Briefing Key Personnel What's New 27 Speeches 34 Key Macroeconomic Indicators Domestic World 59 61 Outstanding Government Debt 62 Market Roundup Macro-Economic Overview Market Overview 40 50 CCIL Indices 74 Primary Market Analysis 76 Milestones 151 154 Money Market Foreign Exchange Market Derivatives Interest Rate Movement Government Securities Market Statistics Corporate Bonds Benchmark Rates 78 116 123 134 137 147 105 81 CONTENTS CONTENTS Managing Director's Message 5 Infocus RBI ANNUAL REPORT 2015-16 Report of the Working Group on Development of Corporate Bond Market in India 7 Article Summary 22 Measuring GDP in a Digitalised Economy The role of collateral in supporting liquidity

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Briefing

Key Personnel

What's New 27

Speeches 34

Key Macroeconomic Indicators

Domestic

World

59

61

Outstanding Government Debt 62

Market Roundup

Macro-Economic Overview

Market Overview

40

50

CCIL Indices 74

Primary Market Analysis 76

Milestones 151

154

Money Market

Foreign Exchange Market

Derivatives

Interest Rate Movement

Government Securities Market

Statistics

Corporate Bonds

Benchmark Rates

78

116

123

134

137

147

105

81

C O N T E N T SC O N T E N T S

Managing Director's Message 5

Infocus

RBI ANNUAL REPORT 2015-16

Report of the Working Group on Development of Corporate Bond Market in India

7

Article Summary 22

Measuring GDP in a Digitalised Economy

The role of collateral in supporting liquidity

STATISTICS

TABLESTABLE 1 : DOMESTIC INDICATORS ......................................................................................................... 59

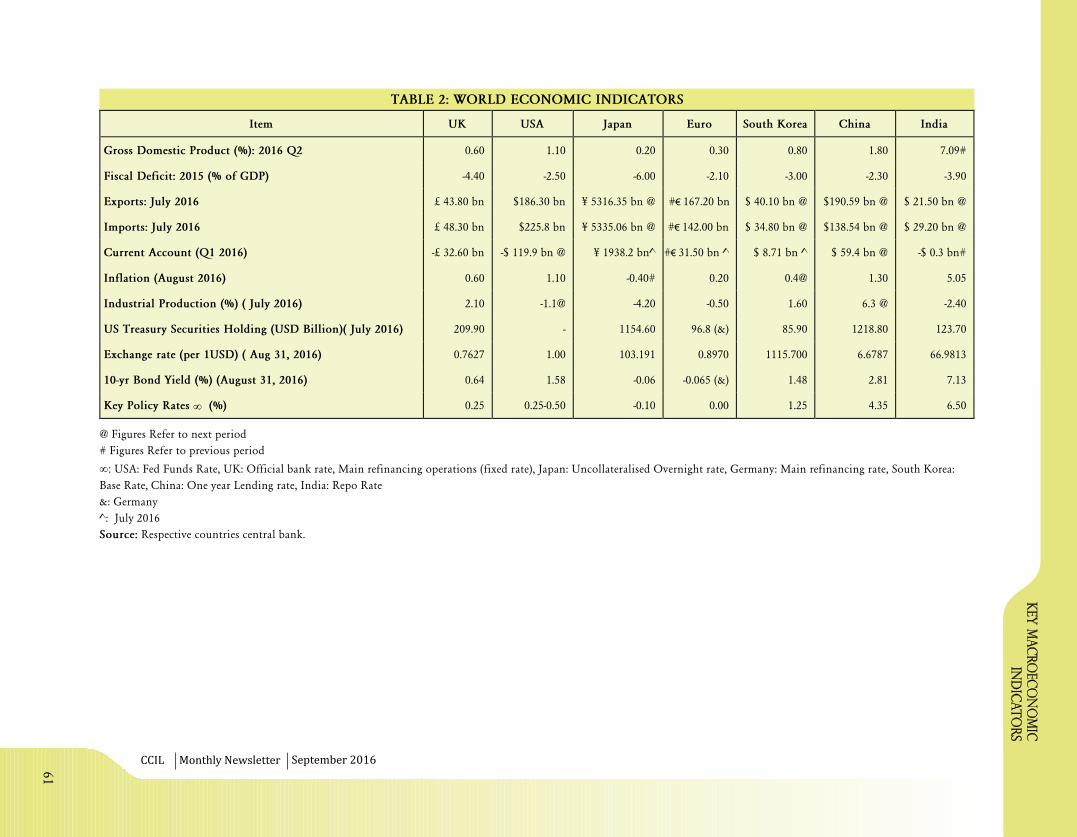

TABLE 2 : WORLD ECONOMIC INDICATORS ...................................................................................... 61

TABLE 3 : OUTSTANDING GOVERNMENT DEBT ............................................................................. 62

TABLE 4 : STATE DEVELOPMENT LOANS (SDLS) OUTSTANDING............................................ 70

TABLE 5 : CONSOLIDATED OUTSTANDING ....................................................................................... 71

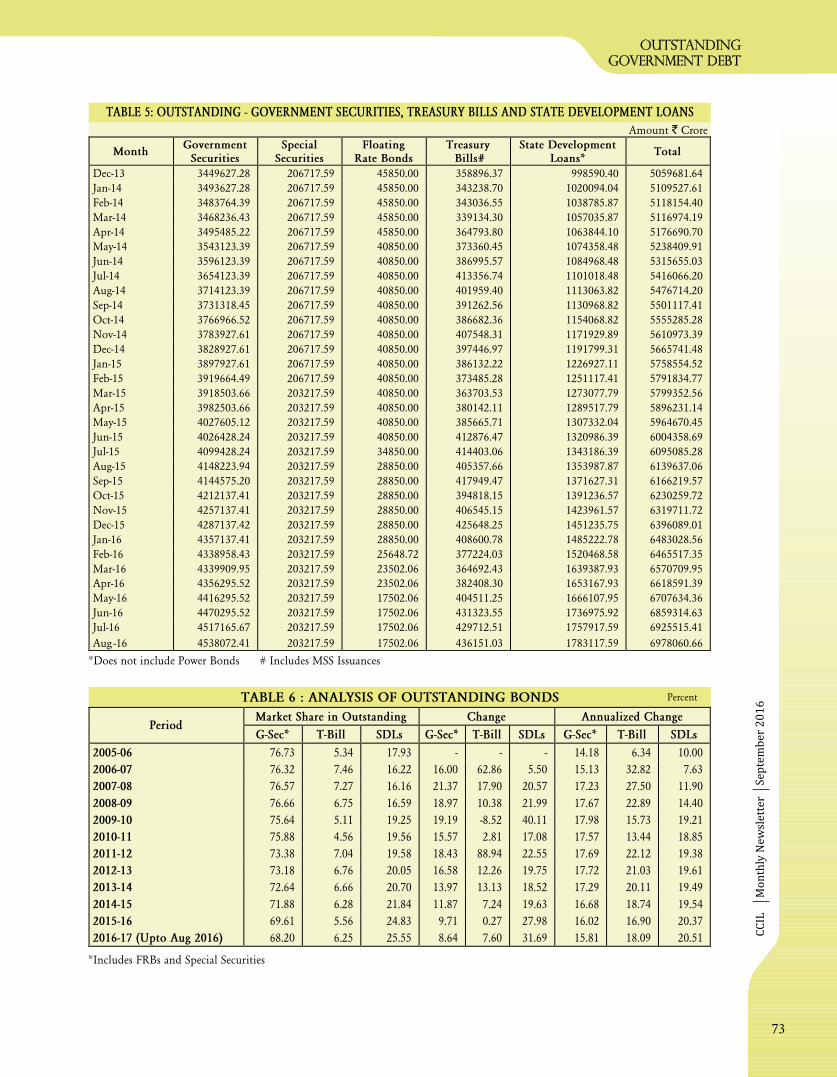

TABLE 6 : ANALYSIS OF OUTSTANDING BONDS .............................................................................. 73

TABLE 7 : INDEX COMPOSITION .............................................................................................................. 74

TABLE 8 : INDEX PERFORMANCE ANALYSIS ..................................................................................... 75

TABLE 9 : SECURITIES & MONEY MARKET (PRIMARY) : COMPARATIVE DATA .................. 76

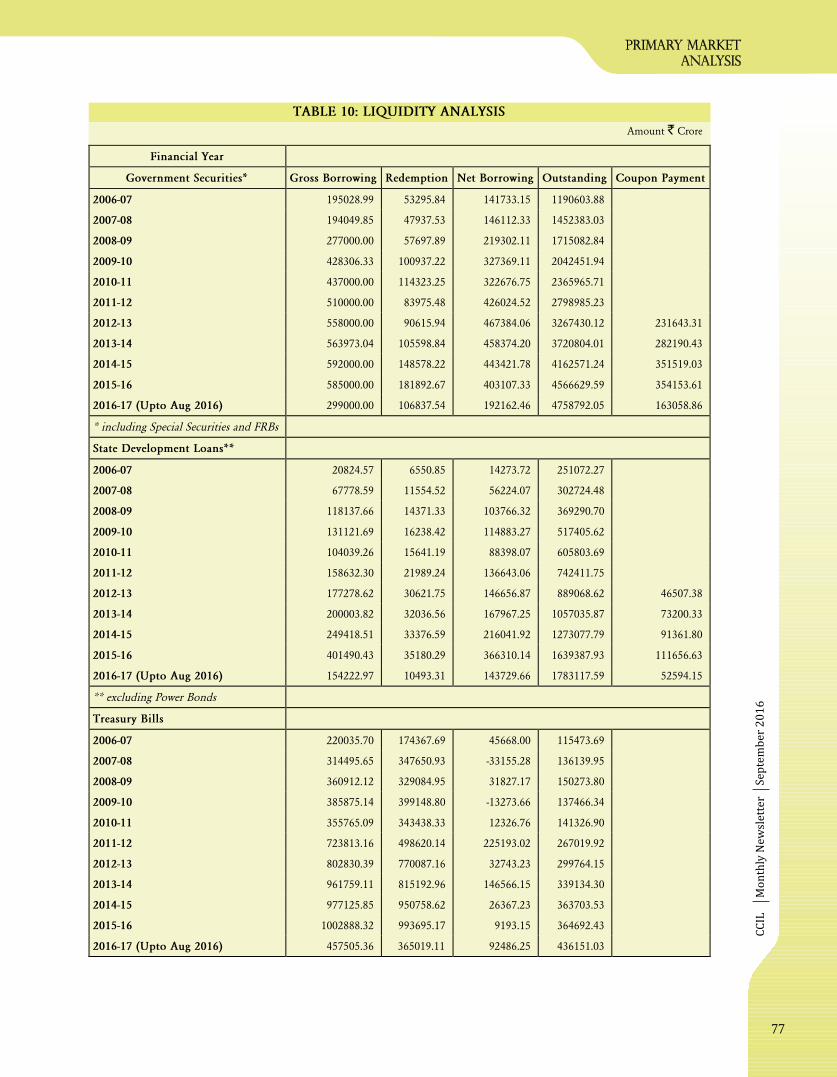

TABLE 10 : LIQUIDITY ANALYSIS ................................................................................................................ 77

TABLE 11 : CCIL SETTLEMENT DETAILS ................................................................................................. 78

TABLE 12 : CATEGORYWISE BUYING ACTIVITY .................................................................................. 79

TABLE 13 : CATEGORYWISE SELLING ACTIVITY ................................................................................ 79

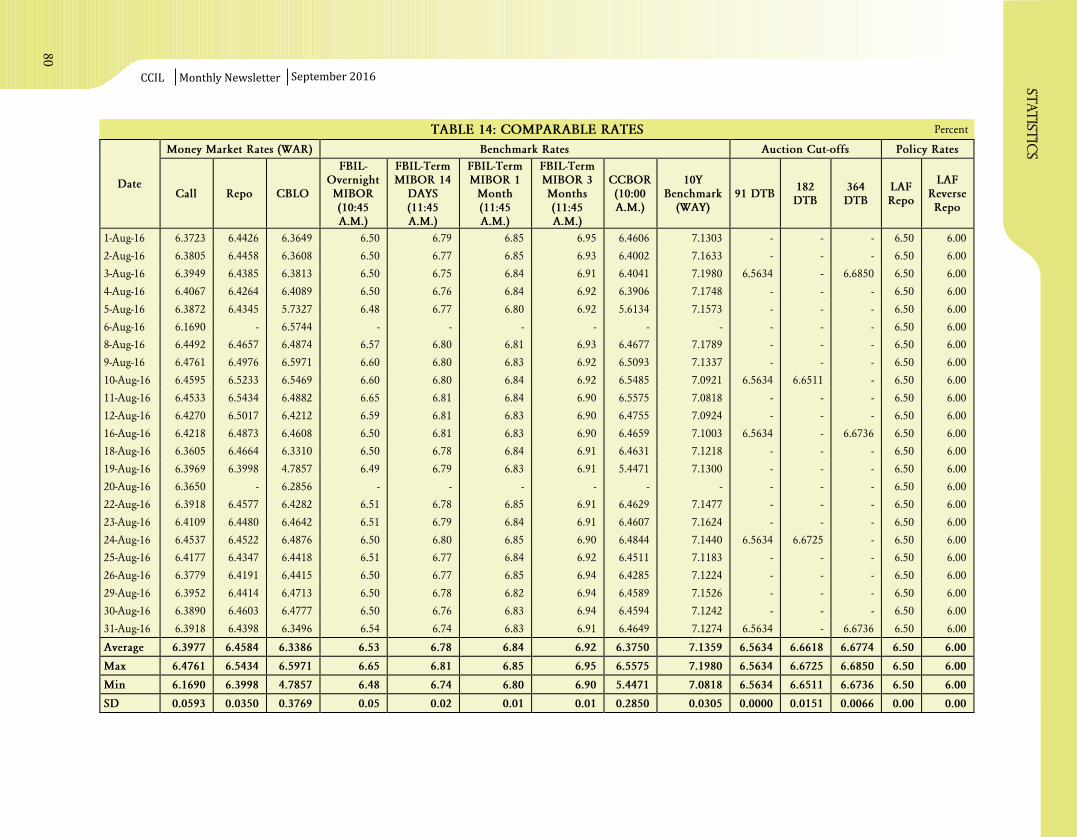

TABLE 14 : COMPARABLE RATES (%) ......................................................................................................... 80

