and alternative species for relief.

• Complete 8' Sticking Stacker Line• Complete Breakdown Unsticking,

Grading Line, and Deadpile Stacking System

• Lumber Breakdown System• Complete Automatic Strapping sys-

tem, Infeed Transfer Deck, Infeed Rollcase, Strapping Machines, and Outfeed Transfer Deck

• Newman EPR-18 Double Surfacer• Weinig Profile Grinder• Industrial PopUp Saw• SSI 160,000 Board Foot Aluminum

Dry Kiln, (2) 50,000 Board Foot Chamber 30,000 Board Foot Chamber.

• Block Kilns with SSI Controls, Fans, and Doors

• 1995 English Waste Fired Boiler• 1976 Cleaver Brooks Package Boiler• (2) Silos with Cyclones and Pipe• Blower System

Call Zach: 931.208.4177

Oct. 19th at 10 AM EDT 11701 McCord RdHuntersville, NC 28078

Huntersville, NCSawmill Equipment Liquidation

At Absolute Auction!

10% Buyer’s Premium for onsite buyers -all items to be paid in full before removal.

Loren Beachy574.825.0704AU10500161

Eugene Hochstetler260.250.4597AU11400005

Jackie Kittrell931.567.0080LIC# 2293

Zach Kittrell931.208.4177Lic# 1959

Complete 8' Sticking Stacker Line•Complete Breakdown Unsticking, Grading Line, and Deadpile Stacking System•Lumber Breakdown System•Complete Automatic Strapping sys-tem, Infeed Transfer Deck, Infeed Rollcase, Strapping Machines, and Outfeed Transfer Deck•Newman EPR-18 Double Surfacer•Weinig Profile Grinder•Industrial PopUp Saw•SSI160,000 Board Foot Aluminum Dry Kiln, (2) 50 Board Foot Chamber (2) 30 Board Foot Chamber.•Block Kilns with SSI Controls, Fans, and Doors•1995 English Waste Fired Boil-er•1976 Cleaver Brooks Package Boiler•(2) Silos with Cyclones and Pipe•Blower System•Flying Dutchman Feed System•Lot of 8' Stacking Sticks•Lot of New and Used Parts andSupplies•Several Tank Mount Air Compressors•Some 20 Prefab Metal Buildings Ranging From 3,500 sq. ft. to 46,000 sq.ft.•Hyster 250 Dual Wheel Forklift, 8' Forks with EnclosedCab•Cat 8000 lb Propane Towmotor•Massey Ferguson 250 Tractor•RX-20 Platform Lift•JLG 40H Pro-Aer Man Lift•Grizzly Surfacer•Portable Office Building

Sellers: Huntersville Hardwood Inc.

• Flying Dutchman Feed System• Lot of 8' Stacking Sticks• Lot of New and Used Parts and

Supplies• Several Tank Mount Air Com-

pressors• Some 20 Prefab Metal Buildings

Ranging From 3,500 sq. ft. to46,000 sq.ft.

• Hyster 250 Dual Wheel Forklift, 8'Forks with Enclosed Cab

• Cat 8000 lb Propane Towmotor• Massey Ferguson 250 Tractor• X-20 Platform Lift• JLG 40H Pro-Aer Man Lift• Grizzly Surfacer• Portable Office Building

American Scissor LiftBand-O-Matic BandertIndustrial Upcut SawYates Floor End Matching MachinesYates-American Flooring MoldersMattison Straight-line Rip SawCarriage Drum DriveYates-American G-55 PlanerYates-American G-50 PlanerScanning SystemFilbert Stowell Band Head RigJackson Cochrane PlanerBenshaw Chipper Braking StarterPoolsen Horizontal Band SawRidgid 300 Pipe ThreaderSpinks ScaleLiftrite Pallet JackWisconsin Gas EngineRiding Tennant SweeperACME 1/2" Plastic Black BandingsCustom Built 4 HB CarriageTyrone-Berry Feed and DriveHanchett SharpenerOverhead Hoist SystemMereen-Johnson GangsawACME Saw SharpenerH 78B Rooftop ChainParker Hydraulic Hose Crimping MachineWarm Gear Winch with Mounting BlocksAJAX Auto Transformer StarterElectric Motors Band SawQL KilnPowermatic Band SawFamco 25R Manual Press

Winston Machinery Incline 5 Strand Transfer DeckWinston Machinery Belt Conveyor6 Strand Green ChainWinston 6 Strand UnscramblerIndustrial Upcut SawsHasko SR-24 Gang SawYates American GrinderMetal DetectorWilliams Patent Crusher and PulveriserCrosscut Solutions Upcut Saws Hasko HSEM-C End Matcher Landen Strapping Machines Flexband Plastic Banding Landen Strapping MachineIngersoll-Rand Air CompressorsTitan Industrial Heavy Duty Shop PressYates American C50 Gang SawDust Bin with Air Lock1992 Industrial Wood Boiler1972 Cleaver Brooks LP BoilerSteam-Pak LP BoilerDeWalt Radial Arm SawLumberline Laser SystemElectric Lift TableCornell UnscramblerCornell Trim SawCAT Forklift20951 Road GraderCart V330B Forklift1998 Ford F-150Whirlwind Upcut SawArmstrong Hand SharpenerVollmer Grinder

Winchester, VA Sawmill/Woodworking Equipment

At Absolute Auction!

Oct. 21st at 9 AM Sellers: Rossi Group

600 N. Kent StWinchester, VA 22601

Call Zach: 931.208.417710% Buyer’s Premium for onsite buyers - all items to be paid in full before removal.

Call 574.825.0704 to receive the Bright Star Bid Book for FREE. This is a detailed catalog that also allows you

to bid on the phone if you can’t attend or bid online.

B o kidB lThis catalog enables you to listen to the auction and bid on the phone.

See inside for details.

Date: August 7th

Date: July 30th Auction start time: 10:00 AM CSTCataloged auction start time: 11:00 AM CST

Auction start time: 9:00 AM CSTCataloged auction start time: 9:00 AM CST

Address:19250 Jaguar

Trail,Bloomfield IA

52537

Address: 2939 Cedar Rd.Seymour IA 52590

Address:10643 Wolcott

Hill Rd.,Camden NY 13316

Call: Eugene at 260-250-4942

Call: Eugene at 260-250-4942Date: August 1st

Auction start time: 10:00 AM ESTCataloged auction start time: 10:00 AM EST

Call: Eugene at 260-250-4942

Tiger cat 235B

Cleereman Carriage 40”, model #40, s/n 40-204, air set works (air over air), 3HB, w/3 Brownsville turners.

In very good condition!

Baker model BBR-O, single head resaw w/return hydraulic drive,

10” capacity

Fox River Hardwoods

ASV RT-65 track machine, almost

new, less than 100 hours

JLD Equipment

1977 Mack Truck, VIN DM685S34900 GVW 56030lbs, 227,218 miles, 1992 Nuova Copma

Model C1830N3LA- Rear Crane Italian made-Metric? 17660 max capacity

Cornell Edger model HEC-36, s/n 783-10-87, w/in-feed & out-

feed, moveable fence, 4 blades, 1 movable, 6’x36’, electric motor

36” CMC Rosserhead slant track Debarker, steel cab, chain drive, 24’ capacity

Formerly Spinks Sawmill

Hyundai 70D-7E Forklift

Loren Beachy574.825.0704AU10500161

Eugene Hochstetler260.250.4597AU11400005

Jackie Kittrell931.567.0080LIC# 2293

Zach Kitrell931.208.4177LIC# 1959

Flooring Machine

Weinig Profimat 22N 5 Head Moulder

40 HP Hydraulic Power Pack

Yates-American Flooring Moulder

Mattison Straight-Line Rip Saw

Oliver Strait-O-Plane

2018 Baker Band Resaw

CAT 950 Wheel Loader

1992 Industrial Wood Boiler

Hasko Matchmaster 4-Sided FSM Moulder

Yates-American G-55 Planer

58” Precision Chipper

Mereen-Johnson Gangsaw

Cornell Automated Cutoff Saw

CAT 920 Wheel Loader

Newman S-382 2-Sided Planer

Barko 160B Stationary KnuckleboomLigna DebarkerKADANT 1500 Bark Shredder56" Husk56” & 60" Circle SawsLigna 2 Saw Edger5 Strand UnscramblerAir Powered Waste DiverterTrim SawSoderhamn 72" ChipperMDI Metal Detector and Fiberglass Section4 Van Loading SystemIngersoll-Rand Screw CompressorSullair Screw CompressorVertical Air TanksSiemens SwitchboardHyster 225 ForkliftBarko 160 CTRK Knuckleboom1989 Peterbilt 3771973 Ford 700 Custom Cab TankerYard Dog2005 Open Top Peerless Walking Floor2012 Open Top Peerless Chip Trailer2007 Open Top Peerless Chip Trailer2000 Open Top ITI Chip TrailerOpen Top Fruehauf Chip Trailer2014 Utility Flat TrailersFast Flat Trailer

Wilkesboro, North Carolina Sawmill Equipment & Rolling Stock

At Absolute Auction!Oct. 28th at 10 AM Sellers: Barnes &

Severt Lumber Co.1016 Congo Rd

Wilkesboro, NC 28697

10% Buyer’s Premium for onsite buyers - all items to be paid in full before removal.