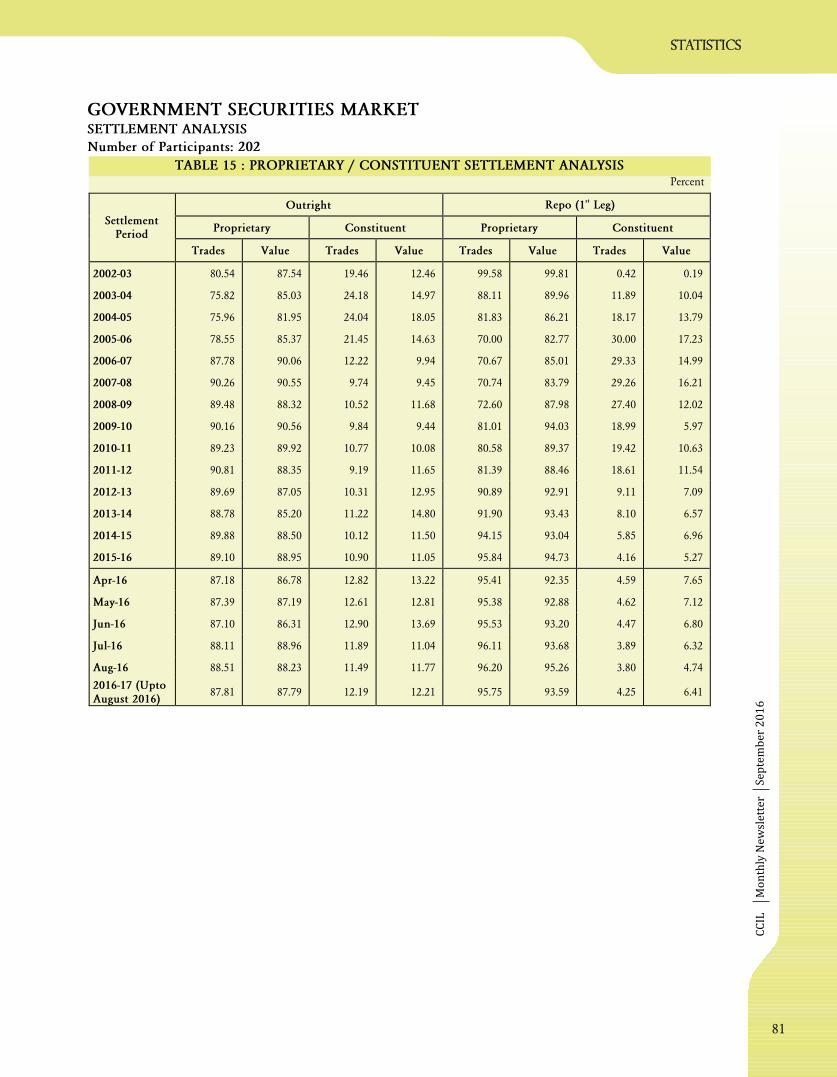

TABLE 15 : PROPRIETARY / CONSTITUENT SETTLEMENT ANALYSIS .......................................... 81

TABLE 16 : DEAL SIZE ANALYSIS ................................................................................................................. 82

TABLE 17 :

TABLE 20 : TENOR WISE ACTIVITY - CENTRAL GOVERNMENT DATED SECURITIES ...... 85

TABLE 21 : NETTING FACTOR - FUNDS ................................................................................................... 86

TABLE 22 : NETTING FACTOR: SECURITIES ........................................................................................... 87

TABLE 23 : LIQUIDITY ANALYSIS FOR CENTRAL GOVERNMENT SECURITIES TRANSACTED

DURING THE MONTH ....................................................................................................... 88

TABLE 24 : MARKET SHARE OF TOP 'N' SECURITIES ........................................................................ 92

TABLE 25 : MARKET SHARE OF MEMBERS IN OUTRIGHT SETTLEMENT ................................. 92

TABLE 26 : MARKET SHARE OF TOP FIVE MEMBERS (CATEGORYWISE) ................................... 93

TABLE 27 : TRADING PLATFORM ANALYSIS OF OUTRIGHT TRADES ........................................ 93

TABLE 29 : MARKET SHARE IN PROPRIETARY TRADES ............................................................... 94

TABLE 30 : MARKET SHARE IN CONSTITUENT TRADES ................................................................ 95

TABLE 31 : TURNOVER RATIO .................................................................................................................... 95

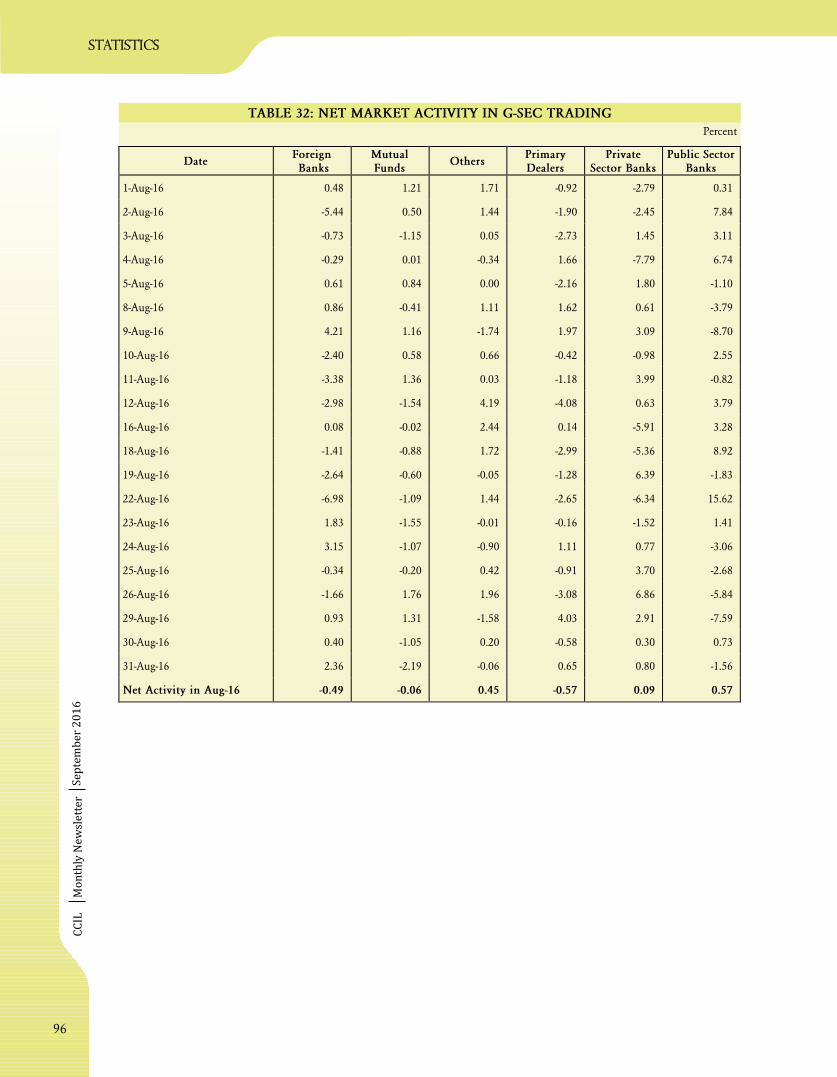

TABLE 32 : NET MARKET ACTIVITY IN G-SEC TRADING ................................................................ 96

GOVERNMENT SECURITIES MARKET

T+2 SETTLEMENT SUMMARY ............................................................................................... 83

TABLE 18: : T+2 TRADES - HISTORICAL SETTLEMENT SUMMARY ............................................... 83

TABLE 19 : INSTRUMENT WISE BREAKUP OF OUTRIGHT TRADES ........................................... 84

TABLE 28 : WHEN-ISSUED TRADING HISTORICAL ............................................................................. 94

TABLE 28A : WHEN-ISSUED TRADING DETAILS .................................................................................... 94

TABLE 33 : TRADING SUMMARY ................................................................................................................ 97

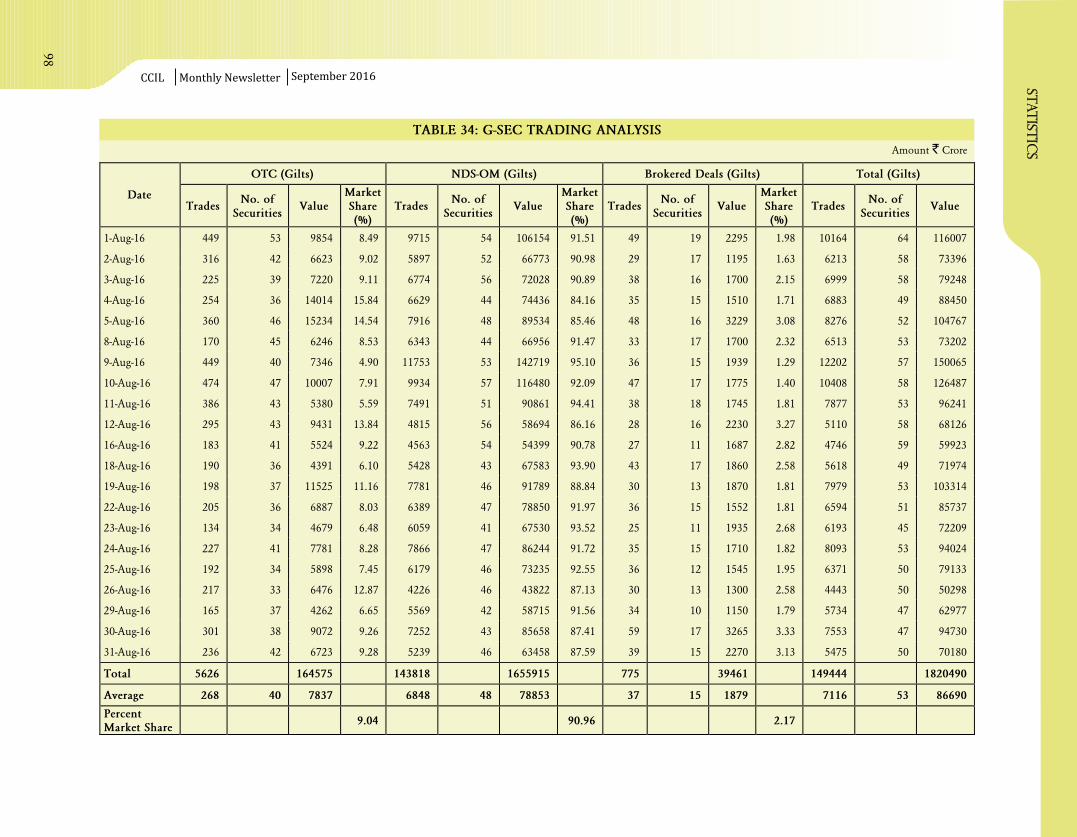

TABLE 34 : G-SEC TRADING ANALYSIS .................................................................................................... 98

TABLE 35 : T-BILL TRADING ANALYSIS ................................................................................................... 99

TABLE 36 : SDL TRADING ANALYSIS ........................................................................................................ 100

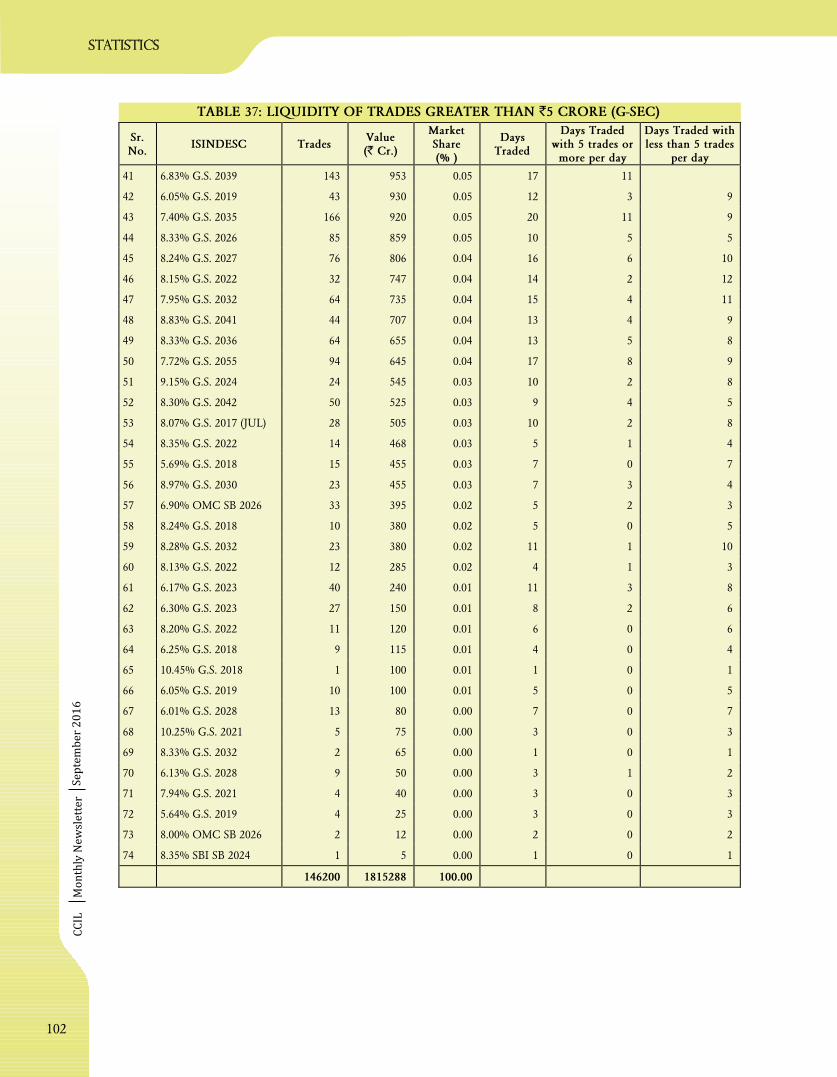

TABLE 37 : LIQUIDITY OF TRADES GREATER THAN 5 CRORE (G-SEC) .................................... 101

TABLE 38 : LIQUIDITY DISTRIBUTION (G-SEC) .................................................................................... 103