CAT 938K Wheel Loader

Volvo L70E Wheel Loader

Volvo L90D Wheel Loader

John Deere 450GTC Crawler Dozer

Volvo L90C Wheel Loader

Hyster 230 Forklift

2007 Kenworth T800

2001 Peterbilt 379

Meadows 4HB Carriage

Ligna Scragg Mill

Ligna Gang Saw

Call 574.825.0704 to receive the Bright Star Bid Book for FREE. This is a detailed catalog that also allows you to bid on the phone if

you can’t attend or bid online.

38 acres offered in two tracts.

Swicegood Group, Inc. (NCAFL 8790)

is handling the real estate

transaction.

B o kidB lThis catalog enables you to listen to the auction and bid on the phone.

See inside for details.

Date: August 7th

Date: July 30th Auction start time: 10:00 AM CSTCataloged auction start time: 11:00 AM CST

Auction start time: 9:00 AM CSTCataloged auction start time: 9:00 AM CST

Address:19250 Jaguar

Trail,Bloomfield IA

52537

Address: 2939 Cedar Rd.Seymour IA 52590

Address:10643 Wolcott

Hill Rd.,Camden NY 13316

Call: Eugene at 260-250-4942

Call: Eugene at 260-250-4942Date: August 1st

Auction start time: 10:00 AM ESTCataloged auction start time: 10:00 AM EST

Call: Eugene at 260-250-4942

Tiger cat 235B

Cleereman Carriage 40”, model #40, s/n 40-204, air set works (air over air), 3HB, w/3 Brownsville turners.

In very good condition!

Baker model BBR-O, single head resaw w/return hydraulic drive,

10” capacity

Fox River Hardwoods

ASV RT-65 track machine, almost

new, less than 100 hours

JLD Equipment

1977 Mack Truck, VIN DM685S34900 GVW 56030lbs, 227,218 miles, 1992 Nuova Copma

Model C1830N3LA- Rear Crane Italian made-Metric? 17660 max capacity

Cornell Edger model HEC-36, s/n 783-10-87, w/in-feed & out-

feed, moveable fence, 4 blades, 1 movable, 6’x36’, electric motor

36” CMC Rosserhead slant track Debarker, steel cab, chain drive, 24’ capacity

Formerly Spinks Sawmill

Call Zach: 931.224.0699Loren Beachy574.825.0704NCAL#10381

Eugene Hochstetler260.350.8953AU11400005

Zach Kittrell931.224.0699Lic# 1959

3 Bunk Log TrailerCarolina Metal Cutting BandsawCarolina Shop PressCarolina Shophand 5000 HoistNorthern Log SplitterMassey Ferguson 1010 TractorSquealer Bush HogCub Cadet Hydrostatic Riding Lawn Mower22" Lawn Boy Self Propelled MowerTahoe GeneratorsBobcat 225G AC/DC Welder 8000W GeneratorHonda GX200 Air CompressorYamaha MZ175 Trash PumpReddy Heater Pro100Sears 55,000 BTU HeaterDaytona Heavy Duty 16-Speed Drill PressDaytona 7500L 8" Bench GrinderElectric Powered Hoist

Real Estate!

53' Van Trailer53' Great Dane Van Trailer1977 48' Fruehauf Van TrailerPeerless Open Top Chip TrailerCurtis-Toledo Air Compressor80 Gallon Beaird Air CompressorBaker DedusterBrewer SizerZurn Air DryerAirco WeldersReed-Prentice MachineLincoln SA-200 WelderBaker Lateral ConveyorsCrosby 3 Saw EdgerSmith Single Head Band Resaw with ReturnDouble Head Smith Band Resaw3 HB Corinth American Carriage3 Strand Brewer Log Deck4 Strand Brewer UnscramblerBaker Belt ConveyorWest Plains Automated Chop SawMagliner Mobile Loading Ramp

Ellington, MO Sawmill ~ Pallet Shop ~ Real Estate

At Auction!Oct. 30th

at 9 AM CST Sellers: Roberts

Pallet Co.607 CR 500

Ellington, MO 63638

Call Eugene: 260.350.8953All items to be paid in full before removal - 10% BP on real estate & equipment.

Loren Beachy574.825.0704AU10500161

Eugene Hochstetler260.350.8953AU11400005

Nathan Lehman574.349.8570AU11000090

Call 574.825.0704 to receive the Bright Star Bid Book for FREE. This is a detailed catalog that also allows you

to bid on the phone if you can’t attend or bid online.