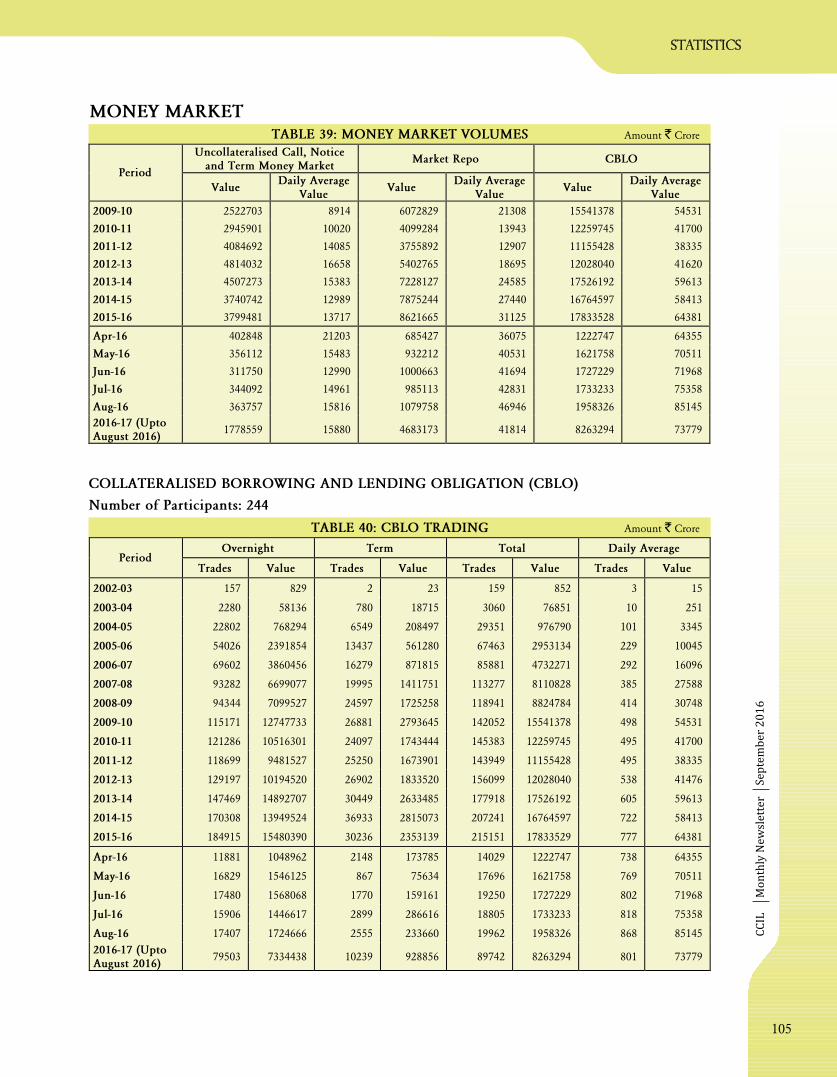

TABLE 39 : MONEY MARKET VOLUMES ................................................................................................ 105

MONEY MARKET

TABLE 40 : CBLO TRADING........................................................................................................................... 105

TABLE 41 : REPO TERM ANALYSIS .............................................................................................................. 106

TABLE 42 : INSTRUMENTWISE SETTLEMENT OF REPO TRADES ................................................ 106

TABLE 43 : CROMS TRADING ACTIVITY .................................................................................................. 107

TABLE 44 : CROMS HISTORICAL SUMMARY............................................................................................ 107

TABLE 45 : TOP 5 SECURITIES - BASKET REPO ..................................................................................... 108

TABLE 46 : TOP 5 SECURITIES - SPECIAL REPO .................................................................................... 108

TABLE 47 : DEALT TRANSACTIONS ON THE NDS-CALL PLATFORM .......................................... 108

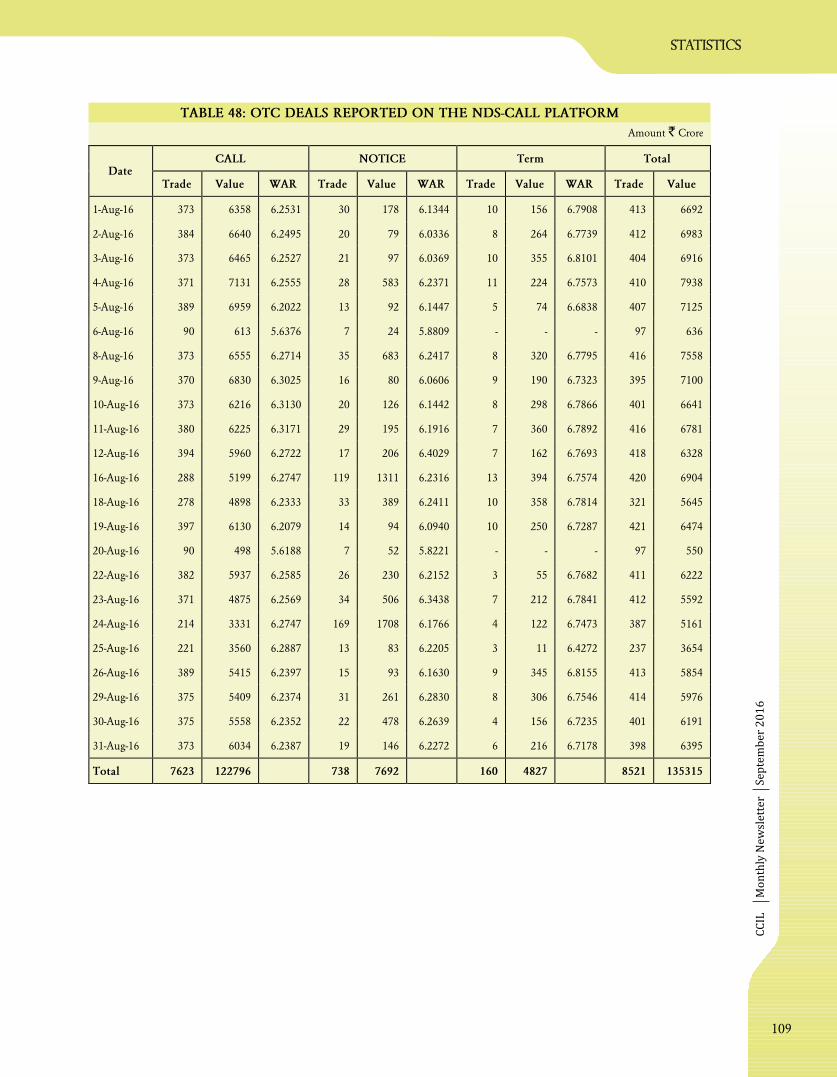

TABLE 48 : OTC DEALS REPORTED ON THE NDS-CALL SYSTEM .................................................. 109

TABLE 49 : UNCOLLATERALISED OVERNIGHT TRANSACTIONS (%) ............................................ 110

TABLE 50 : OVERNIGHT TRANSACTIONS DEALT ON NDS-CALL PLATFORM (%) .................... 111

TABLE 51 : OVERNIGHT TRANSACTIONS REPORTED ON NDS-CALL PLATFORM (%) ........... 112

TABLE 52 : CALL MARKET AND FBIL O/N MIBOR - RATES (%) ....................................................... 113

TABLE 53 : TENORWISE ANALYSIS OF TERM MONEY TRANSACTIONS ........................................ 114

TABLE 54 : NDS-CALL HISTORICAL ............................................................................................................ 115

TABLE 55 : FOREX SETTLEMENT ................................................................................................................ 116

TABLE 56 : FOREX TRADE TYPE ANALYSIS ........................................................................................... 117

TABLE 57 : FOREX DEAL SIZE ANALYSIS ................................................................................................ 117

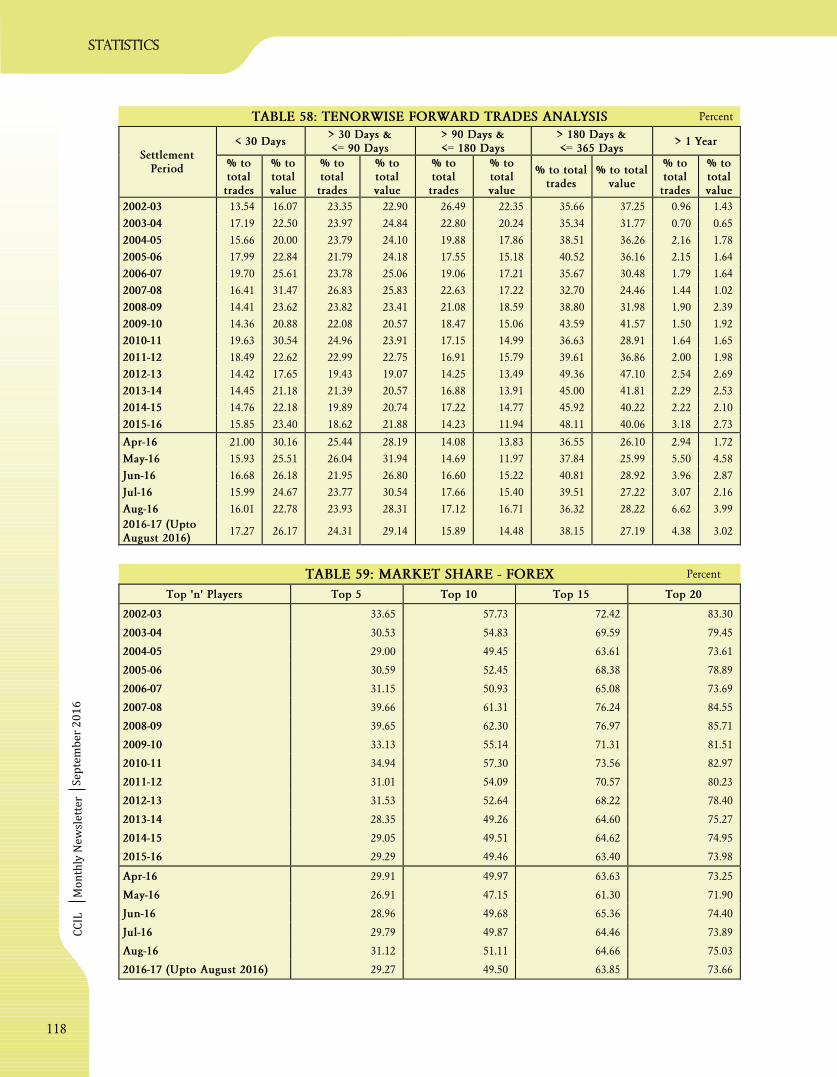

TABLE 58 : TENORWISE FORWARD TRADES ANALYSIS ................................................................... 118

TABLE 59 : MARKET SHARE - FOREX ........................................................................................................ 118

TABLE 60 : CATEGORYWISE FOREX ACTIVITY - DEAL TYPE ........................................................ 119

TABLE 61 : NETTING FACTOR - FOREX ................................................................................................... 119

TABLE 62 : FOREX FORWARD SETTLEMENT STATISTICS ............................................................... 120

TABLE 63 : CLS SETTLEMENT ....................................................................................................................... 120

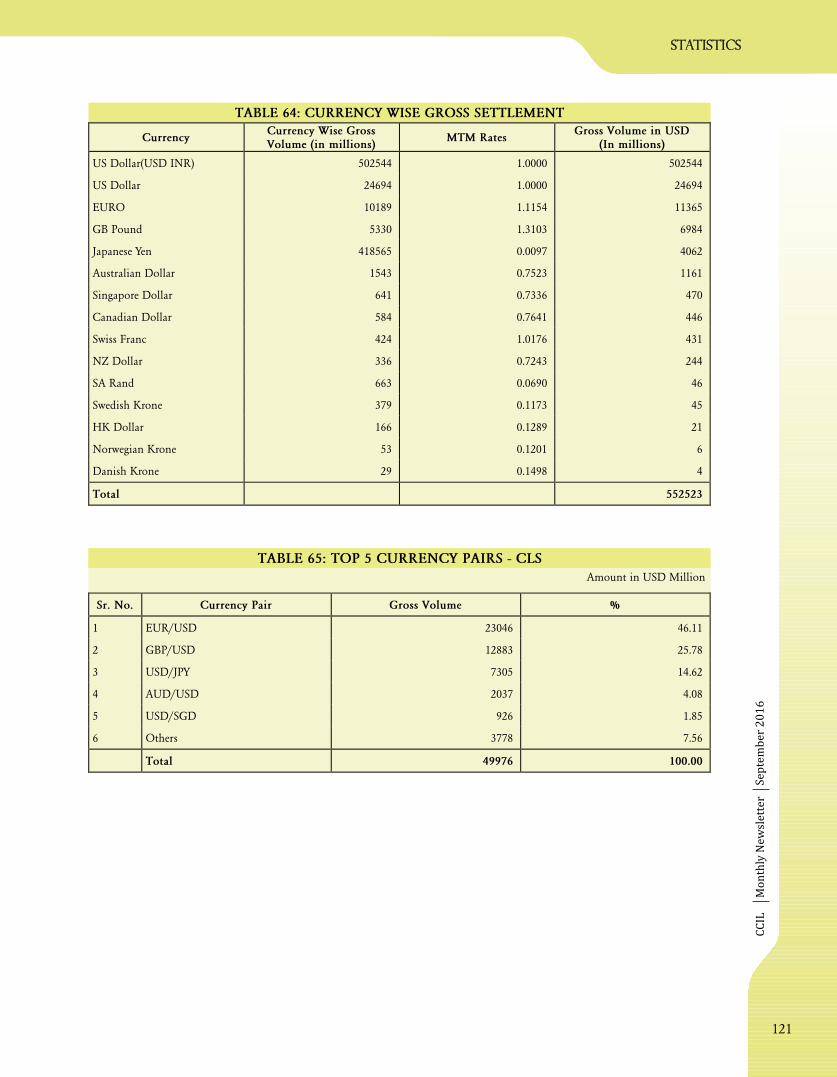

TABLE 64 : CURRENCY WISE GROSS SETTLEMENT ........................................................................... 121