B o kidB lThis catalog enables you to listen to the auction and bid on the phone.

See inside for details.

Date: August 7th

Date: July 30th Auction start time: 10:00 AM CSTCataloged auction start time: 11:00 AM CST

Auction start time: 9:00 AM CSTCataloged auction start time: 9:00 AM CST

Address:19250 Jaguar

Trail,Bloomfield IA

52537

Address: 2939 Cedar Rd.Seymour IA 52590

Address:10643 Wolcott

Hill Rd.,Camden NY 13316

Call: Eugene at 260-250-4942

Call: Eugene at 260-250-4942Date: August 1st

Auction start time: 10:00 AM ESTCataloged auction start time: 10:00 AM EST

Call: Eugene at 260-250-4942

Tiger cat 235B

Cleereman Carriage 40”, model #40, s/n 40-204, air set works (air over air), 3HB, w/3 Brownsville turners.

In very good condition!

Baker model BBR-O, single head resaw w/return hydraulic drive,

10” capacity

Fox River Hardwoods

ASV RT-65 track machine, almost

new, less than 100 hours

JLD Equipment

1977 Mack Truck, VIN DM685S34900 GVW 56030lbs, 227,218 miles, 1992 Nuova Copma

Model C1830N3LA- Rear Crane Italian made-Metric? 17660 max capacity

Cornell Edger model HEC-36, s/n 783-10-87, w/in-feed & out-

feed, moveable fence, 4 blades, 1 movable, 6’x36’, electric motor

36” CMC Rosserhead slant track Debarker, steel cab, chain drive, 24’ capacity

Formerly Spinks Sawmill

Baker 3 Head-Cut-Off Saw

Baker 5 Head Band Resaw w/ Return

2-2015 CAT 914K Wheel Loaders

1 of 4 CAT Forklifts

1 of 2 2012 Freightliner Cascadia 125 CAT D6

Dozer

Gehl 5640 Turbo Skid Steer

Brewer Golden Eagle Gangsaw

w/ Sizer Head

Timberland Machinery Double Head Knotcher

1 of 3 Viking Turbo 505

Pallet Nailers

Jockey Grinder w/ Milwaukee Drill Cleereman 3 HB Carriage Cleereman Cab56" HuskCleereman 3 Saw Vertical Edger52" and 56" Circle SawsHytrol Skate Rolls Curtis Toledo Air Compressor Baker UnscramblerBaker Belt ConveyorBaker ChamferBaker UnscramblerMorgan 2 Head Trim SawBaker 3 Strand Infeed for ResawBaker DedusterCurtis Toledo Air CompressorHorizontal Air TanksBold Design Heat TreatVolvo L50E Wheel LoaderSeveral Loader AttachmentsWiese ForkliftCat D5 Dozer2005 Freightliner Columbia 1202000 Trailmobile Flatbed TrailerEquipment Trailer

44 Acres & Buildings

with a minimum bid of $400,000.

INTERNATIONAL MARKETS

© 2021 Hardwood Market Report

T

Export activity is largely based on individual specifications between buyers and sellers. Factors such as color, tex-ture, lengths, widths, special grade, packaging, consistency of quality and scheduling enter into price negotiations. However, the Hardwood Market Report can serve as a basis for information, and as a reference to domestic market activity and pricing that could contribute in export negotiations.

16 9/24/21

he Chinese government announced last week that it will extend tariff exemptions on hardwood lum-

Exporters are experiencing little to no relief from the container and vessel space shortages that have disrupted activity all year. Loads awaiting containers are stack-ing up in warehouses; congestion is delaying shipments through ports in North America and abroad; and ship-ping costs continue to climb.

In July, US exports of hardwood lumber slid 3% from June but climbed 12% over July 2020 to 114.1 MMBF. Shipments to China declined 29% from last July to a 19 month low of 29.0 MMBF. However, combined ship-ments to all other destinations rose 40% over last July, fueled by large gains to Canada (+56%), the EU27+UK (+121%), and the Middle East/North Africa region (+116%). Notably, exports to the EU27+UK were the strongest for any July since 2006.

The US exported 39.3 MMBF of hardwood logs in July to set a new record for that month. Compared to July 2020, shipments climbed 44% to China, 74% to all other markets, and 57% in total. July exports of Walnut and White Oak logs were both about double July 2020 levels.

White Oak was the most exported lumber species for the third consecutive month in July, with shipments up 62% over last July to 26.6 MMBF. At the same time, weaker shipments to China dropped overall Red Oak exports to 23.7 MMBF – the lowest July level since 2012. This July, Poplar exports were little changed from June (+2%) and July 2020 (+1%), at 15.4 MMBF. Ma-ple exports remained strong in July; YTD volumes were up 99% to Canada, 16% to China, 110% to Mexico, 259% to Vietnam, and 68% overall.

ber and logs imported from the US through April 16, 2022. If the exemptions had not been extended, higher tariffs would have substantially increased costs for US hardwoods in China from September 18th onward. De-spite this news, Chinese markets remain relatively slow. Longtime exporters to China report highly competitive pricing in ongoing business; many not in that category have stopped shipping to China for now.

Business into Vietnam is slow amid that country’s on-going battle with COVID. Restrictions have been eased in Hanoi. However, they remain in effect in and around Ho Chi Minh City, where most of the new cases and deaths are occurring and which is also where much of the country’s wood products manufacturing is located.

Canadian housing markets are performing very well, and consumption of US hardwoods has increased along-side of construction activity. Shipments to Canada sea-sonally slowed in August but have rebounded strongly in September. Exporters report decent demand from Mexico. However, shipments are noticeably stronger to Maquiladora manufacturers that re-export finished goods to the US than to distributors and end users in the interior of the country.

YTD exports of hardwood lumber increased to 9 of the top 10 European destinations through July, with Spain the lone exception. In September, demand has been strong from the UK, and steady from most other Euro-pean markets.

Table 1. US Hardwood Lumber Exports to Leading Countries and Lumber & Log Exports by Species

COUNTRY 2020 2021 Chg. LOGS 2020 2021 Chg.Red OakMapleWalnutWhite OakAshWORLD

45.143.235.325.632.4

223.4

56.851.039.935.526.8

264.7

+26%+18%+13%+38%-17%+18%

ChinaCanadaVietnamMexicoUKWORLD

-16%+61%+4%

+39%+81%+11%

275.0162.4119.581.334.5

827.6

328.7101.1115.2

58.319.1

744.7

YTD 2021 vs 2020 (through July) –– Million Board Feet

Red OakWhite OakPoplarWalnutAshMaple

+5%+31%

-8%+21%-12%+68%

200.4169.599.262.460.749.5

191.7129.7107.951.768.729.5

LUMBER 2020 2021 Chg.

Data: USDA Foreign Agricultural Service Table: HMR

HARD MAPLE

11.5M’ 4/4 #2 Com S1F&Btr 6.2M’ 4/4 #2 Com Brown 10.7M’ 5/4 #1 Com S1F&Btr 5.5M’ 5/4 #2 Com Brown 4.5M’ 8/4 #2 Com Unsel 2M’ 10/4 FAS/Sel 2WH&S1F&Brn 3.0M’ 12/4 FAS/Sel 1&2WH 3.2M’ 12/4 FAS/Sel S1F&Brn

CHERRY 2M’ 4/4 Select 90/70+ Heart 6’ 2M’ 4/4 Select 90/70+ Heart 7’ 24M’ 4/4 FAS/Sel 90/70+ Heart 3.4M’ 4/4 #2 Com Unsel 7.2M’ 5/4 Select 90/70+ Heart 6’ 13M’ 5/4 FAS/Sel 90/70+ Heart 13M’ 5/4 FAS/Sel Sap 3.6M’ 5/4 #2 Com 13M’ 6/4 FAS/Sel Heavy Red 4M’ 7/4 FAS/Sel 12M’ 8/4 FAS/Sel Heavy Red 12M’ 10/4 FAS/Sel Heavy Red

RED OAK - RIFT & QTRD 6M’ 4/4 FAS/Sel Rift 12M’ 5/4 FAS/Sel Rift 6M’ 5/4 FAS/Sel Qtrd 12M’ 6/4 FAS/Sel Qtrd 8M’ 8/4 FAS/Sel Rift

BOULES 10/4 Walnut

17

Growing, Sustainably Harvesting and Manufacturing Hardwoods the Pike Brand Way.

LUMBER COMPANY, INC.

• 719 Front St., Akron, IN 46910• 1-800-356-4554 • Fax: 574-893-7400• www.pikelumber.com

September 2021

Contact us for current prices:

®

Marcus Banning [email protected] Capper: [email protected] Irwin: [email protected] Mulligan: [email protected] Smith: [email protected]

SOFT MAPLE WHAD 3.3M’ 5/4 #2 Com 12M’ 6/4 FAS/Sel

RED OAK 6M’ 4/4 FAS/Sel Mineral 12M’ 4/4 #2 Com 4M’ 4/4 #3A Com 3.5M’ 5/4 Select 6’ 4.4M’ 5/4 Select 7’ 24M’ 5/4 FAS/Sel 8M’ 5/4 FAS/Sel Mineral 24M’ 5/4 #1 Com 12M’ 5/4 #2 Com 7M’ 7/4 FAS/Sel 12M’ 8/4 FAS/Sel WHITE OAK - RIFT & QTRD 12M’ 4/4 #1 Com R/Q 12M’ 4/4 #2 Com R/Q 22M’ 5/4 #1 Com R/Q