TABLE 65 : TOP 5 CURRENCY PAIRS - CLS ............................................................................................. 121

TABLE 66 : TRADING DETAILS - FX CLEAR ............................................................................................ 122

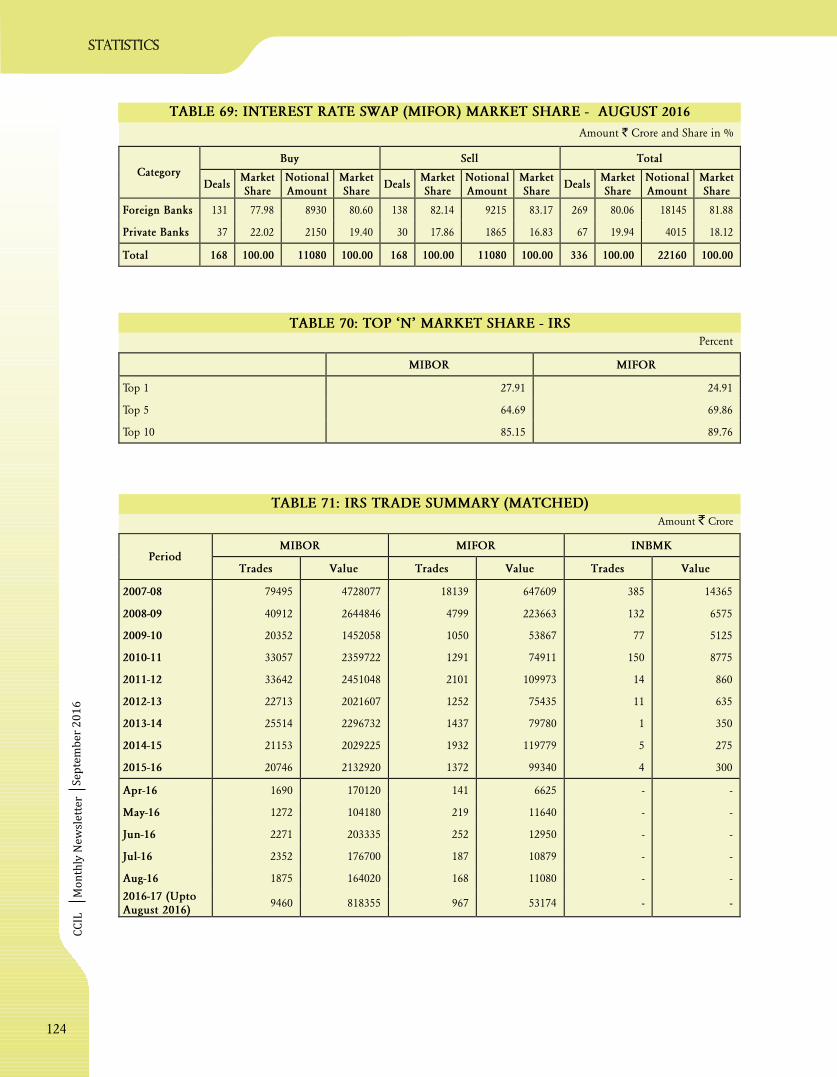

TABLE 67 : INTEREST RATE SWAP TRANSACTIONS (MATCHED) ................................................. 123

TABLE 68 : INTEREST RATE SWAP (MIBOR) MARKET SHARE ........................................................ 123

TABLE 69 : INTEREST RATE SWAP (MIFOR) MARKET SHARE ........................................................ 124

TABLE 70 : TOP ‘N’ MARKET SHARE - IRS .............................................................................................. 124

TABLE 71 : IRS TRADE SUMMARY (MATCHED) ................................................................................... 124

TABLE 72 : OUTSTANDING POSITION IN IRS TRANSACTIONS ..................................................... 125

TABLE 73 : NETTING FACTOR - IRS NON-GUARANTEED SETTLEMENT ................................... 125

TABLE 74 : TRADED VOLUME FOR OTC INTERBANK FCY - INR FORWARDS ....................... 126

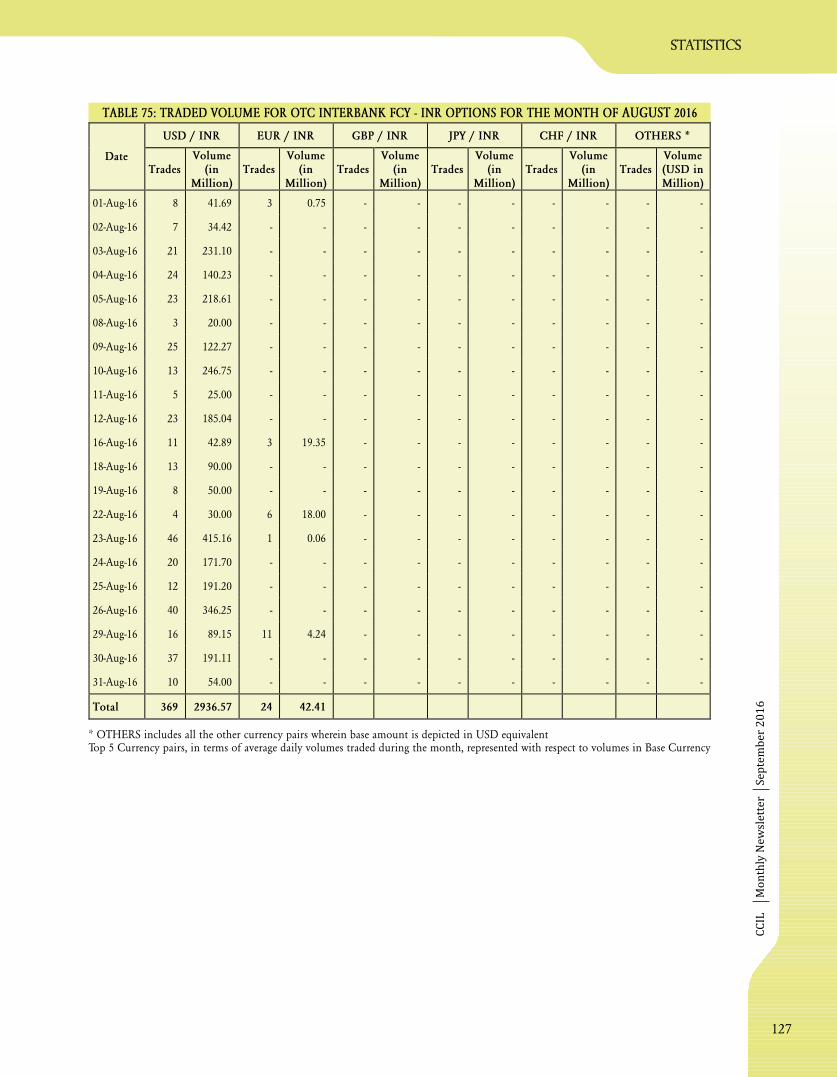

TABLE 75 : TRADED VOLUME FOR OTC INTERBANK FCY - INR OPTIONS ........................... 127

TABLE 76 : TRADED PRINCIPAL AMOUNT FOR OTC INTERBANK FCY - INR CROSS CURRENCY

SWAPS .................................................................................................................. 128

TABLE 77 : TRADED VOLUME FOR OTC INTERBANK FCY - FCY FORWARDS ......................... 129

TABLE 78 : TRADED VOLUME FOR OTC INTERBANK FCY - FCY OPTIONS .......................... 130

TABLE 79 : TRADED PRINCIPAL AMOUNT FOR OTC INTERBANK FCY - FCY CROSS

CURRENCY SWAPS ................................................................................................................. 130

TABLE 80 : TRADED NOTIONAL PRINCIPAL FOR OTC INTERBANK FCY - IRS .................... 131

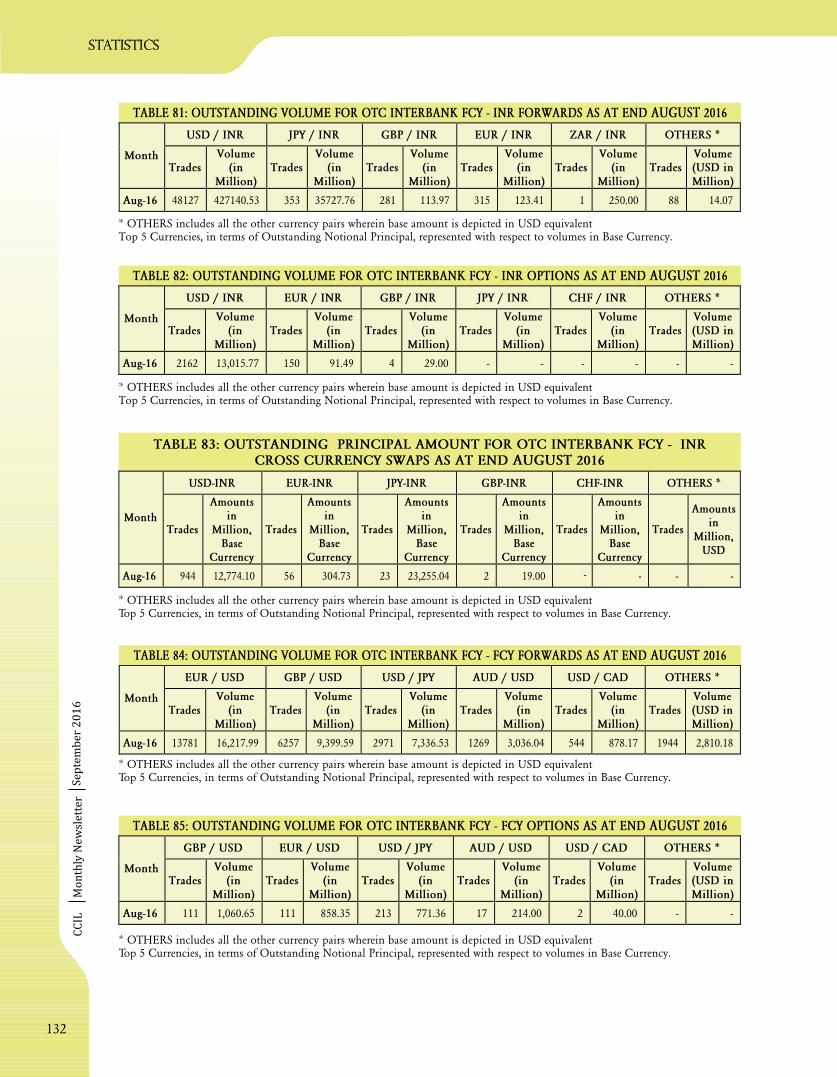

TABLE 81 : OUTSTANDING VOLUME FOR OTC INTERBANK FCY - INR FORWARDS ........... 132

FOREIGN EXCHANGE MARKET

DERIVATIVES

TABLE 82 : OUTSTANDING VOLUME FOR OTC INTERBANK FCY - INR OPTIONS ............... 132

TABLE 83 : OUTSTANDING PRINCIPAL AMOUNT FOR OTC INTERBANK FCY - INR

CROSS CURRENCY SWAPS .................................................................................................... 132

TABLE 84 : OUTSTANDING VOLUME FOR OTC INTERBANK FCY - FCY FORWARDS .......... 132

TABLE 85 : OUTSTANDING VOLUME FOR OTC INTERBANK FCY - FCY OPTIONS ............... 132

TABLE 86 : OUTSTANDING PRINCIPAL AMOUNT FOR OTC INTERBANK FCY -

FCY CROSS CURRENCY SWAPS ......................................................................................... 133

TABLE 87 : OUTSTANDING NOTIONAL PRINCIPAL FOR OTC INTERBANK FCY - IRS ........ 133

TABLE 88 : SPREAD ANALYSIS - SDL .......................................................................................................... 135

TABLE 89 : YIELD MOVEMENT .................................................................................................................... 136

TABLE 90 : PRIMARY MARKET ISSUANCE OF CORPORATE BONDS .......................................... 137

TABLE 91 : ANALYSIS OF CORPORATE BOND ISSUANCE ................................................................ 138

TABLE 92 : RATING ANALYSIS OF CORPORATE BOND ISSUANCES ........................................... 138

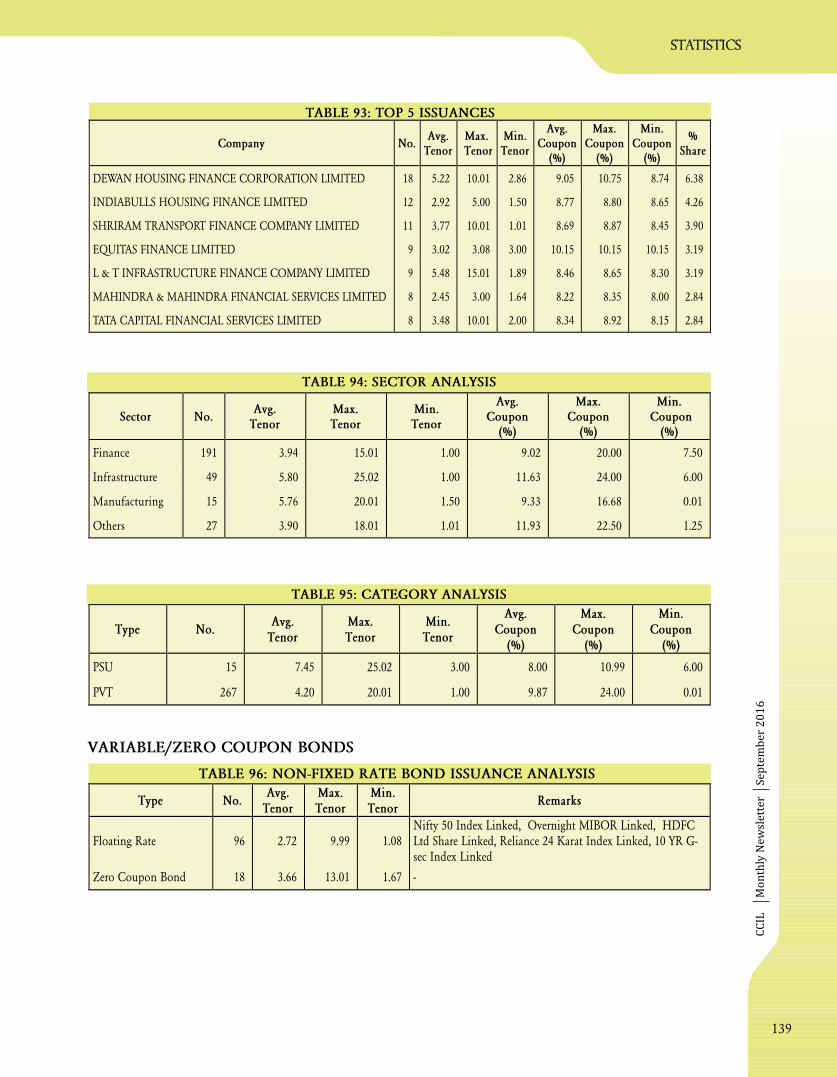

TABLE 93 : TOP 5 ISSUANCES .................................................................................................................... 139