POPLAR 16M’ 4/4 #1 Com 15M’ 4/4 #2 Com 10M’ 5/4 #1 Com 9M’ 5/4 #2 Com 12M’ 6/4 FAS/Sel 9M’ 7/4 FAS/Sel 15M’ 8/4 FAS/Sel 6M’ 10/4 FAS/Sel 15M’ 12/4 FAS/Sel 1.3M’ 16/4 #2 Com

BASSWOOD 3.9M’ 4/4 #1 Com 3.6M’ 4/4 #2 Com 1.6M’ 8/4 #1 Com 6M’ 12/4 FAS/Sel 1.7M’ 16/4 #2 Com

HICKORY 12M’ 4/4 FAS/Sel 1&2WH 11M’ 4/4 #1 Com 11M’ 5/4 FAS/Sel 8M’ 5/4 #1 Com 11M’ 5/4 #2 Com 4M’ 5/4 Rustic 11M’ 6/4 FAS/Sel

WHITE OAK 6M’ 4/4 FAS/Sel 12M’ 4/4 #1 Com 12M’ 4/4 #3A Com Non-Rustic 2.9M’ 4/4 Rustic 4”-6” 6M’ 5/4 FAS/Sel 11M’ 5/4 #2 Com 2M’ 5/4 #3A Com Non-Rustic 5M’ 5/4 Rustic

ASH 12M’ 5/4 #1 Com 12M’ 5/4 #2 Com 6M’ 12/4 FAS/Sel

COFFEENUT 3M’ 4/4 FAS/Sel 2M’ 4/4 #1 Com

WALNUT 14M’ 4/4 FAS1F&Btr 14M’ 5/4 FAS1F&Btr 14M’ 5/4 FAS1F&Btr Sap 6M’ 6/4 FAS1F&Btr 14M’ 8/4 FAS1F&Btr

2016 KMC Track Skidderemail: Kirk Robinson [email protected]

18

P.O. Box 111Spartansburg, PA 16434

KD LUMBER FOR SALE

Snowbelt Hardwoods is FSC certified

Cert# NC-COC-003368

ASPEN ½ T/L 4/4 #1 ComBASSWOOD ½ T/L 4/4 S/B 6’ ½ T/L 4/4 #1 ComCHERRY ½ T/L 4/4 #1 ComSOFT MAPLE 1 T/L 4/4 S/B Sap ½ T/L 4/4 S/B Brown 1 T/L 4/4 #1 Com Sap 1 T/L 4/4 #1 Com Brown

Joe Francois [email protected] Contact: John Hilgemann [email protected] Brady Francois [email protected] Tyler Francois [email protected]

345 Ringle Drive, Hurley, WI 54534 • 715-561-2200 • Fax 715-561-2040email: [email protected]

SNOWBELT HARDWOODS, INC.

RED OAK 1.7M’ 5/4 S/B 10M’ 5/4 #1 Com 2 T/L’S 4/4 S/B 7/8’ 2 T/L’S 4/4 #1 Com 15/16”HARD MAPLE ½ T/L 6/4 S/B #1&2 White 1 T/L 4/4 S/B #1&2 White 1 T/L 4/4 #2A WhiteASH 1 T/L 4/4 S/B White

Drying 8,000,000 BF Basswood per year.

KD Lumber Ash 6/4 2C 8/4 #1CCherry 6/4 #1C 6/4 2CH. Maple 1-2W 5/4 2C 6/4 #1C

H. Maple 1-2W cont’d 6/4 2CHickory 6/4 FAS/Sel 8/4 FAS/Sel 8/4 #1CPoplar 7/4 FAS/1F 7/4 #1C 7/4 2C

Poplar cont’d 8/4 FAS/1F 8/4 #1C 8/4 2C 10/4 FAS/1FRed Oak 5/4 FAS/1F 6/4 FAS/1F 8/4 FAS/1F

Soft Maple 5/4 1/Btr WHND 6/4 FAS/Sel 6/4 1/Btr WHND 10/4 1/Btr WHND 12/4 FAS/Sel SapWhite Oak 4/4 Rustic 6/4 Rustic 8/4 Rustic

Contact: Mark Bennett, Charlie Brenneman, Doug Brenneman Jr. Telephone: 740-397-0573 • Fax: 740-392-9498

51 Parrott Street Ext., P.O. Box 951Mount Vernon, OH 43050

ASH 1 T/L 4/4 Prime 1 T/L 4/4 #2A 2 T/L 7/4 PrimeCHERRY 1 T/L 3/4 Prime Red 1 Face 1 T/L 3/4 Prime 90/50 1 T/L 3/4 ComSel 1 T/L 3/4 #2A 1 T/L 4/4 Prime Red 1 Face 1 T/L 4/4 Prime 90/50 2 T/L 4/4 ComSel 1 T/L 4/4 #2ARED OAK 3 T/L 3/4 Prime 3 T/L 3/4 ComSel 3 T/L 3/4 #2A 1 T/L 4/4 Prime 1 T/L 4/4 ComSel 2 T/L 5/4 ComSel 2 T/L 7/4 PrimeSOFT MAPLE 2 T/L 4/4 #1C SapWALNUT 1 T/L 3/4 #2CWHITE OAK 1 T/L 3/4 Prime 2 T/L 3/4 ComSel 1 T/L 3/4 #2A

www.penn-sylvan.com

Andrew [email protected]

416-606-4641

Marty [email protected]

814-694-2311

814-758-3333

Jeff Taylor: [email protected] (901) 684-1400Zack Taylor: [email protected] (901) 684-1400Kirby Field: [email protected] (601) 885-6257Howell Cox: [email protected] (208) 507-1003

Fax: (901) 684-1404

Specialty Timbers/Cants/Board Road LumberInfo: 2 Sawmills, Clarendon, AR

Dry Kilns, Newman 382, Air Drying Sheds, Fan Sheds, Company Owned Trucks, Total Dry Shipping/Loading Area

KILN DRIED:Memphis, TN

1 T/L 5/4 FAS Red Oak

2 T/L 5/4 #1 Com Red Oak

2 T/L 5/4 #1 Com White Oak

2 T/L 5/4 #2 Com White Oak

1 T/L 4/4 FAS Sycamore

19

SAWMILLS • DRY KILNSRiverton, WV • Petersburg, WV • Princeton, WV • Kingwood, WV

Norton, WV • Hazelton, WV • Cowen, WV • Jacksonburg, WV • Smoot, WV

ALLEGHENY WOOD PRODUCTSP.O. Box 867 • Petersburg, WV 26847Tel: 304.257.1082 • Fax: 304.257.2342

www.alleghenywood.com

Petersburg, WVDean [email protected]

Europe & Middle EastPaul [email protected]

Midwest USADavid [email protected]

Pallet Lumber & TiesLinda [email protected]

Northeast USAGerry [email protected]

ChinaTony Fu011 86 150 9206 [email protected]

Southeast & Western USAKris [email protected]

China/VietnamDemon Yan011 86 156 9213 [email protected]

ASH 5M’ 4/4 FAS/1F Brown CHERRY 12M’ 4/4 FAS/1F Unsel 30M’ 4/4 1 Com 30M’ 4/4 2 ComHARD MAPLE 35M’ 4/4 1 Com Brown 7M’ 4/4 2A Com 35M’ 4/4 2 ComRED OAK • OFF COLOR 30M’ 4/4 FAS/1F 5M’ 6/4 FAS/1F 3M’ 6/4 1 Com

RED OAK • APPALACHIAN 12M’ 4/4 FAS/1F 11”&Wider 70M’ 4/4 1 Com 6M’ 6/4 FAS/1F 6M’ 6/4 2A Com 1M’ 6/4 3A/2B ComPOPLAR 10M’ 4/4 FAS/1F 11”&Wider 10M’ 4/4 2A ComSASSAFRAS 10M’ 4/4 2 Com - BtrWALNUT Steamed 450’ 8/4 FAS/1F 13’-16’ 10” avg. width

HICKORY 5M’ 4/4 FAS/1F White 20M’ 4/4 FAS/1F Calico 10M’ 4/4 1 Com 25M’ 4/4 2A Com 25M’ 4/4 2B/3A ComWHITE OAK 2200’ 4/4 FAS/1F Rift 1500’ 4/4 1 Com RiftWHITE OAK • OFF COLOR TIMBERS AND TIES 7x9 8’-16’ BOARD ROAD 2x8 8’-16’

• ATFS CERTIFIED FORESTS• SURFACING FINISHED OR HIT & MISS• STRAIGHT-LINE RIPPING

• SHRINK WRAPPING• EXPORT PREPARATION • CONTAINER LOADING• MIXED TRUCKLOADS

BLOCKING 2x4 8’-16’ 3x4 8’-16’TRAILER FLOOR REPLACEMENT 2x8 8’-16’ White OakKINDLING & FIREWOOD LUMBER Green and Kiln DriedLIVE EDGE SLABS KD 2” Walnut 2” Poplar

FOR SALE • KILN DRIED

7029 Main St.P. O. Box 105

Frohna,Missouri 63748

USA

PHONE573-824-5272

FAX573-824-5275

Web Site:www.eastperrylumber.com

USED EQUIPMENT FOR SALETyrone SMA-385-C

Hydraulic Gun Carriage Feed System

Email:[email protected]

20

Berkshire, NY 13736Ph: 607-657-8686 - Fax: 607-657-2532

Hardwoods, Inc.