TABLE 94 : SECTOR ANALYSIS ...................................................................................................................... 139

TABLE 95 : CATEGORY ANALYSIS ............................................................................................................... 139

TABLE 96 : NON-FIXED RATE BOND ISSUANCE ANALYSIS ............................................................. 139

TABLE 97 : CORPORATE BONDS TRADING DETAILS ....................................................................... 140

TABLE 98 : HISTORICAL SUMMARY ....................................................................................................... 140

TABLE 99 : TRADING ANALYSIS ............................................................................................................... 141

TABLE 100 : RATING ANALYSIS .................................................................................................................. 141

TABLE 101 : CATEGORY ANALYSIS .............................................................................................................. 142

TABLE 102 : BOND TYPE ANALYSIS ........................................................................................................... 142

TABLE 103 : SPREAD ANALYSIS ...................................................................................................................... 142

TABLE 104 : CATEGORY ANALYSIS - HISTORICAL ................................................................................... 142

TABLE 105 : RATING ANALYSIS - HISTORICAL ......................................................................................... 143

TABLE 106 : SPREAD ANALYSIS - HISTORICAL .......................................................................................... 143

TABLE 107 : TOP 25 TRADED CORPORATE BONDS .............................................................................. 144

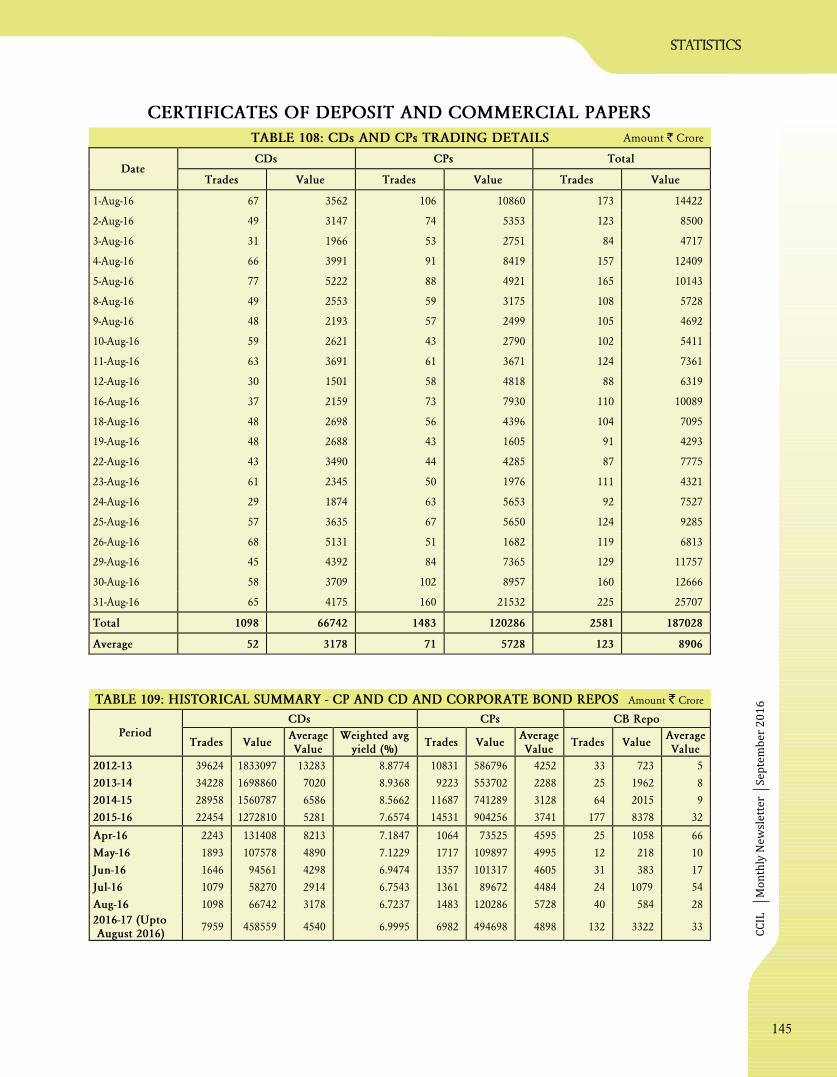

TABLE 108 : CDs AND CPs TRADING DETAILS ........................................................................................ 145

TABLE 109 : HISTORICAL SUMMARY ...................................................................................................... 145

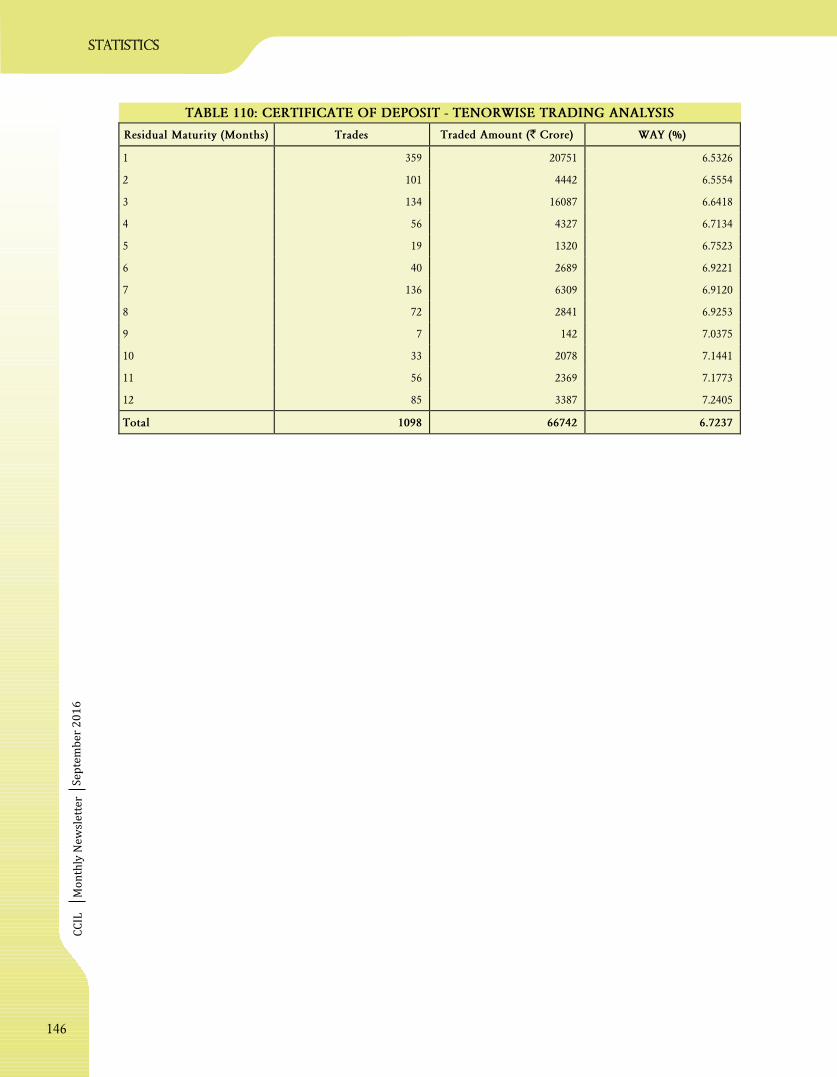

TABLE 110 : TENORWISE TRADING ANALYSIS CDs ................................................................................. 146

TABLE 111 :

TABLE 112 :

TABLE 113 :

TABLE 114 :

CHART 1 : ZERO COUPON YIELD CURVE .............................................................................................. 134

CHART 2 : SOVEREIGN YIELD CURVE ..................................................................................................... 134

INTEREST RATE MOVEMENT

CORPORATE BONDS

CERTIFICATE OF DEPOSIT AND COMMERCIAL PAPERS

BENCHMARK RATES

CHARTS

COMPARISON OF FBIL TERM MIBOR AND CD WEIGHTED AVERAGE RATE (%) 147

148

FBIL FC-RUPEE OPTION VOLATILITY MATRIX RATES - 25 DELTA RISK REVERSAL (%) 149

FBIL FC-RUPEE OPTION VOLATILITY MATRIX RATES - 25 DELTA STRANGLE (%) 150

FBIL FC-RUPEE OPTION VOLATILITY MATRIX RATES - AT THE MONEY (ATM) VOLS (%)

Message from MDMessage from MD

Dear Colleagues,

Financial markets in India have been able to

achieve stability for the last few quarters

with growth slowly picking up and the Indian

Rupee being relatively less volatile vis-à-vis

many emerging market currencies.

Recessionary conditions are gradually

diminishing in Brazil and Russia, but the

near-term outlook is still fragile due to

policy uncertainties and soft commodity

prices. The flow from foreign investors to

Indian markets has been positive and the

equity market has witnessed some buying

which moved benchmark indices northward.

That has been aided by stable rainfall -

almost normal with only a marginal deficit.

The normal rainfall would help in keeping a

rein on inflationary pressures. Oil prices,

which moved upward temporarily, have been

stable and remained below USD50 helping

non-oil emerging countries like India.

Last GDP data release showed a marginal

drop in growth for Q1 of 2016-17. The

inflation data (both CPI and WPI) does not

show any immediate concern for policy

makers. The global commodity price stability

has helped in keeping domestic inflation at

manageable levels. Liquidity pressure has

come down in recent months after infusion of

liquidity by Reserve Bank of India through

OMO auctions and higher Government

spending.

RBI announced new policies for deepening the

corporate bond market. These measures are

intended to aid in market development,

enhance participation, facilitate greater

market liquidity and improve communication.

Accepting many of the recommendations of the

Khan Committee to develop the corporate bond

market, RBI has decided to enhance the

aggregate limit of partial credit enhancement

provided by banks, permit brokers in corporate

bond repos, authorise the platform for repo in

corporate bonds and encourage credit supply

for large borrowers through market

mechanism. Suitable legal amendments may

have to be made in the existing legal framework

in case RBI decides to accept corporate bonds

under current LAF mechanism as collateral.

Banks are also being permitted to issue Masala

Bonds for their capital requirements and for

financing infrastructure and affordable

housing. The FPIs will be eligible to avail the

facility to trade directly in corporate bonds.

These measures are likely to be helpful for

developing the corporate bond market in India.

R. Sridharan

of the month

•

•

•

•

On September 8, 2016, CCIL conducted the 11th cycle of the Portfolio Compression

exercise in the OTC Interest Rate Swaps market. The exercise achieved a compression of

84% and a market-wide reduction of notional outstanding of 2,18,958.79 crore.

FX-SWAP Dealing System registered its highest daily volume of USD 730.00 million on

September 6, 2016.

Trades on the ASTROID (the Anonymous IRS Dealing System) recorded their highest level

of 6,700 crore on September 14, 2016.

CBLO volumes recorded their all-time high volumes of 1,16,232.60 crore on September

15, 2016.

`

`

`

Against the backdrop of a global environment

characterized by weak growth and heightened

financial market volatility, the Indian economy

posted gains in 2015-16 and the underlying

conditions improved, scaling up the growth

momentum. Progress of the southwest monsoon

augurs well for agriculture and the rural economy,

while the seventh pay commission award would

provide a stimulus to consumption spending

within the targeted fiscal deficit. On the external

front, indicators of external sustainability

improved noticeably during the year and foreign

direct investment (FDI) recorded the highest

annual net inflow. On the flipside, sluggishness in

the industrial sector continues, and the capex cycle

and private investment activity remains weak.

Further, the banking sector has been dealing with

stress on account of deterioration in corporate

balance sheets and loan quality, necessitating

efforts to free up credit flows to the productive

sectors of the economy.

The modest acceleration in real GDP growth in

2015-16 was supported by private consumption.

The significant improvement in corporate

profitability, on account of saving on input costs

and sales growth, is expected to boost corporate

saving and translate into investment spending.

However, on the production side, agriculture

weathered two consecutive years of drought

conditions and posted a modest growth during the

year. Industrial output weakened during the year

and consumer non-durables posted a decline after

consecutive years of expansion, mainly on account

of contraction/deceleration in fast moving

consumer goods, reflecting the subdued state of

rural demand. The services sector witnessed a

deceleration across all constituents as new business

orders slowed and exports were impacted by weak

external demand. Notable progress was seen in the

infrastructure space, with electricity generation

recording the highest ever annual capacity addition

in the solar and wind energy segments. There was

significant improvement in the road sector in terms

of new constructions and also in the railways sector

in terms of capital investment, commissioning of

broad gauged lines and electrification of railway

tracks. Major Indian ports recorded the highest

capacity addition during the year.

The inflation conditions which eased in the first

few months of 2016 on the back of the seasonal

decline in prices of fruits and vegetables picked up

again from May 2016 as food prices firmed up

ahead of the onset of the monsoon. Monetary

conditions reflected an interplay of diverse factors

as demand for currency drove up the expansion of

reserve money and muted the money multiplier

which, in turn, moderated the rate of money

supply. Bank credit which was sluggish in the first

half of the year, picked up in the retail segment,

industry and agriculture in the second half of the

year. Timely recognition of the deterioration in

banks' balance sheets through the Reserve Bank's

asset quality review resulted in the overall stressed

assets ratio rising marginally by end-March 2016

from its level a year ago, with a rise in the gross NPA

ratio but a fall in the restructured assets ratio. In the

external sector, a faster pace of contraction in

imports relative to exports and large terms of trade

gains narrowed the current account deficit to 1.1%

of GDP, which was comfortably financed along

with sizable accretion to reserves.

Assessment: 2015-16

RBI ANNUAL REPORT 2015-16

CC

ILM

on

thly

Ne

wsl

ett

er

Se

pte

mb

er

20

16

INFOCUS

7

CC

ILM

on

thly

Ne

wsl

ett

er

Se

pte

mb

er

20

16

Prospects: 2016-17

The near-term domestic outlook appears to be

brighter than the outcome for 2015-16, despite the

weak outlook for the global economy due to the

Brexit referendum. Although a pick-up in

investment activity remains a concern,

consumption is expected to provide support to

aggregate demand and may receive a boost from the

revival of rural demand in response to the well-

distributed southwest monsoon and the seventh

pay commission's award. However, industrial

activity and export demand is likely to remain slack

in the coming months, unless the industrial

activity is supported by the recent Government

measures including 100% FDI in defence, civil

aviation, pharmaceuticals and broadcasting.

Service sector activity is likely to receive a stimulus

in public administration, defence and other

services as public expenditure on wages, salaries

and pensions translates into disposable incomes.

The central government's commitment to the fiscal

consolidation path in 2016-17 has enhanced the

credibility of fiscal policy, thus helping in

anchoring inflation expectations and improving

the business environment. The passage and

implementation of the Goods and Services Tax

(GST) Bill is expected to boost trade, investment

and growth by reducing supply chain rigidities,

encouraging scale economies, cutting down

transportation and transaction costs, as also

promoting efficiency gains.

India's external position seems viable and well-

buffered to sustain a pick-up in non-oil non-gold

imports, although the external environment

continues to pose challenges stemming from large

currency movements, a rising incidence of

protectionist measures, swift and massive

movements of capital and the amplification of

uncertainty by the Brexit vote. Although the

outlook for capital inflows is optimistic with the

recent liberalization of FDI policy, the repayment

of FCNR (B) deposits which is due under the

special swap scheme needs to be managed carefully.

Among the various structural reforms initiated, the

UDAY scheme has provided DISCOMs an

opportunity to regain financial viability. In the

banking sector, the enactment of the Insolvency

and Bankruptcy Code would help sick companies

to either wind up or turn around, and for investors

to exit. Amendments to strengthen the Debt

Recovery Tribunals for speedier resolution of

stressed assets have been passed. Efforts need to be

made to re-energise asset reconstruction companies

(ARCs) by resolving issues relating to their capital

requirements and enabling price discovery for

NPAs/security receipts so that they can be traded in

open, competitive markets that ensure liquidity. In

order to intensify structural reforms in factor

markets, particularly land and labour, initiatives

are being taken by state governments, such as

amendment of labour laws, and a transparent and

viable framework for land acquisition processes.

The National Agriculture Market (NAM), a pan-

India electronic trading platform is an important

step towards improving marketing infrastructure.

India witnessed a moderate pick-up in pace in the

second half of the year despite truncating

investment and persistent global uncertainties.

Government continued its fiscal consolidation

roadmap in 2015-16. Net exports remained muted

in the midst of suppressed global demand. Despite

this, trade deficit dwindled due to the pace of

contraction of imports surpassing that of exports,

and in part due to gains in net terms of trade. A

holistic view of the Indian economy portrays

sound macroeconomic fundamentals buttressed by

slumping inflation and narrowing twin deficits.

Economic Review

INFOCUS

8

The key challenges in the year ahead entail

stimulating private investment and rejuvenating

banking sector while maintaining macroeconomic

stability.

Aggregate demand in urban and rural areas depicts

contrary views on recent income evolution.

Improvement in urban consumption is reflected in

the concurrent surge in sales of passenger vehicles.

By contrast, rural consumption has stagnated, with

two consecutive years of deficient monsoons

having taken a toll on rural incomes. Gross fixed

capital formation remained subdued during 2015-

16. At the same time, several initiatives by the

Government, including 'Make in India', and faster

clearances of stalled projects have revived business

sentiment. Higher rate of increase in gross financial

assets relative to financial liabilities was responsible

for the spike in household net financial saving rate.

Despite two consecutive years of below par rainfall,

GVA from agriculture and allied activities posted a

modest growth in 2015-16. Notwithstanding these

setbacks, the Ministry of Agriculture has placed

food grains production for the year at 0.1% higher

than previous year, mainly due to an increase in

wheat production. At the same time, the favourable

impact of the normal monsoon this year

juxtaposed with the implementation of the seventh

pay commission's recommendations will provide a

fillip to consumption demand.

For the year as a whole, average inflation

plummeted from 5.8% in the preceding year to

4.9% in the current year. A statistical

decomposition of contribution of different

subgroups within CPI indicates that the major

contribution to disinflation emanated from the

food group mainly on account of the government's

adroit supply management policies and also from

the fall in global food prices.

Food constitutes 45.9% of CPI and contributed

50% to overall inflation in 2015-16. Keeping this

in mind, the Government took a couple of

measures to break the food inflation spiral as part

of a comprehensive and rapidly deployed food

management strategy - higher Minimum Support

Prices (MSPs) to incentivise production of pulses;

procurement of pulses with a view to creating

buffer stock; banning exports of most pulses; zero

import duty on pulses and onions; raising

minimum export prices of onions; and allowing

states to impose stock limits for certain essential

commodities such as onions, edible oils and pulses.

The implementation of the revised pay scales under

the seventh pay commission is expected to increase

headline inflation with a cumulative impact of 10

basis points by March 2017 over the baseline

scenario set out in the bi-monthly monetary policy

statement of June 2016 (which excluded the impact

of the seventh pay commission implementation).

This reflects indirect effects emerging from

augmentation in personal consumption

expenditures pushing up aggregate demand. The

full impact on CPI inflation, which mainly comes

through the direct effects of an increase in house

rent allowance when it is affected, will be realised in

a calibrated manner over ensuing months.

Domestic financial markets showed differential

responses across segments, with equity and foreign

exchange markets most affected by global

spillovers, while the debt, money and credit market

were driven by global developments. Money

market rates shifted from a softening bias in the

first half of 2015-16 and hardened in the second

half of the fiscal due to advance tax outflows and

year-end factors. However rates have softened

considerably during the current fiscal i.e. 2016-17

following easing liquidity conditions. During

Financial Markets

CC

ILM

on

thly

Ne

wsl

ett

er

Se

pte

mb

er

20

16

INFOCUS

9

CC

ILM

on

thly

Ne

wsl

ett

er

Se

pte

mb

er

20

16

2015-16, G-Sec yields exhibited slight bearish

trends following the weak rupee, sub-normal

monsoons, oversupply of securities and changing

expectations of a rate hike by the US Fed. However

the fiscal consolidation adherence of the Union

Budget 2016-17, dovish guidance by the US Fed

brought about the easing of yields in the first

quarter of 2016-17, which got further momentum

mid-June 2016 following the Brexit results, lower

inflation concerns due to normal monsoons, easy

liquidity conditions supported by OMO purchases

by the RBI. The corporate debt market has seen a

substantial increase in issuance by corporates,

while there was a decline in the secondary market

turnover. The equity market started on a subdued

note in the first half of 2015-16 affected by

domestic factors like weak monsoon, asset quality

of the banking system, sluggish investment

activity, depreciation of the rupee etc. While the

tide turned at the start of the second half following

the rate cut affected by the RBI in September, the

trend reversed at the start of 2016 following global

turbulence on fears of a China meltdown and flight

of FII capital from emerging markets. The trends

reversed after March 2016 led by increasing

investor optimism about government reforms,

good progress of monsoons and FPI buying in the

market. The rupee showed a depreciating bias

through 2015-16 due to factors like the Greek crisis,

hawkish FOMC guidance, global sell-offs,

devaluation of remnimbi and the subsequent sell-

offs in the Chinese market. During the current

fiscal, the rupee has remained largely range bound

showing a slight depreciation during the

immediate aftermath of the Brexit result. Overall,

the rupee has largely remained a better performing

currency among its peer currencies.

During fiscal 2015-16 indirect tax collections were

around 30% higher than the previous year

supported by higher excise duty collections due to

the upward duty revisions on petroleum products,

modest increase in customs collections and the

increase in service tax due to upward revision in the

service tax rates. On the other hand direct tax

collections recorded a shortfall relative to the

budget estimates. Non-tax revenues and non-debt

receipts from were higher than budgeted. The

budgeted target for GFD-GDP ratio was

maintained at 3.9% as budgeted, with the revenue

deficit at 2.5%, lower than the budgeted 2.8%.

During 2016-17, the buoyancy in tax collections is

budgeted to decline, with an increase in

d i s i n v e s t m e n t p ro c e e d s a n d re c e i p t s

communication services. Expenditure is expected

to pick up in the form up provision for

implementation of One-Rank-One-Pension

(OROP) awards and towards bank capitalization,

while a decline in major subsidies has been

estimated. While key fiscal indicators of State

Governments have deteriorated in 2015-16, the

GFD-GDP ratio for 2016-17 is budgeted to decline

due to a turnaround from a deficit mode to a

surplus mode.

The slump in commodity prices, weak global

demand and a surge in protectionist measures

across advanced and emerging economies led to a

decline in exports by 15.5% in 2015-16, panning

across all constituents and in terms of both volume

and value. Imports also declined by similar levels

led by reduction in oil prices and also gold and

non-oil non-gold imports. Invisibles behaved

diversely in 2015-16, with exports of merchandise

trade related transportation services impacted by

the global deceleration, while tourism and software

exports have remained resilient. On the other hand,

remittance inflows were affected by the sluggish

Government Finances

External Sector

INFOCUS

10

CC

ILM

on

thly

Ne

wsl

ett

er

Se

pte

mb

er

20

16

activity in the gulf region. However, due to the

sharp fall in merchandise trade deficit, current

account deficit was at 1.1% of GDP, the lowest since

2007-08. Buoyed by measures to enhance GDP, FDI

inflows surged to USD 36 billion in 2015-16, the

highest net annual inflow thus far, while net

portfolio inflows turned negative. By the end of

2015-16, India's foreign exchange reserves reached a

record level of USD 360.2 billion. Going ahead, the

external sector outlook will depend upon CAD

remaining under sustainable limits, revival in

exports and ability of the reform measures to instill

confidence among international investors.

A Monetary Policy Framework Agreement (MPFA)

was signed between the Government of India and

RBI on February 20, 2015 which steered the

conduct of monetary policy during 2015-16.

Empowered by the MPFA, RBI set out an agenda

for its monetary policy operations: entrenching a

durable disinflationary process to take consumer

price index (CPI) inflation to the targets set for

January 2016 and March 2017; improving

transmission of the policy rate to bank lending

rates by ensuring appropriate liquidity

management consistent with the monetary policy

stance; and dampening volatility of the WACR and

other money market rates around the repo rate, i.e.,

securing the first leg of monetary transmission.

RBI continued with an accommodative stance for

monetary policy through 2015-16 while keeping

focus on a gradual and durable disinflation path

that was expected to take the CPI inflation below

6% by January 2016. The policy repo rate was

reduced by 25 bps in June 2015 and 50 bps in

September 2015 as the receding inflationary

pressure emanating from benign cereal prices and

moderation in international crude oil prices

opened up space for monetary policy action. With

the target for January 2016 achieved, the focus of

monetary policy shifted to attaining the inflation

target of 5% by the end of 2016-17. Based on an

assessment that the target of 5% inflation by March

2017 was achievable, particularly when the Union

Budget 2016-17 adhered to fiscal consolidation and

announced measures to re-invigorate the rural

economy, upgrade the social and physical

infrastructure, deepen institutional reforms and

improve the environment for business, the policy

rate was reduced further by 25 bps to 6.50% in April

2016, the lowest since March 2011. The policy rate

was kept unchanged thereafter as a sharper-than-

anticipated increase in food prices has pushed up

the projected trajectory of inflation over the rest of

the year.

During 2015-16, a considerable flux in

autonomous liquidity flows necessitated a pro-

active assessment of liquidity conditions and

nimble responses through a combination of regular

facilities and fine-tuning operations in the form of

variable rate repo/reverse repo auctions. Liquidity

conditions generally remained tight during the

second half of the year due to festival related

currency requirements and advance tax outflows in

Q3, followed by balance sheet considerations and

restraint in government spending in Q4. Effective

liquidity management, however, kept the WACR

within +/- 10 bps and +/- 20 bps of the repo rate for

36% and 79% of the total number of trading days,

respectively, during 2015-16. With the institution

of the revised liquidity management framework,

the role of term repo auctions under the liquidity

adjustment facility (LAF) has become significant.

Normal 14-day and fine tuning term repos of

varying tenors ranging from 2 to 56-day accounted

Monetary Policy Operations

Disinflation

Operating Framework

INFOCUS

11

CC

ILM

on

thly

Ne

wsl

ett

er

Se

pte

mb

er

20

16

for about 90% of the average net liquidity injection

under the LAF during the year. Since July 22, 2015,

the Financial Benchmark India Private Limited

(FBIL) has started compiling the Mumbai Inter-

Bank Offer Rate (MIBOR) based on actual data of

the interbank call market transactions covering a

one hour time span from 9.00 a.m. to 10.00 a.m.