Basswood 3M’ 5/4 1C 2M’ 5/4 2AC Cherry 12M’ 4/4 PRM-W 90/50+ 8.5”+ 5M’ 4/4 SEL-N Unsel 34M’ 8/4 FAS/SEL 90/50 Red+ 1M’ 8/4 FAS/SEL Sappy 6M’ 8/4 1C 90/50 Red+ 29M’ 8/4 2AC 90/50 Red + Butternut 1.7M’ 4/4 2AC&BTR Wormy 4M’ 4/4 1C 3M’ 4/4 2AC Hard Maple 7M’ 4/4 FAS/SEL Brown 12M’ 4/4 2AC Sap&Btr 12M’ 5/4 FAS/F1F 1&2 White 3M’ 6/4 2AC Sap&Btr Red Oak 12M’ 4/4 FAS/SEL 5”& wider 12M’ 4/4 FAS/F1F 8.5”& wider 1M’ 6/4 FAS/F1F 12”& wider Soft Maple 5M’ 4/4 1C Brown 15/16” 15M’ 4/4 2AC Brown 7.5M’ 5/4 2AC Unselected 4M’ 6/4 1C&BTR Wormy 2M’ 6/4 1C&BTR Ambrosia 14M’ 8/4 1C&BTR Ambrosia 11M’ 8/4 1C&BTR Wormy Walnut 2M’ 4/4 FAS/F1F 6’ 90/50 ROK rules 2M’ 4/4 FAS/F1F Unselected 15/16” 5M’ 4/4 FAS/F1F Sappy 15/16” 2.5M’ 4/4 1C Unselected 15/16” 2M’ 8/4 2AC Unselected

Custom Rip to Width & Chop to Length options available upon request.

www.tiogahardwoods.com

G. F. HARDWOODS, INC.“A Company You Can Depend On”

9880 Clay County Hwy.MOSS, TN 38575-9724PH 1-800-844-3944FAX 931-258-3517

1 T/L 4/4 1F+ Hard Maple White 3 WEEKS 1 T/L 4/4 1F+ Poplar PROMPT 1 T/L 4/4 1C Poplar PROMPT 1 T/L 5/4 1F+ Poplar 2 WEEKS 1 T/L 6/4 1F+ Poplar 2 WEEKS 1 T/L 6/4 1C Poplar 2 WEEKS 1 T/L 4/4 1F+ Red Oak 1 WEEK

All Material is KD - Rough

Sales Quentin Moss Trevor Graves

1 T/L 4/4 1C Red Oak 1 WEEK 1 T/L 4/4 2C Red Oak 1 WEEK 2 T/L’s 4/4 3A Red Oak PROMPT 1 T/L 4/4 1F+ Soft Maple Unsel 3 WEEKS 1 T/L 4/4 1F+ White Oak 2 WEEKS 1 T/L 6/4 1F+ White Oak Heavy 10’ PROMPT

125 YEAR

S

tplco.com · s4shardwoods.com

Office: St. Louis, MO · 314-231-9343Distribution Yard: Nashville, IL

Fulfilling our customers’ unique set of needs and requirements is our top

priority. Whether it’s Appalachian Hardwood Lumber, S4S, or Moulder Ready Blanks, that’s the Thomas &

Proetz difference. Est.1896

“Consistency & Yield have alwaysbeen our trademark.”

We have the following species available in kiln dried Appalachian Hardwood lumber:

Ray Miller 330-893-3121 EXT. 101 � Email: [email protected] Schmertzler 828-244-5767 � Email: [email protected]

• Red Oak• Poplar• Hard Maple

• White Oak Quarter Sawn• White Oak Flat Sawn• Soft Maple

ASH

12,000’ 4/4 Sel&Btr

1,525’ 4/4 1 Com

2,000’ 4/4 2 Com

1,910’ 8/4 Sel&Btr

RED OAK

6,093’ 4/4 Prime

42’ 4/4 Selects

446’ 4/4 2 Com

432’ 4/4 Framestock

589’ 6/4 Prime

421’ 6/4 2 Com

248’ 8/4 1 Com