Given the market microstructure, thick trading in

the first hour usually elevates MIBOR above

WACR. The FBIL has started generating quote-

based term benchmarks, but their use in pricing of

financial products and transactions is yet to pick

up.

In April 2016, the liquidity management

framework was revised in a move to progressively

lower the average ex ante liquidity deficit to a

position closer to neutrality. RBI assured the

market of meeting the requirements of durable

liquidity and then using its fine-tuning operations

to make short-term liquidity conditions consistent

with the stated policy stance. Accordingly, in Q1 of

2016-17 RBI injected permanent liquidity through

open market operations (outright), more than

offsetting the impact of currency leakage during

the same period. For ensuring non-disruptive

FCNR(B) redemptions, RBI pro-actively injected

liquidity through open market purchase auction

on August 11, 2016. With a view to further

minimising volatility in WACR, as also easing

liquidity management for banks without

abandoning liquidity discipline, the minimum

daily maintenance of the cash reserve ratio (CRR)

was lowered from 95% of the requirement to 90%

effective April 16, 2016. Furthermore, the policy

rate corridor around the repo rate was narrowed

from +/-100 bps to +/- 50 bps.

During 2015-16, as a part of the phased

implementation of the liquidity coverage ratio

(LCR), the minimum required high quality liquid

assets (HQLA) was raised from 60% to 70% of the

total net cash outflow over the next 30 calendar

days under the stress scenario effective January 01,

2016, which correspondingly limited the capacity

of banks to use the excess statutory liquidity ratio

(SLR) securities to access collateralised liquidity

from money markets and RBI. Recognising the

scope for providing greater flexibility to banks

within the prescribed SLR, effective February 11,

2016, RBI allowed banks to reckon additional

government securities held by them up to 3% of

their NDTL within the mandatory SLR

requirement as level 1 HQLA for the purpose of

computing their LCR on top of the 5% permitted

in November 2014. On July 21, 2016, additional

headroom equivalent to 1% of NDTL was provided

within the prescribed SLR. Together, the total carve-

out from SLR available to banks stands at 11% of

their NDTL, including 2% of NDTL available

under MSF.

In response to the reduction in the policy repo rate

by 150 bps during January 15, 2015 through April

05, 2016, the median base rate of banks declined by

60 bps as against a higher decline of 92 bps in

median term deposit rates, reflecting banks'

preference to protect profitability in the wake of

deter iorat ing asset qual i ty and higher

provisioning. The weighted average lending rate

(WALR) on fresh rupee loans declined by 100 bps

(up to June 2016), significantly more than the

decline of 65 bps in WALR on outstanding rupee

loans.

As set out in the agenda for 2015-16, RBI

introduced the Marginal Cost of Funds based

Lending Rate (MCLR) system for scheduled

commercial banks (excluding RRBs), effective

Monetary Policy Transmission

Experience of the MCLR System

INFOCUS

12

CC

ILM

on

thly

Ne

wsl

ett

er

Se

pte

mb

er

20

16

April 1, 2016 whereby all new rupee loans

sanctioned and credit limits renewed would be

priced with reference to the MCLR. As expected,

the MCLR for the overnight segment, one year

segment and up to three-year segment (as on July

31, 2016) was lower by 70 bps, 25 bps and 36 bps,

respectively, than the base rate of 9.65%.

There has hardly been any transmission of a

reduction in the policy rate to the actual lending

rates charged to customers during 2016-17. While

the cost of funding by banks has declined

somewhat leading to a decline in shorter maturity

MCLR, there has been an increase in the term

premia in respect of term loans of one year and

above, thereby attenuating the transmission to

actual lending rates charged to customers.

Moreover, banks may have been loading (i) a higher

credit risk premia on their new customers in order

to attain their desired return on net worth in a

rising NPA environment; and/or (ii) a higher

strategic risk premia on their riskier loans as part of

their business strategy to reorient their lending

operations towards less risky activities. The

consequent rise in the spread is reflected in a near

unchanged WALR in respect of both outstanding

and fresh rupee loans during 2016-17 so far.

In the first bi-monthly policy statement for 2016-

17, RBI set a target for CPI inflation at 5% by

March 2017. The eventual aim is to move towards

4% CPI inflation by the end of 2017-18. To

strengthen the monetary policy framework, the

Union Budget 2016-17 announced the formal

constitution of a Monetary Policy Committee

(MPC) by amending the RBI Act, 1934, which will

be vested with the responsibility of setting the

policy rate. The amended RBI Act, which was

notified in the Gazette of India on May 14, 2016

mandates a MPC to determine the policy interest

rate to achieve the inflation target set by the

Government. MPC is a new institutional structure.

The MPC shall consist of the Governor of RBI, the

Deputy Governor-in-charge of monetary policy,

one officer of the Bank to be nominated by the

Central Board of RBI and three members to be

appointed by the Central Government. Each

member shall have one vote, and in the event of a

tie, the Governor can exercise a casting or second

vote.

In 2015-16, RBI put especial effort towards

fostering a more conducive environment for

adequate flow of credit to priority sectors, in

particular to the micro, small and medium

enterprises (MSME) sector. The committee on

Medium-Term Path on Financial Inclusion

submitted action plan for financial inclusion that

will guide the financial inclusion process going

forward. RBI has set up Financial Inclusion and

Development Department (FIDD) for seamless

implementation of its financial inclusion agenda.

Priority Sector Lending Certificates (PSLCs) will

allow the market mechanism to drive priority

sector lending by leveraging the comparative

strengths of different banks.

In view of the critical role played by regional rural

banks (RRBs) in driving the financial inclusion

agenda, priority sector lending guidelines were

revised for RRBs in December 2015 and an overall

target of 75% of the total outstanding loans to the

priority sector was set for them. RBI advised banks

to review their existing lending policies to the

micro and small enterprises (MSEs) sector and fine-

tune them by allowing for standby credit facilities

in case of term loans, additional working capital

limits, mid-term review of regular working capital

limits and timelines for credit decisions.

Agenda for 2016-17

Credit delivery and financial inclusion

INFOCUS

13

CC

ILM

on

thly

Ne

wsl

ett

er

Se

pte

mb

er

20

16

Financial Inclusion Advisory Committee (FIAC)

was reconstituted in June 2015 for preparing a

national strategy for financial inclusion which

aims at converging financial inclusion efforts of

various stakeholders and PMJDY, apart from

monitoring the progress; (ii) monitoring progress

on FIP; and (iii) monitoring progress on financial

literacy. The Government of India merged

financial inclusion fund (FIF) and financial

inclusion technology fund (FITF) to form a single

financial inclusion fund in July 2015 with a corpus

of 20 billion. The new FIF, which will be

administered by an advisory Board constituted by

the Government, will be maintained by NABARD.

Based on the recommendations of the

Implementation Group on Encouraging Greater

Retail Participation in G-Secs, the Clearing

Corporation of India Ltd. (CCIL) was advised to

enable participation of demat account holders in

NDS-OM. A Working Group set up under the aegis

of the Financial Stability and Development

Council Sub-committee (FSDC-SC) considered

several measures for strengthening participation,

improving market infrastructure and easing the

issuance process for corporate bonds. Unlisted

securities and securitised debt instruments will

shortly be added to the basket of corporate debt for

foreign portfolio investor (FPI) investments.

Covered options against underlying currency

exposures have been allowed. The limits for all

resident individuals, firms and companies to book

foreign exchange forwards and foreign currency-

Indian rupee (FCY-INR) options contracts on the

basis of declaration have been increased from US$

250,000 to US$ 1,000,000. Indian residents having

long term foreign currency (FCY) borrowings were

permitted to enter into FCY-INR swaps with

multilateral or international financial institutions

(MFIs/IFIs), in which the Government of India is a

shareholding member provided such swaps were

undertaken by the MFI/IFI concerned on a back-to-

back basis with an authorised dealer (AD)

Category-I bank in India.

In the when-issued (WI) market, scheduled

commercial banks were allowed to take short

positions, whereas all eligible entities were

permitted to take long positions. Primary dealers

(PDs) were allowed to participate in exchange

traded currency futures market. For a more broad

based participation in OTC derivatives, regulated

entities other than banks and PDs such as mutual

funds and insurance companies have been enabled

to trade in such derivatives on electronic platforms

with guaranteed settlements by the CCIL.

The Financial Benchmarks India Pvt. Ltd. (FBIL)

took over the administration of the benchmark for

the overnight inter-bank rate based on the actual

traded rates, and also started publishing the polled

term Mumbai interbank offer rate (MIBOR) for

three tenors, 14-day, one month and three

months, as well as the FBIL FC-Rupee Options

Volatility Matrix rates. The CCIL trade repository

expanded the public dissemination of data on a

gross basis in pursuit of enhanced transparency.

CCIL has also started disseminating data on short

term USD/INR interbank near maturity swaps.

Agenda for 2016-17 include changes in e-Kuber to

facilitate seamless transfer of g-secs between demat

accounts and subsidiary general ledger/gilt

accounts and operationalising electronic platforms

for repo in corporate bonds in coordination with

the Securities and Exchange Board of India (SEBI),

issuance of final guidelines on introduction of

interest rate options, review of Guidelines on

commercial paper (CP), CDS and STRIPS, as well as

introduction of money market futures.

`

Financial Markets and Foreign Exchange

Management

viz.,

INFOCUS

14

CC

ILM

on

thly

Ne

wsl

ett

er

Se

pte

mb

er

20

16

Additionally, framework for authorisation of

shifting OTC derivatives on to exchanges or

electronic trading platforms will be put in place.

The scope of dissemination of OTC forex

derivative transactions by the CCIL Trade

Repository will also be expanded.

Under the Financial Markets Operations

Department (FMOD), a 56-day variable rate repo

was conducted in January 2016 to expand the ambit

of liquidity adjustment facility. Straight through

processing (STP) was introduced for fixed rate repo,

reverse repo and MSF. Under Section 25 of the

Negotiable Instruments Act, 1881, it was decided to

keep open all money market segments on the

working Saturdays from September 01, 2015.

Reverse repo and MSF are being conducted from

February 19, 2016 on all Mumbai holidays when

the real time gross settlement (RTGS) system is in

operation. From May 02, 2016, the Reserve Bank

reference rate is being computed on the basis of the

volume weighted average of the actual market

transactions that have taken place during a

randomly selected 15-minute window between

11.30 a.m. and 12.30 p.m. every weekday. To address

the volatility in the foreign exchange market,

intervention in the exchange traded currency

derivatives (ETCD) segment commenced in

September 2015.

Under the Foreign Exchange Department (FED),

the guidelines on external commercial borrowings

(ECBs) were rationalised and liberalised during

2015 -16 in tune wi th macroeconomic

developments. Resident importers were allowed to

raise trade credits in INR allowing the transfer of

currency risk to overseas lenders. To facilitate rupee

denominated borrowings/bonds from abroad, a

framework for such issuance has been put in place.

An analogous information technology based

system for monitoring import transactions is being

operationalised.

Furthermore, regulations pertaining to the

employee stock options (ESOP) scheme were

reframed in sync with the SEBI regulations (for

listed companies) and the Ministry of Corporate

Affairs' regulations (for unlisted companies). The

National Pension System (NPS) was made an

eligible investment option for non-resident

Indians (NRIs). As per the foreign direct

investment (FDI) policy amendment by the

Government, sectoral limits on foreign

investments are to be aggregates of both FDI & FPI,

foreign investment in limited liability partnership

(LLP) is permitted under the automatic route for

sectors where 100% FDI is allowed without

attendant FDI-linked performance conditionality,

foreign investment up to 100% under the

automatic route is permitted in the plantation

sector, manufacturing sector given clear definition

as to where foreign investment has been allowed,

single brand retail brick & mortar stores can

undertake sales via e-commerce, and FDI limit in

the insurance sector via automatic route has been

increased to 49%.

To encourage start-up entities, cashless sweat issue

of equity has been allowed if drafted as per SEBI

guidelines, issue of shares against legitimate

payment owed by the investee company permitted

subject to adherence to the FDI policy, having an

escrow arrangement in respect of transfer of shares

between a resident and a non-resident, as well as

start-up having an overseas subsidiary has been

permitted to open an FCY account with a bank

outside India for the purpose of crediting to it

foreign exchange earnings from operations.

Further, payments in foreign exchange arising out

of its own or its subsidiaries' sales/exports have

been allowed as a permissible credit to an Indian

start-up's exchange earners account.

INFOCUS

15

CC

ILM

on

thly

Ne

wsl

ett

er

Se

pte

mb

er

20

16

The Reserve Bank has also liberalised the approval

process for setting up liaison/branch/ project

office in India to ease doing business in the

country. Transfers between non-resident ordinary

rupee (NRO) accounts have been permitted.

Further, NRIs and persons of Indian origin (PIOs)

have been permitted to open NRO accounts jointly

with other NRIs/PIOs. Authorised dealer (AD)

banks have to obtain declarations from their clients

that remittances from their respective NRO

accounts are legitimate and not external

borrowings. Non-residents having a business

interest in India are permitted to open a repatriable

special non-resident rupee (SNRR) account with

balances commensurate with business operations.

An Indian company receiving foreign investment

under the FDI route has been permitted to open

and maintain an FCY account with an AD in India

provided it has impending FCY expenditure, which

however needs to be closed immediately after the

requirements are completed or within six months

from the date of opening of such account,

whichever is earlier.

Despite marginal pick-up in economic growth and

credit off-take, the Indian banking system

continued to battle with the challenge of rising

NPAs during 2015-16. As a supervisory action, RBI

initiated an “asset quality review” during the year

following which banks recognized stressed assets,

there by taking a hit on profitability with higher

provisioning. To foster competition in the banking

system and with an aim to take banking services to

under-served segments of the population, RBI

allowed entry of new players with the establishment

of small finance and payments banks.

To address challenges posed by the recent growth in

banking consumers following the implementation

of the Pradhan Mantri Jan-Dhan Yojana (PMJDY),

for customer services and protection RBI

operationalised the Charter of Customer Rights. It

also undertook a comprehensive review of the

Banking Ombudsman (BO) scheme. Thus, the year

witnessed a slew of policy actions in pursuance of

the three pillars envisaged by the Reserve Bank for

improving the regulation and supervision of the

financial sector, ., strengthening the banking

structure through new players; expanding financial

access; and improving the system's ability to deal

with distress.

The Financial Stability Unit (FSU) within the

Reserve Bank is responsible for macro-prudential

surveillance by conducting periodic stress tests and

other tools, dissemination of information relating

to the status of and challenges to financial stability

through the bi-annual report, namely, Financial

Stability Report (FSR). It also acts as a secretariat to

the Financial Stability and Development Council,

a sub-Committee of the apex institutional

mechanism for financial stability in the country. In

2015-16, the stress testing framework was modified

to incorporate sectoral probability of defaults and

modeling corporate sector distress. The Sub-

Committee of FSDC review various issues which

includes central know your customer registry,

International Financial Services Centre,

development of corporate bond market, peer-to-

peer (P2P) lending, regulation of credit guarantee

schemes, risks in deposit mobilization by multi-

state co-operative societies. A sub-group of FSDC

also looked into the range of issues like legal entity

identifier (LEI), a regulatory framework for NBFC-

account aggregator (AA), securitization, a single

entity undertaking multiple activities.

Regulation, Supervision and Financial

Stability

,

viz

Financial Stability Unit

INFOCUS

16

CC

ILM

on

thly

Ne

wsl

ett

er

Se

pte

mb

er

20

16

Regulation of Financial Intermediaries

Department of Banking Regulation (DBR)

regulates commercial banks and has proactively

addressed both the time and cross-sectional

dimensions of risks to preserve systemic stability. It

also focused on developing an inclusive and

competi t ive banking structure through

appropriate regulatory measures. In 2015-16, the

RBI strengthened the regulatory framework for

dealing with stressed assets, introduced the Scheme

for Sustainable Structuring of Stressed Assets and

passed Insolvency and Bankruptcy Code to

improve the framework for resolution of corporate

entities, partnership firms and individuals in a

time-bound manner. To improve recovery, it

amended many of its Acts.

As an initiative towards financial inclusion

through a bouquet of banking products, including

small credit, small savings and payments/

remittances, the Reserve Bank issued in-principle

approval for setting up of 11 payments banks and

ten small finance banks (SFBs) in September 2015

and October 2015, respectively. The first SFB

license was granted to Capital Small Finance Bank

Limited in March 2016 while the first payment

bank license was granted to Airtel Payment Bank

Ltd. in April 2016. To determine transparent

lending rates and strengthen monetary

transmission, banks were mandated to price their

credit using the marginal cost of funds based

lending rate (MCLR) as the internal benchmark.

In August 2016, RBI released guidelines for on-tap

licensing of universal banks with the objective to

encourage greater competition and innovation in

the system. In February 2016, banks were advised to

comply with the Indian Accounting Standards

converged with IFRS in the preparation of

financial statements for the accounting periods

beginning April 1, 2018. Following the

announc emen t i n th e Fo l l ow ing th e

recommendations made by the Committee to

Review Governance of Boards of Banks in India,

the Banks Board Bureau (BBB - which started

functioning from April 8, 2016) was set up by the

central government with support from the Reserve

Bank to infuse greater professionalism in the

constitution and operation of the boards of PSBs.

For 2016-17, RBI intends to finalize the policy on

prudential and implementation aspects of the

expected credit loss approach, guidelines for

computing exposure for counterparty credit risk

(CCR) arising from derivative transactions and

capital requirements for bank exposures to central

counterparties as well as margin requirements for

non-centrally cleared derivatives.

During 2015-16, steps such as early recognition of

financial distress; prompt steps for resolution and

fair recovery for lenders, risk weights assigning to

exposures to central/state government/s and

claims guaranteed by state governments; risk

weights with respect to investments in corporate

bonds by standalone primary dealers; and strategic

debt restructuring and refinancing of project loans

had been taken.

The Reserve Bank introduced the revised format for

central repository for information on large credits

(CRILC) reporting for improved data collection

from banks from the quarter ended September

2015. A new framework for fraud detection,

reporting and monitoring was rolled out in May

2015. A Central Fraud Registry for the use of banks

was operationalized on January 20, 2016. An

Expert Panel on IT Examination and Cyber

Security, set up by the RBI, is expected to provide

assistance in IT examination/cyber security

initiatives of banks, review examination reports

and suggest actionable items during 2016-17.

INFOCUS

17

CC

ILM

on

thly

Ne

wsl

ett

er

Se

pte

mb

er

20

16

Public debt management

During the year, the Reserve Bank successfully

managed the large borrowing programme of the

central government and the states in an orderly

manner in the face of multiple challenges

including reduction in HTM category of banks'

investments, reduction in SLR in an environment

of tight liquidity, increased issuances by state

governments and global uncertainties.

The central government in consultation with the

Reserve Bank designed a Sovereign Gold Bond

Scheme (SGB) as an alternative to the purchase of

metal gold. The Reserve Bank manages the scheme

on behalf of the Government and issued three

tranches of SGBs during the fiscal year 2015-16.

Further, the Government of India (Ministry of

Power) had formulated the Ujwal DISCOM

Assurance Yojana (UDAY) scheme on November

20, 2015 with the objective to improve operational

and financial efficiency of the state DISCOMs. The

Reserve Bank during 2015-16 issued UDAY bonds

for a total amount of 990 billion with a fixed

spread of 75 bps over the FIMMDA g-sec yield. In

2016-17 so far, the issuance spread ranged between

63-74 bps for 495 billion.

Gross market borrowings of 6,000 billion were

proposed in the Union Budget 2015-16 through

dated securities, of which 150 billion was

allocated for issue of SGBs. The actual gross market

borrowings through dated securities were 5850

billion and the net borrowings were 4406 billion

which funded 82% of the gross fiscal deficit as

against 89 percent in the previous year. The net

market borrowings of the central government, (i.e.,

through dated securities and T-bills) declined to

4,530 billion in 2015-16 from 4,778 billion in

2014-15.

The Reserve Bank continued with the policy of

passive consolidation of g-secs by way of

reissuances. Out of 161 securities auctioned in

2015-16, 154 securities were reissues of the existing

securities. In order to manage the maturity profile

and reduce rollover risks of the government debt in

a proactive manner, buybacks and switches were

conducted in the fourth quarter of 2015-16 for an

amount of 749 billion ( 579 billion in the

previous year). This has modulated redemption

pressures and reduced the quantum of gross

borrowing requirement for 2016-17. Reflecting the

strategy of maturity elongation, the weighted

average maturity of borrowings increased to 16.0

years in 2015-16 from 14.7 years in 2014-15.

Consequently, the weighted average maturity of

outstanding debt increased to 10.5 years in 2015-16

from 10.2 years in 2014-15. To cater to the demand

from long-term investors like insurance companies

and pension funds, a 40-year security was also

issued in 2015-16.

A Medium Term Debt Management Strategy

(MTDS) was formulated by the Reserve Bank in

consultation with the Government and placed in

the public domain on December 31, 2015. The

MTDS has been articulated for a period of three

years (2015-16 to 2017-18). It is premised on three

broad pillars: low costs, risk mitigation and market

development in line with the sound international

practices while factoring in domestic economic

and financial conditions.

The net issuance of T-bills was lower during 2015-

16 than in the previous year. The yields on T-bills

softened during the year reflecting the easing

interest rate regime. Primary Dealers (PDs)

`

`

`

`

`

`

` `

` `

Debt Management of the Central Government

Debt Management Operations

Medium Term Debt Management Strategy

Treasury Bills

INFOCUS

18

CC

ILM

on

thly

Ne

wsl

ett

er

Se

pte

mb

er

20

16

individually achieved the stipulated minimum

success ratio and their aggregate share in T-bill

auctions stood at 75.4% in 2015-16, down from

77.2% during 2014-15.

The Government's WMA limits for the first and

second halves of 2015-16 were fixed at 450 billion

and 200 billion, respectively. The Government's

cash position was largely comfortable as it started

the year with a large cash balance of 1,573 billion.

Recourse to WMA was limited to 16 days in 2015-

16 vis-à-vis 61 days in the previous year (including

16 days of overdraft), reflecting relatively fewer

gaps between receipts and expenditures. The

average utilization of WMA was lower at 187

billion as compared to 236 billion in 2014-15.

Gross market borrowings of the states increased to

2,946 billion during 2015-16 through the issuance

of 298 securities as compared to 2,408 billion

mobilised through 282 securities in the previous

year. Despite increased supply, the weighted

average yield of SDLs during 2015-16 was lower at

8.28% as compared with 8.58% in the previous year,

reflecting the easing interest rate regime. However,

the weighted average spread over the comparable

central government securities increased to 50 bps

from 38 bps during the previous year on concerns

over increased supply due to UDAY bond

issuances.

Investments by states in Intermediate Treasury Bills

(ITBs) of the central government increased during

the year. The daily average investments in ITBs

increased marginally to 749 billion in 2015-16

from 731 billion in the previous year. Further,

while the outstanding amount in Auction Treasury

Bills (ATBs) continued to decline in 2015-16, the

declining trend in investments in ITBs reversed

over the same period. During 2015-16, eleven states

availed Special Drawing Facility (six states in 2014-

15), eleven states availed WMA (10 states in 2014-

15) and nine states availed Over Draft facility from

the Reserve Bank in 2015-16 (10 states in 2014-15).

The monthly average utilization of WMA and OD

by the states was higher during 2015-16 than that

during 2014-15.

Source : www.rbi.org.in

Cash Management of the Central Government

Debt Management of State Governments

Cash Management of State Governments`

`

`

`

`

`

`

`

`

INFOCUS

19

CC

ILM

on

thly

Ne

wsl

ett

er

Se

pte

mb

er

20

16

The Financial Stability and Development Council

Sub-committee (FSDC-SC) in its meeting held on

September 10, 2015 decided to constitute a

Working Group on Corporate Bonds with

representation from the Ministry of Finance,

Government of India and all the regulators with the

remit to guide the implementation of the

recommendations made by all the earlier

committees and suggest further measures that may

be taken to develop the corporate debt market. The

recommendations of the Committee released in

August 2016 are:

1. Frequent debt issuers may club all issuances

during a quarter under the same umbrella ISIN

to enhance liquidity of the issuance. These

issuers may come out with a feasible maturity

structure wherein they can stagger the

redemption amount across the year by

amortizing the repayments. Reissuances to be

exempt from Stamp Duty and review of

Corporate Governance norms for companies

with only listed debt securities.

2. SEBI to have a relook at October 2013

guidelines to clarify on day count convention,

shut period, basis for yield calculation,

calculation of coupon interest and redemption

with intervening holidays with illustrations.

3. Required notification to be issued by RBI by

August-end 2016 to allow FPIs to invest in

unlisted debt securities and pass through

securities issued by securitizations SPVs /

Special Purpose Distinct Entity (SPDE).

4. Amendments in FEMA and SEBI guidelines to

facilitate direct trading in corporate bonds by

FPIs in the OTC segment and on an electronic

platform of a recognized stock exchange, with

no involvement of brokers.

5. Amendment in RBI guidelines so that the credit

exposure of a protection buyer in credit default

swaps shall be on the protection seller.

6. Stock exchanges may operationalize market

making scheme in corporate bonds.

7. Regulated entities like banks, PDs other than

brokers to be encouraged to act as market

makers. RBI to examine members of debt

segment of exchanges to access the repo market

in corporate bonds to enable market making.

8. The Electronic Book Mechanism for private

placement of debt securities, currently

mandatory for issuances over 500 crore, may

be extended to all primary market issuances.

9. An acceptable mechanism for daily valuation

of corporate bond holdings to be developed

either by the Financial Benchmarks India Pvt.

Ltd. (FBIL) or credit rating agencies.

10. The penalty structure in place for default in

delivery of debt securities/funds for trades

subject to CCP clearing to be reviewed in order

to prescribe prudent yet reasonable penalty or

an alternative mechanism of borrowing

through corporate bond repo to be explored to

ensure settlement.

11. CRAs may be mandated to strictly adhere to the

regulatory norms with regard to timely

disclosure of defaults on the stock exchanges

and their own website and also publish credit

rating transition matrix more frequently.

12. Banks may be encouraged to submit loan

overdue information to CICs on a weekly basis

to start with.

13. A centralized database for corporate bonds

covering both primary and secondary market

segments may be established expeditiously in

`

Report of the Working Group on Development of Corporate Bond Market in India

INFOCUS

20

CC

ILM

on

thly

Ne

wsl

ett

er

Se

pte

mb

er

20

16

two phases, for secondary market trades by end

August 2016 and for both primary and

secondary market by end October 2016.

14. Amendments may be carried out in the RBI

Act, 1934 to provide complete clarity on the

legal position relating to netting of OTC

derivat ive contracts . Pending these

amendments, the possibility of permitting

netting keeping in view the existing legal

provisions and banking practices may be

explored expeditiously.

15. An electronic dealing platform with CCP

facility similar to the CROMS platform in the

G-Sec market may be introduced. An electronic

dealing platform without CCP facility may also

be introduced for bonds for which CCP facility

may not be feasible.

16. FIMMDA may consult market participants to

develop a commonly acceptable market repo

agreement for execution among the market

participants by end September 2016.

17. Guidelines on Tripartite repo on corporate

bonds may also be introduced by

depositories/other entities in consultation with

SEBI by end September 2016.

18. Entities authorized as market makers in

corporate bond market, including the brokers,

may be allowed to participate in the repo

market executed on electronic platform linked

to guaranteed settlement

19. Insurance companies and EPFO may be

allowed to invest in AT-1 bonds of banks subject

to prudential limits with credit rating upto

investment grade.

20. The maximum investment ceiling of 2% of the

total portfolio of the funds in AT-1 instruments

stipulated for non-Government PFs may be

reviewed for relaxation.

21. Corporate bond index may be introduced by

the Stock Exchanges/other entities.

22. Initially the upper limit for PCE by the banking